JAPAN NRG WEEKLY

August 11 to August 16, 2020

NEWSTOP Japan’s US LNG volumes to jump on Cameron expansion OIL & GAS JERA appoints American director with green credentials Defense ministry fuel tender avoids scrutiny over low price POWER & NUCLEAR RENEWABLES & OTHER Hokkaido fishermen shift from foe to friend of offshore wind TDK pledges to use only local, hydropower for facility CONTACT US |

ANALYSISPOST UNBUNDLING, IS JAPAN’S POWER GRID ACTUALLY INDEPENDENT? On April 1, 2020, Japan planned to abolish regulated electricity tariffs, freeing the incumbent utilities to compete with new market entrants by lowering rates. However, the plan was predicated on creating a neutral grid industry, which was supposed to cut ties with the 10 dominant power utilities. Evidence suggests that grid companies retain an unhealthy proximity to their ancestor utilities. And the tariffs still remain. We explore why. NUCLEAR RESTARTS IN JAPAN BRING MORE PROBLEMS THEN SOLUTIONS Last week we outlined the bull case for nuclear plant restarts. The industry has recently gained some positive momentum. And yet, we see nuclear’s role in the country’s energy mix dropping to 10% or less by 2030. A mass-restart of nuclear power in Japan faces three major issues: the public, market forces, and a myriad of technical problems. Here is the bear case. HOUSE VIEW COVID has wreaked havoc with Japan’s economy. It shrank an annualized 27.8% in April-June, the worse since 1955. Yet, recent global geopolitical turmoil helped lift oil prices, and that’s mostly good news for Japan’s oil firms and investors. Brent, at $19 in April, has rebounded above $40 since early June. Further support for energy prices could come from the run-up to the US presidential election, US-Iran tensions, a Turkey-Greece dispute over gas, and potential escalation of unrest in Belarus. Japan’s economic recovery is uncertain, yet weakness in non-US oil benchmarks will likely be offset by global tensions. |

NEWS

OIL & GAS

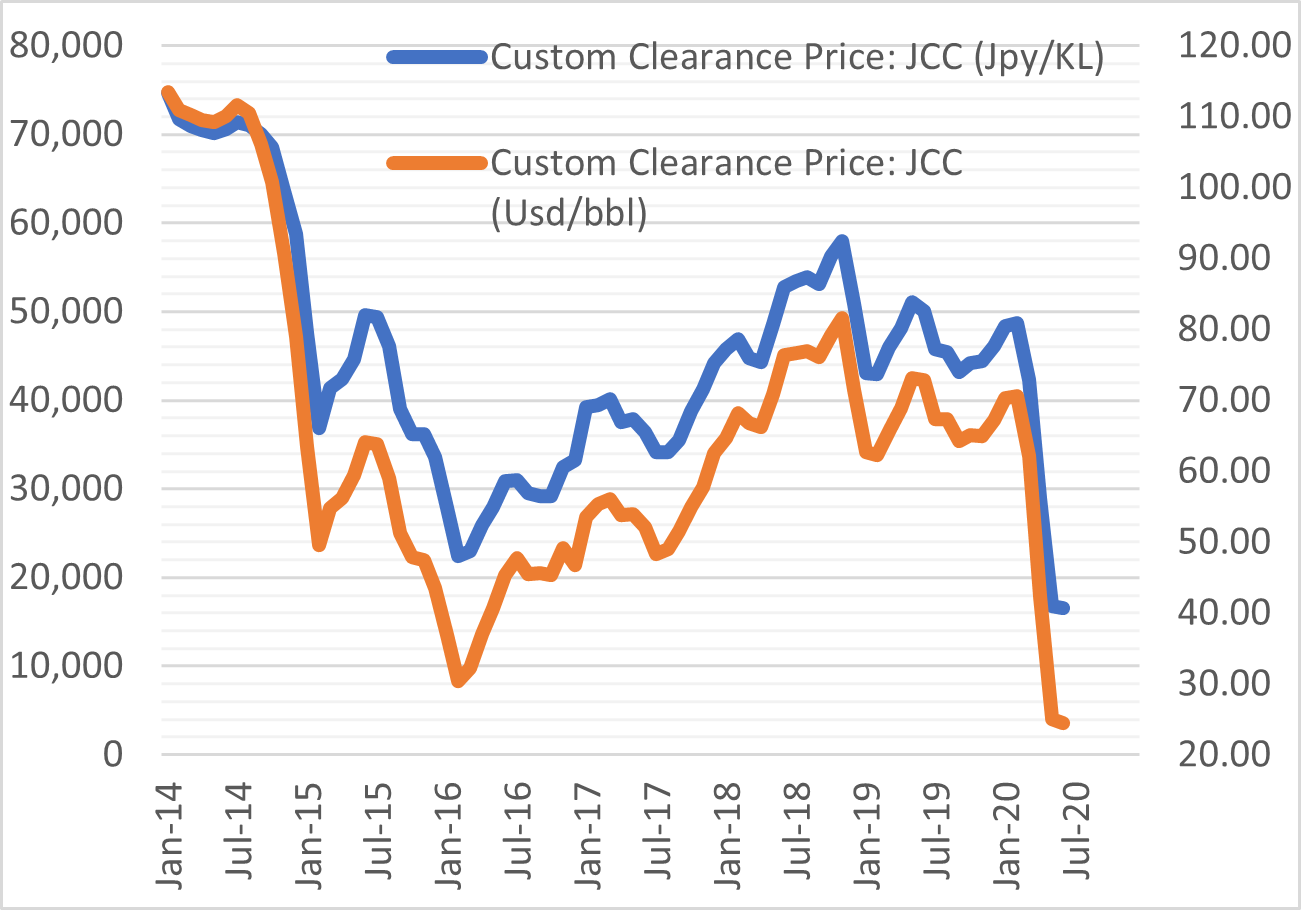

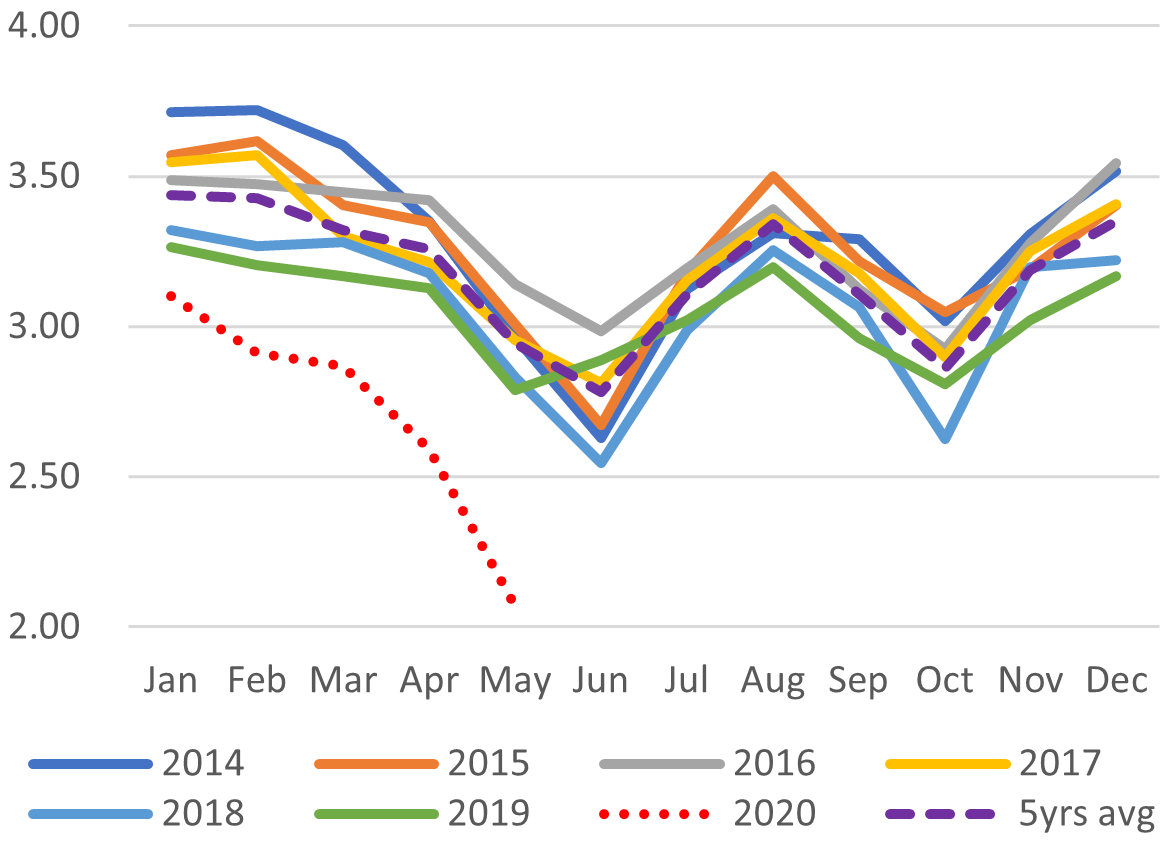

JAPAN OIL PRICE: $24.40 per barrel

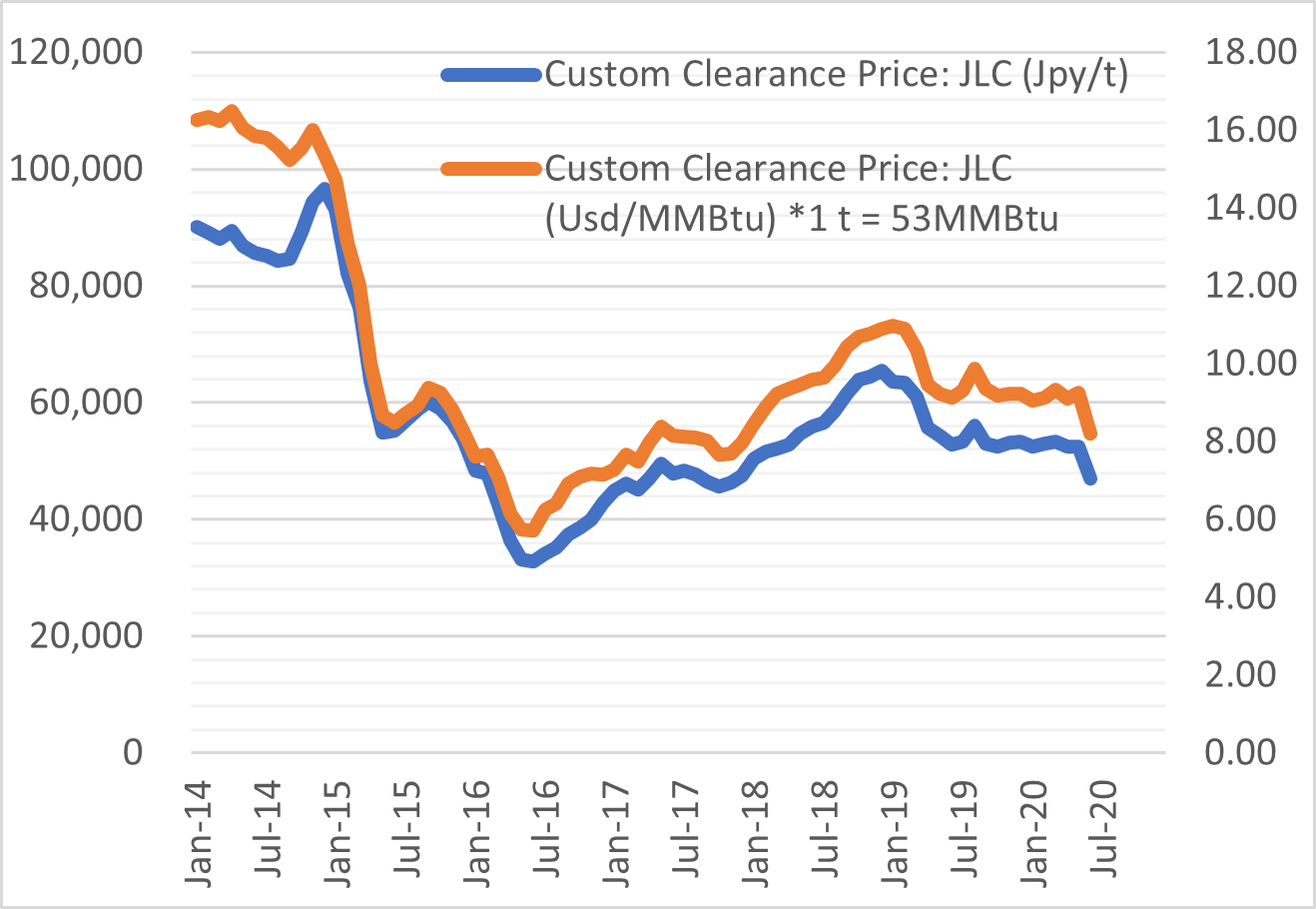

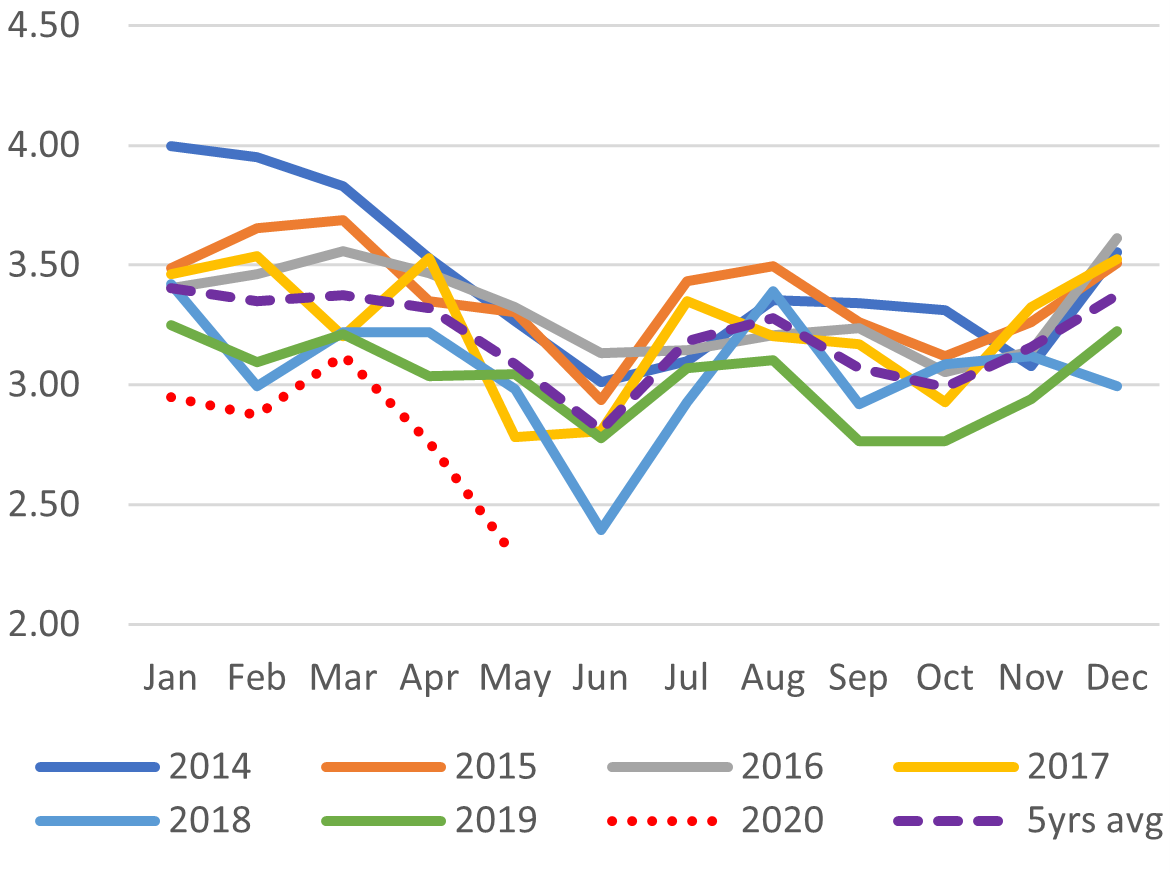

JAPAN (JLC) LNG PRICE: $8.21 per million BTU

Cameron LNG project doubles output (Nikkei, August 11)

- The third and final liquefaction train in the US-based Cameron LNG project, in which both Mitsui & Co. and Mitsubishi Corporation hold stakes, went online on August 10. This doubles the plant’s annual capacity to 12 million metric tons.

- Japan is allotted 4 million tons of total capacity.

- CONTEXT: Japan’s share of Cameron is equal to more than 5% of the country’s total LNG imports. Mitsubishi’s 16.6% stake in Cameron is held via a 70-30 JV with marine shipping group Nippon Yusen (NYK Line). Mitsui and France’s Total also hold 16.6% each, while US-based Sempra Energy is the controlling owner.

- CONTEXT: Japan’s Chiyoda was the engineering, procurement and construction (EPC) lead on the Cameron project. Due to cost overruns and other issues it had a slightly negative impact on investor views of Chiyoda stock.

- TAKEAWAY: This is one of the most important LNG projects for Japan and the US. The Japan portion is bigger than the entire volume of LNG that the nation imported from the US last fiscal year. The Cameron plant was one of the first major post-Fukushima rolls of the dice by Japan to secure large LNG volumes outside its traditional suppliers. And yet, the investment was concluded at a time when US prices of LNG were cheap versus Asian benchmarks. This year’s plummet in oil prices put the trend in reverse. With the US contracts often lacking delivery and price flexibility, it will be curious to see if Japan’s enthusiasm for LNG projects in the US continues.

Mauritius oil spill latest: Fear of further oil spillage (Asahi Shimbun, various, Aug 16)

- The hull of the Japanese freighter stranded off the coast of Mauritius was almost split in two as of Aug. 15 and is cracking further under high waves. Concern of further oil spills are increasing.

- CONTEXT: The Panama-flagged Wakashio bulk carrier, owned by Nagashiki Shipping and chartered by Mitsui OSK, ran aground on a reef off the coast of Mauritious on July 25. Leaks started in earnest a week later. It was carrying about 3,800 tons of oil and 200 tons of diesel from China to Brazil. So far, about 1,200 tons spilled into the water from damaged tanks. Roughly 500 tons were recovered. Early estimates indicate that environmental recovery will take decades.

- Mauritius Prime Minister Pravind Jugnauth pledged to seek damages, and the accident will strongly hamper the tourism-led local economy. Nagashiki Shipping has signaled that it will comply with damage requests.

- The shipper may face damages of about ¥2 billion (USD 19M) due to maritime limits on liability, according to Japanese officials.

- Media reports the vessel neared shore as crew members celebrated a birthday and wanted to get a better wi-fi signal. Repeated warnings from local authorities to the ship were ignored.

- TAKEAWAY: Given current political and geopolitical events, this accident didn’t even make the top Africa news in the global media. The Japan side has apologized, offered to pay and help clean up. Damage to Mauritius’ unique and world-famous ecosystem will be mourned. Yet, we do not see wider industry repercussions at this stage.

JERA appoints David Crane as director (Denki Shimbun, August 6)

- JERA has appointed former NRG Energy CEO David Crane to its Board of Directors.

- Crane brings to JERA his experience gained in the US and UK energy markets, which saw increased competition as a result of deregulation.

- TAKEAWAY: Apart from bringing in a third non-Japanese director to its 10-person board, already a rare proportion for a major Japanese corporate, JERA must be looking to tap into Mr. Crane’s vision for how to lead an “old-energy” firm into renewables. He is famous for turning coal-heavy NRG Energy towards green businesses, such as solar. He is a self-confessed renewables evangelist. This could be a good fit for a coal-heavy firm like JERA, which is just starting to invest in green energy.

Defense ministry’s 2nd shipping fuel tender at closer to market price (Sekiyu Tsushin, August 14)

- Japan’s Ministry of Defense has released the results of its second shipping fuel tender of the year. All successful bids were above ¥40,000 per kiloliter.

- CONTEXT: The first tender drew industry attention because some bids were questionably low, in the mid-30,000s of yen per kiloliter. Most of the diesel supply contracts were won by Nakagawa Shoji trading firm.

Idemitsu strikes oil in North Sea (Sekiyu Tsushin)

- Idemitsu Kosan said one of its test rigs found oil deposits in Norway’s North Sea.

- Idemitsu holds a 20% stake in a production license for area PL882, which was purchased in 2019.

Idemitsu: Chinese lubricants factory goes online (Nikkan Kogyo Shimbun, August 12)

- Idemitsu’s second Chinese lubricants factory, located in Guangzhou, began production.

- The factory has an annual capacity of 120 million liters and was constructed to cater to the increase in demand for lubricants in the Chinese market.

Toho Gas unit actively to promote cogeneration to win clients (Nikkan Kogyo Shimbun, August 14)

- Toho Gas subsidiary Mizushima Gas plans a major marketing push to commercial clients in the Kurashiki area. The subsidiary saw sales drop significantly in the June quarter due to the coronavirus pandemic.

- Based on the results of energy efficiency assessments, Mizushima Gas will actively promote cogeneration (heat and electricity) solutions to commercial clients, as well as encouraging clients currently using other energy sources to convert to LPG.

POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | ||

| of which | applied for restart | 25 | |

| approved by regulator | 16 | ||

| restarted | 9 | ||

| in operation today | 5 | ||

| able to use MOX fuel | 4 | ||

| No. of nuclear reactors under construction | 3 | ||

| No. of reactors slated for decommissioning | 27 | ||

| of which | competed work | 1 | |

| started process | 4 | ||

| yet to start / not known | 22 | ||

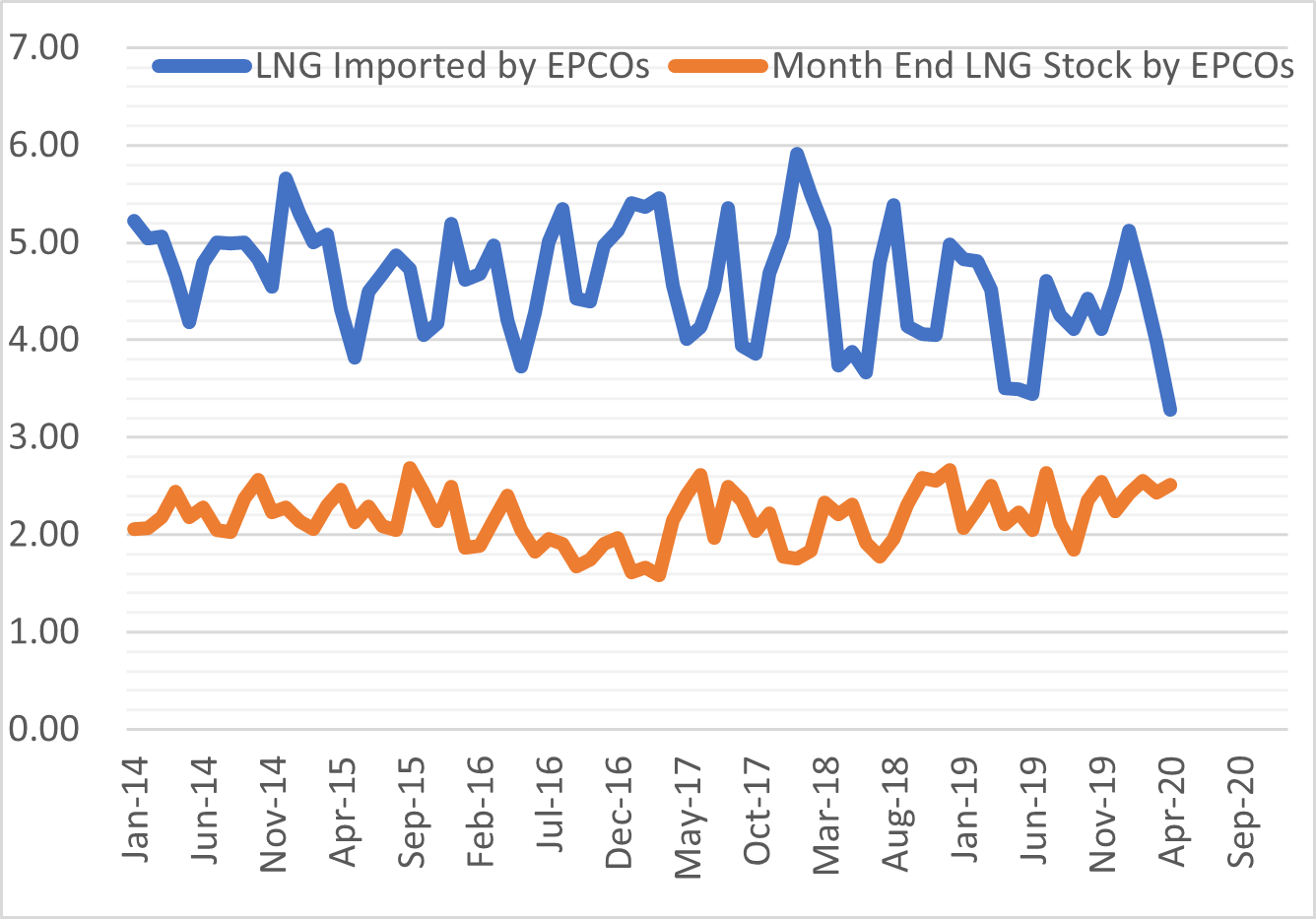

POWER UTILITY LNG IMPORTS VS STOCKPILES

Source: JAIF, as of August 5, 2020

Ex-Keidanren chief Sakakibara lobbies for nuclear, citing risks from LNG and coal closures (Denki Shimbun, August 14)

- Sakakibara Sadayuki, who was recently appointed as an external director of the Kansai Electric Power Co., said energy is a fundamental component of national security. If Japan does away with nuclear power, it could face power shortages in the event that a geopolitical conflict cuts off the LNG supply, he says.

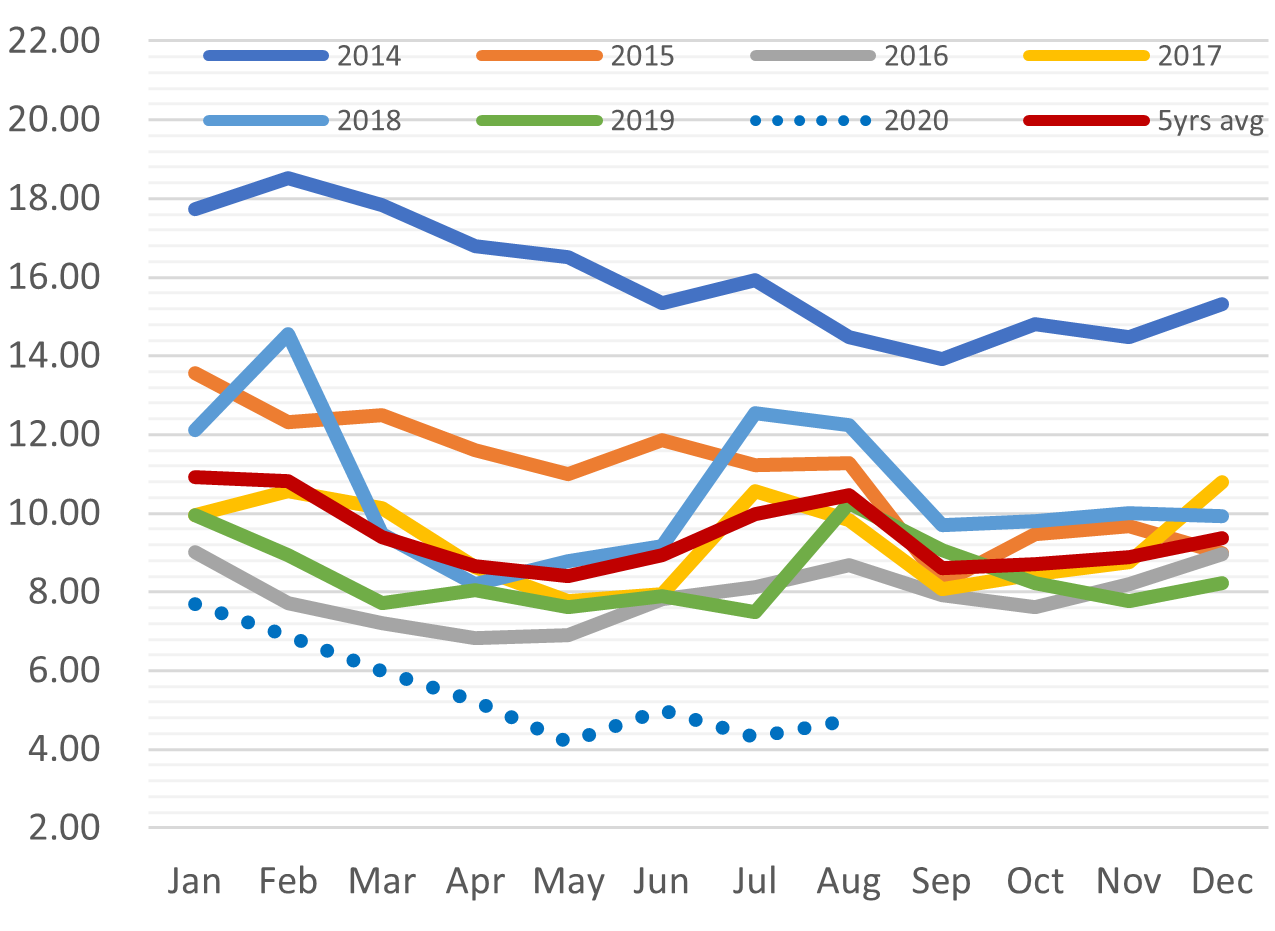

- Japan only stores around two weeks’ supply of LNG, placing it in a vulnerable position, Sakakibara said.

- Japan’s 140 coal-fired power stations play an important role in ensuring stable electricity supply – inefficient plants cannot be turned off overnight, said Sakakibara.

- He also discussed the need to implement reforms at KEPCO to shareholders’ trust after the recent bribery scandals.

- SIDE DEVELOPMENT: Nuclear and coal are inseparable says Research Institute of Innovative Technology for the Earth (Denki Shimbun, August 11)

- The Research Institute of Innovative Technology for the Earth (RITE) deputy chair, Yamaji Kenji, says a lack of progress in bringing nuclear power stations back online means that nuclear plants will be unable to provide the increased demand for baseload electricity that will arise when Japan decommissions its inefficient coal-fired plants.

- However, Yamaji argues that he believes the government will stick to the targets

set forth in the Fifth Basic Energy Plan. He believes the move away from coal will increase pressure to restart nuclear power stations.

- SIDE DEVELOPMENT: Japan Association of Corporate Executives calls for 40% renewables target (Gas Energy Shimbun, August 10)

- The Japan Association of Corporate Executives is calling for the government’s 2030 target for renewable energy use, currently set at 20 to 24%, to be lifted to 40%.

- The Association says it is confident that the official target will be significantly revised in the new basic energy policy due to be released as early as 2021.

- SIDE DEVELOPMENT: Over nine years after the accident, we take an aerial view of the Fukushima Daiichi reactor (Tokyo Shimbun, August 11)

- Aerial photos show the sheer size of the Fukushima site, which has grown over the years as additional decontamination plants have been constructed, and as contaminated soil and debris were brought in from surrounding areas.

- TAKEAWAY: The battle lines in Japan’s nuclear debate are being drawn. Keidanren, the top big-business lobby group, is unwaveringly pro-nuclear since it is dominated by the large electricity utilities. The Corporate Executives Association, or the Keizai Doyukai in Japanese, is the second or third largest business lobby and tends to be market-driven and progressive. These arguments are sure to continue into next year.

Power-to-heat infrastructure would help Japan make renewables a key energy source (Kikkawa Takeo, Gas Energy Shimbun, July 30)

- CONTEXT: This is an op-ed by energy economist, Professor Kikkawa of the Hitotsubashi University.

- While the Japanese government’s commitment to make renewables a major electricity source by 2050 is a welcome, and even revolutionary, development, the government has failed to increase its renewables target from the current 22-24%, suggesting it is in fact not serious about renewables.

- The best way to increase the uptake of renewable energy is to use a market-based approach, rather than feed-in tariffs (FIT).

- The writer advocates the need to replace capacity “vacated” by shuttered nuclear plants with renewables. However, he notes that at present renewable projects require the back-up of thermal generation. Using thermal power plants as a top-up means running them at a fraction of their maximum output, increasing costs.

- Japan will be able to make better use of its infrastructure if it follows the lead of countries such as Denmark and adopts the “power-to-heat” paradigm. Surplus electricity from renewable sources can be converted to heat, which can also be stored for use in other applications.

- Power-to-heat approach will require significant investment in heating pipes.

- TAKEAWAY: It’s highly unlikely for Japan to move away from FIT and Feed-In Premium at this stage and any time soon. However, exploring ways to make renewables projects more effective is a major government goal. Thus, ideas that explore ways to store energy could get further traction.

TEPCO Power Grid signs agreement with Chiba prefectural government to guard against power outages (Asahi Shimbun, August 13)

- TEPCO Power Grid has agreed to deploy mobile backup generators to hospitals and other critical facilities in Chiba in the event of future widespread power outages.

- The move comes after typhoons last year left large swathes of Chiba without electricity for extended periods.

- To reduce the risk of trees falling on power lines and causing power outages, TEPCO Power Grid will also work to cut down trees near power lines.

KEPCO boosts website security after 6 cyber-attacks (Denki Shimbun, August 14)

- KEPCO says it has beefed up security on a website that allows subscribers to monitor their electricity and gas usage, after the site was hacked at least six times.

- The website now uses two-step verification.

- It is believed that all of the cyber-attacks were related.

RENEWABLES & OTHER

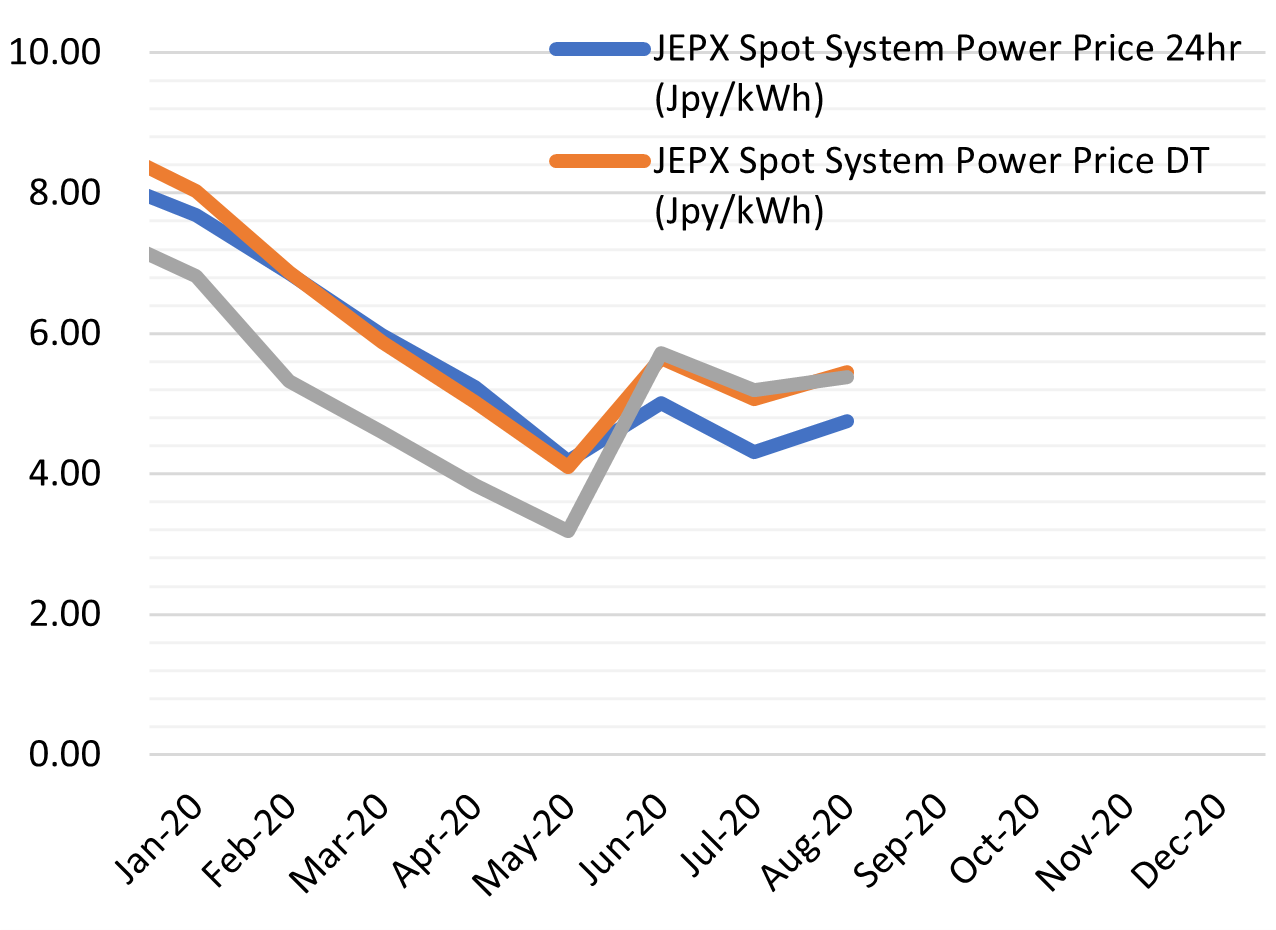

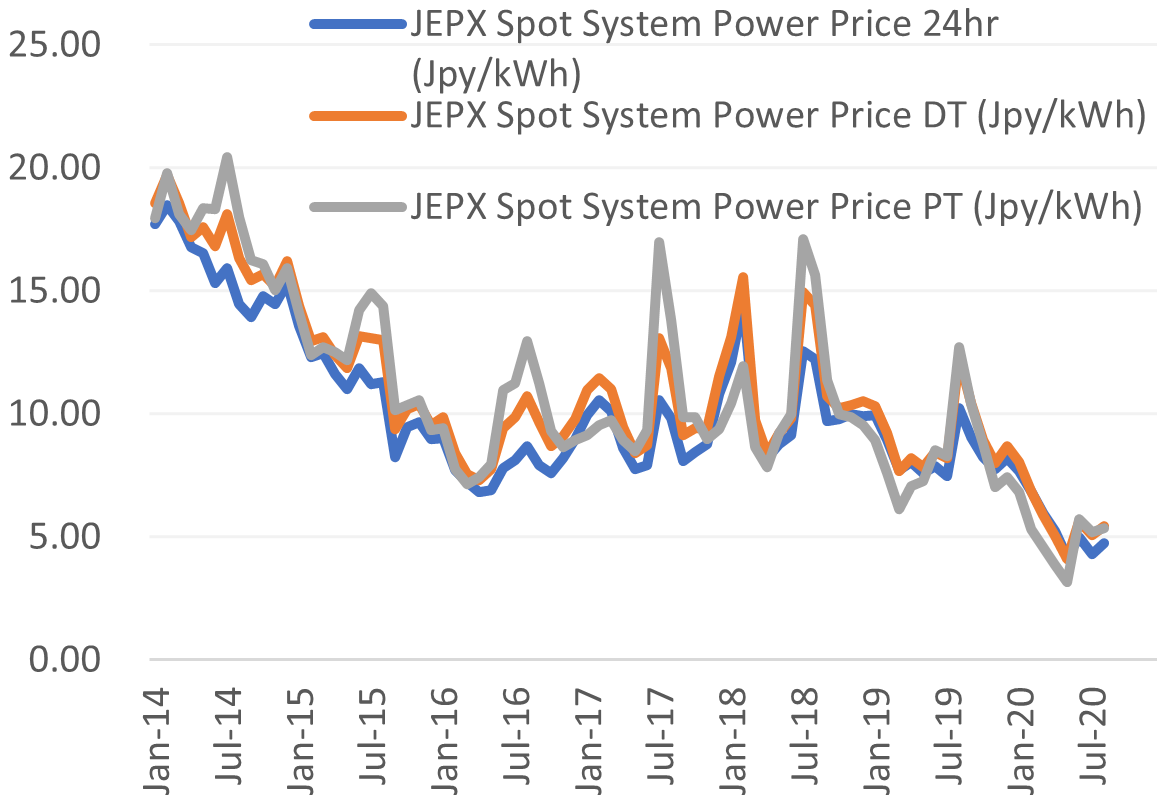

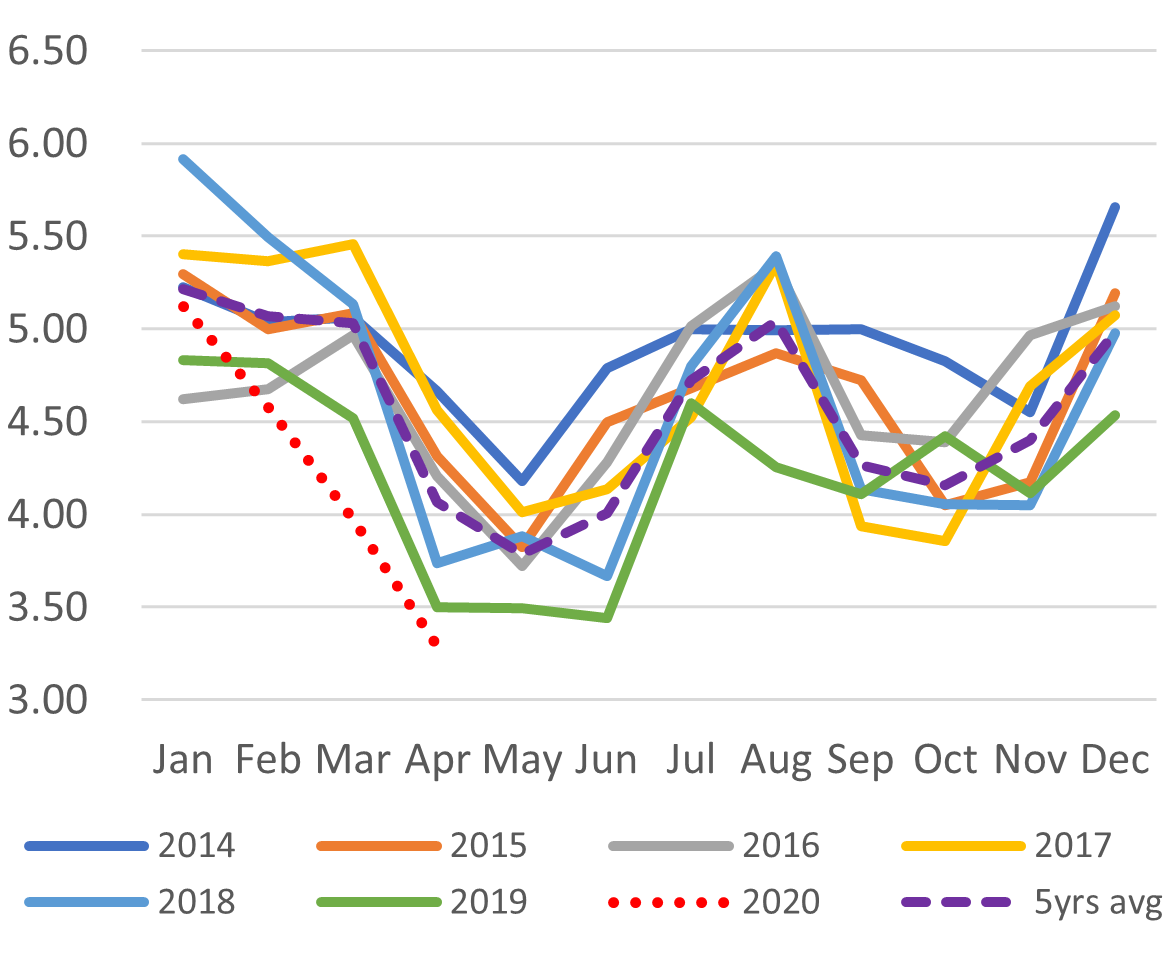

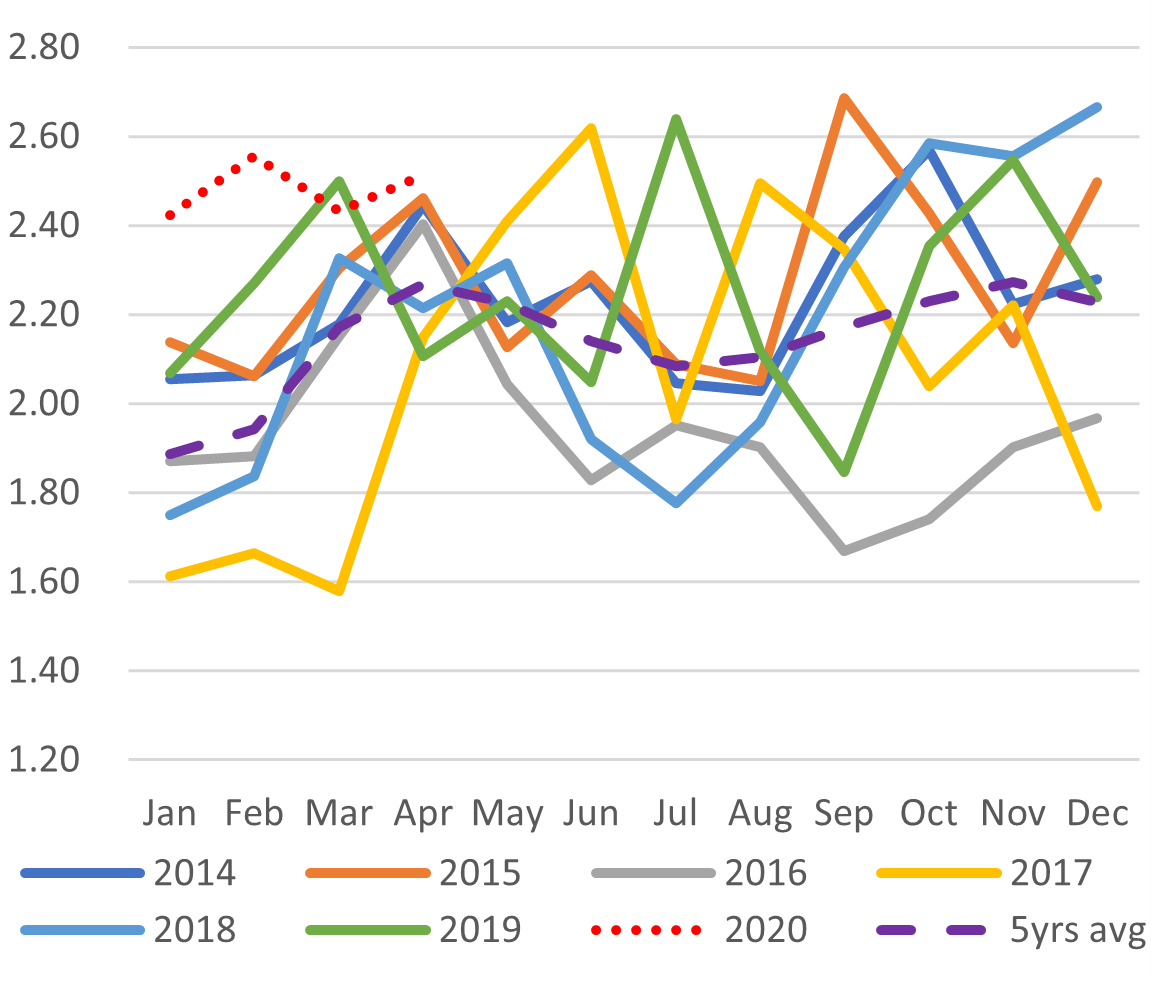

HISTORICAL SPOT ELECTRICITY PRICES (24h)

SPOT ELECTRICITY PRICES (2020)

Major change to energy efficiency policy (Gas Energy Shimbun, August 10)

- In a change of policy direction, the Agency for Natural Resources and Energy says it will now place greater emphasis on the resilience of energy generation and transmission systems, as well as the efficient use of surplus energy generated at off-peak times.

- The committee in charge of energy policy signaled that cogeneration is a topic for future debate, due to its benefits for both efficiency and resilience. The committee is also interested in making greater use of hydrogen produced from renewable sources.

- The comments come in response to major distortions in the current electricity market. In some parts of Japan, the market price of electricity approaches zero at some times of the day and year. Meanwhile, consumers elsewhere in the country are required to reduce their peak electricity consumption during the middle of the day in summer.

- TAKEAWAY: The committee stated that energy efficiency and renewable energy would no longer be treated as separate issues. This seems like an indication that bureaucrats are going to crack down even harder on electricity prices and that renewable energy projects will no longer have a halo effect simply because they are green. A recent METI report shows that the growth in renewables capacity, on the back of the Feed-In Tariff (FIT), has pushed up electricity costs passed on to households via a “green” surcharge to ¥767 per month. That’s up from ¥57 / month in the year before FIT was introduced.

ENEOS, KEPCO, and others establish USD 3.75bn renewables fund (Nikkei Sangyo Shimbun, August 7)

- ENEOS has partnered with Renewable Japan, Tokyu Land Corporation, and the Kansai Electric Power Company to launch a fund for investing in renewable energy.

- The fund will initially focus on solar energy, and aims to procure ¥400 billion in investments in its first five years.

- SIDE DEVELOPMENT: ENEOS records a loss in June quarter over inventory write-down (Nikkan Kogyo Shimbun, August 13)

- ENEOS Holdings reported a ¥4.8 billion loss in its April to June quarter. In the same period a year earlier, ENEOS made a profit of ¥17.3 billion.

- A ¥62 billion write-down in the value of petrochemical inventory contributed to the poor result.

- When the effects of the write-down are removed, the corporation’s energy business made a profit of ¥43.8 billion, up 38% on the same period last year.

- TAKEAWAY: As we forecast in the Aug. 3 report, Japan’s oil and gas industry has been booking heavy write-downs on the value of their hydrocarbon portfolio to reflect the drop in energy prices. One popular response from the industry so far has been to talk up potential investments in renewables. The size of the renewables fund from ENEOS and KEPCO looks impressive. Yet, at present, it looks like large Japanese energy firms are buying a renewables portfolio, rather than developing one. That will surely affect how seriously they view green energy assets.

Hokkaido fishing groups shift from foe to supporters of offshore wind as local economies wane (Asia Nikkei, Aug 10)

- Feature story that tells of dropping local fishing catch due to global warming, and how that is turning the fishermen who once opposed offshore wind farms into backers of the emerging industry.

- SIDE DEVELOPMENT: Deloitte simulates cost of renewable energy projects (Nikkei Sangyo Shimbun, August 12)

- Deloitte Tohmatsu Consulting has released a package that is able to project the cost and output of future renewable energy projects.

- By inputting information on transmission infrastructure and demographics it is also possible to project future trends in installation of renewable generation and storage infrastructure in a given area.

Orix Bank marketing renewable energy investments (Nikkei, August 5)

- Orix Bank has launched a range of financial products aimed at not only institutional investors but also individual investors who wish to invest in renewable energy.

- Products offered will initially focus on solar energy and will be expanded to include wind projects.

- Orix Bank is licensed as a trust bank.

- The move comes after the region was battered by a slew of extreme weather events, including major typhoons and torrential rain.

Vena Energy to build wind farm in Aomori (Nikkei, August 12)

- Singaporean solar operator Vena Energy began construction of a 47 MW wind farm in Aomori prefecture.

- CONTEXT: Vena already operates 450 MW of solar generation capacity around Japan.

TDK pledges to use only locally-generated electricity (Mainichi Shimbun, August 10)

- Manufacturer TDK has pledged to the Akita prefectural government to only use energy generated at local hydroelectric plants in its “TDK Museum” publicity facility.

- TDK says that while the arrangement involves additional cost, it has the benefit of reducing the environmental impact of electricity usage.

- TDK hopes the move will encourage other local companies to do the same.

ANALYSIS & COMMENTARY

|

Post-unbundling, Japan’s grid firms retain unhealthy proximity to ancestor power utilities |

|

| DANIEL SHULMAN, PRINCIPAL, SHULMAN ADVISORY |

On April 1, 2020, Japan planned to abolish regulated electricity tariffs, freeing the incumbent utilities to compete with new market entrants by lowering rates. However, the plan was predicated on creating a neutral power transmission and distribution (T&D) industry, which had cut ties with the country’s 10 dominant power utilities. And therein lies the problem.On the face of it, the unbundling took place, but evidence suggests that grid companies retain an unhealthy proximity to their ancestor utilities.For example, TEPCO Energy Partner, the new deregulated retail arm of incumbent Tokyo-area utility TEPCO, has consistently purchased power that exceeds its customer load. Meanwhile, TEPCO Power Grid, the new T&D company unbundled from the utility, has posted losses since FY 2016 – as a result of buying the surplus from TEPCO EP at a higher price than it would have captured on the wholesale market. It’s almost as if the two companies view themselves as having a shared balance sheet.As a result, the abolishment of tariffs has been postponed by at least a year.

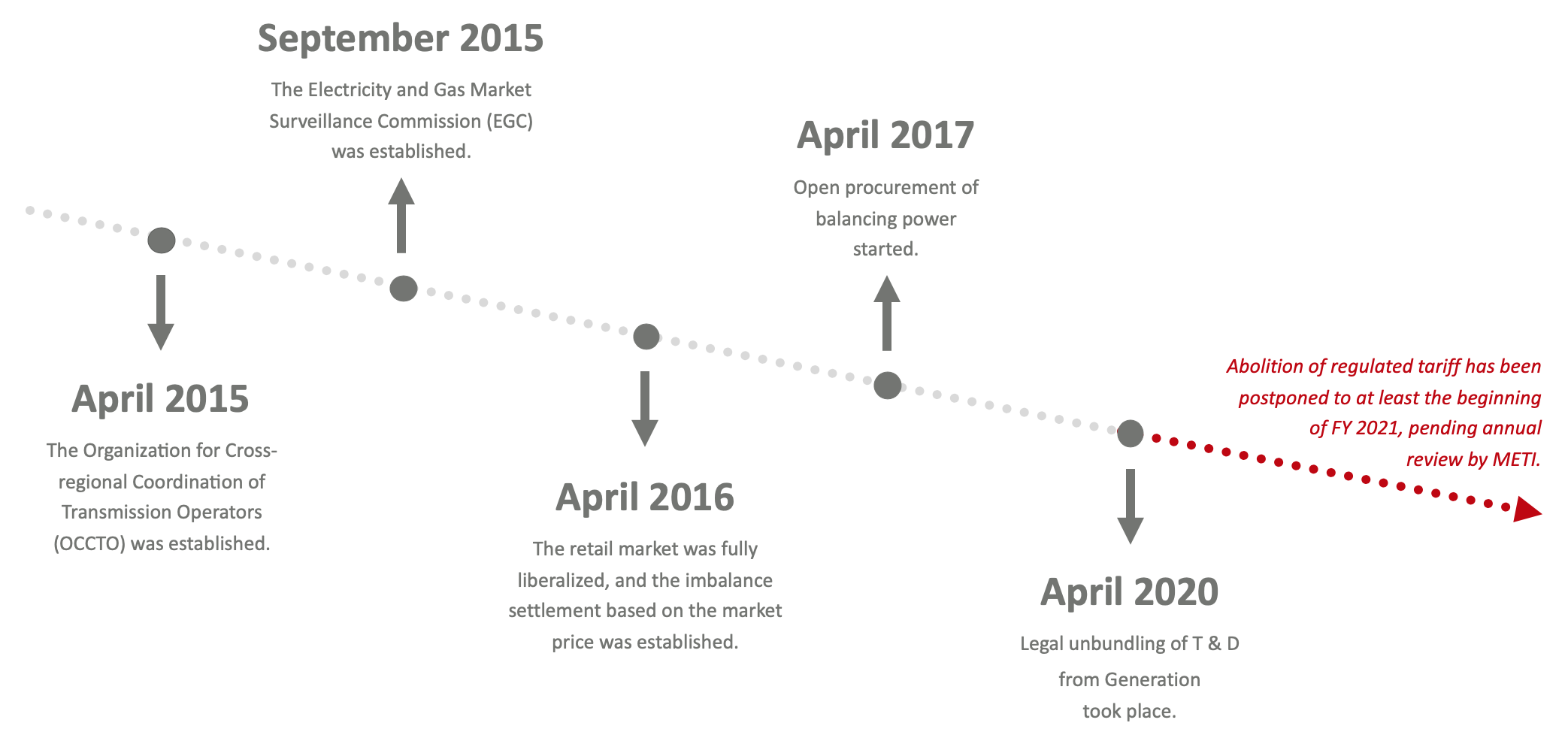

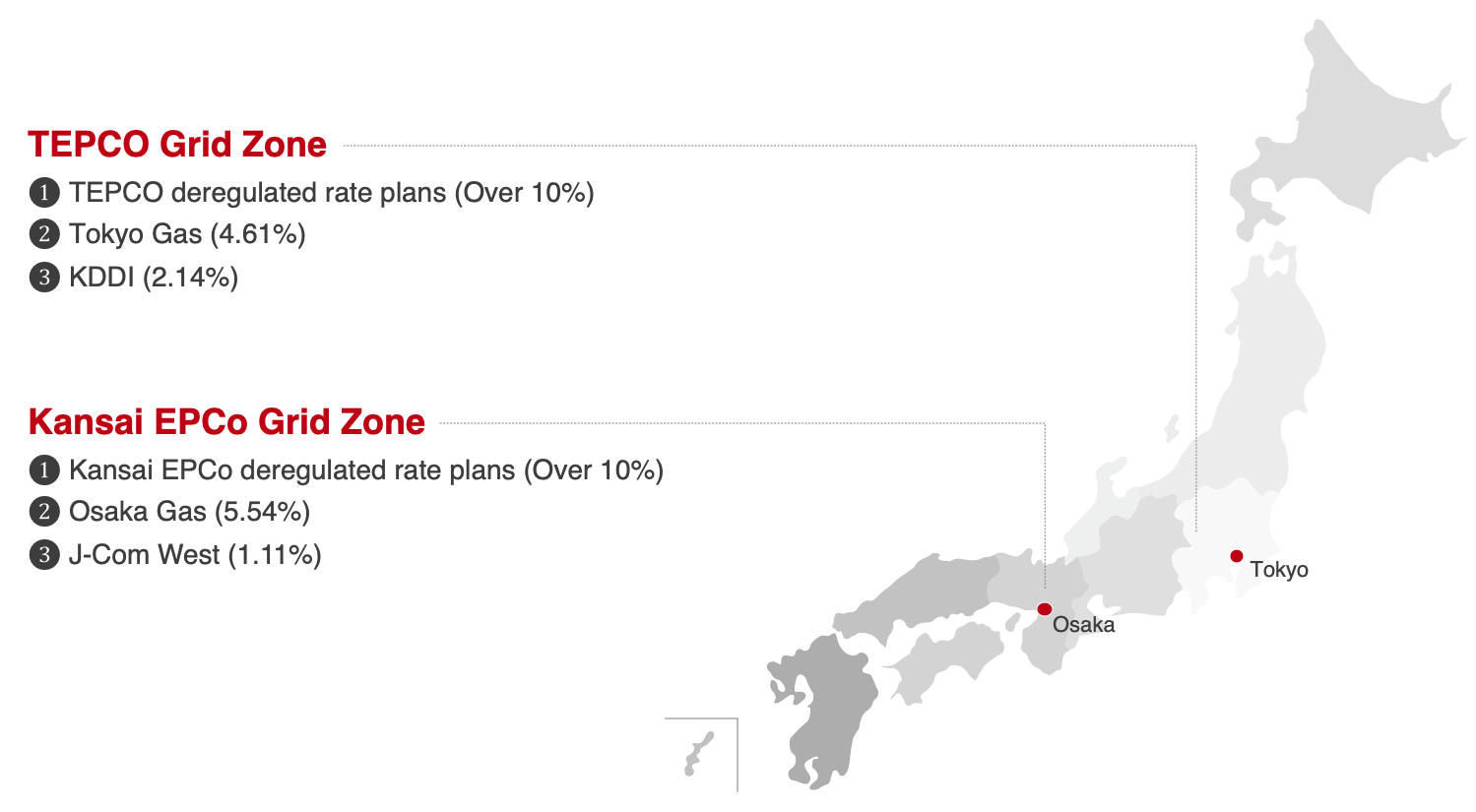

Timeline of the deregulation of the Japanese electricity market Competing on Price In the Ministry of Economy, Trade and Industry’s (METI) original roadmap for deregulation, the incumbent utilities were forced to continue to offer regulated tariff plans for the first four years of the post-2016 market. With incumbent utilities’ rates bloated from years of acting as regional monopolies, new retailers with a modicum of competence could run their businesses for a four-year “grace period”, beating the Electric Power Companies (EPCOs) on price. At the same time, METI granted the incumbents the ability to create new retail companies that could offer deregulated rate plans when the market opened, partially undercutting the stated purpose of the continuation of regulated rate plans for the first four years. Indeed, at the end of 2018, METI found that the new retail arms of the former monopolies had captured about 40% of the customers who had switched away from their old regulated service; in other words, only 60% of customers who had switched away from the incumbents had truly moved to new electricity retailers. When METI set the beginning of FY 2020 as the date to untie the hands of the incumbents and allow them to lower their prices, it left itself an off-ramp by reserving the right to “assess the competitive environment,” and delay the abolishment of regulated tariff if necessary. The criteria for a delay was as follows: In a given grid (former monopoly) zone, there should be two or more retailers with no association with the incumbent who have captured at least 5% of low voltage (residential and small commercial) market share. In July of 2019, it was judged that none of Japan’s nine deregulated grid zones had met these criteria, and therefore regulated tariff should be kept in place for another year. In the two most populous grid zones, TEPCO and Kansai, the competitive retail arm of the incumbent utility had captured more than 10% of market share, as calculated by number of meters.

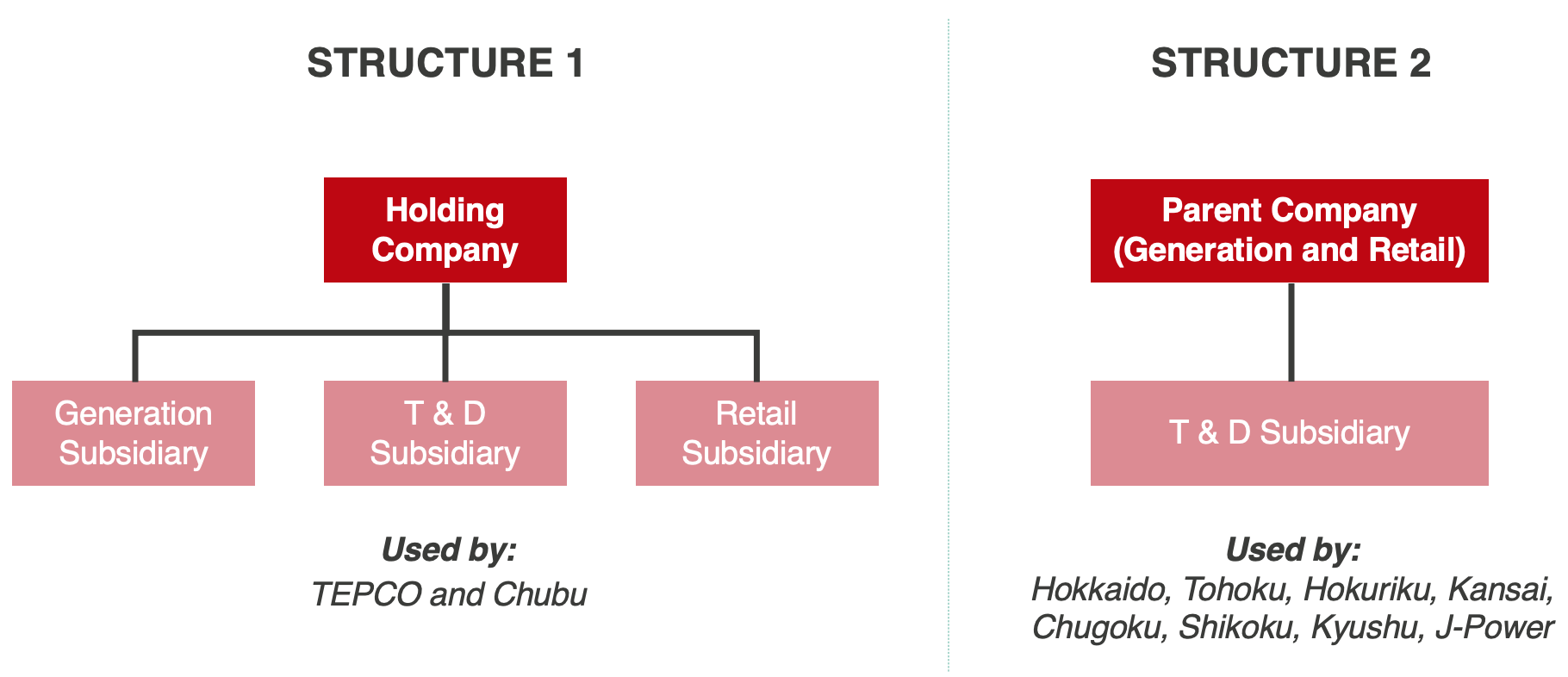

(Source: Ministry of Economy, Trade and Industry) METI plans to make a new assessment each year. Is it any surprise that the incumbents jumped through the gaping loophole which allowed them to start competing from day one of the market by establishing separate retail arms, and have succeeded in using this to stay ahead of the pack? Legal Separation of T&D from Generation As of the first day of FY 2020, all of Japan’s former monopoly utilities had spun T&D off into separate legal entities from their generating companies. However, the manner in which it has been done leaves room for doubt over how fair and unbiased the T&D network will be for non-incumbent players. In the case of TEPCO and Chubu EPCO, both created holding companies which own their respective generation, T&D and retail businesses – each contained in a separate legal entity. The other utilities, however, have created structures in which their generation and retail arms constitute a single company, and that company owns the T&D company.

(Source: Ministry of Economy, Trade and Industry) In either of these structures – particularly the latter – it would seem that an enormous number of granular rules, and correspondingly onerous regulatory reporting and monitoring burden, would be needed in order to assure anything resembling neutrality in the way the T&D companies treat market players not associated with the groups they belong to. Since late 2018, the outsourcing of services between the companies in an incumbent group is nominally prohibited. In reality, the rules allow for so many exceptions – to the point that, under the right conditions, employees can be seconded from one company to another and directors can even sit on the boards of multiple companies within a group. Government officials see the risk TAKEAWAY: It will take time for the complaints to work themselves through the system, but we hope it will return to give all market players greater assurance on the neutrality of access to the grid. |

|

Nuclear Restarts in Japan Bring More Problems Than Solutions |

|

| YURIY HUMBER, DIRECTOR, YURI INVEST RESEARCH |

Last week we outlined the bull case for nuclear plant restarts in Japan. The industry has gained positive momentum after the regulator gave the (almost) go-ahead to begin spent fuel processing. The recent government decision to close older coal-fired plants will also act as a trigger for restarts as nuclear offers emissions-free, baseload power. And yet, it’s hard to see nuclear’s role in the energy mix above 10% by 2030.Mass restarts of nuclear power in Japan face three main issues: public mood, market forces, and technical challenges. (1) PUBLIC ISSUES

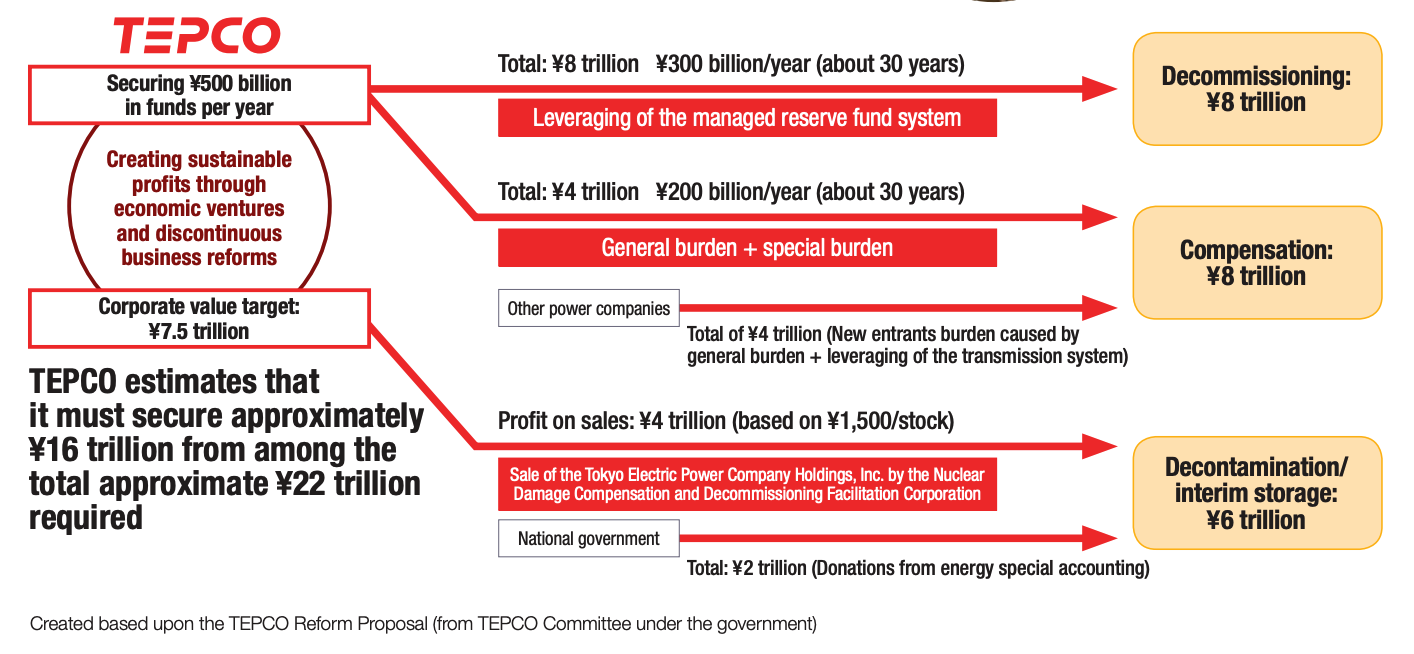

Immense human effort. According to TEPCO figures, more than half a million workers so far were engaged in the Fukushima cleanup operation. Add in the people involved in related cleanups in the neighboring prefectures, and the human resource stretches to almost 1% of the country’s population. The public is on the hook because TEPCO didn’t make provisions. Last month, Japan’s nine utilities with nuclear assets asked the government to pass on another ¥2.4 trillion of costs to the public via additional electricity levies, which would pay for their portion of costs associated with the Fukushima disaster. One of the reasons given for the levy is that TEPCO did not make advanced provisions for such liabilities. Public opinion overwhelmingly against. Given the above, it’s not a surprise that the public oppose the use of nuclear and have a dim view of TEPCO. Even in the latest official polls published by the Japan Atomic Industrial Forum Inc. (JAIF) almost half of those surveyed want nuclear plants to close “over time,” and a further 11.2% want them shut immediately. Those who want a return to a pre-Fukushima reliance on nuclear power account for less than 10% of total. Local political assent needed for restarts. Legally, utilities can restart reactors based on the regulatory approvals alone. In practice, utilities wait for “blessing” from local mayors and prefectural governors, who mostly reflect public opinion and take into account any legal proceedings. (2) MARKET FORCES Nuclear power is no longer a cost leader. Japan’s pro-nuclear government estimated in 2014 that the unit cost of nuclear power was ¥10.1 per kilowatt-hour (kWh). Solar was then seen at ¥24 to ¥29. Within just 5 years, the additional safety features required post-Fukushima have inflated the initial capital outlay for nuclear stations, which suggests that 2014 figure should be revised up 10% or more. Meanwhile, this year’s tariffs on solar projects are down to around ¥12 per kilowatt-hour. A breakthrough in battery storage for renewable energy would make it hard for nuclear energy to compete. Nuclear industry lacks leadership. Major Japanese firms are leaving the field. Toshiba sold off its crown acquisition of Westinghouse, taking heavy losses and effectively ending ambitions of building nuclear plants abroad. IHI, a major parts supplier for the industry, dissolved its nuclear venture with Toshiba. Hitachi froze its UK nuclear project. A year ago, TEPCO proposed to create a national nuclear champion by joining with Chubu Electric, Toshiba and Hitachi. A year on, the project has barely moved with other partners afraid that it could open them up to problems around Fukushima decommissioning and its liabilities. Utilities will argue for nuclear… until they don’t. Industry insiders estimate the cost of power from an existing nuclear plant at ¥1/kWh. It’s clear why utilities lobby to run existing nuclear plants. And yet, if the cost of scrapping the assets entirely is (as usual) passed onto the public, be it as a separate levy or part of the electricity fee, the utilities will have fewer reasons to promote reactors. Especially, if such an action is taken, say, ten years from now to allow time to develop other generation assets. (3) TECHNICAL CHALLENGES Too many questions. This is arguably the biggest reason to be bearish on nuclear restarts in Japan. The domestic industry has not resolved its many, admittedly enormous, technical challenges. And it can no longer ask the public to trust that it will work them out at some later date.

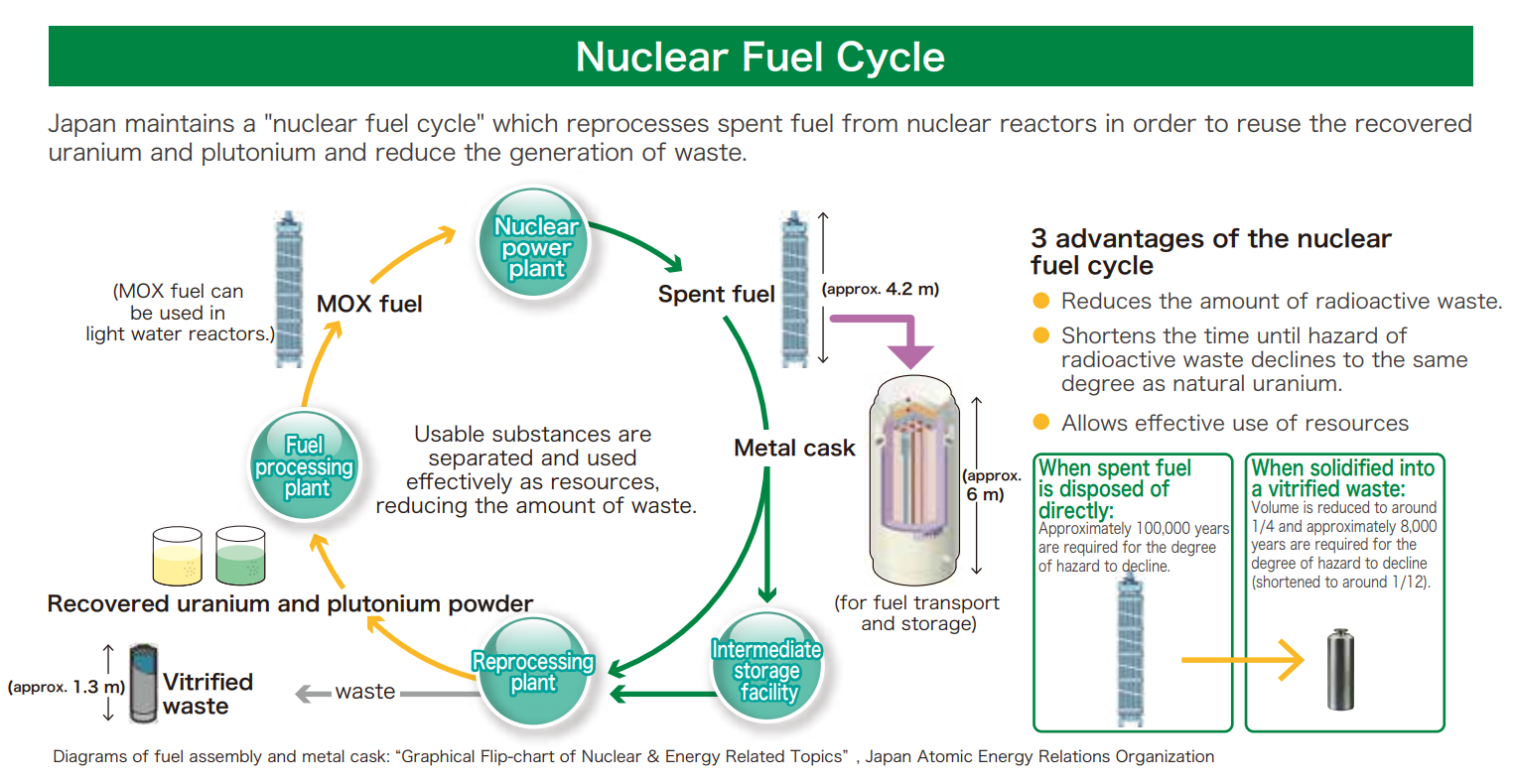

Rokkasho may face more delays. The heart of the nuclear cycle is the Rokkasho complex. The site, operated by Japan Nuclear Fuel Ltd., recently received regulatory approval for new safety measures – a process that took over six years. However, it was not the final hurdle to start spent fuel reprocessing on the site. Japan Nuclear Fuel still needs to get approval for Rokkasho’s design and some of operational measures. It’s unclear how long either will take. Some Japanese media suggest this could yet be “years,” noting that the process involves an inspection of over 10,000 pieces of equipment. Processing fuel will create too much plutonium. Reprocessing spent fuel recovers still-useful uranium and plutonium. The latter can be blended with uranium to create a more potent nuclear fuel known as MOX (Mixed Oxide). However, at full capacity Rokkasho will create seven tons of plutonium a year and Japan does not need that much for MOX fuel. Prior to Fukushima, Japan planned to have at least 16-18 reactors fitted to run on MOX fuel. The 2011 accident led to more stringent rules, and today only 4 of the reactors use MOX. Japan’s plutonium emboldens other countries to do the same. South Korea is holding a 10-year joint study program with the US to explore the feasibility of reprocessing in the country. When the study ends in 2021, South Korea could demand the same rights and in time build its own plutonium stockpile. Deadlines for new safety measures are not met. Many of the utilities will not meet their own dates for completion of new anti-terrorist measures at the nuclear plants, according to a recent report in the Yomiuri Shimbun. The industry regulator has said it will not extend the deadlines. That will affect One more technical reason the reactors would need to stop. CODA: POLITICAL TIMES ARE A-CHANGING Current defense minister, and former foreign minister, Kono Taro has openly criticized the nuclear industry. His recent decision to cancel the purchase of the Aegis Ashore missile defense system showed that he is not fazed by changing tack on a long-term project supported by all of his predecessors and that he makes his decisions based on practical (money) calculations. Kono expressed some of his views on Japan’s nuclear cycle in the summer of 2011, slamming Rokkasho and the industry’s inability to solve its own problems. “Back in 1967 the government was saying that a fast breeder reactor would be ready in 20 years; in the 1970s they said it will take 30 years. What will happen in 2050 is that they’ll say it will probably be available in 70 years,” Kono said. “We’re not going to have it, and we know it.” |

STOCK MARKET PERFORMANCE

| As of close on August 14, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| COSMO ENERGY HOLD. | 5021 JP | 145.89 | 5.91 | 4.81 | -27.94 | |

| ENEOS HOLDINGS INC | 5020 JP | 1,340.57 | 7.51 | 5.28 | -14.16 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 706.24 | 5.61 | 1.28 | -19.22 | |

| INPEX CORP | 1605 JP | 999.06 | 2.58 | 4.53 | -38.79 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 104.82 | 2.06 | -1.13 | -37.07 | |

| Industrials | ||||||

| CHIYODA CORP | 6366 JP | 72.37 | 1.46 | -2.11 | -1.77 | |

| JGC HOLDINGS CORP | 1963 JP | 314.43 | 4.39 | 4.84 | -29.93 | |

| MITSUBISHI CORP | 8058 JP | 3438.71 | 4.66 | -0.02 | -17.91 | |

| MITSUI & CO LTD | 8031 JP | 3042.71 | 6.75 | 7.79 | -6.62 | |

| Utilities | ||||||

| CHUBU ELECTRIC POWER | 9502 JP | 1001.32 | 6.79 | -3.33 | -12.93 | |

| KANSAI ELECTRIC POWER | 9503 JP | 982.85 | 3.05 | -3.64 | -15.51 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 457.11 | 5.36 | 4.22 | 3.73 | |

| J-POWER | 9513 JP | 296.73 | 6.09 | -9.49 | -37.71 | |

| TOKYO GAS CO | 9531 JP | 1062.29 | 11.16 | -6.23 | -8.42 | |

| OSAKA GAS CO | 9532 JP | 880.44 | 6.29 | 0.38 | 2.26 | |

| TOHO GAS CO | 9533 JP | 522.75 | 6.11 | -4.07 | 11.57 | |

| SAIBU GAS CO | 9536 JP | 95.01 | 8.40 | 1.55 | 1.82 | |

| SHIZUOKA GAS CO | 9543 JP | 69.18 | 6.95 | 1.91 | -3.69 | |

| TOKYO ELECTRIC POWER | 9501 JP | 509.42 | 4.62 | -4.23 | -32.12 | |

DATA

Japan Oil Price

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

Domestic Fuel Sales

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

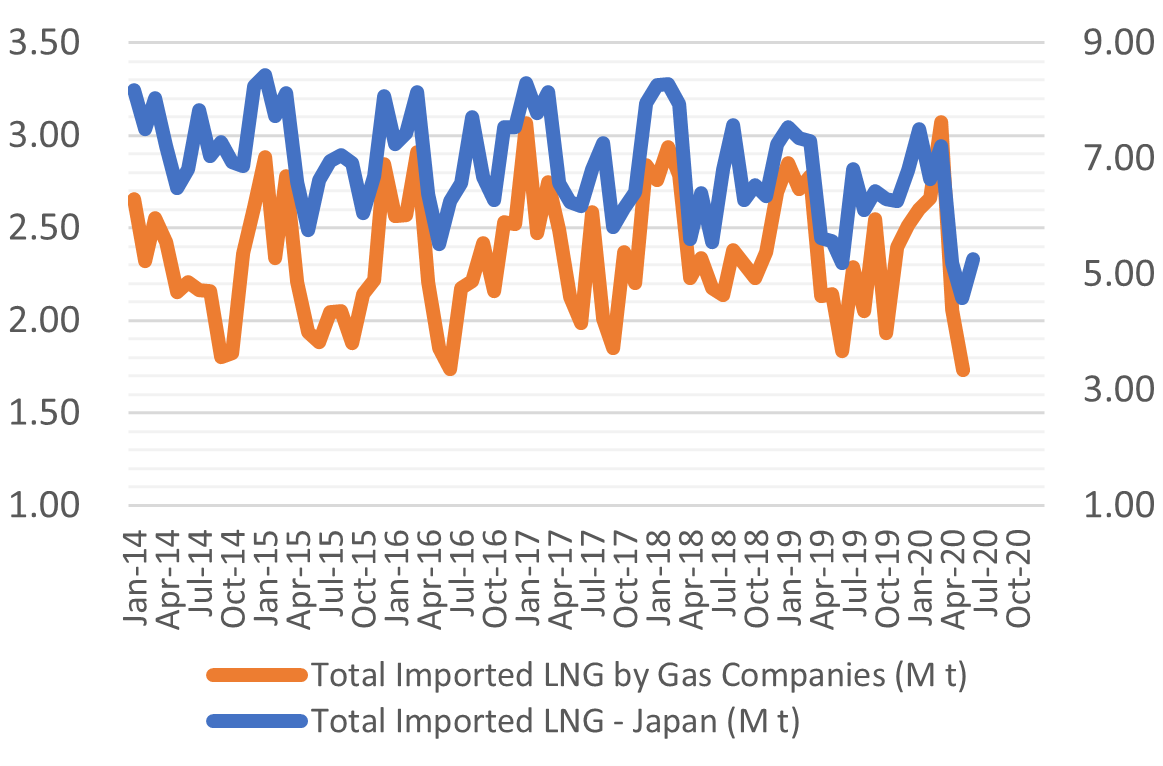

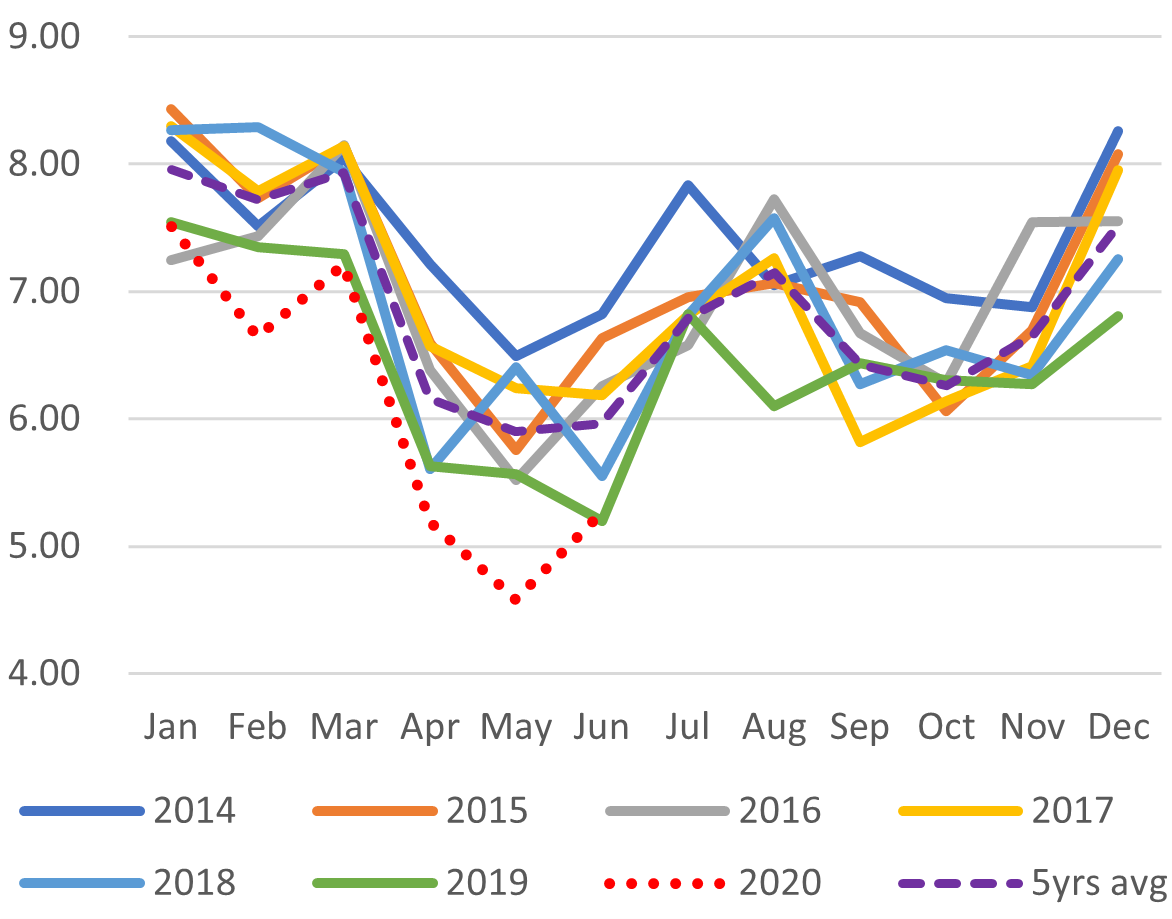

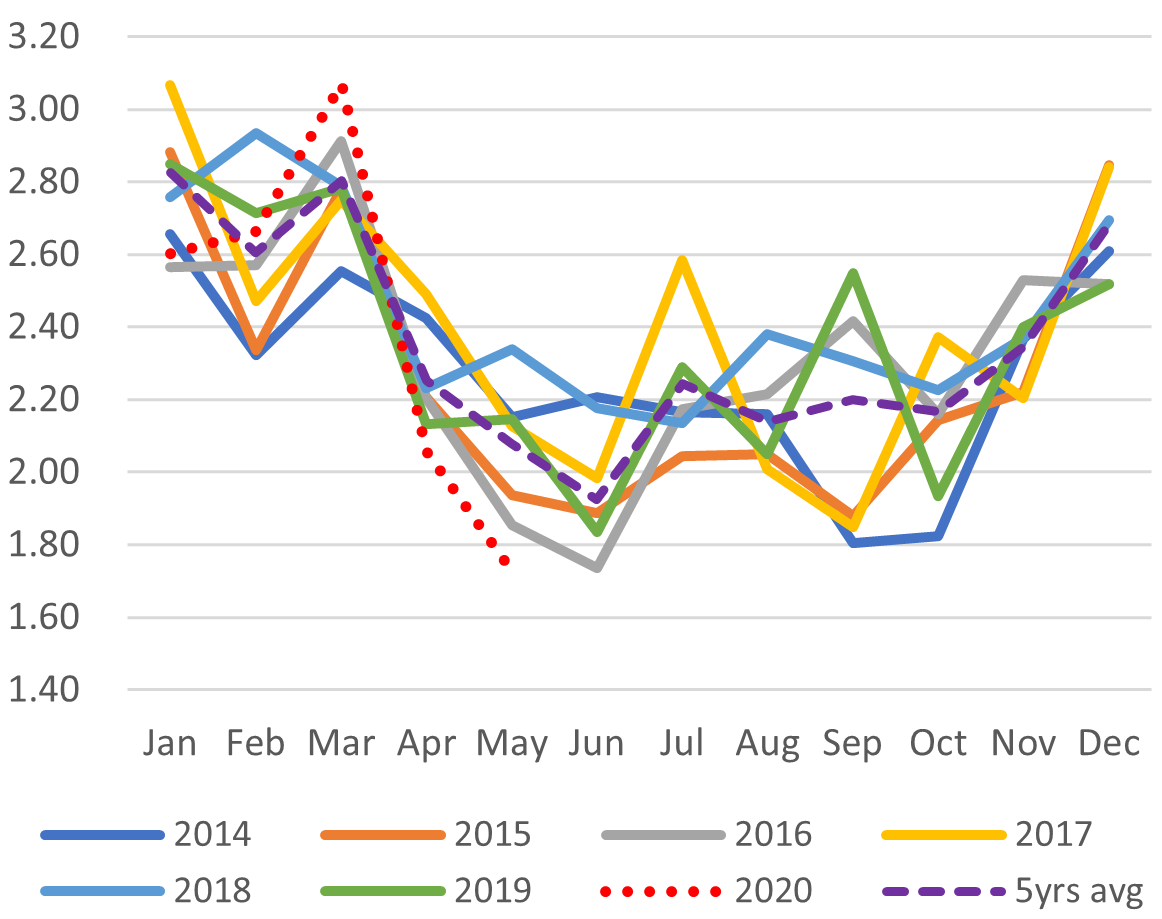

Japan LNG Price

LNG Imports: Japan Total vs Gas Utilities Only

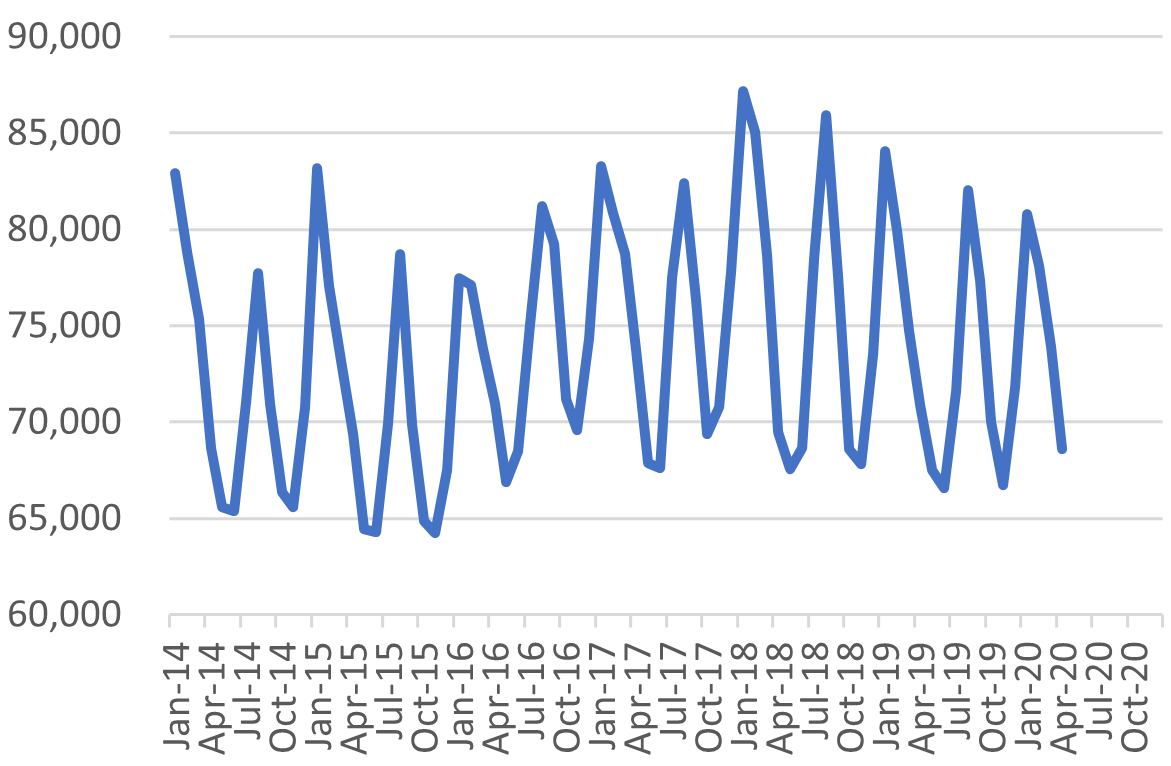

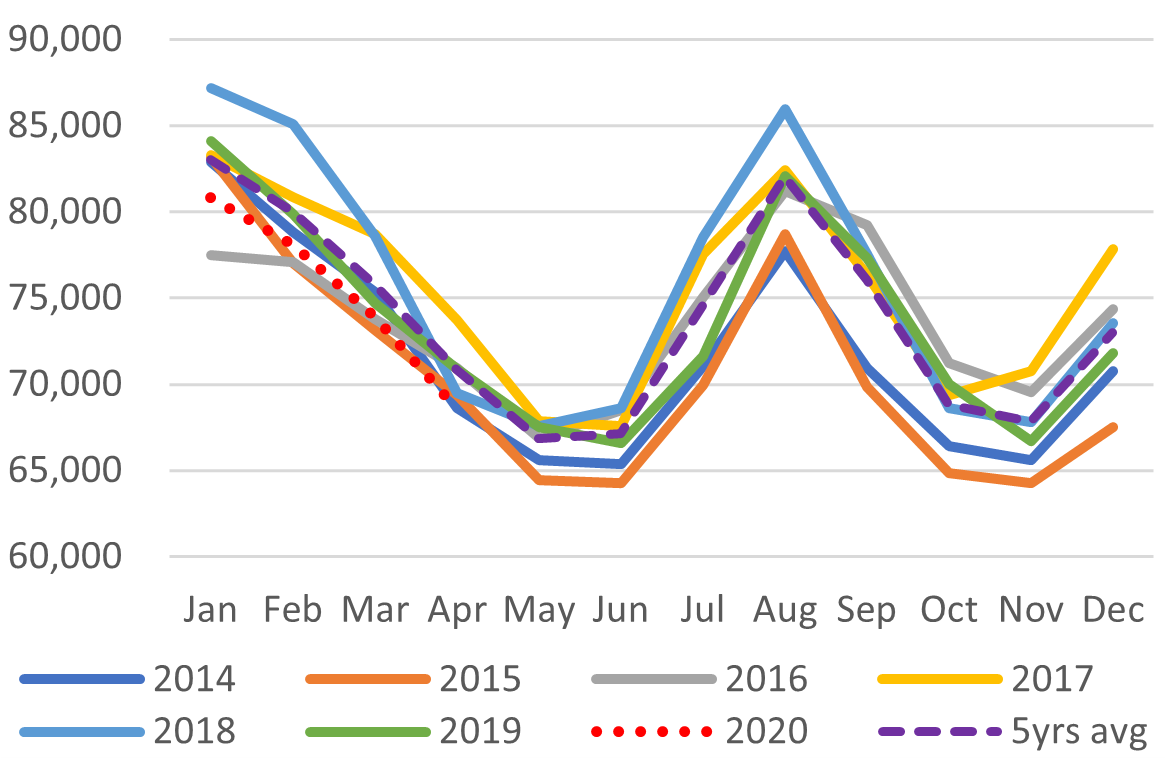

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

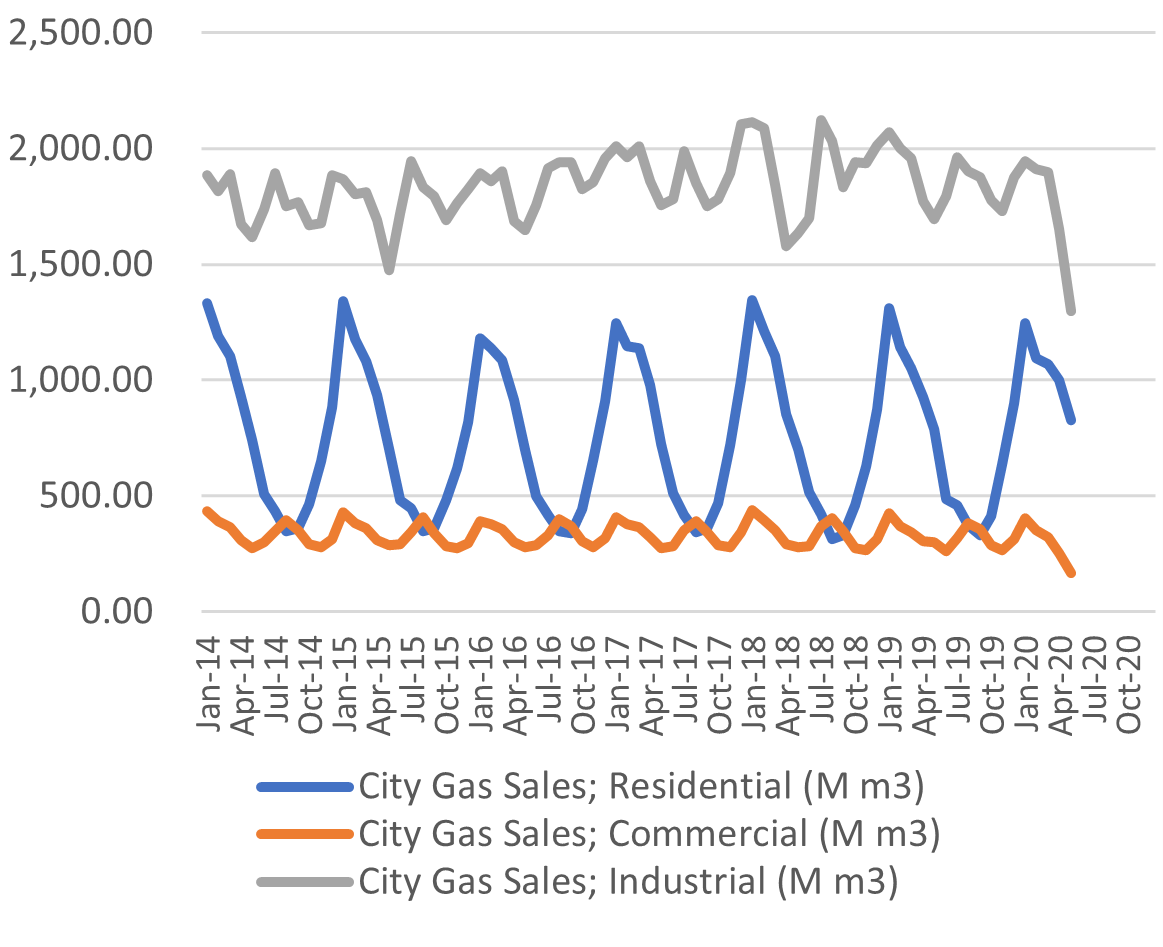

City Gas Sales – Total (M m3)

City Gas Sales by Sector (M m3)

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Ministry of Finance.

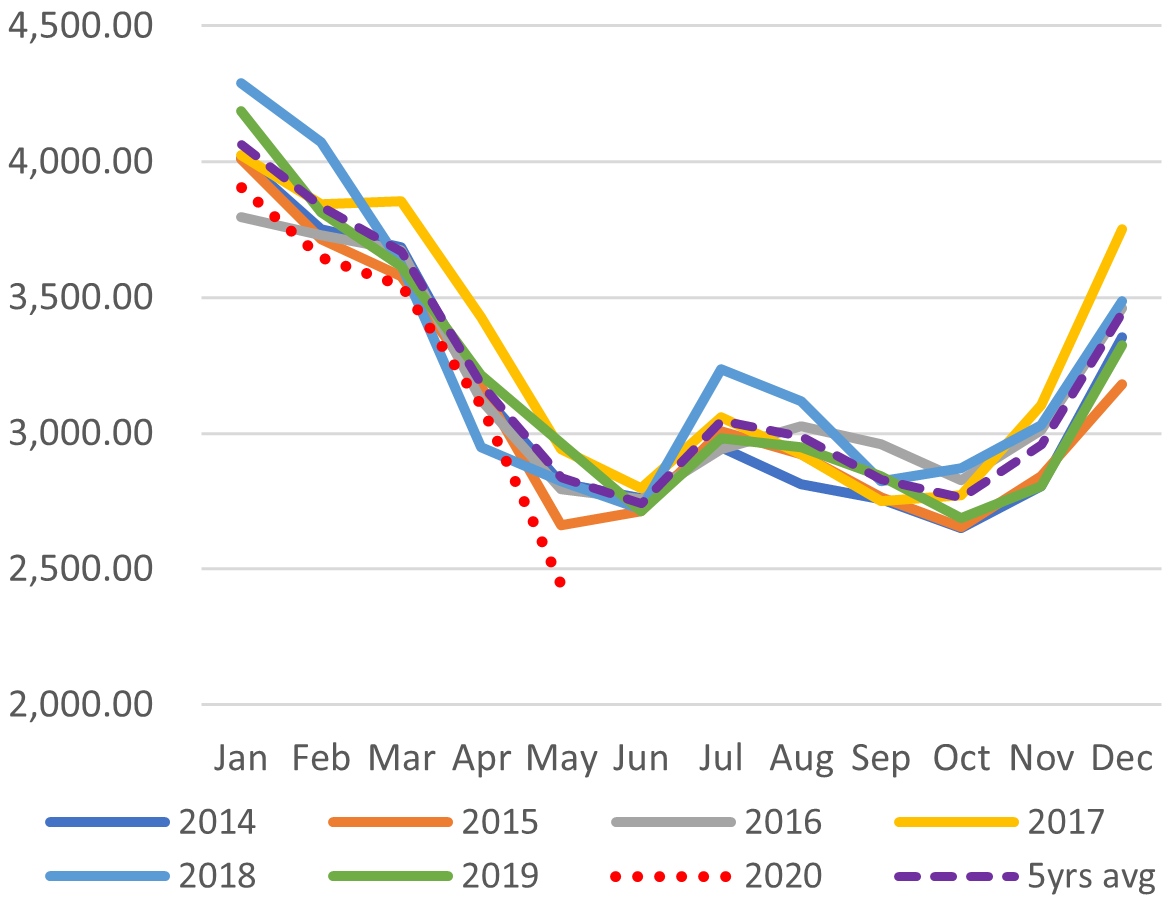

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

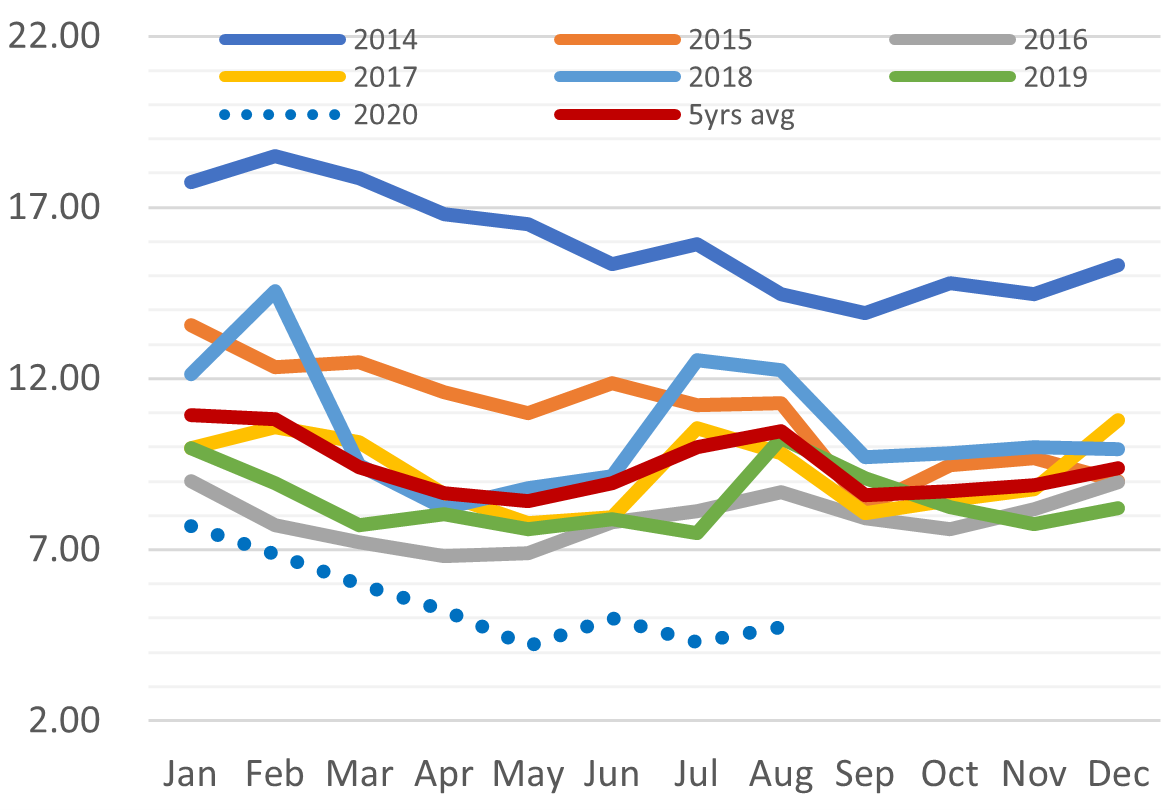

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

DISCLAIMER

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest Research Ltd., which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

Recipients of this report should ensure that they fully understand the legal, tax and accounting implications before making an investment decision and independently determine that the transaction is appropriate based on their own objectives, experience and resources.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided.

In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.