WEEKLY

April 20, 2026

ANALYSIS

NOT JUST ABOUT OIL: IRAN WAR IMPACTS THE SUPPLY CHAIN

- The most acute immediate threat to Japan has emerged in the petrochemical sector, such as the naphtha-ethylene supply chain.

- PM Takaichi faces an unprecedented tumultuous storm of record-high fuel prices, domestic production halts and multiple supply chain disruptions.

FRENEMIES IN TRANSITION: HOW IHI AND MHI ARE SHAPING JAPAN’S AMMONIA BET

- Japan’s push to use ammonia as a power-generation fuel is framed as a technological challenge. But, it may hinge on industrial coordination.

- IHI and MHI are developing competing approaches to ammonia-based power. Such competition could fragment technology pathways, slow standardization, and divide investment, thus weakening the transition.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Japan eyes Pacific sea lane defense as Hormuz crisis exposes supply risk

- Govt seeks roadmap for Energy Security & GX

- Infroneer buys water infrastructure firm for ~¥90 bln

- Japan’s power prices rise as fuel procurement comes under strain

- JEPX intraday market price spikes, volumes down

- ANRE releases finalized FY2024 energy supplydemand results

- METI experts move to curb “phantom” grid connection requests

- Nikkiso supplies liquid hydrogen pump for Kobe demo

- Tokyu to invest billions of yen in BESS portfolio after securing Tokyo subsidies

- West Holdings agrees with Mitsubishi for ¥7 billion BESS fund

- Tokyo Gas signs BESS operation and aggregation deals

- Hulic and CEC partner on 800-site solar portfolio to support off-site PPAs

WIND POWER AND OTHER RENEWABLES

- Chugoku Electric, Toda join wind project

- Invenergy’s Hokkaido wind project enters EIA stage

- KEPCO warns nuclear fleet utilization rate to decline

- TEPCO restarts Kashiwazaki-Kariwa NPP Unit 6

- Japan to support Asian allies’ oil supply with $10 bln package

- March LNG spot contract prices down slightly

- JAPEX lost two cargoes due to war in Iran

- Teikoku Databank survey says naphtha scarcity impacts over 40,000 firms

CARBON CAPTURE & SYNTHETIC FUELS

- Japan’s emissions decline slows as clean power growth weakens

- Metropolitan CCS receives approval from METI for exploratory drilling

EVENTS

Mid-April FIT/FIP Solar Auction #28

Japan Atomic Industrial Forum

(JAIF) Annual conference @ Tokyo

April 24 Green Elements at Work @ Google for Startups

May 3-6 Golden Week (many companies will close from April 29 to May 6)

May 26-28 Japan Energy Summit @ Tokyo Big Sight

June 3 South Korea – Local Elections

June 23-25 “Summer Davos” in Dalian, China

September 14-18 IAEA General Conference 2026

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com. For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Japan eyes Pacific sea lane defense as Hormuz crisis exposes supply risks

(Asia Nikkei, April 17)

- Japan seeks to strengthen defence of Pacific shipping routes as disruptions in the Strait of Hormuz highlight risks to fuel and food imports.

- The govt will set up a panel to revise its National Security Strategy, with protection of sea lanes, particularly routes linking Japan to Australia, likely to become a core pillar.

- Measures under review include surveillance aircraft, island-based radar systems, and expanded cooperation with allies to secure maritime routes.

- CONTEXT: Japan remains highly exposed to fuel imports. It sources over 70% of thermal coal and ~40% of its LNG from Australia.

- TAKEAWAY: These are the beginnings of discussions over how energy transportation needs to be reconsidered in light of the Hormuz disruption. The obvious routes to protect are the ones to its south, not only to Australia but also to Malaysia and Indonesia. The question officials are avoiding is: Against whom Japan needs to defend these routes from. If the answer is China, then the scale of the defense will need a very thorough examination.

Govt seeks roadmap for Energy Security & GX

(Government statement, April 16)

- The govt is considering a roadmap for “Resource & Energy Security & GX” as part of crisis management efforts.

- Japan is accelerating GX investment across 16 priority sectors by integrating policy support and investment strategies, while identifying bottlenecks across the full value chain – from R&D to commercialization and global expansion.

- The roadmap emphasizes “crisis management investment” to enhance energy security, expand decarbonized energy supply, and build globally competitive industries.

- Key measures include:

- continuous R&D support through deployment,

- strengthening GX supply chains,

- creating demand via targeted policies and standards,

- expanding overseas markets through public–private partnerships,

- scaling up decarbonized power and grid investment with improved financing,

- integrating AI with GX to boost efficiency and competitiveness.

- In the growth strategy, roadmaps are being developed for seven key products and technologies: perovskite solar cells, hydrogen, green steel, next-gen geothermal, offshore wind power, next-gen innovative reactors, and GX chemicals.

- CONTEXT: The GX investment strategy focuses on 16 key sectors: 1) steel, 2) chemicals, 3) pulp & paper, 4) cement, 5) automobiles, 6) storage batteries, 7) aircraft, 8) SAF, 9) ships, 10) daily life, 11) resource recycling, 12) AI & semiconductors, 13) hydrogen, 14) next-gen renewable energy (perovskite solar cells, floating offshore wind power, next-gen geothermal), 15) nuclear & fusion energy, and 16) CCS.

Infroneer buys water infrastructure firm for ~¥90 bln amid sector consolidation

(Nikkei, April 14)

- Infroneer Holdings plans to acquire water infrastructure firm Swing for over ¥90 billion, buying out stakes held by Mitsubishi Corp, Ebara and JGC.

- Swing specializes in water treatment plant design, construction and operations. Group revenue for the fiscal year ended March 2025 was ¥82.9 billion.

- The deal comes as Japan’s water infrastructure faces aging assets, straining municipal finances and accelerating the need for private-sector involvement.

- TAKEAWAY: The deal signals accelerating consolidation and privatization in Japan’s water sector. It may have limited direct impact on power generation, but could have several implications. With higher efficiency from upgraded assets, energy intensity per unit of water should fall. With a bigger portfolio, Infroneer may also utilize Swing locations for distributed energy generation. Onsite solar and storage, and wastewater biogas are some options. Water infrastructure can also be considered as facilities with access to water, land and grid connections, which could make them suitable for installing electrolyzers to make hydrogen.

Yanmar to build factory to make emergency generators for datacenters

(Company statement, April 7)

- Yanmar Energy Systems plans a new factory to produce emergency power generators for data centers in Kitakyushu (Fukuoka Pref).

- The firm will expand its customer base beyond data centers to factories and hospitals.

- CONTEXT: In Oct 2025, Yanmar launched the GY175 series, a 2,000 kVA generator model. The firm plans to increase output capacity to 3,000 kVA by 2026 and to 4,000 kVA by 2028; (kVA refers to the apparent generator power capacity).

NEWS: ELECTRICITY MARKETS

Iran conflict pushing power prices, disrupting fuel procurement across sectors

(Japan NRG, April 14)

- CONTEXT: This is a wrap of the various impacts from the Iran conflict on the energy and related sectors in Japan.

- Spot power prices in Tokyo and Chubu rose to their highest levels since the 2022 Ukraine crisis in early April, averaging ¥21.06/ kWh in Tokyo, ¥19.89 in Chubu, and ¥15.02 in Kansai between April 1-14. This reflects LNG supply uncertainty.

- Price pressure is more pronounced in Tokyo and Chubu due to their heavy reliance on thermal generation (70–80%), making power costs more sensitive to disruptions in LNG and oil-linked fuel markets.

- The expiry of long-term contracts between JERA and TEPCO Energy Partner/Chubu Electric Miraiz in March has pushed a greater share of procurement into the spot market, increasing exposure to short-term volatility.

- With power spring demand weak and utilities not yet calling for conservation, industry officials warn that fuel procurement conditions are unstable. Mori Nozomu, head of the power industry group, the FEPC, said a prolonged crisis will lead to tighter power supply and demand. The public may be asked to save electricity during the high cooling demand of the summer.

- In the fuels sector, the govt is maintaining a ¥170/litre gasoline cap to limit pass-through of higher procurement costs despite sharp increases in crude prices linked to the Hormuz disruption. To cut state spending on the subsidies, ANRE has switched its subsidy calculations from the Dubai to the North Sea Brent crude benchmark.

