JAPAN NRG WEEKLY

AUGUST 22, 2022

JAPAN NRG WEEKLY

Aug 22, 2022

NEWS

TOP

- PM Kishida urges new METI chief to tackle energy inflation and repeats the need to secure more nuclear power, but incoming minister sends mixed messages on commitment to nuclear

- Kyushu Electric to launch battery power trades in coming year

as it looks at new options in electricity markets - Foreign shareholders sue Kansai Electric over bribe scandal claiming failure to disclose nuclear-related back payments

ENERGY TRANSITION & POLICY

- METI, MoE set up structures to implement Kishida’s GX initiative

- Govt. seeks to expand FIP scheme to cover mini-solar operations

- Japan’s solar efficiency ratio up, but better maintenance needed

- Ministry prepares net-zero railway council to reform the industry

- Soil carbon capture wins more converts in Japan after rule change

- IHI to develop ammonia turbine with almost zero CO2 emission

- Japanese startup selected as part of UK nuclear fusion program

- Osaka Gas aims to synthesize 90% of supply from waste CO2

ELECTRICITY MARKETS

- Major power utilities max out their scope to raise electricity prices

- Tohoku Electric asks regulator to speed up reactor review process

- Part of TEPCO’s plan for Kashiwazaki-Kariwa NPP gets approved

- JERA agrees to acquire 35% stake in Vietnam renewables utility

- Kansai Electric launches new solar leasing services for households, but forced to abandon plans for new wind farm in the northeast

- Gas utilities keen to diversify into renewables to stay competitive

- JERA and Eurus Energy bring online new wind power projects

OIL, GAS & MINING

- PM Kishida to visit Middle East amid high oil prices

- Russia offers Japan same LNG sale terms after Sakhalin-2 changes

- ENEOS CEO suddenly resigns, prompting speculation

- Imports of LNG dropped by more than a fifth even as stocks rose

ANALYSIS

JAPAN PLEDGES TO BUILD NEXT-GEN NUCLEAR REACTORS BUT TIMELINE RAISES QUESTIONS

Japan unveiled a new nuclear roadmap that outlines the development and construction of new facilities and reactor technologies. The announcement came just days after the minister in charge repeated the long-held position that no new nuclear energy construction projects were on the horizon. Apart from the mixed messaging, there are several concerns around the new roadmap. It lacks details and paints the commercial launch of new technologies two decades from now. Can that still work for Japan? We review.

TOP INTERVIEW:

MEG O’NEILL, CEO OF WOODSIDE ENERGY

Japan NRG sat down with Meg O’Neill, the CEO of Woodside Energy, which has recently merged with BHP’s oil and gas assets to create one of the world’s top 10 independent energy companies. Woodside Energy is also heavily involved in Japan’s energy market and works with Japanese companies on projects in Australia. Meg shared her thoughts on the future of the Japanese market and its standing in Asia, CCUS, potential for “carbon neutral” LNG, hydrogen projects, and other topics.

GLOBAL VIEW

Chinese solar firm holds major IPO. BHP posts record profits on coal prices. EU may ease mining regulation to help green tech. Barclays lowers oil forecast for 2022, next year. Russia’s energy revenue up by more than a third. Adani to invest big in Sri Lanka wind power. Details on these and more in our global wrap.

EVENTS SCHEDULE

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Japan, Events)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Daniel Shulman (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

PM Kishida asks METI minister again to tackle energy inflation and to secure nuclear power

(Government Statement, Aug. 15)

- During a ministerial meeting to combat inflation, Prime Minister Kishida once again asked METI minister Nishimura to bring energy prices under control, as well as to bring nuclear power back online.

- Kishida told Nishimura to list measures to curb gasoline and other fuel cost hikes, as well as to review the impact of fuel subsidies and to ensure that at least nine nuclear reactors will be operational in winter. The PM also called for pursuing other power and fuel supplies, and to mitigate the impact of power cost rises on consumers using applicable subsidy programs.

TAKEAWAY: Listing anti-inflation measures for energy might mean changes in fuel pricing that’ll be taken up by parliament. For example, some lawmakers demanded removal of the gasoline tax. The next parliamentary session will likely focus on regulatory changes associated with the Kishida Clean Energy Strategy, but could include amendments to control inflation and secure energy supplies.

- SIDE DEVELOPMENT:

New METI head sends mixed message on nuclear reactors

(Aug. 12, Sankei Shinbun)- Newly inaugurated METI Minister Nishimura confirmed that, at most, 9 units of nuclear power plants will be restarted this winter. He pledged to support utilities to get approval from local governments and to do the same for more reactors next year, in time for the summer peak.

- However, Nishimura also said that he’d prefer to lessen Japan’s dependence on nuclear energy.

- CONTEXT: Nishimura’s ministry has just unveiled a long-term roadmap for nuclear power development in Japan. This seems to contradict the ministry’s comments on lessening dependence on nuclear power in the future. See our Analysis section for a full takeaway on the issue.

GX framework takes shape at METI and MoE – Pillars of Kishida govt

(Aug. 19, Denki Shinbun)

- The GX Implementation Council will be the central core of Kishida’s energy / low carbon policy. METI and MoE, along with the private sector, are now rapidly consolidating to promote this government platform.

- On Aug. 9, METI and MoE met to improve private investment. Both ministries have GX committees and plan to issue 10-year roadmaps for renewables and nuclear energy.

- At the first GX Council on July 27, Kishida called for securing electricity and gas supplies. He ordered the METI Minister to deploy more renewable energy and power storage, to restart NPPs and further develop nuclear power.

METI proposes to expand FIP to cover mini-solar power stations

(Japan NRG, Aug. 17)

- METI plans to expand the Feed-in-Premium (FIP) to include solar power operators with projects that are just 10 – 50 kW in capacity.

- From this year, operators of over 1 MW in capacity are required to shift to FIP from the Feed-in-Tariff (FIT) system. Those with installations of 50 kW – 1 MW have a choice, they can either shift to FIP or stay with FIT.

- The mini-operators that have business contracts with power retailers and aggregators should also be given a choice to make the shift, METI said. 34% of solar operators serving business customers last year were 10 – 50 kW mini-stations. The Power Tariff Committee, which has oversight on renewable rates, will review the proposal.

