Japan inks several major long-term LNG deals, with the U.S. and Kingdom of Oman; neither expected to have a destination clause

Auctions for offshore wind projects restart after rule changes with four areas opened up for bidding

Tokyo Gas seeks to buy U.S. natural gas producer for $4.6 billion to diversify its upstream asset portfolio

ENERGY TRANSITION & POLICY

METI accelerates plans to start domestic carbon credits market

Bureaucrats seek to raise GHG reduction target for gasoline cars

METI signs hydrogen/ammonia accords with Saudi Arabia, Oman

IAEA reviews treated water at Fukushima site prior to discharge

GX vision sees stand-alone battery business developing by 2030

Japan to relax rules on fast EV chargers

J-Power and GEI to research making pellets from oil palm waste

Osaka Gas to study U.S. e-methane project with local partners

ELECTRICITY MARKETS

Itochu to enter power management business, control batteries

ENEOS to build Japan’s largest energy management system site

NTT Anode, Shizen join forces to use AI in energy management

Mitsubishi Electric and MHI mull merging thermal power divisions

METI may delay expectation for drop in solar generation costs

HSE plans to develop 150 MW onshore wind farm in Iwate

INPEX buys 31.45% of Indonesian geothermal plant from Engie

Toshiba to set up new department to develop next-gen NPPs

Kansai Electric scandal: staff had access to grid operator’s data

OIL, GAS & MINING

JERA narrows list of potential ammonia suppliers to “about 10”

Japan seeks to minimize reliance on China for critical materials

Japan to continue insurance for Russian LNG cargoes

End-of-year LNG stockpiles slightly above year-earlier period

ANALYSIS

TOP INTERVIEW: ENVIRONMENT MINISTRY’S JCM POINT MAN

We sat down with the Ministry of Environment’s Shigematsu Takayuki, the Planning Officer for the Joint Crediting Mechanism (JCM). He spoke about how Japan wants to take the lead in developing high integrity carbon markets around the world, and also on ambitious new plans to evolve and expand its JCM program. This includes allowing some future JCM projects to be fully funded by the private sector.

TOP INTERVIEW: OUTLOOK FROM TOP TRADER OF BATTERY METALS

We spoke with Tomono Junichi, a corporate officer in the Primary Metal Unit of Hanwa Co., Ltd., a key Japanese upstream investor in and trader of the metals used in storage batteries. He offered a 2023 outlook for critical materials such as lithium, nickel and cobalt, and detailed expected changes in the battery supply chain.

2023 GLOBAL ENERGY OUTLOOK

The global economy will continue to face turmoil in 2023, but it’s not all gloom. We expect this year to mark a genuine boom in energy investments in terms of capital allocated to new projects and R&D, state programs, green finance issuances and M&A. More on this and other trends for this year in the full story.

UPCOMING EVENTS

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Yoshihisa Ohno (Japan) Wilfried Goossens (Events, global)

New Energy and Industrial Technology Development Organization

kWh

Kilowatt hours (electricity generation volume)

TEPCO

Tokyo Electric Power Company

FIT

Feed-in Tariff

KEPCO

Kansai Electric Power Company

FIP

Feed-in Premium

EPCO

Electric Power Company

SAF

Sustainable Aviation Fuel

JCC

Japan Crude Cocktail

NPP

Nuclear power plant

JKM

Japan Korea Market, the Platt’s LNG benchmark

JOGMEC

Japan Organization for Metals and Energy Security

CCUS

Carbon Capture, Utilization and Storage

OCCTO

Organization for Cross-regional Coordination of Transmission Operators

NRA

Nuclear Regulation Authority

GX

Green Transformation

NEWS: ENERGY TRANSITION & POLICY

As trial carbon trading draws to a close, METI looks to speed up full market launch

(Denki Shimbun, Jan. 6)

Trial trading of carbon credits started on the Tokyo Stock Exchange in fall 2022 and is due to complete at the end of January 2023. It mostly covers trading in J-Credits.

Between the trial’s start in September and Dec. 8, credits representing a reduction of 34,249 tons of CO2 were traded at an average unit price of ¥1,927/ ton.

METI will now hold interviews with trial participating companies and the Financial Services Agency to identify issues that need addressing before launching the market in earnest. A report on the trial period is due in spring. Based on its contents, bureaucrats will proceed to draw a detailed market design for the emissions trading system.

Full trading is still expected to begin by the end of FY2023.

CONTEXT: The carbon credit market is a pillar of an emissions trading system for trading GHG emission allowances. This market will allow companies that reduced more GHG emissions than planned to sell that excess amount to others that weren’t able to meet their targets.

The government started the offshore wind power auction in four areas: Happo Noshiro in Akita prefecture, Murakami-Tainai coast in Niigata prefecture, Oga-Katagami-Akita coast in Akita prefecture and Saikai-Eshima coast in Nagasaki prefecture.

The government will apply the new FIP system to all four areas. There will be an upper limit on the supply price: ¥19/ kWh for the first three areas, where monopile type foundations are expected to be used, and ¥29/ kWh for Saikai-Eshima, where projects will likely use jacket type foundations. Each auction will be for a 30-year occupancy period.

An explanatory meeting will be held on Jan 13 from 2:00 pm to 4:00 pm.

Bid will be accepted until 5pm on June 30.

CONTEXT: Auction rules were revised last year following the Mitsubishi consortium winning three projects in the December 2021 auction. That decision was highly controversial and led to an uproar in the industry.

METI proposed raising the GHG reduction goal for the transport sector to 60% of gasoline-derived emissions from 55% currently.

In 2023, METI will conduct a fact-finding survey on GHG emissions in the gasoline life cycle; this follows its review of the U.S. and Brazilian bioethanol life cycle.

It proposes to keep the national bioethanol consumption goal at 0.5 mln oil-equivalent kiloliters/ year; Domestic bioethanol supply will probably see meager growth in the next five years.

CONTEXT: METI has been studying the possibility of blending more bioethanol into gasoline to cut vehicle emissions. The proposals comprise the 2023-2027 national green energy goals under the Act of Advancement of Energy Supply Structures. The government opened the goal proposals to the general public for comments. Feedback submissions close on January 17.