- The Hormuz blockade has caused the Dubai crude benchmark to trade at a massive premium (up to $49 per barrel over Brent). Subsidies to wholesalers do not fully cover their actual procurement costs, which has so far meant that sellers must absorb the price difference.

- Oil wholesalers booked around ¥200 billion in losses in a single month across fuel types because fixed retail pricing prevented cost pass-through.

- Supply disruptions are beginning to affect physical fuel availability, with bus operators in Kyushu and elsewhere failing to secure fuel through tenders and being forced into higher-cost or alternative procurement arrangements.

- Smaller transport operators have already adjusted operations, with boat operator Segawa Kisen reducing services due to diesel shortages, indicating that supply stress is moving beyond pricing into logistics constraints.

- SIDE DEVELOPMENT:

- TOCOM launches Chubu power futures trading

- (Exchange statement, Denki Shimbun, April 8-13)

- TOCOM began trading Chubu-area power futures on April 13, adding a third regional market alongside East and West Japan.

- Initial trades totalled 30 contracts (14.7 GWh) for July–Sept delivery, priced at ¥22.20/ kWh (baseload) and ¥28.15/ kWh (daytime).

- CONTEXT: The new products respond to widening regional price gaps in the spot market, allowing participants to hedge using local price exposure. The rival EEX has also launched Chubu area contracts.

JEPX intraday market price spikes, volumes down

(Exchange data, Denki Shimbun, April 16)

- The electricity intraday market recorded a 3.9% MoM drop in average daily volume in March, a third consecutive decline.

- Prices surged on tight supply: the monthly high hit ¥84.68/ kWh on March 14, exceeding February levels, with another spike to ¥80 on March 21.

- The March 14 peak coincided with coal plant outages in both East and West Japan, driving higher trading volumes and price volatility.

- Monthly average price rose to ¥12.84 (+¥1.76 on last month), broadly tracking elevated spot prices amid Middle East-driven fuel cost pressures.

ANRE announces finalized energy supply-demand results for FY2024

(Government statement, April 14)

- ANRE has compiled the final report for FY2024 Comprehensive Energy Statistics.

- Final energy consumption fell by 2% YoY, driven by declines in coal (-3.9%) and oil (-3.8%), while city gas (+3.2%) and electricity (+0.6%) increased. Industrial and transport sectors declined, while the residential sector was flat. Electricity use rose slightly in both industry/ commercial and residential sectors.

- Primary energy supply decreased by 0.5% YoY. Fossil fuels fell (-1.3%) while non-fossil energy rose (+2.5%). Nuclear (+9.6%) led non-fossil growth due to reactor restarts, and renewables also increased.

- Total power generation rose by 0.4%, with the non-fossil share reaching 32.5%.

- Energy-related CO2 emissions fell 1.6% YoY (down 26.6% vs. FY2013) to 910 Mt, the lowest since 1990. The decline was driven by lower energy demand and higher non-fossil use.

- Emissions decreased across all sectors, and power sector carbon intensity improved to 0.45 kg-CO2/ kWh (-1.8%).

- CONTEXT: Comprehensive Energy Statistics is compiled by ANRE, to provide a detailed overview of the country’s energy supply and demand, covering sources such as fossil fuels, renewables, and electricity. The statistics are used to track energy flows, analyze trends, and support policymaking in Japan’s energy sector.

ANRE plans to set support period at 20–40 years for 4th LTDA

(Government statement, April 3, Denki Shimbun, April 14)

- ANRE plans to set the support period for the LTDA scheme at 20–40 years, introducing a 40-year cap to limit the total public cost of long-duration contracts.

- While extending support periods lowers annual payments, it raises total system costs due to higher financing expenses, prompting the cap as a trade-off between investment support and consumer burden.

- The minimum support period will remain at 20 years, with longer terms permitted but not actively incentivized, as project developers face penalties and implicit pressure to prioritise faster cost recovery.

- Recent auction outcomes show a clear shift toward longer-duration bids (21–40 years), suggesting developers are seeking to de-risk projects amid rising capital costs.

- The government is emphasizing that LTDA is intended to support upfront investment rather than provide long-term revenue guarantees, with the cap designed to limit overreliance on extended support and reduce moral hazard.

- CONTEXT: The results of the 3rd auction are expected later this month.

METI experts discuss measures to curb “phantom” grid connection requests

(Government statement, April 16)

- A METI working group for next-gen power grids voiced concern about the growing problem of “phantom reservations” in grid connection contracts. This is where large consumers, particularly data center developers, reserve more grid capacity than they ultimately use, tying up infrastructure and delaying other applicants.

- The working group proposed:

- 1) If a consumer with a phased connection contract fails to reach the contracted power level by the agreed milestone, the unused reserved capacity is released back to the grid; this removes the ability to indefinitely hold capacity without commitment.

- 2) Where a consumer’s final contracted power falls materially short of the originally committed level, financial settlements proportional to the shortfall will be imposed; this introduces a direct cost to speculative or inflated reservation behavior.

- Cases of mismatch between reserved and actual grid capacity across multiple regions include those where infrastructure was built or planned based on demand forecasts but not used, raising costs for all grid users through higher transmission tariffs.

- TAKEAWAY: METI framed the proposals as necessary to ensure grid capacity reaches projects with genuine and timely power needs, and noted that current TSO review processes are struggling under the volume of large-scale connection requests. The proposals could cut both ways: increase the cost of booking grid capacity, but also free up more of the grid for new applications. The key for developers will be to demonstrate to TSOs that their projects are serious, not speculative.

TEPCO to expand and streamline grid infrastructure in FY2026 supply plan

(Company statement, Denki Shimbun, March 28-April 13)

- TEPCO Power Grid will add three new substations to its FY2026 supply plan, as well as upgrades to existing facilities to address demand growth and aging infrastructure.

- Key measures include a 300 MVA transformer addition at Katsunan substation (operational FY2029), while other sites will see capacity reductions or equipment replacement as part of asset optimization.

- Several transformer installations and retirements were rescheduled across the Tokyo area, highlighting ongoing adjustments to balance reliability, cost, and utilization.

- TAKEAWAY: While grid investment continues, TEPCO’s plan shows a shift toward selective upgrades and timing adjustments rather than aggressive expansion. That’s at least in part due to the poor nature of TEPCO Holdings’ finances, but it also speaks to the multiple pressures that the grid operator is under to balance new capacity demand applications in certain areas.

Govt discusses current and future issues under revenue cap system

(Government statement, April 10)

- EGC, the market regulator, is reviewing TSO investment plans for FY2026–2027 and the design of the second regulatory period (from FY2028), focusing on cost control and system stability under the revenue cap framework.

- TSOs are revising near-term investment plans to reflect changing conditions, with the regulator emphasizing the need to maintain supply reliability while improving cost efficiency through stricter optimization.

- The EGC signaled closer scrutiny of grid investment revisions, indicating it will tightly assess any upward adjustments and push for consistent efficiency measures across all operators.

- A key proposed change is a shift from fixed five-year wheeling tariffs to annual adjustments, allowing faster pass-through of rising costs and reducing the risk of financial strain on TSOs.

- At the same time, the regulator is considering maintaining upfront visibility by announcing indicative tariffs for the full five-year period, balancing flexibility for TSOs with predictability for retailers and consumers.

- With tariff reviews for the second period starting in July 2027, any regulatory changes requiring ordinance revisions will need to be finalized by late 2026 to early 2027, setting a tight policy timeline.

- CONTEXT: The revenue cap system sets a maximum amount that TSOs can earn during a specified regulatory period (1st: FY2023–2027, 2nd: FY2028–2032). The cap is based on expected costs and investment needs. They can keep profits if they reduce costs but cannot fully recover excess costs if they overspend.

OCCTO orders power transfer to Kansai area

(Agency statement, April 12)

- On April 12, OCCTO ordered power transfer from Kansai TSO to Chugoku TSO to improve the supply-demand balance in the Kansai area, which was oversupplied.

- Between 10:00 and 12:00, up to 137 MW of electricity was transferred.

- CONTEXT: OCCTO operates inter-area corrective power interchange to adjust actual power flows between regions when real-time supply-demand deviates from plans.

- TAKEAWAY: Power transfer orders by OCCTO are typically issued when supply capacity is insufficient due to increased demand caused by extreme temperatures, severe weather, or equipment failures, requiring power to be supplied from other areas. Even when excess electricity is generated because power output cannot be reduced, as in this case, TSOs may transfer it to other areas for consumption. In the Kansai area, such orders were issued only a few times in 2023 and 2024.

