WEEKLY

APRIL 28, 2025

ANALYSIS

PINK PROSPECTS: WHY JAPAN’S HYDROGEN FUTURE GLOWS NUCLEAR

- While ‘green’ hydrogen is heralded as sustainable, ‘pink’ should be the color of Japan’s clean energy future, according to Dr Venera Anderson.

- ‘Pink’ hydrogen is produced by nuclear-powered electrolysis. Restarting reactors could offer an economic way for domestic hydrogen supply.

BATTERY MAKERS DRIVE BREAKTHROUGHS AS ENERGY STORAGE IS CRUCIAL FOR GRID STABILITY

- Lithium-ion batteries have long dominated energy storage, but they rely on certain materials.

- Top battery makers feel that racing to secure mines or supply chains is not the only way for Japan to compete.

- There is faith in new technology breakthroughs that could flip the script on resource demand.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Power retailers allowed greater scope around use of non-fossil certificates

- Govt launches working group for data center-focused Watt-Bit Coordination

- ANRE announces updates for 3rd round LTDA

- OCCTO gives electricity supply-demand outlook for 2040 and 2050 by source

- EEX posts growth in Japanese electricity futures

- JEPX spot market rebuilds post gross bidding

- Japan Engine final test on ammonia-mixed marine engine

- Hydrogen-powered equipment pilot at Kobe port

- Digital Grid’s IPO on TSO; most funds go to BESS

- Konica Minolta targets PSC breakthrough

- Tokyo Metro Govt outlines subsidy program for grid-scale BESS

WIND POWER AND OTHER RENEWABLES

- Kagoshima Pref seeks promising zone designation

- Toko Tekko enters offshore wind power sector

- Chugoku Electric launches floating offshore wind

- NRA edges closer to approval of Tomari NPP restart

- TEPCO retrieves fuel debris from Fukushima Unit 2

- Petroleum committee’s outlook for FY2025-FY2029

- JERA, Saibu Gas to share LNG via Hibiki Terminal

- Osaka Gas – first gas utility to launch Shore-to-Ship LNG bunkering

CARBON CAPTURE & SYNTHETIC FUELS

- Emissions from energy sector lowest since 1990

- ANRE presents support plan for CCS value chain

- Govt reviews bill for CO2 emissions trading system

EVENTS

May 3-6 May Golden Week Holidays

June 4-5 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 4-6 AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky Expo

June 15-17 G7 Summit @ Kananaskis, Alberta, Canada

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL POLICY AND TRENDS

Retailers to be allowed to use FIT certificates to sub for non-FIT, non-fossil certificates

(Government statement, April 23)

- ANRE will allow retail electricity providers to use FIT certificates as a substitute for non-FIT, non-fossil certificates to meet their obligations.

- Demand exceeded supply in the most recent (3rd round) non-FIT, non-fossil certs auction, creating a risk that retailers will be unable to meet assigned interim targets.

- The price for substitute procurement will be set at ¥1.3/ kWh or higher, the same as the auction cap for non-FIT certs.

- CONTEXT: Of the annual amount of non-FIT certificates issued by power generators (111.8 TWh), almost all have already been allocated, with only about 400 GWh remaining. ANRE estimates that about 80 TWh of FIT certificates remain unsold, and even after deducting the amount to be purchased externally, the impact will be limited.

TAKEAWAY: Retail electricity suppliers are required to boost their proportion of electricity from non-fossil fuel sources to 44% or more by 2030. But, this is difficult to achieve for small and medium-sized businesses that rely on the wholesale power market, so they rely on the purchase of non-fossil certificates to meet quotas. Data centers and real estate developers are other players that consume a large portion of certs. This elevated demand leads to shortages in the certs pools. FIT-related certs represent the bigger portion in the market. However, the renewables sector is shifting from FIT to FIP and other models, while there are also non-fossil certs that represent non-FIT power sources like nuclear.

Govt launches working group for Watt-Bit Coordination

(Government statement, April 21)

- The Ministry of Internal Affairs and Communications (MIC) and METI launched a working group to promote integrated development of power infrastructure and data centers, known as the “Watt-Bit Coordination.”

- The working group includes representatives from major power and telecom companies, including Tokyo Electric Power Grid, NTT, SoftBank, and KDDI.

- Professor Ezaki Hiroshi of the University of Tokyo chairs the group.

- Due to the concentration of data center connection requests in specific regions, the group called to focus efforts on improving the efficient use of existing power grids in the short term — placing data centers in areas with spare grid capacity.

- In the short to mid-term (by 2030), the goal is to develop data center sites that rely on existing grids; in the long term, to expand power and telecom infrastructure.

ANRE announces significant updates for 3rd round LTDA

(Government statement, April 23)

- ANRE announced significant updates for the third round of the Long-Term Decarbonization Power Source Auction (LTDA) in FY2025.

- The goal is to encourage investment in new power sources by addressing rising construction costs due to inflation, interest rate hikes, and currency depreciation.

- Key updates are:

- Adjusted business return rates: The standard business return rate of 5% will be modified based on the construction period.

- Increased bid price cap: The maximum bid price was doubled from ¥100,000/ kW to ¥200,000/ kW to reflect increased construction costs.

- Higher price cap for emerging technologies: The maximum price for hydrogen, ammonia, and thermal power with CCS will be raised.

- CONTEXT: The LTDA bidding system, which aims to promote new investment in decarbonized power sources, was conducted twice since FY2023. The winner of the second auction hasn’t been determined, but a detailed plan for the third auction is underway, reflecting the new 7th Basic Energy Plan.

Idemitsu partners with Toyota to shift from oil to decarbonized energy

(Nikkei, April 22)

- Idemitsu is partnering with Toyota to drive its shift from oil to decarbonized energy. Key efforts include developing solid electrolytes for next-gen EV batteries and building a synthetic gasoline supply chain using green hydrogen and CO2.

- Mass production of battery materials is planned by 2027–2028, with synthetic fuel deliveries to Toyota starting around 2026.

- While cautious about renewables, Idemitsu is investing heavily in four focus areas: solid electrolytes, ammonia, synthetic methanol, and sustainable aviation fuel.

- The company aims to invest ¥800 billion by 2030 to lead Japan’s energy transition.

Denso begins fuel cell power utilization demo

(Company statement, April 22)

- Auto components manufacturer Denso began a demo project using its proprietary solid oxide fuel cell (SOFC) system at a public facility in Okazaki City, Aichi Pref.

- The system supplies power and, in collaboration with Chubu Electric Miraiz, feeds surplus electricity back to the grid at night when excess power is generated.

- SOFC is a fuel cell using ceramic in the core part called “cell stack”, which generates electricity and heat using oxygen in the air and hydrogen reformed from gas.

- CONTEXT: The project is part of an initiative sponsored by NEDO and aims to expand the use of fuel cells through industry-academia-govt collaboration.

Kyuden forms alliance with German startup

(Company statement, April 24)

- Kyuden International, a subsidiary of Kyushu Electric, invested in German startup LiveEO, which uses AI to analyze satellite data. The data is used for infrastructure inspection, such as power lines and railways.

- The investment was made through a fund Kyuden joined in 2023.

- CONTEXT: Kyuden has a pilot project with LiveEO to test satellite-based power line monitoring, and plans to market the service to utilities and railway firms.

ANRE releases new efficiency standards for gas water heaters

(Government statement, April 18)

- ANRE released a report on new energy efficiency standards for gas water heaters.

- The target is based on “thermal efficiency (%),” and manufacturers are required to achieve an average of 87.5% or higher starting FY2028.

- Since the average in FY2022 was 85%, an efficiency improvement of about 3% is required.

NEWS: ELECTRICITY MARKETS

OCCTO forecasts electricity supply-demand outlook for 2040, 2050 by source

(Agency statement, April 18)

- OCCTO announced Japan’s electricity supply-demand outlook for 2040 and 2050 including nuclear, renewables, pumped storage, and battery storage.

- The conclusions are based on studies from the Research Institute of Innovative Technology for the Earth (RITE) and Deloitte Tohmatsu Consulting.

- It assumes an increase in electricity demand due to factors like new data centers, and a significant expansion of renewables.

- Nuclear power is expected to contribute 23–37 GW, factoring in long-term operation and replacement of older plants.

- Renewable energy capacity could reach up to 260 GW by 2050. Solar power is expected to continue to play a major role.

- Supply-demand balance during spring and autumn daytime hours was also considered, noting that surplus power could be managed with pumped storage and batteries.

- CONTEXT: At the previous meeting in February, OCCTO created a model case for demand that took into account uncertainties and other factors, presenting two cases for electricity demand in 2040 (900 and 1,100 TWh), and four cases for 2050 (950, 1,050, 1,150, and 1,250 TWh).

EEX records 119% growth in Japanese electricity futures

(Exchange statement, April 23)

- The European Energy Exchange saw trading in Japanese electricity derivatives jump 119% to 35.7 TWh in Q1, compared to 16.3 TWh a year earlier.

- March recorded 13.6 TWh of electricity trades via futures and options contracts, a monthly record. Last year’s total was 72.9 TWh.

- Earlier this month, EEX launched a central limit order book for the Japanese market, allowing electronic access to real-time prices and liquidity, boosting trading.

- The exchange received the first orders for the book on the day of launch (April 22), and the first trade concluded was related to a Tokyo-based Month Future.

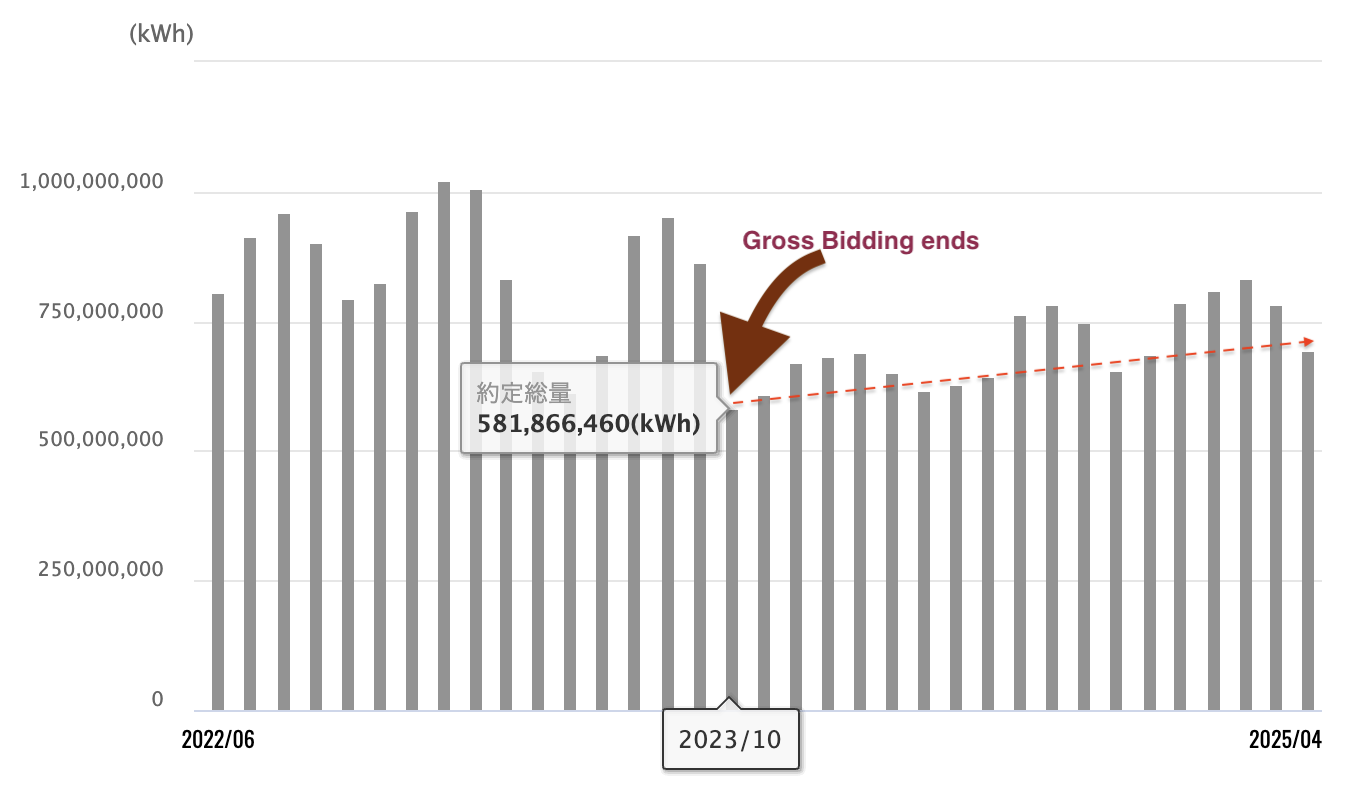

JEPX spot market rebuilds volumes after end of gross bidding

(Japan NRG, Exchange data, April 25)

- The average Japan Electric Power Exchange (JEPX) daily spot market trading in March was up 20% YoY to 781.7 GWh, as trading volumes continue to recover from October 2023 when the practice of gross bidding ended.

- There’s been an upward trend in spot trading volumes over the last 18 months and the average daily totals grew in the five months before March, until early spring brought warmer-than-usual temperatures.

- The March total trading volume was up both YoY (+20%) and MoM (+4.0%) to 24.23 TWh. This accounted for 33.7% of total nationwide electricity demand.

- The average 24-hour system price dropped ¥2.63 from February to ¥11.31/ kWh, with daytime and peak averages falling similarly. It’s set to average closer to ¥10 in April.

TAKEAWAY: As impressive as the March 2025 numbers are, the daily trading volumes are still 6% below same-month 2023 levels and 8% less than in 2022. Volumes are rebuilding after the suspension of gross bidding by the EPCOs in late 2023. Gross bidding, introduced in 2017, forced the generation divisions of EPCO holdings to sell power at marginal cost on the JEPX – with the holding’s own retail arms usually buying it back. The idea was to boost JEPX liquidity and reduce price volatility. Gross bidding accounted for 6% of Japan’s total physical power at one point and 15% of JEPX’s traded volumes, but it had little impact on allowing equal access for new market entrants to wholesale electricity; so, the regulator, EGC, recommended phasing it out. All EPCOs suspended gross bidding effective October 1, 2023. The gradual recovery in volumes is important for improved price discovery. It also indicates natural market growth, partly led by the expansion of market participants, greater reliance on the spot market by power generators, and overall power demand growth.

Average daily trading volumes on the wholesale market (JEPX)

Source: Japan NRG, JEPX data

ANRE announces additional auction for capacity market

(Government statement, April 23)

- ANRE will hold an additional auction for the capacity market in FY2025 (actual supply-demand in FY2026).

- This decision comes as power supply is expected to fall short by about 5 GW due to increased procurement targets and a number of power sources exiting the market.

- This will be the second consecutive year such an auction is held; bidding is set to begin in early June.

- OCCTO presented a draft demand curve showing the new target is about 187 GW, an increase of 8.5 GW (4.8%) from the previous main auction in 2022. However, only 181.6 GW is currently secured, leaving a shortfall.

- Bidding is scheduled for June 4. Results to be announced in late July.

- CONTEXT: The additional auction is used by OCCTO to adjust the amount of secured capacity for future periods. This auction is usually held one year before the supply year to account for updated forecasts of electricity demand, changes in generation capacity, or other developments not foreseen during the main auction.

- SIDE DEVELOPMENT:

- OCCTO begins comprehensive verification of capacity market

- (Agency statement, April 23)

- OCCTO began a comprehensive review of the capacity market, which will assess whether the system has been functioning properly based on the results of past auctions, and will identify areas for improvement.

- Findings are expected to be compiled by late FY2025. Topics include investment predictability, penalties, financial requirements, and policy issues like inefficient coal power. Long-term decarbonization auctions won’t be reviewed.

- Improvements will be applied starting with the FY2026 auction for FY2030 supply.

- CONTENTS: The capacity market system has held five main auctions to date and completed one full cycle of actual supply and demand in FY2024.

ANRE, OCCTO clarify plans for simultaneous market

(Government statement, April 22)

- ANRE and OCCTO updated plans for a simultaneous market, in which electricity supply (kWh) and balancing capacity (Δ (delta) kW) are traded together.

- After deliberating whether to obligate self-scheduled generation to bid in the future simultaneous market system, planners decided it won’t be necessary – provided that power plant operators meet transparency measures, such as registering generation information.

- CONTEXT: Self-scheduled generation refers to power plants where operators can determine whether to start up or switch off facilities themselves, as opposed to following grid operator instructions.

- Officials decided that the new system should impose restrictions on self-scheduled power sources only when necessary, such as when renewable output control or balancing shortages can’t be avoided. In such cases, power allocation will follow a merit order (ie. ranking generation facilities based on price, etc.) instead of giving priority to self-scheduled power sources.

- Other updates:

- Retailers will register desired quantities and prices by area and time slot, but quantity-only bids will also be allowed.

- There’ll be location-specific bidding for certain large-scale power consumers, including pumped hydro storage, economic dispatch for large thermal plants, and highly variable loads like data centers.

TAKEAWAY: The simultaneous market discussions are accelerating, as noted in the Analysis section of the March 31, 2025 issue of Japan NRG. There are still many complex issues to work through, many technical and financial. Contrary to media reports, METI says it’s not under pressure to complete discussions by a particular time frame. Still, it’s expected that the system configurations may be defined in the next year or two.

TEPCO EP considers lowering basic charge for extra-high and high-voltage plans

(Denki Shimbun, April 25)

- TEPCO Energy Partner might lower basic charges for some standard rate plans offered to high-voltage and above customers. The focus is on plans with about 30% exposure to wholesale market price fluctuations, with rate revisions planned for FY2026.

- In addition to enhancing the competitiveness of rate plans based on customer demands, TEPCO EP aims to strengthen proposals for carbon-neutral solutions. This aims to create a rate structure that benefits customers who level out power loads, reduce contracted power, and use electricity efficiently.

- CONTEXT: Since FY2024, TEPCO EP has offered standard high-voltage and above plans with wholesale market exposure levels of 0%, 30%, and 100%. For the 0% and 30% plans, TEPCO EP announced that starting in FY2025, basic charges would increase by about ¥1,000/ kWh of contracted power, bringing the total to around ¥3,000, while lowering the per-unit energy charges.

TAKEAWAY: In the Tokyo metropolitan area, competition for corporate power contracts is intensifying. New power retailers are gaining ground, capitalizing on falling wholesale market prices, and there are also reports of major utilities from other regions “crossing borders” into the market. TEPCO EP needs to offer more diverse solutions to retain its market dominance.

TEPCO PG sets up company for data center business, focus on Kanto

(Denki Shimbun, April 25)

- TEPCO Power Grid created TEPCO Digital Infrastructure to develop and operate data centers in the Kanto region and beyond.

- It will also advise on optimal electrical equipment operations and support companies that run data centers.

- CONTEXT: TEPCO PG has already set up a special purpose company with an NTT Data group company for data center-related operations in the Inzai-Shiroi area of Chiba Pref.

Hitachi Industrial launches new GFM

(Company statement, April 17)

- Hitachi Industrial Equipment Systems began operating its newly developed Grid-Forming Inverter (GFM) at its plant in Narashino City, Chiba Pref.

- GFM can autonomously create and coordinate microgrids, boosting energy resilience for businesses and municipalities.

- At Narashino, Hitachi installed an 82 kW solar system prioritized for power use, integrated with three parallel GFMs forming an AC microgrid.

NEWS: HYDROGEN

Japan Engine final test on ammonia-mixed marine engine

(Nikkei, April 21)

- Japan Engine Corp launched the final trials for a low-speed marine engine that uses a blend of ammonia (up to 95%) and heavy fuel oil, aiming to complete tests by Sept 2025 before shipping in October.

- The engine will be installed on an ammonia carrier under development by Nippon Yusen Kaisha, scheduled for delivery in FY2026.

- CONTEXT: The company has an MoE subsidy to expand production of ammonia fuel engines. The plant is scheduled for completion in 2028.

Hydrogen-powered equipment pilot at Kobe port

(Nikkei, April 24)

- The Ministry of Land, Infrastructure, Transport and Tourism demonstrated a pilot at Kobe port, replacing the diesel engine of a rubber-tired gantry crane (RTG) with a hydrogen-powered engine developed by startup iLabo.

- The hydrogen-powered RTG performed on par with diesel-powered units.

- CONTEXT: Japan’s major ports in Kobe, Tokyo, and Yokohama are accelerating hydrogen trials for port machinery. Tokyo completed a hydrogen fuel cell RTG trial.

- SIDE DEVELOPMENT:

- Hydrogen-only excavator tested on construction site

- (Company statement, April 23)

- A consortium led by Flat Field Corp, Tokyo City University, Kanazawa Institute of Technology, and Oriental Consultants modified a 20-ton Sumitomo SH200-7 excavator to run on a 100% hydrogen internal combustion engine, replacing the original diesel components with hydrogen-compatible parts.

- MoE backs the project, seeking to decarbonize heavy construction equipment.

UCC launches world’s first mass-produced hydrogen-roasted coffee

(Nikkei, April 23)

- CC began the world’s first mass production of hydrogen-roasted coffee, using a custom-built large roaster at its Fuji Factory powered entirely by green hydrogen.

- UCC sells hydrogen-roasted beans to both consumers and businesses, initially pricing a cup at about ¥70–90 higher than conventional roasts.

NEWS: SOLAR AND BATTERIES

Digital Grid’s IPO on TSO; most funds go to BESS

(Denki Shimbun, Nihon Securities Journal, April 23)

- The shares of Digital Grid, an operator of a power trading platform, debuted at ¥5,310 on the Tokyo Stock Exchange’s Growth Market on April 22, 17.4% above the initial offering price of ¥4,520.

- Most funds will go toward capital investment in its transmission grid battery storage business. Digital Grid was listed on the TSO on April 22. It entered the grid battery storage business in 2024.

- Digital Grid uses AI and other software to automate complex operations traditionally handled by power utilities, allowing for cost savings and flexibility in power sourcing.

- By 2030, the company aims to manage 1 GW of aggregated assets, with two customer projects already underway.

- CONTEXT: Digital Grid is a University of Tokyo spin-off founded in October 2017. In August 2023, Digital Grid launched its subsidiary – Digital Grid Asset Management – for development, ownership, and operation of grid storage batteries. It plans to participate in Japan’s wholesale power, capacity, and balancing markets.

Konica Minolta targets PSC breakthrough with innovative film

(Nikkei, April 23)

- Konica Minolta will produce a moisture-blocking film that can double the lifespan of flexible perovskite solar panels to 20 years.

- These panels, known for their lightweight and bendable properties, are vulnerable to degradation from moisture, limiting durability to 10–15 years.

- Konica Minolta developed the film to protect the panels’ sunlight-facing surfaces. Sample shipments begin later in FY2025, with full-scale production in 2027.

- CONTEXT: Konica Minolta sees PSCs as a growth opportunity. Japan is pushing to scale production, aiming for 20 GW of PSC capacity by 2040. Companies like Canon, Sekisui Chemical, Toshiba, and Panasonic are also advancing PSC solutions, with Canon preparing a similar protective coating for mass production in 2025.

TAKEAWAY: The global PSC market is forecasted to grow from ¥37 billion in 2023 to ¥2.4 trillion by 2040, which highlights the sector’s importance in Japan’s energy transition and security strategy.

Tokyo Metro Govt outlines subsidy program for grid-scale BESS

(Government statement, March 31)

- The Tokyo Metropolitan Govt outlined its 2025 subsidy program for grid-connected battery storage systems. Applications will be accepted from Sept 1–30, with the subsidy recipients announced in January 2026.

- The plan is to select five projects at extra-high voltage scale and six at high-voltage scale. Eligible applicants must have an office or branch registered in Tokyo and install a BESS of at least 1 MW directly connected to the TEPCO power grid.

- The subsidy will cover two-thirds of eligible costs (up to ¥2 billion/ project). If using reused EV batteries, the subsidy rises to three-quarters.

- The program’s total budget is ¥13 billion.

Shinden Hightex expands into energy storage, plans BESS in Chiba

(Company statement, April 17)

- Shinden Hightex will build a grid-scale battery storage in Asahi City, Chiba Pref, with an investment of around ¥400 million.

- The output and specifications of the battery have not been disclosed. Construction begins in July; Operations targeted for October 2026.

- CONTEXT: Shinden Hightex has been supplying Li-ion and lead-acid batteries since 2014, sourcing mainly from Japan, South Korea, and Taiwan. It also provides power equipment and modules for industrial and renewable energy sectors.

Tokyu Land, Shizen Energy to develop agrisolar plants

(Company statement, April 21)

- Real estate firm Tokyu Land and renewables developer Shizen Energy set up a JV to develop agrisolar power plants.

- The first project, using vertically mounted solar panels, will be built at Obihiro University in Obihiro City, Hokkaido, with a capacity of 708 kW.

- The new company, ReENE Shizen Farm, aims to develop 10 MW of solar capacity within two years, focusing on underutilized farmland.

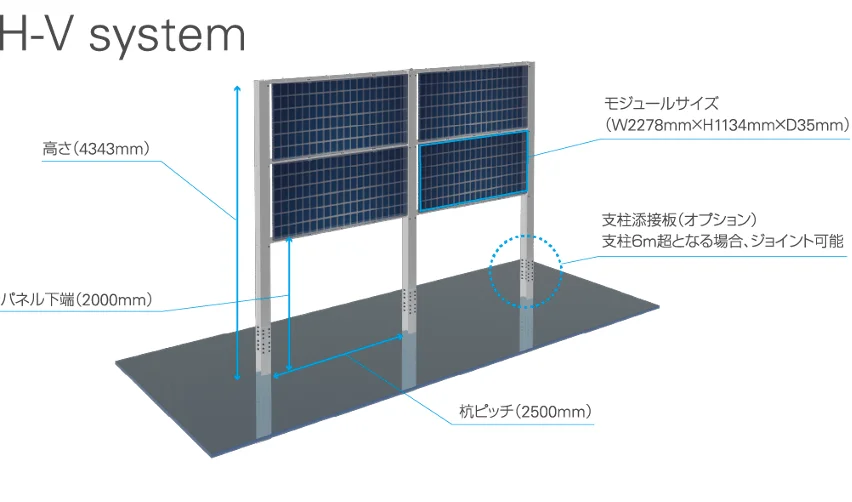

Takamiya develops vertical solar panel for narrow, snowy areas

(Company statement, April 17)

- Takamiya, a scaffolding manufacturer, has developed a vertical solar panel mounting called the H-V system. Designed to occupy minimal ground space, it enables solar power generation on farmland, factory sites, and parking lots.

- The H-V system uses bifacial panels to generate power during peak morning and evening hours — when electricity prices are higher — and is well-suited for snowy regions as snow buildup is minimized.

Hanwha introduces new solar energy service

(Company statement, April 25)

- Hanwha Japan is launching a new solar energy service for households. The plan shortens the contract period for managing and supplying power from 13 to 4 years.

- Customers will only pay for installation costs, with the solar system provided free of charge. Hanwha’s subsidiary, Renex, will handle installation and maintenance.

GS Yuasa develops compact industrial BESS, installs at Honda

(Company statement, April 24)

- GS Yuasa developed a new Li-ion battery storage system for industrial use, designed to be easily installed in limited spaces.

- Unlike conventional container-type systems that require large cranes, the new system uses modular battery units, simplifying installation.

- The system was installed at Honda’s outboard motor factory in Hamamatsu City, Shizuoka Pref, through a Tokyo Gas subsidiary. It consists of ten 200 kWh units connected for a total capacity of 2 MWh, used to store solar-generated electricity.

GS Yuasa’s new compact Li-ion BESS Installed at Honda factory in Hamamatsu City.

West Holdings and TMEIC to develop 20 battery storage stations

(Company statement, April 22)

- West Holdings, one of Japan’s top solar developers, is partnering with TMEIC (a Toshiba and Mitsubishi Electric JV) to build 20 grid-connected battery facilities across Japan by FY2026, totaling 160 MWh in storage capacity.

- TMEIC will supply the battery systems (2 MW/ 8 MWh ) and energy management tech, while West will handle development and land acquisition.

- The first site will be in Sosa City, Chiba Pref, with additional large-scale projects planned in Hiroshima and Kumamoto Prefs.

KDDI Group to build 28 MW grid-scale battery in Mie

(Company statement, April 22)

- au Renewable Energy and Eneres plan to build a 28 MW/ 90 MWh grid battery in Tsu City, Mie Pref. Eneres provides services to help electricity consumers reduce power procurement and operational costs.

- The facility will launch by April 2027, with revenue expected from the wholesale power, capacity, and balancing markets.

- CONTEXT: Eneres is a subsidiary of KDDI, which owns 59%, while J-Power owns a 41% stake. In April 2022, KDDI reorganized its energy-related businesses by establishing au Energy Holdings, under which Eneres now operates.

NEWS: WIND POWER AND OTHER RENEWABLES

Kagoshima Pref seeks ‘promising zone’ designation off Ichikikushikino City

(NHK, TBS, Govt statement, April 25)

- Kagoshima Pref submitted information to the govt recommending the waters off Ichikikushikino City as a candidate site for offshore wind power development.

- The goal is for the area to be designated as a “Promising Zone” – a preliminary step before it is officially recognized as a “Promotion Zone” for project development.

- This follows two years of study and seven meetings involving five cities, one town, and 15 local fishing cooperatives.

- Concerns from some fishers remain, but the prefecture will act to alleviate worries.

- As of March, Kyushu has the following offshore wind designations:

- Promotion Zones: Off Goto City and Saikai City, Nagasaki Pref;

- Preparation Zones: Off Hibikinada, Fukuoka Pref; and Karatsu, Saga Pref.

- CONTEXT: Offshore areas of Ichikikushikino City and neighboring Akune and Satsumasendai Cities have a wind power generation potential of up to 1.5 GW.

TAKEAWAY: Offshore wind development near Kagoshima Pref presents both promising opportunities and notable challenges due to the region’s unique environmental conditions. Offshore areas near Kagoshima have strong wind resources, deep coastal waters ideal for floating turbines, and significant potential for clean energy development. On the other hand, the area faces seismic risks, frequent typhoons, and potential conflicts with local fisheries. Deep waters and extreme weather will require advanced tech and careful environmental and community engagement.

Toko Tekko enters offshore wind power sector

(Nikkei, April 24)

- Toko Tekko, a manufacturer of steel structures and materials, is expanding into the offshore wind power sector. The firm began building a factory for the production of davit cranes used for the maintenance and unloading of offshore wind equipment.

- Toko Tekko plans to leverage the 150 wind turbines planned for installation in Akita Pref as a starting point to compete in a market dominated by foreign manufacturers.

- CONTEXT: Davit cranes are large devices used to transfer parts and supplies from cargo ships to wind turbines.

- By directly supplying davit cranes to customers, the firm aims to grow revenue between ¥5.5 and ¥10 billion.

TAKEAWAY: The offshore wind projects in Akita are growing, with 33 turbines already operational and plans for 149 more. Toko Tekko aims to capture a significant share of the growing demand in this region and expand by targeting nearby areas like Aomori, Yamagata, and Niigata prefectures.

Chugoku Electric launches floating offshore wind project

(Company statement, April 22)

- Chugoku Electric resumed offshore wind development, starting commercial operations of a floating wind turbine off Kitakyushu.

- This is Japan’s second floating offshore wind project and the first using a steel barge-type platform.

- The project involves six firms, including Hiroshima-based Glocal that specializes in floating wind tech. A 3 MW turbine will be used and will sell electricity under the FIT program to Kyushu Electric Power T&D.

- The participating companies aim to quickly develop technologies that reduce generation costs, which are now quite significant.

- CONTEXT: Japan sees floating offshore wind as crucial for decarbonization efforts. Such efforts began in 2014 under a demo program by NEDO to develop a cost-effective, durable floating system suitable for metocean (weather and sea) conditions at depths of 50–100 meters.

TAKEAWAY: Floating wind tech development is gaining momentum in Japan despite fixed-offshore wind projects facing challenges such as rising costs from inflation and geopolitical tensions. Progress in floating wind will be crucial for the broader expansion of offshore wind, particularly given Japan’s deep coastal waters, where traditional fixed-bottom turbines are less feasible.

TEPCO maintains renewables profit target despite offshore wind setbacks

(Nikkei, April 18)

- TEPCO will maintain its ¥100 billion profit target for renewables by FY2030 despite delays in offshore wind projects, having won only one major bid so far. The firm plans to offset this with strong performance in hydropower, including pumped storage and corporate PPA sales.

- CONTEXT: In 2023 TEPCO Holdings pledged to build 6-7 GW of new renewable capacity. In an interview in 2023, TEPCO RP President Nagasawa said the firm was seeking to develop 2-3 GW in offshore wind alone, domestically and overseas.

- Amid stalled nuclear restarts and rising costs, TEPCO is prioritizing renewables and aims to fund future growth through domestic and international partnerships.

- CONTEXT: The cost of offshore wind projects can reach hundreds of billions of yen for large-scale developments. In particular, wind turbine prices have been rising since around 2021. According to BloombergNEF, global procurement costs for wind turbines have increased by 30% over the four years leading up to 2024.

Earthsolar raises ¥630 million to expand renewables projects

(Company statement, April 16)

- Earthsolar, a Tokyo-based renewables developer, raised ¥630 million in a third-party allotment led by Environmental Energy Investment, with participation from capital market firm Mitsubishi UFJ Capital and venture capital firm ANRI.

- The funds will be used to accelerate the development of new renewable energy projects and hire new talent.

- The firm is led by Tomohiro Yamazaki, formerly of Renova, and is developing 50 MW of high-voltage class solar power projects.

Penta-Ocean, MOL Maritex cooperate on wind condition observation

(Company statement, April 21)

- Penta-Ocean Construction and MOL Maritex set up a consortium to conduct wind condition observation work for offshore wind development.

- A floating wind observation tower was installed in September 2024, and data collection has already begun. Observations will continue through FY2025.

LOOOP inks alliance with Tokyu Land Corp

(Company statement, April 25)

- Renewables developer LOOOP signed a capital and business alliance deal with Tokyu Land Corp, one of Japan’s leading real estate developers.

- LOOOP held a third-party allotment of shares to raise funds.

NEWS: NUCLEAR

NRA to approve Tomari NPP Unit 3 restart

(Nikkei, April 23)

- The NRA is set to approve the restart of Hokkaido Electric’s Tomari NPP Unit 3, which has been offline since 2012.

- The NRA plans to present a draft safety review report on April 30, which, after public comments, could lead to formal approval by summer.

- This would be the first reactor to pass the new safety standards since the Shimane Unit 2 reactor in 2021.

- The next steps involve reviews of detailed construction and safety plans.

- Hokkaido Electric aims to restart the plant in 2027, after completing a new seawall. Local approval, including from the Hokkaido Governor, will still be necessary.

- CONTEXT: So far, 17 reactors nationwide have passed the review, with 14 restarted. Unit 3 faced delays in the approval process due to lengthy assessments of whether an on-site fault line is active. In 2021, analysis concluded the fault isn’t active. By 2024, the utility completed its explanations on seismic, tsunami, and design safety.

TAKEAWAY: As Hokkaido’s only operable NPP, Tomari is drawing attention from major tech companies such as chipmaker Rapidus. Coupled with the region’s huge renewables potential, the northern island could become a hub for many companies.

TEPCO retrieves fuel debris from Fukushima Unit 2

(Nikkei, April 23)

- TEPCO retrieved nuclear fuel debris from Fukushima Daiichi NPP Unit 2, using a fishing rod-like device. This time, the process took only a week, compared to over two months during the first attempt in Nov 2024.

- Later in FY2025, TEPCO plans to switch to a versatile robotic arm system to expand retrieval capabilities. Full-scale debris removal won’t begin until FY2028 or later.

NEWS: TRADITIONAL FUELS

Petroleum Product Committee’s outlook for FY2025-FY2029

(Government statement, April 25)

- Total domestic demand for fuel oil will keep declining in the FY2024-FY2029 period, from 136.5 million kiloliters in FY2024 to 122.2 million kiloliters by FY2029.

- Of the various fuels under scrutiny, only jet fuel demand will likely remain stable. This excludes power generation use of C fuel oil.

- Total demand for LPG will fall from 11.99 million tons in FY2024 to 11.40 million tons in FY2029.

- As for sectors, residential and commercial use accounts for 47% of oil fuel demand. Still, it will likely fall by 1.9% to 5.19 million tons in FY2029.

JERA, Saibu Gas to share LNG via Hibiki Terminal

(Company statement, April 22)

- JERA and Saibu Gas announced a collaboration for the Hibiki LNG Terminal.

- It will become of joint use and reciprocal LNG sharing. JERA gains access to the third tank, to help manage energy supply-demand volatility.

- The terminal has a strategic location to expand LNG-related business across Asia and globally. They will also explore long-term energy initiatives, including hydrogen and other next-generation fuels.

- CONTEXT: The partnership follows Saibu Gas’s decision in November to expand the terminal with a third LNG tank. This will help meet domestic natural gas demand and stabilize supply. The third LNG tank is scheduled to begin construction in summer 2025, and be in, operation by Sept 2029. The expansion will cost about ¥50 billion.

TAKEAWAY: As Japan NRG showed in the April 14 and April 21 issues, JERA is expanding both its LNG trading volumes and related infrastructure in Southeast Asia. With more LNG in JERA’s hands, it’s securing terminals for shipments across the continent.

Osaka Gas – first gas utility to launch Shore-to-Ship LNG bunkering

(Company statement, April 21)

- Osaka Gas launched its LNG bunkering business; Japan’s first gas utility to do so.

- The refueling method, called “Shore-to-Ship,” involves supplying fuel to a ship from a land-based facility, enabling large-volume delivery.

- Osaka Gas Senboku Manufacturing Plant (Takaishi City, Osaka Pref) supplied LNG to the LNG fuel carrier Verde Heraldo operated by Mitsui O.S.K. Lines.

- Osaka Gas also plans to enter the “Ship-to-Ship” market.

- CONTEXT: This first supply equaled 1,000 tons of LNG, enough for the vessel’s round-trip journey to Australia. Alternatives to heavy fuel oil, like ammonia, are still not widespread. LNG-fuelled ships are an option to lower CO2 in the shipping sector.

LNG stocks down from previous week, down YoY

(Government data, April 23)

- As of April 23, the LNG stocks of 10 power utilities were 2.11 Mt, down 0.9% from the previous week (2.13 Mt); down 3.2% from end April 2024 (2.18 Mt); and 1.4% down from the 5-year average of 2.14 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Energy consumption and CO2 emissions drop amid shift to renewables

(Government statement, April 25)

- ANRE released final figures for Japan’s energy supply and demand in FY2023.

- Final energy consumption decreased 2.7% compared to the previous year. Petroleum consumption dropped 3%, city gas 2.5%, electricity 2.5%, and coal 2.2%.

- Primary energy supply also shrank, down 4% from FY2022. Fossil fuel supply experienced a significant 7% reduction. Coal decreased by 8.7%, natural gas and city gas by 7.9%, and oil by 5.2%.

- Non-fossil fuel supply rose by 11.1%. This was due to a 51.7% increase in nuclear power and a 6.3% rise in renewable energy (excluding hydro). Renewable energy, including hydro, increased and reached a 19.3% share of total energy supply. This is the highest in 25 years.

- Electricity generation totaled 987.7 TWh, the lowest level since FY2010. The share of non-fossil fuel electricity sources exceeded 30% for the first time since the 2011 Fukushima disaster, reaching 31.4%. The generation mix consisted of 22.9% from renewable energy, 8.5% from nuclear, and 68.6% from thermal (excluding biomass).

- CO2 emissions from energy use fell to 920 million tons. This marks the lowest level recorded since FY1990. Emissions dropped across all major sectors: 4.7% in industry/business, 6.8% in households, and 0.7% in transport.

ANRE presents support plan for CCS value chain

(Government statement, April 24)

- ANRE’s CCS Policy Office gave updates on its support scheme for CCS. The draft model has a framework involving all relevant parties in the CCS value chain.

- The govt proposes principles for risk allocation. EPC contractors and O&M companies should bear risks related to facility construction and operation. Lenders assume financial and stranded asset risks.

- Emitters and storage operators should share liability for CO2 supply mismatches. T&S operators should take on transport-related risks. Potential CO2 leakage remains one of the major concerns.

- An issue under discussion is the potential suspension of CO2 transport and storage. It would force emitters to halt capture operations. The govt is then considering compensation schemes when such suspension is not the fault of the emitter.

- In case of CO2 supply interruption from emitters, these operators may not earn enough to repay loans, leading to stranded assets.

- The govt is considering introducing auctions for CCS service fees. These auctions would include price caps to ensure rational cost structures.

Govt reviews bill for CO2 emissions trading system

(Denki Shimbun, April 24)

- The House of Representatives Committee on Economy, Trade and Industry is working on a bill for a CO2 emissions trading system.

- The system would put a price on CO2 emissions and allow companies to trade emissions permits.

- Companies emitting over 100,000 tons of CO2 a year would have to take part, with actual trading set to begin in FY2027.

- The system will apply to 300–400 companies in steel, power, and chemicals.

- Companies must calculate their annual CO2 emissions. They will then surrender an equal amount of emissions allowances.

Rengo and Sumitomo Forestry to launch SAF feedstock venture

(Company statement, April 23)

- Paperboard box manufacturer Rengo will set up a JV with Sumitomo Forestry to produce and sell bioethanol as a feedstock for sustainable aviation fuel (SAF).

- The firm will build a plant at its subsidiary Daiko Paper in Shizuoka by 2027, using wood chips from construction and demolition waste supplied by Sumitomo Forestry.

- The bioethanol will be sold to oil companies for SAF production, with JAL and other domestic airlines expected as end users.

- CONTEXT: Rengo aims to produce 20,000 kiloliters/ year, expanding further if profitability is confirmed. Japan aims for 10% of total aviation fuel to be SAF by 2030, amid tight global supply and soaring costs of traditional feedstocks like UCO.

BY DR. VENERA N. ANDERSON

Pink Prospects: Why Japan’s Hydrogen Future Glows Nuclear

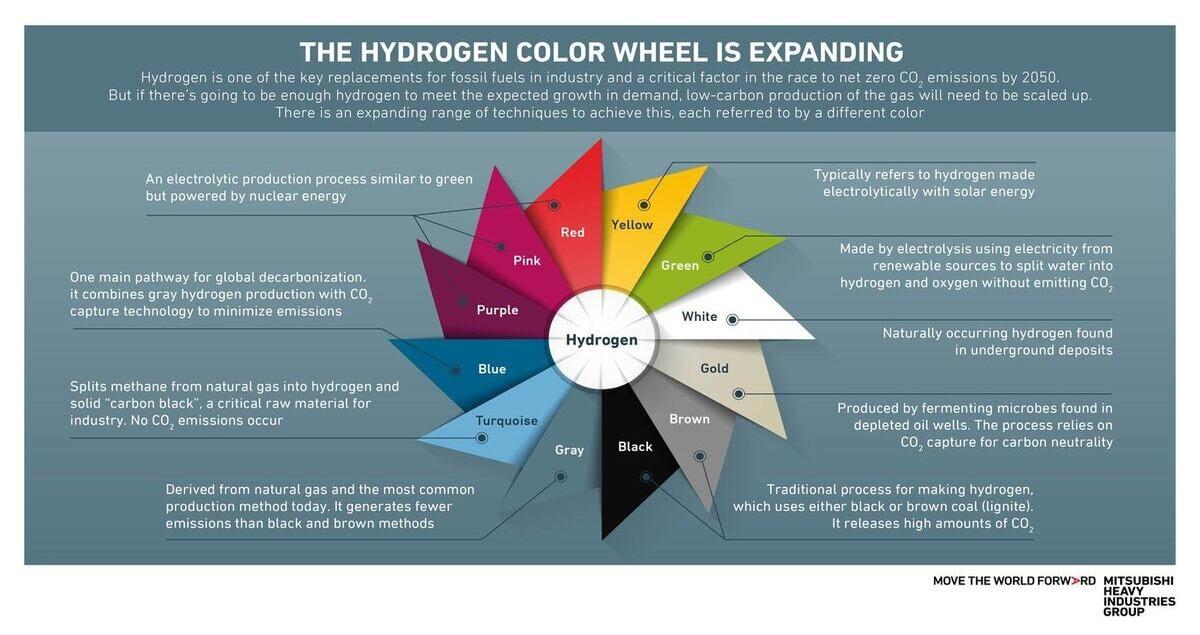

Japan has painted its development of a clean hydrogen society as largely moving from ‘gray’ fuel (the production of which releases emissions) to ‘blue’ (which seeks to capture/ store those emissions) and to ‘green’ (no/ low emissions during electrolysis powered by renewables).

Yet, while ‘green’ hydrogen is often heralded as the sustainable choice, ‘pink’ should be the color of Japan’s clean energy future (2040-beyond) if produced based on a partial circular economy approach. ‘Pink’ hydrogen is produced by nuclear-powered electrolysis. While the country seeks to raise the share of electricity in the mix from renewable sources, nearly 20 GW of nuclear capacity remains unused due to roadblocks in the regulatory or local government processes.

Restarting this capacity — and adding new nuclear facilities tailored for hydrogen production – could offer a practical and economic way to create domestic hydrogen supply without diverting Japan’s scant renewable resources from the power grid.

Japan’s energy dilemma is acute as it imports nearly 97% of its primary energy, relying heavily on LNG and oil shipments, making its primary energy self-sufficiency ratio critically low. Nuclear energy, curtailed post-Fukushima, is being rehabilitated, but the domestic fleet of reactors is aging. The cost of building new reactors makes it difficult to see how they will compete in a liberalized electricity market without certain state support.

According to my research, over the past year using numerous Japanese and global sources and interviews, promoting nuclear as one of the primary power sources for domestic hydrogen production would hit several goals – cost, stability, energy security, and industrial competitiveness. This special column for Japan NRG, based on my thesis submitted to Johns Hopkins University late last year, outlines some of these arguments.

Differentiation of H2 colors based on the production methods and materials

Source: Mitsubishi Heavy Industry Group (2024).

Methodology

Given Japan’s energy and environmental situations, my research sought to explore the best reasonable, practical, and economic future (2040-beyond) source of clean hydrogen for Japan if produced based on a partial circular economy approach. There is a gap in the data and information required for a complete cost-comparative analysis. However, below are a few considerations that could guide policy and business reviews.

During the 2024 Japan Energy Summit & Exhibition, I presented my “Begin at the Beginning” strategy, which builds on my nexus-integrated policies that emphasized domestic clean hydrogen production and its integration with high priority, heavy industry of Japan.

This strategy centers on sustainable hydrogen production from domestic green or pink hydrogen hubs strategically co-located with existing and future wastewater treatment plants. Given the projected decline in freshwater availability, wastewater represents an untapped, renewable, and virtually infinite energy resource.

This analysis draws inspiration from Japan’s mottainai movement (reduce, reuse, recycle, respect) and leverages three theoretical frameworks to guide data selection and comparative analysis of green and pink hydrogen production, based on a partial circular economy approach. My previously developed proprietary qualitative frameworks for the hydrogen sector, including concepts such as the quasi-revolutionary transition for U.S. coastal green hydrogen hubs and nexus-integrated policies for Japan, underpin the methodology.

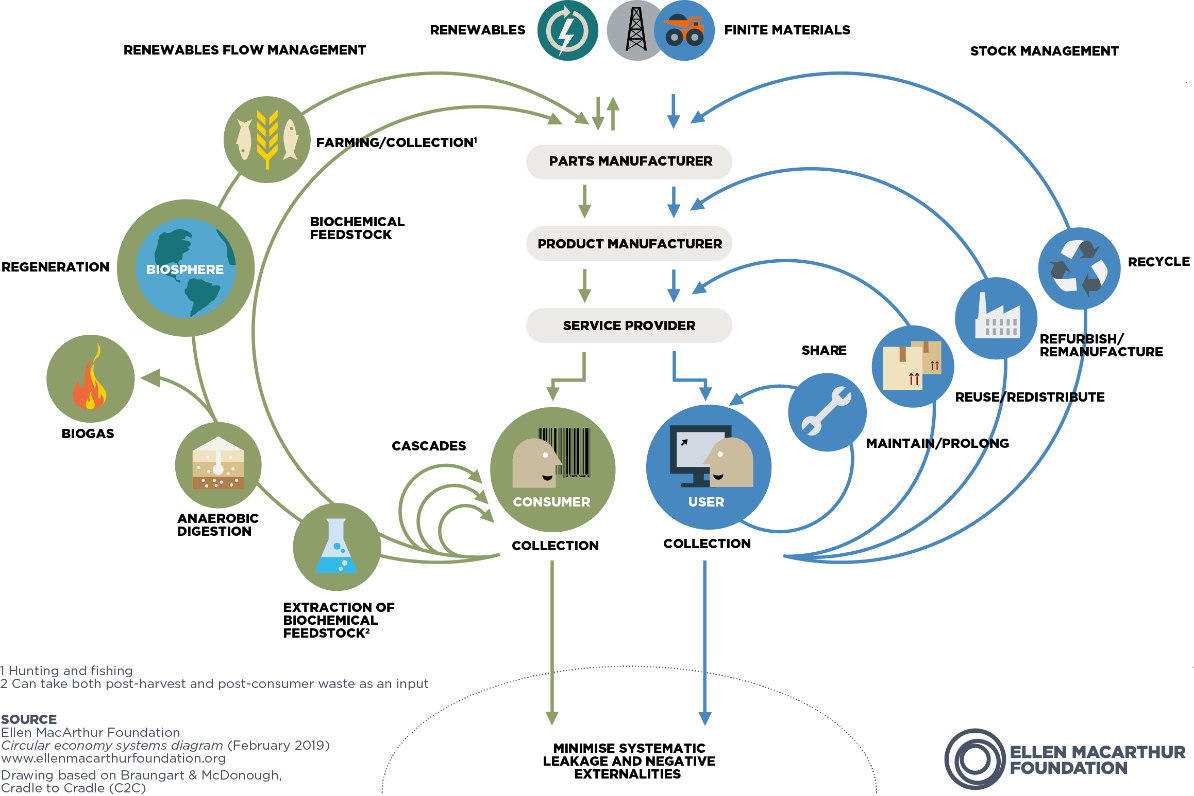

Additionally, the analysis employs the technical cycle outlined in the Ellen MacArthur Foundation’s circular economy diagram to structure comparative assessments. The circular economy model adheres to three core principles: eliminating waste and pollution, circulating materials and products at their highest value, and regenerating nature. It operates through two cycles – biological and technical – that address both material production and consumption alongside sustainable natural resource management.

Circular Economy Systems Diagram

Innovation

One reason for Japan not to limit its domestic hydrogen program to ‘green’ sources is that the volume of renewables that can be connected to electrolyzers without diverting power from direct electricity users is small. Japan’s current generation of ‘green’ hydrogen projects does not exceed 10 MW of capacity. That scale cannot meet even a fraction of Japan’s stated goals of growing hydrogen consumption from 2 million tons a year today to 3 million tons in 2030, 12 million tons in 2040, and 20 million tons in 2050.

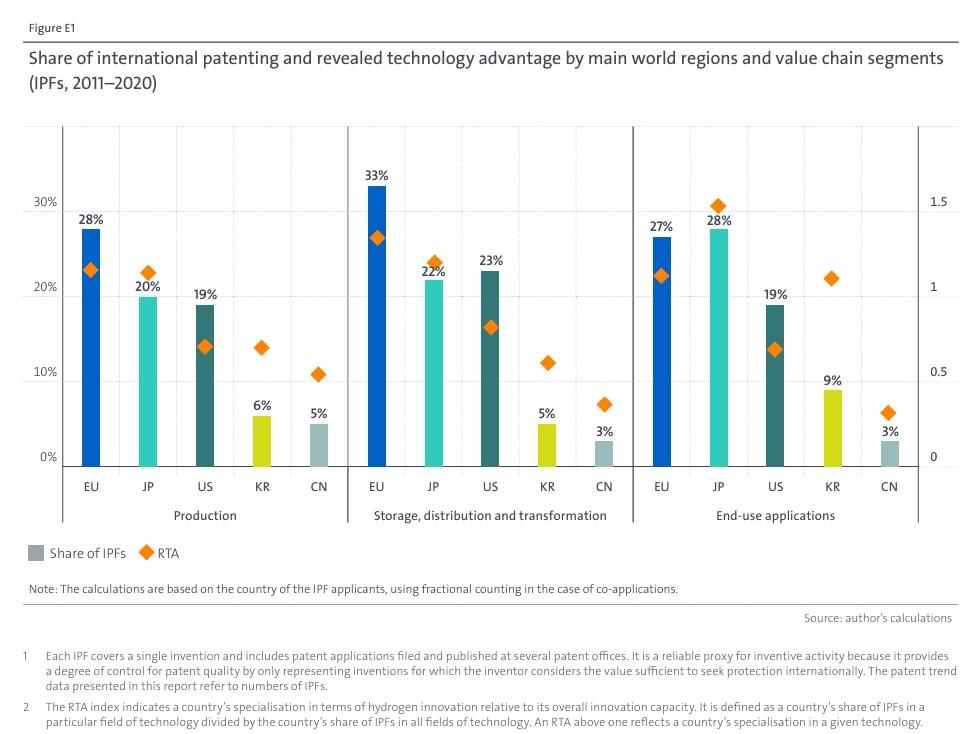

Luckily, scarcity of resources has catalyzed Japan’s R&D. From 2011 to 2020, the country emerged as a top innovator, accounting for 24% of clean hydrogen-related international patent families (IPFs).

Japanese Patents in the Clean Hydrogen Sectors

During the last decade, Japanese clean hydrogen patenting grew faster than in the European Union, with a compound average growth rate of 6.2% versus 4.5%, respectively. In September 2024, the Japan Hydrogen Fund was set up as the first Japanese fund dedicated to developing low-carbon hydrogen. With $400 million from various investors, it seeks to propel some of these innovations to the next level.

Run rates

Another reason to consider nuclear as an alternative to renewables for hydrogen production is the energy efficiency rates of the technologies. Capacity factors, a crucial reliability indicator, reveal a stark contrast: nuclear reactors typically achieve upwards of 90%, compared to wind and solar in Japan, which fluctuate between 25% and 33%.

This reliability dramatically lowers operational costs. For instance, in 2023, Japanese nuclear energy achieved a capacity factor of 28%, still below optimal levels but significantly higher than solar’s 17.2% and wind’s 25.4% capacity factors projected for 2030.

With the restart of more reactors, METI expects the capacity factor of nuclear plants in Japan to reach 70% by 2030.

Lowering grid capex?

The financial advantages of utilizing existing nuclear infrastructure are considerable. Restarting existing reactors and prolonging their operational life can cost between $700 million and $1 billion per reactor, significantly cheaper than constructing new renewable infrastructure. Conversely, expanding solar and wind generation requires significant investment in transmission lines, battery storage, and other grid enhancements.

For instance, TEPCO recently announced a $3.2 billion upgrade of its power grid specifically to support increased renewable energy integration. While grid upgrades are vital for the country to move toward CO2-free electricity in general, the transmission capex nationwide should be lower, with ‘pink’ hydrogen contributing to the energy mix.

Tests of pink hydrogen

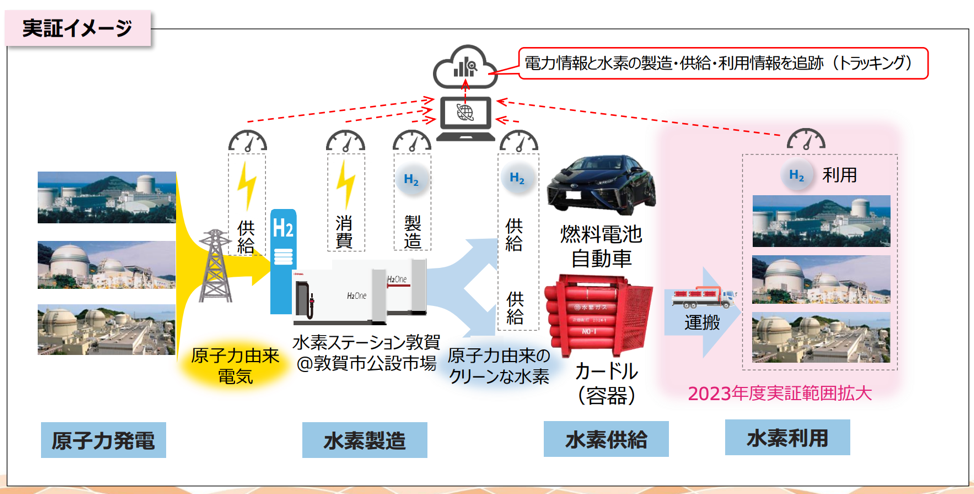

Successful tests of Japan’s home-grown high-temperature engineering test reactor (HTTR) during the 2000s and last year showcase the potential to utilize this technology to support hydrogen production. The HTTR program has now applied for a permit to connect it with a hydrogen system to begin pilot-scale production from 2030.

However, early efforts to make ‘pink’ hydrogen are already underway. Kansai Electric conducted a six-month demonstration (October 2023 to March 2024) that sent about 27.7 MWh of nuclear-derived electricity to a hydrogen system in Tsuruga City. This experiment resulted in a total manufacturing of about 1,570 Nm³ (roughly 140 kg) of hydrogen. Around 990 Nm³ (88 kg) of this hydrogen was utilized within the nuclear plants as fuel for cooling generators and other devices, and about 580 Nm³ (52 kg) was allocated to fuel cell vehicles.

In November 2024, Kansai Electric said that it will use the same approach to manufacture ‘pink’ hydrogen for use in fuel cell ships at the Osaka-Kansai World Expo in Osaka, which started on April 13, and to source hydrogen fuel for co-firing at the Himeji No. 2 Thermal Power Plant. The co-firing tests are due to start this fiscal year.

Japan’s first pink hydrogen demonstration project (Kansai Electric). Source: Kansai Electric (2024).

Japan’s first pink hydrogen demonstration project (Kansai Electric). Source: Kansai Electric (2024).

Environmental impact

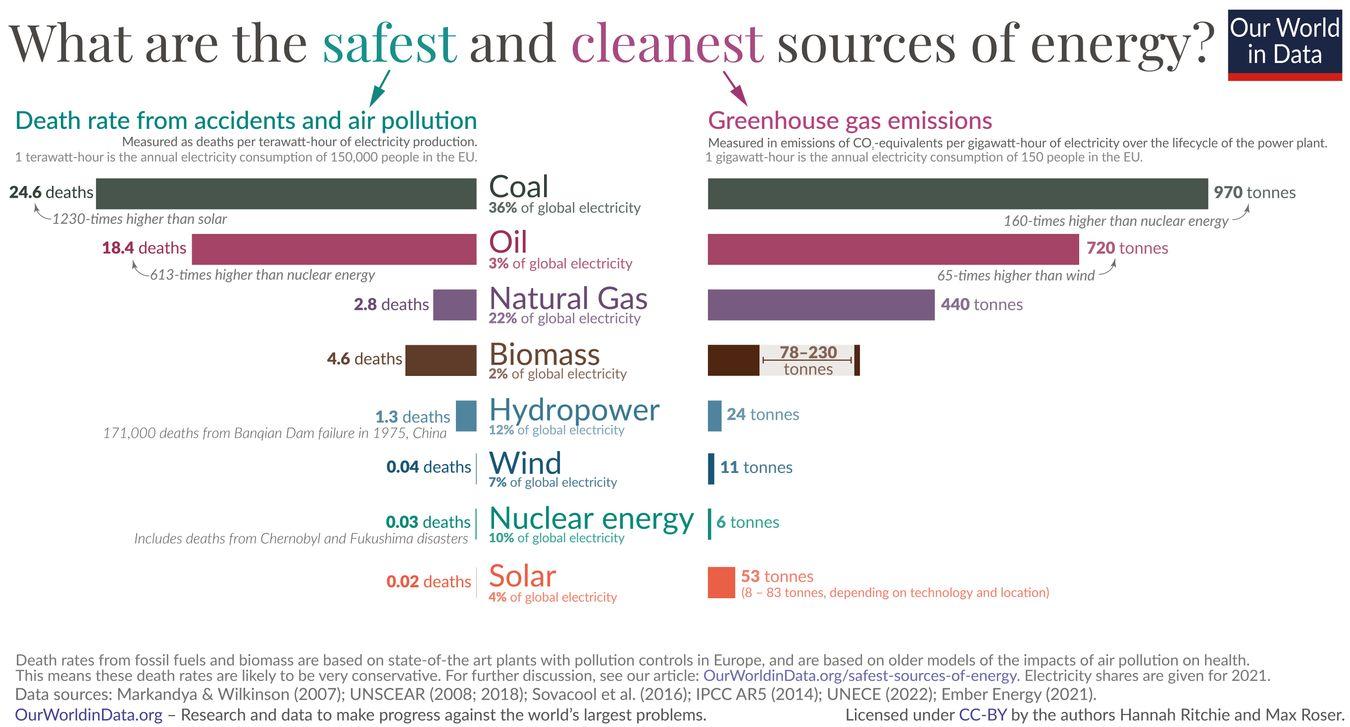

From an environmental standpoint, nuclear energy exhibits significantly lower lifecycle GHG emissions, approximately 6 tons of CO2 per GWh, compared to 8-83 tons for solar power and around 11 tons for wind.

Land use – a critical issue in densely populated Japan – also highlights nuclear advantages. Salvaging existing infrastructure is an important consideration for building both green and pink H2 hubs located next to existing and future water wastewater treatment plants.

Small modular reactors (SMRs), touted as next-generation nuclear technology, also occupy significantly smaller land footprints than extensive solar or wind farms, minimizing ecological disruptions and land acquisition issues. Source: Our World in Data (2020)

Small modular reactors (SMRs), touted as next-generation nuclear technology, also occupy significantly smaller land footprints than extensive solar or wind farms, minimizing ecological disruptions and land acquisition issues. Source: Our World in Data (2020)

Conclusion

In summary, Japan’s energy insecurity, limited land resources, existing nuclear infrastructure, and ambitious climate targets make pink hydrogen not only merely attractive but strategically indispensable.

Nuclear-powered hydrogen production, utilizing a partial circular economy approach, emerges as an economically compelling, practically feasible, and environmentally sound choice based on the chance for innovation, favorable capacity factors, financial advantages and a positive environmental impact. Based on this, pink hydrogen should at the very least complement its green cousin – and, it may even exceed it.

This is a guest column based on a thesis submitted to Johns Hopkins University with the requirements for the degree of Master of Science, Energy Policy and Climate (December 2024) by Dr. Venera N. Anderson. The research study will be presented at the Japan Energy Summit & Exhibition (Tokyo Big Sight, June 18-20, 2025).

The whole version is published on Dr. Venera N. Anderson’s illuminem Voice page: “Green vs. Pink Hydrogen Production in Japan: A Partial Circular Economy Approach” (6-part article): https://illuminem.com/illuminemvoicesprofile/venera-n-anderson

BY MAGDALENA OSUMI

Battery Makers Drive Breakthroughs as Energy Storage is Crucial for Grid Stability

As the grid gets smarter and the demand for clean energy surges, Japan is racing to ensure the power stays on — even when the sun isn’t shining and the wind isn’t blowing. Battery storage, once a backstage player, is now a critical piece of the country’s energy puzzle.

Ask a Tokyo energy planner what tops their agenda and they’ll often list building out the energy storage sector. That’s a national priority, with Japan setting ambitious targets to expand renewable energy sources like solar and offshore wind, and to reduce dependence on fossil fuels. However, the intermittent nature of certain renewables demands scalable storage solutions to stabilize the grid, making battery innovation more important than ever.

Lithium-ion batteries (LiBs) have long dominated energy storage, but their heavy reliance on materials like lithium and cobalt — sometimes sourced through fragile and ethically questionable supply chains — poses a risk to Japan’s energy security and sustainability.

There’s also the competition with China to consider, whose battery makers are linked in supply chains that stretch right to the source of the raw minerals, helping them lower costs.

Still, Japan’s top battery makers feel that racing to secure their own mines or supply chains in Africa and elsewhere is not the only way to compete. There is faith in new technology breakthroughs that could flip the script on resource demand.

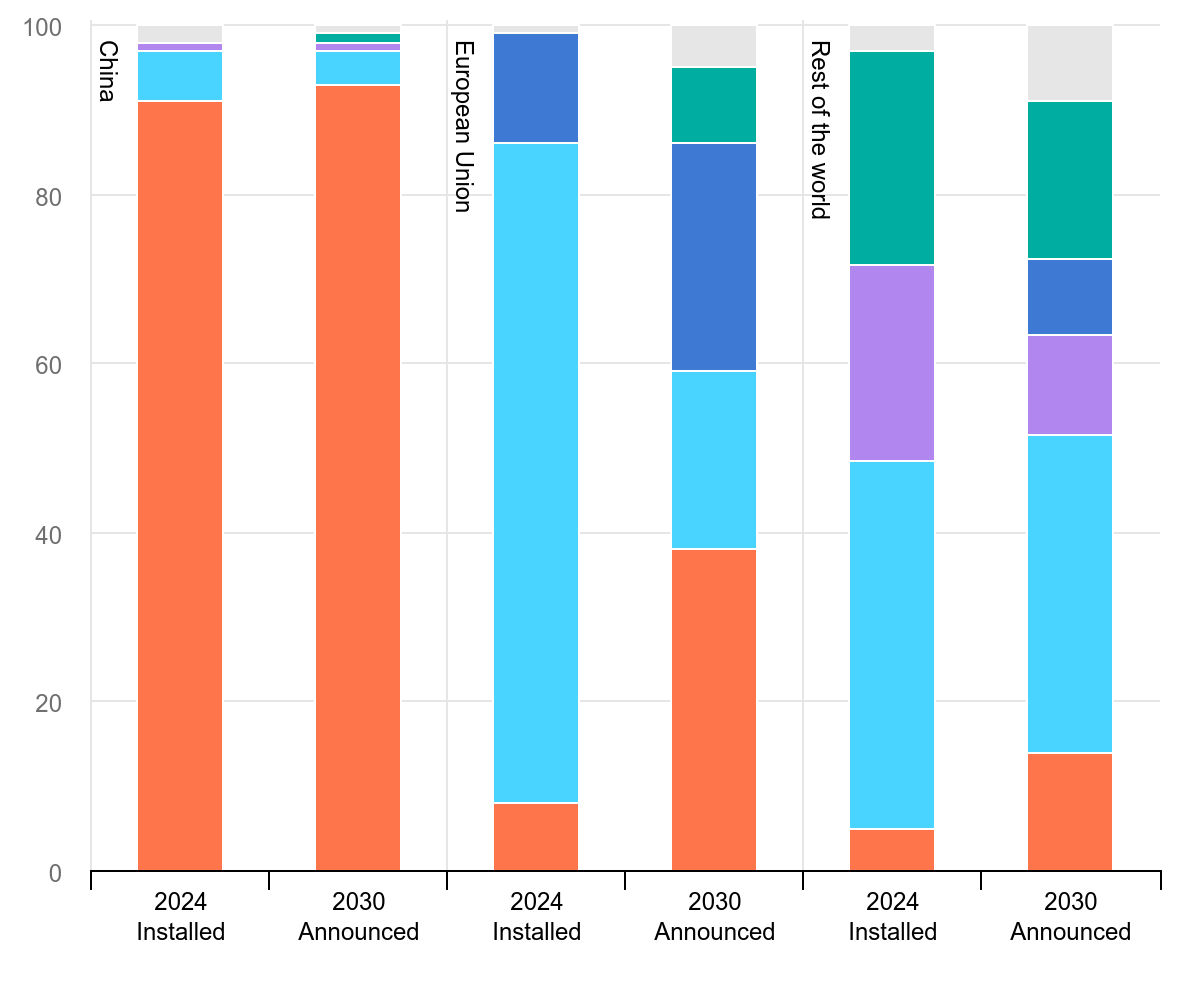

Share of manufacturing capacity by battery producer’s domicile, 2024-2030. Source: IEA

Share of manufacturing capacity by battery producer’s domicile, 2024-2030. Source: IEA

Technology Shift: Beyond Lithium-Ion

Japan’s battery sector is growing rapidly. In 2023, battery shipments surged by 125% year-on-year, fueled by demand across residential, commercial, and grid-scale markets. Yet, vulnerabilities in lithium supply chains — largely dominated by China — have exposed the need for alternative technologies.

The government is reinforcing these industrial efforts with strong policy support. Batteries have been designated as critical materials under the Economic Security Promotion Act, and ¥40 billion (roughly $260 million) has been earmarked in FY2024 to support grid-connected storage deployment through the energy transition bond program.

In parallel, Japan is rolling out a battery industry strategy aimed at securing domestic manufacturing capabilities for lithium-ion batteries. These plans center around accelerating the development of next-generation batteries such as the following:

- Sodium-ion batteries (SiBs), which use abundant, low-cost materials like sodium and eliminate the need for cobalt, offering greater thermal stability and sustainability;

- Vanadium redox flow batteries (VRFBs) and sodium-sulfur (NaS) batteries, which show strong potential for grid-scale, long-duration energy storage.

Companies such as NGK Insulators, Sumitomo Electric, and Toyota are spearheading advances in alternative chemistries, supported by government programs and international partnerships. These public-sector efforts are catalyzing private innovation, helping to scale production and strengthen domestic battery supply chains.

In the words of one domestic battery manufacturer, “we hope to extend the availability of renewables electricity to the 5pm to 9pm period.” Without this longer availability of ‘green’ power on a daily basis, it’s hard to justify major new investments in solar capacity because of the growing trend for curtailments, the manufacturer said.

Regular consumer support for decarbonized electricity would also expand if renewables could cover the late afternoon demand peak, according to the manufacturer.

Solid-state batteries as the next frontier

As tech advancements continue, solid-state batteries (ASSBs) are drawing attention as the next major leap in energy storage technology, promising to overcome many of the limitations of conventional Li-ion batteries. By replacing the liquid electrolyte with a solid material, they offer the potential for significantly higher energy density, faster charging times, enhanced safety, and longer lifespans.

Japan is heavily invested in solid-state battery technology to reclaim its leadership in battery innovation, having pioneered Li-ion batteries in the 1990s. Major automotive players like Toyota, Honda, and Nissan see SSBs as essential for the next generation of EVs, offering faster charging and longer range. Japan’s reliance on imported energy means that high-performance batteries are also crucial for enhancing energy security and supporting renewable energy integration.

The government is backing this push through significant R&D funding and initiatives like the Green Innovation Fund, aiming for commercialization by 2030. Facing intense global competition, Japan views the rapid development of SSBs as critical, with companies like Toyota showcasing prototypes, startups like ProLogium entering the scene, and materials giants such as Sumitomo Chemical and Murata building the supply chain.

Leading developments in this area include:

- Toyota aims to commercialize solid-state batteries for hybrid vehicles by 2027–2028 and is collaborating with Idemitsu Kosan to develop advanced sulfide-based electrolytes;

- Honda built a demonstration facility in Sakura City, preparing for mass production of solid-state batteries in the late 2020s;

- Nissan plans to mass-produce all-solid-state batteries by early 2029, focusing on faster charging, lower costs, and greater safety;

- SoftBank and Enpower Japan have achieved a specific energy of 350 Wh/ kg with their all-solid-state battery, initially targeting drones and HAPS, with future automotive applications in sight.

While challenges such as scaling production and ensuring long-term stability remain, solid-state batteries could offer dramatically higher energy density, faster charging, and improved safety compared to current technologies.

Government support: boosting domestic capacity

Recognizing the strategic importance of energy storage, METI has launched major subsidy programs for grid-connected batteries, residential storage systems, and EV battery production.

The Tokyo Metropolitan Government also announced generous funding initiatives starting in fiscal 2025, targeting projects over 1 MW to enhance grid resilience. Japan has recently introduced several government subsidies and programs to bolster battery energy storage across various sectors. Here’s an overview of the key initiatives:

- In late 2024, METI awarded ¥34.6 billion in subsidies to 27 grid-scale battery energy storage system (BESS) projects. These subsidies cover between one-third and two-thirds of equipment and construction costs, depending on the technology. Eligible projects are 1 MW or larger and can span up to three fiscal years. Notable recipients include Eurus Energy, Terras Energy, and Toyota Tsusho.

- Another program is Home & Commercial Energy Storage. In July 2024, the Japanese government allocated ¥9 billion to support the introduction of energy storage systems for home, commercial, and industrial use. Nine energy aggregators were selected to facilitate this program. Subsidies cover up to one-third of capital expenditure, with a maximum of ¥300 million per commercial and industrial project. The majority of the funding is directed toward the residential system.

- In September 2024, METI approved up to ¥347.9 billion in subsidies for 12 projects aimed at enhancing Japan’s electric vehicle (EV) battery production capacity. This initiative is part of a broader strategy to achieve 150 GWh/ year of domestic battery production by 2030. The subsidies cover various aspects, including Li-ion battery cell production, raw material production, and manufacturing equipment.

Long-duration and grid-scale storage solutions

To strengthen grid resilience and provide stable, long-duration energy storage, Japanese companies are deploying large-scale storage systems, such as one by Sumitomo Electric, which installed a 1 MW × 8-hour VRFB system in Kashiwazaki City, with a second unit expected by spring 2025.

NGK Insulators introduced the NAS MODEL L24 battery, featuring improved durability and lower annual degradation. Eku Energy is also constructing the Hirohara Battery Energy Storage System (BESS) in Miyazaki City, a 120 MWh project set to serve some 63,000 households for four hours starting in 2026.

Battery innovation is also advancing in the residential and commercial sectors. For instance, Kyocera, in collaboration with 24M Technologies, a U.S.-based firm engaged in R&D of batteries for energy storage, commercialized a semi-solid Li-ion battery cell, offering safer, more cost-effective energy storage for homes.

Early signs indicate the investments are paying off. In October 2024, Panasonic reported a 42% rise in energy unit operating profit for Q2, driven by growing demand for storage systems in data centers. Despite a decline in profit from the in-vehicle business, operating income for the key segment, which makes batteries for Tesla, and other automakers, rose to ¥32.7 billion last year.

Background: ethical and environmental drivers

Japan’s pivot to alternative battery technologies is also shaped by environmental and ethical concerns.

There is growing awareness in Japan among experts and organizations about the ethical and environmental problems tied to battery material sourcing, particularly related to mining impacts and human rights. Some groups stress the need for more sustainable resource extraction, while others call for Japan to develop its own alternative resource bases to reduce dependency on problematic global supply chains.

For instance, extracting lithium from salt flats in Argentina and Chile consumes vast amounts of water in already arid regions, while producing battery-grade lithium in China and Australia demands high energy use. Current practices strain ecosystems.

On top of that, mining of lithium and cobalt has been linked to significant ecological damage and human rights violations, particularly in South America and the Democratic Republic of Congo. The issue has been raised in Japan by political scientist Mutsuji Shoji, who warns that while the spread of EVs promotes decarbonization, it also risks overlooking these human rights abuses, such as child labor, associated with cobalt mining in the DRC.

As an example, sodium-ion batteries propose a cleaner, more ethical alternative that will help reduce reliance on geopolitically sensitive regions. There are also advances in sustainable material science, such as biomass-based anodes and machine learning-designed electrodes.

Another solution, backed by the Japan Project-Industry Council (JAPIC), which promotes domestic resource utilization, is development of deep-sea resources, specifically cobalt-rich crusts within Japan’s Exclusive Economic Zone (EEZ). They propose manufacturing mining test equipment by fiscal year 2025 and beginning real-sea excavation tests by 2027, urging both the government and private sector to cooperate closely.

Deep-sea mining, however, also faces a pushback by environmental groups and some global manufacturers.

Building a resilient energy future

Amid soaring electricity demand and the rapid growth of renewables, battery storage is becoming the cornerstone of Japan’s energy transition.

Thanks to breakthroughs in sodium-ion, vanadium flow, and solid-state technologies, and supported by aggressive government programs, Japan is positioning itself as a global leader in next-generation energy storage.

While challenges around scalability and cost remain, the country’s long-term strategy — investing early in diversified battery technologies — could secure energy resilience and technological competitiveness well into the 2030s and beyond.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Elections

‘Australian Gas for Australians’ – Energy takes the main stage in the country’s elections. The soaring cost of electricity is the focus of debates ahead of May’s vote. Peter Dutton, the rightwing leader of the opposition Liberal party, threw his weight behind nuclear power to undermine the Labor government’s “reckless” policies on renewable energy.

China / Renewable energy

Shanghai Electric agreed with Abu Dhabi Future Energy Company (Masdar) and Oman’s Mawarid Group for major renewable energy projects across both Middle Eastern nations. The partnerships will focus on advancing clean energy through technology deployment, localized manufacturing, and multi-sector collaboration. The agreement with Masdar involves the development of a 2GW solar power project in Saudi Arabia.

India / Pumped hydro

Adani Green Energy signed a 40-year PPA for 1.25 GW pumped hydro in Uttar Pradesh, which is India’s most populous state with around 240 million inhabitants.

India / Wind power

NTPC Green Energy awarded a contract to Suzlon involving a 378 MW wind energy project. Following this development, the two companies are now working on projects that will generate a total of 1.54 GW of wind power.

Indonesia / Gas power

Indonesia should cut gas subsidies and enforce carbon pricing mechanisms to enhance the viability of green hydrogen for domestic industries, according to the Institute for Essential Services Reform. Indonesia identified 17 potential sites for green hydrogen production. However, the subsidized gas price of $6 per MMBTU for seven industrial sectors poses a challenge to the competitiveness of green hydrogen.

LPG markets

China’s pivot away from U.S. liquefied petroleum gas under new tariffs is shaking global energy flows, slashing demand, and fuelling a scramble for alternatives across Asia, with Middle Eastern suppliers and rival buyers seizing the moment. The tariff move, effective May 14, is the latest blow in a widening trade dispute between Washington and Beijing.

Philippines/ Gas power

At the request of the Philippine Stock Exchange, ENEX Energy Corp confirmed it is still keen on developing a 1.1 GW gas plant in Batangas.

Southeast Asia / Solar panels

The U.S. announced new tariffs, targeting companies in Cambodia, Thailand, Malaysia and Vietnam, after an investigation begun a year ago when American manufacturers of solar panels accused Chinese companies of flooding the market with subsidized, cheap goods made in SE Asia. Products from Cambodia would face the highest tariffs, of 3,521%, because its companies did not cooperate with the U.S. investigation; products made in Malaysia by the Chinese manufacturer Jinko Solar face duties of just over 41%; rival Trina Solar’s products from Thailand will incur tariffs of 375%.

Vietnam / Solar and BESS

The Ministry of Industry and Trade announced a new round of feed-in tariffs (FIT) for solar power, introducing location-based pricing and, for the first time, incorporating energy storage systems. The updated scheme highlights the growing importance of storage in stabilizing the grid and enhancing energy autonomy.

Wind Power

Over 900 GW of wind power capacity is forecasted to be installed from 2025 to 2030, said the Global Wind Energy Council. It expects a compound average growth rate of 8.8%, which means another 981 GW of wind energy capacity globally by 2030. A total of 117 GW of wind energy was installed in 2024, with China leading with 80 GW.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.