JAPAN NRG WEEKLY

FEB. 28, 2022

JAPAN NRG WEEKLY

Feb. 28, 2022

NEWS

TOP

- PM Kishida announces sanctions against Russia in response to conflict in Ukraine, but says energy flows won’t be targeted

- EU asks Japan for additional LNG shipments; region seeks talks on supplies beyond March as concerns about disruptions grow

- Japan to vet supply chains for chips, batteries under economic security law that’s expected to come into force next fiscal year

ENERGY TRANSITION & POLICY

- CCS is cheaper than ammonia/hydrogen co-firing: CRIEPI analysis

- Tokyo Gas and MHI to test carbon capture for synthetic methane

- Japan to provide ASEAN financing to cut 1 mln tons of emissions

- Nippon Steel says its hydrogen consumption will hit 6-7 mln tons

- METI identifies potential issues in counting carbon in recycled fuel

- Japan to develop next-generation hydrogen engine for airplanes

- Ministry plans creation of “carbon neutral” port in northern Japan

- Solid-state batteries not a game changer: Toyota-backed institute

ELECTRICITY MARKETS

- Cost of nuclear plant upgrades since Fukushima now at ¥5.7 trn

- Price focus of the offshore wind auctions raises security concerns

- Chubu Electric to invest ¥400 bln in global expansion this decade; utility also posted highest January power demand in 17 years

- Enfinity Global buys solar portfolio in Japan valued at $1 bln

- ENEOS, Erex plan massive biomass power facility in Niigata area

- Hitachi group receives one of its largest ever wind power orders

- Kajima, Van Oord join wind farm projects in Akita and Chiba areas

- Japan Nuclear Fuel sets up Tokyo office to speed up reprocessing

OIL, GAS & MINING

- Government considers releasing more oil from reserves

- Japan’s LNG stockpiles rise slightly despite cargo sales to EU

- Aluminum prices hit record after doubling in the last year or so

- Mitsubishi Corp. sells Myanmar natural gas interests

- Japan petrochemicals companies must merge to survive: CEO

ANALYSIS

RUSSIA-JAPAN ENERGY RELATIONS:

TOO RISKY TO BREAK, TOO SMALL TO PARALYZE

In view of the Russian military incursion into Ukraine last week we are providing an overview of the energy and commodity ties between Russia and Japan, as well as a basic assessment of what may and may not be hit by sanctions. This article also provides a recap of the historical and political ties between the two countries, noting what factors have restrained investment and further economic integration. We have also included data for all major commodity imports from Russia.

JAPAN FOLLOWS THE UK DOWN THE POWER DEREGULATION RABBIT-HOLE

Britain’s experiment with privatization in the 1980s, followed by successive bouts of energy market reform throughout the 2000s and 2010s, became a global reference. Unbundling vertically integrated power monopolies and exposing incumbents to upstream/ generation and retail competition was seen as a winning formula. The implosion of the UK’s power retail sector in the last half-a-year may now be giving Japan and other countries food for thought. There is a growing disconnect between commerce and politics.

GLOBAL VIEW

Top investor in Nord Stream 2 gas pipeline wants compensation. Coal prices rising as Russian suppliers struggle to export. Global methane emissions are vastly under-reported, IEA says. U.S. nets a record amount from offshore wind auctions. Details on these and more in our global wrap.

EVENT CALENDAR FOR 2022

Key political and business events in Japan and abroad.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Tom O’Sullivan (Japan, Middle East, Africa)

Mayumi Watanabe (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

War in Ukraine

- Kishida announces sanctions against Russia

(Nikkei, Feb. 25)- PM Kishida announced sanctions against Russia in response to what he described as an attempt to unilaterally change the status quo by force.

- The sanctions include freezing of assets of individuals and financial institutions, suspension of visas, a ban on exports to organizations with military affiliations, and a ban on the export of semiconductors and other goods.

- He added that sanctions won’t directly interfere with Japan’s energy supply, saying that Japan had around 240 days of both strategic and private sector oil reserves, and that gas and electricity providers had two to three weeks of LNG reserves.

- While the PM didn’t rule out scrapping price relief on gasoline, he said all options will be considered to minimize the impact on consumers and businesses.

- SIDE DEVELOPMENT:

Japanese government urges oil producing nations to boost output

(METI press release, Feb 23)- The latest situation in Ukraine has created additional pressure on oil prices.

- Since the stability of oil markets is essential for the stability of the global economy, the Japanese government urges oil producing nations to boost production and cooperate with international organizations and major oil consuming nations.

- SIDE DEVELOPMENT:

EU asks Japan for additional LNG shipments on Russia supply concerns

(Nikkei Asia, Feb. 26)- European Commission has asked Japan to send additional LNG cargos to Europe to hedge against potential disruptions of Russian energy flows.

- This comes after Japan has already diverted some LNG cargos to the EU for delivery in March. The EU and Japan soon plan to discuss supply situation beyond this timeframe.

- Japan’s government plans to survey domestic firms to understand the volumes that are available, but would like to accommodate the EU request.

TAKEAWAY: The Analysis section outlines the Russia-Japan energy ties and notes that Japan itself depends on Russian LNG supplies for about 8-9% of its total. Should Russia decide to renege on its supply contracts due to sanctions, both the EU and Japan would be affected. Further, Japan’s ability to cover any significant drop in Russian gas volumes to Europe is limited.

Rather than Russia unilaterally cutting energy exports, it is possible that flows will be disrupted by sanctions against its financial system and logistics.

- SIDE DEVELOPMENT:

LNG Buyers Struggle to Get Credit for Russian Shipments

(Bloomberg, Feb. 25)- LNG buyers in Asia struggle to secure credit lines from some Singapore banks for purchasing shipments from Russia amid fears of further sanctions. The banks won’t issue a standby letter of credit for buying spot shipments from Russia’s Sakhalin-II export project.

- CONTEXT: Cutting off the ability to purchase LNG from Russia could further tighten the market, exacerbating a run-up in spot rates.

- SIDE DEVELOPMENT:

Expect higher prices not shortages on Ukraine crisis: Japanese energy firms

(Denki Shimbun, Feb. 25)- JERA, which relies on Russia for less than 10% of its LNG requirements and just over 10% of its coal requirements, plans to source commodities from Australia and other producers if supply from Russia is interrupted.

- Kansai Electric, which sources 15% of its coal from Russia, says supply is unaffected.

- Tokyo Gas depends on Russia for about 10% of its natural gas supplies.

- Rather than fuel shortages, skyrocketing prices is what the energy sector fears.

Japan to vet supply chains for chips, batteries under economic security law

(Nikkei, Feb. 26)

- New Japanese economic security law aims to give the government power to review the supply chains for semiconductors, storage batteries, rare-earth elements and other key products in order to lessen foreign dependence.

- Text of the bill was approved by the Cabinet and is expected to be ratified by parliament soon.

- The law, which would come into force around FY2023, seeks to bolster domestic supply chains; safeguarding key infrastructure; promote research in AI, quantum technology and other cutting-edge fields; and limit the public disclosure of patents into sensitive technology that may have military use.

- Impact from the law incudes the need for companies in several industries, including electricity and finance, to give the government advance notice on new equipment and suppliers.

