WEEKLY

June 22, 2026

ANALYSIS

BEYOND HORMUZ: JAPAN’S NEXT ENERGY SECURITY CHALLENGE

- Japan’s total dependence on Middle Eastern oil is no longer sustainable. Tokyo’s initial response has been an aggressive pivot towards petroleum imports from the U.S.

- But this might replace one dependence with another. Japan’s path forward requires building a more resilient system on top of the short-term measures adopted during the crisis.

SODIUM-ION BATTERIES: THE NEXT FRONTIER FOR BESS?

- Lithium-ion batteries dominate across a wide range of energy storage applications. But a new technology – sodium-ion batteries (SIBs) – offers several key advantages over lithium.

- While China has charged ahead in SIBs, Japan has so far overlooked this tech. Is Japan missing a new opportunity, or is this indifference justified?

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- TEPCO narrows capital alliance talks to five groups including SoftBank and KKR

- Japan explores rare-earth mining in Greenland

- EEX to expand power futures and options

- OCCTO reviews balancing market transactions after reforms

- METI accepts temporary power, gas discounts

- Govt ends participation in ammonia co-firing projects, casting doubt on timelines

- INPEX supplies electricity generated from H2

- JERA signs time charter deal with NYK and MOL for ammonia carriers

- Japan mulls EV battery recycling mandate

- Tokyo Century and TESS open 50-MW BESS

- Osaka Gas expands into energy management, EV charging

WIND POWER AND OTHER RENEWABLES

- GWEC: Japan must accelerate offshore wind

- MoE concerned over large Cosmo wind farm

- JRI: Existing flood-control dams could double national hydropower output

- Govt: MOX fuel transport to France progresses

- Kanagawa backs superconducting coil project for future fusion reactors

- U.S. extends Japan’s Sakhalin-2 import license

- Oil import costs hit record high in May

- Uniper privatization draws interest from bidders including JERA

- Australian unions reach deal with INPEX, strike off at Ichthys LNG

CARBON CAPTURE & SYNTHETIC FUELS

- Japan Liquid Carbonic, Ube Materials to conduct CO2 supply chain study

- MoE launches CCU promotion subsidy

EVENTS

June 23-25 “Summer Davos” in Dalian, China

Jun 30-Jul 1 Asia Nuclear Energy & SMR 2026 @

Singapore

Jun 11-Jul 19 FIFA World Cup

July 1-2 4th WFO Asia Pacific Summit @ Tokyo

August Asia-Pacific Economic Cooperation / Energy Ministerial Meeting

Sept 7-10 APPEC 2026, Singapore

Sept 9-11 Smart Energy Week (Autumn) 2026 @ Makuhari Messe (co-exhibiting H2 & FC Expo, Battery Japan, Smart Grid, Wind Expo, CCUS Expo, etc.)

Sept 9-11 Automotive World @ Makuhari Messe

September 14-18 IAEA General Conference 2026 @ Vienna, Austria

October International Maritime Organization –

Net-zero Discussions

Nov 2-5 ADIPEC 2026 @ Abu Dhabi

Nov 3 U.S. Midterm Elections

Nov Publication of International Energy

Agency – World Energy Outlook 2026

Nov 18-19 Asia-Pacific Economic Cooperation –

Leaders Meeting @ Shenzhen, China

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com. For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

TEPCO’S capital alliance centers around five groups including SoftBank

(Nikkei, June 20)

- TEPCO will proceed with capital alliance negotiations with five main groups. SoftBank, domestic fund Japan Industrial Partners (JIP), and three foreign investment funds will begin full-scale due diligence.

- The three overseas funds are KKR and Blackstone, and Global Infrastructure Partners, an infrastructure investment firm under BlackRock.

- TEPCO had accepted a number of partnership proposals earlier this year, but will prioritize these five in talks over a capital partnership. Some have offered to invest more than ¥1 trillion in TEPCO in deals that will require major restructuring.

- The bidders may yet be asked to form a multi-company consortium. The govt is likely to retain a control mechanism such as a ‘golden share’.

- TAKEAWAY: For all its challenges, TEPCO operates the country’s largest power grid, which today is probably its most valuable asset. For infrastructure and financial investors, the appeal would be exposure to long-term network investment, data-center demand, electrification and grid reinforcement, though any deal is likely to come with political constraints. TEPCO’s retail businesses could also offer scale, but their margins remain vulnerable and competition is high. These could be divestment targets. The more sensitive asset is TEPCO’s 50% stake in JERA; the govt is likely to be cautious about letting outside investors gain indirect influence over a company central to Japan’s LNG procurement and thermal-power strategy, especially while TEPCO still faces large Fukushima-related liabilities. It’s likely JERA will be excluded from the deal.

Japan to explore rare-earth mining, visit planned to Greenland

(Nikkei Asia, other reports, June 14)

- The Japanese govt plans to send a high-level delegation to Greenland to study the potential for mining rare earths and other critical minerals.

- METI officials and JOGMEC geologists will meet with Greenland’s govt, visit mines and evaluate deposit sizes and mining costs.

- Japan hopes to find dysprosium (for electric motors), graphite for batteries and other minerals, possibly tantalum and niobium, (used in semiconductors).

- CONTEXT: Greenland holds around 1.5 Mt of rare earths – the world’s eighth-largest known reserves. Rare-earth mining hasn’t begun in Greenland but U.S. and EU firms are exploring. Japanese firms might join their projects.

- TAKEAWAY: Japan hopes to contribute to building a supply chain among major allies. The Greenland mission could pave the way for equity investments by Japanese trading houses, battery-materials companies and producers, similar to the longstanding strategy of securing overseas resource interests through state-owned JOGMEC. Greenland PM Nielsen is eager to cooperate with Japan, while opposed to Chinese investment. While Greenland’s resource potential is significant, commercial production remains years away.

JX Advanced Metals to boost optical chip wafer capacity for DCs

(Company statement, June 16)

- JX Advanced Metals, which specializes in copper, rare metals and semiconductor materials, will boost production for optical chip wafers to meet demand for equipment that can reduce data center (DCs) power consumption.

- By 2030, the firm will invest ¥120 billion to increase capacity for indium phosphide wafers by 7-10 times over the FY2025 figure.

- CONTEXT: Indium phosphide can reduce DC power use by converting electrical signals to optical ones and back.

- TAKEAWAY: The global market for InP wafers is forecasted to exceed $500 million in 2034, nearly triple its 2025 size. JX Advanced Metals and rival Sumitomo Electric Industries each hold an estimated 40% of today’s market. JX has also a stake in Rapidus, the govt-backed chipmaker targeting mass semiconductor production.

Tokyo think tank calls for stronger support for agrivoltaics

(Organization statement, June 8)

- Platinum Network, a Tokyo think tank, recommends speeding up deployment of agrivoltaics – for greater support for agricultural electrification, energy self-sufficiency, and the creation of a national database to track crop yields, solar performance, and project outcomes.

- It also urged policymakers to accommodate emerging tech such as vertical solar installations, movable mounting systems, and PSCs.

- CONTEXT: The recommendations come as Japan reviews its agrivoltaics framework. The group argues that agrivoltaics can help strengthen farm incomes, support decarbonization, and revitalize rural communities.

Hitachi Energy to buy Canadian transformer-parts supplier

(Company statement, June 17)

- Hitachi Energy agreed to acquire Canduct, a Canadian supplier of transformer materials, insulating kits and components.

- Hitachi seeks to expand its North American manufacturing footprint as grid and transformer demand rises, partly driven by data-center construction.

NEWS: ELECTRICITY MARKETS

EEX to expand Japan power futures and options products

(Exchange presentation; Denki Shimbun, June 8-17)

- EEX plans to broaden its Japan power derivatives offering in 2026, including Chubu area day and weekend futures and options.

- The contracts are expected to be structured similarly to Tokyo area products.

- Kansai area day and weekend futures became available on May 26. EEX said more than 4 TWh of Chubu area futures and options have already traded.

- EEX is also considering introducing “European-style” options for Japan power contracts. Unlike the Asian-style options introduced in 2025, which use a monthly average spot price as the reference price, European-style options would reference the spot price at a specific point in time.

- The new options help generators hedge exposure tied to whether plants run or not at specific times, rather than only managing average monthly price risk.

- From Sept 2026, EEX Japan Power products will be tradable in the exchange orderbook from 9 am to 6 pm JST. Transactions registered with EEX during that window will be processed for immediate clearing, avoiding the need to queue trades until European afternoon hours.

- CONTEXT: EEX’s Japan power market has been expanding from Tokyo-area baseload products into broader regional and risk-management tools. The exchange is also preparing wider margin offsets from Q3 2026 between Japan Power, JKM LNG and European energy contracts, and plans to shift in 2027 from the SPAN margining model to a portfolio-based VaR model.

