JAPAN NRG WEEKLY

OCTOBER 19, 2020

JAPAN NRG WEEKLY

October 19, 2020

TOP

- Japan’s nuclear power to dwindle to a single operating reactor;

KEPCO to shut one more unit; Industry lobby group fears all Japan nuclear assets will be split off into a separate entity - JERA director calls for Asian market index for LNG

- METI considers cost of carbon in design of Feed-In Premium;

Govt. panel offers a carbon price target - Minister promises to raise share of renewables in Japan’s energy

mix to “without limit”

OIL & GAS

- JBIC leads USD 1 billion financing for INPEX’s Abu Dhabi oil field

- Japan to offer Mauritius economic support after oil spill

POWER & NUCLEAR

- JERA to go carbon neutral by 2050, shut down inefficient coal plants; Co. sells debut bonds

- Govt. vows to make decision soon on Fukushima water release; Renewable energy firm sues Govt. over Fukushima charges

- Commission finds misleading bid in recent capacity auction

- Tokyo Gas, Cosmo move to expand power retail business

- KEPCO to use VPP and join energy exchange in April

- Japan’s biggest bank to phase out coal power financing

- Mitsubishi says yes to coal/biomass co-firing in Indonesia

RENEWABLES, OTHER

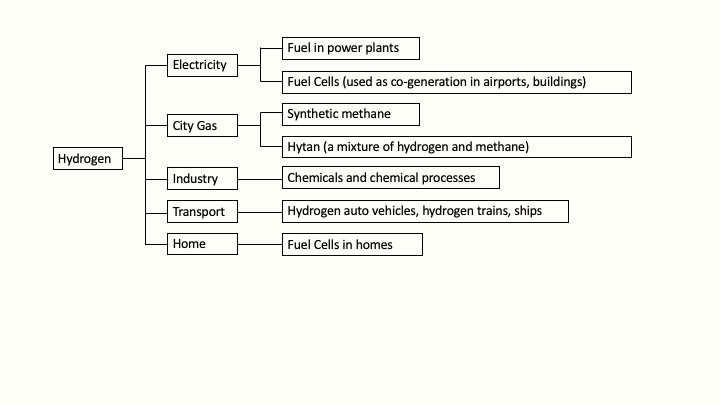

- Australia, Brunei core part of Japan’s hydrogen chain;ENEOS among Japanese firms forming local hydrogen lobby

- Mitsubishi Heavy makes push into carbon capture market

- ENEOS launches campaign to woo solar players exiting FIT; Mitsubishi starts solar farm in Japan and mulls U.S. offshore wind

- Toshiba accelerates work on fuel cells for ships, locomotives

- Kyushu to consider a geothermal plant in Fukushima Prefecture

- Mitsui Sumitomo Insurance, Looop work on weather derivatives

JAPAN HOSTS HEADLINE LNG CONFERENCE

WORLD’S TOP LNG BUYER SEEKS PRICE REFORMS

Arguably the most important Japanese LNG conference took place last week. Officials from the host government and Japan’s top energy firms told a global audience of LNG producers and consumers that they want the fuel’s price to better reflect domestic gas market fundamentals. The Japanese side also called for the creation of a new pricing mechanism that would apply to a broader Asian region, which among other things would help facilitate a better resale market for the fuel. In a bold move, several key Japanese representatives, including METI Minister Kajiyama, noted that they wish to reconsider terms not only for future long-term LNG deals but also ongoing contracts.

JAPAN’S DECARBONIZATION CONCEPT MEANS ITS HYDROGEN DEMAND WOULD JUMP BY 2,600%

There is a limit as to how much Japan can decarbonize its natural gas system and that limit has been reached. Yet, with gas set to remain a key energy source for the economy, despite an increased push into renewables, the country’s main option to cut emissions will be to employ hydrogen. In order to fully decarbonize Japan’s gas industry with hydrogen, it will need more than 2,600% more volume than the country current consumes. Japan’s potential demand would be equivalent to a fifth of the hydrogen available globally on the open market today.

GLOBAL VIEW

Reports by IEA and OPEC, as well as COVID’s impact and China’s moves against Australia are among the international energy developments last week that the NRG team selected for a new digest feature. We will showcase stories that have an impact on prices, on global energy supply and demand, as well as which are relevant for Japanese and international energy investors.

JAPAN NRG WEEKLY

K. K. Yuri Group and Yuri Invest Research Ltd.Editorial Team

Yuriy Humber (Editor-in-Chief)Tom O’Sullivan (Japan, Middle East, Africa)John Varoli (Americas)

Contributors

Mayumi Watanabe

Daniel Shulman

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS

Individual, corporate and academic plans are available. Please contact one of the Editorial Team members or write to nrgnews@yuri-invest-research.com for more details.

ADVERTISING

For marketing, advertising, or collaboration inquiries, please write to nrgnews@yuri-invest-research.com

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest, which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS: OIL & GAS

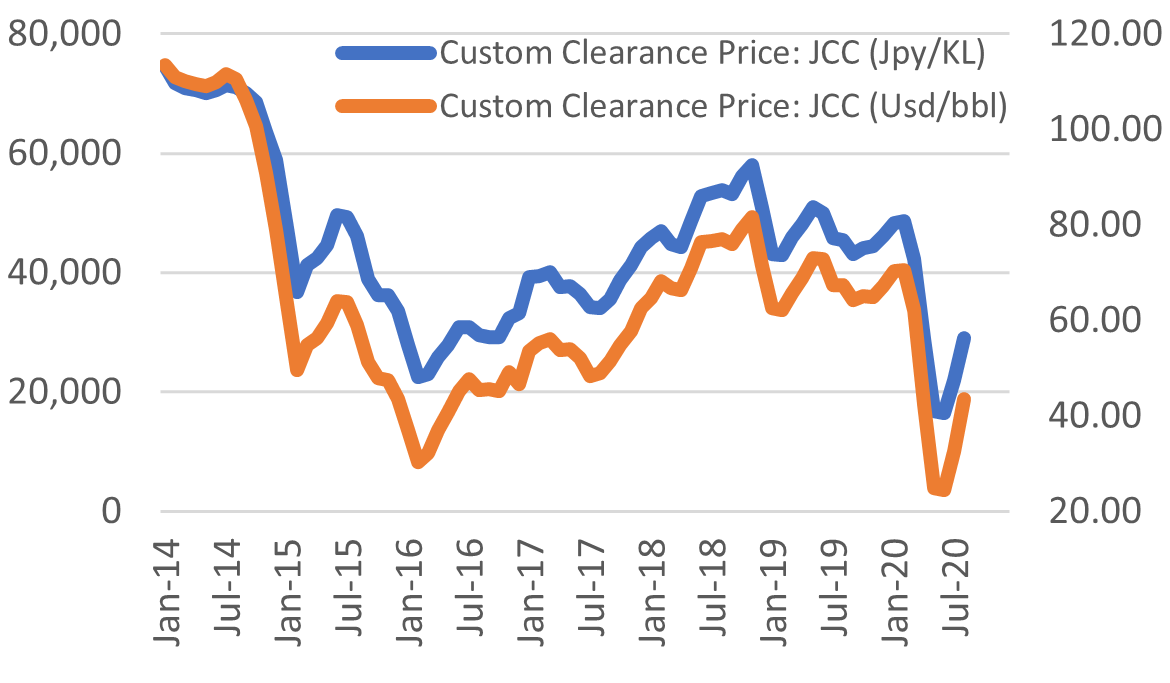

Japan Oil Price: $43.42 / barrel

Japan (JLC) LNG Price: $5.81 per Mbtu

JERA director calls for Asian market index for LNG

(Japan Maritime Daily, October 14)

- JERA Senior Executive Vice President Sato Hiroki called for the creation of an Asian LNG market index. He was speaking at the METI-hosted LNG forum on Oct. 12.

- Sato said that such an index would help improve trading liquidity, as well as grow the LNG market. Currently, buyers who purchase LNG that’s pegged to the price of crude face significant risks when selling LNG at spot prices determined by the Japan Korea Marker, said Sato.

TAKEAWAY: Please see the Analysis section for a full report on the conference.

JBIC leads USD 1 billion financing for INPEX’s Abu Dhabi oil field

(Company press release, Oct. 14)

- The Japan Bank for International Cooperation (JBIC) signed on Oct. 13 three loan agreements totaling up to USD 650 million (JBIC portion) with Japan Oil Development Co. and INPEX Financial Services Singapore, a Japanese and a Singaporean subsidiary of INPEX Corp, respectively.

- The loans are co-financed with private financial institutions, bringing the total co-financing amount to USD 1 billion.

- The money will support onshore and offshore oil fields in Abu Dhabi in which INPEX has a stake.

Japan to offer Mauritius economic support after oil spill

(Nikkei Shimbun, Oct. 16)

- CONTEXT: The Panama-flagged Wakashio bulk carrier, owned by Nagashiki Shipping and chartered by Mitsui OSK, ran aground on a reef off the coast of Mauritius on July 25. It was carrying about 3,800 tons of oil and 200 tons of diesel from China to Brazil. About 1,200 tons spilled into the water. Oil from the ship has now reached mangrove forests and damaged coral, which could take decades to recover.

- The government of Japan is considering providing economic assistance to Mauritius following an oil spill caused by a Japanese-owned vessel.

- The government cannot make a direct payment, since that would acknowledge legal responsibility for the accident. However, the funds could come in the form of non-specific grants or yen-denominated loans.

- As a nation, Japan is not liable for the disaster. The ship owner is the only liable party. However, damage to the Indian Ocean nation’s economy is too severe to be fully made up for through payments from the ship owner and insurance payouts. As such, Japan’s government wants to provide aid as a moral obligation and to minimize any harm to Tokyo’s international credibility.

NEWS: POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 2 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

