JAPAN NRG WEEKLY

APRIL 11, 2022

JAPAN NRG WEEKLY

April 11, 2022

NEWS

TOP

- Japan to phase out Russian coal imports in new sanctions round; PM Kishida says more reliance on renewables, nuclear is needed

- 440 companies join Japan’s carbon trading exchange project; some major emitters included in group that will set project rules

- Japan’s first hydrogen-fired power plant construction is complete; pilot facility will test technical viability and seek ways to cuts costs

ENERGY TRANSITION & POLICY

- METI says ~6.2 GW of renewables capacity was added last year

- Govt. discloses analysis of March 22 power shortages in Tokyo

- Chiyoda spreads its hydrogen transport tech in Singapore market

- Mitsubishi Heavy embarks on $2 bn hydrogen venture in the U.S. and wins approval to test carbon capture at Japan cement plant

- JERA, Abu Dhabi, Germany’s Uniper to study hydrogen transport

- Asahi takes delivery of world’s first battery-propelled tanker

- Mitsui OSK to launch ocean thermal power plant in 2025

ELECTRICITY MARKETS

- METI to boost support for Japan’s nuclear equipment exports

- TEPCO may see CEO change as replacement candidates emerge

- Mitsui to invest in 1.3 GW of wind and solar capacity in India

- Japan’s largest onshore wind farm starts construction in Fukushima

- Renova and JERA submit plans for new offshore wind power plants

- Tokyo Gas, Hokuriku Electric join 112 MW biomass power project

- TOCOM power futures volumes rise in March

- Opinion column: Deregulation to blame for electricity shortages

- Logistics firm vows to be top player in Japan’s renewables market

OIL, GAS & MINING

- Japanese buyers stick to Russian gas, but also look for alternatives

- Prolonged period of high oil prices to push Japan into the red

- ENEOS develops carbon-neutral range of lubricants

- Japan’s LNG stockpiles remain flat, well below four-year average

- Pan Pacific Copper plans record high output this fiscal year

ANALYSIS

HYDROGEN’S DAY OF RECKONING IS APPROACHING;

WHICH TECH WILL WIN OUT IN JAPAN?

The next two years will make or break the fate of hydrogen in Japan, at least as far as the state-led hydrogen economy program plans to meet its 2030 targets. Booming interest in the hydrogen economy has revealed a plethora of technological solutions for both H2 and ammonia. But after years of testing and R&D, it’s decision time. Supply chains from production to transport and storage to consumption must be up and running well before 2030 for Japan to hit its goal of 1% hydrogen-fired generation in the mix. We review Japan’s current tech solutions in hydrogen and ammonia.

RENEWABLES OPERATORS MAY SEE SOME ASSET VALUES JUMP ON CHANGE IN GRID RULES

In some of Japan’s local power grids, developing renewable energy facilities has proved problematic with a lack of spare capacity often cited as the reason. To address the issue, a few years ago a new kind of “non-firm” contract was rolled out. It allowed new power assets to connect to the grid but limited their operations to times where there was spare capacity.

Now, with the government looking to give renewables priority access to the grid, bumping thermal and other CO2-emitting sources down the priority order, the group most likely to benefit could be those with “non-firm” contracts.

GLOBAL VIEW

Asia is leading global growth in floating solar installs. Spanish utility seeks to develop 1 GW of renewables in Colombia. Germany nationalizes Gazprom’s local unit. China buys Russian coal with yuan. Sweden gets funds to build Europe’s first large-scale negative carbon emissions plant. Details on these items and more in our global wrap.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Japan, Events)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Daniel Shulman (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Renewable expansion progress in 2021

(Japan NRG, April 7)

- METI reported capacity expansion of renewables in the fiscal year ending March 2022 and measures to reach the 2030 target of 36-38% share of the national power mix. It also forecasted that the taxpayer burden to complete the renewable plan will be ¥2.7 trillion in FY2022, flat from the previous period.

| New FIT capacity added in 2021 | Target capacity addition till 2030 | Measures | |

| Solar | 2.4 GW | 4-6 GW/year | Solar panels on public buildings, farms, railway stations and airports

Power purchase agreements outside FIT/FIP schemes |

| Onshore wind | 1.3 GW | Over 1 GW/year | Additional auctions if total bids exceeded 1.7 GW

Clarifying rules for properties without identifiable owners, easing forestry rules |

| Offshore wind | 1.7 GW | 3.3 GW till 2030 | Revising auction rules to improve transparency

Increased municipality involvement in projects to speed up decisions Streamline construction safety reviews |

| Geothermal | 0.05 GW | 0.9 GW till 2030 | JOGMEC to support exploration

14 national parks open for surveys |

| Small/medium hydro | 0.5 GW | 0.6 GW till 2030 | Fully utilize digital and AI for more accurate forecast of water flows |

| Biomass | 0.2 GW | 0.2 GW till 2030 | Set up third party review system of potential feeds |

METI discloses analysis of March 22 power shortage

(Japan NRG, April 7)

- METI disclosed details of power generation in the Tokyo and Tohoku areas on March 22 when power shortage hit. Power demand for Tokyo area was forecast at 43 GW, but actual demand was 48 GW. Blackout was avoided as large consumers switched off or shifted to self-generators.

- Tokyo had 41 GW capacity (gas 27.9 GW, coal 5.1 GW, oil 1 GW) and Tohoku 15.9 GW (gas 6.9 GW, coal 3.5 GW and oil 0.6 GW). 80% were thermal power and 20% renewables.

- Gas and coal capacity run rates exceeded 100%.

- In addition, 5.11 GW capacities were offline for maintenance as March heating demand typically starts to wane from winter peaks.

440 companies join GX League – precursor to Japan’s nationwide carbon market

(METI Statement, April 1)

- A total of 440 companies joined GX League that will serve as decarbonization role models and participate in the rule-making of the carbon credit exchange that will trade compliance and high-quality voluntary credits. The companies account for 28% of Japan’s carbon emissions.

- CONTEXT: GX League members that have earned J-Credits from offset projects are limited to Mitsui Group and Yamato Transport.

TAKEAWAY: For a full article on what is the GX League and how it is part of Japan’s first nationwide carbon trading market which was launched earlier this month, see the March 28 edition of Japan NRG Weekly.

Chiyoda spreads hydrogen transport technology in Singapore

(Government Statement, March 31)

- Singapore’s Nanyang University plans to develop hydrogen carriage and extraction technology based on SPERA, a hydrogen transport system using toluene developed by Chiyoda Corporation. Chiyoda is offering the SPERA technology under the Japanese government-backed Asia Energy Transition Initiative. Singapore’s government will be funding the project, eyeing semi-commercialization by the year 2025 and full commercialization by 2030. PSA Corporation, Sembcorp Industries, City Energy, Jurong Port, Singapore LNG Corporation and Mitsubishi Corp will also take part.

