JAPAN NRG WEEKLY

August 24, 2020

NEWSTOP Coal-fired plant closures will hurt more than the utilities Gloves are off in battle to build first offshore wind farm Tepco confirms CEO’s responsibility for nuclear accidents OIL & GAS Japan’s move away from coal will swing it towards LNG Gasoline prices fall for first time in 14 weeks Mauritius oil spill latest: Captain of ship arrested Tokyo Gas buys shale, solar to enact vision Tokyo Gas likely to be LNG supplier for Yokohama project POWER & NUCLEAR Town mulls hosting Japan’s long-term nuclear waste Rival ministries join forces to champion nuclear power Extreme temperatures led to electricity price volatility Hitachi considers restarting UK nuclear project Tohoku Electric to issue “green bonds” KEPCO scandal continues: documents refer to hush money RENEWABLES & OTHER Japan to add more EV charging points Japan could generate 45% of power form renewables: REI Government looks at buying forests to fuel biomass power Idemitsu selected as first supplier for Tokyo energy plan WEBINAR WRAP We hosted our first event, an online seminar to discuss the current state of nuclear power in Japan and its potential development in the future. CONTACT US |

ANALYSISHYDROGEN: JAPAN HAS A PLAN, Japan has taken an active role in engaging to build both a domestic and an international supply chain for hydrogen. That said, all efforts are as yet at a demonstration stage. There is also little progress on so-called green hydrogen, which puts into question the goals of the entire project. COMPANY PROFILE: JERA, THE FORMING OF JAPAN’S NEW ENERGY COLLOSSUS The biggest LNG buyer in the world also owns power assets which equal half the power capacity of the African continent. As the company moves towards an IPO, we consider its strengths and challenges. HOUSE VIEW Two global events over the last week will greatly affect Japan: the California power grid’s failure and BHP’s exit from coal. The former, sparked by an aggressive move into renewables without systemic capacity for backup when the sun sets, will bolster the position of Japan’s incumbent utilities. They will push for either more nuclear power restarts or a government and public acceptance of rising power bills. The second global event is another possible boon for nuclear power in Japan, but it poses a major challenge to Mitsubishi Corp, among other Japanese trading firms. The traders co-invest with global mining majors to secure the nation’s supplies of coal. Now, they will need to consider if it’s worth to do so alone. |

NEWS

OIL & GAS

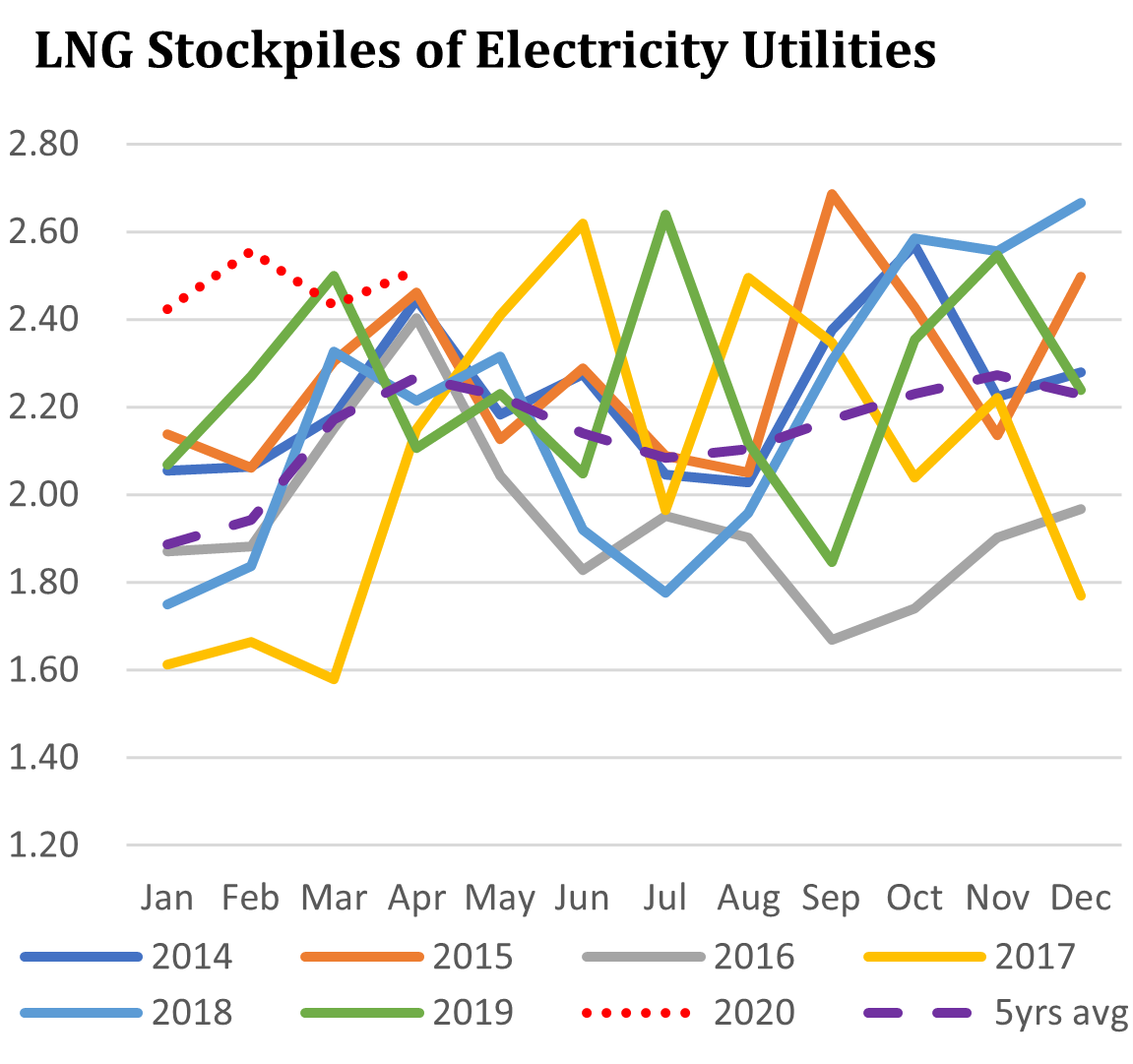

Japan’s move away from coal will swing country towards gas and jack up its price (Takeuchi Junko, International Environment and Economy Institute, August 18)

- CONTEXT: Ms. Takeuchi is a Director and principal researcher at the International Environment and Economy Institute (IEEI). This is an op-ed on the Institute’s website.

- The Japanese government plan to phase out coal-fired power stations was announced in early July with great fanfare and full-page headlines. However, many in the industry have misgivings about the announcement and are hoping for a more transparent policy debate that gives consideration both to Japan’s national interest and the planet.

- Ironically, the deregulation of the electricity market and the adoption of market principles for emissions trading could mean that inefficient coal fired plants are actually replaced with larger (and therefore more efficient) coal-fired plants.

- While proposing to exert rigorous control over renewable generators and thermal generation plants, the government’s policy leaves nuclear power completely at the mercy of the free market. This is ironic because nuclear is the form of energy least compatible with free-market principles.

- In the short term, the policy will mean a much higher reliance on natural gas. This will result in higher energy costs, especially when one considers that the current spate of layoffs in the gas exploration sector could mean that if the global economy recovers around 2025, then there could be a natural gas shortage, causing prices to skyrocket.

Gasoline prices fall for first time in 14 weeks (Nikkei Shimbun, August 19)

- The Agency for Natural Resources and Energy said the national average retail price paid for regular gasoline had fallen for the first time in 14 weeks, to ¥135.5 per liter.

- As the coronavirus epidemic rages, more people are staying at home, resulting in fewer cars on the road. A Tokyo service station owner said customer numbers were down compared to last year.

- Prices are expected to rise slightly next week as petroleum companies pass higher crude prices onto service stations.

- TAKEAWAY: A rapid increase in coronavirus infections during July curtailed a major domestic tourism promotion campaign in the country. The Tokyo governor asked the city residents to refrain from summer travel, in effect dampening demand for all fuel products. A fragile economic recovery and changing work habits are likely to exert downward pressure on prices for the rest of the year.

Mauritius oil spill latest: Captain of ship arrested (Nikkei Shimbun, various, Aug 21)

- CONTEXT: The Panama-flagged Wakashio bulk carrier, owned by Nagashiki Shipping and chartered by Mitsui OSK, ran aground on a reef off the coast of Mauritious on July 25. Leaks started in earnest a week later. It was carrying about 3,800 tons of oil and 200 tons of diesel from China to Brazil. So far, about 1,200 tons spilled into the water from damaged tanks. Early estimates indicate that environmental recovery will take decades.

- Most of the oil spilled into open waters has been recovered, but removing oil from the wetlands and mangrove forests has proved a challenge since chemicals often used for such tasks would further damage the local ecosystem. Onsite teams are looking for other ways to conduct cleanup, with the work likely to take at least half a year.

- The ship has split into two and the bow was towed off to the coast along with the cargo.

- Captain of the bulk carrier, an Indian national, was arrested and brought before a district court in the Mauritius capital city Port Louis.

- SIDE DEVELOPMENT: Visuals of the spill (Asia Nikkei, Aug 21)

- Pictures and graphics, charting the ship’s course, the spread of the spill and key data.

- SIDE DEVELOPMENT: Nippon Yuzen plans to monitor ships in real time (Nikkei Shimbun, Aug 17)

- The Japanese marine shipper opened a center in the Philippines which monitors ships for breakdowns and disrepair using real-time data and AI.

- Crew members that are on furlough between voyages will man the facility and watch over 200 vessels in transit, mainly those of Nippon Yusen.

- The technology will later add functionality to detect if a ship strays off course.

Tokyo Gas buys solar, North American shale gas to enact its 2030 vision (Nikkan Dempa Shimbun, August 18)

- The Tokyo Gas Group is investing over ¥69 billion in large-scale solar power stations in Texas and Illinois, in addition to North American shale gas production, via local subsidiary Tokyo Gas America. The move is part of a plan to triple overseas earnings by 2030.

- In a statement on its corporate vision announced in November, Tokyo Gas says it aims to significantly increase its global renewable energy capacity, which currently stands at 490 MW, to 5 GW by 2030.

- TAKEAWAY: The “5 GW” number seems to be a very popular target among Japanese utilities. JERA, Kyushu Electric and several others have stated the same goal. As such, it feels more like a nice round number and less of a realistic projection based on real projects. Most likely, as their self-imposed deadlines approach, the utilities will simply go out to buy the capacity from independent RE developers.

Tokyo Gas likely to be LNG supplier for Yokohama LNG bunkering project (Rim Intelligence, August 21)

- The city of Yokohama was taking an LNG bunkering project forward.

- An LNG bunkering ship, which was under construction, was expected to have a tank with a capacity of 2,500 cubic meters, or just more than 48mt of LNG.

- LNG for the ship was scheduled to be delivered by Sumitomo Corp. However, sources believe that the trader would initially buy LNG from Tokyo Gas.

POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | ||

| of which | applied for restart | 25 | |

| approved by regulator | 16 | ||

| restarted | 9 | ||

| in operation today | 4 | ||

| able to use MOX fuel | 4 | ||

| No. of nuclear reactors under construction | 3 | ||

| No. of reactors slated for decommissioning | 27 | ||

| of which | competed work | 1 | |

| started process | 4 | ||

| yet to start / not known | 22 | ||

Source: JANSI and JAIF, as of August 23, 2020

Coal plant closures plan could give utilities a sweetener, but hurt industry (FACTA, September Issue)

- Japan has 114 coal-fired power plants that meet the criteria of the Ministry of Economy, Trade and Industry (METI) for being phased out. But, it’s likely that METI minister Hiroshi Kajiyama aims to gradually stop only about 100.

- There are 140 coal-fired plants in total in Japan. Shutting down 100 or so will cut the power capacity of coal generation by half.

- It’s likely that major Japanese utilities knew about this announcement well before and have started preparing for the transformation. Just a week after the METI announcement, JERA President Satoshi Onoda said his company will stop 2 coal plants in Aichi perfection. It’s not possible that he could have acted so quickly without prior warning and coordination.

- Unlike other countries, Japan does not have specific measures in place for achieving its pledge to cut emissions by 26% by 2030. Last September, Minister of Environment Shinjiro Koizumi was unable to explain how Japan is going to achieve its goal at the UN Climate Action Summit. Japan’s actions are out of sync with plans in Europe.

- Japan won’t be able to repeat its 26% target when it comes to the COP26 without coming under heavy criticism from other countries, who will want to know details, according to a power industry executive.

- Coal is still a vital source for Okinawa. The local EPCO relies on coal for 55% of its energy. Hokuriku, Chugoku and Hokkaido EPCOs are also similarly reliant on coal. What’s more, Okinawa and Hokkaido have weak connections to the rest of the country’s grid. They will likely be allowed to keep coal plants as an exception.

- As for Hokuriku and Chugoku EPCOs, they could switch to other sources. Also likely is a merger of Hokuriku with Chubu, and of Chugoku with Kansai EPCO, according to a power industry insider.

- The biggest problems will be for the non-utility power generators. Steel, paper, and chemicals companies also operate generation facilities. In total, manufacturers have around 7.62 GW of coal-fired capacity. METI’s decision will effectively ask them to shut it all down. Some have already complained to METI, but the ministry ignored their pleas.

- TAKEAWAY: If the government goes through with its coal closure plans as promised, they can offer utilities a sweetener for the pain. By shutting all coal-fired capacity below USC standards, they are also taking away the power base of some major manufacturers. Utilities will have the chance to pick up orders that were previously met by some 7.62GW of private generation. And those EPCOs (outside of Hokkaido and Okinawa) that struggle to turn a profit after the industry shift will simply be swallowed by rivals.

TEPCO confirms CEO’s legal responsibility for nuclear accidents (Chunichi Shimbun, August 21)

- In a written submission to Japan’s Nuclear Regulation Authority, TEPCO has said legal accountability for any accident at the Kashiwazaki-Kariwa nuclear plant rests with its CEO.

- TEPCO’s legal counsel issued a statement of opinion stating that the CEO would bear criminal liability, and be liable for compensation, in the event that he neglected to properly mitigate risk.

- SIDE DEVELOPMENT: Residents protest restarting of ageing nuclear plants (Fukui Shimbun, August 21)

- A group of 300 citizens and politicians has filed petitions with the heads of the local bodies in which KEPCO’s Mihama, Ooi and Takahamacho nuclear plants are located, calling on them to disallow the restarting of the plants.

- KEPCO aims to have its nuclear plants running for over 40 years before they are decommissioned.

