WEEKLY

March 2, 2026

ANALYSIS

JAPAN’S CORPORATE PPA MARKET REACHING SCALE – AND A TURNING POINT

- Cumulative power capacity linked to Corporate PPAs in Japan surpassed 3 GW in 2025, with median disclosed project size rising 82% YoY.

- The number of deals made public in the last six months was a third higher than in the first half. The PPA market’s importance will only grow.

- Even as the number of renewable power sources available for PPA deals has increased in the past two years, solar accounted for nearly nine out of ten contracts in 2025.

- So, who were the biggest players in the market last year and what were the key trends?

- This is our extended look at the market.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Govt and 32 firms invest ¥268 bln in Rapidus

- China imposes export controls on 40 Japanese entities amid rising tensions

- Rare earth recycling infrastructure to be subsidized

- OCCTO to revise guidelines for replacement of aging power facilities

- EGC debates whether to continue with contracted pumped-storage operations in balancing market

- TEPCO in talks with potential investment partners

- Kanadevia signs MoU with Indian firm on green H2

- Mitsubishi Shipbuilding delivers first systems for marine ammonia-fueled engines

- INPEX and Osaka Gas begin operations at emethane test facility

- MoE to make environmental/ social guide for solar

- Tohoku Electric signs PPA to supply 7-Eleven

- Leapton Solar creates subsidiary in Vietnam

WIND POWER AND OTHER RENEWABLES

- JERA’s Round 3 offshore wind project expands capacity thanks to larger turbines

- REI urges overhaul of offshore wind zoning to unlock EEZ development

- Chubu Electric to advance wave power

- Govt pledges ¥1 trln for next-gen reactors, fusion

- TEPCO to boost Kashiwazaki-Kariwa NPP Unit 6 to commercial operation

- FEPC forecasts plutonium consumption for FY2026 and FY2027

- Idemitsu to keep oil refineries open until 2030

- Japanese consortium among bidders for Shell’s stake in Australia LNG plant

- INPEX gets environmental approval for Abadi LNG

CARBON CAPTURE & SYNTHETIC FUELS

- MoE selects Marubeni’s large solar project in Tunisia for the JCM credits

- BYWILL and banks to promote J-Credits in Chiba

EVENTS

March 5 Nepal – First Parliamentary Election

March 11 “REVision 2026” symposium by

Renewable Energy Institute @ Tokyo

Mar 17-19 Smart Energy Week Spring 2026 / H2& FC EXPO / PV EXPO / Battery Japan / Smart Grid EXPO / Wind Expo / Biomass Expo / Zero-E Thermal Expo /Decarbonization EXPO 2026 @ Tokyo Big Sight

March 31 End of Japan’s Fiscal Year 2025

Mid-April FIT/FIP Solar Auction #28

Japan Atomic Industrial Forum

(JAIF) Annual conference @ Tokyo

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

CORRECTIONS

In last week’s (Feb 24) issue, in the table on page 23 accompanying the second analysis article, Finding the Right Balance: How Japan is Fine-Tuning the Balancing Market, the price caps for Secondary Reserve (2) and Tertiary Reserve (1) should read ¥7.21. This price level has been in place for these products since 2024 and will remain unchanged in FY2026. The article’s discussion focused solely on the price cap revisions for Primary, Secondary Reserve (1), and the Composite product. The online version of the report has been corrected.

NEWS: GENERAL OUTLOOK AND TRENDS

Govt and 32 firms invest ¥268 bln in Rapidus; state largest shareholder

(Government statement, Nikkei, February 26)

- The Japanese govt and private investors have injected a total of ¥267.6 billion into domestic chipmaker Rapidus.

- This includes ¥100 billion in state equity via the Information-Technology Promotion Agency (IPA), and ¥167.6 billion from 32 private companies.

- The private funding amount exceeded expectations.

- Through its investment, the govt will hold 11.5% of voting rights, becoming the largest single shareholder.

- The govt will hold three types of shares:

- A golden share granting veto power over key management decisions;

- Voting shares (limited to roughly 10% of total voting rights to allow managerial flexibility);

- Special nonvoting shares that can convert into voting shares if the company faces financial distress.

- If Rapidus encounters serious financial trouble, the govt can raise its voting rights to 60%, matching its capital ratio, enabling it to lead in restructuring.

- An additional ¥150 billion in equity is earmarked in the FY2026 budget proposal, bringing total planned state equity for FY2026 to ¥250 billion. Overall public support, including R&D subsidies, is expected to reach about ¥3 trillion.

- TAKEAWAY: Rapidus is now firmly positioned as a state-backed strategic semiconductor project. While the govt has limited its voting rights to preserve operational autonomy, the golden share and conversion mechanism ensure strong oversight and the ability to intervene if needed. This project is also important for the power industry, as Rapidus and the facilities built around them will become important clean energy consumers, driving Hokkaido area demand. The company’s main chip fab alone will require 600 MW of capacity.

China imposes export controls on 40 Japanese entities amid rising tensions

(Yomiuri / Nikkei Shimbun, February 24)

- China’s Ministry of Commerce added 40 Japanese companies and institutions to export control lists, tightening restrictions on dual-use (civil–military) goods.

- The order has immediate effect.

- Twenty entities, including Mitsubishi Shipbuilding, IHI Power Systems, Kawasaki Heavy Industries Aerospace Systems and Japan’s National Defense Academy, were placed on the full export control list.

- Another 20 companies, including Subaru, ENEOS, TDK, Mitsubishi Materials and affiliates of trading houses Itochu, Mitsui and Sumitomo, were added to a “watch list,” requiring Chinese exporters to submit risk assessments and written assurances that products will not enhance Japan’s military capabilities.

- China said the measures aim to curb Japan’s “remilitarization and nuclear ambitions,” linking them to PM Takaichi’s remarks regarding a potential Taiwan contingency.

- CONTEXT: The move follows earlier tightening of Chinese controls on dual-use exports, including rare metals such as tungsten, tellurium and bismuth.

- TAKEAWAY: The measures escalate friction between China and Japan, extending export controls beyond specific materials to named corporate entities. Some companies were caught off guard by the announcement. While Beijing frames the restrictions as narrowly targeted, the inclusion of major industrial, energy and aerospace firms – and even top trading houses, which oversee main trade channels – increases uncertainty around supply chains for advanced materials. China’s goal is not only to restrict trade but to win a propaganda war in which it seeks to paint Japan as returning to militarism. The next step may prompt Japan to increase subsidies to the affected industries to accelerate supply chain decoupling.

Japan to subsidize rare earth recycling infrastructure

(Asia Nikkei, February 24)

- The MoE will launch subsidies to support infrastructure for recycling rare earth materials, including equipment for transport, storage and quality verification.

- The ministry earmarked ¥6 billion in its proposed FY2026 budget to fund demos for recovering rare earths from scrap, such as used EV motors and electronic waste.

- Subsidies will cover collection and storage facilities, and test equipment to verify the quality of extracted rare earths, with projects to be selected through an open call.

- Neodymium, which is essential for high-performance magnets used in EVs, generators and electronics, is a key target. China refines over 90% of global supply, and domestic recycling in Japan remains minimal.

- The ministry also aims to expand annual e-waste recycling volume to 500,000 tons by 2030, up 50% from 2020, including support for port-based handling facilities.

- TAKEAWAY: While recycling remains expensive and underdeveloped, targeted infrastructure support could improve scale and reduce processing unit costs, positioning secondary supply as a complementary pillar alongside overseas procurement and seabed resource development.

Govt selects three new biomass industry cities

(Government statement, February 24)

- Seven ministries – including the MAFF, METI and the MoE – selected three cities that applied to become “biomass industry cities”: Nagara (Chiba Pref), Oyama (Shizuoka Pref) and Saito (Miyazaki Pref).

- CONTEXT: The govt defines a “biomass industry city” as one that aims to be resilient in the face of natural disasters and decarbonized via domestic biomass – from raw material production to collection, transportation, manufacturing and utilization. Since its creation in 2013, a total of 107 cities have been selected across Japan.

| Nagara | Conversion of agricultural residues, food waste, conversion of unused thinned timber into fertilizer, biogas power generation |

| Oyama | Thermal utilization of forest residues and rice husks, biogas power generation from food waste |

| Saito | Biogas power generation from unused thinned timber, bamboo biochar and silage utilization, willow fuel conversion, etc |

- CONTEXT: Biochar is the lightweight black remnants remaining after the pyrolysis of biomass. A form of charcoal, it is intended for organic use. Silage is a method of preserving forage through anaerobic fermentation (without air) in silos.