TAKEAWAY: In theory, this should bring more manufacturing back to Japan and encourage domestic investment in new energy technologies, such as batteries. But Japanese businesses are wary of how the law application will go and of the potential disruptions that will likely follow. Limiting supply of certain goods or materials due to a lack of information about their origin could have serious near-term impact on prices and production. Furthermore, even if repatriated Japanese supply chains would remain dependent on security of raw materials, something that is not guaranteed in today’s more volatile geopolitical environment and with rising resource nationalism. We expect this topic to continue to gather attention over the coming year.

CCS cheaper than ammonia/hydrogen co-firing: CRIEPI analysis

(Japan NRG, Feb. 24)

- Central Research Institute of Electric Power Industry (CRIEPI)’s calculations showed that the power generation cost of carbon capture and storage (CCS) equipped thermal power will be lower than hydrogen or ammonia co-firing.

- CCS-equipped LNG power plants generated power at ¥13.3/ kWh, while the costs of ammonia/hydrogen co-firing of LNG plants came to ¥16.8-25.6 /kWh. CCS-equipped coal power cost was ¥16.5/ kWh, while the costs of ammonia/hydrogen co-firing came to ¥20.8-27.9/ kWh.

- The transport cost of the fuel, possibly from overseas, and the energy consumption for converting the elements into liquids and to gas weigh on co-firing, its analysis showed.

Tokyo Gas and MHI to test carbon capture to help make synthetic methane

(Denki Shimbun, Feb. 25)

- Tokyo Gas will start a demonstration test of carbon dioxide capture and utilization (CCU) with Mitsubishi Heavy Industries in January next year. A CO2 separation and recovery system will be installed at a waste incineration plant in Yokohama City. It will be used as a raw material for synthetic methane.

- Some gas will be used for welding and beverage applications.

- CONTEXT: Methanation does not increase the total amount of CO2 in the atmosphere because it captures CO2 emitted by factories before it’s released.

TAKEAWAY: Synthetic methane, or methanation, has gained attention in Japan for its promise to act as a “renewable” gas. Synthetic methane is seen as a way to decarbonize heat and can utilize existing natural gas infrastructure.

Methanation was discussed at a METI meeting with major gas companies this month. Japan’s top gas utilities aim to have synthetic methane account for 1% of total city gas volumes by 2030, and want to grow that ratio.

Synthetic methane is a cheap alternative to hydrogen in certain sectors. Japanese firms like Osaka Gas are also banking on future R&D to make the cost of synthetic methane more economically efficient than hydrogen.

Japan to provide financing to ASEAN to cut 1 million tons of emissions

(Japan NRG, Feb. 21)

- Japan plans to provide $50 million financing to cut 1 million tons of carbon emissions in the ASEAN region by 2025, Masahiro Ishii of METI told the Clean Energy Future Initiative for ASEAN forum.

- METI and the Asian Development Bank plan an event on transition financing in the first half of this year.

- Japan will transfer decarbonization technologies through energy efficiency projects such as IoT optimization of boiler and factory equipment called RENKEI, zero-emission buildings (ZEB), and microgrids. Pertamina in Indonesia deployed RENKEI, and fertilizer plants in Thailand launched feasibility studies in 2021. Malaysia plans to launch pilot ZEB projects this year.

TAKEAWAY: $50 million is a small sum compared to the EU’s recent decision to grant a $237.6 million non-refundable green transition aid to Vietnam over 2021-2024. At COP26, Vietnam vowed to phase out coal power by 2040s.

Improving energy efficiency is the fastest and less costly means to reduce carbon. Japan is also supporting gradual energy transitions while retaining thermal power systems.

Decreasing power rates for steel, chemicals can help meet net zero goals

(Japan NRG, Feb. 21)

- METI told the Industrial Structure Council for reviewing steel and chemical sectors that decreasing power rates may speed up their transition to a carbon neutral economy. The measure may help develop new technologies while continuing legacy operations.

- Germany has cut power rates for power-intensive industries, which is a good example for Japan. Steel and chemical companies are the two top carbon emitters outside the power sector.

- Council members expressed divided views. The companies are exposed to international competition while breakthrough technologies for zero carbon steel and chemicals have not been established. Panelists pointed out stable steel and chemical supplies are key to national economic security, but there’s a need to see if businesses are efficient. Taxpayers must be convinced these sectors need to be protected.

- CONTEXT: Key breakthrough technologies for steel are replacing coking coal with hydrogen. The Green Innovation Fund will be providing ¥193.5 billion to finance one such tech: the hydrogen reduction process. The Japan Iron and Steel Federation, however, has argued this amount is not enough and overseas rivals get more support.

- CONTEXT: Japanese steel mills run 15 GW of power plants, many coal-fired. Kobe Steel has even been selling surplus coal-fired power to Kansai Electric since 2002.

- SIDE DEVELOPMENT:

Nippon Steel says its hydrogen consumption will hit 6-7 million tons

(Japan NRG, Feb. 21)- Nippon Steel president Hashimoto told the Industrial Structure Council its hydrogen consumption is estimated to hit 6-7 million tons/ year if the hydrogen reduction process replaces the coal-based process.

- METI forecasts national hydrogen demand to be 20 million tons in 2050, suggesting Japan may run short of hydrogen at the expense of steelmaking.

- Hashimoto said Nippon Steel will restructure operations, cutting output of construction and other low value steel by up to 20%.

- Nippon Steel president Hashimoto told the Industrial Structure Council its hydrogen consumption is estimated to hit 6-7 million tons/ year if the hydrogen reduction process replaces the coal-based process.

- METI forecasts national hydrogen demand to be 20 million tons in 2050, suggesting Japan may run short of hydrogen at the expense of steelmaking.

- Hashimoto said Nippon Steel will restructure operations, cutting output of construction and other low value steel by up to 20%.

TAKEAWAY: Nippon Steel, JFE Steel and Kobe Steel dominate domestic production with over 70% of the market. The survival strategy for 40 or so other smaller steelmakers is to focus on energy transition products: Aichi Steel on EV and FCV components, Japan Steel Works hydrogen storages, and Daido Specialty Steel nuclear power furnace structures.

METI identifies potential issues in counting total carbon in recycled fuel

(Japan NRG, Feb. 24)

- METI reported to the Government-Private Council on Methanation key issues counting carbon of recycled carbon fuel, to be shared with the MoE’s task force that determines methods of measuring GHG emissions from CCU.

- The issues are possibly double counting of carbon emissions from recycled carbon fuel (RCF) and when the carbon is captured; counting carbon when RCF trades across borders; and the methodology to measure carbon once it is re-used after long-term capture and storage.

Japan to develop next-generation hydrogen engine for aircraft

(Yomiuri Shimbun, Feb. 19)

- The Education, Culture, Sports, Science and Technology Ministry and the Japan Aerospace Exploration Agency (JAXA) will begin development of a next-generation aircraft engine that uses liquid hydrogen as fuel in fiscal 2022.

- Japan wants to secure the core technologies in order to enhance the international position of its aviation industry.

- The ministry presented its prioritized themes and work schedule in the aviation industry to an expert panel, including the development of hydrogen engines.

Infrastructure Ministry plans carbon neutral port for Yamagata

(Kensetsu Shimbun, Feb. 24)

- The Ministry of Land, Infrastructure and Transport released a roadmap to create a carbon neutral port in Sakata, Yamagata.

- Of the 3.3 million tons of coal that pass through the port annually, 1.8 million tons is thermal coal used for power generation.

- The roadmap calls for the construction of biomass-fired power stations, wind farms and hydrogen storage facilities near the port, the electrification of cranes and other waterside equipment, and the introduction of fuel cell vehicles.

