Japan’s version of Big Oil may have a multi-billion-dollar problem should the residency in the U.S. White House change from November. Japanese total outlay on the U.S. oil and gas sector, which only accelerated in the recent decade, has likely topped $200 billion. Based on the Democrat Party candidate’s announced green energy policies, these assets would face significant reevaluations and possible write-downs should Joe Biden take over from the incumbent.

Between now and the beginning of fiscal 2022, Japan is due to unveil details of a new Feed-In Premium (FIP) electricity pricing system, which will complement the Feed-In Tariff (FIT) contracts that helped almost triple the country’s renewables capacity since 2012. The new system is supposed to create incentives for investors to add energy storage to their solar and wind projects, putting them further on course to compete in the open market without taxpayer aid. The concern is that without a guaranteed level of return, some renewables investors may cool on the Japanese power market.

HOUSE VIEW

Criticized for over a year for a seeming lack of action on climate change, last week Japan struck back. Environment Minister Koizumi Shinjiro hosted a global ministerial web conference that launched a Japan initiative for countries to share experiences in formulating climate-friendly economic recovery packages. Koizumi’s “Platform for Redesign 2020” was a progressive-sounding initiative. It did not, however, stop some conference participants from questioning he depth of Japan’s commitment sdsdsdsdsdsd sdsds. Dsds ds dssd sdsdsdsdsdsdsds sdsds … MORE

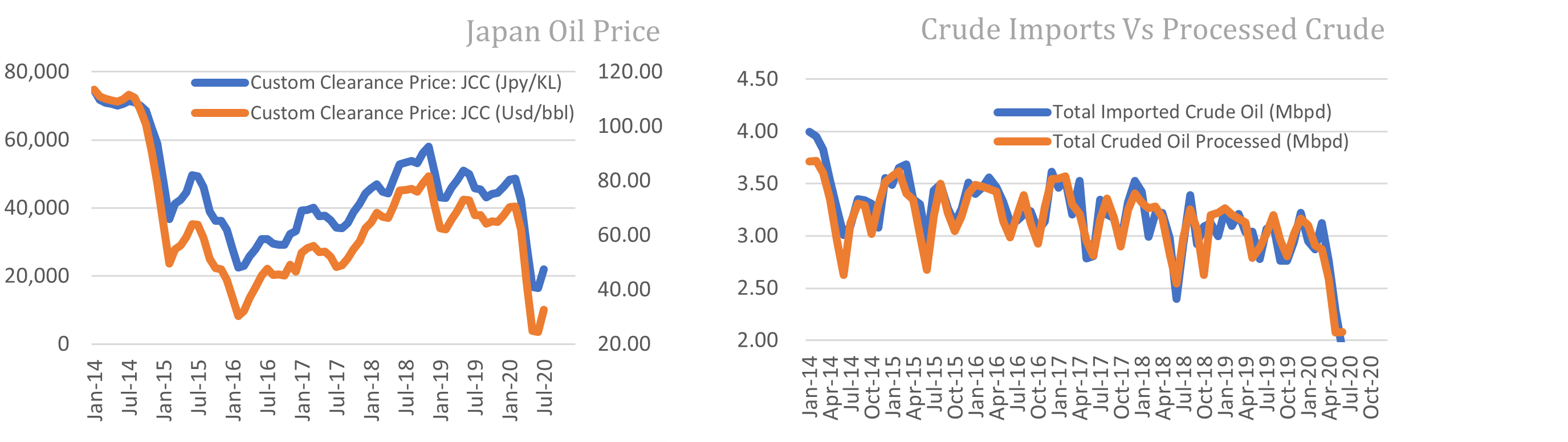

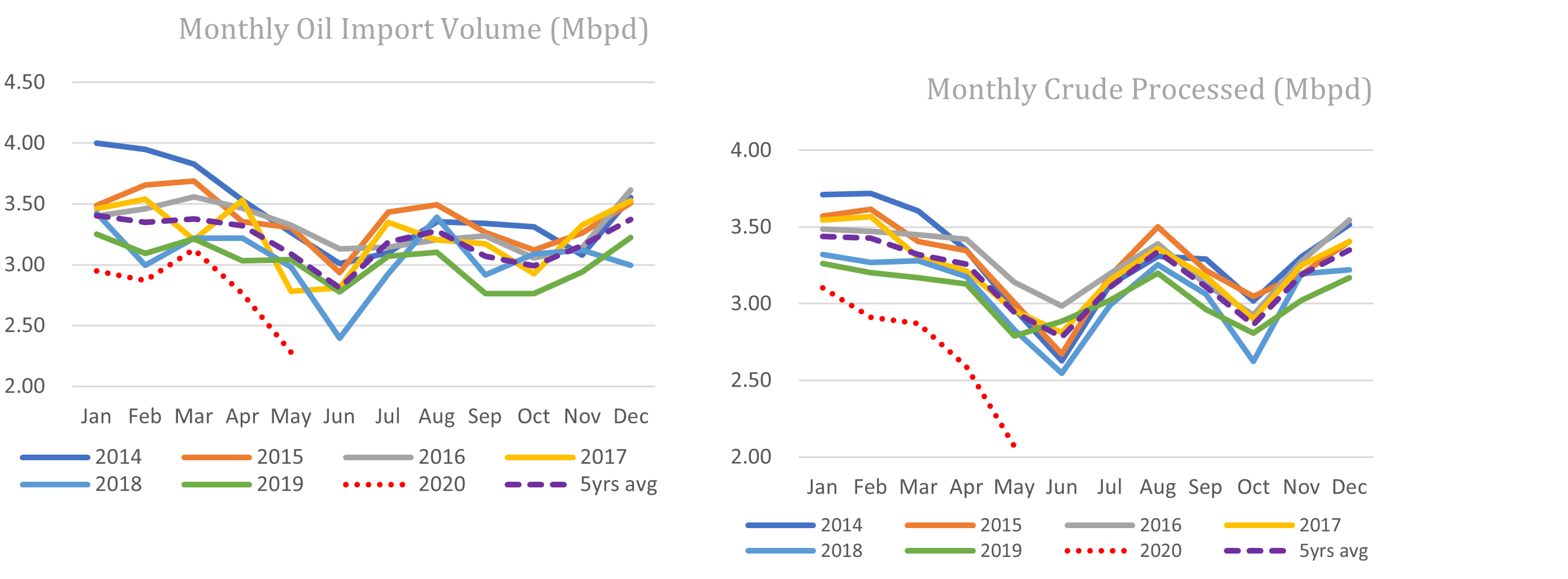

Japan’s oil demand drop is accelerating, driven by the coronavirus pandemic and depopulation, and if that continues the industry will need to consolidate further or shutter refineries, new Eneos President Ota Katsuyuki said in a media interview.

The country’s biggest oil refining firm saw utilization rate of its domestic plants fall to 68% in the April to June quarter.

Eneos may look to convert some refinery locations near the sea into hydrogen import terminals, and install solar panels at other sites, Ota said.

The company must look to expand its business areas, Ota said.

CONTEXT: Eneos was formerly known as JXTG Holdings and used to be one of the world’s largest companies by revenue.

ENEOS President Ota says service stations can be transformed into “delivery hubs” that attend to a range of customer needs.

Ota mentioned the possibility of offering laundromat and delivery services via the ENEOS service station network. These services could be controlled via mobile apps, he said.

ENEOS has released a biodegradable grease for use in tunneling machines, which it developed in conjunction with Obayashi.

ENEOS says the new grease enables operators to reduce the environmental impact of tunnel construction.

TAKEAWAY: The pandemic has forced an issue that Japan’s entire energy complex has struggled to tackle for years: a declining and aging population will not have the same energy needs and infrastructure. Although there have been mergers among domestic refining players in the last five or so years – all the more notable for the intense corporate cultural differences in the industry – the painful issue shuttering capacity has been largely untouched. Comments from the new president of Eneos suggest this may finally be on the agenda. The next big question will be how much Japanese firms will be prepared to invest in site conversions and pivots to chemicals or hydrogen. With global majors such as Saudi Aramco delaying or walking away from new petrochemical and refining investments, this may be a chance for Japanese players to step in, reposition their assets, and secure a place in the next up cycle.

Tokyo Gas, one of the largest buyers of LNG in Japan, said Sept 1 that it has established a new company called TG Global Trading to more actively trade LNG as it looks to strengthen its hand in the global market.

The new company aims to achieve an annual transaction volume of 5 million tons by 2030.

Based in Singapore, TG Global Trading will initially have a staff of 30.

CONTEXT: Japan imported 77 million tons of LNG last year. Of those, about half were brought in by JERA, a company created by Tokyo Electric (TEPCO) and Chubu Electric.

TAKEAWAY: Global diversification by a Japanese conservative utility is a seismic shift. It shows both the realization that the domestic market has little to no room for expanding volumes and that Japan’s know-how in LNG purchases could be carried to other markets. Traditionally, the only Japanese firms to trade energy outside of their home country were the trading houses and they had a mixed record with it. After three decades in Singapore, Mitsubishi Corp. even decided to close its local oil-trading desk after it lost $320 million in supposedly unauthorized transactions. Still, as a buyer of a third of the world’s LNG, Japan is arguably better placed to trade this market. It will also be interesting to see if the Singapore hub will embolden Tokyo Gas, and other Japanese buyers, to shift away from their reliance on long-term LNG deals to more spot purchases.

Mitsubishi Energy buys stake in Taiyo Koyu gasoline station brand (Sekiyu Tsushin, September 1)

Mitsubishi Energy said on Monday it now owned 46% of service station chain Taiyo Koyu after a purchase agreement with a related shareholder.

According to those familiar with the transaction, Mitsubishi’s stake is now the same size as that held by Eneos.

Mitsubishi says it made the investment to help grow its energy supply business by combining resources with Taiyo Koyu’s sales network.

CONTEXT: Until the mid-1980s, Japan had at least 17 gasoline station brands. After a merger of Idemitsu with Showa Shell last year, this official shrunk to just five.

