OCCTO published the “FY2025 Supply Plan” as part of its 2025 Annual Report.

The report was sent to the METI Minister with the following opinions:

Data center demand and coal power-fired plant shutdowns may tighten the mid-to-long-term supply-demand balance, requiring more policies to ensure both decarbonization and stable power supply.

Aging facilities, work style reforms, and an increase in startup/ shutdown frequency have prolonged the repair periods for power stations, impacting the supply-demand balance. It is necessary to consider securing additional power capacity and the cost burdens that come with that.

With regard to grid development to meet large demand, it is necessary to consider fair cost sharing among market participants and review the rules for getting connected to the grid.

CONTEXT: OCCTO annual reports also include: “Overview of Electricity Supply-Demand and Power Grids”; “Electricity Quality”; “Information on Grid Access Services for Power Generation Facilities”; “Results of Required Amount of Regulating Power and Confirmation of Securing Status”. Only the Supply Plan and a Research Study (Reviewing Overseas Simultaneous Markets) are published.

Total reported GHG emissions from large emitters dropped 4.4% to 586 Mt of CO2 in FY2022, down from 613 Mt the previous year.

Large industrial and commercial sites contributed 559 Mt, which adjusts to 530 Mt after accounting for domestic emission reductions and alternative fuels.

Major transport operators accounted for 26.95 Mt of emissions, a slight increase from 25.62 Mt a year earlier.

CONTEXT: The data, covering 12,044 businesses and 1,335 transport operators, is mandated by the Act on Promotion of Global Warming Countermeasures and aims to encourage transparency and voluntary emission reductions among polluters.

Mitsubishi Research Institute (MRI) estimates that relocating data centers to Hokkaido could generate economic benefits of ¥4.4 to ¥9.4 billion by reducing renewable energy curtailment and fossil fuel consumption.

Under a scenario where data center-driven electricity demand in Hokkaido rises from 28.2 TWh in FY2023 to 40–55 TWh by 2040, higher demand would reduce renewable curtailment and CO2 emissions, MRI argues.

Improved renewable utilization could increase annual revenue by ¥400 to ¥900 million for a 500 MW wind power project.

Although lower land costs attract data center operators to rural areas, additional incentives – such as discounted electricity rates – are essential to encourage regional investments due to shorter data center project lead times (3–5 years) compared to some renewable energy projects (around 10 years), according to MRI.

METI approved the General Contribution Amount, the Special Contribution Amount, and Decommissioning Reserve Fund fund for FY2024. This is under the Nuclear Damage Compensation and Decommissioning Facilitation Corporation Act.

The General Contribution Amount is ¥194,695,376,800. Special Contribution Amount: ¥60,000,000,000, and Decommissioning Reserve Fund: ¥262,073,569,688.

CONTEXT: Ministerial approval for these provisions is required each fiscal year.

Company

Percentage

Investment (¥)

TEPCO

34.70%

¥67,550,177,600

KEPCO

20.43%

¥39,767,969,400

Kyushu Electric

10.08%

¥19,625,192,400

Chubu Electric

9.18%

¥17,880,591,000

Tohoku Electric

5.48%

¥10,662,687,000

JAPC

6.08%

¥11,832,121,400

Shikoku Electric

3.98%

¥7,755,122,600

Hokkaido Electric

3.32%

¥6,466,146,000

Hokuriku Electric

2.92%

¥5,675,636,800

Chugoku Electric

2.66%

¥5,174,532,600

Japan Nuclear Fuel Limited

1.18%

¥2,305,200,000

TAKEAWAY: The special contribution from TEPCO for compensation related to the Fukushima Daiichi NPP accident is ¥60 billion for FY2025, which is the fifth-largest amount on record. The decision is based on TEPCO HD’s profit level. The govt estimates that final compensation for disaster victims will total ¥9.2 trillion.

ANRE is revising the manual and guidelines to encourage local govts to use electricity data for disaster relief.

From early April to mid-May, public comments are invited on the proposed revised guidelines, which will come into effect in late May.

CONTEXT: Through the 2024 budget project, ANRE held a demo of the use of electricity data in local govt operations, such as supporting disaster victims in collaboration with Ishikawa Pref, which was affected by the Noto Peninsula earthquake and the heavy rain in Okunoto.

ANRE reported on the electricity supply-demand this past winter, as well as the outlook for FY2025.

In winter FY2024, except for some days in March, power demand didn’t exceed the level expected during a once-in-a-decade cold wave. Demand was similar to last winter in December, higher in early January, and high in February. In March, it was considered to be at a low level compared to the once-in-a-decade benchmark.

For the summer of FY2025, all areas of Japan are expected to be able to maintain a 3% reserve margin. However, due to risks such as extreme weather, international fuel supply problems, and the concentration of thermal power plants along the Tokyo Bay and Pacific coast, the power supply-demand situation remains uncertain.

Future plans include refining monthly supply-demand forecasts and reviewing the coordination of power plant retirements.

TAKEAWAY: OCCTO completed the FY2025 supply plan after receiving input from all the major generators. Based on that, the power supply-demand outlook for summer and winter 2025 shows that all areas are expected to maintain the minimum required 3% reserve margin, even under severe weather conditions (i.e. once-in-a-decade cold or heat). This should add stability to power prices, although unplanned shutdowns due to weather and technical issues are on the increase. The level of caution by the govt will be judged based on whether they issue a power conservation warning this summer or not.

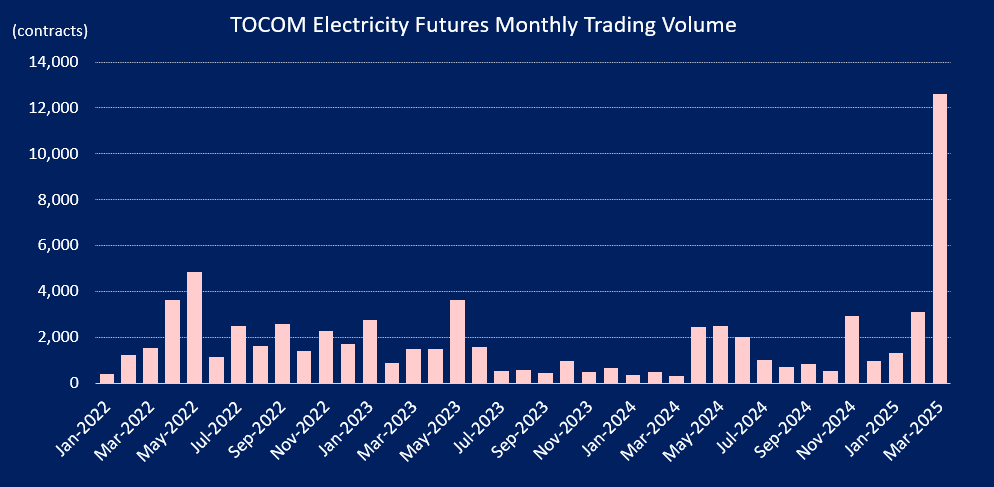

The TOCOM exchange said electricity futures trading in March saw 12,600 contracts change hands, easily surpassing the previous high of 4,853 contracts in May 2022.

CONTEXT: This translates into 901 GWh of volume, more than three times that of May 2022. The exchange has attributed the increase in liquidity to the introduction of marketmakers and the entry of the nation’s major banks into the market.

During the first three months of this year, futures trading on the TOCOM platform has already surpassed the volume for the entire 2024, when 14,969 contracts were sold, representing a little over 2 TWh of electricity.

The most popular power futures contract by far is for East Area Baseload.

Daily average purchase bids on the JEPX spot market rose 8.7% MoM to 1.09 TWh in February, driven by two severe cold snaps that boosted electricity demand.

Daily average sell offers fell slightly by 2.5% to 1.28 TWh, but ample supply – supported by restarted nuclear power plants – prevented tight market conditions.

Total monthly purchase volume declined by 1.8% to 30.4 TWh, while sell volume dropped 11.9% to 35.9 TWh. Demand was particularly high in early February.

CONTEXT: The February trend was followed by weakening demand in March. While not all data is available, the average day-ahead 24-hour spot price for March was ¥11.31/ kWh, down 18.8% from February (¥13.94).

Since the first auction attracted no bids, METI will raise the maximum bid price for backup power capacity auctions to ¥14,399/ kW, more than double the initial ¥6,429.

CONTEXT: This market pays utilities to maintain power plants on standby so that these can be called upon in case of emergency.

The new cap reflects feedback from power generators who said the original cap was insufficient to cover repair and maintenance costs, thereby discouraging bids.

METI carefully set the revised cap based on the average upper limit of previous capacity market auctions (FY2020–24) to ensure incentives remain balanced between the capacity and backup markets. This prevents operational power plants from shifting to backup status solely for higher fees.

The second auction, covering FY2026–27, is scheduled to begin in summer 2025, with separate bidding for eastern and western regions.

METI also confirmed plans for a comprehensive review of the capacity market beginning FY2025, which could lead to adjustments in future backup power pricing depending on market response.

OCCTO will tighten economic penalties in the capacity market starting FY2025 for failing to meet requirements to supply electricity to wholesale power exchanges, etc.

OCCTO will increase the annual assumed duration of capacity commitment notices from the current 30 hours to 90 hours, reflecting actual conditions where notices frequently exceeded initial assumptions. For example, in FY2024, capacity notices averaged 106 hours nationwide due to unusual weather conditions.

The stricter calculation method will be applied retroactively to the main capacity market auctions held between FY2021 and FY2024 (covering electricity supply from FY2025 to FY2028), as well as the additional auctions conducted in FY2024 and FY2025 (covering electricity supply from FY2025 and FY2026).

CONTEXT: OCCTO’s capacity market committee approved the measure on March 27, aiming to ensure fair market operations, enhance reliability, and prevent unintended exits by participants facing higher-than-anticipated penalty risks.

Experts at the power market regulator, the Electricity and Gas Market Surveillance Commission (EGC), recommended significant changes to imbalance charges.

New maximum imbalance fee set at ¥300/ kWh during periods of tight supply (i.e. when reserve margins fall below 3%), starting FY2026;

Maximum fee during periods of relatively tight supply (i.e. when reserve margins hit 8%) will rise to ¥50/ kWh from ¥45 to reflect additional startup costs for backup power;

To mitigate prolonged price spikes, a cumulative pricing threshold mechanism will be activated if an area’s spot market price exceeds ¥200/ kWh in 30 slots over a seven-day period, subsequently lowering the maximum imbalance charge to ¥100/ kWh from the next day.

The adjustments aim to incentivize generators to supply additional capacity while limiting financial risks for smaller electricity retailers.

Some committee experts warned that lower imbalance charges in stressed areas could inadvertently encourage power suppliers to redirect sales to neighboring regions where there may be higher market prices.

CONTEXT: The expert recommendations look set to proceed. They are at the lowest range of what was initially proposed as the maximum imbalance fee. At the previous meeting, experts reviewed the potential for the fee to be as high as ¥600.

Kyushu Electric announced plans to offer negotiated wholesale power contracts in FY2025, accepting applications on an ongoing basis without a fixed deadline.

Two product types will be available: a base-load product (24 hours daily) and custom-made products tailored to buyers’ needs, both with minimum contracted capacity of 100 kW.

Buyers can submit applications via email, after which contract terms will be discussed for two weeks, followed by contract finalization within an additional two weeks.

Power delivery points will be within Kyushu or at the JEPX, with pricing determined through bilateral negotiation; transmission congestion costs to be borne by the buyer.

ANRE plans to lift the high-voltage price controls on Okinawa Electric in April 2026.

The Electricity and Gas Market Surveillance Commission (EGC) also approved the decision, but it called for the following points to be noted:

For three years after the lifting, the EGC will conduct special post-monitoring to ensure no unreasonable price increases.

An appropriate wholesale trading environment must be maintained even after the lifting.

Okinawa Electric agreed to the EGC’s requirements.

TAKEAWAY: Okinawa is the last region to follow through on the liberalization of the market, but to date it has not attracted strong interest from new players due to its small market size and distance from mainland Japan.

The $1 billion Hydrogen Energy Supply Chain (HESC) project, aimed at exporting liquid hydrogen from Australia’s lignite reserves to Japan, is facing critical delays due to regulatory hurdles in Victoria and concerns about its economic viability.

Japan, which initially backed the project with ¥220bn, is shifting focus towards domestic hydrogen production to meet its 2030 pilot phase targets, citing high costs of cooling hydrogen to -253°C for maritime transport.

Environmental opposition to carbon capture and storage has intensified in Australia, influencing a shift in Japan’s commercial approach.

CONTEXT: Kansai Electric’s recent withdrawal from another Australian green hydrogen project highlights growing uncertainties about the economics and regulatory environment involved in this trade.

Ritsumeikan University and Iwasaki Electric, developed a Mist CVD-based coating on titanium substrates to enhance PEM water electrolysis.

The method allows for low-cost production of corrosion-resistant, conductive separators without using precious metals, which are key to reduce costs in PEM electrolyzers used for green hydrogen.

Mitsubishi Materials and Enecoat Technologies have developed a new coating ink for the electron transport layer (ETL) of perovskite solar cells, achieving about 1.5 times higher power generation efficiency than conventional inks.

Of the two main types of PSCs (normal- and inverted-structured), inverted-structured ones are drawing attention due to ease of manufacturing and improved durability.

However, forming ETL on top of the perovskite layer without causing damage has been a challenge.

The new ink enhances efficiency and also prevents erosion of the perovskite layer.

Smart Energy is entering the operation and maintenance business for stationary battery storage systems, aiming to secure contracts for 300 MW and 1.5 GWh of capacity by March 2026. It aims for over a 20% market share.

As METI predicts total battery storage deployment to reach between 14.1 and 23.8 GWh by 2030, Smart Energy seeks to bolster its presence on the market in grid storage, co-located renewables facilities and customer-side installations.

For example, Smart Energy has secured an O&M contract from ENEOS Renewable Energy for the battery storage system at a solar farm in Fukuchi Town, Fukuoka Pref. The BESS has a 2 MW / 10.32 MWh capacity.

CONTEXT: Smart Energy currently manages around 4.6 GW of solar O&M contracts, and has begun securing battery O&M projects. The firm has been receiving contracts from companies without prior solar O&M engagements, which highlights its growing role in Japan’s battery storage sector.

PowerX will provide 20 large-scale power grid-scale battery storage systems (total capacity 55 MWh) for logistics firm Kamigumi. This is PowerX’s second order from Kamigumi, following a previous high-voltage project in Tokyo.

The BESS, which launches in spring 2026, will be installed at Kamigumi’s power storage plant in Kasai City (Hyogo Pref) near its existing 21 MW solar farm.

The BESS will be used for arbitrage trading and transactions in the capacity market and balancing market.

A consortium of nine firms, including railway company JR East, battery producer GS Yuasa, and Mitsubishi Research Institute, set up Hokkaido Sapporo Battery to develop a 10 MW/ 30 MWh grid-scale battery system in Sapporo, Hokkaido, aiming for operation by April 2027.

This project was selected for METI’s FY2024 renewable energy expansion and grid battery storage system subsidy program, receiving ¥1.05 billion in funding.

Their roles will be as follows:

Shikoku Electric-affiliated Yonden Engineering: EPC, O&M support, power negotiations

Aoki Asunaro Construction: Civil works

JR East & JR East Energy Development: Power transaction management

Decarbonization Support Organization: Funding review

WWB: Grid access, land acquisition, regulatory coordination

Chubu Plant Service: O&M support

Mitsubishi Research Institute: Battery operation planning

Fukushima Reconstruction Wind Power, a consortium of nine companies including Sumitomo and Renova, launched operations in Abukuma region (Fukushima Pref).

With a 147 MW capacity, it’s expected to generate 360 GWh annually, operating until March 2045 under the FIP scheme. It is now Japan’s largest wind farm.

The project has 46 GE Vernova wind turbines, (each 3.2 MW). Toshiba Energy Systems supplied the turbines and will manage their O&M.

Sumitomo will buy all generated power and supply it to users via corporate PPAs, with buyers including Okuma Town Hall and silicon wafers producer SUMCO.

In response to articles published by Nikkei on April 2 (online) and April 3 (print), the Japan Wind Power Association requested a correction, citing factual inaccuracies related to the discussion of offshore wind auction rule changes.

JWPA argued that Nikkei misrepresented its role and overstated industry consensus against the rule changes.

The articles claimed that the JWPA conveyed concerns and opinions from its member companies, implying it had taken an official stance against rule changes.

The JWPA said it had not expressed any concerns nor formulated a collective opinion on behalf of its members but simply compiled individual views, which should not be construed as the association’s position.

CONTEXT: The METI guideline revision would allow previously auctioned offshore wind projects – like those won by Mitsubishi in 2021 – to sell electricity at higher prices than initially agreed. Critics, including rival bidders, see this as unfair and a potential “bailout” for Mitsubishi that recently reported large losses on those projects. Public consultation on the changes is open until April 27.

Potentia Energy, co-owned by Enel Green Power and INPEX, fully acquired 1.13 GW of renewables assets across Australia, including 700 MW of wind and solar projects.

The portfolio includes key operational sites such as Warradarge Wind Farm, Greenough River Solar Farm, Albany Grasmere Wind Farm, Clare Solar Farm, etc.

Potentia also has a 7 GW development pipeline in wind, solar, storage, and hybrid projects in Australia.

J-Power inked a 20-year virtual PPA with KDDI, backed by electricity from a new onshore wind farm in Kaminokuni Town, Hokkaido.

Work on the Kaminokuni Third Wind Farm (capacity 51 MW) is set to start in the first half of FY2025, with commercial operations in Sept 2028.

This is the second virtual PPA between the two firms. In December 2024, KDDI and J-Power’s subsidiary, J-Wind, signed a virtual PPA for a 19.5 MW wind farm in Kagoshima Pref, set to begin operations in December 2027.

CONTEXT: Despite rising material costs due to inflation and yen depreciation, the project moved forward, supported by stable revenue from the PPA and a ¥11.98/ kWh subsidy under the FIP scheme. The generated electricity will be sold on the JEPX.

CONTEXT: The firm’s second wind farm in Kaminokuni began operations in May 2024; now J-Power’s domestic wind capacity totals 756 MW across 28 sites.

Mitsui Kinzoku signed a R&D agreement with Helical Fusion that will focus on the “blanket”, an essential component to build a nuclear fusion reactor.

CONTEXT: In 2023, Mitsui Kinzoku invested in Helical Fusion, which aims to begin nuclear fusion generation in the 2030s.

CONTEXT: The blanket is a layer that surrounds the fusion reactor vessel. It absorbs the energy from fusion neutrons being produced in the plasma, and helps boil water via a heat exchanger.

KEPCO said that total FY2024 nuclear power generation was 51 TWh, up from 44 TWh last year. The nuclear power plant capacity use rate rose from 72.9% last year to 88.5% this fiscal year.

CONTEXT: The FY2024 nuclear power generation is the utility’s highest level since the Great East Japan Earthquake in March 2011 that shut Japan’s entire nuclear fleet.

TAKEAWAY: Since 2023, when two reactors at the Takahama NPP restarted, all of KEPCO’s seven operable reactors are in operation. In FY2025 many reactors are scheduled for inspections; thus, the utility’s total power generation is expected to decrease.

Kyushu Electric postponed introducing high-burnup fuel at Genkai NPP to FY2028, instead of the planned FY2026. The delay is due to ongoing NRA reviews.

Fuel replacement occurs during regular inspections every 13 months.

CONTEXT: High-burnup fuel contains uranium-235 with a higher enrichment level. It allows for greater energy output and extends the fuel cycle by about 13 months.

NEWS: TRADITIONAL FUELS

Mitsubishi considers joining Alaska LNG project, but doubts loom

(Japan NRG, April 4)

Bloomberg and Reuters reported that Mitsubishi is evaluating a potential investment into a $44 billion LNG project in Alaska. Yet, the company remains cautious about feasibility.

Mitsubishi President Nakanishi Katsuya acknowledged the project’s complexity, citing the need for a 1,300 km pipeline — twice the length of Mitsubishi’s LNG project in Canada – as well as uncertain future demand in SE Asia.

An Alaskan delegation recently visited Japan to seek investment. Still, Mitsubishi wants thorough due diligence before committing. Nakanishi noted this project has been proposed many times in the past, even before Trump.

CONTEXT: Mitsubishi announced a 3-year plan to invest ¥4 trillion, aiming for a ¥1.2 trillion net profit by FY2027/28. The company will commit ¥1 trillion to sustain capital expenditure and more than ¥3 trillion to growth investments.

Tokyo Gas acquired a 70% stake in Chevron U.S.A. East Texas gas assets. The deal includes a $75 million cash payment and $450 million to fund development.

This deal is part of Tokyo Gas’s strategy to optimize its U.S. shale gas asset portfolio and enhance capital efficiency.

TAKEAWAY: Tokyo Gas will use the gas for trading and supplying power plants. This deal focuses on shale investments in the Haynesville formation (from Texas to Louisiana).

NYK set up a new subsidiary, NYK Energy Ocean Corp (NEO), acquiring 80% shares for ¥76 billion. NEO was formed recently by taking over ENEOS Ocean’s shipping business, excluding crude oil tankers.

NYK Group’s LPG fleet now totals 34 vessels, one of the world’s largest LPG carrier operators. NYK aims to strengthen its LNG/ LPG business.

ENEOS Xplora extended the Production Sharing Contract (PSC) with PetroVietnam for its rights to develop an oil field off the coast of Vietnam for another 25 years. The previous development deadline was April 2025.

PetroVietnam controls the area that includes the oil field.

CONTEXT: ENEOS Xplora got the rights for the block in 1992. Over 250 million barrels of crude oil have been produced to date. Production will now be 3,000 barrels per day, about 10% of ENEOS Xplora’s total crude oil production. This PSC is among the first to be awarded under Vietnam’s updated Petroleum Law.

JOGMEC updated its strategic technology roadmap, emphasizing support for CCS/CCUS projects and low-carbon fuels such as hydrogen as a way to align with the nation’s recently approved 7th Basic Energy Plan.

JOGMEC reiterated its goal of raising Japan’s oil and gas self-sufficiency rate to over 50% by 2030, and over 60% by 2040, while promoting the transition to gas resources and lowering the environmental impact of traditional fuel sources.

Actions include technical assistance for domestic and international CCS/CCUS pilot projects, promoting green hydrogen production and infrastructure, and building Japan’s technical capabilities through advanced research and industry collaboration.

TAKEAWAY: The strategy update is very much in line with ongoing developments, but it also formalizes JOGMEC’s new role as the operating entity that administers METI’s auction and subsidy-driven approach to growing new energy sectors, such as CCS and hydrogen, among others. Traditionally, JOGMEC has been a key player in the gas / LNG sector and also focused on new metals and minerals exploration. That role remains but is now supplemented by tasks across almost the entire energy sector. If NEDO is the distributor of funds for R&D, then JOGMEC is now in charge of supporting early-stage commercial projects.

INPEX and Kanto Natural Gas Development have set up a JV to speed up feasibility studies and engineering for the Metropolitan CCS Project commissioned by JOGMEC. Ownership is INPEX (85%) and Kanto Natural Gas (15%).

The JV will collaborate with Nippon Steel, INPEX, and Kanto Natural Gas to advance CCS.

CONTEXT: Metropolitan CCS will assess CCS for Nippon Steel and other industries in the Keiyo Industrial Zone. The plan entails transporting CO2 via pipelines, and storing it in offshore saline aquifers in Chiba Pref.

The University of Tokyo School of Engineering and INPEX will cooperate on research in oil & gas development, as well as CCS.

The program will develop tracers for checking oil & gas production and CCS. Another area is AI-driven optimization for oil & gas field development and CCS.

Chiyoda Corp won a feasibility study contract from oil & gas company Pilot Energy (Australia) to develop a CO2 supply chain.

Pilot Energy plans to capture and store 700,000 tons of CO2 a year from alumina production facilities in Western Australia. The project aims to liquefy the CO2, transport it, and inject it into depleted offshore oil fields.

Cosmo Oil Marketing inked a sustainable aviation fuel supply deal with Delta Air Lines, the first time Delta will use SAF at airports in the Asia-Pacific region.

CONTEXT: The SAF is developed as part of a NEDO program. The fuel secured international sustainability certifications, including ISCC CORSIA and ISCC EU.

Six major firms – Obayashi, Chugoku Mokuzai, JAL, Boeing Japan, Marubeni, and Mitsubishi Chemical – inked an MoU for a feasibility study on producing and selling SAF, bio-naphtha, and biodiesel from domestic forestry resources.

The project will use Cat-HTR hydrothermal liquefaction tech to convert wood residues into bio-crude, which will then be refined into SAF and other fuels.

The study will run until December, with commercialization targeted around 2030.

ANALYSIS

BY ALEXANDER FARRELL

Renewables and Hydrogen on Display as the World Expo Opens in Osaka

When Expo 2025 opens in Osaka on April 13 it will offer visitors a look at some of Japan’s latest renewable and clean energy solutions.

Hydrogen will feature heavily, with a full green hydrogen supply chain at the NTT and Panasonic Group pavilions among the highlights. On the way to the Expo, visitors will be able to ride Japan’s first commercial hydrogen-powered ferry, operated by Iwatani. Hydrogen, along with carbon capture and reuse (CCU) technologies, will also be part of a methanation demonstration operated by Osaka Gas.

In addition to powering hydrogen production, solar will be on display with perovskite cells (PSCs) from Panasonic and Sekisui Chemical supplying renewable energy. As costs for these flexible photovoltaic cells come down, they significantly expand the potential for solar power’s adoption in heavily urbanized areas.

Another solution on display will highlight the opportunities in the nexus of clean energy and digital tech innovation. Domestic telecoms giant NTT is showcasing a concept that seeks to replace electrical circuitry with photonics, claiming both efficiency gains and a lower demand for energy to sustain it.

Energy demonstrations

A World Expo is an opportunity to gauge some of the latest technology trends, although a practical implementation of the solutions may be decades away. For example, Osaka’s previous Expo in 1970 exhibited cordless phones, magnetic levitation (maglev) rail, local area networking (LAN), and IMAX movies.

The 2025 edition has run into speed bumps with significant cost overruns, construction delays, and some countries withdrawing their participation, but this event should provide valuable insights on where energy and other technologies are heading.

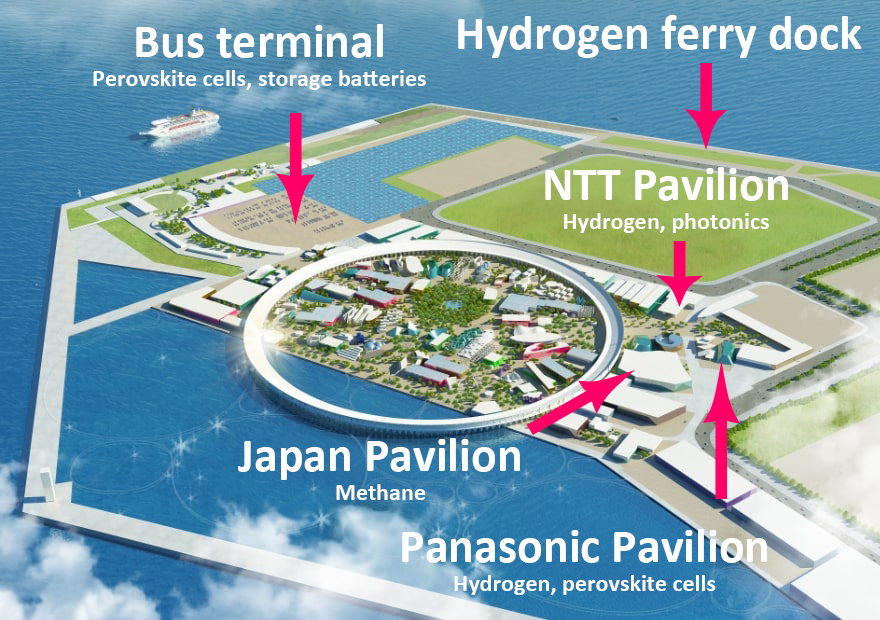

Background image source: Japan Association for the 2025 World Exposition. Detailed venue maps at the Expo website.

Hydrogen supply chain

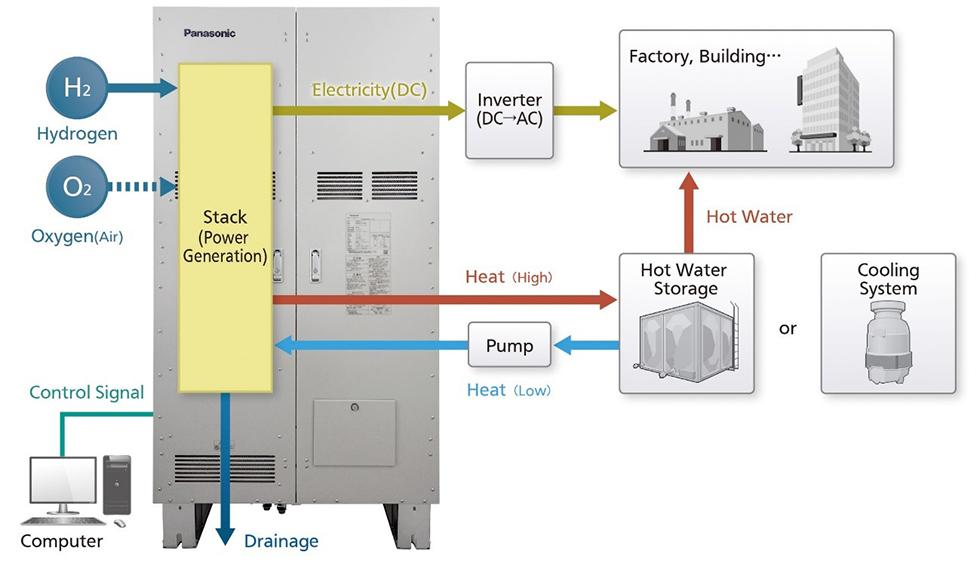

NTT Anode Energy and Panasonic Group are installing a hydrogen supply chain at their pavilions to demonstrate the feasibility of green hydrogen generation with solar power. A 200-meter pipeline that also stores underground telecom lines will transport some of the hydrogen from the NTT Pavilion to the Panasonic Group Pavilion. Panasonic will demonstrate its fuel cell technology at both pavilions.

Panasonic’s H2 Kibou pure hydrogen fuel cell produces electricity by instigating a chemical reaction between highly purified water and atmospheric oxygen. The PH3, a recent model for some overseas markets, is a cogeneration system with a maximum DC power output of 10 kW, with up to 8.2 kW of heat that can warm water up to 60°C.

PH3 power generation mechanism Source: Panasonic

Hydrogen-powered ferry

Iwatani’s hydrogen-powered boat, Mahoroba, will ferry visitors to the north side of Yumeshima, the manmade island hosting the Expo. Running solely on hydrogen fuel cells, this will be Japan’s first commercial operation of a hydrogen-powered boat. Work on this project began in FY2021 with NEDO subsidies.

Hydrogen ferry concept image Source: Iwatani

Perovskite solar cells

Panasonic Group’s pavilion will exhibit an artistic use of perovskite solar cells (PSC).

These cells are strong enough to serve dual functions as structural components in buildings, such as windows. Panasonic is applying its technologies in materials, inkjet coating, and laser treatment to design perovskite cells with a variety of sizes, transparency, and decoration.

Sekisui Chemical will install 257 of its PSCs on 250 meters of roofing at the venue’s bus terminal. This will be the largest combined use of PSCs in Japan.

Sixteen storage batteries will receive the electricity during the day and discharge at night to provide power for the 282 100W LEDs illuminating the bus stops. The batteries have 14 days of capacity to cope with cloudy weather.

Source: Panasonic

Methane

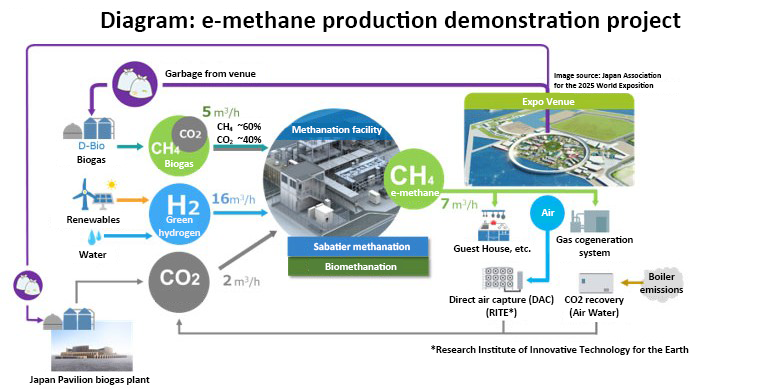

Osaka Gas will power the Japan Pavilion by generating electricity from e-methane fuel that will be produced from CO2 and hydrogen through a methanation system built by Kanadevia (formerly Hitachi Zosen).

The CO2 will come from several sources. One is biogas from garbage collected at the Expo. Another is a direct air capture system installed by the Research Institute of Innovative Technology for the Earth (RITE).

The DAC project is commissioned by NEDO under the Moonshot R&D Program. Thirdly, Air Water will provide a CO2 recovery system that will collect the gas from heating equipment. Electricity generated by renewables will power electrolyzers to make hydrogen.

Source: Osaka Gas

Energy-efficient telecommunications

NTT is installing an All-Photonics Network (APN) to demonstrate how its Innovative Optical and Wireless Network (IOWN) technology platform will provide low-power, high-capacity, low-latency telecommunications.

The concept is to replace electricity in telecommunications with light. Although we already use light to transmit data via fiber-optic cables, relays convert that light to electricity so devices and their chips can handle it.

This conversion increases latency, while the electricity coursing through devices generates heat that must be cooled, which in turn requires more electricity; hence the global rush to boost power generation capacity for large data centers.

The IOWN technology is still far from completion. The service at the Expo will still use the same amount of electricity as current telecommunications tech, but promises to transmit 20% more data. Much more interestingly, it will have 0.5% as much latency, which NTT plans to demonstrate via real-time drone and robot operations, esports competitions, and events where participants far from the venue join via APN to interact in real time.

As early as 2030, NTT has ambitious goals to cut the power consumption of devices by 99% and transmit 125 times as much data, while retaining the 200-fold reduction in latency. However, replacing data transmissions between components and within chips requires a considerable step up from the current semiconductor technology.

Conclusion

As a highly developed but resource-poor country that imports around 90% of its primary energy, Japan has particularly strong incentives to come up with solutions to increase domestic resilience and self-reliance. It has also cemented into law the target of carbon neutrality by 2050.

Renewable and transitional energy technologies pioneered in Japan could find markets in countries with ambitious clean energy goals. Potential buyers also include those with concerns over the security of their supply chains for everything from Middle Eastern oil and gas to Chinese silicon photovoltaic cells.

PSC is a good example of such technologies. METI expects the flexible cells to eventually cost less than their silicon counterparts that are widely used today. The primary ingredient for PSCs also happens to be iodine. Japan has a 30% share of global iodine production, while Chile accounts for much of the rest. PSCs that perform well in Japan’s cities and mountainous terrain could compete well.

If PSCs become cost-competitive against their silicon panels, it would unlock the next set of technologies, such as those related to green hydrogen production at scale, which in turn would bring closer the potential to tap into synthetic fuels, such as e-methane, which is demonstrated at the Japan Pavilion.

Technology evolution is a complex, multi-stage process that often leads to surprise use cases and results. At Expo 2025, organizers are hoping to show some of that magic, and explain the technical and societal aspects behind it.

The World Expo in Osaka runs from April 13 to October 13.

ANALYSIS

BY ANDREW STATTER

Energy Jobs in Japan: Trump and Potential Impact on Energy Jobs

Following the return of Donald Trump to the White House and his predictable actions to roll back clean energy initiatives, we’re constantly asked how we see this impacting Japan and its energy sector’s labour market.

Naturally, when commenting on the future, a certain amount of speculation is necessary. Various moving parts in state policy, investor appetite, and existing partnerships can shift the trajectory of change. That disclaimer aside, overall we see a multitude of factors pointing to a continued increase and further diversification of career opportunities across Japan’s energy industry.

Japan is an energy consumer

Unlike the U,S., with abundant oil & gas reserves and economic opportunity to export these commodities, Japan is a consumer rather than producer of fossil fuels, therefore the same decisions the U.S. makes cannot support Japan to achieve the energy trilemma of secure, cost-effective and sustainable energy.

As Japan still imports over 80% of its primary energy, and has an electricity sector that remains at under 30% penetration of renewables – and barely 40% with renewables and nuclear combined – the demand for non-fossil resources will remain high from an energy independence and security perspective.

LNG is expected to have a new lease on life. Considering the close U.S./ Japan ties, and Japan’s role as a regional LNG trader, this seems inevitable. Japan’s gas utilities, trading houses and other fossil players see an opportunity to improve ties thanks to U.S. production, investments in infrastructure, and increased shipping capacity and volumes – both procured and traded.

Opportunities in clean fuel

With the potential rollback of the IRA in the U.S., many large-scale projects for green hydrogen and ammonia, as well as e-methane, sustainable aviation fuel and other next-generation fuels are facing potentially terminal economic difficulties.

Japan however, remains heavily invested in the ‘hydrogen economy’. Though clean hydrogen will not solve all of Japan’s energy security challenges, as much of the fuel will still need to be imported, industry has huge potential to become a global leader and reignite technology exporting opportunities. Since Japan lost the photovoltaic and battery markets to China, and the domestic wind turbine industry never got off the ground, the focus and pressure from Japan’s industry giants to regain export market share is not to be underestimated.

With Japan invested in the technology and the U.S. dropping projects, this opens the door for increased partnerships from other partners capable of producing clean hydrogen or ammonia at scale. We expect to see a shift in resources from Japanese investors and trading houses away from the U.S. to Australia, Middle East and potentially as far abroad as Canada.

In parallel to this shift in allocation of capital and partnerships, further market entry and investment from private companies into Japan is expected. From an Australian perspective, North Asia is a massive offtake opportunity for commodities. Japan with its stable political landscape and existing infrastructure developed to serve the LNG value chain stands out as the prime candidate to be a regional hub.

The trickle down effect on jobs here is significant. Development, project management, construction, and engineering talent will be required to repurpose or build new port, storage and transportation facilities. Investment and business development professionals will be required both for outbound investment and leading multinational interests in Japan.

Shift in alternative investment funds

The U.S. saw declining investment dollars into clean energy projects in the leadup to the election, and this has accelerated since the result. Europe has seen steady growth, but Asia has seen the biggest uptick in private investment into clean energy over the past 12 months.

Emerging markets in South East Asia attract risk capital, but Japan, despite having lower potential returns, is attracting investment as fund managers look to hedge risks and diversify their portfolios. This is backed up by an increasingly healthy PPA market and opportunities in energy storage. Ares Management’s acquisition of GLP Capital Partners and General Atlantic’s acquisition of Actis are among the examples of diversification and outflows of U.S. capital. We also see direct investments from U.S. platforms such as I Squared Capital, Stonepeak and others coming to Japan.

Though this trend was naturally motivated due to an increase in clean energy demand and the proliferation of energy storage in Japan, we now see changes in the U.S. accelerating it. Opportunities across all key functions of developers – project development, engineering, asset management, investment, procurement etc – are directly increasing. With energy storage in particular, this has second order effects of increasing opportunities for other players in the ecosystem, such as forecasting and optimization solution providers and energy traders.

Chance to double down on GX innovation?

Possibly the biggest loser of the U.S. policy changes will be clean tech companies. Without support for their R&D, manufacturing and other heavy capital investments, the U.S. could hemorrhage up to $50 billion of export revenue due to failed innovation and manufacturing in clean tech sectors, according to Net Zero Industrial Policy Lab.

This naturally creates opportunities elsewhere, and in multiple areas Japan stands to take advantage. Perovskites, next generation battery technologies, floating wind and turbines capable of burning 100% hydrogen are a few examples.

Since PM Suga’s initial Green Innovation Fund, Japan’s political leadership has continued to support innovation across green transformation sectors. And if they double down on this, we will see further opportunities across various areas of R&D and manufacturing.

From a decarbonisation perspective, Japan will not be free of negative effects from the change in the U.S. administration. The clearest illustration will be an almost certain prolonging and increase of Japan’s role as a purveyor of LNG at a regional level.

Looking more broadly though, new opportunities exist in wider partnerships, innovation, export markets and inbound investment into Japanese clean energy infrastructure.

Andrew Statter is a Partner at Titan GreenTech, an executive recruitment agency focused on the clean energy space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Africa/ Energy financing

Chinese financiers are key players in Africa’s energy sector. To date, the China Development Bank (CDB) and the Export-Import Bank of China (Exim Bank), have provided $54 billion of energy finance on the continent. Those funds have primarily been in coal and hydro power, but are now increasingly in renewable energy and natural gas.

Australia / LNG

The govt won’t take action to acquire additional quantities of LNG for Q3 2025 as it feels confident that current volumes are sufficient to cover forecasted demand.

China / Renewables curtailment

China is curtailing more renewable energy capacity. About 6.2% of wind power and 6.1% of solar power were curtailed in the first two months of the year, said the National Energy Administration. In the same period in 2024, just 4% of wind and 4.3% of solar were curtailed.

India / Renewable power potential

Renewable energy generation potential has reached 2,109 GW. The Energy Statistics India 2025 report says the highest potential comes from wind at 1,163 GW (55.17%), followed by solar energy with 748 GW (35.50%), and large hydro with 133 GW (6.32%).

India / Trump tariffs

U.S. tariffs on Indian energy exports present both short-term and long-term challenges, requiring businesses to adopt agile strategies to mitigate risks. The tariffs will likely create upward pressure on the cost of Indian energy exports to the U.S. market, which will lead to less demand, according to Shardul Amarchand Mangaldas & Co.

Indonesia / Floating PV power

PowerChina completed the Cirata Floating PV Power Plant (192 MW), marking the commissioning of the largest facility of its kind in SE Asia. It accounts for 25% of Indonesia’s current renewable energy output.

Offshore wind

The global offshore wind industry is expected to add 19 GW in 2025, recovering from a slowdown in 2024, said Rystad Energy. Capacity additions this year, with sector-wide expenditure projected to hit $80 billion, will be a rebound from last year’s 8 GW.

Philippines / Energy financing

The World Bank approved an $800 million loan targeted to build more renewable energy capacity throughout the country.

Singapore / Power

Singapore’s Energy Market Authority is reviewing how the power market should be managed going forward, with a target completion by 2026.

Vietnam / Renewable energy

The application of a new power purchasing price – which would be implemented retroactively for several years – by Vietnam Electricity, or EVN, puts 173 solar and wind projects at risk of insolvency. The Vietnam Chamber of Commerce and Industry has sent a letter to parliament expressing such concerns.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS:

・OCCTO publishes FY2025 Supply Plan Report

・GHG emissions from major emitters fell in FY2022

・Moving data centers to Hokkaido could save up to ¥9.4 bln

The 2025 edition has run into speed bumps with significant cost overruns, construction delays, and some countries withdrawing their participation, but this event should provide valuable insights on where energy and other technologies are heading.

The 2025 edition has run into speed bumps with significant cost overruns, construction delays, and some countries withdrawing their participation, but this event should provide valuable insights on where energy and other technologies are heading.