WEEKLY

SIXTH ANNIVERSARY ISSUE

June 15, 2026

ANALYSIS

REPOWERING AGING WIND FARMS GIVES SECTOR NEW LEASE ON LIFE

- Some wind power developers are modernizing, or “repowering”, existing wind farms – replacing aging turbines with larger and more efficient machines.

- By increasing generation at wind sites and using existing grid infrastructure, repowering can help bridge the gap between an aging first-generation fleet and green ambitions.

SPOT MARKET ANALYSIS AND IMPACT FROM THE U.S.- IRAN WAR

- Oil and LNG prices have put upward pressure on thermal generation costs, lifting JEPX spot prices in the morning and evening hours. But this time the shock passes through a market that is different from 2022.

- Spot prices are steeper and more volatile, but the balancing market response is even more extreme.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- PM Takaichi to propose energy security principles at G7 summit

- Malaysia and Japan to deepen cooperation on energy security and nuclear power

- China rare earths exports to Japan drop 80%

- Power spot trading ratio rises to record 46%

- Futures trading slows amid uncertainty

- Govt reviews challenges and measures for ensuring stable electricity supply

- Kanadevia consortium to advance green H2

- Kyushu Electric to research natural hydrogen

- Hydrogen fusion startup unveils world’s first prototype heater

- MoE seeks comments on stricter EIA proposal for solar power

- Kyocera Communication to install PSCs

- Takano to conduct R&D on solar cells in space

WIND POWER AND OTHER RENEWABLES

- Regional rivalry begins as METI and Vestas agree on offshore wind turbine production

- Mitsubishi HC Capital and Brookfield launch renewable energy JV

- Cosmo Eco Power inks virtual PPA in wind

- U.S. to use Japan’s capital to advance SMRs

- Onagawa NPP Unit 2 resumes operation

- JERA signs 20-yr LNG deal with Petronas

- Tokyo Gas to open LNG terminal in Malaysia

- Unions extend strike at INPEX’s Ichthys LNG

CARBON CAPTURE & SYNTHETIC FUELS

- Govt to subsidize up to 75% of CCS project construction costs

- NEDO selects Sumitomo for biomass-derived carbon recycling

EVENTS

June 15-17 G7 Summit @ Evian, France

June 17-19 Automotive Engineering Exposition 2026 @ Nagoya, Aichi

Jun 11-Jul 19 FIFA World Cup

June 23-25 “Summer Davos” in Dalian, China

Jun 30-Jul 1 Asia Nuclear Energy & SMR 2026 @

Singapore

July 1-2 4th WFO Asia Pacific Summit @ Tokyo

August Asia-Pacific Economic Cooperation / Energy Ministerial Meeting

September 14-18 IAEA General Conference 2026 @ Vienna, Austria

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

Nov 3 U.S. Midterm Elections

Nov Publication of International Energy

Agency – World Energy Outlook 2026

Nov 18-19 Asia-Pacific Economic Cooperation –

Leaders Meeting @ Shenzhen, China

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com. For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

PM Takaichi to propose energy security tenets at G7 summit

(Yomiuri Shimbun, Financial Times, June 11-12)

- PM Takaichi will propose three energy security principles at the G7 Summit in France on June 15, seeking stronger international cooperation on energy supply resilience amid conflict in the Persian Gulf.

- Proposed principles are:

- Maintaining free and transparent energy trade;

- Strengthen strategic petroleum reserves in coordination with the IEA;

- Enhance cooperation between energy-producing and consuming countries.

- The initiative builds on Japan’s POWERR Asia (Partnership on Wide Energy and Resources Resilience Asia), under which Tokyo supports oil stockpiling and broader energy and critical material supply-chain resilience in Southeast Asia.

- TAKEAWAY: Takaichi is seeking to demonstrate how strategic stockpiles and diversified supply chains have helped shield import-dependent economies such as Japan from external shocks. In METI’s long-term vision, Asian countries would build larger emergency reserves and coordinate their use during supply disruptions, creating a regional energy-security network. By bringing this agenda to the G7, Japan is also reinforcing its ambition to serve as Asia’s leading voice on energy security while linking energy resilience to broader concerns over supply-chain security and economic coercion.

Malaysia and Japan to deepen cooperation on energy security and nuclear power

(Government statement, June 10)

- During a summit meeting, Malaysia and Japan pledged deeper cooperation on energy security and nuclear power.

- PM Anwar Ibrahim and PM Takaichi discussed ways to strengthen resilience against global supply disruptions.

- Takaichi was interested in Malaysia’s preparations to introduce nuclear power – including reactor technology options, site selection, and business arrangements – as a basis for formulating Japan’s support plan.

- TAKEAWAY: The summit elevates Malaysia’s status as a rising SE Asian “middle power,” allowing it to leverage its natural resources while maintaining stable trade and infrastructure flows with allies. Malaysia is critical to Japan’s energy security; its long-term deals account for about 15% of Japan’s total LNG imports and it is an alternative to the Persian Gulf. Also, Malaysia has emerged as a hub for critical minerals, rare earths, and semiconductors, helping Japan build resilient supply chains.

China’s exports of rare earths to Japan drop over 80%

(Nikkei Asia, June 8)

- China’s exports of key rare earths to Japan have fallen over 80% after tighter export controls, forcing Japanese firms to seek alternative supplies from Australia and India, invest in recycling, and develop rare-earth-free technologies.

- TAKEAWAY: China’s dominance in rare-earth processing has exposed Japan’s supply-chain vulnerability, but also accelerated efforts to diversify sourcing and reduce dependence on Chinese materials.

- SIDE DEVELOPMENT:

- U.S. tungsten scrap exports to Japan soar

- (Nikkei Asia, June 11)

- Japan is rapidly increasing imports of recycled tungsten scrap from the U.S. after China’s export restrictions disrupted supplies.

- U.S. tungsten scrap exports to Japan surged 24-fold in early 2026, while prices jumped over fourfold as both Japan and China compete for limited recycled material.

- CONTEXT: Tungsten is used in Japan for steel production, chips for green tech, energy-efficient smart windows, rechargeable batteries, and fusion energy research.

Shin-Etsu Chemical to invest ¥35 bln in domestic rare-earth refining, first in 18 yrs

(Nikkei, June 10)

- Japan’s largest chemical firm, Shin-Etsu Chemical, will invest ¥35 billion to build a rare-earth refining facility in Fukui Pref, its first domestic rare-earth plant in 18 years.

- The project secured ¥17.5 billion in govt subsidies; it aims to strengthen Japan’s ability to process rare earths domestically, reducing dependence on Chinese refining.

- CONTEXT: Japan seeks to set up a secure supply chain for critical minerals and is pursuing rare-earth resource development around Minamitorishima (in the Pacific Ocean) and expanding sourcing from Australia and SE Asia. But refining remains a major bottleneck. China still dominates both rare-earth mining and processing, with over 90% of the world’s refined magnet rare-earth production.

- The planned facility will produce elements such as dysprosium, terbium, and yttrium.

- TAKEAWAY: This news signals a major shift in Japan’s critical minerals strategy from simply diversifying raw material supply to rebuilding domestic processing capacity. While Japan is unlikely to match China’s cost competitiveness in refining, the investment reflects a growing appetite from both govt and industry to prioritize supply security and resilience over lowest-cost sourcing. Sectors likely to benefit include EVs, chips, and defense-related tech.

Survey: over 60% of manufacturing companies feel impact from U.S.-Iran war

(Company statement, June 10)

- Resilire surveyed 500 executives responsible for procurement and purchasing in manufacturing companies.

- 62% said the fallout from the U.S.-Iran war hurts business. Only 7.4% see no impact.

- 40.6% said within six months they’ll reach the limits to sustain operations. Only 4.5% said they’re able to pass on rising costs; 48.2% failed to pass on these costs. Upstream suppliers (parts and materials) struggle more than finished goods producers.

- The main reason why firms hesitate to hike prices is fear of losing clients to competitors (38.1%). Some wait for the right timing to negotiate (35.4%).

- The scale of cost increases threatens profit: 67.2% faced procurement cost increases of 10% or more over the past year, and 21.4% saw costs jump by 30% or more.

- CONTEXT: The firm behind the survey, Resilire, provides a supply chain risk management platform.

NTT and Mitsubishi Materials launch circular economy venture for copper

(Company statement, June 3)

- NTT and Mitsubishi Materials set up NTT Circulust, a circular economy venture that combines the production and sale of recycled metals.

- The new firm will be 66.6% owned by NTT and 33.4% by Mitsubishi Materials. It targets revenue of ¥3 billion by 2030 and ¥30 billion by FY2035.

- The project will start with copper recovered from used IT and telecom equipment, with a digital platform that tracks and shares information on material origin, allocation, and environmental attributes across the supply chain.

- TAKEAWAY: While not an energy project, the venture is relevant to Japan’s energy transition. Copper is a critical material for power grids, renewable energy, EVs, batteries, and data centers. The goals of the new firm align closely with Japan’s Circular Economy Action Plan, which targets increasing recycled copper supply. The focus on traceability and recycled-content verification could also help manufacturers meet growing sustainability reporting and supply-chain disclosure requirements.