- TAKEAWAY: European-style options could be relevant as volatility grows around intraday supply-demand balances, solar output and plant dispatch decisions. The margin-offset changes may also lower the capital burden for firms trading across Japan power, LNG and European energy markets, potentially making the market more attractive to sophisticated and high-volume participants. Battery-focused hedging products would be a logical next step, especially if EEX adapts products being developed in Europe for Japan.

Power futures ease as Gulf risk premium recedes

(Broker and exchange data, June 12-18)

- Electricity futures fell over the past week, led by the Tokyo baseload contract, the country’s most actively traded power product.

- The July contract dropped to ¥20.65/ kWh on June 18 from ¥22.60/ kWh on June 12, down 8.6%, according to prices provided by Tullett Prebon.

- The decline extended across the summer and winter strips. TBL Aug-26 fell 9.6% to ¥20.60; Sept-26 dropped 11.1% to ¥19.65; and Dec-26 fell 12.4% to ¥16.95.

- Kansai and Chubu baseload contracts also weakened. KBL July-26 fell 11.2% to ¥16.60; while CBL July-26 dropped 8.1% to ¥19.85.

- The move followed a sharp easing in LNG-linked fuel risk. JKM swaps also fell over the week, with Aug-26 down 14% to $15.405/ MMBtu from $17.916/ MMBtu.

- CONTEXT: Prices eased after the U.S. and Iran announced an agreement aimed at ending hostilities and reopening the Strait of Hormuz.

- TAKEAWAY: Traders are pricing in a lower probability of near-term supply disruption, though not a full return to normal conditions. After all, the market remains exposed to renewed geopolitical risk, with sporadic hostilities, criticism of the agreement’s terms, and Iran’s stated intention to charge fees for Hormuz passage among the challenges. Meanwhile, the onset of rainy-season weather in central Japan has so far helped restrain temperatures, reducing immediate upside pressure from cooling demand.

OCCTO reviews balancing market transactions after reforms

(Agency statement, June 9)

- OCCTO reviewed transactions in the balancing market since March 14, when the FY2026 market reforms took effect.

- After the introduction of day-ahead trading and 30-minute bidding intervals, bid volumes increased for most products, although shortages remain in Primary and Secondary-1.

- For Tertiary-1, no persistent shortages or major cost increases were observed.

- The 30-minute bidding framework increased flexibility and boosted volumes, but supply shortages and reliance on high-priced resources continue.

- CONTEXT: The balancing market design was revised in FY2026 by moving the transaction timing of the products – Primary, Secondary-1&2, Tertiary-1, and Composite – from weekly auctions to day-ahead trading, and shortening the bidding interval from three hours to 30 minutes. However, concerns were raised that bids could become concentrated in either the composite market or the Tertiary-2 market, as both markets now operate at the same trading time.

- TAKEAWAY: The early results suggest the FY2026 reforms improved the mechanics of the balancing market, but did not remove its underlying scarcity problem. Shorter bidding intervals and day-ahead procurement appear to have increased flexibility and bid volumes, yet shortages in Primary and Secondary-1 show that fast-response balancing resources remain limited. That is important for the planned simultaneous market: combining energy and balancing-capacity procurement may improve efficiency, but it will not by itself create the flexible capacity needed to manage a more variable power system. The next test is whether market design can attract more responsive resources without relying too heavily on high-priced bids.

METI approves temporary electricity and gas bill discount program

(Government statement, June 12)

- METI approved a temporary electricity and gas bill discount for July–Sept 2026.

- The measure allows regulated retail tariffs to be discounted through special exemptions; retailers offering deregulated tariffs will also participate.

- The discounts will be applied directly to monthly bills, reducing energy costs for households and small businesses.

- The support level varies by month, with higher discounts in August.

- Electricity (Low Voltage): ¥3.5/ kWh (July & Sept), ¥4.5/ kWh (Aug)

- Electricity (High Voltage): ¥1.8/ kWh (July & Sept), ¥2.3/ kWh (Aug)

- City Gas: ¥14/ m³ (July & Sept), ¥18/ m³ (Aug)

- TAKEAWAY: METI has implemented electricity and gas bill support programs several times since 2023 to address soaring energy prices and rising living costs. In 2023, large-scale support was introduced to mitigate the impact of soaring energy prices. After 2025, support was provided during peak electricity demand periods in both summer and winter. For this summer, enhanced subsidies will be introduced, exceeding the level of support in summer 2025. While subsidy levels have varied, govt support has become a recurring ad hoc measure during peak-demand periods.

Changes in Subsidy Unit Price

| Program name | Period | Electricity (¥/ kWh) | Gas (¥/ m3) | |

| Low voltage | High voltage | |||

| Electricity/Gas Price Mitigation (global energy crisis and rising fuel costs) | Jan – Aug 2023 | 7.0 | 3.5 | 30 |

| Sept 2023 – Apr 2024 | 3.5 | 1.8 | 15 | |

| May 2024 | 1.8 | 0.9 | 7.5 | |

| Emergency Summer Energy Cost Relief | Aug – Sept 2024 | 4.0 | 2.0 | 17.5 |

| Oct 2024 | 2.5 | 1.3 | 10 | |

| Electricity/Gas Bill Relief in Winter | Jan, Feb 2025 | 2.5 | 1.3 | 10 |

| Mar 2025 | 1.3 | 0.7 | 5 | |

| Electricity/Gas Bill Relief in Summer | July, Sept 2025 | 2.0 | 1.0 | 8 |

| Aug 2025 | 2.4 | 1.2 | 10 | |

| Electricity/Gas Bill Relief in Winter | Jan, Feb 2026 | 4.5 | 2.3 | 18 |

| Mar 2026 | 1.5 | 0.8 | 6 | |

| Electricity/Gas Bill Relief in Summer | July, Sept 2026 | 3.5 | 1.8 | 14 |

| Aug 2026 | 4.5 | 2.3 | 18 | |

Tohoku Electric launches renewable power auction to test green premium

(Company statement, Nikkei, June 9)

- Tohoku Electric will introduce a new wholesale auction system that sells electricity specifically sourced from renewable assets such as hydropower, geothermal, and wind, rather than bundling it with other generation sources.

- The initiative aims to establish a market-based “green premium” by embedding the value of renewable electricity directly into power prices, instead of relying solely on environmental certificates.

- The first auction, July 28, will offer one-year renewable power supply contracts for FY2027. The move comes as firms seek high-quality renewable power with reliable generation characteristics, particularly for energy-intensive users such as data centers.

- TAKEAWAY: The auction is a test of whether buyers will pay a distinct premium for renewable electricity itself, not just for separately procured environmental certificates. That matters because hydro, geothermal and wind can offer different value from generic green claims, especially for data centers and other large users seeking credible, traceable low-carbon supply. If the auction clears at meaningful premiums, other EPCOs may see room to monetize existing renewable assets through wholesale green-power products, creating an alternative to bilateral PPAs and certificate-based procurement.

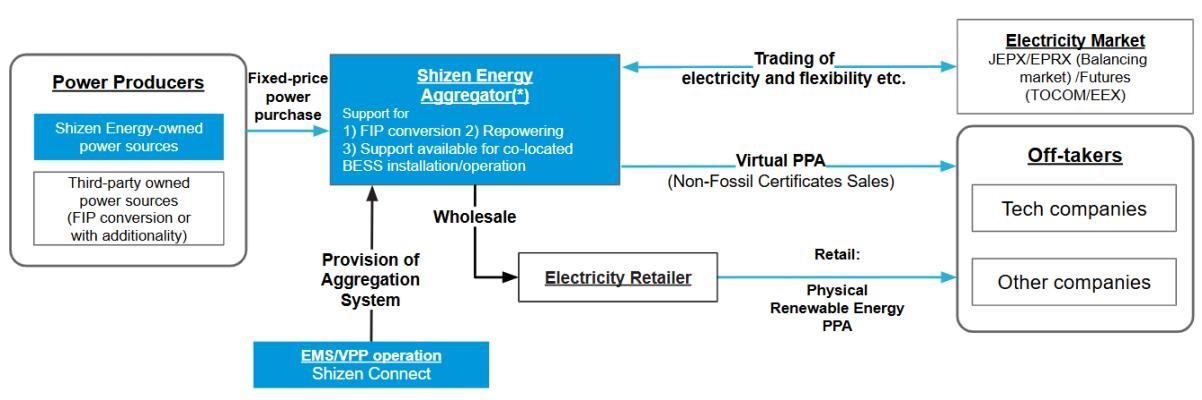

Shizen Energy to expand aggregation business with the support of virtual PPAs

(Company statement, June 11)

- Shizen Energy will expand its aggregation business by purchasing electricity and environmental attributes across Japan at fixed prices, while asset owners will retain ownership of their plants.

- This strategy is expected to increase the number of virtual PPAs signed with off-takers.

- The company aims to aggregate 500 MW by 2030, and 1 GW by 2035.

Suzuyo Shoji backs Greenphard Energy’s AI management platform

(Company statement, June 17)

- Suzuyo Shoji, an energy services firm, inked a capital and business alliance with Greenphard Energy, a startup that uses AI and IoT tech to optimize electricity consumption in refrigeration, cold storage and HVAC systems.