TAKEAWAY: Some experts claim increasing bioethanol content in gasoline would not only help reduce emissions but may also make gasoline cheaper depending on international crude and bioethanol market conditions. However, bioethanol applications are not limited to vehicle fuel but they could potentially expand to bioplastics and sustainable aviation fuel (SAF). Bioplastics and SAF promise better profit margins than vehicle fuel, according to METI findings.

METI minister Nishimura visited Saudi Arabia and Oman at the end of December where he signed a MoC on hydrogen, ammonia, circular carbon economy and carbon recycling.

Nishimura also met with the Omani Minister of Energy and Mineral Resources and signed an MoC on cooperation in the decarbonization sector.

They also discussed overall cooperation in developing Oman-Japan relations; in 2022 the countries celebrated the 50th anniversary of their diplomatic relations.

CONTEXT: METI and JOGMEC are signing hydrogen/ ammonia MoCs with multiple countries and companies that have access to cheap renewable energy in a bid to build diverse supply chains. In the private sector, ENEOS has signed MoCs with Malaysia’s Petronas and Australia’s FMG, and the parties have started hydrogen feasibility studies.

TAKEAWAY: China, Australia, Canada, Norway and the Middle Eastern countries are generally seen as potential green hydrogen/ ammonia supply giants.

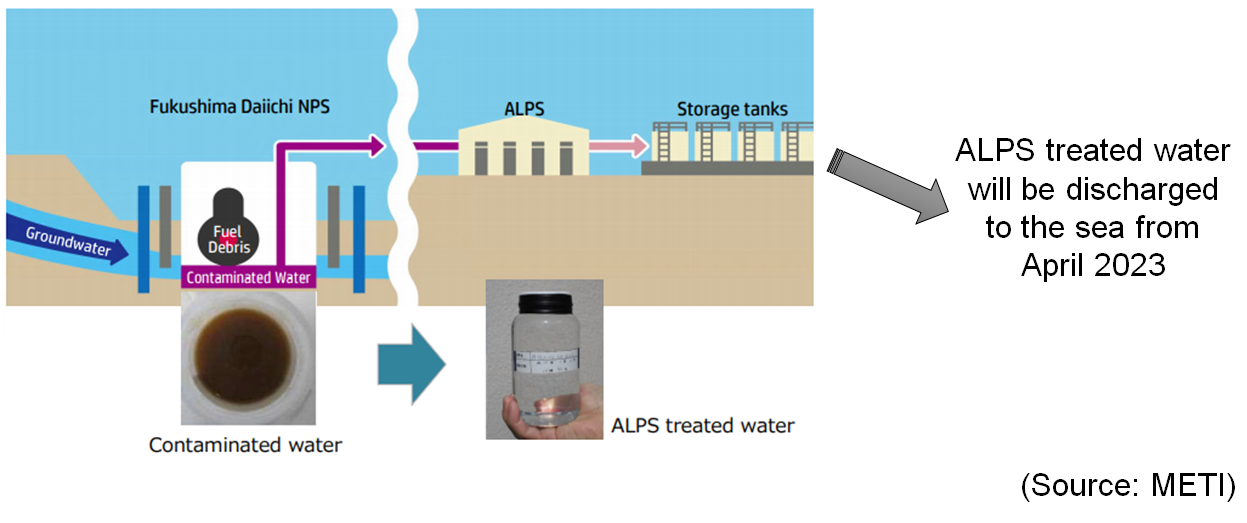

IAEA reviews safety of treated discharged water at Fukushima NPP

(METI statement, Jan. 4)

The IAEA published a safety review of the discharge of ALPS (Advanced Liquid Processing System) treated water at TEPCO’s Fukushima NPP.

The IAEA’s review will continue during and after the ALPS treated water discharge. The IAEA task force consists of IAEA officials and international experts.

The report is intended to instill confidence in the accuracy of the data provided by TEPCO and Japanese authorities.

TAKEAWAY: METI classifies “contaminated water” and “ALPS treated water” differently. “Contaminated water” contains a large amount of radioactive material, but “treated water” has had most radionuclides removed by purification systems (such as ALPS) to meet regulatory standards for discharge, with the exception of tritium, which can’t be removed. There’s no tritium separation technology for treated water with low concentrations and large volumes.

SIDE DEVELOPMENT: TEPCO President: need more credibility before releasing treated water into the ocean (Fukushima Minyu Shimbun, Jan. 5)

TEPCO President Kobayakawa said it’s important to build credibility inside and outside of Japan before releasing the treated water of the Fukushima accident.

The company plans to be transparent about secure safety and reassurances.

However, he added that it’s difficult to judge how much credibility has been built so far, and how to describe the status of the broader public’s understanding.

TAKEAWAY: TEPCO plans to release the treated water in April of 2023. The president’s comments suggest that the company will go ahead with its plans despite some opposition voices from inside and outside of Japan. But this is clearly a very sensitive topic and the government has been at pains to explain that the treated water release plan was approved by several international bodies, including the IAEA. No matter what Japan says, China will likely lodge a protest and, depending on the political relations at the time, there may be some criticism from South Korea also.

Source: METI

NRA to set transition period to new reactor licensing system at “one to three years”

(Mainichi Shimbun, Dec. 26)

The NRA held a meeting with nuclear plant operating companies to discuss their view on the new reactor licensing system. The system keeps the maximum life of a reactor as 60 years but allows the years spent idle post Fukushima to be discounted. It also specifies that all units will need a safety review every decade once they reach 30 years in service.

Companies said they will need time to adjust to the new system. The NRA said it would allow for a one-to-three-year transition to the new rules.

CONTEXT: After the new system is introduced, approvals issued under the old one won’t be eligible. Therefore, all operators with reactors that are 30 years or older will need to pass the new review. This is what the transition period is for.

TAKEAWAY: As of now, 17 reactors have reached the 30 years of service mark and six of them have restarted: Mihama Unit 3 (46 years); Ohi Unit 3 (31 years); Takahama Unit 3 (37 years); Takahama Unit 4 (37 years); Sendai Unit 1 (38 years); and Sendai Unit 2 (37 years). Another four reactors on the list have NRA approval but have not restarted due to local opposition.

GX sees stand-alone battery business developing around 2030

(New Energy Business News, Dec. 27)

The government’s GX strategy forecasts the development of a domestic stand-alone storage battery sector backed by private investment by around FY2030.

The state will support private efforts for commercialization and seek to build a market mechanism that works with distributed power sources like household storage batteries.

Japan to relax rules on fast EV chargers

(Asia Nikkei, Jan. 4)

The govt plans to ease rules around installing fast-chargers for EVs.

Currently, units with an output of more than 200 kW are subject to strict safety measures, which makes installation costly. By the end of 2023, rules around fire and disaster management will be relaxed, thus lowering capex for new fast-charging facilities.

CONTEXT: There are no special regulations for chargers with output of 20 kW or below. Things become progressively stricter above that marker and units with output of 200 kW or more are treated as electrical substations. In November, EVs accounted for just 2% of new vehicle sales in Japan, according to auto industry research firm MarkLines. Potential buyers cite the lack of chargers as the main reason for meager interest.

J-Power and GEI to research making pellets from oil palm waste

(New Energy Business News, Dec. 27)

J-Power and the Green Earth Institute (GEI) will research how to develop pellets using oil palm waste wood. This would create a green chemical/ biofuel business from inedible biomass available at oil palm plantations in Thailand.

CONTEXT: Palm oil is the most widely used vegetable oil in the world. Oil palm plantations, which support this enormous global demand, are regularly replanted to maintain palm fruit yields, and a large amount of tree waste is created each year. The waste is usually buried onsite, but if improperly processed, can emit GHGs.

Osaka Gas to study e-methane project in the U.S. with local partners

(Company statement, Dec. 22)

Osaka Gas signed an MoU with Tallgrass MLP, which operates energy infrastructure such as natural gas pipelines, and Green Plains, which operates bioethanol plants. The three will do a feasibility study for synthetic methane (e-methane) production.

Osaka Gas aims for production of up to 200,000 tons per year by 2030, with a view to liquefy it at the Freeport LNG terminal in Texas and export it to Japan. The process will use biomass-derived CO2 recovered from bioethanol plants owned by Green Plains and blue hydrogen obtained by reforming natural gas.

The partners will also look at opportunities for utilizing green hydrogen.

IHI wins world’s first AiP for ammonia floating storage and regasification barge

(Company Statement, Jan. 5)

IHI, NYK Line and Nihon Shipyard obtained an Approval in Principle (AiP) from ClassNK for their design of an ammonia floating storage and regasification barge (A-FSRB). This apparently is the first such approval globally.

While ammonia is expected to be a potent next-gen fuel that helps with measures to counter global warming, a large initial investment cost is required to secure land for new onshore facilities, including storage tanks and regasification facilities.

A-FSRB offers the advantages of shorter construction time and lower costs in comparison to construction of onshore storage tanks and regasification plants. Offshore floating facilities can receive and store ammonia that has been transported via ship as a liquid, regasify ammonia according to demand, and then send it to a pipeline onshore.

Toshiba to set up new department to develop next-gen NPPs

(Nikkei, Dec. 28)

Toshiba Energy Systems set up an “Innovative Reactor Propulsion Team”, which consists of engineers and marketers tasked with securing orders for the next-gen NPPs.

Toshiba supplies BWR nuclear reactors, the design of the Fukushima NPP.

As construction of new NPPs stopped since the Fukushima accident, the most recent one built by Toshiba is Unit 1 of Higashi-Dori NPP (Tohoku Electric) in December 2005.

TAKEAWAY: Toshiba acquired Westinghouse in 2006 to become the world’s first major global company to sell both BWR (Toshiba) and PWR (Westinghouse). However, Toshiba took on Westinghouse’s huge debts, and their BWR business also faced a crisis. Then, the Fukushima accident set back Japanese NPP suppliers, including Toshiba. One great challenge for this new Toshiba department should be how to retain engineering skills, because construction of next-gen nuclear power plants is only set for the 2030s.

Mitsui and European real estate fund launch $500 million climate friendly fund

(Nikkei, Jan. 9)

Mitsui & Co. and Patrizia SE, a major European real estate fund, have launched an environmentally friendly infrastructure fund, “AECIF,” to invest in the Asia-Oceania region.

The two companies see growth in infrastructure such as renewable energy in the region, and want to set up a $500 million fund (approx. ¥67 billion) by December 2023.

The fund will be managed by Patrizia MBK Fund Management, a 50-50 joint venture in Sydney, Australia.

This is believed to be the first environmentally friendly infrastructure fund established for the Asia-Oceania region. It will focus on six countries and regions, including Australia, New Zealand, Singapore, Taiwan, South Korea, and Japan, with an allocation of 50% for renewable energy.

NEWS: POWER MARKETS

Itochu to enter power management business, remotely control batteries

(Asia Nikkei, Jan. 5)

Itochu will enter the electricity management systems business this year. This will include remotely controlling household storage batteries that source power from solar panels.

Itochu’s VPP (virtual power plant) system hopes to improve energy efficiency and avoid power shortages. The company has sold about 55,000 batteries to homes around Japan.

The trading house (through its GridShare subsidiary) will cooperate with TEPCO Energy Partner and three other power retail firms.

ENEOS to build Japan’s largest energy management system site

(Company statement, Dec. 27)

ENEOS contracted Nippon Koei to build a next-gen energy supply system on the site of a former oil refinery in Shizuoka City. Operations will start in April 2024.

It will consist of large-scale solar generation facilities and storage batteries, as well as an energy management system. The complex promises to be Japan’s largest energy management facility, covering about 42,000 m2.

The complex can work independently from the power grid in times of natural disaster.

SIDE DEVELOPMENT: NTT Anode and Shizen Energy join forces to use AI in energy management (Kankyo Business, Jan. 4)

NTT Anode Energy and Shizen Energy will form an alliance in energy management systems using IoT/AI tech and microgrids.

The partners will offer EV smart charge/discharge services, using their system to find optimal times for charging. Solar power generation equipment and EV recharge/ discharge units (V2B/Vehicle to Building) will be installed in public and private high-voltage power facilities.

