WEEKLY

June 1, 2026

ANALYSIS

WILL LTDA REALLY HELP ACCELERATE JAPAN’S MOVE AWAY FROM FOSSIL FUELS?

- The LTDA auction is meant to promote clean energy by supporting the construction of new decarbonized power capacity. But so far it has helped thermal power even more.

- The reason thermal power can win LTDA subsidies is that each plant must outline how it will later shift to clean fuels. Japan NRG has examined all the roadmaps published by the awarded thermal plant operators so far to review what the transition would look like.

JAPANESE BIOMASS ENERGY AT A CROSSROADS: CONSTRAINTS AND POTENTIAL

- Biomass power is approaching the post-FIT era. The subsidies and cheap fuel imports made many biomass projects bankable. But conditions have changed.

- We examine how the sector’s non-woody biomass facilities – those focused on waste processing and biogas – are faring today and their prospects in the next stage of the sector’s development.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- April data show Japan diversified naphtha imports in face of Middle East disruptions

- Ruling party executive calls for review of gasoline subsidy as state eyes more spending

- Startup focused on sustainable AI data centers wins investors among Japan’s blue-chip firms

- Latest NFC auction results show divergent supply-demand trends

- JERA Cross completes demo of green certs for hourly matching

- OCCTO plans capacity market reform to prevent plant retirement

- Kyushu grid operator seeks to cut curtailments

- PM Takaichi cites Middle East crisis to promote hydrogen and ammonia options

- Sumitomo to invest in large UK BESS portfolio together with Taiwan partner

- Shizen Connect raises ¥2.7 billion to build VPP business

- Tokyo Gas to include CSCs in PPA offer

- JR West starts residential solar program

WIND POWER AND OTHER RENEWABLES

- Cosmo Energy brings FIP-transitioned wind farms into PPA deals

- In a Japan first, Shimizu develops recycling tech for wind turbines

- Osaka court rules again anti-nuclear group

- Idemitsu invests in U.S. fusion power startup

- Chiyoda resumes Qatari LNG plant project

- Woodside may block INPEX bid for Browse

CARBON CAPTURE & SYNTHETIC FUELS

- Osaka Gas launches alliance for carbon credits

- Japanese startup sets up official carbon credits partnership with Laos

EVENTS

June 3 South Korea – Local Elections

June 3-4 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 3-5 AXIA EXPO 2026 (Hydrogen and Ammonia Next-Generation Energy Exhibition/Next-Generation Smart City Exhibition / GX Innovation Exhibition) @ Aichi Sky Expo

June 9-11 APAC Wind Energy Summit @ Hanoi, Vietnam

Jun 11-Jul 19 FIFA World Cup

June 15-17 G7 Summit @ Evian, France

June 23-25 “Summer Davos” in Dalian, China

September 14-18 IAEA General Conference 2026

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

Nov 3 U.S. Midterm Elections

Nov Publication of International Energy

Agency – World Energy Outlook 2026

Nov 18-19 Asia-Pacific Economic Cooperation –

Leaders Meeting @ Shenzhen, China

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com. For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Japan swiftly diversifies naphtha imports as Middle East disruptions persist

(Japan NRG, Government data, May 28)

- Japan’s imports of naphtha, a key petrochemical feedstock, fell 47% YoY in April to about 1.14 million kl, according to customs data.

- Imports from the Middle East declined 79% to roughly 340,000 kl, reducing the region’s share of total imports from around 70% to 30%. Meanwhile, imports from non-Middle Eastern suppliers rose 52% to approx. 800,000 kl.

- The U.S. became Japan’s largest naphtha supplier in April, with imports reaching about 263,000 kl. This volume was up 209-times from a year earlier.

- Significant volumes were also imported from the UAE, Algeria, South Korea and Saudi Arabia.

- CONTEXT: The shift reflects efforts by Japanese buyers to diversify procurement as conflict-related disruptions and shipping risks continue to affect trade flows linked to the Middle East.

- TAKEAWAY: The latest data show how rapidly Japan can reconfigure fuel procurement when energy security concerns intensify. While turning to the U.S. for replacement volumes was an obvious option, the scale of the increase underscores America’s growing ability to act as a swing supplier to Asian markets. For Middle Eastern producers, the episode is a reminder that market share cannot be taken for granted when geopolitical tensions disrupt trade flows. The key question now is whether these shifts unwind once conditions normalize or evolve into a longer-term diversification of Japan’s supply portfolio.

- SIDE DEVELOPMENT:

- Japanese tanker returns from Persian Gulf

- (Japan NRG, May 29)

- The tanker Idemitsu Maru became the first Japanese-linked vessel to return to Japan via the Strait of Hormuz since the outbreak of the U.S.-Israel-Iran conflict, delivering approximately 2 million barrels of Saudi crude oil.

- The vessel had remained in the Persian Gulf for roughly two months due to security concerns. Reports indicate that dozens of Japanese-linked ships remain in the region awaiting safer transit conditions.

- SIDE DEVELOPMENT:

- Ruling party executive calls for review of gasoline subsidy

- (Japan NRG, May 29)

- Acting secretary-general of the LDP Hagiuda Koichi said a review of the subsidy aimed at keeping regular gasoline prices around ¥170/ liter is necessary.

- He said there’s growing support within the party and govt for such a review because of the financial strain it’s placing on the national budget.

- He proposed moving away from a uniform subsidy toward a more targeted system. It should focus on essential workers involved in public transport and social functions.

Govt approves emergency spending ¥513 bln to subsidize electricity, gas bills

(News NNN/ Jiji Press, Cabinet Office, May 26)

- The govt approved spending ¥513.5 billion from its emergency reserve fund to help offset rising energy costs caused by the Middle East conflict.

- The money will subsidize electricity and city gas bills from July to Sept 2026.

- For a typical household, the subsidies will reduce costs by about ¥5,000 over those three months. Subsidy details:

- Electricity: ¥3.5/ kWh discount in July and Sept; ¥4.5/ kWh in August.

- City gas: ¥14/ m3 discount in July and Sept; ¥18/ m3 in August.

- Next week, the govt will submit a supplementary budget of about ¥3 trillion to replenish reserve funds; create a special fund for Middle East-related crises; prepare for continued gasoline subsidies; and include separate support for LP gas costs.

Govt introduces new energy efficiency regulatory scheme for water heaters

(Government statement, May 22)

- ANRE proposed a new regulatory framework to promote energy-efficient and non-fossil fuel water heaters in Japan.

- Starting FY2034, the scheme will introduce a top-runner standard for manufacturers and importers to expand the adoption of high-efficiency systems such as heat pump water heaters, hybrid systems, and residential fuel cells.

- CONTEXT: The residential sector accounts for about 15% of Japan’s final energy consumption, and water heating represents around 30% of household energy use. Therefore, the govt intends to prioritize energy efficiency improvements and decarbonization for the water heaters.

MORGENROT raises funding for sustainable AI data centers

(Company statement, May 21)

- MORGENROT, a startup focused on AI data centers, raised ¥150 million from Mitsubishi HC Capital and SB C&S, bringing total Series B funding to ¥1.25 billion.

- The startup develops tech that optimizes and virtualizes GPU resources for AI.

- Mitsubishi HC Capital will help with AI infrastructure using renewable power. SB C&S will test MORGENROT’s GPU platform “TailorNode”.

- CONTEXT: SB C&S is a wholly-owned subsidiary of SoftBank Corp and operates as a major IT valueadded distributor and manufacturer in Japan.

- TAKEAWAY: The investment highlights growing interest in expanding Japan’s domestic AI infrastructure. As AI deployment accelerates, attention is shifting from model development toward the practical challenges of securing computing capacity, electricity supply, and financing. MORGENROT’s approach aims to improve utilization of existing GPU resources while supporting the development of more energy-efficient AI infrastructure.

Asuene adds functions to help companies streamline sustainability reporting

(Company statement, May 26)

- Climate-tech firm Asuene expanded the capabilities of its carbon footprint management cloud platform “ASUENE,” with new system features designed to streamline corporate compliance with the Sustainability Standards Board of Japan (SSBJ) disclosure requirements.

- The platform, using advanced AI automation and high-resolution data tracking, claims it could reduce the administrative burden of SSBJ compliance by up to 90%.

- The upgrades have three critical functions addressing bottlenecks in sustainability reporting:

- AI-assisted document drafts: By uploading existing company files, such as securities reports, the platform will extract data and analyze climate-related impacts and risks.

- AI financial impact calculation: This feature bridges the gap between environmental data and corporate finance by using a company’s emissions, reduction targets, and Internal Carbon Pricing (ICP) to simulate future carbon tax liabilities.

- Hourly electricity data integration: The platform can sync with 30-minute interval utility data to track real-time power consumption and renewable energy usage.

- CONTEXT: SSBJ standards are Japan’s official framework for corporate ESG reporting. Aligned with global ISSB standards, they require large listed companies to disclose specific environmental, social, and governance risks, such as climate change strategies, GHG emissions, and governance structures in financial filings.

- TAKEAWAY: By translating GHG emissions directly into future financial risks, this will help transform regulatory compliance into a strategic tool for CFOs and global investors looking for rigorous climate transparency.

NEWS: ELECTRICITY MARKETS

JEPX releases latest NFC auction results

(Organization statement, May 22)

- Results of the FY2025 fourth-round NFC auction were released by JEPX.

