JAPAN NRG

WEEKLY

JAPAN NRG WEEKLY

August 31, 2020

TOP

- Japan unveils its biggest hydrogen filling station

ENEOS and JERA launch the commercial site

JERA also files plan for 520 MW offshore wind project - J Power’s new VP positions firm as a hydro, not a coal utility

Co. sees offshore wind as a “challenging” sector - Carbon capture and recycling promotion gaining speed

OIL & GAS

- Fukushima’s new gas-fired power station now online

- Honda to launch its first electric vehicle in October

- Tokyo Gas repairs plan hits 100,000 subscribers

POWER & NUCLEAR

- Total cost of decommissioning Fukushima nuclear plant still unknown

- Japan could employ efficiency tricks to retain some coal capacity

- Tohoku grid forced to buy power from TEPCO in sweltering heat

- Institute of Applied Energy calls for better use of thermal storage

- Expert says Japan already overtaken by South Korea in nuclear

RENEWABLES, OTHER

JAPAN’S LNG PURCHASING STRATEGY NEEDS

A RETHINK: E-TRADING SHOWS ALTERNATIVES

Japan chronically overpays for its energy resources and nowhere has this been more blatant than in its LNG imports. This year, the Japan “premium” ran to over $6 MMBtu, with major losses on for the buyers. With the strong emergence of electronic trading in LNG, there is a chance to Japan to regain its price influence. With other nations embracing the trend, will Japan re-think its strategy?

JAPAN’S THERMAL COAL COSTS LOOK SET TO RISE

AS TRADING HOUSES GET THEIR CANARY MOMENT

A month after Japan said it would shut older coal-fired power plants, the world’s biggest mining firm said it would exit thermal coal production. The result will likely persuade Japanese trading firms to follow BHP out of that door, leaving thermal coal mines to less efficient players. Coal-fired generation is about to get more expensive, adding to the pressures on the sector.

HOUSE VIEW Shinzo Abe’s Legacy

In a bombshell announcement Friday Japan’s longest-ever serving prime minister and architect of Abenomics announced his resignation after almost eight years. Shinzo Abe took office the year after the Great Tohoku Earthquake that devastated a nuclear power plant in Fukushima and crippled the global nuclear power industry. This precipitated a significant overhaul of Japan’s energy policies. Since Prime Minister Abe came to power in 2012 … MORE

NEWS: OIL & GAS

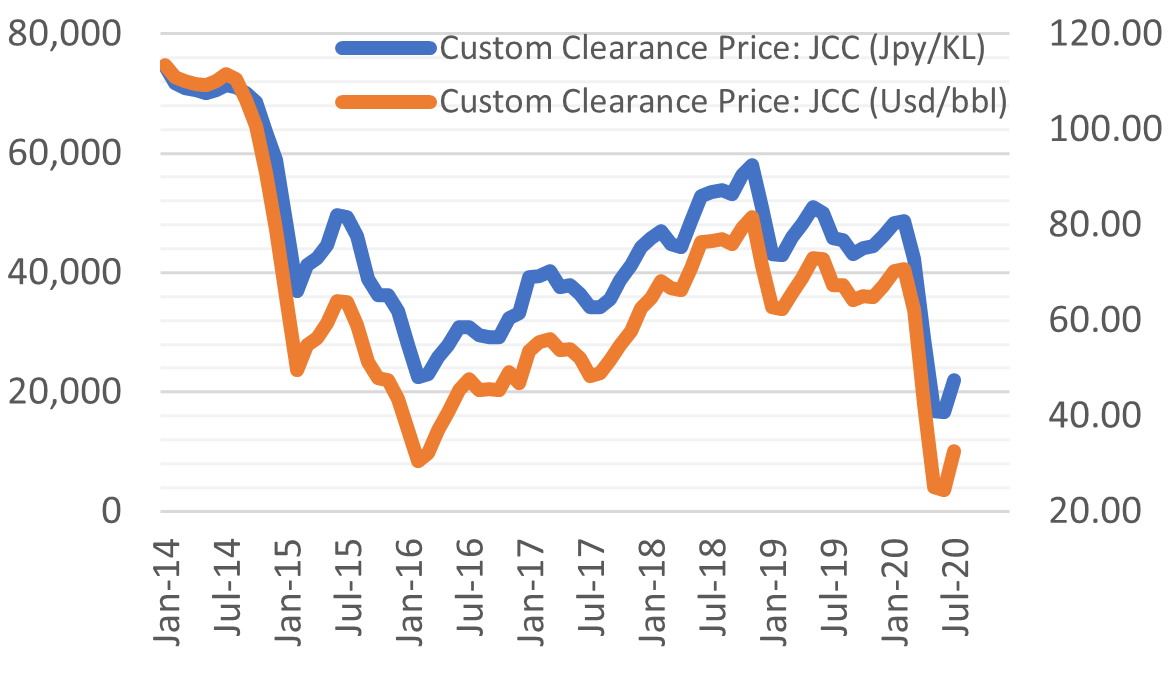

JAPAN OIL PRICE: $32.70 per barrel

JAPAN (JLC) LNG PRICE: $8.21 per million BTU

Fukushima’s new LNG terminal and gas-fired power station now online (Nikkei, August 25)

- Fukushima Gas Power, a joint venture between JAPEX and four other energy companies, said on Aug 24 that the second turbine in a new Fukushima natural gas fired power station, which generates 590 MW, was now fully operational.

- In total, the combined-cycle plant has an output of almost 1.2 GW. The complex is located at Soma Port, Fukushima prefecture.

- CONTEXT: The project is run by the Fukushima Gas Power Co., a JV comprising JAPEX (33%), Mitsui & Co. (29%), Osaka Gas (20%), Mitsubishi Gas Chemical Co. (9%) and Hokkaido EPCO (9%). The consortium came together in 2015-2016.

- CONTEXT: Since the 2011 Fukushima nuclear disaster, the prefecture has made massive strides to show it can become a stronghold for other energy sources and eschew nuclear. Fukushima is already Japan’s No.2 prefecture for solar installations. It’s home to the world’s largest electrolytic hydrogen production site.

- TAKEAWAY: This project reflected the real shift Japan took in the immediate aftermath of 2011 to replace nuclear with LNG. In addition to the power plant, JAPEX built a new LNG import terminal at the site. The key now will be to show that beyond the symbolism, this project had real economic justification. Japan’s total LNG import volumes have dropped every year, bar one, since 2014. Industry calls for nuclear restarts are growing. It will be interesting to see how the Fukushima gas complex fits into JAPEX’s overall gas strategy.

Honda to launch its first electric vehicle in October (Nikkei Shimbun, Aug 27)

- Co’s first mass-produced EV in Japan, the Honda e, will go on sale end of October for a retail price of around ¥4.5 million. The compact car, just 4 meters long, is aimed at city drivers.

- The car travels 300 km on a single charge, less than some rival models.

- Honda targets domestic sales of 1,000 units in the first year.

- CONTEXT: Nissan Motor launched its new electric model, the Ariya, in July as part of a big overhaul in strategy. The car is Nissan’s first electric crossover SUV. Toyota paraded its first Lexus EV earlier this year and Mazda plans to follow with its inaugural EV later this year.

- TAKEAWAY: Predictions that EVs will take over the market have always seemed a little rushed, yet the introduction of new models from so many of the leading Japanese automakers makes it more likely that the EV trend will gain solid footing in the coming years. Gasoline station chains are investing heavily in fast-charging EV infrastructure, with a JV between TEPCO and Chubu Electric also set to unveil a new charging system this year. The grim outlook for domestic oil refineries, already hit by COVID, is only intensifying.

Tokyo Gas repairs plan hits 100,000 subscribers (Denki Shimbun, August 28)

- Tokyo Gas said on Aug 27 that subscribers to its new warranty service had surpassed 100,000.

- Repairs to household gas appliances are free up to ¥30,000 for subscribers to the service. Subscribers are also entitled to discounts when replacing their existing appliances with Tokyo Gas appliances.

- SIDE DEVELOPMENT:Tokyo Gas develops new sintering plant for battery anodes (Nikkan Kogyo Shimbun, August 28)

- Tokyo Gas and the Noritake Company have developed a new, gas-fired sintering furnace for use in the manufacture of anodes used in lithium-ion batteries.

- The furnace offers reduced energy costs of up to 40% in comparison with traditional electric furnaces.

- CONTEXT: Utilities in Japan are progressively seeking new business models and revenue streams to compensate for a shrinking population and deregulation of the gas and power markets.

NEWS: POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 4 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | competed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

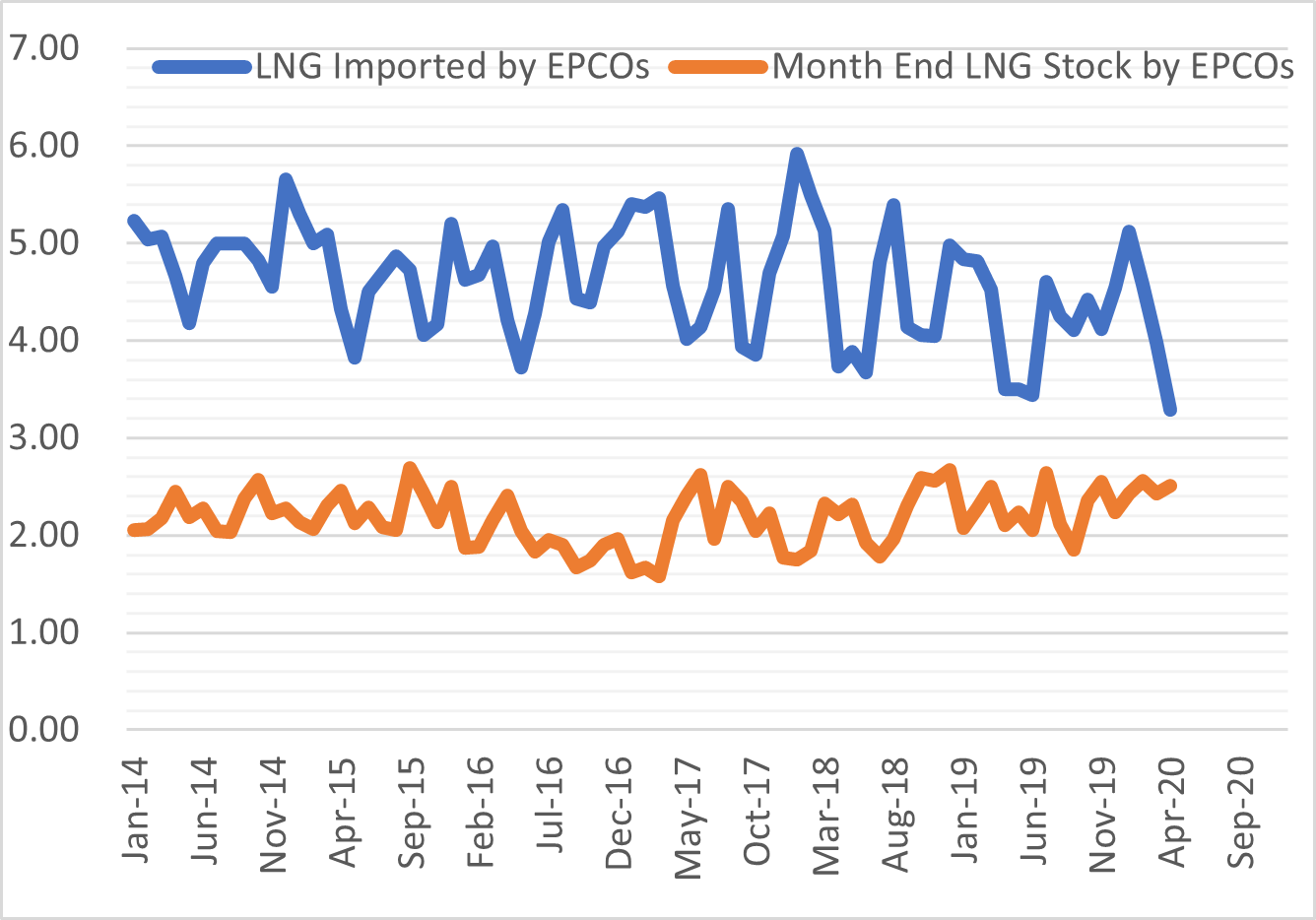

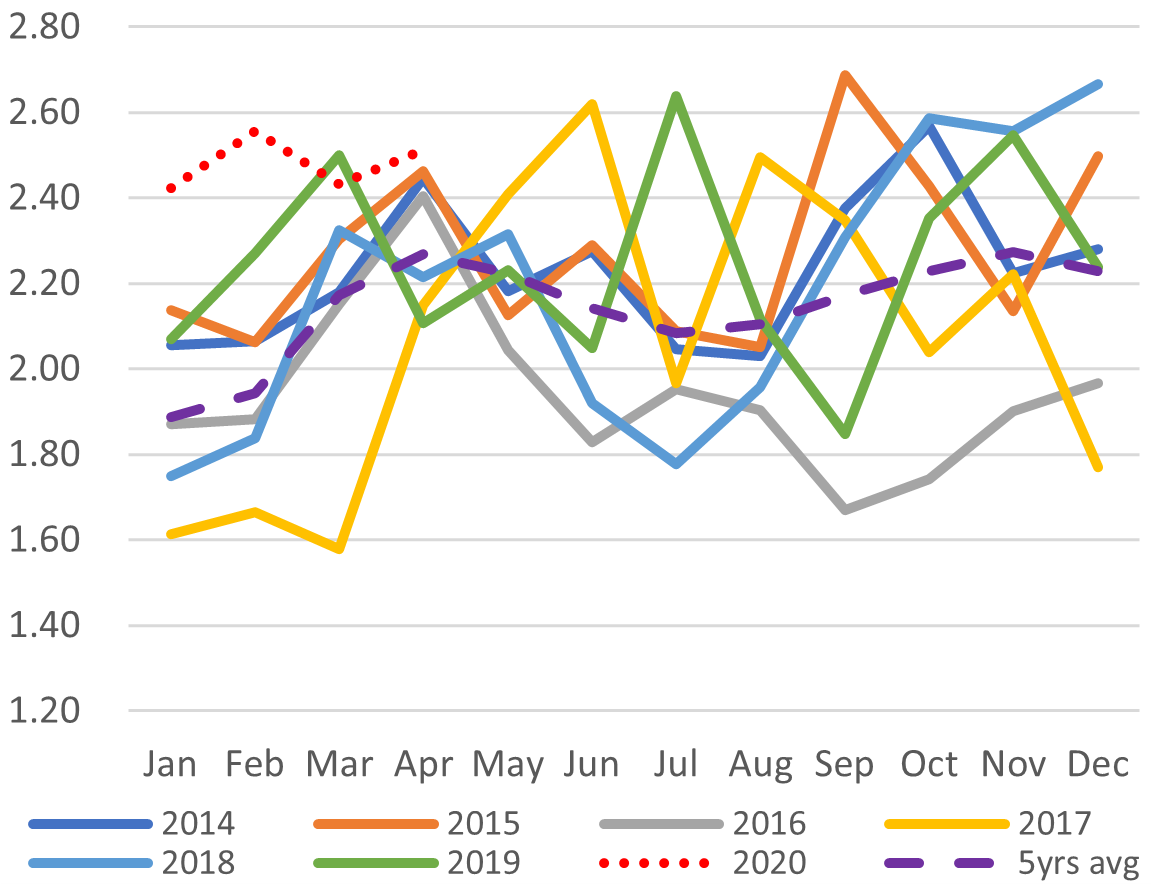

POWER UTILITY LNG IMPORTS VS STOCKPILES

Source: JANSI and JAIF, as of August 23, 2020

J Power’s new vice president talks renewables, coal, and nuclear (Denki Shimbun, August 25)

- New J Power Vice President Sugiyama Hiroyasu says that while many people associate J Power with coal, it actually began as a hydroelectric generator. The company will concentrate more on hydropower in the future, he added.

- Sugiyama says wind is a very challenging sector because of the need to win competitive tenders and make large investments for ever diminishing returns. To remain competitive in the long term, J Power will need to procure power plants as cheaply as possible and keep installation projects as short as possible, he said.

- Sugiyama says that more public support is needed to secure approval for the use of plutonium enriched mixed oxide (MOX) fuel in nuclear reactors, such as the Oma reactor.

- He sees future possibilities for efficiencies by automating the control of hydro dam sluices and thermal power stations.

- SIDE DEVELOPMENT: KEPCO to use laser beams to gauge water levels in hydro lakes (Denki Shimbun special feature, August 28)

- KEPCO has developed a technology that uses a green laser beam fired from a helicopter to judge water levels in hydro lakes.

- The technology is faster and more accurate than traditional boat-based echo sounding.

- TAKEAWAY: J Power has 17 coal-fired units in Japan, of which 9 (about 4.5GW of capacity) were built in the last century. A notable portion of the company’s coal-fired fleet would struggle to continue if Japan goes ahead with plans to shutter less efficient coal capacity. While it is true that J Power also runs 61 hydropower stations in Japan with 8.6 GW of capacity, opportunities to expand domestic hydropower capacity are few.

Hitachi Zosen focus on developing CCUS, a CO2 recycle method (Nikkei, August 28)

- Japan has announced that it will be putting more effort into CCUS (carbon capture and utilization), a strategy of collecting CO2 so that it can be later recycled. Japan believes it has technological strength in this approach and there is interest in it on a global basis.

- There are several methods of how to apply CCUS. One of them is to use methane from city gas. If this development goes well, it will lead to a huge business platform since it can run on existing energy infrastructure.

- One of the leading firms focused on CCUS in Japan is Hitachi Zosen.

- CONTEXT: Hitachi Zosen, despite the name, is not connected to the well-known Hitachi Ltd. engineering and IT conglomerate. Zosen is a manufacturing and engineering group in its own right, formerly famous for its shipbuilding and naval engines. In recent decades, it has pivoted to industrial waste management, especially energy-from-waste technology and environmental solutions.

- SIDE DEVELOPMENT: Hitachi Zosen, Sumitomo Corp. engage in battle to secure sites for offshore wind plants (Nikkei Business Daily, Aug 26)

Total cost of decommissioning Fukushima nuclear plant still unknown (Mainichi Shimbun, August 26)

- TEPCO plans to begin removing molten fuel rods and other debris from reactor number two of the Fukushima Daiichi plant in 2021.

- The project is now projected to cost 27 times more than initial estimates, but the final cost of decommissioning the plant and cleaning up the site, a process that will take between 30 and 50 years, is still unknown.

- Before the accident, TEPCO had estimated the cost of decommissioning all six reactors at ¥294 billion. After the accident, METI estimated it would cost ¥2 trillion to completely decommission the plant. As the project progressed, however, it became clear that this would not be enough to cover the cost of removing debris and processing contaminated water.

- In 2016, METI revised its estimate to ¥8 trillion. While METI staff admit that this figure is not based on a rigorous calculation of costs, they say there is no need to re-revise their initial estimate at the current time. For its part, TEPCO says it is still impossible to predict the full cost of the cleanup.

- CONTEXT: As the costs of the Fukushima cleanup increases, electricity tariffs are being progressively hiked to meet the shortfall.

- Suzuki Tatsujiro of Nagasaki University’s Research Centre for Nuclear Weapons Abolition believes the ¥8 trillion estimate is unrealistic, and points out that the figure has not been revised for nearly four years.

- SIDE DEVELOPMENT: TEPCO said Aug 24 that it received another ¥11.2 trillion from the government to pay out compensation claims related to the Fukushima disaster and for the decommissioning works (Denki Shimbun, Aug 25)

- This is the 103rd request for funding from TEPCO to the government

- SIDE DEVELOPMENT: Hokkaido town becomes flashpoint in Japan’s nuclear waste debate (Asia Nikkei, Aug. 27)

- Mayor of Suttsu, a small town in Hokkaido, suggested the town would welcome the local siting of Japan’s long-term nuclear waste storage facilities. The prefectural authorities immediately responded to say they vehemently oppose the action.

- The mayor has since toned down his welcoming message, while nearby towns raised concerns – in part, because they would not benefit financially from the hosting.

Japan could employ efficiency tricks to retain some coal capacity (Nikkei Energy Next, August 24)

- The government’s announcement of plans to phase out coal-fired power stations shocked the country and the rest of the world.

- As recently as last year, energy minister Kajiyama Hiroshi called for the retention of coal as a power generation option, attracting criticism internationally. Precisely because of Japan’s reputation of being “addicted to coal”, the latest move, seen as a genuine effort to phase out coal power, has been welcomed around the world

- A little-known secret is that various tricks can be used to make coal-fired generation plants look more efficient than they are, therefore creating a rationale to keep such plants operating.

- If biomass is mixed with the coal that is used to fuel power stations, or cogeneration methods (electricity plus heat) are employed, inefficient power stations can be made to appear efficient.

Tohoku Electric Power Network forced to buy power from TEPCO in sweltering heat (Kahoku Shimpo, August 29)

- TEPCO supplied the Tohoku Electric Power Network with an additional 400 MW of electricity on Friday, Aug 28, as the utility came close to running short of power.

- This is the first time the Network has been forced to buy electricity since it was split off in 2012.

- The power shortage was the result of increased air-conditioner use and lower than expected output from solar generation facilities.

Institute of Applied Energy calls for better use of thermal energy storage (Denki Shimbun, August 24)

- Institute of Applied Energy chair, Terai Takayuki, has said more use needs to be made of thermal energy storage in the new, renewable energy environment.

- By converting surplus electricity to heat, which can be easily stored, then converting the heat back to electricity when needed using Carnot batteries or equivalent technology, it is possible to solve peak supply challenges, he said.

- CONTEXT: This is the second notable voice in recent weeks discussing the need to include power-to-heat capabilities in Japan’s energy infrastructure, a strategy that has done well in countries like Denmark.

Japan has already been overtaken by South Korea in nuclear technology (Sunday Mainichi/Economist via Yahoo News, August 24)

- Horizon Nuclear Power, a fully owned subsidiary of Hitachi, is reported to be in negotiations with the UK government concerning the recommencement of a project to construct a nuclear power plant at Wlfa Newydd in Wales.

- Faced with ballooning costs at the under-construction Hinkley Point C plant, the UK government initially approached China to assist with construction of new nuclear plants. However, concerns about energy security and diplomatic pressure from the US caused the UK government to turn to Japan instead. Unfortunately, the cost of the project subsequently skyrocketed, and negotiations between the two governments stalled.

- Ten years after the Fukushima disaster, Japan has yet to finish work on a single new nuclear reactor. As the workforce ages, it is getting harder to train the next generation of engineers.

- Kubota Hideo, a consultant with Tepia Corporation, says that Japan has already been overtaken by South Korea in nuclear technology. One example of that is when the Korea Electric Power Corporation won a bid to export a nuclear reactor to the United Arab Emirates, beating its Japanese rival.

NEWS: RENEWABLES & OTHERS

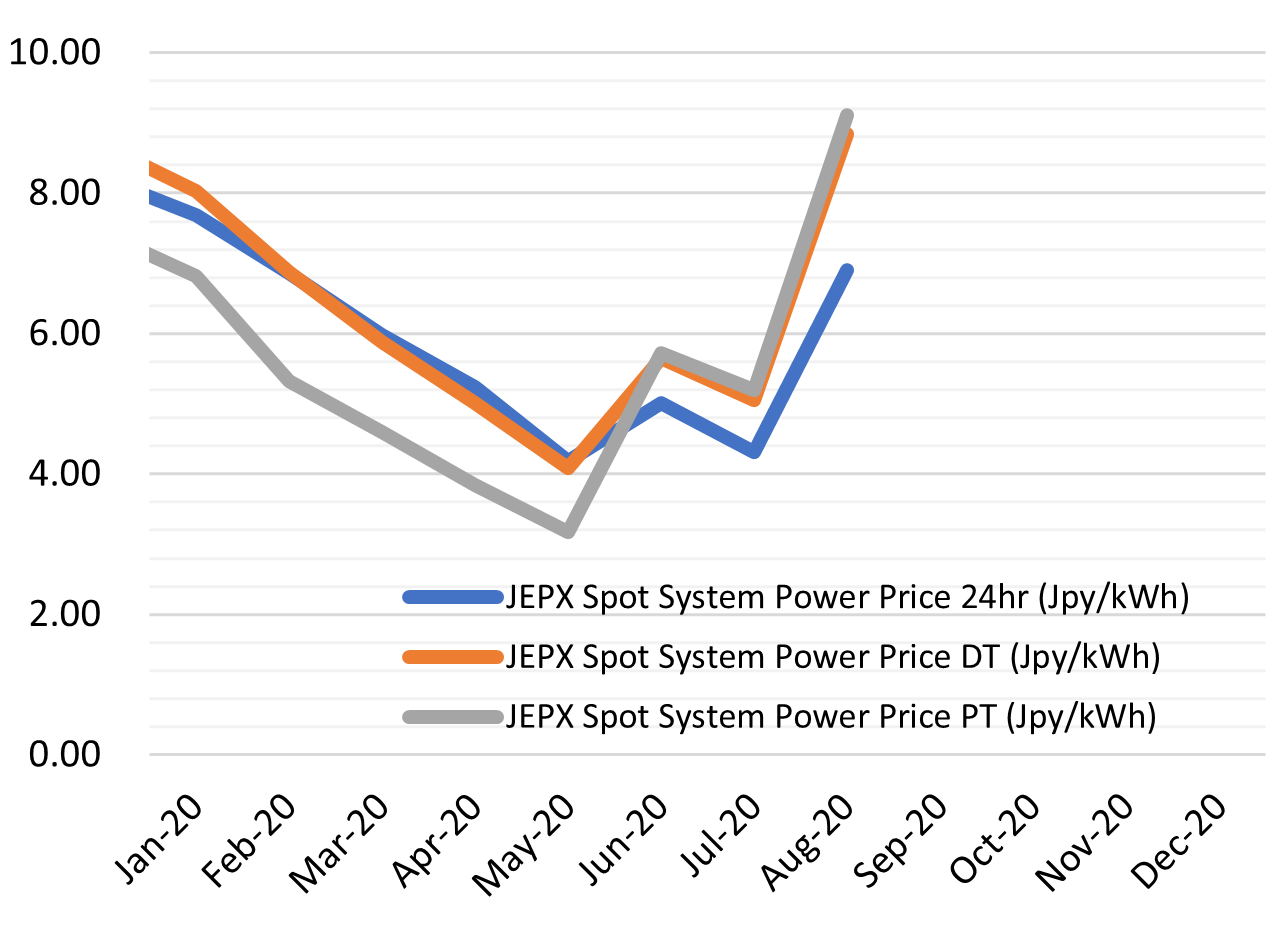

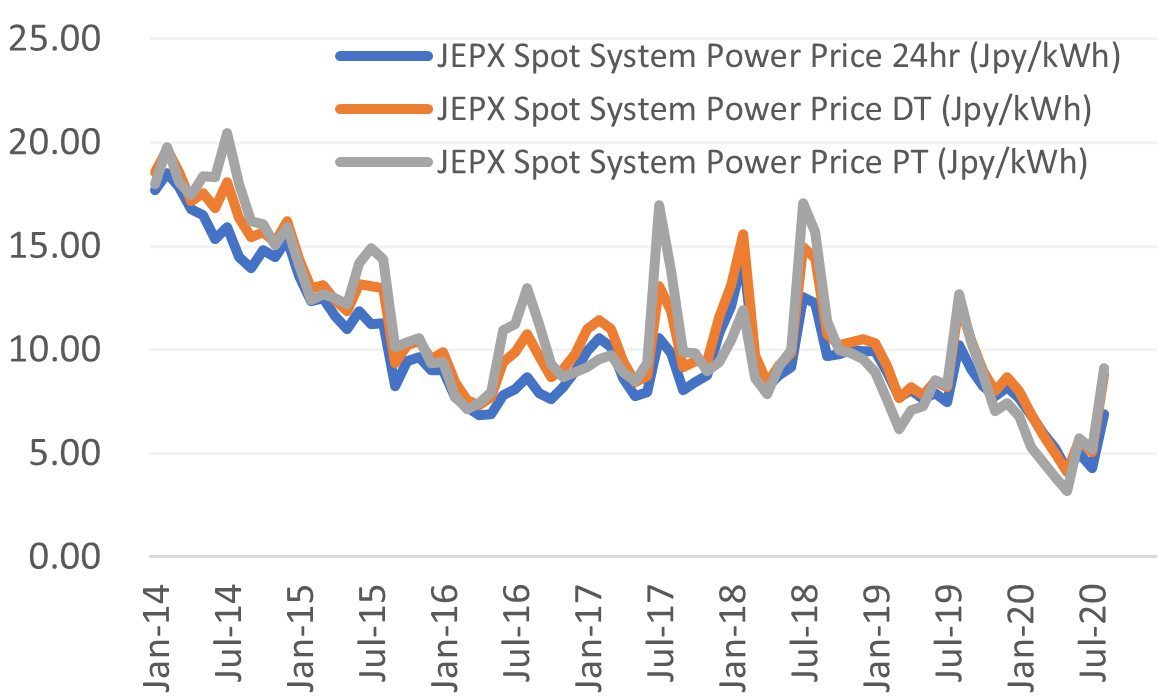

HISTORICAL SPOT ELECTRICITY PRICES (24h)

SPOT ELECTRICITY PRICES (2020)

ENEOS and JERA open hydrogen filling station (Kabushiki News, August 26)

- ENEOS Holdings said on Tuesday it had opened a commercial hydrogen filling station in Tokyo, on the grounds of the Oi power station.

- The station is a joint venture with JERA and will be operated by JERA.

- The hydrogen dispensed is extracted from natural gas.

- CONTEXT: The Oi power plant is owned and operated by JERA. It also houses the JV between ENEOS and JERA, which produces hydrogen from natural gas.

- TAKEAWAY: Although this is announced as a “commercial” level facility, and it is supposed to be the biggest of its kind in Japan, the station itself is small relative to gasoline filling stations, and sits inside JERA’s power plant grounds. Rather than mass-market traffic, most of the clients will be associated with the Tokyo Metropolitan government, which is testing fuel cell buses, as well as fuel cell passenger vehicles connected to the national hydrogen program. Still, this is a notable step for JERA. It is using ENEOS to get a toehold in the retail market. The latter has already built 42 “commercial” hydrogen filling stations, which is almost a third of all such facilities in Japan, and JERA has positioned itself as ENEOS’ fuel supplier – at least in the key Tokyo area.

- SIDE DEVELOPMENT: JERA files environmental assessment plans for its 520 MW offshore wind project in Ishikari Bay, Hokkaido (Company Press Release, Aug 24)

- Co. sees potential for bottom-fixed wind station on shallow sea bed and spare capacity in local power grid

- Project would involve as many as 65 turbines

Tokyo Government invites applications from domestic solar suppliers (Nikkei, August 26)

- On August 28, the Tokyo Metropolitan government will begin accepting applications from households fitted with solar panels or other means of generation and that wish to sell their surplus electricity to the government.

- The government is offering ¥11 per kilowatt hour, slightly higher than the market rate.

- Generators would begin providing the government with electricity after their fixed term feed-in tariffs expire. The government is looking to supply a total of 5000 kW, equivalent to around 1000 households.

- TAKEAWAY: The announced price initially seems like a good deal. The baseload price for electricity in the Tokyo area averaged about ¥9.77 per kWh in 2019, according to JEPIC. And yet, for solar developers, this may be a worrying trend. No one expected Japan to keep its Feed-In Tariffs for renewables at the world-beating ¥40 / kWh as introduced in 2012. And yet, the FIT for solar plants over 2MW has already dropped to ¥12.9 / kWh. Setting a retail marker at ¥11 / kWh, albeit for a relatively small chunk of capacity, is surely another mechanism to push solar developers to offer future projects at lower rates.

COLUMN: We need an energy policy that’s serious about renewables (Nikkei Business, August 24)

- CONTEXT: Author is Nishigawa Shusaku, a senior energy and power analyst at Daiwa Securities.

- 2020 marks a turning point in Japan’s response to global warming: the nation’s basic energy policy has been significantly overhauled.

- While the original 22 to 24% renewables target was seen by some as unrealistic, the feed-in tariffs (FIT) system under which electricity generated from renewables is purchased for a pre-agreed rate has helped to significantly increase the uptake of renewable forms of energy, particularly solar. As coal plants are phased out, the use of energy from renewable sources will need to be increased even further.

- By contrast, the target to source 20 to 22% of electricity from nuclear plants is much more challenging. This represents the output of around 30 nuclear plants. Only nine nuclear reactors are currently [able to] operate in Japan.

- To enable increased use of electricity from renewable sources, we need to move to an approach where electricity is consumed in the region in which it is generated. As things stand, this will necessitate an investment in electricity storage, such as lithium-ion batteries. Such batteries are very expensive, however.

- An alternative solution is rethinking the FIT scheme. If we pay generators a premium for electricity supplied at times of peak demand, rather than paying them a flat rate, then we can use the market to resolve the issue of power shortages at peak times.

Tokyo Gas acquires Singaporean Equis’ biomass ventures (Nikkan Kogyo Shimbun, August 27)

- Tokyo Gas said on Aug 26 that it will acquire two biomass-fired electric power stations from the Equis Group of Singapore.

- The stations are located in Toyama and Chiba, and the transaction will take place in September, for an undisclosed sum.

- The plants will add 126 MW to Tokyo Gas’s total generation capacity from renewables.

- SIDE DEVELOPMENT: KEPCO to use biofuel to power company vehicles (Denki Shimbun, August 28)

- KEPCO said on Thursday it had begun using blended biodiesel for its company vehicles.

- KEPCO endorsed the “Green Oil Japan” declaration, part of an initiative led by biofuel manufacturer Euglena.

Idemitsu, Nihon Unisys, Scrum Ventures collaborate on smart city project (Kensetsu Tsushin Shimbun, August 28)

- A consortium that includes Idemitsu, JR East Japan, Nihon Unisys, advertising agency Hakuhodo, and US-based start-up accelerator Scrum Ventures has launched a project known as SmartCity X that aims to make smart cities the “new normal” around the world.

- Participating local bodies will provide the consortium with an environment to perform proof of concept studies, with a view to launching new services and apps in the future.

ANALYSIS

HONG CHOU HUI, FOUNDER,

HUI’S CONTENT HUB

That stoicism was severely tested when the gulf between spot and long-term rates widened to USD 6 per MMBtu this summer. Even in the short-term market, Japan appeared to overpay. Spot LNG prices in Asia for June deliveries went as low as $1.85/MMBtu, almost half the average $3.80/MMBtu Japan paid for short-term deals in the same month.

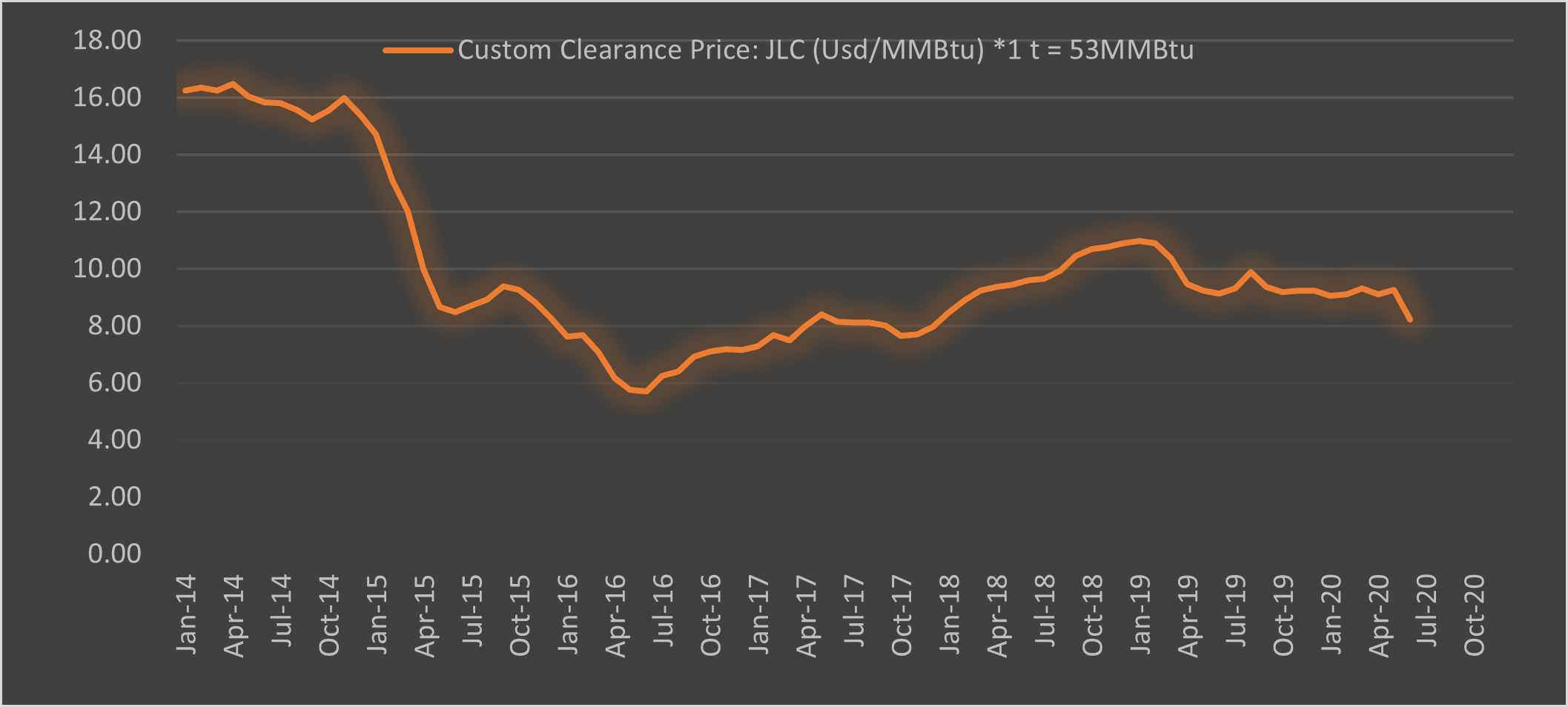

While Japan’s Inpex reportedly sold cargo from its Australian LNG plant for as little as $1.70-$1.75 (DES) earlier this year, Japanese importers via mostly long-term contracts paid on average $8.21 per MMbtu in June, according to official data.

This has had a large impact on the profits of Japanese buyers. The biggest Japanese LNG importer, JERA, alone posted more than 10 billion yen ($90 million) in losses from the resale of LNG cargoes when it announced financial results in July. JERA and Japan’s ministry responsible for energy (METI) spent a lot of time during this summer calling for more “creativity” and flexibility in long-term contracts. Much of Japan’s LNG imports are locked in via contracts of ten years or more; these agreements have a price formula traditionally pegged to oil prices with little or no destination flexibility and no option for buyers to divert cargoes.

JERA and Japan’s ministry responsible for energy (METI) spent a lot of time during this summer calling for more “creativity” and flexibility in long-term contracts. Much of Japan’s LNG imports are locked in via contracts of ten years or more; these agreements have a price formula traditionally pegged to oil prices with little or no destination flexibility and no option for buyers to divert cargoes.

At a recent industry summit, JERA’s executive office Hitoshi Nishizawa appealed to LNG sellers to understand that if Japanese buyers are hurt by the current LNG contract terms, they will find it hard to promote further usage of the fuel in the domestic market.

Mr. Nishizawa wasn’t bluffing, either. With Japan’s July announcement of plans to shutter most of its older coal-fired capacity, a portion of the country’s energy mix is up for grabs. It could go to renewables, nuclear, cleaner-burning coal, hydrogen even, or perhaps LNG.

Turning to LNG could mean an extra 1 million tons or more a year of purchases over the next decade. Yet, it’s hard to see LNG taking over from “old” coal if the terms of long-term contracts remain inflexible. And it’s unlikely that many Japanese buyers will follow the lead of Osaka Gas, which at the start of the year moved an Exxon Mobil-led LNG joint-venture to arbitration in a bid to get lower rates.

Japan could better pressure LNG sellers if it pursued an active role in the growing electronic trading marketplace. A proliferation of new trading platforms has improved transparency and brought much needed liquidity to the sector.

The Covid-19 crisis could be Japan’s best chance to diversify its LNG purchasing portfolio. In utilizing the trading platforms, Japan would become a nimbler buyer, better attuning its purchases to domestic demand. Most importantly, it could regain some of the influence it had when more of the global LNG market was based on long-term contracts.

Last year Japan retained its spot as the biggest LNG buyer, but its sway over Asian LNG pricing, once benchmarked against the Japan Crude Cocktail (JCC), started to give way as early as 2016 on the back of Brent crude crashing below $30/bbl from more than $100/bbl two years earlier. The widely used Platts spot benchmarks now reflect purchases by Taiwan, South Korea, and China, as well as those of Japan.

ELECTRONIC TRADING IS CHANGING THE GAME

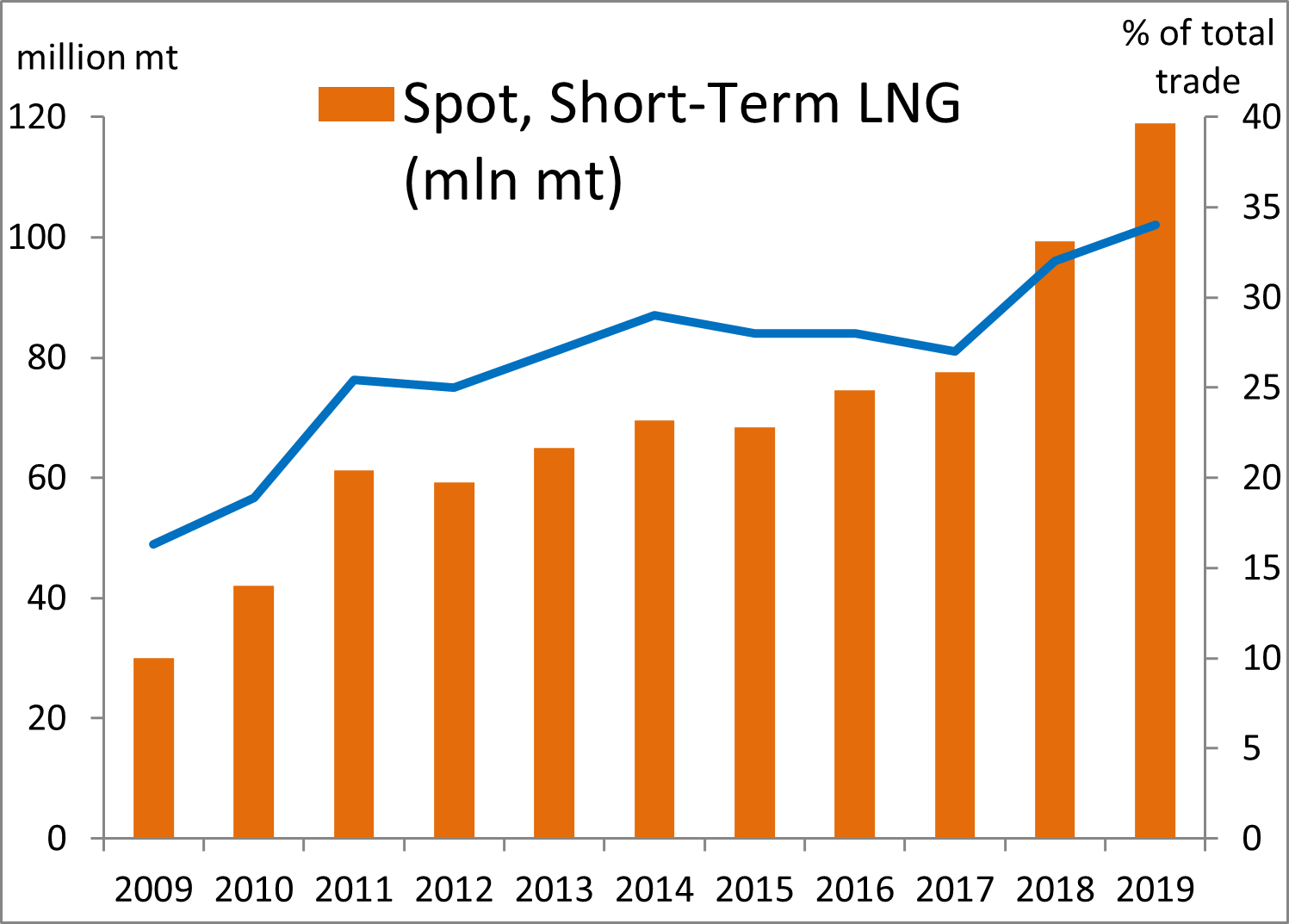

Trading a spot liquefied natural gas cargo usually involves a week-long process where talks begin on a Monday before a deal is inked on Friday. This process was shrunk to seconds thanks to a recent proliferation of electronic LNG trade platforms. Nearly 120 million tons of spot and short-term LNG was traded on such platforms in 2019. This made up 34% of global volumes, which have doubled in the last decade.

Physical transactions executed within a 90-day window comprised over a quarter of global LNG sales last year, an uptick from 17% in 2016, according to GIIGNL statistics.

The market took off around 2016 when, GLX, an Australian startup led by former Shell lawyer, Damien Criddle, announced its intentions to set up an electronic trading platform. The venture promised LNG deals that would forgo the hassle of long flights, meetings, phone calls and late nights. This is becoming even more important in the post-Covid world.

GLX’s successful foray into the domain of trading physical cargoes via an electronic platform, a traditional Platts stronghold, roused the US firm PRA to launch its LNG eWindow with the Intercontinental Exchange, or ICE on 26 July last year. It was used by Vitol to conclude a sale with PetroChina by the month’s end. Earlier the same year, Paris-headquartered data and analytics provider Kpler said it would work with the Powernext, part of Europe’s biggest wholesale electricity bourse, to set up Spark Commodities and its own spot trading platform. Kpler made its product available in the last quarter of 2019 but differentiated it from the earlier two platforms by focusing on LNG freight rates.

Our survey of 32 market participants – buyers, producers, traders and intermediaries – across Asia saw nearly three-quarters are backing Platts to become the trading platform of choice over GLX. Over a third thought Kpler’s product distinctive enough and occupying a niche space in an industry that’s highly reliant on vessels but some felt the product wouldn’t be able to survive competition from Platts, and could eventually be swallowed up by the American PRA or even GLX in a bid to stay competitive.

TAKEAWAY: Electronic trading of LNG is now at a stage of maturity and about half of the market is likely to coalesce around a common electronic marketplace and benchmark within the next five years, according to our survey of market participants. Japan needs to jump into this market before it’s too late or it will be lamenting losses on long-term contracts for many more years to come.

ANALYSIS

YURIY HUMBER, DIRECTOR,

YURI INVEST RESEARCH

Cost of Japan’s Thermal Coal Likely to Rise as BHP Exit Pushes Trading Houses to Reconsider the Fuel

A month after Japan’s government announced plans to cull older, less efficient coal-fired generation, this energy segment is potentially facing a hit on its supplies. The cost of Australian coal, which makes up over 60% of Japan’s thermal coal imports, is likely to rise after BHP Group followed rival Rio Tinto in announcing an exit from mining the mineral.

The news will also likely hasten a restructuring of coal assets at Japanese trading companies like Mitsui & Co., which co-invest with global mining majors to secure supplies of the fuel. Those Japanese utilities least able to switch from coal to gas or other sources, such as Okinawa and Hokkaido EPCOs, and to an extent Chugoku and Shikoku EPCOs, will face the brunt of rising coal costs.

Over the mid-term, the future of Japan’s coking coal supply will also be affected.

| Japan coal imports from Australia (volume) | over 100 million metric tons, three times the next-largest supplier (Indonesia), and over 60% of total, which was 186 million tons in FY2019 |

| Japan spending on coal | ¥2.53 trillion (USD 23.8 billion) |

| Of that, on thermal coal | ¥1.32 trillion |

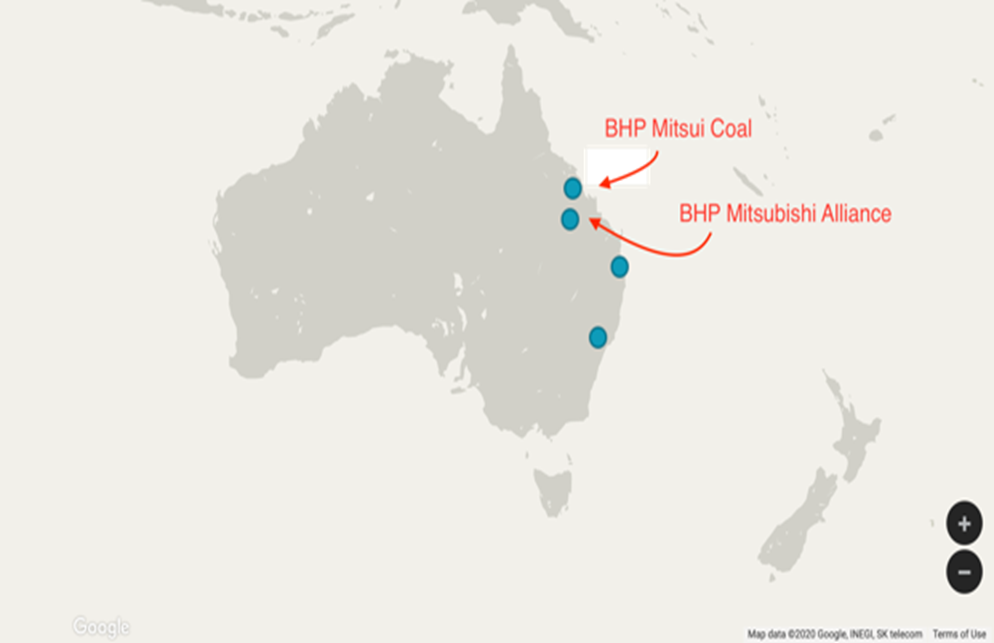

| Mitsui thermal coal assets in Australia | A BMC venture with BHP (Mitsui owns 20%), which runs two mines in Queensland; Mitsui’s equity share of that was 2.1 million tons in FY2019 |

| Mitsui earnings from Australian coal mining | ¥48.5 billion |

| Mitsui thermal coal sales (annual) | 4.2 million tons (FY2019) |

| Mitsubishi’s exposure to Australian coal | 50% stake in BHP Mitsubishi Alliance (BMA) operates seven coking coal mines and a coal terminal in Queensland, Australia; BMA has 30% of global seaborne coal market and is the top producer in Australia. |

| Mitsubishi coal assets book value | ¥650 billion (as of March 31, 2020) |

| Mitsubishi profit sensitivity to mining | Mitsubishi’s Mineral Resource division, which contains BMA, brings in three times the earning of any of the trader’s other units |

| Itochu’s coal exposure | Potential output of over 55 million tons per annum in the five Australian and one Indonesian projects the Co. has invested in; Glencore and BHP are main mining partners |

INEFFICIENT USE OF CAPITAL

BHP announced plans earlier this month to curtail its coal business and exit all assets that mine the fuel for power generation. These mines, which include two that are co-owned with Japan’s Mitsui will be sold or split off into a separate entity.

Similarly, Rio Tinto sold off its last thermal coal assets two years ago – including a mine in which Mitsui also co-invests (Kestrel).

Both BHP and Rio Tinto gave a nod to the environmental issues raised against thermal coal, yet they also both mentioned a business truth: the fuel is no longer a great investment and both firms see better opportunities elsewhere.

As BHP said in its Aug. 18 announcement: “Coal power is expected to progressively lose competitiveness to unsubsidized renewables on a new build basis in the developed world and in China.”

That should come as no surprise to Mitsui, which after all said in 2018 that it would “refrain” from further investments in thermal power and gradually reduce its coal-fired generation assets.

And yet, the exit of BHP is likely to spur Mitsui – and its rivals Itochu Corp., Marubeni Corp., and Sumitomo Corp. – to speed up their own divestments or restructuring of coal assets.

Mitsubishi Corp. has already sold out of thermal coal, after passing on stakes in its Australian assets to Glencore and Sumitomo, and in a separate deal to compatriot Sojitz.

BHP, however, also said that it would stop making significant investments in coking coal. If that stance were to harden, the economic impact on Mitsubishi, Itochu and other traders would be severe.

As it is, the cost structure of thermal coal is likely to rise as the industry passes from the hands of the world’s biggest mining firms, backed by top Japanese traders, to smaller, private firms.

COSTS RISING

Clearly, thermal coal volumes out of Australia would not immediately drop just because BHP exits the business. However, as the most efficient mining firms that can attract cheap capital pass on the assets to smaller, less diverse and often private entities, the cost of capital for the projects will rise.

The buying entities are also unlikely to have the marketing network or access to transport infrastructure that BHP and its peers do, which will also increase the costs of delivery.

Finally, with less global demand for thermal coal, some mines will need to close or shrink, dialing back on the economies of scale.

As Australian thermal coal costs rise, so will its price. And yet, Japanese utilities may not have the luxury of turning to other sources of supply. Japan’s plans to permit only USC coal-fired plants with 43 percent efficiency make it uneconomic to import and burn lower quality, high-sulphur coal.

With the price tag for coal generation rising, and natural gas expected to be depressed for several years, some Japanese utilities may well decide to quit on coal generation.

HOUSE VIEW

In a bombshell announcement Friday Japan’s longest-ever serving prime minister and architect of Abenomics announced his resignation after almost eight years.

Shinzo Abe took office the year after the Great Tohoku Earthquake that devastated a nuclear power plant in Fukushima and crippled the global nuclear power industry. This precipitated a significant overhaul of Japan’s energy policies.

Since Prime Minister Abe came to power in 2012 Japan has deregulated its electricity and gas markets with mixed results. The country has installed over 60 GW of solar power installations but continues to rely on the Middle East, Russia, and other energy suppliers for over 90% of its primary energy inputs, mainly oil, natural gas, and coal.

Growth in other renewables technologies has been anemic. Under Shinzo Abe, Japan signed the Paris Agreement in 2015 but Japan’s carbon emissions have stagnated due to a growing reliance on fossil fuels and delays in reactivating its nuclear fleet.

Japan has not yet committed to carbon neutrality by 2050 unlike some of its peer countries in the developed world. Its position on coal power stations is still ambiguous.

Japan’s critically important automobile industry is still trying to carve out a global leadership position in electric and fuel cell vehicles as EV and FCV developments in other geographies power ahead.

Japan continues to be an energy island with no pipeline or power links with its neighbors unlike the EU where energy transfers across national boundaries are commonplace.

It will fall to Shinzo Abe’s successors to reduce Japan’s external energy dependencies and re-commit to the goals of the Paris Agreement.

STOCK MARKET PERFORMANCE

| As of close on August 28, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| COSMO ENERGY HOLD. | 5021 JP | 139.62 | 2.81 | -31.04 | 8.36 | |

| ENEOS HOLDINGS INC | 5020 JP | 1334.11 | 1.87 | -14.57 | 12.47 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 688.37 | 0.61 | -21.27 | 6.01 | |

| INPEX CORP | 1605 JP | 957.53 | -1.01 | -41.34 | 9.30 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 103.28 | 3.49 | -37.99 | 6.29 | |

| Industrials | ||||||

| CHIYODA CORP | 6366 JP | 69.51 | -1.11 | -5.65 | 6.37 | |

| JGC HOLDINGS CORP | 1963 JP | 297.06 | -0.87 | -33.80 | 7.71 | |

| MITSUBISHI CORP | 8058 JP | 3465.45 | -0.04 | -17.27 | 10.05 | |

| MITSUI & CO LTD | 8031 JP | 3061.60 | -0.11 | -6.04 | 13.28 | |

| Utilities | ||||||

| CHUBU ELECTRIC POWER | 9502 JP | 990.71 | -0.53 | -13.85 | 4.18 | |

| KANSAI ELECTRIC POWER | 9503 JP | 969.71 | 0.39 | -16.64 | 3.15 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 443.36 | -0.21 | 0.61 | 5.77 | |

| J-POWER | 9513 JP | 289.40 | -1.00 | -39.25 | 10.17 | |

| TOKYO GAS CO | 9531 JP | 1024.68 | -0.62 | -11.66 | 3.83 | |

| OSAKA GAS CO | 9532 JP | 850.03 | -2.58 | -1.28 | 4.94 | |

| TOHO GAS CO | 9533 JP | 486.84 | -4.65 | 3.91 | 0.66 | |

| SAIBU GAS CO | 9536 JP | 91.30 | -1.29 | -2.17 | 9.31 | |

| SHIZUOKA GAS CO | 9543 JP | 65.68 | -0.69 | -8.57 | 2.01 | |

| TOKYO ELECTRIC POWER | 9501 JP | 499.78 | 0.65 | -33.40 | 11.07 | |

DATA

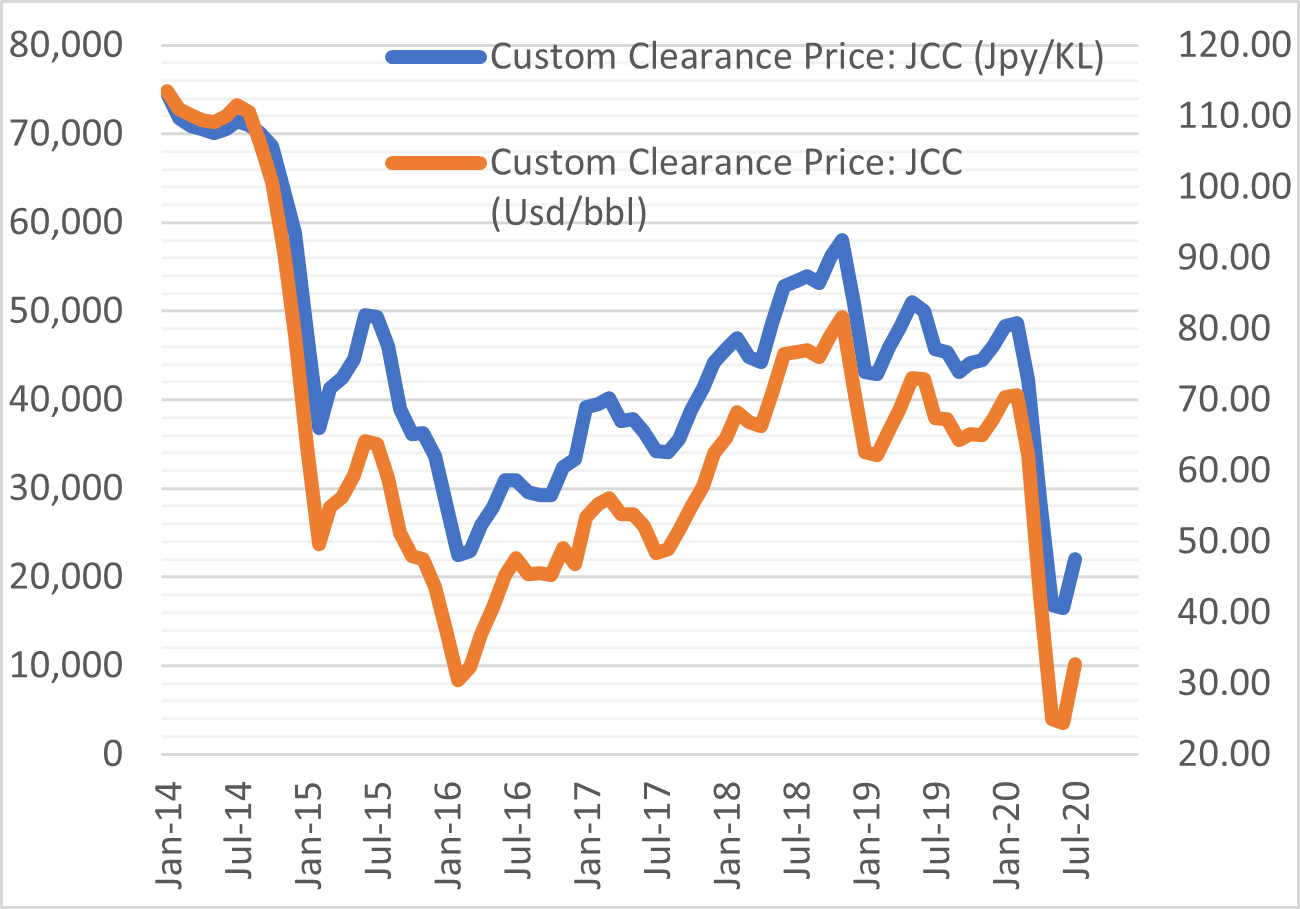

Japan Oil Price

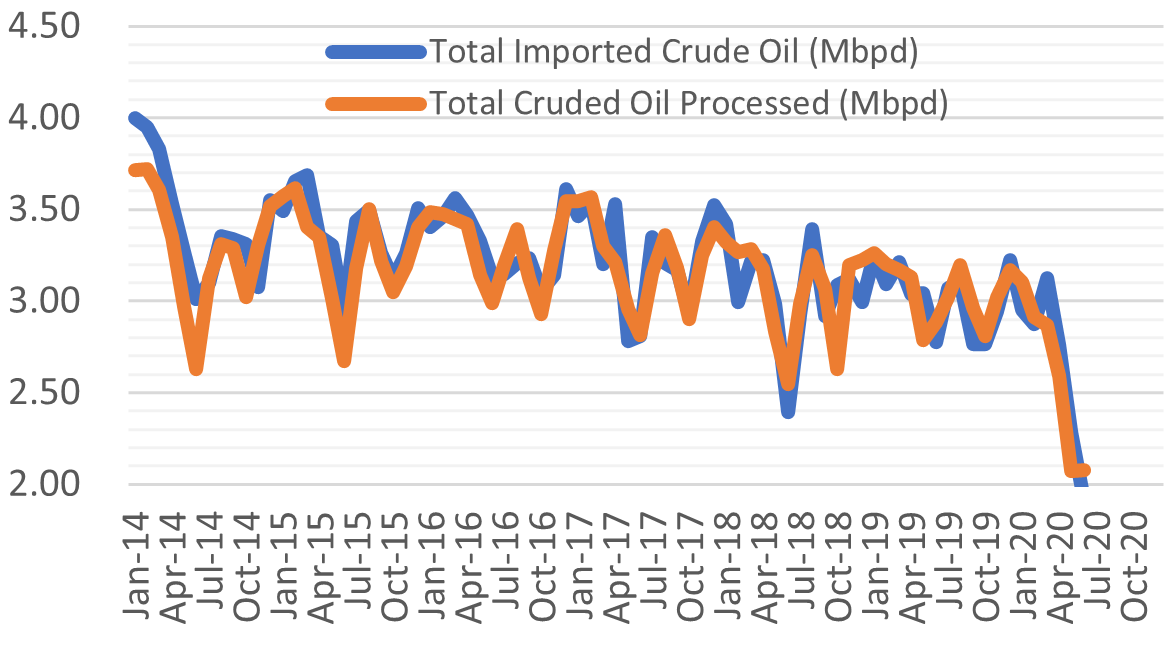

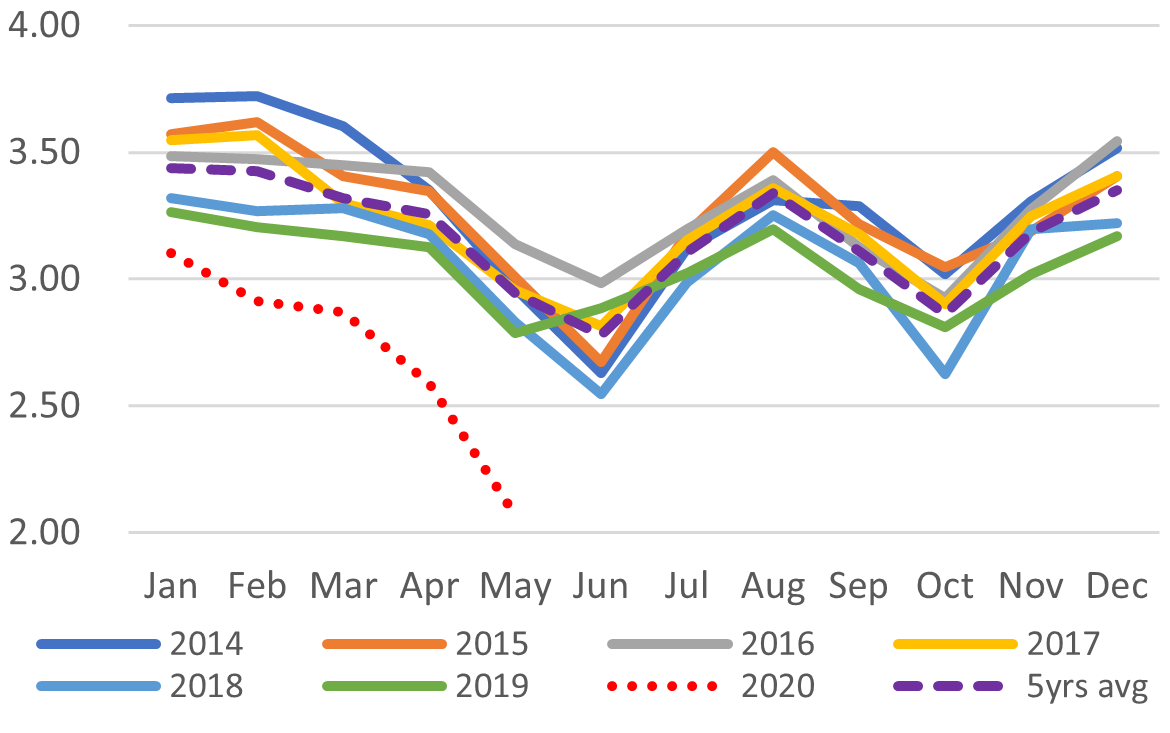

Crude Imports Vs Processed Crude

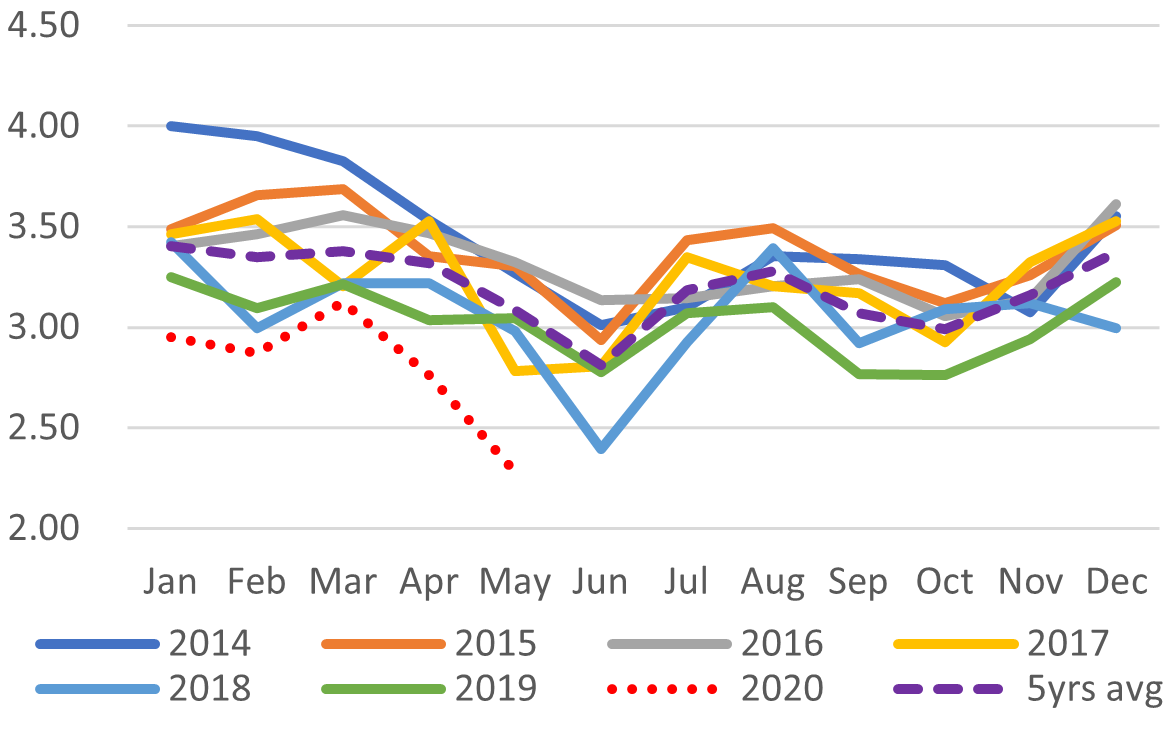

Monthly Crude Processed (Mbpd)

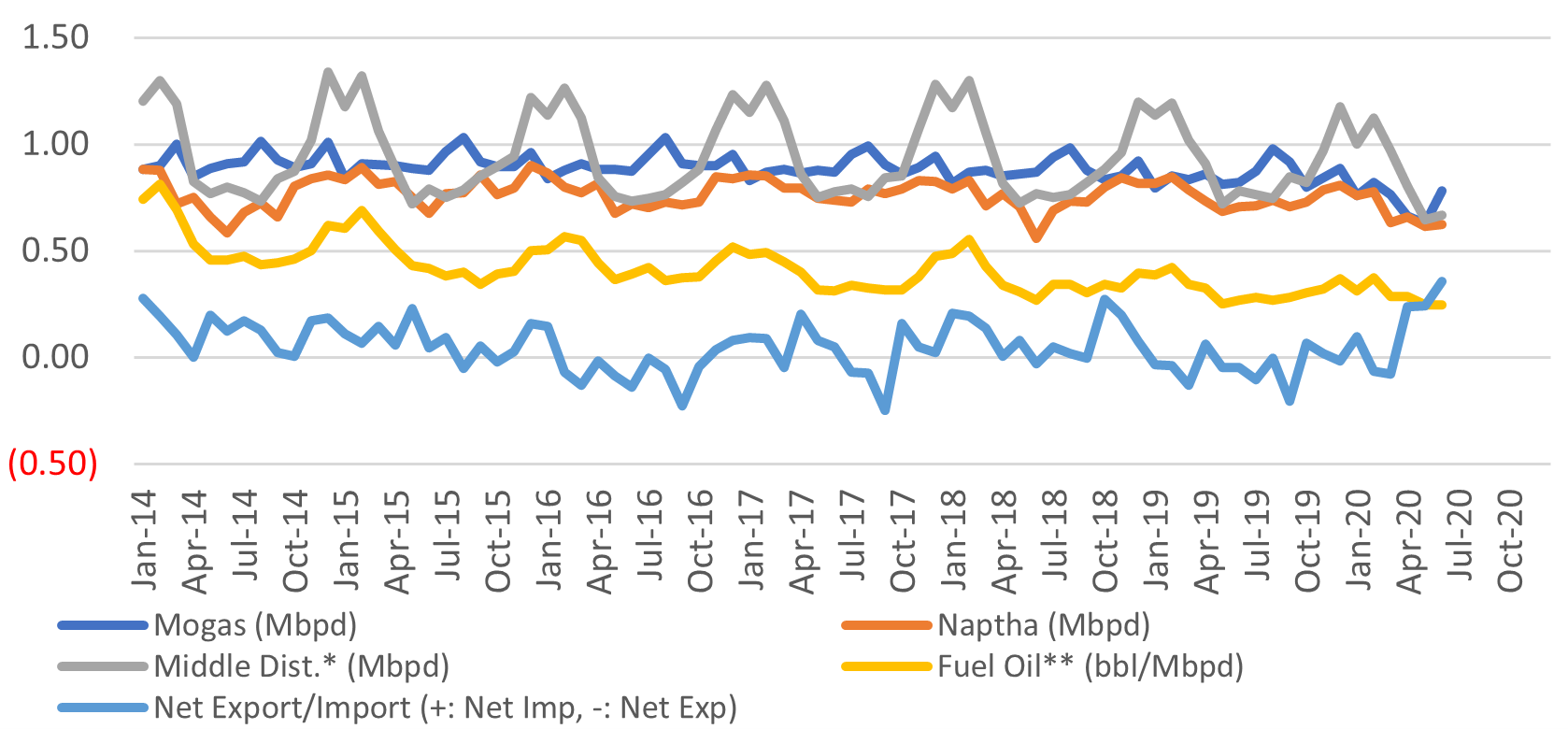

Domestic Fuel Sales

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

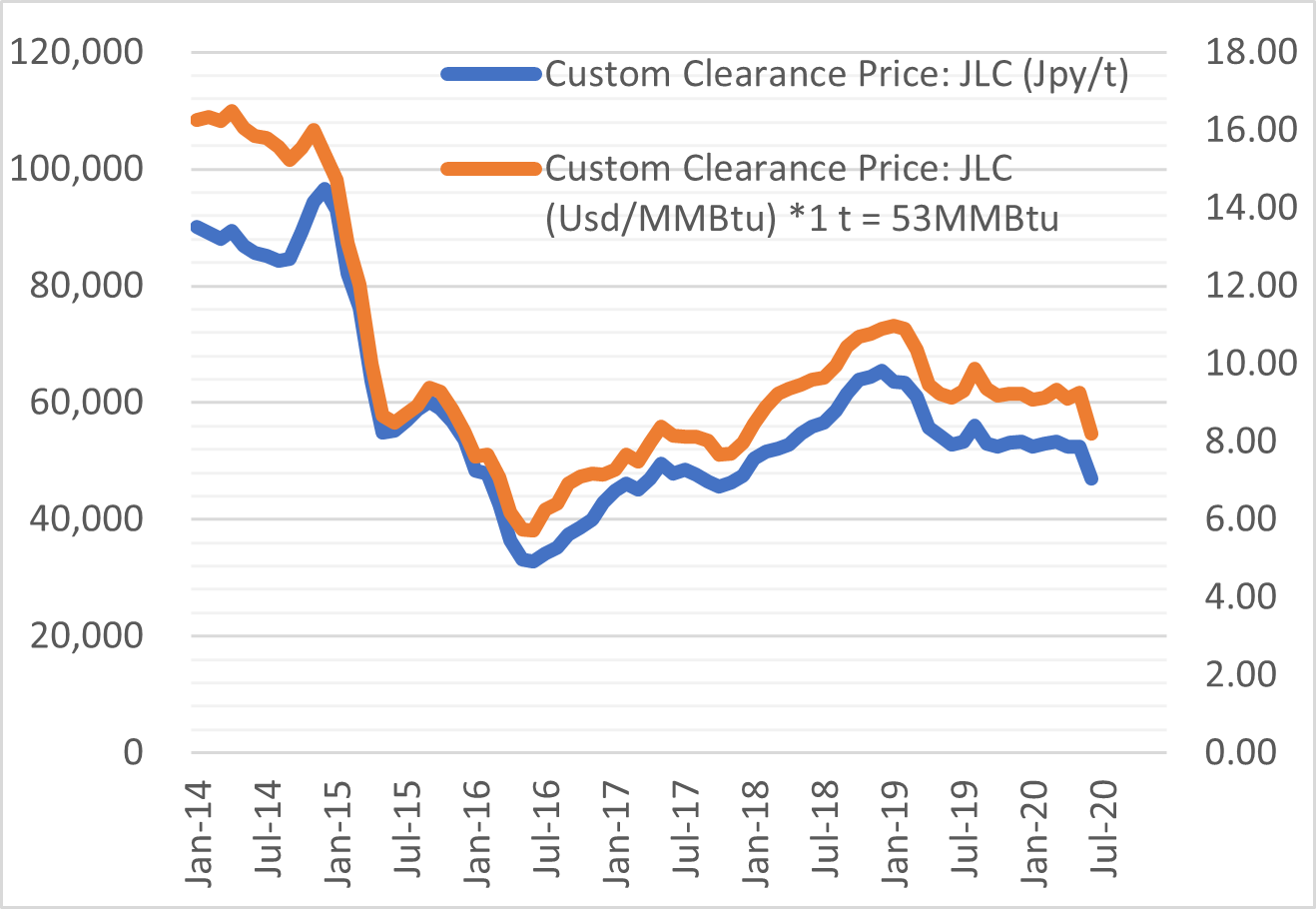

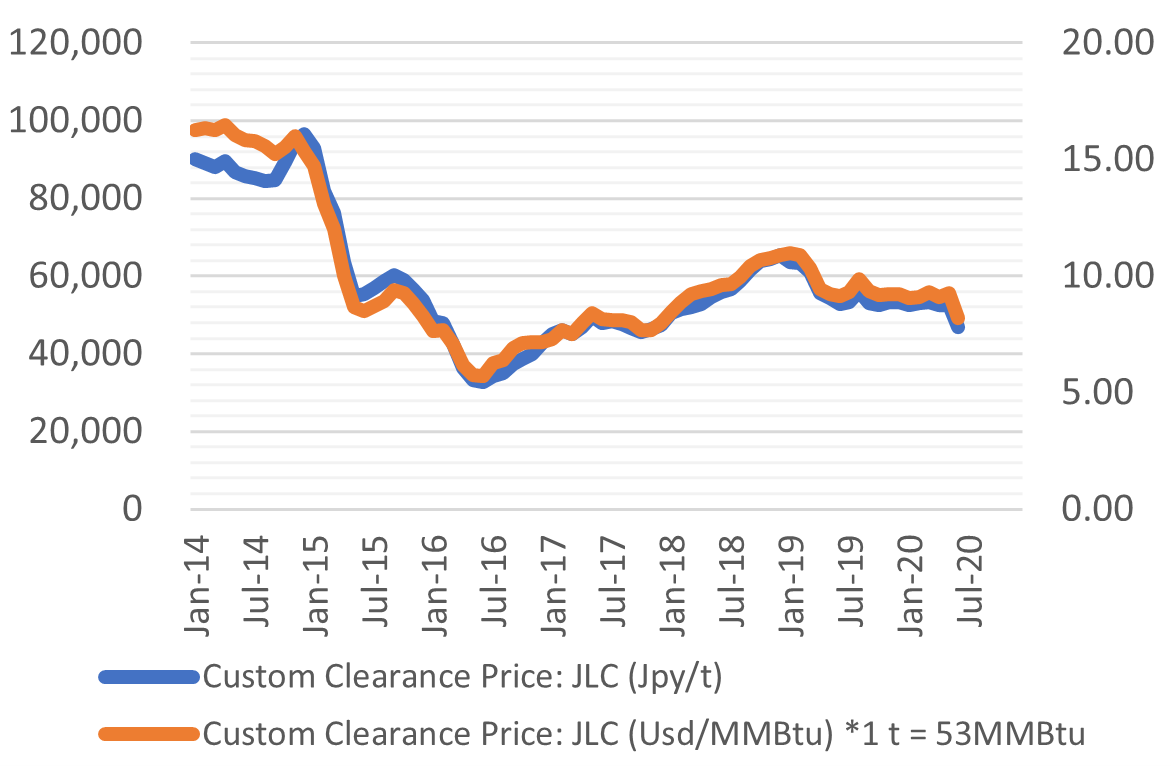

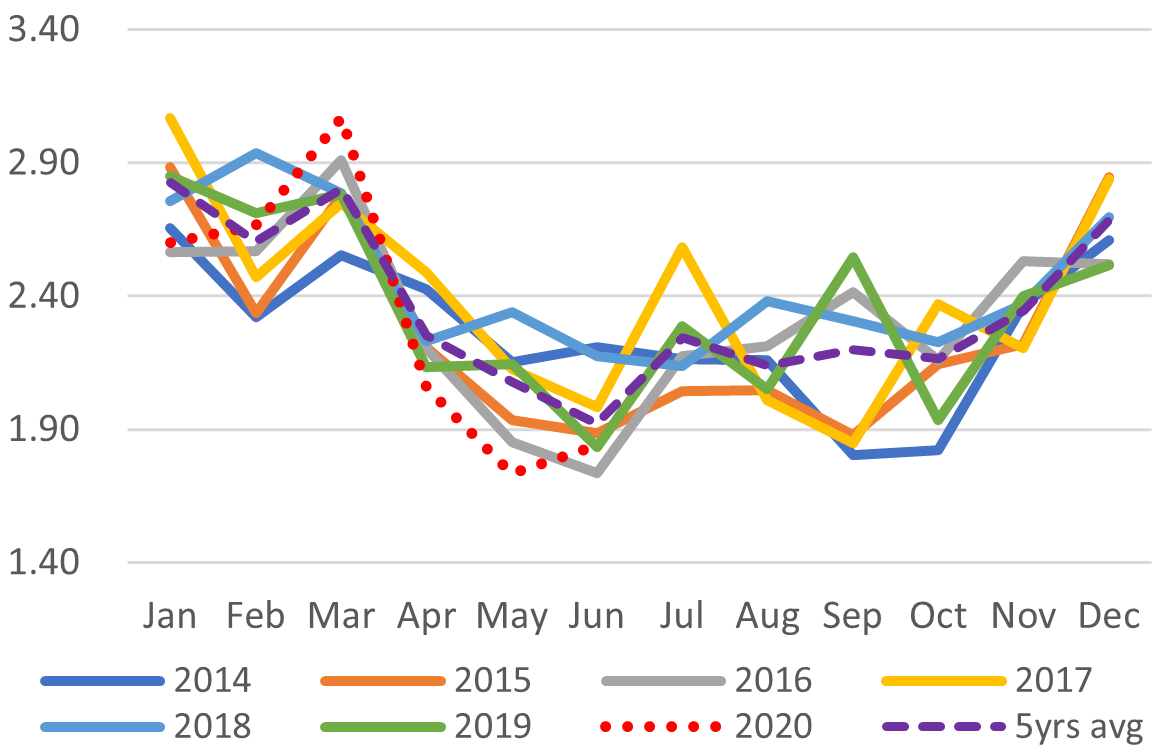

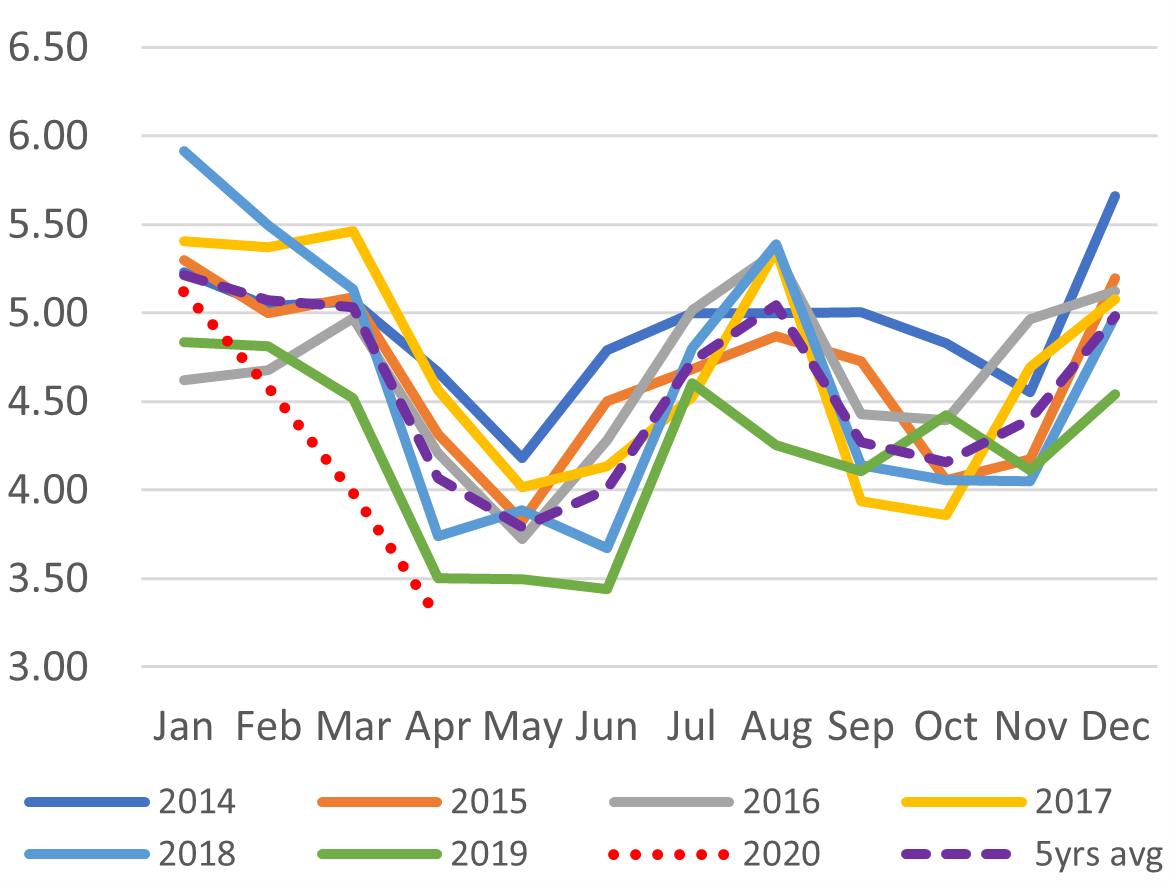

Japan LNG Price

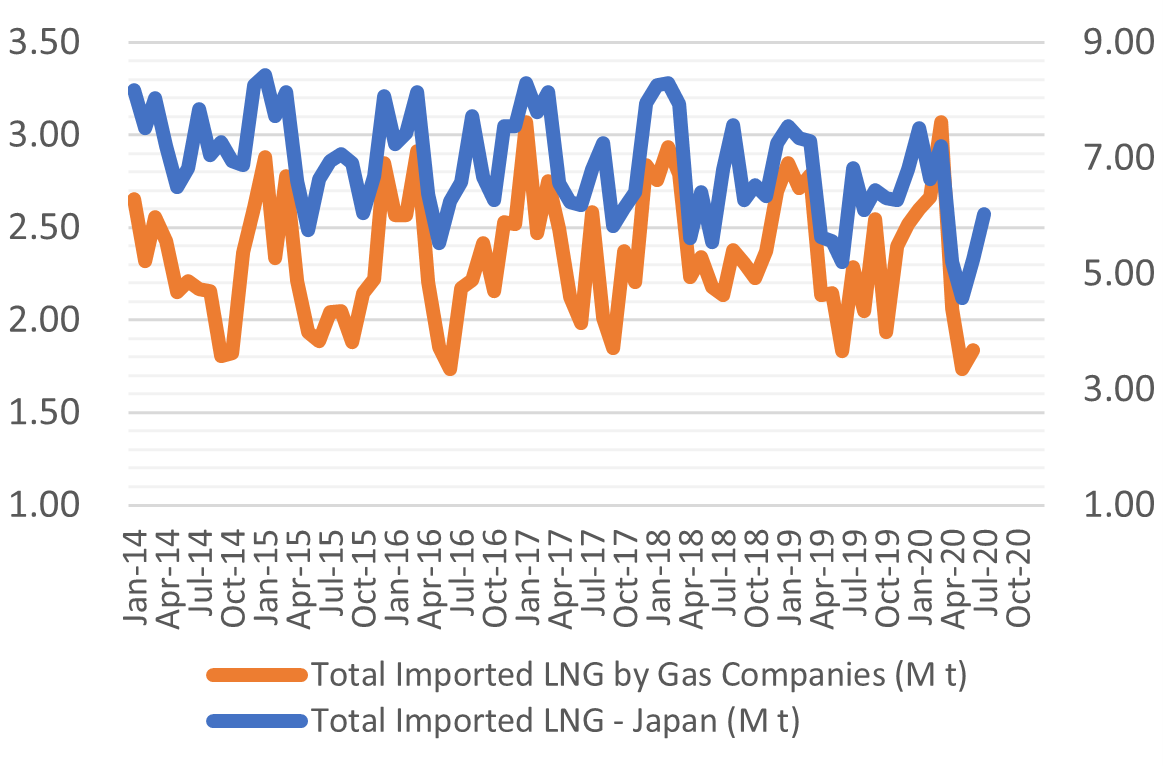

LNG Imports: Japan Total vs Gas Utilities Only

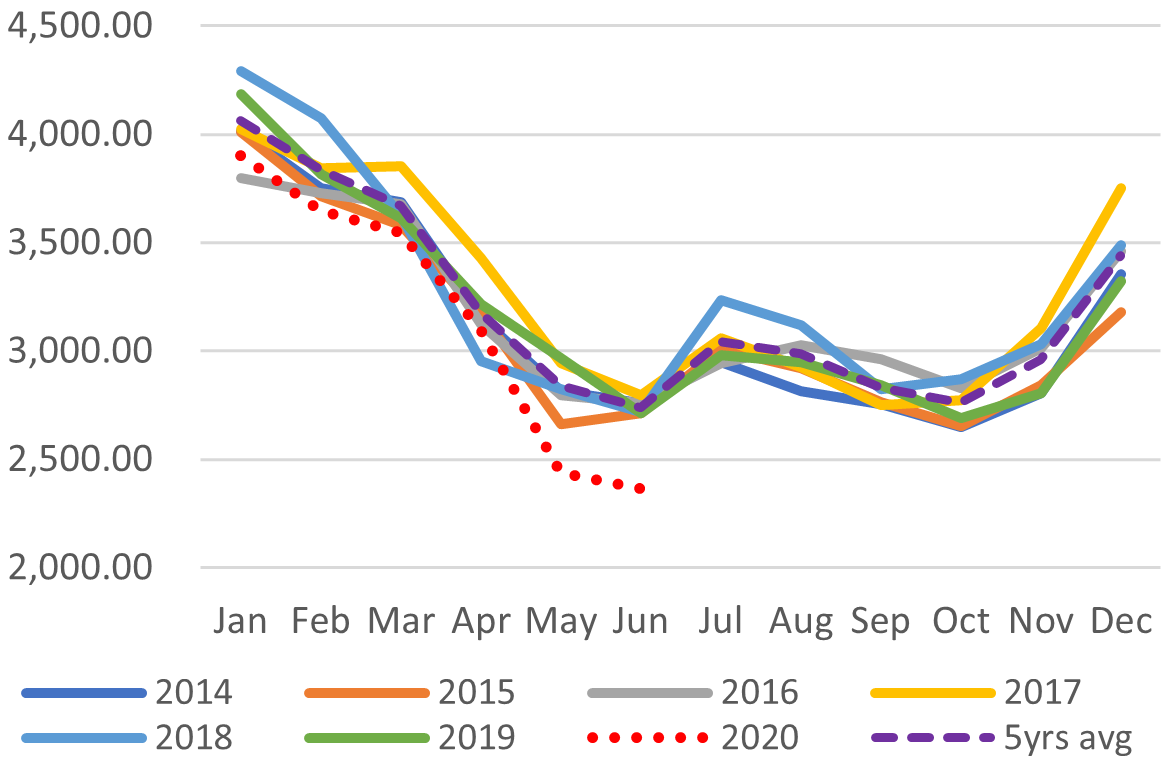

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

City Gas Sales – Total (M m3)

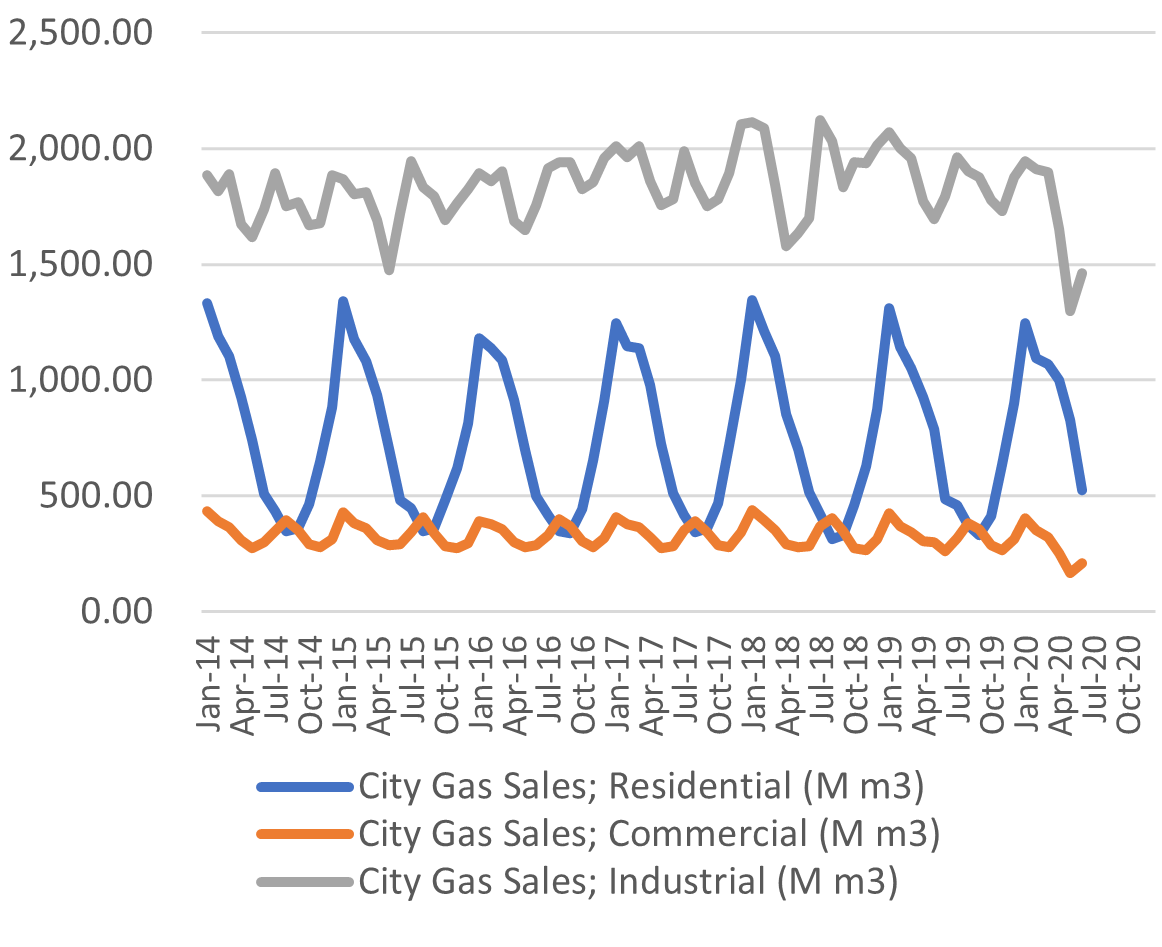

City Gas Sales by Sector (M m3)

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance

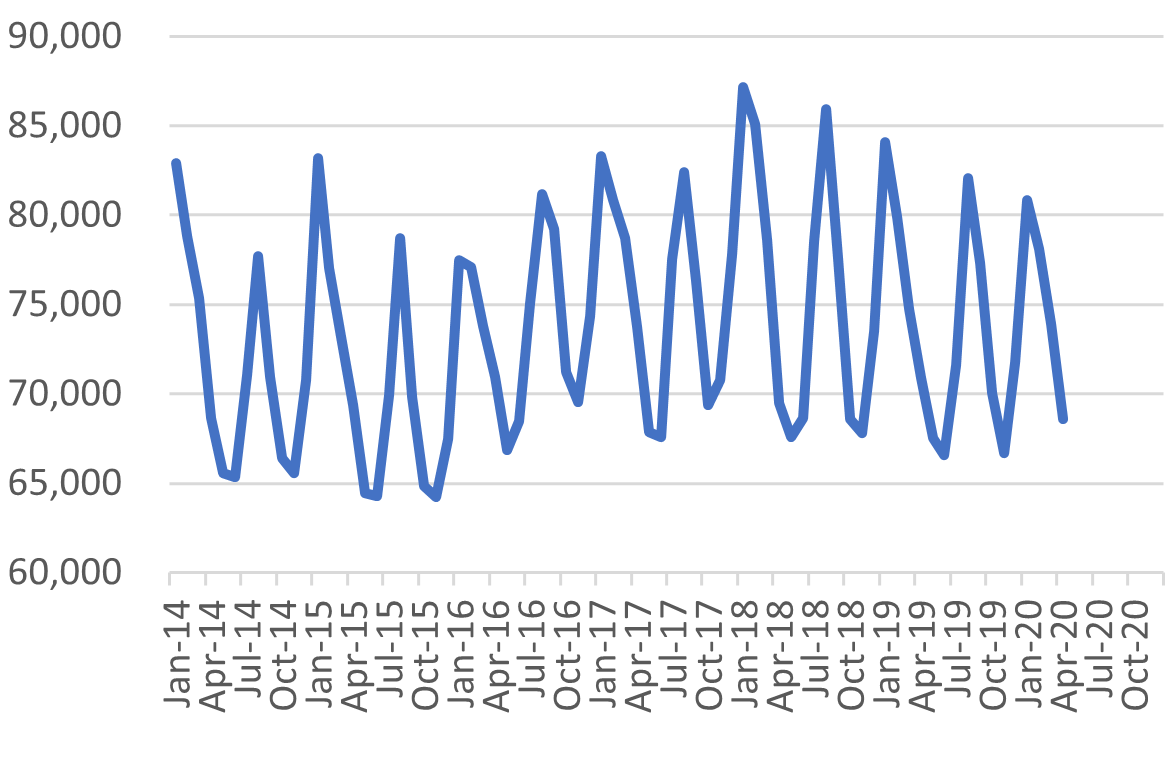

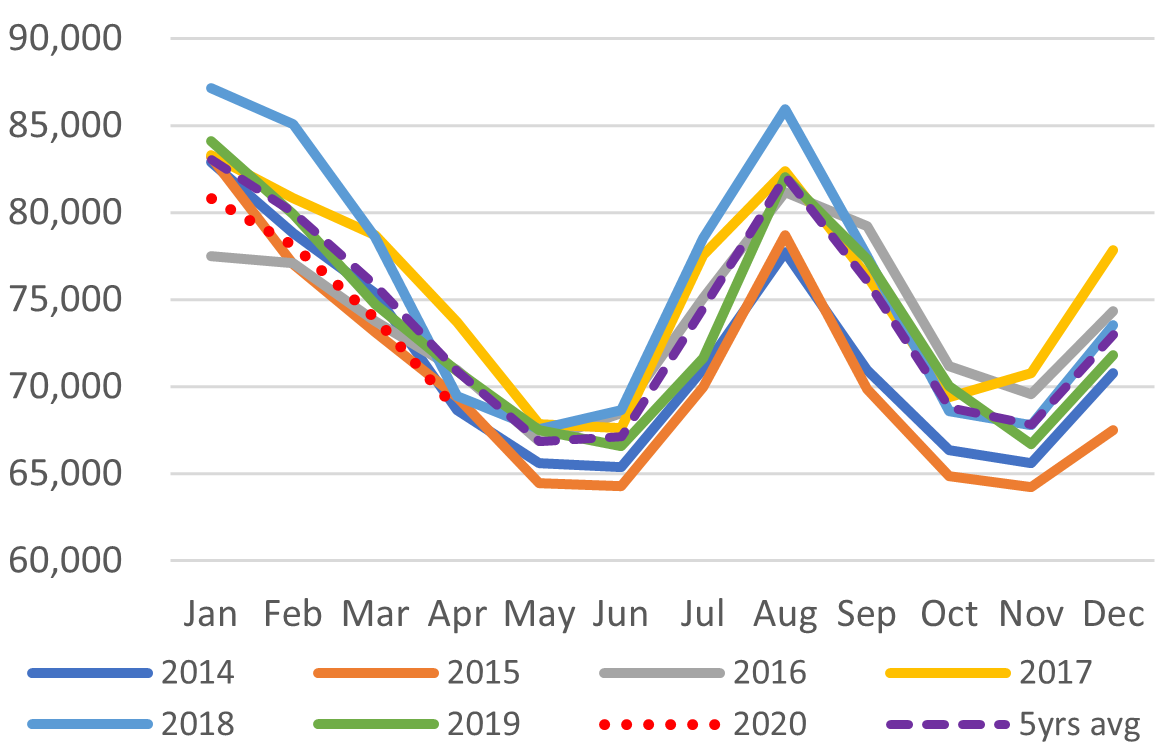

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

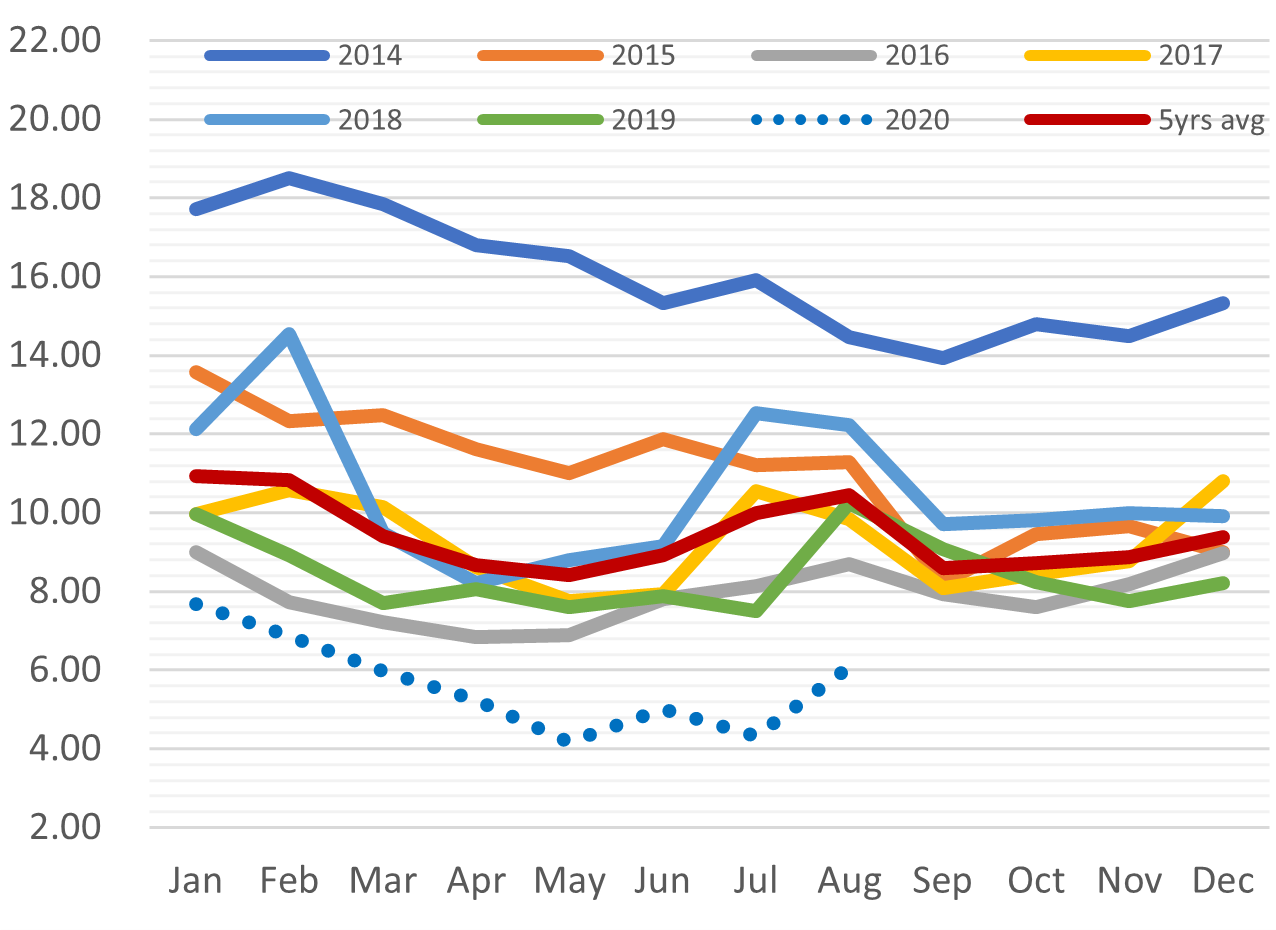

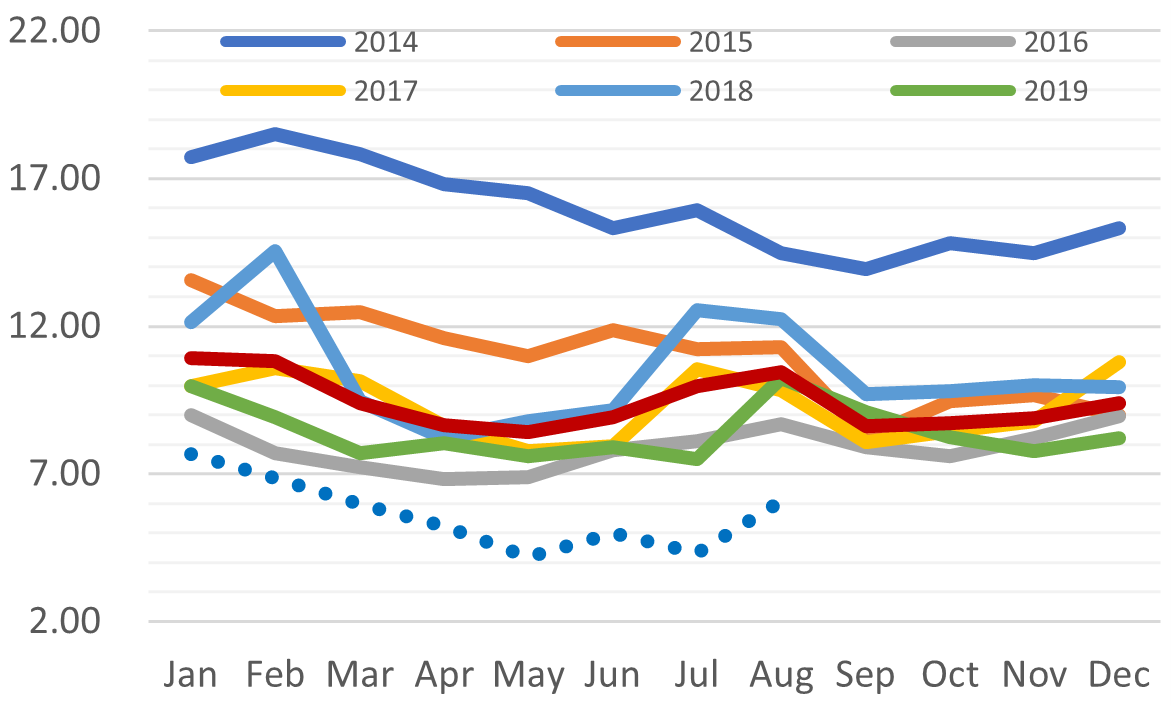

LNG Imports by Electricity Utilities

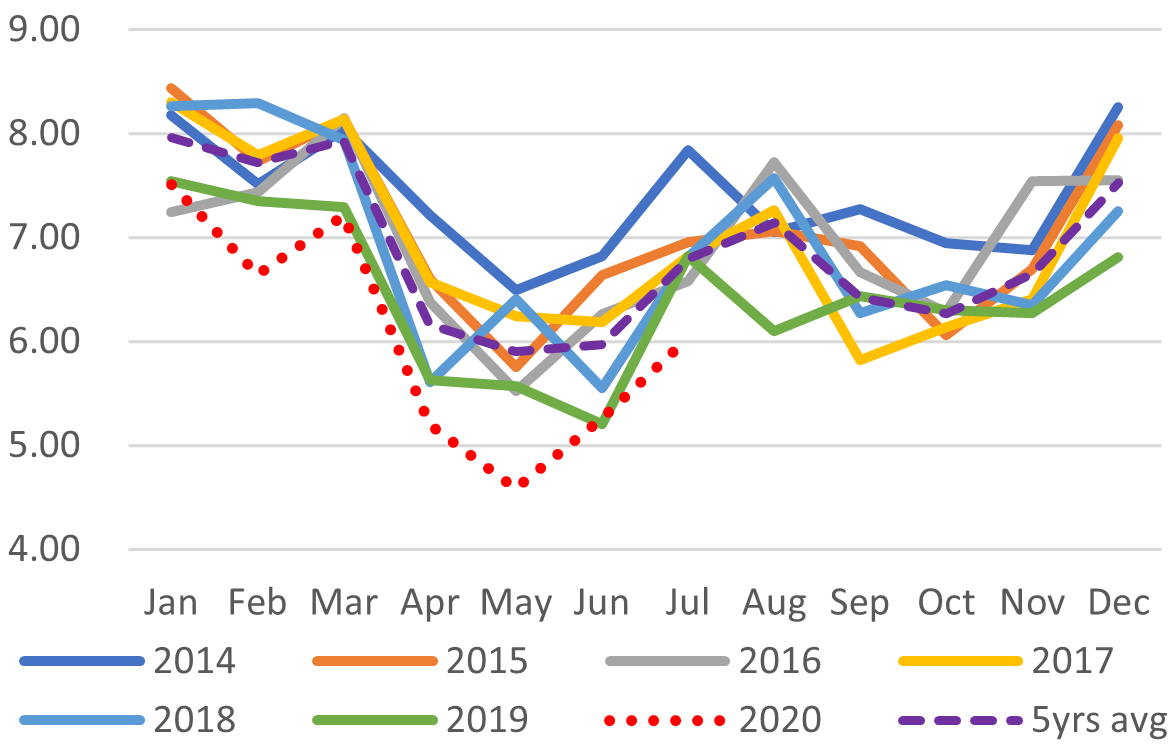

LNG Stockpiles of Electricity Utilities

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest Research Ltd., which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis.

Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

Recipients of this report should ensure that they fully understand the legal, tax and accounting implications before making an investment decision and independently determine that the transaction is appropriate based on their own objectives, experience and resources.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided.

In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004