- CONTEXT: Hydrogen transport and storage technologies are still evolving. See also this week’s Analysis section.

Overview of hydrogen carriage technologies

| Technology | Developed by | Partners | Ship |

| SPERA MCH | Chiyoda Corp. | Mitsubishi Corp., etc | Legacy oil and chemical tankers |

| LH2 (Liquid hydrogen) | Iwatani Corp., Kawasaki Heavy Industries | Marubeni, Kansai Electric, etc | Kawasaki Heavy’s dedicated vessel Suiso Frontier |

| Direct MCH | ENEOS | Chiyoda Corp. | Legacy oil and chemical tankers |

- SIDE DEVELOPMENT:

JERA, Abu Dhabi and Germany’s Uniper begin study of hydrogen transportation

(Denki Shimbun, April 7)- JERA, Abu Dhabi National Oil Company (ADNOC), and German utility Uniper begun a joint study for large-scale marine transportation of hydrogen using the technology of German startup Hydrogenious.

- Hydrogenious has proprietary technology for liquid organic hydrogen carriers (LOHC), which uses benzyl toluene as the medium.

- JERA has invested in Hydrogenious through its U.S. unit.

Mitsubishi Heavy and partner embark on $2 billion hydrogen project in U.S.

(Nikkei Asia, April 5)

- Mitsubishi Heavy Industries (MHI) and U.S.-based Bakken Energy plan to produce more than 300,000 tons of blue hydrogen per year in North Dakota, U.S. as part of a $2 billion project.

- An existing chemical plant in North Dakota will be repurposed to make hydrogen from natural gas. It will capture and store CO2 emitted in the process, with plans to sequester 6 million tons / year.

- The blue hydrogen facility is due to come online by 2027. Mitsubishi Heavy may invest in the project as well as getting involved in construction.

- The project will receive support from the local government.

- SIDE DEVELOPMENT:

Mitsubishi invests in green hydrogen production in Europe

(Nikkei, April 7)- Dutch-based Eneco, an energy company owned by Mitsubishi Corp. and Chubu Electric Power Co., joined a project to create one of Europe’s largest “green” hydrogen production operations.

- Mitsubishi Corp’s investment is expected to be ¥20 – ¥40 billion.

- Eneco aims to produce up to 400,000 metric tons of hydrogen annually by 2030 using electricity generated by offshore wind turbines.

Asahi takes delivery of the world’s first battery propelled tanker

(New Energy Business News, April 7)

- Asahi Tanker, a shipping firm, took delivery of the world’s first battery-electric propulsion tanker. The tanker will be shipped to Kawasaki, where it will undergo power receiving and counter-propulsion tests. It will be ready to sail this month.

- The vessel, measuring 62 meters in length, was built by Koa Sangyo. It will carry heavy oil. Mizuho Lease and Asahi Tanker have a sale-and-leaseback agreement under which Mizuho will own the vessel and lease it to Asahi Tanker in the form of a bareboat charter.

- A second such vessel is scheduled to be delivered in March 2023. It is being built by Imura Shipbuilding.

TAKEAWAY: The fact that a battery-propelled ship is designed to carry heavy oil is a neat summary of the energy transition at this moment.

MHI unit wins approval to test carbon capture tech at a cement plant

(New Energy Business News, April 6)

- Tokuyama and Mitsubishi Heavy Industries Engineering & Construction (MHIENG) signed an MOU for a CO2 capture demonstration test for a cement plant. The MOU is for a CO2 verification test at a cement plant in operation, and the test period is scheduled for nine months starting June 2022.

- The test will utilize MHIENG’s proprietary tech to recover CO2 from exhaust gas at a cement plant operated by Tokuyama in Shunan City.

- For MHIENG, the test will help to verify the efficiency of the tech and help to roll it out on a commercial basis. MHIENG, a unit of Mitsubishi Heavy, developed its CO2 capture tech in collaboration with Kansai Electric.

Shipper Mitsui OSK to launch ocean thermal power plant in 2025

(Nikkei Asia, March 29)

- Mitsui O.S.K. Lines (MOL) aims to launch a large-scale facility that uses ocean thermal energy conversion technology to generate power by around 2025.

- This technology generates power by harnessing the difference in temperatures at the surface of the sea and in deep water. It is estimated that construction of the 1 MW power station will cost several billion yen.

- Mitsui O.S.K. plans to use facilities owned by Okinawa Prefecture for a test and demonstration in April, before building Japan’s first large-scale plant.

- CONTEXT: NEDO estimates that such power source could provide 5% of Japan’s total needs. Its cost is also said to be potentially lower than for offshore wind power generation.

Nissan unveils prototype factory for all-solid-state EV batteries

(Nikkei, April 8)

- Nissan Motor showed online for the first time its next-generation “all-solid-state battery” prototype facility. A pilot production line will be set up in FY 2024 and mass production four years later.

- The automaker says these batteries will charge three times faster and offer twice the range compared to current EVs.

Sompo Japan starts to sell insurance for ammonia transportation

(Kankyo Business, April 5)

- Sompo Japan Insurance began selling insurance specifically for the transportation of ammonia from April 1 this year. On the same day, SOMPO Risk Management, a group company, began offering risk assessment services for facilities handling ammonia.

- The group expects the use of hydrogen and ammonia will increase.

- CONTEXT: This is the first attempt in Japan to develop a dedicated insurance policy for ammonia transportation.

One-Dot Wrap

- The Moray East offshore wind power project, the UK’s largest, has started operation. Kansai Electric and Mitsubishi participate in the project (Kankyo Business, April 7)

- Hitachi Energy launched OceaniQTM, a product, service, and solution designed specifically for offshore wind facilities. It allows for features such as remote monitoring and predictive diagnostics using digital technology. (Kankyo Business, April 7)

- Sumitomo Electric Industries will collaborate with Seaway7, a Norwegian marine construction firm, on offshore wind power generation projects in Asia, including Japan. Seaway7 owns and operates cable laying vessels. Sumitomo Electric provides submarine cables. (Kankyo Business, April 5)

NEWS: POWER MARKETS

Erex competes construction of Japan’s first hydrogen-firing power plant

(Japan NRG, April 4)

- Erex Co., a power retailer and biomass power plant operator, completed construction and started operation of a hydrogen-fired power plant in Fujiyoshida City.

- With an output of 320 kW, the plant is positioned as a demonstration facility to confirm the technical viability of the equipment and to find ways to reduce costs.

- CONTEXT: This is Japan’s first known 100% hydrogen-firing power generator.

