WEEKLY

March 16, 2026

ANALYSIS

BEHIND THE RESTARTS: WHAT ARE THE COSTS OF THE NUCLEAR ENERGY PIVOT?

- The government wants to maximize nuclear power. Achieving that will require significant state support, and the PM is happy to oblige.

- Yet the road to a nuclear revival may not be smooth. Last month, Chubu Electric admitted to falsification of seismic data at its Hamaoka NPP.

- The scale of the reputational damage is uncertain.

SMALL PARAMETER WITH BIG CONSEQUENCES: JAPAN REVISITS NET CONE

- A technical review at METI could tilt the direction of Japan’s power sector for the next decade.

- At issue is a measure that helps determine the price at which new power capacity should be procured to ensure a stable electricity supply.

- But in addition to encouraging new investments, its increase may have unintended consequences.

ASIA PACIFIC REVIEW

This column provides a brief overview of the region’s main energy events from the past week

NEWS

- Govt lists 61 priority technologies in growth strategy

- Labor shortages push up corporate bankruptcies with construction sector failures on the rise

- Tally Group buys energy consultancy Skipping Stone

- EEX power futures trading surges amid Iran war

- ANRE discusses revisions for the 4th LTDA round

- TEPCO curtails renewables for second Sunday in a row, but grid operator’s strategy changed

- Kansai companies to study hydrogen supply chain

- OCCTO solar auction has Manako Solar and X-Elio as the big winners

- ANRE discusses major trends and risks of BESS market

- JERA studies integrating batteries with thermal plants to reduce shutdowns

WIND POWER AND OTHER RENEWABLES

- Vestas inks deal with METI on turbine manufacturing in Japan

- Eurus begins repowering work at Aomori wind farm

- Digital Grid begins wind power aggregation using AI

- TEPCO disconnects Kashiwazaki-Kariwa generator for inspection after fault alarm

- Sumitomo invests in U.S. fusion tech company

- Japan to release record 80m barrels from oil reserves

- ANRE: inventory levels for power and gas utilities consistent with 5-yr averages

- Wholesale gasoline prices raised significantly

- Iran war could reshape Japan’s LNG procurement strategy, IEEJ says

- JERA to sell stakes in Australian LNG projects

CARBON CAPTURE & SYNTHETIC FUELS

- Malaysia hosts CCS events, touts cooperation with Japan

- Toho Gas starts product-scale demo of CO2 separation and capture

EVENTS

Mar 17-19 Smart Energy Week Spring 2026 / H2& FC EXPO / PV EXPO / Battery Japan / Smart Grid EXPO / Wind Expo / Biomass Expo / Zero-E Thermal Expo /Decarbonization EXPO 2026 @ Tokyo Big Sight

March 31 End of Japan’s Fiscal Year 2025

Mid-April FIT/FIP Solar Auction #28

Japan Atomic Industrial Forum

(JAIF) Annual conference @ Tokyo

May 3-6 Golden Week (many companies will close from April 29 to May 6)

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Chief Editor)

John Varoli (Senior Editor, Americas)

Kyoko Fukuda (Data, Events)

Magdalena Osumi (Renewables & Storage)

Filippo Pedretti (Thermal, CCS, Nuclear)

Tetsuji Tomita (Power Market, Hydrogen)

Aglaé Bange (Renewables and Biomass)

George Hoffman (Sales, Business Development)

Tim Young (Design)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

NEWS: GENERAL OUTLOOK AND TRENDS

Govt lists 61 priority technologies in new growth strategy; includes energy

(Asahi Shimbun, March 10)

- The govt identified 61 priority products and technologies across 17 sectors as part of PM Takaichi’s growth strategy focusing on “crisis management investment” and industrial competitiveness.

- The list includes fields such as AI, semiconductors, aerospace, cybersecurity, quantum technology and energy security, though the govt has not yet specified the scale of investment or expected economic impact.

- Among the headline targets, the govt aims to expand domestic semiconductor production to ¥40 trillion by 2040, up from about ¥5 trillion in 2020, extending and significantly raising previous targets.

- Several energy-related technologies are included, notably PSCs, hydrogen, green steel, next-gen geothermal, offshore wind, advanced nuclear reactors and fusion.

- The roadmap sets a goal to capture more than 30% of the global AI robotics market by 2040, positioning itself as a third pole alongside the U.S. and China.

- CONTEXT: The initiative reflects the Takaichi admin’s effort to align industrial policy with economic security priorities, strengthening domestic production capabilities in strategic sectors while promoting long-term economic growth

- TAKEAWAY: Many have wondered what Takaichi’s stance on renewables is. This strategy includes both solar (via PSC) and wind generation, as well as geothermal. In that sense, the current government policy is not shifting away from green electrons. Hydrogen also remains very much in the foreground.

Corporate bankruptcies exceed 800 in Feb as construction failures rise

(Company research, March 9)

- Corporate bankruptcies totaled 851 cases in February, up 11.3% YoY, the first time in 13 years that February failures exceeded 800, according to Tokyo Shoko Research. Total liabilities amounted to ¥133.16 billion, down 22.2% YoY.

- Failures have risen for three consecutive months, reflecting pressure on small businesses as pandemic-era financial support ends and firms begin repaying state-backed loans.

- Labor shortages were an increasingly prominent cause of bankruptcies, with 47 cases linked to staffing shortages, more than double the level a year earlier.

- By sector, service businesses recorded the largest number of bankruptcies at 309 cases, up 31% YoY, while construction failures rose to 169 cases, up 17.3%.

- Among the largest failures was Yonago Biomass Power, a biomass power operator in Tottori Pref, with liabilities of about ¥4.97 billion.

Tally Group acquires energy consultancy Skipping Stone

(Company statement, March 9)

- Australia-based software provider Tally Group acquired Skipping Stone, an energy strategy and consulting firm. Financial terms were not disclosed.

- Skipping Stone will continue under its own brand. The companies aim to combine advisory services with Tally’s energy market software and billing platforms.

- Tally said the acquisition will expand its presence in global energy markets, particularly in North America and Japan, where electricity retail markets have been liberalized and digital platforms for billing and customer management are expanding.

- CONTEXT: Tally entered the Japanese market in 2025, deploying a cloud-based billing system for a large electricity retailer.

- TAKEAWAY: The deal reflects demand from utilities for integrated technology platforms and advisory services as energy markets become more complex due to deregulation, renewables and BESS integration, and new retail products. The interest of investment funds in renewables platforms and data centers has expanded the number of larger clients in the consulting sector.

NEWS: ELECTRICITY MARKETS

EEX power futures trading surges amid Iran war fallout

(Exchange statement, March 9)

- EEX Japan power futures trading surged, as energy markets reacted to the Iran war.

- Total traded volume in the week ending March 6 reached 17.9 TWh, up more than sixfold from the previous week; the number of trades rose sharply to 11,688 lots.

- The spike follows a record trading day on March 3, when market participants rushed to hedge exposure to rising fuel costs and potential LNG supply disruptions.

- Trading was distributed evenly between regions. Kansai-area futures volumes were comparable to Tokyo-area contracts on March 3, diverging from the typical pattern in which Tokyo-area (TEPCO) futures dominate trading.

- Forward power prices also moved sharply higher across the curve. The 2026 summer baseload contract rose more than 50% to about ¥18.5/ kWh, while peakload prices climbed to around ¥21.7/ kWh, reflecting expectations of higher generation costs.

- TAKEAWAY: The unusual strength in Kansai-area contracts indicates traders are also focusing on regional exposure to LNG supply disruptions. Kansai Electric relies on the Persian Gulf for one-sixth of its LNG supply, making the entire Kansai region particularly sensitive to any closure of the Strait of Hormuz.

- SIDE DEVELOPMENT:

- TOCOM power futures ramped up in February

- (Exchange statement, March 9)

- Trading in power futures on the TOCOM rose sharply in February, with total volume reaching 4,043 contracts, nearly three times the 1,419 contracts traded in January.

- The number of concluded trades increased to 111 deals, up from 39 in the previous month. Large negotiated trades accounted for a significant portion of activity. Tokyo-area baseload futures was the most popular traded contract.

- Final settlement prices for February-delivery contracts were ¥11.17/ kWh for Tokyo baseload and ¥10.11 for Kansai.

- Separately, Hokuriku Bank obtained approval for exchange trading and clearing for energy derivatives on TOCOM, allowing the bank to handle customer orders and settlement for power futures transactions.

LNG a big winner as ANRE discusses revisions for the 4th LTDA round

(Government statement, March 4)

- ANRE discussed revisions to the Long-Term Decarbonized Power Sources Auction (LTDA) ahead of its 4th round (FY2026), focusing on LNG capacity procurement, battery supply-chain risks, and project screening for hydrogen and ammonia.

- The government signalled that LNG-only thermal capacity auctions will continue beyond FY2026. Under earlier rounds, the procurement target for LNG-only plants was 6 GW in the first round and about 4 GW combined for the second and third rounds. ANRE said further auctions may be needed to maintain supply adequacy as electricity demand grows and older thermal plants retire.