- By 2030, utilities aim to halve CO2 emissions of the Sakata thermal power plant.

Solid-state batteries will not be a game changer: Opinion

(Nikkei X-Tech opinion, Feb. 22)

- CONTEXT: This is a column by Furuno Shigeo, an executive fellow at SOKEN Inc., which is a research institute founded by the 11 companies of Toyota Group. It pursues R&D in the automotive field, including around the powertrain, fuel cells, and power electronics.

- While many automakers are investing heavily in post-liquid lithium-ion battery research, short battery life and other technical challenges mean solid-state batteries probably won’t make their presence felt until after 2030.

- Toyota announced in September that it’s developing a hybrid vehicle that would have an entirely solid-state battery.

- Nissan plans to build a solid-state battery production line by 2024/25, with a goal of achieving an energy density double that of liquid lithium-ion batteries.

Former Japan Research Institute director skeptical about EVs

(Nikkei X-Tech, Feb 22

- Despite the current hype around electric vehicles (EVs), exemplified by Tesla’s trillion-dollar market capitalization, former Japan Research Institute Director Ikuma Hitoshi believes the EV market is a bubble that will eventually burst.

- Ikuma stresses that EVs are only a means to an end and not the only technology that can help reduce carbon emissions. The debate over EVs ignores the significant carbon emissions and environmental impact from with their manufacture, he said.

- The world’s two largest car markets placed bets on hybrid vehicles as opposed to purely electric cars, and he says it doesn’t make sense to ignore this market.

- In any case, Ikuma believes Japanese auto manufacturers would be unable to build an EV value chain that rivals China’s, which holds significant lithium interests and whose government has invested heavily in EV manufacture.

- Rather than electrifying its vehicle fleet, Japan should leverage its existing transport infrastructure and invest in Mobility as a Service platforms that reduce carbon emissions by combining various forms of transport, says Ikuma.

Tokyo Gas to sell transition bonds

(Denki Shimbun, Feb. 24)

- Tokyo Gas will sell transition bonds in the domestic market. It will issue 10-year and 7-year bonds of ¥10 billion each, with interest rates of 0.359% and 0.26%, respectively.

- The lead managers are Mizuho Securities and Nomura Securities.

Toshiba, Rohm pursue power chip tech to cut energy loss in half

(Nikkei Asia, Feb. 25)

- Toshiba, Denso and Rohm are developing power chip technology that halves electricity loss, and will be on sale by 2030. Toshiba Electronic Devices & Storage will work on chips used for renewable energy and data center servers. The effort will get annual subsidies of ¥30.5 billion ($264 million) over the next 10 years from the state’s Green Innovation Fund.

Chugoku Electric to test EV charger system with Toshiba Energy Systems

(Denki Shimbun, Feb. 25)

- Chugoku Electric will start a demonstration with Toshiba Energy Systems, Yamaguchi Prefecture, REXEV and others to remotely control recharging and discharging of EVs, with the aim of utilizing the results for energy management.

- This will involve remotely controlling multiple EVs in Iwakuni and Hiroshima, and studying their use as storage batteries for electricity from renewable energy sources, as well as the possibility of adjusting supply and demand.

- The demonstration period will last for one year from April 2022.

Mitsui to invest in Air Water industrial gases producer and expand globally

(Sangyo Press, Feb. 25)

- Air Water and Mitsui & Co. will form an alliance to expand their global industrial gas business. Mitsui will invest $40 million in AW America, a wholly-owned Air Water subsidiary, to expand in North America where there is demand for highly efficient compact air separation plants in the suburbs.

NEWS: POWER MARKETS

Cost of nuclear plant safety upgrades since Fukushima now at ¥5.7 trillion

(Mainichi Newspaper, Feb. 25)

- The total cost of safety measures taken by 11 power companies to restart nuclear power plants after the accident at TEPCO’s Fukushima Dai-ichi NPP exceeded ¥5.7 trillion as of January. This is more than twice the amount initially expected.

- The total what’s been spent and is expected to be spent, but there are several companies that do not include certain costs in their calculations, such as for setting up anti-terrorism facilities. So, the figure is expected to increase further.

- The restart of nuclear plants after the Fukushima accident requires compliance with new regulatory standards set by the Nuclear Regulation Authority (NRA). So far, 27 reactors face examination by the regulator with a view for restart.

- Utilities said the costs have exceeded initial expectations due to additional measures requested by the NRA based on its review of the facilities.

- The biggest bill was for Kansai Electric, which restarted five of its seven units.

Mitsubishi’s offshore wind success has some locals upset over the selection process

(Nikkei Business, Feb. 23)

- CONTEXT: In December, winners for the first three auctions of bottom-fixed offshore wind power projects were announced. All three winners consisted of Mitsubishi Corp and a unit of Chubu Electric. The lowest winning bid was ¥11.99/ kWh.

- Some politicians are concerned that excessive focus on the lowest price in the recent offshore wind capacity tenders could lead to future energy security problems. For example, it’s possible that a Chinese consortium, backed by vast funds that support business, could offer the lowest price in a future such tender.

- Among the dissatisfied are locals from Akita Prefecture. They feel other companies were more “sincere” with communities. A fisherman from Yusa, a town whose sea areas will be up for offshore auctions, said if a similar selection process took place as at the end of 2021, many would not support the results.

- Without local buy-in, it will be hard to build up the offshore wind industry.

- A foreign wind operator executive said it took Europe 30 years to lower offshore wind prices to the current levels and that came after a buildup of the local supply chain, local industry, and competition. In Japan, these were the first such tenders, so is it really possible to hit such a low price?

TAKEAWAY: More than two months after the tender results were published the debate about the outcome is still strong. To make sure the sour mood does not derail the industry’s development, the government needs to move ahead with more tender announcements. So far, that hasn’t been forthcoming. The Clean Growth Strategy due to be announced sometime around April may help move the process forward.

Chubu Electric to invest ¥400 billion in global expansion this decade

(Denki Shimbun, Feb. 25)

- Chubu Electric plans to accelerate its overseas business development, said Sato Hiroki, Executive Officer and GM of Corporate Strategy Division.

- Of the ¥400 billion set aside for this to 2030, ¥250 billion will go to renewables, and ¥100 billion to “blue” hydrogen and ammonia investments. The rest will be put into power retail, distribution and new services.

- Over half will go to Europe, where Chubu’s strategy centers on Dutch power retail firm Eneco. The rest will go to Asia with focus on ASEAN countries.

- Chubu Electric has doubled staff at its global business unit in Tokyo, and plans to grow staff numbers further.

- The utility also plans to commercialize CCUS within 10 years.

- SIDE DEVELOPMENT:

Chubu Electric posts highest January power demand in 17 years

(Denki Shimbun, Feb. 22)- Chubu Electric Power Grid (PG) said electricity demand in the Chubu area in January increased 0.6%, YoY, to 12.142 billion kWh, a second consecutive month of YoY increases. The main reason was higher heating demand.

- Low-voltage power demand increased 0.7%, to 4.995 billion kWh, the highest for January since 2005, when records began, due to heating and non-transport industry demand.

Enfinity Global buys 250 MW solar portfolio in Japan at $1 billion enterprise value

(Company statement, Feb. 17)

- Enfinity Global, a renewable energy services company, acquired a 250 MW solar PV portfolio in Japan worth $1 billion.

- The acquisition includes three operational solar power plants (70 MW in total) and five projects currently under construction throughout Japan (180 MW in total). The projects under construction will be in operation in 2023.

