JAPAN NRG WEEKLY

MARCH 22, 2021

JAPAN NRG WEEKLY

March 22, 2021

NEWS

TOP

- Japan’s nuclear industry has mixed week: TEPCO gets major warning from regulator and delays all restart plans, but two other utilities win court battles; yet another court rules against J-Atomic

- Industry association asks govt. to set a $46/ ton carbon price

- Petroleum Association of Japan commits to 2050 net-zero carbon

ENERGY TRANSITION & POLICY

- Government creates panel to pursue underwater grid project

- Euglena sees first flights powered by algae biofuel within a year

- J-Power to cut CO2 emissions by 40% within decade as it turns away from coal and towards hydrogen and renewables

- Japan’s 2017 CO2 emissions report shows little change YoY

- Shipper MOL buys stake in Norway peer to develop CO2 carriers

- Mitsubishi Heavy tests CO2 recovery technology in Norway

- Japan manufacturers claim edge in solid-state and grid batteries

- Mitsubishi Power starts developing ammonia-fired gas turbine; Mitsubishi Corp to source ammonia fuel in Indonesia

- Japan to test waves and noise as new power generation sources

- Marubeni launches vehicle-to-building power service in the UK

- JGC wins contract to build Mongolia’s first solar & storage plant

- SoftBank, U.S. startup Greentech demonstrate next-gen battery

- Sumitomo Corp to develop hydrogen ecosystem in Australia

ELECTRICITY MARKETS

- Prominent energy policy expert casts doubt on future of nuclear

- Iberdrola to join 600 MW offshore wind project with Cosmo, Hitz; ENEOS comes into Itochu wind farm, also in Aomori prefecture

- Hitachi-backed 159.6 MW offshore wind project publishes report

- Chubu Electric, Chudenko buy into Taiwan hydropower project

- Shikoku Electric invests in U.S. energy trading platform startup

- Transmission operators establish capacity market for balancing

OIL, GAS & MINING

- Kawasaki Kisen completes ship-to-ship LNG fueling for its carrier

ANALYSIS

IF GOLDMAN SACHS IS SELLING, IS IT TIME

TO EXIT JAPAN’S SOLAR MARKET?

This year’s marquee deal in Asia-Pacific renewables may well be the potential exit of Goldman Sachs from Japan’s solar market. The bank, known for its investment acumen, has started to sound out potential buyers for a majority ownership in Japan Renewable Energy Corp, a developer of solar and other green energy assets.

The potential sale will have many investors wondering if the Japanese renewables market has turned after a surge in solar capacity over the last 10 years. Certainly, the market’s structure has shifted. Still, Goldman’s likely exit is not only about structural reforms. This is a story about returns expectation.

TEPCO MARKS FUKUSHIMA’S 10-YEAR

ANNIVERSARY WITH A “RED CARD”

On the 10th anniversary of the Fukushima accident another nuclear catastrophe beset TEPCO, casting further doubt on it re-emerging as an operator of atomic power facilities. In a mixed week for the nuclear industry in Japan, TEPCO was issued with a “red rating” by the regulator, the most serious warning, for poor execution of safety measures. This immediately aborts the utility’s plan to restart two of its reactors in spring and rules out the possibility of TEPCO operating a nuclear power plant until at least H2 2022.

With a growing renewables business and options to expand in power transmission, the TEPCO name and current structure looks ripe for change.

GLOBAL VIEW

A selection of global energy-related news.

2021 EVENT CALENDAR

DATA SECTION

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

Sponsored

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI

The Ministry of Energy, Trade and Industry

ANRE

Agency for Natural Resources and Energy

NEDO

New Energy and Industrial Technology Development Organization

TEPCO

Tokyo Electric Power Company

KEPCO

Kansai Electric Power Company

EPCO

Electric Power Company

JCC

Japan Crude Cocktail

JKM

Japan Korea Market, the Platt’s LNG benchmark

CCUS

Carbon Capture, Utilization and Storage

mmbtu

Million British Thermal Units

mb/d

Million barrels per day

mtoe

Million Tons of Oil Equivalent

kWh

Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Japan industry association asks government to set a ¥5,000 ($46) carbon price

(Japan NRG, March 17)

- A price of ¥5,000/ ton of CO2 emissions could boost the development of renewables outside of the FIT system by 17%, according to Japan Climate Change Leadership Partnership (JCLP).

- The comments were made in a March 16 presentation to METI, as part of the meeting of the Next Generation Electricity Network Subcommittee.

- JCLP is an association that consists of 175 companies, including domestic players such as Fujitsu, Orix, Ricoh and Aeon, and overseas companies like Amazon and Google. The group is lobbying to help increase use of renewable energy in Japan.

Government launches panel to plan submarine cables for offshore wind power transmission

(Japan NRG, March 21)

- Last week local media reported that the government is considering the creation of an underwater power grid to connect with the upcoming development of offshore wind power resources. Now, the government has officially set up a committee to consider how to implement the idea.

- This government panel held its inaugural meeting on March 15. It is led by Baba Jumpei, an Associate Professor at University of Tokyo’s Department of Advanced Energy, and a specialist in the application of power electronics and superconductivity for power systems.

- Four more academics make up the core committee members. Six representatives of power utilities and others from the electricity industry make up a list of 11 “observers”.

- The committee has set a target of preparing the master plan for cable installation by spring 2022. A core issue to consider will be how to install such a grid system on Japan’s deep and complex seabed.

TAKEAWAY: Japan’s current grid has several bottlenecks between regions because of low interconnection capacity. Investment in the grid on-land could be expensive as it may require purchase of additional land. In this sense, underwater construction may be cheaper. Still, any deep-sea construction projects are likely to require major expenditure, which is currently guesstimated at a trillion yen. That would prevent the ability of offshore wind power to reduce its costs in Japan in the next decade or so.

Euglena sees first jet flights powered by algae biofuel within a year

(New Energy Business News, March 18)

- Biofuels producer Euglena says it has perfected a bio-jet diesel blend synthesized using algae that satisfies the ASTM D7566 Annex 6 standard.

- Euglena developed the fuel in collaboration with Chevron Lummus Global and Applied Research Associates.

- The fuel was manufactured at Euglena’s biofuel testing plant, the first of its type in Japan.

- The biodiesel will be first used in aircraft later this year.

J-Power says it will cut CO2 emissions by 40% within a decade via hydrogen

(New Energy Business News, March 16)

- J-Power has released what it’s calling “Blue Mission 2050”, a roadmap for transitioning to carbon neutrality.

- Under the plan, J-Power aims to reduce CO2 emissions by 40% by 2030.

- J-Power says it will achieve this goal by utilizing green hydrogen, creating 1 GW of renewable capacity, and further strengthening its electricity network.

- The plan requires J-Power to progressively phase out its obsolete coal-fired power stations and switch existing power stations to natural gas.

Japan publishes detailed account of 2017 emissions, with numbers little-changed from 2016

(Japan NRG, March 17)

- Total reported carbon release of big emitters was almost flat in fiscal 2017, at 689.19 million tons of CO2, according to a report published by METI.

- Those that emit more than 3,000 million tons of greenhouse gases, and have 21 or more staff, are required to report annual numbers. The total of such emitters was also little changed at 12,341 businesses / business units in FY2017.

Shipper MOL buys stake in Norway’s Larvik Shipping to develop liquid CO2 carriers for CCS

(Nikkei, March 20)

- MOL said on March 19 that it will enter the business of shipping liquified CO2. The Japanese shipping company is buying a 25% stake in Norway’s Larvik Shipping and will start joint transport operations in 2024.

- MOL seeks to collect CO2 emissions from steel, cement and other manufacturers, store it and recycle the gas, thus lowering overall emissions into the atmosphere. Carbon Capture, Storage and Recycling is seen as a key technology for helping heavy emitters.

- The investment amount is not disclosed but said to be in the range of several hundred-million yen. MOL will dispatch some shipping staff to its partner.

- The two companies plan to grow the business and eventually work with bigger ships to improve the efficiencies of transporting liquid CO2.

Mitsubishi tests CO2 recovery technology in Norway

(New Energy Business News, March 18)

- Mitsubishi Heavy Industries Engineering has agreed to begin a trial to assess the performance of a carbon-dioxide-absorbing liquid jointly developed by Mitsubishi Heavy Industries and KEPCO at Norway’s CO2 Technology Centre Mongstad.

- The trial aims to evaluate long-term use of the KS-21 amine-based solvent, which is part of the advanced KM CDR process jointly developed by Mitsubishi Heavy Industries and KEPCO.

- Mitsubishi aims to release the solvent for commercial use by the end of the 2021/22 fiscal year.

Japanese manufacturers claim edge in solid-state and grid battery markets

(Nikkei, March 15)

- Sumitomo Electric Industries’ Koganeya Masanobu says Japan leads the world in solid state battery technology and grid battery storage.

- Redox flow batteries, which make use of reactions whereby electricity is released when vanadium and other ions are oxidized, are scalable by simply adding more electrolyte. The ability of these batteries to store a charge for extended periods of time makes them popular with utilities in Europe and the U.S., as well as in Japan. Redox batteries have a useful life of around 20 years.

- NAS batteries are also well suited to grid energy storage applications because of their high capacity and absence of self-discharge. These batteries can also be manufactured without using rare metals.

Mitsubishi Power begins development of ammonia-fired gas turbine

(New Energy Business News, March 17)

- Mitsubishi Power has begun developing a 400 MW gas turbine system that burns pure ammonia. The corporation aims to release a commercial version of the turbine by 2025.

- Mitsubishi Power is also developing a system that uses waste heat from gas turbines to split ammonia into nitrogen and hydrogen, the latter of which can be used to power secondary gas turbines.

- SIDE DEVELOPMENT:

- Mitsubishi to manufacture ammonia as a fuel in Indonesia

- (Asia Nikkei, March 19)

- Mitsubishi Corp to begin producing ammonia as a fuel in Indonesia using an emissions-reducing process within five years. The trading house plans to ship the fuel to Japan.

- Mitsubishi’s part-owned Indonesian ammonia producer, Panca Amara Utama will revamp its process, which currently makes ammonia as a feedstock for fertilizer, to make gas that can be used as fuel in thermal power plants. Ammonia would then be used together with coal for co-firing.

- The Indonesian maker has an annual capacity of 700,000 tons of ammonia.

- Mitsubishi also wants to add carbon capture technology to the site and send the emissions underground through a pipeline.

- JOGMEC and Indonesia’s Bandung Institute of Technology are also involved.

Wave power, noise harnessed to generate electricity in Shimane

(New Energy Business News, March 17)

- A start-up founded by graduates of Keio University that harnesses energy produced by vibration, waves, and even noise to generate electricity, was trailed in Shimane between 1 and 5 March.

- Kanagawa-based Soundpower Corp has patented a technology that uses wave energy to push up a column of water. Water flowing from the top can then be used to generate electricity.

- CEO Hayamizu Kohei says while the experimental unit only has an output of around 1.5 W, if scaled up, the wave generation unit could generate over 300 MW.

Marubeni launches vehicle-to-building power service

(Kankyo Business, March 17)

- Marubeni said on March 15 that it is part of a UK-based “vehicle to building” initiative in which the batteries of electric vehicles connected to charging stations will be used to supply electricity to buildings when power is in short supply.

- When there is a surplus of electricity, as is the case with solar farms during fine weather, the same batteries will be used to store surplus electricity.

Japan’s JGC wins contract to build Mongolia’s first solar and storage facility

(Asia Nikkei, March 20)

- JGC will manage design and construction of the first solar power plant with storage in Mongolia.

- The plant, located in the city of Uliastai, western Mongolia, will have 5 MW of solar power capacity and 3.6 MWh of storage. Local contractor MCS International with work with JGC.

- The Mongolian project qualifies for a carbon credit framework under which assistance to reduce emissions in developing countries is counted toward Japan’s tally. This will mean a 6,423-ton reduction in Japan’s annual CO2 emissions.

Softbank and Enpower Greentech succeed in demonstrating next-generation battery

(Nikkei; March 15, 2021)

- Softbank and US startup Empower Greentech have been jointly working on next-generation batteries since April 2020.

- On March 15, the companies announced that they have succeeded in demonstrating a light and long-life lithium metal battery, which has a mass energy density of 450Wh/kg (about 2x that of other batteries).

- SoftBank also says it will establish a Next-Generation Battery Lab.