Horiba launches hub for equipment for chips

(Company statement, June 11)

- HORIBA STEC, a subsidiary of Horiba, a leader in measurement and analytical tech, opened an energy-efficient semiconductor equipment factory in Kyoto.

- The firm plans to triple its domestic mass flow controller (MFC) production capacity.

- The factory is designed as a ZEB. Its rooftop PV system will use generated electricity on-site, and any surplus renewable power will be converted into hydrogen via water electrolysis, stored, and later used for electricity generation.

NEWS: ELECTRICITY MARKETS

Power spot trading ratio rises to record 46% in May

(Exchange statement, June 8)

- The electricity wholesale market remained highly active in May, with spot transactions accounting for 46% of total power demand, up from 45.4% in April.

- Total electricity demand reached 60.4 TWh, while contracted spot-market volume amounted to 27.8 TWh.

- TOCOM said stronger spot procurement by major utilities and higher cooling demand drove the increase in market activity.

- May was unusually warm across Japan, with the national average temperature 1.37°C above normal, the second-warmest May since records began in 1898.

- Sunshine hours were also above average across the country.

- Despite the higher trading activity, spot prices softened in most regions. Monthly average prices fell in seven of the nine power areas, although Tokyo and Chubu remained elevated at about ¥18/ kWh and ¥16/ kWh, respectively.

- TAKEAWAY: During the shoulder low-demand season, major utilities now tend to reduce thermal power generation to lower emissions and costs, and dip into the spot market more to cover sudden demand surges. See this week’s Analysis section for a deep dive into power markets and the impact of the Iran conflict on trading and volumes.

May power futures trading slows amid market uncertainty and holidays

(Exchange statement, June 8)

- Trading in the TOCOM power futures market declined sharply in May as participants adopted a wait-and-see approach amid geopolitical uncertainty and reduced trading days during the Golden Week holiday period.

- Monthly contract volume fell to 616 lots, down from 1,645 lots in April, while only five annual contracts were traded.

- TOCOM said uncertainty surrounding developments in the U.S.-Iran war and directionless fuel markets contributed to lower liquidity.

- The number of concluded transactions dropped to 34, compared with 117 in April. Nearly all deals were negotiated off-exchange, with only one transaction executed on the exchange itself. Trading focused primarily on June 2026 delivery contracts and summer-quarter products as market participants positioned for expected increases in summer electricity demand.

- No transactions over 100 lots (10 MW) were recorded for a second month in a row. The highestpriced transaction was a July 2026 East Area daytime-load contract at ¥33.05/ kWh; the lowest was a FY2027 East Area baseload contract at ¥15.3.

- TAKEAWAY: The sharp decline in volumes suggests many participants preferred to wait for clearer signals from fuel markets and geopolitical developments rather than lock in forward power prices, leaving liquidity relatively thin. The EEX May data had a similar trajectory, albeit with much higher volumes. The start of the soccer World Cup is another reason some traders cite as depressing volumes as attention gravitates to the event.

- SIDE DEVELOPMENT:

- JEPX intraday market volumes remain elevated in May

- (Exchange statement, June 8)

- Trading in the intraday market remained strong in May; average daily volume rose 9.8% MoM to 24.5 GWh, the second consecutive month above 20 GWh.

- Total monthly traded volume increased 3.5% to 758.6 GWh, while the number of transactions rose 1.8% to a record 308,557 trades. Traded volume represented 1.3% of total electricity demand, up 0.2 percentage points from April.

- The monthly average intraday price fell to ¥14.84/ kWh, down ¥1.20 from April, although prices reached ¥80 on several days during the month.

Govt warns of tight power supply outlook through late 2020s

(Government statement, June 5)

- ANRE said Japan faces tightening electricity supply margins through FY2029 due to rising demand and continued thermal power plant retirements.

- Based on OCCTO’s latest long-term supply outlook, the govt said existing thermal generation will remain essential to maintaining supply security until new low-carbon capacity supported through the LTDA (Long-Term Decarbonized Power Sources Auction) begins entering service at scale.

- To address the risk, ANRE plans to review reserve capacity mechanisms, capacity market design, and measures to retain existing generation resources. It will also examine how to accelerate investment in new capacity while limiting costs to consumers.

- CONTEXT: OCCTO’s latest assessment found that some regions could fall below the 3% reserve margin reliability benchmark before 2030, reflecting growing demand and the retirement of aging thermal plants. The outlook improves in the early 2030s as projects awarded through the LTDA begin commercial operation.

- TAKEAWAY: The discussion highlights a growing policy dilemma. Japan wants to accelerate the transition to low-carbon power, but near-term supply risks mean thermal generation may need to remain online longer than expected. The challenge for policymakers is managing this transition without undermining investment in new decarbonized capacity.

Govt revises capacity market procurement rules

(Government statement, June 5)

- ANRE will revise Japan’s capacity market design by procuring all required capacity through the main auction, eliminating the current practice of reserving 2% of demand for the additional auction held one year before delivery.

- The change was proposed after concerns emerged that future supply shortages could make it difficult to secure sufficient resources through the additional auction. Resources that fail to clear the main auction may retire before the additional auction takes place, while some resources that clear the main auction may subsequently exit the market.

- The review also found that bids from dispatchable resources in the main auction consistently exceed the current bidding cap, while participation in the additional auction remains below its procurement target.

- CONTEXT: Under the current framework, the main auction procures capacity four years ahead of delivery but excludes 2% of forecast H3 demand (the average of the three highest-demand days of the year). That volume is later procured through the additional auction on the assumption that resources such as nuclear power, self-generation and demand response (DR) will become available closer to delivery.

- TAKEAWAY: The reform reflects growing concern over thermal plant retirements and tightening supply margins. By shifting all procurement to the main auction, the govt is prioritizing certainty of capacity procurement over flexibility, reducing reliance on future resource additions that may not materialize.

ANRE proposes further revisions to 4th LTDA

(Government statement, June 5)

- ANRE proposed further revisions to the 4th LTDA (Long-Term Decarbonized Power Sources Auction) design, scheduled for bidding in January 2027.

- Procurement of LNG-fired power will continue beyond the initial three-year period, with a target of 6 GW set to ensure adequate supply capacity.

- The commissioning deadline for LNG projects would be extended from 8 to 11 years to reflect longer construction periods caused by global gas turbine supply constraints.

- The commissioning deadline for LDES (long-duration energy storage) projects will be extended from 4 to 7 years, recognizing that these projects require larger sites and longer development periods than initially assumed.

- The allowable cost of capital for LNG and LDES projects would be increased to better reflect their higher investment and construction risks.

- Rising interest rates have increased financing costs, making the current 5% capital cost benchmark less adequate. The proposal is to raise the base capital cost to 5.4%.

- CONTEXT: Since March, ANRE discussed revisions to LTDA-4. The key discussion points are:

procurement volume for LNG-fired power; contract methodology for BESS; pre-screening requirements for hydrogen and ammonia projects, including incorporation of carbon intensity (CI) values into cofiring requirements; fuels in the decarbonization roadmap; market exit and post-award price competition; maximum program applicability period; funding for wind power facility decommissioning costs; and the definition of CO2 capture rates for CCS. - TAKEAWAY: The revision of the capital cost assumption for all power sources is the issue with the greatest potential impact on bid prices and project economics. For developers of nuclear, CCS, and hydrogen/ ammonia projects, this is likely to be the most critical aspect of the ongoing market design review.

Govt proposes new rules to prevent phantom grid connection requests

(Government statement, June 10)

- ANRE proposed new rules to prevent large electricity users, such as data centers, from reserving transmission capacity they do not actually use (phantom reservation).

- The measures target extra-high-voltage customers with contract demand of 30 MW or more and aim to ensure fair and efficient use of limited grid capacity.

- Key proposals include:

- Release unused reserved capacity when demand plans are reduced. o Impose cost settlements if planned power demand is delayed over a year.

- Limit staged connection contracts to a maximum of six years.

- The new rules are expected to take effect in FY2027, while procedural requirements, including stricter payment and application rules, are planned to start in October 2026.

- CONTEXT: As large-scale electricity demand becomes increasingly concentrated in specific locations, concerns have arisen that speculative (or phantom) reservation of grid capacity could hinder the provision of adequate power supply to consumers and increase wheeling charge burdens.

- TAKEAWAY: The reforms aim to reduce grid capacity hoarding (phantom reservation), improve access for other users, and limit unnecessary transmission cost increases. Customers with 30 MW demand or more will face stricter limits on securing excess future grid capacity and need more credible development plans. While this will improve efficient use of grid capacity, it will also increase the importance of contract and project schedule management for large new projects.

- SIDE DEVELOPMENT:

- ANRE to accelerate grid connections for BESS and other generators

- (Government statement, June 10)

- ANRE finalized measures to accelerate grid connections for BESS and other generation facilities by preventing speculative (phantom) grid reservations.

- A cap on the number of grid connection review applications per developer will take effect on August 1. The limit for each area will range from 5 to 12 applications.

- Starting Oct 1, proof of land-use rights is mandatory for new connection applications.

- Existing facilities will be exempt in certain upgrade and refurbishment cases.

- CONTEXT: The new measures were discussed for about a year amid concerns about the hoarding of grid capacity caused by the rapid increase in grid-scale BESS and renewable energy projects in recent years. At the previous working group meeting in April, ANRE reported that the cap on the application number would be implemented.