- Greenphard’s platform can reduce energy use by over 20% while enabling participation in demand response (DR) programs, helping customers lower costs and generate additional revenue from flexible power demand.

- CONTEXT: The alliance follows Greenphard Energy’s first Series A close in January that raised about ¥230 million from investors including Fujita, Mitsubishi UFJ Trust and Banking, and Nomura Holdings.

- TAKEAWAY: The deal highlights growing interest in AI-enabled energy management, demand response and virtual power plant (VPP) technologies as Japan seeks greater grid flexibility and decarbonization.

Informetis and Kansai Electric partner on next-gen energy flexibility solutions

(Company statement, June 15)

- Informetis, a Japanese energy analytics startup, agreed with Kansai Electric to support the development of next-gen energy management systems.

- The partnership will leverage Informetis’ AI-based Non-Intrusive Load Monitoring tech, which can disaggregate household electricity consumption and combine it with advanced demand forecasting, customer engagement, and device-control capabilities.

- The firms aim to develop solutions that improve energy flexibility, adjusting electricity demand in response to grid conditions and power prices to help utilities manage rising renewable energy adoption while reducing costs for consumers.

- CONTEXT: The deal follows Informetis’ earlier partnership with Chugoku Electric and reflects rising interest among utilities in DR, smart grid tech, and AI-driven energy management. It’s also relevant due to widespread smart meter deployment, while appliance-level energy data is lacking.

Enerbank to support FIT non-fossil certificate joint purchasing project

(Company statement, June 16)

- Kyoto Pref reappointed Enerbank to manage a joint purchasing program for FIT non-fossil certificates, using its Green Ticket platform.

- Enerbank will help clients procure renewables certificates at lower cost.

- The joint purchasing approach aims to reduce both procurement costs and administrative burdens compared with buying certificates individually.

- The prefectural govt and the service provider will hold four explanatory sessions. Applications to join the sessions are accepted here.

NEWS: HYDROGEN

METI ends its participation in ammonia co-firing power generation projects

(Government statement, June 16)

- METI approved ending its ammonia co-firing power generation projects under the Green Innovation Fund conducted by MHI and JERA.

- The firms involved in the tech will continue development at their own expense, aiming to commercialize high-efficiency 50% ammonia co-firing in the 2030s.

- The decision was made after a study revealed that extensive plant upgrades are required, resulting in significant construction delays and higher costs.

- MHI and JERA requested ending the project because the commercial-scale demo is expected to miss GIF’s FY2030 deadline by about five years.

- Another ammonia co-firing project led by IHI and JERA at the Hekinan Power Station – which targets 20% co-firing – remains on track to start in FY2030.

- TAKEAWAY: The decision is a warning that high-ratio ammonia co-firing may be harder to retrofit into existing coal plants than Japan’s policy narrative has implied. If a 50% co-firing system requires more upgrades and cost, and longer construction timelines, then this is more than just about missing the Green Innovation Fund’s FY2030 window. This now splits the ammonia development timeline into two parts. Low-ratio co-firing may still proceed as an incremental decarbonization option, but high-ratio co-firing is moving further into the 2030s and will have to compete for capital against other firm low-carbon power options. That makes ammonia a higher-cost bet on future fuel supply chains, plant conversions, and policy support.

INPEX begins supplying power generated using hydrogen

(Company statement, June 17)

- INPEX began supplying electricity generated using hydrogen from its blue hydrogen and ammonia demonstration project in Kashiwazaki, Niigata Pref, to local utility Kashiwazaki IR Energy.

- This is Japan’s first integrated demonstration covering blue hydrogen and ammonia production, CCUS, and end-use applications.

- The hydrogen and ammonia are produced using natural gas from INPEX’s Minami-Nagaoka gas field in Niigata Prefecture. CO2 generated during production is captured and injected into a depleted reservoir at the Higashi-Kashiwazaki gas field.

- CONTEXT: Kashiwazaki IR Energy was established in March 2022 to support local energy production and consumption in Kashiwazaki.

- TAKEAWAY: The project is significant because it demonstrates a complete hydrogen value chain using domestic natural gas and CO2 storage in depleted gas fields, providing a model for future commercial hydrogen and CCUS projects in Japan. It also supports energy security, decarbonization, and the development of a local hydrogen economy. But the main question remains whether this demo could be scaled in Japan to a commercial size.

JERA signs time charter deal with NYK and MOL for ammonia carriers

(Company statement, June 18)

- JERA signed time charter agreements with NYK Bulkship and Mitsui O.S.K. Lines (MOL) for four ammonia carriers.

- The vessels will transport low-carbon ammonia produced at the Blue Point project in Louisiana to support commercial-scale ammonia 20% co-firing at the Hekinan Thermal Power Station.

- This will be the world’s first long-term deployment of very large ammonia carriers (VLGC), enabling more cost-effective large-scale ammonia transport.

- CONTEXT: JERA’s low-carbon ammonia production project was certified under the Hydrogen Society Promotion Act in Dec 2025 and was awarded govt funding by JOGMEC in Feb 2026.

- TAKEAWAY: The agreement highlights that large-scale ammonia deployment for power generation requires not only production projects but also reliable and cost-efficient transportation capacity. JERA is establishing one of the first integrated ammonia supply chains for power generation, covering production, shipping, receiving, and power generation.

- SIDE DEVELOPMENT:

- NYK, ENEOS install hydrogen FC system for cruise ship

- (Company statement, June 15)

- NYK, Yanmar Power Solutions, and ENEOS will install a hydrogen fuel cell (FC) system for a new dining cruise ship entering service in 2027.

- The project combines hydrogen storage technology from Toyota Motor, hydrogen supply by ENEOS, and system integration by Yanmar.

- CONTEXT: The maritime sector faces pressure to reduce GHG emissions, making low carbon fuel a promising zero-emission solution for ships. FC propulsion is well suited for restaurant ships, where quiet operation and passenger comfort are essential.

Univ of Tokyo tests liquid-based hydrogen storage system

(Company statement, June 2)

- Kono Lab at the University of Tokyo Advanced Science and Technology Research Center, in collaboration with ARM Technologies and AISIN Corp, demonstrated a new energy system for utilizing green hydrogen.

- Hydrogen generated from solar power is directly stored in a proprietary liquid by an original electrolysis device, and utilized as electricity after being transported in polypropylene containers at a regular temperature and pressure.

- The technology stores hydrogen in a non-combustible proprietary liquid at normal temperature and pressure.

- This project aims to build large-scale infrastructure for storage and transport of renewable energy, develop models for supplying next-gen energy to electric vehicles, and spread daily-life practical applications like mobile batteries and help in the establishment of a hydrogen supply chain.

Yamaha agrees with Chubu Electric PM for demos in hydrogen and solar

(Company statement, June 15)

- Yamaha agreed with Chubu Electric Power Miraiz to collaborate on the following:

- A demo aimed at reducing hydrogen production costs through energy management;

- The Enshu Decarbonization Project, which Yamaha launched in Shizuoka Pref, under which Chubu Electric PM will supply 1.32 GWh/ year of surplus solar electricity generated by three Yamaha suppliers.

- Both firms aim to expand the Enshu project to additional suppliers.

- CONTEXT: Yamaha and Chubu Electric PM already collaborate in decarbonizing Yamaha’s supply chain, with renewable electricity menus, off-site physical PPA services and the introduction of infrared heaters instead of gas burners.

NEWS: SOLAR AND BATTERIES

Japan to consider EV battery recycling mandate

(Government statement, Nikkei, June 9)

- The govt will consider making automakers legally responsible for collecting and recycling end-of-life EV batteries. The MoE and METI will set up a working group.

- Currently, recycling is voluntary.

- The plan comes as other countries move toward stricter battery recycling rules.

- CONTEXT: About 13,000 used batteries were recovered in FY2024, but the number of retired EV batteries is expected to spike, from 50,000 in FY2026 to 130,000 in 2030, and 400,000 by 2040.

- The push is driven by concerns related to waste management and safety, resource security, and economic competitiveness.

- TAKEAWAY: Japan is preparing for a wave of EV battery waste and must decide whether voluntary industry programs are sufficient or whether automakers should be legally required to take responsibility for battery collection and recycling. The EU introduced the EU Battery Regulation, which sets recycling and materialrecovery targets for batteries; China is building a nationwide battery traceability system that tracks batteries from production through recycling. Japan recently passed legislation for large-scale solar panel recycling. Since future batteries are expected to contain fewer high-value materials, many countries are shifting from marketdriven recycling toward regulatory systems.

Tokyo Century and TESS to open a 50 MW BESS

(Company statement, June 16)

- Tokyo Century and TESS plan to open a 50 MW / 209 MWh BESS station in Fukuchiyama (Kyoto Pref), expected to start in 2028.

- The BESS will be full-merchant and won’t rely on subsidies.