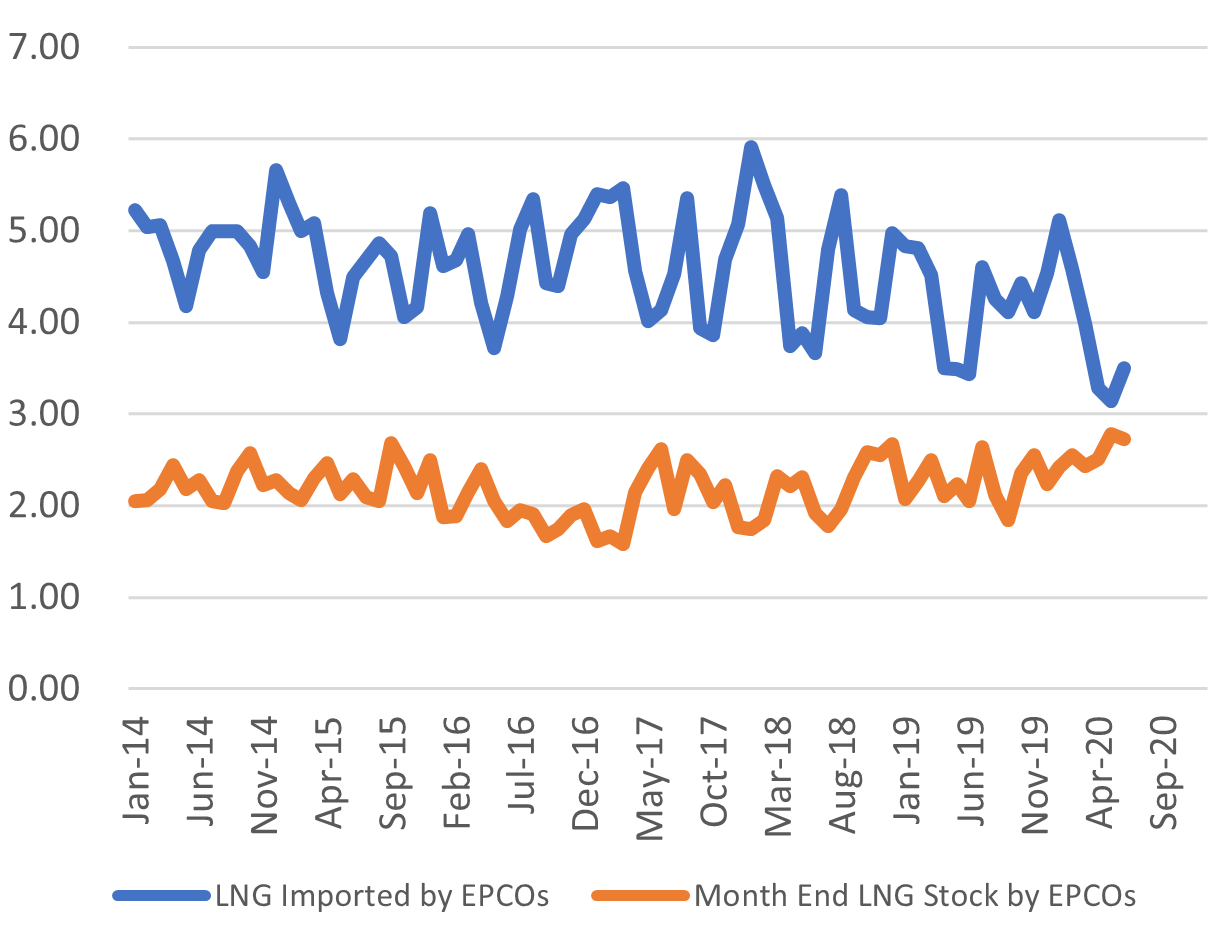

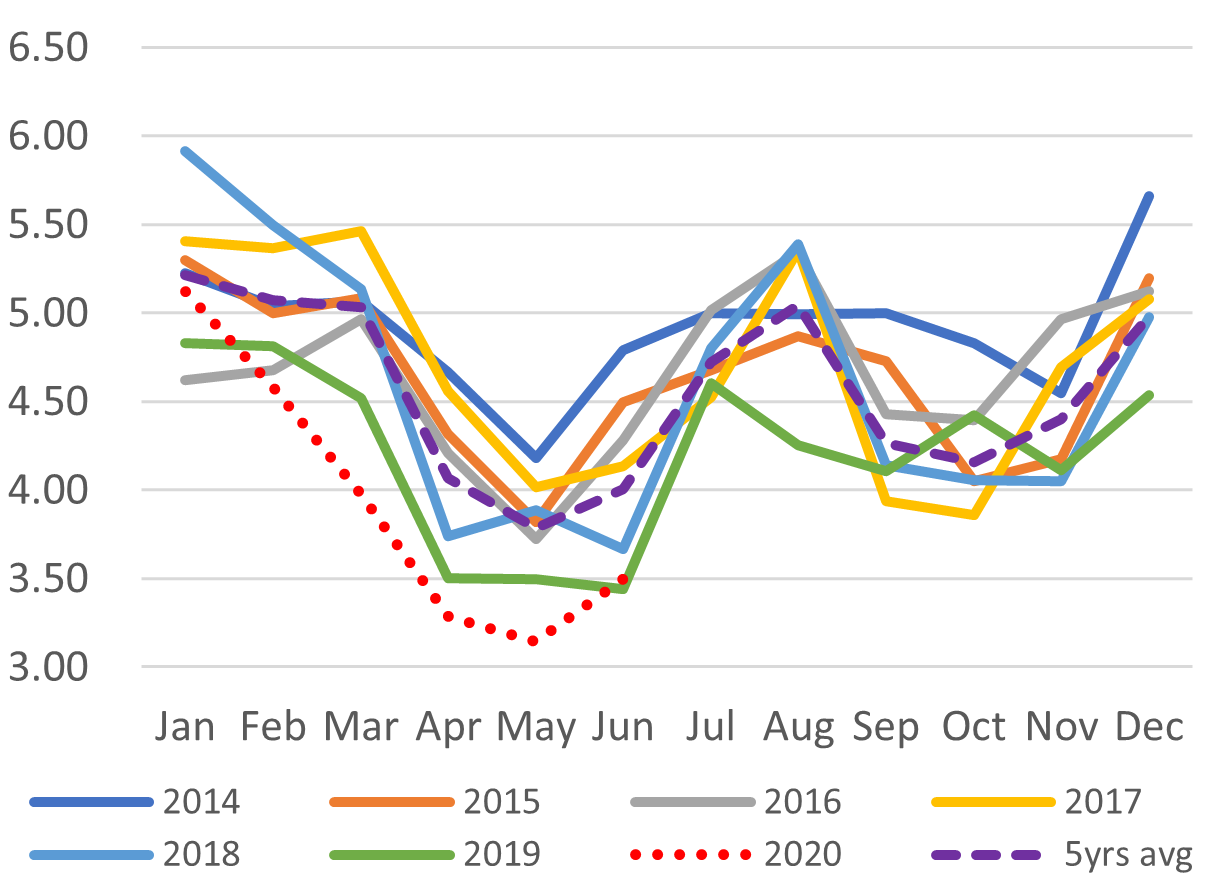

Power Utilities’ LNG Imports Vs Stockpiles

Source: Company websites, JANSI and JAIF, as of Oct. 10, 2020

Japan nuclear power to dwindle to a single operating reactor on Nov. 4

(Asahi Broadcasting Corp., Various)

- Kansai Electric (KEPCO)’s Ohi Unit 4 reactor is due to start regular maintenance from Nov. 4; the work will last two and a half months.

- This will result in all of KEPCO nuclear reactors being offline for the first time in three and a half years.

- KEPCO had hoped to restart Ohi Unit 3 just as Unit 4 went into maintenance and checks. However, a crack was found in the piping, and the Nuclear Regulatory Authority has requested a detailed investigation and an explanation.

- CONTEXT: KEPCO would have needed to insert fuel into Unit 3 by Oct. 15 to restart it in early November.

- SIDE DEVELOPMENTS:

Governor to approve restart of Onagawa reactor

(47 News, October 14)- The Governor of Miyagi is prepared to give his consent to the restarting of Tohoku Electric’s Onagawa Unit 2 nuclear reactor as early as mid-November, sources say.

- Opponents say the prefectural government has ignored residents’ concerns about safety.

- The prefectural assembly is expected to approve a motion to restart the reactor on Oct. 22. After that, the matter will go to the governor’s office.

- CONTEXT: The utility still needs to complete necessary works on the facility to meet the restart requirements. This suggests the actual restart date would be around 2022.

- SIDE DEVELOPMENT:

Nuclear industry fear key lobby group does not fully support them

(Sentaku, October edition)- The Federation of Electric Power Companies is a key lobby group for the industry and its chairman is often seen as an influential figure when dealing with the government. However, currently the chairman is Kyushu Electric’s Ikebe Kazuhiro, and despite being seen as smart and part of the business elite, many from the nuclear circles say he does not seem to know much about their sector.

- The nuclear side believes Ikebe is not supporting them much and this may lead the government to carve out all nuclear assets from the private electricity utilities and merge them into a separate business.

- The utilities that were traditionally strong in the nuclear business in Japan – Tokyo Electric and Kansai Electric — are struggling. Chubu Electric has said it is no longer interested in being part of the Federation. Kyushu is the only major force left and its top executive seems ambivalent on the merits of nuclear power.

TAKEAWAY: While there is a big push both by industry and the government to restart reactors, the public and the NRA have been much harder to get onboard. Several utilities including TEPCO and Chubu Electric have even resorted to loading fuel into their nuclear power plants to keep the technical side on track and meet regulator deadlines. The site of fuel loading into Kashiwazaki Kariwa NPP and Hamaoka NPP is meant to suggest there is progress with the restarts. Until local politicians give their go-ahead, however, this is all smoke but no fire.

TAKEAWAY: As reported in the Oct. 12 edition of the Japan NRG Weekly, Japan had just 3 reactors operating until October. Of those, two belong to KEPCO. The Kansai utility had to shut down Takahama Unit 4 on Oct. 7 to complete upgrades to the facility’s anti-terrorist measures. That unit will now be offline for four months. Now, KEPCO faces the obligation of idling the last of its operating reactors. That will leave Kyushu Electric as the only utility in Japan operating a nuclear facility and it has only one reactor running at present.

While the government designates nuclear energy as an important baseload power source, the legal challenges, technical problems, and issues related to the pandemic have made nuclear an increasingly unreliable source of power, according to some in government.

METI considers cost of carbon in designing Feed-In Premium

(METI public disclosure, Oct. 9)

- The ministry is looking at the design of Feed-In Premium, the successor pricing scheme to Feed-In Tariffs (FIT). Fuel competition, the cost of upgrading power transmissions, are part of the consideration.

- The ministry also notes that both fuel and carbon costs should be part of the cost analysis.

- SIDE DEVELOPMENT:

- METI’s Green Innovation Strategy Panel proposed a cost target for carbon to be around ¥1,000/ton to encourage carbon capture and storage (CCS). The ministry wants to encourage decarbonization efforts by 2050 and wants coal and gas combustion turbines to be fitted with CCS. On Oct. 13, the panel published its findings and a roadmap for carbon capture tech development.

TAKEAWAY: Putting a price on carbon is considered one of the most important ways to stimulate both a reduction in CO2 emissions and the creation of carbon off-set / trading mechanisms that allow industries with low emissions to sell their allowances to larger emitters. According to the World Bank, some 40 countries already use carbon pricing mechanisms, with more planning to implement them in the future.

JERA go carbon neutral by 2050, shut down inefficient coal plants

(NHK News Web, October 13)

- JERA, a joint venture between TEPCO and Chubu Electric, said Oct. 13 that it will transition to being carbon neutral by 2050.

- To achieve the goal, JERA plans to shut down or decommission inefficient coal-fired power plants by 2030.

- JERA will also commence a trial in which ammonia or hydrogen is blended with the fuel used in its remaining thermal plants to improve efficiency.

- Offshore wind will be the leading renewable energy source that JERA invests in.

- JERA says that as Japan’s largest electricity generator it has a social obligation to reduce its carbon emissions. It will also create a transition roadmap for every country it operates in.

- SIDE DEVELOPMENT:

- JERA sells debut bonds, gets rated AA-

- The Japan Credit Rating Agency has rated JERA’s five-year and ten-year unsecured bond issues AA-, saying JERA enjoys a stable outlook.

- The five-year, and ten-year bond issues are worth a total of ¥40 billion. The five-year bonds pay 0.190% interest.

TAKEAWAY: JERA’s announcement on the phase out of “inefficient” coal-fired plants, i.e. those that fall below the ultra-supercritical (USC) ranking, is not so much a corporate strategy as a following of the rules laid out by the key energy ministry, METI. The 2050 marker is also familiar. Still, as owner of the most thermal capacity in Japan, JERA’s pledge is significant in terms of showing how Japanese players want to navigate the energy transition. Big utilities are willing to sacrifice some older coal plants if they can keep the bigger, more modern units and bolster their power efficiency ratings. Hydrogen, in some form, as well as biomass, are seen as two main strategies in boosting their efficiency numbers. For the green option, most of Japan’s incumbent utilities will favor the scale that offshore wind seems to offer over solar.

Japan set to release treated radioactive water from Fukushima into the ocean

(Nikkei, Oct. 16)

- Japanese government will officially decide later this month to release water stored at the damaged Fukushima Dai-Ichi nuclear power plant into the Pacific Ocean.

- CONTEXT: Water naturally enters the nuclear plant site as rain and groundwater and has to be pumped out. It is then processed to remove most of the radiation, but an element called tritium remains because it is not possible to extract. The radiation in the treated water is said to be at minimal levels, but the release has still faced opposition from local fisherman, who fear it will harm the reputation of their catch.

- The government is aware that keeping water at the site will affect further decommissioning work. The storage tanks built to hold the water are almost full and space will run out by 2022. As of mid-Sept., the site held 1.23 million tons of treated water in about 1,000 tanks.

- The release would occur after 2022 and the level of radioactive material in the water would be below international standards.

TAKEAWAY: No matter how safely or gradually the release of the treated water into the ocean would be, Japan will face criticism both domestically and internationally. Expect South Korea and China to be among the prominent voices in what would inevitably be a geopolitical issue.

Renewable energy provider sues government over Fukushima charges

(Mainichi Shimbun, October 16)

- Fukuoka-based renewable energy producer, Green Coop Denki, filed a lawsuit against the state on Oct. 15 demanding the reversal of a decision to impose a levy on power transmission vendors to recover the cost of decommissioning the Fukushima Daiichi reactor.

- According to the plaintiff’s legal counsel, the case is the first of its kind.

- In September, the state approved an increase in the transmission fees paid by Kyushu Electric.

Electricity and Gas Market Commission makes judgment on recent power capacity auctions

(METI public disclosure, Oct. 13)

- CONTEXT: Environmental Ministry gave public voice to numerous complaints from renewable energy retailers earlier this month after recent power capacity auctions, which only started this July, hit the maximum pricing allowed by the government. Retailers said the high prices would need to be passed on to electricity consumers or hit their bottom lines hard.

- The Electricity and Gas Market Surveillance Commission made a report on the recent power auctions. It addressed complaints that the auctions were influenced to attain high prices for power generation companies. The Commission said it could not confirm any suspicious practices, but did note one case in which the operational cost figures provided by the bidder were misleading.

- The Commission ruled that it’s not a problem for the dominant power utilities in Japan’s regions to bid a price level that equals its operational costs.

- METI is concerned that due to the phase out of fossil fuel fired power plants, Japan may be short of power capacity in four years’ time and the auctions are a way to stimulate new construction.

- At the most recent auction, there was 20GW less sold than expected. METI will need to consider how to deal with the gap.

- The Commission noted that the auction for 2024 power capacity had an average price of ¥9,534 per kW, which is twice as high as the U.S. and four times higher than U.K. levels.

Tokyo Gas, Cosmo move to expand power retail business nationwide

(Gas Energy News, Denki Shimbun, Oct. 12 and 16)

- Tokyo Gas said it has started to offer new low-voltage electricity rates for the Kanto, Chubu and Hokkaido areas, tempting new customers with free Amazon online store gift certificates. This is an online-only contract.

- The expansion is the first by Tokyo Gas outside of its home territory of Kanto in terms of low-voltage power retail.

- Within a year the utility plans to offer the service nationwide, except in Okinawa.

- CONTEXT: Tokyo Gas has already become the biggest seller of electricity in Japan outside of the 10 incumbent regional power utilities. It had 2.5 million contracts as of August and aims to expand that to 3.8 million contracts by 2022.

- Oil refining major Cosmo said it has entered the power retail market for business users. It starting selling electricity for corporate customers, targeting both low and high voltage sales nationwide, except for Okinawa.

- Potential clients are all those that the Cosmo Energy Group has existing relationships with.

KEPCO to join energy exchange in April

(New Energy Business News, October 15)

- Kansai Electric Power Company will use a virtual power plant to participate in the energy exchange from April 21.

- KEPCO made the decision to join the exchange after concluding agreements with clients able to exact a high degree of demand response, and performing enhancements to its integrated platform system.

- The energy exchange, on which transmission vendors can sell supply capacity in real time, is expected to facilitate the growth of solar and wind energy.

- SIDE DEVELOPMENT:

DeNA to establish virtual power plant as corporations scramble for piece of 20 trillion-yen market

(Nikkei, October 16)- DeNA, more known for ventures in the video game and sporting markets, plans to become a power company. Other corporations, also eager to have a piece of the energy market, plan similar moves.

- Virtual power plants use artificial intelligence to predict drops in the output of solar and wind plants, and adjust demand accordingly.

- Renewable energy is expected to make up 25% of Japan’s total energy needs by 2050.

Japan’s biggest bank Mitsubishi UFJ to phase out coal power financing

(Bloomberg, Oct. 15)

- The bank will announce plans to phase out lending to coal-fired power projects over the next 20 years, a source told Bloomberg.

- MUFJ has $3.58 billion in loans outstanding on coal projects. The number will drop by half in the fiscal year ending March 2031 and become zero a decade later.

- CONTEXT: Japanese banks are among the biggest lenders to coal-fired power projects and have come under fierce criticism for this in recent years. Shareholders tabled a motion at rival Mizuho bank’s AGM this year to have the bank exit its coal financing activities.

- CONTEXT: Mizuho this year pledged to cut its coal power financing in half by 2030 and make it zero by 2050. Sumitomo Mitsui Financial Group aims to bring coal financing to zero by 2040.

Mitsubishi Power says it is supporting coal/biomass co-firing in Indonesia

(Denki Shimbun, October 15)

- Mitsubishi Power says it will support initiatives to blend biomass with the coal used to power thermal power stations in Indonesia.