- Enfinity Global’s assets in Japan now total 281 MW across nine owned and managed projects, which operate under the FIT.

- PAG, an investment firm, participated in the investment. Nomura served as sole lead arranger and bookrunner.

ENEOS, Erex plan massive biomass facility in Niigata

(Asahi Shimbun, Feb. 24)

- A biomass fired power station is planned as part of a new port in Niigata.

- The construction of the 300 MW plant is financed by ENEOS and Erex.

- It’s hoped this will put Niigata, which is struggling economically, on the map as a renewable energy production and distribution hub.

Hitachi group receives one of its biggest wind power orders

(Kankyo Business, Feb. 24)

- Hitachi Power Solutions (HPS) received an order from Shirakami Wind for 25 wind power generation systems totaling 96.6 MW. The order is one of the largest ever received by the Hitachi Group for wind power generation equipment.

- Shirakami Wind will install 25 wind turbines at four sites in Noshiro City and Happo Town in Akita Prefecture. HPS will deliver the E-115, a single-unit wind power system with an output of 4.2 MW made by its German partner Enercon.

- Shirakami Wind aims to begin operating the projects in 2025.

Kajima and Van Oord to join wind farm project

(Nikkan Kogyo Shimbun, Feb. 25)

- Construction company Kajima will join a government funded project to build wind farms off the coasts of Akita and Chiba.

- Kajima will partner with a local subsidiary of Van Oord from the Netherlands.

Japan Nuclear Fuel sets up shop in Tokyo as work progresses on reprocessing facility

(Nikkei, Feb. 24)

- Japan Nuclear Fuel CEO Masuda Naohiro said the company opened an office in Tokyo to act as a base for engineers and experts liaising with the government in relation to its building a reprocessing plant for spent nuclear fuel in Aomori.

- JNF feels that a presence in Tokyo makes it easier to deal with any issues identified by the authorities.

- JNF aims to complete the facility this year.

Kansai Electric, Lotte sign on-site PPA for solar in Vietnam

(Denki Shimbun, Feb. 25)

- Kansai Electric (KEPCO) and Lotte signed an on-site PPA (Power Purchase Agreement) for solar power generation in Vietnam. The project will reduce emissions and costs by adding 1.2 MW of solar modules to the roof of Lotte’s confectionery factory in the Binh Duong Province, north of Ho Chi Minh City.

- Lotte Vietnam expects to reduce CO2 emissions by 1,300 tons per year.

- The project will be subsidized from MoE’s FY2021 bilateral credit mechanism.

NEWS: OIL, GAS & MINING

Japan weighs joining U.S. to tap oil reserves as crude tops $100

(Nikkei Asia, Feb. 25)

- Japan considers releasing more oil from its reserves in coordination with the U.S. and other countries as crude oil topped $100 per barrel.

- The International Energy Agency is expected to begin talks soon with member nations such as Japan, the U.S. and the U.K. regarding the crisis in Ukraine. Japan plans to respond should the IEA call for a coordinated release of oil.

- Tokyo looks to tap private-sector reserves, which can be deployed more easily, in response to any request by the IEA.

- CONTEXT: Earlier media reports had said that METI plans to bring to market 0.6% of its total strategic oil reserves, equivalent to 260 million liters or 1.6 million barrels. The oil will be sold via tender on March 9 and delivered on and after April 20.

LNG stocks pick up from last week to 1.82 million tons

(Japan NRG, Feb. 23)

- LNG stocks picked up to 1.82 million tons on February 20, up from 1.78 million tons a week earlier. The level was lower than 2.3 million tons last February and the four-year monthly average of 1.98 million tons.

- METI minister Hagiuda said the stocks were enough for the next 2-3 weeks and Japan has diverted some February cargoes to Europe. More March cargoes will be shipped to Europe. No decision on April cargo yet.

Aluminum prices hit record high of $3,450/ ton on Ukraine war

(Japan NRG, Feb. 25)

- Aluminum prices on the London Metal Exchange hit a record of $3,450/ ton following the Russian invasion. Prices averaged $1,700/ ton in 2020 and to $2,550/ ton in 2021.

TAKEAWAY: The continual price surge will likely trigger material substitution by automakers, to switch to galvanized steel that costs less than one third. Aluminum use in car bodies has increased due to light weight requirements of low-emission vehicles. Steelmakers have developed thinner and lighter steel sheets with high-tensile properties to compete against aluminum. Another switching alternative is resin.

The aluminum price surge will also trigger switches in EV battery packaging material and other components.

Mitsubishi sells Myanmar gas interests

(Nikkei, Feb. 18)

- Mitsubishi Corporation is the latest Japanese company to pull out of Myanmar.

- Mitsubishi will halt natural gas exploration in the country.

- The move was prompted by declining production volumes and the recent coup.

- Marubeni, Sumitomo Corporation and Mitsui & Co also suspended work on construction of an LNG-fired power station in Myanmar.

Tokyo Gas starts to supply “carbon neutral” LNG to Seibu Gas

(Denki Shimbun, Feb. 21)

- Tokyo Gas started supplying “carbon neutral” LNG to Seibu Gas. The initial supply of about 70,000 tons of arrived at Seibu Gas’ Hibiki LNG terminal.

- Tokyo Gas became the first company in Japan to introduce CNLNG in June 2019, and has so far provided it to more than 50 users as carbon-neutral city gas.

Japan Petrochemical Companies Must Merge to Survive, CEO Says

(Bloomberg, Feb. 24)

- Jean-Marc Gilson, the Belgian who heads Japan’s Mitsubishi Chemical Holdings Corp., called on Japan’s petrochemical makers to combine assets into a company that can compete globally and invest in emission-reducing technology.

- CONTEXT: Japan has five large chemical companies.

ANALYSIS

BY YURIY HUMBER and

MAYUMI WATANABE

Overview of Russia-Japan Energy Relations:

Too Risky to Break, Too Small to Disrupt, But Metals Trade Key

In view of the events of last week, in which Russian President Vladimir Putin ordered armed forces into Ukraine, we are providing an overview of the energy and commodity ties between Russia and Japan, as well as a basic assessment of potential sanctions.

Russia is one of the world’s most significant suppliers of oil, gas, coal and metals. It is not, however, a significant energy supplier to Japan, despite being a neighbor. In part, this is due to the fact that political relations between two nations have been limited by a number of key factors. Also, Japan is host to U.S. armed forces and is arguably the closest American ally in the Pacific. Another is a post-World War II territorial dispute over the islands north of Hokkaido that Russia calls the Kurils and Japan the “Northern Territories”.

The island chain is close to rich fishing grounds and may have claim to offshore oil and gas reserves, but the resources are not well known and are not thought to be the major issue. The islands have symbolic meaning to both sides.

Previous Prime Minister Abe Shinzo invested a considerable amount of time and diplomacy into brokering a resolution to the territorial dispute, meeting with President Putin at least 26 times during his eight-year tenure. The two appeared to form a warm working relation, but President Putin made it clear that Russia would not cede even part of the disputed territory, leaving the talks at a dead end.

It’s often noted that Japan and Russia still haven’t officially signed a peace treaty after World War II. The two have signed other treaties, however, which acknowledged the end of hostilities, and therefore this alone is not a strong issue for Japanese business operating in Russia. Toyota Motor, Nissan, and Komatsu are some of the Japanese manufacturers that set up factories in Russia over the last 10-15 years. Mitsui & Co. and Mitsubishi Corp. trading houses were early investors in oil and gas projects on the Sakhalin Island.