Sumitomo Corp signs MoU to develop hydrogen ecosystem in Australia

(Japan NRG, March 19)

- Sumitomo Corp. signed a memorandum of understanding with Gladstone Ports Corp, and representatives of the city’s authorities and Australia’s gas networks, to develop a “hydrogen ecosystem”.

- Sumitomo said it will conduct a feasibility study covering the entire hydrogen supply chain to determining the best configuration for hydrogen production and demand creation in the Gladstone region.

- Sumitomo said it sees the local gas and transport infrastructure as key to the project.

- The Japanese trading house will establish a new entity called Energy Innovation Initiative (EII) in April to carry this Gladstone project.

NEWS: POWER MARKETS

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 6 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

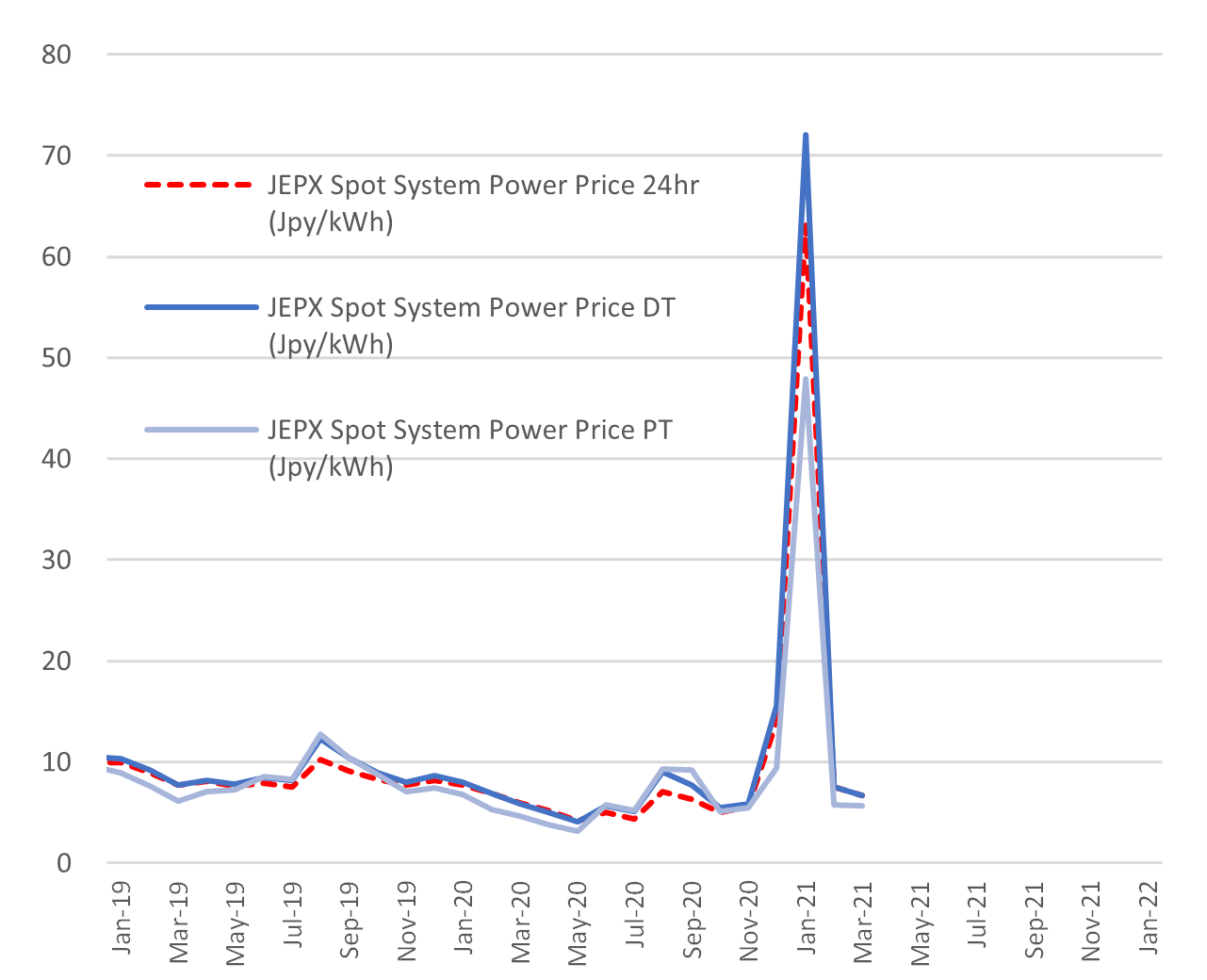

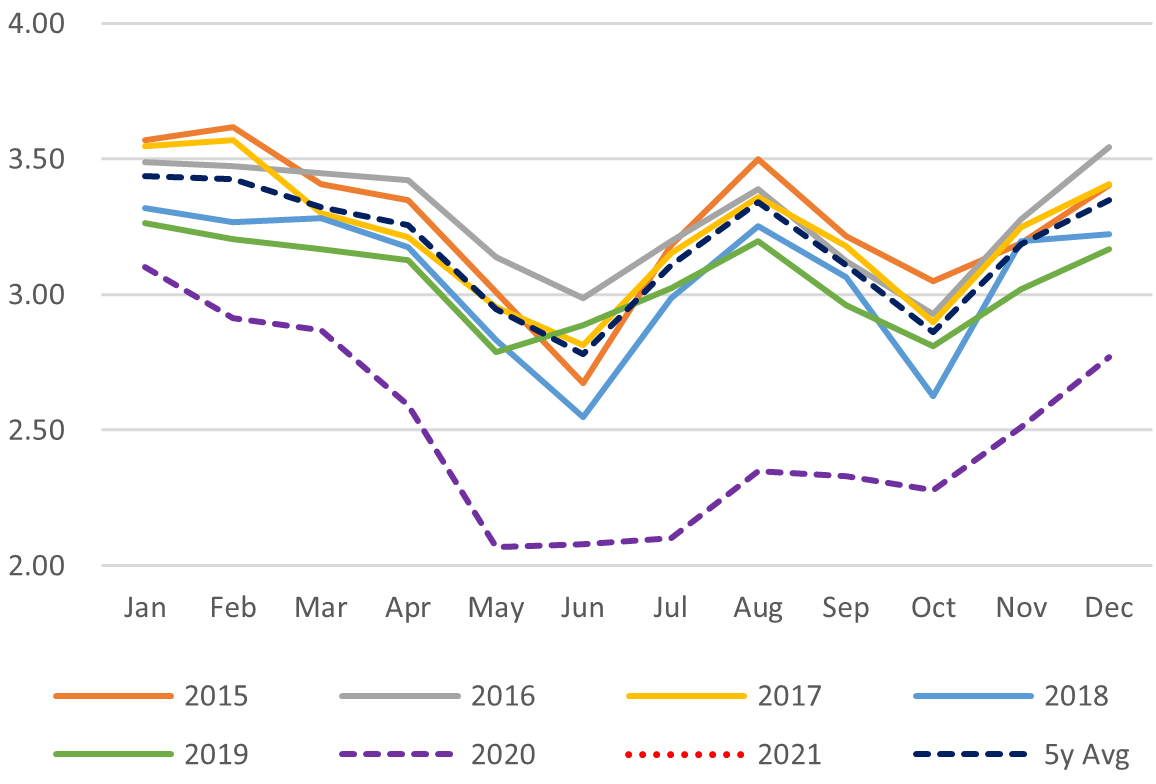

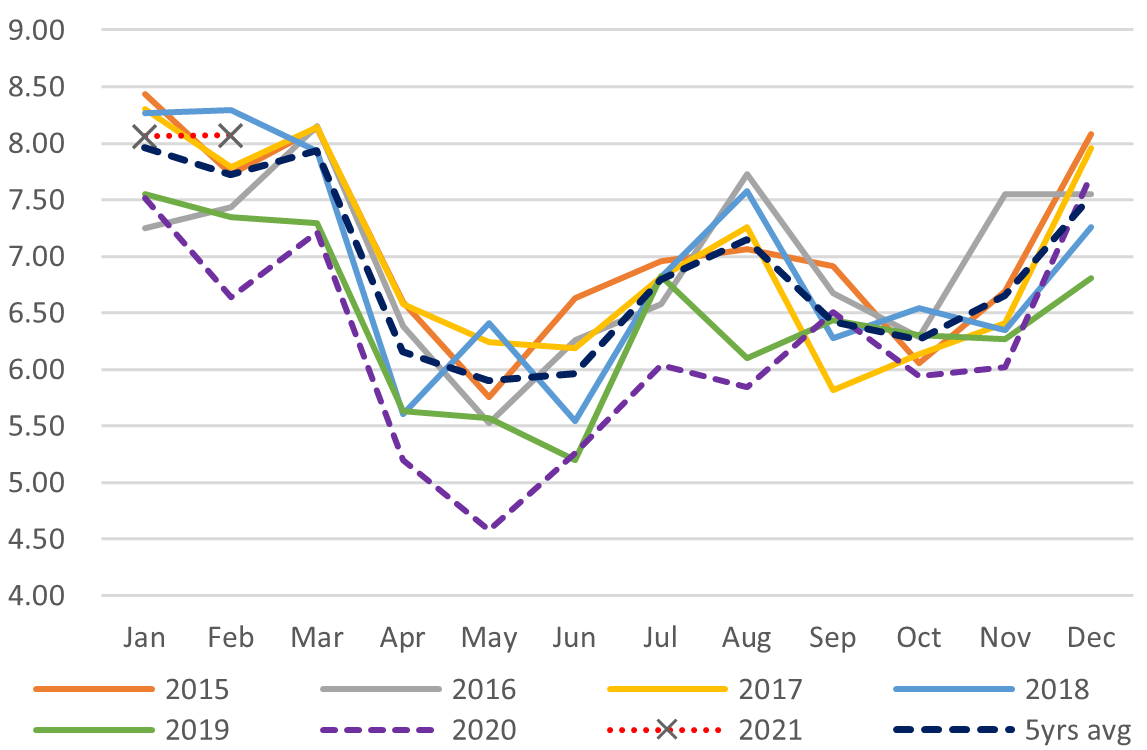

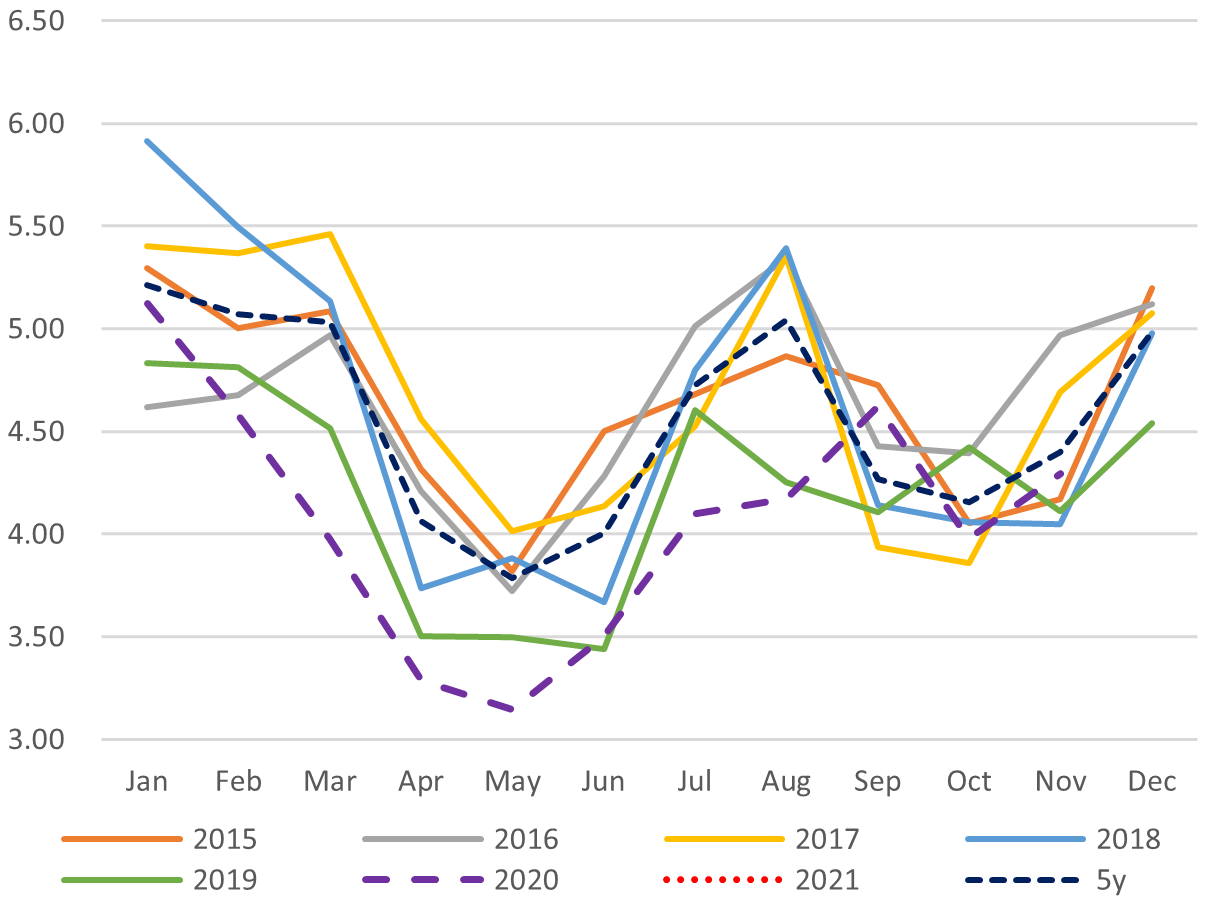

Spot Electricity Prices, Monthly Avg.