- TAKEAWAY: Measures to prevent grid capacity hoarding have entered the implementation phase. BESS and renewable energy developers will need to better manage connection requests and secure site rights at an earlier stage. However, projects with higher development certainty should benefit from faster grid connection processes.

Mitsuuroko to pass along electricity and gas subsidies

(Company statement, June 10)

- Mitsuuroko Group will apply state-funded discounts to electricity and city gas bills for July–Sept 2026 usage (reflected in August–Oct bills) under Japan’s renewed Electricity and Gas Price Relief Program.

- The subsidy will reduce customer bills without requiring an application. Household electricity discount will be up to ¥4.5/ kWh and gas discounts up to ¥18/ m3.

- CONTEXT: The move is tied to a govt support package approved May 26. The policy aims to cushion households and businesses from any increase in fuel and LNG costs.

- Similar announcements are likely to be made (or have already been made) by major utilities and retailers including: TEPCO, KEPCO, Chubu Electric, Osaka Gas, Tokyo Gas and independent power and gas retailers.

NEWS: HYDROGEN

Yamanashi Pref and Kanadevia consortium to advance green H2

(Government statement, Nikkei, June 3)

- Yamanashi Pref, Yamanashi University, Kanadevia, Tomoe Shokai, and Yamanashi Hydrogen launched the LIGHT consortium to accelerate adoption of green hydrogen.

- The consortium will train operators of hydrogen supply systems, study regulatory frameworks, and promote collaboration among industry players, govt and academia.

- CONTEXT: The initiative builds on Yamanashi’s efforts to become a hydrogen hub, including green hydrogen production in Kofu and a major green hydrogen production site in Hokuto. Kanadevia, which is developing a hydrogen equipment manufacturing plant in Tsuru, said the consortium will help create a hydrogen ecosystem combining tech, workforce development, and practical deployment.

Kyushu Electric and Kyushu Univ to research natural ‘white’ hydrogen

(Organization statement, June 9)

- Kyushu Electric and Kyushu Univ will research the potential of white hydrogen generation, aiming to eventually commercialize it.

- On May 29, the project was approved by NEDO, which will provide funding through the end of FY2028.

- CONTEXT: White hydrogen exists naturally underground and can be obtained with minimal CO2 emissions in comparison to manufactured hydrogen. JOGMEC provides financial assistance to Japanese firms exploring natural hydrogen and support for the hydrogen supply chain. White hydrogen is valued for its potential as a low-cost, low-carbon natural resource.

Hydrogen fusion startup unveils world’s first prototype heater

(Company statement, June 12)

- Japanese startup New Hydrogen Fusion Energy unveiled a prototype hydrogen-fusion heater, claiming it generates 500 W of heat from 200 W of electrical input.

- The company says the device is the world’s first heater based on a light-hydrogen fusion principle and achieves a heat output equivalent to 2.5 times its electrical input.

- TAKEAWAY: Claims of room-temperature or light-hydrogen fusion producing excess heat remain highly controversial and have not been accepted by the scientific mainstream. Any reported energy gain would require independent verification and reproducible results before it could be regarded as a breakthrough in fusion technology.

Hoku Energy wins grant for green H2 projects

(Company statement, June 10)

- Hoku Energy, a clean tech firm that develops green hydrogen and ammonia supply chains, was selected for Kitakyushu City’s subsidy for low-carbon hydrogen projects.

- Hoku Energy will assess site conditions, infrastructure availability and related factors for prospective coastal locations, and evaluate the commercial viability of power generation using hydrogen and other low-carbon fuels.

- CONTEXT: Kitakyushu has positioned itself as one of Japan’s leading hydrogen development regions, with plans to attract hydrogen production, import, storage, and utilization projects as part of its industrial decarbonization strategy.

- TAKEAWAY: The project reflects a broader shift in Japan’s hydrogen strategy from supporting production projects toward developing local supply chains and demand hubs. While government targets for hydrogen consumption remain ambitious, infrastructure availability, transport costs, and end-user demand continue to be among the largest barriers to commercial deployment.

NEWS: SOLAR AND BATTERIES

MoE seeks comments on stricter EIA rules proposal for solar power

(Government statement, June 2)

- The MoE is calling for public comments on its plans to lower the threshold for mandatory environmental impact assessments (EIAs) for solar power projects.

- The revised rules take effect on April 1, 2027.

- The proposed changes are:

- The current rule mandating EIAs for projects with at least a 40 MW capacity would apply to projects with at least 20 MW;

- Screening required to determine if an EIA is needed would be lowered from the current range of 30–40 MW to 15–20 MW.

- The ministry is accepting feedback until July 1 here.

- During the transition period, the existing 30–40 MW projects already in the EIA process can continue under current rules.

- Also, projects under 30 MW already undergoing EIA reviews under local ordinances may be allowed to transition into the national EIA process without starting over.

- CONTEXT: Since the current system began in 2020, some solar developments have caused disputes with communities over landslide and flooding risks, prompting local municipalities to introduce their own regulations.

- TAKEAWAY: If approved, the changes might not only increase development costs and project timelines but would also require operators to renegotiate terms for corporate PPAs if approvals take longer.

Kyocera Communication to install PSCs in Shiga and Fukuoka

(Company statement, June 8)

- Kyocera Communication Systems began installing PSCs on six public buildings, such as schools, in Shiga and Fukuoka prefs.

- The effort benefits from MoE subsidies. Sekisui Solar Film supplies the PSCs.

- TAKEAWAY: These PSCs are commercial installations, highlighting the market’s rapid maturation. Such a project is interesting to monitor since this is a real-world application of the new technology, particularly regarding long-term energy conversion efficiency, maintenance costs, and durability in outdoor environments.

- SIDE DEVELOPMENT:

- Shutoko Metropolitan Expressway to test Sekisui’s PSCs

- (Company statement, June 8)

- In the fall, Shutoko Metropolitan Expressway will launch a demo of Sekisui Solar Film’s film-type PSCs installed on a commercial rooftop.

- The project aims to evaluate power generation performance and installation methods.

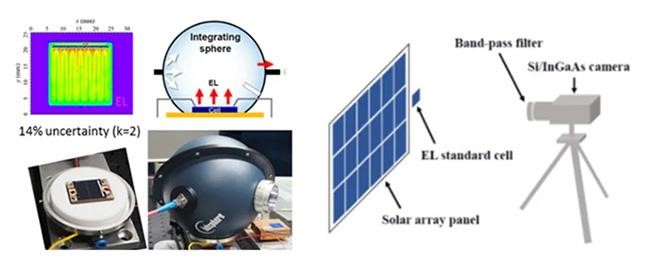

Takano to conduct R&D on solar cells in space applications

(Company statement, June 8)

- Takano will join a JAXA-backed project to develop next-gen solar modules for space applications, aiming to achieve conversion efficiencies of 35–40%.

- Takano will develop an evaluation device based on electroluminescence (EL) tech.

- CONTEXT: EL is an imaging technique used to evaluate the performance of solar cells by analyzing the light they emit when an electric current is applied.

- TAKEAWAY: Such conversion efficiencies exceed those of conventional silicon solar modules, even for tandem PSCs and CSCs. It can be achieved thanks to much higher solar irradiance in space, roughly 40% greater than on the Earth’s surface. However, SSPS (Space Solar Power Systems) faces operational challenges requiring substantial R&D investment, such as maintaining large structures in orbit, performing maintenance or controlling laser transmission and pointing systems, limiting its potential.

(Company statement, June 3)

- iGrid Solutions, Keio University, and Sakai City launched a demo to track and verify locally generated solar power on an hourly basis using international Energy Tag standards and blockchain.

- The pilot will use rooftop solar installations across Sakai City. The demo seeks to verify “hourly matching,” linking renewable power and environmental attributes by location, volume, and time of generation and consumption.

- CONTEXT: Energy Tag is a set of open-source guidelines designed to facilitate the transition to 24/7 carbon-free energy by enabling the tracking of power generation and consumption in real-time or nearreal time.

- TAKEAWAY: This trial fits into a growing trend in Japan toward 24/7 carbon-free energy (CFE) and hourly matching schemes, which is gaining importance as carbon-accounting standards evolve. The news follows announcements from J-Power, Mizuho Bank, Mizuho Leasing and Mizuho Securities, which also recently demonstrated hourly matching for a future 24/7 corporate PPA, using multiple renewable energy sources and digital tracking tech. Also, NTT Anode Energy, NTT Docomo and JERA Cross are among firms that completed demos of hourly matching solar and biomass generation to supply telecom facilities, one of Japan’s first such projects involving biomass power.

Riken Technos subsidiary in Vietnam launches PV system

(Company statement, June 11)

- Riken Vietnam, a subsidiary of Tokyo-based chemical firm Riken Technos, started full-scale operation of a solar power system for factory buildings in Vietnam.

- The firm installed 900 rooftop solar panels, enough to meet 12% of the factory’s total power needs.

- CONTEXT: Riken Technos is historically related to Riken, Japan’s largest institute for natural sciences research. Today it’s an independent, publicly listed firm. Riken Technos supplies the materials enabling electrical infrastructure to function with its electronics segment, producing compounds used for power cable insulation and sheathing or EV wiring harnesses and vehicle electrical systems.