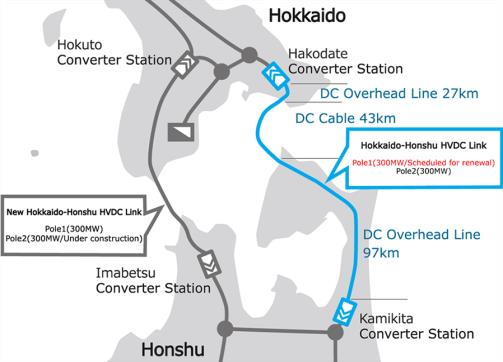

Toshiba wins HVDC upgrade contract for Hokkaido–Honshu interconnector

(Company statement, March 16)

- Toshiba Energy Systems secured an order to supply a VSC-based HVDC system for the renewal of Pole 1 of the Hokkaido–Honshu interconnection link.

- It will replace infrastructure dating to 1979, with equipment deliveries starting in FY2029 and commercial operation in FY2031.

- The link currently provides 600 MW of capacity (in a total 900 MW interconnection), with future expansion set to increase transfer capacity.

- CONTEXT: The interconnector is a key backbone for long-distance transmission, including undersea cables, linking the Hokkaido and Honshu grids. Upgrading interconnection infrastructure is critical to integrating renewables, with more flexible HVDC systems enabling greater power flows between regions.

Marubeni expands power retail footprint in Europe and LatinAm with €200 mln deal

(Company statement, April 17)

- Marubeni, via its UK-based subsidiary SmartestEnergy, acquired an 85% stake in Spain’s Factor Energia for ~€200 million, gaining access to power and gas retail markets across Iberia and Latin America.

- Factor Energia serves 300,000+ customers and sold ~3.2 TWh in 2024, with plans to scale to 10 TWh by 2030, including expansion into larger industrial clients.

- The deal targets fast-growing electricity demand in Iberia, where consumption is expected to rise ~4% annually to 2030, driven by electrification and data center growth, alongside a policy push to reach >80% renewables.

- Marubeni aims to combine SmartestEnergy’s strengths in trading, risk management, and renewable sourcing with Factor Energia’s customer base and digital platform, including AI-driven optimization.

- TAKEAWAY: A number of Japanese trading houses have moved downstream into power retail and trading platforms in liberalized markets, both at home and overseas (mostly in Europe and the U.S.). The idea is to capture value from renewables growth and power market volatility, but the long-term picture is likely tied to new business models resulting from aggregation, BESS, and PPA contracts. However, Japanese firms tend to be more risk averse than their international counterparts in commodities trading.

Shikoku Electric to decommission two oil-fired power plants

(Company statement, April 15)

- Shikoku Electric will decommission two aging oil-fired power plants.

- Anan Station Unit 3 (450 MW) has been inactive since early 2026. Permanent closure is set for June.

- Sakaide Station Unit 3 (450 MW) will be shut later in FY2027, coinciding with the termination of its essential byproduct gas supply from a local factory.

- The plant used a combination of oil and coke oven gas.

- The facilities launched in 1975 and 1973, respectively.

NEWS: HYDROGEN

Nikkiso supplies liquid hydrogen pump for Kobe demo

(Company statement, April 7)

- Cryogenic technologies specialist Nikkiso delivered a liquid hydrogen pump skid for a hydrogen cogeneration (CGS) demo led by KHI and Kobe Steel in Kobe.

- The system forms part of a world-first, next-gen hydrogen fuel supply setup, combining liquid hydrogen pumping, vaporization and gas turbine generation.

- The pump enables efficient high-pressure handling of hydrogen in liquid form, reducing energy use and lowering costs.

- CONTEXT: This NEDO-backed project aims to set up integrated hydrogen supply and utilization models for large-scale power generation and regional energy systems.

IHI partners with U.S. firms on low-carbon boiler conversions

(Company statement, April 14)

- IHI agreed with Babcock Power (U.S.) to develop fuel conversion projects (i.e. retrofits) for power plant boilers, targeting lower-carbon fuels such as ammonia.

- The partnership combines IHI’s ammonia combustion expertise with Babcock’s track record in boiler retrofits, which total over 17 GW of converted capacity globally.

- The companies aim to offer their fuel-switching solutions worldwide.

NEWS: SOLAR AND BATTERIES

Tokyu group to deploy 46-MW BESS portfolio under Tokyo subsidy program

(Company statement, April 8)

- Tokyu will develop 46 MW / 184 MWh of grid-scale battery storage, targeting full operation by FY2027, with total investment of ~¥14 billion.

- The projects were selected for a second consecutive year under Tokyo’s subsidy program supporting large-scale BESS to enable renewable integration.

- Tokyu will handle development and construction, while Tokyu Power Supply will operate the assets, leveraging its retail and balancing expertise to provide flexibility services, absorb surplus renewables, and respond to tight supply conditions.

- CONTEXT: The initiative follows rising curtailment risks in the Tokyo area, where renewable output control was implemented for the first time in March 2026.

- TAKEAWAY: Billions are now flowing into Japan’s BESS sector, which has only taken off in the past 2–3 years. Even large developers are relying on subsidy schemes – such as the LTDA and Tokyo metropolitan program – to de-risk initial projects and establish a foothold. While this offers a relatively conservative revenue base, it provides a more bankable route to deployment than fully merchant exposure, given the scarcity of early-stage large-scale merchant opportunities. As a result, competition for subsidies is intense, and Tokyu securing support for a second consecutive year highlights both execution strength and the tight access to early market entry.

- SIDE DEVELOPMENT:

- West Holdings agrees with Mitsubishi for a ¥7 billion BESS fund

- (Company statement, April 13)

- West Holdings agreed with Mitsubishi UFJ Morgan Stanley to invest in a ¥7 billion fund focused on high-voltage BESS stations owned by West Holdings.

- Other investors include Sumitomo Mitsui Trust Panasonic Finance, MUFG Finance & Leasing, Ricoh Lease, Kyushu Lease Service Group, Toda Construction, Chugin Energy, Japan Land Development, and West Energy Solutions.

- CONTEXT: TMEIC and West Holdings signed a partnership in Feb 2025 to develop 20 BESS stations nationwide totaling 160 MWh, as well as larger-scale projects, including one in Hiroshima Pref (10 MW/ 35 MWh).

Tokyo Gas agrees on 149 MW of BESS in Aomori

(Company statement, April 16)

- Tokyo Gas inked an operation service deal for two BESS in Towada and Hachinohe (Aomori) with a storage battery operator invested in by Hong De Energy Technology.

- BESS capacity will total 149 MW and is expected to start operation in 2029.

- By the early 2030s, Tokyo Gas aims to have 2 GW of BESS installed nationwide.

- SIDE DEVELOPMENT:

- Tokyo Gas agrees with HD Renewable in aggregation and tolling

- (Company statement, April 16)

- Tokyo Gas agreed with HD Renewable Energy on both operation and tolling agreements covering 340 MW of BESS stations.

- Operational service projects include those mentioned above in Aomori Pref, where HD Renewable Energy is responsible for development and construction.

- Other projects are in Miyazaki, Iwate, Miyagi, and Fukushima Prefs, totaling 190 MW; Tokyo Gas will provide aggregation services and pay usage fees over 20 years.

- CONTEXT: HD Renewable Energy has a BESS development pipeline of about 3 GW in Japan, with 400 MW already secured under LTDA.

- SIDE DEVELOPMENT:

- Tokyo Gas agrees with Bison on 240 MW BESS tolling

- (Company statement, April 17)

- Tokyo Gas agreed with Bison Energy on a tolling agreement for a total of 240 MW across four BESS facilities, which are due to start operations in 2029.

- The deal strengthens “long-term revenue prospects” for Bison, which will continue to develop the projects as part of the agreement.

- TAKEAWAY: Tokyo Gas signed several tolling agreements over the past two years, including with Eku Energy in 2024 (Japan’s first such deal) and with Renova and Equis in 2025 for large-scale BESS stations. As tolling agreements enhance revenue visibility and asset value, banks are more willing to engage. With BESS posting sustained annual growth in both installed capacity and grid connection applications, tolling agreements will increase, particularly when coupled with aggregation to maximize revenues despite usage fees.

