JAPAN NRG WEEKLY

SEPTEMBER 14, 2020

JAPAN NRG WEEKLY

September 14, 2020

TOP

- Tokyo Gas invests in U.S. shale to boosts American gas volumes, building up massive hedge against Japanese LNG demand

- Tokyo bourse introduces market-maker program to inject liquidity

in Japanese power trading - Japan promise to roll out new power grid code by 2023; and issues

new guidance for grid rental fees - Equitor helps Japan’s JERA and J-Power transform from fossil fuels

to renewables with offshore wind charge

OIL & GAS

- ENEOS CEO says Japan’s oil demand will halve in 20 years

- Japan’s petroleum fuel prices fall as economy runs out of steam

- Mitsui OSK to set up fund for Mauritius oil spill clean-up

POWER & NUCLEAR

- Governor of area that hosts all of Kansai Electric nuclear plants says confidence in the power company is lost

- Tokyo Gas plots 50%+ boost in electricity clients over two years

- J-Power sells stake in Taiwan gas-fired utility to fund renewables

- Hitachi unveils mobile power plant for natural disasters

- Most cesium released by Fukushima reactors now lies in forests

- OPINION: PM Abe’s successor faces energy conundrum

- TEPCO issued warning over improper power retail practices

RENEWABLES, OTHER

- Tohoku Electric, ENEOS, JRE to invest in 150 MW offshore wind

- Orix buys 20% of India renewables firm for USD 980 million

- Sony to triple use of renewable energy to 15% within five years

- Kawasaki City mulls burning household waste to generate power

- Offshore wind needs mass output or bigger turbines to cut costs

CHEAP JAPAN ENERGY STOCKS OFFER WARREN

BUFFETT-LIKE OPPORTUNITIES

Buffett’s recent $6 billion investment into five Japanese trading houses may be whetting foreign investor appetites for more bargains in the country. The energy sector holds plenty of them. While top global energy names slash dividends or rein in spending, peers in Japan’s oil & gas, shipping and renewables-adjacent space offer both shareholder returns and growth – at valuations close to half their book value.

ENEOS, Japan’s biggest oil player, has a PBR of 0.58 and a dividend yield of 5.35%. For a similar yield from energy firms in the U.S. and Europe, investors pay par book value or more.

FUTURE OF GAS IS NOT (ONLY) IN GAS, MINISTRY SAYS, LAUNCHING NEW 2050 STUDY GROUP

The opening up of Japan’s gas markets in the last three years will help lower the country’s prices for the fuel while growing its use cases. However, it also spells the end of gas as a stand-alone energy sector in Japan.

Meanwhile, Japan’s international clout in natural gas will wane to just 12% of global purchases in 2040. Those are the forecasts released last week by Japan’s METI, which also launched a research initiative to analyze how the domestic gas industry will change in the coming decades.

HOUSE VIEW New Prime Minister

Later today, Japan is expected to have a new prime minister. Most likely, it will be current premier Shinzo Abe’s Chief Cabinet Secretary, Yoshihide Suga. That should be a net positive for energy markets. MORE