Q.ENEST inks bridge loan for scalable distributed PV platform

(Company statement, June 8)

- Q.ENEST Holdings secured a development bridge loan facility from JA Mitsui Leasing to support the acquisition and construction of low-voltage solar projects across Japan.

- The financing follows a ¥9 billion facility arranged by Sumitomo Mitsui Banking Corp in May to fund an 80 MW portfolio of distributed solar assets.

- CONTEXT: Q.ENEST serves as Hanwha Group’s dedicated renewables platform in Japan. Originally part of Hanwha Japan, in 2023, the business was separated into Q.ENEST Holdings for the development and operation of distributed solar and other renewable energy assets.

- TAKEAWAY: The deal highlights growing investor appetite for aggregated distributed solar portfolios in Japan. Rather than financing projects individually, Q.ENEST is establishing a scalable development platform that can continuously acquire, build, and refinance solar assets as the market expands.

REXEV and Machi Mirai launch program for PV assets converting to FIP

(Company statement, June 9)

- Energy tech startup REXEV and Machi Mirai, a renewables aggregator and developer, are launching REXEV e.CYCLE, a service to help PV projects switch to FIP, add BESS, and optimize revenues through aggregation and energy trading.

- The program will cover procedures for FIT-FIP conversion; add batteries to solar plants to store lowvalue electricity and sell when prices are higher.

- TAKEAWAY: The service aims to increase the profitability of existing FIT solar assets by combining FIP conversion with BESS and market optimization, while also returning some value to local communities.

Toda and Eurus Energy launch DR demo in residential BESS

(Company statement, June 10)

- Toda and Eurus Energy launched a DR demo combining a VPP and a cloud-based energy management platform.

- The demo, at Toda’s research center in Tsukuba, combines Eurus Energy’s VPP platform, ReEra, with Toda’s cloud platform.

- Connected to a residential BESS it aims to assess:

- the stability of electricity supply;

- reductions in electricity consumption costs;

- automatic switching to a low-energy mode when no DR request is issued.

UBE and Maxell to produce separators for batteries

(Company statement, June 3)

- UBE Maxell plans to make separators for lithium-ion batteries in Sakai (Osaka Pref).

- This move is due to the rise in demand for BESS in datacenters and xEVs.

- CONTEXT: A separator is a membrane that keeps the anode and cathode separate.

- CONTEXT: An xEV stands for “Electrified Vehicle” and includes all types of electrically powered vehicles (100% electric, plug-in, hybrid, etc).

NEWS: WIND POWER AND OTHER RENEWABLES

Regional rivalry heats up as METI and Vestas agree on offshore wind turbine production

(Nikkei, June 6)

- Muroran, Kitakyushu, and Akita govts launched a competition to attract major wind turbine giant Vestas.

- In March, Vestas and METI agreed to localize offshore wind turbine production.

- Under the MoC, Vestas and METI plan to establish domestic assembly of turbine nacelles by FY2029 and build a full Japanese supply chain and complete turbine assembly by FY2039, subject to sufficient market growth and a stable pipeline of offshore projects.

- The regional rivalry reflects a struggle over who will anchor Japan’s offshore wind supply chain.

Each city is leveraging industrial assets, geographic advantages, etc:- Muroran highlights its steelmaking, shipbuilding, port infrastructure, etc;

- Kitakyushu promotes its offshore wind experience, industrial base, etc;

- Akita has proximity to offshore wind development zones.

- CONTEXT: The stakes are significant as nacelle production could create jobs and attract a broad supplier network spanning electrical equipment, machinery, bearings, logistics, and maintenance services. However, Vestas made clear that investment depends on Japan providing long-term certainty for future offshore wind auctions. Amid delays and project cancellations, the restart of govt tenders will be the key factor determining whether Vestas proceeds with a major manufacturing investment and where it will be located.

- TAKEAWAY: Japan has largely relied on imported turbines and overseas expertise. Domestic nacelle assembly by 2029 could shorten supply chains and improve delivery reliability, but it will not by itself resolve offshore wind deployment bottlenecks. Recognizing this, Vestas has signed agreements with DENZAI and Nippon Express to explore cooperation on installation engineering, heavy lifting, logistics and O&M services. This signals that localization efforts need to extend beyond turbine manufacturing to the broader supply chain necessary to build and operate offshore wind projects.

Mitsubishi HC Capital and Brookfield launch renewable energy JV

(Company statement, June 10)

- Mitsubishi HC Capital and Brookfield Asset Management will form a JV to invest in and operate renewables assets, starting in Europe and expanding globally.

- As its first transaction, the JV will acquire a portfolio of solar and onshore wind projects totaling 570 MW across Europe – UK, Spain, Sweden, Finland, France, and Ireland – for about €400 million.

- Many assets are backed by long-term PPAs with investment-grade customers, providing stable cash flows.

- The JV will later pursue renewables investments across Europe, North America, and Australia, seeking to build a global renewable energy platform.

- CONTEXT: The partners aim to combine Mitsubishi HC Capital’s financing and investment capabilities with Brookfield’s renewable energy development and asset management expertise.

Cosmo Eco Power inks virtual PPA in wind sector

(Japan NRG, June 8)

- Cosmo Eco Power signed a virtual PPA with Furukawa Electric for environmental attributes from the 6.33 MW Enshu Wind Farm under construction in Shizuoka Pref.

- The PPA follows a similar deal signed in April with Fuji Electric, which produces power semiconductors.

- The Enshu wind project, set to launch in H1 of FY2027, will comprise two 4.2 MW turbines. Electricity generated will be sold to the wholesale power market; Furukawa and Fuji Electric will receive the renewables attributes through vPPAs.

- The Enshu region, spanning the coastline of Shizuoka Pref, is a key area for renewables development. It has several established wind and biomass power plants alongside at least one massive offshore wind project in pre-construction phase.

- Cosmo Eco Power is among the firms repowering its fleet, with at least two projects underway, while developing new projects backed by corporate offtake agreements.

- TAKEAWAY: The agreement highlights a broader shift among Japanese wind developers as aging FIT-era assets are repowered and transitioned to FIP-based business models. Developers are now relying on corporate procurement to underpin new and repowered projects. vPPAs allow wind operators to monetize environmental attributes separately from electricity sales, creating a more flexible revenue model than traditional subsidy schemes.

Chubu Electric to invest ¥23 bln in India’s Continuum Green Energy

(Company statement, June 1)

- Chubu Electric will invest about ¥23 billion in Continuum Green Energy, an Indian wind and solar power generation and electricity sales business.

- Continuum supplies electricity to India’s commercial and industrial sector through corporate PPAs. Following regulatory approvals, Chubu Electric will acquire shares.

- CONTEXT: India aims to install 500 GW of renewable energy capacity by 2030; demand from the C&I sector is expected to continue growing. Chubu Electric supports Japanese firms entering the Indian market in procuring renewables.

Gunma expands hydropower PPA program for industrial users

(Nikkei, June 4)

- Gunma Pref launched the 4th round of its “local production, local consumption” PPA, supplying electricity from prefecture-owned hydropower plants to local businesses.

- The new round will provide 150–180 GWh/ year of renewable electricity from April 2027 through March 2030, with eligible large industrial and commercial users able to receive up to 60 GWh/ year.

- Applications are open until July 10

- TAKEAWAY: The initiative reflects a trend toward regional energy resilience and local clean-energy procurement. While small in national terms, prefecture-led hydropower PPAs offer manufacturers a stable source of renewable electricity and help reduce exposure to volatile fossil-fuel prices.

KDDI SmartDrone completes remote offshore wind turbine inspections

(Company statement, June 10)

- KDDI SmartDrone, a subsidiary of KDDI Corp, and Akita Offshore Wind Power demonstrated a remote drone inspection system for offshore wind turbines.

- It used a vehicle-mounted drone dock at the Akita and Noshiro offshore wind farms.

- Operators can remotely launch, recover, and recharge drones from land.

- During the trial, drones inspected turbine blades for dirt, damage, repair marks, etc.

- A turbine blade inspection was completed in 30–60 minutes per turbine, helping reduce maintenance response times and potential shutdowns.

Toshiba firm to procure environmental attributes from geothermal project

(Company statement, June 5)

- Japan Semiconductor, a Toshiba Device & Storage subsidiary, signed a 15-year virtual PPA to procure environmental attributes from the 5 MW Waita No 2 geothermal plant in Kumamoto. The plant began operations in March.

- CONTEXT: Toshiba is adding 24/ 7 geothermal renewable power to its semiconductor manufacturing decarbonization strategy, to diversify beyond solar.

- TAKEAWAY: Compared with solar and wind PPAs, the number of geothermal PPAs is still very small, less than 10. The market has been dominated by one supplier, Kyuden Mirai Energy, which has been offering geothermal PPAs from its existing geothermal portfolio.

NEWS: NUCLEAR ENERGY

U.S. wants to use Japanese investments toward SMRs

(Nikkei Asia, June 12)

- U.S. Commerce Secretary Lutnick said the U.S. will use Japanese investments to advance SMRs.

- As part of Japan’s $550 billion investment pledge in 2025, Tokyo is negotiating to invest up to $40 billion in SMRs built by GE Vernova and Hitachi.

- This is alongside a potential $25 billion investment in NuScale Power. Total Japanese investments in U.S. nuclear projects could exceed $62 billion.

