JAPAN NRG WEEKLY

SEPT. 26, 2022

JAPAN NRG WEEKLY

Sept. 26, 2022

NEWS

TOP

- Winter power supply seen improving due to early unit restarts of nuclear and thermal capacity, but outlook beyond 2023 cloudy

- TEPCO to hike corporate tariffs by as much as a sixth as utilities seek to change electricity pricing model to reflect rising costs

- “Green food” financing scheme launches as the govt. decides to double down on biomass-derived energy raw materials

ENERGY TRANSITION & POLICY

- State-private council on e-fuels created to build supply chains

- Narita Airport starts sourcing local sustainable aviation fuel

- Idemitsu gets subsidy for 250 MW Australian pumped hydro plan

- Japan’s top automakers agree to pay EV-related patent fees as the country prepares to test wireless charging for EVs on roads

- Georgia becomes 22nd nation to join Japan carbon credit scheme

- METI pledges to start design of a test fast reactor in 2024

- Japan govt. keen to create a national nuclear fusion strategy

- Kansai Electric to develop CCS technology for JOGMEC

ELECTRICITY MARKETS

- Major regional utilities push to phase out fuel cost adjustment cap

- Five thermal power plants to come online during 2023: OCCTO

- METI reports errors in estimates for how much capacity will retire

- Kyushu Electric struggled to avoid blackouts in extreme weather

- DMG Mori plans one of Japan’s biggest private solar farms

- Wind turbine startup raises new funding from retail billionaire

- Sumitomo Electric delivers energy storage system to Kawasaki

OIL, GAS & MINING

- LPG, biogas, hydrogen and gasified coal seen as LNG alternatives

- INPEX to explore new domestic natural gas field

- Sempra says will consider blue hydrogen exports to Japan

- Toho Gas makes its first overseas expansion

- August LNG imports slump, but stocks remain seasonally elevated

- Reason behind sudden resignation of ENEOS CEO is revealed

ANALYSIS

TOP INTERVIEW

JERA’S DECARBONIZATION STRATEGY CHIEF

Japan’s top power utility and LNG importer, JERA, has embarked on an ambitious strategy to shift its power plants to burn ammonia and potentially hydrogen. This has already led the company to announce the world’s biggest tender for ammonia supply. Japan NRG sat down with Takahashi Kenji, GM of the Decarbonization Promotion Section at JERA’s Corporate Strategy Dept. to discuss how the ammonia tender is going and the company’s plans to move away from coal. We also talked about the future of CCS, JERA’s outlook for Southeast Asia, and how the company sees “carbon neutral” LNG.

WAS JAPAN’S POWER MARKET DEREGULATION A FAILURE? NEW ENTRANTS FACE FIGHT TO SURVIVE

Japan’s retail electricity market may be facing its greatest crisis since the end of World War II. Rapidly rising energy prices have forced many electricity retailers into bankruptcy or market exit. At the center of this upheaval are companies that sprung up since 2016, the Power Producer and Suppliers (PPSs). These companies came in to challenge the regional utilities, betting that deregulation and a shift to cheaper or renewable power sources would ease the incumbents’ grip on the market. This strategy worked for years but has come unstuck in the last 12 months. How many of the PPS will be able to survive this challenging time? We review the prospects.

GLOBAL VIEW

UN and IRENA outline scale of renewable investment needed by 2030, but UN also tweaks net-zero outlook to allow some coal projects. Germany nationalizes gas importer Uniper. China purchases of Russian oil hits records. Fracking under pressure in Australia. Details on these and more in our global wrap.

EVENTS SCHEDULE

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Yoshihisa Ohno (Japan)

Wilfried Goossens (Events, global)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

Events

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

“Green food” financing starts as govt decides to double biomass-derived energy

(Japan NRG, Sept. 15)

- The Ministry of Agriculture, Forestry and Fisheries is accepting applications for low-interest loans to build sustainable low-carbon food supply chains.

- On Sept. 6, the Kishida Cabinet approved the basic biomass plan prepared in July, doubling the share of biomass power to 2% of total energy by 2030.

- Green food financing aims to reduce consumption of fossil-derived fertilizer by 30% and to increase organic farming areas 25% by 2050.

- A typical project involves recycling livestock manure into energy and fertilizer resources, and reducing methane emissions.

Major biomass materials

|

|

Annual supply |

Reuse rate |

2030 target rate |

|

Livestock manure |

80 million tons |

86% |

90% |

|

Sewer waste |

79 million tons |

75% |

85% |

|

Paper |

85 million tons |

80% |

85% |

|

Food waste |

24 million tons |

58% |

63% |

|

Crop waste |

12 million tons |

31% |

45% |

|

Forest waste |

9.7 million tons |

29% |

Over 33% |

|

Scrap wood |

5.5 million tons |

96% |

96% |

TAKEAWAY: Japan’s biomass supplies could increase as the country’s reuse rate of agricultural waste is 92% and wood scrap 29%. However, obtaining the proper balance between energy and food security requirements will be challenging since biomass demand will outstrip supply.

MAFF has oversight over biomass production, but METI has authority to determine which biomass materials can be used as fuel.

METI’s standard is that inedible material could be fuel, but it’s not so simple. Farms reuse some inedible material for livestock feed or fertilizer. The present METI system does not allow farms to take part in energy policy discussions, which vexes the farming sector.

Biomass market is estimated at ¥500 billion.

See also “Once Trash, Used Cooking Oil Now Center of Tug-of-War Between Food and Jet Fuel” —in the May 23, 2022 issue of Japan NRG.

Government-private sector council on e-fuel launched

(Government statement, Sept. 16)

- A government-private sector council on synthetic fuel was launched to build the sector supply chain and set up a framework to assess its decarbonization impact. Working groups to drive the fuel’s commercialization and design a regulatory framework for it were also established.

- The council comprises Japan Petroleum Association, Japan Automobile Manufacturers Association, as well as the industrial bodies representing gasoline service stations, shipping and aviation sectors. Also included are METI, ANRE, Ministry of Land, Infrastructure, Transport and Tourism, and research institutes NEDO and AIST.

- If 5% of gasoline switches to e-fuel, the amount of carbon reduction would equal that of 3 million EVs, according to Zensekiren (National Federation of Oil Product Business Unions).

TAKEAWAY: So far, the production cost of e-fuel is ¥300-700/ liter. Bioethanol is positioned as a near-term transition fuel until e-fuel commercialization. Bioethanol import costs are one-third of e-fuel costs. See also the analysis “Toyota Has Not Given Up on Gasoline: Automaker Plans to Develop Green Gasoline” in the Sept. 5, 2022 issue of Japan NRG. Nissan Motor has also been developing biofuel cell vehicles.

METI, JFTC clarify electricity rate rule in power trade guidelines

(Government statement, Sept. 20)

- METI and the Japan Fair Trade Commission stated in power trade guidelines that while power operators have the capacity to modify rate structures to reflect fuel costs, they need to be transparent about how they pass on the cost changes.

TAKEAWAY: Overcharging users is typically a consumer issue but becomes a competition issue if the conduct is considered to be an “abuse of superior position” as banned by the Antimonopoly Act. The guidelines might be updated again to ensure competition law compliance in B2B deals as more multi-party demand-response, aggregation and virtual power plants enter the market.

Government publishes human rights due diligence guidelines

(Government statement, Sept. 14)

- METI set guidelines for human rights due diligence throughout supply chains, complying to OECD and International Labor Organization standards and reflecting feedback from 131 individuals and organizations.