NEWS: OIL & GAS

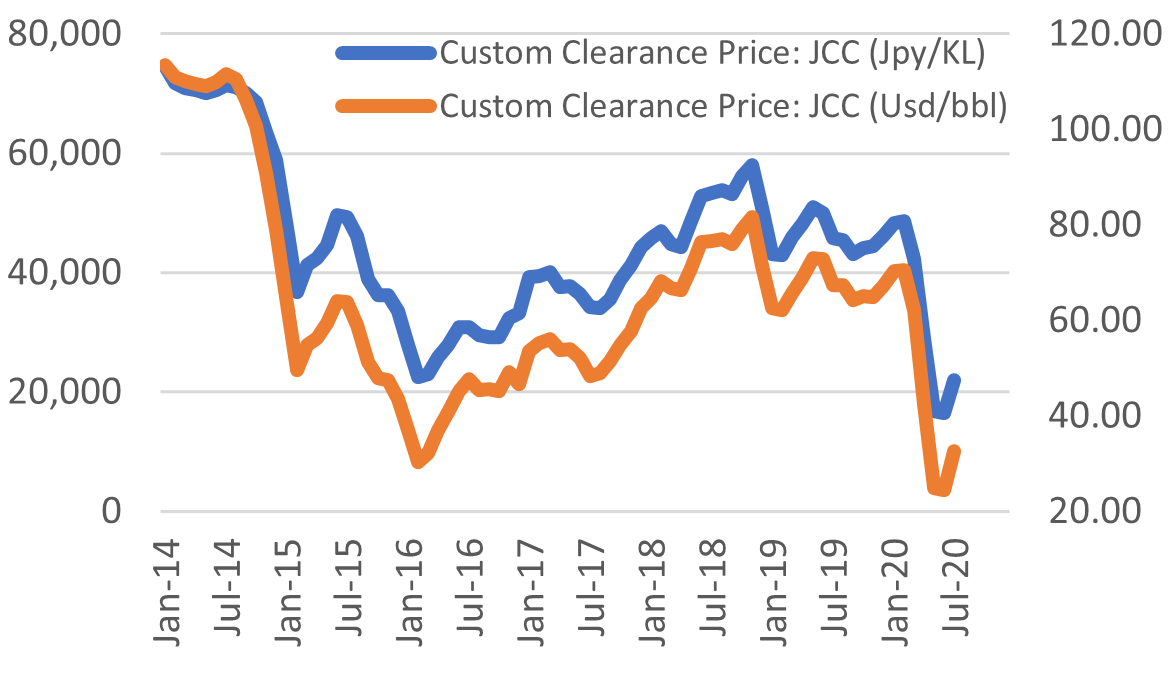

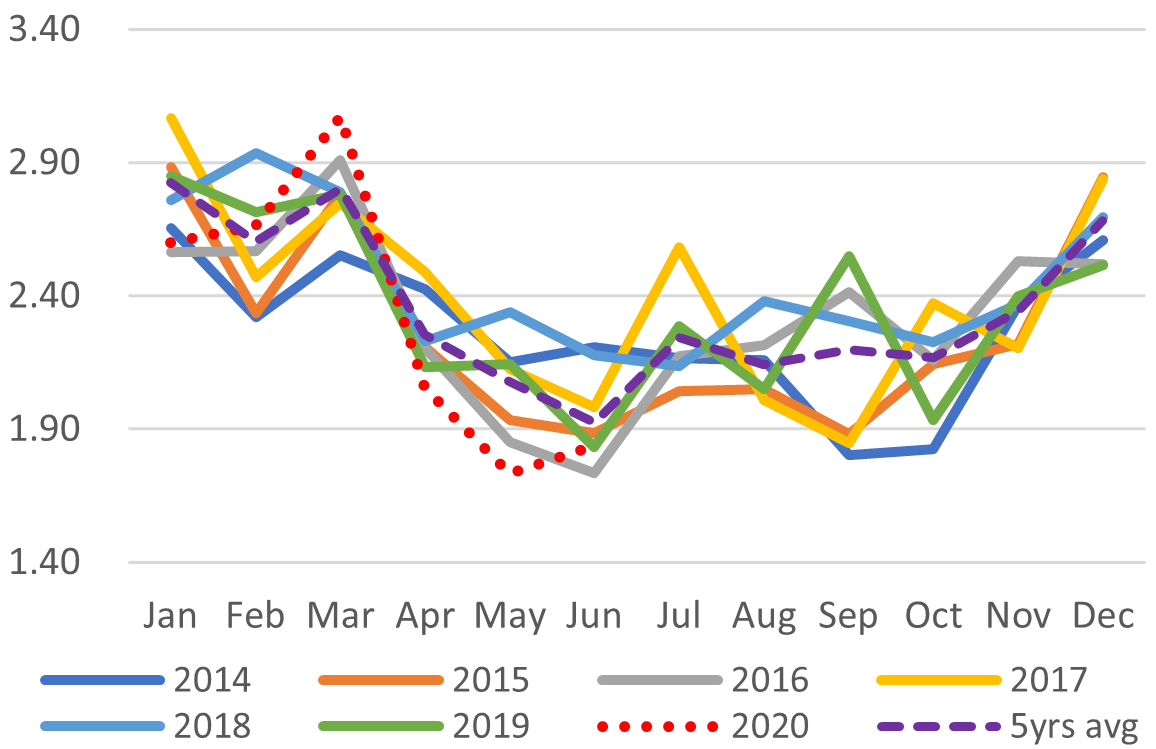

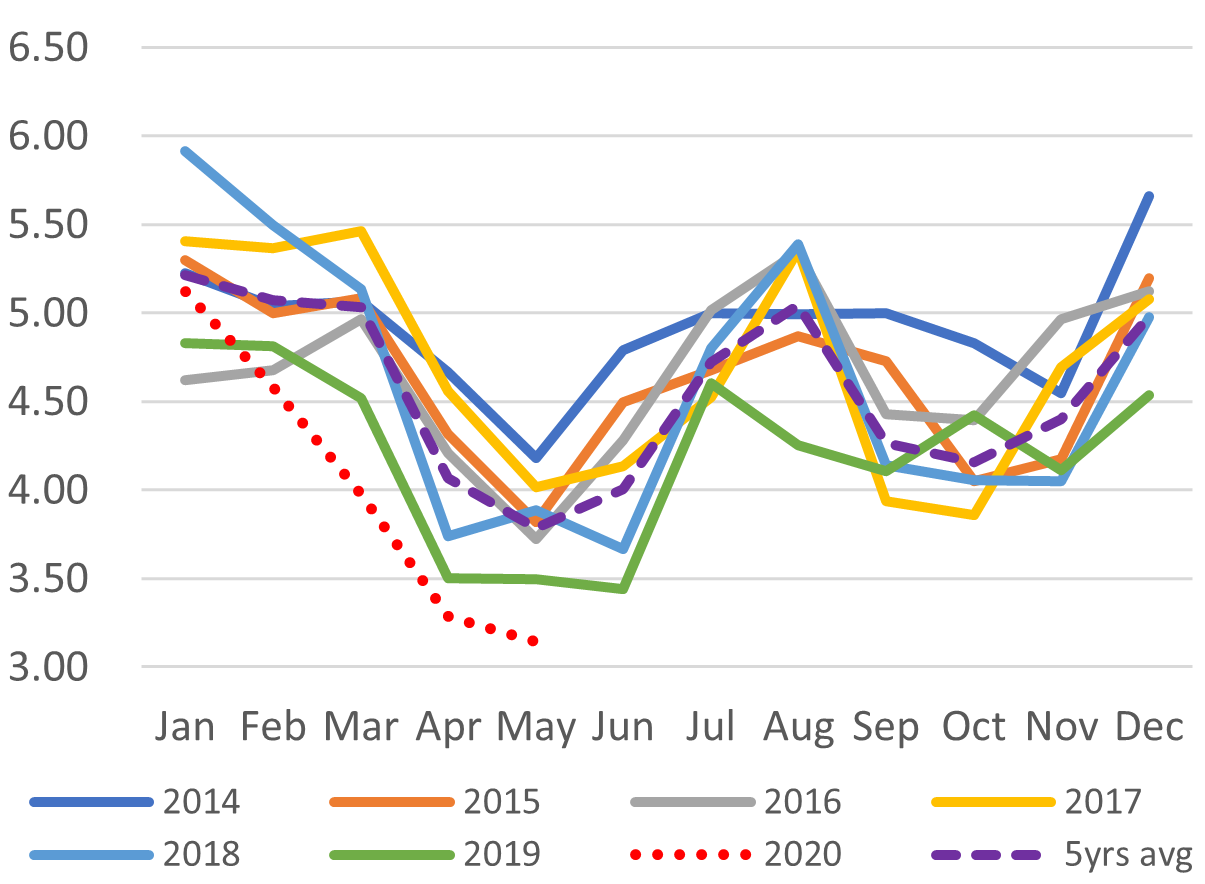

Japan Oil Price: $32.70 / barrel

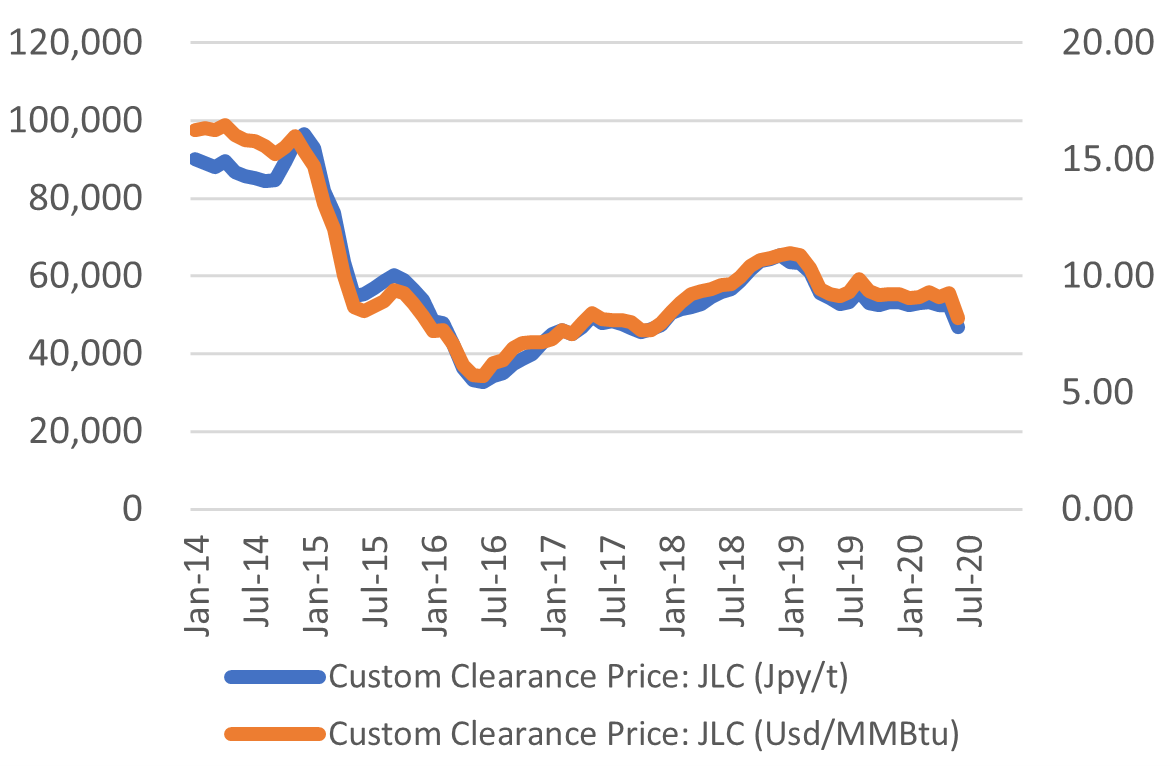

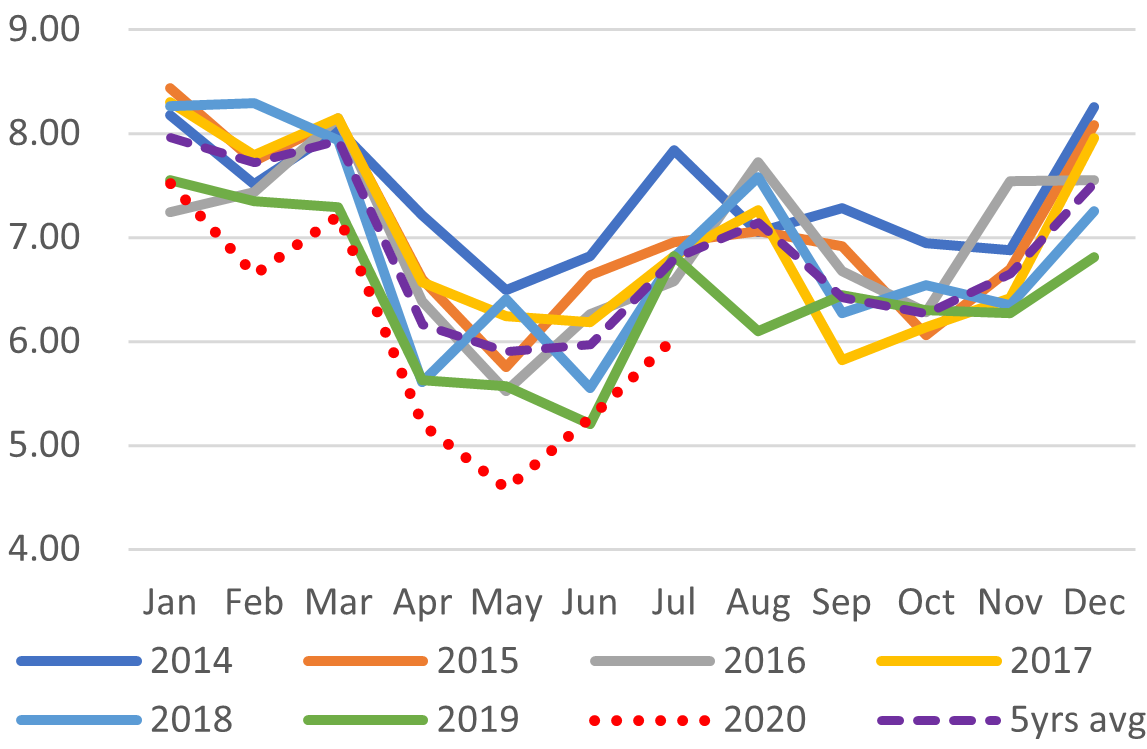

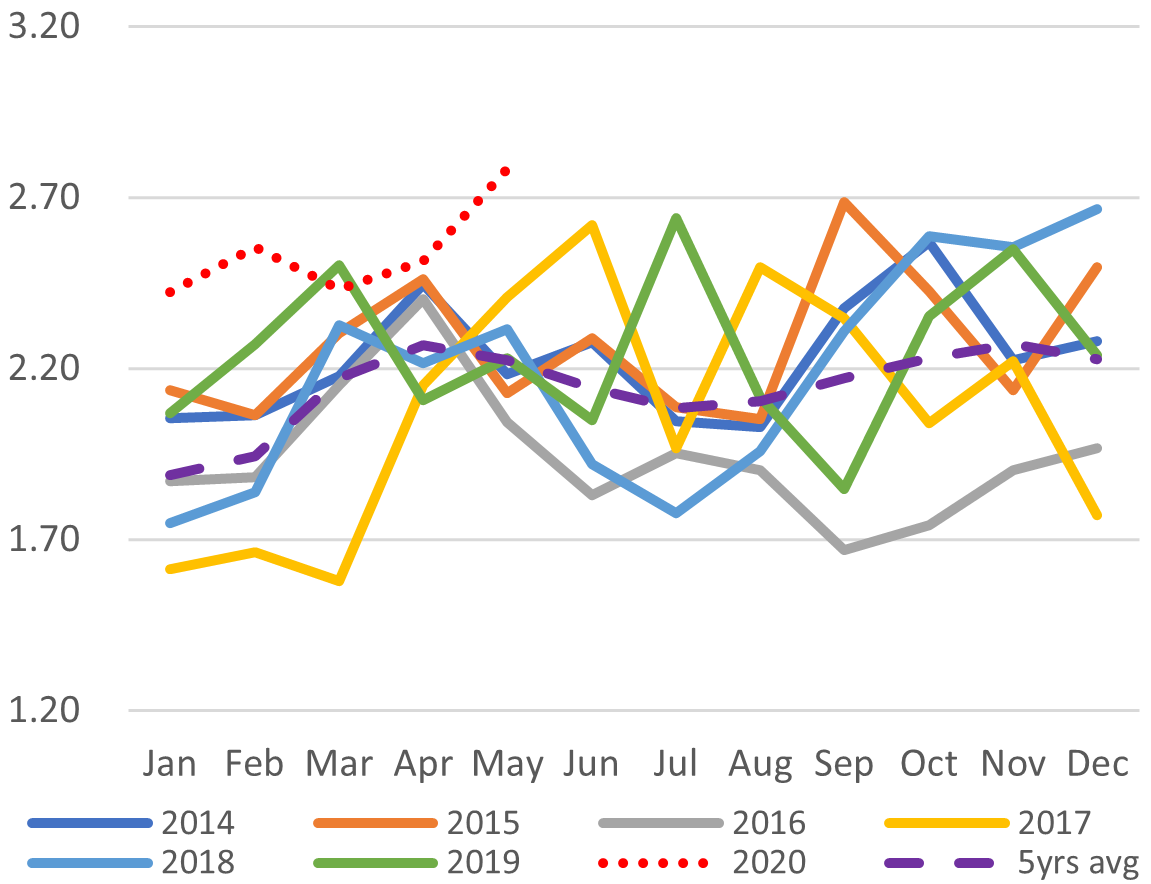

Japan (JLC) LNG Price: $8.21 per Mbtu

Tokyo Gas invests ¥20 billion (USD 180 million) in U.S. shale gas

(Nikkei, September 8)

- Due to a slump in the American gas industry, caused by the coronavirus pandemic, Tokyo Gas was able to acquire these extraction rights from U.S. investor Range Resources for 20% less than first projected.

- The transaction was made through Castleton Resources, a unit of Tokyo Gas America.

- Tokyo Gas raised its stake in Castleton Resources to 70% in July. U.S. gas trader Castleton Commodities International owns the rest.

- In the acquisition of rights from Range Resources, Tokyo Gas spent ¥20 billion and Castleton Commodities another ¥6 billion.

- CONTEXT: The purchase expands annual production capacity of Castleton Resources to 4.7 billion cubic meters, from 2.9 billion cubic meters.

- TAKEAWAY: Tokyo Gas has made a series of shale investments in the U.S. in the last five or so years, partly as a play on the country’s switch to gas from coal for its electricity generation. The scale of the investment, however, is also helping Tokyo Gas use the U.S. gas assets as a hedge against the domestic market. The production levels attributable to Castleton Resources alone run to 3.45 million metric tons of LNG equivalent. That’s equal to almost 4.5% of Japan’s entire LNG import volume.

ENEOS CEO says demand for oil will halve in 20 years

(SankeiBiz, September 4)

- CONTEXT: New company president Ota Katsuyuki gave a series of media interviews, most of which were covered in the Sept. 7 edition of Japan NRG Weekly.

- CEO Ota said ENEOS has taken the bold move of slashing its projection for oil demand in Japan in 20 years’ time to half of current levels.

- Ota sees oil demand never recovering fully to pre-COVID levels.

- ENEOS posted a loss of ¥188 billion in the fiscal year to March, as a result of inventory write-downs on crude oil and lackluster fuel sales.

- TAKEAWAY: Japan’s biggest oil firm made the pessimistic projection on Japan’s oil demand for 2040 even before the COVID crisis. That the new president has reiterated the call indicates that the company started planning for a future less dependent on oil earlier than its international peers, many of which used the 2020 pandemic as a jump-off point. Ota also gave the media hints of where he wants to diversify: hydrogen, solar, petrochemicals. Sceptics says ENEOS’ rivals have already tried some of these moves and the results have been disappointing. Moreover, while Japan’s oil refining margins remain among the best in Asia, it’s harder to convey a sense of urgency. How much ENEOS has absorbed its own forecasts will become clear from its investments over the next two-three years.

Japan petroleum fuel prices fall as economy runs out of steam

(Sekiyu Shimbun, September 10)

- ENEOS, Idemitsu and COSMO have all announced a one yen per liter reduction in fuel prices across the board in response to a fall in the price of crude.

- This is the first reduction in fuel prices for five weeks, and is seen as evidence that the recent bullishness in the market was unsustainable.

- Crude prices seem to be in part reacting to reports that Covid-19 is now out of control in major oil consumer India.

Mitsui O.S.K. to spend ¥1 billion on oil spill cleanup and set up fund for Mauritius relief

(Nikkei Shimbun, Jiji, September 12)

- CONTEXT: The Panama-flagged Wakashio bulk carrier, owned by Nagashiki Shipping and chartered by Mitsui OSK, ran aground on a reef off the coast of Mauritius on July 25. Leaks started in earnest a week later. It was carrying about 3,800 tons of oil and 200 tons of diesel from China to Brazil. About 1,200 tons spilled into the water, and while more than half was recovered early estimates indicate that environmental recovery will take decades.

- Mitsui OSK Lines said Sept 11 that it will spend about ¥1 billion (USD 9.42 million) to help with the clean-up work off the coast, in and around Mauritius. That includes ¥800 million to set up a fund for environmental restoration.

- Co. President Ikeda Junichiro said he felt social responsibility for the accident. The co.’s fund will disperse financing over several years, paying for coral reef recovery and other environmental clean-up efforts.

- Direct monetary responsibility for the accident lies with vessel owner Nagashiki Shipping. However, the firm’s liability under maritime claims cannot exceed 2 billion-yen, which experts say is not enough to cover the work to restore the area.

- Mitsui OSK is also setting up an office in Mauritius next month to post staff who will oversee the cleanup efforts.

NEWS: POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 4 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | competed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

Power Utilities’ LNG Imports Vs Stockpiles

Source: JANSI and JAIF, as of August 23, 2020

Tokyo Commodity Exchange starts market maker program for electricity futures

(Denki Shimbun, September 11)

- The Tokyo Commodity Exchange is introducing a “market maker” program for electricity futures in a bid to boost the liquidity of the futures market.

- Under the system, “market makers”—principally securities firms—will simultaneously provide bids and asks for contracts in electricity futures, thereby facilitating trading in electricity utilities and other traded entities.

- On September 4, the Exchange began accepting applications from market makers in respect of East Area Baseload (24 hours a day, every day) and East Area Peakload (12 hours a day on weekdays).

- The program will begin on October 1.

- CONTEXT: Liquidity of Japan’s power trading reached records this summer. The trading volume of the Japan Electric Power eXchange (JEPX) went above 42% of power demand in June.

Japan promises to roll out new power grid code by April 2023

(Denki Shimbun, September 7)

- An expert committee under the auspices of the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) met on Oct 4 to begin discussing Japan’s new “grid code” — a set of rules that govern the supply of renewable energy to the national grid.

- Consideration will be given to the government’s 2030 “energy mix” targets.

- The committee aims to finalize the technical requirements necessary to address current issues about power quality and the rationalization of output controls in a timely manner, and is working to have the grid code ready to be rolled out in April 2023.

- SIDE DEVELOPMENT: Agency issues new guidance for power grid rental fees

(Denki Shimbun, September 11)- The Agency for Natural Resources and Energy has issued guidance on the level of grid rental fees payable by electricity transmission operators.

- In urban areas, new entrants to the transmission market will pay a rental fee equivalent to the total expected revenue from transmission services provided in the area minus grid maintenance costs. The rental fee includes a levy to ensure universal service is maintained in other regions.

- In mountainous areas where there is less demand, new entrants to the transmission market will receive a subsidy, meaning that these operators will effectively be subsidized by legacy operators.

Fukui Governor says confidence in Kansai Electric not restored

(Nikkei, September 5)

- Fukui Governor Sugimoto Tatsuji says public confidence in Kansai Electric (KEPCO) has not improved in the communities that are home to the utility’s nuclear reactors.

- Referring to the recent spate of workplace accidents in nuclear power stations in Fukui, Sugimoto said KEPCO’s relationship with the community would not improve until it took proper measures against the coronavirus, has put an end to workplace accidents, and did more to support the local economy.

- SIDE DEVELOPMENT: KEPCO CEO pledges improve safety through structural reform

(Denki Shimbun, September 11)- KEPCO CEO Morimoto Takashi held discussions with the Nuclear Regulation Authority on Sept 9.

- Morimoto outlined reforms implemented in response to the recent scandal involving former directors, and explained voluntary action being taken by KEPCO to improve safety.

- The Authority and Morimoto spoke about morale at KEPCO in the wake of the scandal.

- SIDE DEVELOPMENT: Oi plant: Authority to investigate cracks

(Mainichi Shimbun, September 11)- The Nuclear Regulation Authority agreed on October 9 that the operator of the Oi nuclear power plant in Fukui, KEPCO, should provide more information on cracks found in welded sections of pipes attached to the number three reactor and allow the Authority to inspect the affected area.

TAKEAWAY: Fukui prefecture is home to the most nuclear reactors of any one locality in Japan. It hosts all three of Kansai Electric’s operable nuclear stations. Since the outbreak of the graft scandal around KEPCO’s nuclear assets earlier this year, the company has been under attack from civil society. The comments from Fukui’s governor suggest it will be a while before KEPCO can ask for the token (but very important) permission from the prefectural government to restart more of its nuclear reactors.

Tokyo Gas plans to boost electricity subscribes more than 50% in two years

(Sekiyu Shimbun, September 10)

- Tokyo Gas said it has over 2.5 million households now subscribing to its Zuttomo Denki electricity plan.

- The utility’s mid-term business plan through 2022 sets a target of 3.8 million subscribers.

- SIDE DEVELOPMENT: Tokyo Gas subscribers can now pay gas bills using Line

(Denki Shimbun, September 11)- Tokyo Gas said on Thursday it had entered into an agreement with Line Pay that would enable subscribers to pay gas and electricity bills via Line Pay’s cashless payment interface.

- The new service is envisaged to start in early 2021.

- CONTEXT: LINE is the most popular social media communications app in Japan with more than 80 million accounts.

TAKEAWAY: Tokyo Gas seems to have the most aggressive plan for the electricity business. With negative population growth, gaining new clients is a zero-sum game, in which the biggest loser may be Tokyo Electric Power Co. (TEPCO).

J Power sells stake in Taiwanese utility

(Nikkei, September 8)

- J Power said on Sept 7 that it was selling its 39.97% stake in Taiwan’s Chiahui Power Corporation to Chiahui affiliate, Asia Cement.

- The 19.4 billion yen raised by the sale will be invested in renewable energy projects.

TAKEAWAY: J-Power has recently tried to present itself as a hydropower utility, as featured in the Aug 31 edition of Japan NRG Power. In reality, however, the company is heavily reliant on coal-fired generation and its approach to overseas investments to date could be interpreted as a scatter-gun. To rebalance the energy and geographic portfolio, it makes sense to sell a minority stake in one gas-fired station in Taiwan, especially one that sees its power-purchasing agreement expire in less than a decade.

Hitachi unveils mobile power station

(Nikkei Sangyo Shimbun, September 9)

- Hitachi subsidiary ABB Power Grid has unveiled a movable power station that can be transferred to areas that suffer power outages after a natural disaster or where power demand urgently spikes.

- The power station can be deployed within seven days.

- The modular design enables it to be transported by truck.

Tracking cesium released by Fukushima reactor

(Asahi Shimbun, September 7)

- A survey of deposits of radioactive cesium-137 around the Fukushima reactor has found that 70% of cesium-137 released during the accident now lies in the surrounding forest.

- Of the cesium-137 that landed in forested areas, 98% was absorbed by soil and leaf litter, with a mere 2% contained in tree trunks and branches.

- A faster than expected drop in the concentration of radioactive cesium in rivers in the area is attributed to a decrease in the radioactivity of leaves falling into the water.

- Fish in the rivers were also studied. The largest fish were found to contain the greatest concentrations of radioactive cesium.

- CONTEXT: Asahi is Japan’s most left-leaning Top 5 daily. It has closely tracked the fallout from the Fukushima nuclear accident. The issue of radioactive contamination in farm produce, fish and seafood was of particular concern for the local communities.

OPINION: PM Abe successor faces energy puzzle as little progress in nuclear restarts

(Mainichi Shimbun, September 8)

- CONTEXT: This is a long opinion piece in one of the Top 5 dailies in Japan, which seeks to evaluate the state of the energy industry after PM Abe Shinzo’s more than seven years in power.

- When Abe became Prime Minister in 2012, he promised to scrap the commitment made by the previous Democratic Party administration to phase out nuclear power.

- The Abe government proposed to keep nuclear as an important baseload power source and set a target for nuclear reactors to provide 20-22% of all electricity by 2030. This represents an output of around 30 nuclear reactors. To date, however, only nine reactors have been restarted.

- While the government also made renewable energy part of its policy, as of 2018, renewable energy only made up 17% of the energy mix, a long way from the 22-24% target for 2030.

- Abe’s successor will inherit a lot of thorny energy problems, including finding a final storage site for highly radioactive waste.

- One of Abe’s top achievements was reforming Japan’s electricity grid in 2015 to allow surplus electricity generated in west Japan to be used in the east. Abe’s government also deregulated the retail electricity market.

- Environmental economist Oshima Ken’ichi says the rising safety costs associated with nuclear power make it difficult to sell local communities on the idea of restarting reactors. Because nuclear is a drain on power companies’ bottom line, the government needs to support utilities more to enable them to invest in renewables, he says.

TEPCO ordered to reform marketing practices

(Nikkei, September 9)

- TEPCO subsidiary TEPCO Energy Partner said on Wednesday it had been served with a warning by the Ministry of Economy, Trade and Industry’s electricity and gas industry watchdog, and instructed to reform its business practices.

- Between March and December 2019, a telemarketing company contracted by TEPCO Energy Partner signed up consumers for electricity plans without their consent, and engaged in other improper conduct, according to a government probe.

- This is the fourth time that TEPCO Energy Partner has been issued with a warning over its business practices.

NEWS: RENEWABLES & OTHERS

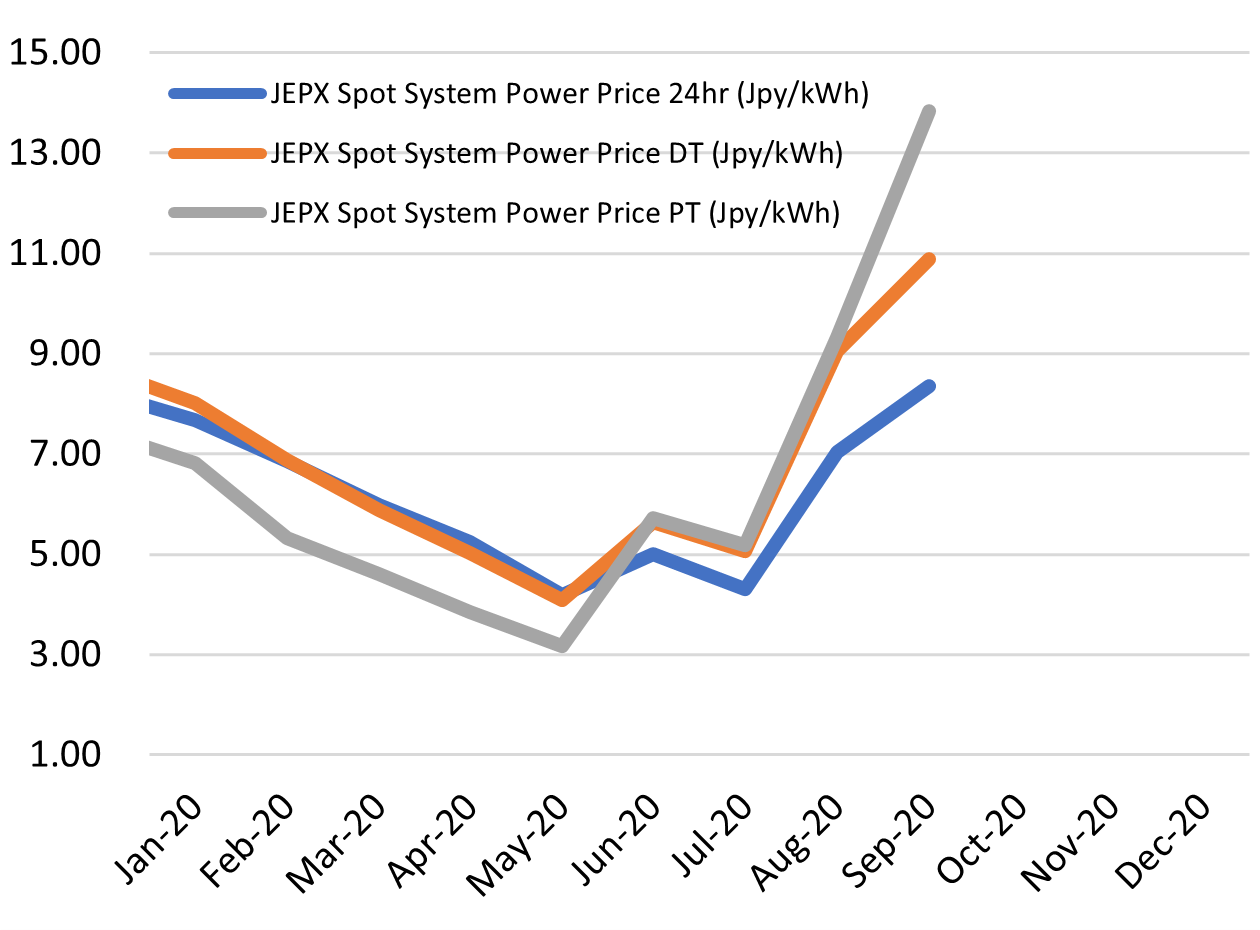

Spot Electricity Prices (24h)

Spot Electricity Prices (2020)

Equinor, JERA and J-Power prepare to bid for Akita offshore wind project

(Akita Sakigake Shimpo, September 10)

- Major thermal generation utility JERA has formed a consortium with electricity wholesaler J-Power and Norwegian energy developer Equinor to bid for offshore wind projects in Akita Prefecture, in the north of Japan.

- The consortium will participate in the government’s tender process for offshore win sites, which is scheduled for November.

TAKEAWAY: The alliance is interesting in that, among other factors, it pools together companies that are more known rooted in fossil fuels. Equinor of Norway changed its name from Statoil two years ago to signal that the oil and gas major would seek to diversify, including into solar and wind projects. JERA is Japan’s biggest LNG importer and has itself only started a gradual tip-toe into renewables. J-Power is heavily reliant on coal-fired generation. Still, in moving ahead of its oil and gas peers into the renewables space Equinor has already gained some reputation in the field and even sold a stake in its US offshore wind projects to BP for over USD 1 billion. It’s likely the Norwegians will also take the lead here.

Orix invests USD 980 million in Indian renewable company

(Nikkei Shimbun, September 11)

- Orix Corp makes its biggest investment overseas in buying about 20% of Indian renewable energy development firm Greenko Energy Holdings.

- Orix will buy new and existing shares, and will transfer its wind power generation business in India to Greenko. Singapore’s GIC Pte holds 65.8% of Greenko, Abu Dhabi Investment Authority has a 16.5% stake and the remainder is held by its founders.

- CONTEXT: Orix is major renewable energy developer in Japan, especially in solar. It is considering acquisition targets in the space in Europe as well.

Sony to triple use of renewable energy to 15% of total within 5 years

(Nikkei, Sept 10)

- Co. said Sept 10 that 15% of the electricity the group uses will come from renewable sources by the middle of this decade. The group will ask its suppliers and contract manufacturers to cooperate.

- Sony is also creating a ¥1-billion corporate venture capital fund to invest in environmental technology startups over the next three to five years.

- Co. says it is important to set achievable goals in the short term, but it still aims to move toward 100% renewable energy in the longer term.

- CONTEXT: Sony is a member of the RE100 initiative, which seeks to have its members source all their electricity from renewable sources.

Tohoku Electric, ENEOS, JRE to invest in 155 MW Offshore Wind Project

(Yuri Invest Research, Sept 11)

- Tohoku EPCO, ENEOS and Japan Renewable Energy Corp (JRE) have agreed to invest in the Happo Noshiro offshore wind power project which aims to set up 155 MW of capacity off the coast of Akita prefecture.

- JRE is currently conducting environment impact assessment and other studies on the site near Noshiro City in northern Japan.

- In July this year, the Ministry of Economy, Trade and Industry (METI) and the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) designated the planned project area as one of “promising four sea areas for which preparations for organizing the council and other actions will start,“ according to JRE.

- The project would see the utilization of 22 turbines, each of 8 MW to 10 MW capacity. Commercial operation is expected after 2024, JRE said.

Kawasaki City may generate electricity from household waste

(Kensetsu Shimbun, September 7)

- The Kawasaki government is considering generating electricity from waste collected in the municipality by 2023/24.

- Power generated could be used to supply the electricity needs of government buildings and facilities.

- It is projected that 120 GWh of electricity could be generated from burning waste every year.

Reducing the cost of offshore wind with a variation on Moore’s Law

(Nikkei X-Tech, September 4)

- There are two main avenues for reducing the cost of wind power. The first involves leveraging the cheaper costs afforded by mass production. The second involves building wind turbines with higher pylons or longer blades—the output of a wind turbine is more or less proportional to the square of the blade length.

- The world’s largest wind turbine is currently the Siemens Gamesa Renewable Energy 14MW, which it is nearly as tall as the Eiffel Tower and sports a turbine diameter of 220 m.

- The trend toward giant turbines will also accelerate the consolidation of the market between a small number of operators.

ANALYSIS

DIRECTOR,

K.K. MATHYOS

With Low Metrics, High Dividend Yields, and Growth StoryWarren Buffett’s recent $6 billion investment into five Japanese trading houses may be whetting foreign investor appetites for more bargains in the country. The energy sector holds plenty of them.

While top global energy names slash dividends or rein in spending, peers in Japan’s oil & gas, shipping and renewables-adjacent space offer both shareholder returns and growth – at valuations close to half their book value. ENEOS, Japan’s biggest oil player, has a PBR of 0.58 and a dividend yield of 5.35%. For a similar yield on energy firms in the U.S. and Europe, investors pay par book value or more.

Foreign investors pulled back from the Japanese market around 2015 after initially backing the economic course of (now outgoing) Prime Minister Shinzo Abe. Part of that was over concerns that PM Abe had failed to push through promise structural reforms. Yet, looking at energy space alone, change has been dramatic.

During PM Abe’s term, Japan has completely liberalized electricity and gas retail, creating the world’s third-largest power market. Japan has tripled its renewables capacity in the last decade and installed the third-most solar capacity. It remains the No.1 importer of LNG, with Japanese firms now starting to expand their trading of the fuel outside the country. Even the “waning” oil industry can boast refining margins that often touch 15%, among the best in Asia.

Government policies and commitments to sensible energy transition are unlikely to change with the new premier. If, as widely expected, Yoshihide Suga takes over the leadership on September, Abe’s No. 3 will likely continue the Abenomics course, focusing on restructuring and a loose monetary policy. This will benefit investors compared with the political uncertainty in, for example, the U.S., where some stock valuations are breaking all records.

Japan is also less vulnerable than some of its international peers on international trade. Exports and imports for Japan as a proportion of GDP are less than international peer economies.

LOW VALUATION METRICS

There is a lot of speculation over why Buffett chose Japan, which he has previously shunned, and the trading houses in particular, as they do not easily fit his preference for a “simple” business. One thing, however, is clear: This is a profitable trade.

A year ago, Buffett’s Berkshire Hathaway sold its first ever bonds in Japan, raising around $4 billion. If that money was put to the purchase of stocks of Mitsubishi Corp., Mitsui & Co., and other trading houses (which earn a significant portion of their income from energy and commodities), the Oracle of Omaha may well be sitting on a positive carry of a quarter of a billion dollars per year. (Based on an average dividend yield of 470 basis points, less funding of 70 basis points).

This may not be a bad investment when there is concern about dividends in the U.S. As speculation mounts over whether Exxon Mobil will cancel its dividend in 2021, most analysts say the company will struggle to keep its returns at the traditionally generous level going forward. Buffett’s total portfolio earns just short of $4 billion in dividends annually and the bulk of the holdings is in infrastructure and energy.

In the other extreme, Saudi Aramco, now the world’s largest oil company by market capitalization, is cancelling large parts of its investments in order to direct cash to dividends to support the Saudi economy in the face of collapsing oil demand and prices. This could hamper its future growth.

Japan’s energy sector provides an oft-overlooked alternative, especially as the country’s firms are also valued at low price-to-book ratios (PBRs) and price-earnings-ratios (PERs) compared to global peers.

Also, as reported in the Sept 7 edition of the Japan NRG Weekly, Japan’s 10 listed electricity companies may be forced to merge, opening up opportunities to earn M&A premia. Chugoku, Tohoku, and Hokuriku EPCs are all considered vulnerable due to their excessive reliance on coal fired-power stations. Aside from the energy mix conundrum, Japanese utilities enjoy resilient demand and health prices (over 20 cents per kWh compared with nine cents per kWh for U.S. electricity companies).

SPENDING LESS TO YIELD MORE

For attractive yields, it’s worth taking a look at Japan’s oil and refining sector. Post-merger with domestic rival Showa Shell last year, Idemitsu’s divided yield runs to 5.1%. Industry leader ENEOS is even more generous with a yield of 5.21% on a PBR of 0.58. ENEOS is also aggressively pursuing hydrogen energy opportunities, including via a tie-up with JERA (the world’s largest LNG buyer), and other business diversifications.

In upstream oil, JAPEX trades at a PBR of less that 0.30. Its 7% cross-shareholding in domestic peer INPEX is worth almost $700 million – equivalent to about 70% of JAPEX’s market capitalization.

Tokyo Gas, Japan’s largest gas company, recently announced that its retail electricity customers had reached 2.5 million, marking a very successful diversification into the adjacent sector since its liberalization. Tokyo Gas has a dividend yield of almost 3%.

In shipping/marine transportation, Nippon Yusen trades at a PBR of 0.64 and Mitsui OSK at 0.51. Both companies could see a remarkable turnaround if a Covid-19 vaccine is found and global trade quickly recovers to pre-pandemic levels.

In infrastructure, JGC forecasting profit to increase this year and has a resilient global order book, but trades at a PBR of 0.72.

If Japan is forced to accelerate nuclear power re-starts to meet carbon reduction goals, beneficiaries would include Hitachi, which recently completed a record $7 billion acquisition of ABB’s power grid business.

Japan’s chemicals and pharmaceuticals sectors, which absorb large commodity inputs, may also offer good inflation-proof returns in a post-Covid world. Many of these companies are global leaders with large international footprints.

At 90 years old, some say Buffett is too old and does not grasp the technology stocks that drive markets today. Whatever your views, it’s hard to argue against his knowledge of the energy space.

About five years ago Buffett sold off his $4 billion holding in Exxon, when the U.S. oil major was around an all-time high of over $100.

It now trades at $36.

ANALYSIS

RESEARCHER,

YURI INVEST RESEARCH

As Ministry Begins Study of Trends to 2050The opening up of Japan’s gas markets in the last three years will help lower the country’s prices for the fuel while growing its use cases. However, it also spells the end of gas as a stand-alone energy sector in Japan.

Meanwhile, Japan’s international clout in natural gas will wane as the country’s share of global purchases will slide to just 12% in 2040, from around a third today.

Those are the intriguing forecasts released last week by the Japanese ministry in charge of energy policy (METI), which launched a research initiative this month to analyze how the domestic gas industry will change in the coming decades.

The research will be conducted by a newly created “Study Group on the Gas Sector in 2050,” which held its first meeting on September 4. The group, comprised of 10 experts, is chaired by Professor Yamauchi Hirotaka of Hitotsubashi University. Other members include Shibata Yoshiaki, a senior economist at The Institute of Energy Economics, and Yoshitaka Mari, the principal sustainability strategist at Mitsubishi UFJ Research & Consulting.

THE GAS STORY SO FAR

The liberalization of Japan’s gas retail, done almost concurrently with the similar opening up of the electricity sector, has already revamped the industry.

Since opening all gas retail to competition from 2017, some 80 new companies have entered the market, according to METI’s report, published to coincide with the creation of the Study Group. New entrants include seven of Japan’s 10 dominant power utilities (EPCOs), 16 LP gas companies, 9 distribution firms, and many others including oil and steel majors.

Households have 35 new gas suppliers to choose from, according to METI.

That is not an insignificant change given that the city gas industry in Japan counted around 200 companies before deregulation, according to Gas Association data. (The figure does not include the thousands of micro sellers, like grocery stores that supply LP gas to a single farm.)

The inflow of such prominent fresh faces that include Japan’s biggest electricity, oil-refining, and other energy majors shows that the “sectoral silos” of energy are breaking down. The future, as METI sees it, belongs to integrated energy companies that work across multiple energy sources and, in addition to gas and electricity, provide associated services.

The unbundling of the six regional gas monopolies, such as Tokyo Gas, Osaka Gas, and Toho Gas, due to be completed by April 2022, will further stimulate competition. METI will seek a similar separation of distribution and retail assets in the smaller gas companies, though rule application in those cases is expected to be looser.

METI plans to review the liberalization program after its completion in April 2022. The goals that the ministry has in mind are: reduced gas rates, more stable supply, a broader gas services menu, and more marketing opportunities associated with the industry.

TOPICS THE “STUDY GROUP ON GAS SECTOR IN 2050” WILL TACKLE

| Gas Industry’s “Identity Crisis” | The role of gas in a low carbon society and in digitized economies |

| What industry stakeholders need to do to fulfill such roles | |

| Supply Stability Issues | A review of the current procurement strategy, which is based on multi-year contracts and pricing pegged to oil prices |

| Solutions for how to deal with supply cuts during a disaster | |

| Use of advanced digital technologies | |

| Building a diversified energy supply system | |

| Advanced Technologies | How AI and IoT will be applied and what new business models this creates |

| What new markets can gas suppliers diversify into | |

| How to serve sparsely populated areas with low demand | |

| What partners can gas firms find in other industries |

THE SHRINKING OF THE GAS GIANTS

While Japan’s gas market will turn more vibrant through new services and competition, it faces many tough challenges ahead.

The country’s goal by 2050 is to cut emissions by 80%, according to METI’s document. As such, the gas business will need to work within an integrated energy company to survive.

In addition to the well-known factors of geopolitical tensions and Japan’s demographic shift, the domestic gas industry will need to integrate new digital tools, such as the Internet of Things (IoT) and AI, plus adapt to lifestyle changes driven by a post-Covid world outlook.

Utilizing IoT and AI should help improve the efficiency of daily operations and market forecasts, as well as aid physical delivery of gas to customers. Technological change, however, is also likely to lead to less energy consumption and industry streamlining.

The new Study Group is tasked with looking for answers to such challenged. And they will need to approach it while keeping in mind the downsizing of Japan’s overall influence in the global gas market.

METI sees China and India replacing Japan as the world’s mega consumers of gas, weakening the latter’s bargaining power. As Japan’s share of global gas purchases shrinks to 12% by 2040, China’s will rise to 26%, METI forecasts.

India’s demand will double the country’s global share to 16% in 2040, from 8% in 2018.

HOUSE VIEW

After the party vote, Japan’s parliament is expected to formally announce a new prime minister on Wednesday, Sept 16.

Ostensibly, the vote is supposed to decide only who serves out the rest of PM Abe’s term as head of the LDP. That term is due to end next September.

Our sources, however, indicate that should Suga be elected prime minister, there is a strong likelihood of him calling a general election on Oct. 25th (nine days before the U.S. presidential election). The date would coincide with a municipal election in Osaka, the heart of Japan’s second-largest economic region.

The emergence of Suga as front-runner has given the ruling LDP a 20-percentage point jump in popularity in recent weeks, the kind of boost it has not seen for a while. If this were translated into electoral gains, the make-up of Japan’s parliament would be locked down and political stability largely secured until the middle of the decade. The biggest opposition parties reunited last week after a three-plus year split. An election next month may leave them with little time to rally support.

For energy investors, the above scenario could be appealing. As a major part of the Abe administration, Suga is unlikely to veer far from policies of his predecessor. His stated perchance for lower household bills is also unlikely to rattle electricity markets, where the trend has been for lower prices since liberalization.

As METI, the ministry in charge of energy, works on a revision of Japan’s 2030 energy mix targets, it would also help to have a premier who will stick around for more than a year. Otherwise, it would be hard to expect progress on major energy issues, such as how to resolve the impasse over nuclear restarts, what to do with weakened power utilities once Japan phases out older coal plants, and how to create a realistic market for offshore wind.

Change often seems more exciting than stability. For long-term energy policies, prospective investors should be happy to stay bored for a while longer.

STOCK MARKET PERFORMANCE

| As of close on September 11, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| INPEX CORP | 1605 JP | 925.36 | -1.14 | -43.31 | -7.38 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 103.68 | 0.72 | -37.75 | -1.09 | |

| ENEOS HOLDINGS INC | 5020 JP | 1324.74 | 0.47 | -15.17 | -1.18 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 706.24 | 2.29 | -19.22 | 0.00 | |

| COSMO ENERGY HOLD. | 5021 JP | 138.43 | 2.00 | -31.63 | -5.11 | |

| Industrials | ||||||

| JGC HOLDINGS CORP | 1963 JP | 291.88 | -0.88 | -34.96 | -7.17 | |

| CHIYODA CORP | 6366 JP | 69.51 | -1.84 | -5.65 | -3.96 | |

| MITSUBISHI CORP | 8058 JP | 3802.71 | -1.14 | -9.22 | 10.59 | |

| MITSUI & CO LTD | 8031 JP | 3309.72 | -1.31 | 1.57 | 8.78 | |

| Utilities | ||||||

| TOKYO ELECTRIC POWER | 9501 JP | 491.75 | -1.29 | -34.48 | -3.47 | |

| CHUBU ELECTRIC POWER | 9502 JP | 1013.83 | 2.65 | -11.84 | 1.25 | |

| KANSAI ELECTRIC POWER | 9503 JP | 997.87 | 1.48 | -14.22 | 1.53 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 458.062 | 2.11 | 3.95 | 0.21 | |

| J-POWER | 9513 JP | 303.86 | 3.75 | -36.21 | 2.41 | |

| TOKYO GAS CO | 9531 JP | 1048.79 | 1.72 | -9.58 | -1.27 | |

| OSAKA GAS CO | 9532 JP | 862.94 | 2.12 | 0.22 | -1.99 | |

| TOHO GAS CO | 9533 JP | 497.93 | 4.31 | 6.28 | -4.75 | |

| SAIBU GAS CO | 9536 JP | 99.85 | 7.92 | 7.00 | 5.09 | |

| SHIZUOKA GAS CO | 9543 JP | 66.82 | 0.11 | -6.97 | -3.41 | |

DATA

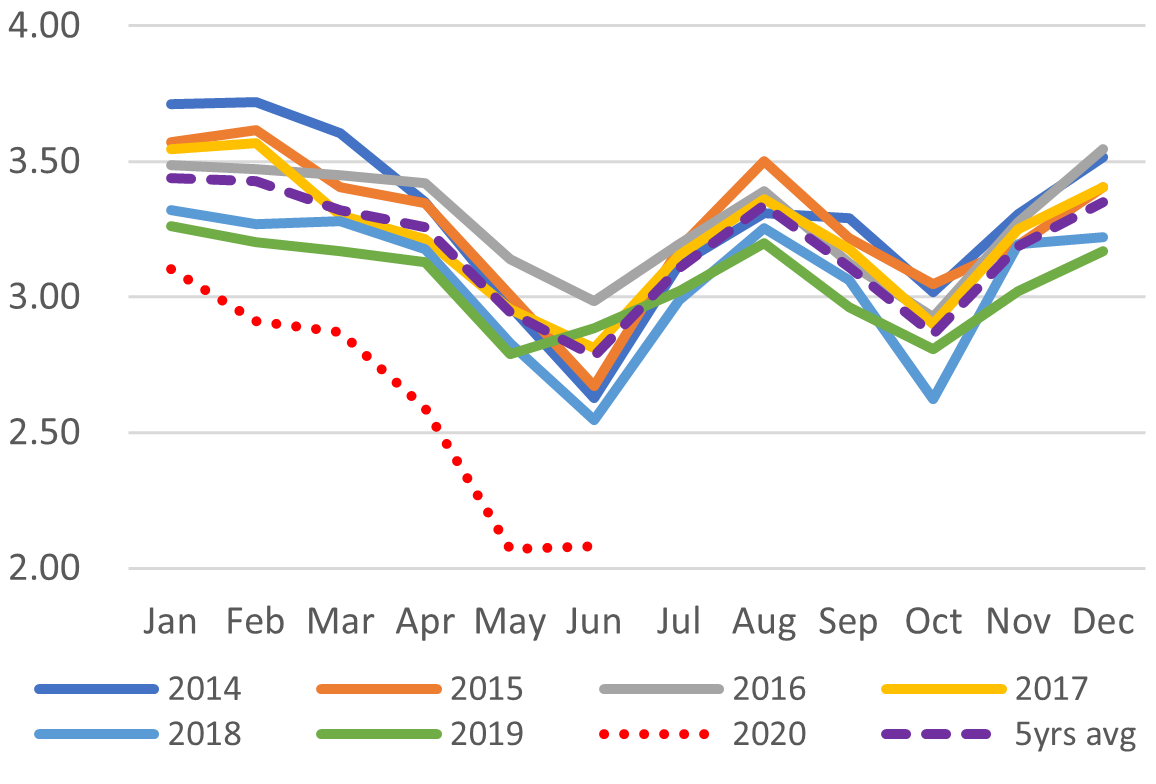

Japan Oil Price

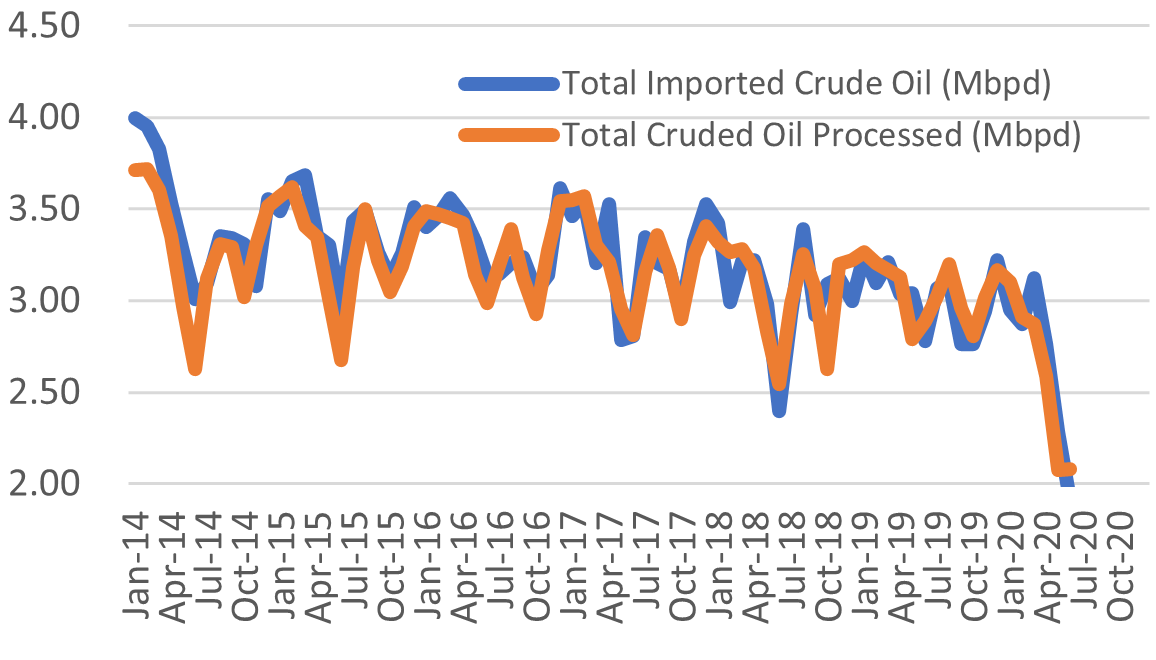

Crude Imports Vs Processed Crude

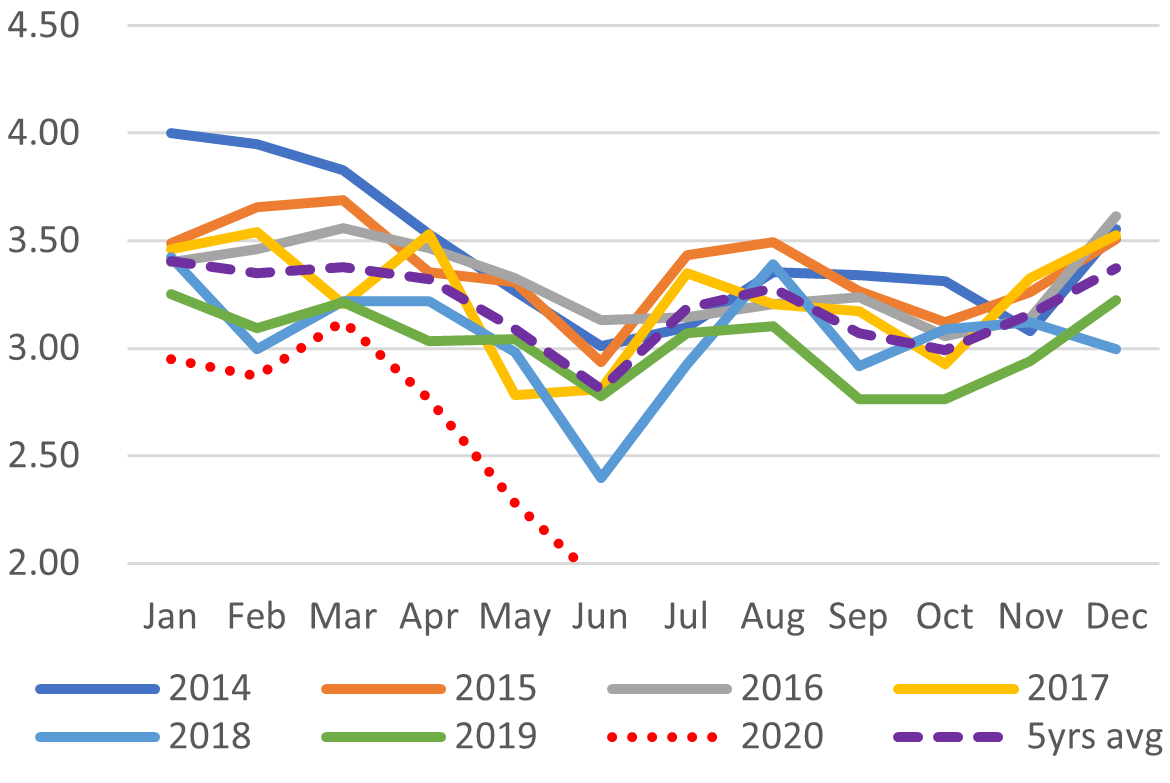

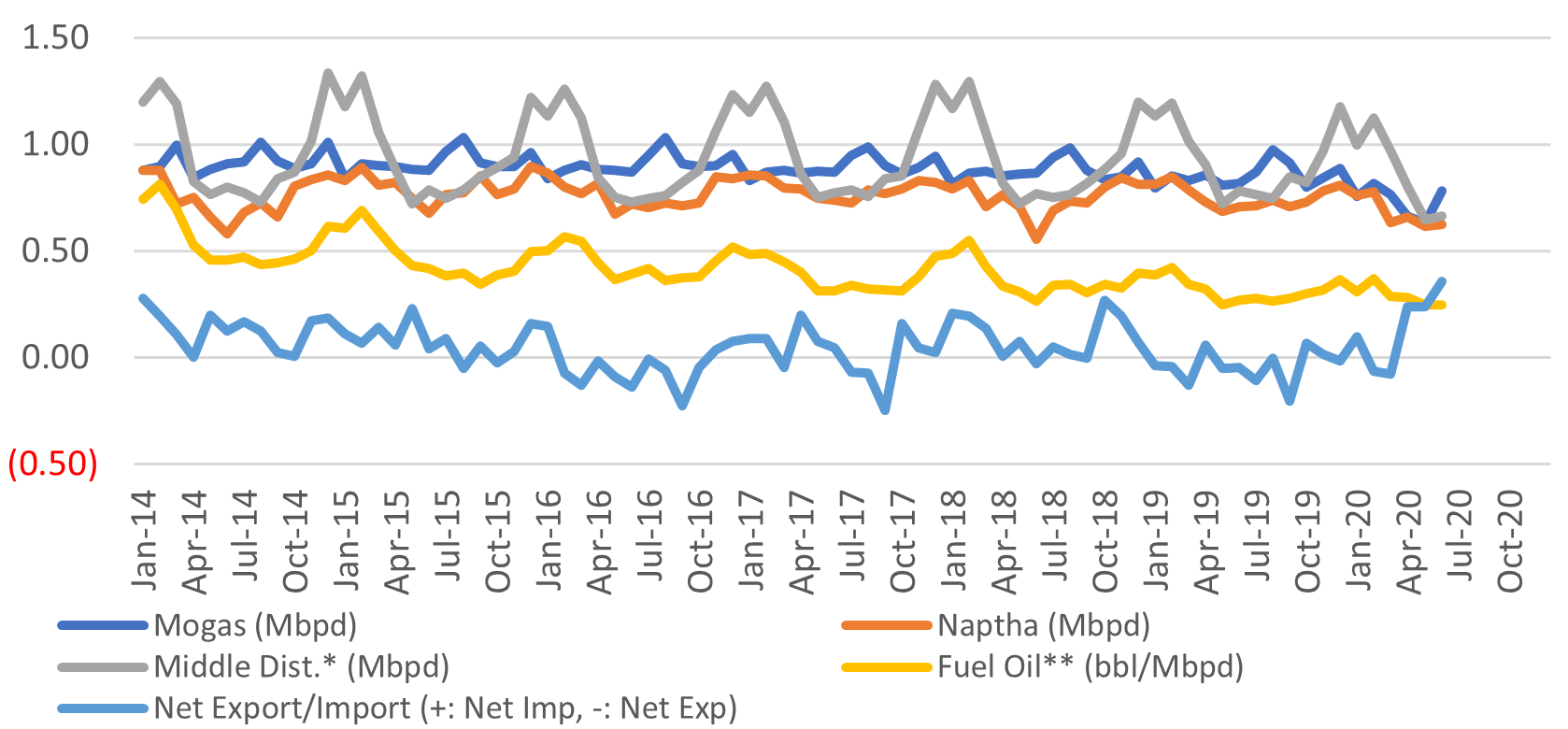

Monthly Oil Import Volume (Mbpd)

Domestic Fuel Sales

Monthly Crude Processed (Mbpd)

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

Japan LNG Price

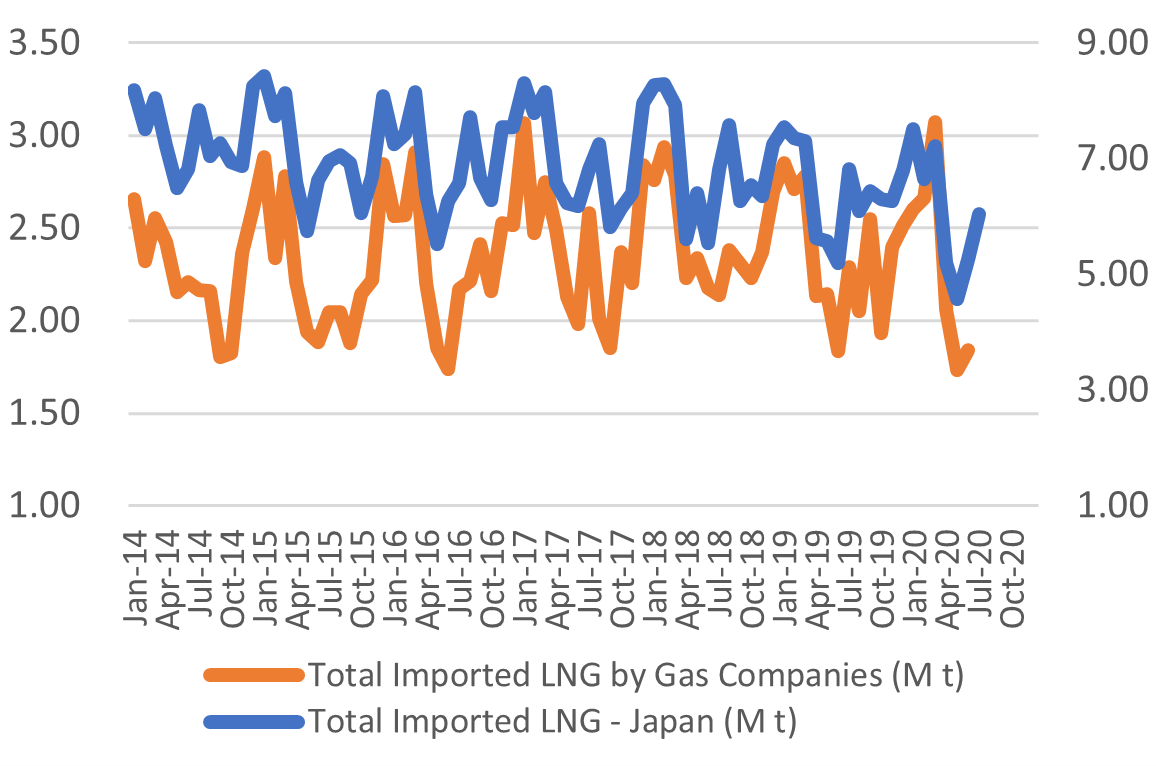

LNG Imports: Japan Total vs Gas Utilities Only

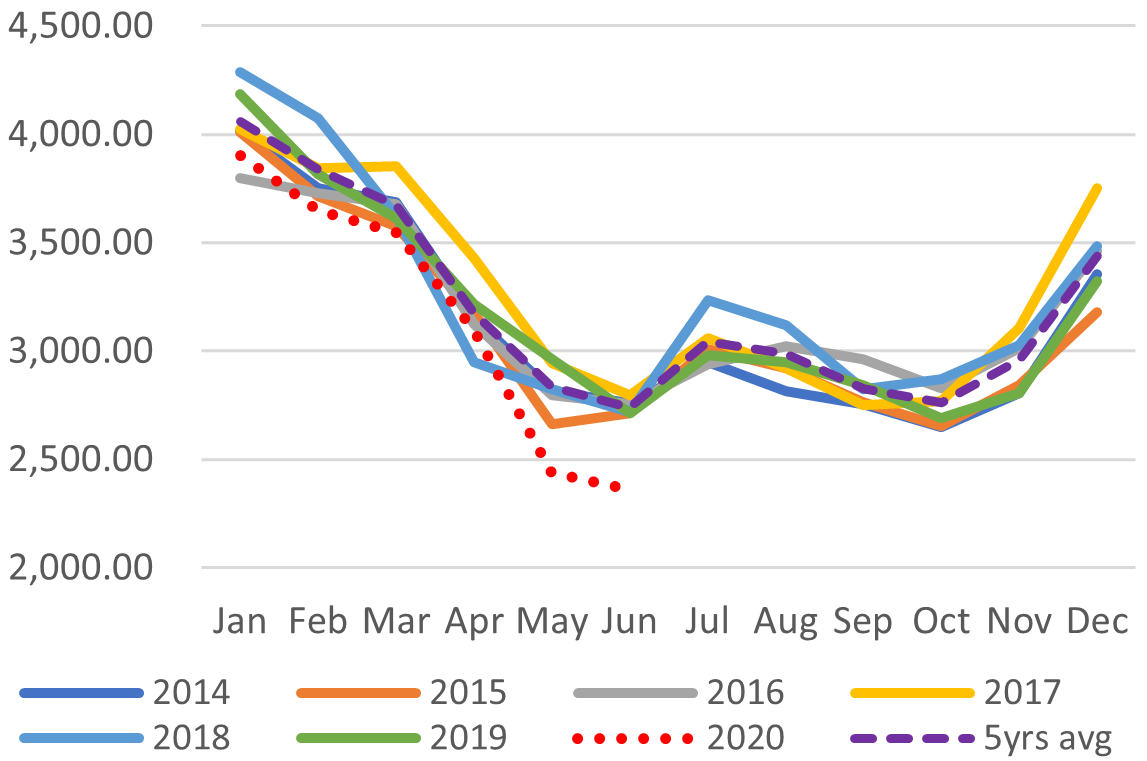

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

City Gas Sales – Total (M m3)

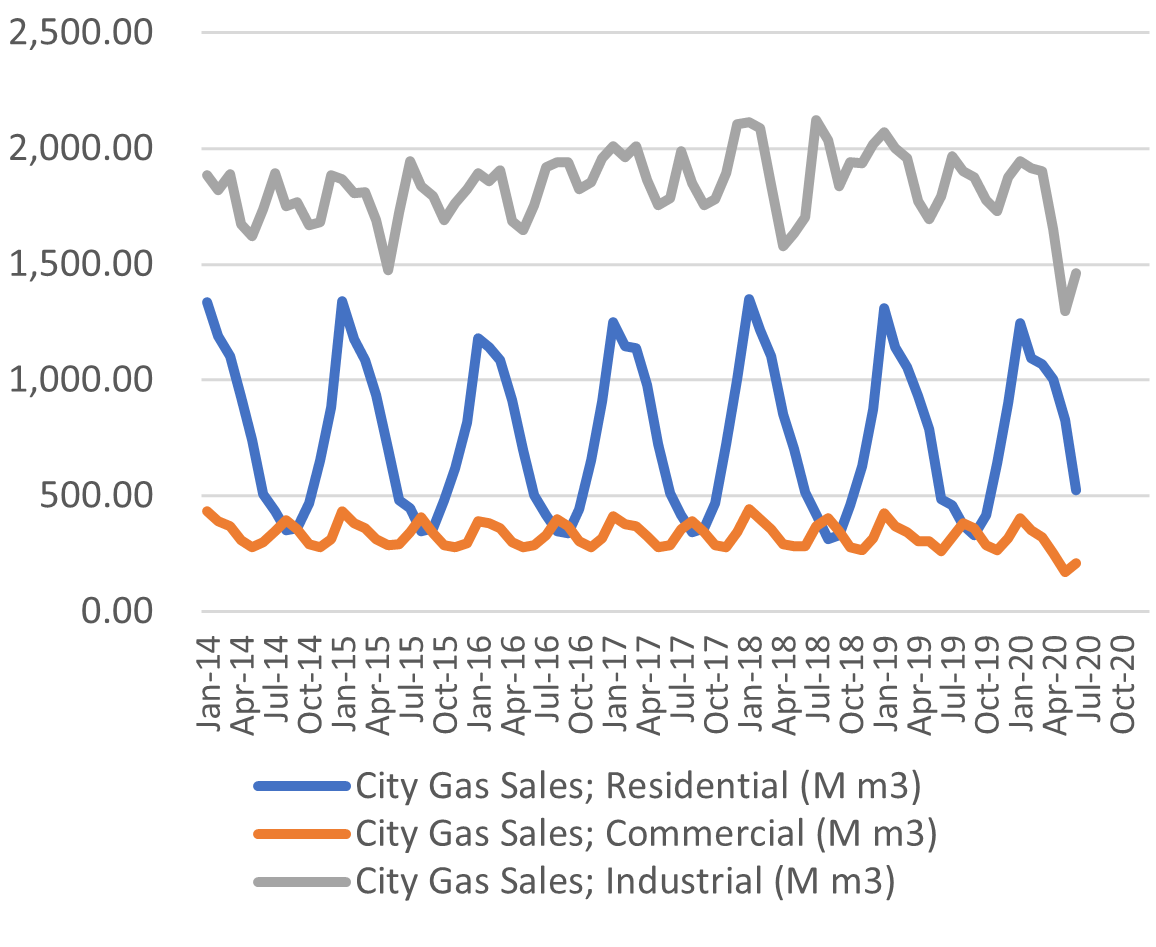

City Gas Sales by Sector (M m3)

SOURCES: the Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

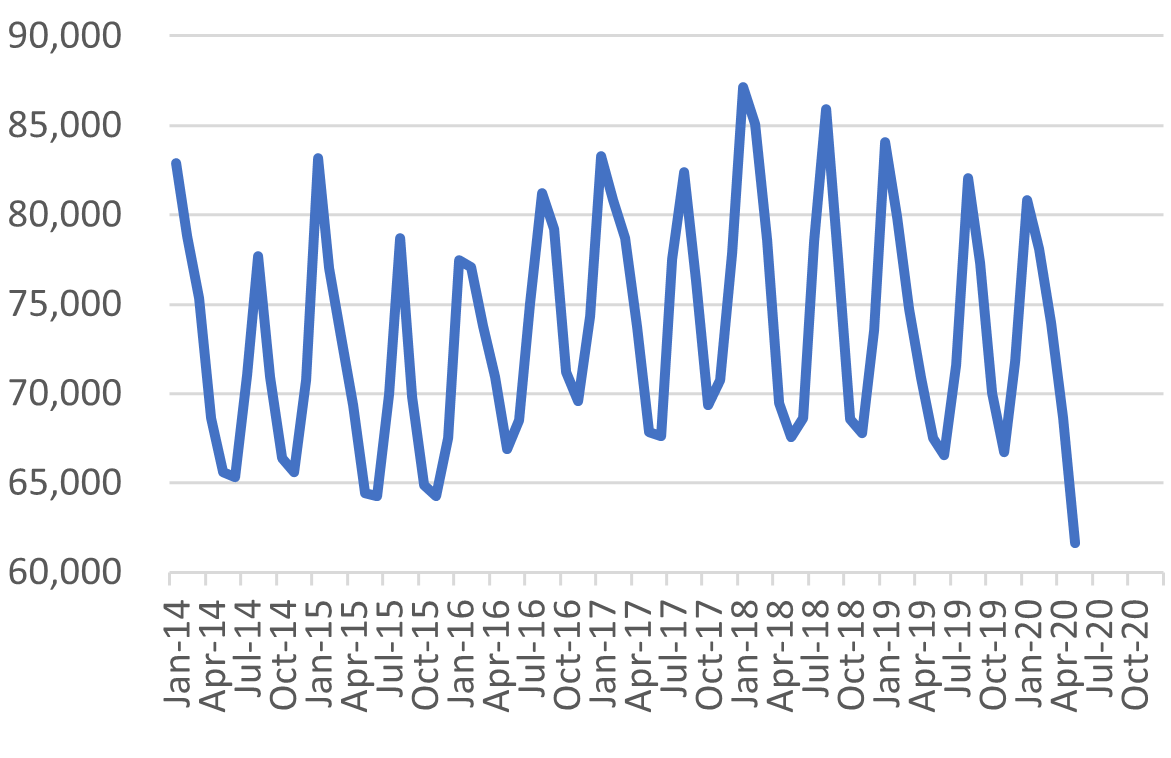

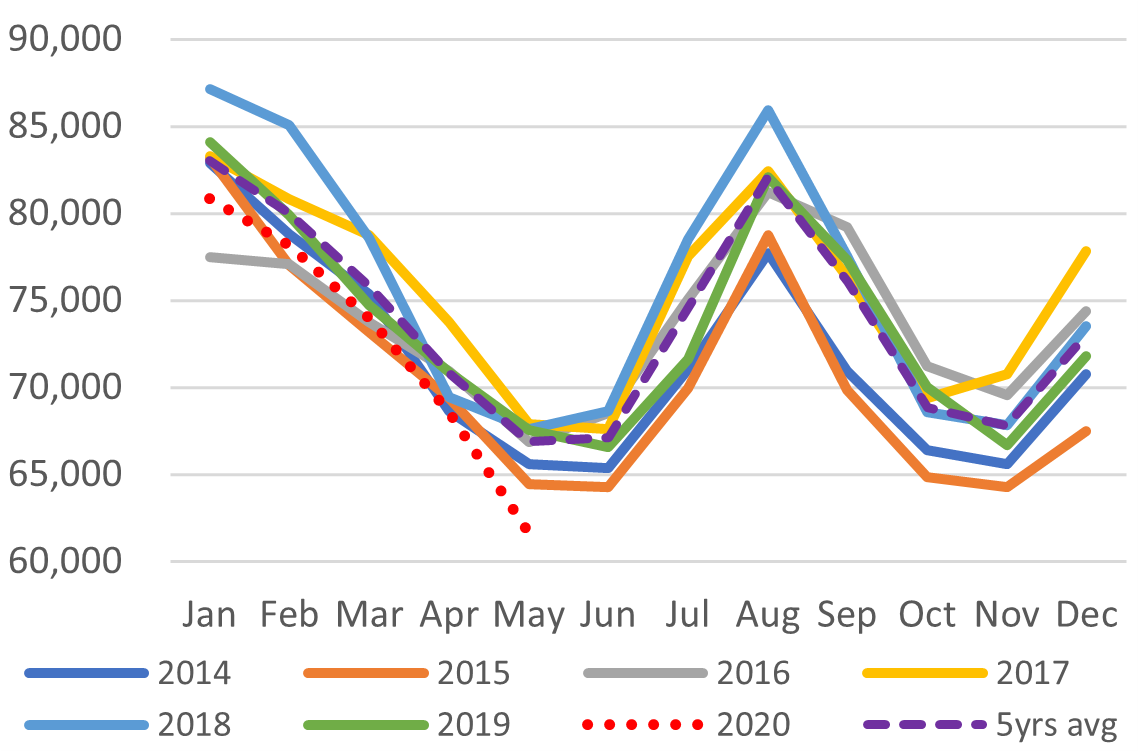

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

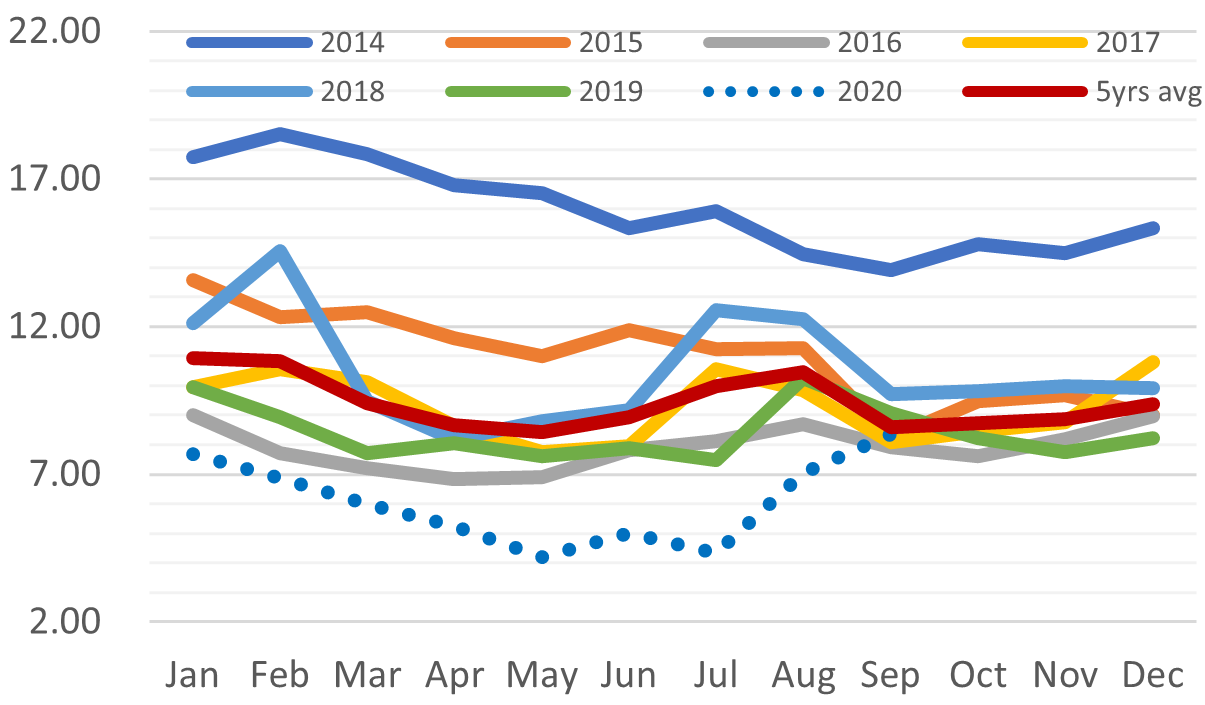

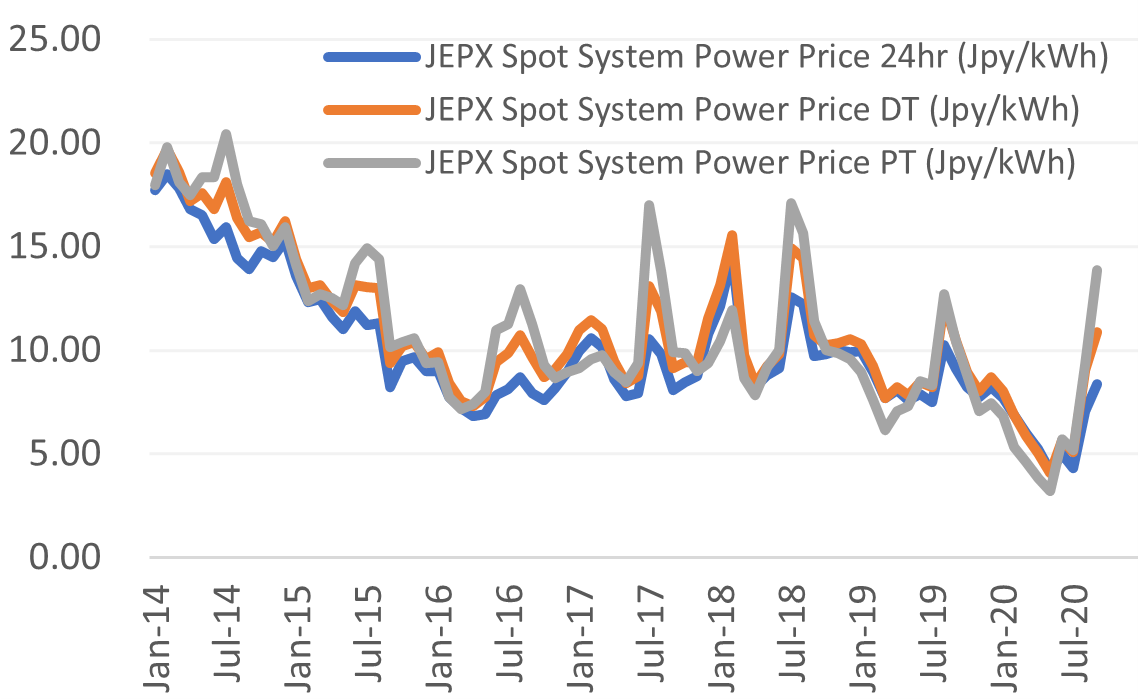

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest Research Ltd., which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis.

Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

Recipients of this report should ensure that they fully understand the legal, tax and accounting implications before making an investment decision and independently determine that the transaction is appropriate based on their own objectives, experience and resources.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided.

In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.