- Japan has not built a new nuclear plant since 2009. Current regulations are not suited for SMRs, causing the country to fall behind the U.S. and China.

- This investment allows Japan to gain SMR tech and export nuclear components.

- CONTEXT: The White House is processing approvals. The first SMR is expected to be built in Tennessee. The U.S. aims to quadruple its nuclear capacity from 100 GW to 400 GW by 2050. It will add 10 large NPPs and deploy over 300 SMRs.

Onagawa NPP Unit 2 resumes commercial operation

(Company statement, June 9)

- Onagawa NPP Unit 2 (825 MW output) completed the final phase of its 12th periodic inspection and resumed commercial operation.

- CONTEXT: The unit was shut for inspection in January, with reactor startup in May. The work included checking reactor components and replacing some fuel assemblies. Periodic inspections are necessary within 13 months of commercial operation.

JNFL says progress made at Rokkasho reprocessing plant

(Nikkei, June 12)

- Numahata Hideki, Executive VP of Japan Nuclear Fuel (JNFL), met with Aomori vice-governor to discuss design and construction plans for the spent nuclear fuel reprocessing plant in Rokkasho.

- The next stages include submitting revisions to get final approval, such as for safety.

- Numahata said the amendment application process should take three to four months.

- CONTEXT: Completion of Rokkasho is targeted for this fiscal year. Actual plutonium-separation should begin in FY2027. The associated MOX Fuel Fabrication Plant should be completed in FY2027.

NEWS: TRADITIONAL FUELS

JERA signs 20-yr LNG deal with Petronas

(Company statement, June 10)

- JERA signed a 20-year LNG sales and purchase agreement with Petronas LNG, a subsidiary of Malaysia’s state-owned Petronas.

- Starting in 2028, JERA will get up to 2 Mtpa of LNG from Malaysia.

- CONTEXT: Malaysia represents around 15% of Japan’s LNG imports. It is the second largest supplier, after Australia (which represents 40%). Takaichi had met with the Australian leader at the beginning of last year, aiming to strengthen LNG procurement with the Oceanian country as well.

- TAKEAWAY: After meeting with Malaysian PM Anwar Ibrahim, Takaichi stressed the importance of strengthening energy partnership with Malaysia, deeming the country a reliable partner amidst a worsening global geopolitical environment. The two also signed agreements on fertilizer feedstocks and critical mineral supply chains.

- SIDE DEVELOPMENT:

- JERA receives first LNG shipment from Barossa

- (Company statement, June 12)

- JERA received its first LNG shipment from the Barossa Gas Project in Australia, arriving at its Futtsu LNG terminal.

- JERA will receive about 0.425 Mtpa.

- JERA has investments in the Wheatstone LNG Project and Scarborough Gas Field.

- CONTEXT: The Barossa Gas Project, offshore Australia’s Northern Territory, began production in 2025. Gas from Barossa is processed at the Darwin LNG plant and exported worldwide.

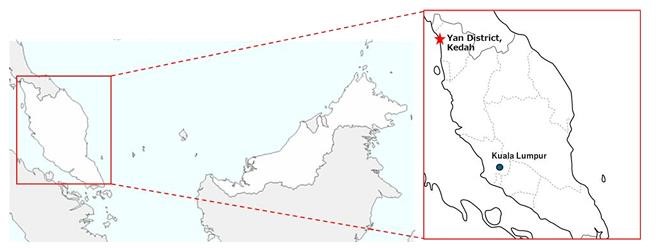

Tokyo Gas to develop LNG terminal in Malaysia

(Company statement, June 8)

- Tokyo Gas agreed with Gas Malaysia Berhad and VTTI to develop the RGT Yan LNG receiving terminal in Malaysia’s Kedah state.

- It uses a floating storage and regasification unit (FSRU).

- The $765 million project is a massive expansion of Malaysia’s energy grid, with 6 Mtpa regasification capacity, moving the country toward full gas market deregulation

- CONTEXT: RGT Yan is owned by Gas Malaysia Berhad (70%); Tokyo Gas (15%), and VTTI (15%). An FSRU stores LNG transported by carrier vessels and sends vaporized gas to thermal power plants and city gas networks. Compared to onshore terminals, FSRUs offer lower construction costs and shorter delivery times.

- TAKEAWAY: Malaysia has been a major producer and exporter of natural gas since the 1970s. However, due to approaching depletion of gas fields and rising electricity demand, the country will most likely have to import LNG. This trend aligns with the aggressive LNG trading by Japanese companies in recent years. Specifically, Tokyo Gas is expanding its presence in Malaysia, developing LNG terminals in Japan and operating an FSRU in the Philippines from 2025. This is part of a broader company plan to develop a South-Asian LNG chain. For more info, see the analysis section of April 21 2025 Japan NRG issue.

Unions to extend strike at INPEX’s Ichthys LNG

(Reuters, June 9)

- Workers at INPEX’s Ichthys LNG in Australia will escalate their strike from four-hour to eight-hour daily stoppages. There will be other work bans.

- The union says INPEX reneged on terms agreed during a mediation session.

- CONTEXT: Ichthys accounts for about 10% of Australia’s total LNG supply. It has an output of 9.3 Mt, and 70% of it goes to Japan, Also, Australia is Japan’s largest LNG supply source.

- TAKEAWAY: Although there have not yet been any repercussions so far, as the strikes have only just begun, a prolonged labor dispute could have serious consequences. INPEX plans to take legal action to block an escalation, warning that an extended strike would disrupt domestic fuel supplies and hurt LNG buyers. Major off-takers include TotalEnergies and Taiwan’s CPC. The facility also supplies domestic gas to Australia’s Northern Territory.

Woodside exercises preemption right and buys stake in Browse project

(Company statement, June 12)

- Woodside will exercise its preemption right to increase its stake in the Browse Gas Project off Australia’s west coast.

- It will get a 10.675% stake from PetroChina that was slated for sale to INPEX.

- Woodside’s stake will rise from 30.6% to 41.27%.

- CONTEXT: Browse is Australia’s largest undeveloped gas resource. It has a potential output of 11.4 Mtpa of LNG, LPG, and domestic gas.

- TAKEAWAY: Woodside’s aim is to pipe gas to the company’s North West Shelf plant, since supply from existing fields is diminishing. INPEX could have routed the gas to its Ichthys LNG project in Darwin. The potential conflict led Woodside to exercise its preemption right.

JGC awarded major contract for Mozambique’s FLNG project

(Company statement, Japan NRG, June 8)

- JGC won an engineering, procurement, construction, installation, and commissioning (EPCIC) contract for Coral North Floating LNG in Mozambique, 50 km offshore.

- LNG production will total about 3.6 Mtpa, starting in 2028.

- Sales are targeted for Europe and China.

- JGC and Technip Energies France will lead project management. Samsung Heavy Industries (SHI) will build the vessel’s hull and handle ship assembly.

- Construction will total about $5 billion. JGC’s share exceeds $1 billion.

- CONTEXT: This is Mozambique’s second FLNG. The first was the Coral South Project. JGC, Technip, and also collaborated on that, which launched in 2022.

- TAKEAWAY: An offshore FLNG plant allows gas extraction from sites without pipeline infrastructure, avoiding local security threats. Onshore projects in Mozambique have faced interruptions due to an insurrection, such as Mozambique LNG led by TotalEnergies.

LNG stocks down over last week, down YoY

(Government data, June 10)

- As of June 7, the LNG stocks of 10 power utilities were 1.8 Mt, down 5.3% from the previous week (1.9 Mt), down 19.3% from end June 2025 (2.23 Mt), and down 15.1% from the 5-year average of 2.12 Mt.

- The rainy season has officially begun across most of the country. Humidity is high, but temperatures are moderate so far, thus limiting air-conditioner use.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Govt to subsidize up to 75% of CCS project construction costs

(Government statement, Japan NRG, June 12)

- The govt is introducing the CCS Cost Difference Support Measure because the cost of implementing CCS is higher than purchasing CO2 emission allowances.

- This system aims to bridge that financial gap and speed up cost reductions.

- The support covers the difference between a “Base Price” and a “Reference Price”. The former is the actual cost per ton of CO2 for separation, transport, and storage. The latter is based on the average trading price on the emissions trading system.

- The Base Price’s formula divides total CAPEX and OPEX by the total expected volume of stored CO2. The formula adjusts for inflation and allows for up to a 10% reserve fund to handle construction cost overruns.

- The govt will subsidize up to 75% of construction costs before operations begin. The subsidy spans 15 years from the start of storage. Operators must pledge to a 10-year business continuity obligation after the 15-year support period ends.

- CONTEXT: The govt has a target to store 6 to 12 Mt of CO2 a year by 2030. To realize this, new facilities must begin construction by FY2027. Currently, five domestic projects are progressing. They include offshore trial drilling in Tomakomai (Hokkaido) and Kujukuri (Chiba). However, CCS requires high initial investments, in the range of ¥100-200 billion for separation/recovery, and ¥100-350 billion for transport/storage.