Hulic and CEC partner on 800-site solar portfolio to support off-site PPAs

(Company statement, April 15)

- Hulic and Clean Energy Connect will invest in an off-site corporate PPA service via an SPC that will operate 800 non-FIT small-scale solar plants totaling 70 MW.

- Annual electricity generation is expected to reach 73 GWh.

Hanwha Japan launches repowering solutions for low-voltage solar assets

(Company statement, April 10)

- Hanwha Japan launched a package to repower low-voltage solar farms.

- Services include repowering works, equipment evaluation and repair, and O&M.

- CONTEXT: This service comes amid rising maintenance costs, as warranties for equipment (PCS, remote monitoring tools, etc) expire for assets installed during the early FIT period. In addition, new regulations require upgrades such as the installation of fences. Equipment that is not properly updated may lead to the revocation of FIT certification, as it can be considered a maintenance deficiency.

- The firm also plans to expand into the BESS business in cooperation with its group company Q.ENEST, an aggregator and electricity provider.

- SIDE DEVELOPMENT:

- Q.ENEST creates solar portfolio for short-term PPAs

- (Company statement, April 10)

- Q.ENEST created an infrastructure portfolio comprising 160 solar farms with a total capacity of 16 MW to support its short-term PPA service.

- Up to 16.3 GWh of electricity and associated environmental value can be supplied annually under corporate PPAs to companies seeking flexible procurement options.

- CONTEXT: A short-term PPA refers to an agreement with a limited duration (typically 1–5 years), compared to more common contracts of around 20 years. Such PPAs are relevant in times of high energy price volatility, or as a bridge solution while awaiting a long-term PPA.

Chemitox files patent to measure PSC power performance

(Company statement, April 14)

- Chemitox filed a patent for a method to measure the voltage of PSCs.

- CONTEXT: There are two main approaches to evaluate the performance of a solar cell. 1) The MPPT (Maximum Power Point Tracking) method continuously tracks the operating point at which a PV cell delivers its maximum power under given conditions of sunlight and temperature. 2) Measuring the current–voltage (I–V) curve by sweeping the voltage over time and recording the corresponding current, allowing the determination of the maximum power point.

NEWS: WIND POWER AND OTHER RENEWABLES

Chugoku Electric, Toda join wind project

(Company statement, April 16)

- Chugoku Electric and Toda Corp bought stakes in the 54 MW Masuda Hikimi wind project in Shimane, joining existing investors MOL and Hokutaku.

- It envisages 13 turbines (4.2 MW each); commercial operation to launch in Jan 2030.

- TAKEAWAY: Recent onshore wind projects seem to have dropped below the 100-MW scale as smaller developments face fewer local stakeholder and NIMBY issues. Regional onshore wind projects continue to attract multi-sector investment consortia, reflecting the need to pool expertise and capital for project execution.

Invenergy’s Hokkaido wind project enters EIA stage

(Company statement, April 1)

- Invenergy’s proposed onshore wind farm in Hakodate, Hokkaido entered the environmental impact assessment (EIA) “method statement” stage, open to public review until May 15, comments accepted to May 29.

- The project, led by Hakodate Torasawa Wind, outlines plans for up to 47 MW of capacity, with as many as 11 turbines (4.3 MW each).

- The area spans 1,120 hectares across Hakodate and nearby towns, with turbine specs indicating rotor diameters of 117–140 m and max heights of nearly 200 m.

- CONTEXT: The project is still in an early regulatory stage. For now, the developer defines the survey methods and impact assessment scope, with turbine siting, grid connection, and final design still under review pending environmental studies and stakeholder consultations.

Mitsui and partners plan pongamia cultivation project in Indonesia

(Company statement, April 14)

- Mitsui O.S.K. Lines, Hasnur, Nipponham, Four Pride, and SPIL Ventures formed a consortium for a pongamia cultivation project in South Kalimantan, Indonesia on a former coal mine site spanning 10 hectares, running from 2026–2031.

- The goal is to study cultivation and reliability of pongamia as a feedstock for biofuel production, develop supply chains, and potential for carbon credit generation.

- CONTEXT: Pongamia grows in humid climates and can be cultivated in Okinawa, hence interest from Japanese firms. For more information, refer to the March 16 issue.

Axpo agrees with Nestlé to supply renewable energy

(Company statement, April 15)

- Axpo agreed with Nestlé Japan to supply electricity and environmental attributes to Nestlé’s factory in Shimada (Shizuoka Pref).

- This is Axpo’s first deal in Japan.

- CONTEXT: Axpo is a Swiss-based energy firm supplying EHV electricity, renewable energy through PPAs, and energy trading services. Nestlé Japan operates three factories in Japan, all powered entirely by renewable energy.

NEWS: NUCLEAR ENERGY

KEPCO nuclear fleet capacity utilization rate to decline

(Company statement, April 10)

- KEPCO said its nuclear power plant capacity utilization rate for FY2026 will be 70.5%, a 10.4% drop YoY.

- This is due to extended regular inspections at Takahama NPP that’s preparing for replacing internal structures in Units 1 and 2, and steam generator replacement work in Units 3 and 4.

- Total electricity generation from the utility’s seven reactors – (Mihama NPP Unit 3, Takahama NPP Units 1-4, Ohi NPP Units 3 and 4) – is forecast at about 40.6 TWh, down from 48.46 TWh in FY2025.

- KEPCO plans to reduce output before regular inspections, starting with Ohi NPP Unit 3, to allow for longer fuel burn and effective use of fuel amid rising uranium prices.

- For new fuel, 292 assemblies will be procured for six plants (excluding Takahama NPP Unit 3, which already has enough stock).

- Also, KEPCO said it will send 4,880 drums of low-level radioactive waste to the Rokkasho reprocessing site.

TEPCO restarts Kashiwazaki-Kariwa NPP Unit 6

(Company statement, April 16)

- TEPCO resumed commercial operations at Kashiwazaki-Kariwa NPP Unit 6 following regulatory approval.

- The unit met all NRA safety inspections and certification requirements.

- In response to past incidents, the utility pledged to improve transparency and safety.

- CONTEXT: Since 2020, TEPCO has faced reprimands for insufficient terrorism countermeasures and is now working to correct the matter.

- TAKEAWAY: The restart marks the first TEPCO reactor restart since the Fukushima disaster in March 2011. It is also the second reactor to restart in eastern Japan, following Tohoku Electric’s Onagawa NPP Unit 2 in Dec 2024. With Kashiwazaki-Kariwa NPP Unit 6, the ratio of nuclear power in the country’s energy mix could reach 10%. Supporters of the restart say it comes at a time when Japan’s energy procurement could benefit from domestic-generated nuclear power.

Ogasawara town accepts literature survey for nuclear waste storage in Pacific island

(Japan NRG, April 14)

- Ogasawara mayor Shibuya Masaaki will accept a “literature survey” – the first of three stages in choosing a nuclear waste disposal site – for Minamitorishima, an island 2,000 km from Tokyo with no civilian population. The entire island is state-owned, which reduces the complexity of land acquisition.

- The selection process will take about 20 years. The second and third phases are the “preliminary” and “detailed” investigations. The first phase offers a grant of up to ¥2 billion; the second – ¥7 billion.

- Shibuya said cooperation depends on the govt making requests to other municipalities to ensure Ogasawara won’t be the sole candidate. But regional governors in other candidate areas resist advancing the survey process.

- He emphasized survey acceptance doesn’t mean a final agreement to build a facility.

- CONTEXT: Japan lacks a permanent solution for spent nuclear fuel that is currently stored in cooling pools at various nuclear plants, and capacity is nearing its limit. The reprocessing plant in Aomori Pref, managed by JNFL, faces prolonged NRA inspections. This makes its 2026 completion goal difficult to achieve.

- TAKEAWAY: Up until now, the selection process relied on an open-call method. Municipalities applied for surveys on a voluntary basis. This method only yielded several candidates – two locations in Hokkaido and one in Saga Pref. This is the first time the govt requests a survey, rather than waiting for municipalities to volunteer.

Yet, the most critical part is yet to come – the transition from literature surveys to physical drilling (phase 2).

The latter requires not only the mayor’s agreement, but also the governor’s. Governor Suzuki Naomichi (Hokkaido) is negative on proceeding to the second stage, as is Saga’s governor. Locals also fear consequences from storing the fuel, such as declining tourism.