Despite these few headline investments, Japanese business has been wary of expanding ties with Russia and further economic integration, and former PM Abe’s efforts did little to turn the tide. Politics serve as a backdrop, but the most acute reason has always been Russia’s business environment, which is viewed by Japan as risky due to the volatility of the local currency, corruption, and geopolitical constraints.

In fact, trade between Russia and Japan is almost half of where it was in 2012. Economic relations were decimated by the 2014 Russian claim to the Crimea and the sanctions that followed.

Finally, Russia is a major wheat exporter. Although Japan is not thought to have direct wheat purchase contracts with Russia, if the latter’s supply does not reach global markets the price of the grain would rise and affect Japanese purchases from other suppliers.

Bottom line: Japan cannot easily substitute Russian supply of aluminum or palladium, and would find it difficult to find alternatives for LNG. However, even if Japanese imports are not disrupted, a major risk for the economy lies in commodity price spikes and inflation.

It’s unlikely that Japan would support sanctions against Russian commodity suppliers, even in areas that it can find other sources of supply. It’s also unlikely that Russia would wish to lose Japan as a buyer by withholding key exports.

The biggest knock-on effect, then, is likely to be on new investments, including in energy, and technology transfer.

Trade

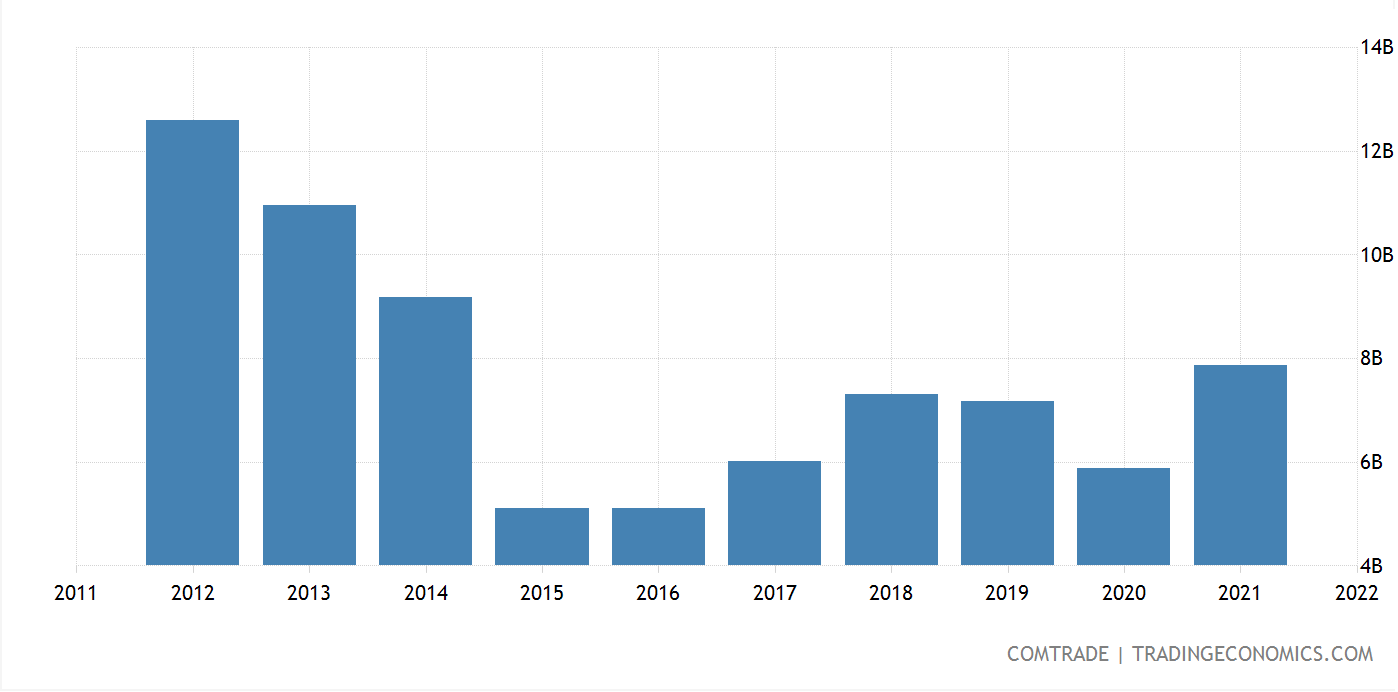

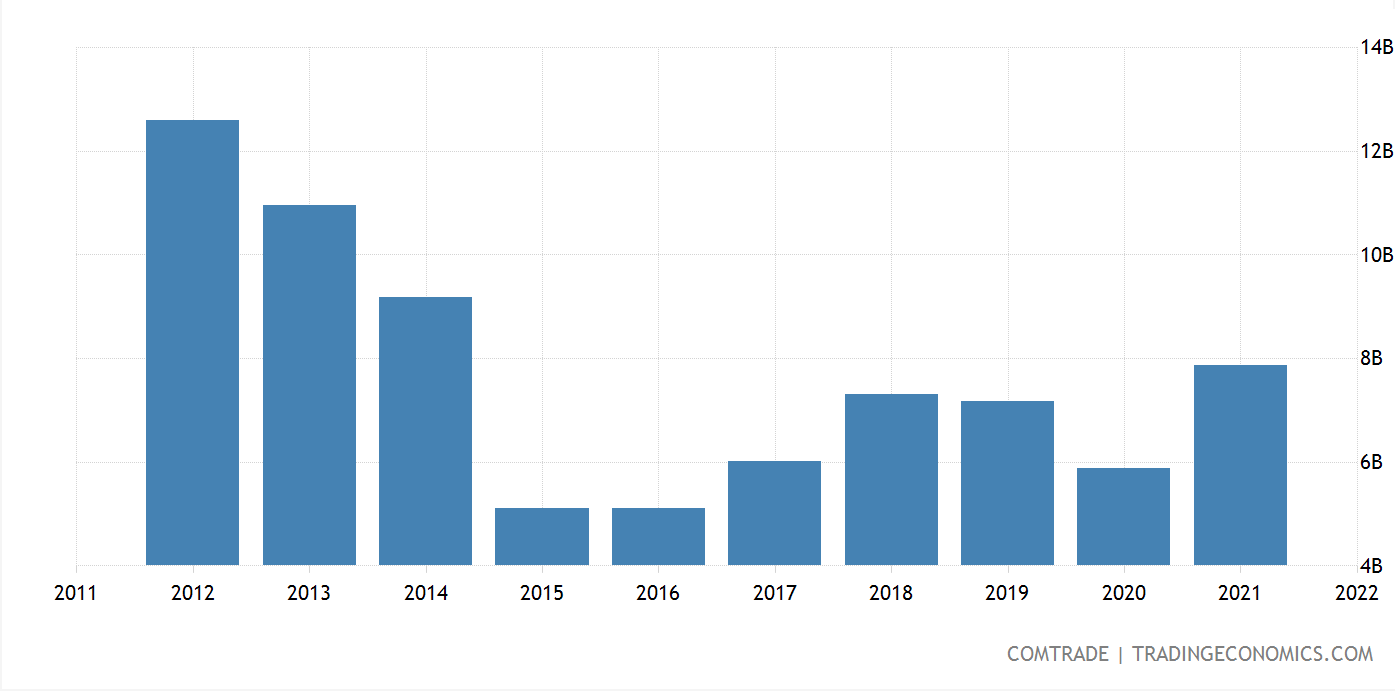

In 2021, Japan exported ¥862 billion worth of goods to Russia while importing ¥1.54 trillion, resulting in a net trade deficit of ¥692 billion. These are just a fraction of Japan’s ¥18 trillion exports and ¥20 trillion imports to and from China.