- The hydrogen is supplied by the startup Hydrogen Technology, which produces the fuel by reacting igneous rock and water. HT’s technology does not emit CO2 during the hydrogen production process.

- If successful, Erex and Hydrogen Technology aim to build a larger demonstration facility that’s five times the size of the current one.

METI boosts support for nuclear exporters

(Nikkei, April 6)

- METI will offer greater support to Japanese businesses that manufacture components and systems for use in nuclear power stations.

- In the past, METI focused on corporations contracted to build entire plants overseas, but recent failures to win such contracts led METI to change its strategy.

- The new policy will be reflected in the government’s draft green energy strategy with a view to its inclusion in the 2023/24 budget.

- Before the Fukushima disaster, Japanese manufacturers exported ¥130 billion annually in nuclear plant components. That figure has since declined six-fold.

Manufacturing major Murata turns to multi-prong strategy in switch to renewables

(New Energy Business News, April 8)

- Murata Manufacturing plans to move to renewable energy across multiple offices and factories through a series of measures.

- Its Sendai facility switched to buying only electricity from renewable sources from Tohoku Electric, and plans to install 600 kW of solar PV and a 900-kWh battery storage system this summer to reduce the burden on the grid. The integrated system will also monitor consumption, weather, power generation forecasts, and conduct an analysis to provide the best energy strategy.

- In the Chugoku area, it signed a green power procurement contract with Chugoku Electric to secure off-site solar-generated power supply. Murata will also procure and use green electricity combined with non-fossil fuel certificates from Chugoku Electric.

TAKEAWAY: Murata is not a widely known consumer brand, but the maker of electronic modules and components is a major domestic manufacturer, and exactly the kind of company that will need to move to low-carbon sources for Japan to succeed in its net zero ambitions. It’s interesting to see the strategy Murata is taking as it seeks to consume up to 50% of its electricity from renewable sources by 2030.

TEPCO CEO change looks likely: Who takes over?

(Diamond, April 4)

- While TEPCO CEO Kobayakawa Tomoaki is now in his sixth term, a recent scandal involving compliance breaches at the Kashiwazaki-Kariwa nuclear power station has given rise to rumors that Kobayakawa will be demoted.

- The person most likely to replace him as CEO is Nagasawa Masashi, a 55-year-old straight talker known for making enemies easily.

- Other contenders are 52-year-old Nagasaki Momoko, who would be the company’s first female CEO, and Moriya Seiji, a 58-year-old finance and accounting expert.

Mitsui to invest in 1.3 GW of renewables in India

(Company Statement, April 6)

- Trading house Mitsui & Co. will invest in a $1.35 billion renewable energy project being developed by ReNew Power Private in India.

- The project will consist of three newly-built wind farms (900 MW in total) and one solar plus battery storage farm (400 MW plus up to 100 MWh), across three states in India.

- The project will guarantee 400 MW of capacity to an Indian central government-owned entity based on a 25-year power purchase agreement.

- The commercial operations are scheduled to start by August 2023.

OPINION: Deregulation to blame for electricity shortages

(Shukan Diamond, April 16 edition)

- CONTEXT: This is an opinion piece by the Shukan Diamond editorial team.

- While recent power cuts around Japan were triggered by an earthquake off the Fukushima coast, a chronic shortage of generation capacity means that it might not even take a natural disaster to cause power outages.

- The electricity sector reform in 2012 is to blame for the chronic capacity shortage.

- Electricity generation and transmission deregulation, and transition to a profit-based model, made legacy power plant operators less financially secure, forcing them to shut oil-fired plants and other aging and little-utilized plants.

- In the five years since 2016, over a gigawatt of capacity—equivalent to the output of one nuclear power station—has been removed from the grid.

- A quick fix to this problem is restarting some of Japan’s idle nuclear reactors. Four nuclear power stations have been approved for restart by their local communities.

- Such a move would free up a total of 4.6 GW of additional capacity.

Logistics operator GLP Japan enters renewables market, vows to become major player

(Kankyo Business, April 6)

- GLP Japan announced a full-scale entry into renewables. In addition to its main business, the development and operation of logistics facilities, the company will promote data centers, and its renewable energy business.

- Going forward, the company aims to become one of the largest renewable energy power suppliers in Japan by making additional investments. In the next five years, the company expects to invest about ¥500 billion to acquire capacity. Its immediate goal is to have 500 MW of capacity by 2024.

- CONTEXT: Last year, the company entered the power retail market by taking over the power retail firm F-Power while it was going through reorganization.

Renova, Sumitomo and others begin construction of Japan’s largest onshore wind farm

(Various, April 4)

- Nine companies including Sumitomo Corp, JR East Energy Development, Shimizu, and Renova have started construction of the Abukuma Wind Farms No. 1, 2, 3, and 4 in the Abukuma region of Fukushima Prefecture through their joint venture Fukushima Fukko Wind Power. With a capacity of approximately 147 MW, it will be the largest onshore wind farm in Japan.

- The project will cost ¥67 billion yen and consist of 46 wind turbines with a total height of approximately 148 m on a ridgeline in the Abukuma region, which spans Tamura City, Okuma Town, Namie Town, and Katsurao Village, Fukushima Prefecture, and is scheduled for completion in the spring of 2025.

- The power generated will be sold via a shared transmission line installed by Fukushima Power Transmission Co.

Renova plans 400 MW offshore wind project in Saga area

(New Energy Business News, April 6)

- MoE made an opinion on the early stage of the environmental assessment for an offshore wind power project planned by Renova off the Karatsu City coast.

- The project will have a maximum output of 400 MW, and occupy about 14,280 ha. There’ll be up to 42 turbines, each with an output of 9,500 kW to 15,000 kW.

- Four types of foundations will be considered: monopile type, jacket type, suction bucket type, and gravity type. Construction is expected to last about 3 years.

JERA plans 356 MW offshore wind power project in Akita area

(New Energy Business News, April 5)

- MoE submitted its opinion on the environmental assessment documents for an offshore wind power project planned by JERA in Akita area. The opinion calls for avoiding or minimizing the impact on the living environment caused by the shadows cast by wind turbines during operation.

- The project will have a maximum output of 356 MW, with 30 wind turbines of 12,000 kW, 26 of 14,000 kW, or 24 of 15,000 kW.

- The project area is approximately 3,230 ha off the coast of Noshiro City and Happo Town, Akita Prefecture, and the foundation structure is bottom-fixed.

Tokyo Gas and Hokuriku Electric join Sumitomo’s 112 MW biomass project

(New Energy Business News, April 4)

- Tokyo Gas and Hokuriku Electric will join in the construction and operation of a woody biomass-fired power plant with 112 MW of capacity that Sumitomo Corporation plans to build in Sendai City, Miyagi Prefecture.

