It’s a strange time for Japanese oil refiners to accept that the journey is over. Japan’s gasoline and diesel consumption are at 95% of pre-Covid levels. The refinery run rates have finally bucked a six-month declining trend. And margins are the envy of all Asia, if not the whole world. And yet, the industry knows that this is the end of the line. As another Japanese oil refinery stops operating this month, industry watchers estimate that a fifth of the country’s entire crude processing capacity, or some 700,000 barrels per day (bpd) of throughput, must be idled in the near to mid-term. This translates into at least three mid-sized refineries out of the 22 units in Japan.

Earlier this year Japan’s buyers felt they got a raw deal on long-term U.S. LNG contracts, but now on the threshold of winter there’s the best opportunity in years to lock in more U.S. supply on the cheap. U.S. producers are ready to accept steep discounts, industry insiders say, and Tokyo Gas’ cut-price acquisition of a U.S. gas project earlier this month showed yet another way how Japanese firms could exploit the situation. With as much as one-tenth of Japan’s annual import volumes bound in long-term contracts that are due to expire by Dec. 2021, Japanese buyers could leverage their negotiating position to rethink supply sources.

EVENT METI’s Annual LNG Conference

One of the premier events in Japan’s LNG conference calendar will be held online, a first. The Oct. 12 event, hosted by the key ministry responsible for energy (METI) will focus on pricing stability and the potential for decarbonization in the LNG sector. Our NRG team will attend and report on the main talking points and developments in the Oct. 19 edition of Japan NRG Weekly. See below for an outline of the main issues.

NEWS: OIL & GAS

Tokyo Gas registers unit to trade LNG, considers global expansion (Dempa Publications, Sept. 29)

Co. set up “TG Global Trading” (based in Tokyo) as a wholly owned subsidiary to handle the sales of LNG to third-party clients. In the future, Co. said it will consider setting up offices for the unit overseas.

Tokyo Gas wants to utilize existing storage tanks and transport vessels’ infrastructure to capture growth opportunities for LNG demand in Asia.

Co. wants to grow third-party trading of LNG to 5 million tons a year by 2030.

CONTEXT: As previously reported, Tokyo Gas is establishing a global LNG trading desk in Singapore. This sets up the trading part, separate from Tokyo Gas’ activities in procuring LNG via mostly long-term contracts for use in Japan in gas-fired power generation and gas sales.

GasTech – View from Japan: LNG prices fall as market growth slows

(Gas Energy Shimbun, Sept. 28)

Gastech, one of the world’s largest LNG conferences, was held in Barcelona from September 7 to 11. For the first time ever, the conference was held online.

The feeling at the conference was that demand for LNG and natural gas in the medium term will remain strong in developing markets.

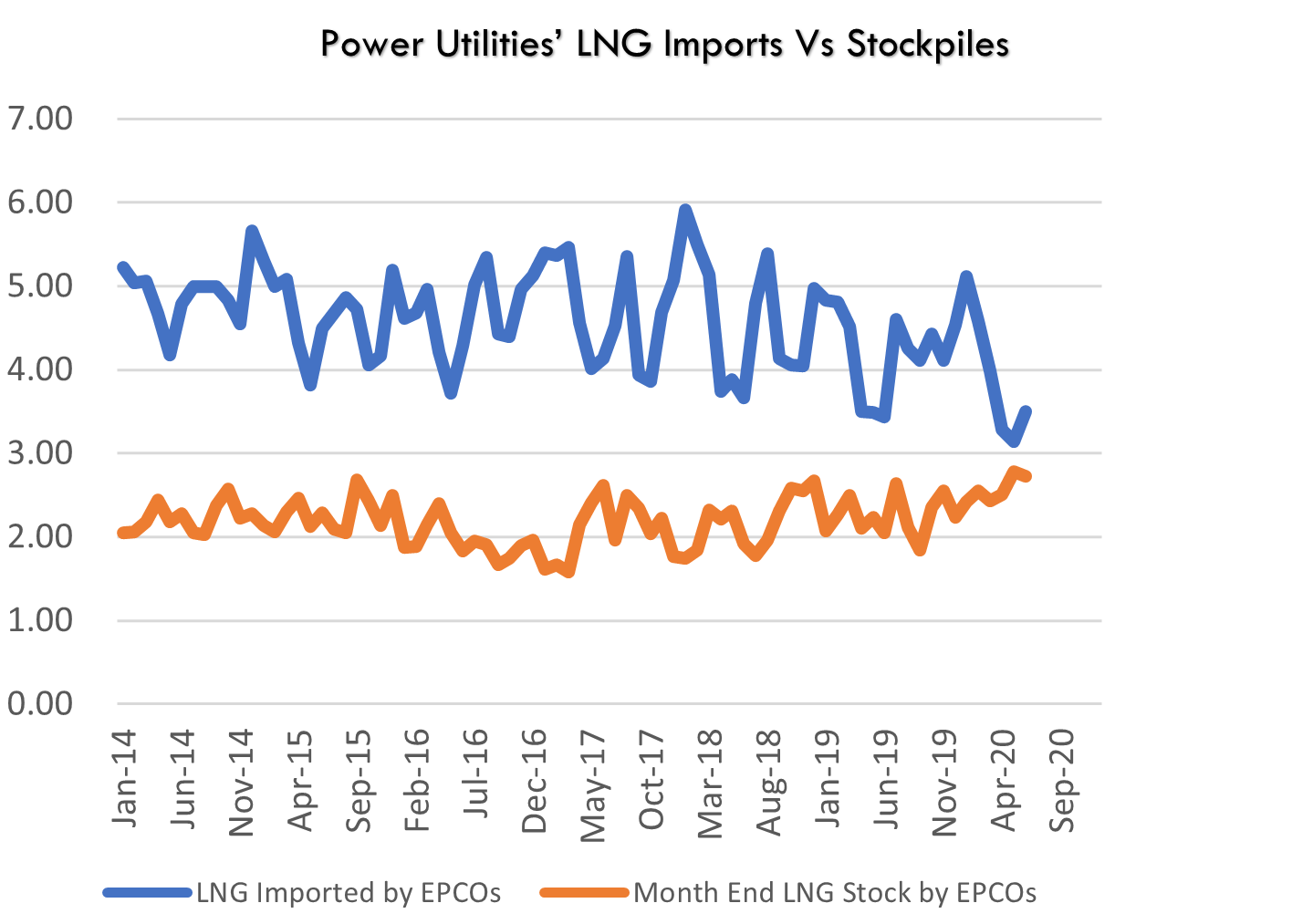

However, the coronavirus pandemic has meant that growth in global LNG imports, which surpassed 180 million metric tons in the first six months of this year, is slowing, with demand only 5% above the figure for the same period last year. Japan’s LNG imports remain at their lowest level in 10 years.

TAKEAWAY: A little more than a week from now Japan will host its own major LNG conference. (See the Events section of this report for more details.) Uncertainty over demand is not only due to the outbreak of COVID. China’s announcement of a 2060 carbon-free goal is the largest but by no means the only major pledge made by a country or corporation in recent months. The concern is especially strong in Japan, which as well as being the top LNG buyer sees the fuel as part of its economic future via related infrastructure exports. It’s curious, however, that a fuel recently seen as a better alternative to coal but too expensive for the developing world is now pinning its future demand on those markets.

NEWS: POWER & NUCLEAR

No. of operable nuclear reactors

33

of which

applied for restart

25

approved by regulator

16

restarted

9

in operation today

3

able to use MOX fuel

4

No. of nuclear reactors under construction

3

No. of reactors slated for decommissioning

27

of which

completed work

1

started process

4

yet to start / not known

22

Surce: JANSI and JAIF, as of Sept. 30, 2020

Will Kashiwazaki-Kariwa be sold? Japan struggles under Japan-U.S. nuclear agreement

(Weekly Economist, Sept. 28)

A Joe Biden victory in the U.S. presidential election will likely result in demands by the U.S. for Japan to reduce its 46 metric ton plutonium stockpile to fulfill its obligations under the Japan U.S. Agreement for Cooperation Concerning the Civil Use of Atomic Energy.

To achieve this, at least 15 reactors would need to be converted to run on plutonium-enriched MOX fuel.

This would likely mean that ownership of two of the reactors at TEPCO’s Kashiwazaki-Kariwa plant would be transferred to the Japan Atomic Power Company.

SIDE DEVELOPMENT: TEPCO considers loading nuclear fuel into Kashiwazaki-Kariwa Unit 7 (Kyodo News, Various, Oct. 3)

TEPCO does not yet have the local green light for reactor restart

Co. is thinking of loading the unit with an eye on a March-April start.

CONTEX: Japan currently has 4 nuclear reactors that are permitted to run on MOX fuel. At present, Japan does not create or process its own MOX fuel and one facility that would do so, the Rokkasho plant, has yet to get the final go-ahead to begin operations.

