WEEKLY

JUNE 2, 2025

ANALYSIS

FROM POLICY TO PRACTICE: JAPAN’S CHANGING APPROACH TO RESOURCE DIPLOMACY

- Japan is no longer just about shielding domestic industries from supply shocks. It’s actively co-architecting markets, picking which technologies scale, and where firms place their bets.

- For foreign and domestic firms, this signals a more activist Japanese industrial policy.

JAPANESE SMRs MOVE FORWARD…

BUT NOT IN JAPAN

- Japanese firms are developing Small Modular Reactors (SMRs), nuclear units that are touted as the sector’s next phase.

- Most developments by Japanese firms, however, are taking place outside of Japan. Only success there will lead to SMR entry to domestic market.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Grid operators offer plan for 9 GW of new data centers capacity

- METI seeks LTDA rounds with stricter rules for BESS and LNG focus

- ANRE eyes funding for large-scale grid upgrade

- Guarantee proposed for ¥1.8 trillion Hokkaido-Honshu subsea power cable

- Japan considers inflation-linked reforms to transmission fee rules

- ANRE holds off on mandatory supply system in the balancing market

- Osaka Gas climbs to No. 2 in power sales ranking

- Air Water to partner with Mikasa City in hydrogen and renewables

- JFE has breakthrough ratio with hydrogen co-firing

- Toshiba launches packages with 90% size reduction for PV inverters

- First PSC demo on thermal power plant enclosure

- Ishizaka Sangyo opens solar panel recycling

WIND POWER AND OTHER RENEWABLES

- Eurus completes Japan’s largest onshore wind farm

- Ministries report on renewable energy expansion

- MOL to join offshore wind project in Taiwan

- IHI and NuScale Power complete module for SMR project in Romania

- KEPCO gets approval for dry storage facility

- Third-party committee says safety satisfactory at Kashiwazaki-Kariwa NPP

- JERA interested in Alaska LNG project

- Kyushu Electric and JERA ink deals for U.S. LNG

CARBON CAPTURE & SYNTHETIC FUELS

- Mitsubishi-backed firm building SAF plant in Texas

- Tanzania signs up as Japan’s 30th partner on JCM carbon credits mechanism

EVENTS

June 4-5 Kyushu Innovation Week / Kyushu GX Decarbonization Expo @ Marine Messe Fukuoka

June 4-6 AXIA EXPO 2025 (Hydrogen and Ammonia Next-Generation Energy Exhibition) @ Aichi Sky Expo

June 15-17 G7 Summit @ Kananaskis, Alberta, Canada

June 18-20 Japan Energy Summit & Exhibition ` Tokyo Big Sight

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Grid operators offer upgrade plans to meet 9 GW of new data center capacity

(Government statement, May 29)

- CONTEXT: METI and the Ministry of Internal Affairs and Communications (MIC) held their third “Watt-Bit” working group meeting to align power grid infrastructure with the rapidly expanding data center (DC) sector.

- The ministries and officials from TEPCO Power Grid and the Japan Data Center Council focused on locations for DCs, which the group says needs an additional 6 to 9 GW of power capacity by 2040.

- TEPCO Power Grid outlined a phased response:

- Short term (to 2030): focus on attracting DCs to areas with existing grid capacity – particularly in Chiba and Tochigi prefs, which together offer about 5 GW of spare capacity.

- Medium-term (to 2035): connect small-scale DCs (under 2 MW) to local distribution substations. This could unlock 1 to 1.5 GW of capacity in eastern Japan, assuming efficient coordination and equipment upgrades.

- Long-term (to 2040): build two to three new high-voltage (500/154 kV) substations in DC-heavy zones, along with land acquisition to support grid-side investment in high-demand areas.

- Authorities raised concern about developers splitting up large DC projects (over 2 MW) into smaller units to avoid grid fees and noted the need to maintain grid fairness.

TAKEAWAY: A full discussion of the Watt-Bit initiative was published in the Japan NRG Analysis section on May 19, 2025. This is one of the most urgent initiatives at the moment and policy discussions are moving quickly. We expect further details on locations and capacity forecasts to be made during the summer. A summary of policy recommendations is likely to be released after the next working group meeting.

- SIDE DEVELOPMENT:

- Vena Group seeks to drive green AI data center expansion

- (Company statement, May 28)

- Singapore-based Vena Energy, a renewables developer, set up a new data center subsidiary, Vena Nexus, and plans similar development in Japan. The focus is on AI-driven data centers powered by renewable energy.

- In February, Vena Energy partnered with Tokyo-based startup Quantum Mesh to set up small-scale renewables-powered data centers.

- This highlights Japan’s growing role in combining renewables and advanced data infrastructure amid rising demand from AI and digital services.

- Vena Energy also aims to expand similar projects across Asia-Pacific, including Thailand, South Korea, and Australia.

METI seeks next LTDA rounds with stricter rules for BESS, LNG focus

(Government statement, May 28)

- METI/ ANRE proposed keeping the third round capacity of the Long-term Decarbonized Power Sources Auction at the level of the previous one: 5 GW.

- Still, key changes include stricter criteria for batteries (BESS), cutbacks in hydrogen/ ammonia and nuclear upgrade capacity, and focus on LNG for power supply.

Key points:

- Battery Storage & Long-duration Storage (LDES):

- Total cap for storage (batteries + pumped hydro + LDES): 800 MW*

- Battery projects must have a discharge duration of at least six hours.

- Projects with three to six hour duration are implemented outside the auction, so will not be targeted.

- The 800 MW* is split into two categories:

- Pumped hydro refurbishment & Li-ion batteries: 400 MW

- New pumped hydro, non-lithium batteries & LDES: 400 MW

This is a drop from previous rounds, where auctioned capacity exceeded the set cap.

- Hydrogen/ ammonia & CCS-fitted thermal power:

- Upper limit: 500 MW

- Price ceiling per kW: ¥134,000 – ¥795,000 (avg: /~¥400,000)

- This is about twice the ceiling price for other sources (¥200,000/ kW).

- The cap was reduced from 1 GW in the previous round to ease public burden.

- Existing nuclear safety upgrades:

- New cap: 1.5 GW (down from 2 GW)

- The last round saw 3.15 GW awarded, exceeding the limit.

- LNG-Fired Power (Exclusive use):

- Cap set a 2.93 GW (including 2 GW originally planned + 930 MW unallocated from the previous round)

- Future auctions (from FY2026) may continue to target 2 to 3 GW to ensure stable supply amid plant retirements and demand growth.

TAKEAWAY: The changes, especially a tighter scope for batteries and requirements than in earlier rounds, showcase much stricter rules on batteries, apparently in response to growing interest from developers and a way to secure more reliant technology. The draft also shows a continued strong preference for LNG, despite initial ministry claims that it’s a transitional power source. The perceived reliability of LNG generation is one of the reasons pushing its extended usage.

ANRE proposes funding method for large-scale grid development

(Government statement, May 23)

- ANRE wants a system to allow part of the costs for large-scale power grid development to be recovered through wheeling charges even before operations begin.

- This would ease cash flow issues for TSOs during long construction periods and avoid investment delays for inter-regional connections and large-scale internal grids.

- ANRE is also considering revising how construction-phase assets are treated in calculating business returns, as rising interest rates increase funding costs.

- CONTEXT: The 7th Basic Energy Plan outlines frameworks to promote development of regional grids and measures to facilitate financing for large-scale interregional power connections. Ensuring stable electricity supply while expanding renewable energy requires enhanced grid development.

Upper House passes GX promo amendment, emissions trading participation mandatory

(Denki Shimbun, May 29)

- The Upper House passed the amended GX Promotion Law, formalizing a national carbon emissions trading scheme (ETS).

- Starting in FY2027, companies emitting over 100,000 tons of CO2 will have to join the ETS; this will impact about 400 major companies in steel, power, and chemicals.

- They’ll have to calculate annual CO2 emissions and offset with emission allowances.

- SIDE DEVELOPMENT:

GX League to expand its framework to retail and other sectors - (Denki Shimbun, May 26)

- METI seeks to revise the structure of the GX League, which involves over 700 companies mostly from manufacturing, energy, and transport.

- The goal is to shift focus from individual company emissions to full supply chain (Scope 3) CO2 reductions.

NEWS: ELECTRICITY MARKETS

Guarantee proposed for ¥1.8 trillion Hokkaido-Honshu subsea power cable

(Nikkei, May 29)

- The govt is considering public debt guarantees to build a subsea power cable connecting Hokkaido and Honshu; total cost is estimated at ¥1.5 to ¥1.8 trillion.

- The cable aims to link Hokkaido’s abundant renewable energy resources (wind, solar) with the high-demand Honshu region, promoting wider renewable energy use and more stable power supply.