TAKEAWAY: FIP is new and there are only 30 or so aggregators, many of which are grids or their affiliates. FIP determines revenues based on spot electricity prices, plus a premium, as opposed to a fixed revenue system under the FIT. As of April, 144 power stations shifted to FIP, and 40,000 stations qualify for the change. Over 700,000 mini-stations have 10 – 50 kW capacity; but, some of these are actually megawatt-scale solar plants split into smaller units for the purpose of regulatory filing.

Japan’s solar efficiency ratio jumps in a decade, but govt. still urges better maintenance

(Japan NRG, Aug. 17)

- Proper maintenance of solar power stations could improve operational efficiency, a survey by the Agency of Natural Resources and Energy showed. About 13% of power operators serving businesses said their output declined by over 10%, possibly due to inadequate maintenance.

- Panels typically guarantee 25-30 years of output. METI will ask the Power Tariff Committee to design a plan to incentivize facility maintenance and upgrades.

- The 2021 power conversion rate of solar operators averaged at 21.1%, compared to 16.5% in 2012-2013.

TAKEAWAY: While most Japanese solar panels are silicon-based and imported, there are new technologies and materials that can provide 30% conversion efficiencies. The main obstacles are cost, battery endurance, and recycling.

Net-zero railway council to be launched

(Government Statement, Aug. 16)

- In the coming weeks the Ministry of Land, Infrastructure, Transport and Tourism plans to set up a government-private sector council to decarbonize railways. The council will draw roadmaps by March 2023 for the industry to reach net-zero.

- There are three main approaches to cut carbon: localizing energy supply and consumption, using rail infrastructure to transport energy, and development of net-zero vehicles. Ideas include using railway terminal facilities to store power, installing pipelines along the track to transport hydrogen, and fuel cell-powered rail vehicles.

- CONTEXT: Germany is ahead of Japan in decarbonizing railway systems, this year launching operation of the world’s first hydrogen-powered rail system. Railways accounted for 4.8% of total transport emissions in 2020.

More companies engage in soil carbon capture

(Japan NRG, Aug. 18)

- Thanks to J-Credit’s authorization of biochar as an offset, more companies are involved in soil carbon capture projects in the farming sector.

- Marubeni started sales of J-credits derived from a soil carbon capture project by Japan Cool Vege Association. The association makes biochar from plant wastes, and farms use it as fertilizer that captures carbon in the soil.

- The trading firm will offer up to 500 tons/ year of biochar offset credits.

- In July, Chubu Electric started a pilot tea plantation to study the effects of biochar.

- Shimizu Corp developed concrete containing biochar and plans to seek J-Credit authorization as “concrete carbon capture”.

TAKEAWAY: The decline in the amount of carbon absorbed by Japanese forests and farmland has brought soil carbon capture into the spotlight as an effective negative emission method. Too much biochar in soil, however, inhibits growth of some crops such as tea and potatoes. Japan’s annual biochar production is around 20,000-30,000 tons. Its main application is fuel, and consumption in agriculture accounts for around 10%.

IHI to develop ammonia gas turbine with almost zero CO2 emission

(Aug. 18, Denki Shimbun)

- Ishikawajima Heavy Industries (IHI) developed an ammonia gas turbine that emits very small amounts of CO2. This is significant because most ammonia applications to date were co-combustion with coal. IHI has been developing ammonia gas turbines for 10 years.

- As a gas, ammonia has only 15% flow-heating value compared with hydrogen. However, as a liquid, the density is 10 times greater, making ammonia’s transportation efficiency much higher. Also, ammonia’s boiling point is higher than hydrogen, so the energy required for liquification is much smaller. For those reasons, IHI developed direct combustion of ammonia rather than taking hydrogen from ammonia.

- CONTEXT: IHI also plans to start 20% co-combustion of ammonia with coal at JERA’s Hekinan Coal-fired Power Plant in 2023, one year earlier than scheduled.

Japanese nuclear fusion startup selected as partner for UK’s STEP program

(Aug. 16, Denki Shimbun)

- Kyoto Fusioneering, a nuclear fusion startup at Kyoto University, was selected as the fifth consortium member by the UK nuclear fusion program STEP (Spherical Tokamak for Energy Production). Kyoto Fusioneering is the only company outside Europe in the list.

- By 2040, STEP plans to start power generation with a prototype reactor. Five candidate locations in the UK are under consideration; the design will be completed by March 2024.

- In the past, Kyoto Fusioneering received several orders from the STEP program.

Morinaga to start internal carbon pricing in 2023

(Company Statement, Aug. 12)

- Food manufacturer Morinaga will start internal carbon pricing (ICP) from 2023 after completing the ICP support program of the MoE. The company also participates in METI’s GX League that will launch the carbon trading platform.

- CONTEXT: Over 200 Japanese companies have introduced ICP but their methodologies are diverse, as reported by Japan NRG in late 2020.

TAKEAWAY: Morinaga’s ICP methodology that may reflect MoE and METI approaches is worth noting. MoE publishes ICP guidelines, which are revised reflecting the results of its annual ICP program. All Nippon Airways, Seibu Holdings and Daiwa House Industry are other participants of MoE’s ICP program. These three companies, however, are not part of the GX League, which is an initiative spearheaded by METI to develop a nationwide offset credit trading platform.

Osaka Gas to synthesize 90% of supply from waste CO2 by 2050

(Okinawa Times, Aug. 16)

- Osaka Gas is increasing its focus on methanation technology.

- By 2050, the company seeks to synthesize 90% of the gas it supplies from CO2 generated as a byproduct of industrial processes.

Sendai joint procurement initiative leads to savings on solar panels

(Kohoku Shimpo, Aug. 18)

- Sendai City launched a joint procurement plan to enable house owners and businesses to purchase solar panels for about 20% cheaper than usual.

- If purchased through the plan, a typical ten, 4 kW panel set will cost less than ¥900,000, which is a savings of about 24%.

Fukushima sets 2040 as total green energy target

(Nikkan Kogyo Shimbun, Aug. 19)

- The Fukushima prefectural government pledged to source 100% of its energy from renewables by 2040, and is promoting solar and wind power.