CONTEXT: The Kashiwazaki-Kariwa plant was one of three nuclear power plants owned by Tokyo Electric (TEPCO) and once ranked as the world’s largest NPP. A 2011 disaster at TEPCO’s Fukushima Dai-Ichi plant tarnished the firm’s reputation with the public and two of TEPCO’s NPPs including the Dai-Ichi will never operate again. The remaining Kashiwazaki NPP has seven reactor units. Of those, five are also unlikely to ever restart due to public pressure and TEPCO has mostly acknowledged this.

What TEPCO had hoped to salvage were the two more recent units at Kashiwazaki. This has also proved a step too far. Units 6 and 7 were approved for restart at the end of 2017. Three years on, TEPCO has failed to gain the tacit approval for restarts from the local authorities. The national government is increasingly certain that for the reactors to ever restart they need to be managed by a different company. Japan Atomic Power Co. is an entity set up by the country to promote commercial use of nuclear power and is jointly owned by Japan’s major electric utilities.

SIDE DEVELOPMENT: Nuclear disaster was fault of TEPCO and government, says appeal court

(Tokyo Shimbun, Sept. 30)

The Sendai High Court has upheld a district court judgment that found the government and the Tokyo Electric Power Co. liable for the Fukushima nuclear disaster. The court ordered over ¥1 billion in damages to be paid to 3,500 plaintiffs.

Both the government and TEPCO appealed the Fukushima District court’s 2017 verdict.

TAKEAWAY: The U.S. has been aware of Japan’s growing plutonium stockpile for years and due to the closure of most of the nation’s nuclear reactors since 2011 the stockpile has not notably increased. It is not clear that a Biden presidency would actually press the button on the issue. However, for those in Japan who support the nuclear complex (which includes spent fuel recycling and MOX fuel usage), the U.S. presidential change would be great cover. Whether it is real or not, Japanese politicians and bureaucrats like to use “outside pressure” as an excuse to move unpopular legislation / processes forward. Biden as president would serve as that trigger.

Minister demands explanation after jump in price at power capacity auction

(Asahi Shimbun, Sept. 30)

CONTEXT: Launched in July 2020, the market enables utilities to bid not for kilowatt hours of electricity, but power capacity. As capacity market trading is allowed for up to four years into the future, it allows the bigger industry players to better manage future revenue than spot electricity trading. The idea is also that it allows power companies to feel more secure about investing in construction of new power facilities.

Bids in a recent capacity tender reached the government imposed maximum of ¥14,137 per kilowatt. Some non-legacy generators expressed shock at the high prices and there were calls for the bidding system to be changed.

Environment Minister Koizumi Shinjiro said on Sept. 29 that he believes the high prices seen on the power capacity trading market will result in households paying even more for electricity.

Koizumi has demanded more transparency about the reason the capacity prices were so high.

Chubu Electric rumored to be interested in Hokuriku EPCO takeover

(Economist Online, Sept. 28)

As Japan’s electricity and gas industries undergo a major restructuring, there is an increasing trend to consolidate generation capacity in western Japan and to invest in beefing up transmission networks in the country’s east.

As acquisitions become more commonplace, Chubu Electric Power Co. is rumored to have its eye on the Hokuriku Electric Power Co.

TAKEAWAY: As reported in the Sept. 7 edition of Japan NRG Weekly, we are very likely moving toward a stage of market consolidation among the major electricity utilities. Since the 2016 deregulation of the electricity market, a few of the 10 incumbent power utilities are struggling, either due to their energy mix or declining regional demand. What’s more, the idea of a Chubu-Hokuriku merger was favored by the METI officials that advised former prime minister Abe Shinzo. It’s an idea that’s unlikely to have waned with the new prime minister and it has also been discussed in several media publications.

Tohoku Electric unveils new zero-carbon retail plan

(Tokyo Yomiuri Shimbun, Sept. 29)

Tohoku Electric has unveiled a new plan known as “Eco Denki Premium” that claims to supply electricity generated with net zero carbon emissions.

The plan asks clients to pay an additional ¥3.3 per kilowatt hour.

Subscribers will receive a certificate to confirm their zero-carbon status.

SIDE DEVELOPMENT: Toho Gas rolls out zero-emissions electricity plan (Nikkan Kogyo, Oct. 1)

Co. promises electricity derived from renewable energy sources and will give certificates to clients as proof

Co. claims to be offering a cheaper zero-emissions plan than rivals

SIDE DEVELOPMENT: TEPCO rolls out zero-emissions electricity plan (Nikkan Kogyo, Sept. 28)

TEPCO Energy Partner, in collaboration with Gunma Prefecture, will start an emissions-free electricity plan based on electricity generated by hydroelectric power plants in the prefecture.

SIDE DEVELOPMENT: Chubu Electric unit rolls out zero-emissions electricity plan (Denki Shimbun, Oct. 2)

Chubu Electric Power Miraiz said it will offer from November an emissions-free electricity plan based on electricity generated by its hydroelectric power plants in the Nagano prefecture.

TAKEAWAY: The cost of electricity is famously expensive in Japan. For some listed corporates, however, this will be seen as a necessary ESG expense that will pay back the value many times over.

Kyushu Electric brings forward restart dates for Sendai No. 1 and No. 2 nuclear reactors

(Jiji, Oct. 1)

Kyushu Electric said units one and two at the Sendai nuclear power plant in Kyushu will go back online one month earlier than initially scheduled, on November 26 and December 26, respectively.

The reactors were shut down to undergo enhancements to bolster resilience against terrorist attacks and similar incidents.

CONTEXT: Should the restarts take place, they would increase the operating capacity of nuclear power in Japan by 55%. For the Kyushu area, however, the impact would be more drastic. It would mean Kyushu Electric has three of its four units up and running.

KEPCO struggles to win public trust, endangering restarts of its nuclear units

(Chugoku Shimbun, Oct. 2)

The Kansai Electric Power Company convened a recent meeting of its Board of Directors in Fukui, which is home to its nuclear power stations, to send a message that it was part of the local community.

While the move was designed to restore confidence in the utility after recent bribery allegations, the process of restoring the public’s trust will likely be difficult.

It also appears likely that none of KEPCO reactors that are currently able to restart, but are down for maintenance, will actually restart soon. This will place further pressure on KEPCO’s revenue.

TAKEAWAY: Kansai Electric has seven operable nuclear reactors. Only two are actually working. In theory, the company can bring online all seven, since it has the approvals from Japan’s nuclear regulator. Last month, it even finished the extra work on older units that extended their 40-year licenses for another 20 years. However, the reality is that KEPCO’s projected timeline for restarting at least two more units may be too optimistic. The company was marred by bribery and fraud allegations, which hit over a year ago. KEPCO is working to present itself as rehabilitated. Reports in the local media suggest that the local public and politicians are not buying it. And, without their consent, it’s very hard for the company to turn on the switch.

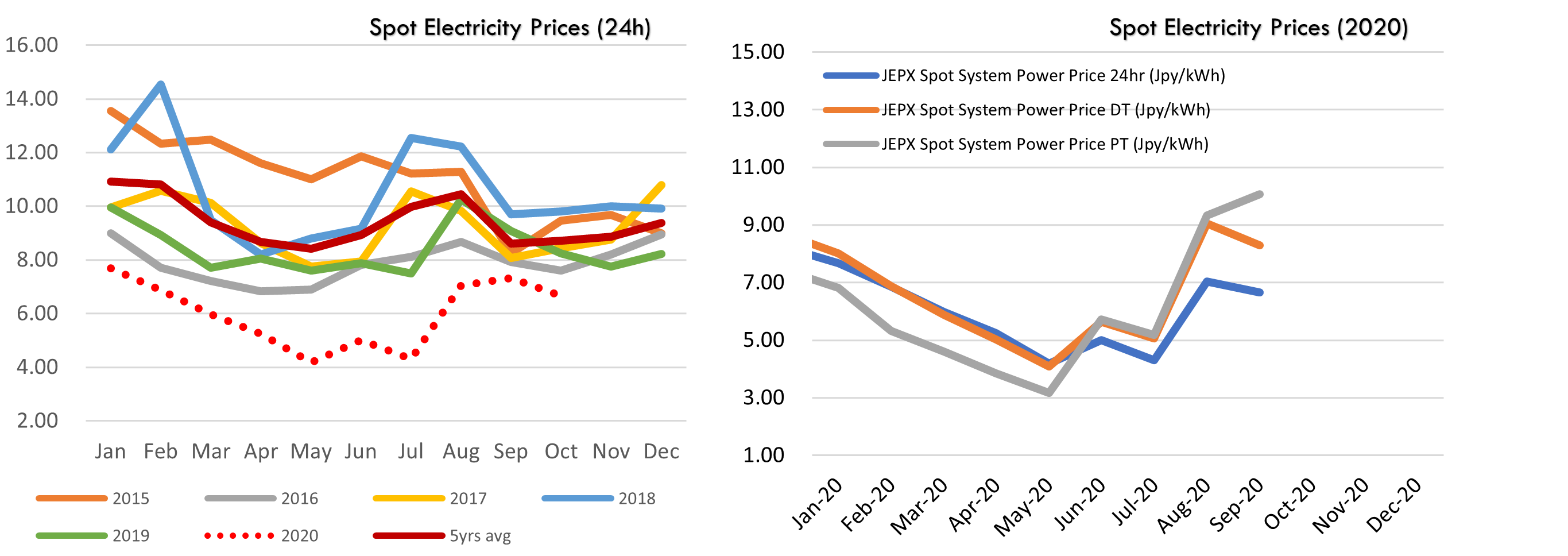

Electricity tariffs to rise for first time in six months

(Tokyo Shimbun, Sept. 29)

Four of Japan’s electricity utilities have said they will raise tariffs in October, in the first such rise in six months.