- Overseen by the national grid operator, the project will be awarded by March 2026, with construction taking six to 10 years.

- TEPCO Power Grid leads the consortium bidding on the project, but requests govt-backed debt guarantees to attract private financing.

- The Basic Energy Plan emphasizes such measures to facilitate financing for large energy infrastructure projects.

- Enhanced interregional power transmission supports Japan’s target to increase renewable energy to 50% by 2040.

- CONTEXT: International precedents exist, such as Germany-Norway subsea cables backed partly by state loans or guarantees.

TAKEAWAY: The Hokkaido-Honshu cable project reflects a critical turning point for Japan’s energy transition. While debt guarantees are a positive step, they are not sufficient on their own. Given the scale and the long construction timeline, more proactive and direct public financing will also be needed. To speed up grid upgrades to improve the transmission network, the govt needs to attract private investment, which proved essential in large-scale interconnection infrastructure like NordLink connecting Germany and Norway.

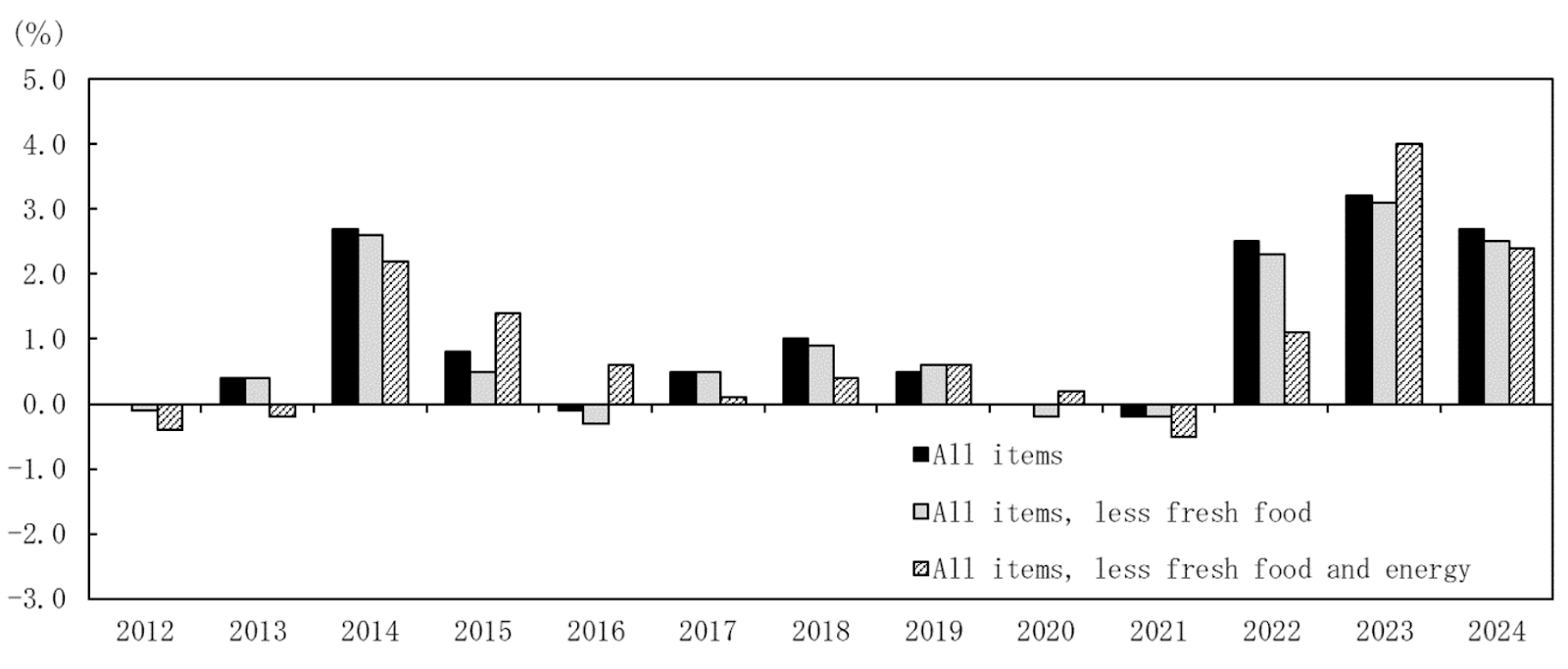

Japan considers inflation-linked reforms to transmission fee rules

(Government statement, May 29)

- The power & gas regulator, EGC, seeks inflation adjustment to the “revenue cap” system that governs how transmission and distribution (T&D) companies recover costs; the goal is to reflect rising prices and labor costs.

- Under current rules, utilities’ revenue ceilings are based on pre-approved expenses; however, recent inflation has driven actual costs higher, prompting calls to refine calculation methods for both current and future regulatory periods.

- The proposal would introduce indicators – such as govt inflation forecasts and labor cost indices – to set revenue limits, with adjustments made retroactively if actual inflation deviates from projections.

- While reforms are slated for what is termed the ‘second regulatory period’ (FY2028–32), the govt is also weighing whether to apply temporary measures to the current period (FY2023–27), where cost pressures are already materializing.

- For FY2023, for example, utilities reported cost increases of about ¥1.5 trillion that can be attributed to inflation, but only about ¥495 billion of this qualifies under the current revenue cap’s expense-based criteria.

- EGC stresses that any adjustments must be transparent and fair to consumers, who are increasingly sensitive to power price hikes.

Consumer price changes in %, YoY

Source: Statistics Bureau of Japan

ANRE holds off on mandatory supply system in balancing market

(Government statement, May 28)

- ANRE will not introduce institutional measures that would partially mandate the supply of power sources to the balancing market, originally planned for April 2026.

- For now, market procurement will proceed by utilizing available power sources and discretionary contracts for pumped storage, among others.

- In FY2026, the trading time for all products is scheduled to be shortened from 3 hours to 30 minutes per block, and weekly products are to shift to day-ahead trading.

- Given the multiple planned system upgrades, it’s believed that proceeding as originally planned could disrupt markets.

- CONTEXT: Since trading began in the balancing market in FY2021, there’ve been frequent shortfalls in meeting solicitation volume, leading to a sharp rise in procurement prices. This impacts both the financial stability of TSOs, who bear the cost of securing balancing capacity, and the burden on consumers.

METI launches new subcommittee for electricity and gas industry

(Government statement, May 23)

- METI created the Next-Generation Electricity and Gas Infrastructure Development Subcommittee under the Electricity and Gas Business Subcommittee of the Advisory Committee for Natural Resources and Energy.

- It will discuss the institutional, market, and competitive environments of the electricity and gas industries in order to develop next-gen energy systems.

- This year, the agenda covers:

- Future direction of the electric power industry and environmental impact

- Approach to institutional design based on review of electricity system reform

- Modernization of the power network

- Review of the gas system reform

- Measures for electricity supply and demand during summer of FY2025

- CONTEXT: The reform of the electricity and gas systems has been hitherto discussed by the Electricity and Gas Basic Policy Subcommittee. Now, further detailed discussions will take place in this new subcommittee.

FIT certificate prices rise as policy shift boosts demand

(Denki Shimbun, May 26)

- FIT certificate prices reached ¥1.3/ kWh in the final FY2024 non-fossil value market auction, matching the cap, and aligning with non-FIT certificates.

- Trading volumes for FIT certificates rose 24.3% to a record 190.7 TWh, while the average price climbed ¥0.27 to ¥0.67/ kWh.

- CONTEXT: Increased demand was driven by a rule change that allows non-fossil value certificates issued under the FIT to count toward utilities’ legally mandated targets for non-fossil energy procurement.

April intraday power trades fall for first time in five months

(Denki Shimbun, May 28)

- JEPX intraday market volume fell 22.7% MoM in April to 18.3 GWh/ day, the first drop in five months.

- The monthly high price hit ¥50/ kWh on April 1, a day of cold, rainy weather.

- The month’s average price was ¥10.83/ kWh. Total monthly trading volume fell 25.2% to 548.9 GWh.

EEX welcomes Okachi as first non-clearing member from Japan

(Company statement, May 27)

- Commodity brokerage Okachi & Co joined the EEX platform as the first Japanese non-clearing member, boosting its clearing network in APAC.

Osaka Gas climbs to No. 2 in latest power sales ranking

(Energy Information Center, May 28)

- In January, Osaka Gas had the sharpest rise among top retail power suppliers, jumping from fourth to second place with 882 GWh in sales, according to the latest sector rankings based on govt data.

- Tokyo Gas retained the top spot, while several firms saw shifts in rank amid fluctuating winter demand. New entrants like au Energy & Life also gained, entering the top ten for the first time this year.

Rank | Company | Sales (GWh) | Previous Rank |

1 | Tokyo Gas | 1,431 | 1 |

2 | Osaka Gas | 882 | 4 |

3 | Ennet | 712 | 2 |

4 | ENEOS Power | 642 | 5 |

5 | Marubeni Power Retail | 638 | 3 |

6 | SB Power | 590 | 8 |

7 | Mitsuuroko Green Energy | 518 | 6 |

8 | au Energy & Life | 508 | 11 |

9 | CD Energy Direct | 464 | 7 |

10 | Halene (Haruené) | 445 | 10 |

NEWS: HYDROGEN

Air Water to partner with Mikasa City in hydrogen and renewables

(Company statement, May 23)

- Air Water and Air Water Hokkaido inked a partnership with Mikasa City, Hokkaido, to promote regional development and renewable energy.

- Air Water is responsible for testing hydrogen purification, and CO2 separation and capture from the extracted gas.

- The partnership covers a wide range; not only hydrogen production but also CO2 reduction, utilization of biomass and snow/ ice thermal energy.

- Mikasa City once flourished thanks to the coal industry. It now promotes underground coal gasification (UCG) and is engaged in low-carbon hydrogen production called the hybrid-UCG (H-USG), which combines coal and woody biomass.

- CONTEXT: UCG involves igniting underground coal directly to generate heat, which then gasifies the surrounding coal. The resulting gas is recovered and used as fuel or as a raw material for hydrogen production. The H-UCG project includes underground gasification of coal, aboveground gasification of mined coal and woody biomass, and the production of hydrogen from the extracted gas.

JFE Engineering achieves breakthrough ratio with hydrogen co-firing

(Company statement, May 29)

- JFE Engineering upgraded its hydrogen co-firing gas engine cogeneration system (JFE-MWM/H series), boosting the max hydrogen ratio from 25 vol% to 45 vol%.

- Achieving a 45 vol% while maintaining the same output as city gas is a world first.

- The cogeneration system has inbuilt flexibility. Even if it’s introduced initially for city gas-only, it can be modified in the future to support hydrogen co-firing.

- CONTEXT: In May 2024, the company began sales of the JFE-MWM/H series, which retrofits conventional city gas-only engines.

Start of design and verification of hydrogen infrastructure at Nagoya

(Company statement, May 27)

- NEDO has approved support for a project called “Design and Verification of Hydrogen Supply Infrastructure for Commercial Use in and Around the Port of Nagoya.” It was submitted by Toyota Tsusho, Taiyo Nippon Sanso, and Toho Gas.

- Toyota Tsusho will be the project manager, verifying the feasibility and economic viability. Taiyo Nippon Sanso will develop design guidelines for the supply infrastructure and test safety. Toho Gas will explore optimal hydrogen compression and storage.

- CONTEXT: A study in 2022 confirmed potential demand of up to 1,500 tons of hydrogen per year for cargo handling and logistics at Nagoya Port.

- SIDE DEVELOPMENT:

- JSE begins work on domestic base for hydrogen supply chain

- Japan Suiso Energy (JSE) began construction of the world’s first commercial-scale domestic hydrogen base as part of an international hydrogen supply chain.

- Located in Ohgishima, Kawasaki City, the facility will include large-scale hydrogen storage (50,000 m³), shipping/ receiving terminals, liquefaction systems, gas transport systems, and tanker loading facilities.

- CONTEXT: JSE is mostly owned by KHI and Iwatani Corp.

Japan explores subsurface hydrogen production using serpentinization

(Nikkei, May 24)

- NEDO will support research by AIST and others to develop a method of producing hydrogen underground by injecting hot water into rock layers, particularly peridotite, which reacts with water to produce hydrogen via serpentinization.

- The released hydrogen can then be collected for use in power generation.

NEWS: SOLAR AND BATTERIES

Toshiba launches packages with 90% size reduction for PV inverters

(Company statement, May 20)

- Toshiba Device & Storage began mass production of four new 650V SiC MOSFET products with their latest silicon carbide chips in compact 8×8 mm DFN packages.

- CONTEXT: SiC MOSFET modules are power electronic devices that combine multiple silicon carbide (SiC) MOSFET (Metal-Oxide-Semiconductor Field-Effect Transistor) chips into a single package or module.

- These reduce volume by over 90% compared to previous models, improving power density for industrial devices like solar inverters.

- SIDE DEVELOPMENT:

- ROHM modules adopted in SMA’s new system

- (Company statement, May 12)

- CONTEXT: ROHM, Japan’s major semiconductor firm, supplies advanced 2kV SiC MOSFET chips known for efficiency and durability. These chips are integrated by Semikron Danfoss into power modules designed for solar energy use.

- Semikron Danfoss now provides these chips to SMA Solar Technology, a German solar inverter firm, for use in its new “Sunny Central FLEX” solar platform.

TAKEAWAY: This collaboration showcases how Japan’s semiconductor expertise is used globally for powering next-gen solar tech. The news about ROHM’s SiC MOSFET modules and Toshiba’s latest SiC MOSFET packages are closely linked as they both highlight advancements in silicon carbide (SiC) semiconductor tech, which is crucial for improving solar systems. SiC MOSFETs offer higher efficiency, smaller size, and better heat resistance than current silicon units, enabling more compact and efficient solar inverters. This reduces power loss, extends lifespan, and boosts power density, thus improving cost-effectiveness.

Japan’s first PSC demo on thermal power plant enclosure

(Company statement, May 29)

- JERA, Sekisui Chemical, and Sanko Metal Industrial began Japan’s first demo of perovskite solar cells (PSCs) installed on a thermal power plant enclosure at the Yokosuka Thermal Power Station.

- The goal is to test PSC durability, efficiency and installation in a difficult location

Ishizaka Sangyo opens solar panel recycling plant in Saitama

(Company statement, May 26)

- Waste treatment firm Ishizaka Sangyo opened a new solar panel recycling facility in Iruma City, Saitama Pref.

- It can process 8.88 tons/ day and uses NPC’s hot knife separation method; it recycles materials like glass, metal, and aluminum from spent solar panels.

TAKEAWAY: Japan’s solar boom has brought clean energy to millions of rooftops, but a looming challenge is approaching: end-of-life solar panels. With many installations from the early 2000s nearing retirement, waste volumes are set to surge around 2030. Ishizaka Sangyo’s new recycling plant in Saitama uses advanced methods to recover valuable materials. However, Japan still lacks clear national regulations mandating panel recycling or producer responsibility. To avoid a future waste crisis, Japan must urgently establish legal frameworks and expand recycling infrastructure in line with solar ambitions.

Startup Nobest launches remote monitoring system for solar farms

(Company statement, May 26)

- Nobest, a startup based in Kawasaki, launched a remote monitoring system for solar power facilities called Nobest IoT.

- It allows operators and maintenance firms to track equipment status and detect faults.

- A key feature is centralized management of multiple facilities and AI-based prediction of weather-related issues.

- The company aims to sign contracts with around 100 firms by 2025 and plans to expand into theft prevention and remote monitoring for hydro and wind power.

TAKEAWAY: The launch of Nobest IoT comes at a timely moment amid rising cybersecurity concerns in the solar sector. With features like AI-based fault detection, centralized management, and domestic development, Nobest IoT seeks to offer a more secure alternative. This aligns with growing global and domestic efforts to protect energy infrastructure from cyber threats and reduce dependence on potentially vulnerable foreign equipment. For instance, Sankei Shimbun reported in May 2024 an incident in which hackers exploited a known flaw in 800 remote monitoring devices, leading to bank account thefts.

Shizen completes rooftop solar PV system in Indonesia

(Company statement, May 29)

- Alam Energy Renewables, backed by four Japanese companies including Shizen Energy, completed a 5 MWp rooftop solar power system for PT Kao’s Karawang factory in West Java, Indonesia.

- CONTEXT: Established in July 2020, Alam Energy is a JV between Shizen Energy, the NiX Group, and Alamport. It offers rooftop solar rental business in Indonesia.

Toyota Tsusho acquires stake in battery components producer

(Company statement, May 16)

- Toyota Tsusho acquired a 34% stake in Fuji Springs (Fuji Hatsujo in Japanese), a leading producer of automotive battery components.

- The two firms collaborate in the U.S. via FTBC, their JV in North Carolina.

- This investment will strengthen battery supply chains and expand production capacity and offerings to meet EV demand.

KEPCO launches battery storage support service

(Company statement, May 28)

- KEPCO launched a service called “Kan-denchi” to support companies developing and operating battery storage facilities. The service will be offered through a new firm with its group construction firm Kindan.

- The initiative aims to help customers use idle land for storage, improve operational efficiency, and reduce costs.

- CONTEXT: KEPCO already operates a battery storage facility in Wakayama and plans two more nationwide amid growing demand.

- SIDE DEVELOPMENT:

- JERA Cross patents battery control tech

- (Company statement, May 22)

- JERA Cross secured a patent for a battery control system that optimizes charging and discharging of renewable energy based on electricity prices and demand.

- It supports stable 24/7 renewable power use and can be integrated with its previously patented “Point 24/7” system to meet specific energy needs of commercial facilities.

Battery system adopted for offshore floating data center pilot

(Company statement, May 21)

- PowerX won an order to supply a battery system (80 kW/ 358 kWh) for a floating offshore data center demo in Yokohama, to be powered by solar.

- The pilot is led by Yokohama City, NYK, NTT Facilities, Eurus Energy, and MUFG Bank, aiming to test the reliability of renewable-powered offshore data centers.

- SIDE DEVELOPMENT:

- PowerX delivers mid-sized BESS to Awakura Electric

- (Company statement, May 22)

- PowerX has delivered its mid-sized industrial storage system, PowerX Cube 360, to Awakura Electric Manufacturing in Okayama Pref, a producer of precision plastic parts for the automotive industry.

- The system stores surplus solar energy from the factory’s rooftop panels (316 kW) and uses it during peak demand times.

NYK completes battery-powered fully electric workboat

(Company statement, May 26)

- The fully electric workboat e-Crea, owned by NYK Line, was completed by the group company, Keihin Dock Co.

- This ship is Japan’s first battery-powered workboat that does not carry a generator.

- It will be operated by Keihin Dock and assist with tugboat docking and undocking operations at the plant.

NEWS: WIND POWER AND OTHER RENEWABLES

Eurus Energy completes Japan’s largest onshore wind farm

(Company statement, Nikkei, May 27)

- Eurus Energy completed Japan’s largest onshore wind power complex in north Hokkaido, installing 107 turbines across six sites with combined capacity of 435 MW.

- The project culminates over 15 years of work and involves ¥105 billion in transmission infrastructure investment to overcome the region’s grid limitations.

- CONTEXT: To address local electricity demand, Eurus is considering building a data center in the area. The firm, which merged with solar-focused Terras Energy in April, now has 5 GW of generation capacity worldwide and plans to double the Toyota Tsusho Group’s renewables capacity to 10 GW by FY2030.

- SIDE DEVELOPMENT:

- J-Power plans wind farm upgrade in Fukushima

- (Company statement, May 23)

- J-Power presented the environmental assessment draft for the new Koriyama Nunobiki Kogen Wind Farm, a replacement for the existing onshore facility.

- The new plant will have a capacity of 69 MW with 16 turbines (4.3 MW each); construction to start in August 2026 and begin operations by February 2030.

- The current facility, operating since 2007, has 33 turbines and 66 MW capacity.

Ministries report on renewable energy expansion

(Government statement, May 27)

- The MoE, MLIT, and MAFF reported on the progress of their respective initiatives at the METI “Subcommittee on Large-Scale Introduction of Renewable Energy and Next-Generation Power Networks.”

- MoE said it is promoting renewable energy by supporting its introduction in public facilities, and promoting energy supply models that utilize local resources.

- MLIT seeks to expand the introduction and use of renewables in infrastructure spaces such as airports, railways, ports, and roads. It is also strengthening policies to encourage the installation of solar power systems in newly built homes.

- MAFF is supporting the development of circular economy regions centered on agriculture, forestry, and fisheries. It promotes the use of woody biomass and the introduction of agrivoltaics.

MOL to join offshore wind project in Taiwan

(Company statement, May 9)

- Mitsui O.S.K. Lines (MOL) will acquire a 10% stake in CI Fengmiao, which is owned by Copenhagen Infrastructure Partners.

- This gives MOL a role in the 495 MW Feng Miao Offshore Wind Farm in Taiwan (33 Vestas 15 MW turbines). MOL’s investment is expected to be ¥25 billion.

- Construction began in March 2025; completion set for late 2027. All output is secured via long-term contracts with major firms like Google and United Microelectronics.

- This is MOL’s second offshore wind investment in Taiwan, after Formosa I. MOL will also provide support vessels and dispatch personnel to gain hands-on experience.

- CONTEXT: The move is part of MOL’s broader 2035 strategy to grow its offshore wind business, which includes investments in floating wind, service operation vessels (SOVs), crew transfer vessels (CTVs), and maintenance.

Offshore wind faces further headwinds due to rising costs

(Nikkei, May 26)

- CONTEXT: This is a trend piece covering some of the recent problems in Japan’s offshore wind sector, such as surging material costs, a weak yen, and a lack of local components and turbines. It notes that developers like TEPCO Renewable Power and Mitsubishi Corp are struggling with profitability on current projects.

- While the govt plans to revise auction rules to allow higher feed-in prices and provide more flexible support, some argue these changes come too late or are insufficient.

- There are also concerns about fairness if new rules are retroactively applied. Without a clear path to financial viability, Japan risks setbacks in its goal to significantly expand offshore wind capacity by 2040.

TAKEAWAY: Although the article primarily captures ongoing debates, the govt should take seriously the negative sentiments expressed by stakeholders toward the proposed changes to future tenders. Progress on projects awarded in the first three rounds has been slower than expected, with most still in the planning phase.

KME and Kyocera seek further expansion in renewables

(Company statement, May 27)

- Kyuden Mirai Energy and Kyocera agreed on further collaboration in renewables.

- On April 1, the firms inked an off-site corporate PPA, under which KME began supplying geothermal electricity to Kyocera facilities. This is Kyocera’s first PPA for geothermal power; it has previously focused on solar PPAs.

- CONTEXT: KME is also active in solar, wind, and hydro, with 1.1 GW of operational and planned projects. Earlier this month it entered the BESS market.

- SIDE DEVELOPMENT:

- Asuene acquires GHG emissions visualization service

- (Company statement, May 27)

- Asuene acquired the GHG emissions visualization service, Sustana, from Sumitomo Mitsui Banking Corp, and plans to integrate it with its own “ASUENE” platform.

Shipping association sets guidelines for GHGs of Ro-Ro ships

(Company statement, May 26)

- Eastern Car Liner, K Line, Mitsui O.S.K. Lines, NYK Line, Wallenius Wilhelmsen, and ClassNK said the Global Ro-Ro Community (GRC), of which they are members, set guidelines for GHG emission intensity from Ro-Ro ships.

- By introducing a standardized calculation method through these guidelines, cargo owners will be able to accurately measure their Scope 3 emissions.

- CONTEXT: There is growing interest in understanding the carbon footprint of products and services across their entire lifecycle. However, there are discrepancies due to differing calculation methodologies. A Ro-Ro (roll-on/roll-off) ship is a type of cargo vessel designed to allow vehicles such as cars, trucks, trailers, etc to be driven on and off the ship under their own power.

NEWS: NUCLEAR ENERGY

IHI and NuScale Power complete wall module for SMR project in Romania

(NikkeiAsia, May 28)

- IHI completed a prototype wall module for a small modular reactor in Romania, in partnership with NuScale Power (U.S.). About 620 of these modules will go into use at the plant, set to open by 2030.

- IHI hopes to more than double its nuclear business sales to ¥100 billion (~$690 million) in the 2030s, with SMRs as a central growth area.

- CONTEXT: Japan’s domestic nuclear sector has stagnated, with no new plants built since 2009. SMRs, which have a capacity of up to 300 MW, are gaining global attention particularly from data centers.

TAKEAWAY: See this issue’s Analysis section.

KEPCO gets approval for dry storage facility at Takahama NPP

(Company statement, May 28)

- KEPCO secured NRA approval to build a dry storage facility for spent fuel (Phase 1) on the premises of Takahama NPP.

- This facility will serve all four units and allow interim storage of spent fuel. Construction should be complete in 2027.

- Each cask can hold 24 spent fuel assemblies that had been cooled for at least 25 years in a pool. Key safety features include natural air cooling and double-sealing lids.

- The facility will store up to 22 casks, equal to 240 tons of spent fuel, for 60 years.

Third-party committee says safety satisfactory at Kashiwazaki-Kariwa NPP

(Nikkei, May 28)

- TEPCO held a meeting of its third-party Nuclear Reform Monitoring Committee that comprises Japanese and international experts. It assessed safety at the Kashiwazaki-Kariwa NPP, and gave a mostly positive conclusion.

- U.S. Nuclear Regulatory Commission’s Dale Klein and Charles Casto inspected Unit 6. Klein remarked that TEPCO must ensure adequate training. Casto said even simple tasks during restart preparation need more attention.

- Klein urged TEPCO President Kobayakawa to provide strong leadership, and give priority to safety over cost.

- CONTEXT: Nagasaki Shinya, an NRA commissioner, also visited the plant. He inspected counter-terrorism measures, made necessary by serious security lapses discovered in 2021. These included unauthorized ID use and malfunctioning intrusion detection systems. This led the NRA to ban operations at the plant until Dec 2023. TEPCO has since added new fences and reduced the number of personnel allowed in restricted areas. It also introduced biometric authentication systems.

Kyushu Electric’s Genkai NPP to restart

(Company statement, May 30)

- Kyushu Electric announced the restart schedule for Genkai NPP Unit 3. The plant has been undergoing periodic inspection since March 28.

- It will restart on June 6, and complete the comprehensive performance test by June 30, after which it can return to normal operation.

Chugoku Electric to invest in disaster prevention in Shimane Pref

(Nikkei, May 30)

- Chugoku Electric will give ¥5 billion toward disaster prevention projects, planned by Shimane Pref for the Shimane Peninsula, and to take place over the next 10 years.

- Plans include building heliports, upgrading fishing ports, and reinforcing roads.

- The initiative comes after the Jan 2024 Noto Peninsula earthquake. Shimane NPP is on the peninsula.

- The total cost will be around ¥10.3 billion over 10 years, with the pref covering ¥5.5 billion with national subsidies.

NEWS: TRADITIONAL FUELS

JERA interested in Alaska LNG project ahead of energy summit

(Bloomberg, May 30)

- JERA expressed interest in purchasing LNG from the long-delayed $44 billion Alaska LNG export project. The move comes ahead of the Alaska Sustainable Energy Conference. Japanese, Taiwanese, and South Korean companies will attend.

- The Alaska project has struggled for decades to secure long-term contracts.

- CONTEXT: The Alaska Sustainable Energy Conference (June 3-5) in Anchorage will focus on various energy issues and not only LNG. Japan’s Vice Minister for International Affairs, Matsuo Takehiko, will attend.

Kyushu Electric inks 20 yr deal with U.S. supplier for LNG

(Company statement, May 29)

- Kyushu Electric signed an agreement with Energy Transfer LNG Export to buy LNG, the firm’s first contract with a U.S. supplier. Energy Transfer will supply up to 1 Mtpa of LNG for 20 years, sourced from Lake Charles LNG in Louisiana.

- It has FOB (Free on Board) delivery with no destination restrictions. Delivery timing can be adjusted according to domestic power demand, and resold when demand is low.

- CONTEXT: Kyushu Electric procured 2.59 Mt of LNG in FY2024, about 70% from Australia.

- SIDE DEVELOPMENT:

- JERA inks deal with U.S. for 2 Mtpa of LNG

- (Company statement, May 29)

- JERA signed a contract with U.S. energy company NextDecade to buy 2 Mtpa of LNG over 20 years, starting when the project begins operation.

- CONTEXT: The deal’s price was not disclosed, but the value could reach ¥100 billion. JERA buys about 36 Mtpa of LNG, most of it from Australia.

TAKEAWAY: This deal was announced on the same day as Kyushu Electric’s one from Lake Charles. For such companies, securing long-term agreements is a way to cover themselves from future market shocks. But, there is politics at play – Trump wants Japan to buy more American LNG. Also, these contracts come without destination clauses. This is crucial because Japan’s own LNG demand is shrinking, while cross-border trading is intensifying.

MOL wants govt help after EU sanctioned LNG tankers

(Bloomberg, May 27)

- Mitsui OSK Lines (MOL) seeks govt help after the EU sanctioned three of its LNG tankers linked to Russia’s Yamal LNG. The project is not under sanction.

- The EU included the vessels in its 17th round of sanctions.

LNG stocks up over previous week, up YoY

(Government data, May 28)

- As of May 25, the LNG stocks of 10 power utilities were 2.16 Mt, up 9.1% from the previous week (2.07 Mt), up 4.4% from end May 2024 (2.07 Mt), and 0.9% down from the 5-year average of 2.18 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Tokyo Govt and Tokyo Gas ink partnership for carbon neutrality

(Government statement, May 26)

- The Tokyo Metropolitan Govt and Tokyo Gas signed an agreement to accelerate efforts at carbon neutrality. This includes:

- Measures to stabilize energy supply and demand

- Expansion of renewable energy utilization

- Utilization of green hydrogen

- Promotion of biofuels and synthetic fuels

- The main goal is to realize a “decarbonized city” that serves as a global model.

- CONTEXT: Tokyo is implementing energy-saving technologies, hydrogen-related technologies, and other initiatives that contribute to green transformation (GX), aiming to achieve carbon neutrality by 2050. Tokyo Gas says that “balancing stable energy supply and decarbonization” is one of its three core strategies.

Mitsubishi-backed e-fuel firm building SAF plant in Texas

(Company statement, May 20)

- Mitsubishi and the JOGMEC-backed e-fuel producer Infinium inked a final investment decision to build its second plant in Texas.

- The “Roadrunner” will produce 23,000 tons annually of e-SAF (sustainable aviation fuel) starting in 2027, making it one of the world’s largest facilities. The plant will use green hydrogen and CO2 to create low-carbon synthetic fuel.

Japan and Tanzania agree on JCM, marking 30th partner country

(Government statement, May 28)

- Japan and Tanzania inked an MoC on the Joint Crediting Mechanism (JCM), making Tanzania the 30th partner country.

- CONTEXT: The scheme supports developing nations with Japanese low-carbon techs and infrastructure, generating emission reduction credits.

MHI agrees with Uzbekistan for decarbonization study

(Company statement, May 26)

- Mitsubishi Heavy Industries (MHI) signed an MoU with the Ministry of Energy of Uzbekistan to study a plan to ensure a stable supply of electricity.

- The project will focus on retrofitting existing MHI-supplied plants, developing hydrogen-ready gas turbine systems, and assessing future carbon-neutral energy infrastructure for Uzbekistan’s goal to raise renewable energy to 54% by 2030.

ANALYSIS

BY PARUL BAKSHI

Japan’s Resource Diplomacy Evolves Into Market Architecture

Japan’s natural resource diplomacy is no longer just about shielding domestic industries from supply shocks. Rather, it’s now actively co-architecting markets, shaping which technologies scale and where companies place their bets.

After decades of debating new ways to access critical minerals, Japan is starting to wield its institutional tools more assertively – making direct investments, underwriting high-risk ventures, and expanding state finance to influence global supply chains. This marks a shift from strategic intent to operational action.

Two recent deals illustrate this. JOGMEC backed a rare earth refinery in France – its first support for a stand-alone overseas processing facility. Meanwhile, the Japan Bank for International Cooperation (JBIC) committed $466 million to Chile’s state copper giant, Codelco, as part of a larger co-financing package to secure supplies for Japanese firms.

Such moves go beyond raw material access. They reflect Tokyo’s recognition that mineral security today means engaging across the value chain. What began in the 2010s as risk mitigation has matured into a state-enabled resource diplomacy ecosystem – one suited for an era of geopolitical fragmentation and technological chokepoints.

Seen this way, Japan’s resource push is not just about extraction, but systems-building. It favours selective interdependence and strategic sovereignty without full decoupling from China. For foreign and domestic firms alike, this signals a more activist Japanese industrial policy – full of opportunity, but governed on tighter terms.

From minerals to strategy

Japan’s status as a high-tech manufacturer has long demanded a strategic approach to mineral security. Applications in batteries, solar panels, wind turbines and hydrogen electrolyzers have only heightened this need, linking mineral inputs to clean energy and industrial goals.

Anchored by METI’s 35-item critical minerals list, which was updated in 2024 to include uranium, Japan’s mineral diplomacy now underpins the broader Green and Digital Transformation strategies (ie GX and DX). These aim to mobilize ¥150 trillion in public–private investment for net zero, while upgrading Japan’s digital and industrial base.

The alignment of climate, digital, and industrial goals reframes minerals as strategic enablers of techno-industrial competitiveness. This evolution occurs amid escalating supply chain politics with Washington’s tariffs and Beijing’s export curbs casting a long shadow on economic planning.

Japan’s own 2010 rare earths shock – when China suspended exports during a maritime dispute – triggered a decade of diversification and long-term offtakes, much of it led by the then-named Japan Oil, Gas and Metals National Corporation, which in 2022 was renamed Japan Organization for Metals and Energy Security to reflect a renewed focus.

Today, JOGMEC and JBIC – Japan’s chief state-backed financial tools – have seen their mandates expand accordingly. Both are now central to Japan’s economic security strategy, taking on roles well beyond their historical remits.

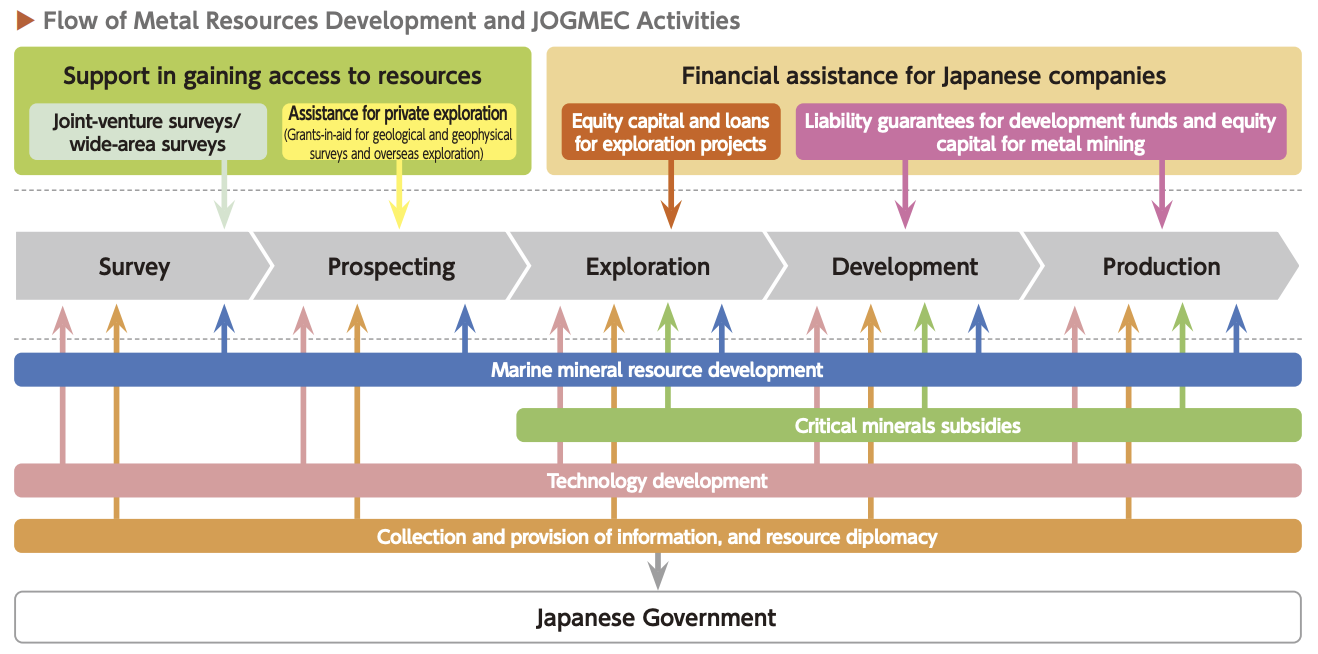

Flow of metal resources development & JOGMEC activities

Source: JOGMEC

Finance arms of mineral strategy

JOGMEC’s legal cap on overseas equity stakes was lifted from 50% to 75% in 2022, alongside new authorization to issue debt guarantees. That has allowed it to chase riskier, priority projects – particularly in lithium, cobalt and rare earths. The organization spans the full development cycle from exploration to production, with government-backed insurance and resource diplomacy to match.

Between 2004 and 2020, JOGMEC participated in more than 100 projects, deploying over $600 million across 15 countries. Its stockpiling policy was also revised in 2020, allowing it to release or acquire reserves in response to supply shocks, with terms kept confidential to avoid market disruption.

JBIC, meanwhile, repositioned itself as more than just a financier of Japanese firms overseas. Its latest business plan (FY2024–26) highlights carbon neutrality, semiconductor resilience and global supply chain robustness. JBIC now backs clean tech, digital infrastructure, and even global startups – supporting both large corporates and export-focused SMEs. Its toolkit includes debt, equity and bilateral project finance.

The pair have complementary roles: JOGMEC absorbs upstream risk; JBIC builds out the midstream and downstream. Together, they underpin Japan’s broader policy framework, shaped by the 2022 Economic Security Promotion Act. This legislation formalized cross-ministry coordination and introduced “specified important materials,” giving the state broader authority to intervene in strategic supply chains.

These tools are now deployed alongside credit lines, industrial subsidies, and foreign aid – designed not only to build resilience, but to exert influence over infrastructure, technologies, and commercial norms.

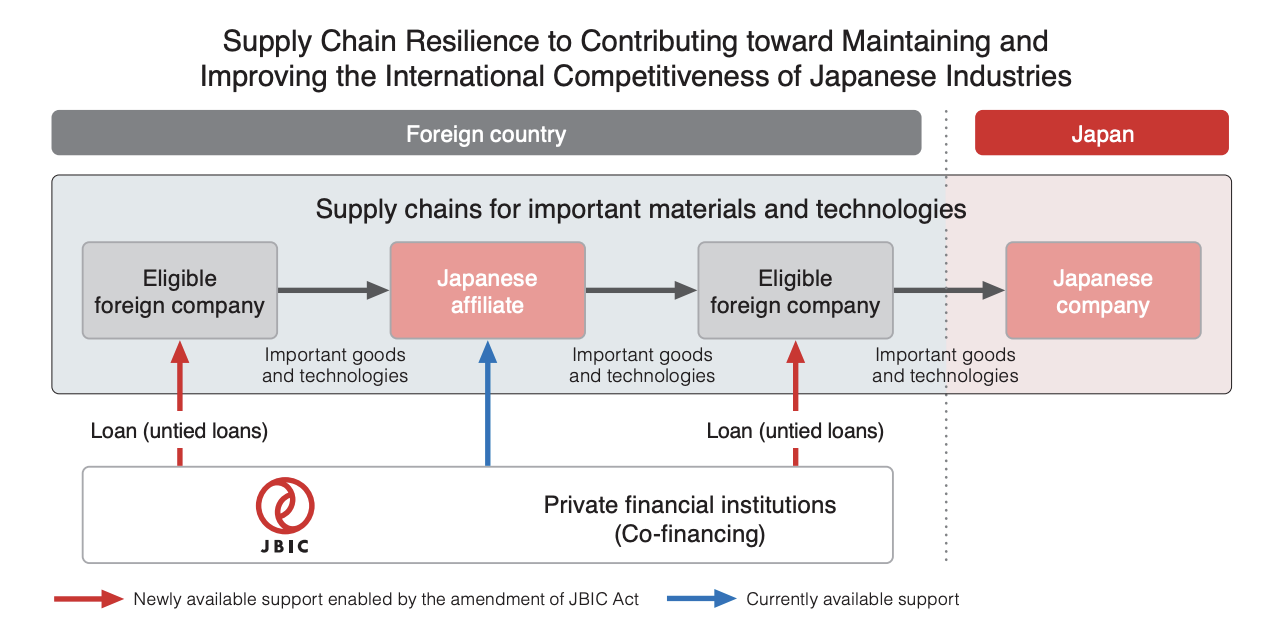

JBIC’s role in global supply chain reconstruction

Source: JBIC

From access to architecture

Japan’s approach has evolved from mineral access to ecosystem design. This shift is evident in its geographically tiered strategy, outlined in the GX Diplomacy Guidelines. Stable countries like Australia and Canada receive direct investment. Chile, Peru, and the Philippines are targeted via public–private dialogues. Higher-risk markets, particularly in Africa, are accessed through trilateral or multilateral initiatives with allies.

Bilateral and multilateral partnerships are multiplying. A 2023 mineral supply chain agreement with the U.S. expanded into a pact with South Korea covering semiconductors and critical minerals. Japan is investing in mineral processing centers in Vietnam and co-developing nickel value chains in the Philippines. Ties with France and the UK are deepening, and joint ventures in Africa are being negotiated.

Japan’s traditional commodity procurement agents, the trading houses, are also active. Sumitomo Corp has worked to procure rare earth elements in Kazakhstan and Vietnam, and in February 2023 signed an exclusive rare earths deal for Japan with MP Materials.

In a quid pro quo, Japan’s overseas aid went to port infrastructure in Madagascar to facilitate nickel extraction. Meanwhile, Japan remains a founding member of the Minerals Security Partnership (MSP) and the Quad’s Critical Minerals Working Group – efforts that seek to set global standards for ESG, traceability, and sustainable mining.

At the G7 in Hiroshima in 2023, Japan pushed through a Five-Point Plan for Critical Mineral Security, backed by ¥200 billion in commitments. Regional frameworks like the Asia Zero Emissions Community (AZEC) and the Asia Energy Transition Initiative (AETI) embed mineral supply into broader decarbonization efforts.

The result is a web of projects, institutions and rules – what might be called curated interdependence. Japan is building trust-based supply chain ecosystems, while limiting exposure to volatility and techno-nationalist blocs. The real strategic asset is no longer just the mineral, but the platform, the rules, and the alliances that govern it.

Signals to business

For companies, Japan’s resource diplomacy introduces a new landscape of signals and incentives. Domestic firms in strategic sectors are likely to benefit from subsidies, insurance, and joint ventures, especially where market risks are high or technologies remain pre-commercial.

Through METI’s ¥2 trillion Green Innovation Fund, administered by NEDO, Japan is bankrolling early-stage projects such as Sumitomo Chemical and JERA’s lithium-ion battery reuse process. The Critical Minerals Subsidy Scheme overseen by JOGMEC covers up to half of eligible costs for approved ventures.

Foreign firms face a different dynamic. They may encounter more scrutiny – or encouragement – to form partnerships with Japanese counterparts. This is not protectionism as much as it is market design. Japan wants control over how and where risk is sourced, and where value accumulates.

This design extends overseas. State funding is increasingly tied to JVs in third-country markets. In Australia, JBIC backed Japanese investments in Lynas, helping it become the first commercial producer of heavy rare earths outside China. The Japan–France Rare Earth Corp, a public-private partnership between JOGMEC, Iwatani, and France’s Caremag, is building a rare earth separation facility in France that could eventually meet a fifth of Japan’s demand for certain oxides like dysprosium and terbium.

Japan’s involvement is not just financial. It includes diplomatic facilitation and demand-side guarantees to stabilise investor expectations – ensuring private capital flows into projects aligned with national priorities.

Where technologies are promising but risky, the state is offering incentives to co-develop and de-risk them – shaping entire ecosystems, not just single ventures. The goal is to embed innovation within Japan’s supply chains, not outsource it.

Foreign investors, especially those in projects with environmental or social footprints, will need to interpret where Japan signals openness – and where it expects tighter alignment on ESG, data sharing, or strategic autonomy. Japanese firms themselves are being pushed to meet higher standards, disclose more, and demonstrate compliance.

This may raise long-term costs, but it also offers reputational rewards in a global market hungry for verified, responsibly sourced minerals.

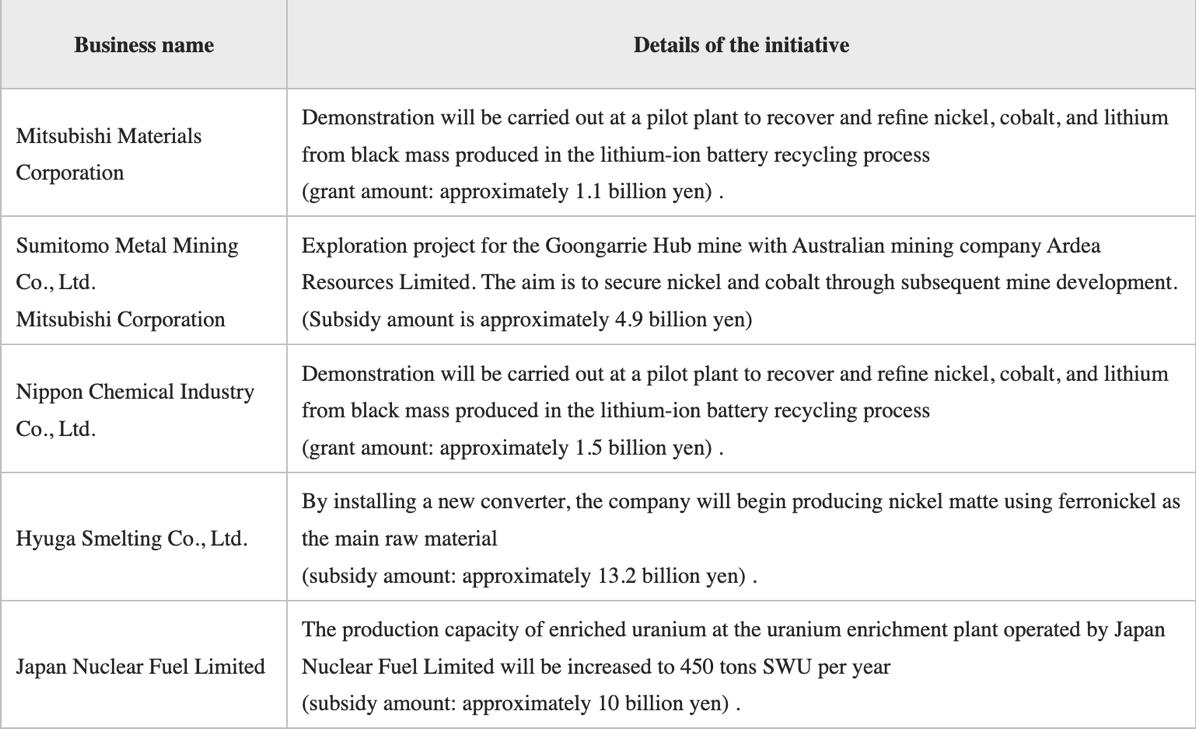

Critical Minerals Subsidy Scheme projects

Source: JOGMEC

A platform strategy

Ultimately, Japan is betting on interdependence – not through laissez-faire openness, but rather through curated collaboration. From lithium mines to rare earth refineries, from trading house diplomacy to bilateral rulemaking, Tokyo is building a system that mixes industrial logic with statecraft.

Industries tied to clean energy, digital infrastructure, and critical materials will increasingly find themselves nested within these state-backed ecosystems – sheltered from certain market risks, but subject to more oversight. That duality is what makes Japan’s new resource diplomacy not just a geopolitical hedge, but a market-shaping force.

Dr. Parul Bakshi is a Japan Foundation Indo-Pacific Partnership Fellow at the University of Tokyo’s Institute for Future Initiatives and a Visiting Research Fellow at the Oxford Institute for Energy Studies.

ANALYSIS

BY FILIPPO PEDRETTI

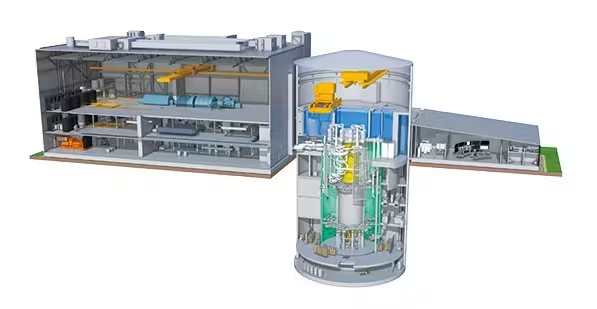

Japanese SMRs Move Forward but Not in Japan

Japanese firms are developing Small Modular Reactors (SMRs), nuclear units that are touted as the sector’s next phase and best bet to further spread nuclear power across the globe, especially to cash-strapped countries. Most significant developments by Japanese companies, however, are taking place outside of the country.

With a capacity of under 300 MW, SMRs comprises diverse kinds of technologies, including conventional reactors such as BWRs/PWRs and experimental ones. They are modular, meaning the components can be mass-produced and assembled on site.

Hyped as a game changer for the nuclear industry, the SMR is still an underdeveloped technology, with only Russia and China having commercially operable reactors. In April, however, the technology took a big step forward in G7 countries, when a project using GE Hitachi Nuclear Energy’s BWRX-300 secured permission to begin construction in Canada.

Another Japanese firm is in talks to build an SMR in the U.S. based on Japan’s own innovative gas-cooling technology. That project is still in the early stages, but it’s already attracting attention from big energy users, such as data center companies, which are eager to find solutions to their power hungry business.

Proponents of SMRs hope such projects will pave the way to develop a safer, easier to deploy nuclear power source that can balance out the rising wave of variable renewable energy. With Japan’s domestic nuclear sector slow to reemerge, success abroad is seen as vital to realizing SMRs in a real, commercial setting. A positive track record of SMRs operating overseas would pave the way to the tech’s introduction in Japan’s home market.

The model

One of the most advanced and prominent Japanese SMR projects abroad is the BWRX-300, which is a 300-MWe developed by GEH, a joint venture between U.S.-based GE Vernova and Hitachi. The model includes components from GEH’s Economic Simplified Boiling Water Reactor (ESBWR) and Advanced Boiling Water Reactor (ABWR).

One of its most attractive features is the passive safety mechanism. Conventional reactors rely on active cooling systems, but the BWRX-300 can shut down and cool itself through natural circulation. This is obtained through a system that provides natural circulation of water to cool the reactor without the need of an active operator. This is crucial in case of an earthquake or tsunami. In addition, this feature helps to lower costs.

Source: GE Hitachi Nuclear Energy

The first BWRX-300 is already on the path to realization. Last month, Ontario Power Generation (OPG) secured a permit to build the first one at its Darlington New Nuclear Project site. This project is slated to become a hub with up to four SMRs, with units 2 through 4 scheduled to begin operations between 2034 and 2036. The max licensed capacity of the site is 4,800 MW, so in time further reactors may be added.

GEH will provide in-core structures, a control rod drive mechanism, and a control rod drive hydraulic unit. Japanese suppliers will provide major components, and by doing so, also help develop human resources in Japan that can specialize in the sector. By building experience in working with the new reactor model, the company will gain know-how and expertise for further development of SMRs in Japan.

If successful, the first BWRX-300 will serve as the pathfinder for future SMR deployments in the province and then across Canada.

Permits and costs

In 2021, OPG selected GEH’s predecessor as its technology partner. After preparatory work such as foundation digging, the permit from the Canadian Nuclear Safety Commission finally allowed the company to proceed. The licence is valid until the end of March 31, 2035 and is part of the regulatory oversight to govern the project.

The CNSC’s decision followed an extensive two-part public hearing in October 2024 and then in January 2025. All submissions and perspectives were considered, including those from local residents, environmental experts, and Indigenous groups.

In 2022, the company applied for the current permit, which pertains to construction only. Before progressing to reactor operation, the company must secure another permit for operations. GEH and OPG expect the reactors to start about FY2029 or FY2030 and to operate for around 65 years.

Costs for the Darlington project could reach $15 billion, including from licensing and construction to interest on financing. The first SMR unit is forecasted at $4.45 billion, and related infrastructure costs will be $1.17 billion, for a total of $5.62 billion.

The cost estimates for the second, third, and fourth SMRs are not yet finalized, but OPG expects each successive unit to be less costly with the fourth unit estimated at $3 billion.

The above figures are much higher than previous GEH’s estimates, which were around $2,250-2,500/ kW, or $700 million-$750 million for a single 300 MW unit. Such a price tag made the units competitive with other energy sources, especially thermal ones like gas.

Still, OPG thinks it can keep the electricity cost to around $0.1088/ kWh. While higher than the $0.09/ kWh of GEH earlier estimates, according to OPG this will both be enough to recover the investment and stay competitive with other sources, especially renewables.

More projects

Meanwhile, across the Atlantic in Europe the BWRX-300 is gaining traction in the UK’s plans for a fleet of SMR facilities. The government shortlisted three potential SMR technologies, with the BWRX-300 a contender. The others are from Holtec and Rolls-Royce. Westinghouse was also on the list, but dropped out in April.

Meanwhile, across the Atlantic in Europe the BWRX-300 is gaining traction in the UK’s plans for a fleet of SMR facilities. The government shortlisted three potential SMR technologies, with the BWRX-300 a contender. The others are from Holtec and Rolls-Royce. Westinghouse was also on the list, but dropped out in April.

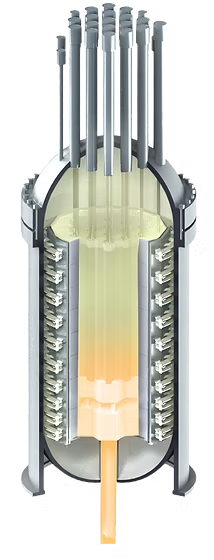

Some SMRs are eschewing the traditional BWR and LWR nuclear technologies and experimenting with very different systems that claim to be even safer and more agile.

Recently, Coral Capital invested in ZettaJoule, a Japanese startup developing an SMR built on a high-temperature gas reactor (HTGR). The company recently secured follow-on funding led by Globis Capital Partners, with participation from Archetype Ventures, HAX, etc.

Unlike reactors relying on water cooling, ZettaJoule’s proposed design uses helium as a coolant and graphite as a moderator. This enables the reactor to operate at high temperatures, up to 900°C, and should also minimize meltdown risks.

ZettaJoule intends to unite Japanese suppliers and international regulators and investors. The startup is partnering with a U.S. university to build a demo reactor in Texas by the early 2030s, with plans for commercial deployment later that decade.

Source: ZettaJoule

Getting a permit for new technology takes years – five or more. But ZettaJoule’s plan to have the initial reactor project in the U.S. as a research facility should expedite permissions to as little as 12-15 months, according to the company.

The permit application should also be helped by the fact that Japan has operated such tech for decades. And once a research reactor has a track record working in the U.S., securing approval for a commercial-scale unit should be easier, according to ZettaJoule.

The startup has assembled an international and experienced team spanning several disciplines. It is led by an ex-Sumitomo Corp strategist for commercialization with a former senior Mitsubishi Heavy Industries executive as the deputy CEO. JAEA’s HTGR pioneers and former nuclear regulators from Canada and the U.S. are among those managing the technical and policy challenges ZettaJoules faces.

The level of seniority among ZettaJoules leaders signals a further change in Japan’s attitude towards SMRs, whose research was also affected by the negative opinion towards nuclear power in the wake of Fukushima in 2011.

After the post-Fukushima cold approach towards nuclear power, SMRs included, change in attitude began also thanks to companies like engineering giants IHI Corp and JGC Holdings, which took part in the SMR business through investment in the U.S. specialist NuScale. They made an investment of $20 million and $40 million each. Just a few days ago, IHI said it completed a prototype wall module for NuScale’s SMR plant project in Romania set to open by 2030. IHI too hopes that it will bring such technology and related expertise to Japan.

Other Japanese firms reportedly working on SMR projects include Toshiba and MHI. The latter is believed to be developing a PWR-type SMR unit.

Conclusion

On paper, SMRs promise to be a flexible and cheaper alternative to traditional large-scale nuclear reactors that often face delays to regulatory hurdles and community opposition. SMRs could be suitable for powering remote communities and supporting industrial operations, especially in helping to meet the growing energy demand that is accompanying the rise of generative AI.

However, G7 nations have not made SMRs a priority. Only Russia and China have commercial SMR operations, with the former starting in May 2020, and China following in December 2023. But if technologies such as those promoted by GEH and ZettaJoule prove themselves commercially viable, this could open the door to a new wave of enthusiasm for nuclear power, including in Japan.

That’s still a large “if”. An SMR flagship project by Nuscale in the U.S. was recently cancelled due to an almost doubling of costs to $9.3 billion. And while SMR construction costs tend to be less than for conventional reactors, SMRs still need to show their profitability in cost-per-output terms, something difficult given the loss of economy of scale.

Relying on progress overseas is not the easiest path for Japanese industry, but it may be their only option at present. Japan’s nuclear regulator remains extremely conservative and slow to engage in new technology reviews. The government lacks a detailed strategy or roadmap for SMRs. Aside from a very general timeline, Tokyo energy planners have on occasion made scattered remarks about the potential to substitute aging reactors with smaller versions.

The cooler reception to SMRs inside Japan despite momentum for the technology overseas is in part due to the nuclear sector’s general difficulties at home. Most politicians are wary of bringing up new nuclear facilities when the majority of the existing ones have yet to restart. The same is largely true for domestic nuclear plant operators, which have yet to recoup the vast sums spent on fortifying existing stations to meet stricter safety standards.

And so it is left to the technologists to forge ahead – overseas. As ever, they will be judged on how well their projects deliver in terms of cost and time. Industry leaders know that the road ahead is long and far from simple. Betting on SMRs as a near-term solution for Japan at this point is little more than wishful thinking.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Asia / Fossil fuels

The Asia Clean Energy Coalition said the region “remains heavily reliant on fossil fuels”, with over 85% of its energy still sourced from non-renewable sources.

Asia / LNG

Imports of LNG to Asia are stable, on track to reach 22.53 Mt in May, up slightly from 21.89 Mt in April, according to commodities analysts at Kpler.

Australia / LNG

Viva Energy received an environmental permit for its proposed LNG terminal in Geelong. It will enable the market in Victoria to connect to supply sources in north Australia.

China / Coal

China is producing more coal than it can consume, resulting in a 42% YoY increase in mine stockpiles and a 25% annual rise in inventories at northern Bohai area ports.

China / Hydrogen

Oil and gas major Sinopec unveiled a $690 million venture capital fund to support early-stage hydrogen investments and technologies.

China / Russian gas

Gazprom delivered the first 100 bcm of natural gas via the Power of Siberia pipeline, as part of contracted volumes exceeding 1 trillion cubic meters. In 2027, Gazprom will start deliveries of gas to China via a second pipeline – the Far Eastern route.

India / Coal imports

Coal imports decreased 7.9 % in FY2025, totalling 244 Mt. This drop resulted in foreign exchange savings of about $7.93 billion.

India / Solar and BESS

Sembcorp Industries won a 150 MW solar power project with a 300 MWh BESS, and a 25-yr PPA with SJVN. The firm now has a total of 6.3 GW renewables capacity across India.

Malaysia / Power generation

ACWA Power agreed with the govt to develop up to 12.5 GW of power generation capacity by 2040. Total investment will reach $10 billion.

Singapore / Carbon credits

Singapore inked a deal with Paraguay on carbon credits cooperation. This is its seventh partner; others are Papua New Guinea, Ghana, Bhutan, Peru, Chile, and Rwanda.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.