- The initiative has extensive local support, as evidenced by the fact that of the 900 members of a renewable energy association led by the prefectural government, 600 are local businesses.

- A solar panel operation and maintenance working group aims to extend the lives of PV panels through better maintenance, and to provide better options for recycling the panels at the end of their lives.

Renewables blind spot evokes memories of oil crisis

(Weekly Economist, Aug. 23)

- On June 27, unseasonably high temperatures caused demand for electricity across the TEPCO network to reach 52.5 GW – more than 10% above the peak demand in June in any of the last 10 years.

- Heavy investment in renewables in the wake of the Fukushima disaster meant that by 2016, the government no longer needed to call on consumers to conserve electricity, even without a single nuclear reactor operating.

- The Agency for Natural Resources and Energy blames structural factors for the return to electricity shortages in recent years.

- When it became clear that Japan’s nuclear power stations wouldn’t be restarted anytime soon, many new coal and gas fired power stations were planned.

- However, the subsequent rapid growth in renewables caused many of these plans to be scrapped amid poor profitability forecasts.

- Between 2017 and 2031, a net 25-GW decrease in total capacity of thermal power stations is projected.

- According to energy expert and International University of Japan lecturer Kikkawa Takeo, the government’s failure to articulate a clear policy on nuclear energy has meant that energy companies’ hands are tied.

- Kikkawa says it is counter-productive to respond to the energy crisis with subsidies such as those on gasoline. Rather, energy users need to be encouraged to conserve.

- While this approach means pain in the short term, in the long-term, it brings about the changes needed to create a low-carbon economy.

- During the oil crises of the 1970s, Japanese automakers’ efforts to conserve energy contributed to their phenomenal international growth.

NEWS: POWER MARKETS

Kyushu Electric to launch battery power trades in 2023

(Japan NRG, Aug. 18)

- In 2023, Kyushu Electric plans to launch battery power trading after its 4.2 MWh battery power storage system becomes operational, the company told Japan NRG.

- In a bid to build new business models, Kyushu Electric plans to trade battery power on the Japan Electricity Power Exchange (JEPX), the capacity market and the supply-demand balancing market.

- The system will initially store power generated by the grid, and will be open to solar operators outside of the Kyushu Electric group.

- The storage system, jointly run with NTT Anode Energy and Mitsubishi Corp, will be installed in the Tagawa district of Fukuoka prefecture by February 2023.

- CONTEXT: Kyushu Electric runs one of the world’s largest power storage systems. Located in Buzen, it has 300 MWh in capacity. The Kyushu area also has the highest renewable output curb rates among Japan’s regional grids.

Foreign shareholders sue Kansai Electric for not reporting bribe scandal

(Aug. 18, Nikkei)

- Kansai Electric reported that foreign shareholders filed a lawsuit against its U.S. subsidiary for not reporting in its securities filing that more than 80 employees including board members accepted bribes from the deputy mayor of Takahama City, where the utility’s Takahama NPP is located.

- The lawsuit, filed by 82 foreign KEPCO shareholders, seeks ¥24 billion in compensation.

- CONTEXT: The bribe scandal came to light in September 2019. Moriyama Eiji, a former deputy mayor of Takahama City, was linked to bribes in the amount of ¥370 million. He sought to win orders for his construction business. Moriyama was deceased by the time of the revelations.

TAKEAWAY: The lawsuit opens a very embarrassing chapter for the utility, which thought it was finally able to move on after personnel changes and a long process of rebuilding trust with the local community. At the very least, it will keep the issue in the public spotlight, potentially complicating further reactor restarts.

All 10 major power companies max out fuel surcharge

(Kyodo, Aug. 17)

- Chubu Electric is expected to raise domestic tariffs in October.

- This means that none of Japan’s 10 major electricity companies can pass on any additional increases in fuel costs according to government rules.

- This is the first time this has happened since 2009.

Tohoku Electric asks Authority to speed up Higashidori approval process

(NHK, Aug. 17)

- Tohoku Electric requested the NRA to identify issues preventing the restart of its Higashidori Unit 1 reactor in Aomori.

- Tohoku Electric said the vetting process needs to be more efficient.

- The process has so far taken over nine years.

- SIDE DEVELOPMENT:

Nuclear regulator turns 10

(Yomiuri Shimbun, Aug. 14)- To mark 10 years of the Nuclear Regulation Authority, the Yomiuri Shimbun asked top specialists what they think of the NRA.

- Former Chief Cabinet Secretary Shiozaki Yasuhisa says the establishment of an independent regulator was a good thing because previously METI was expected to simultaneously promote and regulate the industry, with the result that there was no objective regulation.

- However, autonomy doesn’t mean that you have no contact with Diet members, says Shiozaki. To date, the NRA has never held discussions with any government representatives. The NRA should take a more balanced approach, and stop unreasonably delaying reactor restarts at a time when there are power shortages, says Shiozaki.

Kashiwazai-Kariwa NPP wins approval for severe accident countermeasures

(Denki Shimbun, Aug. 18)

- Nuclear regulator, the NRA, approved modification of mandatory nuclear reactor severe accident countermeasures for units 6 and 7 of TEPCO’s Kashiwazaki-Kariwa NPP. This is the second such approval of a modification for a boiling water reactor (BWR), along with Tokai No. 2 NPP of Japan Atomic Power Co.

- TEPCO applied for this modification in December 2014. Four major revisions were required and the application was approved after 8 years of discussion. However, under NRA rules, TEPCO must get approval for its next review, which is for the design and construction required for accident countermeasures.

- The NRA is reviewing modifications for unit 2 of Onagawa NPP (Tohoku Electric Power) and unit 2 of Shimane NPP (Chugoku Electric Power). Tokai No.2 NPP, which already secured approval for the first stage, is on the next review.

TAKEAWAY: These are very small steps towards a restart of TEPCO’s only operable nuclear power facility, but they represent arguably the most progress the utility has seen in this area for a while. Last year’s estimates for a restart of the Kashiwazaki Kariwa NPP in the second half of 2022 are, of course, wide of the mark. However, the restart of at least one unit next year is now not impossible.