- All available non-FIT NFCs without renewable attributes (i.e. nuclear) and non-FIT NFCs with renewable attributes were contracted, indicating continued tight supply in both markets. Prices for both reached the upper limit of ¥1.3/ kWh.

- Contracted volume for non-FIT NFCs without renewable attributes reached about 2.0 TWh, roughly double the previous round, while volume for non-FIT NFCs with renewable attributes rose about 28% to 1.05 TWh.

- Purchase bid volume for non-FIT NFCs without renewable attributes totaled about 3.7 TWh, exceeding available supply by nearly twofold. Demand for non-FIT renewable NFCs remained above supply despite a decline from the previous round.

- In the FIT NFC auction, contracted volume fell 5% to about 18.0 TWh. The average contract price was ¥0.44/ kWh, while the highest contract price remained at ¥4.00/ kWh.

- TAKEAWAY: The auction again highlighted the contrast between Japan’s NFC markets. Non-FIT certificates remained supply-constrained, with all available volumes sold and demand exceeding supply in both renewable and non-renewable categories. By contrast, the FIT NFC market remained heavily oversupplied, with only around 22% of offered volumes contracted despite unchanged maximum prices. The results suggest that buyers continue to place a premium on scarce non-FIT certificates while abundant FIT certificates face persistent downward pressure on pricing.

- SIDE DEVELOPMENT:

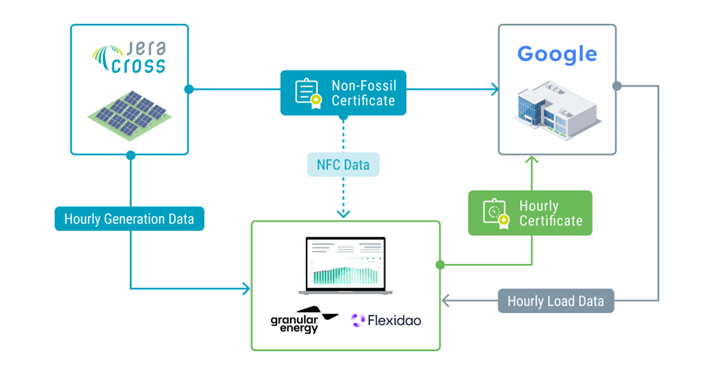

- JERA Cross completes demo of green certificates providing hourly matching

- (Company statement, May 26)

- JERA Cross completed a demonstration of granular certificates based on the Granular Scheme Standard, which tracks renewable energy generation and consumption on an hourly basis.

- CONTEXT: Developed by UK-based EnergyTag, the Granular Scheme Standard enables companies to match electricity consumption with renewable generation on an hourly basis rather than annually or monthly. The approach is increasingly viewed as a more rigorous method of demonstrating actual decarbonization.

- Using NFCs and solar power supplied by JERA Cross, the demo used the certificates to track hourly alignment between electricity demand and renewables generation.

- TAKEAWAY: The demo reflects a potential shift in voluntary carbon and renewable energy markets toward measuring the quality – not just the quantity – of renewables procurement. While annual matching remains the dominant standard in Japan, hourly matching could emerge as a premium product for large corporates seeking more credible decarbonization claims and alignment with evolving international reporting frameworks. However, there are several operational constraints that push up the cost of increasing the frequency of matching.

OCCTO plans capacity market reforms to prevent plant retirements

(Denki Shimbun, May 29)

- OCCTO plans to increase procurement volumes in the capacity market’s main auction, citing concerns that power plant retirements could outpace new capacity additions.

- Under the current system, 2% of forecast peak demand (H3 demand) is withheld from the main auction and procured later through an additional auction held one year before delivery. OCCTO now proposes procuring the full amount in the main auction instead.

- The proposal follows analysis showing that around 3% of capacity procured in past auctions has exited the market before the delivery year. OCCTO warned that continued retirements could make it difficult to secure sufficient capacity through the current framework.

- OCCTO also proposes raising the bidding cap for dispatchable resources in the main auction to 5% of H3 demand from the current 4%, reflecting strong participation from such resources in recent auctions.

- CONTEXT: Japan’s capacity market secures supply four years ahead of delivery through a main auction, with additional auctions held closer to the delivery year to replace capacity lost through retirements or other market exits.

- TAKEAWAY: The proposed changes reflect growing METI concern that thermal power plant retirements are accelerating as operators face aging fleets, decarbonization pressures, and uncertain profitability. By procuring more capacity earlier, OCCTO hopes to reduce the risk of supply shortages and improve investment visibility for generators.

OCCTO reports on cross-regional grid development plans

(Agency statement, May 22)

- OCCTO reported on the major cross-regional transmission reinforcement projects as of Q1 of FY2025.

- The five projects cover the following interconnections: Tokyo–Chubu (+900 MW), Tohoku–Tokyo (+4.55 GW), Hokkaido–Honshu (+300 MW), Chubu–Kansai (+3 GW), and Chugoku–Kyushu (+1 GW).

- Most projects are on schedule, but the Tokyo–Chubu project faces a delay, with final operation now expected in or after March 2030 (changed from December 2028).

- The report also notes that estimated construction costs rose for some projects, especially the Tokyo– Chubu and Tohoku–Tokyo interconnections.

- CONTEXT: OCCTO reports on the progress of cross-regional grid development plans are quarterly. The delay in the Tokyo–Chubu interconnection is due to prolonged land negotiations for the Sakuma Higashi transmission line reinforcement project, a key bottleneck. The delay was exacerbated by heavy rain damage in April 2024.

- TAKEAWAY: Cross-regional transmission reinforcement projects are vital for bridging the gap between remote renewable energy production hubs, such as Hokkaido and Tohoku, and major energy demand centers such as Tokyo. These upgrades prevent green energy waste, strengthen disaster resilience, and support the nation’s decarbonization goals. OCCTO’s quarterly reporting on the progress of development plans is important not simply for sharing construction updates, but for ensuring the stability of the overall power system, investment predictability, and the effective implementation of energy policies.

- SIDE DEVELOPMENT:

- OCCTO evaluates Hokkaido-Honshu HVDC interconnection Japan Sea route

- (Agency statement, May 22)

- OCCTO evaluated the cross-regional grid enhancement plan for a new HVDC interconnection route between Hokkaido and Honshu via the Sea of Japan route. o It concluded that a multi-terminal HVDC configuration without DC circuit breakers is technically feasible and preferable due to lower construction costs, shorter construction time, and improved resilience against AC system faults.

- The plan also includes reinforcement of the Shiribeshi transmission line and installation of grid stabilization systems in Hokkaido and Tohoku to address blackout and frequency stability risks associated with HVDC outages.

- CONTEXT: The qualified operators – Hokkaido Electric Power Network, Tohoku Electric Power Network, TEPCO Power Grid, and J-POWER Transmission Network – are continuing to examine the implementation plan for this project. Although the original deadline for submitting the plan was December 26, 2025, it was extended by one year to allow the utilities to address financing and other challenges.

- TAKEAWAY: The adoption of a multi-terminal HVDC system indicates growing confidence in advanced HVDC technologies and could influence future transmission projects in Japan.

Kyushu Grid to cut solar curtailment with near real-time control

(Company statement, Denki Shimbun, May 27)

- Kyushu Electric Power Transmission and Distribution will introduce a new curtailment system for extra-high-voltage renewable generators from 1 June, allowing output control decisions to be made 15–30 minutes ahead of actual conditions rather than based on forecasts one to two hours in advance.

- The utility expects the new approach, the first of its kind in Japan, to reduce annual renewable curtailment by several percent. It will initially focus on solar power, which accounts for 12.61 GW of installed capacity in Kyushu as of September 2025.

- Kyushu curtailed around 750 GWh of renewable generation in FY2024, equivalent to a 4.8% curtailment rate. The new system will incorporate near real-time weather and demand data to determine the minimum level of output restrictions required.

- The utility has also begun operating a new transmission-disconnection system that allows greater power exports from Kyushu to Chugoku via the Kanmon interconnector. The system now includes variable renewable generation in its control calculations and has increased transfer capability by up to 300 MW.

- TAKEAWAY: Kyushu remains Japan’s most advanced region for renewable curtailment management because of its exceptionally high solar penetration and frequent oversupply conditions. The move reflects a broader shift from blunt curtailment measures toward more sophisticated real-time grid management, allowing more renewable electricity to remain on the system without compromising reliability. If successful, similar systems could eventually be expanded to lower-voltage solar installations and adopted by other transmission operators facing growing curtailment volumes.

Hokuriku Electric gas rationing at Toyama Shinko plant while planning a new unit

(Japan NRG, May 28)

- Hokuriku Electric is preparing to build a new LNG-fired Unit 2 (630 MW) at the Toyama Shinko power plant, targeting the start of operations in FY2033.

- The unit will use combined-cycle technology incorporating both gas and steam turbines and is expected to achieve a generation efficiency of 64%, among the highest levels in the industry. Compared with conventional coal-fired generation, the facility could reduce CO2 emissions by roughly 2 Mtpa.

- The plant currently relies on a single LNG storage tank, requiring the company to manage generation output around fuel inventory levels and LNG delivery schedules.

- CONTEXT: Hokuriku Electric procures LNG from a single supplier in Malaysia. The new unit would more than double the utility’s LNG requirements, prompting the company to explore alternative procurement options. One possibility is a “tankless” arrangement under which LNG would be supplied via pipelines connected to third-party storage facilities, including INPEX’s terminal in Niigata. LNG must be stored at approximately -162°C, resulting in boil-off gas over time. Reducing on-site storage requirements could help lower associated operational costs and fuel losses.

- TAKEAWAY: The project illustrates how Japanese utilities are attempting to balance energy security, decarbonization, and affordability. While the new LNG unit would significantly reduce emissions compared with coal-fired generation and improve efficiency, Hokuriku Electric is also preserving the option of future hydrogen use by reserving space for related infrastructure. At the same time, the utility continues to pursue renewables expansion and seeks the restart of Shika NPP Unit 2, highlighting a broader strategy of combining LNG, renewables, and nuclear power rather than relying on a single pathway.

Osaka Gas jumps to No. 2 ‘new entrant’ power retailer; SB Power also gains

(PPS Net, May 27)

- Osaka Gas expanded electricity sales 52% MoM to 865 GWh in January, gaining in the nationwide rankings. It rose to be the second-largest retailer among shin denryoku, or new market entrants, and 11th overall.

- Tokyo Gas remained the top ‘new entrant’ with 1.52 TWh sold. SB power was the other big mover, jumping from 10th to fifth.

- CONTEXT: TEPCO remains Japan’s biggest seller of electricity, via TEPCO Energy Partner unit that sells ten times the volume of Tokyo Gas. Kansai and Chubu Electric are the other dominant retailers. The EPCOs, apart from Okinawa Electric, make up the first nine places in power sales rankings, with Tokyo Gas completing the top 10.

NEWS: HYDROGEN

PM Takaichi cites Middle East crisis to promote hydrogen and ammonia

(Nikkei, May 29)

- PM Takaichi said Japan should turn the current Middle East crisis into an opportunity by expanding its energy options, including hydrogen and ammonia.

- The remarks came during a meeting with governors involved in hydrogen-related initiatives, including Tokyo Governor Koike and Aichi Governor Omura. The governors submitted proposals calling for a stronger investment environment for hydrogen projects.

- Koike stressed the importance of energy policy from a national security perspective, while Omura said the prime minister expressed support for broadening Japan’s energy sources in response to geopolitical risks.

- TAKEAWAY: The meeting did not produce new policy measures, but it illustrates how energy security is increasingly being used alongside decarbonization as a justification for hydrogen and ammonia development. As concerns over Middle Eastern supply disruptions grow, proponents of alternative fuels are seeking to position hydrogen not only as a climate solution but also as a strategic tool for reducing Japan’s dependence on imported fossil fuels.

NEWS: SOLAR AND BATTERIES

Sumitomo to invest in almost 700 MW of BESS in the UK

(Company statement, May 27)

- Trading house Sumitomo and Taiwan-based TPK HD invested in Summit Transition Partners, and agreed with local partner Gresham House Energy Storage Fund to develop five large-scale BESS projects in the UK, totaling 694 MW of installed capacity.

- The projects are:

- Elland 2: 100 MW / 200 MWh

- Cockenzie: 240 MW / 480 MWh

- Monet’s Garden: 57 MW / 114 MWh

- Lister Drive: 57 MW / 114 MWh

- Ocker Hill: 240 MW / 480 MWh.

- CONTEXT : Gresham House Energy Storage Fund’s track record of about 1 GW of BESS represents around 15% of the UK’s installed BESS capacity (about 7 GW).

- SIDE DEVELOPMENT:

- CEC secures ¥19.5 Bln for non-FIT solar plants across Japan under off-site CPPAs

- (Company statement, May 28)

- Clean Energy Connect (CEC), a Japanese clean energy service provider, secured ¥19.5 billion in project finance from SBI Shinsei Bank to develop roughly 1,600 non-FIT, smallscale solar power plants across Japan under off-site corporate PPAs.

- Bringing CEC’s cumulative funding to ¥80.6 billion, the initiative will generate 146 GWh of green electricity annually.

- TAKEAWAY: This project offers tech giants and major corporations like Google and Amazon a fast, scalable way to meet their RE100 mandates by utilizing scattered, abandoned farmlands. The project builds entirely new, subsidy-free generation capacity, providing crucial “additionality” to Japan’s power grid while advancing the infrastructure needed for real-time, 24/7 carbon-free energy tracking.

Shizen Connect raises ¥2.7 billion to expand VPP business

(Company statement, May 25)

- Shizen Connect raised ¥2.7 billion in a third-party allotment of new shares as part of its Series A round, and agreed with six companies to expand its VPP business.

- Fundraising resulted in 10 new shareholders, bringing total funding to ¥3.26 billion.

- Partner companies will use Shizen Connect’s platform for the following:

| Facilities aggregated in VPPs | Large electricity and gas companies | Manufacturers, IT companies, real estate, transport operators |

| Grid-scale BESS | Osaka Gas, Tokyo Gas, Shikoku Electric, Hokuriku Electric, JERA | Shin Nippon Air Technologies, Tokyu Fudosan, Nishi-Nippon Railroad, Biprogy, unnamed company |

| Residential DR and BESS, EVs, EcoCute* | Osaka Gas, Kyushu Electric, Shikoku Electric, Hokuriku Electric, Hokkaido Electric, Tokyo Gas | Daikin, Panasonic |

| Commercial and industrial BESS | JERA | Nishi-Nippon Railroad, unnamed company |

| BESS for datacenters | JERA | Tokyu Fudosan |

| EV buses | Shikoku Electric | Nishi-Nippon Railroad |

*heat pump and water heating system

- CONTEXT: According to ANRE, cumulative BESS installations are expected to reach a total of 50 GWh by 2030, equivalent to 8.5% of households’ daily electricity demand. This estimate includes 14.1–23.8 GWh of grid-scale storage, 24 GWh of residential storage, and 2.9 GWh of commercial and industrial BESS. This highlights the importance of VPPs to integrate distributed BESS assets.

- SIDE DEVELOPMENT:

- ENEOS Power chooses Shizen Connect’s DR services in BESS

- (Company statement, May 28)

- ENEOS Power chose Shizen Connect’s device-controlled DR (demand-response) service for their FIT installation plan campaign for residential BESS.

- Via cloud-based remote control of residential BESS, ENEOS will use the service for:

- DR control during periods of power supply-demand balance

- DR control to boost electricity consumption at times of surplus power generation.

- This brings the combined market share of electricity retailers using Shizen Connect’s platform to about 38%.

Manoa Energy sells three battery storage projects in Japan

(Company statement, May 29)

- Manoa Energy announced the sale of three high-voltage BESS projects in Japan, including two in Kyushu and one in the Kansai region.

- The company did not disclose the buyer, project capacities, transaction value, or development stage. Manoa said the deal strengthens its track record in originating, developing, constructing, and selling high-voltage battery assets.

- CONTEXT: Manoa is backed by Hong Kong-based infrastructure investor Brawn Capital and is developing roughly 1 GW of battery storage projects across Japan. The company brought its first extrahigh-voltage standalone BESS project, the 50 MW / 104 MWh Helios facility in Hokkaido, into commercial operation in December 2025.

- CONTEXT: Brawn Capital has previously indicated that it intends to recycle capital through partial or full divestments of completed storage assets while continuing to expand its Japanese development pipeline. A majority stake in the Helios project was sold earlier to Taiwan’s HD Renewable Energy.

- TAKEAWAY: The transaction is another sign that the grid-scale battery market is maturing from pure development into an active asset trading and capital recycling market. Developers increasingly aim to originate projects, secure grid connections and permits, and then sell them to infrastructure investors, utilities, or longterm asset owners. Kyushu remains among the most attractive regions for battery investment because of renewable curtailment risks, volatile power prices, and growing opportunities in balancing, capacity, and wholesale power markets.

Nippon Electric Glass develops ultra-thin cover for satellite solar panels

(Company statement, May 20)

- Nippon Electric Glass launched “Starveil,” a new brand of ultra-thin cover glass designed for satellites and space equipment.

- The glass is light, UV-resistant, and aims to protect sensitive space hardware such as satellite solar panels while reducing weight and improving durability.

- NEG is a world leading specialty glass producer, supplying advanced materials for chips, displays, electronics and energy applications.

- The firm had ¥311 billion in revenue in FY2025.

- TAKEAWAY: This news shows that Japan is expanding into the commercial space industry through advanced materials manufacturing. As satellite launches and space infrastructure demand increase globally, specialized components like radiation- and UV-resistant glass are crucial. The move also reveals how traditional industrial companies are repositioning toward high-growth sectors such as aerospace, semiconductors, and advanced energy tech.

Tokyo Gas to include CSCs in PPA offer (Company statement, May 26)

- Tokyo Gas unveiled a construction method for installing CSCs on building walls.

- It’s doing a field test at an artificial light-based plant operated by Green Factory TFK, a subsidiary of Tokyo Fudosan.

- The company aims to incorporate wall-installed CSCs into its “Hinatao Solar” offer.

- CONTEXT: “Hinatao Solar” is a solar PPA service enabling customers to install solar PV systems without upfront costs. Until now, installations had been limited to rooftops. CSCs are provided by PXP.

