METI says that Japan can play a key role by assisting partner countries to align with their NDCs, and help verify compatible technologies, and manage carbon risks.

The ministry also said the IEA sees Japan’s Climate Transition Bonds (JCTBs) as offering a model for emerging economies to provide govt-backed credit support. However, more needs to be done to improve general understanding of the value of transition finance and what partner countries should expect.

CONTEXT: The IEA urges transition finance to integrate with sustainable finance frameworks. In 2024, global energy investment likely exceeded $3 trillion. Two-thirds were for clean energy, though 85% was in advanced economies and China.

Japan’s emissions trading system (GX-ETS) will be mandatory in FY2026 for about 300-400 companies, those emitting over 100,000 tons of CO2 a year. These firms account for about 60% of Japan’s GHGs.

Firms must match their emissions with govt-allocated allowances, traded in a market run by the GX Promotion Organization.

A price ceiling/ floor will stabilize costs, and there will be fines for non-compliance. Additionally, the govt will introduce a fossil fuel levy in FY2028.

CONTEXT: These moves are part of the amended GX (Green Transformation) Promotion Law. There are concerns over double burdens (e.g., power sector costs), which will be the target of future legislation.

ANRE drafted an action plan and policy to promote use of bioethanol in gasoline, so that it will have up to 10% bioethanol by FY2030, aiming for up to 20% by FY2040.

A trial introduction in select regions by FY2028 will identify issues and support rapid expansion as compatible vehicles become more common.

NTT, NTT West and QTNet, a subsidiary of Kyushu Electric, demonstrated that IOWN’s All-Photonics Network (APN) enables high-capacity, low-latency communication across geographically dispersed data centers.

CONTEXT: The IOWN (Innovative Optical and Wireless Network) is an initiative for networks and information processing infrastructure including terminals.

In a test between data centers in Fukuoka and Osaka (600 km apart), downtime during live migration was reduced and renewable energy use improved by up to 31%. The firms say the test proved that the tech allows optimal workload placement based on renewables availability.

NTT’s algorithm generated optimized workload plans within 2 minutes, enabling dynamic processing shifts every 30 minutes based on real-time power conditions.

Tesla will launch a virtual power plant (VPP) business across Japan, managing small-scale batteries collectively.

Batteries will be provided to businesses for free. They will be centrally controlled to charge during periods of high renewables generation and discharge during peak electricity demand.

Tesla has partnered with Fukuoka-based Global Engineering and Fuyo Lease, aiming to install 100 units by FY2025. The program builds on a pilot in Okinawa.

This initiative lays the groundwork for Tesla’s vision of a “virtual power company” that aggregates large numbers of batteries to supply power on demand.

Japan plans to promote VPPs by launching a system in FY2026 to help battery operators trade their electricity. The balancing market will allow aggregated small-scale power sources to participate.

CONTEXT: VPP operators manage dispersed small-scale batteries in homes and offices to balance regional electricity supply and demand. Batteries are charged during the day when solar power is abundant and discharged during high-consumption periods like evenings.

TAKEAWAY: Japan’s greater reliance on renewable energy sources like solar and wind requires more deployment of batteries that can store and discharge power on demand to stabilise supply. Currently, the government’s efforts are directed at larger battery projects and longer duration energy storage. Tesla sees a way to achieve scale through aggregation and management of many small-scale units. Also, the company has started its business in the Kyushu region, one of the worst for green power curtailments.

TOCOM electricity futures trading down as hedging activity eases

(Exchange data, June 10)

TOCOM power derivatives trading slowed as forecasts for stability in the electricity supply demand balance eased interest in hedging. Summer reserve margins are forecast by OCCTO at above 7% across all regions even under severe heat scenarios.

TOCOM May trading volumes dropped sharply to 176.2 GWh (2,514 contracts) in May, down nearly 80% from April’s 863.6 GWh (12,351 contracts).

Newly introduced annual contracts for FY2026 began trading on May 26, with initial deals executed for East and West base-load products at ¥13.30/ kWh (East) and ¥11.35/ kWh (West).

May saw a total of 82 transactions, much lower than April’s 393, impacted by holidays and Japan Power Week events. Off-market (negotiated) transactions remained dominant – 69 of these deals – including various trading periods such as summer, winter, and irregular durations tied to specific retail contracts.

Open interest at month’s end remained high at 830 GWh, down just 8.5% from April’s record.

JEPX average daily sell orders for May decreased 2% MoM to 1.126 TWh, while buy orders fell 3.4% to 827 GWh.

Total monthly sell orders rose slightly by 1.2% to 34.92 TWh; buy orders edged down 0.1% to 25.64 TWh.

Sell volumes were impacted by holidays and power plant maintenance but supported by increased solar power generation. Buy volumes remained subdued due to unstable weather despite rising demand towards the end of May.

Daily buy order peaks were around 900 GWh on May 20-21, driven by increased air-conditioning demand as many regions experienced summer-like temperatures.

Tokyo Metropolitan Govt and Tokyo Commodity Exchange (TOCOM) released results for FY2025 first round of bidding for Tokyo Green Hydrogen Trial Trading.

Bidding was held for two separate categories: the trailer transport course (2,484 Nm3/ unit), and the cylinder cradle transport course (263 Nm3/ unit).

CONTEXT: A cylinder cradle refers to a set of gas cylinders bundled together for bulk transportation and supply of industrial gasses.

The results are as follows:

Bidding Classification

Trailer Transport Course

Cradle Transport Course

Supply side

Number of bidders

1

1

Winning bid

¥280/ Nm3

¥355/ Nm3

User side

Number of bidders

2

3

Winning bid

¥100/ Nm3

¥280/ Nm3

Delivery conditions of winning bid

Transport twice a week

Total of 6 transports

CONTEXT: Tokyo has set up a trial exchange to trade specifically green hydrogen; suppliers and users bid, and the govt covers the price gaps between them. The first bid was held in December 2024. One supplier won the bid at a common price of ¥300 for both courses. On the user side, two companies won in the trailer category at ¥89/Nm³, and two companies won in the cradle category at ¥230/ Nm³.

TAKEAWAY: Although the bids show the vast gap between what producers can offer and what users are willing to pay, this also brings necessary transparency to green hydrogen pricing, at least in the domestic context. This valuable reference price can be utilized by both the supplier and user sides to plan for the future, and for the government to understand the scale of public support needed to bridge the cost gaps between fossil and green fuels.

In 2027, Suntory Holdings plans to enter the green hydrogen business, collaborating with Yamanashi Pref and local firms to establish Japan’s first integrated model from production to sales.

Suntory plans to start production of green hydrogen at its facility in Hokuto; annual capacity 2,200 tons.

The company unveiled a “vision” for the green hydrogen business based on what it claims will be the largest domestic green hydrogen production site with a 16 MW facility. Suntory is working with Toray Industries, TEPCO and TEPCO Energy Partners, Kanadevia, Siemens Energy, Kaji Tech, Miura Co., Nichicon, and the Yamanashi Hydrogen Company.

Using its Yamanashi Model P2G (Power-to-Gas) system, which makes hydrogen from power delivered via renewable energy sources, Suntory plans to expand supply to local consumers and Tokyo-based businesses.

TAKEAWAY: Suntory’s production plans were largely unveiled last year, but the company is taking steps to promote the move as more than a green branding exercise. The drinks maker and the regional authorities want to spread the use of green hydrogen to a wider set of manufacturers in Yamanashi, which would help build up the local transportation and storage infrastructure and lower costs for all parties.

In a world-first breakthrough, a Tokyo University research team led by Professor Nishibayashi synthesized ammonia at room temperature and atmospheric pressure using only nitrogen from air, water, a reducing agent, and light.

This method bypasses fossil fuels and avoids CO2 emissions, making it a potential game-changer for clean energy production.

Unlike the century-old Haber-Bosch process that needs high temperatures and fossil fuel-derived hydrogen, the new method relies on nitrogen-fixing bacteria in roots.

TAKEAWAY: If made practical, this technology could decentralize ammonia production, such as installing synthesis devices in vehicles or homes, where sunlight, air, and water can be converted into ammonia fuel on-site, opening the door to “making energy from air.”

The Kushiro municipal govt officially stated opposition to large-scale solar projects that do not harmonize with the local environment.

While the city supports the energy transition, it wants to protect natural ecosystems, including the Kushiro Wetlands, a national park.

TAKEAWAY: This decision aligns with the trend in many localities of switching to smaller scale solar projects, due to a combination of economic, regulatory, environmental and other factors. One reason developers are moving away from large-scale projects is limited land availability. Such projects also face local opposition due to visual impact, land use conflicts, and environmental degradation. While this is common globally, the opposition is stronger in Japan due to the mix of factors such as environmental sensitivity and land scarcity.

TEPCO, in partnership with Hong Kong real estate giant ESR Group, has secured financing of ¥1.1 billion from Taiwan’s Bank SinoPac for a 10 MW rooftop solar project in Singapore.

The JV seeks ¥3.9 billion to support a total capacity of 40 MW. Multiple corporate PPAs have been signed.

CONTEXT: TEPCO aims to deploy 100 MW of rooftop solar across APAC.

TESS Engineering began supplying 100% renewable electricity to facilities of machine tools manufacturer DMG Mori’s Iga and Nara via on-site solar PPA systems.

A total of 16 MW of solar capacity has been installed, covering about 30% of each site’s annual power needs.

Both sites are equipped with batteries to store surplus energy and provide emergency backup power during outages.

TAKEAWAY: The project reflects a growing interest in PPAs involving large-scale solar installations that cover entire factory or facility rooftops.

Aisin began a demo of perovskite solar panels at its Anjo plant in Aichi Pref. The panels weigh one fifth and cost one-hundredth to install compared to conventional units. They can be mounted on walls, pillars, or roofs using ordinary screws.

Aisin plans to conduct a one-year trial, aiming for test sales in 2028, and full commercialization by 2030.

CONTEXT: PSCs are mainly made with domestically sourced materials like iodine, which aligns with Japan’s economic security goals.

Aisin also launched a joint experiment with construction firm Obayashi Corp, testing durability and ease of installation methods. Future targets include sales to factories and warehouses, with further expansion to homes and vehicles.

The Kyoto University startup, Enecoat Technologies, is building its first mass-production plant for flexible perovskite solar cells in Uji City, Kyoto Pref, aiming to launch output in summer 2026.

Investing about ¥10 billion, the startup targets high-value applications like vehicle-mounted solar panels.

Enecoat collaborates with Toyota to develop solar roofs for EVs, having achieved 30% conversion efficiency in small cells.

CONTEXT: As competition increases, including from Sekisui Chemical, Panasonic, and Chinese firms, Enecoat has focused on high-end, automotive applications.

Kobe municipal govt installed perovskite solar cells within the restricted area of Kobe Airport, the first at an airport in Japan.

The project has 50 lightweight, 1-meter square film panels, placed on weed-control sheets. In partnership with Sekisui Chemical, the demo runs until March 2027.

The goal is to explore renewable energy use in urban areas with limited space.

Daiwa Energy & Infrastructure (DEI) acquired a 49% stake in two large-scale battery energy storage projects under development by Enfinity Global: 250 MW in Texas and 130 MW in Italy.

This is DEI’s first investment in Italy. The projects begin operations in late 2026.

Singapore-based renewables firm Gurīn Energy will collaborate with France’s Saft on providing BESS for its first Japanese project in Soma City, Fukushima Pref.

This will provide over 1 GWh of storage to help integrate renewables into Japan’s grid.

The BESS will be installed, commissioned and serviced by Saft, a wholly-owned subsidiary of TotalEnergies.

The project is expected to provide over 240 MW of power for four hours. Construction begins in 2026.

CONTEXT: Demand for energy storage is on the rise and is crucial to achieve Japan’s goal of 40-50% of renewables in its national energy mix by 2040.

Sungrow Japan won an order from Toshiba Energy Systems for battery storage systems for two large-scale projects in Sapporo, totaling 100 MW installed capacity and 351 MWh of storage capacity. This is among the largest in Japan.

The projects, led by Kansai Electric, JA Mitsui Leasing, and Sparx Group, aim to start operations in April 2028.

Sungrow’s cumulative grid-scale storage orders in Japan now exceed 1.2 GWh.

SIDE DEVELOPMENT:

Sun Village signs key deals with SMFL, JIF to advance grid-scale BESS projects

(Company statements, June 3 / June 6)

Sun Village inked two key deals to advance grid-scale BESS in Japan:

With SMFL Mirai Partners, Sun Village agreed to transfer three high-voltage battery storage assets (each 2 MW / 8.3 MWh) in Mie and Fukushima Prefs. These facilities will begin operation later this year or early next, participating in Japan’s wholesale, balancing, and capacity markets.

With the Japan Infrastructure Fund, Sun Village agreed to develop grid-scale BESS and convert FIT solar plants (especially in output-constrained Kyushu) to the FIP with battery additions.

Kyushu Electric will cooperate with Ocean Power Grid to develop electricity storage vessels. The startup is a subsidiary of PowerX.

The vessels are designed to store electricity generated from sources like offshore wind and deliver it to areas of demand. The first vessel is scheduled for completion in 2027.

CONTEXT: Use of these vessels would efficiently utilize excess power in island regions not connected by undersea cables. Kyushu Electric began collaborating with PowerX on maritime power transmission in 2023.

TAKEAWAY: PowerX sees batteries as a useful technology for short-distance marine transport. The company’s current manufacturing focus is on grid-scale batteries but as Japan’s renewables sector expands in the 2030s through offshore wind, it believes the market opportunities will open in this field also. For offshore wind developers, there may be several options to consider, however, and the economics of ships as ‘electricity carriers’ has yet to be tested.

(Company statement, Government statement, June 10)

GE Vernova International inked an MoU with Eurus Energy to promote renewables and build data centers (DC) in north Hokkaido.

In the area of Wakkanai City, Eurus will explore building large renewable-powered DCs with GE Vernova.

CONTEXT: Eurus is developing five wind farms in north Hokkaido, totaling 1.8 GW of capacity. These wind farms could power DCs.

GE Vernova and METI also launched a public-private framework to cooperate on supply chain development, energy security, and innovation, focusing on wind power, hydrogen and ammonia, CCS, power grid improvements, and nuclear power.

CONTEXT: Former METI Minister Saito Ken, a member of the House of Representatives, spoke at the Energy Forum.

He pointed out that renewable energy discussions began before the March 2011 Fukushima nuclear disaster. The FIT system was approved by the cabinet on the morning of the earthquake, before the disaster occurred.

Japan used to be a leader in solar panel technology, but most solar panels are now manufactured in China, which dominates global markets with low-cost products.

Japan’s loss of competitiveness is partly due to its preference for cheaper foreign products. However, China’s practices are considered unfair. There is a debate about whether Japan should use subsidies to protect domestic jobs and technology; but doing so could lead to a subsidy war.

Japan Nuclear Fuel (JNFL) expects to complete its nuclear fuel reprocessing plant in Rokkasho in FY2026.

CONTEXT: The facility was originally scheduled for completion in 1997, but the plant has since faced 27 delays.

The facility currently holds about 99% of its 3,000-ton capacity of spent nuclear fuel. Due to the delays, power companies have to store spent fuel on-site at their plants.

KEPCO revised its spent fuel shipment plans based on the 2026 target. It received approval from Fukui Pref, which allows continued operation of three aging reactors: Takahama units 1 and 2, and Mihama unit 3. An NRA review is ongoing.

CONTEXT: The nuclear fuel reprocessing plant will extract uranium and plutonium for reuse in power generation. Thus, Japan considers the Rokkasho plant as a vital facility in its nuclear cycle.

TAKEAWAY: Given the many past delays, concern around the plant’s operations persist. This has had repercussions on the EPCOs. For example, KEPCO placed the facility’s completion at the center of its spent fuel management plans, trying to assure Fukui Pref that it will eventually send the spent fuel outside of the prefecture borders. Still, continuing to rely on Rokkasho’s plant completion has led critics to question KEPCO’s intentions.

A meeting of the 7th Spent Fuel Countermeasures Promotion Council highlighted the govt’s priorities in advancing the nuclear fuel cycle and spent fuel management.

It called for continued safety reviews. On the Rokkasho reprocessing plant, it urged JNFL to adhere to its plans.

Tohoku Electric secured approval for a dry storage facility at Onagawa Unit 2 (targeting 2028/2032 operation).

KEPCO applied to the NRA to install a second dry storage facility at Takahama NPP in Fukui Pref. The first facility received approval in May, and the company aims to have the second one operational around 2030.

Dry storage facilities hold spent nuclear fuel removed from cooling pools. KEPCO says they’re necessary to help the smooth transfer of spent fuel to interim sites.

CONTEXT: KEPCO is also applying for the Mihama and Oi NPP. The company has now completed all planned applications for dry storage facilities.

TEPCO got NRA approval for test operations of safety systems at Unit 6 of Kashiwazaki-Kariwa NPP.

CONTEXT: This is needed to confirm the plant’s status before restart.

TAKEAWAY: After the announcement, investor sentiment toward TEPCO turned bullish. With Unit 6 closer to restart, TEPCO hopes for a financial recovery. Also, local political support emerged for Tokai No. 2, with the mayor supporting a restart if regulations are met.

Kyushu Electric inspected a valve that caused an error on June 3, as well as three other valves.

After resuming generation, the plant will do adjustment operations to confirm performance. After increasing output, it will complete a comprehensive load performance test by July 10, and then the plant will return to normal operation.

CONTEXT: Genkai NPP Unit 3 is under its 18th periodic inspection since March 28.

Hokkaido Electric plans to build a port as part of safety measures for the Tomari NPP Unit 3. Located outside the NPP premises, it will serve nuclear fuel transport ships.

This contained port would prevent drifting of vessels during a possible tsunami.

CONTEXT: Tomari NPP Unit 3 aims to restart in 2027. Port construction will begin soon after and take around four years. In January, the utility proposed building the external port in response to regulator concerns. In April, the NRA issued a draft review indicating the plant passed its safety inspection.

JERA will boost purchases of U.S. LNG, seeking to triple supply up to 10 Mtpa by the early 2030s. This will raise the U.S. share in JERA’s LNG imports from 10% to 30%.

JERA has agreed to buy up to 3.5 Mtpa of LNG from three U.S. suppliers: Sempra Infrastructure (Port Arthur Phase 2, Texas) – 1.5 Mtpa; Commonwealth LNG (Louisiana) – 1 Mtpa; and Cheniere Energy (Corpus Christi, TX & Sabine Pass, LA) – 1 Mtpa. This is in addition to the 2 Mtpa deal with NextDecade’s Rio Grande project in Texas.

Annual value of these deals is about ¥400 billion ($2.76 billion).

CONTEXT: Japan is diversifying supplies due to uncertainty over future Russian LNG supply and dependence on Australia. It also reflects U.S. efforts, particularly under Trump, to expand LNG exports to allies.

Despite U.S. pressure, JERA remains hesitant about investing in Alaska’s $44 billion LNG project, citing complex conditions. Currently, JERA’s U.S. LNG sourcing comes from the Gulf Coast.

CONTEXT: While contracts with NextDecade and Commonwealth are binding, those with Sempra and Cheniere are not. Together they total 5.5 Mt of LNG per year. Since JERA aims to buy 35 Mtpa of LNG by 2035, this is more than 15% of the target.

TAKEAWAY: JERA’s deals, like Kyushu Electric’s long-term deal with Lake Charles, are no surprise. JERA said it was considering reducing dependence on Australian imports through more U.S. supply. The latter is seen as more reliable and, with Trump in the White House, it’s likely that LNG projects in the U.S. will continue to receive quick approvals. At this point, the various deals could be seen as a cautious rebalancing of the portfolio. Is JERA saving some of its powder for the Alaska LNG project, or is it waiting on improved terms from non-U.S. supply? Either way, decisions on the future of Japan’s LNG sourcing from Russia’s Sakhalin projects will need to be made this year.

Mitsubishi Corp will begin importing LNG from Canada in the coming weeks; this is that country’s first large-scale LNG export to Japan.

The gas will come from the LNG Canada Development facility in British Columbia, owned by Shell, Petronas, China National Petroleum Corp, Korea Gas Corp, and Mitsubishi.

CONTEXT: The latter holds a 15% stake in the project and has secured 2.1 Mtpa in offtake. With it, Mitsubishi’s total LNG capacity will expand from 12.8 to 14.9 Mtpa.

TAKEAWAY: Japan’s reliance on LNG from Australia (38% in FY2024) highlights the need for diversification. These deals increase buying options and reduce supply risks. Canadian LNG offers logistical advantages: shorter shipping times (10 days) and a route that avoids choke points like the Panama Canal. Also, U.S. policy on LNG may shift after Trump, while imports from the Middle East could be impacted by hostilities. All of this makes Canada’s LNG supply very attractive for Japan.

Mitsui O.S.K. Lines (MOL) and Samsung Heavy Industries received Approval in Principle (AiP) from Lloyd’s Register for a LNG carrier. It is equipped with a 300kW solid oxide fuel cell (SOFC) supplied by Bloom Energy.

The vessel will be delivered in FY2027, and use SOFC as an auxiliary power generator.

CONTEXT: SOFCs convert fuels like natural gas, hydrogen, methanol, or ammonia into electricity and heat. There is no combustion, so it reduces GHG emissions, NOx, SOx, and methane slip.

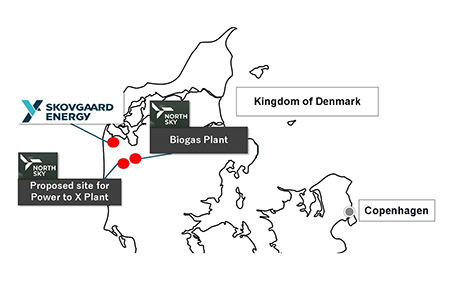

Sumitomo created a JV with Danish firm Skovgaard Energy to produce biogas, as much as 40 million Nm3 of per year, mainly using cattle manure, and also to develop e-SAF using biomass-derived CO2 and green hydrogen.

This is Sumitomo’s first step into biogas production, aligning with Denmark’s goal of 100% biogas in its national gas grid by 2030.

As of June 8, the LNG stocks of 10 power utilities were 2.34 Mt, up 4% from the previous week (2.25 Mt), up 9.9% from end June 2024 (2.13 Mt), and down 11.4% from the 5-year average of 2.1 Mt.

CONTEXT: Tokyo area’s rainy season has officially begun. It usually lasts until mid July.

METI discussed govt-business risk-sharing in support of the CCS sector, by covering the cost gap between actual CCS costs and mitigation costs.

At first, it will focus on pipelines, and then, separately consider ship-based transport. This long-term support would end when CCS becomes more cost-effective.

Support will cover capital and operational costs per ton of CO2, calculated as the difference between a standard price and a reference carbon price.

METI will select projects on a yearly basis, based on value and not only bid price, with early CAPEX support available. After the support period, companies must continue operations for the same duration or repay the funds.

Asuene and Daikin Industries will cooperate on decarbonization and energy efficiency services in Japan and North America.

As part of Asuene’s Series C2 funding round, Daikin invested through a third-party allotment, bringing Asuene’s total funding to ¥10.6 billion.

The partnership will combine Asuene’s CO2 tracking and consulting services with Daikin’s HVAC and building management solutions to offer integrated, end-to-end decarbonization support.

By 2028, Seiko Epson will launch compact carbon capture devices, about the size of office copiers. Epson’s machines don’t need heat, lowering energy consumption.

They will be using a 10-nanometer film based on inkjet printer technology to capture CO2 from factory exhaust or from the air.

CONTEXT: Estimates say Japan’s carbon capture market will grow from $12.6 billion in 2030 to $245 billion in 2050. KHI has also developed a compact unit capturing over 5 kg/ day of CO2 from the air.

ANALYSIS

BY JAPAN NRG TEAM

Power, Politics, and Patience: Inside Japan’s 2025 Energy Shift

Four months after Japan signed off on its revised energy strategy, the government shows little sign of deviation — despite mounting geopolitical frictions, war-driven supply risks, and policy reversals elsewhere. Tokyo’s stance is pragmatic: it remains committed to the long slog of energy transition, but not at the expense of economic stability or energy security. Japan, in effect, is walking a narrow path between resilience and reinvention.

Already in 2025, developments are piling up across the sector. Power trading volumes are surging as derivatives markets deepen. Interest in grid-scale batteries is rising — but so are doubts about the profitability of some subsidized BESS projects and their grid connection.

Meanwhile, Japan is nudging forward with a hydrogen subsidy scheme few currently fully understand and fewer still will be able to access and build around. Nuclear plants are edging back online, though coal and gas seem to remain indispensable. The power grid is due for a long-awaited upgrade.

The following outlines key movements in Japan’s energy landscape this year, from LNG and nuclear to electricity markets, hydrogen and ammonia. The themes are familiar: slow acceleration, cautious innovation, and a government hoping that coordination can do what speed alone cannot.

Yuriy Humber

Policy and Strategy

Strategist’s memo: Signals amid the summer haze

Japan’s energy policy remains largely on track, with ministries rolling out subsidy frameworks, auction tweaks, and infrastructure reviews across the power, hydrogen, and grid sectors. Execution remains uneven, but directional commitment is clear.

The macro backdrop is giving Tokyo breathing room. Global energy prices are lower YoY, and the yen’s 9% strengthening helps offset import costs on paper. But that’s not how it feels to households: gasoline prices are up over 6% YoY and more persistently elevated than at any point since 1990. The government’s move to reintroduce fuel subsidies is more political than economic.

Electricity price volatility has been muted since the shocks of 2021–22, but summer 2025 may bring a spike. Demand is higher during hot months, and the forecast calls for a hotter-than-average July–September, with uncertainty over rainfall in East Japan. Markets may test the system’s resilience just as policymakers are refining reforms.

Politically, Prime Minister Ishiba heads into the July Upper House election with weak but steady support. His government has positioned itself as a stabilizing force amid trade friction with Washington, where LNG diplomacy is back in vogue, and is doubling down on ties with Europe. Japan remains open to new energy partnerships, especially in hydrogen and grid innovation, but is wary of repeating past overcommitments.

Magdalena Osumi Renewables (Wind Power / Solar Power / Energy storage)

WIND POWER

Japan passes a bill allowing offshore wind projects in its EEZ

METI / MLIT discusses further support for projects awarded via public tender

Developers reassess projects in the pipeline amid economic challenges

The Diet passed a bill amending the Act on Promoting the Utilization of Sea Areas, enabling offshore wind projects to be developed in Japan’s Exclusive Economic Zone (EEZ), both fixed-bottom and floating technologies. Spanning about 4.48 million square kilometers, the EEZ is more feasible for development due to fewer permitting conflicts with stakeholders such as fisheries or local governments.

This news comes at a critical time, as Japan’s offshore wind sector faces headwinds due to a weak yen, rising global costs, and an uncertain regulatory framework. Earlier this year, a consortium led by major trading house Mitsubishi, winner of Round 1 of a public offshore wind tender, announced its possible withdrawal, casting doubt on its awarded projects.

On June 3, METI and MLIT discussed support following feedback on revised auction guidelines. A key issue was whether Round 1 projects, originally awarded under the Feed-in Tariff (FIT), should be allowed to transition to the Feed-in Premium (FIP). This faces strong opposition from some stakeholders who argued it could erode trust in the policy process.

Developers also raised concerns about the need for improved offtaker support and clearer mechanisms for adjusting prices in zero-premium FIP projects. Without enhanced state support, industry players warn of broader delays and supply chain disruptions, especially affecting Round 2 and Round 3 projects.

Japan NRG discussed these challenges in more detail, including floating wind and regulatory hurdles, in recent issues on February 25 and April 14.

SOLAR POWER

Agrisolar projects and rooftop solar installations on the rise

Perovskite cells promoted as a new driver for renewables

Regulations delayed in mandating recycling of end-of-life solar panels

Japan needs to install at least 7 GW of solar power annually

With limited suitable land for large-scale solar warms, Japan is boosting agrisolar and rooftop solar installations. Both options help to grow total renewables capacity without taking up any more land. Also toward that goal, Japan is betting on perovskite solar cells, particularly film-type technologies. Sekisui Chemical, Toshiba, Kaneka, EneCoat Technologies, and Aisin are among key players in this field.

JERA, Sekisui Chemical, and Sanko Metal Industrial launched a PSC demo at a thermal power station in Kanagawa Prefecture in late May. Earlier that month, ANRE unveiled plans to boost demand for next-gen PSCs. More on this in the March 10 issue.

Momentum is also building around both on-site and off-site power purchase agreements (PPAs), including virtual PPAs, reflecting growing corporate demand for decarbonized power.

In the context of the rapid expansion of data centers, Japan must significantly scale up solar deployment, between 5 to 7 GW annually by 2030. From 2030 onward, annual installations must ramp up to 10 to 16 GW (AC) to reach between 203 and 280 GW (AC) by 2040.

While concerns continue to arise in Japan over mass disposal and landfill use of solar panels, which are expected to reach the end of lifespan in the 2030s, the government has yet to clarify who is responsible for their disposal. The MoE and METI decided to delay the implementation of legislation mandating solar panel recycling.

BATTERY ENERGY STORAGE

BESS wins big in the the second clean capacity auction (LTDA)

Battery players grow skeptical over profitability of some LTDA projects

Government shifts focus to longer duration energy storage / batteries, while developers see technological and economic challenges

Japan sees renewed interest in alternative battery technologies

Recent developments in Japan’s renewable energy sector highlight a growing demand for battery energy storage systems (BESS), driven partly by transmission constraints and the need to stabilize variable renewable output across a fragmented grid system.

In the second round of the Long-Term Decarbonized Power Sources Auction (LTDA), 27 out of the 38 winning bids were BESS projects. While most projects offer storage durations of 3–6 hours, only six included systems capable of operating for 6 hours or more. Results suggest that the current design of the LTDA scheme may be losing appeal, particularly as developers confront mounting economic and technological challenges.

Developing BESS with durations beyond six hours presents significant challenges. Most commercial systems use Li-ion batteries, which are optimized for 1–4 hour applications. Extending operation to 6+ hours introduces risks such as thermal management issues, faster battery degradation, and reduced efficiency.

Longer-duration BESS requires significantly more storage capacity, leading to higher capital costs without guaranteed returns. To make such projects viable, developers must combine multiple revenue streams (arbitrage, grid services, capacity payments). In response, interest is growing in non-traditional battery chemistries and configurations, for instance using nickel, signaling a shift toward more diverse and flexible energy storage solutions.

Conventional energy, low-carbon technologies

Filppo Pedretti

LNG

JERA is boosting long-term U.S. LNG imports to around 30% of supply by 2030

Japan mulls joining Alaska LNG project, despite cost and viability concerns

Mitsubishi-backed LNG Canada due to deliver first cargo to Japan by July

Japan’s LNG trading strategy shifts from imports to regional supply role

For Japan’s LNG sector, the most important news comes from the other side of the Pacific. The U.S. will boost LNG production by supporting shale gas and fossil fuel expansion. More LNG coming from the U.S. via contracts without destination clauses, also a political necessity to ease Trump’s tariffs, indicates that Japan will sell more of this LNG to third-countries. Domestically, the country is facing declining LNG demand as nuclear power reactors come on-line, along with expanding renewables capacity.

A key part of Trump’s LNG policy revolves around the Alaska LNG project, which should transport gas to Asia via pipeline. Construction should begin in 2026 and production in 2031. Japanese investors are reported to be considering participating in it, but there are worries about cost overruns and competitiveness compared to alternatives. LNG Canada, for example, is about to start shipping the fuel to Japan. The Mitsubishi Corp-backed project is already looking to expand capacity in the future.

Overall, Japan will focus less on procurement and more on strengthening its LNG trading capabilities.

NUCLEAR POWER

Latest clean capacity auction has three nuclear reactors among the winners, signaling renewed policy support for the sector

TEPCO wins regulator clearance for test operations at Kashiwazaki‑Kariwa NPP, but utility struggles to restart it earlier than this winter

Japan Atomic’s Tokai No. 2 NPP edges closer to restart after passing NRA review and local mayor’s endorsement

Japan’s youngest reactor, Tomari NPP Unit 3, cleared NRA screening after 11 years

In April, OCCTO’s Long-term Decarbonized Power Sources Auction signaled a renewed push for nuclear energy in Japan. Among the winners were three nuclear reactors – Tomari 3, Kashiwazaki-Kariwa 6, and Tokai No.2. For TEPCO.

TEPCO is pushing for the restart of either Units 6 or 7 of Kashiwazaki-Kariwa.In the meantime, public hearings in Niigata Pref through August 31 suggest no decision until fall. This means, best scenario dictates operations will restart during winter.

TEPCO also has stakes in Tokai No. 2, operated by Japan Atomic Power (JAPC). The town’s mayor recently stated that he will support a restart, provided consent from the govt and safety is guaranteed.

Further north, Tomari 3, operated by Hokkaido Electric, received NRA safety approval after 11 years. Final clearance and local consent are pending, but restart is set to FY2027.

Electricity markets, hydrogen/ammonia

Tetsuji Tomita

ELECTRICITY MARKETS

METI launched a new subcommittee to design next-gen electricity systems and improve market structures

OCCTO started reviewing long-term cross-regional grid plans

Officials debate the structure of a future “Simultaneous Market” to combine spot, balancing and capacity trading

ANRE plans new funding tools to develop large-scale regional and interregional grids

MIC and METI launched a public-private council to align power and telecom infrastructure for data center growth

In late March, METI/ ANRE completed a review of the electricity system reform and outlined measures for addressing issues. In May, a new subcommittee launched and discussions on the system design began. The main points concern the institutional, market, and competitive environments of power industries in order to develop next-gen energy systems.

OCCTO began discussing the long-term outlook for cross-regional grid development review. In preparation for the third master plan, it will discuss whether to revise the assumptions and scenarios in the current long-term outlook. The policy includes the ideal state of the nationwide grid systems over a 10-year period and the approach to achieving it.

Japan’s current two-market system has become increasingly inefficient; thus, a “Simultaneous Market” to integrate these two markets is now considered. The 7th Basic Energy Plan outlines frameworks to promote the development of regional grids and measures to facilitate financing for large-scale interregional power connections.

In March, the Ministry of Internal Affairs and Communications (MIC) and METI launched the Public-Private Council on Watt-Bit Coordination Roundtable to shepherd stakeholders in the power and communication sectors into coordinating their activities, aiming to improve the efficiency of new infrastructure built to support data centers.

HYDROGEN / AMMONIA

Japan launched ¥3 trillion CfD scheme to subsidize clean hydrogen/ammonia supply; initial round over-subscribed with both domestic and overseas projects in the running

Initial CfD application window closed in March, but a separate hub development support program is open to late June

Next year’s clean capacity auction (LTDA) to be revised to give more favorable terms for power plans keen to switch to hydrogen or ammonia

After the Hydrogen Society Promotion Act took effect in October 2024, government initiatives aimed at establishing a low-carbon hydrogen supply chain began, including “support focusing on price differences (CfD)” and “hub development support.”

Applications for the CfD program closed at the end of March and are currently under review. Applications for the Hub program are being accepted until the end of June.

The government is discussing updates for the third round of the Long-Term Decarbonized Power Sources Auction (LTDA) in FY2025. The target power sources include hydrogen/ ammonia co-fired thermal power. Due to the maximum bid price, companies found it difficult to participate. Therefore, the maximum price for hydrogen and ammonia fuels will be raised.

ANALYSIS

BY GEORGE HOFFMAN

Modular Data Centers Seek to Reshape Japan’s AI Infrastructure Boom

As demand for AI explodes, so does the need for new infrastructure. But building a conventional data center can take three to five years – an eternity in the age of generative AI, where chip designs evolve every quarter and competitive advantage can hinge on milliseconds.

One Japanese firm, Getworks, thinks it has a faster answer. Rather than constructing massive hyperscale facilities from scratch, the company assembles modular, container-style data centers in factories and ships them out for near-instant deployment. It’s a plug-and-play model for the AI age – compact, mobile, and quick to install.

Getworks is not alone in recognizing the opportunity. Japan’s digital infrastructure is straining under a perfect storm of forces: surging AI workloads, growing cloud adoption, and aging corporate IT systems. As the government pushes for “digital transformation” and firms rush to modernize, the country faces a compute crunch. Modular data centers – faster to build, easier to cool, and more flexible in where they operate – offer one possible solution.

Speed, however, is only part of the appeal. Getworks also seeks to align with broader shifts in energy and infrastructure policy. Its container units are designed to run on distributed renewable sources, such as solar and biomass, and to be sited in regions with surplus power – rather than adding to the load in grid-congested cities. That decentralization model, if it scales, could support both carbon goals and resilience against grid strain or seismic disruptions.

With public cloud spending expected to double by 2029 and GPU server demand rising at over 40% a year, Japan’s data center market is poised for transformation. The race to create that new infrastructure is on.

The AI-fueled GPU surge

The rise of generative AI has transformed GPUs (graphics processing units) from a niche tool for research labs into a central pillar of modern computing. Once the domain of university clusters and deep-pocketed startups, GPU servers are now being snapped up by sectors ranging from pharma to finance, as companies race to build, fine-tune, or deploy large language models (LLMs).

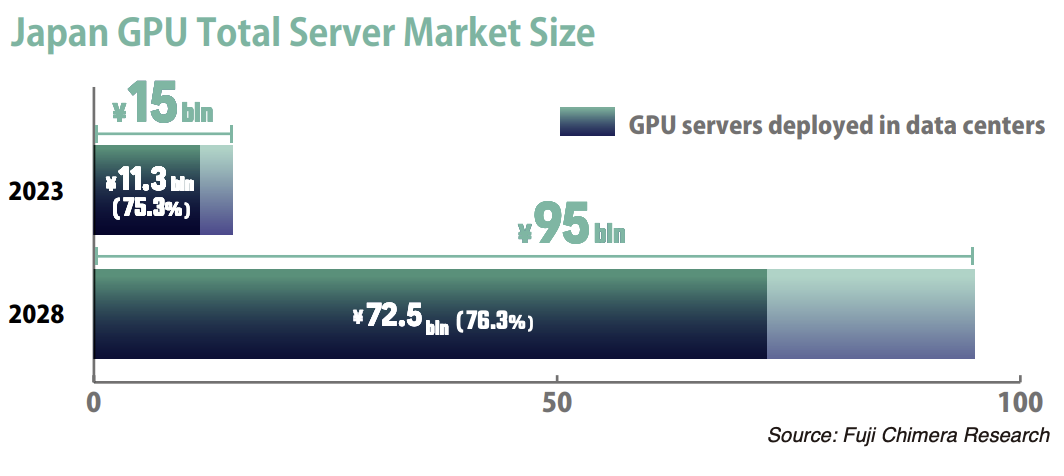

Japan is no exception. The domestic GPU server market is projected to grow at 44.7% annually between FY2023 and FY2028, reaching ¥95 billion in shipment value, according to Fuji Chimera Research. By then, more than 75% of those servers will be deployed inside data centers.

It’s not hard to see why. GPU servers are purpose-built for compute-heavy tasks like AI model training, robotics, autonomous driving, and scientific simulation. But their appetite for electricity and cooling makes them unsuitable for most corporate server rooms. A single high-end GPU server can consume the same power as 40 conventional CPU servers – while generating significantly more heat in the process.

As a result, deployment is shifting toward dedicated data centers, whether collocated or cloud-based.

Power and cooling

As Japan’s AI ambitions scale up, its power grid is feeling the strain. GPU servers don’t just demand more energy – they concentrate that demand in smaller spaces, producing intense heat loads that push conventional cooling systems to their limits.

Industry figures point to a coming crunch. IDC estimates that a single hyperscale deployment focused on GPUs could soon require more than 200 MW of dedicated capacity – roughly equivalent to the power usage of 170,000 Japanese households. That figure covers compute loads alone; cooling, networking, and backup systems add yet more pressure.

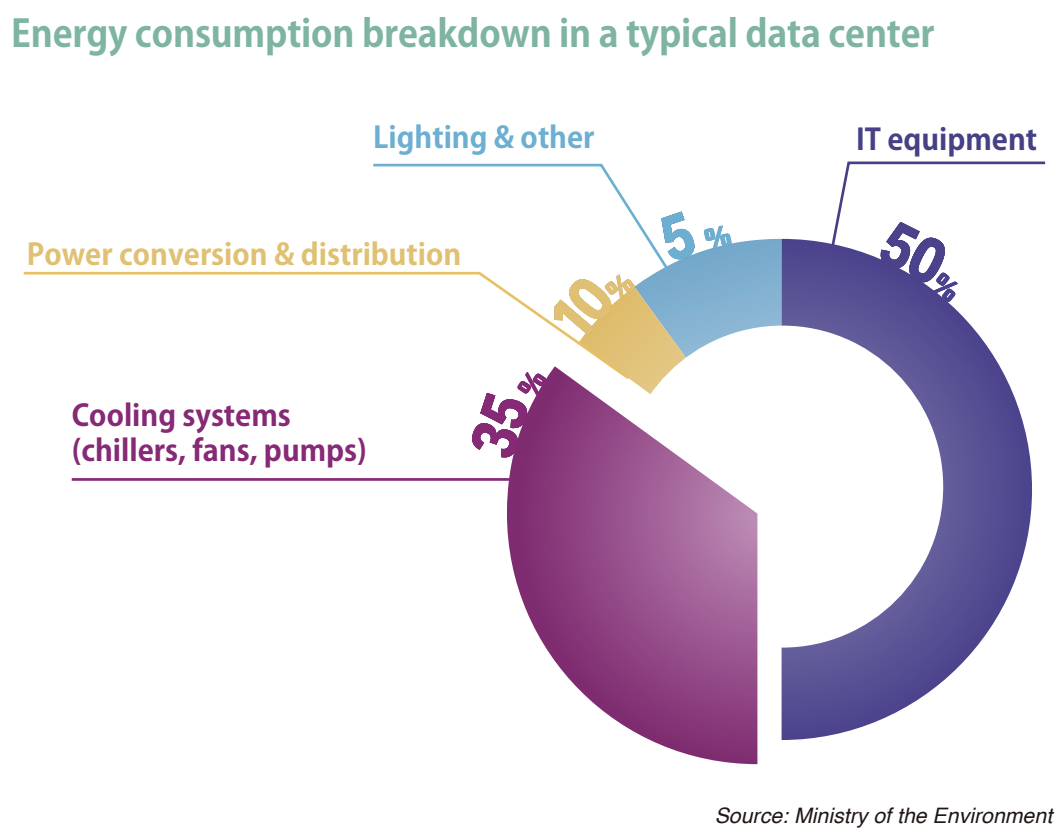

In a typical data center, cooling accounts for 30–40% of total electricity use. Chillers, fans, and pumps keep servers from overheating – but they also drive up costs and reduce efficiency. Japan’s older data centers, designed before the AI boom, often lack the capacity or layout flexibility to accommodate new cooling technologies.

Liquid cooling and immersion systems are gaining popularity internationally for their efficiency and smaller footprint. But adoption in Japan remains sluggish. One barrier is technical: low-temperature water systems risk condensation unless carefully engineered. Another is fragmentation: server makers still use different specs for pressure, flow, and temperature, which complicates data center design.

Firms like Getworks argue that starting from a clean slate offers an advantage. Its units are preconfigured for liquid cooling and optimized for high thermal loads. Whether this makes a measurable impact on power usage effectiveness (PUE) across deployments remains to be seen. But in a market where the ability to cool efficiently can make or break a facility, design choices matter.

Modularity and decentralization as an edge

Unlike the vast plains of the American Midwest or Northern Europe, Japan is a mountainous archipelago with dense urban cores and limited land availability. Its major population and business hubs are far from the renewable-rich regions of Hokkaido or Kyushu, where solar, wind, and biomass generation is concentrated.

That mismatch creates bottlenecks. Grid congestion during peak solar production in summer, strain from urban energy demand, and vulnerability to seismic disruptions all make centralized data center construction a risky, expensive proposition. The government, keen to diversify and decentralize digital infrastructure, is offering support for regional computing hubs that can operate independently from the big city Tokyo-Osaka axis.

Modular data centers fit this vision. Because they are built off-site and assembled quickly, they can be deployed in remote or infrastructure-limited areas. Their compact size and flexible siting requirements allow them to piggyback on local energy sources or integrate directly with surplus renewables. For companies looking to reduce latency, improve resilience, or bypass grid constraints, that flexibility is attractive.

Getworks is attempting to position itself as a solution. Its container-based systems are designed to run on 50–500 kW per unit, allowing clients to scale up gradually or deploy in clusters. The firm says it is fielding inquiries for multi-megawatt projects, including from clients seeking alternatives to long construction timelines or expensive real estate in urban cores.

As Japan’s data center market shifts from a handful of hyperscale builds to a more distributed network of edge and regional nodes, modular approaches may offer a middle path: fast-to-deploy, semi-permanent infrastructure that can grow alongside demand.

Green ambitions and energy trade-offs

Most data centers still rely heavily on grid power, which in Japan’s case comes largely from gas and coal-fired generators. In rural areas, limited transmission infrastructure makes large-scale expansion difficult.

Getworks sees an opportunity in this mismatch. The company prioritizes renewables integration into its modular facilities, aiming to site them near solar, biomass, or other distributed energy sources. This is not purely a climate play. For many locations, clean energy is the only viable source of capacity – especially for rapid-deployment builds far from city grids.

To burnish its green credentials, the company also incorporates liquid cooling and even groundwater-based heat exchange – a rare method in Japan. By drawing water from wells to manage server temperatures and recycling waste heat, the company hopes to cut energy overhead and improve PUE. Whether these systems can be scaled cost-effectively across multiple deployments is yet to be tested.

Source: Getworks

Conclusion

Japan’s digital future is arriving faster than its infrastructure can keep up. As companies race to deploy generative AI, modernize legacy IT systems, and absorb ever-growing volumes of internet traffic, demand for data center capacity is outpacing supply.

Container-based data centers won’t replace hyperscale campuses, but they could play a vital supporting role. Their speed, modularity, and adaptability make them well-suited to regions where land is scarce, energy is constrained, or compute demand is fragmented. In Japan’s underdeveloped mid-sized data center segment, they may help fill the gap.

They also represent a potential new class of customer for renewables developers. Unlike urban hyperscalers tethered to congested grids, modular data centers can be deployed closer to wind, solar, or biomass assets in rural areas, and connected through PPAs. That pairing could make the economics of clean power more viable outside Japan’s urban cores.

The above is a shortened adaptation of a GxxD series report titled “Cool. Scale. Compute.”

K.K. Yuri Group, the company that operates the Japan NRG platform, also publishes the GxxD series of research to cover the intersection of digital and clean energy technologies in Japan. To see more information about the series and the full version of the original report, please check: https://www.yuri-group.co.jp/gxxd

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Power bills

Cash-strapped citizens were warned the “cold hard truth” is that electricity prices will rise this winter; the average family will pay $1,830 more a year.

China / Oil

CNOOC launched production at Weizhou 5-3 Oilfield, which is located in the Beibu Gulf Basin, South China Sea.

China / Solar power

Solar panel producers grapple with oversupply and price reforms. The country’s top producers face billions of dollars in losses as competition has pushed prices below cost level.

China / Grid infrastructure

The Hami-Chongqing ±800 kV ultra-high voltage DC transmission project was launched, linking eastern Xinjiang’s Hami with Chongqing in the southwest.

India / Coal

Coal stockpiles are swelling as more and more renewable energy comes online, energy storage projects built, and a renewed push for nuclear.

Indonesia / Geothermal

PT Pertamina Geothermal Energy posted a net profit of $160 million for FY2024, down from $163.6 million in FY2023.

Laos / Energy policy

The govt announced four key strategies to expand domestic power generation and address the electricity shortage. The first measure is completing the Nam Ngum 3 Hydropower Plant.

Singapore / Subsea cables

Singapore Energy Interconnections and Kim Heng Ltd inked an MoU to operate, repair, and maintain subsea power cable systems installed in the ASEAN region.

South Korea / Energy policy

New president Lee Jae-myung is reviewing the national energy policy, aiming to rebalance nuclear regulations, without immediately shutting down reactors.

UAE / Power capacity

Total national power capacity is expected to hit 79 GW by 2035, growing at a compound annual rate of 3.4% from 2024, reports GlobalData.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS:

・Japan can play key role in transition finance in Asia

・300-400 high-emitting firms seen joining the GX-ETS carbon trading mechanism

・Higher biofuel blending to start in a few years

To burnish its green credentials, the company also incorporates liquid cooling and even groundwater-based heat exchange – a rare method in Japan. By drawing water from wells to manage server temperatures and recycling waste heat, the company hopes to cut energy overhead and improve PUE. Whether these systems can be scaled cost-effectively across multiple deployments is yet to be tested.

To burnish its green credentials, the company also incorporates liquid cooling and even groundwater-based heat exchange – a rare method in Japan. By drawing water from wells to manage server temperatures and recycling waste heat, the company hopes to cut energy overhead and improve PUE. Whether these systems can be scaled cost-effectively across multiple deployments is yet to be tested.