CONTEXT: Optimization services help to shift power demand outside of peak times, thereby lowering costs.

Mitsubishi Electric and Mitsubishi Heavy mull merging thermal power generation divisions

(NHK, Dec. 28)

Mitsubishi Electric and Mitsubishi Heavy Industries (MHI) will study setting up a JV to integrate their thermal power generation businesses by April 2024. Mitsubishi is expected to become the majority shareholder of the new company.

The JV will cover planning, design, development, manufacturing, sales, and after-sales service of large generators and related equipment used in power generation.

CONTEXT: MHI leads the global market share for large power plant turbines, but it relied on Mitsubishi Electric to supply the generators. In 2016, MHI and Hitachi pooled their thermal power assets into one company, but Hitachi sold its stake in the business to MHI in 2019.

TAKEAWAY: Mitsubishi Electric and MHI were part of the same Mitsubishi zaibatsu conglomerate before a forced split post World War 2. After a largely fractious MHI-Hitachi partnership, the latest proposed deal would consolidate the thermal power business capacities of three of Japan’s top engineering companies.

METI may delay expectation for drop in solar cost, and creates new PV categories

(New Energy Business News, Dec. 27)

METI’s pricing committee met at the end of December to discuss solar power generation. The committee proposed delaying the ministry’s ¥7/ kWh price target for solar generation from FY2025 to FY2028.

The ¥7 target was set in FY2018. The committee still believes that very cost-effective projects will be able to reach ¥5/ kWh in 2028.

The committee also suggested splitting PV generation into two distinct groups: ground-mounted and rooftop-mounted. New classifications for perovskite and other next-gen solar cells will also be considered later and adopted under the FIT/ FIP systems to help stimulate demand for the technologies.

HSE plans to develop 150 MW onshore wind farm in Iwate

(New Energy Business News, Jan. 5)

HSE plans to develop an onshore wind farm in the vicinity of Karume-cho, Iwate Prefecture. The maximum output is 150 MW.

Construction will begin in FY2026 and operation in FY2028. In the surrounding area, Tokyu Land, Invenergy, and others are also planning wind projects.

CONTEXT: HSE is 85% owned by Mitsubishi HC Capital.

INPEX to acquire 31.45% stock of Indonesian geothermal plant from Engie

(Denki Shimbun, Jan. 5)

INPEX invested in Rajabasa Geothermal, its fourth geothermal power plant in Indonesia.

Rajabasa was founded by Indonesia’s PT Supreme Energy (19.10%), Sumitomo Corp (40.45%) and Engie (40.45%). INPEX acquired 31.45% and Sumitomo acquired 9% from Engie.

INPEX also opened an office in Jakarta on Oct 10.

CONTEXT: Engie sold all shares of this project to two Japanese companies, and Sumitomo became the largest shareholder.

Kansai Electric gained unauthorized access to customer information since 2016

(Kansai TV, Dec. 28)

Kansai Electric gained unauthorized access to new power market client information that’s managed by Kansai Transmission and Distribution, Inc.

Since 2016, Kansai Electric employees were able to gain unauthorized access to company names, staff names and phone numbers of new power market players.

Between Dec 6 and 12 of 2022 alone, 329 Kansai Electric employees and outsourcing company staff accessed about 1,300 data entries.

TAKEAWAY: This is the latest scandal to hit Kansai Electric and while it is not directly related to the nuclear industry, experts worry that the company needs to take compliance more seriously before applying to extend the operational life of its NPPs. The discovery will also vindicate those that doubt the unbundling of the EPCOs, the major regional power utilities. With an antitrust probe against several of the EPCOs ongoing, the timing of this scandal is highly unfortunate for Kansai Electric.

Residents appeal to stop the restart of Kansai Electric’s Mihama nuclear reactor

(MBS News, Jan. 4)

On Jan 4, nine residents of Fukui, Shiga and Kyoto prefectures filed an immediate appeal to the Osaka High Court to overturn the Osaka District Court ruling to dismiss their appeal to stop operation of Unit 3 of Mihama NPP.

Unit 3 is the only reactor to operate beyond its original 40-year license in Japan at present. The residents claim the NPP is dilapidated, and there are active faults at the site.

The Osaka Court ruled on Dec 20 that the measurement of age degradation by the NRA is reliable; thus, more safety measures aren’t required under new IRA standards.

TAKEAWAY: After 10 years of cessation following the Fukushima accident, Unit 3 at Mihama restarted in June 2021. This NPP is the oldest in operation in Japan, so Kansai Electric has to be vigilant to prevent even the slightest problem. Any issue can negatively impact the entire nuclear industry.

Mitsubishi CEO wants more renewables and energy security

(Asia Nikkei, Jan. 2)

Mitsubishi CEO Nakanishi Katsuya says the company will spend ¥1.2 trillion on renewables by FY2024. He sees renewables and nuclear as key to Japan’s energy security.

He said Japan has tempered gas prices hikes thanks to long-term LNG contracts.

He said Mitsubishi is keen to invest in hydrogen and ammonia projects to supply Japan.

NEWS: OIL, GAS & MINING

JERA has narrowed its potential ammonia suppliers down to 10 companies

(Diamond, Jan. 7)

JERA President Onoda said the company has narrowed the number of potential suppliers of ammonia on a long-term contract, which it announced as a public tender in 2022. It is now looking at proposals from about 10 companies.

JERA’s preparations to move its thermal power plants to use fuel ammonia is progressing well and the company needs a broad supply chain that will allow large quantities of the fuel to be imported, Onoda said.

Japan strikes several key LNG deals

(Japan NRG, Dec. 29)

INPEX and JERA agreed to a major long-term LNG supply deal, reversing a trend of Japanese firms running down such contracts.

While domestic demand has softened over the past few years due to Covid, high LNG prices and the restart of more nuclear capacity, the government is supporting gas imports. For example, JOGMEC will assume the investment risk in new upstream projects, and buy “spare” LNG cargoes if domestic demand lags. This encourages Japanese importers to make purchases based on a high-demand scenario, covering the risk of losses.

SIDE DEVELOPMENT: INPEX inks 20-year LNG deal with Venture Global in the U.S. (Japan NRG, Dec. 28)

Japan’s top oil and gas explorer, INPEX, agreed to buy 1 mln tons of LNG per year for 20 years from Venture Global in the state of Louisiana.

The deal is on the basis of “free-on-board”, which means the buyer has flexibility to choose the cargo’s destination.

Mitsui, Itochu and JERA, and Oman LNG signed a contract to supply 2.35 mln tons/ year of LNG over a 10-year period. The METI minister and Oman’s Energy Minister Salim Al-Aufi attended the signing ceremony.

The countries will continue negotiations on more issues such as shipping schedules.

The contract is unlikely to include a destination clause and would allow Japanese buyers to sell the cargoes outside of Japan, a source close to the talks told Japan NRG.

JERA alone accounts for 0.8 mln tons of the deal total.

METI minister Nishimura said Oman’s location makes it less likely to be affected by geopolitical factors.

Other Japanese companies are also in talks with Oman on LNG supply. Mitsui, Itochu, Mitsubishi and Osaka Gas all have stakes in an LNG project in Oman.

CONTEXT: 2.35 mln tons/ year is nearly equivalent to the current import amount from Oman. Oman currently provides less than 3% of Japan’s total LNG imports.

TAKEAWAY: The deals will help Japan find alternative supplies to Russian gas. However, both the Oman and the U.S. deals won’t start deliveries until around 2025. They’ll total under 3.4 million tons, compared to the 6 million tons or so that Russia sends to Japan each year. Also, several Japanese long-term deals are expiring. JERA decided not to renew a 5.5 mtpa deal with Qatar at the end of 2021, while Itochu has an 0.7 mtpa Oman contract that expires in 2025. So, from Tokyo’s point of view, the new deals create necessary options in a very tight market. But they cannot be used to walk away from Sakhalin-2 LNG cargoes.

Tokyo Gas seeks to buy U.S. natural gas producer for about $4.6 billion

(Reuters, Jan. 4)

A unit of Tokyo Gas is in talks to buy U.S. natural gas producer Rockcliff Energy for about $4.6 billion, including debt. The seller is equity firm Quantum Energy Partners.

The all-cash deal may be announced later this month.

The buyer would be Houston-based TG Natural Resources, which is 70% owned by Tokyo Gas and 30% by Castleton Commodities International.

Rockcliff produces over 1 billion cubic feet per day of natural gas from the Haynesville shale formation in Louisiana and East Texas.

CONTEXT: Tokyo Gas sold minority stakes in several Australian LNG projects at the end of 2022. The U.S. deal would give it more exposure to upstream operations.

Japan seeks to minimize reliance on China for critical raw materials

(Asia Nikkei, Dec. 21)

Japan designated 11 areas, including semiconductors, batteries and machine tools as “strategically critical” and vowed to lessen reliance on China for supplies.

Bolstering national security means finding new supply options and building stockpiles.

The change will affect battery manufacturers such as Panasonic, which had sourced much from China, for example, raw materials like graphite. Tokyo will lend as much as ¥1 trillion in support for companies to invest in new mining to diversify sources.

The initiative is spearheaded by Economic Security Ministry Sanae Takaichi. The risk of conflict over Taiwan is one concern driving the policy change.

CONTEXT: Around the start of the previous decade, China banned the export of rare-earth metals to Japan over border disputes. This spurred some Japanese firms to research machinery and motor designs that utilize less rare-earths or rely on those elements more readily available.

Japan to continue insurance for Russian LNG cargoes

(Nikkei, Dec. 30)

After concerns that Japanese insurers will need to stop covering ships sailing though Russian waters from Jan. 1, the companies seem to have reversed direction.

METI’s Agency for Natural Resources and Energy asked the three main insurers to continue offering war-risk coverage so as not to disrupt energy deliveries.

Tokio Marine & Nichido Fire Insurance, Sompo Japan Insurance and Mitsui Sumitomo Insurance relented and will keep the insurance available but scaled back the coverage.

Japan imported 0.45 mln tons of LNG from Russia in Nov, out of the 5.55 mln tons total. Australia Imports were 2.31 mln tons; Malaysia 1.12 mln tons; Brunei 0.26 mln tons.

As of Dec 25, LNG stocks of 10 power grids stood at 2.41 mln tons, down from 2.44 mln tons a week earlier. The end-December stocks last year were 2.34 mln tons. The five-year average for this time of year is 1.84 mln tons.

METI has not updated figures for Jan 1.

INTERVIEW

BY MAYUMI WATANABE

TOP INTERVIEW: MOE’s Point Man for the JCM Program Outlines Expansion Plans

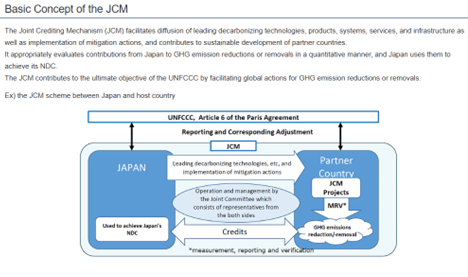

Japan expects to facilitate the development of high integrity carbon markets around the world. Such an approach could allow financing from wealthy nations to flow to decarbonizing technology and infrastructure in developing economies. The end result should be more funds for the latter and also a reduction in global GHG output. But there are several challenges to orchestrating this kind of exchange.

One of the countries with the most experience in international carbon transfer happens to be Japan. It has implemented the Joint Crediting Mechanism (JCM) for a decade, which is a program that promotes the deployment of decarbonizing technology and infrastructure by verifying credits for and funding projects conducted by Japanese firms to reduce GHG emissions in JCM Partner countries. The credit for the GHG emission reduction is allocated between the JCM Partner country where the project takes place and Japan.

This year, the topic of carbon credits will likely reach a whole new level: 2023 is the inaugural year for implementing the carbon market mechanism alignment according to the rules of Article 6 of the Paris Agreement. Japan NRG sat down with the Ministry of Environment’s Shigematsu Takayuki, the Planning Officer for JCM, to discuss the evolution of the mechanism and its expansion.

EXPANDING THE JCM PROGRAM What’s exciting about 2023?

In 2023, the Paris Agreement Article 6 Implementation Partnership will start its activities. While the programs related to it will only just get started, Japan will celebrate a decade of operating the JCM. Under the JCM scheme, Japan is facilitating diffusion of leading decarbonizing technologies and infrastructure, etc. as well as implementation of mitigation actions in partner countries. The JCM contribute to the achievement of both countries’ NDCs while ensuring the avoidance of double counting through corresponding adjustments. Only Japan and Switzerland have experience with such international frameworks. Japan will be happy to help other countries understand the workings of an exchange mechanism and develop things further.

The JCM program has a 2030 goal of registering credits equivalent to the reduction of 100 million tons of CO2. You also hope to boost the number of participating countries to 30 from the current 25. What’s the latest status of the program?

As of December 2022, a total of 227 emissions-reduction projects have been implemented in 17 countries. These projects are expected to generate credits cumulatively equivalent to 19 million tons of CO2 by 2030. It’s a significant number but far short of the ultimate goal. So, we need more projects, and we need bigger projects. Of course, small projects are just as important and they add up, but bigger projects do have better cost efficiency.

On the other hand, many small and medium-sized companies are also participating in JCM, expanding projects in collaboration with partner countries and contributing not only to GHG reduction but also to SDGs such as sanitation and food issues.

With that in mind, we plan to expand the scope of JCM to include projects that are fully funded by the private sector. The existing 227 projects all received government grants. We want to increase the number of private companies that implement the JCM scheme but do so entirely on their own. We plan to publish guidance that will elaborate what companies need to take note of when registering their emission reductions; how to apply the JCM rules; what are the verification processes, and how to avoid double counting of credits. This guidance will be released and formally announced before March 2023. The business community, represented by the Japan Business Federation (Keidanren), has been supportive of JCM’s growth.

Non-Japanese entities have had limited access to JCM so far since all projects must involve a Japanese company. That’s because the projects receive government grants. We have a platform that matches global businesses with Japanese companies to carry out JCM projects. This platform is called “JCM Global Match”.

JCM was intended to transfer technology to developing countries but there is no rule that clearly excludes UNFCCC’s Annex I parties[1]. Such categorization may not be that relevant anyway as situations change. If there’s a need to include projects in industrial economies as part of the JCM program, that could be possible. But at this very moment, demand for JCM implementation comes from developing nations.

JCM projects can be categorized into: energy efficiency, renewable energy, waste, and transport. Most projects fall into the first two categories. We haven’t touched CCS (carbon capture and storage) tech as a means to cut emissions, but we could go into that direction in the future.

For now, we plan to reach out to countries in Africa, Central and South America and the Pacific islands as a way to boost JCM’s partnership network to 30 countries by 2025. Most countries have announced nationally determined contributions (NDCs) and need to reduce emissions. They may have their own initiatives, but JCM would be another option. Developing countries are attracted by the financial and technology support that Japan offers via JCM.

MARKET OPPORTUNITIES

Will credits verified via JCM be integrated with the Japanese carbon trading market, which is in a trial phase[2] on the Tokyo Stock Exchange?

There is a possibility, but it’s not confirmed. The purpose of offset credits is to stimulate ever higher emission reduction goals. Credits are not meant to reduce carbon volumes with money. We need to strengthen our ambition to pursue further GHG emission.

GLOBAL COOPERATION At COP27, Japan established the Paris Agreement Article 6 Implementation Partnership with 40 countries and 23 institutions. What activities are planned for it in 2023?

2023 will be the inaugural year for the Implementation Partnership. We’ll begin by deepening our understanding of Article 6 and offering support to create high integrity carbon markets.

The most challenging part of implementing an Article 6 framework is setting the institutional arrangements to authorize and allocate credits among parties while avoiding double-counting, and establishing methodologies for new technologies such as CCS.

The methodologies used for renewables and for energy efficiency are similar across countries. With that, it should be possible to disseminate JCM methodologies more globally.

How do you see the carbon market evolving under Article 6 implementation?

New types of credits may emerge within the Article 6 framework. Japanese tech might find application in Australia and the U.S., for example. As the scope of credits expands, it’s important to ensure that there is no double counting. Credits will also likely become more diversified. There will be so-called “good” credits and “bad” credits. The former credits are backed by solid processes and systems, and have credibility.

I also believe credits could be worth more than their “face value.” We should look into the various positive impacts these projects have. For example, how much they help local residents by reducing air pollution and improving sanitation.

At the time of the interview, 46 countries and 24 international organizations are part of the Implementation Partnership. Among the major emitters, the U.S., India, and Germany have joined. Among the organizations involves are UN entities, financial institutions such as the World Bank and the Asian Development Bank, and the International Emissions Trading Association. One of our goals is to increase the membership number to 100. We have received several inquiries from the private sector and are discussing ways to involve them in the Partnership.

These are mostly industrial economies that are seen to be less vulnerable to climate change ↑

We will reach out for collaboration through newsletters and through an information platform, which will launch next year. That will report on our progress as well as offering insights on how to effectively run Article 6 initiatives at international forums and so on.

INTERVIEW

BY MAYUMI WATANABE

TOP INTERVIEW: Japan’s Top Trader of Battery Metals Discusses 2023 Outlook

Raw material prices have skyrocketed in the last 18 months, causing a headache for both consumers of fossil fuels and clean energy tech. The price of solar projects, for example, is up by a third in some cases, while wind turbine and battery makers have struggled to turn a profit despite strong demand for their products.

This year promises to be less volatile for raw materials, but it’s too early to breathe a sigh of relief. Japan NRG spoke with Tomono Junichi, a corporate officer for the Primary Metal Unit at Hanwa Co., Ltd., a key Japanese upstream investor and trader of metals used in batteries. He offers a 2023 outlook for critical materials such as lithium, nickel and cobalt, and details expected changes in the battery supply chain.

2023 PRICE OUTLOOK

In 2023, LNG and other fossil fuel prices are forecast to stay high. What’s your outlook for battery metals such as lithium, nickel and cobalt?

The price direction for these metals is generally on the up. It’s hard to see prices decline with such robust demand for batteries. I see lithium trading in the $70-90/ kg range compared to $30-85/kg during 2022. Prices are at historically high levels but demand continues to grow. Market records could be broken again.

My nickel outlook is for $22,000-32,000/ ton in 2023, and $15-30/ lb for cobalt. That compares with a range of $20,000-$48,000 for nickel and $18-38/ lb for cobalt last year.

Spot lithium supplies are extremely tight. Consumers need to book material via long-term contracts because spot sellers are difficult to find. Suppliers are prioritizing deals with long-term customers. Even if you offer double the current spot price, you might still struggle to find a willing seller. For new market entrants that’s especially tough. Sellers will typically run checks on new prospective clients before deciding on whether to accept them as a buyer.

Nickel is easier to procure. New supply sources have emerged in Indonesia thanks to the emergence of a new remelting and processing technique that refines Class-III nickel matte into Class-I battery grade material. So, it’s likely that nickel supplies will ramp up in 2023.

The cobalt market is soft, presently trading at around $19/ lb. Cobalt has trended down since the summer of 2022 due to weak demand for digital devices in China. However, the spread of Covid in China could actually hit the metal’s supply side pretty heavily. China accounts for 60% of the world’s intermediate cobalt processing capacity. It would make cobalt prices very volatile this year and the development of the pandemic in China could cut both ways.

In 2022, lithium-ion battery prices rose to $151/kWh from $141/kWh in 2021, according to BNEF, which expects the rally to continue this year. My outlook is in line with their forecast, which is for $152/ kWh in 2023.

Raw materials are perennially in a boom-then-bust cycle. Do you currently see any chance of prices suddenly plunging to levels that are below cost of production?

I don’t see any chance of that happening, unless there’s some major incident. Nickel production costs are around $15,000/ ton or less. I could see nickel hitting $18,000, but not $12,000 or less. Likewise, I don’t think we’ll see lithium drop below $70/ kg thanks to EV demand. Cobalt may slide somewhat but will likely stop at $15/ lb.

How will high metal prices affect the battery supply chain?

The battery business model is showing its limitation because a rise in battery demand is not leading to lower costs. An economy of scale was supposed to emerge as the rollout of EVs led to higher demand and hence lower costs. But the rising demand for batteries is actually increasing their cost. EV makers like Tesla are raising prices. So, the obvious question is: how will that impact EV demand? Will buyers accept the elevated price tags, which end up being even higher because of rising interest rates?

We have to see if automakers manage to sell several million units of EVs a year and retain the sector’s momentum despite cost increases. Even if EV demand momentum holds, raw material supply volumes will not be able to keep up with demand. You can’t use just any lithium, nickel or cobalt to make batteries. These metals have to be of a certain purity and other quality standards, otherwise the batteries could explode.

METI’s vehicle decarbonization goals

VEHICLES LESS THAN 8-TON IN WEIGHT

TRUCKS OF OVER 8 TONS

2030

Electric vehicles to account for 20-30% of new car sales

Sales to reach 5,000 electric vehicles

2040

All new car sales to be either EVs or other non-fossil fuel autos

Target to be set in 2030

Source: METI

ALTERNATIVES FOR ELECTRIC VEHICLES

But industry needs cheaper battery solutions. Do they exist?

Presently, EVs dominate battery demand. Storage batteries for power utilities have a very negligible market share. There is talk of sodium-ion batteries as a cheaper alternative to lithium-ion batteries. For storage battery systems, new technologies such as vanadium-based redox flow and NAS (sodium sulfide) batteries have been developed. But these technologies are in their infancy. Their commercial installations are limited in number and are unlikely to impact lithium-ion battery demand at least in the next year or so.

One recent trend in EV batteries is to use less cobalt and more nickel, in part due to safety issues. But if cobalt prices soften, could the trend reverse?

That’s impossible. That said, each time industry has looked to increase its consumption of cobalt prices have jumped. Such volatility prevents a stronger move to cobalt.

SUPPLY CONSTRAINTS

The spread between lithium carbonate, the raw material, and lithium hydroxide, which goes into batteries, has been unstable. How has this affected the supply chain?

Lower hydroxide prices have benefited battery makers and carmakers. Higher carbonate prices hurt profit margins for hydroxide producers. At the moment, hydroxide trades above carbonate. The spread flips back and forth.

Constraints on the raw material supply chain suggests Japan should make more upstream investments in mining to secure access to the so-called “minor” metals (such as rare earths) needed for batteries. And yet, Japanese investors tend to focus primarily on base metals (iron, copper), with Hanwa, Toyota Tsusho and Sojitz the exceptions. Why so?

Rare earth metal projects are smaller in size and market volume compared to base metals, so perhaps companies find them to be less attractive on an economic basis? My strategy has been to get our hands on anything that has to do with batteries and be a step ahead of the others. Hanwa has developed a complete rare metal supply portfolio including scrap.

There are plenty of “minor” metal deposits waiting to be explored around the world. What could governments overseas do to attract Japanese investments?

Japan is starting to look around and is making some progress. For example, there was recent news about a Japanese trading house forming a JV with a Canadian exploration company to develop nickel deposits in Canada. I think subsidies will be key to attract Japanese investors. I’ve heard provinces in Canada are offering subsidies. Many governments in South America don’t have deep enough pockets to offer the same, but they can still take measure to guarantee lower development costs. That would certainly be appreciated.

GLOBAL ANALYSIS

BY JOHN VAROLI

2023 Global Energy Outlook: Key Trends and Concerns

The global economy will continue to face turmoil in 2023 in part due to recent underinvestment in energy. The good news is that the issue is now widely acknowledged and both state and private funds are starting to pour into all forms of energy. We expect this year to mark a genuine boom in energy investments in terms of capital allocated to new projects and R&D, government programs, green finance issuances and M&A.

Looking back on Japan NRG’s 2022 predictions from a year ago, we successfully recognized the trend toward more nuclear and fossil fuels in the global energy mix. However, like most everyone else, we didn’t expect such a drastic shift. The speed of change was dictated by a black swan event — the outbreak of full-scale war in eastern Europe. Since then, global energy systems have undergone a real-life stress test as sanctions and geopolitics upended decades-old trade flows.

What we also couldn’t foresee was the unprecedented levels of state intervention in energy markets. Governments on both sides of the new geo-political divide no longer hesitate to take action to control markets through price levers (e.g. caps), supply-side manipulation (e.g. stock releases and the creation of new reserves), and political filters. Talk of a decoupling between the U.S. and China simmered for years, but the war in Ukraine led to an open demarcation of consumers as belonging to “friendly” and “unfriendly” nations. This trend will surely accelerate in 2023.

The 2022 trend that households felt most prominently, however, was a return of high energy prices. That theme will continue this year despite government attempts to use subsidies to shield consumers. Should the IMF’s grim economic outlook for the first half of 2023 hold true, a slowdown in Europe, China and the U.S. will help cool energy prices in the latter part of the year.

Energy pragmatism and security concerns will remain the dominant government and corporate guidance. While the pace of investments in clean energy projects will also rise, their immediate impact will be less pronounced. Most obviously this will put further pressure on state and business leaders to explain how they can reach 2030 emission reduction goals. The answer will increasingly be via some form of carbon credits and/or taxation. The latter assumes a stronger economy, so the former will likely gain more traction in the near term.

Let’s take a look at the major energy sectors and their prospects for 2023.

Nuclear

In 2022, the ghosts of the 2011 Fukushima accident were banished. Many countries now embrace nuclear power, seeing it a vital component of a reliable, carbon-free energy system. The U.S. — which has the world’s largest nuclear fleet, with 93 reactors — saw private investment grow with federal support. New legislation will inject about $40 billion into nuclear power over the next decade. Nuclear sceptics in Europe are also becoming reluctant converts. None more so than Germany, which postponed closing its three remaining nuclear plants until April and then sparked a debate around further extensions. France, Poland, Romania and the Netherlands are among the EU nations planning to add new nuclear facilities. Meanwhile, the vast size of China’s plans could see it emerge as the nuclear industry leader by the end of this decade.

Oil

This year will be another bonanza for energy companies trading in fossil fuels, though without the wild profits seen in 2022. Barring an unexpected geopolitical event, there shouldn’t be a sharp spike in oil prices, which will probably hover between $80 and $100/ barrel. Even more significant is that a new and unusual era in oil markets will coalesce in 2023. Due to western sanctions on Russian exports the global oil market will split. Russian energy exports that once flowed to the EU now head to India and China. U.S. exports will increasingly flow to Europe and to Asian allies. How prices are formed in these two markets will impact us for years to come.

LNG/ Gas

The record prices of 2022 are unlikely to repeat, but LNG and natural gas will enjoy another robust year. Prices should remain high but stable. EU countries lowered dependence on Russian gas by turning to Norway and the U.S., along with accelerating plans to build clean energy sources. But without Russian supplies it will be difficult to refill Europe’s storage facilities in the run-up to next winter. Japan is forging ahead with LNG, thanks to its latest slew of major deals, and is back as the world’s top importer based on last year’s volumes.

Coal

Just a year ago, the industry seemed in terminal decline, but 2022 was coal’s best year in over a decade. According to FT data, total earnings of the world’s 20 largest coal miners hit $98 billion in 2022, compared to $28 billion in 2021. Major economies such as India, China and even Germany will continue to increase coal use in 2023 because they’re far from installing sufficient clean energy capacity. Japan is in no rush to retire coal-fired power plants and will continue to rely on them for backup when power demand surges and LNG reserves dwindle. Since energy security and pragmatism will remain paramount in 2023, coal can count on another strong year.

Solar and Wind

By the end of 2023, renewables are expected to account for nearly 33% of the world’s electricity production, with solar PV’s reaching almost 60% (about 697 GW) of growth, according to the IEA. The high prices for energy manifest the benefits of energy efficiency and are stimulating new technologies to reduce consumption. However, high prices for everything is a double-edged sword, also making the building of clean energy capacity more costly. State subsidies are seen as a cure and the Inflation Reduction Act in the U.S. will provide a shot in the arm for the domestic renewables industry. But it has also upset the EU and Japan, which fear the U.S. will lure clean energy firms away from their shores.

The U.S. plans to build 57 GW of new wind and solar capacity in the next two years. That should help to influence other countries to stay the course on the energy transition. But the U.S. is not the only big spender on green tech. The EU has a €300 billion clean energy strategy to phase out Russian fossil fuel imports. China plans a 33% increase of solar and wind capacity this year, and Japan’s offshore wind tenders are set to finally resume in 2023 after a year-long debate over rules. With all the major markets seeking to accelerate the rollout of wind and solar at the same time, China is likely to be a major winner in global equipment orders because of its market size.

Hydrogen

More than any region of the globe, the EU is betting big on hydrogen to power its energy transition. The bloc has set up a €3 billion investment vehicle to “guarantee the purchase of hydrogen” by spurring demand. Also, Norway and Germany plan to build a blue hydrogen pipeline between the two countries by 2030, and the EU’s recent $50 billion green hydrogen deal with Kazakhstan could be an energy gamechanger for the bloc. In 2023, this energy source will continue to enjoy much favor from governments and private investors.

Biomass

For the first time in many years, high energy prices led to a record number of people losing access to modern energy. As many as 100 million people, mostly in Africa and India, will turn to traditional biomass for simple tasks such as cooking and heating. However, even in Europe, wood burning made an ignominious comeback this winter. A more positive industry development is seen in the biofuels sector with global aviation urgently seeking non-fossil options for jet fuel. Though over a decade in the making, Sustainable Aviation Fuel usage looks likely to finally take off, with Japan eager to be a leader in this sector.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS

・Japan inks several major long-term LNG deals, with the U.S. and Kingdom of Oman; neither expected to have a destination clause

・Auctions for offshore wind projects restart after rule changes with four areas opened up for bidding

・Tokyo Gas seeks to buy U.S. natural gas producer for $4.6 billion to diversify its upstream asset portfolio

TOP INTERVIEW:

TOP INTERVIEW: