Most energy discussions center on the supply or demand of electricity or molecules. Yet without the critical raw materials (CRMs) to build power supply generation facilities, the planning of future energy systems is moot. Japan is a net importer of most critical minerals used in clean energy technologies. Japan’s self-sufficiency in key critical resources is slipping. If Japan fails to secure access to CRMs, then it might also need to adjust its energy strategies.

Copper means a lot to Japan, which has a total copper refining capacity of 1.7 million tons/ year, the world’s second largest after China. The main concern is surging demand, driven by diversified power transmission networks, as well as a surge in AI-driven data traffic. In June, ANRE decided to drive more investments into overseas copper mines by increasing state ownership of future projects. Also, it launched efforts to encourage new businesses in the metal recycling industry. Can other measures, especially on the demand side, be implemented to help manage possible shortages?

ASIA ENERGY VIEW

A wrap of top energy news that impacts other Asian countries.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2024.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Kyoko Fukuda (Japan) Magdalena Osumi (Japan Filippo Pedretti (Japan) Tim Young (Japan)

The METI subcommittee tasked with revising guidelines and criteria for the next rounds of the long-term decarbonized power auction (LTDA) has proposed to increase capacity to 5 GW for the next auction, now planned for January 2025. OCCTO will begin accepting applications in October.

If the proposal is approved, capacity allocated by category will be as follows:

BESS (3-6 hours) – up to 750 MW

BESS (over 6 hours) – up to 750 MW

Renovation of existing thermal power plants – up to 1 GW

Investment in safety for an existing NPP – up to 2 GW

The decision to change criteria for nuclear power is part of efforts to accelerate the process of restarting nuclear power plants.

CONTEXT: Since some LTDA categories, such as upgrades of existing thermal plants, receive less interest than expected, the govt plans to improve the remuneration rate, the refund rate for other market revenues, and the maximum price. However, it warned that improving the incentives will need to be balanced without putting much more burden on consumers, or distorting the fairness of other markets. So, changes won’t be immediate, but will be part of an ongoing review.

TAKEAWAY: The review will likely take a while and seek to gather opinions from market participants before finalizing the criteria for Round 2. METI has been encouraged by the strong BESS showing, but also wants LTDA to support a wide range of generation sources, including hydro, nuclear, as well as a revamp of thermal generation via ammonia co-firing and similar.

METI selected nine Advanced CCS Projects for Commercialization to receive support from carbon capture to storage, aiming to realize their commercialization before 2030. Their total storage capacity is 6-12 mln tons/ year of CO2.

Out of the nine, seven have been under the METI Advanced CCS Project program launched in 2023. The two new projects are in Malaysia: Sawarak Coast Project (JAPEX, K-Line, JGC Holdings, Petronas CCS Ventures, etc); and the Southern Malaysian Offshore Project (Mitsui & Co, Chugoku Electric, Kansai Electric, etc.)

METI doesn’t plan more projects unless there are changes that make it difficult to hit the 2030 storage capacity goal.

As the Seventh Basic Energy Plan is being written, verifying the cost of combined energy sources will be an important area to be discussed and determined.

Also, the cost of combined energy installations, such as pairing of renewable energy and batteries, may also be included in the new Plan, according to officials.

This cost verification will cover not only each individual power source, but also their cost impact on the broader energy system (a measure known as the “system cost”). These calculations are said to be more complex than those prepared previously.

METI’s “Power Generation Cost Verification Working Group,” which was established to write the 6th Basic Energy Plan, calculated the expected kWh cost of each power source for 2030 by taking into account the cost of capital, fuel, operation and maintenance expenses.

In the wake of PM Kishida’s recent announcement of the resumption of subsidies for electricity and gas rates, ANRE said it’s concerned the decision may have been abrupt as the PM hadn’t discussed it with METI.

METI and ANRE are now working with the ruling LDP policy council to determine the subsidy amount; ANRE hopes to finalize the details by the end of June.

The subsidy is expected to be applied for three months starting August in order to meet increased power demand due to prevalent air conditioning use.

CONTEXT: Japan introduced its subsidy program for fuel prices in January 2022 and subsidies for electricity and gas bills in early 2023. The programs were originally set to end in September 2023, but were extended to deal with new price increases.

TAKEAWAY: Kishida’s move has also drawn backlash from utilities; as they suspect the resumption is a political ploy ahead of the LDP leadership race in September.

ANRE will review the mechanism for publishing a power capacity reserve margin for the wider region as the energy agency looks to improve the reliability and practicality of reserve figures that are used in weekly planning by grids and utilities.

This summer, amid its monitoring results, OCCTO will start to publish energy system reserve margins that include any power sources that are available to start up.

CONTEXT: Smooth operation of the electricity system requires some power plants or capacities to be available as a reserve in case of a sudden surge in demand and to meet peak demand times.

Since April, utilities that signed up to make power capacity available as a backup are notified when the reserve margin drops below 8%.

As ANRE looks to improve the use of reserve margin data, it will also start to reflect in the regional reserve numbers those generation units that have been shut due to balancing needs. The latter will be stated in a separate frame in the kilowatt (supply capacity) monitoring published weekly by OCCTO.

The Electricity and Gas Market Surveillance Commission (EGC) determined that since April procurement rates for weekly products have been very low in the supply-demand adjustment (balancing) market in Tokyo and Chubu.

All five products became available from April, but the watchdog confirmed that the two areas had extremely low primary adjustment capacity and secondary procurement rates for weekly products compared to other areas.

The EGC’s committee reviewing the procurement status on June 25 discussed the idea of settling start-up costs ex-post (post-delivery) instead of including them in the delta kilowatt price. The move could mitigate the risk of omission of start-up costs.

TSOs said they can’t accurately forecast power demand and supply, especially when it comes to supply of renewables, and potential troubles of hydro, thermal and nuclear power sources. It turned out they were operating close to the deadline/ gate close (GC) to minimize imbalances.

JOGMEC inked an MoC with Bureau Veritas Japan (BVJ), a certification services provider, which has a focus on offshore wind units.

The goal is to effectively use JOGMEC site survey results for offshore wind project development.

CONTEXT: Since April 2023, JOGMEC has conducted bathymetry, identification of sea floor objects, wind conditions, meteorological, and oceanographic site surveys for offshore wind development as part of the Japanese Centralized System. The results are provided to offshore wind developers that participate in public tenders.

TAKEAWAY: As Japan seeks to build almost 10 GW of offshore wind power by late FY2030, speeding up project development is crucial. Developers rely on the Centralized System that reflects the criteria set by the government. This MoC with BVJ reflects concerns over the accuracy and accessibility of the government approved data.

In Q1 2025, Mitsubishi Power will launch ACES Delta, a green hydrogen facility in the U.S.

(Japan NRG, June 26)

Speaking at a Reuters energy conference in New York, William Newsom, CEO of Mitsubishi Power Americas, said the company’s Advanced Clean Energy Storage Hydrogen Hub (ACES Delta) will launch in Q1 2025 in Delta, Utah.

Newsom said that the ACES hub will convert over 220 MW of renewable energy to 100 metric tons per day of green hydrogen, which will then be stored in two salt caverns capable of holding more than 300 GWh of dispatchable clean energy.

ACES Delta will support the Intermountain Power Agency’s IPP Renewed Project, an 840 MW hydrogen-capable gas turbine combined cycle power plant that will initially run on a blend of 30% green hydrogen and 70% natural gas starting in early 2025 and expanding to 100% green hydrogen by 2045.

CONTEXT: ACES Delta is a JV with Chevron through its wholly-owned subsidiary, Magnum Development. Chevron has a majority stake. Once operational, ACES will be the largest hydrogen storage hub in the U.S. Mitsubishi Power hopes to replicate the project across the U.S.

Alhytec and Hotel Mikazuki signed a deal to use hydrogen made from aluminum hydroxide to run the hotel’s energy systems starting 2026. Used beverage and food containers and other aluminum industrial wastes will be the feedstock.

CONTEXT: Alhytec is a startup in Takaoka city, which has a cluster of aluminum building material and auto components makers. In May 2021, the company commercialized equipment that continuously converts aluminum hydroxide to vehicle-grade hydrogen. See also Analysis “Toyota-backed firm hopes to utilize aluminum to produce hydrogen-based energy”, in the June 14, 2021 issue of Japan NRG.

TAKEAWAY: The Alhytec system produces 27 kg of hydrogen per hour from 270 kg of aluminum hydroxide; not a large amount. However, the capacity to output low-cost small-volume hydrogen from household materials could develop into interesting markets. For example, tech startup Gita is developing hydrogen-fueled kickboards and bicycles, using metal hydride as a hydrogen carrier to improve safety. There are also studies to use methanol as a carrier of hydrogen for small off-grid power systems.

Sumitomo Electric Industries has developed electrodes for green hydrogen electrolysis systems that cut power consumption by 10%.

The electrodes are made of nickel-coated urethane resin with nanosized holes, which increase the electrodes’ interactions with water.

The company plans commercialization in 2025.

CONTEXT: Electrolyzer component development is heating up thanks to market entries from the battery sector. Nickel is the key electrode raw material, but Japanese companies have also been exploring the use of titanium, stainless steel and other cheaper materials. Only a handful have reached commercialization.

TAKEAWAY: Power consumption is an important green hydrogen cost factor, along with the endurance of the electrodes, the cost of manufacturing the electrodes, etc.

Mitsui & Co inked a loan with the Japan Bank of International Cooperation and Sumitomo Mitsui Banking Corp for financing the construction of a 1 mln tons/ year ammonia plant in the UAE.

The two banks will provide up to $27 mln in total.

Plant construction is underway and ammonia production will begin in 2027. A CCS facility will begin operations there in 2030.

The project is owned by Abu Dhabi National Oil, GS Energy, Fertiglobe and Mitsui.

TAKEAWAY: JBIC’s key role is to support industries in developing economies, but in 2022 its scope expanded to financing ammonia projects in industrialized economies.

Itochu plans to build a global supply chain of direct reduced iron (DRI) by shipping iron ore from Brazil to the UAE, then processing it into DRI and supplying it to Japanese steel makers. It will conduct feasibility studies with Emirates Steel Arkan and other corporations.

They plan to bring onstream a 2.5 mln tons/ year DRI processing plant in 2027.

CONTEXT: DRI, which uses natural gas or hydrogen as reducing agents, has a lower carbon footprint than the current process that uses coal in blast furnaces.

TAKEAWAY: The success of DRI supply chains depend on access to high-grade iron ore with over 92% iron content, because lower-grade ores are not suitable for the process. Itochu owns stakes in Brazilian and Canadian mines with DRI-grade iron ore deposits. Sumitomo Corp also owns DRI-grade iron ore assets in Brazil and could build a similar supply chain.

Solar car cuts 80 kg of CO2 per year: study

(Japan NRG, June 26)

A solar car cuts 80 kg of CO2/ year, according to studies by Murakami & Co, which has been test driving Mitsubishi-model EVs mounted with solar panels in northeastern Japan since 2023.

The vehicle is totally emission-free as it’s fully powered by rooftop solar panels. However, it can’t travel more than 20 km due to limits on solar capacity.

The company, together with local authorities and financial institutions, are test driving five solar EVs in Fukushima and Iwate prefs.

CONTEXT: On average, one gasoline-fueled passenger vehicle emits 1.2 tons of CO2 when it travels 8,000 km.

TAKEAWAY: Murakami & Co plan to commercialize solar-car services in 2025. The study shows consumer behavior must change to make use of zero-emission cars. A company official told Japan NRG that the most difficult change has been promoting the habit of parking the cars outside the garage for solar power generation.

U.S. hedge fund Citadel will buy its first company in Japan, acquiring all of Tokyo-based market maker Energy Grid. The acquisition will be completed between July and Sept. The purchase price has not been disclosed.

More than 80 customers of Energy Grid, which was founded in 2021, include major electric utilities as well as new players mainly engaging in electricity retailing.

According to Nikkei, as of July last year, Energy Grid saw an electricity trading volume of 9.8 TWh, worth ¥230 billion (about $1.4 billion).

The acquisition is led by Citadel’s Commodities business, whose focus is on assisting energy producers and consumers manage commodity risks.

CONTEXT: Recent price volatility in the electricity market shows a growing demand for risk-hedging, drawing interest from major hedge funds. Citadel had closed its last office in Tokyo as part of its restructuring in the aftermath of the collapse of Lehman Brothers. But it continued to invest in Japanese shares from overseas.

TAKEAWAY: The Japanese stock market is seeing more foreign investors pushing for corporate governance changes. Citadel’s entry into the Japanese market could encourage other overseas investors to follow suit.

JERA completed a field test of 20% ammonia co-firing at Unit 4 (capacity 1 GW) at the Hekinan coal power thermal plant in Aichi Pref. The test began in March. IHI and NEDO also participated.

The NOx release level was not higher than the amount from coal firing; sulfur oxides release was cut 20%, and N2O release was below the threshold for detection.

JERA’s next goal is to establish, by March 2025, technologies to consolidate ammonia’s position in thermal power generation.

CONTEXT: This was the world’s first field study of 20% ammonia co-firing at a GW-sized thermal power plant, provoking protests from climate activists. If co-firing operators receive state subsidies, METI will have oversight on safety issues. If no subsidies, then municipalities of co-firing sites will have authority.

TAKEAWAY: JERA did not elaborate on the actual NOx and N2O release levels, but more disclosure will be required if offset credits are to be issued for ammonia co-firing.

At its Nanyo thermal plant in Shunan city (Yamaguchi Pref), Tosoh plans to shift to ammonia co-firing from coal power generation.

The company will begin designing the co-firing facilities in 2025, and plans to bring it online about 2030.

Idemitsu will import ammonia and supply the Nanyo plant via pipelines.

CONTEXT: Tosoh, together with Nippon Zeon and Tokuyama that also operate coal power plants in Shunan, plan to create a 1 million/ year ammonia demand in the area by shifting to 20% ammonia-coal co-firing. Tosoh has also budgeted ¥6 billion for carbon capture and utilization facilities in Nanyo.

TAKEAWAY: The Shunan ammonia project may be one of Japan’s most cost-efficient since most of the capital-intensive infrastructure is already in place. The port is big enough for ammonia imports and a LPG pipeline already connects the three company plants with Idemitsu. Provided the LPG pipelines satisfy ammonia safety requirements, users only need to install ammonia burners and other facilities for co-firing.

JERA will address electricity supply-demand challenges this summer based on the forecast by METI’s Electricity and Gas Basic Policy Subcommittee.

For example, JERA plans to avoid scheduling thermal power plant repairs and inspections during summer. But JERA is conducting soundness checks and patrols of boilers and other equipment. This will help mitigate the risk of power facility outages.

Still, the company will forge ahead with construction of new thermal power stations. For example, Goi Thermal Power Station (Chiba Pref) launches in August.

With a total generation capacity of 2.34 GW, Goi will have three units, each 780 MW, using LNG as fuel. Unit 2 is scheduled to launch in November. Unit 3 in March 2025.

ENEOS Renewable Energy was the biggest winner in the 20th auction for solar power generation under the FIP. The firm was awarded up to 15.15 MW capacity.

ENEOS’ bids were the lowest, ranging between ¥4.55/ kWh and ¥6.52/ kWh for a total of 10 projects. There were 47 winning bids in the 20th round.

The highest successful bid was ¥8.84/ kWh, slightly below the cap of ¥9.20/ kWh.

The weighted-average bid was at ¥6.84/ kWh. In the previous round, the weighted-average bid was ¥5.11/ kWh, but this number was ‘distorted’ by a zero-yen bid among the winners.

The bidding was for FIP PV installations with an output of 500 kW or more, and FIT PV installations with an output of between 250 kW and 500 kW.

TAKEAWAY: The auction is another example of the trend among large companies to use the tender as a way to secure grid connectivity while securing better price deals under PPAs or other contracts. The biggest winner in the previous auction, the last in FY2023, offered ¥0/ kWh. Auctions held in the past few years showed a tendency for operators to bid below ¥7/ kWh, which many say is not a feasible level at which to run a solar power plant.

On June 21, OCCTO instructed Tokyo Electric Power Grid to transfer power to cover the tight supply and demand balance in the Tohoku region.

Up to 850 MW was ordered from 1:00 p.m. to 4:30 p.m., and an additional 250 MW from 2:00 p.m. to 2:30 p.m. The area reserve ratio was at risk of falling below 3% due to the weather and a drop in solar power generation.

The balancing market continues to be short of bids for tertiary adjustment capacity, which corresponds to forecast errors for renewables.

CONTEXT: When the area reserve ratio is likely to fall below 3%, there is a rule that OCCTO instructs tight supply and demand adjustment. Tohoku Electric received balancing power transfer from TEPCO PG for 3 consecutive days from June 11 to 13 due to a combination of increased area demand and supply capacity shortages caused by rising temperatures. Among the causes are the closures of thermal and other power plants for inspections and repairs in June, which is the off-peak season.

Spot market: Supply-demand balance eases in May despite thermal power outage

(Japan NRG, June 26)

JEPX data show that the average daily input into the spot market in May was 1.07 TWh, down 1.2% MoM; the average daily bid was 793.42 GWh, up 0.5% from April.

Total monthly input was 33.28 TWh, up 2.1% from April, for items sold; and 24.59 TWh, up 3.8% for purchased items.

Although the industry saw shutdowns of thermal power plants in the off-peak season more than in the previous months, the increase in solar power generation compensated for those shortages, which helped ease the supply-demand balance for sales.

The largest item on the sellers’ list was 3.76 GWh from 11:30 to noon on May 3, during the Golden Week holiday period, which had three sunny days and which led to an increase in solar power generation.

The highest contract volume on the buyers’ list was 23.01 GWh from 11:00 to 11:30 on May 23; while the smallest was 10.41 GWh on May 4, from 8 to 8:30.

J-Power sold its 50% stake in Green Country Energy (in the state of Oklahoma) along with its partner company’s interest, to Public Service Company of Oklahoma, which is owned by American Electric Power

The Green Country power plant is a gas-fired power plant, (capacity 795 MW).

The sale is to be completed by June 2025. The financial impact will be reflected in the FY2025 results.

IHI and the Electricity Generating Authority of Thailand inked an MoU on biomass co-firing, biomass feed selection and biomass pellet production. The co-firing is planned at the Mae Moh power station in Thailand.

CONTEXT: Mae Moh (2.2 GW capacity) is fueled by lignite coal. The companies are considering eucalyptus and acacia as possible biomass to be mixed with lignite.

Kyushu Electric and the Ministry of Land, Infrastructure and Transport will explore pumped storage power generation using two dams in the Chikugo River system.

The proposed new power plant would use Shimouke Dam (Hita City, Oita Pref) as the upper reservoir and Matsubara Dam (Hita City) as the lower reservoir.

The goal is to use it as a peak power source when supply and demand are tight.

If approved, the project will be the area’s fourth pumped storage power plant.

CONTEXT: The Kyushu area is expected to have the highest renewable energy curtailment in FY2024, at 6.1%. Reducing curtailment can be achieved by expanding the supply and demand adjustment function of pumped storage.

Nikkei surveyed about 100 Japanese executives on NPPs. The majority support construction of new NPPs; over 70% also favor the restart of existing ones.

Also, more than 80% think Japan should increase its renewable energy goals.

Executives showed dissatisfaction over Japan’s reliance on coal and gas, saying this exposes electricity prices to global fluctuations. They stressed the need for expanding nuclear power for stability.

KEPCO received NRA approval for a long-term facility management plan on aging measures for Units 3 and 4 at Oi NPP.

The approval is based on the revised Reactor Regulation Act that requires a technical evaluation of equipment every 10 years for NPPs operating more than 30 years.

CONTEXT: This is the first reactor approval under the new “Green Transformation Decarbonization Power Supply Act” that allows for NPP operation beyond 60 years. KEPCO also made a similar application for its Sendai NPP.

It was just revealed that on June 12 the emergency gas treatment system at Tohoku Electric’s Onagawa NPP Unit 2 activated during an inspection of the air conditioning system. No radiation was detected. The source of the issue is unclear.

CONTEXT: The NPP is set to restart about September. It’s unlikely this incident will cause any delay. The NPP’s restart has been delayed twice since approval in 2020.

Mitsui & Co, via its subsidiary Mitsui E&P USA, acquired an unconventional gas asset (often referred to as shale gas) from U.S. energy companies Sabana and Vanna. The companies did not disclose the financial terms of the deal.

This asset, named Tatonka, is in Texas and has access to the Gulf Coast industrial area. Mitsui plans to develop it for full-scale production after 2026.

CONTEXT: An “unconventional gas asset” is obtained from sources that need advanced extraction techniques, such as hydraulic fracturing (fracking) or horizontal drilling. Sources include shale gas, tight gas, and coalbed methane. They’re more challenging to produce compared to conventional gas reservoirs.

In 2023, Mitsui bought a 92% stake in a shale gas asset in South Texas from Silver Hill Eagle Ford. Also in 2023, Tokyo Gas acquired Rockcliff Energy for about $2.7 billion to expand its U.S. shale business.

Lundin Mining acquired a 19% stake in the Caserones copper-molybdenum mine in Chile from JX Metals, exercising its option to increase its stake from 51% to 70%.

CONTEXT: Caserones was funded by Japan Bank of International Corp, and JOGMEC was the debt guarantor. The investment decision was made in 2011 when its copper deposit accounted for 11% of Japan’s copper ore requirement.

TAKEAWAY: The mine also had reserves of molybdenum, which at the time was positioned to what lithium or nickel are today, critical to the economy. However, the mine’s drawback was its remote location that inflated the costs of bringing ores to Japan.

Chiyoda Corp appealed to a U.S. court to resume part of the Golden Pass LNG project in Texas. Construction froze in May when Zachry Industrial went bankrupt.

The remaining partners will take over the construction and complete the project.

Chiyoda reported a consolidated net loss of ¥15.8 billion for FY2023. It had a profit of ¥15.1 billion in FY2022.

The project, owned by QatarEnergy and ExxonMobil, is valued at around $10 billion.

NYK and PT Pertamina International Shipping signed an MoU to collaborate on LCO2 and LNG transportation.

NYK and PIS will study the transportation of LCO2 to and from Indonesia. The market is storage operators and CO2 emitters like Pertamina.

TAKEAWAY: LCO2 carriers are emerging worldwide to service the CCS industry. They’re smaller than LNG tankers thanks to pressure chamber constraints. Their goal is to transport CO2 from emitters to storage sites. However, there’s currently a shortage of port infrastructure. While such carriers are expected to increase in number, issues remain with shipping costs and logistics.

LNG stocks of 10 power utilities were 2.08 mln tons as of June 23, down 2.8% from the previous week (2.14 mln tons). This is the same as a year ago (2.08 mln tons), and 3.5% up from the 5-year average of 2.01 mln tons.

Power companies are preparing for the peak demand period in July and August when air condition demand is the highest due to hot weather.

ANALYSIS

BY PROFESSOR ANDREW DeWIT

The 5Ds of Critical Raw Materials in Japan

On June 7, the energy agency (ANRE) made a startling admission about Japan’s vulnerability in critical raw materials. A mere three years after trumpeting a heightened focus on boosting the nation’s self-sufficiency in the materials needed to decarbonize energy systems, the agency quietly confessed that the goals were unreachable.

Most energy discussions center on the supply or demand of electricity or molecules, as well as the associated costs. Yet without the critical raw materials (CRMs) to build power supply generation facilities, the planning of future energy systems is moot. Japan is a net importer of most CRMs used in batteries and EVs, solar and wind generation equipment, and other clean energy technologies.

ANRE’s admission comes at an important juncture. Deliberations over an update to the national Basic Energy Plan are ongoing, and influential policy experts, such as those at the Institute of Energy Economics, Japan (IEEJ), argue that CRM security should be made equivalent to national security. An extension of this logic suggests that if Japan fails to secure adequate access to certain CRMs, then it might also need to adjust its energy strategies.

Japanese diplomats and businesses have been active in securing the supply of CRMs, striking deals with the U.S. and EU to collaborate on development and procurement. Also, the state resource company JOGMEC has had its remit expanded from hydrocarbons to CRMs.

Data from ANRE, however, suggests that the above activity has yet to bear fruit. Meanwhile, Japan’s self-sufficiency in key critical resources is slipping.

Copper shock

ANRE published its recent concerns in a document titled “Future directions in mineral resource policy,” noting that Japan’s current energy strategy aims for an 80% self-sufficiency in copper and other base metals largely via Japan’s offtake from collaborative overseas projects. By 2050, that ratio is supposed to hit 100%.

But a mere three years after Japanese officials announced the above targets, ANRE’s data show that Japan’s self-sufficiency in copper has in fact plummeted from about 58% in 2014 to around 40% in 2022. Recent initiatives are expected to bolster the ratio to roughly 48% in 2023, and then help it head for a likely peak of about 54% in 2030. But after that, it is projected to decline to under 40% in 2040.

Japan’s oft-cited policy goals in copper and other CRMs are thus questionable, leaving Japan more vulnerable to supply shocks and other risks. Japan is over-invested in regions with depleting mines, and ill-equipped to assess the full slate of factors driving demand and then respond adroitly.

ANRE clearly understands these core facts. Even so, it seems that the agency isn’t yet sufficiently apprehensive because it underplays or overlooks several huge drivers of CRM insecurity. This does not refer, however, to the high dependence on Chinese-dominated supply chains, even though IEA and Japanese data show that the dependence has worsened over the past few years.

Dependence on China is quite problematic, but there’s already extensive literature on that. Rather, below is an overview of Japan’s dire critical mineral challenges as the 5Ds of decarbonization, digitalization, defense, demographics, and debt.

Decarbonization: Japan’s official decarbonization goals include nearly halving emissions between 2103 and 2030, and then achieving net zero by 2050. As with other developed countries, Japan’s climate goals imply a major increase in CRM demand to build a vast new infrastructure of clean generation, transmission, storage, and end-use electrification. For example, Japan plans to raise solar, wind and other renewable energy shares in its power mix, from 21.7% in 2022 to between 36-38% by 2030, and even more in subsequent years. Also, their intermittency will be addressed with battery storage and expansion of the transmission grid.

Missing from these and other energy-transition ambitions is a Japan-specific assessment of how much copper, silver, nickel, rare earths and other CRMs are likely to be required. JOGMEG and the IEEJ released a scoping study in 2022, but they used IEA and other global macro level data to project material demand from EVs, solar, wind, and other technologies. Yet decarbonization in Japan will almost certainly require a much higher density of CRMs per unit of emissions reduction/clean energy than the global average, especially if Japan’s decarbonization is centered on distributed solar and offshore wind.

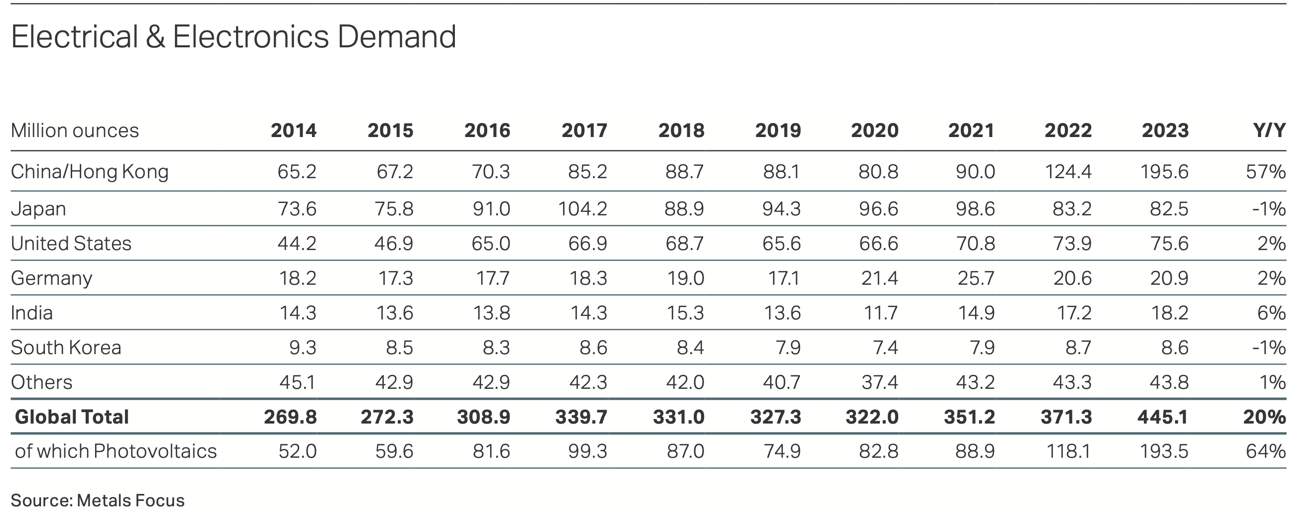

Japan’s high CRM density of decarbonization is not merely driven by the country’s need for a multi-trillion yen expansion of copper-intensive cables to link distant offshore wind generation with urban power consumption centers. Beyond copper, cobalt, rare earths, and other much-discussed CRMs, many other materials matter. For example, BloombergNEF estimates that silver use in solar is roughly 12 tons/GW of capacity. Solar’s consumption of global silver production rose from 5% in 2014 to 14% in 2023, while silver’s cost per solar module has reached 11%, further squeezing manufacturers’ already strained profitability. And Figure 1 shows that solar’s demand for silver was up a startling 64% between 2022 and 2023, and that Japan’s consumption share declined by 1% while Chinese demand grew by 57%. China is willing to pay a double-digit premium for silver whereas Japanese producers struggle with a devaluing currency already at 50-year lows in purchasing power.

Silver demand in electrical and electronics

Source: Silver Institute

To be sure, Japan hopes to innovate low-cost and large-scale manufacturing of iodine-based perovskite solar by 2040. But that is decades away, and meanwhile, silver is also increasingly needed in EVs, chargers, and many other decarbonization-related technologies.

Digitalization: Digitalization ramps up demand for CRMs because data centers are material-intensive and require large increases in power generation to satisfy Chat GPT and other innovations’ voracious appetite for electricity. The ANRE document effectively concedes that policymakers overlooked digitalization when they formulated their self-sufficiency targets. In 2022, Japan’s total copper consumption was roughly 1 million tons, but by 2030 that’s projected to rise to well over 1.4 million tons.

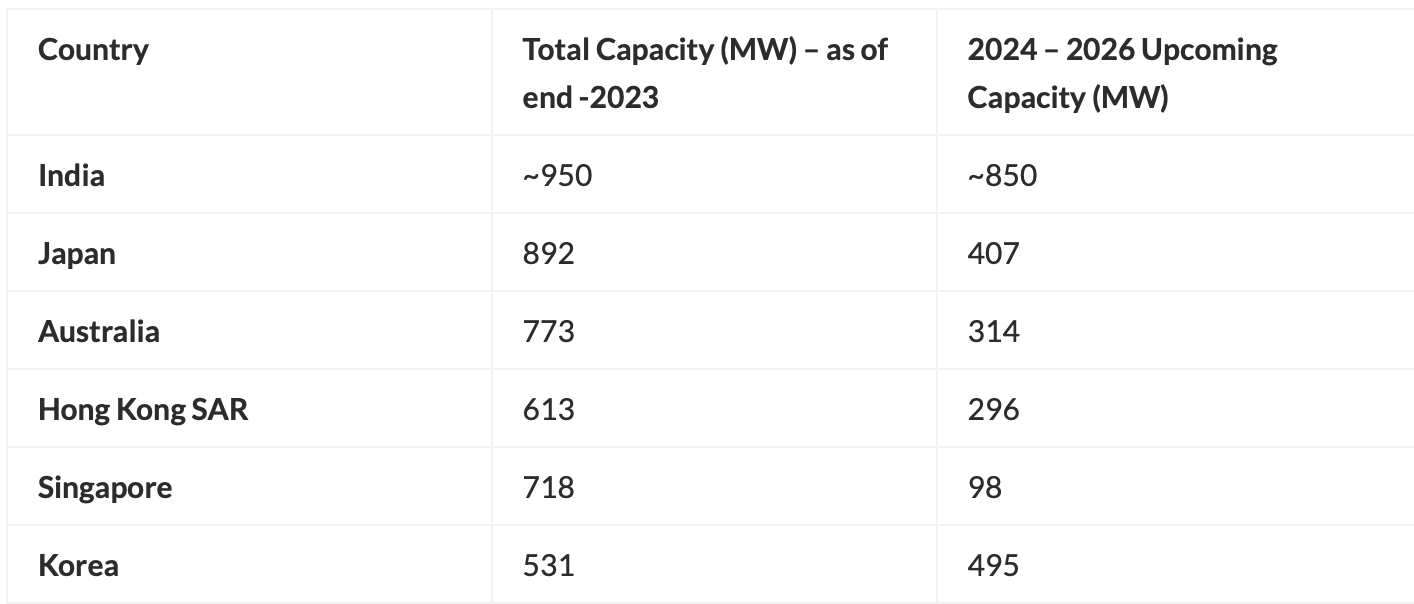

A big share of the increase in copper owes to EVs along with renewables and power systems. But digitalization and AI are now expected to require a lot more, likely quintupling globally to 1 million tons by 2030. Drilling down on demand numbers, we find that most reliable estimates suggest each MW of data center power capacity requires between 20 to 40 tons of copper. Relatedly, one oft-cited new survey “Asia Pacific Data Center Trends” suggests that Japan will add 407 MW of new data center capacity between 2024 and 2026, a major increase over late 2023 total capacity of 892 MW.

Asia Pacific Data Center Trends, 2024-26

Source: CXOToday

Japan’s expansion of digitalization has a large CRM footprint on its own, and implies a lot of new (and ideally clean) power generation to operate those assets and ancillary infrastructure. The ANRE data indicate that Japan’s copper consumption for construction and other conventional uses will hover at about 800,000 tons/ year, reflecting its aging and shrinking society. And copper for conventional vehicles is slated to plunge from 200,000 tons/ year in 2022 to well under half that in 2030 and even less in 2040. Conversely, Japan’s 2 Ds of decarbonization and digitalization will add at least 500,000 tons/ year by 2030 and upwards of 600,000 tons by 2040.

Defense: Increasing expenditures on weapons systems and ammunition is another area of significant CRM demand. The authoritative “SIPRI Trends in World Military Expenditure, 2023” reveals that global military spending grew 6.8% to an all-time high of $2.44 trillion. Various observers and institutions, including such diverse agencies as the Carnegie Endowment for International Peace and the Modern War Institute at West Point, are beginning to analyze the impact of rising military demand on geopolitically fraught CRM supply chains.

The ANRE document does not scope Japan’s military demand for copper, and indeed few analysts try to quantify defense demand for CRM. But highly regarded copper expert Simon Hunt’s firm, Simon Hunt Strategic Services, has estimated that defense demand consumed 9% of global copper in 2021 — 2.186 million metric tons — and was growing at 14% YoY. Meanwhile, Japan’s FY 2024 defense budget has risen to 1.6% of GDP or ¥8.9 trillion, rising at its fastest rate in 50 years.

Japan’s defense spend includes buying up or building a significant number of new fighter aircraft, warships, tanks, missiles, ammunition, and other CRM-intensive weapons systems. Given the scale of CRM in high-tech national defense, coupled with the rapid expansion of Japanese spending, the next iteration of ANRE’s work on mineral resources should include some numbers on defense demand.

Demographics: Japan’s shrinking and aging population is another 5D challenge for critical minerals. Ordinarily, Japan’s demographic shift would mean declining demand for copper and other CRM, as fewer and older citizens mean lower levels of per-capita consumption. But the potential for more compact and resource-efficient lifestyles is not reflected in the ANRE data that suggest a plateau, but not a decline, in annual copper demand outside of decarbonization and digitalization.

Japanese urban space has a high per-capita footprint of CRM in water, sanitation, transport, and other critical infrastructures. A more spatially compact urbanization has long been a policy goal of central agencies that govern infrastructure, urban planning, local finance and related areas.

Their policy goals would help moderate the rising costs of maintaining aging infrastructures, and help free up a lot of pipes, wires, and electric motors for recycling. But outside of a few communities, Japan’s demographic shift is marked by a startling increase in single-person households – from 20% in 1980 to 38% in 2020 – and the stubborn stickiness of cities’ and towns’ spatial extent.

Japan’s demographics have another challenging aspect. Since Japan doesn’t mine CRM domestically, it relies on its scarce human capital and networks to facilitate overseas projects. Even so, ANRE wants to expand Japan’s projects beyond reliance on the resource majors and conventional regions (eg, Latin America) to include a strong shift to working with junior mining firms in Africa and other frontier regions.

Moreover, ANRE hopes to bolster the intelligence-gathering capabilities of Japan’s JOGMEC and businesses involved in resource security. Yet the demographic challenge again becomes significant, as Japan already has a thin bench of talent capable of doing the work involved in securing CRM.

Moreover, those people are aging and on the cusp of retirement, while the academic institutions that should be training a lot of new recruits are in fact shrinking. ANRE urgently wants to foster many more skilled personnel capable of working in an increasingly dynamic and diverse environment, but that is a tall order for at least the next decade or two.

Debt: Perhaps the most forbidding of the 5Ds is Japan’s unmatched public debt, well over 260% of GDP and costing 22% of public spending in debt retirement even at ultra-low interest rates. ANRE and other agencies understand that increasing security in CRM will require a lot more public money, and in fact, recently increased JOGMEC’s capability to underwrite overseas initiatives.

More money is essential. The very high volatility of CRM prices has often left government-backed Chinese firms in the catbird seat, as their market-driven competitors were driven into bankruptcy and Chinese firms swooped in to buy up intellectual property and projects on the cheap. China has also built dominance in CRM mining and refining through decades of financing a comprehensive industrial policy of funding new technologies, training legions of experts, providing various carrots to foreign governments, and other strategies. Japan’s ANRE and others want to undertake that public-private approach.

But mining and refining projects are increasingly expensive, their costs driven up by local communities’ understandable desire for better returns, longer lead times, increased environmental rules, more costly water, and higher energy inputs in mining and processing declining ore grades. Finding a lot more public money in Japan confronts the probable increase in debt-finance payments coupled with the rising costs of social security, national defense, and myriad other areas. Worse yet, deep devaluation of the yen – if protracted – means that available funds buy far less in the way of overseas initiatives and offtake.

In summary, Japan’s CRM needs are expanding even as the daunting 5Ds of challenges complicate the country’s ability to secure adequate supplies. The existence of these constraints does not, of course, mean that decarbonization is impossible. Rather, the constraints suggest that many difficult tradeoffs will have to be made on the means of decarbonization and perhaps even the extent of digitalization.

Japan has perhaps been moving in this direction for some time. For example, Toyota credibly argues that decarbonizing mobility is better served by including a large role for CRM-lite hybrids rather than insisting on 100% CRM-intensive EVs. So to end on an optimistic note, the potential upside of Japan’s 5Ds could be a powerful return to the resource-efficiency that Japan once embodied.

ANALYSIS

BY MAYUMI WATANABE

Potential Copper Shortages Loom: Demand-side Measures Are Needed

The International Copper Study Group (ICSG) forecasts that this year will see a 162,000-ton copper surplus globally, and a 94,000-ton surplus in 2025. Nevertheless, the U.S. and the EU classify copper as a critical mineral vulnerable to supply risks. The main concern is surging demand, driven by diversified power transmission networks, as well as a surge in AI-driven data traffic globally that will outpace supply growth.

Copper means a lot to Japan, which has a total copper refining capacity of 1.7 million tons/ year, the world’s second largest after China. Japan is also the world’s fourth largest exporter of refined copper products called copper cathode. However, the country’s four copper cathode producers rely entirely on imports for the ore concentrate.

In June, the Agency of Natural Resources and Energy (ANRE) decided to drive more investments into overseas copper mines by increasing state ownership of future mining projects. Equally significant, it also announced a plan to launch a framework that will encourage new businesses in the metal recycling industry.

Will these measures be sufficient to secure Japan’s copper concentrate needs, which are about five million tons/ year? Can other measures, especially on the demand side, be implemented to help manage possible shortages?

ICGS global refined copper balance (tons)

2011

-214,000

2012

-421,000

2013

-272,000

2014

-414,000

2015

-153,000

2016

-152,000

2017

-261,000

2018

-404,000

2019

-382,000

2020

-479,000

2021

-458,000

2022

-461,000

2023

-3,000

2024 (forecast)

162,000

2025 (forecast)

94,000

Copper threat

On June 7, ANRE told the Sub-committee on Resources and Fuel about the plan to raise state ownership of copper mining projects overseas. Presently, the Japanese state can own up to 50% of such projects, but now the cap will be increased to 75% by late FY2024.

This will help to financially support a dozen copper upstream players – consisting of six producers and six trading houses – to acquire interests in untapped resources, notably in Africa, which is the new copper frontier. In the last three years, Japanese companies have sold mines in Chile and Canada because they were running operating losses.

After the sale, Japan’s copper ore self-sufficiency rate fell to less than 40%, far from the 2030 goal of 80%. Copper producers also said that the mines’ bargaining power in ore price negotiations is getting stronger.

Even if copper cathode prices rise on strong demand prospects, the producers will be paying more for the ores. Ideally, they need to have direct access to ore resources.

Recent copper mine sales

Sellers

Mine name

Year of sale

Sumitomo Metal Mining, Sumitomo Corporation

Sierra Gorda (Chile)

2021

JX Nippon Mining

Caserones (Chile)

2023

Dowa Metal Mines

Cariboo Copper (Canada)

2024

Japanese companies hold stakes in 20 copper mines overseas, mostly in South America. Japan imports about five million tons/ year of copper ore concentrate to produce 1-1.5 million tons/ year of cathode for domestic and export markets.

This amount is not expected to change significantly as domestic refining facilities are unlikely to be expanded. Even if domestic demand rises 30% to 1.35 million tons in 2040 (over 2022), this is within the capacity of the present facilities of roughly 1.7 million tons/ year.

New copper ore frontiers: Africa and at home

Copper cathode can be produced by remelting scrap, but copper concentrate contains other metals. Chilean copper concentrate contains gold, silver, sulfuric acid and rare metals that are classified as “critical resources” in some countries; these include selenium, molybdenum, and rhenium.

Africa is a new frontier for copper concentrate. Over 50 years ago, ENEOS group had a project in Rhodesia (Zimbabwe) but political turmoil forced it to exit. Today, Japan does not import any copper concentrate from Africa. However, new overseas mine projects in the last decade were mostly in Africa.

The increased Japanese state ownership of mining projects is effective in managing country risks; for example, many African governments have assertive mining policies. Although Africa is geographically far from Japan, it is important in order to diversify supply sources as much as possible to reduce risks. These include resource nationalism-driven raw material export halts, as well as damage to ports and mines due to armed conflicts and weather, etc.

Shipping is often delayed by labor strikes, so Japanese copper producers keep high concentrate inventories for several months. However, it is always more reassuring to have suppliers closer to home. Having local supplies is important, and recycling is a solution in this matter.

Japan’s copper recycling rate is over 80%, reproducing about 1 million tons / year. On June 7, ANRE said it will design a framework to encourage more recycling businesses because labor shortages have led to closures of recycling firms.

Upstream development and recycling have been a core strategy for all metals industries. Other actions include export restrictions and restart of domestic copper mines. Japan exports around 0.4 million tons/ year of recycled copper, which is nearly half of domestic recycled supplies. China is the biggest buyer.

The last of Japan’s copper mines closed in 1994 due to high operational costs. But according to the National Institute of Material Science, Japan has 38 million tons of copper ore deposits, or about 8% of the global reserve.

Demand-side measures

Upstream development, recycling, and export controls are supply-side measures. There are also demand-side measures to decrease copper consumption and switch to other materials, but governments have not been keen to act since they strain consumers. Demand-side measures, however, are needed since there are limits to supply growth.

In the past, demand measures were implemented as a last resort when there was a buying frenzy caused by supply tightness. In 1938, Japan began to regulate copper usage and launched a ration system amid shortages caused by the Depression and World War 2. Post 1945 there was no crisis that triggered copper demand measures, but there was a crisis hitting other resources.

In 2022, the Ministry of Environment launched programs to curb helium gas consumption for water and air quality analysis, as geopolitical tensions in the Persian Gulf region cut supplies from Qatar, Japan’s major import source. The plans to purchase helium from Russia ceased due to the Ukraine invasion.

The MoE programs consisted of substitution, usage reduction and increased recycling. Other helium users also made switches: Argon for optical fiber and semiconductor manufacturing; hydrogen and nitrogen for leak tests, etc. In the end, helium rationing was avoided, but consumers continue conservation measures.

MoE helium measures

Substitution

Hydrogen for gas chromatographic separation

Nitrogen for the atmospheric pressure gas chromatography process

Use solutions or solids where applicable

Usage reduction

Use of gas saver device or switch to nitrogen during stand-by;

Turn off the analysis equipment when not used;

Reduce the use frequency by combining several tests into one;

Replace 99.95% helium filter with 99.999% device:

Install gas savers to all analysis equipment

Shift to equipment with helium freezing function

Recycling

Collect gas residue in the equipment after use, if possible; capture helium in the room.

Possible copper demand-side measures

Driven by high prices, Japanese copper consumers have been practicing demand-side approaches voluntarily. Automotive manufacturers have set a price threshold, such as Grade-A copper cathode at $100,000/ ton to start looking for substitutions. This might be a one-time process or may become a permanent practice.

For example, radiators used in air conditioning were made of copper; but aluminum, which costs one third of copper, replaced it almost entirely. Aluminum’s electricity conductivity is lower than copper, but it is lightweight. Similarly, copper cables have been replaced by aluminum for installations where weight becomes an issue.

The woes over availability of fossil fuel, electricity, and battery metals are driving resource saving solutions. For copper, one solution is removing copper cables in buildings, and installing wireless microwave power transmission systems. This is a new technology. Radio wave frequency licensing for power transmission only began in 2022.

But there are mounting issues to clear such as health concerns if exposed to microwave transporting power. Another approach sought by tech startups is appliances that do not require electricity but rather run on kinetic energy and other energies, thus eliminating any need for power transmission lines or batteries.

There is no single solution to resource strategies. Instead, multiple and diversified approaches from both the supply and demand sides are seen as optimal strategies. This is widely understood in theory, but in practice consumers have been reluctant to explore substitutions and other demand-side measures until hit by critical situations.

Demand-side measures imposed costs for buying new equipment and changing processes. However, the war in Ukraine and mounting geopolitical tensions elsewhere are gradually changing this mindset. More businesses are becoming aware that they need to intensify efforts to safeguard supply chains and find substitutes for critical raw materials.

Copper has become expensive at $10,000/ ton. The accelerating race over untapped African copper reserves may change buyer awareness on copper consumption. But there are positive sides to this development. Just as the green transformation drives innovations to resolve climate issues, resource supply constraints may open new opportunities and a suite of new solutions.

ASIA ENERGY REVIEW

BY JOHN VAROLI

This weekly column focuses on energy events in Asia and the Pacific

AI / Electricity usage

Bill Gates urged not to worry about the amount of power to run new generative AI systems. Data centers will drive a rise in global electricity usage of between 2-6%, but Gates believes that investments in sustainable energy can offset increases in data center emissions. In May, Microsoft said its GHGs had risen by a third since 2020, mostly due to new data centers.

APAC / Energy consumption

In 2023, APAC consumed 78% of the world’s total energy, according to the Statistical Review of World Energy.

Asia / AI

To promote the wider adoption of AI, companies that run data centers in Asia must invest over $100 billion to expand their capacity through 2030, said Mayank Maheshwari, an energy analyst at Morgan Stanley.

China / Coal

China’s growing LNG imports haven’t reduced or slowed the growth of its coal consumption. Since 2017, China’s coal demand has increased more than LNG imports every year. In the power sector, which accounts for 60% of China’s total coal usage, since 2015 the share of natural gas generation has remained at 3%.

China / LNG

China has taken advantage of low spot market prices to boost the amount of gas in storage. As storage fills and spot prices rise, China’s intake is likely to taper over the summer. The country bought a record 55 MMT of gas from overland pipelines and sea-borne LNG in the first five months of 2024.

Coal

APAC was a major contributor in global coal production in 2023, accounting for 79% of total output, said the Statistical Review of World Energy. APAC’s output was up 6% over 2022. Activity was mostly in Australia, China, India, and Indonesia, which accounted for 97% of the region’s production.

Indonesia / CRMs

BASF pulled out of a $2.6 billion nickel-cobalt refining complex in Weda Bay. Activists highlighted the plight of uncontacted people in the area. Despite the scrapping of the refinery project, Weda Bay Nickel – the world’s biggest nickel mine – is set to continue. The nickel is destined for EV car batteries.

Malaysia / Taiwan / Renewables

Malaysia’s Solarvest inked a partnership with GreenRock Energy (Taiwan) to develop 1 GW of renewable energy projects in their respective countries over the next five years.

South Korea / SMRs

South Korea seeks to become a significant player in the construction of small modular reactors (SMRs). The govt will provide $216 million to develop an SMR industrial hub to be built in Gyeongju, which will include manufacturing technology.

2024 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

First market trading day (Jan 4)

IEA “Renewables 2023: Analysis and Market Forecast to 2028” released (Jan 11)

Renewable Energy Exhibition (Jan 31 – Feb 2)

Taiwan presidential election (Jan 13)

Japan’s Diet convenes

IEA “Electricity 2024 / Analysis and Forecast to 2026” released (Jan 24)

February

CFAA International Symposium (Feb 2)

India Energy Week 2024 (Feb 6-9)

Lunar New Year (Feb 10-17)

Indonesia presidential election (Feb 14)

Japan-Ukraine Conference for Promotion of Economic Reconstruction (Feb 19)

FIT/FIP solar auction (Feb 19 – March 1)

Smart Energy Week (Feb 28-Mar 1)

March

Announcement of auction result for Offshore Wind Round 2 (for Akita Happo-Noshiro Project)

Onshore wind auctions (March 4-15; results on March 22)

International LNG Congress (LNGCON) 2024, Milan, Italy (March 11-12)

Russian president election (March 15-17)

World Petrochemical Conference, Houston, TX, USA (March 18-22)

IAEA Nuclear Energy Summit @ Belgium (March 21)

Ukraine presidential election (due before March 31)

Happo Noshiro, Murakami-Tainai, Oga-Katagami-Akita and Saikai-Eshima wind project auctions close (June 30)

July

Tokyo governor election (July 7)

7th Basic (Strategic) Energy Plan draft published (expected)

August

7th Basic (Strategic) Energy Plan draft presented to Cabinet (expected)

September

Global Offshore Wind Summit Japan 2024, Sapporo, Hokkaido (Sept 3-4)

The United Nations Summit of the Future (Sept 22-23)

Gastech 2024, Houston, TX (Sept 17-20)

IAEA General Conference

GX Week in Tokyo (expected late Sept to October)

Asia Green Growth Partnership Ministerial Meeting

Asia CCUS Network Forum

International Conference on Carbon Recycling

International Conference on Fuel Ammonia

GGX x TCFD Summit

October

IEA World Energy Outlook 2024 Release

BP Energy Outlook 2024 Release

Innovation for Cool Earth Forum (expected)

Connecting Green Hydrogen Japan 2024 (Oct 16-17)

Japan Wind Energy 2024 Summit (Oct 16-17)

Solar Energy Future Japan 2024 (Oct 16-17)

Japan Mobility Show (Oct 25-Nov 5)

November

US presidential election (Nov 5)

COP 29 in Azerbaijan (Nov 11-22)

Abu Dhabi International Petroleum Exhibition Conference (ADIPEC) 2024, Abu Dhabi, UAE (Nov 11-14)

APEC 2024 @ Lima, Peru

International Conference on Nuclear Decommissioning (TBD)

G20 Rio de Janeiro Summit (Nov 18-19)

Offshore Energy Exhibition & Conference (OEEC) 2024, Amsterdam, the Netherlands (Nov 26-27)

Biomass & BioEnergy Asia Conference (TBD)

European Biomethane Week 2024

December

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.