- TAKEAWAY: Several extra-high-voltage BESS projects in Japan no longer require subsidies. The fact that this project is developed on a fully merchant basis shows investors are confident that market revenues, without support of a tolling agreement or other long-term revenue guarantees, suffice to justify financing.

JinkoSolar sets new perovskite-silicon tandem efficiency record

(Company statement, June 17)

- JinkoSolar achieved a 34.82% conversion efficiency for its N-type TOPCon perovskite-silicon tandem solar cell, beating its own world record of 34.76%.

- The result highlights progress in combining commercially proven TOPCon silicon tech with next-gen PSC materials.

- CONTEXT: While PSCs currently represent a negligible share of Japan’s installed solar capacity, globally, TOPCon accounts for over half of new solar cell production capacity; many modules imported into Japan from Chinese manufacturers such as JinkoSolar and LONGi are based on TOPCon.

- TAKEAWAY: JinkoSolar’s milestone reflects global competition in perovskite tech and the race to bring next-gen high-efficiency solar cells from the laboratory to mass production. The development is relevant as Japan is investing heavily in this technology. Sekisui Chemical leads Japan’s efforts to commercialize light, flexible PSCs.

The govt sees perovskites, including tandem structures, as a key tech for expanding domestic solar deployment on building facades, rooftops, and space-constrained sites.

Enerbank launches collective-purchasing program for solar

(Government/Company statement, June 15)

- Enerbank launched Solareco, a group-purchasing program for business solar installations.

- The goal is to support Saitama City by helping local businesses install rooftop solar through a collective procurement program.

- TAKEAWAY: Saitama is one of Japan’s more proactive municipalities on distributed solar, combining rooftop solar promotion, innovative PPA structures, public-asset solar development, and group procurement programs to accelerate local decarbonization.

Kyocera’s PV system selected for demos in Tokyo

(Company statement, June 17)

- Kyocera’s lightweight PV system was chosen by the Tokyo Govt under its support program for new energy technologies.

- The system, which uses silicon solar cells, can be installed on factory and warehouse rooftops.

- Kyocera is currently conducting a demo with Denso on a slate roof and plans others in the Tokyo area.

- TAKEAWAY: A conventional silicon PV system installed on a rooftop, including the mounting structure, adds between 15 and 25 kilos per sq/ meter. This can pose challenges for warehouses with lightweight metal roofs, or roofs made of more fragile materials such as slate. Kyocera’s system does not use glass, significantly reducing the weight of the PV module, as glass typically accounts for around 50–75% of a conventional module’s weight.

- SIDE DEVELOPMENT:

- Sumitomo launches lightweight solar installation services

- (Company statement, June 17)

- Sumitomo Fudosan, TEPCO and Denkosha launched a service offering solar PV and battery installations with no upfront costs, as well as maintenance, repair and replacement support.

- The solar PV modules are ultra-lightweight, weighing only one-sixth as much as conventional panels.

Osaka Gas expands into energy management, EV charging

(Company statement, June 16)

- Osaka Gas and Sumitomo Mitsui Auto Service will collaborate on new EV services that combine fleet management, smart charging, and battery analytics.

- They’ll develop services that optimize EV charging and electricity costs using vehicle usage schedules and energy management systems.

- CONTEXT: Sumitomo Mitsui Auto Service is one of Japan’s largest vehicle leasing and fleet management firms, focusing on EV deployment.

- TAKEAWAY: The move addresses two major barriers to EV adoption: high charging/ energy costs, and uncertainty around battery condition in used EVs. This partnership highlights growing convergence of mobility, energy management, and battery data services, which are needed to build the infrastructure for large-scale EV adoption that would cover smart charging, battery valuation, and VPP-ready fleet management.

Hanwha Japan launches AI tools to speed up residential solar sales and design

(Company statement, June 10)

- Hanwha Japan, a subsidiary of Hanwha Corp (South Korea), announced two AI-powered web tools to help solar installers and home builders design and sell residential rooftop PV systems more efficiently.

- PVMap uses AI to analyze roof shapes from map data and generate panel layouts, system size recommendations, and generation forecasts.

- AutoDraft uses AI to create solar design drawings from uploaded housing plans, reducing engineering workload and speeding up quotations.

- CONTEXT: Hanwha will unveil the tools at ENERICH on July 2 in Tokyo.

- TAKEAWAY: This is another example of AI applied to Japan’s distributed energy sector: not in grid operations, but in reducing the soft costs of rooftop solar deployment, and which can help accelerate residential solar adoption.

Kanagawa Pref selects Tokyo Gas and PXP for CSC demo

(Company statement, June 17)

- Tokyo Gas and PXP were chosen by Kanagawa Pref under its carbon-neutral R&D promotion program for a second consecutive year.

- Both firms will conduct a demo to study installation methods on walls made of various surfaces and materials.

- CONTEXT: Last year, Tokyo Gas and PXP focused on CSC installations on rooftops.

NEWS: WIND POWER AND OTHER RENEWABLES

GWEC: Japan must accelerate offshore wind deployment for energy security

(Organization statement, June 9)

- In its 2026 report, the Global Wind Energy Council (GWEC) urged Japan to accelerate offshore wind projects to establish a large-scale domestically sourced renewables supply ecosystem as an energy security imperative.

- GWEC noted that deployment is slower than needed.

- Key challenges are complex permitting and seabed approval procedures, grid connection and investment uncertainty, and financing risks stemming from unclear tender and revenue mechanisms.

- GWEC said Japan should: o Streamline permitting and approvals; o Improve auction design; o Provide long-term investment certainty; o Treat offshore wind as critical national energy-security infrastructure.

- CONTEXT: The report said total global wind capacity – mostly onshore wind – hit a record 165 GW in 2025, up 40% YoY, led by China, U.S. and India. There are 28,395 wind turbines installed across 57 countries.

- TAKEAWAY: Japan had 6.43 GW of installed wind capacity at the end of 2025, including 1.28 GW in Hokkaido, driven mainly by onshore wind growth. Offshore wind capacity rose to just over 0.5 GW in 2026 following the commissioning of the 220 MW Hibikinada and 16.8 MW Goto floating wind projects. Japan’s offshore wind targets are 10 GW by 2030 and 30–45 GW by 2040, but GWEC forecasts only 3.5 GW by 2030 and 8.4 GW by 2035 coming online, reflecting slower-than-expected deployment due to auction-design and project challenges that emerged after the first auction round.

- SIDE DEVELOPMENT:

- Japan, UK strengthen economic security and energy ties

- (Japan NRG, Nikkei Asia, June 15)

- Japan and the UK signed an economic security declaration to strengthen cooperation in energy, advanced technologies, and supply chains.

- Japanese firms plan to invest up to £9 billion in 5.9 GW of UK floating offshore wind projects, including with Ossian, Green Volt, and Erebus.

- The two countries will also cooperate on offshore wind supply chains, next-gen nuclear power, critical minerals, semiconductors, and AI.

- TAKEAWAY: The agreement strengthens Japan-UK cooperation on energy security and clean energy, while helping Japanese firms gain expertise in floating offshore wind, which will play an important role in the country’s overall offshore wind expansion.

MoE raises concerns over 215 MW Cosmo Eco Power wind farm

(Government statement, June 12)

- The MoE issued a statement to METI on Cosmo Eco Power’s plan for its Shimamaki–Kuromatsunai Second Wind Farm in Hokkaido.

- The project could reach 215 MW with up to 50 turbines, (each 4.3 MW). Construction would begin in May 2031, with operations to start in April 2035.

- The MoE called for closer coordination with nearby wind projects, assessment of impacts on residents, and stronger measures to protect wildlife.

- CONTEXT: The area has several wind projects involving JERA and Japan Wind Development. Hokkaido Electric and Invenergy projects also face environmental assessment. Another Cosmo Eco wind farm (Shimamaki–Kuromatsunai) is being built and expected to start operations in 2029.

- TAKEAWAY: The Shimamaki–Kuromatsunai region in southwestern Hokkaido is becoming a major wind power hub, with several existing, under-construction, and proposed projects totaling hundreds of megawatts of capacity. The region enjoys prevailing south and southeast winds in the spring and summer, shifting to gusty west or northwest winds in the fall and winter, with speeds ranging between 10–20 mph.

JRI: Existing flood-control dams could double Japan’s hydropower output

(Organization statement, June 16)

- The Japan Research Institute (JRI) published a report saying that Japan can reduce its dependence on imported oil and strengthen energy security by better using domestic “mountain resources” such as hydropower, biomass, and geothermal energy.

- No major new dam construction would be required.

- CONTEXT: Japan currently generates about 73.5 TWh of hydropower annually, representing 7.4% of total electricity generation.

- Of Japan’s 588 flood-control dams, only 173 have commercial hydropower facilities. Most floodcontrol dams are operated for flood management, not power generation, leaving significant untapped potential.

- JRI estimates that existing flood-control dams could help increase power generation by 64.3 TWh/ year, matching current national hydropower output. With more upgrades, generation could increase by 126.9 TWh.

- JRI recommends:

- Converting dams into “hybrid dams” that optimize both flood control and power generation using weather forecasting and advanced water management;

- Improving turbine efficiency;

- Raising dam heights and increasing reservoir capacity;

- Upgrading existing infrastructure instead of building new dams, thus reducing environmental impacts.

- SIDE DEVELOPMENT:

- KEPCO resumes operation of repowered Jikumaru hydro plant

- (Company statement, June 18)

- KEPCO resumed operations of its repowered Jikumaru Power Station hydropower plant in Bungoono City, Oita Pref.

- Until May 2021, the 105-old plant operated with a 12.5 MW capacity under the FIT, until it was shut down for refurbishment.

- CONTEXT: KEPCO has 139 hydropower assets across Japan; total capacity 3.6 GW.

- TAKEAWAY: KEPCO has been modernizing more than a dozen of its hydropower assets, aiming to increase renewable electricity generation. The move highlights the growing focus on hydro refurbishment as a low-cost decarbonization strategy, a trend gaining momentum alongside the modernization of other aging renewables assets such as wind power systems.

eRex Cambodia hydropower project close to completion

(Company statement, June 8)

- Japanese power producer eRex began reservoir filling at its hydropower project in Cambodia, the final step before operations begin.

- The 80 MW plant, in Pursat Province, will launch in Jan 2027. The electricity will be sold to the state utility under a 35-year PPA.

- The dam’s reservoir can store 1.2 billion cubic meters of water, about 1.8 times larger than Japan’s Tokuyama Dam.

- eRex invested $240 million in the project, and it also plans to develop biomass and solar power projects in Cambodia by FY2027.

- TAKEAWAY: This is a significant overseas renewables project for a Japanese energy company. It strengthens eRex’s position in SE Asia and supports Cambodia’s growing demand for low-carbon electricity.

Kyuden Mirai and Shikoku Electric launch tidal power demo off Goto Islands

(Company statement, June 12)

- Kyuden Mirai Energy and Shikoku Electric will do a large-scale tidal energy demo in Naru Strait between Hisaka and Naru islands in the Goto archipelago.

- Supported by the MoE, the project will deploy a 1.1 MW tidal turbine on the seabed in October to evaluate reliability, maintenance requirements, and economics ahead of potential commercialization in the early 2030s.

- CONTEXT: The initiative builds on Kyuden Mirai Energy’s previous tidal power trials in the same waters conducted since 2019.

- TAKEAWAY: Japan sees tidal energy as a promising source of predictable marine renewable power, particularly in regions with strong currents such as western Kyushu, the Goto Islands, and parts of the Seto Inland Sea. While Europe has demonstrated multi-year continuous operation of tidal turbines, Japan’s tidal sector remains at the demo stage. The addition of Shikoku Electric broadens industry participation and could help speed up domestic supply chains, tech development, and future deployment of marine energy projects.

NEWS: NUCLEAR ENERGY

Govt says MOX fuel transport to France is progressing

(Government statement, June 18)

- FEPC and JNFL reported on the status of Japan’s spent fuel management and reprocessing efforts.

- For dry storage, Shikoku Electric began operations at its Ikata facility in July 2025 and now stores 4 casks.

- Tohoku Electric received its installation modification permit for Onagawa in May 2025. Kyushu Electric applied for its permit for Sendai in October 2025.

- For intermediate storage, TEPCO said its facility is unlikely to reach its initial 5,000-ton plan. Interoperator cooperation is needed.

- In March, Aomori Pref said the environment for intermediate storage was not yet ready. This led operators to pledge an “All-Japan” support system to back the completion of JNFL’s reprocessing plant.

- Kansai Electric is preparing to transport spent MOX fuel to France and completed two out of 12 planned TN-Eagle transport casks, with the rest under construction. The completed casks will arrive at the Takahama NPP in autumn, with shipments to France planned to start in FY2027.

- CONTEXT: Minister Akazawa said the govt will strengthen progress monitoring of the Rokkasho nuclear fuel reprocessing plant and will coordinate with industry to support its completion.

Kanagawa backs superconducting coil project for future fusion reactors

(Company statement, June 17)

- Japanese superconducting startup Nippon Superconductor Applied Development was chosen for Kanagawa Pref’s carbon-neutral R&D program to develop low-loss superconducting coils for future fusion reactors.

- The firm will use its proprietary flexible superconducting wire to build and test low-loss fusion reactor coils.

- The project aims to show that the wire generates less heat under fluctuating magnetic fields, a major challenge for fusion systems.

- TAKEAWAY: While still early-stage, the project supports Japan’s long-term ambitions in fusion energy, an area receiving growing govt and private-sector investment. If successful, the tech could improve the efficiency and practicality of superconducting magnets, which will be a critical component in future fusion power plants.

KEPCO reports on Mihama NPP steam leak

(Company statement, June 19)

- KEPCO reported its findings from an inquiry about the May 8 mishap at its Mihama NPP Unit 3 high-pressure turbine.

- The incident resulted in a manual reactor shutdown, though there was no radioactive impact on the environment.

- Operators discovered a 1 cm by 8 cm hole in the governor-side closure cap of the turbine casing. The cap’s original thickness of about 20 millimeters had thinned to roughly 1 millimeter in some areas.

- The company will replace the caps, to be treated with a corrosion-resistant stainless steel lining on the inside.

- SIDE DEVELOPMENT:

- JAEA reports fires at Tokai-mura

- (Nikkei, June 19)

- The Japan Atomic Energy Agency reported two electrical fire-related incidents at its facilities in Tokai-mura on June 15.

- Both occurred outside radiation control areas and involved no actual flames or smoke. They happened within a dozen meters of sensitive areas.

- On June 19, JAEA reported a fire at its Nuclear Science Research Institute in Tokai Village, Ibaraki Pref, inside a radiation-controlled area. There was no radiation leak. After the shut down of surrounding equipment, the fire extinguished itself.

NRA reviews Shimane NPP’s Unit 3 seismic data

(Denki Shimbun, June 15)

- The Nuclear Regulation Authority held a meeting to review the safety of Shimane NPP’s Unit 3.

- Chugoku Electric refuted the existence of an active fault believed to be near the facility’s southern boundary.

- Regulators requested further clarification and documentation from the utility. To conclude verification, officials plan to conduct a final on-site inspection.

NEWS: TRADITIONAL FUELS

U.S. extends Japan’s Sakhalin-2 import license

(Denki Shimbun, June 17)

- The U.S. Treasury permitted Japan to continue with the Sakhalin-2 oil and gas project in Russia until Dec 18, 2026. This is the second extension.

- CONTEXT: Sakhalin-2 accounts for about 9% of Japan’s total LNG imports. The U.S. generally bans Russian energy transactions as part of sanctions. But, it has maintained an exception for Japan’s gas imports from this project.

- TAKEAWAY: The extension reflects Washington’s continued tolerance of Japan’s Sakhalin-2 exposure because the project remains difficult to replace quickly. Sakhalin-2 supplies roughly 9% of Japan’s total LNG imports, and that supply can’t be easily replaced. Alternatives are costlier and-or of lower quality, as Sakhalin gas has high calorific value. Also, powerful and politically-connected trading houses Mitsui and Mitsubishi hold equity stakes in Sakhalin-2.

Japan’s oil imports costs hit record high in May

(Government statement, Japan NRG, June 17)

- In May, Japan’s crude oil import unit price reached a record high of ¥114,076 per kiloliter, a 67.2% YoY increase. Oil imports from the Middle East plummeted 61.9%.

- To compensate for lost supply, Japan increased oil imports from the U.S. and SE Asia. But, these alternative sources are more expensive due to longer transport distances, higher shipping fees, and increased insurance premiums.

- The MoF reported that soaring costs of crude oil procurement contributed to a trade deficit of ¥378 billion, Japan’s first trade deficit in four months. Total imports rose 12.5% to ¥9.89 trillion, while exports grew 17% to ¥9.51 trillion, supported by semiconductor and automobile sales.

- CONTEXT: Global oil prices remained high through May. The recent U.S.-Iranian peace memorandum has caused prices to drop below $80 per barrel. Experts believe this will lower Japan’s import costs, though it is uncertain how long it will take to return to pre-conflict price levels.

- TAKEAWAY: For more info, see this issue’s Analysis section.

Uniper privatization draws interests from bidders including JERA

(Bloomberg, June 18)

- Germany’s Uniper attracted 10 bidders, including JERA, KKR, Equinor, RWE, Vattenfall, and TotalEnergies.

- Vattenfall is interested in Uniper’s Swedish hydro and nuclear assets.

- CONTEXT: Uniper was nationalized during the 2022 energy crisis. Its sale is a major step for the German govt, as Uniper remains a key gas importer and power plant operator. Even after the sale, the govt plans to keep about a 25% stake.

Marubeni acquires U.S. natural gas producer EagleRidge Energy

(Company statement, June 17)

- Marubeni Corp acquired 100% ownership of EagleRidge Energy, a natural gas development and production firm operating in Barnett Shale in Texas.

- Barnett Shale daily production will be 170 million cubic feet of natural gas, or about 1.3 Mtpa of LNG, equal to 19 LNG carriers.

- CONTEXT: Barnett Shale is a major U.S. gas basin with a long production history and stable output. It’s close to Gulf Coast export terminals.

Australian unions reach deal with INPEX, strike off at Ichthys LNG

(Reuters, June 17)

- Australian unions reached a deal with INPEX to end strikes at the Ichthys LNG facilities, with all strike action ceasing.

- The agreement includes a 3% annual pay rise above the consumer price index. There are guarantees that permanent jobs won’t be outsourced to low-wage contractors.

- Cargo loading has already restarted, and the second production train should be back online within days.

- CONTEXT: The strike began on June 2 and disrupted shipments, forcing the shutdown of one production train and causing three cargoes to miss loading. This caused an estimated $200 million in lost earnings.

- TAKEAWAY: Ichthys accounts for about 10% of Japan’s LNG imports. Japan’s govt was concerned because longterm disruption would have impacted Tokyo. METI said the govt kept close contact with INPEX and major utilities, making contingency plans and looking into procuring alternative supplies. The success of the strike might embolden unions at other LNG projects.

Kanadevia and AIST launch demo of gas generation from sludge

(Company statement, June 17)

- Kanadevia and AIST began a demo at a sewage treatment plant in Kagoshima City to test the feasibility of generating fuel gas for self-supplying electricity to the facility.

- The partners aim to produce fuel gas, including hydrogen, from dewatered sewage sludge using olivine as a catalyst.

- CONTEXT: Olivine is a magnesium iron silicate mineral primarily used as an additive in the steel industry.

LNG stocks up from previous week, down YoY

(Government data, June 17)

- As of June 14, the LNG stocks of 10 power utilities were 2.04 Mt, up 13.3% from the previous week (1.8 Mt); down 8.5% from end June 2025 (2.23 Mt); and down 3.8% from the 5-year average of 2.12 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Japan Liquid Carbonic, Ube Materials to conduct CO2 supply chain study

(Company statement, June 5)

- Japan Liquid Carbonic, an industrial gas firm, and Ube Materials, a specialty materials producer, were chosen for a NEDO-funded study on building a CO2 supply chain centered on the Ube–SanyoOnoda industrial region in Yamaguchi Pref.

- The goal is to capture CO2 from cement, waste, and sewage facilities, aggregating it at Japan Liquid Carbonic’s Ube plant.

- The CO2 will be supplied to industrial users and new carbon-recycling applications such as carbonates, polycarbonates, and methanation.

- CONTEXT: The Ube-Sanyo-Onoda region faces a shortage of industrial CO2 because existing sources associated with petroleum refining and ammonia production are being phased out or shut down. The project seeks to secure alternative CO2 sources from other local industries.

- TAKEAWAY: Through this project, captured CO2 would continue to serve existing markets such as beverages, welding, neutralization chemicals, and agriculture, while also supporting new carbon recycling applications. If successful, the model could be expanded to other regions in Japan facing similar shortage-related issues. Potential new uses include: carbonate production, polycarbonate manufacturing, methanation, which combines CO2 and hydrogen to produce methane for boilers and city gas systems and other CCU tech.

- SIDE DEVELOPMENT:

- MoE launches CCU promotion subsidy

- (Government statement, June 12)

- The MoE launched its program to promote use of CCU technology, to support businesses acquire equipment and to create regional CCU projects.

- Subsidies cover up to 1/2 for SMEs; up to 1/3 for others. Applications are accepted from June 12 to Aug 7, 2026.

- CONTEXT: CCU stands for Carbon Capture and Utilization. The tech captures CO2 from industries and re-uses it in a variety of products such as fuels, construction materials, plastics, etc. Unlike CCS (Carbon Capture and Storage), CO2 is not buried underground, but is part of a circular economy.

JRI launches carbon price forecasting to help firms meet GX-ETS requirements

(Organization statement, June 17)

- The Japan Research Institute (JRI) launched a carbon price forecasting service that projects future carbon costs under the GX Emissions Trading System (GX-ETS), fossil fuel levies, and other carbon-pricing mechanisms.

- The service will help companies quantify the financial impact of emissions, benchmark internal carbon prices, and make decisions on decarbonization investments across sectors from energy to steel, chemicals, and cement.

- CONTEXT: JRI is a Japanese policy and business consultancy that focuses on long-term economic, energy, environmental, and industrial strategy. The revised GX Promotion Act has formalized the GX-ETS and will introduce a fossil fuel levy from 2028, increasing the cost of CO2 emissions for companies.

- TAKEAWAY: Carbon pricing in Japan is becoming material enough that companies now need long-term carbon cost forecasts for budgeting, investment planning, and competitiveness. The launch reflects growing demand for quantitative tools to manage future carbon liabilities under the GX framework.

Sustech and TEPCO EP partner on corporate decarbonization support

(Company statement, June 15)

- Sustech, a Tokyo-based climate-tech firm, will join TEPCO Energy Partner to help corporate customers accelerate carbon neutrality efforts.

- The two firms will provide support from GHG emissions accounting and visualization to roadmap development, emissions reduction measures, and progress tracking.

- The goal is to help move companies beyond emissions reporting by identifying reduction opportunities and implementing strategies tailored to each customer’s energy use and emissions profile.

- CONTEXT: In 2022, TEPCO EP launched TEPCO CN Design as a one-stop carbon neutrality support service for corporate customers, from strategy development to renewables procurement and energy efficiency measures.

- TAKEAWAY: The deal reflects the rapid expansion of Japan’s carbon-management software market under pressure to measure, disclose, and reduce emissions across operations and supply chains. By combining energy data with emissions analytics, utilities are positioning themselves as decarbonization service providers rather than simply electricity suppliers.

ANALYSIS

BY FILIPPO PEDRETTI

Beyond Hormuz: Japan’s Next Energy Security Challenge

Whether the conflict in the Persian Gulf is over, merely paused, or continuing under another form remains unclear. What is certain is that Japan will face lasting consequences.

The country’s overwhelming dependence on Middle Eastern oil is no longer tenable. The concentration of refining capacity around a narrow range of crude grades has become a strategic vulnerability. So too has a largely hands-off approach to securing upstream supply.

The lessons from the conflict, however, extend beyond oil. War in one of the most crucial regions for global supply chains for a number of crucial commodities – not just oil – has exposed vulnerabilities across the economy. Japan is still in the early stages of grappling with rising costs, supply disruptions and logistical bottlenecks.

Tokyo’s initial response has been an aggressive pivot towards petroleum imports from one of the conflict’s main participants – the U.S. But this is unlikely to be a long-term solution. There is too much at stake to allow one dependence to be replaced with another, especially with an ally that has an aggressive transactional nature.

Japan’s path forward will require more than emergency procurement. The challenge now is to build a more resilient system on top of the short-term measures adopted during the crisis.

A congested strait and alternative supplies

The end of April brought a dim sign of hope for global oil markets, especially for Japan.

On April 28, the first Japanese carrier passed through the Strait of Hormuz. The Idemitsu Maru, a crude carrier owned by Idemitsu Kosan, transited the strait with permission from Iran. On May 25, that ship docked at a pier off the coast of Chita City.

On June 3, a second vessel, Eneos Endeavor, arrived in Kagoshima carrying 2.15 million barrels of Kuwaiti and UAE crude before heading to the Negishi refinery in Yokohama. JERA also breathed a sigh of relief when in mid May the Mraweh delivered the first postblockade Persian Gulf LNG cargo to the port of Futtsu.

Still, industry insiders worry that as of early June, an estimated 38 Japan-related vessels remain trapped and immobilized in the Persian Gulf. Overall shipping volumes through Hormuz remain at a mere 4% of normal levels transported through the strait.

As for Japanese oil imports, which are almost entirely from the Persian Gulf, METI data revealed that April crude imports plummeted 65.7% YoY, the lowest import volume since 1989. Meanwhile, U.S. oil sales to Japan surged in May, hitting a record high of 800,000 barrels per day, more than triple the pre-war monthly average.

After oil, one of the most impacted commodities is naphtha. Due to the Hormuz disruption, Japan’s overall naphtha imports fell 47% YoY in April. Imports from the Middle East, which previously accounted for 70% of Japan’s import supply, plummeted 79%. To compensate and ease supply anxieties, Japan increased naphtha procurement from outside the Persian Gulf by 52%. Naphtha imports from the U.S. surged 209-fold to become Japan’s top supplier.

Japan sources 40% of its naphtha domestically, but here too, the situation has not been favorable. Due to a period of scheduled facility maintenance, production in April plummeted 22.8% YoY. On June 2, METI’s Minister Akazawa Ryosei said that domestic production will likely return to normal levels by July once maintenance concludes.

| Procurement Source | April 2026 Volume | Year-over-Year Change |

| Total Naphtha Imports | 1.14 million kL | -47% |

| Middle East | 340,000 kL | -79% |

| Non-Middle East (alternative) | 800,000 kL | +52% |

| U.S. only | 270,000 kL | +20,800% (209-fold) |

| Period | Oil barrels per day from the U.S. |

| Pre-Crisis Average | Under 230,000 |

| March 2026 | 370,000 |

| April 2026 | 600,000 |

| May 2026 | 800,000 |

| Country of Origin | Year-on-Year Crude Oil Import Volume Change | Baseline Pre-Crisis Import Share (2025) | Primary Strategic Vulnerability |

| UAE | -22% | 43.3% | Blocked behind Hormuz chokepoint; partial rerouting via Fujairah. |

| Saudi Arabia | Constrained | 39.4% | Buffered via the East-West and SUMED alternative pipelines. |

| Kuwait | -64% | 6.2% | Complete entrapment within the Persian Gulf maritime zone. |

| Qatar | -81% | 4.2% | Critical gas infrastructure damaged; processing lines offline. |

Shipping bottlenecks

Substituting Persian Gulf supplies, such as oil, is fraught with logistical hurdles. For example, sourcing crude from the U.S. more than doubles the transit time. Because vessels are tied up on these longer voyages, the fleet’s annual carrying capacity is halved, creating a shortage of available tankers and inflating freight and insurance costs.

Shipowners are demanding massive premiums or outright refusing to sail into the dangerous Persian Gulf. Between March and May, an estimated 50% of Japanese crude tankers returning from the Middle East (15 out of 33) avoided the Gulf altogether. Instead, they engaged in “Ship-to-Ship” (STS) mid-ocean transfers in the waters off Malaysia and India.

STS adds roughly $100,000 in costs and takes days to complete, but it remains cheaper and faster than re-routing tankers around the Cape of Good Hope, a 50-day journey. Major Asian consumers also shifted to LPG from the U.S., and Japanese LPG import prices reached a record high in April, hitting ¥115,660 per ton – a 21% increase over the previous month. The sudden shift to U.S. suppliers has inflated shipping costs. Spot freight rates between the U.S. and the Far East soared to 1.9 times pre-crisis levels.

Domestic and international moves

By the end of April, the Nikkei Commodity Index hit a record high of 294.18 (up 3.5% over March), driven by a 18% climb in the chemical index. The hit was felt in sectors working with naphtha and its derivatives, such as propylene.

A May report by the Yokohama Research Institute warned that if naphtha imports from the Middle East remain severed without adequate substitution, it could drag down Japan’s economic growth by -0.7% percentage points. In highly industrialized regions like Kanagawa Prefecture, the downward pressure could reach -0.8%, creating a risk of economic recession.

Also, state fuel subsidies reinstated in March to cap retail gasoline prices at ¥170 per liter are burning through coffers. Economic models forecast that the ¥800 billion allocated from the FY2025 reserve fund could be completely exhausted by late June.

In response, METI set up a cross-bureau crisis hotline. By May 15, a team of 50 bureaucrats had fielded roughly 2,600 complaints from businesses suffering from fuel and chemical shortages. Surveys by private entities also show widespread damages and fears for the future.

Faced with these pressures, Prime Minister Takaichi convened meetings in mid-May to discuss a supplementary budget to extend subsidies for fuel, electricity, and gas through the peak summer months of July to September.

But Tokyo’s attention is not only inwards. It’s using its financial power to stabilize regional supply chains that are vital for the country. For example, a collapse in Southeast Asian manufacturing would sever Japan’s supply of critical medical goods.

To prevent this, Tokyo set up a $10 billion financial support framework via the Japan Bank for International Cooperation (JBIC) to help regional neighbors procure alternative crude. For example, Idemitsu supplied 4 million barrels of crude to the Nghi Son refinery in Vietnam, ensuring the continued flow of downstream plastics back to Japan.

Japan and South Korea agreed to activate the ‘Partnership On Wide Energy and

Resources Resilience’ (POWERR Asia). In a summit in late May, Takaichi and President Lee Jae Myung agreed to establish joint crude oil procurement frameworks and reserves under this initiative.

Only about 40% of the oil procured by Japan is secured through equity interests held by Japanese companies. Successive energy plans have targeted raising that figure to 60%, but progress is slow.

Corporate forecasts and action

Japanese firms are eager for a diplomatic solution between the U.S. and Iran. ENEOS initially set its FY2027 forecasts on the assumption that Middle East disruptions would be resolved in May. INPEX pushed its normalization outlook to July. JAPEX, however, has a more grim assessment – that Iraqi oil production will remain halted for the entire fiscal year.

The war also lowers chances of moving forward with decarbonization. On May 12, Idemitsu Kosan cancelled planned refinery closures. The company had pledged an unprecedented ¥1.8 trillion investment over the next five years, dedicating a third of it to maintaining all six of its domestic refineries through 2030. Now, Idemitsu executives argued that maintaining robust domestic refining capabilities is critical for national security.

Mitsubishi Corp similarly relaxed its strict 2030 decarbonization goals, pivoting aggressively back to natural gas and LNG investments to ensure supply stability in a volatile world.

Yet, while current energy costs are high, energy companies still maintain a positive outlook and believe in slight stabilization. Many companies estimate the average crude oil price for FY2026 will settle around $80 per barrel, roughly 10% lower than current levels.

However, there is significant variance in quarterly forecasts across the sector. ENEOS anticipates prices will drop to $80 by June, whereas Idemitsu expects a decline to $65 by the first quarter of the following year.

The danger is that a fall in prices will be mistaken for a return to normality. For refiners, utilities and trading houses, cheaper crude would ease balance-sheet pressure and make familiar procurement routes attractive again. But the strategic problem exposed by the Gulf crisis would remain unresolved.

Real security from real diversity

The lag between rising crude costs and consumer price hikes often spans roughly six months. The Iran conflict compressed that timeline to barely eight weeks.

This rapid shock has exposed the acute vulnerability of Japan’s maritime lifelines and the bottleneck of having all the nation’s refineries configured to process similar oil grades.

Tokyo has responded quickly, securing supply by pivoting to its trusted ally, the U.S. Yet, the shift needs to be carefully calibrated so as to avoid a new round of dependency. True diversification means developing supply relationships with producers such as Canada, Brazil, Malaysia and others, while investing in the storage, logistics and refinery upgrades needed to make those supplies commercially viable.

Such investments may appear costly in a period of easing oil prices. Markets are already betting that additional production from the U.S. and the UAE, combined with weaker global demand, will push crude prices lower next year. If that happens, the temptation will be to return to familiar suppliers and established procurement patterns.

That would be a mistake. The lesson of the past several years is that resilience carries a cost. Redundancy, spare capacity and diversified supply chains often look inefficient until the moment they become indispensable.

The market alone is unlikely to deliver that outcome. Once the immediate crisis fades, commercial incentives will favour the cheapest and most familiar options. If Japan wants genuine energy security rather than temporary relief, the state will need to take the lead – using financing, diplomatic support and industrial policy to build supply chains that private actors may not create on their own.

While the price will be higher, so will energy security be enhanced.

ANALYSIS

BY AGLAÉ BANGE

Sodium-Ion Batteries: The Next Frontier for BESS?

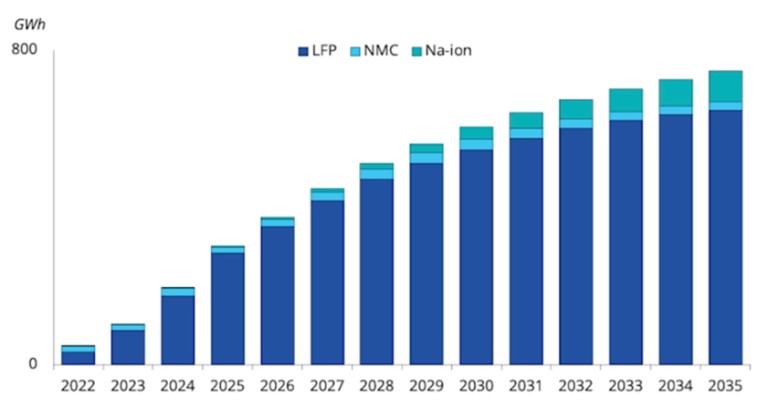

Lithium-ion batteries (LIBs) are dominant across a wide range of energy storage applications, but a new technology could pose a serious challenge. Last year, following major strides by Chinese manufacturers, sodium-ion batteries (SIBs) made a strong entrance on the market, offering several key advantages over lithium.

In 2025, SIBs accounted for less than 1% of global battery energy storage production, but their share could grow significantly by 2030. Free from nickel and cobalt, and instead relying on more abundant and affordable materials, SIBs are also less prone to fire and can retain most of their performance across a wider temperature range.

Given these advantages, LIB manufacturers are taking notice. Yet, so far, Japan appears to have overlooked SIBs. Despite a desire to compete with China in the clean energy sector, seen by strong state support around, for example, perovskite solar cells, and heightened concern over critical metals supply, Japan has shown surprisingly limited interest in developing SIBs domestically.

Is Japan missing a strategic new opportunity, or is its indifference justified?

SIBs: How do they work?

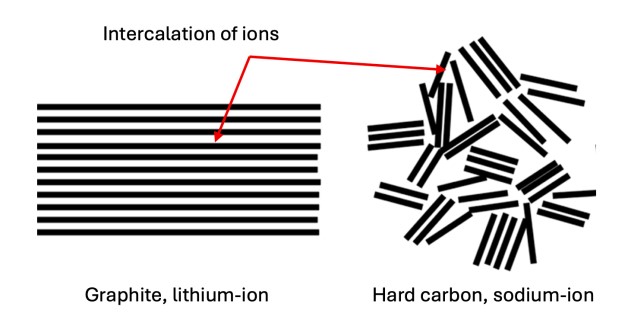

SIBs consist of a negative anode, a positive cathode, an electrolyte, and a separator; ions move between the anode and cathode during charging and discharging. Both sodium and lithium are alkali metals and share similar electrochemical properties.

A major difference, however, lies in density. Sodium ions are roughly 35% larger than lithium ions; this means that fewer ions can be stored within a battery cell. This size difference has important implications for the materials used in the anode.

In LIBs, the anode is made of graphite, an inexpensive material with a structure able to accommodate lithium ions. Conversely, sodium ions are too large to properly adhere within graphite, a process referred to as intercalation.

Since 2000, the industry has known about ‘hard carbon’ – a material capable of accommodating sodium ions effectively. Unlike graphite, hard carbon contains numerous pores and irregular spacings where sodium ions can intercalate despite their bigger size.

This innovation should have spurred manufacturer interest, yet for years the battery industry gave SIBs the cold shoulder. LIBs, due to their higher density (150 Wh/ kg – 300 Wh/ kg), simply offered better performance. In the case of EVs, this accounted for a substantial difference in potential vehicle range.

However, recent concerns around lithium supply has led the industry to reconsider its initial position.

Early developments in China

In 2019, the first SIB system – a 30 kW / 100 kWh BESS station – was installed in a research center in Jiangsu province, with the support of battery manufacturer HiNa as part of a broader wave of R&D investment across China.

Momentum accelerated in favor of SIBs in late 2022. Lithium chemical spot prices surged to a peak of around $80,000 per ton, before falling back to about $19,000 by the end of 2023. This led to concerns over the vulnerability of lithium supply chains, making the search for alternatives to LIBs more urgent.

Last May, Chinese battery manufacturer CATL signed a 60 GWh supply agreement with energy storage integrator HyperStrong. It is now preparing for the commercial rollout of its new sodium-ion battery model, Naxtra. Unveiled in 2025, commercial sales of Naxtra are expected to begin by this year’s end. BYD has also joined the fray, starting to build a sodium-ion battery plant in 2024.

This innovation push is not remaining locked inside the Chinese market – quite the opposite. As sodium-ion batteries enter commercialization, Chinese manufacturers are keen to offer them to Japanese consumers as an alternative option for EVs and even for BESS. One of the top Chinese players, HiTHIUM, told Japan NRG it presented sodiumion products in Japan as early as last year and found interest from developers seeking technology options aligned with Japan’s policy support for non-lithium storage under the latest LTDA framework.

HiTHIUM has ambitious plans for the Japanese market and intends to offer sodium-ion and other battery chemistries as part of its sales push.

Sodium-ion batteries and Japanese market of EVs

Naxtra by CATL is an improved sodium-ion battery model that addresses one of the technology’s main limitations for both stationary storage and EVs: energy density. Naxtra’s energy density is 175 Wh/ kg, a level that rivals lower-end lithium-ion batteries. Previous SIBs typically offered energy densities of no more than 160 Wh/ kg.

SIBs offer a number of other competitive advantages:

| Criteria | Sodium-ion (Na-ion) | Lithium-ion |

| Resources | Sodium (salt) : Abundant* | Lithium/ Cobalt: rare and localized |

| Cost | Low (cheap materials) | High (critical minerals) |

| Energy density | Average (100~175 Wh/ kg) | High (150~300 Wh/ kg) |

| Resistance to extreme temperatures | Excellent (from -20°C to +70°C) | Reduces performance by 20-40% |

| Safety | High | Risk of thermal runaway |

| Charging speed | Rapid (an 80% charge achieved in 15 min for the Naxtra model) | Average |

In Japan, SIB’s properties could carry a competitive advantage for operations in the colder climates of northern Tohoku and Hokkaido. If SIBs are priced more reasonably, they could also emerge as a serious competitor to lead-acid batteries, which are still used in EVs to power auxiliary systems (such as door locks, security systems, windscreen wipers, etc).

Lead-acid batteries are widely used in Japan due to their low cost and well-established recycling chain. This chemistry, however, has a relatively limited lifespan as batteries with it naturally degrade over time due to positive grid corrosion, sulfation, and electrolyte loss. Once a battery drops below 80% of its original capacity, it reaches an end-of-life and becomes highly unreliable, risking sudden failure.

Domestic SIBs: to remain a niche?

Japan is not entirely absent from sodium-ion batteries. Its activity, however, looks very different from China’s. Rather than a coordinated push into mass production for EVs or grid storage, Japan’s sodium-ion efforts remain scattered across university research, specialty industrial cells and small consumer products.

The strongest domestic research base is in materials. Japan Science and Technology Agency’s GteX program includes a sodium-ion battery project led by Professor Shinichi Komaba, one of the country’s leading researchers in the field.

The project brings together universities and research institutes including the University of Tokyo, Waseda, Nagoya University, NIMS and RIKEN. Its goal is to develop lithiumfree batteries that avoid the resource constraints and geopolitical risks associated with lithium-ion supply chains.

There have been several breakthroughs. Tokyo University of Science has reported progress on hard-carbon anodes, one of the key bottlenecks for SIBs. Earlier work by Komaba’s group reported a hard-carbon electrode with unusually high sodium storage capacity. More recent research suggests that sodium insertion into hard carbon can be intrinsically fast, potentially supporting higher-rate charging.

Commercialization in Japan, however, remains limited and niche. Nippon Electric Glass sells an all-solid-state sodium-ion secondary battery based on oxide materials. Its appeal lies less in mass-market scale than in safety and durability.

The company targets applications such as electronics, mobility, stationary uses, energy harvesting and equipment operating in harsh environments. The battery contains no lithium, nickel or cobalt, uses no liquid electrolyte, and can operate in high-temperature environments of up to 300°C.

Elecom has taken sodium-ion into consumer electronics. Its 9,000 mAh sodium-ion mobile battery is marketed around long life, safety and temperature tolerance. The product offers 5,000 cycles and can operate from -35°C to 50°C, making it useful for outdoor, emergency and cold-weather applications.

A similar pattern can be seen in motorcycles where one of the distributors, Navic, offers a SIB product that is lighter and more cold-resistant than the regular lead-acid batteries used in bikes.

There is little evidence to indicate that Japanese manufacturers are working on SIBs for grid-connected energy storage, however. That sector is dominated by LIBs with a handful of sodium-sulfur (different from SIBs) and vanadium redox projects filling at the edges.

Better application?

Japan’s lack of interest in SIBs, in contrast to the Chinese battery makers, seems justified at this stage. SIB’s advantage currently lies in use cases where safety, cycle life, lowtemperature performance, supply-chain resilience and lower material risk matter more than energy density.

Even in China, lithium-ion batteries still dominate most product line-ups, and few expect sodium-ion to take substantial market share over the coming decade. Lithium-ion batteries, especially LFP, continue to benefit from scale, falling material costs, established bankability and a mature production ecosystem. For two-to-four-hour BESS, they’re difficult to displace.

One area worth watching, however, is long-duration energy storage (LDES). As storage duration increases, energy density becomes less decisive, particularly for stationary projects where space and weight are secondary concerns. Cost, safety, cycle life, temperature tolerance and materials availability become more important. On those metrics, sodium-ion could develop a stronger case than it has in EVs or compact consumer devices.

That does not mean SIBs would immediately dominate LDES. They will have to compete with other alternatives, including flow batteries, sodium-sulfur batteries and emerging non-lithium chemistries.

Source : Argus Media

*NMC being also a lithium-ion battery type, alongside LFP, the most common chemistry

Conclusion

Japan’s battery makers have poured time and money into solid-state batteries, while showing far less interest in sodium-ion. For now, that caution is understandable. SIBs offer advantages in safety, cycle life, low-temperature performance and material security, but they are unlikely to overturn the battery industry’s current trajectory. Lithium-ion batteries, especially LFP, remain cheaper at scale, more mature and more bankable for mainstream BESS projects.