Kyushu Electric enters stage 2 of decommissioning for Genkai NPP

(Company statement, April 13)

- Kyushu Electric transitioned to the second stage of decommissioning for Genkai NPP Units 1 and 2, part of a four-stage decommissioning plan. It will dismantle equipment contaminated with radioactive material.

- The primary focus of Stage 2 is the removal of reactor peripheral equipment such as pumps and coolers with low levels of radioactivity. This phase will end by FY2040.

- CONTEXT: Stage 1 began in 2017 for Unit 1, and in 2020 for Unit 2. It focused on non-contaminated secondary systems. Stage 2 is the first time when decommissioning addresses equipment exposed to radiation.

NEWS: TRADITIONAL FUELS

Japan to support Asian countries oil supply with $10 billion

(Japan NRG, April 16)

- Japan will create a $10 billion (¥1.6 trillion) support package to help them cope with rising crude oil prices linked to the Middle East conflict.

- The announcement came at the AZEC+ online summit.

- The aid will go through JBIC and institutions such as NEXI, to help Asian nations secure crude oil from the U.S.

- PM Takaichi says support equals ASEAN’s annual crude imports, 1.2 billion barrels.

- Other targeted actions are securing manufacturing bases for medical products.

- Tokyo will share its oil stockpiling and release systems to boost regional reserves.

- TAKEAWAY: Tokyo is concerned that fuel shortages in SE Asia could disrupt its supply chains for medical and industrial goods, including petroleum-derived products. Japan’s cautious approach to energy security via holding larger than recommended oil stockpiles is paying dividends: it allows the country to help allies and to use that for supply security in other products. In a fragmented world economy, such trade ties are one measure of security. The decision also shows just how intertwined energy and industrial supply chains are. Japan is also using its financial strength to stabilize fuel access and protect downstream industries.

- SIDE DEVELOPMENT:

- March LNG spot contract prices down slightly

- (Denki Shimbun, April 13)

- JOGMEC reported the average contract price for LNG spot deals made by Japanese companies in March (for delivery in March or later) — $10.8 per million BTU (preliminary), a little lower than February’s final average spot contract price of $11. o The Iran war impact has not yet appeared in the data.

- For reference, the average arrival price in Japan for Feb was $10.4 per million BTU.

Sojitz enters U.S. biomethane market via Fidem investment

(Company statement, April 1)

- Trading house Sojitz acquired a stake in Fidem Energy (U.S.) to enter the biomethane business, with Fidem becoming an equity-method affiliate.

- Fidem produces biomethane from landfill gas, with existing operations in Tennessee and a broader pipeline of development projects.

- In the U.S., biomethane demand rose 24% in 2025, driven by decarbonization and energy security needs, with growth expected to continue.

- Sojitz aims to expand production of the fuel in America and also export biomethane to Japan and across Asia.

- CONTEXT: Biomethane is nearly chemically identical to natural gas and fully interchangeable, but produced from waste (landfill gas, biogas).

- TAKEAWAY: With an abundance of cheap shale gas as a bioproduct of oil drilling, biomethane is a policy-driven niche product in the U.S. It works in the North American market in regions with incentive schemes or for firms complying with Renewable identification numbers (RINs) as credits. Sojitz sees this more as a low-carbon gas play. It could either export the gas – which can be utilized as a drop-in solution in thermal power infrastructure – or just sell the environmental value. Either way, Japanese utilities would be able to cut emissions while preserving LNG-based power systems and infrastructure.

JAPEX lost two cargoes due to war in Iran, resorted to spot purchases

(Company statement, Japan NRG, April 17)

- Due to tensions in the Strait of Hormuz, JAPEX was unable to receive two LNG cargoes in Q1 of FY2026.

- JAPEX bought substitute cargoes from other regions on an unplanned spot contract basis. These purchases have raised procurement costs.

- JAPEX participates in the Garraf oil field in south Iraq via a subsidiary. Following a force majeure issued by Iraq, all production and shipments at the site halted.

- The Iran war has driven up global crude oil prices, contributing to increased revenue and profits for JAPEX.

- JAPEX is securing alternative LNG supplies on the spot market from areas outside the Middle East to ensure power generation at its Fukushima Natural Gas Power Plant. The same goes for natural gas distribution to factories and city gas networks.

Teikoku Databank survey says naphtha scarcity impacts over 40,000 firms

(Organization statement, April 17)

- Teikoku Databank studied the effects of the scarcity of naphtha in Japan, concluding that it could be disrupting the supply chains of 46,741 companies, which accounts for 30% of the country’s entire manufacturing sector.

- The chemical and petroleum/ coal products sector faces the most severe exposure, with 67% of companies affected.

- The second most vulnerable sector is rubber product manufacturing, with 52% of businesses affected. The pulp, paper, and paper-processed goods sector is also reliant on naphtha supply, with 49% of such companies facing potential disruptions.

- The study notes that the naphtha supply crisis is threatening SMEs in particular.

- SIDE DEVELOPMENT:

- Companies face naphtha supply disruptions despite govt reassurances

- (Reuters, April 16)

- Japanese companies relying on naphtha are halting orders and cutting production due to supply disruptions, contradicting govt assurances of sufficient supply.

- Over a dozen firms, including Toto and Asahi Kasei, have had delivery disruptions or raised prices. A survey found only 2.7% of companies can get thinner solvents as usual.

- The govt claims Japan has enough naphtha for four months and is working to secure nonMiddle Eastern supplies.

- Despite this, Toto suspended orders for bathroom units. Rivals like Panasonic have flagged delivery impacts.

- Unlike South Korea and Thailand, Japan has not called for conservation measures. o Govt officials admit that conservation should be urged. But, the prime minister’s office has blocked such messaging. Naphtha-dependent companies’ shares are underperforming the Nikkei benchmark.

- TAKEAWAY: See the analysis section for more information.

LNG stocks up from previous week, up YoY

(Government data, April 15)

- As of April 12, the LNG stocks of 10 power utilities were 2.29 Mt; up 3.2% from the previous week; up 14.5% from end April 2025 (2 Mt), and up 8% from the 5-year average of 2.12 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Japan’s emissions decline slows as pace of new clean power capacity weakens

(Government statement, April 15)

- Japan’s FY2024 GHG emissions fell 1.9% YoY to ~1.046 billion tons (CO2e, excluding sinks), or ~994 million tons including forest absorption, marking the first time net emissions dropped below 1 billion tons. The data comes from the National Institute for Environmental Studies and the MoE.

- CO2 emissions alone fell 1.7% YoY, continuing a longer-term decline, with total emissions now ~28.7% below 2013 levels (net basis).

- Carbon absorption from sinks such as forests totaled 52.3 Mt in FY2024, remaining stable YoY. Blue carbon – carbon captured by coastal and marine ecosystems – remains modest but is considered to be a promising means of reducing emissions.

- Main decrease drivers include reduced industrial output and a rise in renewable energy and nuclear power, which account for over 30% of the national energy mix.

- CONTEXT: The nation’s emissions need to decline by another 17 percentage points to meet Japan’s 2030 GHG targets.

- Power mix improvements continued in FY2024 but modestly: renewables rose to 23.1% (+0.2 percentage points) and nuclear to 9.4% (+0.9 ppt), but generation gains were limited. By sector, emissions declined across the board:

- Industry: -2.5% (largest share)

- Transport: -1.6%

- Households: -0.7%

- Energy conversion: -2.5%, thanks to efficiency gains and gradual fuel switching.

- TAKEAWAY: This was the first year that Japan’s emissions fell below the 1-billion-ton level when including sinks, a notable milestone. Even more interestingly, Japan’s emissions seem to have structurally decoupled from economic growth. The ratio of GHG to GDP has been declining for 12 years straight now – ever since FY2013. Since that year, GDP has gained 4.8% while GHG emissions are down 24.9%, according to MoE data. Beyond natural carbon capture, CCS technologies are gradually introduced, although the market remains at an early stage. The govt also seeks to promote deployment, setting a target of capturing 6–12 Mt of CO2 per year by 2030, and 120–240 Mt by 2050.

Metropolitan CCS receives approval from METI for exploratory drilling

(Company statement, Japan NRG, April 17)

- Metropolitan CCS, a JV between INPEX and Kanto Natural Gas Development, received METI approval to conduct exploratory drilling for CCS.

- Drilling will take place offshore Kujukuri, Chiba Pref. This will be the second project of its kind in Japan, following a similar one off Tomakomai, Hokkaido.

- The project involves capturing CO2 emitted from heavy industrial sources in the Tokyo Bay area such as Nippon Steel’s East Nippon Works.

- Nippon Steel will be responsible for CO2 separation and capture. Metropolitan will handle transportation and subterranean storage.

- Captured CO2 will be sent via underground pipelines for storage in offshore Kujukuri.

- The project aims to store up to 5 million tons of CO2 a year, about 0.5% of Japan’s total annual emissions.

- The final goal is to begin CO2 storage by the early 2030s, with an anticipated lifecycle spanning 20 to 30 years.

Mitsui agrees with Shell on environmental value for transport companies

(Company statement, April 9)

- Mitsui O.S.K. Lines agreed with Shell Trading Rotterdam on environmental attributes for customers seeking to reduce emissions from vessel operations.

- These attributes are verified to ensure reliability and transparency, then registered by a third party, 123Carbon, under a book-and-claim model.

- Shell will register the attributes in 123Carbon’s registry, while Mitsui will convert them into tradable values.

- CONTEXT: 123Carbon is a Netherlands-based platform that manages and allocates environmental attribute certificates in the transportation sector. The book-and-claim model separates the physical fuel (SAF, marine fuel, etc) from the associated emissions reduction value, tracked via a registry. This allows companies to support decarbonization without being physically connected to the fuel supply. The fuel is used at the point of production, while the environmental value is transferred to a user elsewhere. This approach is part of the MBM (Market-Based Measures) program, created in 2023 by the Smart Freight Centre to standardize the accounting and reporting of transport-related GHG emissions and to deploy low emission transportation services.

- Mitsui plans to expand this service to air and land transportation.

- TAKEAWAY: Domestic environmental value is hardly applicable in maritime transport, as sea vessels do not run on electricity but on bunker fuels. This explains why the use of domestic environmental value in maritime projects remains very limited. One example in 2023 involved Marubeni and Asahi Tanker, where a project was approved under the J-Credit scheme. However, it involves an electric tanker not intended for international shipping which favors globally recognized frameworks, primarily based on European standards or private systems such as 123Carbon, which Mitsui relies on.

Kimura Chemical joins consortium to produce bioethanol for SAF

(Company statement, April 6)

- Kimura Chemical Machinery joined the J-BAS consortium (Japan Bio Alcohol from Sorghum) that aims to produce bioethanol from sorghum.

- The company will contribute by introducing a heat pump-based bioethanol distillation system that reduces carbon emissions.

- CONTEXT: Sorghum (a herbaceous plant) is fermented into bioethanol, and then converted into SAF. The MLIT set a target for SAF to account for 10% of fuel used by Japanese airlines by 2030, requiring initiatives such as J-BAS to develop efficient and cost-effective production processes.

ANALYSIS

BY FILIPPO PEDRETTI

Not Just About Oil: Iran War Impacts The Supply Chain

For Japan, the fallout from the U.S.-Israel war on Iran is not limited to an energy crisis precipitated by the closure of the Strait of Hormuz.

After all, oil and natural gas are not only consumed as fuels; they are also critical industrial inputs. The most immediate vulnerability has emerged in the nation’s petrochemical sector, particularly the naphtha-to-ethylene supply chain.

Natural gas is also essential for fertilizer production, creating knock-on effects not just for Japan but across import-dependent Asian economies such as South Korea and the Philippines. Other exposed sectors include semiconductor production and automotive manufacturing.

The government of Prime Minister Takaichi, in power for only six months, now faces an unprecedented storm of record-high fuel prices, domestic production halts and multiple supply chain disruptions.

Oil and LNG — reservoirs don’t solve everything

A spike in global oil benchmarks is the immediate economic impact of the Iran war. On February 27, the day before the sneak American/ Israeli attack on Iran, the West Texas Intermediate (WTI) price stood at $64.85; by March 9, it surged to a peak of $113.28. Fuel costs, from buses to airlines, escalated quickly, with the latter estimating ¥30 billion in extra monthly costs at the beginning of April. Farmers across the globe are facing the brunt of the cost spike, with shortages in supplies for fueling greenhouses and tractors. METI has requested wholesalers to supply fuel to critical facilities, such as hospitals.

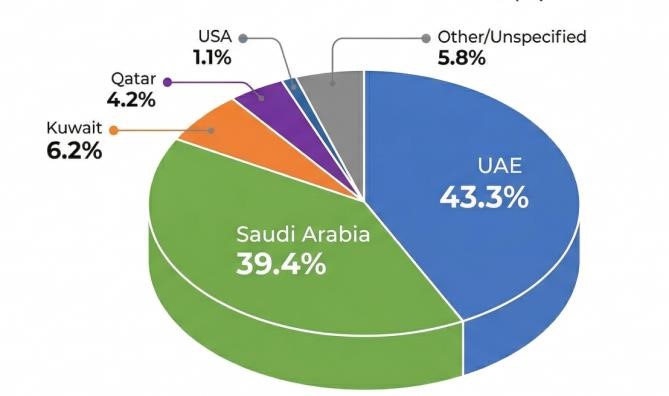

Japan’s reliance on Middle East crude oil stood at 94% in 2025. The UAE and Saudi Arabia alone provided 82.7% of Japan’s total oil imports.

To rectify the situation, Takaichi has tapped into Japan’s ample emergency oil reserves. As of late 2025, Japan maintained a buffer equal to 254 days of consumption. This includes state (146 days), private (101 days) and joint-producer stockpiles (7 days).

Between March 16 and 26, private-sector and state-held reserve releases began, with about 8.5 million kiloliters of state-held crude sold to the big four refiners (ENEOS, Idemitsu Kosan, Cosmo Oil, and Taiyo Oil) for a total of ¥540 billion. Such reservoirs, however, are mostly heavy crude, which requires more time and cost to refine.

In May, METI plans more releases from reserves.

Unlike oil, Tokyo’s LNG procurement strategy is more diversified. Only 10.8% of Japan’s LNG imports originate in the Middle East, with just 6.3% (4 million tons a year) transiting the Strait of Hormuz, according to METI. Incidentally, that’s also the number of tons METI claims are held by Japanese power and gas companies in their reserves, although the weekly stocks data released by the ministry points significantly lower.

If oil is essential for Japan’s transport and logistics, then natural gas is the fulcrum of the nation’s electricity markets. It is usually marginal LNG-fired generation that sets the system price most times of the day. The wholesale power price feeds into the cost for consumers.

| Country | LNG Imports (Mt) | Share of Japan’s Total LNG Imports |

| Qatar | 3,416,860 | 5.26% |

| Oman | 2,932,388 | 4.51% |

| United Arab Emirates | 665,263 | 1.02% |

| Total (3 countries) | 7,014,511 | 10.79% |

Due to higher LNG prices, Tokyo Gas and ENEOS have stopped accepting new electricity supply contracts for large facilities. Even Hiroshima Gas, which sources half of its LNG from Sakhalin-2, said its LNG costs were rising due to higher global oil prices.

The naphtha-ethylene shock

Naphtha is the essential feedstock for producing ethylene and propylene, and is used in a wide range of sectors, especially crucial in the medical industry.

Japan produces about 40% of its domestic demand for naphtha domestically, but imports more than 40% from the Middle East; the remaining 20% is imported from other regions. Further complicating this equation is the fact that over 90% of the crude oil used as feedstock for domestically produced naphtha is imported from the Middle East.

In response to the disruption caused by the war, Japan’s ethylene production facilities have slashed production to conserve inventory. The plants’ operating rate was 75.7% in February, declining since then. 70% is the minimum rate needed to maintain facilities.

| Company | Facilities |

| Idemitsu Kosan | Chiba and Tokuyama facilities |

| Mitsubishi Chemical | Ibaraki Pref facility |

| Mitsui Chemical | Chiba and Osaka facilities |

The current 70% surge in raw naphtha costs (reaching $1,118 per ton) have induced companies such as Toray to introduce a surcharge pricing system for resins and carbon fiber that allows price adjustments within one month.

Mitsubishi Chemical and Mitsui already are seeking supply sources other than the Middle East, such as the U.S. and Africa. Instead of selling on the open market, INPEX will prioritize supplying Japan with an appropriate type of crude oil from Australia, to refine it into naphtha and gasoline.

Despite the disruptions, in a bid to avoid possible anxiety, Japan’s government insists that naphtha supplies are stable. Inventories cover four months of domestic demand, extending to more than six months when including domestic production, Takaichi told the media.

Nevertheless, distribution bottlenecks due to hoarding have appeared. In mid April, TOTO suspended new orders for some products due to unstable procurement of solvents including naptha. There has been no resumption to date. Also, LIXIL said that high costs for petroleum-derived materials may lead to restrictions on production.

The aluminum shock

UAE, Qatar, and Bahrain account for approximately 9% of global primary aluminum production. Japanese automakers rely on the region for 30% of their total supply.

Japanese aluminum buyers have been forced to accept record-high delivery premiums. For the second quarter of 2026, premiums surged to $350-$353 per metric ton above the London Metal Exchange (LME) cash price. This is an 80% increase from the first quarter and the highest level in 11 years.

| Country (export to Japan) | Aluminum Import Volume (Metric tons) | Value in JPY |

| UAE | 400,305 | ¥168.5 billion |

| Qatar | 54,709 | ¥23.5 billion |

| Oman | 42,989 | ¥17.3 billion |

| Saudi Arabia | 41,444 | ¥16.7 billion |

| Bahrain | 36,051 | ¥15.4 billion |

| Middle East total | ~580,000 | ¥242.7 billion |

Toyota Motor has announced a production cut of nearly 40,000 units for Middle Eastbound vehicles over a two-month period. Automakers have attempted to substitute virgin aluminum with scrap metal. But, the technical requirements for high-performance components make widespread substitution difficult.

Conclusion

Iran and Saudi Arabia rank sixth and second, respectively, among the world’s largest oil producers. The outbreak of hostilities has sent shockwaves across Asia, where many economies remain highly exposed to fuel import disruptions. The Philippines and Bangladesh hold reserves equivalent to just 45 days and one month of consumption, respectively, while Pakistan, Thailand, Indonesia and South Korea have already introduced energy-saving measures. Japan, with comparatively larger stockpiles, is better positioned – but far from insulated.

The coordinated release of 400m barrels from the strategic reserves of 32 IEA member countries has done little to stem price volatility. Brent crude briefly retreated from peaks above $110 but remains close to $95–100 per barrel, well above pre-conflict levels.

Forecasts suggest that a sustained rise in crude prices could lift Japan’s inflation by 0.3– 0.4 percentage points and shave up to 3% off GDP. A temporary ceasefire in early April pushed prices below $100, raising hopes that the worst had been avoided. But the collapse of talks days later quickly reversed the trend.

This volatility reflects the reality that oil prices are now driven as much by political signals as by physical supply. Statements from Washington and Tehran continue to shift daily, and markets move in lockstep.

For now, Japan’s strategy is to manage the energy shock through a combination of stockpile releases and energy subsidies. The government has already put to work ¥800 billion from the contingency reserve of the FY2025 budget to protect consumers.

These are measures that buy time – perhaps another two-three months of tenuous stability. They won’t resolve the underlying problem that the fate of a key energy route is beyond Japanese control. As such, the government is looking for mid and longer-term solutions.

Perhaps the most obvious is beginning a review of how to shift Japan’s procurement away from the Gulf. This would likely lead to more oil imports from the U.S., as well as Southern Asia. So far, a rethink on Russian oil imports, curtailed after the 2022 start of the Ukraine war, has not entered public Japanese discussions.

Switching oil suppliers will come at a cost. Switching suppliers means handling different crude grades, requiring investment to reconfigure refining capacity. Tokyo is likely to absorb these costs as part of a broader energy security strategy.

The more fundamental question is how far Japan can truly de-risk oil and gas. With geopolitics affecting many key producers – from Russia to Iran and Venezuela – alternatives are limited. Meanwhile, Japan’s economy remains structurally dependent on imported fuels.

If geo-political conflict and instability become the new-normal, then future supply chain disruptions are inevitable. Preparing for that future will require not just diversification of suppliers, but a sustained shift in the energy mix itself.

ANALYSIS

BY TETSUJI TOMITA

Frenemies In Transition: How IHI and MHI Are Shaping Japan’s Ammonia Bet

Japan’s push to use ammonia as a power-generation fuel is often framed as a technological challenge. In reality, it may hinge just as much on industrial coordination.

Two of the country’s most important engineering firms – IHI and Mitsubishi Heavy Industries (MHI) – are developing competing approaches to ammonia-based power. Their strategies are not directly opposed, but neither are they fully aligned.

This carries some risks for a market barely out of the demonstration phase. If competition between the two fragments technology pathways, slows standardization, or divides investment, it could weaken the very transition they are meant to enable.

Ammonia has attracted attention as a carbon-free fuel that can be introduced into existing thermal power infrastructure, offering a relatively smooth pathway to decarbonization. For policymakers, this compatibility is critical: it allows Japan to cut emissions while maintaining energy security and continuing to utilize its large installed base of coal and gas-fired assets.

As such, government support has been extensive, spanning multiple programmes under SIP, NEDO, and the Green Innovation Fund, with both IHI and MHI playing central roles. Yet beneath this coordinated policy push, a more complex industrial dynamic is emerging.

Framing the divergence

While both companies are advancing ammonia-based power generation, their approaches differ fundamentally not only in technology, but in how they envision the transition unfolding and commercialization.

At its core, the divergence reflects two pathways:

- A technology-led approach, focused on solving combustion challenges and enabling early deployment; and

- A systems-led approach, focused on integrating ammonia into large-scale and commercially viable power infrastructure.

This distinction runs through both coal-fired power and gas turbines of the two engineering majors, shaping how ammonia is likely to be adopted across Japan’s power system.

Comparison of Ammonia Power Technologies and Strategies: IHI vs. MHI

| Category | IHI | MHI |

| Core Strength | Combustion technology (burners, flame control) | System integration (GTCC, full plant) |

| Strategic Focus | Advanced ammonia combustion (high co-firing → 100% firing) | Practical deployment & commercialization |

| Coal Power Boilers | Develops ammonia burners; achieved 20% cofiring at commercial scale | Optimizes full plant systems; enables retrofit of existing plants |

| Gas Turbines | Advanced at small-to-mid scale | Gradual transition (natural gas → hydrogen → ammonia) |

| Scale Advantage | Solve combustion challenges directly | Strong in large-scale systems and EPC |

| Role in Market | Innovation driver | System integrator & deployer |

| Positioning | Innovation leader | Deployment/commercialization leader |

Coal-fired power: retrofit vs system optimization

In coal-fired power, ammonia co-firing represents the most immediate pathway to reducing emissions, precisely because it leverages existing infrastructure.

IHI has positioned itself at the center of this approach. Building on SIP projects dating back to 2015, it has developed burners and combustion control technologies for co-firing ammonia with pulverized coal. These systems have demonstrated commercial-scale viability while keeping NOx emissions at or below levels seen in coal-only combustion.

This was validated at JERA’s Hekinan plant, where co-firing tests achieved performance comparable to coal-only operation. While the target was a 20% ammonia mix (on a heat basis), tests reached as high as 28%.

IHI’s roadmap now targets 50% co-firing and eventually 100% ammonia combustion. JERA’s timeline reflects this trajectory: commercial 20% co-firing at Hekinan Units 4 and 5 by around FY2029, rising to 50% by 2035 and full ammonia firing by 2050.

Beyond JERA, IHI is expected to support similar retrofits, including at Hokkaido Electric’s Tomatoh-Atsuma plant, which is targeting 20% ammonia co-firing by FY2030 at its 700-MW Unit 4. Ammonia supply will arrive thanks to Mitsui & Co, which already received state CfD subsidies to source the fuel from Louisiana, U.S. for use at the power plant and other industries in the Tomakomai area.

MHI, by contrast, has focused less on early-stage co-firing and more on system-level integration. It did not participate in the original SIP program from which ammonia cofiring was born. Instead, the firm has taken a different tack.

MHI’s strategy centers on developing ammonia-capable combustion systems and optimizing entire plants, with an emphasis on retrofitting and scaling existing assets rather than leading early combustion breakthroughs.

This isn’t just a technical point. It’s a trajectory that refelects the two main pathways to decarbonization. One is through incremental retrofitting, which enables faster near-term deployment, and another is through system-level redesign, which could offer better long-term efficiency and scalability.

In practice, the former lowers barriers to early adoption but may face limits at higher ammonia ratios. The latter is more comprehensive, but requires longer lead times and greater coordination across plant systems.

MHI is also working with JERA under a GI Fund project to develop high-ratio ammonia co-firing using single-fuel burners. By FY2024, it had developed burners capable of 100% ammonia combustion and established a basic plan for full-scale demonstration.

A decision is now pending on whether to proceed with testing at a JERA-owned coalfired unit manufactured by MHI. The goal is to verify co-firing ratios of 50% or higher by FY2028 using two commercial-scale units with different boiler types.

If successful, MHI could offer higher co-firing ratios than IHI by the end of the decade – provided existing coal infrastructure remains in use.

Gas turbines: competing transition pathways

The divergence between IHI and MHI becomes even more pronounced when we turn to gas turbines, where ammonia faces greater technical challenges. IHI has pursued direct ammonia combustion, demonstrating a 2-MW turbine operating on 100% ammonia in 2022, reducing GHG emissions by more than 99%.

From July 2024, IHI held long-term durability tests for deployment of the turbines at its Aioi Works. This confirmed that the system achieved the planned power output while significantly suppressing N2O and NOx emissions, and performance comparable to natural gas systems. The technology has already been used for on-site power generation, including applications linked to World Expo 2025 in Osaka.

IHI is now working with GE Vernova to scale this approach, targeting commercialization of 100% ammonia-capable F-class turbines (88–300 MW) by 2030. In March 2026, fullscale combustor testing under simulated operating conditions demonstrated feasibility.

MHI, meanwhile, has taken a phased approach rooted in its long experience with hydrogen-capable turbines. The MHI group has worked on gas turbines capable of handling by-product gases containing hydrogen since as far back as the 1970s in response to customer demand from refineries and steelworks.

MHI’s strategy involves either decomposing ammonia into hydrogen and nitrogen or transitioning gradually from natural gas to hydrogen and then ammonia within integrated gas turbine combined cycle (GTCC) systems.

Since 2021, development has been underway for a 40 MW-class gas turbine system that uses 100% ammonia. A prototype combustor was developed, and a large-scale, highpressure ammonia supply system was installed at the Hitachi (Katsuta) test facility to enable full-scale testing. These tests showed stable operation with ammonia-only fuel use.

To summarize, the technical efforts of IHI and MHI are approaching ammonia combustion from different angles. This raises the broader strategic question: will ammonia emerge as a primary fuel, as IHI’s approach suggests, or as part of a hydrogenmediated system, as implied by MHI’s pathway?

The answer has implications not only for technology development, but also for infrastructure investment and supply chain design.

A system under parallel development

Taken together, these approaches suggest that Japan is not pursuing a single ammonia strategy, but multiple parallel ones.

Policy support mechanisms, including price-gap subsidies and infrastructure funding, enable both pathways simultaneously. Ammonia supply projects, particularly imports from the U.S., are being developed with the expectation of large-scale future demand.

At the same time, coal-fired power plants selected under the LTDA scheme are expected to adopt ammonia co-firing, with boilers supplied by both IHI and MHI. This creates a system in which early deployment is driven by retrofit-based co-firing, while longer-term scaling depends on integrated system performance.

In principle, this dual-track approach supports both innovation and commercialization. In practice, it also introduces coordination challenges – particularly around technology standards, fuel specifications, and investment signals.

Coal-fired power plants for retrofitting with ammonia co-firing, awarded to LTDA

| Round (Year) | Company | Plant Name | Capacity (MW) | Boiler Type | Boiler Maker | Decarbonation Roadmap |

| 1st FY2023 | Hokkaido Electric | Tomato- Atsuma Unit 4 | 700 | Pulverized Coal – USC | IHI | 20%: 2030- 50%: late 2030s 100%: 2040s |

| JERA | Hekinan Unit 4 | 1,000 | Pulverized Coal – USC | IHI | 20%: 2027- 50%: mid-2030s 100%: late 2040s | |

| JERA | Hekinan Unit 5 | 1,000 | Pulverized Coal – USC | IHI | 20%: 2029- 50%: early 2030s 100%: late 2040s | |

| Kobelco Power Kobe | Kobe Unit 1 | 700 | Pulverized Coal – SC | MHI | 20%: 2029- 100%: 2040s | |

| Kobelco Power Kobe | Kobe Unit 2 | 700 | Pulverized Coal – SC | IHI | 20%: 2029- 100%: 2040s | |

| 2nd FY2024 | Shikoku Electric | Saijo Unit 1 | 500 | Pulverized Coal – USC | MHI | 20%: 2030- 50%: late 2030s 100%: late 2040s |

Conclusion

The comparison between IHI and MHI reveals a complementary industrial structure, but not a fully coordinated one.

IHI is pushing the technological frontier of ammonia combustion, enabling early deployment through burner innovation. MHI, by contrast, is building the systems needed to scale that technology across large, complex power assets.

In principle, this division of labor could accelerate Japan’s ammonia transition. In practice, its success will depend on how well these parallel approaches align.

If they converge, they could create a coherent pathway from pilot projects to large-scale deployment. If they diverge, they risk slowing standardization, fragmenting investment, and weakening confidence in ammonia as a viable decarbonization fuel.

Ammonia-Fired Power R&D History

IHI began developing ammonia–pulverized coal co-firing technology for coal-fired boilers under the SIP in 2015. After the SIP project ended in FY2018, the work continued from FY2019 as a NEDO project in collaboration with CRIEPI (Central Research Institute of Electric Power Industry) and Osaka University, focusing on multi-burner ammonia co-firing technology. Based on these results, IHI and JERA launched a demonstration project in FY2021 as a NEDO project to achieve 20% ammonia co-firing in a 1 GW coal-fired power plant.

From April to June 2024, Unit 4 (1 GW) at JERA’s Hekinan plant successfully demonstrated 20% ammonia co-firing, confirming operational and environmental performance equivalent to coal-only operation. The test also showed comparable operational flexibility (minimum load of 400 MW, ramp rate of 10 MW/ min), with a maximum co-firing ratio reaching 28% at 600 MW output.

In parallel, since FY2021, a commercialization project has been underway under the GI Fund to establish high-ratio ammonia co-firing technologies. Construction is ongoing to enable commercial 20% ammonia co-firing at Units 4 and 5 of Hekinan by around FY2029.

JERA was certified in December 2025 under Japan’s support scheme for low-carbon fuels based on price-gap compensation (under the Hydrogen Society Promotion Act). It plans to use low-carbon ammonia produced in Louisiana (“Blue Point”) as fuel at Hekinan. In March 2026, JERA gained approval under a hub development support program to build and operate an ammonia supply base in the Hekinan area, securing fuel supply infrastructure.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Fuel crisis

PM Albanese visited Singapore, Malaysia, etc, in order to maintain supplies of fuel and fertilizer. Australia imports about 80% of its refined fuels from Singapore, South Korea and Malaysia, which in turn depend on crude oil imports from the Middle East.

Australia / Oil Refinery

A major fire hit Viva Energy’s Geelong refinery, which can process up to 120,000 barrels of oil a day, including diesel, LPG, jet fuel, avgas, etc. The refinery is one of two facilities that can refine fuel domestically.

China / Clean energy

China wants to double non-fossil fuel energy by 2035 over 2025 levels. A hydropower project in Tibet and desert-based renewable hubs will help build clean-energy generation.

China / Energy crisis

China will continue to diversify energy imports and boost reserves to enhance its capacity to cope with an “emergency situation”, said Wang Changlin of the state economic planner.

India / Oil

Indian refiners are settling payments for cargoes of Iranian oil purchased under a temporary U.S. sanctions waiver using Chinese yuan through Mumbai-based ICICI Bank, said Reuters.

India / Oil & Gas

The U.S. is stepping up efforts to sell oil and gas to India as it faces supply disruptions from the Middle East.

LNG

U.S. LNG exports are expected to grow 28% by the end of 2027 as five LNG export projects start operations and ramp up production, said the EIA. In 2026, exports of U.S. natural gas will grow 18% to 18.7 billion cubic feet per day.

Oil

The White House is urging U.S. oil producers to boost output to compensate for losses to global supply due to the war against Iran. Energy Secretary Wright met with a dozen executives, including from Exxon Mobil, Chevron and Continental Resources.

South Korea / Oil

South Korea secured 273 million barrels of crude oil from the Middle East and Kazakhstan through year’s end, and also secured 2.1 million metric tons of naphtha.

Taiwan / Geothermal

National Taiwan University estimates the country’s recoverable geothermal resources at more than 33 GW. Current installed capacity stands just under 10 MW.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.