WEEKLY

May 18, 2026

ANALYSIS

NUCLEAR, BESS (AND LNG) REMAIN BIGGEST WINNERS IN LATEST LTDA AUCTION

- The direction of the Long-Term Decarbonized Power Sources Auction (LTDA) is clear: nuclear provides the backbone, and battery storage supplies the flexibility.

- This chimes with the govt’s twin priorities of securing dispatchable generation while preparing the grid for a much larger share of intermittent renewables.

WILL JAPAN RETURN TO RUSSIAN OIL SUPPLIES?

- With global oil and gas markets in their third month of crisis, G-7 countries have made cautious overtures to Russia hoping to stabilize crude oil supplies.

- Russia may not become a major supplier to Japan again in the near term. But latest developments suggest Tokyo won’t close the door completely.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- METI says officials may visit Russia late this month

- Japanese firms develop tech for more efficient nextgen power chips

- JX bets future on electrification, moving away from fuel-reliant ENEOS

- LTDA to sponsor new NPP, retains BESS interest with 19 winning bids

- Power futures for June jump as summer approaches, amid persistent Iran risk

- Eneres launches market-linked PPAs for clean power

- Chemicals firm to invest in local hydro in Nagano

- Akasaka DHC launches hydrogen-based heat source facility

- PSC study forecasts 12.5 GW deployment by 2040

- Firms launch first agrisolar demo using PSCs in rice farming

- Sumitomo to expand business in battery recycling

- Mitsui Fudosan invests in DR system for BESS

- Japanese researchers achieve record efficiency with perovskite-CIGS cells

WIND POWER AND OTHER RENEWABLES

- Sumitomo begins commercial operation of 500 MW wind farm in France

- OKA secures SEP vessel for large Akita wind farm

- METI releases subsidy results to promote geothermal

- Tohoku Electric stops reactor soon after restart to investigate steam leak

- KEPCO investigates steam leak at Mihama NPP

- METI says oil supply diversification results rapidly improving, easing pressure on further stock releases

- INPEX scales back investments due to Iran conflict

- Idemitsu Kosan reverses plan to close refineries

- ENEOS to acquire Chevron’s fuel businesses in APAC

CARBON CAPTURE & SYNTHETIC FUELS

- ENEOS trades SAF environmental value with partners

- Mitsui selects Planet Savers for its DAC tech

EVENTS

June 3 South Korea – Local Elections

June 23-25 “Summer Davos” in Dalian, China

September 14-18 IAEA General Conference 2026

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

Nov 3 U.S. Midterm Elections

Nov Publication of International Energy

Agency – World Energy Outlook 2026

Nov 18-19 Asia-Pacific Economic Cooperation –

Leaders Meeting @ Shenzhen, China

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com. For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

METI says officials may visit Russia late this month

(Japan NRG, May 14)

- METI said govt officials may visit Russia later this month to support Japanese companies operating there.

- METI said the trip is not aimed at building new ties with Russia and reaffirmed its commitment to G7 sanctions.

- TAKEAWAY: For a more detailed look at Russian-Japanese energy relations, please look at this issue’s Analysis section.

Patentix and JTEKT Thermo Systems develop tech for more efficient next-gen power chips

(Company statement, May 13)

- Patentix and JTEKT Thermo Systems have developed a new 6-inch deposition system capable of forming single-crystal r-GeO2 (rutile-type germanium dioxide) films on silicon substrates – an important step toward commercializing next-generation power semiconductors.

- The breakthrough enables high-quality heteroepitaxial growth using a proprietary deposition method, paving the way for lower-cost, high-efficiency vertical power devices based on GeO2-on-Si technology.

- CONTEXT: Patentix is a deep-tech company developing advanced semiconductor materials and deposition technologies. JTEKT manufactures industrial thermal processing equipment used in semiconductor and advanced materials production.

- TAKEAWAY: The collaboration marks progress in scaling production technologies for next-generation semiconductor and solar materials, including perovskites. The technology could improve the performance and compactness of solar inverters, EV power modules and grid equipment by increasing voltage tolerance, reducing power-conversion losses and improving overall energy efficiency.

Mitsui Fudosan enters India’s data center market with 200 MW portfolio

(Company statement, May 12)

- Mitsui Fudosan, a major Japanese real estate developer, entered India’s data center market by investing in a 200 MW portfolio via its Singapore subsidiary fund managed by CapitaLand Investment.

- The project includes four data centers across Mumbai, Chennai, and Hyderabad, with a total capacity of about 200 MW.

- CONTEXT: India’s data center capacity has expanded from about 375 MW in 2020 to around 1.5 GW in 2025, and is expected to continue rising sharply.

JX Advanced Metals to reduce ENEOS ownership

(Company statement, May 11)

- JX Advanced Metals Corp announced a share buyback of up to ¥250 billion to reduce ENEOS’s stake from 42.38% to about 36% and increase management independence.

- The move aims to strengthen JX’s focus on semiconductor materials, funded via convertible bonds, while enabling more aggressive investment in growth areas.

- JX’s operating profit in FY2025 from semiconductor-related business showed strong growth, up 37% to ¥71 billion. The firm forecasts further growth in FY2026.

- CONTEXT: JX Advanced Metals has been involved in energy through its roots in mining and copper smelting, which supply key materials for energy systems (copper for power grids, electronics, and renewables).

- TAKEAWAY: The move signals how value within the energy sector is shifting from fuels toward electrification supply chains. While ENEOS remains centred on refining and oil, JX Advanced Metals is increasingly focused on semiconductor materials and copper-based technologies that underpin EVs, power grids and data centres.

NEWS: ELECTRICITY MARKETS

LTDA to sponsor new NPP, retains BESS interest with 19 winning bids

(Government statement, May 13)

- OCCTO announced results of the third round (FY2025) of its LTDA, with a total of 32 projects: 28 in the decarbonized sources category, and four LNG projects.

- In terms of secured capacity, LNG emerged as the leader, followed by nuclear power and energy storage. Total capacity allocated this year was 4.26 GW for decarbonized power sources from nuclear to BESS, and 3.03 GW for LNG.

- The awarded capacity by type of power generation are as follows: o Nuclear – 1.94 GW for one new plant under construction and safety upgrades at an existing plant;

- BESS (using Li-ion batteries) – 551.47 MW;

- Other energy storage systems (tech other than Li-ion batteries) – 699.65 MW; o Ammonia co-firing upgrades for thermal plants — 263.63 MW;

- Pumped storage – 453.44 MW for two projects: one newly built (185.89 MW) and for replacement of an existing one (267.55 MW);

- Dedicated hydrogen combustion – 253.05 MW; o Dedicated biomass combustion – 100.92 MW.

- CONTEXT: All winners are listed in the table in the Analysis section.

- While as many as 19 of a total 28 decarbonized power source bids went to energy storage systems, with 10 BESS projects using Li-ion batteries and nine using tech other than Li-ion, cumulative capacity allocated in this category was only 1.25 GW.

- Among winning BESS bids were major international firms like Stonepeak and CHC, and entities registered at the same address as HDRE.

- Japanese firm Shirokuma Power, whose 11 projects won in the FY2024 auction, was also among the winners in Round 3.

- Despite high expectations for the introduction of new clean energy options like hydrogen or ammonia, there were only two dedicated hydrogen combustion plants, operated by CEF H2 and Hoku Energy. They won 253.05 MW of capacity.

- Two thermal-plant conversion projects for ammonia co-firing also won awards with 263.63 MW.

- For the first time, OCCTO chose a newly built nuclear project – J-Power’s Oma NPP in Aomori Pref; the second winning bid was Hokkaido Electric’s Tomari NPP Unit 1.

- TAKEAWAY: Please see this issue’s Analysis section for more on LTDA R3 results.

Power futures rise as summer approaches, amid persistent Iran risk

(Japan NRG, May 14)

- Power futures rose steadily this week as traders priced in tighter summer balances and continued uncertainty around the Iran conflict. Tokyo baseload (TBL) June 2026 contracts rose to ¥21.30/ kWh on May 14, up from ¥20.35 on May 8, and ¥20.65 on May 11, according to Tullett Prebon data.

- The sharpest move remains between May and June delivery contracts, highlighting expectations for seasonal tightening as cooling demand rises. Tokyo May baseload traded at ¥16.95 on May 14, implying a ¥4.35 MoM jump into June. Kansai baseload (KBL) June contracts rose to ¥16.55 from ¥15.85 a week earlier, while Chubu baseload (CBL) June rose to ¥20.05 from ¥19.20.

- Peak contracts also strengthened. Tokyo peak (TPK) June contracts climbed to ¥27.35 on May 14 from ¥26.10 on May 8, while Kansai peak (KPK) rose to ¥21.50 from ¥21 over the same period.

- Far-curve contracts showed more limited movement, suggesting the market still sees the current tightening primarily as a summer and near-term fuel risk issue.

- CONTEXT: Japanese power futures are increasingly sensitive to LNG and oil market volatility since the Iran war began. Japan relies on imported LNG and thermal fuels for marginal power generation, particularly during summer peak demand periods.

- TAKEAWAY: The widening gap between May and June contracts indicates that traders expect tighter supplydemand conditions going into summer. Also, Japan Meteorological Agency’s two-week outlook sees higher-thanaverage temperatures, which overlaps with persistent geopolitical fuel risk, particularly for LNG-linked thermal generation. Tokyo contracts continue to trade at a premium to Kansai and Chubu, reflecting the fact that there is less spare capacity in the TEPCO area.

- SIDE DEVELOPMENT:

- TOCOM power futures volumes fall as fuel volatility deters large positions

- (Exchange data, May 14)

- In April, TOCOM electricity futures trading volumes fell to 1,645 contracts, down from 1,981 contracts in March, with trading limited entirely to monthly contracts after no annual contracts were traded that month. Market players cited uncertainty over the Iran war and fuel markets, saying volatility made it difficult to take large positions.

- Trading remained overwhelmingly OTC-based. Of 117 total deals in April, 116 were negotiated off-exchange. Most involved small lots of 10 contracts or less, suggesting participation was driven primarily by smaller retailers rather than large utilities.

- TOCOM launched Chubu-area power futures trading on April 13, with initial transactions recorded in both baseload and peakload Summer 2026 contracts. Still, for now East Japan contracts dominate activity. East-area baseload accounted for 1,381 contracts out of the total 1,645 traded.

Spot power prices jump on fuel risk, utility procurement shifts

(Exchange data, May 14)

- Spot power prices rose sharply in April across almost all regions as Middle East tensions pushed up fuel costs and changes in utility procurement behavior increased spot market dependence.

- Eight of JEPX’s nine regions reported MoM price rises; Tokyo and Chubu rose by more than ¥5/ kWh. Tokyo monthly average prices climbed into the ¥20/ kWh range.

- Market participants said major retailers increased spot market procurement after long-term bilateral contracts between major utilities and generators expired at the start of FY2026. Buy bids reportedly increased at levels such as ¥50 and ¥80, particularly affecting Tokyo-area prices.

- Spot procurement ratios versus total electricity demand also rose sharply to around 45% in April from roughly 30–35% previously.

- Weather conditions also supported higher prices. Japan’s average April temperature was 1.89°C above the long-term average, making it the country’s third warmest April on record after 2024 and 1998.

- CONTEXT: March saw the expiry of long-term internal supply agreements between JERA and the retail arms of TEPCO and Chubu Electric, which boosted spot market procurement by these retailers, contributing to tighter bidding and higher prices in Tokyo and Chubu. At the same time, power prices mirror fuel market volatility. According to March trade statistics, crude oil import prices rose ¥3,307 MoM to ¥67,695/ kL, LNG rose ¥2,702 to ¥88,092/t, and coal increased ¥486 to ¥19,392/t.

Eneres launches market-linked PPAs for flexible clean power

(Company statement, May 11)

- Eneres, an energy solutions provider, launched two market-linked offsite PPA products, using renewable power from its FIP support scheme.

- The goal is to make corporate clean energy procurement more flexible and accessible.

- Services include a physical PPA, where both electricity and environmental value prices track wholesale market rates; and also a virtual PPA without contract-for-difference (CfD) that provides only environmental attributes without price settlement risk.

- Both options allow short-term contracts from one year and price flexibility; previously, fixed PPA pricing was not competitive with local electricity tariffs.

- SIDE DEVELOPMENT:

- Eneres signs PPA with Sumitomo Heavy Industries

- (Company statement, May 14)

- Eneres signed an offsite (physical) PPA with Sumitomo Heavy Industries to redistribute surplus solar power generated at a Chiba plant (~600 kW) to other group facilities in Tokyo and Yokohama.

- Using aggregation and forecasting tech, the scheme maximizes use of excess renewable power that would otherwise be wasted.

Tosoh starts 74 MW biomass power plant in Yamaguchi

(Company statement, May 8)

- Tosoh launched a 74 MW biomass plant in Shunan (Yamaguchi Pref), using wood chips, wood pellets, and RPF.

- CONTEXT: RPF is a solid fuel made from industrial non-recyclable paper and plastics, used in boilers in power plants, or furnaces in lime, paper or steel industries.

J-POWER raises Thai cogeneration portfolio with stake in new projects

(Company statement, April 27)

- J-POWER will participate in two gas cogeneration projects in Thailand via its local subsidiary, acquiring 49% stakes from Electricity Generating Public Co (EGAT).

- The projects are operated by Klongluang Utilities in Pathum Thani (122 MW) and Banpong Utilities in Ratchaburi (256 MW).

- Combined, they add 378 MW of capacity. Both operate under Thailand’s small power production scheme, about 9.33 GW total as of January.

- CONTEXT: With this deal, J-POWER expands its Thai cogeneration portfolio to 10 projects, strengthening its presence across gas, biomass, and solar.

Toagosei to develop small power plants across Nagano Pref

(Company statement, May 11)

- Chemical firm Toagosei and Mori to Mizu no Chikara Corp agreed to develop multiple small hydropower plants in Nagano Pref.

- Mori to Mizu no Chikara is a Nara-based renewables firm focusing on small-scale hydro projects. It targets a total annual generation of ~30 GWh.

- Typical installations range from tens of kW to several MW.

- TAKEAWAY: Since they benefit from high utilization rates (50–90%), such plants could prove more stable power suppliers than solar. The initiative supports Toagosei’s goal to halve CO2 levels by 2030 over 2013 levels; this aligns with Japan’s push for distributed renewables in regions like Nagano, where small hydropower plays a major role in energy supply.

Beyond Next Energy launches post-FIT revenue forecasting service for power sales

(Company statement, May 8)

- Consulting firm Beyond Next Energy launched a support service for forecasting post-FIT electricity sales revenue beyond 2032.

- After FIT contracts expire, renewable power plant owners can continue selling power through wholesale markets or corporate PPAs, invest in batteries or repowering to capture additional market revenues, sell the assets, or retire the plant.

- Beyond Next Energy supports these decisions by providing 30-minute interval long-term electricity price forecasts and post-FIT revenue simulations through 2050.

- CONTEXT: Japan introduced the FIT scheme in 2012, requiring utilities to buy renewable electricity at fixed prices for 20 years. High solar FIT prices, initially set at JPY 40/kWh, accelerated solar deployment. From 2032 onward, FIT contracts will begin expiring, with about 7 GW of mainly solar projects expected to enter the post-FIT phase during 2032–2033.

- TAKEAWAY: So far, only a limited number of renewable power operators have switched from FIT to FIP before FIT expiration. However, interest in early FIP transition is increasing due to curtailment risks, battery storage opportunities, and potential gains from wholesale electricity markets and balancing services. The govt is also encouraging a shift to the FIP scheme. Therefore, such services will likely become more common as they assist businesses still under the FIT scheme when planning operations.

Sassor launches custom aggregation system development service

(Company statement, May 13)

- Sassor, a Tokyo-based energy tech firm, launched a custom aggregation service to help energy operators build in-house Virtual Power Plant (VPP) platforms to integrate storage (grid-scale, colocated, and LV batteries), other renewables, and distributed energy resources (DER).

- The system supports tech like OpenADR (Automated Demand Response), AI-based control, and market-linked optimization, enabling participation in Japan’s wholesale, balancing, and capacity markets with bidding, forecasting, and revenue simulation.

- The goal is to shift operators from outsourced aggregation to self-owned systems, improving profitability, data utilization, and flexibility while supporting scalable integration of batteries, EVs, and other DER assets.

- CONTEXT: Sassor is a resource aggregator, handling software infrastructure instead of focusing solely on trading.

- TAKEAWAY: This new service helps Sassor expand its customer base and compete with bigger aggregators such as E-Flow or Toshiba ESS. As battery storage capacity continues to grow at double-digit rates, and participation balancing and capacity markets expands, more operators need in-house systems to manage and monetize distributed energy resources. This trend confirms that aggregation is now a core function rather than an outsourced service.

Tokyo Govt to promote use of DC waste heat

(Government statement, May 11)

- The Tokyo Govt launched a public call for a new program to promote the use of waste heat from data centers (DCs).

- It aims to support new technologies and services that utilize increasing waste heat from advanced servers, while improving energy efficiency.

- Selected companies will receive financial support of up to ¥5.2 billion in total for FY2026–2027.

- Applications will be accepted from May 22 to June 18, 2026.

- CONTEXT: Growing heat generation and power consumption by data centers driven by AI GPU servers is a key challenge. Challenges center on growing electricity use for cooling, and unused exhaust heat released into the atmosphere.

Three TSOs launch METI-supported project on DR utilizing smart meters

(Company statement, May 11)

- Three TSOs in Tokyo, Chubu, and Kansai were again chosen for the METI demo on demand response (DR) utilizing smart meters.

- Last year’s tests successfully controlled distributed energy resources (DERs) to charge during lowprice periods and discharge during high-price periods in the wholesale electricity market.

- The project will improve large-scale DER control systems, as well as verify grid congestion management and balancing market use cases.

- TAKEAWAY: The project could reduce the cost of residential demand response by using existing smart meter infrastructure and accelerate aggregation of DERs for future virtual power plant (VPP) development. It also reveals the growing role of smart meters in DER control and the importance of cybersecurity and standardized infrastructure.

NEWS: HYDROGEN

Akasaka DHC launches hydrogen-based heat source facility

(Company statement, May 12)

- Akasaka District Heating and Cooling (DHC) of the TBS Group began full-scale commercial operation of a hydrogen-based heat source facility using green hydrogen, the first such project by a DHC operator in central Tokyo.

- The facility receives green hydrogen from a production site in Yamanashi Pref and stores it in two hydrogen storage alloy tanks with a capacity of 1,350 Nm3 each.

- Hydrogen will be utilized for power generation with fuel cells and for heat supply through a hydrogen co-firing boiler.

- The Tokyo Govt supports the facility.

- CONTEXT: Akasaka DHC supplies chilled water, steam, and electricity from two underground plants to buildings in Tokyo’s Akasaka 5-chome area, including the Tokyo Broadcasting System (TBS).

- TAKEAWAY: This project is set within urban energy infrastructure and aims to demonstrate that green hydrogen can be commercially integrated into DHC systems. The question, as always, is how much of the state subsidies are required to make it work economically. If the number of similar projects grows, it would be a good sign that Tokyo can create real use cases for hydrogen beyond heavy duty transport mobility. So far, many such projects are one-of-a-kind and their economics are not fully transparent.

NEWS: SOLAR AND BATTERIES

Japan study on PSCs forecasts 12.5 GW deployment by 2040

(Company statement, May 8)

- Japan’s 2026 study on tandem perovskite solar cells forecasts about 12.5 GW cumulative deployment by 2040, with strong growth driven by both new installations and replacement of aging conventional silicon panels.

- CONTEXT: Japan targets up to 20 GW of PSC capacity by 2040.

- The findings by Yano Research Institute show that to reach national solar targets, improving efficiency through tandem tech is essential.

- Results clarify that adoption will vary by use: flexible PSCs for new applications (buildings or curved surfaces), and perovskite/ silicon tandems as replacement for existing systems.

- The study positioned CIGS (copper indium gallium selenide solar cells) as a key tandem partner for PSCs, especially when silicon becomes too heavy or rigid. Technically, CIGS acts as a bottom cell in tandem structures, enabling high efficiency (25% achieved; over 28% potential).

- TAKEAWAY: The study highlights growing global competition especially from cheaper overseas products and suggests that Japanese firms secure early market share by targeting applications with ~10-year durability rather than waiting for 20-year lifespans. Overall, this industry’s success will depend on faster commercialization, strategic niche adoption, and solving key technical challenges like durability and moisture resistance.

- SIDE DEVELOPMENT:

- Japanese researchers achieve record 25% efficiency of perovskite-CIGS cells

- (Company statement, May 8)

- Researchers at Tokyo City University and The National Institute of Advanced Industrial Science and Technology (AIST) achieved a 25.14% world-record efficiency in a 1 sq cm two-terminal perovskiteCIGS tandem solar cell.

- The previous record was 24.6%. The tech relies on a newly developed carrier recombination layer and barrier layer that enhances crystal quality and voltage performance at the perovskite–CIGS interface.

- Further work will focus on improving output, material composition, and durability.

- TAKEAWAY: The results show a lightweight, flexible thin-film tandem architecture with high efficiency, suitable for use on curved surfaces, building integration, EVs, and drones.

Firms launch first agrisolar demo using PSCs in rice farming

(Company statement, Nikkei, Chiba University, May 11)

- Sekisui Solar Film (a wholly-owned subsidiary of Sekisui Chemical) and TERRA, operator of agrisolar businesses, launched a pilot project at Chiba University to test agrivoltaics using perovskite solar film installed above rice fields.

- The 3-year experiment will evaluate durability, crop yield, and quality while generating electricity for the university.

- This is Japan’s first such setup using PSCs in rice farming.

- The project also aims to reduce heat stress on rice and lower methane emissions.

- CONTEXT: TERRA and Sekisui Chemical produced this ultra-light, flexible perovskite solar film with an adaptable mounting structure for locations where rigid cells can’t be installed. SSF, which in FY2025 commercialized its SOLAFIL film-type PSCs, seeks to launch a 100 MW-scale production line in FY2027.

- TAKEAWAY: While this perovskite film achieves about 15% conversion efficiency, which is lower than conventional silicon panels (~20%), its lightweight, flexible form and suitability for farming environments are key advantages, alongside durability and crop impact (i.e. through lower heat stress in power generation). Sekisui’s film achieved roughly 1/10th the weight and 1/20th the thickness of silicon.The new tech unveils new use possibilities on surfaces such as curved roofs, warehouses, factories or facades, and even vehicle roofs.

Shizuoka demo signals new trends in PSC deployment

(Organization statement, April 27)

- The University of Electro-Communications and Shizuoka Pref launched a pilot project installing suspension-type cylindrical perovskite solar modules over steep tea fields to enable both farming and power generation.

- The flexible perovskite sheets are enclosed in tubeshaped modules that provide stable power regardless of sun angle while allowing light, wind, and rain to pass through, making them suitable for steep, soft terrain and agricultural use.

- TAKEAWAY: While this project is promising, the tech isn’t yet deployable. Still, the project, similar to the one by Sekisui and TERRA, shows strong interest in unconventional usage of PSCs. In recent years, Sekisui, the leader in perovskite development, has tested resistance to salt damage and wind. Field tests across floating systems, coastal sites, buildings, and agriculture show stable performance in real-world conditions, though long-term degradation and durability beyond 10 years remain key uncertainties.

- SIDE DEVELOPMENT:

- Toyo Seikan, TNO ink deal with Perovion for global deployment of PSCs

- (Company statement, May 15)

- Toyo Seikan Group, Perovion Technologies, and TNO agreed to form a partnership to accelerate the global commercialization of PSCs.

- This combines Toyo Seikan’s materials tech, Perovion’s PSC production, and TNO’s R&D expertise to support mass production and supply chain development.

- The goal is to scale PSC panels for mass production and supply in Europe and Japan.

Sumitomo to expand business in battery recycling

(Company statement, May 15)

- Sumitomo Corp will join the battery recycling business alongside Sumitomo Metal Mining and JOGMEC, with operations expected to begin in 2030.

- CONTEXT: Sumitomo Metal Mining plans to recycle used lithium-ion batteries imported from Australia by crushing them in Japan into a material known as “black mass,” before extracting cobalt and nickel.

- These metals extracted could be reused in the EV industry in a circular economy.

- TAKEAWAY: Recycling lithium-ion batteries, much like that of solar PVs, is a pressing issue for Japan, which promotes deployment of EVs, stationary BESS, and other applications. Sumitomo Metal Mining’s process is based on hydrometallurgy, allowing the isolation of critical materials while helping prevent waste accumulation. Other major players active in the sector include Dowa HD and JX Advanced Metals.

- SIDE DEVELOPMENT:

- Edion launches solar recycling as part of nationwide system

- (Nikkei, May 13)

- Edion opened a solar panel recycling plant in Fukuyama, Hiroshima Pref, operated by its subsidiary ER Japan.

- The facility dismantles and processes used panels, separating materials like glass, silver, and copper for reuse.

- The plant can handle about 240 panels per day and aims to recycle 40,000 panels (around 800 tons) annually by 2035, with profitability targeted within 3–4 years.

- CONTEXT: The move comes as panels sold since 2007 approach their 20-year replacement cycle. Edion is building a nationwide collection system, including panels sold by other firms, to support large-scale recycling.

Q.ENEST Holdings sets up solar power fund

(Company statement, May 12)

- Q.ENEST Holdings (part of Hanwha Japan) set up and financed an ~80 MW low-voltage solar power fund in Japan, raising about ¥9 billion through a syndicated loan arranged by Sumitomo Mitsui Banking Corp.

- The fund will invest in distributed solar plants nationwide and use Q.ENEST’s own electricity retail platform as a buyer of the generated power.

- This will enable a green electricity supply model combining power generation and retail that offers stable pricing to customers while managing market risks.

- Hanwha Japan is a subsidiary of South Korean conglomerate Hanwha Group, which operates with a strong focus on renewables; in Japan it mainly focuses on solar power.

REXEV and partners supply electricity to the grid via EV platform

(Company statement, May 11)

- REXEV, together with Kyocera, Shonan Power and TEPCO, installed a next-gen energy management platform for EVs in Odawara (Kanagawa Pref); it uses a model based on electricity supplied from BESS and solar PVs to the grid.

- The platform monitors consumption in real time, supplying electricity to the grid via the balancing market while retaining stored electricity during less profitable hours.

- The panels are supplied by Kyocera, and the BESS by Shonan Power.

ReAxel Technologies starts test service for recycling rare earth minerals from EVs

(Company statement, May 15)

- ReAxel Technologies launched a pilot-scale recycling testing service for rare earth materials recovered from used EV and HEV motors.

- CONTEXT: ReAxel is a Japanese startup focused on building a resource recycling system for the automotive industry, specifically targeting rare earth magnets in EV and hybrid vehicle (HEV) motors.

- The service targets automakers, suppliers, and materials companies, and generates real-world data on the feasibility, cost, and quality of recycled rare earths, particularly in response to tightening regulations such as the EU’s Critical Raw Materials Act.

- The initiative reflects growing demand to build circular supply chains for critical materials like neodymium and dysprosium.

Mitsui Fudosan invests in DR system for BESS

(Company statement, May 11)

- Mitsui Fudosan invested in Exergy Power Systems, selected for its Exergy Battery®, a storage-based demand response (DR) system used with distributed power sources and electricity demand sites.

- CONTEXT: Mitsui Fudosan conducts field tests with Exergy Power Systems in Kashiwa (Chiba Pref) under the Kashiwa-no-ha smart city project. Since 2025, the two companies have deepened collaboration in the aggregation and trading of demand-side BESS in Kashiwa.

Nagoya Electric Works agrees with PXP in CSCs in road infrastructure

(Company statement, May 12)

- Nagoya Electric Works agreed with PXP to invest in CSCs in order to decarbonize road infrastructure, particularly in equipment where installing solar modules is difficult, such as information signs or security monitoring devices.

- CONTEXT: The agreement follows a demo involving CSCs installed on roadside cameras and information signs, the results of which were reviewed last March (Japan NRG report – Dec 1, 2025). Following positive results, Nagoya Electric Works decided to formalize its partnership with PXP, which is expanding its customer base.

NEWS: WIND POWER AND OTHER RENEWABLES

Sumitomo begins commercial operation of 500 MW wind farm in France

(Company statement, May 11)

- Sumitomo and its partners began commercial operation of the Noirmoutier Offshore Wind Farm in France, in the Bay of Biscay.

- The 500 MW wind farm (61 turbines, 8.4 MW each) will operate for 25 years under a fixed-price PPA with Électricité de France (EDF).

- Ocean Winds has a 40% stake, Sumitomo Corp (29.5%), Allianz Global Investors (20.25%), and other shareholders.

- TAKEAWAY: For Japanese developers like Sumitomo, overseas projects are important for gaining experience since domestic offshore wind continues to face bottlenecks in ports, installation vessels, etc. Also, the project shows Europe’s ability to deliver large-scale offshore wind projects on time under bankable fixed-price PPAs.

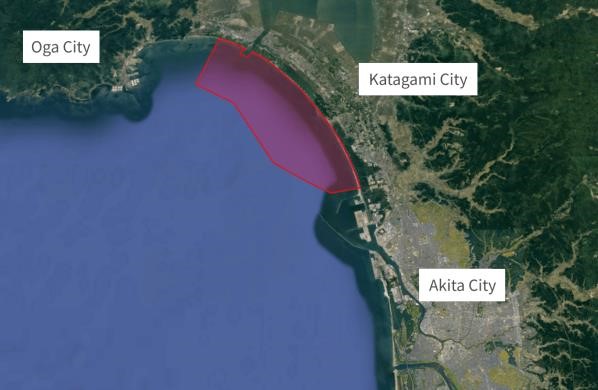

OKA secures SEP vessel for 315 MW Akita wind farm

(Company statement, May 13)

- Oga-Katagami-Akita Offshore Green Energy (OKA), a consortium building a 315 MW offshore wind project in Akita Pref, inked a charter deal with Penta-Ocean Construction for an SEP vessel to be used for turbine installation works.

- The consortium comprises: JERA Nex bp Japan, J-Power, Tohoku Electric and Itochu. METI awarded the project to OKA in Round 2 of the offshore wind tender.

- It’s located off the coast of Oga, Katagami, and Akita cities, and will use 21 Vestas turbines, (15 MW each), and will begin commercial operations in June 2028.

- TAKEAWAY: This chartering of an SEP is a critical de-risking step for Japan’s offshore wind plans, where limited installation vessel availability and port constraints are major bottlenecks. By securing installation capacity early, the OKA consortium reduces execution risk that has delayed or complicated other projects. The move also highlights a shift toward tighter control over construction logistics in a market where supply chain and infrastructure gaps, rather than permitting, are seen as a key constraint on offshore wind deployment.

METI releases subsidy results to promote geothermal energy

(Organization statement, May 11)

- METI announced the projects chosen for its FY2026 geothermal power generation subsidy program. They are the following:

| Company | Location |

| Foundation Ground Consultants | Rausu, Hokkaido |

| Akita Pref | Akita Pref |

| Foundation Ground Consultants, Obayashi | Moyoko, Niigata Pref |

| Takanoyu Onsen | Yuzawa, Akita Pref |

| Oyasu Geothermal | Yuzawa, Akita Pref |

| Oita Pref | Oita Pref |

- The subsidy promotes a better understanding of geothermal power generation among residents living close to geothermal sites (seminars, study sessions, exhibits, etc).

- TAKEAWAY: Takanoyu Onsen hosts a geothermal resource development site near its thermal spring facilities, where a hot water supply system is planned. This suggests that some spring operators might agree to geothermal facilities near their resorts. Similar openness toward geothermal power has also emerged in Kusatsu, a thermal springs town in Gunma Pref.

NEWS: NUCLEAR ENERGY

Tohoku Electric shuts Onagawa NPP Unit 2 soon after restart

(Company statement, Nikkei, May 17)

- Tohoku Electric restarted Onagawa NPP Unit 2 on May 11 after completing periodic inspections. It was due to begin power generation soon and resume commercial operation in early June.

- However, on May 15, steam was detected from a tank connected to the steam separation system used for turbine operations. Closing a related valve did not stop the leak.

- The company said the issue occurred before an earthquake struck Miyagi Pref later that evening and is unrelated to the quake.

- As a precautionary measure, Tohoku Electric shut down the reactor to investigate the steam leak. The utility said no external release of radioactive materials or impact on surrounding areas was confirmed.

- CONTEXT: In January, operations were suspended for reactor core and cooling system inspections.

KEPCO investigates steam leak at Mihama NPP Unit 3

(Company statement, May 12)

- KEPCO reported a steam leak near the turbine of Mihama NPP Unit 3, caused by damage to a cap used to seal the turbine cover.

- An inspection during maintenance in Dec 2021 did not find localized corrosion on the cap’s inner surface. So thickness measurements were not taken at that time.

- CONTEXT: The steam leak led to a manual reactor shutdown, with no abnormal ambient radiation levels. The unit began commercial operation in 1976 and will mark 50 years of operation in 2026.

NEWS: TRADITIONAL FUELS

METI accelerates oil diversification strategy as reserve pressure eases

(Government statement, Japan NRG, May 15)

- METI and ANRE outlined Japan’s latest response measures to secure stable fuel supplies amid continuing tensions in the Middle East.

- The govt said crude procurement diversification is progressing rapidly. Alternative sourcing accounted for around 25% of procurement in April, and is expected to reach about 60% in May, and more than 70% in June. METI said imports from the U.S. alone are expected to increase to roughly eight times last year’s level in June.

- Replacement supply is being secured from a widening group of producers including the U.S., Africa (Nigeria, Angola), Central Asia (Azerbaijan, Kazakhstan), Latin America (Ecuador, Mexico) and the Asia-Pacific region.

- METI added that procurement routes are also diversifying, with greater use of bypass infrastructure such as Saudi Arabia’s East-West pipeline and Egypt’s SUMED pipeline.

- An Azeri crude tanker carrying 648,000 barrels for ENEOS refineries arrived in Japan on May 12, marking one of the first Central Asian crude shipments secured since the Iran conflict intensified earlier this year.

- Azeri crude has refining characteristics similar to Middle Eastern grades.

- The ministry said diversification efforts are reducing pressure on strategic reserves and improving the outlook for stable supply through the end of the year, including for petrochemical feedstocks such as naphtha.

- The govt therefore sees less immediate need for additional reserve releases.

- The materials also emphasized the strategic importance of Japanese upstream equity interests and JOGMEC-backed projects. METI highlighted that Japanese firms are prioritizing crude and condensate supplies from projects in Kazakhstan, Azerbaijan and Australia where Japanese companies hold stakes.

- On gas supplies, the govt said Japan remains in a relatively stable position. More than 90% of LP gas imports come from countries outside the Middle East, primarily the U.S., Canada and Australia, while LNG inventories are currently equivalent to roughly one year of Hormuz-exposed imports.

- METI nevertheless stressed the need to strengthen LNG storage capacity and broader fuel supply-chain resilience.

- CONTEXT: The govt is also considering extending stockpiling obligations to naphtha as part of a broader review of strategic fuel-security measures.

- SIDE DEVELOPMENT:

- Govt to ask business groups to limit lubricant use; won’t release stocks this month

- (Jiji Press, May 14)

- The govt asked business and auto industry groups to limit lubricant oil purchases to last year’s levels to ensure stable supply.

- Due to progress with alternative procurement, the govt will not release extra state oil reserves this month.

INPEX scales back investments due to tensions in Iran

(Company statement, Japan NRG, May 13)

- Driven by surging oil prices, INPEX upgraded its consolidated FY2026 net profit forecast, ranging from ¥350 billion to ¥450 billion, a rise of ¥20 billion to ¥120 billion over the previous estimate of ¥330 billion.

- These forecasts assume Strait of Hormuz disruptions will normalize by July; but INPEX director Yamada Daisuke cautioned that this timeline is uncertain.

- The Iran war forced INPEX to scale back its FY2026 growth investment, now ¥50 billion lower than before, to ¥800 billion. Investments for maintenance, renewal, and production increases at oil fields in the UAE face delays.

- INPEX reacted to the war with plans to focus on crude supplies to Japan from oil fields where it holds stakes in Kazakhstan and Azerbaijan.

- CONTEXT: In February INPEX assumed an average crude oil price of $63 per barrel, but has revised this upward, now expecting a price in the range of $70 and $83 per barrel. Also, it adjusted exchange rate forecasts to¥154 – 156 to the dollar.

- SIDE DEVELOPMENT:

- INPEX gets stake in gas field off coast of Western Australia

- (Company statement, May 15)

- INPEX will get a 10.67% stake in a gas field off the coast of Western Australia from a subsidiary of PetroChina. It includes titles over the Brecknock, Calliance and Torosa fields.

- The stake is part of Browse LNG, one of the biggest projects in Australian history, with production expected to begin after 2030.

- The field is estimated to contain 13.9 trillion cubic feet of natural gas and 390 million barrels of condensate.

- The project’s operator is Australia’s Woodside Energy (30.6% stake), with BP as the largest shareholder (44.33%).

- CONTEXT: The acquisition strengthens INPEX’s base in Australia, where it already holds interests in Ichthys LNG. INPEX has close ties to the Japanese govt, which has about a 20% stake and a “golden share” allowing veto power over key decisions.

Idemitsu Kosan reverses plan to close refineries

(Nikkei, May 12)

- Idemitsu Kosan reversed a plan to close refineries, citing a slower decline in oil demand and heightened energy security risks due to the Iran war.

- The firm scrapped its 2030 target to keep fossil fuel profits below 50% of total profit, returning to a more pragmatic approach.

- In its new medium-term plan, Idemitsu will invest a record ¥1.8 trillion, with ¥590 billion for refinery operations, a 30% increase over the previous plan.

- The firm operates six of Japan’s 19 refineries, which will run until 2030.

- Idemitsu is diversifying crude sources from South and North America. Having many refineries allows it to process different crude grades. The plan was to cut capacity by 300,000 barrels per day (10% of Japan’s total) by 2030, but security concerns and slower decarbonization have shifted priorities.

- Idemitsu will keep investing in LNG, next-gen fuels, and solid-state battery materials for EVs. Its GHG reduction target has been lowered.

Tokyo Gas inks deal with Shizuoka Gas to sell LNG

(Company statement, Japan NRG, May 8)

- Tokyo Gas agreed to sell LNG to Shizuoka Gas for five years or more.

- Starting 2027, Tokyo Gas will supply five LNG cargoes per year (equal to 300,000–350,000 tons).

- Shizuoka Gas said the volume will cover about 25% of its annual LNG purchases.

- The LNG will come from projects with which Tokyo Gas already has contracts.

- The delivered LNG will be on a DES (Delivered Ex-Ship) basis, where the seller arranges the vessel and delivers it to the unloading point.

- Shizuoka Gas may resell the LNG under the contract.

- CONTEXT: This is the first mid-to-long-term LNG deal between the two firms. Shizuoka Gas had some existing LNG procurement contracts expiring; so it has been looking for replacement suppliers.

- CONTEXT: Tokyo Gas does not rely on the Middle East for its supplies, which total around 12 Mtpa. Half of its purchased volume comes from Australia; Malaysia, U.S., and Russia account for the other half.

NYK Line eyes expanding tanker fleet for procurement beyond Middle East

(Nikkei, May 13)

- NYK Line is considering expanding its oil tanker fleet to meet rising demand for petroleum imports from outside the Middle East.

- The Iran–U.S. war reveals the risks of relying heavily on Middle Eastern crude, prompting Japanese oil firms to diversify procurement sources.

- NYK expects the shift to continue even if traffic in the Strait of Hormuz normalizes.

- Since sourcing oil from regions like the U.S. and Africa requires longer routes and more ships, NYK Line may add very large crude carriers.

- CONTEXT: The information is based on Nikkei’s interview with CEO Soga Takaya.

- SIDE DEVELOPMENT:

- ENEOS oil tanker passes through Hormuz

- (Nikkei, May 14)

- An oil tanker owned by ENEOS passed through the Strait of Hormuz, the second Japanese company after Idemitsu to do so since the strait was blocked.

- According to ship tracking data, ENEOS Endeavor sailed from the Persian Gulf into the Gulf of Oman as of 9:00 a.m. on May 14.

- The tanker departed Kuwait in late Feb and will arrive in Japan around June 3. ENEOS cited safety for not commenting on the vessel’s status.

- CONTEXT: Idemitsu’s tanker Idemitsu Maru passed through the strait in late April, thanks to Iranian permission.

ENEOS to acquire Chevron’s fuel businesses in APAC region

(Company statement, May 14)

- In a ¥336 billion ($2.17 billion) deal, ENEOS agreed with Chevron to acquire 100% stakes in its downstream fuel and lubricants businesses across SE Asia and Australia.

- The deal covers operations in Singapore, Malaysia, the Philippines, Vietnam, Indonesia, and Australia, and includes a 50% stake in the Singapore Refining Co.

- The transaction is expected to close in 2027, subject to regulatory approvals.

- The acquisition strengthens ENEOS’s overseas portfolio amid declining fuel demand in Japan, taps into growth in SE Asia and expands trading opportunities in Australia.

- The firm also plans to maintain and develop the Caltex fuel retail and lubricant brand.

Cosmo Energy net profit rises, diversifies oil imports

(Company statement, Japan NRG, May 12)

- Cosmo Energy reported a FY2025 net profit of ¥74 billion, up 28% YoY, and above market expectations; this was helped by reduced valuation losses on oil reserves and improved refining margins.

- For FY2026, the firm forecasts a 41% drop in net profit to ¥44 billion, assuming normalized crude supply from Sept and an oil price of $89 per barrel. This would reduce margins on petroleum product sales.

- CONTEXT: Cosmo Energy expects to secure a stable supply of crude oil from Sept onward, from the U.S., Mexico, etc. The firm is shifting away from Middle Eastern supplies after the Strait of Hormuz blockade.

Okayama Gas raises prices for first time in 26 years

(Nikkei, May 13)

- Okayama Gas raised its gas prices by 10.7% due to higher oil product costs and inflation for equipment maintenance.

- This hike applies to all customers, including household and commercial accounts. For a typical household, the base rate will rise from ¥1,354 to ¥1,893.

- This is the first hike in 26 years.

Osaka Gas launches ship-to-ship LNG bunkering service

(Company statement, May 14)

- Osaka Gas launched its first ship-to-ship LNG bunkering service at JFE Steel West Japan Works in Fukuyama, Hiroshima.

- Its LNG bunkering vessel Seto Azure can now supply LNG fuel directly to ships at sea.

- Osaka Gas now offers all three LNG fueling methods: truck-to-ship, shore-to-ship, and ship-to-ship, able to accommodate various port conditions and vessel operations.

- TAKEAWAY: The move comes as demand for LNG-fueled ships grows globally due to stricter emissions regulations; LNG can reduce emissions by about 30% compared to heavy fuel oil. Osaka Gas aims to strengthen fueling infrastructure in Japan, where supply systems have so far been limited.

LNG stocks up from previous week, down YoY

(Government data, May 13)

- As of May 3, the LNG stocks of 10 power utilities were 2.07 Mt, down 4.6% from the previous week (2.17 Mt at April 26), down 10.8% from end of May 2025 (2.32 Mt) and down 4.6% from the 5year average of 2.17 Mt.

- (No announcement was made on May 6 due to the national holiday.)

- As of May 10, LNG stocks were 2.12 Mt, up 2.4% from the previous week, down 8.6% YoY, and down 2.3% from the 5-year average.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

ENEOS trades SAF environmental value with partners

(Company statement, May 11)

- ENEOS agreed with Furukawa Electric and Sumitomo Warehouse to trade SAF environmental value under the Tokyo Govt’s effort to promote SAF use in air freight.

- Sumitomo Warehouse acts as the freight forwarder and Furukawa Electric as the shipper, while ENEOS issues certificates corresponding to the emissions reductions equivalent to the amount of SAF used by each company.

- TAKEAWAY: In 2023, Japan was the world’s fourth-largest air cargo market, handling 4.6 million tons through its airports, much of it consisting of high-value goods such as pharmaceuticals and semiconductors. Given the sector’s high emissions intensity, companies are seeking to reduce their Scope 3 emissions through the use of SAF in Japan. The industry is at an early stage and still relies largely on environmental certificates, although companies such as DHL Express began directly using SAF produced in Japan in 2025.

Mitsui selects Planet Savers for its DAC tech

(Company statement, May 12)

- Mitsui & Co’s Co-creation Fund will support Planet Savers, aiming to speed up commercialization of its zeolite-based Direct Air Capture (DAC) tech.

- Planet Savers is developing a low-cost DAC system using zeolite materials. It is fully electric, requires no heat or water, and is suited for dry and cold regions, helping reduce energy and material costs.

- Through the fund, Mitsui will support development and expand use of captured CO2 in areas like agriculture, aiming to scale up DAC technology for wider industrial adoption and climate impact.

Sanyo Chemical launches flow-improvers for biodiesel

(Company statement, May 7)

- Sanyo Chemical added two new products to its Neoprever lineup of low-temperature flow improvers for soybean- and palm oil-derived biodiesel fuel.

- Neoprever HBF-201 and Neoprever HBF-301 pledge to improve fuel performance in cold environments by inhibiting crystal growth and aggregation depending on the fuel’s fatty acid composition and crystallization behavior, reducing the risk of filter and pump clogging.

- TAKEAWAY: Conventional FAME (Fatty Acid Methyl Ester), a type of biodiesel, is prone to clogging at low temperatures due to the crystallization of fatty acid-derived components. This leads to maintenance issues that have limited its large-scale use in industrial applications. Thus, FAME is used mainly in low blends such as B5. Products of this kind could help support wider adoption of FAME.

ANALYSIS

BY JAPAN NRG TEAM

Nuclear, BESS (and LNG) Remain Biggest Winners in Latest LTDA Auction

Three years in, the direction of the Long-Term Decarbonized Power Sources Auction (LTDA) is clear: nuclear provides the backbone, while battery storage supplies the flexibility, chiming with the government’s twin priorities of securing dispatchable generation while preparing the grid for a much larger share of intermittent renewables.

Nuclear was the largest winner within the decarbonized category by capacity, but battery energy storage systems (BESS) dominated by project count. Storage projects accounted for roughly 60% of all successful bids in the FY2025 tender, the long-awaited results of which were released May 13.

By 2040, Japan’s energy strategy sees renewables accounting for 40-50% of the national power mix, driven mainly by an expansion of solar and wind. That shift will require far more storage and grid flexibility to absorb intermittent output.

At the same time, AI-driven growth in power demand, delays in restarting nuclear plants, and concerns that renewable deployment may fall short of official targets are convincing policymakers that dispatchable thermal generation cannot yet be phased down too quickly.

The LTDA increasingly reflects this balancing act. Rather than functioning as a conventional renewable-energy support scheme, the auction is evolving into a financing mechanism for capital-intensive technologies that struggle to secure private funding on purely merchant terms. In exchange for stable support over two decades, developers accept limits on upside market revenues – effectively trading profitability for predictability.

That dynamic helps explain the composition of this year’s winners. Technologies with large upfront costs, uncertain future revenues, or unresolved fuel supply featured prominently. Hydrogen and ammonia projects are a case in point: Despite substantially improved support conditions in Round 3, only four projects bid. All four were selected, compared with an overall auction award rate of 67%, suggesting a still-limited project pipeline.

Overall, OCCTO awarded 7.299 GW of capacity from 10.856 GW of bids. Of the 32 successful projects, 28 fell into the “decarbonized power source” category, totaling 4.261 GW, while four LNG-only thermal projects accounted for another 3.038 GW.

LTDA Results by Energy Sector (in terms of kW awarded)

| Energy source | R1 (FY2023) | R2 (FY2024) | R3 (FY2025) |

| Nuclear power | 1,315,707 | 3,153,107 | 1,939,123 |

| Hydrogen and ammonia | 825,582 | 94,600 | 516,687 |

| BESS | 1,092,076 | 1,370,036 | 1,251,127 |

| Pumped hydro | 576,937 | 360,646 | 453,439 |

| LNG | 5,756,320 | 1,314,644 | 3,037,866 |

Nuclear towers over others

While the LTDA auction was initially considered especially favorable for energy storage, in recent rounds it has expanded to cover almost every power source. None have benefited as much as nuclear, which in Round 3 secured close to half of the total from the decarbonized bucket: 1.94 GW across two projects.

This year’s results include the first-ever LTDA award for a new-build reactor. The project, J-Power’s Oma Power Plant in Aomori Prefecture, is an 1.38 GW Advanced Boiling Water Reactor due to run entirely on MOX fuel, which is a recycled nuclear fuel that contains a blend of plutonium and depleted uranium oxides.

The Oma project itself is decades old. Plans for its full-MOX configuration date back to a 1995 decision by the Japan Atomic Energy Commission, but construction has faced repeated delays since the 2011 Fukushima disaster.

The other project is to help Hokkaido Electric upgrade safety measures at its 558-MW Unit 1 of Tomari NPP. The station’s Unit 3 is expected to restart next year to help power a nearby semiconductor fabrication plant. But the utility has struggled for years to secure regulatory approval for the facility and has committed to major additional safety investments as part of the process.

BESS expansion continues

Energy storage secured about 40% of the “decarbonized” capacity awarded (1.25 GW), but it dominated participation, accounting for 19 of 28 awarded projects. Last year’s concerns that BESS developers will desert the auction due to stricter bid requirements has not materialized.

Of the BESS winners, 10 were for Lithium-ion batteries (551 MW) and nine for nonLithium storage systems (700 MW). OCCTO does not disclose the specific chemistry behind the non-lithium-ion category in the winning list, so it should not be assumed that every project is a long-duration energy storage (LDES) – systems capable of delivering electricity over extended periods, typically ten hours or more. Still, the result points to a policy preference for broader storage diversity and longer-duration flexibility, especially after tighter rules were introduced to curb shorter-duration battery bids.

For LDES, battery chemistries other than Li-ion are often seen as more suitable. These include vanadium redox flow batteries, which are already visible at several projects in Japan.

OCCTO also applied a supply-chain concentration rule limiting the share of awarded battery capacity from cells manufactured in any single foreign country or region, excluding Japan, to below 30% in each battery category.

In terms of operators, this time the major winners included HEXA, Stonepeak, and Singapore-based CHC, which secured at least 287 MW across five projects. Several projects registered to the Japanese address of Taiwan’s HDRE were also visible.

While domestic developers – Bison Energy, Shirokuma Power, and TEPCO – remained among the leading recipients, non-Japanese firms proved their growing presence in the battery market, with winning streaks continuing from previous LTDA rounds.

The results underlined how competitive Japan’s storage market has become, attracting global infrastructure investors, domestic renewable developers and aggregators.

Weak yen and costs hurt hydrogen

| Fuel theme | Awardee | Project | Awarded capacity |

| Ammonia co-firing retrofit | Hokkaido Electric | Tomatoh-Atsuma Unit 4 | 132.2 MW |

| Ammonia co-firing retrofit | Kobelco Power Kobe | Kobe Power Plant Unit 1 | 131.4 MW |

| Hydrogen-only combustion | CEF H2 | Miike Power Plant | 146.4 MW |

| Hydrogen-only combustion | Hoku Energy | Daiichi Power Plant | 106.7 MW |

Despite high expectations for clean sources such as ammonia and hydrogen, this year’s auction saw only two winning bids in each category. The awarded capacity totaled 263.63 MW for ammonia co-firing upgrades and 253.05 MW for dedicated hydrogen combustion.

In the first two rounds, bid volumes for hydrogen and ammonia projects fell well short of targets. To address this, the government revised the rules from the third round onward – raising price caps, expanding cost coverage (including fuel), and introducing inflation and interest rate adjustments. These changes attracted greater interest.

The result was positive, but modest. The two hydrogen-only combustion projects were

CEF H2’s Miike Power Plant, at 146 MW, and Hoku Energy’s Daiichi Power Plant, at 107 MW. The two ammonia co-firing retrofits were Hokkaido Electric’s Tomatoh-Atsuma Unit 4, at 132 MW, and Kobelco Power Kobe’s Kobe Unit 1, at 131 MW.

Although bids exceeded the procurement target, suggesting some success of the reforms, overall participation remained limited, highlighting ongoing challenges around construction, retrofit costs, and fuel procurement.

CEF H2 had previously secured support for hydrogen co-firing at Miike before withdrawing and returning with a hydrogen-only project. The company now plans both a hydrogen retrofit of Unit 2 and a dedicated hydrogen Unit 3 supported by adjacent green hydrogen output.

Hokkaido Electric’s Tomatoh-Atsuma Unit 4 (700 MW) had already secured support in FY2023 for 20% ammonia co-firing. In this round, it won additional support to raise the co-firing ratio to 40% by FY2032, backed by both CfD-based price support for ammonia supply and infrastructure subsidies in the Tomakomai area.

Similarly, Kobelco Power Kobe’s Unit 1 had secured an award in FY2023 before withdrawing and later resubmitting under the same category. Under capacity market rules, operators may withdraw without penalty if supporting schemes are not finalized, though resubmitted bids must meet original conditions.

For the fourth LTDA auction, METI is moving toward a pre-screening process for hydrogen, ammonia and CCS projects. The proposed requirements include consideration of Japanese equity upstream participation and contribution to Japan’s industrial competitiveness. METI is also considering whether annual co-firing requirements should be measured not simply by hydrogen/ ammonia usage, but by carbon-intensity benchmarks.

That means future hydrogen and ammonia bidders will likely need more concrete procurement plans, upstream partnerships, and credible low-carbon fuel certification. The number of bids may fall, but the quality and bankability of those bids should improve.

Biomass remains under pressure

Biomass was a marginal winner. Only one project cleared: eREX Niigata, at about 101 MW. A larger, similar project by the company in the same area was canceled last November due to soaring construction costs linked to the weak yen.

That result is consistent with the broader pressure on biomass developers from fuel costs, currency weakness and construction inflation. Unlike storage, where investor appetite remains strong, or nuclear and LNG, where major incumbents can carry large balance sheets, biomass faces a tougher procurement and fuel-supply equation.

LNG Prevails

The largest winner by capacity was LNG-only thermal. Four LNG projects cleared for a combined 3.038 GW: Hokuriku Electric’s Toyama Shinko LNG Unit 2, Kyushu Electric’s New Kokura Unit 6, and JERA’s Sodegaura New Units 1 and 2. JERA alone secured 1.554 GW, the largest corporate winner in the auction.

This may look counterintuitive in a decarbonization auction, but it reflects LTDA’s dual role as both a decarbonization and an energy-security mechanism. LNG-only thermal is treated separately from the ‘decarbonized’ bucket but remains eligible as so-called transitional capacity. This means, operators must commit to begin decarbonization measures at their LNG facilities within 10 years and fully decarbonize them by 2050.

The LNG awards were a sharp increase from the previous round. In the FY2024 auction, LNG-only thermal cleared 1.315 GW; in FY2025, it more than doubled to 3.038 GW. By contrast, decarbonized awards fell from 5.030 GW in FY2024 to 4.261 GW in FY2025.

This indicates that Japanese energy planners are not ready to let thermal capacity disappear and that expectations for a transition to cleaner fuels remain strong. The risk is that this “future decarbonization” is dependent on fuels and carbon-capture technologies for which the supply chains are not yet commercially mature.

Regional winners

Regionally, the auction was concentrated. Tohoku had the largest awarded volume, at about 1.966 GW, driven mainly by J-Power’s Oma nuclear project. Tokyo followed with about 1.822 GW, largely reflecting JERA’s Sodegaura LNG awards and TEPCO Renewable Power’s Shiobara pumped-storage replacement.

Kyushu secured about 1.211 GW, helped by Kyushu Electric’s New Kokura LNG project and CEF H2’s Miike hydrogen project. Hokkaido also stood out, not just for volume but for diversity: Tomari nuclear safety investment, Kyogoku pumped storage, and TomatohAtsuma ammonia co-firing.

Kansai was the clear outlier. OCCTO’s regional chart shows about 1.844 GW of bids from Kansai, but only about 131 MW awarded.

| Region | Awarded capacity | Award rate vs regional bids |

| Tohoku | 1.966 GW | ~71% |

| Tokyo | 1.822 GW | ~79% |

| Kyushu | 1.211 GW | ~94% |

| Hokkaido | 1.016 GW | ~96% |

| Hokuriku | 0.759 GW | ~83% |

| Chugoku | 0.272 GW | ~69% |

| Kansai | 0.131 GW | ~7% |

| Shikoku | 0.075 GW | ~35% |

| Chubu | 0.047 GW | 100%, but from a very small bid base |

Where LTDA goes next

For Round 4, three changes matter most. First, hydrogen and ammonia projects are likely to face tighter scrutiny, especially around low-carbon fuel supply and carbonintensity verification. Second, offshore wind may enter the LTDA framework on an exceptional basis for struggling zero-premium projects from earlier seabed auction rounds. Third, LNG will remain politically and commercially important, but its long-term eligibility will depend on whether Japan can make the promised fuel-switching pathway credible.

The FY2025 auction therefore sends a mixed but useful signal. Nuclear and LNG won the megawatts. Storage won the project count. Hydrogen and ammonia won a foothold. Offshore wind may be next in line for rescue through LTDA.

As such, the LTDA is increasingly becoming a map of Japan’s power-sector anxieties. Rather than picking winners, the auction is gradually becoming a catalogue of the transition risks the government fears the market cannot solve alone.

| Company name | Project | Category | Capacity (kW) | |

1 | J-Power | Oma Nuclear Power Plant | Nuclear Power | 1,381,275 |

2 | erex | erex Niigata (tentative name) | Dedicated biomass combustion | 100,926 |

3 | Hokkaido Electric | Tomari Nuclear Power Plant Unit 1 | Nuclear Power (safety measure investments for existing nuclear facilities) | 557,848 |

4 | Hokkaido Electric | Kyogoku Pumped Storage Power Station Unit 3 | Pumped-storage (newly built) | 185,889 |

5 | Hokkaido Electric | Tomatoh-Atsuma Power Station Unit 4 | Retrofit of existing thermal power plant (conversion to ammonia cofiring) | 132,200 |

6 | CHC Japan | Masuda City Energy Storage Facility | BESS (Li-ion) | 75,633 |

7 | CHC Japan | Shintomi Town Energy Storage Facility | BESS (Li-ion) | 36,722 |

8 | Kobelco Power Kobe | Kobe Power Plant, Unit 1 | Retrofit of existing thermal power plant (conversion to ammonia cofiring) | 131,433 |

9 | HEXA Energy Services | HC25 Chigoku No.1 Energy Storage facility | Energy storage systems (excluding Li-ion batteries) | 46,927 |

| 10 | HEXA Energy Services | HC25 Tohoku No.2 Energy Storage Facility | Energy storage systems (excluding Li-ion batteries) | 43,543 |

| 11 | CEF H2 | Miike Power Plant | Hydrogen-only combustion | 146,400 |

| 12 | NRE-54 Investment LLC | NRE Nakagawa No. 2 Battery Storage Facility | BESS (Li-ion) | 46,828 |

| 13 | Stonepeak Kingdom Holdings | Kingdom-3 | Energy storage systems (excluding Li-ion batteries) | 95,582 |

| 14 | Stonepeak Kingdom Holdings | Kingdom-6 | Energy storage systems (excluding Li-ion batteries) | 45,931 |

| 15 | Stonepeak Kingdom Holdings | Kingdom-1 | BESS (Li-ion) | 32,778 |

| 16 | LLC Battery Storage Facility No. 1 | Battery Storage Facility No. 3 | Energy storage systems (excluding Li-ion batteries) | 36,722 |

| 17 | LLC Battery Storage Facility No. 3 (*Bison Energy) | Battery No.116 GridConnected Energy Storage Facility | Energy storage systems (excluding Li-ion batteries) | 141,527 |

| 18 | LLC Battery Storage Facility No. 3 (*Bison Energy) | Battery No.23 GridConnected Energy Storage Facility | Energy storage systems (excluding Li-ion batteries) | 140,098 |

19 | Hoku Energy | Energy Storage System No. 1 | Hydrogen-only combustion | 106,654 |

| 20 | Homodeus LLC | HD No.1 | BESS (Li-ion) | 45,192 |

| 21 | Polar Bear LLC (*Shirokuma Power) | Shirokuma 33 | BESS (Li-ion) | 33,737 |

22 | Polar Bear LLC (*Shirokuma Power) | Shirokuma 36 | BESS (Li-ion) | 30,128 |

| 23 | ZEUS LLC | ZEUS-A | Energy storage systems (excluding Li-ion batteries) | 75,165 |

| 24 | ZEUS LLC | ZEUS-B | Energy storage systems (excluding Li-ion batteries) | 74,163 |

| 25 | CS Aomori Hachinohe ESS LLC | CS Aomori Hachinohe ESS No. 2 | BESS (Li-ion) | 90,734 |

| 26 | Battery Park 15 LLC (*HDRE) | Kagoshima Satsumasendai Energy Storage Facility | BESS (Li-ion) | 45,705 |

| Company name | Project | Category | Capacity (kW) | |

| 27 | Battery Park 20 LLC (*HDRE) | Miyagi Ishinomaki Energy Storage Facility No. 2 | BESS (Li-ion) | 114,012 |

| 28 | TEPCO Renewable Power | Shiobara Power Plant Unit 2 | Pumped storage (replacement) | 267,550 |

| Company name | Project | Category | Capacity (kW) | |

1 | Hokuriku Electric | Toyama Shinko Thermal Power Station | LNG | 583,750 |

2 | Kyushu Electric | Shin-kokura Power Plant Unit 6 (tentative name) | LNG | 900,000 |

| 3 | JERA | Sodegaura Thermal Power Station Unit 1 | LNG | 777,058 |

4 | JERA | Sodegaura Thermal Power Station Unit 2 | LNG | 777,058 |

ANALYSIS

BY JOHN VAROLI

Will Japan Return to Russian Oil Supplies?

With global oil and gas markets in their third month of crisis due to war in the Middle East, and with no end in sight as the warring parties show little sign of compromise, G-7 countries have been making cautious overtures to Russia in a hope to help stabilize supplies of crude oil. These efforts are opening opportunities for Japanese companies.

In early March, the White House issued a temporary sanctions waiver allowing countries to purchase Russian oil and petroleum products already at sea to help steady global energy markets. That exemption expired May 16 when the White House failed to renew it.

In early May, Taiyo Oil and Idemitsu Kosan resumed purchases of oil from Russia’s Far East, from the Sakhalin-2 project not far from Japanese shores. Then on May 9, the Ministry of Economy, Trade and Industry (METI) said a delegation from Tokyo plans to visit Moscow in coming weeks to discuss business relations. Even if largely technical in nature, the meeting would represent the clearest sign yet of a limited thaw in JapanRussia economic relations since Moscow invaded Ukraine in early 2022.

Geography remains one of the central realities shaping Japan’s energy policy. Resourcerich Russia sits directly to Japan’s north – its closest neighbor, while Tokyo remains heavily dependent on imported fossil fuels for energy security. In purely economic terms, deeper energy cooperation between the two countries would appear logical.

Politics, however, has consistently complicated that logic.

Japan and Russia have never formally signed a peace treaty following the Second World War, due to the long-running territorial dispute over the islands Russia calls the Kurils and Japan refers to as the Northern Territories. More importantly, Japan’s security alliance with the U.S. closely constrains Tokyo’s room for maneuver on Russian policy.

For Washington, with abundant domestic oil and gas resources, energy security is a strategic advantage. For Japan, which imports more than 80% of its primary energy, it remains a structural vulnerability.

As a result, Tokyo has often pursued a more pragmatic approach behind the scenes, seeking exemptions or preferential treatment for projects considered critical to national energy security, particularly Sakhalin-2 LNG exports.

Russia, meanwhile, also has incentives to diversify its customer base. China and India now dominate purchases of Russian crude, allowing both countries to negotiate steep discounts given Moscow’s limited alternative export options. Expanding sales to Japan would modestly strengthen Russia’s bargaining position in Asian energy markets.

Mission to Moscow

In its announcement last week, METI said the goal of its mission to Moscow is to support Japanese companies that have already been operating in Russia for years, to guarantee the safety of those assets from possible nationalization.

METI said it’s “coordinating efforts to facilitate communication with the Russian side” and that representatives from relevant companies may also be present. One official emphasized: “We will firmly support Japanese companies operating in Russia.”

In a social media post, METI made it clear that Tokyo will continue to follow

Washington’s lead on policy towards Russia. “New cooperative relations with Russia” are not on the table and “Japan will continue to implement sanctions against Russia in coordination with the Group of Seven.”

Major Japanese energy sector assets in Russia include:

Sakhalin-2 (LNG and oil): Russia’s state-owned Gazprom holds ~77.5%; Mitsui & Co. has 12.5% and Mitsubishi Corp 10%. This project continues to supply Japan with nearly 9% of its natural gas, or around 6 million tons a year. Current U.S. sanctions waivers on purchases run until June 18, 2026. Taiyo Oil’s purchase came from this project.

Sakhalin-1 (primarily oil): Russian state-owned Rosneft holds ~50%,; India’s ONGC 20%; and the Japanese consortium SODECO holds 30% (JAPEX, Itochu, Marubeni, INPEX).

Arctic LNG 2 (only LNG): Russia’s Novatek holds 60%; TotalEnergies 10%, China’s CNPC and CNOOC also each have 10%, and Mitsui/ JOGMEC hold 10% via joint vehicle. The project was frozen by U.S. sanctions soon after it began operations. Output has resumed and gradually grown, though Japan has not received any of this fuel due to sanctions.

Before 2022, Russian oil was Japan’s “Plan B” – an alternative source to counter overreliance on Middle East supply. Russia supplied around 3%–6% of Japan’s crude oil, and there were plans to grow that share via Sakhalin projects, as well as projects in Siberia and elsewhere.

In 2019, Japan bought 9.38 million tons of oil from Russia, which is under 0.2 million barrels per day, or roughly 6% of national consumption. Imports fell sharply during Covid, before collapsing to nearly zero after the invasion of Ukraine in February 2022.

The Chinese factor

As the global energy crisis deepens and Russian crude remains among the cheapest available on international markets, Tokyo may be tempted to cautiously expand purchases from Moscow despite ongoing geopolitical tensions.

Another important consideration is China, whose refiners have secured large volumes of Russian oil at substantial discounts, helping support industrial competitiveness at a time of rising global energy costs. Japanese policymakers are well aware that higher energy prices further weaken the competitiveness of domestic manufacturing relative to China.

Tokyo also faces a broader strategic balancing act. Reducing dependence on Middle Eastern crude by increasing purchases from the U.S. would improve geopolitical alignment with Washington, but risks simply replacing one external dependency with another.

More critically, Japanese officials remain concerned about the future ownership structure of projects such as Arctic LNG 2, Sakhalin-1 and Sakhalin-2.

There is strong reluctance in Tokyo to abandon these assets entirely and risk seeing Japanese stakes transferred to Chinese companies, further strengthening Beijing’s influence over regional energy infrastructure and Arctic shipping routes.

That consideration appears to have been one of the key arguments used by Tokyo in securing continued U.S. flexibility on Sakhalin-related sanctions.

Russia seeks more Asian sales

In early May, Japan’s fourth-largest oil refiner, Taiyo Oil, made a spot purchase of oil from Sakhalin-2. The company said it is acting under instructions from the energy agency, ANRE, as part of Japanese efforts to diversify procurement and ensure supply stability amid the turmoil in the Middle East.

Sakhalin Blend is lighter than many Middle Eastern crude grades and can be processed relatively easily by Japanese refiners. Before the Ukraine war, Taiyo had regularly handled Sakhalin crude and said the latest cargo posed no operational difficulties.

The Omani-flagged tanker Voyager departed from southern Sakhalin Island carrying the shipment. Although the vessel itself is subject to U.S. sanctions, Taiyo said it confirmed that transport related to Sakhalin-2 remains permissible under existing exemptions.

Russia is also seeking to broaden energy sales elsewhere in Asia. Indonesian President Prabowo Subianto met Russian President Vladimir Putin in Moscow in April and reportedly requested additional petroleum product supplies.

The push comes as Russian oil revenues continue recovering despite western sanctions. According to Finland’s Centre for Research on Energy and Clean Air, Russian seaborne crude export revenues rose 115% in March compared with previous levels, while overall fossil fuel export revenues climbed 52% to their highest monthly level in two years.

At the same time, Ukraine has intensified attacks on Russian oil infrastructure, targeting export terminals and refining assets linked to European trade routes. Drone attacks, often using NATO airspace, pounded oil terminals near Saint Petersburg on the Gulf of Finland, adding another layer of uncertainty to global crude markets.

Keeping options open

For now, Japan’s renewed purchases of Russian crude is less a geopolitical realignment than a pragmatic response to worsening energy security risks.

Tokyo remains aligned with the G7 on sanctions policy and continues to view Russia through the broader framework of U.S.-led strategic coordination. But the combination of Middle East instability, structurally high import dependence and intensifying competition with China is pushing energy security concerns back to the forefront of policymaking.

The result is likely to be a carefully managed middle path: maintaining sanctions compliance publicly while preserving access to strategically important Russian energy projects wherever possible.

Russia may therefore not become a major supplier to Japan again in the near term. But the latest developments suggest Tokyo is increasingly unwilling to close the door completely.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Data centers

State and federal energy ministers agreed that data centers across the country should “fully offset” their electricity demand through investments in new renewable power generation and energy storage. Queensland disagreed, however.

Australia / LNG

Some workers at Woodside Energy’s Karratha gas plant and Pluto LNG facilities in Western Australia will begin strike action starting Wednesday, said the Offshore Alliance workers union.

China / LNG