JERA to acquire 35% stake in Vietnam renewable developer Gia Lai

(Company Statement, Aug. 17)

- JERA acquired a 35.1 % stake in Vietnam’s Gia Lai Electricity.

- Gia Lai, which is listed on the Ho Chi Minh Stock Exchange, has 600 MW of hydro, solar and wind power plants. By 2025, it hopes to have 1.7 GW of capacity.

- TEPCO will dispatch two directors to Gia Lai, and monitor the company via JERA Energy Vietnam Co., hoping to jointly develop renewable energy projects.

TAKEAWAY: Japanese media is reporting that JERA paid about ¥15 billion for the stake in Gia Lai and may partner with the Vietnamese utility on new renewables projects. The structure seems similar to JERA’s Sept. 2021 investment in Aboitiz Power in the Philippines. It is interesting to note that JERA’s renewables strategy is much more focused on Southeast Asia than Japan at this moment.

Kansai Electric launches new solar leasing service

(Denki Shinbun, Aug. 16)

- Kansai Electric began a new solar service menu called “Happy-e Set Solar Regi”, which is part of “Happy-e Set”, a 10-year contract power supply campaign for household consumers combined with new technologies such as EVs, and ECO CUTE (a popular water heating and supply system that uses heat pump technology).

- Registration begins in October for the Kansai area. Electricity generated by the PV panels will be for home use; surplus power can be sold on the FIT system.

- After the 10-year lease expires, the equipment will be handed over to the customer.

Kansai Electric forced to abandon wind plans after just two months

(FNN, Aug. 17)

- Two months after announcing the project, Kansai Electric will abandon plans to build a major wind farm in Miyagi; the move that highlights the difficulties of building renewable infrastructure.

- While the site was chosen for its excellent wind conditions, the proposal met with fierce opposition from residents concerned about visual pollution.

- Under the proposal, some turbines would have been erected in a national park.

- Tohoku University lecturer Nakata Toshihiko says the case highlights problems with the environmental assessment process requiring operators to submit detailed plans at the outset, rather than negotiating details with residents.

Mihama NPP leak caused by loose bolt

(Asahi, Aug. 16)

- Kansai Electric said that a radioactive water leak from Unit 3 of its Mihama NPP was caused by failure to tighten a bolt used to secure a pressure vessel.

- It’s still not known when the reactor will start.

Gas companies diversify into renewables to stay afloat

(Weekly Economist, Aug. 16)

- CONTEXT: This is an opinion article by Yoshida Ai.

- Establishing new, greener revenue sources is a top priority for gas companies. By supplying both gas and electricity, Tokyo Gas and Osaka Gas both aim to grow into fully fledged energy providers that rival major power companies.

- In October 2021, Osaka Gas launched a power purchasing agreement (PPA) brand in conjunction with Osaka-based manufacturer Yamazen. Meanwhile, Tokyo Gas already has PPAs with dozens of schools.

- Next 21, an experimental housing development operated by Osaka Gas, uses EVs to manage energy resources.

- Both Tokyo Gas and Osaka Gas also plan major offshore wind farms.

Celebrity economist urges Tokyoites to install roof-mounted solar

(Mainichi ga Hakken, Aug. 17)

- CONTEXT: This is an article by celebrity economist Morinaga Takuro.

- Around half of all new residential buildings in Tokyo will soon be required to have roof-mounted solar panels.

- The average household can save ¥92,000/ year by installing a 4-kW system.

- This means that the initial investment will be recouped in 10 to 15 years even before subsidies. This should make solar a no-brainer.

- With 90% of roofs still empty, Takuro urges all those who haven’t yet installed solar panels to do so.

JERA’s Taiwanese wind farm goes online

(Nikkei, Aug. 17)

- The Formosa 2 wind farm, in which JERA owns a 49% stake, began supplying the Taiwanese grid with electricity.

- The farm will reach its full output of 380 MW by year’s end.

Eurus Energy’s Kamikatsu Kamiyama wind farm goes online

(Company Statement, Aug. 12)

- Eurus Energy began operation of the 34.5 MW onshore Kamikatsu Kamiyama wind farm, supplying power to Shikoku Electric.

- The wind farm is Shikoku’s largest and has 15 units of 2.3 MW mills made by Enercon.

NEWS: OIL, GAS & MINING

PM to visit Middle East amid high oil prices

(Nikkei, Aug. 19)

- Later this month, PM Kishida will visit Qatar, Saudi Arabia, Tunisia and the UAE.

- With Japan dependent on the Middle East for 90% of its crude oil, there’s a need to discuss price stability with the UAE and other oil producing nations.

- Kishida also expressed interest in the possibility of major increases in LNG supply by Qatar’s state-owned oil and gas companies.

Russia’s new Sakhalin-2 entity offers same terms

(Nikkei, Aug. 17)

- The newly-established entity in control of Russia’s Sakhalin 2 gas project is offering Japanese utilities the option to purchase gas on the same terms as they enjoyed before the project changed hands.

- New METI Minister Nishimura met with Mitsubishi Corp CEO Nakanishi to request investing in the newly established entity to maintain Mitsubishi’s involvement.

- Nishimura said he’s not aware of the imposition of any new terms or conditions that would make it difficult to perform the agreement.

ENEOS CEO Sugimori resigns

(Nikkei; Aug. 13)

- ENEOS Holdings CEO Sugimori Tsutomu resigned for personal reasons and won’t be replaced

- for the time being.

- Sugimori also resigned as an ENEOS director and his positions in the Petroleum Association of Japan and Keidanren.

- CONTEXT: Idemitsu vice-chair Kito Shunichi has taken over as head of the Petroleum Association of Japan for the time being.

SIDE DEVELOPMENT:

Speculation around ENEOS chair’s sudden resignation

(Oak Capital Investment, Aug. 14)- Sugimori’s retirement has given rise to speculation that he will soon be the subject of a tabloid scoop.

- Let’s consider the possibilities. Sugimori’s departure seems unlikely to be due to illness. Possibilities include ties to the controversial Unification Church, or former Minister of Economy, Trade and Industry Haguida Koichi, or even Olympic bribes.