- Sumitomo will own 50%, while Tokyo Gas and Hokuriku Electric will each take a 25% stake. Construction of the power plant is scheduled to start in April, with operations scheduled to commence in October 2025. JGC Corp will be in charge of the EPC work for the power plant.

- CONTEXT: This is Hokuriku Electric’s first investment in a biomass power plant.

TOCOM power futures volumes rise in March

(TOCOM Statement, April 8)

- Trading volumes of power futures on the Tokyo Commodity Exchange rose to 1,511 lots in March, compared to 1,201 lots in February, following a spike in demand for energy commodities. There was also demand for price hedging over the longer term, including off-peak seasons before summer.

- The March 2022 contracts settlements were: ¥30.76/kWh for east area baseload; ¥25.44 for west area baseload; ¥31.99 for east area day-time load; and ¥26.03 for west area day-time load. The east area baseload price tripled from August last year.

Chubu Electric and NGK join capacity market

(Nikkei, April 5)

- Chubu Electric Power Miraiz and NGK will service the capacity market.

- The companies will operate a virtual power plant that centrally controls multiple solar farms and storage batteries, enabling them to sell surplus capacity to the grid.

- The storage batteries have a rated output of 4.4 MW.

- Japan’s annual capacity market is worth over ¥100 billion.

NEC Capital, Nissin invest in Okinawa startup to remotely control solar power plants

(New Energy Business News, April 8)

- NEC Capital Solutions, Nissin Systems, and the Okinawa Development Finance Corporation invested ¥130 million in Okinawa startup Nexstems, which is developing an “area aggregation business.”

- Area aggregation optimizes the supply-demand balance in an area by monitoring the demand and supply of electricity in real time and adjusting the amount of electricity generated by solar power facilities through remote control. This will be a core tech in the renewable energy service provider business (RESP business).

Kansai Electric nuclear capacity operating rates highest since 2011

(Denki Shimbun, April 7)

- Kansai Electric announced the results of its nuclear power plant operations for fiscal 2021 that ended in March. The utilization ratio was approximately 61.0%, the highest since the 2011 earthquake and Fukushima disaster.

7 tons of copper cables stolen from solar power plant

(NHK, April 4)

- 7 tons of copper cables, stretching 2.5 km, were stolen from Ota Solar Power Station in Gunma Prefecture.

- The cables were worth ¥13 million.

- CONTEXT: The solar power plant is likely to have purchased the cables at ¥13 million, but the thieves won’t be able to sell at the same value since cables, once used, are sold as scrap. 7 tons of copper scrap is less than half of the nameplate cable price.

- SIDE DEVELOPMENT:

Aluminum to replace copper cables stolen from solar farms

(Nikkei, April 5)- Furukawa Electric will supply solar farm operator TEC Energy with aluminum cables to replace copper cables recently stolen from TEC’s Ibaraki solar farm.

- It was the latest hit in a spate of thefts targeting solar farms, following a surge in the price of copper.

Fisheries association vehemently opposed to tritium release

(NHK, April 5)

- The head of the National Federation of Fisheries told METI Minister Haguida that the Federation is strongly opposed to any discharge into the sea of radioactive tritium from the site of the Fukushima disaster.

- Federation chair Kishi Hiroshi told the Minister that the Federation’s position has not changed one iota in the past year.

- The Minister asks for more understanding of the government’s position, saying that discussions between stakeholders has closed the distance between them.

NEWS: OIL, GAS & MINING

WAR IN UKRAINE:

Japan will phase out Russian coal imports in latest round of sanctions

(Nikkei Shimbun, April 8)

- PM Kishida announced that Japan will phase out coal imports from Russia in response to the latter’s invasion of Ukraine and reported war crimes.

- The coal ban is part of a broader import restriction against Russian products, which will include Russian wood, machinery, and even vodka.

- The schedule for the phaseout is not yet clear, with PM Kishida saying that it will be done in consultation with the power generation, cement and steelmaking sectors, which will need to find alternatives.

- In order to avoid problems with coal supply for power generation, Kishida said: “we will make maximum use of renewables, nuclear, and other power sources that are highly effective for energy security and decarbonization.”

- The latest sanctions also ban new investments in Russia.

- Several power utilities in Japan said they will stop new spot or long-term contract purchases of coal from Russia.

TAKEAWAY: PM Kishida continues to act quickly and largely in lockstep with Western allies in the G7. Russian coal accounts for only about 13% of Japan’s supply (but as much as a third in the thermal coal segment). It won’t be simple to replace these volumes because today’s market is very tight, coal prices are the highest in decades, and buyers tend to require particular grades of coal for their specific needs. Some goal grades are only suitable for power generation, for example, and power facilities also tend to be “tuned” to operation on coal that has specific characteristics in terms of energy, ash, moisture and other content. That means we’re unlikely to see all Russian coal supplies vanish from Japanese ports for four to six months.

In the meantime, Japan’s coal supplies will be at risk, despite the country’s ample stockpiles. Should Russia’s government decide to disrupt coal exports to Japan in retaliation for the embargo, problems will compound in the domestic and broader Asian markets. At the very least, we can expect continued increase in coal prices, and as a result further increase in electricity prices.

For some, the key comment from PM Kishida related to nuclear power. Yet as discussed previously, Japan’s central government does not have direct control over reactor restarts and there’s not yet enough evidence to suggest a pick-up in the pace of restarts.

Japanese buyers stick to Russian gas, but cast eye for alternatives

(Yomiuri Shimbun and Financial Times, Apr 8-10)

- Tokyo Gas CEO Uchida Takashi said that his company intends to continue to source LNG from the Sakhalin 2 project in Russia.

- Uchida said any interruption in gas imports will jeopardize residential gas supply.

- Gas from the Sakhalin 2 project makes up around 8% of Japan’s total LNG imports.

- Hiroshima Gas relies on Sakhalin 2 for half its long-term contract volumes, but it may ask Malaysian suppliers to increase volumes or deliver ahead of schedule in case of problems with Russia.

- Osaka Gas said it will ask for earlier deliveries from Australia and U.S. producers in case of disruptions to Russian supply.

TAKEAWAY: Today’s global LNG market is like a zero-sum game. If Japan is pressured by Western allies to reject Russian supplies, it will need to secure similar volumes from elsewhere. At a time when the EU and the UK, among others, are seeking alternative suppliers to Russia, this simply adds more eager bidders for the same available LNG volumes. At some point, demands for a complete exodus from Russian natural gas will need to be seen in this context.