TAKEAWAY: The guidelines apply to B2B activity, meaning Japanese investments into Russian energy projects possibly aren’t covered since the deals involve the state, according to a business lawyer.

(Government statement, Sept. 13)

- Georgia is the 22nd nation to join the JCM scheme

- Japanese trading houses have considered investing in Georgian mines for steel raw materials.

Airport begins using locally-made green fuel

(Business Insider, Sept. 21)

- Narita Airport had its first-ever local sustainable aviation fuel (SAF).

- Produced by Japanese manufacturer Euglena, the SAF comprises 10% biofuel sourced from algae and discarded cooking oil.

- Euglena plans to increase the percentage of biofuel in the mix to 30%.

Idemitsu to receive subsidies for 250 MW Australian pumped hydro project

(The Chemical Daily, Sept. 21)

- Idemitsu will receive subsidies worth up to AU$9.5 million for a project to convert a disused coal mine into a pumped hydro facility in New South Wales.

- The project will store energy by pumping water between two ponds that are a vertical distance of 500 meters apart.

- Idemitsu plans to operate the facility in partnership with AGL Energy.

Japanese automakers to pay Avanci connected-car technology fees

(Avanci statement, Sept. 21)

- Toyota Motor, Nissan Motor and Honda Motor agreed to pay fees to license telecom technology patents to Avanci, a U.S.-based consortium consisting of global wireless tech firms. NTT DoCoMo, Mitsubishi Electric and Fujitsu are Avanci members.

- The automakers will pay fees for 2G, 3G and 4G licenses but not 5G.

TAKEAWAY: Avanci licenses don’t include wireless power transmission technologies for EV charging stations. Also, Samsung and Huawei are among the telecom technology giants that are not part of Avanci as they have their own licensing policies.

Automakers paying for patents required for telematic control units reduces the cost burden on unit manufacturers. In the past, component suppliers were expected to pay all license fees. Automakers will pass on the increase for licenses and raw materials; the license cost is negligible compared to battery costs.

Japan to test wireless charging for EVs on roads

(Asia Nikkei, Sept. 20)

- Construction group Obayashi and auto parts supplier Denso aim to add coils below the road surface and introduce a working wireless road charging system by 2025.

METI pledges to start design of test reactor for sodium-cooled fast reactor in 2024

(Denki Shimbun, Sept. 14)

- In 2024, the Agency for Natural Resources and Energy will work on a prototype design for a sodium-cooled fast reactor.

- The Fast Reactor Design Working Group decided that the sodium-cooled fast reactor is a better option than the light-water cooled fast reactor and the Molten-Chloride Fast Reactor. The decision was based on the following criteria: 1) established technology; 2) marketability after starting business operation; 3) production cooperation with relevant organizations at home and abroad; 4) regulation issues.

TAKEAWAY: Fast-reactor technology is at the center of Japan’s national nuclear policy because it’s considered the best solution not only for power supply, but also for radioactive waste. However, since the technical issues at the Monju prototype fast breeder reactor in 1995, the technology has been out of favor. The government decided to decommission Monju in late 2016. The fate of Japan’s sodium-cooled fast reactor may depend on the success of the U.S. startup TerraPower’s collaboration with JAEA and MHI.

Japan to work on nuclear fusion strategy

(Denki Shimbun, Sept.14)

- The government discussed a nuclear fusion strategy, to be finalized in April 2023.

- Securing equipment was discussed, to give Japan an edge over other countries.

- Nuclear fusion technology is being developed at ITER in France. The U.S., UK and China have all made nuclear fusion a priority.

Kansai Electric to develop CCS technology for JOGMEC

(Denki Shimbun, Sept. 20)

- Kansai Electric will study the technology and costs involved to create a value chain for CCS (Carbon capture and storage). The plan is to capture CO2 from thermal power plants; then send it via pipeline to liquidization facilities, and to storage by ship.

- JOGMEC sponsored the research. Kansai Electric will submit a final report by the end of February 2023, and make a detailed plan for the technology if the business side is viable.

- The Council for Long-Term CCS Roadmap plans to start domestic CCS use by 2030.

NEDO, RITE and MHI Engineering developed DAC test facility

(Denki Shimbun, Sept. 21)

- NEDO, RITE, and Mitsubishi Heavy Industries (MHI) developed a test facility for Direct Air Capture in RITE’s headquarters (Kizugawa city, Kyoto).

- This test facility will be able to capture a few kilos of CO2 from the air, but it still needs to make a final decision on a high-performance absorber, which is under development at RITE.

- Direct capture of CO2 is very difficult as its concertation in open air is low. However, a facility that can capture 10 tons of CO2/ day is planned for the late 2020s.

- This is a part of NEDO’s Moonshot R&D Program.

Mitsui enters green hydrogen, ammonia markets in Australia

(Company Statement, Sept. 16)

- Mitsui will acquire a 28% interest in the Yuri project, the industrial-scale renewable hydrogen project in the Pilbara region of Western Australia being developed by France’s Engie.

- It includes an 18 MW solar power plant and a 10 MW electrolysis facility that will produce 640 tons of ammonia annually.

- That ammonia will be sold to the local plant of Yara International, one of the world’s largest producers of nitrogen-based fertilizers, that will begin operation in 2024.

Australian ammonia to be exported to Japan

(Denki Shimbun, Sept. 16)

- JOGMEC, Marubeni, Hokkaido Electric, Tohoku Electric, Hokuriku Electric and Kansai Electric are continuing work on a feasibility study to supply Australian ammonia to Japan.

- This project was started in 2021, and focuses on natural gas reformulation equipment and ammonia production technology. The second stage of the study is scheduled to finish by February 2023.

- The six Japanese companies concluded collaborative research with Woodside Energy to produce ammonia from natural gas for export to Japan. The emitted CO2 is meant to be offset with CCUS and local afforestation.

JNFL approves new design of planned MOX fuel plant

(Denki Shimbun, Sept. 16)

- Japan Nuclear Fuel Ltd (JNFL) said that the NRA approved construction of a MOX fuel production plant that meets the new regulations passed after the Fukushima accident.

- This plant will be built near the Spent Nuclear Fuel Reprocessing Plant. Its construction started in October 2010, but stopped after Fukushima.

- This MOX fuel plant is scheduled to begin operation in the first half of 2024.

TAKEAWAY: MOX fuel would be used at NPPs such as units 3 and 4 of Takahama NPP (Kansai Electric), unit 3 of Ikata NPP (Shikoku Electric), or unit 3 of Genkai NPP (Kyushu Electric). J-Power’s Ohma NPP (under construction) plans to use 100% MOX fuel.

METI to reconsider “40-years rule” for nuclear reactors

(Sankei Shimbun, Sept. 22)

- At a Nuclear Energy Subcommittee meeting, METI said there’s no scientific evidence to limit operation of NPPs to 40 years and that it wants to reexamine the rule together with the NRA.

- In August, PM Kishida called for a review of the “40-year rule” for NPPs.

- If a 40-year limit was applied to all reactors in Japan, only three would be operating by 2050. Before Fukushima, there was no limit on the operational period.

TAKEAWAY: In the U.S., reactors can operate for up to 80 years. In the UK, there’s no limit, but each unit is evaluated every 10 years. If Japanese reactors are to operate for a much shorter period than other countries, this gives a wrong impression about nuclear safety in the country. It would be a tacit admission that Japan’s nuclear equipment is unreliable.

This also comes at a time when public opinion is turning more positive on nuclear energy than it has been since the Fukushima disaster. The latest poll by the Nikkei, published on Sept. 19, showed 53% of the respondents support Kishida’s recent call to build next-generation reactors with only 38% against.

|

US |

No legally binding limit |

Six reactors have cleared regulatory reviews to run up to 80 years; 9 are under review |

|

UK |

No legally binding limit |

Safety reviews every 10 years |

|

France |

No legally binding limit |

Safety reviews every 10 years; 20 out of 56 reactors have been running for over 40 years |

|

Netherlands |

Plants’ operational periods written in law, but no limit |

Plans to extend reactor operating lives to beyond 60 years |

|

South Korea |

No legally binding limit |

Safety reviews every 10 years |

Source: METI

IEEJ report highlights decarbonization challenges

(Gas Energy News, Sept. 19)

- The Institute of Energy Economics, Japan (IEEJ) reported that the high cost of renewable energy in Japan is a hurdle for businesses trying to reduce GHGs.

- Limited available land and restricted grid access are the reasons for renewable energy’s high costs.

- The report also criticized carbon-neutral certification and power purchasing agreements (PPA), calling for better tracking of carbon-neutral certificates.

- The government should issue guidelines on the use of PPA to dispel concerns around the creditworthiness of the corporations that use them, says the report.

NEWS: POWER MARKETS

TEPCO to hike corporate tariffs by up to 14%

(Nikkei, Sept. 20)

- TEPCO’s retail arm TEPCO Energy Partner plans to raise tariffs to corporate subscribers by between 12 and 14% in April.

- The increase is the result of a move to a new pricing scheme that more closely reflects actual generation costs by tracking volatile fuel costs and JEPX price.

- In future, corporate tariffs will be revised monthly on the basis of wholesale energy prices. And yet, while a 50% drop in wholesale prices will only cause corporate tariffs to fall by around 6%, if wholesale prices go up another 50%, corporate tariffs will rise by up to 36%.

- Wholesale energy prices are now around three times higher than last year. Currently, TEPCO is selling electricity at much lower prices than purchased for some contracts.

- SIDE DEVELOPMENT:

EPCOs push nuclear restarts by threatening greater price hikes

(Sentaku, September edition)- Electricity price hikes are imminent. In May, Kyushu Electric said it will abolish the fuel cost adjustment system starting October, earlier than any others. The average fuel price exceeded the ceiling price by 1.5 times as of September’s rate calculation, making it impossible for companies to cover the fuel cost increases on their own.

- From November onwards, the fuel cost adjustment cap will be phased out by Chubu, Hokkaido and Tohoku EPCOs.

- Also, TEPCO, Kansai Electric and Chubu Electric said they’ll raise rates for corporate customers starting 2023.

- Under these circumstances, “negative opinions about restarting nuclear power plants are dissipating”, says a senior EPCO executive. Nuclear is needed to avoid price hikes.

TAKEAWAY: The 10 major EPCOs have ¥5 trillion in cash, and reserves exceed ¥2 trillion. This makes their calls for raising electricity prices suspect in the eyes of many in the media as the perception remains that EPCOs must primarily serve a social role. The companies will argue that since deregulation they cannot be expected to both compete in an open market and act in the greater public good while suffering losses. PM Kishida and his government will be wary of pushing utilities to continue absorbing rising costs ahead of a crucial winter period. A compromise solution via subsidies to EPCOs to reign in power bills is likely.

- SIDE DEVELOPMENT:

Ex-KEPCO president fears JFTC’s decision over “electricity cartel”

(Sentaku, September edition)- KEPCO is anxious about the pending decision of Fair Trade Commission (JFTC) on the alleged cartel of four EPCOs (KEPCO, Chubu Electric, Chugoku Electric and Kyushu Electric) that want to remove the cap on the fuel cost adjustment system allowing to pass fuel costs onto electricity prices.

- KEPCO’s Takashi Morimoto was said to be in charge of the cartel. In April he stepped down and while he’s no longer chairman, he can’t avoid the lawsuit if KEPCO is ordered by the JFTC to pay a surcharge.

- On Aug 1, three members of the management team of KEPCO, including former chairman Shosuke Mori, were deemed liable for prosecution for accepting money and goods in relation to the company’s NPPs. The PM’s office is worried that continued loss of confidence in KEPCO will lead to public discontent over the energy crisis.

Winter power supply to improve thanks to early plant restarts

(Government statement, Sept. 15)

- Power supply in Jan-Feb will improve as restarts of Kansai Electric’s Takahama nuclear and Tohoku Electric’s Shinchi thermal power stations are moved forward, said the Organization of Cross Coordination of Transmission Operators (OCCTO). Also, power operators sought 1.6 GW more supplies from third parties, raising power reserve rates above the critical 3% threshold.

- OCCTO previously forecast that the reserve rates for all areas except Hokkaido and Okinawa were 1.5-1.9% in January, and 1.6-3.4% in February. Thanks to the restarts and additional third-party supplies, reserve rates improved to 3.4-4.8% in January and 4.1-6.4% in February.

- OCCTO also noted regional grids in Tohoku and Tokyo areas, which seek over 1 GW of additional supplies, could source only 779 MW since some bids were above the price cap. METI is studying raising the cap since restarts of old thermal plants may be costly.

- OCCTO forecasts that reserve rates will hold above 3% in the year to March 2024, but it will be tight in Tokyo and Chubu during summer

Updated power reserve rates in % (previous forecast dated June 30)

|

|

January |

February |

|

Hokkaido |

7.9 (6.0) |

8.1 (6.1) |

|

Tohoku |

3.4 (1.5) |

4.1 (1.6) |

|

Tokyo |

3.4 (1.5) |

4.1 (1.6) |

|

Chubu |

4.8 (1.9) |

6.4 (3.4) |

|

Hokuriku |

4.8 (1.9) |

6.4 (3.4) |

|

Kansai |

4.8 (1.9) |

6.4 (3.4) |

|

Chugoku |

4.8 (1.9) |

6.4 (3.4) |

|

Shikoku |

4.8 (1.9) |

6.4 (3.4) |

|

Kyushu |

4.8 (1.9) |

6.4 (3.4) |

|

Okinawa |

33.1 (39.1) |

34.4 (40.8) |

TAKEAWAY: OCCTO’s figures show Japan could live through the coming winter but needs to come up with new approaches for 2023 and beyond.

Plant restarts were brought forward by curtailing the maintenance period or changing their schedules. Some experts warn that if this measure continues, risks of unplanned plant shutdowns will increase. Seeking third-party supplies would cost the grids ¥105 billion this winter.