Source: Company websites, JANSI and JAIF, as of March. 15, 2021

A mixed week for the nuclear industry in Japan:

- TEPCO gets a red card from the regulator, a major rebuke from the prime minister, stops construction of a new nuclear power plant (See Analysis section for full story and our takeaway)

- TEPCO now cannot restart any nuclear reactors until at least late 2022, which may require JERA to import more LNG

- Courts lifts restrictions from Kansai Electric to proceed with restarts at its three NPPs

- Courts allow Shikoku Electric to resume operations of Ikata NPP

- Courts bar operations at J-Atomic’s Tokai Dai-Ni NPP (which is not operating at present)

- A prominent energy policy expert in Japan casts doubt on future of nuclear industry in the country

- SIDE DEVELOPMENT

TEPCO’s Kashiwazaki plant anti-terrorism measures woefully deficient

(NHK, March 16)- A Nuclear Regulation Authority audit of alarm systems fitted to the Kashiwazaki-Kariwa nuclear power station to prevent intruders has revealed that multiple alarms have failed since March 2020.

- Despite being aware of the malfunctions and of the fact that the stopgap security measures taken in lieu of the alarms were not effective, TEPCO security personnel did not attempt to rectify the situation, says the Authority.

- In an unprecedented move, the Authority has assigned the plant the lowest counterterrorism defense rating on its four-point scale, in view of the fact that the plant was left vulnerable to intruders for a significant period of time.

- NRA chairman was quoted by media wondering if TEPCO has a lack of knowledge or is not even trying when it comes to nuclear facility management.

- SIDE DEVELOPMENT

PM Suga questions if TEPCO should run nuclear facilities

(Mainichi Shimbun, March 20)- Prime Minister Suga has censured TEPCO over a recent scandal involving security breaches at its Kashiwazaki-Kariwa nuclear power station.

- The revelations force one to “question whether TEPCO is actually qualified to run a nuclear power plant,” said Suga.

- SIDE DEVELOPMENT

TEPCO delays construction of new Higashidori reactor

(Too Nippo, March 20)- The head of TEPCO Holdings’ Aomori office said that construction on Unit 1 of the Higashidori nuclear power station will not start during the current financial year.

- The announcement comes in the wake of a series of scandals involving TEPCO.

- SIDE DEVELOPMENT

Court backs Kansai Electric and throws out residents’ petition to shut down its NPPs

(Tokyo Shimbun, March 17)- The Osaka District Court on March 17 dismissed a petition filed by residents of Fukui and surrounding prefectures to have the Mihama, Takahama and Ohi nuclear power plants turned off.

- The court said the residents’ petition lacked grounds because they had failed to explain the actual risk of a nuclear fallout event occurring.

- SIDE DEVELOPMENT

Court gives green light to turning on Shikoku Electric’s Ikata Unit 3

(NHK, March 18)- The Hiroshima High Court has overturned a provisional disposition imposed last year in relation to the Unit 3 reactor at the Ikata nuclear power station in Shikoku, saying that the probability of a natural disaster serious enough to jeopardize the reactor’s safety was “not high”.

- Last year’s disposition was issued in response to a petition filed by residents of nearby Hiroshima and ordered the reactor to remain off, citing earthquake and volcanic eruption as specific risks.

- Counsel for the plaintiffs in last year’s action said that because, scientifically speaking, the risks in question are impossible to fully demonstrate, by placing the burden of proof on local residents, the court has effectively blocked the residents’ path to stopping the reactor.

- Shikoku Electric welcomed the decision as “fair”.

- Ehime Mayor Takakado refused to comment on the decision, saying it was a matter for the judiciary. Takakado did express concerns about the technical skills lost when reactors remain switched off for extended periods.

- SIDE DEVELOPMENT

Mito court says no to J-Power reactor restart at Tokai Dai-Ni

(NHK, March 18)- The Mito District Court found on March 18 that approval should not be granted for the restart of the Tokai Dai-Ni nuclear power plant, on the grounds that no suitable plan was in place to evacuate residents living within a 30km radius of the plant in the event of an emergency.

- The decision is a victory for the plaintiffs, a group of 224 residents of surrounding regions who sued the Japan Atomic Power Company over concerns about the plant’s safety in a major earthquake. The plaintiffs say the decision shows the lessons of the Fukushima disaster have not been ignored.

- Counsel for the plaintiff called the decision unexpected and historic.

- In a statement, Tokaimura Mayor Yamada Osamu said he believes the stakeholders are working hard to improve evacuation arrangements for the plant. Yamada also stressed the importance of forming agreement with the local community.

- The Japan Atomic Power Company says it will appeal the decision.

- SIDE DEVELOPMENT

OPINION: Fukushima 10 years on: Does nuclear still have a future in Japan?

(World Economic Review, March 15)- CONTEXT: This is a column by Prof. Kikkawa Takeo at the Graduate School of Commerce and Management, Hitotsubashi University.

- At the time of the Fukushima nuclear disaster, there were 54 nuclear power plants in Japan and another three under construction. Today, 21 of these 57 have been slated for decommissioning, and a mere nine reactors have been given the go-ahead restart under the government’s new, stricter rules.

- The government’s current basic energy outlook calls for up to 60% of electricity from renewables, 10% from hydrogen and ammonia, and the remaining 30 to 40% from nuclear sources by 2050, although the government has described this “plan” as a mere point of reference for encouraging discussion.

- While Prime Minister Suga’s carbon neutral declaration has created optimism amongst the nuclear power lobby, this optimism will likely prove unwarranted. Indeed, METI Minister Kajiyama himself has not changed his opposition to building new reactors as a replacement for aging assets. And without investment in new reactors, the government’s much vaunted small modular reactor (SMR) program is a mere pipe dream.

- By placing the blame for the disaster squarely on TEPCO, the government has attempted to frame itself as the “good guy” bringing the “villain” (the nuclear industry) to justice. This also explains the government’s reluctance to issue clear guidelines on nuclear policy.

- It’s hard to see a future for nuclear power in Japan.

Iberdrola says plans to develop 600 MW offshore wind farm in Japan with Cosmo and Hitz

(Japan NRG, March 17)

- Spanish utility says it is pursuing its second deal in Japan’s power market by coming into a project to develop a 600 MW offshore wind power plant.

- The Seihoku-oki wind farm, in Aomori prefecture, is run by a unit of Cosmo Energy, and engineering firm Hitz. After the deal is completed in six months, Iberdrola and Cosmo will share project leadership, with “similar voting rights”, the utility said. Hitz will also remain in the project.

- The project will enter round two of the capacity auction planned by the Japanese government either this or next year, according to Iberdrola.

- CONTEXT: Iberdrola acquired all of Acacia Renewables last year, which has 3.3 GW in offshore wind project pipeline in Japan. Macquarie’s Green Investment Group is a partner for Iberdrola in the Acacia portfolio.

- SIDE DEVELOPMENT:

ENEOS joins forces with Itochu, Hitachi Zosen in Aomori wind farm project

(Kankyo Business, March 18)- ENEOS said on March 17 that it would participate in a project to build a 57 MW wind farm in Rokkashomura, Aomori. The project was launched by Itochu and Hitachi Zosen.

- The farm is expected to begin supplying the grid in 2024.

Hitachi-backed offshore wind project publishes environmental assessment

(New Energy Business News, March 19)

- Wind Power Energy published an environmental assessment for the Kashima Port Offshore Wind Power Generation Project, which aims to build 159.6 MW of wind power capacity near Kashima Port in Ibaraki Prefecture. Construction will begin in 2024 and operation in 2026.

- Kashima’s plan involves installing 19 wind turbines with a single unit output of 8,400 kW, or 10 wind turbines with a single unit output of 14,000 kW.

- Wind Power Energy has been selected by Ibaraki Prefecture as a business operator. Hitachi Wind Power has a 51% stake, Wind Power Group has a 33.4% stake, and Tokyo Gas has a 15.4% stake in the operating company.

Chubu Electric and Chudenko to buys stake in Taiwan hydropower project

(New Energy Business News, March 15)

- Chugoku Electric and Chudenko Corporation have decided to jointly participate in a hydroelectric power generation project in Hualien County, Taiwan. This is the second time that the two have jointly participated in an overseas power business).

- A JV of the companies has taken a 25% stake in Taiwan Foxlink group company Yongho Investment Holding.

- The company plans to start operation of two hydroelectric power plants in Hualien County with a of 37.1 MW capacity by the end of 2024.

Shikoku Electric to invest in trading platform LO3 Energy

(New Energy Business News, March 19)

- Shikoku Electric has invested in US startup LO3 Energy, the company behind the blockchain-based Pando energy trading platform.

- LO3 implements solutions that enable electricity to be traded locally.

Transmission operators establish capacity market to balance supply and demand

(New Energy Business News, March 19)

- A consortium of nine transmission operators, including TEPCO Powergrid, has established a nationwide market for trading transmission capacity that covers everywhere in Japan except Okinawa.

- Transmission operators adjust for minute-by-minute discrepancies between forecast and actual supply and demand to ensure that supply and demand are balanced across the grid.