TAKEAWAY: The number of Japan’s gasoline brands is, in effect, scaling back to the three industry majors (Eneos, Idemitsu, and Cosmo). The other two, Taiyo Koyu and Kygnus, can hardly be views as independent. Taiyo is now almost entirely controlled by the Eneos empire. Mitsubishi is one of the original entities that went on to create the current Eneos brand through a series of industry mergers in the last two decades. With Eneos and Mitsubishi holding 92% of Taiyo, how long the latter remains a high-street brand is a moot point. Meanwhile, 20% of Kygnus is held by Cosmo and its parent firm San-Ai Oil has relations with Eneos too. With the global pandemic adding to the ongoing issue of rural depopulation in Japan, this ongoing gasoline industry consolidation seems inevitable and likely to result in more station closures.

NEWS: POWER & NUCLEAR

No. of operable nuclear reactors

33

of which

applied for restart

25

approved by regulator

16

restarted

9

in operation today

4

able to use MOX fuel

4

No. of nuclear reactors under construction

3

No. of reactors slated for decommissioning

27

of which

competed work

1

started process

4

yet to start / not known

22

Source: JANSI and JAIF, as of August 23, 2020

Sacrificing coal, METI plans nuclear revival and mergers of weaker power utilities (Zaiten, September edition)

The Ministry for Economy, Trade and Industry (METI) announced that Japan will phase out coal-fired power generation, which climbed to over 30% of the total since the 2011 Fukushima disaster. But, this is a bluff.

METI’s line is that the government and the private sector will work together to bring online renewable capacity, such as wind power stations. However, there is no way that generation that is at the mercy of the weather can replace 70% of Japan’s coal-fired baseload capacity. In truth, the announced line on coal is simply a scheme to bring back online nuclear power.

The government also really wants to get construction of new nuclear plants going as that will create jobs – including for retiring bureaucrats from METI. The ministry has always favored the nuclear sector.

Unless METI gets the nuclear fleet back online, Japan could have zero nuclear reactors active by 2049 based on current licensing terms.

PM Shinzo Abe and the ruling party was afraid to lose popular support over openly backing nuclear restarts and new nuclear construction; thus, the politicians did not help METI, says a highly placed bureaucrat, now retired.

Assistant to the PM, Takaya Imai, turned the situation around, bringing more political support to METI, which is now finally moving to push through nuclear restarts.

Imai is the same person who persuaded Toshiba to buy Westinghouse. Due to the 2011 Fukushima nuclear plant accident, Toshiba’s nuclear division went down the drain, but Imai brushes this off. He continues to tell those in his circle that “Japan needs nuclear power because we have no natural resources.”

Imai is said to have hand-picked the METI bureaucrats who now oversee his nuclear restart plan. His picks are Shin Hosaka, now secretary of the energy bureau, and Yuji Iida.

Imai’s plan is to keep nuclear’s role in the energy mix at 20-22%. Nuclear will be positioned as an “economic and stable source of energy.”

Imai wants first to restart construction of the Higashidori and Oma nuclear plants. Then, he will push for one reactor to be added at each of the Mihama and Tsuruga nuclear plants.

The biggest losers in the culling of coal-fired stations are Chugoku, Tohoku and Hokuriku electric power companies (EPCOs). These three already face a drop in their catchment area population and sluggish local economies. They will struggle to raise financing to build new coal or nuclear plants.

As such, METI plans to merge Tohoku with Tokyo Electric (TEPCO) and change the company name to Higashidori Electric Power Co. This will rebrand TEPCO, whose brand was tarnished by the Fukushima disaster. METI believes the rebranding will reduce public opposition to the company and nuclear power in general.

The reorganization plan for Chugoku is a merger with Kansai Electric Power Co (KEPCO). Hokuriku would merge with Chubu EPCO. Chugoku and Hokuriku have large hydropower capacity, so that would give KEPCO and Chubu a bigger renewable energy portfolio.

Since the METI knows the weak spots of KEPCO and Chubu, the companies probably have no choice but to follow METI requests for an industry reorganization.

Tokyo Gas hits 2.5 million electricity subscribers (Denki Shimbun, September 4)

Tokyo Gas said it now has over 2.5 million electricity subscribers.

Tokyo Gas entered the electricity retail market in April 2016, and currently waives its basic service charge for new subscribers for the first three months.

Tokyo Gas sold 670 GWh of electricity in May, making it Japan’s leading non-legacy domestic electricity retailer.

TAKEAWAY: Japan’s power demand is around 1,000 TWh a year. Tokyo Gas power sales, projected on an annual basis, indicate the company retails not far from 1% of the Japanese total. All this for a company that retailed zero electricity five years ago. Of course, being the biggest utility (after TEPCO) in the most populated zone has helped. Tokyo Gas has probably been one of the biggest beneficiaries of the downfall at Tokyo Electric (TEPCO). However, the gas utility is also proof that deregulation has worked and that the market could be heading into a new phase of reorganization.

Okinawa Electric digs in on coal, seeks to blend biomass with coal to improve efficiency (Denki Shimbun, August 25)

A new director at Okinawa Electric Power Co., Hisagai Hiroyasu, said that while the company remains committed to fighting global warming, he believes coal-fired thermal remains an important power source for the region from the perspective of stability and economics.

The utility will blend biomass fuel with coal, and employ smart technologies to more precisely control turbines, to reduce the environmental impact of its operations.

CONTEXT: Okinawa is the most reliant of Japanese utilizes on coal-fired generation with about 60% of its electricity coming from burning the mineral.

Mitsubishi Hitachi Power Systems has become a wholly-owned subsidiary of Mitsubishi Heavy Industries and changed its name to “Mitsubishi Power”

CEO Kawai Ken said that while services related to coal-fired power stations currently account for 40% of the company revenue, this will increase to 80%.

Kawai is concerned about impact on the industry from Japanese government’s decision to phase out 90% of coal-fired generation plants by 2030/31. He says his company will need to become leaner to adapt.

Kawai says that both in Japan and in Southeast Asia, his company will adapt to the transition to renewables by switching to greener generation technology.

Still, demand for services that boost the efficiency of thermal plants will likely remain, says Kawai. In a major shift, his company intends to make these services a core source of revenue.

TAKEAWAY: Ever since Japan’s energy ministry, METI, unveiled plans this summer to shutter old and “inefficient” coal-fired generation, the internal debate on what this will mean in practice has been incessant. Okinawa Electric, with no grid connection to the rest of Japan and reliant on coal-fired generation like no other utility, has the most to lose if METI applies its “inefficiency” criteria. One way to work around it, from the Okinawa company’s standpoint, is to boost the energy efficiency figures of its plants with the biomass add-on. Employing new IT-led tech from companies like Mitsubishi Power will also boost the results and gain political sympathy. Lobbying and the nature of Okinawa’s politics will do the rest. Bottom line: It’s hard to see Okinawa losing even half of its coal-fired capacity in the next decade.

Japan’s nuclear Regulation Authority has given a stamp of approval to a new intermediary storage facility for spent fuel rods in Aomori.

The facility is scheduled to open during 2021/22, and is duly operated by TEPCO and the Japan Atomic Power Company.

TAKEAWAY: As covered in previous issues of Japan NRG Weekly, one of the major problems for Japan’s nuclear complex is a lack of storage for used nuclear fuel. The country’s nuclear power plants host around 16,000 tons of spent fuel and that is seem as close to the limit. Adding a brand-new facility for storage is an important short- to mid-term solution for the nuclear industry as it lobbies for more reactor restarts.

CONTEXT: The author is the head of the Japan Food-Journalists Association and a former editorial board member of the Mainichi Shimbun, one of Japan’s big five broadsheets.

Japan was recently awarded the satirical “Fossil of the Day” award in criticism of its reliance on fossil fuels. If anything, the fact that we were chosen for this award should be celebrated, because for a resource-scarce country like Japan, coal-fired power stations remain an essential part of energy security.

For countries in the EU, home of the “Fossil of the Day” award, divesting in coal serves the national interest because it opens up possibilities for new local industries. The ability to share solar and wind generated power over a wide area makes renewable energy a relatively stable option.

In Japan, however, circumstances are very different. Being a small island nation, Japan is unable to trade electricity with other countries in the region.

Keeping coal, of which there are abundant reserves in Australia and in other countries, as part of Japan’s energy mix also reduces our reliance on Middle Eastern oil.

The government’s 2030 energy plan requires electricity generated from coal to be just 26% of Japan’s total. Coal currently comprises a much larger percentage, so without phasing out older coal-fired facilities, achieving this 2030 target may be very difficult, especially when coal-fired plants currently under construction came online.

The government is actively encouraging the growth of offshore wind projects, which are able to convert a higher percentage of energy received into electricity compared to other forms of renewable energy.

Local bodies and industry groups are calling for even more aggressive renewables targets. The Renewable Energy Council (Shizen Enerugi Kyogikai), whose members include 34 of Japan’s 47 prefectural governments, is calling for a target of at least 40%.

Author is Rebecca Mikula-Wright is executive director of the Asia Investor Group on Climate Change.

Author cites ING bank to say that while many European governments have planned their COVID stimulus packages based on climate change investments, Japan’s green measures accounted for just 0.02% of the overall economic support.

Japan’s financial institutions need to consider their role in climate change.

TAKEAWAY: See our extended House View commentary for more assessment on this topic.

TEPCO Holdings says it will launch a new service in 2021 aimed at “virtual power producers” (VPP), which trade power between producers, consumers, and storage units.

As VPPs tend to lack expertise in adjusting output to meet grid demand, for a fee, TEPCO will help VPPS optimize their supply to the grid.

The market for electricity provided by VPPs is forecast to reach ¥80 billion by 2030.

CONTEXT: The VPP business in Japan is expected to begin in earnest from next fiscal year (starting in April, 2021) to cover excess supply and demand in electricity. Several companies are considering entering the market, including TEPCO, Kansai Electric (KEPCO) and German’s Sonnen, a unit of Royal Dutch Shell.

The five former Kansai Electric (KEPCO) board members being sued by shareholders for ¥2 billion in damages in relation to allegations of impropriety say they will defend themselves in legal action.

Asserting that they merely took custody of the funds in the interests of facilitating KEPCO’s nuclear generation operations, the former directors deny legal liability.

CONTEXT: KEPCO is embroiled in one of its biggest ever scandals as dozens of former executives are accused of bribery and improper use of corporate funds, most of which is related to the utility’s nuclear assets.

The Agency for Natural Resources and Energy, which is a part of METI, has suggested it may pay less for power generated by offshore wind farms than originally thought.

A lower bid price could render the business case of favorites TEPCO and Obayashi untenable and open up the possibility that the tender will go to another contractor.

On August 19, a METI expert committee was convened to discuss electricity procurement prices. The ¥12 per kilowatt hour feed-in tariff (FIT) recommended by the committee was significantly lower than the expected tariff of ¥36 per kilowatt hour.

The METI committee cited the example of wind power leader Europe, where investments in infrastructure have significantly reduced the cost of generation. This comparison was vigorously rejected by the Japan Wind Power Association, of which TEPCO is a member, which said conditions in Japan and Europe were too different to allow comparison.

Tokyo Electric (TEPCO Holdings) said it was developing a technology that would enable floating offshore wind turbines to be constructed up to 30% cheaper than in Europe.

TEPCO’s focus is on turbines in the 10 MW class.

TEPCO is experimenting with turbines with oval hulls which tend to be less buffeted by high waves. It may involve Tokyo University and Penta-Ocean construction in its research.

TAKEAWAY: METI, Japan’s energy ministry, has said it wants to see 1 GW of offshore wind capacity built in the country over the next decade. As Japan has yet to construct from scratch a single commercial-scale offshore wind project, many in the power industry believe higher tariffs are vital to ensuring there is initial momentum to realise the plans. A FIT of ¥12 per kWh would make most solar power developers in Japan nervous, and the country has 55 GW of solar capacity under its belt. Proposing such a low price for offshore wind is almost unbelievable. Meaning, we would expect tariff negotiations to continue and the bureaucrats’ tariff to sweeten over time.

Solar plants at center of litigation amid deforestation, accidents (Nikkei, August 31)

A spate of accidents relating to large-scale solar generation facilities is making local bodies more wary about allowing the construction of such facilities.

In 2018, a sloping section in Kobe that had been cleared of trees to accommodate solar panels collapsed in torrential rain, disrupting bullet train services.

Many local bodies are now requiring generators to deposit a bond to cover the cost of removing the panels at the end of their lifetime. An ordinance introduced by some local bodies in 2019 prohibited the erection of solar panels on steep sections.

The town of Ito is currently the center of a dispute between the government, residents, and a solar project consortium including South Korea’s Hanwha Group. The town was slow to introduce legislation to regulate the solar industry, and is now being sued by the consortium over its refusal to issue a permit for a solar power facility.

In the early days of solar generation, the industry was subject to few regulations. This is attributed to significant goodwill in the community, and the assumption that operators would exercise common sense, says one local body politician. Meanwhile, operators claim that solar panels are a good way to make use of uncultivated land, and the risk of accidents is low if they are installed correctly.

Idemitsu says it has begun cultivating sorghum in Australia for use in biomass fired power generation.

The trial is being performed on an unused area of land belonging to the Ensham coal mine in Queensland, Australia, which is 85% owned by Idemitsu.

Some of the sorghum cultivated will be made into pellets which can be mixed with coal use for fuel in power stations.

The Queensland state government, which aims to increase its biomass exports, has provided Idemitsu with an AUD 20,000 grant for the project.

TAKEAWAY: Biomass is seen as a side-car to coal-fired thermal generation and a key component to improving coal’s energy efficiency figures. As Japan’s government embarks on a cull of its older, less efficient coal-fired units, most utilities will be clamoring for ways to game the system. Idemitsu could be cultivating a very profitable business line.

SB Power to switch entirely to renewable energy (Denki Shimbun, September 4, 2020)

SB Power, a subsidiary of SoftBank, announced on September 1 that from October 1 it will switch to 100% renewable energy, without any changes to pricing.

The company will offset its CO2 emission by using non-fossil certificates from renewable energy.

CONTEXT: Softbank, controlled by billionaire Son Masayoshi, has been one of the earliest and biggest investors in renewable energy in Japan after the 2011 Fukushima nuclear accident.

TEPCO markets zero emissions electricity generated in Saitama (Sekiyu Tsushin, September 2)

TEPCO Energy Partner and the Saitama Prefectural government have entered into an agreement that will allow commercial customers in the Saitama region to use locally-generated, zero emissions electricity.

The electricity is sourced from domestic solar generators that are no longer on the FIT scheme and solar-generated electricity supplied by the water board.

Despite high expectations from energy markets, due to the effect of COVID Hitachi’s acquired ABB Power grid business will likely be loss-making in the first year. However, Hitachi have bought “hidden” assets, such as software, worth 500 billion yen, and this will come out as a benefit for the company.

Hitachi’s asset ratio is now up to close to 20%, which has huge potential to change the future of the company’s business model.

Although Hitachi paid the most ever in the ABB deal and sees initial losses, looking beyond that into the future, it seems that they acquired a very strong business.

Hitachi ABB Power Grid received 4 electric power substation orders from EDF Renewables, a major renewable energy company in France.

The Hitachi unit will supply high tension breakers, transformers, gauges, and surge arrestors for use in substations that convert 20,000 volts power generated by wind turbines to the 110,000 volts used by the grid.

The value of the order, due by the end of 2021, was not disclosed.

ANALYSIS

DANIEL SHULMAN, PRINCIPLE, SHULMAN ADVISORY

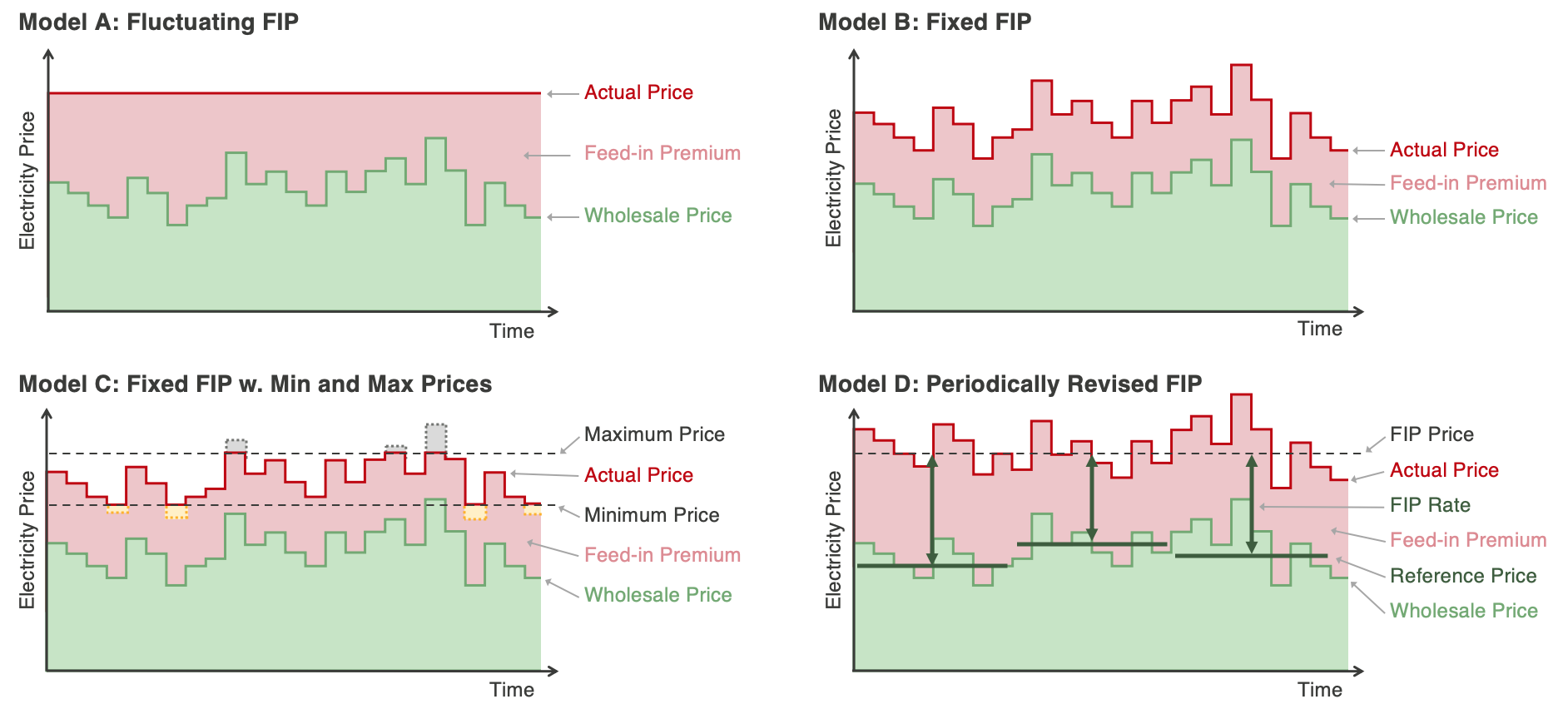

Transition to Feed-In Premium: What the Shift in Electricity Market Pricing System Means

Between now and the beginning of fiscal 2022, Japan is due to unveil details of a new Feed-In Premium (FIP) electricity pricing system, which will complement the Feed-In Tariff (FIT) contracts that helped almost triple the country’s renewables capacity since 2012.

The new system is supposed to create incentives for investors to add energy storage to their solar and wind projects, putting them further on course to compete in the open market without taxpayer aid. The concern is that without a guaranteed level of return via the FIT scheme some renewables investors may cool on the Japanese power market.

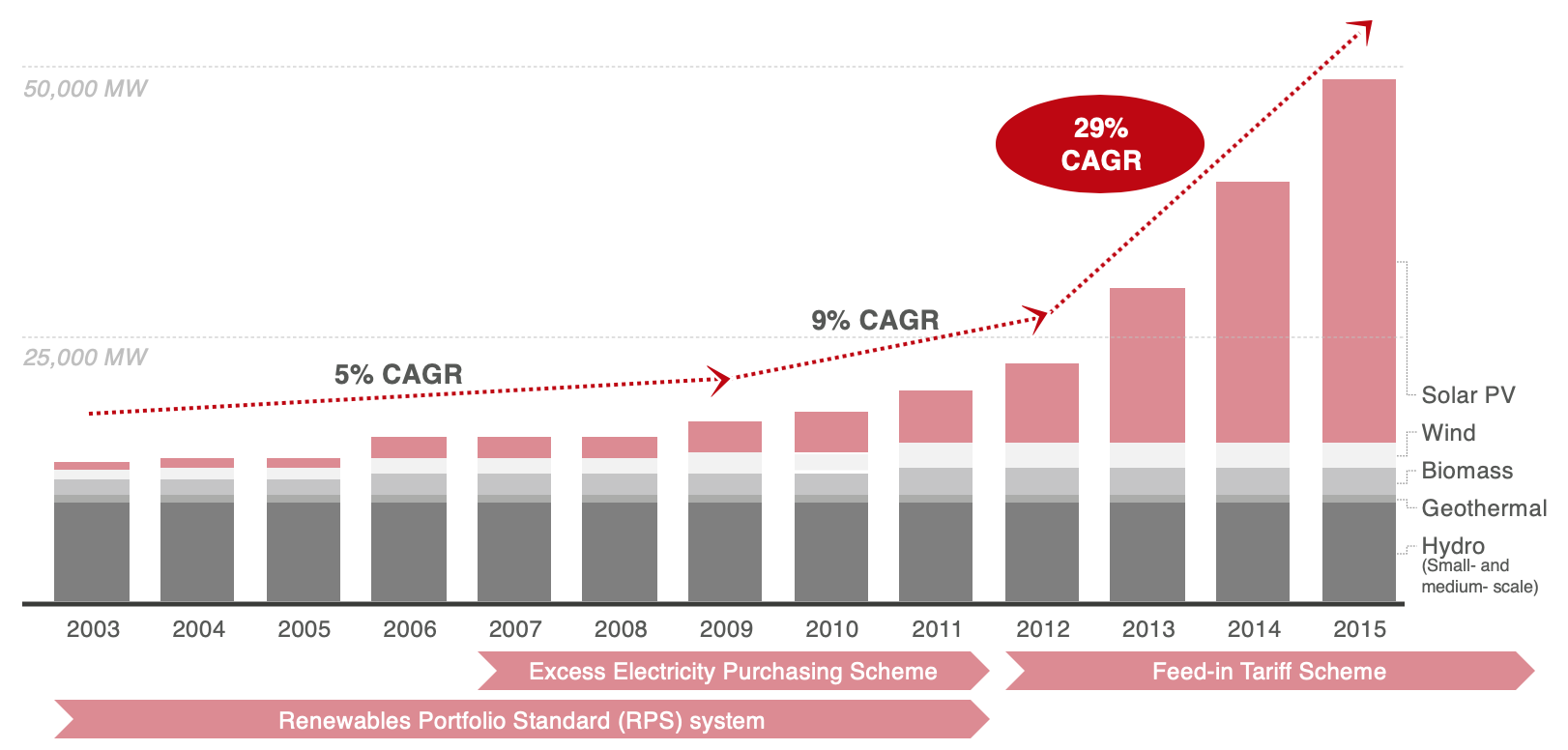

FIT STARTED THE REVOLUTION Until 2009, Japan’s foray into renewables outside of hydropower was negligible. That year, the industry started to grow with the introduction of a net metering program to purchase excess residential solar generation. Yet, it was not until the introduction of the FIT scheme in 2012, spurred on by the Fukushima nuclear disaster the previous year, that the domestic renewables industry took off.

Source: Agency for Natural Resources and Energy.

The initial residential net metering scheme that preceded FIT was merged with the new system. However, beginning in November 2019, those residual net metering contracts began to expire. By 2023, the same will be true for roughly 1.65 million residential solar contracts.

Japan needed to find a way to make sure these solar producers can continue to sell their excess generation to the grid. For this, and several other reasons, the Ministry for Economic, Trade and Industry (METI) decided to evolve the FIT system into FIP.

Where FIP is different is the incentives it creates for power generators. With FIT, with its guaranteed and often above-market kWh rates, renewable generators have no incentive to improve their projects by investing in energy storage. And yet, the latter would play an important role in optimizing the entire Japanese power supply system through a more stable supply from renewable sources and through the aggregation of business models.

Likewise, current FIT contracts do not lend themselves to pushing investors to improve the accuracy of their generation forecasting or to install better output adjustment controls. The contract always pays out the same per KWh and the responsibility for balancing generation sources lies with the grid operators.

However, given the fragmented and isolated nature of the Japanese power grid, creating incentives for more commitment from the generation side makes sense.

As renewables projects grow through energy storage, they will also improve their efficiency and cash flow. The government hopes that this will push the renewables industry in the direction of self-reliance, dispensing with the need for locked-in feed-in tariff rates, which are passed onto the Japanese electricity consumer via surcharges.

By 2018, 11% of the residential electricity bill and 15% of the commercial and industry bill were made up from the surcharges that go on to support the FIT program. Clearly, further increase in the burden of ratepayers must be avoided. Without such rate payer support, renewables start to compete on a more level playing field, which in the end strengthens the industry’s case for Japan to rely more on solar, wind and other renewable energy sources.

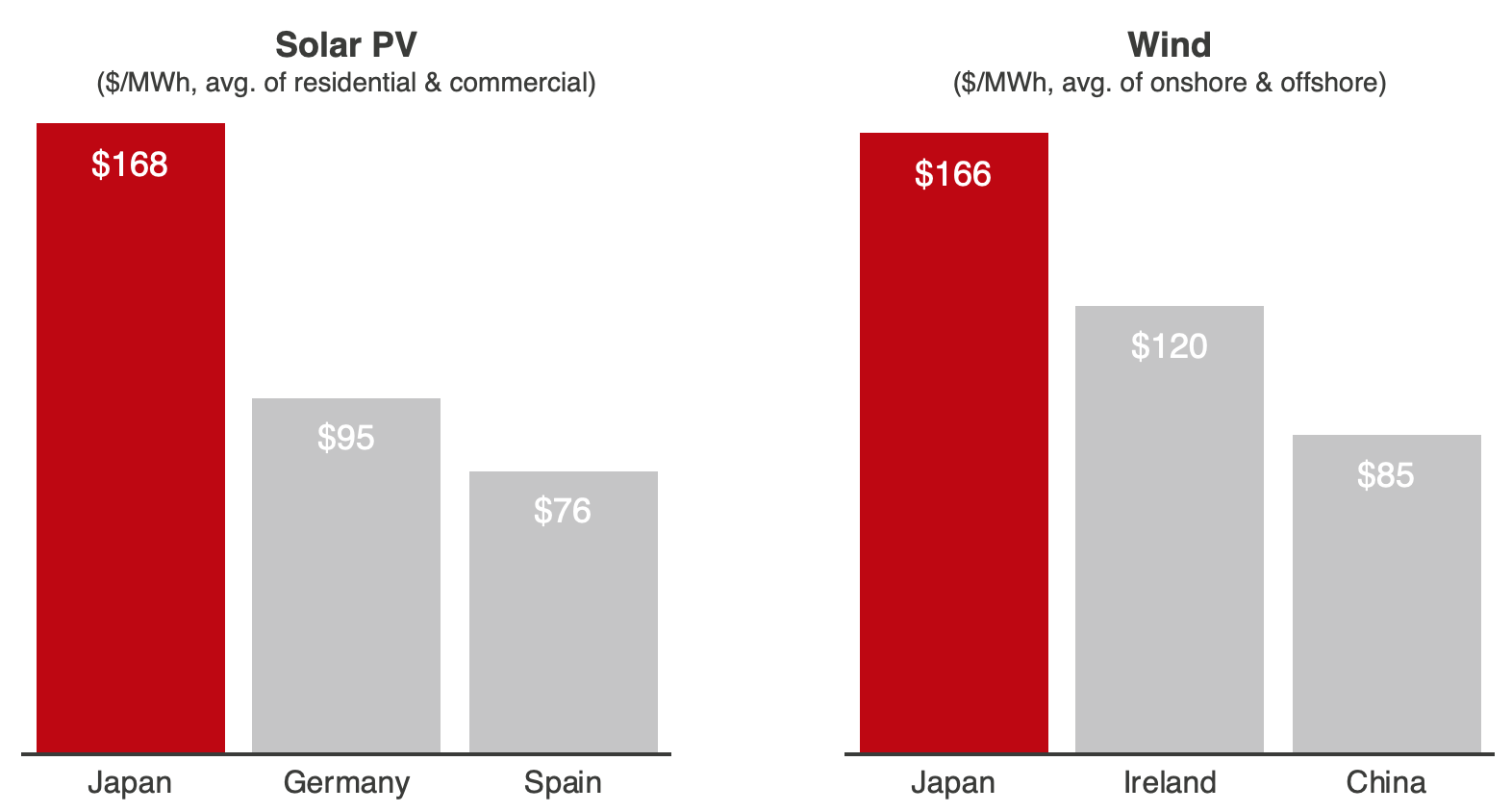

REALITY CHECK The idea that FIP will push renewables to operate at grid-parity, or at free market rates, is not meshing well with the actual levelized cost of energy (LCOE) for Japanese renewables projects. The measure, which allows us to compare the cost of electricity from different sources, shows that padded by the 10-year and 20-year FIT contracts, Japan’s LCOE remains stubbornly high on a global basis.

So, can the move to FIP sustain the growth of renewables in Japan and allow the sector to hit its 2030 targets? Certainly, there are some developers and asset managers who have refined their businesses to a level where they can grow and thrive in this brave new FIP world. But, will there be enough such industry players?

Without a guaranteed return on investment, and faced with the many regulatory hurdles and administrative issues, will some of the current renewables operators and investors in Japan be tempted to quit? This remains an open question.

Levelized Cost of Energy for Renewables

Source: Ministry of Economy, Trade and Industry

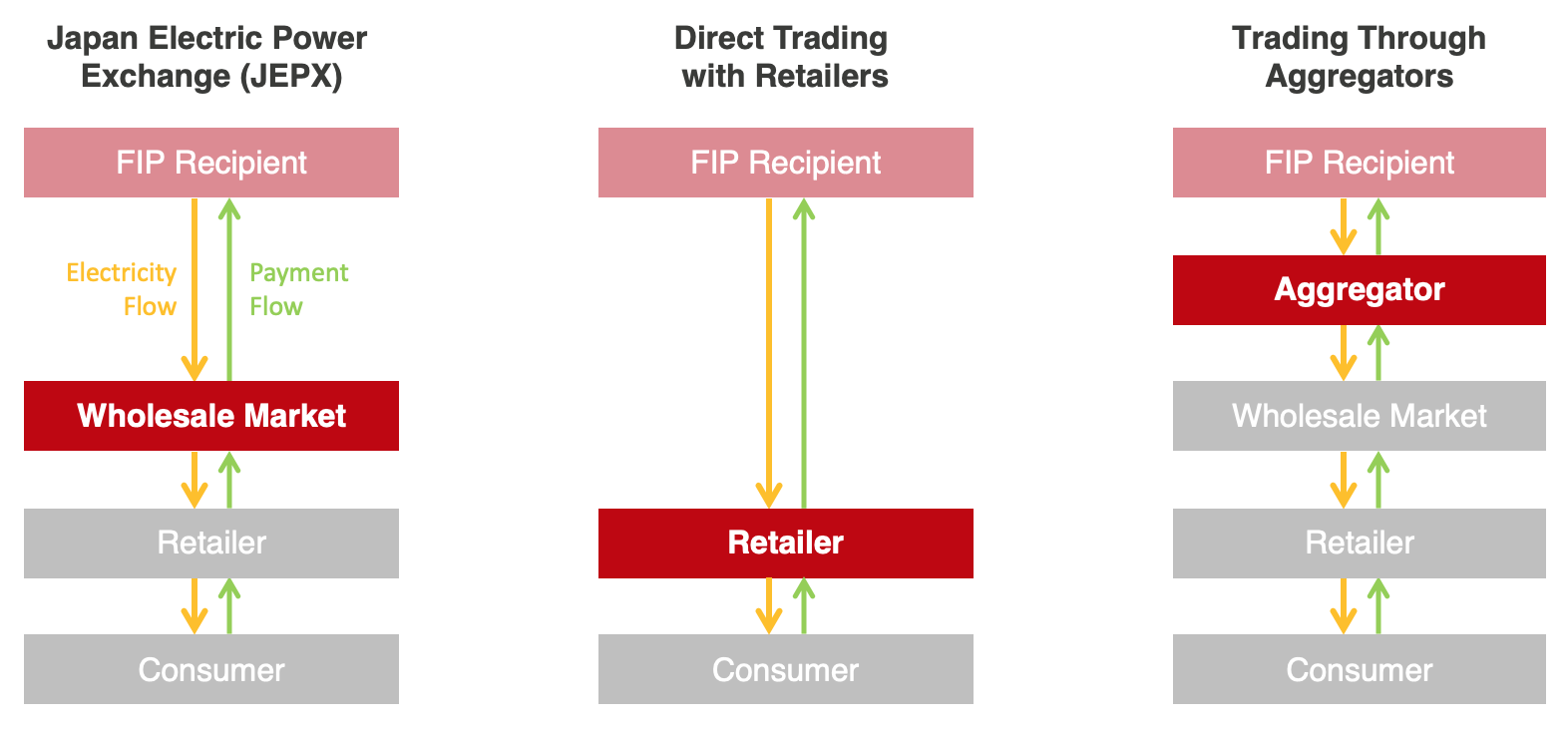

MODELS FOR TRADING POWER UNDER FIP METI envisions FIP-approved generators selling power through three channels: wholesale on the Japan Electric Power Exchange (JEPX), bilateral contracts with electricity retailers, and to aggregators who can then sell on JEPX.

Source: Ministry of Economy, Trade and Industry

However, because of minimum volumes required in order to trade on JEPX, and the complexity of integrating variable renewables into the portfolios of retailers, METI anticipates that the most important trading channel for small-scale generators will be via the aggregators. The latter are the market players that METI most wishes to incentivize through the FIP.

STRUCTURE OF THE FIP MODEL METI is still in the process of finalizing the details, but according to the information released so far, we know that the ministry has looked at several models and assessed them in terms of:

Investment Incentive – Will the model offer investors acceptable returns?

Market Integration – Will the model push renewables to compete on the market without as much help from taxpayers?

Source: Ministry of Economy, Trade and Industry

METI appears to have settled on Model D, as seen above, having concluded that it does the best job of incentivizing investment while also pushing renewables toward greater market integration.

PRICING OF THE FIP METI is considering two approaches to defining the actual yen value of the premium. Categorization by generation type and output capacity Auction system

Though not yet written in stone, METI appears inclined to use the auction system, which would most likely be based on the existing system which has been implemented in recent years even as FIT is still in place.

Still, given the lackluster results of the auctions that were held so far, it’s safe to assume that METI will refine and adjust the system quite a bit before pinning the success of FIP to it.

In any event, it’s clear that there will be a premium component determined either by the Procurement Price Calculation Committee or through an auction, and that there will be a reference price component, which will be derived from average market price over a period of time that has yet to be determined.

ANALYSIS

JOHN VAROLI DIRECTOR, NORTH AMERICA YURI INVEST RESEARCH

Joe Biden Win Could Spell Billion-Dollar Headache for Japan’s Oil and Gas Complex

Japan’s version of Big Oil may have a multi-billion-dollar problem should the residency in the U.S. White House change from November. Japanese total outlay on the U.S. oil and gas sector, which only accelerated in the recent decade, has likely topped $200 billion.

Based on the Democrat Party candidate’s announced green energy policies, these assets would face significant reevaluations and possible write-downs should Joe Biden take over from the incumbent Donald Trump.

While Japanese money has started to flow into solar and other renewables projects in North America, it is small compared to decades of investments in U.S. oil exploration and gas pipelines. Since 2011, Japan has also made billion-dollar bets on U.S. shale and LNG infrastructure.

Just a year ago, Osaka Gas became the first Japanese firm to buy a U.S. shale gas driller, paying $610 million. Seven & I Holding bet a whole $21 billion this summer to take a U.S. gasoline station network off the hands of Marathon Petroleum.

GONE IN 60 DAYS?

With less than 60 days to go before Americans head to the polls, the outcome of the U.S. presidential race will certainly be one of the most hotly contested in the country’s history. The outcome will also be closely watched in Japan, which has significant foreign direct investment in the United States as well as being one its closest trading partners.

On just about every major issue the two candidates are poles apart, and those differences are especially stark in terms of energy policy.

President Trump’s stance is clear and if re-elected no major deviations are expected. Hoping to appease Trump’s concerns about trade imbalance, Japan only increased outlays into the American oil and gas infrastructure, touting its role in U.S. job creation. The two countries even joined forces to promote LNG and its infrastructure in the Indo-Pacific and sub-Saharan Africa, signing the Japan-United States Strategic Energy Partnership (JUSEP) in 2018.

The energy outlook of Biden seems cardinally different.

The former VP of former President Barack Obama, Biden is set to continue the latter’s clean energy initiatives. The main difference, however, seems to be an acceleration of the shift toward a “green energy revolution,” which became a top priority of the Democratic Party a few years ago under intense pressure from younger and more militant members.

In contrast to Trump’s commitment to fossil fuels, especially Big Oil, the soft-spoken Biden speaks about energy and climate with a religious zeal, utilizing terms such as “clean energy revolution” and “environmental justice,” which he says will be “a priority across all federal agencies.”

Biden has promised to “hold polluters accountable.”

IT’S GREENER ON THE OTHER SIDE

Obviously, a Biden presidency means a boon for the entire renewable energy sector, and Biden promises to “take executive action on Day 1 to not just reverse all of the damage Trump has done, but go further and faster.” To show that he’s sincere, Biden says he is not accepting contributions from oil, gas and coal companies.

While Trump has dismissed the notion of climate change, Biden says he wants to direct $1.7 trillion in spending to fight against it. Biden says he “will act on climate immediately and ambitiously.”

In his first year in office, Biden promises to push the U.S. to rejoin the Paris Climate Agreement, and enact laws that “put us on an irreversible path to achieve economy-wide, net-zero emissions no later than 2050.”

Biden wants to invest $400 billion over the course of the next decade in clean energy innovation, which will “accelerate the deployment of clean technology throughout our economy.” This envisions incentives for better energy efficiency and on-site clean power generation, as well as an establishment of half a million new power charging outlets within a decade to usher in the electric vehicle era.

The carbon footprint of U.S. building stock should be reduced 50% by 2035, according to Biden’s policies.

Renewables executives in the U.S. say they are excited about how the country’s approach to energy will change.

Certainly, that will encourage Japan’s renewable energy players – both in terms of lobbying for more green reforms at home, and in terms of broadening the range of investment opportunities abroad.

But, first, there will be a reckoning over North American fossil fuel investments that are thought to exceed $200 billion.

WHAT IS THE ORACLE’S MESSAGE? In addition to Japanese trading companies, led by Mitsubishi Corp. and Mitsui & Co., the nation’s power and gas utilities, and oil refiners may need to reappraise their U.S. energy investments.

Two of Japan’s big three lenders, MUFG Bank and Mizuho Bank, feature in the Top 10 banks globally in terms of outstanding loan exposure to fossil fuel companies. Both banks may have added $100 billion of incremental exposure since the Paris Agreement was signed in 2015.

Mizuho may also be the largest global lender to the coal sector, according to NGO calculations. Japan’s big three banks account for one third of all direct lending to coal power plant developers.

None of the above is likely to have escaped Warren Buffet as he met his 90th birthday by announcing a position of over $6 billion in the five biggest Japanese trading companies. The firms are Japan’s largest investors in U.S. oil and gas.

So, why would the Oracle of Omaha bet so heavily on “old energy” and Japan in the run-up to the U.S. presidential election? He would surely be aware that U.S. oil and gas portfolio risk would weigh heavy on the companies in fiscal Q4 if there were to be major political change.

Decoding the meaning of oracles is a thankless task. Japan’s version of Big Oil will be hoping that whichever way the election goes, change will come about slower than words.

HOUSE VIEW

Japan’s carbon-free promises are best taken with a pinch of salt.

Criticized for over a year for a seeming lack of action on climate change, last week Japan struck back. Environment Minister Koizumi Shinjiro hosted a global ministerial web conference that launched a Japan initiative for countries to share experiences in formulating climate-friendly economic recovery packages.

This was meant to show Japan as a leader in climate change action and to counter European criticism that Japan was putting the issue on hold due to the Covid-19 pandemic. Several European nations had incorporated climate-friendly measures in their pandemic stimulus packages.

Minister Koizumi’s conference, a filler of sorts for COP26 which was delayed to next year, indicated that Japan is finally learning the art of spin.

Koizumi said that Japan is no longer supporting coal-fired generation, is pursuing green hydrogen, and embracing renewable energy at all levels. Apparently, there are now 150 zero-carbon cities in Japan, covering half of the population. Japanese firms are the most active globally in the task force on climate-related financial disclosures (TFCD) scheme. And even Japan’s defense sector is switching from diesel to renewables.

Minister Koizumi then executed the ultimate policy trick of unveiling a new progressive-sounding initiative (“Platform for Redesign 2020″) and then explained how its wording carries deep layers of meaning. “Redesign”, in this context, refers to decarbonization, to running a sustainable economy, and to decentralization of society, he said.

Environmental ministers from 25 countries and UN officials mostly nodded in approval.

Of course, the reality is not quite so rosy. Japan has not abandoned coal. It announced plans to close older, less-efficient coal stations (with exceptions for some regions). New coal plants are under construction, and while Japan tightened restrictions on coal-fired technology exports, these new standards merely reflect the specs of its current export models.

Japan does have a test-size project in green hydrogen, but most of the hydrogen projects it supports are based on coal or gas.

The UN Secretary General Antonio Guterres took the opportunity to offer Minister Koizumi a gentle rebuke. In a video message, he said there was no rationale for coal power, especially for Japan.

Others participants poked in other sensitive areas. Mark Carney, a COP26 Finance Advisor, urged Japan’s mammoth funds, such as the world’s largest pension fund, the GPIF, to be more transparent. “How is the money invested? What kind of emissions are they financing?” Carney asked.

Earlier this summer, several European pension and wealth funds fought to get Japan’s Mizuho bank to stop financing coal projects. GPIF is not known for such climate-driven activism.

Of course, in many ways the criticisms against Japan simply reflect different levels of involvement on the issue in Europe and in Asia.

Last week, Germany announced plans to auction 67 GW of renewables capacity by 2028. Of that, 31.3 GW will be in offshore wind. By 2030, Germany expects to generate 65% of its electricity from renewable sources.

In comparison, Japan’s plan is for renewables to make up just 22%-24% of power capacity. Japan’s push into solar is decelerating and the country targets just 1 GW of new offshore wind a year.

Japan’s ambitions are not dissimilar to others in Asia. South Korea’s 2030 target for renewables is only 20% of total. China’s target is among the most ambitions at 35%.

This is not to say that Japan has failed to make progress on climate change. Much has been invested into carbon capture, use and storage (CCUS) and Minister Koizumi was right to note it.

However, if Japan is to take the lead in climate change in a meaningful way, the country needs to do more than simply wait for the population to agree to restarting nuclear power plants.

With a change in the premiership underway and a US presidential election to come, it’s hard to see Japan making major changes in its energy policy over the next six months. Still, now that Minister Koizumi has unveiled the Platform, it’s time for the Redesign to whirl into action.

STOCK MARKET PERFORMANCE

As of close on September 4, 2020

Ticker

Market Cap

1W (%)

MTD (%)

YTD (%)

billions of yen

Energy

INPEX CORP

1605 JP

943.05

-4.29

-42.22

-3.17

JAPAN PETROLEUM EXPL.

1662 JP

103.62

-1.68

-37.79

0.89

ENEOS HOLDINGS INC

5020 JP

1324.42

-1.35

-15.19

6.22

IDEMITSU KOSAN CO LTD

5019 JP

686.58

-1.33

-21.47

2.67

COSMO ENERGY HOLD.

5021 JP

135.80

-4.76

-32.92

-1.42

Industrials

JGC HOLDINGS CORP

1963 JP

292.65

-3.59

-34.78

-2.84

CHIYODA CORP

6366 JP

70.55

-2.17

-4.24

-1.09

MITSUBISHI CORP

8058 JP

3888.14

4.16

-7.18

18.34

MITSUI & CO LTD

8031 JP

3350.07

1.93

2.81

17.53

Utilities

TOKYO ELECTRIC POWER

9501 JP

503.00

0.32

-32.98

3.30

CHUBU ELECTRIC POWER

9502 JP

995.25

0.27

-13.46

6.14

KANSAI ELECTRIC POWER

9503 JP

992.24

1.25

-14.70

4.04

KYUSHU ELECTRIC POWER

9508 JP

452.37

1.60

2.66

4.26

J-POWER

9513 JP

294.35

0.56

-38.21

5.24

TOKYO GAS CO

9531 JP

1037.07

-0.53

-10.60

8.52

OSAKA GAS CO

9532 JP

857.94

-0.68

-0.36

3.57

TOHO GAS CO

9533 JP

493.18

0.00

5.26

0.11

SAIBU GAS CO

9536 JP

91.18

-0.45

-2.29

4.03

SHIZUOKA GAS CO

9543 JP

66.59

0.11

-7.29

2.94

DATA

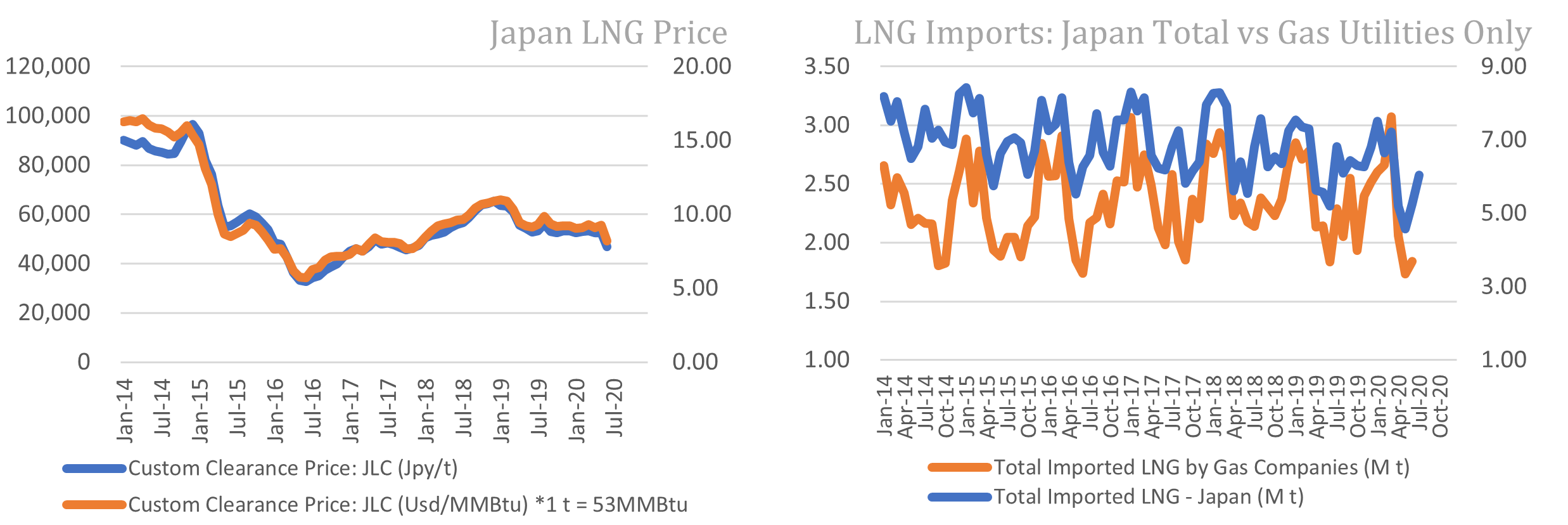

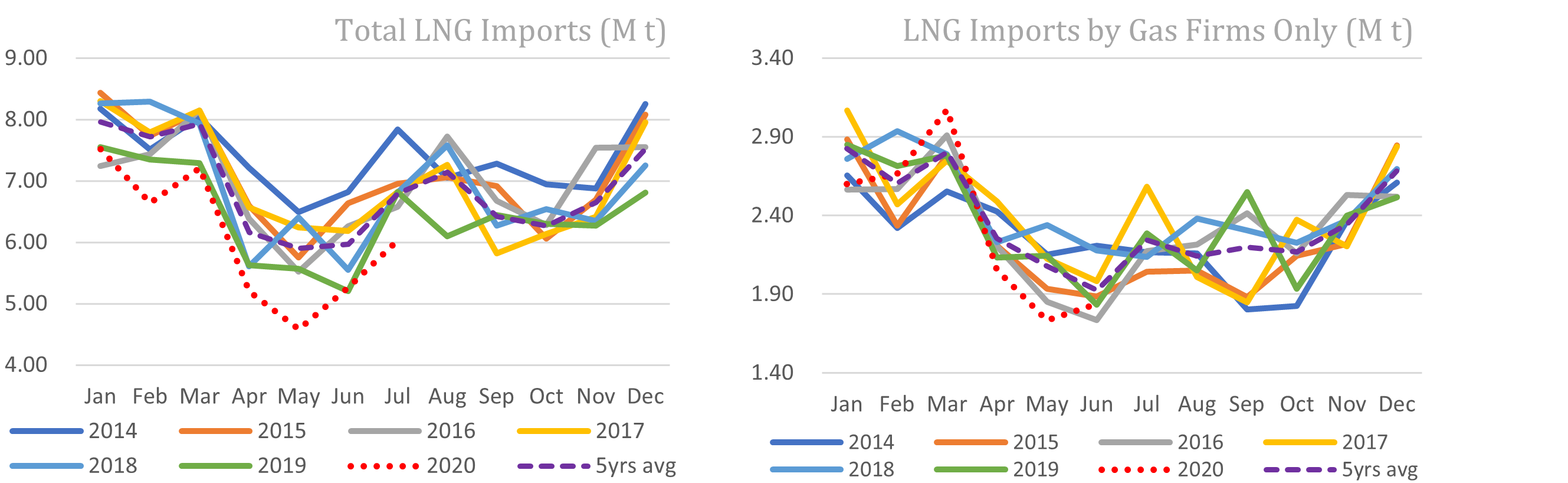

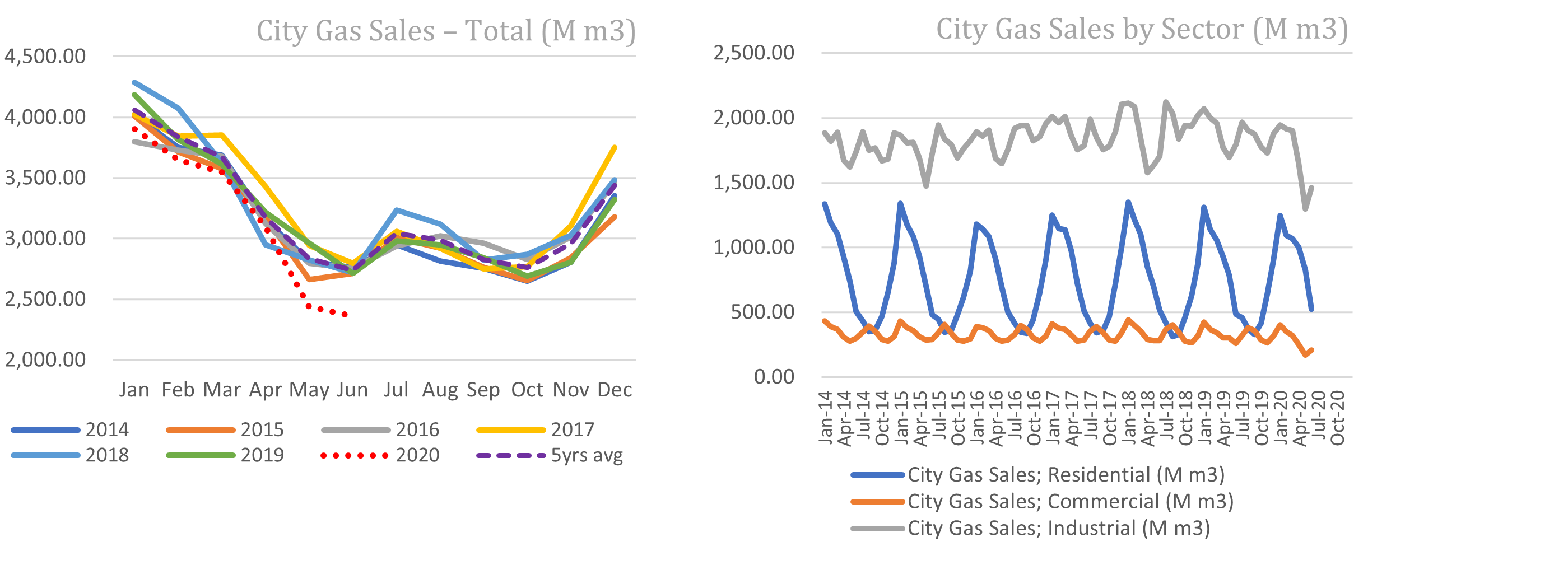

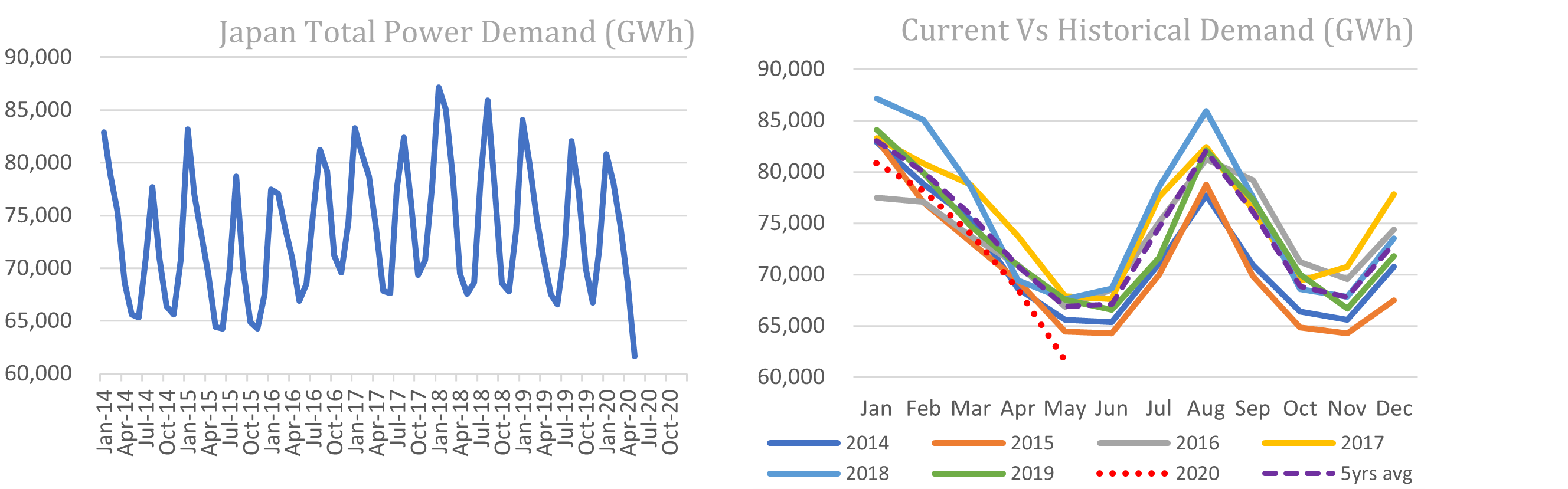

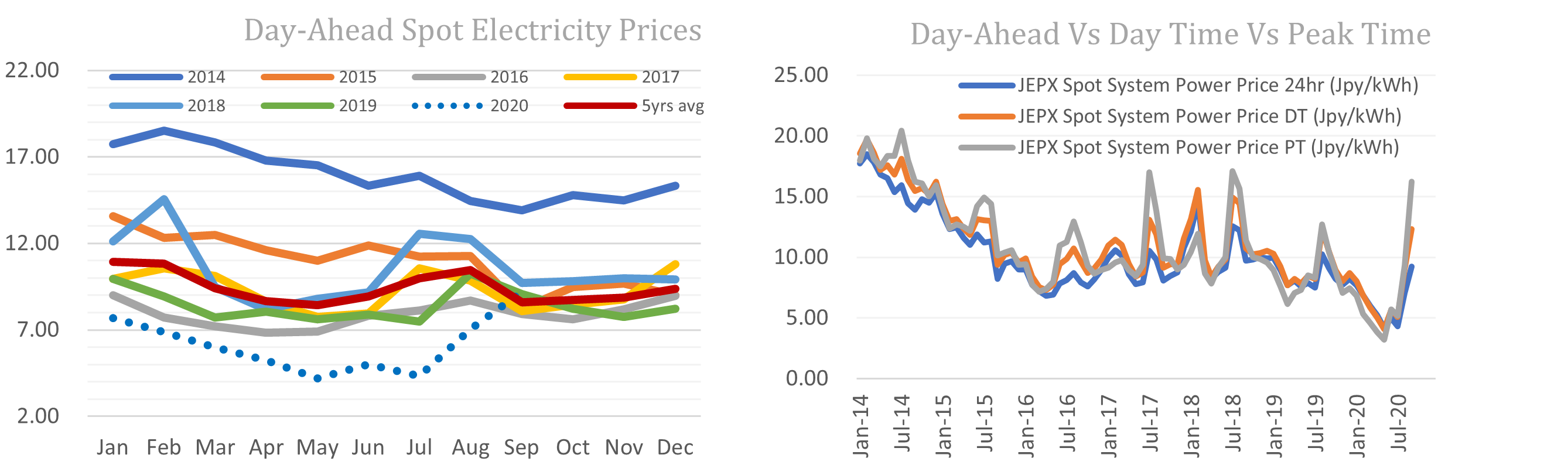

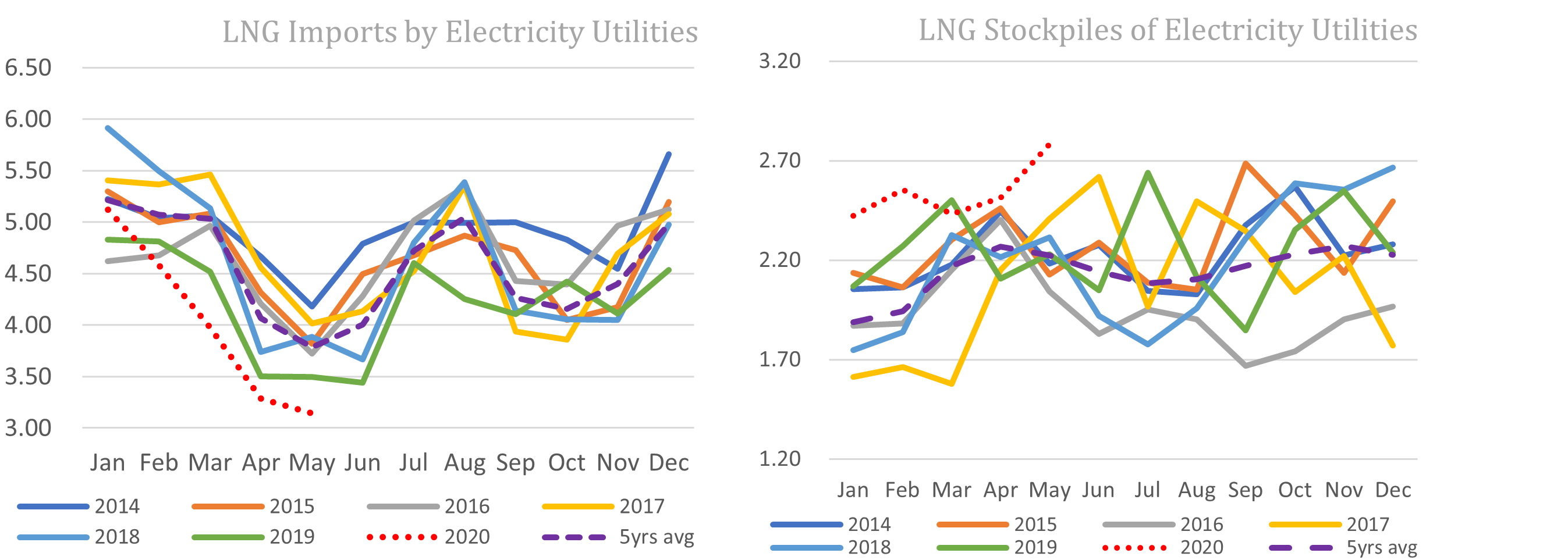

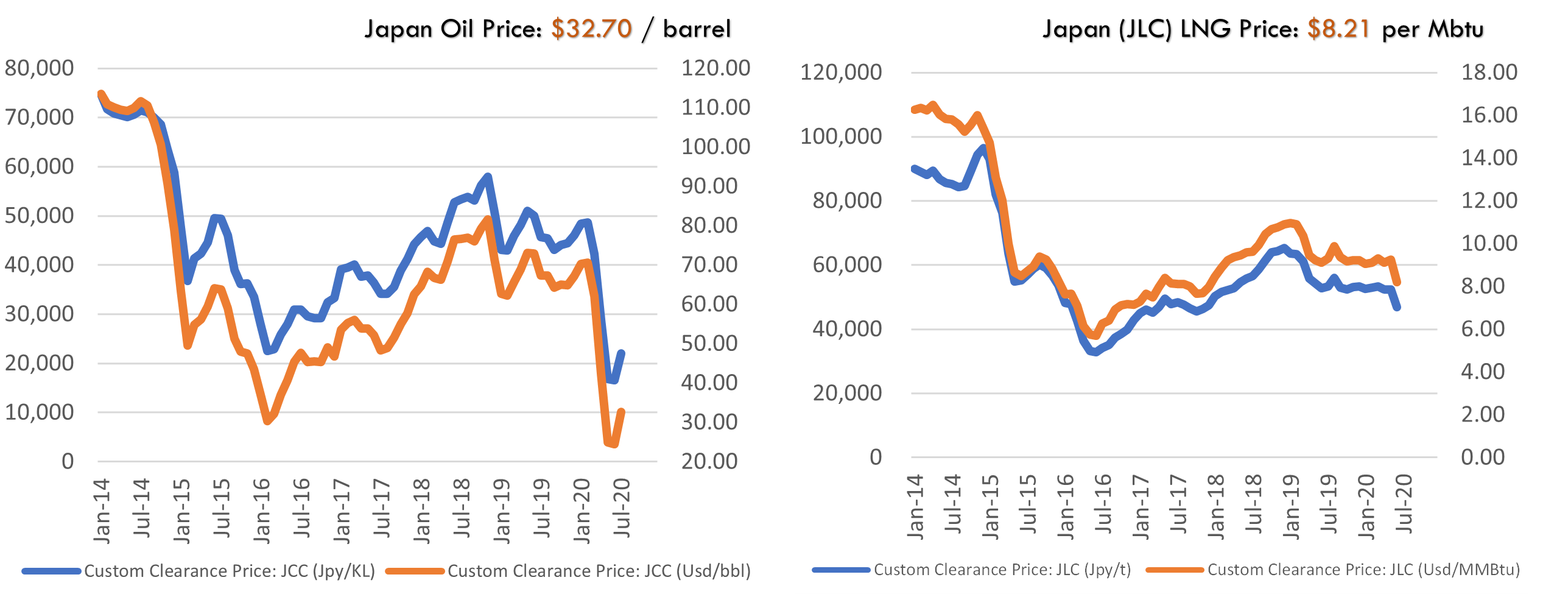

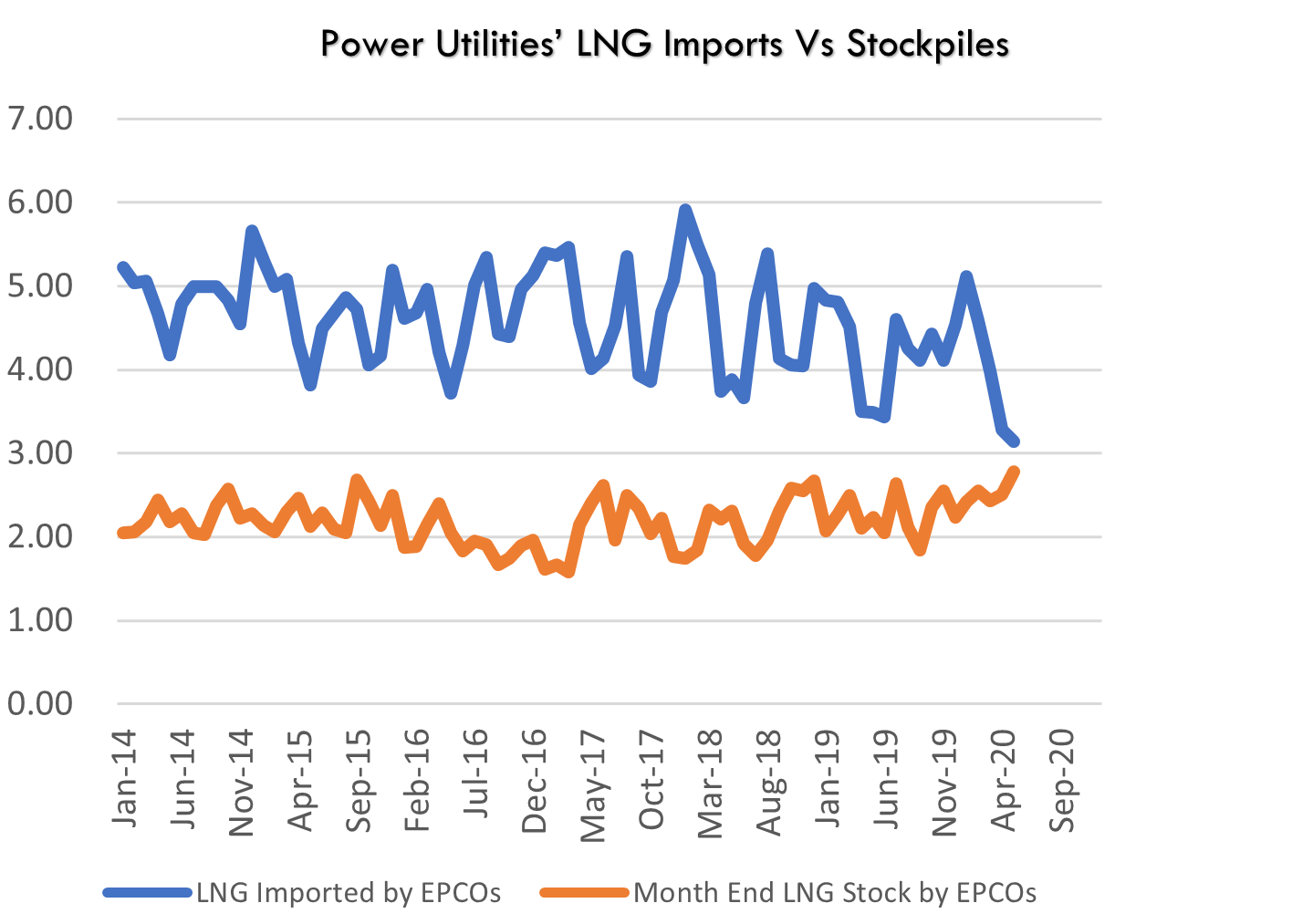

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance

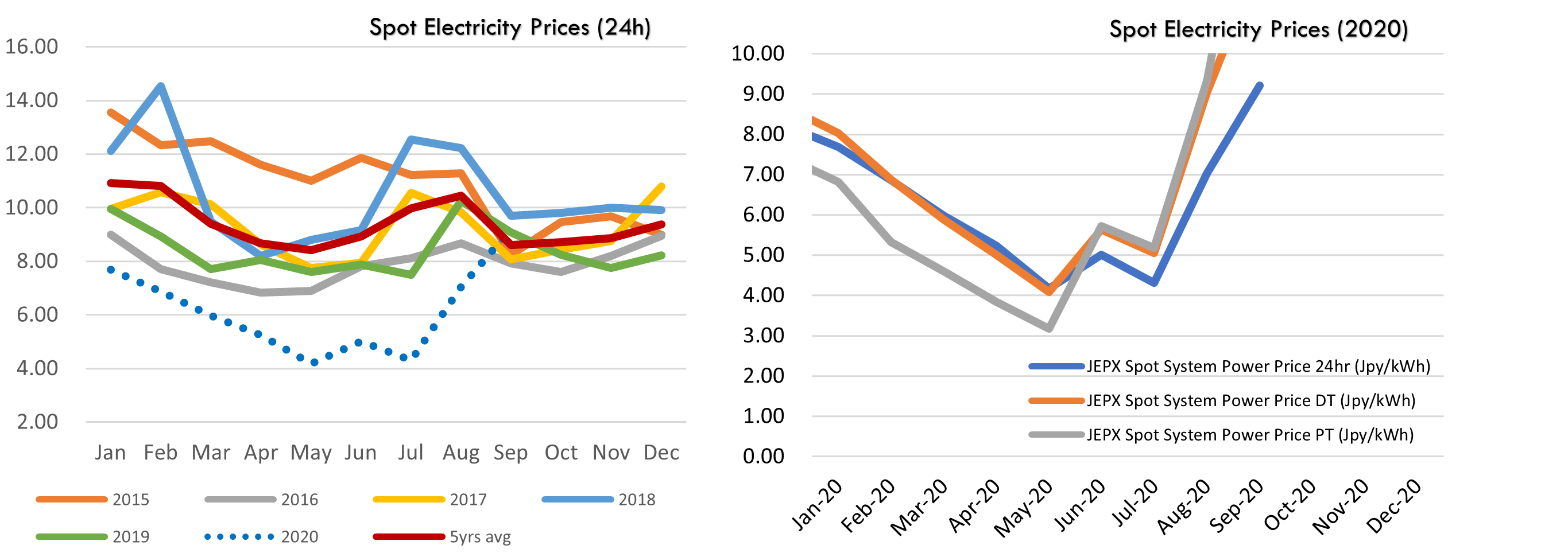

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest Research Ltd., which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis.

Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

Recipients of this report should ensure that they fully understand the legal, tax and accounting implications before making an investment decision and independently determine that the transaction is appropriate based on their own objectives, experience and resources.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided.

In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

JAPAN NRG WEEKLY SEPTEMBER 7, 2020 JAPAN NRG WEEKLY September 7, 2020 NEWS TOP OIL & GAS POWER & NUCLEAR RENEWABLES, OTHER ANALYSIS JOE BIDEN WIN COULD SPELL BILLION-DOLLAR HEADACHE FOR JAPAN’S OIL & GAS COMPLEX Japan’s version of Big Oil may have a multi-billion-dollar problem should the residency in the […]

Source: Ministry of Economy, Trade and Industry

Source: Ministry of Economy, Trade and Industry