Five thermal power plants to come online in 2023

(Government statement, Sept. 15)

- OCCTO said five thermal power plants will start commercial operation in 2023: four in the Tokyo area and one in Shikoku; with a total capacity of about 3 GW.

|

Area |

Power station |

Capacity |

Commercial service launch |

|

Tokyo |

Anegasaki 1 |

647 MW |

February |

|

Anegasaki 2 |

647 MW |

April | |

|

Anegasaki 3 |

647 MW |

August | |

|

Anegasaki 4 |

650 MW |

June | |

|

Shikoku |

Saijo 1 |

400 MW |

June |

METI reports errors in figures estimating how much power capacity will retire

(Government statement, Sept. 15)

- METI reported errors in the figures of scrapped and new thermal capacities published last year and used for policy debates. For example, it said that from 2021 to 2030 the scrapped thermal capacities will total 27.65 GW when it should be 43.33 GW. It had put new thermal capacity higher and decommissioned capacity lower than the actual. The corrections are in the table below.

|

2016-2020 |

Corrected as |

Previous figure |

|

New capacity |

14.99 GW |

15.53 GW |

|

Decommissioned capacity |

16.72 GW |

16.55 GW |

|

2021-2030 | ||

|

New capacity |

14.31 GW |

14.44 GW |

|

Capacity to be decommissioned |

43.33 GW |

27.65 GW |

- METI said that miscounting occurred when new plant operations were delayed into the new fiscal year; also, plants that suspended operations were not included in the decommissioned figure, and some plants that will be decommissioned were not included.

TAKEAWAY: A deliberate error or an honest mistake? That’s the question most are asking around this issue. Part of the issue here is that METI’s definitions are confusing. New capacity means all newly planned installations of grids and non-grid operators. Decommissioned capacities include only those of key regional grids that haven’t operated for 45 years.

METI provided a list of thermal power plants of the major grids as of September, which is not a full list as plants owned by manufacturers and other non-grid businesses, mostly coal plants, aren’t included.

Kyushu Electric struggled to avoid blackouts amid extreme weather

(Denki Shimbun, Sept. 16)

- While Kyushu Electric can count on power from restarted nuclear power plants, its system remains vulnerable during extreme weather events.

- This summer, Kyushu Electric faced unexpected hot weather and needed emergency power supply from other EPCOs.

- Kyushu Electric needed power in the evening when solar output dropped but demand didn’t. On Sept 12, other EPCOs supplied up to 700 MW; and on Sept 13 up to 400 MW.

- This was the first emergency power supply since January 2021 when the power reserve of the Kyushu area fell to minus 0.8 due to unexpected cold weather.

- Takeaway: If Kyushu Electric hadn’t been rescued, the power reserve might have fallen to minus 1.6% on Sept 12, and zero on Sept 13. This would have resulted in a blackout. Japanese politicians must think more seriously about security of the electric power supply, rather than saying “no more nuclear power” or ”more renewable energy”.

DMG Mori plans solar farm to lower emissions

(Nikkei, Sept. 20

- Major equipment manufacturer DMG Mori plans to build a 13 MW solar farm near its Mie factory in 2025 in a bid to lower its carbon emissions.

- CONTEXT: The farm will be one of Japan’s largest private solar farms.

Wind turbine startup raises ¥1.2 billion for revolutionary technology

(PR Times, Sept. 22)

- Tokyo-based Challenergy raised ¥1.2 billion from the Maezawa Fund.

- The money will be for R&D of “magnus” vertical axis wind turbines that are able to generate electricity from strong winds, even during typhoons.

- The Maezawa Fund is led by billionaire and space tourist Maezawa Yusaku.

Sumitomo Electric delivers energy storage system to Kawasaki Thailand

(NNA Asia, Sept. 23)

- Sumitomo Electric delivered a 550-kWh energy management system to Thailand-based Kawasaki Motors Enterprise.

- The system will form part of services provided under a third-party on-site power purchasing agreement (PPA).

- Sumitomo has not disclosed how much it was paid for the system.

NEWS: OIL, GAS & MINING

LPG, biogas, hydrogen and gasified coal as alternatives to LNG

(Japan NRG, Sept. 15)

- METI is looking into LPG, hydrogen, biogas, synthetic methanol as potential substitutes of LNG. LPG has already been used by some city gas utilities as LNG substitutes and it could meet up to 1.5% of Japan’s total LNG demand, according to the Japan Gas Association. The utilities need to react the gas with nitrogen to adjust the different heat levels of the two gases.

- Professor Matsuhashi Ryuji of Tokyo University proposed state-funded research to gasify coal.

- CONTEXT: Japan consumes 1.5 million tons/ month of LPG. Half of those are imports.

INPEX to explore new domestic natural gas field in Japan

(Asia Nikkei, Sept. 22)

- INPEX plans to start exploring a new domestic gas field in November amid rising prices for the fuel and energy security concerns.

- Gas reserves have already been confirmed in an area near the Minami-Nagaoka gas field, one of the country’s largest. Now INPEX will conduct a prospecting survey in the area until next summer with a plan to start output in 2026.

- The next challenge will be to estimate how much the field can produce. Details around volumes and investments are not disclosed.

- CONTEXT: If this gas field goes live in 2026, it will be Inpex’s first in 16 years.

Sempra considers blue hydrogen exports from US to Japan

(Asia Nikkei, Sept. 20)

- Sempra Energy is considering the export of hydrogen made from LNG with deployment of carbon capture to Japan and other parts of Asia, Sempra Infrastructure President Dan Brouillette told Nikkei.

- Sempra could use its Cameron LNG plant in Louisiana to develop hydrogen.

- CONTEXT: Trading houses Mitsui and Mitsubishi and the shipper Nippon Yusen are investors in the Cameron LNG project.

Toho Gas expands to Thailand

(Nikkan Kogyo Shimbun, Sept. 23)

- Toho Gas began selling gas to commercial subscribers in Thailand in a JV with Shizuoka Gas.

- CONTEXT: This represents Toho Gas’ first ever overseas venture.

- Toho aims to tap into growing demand for gas in the nation.

LNG stocks rise to 2.62 million tons

(Government data, Sept. 21)

- LNG stocks of 10 power grids stood at 2.62 million tons as of Sept. 18, up from 2.4 million tons a week earlier. The end-September stocks last year were 2.46 million tons. The five-year average for this time of year is 1.94 million tons.

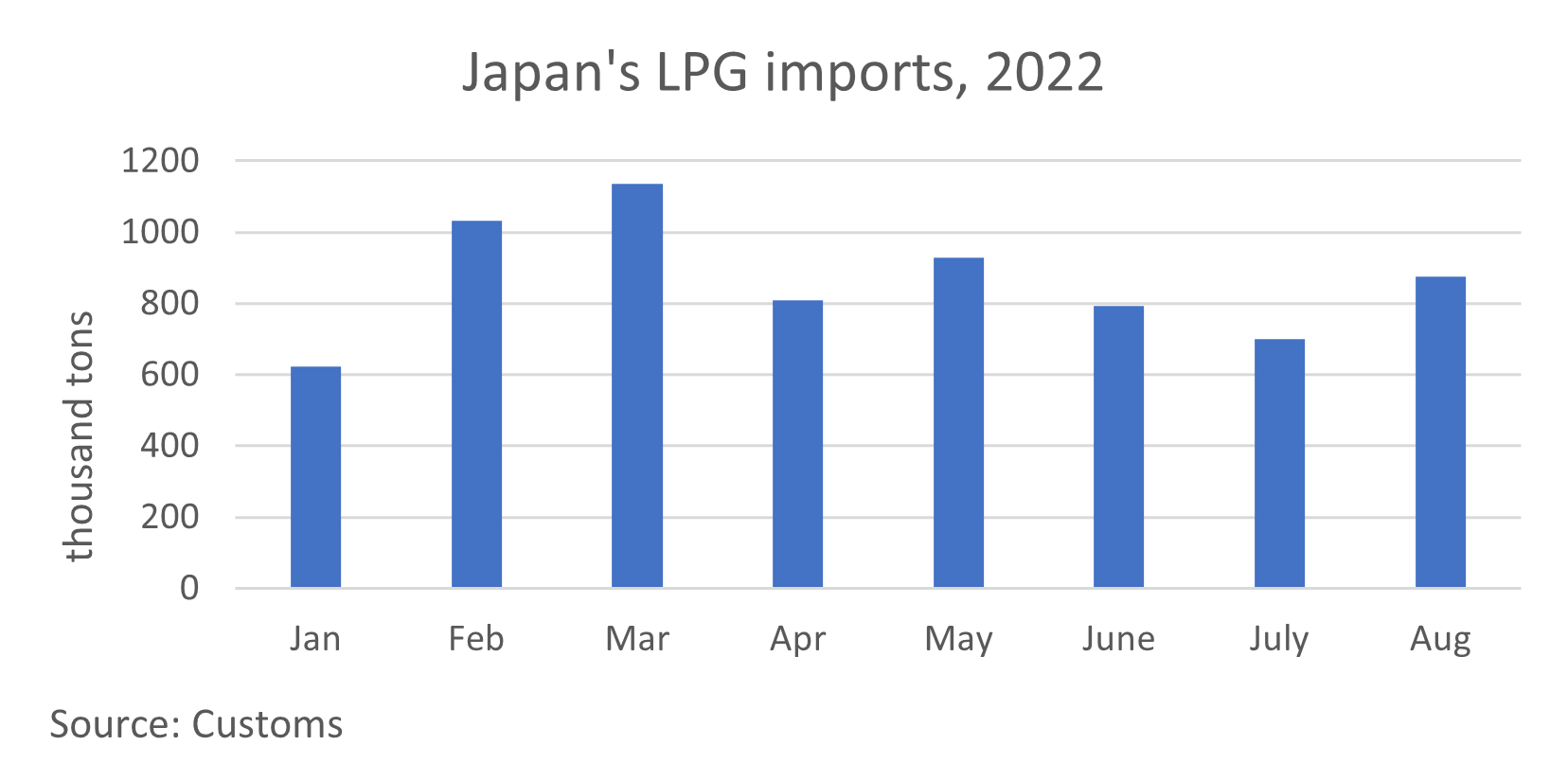

Japan’s Aug LNG imports slip, coal, crude rise, LPG jumps

(Government data, Sept. 15)

- Japan imported 6.27 million tons of LNG in August, down 0.4% from a year ago. Crude oil imports were 13.72 million kiloliters, up 1.5%, while thermal coal imports were 12.28 million tons, up 16.3%. LPG imports surged 34.3% to 0.88 million tons.

Sojitz, JOGMEC invest $9mln in Lynas Rare Earths in Australia

(Company statement, Sept. 20)

TAKEAWAY: Lynas has one of the world’s largest deposits of neodymium used for low emission vehicles and wind power systems, as well as lanthanum for some all-solid-state battery types.

Marubeni invests in a promising metals exploration company in Alaska

(Company Statement, Sept.21)

- Marubeni agreed to buy 19.99% of Canadian metals exploration company Valhalla Metals for about C$8.3 million.

- Valhalla owns exploration assets in the Ambler Mining District in northwestern Alaska, U.S. The area is well known for the existence of one of the foremost volcanogenic massive sulfide (VMS) deposits and contains some of the highest grade copper and other metals (zinc, lead, gold, and silver) in the world.

- CONTEXT: Marubeni considering the mining investment part of its core approaches to building a decarbonization business.

Sexual assault behind ENEOS CEO’s sudden resignation

(Asahi Shimbun, Sept. 21)

- Major tabloid Shukan Shincho has revealed the circumstances behind the sudden resignation of ENEOS CEO Sugimori Tsutomu in August.

- Shincho reports that Sugimori, while drunk, groped and forcibly undressed an employee at an Okinawan hostess club in July in a violent attack that left the woman with a broken rib.

- Both ENEOS and Sugimori have acknowledged that the reports are true.

- ENEOS learned of the assault after being contacted by the victim’s lawyer.

- SIDE DEVELOPMENT:

ENEOS shouldn’t have covered up sexual assault

(Sankei Shimbun, Sept. 23)- CONTEXT: This is an opinion piece by the Sankei editorial board.

- Prior to details of Sugimori Tsutomu’s sexual assault offences coming to light, ENEOS concealed the truth behind the former CEO’s resignation, saying only that Sugimori had resigned for “personal reasons”.

- The fact that the leader of one of Japan’s largest energy companies assaulted a woman is unacceptable, but ENEOS made a fatal mistake in refusing to disclose the reason for Sugimori’s resignation at the time.

- CEO appointments are core to corporate governance, and the scandal suggests that all is not well with ENEOS’ corporate governance.

ANALYSIS

BY MASUTOMO TAKEHIRO

TOP INTERVIEW: JERA’s Head of Decarbonization Strategy

Japan NRG sat down with Takahashi Kenji, GM of the Decarbonization Promotion Section at JERA’s Corporate Strategy Dept. to discuss what Japan’s biggest thermal power utility and top importer of LNG thinks about the development of ammonia / hydrogen and other energy issues.

WORLD’S TOP AMMONIA TENDER

You announced the world’s biggest global tender for ammonia — to provide 0.5 million tons a year. How was the response?

We asked about 30 companies to submit proposals. We received proposals from almost all of them. Actually, since we made the tender information public, we received interest from more than twice as many companies. In total, nearly 100 companies expressed interest. However, we will be closely examining their proposals to see how much they can realistically supply and at what price. We will then deepen our discussions in order to conclude a proper contract.

What’s your early impression of the prices offered?

We see that the price of the underlying raw material, for example in the case of blue ammonia it’s natural gas, will be affected by when supply actually starts. So, first we need to determine the conditions under which that gas will be supplied and the basis of its long-term price. It’s not a simple matter of evaluating the offers as high or low at this point.

AMMONIA PURCHASING PARTNERSHIP

JERA has partnered with two other Japanese utilities (Kyushu Electric and Chugoku Electric) for joint procurement of ammonia. What is the thinking behind that?

All three companies seek to utilize ammonia for co-firing at coal-fired power plants and need to establish an ammonia supply chain. So, we said we’ll consider the possibility of joint procurement in the future. Also, state support is very important in such initiatives. We believe that working with several other companies, we’ll have a better chance of winning government support. We started as the three of us, but we’d like to invite other interested utilities to join with us and expand the group.

What kind of government support do you seek?

The government is currently looking at concrete measures to support companies in this sector, with the Hydrogen Policy Subcommittee and the Fuel Ammonia Policy Subcommittee leading the discussions. With that in mind, we’ll ask for state support.

PROGRESS IN CO-FIRING

You’re testing ammonia co-firing at the Hekinan coal plant. Are you satisfied with progress so far? Any issues?

We initially planned to test 20% co-firing at the Hekinan Plant in FY2024. However, we want to accelerate the schedule. After discussions with our partner IHI, we agreed to move up the timeline by a year. We now believe we can start tests in the second half of FY2023.

JERA’S Hekinan Thermal Power Plant

Source: JERA

It seems as though the 20% co-firing level is very achievable. Is that right?

Yes, for 20% co-firing, we will install a burner that’s already been confirmed as able to achieve the same combustion as if we used only coal, and without increasing NOx [emissions]. Installing it at the station will build knowledge on how to control the technology as a whole.

What are the main challenges for JERA in moving towards widespread use of co-firing? Is it price, or the technical side, or supply chain logistics?

If we end up with a co-firing rate of only 20%, that will cut CO2 emissions only slightly. So, this is only a mid-way point. Our next big step is moving to more than 50% co-firing. With support from the Green Innovation Fund, we’re working with IHI and separately with Mitsubishi Heavy Industries to develop a burner that can accommodate 50% and higher. If development goes smoothly, we’ll move to demonstration tests.

IHI has developed a third of the boilers used in Japan and Mitsubishi Heavy Industries the rest. So, if tests are successful, I believe we can adopt the technology at all domestic coal-fired plants.

When do you expect to hit 50%?

Under the current Green Innovation Fund scenario, a burner will be developed by 2024 and demonstration tests completed by 2028. Once the tests are done, we’d like to roll out ammonia power generation as soon as possible, so that by the first half of the 2030s the main fuel used at existing coal plants is ammonia.

So, the technological aspect of the project the biggest challenge?

That’s right. We can’t discuss prices in detail until the technology is fully developed.

Where will you introduce commercial scale co-firing first – in Japan, the U.S. or elsewhere?

I think Japan will be first.

AMMONIA OR HYDROGEN?

Does ammonia as a power fuel make more sense than hydrogen?

In the U.S., if existing gas pipelines were switched to hydrogen, there’s a possibility that this can be more efficient. The same can be true for Europe. For Japan, bringing hydrogen by pipeline is not an option. So, you need to look at the most suitable and cost-effective carrier that can travel via marine transport.

As a consumer, we’re neutral on the carrier and technology. But in terms of where we can cut CO2 emissions the most, ammonia is superior. Because if you want to deploy co-firing at coal power plants, you cannot use hydrogen.

And, after that, from a Japan standpoint, it’s about which hydrogen carrier has the lowest cost when shipped across the sea.

HOW TO PRICE AMMONIA

There are many global benchmarks for natural gas and oil. But ammonia does not yet have those common benchmarks. So, how do you begin to evaluate its price?

Unlike other hydrogen-related products, ammonia is widely sold as a feed for fertilizer. So there is a track record there to a certain extent, including with ammonia spot prices.

However, this time we’re talking about ammonia as a power fuel. That’s not the same as a short-term market that trade ammonia as a raw material. So, we need to study which mechanism is most suitable to create a stable supply chain and support consumption over a period of time.

Natural gas has become a global market. Ammonia is still mostly traded locally. Will it follow in the footsteps of natural gas?

Part of the global ammonia production goes into making urea and I don’t think the contract pricing of that segment will change much. But the 20 million tons or so of ammonia that trades on the open market is much more volatile, responding to the supply-demand balance. That makes it a global rather than a local market. However, we’re talking about very short-term transactions. Which is not what you need for fuel procurement, which needs to be structured globally and with long-term transactions.

FUTURE OF CCS

If we move to co-firing and eventually 100% ammonia generation, will there be any need for CCS? Can co-firing and CCS co-exist?

If we are talking about using co-firing and CCS in coal-fired power generation, then it’s one or the other. If both are used, it’s a waste of resources and equipment. The first thing to estimate is which is the cheaper option.

Furthermore, the cost of running 100% ammonia firing or, say, 50% will be different. Whichever is the cheaper route will likely win.

ASIA STRATEGY

Japan’s government is promoting its Asia Zero Emission Community initiative. Does JERA have any specific plans to deploy ammonia and related technologies in Asia?

We’re in dialog with various power companies in which JERA has invested. But this is not just about promoting hydrogen, it’s about finding the most rational way to get to carbon neutrality.

If we suddenly ask people to burn hydrogen, which is extremely expensive, they may disagree. We should start with what is possible. Japan and other Asian countries should work toward carbon neutrality while ensuring supply without energy shortages.

We’ve received many requests from Asian countries that want to test ammonia co-firing, and we’re now in conversation around that. We’re also working with JICA to study roadmaps for carbon neutral power generation in Indonesia, among other countries.

This year JERA invested in a power company in Vietnam. Last year, you also invested in Aboitiz Power in the Philippines. Is this a strategy to expand renewable energy in Southeast Asia?

Yes, it is. We are not only going to use hydrogen and ammonia. We’ll also renewables, as long as they are inexpensive. However, we do need to balance this. Without it, we may not be able to provide stable power supply. So, we need to do both.

I believe we need to start with low-carbon energy and then move to decarbonization. We can use LNG to complement renewables. We could also use ammonia for existing coal-fired power plants. For new facilities, we could combine renewables with high-efficiency thermal power plants that could switch to hydrogen in the future. This is a trend that’ll likely develop further.

Furthermore, if a country has the potential for carbon capture, it may be possible to cover CO2 emissions with CCS without going to the trouble of introducing hydrogen. Or, if biomass resources are large, CCS could be combined with biomass.

We’ll use our knowledge and experience to determine the best combination for each country. Hydrogen and ammonia are just two of the options.

SHAREHOLDER ACTIVISM

Japan saw more activists at this year’s AGMs pushing companies to stop using coal. You plan to move away from coal gradually. But what do you say to those who want an exit today?

I think stable energy supply is the first priority. Only after this we can talk about decarbonization and costs.

We can stop using coal and move to only natural gas, and then introduce renewables as much as possible. But, if at this point we have no way to adjust our energy supply, then we hit a ceiling. So, I think there is a certain limit to what can be done.

Say we exit coal today and cover the gap with natural gas. The moment this happens we’ll be in a very difficult position due to stability of supply and cost issues. We will be taken advantage of in that situation. So, we will use both gas and coal. However, we will naturally stop using inefficient coal-fired thermal plants, and pick high-efficiency thermal plants to reduce emissions. Coal-fired power is necessary to ensure stable energy supply, and also to maximize the use of low-carbon natural gas.

“CARBON NEUTRAL” LNG

There is a fairly new product called “carbon-neutral” LNG that’s being actively promoted by some Japanese energy companies. JERA has not entered this sector so far. Do you have a different outlook on this topic?

Yes, we are not going to use it. We believe credits based on Scope 1 emissions, which relates to direct emissions, should not be used to reduce [someone else’s] Scope 1 emissions. The first thing to do is to tackle Scope 1 emissions.

ANALYSIS

BY YOSHIHISA OHNO

Was Japan’s Power Market Regulation a Failure?

New Industry Entrants Face Their Toughest Survival Test Yet

Japan’s retail electricity market may be facing its greatest crisis since the end of World War II. Rapidly rising energy prices over the past six months have forced many electricity retailers into bankruptcy or to exit the market, leaving many customers scrambling to find other service providers.

At the center of this upheaval are companies that sprung up since 2016, the Power Producer and Suppliers (PPSs). These companies came in to challenge the regional utilities, betting that deregulation and a shift to cheaper or renewable power sources such as solar would ease the incumbents’ grip on the market.

As long as the power prices were trending down for most of the last six years, that premise held. As a result, hundreds of PPS firms took over nearly a quarter of Japanese power sales.

The recent jump in fossil fuel prices, however, has bucked the trend. PPS firms without their own power resources, along with their sophisticated business models or price-hedging capabilities, have crashed. Many are now losing money in a market that combines heightened price volatility with pockets of supply disruption.

Japan has 737 PPS firms registered today. As many as 70-80% of those active in the market are unlikely to survive the ongoing flux and uncertainty. This winter could precipitate industry consolidation.

Deregulation gave rise to the PPS

After the end of World War II, Japan’s power supply system was dominated by 10 regional power companies that were strictly regulated by the government. The utilities were vertically integrated, covering everything from fuel purchasing to generation, transmission and retail of electricity.

Hand-in-hand with the expansion of its heavy power machinery groups such as Toshiba, Hitachi or Mitsubishi, Japan was able to build a world-class electrical power system mostly using homegrown technology.

The 10 regional utilities focused entirely on stable supply. This resulted in Japanese firms boasting the lowest rate of power blackouts in the world. But this stability came at a cost. Japan’s electricity prices regularly clocked in at several levels of magnitude higher than in the U.S. and Europe.

As Japan’s bubble economy burst and domestic manufacturers could no longer compete on quality alone, cost of energy became a hot potato issue. Cue an August 1993 assessment by the predecessor of the Ministry of Internal Affairs and Communications that Japan’s electricity prices were too high compared with overseas markets and should be reduced.

Reform began in earnest in 1995 with an overhaul of the Electricity Business Act. This led to a change in the system of electricity rates, establishing the foundation for market price mechanisms. It also opened up the generation market to Independent Power producers (IPPs) and promised more deregulation via a detailed roadmap.

Deregulation Schedule as of 1995[1]

- March 2000: Retail of high-voltage electric power (6 kV)

- April 2004 – April 2005: Retail of extra high-voltage power (20 kV~140 kV)

- Start discussion after 2007: Retail of all electric power

-

Power voltage classification follows that of Tokyo Electric Power ↑

At a Cabinet meeting of February 2014, it was officially decided to deregulate all electric power by April 2016.

Dependent on the high-voltage market

The official birth of the PPS system in Japan could be set as May 1999, when another revision to the Electricity Business Act recognized PPS as a new power supplier category.

This watershed moment forced regional power utilities to open up their transmission networks to new entrants. These tended to be entities related to major Japanese conglomerates and included Diamond Power (Mitsubishi Corporation), Summit Energy (Sumitomo Corporation), Ennet (Tokyo Gas, Osaka Gas, NTT Facilities), and Erex (Nittan Capital, Mitsui & Co.).

It also briefly saw the market entrance of major overseas developers. The notorious Enron Corp. planned to build four gas and coal thermal stations across Japan before its spectacular collapse in 2001.

New entrants gained a small share of the market for industrial / commercial users but failed to make headway beyond contracts with allied or related companies. Regional utilities zealously kept control of the market through their power over the grid.

The total deregulation of 2016 was meant to address this as it asked the regional utilities to split off their transmission businesses. In practice, most reorganized as holding companies, keeping generation and grid companies separate within the same group.

Still, the April 2016 deregulation of the retail market engendered a lot of hope. With it, hundreds of new firms applied for a license to retail electricity. Among these were oil and gas companies, communication companies, real estate companies, trading companies, financial companies, and even local authorities. Established overseas energy giants won a permit alongside entities that officially employ just a few staff or that operate in completely unrelated sectors.

This wave of entrants, often referred to in Japanese as shindenryoku or “new electricity firms”, often practiced an asset-lite model. Most of them owned no generation capacity and could undercut the major utilities through their lower cost base. The new PPS firms began to quickly capture market share. In the first year, from April 2016 to March 2017, a total of 2,953,663 contracts switched from regional power companies to PPS. The next fiscal year, switching totaled 3,270,771 and remained at a similar level for the next three years.

In essence, about 3 million contracts have switched power suppliers annually since full market deregulation in April 2016.

Curiously, while the full deregulation (i.e., access to households) was the trigger for the quick growth in PPS firms, more than half of the electricity they sold was in the form of high-voltage contracts – a market segment that opened as far back as March 2000.

The reality was that corporate clients were far more interested in hearing about new options than households. The latter tend to be reluctant to switch providers and more conservative, while businesses tend to be more price-responsive. And yet, most PPS firms lacked the capacity to supply enough electricity to extra high-voltage customers, making them reliant on the wholesale market for volume.

Bankruptcies looming

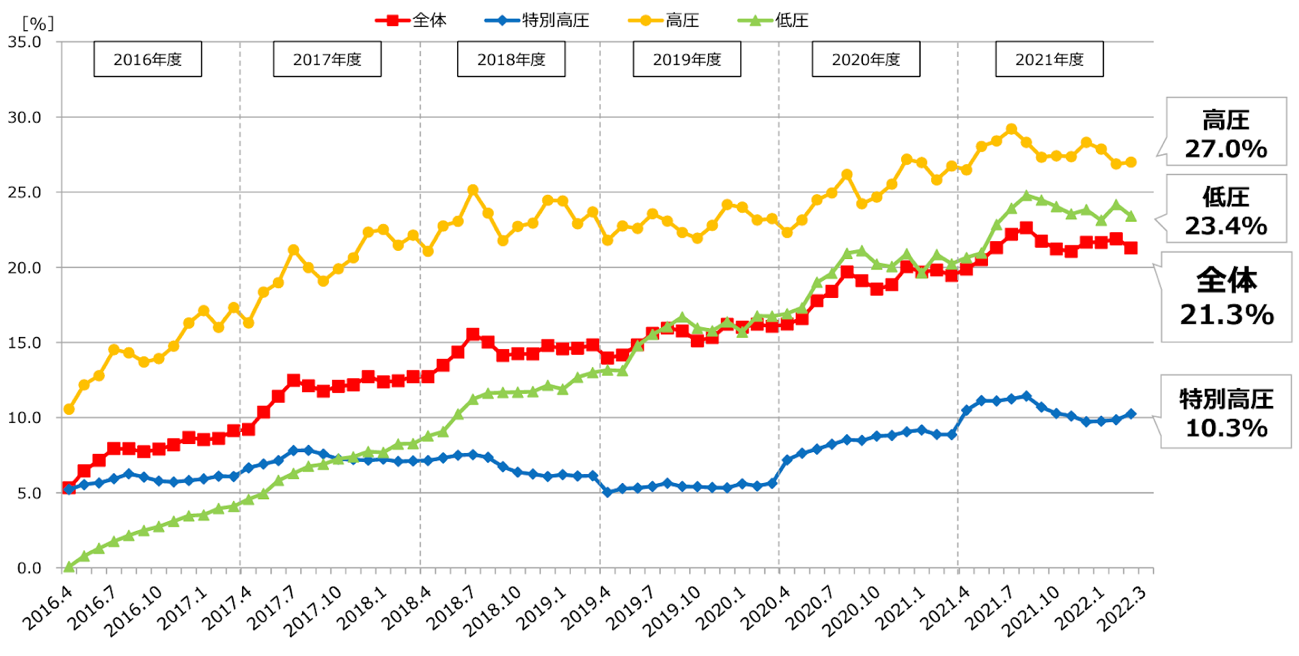

When deregulation began PPSs supplied only 5% of Japan’s total electricity, but by December 2020 their market share increased, reaching a high of 20%. After a short dip, the share grew again and hit a record 22.6% in August 2021.

Since then, the share has started to slide. The latest official data released is for March 2022, which says the market share of independent retailers (not connected with one of the 10 major power utilities) was 21.3%. By now, it’s notably less.

After Moscow’s late February invasion of Ukraine, and the subsequent western economic sanctions targeting Russia’s energy sector, Japan’s wholesale power prices have spiked sharply. A major earthquake and unexpected troubles at aging thermal stations have added to power market disruptions since then.