NEWS: OIL, GAS & MINING

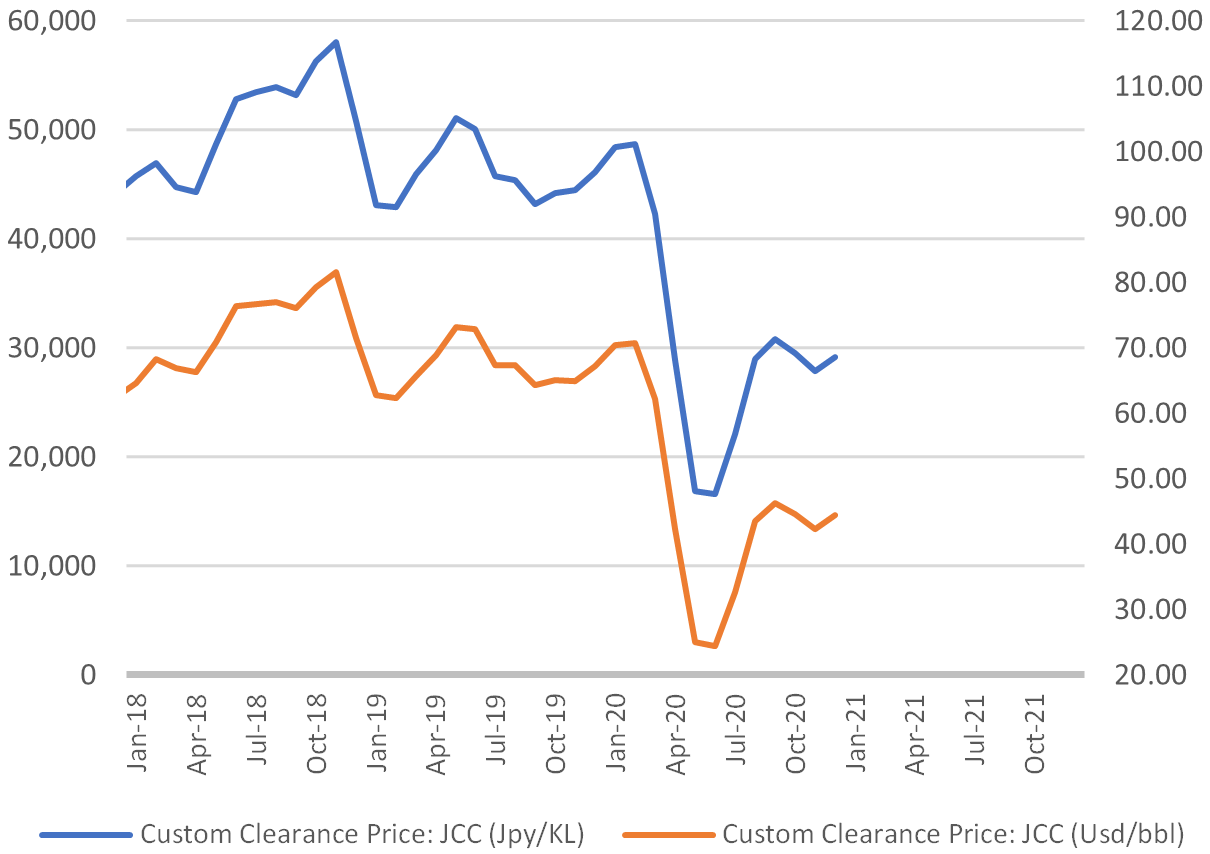

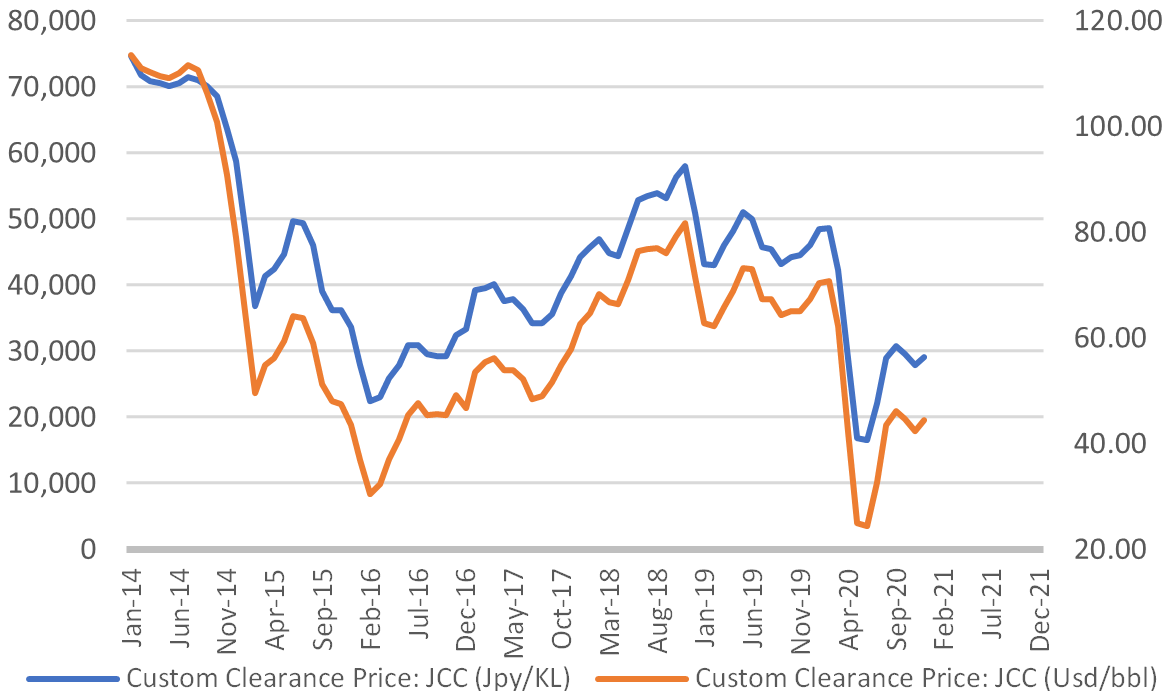

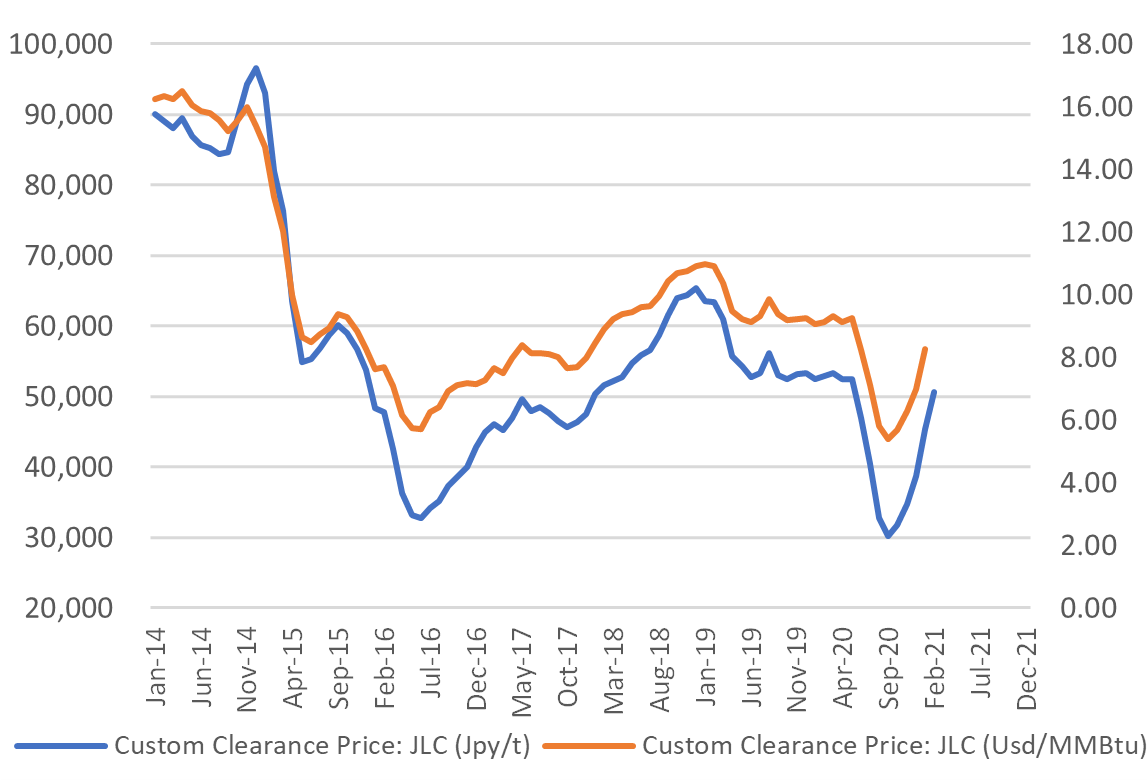

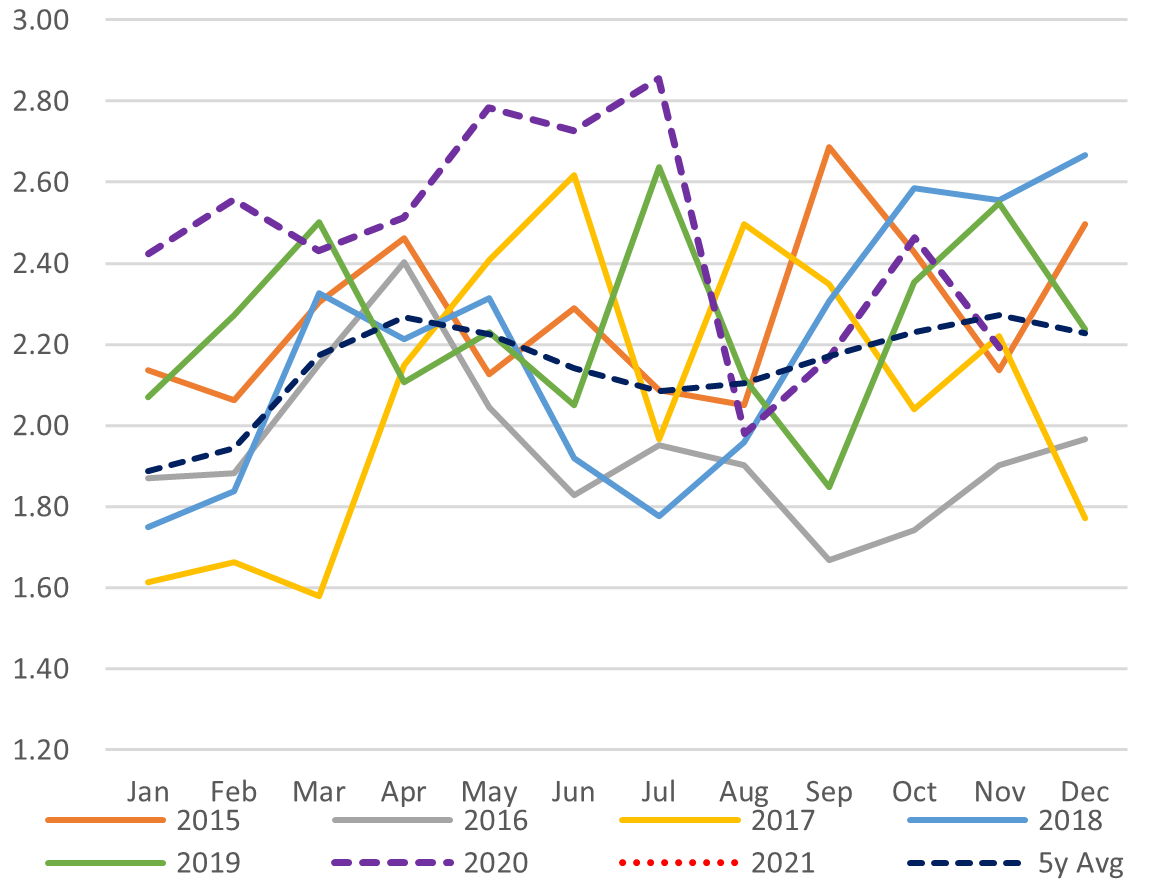

Japan Oil Price: $50.09/ barrel

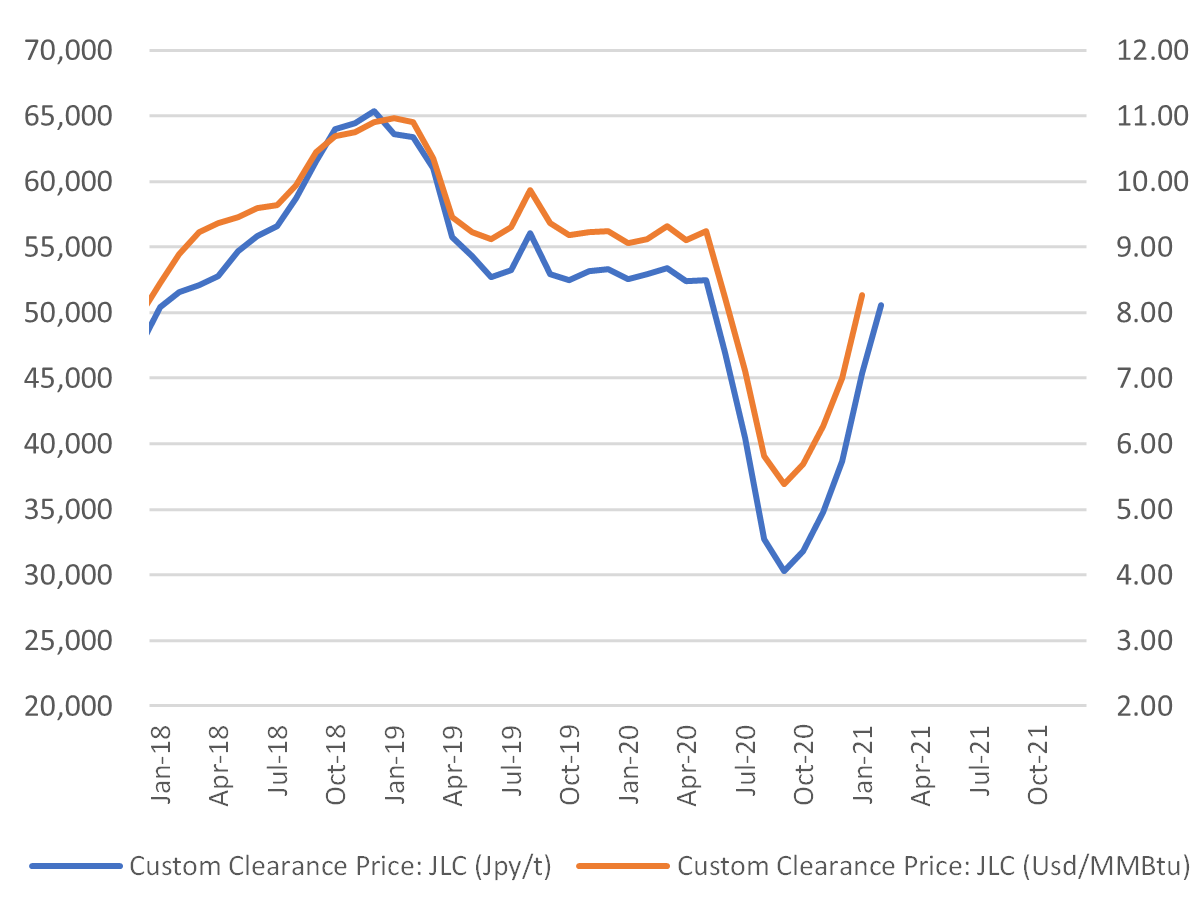

Japan (JLC) LNG Price: $8.27/ mmbtu

Petroleum Association pledges net zero CO2 emissions by 2050

(Sankei Biz, March 19)

- On March 19 the Petroleum Association of Japan announced a new vision in which it aims to reduce its net CO2 emissions to zero by 2050.

- The Association aims to achieve this goal by accelerating the decarbonization of its supply chain and the decarbonization of petroleum products, as well as researching and developing green technologies, specifically green hydrogen and the capture, storage and reuse of carbon.

Kawasaki Kisen completes ship-to-ship fueling for its LNG-powered carrier

(Denki Shimbun, March 17)

- Kawasaki Kisen, also known as K-Line, said that it completed a ship-to-ship LNG fueling operating for its recently commissioned car carrier, the Century Highway Green. The fuel was provided from the bunkering ship Kaguya, which made Japan’s first such LNG transfer at sea in October last year. This is the second ship-to-ship transfer for Kaguya.

- Kaguya is based at JERA’s Kawagoe thermal power plant and plans to supply LNG-powered vessels moored in the Chubu region.

- LNG bunkering in Japan is carried out by a joint venture between JERA, NYK Line, Kawasaki Kisen, and Toyota Tsusho. The JV procures LNG from JERA and operate the Kaguya.

ANALYSIS

BY ESWAR MANI

MANAGING PARTNER

MANI KAPITAL

If Goldman Sachs is selling,

Is it time to exit Japan’s solar market?

This year’s marquee deal in the Asia-Pacific renewables space may well be the potential exit of Goldman Sachs from Japan’s solar market. The bank, known for its investment acumen, has started to sound out potential buyers for its majority ownership in Japan Renewable Energy Corp (JRE), a developer of solar and other green energy assets. The potential sale will have many investors wondering if the Japanese renewables market has turned after a surge in solar capacity over the last 10 years. Certainly, the structure of this market has shifted.

Still, Goldman’s likely exit is not only about structural reforms, but also a reflection of the ESG momentum. Many European pension funds and other institutional investors have taken to supporting ESG themes and threatening a withdrawal of funding from firms and investment vehicles that do not engage.

With Japan’s investable pool of renewable assets still shallow, sizeable investment options inside the country are slim. The expected return (and perceived risk) of Japan solar has significantly decreased since JRE was formed.

This JRE sale will be the deal that people will not want to lose, even if it makes them bid irrationally in the end to secure the bragging rights. For Goldman, it will mean collecting significant financial gains.

How it started

Goldman’s entry timing was favorable. At the start of the previous decade, the renewables industry, and especially solar, was in a funk. One of the early front-runners in solar adoption, Spain, had recently reneged on government-subsidized tariffs for renewable energy. Germany had started decreasing their own tariffs to mirror a drop in solar panel prices and construction costs.

Goldman was one of the earlier investors to build an institutional business in Japan around a new renewables tariff system introduced soon after the 2011 Fukushima disaster. It registered Japan Renewable Energy (JRE) in 2012, the same year that the country introduced the then world’s highest Feed-In Tariff; a guaranteed price at which an operator of a solar or wind generation facility can sell their electricity over a period of 20 or so years.

In less than a decade, JRE has built a portfolio of almost 420 MW, with another 410 MW currently under construction. In 2017, Singapore’s sovereign wealth fund GIC agreed to buy a 25% stake in JRE.

The Fukushima disaster switched sentiment. Germany and several others vowed to quit nuclear energy. The immediate winner was renewables. Even as Japan turned to fossil fuels to fill in the gap vacated by nuclear, the then ruling party hastily put together the FIT scheme to scale the renewable energy industry in Japan.

All experienced European and other global players were only too happy to bring their knowhow to Japan.

How it’s going

Japan’s renewables capacity has certainly grown and the electricity market’s unbundling has further diversified the industry that hitherto had been dominated from generation to retail by 10 vertically integrated utilities.

However, while the market has developed and Japan’s government predictably followed the European model of lowering the FIT price over time, some of the trend lines from Europe have not carried over.

(1) Balance of Systems costs (non-solar panel costs) have not decreased in Japan in line with the rest of the world. One reason is the often-long chain between the prime Engineering, Procurement, and Construction (EPC) contractor and the company that sends workers to the site; so, the project has a lot of mouths to feed. There is no legal limit on the number of subcontractors, and banks tend to lend only if there is a blue-chip general contractor on the paperwork.

(2) A bankable general contractor decreases the perceived risk of the construction process of the solar power plant. The risk, and therefore the expected return, between operational projects and those under construction with debt financing locked in is slim, reflecting a high degree of confidence in project execution.

JRE has as much capacity under construction as it does in operation. Bidders will likely need to price its entire asset base as if it is all online.

How it will be – the biggest unknown

The FIT business model is being phased out. From next April, most new renewables projects will need to apply for a Feed-In Premium (FIP), a less generous mechanism that tends to reward renewables operators that also invest in storage. The stated goal of the government is to have the FIP also expire and for solar, wind and other renewable sources to compete for consumers in the open market.

Current investors in renewable energy in Japan bid for a FIT price that is almost four times lower than the original.

Still, Goldman was not alone among investors eager to snap up early FIT certificates at world-beating prices. Plenty of domestic and overseas prospectors entered the field and were rewarded with 93 GW of FIT-certified projects. Of that, only about 58 GW is online or close. The true operational capacity may be much less, with a substantial number of solar power plants poorly managed.

The remaining FIT-certified capacity could be construed as market overhang for the Goldman deal, but several factors preclude this. While FIT certificates were relatively easy to obtain, initially, getting access to land rights, a grid connection and securing relevant permits was not.

Moreover, METI has begun a campaign to cancel FIT certificates for those that are deemed to be sitting on them but not acting towards project realization. This move may be due to feedback from the big power utilities, which argue that there is already sufficient capacity in overall generation assets (including new coal power plants).

As a consequence, FIT certificates for projects not deemed as progressing by April 2022 will be canceled or asked to re-apply – at the current, lower FIT price. In addition, today’s solar FIT certificates are awarded with an “unlimited curtailment risk”. This means that if even if a new entrant renewables generator produces power, the grid – still controlled by units of the 10 legacy power utilities – can decide not to accept it.

Banks have been scratching their heads around curtailment and only a handful of unlimited curtailment projects have been awarded limited-recourse project finance.

Many players with deep pockets have tried to get around the roadblocks to debt financing and expedited construction by building the projects themselves, obtaining financing after project completion. This likely means having to bundle and cross-collateralize several projects together, which makes it tough to later sell them individually.

Conclusion – Lots of bidders, leaks abound

With the pool of existing FIT-approved projects set to shrink, and the valuation of new projects uncertain, the liquidity of the world’s No. 3 solar market is being tested. Goldman’s asset should prove attractive and gather a significant number of bidders.

The sell-side bankers will need to identify whether potential bidders are spurious or legitimate before opening up details of all projects for the suitors. This will affect not only project values after divestiture, but also the investment of Goldman’s partner, GIC.

While Goldman’s sale seems logical if opportunistic, the bank will likely not want to indicate that it is exiting Japanese renewables completely. The bank has other structural options. The margins from a JRE sale today, however, are probably too good for Goldman to resist.

If Goldman Sachs is selling, is it time to exit Japan’s solar market? The answer primarily depends on your return expectation.

ANALYSIS

BY TOM O’SULLIVAN

TEPCO Marks Fukushima’s 10-Year Anniversary With “Red Card”

Casting Doubt on its Nuclear Strategy

On the 10th anniversary of the Fukushima accident another nuclear catastrophe beset TEPCO, casting further doubt on it re-emerging as an operator of atomic power facilities.

In a mixed week for the nuclear industry in Japan, TEPCO was issued with a “red rating” by the regulator, the most serious warning, for poor execution of installing safety measures. This immediately aborts the utility’s plan to restart two of its reactors in spring and rules out the possibility of TEPCO operating a nuclear power plant until at least H2 2022.

The latest in a long list of TEPCO missteps, after a concerted recent campaign to buy goodwill with locals near its nuclear plants, may mark the end of the line for TEPCO as it stands today. With a growing renewables business and options to expand in power transmission, the TEPCO name and current structure looks ripe for change.

Last week, Japan’s Nuclear Regulatory Authority (NRA) issued TEPCO with the worst of four possible ratings. The status was assigned to TEPCO’s only operable nuclear facility, the Kashiwazaki-Kariwa NPP in Niigata prefecture, because of deficiencies relating to physical security of nuclear materials.

TEPCO is the first company to receive a “red rating.” NRA noted that a probe into the deficiencies at the NPP will now take at least a year. METI confirmed that the facility is not currently fit to operate, causing TEPCO’s stock to fall 10% on Wednesday knocking $500 million off shareholder value.

Delaying restarting Kashiwazaki to late 2022 means it will be 10 years since the NPP’s Units 6 was operating, and more than 11 years for Unit 7. Three of the facility’s four oldest reactors have been offline since 2007, never restarted after a separate earthquake that same year damaged equipment.

Even with regular maintenance, restarting a nuclear plant after such a long layoff is technically challenging.

Given the cost of ongoing maintenance, safety checks, and additional investment in new safety measures, the business case for TEPCO restarting Kashiwazaki is also fading.

Once a fully private company and the world’s third-largest utility, TEPCO is now under the control of the government. Its main shareholder is the state Nuclear Damage Compensation and Decommissioning Facilitation Corporation (NDF).

The utility’s state-mandated task is to operate its power business and generate cash to pay for the Fukushima accident compensation and the decommissioning costs for the wrecked Dai-Ichi NPP, as well as the nearby Dai-Ni NPP site. However, Fukushima decommission cost estimates have jumped to $74 billion, compensation payments to $80 billion, and area decontamination and storage to $60 billion.

This puts the total Fukushima accident-related costs at over $200 billion, with the decommissioning timetable expected to take another 30 to 40 years.

NDF has already injected almost $100 billion into the company through over 100 separate fund-raising rounds to help it meet the Fukushima liabilities while also remaining as a solvent business. TEPCO took cumulative losses of $25 billion in the three years following the 2011 accident.

Ten years after Fukushima, TEPCO is still Japan’s largest power utility with sales of 220 TWh ($57 billion) for FY2019 compared with a peak of 292 TWh before the accident. TEPCO continues to service almost one quarter of Japan’s total electricity consumption though it has lost more customers than any other power utility since consumers were allowed to switch providers in 2016.

TEPCO now has a peak load of 55 GW for its catchment area of nine prefectures that includes greater Tokyo, compared with a 62 GW peak load in 2007. It has 31,000 staff and over $100 billion in assets.

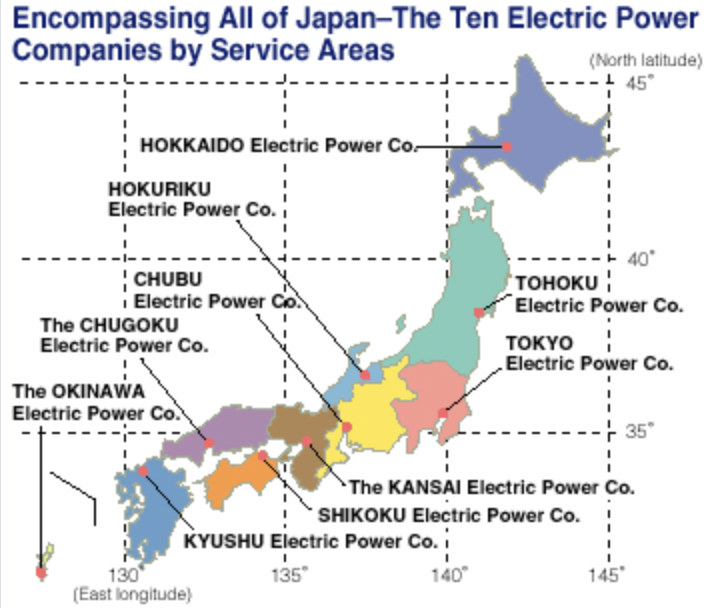

TEPCO Service Area

All three of TEPCO’s NPPs have been closed since 2011.

Until Covid-19 hit, TEPCO had hoped to rebuild its profit to $3 billion per annum by 2027. The pandemic reduced TEPCO’s electricity sales by 10% YoY. Profits in 1H FY2020 were down 65%. Management had also hoped to increase TEPCO’s stock market capitalization 15-fold to $75 billion by 2027.

Even before Covid, TEPCO has struggled to rebuild its business. One of its electricity sales agents was reprimanded last year for dubious sales practices. The retail unit has lost over 15% of its sales to competitors in the last five years, and now faces the possibility of being split off from TEPCO and sold in the near future. ENEOS is seen as a possible buyer.

Meanwhile, TEPCO’s plans to expand into the gas distribution business in new areas have mostly failed. The firm’s retail gas business in Kansai may be stalling due to low subscriber numbers.

In the last five years, the company has separated into five legal entities: TEPCO Holdings, TEPCO Fuel and Power, TEPCO Power Grid, TEPCO Energy Partner, and TEPCO Renewable Power.

TEPCO’s thermal generation assets (41 GW) were transferred to a new entity, JERA, in April 2019, including its four LNG terminals, for $8 billion. The thermal generation assets of Chubu Electric (24 GW), TEPCO’s adjacent utility, were also consolidated into JERA (Japan NRG profiled JERA in our Aug. 24, 2020 edition).

TEPCO had hoped to list JERA and raise cash, but Covid-19 stalled those plans.

TEPCO’s only remaining generation assets of any significance are in hydropower: 10 GW at 164 locations. The net book value of fixed assets was $70 billion at the end of FY2020, including the residual value of its nuclear fleet.

TEPCO now buys its electricity mainly from JERA, paying $17 billion for power during FY2019, and purchases of electricity sourced from renewables is expected to be almost $6 billion this fiscal year.

TEPCO was one of Japan’s first major utilities to announce plans to become carbon neutral by 2050. As part of this plan, it aims to install 7 GW of renewable generation by 2030.

Energy transition has offered other avenues for TEPCO to revitalize, with the utility seizing on its size and network to tap into a diverse set of partnerships. Below is a selection of new energy joint ventures TEPCO is pursuing:

- In addition, TEPCO has vowed to create a new business around nuclear reactor decommissioning in Fukushima prefecture.

Outside Japan, TEPCO recently won a substation contract in Thailand and also has investments in Vietnam.

At core, TEPCO still has the biggest slice of the world’s No. 3 electricity market. What’s more, the country’s 2050 net-zero emissions pledge and the associated move to greater electrification present the utility with a growing market and new business opportunities.

The hope that nuclear energy can be a money-spinner for TEPCO diminished last week. NRA’s ruling is only the latest in a series of red cards shown to TEPCO’s nuclear business.

If TEPCO is to raise $200 billion or more in needed to pay for the Fukushima cleanup, it needs to pass the Kashiwazaki NPP to a more proficient operator.

The Japanese government also urgently needs to address its strategy for managing the country’s nuclear assets in a consistent manner and implementing reforms to the national grid system and TEPCO’s roles in those initiatives.

Japan must also keep electricity costs at an internationally competitive level.

GLOBAL VIEW

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Coal

Methane leaks from planned coal mines could have a bigger climate impact than carbon emissions from U.S. coal plants, the nonprofit Global Energy Monitor said in a report.

Biofuels

U.S. President Joe Biden’s green fuel push using edible oils is helping drive up vegetable oil prices that are already near record highs, hitting key cost-sensitive consumers in India and Africa and stoking global food inflation fears.

Renewables / Hydrogen

1). Apple said that it allotted $2.8 billion raised from green bonds last years to fund 17 projects with 1.2 GW of renewable energy capacity.

2). Germany and Canada said they will jointly develop projects in green hydrogen that utilize Canadian hydroelectric power with an eye on the fuel’s export to Germany.

3). Planned investment in clean energy must increase by 30% to a total of $131 trillion by 2050 to avert catastrophic climate change, International Renewable Energy Agency (IRENA) said in its annual report. The agency especially advocated the need to scale up hydrogen production.

LNG

Asia became the main destination for U.S. LNG exports last year as volumes to the region rose 67% YoY in 2020. Asia accounted for almost half, or 3.1 Bcf/d, of all U.S. LNG exports, according to the U.S. Energy Information Administration

Aviation

U.S. airlines United and Delta said they may stop bleeding cash as soon as this month as air travel starts to recover. This month American airports had some of their busiest days since March 2020.

Australia

Australia’s Fortescue Metals Group, the world’s No.4 iron ore miner, outlined a plan to become carbon neutral by 2030, bringing forward the target by 10 years. The company aims to start producing green hydrogen as soon as 2023.

China

1) China published its next five-year energy plan, which sees to boost the share of non-fossil sources in the country’s energy mix (including nuclear and hydropower) to around 20% in by the end of the period, up from about 15.8%.

2) Factory and retail sector activity in China was strong in the first two months of this year, beating expectations. Industrial output was up 16.9% YoY.

Egypt

Shell agrees on deal with units of Cheiron Petroleum and Cairn Energy to sell onshore upstream assets in the country for $646 million.

India

Officials close to Prime Minister Modi are debating whether to set a 2050 net-zero-emissions target, similar to the pronouncements of most of the world’s major economies in the last six months. Such a target would mean an overhaul of the Indian economy, which currently relies on coal. The deadline might even be set at 2047, which would mark the centenary of India’s independence from British rule.

Russia

The price at which Gazprom supplies gas to China dropped below $120 per 1,000 m3 in January as it is tied to the oil price with a nine-month time lag. That price was a fifth of Asian LNG price at the time.

Thailand

Thai authorities are drafting a master plan to help the country reach zero net carbon emissions by 2050, and will present a draft during next month. Changing the power industry’s fuel mix and a move into EVs are expected to feature.

UAE

ADNOC banned engineering giant Petrofac from competing for new contracts in UAE after one of its former executives pleaded guilty to charges of making bribes to secure business. UAE accounts for 10% of Petrofac’s revenue.

UK

BP said it aims to build Britain’s largest hydrogen plant by 2030 as part of the country’s push to boost use of the fuel and cut emissions. The plant in northern England will have capacity of up to 1 GW of blue hydrogen, about a fifth of Britain’s target by the end of the decade.

U.S.

1) Jane Lubchenco, a marine ecologist with wide federal government experience, has joined the Biden administration to lead climate and environment efforts at the Office of Science and Technology Policy, the White House said on Friday.

2) Three environmental groups filed a false advertising complaint against Chevron with the Federal Trade Commission on Tuesday, alleging that the U.S. oil major has overstated its investment in renewable energy and actions to curb greenhouse gas emissions.

3) The U.S. Environmental Protection Agency said it will require power plants in a dozen states to cut their smog emissions starting this year as part of an effort to help areas of the country that are downwind of polluting industry.

EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy.

| February | Approval of Fiscal 2021 Budget by Japanese parliament including energy funding projects;

CMC LNG Conference |

| March | 10th Anniversary of Fukushima Nuclear Accident;

Smart Energy Week – Tokyo; Quarterly OPEC Meeting; Japan LPG Annual Conference; Full completion of all aspects of the multi-year deregulation of Japan’s electricity market; End of 2020/21 Fiscal Year in Japan; |

| April | Japan Atomic Industrial Forum – Annual Nuclear Power Conference;

38th ASEAN Annual Conference-Brunei; Japan LNG & Gas Virtual Summit (DMG)-Tokyo Three crucial by-elections in Hokkaido, Nagano & Hiroshima – April 25th |

| May | Bids close in first tender for commercial offshore wind projects in Japan;

Prime Minister Suga to visit the U.S.-tentative |

| June | Release of New Japan National Basic Energy Plan-2021;

G7 Meeting – U.K. Forum for China-Africa Cooperation Summit (Senegal) |

| July | Tokyo Metropolitan Govt. Assembly Elections;

Commencement of 2020 Tokyo Olympics |

| August | Hydrogen Ministerial Conference in conjunction with IEA World Economic Forum in Singapore – Deferred from May |

| September | Ruling LDP Presidential Election;

UN General Assembly Annual Meeting that is expected to address energy/climate challenges; IMF/World Bank Annual Meetings (multilateral and central banks expected to take further action on emissions disclosures and lending to fossil fuel projects); End of H1 FY2021 Fiscal Year in Japan; Japan-Russia: Eastern Economic Forum (Vladivostok)-tentative |

| October | Last possible month for holding Japan’s 2021 General Election;

METI Sponsored LNG Producer/Consumer Conference; Innovation for Cool Earth Forum – Tokyo Conference; Task Force on Climate-Related Financial Disclosure (TCFD) – Tokyo Conference; G20 Meeting-Italy |

| November | COP26 (Glasgow);

Asian Development Bank (‘ADB’) Annual Conference; Japan-Canada Energy Forum; East Asia Summit (EAS) – Brunei |

| December | Asia Pacific Economic Cooperation (APEC) Forum – New Zealand;

Final details expected from METI on proposed unbundling of natural gas pipeline network scheduled for 2022. |

DATA

Japan Oil Price

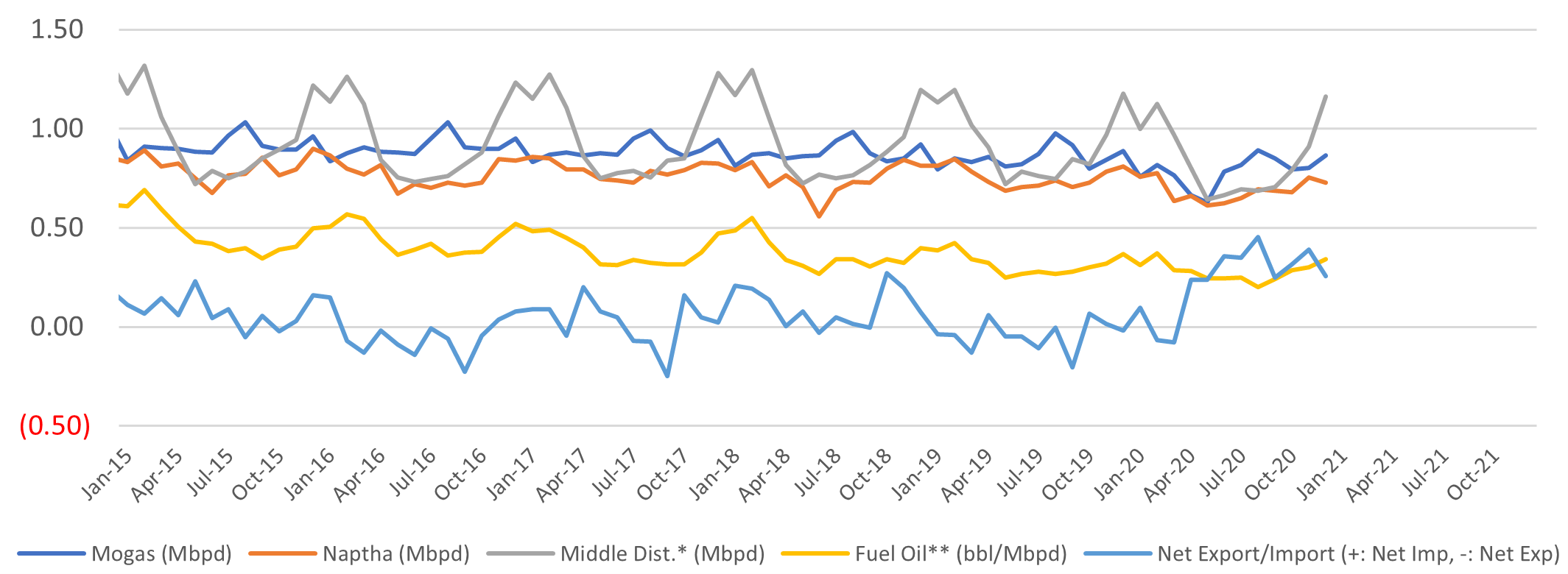

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

Domestic Fuel Sales

SOURCES: Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

Japan LNG Price

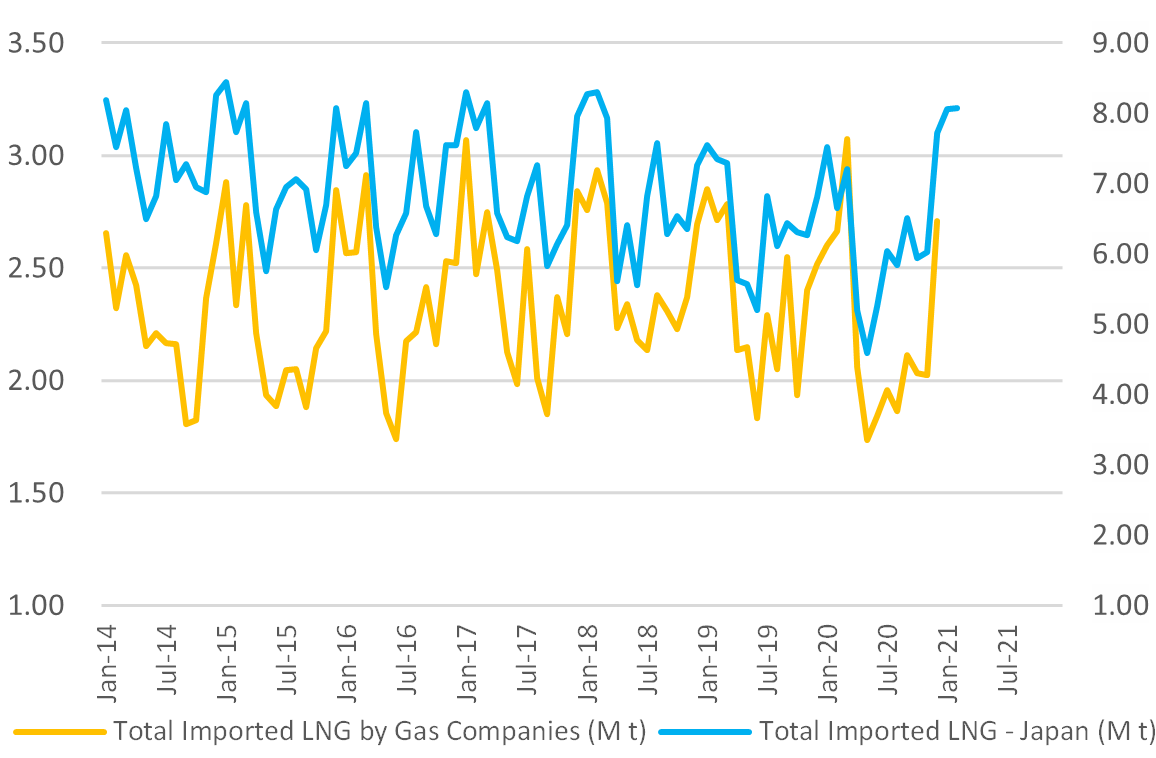

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

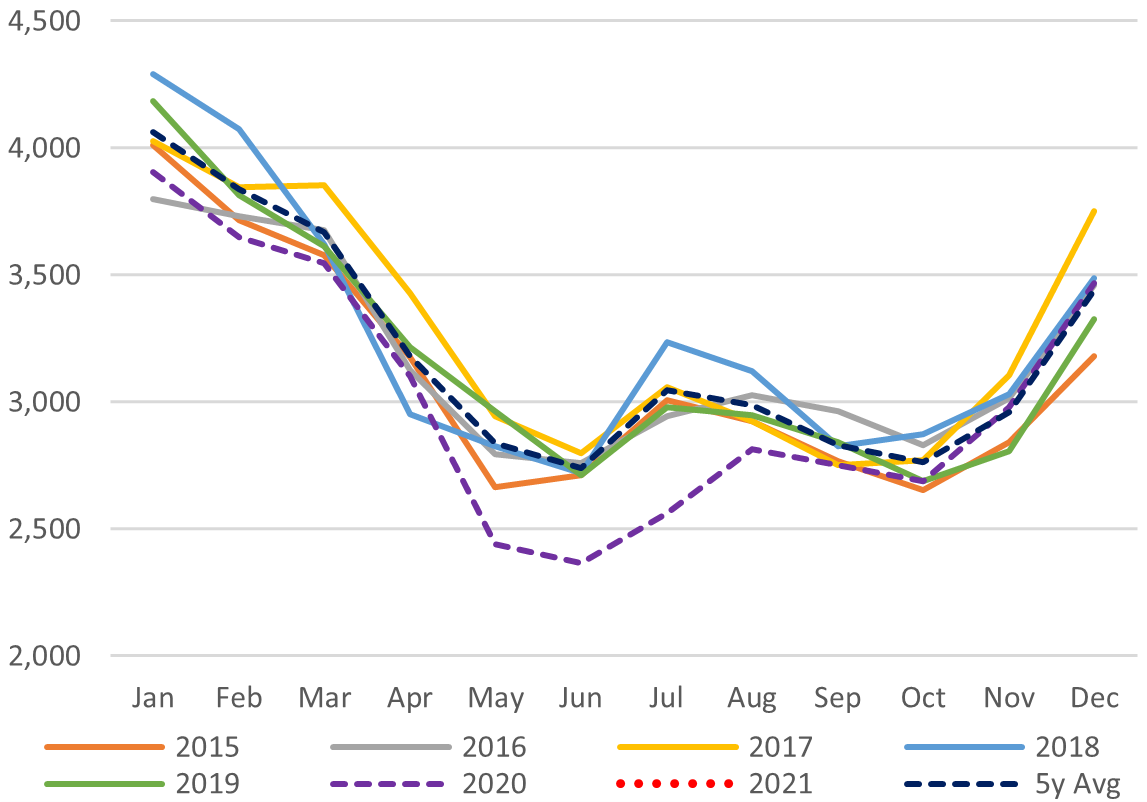

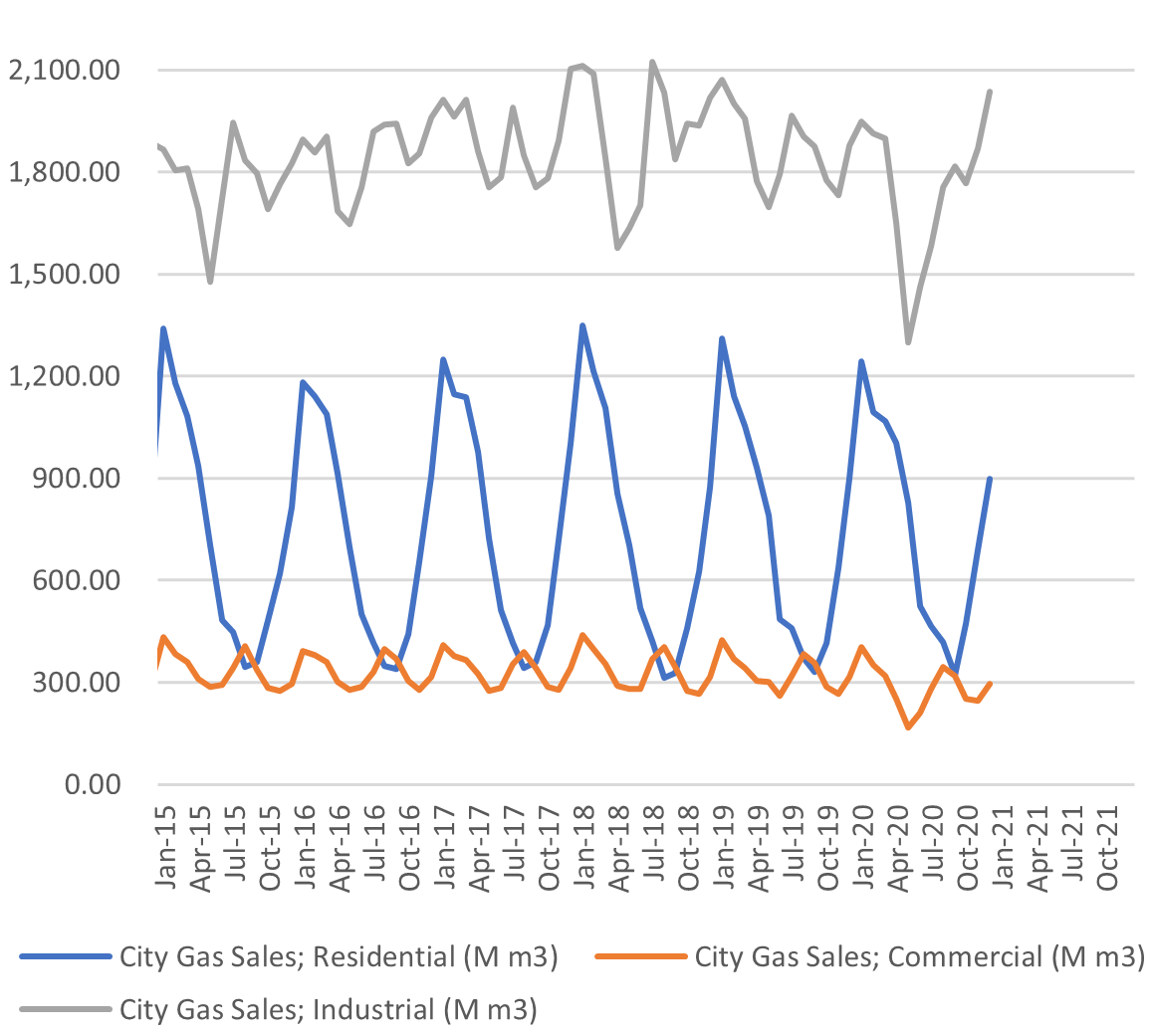

City Gas Sales – Total (M m3)

City Gas Sales by Sector (M m3)

SOURCES: Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

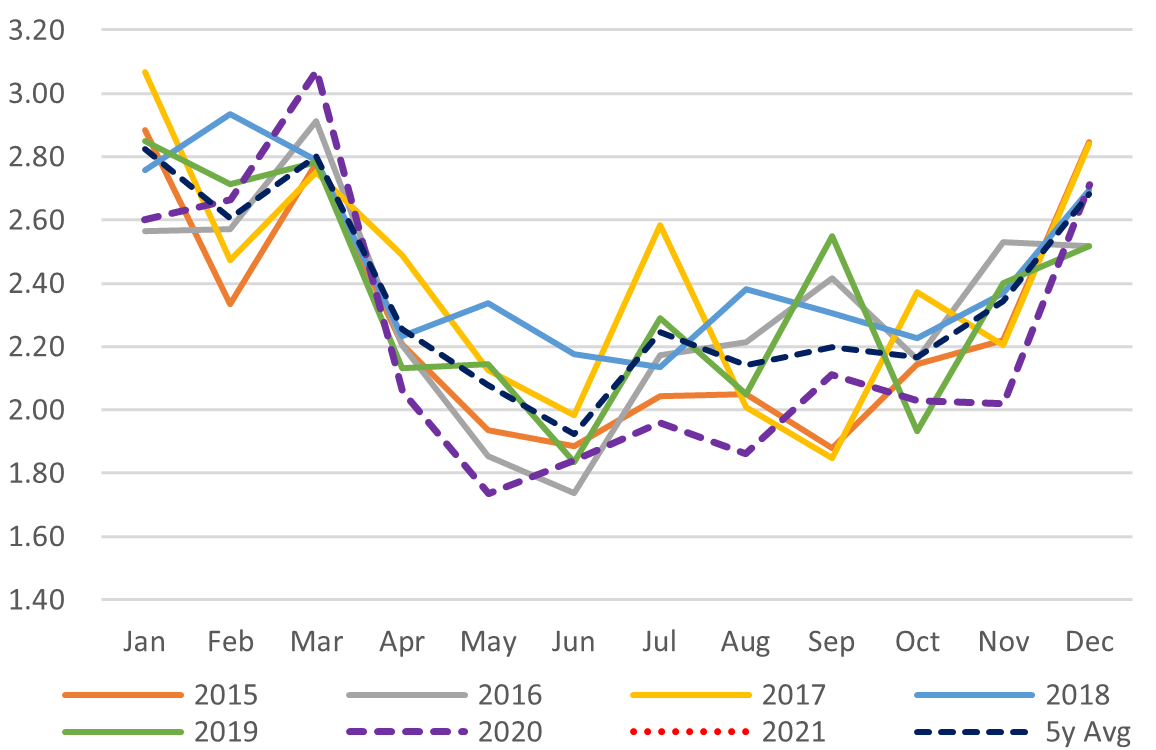

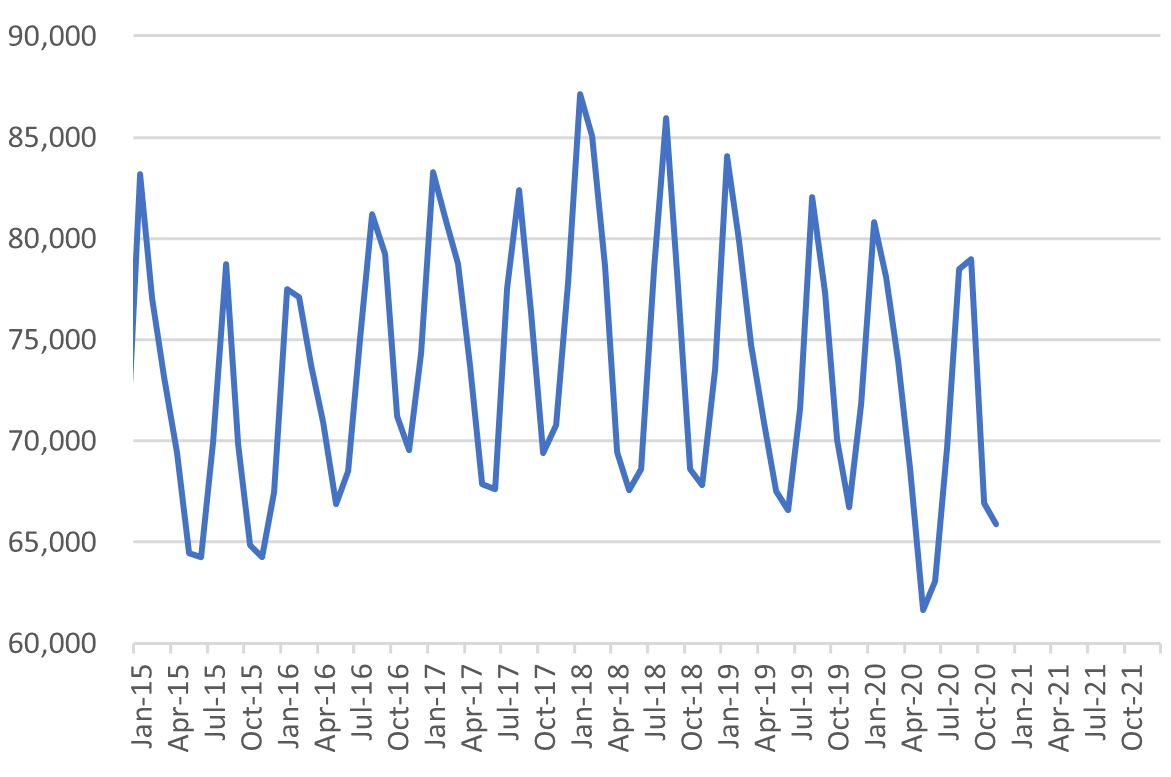

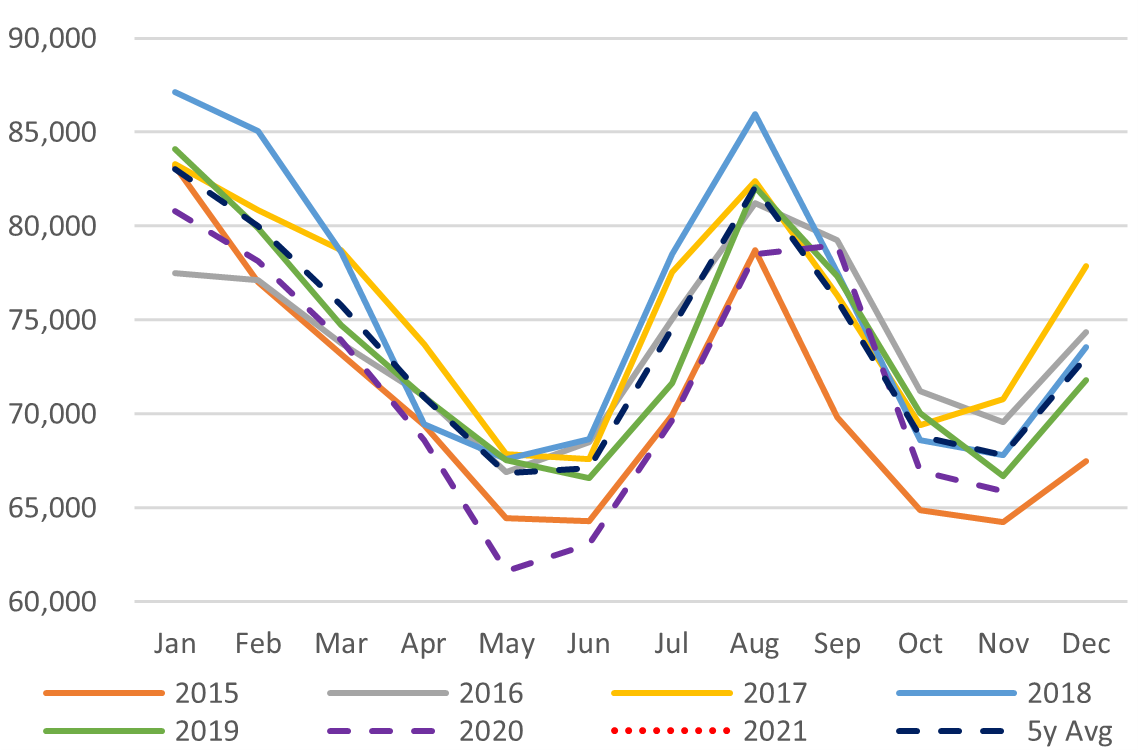

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

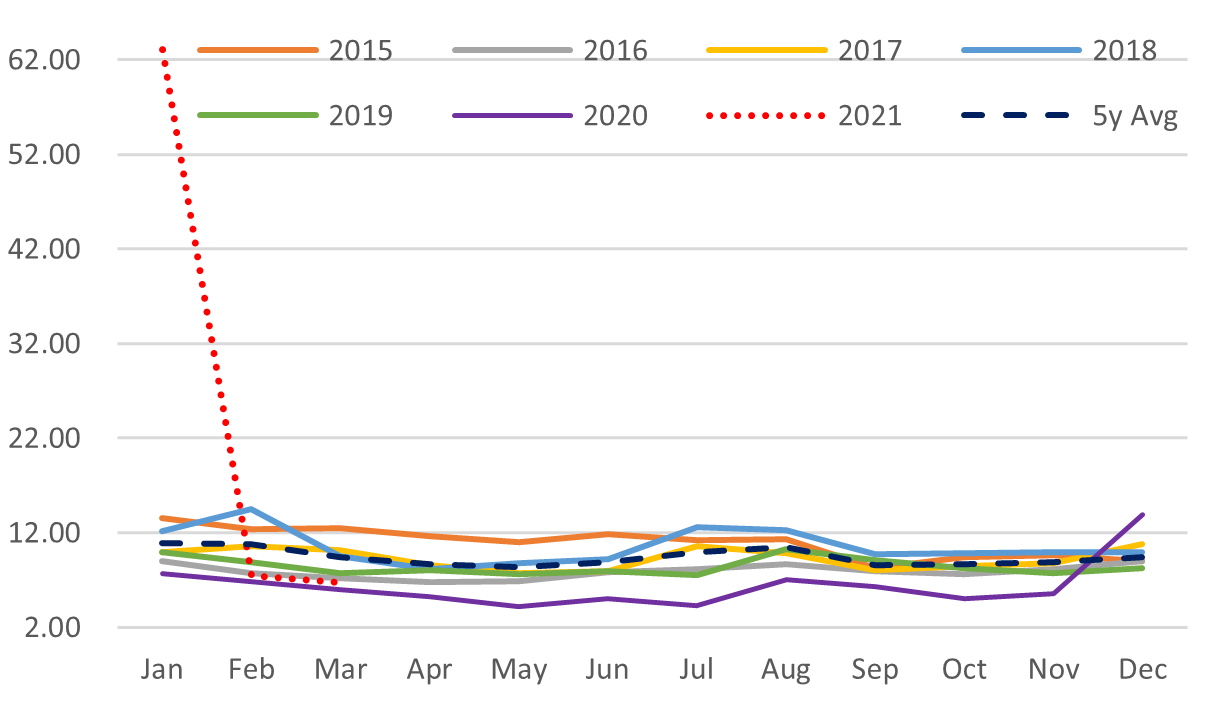

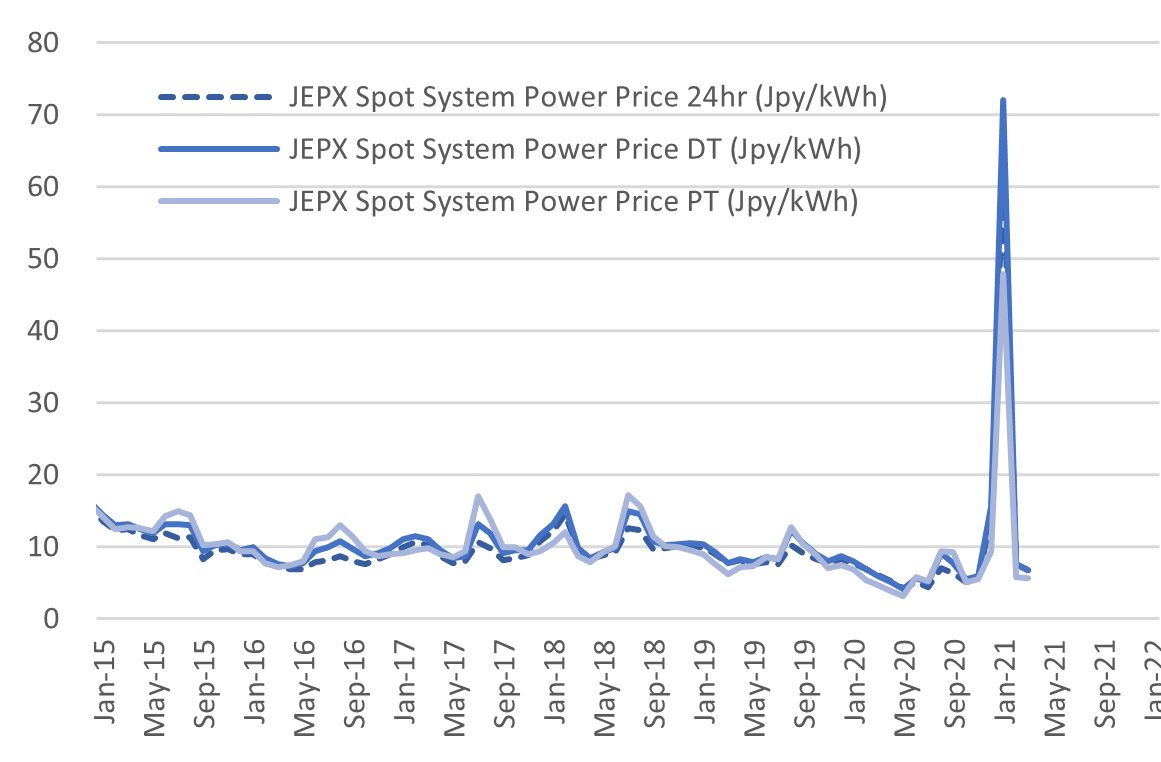

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.