It’s also questionable how much Japan’s energy buyers can request earlier deliveries from non-Russian sources. Without a long-term storage facility, balancing the timing of deliveries is hard.

Global LNG market shortages are expected if Russian LNG volumes do not enter the market somewhere (for example: China or India, which could free up some of the volumes those buyers would have procured elsewhere).

We expect curtailment of industrial output to conserve gas to become an increasingly regular topic, if not a reality, going forward this year.

Prolonged period of high oil prices to push Japan into the red

(Nikkei Asia, April 9)

- Japan’s current-account balance is poised to dip into the red on an annual basis for the first time in decades should energy prices climb further, according to a Nikkei estimate.

- If crude oil surges back to $130 a barrel and the yen hovers at 120 against the dollar, Japan could face a current-account deficit of ¥16 trillion, or $130 billion, for fiscal 2022, calculations show. The costlier oil imports are seen outweighing the boost to exports from a weak yen.

- Japan last logged a current-account deficit for a calendar year in 1980, with no fiscal year deficit on record going back to 1996.

ENEOS develops carbon-neutral lubricant

(Chemical Daily, April 8)

- ENEOS has developed a new carbon-neutral range of lubricants.

- Manufactured exclusively from plant oils, the lubricant range includes automotive lubricant, industrial lubricant, and grease.

- ENEOS is ramping up its procurement and manufacturing capacity with a view to release the lubricant commercially in 2022/23.

Japan’s LNG stocks remain flat at 1.65 million tons

(Government Statement, April 6)

- Japan’s LNG stocks stood at 1.65 million tons as of April 3, flat from 1.66 million tons a week ago. The end-April stocks last year were 2.01 million tons and the four-year average was 1.90 million tons.

Pan Pacific Copper plans record high output for April-September

(Japan NRG, April 1)

- Japan’s largest copper producer, Pan Pacific Copper, plans to produce 307,700 tons of copper cathode in April to September 2022, which is a record high. Six Japanese copper producers plan 805,000 tons of output in April-September, up 5% YoY.

- SIDE DEVELOPMENT:

Sumitomo Metal Mining expects less nickel output in 2022 due to plant maintenance

(Company Statement, April 1)- Sumitomo Metal Mining plans to produce 55,500 tons of nickel cathode in April 2022-March 2023 period, down from 57,000 tons forecast for the previous period. Its Niihama Nickel Refinery will be closed for maintenance in May and in November.

Hanwa signs lithium carbonate offtake deal with Lake Resources

(Company Statement, April 1)

- Hanwa will purchase 15,000-25,000 tons/year of lithium carbonate and hydroxide for 10 years from the Kachi site in Argentina, for Asia wide sales.

- CONTEXT: Japan’s annual lithium carbonate imports are around 20,000 tons. Toyotsu Lithium plans to bring onstream a 10,000 ton/year lithium hydroxide plant in Fukushima this year.

JGC to expand Taiwanese LNG terminal

(Nikkei, April 6)

- JGC Holdings won a contract to expand work on an LNG terminal in Taiwan.

- JGC will partner with a local construction contractor on the ¥60 billion project.

- Taiwan aims to increase its reliance on LNG for electricity generation to 50% by 2025, up from 30% currently.

ANALYSIS

BY MAYUMI WATANABE

Hydrogen’s Day of Reckoning Is Approaching in Japan;

Which Technologies Will Win Out?

The next two years will make or break the fate of hydrogen in Japan, at least as far as the state-led hydrogen economy program plans to meet its 2030 targets.

The goal is for hydrogen-fired power generation to have a nominal but noticeable place in the national electricity mix, at 1% of the total by 2030. Instead of building new power capacity oriented on hydrogen, most of that 1%, which is equivalent to 9-10 TWh of electricity, will come from so-called co-firing. This assumes that some gas power plants will add hydrogen into their fuel mix and some coal plants will do the same with its cousin, ammonia.

The challenges were, and remain, picking the most reliable, cost-effective, and environmentally clean technology. Booming interest in the hydrogen economy has revealed a plethora of technological solutions for both H2 and ammonia.

After years of testing and R&D, it’s decision time. Supply chains from production to transport and storage to consumption must be up and running well before 2030 for Japan to hit that 1% target. Here, we review some of Japan’s current solutions in hydrogen and ammonia.

Imports and domestic sources

Japan’s hydrogen economy program calls for the fuel, or ammonia, to account for 1% of national power generation and be used in manufacturing processes by replacing fossil fuels. The assumption is that hydrogen production costs will drop to ¥30/ Nm3 by 2030, from the current ¥170/Nm3 for hydrogen, and to ¥15-20/ Nm3 from ¥25-30/Nm3 for ammonia.

Most of Japan’s ammonia and hydrogen demand is expected to be met with overseas supply. While the government expects to initially use blue hydrogen that’s made from natural gas, after 2030 the outlook is for green hydrogen (made with renewables) to become more popular.

With few low-cost renewable energy facilities, Japan doesn’t expect to become a significant producer of green hydrogen. Since the hydrogen will originate from natural gas and be utilized by gas-firing power plants for co-firing, Japan plans to lean on its fossil fuel infrastructure.

According to oil refining major ENEOS, by 2030 Japan will require 300,000 tons of hydrogen for gas power plants’ co-firing. ENEOS will convert its refineries into hydrogen supply bases. The company’s desulfurization units could be used for dehydrogenation (turning hydrogen from liquid to gas); its port terminals, piers, pipelines and storage tanks can offload and store H2.

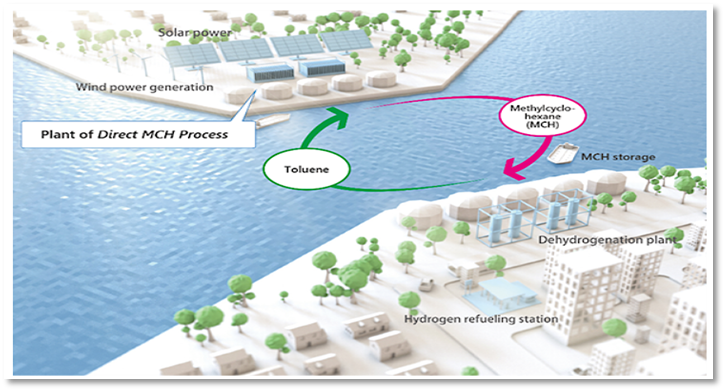

Crucially, seven ENEOS refineries are located on the Pacific coast, close to half of Japan’s gas-fired power plants. ENEOS has 12 crude oil tankers and 15 chemical tankers that can be adapted to carry hydrogen. The company favors MCH technology for transport, which it believes it can secure in large quantities from Saudi Arabia, Australia and Southeast Asia.

MCH (Methylcyclohexane), already a widely used compound, can also be produced when converting hydrogen into a liquid using an element called toluene. This turns hydrogen into a compound that’s relatively easy to transport.

Liquid or compound?

Five years ago, most efforts focused on finding ways to transport H2 in liquid form. Kawasaki Heavy Industries built the world’s first liquified hydrogen carriers, the Suiso Frontier, which set sail in 2021. Japan’s largest hydrogen producer, Iwatani Corporation, now uses the liquified form to transport locally produced hydrogen to fuel cell vehicle service stations.

Cooling hydrogen to the point of liquefaction (-253°C) is energy intensive. Initially, it was better because it had lower energy losses (25-35%) compared to MCH (35-40%). But MCH’s advantage is that it’s condensed by 500-fold; so, one liter of MCH can store 500 liters of hydrogen that can be transported at room temperature and pressure, avoiding the cost of cooling pure hydrogen.

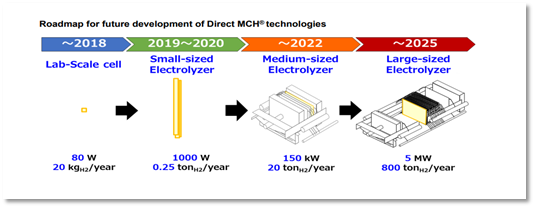

MCH is also safe due to limited chemical reactions regardless of ambient pressure or temperature changes. Now, ENEOS says it found a way for MCH to make up the energy losses by developing a green hydrogen process it calls Direct MCH.

Source: ENEOS

At present, green MCH has two steps: water electrolysis powered by renewables to separate hydrogen from water, and then toluene hydrogenation. Direct MCH allows for a direct reaction of toluene with water instead of hydrogen, eliminating the need to store hydrogen in tanks before the next toluene hydrogeneration phase. As a result, the cost of MCH is halved.

The company believes the innovation will help achieve the ¥30/ Nm3 goal. It’s also developing MW-class large electrolyzers by expanding the electrode area and stacking cells. In 2021, ENEOS and Origin Energy conducted a trial run of Direct MCH in Australia. Solar powered the electrolyzer, producing 4 liters of MCH, then shipped to Japan to power a FC vehicle.

Source: ENEOS

Breakthrough ammonia technologies

Japan’s ammonia demand is 1 million tons/ year, which might triple by 2030. Ammonia is manufactured using the Haber-Bosche process. Japanese manufacturers have to pay license fees to European firms for the process, so they’ve looked for an alternative for years.

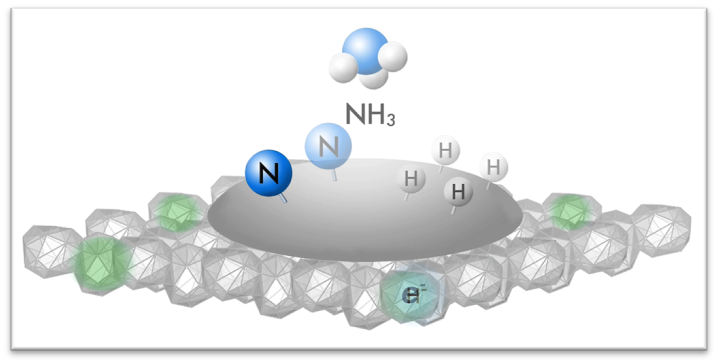

Recently, startup Tsubame BHB developed an electride catalyst that produces ammonia at a lower temperature and pressure than Haber-Bosche. It can produce the gas at 300-400°C and in a 3-5 MPa environment, compared to Haber-Bosch’s 400-500°C and a 20 MPa requirement.

So far, the catalyst has been used in smaller manufacturing plants with output of 500 to 50,000 ammonia tons/ year. Tsubame BHB has yet to find a way to apply the process to bigger facilities. The new catalyst raises cost issues, however. It contains platinum group metals that are expensive and not easy to secure, with Russia one of the major global suppliers. The process also generates nitrates and nitrites, which are toxic.

Graphic: Tsubame BHB

Another Japanese oil refinery major, Idemitsu, says it has a better solution — a process that will employ molybdenum instead of PGMs. Idemitsu’s catalyst is dinitrogen-bridged dimolybdenum, a combination of molybdenum dioxide and nitrogen. The company manufactures compounds with a similar composition for its oil products. Molybdenum is commonly found in copper ores and costs $20-30/ kg, a clear price advantage against the $10/ gram for ruthenium, a PGM.

Challenges still remain. Idemitsu needs to improve the energy efficiency of its ammonia production process and find a way to control the toxic substances generated as a byproduct. The oil refiner hopes to complete development by 2024 and to have a cartridge-based system that allows the scaling up of output by 2028. Tsubame BHB also hopes to develop a PGM-free version of its catalyst by 2024, and aims to be ready for pilot tests by 2027.

Japanese academics have stepped up research on new non-PGM catalysts. New possibilities include compounds composed of nickel, copper, manganese and others. Main challenges are improving the endurance and life cycle of the compounds, scaling up the process, as well as improving energy efficiency.

Catalyst technologies in academic development in Japan

| Nickel lanthalum oxide (NiLaN) | Tokyo Institute of Technology |

| Perovskite material (BaCeO3-xNyH2) | Tokyo Institute of Technology |

| Copper oxide on aluminum silicates and silica oxides (CuOz/3A2S) | Kumamoto University |

| Copper and nickel ions embedded in manganese dioxide compound | Yamaguchi University |

Build it and they will come

Despite all these advances and progress, industry insiders and experts are concerned that all efforts to create abundant hydrogen and ammonia suppliers will fall flat if the promised demand does not materialize. As one METI committee panel on the matter noted, nearly all the R&D in the space is heavily weighted towards production. There’s much less innovation among industries to actually deploy the hydrogen.

Consumers in the power sector, such as JERA, have committed to moving towards hydrogen and ammonia in the mid-to-long-term, but are still guessing on timelines and volumes. Much depends on the technical testing of co-firing, such as the one JERA started at its Hekinan coal-fired power station last year.

If it goes well, JERA hopes to accelerate full commercialization of co-firing before a self-imposed 2030 deadline. In fact, the power utility this February launched a global tender for “up to” 500,000 tons of ammonia per year from FY2027. But ultimately, JERA’s decision will depend on the cost of this ammonia, as well as the co-firing pilot projects.

Despite the many uncertainties, the window of opportunity to hit the 2030 net-zero targets is closing. In the next two years, Japan may simply need to take a leap of faith.

ANALYSIS

BY DANIEL SHULMAN

PRINCIPAL

SHULMAN ADVISORY

Renewables Operators May See Some Asset Values Jump

On Change in Grid Rules

In some of Japan’s local power grids, developing renewable energy facilities has proved problematic with a lack of spare capacity often cited as the reason. To address the issue, a few years ago a new kind of “non-firm” contract was rolled out. It allowed new power assets to connect to the grid but limited their operations to times where there was spare capacity in the transmission system.

As such, owners of “non-firm” contracts were the first in line to have their operations curtailed in times of weak demand or oversupply.

Now, with the government looking to give renewables priority access to the grid, bumping thermal and other CO2-emitting sources down the priority order, the group of power facilities likely to benefit the most could be those with a “non-firm” contract. Once owners of an arrangement that offered only a partial operating schedule, developers and investors behind plants with a “non-firm” contract could now see material upside in the value of their assets.

The change could also have a significant impact on coal and gas-fired power plants in areas with a large volume of such contracts. The Tokyo power grid, in particular, may see a strong shakeup in run rates among various power plants.

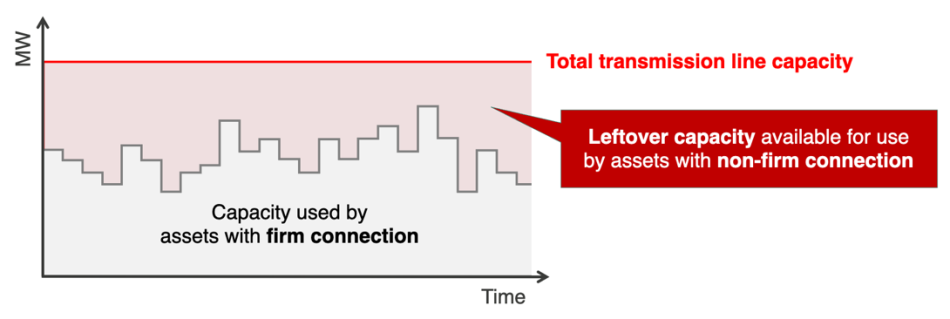

Fluctuation in firm capacity use and non-firm availability

How the system works today

With a big surge in interest from developers in building solar and wind power plants over the last decade, local transmission system operators, or TSOs, have struggled with how to accommodate the newcomers while reserving grid capacity for existing suppliers.

When a generation asset is brought into operation, a grid connection request must be addressed to the TSO in charge of the area. The TSO evaluates the grid connection costs, which include checks that the capacity of the network allows the new power source to be effectively transmitted and/or distributed, as well as the actual cost of connecting the asset to the correct voltage branch of the grid.

If there is not enough network capacity to accommodate the asset, two options are available to the TSO. It might consider upgrading the grid, especially if several generating assets were able to share the grid upgrade costs. Alternatively, it can offer the developer a non-firm contract.

Assets under a non-firm transmission contract can send power through the grid only when there is capacity left after other (firm contract) power sources have dispatched their power. This means that when grid capacity is reached, non-firm assets will be curtailed.

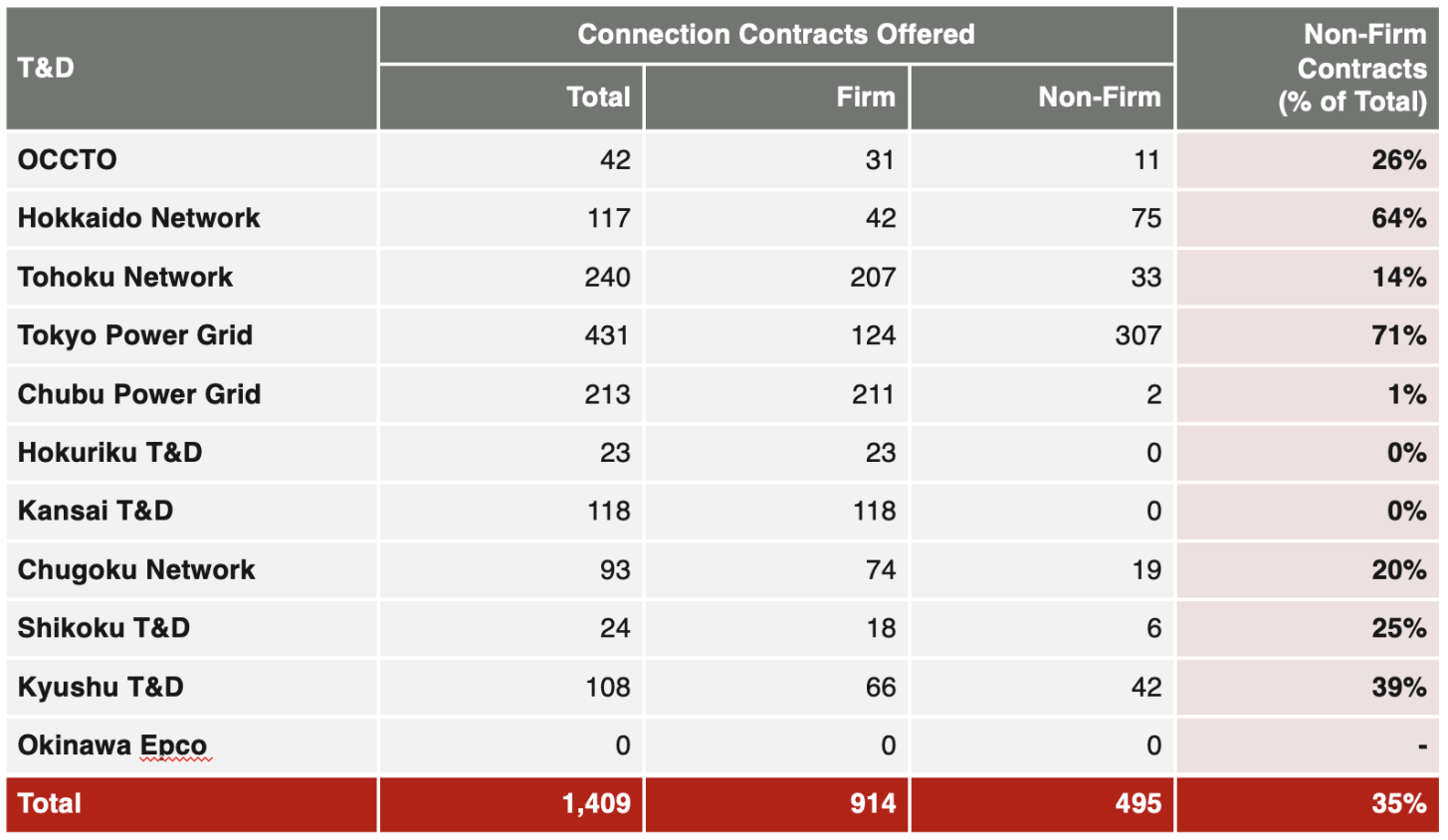

This system was originally applied to areas with a significant shortage of capacity, including the Tokyo area from September 2019, and Tohoku and Kyushu from 2020. From January 2021 it was deployed nationwide for the bulk power system of each area and soon after that was extended across all three levels of the grid.

Such an un interruptible transmission system was created to increase the amount of renewable assets connected to the grid. As much as 98% of the 855 connection requests in FY2020 were for renewable assets, and the period from April 2021 to end-September 2021 saw even more connection requests.

Instead of refusing the connection of some of these renewable assets, the TSOs offered non-firm contracts. Out of the 1409 connection requests during this period, 497 non-firm contracts were offered – a nationwide average of 35%, with considerable variation among regions.

In theory, such a system allows for the integration of more renewable power on the grid, but the increased curtailment risk means a project may not getting funded or commissioned.

Non-firm assets are also currently not allowed to participate in the capacity and balancing markets, reducing monetization options.

Under the current rule, coal assets under a firm contract could keep producing power during periods of grid congestion, while renewable assets under a non-firm contract are curtailed.

Reforms of the rules

METI is now changing the system to support growth in green power sources. From April 2022, only non-firm transmission contracts will be given to all forms of generating assets connecting to the bulk power system nationwide, and this will be extended to the local power system layer by the end of FY2022.

From December 2022 the curtailment order will be modified for non-firm assets as well as for adjustable power assets. From FY2023 these rules should be extended to all assets, including assets under firm-contract.

The new curtailment order will be as follows:

- The first assets that will be curtailed will be thermal power plants that have been appointed as priority curtailment assets by the TSOs, thermal power plants with online curtailment control system, pumped hydro, and batteries

- After that thermal power plants with no online controls will be curtailed

- Followed by biomass power plants

- Followed by PV and wind power plants

- And finally other plants such as nuclear, hydropower and geothermal

Within each category, plants with the highest marginal cost of generation will be curtailed first. This will have the added benefit of reducing the power wholesale market price as the price is equal to the marginal cost of the most expensive asset cleared for a given interval on the market.

In addition to the change in curtailment priority order, non-firm assets will be allowed to participate in both the capacity market (from this year for delivery in 2026) and the balancing market. METI plans to monitor and review the results of these changes in FY2022 and FY2023.

Impact

These changes should have several effects. Renewable assets developed over the last two years with non-firm contracts but not commissioned due to the associated risks are likely to move forward.

In future, curtailment of renewable assets will be reduced considerably from where it would have been under the old system – although as renewable penetration increases, curtailment risk is still expected to increase compared to recent years, apart from in the Kyushu area.

Finally, the economics of fossil fuel generation plants are going to be further squeezed as curtailment increases. These assets will have to find new sources of income, potentially through the balancing market.

For now, victory in the competition to grid access goes to renewable energy operators. But there is one eventuality that has yet to be explained by the government under the changing rules of the game. What will happen to fossil fuel generation plant curtailment orders when, or if, METI’s vision of ammonia fuel and/or carbon capture materializes?

If the premise for curtailment orders changes to include a plant’s environmental criteria, as well as its marginal costs, we may see another shift in grid access hierarchy.

Firm and non-firm transmission contracts in Japan (April – September 2021)

Source: METI

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Asia/ Floating solar power

Asia is leading global growth in floating solar installations, said Fitch Solutions. There are now 22 such projects, with expected total installed capacity of 10 GW, up 37.5% from early 2021. Among the leading projects is China’s 320 MW Huaneng Power International.

Colombia/ Renewables

Spanish solar developer Grenergy issued €52.5 million of green bonds to finance renewables projects. In total, Grenergy plans to invest more than $700 million in Colombia to develop a portfolio of 1 GW of renewable projects that are currently at different stages of development.

Europe/ Solar power

The EU has the potential to add 39 GW of solar power under an “accelerated high scenario” that in 2022 would add 23.3 GW of rooftop and 15.7 GW of utility-scale solar, said SolarPower Europe. This accelerated scenario could see global solar capacity reach 1 TW by 2030.

Germany/ Gas storage

Berlin nationalized Gazprom Germania, the local subsidiary of the Russian gas group that operates some of Germany’s largest natural gas storage facilities. The government cited the company’s alleged “unclear legal relationship and its violations of its reporting obligations”.

Global solar and wind power

Wind and solar generated 10.3% of global electricity in 2021, twice more than 2015, said Ember Research. Denmark and Luxembourg led electricity generation from renewables, at 52% and 43%, respectively. 50 countries now produce 10% of their electricity from wind and solar, up from 43 in 2020.

LNG/ Infrastructure investments

Miami-based I Squared Capital closed its $15 billion infrastructure fund. The LNG sector is said to be top on the fund’s priority list, as it hopes to capitalize on Europe’s need for alternative gas supplies from Russia, as well as Asia’s growing appetite for LNG.

Russia/ Coal exports

In March, several Chinese firms purchased Russian coal with yuan. The shipments will arrive this month and are the first commodity shipments purchased in China’s currency since the war in Ukraine began. According to the Bank for International Settlements, 90% of foreign-exchange transactions in 2019 were in U.S. dollars, compared to just over 4% for the yuan.

Sweden/ Carbon capture

The EU gave €180 million to Stockholm Exergi to build Europe’s first large-scale negative carbon emissions plant. When completed, the bio-energy with carbon capture and storage (BECCS) at the company’s KVV8 bio-cogeneration plant will have an annual capture capacity of almost 800,000 tons of CO2.

Switzerland/ Carbon capture

Climeworks, the Swiss carbon capture startup, raised CHF 600 million. Financing was led by Partners Group , GIC, and Swiss Re, with participation from Baillie Gifford, Carbon Removal Partners, Global Founders Capital, and Climeworks’ anchor shareholder, BigPoint Holding.

Taiwan/ Renewables

The government and state-controlled companies will invest $32 billion through 2030 to develop renewable technologies, grid infrastructure and energy storage. The country plans to reach net-zero emissions by 2050. By 2026, it has a goal to produce 20% of power from renewables.

U.S./ Energy transition

NextEra Energy sold its 156-mile natural gas pipeline in Texas for about $200 million, and will invest the transaction proceeds “to acquire higher-yielding renewable assets,” said NextEra CEO John Ketchum.

Zimbabwe/ Coal power

RioZim Ltd, one of the country’s biggest mining and energy companies, had planned to work with China to build a major coal-fired power plant. Beijing, however, pulled out because it’s scaling back overseas funding, forcing nations in Africa and Asia to rethink energy plans.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.