- SIDE DEVELOPMENT:

- JFE Engineering and partners launch solar PPA using CSCs

- (Company statement, May 27)

- JFE Engineering, Urban Energy and Tokyo Century launched a solar PPA service in Myoko (Niigata Pref).

- CSCs have been installed on the city’s household waste management center to supply public buildings until 2028.

- TAKEAWAY: So far, PXP’s CSCs have been used in field tests only; their integration into a commercial PPA service is a major breakthrough. Tokyo Gas and companies in Myoko chose these cells for their flexibility, a wide range of possible installation methods, and the fact they don’t require ground-mounted structures, thus reducing costs and installation complexity.

Nippon Fine Chemical launches new HTM for inverted PSCs

(Company statement, May 28)

- Nippon Fine Chemical developed and launched the Spirokite™-TTB (of Spiro-TTB), a new hole transport material specifically designed for inverted-structure PSCs.

- The new material allows the firm to expand its business into inverted-structure cells and next-gen PCS/ silicon tandem cells.

- CONTEXT: When sunlight hits the perovskite layer, it generates electrons (negative charges) and “holes” (positive charges). A Hole Transport Material (HTM) is a crucial chemical layer responsible for smoothly extracting and moving those positive charges to the electrical contact to generate electricity. PSCs come in two architectures: regular (n-i-p) and inverted (p-i-n). Spiro-TTB is specifically engineered for the inverted structure, where the layers are stacked in the reverse order compared to traditional cells.

- TAKEAWAY: The inverted structure is preferred when building PCS/ silicon tandem cells, which stack PSC directly on top of a traditional silicon cell to capture different wavelengths of light. Tandem cells are the holy grail of next-gen solar tech as they can exceed the efficiency limits of standard silicon panels. Nippon Fine Chemical’s new material also directly supports production of longer-lasting, commercially viable perovskite panels. Overall, the tech may help Japan secure a domestic, high-quality supply of advanced chemical materials, vital for the tech’s deployment. This would mean Japan’s solar manufacturers could have a reliable, specialized supplier for major types of perovskite structures, which is crucial for PSC’s commercialization.

Kyushu Electric Group launches one-stop service for used solar panels

(Company statement, May 27)

- Five companies from the Kyushu Electric group launched a new one-stop service for handling used solar panels – from removal and transportation to reuse and recycling.

- This will allow solar power operators to avoid coordinating with multiple contractors.

- The service applies to ground-mounted commercial solar panels (10kW or larger) within Kyushu and Yamaguchi Pref. Expansion of coverage is planned in the future.

JR West launches Japan’s first railway-backed residential solar program

(Company statement, May 25)

- JR West, which operates in western Honshu, and renewables firm Hachidori Solar launched Japan’s first railway-backed residential solar program, providing solar and battery systems with zero upfront cost.

- The service is available across Hiroshima, Yamaguchi, and Okayama prefs.

- This initiative aims to transform local homes into “micro-power plants,” building a decentralized energy infrastructure across regional Japan.

- CONTEXT: Hachidori Solar offers climate-tech, and zero-initial-cost rooftop solar panel and battery storage services for households and businesses.

- TAKEAWAY: The partnership is significant as it scales green energy from individual homes to entire communities by leveraging JR West’s massive regional network and trusted brand. By driving energy self-sufficiency in areas with limited local subsidies, it directly shields households from rising electricity costs, strengthens disaster resilience along railway lines, and acts as a blueprint for local economic sustainability.

Q.ENEST launches aggregator of BESS

(Company statement, May 22)

- Q.ENEST launched an aggregation service for BESS.

- As its first project, the firm began aggregating its own 2 MW / 8 MWh BESS station in Sano (Tochigi Pref) to optimize its AI platform and control of battery charge/discharge.

- In cooperation with its partner Hanwha Japan, Q.ENEST will:

- operate across three electricity markets (capacity, balancing, and wholesale);

- assist with offtake and tolling based on its track record with 100 MW of capacity;

- cooperate with battery, PCS, and EMS manufacturers.

- TAKEAWAY: This decision illustrates a trend in which battery manufacturers and operators are launching in-house aggregation services. PowerX also embraced this strategy.

XSOL launches guarantee service for residential solar systems

(Company statement, May 22)

- XSOL, a Japanese solar system provider, launched a performance guarantee service for residential PV installations. The scheme compensates homeowners if actual electricity generation falls below the company’s projected output under specified conditions.

- The guarantee applies to solar systems designed and sold by XSOL and provides coverage for five years, with compensation of up to ¥3 million. Coverage primarily relates to equipment defects, design errors, or installation issues, and excludes factors such as natural disasters and weather-related fluctuations in solar irradiation.

- XSOL supplies solar and battery storage systems for residential and commercial customers across Japan.

- TAKEAWAY: The new service addresses a key barrier to residential solar adoption: uncertainty over whether a system will perform as promised. By assuming part of the performance risk, XSOL is effectively backing its own engineering and installation quality. The move reflects growing competition in the residential solar market, where providers are increasingly differentiating themselves through warranties, guarantees, financing packages, and integrated battery offerings rather than panel hardware alone.

NEXTES obtains fire-resistance certification for lithium-ion battery packs

(Company statement, May 27)

- NEXTES obtained a fire-resistance certification for its lithium-ion battery pack.

- Granted by the Hazardous Materials Safety Techniques Association, the certification indicates that the battery pack demonstrates enhanced fire safety performance.

- TAKEAWAY: Fire safety remains a critical consideration for grid-scale battery projects, particularly in the EHV segment where installations are becoming larger and more concentrated. Independent certification can provide additional assurance to project developers and stakeholders regarding system safety.

NEWS: WIND POWER AND OTHER RENEWABLES

Cosmo Eco Power and NSE introduce PPA deals for FIP-transitioned wind farms

(Company statement, May 28)

- Cosmo Eco Power, a subsidiary of Cosmo Energy, and Nippon Steel Engineering have developed and launched a new off-site PPA scheme using multiple onshore wind farms that transitioned to the FIP.

- By combining three different wind farms located across Aomori, Yamagata and Akita prefs, including one self-operated by Cosmo Eco Power and two externally aggregated, the scheme mitigates the inherent volatility of wind energy.

- This blending improves the hourly matching ratio, aligning electricity consumption with green generation on an hourly basis.

- Cosmo Eco Power acts as the aggregator to secure the wind power, while Nippon Steel Engineering leverages its experience to manage the wheeling and retail supply.

- The end-consumer is Kioxia Iwate, which will receive this power at its facility in Kitakami City. During hours when wind generation falls short of demand, Nippon Steel Engineering will bridge the gap using market-sourced electricity enhanced with wind-derived non-fossil certificates.

In Japan’s first, Shimizu develops recycling tech for wind turbines

(Company statement, May 25)

- Shimizu Corp, one of Japan’s five biggest general contractors, said it developed the country’s first chemical recycling tech for used wind turbine blades.

- Together with industrial waste disposal firm Otaki Shoten, Shimizu created a process that crushes discarded blades, recycling them into agents used in steel making.

- It aims to reduce environmental impact compared with landfill disposal or thermal recycling, both of which are huge CO2 emitting processes.

- The recycled material can replace limited resources such as coke used in steelmaking.

- The firm plans to propose recycling and disposal solutions for aging wind turbines and to capture around ¥20 billion/ year in wind power-related orders, including both new construction and replacement projects.

- TAKEAWAY: Since wind turbine blades are made from difficult-to-recycle composite materials such as fiberglass- or carbon-fiber-reinforced plastics, disposal is a major issue; aging wind turbines will need to be replaced from the 2030s. The issue has gained additional attention following recent wind turbine blade accidents in Akita Pref, including a fatal 2025 incident in Akita City.

Obayashi receives ClassNK for hybrid steel-concrete TLP for floating wind tech

(Company statement, May 25)

- Obayashi, one of Japan’s five major construction firms, received Approval in Principle from ClassNK for a hybrid steel-concrete TLP (Tension Leg Platform) floating offshore wind support structure.

- This is the first such certification globally for such a hybrid design.

- CONTEXT: The project is part of a govt-backed program led by NEDO to accelerate next-gen floating offshore wind tech.

- The TLP design uses tensioned mooring lines to stabilize the floating platform. This improves power generation efficiency and reduces ocean area usage compared with conventional floating wind systems.

- Obayashi estimates 25% lower construction costs versus steel semi-submersible designs, 8% higher power generation efficiency, and reduced impact on fisheries due to a smaller mooring footprint.

- By 2028, the firm aims to conduct real-sea demo testing with an installed turbine.

Panasonic partners with German firm in cybersecurity database for renewables

(Company statement, May 25)

- Panasonic HD and German computer science company Fraunhofer developed a database to visualize the impact of cyberattacks on renewable energy systems.

- The platform, “Data4Cyber”, synchronizes empirical data, analyzes the impact of cyberattacks on energy systems, and builds plausible attack scenarios (fraudulent price signals, falsified equipment commands, etc.).

- The database compiles:

- telecom data, such as IoT messages;

- control data, such as EMS data;

- physical process data, such as solar power generation levels or battery state-of-charge data.

- Potential customers include electricity companies, equipment manufacturers, cybersecurity companies, and research institutions.