Trade with Russia has recovered in the last five years after the post-Crimea sanctions, especially in terms of exports, which are up 56% since 2016.

Japan Exports to Russia, in USD

Energy supply

There are no gas or oil pipelines between Russia and Japan, though several projects have been proposed. This lack of infrastructure is one reason for the relatively small volumes of Russian oil and gas in Japan, but the key factor has always been concern about geopolitical risk.

In the last five years, Russian companies have offered Japanese investors stakes in several new LNG developments – in Vladivostok and in the Arctic. In 2019, Mitsui and state-owned JOGMEC Corp. jointly acquired 10% of the Arctic LNG 2 development, which is led by Russia’s Novatek. The Project will commence production starting in 2023, with LNG aimed for delivery mainly to Asia and Europe. Japanese banks are among the major financiers of the Arctic LNG 2 project.

Russia and Japan have also signed various agreements in the nuclear sector, though there are no major bilateral projects between the two at this moment.

LNG

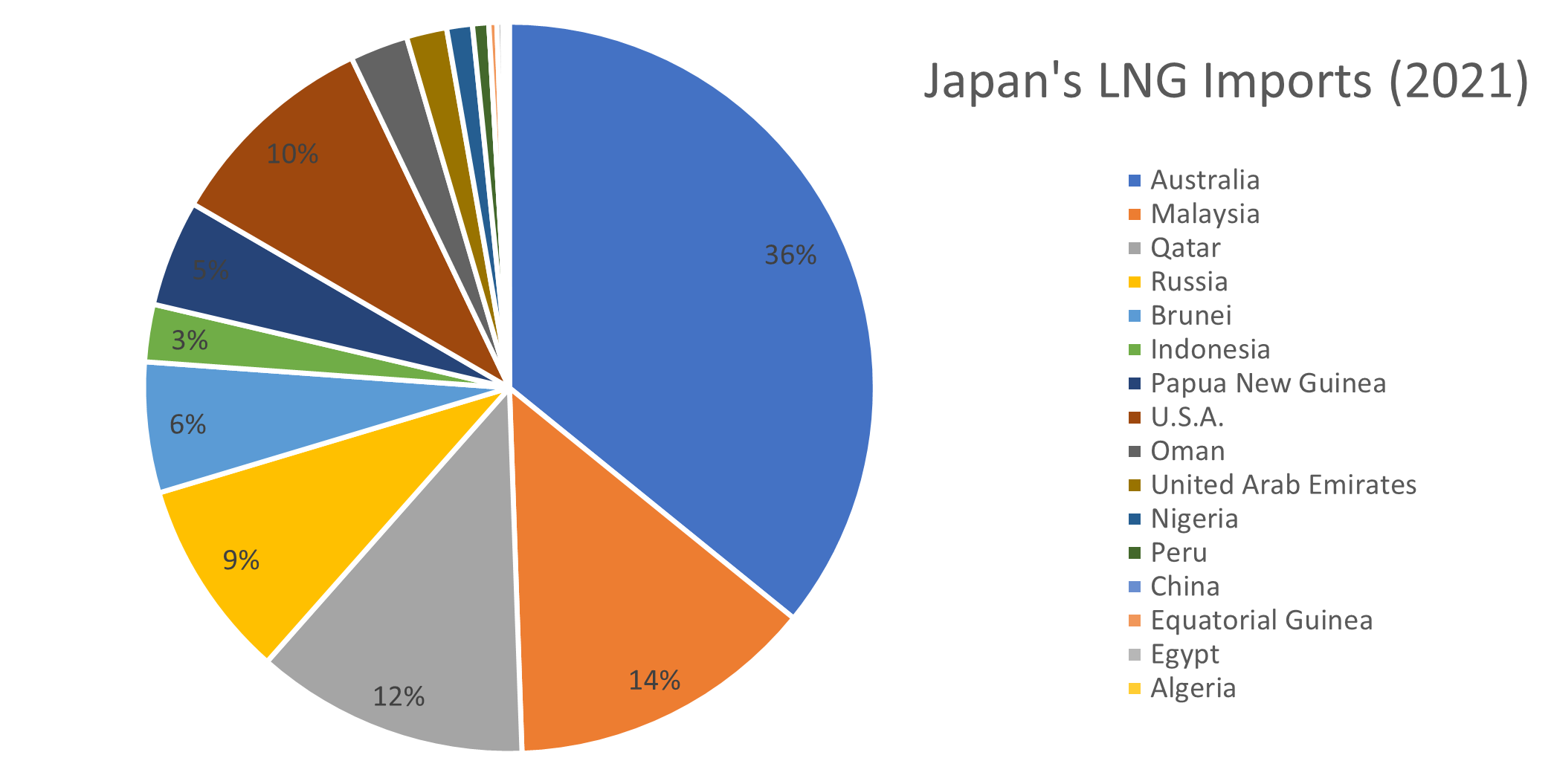

Pre-pandemic, Russia accounted for 8% of Japan’s LNG imports, with about 6.4 million tons of the fuel. Last year, this share was slightly higher at 9%, but the volume was only slightly higher at 6.57 million tons. Almost all Russian LNG that comes to Japan is sourced from the Sakhalin developments in which trading houses Mitsui and Mitsubishi are co-investors.

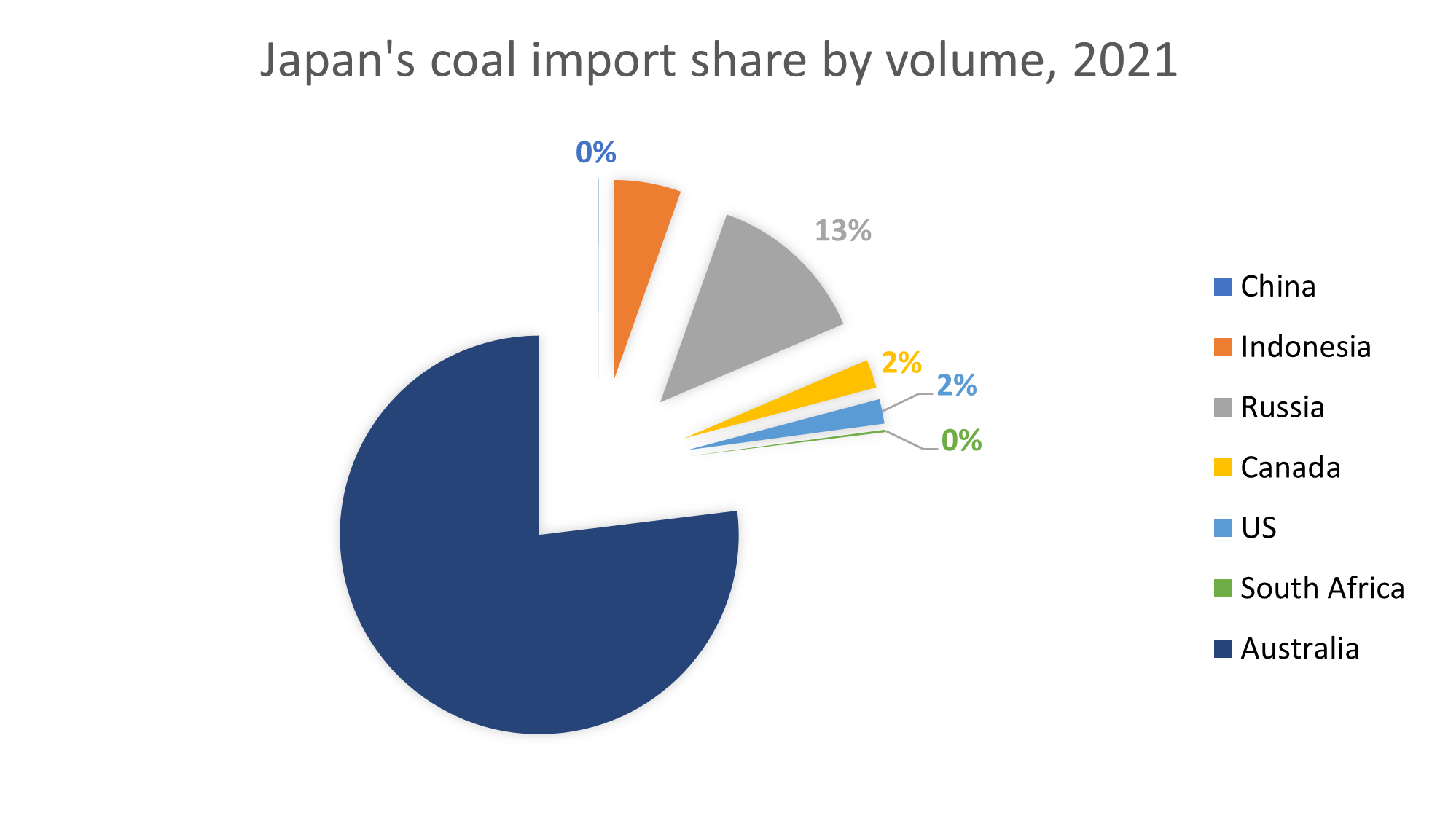

Coal

Russia supplied 13.8 million tons of coal to Japan, 13% of the total imports, and worth just over ¥190 billion. Russia has high-quality hard coking coal deposits with grades suitable for steelmaking. However, Japan’s market is dominated by Australian supply in both coking and thermal coal.

Crude

Russia accounted for 4% of Japan’s total oil imports in 2021; the volume was the lowest in over a decade.

Metals supply

Russia is the world’s biggest supplier of palladium, and one of the largest producers of nickel and aluminum. Japanese firms are major buyers of aluminum, but have alternatives in other metals.

Aluminum

Russian supplies account for 20%, or the largest share of Japanese imports of aluminum ingot and alloys. They mostly go to the automotive sector (car bodies and auto components) and cannot be easily replaced.

Platinum and nickel:

Negligible volumes from Russia. Just 24 kg of platinum in 2021, from a total of over 35 metric tons. Nickel’s 583 tons were also a fragment of the 51,454 tons that Japan imported last year.

| Nickel | Ingot | Scrap | Total |

| Russia | 240 | 343 | 583 |

| Total | 40970 | 10484 | 51454 |

Palladium

Russia accounts for about 35% of Japan’s imports of the metal used in catalytic converters and other parts of the auto supply chain.

ANALYSIS

BY SEB KENNEDY

FOUNDING EDITOR

ENERGY FLUX

Japan Follows the UK Down the Power Deregulation Rabbit-Hole

I once interviewed an economist in Tokyo about Japan’s energy market deregulation. I asked him which country or market Japanese government officials looked to as an example of successful electricity and gas market liberalization. Without hesitating, he said: “The UK.”

Britain’s experiment with privatization in the 1980s, followed by successive bouts of energy market reform throughout the 2000s and 2010s, became a global reference. Unbundling vertically integrated monopolies and exposing incumbents to upstream/generation and retail competition was seen as a winning formula. Cutting the red tape unleashed market efficiencies, which lowered prices for end consumers — until energy markets crunched, that is.

I wonder what the same Japanese economist would make of the implosion of the UK energy retail segment. Regulator Ofgem recently approved an eye-watering 54% increase in the retail price cap, which will push millions of households towards energy poverty. Further rises are expected in October, and with increasing frequency thereafter to keep up with an erratic market.

The regulator was caught between competing priorities: protect customers, or allow loss-making suppliers to recover ballooning wholesale costs from consumers. After bailing out major independent utility Bulb, political appetite for further intervention is low. Ofgem chose to hike the cap to prevent further supplier failures. Cue much hot air from politicians (although sadly not enough to keep the homes of energy-poor Britons warm this winter).

The 2021-22 winter won’t be a one-off. The combination of liberalization and decarbonization is a recipe for volatility. The switch to short-term market-based gas pricing slashed billions of dollars off European import costs over the past decade, only for those savings to be almost entirely wiped out in a matter of months when global LNG prices spiked last autumn. Wholesale gas and power prices remain inflated and the cost to consumers will keep stacking up until the market cools off and losses are settled.

Red tape meltdown

Regulators and politicians will need to get used to making difficult trade-offs as the energy transition progresses. Import-dependent Japan is facing the same challenges. All of Japan’s 10 regional utilities slashed their earnings estimates for this business year on soaring oil, gas and coal prices.

Japan arrived late to the deregulation party, thanks partly to the physical segmentation of its power grid into two distinct networks running at different frequencies, and the lack of interconnection between regional natural gas distribution networks. These barriers perpetuated the natural monopolies presided over by state-run or municipal utilities.

The Fukushima nuclear disaster of 2011 was like an electric shock to Japan’s leisurely deregulation agenda. The slow-burn liberalization of energy retail and trade gained momentum after the 2011 earthquake, tsunami, meltdown and subsequent shutdown of the entire nuclear fleet. Operator of Fukushima nuclear plants, TEPCO, had long resisted liberalization, as had many of the EPCos. But TEPCO’s bailout and partial nationalization swept away that resistance, accelerating the legal unbundling of transmission and distribution networks and ushering in competition across all energy retail segments.

Silent nuclear fallout

The post-Fukushima nuclear shutdown forced Japan to buy vast volumes of LNG from global suppliers to replace lost capacity. But it is less widely appreciated that the wave of deregulation that followed eroded the confidence of incumbent utilities to commit to long-term procurement of energy from global suppliers.

The old monopoly structure gave regulated utilities domestic demand certainty. The obligation to meet the needs of a captive consumer base created a fixed demand anchor, which drove EPCos to sign long-term LNG supply and purchase agreements with global sellers.

Retail competition means that that certainty is diminishing, exacerbated by demographic changes and the decarbonization megatrend. Japan is ramping up its renewables deployment to help meet the CO2 reduction targets, all the while unsure when most of its nuclear reactors can be restarted.

Japan’s commercial nuclear fleet has dwindled to 33 reactors today, of which only seven are currently operational. The government is committed to restarting the rest but the outlook for doing so is shrouded in uncertainty, amid continued skepticism around nuclear among the population and strict safety requirements that the facilities struggle to adhere to.

Fickle demand

Japan, for a long time the world’s biggest LNG importer, was last year overtaken by China and its role in global gas markets is fading. Overall gas consumption peaked in 2014 at 124.8 billion cubic meters (Bcm), and has since fallen to 104.4 Bcm in 2020 according to BP data. Japanese LNG imports peaked in 2015 at 84.75 million tons, and fell to 74.46 mt in the pandemic year of 2020.

These factors prompted TEPCO and Chubu Electric to join forces and launch joint venture JERA to boost their LNG buying power in international markets. JERA has since evolved to become one of the world’s largest LNG buyers, with an annual transaction volume of around 40 million tons and sales of ¥2.7 trillion ($24.5 billion).

With rising commodity exposure and uncertainty over long-term demand trends in its home market, risk management shot up the priority list for JERA. In response, the company merged its LNG trading and optimization activities with those of EDF Trading in 2019, giving rise to JERA Global Markets – which today operates one of the largest seaborne energy portfolios in the world.

JERA’s highly sophisticated trading, optimization and risk management operation can mitigate the downside risks of being caught long on LNG or coal in a global slump. But it can’t nullify them completely.

So JERA’s recent decision not to renew a 25-year LNG sales and purchase agreement (SPA) with Qatar must be understood in the context of market liberalization, Japan’s overall diminishing and uncertain domestic gas demand profile, and increasing seasonal swings in demand. The view is that demand is fickle, so contractual flexibility trumps certainty.

JERA’s decision led to much diplomatic soul-searching in Tokyo and Doha. Qatar helped keep the lights on in Japan by sending JERA wave after wave of spot LNG on top of the amount it had contracted for. Riled by the snub, Qatar is quite happy to be courted by the Biden administration as a potential savior should Russia’s invasion of Ukraine disrupt gas flows into Europe.

The Japanese government wants to be seen helping too, and asked Japanese LNG buyers to divert LNG cargoes to Europe. JERA was apparently eager to help, probably because it was diverting its US LNG cargoes to Europe anyway. Wholesale gas prices on TTF, the European benchmark hub, are still comparable to spot prices in Asia and the cost of transit is lower due to the shorter distance, so Europe offers better margins.

Rudderless juggernauts

The bigger question for Tokyo is how to reconcile the commercial priorities of companies operating in a liberalized market with the strategic priorities of government. This question is further complicated by a structural dependency on energy imports – a situation facing both the UK/Europe and Japan.

Due to its geography, Japan lacks natural resources like oil and gas – hence the original push to power the island with nuclear in the 1960s. In Europe, declining domestic oil and gas production is posing enormous strategic challenges.

Energy is the lifeblood of modern industrial economies. The world’s most advanced economies took a relaxed approach to energy security and now often find themselves competing in spot markets for scarce winter supplies of oil, gas and coal.

Privatization and deregulation meant outsourcing security of supply to ‘the market’. Having embraced liberalization, the UK and Japan find themselves more exposed to volatility, supply disruptions and domestic political repercussions whenever global markets tighten.

This is problematic, because markets need more guidance than ever to navigate the many contradictions at the heart of the energy transition. Expect the commercial-political disconnect over energy to become increasingly pronounced.

This article was first published in Energy Flux, an independent newsletter about the global energy transition (www.EnergyFlux.news). Energy Flux offers thoughtful and balanced analysis of decarbonisation policies, and the trade-offs at the heart of the push for net zero.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Aviation/ Hydrogen fuel

By the end of 2026, Airbus will test a superjumbo A380 with hydrogen-powered jet engines. The aviation industry is facing pressure to meet zero-emission targets by 2050. Aviation accounts for about 2.4% of global emissions.

Europe/ Natural gas

Top energy companies are buying more Russian gas, despite Russia’s invasion. As prices rose more than 60% this week, power companies are making long-term contracts with Gazprom. Russian gas imports are cheaper than spot gas traded at European hubs.

Europe/ Wind power

A record 17.4 GW of wind power capacity was installed in 2021, up 18% YoY, said WindEurope, adding that it’s not enough to meet energy and climate goals. By 2030, the EU wants to cut GHG emissions by 55%.

Fossil fuels/ Financing

Blackstone said its private equity arm is ending investment in oil and gas exploration and production. Blackstone’s credit arm will follow suit.

Germany/ Nord Stream 2

Wintershall Dea, a top investor in Nord Stream 2, wants compensation for its €730 million investment, if the pipeline doesn’t become operational. The German group is one of five lenders to Gazprom for the project. The other four are Shell, Uniper, Engie and OMV. The German government suspended Nord Stream 2 approval, due to Russia’s invasion of Ukraine.

Iraq and Kuwait/ Renewable energy

Iraq and Kuwait plan renewable energy projects. Kuwait is developing a low-carbon strategy for 2035, to focus on blue and green hydrogen. Also, the country plans 2 GW in wind and solar capacity. Iraq is considering renewables as a way to end imports of Iranian gas and electricity.

Methane emissions

Global methane emissions from the energy industry have been under-reported by 70%, the International Energy Agency said. Many GHG emissions totals submitted to the United Nations by member states “have not been updated for years.”

Russia/ Coal

Coal prices are rising as the Russia-Ukraine war worsens. Also, Russian coal producers face difficulties getting coal to their own export terminals. The country’s largest producer, Kuzbassrazrezugol, asked customers to be allowed to postpone deliveries for the 1Q and 2Q of 2022. Russia has a 20% share of global coal sales.

South Korea/ Solar power

LG Electronics will end its solar panel business. The company said that cheaper panels from Chinese rivals have made it difficult to compete.

Ukraine/ Nuclear power

The International Atomic Energy Agency said “unidentified armed forces” took control of the abandoned Chernobyl nuclear power plant. The agency called for “maximum restraint” to avoid risk at the facility. It added that Ukraine’s four operational nuclear power plants are secure.

U.S./ Wind power

The U.S. netted a record $4.37 billion from its largest-ever sale of offshore wind development rights — for areas off the coasts of New York and New Jersey. On offer were six leases covering 488,000 acres. Once completed, the project could produce about 7 GW.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

| January | OPEC quarterly meeting;

JCCP Petroleum Conference – Tokyo; EU Taxonomy Climate Delegated Act activates; Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

| February | Chinese New Year (Jan. 31 to Feb. 6);

Beijing Winter Olympics; South Korea joins RCEP trade agreement |

| March | Renewable Energy Institute annual conference;

Smart Energy Week – Tokyo; Japan Atomic Industrial Forum annual conference – Tokyo; World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

| April | Japan Energy Summit – Tokyo;

MARPOL Convention on Emissions reductions for containerships and LNG carriers activates; Japan Feed-in-Premium system commences as Energy Resilience Act takes effect; Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

| May | World Natural Gas Conference WCG2022 – South Korea;

Elections: Australian general election; Philippines general and presidential elections |

| June | Happo-Noshiro offshore wind project auction closes;

Annual IEA Global Conference on Energy Efficiency – Denmark; UNEP Environment Day, Environment Ministers Meeting – Sweden; G7 meeting – Germany |

| July | Japan to finalize economic security policies as part of natl. security strategy review;

China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong; Czech Republic assumes presidency of EU; Elections: Japan’s Upper House Elections; Indian presidential election |

| August | Japan: Africa (TICAD 8) Summit – Tunisia;

Kenyan general election |

| September | IPCC to release Assessment and Synthesis Report;

Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.; Japan LNG Producer/Consumer Conference – Tokyo; IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

| October | EU Review of CO2 emission standards for heavy-duty vehicles published;

Chinese Communist Party 20th quinquennial National Party Congress; G20 Meeting – Bali, Indonesia; Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

| November | COP27 – Egypt;

U.S. mid-term elections; Soccer World Cup – Qatar; |

| December | Germany to eliminate nuclear power from energy mix;

Happo-Noshiro offshore wind project auction result released; Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26; Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.