- Government modelling suggests that in a scenario where electricity demand reaches about 1,100 TWh by 2040, Japan could still face a supply shortfall of roughly 13 GW even if all ageing thermal capacity is replaced.

- Battery procurement rules may also change. While the third auction round introduced a cap limiting battery cell manufacturing from any single country or region (outside of Japan) to less than 30% of total awarded capacity, ANRE now argues that geographic diversification alone does not mitigate supply-chain risk because top battery makers operate factories across multiple countries.

- Instead, the government is considering prioritizing projects that use lithium-ion cells produced by manufacturers certified under the Economic Security Promotion Act, which requires approved plans to ensure stable battery supply. If adopted, the existing 30% manufacturing-location cap would no longer apply to lithium-ion batteries.

- For hydrogen and ammonia projects, the govt is mulling introducing pre-screening of fuel supply chains to ensure only projects with credible fuel procurement plans enter the auction. The screening criteria may align with those used in the CfD hydrogen support framework.

- The LTDA guidelines may also be revised following recommendations from the market regulator, EGC. Proposed changes include limited flexibility in market-price rules for bilateral contracts, adjustments to non-discrimination rules, improved monitoring of variable costs, and clearer procedures for monitoring outcomes and appeals.

- CONTEXT: Bidding for the third LTDA round (FY2025) concluded in January and the EGC is currently reviewing bid prices. Results are expected in April, while preparations for the FY2026 auction are under way.

- TAKEAWAY: The LTDA launched in FY2023 to procure “decarbonized” capacity, positioning it as a mechanism separate from the main capacity market, which is open to all technologies. Since then, however, the scheme has evolved into a broader energy security and industrial policy tool. It increasingly serves as a vehicle for METI to address structural concerns in specific sectors that are difficult to tackle through existing market mechanisms. Officials now appear increasingly concerned about maintaining dispatchable capacity as electricity demand rises and ageing thermal plants retire. As a result, what was initially framed as temporary support to encourage construction of new gas-fired plants is entering its fourth year with no clear end date. Meanwhile, tighter screening of battery supply chains and hydrogen fuel procurement suggests that future LTDA rounds will place greater emphasis on supply-chain resilience and project feasibility alongside emissions reduction. More detailed discussions are likely to begin after the Round 3 results are announced.

Spot power prices fell across all regions in February

(Exchange data, March 9)

- JEPX spot prices declined in all nine regional markets in February, as unusually warm weather weakened electricity demand while power supply remained ample.

- Temperatures were well above seasonal norms, with northern Japan recording its warmest February since records began in 1946, reducing heating demand.

- Strong solar output also weighed on prices. Sunny conditions and limited rainfall helped increase renewable generation, adding to downward market pressure.

- The softer demand environment led to heavy selling in the spot market, with daily trading reaching record levels.

- In some regions, prices fell close to zero. Shikoku and Kyushu recorded prices as low as ¥0.01/ kWh even on weekdays, reflecting oversupply conditions in local systems.

- CONTEXT: The weak spot market contrasted with mixed movements in fuel prices. Oil and coal prices rose slightly, while LNG prices declined during the month.

- TAKEAWAY: Events in the Middle East have distorted domestic market signals, at least in futures trading, but February’s spot market illustrates well how weather-driven demand swings and growing solar output are increasingly shaping power prices. With renewable capacity continuing to expand steadily, periods of near-zero prices during mild weather conditions are more frequent. The TEPCO area recorded its first two cases of curtailment earlier in March.

OCCTO discusses updates to long-term electricity supply-demand scenarios

(Agency statement, March 10)

- OCCTO discussed how long-term electricity supply-demand scenarios should be utilized and updated.

- The survey on how stakeholders use scenarios for 2040 and 2050 showed that these are guiding long-term planning for generation, grids, and policy; but stakeholders want clearer assumptions, regular updates, and more regional detail.

- Starting January, monitoring is tracking key indicators, electricity demand, renewables, capacity, and storage adoption, to compare actual developments with scenario assumptions, and revise scenarios if needed.

- CONTEXT: Starting the latter half of FY2025 through FY2026, OCCTO will allocate the components defined in the nationwide scenarios in July 2025 by area, taking interconnections into account, and develop area-specific scenarios.

- TAKEAWAY: The OCCTO Study Group on Future Electricity Supply-Demand Scenarios analyzes Japan’s longterm electricity supply and demand for 2040-2050 under multiple scenarios. It provides reference data for investment, policy, and decarbonization planning. The first report in July 2025 had scenario-based demand forecasts, supply capacity, and system considerations. The focus is on uncertainty and long-term guidance, not regulatory decisions. OCCTO is preparing regional electricity supply-demand scenarios that capture local differences in demand, renewable potential, and grid capacity. These area-specific scenarios offer policymakers and grid operators detailed insights to help plan infrastructure, ensure sufficient resources, expand transmission, integrate renewables, and design regional decarbonization strategies.

TEPCO Grid curtails renewables for second Sunday in a row

(Company data, Japan NRG, March 8)

- TEPCO Power Grid implemented a second renewables curtailment on March 8, a week after its firstever intervention in the Tokyo-focused region.

- Curtailment totaled about 4.18 GWh, almost double the 2.28 GWh curtailed on March 1. The maximum curtailed output reached 1.08 GW, lower than the 1.84 GW peak recorded on March 1, but the restriction lasted longer.

- Solar accounted for the vast majority of curtailed generation, with wind contributing a smaller share (~228 MWh).

- CONTEXT: The TEPCO region has over 21 GW of installed renewable capacity, mostly solar. Rapid growth of rooftop and utility-scale PV has begun to create occasional oversupply conditions during mild weather and low weekend demand.

- TAKEAWAY: The March 8 event confirms our thesis from last week that curtailment in the TEPCO system is likely to become a regular occurrence. Compared with the first curtailment on March 1, the grid operator limited output for a longer period rather than imposing a sharper peak cut. This indicates a shift to a preventative approach rather than reactive curtailment, mostly so as to minimize grid stress. As daylight hours lengthen, the Tokyo grid needs much more flexibility, especially via battery storage creating business opportunities for BESS. We estimate that curtailments will be most evident when solar’s share of the electricity mix approaches 50%. Ironically, the restart of the Kashiwazaki Kariwa NPP may accelerate curtailment frequency.

Tohoku grid to introduce uniform partial curtailment of renewables

(Company statement, March 6)

- Tohoku Electric Power Network will introduce uniform partial curtailment of renewable generation starting April as renewable capacity expands in the Tohoku–Niigata grid area.

- The measure will apply mainly to solar and wind projects under unlimited curtailment rules (nonfirm contracts) or outside the FIT scheme, with output reduced proportionally across eligible facilities rather than stopping plants sequentially.

- The change follows projections that annual curtailment days for older FIT solar and wind projects could exceed the 30-day compensation threshold in FY2026 due to rising renewable capacity connected to the grid.

- Projects operating under earlier FIT rules will continue to be curtailed on a rotational basis to keep annual curtailment within the 30-day limit, while wind projects under newer rules will remain capped at 720 hours of curtailment per year.

Two power plants selected in FY2025 reserve power source procurement

(Agency statement, March 10)

- OCCTO announced the results of the FY2025 reserve power procurement auction for delivery in FY2026 and FY2027.

- The auction was divided between the eastern (50 Hz) and western (60 Hz) grid areas, with 1 GW procured in each. No bids were submitted in the eastern area, while two bids were received in the western area and both were awarded contracts.

- Awarded projects were:

- JERA’s Chita No.2 Unit 2: LNG-fired (June 2027 to May 2028);

- Kansai Electric’s Gobo Unit 3: Oil-fired (March 2028 to Feb 2031);

- The total awarded value was not disclosed because fewer than three bidders were selected.

- CONTEXT: The reserve power procurement scheme maintains mothballed or suspended power plants that can be reactivated during supply emergencies. Introduced after the March 2022 power supply crisis, it is designed to address risks not covered by the capacity market and to supplement supply when procured capacity falls short of requirements. Plants contracted under the scheme remain idle but available until activation.

- TAKEAWAY: The first auction in FY2024 received no bids, largely because the price cap was considered too low (¥6,429/kW) and technical requirements too strict for plant operators. In response, OCCTO revised the rules by raising the price cap (to ¥14,399/kW) and introducing categories based on start-up time, allowing a wider range of plants – including those requiring refurbishment – to participate. The revised price cap is now linked to the capacity market benchmark price, replacing the earlier methodology based on the average clearing price. The fact that two power plants were awarded in the western area for the first time suggests that the rule changes were partly effective. However, the absence of bids in the eastern area indicates that the scheme may still need further adjustments.

NEWS: HYDROGEN

Kansai companies to study hydrogen supply chain

(Company statement, March 11)

- Kansai Electric, West Japan Railway (JR West), NTT and others agreed to a study and demo project to build a hydrogen supply chain in the Kansai region.

- The project brings together 12 companies – including Panasonic, KHI, Kobe Steel and Nippon Express – to explore large-scale hydrogen transport and infrastructure development.

- The concept includes using existing infrastructure, such as JR West railway corridors and NTT underground telecom conduits, to transport hydrogen across the region.

- On the supply side, Kansai Electric is studying hydrogen procurement from Australia, while Kobe Steel may develop facilities to receive liquefied hydrogen containers, with demand expected from Panasonic fuel cells and KHI industrial users.

- TAKEAWAY: The project reflects growing efforts by Japanese companies to build credible regional hydrogen supply chains ahead of government support schemes. In particular, developers are increasingly focusing on demonstrating integrated supply, transport and demand arrangements, which could become important as the government considers introducing stricter feasibility screening for hydrogen projects in the 4th round of the LTDA. Projects with clearer supply chains may have an advantage in future subsidy competitions.

NEWS: SOLAR AND BATTERIES

OCCTO solar auction concludes, Manako Solar and X-Elio big winners

(Organization statement, March 6)

- OCCTO’s FY2025 4th round tender – for FIP solar projects of at least 250 kW – ended with just 11 among 23 bids securing capacity.

- Winning prices hovered between ¥0.00/ kWh to ¥6.49/ kWh; weighted average price was ¥4.61/ kWh.

- The top winner for a single asset was Manako Solar, with 29.9 MW awarded. X-Elio was awarded a similar capacity of 30 MW, split between two assets.

- Total capacity submitted for bidding amounted to 162 MW, capped at 79 MW with a ceiling at ¥8.69/ kWh.

| Company name | Bidding price (¥/ kWh) | Capacity (kW) |

| Hinomoto Power Generation | 0.00 | 400 |

| Eurus Energy HD | 3.90 | 400 |

| Enelution | 3.98 | 445.5 |

| Nemuro Nishihama Solar | 4.46 | 16,000 |

| Manako Solar | 4.46 | 29,900 |

| X-Elio 23 | 4.67 | 19,999 |

| X-Elio 25 | 5.12 | 9,999 |

| Enelution | 5.98 | 495 |

| Daiichi Solar Power Generation | 6.48 | 400 |

| Daiwa House Industry | 6.49 | 888.8 |

| Daiwa House Industry | 6.49 | 72.7 |

ANRE discusses major trends and risks of BESS market

(Organization statement, March 5)

- ANRE discussed future trends in demand-side battery energy storage systems (BESS) for residential, commercial and industrial use, as well as risks affecting the broader battery industry and measures to ensure long-term business sustainability.

- The main concerns identified include: o supply-chain risks for battery components and raw materials;

- business sustainability for grid-scale BESS, given the roughly 24 GW of grid connection applications so far;

- battery recycling and lifecycle management; o geopolitical and cybersecurity issues.

- ANRE also noted that about 24 GW of grid-scale BESS projects have applied for grid connection so far, raising questions about project viability and market sustainability.

- To address supply-chain risks, the govt introduced additional requirements for battery projects participating in the 3rd LTDA:

- obtaining a 1-star certification under the JC-STAR security framework;

- a cap limiting lithium-ion battery cells manufactured abroad in a single country or region to less than 30% of total awarded capacity;

- limiting li-ion battery projects to systems with at least 6 hours of duration.

- ANRE also highlighted broader efforts to strengthen Japan’s battery ecosystem, including securing upstream mineral supplies such as lithium, graphite, nickel and cobalt, improving domestic battery manufacturing competitiveness, and expanding recycling and reuse frameworks.

- ANRE estimates that demand-side BESS capacity, currently about 4 GW, could reach up to 33 GW by 2040, while DR resources could expand to around 15 GW.

- CONTEXT: According to Japan NRG’s database, more than 1 GW of stationary BESS is currently operational, with an additional 3 GW expected to come online by 2030 based on current announcements. Total installed capacity is forecast to reach 6–7 GW by 2030.

- TAKEAWAY: The discussion highlights how Japan’s battery policy is expanding beyond grid storage deployment to encompass supply-chain security, industrial competitiveness and lifecycle management. While large volumes of BESS projects are seeking connection, the government appears increasingly focused on ensuring that the battery ecosystem, from upstream minerals to recycling, remains resilient and economically viable. This broader approach mirrors similar changes in other METI policies, such as with the LTDA, where supply-chain resilience and project feasibility are becoming increasingly important alongside decarbonization goals.

ENEOS Power to become aggregator of EHV BESS

(Company statement, March 10)

- ENEOS Power agreed with Mirai Tokyo Energy Storage to act as the aggregator for its extra high voltage BESS station in Yokohama.

- The station (capacity 12 MW) is scheduled to start operations in 2029 with electricity to be traded in the wholesale, supply–demand adjustment, and capacity markets.

- CONTEXT: ENEOS Power became an aggregator in July 2025; with experience in electricity trading via its large-scale BESS project in Muroran, Hokkaido.

- TAKEAWAY: Large developers are increasingly seeking to integrate the entire BESS value chain to capture greater revenues and reduce costs associated with relying on an external aggregator. In addition, as shown by ENEOS Power, conducting trading activities internally allows them to gain experience that can later be leveraged to provide external aggregation services to developers which do not integrate, thereby gaining a competitive advantage.

JERA studies integrating batteries with thermal plants to reduce shutdowns

(Denki Shimbun, March 9)

- JERA is considering large-scale battery installations at thermal plants to allow units to continue operating at minimum load instead of shutting down during periods of low electricity demand.

- This allows surplus electricity to be stored in batteries, helping balance fluctuations in renewable generation, and reducing repeated start and stop of thermal units.

- The number of start-stop cycles at JERA’s domestic gas-fired plants has risen sharply, reaching about 12,500 in FY2024. That’s around 2.5 times the level a decade earlier, reflecting growing renewable variability.

- The company plans to begin simulations of combined gas-thermal and battery operation and evaluate potential installation sites and scale, although the timing of deployment remains undecided.

Power Pool invests ¥4.5 billion to develop BESS assets

(Company statement, March 6)

- Taoke Energy’s subsidiary, Power Pool, created Japan Power Storage to invest ¥4.5 billion to develop six of its own BESS stations. The fund uses a GK-TK scheme.

- CONTEXT: A GK-TK scheme aims to secure real estate (private placement funds) in which a LLC is used as a SPC, with funds raised from investors using an anonymous partnership agreement. This scheme is often used in BESS assets.

- Compass Capital manages the assets, while Power Pool provides aggregation services. Taoke Energy owns 20% of the fund and provides O&M services.

- CONTEXT: Taoke Energy is a growing player in the BESS market, totaling 60 HV projects (2 MW / 8 MWh) in its pipeline, of which 21 are planned for interconnection from FY2026 onward.

PowerX raises ¥1.1 billion to develop electric carriers for batteries

(Nikkei, February 27)

- PowerX’s subsidiary Ocean Power Grid raised ¥1.1 billion to develop electric carriers designed to supply batteries for BESS and datacenter projects on remote islands.

- Ocean Power Grid aims to launch the carrier in 2028, with an initial test planned at Yakushima (Kagoshima Pref).

- CONTEXT: The funding was provided by NYK Line, PowerX, Kraftia, CEPCO-R (affiliated to Chubu Electric), Tatsumi Shokai, Development Bank of Japan, and Mizuho Financial Group.

- TAKEAWAY: Remote islands in Japan most often rely on local diesel generators for electricity supply when not connected to the mainland grid via subsea transmission cables. While renewable energy projects are being deployed, including on Yakushima, where almost 100% of electricity is generated by hydropower, many islands still lag in terms of decarbonization. Thus, BESS projects are expected to expand. The Oki Islands are using Sumitomo Electric’s vanadium redox flow batteries.

XSOL to launch low-reflection PV

(Company statement, March 5)

- XSOL will launch new VOLTURBO PV models with these features:

- A 90% anti-reflection rate;

- Conversion efficiency of up to 23%;

- High-voltage modules, enables installation even on small or odd shaped roofs;

- The models received the 2025 Good Design Award.

- CONTEXT: TOPCon (Tunnel Oxide Passivated Contact) is an N-type solar cell technology using a thin tunnel oxide layer to reduce charge loss, achieving higher conversion efficiency than conventional P-type PERC cells. The technology can perform well even under low-light or high-temperature conditions and offers long-term output warranties of up to 30 years.

- TAKEAWAY: Low-reflection PV modules are important to improve solar energy’s social acceptance. Complaints over glare from PV panels, both in residential areas and at large-scale solar projects, are growing. In Fukushima Pref, glare from PVs at the 60 MW Sendatsuyama project ignited criticism for creating road hazards and degrading the landscape.

Toshiba to launch new performance monitoring tool for solar installations

(Company statement, March 11)

- In April, Toshiba will launch a new monitoring tool for renewable power generation.

- The product, designed for O&M providers, offers performance ratio analysis for PCS (Power Conditioning Systems) and operating rate management functions for solar power plants. It enables users to reduce O&M workloads, access real-time electricity generation data, detect equipment damage, and generate maintenance schedules.

- Toshiba will expand use of these tools to BESS, hybrid solar-plus-storage plants, and wind power projects.

Marubeni, Power X and Nishimu Electronics to add cybersecurity package for BESS

(Company statement, March 3)

- Nishimu Electronics Industries, Marubeni Power Retail, and PowerX agreed to roll out a package that adds cybersecurity configuration.

- The package will be applied to the Mega Power 2500 battery made by PowerX.

- CONTEXT: The Mega Power 500 battery was certified under the JC-STAR cybersecurity system at Level 1 (self-declaration of cybersecurity measures for IoT devices). This model was supplied to Marubeni’s Mibugawa Ina BESS station, in Nagano Pref, in 2024.

- The companies also propose a scheme to recycle used solar PVs and BESS.

SankyoTateyama, Aisin and Yamashita test window-type PSCs

(Company statement, March 10)

- SankyoTateyama, Aisin, and Yamashita Sekkei are doing R&D and demos on PSCs designed for installation on windows, aiming to combine aesthetics with efficiency.

- These PSCs can be installed in residential or commercial buildings, and are designed to reduce heat exposure through windows while blending with the architecture.

NEWS: WIND POWER AND OTHER RENEWABLES

Vestas inks deal with METI on potential turbine manufacturing in Japan

(Company statement, March 9)

- Danish manufacturer Vestas agreed with METI to explore domestic manufacturing of wind turbine components, for final assembly of turbine nacelles in Japan by FY2029, contingent on securing sufficient orders from offshore wind projects.

- They also agreed to develop a roadmap for full nacelle assembly in Japan by FY2039, subject to continued offshore wind market growth and clearer long-term visibility for project auctions.

- Vestas also agreed with Nippon Express and DENZAI to strengthen logistics and heavy-lift engineering capabilities for wind turbine construction and maintenance.

- CONTEXT: Japan imports nearly all wind turbines used in offshore projects, but the govt wants at least 60% of the supply chain to be local. Vestas claims to have installed more than 1.8 GW of wind capacity in Japan and has 685 MW under construction.

- TAKEAWAY: METI is pursuing such deals with major turbine manufacturers, but global players have been hesitant to commit due to unclear project pipelines and a dearth of confirmed turbine orders. This latest accord has more detailed plans, which are contingent on industry and auction progress. Wind turbine makers typically localize nacelle assembly first because it is the most valuable and logistically efficient part of the turbine to produce domestically. The nacelle holds the generator, gearbox, power electronics and control systems, which comprises a large share of the turbine’s value. Still, it is relatively compact unlike bulky and difficult to transport blades. Establishing nacelle assembly allows manufacturers to integrate imported components with locally sourced parts, such as steel structures, bearings, and so on.

- SIDE DEVELOPMENT:

- Nippon Express signs wind logistics cooperation deal with Vestas

- (Company statement, March 11)

- Nippon Express inked an MoU with Vestas to cooperate on logistics for wind power projects in Japan.

- The partnership will focus on transport, port handling, storage and delivery of wind turbine components, as well as logistics support for O&M after projects enter service.

- CONTEXT: Handling wind turbine equipment requires specialized logistics due to the large size and weight of components such as blades and towers, requiring coordinated transport routes and port operations.

Eurus begins repowering work at Aomori wind farm

(Company statement, March 10)

- Eurus Energy started repowering construction at the 50 MW Eurus Noheji Wind Farm in Aomori Pref, replacing turbines installed in 2008.

- The project will remove 25 turbines (2 MW each) and install 12 larger Siemens turbines (4.3 MW each), maintaining a grid connection capacity of about 50 MW.

- Commercial operation of the new wind farm is scheduled for April 2029.

Cosmo publishes environmental assessment for wind farm in Aomori

(Company statement, February 27)

- Cosmo Energy published the environmental impact assessment for its Yokohamacho Wind Farm project (Aomori Pref). It’s open for public view until March 26, 2026.

- The 60 MW onshore wind farm will have up to 13 turbines, each 4.3 MW to 5.5 MW.

- The project covers 569 hectares, with about 24.6 hectares for land modification.

- Construction begins this month, with trial operations expected in December 2029 and commercial operations targeted for March 2030.

- SIDE DEVELOPMENT:

- Yokogawa wins control system and battery order for wind project

- (Company statement, March 5)

- Yokogawa Electric won an order to supply a power plant controller and battery system for Cosmo Eco Power’s Shimamaki–Kuromatsunai wind farm in Hokkaido.

- The 95 MW project is scheduled to begin operations in 2029.

- Yokogawa will deploy a power plant controller developed by its subsidiary BaxEnergy.

- TAKEAWAY: Wind projects in Hokkaido face some of Japan’s strictest grid connection requirements as they must help maintain grid frequency stability.

Digital Grid begins wind power aggregation using AI forecasting

(Company statement, March 9)

- Digital Grid began providing aggregation services for wind power generation, adding to its similar service in the solar power segment.

- The firm developed an AI-based system that predicts wind generation using real-time weather data, enabling automated balancing of electricity supply and demand.

- The service allows wind power producers to integrate generation forecasts, balancing operations and electricity sales on the JEPX via the company’s Digital Grid Platform.

- CONTEXT: Wind generation typically exhibits greater output variability than solar due to changing weather conditions and more seasonal variation.

MOL enters European offshore wind support vessel market

(Company statement, March 9)

- Mitsui O.S.K. Lines (MOL) will enter the European offshore wind service operation vessel (SOV) market by jointly owning two vessels scheduled for delivery in 2027.

- The company will invest in Deutsche Offshore Schifffahrt, an offshore vessel developer and operator that’ll manage the ships.

- The vessels will support offshore wind farm operations by transporting technicians and providing accommodation and maintenance services at sea.

- CONTEXT: MOL also entered Taiwan’s SOV market as it sees non-shipping opportunities as a way to reduce earnings volatility tied to shipping markets.

Tokyo Gas unit signs offshore wind deal with IX Renewables consultancy

(Company statement, March 12)

- Tokyo Gas Engineering Solutions (TGES) inked an MoU with Dutch consultancy IX Renewables to bid jointly for consulting and engineering contracts at offshore wind projects in Japan and overseas.

- TGES has experience in energy infrastructure engineering and Japan’s regulatory requirements; while IX brings offshore wind expertise in Europe and Taiwan.

Octopus Energy to supply over 150 GWh of hydroelectricity

(Company statement, March 3)

- Octopus Energy was re-selected to supply hydroelectric power under Gunma Pref’s local production and consumption PPA.

- The company aims to supply 156 GWh of electricity to seven companies across 11 locations, including JR East, over three years starting in April.

- CONTEXT: Gunma’s local production and consumption PPA program supplies electricity generated by local hydropower plants to businesses in the prefecture.

J-POWER tests herbaceous fuel for co-firing biomass

(Company statement, March 10)

- J-POWER made a demo of biomass co-firing using erianthus as a fuel at one of its coal-fired power plants in Nagomi (Kumamoto Pref).

- CONTEXT: Erianthus is a perennial grass that grows wild in tropical regions and is a vigorous energy crop. A relative of sugarcane, it’s promising for biomass applications. It has attracted J-POWER’s interest because its production yield can be roughly twice that of wood pellets on average (up to about 30 tons/ha), and it can be cultivated with relatively limited fertilizer use and labor in the Kanto region and further south.

- TAKEAWAY: Research is being conducted by NARO (National Agriculture and Food Research Organization); one of its projects led to the commercialization of erianthus for bioenergy in 2017, when it was used to fuel boilers at hot spring facilities in Tochigi Pref. However, the use of erianthus for large-scale biomass applications has not yet been commercialized and remains at the demo stage. The biomass market in Japan, and globally, remains dominated by traditional fuels (wood pellets, PKS, forest or agricultural residues).

NEWS: NUCLEAR ENERGY

TEPCO disconnects Kashiwazaki-Kariwa generator for inspection after fault alarm

(Company statement, NHK, March 13-15)

- TEPCO disconnected the generator at Kashiwazaki-Kariwa nuclear power plant Unit 6 from the grid after an alarm indicated a possible ground fault.

- The alarm occurred around 4 p.m. on March 12 while the reactor was operating at constant thermal output. To conduct a detailed probe, TEPCO disconnected the generator from the transmission system at about 12:30 p.m. on March 14.

- Following the disconnection, reactor output was reduced to about 20%, although the reactor itself was not shut down.

- According to media reports, the delay is expected to push back the start of commercial operation, originally scheduled for March 18. TEPCO plans to review the schedule and submit a revised application to the Nuclear Regulation Authority.

- No abnormalities have been reported in the reactor itself.

- CONTEXT: Unit 6 restarted on January 21 and began trial power transmission on February 16. Reactor output had gradually increased and was nearing full capacity ahead of planned commercial operation on March 18.

- TAKEAWAY: Kashiwazaki-Kariwa remains the most politically sensitive nuclear restart in Japan. Even minor technical issues are likely to trigger additional scrutiny from regulators and local stakeholders, increasing the likelihood of schedule delays.

As Japan NRG has said many times, it is unrealistic to expect that this restart will go in accordance with plans. While generator faults are relatively common during restart testing, they usually do not affect reactor safety systems.

Sumitomo invests in U.S. fusion tech company

(Company statement, March 10)

- Sumitomo Corp invested in SHINE Technologies, a U.S. fusion technology company to collaborate on commercializing fusion-related technologies such as medical isotopes used in healthcare and neutron imaging technologies

- The investment turns earlier cooperation into a partnership with equity participation.

- Sumitomo will support SHINE Technologies in expanding in Japan and across Asia.

- The partnership also aims to advance nuclear waste recycling technologies.

NEWS: TRADITIONAL FUELS

Japan to release record 80m barrels from oil reserves as soon as March 16

(Japan NRG, March 11)

- Japan will begin releasing oil from national petroleum reserves as early as March 16, tapping both private-sector and state stockpiles in response to supply risks stemming from the Iran conflict.

- METI minister Akazawa said the sales will be conducted at prices based on levels before the start of the Middle East war and officials will oversee the process.

- PM Takaichi plans to release about 80 million barrels, equal to 45 days of domestic demand, the largest drawdown of Japan’s reserves on record.

- The first phase will draw on private-sector inventories, which account for 101 days of national oil demand. The govt will release 15 days’ worth of these private stocks immediately, as they can be distributed quickly without additional logistical transfers.

- A second phase will involve the release of about 30 days of state-held reserves, likely between late March and early April. Japan stores these national reserves across 10 facilities nationwide and in leased storage tanks.

- To accelerate the process, the govt will allocate crude through negotiated contracts rather than competitive bidding, aiming to begin deliveries within a month of the decision. This approach aims to prevent the aftermath of Russia’s 2022 Ukraine incursion, which also led to Japanese stockpile releases but was delayed by several weeks due to bidding.

- The govt seeks to keep gasoline contained to around ¥170/ liter. Retail prices have already risen to about ¥161.8, with officials warning they could exceed ¥180–¥200 if crude prices continue climbing.

- CONTEXT: Japan held oil reserves equivalent to 254 days of domestic demand at the end of December. The release will be the largest of the seven emergency drawdowns Japan has conducted, most coordinated with the International Energy Agency.

- SIDE DEVELOPMENT:

- G7 Energy Ministers meet to discuss release of oil reserves

- (Government statement, Japan NRG, March 10)

- METI’s Minister Akazawa attended the G7 Energy Ministers online meeting to discuss market stability and potential coordination on reserve releases.

- The ministers confirmed a joint statement to strengthen international coordination.

- TAKEAWAY: The Iran war is causing volatility across global energy markets – even those usually insulated from Gulf supply disruptions. West Texas Intermediate crude futures, which reflect the price of oil delivered in the U.S., briefly exceeded $110/ bbl, the highest level in four years. The surge reflects mounting uncertainty around physical deliveries as Gulf producers, international oil majors and traders declare force majeure after production and export facilities were idled. Iranian drone strikes have reached as far as southern Oman, prompting some exporters to clear tankers from ports to reduce the risk of attacks. Despite U.S. pressure, Iran continues to control access to the Strait of Hormuz, meaning that most oil currently transiting the passage is Iranian. It is unclear how quickly oil released from strategic reserves by IEA members will reach markets and offset disrupted shipments. For example, it takes 20-25 days for tankers to transport oil from the Middle East to Japan. Even at 80m barrels, the planned releases are small compared with the 15–18m b/d of crude normally passing through the Strait. While attention has focused on crude and LNG, the next shock may come from refined products and petrochemical feedstocks. Disruptions to refining could tighten naphtha supplies, constraining production of key industrial materials such as ethylene and amplifying the economic impact.

ANRE: inventory levels for power and gas utilities consistent with 5-yr averages

(Government statement, March 10)

- ANRE took stock of the current landscape of LNG imports and risks to energy stability in the wake of the Iran war and a sharp spike in global spot prices.

- ANRE said inventory levels for power and gas utilities remain consistent with five-year averages. To safeguard the nation, the govt has established cooperative frameworks for resource sharing, and boosted fuel monitoring to prevent potential electricity shortages.

- Japan has two primary frameworks, created in 2021, to address potential disruptions. The Regional Cooperation Scheme and the National Cooperation Scheme.

- The first envisions partnerships among power and gas companies in a specific region. They share LNG terminals, have terminals located close to one another, or transport gas via pipelines. If operators cannot manage supply shortages, ANRE will intervene.

- Also, a temporary “kWh monitoring” system was implemented, whereby the fuel inventory and procurement status of power generation operators are checked. This is to compare the nation’s power generation capacity against predicted demand.

- The results of this temporary monitoring would come around early April.

- CONTEXT: Japan relies on the Middle East for about 10.8% of its LNG imports. Around 6.3% (about 4 Mtpa) of the total passes through the Strait of Hormuz. But more than 95% of its oil imports come from the Middle East, almost 44% of it from the UAE, the biggest exporter. Saudi Arabia follows with a little more than 40%, and Kuwait represents around 6% of Japan’s total imports, followed by other ME countries such as Qatar and Oman.

ENEOS raises gasoline wholesale prices sharply after Iran attack

(Nikkei, March 11)

- ENEOS notified affiliated service stations that it will raise gasoline wholesale prices by ¥26/ liter for deliveries between March 12-18, reflecting the surge in crude oil prices following the attack on Iran.

- A price increase of more than ¥20/ liter is unusual in Japan’s fuel market.

- The company had already informed dealers of a ¥2.5/ liter increase for shipments between March 5-11, also linked to rising crude prices and exchange-rate movements.

Iran conflict could reshape Japan’s LNG procurement strategy, IEEJ says

(Think tank report, March 10)

- War in the Middle East and the Strait of Hormuz closure could trigger unprecedented disruption in global LNG markets, said the Institute of Energy Economics, Japan.

- CONTEXT: The shutdown of Qatar’s Ras Laffan export hub, the world’s largest LNG production complex, has affected roughly 20% of global LNG supply, pushing Asian spot LNG prices above $25/ MMBtu and oil prices above $100 per barrel.

- In the short term, the main effects would be physical disruption to shipping routes, surging insurance premiums for LNG carriers and panic-driven price volatility.

- Japan could see LNG import prices rise with a three-month lag, as most long-term contracts remain linked to crude oil prices.

- The impact on physical supply to Japan may be partly mitigated because the conflict erupted after the winter peak demand season in Asia. Weak spot buying from China could also ease pressure on cargo availability.

- Longer term, the crisis may accelerate structural changes in global markets. Buyers may cut reliance on Middle Eastern LNG and diversify procurement toward North America, Canada, Mexico and Alaska projects.

- Japan may also reconsider maintaining imports from Russia’s Sakhalin-2 LNG project as part of a broader energy security strategy.

- The think tank also expects greater emphasis on flexible LNG contracts that allow cargo redirection during emergencies. U.S. LNG priced against Henry Hub may gain competitiveness relative to oil-linked contracts.

Gas benchmarks drop after Trump says Iran war to end soon

(Denki Shimbun, March 12)

- President Trump said the U.S. war against Iran might soon end. Since then, futures prices for power-generation fuels began to fall.

- The European gas benchmark Title Transfer Facility (TTF) dropped on May contracts.

- The LNG benchmark Japan Korea Marker (JKM) also dropped on May contracts.

- TTF fell 15.5% (from $18.88 to $15.96/ million BTU). JKM fell 17.8% (from $21.48 to $17.66).

- Prices are driven more by market psychology and speculation than by supply-demand fundamentals. This means prices could rise again depending on developments in the conflict or political statements.

- TAKEAWAY: JKM correlates with Japan’s spot electricity prices. So, domestic power utilities are watching them closely. Australian thermal coal futures also rose, but have since fallen from $137.65 to $131.55/ ton, about a 4% drop. Some market observers suspect that resource producers may have raised prices.

JERA to sell stakes in Australian LNG projects

(Company statement, March 12)

- JERA plans to sell its stakes in two Australian LNG projects, Gorgon LNG and Ichthys LNG. The buyer is MidOcean Energy, a U.S.-based LNG company.

- The deal still needs state and partner approvals. Even after selling its shares, JERA will continue purchasing LNG from both projects.

- JERA will instead focus on other major LNG investments in Australia, such as Wheatstone LNG (operated by Chevron), Barossa (operated by Santos), and Scarborough (operated by Woodside)

- CONTEXT: JERA has a 0.735% stake in Ichthys LNG Project and 0.417% in Gorgon LNG Project. The first is operated by INPEX, the second by Chevron. JERA currently gets around 3 Mtpa of LNG from such projects.

- TAKEAWAY: With global LNG demand expected to grow, upstream LNG assets are now more valuable and sought after. By divesting minority stakes now, JERA can monetize these assets at favorable conditions and redeploy capital toward more strategic LNG investments. JERA still maintains LNG supply contracts from these projects, since Australia remains crucial to Japan. The transaction may also strengthen JERA’s relationship with MidOcean Energy. The latter has LNG upstream holdings in Canada and South America and is expanding, creating potential for future collaboration or co-investment opportunities.

- SIDE DEVELOPMENT:

- JERA says Iran war won’t affect LNG procurement this spring

- (Denki Shimbun, March 10)

- Okuda Hisahide, president of JERA, said the Middle East war is unlikely to impact LNG procurement this spring because the firm already took supply-security measures.

- He said the rise of the WTI oil benchmark above $100/ barrel could push LNG prices higher, depending on whether the crisis is short- or long-term.

- Okuda said JERA will maintain its LNG relationship with QatarEnergy (3 Mtpa).

METI works toward reduction of gas-related fatalities

(Government statement, March 10)

- METI outlined the Liquefied Petroleum Gas (LPG) Safety Enhancement Plan 2030 to achieve zero gas-related fatalities and reduce accidents by 2030.

- Documents note that major accidents have remained minimal since 2021.

- Initiatives include measures against CO poisoning, equipment failures, and damage by natural disasters.

- SIDE DEVELOPMENT:

- METI assesses gas-related incidents and proposes related targets

- (Government statement, March 9)

- METI tested the impact of gas system reforms on safety, confirming that liberalizing the city gas market hasn’t led to an increase in accidents. Incidents are down.

- METI sets targets for 2030, such as keeping fatal accidents to less than 1 per year.

- Replacement of aging infrastructure is a key component of the plan. It also includes new measures for responding to pressure rise accidents.

Nippon Steel agrees with Australian firms for biofuel production

(Company statement, March 10)

- Nippon Steel Trading agreed with Energreen Nutrition and Green Biotechnology Solutions, which grow pongamia in Queensland, to develop biofuel production.

- CONTEXT: Pongamia is a drought-resistant legume tree that produces seeds with up to 40% oil content, making it a promising feedstock for biodiesel and SAF. Able to grow on degraded land and requiring relatively little fertilizer, it can achieve oil yields of around 5–10 tons/ ha, outperforming traditional crops such as palm (3.8 tons/ ha).

- SIDE DEVELOPMENT:

- Aktio and Japan Caterpillar manufacture biodiesel backhoe

- (Company statement, March 11)

- Aktio and Japan Caterpillar manufactured a biodiesel-powered backhoe.

- CONTEXT: Biodiesel-powered construction machinery has been commercialized on a small scale since the 2020s. Electrification is spreading as a way to decarbonize construction equipment, as electric motors are quieter and generate fewer vibrations.

LNG stocks down from previous week, flat YoY

(Government data, March 11)

- As of March 8, the LNG stocks of 10 power utilities were 2.12 Mt; down 3.2% from the previous week (2.19 Mt); no change from end March 2025 (2.12 Mt), and up 6% from the 5-year average of 2 Mt.

NEWS: CARBON CAPTURE & SYNTHETIC FUELS

Malaysia hosts CCS events, focuses on cooperation with Japan

(Denki Shimbun, March 10)

- A two-day event in Kuala Lumpur focused on cross-border CCS projects. The event was co-hosted by JBIC and Malaysia’s Petroliam Nasional Berhad.

- It covered policy developments, technology, and finance to store captured Japanese CO2 in Malaysia. Participants included companies from sectors such as power generation, steel, shipping, and finance.

- CONTEXT: Malaysia is promoting CCS as a key measure for carbon neutrality. Infrastructure is developed at Kuantan Port to receive liquefied CO2 ships and serve as a hub for a CCS project supported by JOGMEC.

- TAKEAWAY: Both govts are strengthening cooperation. In October, METI and Malaysia’s economy ministry signed an MoU on CCS, aiming to realize cross-border CCS projects in the 2030s. Japanese officials emphasized that CCS is an area where Japanese technology and private finance can play a major role.

Toho Gas starts product-scale demo of CO2 separation and capture

(Company statement, March 11)

- Toho Gas started a product-scale demo of a CO2 separation and capture system that targets exhaust gases from customer factories.

- It combines membrane separation tech that allows CO2 to pass through a membrane and physical adsorption tech which uses adsorbent materials to capture CO2.

- Toho Gas is developing membrane separation equipment.

- NGK Insulators is developing the membrane used in the separation equipment.

Mitsubishi Chemical cuts ethylene output amid naphtha supply concerns

(Kyodo News, Japan NRG, March 9)

- Mitsubishi Chemical reduced ethylene production at a petrochemical complex in Ibaraki Pref, citing difficulties with the feedstock naphtha as the Iran war disrupts supply chains.

- On March 6, the company began lowering output at the site, which has an annual capacity of 485,000 tons, about 8% of Japan’s total ethylene production capacity.

- CONTEXT: Japan relies heavily on imported naphtha, with about 60% sourced overseas, of which 70% is from the Middle East.

- Mitsubishi Chemical said the move is intended to avoid a full shutdown if naphtha procurement worsens, and the company has already notified major customers.

- Idemitsu Kosan also warned business partners that two of its ethylene plants could be suspended if the effective closure of the Strait of Hormuz continues.

- TAKEAWAY: Japan’s ethylene production capacity totals roughly 6 to 6.5 million tons (Mt) per year, which means the slowdown or closure of Mitsubishi Chemical and Idemitsu facilities would greatly impact domestic output. Reduced rates tighten supply downstream for petrochemicals such as polyethylene, polypropylene, ethylene oxide and styrene, which are used in packaging, automotive plastics, synthetic fibers and chemical intermediates.

ANALYSIS

BY FILIPPO PEDRETTI

Behind the Restarts: What Are the Costs of the Nuclear Energy Pivot?

Almost nine years after receiving initial regulatory approval, Tokyo-based utility TEPCO was expected this week to bring its only remaining nuclear facility back into commercial operation. The restart of Unit 6 at the Kashiwazaki-Kariwa nuclear power plant would mark the company’s first since the 2011 disaster at Fukushima Daiichi – also a TEPCO facility – froze Japan’s entire nuclear sector.

That timeline has already slipped. On March 14, TEPCO disconnected the generator at Unit 6 from the grid after an alarm indicated a minor ground fault. The reactor itself was not shut down, but output was reduced while TEPCO investigated. The incident is unlikely to affect reactor safety, yet it illustrates how even small issues can delay the carefully choreographed nuclear restart program.

Kashiwazaki-Kariwa’s return, along with other planned restarts such as Unit 3 at the Tomari plant, forms part of a broader national push to raise nuclear’s share of the power mix from roughly 9% today to 20% by 2030. Achieving that target will require significant state support and spending. Luckily, Prime Minister Takaichi’s administration appears happy to oblige.

The government wants to maximize nuclear generation as Japan scrambles to accelerate decarbonization, meet rising electricity demand driven by the AI boom, and reduce dependence on energy imports from the Middle East.

Yet the road to a nuclear revival may not be smooth. Last month, Chubu Electric admitted to systemic falsification of seismic data at its Hamaoka nuclear power plant, reigniting concerns over the governance and reliability of Japan’s nuclear operators.

The scandal comes just as policymakers hoped the industry was finally moving beyond the shadow of Fukushima. The scale of the reputational damage remains uncertain, but the burden now falls on both utilities and the government to rebuild trust among local communities, whose support will be essential if further restarts are to proceed.

Financing the nuclear future

Japan’s nuclear revival will be financed less by markets than by the state.

Until 2022, nuclear power faced strong opposition in Japan at both the national and local levels. The energy shock that followed Russia’s invasion of Ukraine in February that year inadvertently delivered a major public-relations boost to the sector. As energy bills surged, Japanese consumers proved more receptive to nuclear power’s promise of easing the burden.

The government’s 7th Basic Energy Plan, released in 2025, codified that shift. It calls for raising nuclear’s share of the power mix to 20%, up from less than 9% today. Achieving this will require extending the operating life of existing reactors beyond 60 years and constructing new reactors at the sites of decommissioned ones.

Those ambitions carry a steep price tag. Large-scale reactors cost between ¥2 trillion and ¥6 trillion to build, while even small modular reactors (SMRs) are estimated at ¥1–2 trillion. Faced with such costs, private financing alone is unlikely to suffice. PM Takaichi’s government has therefore opted for a state-led funding model.

The plan centers on the grid oversight body, OCCTO, which would raise funds with state guarantees. In December policymakers proposed shifting to a “fiscal loan” model, under which the government would lend funds via the Fiscal Investment and Loan Program (FILP). Public money, sourced from taxes and FILP, would flow to OCCTO, which would then on-lend it to utilities.

The Energy Agency has already requested ¥54 billion in the FY2026 budget to launch the system. The funds would support loans to utilities for “supply capacity” and “grid reinforcement.”

Under the scheme, OCCTO effectively becomes a financial intermediary while preserving the familiar formula of “national policy, private management”. By routing capital through OCCTO rather than taking equity stakes, the government can support nuclear investment while avoiding the optics of nationalisation – despite TEPCO having been effectively nationalised since 2012.

| OCCTO funding pillar (2026 Request) | Amount (¥ billion) | Intended Use |

| Power supply capacity loans | 24 | Restarts and new reactor development |

| Transmission/grid investment | 30 | Integration of baseload and regional grids |

| Total | 54 |

The long road ahead

As it seeks to win over skeptical host communities, the government has framed nuclear power as an indispensable baseload energy source. Yet the numbers suggest that the sector still has a long way to go before delivering the promised benefits.

In principle, nuclear reactors are well-suited to baseload generation. Plants are typically designed to operate at capacity factors above 70–80%. Japan’s 14 currently operating reactors achieved roughly that level in 2024, posting an average capacity factor of just over 80%.

The picture looks different, however, when considering the country’s entire operable fleet of 33 reactors. Across those units, the average output in 2024 was just 30.6%, reflecting regulatory delays and safety-related shutdowns. That is far below the level required for efficient operation on a per-unit basis.

Low utilization carries financial consequences. When reactor fleets operate at ~30% capacity, the costs of safety upgrades, maintenance and staffing must be spread across a much smaller volume of electricity, pushing up the cost per kilowatt-hour, thus eroding nuclear competitiveness against both renewables and thermal power.

To help bridge this economic gap, the government has begun deploying financial support. Through OCCTO, it has arranged ¥54 billion in financing and is considering additional direct subsidies aimed at keeping nuclear generation competitive.

The challenge becomes clearer when looking at the state’s 2030 target. For nuclear power to supply roughly 20% of Japan’s electricity, the entire operable fleet (around 33

GW) would need to run at around an 80% capacity factor. That would produce roughly 230 TWh annually (33 GW × 0.8 × 8,760 hours), out of the roughly 1,000 TWh generated by the nation’s power sector each year.

What’s more, new construction is irrelevant to the 2030 state target. Even if new reactors were approved and construction began immediately, they would be unlikely to connect to the grid before the 2040s.

One step forward, one step back

The government has shown little hesitation in directing funds toward nuclear restarts, and Kashiwazaki-Kariwa, once the world’s largest nuclear power plant by capacity, sits at the centre of that strategy.

Yet the plant embodies some of the political complications that continue to dog the nuclear revival. Although located in the service territory of Tohoku Electric,

Kashiwazaki-Kariwa supplies electricity to TEPCO’s customers in the Tokyo metropolitan area. For local communities, this arrangement feels one-sided: Niigata hosts the plant and its risks, while the electricity flows to the capital.

TEPCO’s position as an ‘outsider’ utility has further complicated matters. Unlike regional operators, the company is not deeply embedded in Niigata’s local political and community networks, something critics say has contributed to shortcomings in evacuation planning and broader crisis preparedness.

To ease local concerns, the government has offered substantial financial support. Niigata Pref is set to receive ¥100 billion from TEPCO over ten years, alongside central government funding for evacuation roads within a 30-kilometre radius of the plant. Comparable support has not been extended to other nuclear host regions.

These payments come on top of TEPCO’s already vast financial obligations stemming from the Fukushima disaster. The government estimates compensation,

decommissioning and cleanup costs at around ¥23.4 trillion, though some independent analysts believe the eventual bill could be higher. Much of that burden is ultimately being recovered through higher electricity tariffs and public funds.

| Niigata Accord Component | Funding Source | Strategic Goal |

| Revitalization fund | TEPCO (¥100bn) | Local economic development |

| Evacuation infrastructure | Central govt (Special) | Seismic/ Snow-resilient roads |

| Monitoring team | Cabinet secretariat | Oversight of TEPCO governance |

| Three power laws reform | Legislative change | Increased recurring grants |

Conclusion

Japan’s nuclear revival increasingly resembles an industrial policy project rather than a market-driven investment cycle. Even Kansai Electric President Mori has acknowledged that large nuclear projects are effectively unbankable without government backing. In practice, that leaves the state as the sector’s lender, guarantor and, ultimately, its risk bearer.

PM Takaichi appears prepared to assume that role. In late February, the government announced plans to allocate more than ¥1 trillion to accelerate the commercialization of next-generation reactors and fusion tech. A detailed public investment roadmap is expected later this year.

Much of that funding will flow toward technologies that remain far from commercial deployment. The roadmap elevates fusion from laboratory research to a pillar of national industrial policy. Yet even the most optimistic projections place fusion power on the grid no earlier than the latter half of the century.

Over this “state-policy, private-management” model looms a governance challenge that cannot be ignored. Chubu Electric’s recent admission that it falsified seismic data at the Hamaoka NPP has reignited concerns about the industry’s credibility. The NRA has launched a comprehensive review, and the full extent of the damage to public confidence remains uncertain.

That reputational risk carries financial implications. If taxpayers are expected to shoulder a growing share of nuclear power’s costs – through subsidies, guarantees and higher electricity tariffs – public trust becomes an economic prerequisite rather than merely a political aspiration.

In a way, the Hamaoka episode encapsulates the two structural constraints facing Japan’s nuclear sector: persistent public skepticism and the operational bottlenecks that continue to keep much of the reactor fleet offline. Both undermine the utilization rates needed to make nuclear power economically viable.

For now, the government’s roadmap assumes those obstacles can be overcome. But it offers little contingency planning should restarts stall – as Kashiwazaki Kariwa has demonstrated time and again – or public opposition intensifies. A credible fallback strategy – whether expanded renewables, grid-scale storage or alternative decarbonization pathways – remains largely absent from the discussion.

ANALYSIS

BY TESTUJI TOMITA

A Small Parameter with Big Consequences: Japan Revisits Net CONE

Sometimes the smallest technical decisions can change everything.

Buried in discussions of a working group under METI is a technical review that could tilt the direction of Japan’s power sector for the next decade. At issue is a measure known as Net CONE, short for the Net Cost of New Entry.

This benchmark helps determine the price at which new power capacity should be procured to ensure a stable electricity supply. In simple terms, when Net CONE is high, companies have a stronger incentive to build new power plants. If it is set too low relative to developers’ expectations, investment slows.

Capacity auctions in recent years suggest we’re at an inflection point. Despite growing electricity demand from semiconductor production facilities and data centers, auction results indicate that the benchmark underestimates the cost of bringing new generation online.

That has pushed policymakers to consider revising Net CONE – its first major reassessment since the capacity market framework was drafted in the late 2010s.

This revision carries risks. With incumbent utilities controlling nearly 80% of the power market, a higher Net CONE also translates into a significant revenue tailwind for existing fossil-based assets. This could end up “overcompensating” the depreciated older plants and inadvertently extending the lifespan of carbon-intensive generation, thus complicating Japan’s long-term decarbonization goals.

Auction results trigger policy review

In January 2026, the results of the sixth capacity market main auction (a tender held in FY2025 for FY2029 delivery) were announced. Even before the results were released, policymakers had begun reviewing the outcome of the previous year’s auction and saw an emerging need to adjust market design.

Net CONE is highly sensitive to trends in construction, maintenance, operating, and capital costs. And all these have been heading considerably higher in recent years.

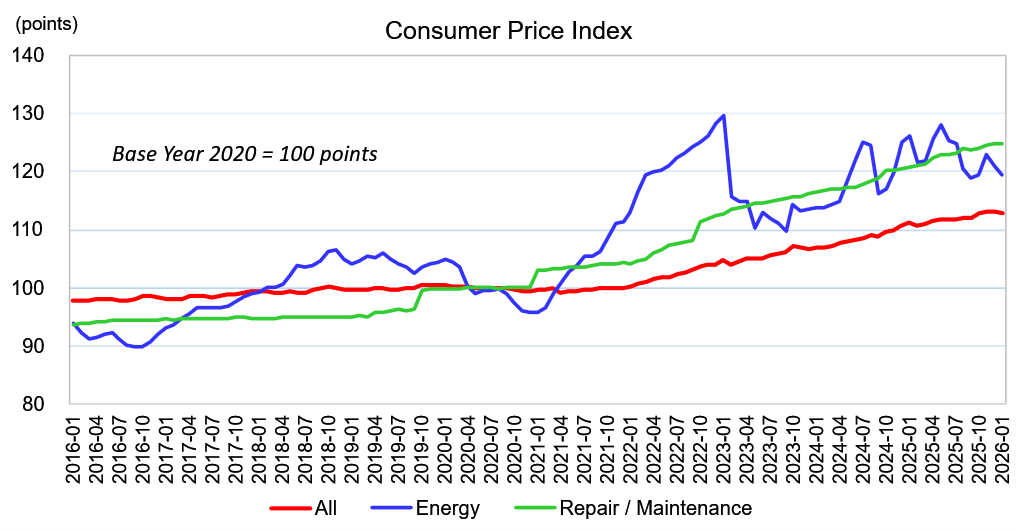

Japan’s consumer price index has risen steadily since 2022, reaching around 112 by 2025 (2020=100). The broader inflation trend has raised operating and maintenance costs across the power sector.

Consumer Price Index Trends

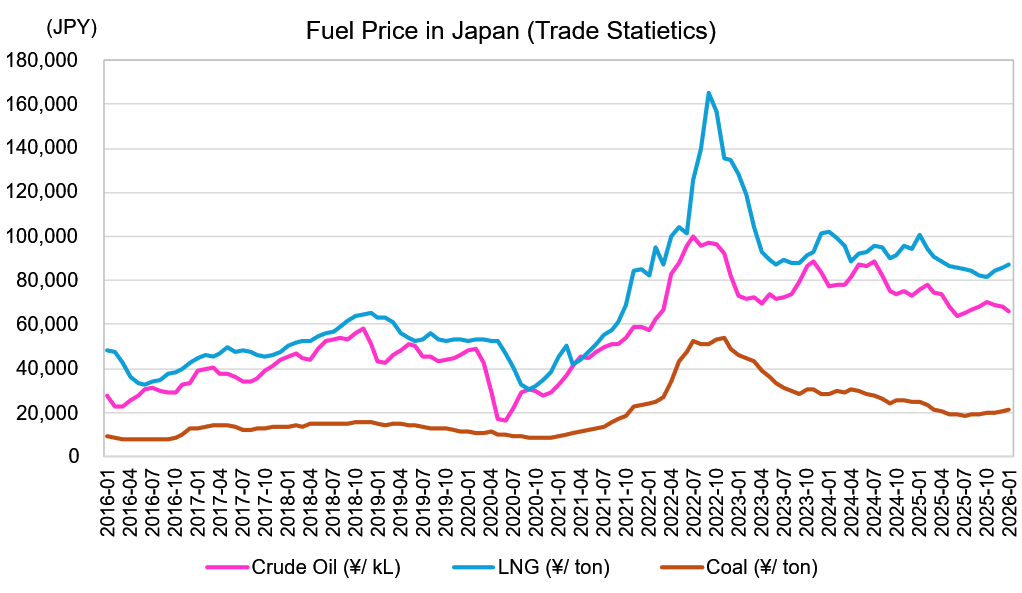

Fuel markets have also added volatility. The start of the Russia-Ukraine war in 2022 was followed by a huge jump in the price of oil and natural gas. And while trade statistics suggest prices softened by 2025, fuel benchmarks began rising again this year as conflict broke out in the Middle East. Following Iran’s effective closure of the Strait of Hormuz, crude oil has surged sharply, which six months down the line is likely to translate into increased costs for power producers and consumers.

Fuel Price Trends

Inflationary environment

The Iran war is only the latest factor among a host of macroeconomic pressures indicating that the calculations behind the current Net CONE are now obsolete. The benchmark no longer reflects the true cost environment for generators, and capacity auction bids confirm this is fast-emerging as the mainstream view in the power industry.

The number of times that bids in the 6th capacity main auction exceeded Net CONE was up 1.6 times over the previous year. The jump from the 4th auction to the 5th was even more profound – roughly a 400% increase.

In Japan’s capacity market framework, Net CONE is calculated by subtracting expected revenues from other markets from the gross cost of building new generation capacity. The benchmark therefore functions as an indicator of the price level required to support investment in new power plants while avoiding excessive returns to existing facilities.

Net CONE and Contract Price in Each Year Capacity Market Main Auction

(Unit: ¥ / kW / year)

| Round | 1st | 2nd | 3rd | 4th | 5th | 6th | |

| Auction Year | FY2020 | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 | |

| Actual Supply Year | FY2024 | FY2025 | FY2026 | FY2027 | FY2028 | FY2029 | |

| Net CONE | 9,425 | 9,372 | 9,557 | 9,769 | 9,875 | 10,075 | |

| Price Cap | 14,137 | 14,058 | 14,335 | 14,653 | 14,812 | 15,112 | |

|

Area Price | Hokkaido | 14,137 | 5,242 | 8,749 | 13,287 | 14,812 | 14,972 |

| Tohoku | 3,495 | 5,833 | 9,044 | 15,111 | |||

Tokyo | 5,834 | 9,555 | |||||

Chubu | 5,832 | 7,823 | 10,280 | 12,388 | |||

Hokuriku | 7,638 | 8,785 | |||||

Kansai | |||||||

Chugoku | |||||||

Shikoku | |||||||

Kyushu | 5,242 | 8,748 | 11,457 | 13,177 | 14,137 | ||

| Total Average Price (after transitional deduction) | 9,534 | 3,109 | 5,226 | 7,847 | 11,134 | 13,303 | |

It’s little surprise that generators are bidding higher. They face higher costs to maintain aging power plants, labor shortages, and with the Bank of Japan raising rates now a higher cost of capital. As a result, the Net CONE-based reference price and price cap – established when the capacity market was designed in 2020 – are out of touch with today’s realities.

All of which means lower capacity procurement in the market and low motivation to invest in new plants.

Policy options

In reviewing the current framework, the government identified three main options:

- Revising Net CONE: Under the current framework, the cap is set at 1.5 times Net CONE. Updating the benchmark would better reflect current cost conditions and automatically raise the price cap. This could allow resources that previously failed to clear the auction to be procured, improving supply adequacy and restoring the relevance of the indicator price. However, because these payments are funded through charges on electricity retailers, a sharp increase would raise their burden and ultimately be reflected in higher power prices for consumers.

- Revising only the price cap: This could allow higher-priced bids to clear without altering the reference benchmark. But relying on cost assumptions dating back to 2015 could undermine the credibility of the indicator price, and determining an appropriate cap level would remain challenging.

- Maintaining the current framework: This would avoid sudden increases in retailers’ costs. However, it would do little to address emerging concerns about supply adequacy, and would leave the underlying benchmark increasingly detached from current cost conditions.

At present, discussions suggest the government is most likely to go with Option 1.

Revisiting the cost assumptions

The current Net CONE calculation relies on a cost estimate methodology developed by the Power Generation Cost Verification Working Group in 2015. This has been retained largely because it is considered technically neutral and broadly reliable, and no clear alternative methodology has emerged.

However, a decade of cost evolution has rendered the original assumptions insufficient.

As an example, total unit costs for model LNG plants have surged from ¥132,100/ kW in 2015 to ¥297,700/ kW in 2025, while CO2 mitigation costs have experienced a nearly five-fold increase in the same period.

Comparative Estimation of LNG Thermal Power Generation Costs

| Release Year | May 2015 | Sep 2021 | Feb 2025 |

| Estimated Year | 2014 | 2020 | 2023 |

| Generation Cost (¥ / kWh) | 13.7 | 10.7 | 19.1 |

| Capital Cost (¥ / kWh) | 1.0 | 1.3 | 2.1 |

| Total Cost per unit (¥1,000 / kW) | 132.1 | 176.8 | 297.7 |

| Construction Cost (¥1,000 / kW) | 120 | 161 | 268 |

| O&M Cost (¥ / kWh) | 0.6 | 1.2 | 1.8 |

| Total Cost per unit 40 years (¥1,000 / kW) | 84.3 | 166.6 | 255.3 |

| Fuel Cost (¥ / kWh) | 10.8 | 6.4 | 9.0 |

| Total Cost per unit 40 years (¥1,000 / kW) | 1,500.0 | 893.1 | 1,244.8 |

| CO2 Mitigation Cost (¥ / kWh) | 1.3 | 1.8 | 6.1 |

| Total Cost per unit 40 years (¥1,000 / kW) | 177.3 | 236.4 | 843.8 |

| Policy Expense (¥ / kWh) | 0.02 | 0.1 | 0.1 |

| Model Plant | |||

| Generation Capacity (MW) | 1,400 | 850 | 600 |

| Capacity Factor (%) | 70 | 70 | 70 |

| Generation Efficiency (%) | 52.0 | 54.5 | 54.9 |

| Operational Years | 40 | 40 | 40 |

Applying the 2025 cost markers to the current framework suggests a “True Net CONE” of approximately ¥20,500/ kW, which is double the current FY2025 level of ¥10,075/kW. And, if the latest METI working group figures are applied, Net CONE would be expected to extend its upper price cap to ¥31,000/ kW.

Mitigating cost impact on consumers

On January 30, OCCTO presented a detailed outline of potential reforms and mitigation measures. At the March 4 advisory committee meeting, experts subsequently presented METI with a proposal to raise both Net CONE and the price cap in order to reflect rising generation costs and maintain investment incentives.

In determining the final direction, policymakers must weigh the impact of raising the benchmark against the potential burden on electricity retailers.

Several mitigation mechanisms are under discussion. These include gradually increasing Net CONE over several years and introducing limits to the single-price clearing range, with higher-priced bids cleared under a multi-price mechanism to reduce volatility in total procurement costs.

Net.. zero?