Rarely does the relationship in energy between Japan and Singapore garner much attention. But the two have a potent tandem that drives developments in Asian energy markets.

Japan’s technological prowess complements Singapore’s financial and logistical strengths.

ANRE published its review of electricity market reforms over the past decade. Results indicate success in achieving the main aims of ensuring a stable power supply, reigning in power rates, and offering consumers more choice.

Yet beneath this positive headline lies a critical challenge: how to ensure sufficient capacity and stability in increasingly complex power markets without giving up on the energy transition?

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

The Financial Services Agency (FSA) will postpone mandatory sustainability disclosure requirement for Tokyo Stock Exchange Prime-listed companies with a market capitalization below ¥500 billion. A final decision on whether to mandate disclosure for these companies will come within a few years.

The plan was to ask all Prime-listed firms to disclose sustainability data by FY2030. Now, the obligation will come in phases. Companies with market caps over ¥3 trillion must start in FY2026. Those between ¥1 trillion and ¥3 trillion in FY2027. And those between ¥500 billion and ¥1 trillion could need to start from FY2028, though that timeline may now change.

The FSA noted that about 45% of firms in the ¥500 billion–¥1 trillion range have foreign ownership above 30%. This is in contrast to less than 30% in the ¥300–500 billion range. Foreign investors tend to demand sustainability data.

CONTEXT: Sustainability disclosure is corporate information about environmental, social, human rights, and governance practices. While companies have included some of this in their securities reports, there were no clear standards until now. Starting FY2027, companies will need to disclose more detailed data. They include Scope 3 GHG emissions and climate-related risk strategies. This will be on the basis of new guidelines set by the Sustainability Standards Board of Japan (SSBJ).

Mitsui O.S.K. Lines (MOL), signed a MoU with Kinetics, a clean energy and infrastructure initiative by Karpowership, to develop the world’s first integrated floating data center platform.

The project will involve retrofitting used vessels into mobile data centers that will receive power from Karpowership’s LNG-fueled ships. It’s also possible to integrate onshore grids, solar farms, or offshore wind depending on location.

The first floating data center will launch in 2027, with a capacity of 20 to 73 MW. It will connect to land-based internet exchanges and submarine cables.

The vessel for the data center will weigh 9,731 tons, with a length of 120 meters.

TAKEAWAY: The offshore model offers several advantages – independent of local electricity supplies; and avoids the need for expensive and limited land acquisition in metropolitan areas. Also, while a typical land-based data center may take four years to build, the conversion of a used vessel takes about one year. And the floating platform allows for mobility. And yet, while this offers respite for a while, it’s not clear how much scale such offshore centers can offer in the longer-term.

J-Power and Hitachi inked an MoU to develop a renewable energy-powered AI data center.

The move is part of collaborations under the “watt-bitt” model for renewables to power the increasing high-energy needs of data centers and grow domestic cloud supplying industries.

ANRE proposed mandating electricity retailers to secure a certain amount of supply to support smooth mid- to long-term trading.

Under the current Electricity Business Act, retailers are obligated to secure sufficient power supply capacity. The new system requires retailers to secure 50% of expected demand (kWh) three years before the actual supply year, and 70% one year prior.

To encourage compliance, the system will be reviewed with a focus on clarifying that a violation of this requirement could be grounds for revoking a retailer’s registration.

CONTEXT: Currently, the JEPX operates a baseload market and a forward market – the markets that allow for mid- to long-term power procurement. But, there are issues with this setup, such as a lack of options to secure supply capacity in the shorter term.

TAKEAWAY: Requiring retailers to secure both capacity-based supply (kW) and energy-based supply (kWh) in an integrated manner should improve the predictability of electricity sales volumes for generators, and help foster a favorable environment for long-term fuel procurement contracts and encouraging investment in power sources. However, some retailers will see the new structure as locking them into a system that favors the bigger power producers as well as retailers with captive generating capacity. The energy agency will need to be wary of balancing its desire to support stable power supply with the need to allow market signals to play their role in a liberalized sector.

TOCOM power futures trading surges on geopolitical risks

(Exchange data, July 8)

Electricity futures trading on the TOCOM surged in June, with traded volume jumping 4.3-fold from May to 766 GWh.

Middle East tensions likely spurred trading, with large volumes (705 contracts totaling 618 GWh) executed for FY2026 delivery, mostly on June 19 and 20.

Open interest (positions not offset by opposing trades) hit a record high of 1.5 TWh at month-end, up 79.2% from May.

Prices rose significantly due to tight summer supply and increased demand; notably, Western-area baseload futures for July increased by ¥1.58/ kWh.

Average daily contracted volume in Japan’s intraday electricity market fell 14.3% MoM to 16.8 GWh, marking the first decline in two months.

Monthly contracted volume dropped 17.1% to 504 GWh, with average daily transactions down 1.7% to 8,375, representing just 0.7% of total electricity demand across nine regional markets.

The average monthly contract price rose by ¥1.43 to ¥11.26/ kWh, ¥0.39 higher than the spot market price; prices rose notably from mid-month amid greater cooling demand due to high temperatures.

The highest price recorded was ¥50/ kWh on June 17, reflecting tight supply-demand conditions as temperatures climbed nationwide.

June heatwave spikes spot electricity demand in Japan

(Exchange data, June 8)

The electricity spot market saw sharp increases in buying bids in late June as persistent high temperatures boosted demand, with buying volumes up 11.4% month-on-month.

Average daily buying volume reached 921.27 GWh, peaking in mid-to-late June amid hot weather conditions, causing a brief narrowing of the supply-demand gap and pushing system prices to monthly highs.

Nighttime supply rose notably by 8.8%, indicating recovery in thermal power generation ahead of peak summer demand.

Enaris, a subsidiary of KDDI, pledged to continue its research with Shibaura Institute of Technology to advance resource control technologies.

This comes in anticipation of FY2026, when “low-voltage resources” such as EVs and residential storage batteries will be permitted to participate in the supply-demand adjustment (i.e. balancing) market. The goal is to expand the number of controllable low-voltage resources and further enhance control precision.

The project will also leverage the computational capabilities of control terminals attached to batteries and other devices.

CONTEXT: The research began in 2024 using Shibaura Institute’s distributed processing control technology known as MEC-RM.

TAKEAWAY: The aim is to improve control precision and increase the volume of adjustable capacity that can be offered to the market. This should offer new balancing levers to TSOs, but will also make the calculations more complex.

METI has revised the plans and budgets of some hydrogen and ammonia-related projects supported by the Green Innovation Fund.

The Hydrogen Co-Firing Power Generation Demonstration will be discontinued due to the lack of new technologies that need testing and ongoing demos worldwide. Meanwhile, plans and budgets for developing large-scale hydrogen liquefiers and direct MCH electrochemical synthesis will be revised. The total project budget will be adjusted from ¥325 to ¥321 billion.

Both the Fuel Ammonia Supply Chain Establishment project and the Green Ammonia Electrochemical Synthesis project, despite achieving valuable results such as catalyst development and the discovery of reducing agents, will be terminated due to a significant shortfall in achieving targets. The total project budget will be revised from ¥71.27 billion to ¥69.8 billion.

Mitsubishi Heavy Industries Engine & Turbocharger (MHIET) will launch a new gas cogeneration system with a power output of 450 kW, capable of hydrogen co-firing, and jointly developed with Toho Gas.

The hydrogen mixing ratio is set at a maximum of 15% to minimize the extent of modifications required from conventional gas engines.

The system offers two operation modes: a city gas 13A-only mode and a hydrogen co-firing mode that can be switched freely during load operation.

CONTEXT: In August 2021, the two companies completed Japan’s first trial of a system with a power output of 450 kW and a hydrogen co-firing ratio of 35%.

IHI and Vopak will set up a JV to build and operate an ammonia terminal, aiming for commercial operation by 2030. No location has yet been chosen.

The terminal development aims to facilitate the receiving and storing of imported ammonia within Japan and to facilitate the establishment of a system for stable supply of such ammonia in Japan.

It will also serve as a hub for marine transportation.

Tokyo-based iGrid Solutions launched “Circular Power,” a service that aggregates surplus solar electricity from 1,200 distributed locations, enabling businesses without their own generation assets to procure low-carbon power at fixed rates.

Aimed at companies pursuing decarbonization targets, the service enables procurement of third-party solar power under long-term contracts, helping firms lower emissions without needing to install their own generation systems.

The Tokyo Metropolitan Govt will invest in a 80 MW grid-scale battery project in Kashima City, Ibaraki Pref, its first investment via its public-private Energy Creation and Storage Promotion Fund.

The project will cost ¥4 billion, and operation is expected to begin in Sept 2028.

The Fund totals ¥9 billion, with ¥2 billion from Tokyo, and is managed by Itochu and UK-based Gore Street Capital’s JV – GI Energy Storage Management. Other investors include NCS RE Capital, Tokyu Fudosan, Tokyo Century, Honda, and Bank of Yokohama.

The Fund aims to invest in grid-scale and co-located renewable storage projects mainly in the Kanto region.

Renova will freeze development of new large-scale biomass power projects that use wood as fuel. The decision comes as fuel costs remain high and government subsidy conditions are stricter.

Large-scale biomass projects using imported fuel are now ineligible for subsidies.

Moving forward, Renova will prioritize developing smaller-scale solar, battery storage, and onshore wind projects, as well as improving profitability of its existing biomass operations.

CONTEXT: Biomass power generation expanded under the FIT, which began in 2012. Historically, fuel for these projects has included domestic thinning materials and waste, as well as imported wood pellets from North America and SE Asia.

JAPEX, which operates large-scale biomass facilities at four domestic locations, has also confirmed it has no new development plans at present.

TAKEAWAY: According to METI, the amount of woody biomass power generation eligible for state subsidies has been decreasing year by year. In 2024, state subsidies for biomass power generation declined for the first time in four years, attributed to fewer new plans, project cancellations, and the closure of power plants.

Osaka Gas began operation of the Sodegaura Biomass Power Plant in Chiba Pref (output 75 MW), one of the largest such facilities in Japan.

The plant’s launch was delayed two years due to a fire.

The plant is part of Daigas Group’s overall 3.74 GW renewables portfolio, which continues to grow as the firm aims for a total of 5 GW capacity by FY2030.

A consortium of Marubeni-led MM Capital Infrastructure Fund II (41.75% share), Daiwa Energy (41.75% share), and Mizuho Leasing (16.5% share) acquired a 50% stake in TotalEnergies’ 604 MW renewables portfolio in Portugal.

The portfolio is one of south Europe’s largest and most geographically diverse, and includes 31 assets including onshore wind, solar PV, and small hydro projects.

TotalEnergies will retain a 50% stake, and will manage and operate the assets.

As a part of its ¥1.5 trillion (£7.5 billion) MoU with the UK govt, Sumitomo will invest in the Galloper Wind Farm project, in hydrogen production, in CCS projects in the North Sea, and in fusion collaboration with Tokamak Energy.

While the announcement doesn’t offer a project-level breakdown, the UK govt confirmed the funding will support clean energy and infrastructure through 2035.

Helical Fusion raised ¥2.3 billion via a third-party allocation of shares.

This brings total capital, including grants and loans, to ¥5.2 billion ($35 million).

The funds will help develop core equipment that converts fusion energy into heat. The goal is to build a demo reactor in the early 2030s.

Helical Fusion is developing a helical-type fusion reactor, which uses spiral-shaped coils to control plasma with magnetic fields. It should allow continuous 24/7 operation, high energy efficiency, etc.

CONTEXT: The funding round received backing from VC firms — SBI Investment and Keio Innovation Initiative.

Mayor Kataoka Haruo of Suttsu, Hokkaido, said he’s concerned about the method of selecting final disposal sites for nuclear waste. Suttsu was one of the first municipalities to complete the initial literature survey phase.

He said the federal govt’s approach incites divisions in communities, as in his town.

Kataoka called for the national govt to choose many candidate sites and then seek cooperation from local govts. This would put responsibility back on the national level, and could encourage debate and greater public understanding.

TAKEAWAY: The government has tried to utilize the ‘Scandinavian’ model of encouraging local governments to declare their interest in hosting a nuclear waste hub in return for ample subsidies. However, as the Suttsu mayor says, this has a number of drawbacks in Japan, where even small local opposition can derail huge infrastructure initiatives. Many look to and even expect the national government to take responsibility for a major facility such as a nuclear waste hub and it will likely require a more active Cabinet to bring to light. It should be noted, however, that one reason the national government tries to steer clear of this topic is the fear that it will be taken up as an issue by opposition parties and used to drive down government popularity.

In September, Niigata Pref will survey public opinion on the restart of TEPCO’s Kashiwazaki-Kariwa NPP.

This will help Gov Hanazumi’s decide whether or not to give consent for the restart.

Besides the survey, discussions with local mayors will conclude by Aug 7, and public hearings will go on until Aug 31.

TAKEAWAY: Last month TEPCO suspended efforts to restart Unit 7 due to delays in anti-terrorism facility construction, subsequently unable to meet the stated deadline. Thus, the utility decided to shift focus to preparing Unit 6, and it estimates two months are needed from the moment of approval to begin commercial operation. However, a new public opinion survey further delays any potential restart date, now unlikely to happen by year’s end.

This development also shows the ‘mastery’ of Gov Hanazumi, who has managed to delay and obfuscate the restart issue for years. He has always hinted at wanting to shift the responsibility for greenlighting the restart to the public and while his call for a referendum was denied by state officials, this public opinion survey is in fact a similar move.

West Australian Premier Roger Cook visited Japan to promote his region’s LNG exports and CCS opportunities. The Australian govt is considering building an east coast gas reservation, raising Japanese concerns that it could threaten energy security and long-term investment.

Australia is now prioritizing domestic gas supply, and Cook warns that investment in the sector might drop if Australia restricts LNG exports.

CONTEXT: Japan is highly dependent on Australian LNG. West Australia alone has been a key supplier, accounting for 28% of Japan’s total LNG imports in 2023. In total, all of Australia accounts for about 40% of Japan’s LNG imports.

Cook reassured Japan that West Australia remains a stable partner, as long as domestic gas supply commitments are upheld.

Cook pointed to further trade opportunities with Japan in hydrogen, ammonia, and critical minerals.

INPEX is advancing the $20 billion Abadi LNG project in Indonesia’s Maluku province. It will produce 9.5 Mtpa of LNG, making it Indonesia’s second-largest LNG project. Inpex (65% stake) leads development with partners Pertamina and Petronas.

Construction could start in 2027, with production by the early 2030s. Gas will be drilled offshore and piped 180 km to onshore liquefaction facilities. Inpex will need to hire 10,000 workers for full-scale construction.

CONTEXT: Abadi could become a second major revenue source for INPEX, along with Ichthys LNG in Australia, which currently accounts for 60% of profits.

Petronas shipped its first cargo from the LNG Canada facility in Kitimat, British Columbia. The cargo is headed to Japan.

With a 25% stake in the LNG Canada project, Petronas aims to diversify its supply portfolio. The facility uses hydro-powered electricity and advanced methane control systems.

CONTEXT: LNG Canada is a JV of Shell, Petronas, PetroChina, Mitsubishi Corp and KOGAS. This is Canada’s first major LNG project, with a 14 Mtpa capacity. Mitsubishi will offtake 15% (2.1 Mtpa) and supply to Japan through its subsidiary, Diamond Gas International.

CONTEXT: The story covers the main status of the Alaska LNG project, noting that the backers are making headway in planning the 1,300-km pipeline to transport gas from north Alaska to Anchorage. From there, once a liquefaction plant is added, it can travel to Asia, with potential interest from Japan and South Korea. The LNG plant’s capacity is expected to be 20 Mtpa, equal to roughly 30% of Japan’s yearly demand.

Alaska LNG operating company, Glenfarne plans to make a FID on the first phase of the project by end of 2025. Gas deliveries to Anchorage should begin by late 2028, and LNG exports to Asia could start in 2030.

The pipeline is considered one of the project’s top challenges. Construction costs are estimated at $11 billion, about a quarter of the total $44 billion project cost.

Thailand’s PTT inked a non-binding deal to buy 2 Mtpa of LNG for 20 years. Taiwan’s CPC agreed in principle to buy 6 Mtpa. Japanese and South Korean companies are reportedly also seen as likely investors or buyers.

Chiyoda Corp will no longer take on massive, overseas trillion-yen LNG projects, and will diversify by focusing on smaller-scale projects, said company President Ota Koji.

In recent years, the company has been hit with heavy losses due to construction delays at Cameron LNG, as well as losses with the Golden Pass LNG project, both in the U.S.

The Cameron LNG construction suffered from a labor shortage. Golden Pass LNG was a JV with U.S. firm Zachry Industrial, which went bankrupt due to rising costs.

Chiyoda aims for an average consolidated net profit of ¥15 billion per year. It will strengthen risk management at the contract stage. Traditional contracts required contractors to bear all post-signing cost increases. This will now be re-evaluated together with customers for fairer risk-sharing.

As of July 6, the LNG stocks of 10 power utilities were 2 Mt, down 7% from the previous week (2.15 Mt), up 3.1% from end July 2024 (1.94 Mt), and 7% down from the 5-year average of 2.15 Mt.

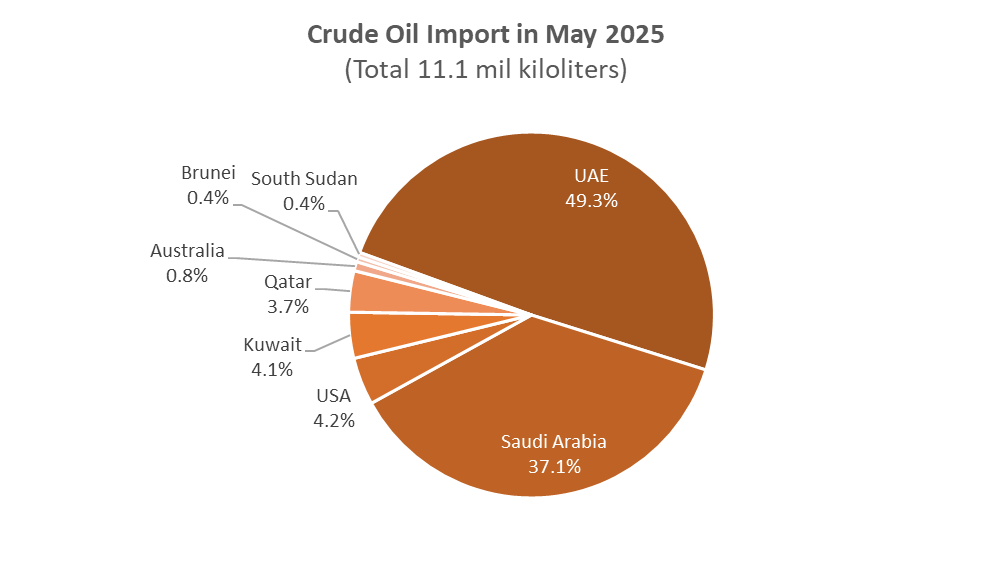

In May, Japan imported 11.1 million kiloliters of crude oil, down 10.4% MoM and up 3.5% YoY. As usual, nearly 95% of the total crude oil imports came from the Middle East, and the UAE was the top supplier.

For the past three months (March-May), imports from the U.S. jumped from 50-80 million kiloliters to 330-465 million kiloliters. Meanwhile, imports from Kuwait and Qatar halved this month (compared to April), and none came from Oman.

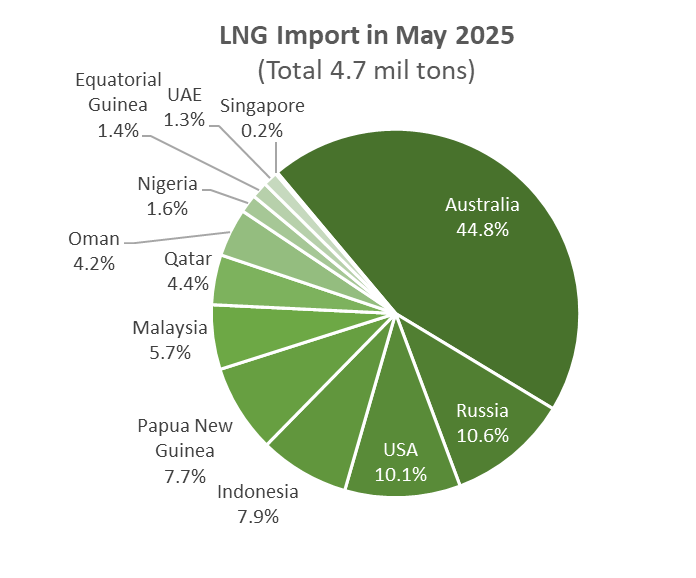

LNG imports in May totaled 4.7 Mt, down 13.2% MoM, and down 4.3% YoY. Imports from the U.S. jumped 2.6-fold (from 0.19 Mt to 0.5 Mt), while those from Malaysia dropped to one-third (0.82 Mt to 0.26 Mt). Shipment from Equatorial Guinea arrived for the first time in 2025.

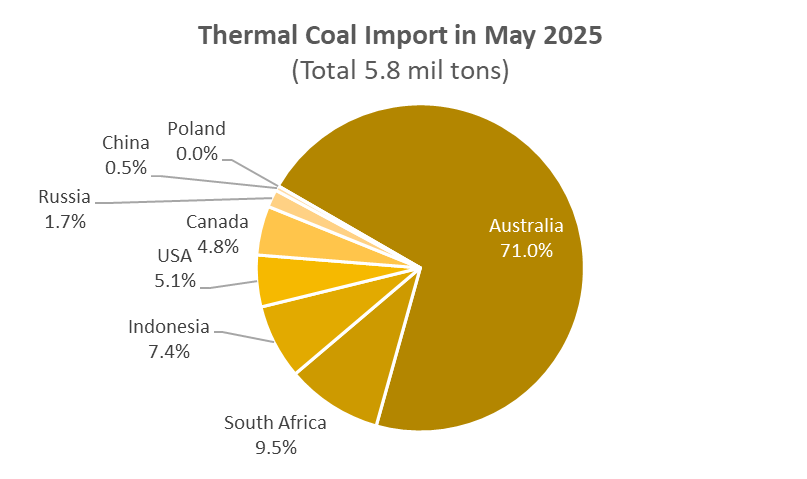

Thermal coal imports in May decreased to 5.8 Mt, down 22.2% MoM, and down 3.7% YoY. Imports from Australia were down 28%, and from Indonesia down 52% over April. South Africa’s volume hiked four-fold (from 0.14 Mt to 0.55 Mt), and Russia jumped 46% (0.07 Mt to 0.1 Mt). Japan started to import from Poland for the first time, but the volume was almost nil.

METI said that for the legal and regulatory carbon storage framework, three main approvals are required: 1) CO2 Storage Project Permit; 2) Implementation Plan Approval; 3) and Safety Regulations Submission and Review. These fall under the CCS Business Act.

Project operators must put in place safety measures on land excavation for storage projects and must be careful of storage of CO2 in geological formations.

Safety measures include handling of explosives and fire hazards. These mirror measures for exploratory drilling.

For permits and implementation plans, operators must prove technical and financial capabilities and provide proper CO2 storage methods and monitoring, as well as measures to prevent leakage and ensure safety. Finally, operators must show that there is no conflict with other industries or public interest and no alternative disposal method in marine areas.

Monitoring needs to confirm CO2 storage conditions (e.g., pressure, temperature). Operators must inject CO2 and conduct continuous monitoring.

The Safety Subcommittee will continue reviewing safety obligations for CO2 storage. They will reference international standards and Japan’s Tomakomai demo project. The goal is to complete the guidelines at least by the end of summer.

Trading house Sumitomo committed new funding to develop a CO2 transport pipeline for the Peak Cluster carbon capture project, to be done via its UK subsidiary Summit Energy Evolution Ltd.

It will capture and transport 3 Mtpa of CO2 from four major cement and lime plants.

CONTEXT: Six companies will contribute £60 million (¥12 billion) to fund research and design costs. Construction routes are being studied with an FID targeted for 2028 and project completion planned for 2031. Extra funding will need to come after FID for construction. A separate consortium will develop the pipeline and storage facilities from Liverpool to the seabed.

Mitsubishi Heavy Industries (MHI) won a contract from Hokkaido Electric for the basic design (FEED) of what will become Japan’s largest CO2 capture plant, at the Tomato-Atsuma Power Station.

The facility will capture 5,200 tons of CO2 per day using MHI’s tech.

The captured CO2 will be stored offshore near Tomakomai, in cooperation with Idemitsu Kosan and JAPEX.

CONTEXT: This is part of one of Japan’s advanced CCS projects and it aims to store 1.5–2 Mtpa by 2030.

On July 7, as part of the Fry to Fly Project, domestic SAF was supplied to an ANA flight traveling from Haneda Airport to Taipei.

The SAF is mass-produced at Cosmo Oil’s refinery in Sakai City, Osaka Pref, using waste cooking oil partially collected in collaboration between JGC and the TMG.

CONTEXT: The Fry to Fly Project seeks a world where aircraft fly on SAF derived from waste cooking oil. It was proposed and is managed by JGC, and now includes over 200 companies, municipalities, and organizations in Japan.

TAKEAWAY: JGC aims to accelerate decarbonization in the aviation industry by more collaboration between companies and local governments, promoting the collection of waste cooking oil, and expanding the use of SAF in Japan. The Cosmo SAF refinery started trial operation in January 2025, becoming the first in Japan to produce SAF at a commercial scale.

Cosmo Energy became the first oil refiner in Japan to join the CO2 emissions reduction programs offered by Japan Airlines (JAL) and All Nippon Airways (ANA).

This initiative aims to reduce CO2 emissions from business travel by Cosmo Energy Group employees through the purchase of emission reduction certificates under JAL’s and ANA’s SAF programs.

CONTEXT: Compared to petroleum-based jet fuel, SAF is expected to reduce CO2 emissions by up to 84%.

ANALYSIS

BY JOHN VAROLI

Dynamic Duo: Japan and Singapore Drive Energy in East Asia

News and analysis about Japan’s foreign relations in the energy sector are often dominated by partnerships and deals with Australia, China, Qatar, the U.S., and UAE. Rarely does the bilateral relationship between Japan and Singapore garner much attention.

But these two countries, despite their differences, have developed a potent tandem that’s driving developments in regional and global energy markets in ways that don’t always grab headlines. While energy deals between the two countries don’t register in billion-dollar figures – as they do with Australia and the U.S. – Tokyo’s relationship with Singapore is a cornerstone of regional energy cooperation and development in East Asia.

Despite contrasting geographic profiles, both nations are resource-scarce and function with trade-dependent economies. As well as becoming energy hubs, Japan and Singapore also share a deep dependence on thermal power plants and, hitherto, a strong reliance on natural gas. Today, however, they are united in exploring alternatives in hydrogen, battery energy storage, and pioneering the energy transition in the region.

Japan’s technological prowess in CCS, hydrogen, and renewables complements Singapore’s financial, trading and logistical strengths. Japan NRG explores their collaborative efforts in a number of sectors and the impact across the Asia Pacific.

LNG and foundations of energy cooperation

The convergence of business needs – Japan as a major energy consumer and Singapore as a critical node in energy trade – is the bedrock of this half-century partnership. Singapore’s location along major maritime shipping lanes and its development of Jurong Island as a hub for energy and petrochemicals since the 1960s have made it a vital partner for Japan.

Despite determined efforts in greening its energy sector, Japan remains heavily reliant on LNG imports for power generation. In addition, Japanese companies are increasingly looking for LNG trading opportunities to countries across Asia. Singapore plays a pivotal role as a hub, hosting LNG trading operations for companies such as JERA, Japan’s largest utility, as well as global majors such as BP, and ExxonMobil.

In March, the city-state’s importance for Japan’s energy strategy was ramped up a notch when the natural gas and coal trading operations of JERA merged with France’s EDF to form the Singapore-based firm JERA Global Markets – 66.7% owned by JERA, with the remaining stake held by EDF Trading.

Investments in Singapore’s energy infrastructure

The second pillar of Japan-Singapore energy relations is the ownership and operation of Singapore’s energy assets, particularly in electricity generation.

In late 2008, Marubeni led a consortium that included Kyushu Electric, Kansai Electric, the Japan Bank of International Cooperation (JBIC), and GDF Suez (now Engie) to acquire Senoko Power from Singapore state-owned Temasek Holdings. The consortium, known as Lion Power Holdings, was controlled by Marubeni and Engie holding 30% each.

In late June, trading house Marubeni increased its stake in Senoko from 30% to 50% by acquiring the Lion Power shares from Kyushu Electric, KEPCO, and JBIC. Senoko, with its 2.6 GW capacity, supplies about 18% of Singapore’s electricity, making it the state’s second largest power provider.

That deal has positioned Marubeni as a 50/50 co-owner along with Sembcorp Utilities, a subsidiary of Singapore’s state-owned Sembcorp Industries. This deal highlights deepening trust and collaboration between firms from the two nations, leading to a symbiotic dynamic – meeting Singapore’s need for stable electricity with Japan’s constant pursuit of overseas investment opportunities.

Finally, Japanese investors in Singapore’s power sector are a counterbalance to Chinese firms. Huaneng Power International owns Tuas Power, the city-state’s largest power company, with a 20% market share.

BESS and AI boom in Japan

Both nations are investing heavily in renewable energy and energy storage. Singapore-based firms with backing from global investors – such as Peak Energy, Gurīn Energy, and Vena Energy – are making significant inroads into Japan’s renewables market, particularly in solar and battery energy storage systems (BESS).

The ambitions of Singaporean players align with Japan’s push to combine renewable energy with advanced technology, particularly as AI and digital services drive energy consumption.

In mid June, Peak Energy acquired a portfolio of ready-to-build, high-voltage solar farms in Tokyo and Tohoku, with a combined capacity of 48 MW. These facilities, equipped with BESS, are set to be operational between 2026 and 2028 and will supply power to corporate customers through long-term power purchase agreements (PPAs).

Also in mid June, Gurīn Energy, in collaboration with France’s Saft (a TotalEnergies subsidiary), said it is developing a project in Soma City, Fukushima Prefecture, that will provide over 1 GWh of storage capacity to integrate renewables into Japan’s grid.

In late May, Vena Energy added to its 1 GW of operating solar capacity in Japan, as well as wind and battery ambitions, by creating a data center subsidiary, Vena Nexus. The new entity has some Japanese assets in its pipeline and among these is a partnership with Tokyo-based startup Quantum Mesh, with whom Vena is developing small-scale, renewables-powered data centers for AI-driven and digital infrastructure.

Vena Energy’s ambitions extend beyond Tokyo, but the Japanese business is one of the firm’s largest.

Rooftop solar, transition finance and eye on India

Singapore’s role as a financial and operational hub underscores its importance as a springboard for Japanese players to connect with other Asian markets.

In early June, TEPCO, in partnership with Hong Kong’s ESR Group, secured ¥1.1 billion in financing from Taiwan’s Bank SinoPac for a 10 MW rooftop solar project in Singapore, with plans to expand to 40 MW through an additional ¥3.9 billion.

Supported by multiple corporate PPAs, this joint venture reflects TEPCO’s goal to deploy 100 MW of rooftop solar across the Asia-Pacific, leveraging Singapore’s favorable investment climate and demand for clean energy.

Japan’s Climate Transition Bonds (also known as GX Bonds) have been highlighted by the International Energy Agency (IEA) as a model for emerging economies, offering government-backed credit support to facilitate clean energy spending. As a global financial center, Singapore can play a role in facilitating the trading of GX Bonds.

The Japanese government aims to issue ¥20 trillion worth of GX bonds over the next decade to support decarbonization across multiple sectors. A significant portion of the proceeds (over 50%) is allocated to energy transition R&D.

Meanwhile, firms from Japan and Singapore are exploring joint investments in third countries to counterbalance the limitations and even shrinking in their domestic businesses. As part of Osaka Gas’s broader strategy to expand its energy business in emerging markets, Osaka Gas Singapore has invested in Singapore-based AG&P City Gas, which is developing 12 city gas distribution concessions in South India and Rajasthan. (The company’s subsidiary in India is known as AG&P Pratham.)

In 2024, AG&P secured exclusive gas distribution rights covering 10% of India’s land area, and targets annual sales of 3.5 billion cubic meters by 2030. Toward that goal, the company is laying a 100 km gas pipeline in Chennai. But it’s also expanding into renewables, planning to develop 400 MW solar and wind power capacity in India by 2028.

This robust international strategy, driven by Japan’s shrinking domestic market, saw Osaka Gas’s non-Japan revenue surge from ¥18.7 billion in FY2016 to ¥116.4 billion in FY2024.

CCS partnership

In August 2024, during the 2nd Asia Zero Emissions Community (AZEC) meeting in Indonesia, METI Minister Saito Ken and Singapore’s Second Minister for Trade and Industry, Dr. Tan See Leng, agreed to cooperate on carbon capture and storage.

Japan, a leader in CCS technology innovation, is well placed to support Singapore’s ambitions to decarbonize its energy-intensive industries, including power generation, chemicals, and waste management.

Constrained by limited land and domestic renewable energy potential, Singapore views CCS as a vital tool for reducing emissions while maintaining its role as a regional energy hub. The two countries will develop common standards for CCS, fostering a market for CCS solutions across the Asia-Pacific.

Conclusion

While only a city-state with a population of just under six million, nearly 21 times less than Japan’s 125 million people, Singapore occupies an outsized place in Japan’s regional energy strategy.

While much is said about Singapore’s geographic location, part of its allure for Japanese players is the state’s high levels of efficiency and services, and low levels of corruption. The stability of local business relations is another trait valued by Japanese firms. (Singapore ranks No 3 globally for least corruption; while Japan ranks 20th.)

Of course, Singapore has attracted investors from various locations due its finance and trade focus. That kind of international environment, and a cosmopolitan lifestyle, has endeared the city-state to many of Japan’s business and financial elite.

It is the similarity of Singapore’s approach to energy – the focus on security of supply and affordability, in addition to decarbonization – and the proximity to the fast-growing markets of Indonesia and Malaysia, for example, that has led Japanese energy companies to consider the city state a vital hub for their Asian business expansion.

ANALYSIS

BY TETSUJI TOMITA

The Balancing Act for Energy Planners Continues a Decade into Reforms

In late March, the energy agency (ANRE) published its long-awaited review of electricity market reforms carried out over the past decade, and set out future priorities. The results indicate success in achieving the main aims of ensuring a stable power supply, reigning in power rates, all while offering consumers more choice.

Yet beneath this positive headline lies a critical challenge: how to ensure sufficient capacity and stability in ever more sophisticated power markets without giving up on the energy transition?

ANRE’s review also underscored persistent vulnerabilities, especially around maintaining adequate supply and stable prices as Japan pushes ahead with the twin national strategies: digital transformation (DX) and green transformation (GX). These strategies aim for a rapid shift toward decarbonized infrastructure, but also place greater strain on Japan’s already tight electricity grid – a concern echoed in this year’s 7th Basic Energy Plan.

Japan NRG takes a deeper look at the agency’s concerns and how they relate to the main developments in the electricity sector and markets.

Supply capacity shortage

In recent years, a number of factors worry Japanese energy planners regarding available power supply and capacity. First, the decommissionings and suspension of aging thermal power plants has gained momentum. At the same time, the rollout of renewables and new thermal power sources has not kept pace with state targets, resulting in a discrepancy between supply and demand.

Over the past decade, Japan has reduced reliance on thermal power generation, with a net loss of about 21 GW of LNG, coal, and oil-fired capacity. Meanwhile, new solar capacity coming online has slowed, dropping to about 6 GW a year in 2022, from a high of nearly 11 GW in 2015. This is partly due to less land availability, rising costs, the phasing out of tariffs, and an intensifying grass-roots opposition in certain localities due to resident concerns.

Second, structural changes on the demand side have had an impact. Prolonged summer heat and winter cold, combined with economic recovery after the Covid pandemic, have led to rapid increases in electricity demand, making it more likely for peak demand to exceed initial projections. This has resulted in growing instances of a decline in reserve margins.

In summer 2024, for example, there were at least three incidents when large volumes of electricity had to be transferred quickly between the major regions into which Japan’s power system is split. On July 1, Kansai’s transmission system operator warned that its reserve margin was due to fall below 3%, a red line; Kansai received nearly 1.5 GW of power from the Chubu region to improve the power balance.

Third, there is a shortage of balancing capacity in the supply-demand adjustment market, the Electric Power Reserve Exchange (ERPX), that helps to cope with the output fluctuations of renewable energy. The rollout of flexible resources such as storage batteries is taking time, especially because of grid connection bottlenecks and trouble with raising project financing.

Meanwhile, the cost of expanding pumped hydro storage – where possible – is substantial. This has led to situations where sudden imbalances in power supply and demand cannot be promptly addressed.

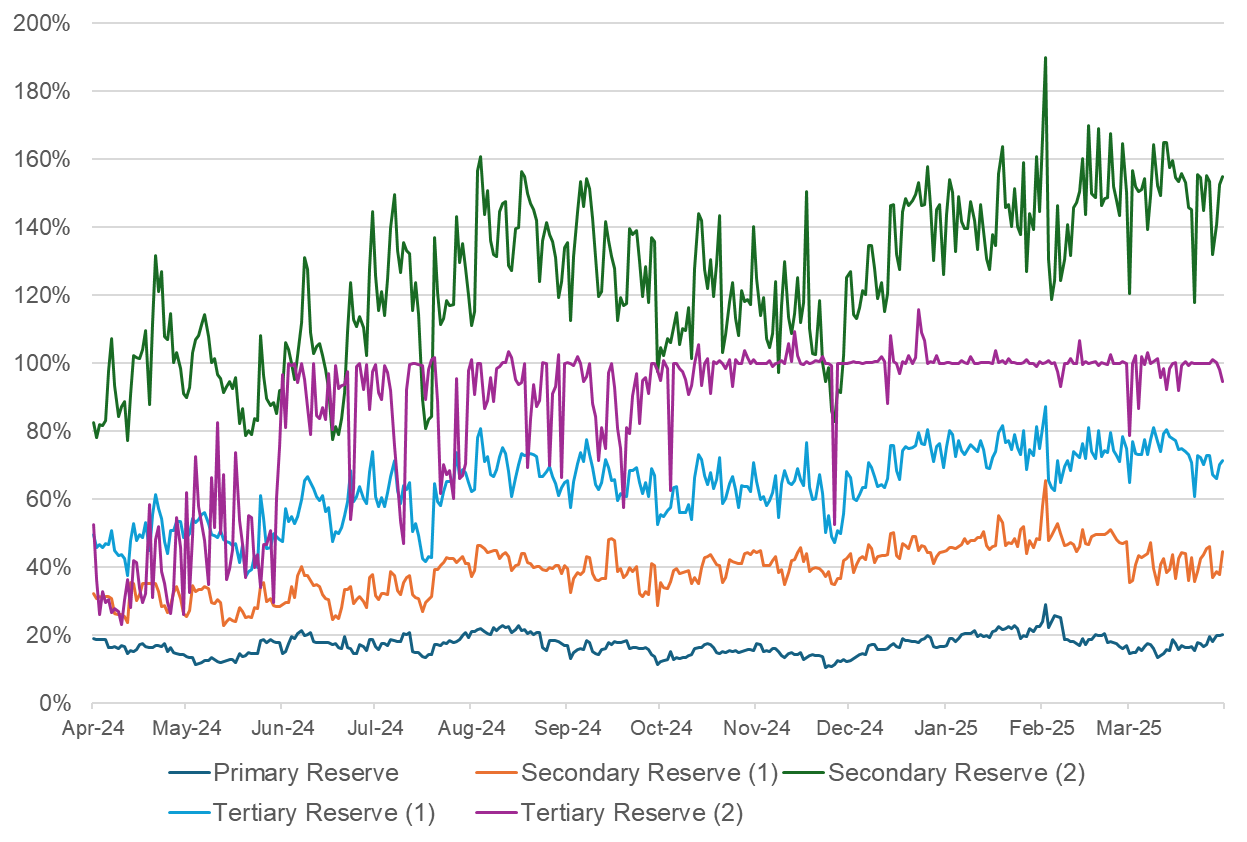

The gaps in the EPRX market could be illustrated by tracking the procurement ratio for its various products. In other words, by considering how much certain power generation sources are underutilized while others are over-relied upon. Based on the procurement ratio for each EPRX product during FY2024, which is calculated by dividing the daily contracted capacity by the solicited capacity (i.e. required balancing capacity), we can see:

Clear shortage of capacity for certain types of energy;

Reliability concerns when integrating variable power sources;

Frequent forecast errors or grid fluctuations that need rapid response;

Challenges in forecasting short-term balancing needs or intermittent asset availability.

Balancing Capacity Procurement Ratio in the EPRX (FY2024)

NOTE: The procurement ratio is calculated by dividing the daily contracted capacity by the solicited capacity (required balancing capacity).

Reserve Product

Response Time

Duration

Typical Power Sources

Usage

Primary Reserve(FCR – Frequency Containment Reserve)

Within 10 seconds

≥5 min

• Battery Energy Storage Systems (BESS) • Fast-ramping gas turbines (online)

Automatic real-time frequency control

Secondary Reserve (1)(S-FRR – Synchronized Frequency Restoration Reserve)

Within 5 minutes

≥30 min

• BESS • Gas turbines, hydro plants • Aggregated DERs (EVs, batteries)

Balances within-settlement deviations

Secondary Reserve (2)(FRR – Frequency Restoration Reserve)

The outcome of the above suggests there are opportunities to invest further in fast-response technologies like BESS that can support the consistently high and volatile secondary reserve categories, which offer drive price premiums and potentially attractive returns.

Measures for stable electricity supply

To ensure a stable electricity supply, the government is working on institutional measures, such as the capacity market, the long-term decarbonized power sources auction (LTDA), and development of short-term markets.

The current capacity market system is designed to secure future supply capacity through bidding and contracting four years in advance. However, incentives for suppliers are limited. In response, revisions are being made to enhance supply effectiveness, including commitments for dispatchable resources and differentiated treatment based on the results of effectiveness tests.

The LTDA was introduced to achieve secure, decarbonized supply capacity, thereby encouraging investment by providing long-term revenue stability for cleaner power sources expected to play a big part in future electricity supply (e.g., offshore wind, nuclear power, etc). The LTDA has so far held two rounds and a third is expected to begin in autumn.

For the short-term market, the introduction of a simultaneous market is under consideration, where supply capacity (kWh) and balancing capability (delta-kW) are contracted simultaneously. This enables optimal resource allocation based on information provided by power generators (such as startup costs, minimum output costs, and incremental cost curves), while taking into account transmission constraints.

Ensuring stability in both supply volume and price

Achieving a stable electricity supply requires a balanced approach to both volume and price.

Reliable supply capacity must be maintained over the medium to long term, and this involves promoting new power sources, extending the life of existing facilities, and expanding flexible resources such as storage batteries and demand response mechanisms.

On the other hand, according to the ANRE review, extreme fluctuations in power prices pose risks for both consumers and businesses. Japanese power officials worry that the current power market design relies too heavily on spot market price signals, which has in the past three years or so led to the collapse of many electricity retailers when prices surged.

To address this issue, officials want to see retailers and other power participants utilize a broader range of contracting options. This includes making more use of the baseload market, futures contracts, and paying more attention to bilateral options such as PPAs.

Future discussions

Following the presentation of ANRE’s review in March, the “Subcommittee for the Development of Next-Generation Electricity and Gas System Infrastructure” was established to examine the future institutional framework, business environment, market structure, and competitive landscape for the electricity and gas industries.

Also, in June the “Working Group on Institutional Design Based on the Review of the Electric Power System Reform” was formed to engage in more detailed discussions on policy and system design.

The subcommittee and working group will grapple with the following eight issues.

1. Securing fuel necessary for stable supply

2. Planned development of intra-area transmission systems

3. Facilitating financing for large-scale transmission system development

4. Development of markets enabling optimal short-term supply-demand operation

5. Clarifying the responsibilities, roles, and discipline of retail electricity providers

6. Markets and mechanisms to promote medium- to long-term transactions

7. Identifying issues related to the removal of transitional tariffs

8. Financing for investments in power sources and transmission systems

Items 1, 4, and 6 are issues related to ensuring stability of power supply.

Conclusion

While electricity system reform has brought diversity and efficiency to the market, officials feel the fundamental issue of creating and maintaining stable power supply needs further measures.

Policy focus seems likely to double down on supporting new, and ideally flexible, capacity installations both over the short and the medium term, with subsidy mechanisms attuned to that. Market and regulatory designs will be geared toward encouraging new investment.

Many familiar with operations in mature power markets overseas continue to hope for more bold measures in market design, such as the introduction of negative pricing. ANRE’s focus on supply and price stability does not suggest the energy planners are keen to introduce such approaches in Japan as yet.

Still, with more and cleaner capacity required, an evolution in domestic energy policy is likely as long as the government feels confident that the changes will not pass along undue price volatility to the population.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / natural gas

The govt plans to reexamine key measures introduced by previous administrations to help formulate its Future Gas Strategy, which maps the govt’s plan for how gas will support the economy’s transition to clean energy.

China / Nuclear

Brazil and China General Nuclear Power Group agreed to cooperate on energy transition efforts and the peaceful and sustainable use of nuclear mineral resources in Brazil.

China / Solar and wind

China is developing a total of 1.3 TW of utility-scale solar and wind capacity, according to Global Energy Monitor; this is 75% of all such capacity under construction globally.

India / Oil

India’s oil consumption totalled 122 Mt in the first six months of 2025 unchanged from the same period in 2024:

India / Solar and wind

India recorded an additional 21.9 GW of new solar and wind capacity in the first half of 2025, reflecting a 56% increase from last year.

Indonesia / Nuclear

The country’s chamber of commerce called on the govt to consider collaborating with Canada and South Korea on the development of NPPs.

Philippines / LNG

LNG imports are set to increase by 508% from 2025 to 2029, driven by the decline of domestic supply from the Malampaya gas field.

Singapore / Petrol

Aster Chemicals and Energy, a JV between Chandra Asri Group and Glencore, is in talks to buy ExxonMobil Corp’s petrol stations in Singapore in a $1.2 billion deal

Taiwan / Offshore wind

Ørsted raised a total of $3 billion for the 632 MW Greater Changhua 2 offshore wind farm, secured through 25 banks and five export credit agencies.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

NEWS:

・FSA to postpone mandatory sustainability disclosures for small companies

・MOL and Kinetics ink MoU for world’s first floating data center platform

・J-Power and Hitachi sign MoU for renewable-powered data centers

May Oil/ Gas/ Coal trade statistics

May Oil/ Gas/ Coal trade statistics