- Mitsubishi signed a memorandum with Indonesia’s state electricity company, PLN, committing to the project. Mitsubishi Power will help select biomass feedstocks and evaluate their combustion performance and economy.

- The Indonesian government aims to reduce the country’s carbon emissions by both increasing renewable electricity sources and closing down coal-fired plants. The blending of biomass in fuel is seen as another effective option for reducing carbon emissions.

NEWS: RENEWABLES & OTHERS

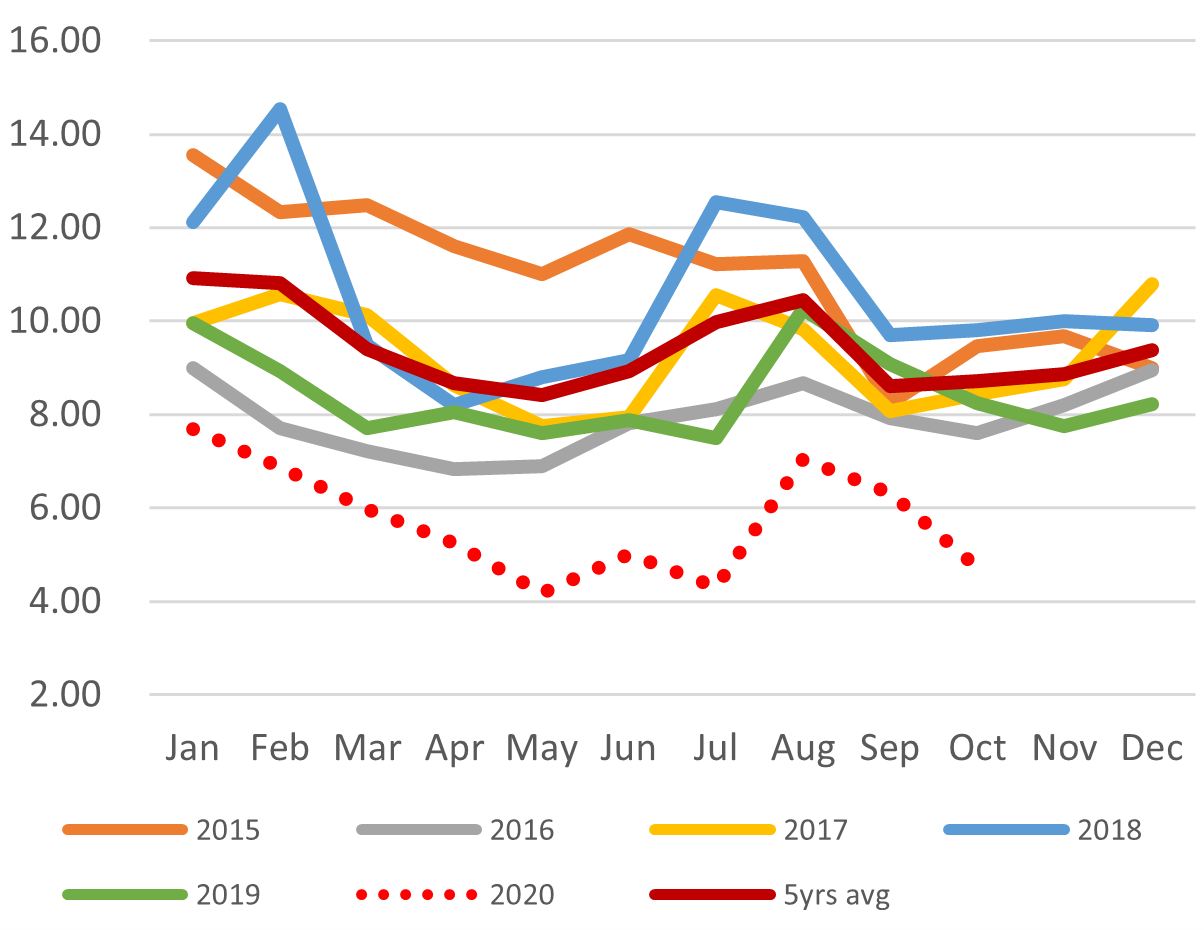

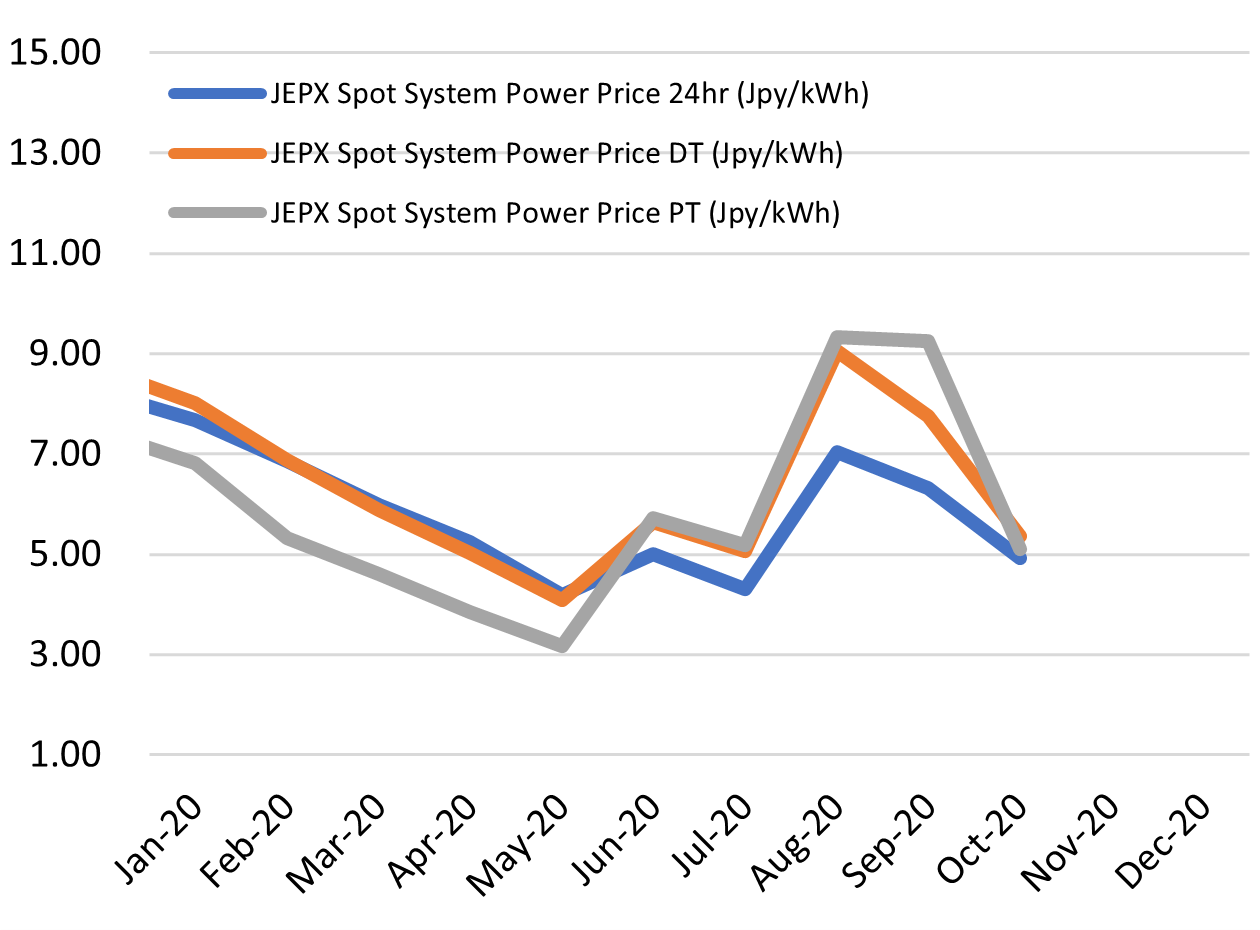

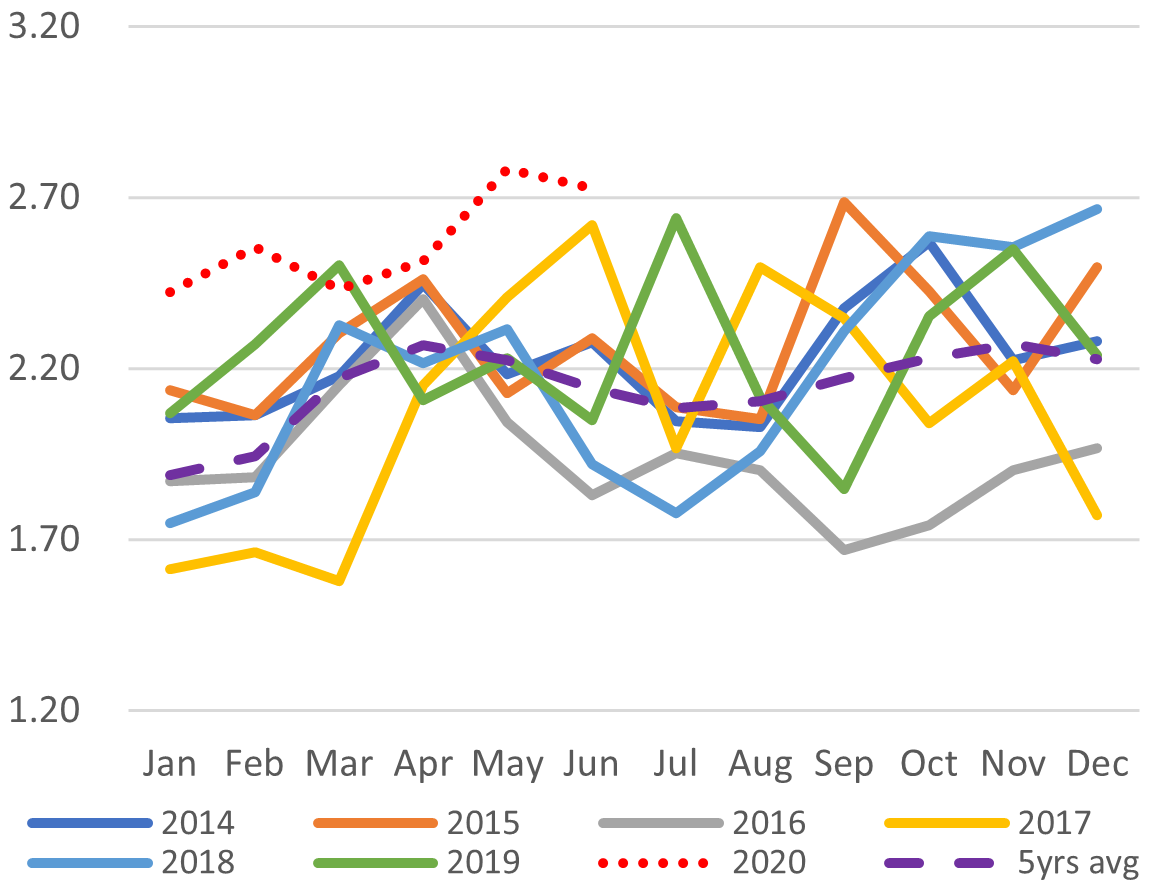

Spot Electricity Prices (24h)

Spot Electricity Prices (2020)

Minister promises to raise share of renewables in Japan’s energy mix “without limit”

(Nikkei Asia, Oct. 13)

- METI minister Kajiyama Hiroshi, the key decision maker on energy, said he wants to make renewables a “major power source” for Japan, as well as increase their share in the country’s energy mix. He will not set an upper limit for green power.

- Kajiyama spoke in an interview with Nikkei Asia. He said the government has just started discussions on the new energy mix vision and will consider new policy goals.

- CONTEXT: Japan’s current 2030 energy mix is under review by Kajima’s ministry. To date, METI has kept the renewables share of the total energy mix at 22% to 24% by fiscal 2030. It was at 17% in 2018.

- The government will consider allocating more funds to support development of battery storage tech and offshore wind, which Kajiyama said has the greatest potential for Japan among renewable sources.

- The minister also noted that the variability of wind and solar power remains a concern for the government and industry.

- On nuclear energy, Kajiyama said he would “do his best” to restart the country’s nuclear reactors over the next decade, but was cautious about the idea of adding new nuclear stations.

Australia and Brunei to form core of Japan’s hydrogen supply chain, minister says

(Nikkei Shimbun, Oct. 15)

- Japan wants to build a global supply network for hydrogen, and considers Australia and Brunei as its core members. The country aims to import 300,000 tons of the fuel a year by 2030, METI minister Kajiyama Hiroshi said at a virtual Hydrogen Energy Ministerial Meeting on Oct. 14.

- Japan is placing a lot of its trust in hydrogen development from lignite coal, a cheap, poor quality mineral that is not widely used or transported. Extracting hydrogen from lignite coal – and separating the CO2 from the process via carbon capture technology, will lead to a lowering of hydrogen production costs, according to Kajiyama.

- Japan wants hydrogen to be cost-competitive with fossil fuels such as LNG. The government aims to drop production cost to ¥30 per Nm3 (“normal cubic meter”) by 2030.

- CONTEXT: Japan is already working with Australia on a trial project to separate hydrogen from lignite. The world’s first ship specifically designed to transport hydrogen is being built by Kawasaki Heavy Industries, and it will start bringing hydrogen to Japan from February-March next year.

- CONTEXT: Australia is Japan’s biggest supplier of coal. As Japan moves away from burning coal to hydrogen, it makes sense for both nations to cooperate on hydrogen. Australia has signed agreements with Japan and South Korea on the concept of establishing an international hydrogen supply chain.

TAKEAWAY: Hydrogen is seen as a competitor to LNG, yet the fuel can complement the existing gas infrastructure. As mentioned in our commentary in this week’s Japan NRG report, hydrogen could be the way for Japan’s gas and power industries to decarbonize. But for that to happen, Japan needs to increase its consumption. Government estimates say demand must hit at least 5 million to 10 million tons for the cost level to drop. The goal is ¥17 / kWh for power generated from hydrogen by 2030.