- TAKEAWAY: This news echoes the recent launch of JC-STAR. Beyond its primary use for day-to-day monitoring, this type of solution may also help simulate cyberattacks on equipment and assess system resilience, supporting compliance and certification processes.

TEPCO RP resumes operation of Minakami hydro plant after upgrade

- TEPCO Renewable Power resumed commercial operation of the Minakami Hydropower Station, Gunma Pref, after a large-scale modernization.

- The power station had been offline since July 2023.

- The station’s main equipment is installed underground and can generate up to 19 MW using a max water flow of 16.7 cubic meters per second.

- CONTEXT: Built in 1953 as part of Japan’s postwar hydroelectric development, the plant is a run-ofriver hydroelectric facility. Along with the nearby Fujiwara Power Station, it plays a role in regulated water releases along the Tone River system.

NEWS: NUCLEAR ENERGY

Osaka court rules in favor of the govt in Ohi NPP case

(NHK, May 28)

- In a lawsuit over the operating license for KEPCO’s Ohi NPP Units 3 and 4, the Osaka High Court ruled in favor of the govt.

- It overturned a 2020 district court decision that ordered the revocation of the reactor installation permit.

- Residents argued the plant lacks sufficient safety features. The case centered on the “reference seismic ground motion” used in the plant’s earthquake design.

- The govt argued that post-Fukushima safety standards account for uncertainties in fault evaluations.

- CONTEXT: Unit 3 is currently operating, while Unit 4 halted for routine inspection; it will restart commercial operation in late June.

Idemitsu Kosan invests in U.S. fusion power startup

(Company statement, May 28)

- Idemitsu Kosan invested in Thea Energy, a U.S. startup for fusion power that uses a unique stellarator device.

- The investment aims to acquire early-stage knowledge on technology and commercialization.

- CONTEXT: Thea Energy is a spin-off from Princeton University’s Plasma Physics Laboratory. It uses planar electromagnetic coils and digital twin control to simplify stellarator design, reducing cost and maintenance complexity. The company plans a demo unit after 2027.

NRA plans penalties for false applications during safety reviews

(Nikkei, May 27)

- The NRA plans to introduce penalties for false applications by operators during safety reviews for NPPs. It seeks to revise the Reactor Regulation Act by 2027, allowing criminal complaints for malicious cases.

- At the moment, falsified documents only result in inspections, rejection of the application, or extra checks.

- The NRA says detecting intentional fraud is difficult. Stronger deterrence is essential.

- CONTEXT: This decision follows an incident involving Chubu Electric when it falsified seismic data in the review for restarting the Hamaoka plant. Six on-site inspections were made at Chubu Electric’s main office. The full picture remains unclear as the utility’s third-party committee has not yet released its report. Still, the penalties won’t apply to Chubu Electric’s incident.

NEWS: TRADITIONAL FUELS

Chiyoda resumes construction at Qatari LNG plant

(Nikkei, May 25)

- Chiyoda Corp resumed construction at its North Field East (NFE) LNG plant in Qatar, a JV with French company Technip Energies.

- This is Chiyoda’s largest project, expected to produce 32 Mtpa LNG. After the U.S./ Iran ceasefire in early April, companies are returning to the region.

- CONTEXT: In mid March, Chiyoda evacuated 160 expatriates. A missile attack on the Ras Laffan Industrial City on March 18 caused no damage to the staff or facilities. With new safety measures in place, Chiyoda wants all its expat workers back on site by May. Other Japanese firms, such as Sojitz, are bringing back personnel.

Woodside Energy likely to block INPEX’s effort to take a stake in Browse LNG

(Japan NRG, May 26)

- Woodside Energy is likely to exercise its pre-emptive rights to block PetroChina’s sale of its 10.67% stake in the Browse LNG project to INPEX.

- CEO Liz Westcott confirmed that Woodside is evaluating whether to intervene and could match INPEX’s bid.

- Woodside operates Browse and already holds a 30.6% share.

- CONTEXT: INPEX struck a deal on May 20 to buy PetroChina’s stake in Browse, Australia’s largest undeveloped gas resource, with 14 trillion cubic feet of gas. It could cost $35 billion to develop.

- TAKEAWAY: There is potential for a conflict over where to process the gas. As supply from existing fields diminishes, Browse gas resources should serve as backfill for the North West Shelf LNG facility that Woodside operates. But, analysts speculate that if INPEX finalizes the deal, it may instead try to route the gas to its own Ichthys LNG plant in Darwin. By stepping in to block the sale, Woodside would cut the threat of gas redirection.

- SIDE DEVELOPMENT:

- Unions call off planned strike at INPEX’s Ichthys LNG facility

- (Reuters, May 26)

- Unions called off a planned strike at INPEX’s Ichthys LNG facility in Darwin Australia.

- The Australian union Offshore Alliance had served the Japanese gas giant with a strike notice. They demanded wage increases and higher allowances.

- TAKEAWAY: Australia is Japan’s largest supplier of LNG. Disruption at the 9.3-million-metric-ton Ichthys facility would be particularly damaging right now. Japan is facing a potential energy supply crunch due to the effects of the Iran war and the upcoming summer demand.

JGC and Honeywell cooperate on FLNG standardization

(Company statement, May 26)

- JGC Holdings and Honeywell will collaborate on floating LNG, to work on a standardized design package for production, storage, and offloading facilities.

- FLNG facilities are often custom-designed to match customer demands. While this approach addresses unique conditions, it extends project schedules and raises costs.

- By relying on standard specifications, post-order engineering work becomes shorter. The new package could cut the time from order to delivery by more than one year.

Taiyo Oil and Nagasaki Kogyo to convert waste plastics into oil and chemicals

(Company statement, May 26)

- Taiyo Oil and Nagasaki Kogyo will convert waste plastics into usable oil that will be processed into chemical raw materials to make home appliances and automobile parts.

- The processing will begin in FY2027, and it will annually handle 800 tons of business-discharged waste plastic.

- TAKEAWAY: This method allows reuse of waste plastics before they’re too difficult to recycle, such as too dirty or containing mixed materials. The plan is to source raw materials from waste rather than relying on imported petroleum; hence, mitigate geopolitical risks and strengthen domestic economic security.

LNG stocks down from previous week, down YoY

(Government data, May 27)

- As of May 24, the LNG stocks of 10 power utilities were 1.95 Mt, down 4.4% from the previous week (2.04 Mt), down 15.9% from end May 2025 (2.32 Mt), and down 10.1% from the 5-year average of 2.17 Mt.

- For the past four weeks, LNG stocks were 8-16% lower (average 12%) YoY.

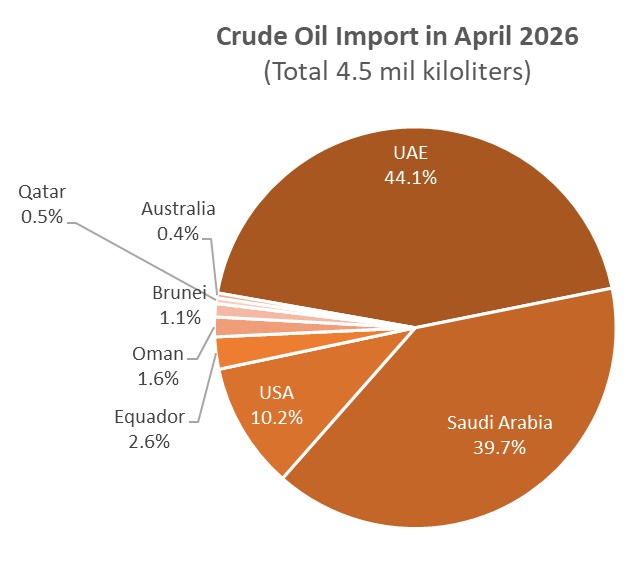

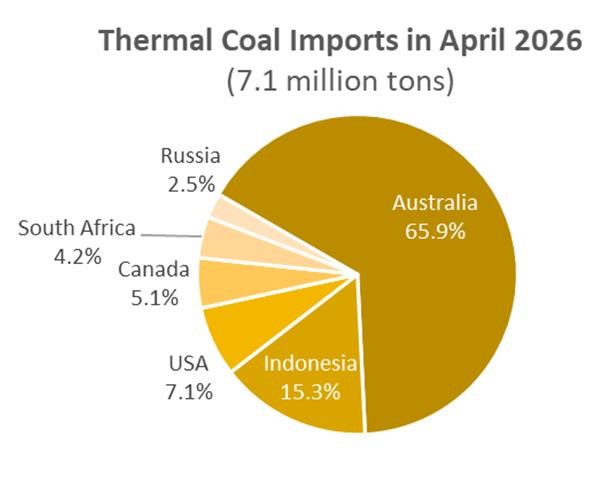

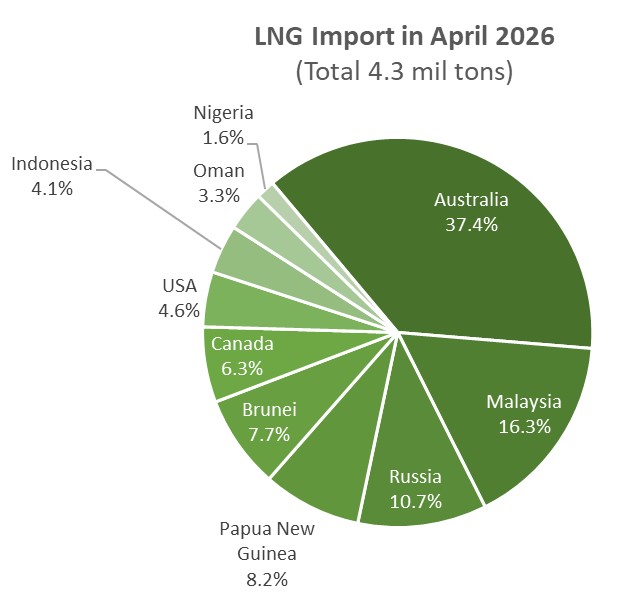

April Oil/ Gas/ Coal Trade Statistics

(Government data, May 28)

| Imports Volume YoY Value (Yen) YoY | ||||

| Crude oil | 4.5 million kiloliters (28.2 million barrels) | -63.7% | 454.3 billion | -50% |

| LNG | 4.3 million tons | -20.6% | 379.5 billion | -20.2% |

| Thermal coal | 7.1 million tons | -4.5% | 148.3 billion | 9.9% |

- As it takes about 40 days to transport crude oil from Middle Eastern countries to Japan, it has taken time for the hostilities at the Strait of Hormuz to be reflected in the imported volumes.

- In April, Japan received 4.5 million kiloliters of crude oil, down 63.7% YoY. The UAE and Saudi Arabia were still major suppliers, but their volumes (YoY) dropped 55.3% and 66.9%, respectively. Imports from Qatar dropped 92.5% MoM. Nearly 86% of crude oil came from Middle Eastern countries.

- LNG imports in April totaled 4.3 Mt, down 27.3% MoM (5.9 Mt) and down 20.6% YoY. About 75% of Japan’s LNG imports came from APAC. A small volume (3.3%) came from Oman, but none from UAE and Qatar. In spring, demand for LNG usually decreases as the heating season is over.

- Thermal coal imports decreased to 7.1 Mt, down 16.4% MoM, and down 4.5% YoY. Imports from Australia dropped 24.8%, but imports from Russia tripled but on small volumes (from roughly 59,000 to 187,000 tons). Both Canada and the U.S. also increased deliveries, but the impact was not significant. The yen-based price per ton increased to ¥20,877 for the month, up 7.4% MoM, and up 15% YoY.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Osaka Gas launches alliance for high-quality carbon credits

(Company statement, May 20)

- Osaka Gas and several partners launched the ARC Coalition, a new international alliance to expand the market for high-quality carbon credits.

- Members include Bain & Company, CATL, Mitsubishi Corp, and Tencent.

- The group aims to aggregate demand for carbon credits, especially in Asia, helping to finance early-stage climate projects that reduce emissions and support biodiversity.

- It also aims to improve transparency in the carbon credit market with stricter standards, and to help firms access carbon credits more easily.

- It targets procurement of more than 10 million tons of credits by 2030.

- TAKEAWAY: Japanese energy firms seek to shape the rules and financing structure of Asia’s carbon credit market. For Osaka Gas, this alliance supports efforts to offset emissions from continued LNG use while scaling lower-carbon fuels like e-methane and hydrogen. It also reflects Japan’s preference for market-based transition mechanisms rather than rapid fossil fuel phaseouts.

- SIDE DEVELOPMENT:

- Carbon credit firm Green Carbon for study in Thailand

- (Company statement, May 26)

- Green Carbon, a climate-tech company focused on nature-based carbon credits, signed an MoU with Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ).

- The partners will study the feasibility of applying Enhanced Rock Weathering (ERW) in Thailand’s agriculture sector, particularly rice farming. The research will assess scientific, environmental, and regulatory aspects of ERW, but is not intended to generate carbon credits or support commercial projects at this stage.

- The initiative forms part of GIZ’s climate-smart agriculture activities in Thailand and aims to support around 250,000 farmers through emissions reductions, lower agricultural input requirements, and reduced environmental impacts.

- CONTEXT: GIZ operates the “Thai Rice: Strengthening Climate-Smart Rice Farming” program with support from the Green Climate Fund (GCF), the world’s largest multilateral climate fund under the UN Framework Convention on Climate Change.

- TAKEAWAY: The project reflects growing interest in ERW as a potential carbon removal pathway in Asia, but remains at an early research stage. For Green Carbon, the study provides an opportunity to evaluate whether the technology can be deployed at scale in one of Southeast Asia’s largest agricultural regions.

Kamei and Euglena supply biofuel to vessels in Tokyo ports

(Company statement, May 21)

- Kamei and Euglena began supplying HVO (Hydrotreated Vegetable Oil) fuel to vessels in Keihin Ports.

- The fuel is supplied Ship-to-Ship (STS), whereby bunkering is carried out by vessel rather than directly at port facilities.

- CONTEXT: Keihin Ports refer to Yokohama and Kawasaki (Kanagawa Pref). The fuel, “Susteo”, is a 100% HVO biofuel produced from UCO and is a drop-in solution.

- TAKEAWAY: The supply arrangement brings HVO into Japan’s largest port cluster without requiring dedicated new infrastructure. By using STS bunkering, suppliers can test demand and operational procedures before committing to larger investments. Success in the Keihin area could provide a model for expanding marine biofuel supply to other major Japanese ports.

Cosmo to supply SAF to Haneda Airport

(Company statement, May 27)

- Cosmo Oil Marketing’s plan to supply SAF to Haneda Airport (Tokyo) was selected under the Tokyo Govt’s FY2026 domestic SAF promotion program.

- The project aims to collect used cooking oil (UCO) as feedstock and produce biofuels through Saffaire Sky Energy, a company established by Cosmo Energy together with JGC Holdings and Revo International.

- CONTEXT: Japan has a goal to have SAF account for 10% of all jet fuel by 2030.

- SIDE DEVELOPMENT:

- City in Osaka Pref to collect oil to produce biodiesel and SAF

- (Organization statement, May 18)

- Toyonaka (Osaka Pref) agreed with Ueda Oil & Fats to collect UCO from households at collection points in local stores.

- The oil will be recycled into biodiesel and, from FY2028 onward, into SAF, when ENEOS plans to begin production at its Wakayama plant.

Jizoku inks MoU with Laos for reforestation under JCM

(Company statement, May 26)

- Jizoku, a startup focused on managing carbon credit projects in agriculture and forestry, signed an MoU with Laos’ Ministry of Agriculture and Environment to develop reforestation projects.

- The deal is under the JCM carbon credit scheme.

- Jizoku is the first Japanese startup to establish an official partnership with Laos.

- The goal is to generate large-scale carbon credits through reforestation in Laos.

- CONTEXT: Under the JCM, Japan provides financing and tech to developing countries and shares the resulting emissions reductions as carbon credits. Jizoku plans to use experience from JCM projects in Vietnam to expand such projects in Laos.

Idemitsu Kosan and Mori Solar BioRefinery to produce alcohol-to-jet SAF

(Company statement, May 27)

- Idemitsu Kosan agreed with Mori Solar BioRefinery to develop a domestic supply chain for ATJ (Alcohol-to-Jet)-based SAF using bioethanol.

- CONTEXT: Mori Solar BioRefinery is a JV established in 2025 to produce SAF. JAL also invested in a similar demo with the company last October.

- TAKEAWAY: ATJ can be made from various feedstocks, including bioethanol derived from woody biomass, as in this demo, and from non-edible crops and waste materials. The ability to source a wide array of feedstocks domestically enables stability of supply, a significant advantage given Japan’s well-known dependence on imported energy resources. For more information on the advantages of domestic biomass, see this issue’s Analysis section.

JAL and partners launch demo of rice oil-based biodiesel in Yamagata

(Company statement, May 28)

- JAL, Showa Sangyo, Phytochem Products, and Tohoku University launched a demo using rice oil-based biodiesel to power a JAL tug at Yamagata Airport.

- CONTEXT: An airport tug is a vehicle used to transport luggage carts or cargo across the tarmac, or to maneuver aircraft for the biggest models.

- The fuel was upcycled by Showa Sangyo using an ion-exchange resin method to extract rice bran fatty acids, a byproduct of rice oil production, as the raw material.

- The demo is scheduled to run until May 2027.

Chubu Electric group offer CO2-free power under ‘furusato noze’

(Company statement, May 22)

- Chubu Electric Power Miraiz and Omaeaki City, Shizuoka Pref, launched a hometown tax donation reward program offering residents CO2-free electricity generated from a local wind farm.

- People who donate to Omaezaki through Japan’s “furusato nozei” system can receive electricity sourced from the city’s wind power plant.

- CONTEXT: Furusato nozei lets residents redirect part of their taxes to municipalities in exchange for local gifts, with nearly all of the donations refunded through tax deductions.

Microwave Chemical reduces iron ore at bench scale, advancing low-carbon steelmaking

(Company statement, May 26)

- Microwave Chemical successfully reduced 15 kg of iron ore using microwave-based smelting, a step toward lower-carbon steel production.

- CONTEXT: The firm is an Osaka University startup transforming the chemical production industry by using microwave tech to heat materials from the inside.

- TAKEAWAY: As iron ore absorbs microwaves, the tech could lower energy consumption and CO2 emissions while also supporting hydrogen- and biomass-based steelmaking.

Nichikon launches CO2 reduction aggregation service for residential solar, storage

(Company statement, May 25)

- Nichicon, a Kyoto-based manufacturer of electronic components, launched a new service that aggregates the CO2 reductions generated by its residential solar and storage system users, converts them into environmental credits (J-Credits), and sells them to corporations looking for green offsets.

- In return, participating homeowners who self-consume clean energy will receive ¥1,200/ year in digital gifts.

- TAKEAWAY: The initiative creates a crowdsourced, decentralized environmental asset model, turning everyday households into active participants in the clean energy market.

ANALYSIS

BY MAGDALENA OSUMI

Will LTDA Help Accelerate Japan’s Fossil Fuel Transition?

Even as parts of Asia revert to coal amid Middle East tensions and energy security concerns, Japan’s decarbonization strategy still assumes that large-scale international supply chains for hydrogen, ammonia, e-methane, and CCS can be developed on schedule despite a fragmented global energy landscape.

To support that transition, the government has made coal- and LNG-fired power plants eligible for subsidies under the Long-Term Decarbonized Power Auction (LTDA), provided operators commit to eventually transitioning toward fully decarbonized operation. Across the first three LTDA rounds, LNG-related projects alone have secured 10.1 GW of capacity.

Yet the latest auction results also expose the fragility of those plans. Three hydrogen and ammonia projects selected in LTDA Round 3 were rebid after earlier versions won support in the first auction two years ago, only to be cancelled, delayed, or substantially redesigned.

The LTDA framework assumes that Japan can gradually replace imported fossil fuels with imported low-carbon molecules, including hydrogen, ammonia, and synthetic methane. But building these supply chains will require vast new infrastructure networks, long-term overseas partnerships, and stable geopolitical conditions over decades.

The current Middle East crisis underscores how vulnerable that assumption may be. Japan NRG reviewed the published LTDA roadmaps to examine how utilities expect Japan’s thermal power sector to evolve over the coming decades.

Phased transition strategy shows logistical uncertainty

Utilities participating in the LTDA are required to publish decarbonization roadmaps on how their subsidized thermal assets will transition to fully low-carbon operation. The facilities include existing plants that will be retrofitted to burn clean fuels and new generators.

For this analysis, we inspected the 18 thermal power projects (excluding nuclear) that have already published roadmaps. Those for projects selected in the third auction round, which was announced last month, are due to be released this summer.

Based on public roadmaps, thermal operators in Japan are in no rush to switch to cleaner alternatives. Most operators plan to adopt phased transition strategies built around LNG, coal, and the co-firing of largely blue ammonia during the 2030s, before exploring green alternatives in the 2040s.

Part of this delayed energy transition closer to mid-century comes from uncertainty over fuel supply and associated costs. Several companies, including KEPCO and Tokyo Gas, have proposed multiple transition scenarios for the same sites that vary based on future fuel availability, CCS deployment, carbon pricing, and government support. In some cases, the idea is to move to hydrogen conversion; in others, there’s a preference for ammonia co-firing, e-methane blending, or the option to keep the facility as a pure LNG plant but paired with carbon capture technology.

This uncertainty reflects the limited maturity of the underlying fuel supply chains. Many of the projected hydrogen, ammonia, and e-methane volumes depend on overseas production projects, shipping infrastructure, and import networks that remain either under development or commercially unproven.

The contrast is visible in LNG procurement. Earlier this year, a key supporter of ammonia as a fuel – JERA – signed a 27-year agreement with QatarEnergy for 3 million tons per year of LNG beginning in 2028. This is one of multiple long-term LNG offtake deals that JERA has across close to a dozen countries. By comparison, JERA has announced only one major offtake deal in ammonia so far.

Many Japanese utilities are still searching for long-term suppliers of hydrogen and ammonia needed to support future co-firing plans.

Estimating future fuel demand

To assess how the LTDA mechanism could affect Japan’s future power mix and fuel demand, Japan NRG modeled indicative fuel requirements for LNG- and coal-fired projects awarded in the first two LTDA rounds. The analysis covers roughly 6.8 GW of LNG-related capacity and 3.4 GW of coal-fired capacity, based on disclosed project roadmaps and auction results.

The estimates are intended as scenario-based projections rather than firm forecasts. They assume average utilization rates of around 65% for LNG-fired assets and 50% for coal-fired assets, broadly reflecting recent thermal plant operating patterns and the expectation that LTDA-supported plants will increasingly operate as mid-merit / balancing resources rather than continuous baseload generators. It also reflects Japan’s strategy to promote renewables.

Fuel demand was estimated using plant capacity, assumed operating rates, disclosed cofiring targets, and energy-equivalent replacement ratios. For LNG assets, the analysis considers a gradual transition from conventional LNG generation toward hydrogen blending, dedicated hydrogen combustion, or CCS-linked operation. For coal assets, the main pathway is ammonia co-firing followed by potential dedicated ammonia combustion.

The results should therefore be read as a measure of scale: even relatively modest cofiring ratios imply significant new clean-fuel demand, while full conversion would require fuel supply chains far larger than those currently available. Because e-methane deployment remains less clearly defined in current project disclosures, the analysis assumes only limited adoption through the 2040s and treats it separately from the main LNG-hydrogen pathway.

Estimates of Annual Fuel Demand Across the LTDA-Sponsored Fleet

| LNG Transition Timeline | Hydrogen Blend Ratio | Remaining LNG Demand (mpta) | Estimated Hydrogen Requirement (mpta) |

| 2030 (Early phase) | 10% Blend | 4.5 | ~0.1 |

| 2040 (Scale-up phase) | 20% Blend | 4.0 | ~0.2 |

| 2040 (High-blend case) | 50% Blend | 2.5 | ~0.5 |

| 2050 (Full conversion) | 100% | 0 | ~1.0-1.2 |

- Hydrogen demand estimates are based on energy-equivalent replacement of LNG using assumed hydrogen blending ratios, plant utilization rates, and disclosed transition pathways for LTDA-supported assets. Lower blend ratios in the 2030s imply relatively modest hydrogen demand, while higher blend ratios and eventual dedicated hydrogen combustion significantly increase fuel requirements.

| Coal Timeline Horizon | Facility Utilization Ratio | Ammonia Blend Ratio | Remaining Coal Demand (mtpa) | Estimated Ammonia Requirement (mtpa) |

| 2030 (Early Phase) | 50% | 20% Blend | 4.0 | ~1.3 |

| 2040 (Scale-up Phase) | 50% | 50% Blend | 2.5 | ~3.3 |

| 2050 (Full Transition) | 50% | 100% | 0 | ~6.5 |

- Ammonia demand estimates are based on energy-equivalent replacement of coal through assumed co-firing ratios and eventual dedicated ammonia combustion. Actual fuel demand will depend on plant operating rates, conversion timelines, and future dispatch patterns.

Takeaway 1 – Slow and steady shift

The submitted roadmaps show a major logistical inflection point emerging between 2035 and 2045. Until then, there is little thermal transition to speak of as LNG and coal dominate the remainder of this decade and the first part of the 2030s.

Even when a shift starts to take place, most projects will introduce initially low-ratio cofiring rather than seeking an immediate full conversion. This should allow operators to utilize the existing thermal infrastructure while gradually introducing ammonia, hydrogen, or e-methane and keeping the CCS option in place.

Earlier this year, a separate METI-funded CfD subsidy scheme for hydrogen clusters started to announce awards for construction of storage facilities, pipelines, transport devices and systems and other infrastructure required for hydrogen / ammonia adoption.

With ammonia transport and storage much easier to implement using existing technologies, it is little surprise to see LTDA winners bank on ammonia for their nearterm transitions, particularly for coal-fired assets.

Hydrogen deployment remains comparatively limited until the 2040s. Many of the more ambitious full-conversion plans remain contingent on future fuel availability.

Takeaway 2 – Blue fuels depend on CCS

Most utilities envision scaling up blue hydrogen and blue ammonia during the 2030s before eventually transitioning toward green fuels as supply chains mature and costs decline.

That strategy, however, makes carbon capture and storage (CCS) a central requirement for the transition. Low-ratio co-firing still leaves most emissions tied to fossil fuels, while many future fuel supply plans depend on overseas CCS-linked production projects in countries such as Australia and Malaysia.

Many utilities draw roadmaps based on future hydrogen and ammonia supply chains that remain only partially developed.

Takeaway 3 – Coal and LNG follow different paths

Most LNG-based assets target hydrogen, e-methane, or CCS pathways, while coal-fired units lean heavily toward ammonia as the latter is seen as more compatible with existing coal boiler infrastructure.

Key coal-transition projects include:

- JERA’s Hekinan Units 4 and 5

- Hokkaido Electric’s Tomatoh-Atsuma Unit 4

- Kobelco Power Kobe’s Kobe plant

These coal assets plan to introduce ammonia co-firing at 20% by 2030; upgrade to 50% firing in the mid-2030s; and achieve full ammonia combustion during the 2040s. All three stations, operated by three different utilities, mention use of green ammonia only at the latter stages.

Notably, the transition pathway for the coal-fired plants is entirely different from those that burn LNG and has earlier timelines. However, both sets of plans require major investments in new storage tanks, import terminals, shipping infrastructure, and port upgrades.