July LNG, coal imports fall, oil up slightly

(Government Data, Aug. 17)

- July LNG and thermal coal imports were down from a year ago, but oil was up slightly. Japan imported 6.1 million tons of LNG, down 22.7%, YoY. Thermal coal imports were 9.4 million tons, down 4.1%. Crude oil imports were up 3.8% to 11.5 million kiloliters.

LNG stocks rise to 2.39 million tons

(Government Data, Aug. 17)

- LNG stocks of 10 power grids stood at 2.39 million tons as of Aug. 8, up from 2.3 million tons a week earlier. The end-August stocks last year were 2.43 million tons. The five-year average for this time of year is 1.85 million tons.

ANALYSIS

BY YOSHIHISA OHNO

Japan Pledges to Build Innovative Next-Gen Nuclear Reactors

But May Struggle to Maintain Industry Standing

Japan unveiled a new nuclear roadmap that outlines the development and construction of new facilities and reactor technologies.

The announcement came just days after the minister in charge repeated the government’s long-held position that no new nuclear energy construction projects were on the horizon, and that the dialog around this was unresolved.

This is not the only mixed message emanating from Japan on its nuclear policies. PM Kishida is urging progress on nuclear energy to ease the nation’s reliance on fossil fuel imports, yet METI’s roadmap speaks of commercial prospects that are at least a decade or two away.

What’s more, the technologies depicted in the roadmap seek to maintain METI’s ambition to develop the holy grail of nuclear technology – a so-called closed fuel cycle, in which there is little waste and the uranium is recycled. And yet, the timelines presented by the ministry are hardly reassuring that this goal will be achieved.

Background

Unlike most countries, Japan has developed several reactor types domestically. In addition to the Pressurized water reactor (PWR) system popular in most countries, it deploys the Boiling Water Reactor (BWR) technology.

It has also developed a number of other reactor technologies, such as one of the world’s most advanced high-temperature gas-cooled reactors, and several versions of fast and fast breeder reactors.

The Fukushima disaster, however, threw Japan’s nuclear R&D into disarray. Most work stalled without state funding and a number of the industry’s top firms announced exits or strategic shifts to other parts of the energy space.

It was not until the recent U.S. development of Small Modular Reactors (SMRs) and a revived interest in fast reactors that Japanese nuclear firms saw the chance for a revival. So far, collaborations with the U.S. Department of Energy, and American startups like NuScale and TerraPower, backed by Bill Gates, are the most prominent announcements, even if details are few and far between.

Still, such collaborations have little relevance without the potential to build new technologies. Until recently, with the public mood mostly against nuclear, few Japanese politicians were willing to discuss openly the need to replace the country’s aging reactors or build new units altogether.

The growing energy crisis has changed the dynamics. At the inaugural meeting for his Green Transformation (GX) Council on July 27, PM Kishida said the country faces an energy crisis as bad as the 1970s oil shock and must be more active in bringing

more of the nation’s nuclear stations online. Kishida’s support for nuclear energy has grown more frequent and vocal with rising energy prices, especially since Russia’s invasion of Ukraine in February, as well as subsequent economic sanctions, this year rocked fossil fuel markets.

Just two days after the GX meeting, however, METI held a session of the innovative reactor working group where then METI Minister Hagiuda stated that there’s still no consensus for replacing or constructing new nuclear power plants (NPPs). That type of ambiguity unnerves investors and corporate leaders.

Sensing this, on Aug. 9, METI clarified the situation and announced the new roadmap – the Development and Construction of Innovative Nuclear Power Plants. It is the first government pledge since the Fukushima accident in 2011 to build a new reactor.

Five key technologies

The latest roadmap clearly indicates that METI plans to reduce the size but maintain Japan’s nuclear industry, along with major international suppliers.

The roadmap centers on five nuclear power technologies. These are the advanced light water reactors, small modular reactors (SMR), fast reactors, high temperature gas-cooled reactors (HTGR), and nuclear fusion reactors.

According to METI bureaucrats, some of the five reactor types, if not all, are expected to be fully functioning and a commercial reality by the 2040s.

Beyond that, details are scant. Only the advanced light water reactors are given a deadline for commercial operations, which is described as “in the 2030s”. This technology is essentially a modified version of the LWRs already in use in Japan and also widely used in the U.S., Europe and Russia. As such, building them is considered the most practical and realistic first step.

Curiously, the roadmap does not promote the development of advanced BWRs, a reactor system that is already installed at units 6 and 7 of the Kashiwazaki-Kariwa NPP (Tokyo Electric; unit 5 of the Hamaoka NPP (Chubu Electric); unit 2 of the Shika NPP (Hokuriku Electric); and unit 3 of the Shimane NPP (Chugoku Electric).

While these are not considered to be the most advanced commercial reactor technologies to date, Japan has a good record in building advanced BWRs on-time and on-budget.

The reason is likely that the site of the 2011 accident, the Fukushima Dai-Ichi NPP, employed the much earlier BWR technology and as such there is less confidence about the system, at least in terms of presenting it to the public.

Slow rollout

The need for public acceptances of nuclear technologies is possibly the reason for such long lead times outlined in the roadmap for new reactor types. The timeline for HTGR and SMR construction is extremely leisurely. A demo plant for the former may come during the next decade and the latter during the 2040s. Details of commercial plants are not even discussed.

That jars when considering the international context. In July 2021, China began construction of the Linglong One 125 MW SMR, which is the world’s first commercial SMR, at the Changjiang NPP. In the UK, Rolls-Royce’s SMR design was accepted for review in March 2022. In July, the U.S. Nuclear Regulatory Commission gave final certification for NuScale’s SMR.

As for HTGRs, China’s test project at Shidaowan was connected to the grid on Dec. 20, 2021. Japan’s HTGR demonstration plant was offline for about a decade and was only switched back on earlier this year to operate in a limited R&D setting.

Given such long lead times set for new technologies, Japanese power utilities are likely to stick with the LWR designs they already deploy – and which are already approved by the regulator. METI experts have urged regulator representatives to be involved in new technology discussions, though it’s unclear how much this will speed up the process.

Without a strong domestic market, Japanese nuclear firms will need to work with overseas players to survive, thus reducing them to the role of supplier for specific components as opposed to provider of the reactor platform.

Fuel cycle ambitions

Perhaps the most curious part of METI’s roadmap is its inclusion of fast reactors. The premise of the technology is that it can run on recycled fuel, or even create fuel during the thermal process. This would cut the volume of raw uranium Japan needs to buy to create the fuel, improving energy security, while also cutting the volume of fuel waste.

Finding a place to store nuclear waste remains an unresolved issue in Japan.

The key part of such a virtuous fuel recycling strategy, known as the closed fuel cycle, is that it requires a spent fuel processing facility. The Rokkasho plant in northern Japan recently announced its 26th delay to launch.

Also, Japan’s history of fast reactors is far from reassuring. A large test plant, called Monju, was built near the Tsuruga NPP in Fukui Prefecture but after 15 years of accidents and mishaps it was slated for decommissioning in Dec. 2016.

Japan’s collaboration in fast breeder reactors with France was abandoned two years later. The 600 MW Advanced Sodium Technological Reactor for Industrial Demonstration (ASTRID) was due to be realized in France with Japan’s help, but the project was closed in November 2018.

Despite the setbacks, METI has kept its faith in fast reactors and prominently features them in the roadmap. The benefits of the closed fuel cycle are, of course, one reason. Another is more complex. Japan’s PWR and BWR reactors hold thousands of spent fuel rods that amount to over 15,000 tons of material.

The rods are kept inside cooling pools on the understanding that they will go to Rokkasho for reprocessing, and thus, leave no nuclear waste behind at nuclear power stations. If the fast reactor vision is canceled, then used fuel rods would be reclassified as nuclear waste and the utilities’ license to operate NPPs could be canceled with it.

ANALYSIS

BY JOHN VAROLI

TOP INTERVIEW: Australia’s Largest Listed Energy Company

Japan NRG sat down with Meg O’Neill, the CEO of Woodside Energy, which has recently merged with BHP’s oil and gas assets, to create one of the world’s top 10 independent energy companies. Woodside Energy is also heavily involved in Japan’s market energy and works with Japanese companies on projects in Australia. Meg shared her thoughts on future development of the Japanese market and its standing in Asia, among other topics.

GLOBAL LNG STRATEGY

In light of the merger with BHP’s oil and gas assets, and the tumult in global gas markets, how has your LNG strategy changed over the past 6 months?

Our strategy is to thrive through the energy transition with a low-cost, lower-carbon, profitable, resilient and diversified portfolio. This strategy remains unchanged following the merger with BHP’s petroleum business, with Woodside becoming a bigger supplier of the energy that the world needs now and will demand in the future.

The merger delivers a diverse portfolio of quality operating assets, plus a suite of growth opportunities across oil, gas and new energy that promises ongoing value for our shareholders.

Completion of the merger will enable Woodside to play a more significant role in the energy transition. With less carbon emissions than other fossil fuels, such as coal and oil, natural gas can help the world transition towards a lower carbon future. Gas accounts for more than 70% of Woodside’s production post completion of the merger.

JAPAN MARKET OUTLOOK

How do you view the Japanese market?

Woodside’s relationships with Japan date back to the critical Japanese investment in the Woodside-operated North West Shelf Project in the 1980s, when Japanese buyers underpinned the project by signing long-term gas supply agreements.

We have delivered safe, reliable, competitive LNG to Japan for more than 30 years. Our long-term relationships between energy suppliers and customers in Australia and Japan are built on trust and mutual respect. These relationships remain important as we see a significant ongoing role for Woodside’s LNG production to support our customers’ decarbonisation commitments.

This aligns with the Japanese Government’s “Outline of Strategic Energy Plan” published in October 2021, which assumes that LNG, while reducing from 37% in 2019, still makes up 20% of Japan’s electricity generation mix in 2030.

At Woodside, we are investing in new energy products and lower-carbon services to reduce customers’ emissions, including but not limited to, hydrogen, ammonia and carbon capture, utilisation and storage.

We have targeted $5 billion investment in new energy products and lower-carbon services by 2030. A key component of Woodside’s strategy to invest in new energy products and lower-carbon services is to work with potential customers to develop demand for new sources of energy.

Japan is seeking to decarbonise its economy by leveraging hydrogen energy in transportation, industry, power production, and other fields. Woodside’s recent Japanese collaboration highlights include:

- A new export project consortium with Japan’s IHI Corporation and Marubeni Corporation in connection with H2TAS, a proposed 100% renewable ammonia project to be located in Tasmania’s Bell Bay region, allowing expansion of the previous concept to export scale while also providing local supply.

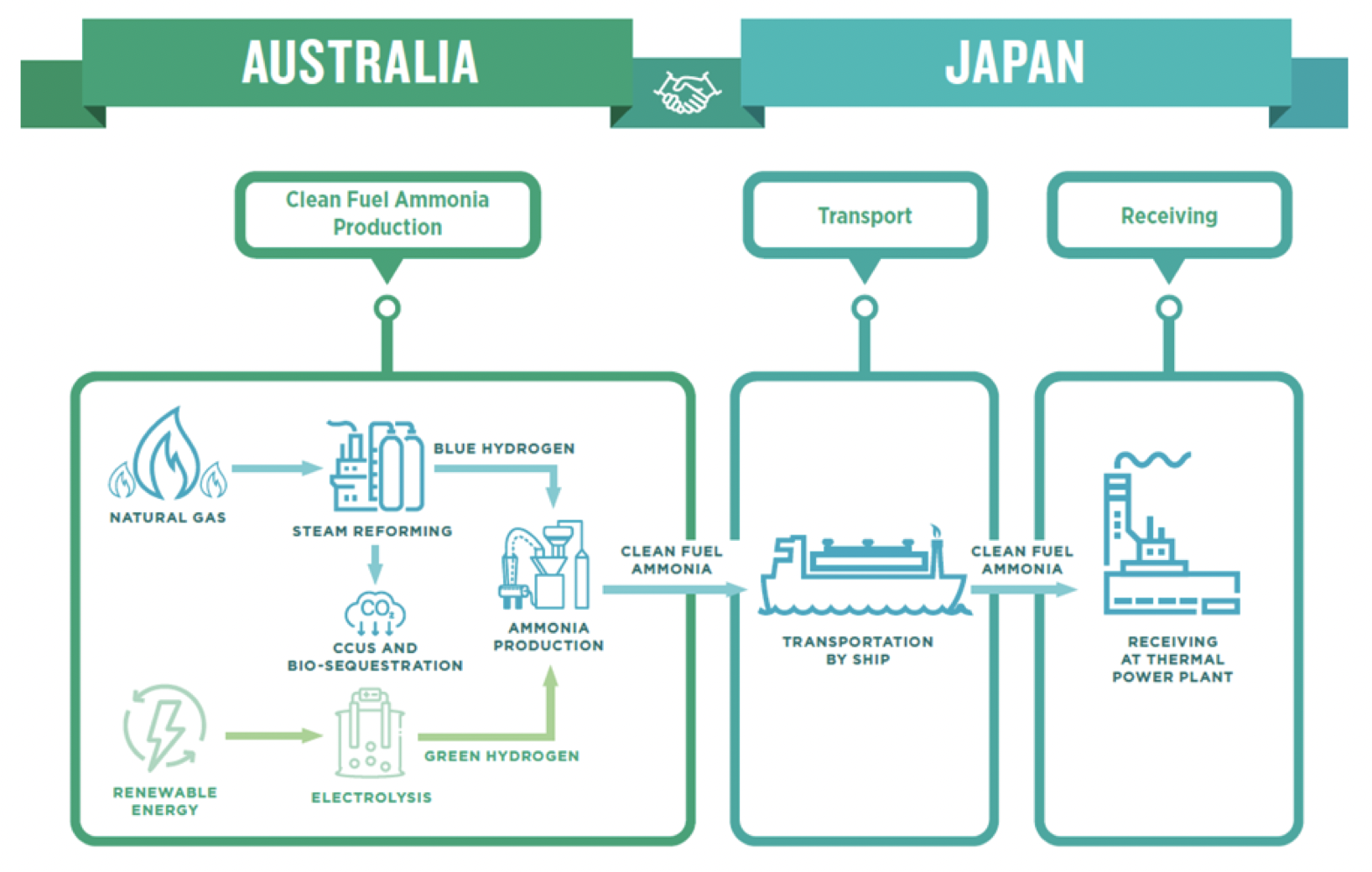

- A joint feasibility study to establish a clean fuel ammonia supply chain from Australia to Japan with Japan Oil, Gas and Metals National Corporation, Marubeni Corporation, Hokuriku Electric Power Company and The Kansai Electric Power Co., Inc.

- A MoU with Keppel Data Centres, City Energy, Osaka Gas Singapore and City-OG Gas Energy Services to study the feasibility of a liquid hydrogen supply chain to Singapore and potentially Japan from Woodside’s proposed H2Perth project, a world-scale liquid hydrogen and ammonia production facility on 130 hectares of industrial land in southern metropolitan Perth.

Is Japan less important now than the China market?

We supply a growing base of customers primarily in the Asia-Pacific region, including Japan and China. Both are important markets for Woodside.

What’s your more general view on Asian demand?

In the Asia–Pacific region, where 1.5 billion people are expected to enjoy better living standards and join the middle class by 2030, energy use is expected to increase. Woodside’s LNG can help Asia to decarbonise, for example by replacing coal, supporting renewables, and in hard to abate uses.

Scarborough gas, processed through Pluto Train 2 project, will be one of the lowest carbon intensity projects for LNG delivered to customers in North Asia. The Scarborough reservoir contains only 0.1% CO2, and Scarborough gas processed through the efficient and expanded Pluto LNG facility supports the decarbonisation goals of our customers in Asia.

CARBON CAPTURE TECH OUTLOOK

The latest G7 environment Ministers memo calls for abatement of the gas industry. Are you ready to move towards carbon capture at your new / existing projects? Are your buyers asking for this?

The G7 Leaders’ Communique (issued 28 June 2022) acknowledges the role of LNG in supporting global energy security as major consumers phase out reliance on Russian gas and transition to a cleaner future. Since the crisis in Europe has unfolded, LNG customers in Asia have sought to ensure they are securing energy from reliable and credible sources, highlighting the positive contribution that Australian producers can make and strengthening the case for Woodside’s established and emerging projects, such as Scarborough.

We recognise that while unabated natural gas can help countries move towards net zero greenhouse gas emissions, it cannot help them reach net zero on their own because most end uses of natural gas result in greenhouse gas emissions. To reach net zero these residual greenhouse gas emissions need to be abated, such as through carbon capture, utilisation and storage (CCUS).

We are working to develop our carbon capture and storage (CCS) capabilities and have established a dedicated team to build relationships and assess opportunities for the large-scale deployment of CCS.

Woodside has established a consortium with bp and Japan Australia LNG (MIMI) Pty Ltd to assess the opportunity to develop a large-scale, multi-user project near Karratha, Western Australia. The consortium will assess the technical, regulatory and commercial feasibility of capturing carbon emitted by multiple industries located near Karratha on the Burrup Peninsula and storing it in offshore reservoirs in the Northern Carnarvon Basin.

CARBON CREDITS AND “CARBON NEUTRAL” LNG

What’s your stance on carbon credits? There have been a lot of reports questioning the credibility of some forestry or other credit schemes. Are you still confident in credits? Any source of credits you particularly support?

Woodside established a carbon business in 2018 to develop a sustainable offset portfolio in support of our base business and new energy projects. We acquire offsets from carbon markets and also have been originating our own since 2012, managing them on a portfolio basis to optimise the cost of meeting both regulatory and corporate targets.

Woodside recognises that there are important conditions on the use of offsets: The emissions reduction hierarchy should prioritise avoiding and reducing emissions before offsetting them. Offsets must be scientifically verified and accurately accounted for using robust methodologies.

Does “carbon neutral” LNG have a future?

Woodside has a three-point Scope 3 emissions plan to invest in new energy products and lower-carbon services, support our customer and supplier emissions reduction and promote global measurements and reporting.

Some activities to achieve this include partnering with customers on data-sharing and technical collaboration and developing bilateral tracking and reporting methods with customers where we have agreed to deliver carbon-offset cargoes.

NEW BUSINESS OPPORTUNITIES

If there’s one non-LNG field, or segment, that you’d love to be involved in today, what would it be?

While we see a significant ongoing role for Woodside’s LNG production, we’re also investing in new energy products and lower-carbon services to reduce customers’ emissions, including but not limited to hydrogen, ammonia and CCUS.

Woodside is progressing a number of opportunities as part of a developing portfolio of new energy products and lower-carbon services. They include:

- H2Perth – a proposed world-scale hydrogen and ammonia production facility in southern metropolitan Perth, Western Australia.

- H2OK – a proposed liquid hydrogen production facility in Ardmore, Oklahoma.

- H2TAS – a proposed 1.7 GW renewable hydrogen and ammonia production facility near Bell Bay, northeast Tasmania.

Woodside is also working with Heliogen, a U.S.-based concentrated solar thermal (CST) energy developer, to build a 5 MW commercial scale single module demonstration facility in California. Heliogen’s AI-enabled technology has the potential to overcome the challenge of intermittency in solar power generation and offer nearly 24/7 power supply.

Woodside Energy together with JOGMEC, Marubeni and two Japanese power utilities are studying the feasibility of an ammonia supply chain between Australia and Japan

Source: JOGMEC Corp

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

China/ Solar energy

Haitai Solar completed its IPO, with 53.82 million shares now trading on the Beijing Stock Exchange. The new capital injection will help the solar power capacity and storage manufacturer strengthen its position in renewable energy.

Coal/ Record profits

Mining giant BHP delighted investors as surging coal prices pushed profits up by 26%. The Australian company declared a final dividend of $8.9 billion, or $1.75/ share, the highest disbursement in its 137-year history.

EU/ Clean energy metals

The EU wants to lower regulatory barriers to mining and production of green energy infrastructure materials such as lithium, cobalt and graphite that are needed for wind farms, solar panels and EVs.

Germany/ Natural gas

Energy company Uniper, which last month secured a €15 billion state bailout, is reported to be close to bankruptcy following a six-month loss of €12.3 billion. This is mainly due to problems with Russian gas supplies that forced Uniper to buy at higher prices elsewhere.

Greece/ Solar power

PPC Renewables is inviting bids to build a 550 MW solar power plant, which will be Greece’s largest PV facility. The estimated €216 million project will operate without state subsidies and sell electricity through power purchase agreements (PPAs).

Greenland/ Clean energy metals

Billionaires Jeff Bezos, Michael Bloomberg and Bill Gates are backing Kobold Metals, a California mining startup that will search for clean energy metals in Greenland’s Nuussuaq Peninsula, which might have major deposits of nickel and cobalt.

Oil/ Global markets

Barclays lowered its Brent price forecast by $8/ barrel for 2022 and 2023, expecting a surplus of crude over the near-term due to “resilient” Russian supplies. Barclays sees Brent averaging $103 this year and next. In related news, energy-rich Middle East states are set to earn as much as $1.3 trillion in additional oil revenues over the next four years, according to the IMF.

Russia/ Energy earnings

Higher oil export volumes to China and India, as well as rising gas prices, will boost Moscow’s earnings from energy sales to $337.5 billion in 2022, a 38% rise YoY, according to the country’s economy ministry.

Russia/ Natural gas

As Gazprom’s natural gas export and production continues to fall, European gas prices might rise by 60% to more than $4,000 per 1,000 c3/m this winter. Overall, Gazprom’s production was down 13.2%, YoY, to 274.8 billion c3/m.

Sri Lanka/ Wind power

Adani Green Energy secured provisional approval to invest over $500 million in two wind projects. Sri Lanka has been besieged with many economic woes and social unrest precisely due to the energy crisis.

Spain/ Renewable energy

Iberdrola’s €300 million, 590 MW Francisco Pizarro clean energy project began operations. It’s Europe’s largest PV project. Across Spain, Iberdrola has installed capacity of more than 19.3 GW. The company will spend €14.3 billion by 2025 to build more renewable capacity.

UK/ Coal power

Britain’s National Grid agreed with power generators Drax Group and EDF to extend the life of four coal-fired power units at two plants as a “last resort” in case other sources can’t provide enough electricity as the country faces an energy crisis in winter.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

| January | OPEC quarterly meeting;JCCP Petroleum Conference – Tokyo;EU Taxonomy Climate Delegated Act activates;

Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

| February | Chinese New Year (Jan. 31 to Feb. 6);Beijing Winter Olympics;South Korea joins RCEP trade agreement |

| March | Renewable Energy Institute annual conference;Smart Energy Week – Tokyo;Japan Atomic Industrial Forum annual conference – Tokyo;

World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

| April | Japan Energy Summit – Tokyo;MARPOL Convention on Emissions reductions for containerships and LNG carriers activates;Japan Feed-in-Premium system commences as Energy Resilience Act takes effect;

Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

| May | World Natural Gas Conference WCG2022 – South Korea;Elections: Australian general election; Philippines general and presidential elections |

| June | Happo-Noshiro offshore wind project auction closes;Annual IEA Global Conference on Energy Efficiency – Denmark;UNEP Environment Day, Environment Ministers Meeting – Sweden;

G7 meeting – Germany |

| July | Japan to finalize economic security policies as part of natl. security strategy review;China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong;Czech Republic assumes presidency of EU;

Elections: Japan’s Upper House Elections; Indian presidential election |

| August | Japan: Africa (TICAD 8) Summit – Tunisia;Kenyan general election |

| September | IPCC to release Assessment and Synthesis Report;Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.;Japan LNG Producer/Consumer Conference – Tokyo;

IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

| October | EU Review of CO2 emission standards for heavy-duty vehicles published;Chinese Communist Party 20th quinquennial National Party Congress;G20 Meeting – Bali, Indonesia;

Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

| November | COP27 – Egypt;U.S. mid-term elections;Soccer World Cup – Qatar; |

| December | Germany to eliminate nuclear power from energy mix;Happo-Noshiro offshore wind project auction result released;Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26;

Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.