For many PPS that once offered cheap contracts to win market share, this is an unsustainable scenario. Buying volume on the market at current elevated prices has led to losses even at the electricity retail units of major Japanese energy companies.

Among those announcing bankruptcy earlier was Synergiapower, established by Tohoku Electric and Tokyo Gas. Veteran developer of solar power projects, West Holdings said it will halt its power retail operations due to difficulty in procuring supply. Also, the power trading unit of e-commerce giant Rakuten Group paused the process of taking on new customers.

Some PPS signed up clients to market-linked pricing – a winner in times of calm, but a burden during an energy crisis. Consumers were shocked to see their electricity bill jump five or ten times as a result.

In a few cases, some PPSs reportedly misled customers by promising not to change the electricity price, but failed to mention that fuel costs would be an additional cost item. From March to June 2022 nearly 300,000 subscribers switched back to their regional utility.

At this rate, about 70 to 80% of the PPSs might not survive the current period of price volatility. Those with strong engineering and technology backgrounds and deeper pockets are more likely to stay in the business.

Why are so many PPSs facing potential disaster? The answer could be as simple as the fact that their power model was too easy. Most PPSs in Japan don’t generate their own power or have any engineering capacity, leaving them with little resources or experience in resolving crises. The era of simply buying power on the wholesale market and reselling it at a premium to consumers is over.

What happens next

The main goal of power market deregulation, as stated by the government, was to increase competition and thus lower the electricity price. At present, with power prices rising, many PPSs are left confused and ill equipped to continue.

To adjust, some PPS are trying out new business models, such as offering price plans linked to the market price. This leaves them competing with the major utilities only based on the customer service experience, a thin platform to build on.

The knee-jerk reaction by regulators and politicians, as well as consumers, could see regional utilities win back some of the market share taken by PPS over the years. Meanwhile, METI bureaucrats will grow more cautious on deregulation and look at the troubles in European markets, such as the UK, as further justification.

Those PPS that wish to continue in the market will surely now look to invest in power generation or batteries, seeking to secure captive capacity, or ally with power firms that have such access. With the Japanese retail market still lacking digital billing and sophisticated analytical products, PPS could add value through embracing new value-added services.

The great contraction in PPS numbers will surely mark the start of a more complex and innovative phase for the sector. The era of buy-low-sell-high outfits is gone.

Wholesale Electricity Market Share Held by “New Power Retailers” (Non-EPCos)

Red: Total; Blue: Special High-Voltage; Yellow: High-Voltage; Low-Voltage

Source: METI

Source: METI

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Australia/ Fracking

Origin Energy’s retreat from a major fracking project in the Northern Territory has led to a loss of $90 million. Facing intense criticism from environmental groups, Orion sold its majority stake in the Beetaloo Basin shale gas project for $60 million.

Australia/ Net zero

Leading iron ore producer Fortescue Metals Group will spend about $6 billion by 2030 to reach net-zero targets. By converting vehicles to hydrogen fuel the company will reduce operating costs by $818 million a year. Total cost savings would reach $3 billion by 2030, with its net-zero investment recouping costs by 2034.

China/ Oil and gas imports

China spent a record-breaking $8.3 billion in August importing Russian oil products, gas, and coal, a 68% increase YoY. Chinese buyers have purchased a record-breaking $44 billion of Russian energy in the six months since Moscow’s forces invaded Ukraine.

Coal power

UN Secretary General António Guterres called again for holding “accountable fossil fuel companies and their enablers that continue to invest and underwrite carbon pollution.” But the Financial Times reports that the UN’s Race to Zero project has quietly made major changes, including ending a ban on support for new coal projects.

EU/ Energy crisis

European governments have earmarked almost €500 billion this year to protect citizens and companies from the economic impact of soaring gas and power prices, reports Bruegel, the Brussels-based think tank.

EU/ Green energy lawsuit

Greenpeace, Client Earth and the World Wildlife Fund filed lawsuits over the EU’s labelling of gas and nuclear as “green” energy regarding investment into climate-friendly projects. These NGOs claim that the “fake green” labels are incompatible with EU climate laws.

EU/ Hydrogen energy

About €5 billion was approved for hydrogen projects, with a further €7 billion more of investments expected from the private sector. The EU will support the research, deployment and construction of hydrogen infrastructure.

Germany/ Natural gas

Germany will nationalize gas importer Uniper, raising the rescue bill to €29 billion. The deal brings the total cash pumped into Germany’s three biggest importers of Russian gas to at least €40 billion. In related news, Berlin nationalized the German subsidiary of Russia’s Rosneft, putting three refineries into a trusteeship.

Renewable energy

By 2030, annual investments of $1 trillion in renewable power and $130 billion in hydrogen will be needed to combat climate change, says a report by IRENA, IEA and the UN. Every year the world needs to add four times the amount of renewable energy deployed in 2021.

Russia/ Natural gas

In late December, Gazprom plans to launch the giant East Siberian Kovykta field, crucial for plans to boost gas sales to China. The company also said its reserves replacement ratio will exceed 100% this year, suggesting it will add more reserves than it will use up.

UK/ Fossil fuels

High energy prices have boosted UK small-cap fossil fuel companies. Seven of the 10 top performing stocks on London’s junior Aim market are fossil fuel companies. Companies such as Union Jack Oil and Angus Energy are among the top performing stocks on Aim.

Ukraine/ Nuclear power

Russian forces fired a missile that just missed the Pivdennoukrainsk NPP in south Ukraine’s Mykolaiv region. This came after the UN warned that Ukrainian shelling of another nuclear power plant occupied by Russian troops also risks a serious incident.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

|

January |

OPEC quarterly meeting; JCCP Petroleum Conference – Tokyo; EU Taxonomy Climate Delegated Act activates; Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

|

February |

Chinese New Year (Jan. 31 to Feb. 6); Beijing Winter Olympics; South Korea joins RCEP trade agreement |

|

March |

Renewable Energy Institute annual conference; Smart Energy Week – Tokyo; Japan Atomic Industrial Forum annual conference – Tokyo; World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

|

April |

Japan Energy Summit – Tokyo; MARPOL Convention on Emissions reductions for containerships and LNG carriers activates; Japan Feed-in-Premium system commences as Energy Resilience Act takes effect; Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

|

May |

World Natural Gas Conference WCG2022 – South Korea; Elections: Australian general election; Philippines general and presidential elections |

|

June |

Happo-Noshiro offshore wind project auction closes; Annual IEA Global Conference on Energy Efficiency – Denmark; UNEP Environment Day, Environment Ministers Meeting – Sweden; G7 meeting – Germany |

|

July |

Japan to finalize economic security policies as part of natl. security strategy review; China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong; Czech Republic assumes presidency of EU; Elections: Japan’s Upper House Elections; Indian presidential election |

|

August |

Japan: Africa (TICAD 8) Summit – Tunisia; Kenyan general election |

|

September |

IPCC to release Assessment and Synthesis Report; Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.; Japan LNG Producer/Consumer Conference – Tokyo; IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

|

October |

EU Review of CO2 emission standards for heavy-duty vehicles published; Chinese Communist Party 20th quinquennial National Party Congress; G20 Meeting – Bali, Indonesia; Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

|

November |

COP27 – Egypt; U.S. mid-term elections; Soccer World Cup – Qatar; |

|

December |

Germany to eliminate nuclear power from energy mix; Happo-Noshiro offshore wind project auction result released; Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26; Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.