- TAKEAWAY: Biogas production in Japan is concentrated in small, decentralized projects (around 0.5 MW on average), often located in small or mid-sized towns operating their own local facilities. A 1.6 MW plant in Kumamoto Pref is scheduled to start operations in July 2029 and to generate about 12 GWh annually. But projects exceeding 1 MW are rare. As a result, Most biomass generation capacity still sits in large plants burning wood residues or imported biomass, rather than in small biogas installations. The govt also sees small-scale biogas plants as instruments for both decarbonization and rural revitalization.

NEWS: ELECTRICITY MARKETS

OCCTO to revise guidelines for replacement of aging power facilities

(Agency statement, February 24)

- OCCTO outlined plans to revise its guidelines for replacing aging T&D facilities, as part of preparations for the Third Long-Term Cross-Regional Grid Development Policy and the second revenue cap regulatory period.

- Under the revenue cap system, TSOs must align business plans with the guidelines, and regulators assess whether renewal investments are sufficient based on quantified asset risk.

- Facility risk is defined as the annual failure probability multiplied by the impact of failure for each asset. This framework allows TSOs to assess asset condition and prioritize renewals.

- In the first regulatory period (FY2023–27), maintenance plans aim to ensure total future risk does not exceed current levels. For the second regulatory period (FY2028–32), the committee will continue in-depth discussions on mid- to long-term issues, including refinement of risk parameters and broader scope.

- CONTEXT: The guidelines provide a standard methodology for quantifying facility risk based on failure probability and impact. The current version was prepared in December 2021.

- CONTEXT: The revenue cap system limits total utility revenue over a five-year period to promote cost efficiency and stable wheeling tariffs. The second regulatory period will run from FY2028 to FY2032.

EGC discusses contracted pumped-storage operation in balancing market

(Government statement, February 20)

- The power market regulator, EGC, reviewed the operation of negotiated pumped-storage contracts in the FY2025 balancing market and debated their treatment from FY2026 onward.

- TSOs argued that negotiated contracts help secure stable balancing capacity at lower cost through portfolio procurement, and said current volumes have not excessively constrained market participation.

- Battery operators countered that deducting contracted pumped-storage volumes from the balancing market has reduced trading opportunities and weakened investment incentives.

- Contracted pumped-storage operators, meanwhile, warned that terminating contracts could raise costs and increase revenue uncertainty.

- Commissioners expressed divided views. Some questioned whether negotiated contracts remain justified as the balancing market moves to full day-ahead trading, arguing that they may suppress competition and distort price signals. Others said combining long-term contracts with market procurement is not inherently inconsistent with market principles, particularly given cost differentials.

- No formal conclusion was reached at this meeting. The commission will continue reviewing the necessity, scale and design of negotiated contracts after hearing further input from balancing service providers.

- CONTEXT: Balancing power is procured competitively via the market. Negotiated pumped-storage contracts were introduced as an exceptional measure to supplement volumes that could not be secured through market procurement. The contracted volume is deducted from balancing market procurement requirements.

TEPCO explores alliances; Bain and KKR among potential partners

(Facta, March 2026 issue)

- TEPCO Holdings is considering cooperation with investors for renewable energy. Domestic funds such as Japan Industrial Partners and the Japan Investment Corp, as well as U.S. private equity firms including Bain Capital and KKR, are among those showing interest. No formal agreements have been announced.

- TEPCO aims to avoid asset sales, and instead use partnerships to secure investment capital. The company plans roughly ¥6 trillion in investments in nuclear and renewable power to bolster longterm earnings capacity.

- TEPCO’s financials remain challenging. As of end-2023, Fukushima-related costs were estimated at ¥23 trillion; the utility is responsible for about ¥17 trillion.

- Kashiwazaki-Kariwa NPP’s full restart, seen as central to earnings recovery, has faced setbacks, and retail electricity sales remain 20% below pre-liberalization levels.

- In the past, TEPCO sought alliances with NTT and ENEOS, which didn’t materialize.

- CONTEXT: TEPCO secured METI approval for a new business plan that forecasts generating ¥500 billion annually from earnings and cash to cover Fukushima costs.

- TAKEAWAY: Reported investor interest remains preliminary, and structural constraints, such as state oversight and restart uncertainty, limit the scope and speed of any deal. More importantly, investors want to ensure that their capital is walled off from company liabilities and yet retain some form of state guarantee.

Chubu Electric invests in offshore “power transport vessel” startup

(Company statement, February 27)

- Chubu Electric will invest in a third-party share allotment by Kaijo Power Grid, a Tokyo-based startup developing a novel offshore electricity transmission model – “electricity transport vessels” equipped with large-capacity onboard batteries that store power generated by offshore wind, and transport it to demand centers.

- This concept aims to address grid connection constraints, and is a solution for offshore wind projects in areas where submarine cable installation is difficult due to seabed conditions or deep waters.

- Founded in 2024, Kaijo Power Grid develops and sells the vessels, as well as operates marine power transport and electricity sales businesses.

NEWS: HYDROGEN

Kanadevia signs MoU with Indian firm on green H2 production

(Company statement, February 27)

- Kanadevia signed an MoU with Infistar Energy, an Indian oil, mineral resources and renewable energy developer, to explore green hydrogen production in Uttar Pradesh.

- Kanadevia aims to support hydrogen deployment in India through the provision of its equipment and services.

- CONTEXT: Kanadevia plans to build a mass-production facility in Tsuru City for water electrolysis stacks, a core component of hydrogen production systems. India is targeting annual green hydrogen production capacity of 5 Mt by 2030.

Mitsubishi Shipbuilding delivers first systems for marine ammonia-fueled engines

(Company statement, February 24)

- Mitsubishi Shipbuilding delivered its first ammonia fuel supply system (AFSS) and ammonia gas abatement system (AGAS) to Japan Engine Corp for installation on an ammonia-fueled marine engine.

- The AFSS ensures stable and safe ammonia fuel supply, while the AGAS safely treats surplus ammonia during fuel switching. Both systems feature integrated remote and automatic control to enhance safety and efficiency.

- CONTEXT: Japan Engine is a manufacturer of large marine diesel engines. MHI, a parent company of Mitsubishi Shipbuilding, is a shareholder. Japan Engine has been developing an ammonia-fueled engine since 2021. Mitsubishi Shipbuilding inked an order from Japan Engine in April 2024 for AFSS and AGAS.

- TAKEAWAY: Ammonia-fueled marine engines can play a role in decarbonizing the shipping industry. Currently, most ships run on petroleum-based fuels, and pollution from shipping accounts for about 3% of global GHGs, emitting about 1 billion tons of CO2 annually. Also, methane emissions from ships doubled between 2018 and 2023. If the shipping industry were a country, it would rank as the 6th largest emitter, comparable to Germany. Forecasts claim that, if unchecked, emissions by 2050 could rise by up to 130% over 2008 levels.

KHI’s automated liquefied H2 bunkering tech selected for GI Fund project

(Company statement, February 20)

- The Green Innovation (GI) Fund selected Kawasaki Heavy Industries (KHI) for Development of Automated Liquefied Hydrogen Bunkering Technology.

- This demo will build onshore facilities for liquefied hydrogen bunkering and develop technologies to optimize and automate the entire bunkering process.

- It aims to minimize boil-off gas (BOG) generated during fueling at -253°C and establish safe, efficient, and rapid automated bunkering.

- The total project cost is about ¥2.07 billion, with NEDO’s support capped at about ¥1.54 billion; the project will run from FY2025 to FY2030.

- CONTEXT: KHI, Yanmar Power Solutions and Japan Engine have been developing marine hydrogen engines and fuel supply systems with tanks. Building large hydrogen-fueled ships requires bunkering facilities to supply liquefied H2 from shore.

- TAKEAWAY: KHI already developed the world’s first liquefied hydrogen carrier, Suiso Frontier. The automated liquefied hydrogen bunkering technology strengthens the midstream and port-side infrastructure necessary to scale up hydrogen maritime logistics. This would position KHI as a full hydrogen maritime value-chain provider.

NGK, Chubu Electric sign agreement for ammonia-fueled kiln

(Company statement, February 24)

- NGK Insulators and Chubu Electric agreed to collaborate on the commercialization of an ammoniafueled kiln for ceramics production.

- The partners will assess technical challenges and potential solutions for using ammonia in hightemperature ceramic firing. Chubu Electric will study ammonia supply logistics and exhaust treatment systems, including NOx mitigation.

- CONTEXT: Ammonia benefits from established transport and storage infrastructure, making it attractive as a decarbonized fuel option. However, its slow combustion characteristics and NOx emissions present technical hurdles. While ammonia combustion technology is advancing in power generation and industrial applications, commercial ceramic kilns have not yet been realised.

- TAKEAWAY: NGK has been developing hydrogen-fired ceramic kilns since 2021, including installation of a large test furnace in 2023 to advance mass-producible hydrogen regenerative burners targeting 50% energy savings. With development now proceeding in parallel for hydrogen- and ammonia-fueled systems, the initiative underscores growing competition between the two fuels in industrial heat. Commercialisation timelines, and relative cost performance, will determine which pathway gains traction first.

INPEX and Osaka Gas begin operations at e-methane test facility

(Company statement, February 24)

- INPEX and Osaka Gas began operations at a CO2 methanation test facility in Niigata, designed to process 400 Nm³ of CO2 per hour – equivalent to the annual gas consumption of around 10,000 households.

- The facility produces synthetic methane (e-methane) with a methane concentration of 96%, meeting the project’s target specification for grid injection.

- The CO2 used in the process is captured at INPEX’s Koshijihara Plant. The facility has been certified by the Japan Gas Association, enabling issuance of clean gas certificates for the synthetic methane produced.

- CONTEXT: The project has been under development since 2021 as part of a NEDO-backed program aimed at commercialising CO2 methanation for city gas decarbonisation. Construction of one of the world’s largest test facilities of its kind began in 2023.

- TAKEAWAY: The launch marks a tangible step toward scaling e-methane as a drop-in decarbonisation option for Japan’s existing gas infrastructure. Alongside INPEX’s blue hydrogen and ammonia demonstration in Kashiwazaki, the project forms a core pillar of the company’s hydrogen-centered decarbonized energy strategy. The key test now will be cost competitiveness and the ability to secure stable CO2 and hydrogen supply at commercial scale.

NEWS: SOLAR AND BATTERIES

MoE to publish environmental and social guide for solar

(Government statement, February 20)

- The MoE is soliciting public comments on a draft guide detailing measures to reduce the environmental impact of large-scale solar projects across all stages, from site selection and design to construction, operation and decommissioning.

- The guide supplements existing solar environmental guidelines by focusing specifically on impacts to animals, plants and ecosystems, and provides stage-by-stage checklists, case studies and mitigation examples.

- Developers are encouraged to consult municipalities and prefectures at the site selection stage and to confirm zoning, local ordinances and environmental sensitivities in advance. The draft also directs developers to use national biodiversity mapping tools such as the Environmental Assessment Database System (EADAS) to identify sensitive habitats and protected areas.

- Where impacts cannot be avoided, the guide outlines mitigation and compensatory measures, including habitat creation and adaptive management with ongoing monitoring. Early-stage ecological surveys are recommended where existing data are insufficient.

- The draft also situates solar development within the broader biodiversity policy shift following the Kunming–Montreal Global Biodiversity Framework and growing TNFD-related disclosure expectations.

- TAKEAWAY: This guideline is aimed at large-scale solar farms. While non-binding, the guide signals tighter expectations for ecological due diligence in solar siting and stronger coordination with local governments. As municipalities increasingly introduce zoning rules and coexistence ordinances for renewables, the document may raise development costs and timelines for greenfield projects, particularly in forested or semi-natural areas. At the same time, it aligns solar policy with Japan’s “nature-positive” positioning and evolving corporate biodiversity disclosure standards.

- SIDE DEVELOPMENT:

- Review of Blue Leaf Energy’s 100 MW solar project begins

- (Company statement, February 25)

- The govt began reviewing Blue Leaf Energy’s environmental impact assessment methodology for its planned 100 MW solar power plant in Ashibetsu (Hokkaido).

- The project site covers 115 hectares, with 154,000 crystalline silicon solar panels.

- The plant is expected to start operations in FY2031.

- CONTEXT: Blue Leaf Energy’s environmental impact assessment methodology is expected to be subject to strict scrutiny. An online petition seeks to halt construction. In October, the MoE objected to the site’s proximity to residential areas and forests.

Tohoku Electric signs off-site PPA to supply 7-Eleven stores

(Company statement, February 20)

- 7-Eleven Japan signed a corporate PPA with Shirokuma Power, Eurus Energy and Tohoku Electric to supply renewable energy to 1,800 stores in Tohoku and Niigata.

- Annual supply is expected to total about 59 GWh, with 25-year contracts from each plant’s commercial start date.

- Supply will come from a 13 MW wind farm in Higashidori (Aomori) backed by Eurus Energy, two wind projects in Niigata (3.9 MW combined), and two solar plants in Miyagi and Iwate (2.2 MW combined).

- The solar projects launched last month, with wind projects to start in 2027.

- CONTEXT: By 2030, 7-Eleven aims to slash by half CO2 emissions from store operations. This PPA marks the firm’s first use of wind power under a PPA.

Leapton Solar creates subsidiary in Vietnam amid rising demand

(Company statement, February 17)

- Kobe-based Leapton Solar set up a subsidiary in Vietnam amid rising demand for solar installations, especially on factory rooftops.

- Within five years, the firm aims for installed capacity equivalent to 500 MW.

- CONTEXT: Leapton Solar originally sold solar modules, but has since diversified its portfolio to offer EPC, electricity sale, PPAs, and financial partnerships. Vietnam has set a goal of 46 to 73 GW in installed solar capacity by 2030.

au Energy & Life agrees with REDER to develop next-gen residential BESS

(Company statement, February 20)

- au Energy & Life agreed with REDER to develop next-gen residential BESS services and EMS methods, including applications for disaster resilience.

- CONTEXT: au Energy & Life is a major telecom company in Japan. REDER specializes in PPA support in solar energy and BESS. It gained expertise in Okinawa’s harsh climate conditions, in collaboration with NEXTEMS. REDER also has knowledge in local area aggregation.

Blue Sky Energy and Remixpoint pilot low-voltage solar aggregation with BESS

- Blue Sky Energy, in collaboration with Remixpoint and its subsidiary Seal Engineering, will launch a project to optimize operation of 10 low-voltage solar power plants in Shibushi (Kagoshima Pref) via installation of BESS.

- The project will use “Tensor Cloud” as the aggregation operating system.

- The power plants are owned by Blue Sky Energy and Remixpoint.

- CONTEXT: Fukuoka-based Tensor Cloud streamlines operation of post-FIT renewable assets (charge/discharge scheduling, high frequency electricity generation and price forecasts, financial planning).

GS Yuasa to invest more than ¥70 billion in lithium-ion batteries

(Company statement, February 18)

- Kyoto-based GS Yuasa will invest over ¥70 billion to expand mass production and R&D of stationary lithium-ion batteries.

- The project includes a ¥24.8 billion subsidy from METI under its battery supply assurance program.

- Annual production capacity equivalent to 2 GWh is scheduled to begin in October 2028.

- TAKEAWAY: The investment underscores Japan’s push to build domestic storage manufacturing capacity with govt backing. While GS Yuasa already has more than 400 MWh of installed battery systems in Japan, including large-scale projects in Hokkaido and Kyushu, the planned 2 GWh annual capacity marks a significant scale-up. At the same time, competition from Chinese suppliers is intensifying: in 2025, Sungrow agreed to supply 500 MWh of BESS systems across Japan. The move positions GS Yuasa to defend its share in a market where cost competitiveness and volume scale are becoming decisive.

Sumitomo Electric and Nissin Electric launch new BESS featuring EMS

(Company statement, February 24)

- Sumitomo Electric and Nissin Electric sold their first BESS model featuring EMS developed by Nissin Electric.

- The EMS enables parallel operations of up to nine Sumitomo batteries at a lower cost than conventional BESS.

- The unit was supplied to a childcare center in Ishikawa (Fukushima Pref), which also serves as an evacuation shelter. It will help secure power in case of emergencies.

- Both companies plan to expand sales to small- and medium-scale factories, office buildings, and to commercial and public facilities.

- SIDE DEVELOPMENT:

- LifeOne acquires 10 properties to build BESS stations

- (Company statement, February 24)

- LifeOne acquired 10 properties from ENEOS to build BESS stations in Aichi, Ibaraki, Gunma, Kagoshima, Miyagi and Akita Prefs.

- With a total surface of about 15,000 m2, projects are likely to be relatively small (within the 2 MW range). Installed capacities have not yet been disclosed.

- CONTEXT: LifeOne is a renovation company, but has expanded into BESS assets.

GBP launches soundproof panels for BESS stations

(Company statement, February 25)

- GBP launched soundproof panels for BESS stations, using a dual-layer solution.

- The goal is to give developers greater flexibility in site selection and to mitigate risks associated with noise emissions.

- The standard panel height is 3 meters, but it can be customized from 2 to 4 meters.

NEWS: WIND POWER AND OTHER RENEWABLES

JERA’s Round 3 offshore wind project expands capacity thanks to larger turbines

(Company report, Feb 10/23)

- JERA submitted a draft environmental assessment (準備書) for its Tsugaru offshore wind project, with capacity rising to 615 MW from 600 MW in earlier plans.

- The site – awarded to JERA in Round 3 of a state tender – will deploy 41 turbines, each 15 MW. The project was conceived with 480 MW capacity using 60 turbines (each 8 MW), but later revised to 600 MW after site occupancy rules confirmed that grid capacity of that scale had been secured.

- At assumed capacity factor of ~30%, Tsugaru is expected to deliver 1.58 TWh/ year.

- CONTEXT: This is about 0.16% of Japan’s electricity consumption.

- The turbines will use monopile foundations with a max seabed penetration of about 40m and a diameter of 9.5m. Subsea cables will be buried 3m below the seabed.

- CONTEXT: The draft also lists several other offshore wind projects planned or under review nearby, suggesting the Tsugaru coast could evolve into an offshore wind cluster of roughly 3–4 GW if other projects proceed.

- TAKEAWAY: The submission of a draft assessment is the start of detailed impact modelling under the Environmental Impact Assessment Act. The project now moves into the legally prescribed third stage of a fourstep process (配慮書 → 方法書 → 準備書 → 評価書)、 bringing it closer to construction. This also triggers formal public review. Local govts, residents and fishing cooperatives can submit opinions. In 2024, Japan NRG published a report on how long each stage of this process can take (available for a fee on request).

REI urges overhaul of offshore wind zoning to unlock EEZ development

(Company statement, February 13)

- The Renewable Energy Institute proposed a two-stage, nationally led sea-area selection system to accelerate offshore wind deployment in Japan’s offshore waters and EEZ, arguing that the current prefecture-led model is ill-suited to floating projects and wide-area coordination challenges.

- The Cabinet Office would first use integrated cross-ministerial data to identify and publicly map “candidate areas” via the “Umi-Shiru” marine platform, separating technical screening from political negotiation.

- In a second stage, prefectures (in territorial waters) or METI (in the EEZ) would conduct stakeholder coordination and designate promotion or recruitment zones.

- REI calls for stronger fisheries integration, including nationwide surveys of fishing activity, clearer data governance rules, national-scale impact monitoring and the creation of a govt-led fisheries fund to address unforeseen wide-area impacts.

- The think tank also proposes a neutral fisheries coordination body, national sea-use safety guidelines, clearer frameworks for community benefit funds and the extension of power-source location subsidies to offshore wind, positioning offshore projects as part of a broader marine planning strategy rather than standalone developments.

- TAKEAWAY: REI’s proposal is technically logical: a national, data-driven zoning model would reduce uncertainty, front-load conflict screening and make offshore wind pipelines more predictable. Clearer EEZ procedures and a govt-backed fisheries risk framework would likely be welcomed by industry, as they address one of the biggest structural barriers to floating projects. Whether it is politically realistic is another matter. The Cabinet Office – whose core secretariat is around 1,300 staff and largely plays a coordination role – is smaller than ministries such as METI, as well as MLIT and MAFF. It is far from clear if those ministries would cede authority over zoning and sea-use decisions. Expanded data collection, national-scale fisheries monitoring and a compensation fund would require sustained budget commitments. Without strong political backing and dedicated funding, the proposal risks becoming an additional procedural layer rather than the accelerator that REI envisions.

Kajima and Kanadevia secure ClassNK for hybrid floating wind foundation design

(Company statement, February 26)

- Kajima and Kanadevia set a new design methodology for a hybrid steel-concrete structure used in floating offshore wind turbine foundations, with ClassNK issuing technical certification – the first of its kind in Japan for a floating structure.

- The design applies a composite structure to the central column of a semi-submersible floating platform, aiming to improve cost efficiency.

- Certification confirms the methodology meets requirements relevant to wind farm approval under domestic regulations.

- The firms were selected for the program’s Phase 2, which will include a demo off Aichi Pref using the semi-submersible design.

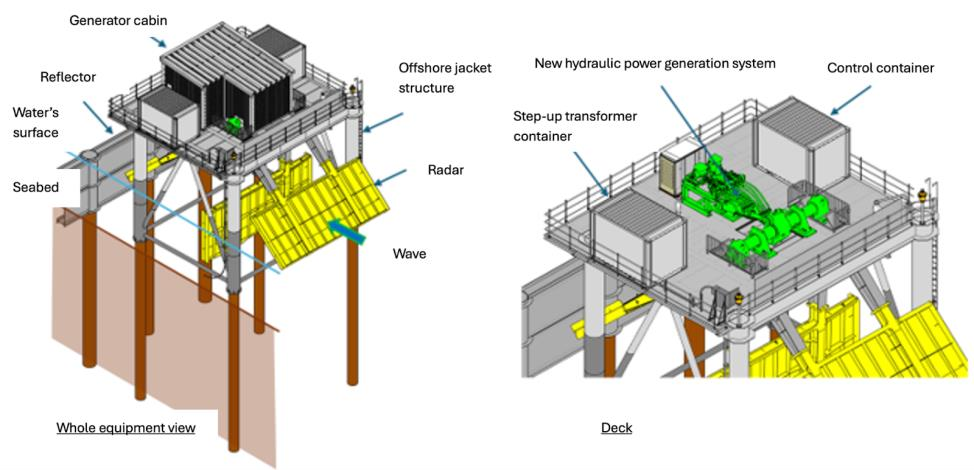

Chubu Electric agrees with e-Wave R&D to advance wave power

(Company statement, February 25)

- Chubu Electric agreed with eWave R&D to develop wave power machinery (0.1 MW) under NEDO’s project for developing new energy.

- The device will be deployed in 4–5 meters of water, using a new hydraulic power generation system that converts wave motion into electricity.

- Research will be conducted in coastal areas of Noshiro (Akita Pref) from April 2026 to March 2030, facing the open ocean.

- Chubu Electric will oversee coordination and marine structure design, while e-Wave R&D will handle electrical systems and control validation.

- CONTEXT: Chubu Electric and e-Wave R&D are members of the Ocean Energy Joint Research Group headed by Tokyo University.

- TAKEAWAY: Wave power remains commercially unproven in Japan, but the project reflects growing interest in diversifying renewable options beyond solar and wind. To date, there is no commercial wave power facility in the country. However, wave power is endorsed by the govt for its potential low-cost and high efficiency supply capacity. With about two-thirds of its population living in coastal areas and almost 30,000 km of coastlines, Japan has a high potential for wave power generation: theoretical total available power could range above 100 GW. This project’s emphasis on domestically developed technology and consortium participation aligns with Japan’s broader push for energy security and strategic autonomy.

Yamato Mobility and Bell Energy to develop EV conversion trucks

(Company statement, February 24)

- Yamato Mobility agreed with Bell Energy to develop EV trucks equipped with a conversion platform and energy supply functions.

- Once commercialized, trucks will supply power for industrial sites or outdoor events.

- CONTEXT: EV truck conversion refers to replacing internal combustion engines with electric motors, controllers and battery packs.

- SIDE DEVELOPMENT:

- Northern Iwate Transportation to introduce EV buses powered by hydroelectricity

- (Iwate Nippo, February 24)

- Northern Iwate Transportation launched an EV bus in the Morioka area (Iwate Pref) that runs on electricity generated from local hydropower.

- In July, the company will introduce two buses to serve Morioka and nearby cities.

NEWS: NUCLEAR ENERGY

Japan to invest ¥1 trillion for advanced reactors and nuclear fusion

(Denki Shimbun, February 26)

- PM Takaichi said the govt will spend over ¥1 trillion in the nuclear sector to speed up commercialization of next-gen reactors and fusion energy.

- Investment-promotion measures will be announced this summer.

- Speaking before the Diet, Takaichi also addressed high-level radioactive waste stored in Aomori Pref, stressing the govt will ensure operators adhere to removal deadlines. Current agreements set storage for 30–50 years before transfer to final disposal.

- CONTEXT: Takaichi also said the govt will enact specific R&D and installation plans for next-gen reactors. This includes reactor replacement at NPP sites that are slated for decommissioning. Efforts will accelerate to restart reactors that the NRA deems safe, alongside improving public communication.

METI details roadmap for next-generation reactors, reiterates role of HTGRs

(Government statement, February 26)

- METI released an updated development roadmap for next-generation reactors, building on its 2022 framework that identified five priority technologies – advanced light-water reactors, SMRs, fast reactors, high-temperature gas-cooled reactors (HTGRs) and fusion – as central to Japan’s long-term energy strategy.

- For advanced light-water reactors, METI noted that since the 2022 roadmap, state-backed R&D has progressed and the technology is broadly ready for deployment. Now it is up to utilities to move forward with investment decisions to replace old reactors with new units while gathering host community consent and regulatory approvals.

- On SMRs, METI acknowledged that overseas projects are advancing while domestic regulatory standards remain underdeveloped, and stressed the need to adapt designs to Japan’s seismic conditions and clarify licensing pathways. SMRs could be used as an alternative to coal for on-grid power and replace diesel in the mining sector.

- For fast reactors, key milestones include a 2026 fuel selection (oxide vs metal) and a 2028 decision on whether to proceed to basic design for a demo reactor.

- METI reiterated support for HTGRs as a platform for industrial decarbonisation, highlighting 950°C heat output and plans to begin hydrogen production testing using HTTR around 2028, with a broader demo roadmap extending into the 2030s. HTTR is framed as relevant for chemical/ petrochemical complexes.

- Across all reactor types, the ministry identified supply-chain erosion, workforce shortages and regulatory predictability as cross-cutting challenges.

- TAKEAWAY: While this roadmap goes over similar ground to the 2022 version, there is a shift from technical discussion to practical project considerations. The working group is going over what needs to happen for the reactors to actually be built. The answer to that lies in creating the right conditions to unlock finance, ease regulatory processes and siting, and encourage supply chains. Most of these will require considerable state involvement – especially via public credit support for the large investments. The struggles of Kansai Electric to raise funds for new reactor construction via equity sales show the limits of private funding alone. Further, METI acknowledges the need to provide a more detailed outlook for the nuclear sector in Japan to support investments. Most of all, the nuclear sector needs at least one – and ideally several – new project(s) to move from discussion to implementation.

TEPCO to boost Kashiwazaki-Kariwa NPP Unit 6 to commercial operation

(Nikkei, February 26)

- On March 3, TEPCO will increase output of Kashiwazaki-Kariwa’s Unit 6 to 1.356 GW, matching its level during commercial operation.

- The utility plans to maintain this output and transition the reactor to full commercial operation on March 18.

- Unit 6 began full-scale power generation on Feb 16, raising output to 50% of its rated capacity.

Output will increase to 100% on March 3. - SIDE DEVELOPMENT:

- NRA issues evaluation on security breach at Kashiwazaki-Kariwa

- (Company statement, February 24)

- The NRA issued an evaluation on a security breach at TEPCO, rating the incident as “white”, meaning that “improvement under supervision” is required.

- The breach involved a TEPCO employee who copied and removed confidential documents on nuclear material protection.

- The NRA said the actions were intentional but that no documents were leaked.

- CONTEXT: The unauthorized actions began in 2020. TEPCO reported the issue to regulators in June and Oct 2025, leading to an NRA inspection that ended in January.

- TAKEAWAY: Despite the violation, the incident likely won’t delay restart of Unit 6 set for March 18. Still, the incident highlights persistent challenges with security. TEPCO remains under pressure to show its improvements are sustainable and not temporary fixes. The NRA will finish its evaluation in March.

FEPC forecasts plutonium consumption for FY2026 and FY2027

(Company statement, February 20)

- The FEPC released a roadmap for the Pluthermal Program between FY2026-2028, outlining how major utilities intend to manage plutonium stockpiles.

- The plan emphasizes recycling nuclear resources, and sets allocation of plutonium usage across various regional power stations.

- CONTEXT: As of late FY2025, the amount of plutonium stockpiled by major power firms is about 40 tons. Energy providers aim to use MOX fuel in 12 reactors by 2030.

- Furthermore, the reports highlight the importance of securing local consent, and fostering interoperator cooperation to redistribute stored fuel volumes.

- The amount of plutonium to be consumed in both FY2026 and FY2027 is 0.7 tons, with the use of MOX at KEPCO’s Takahama NPP.

- CONTEXT: Japan pledges not to hold surplus radioactive material without a specific purpose. So, these initiatives are vital for maintaining transparency of the nuclear fuel cycle. While this updated 3-year roadmap reflects logistical constraints in overseas reprocessing, it reaffirms a commitment to sustainable nuclear power generation.

Yamaguchi Court dismisses challenge seeking to halt Ikata NPP

(Company statement, February 26)

- The Yamaguchi District Court dismissed a challenge to halt operations at Ikata NPP.

- The dispute centers on potential risks posed by active seismic faults near the facility, as well as potential danger of volcanic activity from Mount Aso.

- The plaintiffs say the plant sits on unstable ground and remains vulnerable to eruptions. Shikoku Electric contends that safety assessments met necessary standards.

- CONTEXT: This ruling follows a complex history of temporary injunctions. It overturned decisions on the site’s third reactor, operational since 1994. The decision allows the utility to continue generation despite ongoing public concerns.

NEWS: TRADITIONAL FUELS

In major reversal, Idemitsu to keep oil refineries open until at least 2030

(Asia Nikkei, February 28)

- Idemitsu Kosan is reversing its earlier plan to close domestic refineries, deciding to maintain operations at its six remaining refineries (in Hokkaido, Chiba, Kanagawa, Aichi, and Mie prefs) until at least 2030, with potential extension to 2035.

- The reversal stems from slower-than-expected EV adoption in Japan, where the current EV penetration rate is only about 2% and forecasts indicate gasoline demand will remain roughly flat rather than decline sharply.

- The 2022 plan targeted a 20% reduction in refining capacity by 2030 (potentially closing 1–2 refineries), driven by anticipated EV-driven drops in gasoline demand.

- CONTEXT: Similar trends appear among other refiners: ENEOS Holdings plans to keep refineries open until at least 2028 and Cosmo Energy Holdings until 2030. According to the Petroleum Association of Japan, as of March 2025, there were 19 refineries in Japan with a combined refining capacity of 3.11 million barrels per day. This represents a 20% drop over the past 10 years. Also, Japan has about 27,000 gas stations, a decline of 20% over the past 10 years.

- TAKEAWAY: Other factors supporting gasoline demand include lower prices, a slowdown in gas station closures, potential exports of surplus products (like naphtha) to growing Asian markets, and global policy adjustments (e.g., U.S. subsidy cuts and EU retreat from 2035 ICE vehicle bans) that are slowing broader decarbonization momentum. But while current gasoline demand supports a policy of maintaining refining capacity, the fact is aging facilities and long-term demand decline are nevertheless limiting new investments into the sector.

Japanese consortium among bidders for Shell’s stake in Australia LNG plant

(Bloomberg, February 26)

- A consortium of Japanese companies, including Tokyo Gas, is among bidders for Shell’s 16.67% stake in the A$34 billion North West Shelf project in Western Australia.

- The Japanese group is competing with suitors that include Adnoc’s XRG investment arm and MidOcean Energy (backed by Saudi Aramco).

- The North West Shelf LNG plant, operated by Woodside, is Australia’s oldest and largest LNG facility. Other partners include BP, CNOOC and a Mitsui–Mitsubishi JV.

- Shell is reviewing the project as it transitions toward a third-party tolling model, under which buyers pay a liquefaction fee rather than hold upstream equity. Shell previously exited Browse LNG in 2023 that intended to supply gas to the facility.

- TAKEAWAY: Views on Australia’s future LNG supplies are split among Japanese buyers, but the biggest seller to Tokyo still offers supply security at a time of tighter global competition for gas. Tokyo Gas is also trying to gain a stronger position in upstream and liquefaction assets as it contemplates more third-party trading in Asia.

INPEX secured environmental approval for Abadi LNG

(Company statement, February 20)

- INPEX secured environmental approval from the Indonesian govt for the Abadi LNG project in the Arafura Sea.

- The company can proceed with drilling as well as processing facilities and liquefaction plants. The venture aims to produce 9.5 Mtpa of LNG.

- To ensure sustainable operations, the project uses CCS to reduce GHGs. Following approval, the operator will begin preparatory development work at the site.

Shizuoka Gas to invest ¥107 billion, focus on shale gas in the U.S.

(Nikkei, February 24)

- Shizuoka Gas will invest a record-breaking ¥107 billion over the next three years.

- As the domestic city gas market has reached maturity, the firm seeks profits via international expansion and diversified services.

- Key focus areas include the development of shale gas interests in the U.S.

- Also, it focuses on the acceleration of M&A in the housing and engineering sectors. The firm already acquired Kyowa Fudosan, a real estate firm based in Hamamatsu.

- By 2028, the company aims to achieve a consolidated ordinary profit of over ¥13 billion and an 8% return on equity.

LNG stocks same as previous week, down YoY

(Government data, February 25)

- As of Feb 22, the LNG stocks of 10 power utilities were 2 Mt; the same as the previous week (2 Mt); down 1.5% from end Feb 2025 (2.03 Mt), and down 6.5% from the 5-year average (2.14 Mt).

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

MoE selects Marubeni’s 130 MW solar project in Tunisia under JCM

(Company statement, February 20)

- The MoE selected Marubeni for its 130 MW solar power plant project in Gabès (central Tunisia) under the 7th round of the JCM program.

- Electricity is to be sold to the Tunisian Company of Electricity and Gas.

- CONTEXT: Tunisia’s solar installed capacity amounts to about 773 MW. The govt plans to increase that up to 1.5 GW by 2030. The current top facility is a 120-MW plant in Kairouan, commissioned in December 2025 by AMEA Power.

BYWILL and banks to promote J-Credits in Chiba

(Company statement, February 18)

- BYWILL, Choshi Shinkin Bank and Choshi Shoku Credit Union agreed with the city of Choshi (Chiba pref) to promote J-Credits and business models that include environmental value.

- This agreement aligns with the city’s decarbonization commitments.

- SIDE DEVELOPMENT:

- BYWILL and Mitsui Sumitomo to promote J-Credits in Kumamoto

- (Company statement, February 17)

- BYWILL and Sumitomo Mitsui signed a similar deal with the city of Asagiri (Kumamoto Pref).

- This agreement also aligns with the city’s decarbonization commitments.

- CONTEXT: These agreements with municipalities are part of broader initiatives driven by the MoE, such as the “Decarbonization-Leading Regions” program.

ANALYSIS

BY KYOKO FUKUDA and YURIY HUMBER

Japan’s Corporate PPA Market Reaching Scale – And a Turning Point

Cumulative power capacity linked to Corporate PPAs in Japan surpassed 3 GW in 2025, with median disclosed project size rising 82% YoY, reflecting the growing weight of large-scale corporate offtakers.

While the average size of PPAs shrank a little in the second half of 2025, likely due to political and regulatory uncertainties, the pace of the deal-making was unaffected. The number of deals made public in the last six months was a third higher than in the first half, according to data collected by Japan NRG.

The PPA market’s importance is only set to grow in Japan. With the feed-in tariff (FIT) to be phased out for utility-scale solar farms starting FY2027, developers are increasingly looking to secure anchor electricity buyers to underpin financing for new projects. Even as the number of renewable power sources available for PPA deals has grown in the past two years, solar accounted for nearly nine out of ten contracts in 2025, Japan NRG’s database shows.

What’s more, volatility in fossil fuel import prices since 2022 has narrowed the cost gap between grid electricity and renewable PPAs, making fixed-price contracts more attractive to industrial users seeking price stability. Solar-based corporate PPAs in 2025 were priced to be competitive with conventional tariffs, reinforcing their role not only as decarbonization tools but also as a means of securing hedged long-term energy supply.

Japan NRG began tracking publicly announced PPA deals in the calendar year 2023. Our database collects information on details published by companies, the media, or official sources. It contains parameters such as electricity volumes, forecasted CO2 savings, type of contract, and the sector background of buyers and sellers.

So, who were the biggest players in the market last year and what were the key trends?

Background: What is a PPA

A corporate PPA is typically a 10- to 20-year contract between a company and a power producer. It can be structured as either physical or virtual. In a physical PPA, the buyer directly secures electricity from a specific project. This may be delivered via the grid from an offsite renewable plant, or generated onsite – for example, through solar panels installed on a factory roof. In both cases, the company is contractually tied to the output of a specific generating asset.

A virtual PPA, by contrast, is a financial contract for difference. The generator sells its power into the wholesale market, while the corporate buyer continues to procure electricity from its usual retailer. The two parties then settle the difference between a fixed contract price and the market price. This structure allows the buyer to claim the environmental attributes of the renewable project – effectively saying it runs on 100% green power – even though the physical electricity it consumes may come from the broader grid mix.

PPA prices

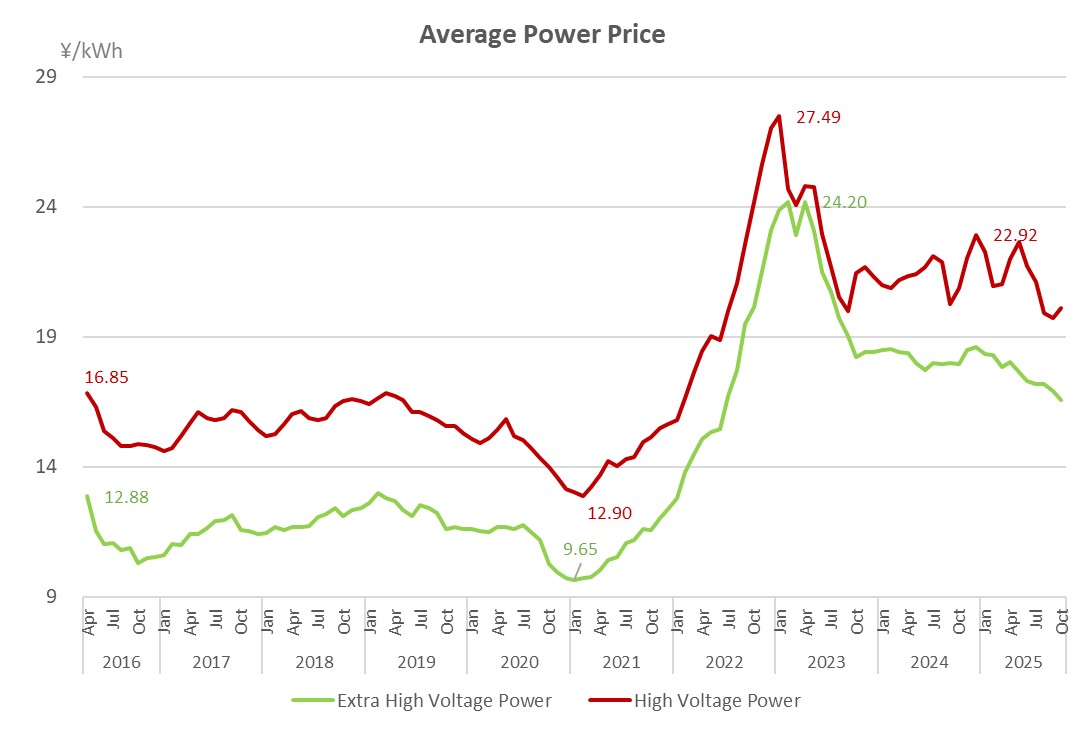

Japan NRG does not collect PPA prices since they are not publicly disclosed. For guidance on price levels, please see below the average price extra-high-voltage power (i.e., 20,000 volts in scale and contracts for 2 MW or more) and high-voltage power (i.e., 6,000 volts in scale and contracts of between 50 kW and 2 MW). Both are for industrial or corporate users.

Based on third-party sources cited by the Renewable Energy Institute (REI), corporate PPA pricing in Japan has stabilized at levels competitive with conventional grid power. For on-site solar PPAs, typical contract prices in 2025 are estimated at ¥12–15/ kWh (tax included), with smaller systems (below 50kW) sometimes closer to ¥20/ kWh. For off-site physical solar PPAs, the underlying generation cost is in the range of ¥13–16/ kWh (excluding tax).

After adding wheeling charges, retailer margins and the renewable surcharge, the delivered cost to large customers typically reaches about ¥22–25/ kWh for special highvoltage users and ¥26–29/ kWh for high-voltage users – levels now in line with post2022 grid electricity tariffs, especially given ongoing fossil fuel price volatility.

PPA market size

Japan NRG estimates that prior to 2023, there were no more than 100 PPA agreements signed in Japan. The first began to appear in Japan around late 2020. Today, the total number of publicly disclosed PPA deals stands close to 750, covering 2020 to 2025.

Our PPA tracker data set contains 192 deals for 2023; 226 for 2024; and 233 in 2025. The total capacity of PPA deals monitored by Japan NRG now covers 3.53 GW. Counting pre-2023 deals is unlikely to significantly change this number since the size of most of the early PPA contracts in Japan was below 1 MW.

Some market players suggest that the “real” amount of capacity tied to PPA deals in Japan is actually twice the above amounts, because most contracts are not disclosed. As there is no data to confirm this, we rely on public information for this analysis.

Overview: Market grows

The data used for the 2025 analysis was compiled by the end of January 2026. Disclosure levels of PPA deals in Japan vary widely. In 2025 alone, we identified 233 separate PPA deals. Many of these contracts covered multiple locations, including retail chains, restaurant networks, railway stations and group subsidiaries, together spanning more than 2,100 sites.

Also, over 130 deals were made in the second half of 2025, suggesting an acceleration. Large retail and service operators accounted for most multi-site contracts. Tokyu Group’s retail segment alone covered around 800 sites, while Tokyu Land (real estate) covered 80, Daiso Industry 120, Skylark Holdings nearly 400, and Koshidaka more than 100 locations. Railway operators including JR East, West, Kyushu and Hokkaido also signed PPAs covering extensive station and facility networks, though exact site counts were not always disclosed.

For database purposes, a single announcement – regardless of how many sites it covers – is counted as one deal in terms of generation capacity and CO2 reduction.

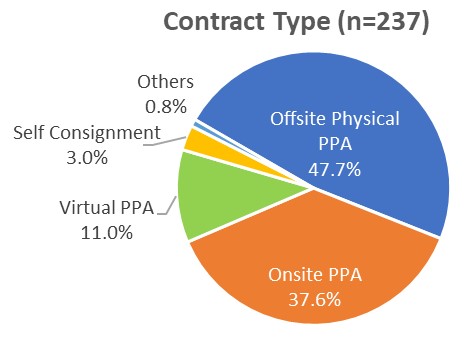

Contract types: shift to offsite PPAs

Of the 233 deals announced in 2025, contract types were distributed as follows:

| Contract Type | Number of Projects |

| Offsite Physical PPA | 113 |

| Onsite PPA | 89 |

| Virtual PPA | 26 |

| Self-consignment | 7 |

| Others (hybrid structures) | 2 |

| Total | 237* |

(*Total exceeds 233 due to two hybrid contracts spanning multiple structures. All percentage shares below are calculated against the 233 primary contracts.)

Offsite physical PPAs accounted for roughly 47.7% of projects in 2025, overtaking onsite PPAs (37.6%). Virtual PPAs represented 11%, while self-consignment remained marginal at just 3%.

This marks a clear shift from 2024, when onsite PPAs dominated at nearly 60% of contracts and offsite physical PPAs accounted for just over 30%. The 2025 reversal suggests that larger-scale, grid-delivered projects are gaining traction, likely reflecting both developer scale-up and growing corporate appetite for higher-capacity contracts.

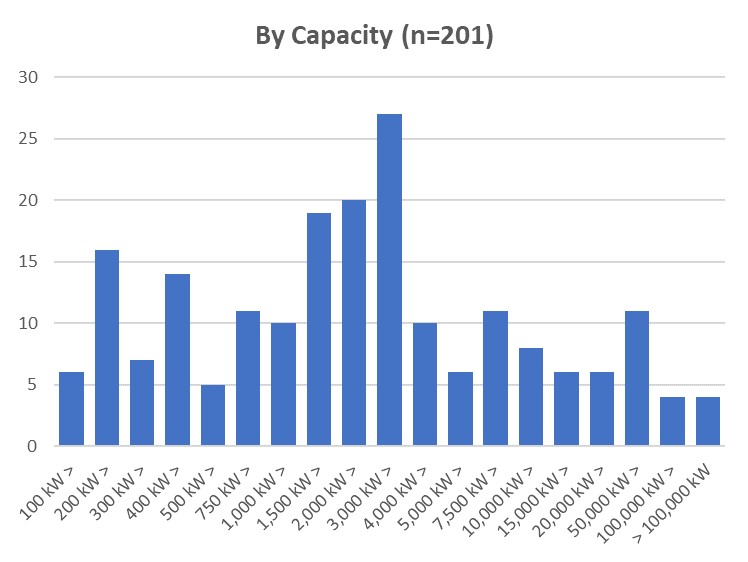

Capacity: median size doubles

Of the 233 projects announced in 2025, a total of 201 disclosed generation capacity. The median project size rose sharply to 1,846 kW – almost double 2023 levels.

| Year | Projects | Median Capacity |

| 2023 | 178 | 769 kW |

| 2024 | 184 | 1,013 kW |

| 2025 | 233 | 1,846 kW |

Total announced capacity in 2025 reached about 1.85 GW, a sharp increase from the 691 MW in deals disclosed in 2024.

The distribution remains broadly stable:

- Around one-third of projects are below 1 MW

- Nearly half fall between 1 MW and 10 MW

However, 2025 stands out for the emergence of very large-scale deals. Four projects exceeded 100 MW – none had done so in 2024. This suggests the market’s structural scaling-up, driven in part by major corporate offtakers and financing-backed utility-scale renewable projects.

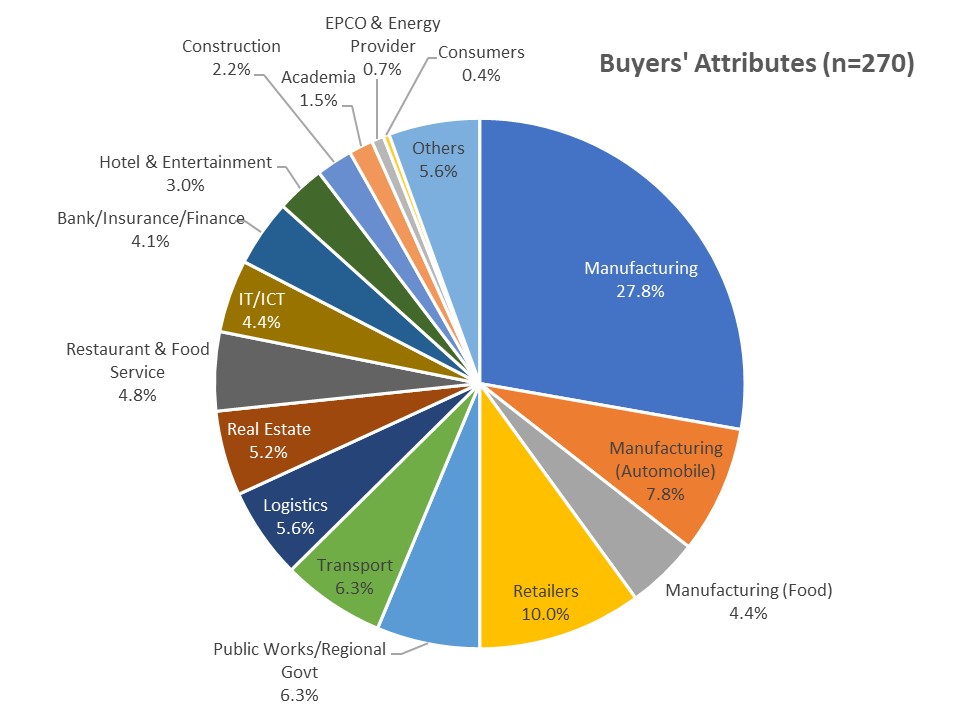

Buyers: manufacturers lead volume, retailers dominate scale

Across the 233 deals, 270 unique buyers were identified.

Manufacturing was the most active sector, accounting for 108 contracts. Within manufacturing:

- 21 were automotive companies

- 12 were food manufacturers

- The remainder spanned a broad industrial base

Retail, public/ regional authorities, and transport operators followed in deal count.

In capacity terms, however, large corporate buyers dominate:

- Aeon Group (retail) contracted about 200 MW of solar capacity.

- Sumitomo Mitsui Banking Corporation and Kyocera’s Kagoshima factory each secured around 197.5 MW from geothermal sources.

- 7-Eleven Japan contracted 140 MW of hydropower in Hiroshima and Yamaguchi prefectures.

The data show that while manufacturing signs the most contracts numerically, large retailers and financial institutions account for some of the largest single-capacity agreements.

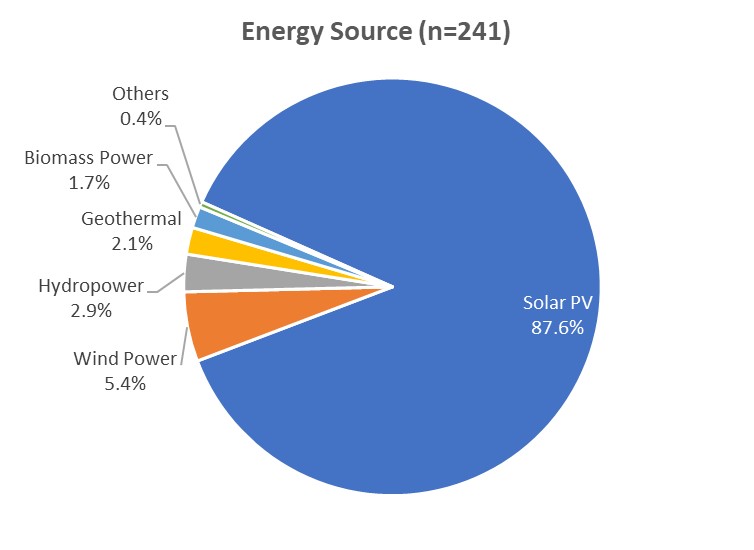

Energy sources: solar still dominant

Solar PV remained overwhelmingly dominant in 2025, accounting for 211 projects.

| Energy Source | Projects |

| Solar PV | 211 |

| Wind | 13 |

| Hydropower | 7 |

| Geothermal | 5 |

| Biomass | 4 |

| Others (hybrid) | 1 |

Solar represented roughly 88% of total contracts – consistent with cost competitiveness and ease of deployment.

However, 2025 showed increased diversification:

- Geothermal featured prominently in several high-capacity contracts.

- Biomass PPAs appeared for the first time since tracking began.

- Hybrid structures combining solar and wind also emerged.

This suggests early-stage diversification beyond utilityscale solar, particularly for larger corporate buyers seeking baseload / dispatchable attributes and balance.

Power providers: EPCOs gain

Japan NRG identified 338 unique power providers across the dataset.

Nearly half are renewable-focused developers or EPCO’s subsidiaries. However, participation from traditional energy suppliers increased significantly in 2025.

The share of utility-affiliated suppliers (e.g., Tokyo Gas, Osaka Gas, JERA, J-Power) rose from 14% in 2024 to 23% in 2025. This indicates that major energy incumbents are increasingly entering the corporate renewable supply space alongside independent developers.

Regional EPCOs maintained steady involvement:

- Kansai (11 projects)

- Tohoku (9)

- Chugoku (5)

- Hokuriku (5)

- Kyushu (5)

- Hokkaido (4)

- Shikoku (3)

- Okinawa (2 — first appearance)

Among renewable-focused suppliers, Chubu Electric Power Miraiz (16 projects) and TESS Group (15 projects) were particularly active, followed by Chugin Energy, NTT Anode Energy and others.

The growing presence of gas and utility majors suggests the corporate PPA market is transitioning from niche developer-led activity toward mainstream energy market integration.

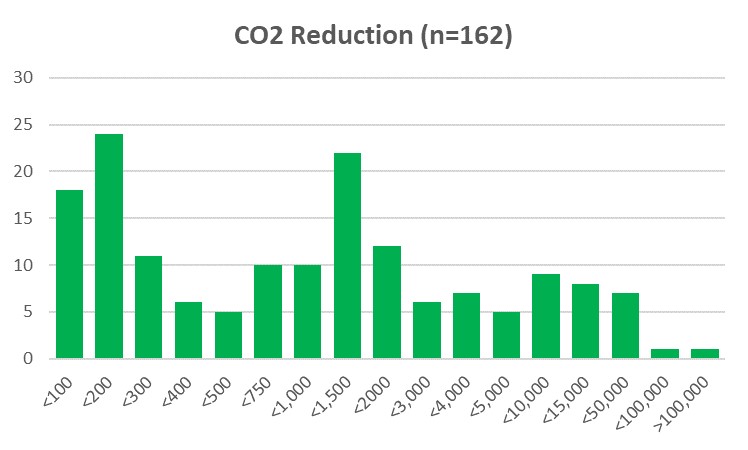

CO2 reduction: the law of large numbers

Of the 233 projects, 162 disclosed emission reduction forecasts. Together they indicate potential annual reductions of 673,717 tons of CO2.

- Average reduction per disclosed project: ~4,159 tons/year

- Median reduction: 930 tons/year

The large gap between mean and median reflects the influence of a small number of very large contracts.

The largest disclosed reduction came from JR East, which signed a virtual PPA with Daigas Energy’s biomass plant in Wakayama, targeting 150,000 tons of CO2 reduction annually.

The second largest came from Isuzu Motors, whose offsite physical PPA with Tokyo Gas (13 MW capacity) is expected to reduce 50,000 tons annually. This indicates that while many PPAs are modest in scale, a handful of very large industrial and transport-sector agreements drive a disproportionate share of emissions impact.

Conclusion

Japan’s corporate PPA market has reached meaningful scale, with over 3.5 GW of disclosed capacity now tied to long-term contracts. Yet internationally, it remains relatively small. Australia procured 3.4 GW in the first eight months of 2024 alone, largely driven by a single dominant buyer, Rio Tinto.

Japan shows a similar pattern of concentration. A limited number of heavyweight offtakers – railway operators, automakers, major retailers and financial institutions – account for a disproportionate share of contracted capacity. As elsewhere, scale depends less on the breadth of participation than on the willingness of large energy users to sign long-duration, high-capacity agreements.

The underlying economics are shifting in favour of such contracts. The phase-out of the FIT regime and transition to FIP has pushed developers toward market-based revenue streams, making corporate PPAs central to financing new green power. Meanwhile, persistently elevated fuel costs and the start of carbon pricing from FY2026 have narrowed the cost differential between grid power and fixed-price renewable supply.

Today, PPAs are instruments of price stability and project bankability.

The next stage of the market will likely be defined by diversification and system integration. Solar still dominates deal count, but utility-scale rollout is facing mounting regulatory and grid constraints. As buyers seek larger, more stable supply blocks, wind, geothermal and hydropower are poised to play a bigger role, and we will likely see generation + storage options also on the table. Even conventional generators may look to structured long-term contracts as heavy industry demands certainty at scale.

Japan’s PPA market remains smaller than the major European, U.S. or Australian markets, which have seen cumulative tens of gigawatts of corporate renewable contracts. Yet with a large base of green capacity not yet tied to long-term offtakes, Japan has the foundations for a steep growth trajectory.

ASIA ENERGY REVIEW

BY JOHN VAROLI

A brief overview of the region’s main energy events from the past week

Australia / Solar

Lightsource bp sold a portfolio of Australian solar assets to Aula Energy. The deal includes five operational solar PV projects with a combined capacity of 1.03 GW. The projects are located across New South Wales, Queensland and Victoria.

China / Emissions

China’s CO2 emissions have been flat or declined for 21 consecutive months, even as electricity demand grows. Carbon Brief said annual emissions dropped 0.3%. China accounts for roughly one-third of global CO2 emissions, more than any other country.

China / Renewables

China plans to build 10 renewable energy projects in Kazakhstan; total capacity 246 MW, and led by the construction of wind farms equipped with energy storage systems.

Fossil fuels

Oil, gas and coal are projected to account for 41% to 55% of global energy consumption by 2050, reports McKinsey. All of its three scenarios point to long-term warming between 1.9°C and 2.7°C by 2100, insufficient to keep global warming within 1.5°C.

India / Energy transition

The IEEFA and Ember found that 21 states, which account for 95% of India’s power demand, are making the energy transition. Karnataka and Kerala lead decarbonization, with a higher renewable energy share in procurement and lower power sector emissions.

India / Natural gas

India’s ambassador to Canada said his country wants to buy any energy product it can from Canada, especially natural gas. He urged Ottawa to streamline approvals for energy export projects so that India can tap into new supplies.

Indonesia / Thermal power

RATCH Group said its subsidiary RH International sold 5% each in PT Paiton Energy and Minejesa Capital, and also sold 24.5% in IPM Asia for $85 million. This reduces the group’s investment proportion in the Paiton Energy thermal power plant business in Indonesia.

Malaysia / Renewables

Malaysia’s installed renewable energy capacity reached 32%, surpassing the 31% target set for 2025, according to Maybank Investment Bank Berhad.

Thailand / Natural gas

The Thai govt suspended 4 GW of gas-fired power capacity and has delayed a new plant from coming online, a major shift in its energy strategy amid electricity oversupply and tougher climate commitments. Thailand has pledged 47% emissions cuts by 2035.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Hulic Ochanomizu Bldg. 3F, 2-3-11, Surugadai, Kanda, Chiyoda-ku, Tokyo, Japan, 1010062.