Other utilities such as Chubu Electric Power are continuing to lower their electricity tariffs.

All Japan’s major gas utilities will lower their tariffs in October, citing lower LNG prices.

Toshiba runs Australia trial to diagnose useful life of thermal power plant

(Denki Shimbun, Sept. 30)

Toshiba Energy Systems says it has developed a system that can predict the useful life of a thermal generation plant and diagnose and foresee faults.

In a project sponsored by the New Energy and Industrial Development Organization, Toshiba is trialing the system at the Vales Point power station in New South Wales, Australia. The trial will continue until March 2022.

OPINION: Why phase-out of coal plants is actually soft on polluters

(Toyo Keizai, Sept. 30)

CONTEXT: This is a Q&A article with Yamaka Kimo, head of the Enerugii Senryaku Kenkyuujo [Energy Strategy Laboratory], based on his views about the country’s energy policies.

According to Yamako, the much-trumpeted phase-out of coal-fired power is not as radical as it sounds. The big top-line numbers cited for coal plant closures actually include plants that have already been decommissioned or closed on a temporary basis. This contrasts with the decision in Germany and the U.K. to shut down all coal-fired power stations.

The government aims to reduce electricity generated from burning coal, currently at 32%, to 26% by 2030. While some think-tanks and analysts believe the 26% figure could be lowered even further, this is an unknown quantity. The government may be unable to achieve further reductions in this time frame.

While the government’s policy calls for over 20% of power from nuclear by 2030, many say Japan’s nuclear output could fall significantly, even to just 5% of total consumption. This means the government will be forced to increase supply from renewables sources to meet emissions targets.

METI recently said it will create a “capacity market” for the trading of power generation. Unlike the capacity markets that operate in the U.S. and elsewhere, the Japanese model does not mandate that the capacity bought on this market has to supply the wholesale electricity market. Japan’s capacity market is actually seen as a lifesaver for coal-fired stations, because it guarantees that they will be able to not only cover their overheads, but also turn a profit.

SIDE DEVELOPMENT: Coal-fired power stations scramble to improve efficiency (Nikkei, Oct. 2)

Some 114 of Japan’s 140 coal-fired power stations, accounting for around half the total coal capacity, are classified as “subcritical” or “supercritical”. Subcritical and supercritical technologies date from the 1960s and 1980s, respectively. Both are now classified as inefficient by the Japanese government.

Only a handful of stations, all of which were constructed in or after the 1990s, are classified as “ultra-super critical”, and therefore efficient.

The government’s decision to phase out inefficient coal power has shocked industry. Steelmakers are among the manufacturers lobbying the government for an exemption from environmental targets.

As most coal-fired power stations are already fully depreciated, they are very profitable for utilities. Coal power also represents a stable source of electricity that is well suited to smoothing out the fluctuations in output from renewable sources.

EDITORIAL: Japan needs to revise its stance on nuclear exports

(Tokyo Shimbun editorial, Sept. 28)

CONTEXT: This is an editorial article in a left-leaning daily. The paper is national, yet as the name suggests it is more focused on the Tokyo region.

Japan has bountiful wind, sunshine, and geothermal energy, in addition to technical prowess. According to the International energy agency, Japan’s electricity output from renewable sources is trending up, even amidst the coronavirus pandemic.

Hitachi’s plans to build two 1.3 GW nuclear plants in Wales were put on hold after tougher safety requirements in the wake of the Fukushima disaster made the project financially unviable.

While Hitachi did not formally cancel the project at that time in deference to the Japanese government’s policy of promoting nuclear infrastructure exports, in recent years the explosion of renewables in the U.K. has reduced the need for nuclear power, and Hitachi has now pulled the plug on the project.

With Toshiba having already exited nuclear power abroad and Mitsubishi Heavy Industries considering a withdrawal from its Turkish reactor project, Japan’s nuclear export program is basically finished. Prime Minister Suga’s government should delete the word “nuclear” from its infrastructure export policy right now and replace it with “renewable energy”.

NEWS: RENEWABLES & OTHERS

Japan targets development of commercial hydrogen-power technology by 2040

(Kankyo Business, Sept. 30)

State-run entity NEDO (New Energy and Industrial Technology Development Organization) said it will develop a highly efficient, zero-emission system to generate electricity from hydrogen, with a view to commercialization as early as 2040.

The closed-cycle system will burn hydrogen at 1,400°C to achieve efficiencies of up to 68%.

CONTEXT: In 2018, Japan turned on the world’s first heat and power hydrogen-fired facility in an urban area with the launch of a test project in the city of Kobe. The plant used 100% hydrogen fuel. Meanwhile, major engineering firm Mitsubishi Hitachi Power Systems has developed a generation plant that can flexibly use hydrogen and natural gas together. The major challenge here is cost of electricity.

SIDE DEVELOPMENT: Saudi Arabia Sends Blue Ammonia to Japan in World- First Shipment (Various, Sept. 29)

CONTEXT: Blue ammonia is a feedstock for hydrogen created from natural gas. This process is labelled as “blue hydrogen” to note that emissions from burning gas in the manufacture of hydrogen are captured and stored, or reused. Hydrogen made from burning gas without the carbon capture element is called grey hydrogen.

The shipment is part of a pilot study conducted by the Institute of Energy Economics Japan and Saudi Aramco in partnership with Saudi Basic Industries Corp. The feedstock sent to Japan will be used for power generation.

The pilot project aims to show how hydrocarbons can be converted to power without triggering the release of carbon dioxide emissions.

The first shipment carries 40 tons of blue ammonia.

TAKEAWAY: Saudi supply is not the only one aiming for the Japanese market. Brunei, Australia and Russia are among the countries that have already sent or aim to supply Japan with some form of hydrogen. Of issue going forward will be the energy source used in the manufacture of the hydrogen. However, this may be more of an issue for the suppliers than Japan.

Bidders in offshore wind farm tender protest low tariff advice

(Diamond Online, Sept. 28)

CONTEXT: As reported in the previous edition of the Japan NRG Weekly, on Sept. 15, a key government panel turned in its offshore wind pricing recommendations to METI and the Agency for Natural Resources and Energy. One of the main points was advice to set a ceiling for offshore wind feed-in tariffs at ¥29 per kilowatt hour.

The price ceiling was a far cry from the ¥36 various offshore wind operators were expecting. A wind lobby group petitioned the government to reconsider, but the bureaucrats stood fast in the face of criticism.

The ceiling rate was made lower than industry expectations partly because METI has already committed to ¥3.8 trillion in FIT payments for renewable energy projects. The ministry is now trying to conserve costs.

Ironically, some latecomers to the bidding for offshore wind projects were trying to push for a lower rate than the ¥36 proposal. These parties saw the price as being too favorable to TEPCO and Obayashi. However, even these latecomers are now not sure they can turn a profit.

TAKEAWAY: Many of these kinds of stories in Japanese media are part of a lobbying campaign on both sides. The tariffs are still in a negotiation period and both the government and various business players are trying to scare others into giving in. Operators want higher FIT to make their projects more profitable. The government doesn’t want to be seen as a pushover and create the problems that the solar market attracted after it unveiled the most lucrative FIT in the world. A final decision from METIC is due before April 2021. It is likely to reflect closely the recent advisory panel recommendation of a ¥29/kWh ceiling. It is also likely that industry players will find a way to make it work.

Japanese secondary market for solar-generated electricity to reach 1.2 GW in 2021/22

(Mega Solar Business, Sept. 19)

The Yano Research Institute is predicting that the Japanese secondary market for solar generated electricity, which was estimated to be 730 MW in 2019/20, will reach 1.2 GW during the next financial year.

In its report, the Institute characterizes the secondary market for solar farms as a sellers’ market, and says ongoing demand is expected from infrastructure investment funds and individual investors.

CONTEXT: Japan has become the world’s third-largest market in terms of solar capacity within less than a decade. The secondary market allows both electricity and non-electricity companies to operate renewable energy assets without taking on the initial development risks.

Sumitomo Corporation plans wind farm off U.K. coast

(Nikkei, Sept. 29)

Sumitomo Corporation said it had joined a project to establish a wind farm off the U.K. coast, which aims to start feeding power to the grid in 2030.

Sumitomo says it has joined a consortium of European companies that includes Germany’s RWE Renewables and Siemens. The consortium has obtained the necessary leases in the North Sea.

The farm will generate 350 MW. Sumitomo holds a 12.5% stake in the project.

TAKEAWAY: With so many potential new projects available in offshore wind in Japan, why does Sumitomo invest in the U.K. market? Clearly, in the U.K. there is more regulatory clarity, a more organized offshore industry, and the profit potential is easier to grasp. However, Sumitomo’s investment is probably in part a learning exercise that can help the company reinvest the know-how into the Japanese market at a later date.

Denyo and Toyota to develop fuel-cell powered commercial vehicle

(Nikkei, Sept. 17)

Generator manufacturer Denyo is collaborating with Toyota to develop a fuel-cell powered vehicle that runs on electricity generated from hydrogen gas.

The manufacturers believe that commercial vehicles need to be converted to run on fuel cells in order to reduce carbon emissions and prevent atmospheric pollution.

The system will be trialed on a Dyna truck, using the fuel cell system from the Toyota Mirai.

TAKEAWAY: California has recently announced a complete ban on gasoline engine vehicle sales on its territory by 2035. The zero-emissions plan is due to hit Japanese carmakers very hard since few have a strong track record in electric cars and most do not even have an EV available in the U.S. market. Japan’s top industry player, Toyota Motor, recently said it would reach its EV sales target five years earlier than initially planned. However, Japanese automakers do not necessarily see “zero-emissions” as only meaning EVs. There has been a strong push to develop fuel-cell vehicles in Japan, as some even experiment with novel solutions such as burning aluminum in cells. The most recent developments center on hydrogen. Toyota’s green auto sales targets also include its projections for hydrogen fuel-cell cars. Still, Toyota and its domestic peers will need to move fast to popularize fuel cells before the trend for EVs overtakes the auto market.

Kyushu Electric takes delivery of biomass fuel transport ship from Erex

(Erex press release, Sept. 30)

Erex has delivered the Ibuki, a 2,300 metric ton cargo ship, which will be used to transport biomass pellets to Kyushu Electric’s Buzen power station.

At 3,200 cubic meters, the under-deck area is 30% larger than usual to allow the lightweight pellets to be transported efficiently.

Japan has potential to combine farms and solar plants. Why has it not worked?

(Smart Japan, Sept. 28)

Since its inception, agricultural solar sharing, in which horticulturalists collaborate with a solar farm operator to erect solar panels on cultivated land, has faced issues with obtaining finance.

While banks are relatively relaxed about lending to operations in which the same entity both cultivates the land and owns the solar panels, when the two sides of the operation are run by different entities, it is a different story.

It costs around ¥15 million to install solar panels above a 2,000 m² rice paddy. When you consider that, in 2015, only 29,000 farms achieved an annual turnover of ¥10 million or more, and a mere 3,500 farms made at least ¥50 million, you can see how difficult it is for farmers to raise these levels of capital.

ANALYSIS

MAYUMI WATANABE, RESEARCHER, YURI INVEST RESEARCH

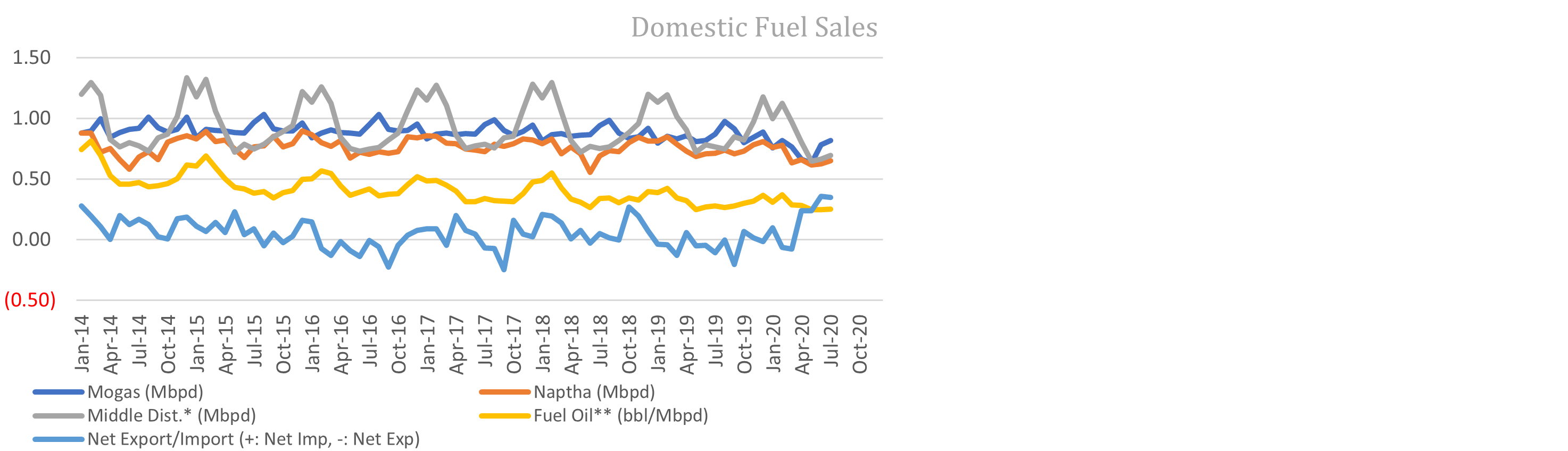

Japan’s Oil Refinery Firms Prepare for Energy Transition Despite Sector Currently Enjoying World-Beating Profits

It’s a strange time for Japanese oil refiners to accept that the journey is over. Japan’s gasoline and diesel consumption are at 95% of pre-Covid levels. The refinery run rates have finally bucked a six-month declining trend. And margins are the envy of all Asia, if not the whole world.

And yet, the industry knows that this is the end of the line. As another Japanese oil refinery stops operating this month, industry watchers estimate that a fifth of the country’s entire crude processing capacity, or some 700,000 barrels per day (bpd) of throughput, must be idled in the near to mid-term. This translates into at least three mid-sized refineries from Japan’s 22 units.

The refineries will need to close or transform into an entirely different facility. For the record, conversions have generally not fared well in Japan. Last year, ENEOS’s Muroran refinery, given a new lease of life in 2014 as Japan’s largest paraxylene facility, stopped production. It could not survive competition and was recast again as a storage terminal.

The issue of what to do with excess oil refining capacity during a period of energy transformation away from petroleum is not limited to Japan. The onset of the Covid pandemic has accelerated the global shift away from gasoline in transport, while also vastly undercutting demand in the current no-travel, work-at-home era.

U.S. inventories of distillate (diesel, jet fuel, gasoil and heating oil) are at the highest level since almost the early 1980s. In Europe, margins for refining crude into gasoil are down to USD 3/barrel, from USD 16 at the start of the year, according to Reuters data. That’s probably not enough to cover costs, Reuters analyst John Kemp notes.

Global oil majors have one after another announced plans to idle or convert crude refining facilities. In late September, Total pledged more than 500 million euros to convert its Grandpuits, France, refinery into a zero-crude platform for biofuels and bioplastics as soon as next year. Marathon, the top U.S. oil refiner, said last week it will cut 12% of its workforce due to the slump in fuel consumption since COVID hit.

The “nice” problem for Japan’s oil refiners is that their current situation is not that bad, in comparison. If anything, this year’s pandemic-induced demand drop had little impact on the refining margins of the three dominant industry players: Idemitsu Kosan, ENEOS, and Cosmo Energy. Their margins remained high, quickly recovering to above ¥10/liter, and oscillating around ¥15 since.

That’s five or more times higher than levels in Europe. As a result, Japan’s three oil refining firms have forecast sales declines of a quarter to a third during this Covid-afflicted financial year ending March 2021. Jefferies brokerage has kept both Idemitsu and ENEOS as a Buy, and Cosmo a Hold in its stock recommendations.

WHICH REFINER BLINKS FIRST?

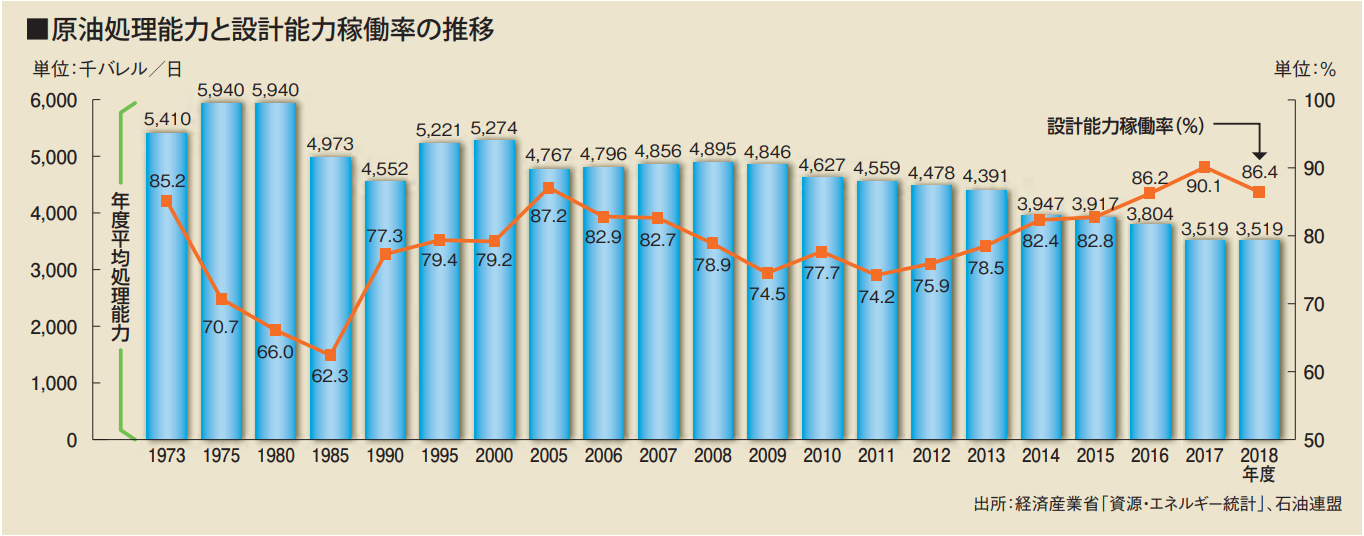

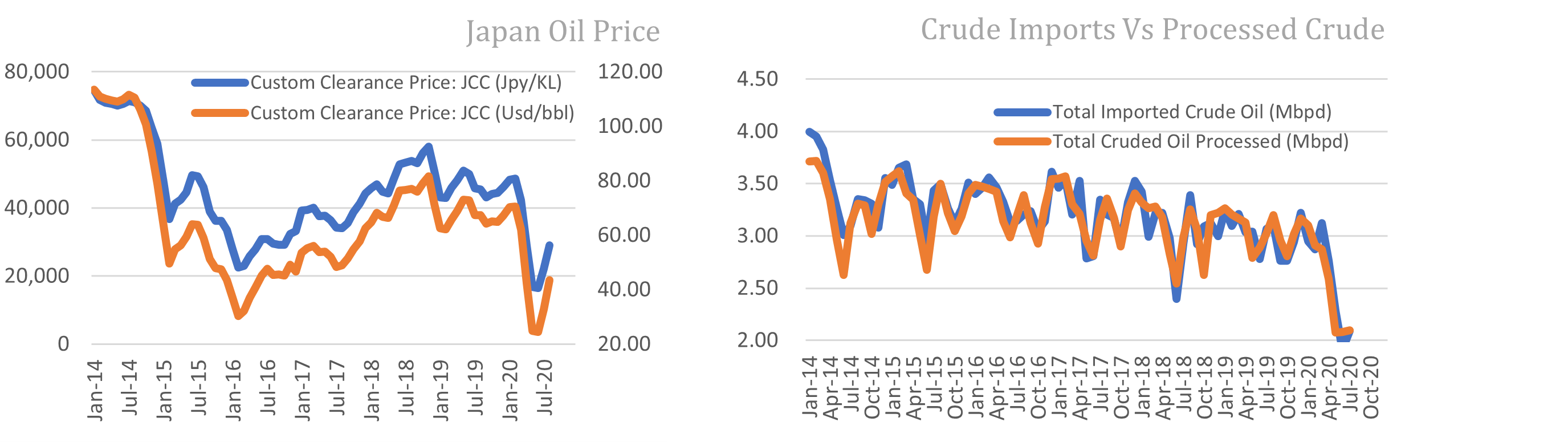

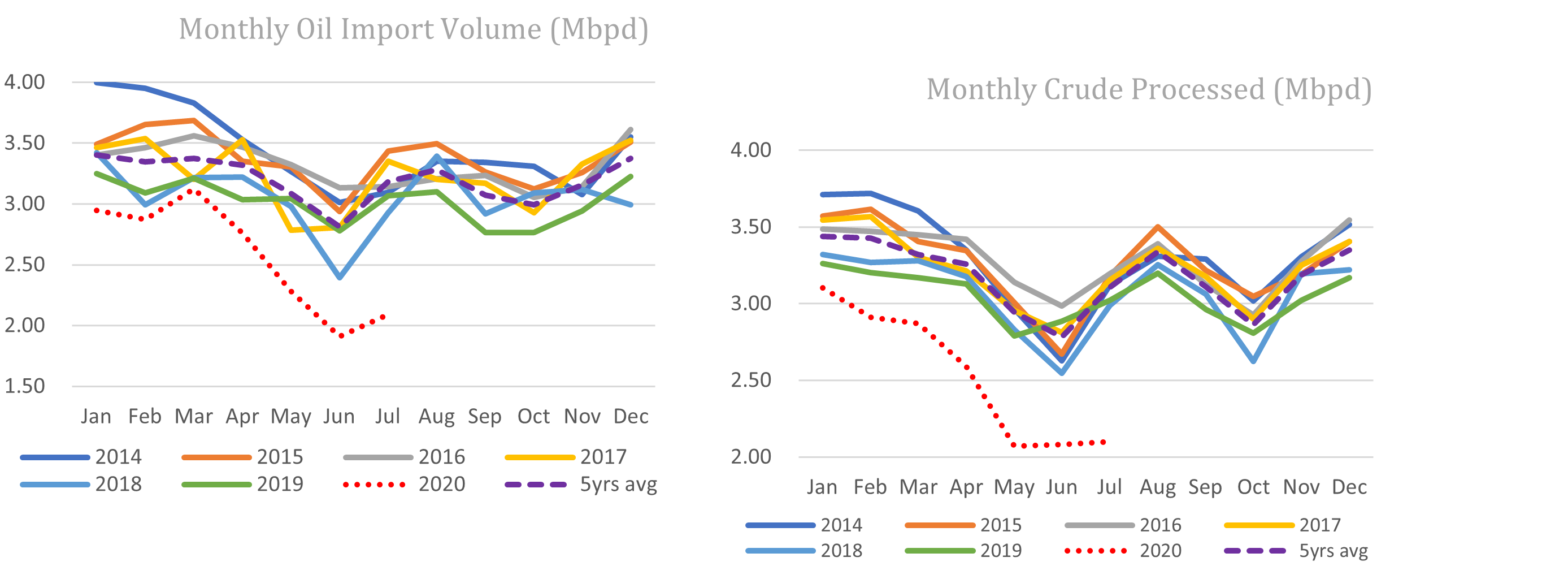

Japanese oil refinery run rates edged up to 59.6% in July 2020 from 59% in June, the first rise in six-months, according to Ministry of Economy, Trade and Industry (METI) data. Ministry officials told Japan NRG Weekly that this probably signaled that the demand drop post-Covid has bottomed out.

It’s unlikely that refinery run rates will quickly return to their 80-90% levels, but it feels that the worst may be over. For now.

That said, it’s clear that further refinery closures in Japan can and should happen, and new ENEOS President Ota Katsuyuki only confirmed the plans in recent media interviews.

In fact, the first refinery closure is already cued up. ENEOS, formerly known as JXTG Holdings and JXTG Nippon Oil & Energy Corp., said in July 2019 that it will cease primary refining operations at its Osaka facility and repurpose it as an asphalt-fueled electric power station. Due to new refineries starting up in Asia, the Osaka plant, operated as a JV with Petro China, was no longer finding enough demand.

This month the Osaka oil refinery will retire, leaving Japan with around 3.4 million bpd of processing capacity, down from 5.6 million bpd in the 1980s. Back then, Japan provided almost one in ten of the world’s petroleum products.

Utilization Rates of Japanese Oil Refineries (Orange) and Total Capacity (Blue, in 000s of bpd)

Source: Petroleum Association of Japan 2019 report, METI

With the need to close a further three or so mid-sized oil refineries, the question is which ones come next.

With scale affecting operational economics, one would expect the dial to fall on the smallest facilities. However, this has not been the case so far in Japan. Closures are more likely to be driven by regional supply competition.

For example, the 115,000 bpd Osaka facility is Japan’s fourth smallest, yet it operated in one of the most oversupplied hubs of the country. Tokyo is another overly concentrated region, especially the recent ENEOS merger with smaller rival TonenGeneral. At present, ENEOS has four facilities serving a post-Covid Tokyo metropolis, where gasoline and truck fuel demand plummeted 20% in the aftermath of the pandemic, according to the Petroleum Association of Japan data.

The three refineries below the Osaka one in terms of output capacity are the 70,000 bpd Keihin refinery, the 86,000 bpd Yokkaichi refinery, and the 100,000 bpd Sakai refinery.

The last two belong to Cosmo Energy. The smallest of the three Japan oil refining majors, it has fared better than domestic rivals during this year. While Idemitsu was still processing its merger with Showa Shell and ENEOS was doing the same after taking over the TonenGeneral business, and thus doubling its Tokyo-area capacity, Cosmo only had to focus on cutting facility operating costs. It did not need to deal with post-merger redundant capacity.

Cosmo has also been smart in forging alliances with its larger rivals, such as building a pipeline in China that it shares with ENEOS. Cosmo and Idemitsu have an alliance based on an understanding for production sharing in the Yokkaichi area, another very busy refining hub where Cosmo and Idemitsu have neighboring facilities.

As a result of its smart maneuvers, Cosmo achieved a run rate of 71.9% during the April to June period. ENEOS’ 11 facilities averaged 68%; Idemitsu had 70%.

PLANNING FOR THE NEXT STEP According to ENEOS, all Japanese refineries face one of two scenarios: scale down of production, or closure and conversion into a petrochemical facility, hydrogen terminals, or power plant.