ENEOS, KEPCO in hydrogen group seeking to build Japan industrial chain

(Response, Oct. 14)

- A consortium comprising ENEOS, Iwatani, Kawasaki Heavy Industries, Kobe Steel, Toshiba, Toyota, Sumitomo Mitsui Financial Group, and Mitsui & Co. is preparing to establish a group that will be known as the Hydrogen Value Chain Council and will lobby for the advancement of hydrogen technology.

- The Council will work to stimulate demand for hydrogen, reduce costs by way of technological innovation and the scaling-up operations, and provide finance to hydrogen industry operators.

- CONTEXT: ENEOS operates a network of 44 hydrogen filling stations nationwide. Iwatani enjoys the largest share of the Japanese hydrogen market. JR East, Hitachi, and Toyota have already started developing test trains with hydrogen fuel cells and storage batteries.

Mitsubishi Heavy makes push into carbon capture market

(Nikkei, Oct. 13)

- Mitsubishi Heavy Industries is increasing efforts to sell carbon capture technology globally after three decades of research in the field. The company began a trial of the tech at a biomass power station in the U.K.

- The trial will run for a year and capture 300 kg of CO2 per day. The goal is to reach negative net emissions at the facility.

- Mitsubishi Heavy hopes that the latest iteration of its carbon capture tech meets the cost and efficiency requirements of the market, and sees tighter environmental regulations globally as a chance for a commercial breakthrough in this field. MHI’s target for this tech to be judged as effective on a commercial level is 2027.

- MHI has delivered 14 carbon capture facilities in markets including Europe, the U.S., Southeast Asia and India, and more are under construction in Russia and Bangladesh.

- CONTEXT: The IEA said last month that meeting climate change goals will be “virtually impossible” without the employment of carbon capture.

ENEOS launches campaign to woo solar generators leaving feed-in tariff scheme

(New Energy business News, Oct. 12)

- CONTEXT: The Feed-in Tariff guarantees pricing for a set period of time. Usually 20 years, but in some cases less.

- ENEOS has launched a new electricity purchasing plan in Kyushu that offers solar generators an additional 2 yen per kilowatt hour until September 2021.

- After September 2021 the tariff reverts to ¥8 / per kilowatt hour.

- Outside Kyushu, ENEOS is currently paying ¥11 /kWh in Hokkaido, Tohoku, and Tokyo, and ¥10 / kWh in the sunnier Kansai, Hokuriku, and Chugoku regions.

Mitsubishi opens 60 MW solar farm in Fukushima

(New Energy Business News, Oct. 12)

- A new solar farm in Namie, Fukushima, a joint venture between the Mitsubishi Research Institute and Mitsubishi UFJ Lease & Finance, is now supplying the grid.

- The farm is located on a 900,000 m² site. Namie was evacuated after the 2011 nuclear disaster, and some restrictions still remain in place.

- The Mitsubishi Research Institute holds a 19% stake in the venture, with the remainder owned by Mitsubishi UFJ Lease & Finance.

- SIDE DEVELOPMENT:

Mitsubishi Corp. explore offshore wind project on one of the Great Lakes

(Various, Oct. 15)- A unit of Mitsubishi has looked at setting up a wind project on Lake Erie and connecting it to New York State. The idea has been around for a couple of years but has so far met with local opposition.

Toshiba accelerates work on fuel cells for ships, locomotives

(Toshiba Energy Systems press release, Oct. 8)

- Toshiba Energy Systems has been awarded a tender by the New Energy and Industrial Technology Development Organization to develop fuel cells for large vehicles, including ships, locomotives, and construction equipment.

- Development will be based on Toshiba’s standard H2Rex-Mov module, a compact, lightweight and powerful 200 kW hydrogen fuel cell.

- Fuel cells need to be made lighter and more vibration resistant so they can be used to power vehicles, says Toshiba.

Kyushu to study potential to build a geothermal power plant in Fukushima Prefecture

(Shin Energy Shimpo, Oct. 16)

- Kyushu Electric will start a geothermal resource survey from the end of October around Yanaizu Town, Fukushima Prefecture. The area is considered to be promising and already has one geothermal plant run by Tohoku Electric.

Mitsui Sumitomo Insurance collaborates with Looop on weather derivatives

(Nikkan Kogyo Shimbun, Oct. 15)

- Mitsui Sumitomo Insurance has released a range of weather derivatives in conjunction with Tokyo-based independent power company Looop.

- Weather derivatives pay dividends proportional to the degree to which actual weather diverges from contractually agreed projections, and are used to hedge against spikes and dips in supply and demand resulting from unusual weather events.

- Looop offers services that enable factories and commercial facilities to enjoy reduced power bills in exchange for having solar panels installed on their roofs.

Hokkaido Governor criticizes Copenhagen Infrastructure environmental assessment

(New Energy Business News, Oct. 14)

- In an opinion submitted in response to CI Hokkaido’s environmental assessment of the wind farm it plans to construct off Ishikari, the Hokkaido government said CI failed to adequately describe the consultation process it conducted with local residents.

- The government has requested CI to provide more information. The planned 1GW wind farm will be located 3 km offshore.

EDITORIAL: Both renewables and nuclear needed to decarbonize

(Nikkan Kogyo Shimbun editorial, Oct. 15)

- Japan’s energy policy is founded on the principles of safety, stability, economics, and environmental protection. However, Japan is self-sufficient for only 12% of its energy needs, which means that Japan’s energy security is exposed to the risks of protectionism amongst oil producing nations and Middle East instability.

- A staggering 77% of Japan’s electricity is generated from fossil fuels. As the rest of the world moves away from carbon, if the Japanese government does not become more aggressive in shutting down coal-fired power plants, Japan could be left behind.

- Restarting nuclear reactors where it is safe to do so is essential in order to decarbonize our economy while at the same time becoming more energy self-sufficient.

- Whether it is establishing hydrogen infrastructure or developing smaller, safer nuclear reactors, Japan must become more innovative if it is to survive in the international energy market. If the country can’t do that, then it will pay the price in the form of higher electricity costs.

ANALYSIS

DIRECTOR,

K.K. MATHYOS

World’s Top LNG Buying Country Seeks Pricing Reforms

Japanese companies, encouraged by the government, are proactively racking Arguably the most important Japanese LNG conference took place last week. Officials from the host government and Japan’s top energy firms told a global audience of LNG producers and consumers that they want the fuel’s price to better reflect domestic gas market fundamentals. The Japanese side also called for the creation of a new pricing mechanism that would apply to a broader Asian region, which among other things would help facilitate a better resale market for the fuel.

In a bold move, several key Japanese representatives, including METI Minister Kajiyama Hiroshi, noted that they wish to reconsider terms not only for future long-term LNG deals but also ongoing contracts.

Producers in turn offered to consider innovations such as permitting buyers to sign contracts as a group.

The LNG Producer Consumer Conference, hosted by one of Japan’s most influential ministries in the energy sphere, METI, took place online for the first time since its 2011 inception. Minister Kajiyama led the key note speeches, promoting Japan’s recent initiative to seek a lowering of emissions across the LNG value chain, but also called for more understanding from the producer side on flexibility of price and destination.

With almost 88% of Japan’s LNG purchases locked into long-term contracts, which have strict destination and pricing clauses, many Japanese posted massive losses this year as the coronavirus pandemic sapped demand. The biggest Japanese LNG importer, JERA, alone posted more than 10 billion yen ($90 million) in losses from the resale of LNG cargoes when it announced financial results in July.

METI’s conference included speeches by H.E. Saad Sherida, Minister of State for Energy Affairs, Qatar, and Fatih Birol, the Executive Director of the International Energy Agency (IEA). Total, Cheniere, Petronas, and Woodside represented the upstream gas industry.

Japanese natural gas industry participants included JERA, the world’s largest buyer of LNG, Mitsubishi Corporation, and Tokyo Gas. Japan’s finance industry was represented by Japan Bank for International Cooperation (JBIC), which has just agreed to finance a major LNG project in Mozambique and NEXI, Japan’s state-run export insurance corporation.

LNG Producer-Consumer Conference 2020

Source: LNG Producer-Consumer Conference 2020 website

The conference was held at a time of enormous difficulties as upstream developers struggle with low oil prices and a collapse of almost 10 mbpd in global oil demand.

IEA’s Birol said that the fall in energy demand in 2020 had no parallel in history, and that all fuels and all technologies were impacted. The largest oil producer in the U.S., ExxonMobil, has seen its market capitalization fall by 50% year-to-date and was ejected from the Dow Jones Industrial Average for the first time in over a century. Chevron, which is more invested in natural gas, has overtaken ExxonMobil in terms of market capitalization.

Globally, the natural gas industry has generally fared better than oil, but Japanese buyers are still trying to renegotiate long-term, oil–indexed contracts. Meanwhile, more liquidity is flowing into Asian spot markets, where prices are less than half those of long-term contracts.

Natural gas is expected to continue to replace coal in the global electricity mix as pressures mount to reduce carbon emissions. China has committed to peak emissions by 2030, and as a result global gas demand has increased since June 2020. However, the LNG industry has also suffered from over-supply this year due to an excess of new projects in 2018 and 2019, and lower pandemic-induced demand in 2020.

Birol said that he expects global natural gas demand to recover to pre-Covid levels by 2021 and that Asia will continue its role as the major growth region.

DEMANDS FROM BOTH SIDES

JERA led the conference’s calls for a single LNG pricing index (Asian LNG Market Index: ‘ALMI’) that would work across the Asia Pacific region and offer greater flexibility in destination clauses.

These were also common themes in previous conferences. Currently, over 70% of LNG purchase contracts are oil-indexed. TTF and NBK are the prevailing gas indices in Europe, and Henry Hub is the most liquid index in the U.S. JKM is the prevailing index in Japan with calls at the conference for greater adoption of the Platts MOC pricing index.

Producers acquiesced, to a point. Petronas, Malaysia’s state-owned oil and gas monopoly, said it has already adopted a Chinese LNG index for settlement with its Chinese buyers and would include more local markers if they were judged fair and transparent.

Despite the Covid-19 downturn, Qatar announced that it is committed to increasing its annual supply from 110 million tons this year to 127 million tons by 2027. Qatar is Japan’s second largest supplier of liquefied natural gas, and concessionally agreed to reschedule and defer cargos to its suppliers this year given the difficult environment.

Total is pushing ahead with investments in Mozambique, Arctic II, and Nigeria Train 7. Mitsui is investing in Mozambique alongside Total, with JBIC providing $3 billion of the $15 billion overall financing and NEXI providing the export credit insurance.

Cheniere’s Anatol Feygin, representing U.S. LNG exporters, underlined the continuing commitment of the U.S. to service the needs of LNG importers in Asia. Cheniere’s stock price collapsed by 50% in March at the peak of the pandemic, but has since recovered.

Carbon capture and sequestration were also leading themes this year, as was eliminating methane leaks and improving efficiency in LNG-to-power generation. The use of natural gas infrastructure, including shipping and pipelines, for hydrogen transportation was also discussed as efforts to decarbonize the power sector across Asia Pacific gather pace.

This year’s conference served to underline the Japanese government’s continuing important annual intermediation role between LNG producers and consumers to ensure market stability for the world’s largest importer of LNG fuel, and to promote greater use of LNG throughout Asia Pacific.

METI is expected to announce a new energy mix early next year and it remains to be seen what LNG’s share will be. Minister Kajiyama gave a hint of what is to come in his speech and subsequent media interviews.

Japan will raise the share of renewable power to an unlimited ratio in the mix, Kajimaya told the Nikkei (see the News section for more details). However, Japan will also need an energy source that can be relied upon whatever the weather, the minister noted.

ANALYSIS

RESEARCHER, JAPAN

YURI INVEST RESEARCH

Japanese Hydrogen Demand Would Jump by 2,600%

There is a limit as to how much Japan can decarbonize its natural gas system and that limit has been reached. Yet, with gas set to remain a key energy source for the economy, despite an increased push into renewables, the country’s main option to cut emissions will be to employ hydrogen.

In order to fully decarbonize Japan’s gas industry with hydrogen, it will need more than 2,600% more volume than the country current consumes. Japan’s potential demand would be equivalent to a fifth of the hydrogen available globally on the open market today.

These calculations formed part of the latest discussions of the “Study Group on the Gas Sector in 2050,” a forum created by Japan’s Ministry for Economy, Trade and Industry (METI). Japan NRG Weekly first reported on the Group’s development in the Sept. 14 edition of the report.

The Group held its latest meeting on Oct. 6, with presentations from the two biggest sector utilities, Tokyo Gas and Osaka Gas, as well as from engineering companies, academics and industry experts.

The Group’s main goal is to conceptualize the transition of the gas industry in the age of energy transition. Gas will be a key source for Japan up to and beyond 2050, much like in the rest of the world, said Akimoto Keigo, the chief researcher of RITE Systems Analysis Group and a member of the Study Group panel. Akimoto noted in his presentation that the IEA sees gas retaining a 14% to 20% share of total energy demand globally in 2070.

However, maintaining reliable supplies of gas well into the future is at risk as more recent environmental activism has denounced all fossil fuels, including gas. It’s no wonder that METI Minister Kajiyama Hiroshi told an LNG conference last week that the “clean fuel needs to get cleaner”. As a result, Japan has recently initiated a campaign to lower emissions from gas fields, LNG tankers, and other parts of the industry chain.

GREATER RELIANCE ON IMPORTS INEVITABLE

Most of the gas supply chain lies outside of Japan, which imports the overwhelming majority of its gas. Once the fuel enters Japan, however, there is little fat to trim in terms of emissions cuts, according to the Japan Gas Association. The shift to LNG from other gas types and improved energy efficiency of the domestic infrastructure (now at close to 99.5%) have exhausted the traditional ways to lower the industry’s carbon footprint.

In fact, Japan’s emissions from gas will rise in 2021 as more co-generation systems go online, the Association told the Study Group.

And yet, the country’s gas firms are being urged to reduce emissions further to 11.1g per cubic meter of gas within a decade. That’s 88% below the 1990 level.

The solutions are few. Methanation and power-to-gas system integration are some means through which gas companies can decarbonize using existing infrastructure, and synthetic methane would work even better than hydrogen. Gas operators can also connect their systems to renewable energy generation units, combine heat and power, and run virtual power plants, Shibata Yoshiaki, a senior economist at the Institute of Energy Economics, Japan, told the Study Group.

Such choices are not open to power generators, which emit almost double the carbon. While Japan’s gas companies combined produce 80 million tons of carbon / year, the nation’s gas-fired power plants emit around 150 million tons. Japan’s greenhouse gas emissions totaled1.24 billion tons in the fiscal year from April 2018 to March 2019, according to the Environment Ministry.

To eliminate the 80 million tons of carbon in Japan’s gas system, which utilizes 38 billion m3 of gas, the country would need to employ 134 billion Nm3 of hydrogen and 43 billion Nm3 of methane, according to Shibata. Japan’s LNG-fired power plants would require almost double those amounts.

Thus, Japan’s total hydrogen demand would balloon to 400 billion Nm3. Currently, Japan’s annual consumption is 15 billion Nm3, most of which is used for ammonia and petrochemical industries. The global supply of hydrogen in the open market stands at around 2 billion Nm3, according to studies by Japan’s New Energy and Industrial Technology Development Organization (NEDO) and France’s IFRI.

So far, Japan’s efforts to enlarge hydrogen production capacity has focused on supporting the creation of manufacturing facilities abroad, mainly in Australia and Brunei, as reported in the Aug. 24 edition of Japan NRG Weekly. These facilities tend to rely on fossil fuel sources to power hydrogen production.

Last week, however, Japan’s biggest engineering firm, Mitsubishi Heavy Industries (MHI), said that it has invested in Norway’s Hydrogen Pro, a maker of hydrogen production equipment. This will gain MHI exposure to the production and supply of “green hydrogen”, as the fuel is referred to when its production relies on renewable power sources.

In fact, the only hydrogen production facility of note in Japan is designated as green. Started in March this year, the Fukushima Hydrogen Energy Research Field (FH2R) is the world’s largest water electrolysis facility. However, its output is just 900 tons / year (about 10 million Nm3).

ALTERNATIVE APPROACHES

Another approach would be to mix hydrogen with LNG on a 50-50 basis, which would significantly cut hydrogen demand. Japan has brought online a 1 MW hydrogen cogeneration system in Kobe in 2018 and a hydrogen-gas turbine is currently being tested by NEDO.

All these options need to be on the table since NEDO forecasts that Japan will only have 12-18 billion Nm3 of hydrogen supplies in 2030, mostly sourced from local oil refineries, steel mills and soda makers.

Moreover, volumes alone would not solve all of Japan’s decarbonization goals. The country’s power plants, for example, have limited operational flexibility to use domestically processed methane. Transport of hydrogen to the power plants is another issue.

Existing power facilities could accommodate MCH hydrogen and liquid ammonia, but if the feedstock is liquid hydrogen then new facilities would have to be built, Shibata noted in his presentation.

There are other ways to decarbonize. Japan is spending significant resources on the development of carbon capture and storage.

If all else fails, there is a way to pay for the carbon problem to go away. Japan could switch its LNG imports to “carbon-neutral” LNG via the use of carbon credits, Shibata suggested.

GLOBAL VIEW

Below are some of the international energy developments from last week that the NRG team is monitoring because of their possible impact on energy supply and demand, and energy prices, as well as possible relevance for Japanese and international energy investors.

The IEA released its Annual World Energy Outlook last week predicting that energy demand may not recover from COVID-19 until 2025 with coal now expected to fall below 20% of the global energy mix for the first time since the Industrial Revolution. Achieving Net-Zero Emissions by 2050 would also require significant additional action.

OPEC:

The OPEC Secretariat released its 2020 Oil Outlook last week predicting that oil demand in OECD countries will now plateau between 2022 and 2025 and then decline by 25% by 2045.

Covid-19:

The John Hopkins dashboard is indicating almost 40 million infections globally. Europe and the U.S. appear to be suffering a severe second wave of infections that could further throttle international energy demand due to new lock-down restrictions. In the last week, France is exceeding 30,000 new cases per day, the U.S. 60,000, and Italy 10,000. Jarand Rystad of Rystad Energy, one of the world’s leading experts on the impact of COVID-19 on the global energy complex, estimates that real global infections may even be above 200 million.

China:

1) Speculation is growing that China may ban the import of Australian thermal and coking coal.

2) The market capitalization of Chinese publicly listed companies exceeded $10 trillion for the first time this week (twice that of Japan) making it easier for the Chinese energy complex to expand in Asia Pacific and globally through the national Belt and Road initiative and other B2B schemes.

Vietnam & Indonesia:

The two ASEAN countries will host the new Japanese prime minister on his first overseas trip this week. Japan has significant energy investments in both countries.

Australia/New Zealand:

A traffic corridor will open between New Zealand and Australia this week brightening the outlook for regional airlines and jet fuel consumption. The New Zealand Labor Party is also expected to win a resounding victory in Saturday’s general election. In September the NZ prime minister committed to 100% renewable energy by 2030.

Russia/Eastern Europe/Central Asia:

1) Opposition parties in Belarus are calling for a national strike to commence on Oct. 26 that could disrupt energy transfers from Russia into Europe. The intensifying conflict between Armenia and Azerbaijan over Nagorno-Karabakh could also disrupt oil and natural gas pipelines from the Caspian region into Turkey and beyond.

2) Europe has imposed further sanctions on Russia because of the attempted murder of Alexei Navalny although the NordStream 2 pipeline is not included in this latest round of sanctions.

Middle East:

The Israeli parliament has approved the normalization of relations with the UAE and a first cargo vessel arrived from UAE to Haifa. There is growing speculation that Saudi Arabia could now imminently follow Bahrain and the UAE in normalizing relations with Israel. This could facilitate more trade and investment from Asia into the region, and the Abraham Accords may be regarded as one of the outstanding foreign policy achievements of the current U.S. administration. Last week, Secretary Pompeo committed to build a new U.S. embassy in Riyadh, emphasizing the two energy superpowers’ close ties.

Europe:

Negotiations between the U.K. and the EU over Brexit appear to be collapsing with the likelihood of ‘No-Deal’ gaining momentum. This could complicate energy and electricity transfers and trade between the U.K. and continental Europe from Jan. 1, 2021. Toyota and Honda recently demanded that the U.K. underwrite any tariff costs the two auto giants might incur from Brexit.

Americas:

1) Array Technologies, a New Mexico-based solar asset-tracking company for utility-scale solar projects, conducted an initial public offering on the NASDAQ last Thursday. It rose 45% on the first day of trading. This was the largest ever IPO by a New Mexico company, which now boasts a market capitalization of $5 billion.

2) Mexico announced it may halt further foreign private sector investments into its oil and gas and electricity sectors.

3) Schlumberger, the U.S. oil and gas services company that is regarded as a bellwether for the U.S. oil and gas industry, announced dismal Q3 results and its stock price fell by 9% on NYSE on Friday, its worst performance in 13 years. The U.S. shale sector has suffered almost 40 bankruptcies year-to-date.

STOCK MARKET PERFORMANCE

| As of close on October 16, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| INPEX CORP | 1605 JP | 786.73 | -5.46 | -51.80 | -10.62 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 97.96 | -7.30 | -40.31 | -2.39 | |

| ENEOS HOLDINGS INC | 5020 JP | 1195.20 | -4.10 | -21.28 | -4.85 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 657.09 | -2.90 | -22.87 | -6.69 | |

| COSMO ENERGY HOLD. | 5021 JP | 132.75 | -3.33 | -34.43 | -4.28 | |

| Industrials | ||||||

| JGC HOLDINGS CORP | 1963 JP | 238.22 | -6.89 | -46.91 | -15.61 | |

| CHIYODA CORP | 6366 JP | 62.99 | -3.20 | -14.49 | -9.36 | |

| MITSUBISHI CORP | 8058 JP | 3650.42 | -2.94 | -10.60 | -2.21 | |

| MITSUI & CO LTD | 8031 JP | 3083.06 | -2.02 | -3.36 | -2.30 | |

| Utilities | ||||||

| TOKYO ELECTRIC POWER | 9501 JP | 472.46 | 3.52 | -37.04 | -3.29 | |

| CHUBU ELECTRIC POWER | 9502 JP | 938.03 | -2.52 | -16.88 | -5.54 | |

| KANSAI ELECTRIC POWER | 9503 JP | 936.86 | -1.77 | -17.52 | -3.30 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 440.99 | -2.41 | 1.89 | -2.78 | |

| J-POWER | 9513 JP | 273.66 | -3.11 | -41.33 | -8.85 | |

| TOKYO GAS CO | 9531 JP | 1037.95 | -1.68 | -9.42 | -0.03 | |

| OSAKA GAS CO | 9532 JP | 824.61 | -1.59 | -3.08 | -3.29 | |

| TOHO GAS CO | 9533 JP | 554.43 | 1.94 | 18.94 | 7.04 | |

| SAIBU GAS CO | 9536 JP | 94.90 | -3.84 | 2.97 | -5.39 | |

| SHIZUOKA GAS CO | 9543 JP | 69.56 | -1.30 | -3.16 | 0.33 | |

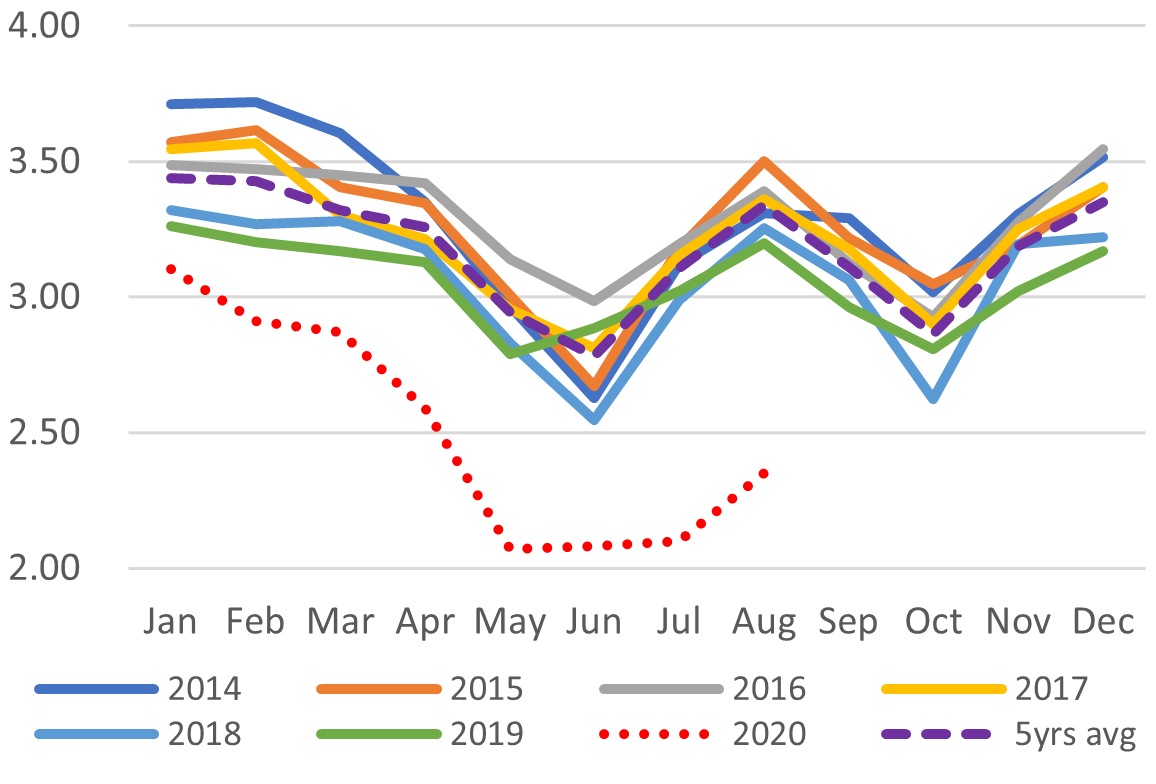

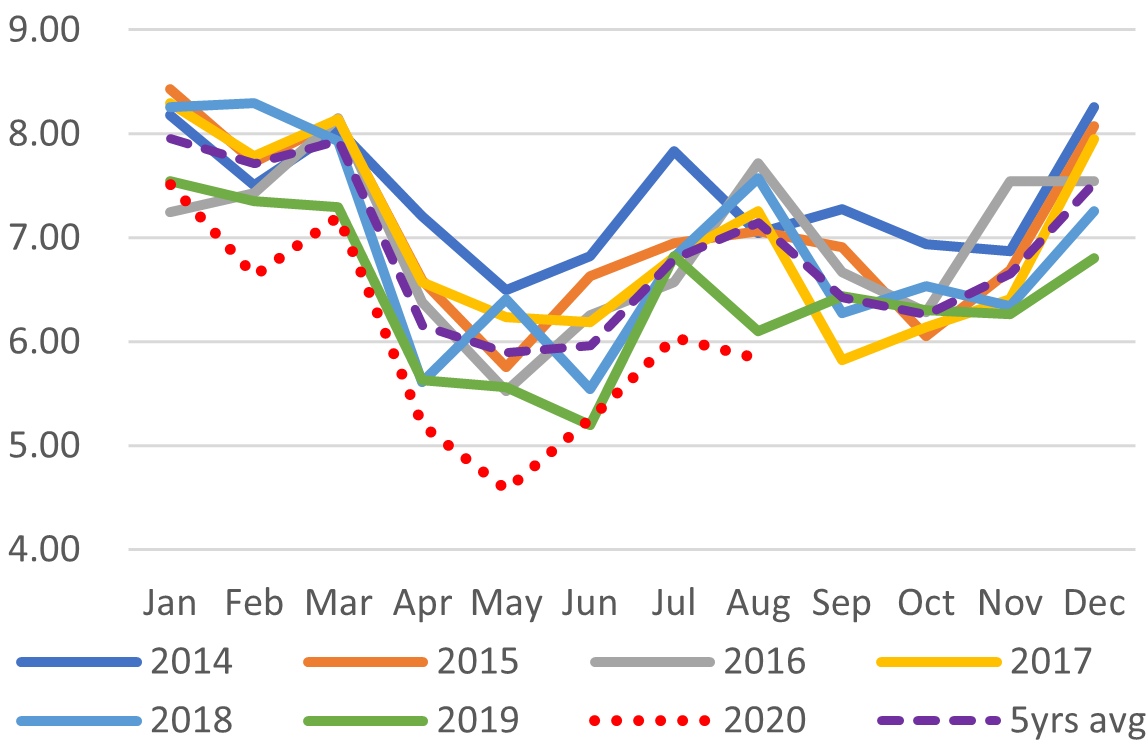

DATA

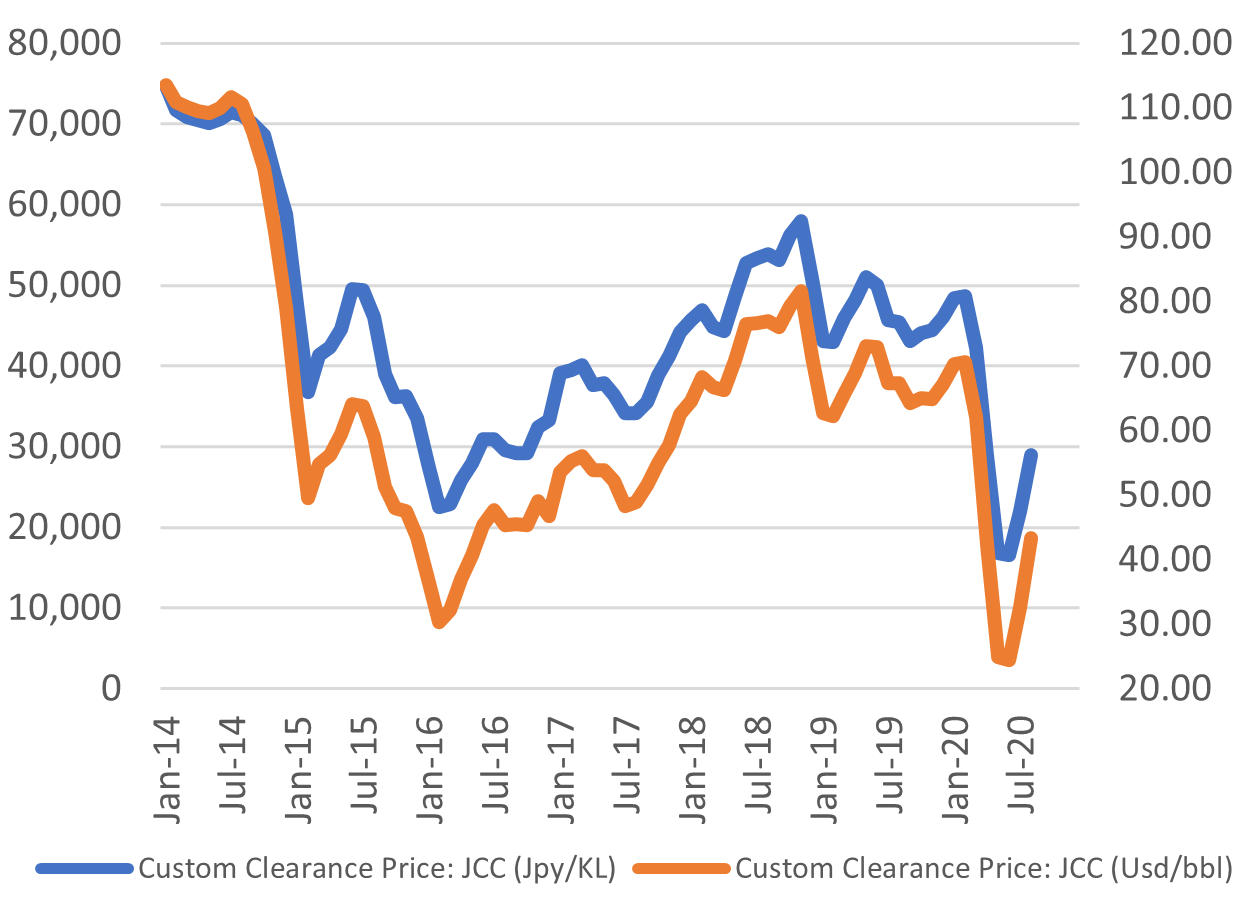

Japan Oil Price

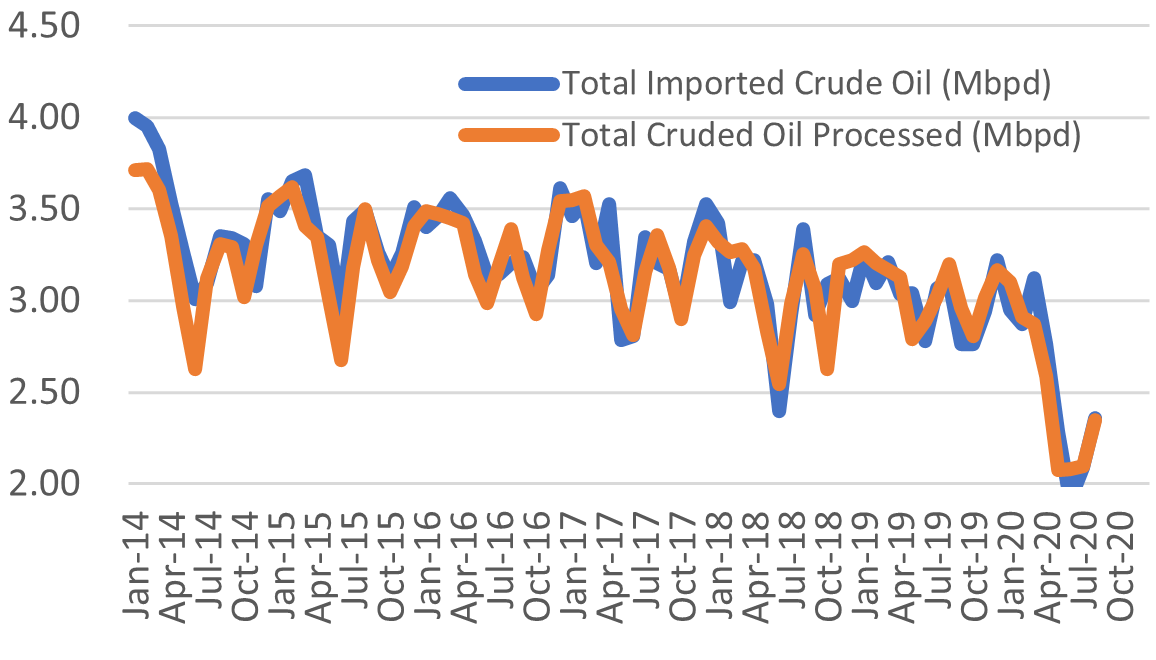

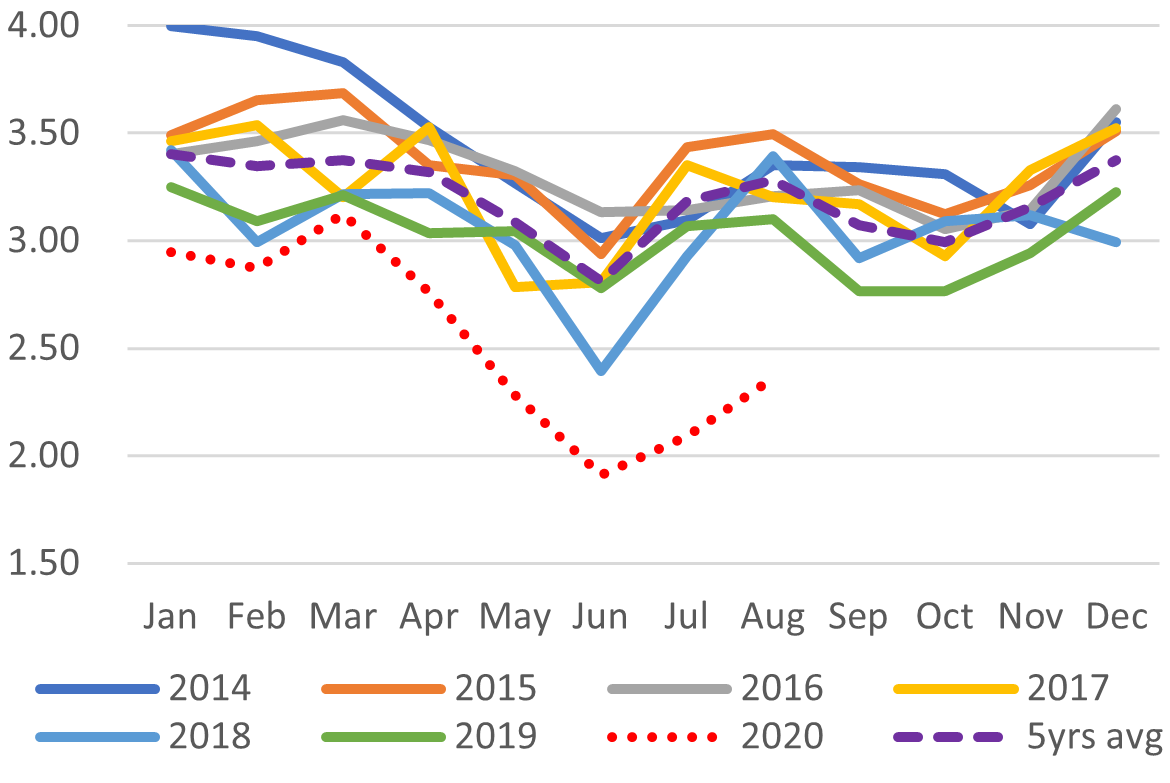

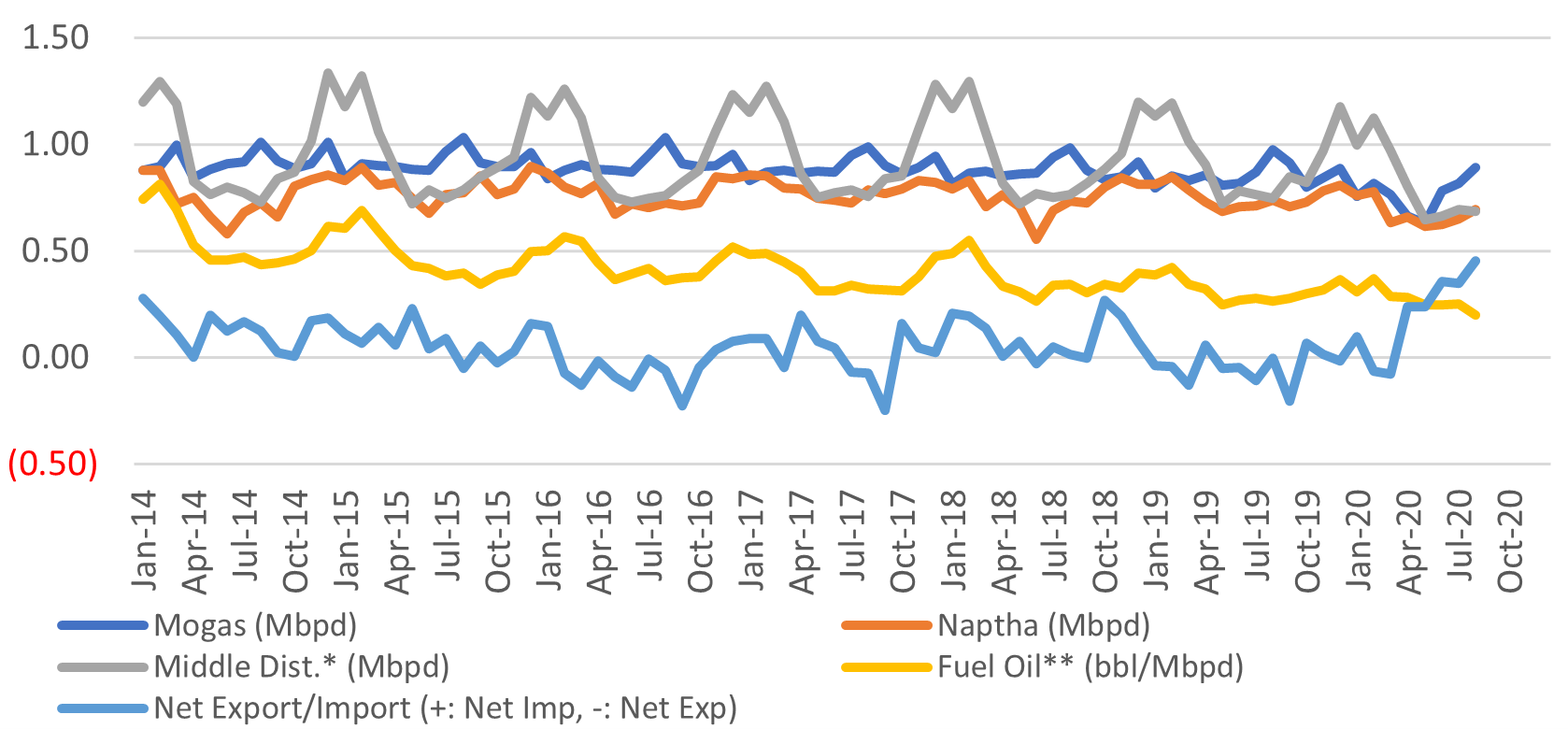

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

Domestic Fuel Sales

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

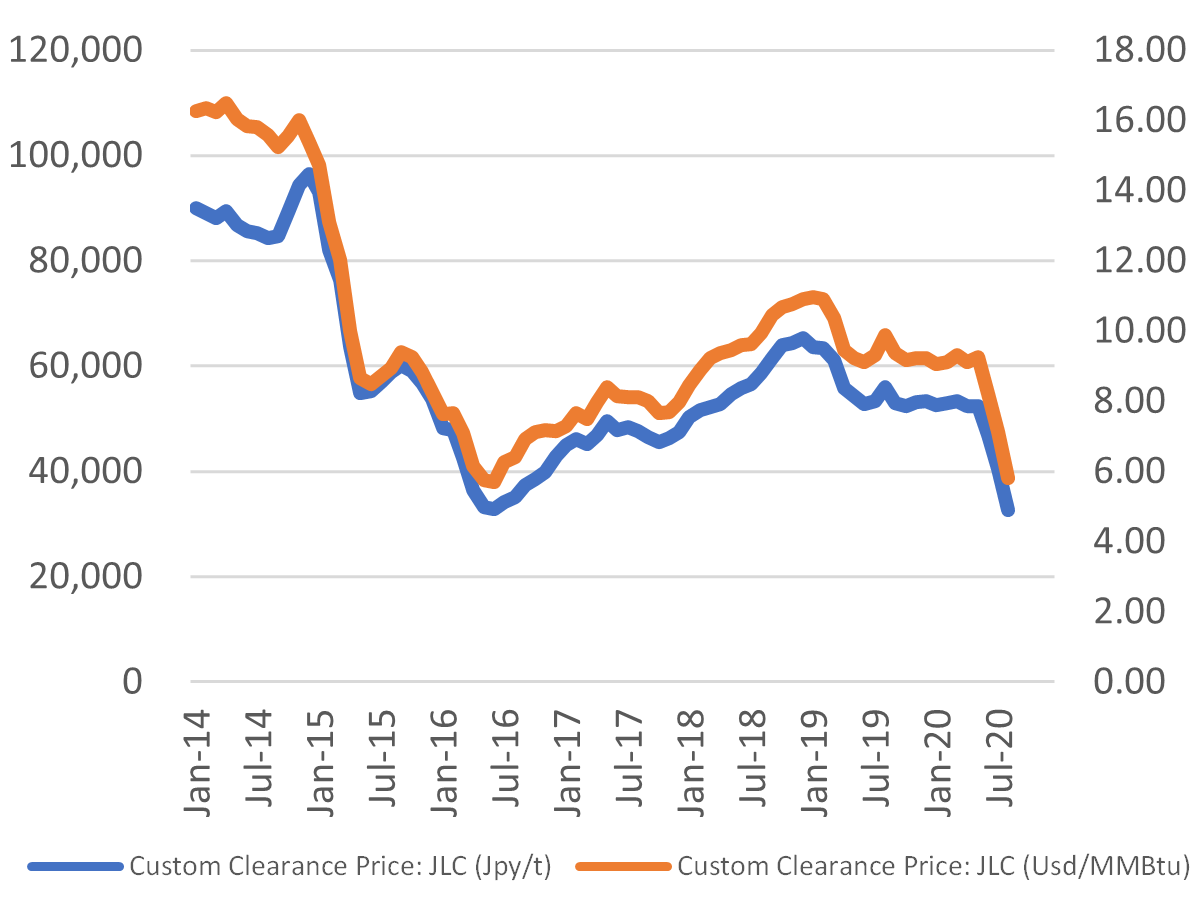

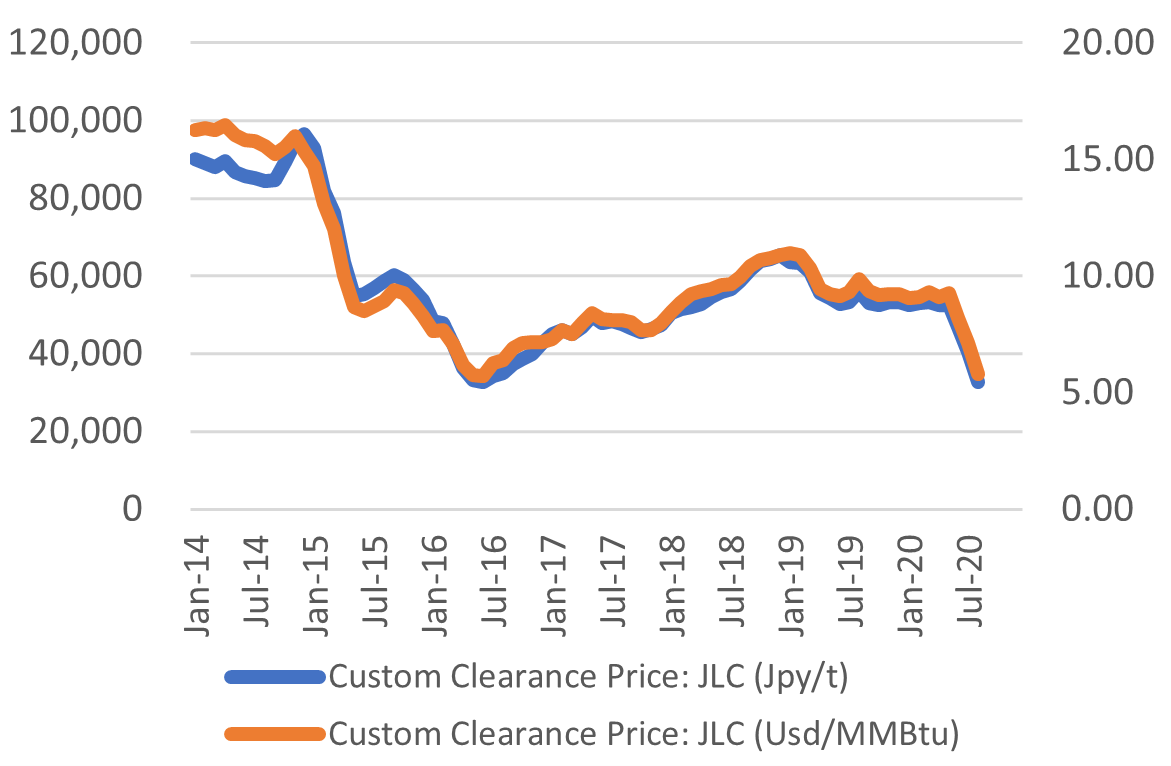

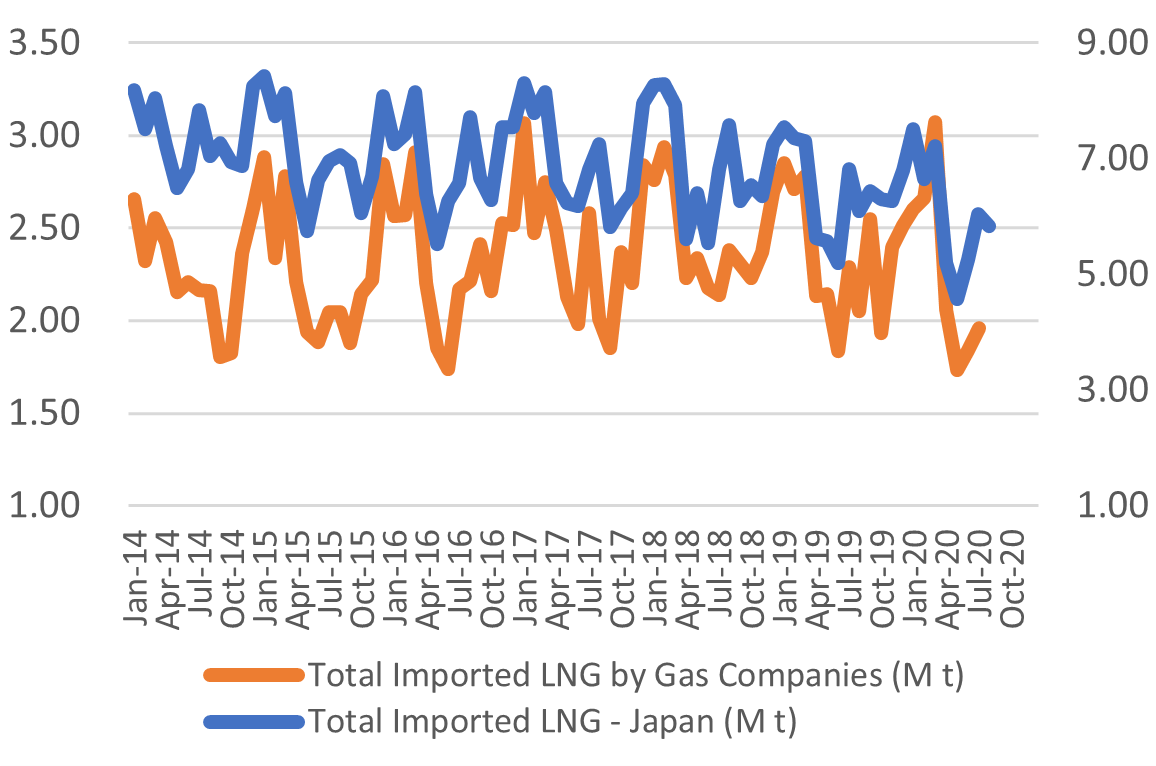

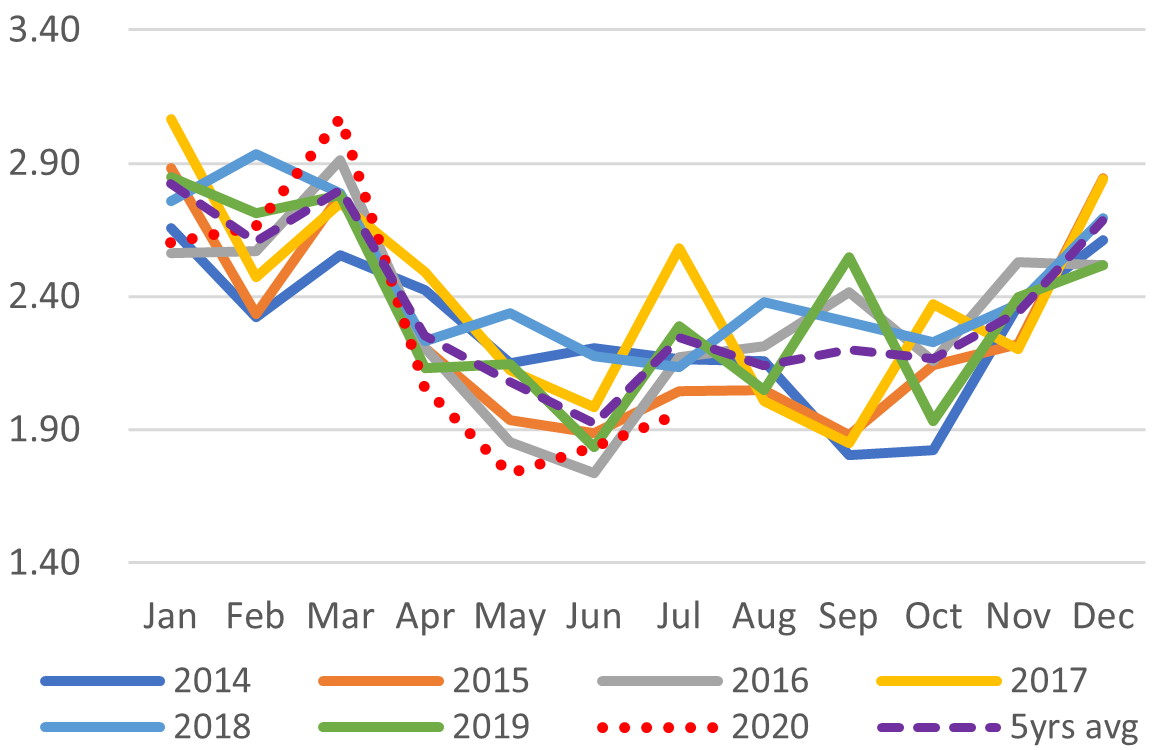

Japan LNG Price

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

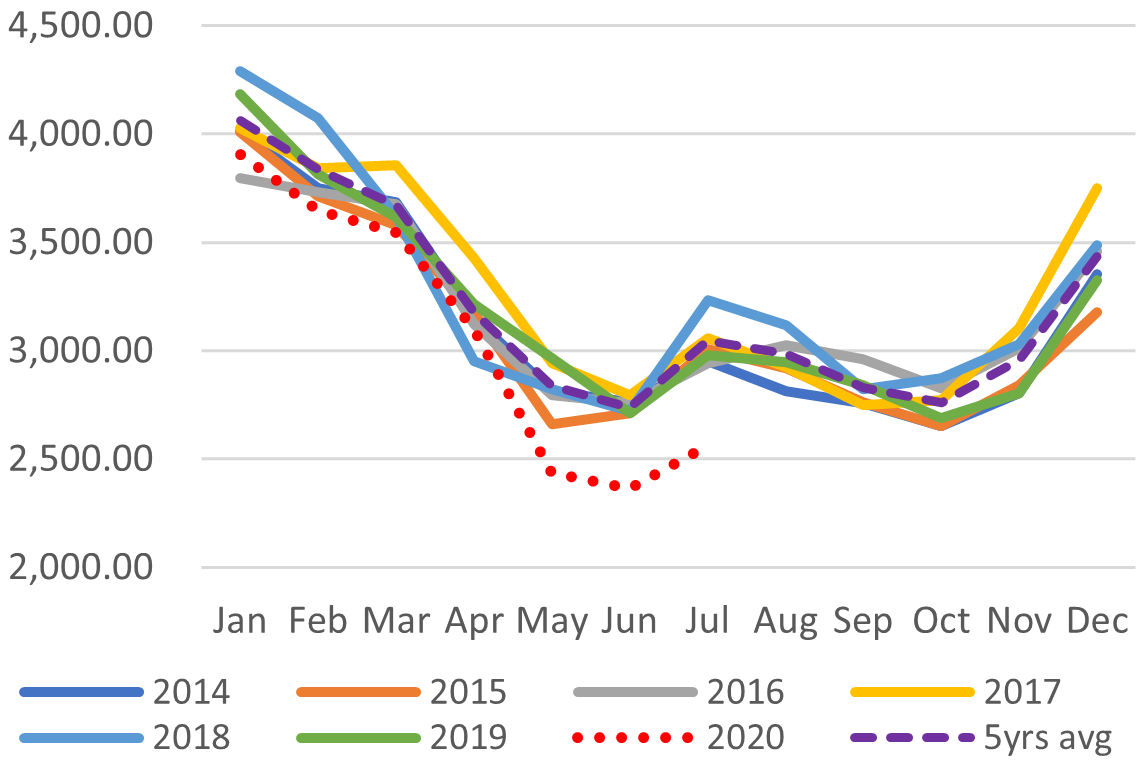

City Gas Sales – Total (M m3)

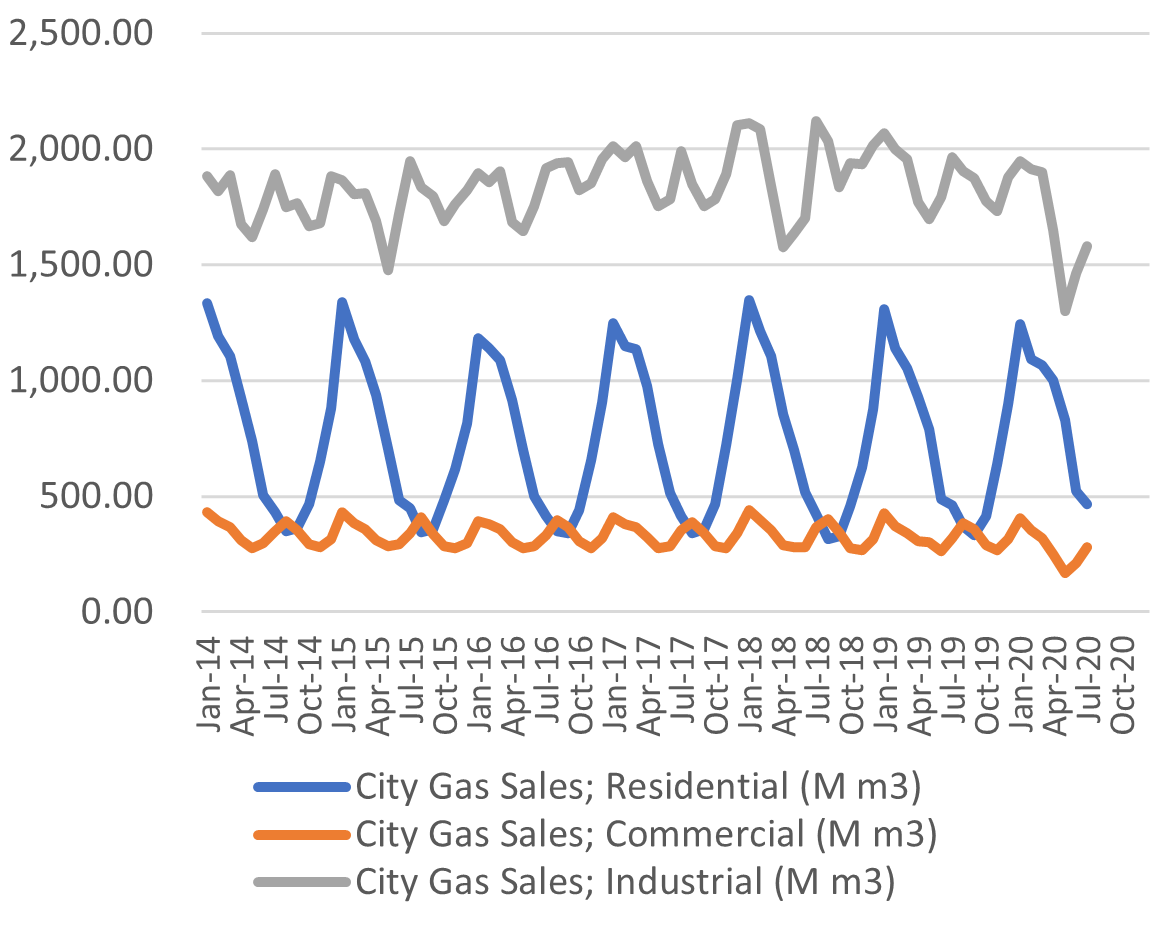

City Gas Sales by Sector (M m3)

SOURCES: the Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

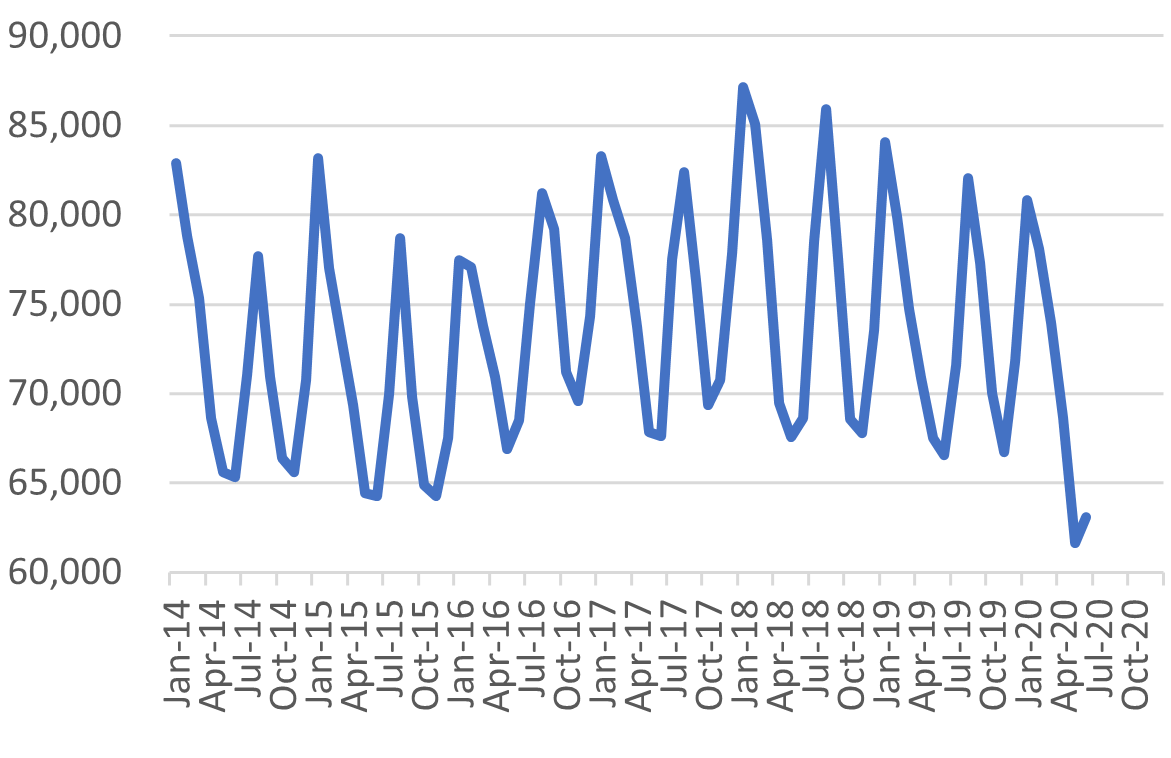

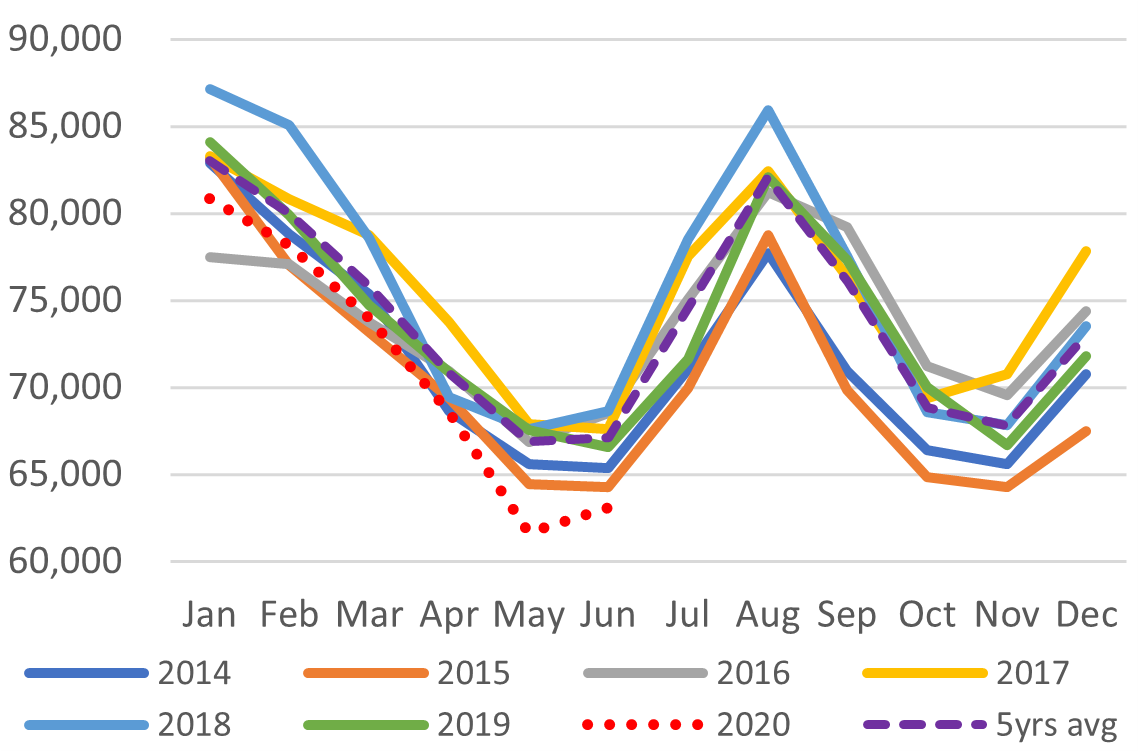

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

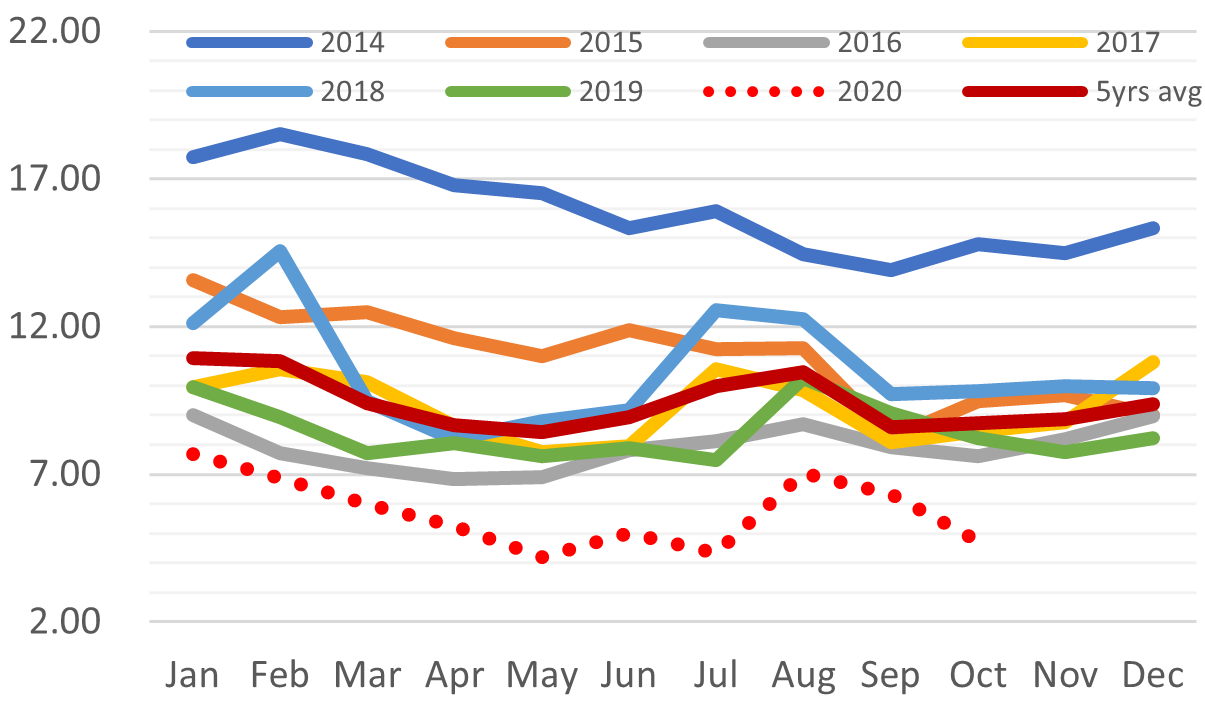

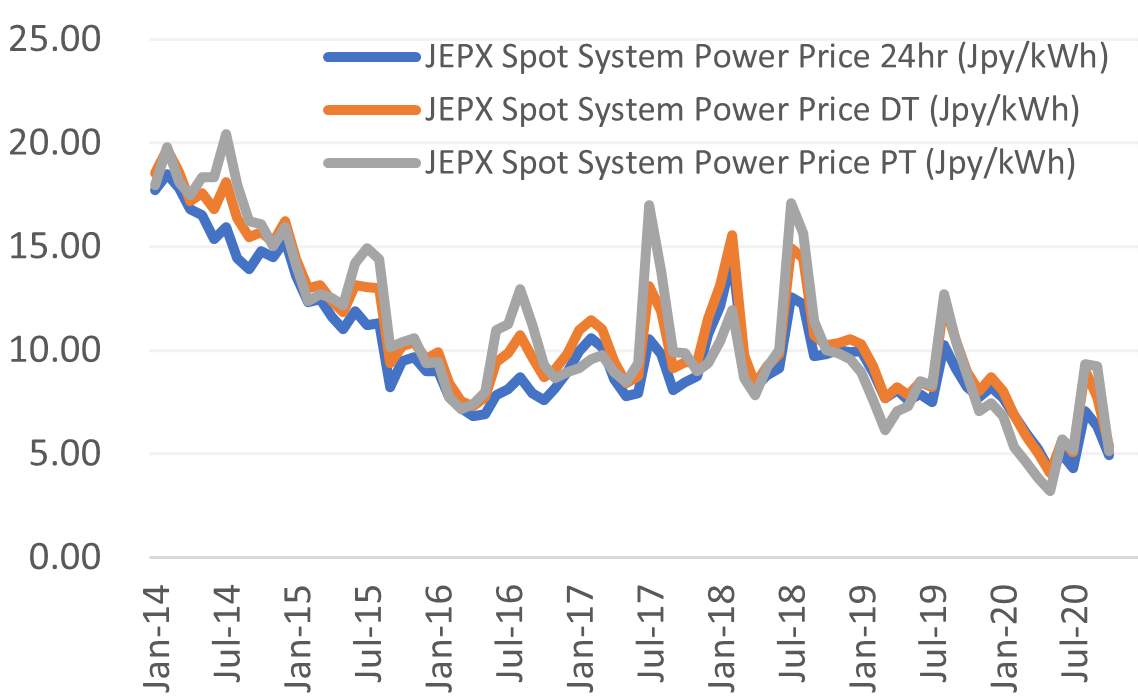

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange