Trading house Mitsui will launch an AI-driven commodity futures trading system by late March, leveraging proprietary generative AI to predict market trends and conduct purchases automatically.

The goal is to stabilize procurement costs for energy firms and other clients, and to enhance prediction accuracy, and to commercialize the system by 2026.

Initially, it will be deployed at Mitsui’s global offices, such as in New York, focusing on metals and energy resources.

Mitsui plans to further enhance its performance by adding commodity-specific algorithms; toward that goal, Mitsui will host a contest this month via AI community platform Kaggle, inviting global experts to contribute.

CONTEXT: While AI trading is common in equities, its application in futures is in the early stages. U.S. agribusiness conglomerate Cargill is exploring AI for futures trading. A unique aspect of Mitsui’s approach is the use of generative AI to automatically generate and refine trading algorithms.

CONTEXT: Jointly developed with Preferred Networks, the AI system has been in trial since 2021, consistently turning a profit on trades. Its development comes as rising geopolitical risks and climate change make the commodity markets more volatile, highlighting the need for innovative, resilient trading strategies.

The govt approved a bill to amend the Renewable Energy Sea Area Utilization Act, expanding the permitted areas for offshore wind power installations from territorial waters to the exclusive economic zone (EEZ).

Under current law, developers awarded designated sea areas can hold exclusive rights for up to 30 years. To facilitate floating wind expansion, the govt will allow long-term operations in the EEZ.

While fixed-bottom wind turbines are standard in territorial waters, floating wind turbines will be the primary option in the EEZ’s deeper waters.

CONTEXT: While offshore wind development is progressing in the northern areas of the Sea of Japan, the country’s deep waters limit suitable locations. Projects in Europe, with much shallower coastal waters, have widely adopted fixed-bottom turbines. This is why floating tech is still in early demo stages globally.

TAKEAWAY: The passage of this bill will accelerate floating wind tech development amid turmoil in the sector related to the fixed-bottom offshore wind projects awarded to Mitsubishi Corp in the first round of public tenders in 2021. The trading firm said it needs improved terms to complete the projects or quit the sector. Others in the industry would see preferential treatment to Mitsubishi as a major signal that the Japanese market is biased towards domestic, government-friendly companies. But finding a way to help Mitsubishi to complete the round one projects without altering the tender framework will be tricky. In this context, the floating wind space offers the government a clean slate – a chance to make a new tender system that learns from the mistakes of the past.

Sumitomo Mitsui Financial Group (SMFG) will exit the Net-Zero Banking Alliance (NZBA), becoming the first Japanese bank to withdraw amid growing U.S. political pressure on institutions. Nomura Holdings is also considering leaving.

Japan’s other megabanks, MUFG and Mizuho, are also reassessing their membership, as they believe that staying in the alliance could pose business risks in the U.S.

CONTEXT: The NZBA was convened in 2021 by the UN Environment Programme finance initiative. It seeks to support the net-zero by 2050 target and counts over 100 global financial institutions in more than 40 countries.

Several U.S. lenders have withdrawn from the alliance in recent months due to the White House’s change in direction on climate action.

SMFG says it will continue decarbonization efforts independently and maintain its 2030 sustainable finance targets.

TAKEAWAY: It is no surprise that Japanese financial institutions are following those in the U.S. in leaving the NZBA so as not to irritate the new White House. Beyond the optics, the change might not be drastic. A European Central bank report last year said that being a signatory to the NZBA has had little impact on climate action results. One area to watch will be any impact on green and transitional financing, and whether some international lenders review earlier promises to stop giving loans to the oil and gas industry.

Akihiro Ondo, managing director and CEO of Mitsubishi Power Asia Pacific said in an interview that:

Natural gas remains essential as a bridge fuel, and Mitsubishi Power is deploying GTCC plants to enhance efficiency and cut emissions.

In Thailand the company installed 10 J-Series Air Cooled (JAC) gas turbines, which can help reduce CO2 emissions by up to 65% compared to coal.

The company is also accelerating hydrogen adoption. Its turbines can co-fire 30% hydrogen, with a goal of 100% hydrogen combustion by 2030.

Mitsubishi Power engages in public-private partnerships and international initiatives like AZEC, and also collaborates with leading utilities such as TNB Genco (Malaysia), EGAT (Thailand), and PLN (Indonesia).

Based on the scenarios of the Central Research Institute of Electric Power Industry (CRIEPI), Research Institute of Innovative Technology for the Earth (RITE), and Deloitte Tohmatsu Consulting, OCCTO has accumulated several long-term power demand forecasts.

Two scenarios for 2040: 900 TWh and 1,100 TWh

Four scenarios for 2050: 950, 1,050, 1,150, and 1,250 TWh

To allow stakeholders to choose a model that suits their purpose and to customize the model as needed, a breakdown will be set for each element.

CONTEXT: The scenarios will be shared among relevant parties, including state agencies and power companies, and will serve as a reference for the smooth implementation of long-term decarbonized power source auctions and systematic power source development. Since their purpose is different from that of METI’s Basic Energy Plan, OCCTO’s Supply Plan and Master Plan, these are developed without necessarily assuming consistency.

CONTEXT: These three organizations developed scenarios that include direct air capture (DAC) and hydrogen production, which could impact electricity demand.

TAKEAWAY: The number of scenarios and the range of the figures are too broad to allow for deep insight, but once again they show how uncertain future demand is in the face of AI and other processes. It’s likely that companies and organizations will cherry pick the data that suits them when citing OCCTO forecasts.

ANRE will lift the high-voltage price controls on Okinawa Electric. The proportion of new power suppliers reached 12.2% in the high-voltage sector, comparable to that on the mainland, so it was decided to lift price controls in Okinawa’s high-voltage sector just as on the mainland.

The necessary measures for cancellation will be considered by the Electricity and Gas Market Surveillance Commission (EGC).

CONTEXT: Retail liberalization in the Okinawa area was implemented in March 2000 for “customers consuming 20,000 kW or more of electricity and receiving it at 60,000 V or more”, and was extended to extra-high voltage (2000 kW or more) in April 2004. But price controls remain in place for the high and low voltage sectors. On the mainland, extra-high voltage (2000kW or more) was deregulated in March 2000, high voltage (500kW or more) in April 2004, high voltage (50 kW or more) in April 2005, and all retail electricity, including low voltage, in April 2016.

The EGC discussed the issue of “non discrimination against buyers inside and outside of the major power companies” when large EPCOs impose conditions that restrict supply within a specific area in wholesale trading.

There are four main sales methods used in trading between power generation companies and retail companies: (1) uniform price sales, (2) bidding, (3) brokerage, and (4) bilateral negotiations.

If the set value for the area supply restriction is lower than the new power company’s market share, there is no concern as long as “non discrimination” conditions are met. The exception is for uniform price sales, which are beneficial to the company’s own retail sales.

If the set value for the area supply restriction is higher than the new power company’s market share, depending on the sales method, the conditions will be favorable for the company’s own retail sales.

CONTENTS: In December, in response to emerging issues and needs, a proposal was made to “allow the imposition of conditions such as area restrictions on a certain amount of wholesale trading as long as they do not indiscriminately violate internal and external trading.”

Osaka Gas will build a third unit at the Himeji Natural Gas Power Plant (Himeji, Hyogo Pref). This is a JV with the Development Bank of Japan, SMFL Mirai Partners, and Mizuho Leasing. Launch is planned for FY2030.

The new unit won a bid in April under the govt’s long-term decarbonization power auction. The plant’s first and second units are already under construction and will start in 2026.

Power generation capacity will be 620 MW, or about 20% of Osaka Gas’s domestic thermal power capacity. The company is considering using e-methane in the future.

The Federation of Electric Power Companies of Japan urged the govt to consider “exceptional measures” for phase-out of inefficient coal-fired power plants by 2030.

FEPC submitted its opinion as part of the public comment process on a draft report by ANRE calling for strengthening measures to speed up the phase-out of inefficient coal power. Yet, FEPC opposed a fixed deadline, requesting “some discretion and time flexibility” for operators.

It emphasized that existing thermal power plants remain essential for stable electricity supply. It called for revisions to the capacity market and reserve power systems to ensure plants can remain operational even at lower run rates.

CONTEXT: The G7 agreed to phase out coal plants without emissions reduction measures by 2035. Yet, Japan still relies on coal for about 30% of its electricity generation and is the slowest among G7 nations in reducing coal dependence.

Starting 2028, ANRE will launch a system to charge customers ¥44,000 who refuse to install smart meters.

CONTEXT: As of late FY2023, Japan’s total number of installed smart meters is about 81.5 million, of which refusals were 40,000 (0.05%). In the Tokyo area, where the number of smart meters installed was high, the number of refusals was also particularly high, at about 21,000.

JERA, ENEOS, and Kyushu Electric completed replacement work at Goi Thermal Power Station. Unit 3 began commercial operations on March 1, 2025.

This marks the full operation of all three units, totaling 2.3 GW. Unit 3 uses a LNG-fired gas turbine combined cycle (GTCC) system with 780 MW capacity.

NEDO welcomed participants in R&D projects to expand hydrogen adoption and strengthen industrial competitiveness. Applications are accepted until April 7, 2025.

The initiative focuses on: (1) foundational technologies for fuel cells and water electrolysis; (2) next-gen element technologies for fuel cells and hydrogen storage; and (3) commercialization and production systems for practical applications.

This project runs from 2025 to 2029, aiming to accelerate innovation in hydrogen production, storage, and fuel cell development, particularly for heavy-duty vehicles.

Nomura Real Estate and Hitachi installed a green hydrogen power generation system (G-HES) at Blue Front Shibaura in central Tokyo, in collaboration with Tokyo University’s Research Center for Advanced Science and Technology.

The system produces, stores, and utilizes green hydrogen generated from 100% solar power and operates independently of the power grid.

G-HES features a 9.6 kW hydrogen production unit, a 100 Nm³ hydrogen storage alloy tank, a 5 kW fuel cell, and a storage battery.

CONTEXT: The system was selected for the MoE’s subsidy program in FY2023 to support the adoption of renewable hydrogen technologies.

Researchers from Tohoku University, Hokkaido University, Wakayama University, and the High Energy Accelerator Research Organization (JASRI) developed a method to separate hydrogen isotopes (H₂ and D₂) at room temperature using a manganese complex and Kubas interaction.

The technique doubles the adsorption energy difference (4.2 kJ/ mol) compared to existing materials, allowing for more efficient separation of hydrogen and deuterium gas at room temperature.

Deuterium is essential for semiconductor manufacturing, and nuclear research, but production methods require significant energy, involving hazardous substances.

CONTEXT: Deuterium is a rare and stable hydrogen isotope used in nuclear fusion energy. Since only one out of 6,420 hydrogen atoms, on average, is a deuterium isotope, producing it in sufficient quantities is difficult.

Chugai Ro Kogyo is advancing ammonia combustion technology for industrial furnaces, particularly in steel mills, as part of a NEDO-backed project.

By 2031, Japan aims for ammonia to account for 50% of industrial furnace fuel, with Chugai Ro working toward 100% mono-fuel combustion.

Ishii Iron Works, a major ammonia storage tank manufacturer, is investing ¥3.5 billion in R&D and capital projects through 2026, with plans to develop Japan’s largest 100,000-ton ammonia tank in collaboration with a steel company.

JFE Engineering was awarded Japan’s first FEED contract for a 10 km clean ammonia pipeline to connect Idemitsu Kosan’s Tokuyama Plant with facilities in the Shunan Petrochemical Complex, aiming to supply over 1 Mtpa of ammonia by 2030.

JFE Engineering will apply its expertise in pipeline construction.

CONTEXT: Idemitsu Kosan has been collaborating with companies in the Shunan Petrochemical Complex since 2022, working on coal-to-ammonia fuel conversion for thermal power plants.

(New Energy Business News; Government statement, March 7)

The Tokyo Metropolitan Govt announced subsidy recipients for its FY2024 program, aimed at supporting large-scale grid storage battery installation.

The program will support 12 projects with a total installed capacity of 180 MW and storage capacity of 595.3 MWh. The total subsidy is ¥13 billion. The list of selected businesses is in the table below.

PowerX, a Tokyo-based startup specializing in battery storage, said it raised ¥3.17 billion in the latter half of its Series C round.

Combined with funds raised in the first half held in Sept and Nov 2024, the company secured a total of ¥5.63 billion in its Series C round. PowerX’s cumulative capital raised since its founding has reached ¥29 billion.

The current funding round included existing investors such as Itochu, Mitsubishi UFJ Bank, and Imabari Shipbuilding, as well as new backers like Toyota Tsusho.

The funds will help expand its partner factory in Okayama Pref that assembles batteries. PowerX is also considering installing new equipment at its own facility.

CONTEXT: PowerX primarily assembles and sells stationary batteries and fast chargers for EVs. A subsidiary is also developing electric transport ships that use battery storage to transfer electricity.

Tokyo Gas will launch a service to operate grid-scale battery storage systems, and has been contracted to manage the operation of two battery storage facilities being developed by renewables firm Renova, set to begin operations in FY2028.

Tokyo Gas inked a deal to manage their operations for over 20 years from FY2028 onward. Total capacity is expected to reach 165 MW – 75 MW in Shuchi District, Shizuoka Pref, and 90 MW in Tomakomai City, Hokkaido.

Tokyo Gas will forecast renewables market prices, and optimize the charging and discharging of the batteries to maximize revenue by determining the best time and amount of electricity to sell on the power market.

CONTEXT: Tokyo Gas aims to use its partnership with Renova as a stepping stone to expand its grid battery operation services to other firms. With the growing share of solar and other renewables, the role of grid-scale batteries for energy storage and discharge is increasingly important in Japan.

Osaka Gas invested in a JV set up last year by Mitsubishi HC Capital Energy and Samsung C&T. It will develop a 25 MW/ 50 MWh grid-scale power storage system in Chitose City, Hokkaido Pref.

Before the investment, Mitsubishi HC had a 90% stake and Samsung 10%. Osaka Gas will acquire 5% from Mitsubishi HC Capital Energy.

Osaka Gas joined the JV as operator and aggregator, overseeing transactions through the wholesale electricity market, capacity market, and balancing market.

Construction work of the BESS facility begins in April, and will launch in January 2027. The facility will use Tesla’s Li-ion batteries.

CONTEXT: This is the third BESS facility in which Osaka Gas has invested. In 2023, it partnered with trading house Itochu and Tokyo Century to develop a 11 MW/ 23 MWh BESS in Osaka Pref. Last year, it partnered with Mizuho Lease, JFE Engineering, and Kyushu Steel to develop another 2 MW/ 8 MWh power storage station in Saga Pref. Both are expected to launch in FY2025.

Japan Trex, a truck manufacturer, installed a 1.8 MW sodium-sulfur (NAS) battery – the largest in the Chubu region – at its new factory that launched in January.

The BESS was installed with cooperation from Chubu Electric Power Miraiz. The firm is using NAS batteries developed by NGK Insulators.

The 750 kW rooftop solar panels charge the NAS battery during low-demand periods, with stored energy discharged during peak hours.

Tohoku Electric and its partners launched commercial operations at the Yatogo Storage Power Station in Kumagaya City, Saitama Pref.

The facility has a 1.96 MW output and 7.46 MWh storage capacity.

This is the first time the Tohoku Electric Group is operating a battery storage business based on market transactions.

The company is also building two additional storage facilities – Nirazuka Storage Power Station in Isesaki City, and Kozumida Storage Power Station in Ota City, both in Gunma Pref. Operations are slated to begin by June 2025.

Niimi Solar (Okayama Pref), which develops and sells solar power systems, obtained patents in China and India for its pyrolysis device for used solar panels.

The device, which uses superheated steam at over 600°C to separate adhesives from glass panels, can recycle 95% of a panel’s material without CO2 emissions.

The firm seeks to expand sales in China and India.

CONTEXT: In Japan, a surge in decommissioned solar panels is expected from the 2030s onward given that a large number of solar farms and systems were established in the early 2010s around the time the govt introduced the FIT scheme. By leveraging its tech, the firm aims to meet recycling requirements.

Mitsubishi Corp, which made headlines last month when it said that it may scrap three large-scale offshore wind projects awarded the first tender in 2021, is set to review the plans in question, possibly this summer.

The issue was debated during an Akita Pref Assembly meeting of a special budget committee. Akita Pref’s Gov Satake said; “There’s no need to be overly pessimistic, but it’s something that needs to be closely monitored.”

Citing discussions with Mitsubishi, Satake said the trading house aims to finalize the issue this summer. Kahoku Shimpo, a regional newspaper, said Satake cited Mitsubishi as saying a decision is expected between summer and fall 2025.

CONTEXT: Mitsubishi said last month it will entirely reassess the project due to a major cost increase, mainly due to a surge in material prices beyond initial expectations.

Two of the three projects that the Mitsubishi-led consortium won are planned off the Akita Pref coast:

478.8 MW – off the coast of Noshiro City, Mitane Town, and Oga City

819 MW – off the coast of Yurihonjo City

Mitsubishi took a ¥52.2 billion impairment charge on its domestic offshore wind projects in the nine-months ending in December 2024. Chubu Electric, the majority owner of C-Tech, another member of the Mitsubishi wind consortium, also announced it took offshore wind-related impairment losses of ¥17.9 billion.

During the meeting, lawmakers voiced a need to support local firms planning to participate in the offshore wind projects now under review.

An assembly member said that following the reassessment, “we will continue to work on matching the power generation business with local businesses.”

Amid the financial struggles faced by the offshore wind industry, METI is revising the tender format to allow rising construction costs to be reflected in the electricity purchase price for future operator selections.

TAKEAWAY: One potential solution to help improve the economics may be for METI to switch the FIT-based agreements to FIP. This may still not be enough to pull the project numbers into the black. It would also encourage Round 2 winners also to ask for business plan changes to cope with rising costs. Ultimately, METI and Mitsubishi have to find a solution that does not look like favoritism. Still, it looks like the option of leaving Mitsubishi to deal with the issues by themselves or having them walk away from the projects altogether is not seriously under consideration, which should be a positive for the sector as a whole.

ANRE proposed to allow “zero-premium projects” that bid ¥3/ kWh in the govt’s offshore wind tender to bid in the capacity market main auction.

It’s expected that no FIP subsidies will be provided, except for the balancing cost equivalent, so that even if participation in the capacity market main auction is allowed, there’ll be no problem of double recovery of fixed costs.

Zero-premium projects will be allowed to participate in the capacity market during the FIP program period, but on the condition that they waive the FIP grant equal to the balancing cost.

The impact on the capacity market of zero premium bids includes issues such as the handling of supply curves and the adjustment factor for offshore wind power; but these will be improved based on future performance data.

CONTEXT: Under the current system, offshore wind is also able to participate in the capacity market, but FIT/FIP projects, including those publicly solicited under the Marine Renewable Energy Act, are not allowed to participate during the period in which the FIT/FIP system is in place, in order to avoid double recovery of fixed costs.

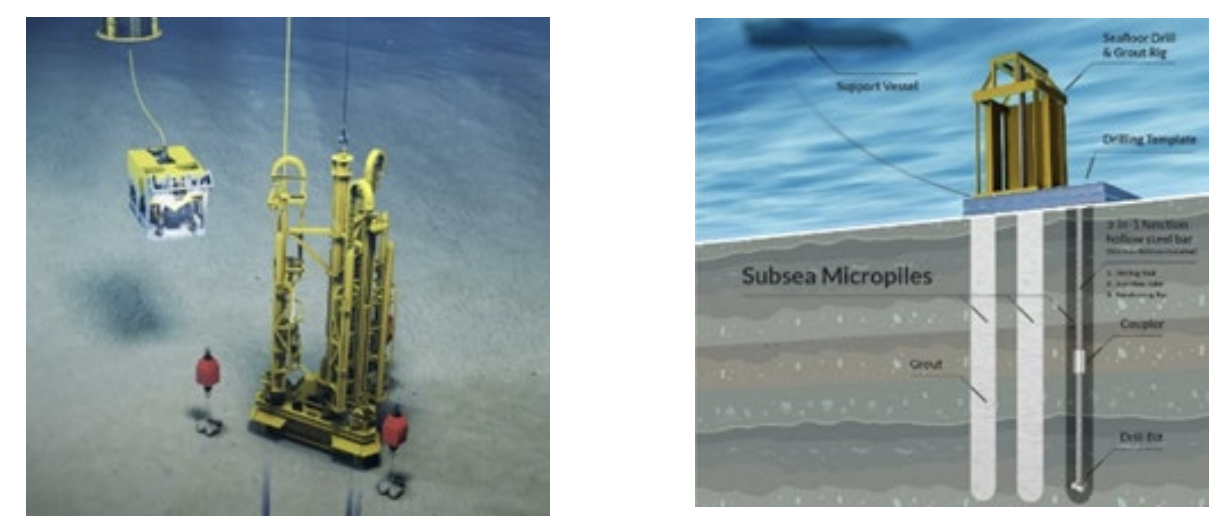

Marubeni-Itochu Steel (MISI) has invested in Ireland-based Subsea Micropiles, a firm specializing in the development, production, and installation of mooring anchors for floating offshore wind and oil & gas applications.

In collaboration with the Scottish National Investment Bank, the group will invest a total of €11 million, with MISI contributing €3 million.

Subsea Micropiles plans to leverage its patented tech to reduce the weight of mooring anchors. This could lower overall costs, including those related to installation vessels, shorten construction timelines, and ensure adaptability to various seabed conditions.

CONTEXT: Marubeni-Itochu Steel aims to expand into Europe’s offshore wind-related market. MISI launched in 2001 via the merger of steel business divisions spun off by trading companies, Marubeni and Itochu, and which is equally owned by the two firms.

TAKEAWAY: Although floating offshore wind tech in Japan is still in its early stages, with only small-scale demo projects underway, investing in Subsea Micropiles will support the firm and its parent trading houses in building a supply chain and related technology. While bottom-fixed offshore wind projects are still the main vector of development, floating wind is seen as the next key driver for Japan’s renewable energy growth. The govt is expected to open bids for floating offshore wind projects within two to three years. This requires interested companies to develop the capabilities and infrastructure to handle floating projects in the future.

Kyushu Electric received NRA approval for the Long-Term Facility Management Plan for Genkai NPP Unit 3. The utility submitted it on Aug 30, 2024, and submitted a revised application on Feb 17.

The plan calls for measures to manage aging degradation of nuclear reactor facilities, and includes inspection methods and results to assess current degradation.

Also, it pertains to methods and results of future degradation prediction and evaluation. Specific measures to manage degradation are also under its scope.

CONTEXT: This approval is crucial for continuing operation after the 30-years mark. Genkai NPP Unit 3 has had a technical evaluation for aging degradation. Kyushu Electric got approval for the amendments to reactor safety regulations in March 2024.

KEPCO’s Takahama NPP Unit 2 resumed full operation. The unit had its 28th periodic inspection starting November 2024, and began test operations on Feb 10.

With the comprehensive load performance test, the periodic inspection has concluded.

The MoE will begin site selection in FY2025 for disposal of contaminated soil from Fukushima. There are 14 million cubic meters in total.

The govt aims to reduce this volume by recycling before disposing outside Fukushima by 2045. As of FY2023, decontamination costs exceeded ¥5.6 trillion, with funding supported by TEPCO bonds and electricity taxes.

Site selection will conclude by 2030, followed by candidate site evaluation. Volume reduction is crucial – without it, a 50-hectare site would be required to accommodate the waste.

CONTEXT: In the wake of the Fukushima disaster, radioactive material spread widely, contaminating soil. Decontamination efforts removed surface soil, leading to massive amounts stored in temporary sites. In 2014, Fukushima Pref agreed to an interim storage facility, now holding 14 million m3 of contaminated soil. The govt plans to complete disposal outside Fukushima by March 2045.

Helical Fusion delivered its new test device, GALOP (GAs-driven Liquid metal OPeration), to its facility at the National Institute for Fusion Science in Gifu Pref.

Developed with the support of Sukegawa Electric, it will test a novel liquid metal blanket, a component for extracting energy from nuclear fusion reactions.

CONTEXT: Helical Fusion’s goal is to achieve the world’s first commercial fusion reactor by 2034. The blanket component serves the role of converting energy into usable heat and shielding the reactor’s interior. The system circulates a liquid metal mixture of lithium and lead using gas pressure. It allows for reactor protection and the integration of corrosion-resistant ceramic materials.

KEPCO explained why the readings from the exhaust stack gas monitor at Oi NPP Unit 3 rose on Feb 27 – it was due to gas leaking from a protective bag on the piping during sample measurement.

They were replacing a device to measure radioactive gaseous waste samples and had covered the pipes with protective bags, but gas leaked into rooms and readings rose.

CONTEXT: Exhaust gas monitor monitors radioactive gaseous waste.

Mitsubishi seeks a final investment decision (FID) to expand LNG Canada, possibly doubling capacity to 28 Mtpa. The company has a 15% stake in LNG Canada, which is set to start production in mid-2025. Mitsubishi sees the project as important due to its low emissions and proximity to Asian markets.

The company is focusing on expanding existing assets rather than building new LNG facilities, citing rising EPC costs. Key projects include LNG Canada Phase 2. Also, they include expansion of the Cameron LNG facility in the U.S. and connecting Browse gas fields to Australia’s North West Shelf.

CONTEXT: The Basic Energy Plan anticipates LNG playing a key role in the energy transition, forecasting Japan will need 53-74 Mtpa of natural gas by 2040-41.

CONTEXT: LNG Canada is building a LNG plant in British Columbia, production capacity of 14 Mtpa. Shipments are due to start in the middle of 2025. It will serve as a new energy source for supplying Canadian shale gas to Asia, particularly Japan. A key feature is that it can supply Japan without travel via the Panama Canal, reducing time and costs.

Nippon Gas acquired Kadokura Shoten, a Tokyo-based retailer and wholesaler of LP gas that serves about 3,000 retail customers, mainly in Chiba and Ibaraki.

Nippon Gas serves about 2 million customers across LP gas, electricity, and city gas.

CONTEXT: Due to a chronic shortage of delivery personnel, the cost of LP gas cylinder distribution is rising. Nippon Gas aims to improve delivery efficiency by expanding its scale through M&A.

As of March 2, the LNG stocks of 10 power utilities were 1.97 Mt, up 2.1% from the previous week (1.93 Mt); up 33.1% from late March 2024 (1.48 Mt), and down 3% from the 5-year average of 2.03 Mt.

CONTEXT: It snowed in Tokyo a little this week, a rare sight in March. Power companies were careful not to reduce their stocks too hastily.

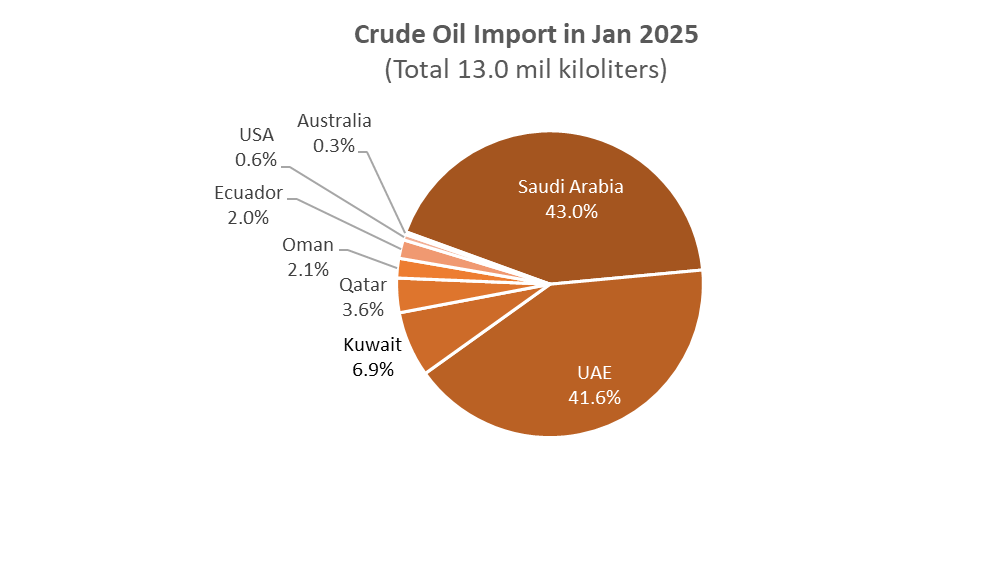

Japan imported 13 million kiloliters of crude oil in January, 9.2% less than in December 2024 and 9.8% more YoY. This month, Japan purchased crude oil from fewer countries than in 2024 (down from 14 countries to 8 countries); over 97% came from the Middle East. Earlier this fiscal year, Japan was trying to import from as many countries as possible, hedging risks.

January LNG imports totaled 6.6 Mt, up 4.4% over December 2024 (6.4 Mt), and up 8.7% YoY. Nearly 40% of LNG was sourced from Australia, followed by Malaysia. In total, over 70% came from Asia Pacific. The number of country suppliers halved (from 20 to 10) compared to 2024. Those (no-import) countries only provided Japan with 3.3% of the total.

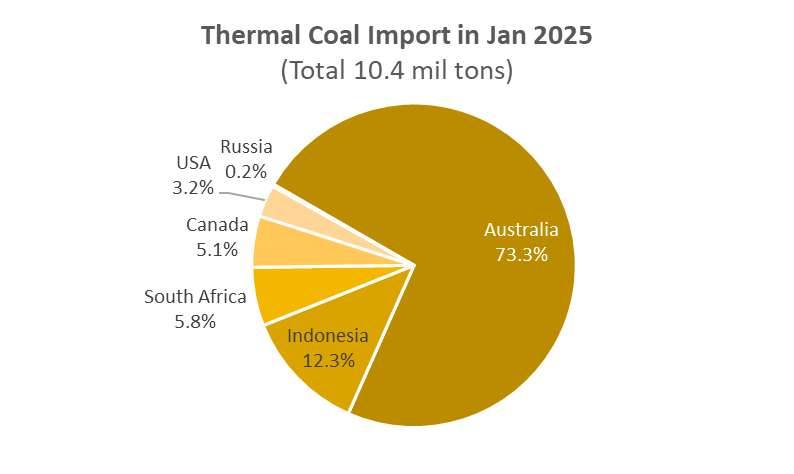

Thermal coal imports in January decreased to 10.4 Mt, down 5.1% from December 2024 (11 Mt), but up 4.5% YoY. The number of country suppliers dropped from eight to six; total imports from these countries had been under 0.3% in 2024.

METI and ANRE proposed a plan for the CCS support system, seeking to increase storage volumes after project initiation to leverage economies of scale.

For OPEX support, the plan focuses on the gap between the standard operating cost price and the reference price for CO2 mitigation costs. They propose an auction-based system. A uniform benchmark reference price will be set to enhance predictability.

The plan clarifies the relationship between CCS support and long-term decarbonization power source auctions. The goal is to adjust bid amounts based on CCS support status. Also, they aim at exempting market exit penalties if CCS support is not obtained or is lower than expected.

Cosmo Energy, Japan’s third-largest refiner, is set to launch the country’s first domestic production of sustainable aviation fuel in April. Cosmo will produce SAF from used cooking oil at its Sakai refinery.

The company aims to boost SAF supply to 300,000 kilolitres by 2030. The project has secured clients such as airline companies JAL and ANA.

CONTEXT: Japan aims to replace 10% of jet fuel with cleaner alternatives.

ANALYSIS

BY TETSUJI TOMITA

Technology Development Trends for Ammonia-fueled Ship

Maritime transportation accounts for 90% of the world’s trade and about 3% of its emissions. For Japan, it is even more vital, sustaining imports of food and fuel, and exports of machinery on which the nation’s economy stands. Sea transport carries 99% of Japan’s trade.

Demand for shipping has historically grown faster than the global economy, but solutions to clean up the industry’s carbon footprint have been slow to reach fruition. The International Maritime Organization (IMO) has a greenhouse gases (GHG) reduction strategy that calls for a cut in CO2 emissions of 20-30% by 2030 (compared with 2008 levels), 70-80% by 2040, and virtually zero by 2050. Which technologies and fuels can help meet these targets is unclear.

In Japan, ammonia has emerged as a compelling – if challenging – alternative to heavy fuel oil. Ammonia contains no carbon, meaning that when burned it emits no CO2. In theory, widespread use of ammonia could enable zero-carbon voyages.

The ships Japanese companies are ordering today tend to run on LNG or LPG as lower-emissions alternatives to conventional oil-based fuels. But within the next two-three years, manufacturers are promising shipping technologies that will give the sector the option to shift to ammonia.

As in power generation, the next-generation fuel of choice for shipping is yet to emerge but recent developments suggest that ammonia-fueled shipping is picking up pace. Japan NRG looks at the state of play in this technology segment.

Background: Why ammonia?

Burning ammonia in an engine is not as straightforward as diesel. Ammonia is notoriously difficult to ignite – it has a low flammability, a high autoignition temperature, and a slow flame speed. In practical terms, this means a ship’s engine often needs a pilot fuel (typically a bit of diesel or another fuel) to get ammonia combustion going. Even once ignited, pure ammonia flames tend to be unstable or “flame retardant.”

The combustion chemistry of ammonia also introduces new pollutants. Unlike oil-based fuels, ammonia doesn’t emit CO2, but it can produce nasty byproducts: nitrogen oxides (NOx), unburnt ammonia, and nitrous oxide (N2O). NOx is a familiar air pollutant from diesel exhaust, and unburned ammonia (ammonia “slip”) is toxic. N2O is a greenhouse gas about 265 times more potent than CO2 on a 100-year basis.

While the technical and emissions factors are huge challenges, Japanese engineers have been working to address them on multiple fronts. These include designing dual-fuel engines (i.e. similar to the co-firing strategy in power generation), and introducing equipment such as selective catalytic reduction (SCR) units to scrub NOx from ship exhaust. Focus on new safety systems is pushing R&D to come up with extra containment and detection, as well as materials that are more resistant to ammonia’s corrosiveness.

Major R&D projects in ammonia-fueled shipping

Under the Strategic Innovation Promotion Program (SIP), an inter-ministerial research and development project led by the Cabinet Office from FY2014 to FY2018, the National Institute of Maritime, Port and Aviation Technology (MPAT) and JEF Engineering each conducted basic research on the combustion of ammonia in marine diesel engines.

The “Green Innovation Fund Project” was launched in FY2021, and as part of the “Next-generation Ship Development” project, the “Development of ammonia-fueled ships” is held in parallel with the development of hydrogen-fueled ships. (See Table)

The “development of ships with ammonia-fueled domestic engines” will be conducted jointly by Nippon Yusen (NYK), Japan Engine Corp (J-ENG), IHI Power Systems, and Nihon Shipyard (NSY). The domestic-use tugboat was converted from a NYK LNG-fueled ship and equipped with an engine (1600 kW) developed by IHI Power Systems, and was completed in August 2024.

For ocean-going ammonia-fueled ships, J-ENG is in charge of developing the main engine (8000 kW) and IHI Engine – the auxiliary engine (1300 kW). NYS will build the first one at the shipyard of its parent company, Japan Marine United (JMU), with completion scheduled for November 2026.

The R&D and rollout of ammonia-fueled ships is spearheaded by a group consisting of trading house Itochu, J-ENG, Mitsui E&S, Kawasaki Kisen Kaisha (K Line), and NS United Kaiun Kaisha. The aim is to introduce ammonia-fueled ships into ports by 2028. This would allow Japan to take global leadership in the technology, able to offer new propulsion systems and hulls specific to ammonia use.

While European shippers and governments are pushing ahead with the introduction of methanol-fueled shipping, Japan hopes to forge ahead with ammonia to maintain the country’s maritime industrial strength in the age of zero-emission ships. Both methanol and ammonia are so-called hydrogen carriers.

Meanwhile, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) is promoting the development of ammonia direct combustion engines through its own “Transport Technology Development Promotion System,” with JFE Engineering conducting “Research on the Expansion of Ammonia Fuel Applications in Ships” and Mitsui E&S conducting “Research on the Expansion of Ammonia Fuel Applications in Ships” in FY2023-2024.

In addition, in January, MLIT, in cooperation with MoE, announced the winners for the “Zero-Emission Ship Construction Promotion Project” that aims to promote the introduction of these ships to the market, reduce CO2 emissions, strengthen industrial competitiveness and promote economic growth by supporting the development of production facilities and other equipment, as well as to establish a domestic supply system for these ships. This includes J-ENG and Daihatsu Diesel as developers of ammonia fuel engines.

Breakthroughs

The biggest problem with ammonia-fueled engines is their flammability, but J-ENG has achieved advanced combustion control by injecting ammonia fuel between the highly flammable pilot fuel and post fuel injection using its unique “layered injection technology,” which makes it possible to optimize the ammonia co-firing ratio and suppress the generation of nitrous oxide.

To reduce the amount of CO2 emitted by ammonia-fueled engines to an absolute minimum, IHI Power Systems increased the proportion of ammonia fuel in the test, achieving a maximum co-firing rate of 95%. In addition, the GHG reduction rate for ammonia combustion is more than 90% compared to heavy fuel oil.

Other achievements include the realization of ammonia operation performance in response to load fluctuations, as well as the confirmation of zero ammonia leakage from the actual engine during operation and after shutdown. This means that the problems associated with the use of ammonia as a fuel have been overcome. As a result, ClassNK issued the world’s first type approval for an ammonia-fueled engine.

In February, ClassNK also issued an approval in Principle (AiP) to NYK Line and Seatrium Ltd for the design of an ammonia-fueled bunkering vessel slated for use in Singapore. When built it will become the world’s first ammonia-fueled bunkering vessel.

Conclusion

Ammonia is not the only alternative vying for the maritime shipping industry’s future. Hydrogen is an obvious contender, able to be used in fuel cells or combusted in engines, yielding only water. A few demonstration vessels are testing hydrogen fuel cells, but storing enough hydrogen onboard an ocean-going ship is a formidable challenge – liquid hydrogen needs to be kept at –253°C, and even then it contains only about one-third the energy per volume of LNG. In practice a ship would need huge, heavily insulated tanks for hydrogen, eating into cargo space.

Biofuel (biodiesel) is a more practical fuel than hydrogen and ammonia because it has the advantage that existing diesel engines can be used without major modifications. However, it is still in the development stage, and companies such as NYK are still conducting test runs.

To meet the IMO’s upcoming greenhouse gas reduction targets, shipping companies must act soon. Furthermore, the urgency to reduce CO2 from the transportation of goods and the broader supply chain will increase from late FY2027, when large companies will be required to disclose sustainability information.

Although both hydrogen and ammonia are promising decarbonized fuels, fuel supply and cost, as well as technology development, will decide which becomes the more popular. At present, Japan is promoting both fuels equally. Ammonia, however, is thought to have the edge in terms of storage and transportation as a marine fuel.

Green Innovation Fund Projects on Next-generation Ship Development

Classification

Themes

Main Members

Period

1.Development of hydrogen-fueled ships

Development of marine hydrogen engine and MHFS (marine hydrogen fuel tanks and fuel supply systems)

Development of hydrogen fuel engine

· Kawasaki Heavy Industries (KHI)

· Yanmer Power Technology

· Japan Engine Corporation

FY2021 – 2030

Development of hydrogen fuel tank and fuel supply system

· Kawasaki Heavy Industries (KHI)

2.Development of ammonia-fueled ships

Development of ships with ammonia-fueled domestic engines

Development and operation of ammonia-fueled tugboat (coastal ship)

· NYK Line (Nippon Yusen)

· IHI Power Systems

FY2021 – 2027

Development and operation of ammonia-fueled ammonia carrier (ocean-going ship)

· NYK Line (Nippon Yusen)

· Japan Engine Corp

· Nihon Shipyard

· IHI Power Systems

FY2021 – 2027

Integrated project for development and social implementation of ammonia-fueled ships

Development of ammonia-fueled ships, operation, fuel production, and fuel supply bases

· ItochuCorp

· Nihon

Shipyard

· Mitsui E&S Machinery

· Kawasaki Kisen Kaisha (K Line)

· NS United Kaiun Kaisha

FY2021 – 2027

Development of N2O reactor installed on ammonia-fueled ships

Developed device to remove N2O and catalyst used

· Kanadevia

· Nippon Yusen

FY2024 – 2027

Development of peripheral equipment for constructing a supply chain using ammonia-fueled ships

Development of high-sensitivity measurement of ammonia, detection of trace leaks, and recovery and reuse technology

· Itochu

· Fuji Electric

FY2024 – 2027

3.Preventing methane slip on LNG-fueled ships

Development of methane slip reduction technology from LNG fueled vessels by catalyst and engine modification

· Hitachi Zosen

· Yanmer Power Technology

· Mitsui O.S.K. Lines

FY2024 – 2026

Source: NEDO “Green Innovation Fund Projects”

ANALYSIS

BY MAGDALENA OSUMI

Japan Bets on Next-gen Solar Power Tech as Key Driver for Clean Energy

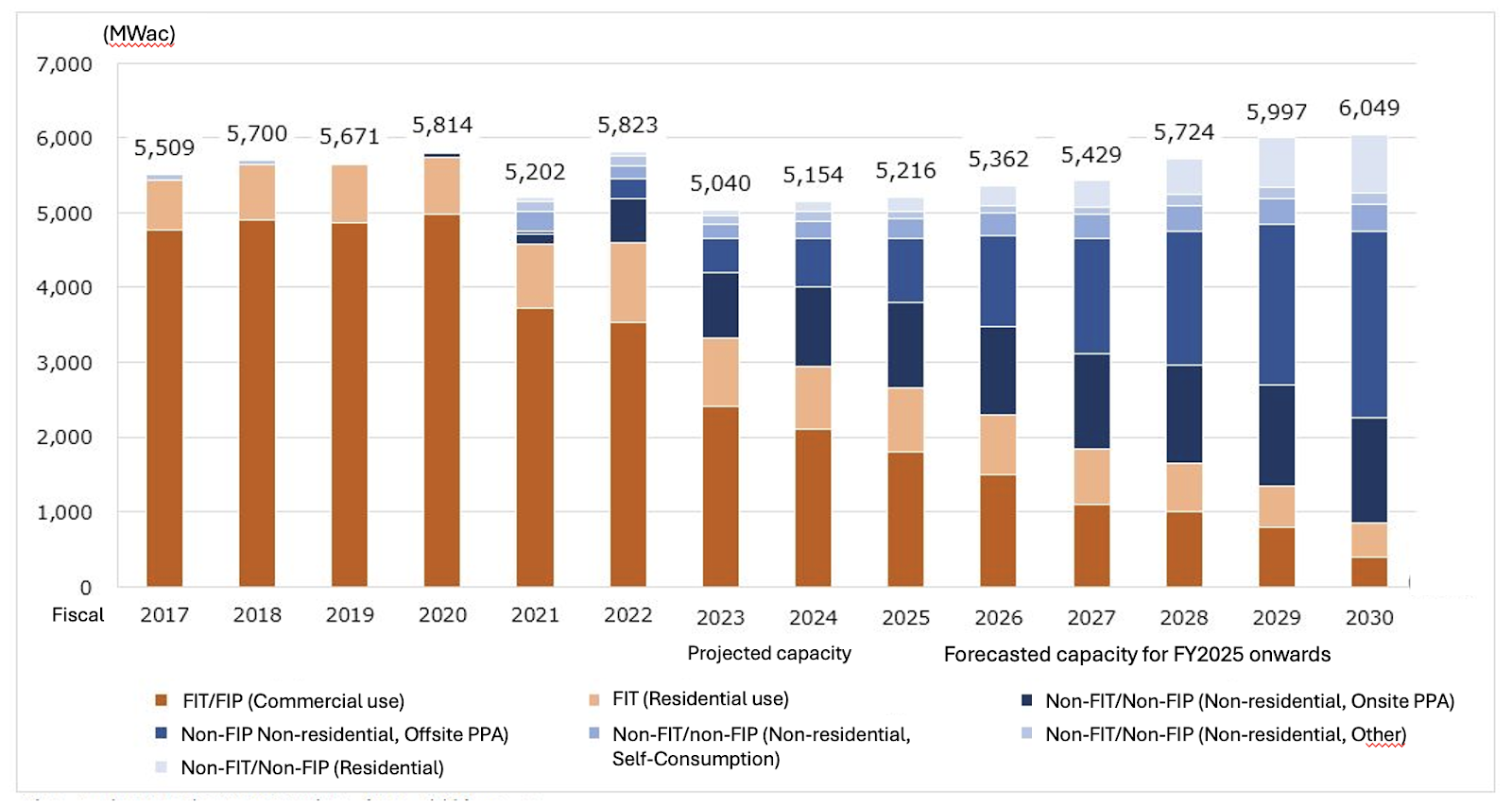

While solar energy’s global momentum has accelerated, the sector development in Japan has been strained in recent years due to land, cost and local community issues. New installations in Japan dropped to only about 1.5% of the world’s total in FY2023, compared to 9.5% in FY2016.

Still, several factors suggest the declines in the Japanese market have peaked, and a revival in the pace of new development will follow. One of the drivers will be the underutilized rooftop solar market – for residential, public and industrial buildings. Another, a greater embrace of hybrid business models, such as agri-solar. On top of that, a nascent shift in solar technologies and materials is touted as the next cost-efficiency opportunity.

Globally, solar PV now provides 6% of electricity. After a 68-year climb to reach 1 TW, solar doubled that capacity within two years and is projected to hit 8 TW installed by 2030, according to Global Solar Council figures. Within this decade, solar power generation is forecast to take a 12% share of the global electricity mix aided by growth trends also for batteries and storage.

In Japan, solar’s share hovers at around 10% of the mix, but the Cabinet’s newly approved Basic Energy Plan targets a 20–29% share by 2040. While challenges for embracing more solar power remain, especially in terms of grid connections and balancing, a rise in corporate interest in Power Purchasing Agreements (PPAs) and steps towards better integration of solar PVs with storage and public or industrial facilities are starting to pay dividends.

Japan NRG takes a look at some of the latest trends in the sector, starting with a regulation that will take effect this April.

Resurgence of solar power

Since the 2011 Fukushima disaster, Japan has become one of the top five solar energy markets. Yet, in recent years, large-scale wind power projects have attracted more investor attention as solar tariffs dropped to single-digit levels in terms of yen per kilowatt-hour. Also, the difficulty in accessing new land, among other factors, has put the brakes on project development pipelines.

With the wind sector yet to navigate its own development challenges, government attention is starting to shift to how it can revive momentum in the renewables space overall.

Starting April 1, new detached houses in Tokyo will be required to install solar power systems. This regulation, affecting about 50 developers and new residential buildings with a total floor area of less than 2,000 square meters, supports Japan’s broader goal of sourcing 50% of its energy from renewables by 2040; Tokyo aims to achieve this by 2030.

A similar ordinance is already in place in Kyoto, which mandates the installation of PV power systems or other renewable energy equipment for new or expanded buildings with total floor areas between 300 and 2,000 square meters. In return, the city offers subsidies to cover the installation costs.

Other local authorities are considering similar measures, but in the case of Fukuoka City, the thinking is evolving to combine the rooftop drive with a desire to nurture new technologies.

Fukuoka has announced plans to install perovskite solar cells (PSC) on a public building’s exterior walls, the first of its kind in Japan. This project is a collaboration with Sekisui Chemical, one of the leading manufacturers of PSC and one of the Japanese firms that has vowed to bring the technology to commercial-scale mass production in the next year or so.

Sekisui will monitor the waterproof performance and power generation efficiency of the film-type perovskite system installed in Fukuoka and make a final evaluation by April 2026.

Image of completed renovation of Osaka Head Office

(Film-type perovskite solar cells are outlined in red)

Separately, Fukuoka City will also install PSC on the roof of the local Kashii-hama Elementary School’s gymnasium before April 2025. This system will cover 200 square meters with an output of 20 kW, making it the largest building-mounted installation of its kind in Japan. Further, the city has allocated ¥2.1 billion in its FY2025 initial budget to introduce PSC at three other municipal facilities.

Perovskites promises

Expectations for PSC among Japanese officials are high with METI banking on the home-grown tech to be one of the catalysts for the domestic green capacity rollout. Curiously, the 20-40 GW target for PSC installations by 2040 is not too dissimilar to the 30-45 GW targets put on offshore wind by the same timeframe. Strong progress in both sectors will be needed if the country is to meet its 73% emissions reduction by the end of the next decade.

One advantage that Japan has in bringing down the cost of PSC is its iodine supply. The country controls 30% of global iodine production, a key material in perovskite cells, second only to Chile. This positions Japan to develop a secure domestic supply chain and reduce reliance on foreign imports.

There’s also progress in making cheaper solar cell components. Silver paste currently accounts for nearly 30% of the material cost in solar cells. Material Concept, a startup from Tohoku University in Sendai, wants to offer a similar product made from copper, which could bring down the price by half.

Copper paste is used as a wiring material in solar cells and, like silver, has high conductivity. It was previously unsuitable due to its tendency to bond with silicon, but Material Concept has developed a proprietary alcohol-based solution that solves the issue.

With an investment of several hundred million yen in production facilities at its university headquarters, Material Concept plans to expand its production capacity from 10 kg/ month to 4 tons/ month. The startup seeks to raise ¥340 million through a third-party allotment of shares to finance the expanded production facilities, which will lower manufacturing expenses through scale.

Efficiency breakthroughs

Perovskite technology faces hurdles such as durability and scalability, but research is making strides. In December 2024, a research team from Kyoto University and Oxford University published a paper in Nature on improving the performance of perovskite solar cells. The study utilizes a method called the “tandem structure,” which involves layering multiple perovskite crystal layers with different properties. This approach achieved a maximum conversion efficiency of 29.7%, surpassing the conventional range of 24 – 27%.

In the residential solar power sector, the highest conversion efficiency is currently around 22.5% (as of 2024). This makes the 29% efficiency mark a groundbreaking achievement.

The doubling of PSC layers or their combination with traditional silicon PVs (known as the tandem structure) will be one of the main ways the solar sector will move forward and Japan is in a position to lead the global industry in this tech, Xavier Daval, a director at the Global Solar Council (GSC) told the Renewable Energy Institute (REI) forum in Tokyo last week.

The smaller scale of PSC at this moment could also be an opportunity to apply the tech to narrow spaces. For example, Tokyo’s new rooftop regulation is for buildings with roof areas smaller than 20 square meters or those with structural limitations, but the lightweight, film-thin properties of PSC broaden its potential application.

Japan’s long-term solar outlook

Commercialization of next-gen technologies isn’t a given. Even in China, which almost entirely dominates the current solar PV technologies, full-scale mass production of PSC has not yet been achieved. Chinese firms like DaZheng Micro-Nano Technology are expected to move to large-scale PSC output in 2025. Japanese manufacturers, including Toshiba, Sekisui Chemical, and Panasonic, are expected to follow suit between 2025 and 2026.

Aware of the challenges in commercializing next-gen solar tech in the face of China’s dominance in current technologies and state resources, METI is focusing on directing its own support to domestic players who could make up a Japanese PSC supply chain. Around ¥55 billion was allocated for this task in the FY2024 budget, with more funds expected this year.

A PSC-specific tariff, like a FIT, will also be made available to kickstart domestic projects since perovskite cells are expected to be more costly than traditional silicon-based panels.

These are as yet small steps towards a Japanese solar revival from a manufacturing and an installation standpoint. But they are genuine efforts to move forward. As global competition intensifies, innovation and regulatory support will determine whether Japan can be a leader in the next-generation of solar technology.

Source: Yano Research Institute

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Offshore wind

Novocastrian Wind Pty, a partnership between Equinor and Oceanex Energy, received the feasibility licence for their planned offshore wind farm project for the Hunter offshore wind area. The feasibility licence is granted for up to seven years and Novocastrian Wind must use this time to obtain all necessary approvals.

Australia / Renewables

Australia has approved three renewable energy projects in New South Wales with a total capacity of over 2.4 GW. The projects include the 1.33 GW Liverpool Range Wind Farm near Coolah, within the Central West Orana Renewable Energy Zone; the 700 MW Spicers Creek Wind Farm Project near Gulgong, also within the Central West Orana Renewable Energy Zone; and the 372 MW Hills of Gold Wind Farm near Nundle.

China / Energy imports

Energy imports fell at the start of 2025, after last year’s record shipments of coal and gas created an overhang of supply and demand for oil continued to ease. Crude oil imports fell 5% YoY in January and February to 83.85 Mt as buyers sought alternative supplies after the U.S. tightened sanctions on Russian and Iranian cargoes.

China / Renewables

China’s newly installed renewable energy capacity accounted for 86% of its total new additions in 2024. The National Energy Administration said the cumulative installed capacity of renewable energy made up a record high of 56% of China’s total capacity.

India / Renewables

In 2024, India issued a record-high of 73 GW of utility-scale renewable energy capacity, a major rise from 58 GW in 2023, reported the Institute for Energy Economics and Financial Analysis (IEEFA) and JMK Research & Analytics.

India / Solar power

Solar is expected to continue dominating India’s renewable energy generation, with about 32.3 GW of new capacity to be added in 2025. According to JMK Research, this will include 22.8 GW from utility-scale, 7.5 GW from rooftop solar, and 2 GW from off-grid components.

Indonesia / Oil refinery

Indonesia plans a massive $12.5 billion refinery project, aiming to cut imports, boost energy security, and improve refining muscle. The 531,500 bpd facility will be one of the largest in SE Asia.

Singapore / Power plant

Keppel Core Infrastructure Fund (KCIF) acquired a 39% stake in the Keppel Merlimau Cogen Plant (KMC), its first power sector asset. Keppel Infrastructure Trust will continue to hold 51% of KMC, with the remaining 10% retained by Keppel Ltd.

Southeast Asia / Renewables

A greenfield renewable energy platform formed by Sustainable Asia Renewable Assets, which is a JV of British International Investment, Dutch development bank FMO, and Swiss investment company SUSI Partners, could invest as much as $700 million to build solar, wind and hydro plants across SE Asia that will generate 500 MW of clean power, starting with the Philippines and Vietnam.

South Korea / Energy cooperation

The Philippines and South Korea launched an initiative to fuel cooperation for a more resilient energy system. It will focus on renewable energy integration and grid modernization, and more.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS

• Mitsui to launch AI-driven commodity futures trading by end of March

• Japan approves bill to expand offshore wind to EEZ

• First Japanese bank to withdraw from global net-zero banking alliance

Sekisui will monitor the waterproof performance and power generation efficiency of the film-type perovskite system installed in Fukuoka and make a final evaluation by April 2026.

Sekisui will monitor the waterproof performance and power generation efficiency of the film-type perovskite system installed in Fukuoka and make a final evaluation by April 2026.