As such, ammonia and hydrogen generation facilities will likely remain subsidydependent at least until the 2040s – or create new revenue options either through the inclusion of their facilities in non-fossil certificates or similar, carbon credits, or PPAs with anchor clients willing to pay a premium to secure clean dispatchable power.

All the above will require substantial business development efforts, which perhaps explains why despite improved support conditions in LTDA Round 3 – including higher price ceilings and expanded CCS eligibility – only four hydrogen and ammonia projects participated in the auction. Most Japanese utilities seem at present uncomfortable with the sector risk and prefer to wait for further state support.

Bidding in the LNG category of the LTDA also obliges utilities to agree to eventually move to at least a 20%-ammonia or 10%-hydrogen co-firing on a calorific basis, but the auction’s long lede timelines give major utilities confidence that fuel procurement and pricing solutions will be found over the next two decades.

The long timelines embedded within the LTDA framework also give utilities flexibility to delay full fuel transitions if supply-chain development or economic progress more slowly than expected.

Conclusion: LTDA provides gradual, hedged bets

The first three LTDA rounds suggest Japan is pursuing a layered and highly gradual thermal transition rather than a rapid replacement of fossil-fuel generation.

LNG remains central to the power mix, ammonia has emerged as the primary near-term decarbonization pathway for coal assets, while hydrogen deployment remains comparatively limited and concentrated in longer-term conversion plans. At the same time, the growing role of battery storage and nuclear restart projects highlights the extent to which Japan is relying on multiple parallel technologies to preserve system stability during the transition.

The auction results also suggest that much of the deeper decarbonization envisioned in utility roadmaps remains back-loaded into the 2040s, when many projects aim to scale dedicated hydrogen, ammonia, e-methane, or CCS-linked generation.

Rather than signaling a rapid exit from thermal power, LTDA increasingly appears designed to extend and gradually adapt Japan’s existing thermal infrastructure while alternative fuel supply chains and low-carbon technologies mature.

The transition pathways illustrate how Japanese utilities are pursuing different decarbonization strategies depending on existing infrastructure, fuel access, and technology preferences, rather than converging around a single national transition model.

| Transition pathway | Representative projects | Long-term target |

| Hydrogen track | Hokkaido (Ishikari 2 & 3), JERA (Chita 6 & 7), Tohoku (Higashi- Niigata 6), KEPCO (Nanko 1-3; Scenario No. 2), Shikoku (Sakaide 5), Chugoku (Yanai), Zero Watt Power (Scenario No.1) | Dedicated blue/green hydrogen combustion |

| Ammonia track | JERA (Hekinan 4 & 5), Hokkaido (Tomatoh 4), Kobelco Power (Kobe PP 2), Zero Watt Power (Scenario No.2) | Dedicated ammonia combustion |

| e-methane track | Toho Gas (Unit 1), Tokyo Gas (Chiba; Scenario No. 1), Osaka Gas (Himeji 3), Zero Watt Power (Scenario No.3) | High-ratio or full e-methane utilization |

| CCS-linked LNG track | KEPCO (Nanko 1-3; Scenario No. 1), Tokyo Gas (Chiba; Scenario No. 3) | Continued LNG operation paired with carbon capture |

ANALYSIS

BY AGLAÉ BANGE

Japanese Biomass Energy at a Crossroads: Constraints and Potential

Biomass power is approaching a post-subsidy test. The feed-in tariff, introduced after the Fukushima disaster to accelerate renewable energy investment, helped make biomass projects bankable.

More than a decade later, many assets are midway through their FIT support periods, and operators are weighing how the sector can remain viable once tariffs expire.

This matters because biomass is no longer marginal. It accounted for 4.1% of Japan’s energy mix in 2023, while METI’s latest Basic Energy Plan sees that share rising to 6% by 2040. But with many plants still dependent on subsidy-backed revenue to offset high fuel, logistics and operating costs, the post-FIT era could bring contraction rather than growth.

That concern is more acute since METI abolished FIT support for woody biomass assets above 10 MW this fiscal year. Industry participants report stagnation, and even declining activity, as inflation and rising fuel costs weigh on project economics. The result is a sector caught between policy targets and commercial uncertainty: the mechanisms that supported biomass power growth are being withdrawn before a clear post-FIT model has emerged.

For now, large woody biomass plants still dominate installed capacity. But the more relevant question for the sector’s next phase may be whether smaller, domesticfeedstock projects can develop into a durable alternative. Sewage sludge, municipal waste, agricultural residues and biogas offer an advantage that imported biomass doesn’t: locally sourced fuel.

That makes these projects attractive in an uncertain geopolitical and energy-security environment. Sludge-based plants and farm-scale biogas systems can turn domestic waste streams into power, heat or self-consumed energy, while supporting local economies. But they also show the limits of Japan’s biomass opportunity. Projects are typically small, difficult to scale and often dependent on lengthy subsidy application processes.

Over the next few years, Japan’s biomass sector will need more than broad policy targets. To hold onto existing capacity – and expand toward METI’s 2040 goal – it will need clearer post-FIT support, more workable subsidy frameworks and business models suited to smaller domestic-resource projects. Without that, biomass risks remaining a useful but constrained complement to solar, wind and other renewable energy sources.

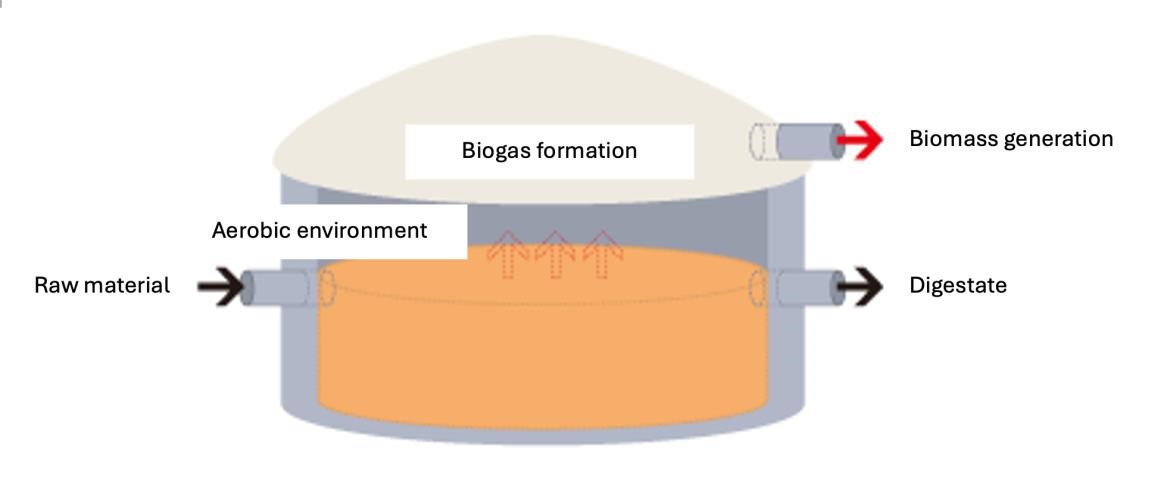

Generating gas from sludge

Sludge-based power generation shows what this smaller, domestic-feedstock model looks like in practice. Unlike large imported-wood biomass plants, these facilities are built around municipal waste, with fuel generated locally and converted into power close to its source.

The trade-off is scale: the 2 MW Funabashi plant in Chiba Prefecture illustrates both the value of this model and its limits. Operated by Funabashi Biomass Energy, with technical support from France’s Veolia, the plant sits on the grounds of the Nishiura Sewage Treatment Plant in Funabashi, east of Tokyo, in an industrial area.

Nishiura has been in service since 1976 and is designed to treat up to 81,000 m³ of wastewater per day for a population of 110,700 people. The power project, commissioned in 2019, was developed to use digestion gas from the sewage treatment process that had previously been an underused biomass resource, while also helping renew ageing city-owned digestion facilities.

The scheme shows how FIT made such local projects workable. Structured as a privately built and operated project, it uses 20 years of FITbacked electricity sales to support the design, construction and maintenance of digestion-gas generation equipment. Funabashi City supplies digestion gas from the sewage treatment plant to the project company, which converts it into electricity for sale to TEPCO.

On site, the process is compact. Municipal sludge is warmed, mixed and treated in large concrete digestion tanks, producing methane-rich gas that is sent through pipelines to storage and generation equipment. Staff said the operation can be run by three people, with much of the monitoring handled remotely. The generation facilities occupy a small corner of the much larger sewage complex, giving the project a very different feel from Japan’s port-side biomass plants running on imported wood pellets.

That compact footprint is part of the appeal. In a sector facing labor constraints as well as fuel-cost pressure, Funabashi offers a model that is local, automated and closely tied to existing public infrastructure. For municipalities, it is a way to monetize a waste stream, cut emissions and update ageing equipment without building a large standalone power plant.

But the same local character is also the constraint. Plant staff told Japan NRG that scaling up production would be difficult because sludge supply depends on the municipality, and the local population is declining.

The same demographic constraint is evident in wasteto-energy (WtE). In 2023, Japan had 1,004 waste treatment facilities, 40.9% of which were equipped for power generation, according to the Funabashi BE’s 2 MW sludge-based biomass plant