- TAKEAWAY: In the past few years, Japan has built a regulatory CCS framework, such as the 2024 CCS Business Law. But, the industry still faces daunting challenges. Capturing and storing CO2 does not provide profit, it is only a cost item at this stage. A solution is carbon pricing. But, full-chain CCS will likely cost ¥10,800-¥18,200/ ton of CO2 by 2030. In contrast, nationwide voluntary carbon credits are only trading between ¥5,000 and ¥6,000. The current carbon price is too low to close the gap. To have the industry running, significant govt financial backing is essential – and these measures confirm this. Another imperative is to tighten the GX-ETS, raising the floor price of domestic carbon credits.

NEDO selects Sumitomo for biomass-derived carbon recycling

(Company statement, June 4)

- NEDO chose Sumitomo Heavy Industries to promote cross-industry collaboration on carbon recycling in Sakata (Yamagata Pref).

- The project aims to build a carbon supply chain by assessing uses for CO2 emitted from biomass power plants.

- Other participants include Yamagata pref, Sakata City, Maeta Concrete Industry, Toho Acetylene, and Yamagata Bank.

- Sumitomo Heavy will oversee the project; Toho Acetylene will handle LCO2 distribution; and Maeta Concrete Industry will work on carbon fixation in concrete.

- TAKEAWAY: The cement industry is one of the most carbon-intensive sectors, generating about 2.4 billion tons of emissions globally each year. In Japan, cement production ranks third in industrial carbon emissions. Biomass is regarded as a renewable energy source because its emissions are considered part of the natural carbon cycle. If emitted CO2 is captured and permanently stored or incorporated into materials, it can result in negative emissions while also helping reduce the carbon footprint of cement production.

Carbon EX agrees with SMBC on expansion of J-Credits

(Company statement, June 10)

- Carbon EX agreed with SMBC to support the creation and sale of J-Credits through the operation of its AI platform.

- The platform provides end-to-end support to companies, from project design and registration to identifying potential buyers.

- TAKEAWAY: Banks tend to show greater interest in providing services related to J-Credits than NFCs, as J-Credits extend beyond renewable power generation. Projects eligible for J-Credits can include high-efficiency boilers, agriculture, or energy-saving measures in commercial buildings. This broad range of applications expands the pool of potential clients. Another reason is that J-Credits involve more administrative procedures, creating additional demand for the support and advisory services that banks can provide. SMBC has signed several other agreements related to J-Credits, including with BYWILL and the Tokyo Govt.

Archeda and Aboitiz seek to develop forest carbon model in SE Asia

(Company statement, June 9)

- Japan-based Archeda, an AI firm specializing in carbon-credit MR (measurement, reporting, and verification), signed an MoU with Aboitiz Foundation, the sustainability arm of Aboitiz Group, to develop high-integrity forest carbon projects in the Philippines.

- The goal is to improve transparency, measurement accuracy, and credibility of forest carbon credits in the Philippines.

- Archeda will provide satellite-based monitoring and AI analytics to support forest carbon credit development, with the Japan–Philippines JCM as the framework.

Green Carbon launches Vietnam JCM rice-carbon project

(Company statement, June 9)

- Green Carbon, a Tokyo-based climate-tech and carbon credit developer, is partnering with Korea Investment Holdings to launch an AWD (Alternate Wetting and Drying) rice cultivation project in Nghe An Province, Vietnam.

- The goal is to reduce methane emissions from rice paddies and generate carbon credits under Japan’s Joint Crediting Mechanism (JCM).

- The firms plan to develop an approved JCM methodology for Vietnam’s agricultural sector and eventually issue JCM credits.

- CONTEXT: The project comes as both Japan and Vietnam increase cooperation on low-carbon growth and seek to expand JCM-based emissions reductions, especially in agriculture, where AWD is a key tool for methane abatement in rice farming.

NYK Line launches demo of vessel running 100% on biofuel

(Company statement, June 2)

- NYK Line launched a 1-yr demo of B100 fuel made from FAME (Fatty Acid Methyl Ester) derived from used cooking oil.

- The trial aims to assess the fuel’s impact on the vessel’s engine performance and the safety of vessel operations.

- CONTEXT: NYK Line has previously conducted demos using B24 and B30 blends (the numbers indicating the percentage of biofuel in the fuel mix).

ANA and partners produce biogas with food residues in Hokkaido

(Company statement, June 5)

- ANA Foods, Urban Energy, J&T Recycling and Sapporo Bio Food Recycling agreed on a waste management scheme in Sapporo using Urban Energy’s Sodenwari® model.

- Residues from banana processing are collected and used as feedstock for biogas production through methane fermentation.

- CONTEXT: Urban Energy and J&T Recycling are subsidiaries of JFE Engineering. Urban Energy has been operating its circular model since 2017.

Mitsubishi Electric and VTT develop DOC technology

(Company statement, June 11)

- Mitsubishi Electric and VTT Technical Research Centre are working on a Direct Ocean Capture (DOC) system that removes CO2 from the atmosphere via seawater.

- The system uses an acidification approach to recover gaseous CO2. This enables both CCS and CCU for synthetic fuels or industrial feedstocks.

- The design integrates with existing seawater intake infrastructure.

- Field tests are planned; Mitsubishi Electric seeks partners.

ANALYSIS

BY MAGDALENA OSUMI

Repowering Aging Wind Farms Gives Sector New Lease on Life

Over a third of planned onshore wind projects in Japan face delays, permitting risks or other development hurdles, according to industry body Japan Wind Power Association. While discussions about future growth often focus on turbines planned for new sites, many existing assets have reached an age when upgrade investments or full replacement is now vital.

Some wind power developers and asset owners are deciding to modernize, or “repower”, existing wind farms – a strategy that can unlock substantial gains in energy production without many of the hurdles associated with greenfield projects.

Repowering typically involves replacing aging turbines with newer, larger and more efficient machines while leveraging existing site infrastructure, grid connections and operational experience. Such an opportunity over the next decade exceeds 1 GW in power capacity.

In mature wind markets such as Germany and Denmark, repowering is an important tool for extending the life of established wind sites and maximizing energy output from limited land resources. By increasing generation at proven wind sites and making more efficient use of existing grid infrastructure, repowering can help bridge the gap between an aging first-generation fleet and the country’s future renewable energy ambitions.

Background: Overhaul needs rising

As of December 2025, Japan had about 6.5 GW of installed wind capacity and 2,866 operating turbines.

The onshore wind sector began expanding after the first commercial wind projects came online in 1999. Growth was driven by government support programs, the Renewable Portfolio Standard (RPS) introduced in 2003, and later the Feed-in Tariff (FIT) scheme.

On top of that, Japan hosted the Kyoto Protocol in 1997 and committed to greenhouse gas reductions. As a result, renewable energy, including wind power, received greater policy attention in the late 1990s and early 2000s. Wind power was then viewed as one of the practical technologies available for reducing CO2 emissions.

Today, onshore projects account for more than 90% of Japan’s installed wind capacity – the remainder is offshore – and most developments rely on government-backed support mechanisms such as FIT.

As those projects approach 20–25 years of operation, operators face a critical decision: continue operating aging equipment with rising maintenance requirements, undertake life-extension measures, or replace first-generation turbines with modern machines capable of producing significantly more electricity from the same site.

The timing is highly relevant given Japan’s long-term energy ambitions. Under its 2040 energy strategy, the government aims to raise the share of renewables in the power mix to 40–50%, with wind power expected to contribute 4–8% of the national total. Achieving these goals will require not only the successful deployment of new projects but also an optimization of existing renewable energy assets.

In Europe, repowering has become a common theme, especially in markets such as Germany, Denmark and Spain. Among the latest to undergo the revamp is the first phase of the Montes de Cierzo wind project in Navarra, Spain, where Europe’s largest renewables firm, Statkraft, said it recently replaced 44 old turbines with 10 new ones thus boosting installed capacity 50% to 90 MW. The project will also add batteries.

Major developments

Currently, Japan only has a handful of confirmed, large-scale onshore wind repowering projects, led by the country’s largest wind developer Eurus Energy, 100% owned by trading house Toyota Tsusho. Along with electricity generator J-Power, Eurus was one of the first companies in Japan to restart modernized wind farms in 2022.

The repowering opportunity extends to around 1 GW of the existing onshore fleet, with many candidates due to emerge during 2025–2035, according to Japan NRG estimates based on a review of sector data.

Repowering decisions are typically triggered by a combination of end of design life (20– 25 years), rising O&M costs, lower turbine availability, FIT or PPA expiration and availability of much larger modern turbines. So far, Eurus has modernized two projects, with two more reconstructions underway.

Cosmo Eco Power relaunched its Shin-Iwaya wind project in March 2025; it was operational from February 2003 to March 2023 as Iwaya Wind Park. The old installation had 18 Neg Micon NM64c/ 1500 turbines (total capacity 27 MW). The updated site uses seven GE Vernova 4.3 turbines (total installed capacity 30 MW, though curtailed at 27 MW).

Cosmo Eco Power has five more wind farms built between 2001 and 2009, with cumulative capacity at nearly 30 MW. Any one of these is a candidate for repowering with one having completed the Environmental Impact Assessment (EIA).

Here’s a brief overview of recently repowered projects:

Nikaho-kogen Wind Power in Akita Prefecture

- Original start of operation: December 2001

- 15 × 1.65 MW turbines

- Total capacity: 24.75 MW

Repowered project (March 2024)

- 6 × 4.3 MW Siemens Gamesa turbines

- Total capacity 24.75 MW

Eurus Kamaishi Wind Farm in Iwate Prefecture

- Original start of operation: December 2004

- 43 × 1 MW Mitsubishi Heavy Industries turbines

- Total capacity: 43 MW

Repowered project (March 2026)

- 11 × 4.2 MW Vestas turbines

- Total capacity ~46 MW class

- Much lower turbine count and higher efficiency

Eurus Nishime Wind Farm in Yurihonjo City, Akita Prefecture

- Original start of operation: November 2004

- 15 × 2 MW Vestas turbines

- Total capacity: 30 MW

Repowered project (March 2026)

- 7 × 4.3 MW Siemens turbines

- Same nominal capacity (~30 MW)

- Larger turbines, fewer units, improved maintenance efficiency

Eurus Mameda Wind Farm in Aomori Prefecture

- Original start of operation: October 2003

- 6 × 1.75 MW turbines

Repowering underway

- Three original turbines to be replaced with two 4.3 MW Siemens turbines

- Commercial operation expected in 2027

Replacing older turbines with fewer but larger ones is often more cost-effective than developing projects from scratch, particularly given Japan’s nonexistent domestic turbine manufacturing base and limited supporting infrastructure. Early Japanese wind farms often used 600 kW–2 MW turbines. Today’s standard models are at 4-6 MW capacity.

For now, projects by major operators such as Eurus Energy and Cosmo Eco Power point to what could become a much larger market over the next decade. In the best cases, output can rise far faster than nameplate capacity, especially where old turbines are replaced with taller, larger-rotor machines.

Recent repowering projects at Kamaishi and Nishime, now rebuilt and operational, illustrate this trend. Developers replaced small 1–2 MW turbines with fewer units but each with a capacity over 4 MW, boosting output and maintenance efficiency while leveraging existing infrastructure and grid transmission and permits.

Another example of the makeover is Eurus’s Tomamae Wind Farm in Hokkaido. The original project had 19 Siemens/Toshiba 1-MW turbines and one 2-MW unit. The developer is now using General Electric’s 4.2 MW turbines. The repowered configuration utilizes five turbines to reach a capacity that’s actually 1 MW less than previous, but generation volumes are expected to increase by roughly 20%.

Standard wind turbines from early 2000s

FIP transition as prelude to market overhaul

The gradual shift of the wind industry from FIT to FIP is expected to improve the incentives for repowering. Many projects commissioned during the first major wave of wind development in the early 2000s and 2010s are now approaching the end of their FIT contracts, prompting operators to assess whether to extend asset life, refurbish existing turbines or replace them with newer, higher-capacity models.

The earliest FIT-supported onshore wind projects will begin reaching the end of their 20year FIT terms starting 2032. But many pre-FIT projects are already 15–25 years old and at an age where major refurbishment or repowering are economic considerations.

This is especially relevant because during periods of grid congestion the priority dispatch guidelines favor FIP projects over those on older FIT plans. This means FIT projects face mandatory output curtailment first before any FIP projects are curtailed.

The shift to FIP also encourages operators to improve performance and lends itself to considerations around adding battery storage. A bolt-on BESS can reduce imbalance risk, improve capture prices and make market-based offtake structures like VPPAs more attractive.

Conclusion

With hundreds of small wind farms now at the end of their operational life, repowering offers a cost-effective way to help Japan meet net-zero targets while also upgrading the technology, shrinking wind’s footprint and notably boosting electricity volumes.

For developers, the attractiveness of repowering includes the chance to reduce administrative issues outside of their control, such as grid interconnection bottlenecks, while upgrading asset economics. In fact, the grid connection alone makes older wind farms value higher than their capacity numbers suggest.

Whether or not repowering ultimately becomes a niche strategy or a major source of new wind generation will depend on the timescale of conversions, business model upgrades, and how much operators wish to embrace larger turbine technologies.

The availability of turbines is another factor that will play a role at a time when much of the supply chain has refocused around offshore wind models.

Japan’s bigger targets for wind lie in the offshore revolution that has yet to take off. But in the near-term, the sector’s most practical and bankable gains will come from existing wind farms already on land.

Below is a list of the oldest onshore wind farms selected for and/ or seen as strong candidates for repowering:

| Wind Farm | Operator | COD | Original capacity (MW) |

| Rokkashomura Wind Farm phase I (planned repowering) | Japan Wind Development (completed EIA for 33 MW wind farm in 2025) | 2003 | 30 (20 GE 1.5 MW turbines) |

| Aoyama Plateau Wind Farm (planned repowering) | (planned replacement with 7 × 2.3 MW turbines) | 2003 | 15 (20 × JFE Engineering 750 kW units) |

| Soya Misaki Wind Farm | Eurus Energy | 2005 | 57 |

| (Japan’s largest onshore wind farm, currently undergoing repowering demolition) | (restart planned for 2029) | (57 × MHI 1 MW turbines) | |

| Green Power Kuzumaki Wind Farm (Japan’s first large-scale wind farm at an elevation of more than 1,000 m) | J-Power | 2003 | 21 (12 × Vestas 1.75 MW) |

| Nunobiki Plateau Wind Farm | J-Power | 2007 | 65.98 (33 Enercon E-70 2MW and 2.3 MW turbines) |

| Choshi Wind Farm | Japan Wind Development | 200 | 13.5 (9 × 1.5 MW) Turbines: REpower Systems SE (now part of Senvion SE |

| Tahara Rinkai Wind Farm | J-Wind TAHARA (J- Power affiliate) | 2005 | 22 (11 × Vestas 2 MW) |

| Irouzaki Wind Farm | J-Power | 2010 | 34 (17 Vestas 2 MW turbines) |

| Aso Oguni Wind Farm (first large-scale wind plant allowed to operate in a Japanese national park) | J-Power (moving forward with scoping and replacing plan) | 2007 | 8.5 portion (5 × 1.7 kW Vestas turbines) |

| Iwata Wind Farm | Cosmo Eco Power | 2009 | 15 (5 Vestas 3 MW turbines) |

Right: Green Hill Wind Park in Hokkaido

Below: Nunobiki Plateau Wind Farm, 33 Enercon E70/ 2 MW

Credit: Yonezawa Yamagata

https://commons.wikimedia.org/wiki/

File:Nunobiki_wind_farm_1389924513.jpg

{kind=link}

ANALYSIS

BY TETSUJI TOMITA

Balancing / Spot Market Analysis and Impact from the U.S.-Iran War

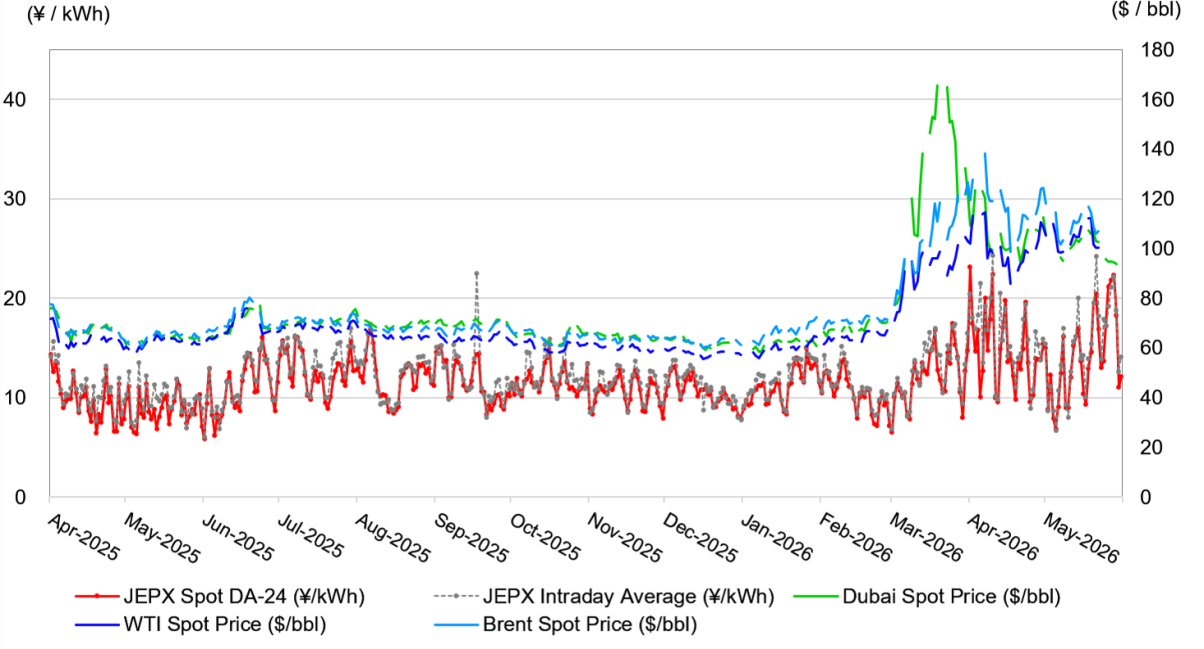

Japan’s electricity market has seen this movie before. In 2021, scarce LNG helped send wholesale prices to emergency levels and forced regulators to impose a ¥200/ kWh cap. In 2022, Russia’s invasion of Ukraine triggered another energy shock, exposing how little hedging capacity many retailers had and how thin Japan’s forward market still was.

The situation around the U.S.-Iran war is different. Oil and LNG prices have again put upward pressure on thermal generation costs, lifting JEPX spot prices in the morning and evening hours when fossil-fuel plants still set the marginal price. But this time the shock passes through a market that is more liquid, more hedged and more financially aware than it was three years ago.

That has changed the shape of the stress. Spot prices have become steeper and more volatile, but the balancing market response is even more extreme. Fast-response products with greater battery and hydro participation have shown how they are less directly exposed to fuel costs, while longer-duration and energy-heavy reserve products remain tied to thermal economics.

The result is a more nuanced test of the electricity market reforms since 2016. The question is no longer whether fuel shocks raise power prices. They clearly do. It’s more about whether Japan’s maturing power market can absorb that shock – and where imported fuel still sets the price of flexibility.

JEPX spot DA-24 prices vs. crude oil spot prices

Impact on JEPX spot and intraday market

The most direct consequence of the oil price surge has been an increase in thermal generation costs. LNG-fired power plants continue to play a key role as marginal generators in Japan’s electricity system, especially during periods when renewable output is insufficient.

As crude prices increased following the conflict, the oil-linked LNG prices also rose, leading to higher procurement costs for power producers. These increases have fed into JEPX spot prices with the effect pronounced during morning and evening peak demand periods. That’s when thermal generation often sets the market clearing price.

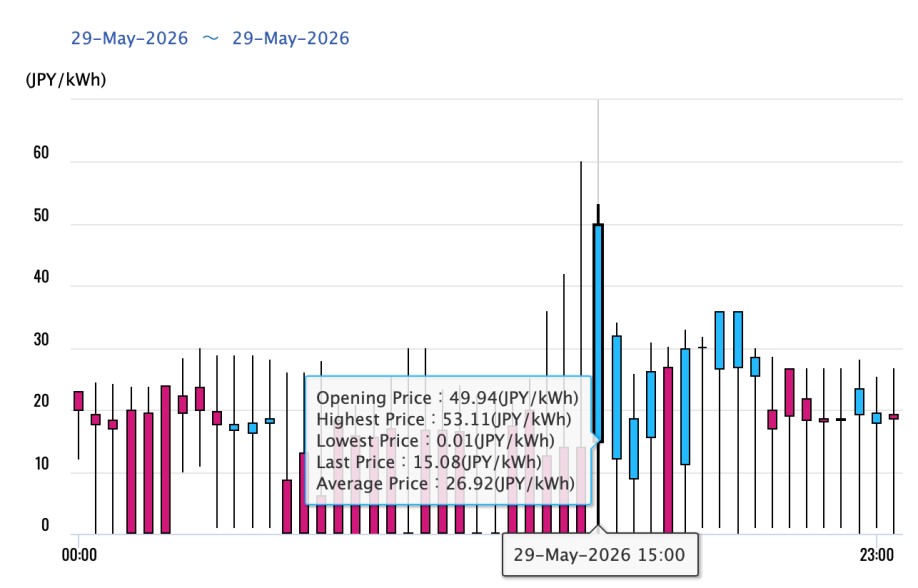

Although abundant solar generation continues to suppress prices during daylight hours, the spread between midday and evening prices has widened considerably. For example, on the last Friday of May, the 29th, wholesale electricity traded at ¥8.12/ kWh at noon; at ¥31.04 at 6:30pm; and ¥0.01 at noon the following day.

The intraday market has been even more sensitive to the effects of fuel price increases. Because the market reflects near-real-time supply-demand conditions, participants must continuously adjust their positions in response to renewable forecast errors, unexpected demand fluctuations, and operational constraints.

Taking the same example of May 29, intraday prices at 3pm ranged from a low of ¥0.01 to a high of ¥53.11, with the average at ¥26.92.

Intraday Market pricing chart

Higher fuel costs have encouraged thermal generators to maintain larger operational reserves and to be more selective in offering volumes to the market. In fact, in May, the ratio of spot power relative to total electricity demand rose to 46% as the major utilities dialed back their thermal plants and instead relied on JEPX to cover odd spikes in air-conditioner-led demand.

The lower available liquidity – especially in the intraday market – contributed to sharper price movements.

Still, the contrast with 2022 is important. Traders say Japan’s power futures market has become more usable since the Ukraine crisis, with more participants, better liquidity and more credible forward prices. That has allowed retailers and trading desks to reduce exposure, manage VaR and adjust hedges across power, LNG, oil, coal and related basis risks.

The latest shock has not produced the same sense of market paralysis, but it shifted attention to a different constraint: Japan’s power market may now have better prices and deeper hedging tools, but its collateral, clearing and credit-risk practices still need to catch up.

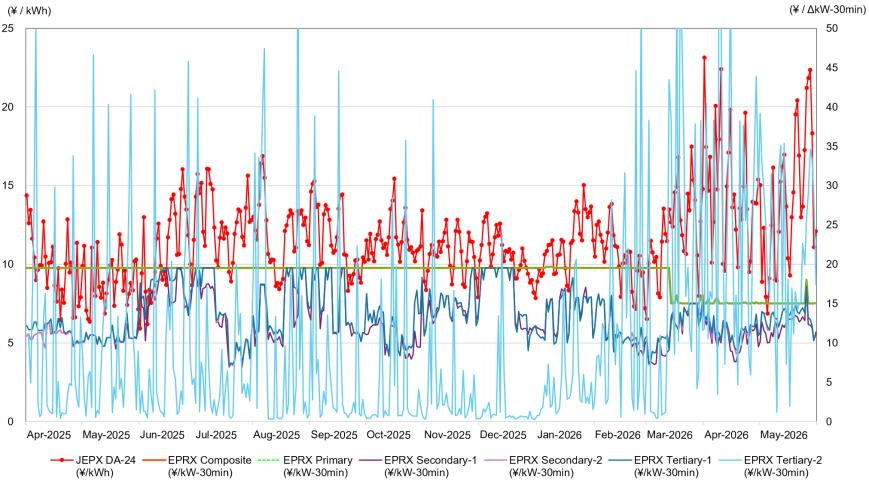

Impact on Balancing Market (EPRX)

Balancing service providers determine their bidding strategies by comparing potential revenues from JEPX with that available via the EPRX. Naturally, this follows that increases in wholesale electricity prices raise the opportunity cost of providing balancing services, placing upward pressure on EPRX clearing prices.

So far, Primary Reserve is the least affected balancing product. Since it mostly compensates providers for maintaining available capacity rather than delivering significant amounts of energy, fuel price increases have had only a limited direct impact. Nevertheless, higher standby and operational costs for thermal units have contributed to modest bid increases.

The impact on Secondary Reserve-1 has also been relatively small. This product increasingly relies on BESS and pumped-hydro resources, both of which are less exposed

to fuel cost fluctuations. However, gas-fired units participating in this segment experience increased operating costs, which creates some upward pressure on prices.

Secondary Reserve-2 has been more significantly affected. This product often requires sustained output adjustments over longer durations, making fuel consumption a more important component of service provision costs.

Tertiary Reserve-1 has experienced substantial upward pressure due to both fuel cost increases and rising JEPX prices. Since many providers are thermal generators, operators must consider whether participating in the balancing market is more profitable than selling electricity into the wholesale market. As the latter rises, balancing market bids also compensate for the higher opportunity cost of withholding capacity from JEPX.

Comparison of JEPX spot prices and EPRX highest awarded prices

Among the balancing products, Tertiary Reserve-2 has likely been the most affected.

This product frequently requires actual energy delivery, making fuel costs a direct determinant of profitability. As LNG and oil prices have risen, providers have incorporated these higher costs into their bidding strategies, leading to rising awarded and clearing prices. As such, Tertiary-2 is the product that most mirrors spot market conditions also because it is procured to manage forecast errors.

Effects of FY2026 market reforms

Starting in FY2026, rules governing the balancing market were revised. The following changes took effect on March 14.

- All balancing products shifted to day-ahead trading: Previously, Primary, Secondary1 & -2, and Tertiary-1 were procured on a weekly basis, while Tertiary-2 was traded day-ahead. From FY2026, all products are traded in the day-ahead timeframe.

- Introduction of a Composite for all products: All products are now procured through a new composite market framework, improving procurement efficiency and flexibility.

- Trading granularity shortened to 30-minute blocks, allowing for more precise balancing.

- Revision of bidding price caps for fast-response products: The price cap for Primary, Secondary-1, and Composite was reduced from ¥19.51/ ΔkW·30 min to ¥15/ ΔkW·30 min, while the caps for Secondary-2 and Tertiary-1 remain at ¥7.21. Tertiary-2 continues to have no price cap.

- New rules facilitate the participation of distributed energy resources (DERs), batteries, demand response (DR), and low-voltage supply, while enabling broader inter-regional procurement of balancing capacity.

- The treatment of startup costs and other post-settlement items has also been updated to align with the new market design and to improve transparency.

Following the shift of all balancing products to day-ahead, the EPRX market became more sensitive to short-term supply-demand conditions reflected in the spot market.

Tertiary-2 prices increased across all areas in April compared with the FY2025 average before the market change. This was likely because bids shifted to the Composite Market, which offers a higher probability of clearing, allowing more of the high-priced bids to succeed in Tertiary-2.