- SIDE DEVELOPMENT: Kansai Electric targets nuclear plant restarts (FBC, Aug 21)

- Mihama No. 3 nuclear reactor from January 2021

- Takahama No. 1 nuclear reactor from March 2021

- TAKEAWAY: One of the key problems that arose from the 2011 Fukushima disaster was that no party – neither TEPCO executives nor government officials – would accept the blame. This huge abstention of responsibility massively impacts on public trust and the willingness of local officials to sign off on further restarts of nuclear power plants. TEPCO’s document is a small gesture, but highly significant. The local Niigata governor now has someone to blame if the restart of the world’s largest nuclear power plant goes awry.

Town mulls putting hand up to host Japan’s long-term nuclear waste facility (NHK, Aug 13)

- CONTEXT: Japan has not yet selected or even began the process of selecting a place to store its high-radioactive nuclear waste. Officials had hoped that municipalities might be attracted to hosting such a facility in return for state money. However, mayors who have suggested the idea publicly have tended to lose their next election.

- The town of Suttsu, on the northern island of Hokkaido, has entered the first stage of deliberation over whether to put its hand up to host Japan’s long-term nuclear waste facilities. The mayor, Mr. Kataoka, said he will consider inviting the national authorities to conduct a suitability survey on land in the municipality.

- The prefectural government of Hokkaido has voiced its opposition to such plans.

- CONTEXT: The town has a population of about 3,100 people. It’s likely the project will not proceed unless Hokkaido prefecture government approves and that is unlikely since the region is the country’s breadbasket.

Rival ministries join forces to fight emissions, pick nuclear as their champion (Diamond Online, August 21)

- Japan’s Ministry of Economy, Trade and Industry has historically had a bad relationship with the Ministry of the Environment, which it saw as an annoyance that threatened to destroy the economy with its advocacy of environmentally friendly policies. METI also looks down on the much smaller Ministry of the Environment, whose budget was only a quarter of the size of METI’s.

- However, these former rivals were forced to work together when the Paris Agreement for the combating of global warming was signed in 2015. In order to achieve Japan’s nationally determined contribution (NDC) — namely a 26% reduction in CO2 emissions by 2030 — the Ministry of the Environment needed to bring METI, which oversees energy policy, to the table.

- The two ministries have now agreed to jointly push for more nuclear power, including through construction of new stations. Officials believe this offers a stable supply of power with zero CO2 emissions, and therefore aligns with their respective goals.

- TAKEAWAY: Initially, Japanese officials thought the Paris goals would be delayed due to damage to the global economy from the coronavirus pandemic. Climate action was delayed after the 2007-2008 financial crisis. However, many western governments have not backed down. In fact, the EC has stuck to its policy of effecting a green recovery that balances economic actions with environmental conservation. In the US too, the Democratic presidential candidate Mr. Joe Biden, has talked up climate issues. Japanese officials now fear they will need to meet or even raise Japan’s NDC. Their current answer is: let’s restart more nuclear reactors. But, as discussed in the NRG Weekly in the last two editions, that is easier said than done.

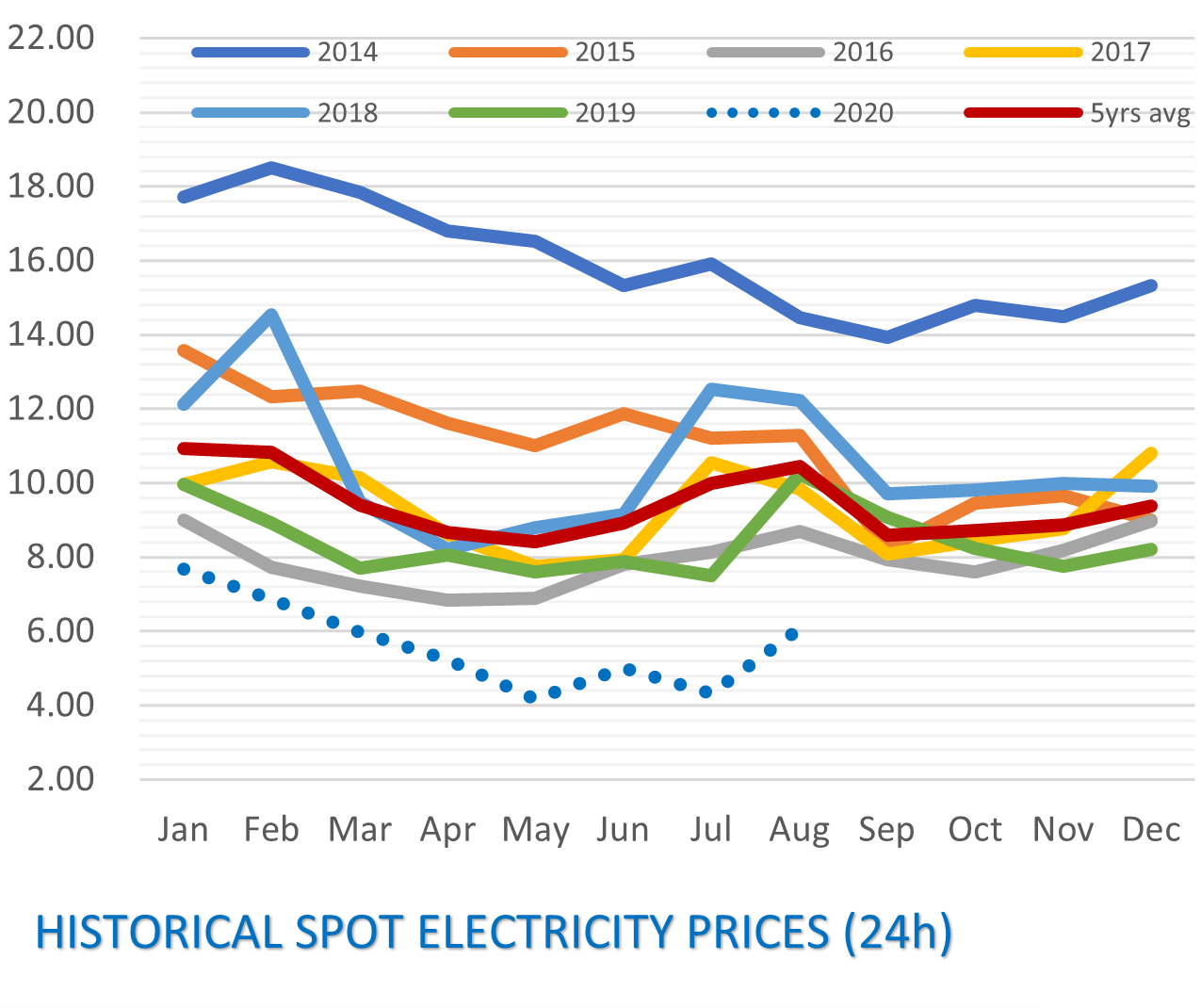

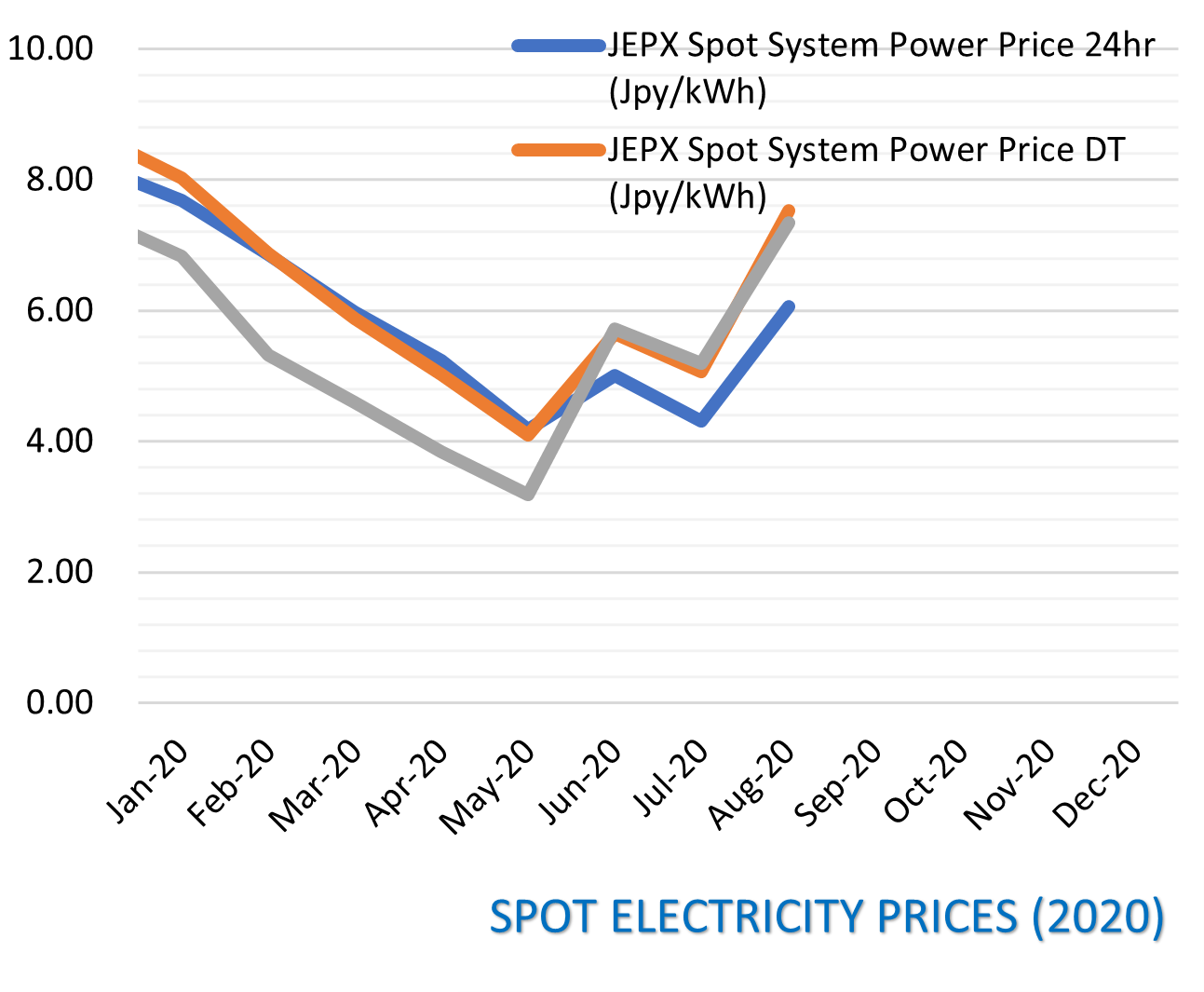

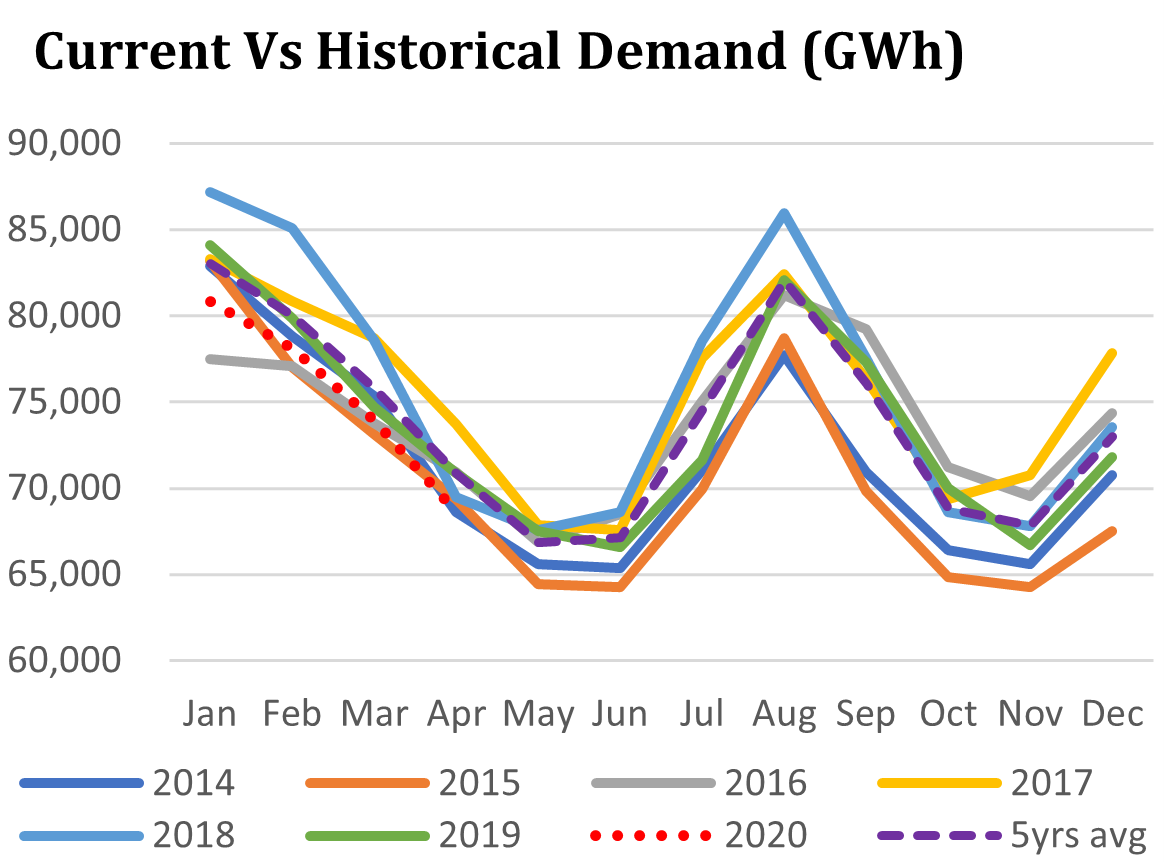

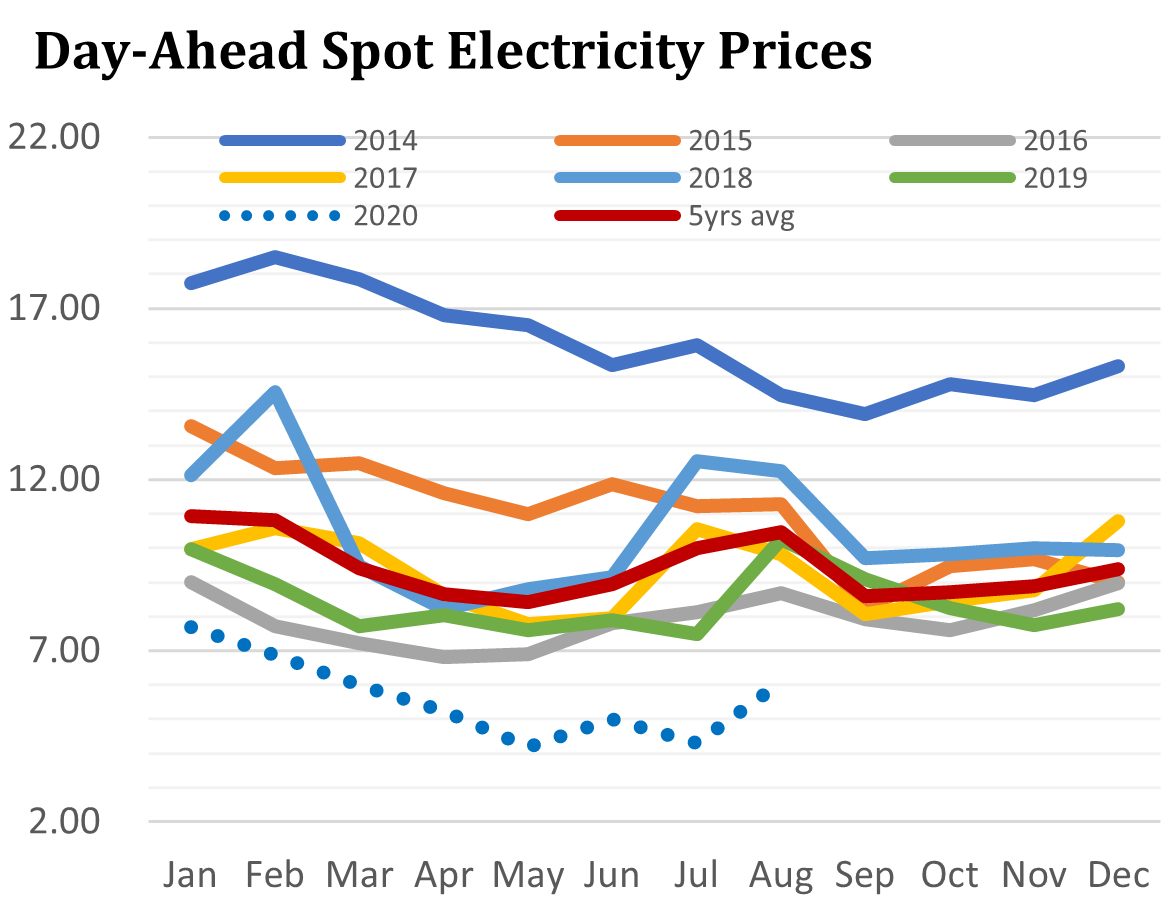

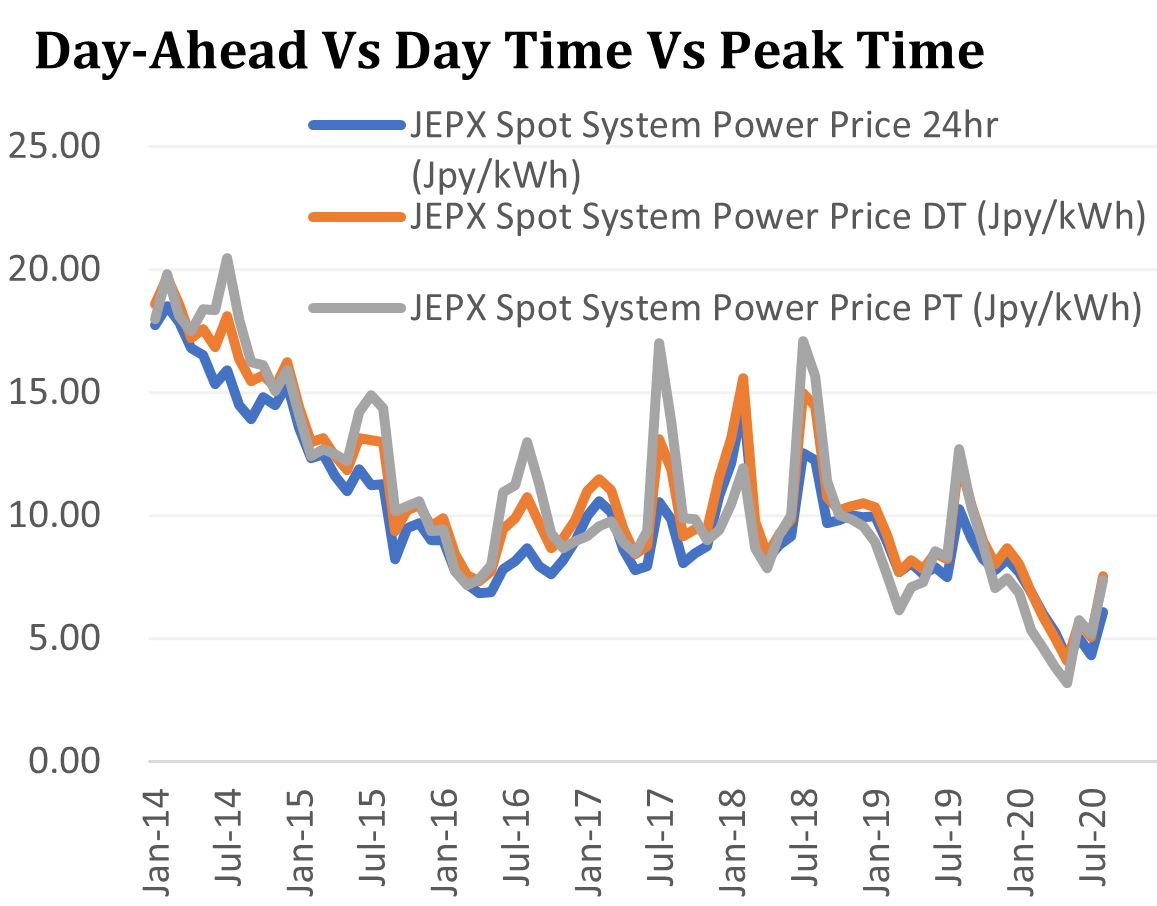

From heat to stove: Extreme temperatures boost electricity price volatility (Yuri Invest Research, Aug 23)

- Days after parts of Japan matched the nationwide record for temperature highs, and two-thirds of the country recorded daytime peaks above 35 degrees Celsius, parts of the northern Hokkaido prefecture posted lows of just 4.9 degrees in the morning.

- The Kamikawa region of Hokkaido had its coolest August in years, according to the Japan Meteorological Agency. That compares with record-tying 41.1 degrees in Hamamatsu, a city about 260 kilometers south of Tokyo, on Aug. 17.

- Japan’s day-ahead peak electricity prices jumped as high as ¥23.05 / kWh on the JEPX on Aug 17, up five times on the previous day. Peak prices stayed above ¥10 for five days – the longest such streak since Oct 10, 2019 – before dropping back to ¥4.65 on Aug. 23.

Hitachi considers restarting UK nuclear project based on new financing model (Kyodo, Aug 17)

- Hitachi Ltd., via its subsidiary Horizon Nuclear Power, is interested in returning to a nuclear power plant building project in the UK. The project is for the Wylfa Newydd NPP on the island of Anglesey, in northern Wales.

- Hitachi froze the project in January 2019, deeming it uneconomic. However, the UK government is said to be willing to adopt a new financing scheme for nuclear power, which will pass on initial investments sunk into construction to the consumers via their electricity bills.

- The project is for two ABWRs with a nameplate capacity of 2,760 MW.

- TAKEAWAY: Hitachi has almost given up on overseas nuclear ambitions, despite the pro-nuclear stance of chairman Nakanishi Hiroaki. The dramatic failure of domestic rival Toshiba, which had to take write-downs of $6.3 billion on its US nuclear unit, made Japanese companies wary of engaging with further atomic projects outside Japan. However, due to recent US-China tensions, letting Chinese firms handle the UK’s next generation of nuclear construction is no longer an option. This opens the door for Hitachi, but the company knows it has the upper hand in negotiations. It will surely ask for generous financial guarantees before proceeding.

Tohoku Electric Power Company to raise ¥10 billion in second “green bond” issue (Kankyo Business Online, August 20)

- Tohoku Electric Power Company said on August 17 it would issue a second tranche of ten-year “green bonds”, which will finance investment in renewable infrastructure.

KEPCO document refers to hush money (Asahi Shimbun, August 18)

- KEPCO’s compliance committee has determined that former chair Mori Shosuke acted alone in making secret payments to directors to compensate for salary cuts imposed when KEPCO hiked electricity tariffs in 2013.

- The head of the committee condemned Mori for “having no qualms about engaging in conduct that betrayed the community’s trust.”

- A document written by Mori instructs the recipients of payments to keep them secret, saying that the public disclosure of the payments could cause “misunderstanding”. The committee says the document is evidence that the payments were hush money.

- CONTEXT: More than 20 former executives of Kansai Electric (KEPCO) are being sued by shareholders for allegedly diverting company revenue to pay personal taxes and top up their salaries. The executives were also found to be involved in graft related to the utility’s nuclear power assets.

RENEWABLES & OTHER

The gloves are off in the battle to build Japan’s first offshore wind farm (Diamond Online, August 18)

- Construction Giants Obayashi and Sumitomo are both vying for the right to build a wind farm off the coast of Akita, an area whose high winds have transformed it into a gold mine for renewable energy.

- In order to succeed, however, the successful bidder will have to form a good relationship with the local fishing cooperative. Many local fishermen are unhappy about the way fisheries have been “sold” to the wind farm project.

- Obayashi began negotiating with the fisheries cooperative in 2016, and felt confident of winning the project. However, in 2019, Sumitomo, another company with a long relationship to the region, entered the competition to win the tender.

- We believe Obayashi has the highest chance of winning the tender for the Oga windfarm, while the consortium comprising Renova, Tohoku Electric Power, Cosmo Eco Power, and JR East Energy Development has the best chance of winning the tender for the Yurihonjo windfarm.

- CONTEXT: No Japanese construction company has significant experience with major offshore wind farm projects, so simply winning a tender for such a project does not guarantee success, especially given the need to keep costs under control for the 30+ year lifespan of the project.

- SIDE DEVELOPMENT: Marubeni’s offshore windfarm—what is the key to success? (Diamond Online, August 19)

- Japan’s electricity, construction, and trading sectors have all made significant investments for the purpose of winning tenders for wind farm projects.

- The first such project will be a 140 MW wind farm off the coast of Akita, an area known for its high winds. The project is being managed by a consortium of companies that includes Marubeni.

- Preparation is key to the success of the project. With each wind turbine weighing hundreds of tons, the yard in which the turbines are stored needs to be on very firm ground.

- SIDE DEVELOPMENT: Choshi offshore wind farm brings both hope and challenges (Nikkei, August 18)

- A newly constructed wind farm off the coast of Chiba features wind turbines that are two meters in diameter, and whose highest points are 126 meters above sea level.

- Originally built by NEDO to study wind speeds, wave heights, and earthquake proofing-issues, the facility was later assigned to TEPCO, which has operated it on a commercial basis since January.

- The wind farm achieves a utilization ratio of around 30%. This is around 50% higher than would be expected with an inland wind farm.

- TEPCO plans to install 7 GW of wind generation capacity in Japan by the mid-2030s, of which around 3 GW will be offshore. This suggests that the Choshi farm could grow to become TEPCO’s first large-scale offshore wind farm.

- TAKEAWAY: Offshore wind is clearly one of the hottest developments in energy in Japan. A lot of expectations from officials and industry players are riding on this energy source. So far, however, there are few assets in operation that can prove the viability of offshore wind and demonstrate how it fits into the current energy mix.

Japan to add more electric vehicle charging points to reduce wait times (Mainichi Shimbun, August 19)

- Idemitsu is among operators investing in electric vehicle recharging points in the hope it will reduce waiting times for drivers, as well as creating a new source of revenue.

- e-Mobility Power, a joint venture between TEPCO and the Chubu Electric Power Company, is developing a new charging system that will be rolled out later this year.

- The JV plans to double its current network of charging points by 2025, by which time it will have 14,000 rapid chargers. Some of these will be installed in Cosmo service stations, as part of an agreement with Cosmo Holdings.

- TAKEAWAY: Japan has been slow to roll out EV infrastructure largely due to industry leader Toyota betting that the future lies in hybrids and fuel cell vehicles (FCV). Toyota also has equity and a degree of control over half the Japanese auto brands. Of the top brands, only Nissan has consistently trumpeted pure EVs. This may now change as the US experiences a boom in EVs not only for passenger cars but also pick-ups and larger vehicles. Some industry experts say Toyota’s stance on EVs is likely to change. The fact that major oil and power companies in Japan are working together to build out the EV infrastructure suggests that this is indeed the case.

Japan could generate 45% of electricity from renewables by 2030—Renewable Energy Institute (Mega Solar Business/Nikkei BP, August 18, 2020)

- Softbank Group CEO and Renewable Energy Institute Chair Son Masayoshi has released a proposal on energy policy in which he claims that Japan will be able to generate 45% of its electricity requirements from renewable sources by 2030.

- According to the proposal, if Japan pursues the status quo, renewables will only account for around 30% of the 980TWh projected to be consumed in 2030/31.

- SIDE DEVELOPMENT: Transmission grid key to uptake of renewable energy (Nikkei, August 19)

- While the cost of investing in renewable technologies remains high, it is projected to decrease in the medium term as Japan moves to a system of competitive tenders.

- Because legacy generators receive preferential access to the grid, solar-generated electricity often goes unused.

- While there will be no doubt about the merits of renewable energy once grid access becomes fairer, significant investment in transmission infrastructure needs to be carried out in order to transport electricity from locations best suited to renewable generation to population centers.

- Japan’s excellent power storage infrastructure means there is a lot of capacity for storing electricity generated overnight by wind farms.

- TAKEAWAY: Mr. Son was an early investor in renewables after the 2011 Fukushima nuclear disaster, and he was one of the key people in pushing through the introduction of a feed-in tariff system in Japan. That said, he remains a divisive figure, especially in government circles, and he is unlikely to hold significant sway over state policy.

Government discusses purchase of forests to fuel biomass power generation (Tokyo Shimbun, August 19)

- The Agency for Natural Resources and Energy today began reviewing the possibility of purchasing forestry land to provide feedstock for biomass electricity generation.

- The government envisages the creation of an “energy forest” planted with broadleaved and fast-growing trees suitable for biomass feedstock.

- CONTEXT: Burning forest for fuel has not yet received the same criticism or scrutiny in Japan that it attracted in the US, not least with the 2019 documentary, Planet of the Humans, promoted by Oscar-winning filmmaker Michael Moore.

- SIDE DEVELOPMENT: “I knew the world would change”—Erex CEO (Nikkei Sangyo Shimbun, August 19)

- Electricity retailer Erex was established in 1999 and chiefly generates electricity from biomass.

- Current CEO Honna Hitoshi said he always remained open-minded about the energy business, believing change was on the way. He was proved right some years later when the global shift away from fossil fuels began.

- In 2018 Erex surprised the market when it announced a major biomass fired power station project that would not be reliant on feed-in tariffs. Homma says he wanted to create the foundations for self-sufficient renewable power generation in Japan.

- CONTEXT: Japan only has about 5 GW of bio-energy power capacity, or one-tenth of its solar generation. The current energy outlook for 2030 sees the industry adding just 1-2 GW of biomass.

Idemitsu Green Power selected as first supplier for Tokyo government’s energy plan (Jiji, August 21)

- Idemitsu subsidiary Idemitsu Green Power has been selected as the first supplier to provide electricity under the Tokyo Metropolitan government’s 100% renewable energy scheme.

- Idemitsu Green Power will purchase electricity generated from renewable sources under the feed-in tariff scheme, and on sell it to the Tokyo Metropolitan government for use and resale.

- Tokyo has pledged to source 100% of the electricity used at government-owned facilities from renewable sources by 2050.

ANALYSIS & COMMENTARY

| Japan is Gingerly Moving Into Hydrogen: How serious is it? | |

| KUMIKO SHIBAOKA,HEAD OF RESEARCH,SHULMAN ADVISORY | Much activity – and much hype – has surrounded the push towards the adoption of hydrogen as a key fuel in Japan. We look at how much progress has actually been made.

POLICY In December 2017, Japan’s “Basic Hydrogen Strategy” was approved by the Cabinet. It has two main goals. 1) Reduce dependence on imported energy sources. Cost of imported fuels for energy skyrocketed after the 2011 Fukushima disaster, while the country’s level of energy self-sufficiency sank to the 6 – 7% range in the post-Fukushima decade, putting Japan second to last in the list of 34 OECD member countries. 2) Achieve carbon emissions reduction targets. The government has vowed as part of the Paris Agreement to cut the nation’s FY2030 emissions by about 25% compared with FY 2005 levels. MAIN PROJECTS AND COSTS Japan has taken an active role in engaging to build both a domestic and an international supply chain for hydrogen. That said, all efforts are as yet at a demonstration stage. On the domestic front, Japan unveiled the world’s largest electrolytic hydrogen production site in February of this year. The Fukushima Hydrogen Energy Research Field (FH2R) facility is primarily powered by on-site solar panels. The pilot project was meant to supply hydrogen for the now postponed 2020 Tokyo Olympics flame, as well as for the various fuel cell vehicles and stationary fuel cell power supply systems that were slated for use at the games. Internationally, Japan kicked-off its hydrogen efforts by teaming up with Australia back in 2015. The two countries plan to build hydrogen production, gasification and loading facilities in Australia, and receiving facilities in Japan. The production facilities will run on brown coal, utilizing an Integrated Coal Gasifier Combined Cycle (IGCC). First shipments to Japan are due this fall. Japan has even created the world’s first dedicated hydrogen tanker. Japan is testing a different hydrogen strategy via a project in Brunei. Last year, Japan received the first shipment of hydrogen in the form of methylcyclohexane (MCH). That compound, which combines hydrogen with toluene, can be shipped via conventional tankers. However, it requires processing on arrival in Japan to extract the hydrogen. As all the projects start to ramp up, Japan expects prices for hydrogen to fall. There is some evidence for that already. In 2017, Japan procured about 200 metric tons of hydrogen at a price of ¥100 / Nm3. The 2030 target is to procure 300,000 tons at a price of about ¥30 / Nm3, with the longer-term target of bringing that down to 20 yen. By comparison, the price of natural gas, when adjusted to the calorific value of hydrogen, currently stands at about ¥16 / Nm3.

Vehicles Japan set ambitious targets for the proliferation of hydrogen fuel cell vehicles (FCV) and supporting infrastructure throughout the country. In 2018, about 3,000 FCVs were registered in Japan. They can fill up at 132 fueling stations. The government wants FCV numbers to jump to 200,000 by FY 2025 and 800,000 by FY 2030. This is expected to cut the price difference between FCVs and hybrid vehicles (HV) from the current average of ¥3 million to about ¥700,000. The strategy sees the gap shrinking due to the lower cost of components and more FCV auto models, with appeal to the mass market. In line with greater public use of FCVs, Japan wants to bolster hydrogen station numbers to 320 stations by FY 2025 and 900 by FY 2030. The idea is that by reducing the cost of construction of hydrogen stations from ¥350 million to ¥200 million and cutting their operating costs by more than half by FY 2025, these facilities will be able to operate as fully commercial ventures independent of state support by the second half of the 2020s. Power Generation In 2018, Japan turned on the world’s first heat and power hydrogen-fired facility in an urban area with the launch of a test project in the city of Kobe. The plant used 100% hydrogen fuel. Work to improve the plant’s efficiency is ongoing. Meanwhile, major engineering firm Mitsubishi Hitachi Power Systems has developed a generation plant that can flexibly use hydrogen and natural gas together. The major challenge here is cost of electricity. As of 2019, the unit price for electricity produced in hydrogen-fired plants in Japan was ¥52 / kWh. The government aims to bring it down to ¥17 / kWh by 2030, and subsequently to bring it down to parity with other forms of thermal power. EXPORT POTENTIAL Japan sees hydrogen-related technologies as something that could grow into an export industry. The dedicated liquefied hydrogen tanker in the Australia-Japan demonstration project was built by Kawasaki Heavy Industries. Hydrogen is cooled even further than LNG. The former’s temperature has to be brought down to minus 253° C for transport on a ship. The resulting liquid hydrogen is just 1/800 the volume of hydrogen in its gaseous form. On the power generation side, Mitsubishi Hitachi Power Systems this year recorded a sale of its hydrogen-enabled combined cycle gas turbine plant technology. The buyer, a US IPP, initially plans to keep the fuel ratio at 30% hydrogen and 70% natural gas. If all goes well, the plant will shift to 100% hydrogen-generation by 2045. The ability to run both fuels is a risk-hedge for utilities, with future energy economics unclear. TAKEAWAY Taken at face value, Japan appears to be moving aggressively towards its goal of “realizing a hydrogen society”. The government targets are aggressive and industry appears to be on board. However, as most Japanese investment is in plants overseas that work only on a demonstration level, it’s hard to accept this as a serious effort. The goal of the hydrogen strategy was to improve energy independence. This will require a rollout of large-scale domestic hydrogen production. Equally, the other target of using hydrogen to cut emissions requires Japan to secure so-called green hydrogen. There does not appear to be an aggressive plan for that. Meanwhile, Japan is logging extra carbon emissions from the transport of hydrogen. |

| Company Profile: JERA,

Japan’s New Power Colossus Paving its Way to an IPO | |

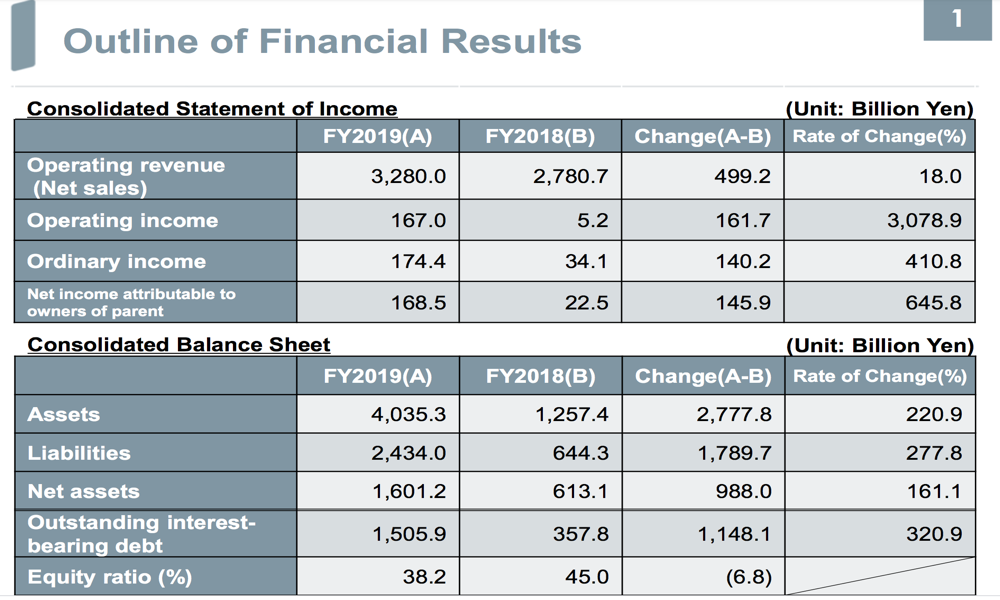

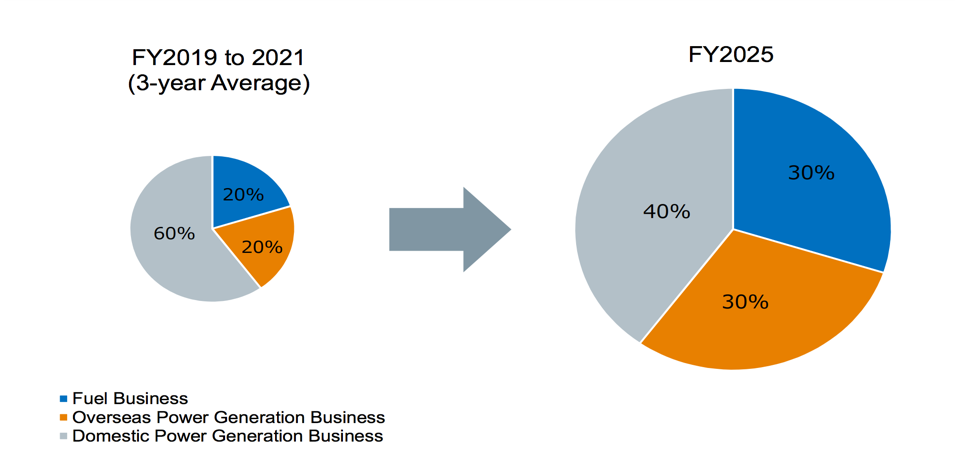

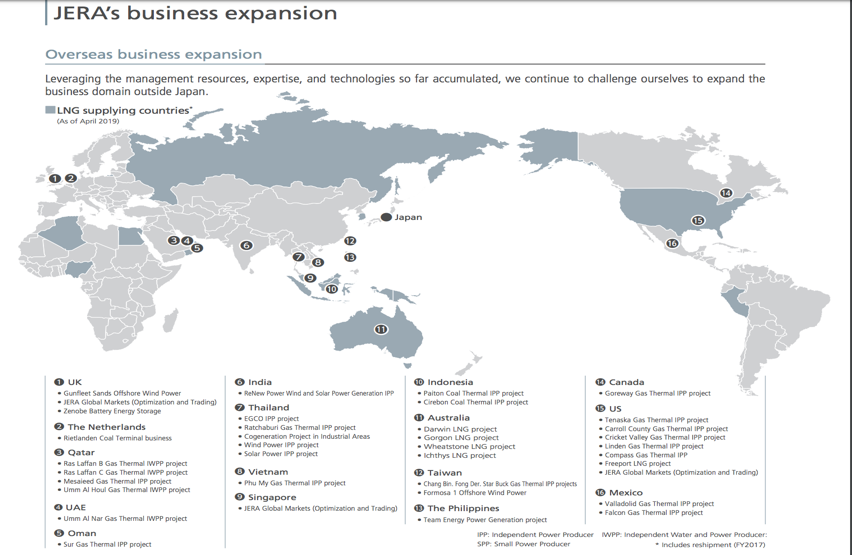

| TOM O’SULLIVAN,DIRECTOR,K.K. MATHYOS | Company OutlineJapan’s JERA was born in 2015 as a 50/50 joint venture between Chubu Electric Power (‘Chubu EPC’) and Tokyo Electric Power (‘TEPCO’) to create a separate thermal power generation operating conglomerate, and to consolidate LNG and coal purchasing power in a single entity. JERA was established in the aftermath of the devastating 2011 Tohoku earthquake, tsunami, and nuclear accident that crippled Japan’s nuclear power industry and seriously damaged the reputation of Japan’s largest electricity company, TEPCO.The creation of JERA, which may have been initiated by the Ministry of Economy Trade & Industry (‘METI’), broke TEPCO into a ‘bad bank’ and a ‘good bank,’ with the ‘bad bank’ retaining the inactive nuclear portfolio, and the residual thermal generation portfolio switching to JERA.After only five years JERA is already Japan’s largest supplier of electricity and bigger than most national state electricity systems, with 26 separate generating stations and a combined domestic and international generation capacity of 76 GW, which equals almost 50% of the power capacity of the African continent. It currently produces around 200 TWhs of power per annum, comprising almost one fifth of Japan’s overall electricity demand.It is also the largest acquirer of LNG in the world at 35 metric tons per annum, buying from 17 different countries and operating 18 LNG vessels. JERA owns eight LNG receiving terminals and controls 40% of Japan’s LNG tank capacity. JERA’s interests span from upstream natural gas investments to renewable energy generation. It is invested in five natural gas upstream projects. In Australia JERA is invested in Wheatstone, Ichthys, Gorgon, and Darwin LNG, and in the US, in the Freeport LNG terminal. JERA still owns 10GW each of legacy coal and oil generation capacity. In renewable energy JERA is expanding into wind power and is also investing in power storage capacity. Financials JERA, which is mainly a B2B business, has revenues of $34 billion, a balance sheet of $36 billion, and expects to generate a profit of close to $2 billion by 2025. It also expects to increase its operational renewable energy generation assets to 5GW over the next five years.  The market capitalization of Chubu EPC and TEPCO is now respectively $9.3 billion and $4.6 billion. JERA might be expected to command a valuation of between $10 billion and $15 billion if it were to IPO. TEPCO is now over 50% owned by the Japanese government and hence JERA is 25% state-controlled. Floatation on the Japan Stock Exchange would monetize some of the Japanese government’s stake in TEPCO. JERA’s Revenue Split  International Footprint Overseas, JERA operates in Singapore, Thailand, Netherlands, Australia, the US, and more recently in Bangladesh, where it has just secured $700 million of funding from Japanese financial institutions for an LNG–to-power project located 40 km from the capital, Dhaka. Domestically, JERA operates thermal power plants in eight Japanese prefectures: Niigata, Fukushima, Ibaraki, Chiba, Kanagawa, Tokyo, Aichi, and Mie. The largest thermal power plant in the portfolio has a capacity in excess of 5GW.  Management Toshiro Sano from TEPCO serves as chairman and Satoshi Onoda from Chubu EPCO serves as president. JERA has recently appointed David Crane, former NRG Energy CEO, to its Board of Directors. Crane is expected to bring experience gained in the US and UK energy markets that saw increased competition as a result of deregulation. Crane is now a self-confessed renewables evangelist. Other non-Japanese members of the JERA board are Hendrik Gordenker, a former White & Case Lawyer, Mike Winkel, a former member of the E.ON Management Board, and David McFarlane, a former EdF Trading executive. Challenges The strategic issues for JERA as we see them are as follows: 1. It is locked into long-term natural gas procurement contracts at a time when natural gas prices are very low. 2. It has 20GW of oil and coal generation capacity, which may need to be decommissioned in the short to medium term. 3. Most of its power is sold B2B to TEPCO and Chubu. 4. Its renewable energy portfolio is too small and overall RE aspirations might be too narrow. 5. Its thermal plant portfolio may be too concentrated in an era when electricity is becoming more distributed and decentralized. 6. It may have too much Australian exposure. 7. The lack of a retail business means that its retail data and digital reservoirs are limited, inhibiting its ability to cross-sell. On the positive side, JERA is building an aggressive international portfolio of assets. But, going forward, and prior to any IPO, the company will need to ensure that its portfolio addresses risk from the Five ‘D’s: 1). Decarbonization 2). Decentralization 3). Digitalization 4). Depopulation 5). Disaster |

NRG Weekly Event

Summary of the Webinar: “Outlook for Nuclear Power in Japan”

Hosted on 20 August 2020

NRG Weekly on Aug. 20 hosted its first webinar on the outlook for nuclear power in Japan, building on interest in the topic that arose from commentaries in our Aug. 17 and Aug. 11 editions.

NRG Weekly presented an analysis of the history of nuclear power in Japan, current status of re-starts, factors that are impacting re-starts, and our assessment of the government’s plans for nuclear power in 2030, the next target date for Japan’s revised energy mix.

Four leading experts on energy and nuclear power joined the webinar to add their views.

Nobuo Tanaka (Former Head of International Energy Agency and former Chairman of the Sasakawa Peace Foundation);

Vincent DuFour (General Representative Japan & Korea for EdF, which is the largest operator of nuclear plants in the developed world);

Tomas Kaberger (Board Member of Vattenfall, the Swedish utility that operates several nuclear power plants, and Chair of the Board of the Renewable Energy Institute); and

Shaun Burnie (Senior Nuclear Specialist, Greenpeace)

Webinar participants included nuclear energy experts from the UK, France, and the United States, all of which have significant investments and dependencies on nuclear energy in their respective national electricity mixes. All G7 countries with the exception of Italy are invested in nuclear energy.

There was an extensive discussion between the guest experts on decarbonization of the energy mix, existing and new nuclear technologies, the nuclear fuel cycle, spent fuel storage capacity, impacts on the nuclear industrial base, international cooperation, economics of nuclear power, and an assessment of Japan’s national energy policies with respect to nuclear power.

With the 10th anniversary of the 2011 Fukushima Nuclear Accident only seven months away, Japan is facing unique energy challenges – only four nuclear reactors are currently operating, two in Kyushu and two in Kansai,. To meet the government’s nuclear energy targets at least another 20 reactors may need to be restarted over the next decade. Japan is also struggling to meet its decarbonization goals as defined in the Paris Agreement.

Recently, Japan’s Nuclear Regulation Authority gave approval to new safety measures put in place at the Rokkasho complex in the north of the country, which many saw as one of the final steps to begin the reprocessing of spent nuclear fuel in Japan. The complex has been blighted by cost and scheduling delays to the point where it is almost a national embarrassment. And yet, the day after we hosted the webinar, the operator of Rokkasho announced a 25th delay to its operating schedule, putting back the starting date by another 12 months.

For further information on the Aug. 20 webinar and future NRG Weekly events please feel free to reach out to Yuriy Humber or Tom O’Sullivan directly, or contact us at nrgnews@yuri-invest-research.com .

STOCK MARKET PERFORMANCE

| As of close on August 21, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| COSMO ENERGY HOLD. | 5021 JP | 136.99 | -3.92 | -32.34 | -1.82 | |

| ENEOS HOLDINGS INC | 5020 JP | 1,307.62 | -2.95 | -16.27 | 3.19 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 691.34 | -1.53 | -20.93 | 0.30 | |

| INPEX CORP | 1605 JP | 964.69 | -2.71 | -40.90 | -0.63 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 100.76 | -4.55 | -39.50 | -5.67 | |

| Industrials | ||||||

| CHIYODA CORP | 6366 JP | 71.33 | -1.08 | -3.18 | -2.84 | |

| JGC HOLDINGS CORP | 1963 JP | 301.99 | -4.51 | -32.70 | 2.37 | |

| MITSUBISHI CORP | 8058 JP | 3,432.02 | -0.06 | -18.07 | 2.08 | |

| MITSUI & CO LTD | 8031 JP | 3,030.69 | -0.42 | -6.99 | 7.72 | |

| Utilities | ||||||

| CHUBU ELECTRIC POWER | 9502 JP | 998.67 | -0.04 | -13.16 | -0.87 | |

| KANSAI ELECTRIC POWER | 9503 JP | 965.96 | -1.20 | -16.96 | -1.81 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 447.63 | -0.84 | 1.58 | 3.40 | |

| J-POWER | 9513 JP | 294.16 | 0.31 | -38.25 | -5.41 | |

| TOKYO GAS CO | 9531 JP | 1041.27 | -0.70 | -10.23 | -9.50 | |

| OSAKA GAS CO | 9532 JP | 872.94 | 0.14 | 1.39 | -0.43 | |

| TOHO GAS CO | 9533 JP | 506.38 | 0.10 | 8.08 | -5.61 | |

| SAIBU GAS CO | 9536 JP | 91.33 | -2.07 | -2.13 | -3.61 | |

| SHIZUOKA GAS CO | 9543 JP | 66.82 | -0.79 | -6.97 | 0.92 | |

| TOKYO ELECTRIC POWER | 9501 JP | 496.57 | -1.90 | -33.83 | -2.83 | |

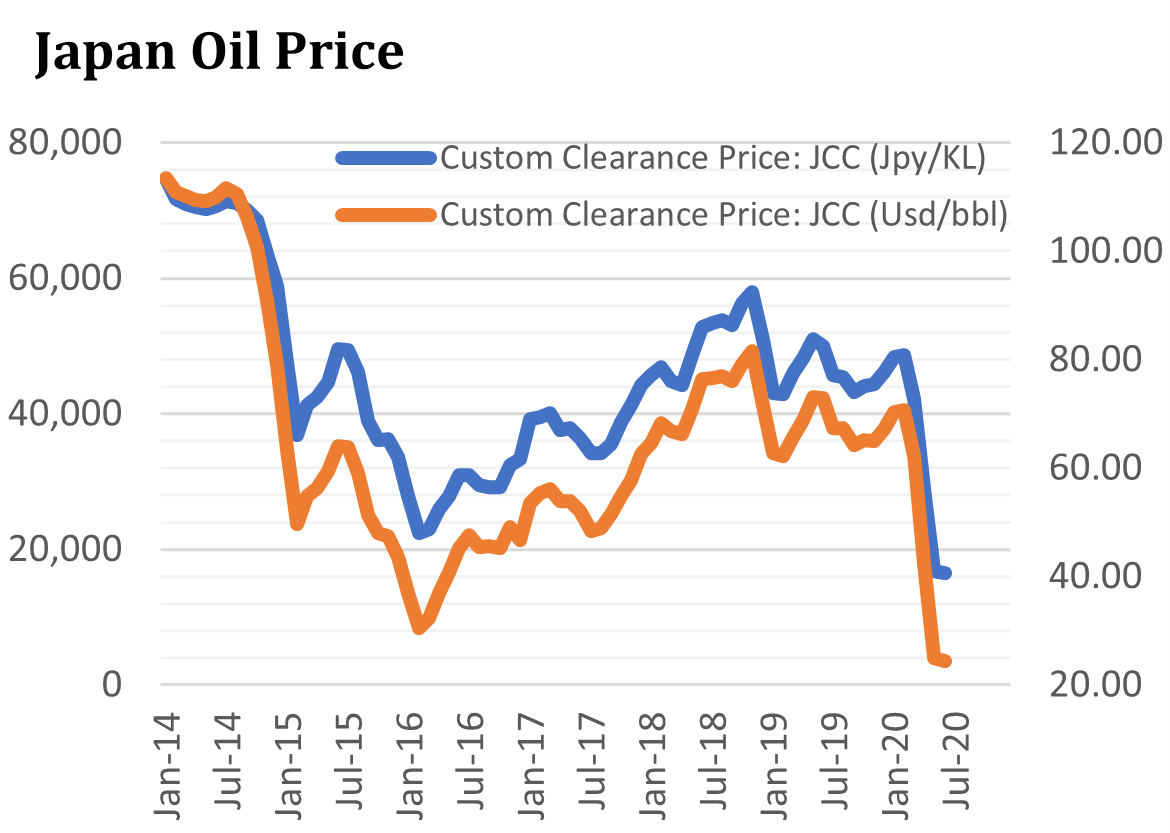

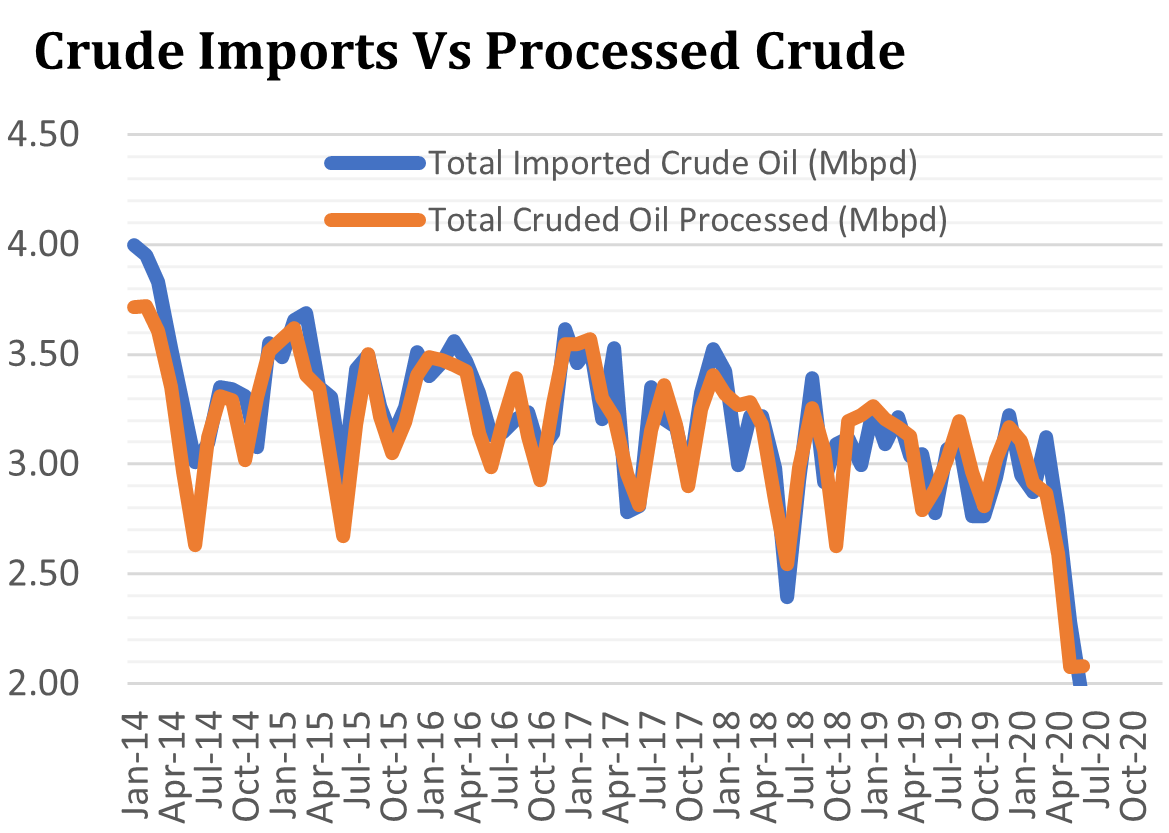

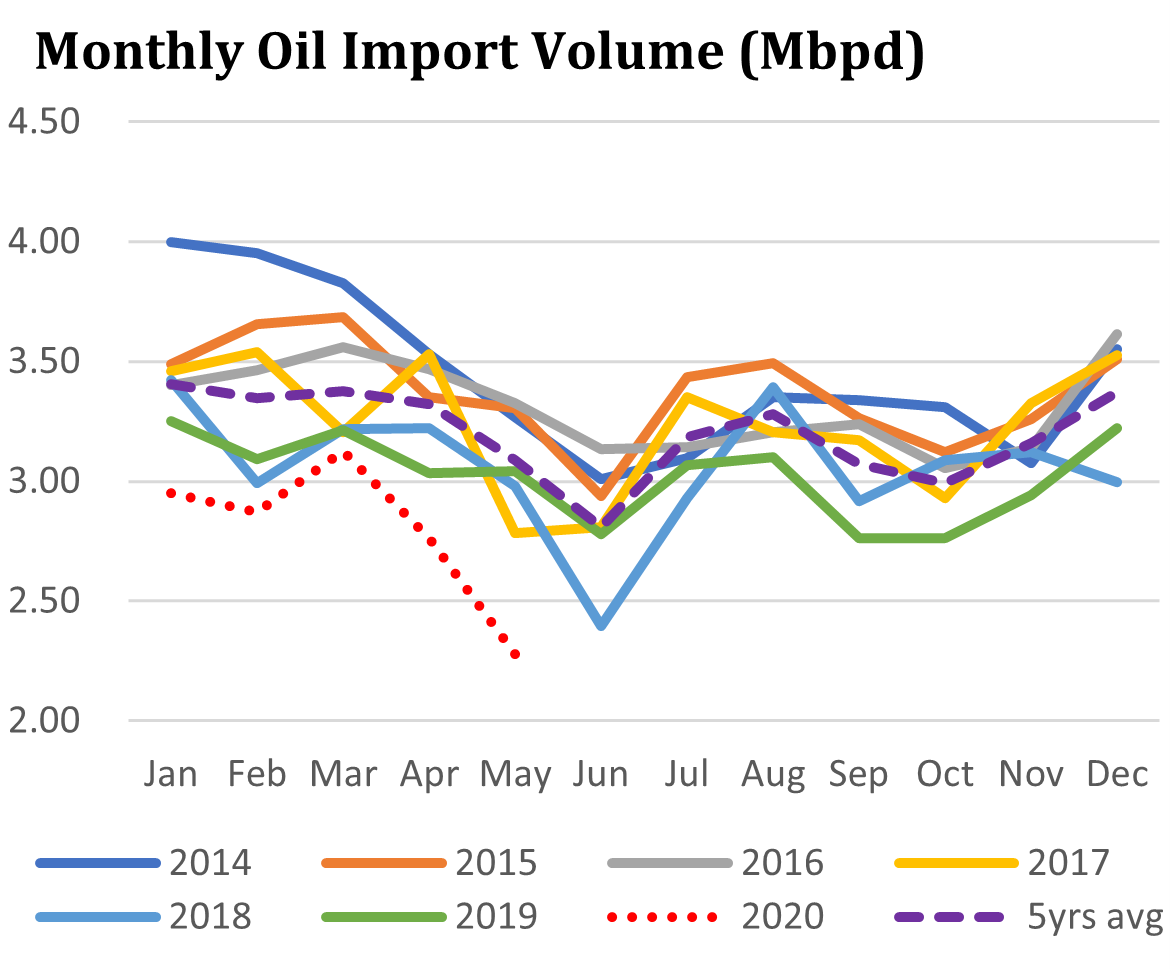

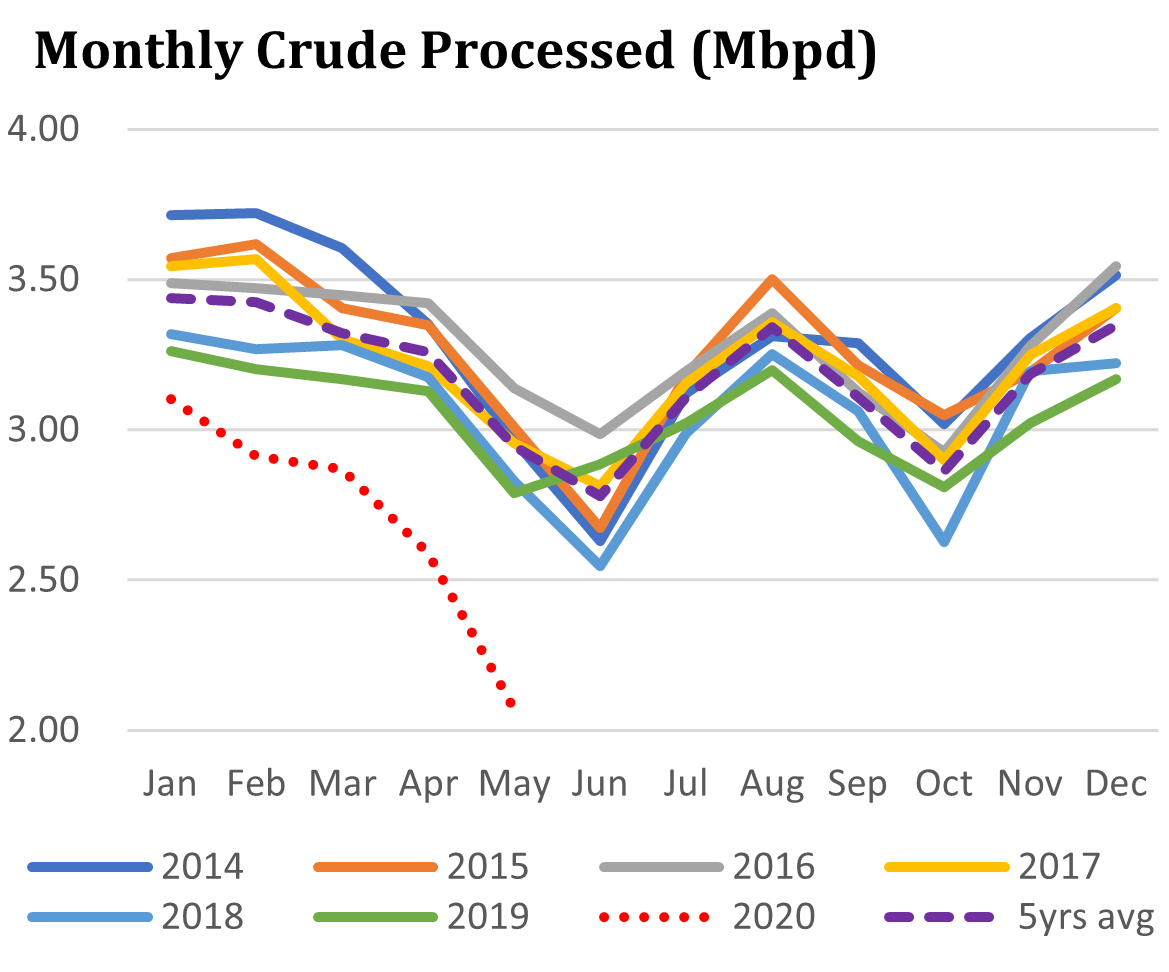

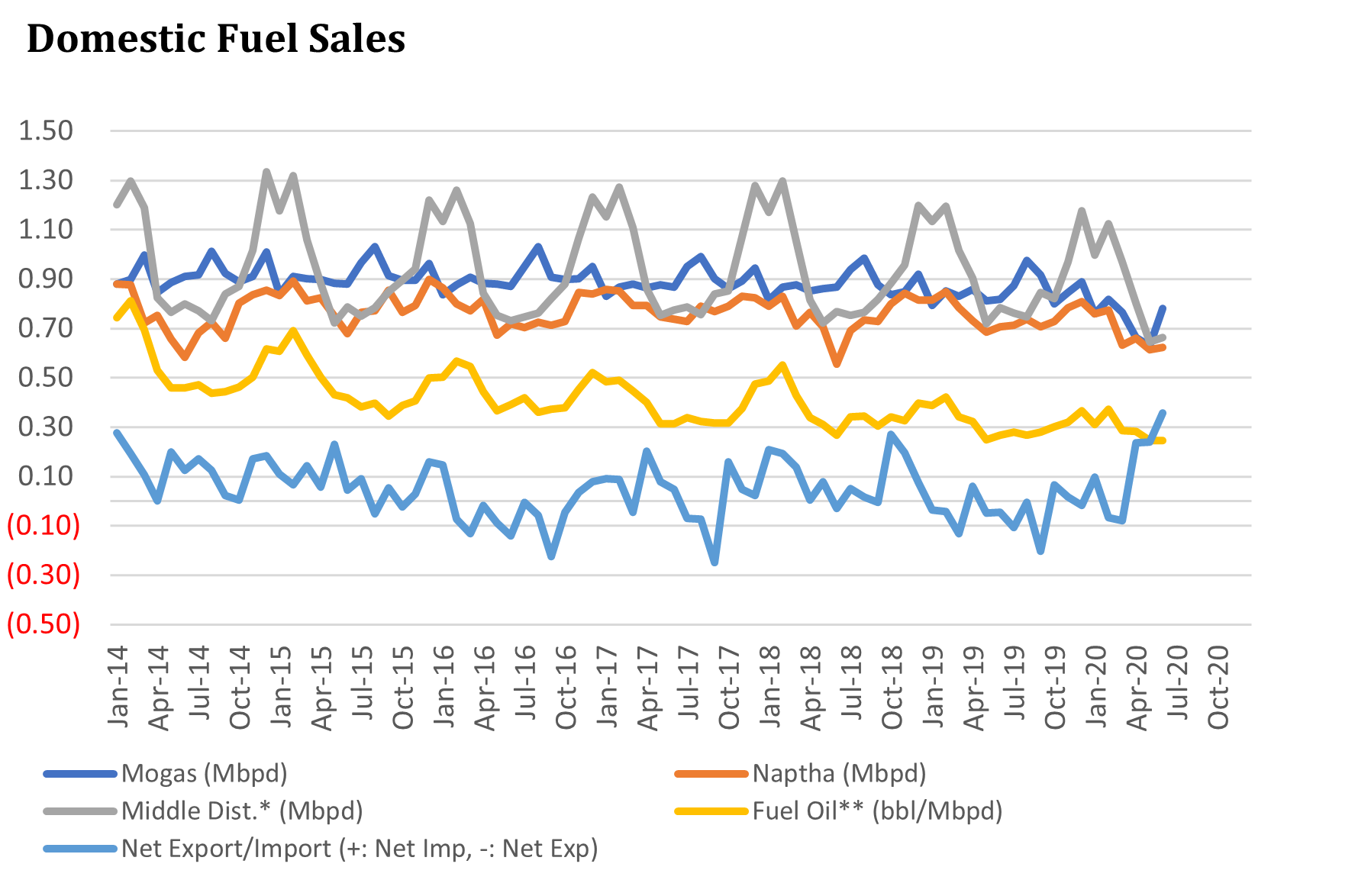

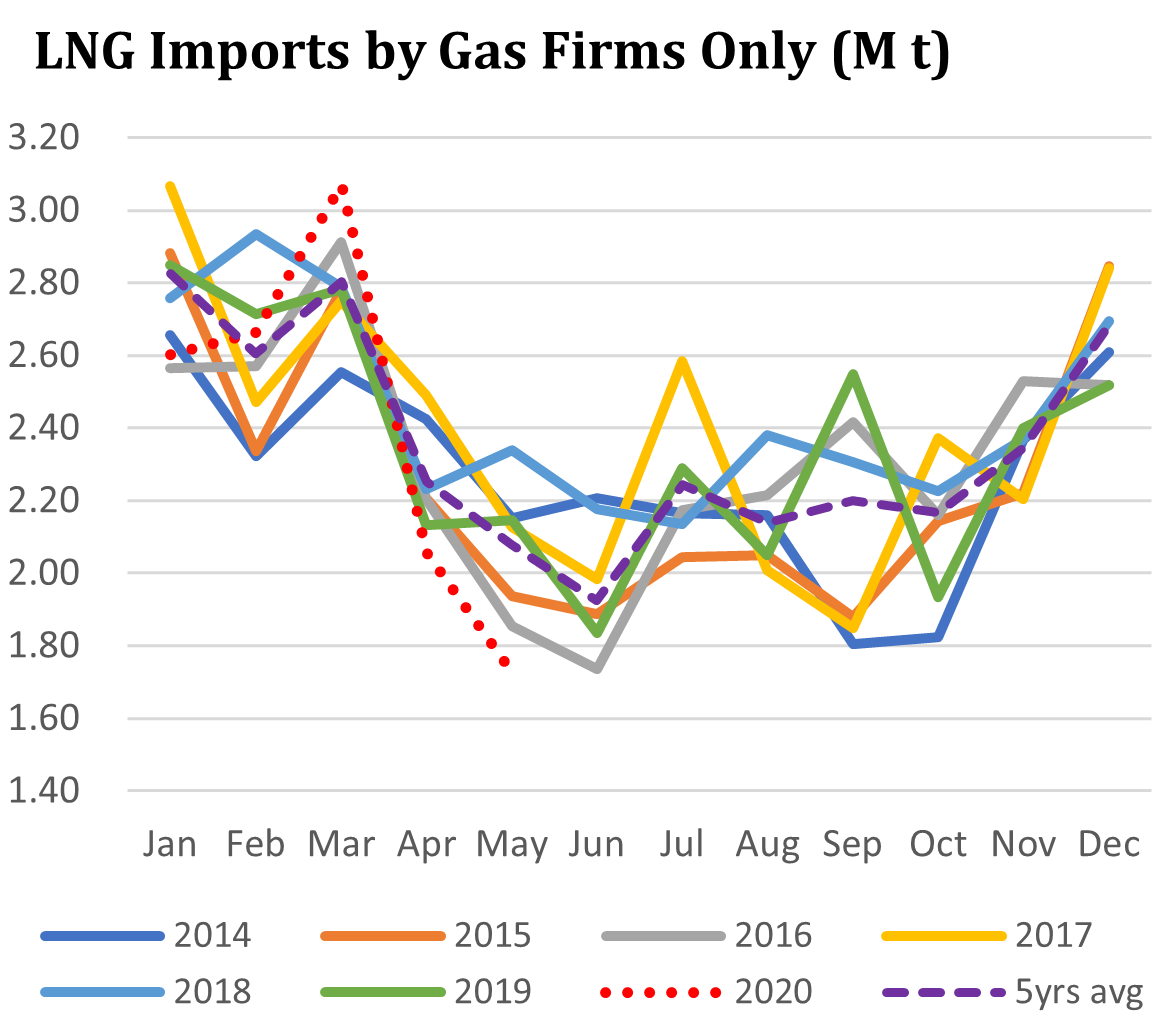

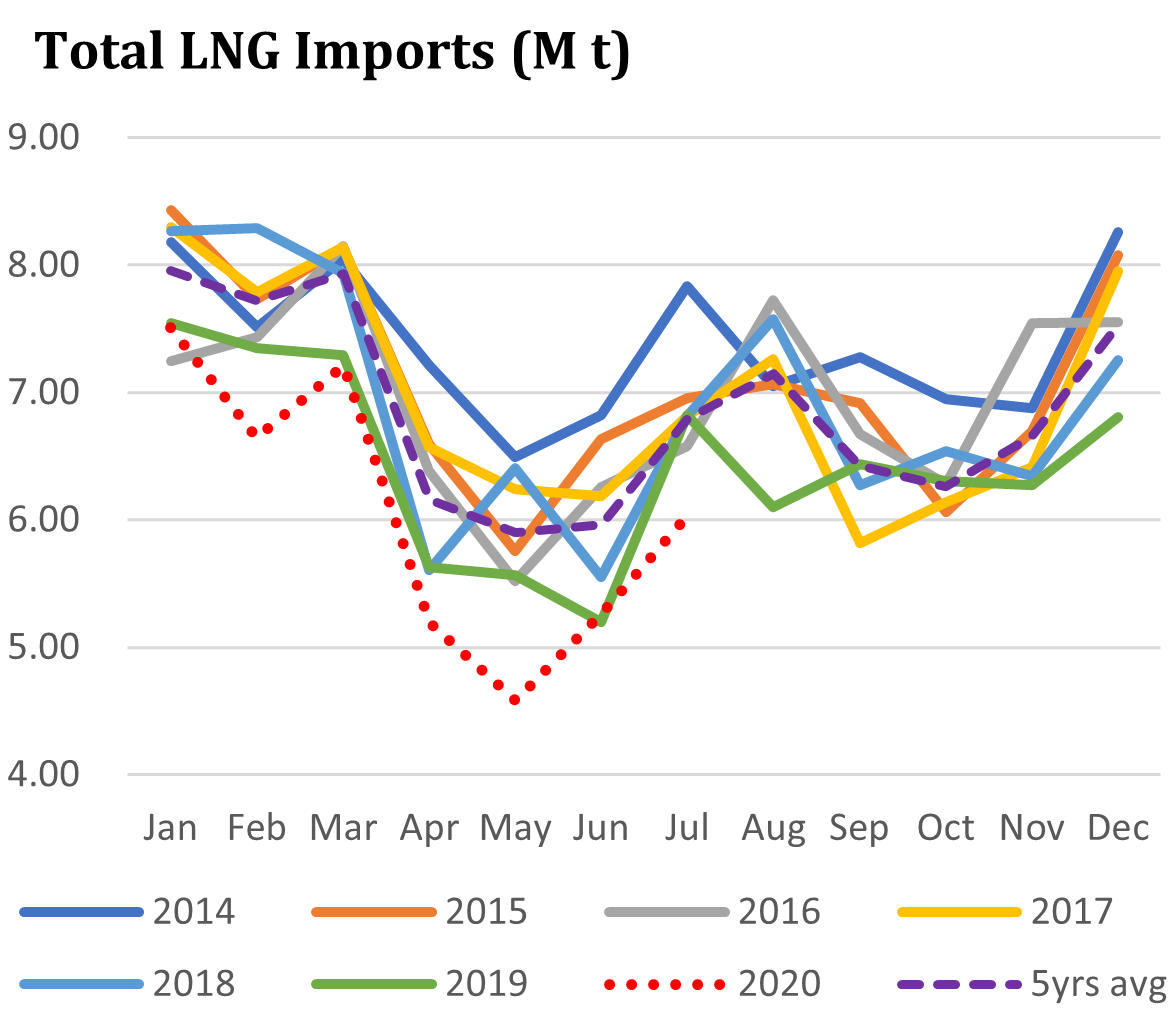

DATA

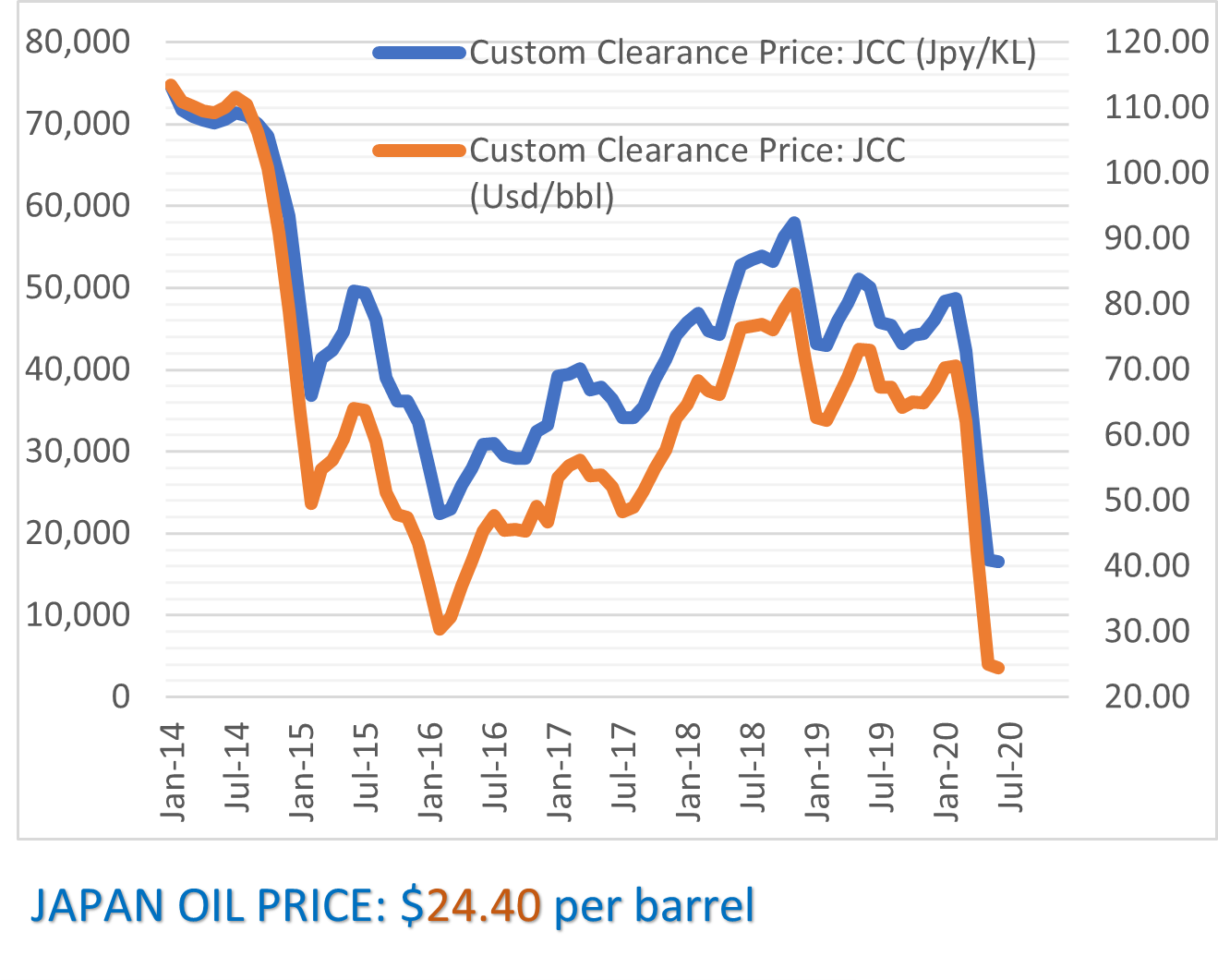

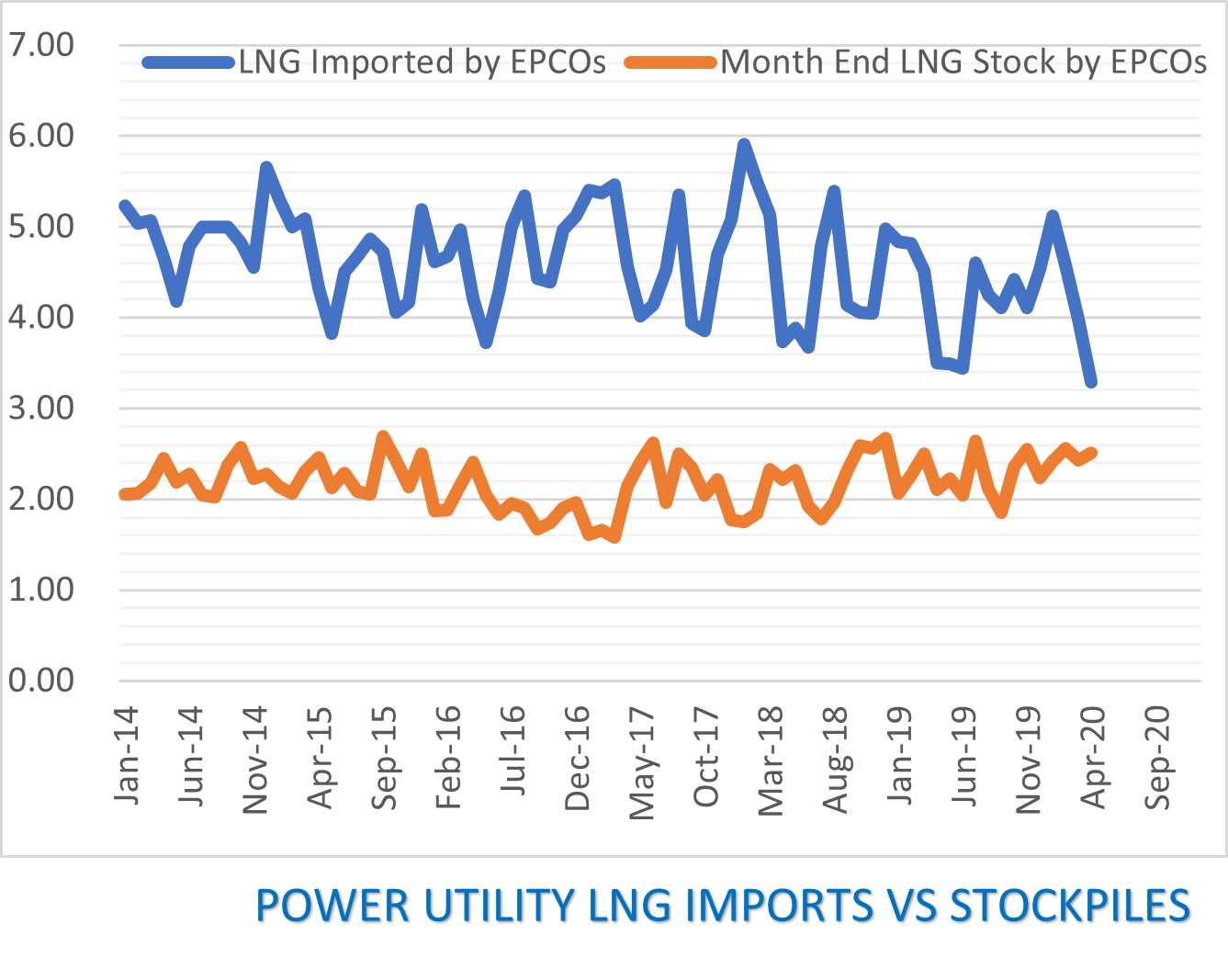

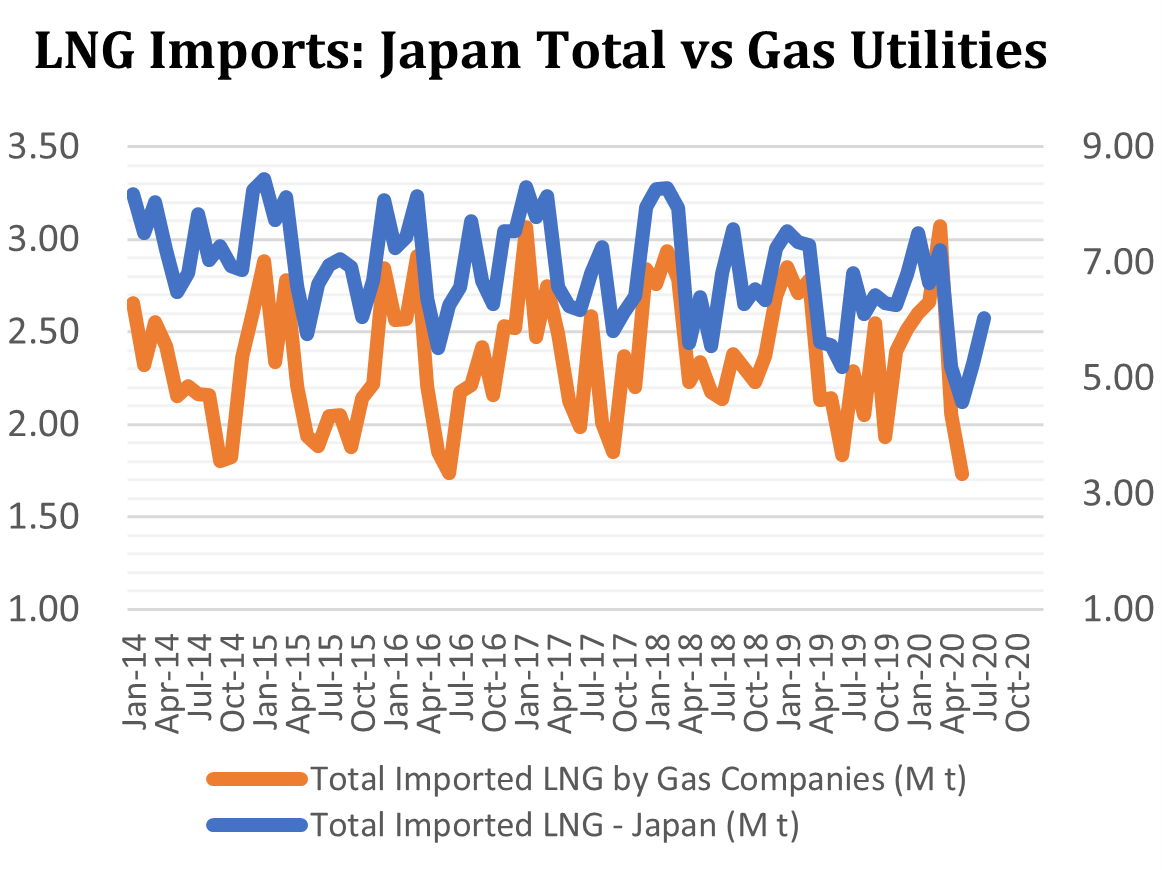

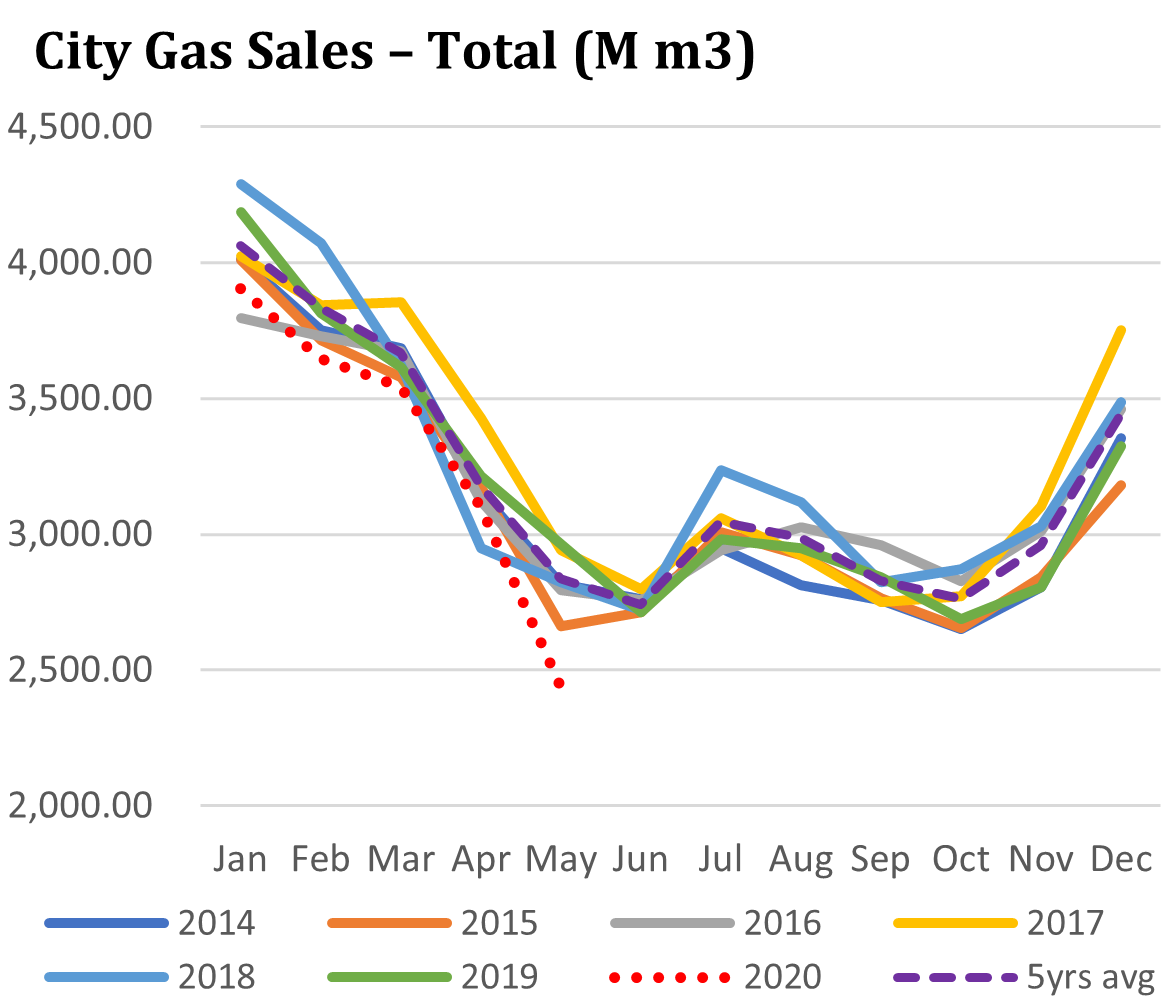

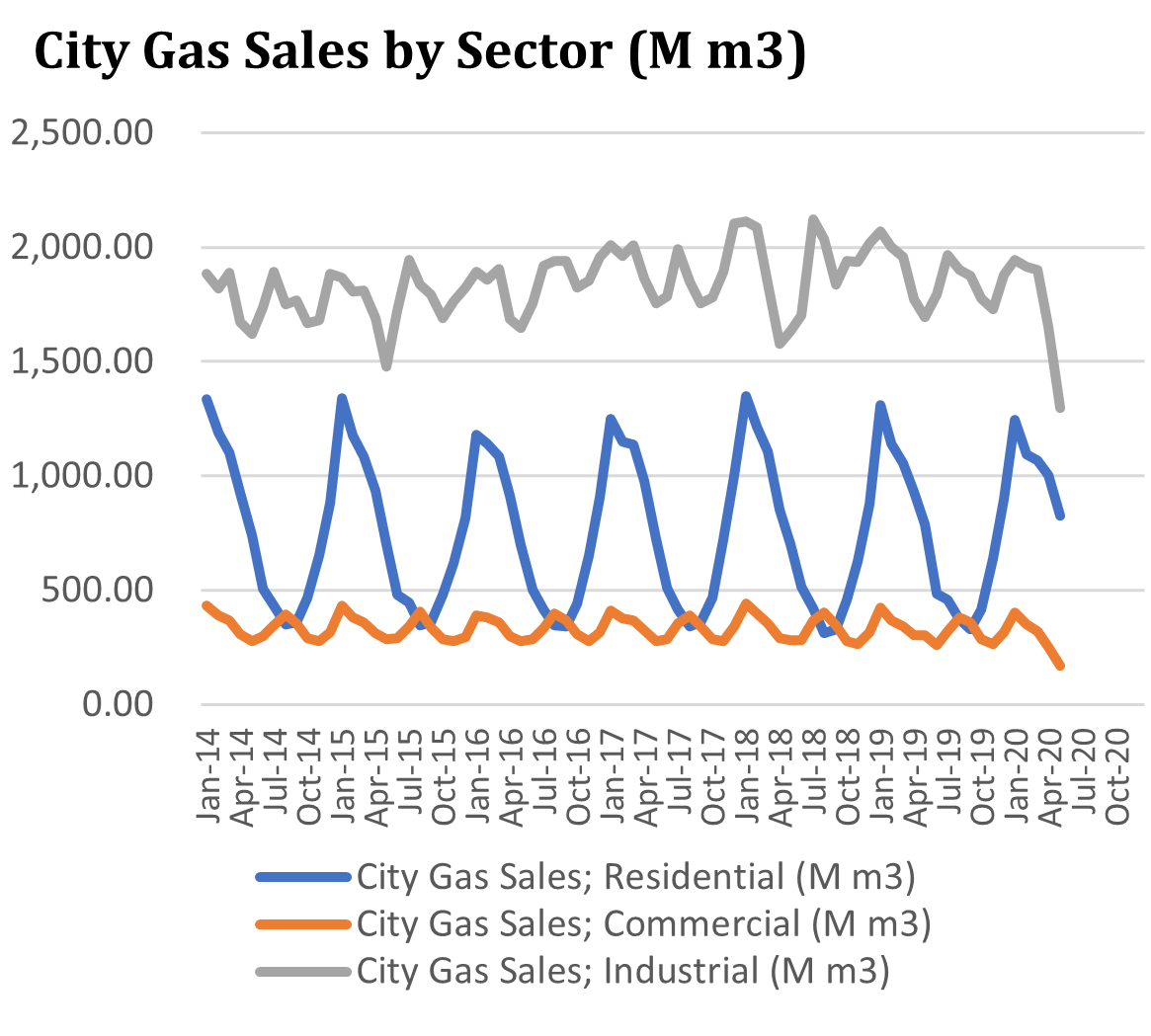

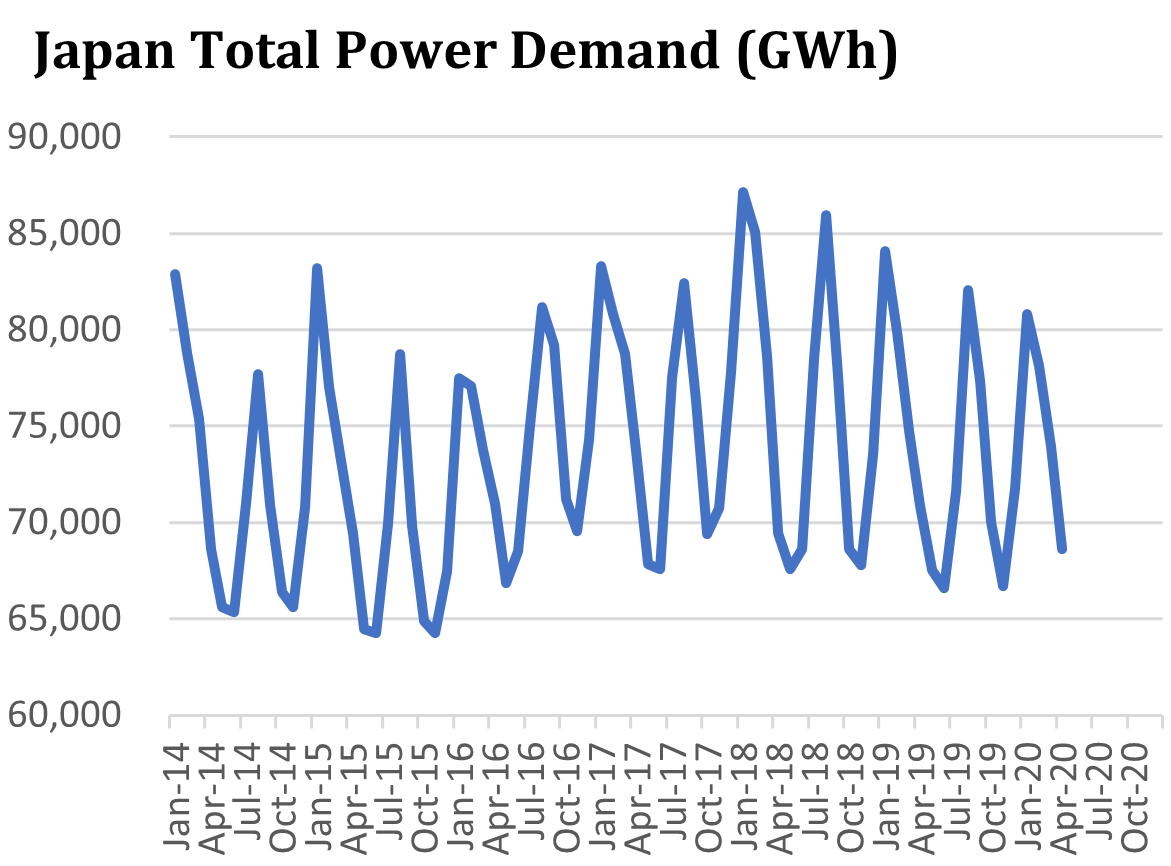

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

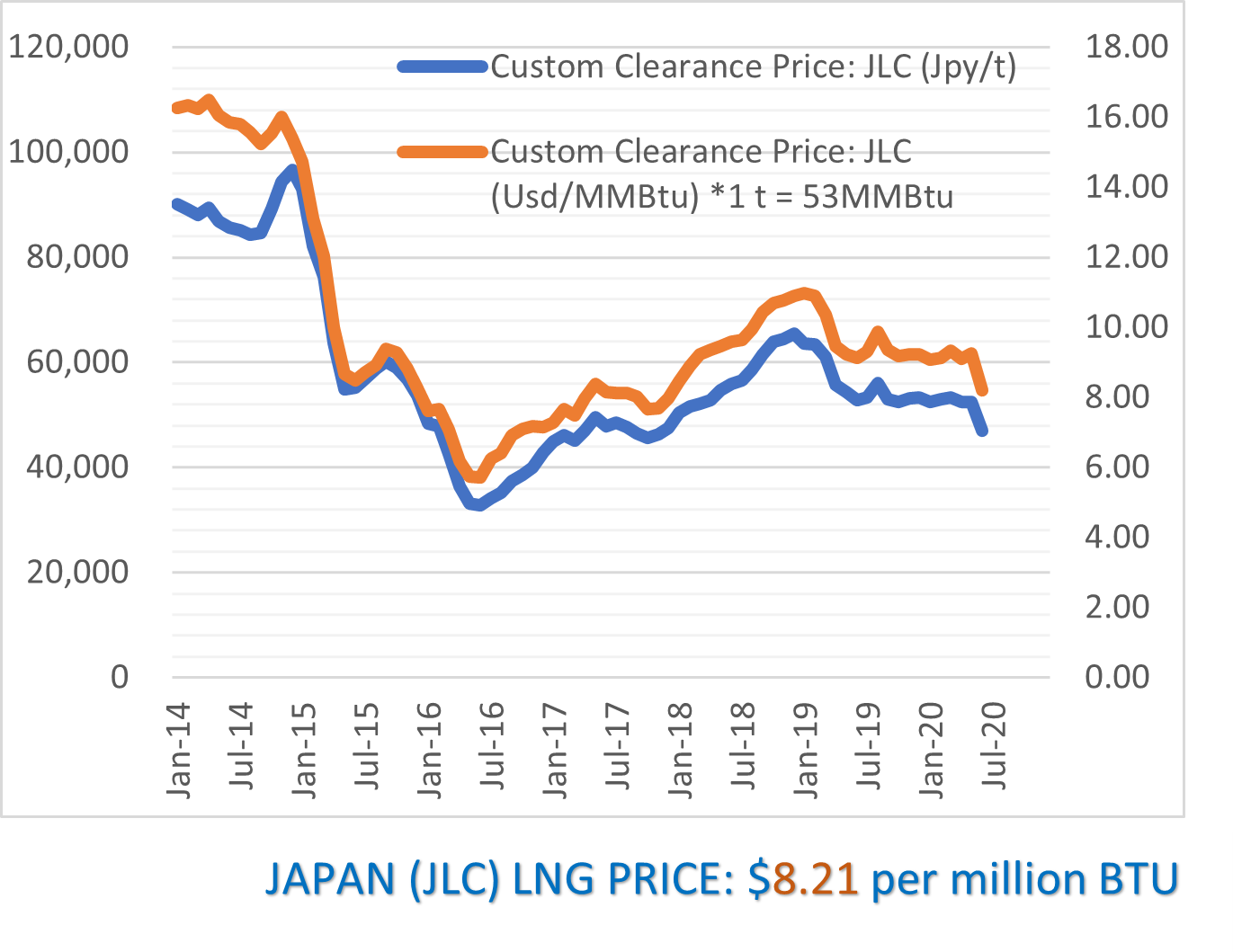

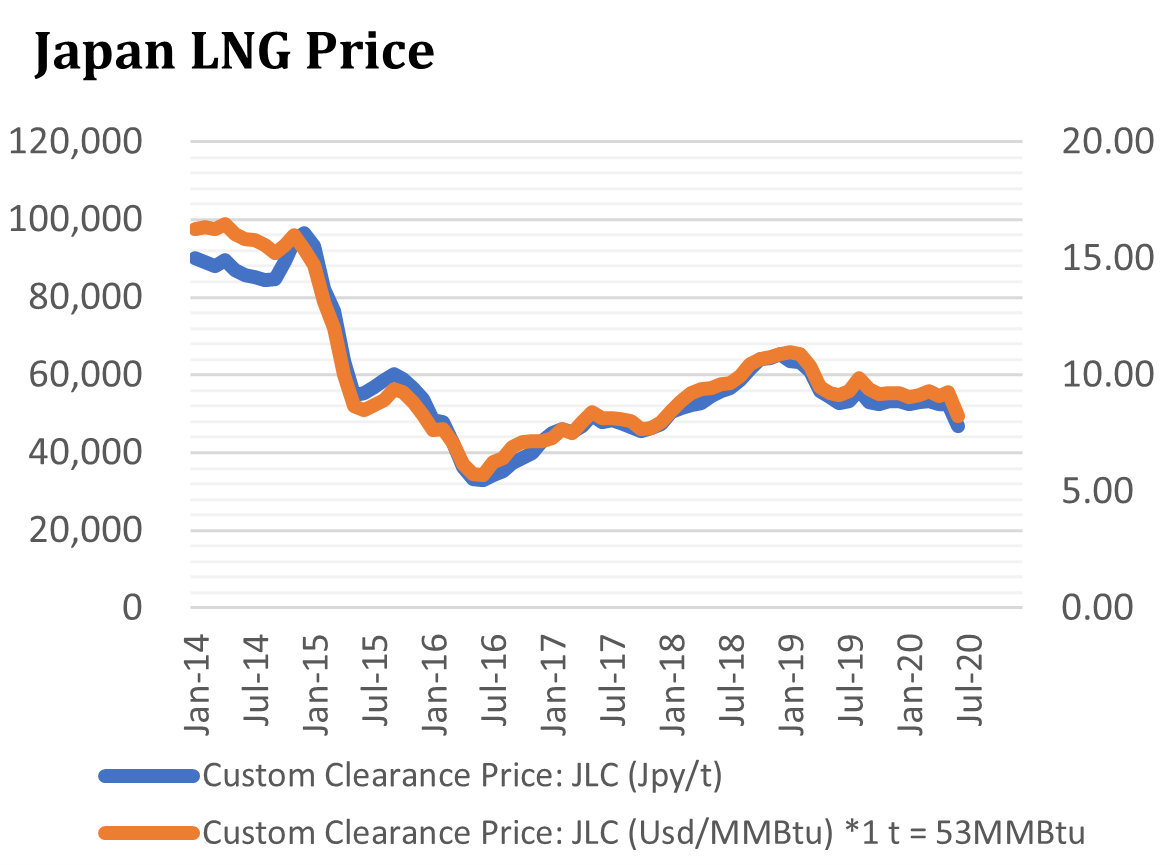

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Ministry of Finance.

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

DISCLAIMER

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest Research Ltd., which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

Recipients of this report should ensure that they fully understand the legal, tax and accounting implications before making an investment decision and independently determine that the transaction is appropriate based on their own objectives, experience and resources.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided.

In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.