The costs of conversion will run into hundreds of millions, if not billions of dollars. That alone will not guarantee a happy rebirth, as ENEOS’s experience with the Muroran refinery showed. Before Covid, a major global campaign was to cut the use of plastics and this year Japan has mandated charges on plastic bags handed out at shops.

To be sure, the money all three Japanese refinery companies are making today is still considerable. In terms of securing future income in new business areas, it may be those who first brave the jump will seize the advantage.

ANALYSIS

JOHN VAROLI, DIRECTOR, NORTH AMERICA YURI INVEST RESEARCH

Hit Hard by the Pandemic, U.S. Offers Bargain LNG Deals That Japan Could Use to Rebalance Its Import Portfolio

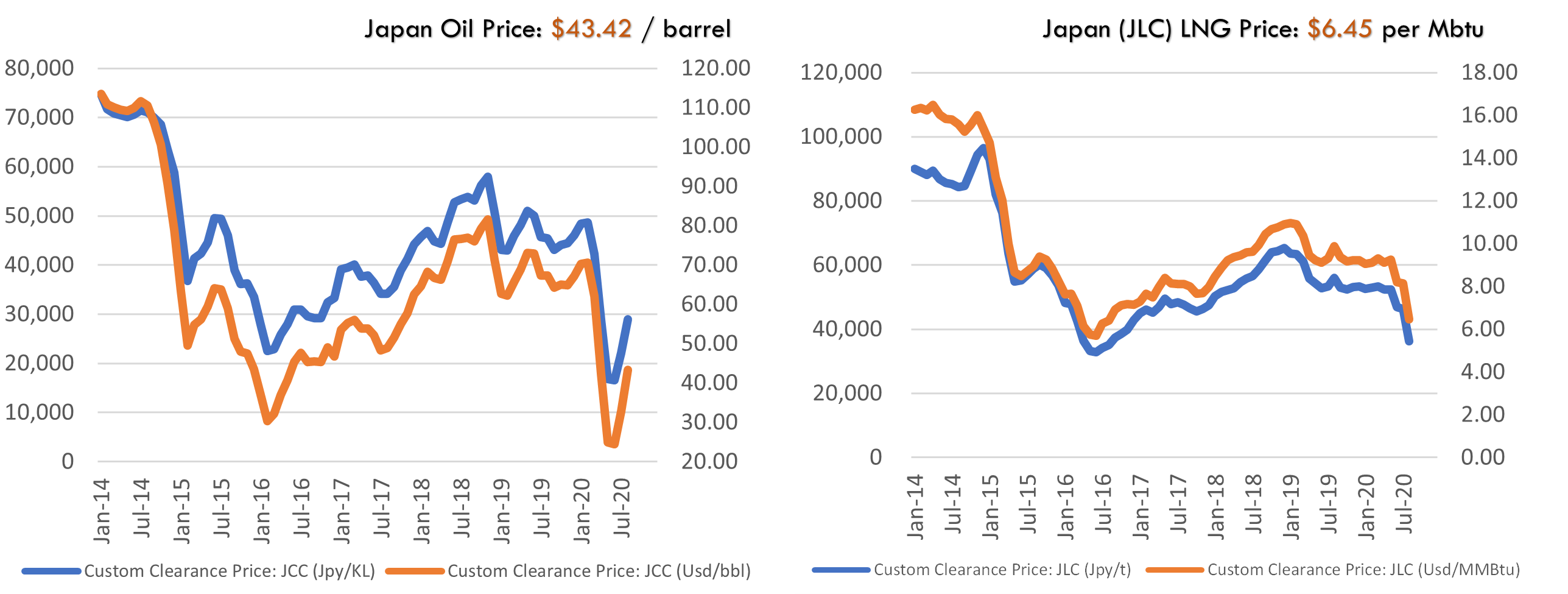

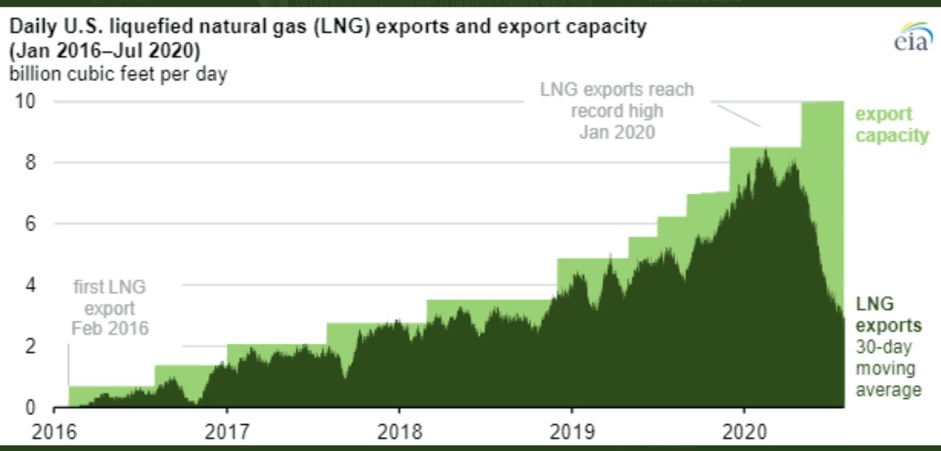

Earlier this year Japan’s buyers felt they got a raw deal on long-term U.S. LNG contracts, but now on the threshold of winter there’s the best opportunity in years to lock in more U.S. supply on the cheap. U.S. producers are ready to accept steep discounts, industry insiders say, and Tokyo Gas’ cut-price acquisition of a U.S. gas project earlier this month showed yet another way how Japanese firms could exploit the situation.

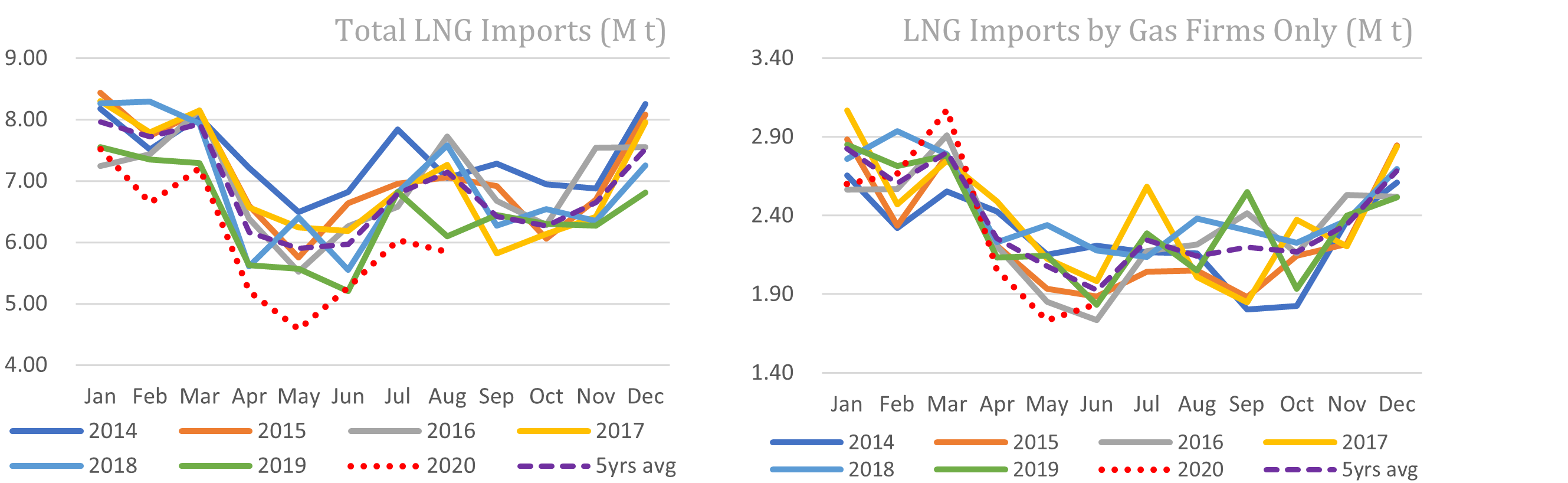

A pandemic-induced economic downturn and milder temperatures have hurt Japan’s LNG demand this year. Still, the nation is likely to remain the premium importer for the near term. And with a reported 7 million metric tons of LNG import contracts due to expire by December 2021 – equivalent to one-tenth of Japan’s annual imports – Japanese buyers could leverage their negotiating position to rethink supply sources.

Now’s a perfect storm for Japanese bargain-hunting, said Rudolf Huber, president at LNG Europe – Institute for Methane Fuels in Austria. “The U.S. currently doesn’t really make money out of LNG exports, and now is a good time for Japanese buyers to get advantageous long-term deals with U.S. producers,” said Huber.

“[U.S. producers] are willing to give as much as possible in order to get their project sanctioned.”

The current U.S. administration is making a major push to expand LNG exports. For example, in mid-July it authorized export from a proposed $10 billion LNG terminal and pipeline project in Jordan Cove, Oregon. This is despite many doubting the economic viability of the complex. It seems that Jordan Cove is yet another example of LNG being used as “freedom gas” to bolster the energy security of allies, including Japan, and to compete with new sources of the fuel from nations like Russia.

“Japan continues to benefit from the abundance of U.S. LNG supply in the global market, which has brought down spot prices to historic lows,” said Ruth Liao, LNG editor of the Americas for Independent Commodity Intelligence Services (ICIS).

“This has been a challenge for the long-term offtakers, which had to cancel cargoes this summer as a result of uneconomic market conditions, but higher demand and spot prices should be supportive of more LNG to Asia.”

Source: EIA

“Cargo cancellations expected in October are at the lowest level since the spring. Meanwhile, Asian spot LNG has broken through USD5/mmbtu on expectations of more buying ahead of the winter season.

CHINA LNG DEMAND GROWTH TO HELP OR HURT JAPAN?

In 2019, Japan was the world’s largest LNG importer, receiving 105 billion cubic meters (about 77.2 million tons), or 21.7 percent of global LNG imports. China was a distant second. The top five LNG exporters in 2019 were Qatar, Australia, the U.S., Russia and Malaysia.

China, however, remains the elephant in the room. The Trump administration has singled out China as America’s arch nemesis, but it’s also the fastest growing LNG market. One of the few long-term contracts signed this year was for a 15-year supply of 500,000 tons per annum to China’s Shenenergy Group., with U.K.’s Centrica Plc. the provider.

This year alone, China’s LNG imports are expected to grow 10% to new highs as its economy recovers from the pandemic.

In contrast, Japan’s long-term demand is in question due to depopulation and a changing energy mix. At China’s current pace, it will overtake Japan as the top global importer within two years.

So, will Washington compromise geopolitical strategy to score a better business deal?

Probably not. Even aside from China’s recent national commitment to a zero-carbon target in 2060, the world’s most popular nation is a tricky customer for most sellers.

Geopolitical tensions could spill over into sanctions. It would not be the first time the U.S. had blocked energy sales to force an issue.

What’s more, Huber believes China could easily switch its current interest in LNG to more coal in the face of economic difficulties. Since 2007, the country brought online around 40 GW to 80 GW in new coal capacity per year. It’s hard to imagine such vast investments would be left idle any time soon. In fact, Chinese industry insiders told Bloomberg last week they expect it will be business as usual for coal firms in the country for many more years to come.

“Just let China’s economy take another hit, just let the conflict with the U.S. deepen and China won’t touch U.S. LNG anymore,” Huber said. “Japan has no such growth and is hard to deal with, but it’s also a safe bet. China has burnt us many times so far.”

This leaves Japan as a “premium buyer,” Huber said.

With few natural resources, no pipeline connections to other countries, and one of the world’s highest renewable energy bills, Japan is also seen as a safe bet to long-term LNG purchases. What’s more, Japanese utilities traditionally pay more to lock in volumes.

NEW STRATEGIC AIMS FOR JAPAN BUYERS

The U.S. only started mass exports of LNG in 2016, although Japan had one legacy contract with U.S. in the 1960s (the former Kenai LNG Plant in Alaska).

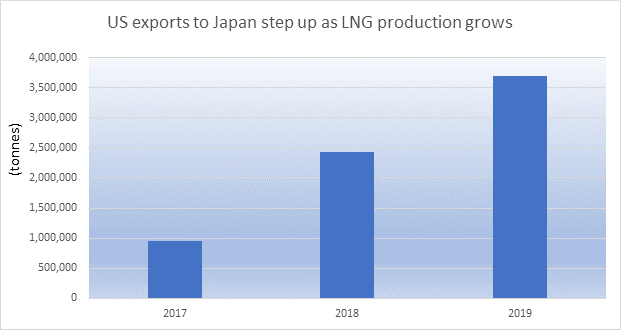

At present, Japan’s biggest LNG offtake and investment deals in the U.S. include the JERA and Osaka Gas involvement at Freeport LNG in Texas (15 million tons per annum – mtpa); Mitsui and Mitsubishi Corp participation in Cameron LNG, Louisiana (13.5 mtpa); and Tokyo Gas and Sumitomo Corp presence at Cove Point LNG in Lusby, Maryland, close to Washington D.C.

Source: ICIS

This summer, Tokyo Gas showed that the list of Japanese investments in U.S. gas may yet grow for reasons other than imports of the fuel to Japan. The gas company raised its stake in U.S.-based shale gas operator Castleton Resources to 70% and spent $188 million to acquire a gas field in Louisiana on the Gulf of Mexico.

The deal, which was said to occur at a 20% discount, was meant to increase Tokyo Gas’ exposure to American gas demand as a hedge against future weakening in the domestic outlook.

With Japanese companies investing in new LNG locations such as Mozambique, their domestic needs for more U.S. supply is low.

However, in addition to the near-term expiry of contracts with high-cost suppliers like Qatar, Japanese firms have become more aggressive in pursuing LNG infrastructure and supply deals in southeast Asia.

That signals that the geopolitical relationship with the U.S., and role of American companies as partners in LNG infrastructure, could pave the way for more strategic U.S. investments by Japanese firms. New U.S. offtake agreements too may no longer depend only on whether the fuel needs to be burned in Japan.

Japan’s Ministry of Economy Trade & Industry will host its 9th LNG Producer-Consumer Conference for the first time in a virtual format on Oct. 12th.

The conference will be held against the backdrop of significant difficulties in the oil and gas sector, caused mainly by the pandemic-induced disruption to oil consumption and the accelerating push for decarbonization.

No new FIDs for natural gas projects have been approved so far in 2020.

Oil prices are currently trading below $40/barrel with 70% of natural gas contracts still oil-indexed. Spot LNG prices in Asia Pacific are also very low at $5 mmbtu, well below the breakeven levels required by LNG suppliers to generate returns on infrastructure investments made over the last several years. US natural gas prices are around $2.40 mmbtu.

However, despite the pandemic, global LNG volumes are still expected to increase by around two percent year-on-year in 2020 to over 350 million tons with overall global LNG trade valued at between $150 to $200 billion in 2020.

Increases in LNG demand are mainly driven by Asia. Japan’s LNG imports in 2019 were 77 million tons and cost $44 billion. JERA is now Japan’s largest LNG importer. Global LNG volumes are still expected to double over the next 20 years as the energy transition takes hold and natural gas replaces coal for electricity production.

The Japanese government is expected to use this year’s LNG conference to push for further expansion and construction of LNG facilities across Asia-Pacific to supplement domestic natural gas production. To this end, Japan has committed to $20 billion of financing and to the training of up to 1,000 staff, mainly in ASEAN countries. Energy ministers from Cambodia and Myanmar will be among those making an address at this year’s conference.

There are currently 21 LNG exporting countries and 42 LNG importing countries; the industry numbers 427 liquefaction facilities and 920 regasification plants. Australia, Qatar, and the U.S. continue to dominate the export market.

Angola, Russia and Papua New Guinea are recent new suppliers delivering significant volumes to the global LNG market. JOGMEC is financing LNG facilities in Russia, including at Yamal and Arctic LNG 2, and has provided over $7 billion of credit for LNG development globally. Japan has also invited energy ministers from Nigeria and Tanzania to address the Oct. 12th LNG event.

Three of Japan’s trading companies, Marubeni, Mitsui and Mitsubishi – all large LNG investors and intermediaries, will also address the conference. Mitsui is expected to use it as a platform to announce that the company will become carbon-neutral by 2050.

Mitsui is in 11 LNG projects in nine countries with a recent major investment in Mozambique LNG. Warren Buffett recently announced a $6 billion investment in Japan’s trading companies, thought to be driven mainly by their global energy businesses.

Japan’s role in shaping the global LNG industry will again be on display on Oct. 12. Japan NRG’s team will be participating in it for the ninth consecutive time since the conference’s inception in 2012.

STOCK MARKET PERFORMANCE

As of close on October 2, 2020

Ticker

Market Cap

1W (%)

MTD (%)

YTD (%)

billions of yen

Energy

INPEX CORP

1605 JP

798.72

-4.94

-51.07

-15.30

JAPAN PETROLEUM EXPL.

1662 JP

94.42

-0.44

-42.47

-7.53

ENEOS HOLDINGS INC

5020 JP

1207.80

-2.98

-20.45

-6.20

IDEMITSU KOSAN CO LTD

5019 JP

663.94

-2.95

-22.07

-0.76

COSMO ENERGY HOLD.

