WEEKLY

OCTOBER 6, 2025

ANALYSIS

GREEN H2 PRODUCTION: WATER ELECTROLYSIS TECHNOLOGY TRENDS AND OUTLOOK

- Japan certified its first low-carbon hydrogen supply plan, approving subsidies that will use wind power to produce green hydrogen through electrolysis. But Japan’s potential hydrogen consumers are cautious due to costs.

- Japan NRG takes a look at the development of the green hydrogen production tech, comparing advantages and challenges, and potential.

ENERGY JOBS IN JAPAN: FEATURES OF TOP LEADERSHIP TALENT FOR THE TRANSITION

- Technological innovation, evolving regulations, and geopolitical dynamics are accelerating change in the energy sector.

- Having the right strategy and ability to execute is critical. Talent is the key to get ahead. The line between success and failure often is defined by leadership, rather than dollars and technology.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- PV installations in 2024 drop, while global growth continues

- Firms using renewables and nuclear to get subsidies of up to 50% of capital investment

- JERA decommissions 3.2 GW of old thermal power

- OCCTO reports survey results for balancing market regulation changes

- Marubeni sets up new power trading JV

- First two certified projects for low-carbon hydrogen/ ammonia CfD announced

- Isuzu, Toyota to develop next-gen fuel cell buses

- Shizen Energy signs 20y PPA deal with Microsoft

- ENEOS and Octopus Energy sign a PPA

- MSFL acquires two BESS from West Holdings

WIND POWER AND OTHER RENEWABLES

- METI Council explores further initiatives to promote geothermal energy

- METI and MLIT add new zones for offshore wind

- Developers want offshore wind to join LTDA’s 20-year fixed revenue

- Eurus proceeds with EIA for offshore wind farm

- METI experts say 55 GW of nuclear capacity may need be replaced by FY2040

- Advanced reactor working group moves forward

- Niigata Pref releases public opinion survey for the Kashiwazaki-Kariwa NPP restart

- Zero Watt Power acquires Surukawa Energy Center and its biomass facilities

CARBON CAPTURE & SYNTHETIC FUELS

- Hard-to-abate sectors give feedback on ETS future developments

- Mazda downgrades carbon neutrality plans from ammonia to LNG; keeps it an option for future

EVENTS

Oct 8-9 Innovation for Cool Earth Forum @ Westin Hotel Tokyo IEA World Energy Outlook 2025 Release

Oct 15-16 Japan CCUS Summit

Oct 15-16 Connecting Green Hydrogen Japan

Oct 15-17 Global Offshore Wind Summit – Japan @ Akita Prefecture

Nov 10-21 COP30 @ Belem, Brazil

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

PV installations drop in 2024, while global growth continues

(Organization statement, September 17)

- Findings by research firm RTS show that in 2024 Japan installed about 5.6 GW of solar PV systems (DC), down 11% over 2023.

- Of this, 1.2 GW was residential and 4.4 GW industrial and utility-scale, bringing cumulative national capacity to 97 GW, the fifth largest globally.

- Under the FIT/FIP, cumulative certified capacity reached 75.1 GW and cumulative operational capacity 70 GW, with a high operational rate of 93–95%. Large-scale FIT projects dropped, while PPA-based non-FIT installations and residential/ non-residential deployments slightly increased.

- Solar module shipments totaled 5.47 GW, down 6.4%, with JinkoSolar’s leading market share at 20%.

- CONTEXT: The Japanese solar market is seeing growth in PPA projects, FIP with storage, O&M, recycling, aggregation, perovskite module testing, and virtual PPAs, signaling diversification beyond FIT-based deployment.

- Meanwhile, globally, 2024 PV installations reached a record 602 GW (DC), up 32% over 2023, bringing cumulative capacity to about 2.2 TW.

- Last year’s growth was driven by falling solar module prices and accelerated renewables adoption, with China (357 GW), the U.S. (47 GW), Germany (16.7 GW), India (32 GW), and other countries contributing significantly.

- Worldwide solar module production rose 23% to 757 GW, led by China (628 GW, 83% of the total), with crystalline silicon modules dominating (~98%).

- Asia-Pacific accounted for 65% of new installations, Europe 18%, the Americas 14%, and the Middle East & Africa 3%.

- SIDE DEVELOPMENT:

- Govt reconsiders plan to mandate solar panel producers to cover recycling cost

- (Nikkei, October 3)

- The govt is reconsidering a plan to require solar panel manufacturers to cover recycling costs, due to legal and practical challenges.

- A new proposal would instead make recycling a voluntary duty for panel owners, with reporting obligations for large-scale power producers.

- CONTEXT: Currently, the recycling rate for used solar panels is 54%, much lower than, for instance, home appliances. The volume of discarded panels is expected to peak at 472,000 tons in 2042. Limited recycling infrastructure and high costs (¥8,000–¥12,000/ kW) are major challenges.

TAKEAWAY: Japan’s solar power market has slowed for several years now mainly due to a drop in tariffs, a shrinking pool of easily accessible land, and the gradual transition to market-linked mechanisms such as FIP and PPAs. The incoming prime minister, Takaichi, has said that she wants to focus on protecting national security by reducing Japan’s reliance on overseas panels. In effect, this means stifling imports of the Chinese products. The problem is, the perovskite home technology that Takaichi says she wants to promote is not yet at the stage of replacing silicon modules on a multi-MW basis. So, we expect the solar market to continue with the current reliance on Chinese models, but the cost of doing so may well increase, which would have a knockon effect on PPA pricing. Meanwhile, other govt support systems (see news item below) are actually trying to accelerate solar installations.

Subsidies for firms using renewables and nuclear, up to 50% of capital investment

(Nikkei, October 3)

- METI will launch a support program for companies utilizing decarbonized power sources, such as wind, solar, and nuclear energy, by subsidizing investment in advanced technologies.

- Firms that sign long-term renewables procurement deals with power firms, or set up factories near decarbonized power plants, will get higher evaluations.

- METI will accept applications in 2026, aiming to begin subsidies that year.

- Regarding investments, priority will be given to those contributing to decarbonization or strengthening economic security, such as factories related to semiconductors, robotics, biotechnology, and similar fields.

- The goal is to foster clusters of decarbonization-focused industries in areas with robust renewable energy generation, such as Hokkaido and Tohoku, or regions with restarting nuclear plants, like Hokuriku and Kyushu.

ANRE talks on standards for imported wood for biomass

(Government statement, September 30)

- ANRE’s working group discussed standards on imported wood for biomass that would be easy to adopt for domestic businesses and recognized both nationally and internationally. Parties agreed on the following:

- Ascertaining overall wood usage status in Japan;

- Checking trends in other countries.

- New standards will be based on wood biomass certification guidelines (2012), Renewable Energy Measures Act (2017) and business plan guidelines for biomass power generation (2017).

MOL, etc achieve high-precision seabed observation of cold discharge water

(Company statement, September 29)

- Mitsui O.S.K. Lines, the University of Tokyo, University of the Ryukyus, and Japan Science and Technology Agency (JST), made an environmental assessment on the impact of cold wastewater from ocean thermal energy conversion (OTEC).

- CONTEXT: OTEC generates power by using temperature difference between warm surface seawater and cold deep seawater. It requires large amounts of deep seawater.

- This method replaces traditional diver-based visual surveys and allows large-scale, efficient, and rapid mapping of seafloor topography and coral distribution.

NEWS: ELECTRICITY MARKETS

JERA decommissions four aging thermal power units, total of 3.2 GW capacity

(Company statement, September 30)

- JERA decommissioned Anegasaki Units 5 & 6, Sodegaura Unit 1, Chita Unit 5, and Hirono Unit 2. They have a combined capacity of 3.2 GW.

- All four had been in long-term shutdowns and were too degraded for restart, so their closure has no impact on current supply stability.

- CONTEXT: Since FY2020, JERA has installed or replaced 7.3 GW of capacity and is building Chita Units 7 & 8 (1.3 GW, by FY2029). Plans also call for new Sodegaura Units 1–3 (about 2.6 GW), with environmental assessments starting.

TAKEAWAY: Hirono Unit 2, located in Fukushima, was JERA’s last oil-fired plant in the Tokyo area. Other companies are also retiring aging thermal plants to cut maintenance costs. For example, Kansai Electric and J-Power are phasing out oil- and coal-fired units. Oil-fired stations are often used as peaker plants in Japan, helping to manage short periods of high consumption.

- SIDE DEVELOPMENT:

JERA sells gas-fired power plant stakes in U.S.

(Nikkei, October 3)- JERA will sell its 20% stake in a large gas-fired power plant – Carroll County Power Plant in Ohio – with a generation capacity of 700 MW.

- The buyer is U.S. investment firm Strategic Value Partners. The sale amount has not been disclosed.

- In September, JERA also sold its stakes in three large gas-fired power plants, jointly owned with Itochu Corp, to Itochu and local energy companies.

- CONTEXT: The U.S. is experiencing a surge in electricity demand due to the construction of new data centers. Excluding the stake being sold, JERA now owns nine power plants in the U.S.

OCCTO reports survey results for balancing market regulation changes

(Agency statement, September 26)

- OCCTO reported the results of a survey on preparations for the balancing market regulation changes starting in FY2026.

- Regarding preparation for next fiscal year, most operators are expected to complete new system and workflow updates in time, so major trading disruptions are unlikely. It’s expected that some bid imbalances across products will still occur.

- Day-ahead trading and 30-minute units may boost bids in the combined market but reduce them in the Tertiary(2) market, with shortages persisting in Primary, Secondary(1), and combined products.

- Regarding the impact of off-market reserve deductions, over 70% of participants reported no major impact from deducting non-market adjustment capacity.

- CONTEXT: Starting FY2026, the balancing market will shift trading of Primary, Secondary(1), Secondary(2), Tertiary(1), and composite reserves from weekly to day-ahead, and trading units will change from 3-hour blocks to 30-minute slots. Since June, off-market reserve deductions have been applied to weekly products.

Sharp launches AI battery control service aligned with FIT

(Company statement, September 24)

- From Oct 1, Sharp updated its Cocoro Energy cloud HEMS service to support Japan’s revised FIT system, the first in the industry to do so.

- It will be the first service to align with the new two-step FIT for residential users. In the revised FIT, electricity is purchased at a higher fixed price for four years, then shifted to market-based pricing for six years. Sharp’s AI automatically optimizes charging and selling behavior under this two-tier system.

- During the first four years, the AI prioritizes selling solar power while charging only as needed. Once the rate drops, it switches to self-consumption mode without user input. By learning household patterns and using cheaper night-time electricity for charging, the system maximizes surplus solar sales and minimizes power purchases from utilities.

Nissan Motors develops subsidiary to include sales of high voltage electricity

(Company statement, September 25)

- Nissan Motors will expand Nissan Denki to include sales of high-voltage electricity to distributors and corporate partners, via Nissan Trading.

- This could cut customer emissions by up to 90%, since most stem from power consumption to operate stores.

- Nissan Motors also broadened its low-voltage electricity sales for households to cover all of Japan, excluding Okinawa and remote islands.

TAKEAWAY: Nissan has embedded climate strategy across its entire value chain, from raw material extraction to product disposal. As for renewable energy use, the company is promoting carbon emissions management by installing solar PV at its dealerships in Japan. Nissan is not alone in entering the renewable electricity business; Volkswagen and Tesla both launched similar services in 2025. Beyond meeting climate targets, expanding this business could also serve as a lever to strengthen Nissan’s financial performance.

Marubeni Power Trading to profit on growing electricity demand

(Company statement, October 1)

- Marubeni Power Retail and Smartest Energy set up Marubeni Power Trading to combine Marubeni Power Retail’s Japanese customer base and Smartest Energy’s expertise in energy trading.

- CONTEXT: In its latest mid-term management strategy, Marubeni aims to boost consolidated profit from wholesale and retail power trading from ¥19 billion in 2025 to ¥30 billion in 2028. The driver is expected to be the expansion of data centers and semiconductor factories.

Hokuriku Electric suspends power station unit due to minor damage

(Company statement, September 29)

- Hokuriku Electric suspended operations at Tsuruga Thermal Power Station Unit 2 due to a steam leakage inside the boiler.

- Hokuriku Electric expects to secure sufficient capacity from other thermal power plants, as well as hydro.

- CONTEXT: Tsuruga (700 MW) also suspended operations in 2019 and 2018 due to similar causes. It took two months to resume operations in 2019 and ten days in 2018. It is one of the main power generation facilities in Nanao City, Ishikawa Pref.

NEWS: HYDROGEN

First two certified projects for low-carbon hydrogen/ ammonia CfD announced

(Government statement, September 30)

- ANRE announced the first two certified projects for low-carbon hydrogen/ammonia price difference support (CfD) program.

- Project 1 (Hydrogen): Toyota Tsusho / Eurus Energy / Iwatani / Aichi Steel

- A manufacturing SPC backed by Toyota Tsusho, Eurus Energy, and Iwatani will procure onshore wind power electricity and use it for electrolysis at Aichi Steel’s Chita Plant to produce low-carbon hydrogen.

- The hydrogen will power Aichi Steel’s production of specialized steel.

- Annual supply: 1,600 tons.

- Project duration: Aug 2030 to July 2055.

- Project 2 (Ammonia): Resonac / Nippon Shokubai

- Resonac plans to gasify waste plastics and waste clothing at its Kawasaki Plant and use hydrogen obtained as feedstock to make low-carbon ammonia.

- The firm will also be the main consumer, producing and selling ammonia derivatives as raw materials for textiles.

- Annual supply: 20,815 tons (3,234 tons of hydrogen equivalent).

- Project duration: April 2030 to March 2055.

- Both projects will start hydrogen / ammonia supply in FY2030 and have support for 15 years. After support ends, fuel supply must continue for an additional 10 years.

- Several projects are expected to be selected for CfD certification this fiscal year.

- CONTEXT: The Hydrogen Society Promotion Act, enacted in May 2024, set up a framework to expand the use of low-carbon hydrogen, ammonia, and other fuels. ANRE invited applications for projects to cover the price gap between conventional fossil fuels and low-carbon fuels; there were 27 applications with plans far exceeding the support budget of ¥3 trillion.

TAKEAWAY: With its large budget, the CfD program attracts attention even from overseas. There has been strong interest in which projects will be approved, and the announcement was long awaited. According to ANRE sources, the detailed business plans described in the applications made the selection very difficult. These first announcements come about six months after the application deadline. It is unclear how many projects will be selected in total, but the program is important for identifying Japan’s main hydrogen and ammonia suppliers and users. The first two selected projects are small-scale, but they are fully domestic; there was always an expectation that METI would green-light at least a few all-domestic projects. Large-scale supply projects will require fuel imports. The timing of the next announcement is unknown. See the Analysis section for a deeper dive into the hydrogen story and its context in Japan.

Isuzu, Toyota to develop next-gen fuel cell buses

(Company statement, September 29)

- Isuzu Motors and Toyota will develop next-gen fuel cell buses.

- Production begins in FY2026 at the J-Bus Utsunomiya Plant.

- This bus is based on the full-flat BEV route buses that Isuzu and Hino released in 2024, combined with Toyota’s fuel cell system.

- CONTEXT: Isuzu seeks to commercialize next-gen FC buses to expand bus options for carbon neutrality. Toyota views hydrogen as a key energy source, and develops production, transport, storage, and usage.

NEWS: SOLAR AND BATTERIES

Shizen Energy signs 20-year long PPA deal with Microsoft

(Company statement, October 3)

- Microsoft signed a new 20-year PPA with Shizen Energy, securing renewable electricity from three planned solar farms. Together with an earlier deal in 2023, Microsoft’s total contracted capacity with Shizen now reaches 100 MW.

- The 2023 virtual PPA was for 20-years from a 25 MW (AC) solar plant in Inuyama, Aichi Pref. This was Microsoft’s first PPA in Japan.

- In the 2023 project Shizen secured ¥11 billion in financing from Société Générale, Japan’s first case of such financing for a VPPA combined with non-fossil certificate sales and a long-term power sales contract.

- The company also signed a renewable energy deal with Google in May 2024.

- CONTEXT: The move aligns with Microsoft’s goal to cut more CO2 than it emits by 2030, as its energy demand grows from AI-driven data centers.

- SIDE DEVELOPMENT:

- ENEOS and Octopus Energy sign a PPA

- (Company statement, September 30)

- ENEOS and Octopus Energy signed a PPA. Octopus will install solar generation equipment on ENEOS-owned rental properties, with the electricity sold to tenants.

- Initial installations are planned in Tokyo, Kansai, and Tokai regions, with nationwide expansion expected.

- CONTEXT: ENEOS is aligned with the ZEH (Net Zero Energy House) initiatives, and seeks certification for its apartment complexes.

MSFL acquires two large-scale BESS from West Holdings

(Company statement, September 30)

- Mitsui Sumitomo Finance & Lease (FL) acquired two large-scale battery storage plants developed by solar power specialist West Holdings.

- Both are located in Yamaguchi and Kumamoto Prefs, with combined storage capacity of 20 MWh. They’ll be operational by November and will be run by SMFL Mirai Partners, a renewables subsidiary of Mitsui Sumitomo FL.

- Toshiba Energy Systems will be the aggregator, handling electricity trading.

- CONTEXT: Mitsui Sumitomo FL plans to recover its investment and generate profits over 20 years through electricity sales. While SMFL Mirai Partners previously focused on acquiring and operating West Holdings’ solar plants, it now aims to expand into storage batteries. By 2030, it plans to invest ¥200 billion in large-scale BESS, including buying facilities developed by West Holdings and others.

TAKEAWAY: More firms operating solar plants are adding BESS to their portfolios as a way to increase profits by adding an option to store the renewables-derived electricity. However, most non-Japanese players tend to see the future of the BESS market in large-scale projects, expecting market saturation for smaller projects in the coming few years.

- SIDE DEVELOPMENT:

- J-Power begins work on its first BESS in Japan

- (Company statement, October 1)

- J-Power began building the Hibikinada power storage plant in Kita-Kyushu, Fukuoka Pref, the company’s first in the domestic market.

- Operations are slated to begin in 2028, with a power capacity of 10 MW, and storage capacity of 43 MWh.

TAKEAWAY: Most online BESS projects in Japan range between 2 and 8 MW; thus, this one is larger than usual. Storage facilities are essential in the Hibikinada area, which is designated as a ‘promising zone’ for wind power. The area has one offshore wind farm, which began operations in August. While J-Power is mainly active in solar, it’s expanding into battery storage to meet the growing demand for renewables.

- SIDE DEVELOPMENT:

- KEPCO, SPARX and JA Mitsui Lease to invest in two BESS

- (Company statement, September 25)

- KEPCO, SPARX and JA Mitsui Lease will invest in two BESS facilities in Mito, Ibaraki Pref (50 MW/ 175.5 MWh), and Hamamatsu, Shizuoka Pref (30 MW/ 110.3 MWh), targeting commercial operation in June 2029 and June 2028, respectively.

- Both projects will deploy Kansai Electric’s kan-denchi one-stop solution, which provides battery diagnostics, operational support, and power market participation services.

- The Kansai utility wants to expand this service nationwide, positioning itself as a comprehensive service provider in Japan’s energy storage market.

Kanematsu acquires stake in solar firm Alam Energy Indonesia

(Company statement, September 25)

- Trading house Kanematsu acquired a 25% stake in solar company Alam Energy Indonesia through a third-party share allotment and share transfer deal.

- The new shareholder structure is:

- Shizen Power Group, 38.25%,

- Alam Nix Renewables, 36.75%,

- Kanematsu, 25%.

- CONTEXT: Alam Energy Indonesia, established in 2019, develops and operates rooftop solar rental projects in Indonesia, and has a total capacity of 30 MW.

JinkoSolar and LONGi reach an agreement on patents

(Company statement, September 19)

- Chinese companies JinkoSolar and LONGi Green Energy Technology reached an agreement over legal disputes on solar technology patents.

- Both agreed to:

- Terminate ongoing patent-related legal proceedings;

- Cooperate in a cross-licensing agreement for core patents owned by each company.

TAKEAWAY: JinkoSolar and LONGi have a strong presence in Japan; thus, this agreement has ramifications for the country’s solar market. JinkoSolar holds a 26% share of Japan’s solar market, and LONGi has stable distribution in several prefectures (Fukushima, Yamagata, Aichi, Kumamoto, Fukuoka, and Miyagi).

Kuraray signs deal with Tokyo Gas to procure renewable certificates in the U.S.

(Company statement, October 1)

- A U.S. subsidiary of Kuraray, a specialty chemical company, signed a 10-year virtual PPA with Tokyo Gas America, starting this month.

- Kuraray will procure 300 GWh of renewable energy certificates annually from the Actina Solar Project in Wharton County, Texas, with a max. capacity of 630 MW.

- The agreement will offset about 70% of Kuraray’s U.S. electricity consumption and around 40% of the company’s total global electricity use.

Sapporo seeks contractors to study solar power on unused municipal land

(Government statement, September 22)

- Sapporo City seeks contractors through a tender to study introduction of solar power facilities on unused municipal land.

- The goal is to assess feasibility, capacity, contractual issues, and conditions for introducing solar power facilities via off-site PPA.

- Target sites are seven locations, for 20 MW total capacity, including:

- Yamamoto Treatment Plant (10 MW)

- Rainwater Retention Site (4 MW)

- Near Satorando (1 MW)

- Proposal submission deadline is Oct 14. Construction should start between FY2027–2029, with operations beginning by FY2030.

- CONTEXT: Sapporo was chosen as a Decarbonization Hub by the MoE, and seeks to install 32 MW of solar capacity on municipal sites and unused land by 2030.

TEPCO and Metropolitan Central agree on solar energy management

(Company statement, September 10)

- TEPCO agreed with Metropolitan Central Wholesale Market to monitor the deployment in Tokyo of solar power generation across its facilities, implement peak shaving through EMS (Energy management systems) combining renewables and storage batteries, and support battery charging using renewable energy.

- TEPCO will consider the feasibility of more advanced energy management when combining storage batteries with EMS.

NEWS: WIND POWER AND OTHER RENEWABLES

METI Council explores further initiatives to promote geothermal energy

(Government statement, September 26)

- METI’s Council for the Promotion of Next-Generation Geothermal Energy discussed measures to promote new geothermal technologies.

- The main direction includes increasing installed power capacity, addressing commercialization issues (financing, safety guidelines, etc.) and reducing drilling and production costs.

- The govt will continue to promote the following:

- Increasing installed power capacity to 1.4 GW by 2040, and 7.7 GW by 2050 in 118 areas;

- For technology support – developing efficient heat recovery and power generation systems for both supercritical and EGS;

- For cost optimization – reducing next-gen geothermal power generation costs to the level of conventional geothermal (¥13.8 – ¥36.8/ kWh), with a long-term target of ¥12 – ¥19/ kWh.

- CONTEXT: The Council is considering measures in the framework of the 7th Basic Energy Plan. Looking to 2050, its objective is to hold public-private discussions to expand geothermal power generation.

METI and MLIT update zones for offshore wind development

(Government statement, October 3)

- METI and MLIT updated sites for offshore wind power development under the Renewable Energy Sea Area Utilization Act.

- Two newly designated “Promising Zones”:

- Offshore Akita City (Akita Pref)

- Offshore Hibikinada (Fukuoka Pref)

- Three new “Preparation Zones”:

- Offshore Asahi City (Chiba Pref)

- Offshore Goto South (Nagasaki Pref, floating)

- Offshore Ichikikushikino (Kagoshima Pref)

- In addition, three zones were selected for JOGMEC-led site surveys (wind, seabed, ocean conditions) to accelerate offshore wind development. They are:

- Area off the coast of Akita City (Akita Pref)

- Offshore Asahi City (Chiba Pref)

- Offshore Hibikinada (Fukuoka Pref)

- The govt stressed that selection as a survey area does not automatically mean designation as a “promotion area” under the Renewable Energy Sea Area Utilization Act; that requires separate procedures.

- CONTEXT: Proposals came from eight candidate areas earlier, and after expert review, these three were chosen. Japan now has 12 ‘promotion areas’, nine ‘promising areas’ and 17 ‘preparation areas’.

Developers want offshore wind to join LTDA’s 20-year fixed revenue

(Reuters, September 29)

- Offshore wind developers are asking to join the govt’s long-term decarbonized power sources auction (LTDA) that offers up to 20 years of fixed revenue. It currently excludes offshore wind projects.

- The request follows Mitsubishi’s withdrawal from three major projects due to soaring costs, raising concerns about the sector’s viability.

- The govt pledged to review the issues, ease regulations, and set a new framework by year-end to support its 2040 goal of 45 GW offshore wind. As a solution, METI is considering allowing changes in suppliers, including for turbines, and allowing offshore wind farms to operate beyond an original timeframe of 30 years.

- An industry player called participation in LTDA “a life vest for the industry.”

- Analysts say inclusion in the LTDA could stabilize investment and allow Japan to capitalize on its floating wind potential over the next decade. However, METI has not clarified how it will respond.

Eurus Energy proceeds with EIA for 397 MW offshore wind farm

(Company statement, September 26)

- Eurus Energy issued an environmental impact assessment methodology document for a fixed-bottom offshore wind project near Kujukuri Town, Chiba Pref; it submitted this to METI and the local governments.

- The company’s plans were for a project with up to 35 turbines, (12-22 MW each); total capacity up to 450 MW. But, due to grid connection restraints, the project will likely be capped at 397 MW.

- CONTEXT: The site is about 10 km off the coast and is located in an area that was added to the list of ‘promising zones’ in 2022.

- The site has not yet been auctioned and several other firms are making studies in the same area, which means they will likely bid in the same tender.

- TEPCO Renewable Power submitted its EIC document for the same site in Dec 2023, planning a wind farm (465 MW capacity) with 24 – 31 turbines.

- CONTEXT: The area was added to the previous zone in Chiba Pref off the coast of Choshi City, which was awarded to a Mitsubishi-led consortium that recently withdrew from offshore wind projects.

JERA Nex transfers ownership in wind farm project in Hokkaido

(Company statement, October 1)

- JERA Nex transferred part of its ownership in Ishikari wind farm (Hokkaido) to Hokkaido Electric and Tohoku Electric.

- The project will now be operated by JERA, Green Power Investment, Hokkaido Electric and Tohoku Electric.

- The project, in operation since 2024, has eight 14 MW turbines, for a total capacity of 112 MW.

NYK signs long-term deal to provide CTV for offshore wind operations

(Company statement, Nikkei, September 29)

- NYK signed a long-term contract to provide a crew transfer vessel (CTV) for offshore wind power operations off Akita Pref.

- Nikkei reports the contract is for over 10 years, though this is not officially disclosed.

- The contract is with OGA Offshore Green Energy, a consortium backed by JERA, J-Power, Tohoku Electric, and Itochu.

- The 28-meter CTV is based on a design from Sweden’s Northern Offshore Services, and adapted by NYK for Japan’s conditions.

TDK Ventures and Toyota Ventures invest in North American geothermal

(Company statement, September 17)

- Rodatherm closed an oversubscribed $38 million Series A funding round, led by Evok Innovations, and included TDK Ventures and Toyota Ventures, etc.

- The funds will go to Rodatherm’s pilot geothermal system in Utah, U.S., and will enable expansion to a full 100 MW system.

- Since 2022, Rodatherm has developed in the US and Canada a closed-loop geothermal system optimized for hot sedimentary basins.

Mitsui transfers shares to K&O Energy to expand geothermal business

(Company statement, October 2)

- Mitsui’s subsidiary, Mitsui Mineral Resources Exploration, transferred 33.4% of its shares to K&O Energy, to boost the company’s geothermal value chain and expand order volumes.

- MMRE provides consulting services in mineral, geothermal, and water resource exploration and development.

NEF releases auction results for subsidy allocation for hydro power

(Organization statement, September 16)

- The New Energy Foundation announced auction results to allocate subsidies to companies/ prefectures that make surveys for potential hydropower plant projects.

- Of seven companies/ prefectures with a total of 50 projects, six covering 49 projects won. They are:

Survey area | Company | Project name |

Hokkaido | Kit Blue | Kamieuchi Village, Ninomega River – Small Hydroelectric Power Plant Feasibility Assessment Survey Project |

Akita | Akita Pref | Akita Pref Small Hydroelectric Power Plant Introduction Feasibility Study Project |

Shimane | Shimane Pref | Obe Power Plant Renewal Project Feasibility Assessment Survey Project |

Kochi | Kochi Pref | Project to outline possible sites for introducing small hydroelectric power generation in the Monobe River system |

Oita | Oita Pref | Feasibility study for the Yabakei Power Plant renewal project |

Miyazaki | Miyazaki Pref | Feasibility study for the Shimoaka Power Station renewal project |

NEWS: NUCLEAR ENERGY

METI says 55 GW of nuclear power capacity to be replaced by FY2040

(Denki Shimbun, October 2)

- METI’s Nuclear Subcommittee began discussions on the future for nuclear power, focusing on next-gen innovative reactors.

- FEPC said to ensure a stable electricity supply by FY2040 Japan should replace 55 GW of nuclear power capacity.

- Nuclear power is expected to maintain a 20% share of Japan’s electricity mix through 2040.

- Nuclear power will need continuous, long-term development and installation. The industry should take into account the long lead times for nuclear projects and the decline in capacity after 2040.

- Industry representatives commented on the decline in new plant construction, which puts pressure on vendors in the nuclear supply chain.

- Some members suggested that setting a clear replacement target of around 55 GW would be an effective way to provide policy direction. Others emphasized that Japan should not fix a single scenario but prepare many options.

- SIDE DEVELOPMENT:

- METI’s advanced reactor working group moves forward

- (Government statement, October 3)

- The group discussed the latest developments in next-gen reactors. Among the items highlighted were that:

- Hitachi GE Vernova is progressing with two next-gen light-water reactor models: the large-scale HI-ABWR and the small modular reactor (SMR) BWRX-300.

- Canada’s Ontario Power Generation will build the first BWRX-300, targeting operation by 2030. It willbe the first SMR to reach this stage in the West.

- Toshiba Energy Systems is working on aboiling water reactor, the iBR, that aims to operate autonomously for up to a week in case of an accident.

- CONTEXT: Some Japanese players have taken a different tack. Instead of developing new technologies, companies such as JGC, in partnership with IHI and NuScale Power, wants to adapt the U.S.-designed NuScale SMR for global markets. The idea is to develop a version of the NuScale plant with enhanced seismic resistance for potential use in Japan. NuScale’s Japanese partners want to study how to reconcile the differences between the U.S. and Japan in nuclear safety regulations and quality assurance standards.

TAKEAWAY: As these expert panel discussions show, major nuclear players are advancing diverse SMR and next-gen reactor designs but, the real momentum remains overseas – not in Japan. Despite technical progress, Japan still lacks a clear domestic SMR strategy, which has pushed companies to build credibility and experience overseas before the technology may take root at home. For more information, see Japan NRG’s June 2 analysis section.

Niigata Pref releases public opinion survey for Kashiwazaki-Kariwa NPP restart

(Nikkei, October 2)

- Niigata Pref released a report on the public opinion survey carried out around the restart of TEPCO’s Kashiwazaki-Kariwa NPP.

- 37% of residents that answered the survey agreed (including “somewhat agreed”) that conditions for a restart are now in place, but 60% disagreed.

- 48% said the NPP should not restart under any circumstances, while 50% disagreed with that view, showing a split in opinion.

- Over 90% worry about the increase of spent nuclear fuel and around the compensation/ reputational damage in the area should a nuclear accident occurs. More than 90% want stronger disaster-prevention measures such as evacuation routes, radiation protection facilities, and snow removal systems. Only 55% felt current safety measures were enough.

- 69% are uneasy about TEPCO operating the facility.

- Niigata Pref Assembly will discuss the result. The governor will make a decision after considering the survey, public hearings, and discussions with mayors.

TAKEAWAY: Any kind of restart of TEPCO’s Kashiwazaki-Kariwa NPP remains uncertain despite the various efforts by the utility and the national government. Governor Hanazumi maintains a cautious stance, saying he will make a decision “at an appropriate time.” The ruling party in the regional assembly is pushing for a swift decision, but the governor will likely wait for the survey’s final report after November, buying time. A potential assembly resolution on the restart is a key focal point, likely during the December session. A final decision on the restart within this calendar year looks unlikely.

- SIDE DEVELOPMENT:

ANRE to explain evacuation measures for Kashiwazaki-Kariwa NPP

(Nikkei, September 29)- ANRE chief Murase Yoshifume offered to attend the Niigata Pref Assembly’s session to explain evacuation procedures for Kashiwazaki-Kariwa NPP.

- His goal is to speed up discussions and gain local consent.

- TEPCO hopes to restart Unit 6 as early as this winter, saying it will be ready by mid-October from a technical point of view.

NEWS: TRADITIONAL FUELS

Kyushu Electric postpones restart date for Genkai NPP Unit 4

(Company statement, September 29)

- Kyushu Electric postponed restart of Genkai NPP Unit 4.

- During an inspection of the main steam system, a problem was found in one of the valves. As a precaution, there will be more inspections.

- Since July 27, Genkai NPP Unit 4 has had its 17th periodic inspection. The reactor restart was planned for Sept 30, and power generation on Oct 2.

- SIDE DEVELOPMENT:

- Ikata NPP Unit 3 to begin regular inspection

- (Company statement, October 3)

- Shikoku Electric will begin a regular inspection of Ikata NPP Unit 3 (Ikata Town, Ehime Pref) on Oct 11, covering the reactor, facilities related to radioactive waste, and replacement of 44 fuel assemblies out of a total of 157 with new uranium.

- Power transmission will resume in late December, inspection ends in January.

- The spent nuclear fuel will be stored for cooling and later transported to a reprocessing plant for eventual recycling as fuel.

Zero Watt Power acquires Surukawa Energy Center and its biomass facilities

(Company statement, September 22)

- Zero Watt Power wholly acquired Surukawa Energy Center, which operates a biomass power plant (85 MW) in Shizuoka Pref fueled by wood pellets.

- Surukawa Energy Center’s overall annual power capacity now equals 600 GWh.

LNG stocks down from previous week, no change YoY

(Government data, October 1)

- As of Sept 28, the LNG stocks of 10 power utilities were 1.83 Mt, down 2.7% from the previous week (1.83 Mt); no change from end Sept 2024 (1.83 Mt); and down 10.7% from the 5-year average of 2.05 Mt.

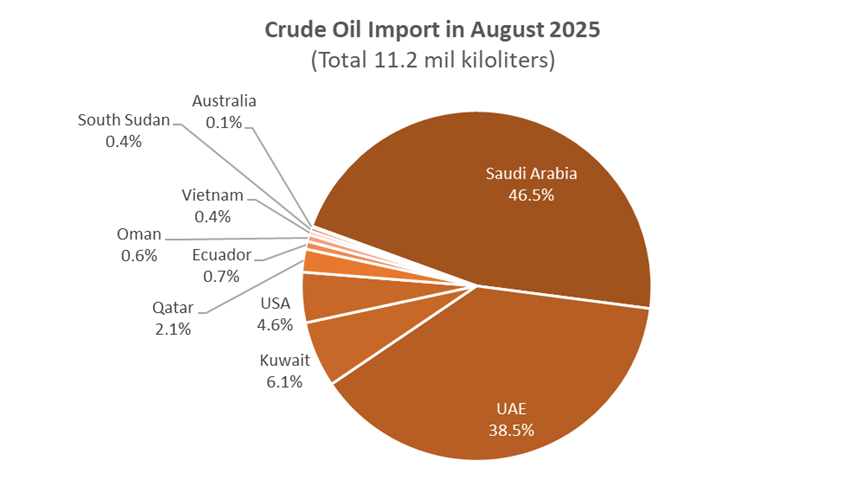

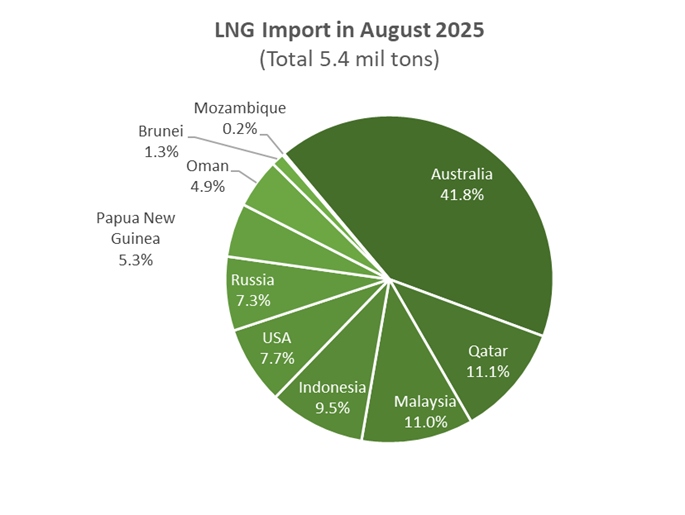

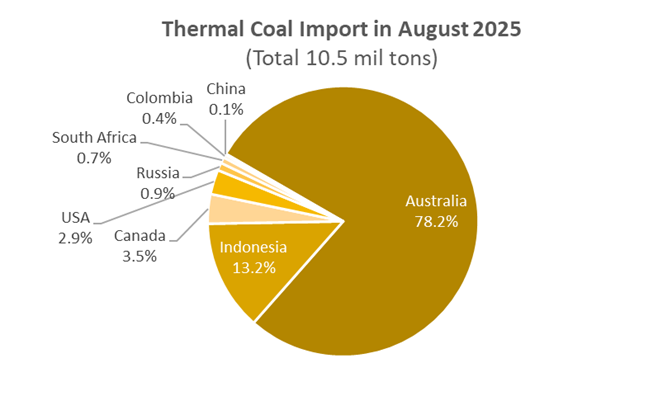

August Oil/ Gas/ Coal trade statistics

(Government data, September 26)

Imports | Volume | YoY | Value (Yen) | YoY |

Crude oil | 11.2 million kiloliters | -2.5% | 749.2 billion | -21% |

LNG | 5.4 million tons | -6.5% | 453.5 billion | -16.4% |

Thermal coal | 10.5 million tons | 13.7% | 187.7 billion | -13.1% |

- Japan imported 11.2 million kiloliters of crude oil in August, down 2.5% from July and down 2.5% YoY. Over 94% of total crude oil imports came from the Middle East, led by UAE, followed by Saudi Arabia. For the first time this year, a small volume came from Vietnam.

- LNG imports in August totaled 5.4 Mt, up 1.7% over July (5.3 Mt) and down 6.5% YoY. Over 40% came from Australia; together with other Asian countries, LNG imports from Asia & Pacific amounted to almost 70%.

- Thermal coal imports in August rose to 10.5 Mt, up 8.4% from July. Electric power companies ramped up thermal coal purchases to prepare for peak power demand for air conditioners during the summer. For the first time in 2025, a small volume came from Colombia.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Hard-to-abate sectors comment on ETS developments

(Government statement, October 2)

- The govt unveiled benchmark proposals for its ETS, targeting hard-to-abate sectors such as aluminum, lime, carbon black, and rubber. A key development is the move towards technical, industry-specific rules.

- For aluminum, correction factors for furnace size and production cycles are needed; for lime, separate benchmarks for process and energy-related emissions.

- The carbon black industry mentioned external factors that will increase its carbon footprint, requiring a compensatory correction. The rubber industry is against a simple product-based benchmark, asking the govt to use “CO2 per unit of heat input”.

- The aluminum industry warned about the massive overseas outflow of aluminum scrap. It is a valuable domestic low-carbon resource. They urge policies to keep this scrap in Japan to fuel a circular economy and reduce reliance on imported primary aluminum. The carbon black industry highlights intense competition from China.

- They all stressed that the ETS must not undermine the competitiveness of domestic producers. This would only shift production and emissions abroad.

Mazda updates roadmap for carbon neutrality, will use LNG instead of ammonia

(Automotive world, September 30)

- Mazda Motor updated its 2030 carbon neutrality roadmap at production plants, which account for about 75% of its CO2 emissions.

- Earlier, they had opted for switching from coal to ammonia at Hiroshima Plant. But now, Mazda will adopt a gas cogeneration system powered by LNG-based city gas, which can later also switch to hydrogen.

- The company partnered with Kawasaki Heavy Industries to design this system. Mazda will phase out coal-fired power plants at the Hiroshima and Hofu facilities by 2030.

TAKEAWAY: Ammonia is seen as a key technology in decarbonization in power generation and transportation. However, with fuel deliveries and pricing uncertain, some manufacturers are turning to the near-term solution of burning natural gas, with the optionality of switching to H2 or ammonia in the future. This news suggests that industrial buyers in Japan are not certain of securing necessary volumes of ammonia by 2030 to switch directly to this fuel and away from coal.

Sumitomo Forestry and NTT Docomo to cooperate on J-Credits

(Nikkei, October 1)

- Sumitomo Forestry and NTT Docomo Business agreed with Shioya Town (Tochigi Pref) on a project to generate and sell govt-certified carbon credits (J-Credits).

- The town will get credit rights from local forest owners, selling them via an online platform operated by the two companies. Forest owners will get part of the revenue.

- Shioya Town, where about 60% of land is forest or wilderness, has around 6,500 hectares of private forest, but 98% is not yet using J-Credits.

- CONTEXT: Issuing J-Credits requires technical expertise and effort to find buyers, which is difficult for individual forest owners. By letting the town handle issuance and sales on their behalf, owners can gain income without extra cost or administrative burden.

- SIDE DEVELOPMENT:

Toho Gas and Green Carbon launch carbon credit project in Philippines - (Company statement, September 29)

- Toho Gas and Green Carbon began a field test in Bohol, Philippines to generate carbon credits under the Joint Crediting Mechanism (JCM).

- The project applies the Alternate Wetting and Drying (AWD) method in rice paddies that reduces methane emissions by draining and reflooding fields.

- Toho Gas will use carbon credits as a carbon-offset for city gas.

ANALYSIS

BY TETSUJI TOMITA

Green Hydrogen Production: Water Electrolysis Technology Trends and Outlook

Japan has certified its first low-carbon hydrogen supply plan, approving subsidies for a project that will use wind power to produce green hydrogen through electrolysis. Led by Toyo Tsusho, Eurus Energy, Iwatani and Aichi Steel, the venture aims to make 1,600 tons a year from 2030 to help decarbonize specialty steelmaking.

Though small, the fact that the first award from the Contract for Difference (CfD) hydrogen support scheme is for a green fuel project is significant. While it’s almost certain that most of Japan’s hydrogen and ammonia consumption over the coming decade will rely on imports and cheaper blue fuels – derived from natural gas with the emissions captured – policymakers are signalling that green fuels, too, will have a role despite their high costs.

That support also dovetails with Japan’s efforts to develop domestic electrolysis technology. State-backed projects are advancing alkaline, PEM and solid oxide designs, aiming to cut costs and improve durability. The new certifications highlight why such innovation matters: only with cheaper and more efficient electrolyzers can green hydrogen compete with imported blue alternatives.

In contrast to the enthusiasm of policymakers, Japan’s potential hydrogen consumers are cautious about switching to a green fuel. Green hydrogen is often double or more the cost of the blue fuel. Meanwhile, when considered among a broader array of options, hydrogen’s energy losses during conversion weaken competitiveness with direct electrification pathways.

Advocates, however, say that hydrogen – and green hydrogen in particular – will play a major role in the decarbonization of hard-to-abate industries such as cement and steelmaking, as well as a feedstock for ammonia production. And thus the anointment of a domestic green steel project for initial CfD funds holds strategic significance. It is the first time that Tokyo has formally certified supply chains for hydrogen and ammonia.

Japan NRG takes a look at the development of the green hydrogen technologies, comparing advantages and challenges, and highlighting their potential.

The second project selected by METI for CfD funds, also approved on 30 September, aims to produce low-carbon ammonia from waste plastics and textiles. Renac and Japan Catalyst will gasify discarded material at Kawasaki to generate over 20,000 tons of ammonia annually – equivalent to 3,200 tonnes of hydrogen – and feed it into textile and recycling supply chains. This is not strictly speaking a ‘green’ fuel, but it does fit with the circular economy approach. Both the Aichi Steel and the Renac projects will run until 2055.

Electrolysis in green hydrogen

Electrolysis involves splitting water molecules into hydrogen and oxygen using electricity. When powered by renewable energy sources such as wind, solar, or hydropower, the resulting hydrogen can be classified as green. Unlike fossil-based hydrogen production, this process generates no direct CO2 emissions.

Electrolyzers also provide value by offering demand-side flexibility to power systems, absorbing excess renewable generation, and supplying hydrogen for industries that are otherwise difficult to decarbonize, such as steelmaking, refining, fertilizer production, and long-distance transport.

Understanding the strengths and limitations of these various technologies is essential for guiding investment and policy decisions. Scaling up electrolytic hydrogen production faces major challenges. Costs remain high, with electrolyzer systems contributing significantly to overall hydrogen prices. Improvements in efficiency, durability, and the ability to rapidly respond to variable renewable electricity also impact competitiveness.

With a levelized cost of hydrogen (LCOH) ranging from $3–5/ kg in optimal regions, equivalent to ~$90–150/ MWh, driven by high electrolyzer costs and ~70% electrolysis efficiency, green hydrogen is 1.5–3 times more expensive than unsubsidized renewable electricity.

That LCOH is projected to decline to $2–4/ kg (~$60–120/ MWh) due to cheaper electrolyzers (30–50% cost reductions) and falling renewable costs, particularly in regions with abundant solar or wind resources.

Overseas, some water electrolysis systems operate at a scale of several tens of megawatts, while Japanese projects tend to be no more than 10 MW. This is largely due to Japan’s more expensive renewables electricity. So, it has fallen to NEDO and the Green Innovation Fund to help find a competitive advantage in the electrolyser part of the value chain.

Water electrolysis technology development

The four prevailing green hydrogen electrolysis technologies differ significantly in their design, operating principles, performance characteristics, and commercial readiness. These are electrolysis (AWE), proton exchange membrane electrolysis (PEM), solid oxide electrolysis cells (SOEC), and anion exchange membrane electrolysis (AEM).

Table. Comparison of electrolysis technologies

Feature | AWE | PEM | SOEC | AEM |

Technology maturity | Commercial, decades of deployment | Commercial, scaling rapidly | Demonstration stage, pilots in EU/US | Early-stage, R&D and pilots |

Operating temperature | 60–90°C | 50–80°C | 600–850°C | 40–80°C |

Efficiency (LHV) | 60–70% | 65–75% | 80–90% (with heat integration) | 65–75% (target) |

Dynamic response | Slow | Fast | Moderate | Fast |

Stack lifetime | 60,000–90,000 h | 30,000–60,000 h | 10,000–30,000 h | <10,000 h |

Key materials | Nickel-based | Iridium, platinum | Ceramic oxides, perovskites | Nickel, cobalt, iron |

System cost | Lowest | High | Highest | Potentially low |

Best applications | Large, stable plants | Renewable integration, mobility | Industrial integration, e-fuels | Emerging distributed H₂ |

Major manufacturer | Asahi Kasei, Tokuyama, Thyssenkrupp, etc. | Kanadevia, Toyota Motor, Siemens, etc. | Sumitomo Electric, MHI, Enapter, etc. | MHI, Denso, Sunfire, etc. |

Source: Japan NRG based on METI, NEDO materials

1) AWE is the most established hydrogen production method, using an alkaline solution (KOH or NaOH) with nickel electrodes and a diaphragm. Robust, reliable, and relatively low-cost, it achieves 60–70% efficiency with lifetimes over 60,000 hours, making it suitable for large-scale hydrogen production from stable power sources.

Operating at low current densities, however, slows response which makes AWE tricky to integrate with variable renewable sources; it also requires maintenance due to liquid electrolytes. While still widely used, newer projects often prefer more flexible alternatives.

2) PEM is the second most commercially advanced hydrogen production technology, using a solid polymer membrane instead of a liquid electrolyte, operating at 50–80°C and high current densities for compact, high-output systems. PEMs can ramp up or down in seconds, suitable for intermittent renewable power and grid support.

Efficiency ranges from 65–75%, with stack lifetimes up to 60,000 hours. Challenges include high costs due to scarce materials like platinum and iridium, and the need for ultra-pure water. Advances in materials and scaling are expected to lower costs. PEM technology is deployed worldwide in multi-megawatt plants and hydrogen stations, with further growth anticipated alongside renewable energy expansion.

3) SOEC electrolysis operates differently from low-temperature systems, using a solid ceramic oxide electrolyte that conducts oxygen ions at 600–850°C. Steam is used as the feed, and high thermal energy reduces the electricity needed to split water. This enables SOEC to reach high efficiencies, often above 80% and potentially 90% when paired with industrial or nuclear waste heat.

They can also co-electrolyze steam and CO2 to produce syngas for synthetic fuels, supporting e-fuels for aviation and shipping. However, SOEC is a less mature technology than AWE or PEM. High temperatures stress ceramics, limiting stack lifetimes to 10,000–30,000 hours and reducing flexibility. Manufacturing complexity and high costs hinder large-scale deployment. Despite this, SOECs attract strong interest in Europe, the U.S., and Japan for their efficiency and industrial integration potential.

4) AEM is a newer technology combining the advantages of AWE and PEM. Like PEM, it uses a solid polymer membrane but conducts hydroxide ions (OH–) under alkaline conditions, allowing non-precious metal catalysts like nickel, cobalt, or iron, which can reduce costs. AEM electrolyzers operate at low temperatures with efficiencies of around 65–75%, and support fast response and compact design.

Durability is limited, however, with membranes often lasting under 10,000 hours. Multi-megawatt scaling has also proved tricky so far. If research improves the membrane and stack durability, AEM could become a cost-effective alternative to PEM for distributed or mid-scale applications. Currently, it is a promising technology that needs further refining.

Outlook for technology development

Over the next decade, all four technologies are expected to improve, though at different paces. Alkaline systems will likely retain their role in large-scale, low-cost hydrogen projects, particularly where renewable power is relatively stable. PEM is projected to scale rapidly, benefitting from falling catalyst loadings and economies of scale.

AEM’s trajectory will depend on breakthroughs in membrane durability, with successful developments potentially positioning it as a disruptive competitor. SOEC, meanwhile, is expected to expand in niche applications involving industrial integration, nuclear power, or synthetic fuel production, gradually moving toward larger commercial deployment.

Policy support, research funding, and international collaboration will be decisive in shaping outcomes. Governments in Europe, Asia, and North America are investing in electrolyzer deployment targets, which will help drive down costs across the industry.

Simultaneously, supply chain constraints, particularly around iridium and platinum for PEM systems, could accelerate the push toward AEM and other alternatives.

Conclusion

Green hydrogen production through water electrolysis stands at the center of global decarbonization strategies. Alkaline, PEM, AEM, and SOEC technologies each present unique advantages and challenges, with their relative roles likely to evolve as costs fall.

In the near term, AWE and PEM will dominate commercial deployments, with PEM growing fastest due to its compatibility with VRE integration. AEM may achieve competitive scale if technical challenges are overcome, while SOEC promises exceptional long-term potential for industrial integration and synthetic fuel pathways.

Ultimately, a diversified technological portfolio is likely to emerge, where different electrolysis technologies complement one another, depending in large part on the industry in question.

This continued technological innovation from the private sector, combined with state policy that provides additional support and frameworks, will be critical to unlocking the potential of green hydrogen as a decarbonization pathway.

ANALYSIS

BY ANDREW STATTER

Energy Jobs in Japan: Features of Top Leadership Talent for the Energy Transition

Technological innovation, shifting economics, evolving regulations, and geopolitical dynamics are accelerating change across the energy sector. While perspectives differ on how quickly and deeply these transitions will unfold, the effort to reconcile energy security, cost competitiveness, and long-term decarbonization goals is creating uncertainty about the industry’s future.

From a macro perspective the energy industry continues to grow, attracting new companies and talent. But if we look deeper the changes in market segments are rapid and significant. We’ve seen solar boom from almost zero, Japan being the fourth largest country for capacity deployed followed by a slowdown with the transition from FIT to a market based system, and finally shifting back into growth mode, with a stronger focus on a distributed asset model.

The promise of 30-45 GW of offshore wind by 2040 attracted dozens of domestic and international players, but this segment is facing major headwinds with increasing costs, cancelled projects and market exits. Energy storage is now booming and attracting billions in new investment, yet there is a limit to how much storage capacity Japan will need to balance the grid, stretch out the power curve and provide critical backup.

In a constantly changing, and increasingly competitive market, having the right strategy and ability to execute is critical. With an abundance of capital entering the market, technologies the same or similar from project to project, talent becomes the key to get ahead. The line between success and failure often is defined by leadership, rather than dollars and technology.

Shifting mindsets for a shifting market

Leaders across the energy sector, from emerging new-energy startups to established oil and gas companies, must address these unprecedented and evolving challenges. This includes balancing traditional and innovative business models, risk profiles, and corporate cultures.

In the past, developers could rely on subsidies, project revenue was relatively simple to forecast and therefore lever with debt. Today however, challenges from curtailment, customer demands, shifting regulatory requirements and technological advancements make project development, delivery and financing more complex. Successfully deployed strategies in the past are not a guarantee of success in the future. Teams need to be built out with new capabilities that were not necessary just a few years ago.

Success in today’s transforming energy sector will require different qualities than in the past. Leaders will face new expectations on strategy, execution and how they hire and build their teams. Below are three of the top qualities that companies look for when hiring for leadership talent.

Ability to design, build and retain a winning team

A team’s makeup in a typical independent power producer today is different from just a few years ago. Naturally the core members who cover land acquisition, project development, engineering and project financing remain. But now there is a greater emphasis placed on strategic procurement, data analytics, market research and offtake origination and negotiation.

As the business, and thus the makeup of the team is more complex, the leader of the past, who only knows core development and execution of projects, is left behind. As one client told me recently: ‘I need someone who can run a company, not just a development platform’.

What is required to achieve this?

- Broad understanding of all the moving pieces of a modern, market-based energy developer and supplier. This includes offtake strategy, regulatory affairs, risk management, supply chain development and others.

- Ability to craft and communicate a vision. Developers, engineers and data scientists tend to think in different ways and value different things. Communicating a clear, compelling vision and purpose to unite all the moving pieces becomes critical.

- Empower over dictation. The leader is not necessarily expected to be an expert in every aspect of the business. The leader hires experts who know more, and gives them the tools, support and freedom to execute is the leader who attracts and retains the best talent.

- Foster an environment of collaboration and sharing. As new functions come into the business, their purpose, value and needs must be shared with the existing team. Integrating the new talent into teams, and having existing resources become well versed in what the new functions do, is necessary to have a smooth operation and avoid silos.

Leaders who can identify top talent across all key functions and bring them to a new organization command a lot more value than those who join a new firm solo.

Commercial innovation to create shared value

To succeed in the evolving energy landscape, leaders may need to move beyond a win/lose mindset that was prevalent in the earlier, fixed revenue business model reliant on subsidies. Today, greater progress can come from adopting a win/win “growth mindset” that emphasizes pursuing new sources of value — collaborating with suppliers, customers, and stakeholders to deploy innovative co-creation plans and solutions, develop new products and services, and ultimately build markets that do not yet exist.

This can be seen for example in revenue sharing offtake models that have become prevalent in advanced energy markets such as the UK or Australia, where the developer and offtaker will share the risk, but also the profits of trading energy from renewable and storage assets.

New fuels such as hydrogen are another example where co-creation and commercial innovation is necessary. Without shared vision, investment and accountability across upstream, midstream and downstream segments, projects will stagnate and ultimately fail to be delivered.

Leaders who are able to learn from other markets and apply lessons to Japan are gaining value. Management professionals in Japanese firms who have been seconded to joint ventures in advanced overseas markets for example are in high demand.

As there is often not yet a clear blueprint for these co-created business models where developer, offtaker, financiers and supply chain players need to collaborate with each other, creativity and innovation in commercial negotiations has become a core value driver for leadership talent.

Put simply, the one who gets hired is the one who listens, thereby understanding the needs of all stakeholders and structure agreements that share risk, providing benefit to each player. In contrast, those who push their own agenda, chase the short-term gain and take a zero-sum approach to negotiations are often passed over.

Ability to execute

At the end of the day, a wonderful strategy and quality team will not save the leader if business results fail to follow. Delivering on targets, winning projects, generating profit is still king.

Results are quantifiable and clear. How many projects in a competitive bid were won, how many MW was built, how much offtake was signed or how many projects were sold and at what margin can be measured and compared.

Recent results are more valuable than historic results — 50 MW delivered now in an innovative offtake strategy with distributed assets, for example, is worth more than 500 MW of big FIT projects years ago. As the market has become more competitive and complex, past success is not seen to automatically translate into future results.

Companies are run by investors, whether a private equity investor, venture capital player or shareholders of a publicly traded company. Investors want to see the track record, both historical and recent, to be comfortable with the decision that hiring a certain leader will ultimately lead to maximization of profits.

Real results, and the ability to clearly articulate how those results came about, and why we can expect them to translate into future success is critical in leadership hiring decision making.

Andrew Statter is a Partner at Titan GreenTech, an executive recruitment agency focused on the clean energy space.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / BESS

The National Electricity Market achieved multiple battery energy storage records on 27-28 Sept, with total storage capacity reaching 6.6 GWh for the first time.

Australia / Oil & Gas

The oil & gas sector is forecast to pay AU $22 billion in taxes and royalties to state and federal govts in 2024–25, the industry’s highest annual tax contribution to date.

China / Natural gas

China became the world’s largest gas importer following the govt’s decision to convert urban heating systems from coal to reduce pollution and CO2 emissions. Imports increased to a record 130 Mt in 2024, up from zero less than two decades ago.

China / Nuclear power

Nuclear electricity generation rose at an average rate of 12% per year since 2005. China is now the world’s second-largest nuclear generator after the U.S., and has 59 operating reactors with a combined capacity of 56.7 GW.

China / Shale gas

China’s largest shale gas production base in the south Sichuan Basin in Sichuan province, achieved a total output exceeding 100 billion cubic meters.

India / Hydropower

The Central Electricity Authority, which approves construction of large dams, will hire external experts to speed up project designs across the country.

India / Renewables

Solar Energy Corp of India is tendering 1.2 GW of renewables projects coupled with energy storage to supply a total 4.8 GWh of electricity across four peak hours daily.

South Korea / Hydrogen

Work began on the $580 million Gangdong Hydrogen Fuel Cell Power Generation Project. It’s slated for completion by 2028.

Taiwan / Naphtha

Imports of Russian naphtha surged, making Taiwan the world’s largest buyer. Russian purchases by Formosa Petrochemical Corp rose from 9% of its total in 2021 to 90% in H1 of 2025.

Singapore / Electricity

More electricity retailers are offering plans with less costly rates during off-peak hours, which analysts say could lead to even cheaper plans amid stiffer competition.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 101-0062.