Most government energy policies focus on supply, but as energy systems shift to renewables, adjusting power demand will become just as important. Fortunately, this is an area that Japan has experience in, and will develop significantly in 2024. Starting this year, the government has decided to make shifting the time of power usage a more regular feature of the market in Japan, and not just as a tool for navigating short-term supply pinches. In April, big power users will be required to start reporting their demand-response (DR) activities.

The win or lose nature of many renewable energy projects presents challenges for employers and employees alike. As a company seeking to win an auction, building up a skilled team with technical expertise and commercial know-how is necessary. However, deciding which positions to prioritize, and what size of team to invest in can be challenging. For employees, managing the risk of joining a firm that may or may not win a project is a tough choice. How can you ensure that the work you do adds value to your CV regardless of auction results?

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Wilfried Goossens (Events, global) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

METI published the interim report on the hydrogen / ammonia policies, including the criteria for hydrogen / ammonia hubs. Municipalities selected as the hub receive state funding to build infrastructure.

METI plans to choose eight sites – three big and five mid-sized hubs – and will start the selection process this summer.

The criteria include:

Demand for over 10,000 metric tons / year of low-carbon hydrogen

Resourceful, efficient infrastructure and utilization of net zero assets

Carbon intensity of hydrogen at the site will be below the threshold

Mid- and long-term plans for building infrastructure that can integrate new carbon recycling and CCUS technologies

At least a 10-year commitment to supply hydrogen / ammonia as required.

CONTEXT: Asia Nikkei reported the govt plans to spend ¥3 trillion ($20.3 billion) over the next 15 years to subsidize clean hydrogen.

Japan Petroleum Exploration (JAPEX), Mitsubishi Gas Chemical, Mitsui OSK Lines, IHI, and Mitsui & Co launched a study to explore the potential to create an ammonia supply hub in the Soma area of Fukushima Pref.

It will assess Soma as a base to import, store and reload ammonia for delivery to the final destinations, as well as demand of hydrogen and ammonia in the wider Soma area. They’ll also survey users in the hard-to-abate sectors on their net zero plans.

Kagawa Pref set up a council composed of businesses and municipalities to promote net zero initiatives such as transition to hydrogen energy in the Bannosu Coastal Industrial Park.

CONTEXT: Kawasaki City (Kanagawa Pref), Yamaguchi Pref, Tomakomai City (Hokkaido), etc are expected to raise hands as the hubs.

METI will submit a CCS project proposal to the Diet outlining a permit system for drilling and storage, with operators responsible for compensation in case of accidents.

The bill has two main components. One is a licensing system for drilling and storage. The other is regulations for storage operators. It aims to establish CCS projects by 2030 and has provisions for monitoring and management tasks.

CONTEXT: The govt estimates that burying 120-240 mln tons of CO2 annually is necessary for the 2050 decarbonization goal.

TAKEAWAY: A key issue of the proposal is related to operator liability. According to the bill outline, operators will be held liable for any damage of the carbon storage operation. This applies both in case operators cause damage with malice or without malice. Project operators will likely need to find someone willing to insure the projects, and enter in an insurance plan, which will add to the already high expenses of CCS projects. State support, especially through JOGMEC’s funds, seems essential to launch the CCS economy.

Toshiba Energy Systems & Solutions (ESS) installed a compact CO2 capture system (3.1 by 2 by 2.8 meters) at Tokyo Gas Senju Techno Station. Operations begin in March and it will capture around 5% concentration CO2 emissions from a gas cogeneration system.

Toshiba’s CC technology employs post-combustion capture methods, and features an amine-based solvent for CO2 capture. The compact system is part of Toshiba’s efforts to meet increasing demand for small-scale CC systems.

Chiyoda Corp, Nippon Yusen Kabushiki Kaisha (NYK), and Knutsen NYK Carbon Carriers (KNCC) completed a CCUS study that focuses on liquefaction, temporary storage, and marine transportation of CO2. Three methods were examined: elevated pressure (EP), medium pressure (MP), and low pressure (LP).

The study concluded that cylinder tanks for onshore storage reduces construction time, and also optimizes land use, lowers investment and operating costs, and enhances energy efficiency.

Prof Miyasaka developing tech to control Perovskite solar cell performance

(Japan NRG, Feb 1)

Prof Miyasaka Tsutomu of Toin University of Yokohama, also known as the father of perovskite solar cells (PSC), is developing technologies to improve control over grains comprising the perovskite crystals. PSC power conversion efficiency remains lower than that of silicon-based PV.

Boundaries between grains allow moisture and other substances to penetrate into the perovskite layer, causing performance and quality issues. Miyasaka is exploring ways to enlarge the grain size and to make the surface more uniform using a technique called “passivation”.

Passivation is minimizing the impact from the barrier between the grains. Miyasaka is testing caffeine, glycine, and hydrazine as possible solutions.

Electrical performance may be improved by doping the indium tin oxide layer, which lies below the perovskite layer, with potassium.

Prof Miyasaka is also exploring lead-free PSC, using tin.

SIDE DEVELOPMENT ENEOS eyes producing Perovskite material at gas fields (Japan NRG, Jan 29)

ENEOS group company JX Nippon Oil and Gas Exploration seeks to be a supplier of Perovskite solar cell (PSC) raw materials using iodine found in gas fields.

Last month, the company donated ¥2 million to Niigata University to increase engagement with researchers. In September last year, it inked a development agreement with Godo Shigen, Japan’s largest iodine producer.

JX Nippon Exploration produces 220 metric tons / year of 99.7%-purity iodine at its Nakajo oil / gas field (Niigata Pref); INPEX has a larger production of 600 tons / year at Chiba and Niigata pref gas fields.

CONTEXT: Japan is the world’s second largest iodine producer with 10,000 tons of annual output. Policymakers hope that the country’s energy self-sufficiency will rise with the rollout of PSC technology. According to Prof Miyasaka’s calculations, if PSC raw material costs are reduced to ¥200 / m2, power could be generated at ¥6-7 / kWh, below the current levels of about ¥10 / kWh for solar PV. For PSC production, iodine needs to be refined into 99.999% purity and all possible moisture must be removed. Currently, 99.7% iodine powder costs around ¥40-50 per gram, while perovskite-grade lead iodide costs ¥3,000-4000 per gram.

Ricoh will conduct a year-long field study of perovskite solar cell-powered outdoor lighting in Ota City (Tokyo) and Atsugi City (Kanagawa Pref) to measure impact of temperature, humidity and illuminance on module performance at night.

TAKEAWAY: The field study will use Ricoh PSC modules made to generate power for night lights. Perovskite crystals also generate light and could be used as light emitting diodes (LED), but this study will focus on their performance as a power source.

Fuel Cell System Manufacturing, a JV between Honda and General Motors, began production of the first hydrogen fuel cell system in Michigan, U.S.

The system is a third the cost of the system that Honda used in its 2019 FCEVs. It will be installed in the new FCEVs that Honda plans to launch by late 2024.

The company plans to expand the use of the system, focusing on four application areas, including commercial vehicles, stationary power sources, and construction machinery.

Asahi Kasei plans to increase its manufacturing capacity of electrolyzers. It will bring onstream a pilot manufacturing plant in Kawasaki City (Kanagawa Pref) in spring 2024, and will start taking commercial orders in 2025.

Initially, it will have an annual capacity for 1GW of electrolyzers, which will be expanded to 2 GW during the fiscal year ending in March 2026.

In Oct 2023, Toray Industries raised the output capacity of catalyst-coated membranes, a core electrolyzer component, at its German plant by 3.5 times to 1.4 GW. The annual capacity will be increased further to 3 GW in 2025.

TAKEAWAY: Asahi Kasei uses alkaline water electrolysis tech while Toray focuses on proton-exchange membrane (PEM) tech; they’re direct competitors. Apart from capital and operational costs, stability and ease of maintenance, the consistent quality of hydrogen being produced is a key factor when it comes to choosing electrolysis tech, one green hydrogen project stakeholder told Japan NRG. Buyers typically seek 99.99% purity guarantees, rather than the vehicle-grade purity of 99.97%.

SIDE DEVELOPMENT: Hokkaido Electric, ENEOS to build 100 MW green hydrogen plant (Japan NRG, Jan 30)

Hokkaido Electric and ENEOS plan a 100 MW green hydrogen plant in Tomakomai City (Hokkaido), and will start offering its supply to factories in the local industrial complex by 2030, said an ENEOS official at a hydrogen event in Tokyo.

Preliminary studies were done in 2022-2023.

CONTEXT: If built, this will be Japan’s largest green hydrogen plant.

In April, Kawasaki Heavy Industries will start a review of a digital management system that can be used for a hydrogen trading platform in domestic and international markets.

The platform will manage hydrogen qualities such as the gas origin, GHG data in the supply chain stages, distribution routes, relevant certifications, etc.

The company plans to commercialize the system in about 2028.

TAKEAWAY: Currently, hydrogen without any climate attributes sells at about the METI price benchmark of ¥100 / NM3. Green hydrogen’s pricing is far from transparent, and varies according to the delivery location, volume, applications, solar power costs, etc. This platform, if successful, would contribute to market transparency.

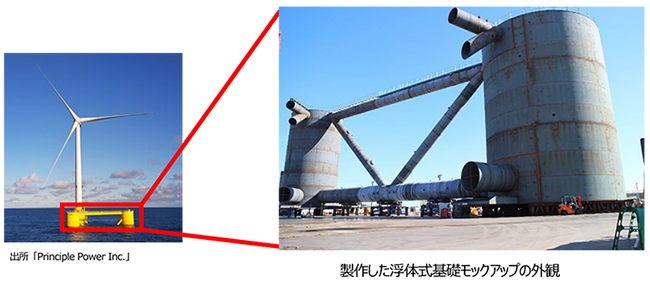

Tokyo Gas completed a trial of offshore wind floating foundations, seeking to develop a low-cost construction tech suitable for larger wind turbines (15 MW scale), severe weather and sea conditions, and suitable for mass production.

The project used a semi-submersible floating foundation and a hybrid mooring system that combines steel mooring and synthetic fiber mooring ropes. The tech is expected to help expand floating offshore wind power in Japan.

TAKEAWAY: The project receives NEDO funding from FY2021 to 2024. NEDO is also funding TEPCO, which is developing a similar tech called “large floating spar”.

Mitsui Mining to triple solid battery electrolyte production

(Japan NRG, Jan 31)

Mitsui Mining and Smelting plans to triple its output capacity of sulfide solid electrolytes for all-solid-state batteries. The electrolyte, called A-SOLiD, is made of argyrodite which consists of lithium, halogen element and phosphorus.

Mitsui began A-SOLiD production in 2021, for sample shipments. The product development is not yet complete as improvements are needed to cut costs; but demand is strong, a company official said.

In November last year, Maxell began commercial shipment of A-SOLiD containing solid batteries to Nikon. It is sized 1 cubic centimeter and has a 8 mAh capacity.

TAKEAWAY: Sulfide solid batteries operate under high temperatures of 125 C, which was not possible for lithium-ion-batteries. Maxell plans to develop 5,000 mAh capacity solid batteries by 2030, and eyes storage batteries for solar farms as its key market.

Hitachi and Iwamizawa City, (Hokkaido Pref), began testing a system to circulate renewable energy obtained from self-supporting nanogrids using a portable AC/DC combination battery developed by Hitachi.

The firm began testing the new tech on Jan 25 in Iwamizawa City. The project is done jointly with Iseki, one of Japan’s largest farm machinery producers. The system seeks to supply renewable energy to dispersed farmlands.

Iwamizawa city also plans to use the batteries at EV charging stations.

The Japan Gas Association (JGA) is committed to tackling climate change by seeking to replace 90% of natural gas with e-methane by 2050. JGA said this in an open letter to the GHG Protocol Secretariat on Jan 25.

It suggests including a market-based approach for carbon recycled fuels in Scope 1 emissions reporting. Examples are e-methane, e-fuels, and SAFs. JGA received appreciation from the GHG Protocol Secretariat for their proposal.

Hydrogen burner startup to open restaurant in Tokyo

(Japan NRG, Jan 30)

H2&DX Inc, a Tokyo-based startup developing hydrogen burners, plans to open a restaurant in Tokyo in April with a fully hydrogen-fueled kitchen, Fukuda Mineyuki, the company founder, told JapanNRG.

The company will also seek tenants for hydrogen-fueled kitchens.

In 2023, H2&DX developed and installed a hydrogen-based kitchen system to Madoka-no-Mori, a luxury inn in Hakone township (Kanagawa pref). It uses 99.99% hydrogen contained in gas cylinders, delivered by trucks once a week.

The operation cost of the inn’s kitchen increased 2.5-fold compared to conventional gas and power systems, according to Fukuda.

TAKEAWAY: The burner can accommodate hydrogen with lower purity but the company is forced to use premium-grade 99.99% hydrogen for fuel cell batteries and FC vehicles, since it’s the only grade available on a commercial basis. Similarly, most hydrogen boilers run on a lower grade 90% hydrogen as long as the gas does not contain sulfur, nitrogen, etc.

The International Atomic Energy Agency (IAEA) completed a safety review of TEPCO’s discharge of Fukushima NPP’s treated water into the sea. The discharge was found to be consistent with international safety standards.

The IAEA will continue its multiyear safety review, and will remain present at Fukushima to check the discharge.

CONTEXT: China, Russia, South Korea and Fukushima’s fishermen have all spoken against the release. In autumn, China and Russia banned Japanese seafood imports. In 2022, China was Japan’s biggest market for fish, with more than $500 mln worth of exports. Russia only accounted for $1.7 mln worth of Japanese seafood exports. Japan plans to use the IAEA report in its talks with China to end the latter’s ban.

Five EPCOs plan electricity rate hikes for households in March; three to drop rates

(Nikkei and Japan NRG, Jan 30)

Five major EPCOs plan to raise electricity rates for March billing (which relates to Feb power usage). The five are: Chubu Electric, TEPCO, Tohoku Electric, Okinawa Electric, and Hokkaido Electric.

An average household bill, as modeled by the companies themselves and based on low-voltage rates, will be affected by the following amounts:

Company name

Forecast change in avg. household payment in March (¥)

Current monthly spend

Chubu Electric

133

¥7,291

TEPCO

72

¥7,560

Tohoku Electric

47

¥7,545

Okinawa Electric

21

¥8,009

Hokkaido Electric

7

¥8,318

However, three other firms – Hokuriku, Chugoku and Shikoku Electric – are set to drop power rates to reflect declining coal prices. The gap also stems from the more varied power supply mix the firms use to generate power.

Company name

Forecast change in avg. household payment in March (¥)

Current monthly spend

Hokuriku Electric

-12

¥6,581

Shikoku Electric

-5

¥7,272

Chugoku Electric

-5

¥7,197

Kyushu Electric and KEPCO do not plan changes. Their average household bill will remain unchanged at ¥6,136 and ¥6,146, respectively.

At least four gas companies also announced increased price plans for March, reflecting price hikes for LPG and LNG. The average monthly household gas bill will increase by around ¥100.

Tokyo Gas: up ¥125;

Shizuoka Gas: up ¥106

Toho Gas: up ¥133

Keiyo Gas: up ¥99

CONTEXT: The companies cited rising prices of LNG and crude oil during October to December 2023 as the reason for rate increases. Household electricity prices for major power firms consist of two types: liberalized rates, which allow utilities to freely set prices, and regulated rates, which require state approval.

TAKEAWAY: The five major EPCOs that announced electricity price hikes already raised prices last year due to the global energy crisis and yen depreciation that had an impact on the costs of LNG, coal, oil and other commodities. Last year in May, the govt approved the requests from seven major utilities to raise monthly electricity bills for standard households by 14% to 42% from June 2023. Those were: Tohoku Electric, Hokuriku Electric, Chugoku Electric, Shikoku Electric, Okinawa Electric, TEPCO and Hokkaido Electric.

METI’s Power Tariff Committee on procurement costs set the purchase prices under Feed-in-Tariff for after FY2024. Below is a summary of the new price parameters introduced by the ministry.

In FY2025, the price for solar power was set at ¥15 / kWh for capacity under 10 kW. Outside of 10 kW, prices in FY2025 and beyond were set at ¥10 for ground-mounted PVs of a capacity under 50 kW; ¥8.9 for 50 kW and above, and ¥11.5 for roof-mounted PVs.

As for the solar tariff auctions, during FY2024 they will be held four times, targeting facilities with capacity of 250 kW or more for ground-mounted installations under the FIP system. The max supply price is set at ¥9.20 for the initial round; it will be decreased to ¥9.13, ¥9.05, and ¥8.98 in the following rounds. The initial amount of capacity offered will be 93 MW.

The price for onshore wind power has now been set as far as FY2026. It was ¥14 in FY2024 and ¥13 in FY2025 for a capacity of less than 50 kW. In FY2026, the cap will drop to ¥12 via the FIT scheme. For onshore wind capacity of over 50 kW, the same price cap will be applied but via the FIP mechanism.

For replacement onshore wind capacity, the price for FY2024 has been set at ¥12 / kWh. Both FIT and FIP systems can be used. Only one auction round is planned for FY2024 with 1 GW on offer.

Offshore wind power projects that aren’t subject to the Act on Promoting the Utilization of Sea Areas will be subject to a bidding system from FY2025. However, the cap on supply price will not be disclosed before the end of FY2024.

For floating wind power, METI agreed to maintain both FIT and FIP prices at ¥36 / kWh at least through FY2026.

For geothermal power generation, there is a similar approach. The current tariff levels were extended for a further year to FY2026 across nearly all categories.

The Electricity and Gas Market Surveillance Commission approved the application submitted by OCCTO for a ¥12 billion loan to cover monthly subsidies to power firms that purchase electricity from renewable generators.

This is the first time OCCTO has applied to borrow funds. On Jan 17, it applied for the METI minister’s approval, and expects the decision shortly. EGC operates under METI. If approved, OCCTO should receive the funds by the end of March.

In its application OCCTO said the monthly “adjustment subsidy” has increased due to a decline in the so-called avoidable costs, which are linked to wholesale electricity prices that have been trended down. Meanwhile, income from the renewables levy has dropped after the rate of the levy was lowered by METI.

The above has created a situation in which there is a gap between income and expenditure, which could see OCCTO run out of funds.

CONTEXT: In 2012, Japan introduced a Feed-in Tariff (FIT) mechanism under which operators of renewables facilities are guaranteed a fixed payment for their electricity. The power goes to the major grids / utilities, which can utilize it or sell it on the market. The losses incurred from buying FIT or similar electricity at fixed prices are meant to be compensated by funds raised from the nationwide renewables levy, the unit price of which is set each year by the government. Part of the compensation calculation, however, takes into account the so-called avoidable (also called avoided) costs, which refers to expenditure that power utilities avoided because they procured electricity volumes without having to spend money to generate it themselves. Since the avoidable cost is linked to the cost of operating power plants and spot power prices, a decline in the market price of electricity affects the adjustment subsidy.

According to OCCTO, it has about ¥460 billion cash on hand, but anticipates a shortfall of about ¥20 billion already in April. The difference between the income raised from the levy, etc. and the amount paid out in adjustment subsidies in the last three months is estimated at ¥160 billion per month.

If METI approves the loan, the lender and borrowing rate will be decided via a tender.

JEPX’s Intraday Market saw a 38.2% (MoM) increase in December’s average daily volume traded, reaching 17.38 GWh.

The increase was likely related to the peak demand season, which increased supply capacity, and a growing need for replacement of older LNG-fired power plants.

The monthly contract also saw volumes rise 42.8% to 539 GWh, as the number of contracts was up 26.1% to 204,515.

In December, more capacity came online as thermal and hydropower plants that had completed inspections and repairs resumed operations. The increase in contracts may have resulted from the replacement of thermal power in the hour-ahead market as part of an effort to reduce fuel consumption.

The monthly average contract price was down ¥1.53/ kWh to ¥12.81/ kWh. This is ¥0.41/ kWh higher than the system price in the spot market.

December’s highest price was ¥45/ kWh, which was reached on Dec 5.

EPCOs and TDGC to incorporate the association that runs the balancing market

(Japan NRG/Denki Shimbun, Jan 26)

Nine EPCOs and the Transmission & Distribution Grid Council (TDGC) agreed to incorporate EPRX, the entity that manages the balancing market. The business entity will start operation on April 1, 2024.

EPRX will trade all categories of adjustment power from FY2024 and cover its operating costs from trading commissions. The founding entities of the business will also make an undisclosed cash injection.

CONTEXT: Created in 2021, EPRX has hitherto been operated by a voluntary organization. Having a business entity in charge is expected to clarify the platform’s responsibilities and speed up decision-making.

Kyushu Electric’s Genkai NPP Unit 3 (PWR, 1.18 GW), which has been suspended for regular inspections, resumed power generation on Feb 2.

Gradual adjustments will be made to confirm the functionality of equipment, with the expectation of returning to normal operation by Feb 29.

TAKEAWAY: After the restart, power generation using MOX fuel was halted. This was due to difficulties in securing plutonium from the French supplier. The inspection involved replacing MOX fuel with uranium fuel. Power generation will proceed with uranium fuel until further notice. Kyushu Electric aims to restart pluthermal (MOX) power generation by FY2026.

Over the course of FY2018 to FY2022, 149 solar power plants violated Japan’s Forest and Forestry Basic Act. Of the total, 20% or 30 of the farms have still not taken action 9 years after being called by the govt to accord with the law, according to a survey carried out by Nikkei.

Of the 149 farms, 46 had no permit to operate at space exceeding 10,000 m2, while another 86 were not compliant with safety regulations.

CONTEXT: Nikkei points out that due to poor communication between municipal and central govt bodies, relevant ministries appear to have no updates on the current situation.

EGCO Cogen, a JV between J-Power and Electricity Generating Public (EGCO) finished replacement construction for a gas cogeneration power plant in Thailand.

The original power plant has been operational since Jan 2003, supplying electricity to the Electricity Generating Authority of Thailand. The PPAs expired last month; thus, EGCO signed new PPAs and began the replacement, with 74 MW capacity.

The power plant has ownership of 80% EGCO and 20% J-Power. EGAT and industrial users near the power plant are the primary customers.

On Jan 31, fire broke out at JERA’s 1.07 GW Taketoyo thermal power station, inside a boiler area. A belt conveyor carrying fuel (woody biomass and coal) caught fire. The plant stopped power generation and the fire was put out after five hours.

Hitachi Zosen Inova secured orders for biogas plant equipment in the UK – there are three from Bio Capital, including gas upgrading units and CO2 liquefaction systems.

The projects aim to produce purified biomethane and will be completed by 2025. Hitachi Zosen Group’s plans to invest around ¥75 billion in biogas under its 2025 medium term management plan.

Solar power firm Blue Sky Solar acquired all shares of Act Electric (Toyohashi City, Aichi), as it seeks to expand, especially in the Chubu area. The goal is to build a company capable of undertaking 1 GW of O&M and developing 100 MW of solar capacity annually by 2028.

CONTEXT: Act Electric, established in 1992, operates a community-based electrical construction business in Aichi Pref. It has deep experience in solar power generation. Blue Sky Solar has over 100 repowering projects; total capacity of over 150 MW.

Infroneer, a subsidiary of general contractor Maeda Corp, a civil engineering group, has completed the acquisition of shares in wind power generation firm Japan Wind Development.

The shares were bought from U.S. private equity firm Bain Capital; the deal is estimated at $1.5 billion. Infroneer secured a ¥218.4 billion loan for the buyout.

CONTEXT: JWD has over 3 GW of new wind power developments and is involved in wind farm maintenance. Japanese regulators advised to conduct a legal compliance review following a bribery scandal involving JWD’s former head who admitted to the allegations and resigned.

U.S., Europe, and Japan business groups urged the Biden administration to reverse its decision to freeze approvals for new LNG export facilities licenses. They include the U.S. Chamber of Commerce, BusinessEurope, and Japan’s Keidanren.

METI officials expressed concern about potential delays at facilities awaiting approval. Japan does not expect an immediate impact on its LNG procurement. Yet, the govt is in discussions with U.S. counterparts to address the situation.

They emphasized growing global demand for more LNG supplies. The U.S. became the top LNG exporter in 2023, serving as a critical supplier to Europe. The impact of the approval freeze on global gas markets is expected to be minimal until at least 2027, according to Goldman Sachs.

CONTEXT: U.S. President Joe Biden halted approvals for new LNG projects, a move praised by climate activists. The pause is aimed at evaluating both economic and environmental impacts. It could delay decisions on new projects until after the Nov election. The U.S. Dept of Energy will conduct a review, followed by a public comment period. The pause affects at least four projects with pending approvals.

TAKEAWAY: Japan seeks to understand the impact of the U.S. decision on projects in which Japanese companies have offtake agreements. One of those is Venture Global’s Calcasieu Pass 2 (CP2) project, in which JERA and INPEX both have 20-year purchase agreements for 1 million tons a year. CP2 alone would boost the U.S. current LNG export volumes by a fifth. In Dec, the two Japanese companies had urged the U.S. to hurry approvals for the project, mentioning its importance for Japan’s energy security.

CONTEXT: The publication is a monthly magazine that offers a behind the scenes look at major corporate events and tends to offer a dramatic narrative.

The recent ouster of President Saito Takeshi due to a sexual harassment scandal was part of a coup d’etat. There’s a power struggle linked to the firm’s future strategy.

The two most likely candidates to succeed Saito are Vice President Miyata Tomohide, the acting president, and Vice Chair Ota Katsuyuki. The article expects the winner to be Ota because he has no ties to the original Nippon Oil business that still forms the core of ENEOS, and because during his brief stint as President, Ota tried to shift the group away from fossil fuels to renewables.

Ota oversaw the acquisition of Japan Renewable Energy Corp from Goldman Sachs and shuttered a large oil refinery.

Any strong reforms at ENEOS could face a backlash, as many of its executives are from the Nippon Oil business and are of a more traditional mindset. If the internal struggles get out of hand, METI might step in and appoint an outsider to lead the firm.

Japan Marine United (JMU) delivered Japan’s first large bulk carrier using LNG as the main fuel to Nippon Yusen Kaisha (NYK). This is the first domestically built LNG-powered ship of the Cape Size bulk carrier category.

The vessel emits 25-30% less CO2 compared to current petroleum fuels, and has 75% lower NOx emissions during operation.

LNG stocks of 10 power utilities stood at 2.16 mln tons as of Jan 28, down 13.3% from 2.49 mln tons a week earlier. This is the second consecutive week that the LNG stock level decreased.

This is 9.6% down from the end of January 2023 (2.39 mln tons), and 13.1% higher than the 5-year average of 1.91 mln tons.

CONTEXT: With LNG imports just under 6 million tons in January, Japan’s total was the lowest for that month since 2009, according to Bloomberg. Reasons cited for this drop are nuclear reactor restarts, higher renewables output, and energy-savings efforts.

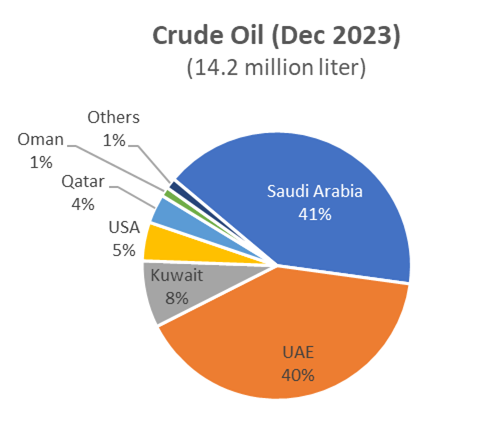

In December, Japan imported 14.2 mln kiloliters of crude oil, of which close to 95% came from the Middle East. Saudi Arabia and UAE accounted for more than 80%.

CONTEXT: Japan’s imports have been as much affected by swings in commodity prices as in the national currency. The yen traded at ¥132.7 to 1 USD at the end of 2022, but weakened to ¥141.8 by the end of 2023.

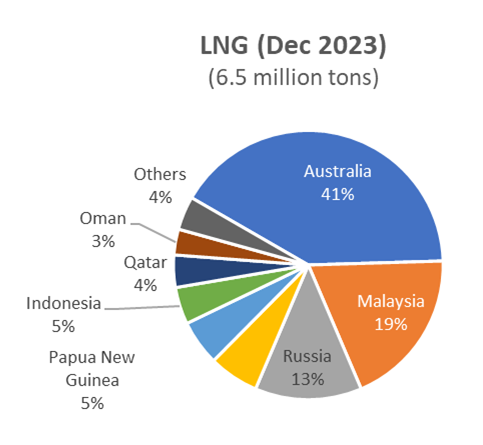

LNG imports in December amounted 6.5 mln tons and over 40% came from Australia. Total volume was up 7.2% YoY, but total value dropped nearly 20%.

Japan’s oil imports were 147.6 mln kiloliters, down 7.1% YoY; Saudi Arabia was the top exporter supplying 60 mln kiloliters, or 40.8% of the total.

LNG imports were 66.2 mln tons, down 8.1% YoY; Australia was the top exporter at 27.5 mln tons with a 41.6% share.

Thermal coal imports were 101.5 mln tons, down 11.9% YoY; Australian coal imports were 71.3 mln tons with a 70.2% share. The total coal imports, including coking coal, were down 8.8% YoY to 167 mln tons.

Japan’s rare earth imports from China rise in 2023

(Government data, Jan 30)

Japan imported 7,784 metric tons of rare earths in 2023; of that amount 5,700 tons, or 73%, were sourced from China. 2022 imports were 8,123 tons; 5,494 tons, or 68%, were from China.

In terms of monetary value, the 2023 imports were worth ¥47.5 billion, compared to ¥77 billion a year earlier.

SIDE DEVELOPMENT: Japan’s 2023 fuel ammonia imports down 31% YoY (Government data, Jan 30)

Japan imported 187,266 metric tons of fuel-grade ammonia in 2023, down 31% from 270,214 tons a year earlier. Indonesia was the largest source, with 131,000 tons.

The 2023 total import value was ¥15.3 billion, which is less than half of the ¥34.6 billion in the previous year.

ANALYSIS

BY CHISAKI WATANABE

Japan Faces Surge in Demand-Response Tech Amid Changing Power Markets

Most government energy policies focus on supply, but as energy systems shift to renewables, adjusting demand for electricity will become just as important. Fortunately, this is an area that Japan has experience in, and it’s expected to develop significantly in 2024.

On March 22, 2022, consumers in eastern Japan, including the Tokyo area, were asked by the government to drastically reduce power usage. This came a week after a 7.4-magnitude quake off the Fukushima coast that triggered a shutdown of numerous thermal plants. After an immediate loss of power to 2.2 million homes in central and northern Japan, the situation soon recovered.

Then suddenly came a bout of unseasonably cold weather that threatened to overwhelm the energy grid. This situation was resolved thanks to a now familiar practice of setsuden, or appeals for energy conservation from the government and power utilities.

The approach has been used numerous times in the past – most famously after the March 11, 2011 earthquake and tsunami that also sparked the Fukushima nuclear accident. Despite a scorching summer in 2011, demand for electricity in the Tokyo area registered volumes of close to a quarter below a year earlier.

Starting this year, the government has decided to make shifting the time of power usage a more regular feature of the power market in Japan, and not just as a tool for navigating short-term supply pinches. In April, big power users will be required to start reporting their demand-response (DR) activities.

Case Study: March 2022

The energy shortage in March 2022 was illustrative for a number of reasons, one of which was that a number of foreseeable and unexpected factors collided to exacerbate the situation.

In addition to halting the operation of 14 thermal power generation units immediately after the March 16, 2022 earthquake, with some of them offline for weeks thereafter, the main power utilities involved – TEPCO and Tohoku Electric – had to contend with a spell of gloomy weather that notably cut generation from solar farms. At the same time, a number of thermal power plants had undergone regular maintenance work, which is usually scheduled for March because it comes after the peak power demand winter period.

With power supply severely constrained, TEPCO was down to its last backup option of pumped storage hydro units to keep the lights on in the capital. The situation was dire. To avert blackouts, TEPCO asked companies with onsite power generation to boost output. It also asked about 400 manufacturers of raw materials such as steel, chemicals, and industrial gas, to reduce power use.

This effort to shift power consumption is one example of DR – an attempt to influence power use by consumers to complement actions on the power supply side.

While the March 2022 event is irregular, its lessons are more applicable on a more daily basis. As more variable renewable energy sources such as solar and wind are added to the grid, there’s an increasing need to match supply and demand. Changes in weather, accidents at power plants, as well as troubles with transmission lines can also impact supply.

Rather than relying on new generation capacity to improve resiliency in time of a supply crunch, DR programs can be deployed to let power users play a role in balancing supply and demand at a cheaper cost. Consumers can take measures such as shifting their power demand from peak times to less congested periods and charging batteries. In return for helping to balance the grid, consumers can receive monetary or price incentives.

Policy action

Several policy developments are pushing further DR implementation. A revision to the act on energy saving that took effect in May 2022 is expected to promote the roles that DR can play since it stipulates large-volume power consumers to report efforts to optimize power demand.

Starting FY2024, it will become mandatory for large-volume power users to report how many times they have implemented DR programs in the past year. Starting FY2025, they’ll be also asked – though on a voluntary basis – to report more details, such as how much power demand they were able to shift by implementing DR.

Of course, such cooperation should be rewarded. Power consumers – whether commercial, industrial, or residential – can be compensated by roughly two types of mechanisms called “economic DR.” One is a “price-based” type in which rates are increased during peak periods. The other is an “incentive-based” mechanism in which customers agree to shift power demand based on a contract with power companies and get compensated, says METI.

Table 1: Types of Economic DR

Price-based

Incentive-based

Power rates will be raised during peak periods to urge customers to reduce demand

Based on a contract, customers will be paid for reducing power usage upon getting a request from utilities

Pros

Easy to operate, can be applied to a large number of customers

Guaranteed results because it is based on a contract

Cons

Uncertain results, as the method depends on customers’ reactions each time

The method is relatively time-consuming, difficult to apply for small-volume power users

Sources: METI, IEA

Mechanisms and trading

Individual efforts to reduce or shift electricity use in DR programs are supported by “aggregators” in charge of controlling the flow of electricity on behalf of power consumers and transactions with Transmission System Operators and power retailers. Eneres and Energy Pool Japan are among some 60 companies registered with METI as aggregators.

Conserved electricity through DR efforts can be traded on power markets. Until last year, TSOs procured power sources for category I’ in order to prepare for once-in-a-decade level of cold or hot weather through a public offering of ancillary services, which are used to ensure the reliability of power systems. The share of DR in procured capacity in that category was on the rise, reaching about 2.5 GW (about 66% of the total) in 2023, said METI.

Starting this year, the equivalent of category I’ power sources will be procured from the capacity market following rule changes. A total of 4.15 GW of dispatchable resources have been awarded for FY2024, 4.75 GW for FY2025 and 5.84 GW for FY2026. The capacity market is designed for procurement of power capacity through a four-year forward auction; the dispatchable resources include demand response, storage batteries, and any power generation with a capacity of less than 1 MW.

Table 2: Procured DR capacity from the ancillary service public offering through 2023 and dispatchable resources awarded in the capacity market from 2024 (in MW)

(NOTE: “dispatchable resources include DR and others)

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

958

961

893

1,289

1,759

2,290

2,520

4,150

4,750

5,840

Sources: METI, OCCTO

Furthermore, the conserved electricity can be sold on the balancing market. Low-voltage power resources such as residential storage batteries, EVs, and heat pumps have not been allowed to take part in the balancing market. The government, however, will change this and allow them to start trading in FY2026. This will expand the scope of DR participation for residential power users. Currently, they can take part in the “economic DR” programs mentioned above.

DR-ready as the wave of the future

METI is also looking at how to promote residential equipment such as ACs, heat pumps, storage batteries, and EV chargers to be “DR-ready” so their usage can be controlled remotely. Some ACs sold in Japan are DR-ready. Adding the remote control function to all ACs would help since such equipment accounts for the largest share – more than 30% – in residential power use.

In April, TEPCO will launch a two-month DR field study to encourage customers to shift to daytime, instead of nighttime, when switching on residential heat pump water heaters. This would boost daytime electricity use at the time when generation of renewable energy, such as solar power, is traditionally higher. Doing so could help the utility avoid curtailing renewable energy output

Participants can earn loyalty points worth ¥2,500, to help compensate for the expected increase in their electricity bills for shifting to daytime instead of nighttime use when rates are cheaper. The utility also plans to announce in February details of a separate DR program for households that won’t require water heater ownership.

Another positive development that encourages demand response is the planned nationwide installation of next-generation smart meters that begins in FY2025. This will allow for collecting data from demand-side resources such as inverters for solar panels and EV chargers, and this could increase the volume of resources for the balancing market.

Switching on residential water heaters at night or setting the air conditioner’s temperature lower in summer may sound like a small step, but given the numbers of these machines already in use in Japan – 90 million ACs, and 5 million heat pump water heaters – there’s the potential for the aggregated capacity to help balance power supply and demand.

As Japan strives to hit 2030 interim climate targets, as well as final ones in 2050, every effort at energy efficiency will be crucial to realizing those goals.

ANALYSIS

By ANDREW STATTER

Jobs in Japan: Increased Market Volatility = Increased Mobility?

Large scale auctions for offshore wind sites, long-term decarbonisation auctions for energy storage capacity, and CfD scheme for hydrogen projects are facilitating the growth of various clean energy projects across Japan’s energy systems, and attracting healthy interest from domestic and international firms alike.

The win or lose nature of these schemes presents challenges for employers and employees alike. As a company seeking to win an auction, building up a skilled team with technical expertise and commercial know-how is necessary, however deciding which positions to prioritize, and what size of team to invest in can be challenging.

For employees, managing the risk of joining a firm that may or may not win a project is a tough choice. How can you ensure that the work you do adds value to your CV regardless of auction results?

Desire to work on winning projects

Naturally, offshore wind industry talent wants to work on projects that will be realized. In the three Round 2 offshore areas to be granted rights in December of 2023, nine firms across three consortiums were successful. One more offshore area will be decided by March of this year.

Over 20 firms will ultimately be unsuccessful with their Round 2 bids, and multiple other firms have worked for over a year to develop projects in preparation for their bids, only to decide against bidding for various economic and competitive reasons. The impact was quick in coming. Within two weeks of the results, about a dozen employees of a major Japanese developer that failed to secure their project have left the company.

One of the winners, however, announced over 30 newly opened positions in the same timeframe and are now interviewing dozens of professionals each week. Over 50% of professionals who submitted applications to one multinational developer prior to the auction result withdrew their interest within a week of that firm failing to secure a win in their offshore zone.

The high costs to develop projects, and all or nothing risk that comes with capital intensive segments such as offshore wind, reveal the risks that employees face. This can be demonstrated by large-scale downsizing and complete market exits for some multinational developers, as well as a large number of Round 1 bidders opting to sit out of Round 2 auctions.

With massive oversubscription of energy storage projects in Japan’s long-term decarbonisation auctions, the potential for a repeat of this pattern of talent drain to project winners is high. Notably, this trend was less pronounced in the solar boom a decade ago.

Under that FIT market scheme, developers were able to secure projects year round, leading to more consistent, albeit smaller wins that allowed businesses to maintain a team that matched their portfolio. The annual auction system creates a fair and level playing field and increases visibility for developers; however, the balance of building and retaining talent becomes more challenging.

Hiring enough to win while managing cost

Developing a team that’s capable of developing quality projects and submitting bids with a high chance of success is a serious investment. The challenge is that there’s nothing to pay for that investment until project wins are secured. So, how to build a strong team and keep costs down?

A few things to keep in mind:

A team that lacks strong local capabilities will make finding and securing development partners more difficult;

Due to the intense workload in the months leading up to bid submissions, the work-life balance and strain on a team that’s too lean can cause internal problems;

On the other hand, the cost of salaries, social insurance, equipment and office space for 40, 50+ staff is hard to justify if the bid is unsuccessful and the next opportunity is another 12 months away.

Talent retention in a cutthroat market

As previously mentioned, strong talent wants to work on projects that will be developed and constructed. Losing talent to winners after a tender result is announced is a risk that’s impossible to eliminate. However, steps can be taken to mitigate this risk and keep top performers under your roof.

Clear vision and long-term commitment. Talent is more likely to stay if there’s a clear roadmap and pipeline of projects in the next auction, or early stage projects not yet subject to auctions. Holding meetings on the firm’s future direction and not committing to the next auction is a sure way to get a stack of resignation letters on your desk.

Get your team involved at a regional level. Multinational firms primarily hire bilingual talent. If yours has interest in other APAC markets, giving your team the chance to have input on projects outside Japan significantly increases your chances of retaining them in the case you fail to secure a project in the Japanese auction systems.

Diversity of projects. Firms that have developed a range of asset types hold a different risk profile and can repurpose talent if a key auction-based project is unsuccessful.

Employees: How to secure your value regardless of company results?

This is one of the most common concerns we see for professionals moving to firms dealing with project materialization risk, irrespective of whether it’s in wind, energy storage, hydrogen or other areas. There is a oft-held view that if a firm fails to secure a project, then the experience and value of its team members falls behind. This would make it harder to secure employment.

At Titan, our view is that this risk is minimal, due to the fact that these markets are young and demand for talent is high, and that inherently there are more losers than winners in such auction systems.

Some points to consider when choosing a firm and selecting a role to ensure that you continue to build value regardless of company results:

Wider roles are better. Since many segments of energy transition sectors are in their infancy, employers gravitate toward talent who can wear multiple hats. Having the ability and mindset to work broadly, and communicate across functions and languages, is a key asset.

Take on roles that shift with the project. Energy projects are divided into phases – if you are able to stick with a project through origination, into development and then into execution, you’ll build more value than through sticking to origination repeatedly.

Look at that firm’s commitment. If it’s strong for multiple projects over a long period of time, you’ll likely have workstreams in more than one project; hence, in case your main project dissolves, you’ll be able to pick up work in the next projects, rather than having ‘dead time’ while your next steps are decided.

Target multiple small wins. For example, we see a trend of professionals in offtake / CPPA favoring solar or BESS over offshore wind for the reason that they can start racking up a track record of small wins, rather than leaving themselves open to the binary risk inherent in larger, more complex offshore projects.

Does job ‘hoppiness’ matter less?

One of the age old questions in Japan is how long a professional needs to remain with a firm in order not to be considered a ‘job hopper’. In the current market, this notion is changing from ‘time in role’ to ‘achievements in role.’

As there’s a larger number of firms in the Japanese energy market looking to develop projects in an increasingly competitive landscape, this naturally correlates to increased mobility. Rather than looking at years in role when judging candidates, it becomes more important to look at years in function, and put the spotlight on what that person has achieved even if it was across two or three different employers.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific, and all that impact markets in the region.

Australia / Renewable energy

EDP Renewables acquired local renewables firm ITP Development, including 1.5 GW of renewable energy assets with a pipeline of wind and solar projects, and the option to co-locate battery energy storage systems (BESS).

Bangladesh / LNG

Summit Group said that in 2023 it inked two agreements to supply 1.5 mln tons of LNG annually to the energy-starved south Asian country (population 170 mln) and a Floating Storage Regasification Unit with a capacity of 170,000 m3.

China / Renewable energy

In 2024, China’s installed wind and solar capacity will overtake coal for the first time. The China Electricity Council said wind and solar would make up around 40% of installed power generation capacity, compared with coal’s expected 37%. In 2023, wind and solar were 36% of capacity, and coal was just under 40%.

India / Green hydrogen

NTPC Green Energy inked a MoU with the state of Maharashtra to develop green hydrogen projects with a potential investment of $10.5 billion. The deal includes derivatives like green ammonia and green methanol of around 1 mln tons annual capacity, as well as 2 GW of pumped storage projects and the development of renewable energy projects.

Malaysia / Energy trading

State-owned oil and gas company Petronas is hiring traders to expand its derivatives business. Building out derivatives trading would represent an attempt to develop a more sophisticated trading operation, alongside existing production and refining businesses.

Malaysia / Natural gas

TotalEnergies will buy OMV’s 50% stake in Malaysia-focused SapuraOMV for $903 million. The main assets are its 40% stake in the natural gas block SK408, and a 30% stake in block SK310, both located offshore of Sarawak.

Philippines / Tidal power

Inyanga Marine Energy Group was selected to build SE Asia’s first tidal power generation plant, a 1-MW station in the Philippines. Completion is planned for 2025.

Singapore / Power systems

The Energy Market Authority selected YTL PowerSeraya to develop a 600-MW hydrogen-ready Combined Cycle Gas Turbine, to be commissioned by end-2027. YTL will build, operate and own the project.

Southeast Asia / Solar power

BlackRock’s Climate Finance Partnership fund is partnering with Ditrolic Energy to develop solar power across Asia-Pacific. The fund, which has raised $670 mln, will accelerate Ditrolic’s 1 GW-plus solar pipeline in Malaysia, Bangladesh, Indonesia and Philippines.

South Korea / Offshore floating wind

Copenhagen Infrastructure Partners (CIP) signed a deal for floating wind structures with HSG Sungdong for its 1.5 GW Haewoori offshore wind project in South Korea. The non-binding MoU will explore opportunities to optimize production of floating foundations.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

Japan’s Diet convenes (January)

The first Long-Term Decarbonization Power Source Auction

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

February

India Energy Week 2024 (Feb 6-9)

Smart Energy Week (Feb 28-Mar 1)

Lunar New Year (Feb 10-17)

CFAA International Symposium (Feb 2)

Indonesia presidential election (Feb 14)

FIT/FIP solar auction (Feb 19 – March 1)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

March

Announcement of the last auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro area)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan (March 11-12)

Russian presidential election (March 15-17)

Ukraine presidential election (due before March 31)

World Petrochemical Conference, Houston, TX, (March 18-22)

End of Japan’s fiscal year 2023 (Mar 31)

April

Details of 2024 capacity auction results released

Japan Atomic Industrial Forum (JAIF) Annual Conference

Global LNG Forum (Apr 15-16), Madrid, Spain

Global Hydrogen & CCS Forum (Apr 17-18), Madrid, Spain

World Energy Council (WEC), Rotterdam, Netherlands (Apr 22-25)

May

May Golden Week holidays (May 3-6)

World Hydrogen Summit (May 13-15)

June

Japan Energy Summit & Exhibition (June 3-5)

G7 Summit in Italy

International Conference on Oilfield Chemistry and Chemical Engineering (IOCCE), Tokyo (June 10-11)

American Nuclear Society (ANS) Annual Conference, Las Vegas (June 9-12)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX, USA (Sep 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

U.S. presidential elections (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

JAPAN NRG WEEKLY FEB 5, 2024 JAPAN NRG WEEKLY FEB 5, 2024 NEWS TOP ENERGY TRANSITION & POLICY ELECTRICITY MARKETS OIL, GAS & MINING ANALYSIS JAPAN FACES SURGE IN DEMAND-RESPONSE TECH AMID CHANGING POWER MARKETS Most government energy policies focus on supply, but as energy systems shift to renewables, adjusting power demand will become just […]