5021 JP

126.56

-3.86

-37.49

-6.80

Industrials

JGC HOLDINGS CORP

1963 JP

270.62

-5.86

-39.69

-7.53

CHIYODA CORP

6366 JP

63.26

-4.71

-14.13

-10.33

MITSUBISHI CORP

8058 JP

3719.51

-3.23

-8.91

-1.86

MITSUI & CO LTD

8031 JP

3079.63

-4.02

-3.47

-6.11

Utilities

TOKYO ELECTRIC POWER

9501 JP

453.18

-6.00

-39.61

-9.90

CHUBU ELECTRIC POWER

9502 JP

947.50

-4.97

-16.04

-2.98

KANSAI ELECTRIC POWER

9503 JP

939.67

-4.01

-17.27

-3.01

KYUSHU ELECTRIC POWER

9508 JP

448.10

-2.22

3.53

0.85

J-POWER

9513 JP

286.66

-5.25

-38.54

-0.54

TOKYO GAS CO

9531 JP

1042.60

-4.79

-9.02

1.77

OSAKA GAS CO

9532 JP

829.61

-6.59

-2.49

-2.14

TOHO GAS CO

9533 JP

534.37

-7.19

14.64

8.91

SAIBU GAS CO

9536 JP

97.02

-7.22

5.27

7.73

SHIZUOKA GAS CO

9543 JP

69.26

-6.29

-3.58

4.00

DATA

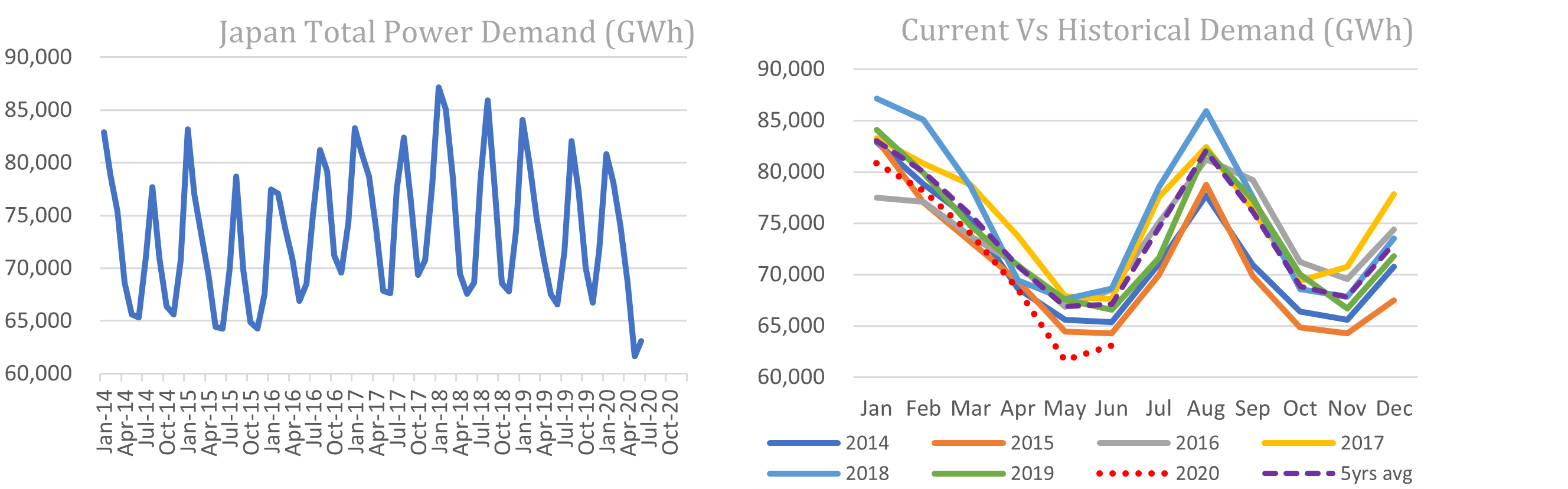

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

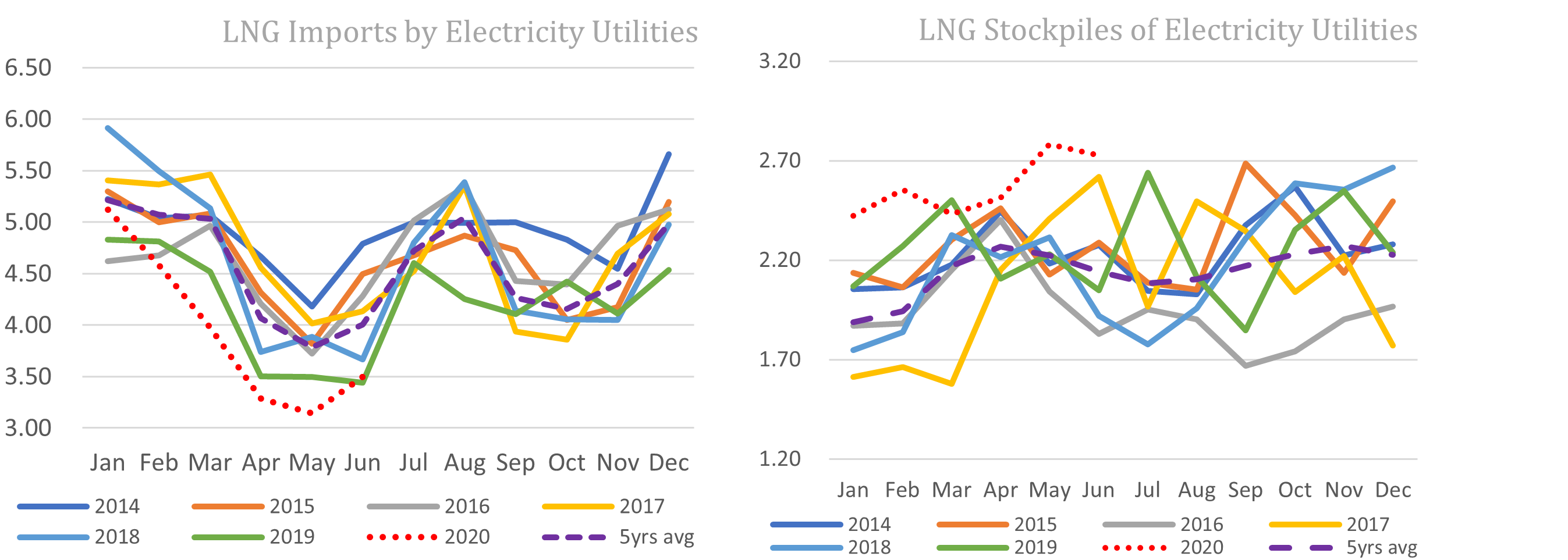

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance

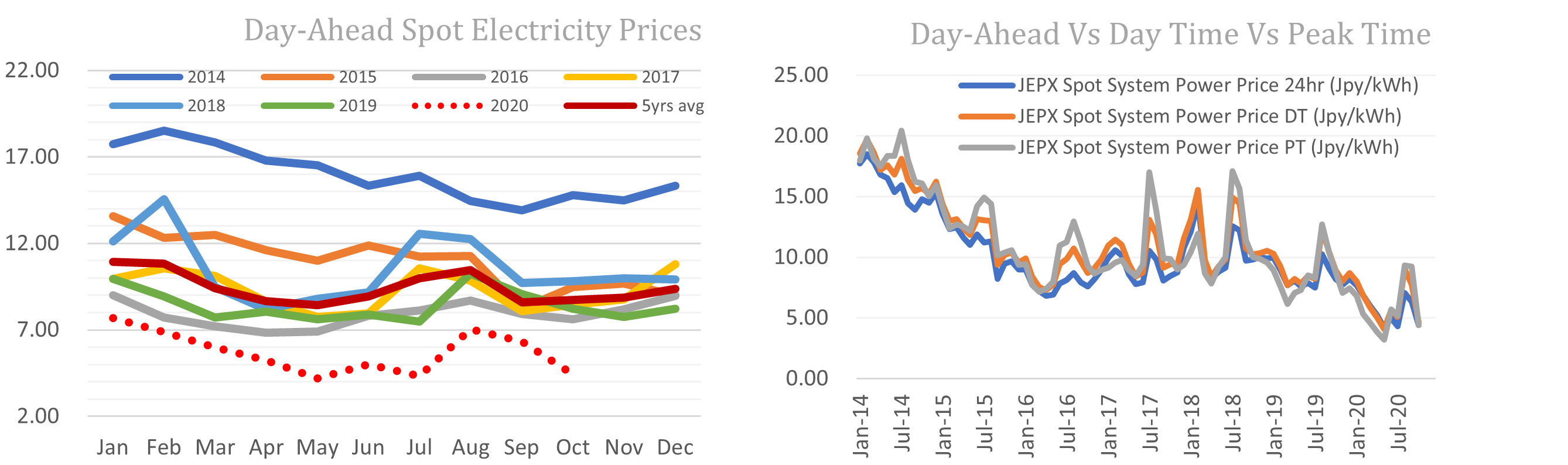

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged.

This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest Research Ltd., which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis.

Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

Recipients of this report should ensure that they fully understand the legal, tax and accounting implications before making an investment decision and independently determine that the transaction is appropriate based on their own objectives, experience and resources.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided.

In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

JAPAN NRG WEEKLY OCTOBER 05, 2020 JAPAN NRG WEEKLY October 5, 2020 NEWS TOP OIL & GAS POWER & NUCLEAR RENEWABLES, OTHER ANALYSIS OIL REFINERIES READY FOR TRANSFORMATION DESPITE THE CURRENT WORLD-BEATING PROFITS It’s a strange time for Japanese oil refiners to accept that the journey is over. Japan’s gasoline and […]

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange