JAPAN NRG WEEKLY

OCTOBER 26, 2020

JAPAN NRG WEEKLY

October 26, 2020

| NEWS TOP

OIL & GAS

POWER & NUCLEAR

RENEWABLES, OTHER

| ANALYSIS TOKYO GAS UNLEASHES GLOBAL STRATEGY AS It has taken a decade longer than planned, but Tokyo Gas, Japan’s top gas utility, is finally transforming into a global player. The company’s cautious international expansion has accelerated in the last 12 months or so, with major acquisitions and investments in gas and renewables. More are expected to follow. JAPAN STARTS POWER CAPACITY MARKET AUCTIONS; FIRST ROUND: GENERATORS WIN, RETAILERS LOSE This summer Japan launched the Power Capacity Market, a new mechanism aimed at supporting future investment in new generation facilities. The results of the first capacity auction, however, have created a mini-scandal. The high bids indicate that the average electricity bill in Japan will need to rise. The alternative is for some power retailers to accept massive losses. Environment Minister Koizumi Shinjiro has vowed to investigate the matter, which is quickly turning into a battle between large generation companies that rely on thermal and nuclear assets, and smaller retail firms, many of which support renewables. How the standoff is resolved could determine not only the size of future Japanese electricity bills, but also the new balance of power across the entire industry. GLOBAL VIEW Cathay Pacific layoffs, Taiwan arms sales, and UAE oil shipments via Israel are just some of international energy developments picked out by the NRG team. |

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group and Yuri Invest Research Ltd.

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Contributors

Mayumi Watanabe

Daniel Shulman

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. For further details, or to discuss marketing, advertising, or collaboration opportunities, please contact one of the Editorial Team members or write to nrgnews@yuri-invest-research.com

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked Yuri Invest Research Ltd. or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Invest, which retains all copyright to the content of this report.

Yuri Invest Research Ltd. is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Invest Research Ltd. or its partner K.K Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

Yuri Invest Research Ltd.: Room 602, Wah Yuen Building, 149 Queen’s Road Central, Central, Hong Kong.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS: OIL & GAS

Total starts supplying “carbon neutral” LNG from Ichthys project

Total starts supplying “carbon neutral” LNG from Ichthys project

(NNA Asia, Oct. 23)

- The first shipments of carbon neutral LNG from the Australian Ichthys project are on their way to China, courtesy of French energy giant Total SE.

- The shipments are destined for the China National Offshore Oil Corporation, with all carbon offset through the use of carbon credits.

- The Ichthys project is operated by Japan’s INPEX Corp.

TAKEAWAY: Carbon neutral LNG will become a major trend in coming years as key buyers in Japan and China, as well as in Europe, look to comply with the national commitments to net zero carbon emissions by 2050. Japan’s main energy ministry, METI, last month called for the global LNG industry to start cutting emissions throughout the supply chain. LNG buyers will increasingly start to request this “carbon-free” label and the easiest way to attach it will be via offsets.

Marubeni, JERA sell stakes in Squadron Energy’s Australian LNG project

(Reuters via Yahoo Japan News, Oct. 20)

- Squadron Energy, an energy company owned by Australian billionaire Andrew Forrest, said on Oct. 20 that it had acquired JERA and Marubeni’s stakes in the Port Kembla LNG import hub in New South Wales.

- Marubeni formerly owned a 30.1% stake in the operation, while JERA owned a 19.19% stake. Squadron did not disclose how much it paid for the shares.

- Squadron said it will accelerate its development of the facility as part of its goal to supply 70% of New South Wales’ gas requirements by late 2022.

TAKEAWAY: Marubeni and JERA only signed an MOU with Squadron Energy for the project in Feb. 2018. At the time, both said they were excited about the prospect of developing a Floating Storage and Regasification Unit (FSRU) in New South Wales to deliver gas to local customers. While the Australian partner said that JERA and Marubeni remain open to exploring future tie-ups, the exit shows that Japanese interest in new investments in upstream gas and LNG in Australia has cooled. Aside from questions around local demand and the post-pandemic economic funk, Japanese firms see that on a relative cost basis there are many global opportunities.

- SIDE DEVELOPMENT:

JERA launches LNG bunkering operation

(Denki Shimbun, Oct. 23)- JERA said on Oct. 21 that it was now providing LNG bunkering (supply) services to shipping operators Kawasaki Kisen, Toyota Tsusho, and NYK line.

- The first LNG was provided when a JERA bunkering vessel, the Kaguya, refueled Sakura Leader, an LNG-powered car transporter on Oct. 20.

Sale of Sendai Gas likely to raise at least ¥400 billion, attracts Tokyo Gas, JAPEX

(Nikkei Shimbun, Oct. 24)

- Sendai city’s gas business supplies more than 7 million homes in 34 municipalities in Miyagi Prefecture, making it the largest public gas asset left in Japan since the full liberalization of gas retail began in 2017.

- The size of the Sendai city gas market is around ¥300 billion yen, and the minimum bid will probably be around ¥400 billion yen.

- The deadline for bids is Oct. 29. The city government expects to start talks with the leading bid around May 2021.

- Tokyo Gas has formed a special company for the bid as it seeks to expand in northeast Japan. It will bid as a 4-member consortium together with JAPEX, Tohoku Electric, and a local energy company. No other notable bidders are as yet known.

TAKEAWAY: We reported on Tokyo Gas’ interest in bidding a few weeks earlier in the Oct. 12 edition, however, the estimate of price seems to be new. There are very few public gas assets left to buy in Japan, which is possibly the reason for the near USD 4 billion price estimate. The sale was originally considered in the first decade of the 21st century, but was delayed due to the global financial crisis.

Idemitsu sells Norway oil interest for about $125 million

(Sekiyu Tsushinsha, Oct. 22)

- On Oct. 22, Idemitsu Kosan signed a sales agreement to transfer part of its interests in Barents Sea fields to Swedish oil company Lundin.

- The sale amount is seen at around USD 125 million.

- Idemitsu retains stakes in the fields related to the sale. The exact date for when the rights will transfer to Lundin will depend on approval from the Norwegian government.

- The partial sale was made based on Idemitsu Kosan’s long-term strategy for the Norwegian business and the need to reduce development costs for oil fields.

- Idemitsu won the rights to the fields in 2013 and 2014 tenders.

IT and e-commerce giant Rakuten enters domestic gas market

(Nikkan Kogyo Shimbun, Oct. 23)

- Mobile phone operator Rakuten Mobile said on Oct. 22 that it will enter the domestic gas retail market.

- Rakuten Mobile has entered into agreements with Tokyo Gas, Toho Gas, and the Kansai Electric that will allow it to provide gas retail services.

- The service will be known as “Rakuten Gas” and tariffs will be similar to those offered by the three gas providers.

TAKEAWAY: As of last month, Japanese households had 35 new companies offering gas sales compared with three years ago, when the market was deregulated to bring competition to the big gas utilities. Rakuten is one of the largest Japanese firms and often positions itself as a major disrupting force. It is currently gearing up to become the fourth national mobile phone carrier in Japan and plans to engage in price-cutting to seize market share. In gas, however, the expected increase in competition from the entry of new players has yet to materialize. As Rakuten’s gas supplier list shows, the IT company will rely on the companies that dominate the market to provide it with white-list services. Apart from offering yet another loyalty points scheme for the gas consumer, it’s hard to see what Rakuten brings to the table.

INPEX and JAPEX rally on improved demand projections

(Minkabu Press, Oct. 23)

- Shares in INPEX and Japan Petroleum Exploration (JAPEX) have rallied in response to a jump in the price of 12-month WTI crude futures.

- Lower than expected unemployment numbers in the U.S. have created optimism in oil markets, and this grew when Russian President Vladimir Putin said his country would not increase oil production.

NEWS: POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 2 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

Source: Company websites, JANSI and JAIF, as of Oct. 21, 2020

Kansai Electric rushes repair work on damaged nuclear reactor pipe ahead of schedule

(Fukui Shimbun Online, Oct. 19)

- The Kansai Electric Power Company (KEPCO) said recently-discovered damage to a pipe forming part of the Ohi No. 3 nuclear unit will be repaired during the scheduled inspection currently underway.

- Scratches up to 4.6 mm deep were discovered in a weld, at a forked section of plumbing used to transport steam. The pipe is only 14 mm thick. Works to remove the damaged section will begin in the last part of this month.

- The No. 3 reactor’s restart date is listed as “undecided”. It’s expected to take quite a while to restart.

- CONTEXT: KEPCO originally said the pipe would not be replaced until the reactor’s next periodic inspection. The repair work has been brought forward since the company faces the prospect of having all of its nuclear reactors out of action for various reasons.

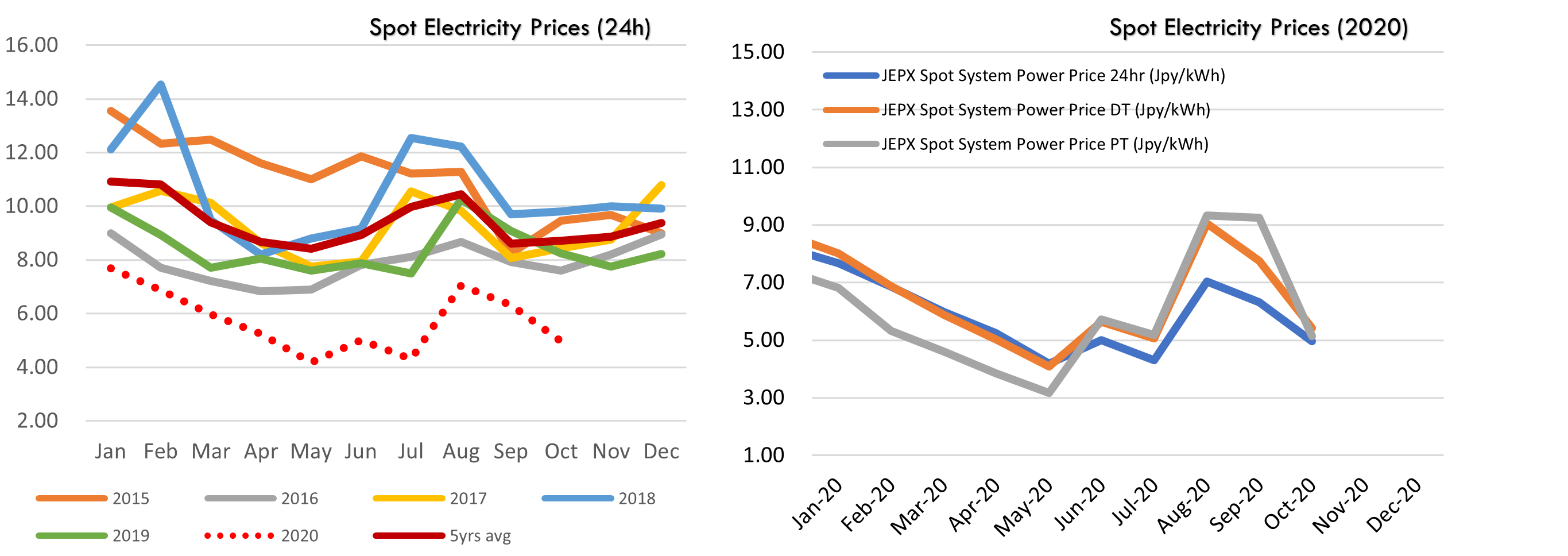

TAKEAWAY: As reported earlier, KEPCO will need to stop Ohi No. 4 reactor on Nov. 3 for regular maintenance. That will mean the utility will have none of its seven reactors in operation, with the earliest restarts seen around February. In nationwide terms, Japan will be left with just one operating nuclear reactor as it heads into what is forecasted to be a colder-than-usual winter. LNG will benefit from this in the near-term as the run up in prices in the last month is showing.

- SIDE DEVELOPMENT:

Mihama City special nuclear commission starts visit to inspect nuclear plant

(Yomiuri Shimbun, Oct. 22)- Officials from the city’s special committee started an inspection of the facility on Oct. 21

- This comes after Mihama’s No. 3 reactor was granted a 20-year operating life extension by the nuclear regulator

- SIDE DEVELOPMENT:

Takahama Nuclear Power Plant future is in KEPCO’s hands, Fukui Governor

(Denki Shimbun, Oct. 23)- Fukui Governor Sugimoto Tatsuji said at a press conference on Oct. 22 that the future of the Takahama nuclear power plant was now in the hands of KEPCO and the Japanese government.

- The Ministry of Economy, Trade and Industry had asked the Fukui government to cooperate on a review that could see the reactor operated beyond its 40-year design lifespan.

- Sugimoto did not explicitly state how approval (or disapproval) from local residents will influence the decision to extend the life of the nuclear plant.

- When asked about a KEPCO proposal to store spent fuel rods outside the prefecture, Sugimoto only said that he would consider proposals on a case-by-case basis.

- CONTEXT: KEPCO, like most Japanese utilities with nuclear assets, is running out of space to store spent fuel before it is sent to be processed. The utility’s nuclear plants are concentrated in Fukui prefecture, but the utility has faced opposition from the locality when discussing plans to build a new facility to store used fuel on an interim basis. KEPCO has looked at candidate sites in other prefectures for close to two decades. However, there remains fierce opposition in other prefectures to accepting its nuclear fuel.

TAKEAWAY: By law, nothing stands in the way of KEPCO restarting several of its older reactors, which have won the nuclear regulator’s approval for a 20-year operating life extension. However, it is customary to get the green light from the local governor and town mayor before a nuclear reactor goes back online. The comments from Fukui’s governor indicate that he is not willing to accept the responsibility for restart approval. The governor saying the ball is in KEPCO and the government’s court is a move that challenges the accepted order of nuclear restarts in Japan. On the one hand, it opens the window for the utility and the government to step up and make that restart happen by themselves. If they do, it could begin a precedent of “bypassing” the process of seeking agreement from local governments. The problem is, if KEPCO and the national government make this decision unilaterally, they will open themselves up to the local population’s direct ire with no filter in the form of municipal and regional governments. Which is, of course, what the Fukui governor is challenging them to do.

Tokyo Gas enters power market in Hokkaido, woos solar generators with post-FIT pricing

(New Energy Business News, Oct. 21)

- Tokyo Gas has launched an electricity plan in central Japan and Hokkaido in which subscribers receive up to 5% Amazon points on electricity purchased.

- Tokyo Gas is also enhancing services offered to solar generators who have left the Feed-In Tariff (FIT) scheme and wish to sell surplus electricity.

- Subscribers who purchase storage batteries are entitled to join a support plan, which enables them to sell electricity at a premium rate of ¥23 per kilowatt hour for the first six months.

- SIDE DEVELOPMENT:

Tokyo Gas, Osaka Gas, others form group to find ways to run renewables without FIT

(Denki Shimbun, Oct. 20)- Five companies that also include Tokyu Fudosan formed the FOURE collective, which among other issues will look at business models that will allow renewable energy projects to be profitable without relying on FIT.

Hitachi CEO explains ABB Power acquisition and future plans

(Nikkei Asia, Oct. 22)

- CEO Higashihara Toshiaki says the ABB Power Grid business represents “a black ship that we brought in from outside to change Hitachi.” CEO says Hitachi can learn from ABB’s management style, with local teams leading businesses while headquarters keeps a grip on governance.

- Acquisition will require 10 years to make return on investment.

- Hitachi CEO named energy as one of the company’s four key pillars (infrastructure, rail, and healthcare being the others).

TEPCO gets additional ¥13 billion from compensation body for Fukushima

(Denki Shimbun, Oct. 23)

- Sugimoto TEPCO Holdings said on Oct. 22 that it had received an additional ¥12.9-billion payment from the Nuclear Damage Compensation and Decommissioning Facilitation Corporation to meet a shortfall in compensation payouts.

- The latest payment is on top of the ¥190 billion of government grants and ¥9.4 trillion of NDCDF payouts already received.

- CONTEXT: The latest payment means that the government has already passed more than USD 96 billion to TEPCO to deal with the fallout from the 2011 Fukushima nuclear disaster.

Waste from Shiga nuclear reactor departs for Rokkasho Processing Plant

(Mainichi Shimbun, Oct. 21)

- Hokuriku Electric said on Oct. 19 that a shipment of low-level radioactive waste from its Shiga reactor was now on its way to the Rokkasho reprocessing plant in Aomori, and is scheduled to arrive on Oct. 21.

- In addition to 480 steel drums containing low level waste, the shipment also contains metallic and plastic waste that was generated during the reactor’s scheduled inspection.

Kansai Electric trials adding parcel delivery boxes to utility poles

(NHK News Web, Oct. 21)

- Kansai Electric is trialing a new scheme in which smart lockers are attached to power transmission poles. Couriers can use the lockers for deliveries addressed to local residents who are not at home when the courier calls.

- While these are not the first smart lockers that can be used for parcels, the power poles could prove to be a convenient space for delivery boxes since they can be easily located by both couriers and residents.

TAKEAWAY: Unlike many other countries, Japan keeps its power lines above ground and as a result the towns and cities are stuffed with electricity cables on poles on most streets. The idea of using this existing asset for an entirely new business line is a great (if rare) example of innovation by a major power utility in Japan. While this is at a very early stage, it would be interesting to see how else utilities can leverage their network to expand business opportunities and generate more income.

NEWS: RENEWABLES & OTHERS

Japan to announce 2050 zero emissions target

Japan to announce 2050 zero emissions target

(Nikkei Shimbun, Oct. 22)

- The Nikkei ran a scoop revealing that Prime Minister Suga will announce on Oct. 26 that Japan will commit to reducing effective greenhouse gas emissions to zero by 2050, thereby matching the EU’s 2019 commitment to become carbon neutral by the middle of the century.

- The zero emissions target pertains to net CO2 emissions after tree planting and other carbon offsets have been factored in.

- The government is expected to announce support for large-scale battery storage for renewable energy projects and will try to attract foreign firms with the technology to come to Japan.

- The govt. is aware that moving away from coal will mean the cost of electricity will go up, but there was also a concern that should Democratic Party candidate Joe Biden win the U.S. election and go on to make a carbon-free pledge, Japan would be left behind.

- CONTEXT: The new target replaces the government’s previous target which only called for an 80% reduction in emissions by 2050. It was criticized by the EU and other nations for being noncommittal.

- CONTEXT: The groundwork for the announcement came two weeks ago, when the Minister of Economy, Trade and Industry Kajiyama Hiroshi said in an interview that Japan will soon review its energy mix outlook. Kajiyama said that renewables will be re-classified as a “main” source of electricity and the sector will be free to grow “without limit.”

- SIDE DEVELOPMENT:

Japan will make renewable energy its “main power source”: Minister

(Nikkei, Oct. 19)- The government currently aims to make renewable energy its ‘main power source,’ but “[they] cannot make investments because there are too many restrictions,” Kono Taro, Japan’s minister for administrative reform and regulatory reform, said in an interview.

- Kono said that he had directed the ministries involved in the decision-making process to sort out the issues, with the idea of amending laws and easing regulations – especially as related to access to land, ports and coastlines.

- Currently, only areas that are designated by the govt. as available for offshore wind development are open to investors. Companies cannot choose the locations themselves, even if they see good opportunities in other areas.

- Other areas subject to Minister Kono’s review include agricultural and local body regulations, which currently limit the erection of solar panels on wasteland and uncleared land, the Forestry Act, which prohibits the construction of wind turbines in national forests, as well as shipping legislation, which prohibits the use of foreign-flagged vessels to transport parts for offshore wind farms.

TAKEAWAY: As predicted by Japan NRG in the Sept. 28 edition, incoming prime minister Suga would move quickly to resolve some of the country’s key energy issues and few were as big as what to do about emissions goals. Japan has managed to more than triple its renewables capacity in the last decade and assemble the world’s third-largest solar capacity, but it still relies on burning fossil fuels for 70% of total electricity. Renewables still account for only about 17% of the nation’s energy mix.

- Japan NRG will explore the deeper implications of Japan’s 2050 commitment in next week’s edition. However, here are a few quick points to consider. As soon as Japan’s government makes the announcement, major companies in the country will need to fall in line and make the same commitment, whether in private or in public.

- Japan will most likely consider introducing a carbon tax or an emissions trading scheme to allow heavy energy users that cannot avoid emissions to purchase offsets. Ammonia and hydrogen have already been mentioned as candidates to help decarbonize the domestic power and gas industries (See our Oct. 19 edition for details).

- More government support will be thrown behind battery storage, fuel cells, and carbon capture technology, all of which are under development in Japan.

- The key headache and hard-to-predict variable, however, will remain nuclear power. Japan has the world’s fourth-largest nuclear power capacity, yet since the 2011 Fukushima disaster most of the reactors rest idle. The big utilities want to see the reactors back on line, as the Federation of Electric Power Companies of Japan repeated last week. However, how many reactors the government and industry can restart in the face of negative public opinion will dictate how much burden will fall on the other parts of the decarbonization program.

Companies slashing carbon emissions see 15% rise in market cap

(Nikkei Asia; Oct. 18, 2020)

- 137 global investors that hold $20 trillion in assets called on over 1,800 companies to set science-based targets for cutting emissions.

- The top 30 corporations that cut carbon emissions from 2014 to 2018 saw their market caps increase by 15% as of September this year compared to December 2017. But the top 30 companies that increased their carbon emissions from 2014 to 2018 saw their market cap decrease by 12% over the same period.

- Among the Japanese firms seeking the same, Hitachi divested from the gas-turbine business and aims to be carbon neutral by fiscal 2030.

ENEOS among group seeking to commercialize fuel cell ship technology by 2030

(New Energy Shimpo magazine, Oct. 10)

- ENEOS, Nippon Yusen, Toshiba, Kawasaki Heavy Industries and ClassNK have joined forces to develop a 150-ton ship that can carry up to 100 passengers and operate on a 500kW hydrogen fuel cell.

- The goal is to develop a marine transport vehicle that has zero emissions.

- Testing of the technology is set for June 2024. Initially, the partner companies will run a feasibility study on fuel cell battery powered ships. Work on the designs for the actual ship and its supply stations will start in 2021, with the manufacturing phase slated for 2023.

- Verification trials will last for six months and will be conducted in the Yokohama Bay area.

- The companies involved believe that commercialization of fuel cell powered ships can occur around 2030.

- CONTEXT: Japan is currently working on fuel cell cars, buses, trains, and now ships. Toyota Motor is one of the biggest proponents of fuel cell vehicles.

Etrion considers sale of entire Japan solar portfolio

(Company Press Release, Oct. 21)

- The Geneva-based independent solar projects developer and operator said it is exploring the sale of its entire Japan portfolio.

- The company engaged Mitsubishi UFJ Morgan Stanley Securities as financial advisor to assist with the potential sale of the company’s 57 MW operating solar portfolio and its 45 MW solar park under construction in Japan.

TAKEAWAY: Etrion was one of the earliest investors into the Japanese solar market once the country introduced the Feed-In Tariff (FIT) scheme to encourage more development of renewable energy. The Swiss-based company partnered with Hitachi High-Tech in 2012 to develop a pipeline of solar assets in Japan and originally expected to have as much as 300 MW of capacity either ready or under construction by 2017. The exit, should it materialize, would inject more liquidity into the secondary market for solar assets in Japan.

Erex establishes Indonesia facility to procure fuel for biomass power plants

(New Energy Business News, Oct. 23)

- A joint venture between a subsidiary of Indonesian energy company DSN and Erex’s Singaporean subsidiary will facilitate the sustainable, long-term, and economic procurement of palm kernel shells for use in biomass fired power plants operated by the Erex group.

- The newly formed company will establish a palm kernel shell stockpile on Borneo and is scheduled to commence shipments in Sept. 2021.

- CONTEXT: Erex is one of Japan’s biggest operators of biomass power plants. The company has four plants and is building two more. With their completion, it will have about 350 MW of biomass power capacity in Japan.

Dai-Ichi Life to invest ¥11 billion in renewable infrastructure fund

(Kankyo Business Online, Oct. 19)

- Insurance company Dai-Ichi Life said on Oct. 14 it will invest ¥10.5 million in the Global Renewable Power Fund III, an infrastructure fund operated by BlackRock Real Assets and focused on renewable energy.

- Through the investment, Dai-Ichi Life aims to make a positive contribution to efforts to stem climate change.

- CONTEXT: The Global Renewable Power Fund III invests in the construction and operation of solar, wind, and other renewable energy facilities in the OECD.

Toshiba and Panasonic to manufacture lithium-ion batteries in Tokushima

(New Energy Business News, Oct. 19)

- Prime Energy & Solutions, a joint venture between Toyota and Panasonic, will start manufacturing lithium-ion batteries for use in hybrid vehicles at a Tokushima factory in 2022, and will eventually ramp up production to 500,000 units per year.

- Prime Energy & Solutions is 51% owned by Toyota. Panasonic holds the rest.

KEPCO to develop drone-based monitoring system for offshore wind farms

(New Energy business News, Oct. 22)

- Kansai Electric will research and develop a drone-based solution for maintaining offshore wind farms.

- The project was commissioned by the New Energy and Industrial Technology Development Organization (NEDO) and will run until 2022. The system aims to enable remote inspection of turbines that are shut down after lightning strikes or other events.

- CONTEXT: Traditional, ship-based maintenance of turbines is time-consuming, and often needs to be postponed due to rough conditions.

Tokyu pulls out of wind project citing poor profitability

(New Energy Business News, Oct. 23)

- The Miyagi Prefectural government says a project to build a wind farm along the Yamamoto coast has been cancelled and will not be renewed.

- Tokyu Land Corporation, who had been selected to construct the wind farm, withdrew from the project citing poor profitability.

- The project would have involved 12 turbines being erected along the coast in very shallow water, with a maximum output of 52 MW.

ANALYSIS

MAYUMI WATANABE,

RESEARCHER, JAPAN,

YURI INVEST RESEARCH

Tokyo Gas Unleashes Global Strategy as Its Long-Time

Ambitions in LNG and Beyond Finally Move Forward

It has taken a decade longer than first planned, but Tokyo Gas, Japan’s biggest natural gas utility, is finally transforming into a global player. The company’s slow burner international expansion has accelerated in the last 12 months, with major acquisitions and investments both in gas and renewables. More are expected to follow.

Despite the pandemic, the gas utility, which is Japan’s second-largest LNG importer, has had a breakout year. In addition to emerging as the biggest domestic seller of electricity outside of the power utilities, Tokyo Gas struck deals to bolster its U.S. gas output by over 240%, doubled its global renewables portfolio, and won approval together with a local partner to build the first LNG import facility in the Philippines.

Last month, Tokyo Gas also set up its first global LNG trading unit in Singapore, which is charged with building almost from scratch a 5 million tons per annum (mtpa) physical trading business by 2030. It will add to the 17 mtpa of LNG that the company already purchases – a number that’s equivalent to the entire import volume of France or Spain.

The sudden burst of activity is almost 10 years behind schedule. Back in 2011, Tokyo Gas declared that in fiscal 2020, which ends in March 2021, it will earn a quarter of its profits from overseas projects. At the time, the non-Japanese earnings made up a 10% share. The rationale was simple: the domestic market is due to shrink, in line with Japan’s population decline.

Despite the overseas growth goal, Tokyo Gas ended up scaling back its global ambitions. In 2017, the non-Japanese profit share for FY 2020 was cut to 20%. Management decided that achieving the 25% ratio would need to wait until 2030.

As we enter the second half of FY 2020, even the scaled back target is likely to be missed – and not by a little. Tokyo Gas earlier forecasted a multi-year low operating profit from the overseas business of ¥2.4 billion. The company-wide business operating profit is forecast at ¥73 billion.

Still, there is reason to be optimistic about Tokyo Gas turning the results around. Despite a flurry of recent deals, the company is relatively disciplined in its investment decisions. It has consistently kept its sites on markets in South and Southeast Asia, as well as in North America, and avoided getting drawn into a broader global spree.

What’s more, Tokyo Gas has made smart decisions on structuring its investments in the upstream gas business overseas. Unlike most Japanese gas companies, Tokyo Gas asked for offtake contracts from upstream LNG facilities either on an FOB or ex-ship basis. This means, the buyer assumes responsibility for the fuel at the port, which allows Tokyo Gas to ship the gas to other Asian markets when needed, rather than being forced to deliver only to its own domestic facilities.

Flexibility became a key issue for LNG buyers this year as the pandemic-induced economic slowdown strongly affected demand. Some Japanese buyers were left paying million-dollar bills for LNG contracts they could not accept due to the drop in demand.

UPSTREAM

The LNG value chain is the core of Tokyo Gas’ overseas business portfolio. It starts with upstream gas field developments, and continues through to LNG facilities, transportation and import terminals, all the way to gas-fired power plants.

In the upstream, Tokyo Gas has invested in five LNG projects in Australia. Each is limited to a minority stake of less than 5%.

| Project name | Tokyo Gas % share | Offtake volume | Expiry date for offtake contracts |

| Darwin LNG | 3.36% | 1 million mt/year | 2023 |

| Pluto LNG | 5% | 1.5-1.75 million mt/year | 2024 |

| Gorgon LNG | 1% | 1.1 million mt/year | 2041 |

| Queensland LNG | 1.25% of gas production and 2.5% of the second LNG train | 1.2 million mt/year | 2035 |

| Ichthys | 1.575% | 1.05 million mt/year | 2032 |

To strengthen LNG sales, in July 2016 Tokyo Gas established a joint venture with LNG Vietnam for procurement and local sales of the fuel. Tokyo Gas owns 10% of the JV, with the rest held by two local energy firms.

MID-STREAM

In this sector, Tokyo Gas’ assets are comprised mainly of LNG terminals in South and Southeast Asia. In 2012, Tokyo Gas designed an LNG terminal for Petro Vietnam Gas, a project that led to the creation of LNG Vietnam.

In 2018, Tokyo Gas was awarded an LNG terminal management contract by Thailand’s PTT LNG Company, which spans until December 2021. The contract is for managing the Nong Fab LNG terminal.

The most recent of the LNG terminal deals is Tokyo Gas’ agreement to work with First Gen of the Philippines to build a floating offshore terminal, which is slated for completion in 2022. Tokyo Gas has a 20% stake in the project.

Future projects may be in Vietnam and Bangladesh. In 2019, supported by Japan’s Ministry of Economy, Trade and Industry (METI), Tokyo Gas completed a feasibility study for the building of an LNG terminal in the Cai Mep-Thi Vai port area in Vietnam. The company also conducted a feasibility study for an onshore LNG terminal planned by the Bangladesh Oil, Gas and Mineral Corporation.

DOWN STREAM

Tokyo Gas has engaged in gas retail and facility management projects in Vietnam, Thailand, Malaysia and Indonesia. It has generally taken ownership ranging from a quarter to a third in downstream projects.

In July 2017, Tokyo Gas acquired 24.9% of PetroVietnam Low Pressure Gas Distribution Joint Stock Company, which supplies gas to manufacturers.

In January 2018, the Japanese firm took a 30% stake in Gulf WHAMT, a privately-owned gas utility in Thailand. In January 2020, Tokyo Gas was awarded the One Bangkok project to supply air conditioning and energy to a business complex in the capital of Thailand, which is slated for completion in 2023. The contract is for 30 years.

In February 2018, Tokyo Gas set up JV Gas Malaysia Energy Advance, which provides gas cogeneration services in Malaysia. Tokyo Gas has a 34% share.

NORTH AMERICA

In North America, Tokyo Gas has so far preferred to focus on shale and renewables, investing in three gas projects, which are targeting the domestic market.

| Project Name | Ownership | Volume |

| Quicksilver | 25% | 275 million cubic feet/day, shale |

| Eagle Ford | 25% | 200,000 mt of LNG |

| Castleton Resources | 70% | 7 million cubic meter/day, shale |

Not a notable player in the Japanese renewable scene, in Dec. 2019, Tokyo Gas took on a 50% share in five solar and wind projects in Mexico that have a total capacity of 721MW. The Japanese company’s partner in the deal is ENGIE.

This year, Tokyo Gas went one step further to take on the full 631MW solar project in Texas and committed for the first time to develop the station from construction stage to commercial operations. The plant is the biggest renewable facility in the U.S.

With the Aktina solar farm in Texas, Tokyo Gas will see its renewable capacity jump to 1.2GW. It was 490MW last year.

By 2030, the company expects to be in charge of 5GW of renewable capacity, half of which should be overseas.

That leaves plenty of room for more deal-making.

ANALYSIS

DANIEL SCHULMAN,

PRINCIPLE,

SCHULMAN ADVISORY

Japan Launches the Electricity Capacity Market Auctions;

First Round Results: Generators Win, Retailers Lose

This summer Japan launched a Power Capacity Market, a new mechanism aimed at supporting future investment in new generation facilities. The results of the first capacity auction, however, have created a mini-scandal since announced last month. The auction’s high bids indicate that the average electricity bill in Japan will have to rise to compensate for new construction; otherwise, the alternative is that some power retailers will face massive losses.

Environment Minister Koizumi Shinjiro has vowed to investigate the incident, which is quickly turning into a battle between large generation companies that rely on thermal and nuclear assets, and smaller retail firms, many of which support renewables. How the standoff is resolved could determine not only the size of Japanese consumers’ future electricity bills, but also the balance of power across the entire industry.

THE PURPOSE AND STRUCTURE OF THE NEW MARKET

The capacity market initiative is part of a broader set of government measures in the last five years to liberalize the electricity industry, and in the process try to lower the average power bill.

Several new market structures have been put in place since 2016. These include a balancing market, a baseload market, interconnection usage auctions, and a non-fossil value market.

The capacity market is the latest mechanism to help the industry transition to open competition.

The market trades generation capacity (MW) rather than volume (MWh). Through annual auctions, power generation companies are able to bid on contracts for supplying capacity four years ahead, (e.g. the first auction held in FY2020 was for capacity to be provided in FY2024). That gives power companies baseline revenue they can rely on in the future rather than having to depend on short-term gains from the day-ahead wholesale market.

The rationale is that with a more secure revenue stream, utilities are better able to justify long-term investments in large-capacity plants that are necessary for the stable supply of power.

The auctions are organized by the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) and are held in the single-price auction format. In other words, all selected bidders are paid the price offered by the highest selected bidder. Power generators that work under feed-in-tariff contracts (which are mostly used for renewable energy projects) are not eligible for the auction.

Though the auction covers the entire country, areas with insufficient supply reliability are treated as separate markets, allowing generators to place higher bids in those zones. For each auction, OCCTO sets a target capacity to procure and a target price per kilowatt that is equal to the net cost of new entry. This means the cost of building a new power plant after accounting for wholesale and ancillary market revenues.

The maximum bid price at the auction is set at 1.5 times the target price.

When putting forward their bids, power generators are limited to submitting a price level that only covers their asset’s “operating costs.” However, in the first auction, generators were able to include corporate, business, and property taxes; labor costs; maintenance and repair costs; and power producer-side base charges as operating expenses. At the same time, generators were required to subtract revenues generated from these power plants through other markets (day-ahead, etc.) from their submitted bids.

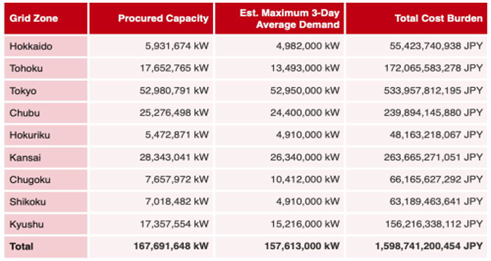

Results of the first capacity auction by grid zone

Source: Ministry of Economy, Trade and Industry

WHO PAYS FOR THE NEW CAPACITY?

While a small portion of the capacity “operating costs” will be borne by companies that transmit the electricity, the majority of the burden falls on power retailers, who are expected to pass the charges on to consumers through increased prices.

To ease the burden on retailers and, to some extent, transmission and distribution companies, the government has implemented “transitional measures.” These include asking generators with power plants built in FY2010 or earlier to receive the money they are owed for capacity over a period of several years. At the same time, the government has allowed generators affected by this charge to inflate their “operating costs,” the basis of their bid price, to compensate for this delay.

FIRST RESULTS

In the first capacity market auction held earlier this year, there was 177,470 MW of capacity on offer for FY2024. The target price was set at ¥9,425 /kW and the maximum price at ¥14,138 /kW. Based on lower supply reliability, the Kyushu area was separated from the rest of the market into a separate auction.

The government managed to secure 167,691 MW of capacity, or 94.4% of the target, through the auction at a procurement price of 14,137 yen/kW. In the national auction (excl. Kyushu), 97% of bids were accepted. In Kyushu, all bids were accepted.

Stable power sources including thermal, nuclear, geothermal, and biomass power plants accounted for 94.8% of the procured capacity. About 95% of the bids above ¥14,000 came from oil- and LPG-fired thermal power plants.

While the procurement price ended up being only one yen lower than the maximum allowed bid, accounting for the transitional measures “discount,” which applies to about 78% of the selected bidders, the average effective procurement price of the first auction added up to ¥9,534 /kW. Compare that to the average bid prices of ¥6,694 /kW in the Kyushu area auction.

The total cost of the capacity “sold” at the auction comes to ¥1.6 trillion. Power retail firms are expected to cover ¥1.47 trillion of that; transmission companies the rest. It is not surprising, that generators were pleased – retailers protested.

Retail firms are appealing to the Agency for Natural Resources and Energy (ANRE) to find a way to correct what they call deficiencies in the market design. One of the heaviest arguments is that the auction gave plant operators far too much scope to calculate their “operating costs.” In some cases, generators even included corporate taxes as part of those.

The Electricity and Gas Market Surveillance Commission, part of the Ministry of Economy, Trade and Industry, pointed out that in their bids, power generators included maintenance costs covering multiple years. This inflated their bids, as did the compensation for getting the capacity payments drawn out over time.

Considering that this was the first auction in an entirely new market structure, imperfections were to be expected.

The question, however, is to what extent these imperfections were the result of the need to learn through trial and error, and to what extent they were the result of the large utilities that enjoyed monopoly power prior to deregulation still wielding too much power.

For now, the ministry has committed to reexamining the auction process. It is likely that plant operators will need to be more cautious about what is included in their operating costs in future auctions.

Part of the resolution, however, will reflect how the government is willing to balance the interests of the larger thermal and nuclear generation utilities with those of new industry players, many of which are supporting and investing in renewable energy sources.

GLOBAL VIEW

Below are some of last week’s most important international energy developments that are being monitored by Japan NRG because of their potential to impact energy supply and demand, as well as energy prices, and for possible relevance for Japanese and international energy investors.

China/Hong Kong/Taiwan:

1). Cathay Pacific, Hong Kong’s flagship airline, announced 8,500 layoffs last week, as well as the closure of Dragon Air, further worsening the outlook for regional airlines and jet fuel consumption. Separately, Japan is discussing with China a phased reopening of a travel corridor between the two countries. Almost 10 million Chinese nationals visited Japan in 2019.

2). The recent U.S. decision to sell $1.8 billion of defense equipment to Taiwan could provoke Chinese retaliation and worsen tensions in sea routes around Taiwan that are used for shipping oil, LNG, and coal to Japan and South Korea. Separately, Taiwan’s ruling DPP Party may consider adopting a carbon neutrality commitment by 2050 and has pledged to phase out nuclear power by 2025.

3). Xi Jinping’s recent U.N. announcement about achieving carbon neutrality by 2060 is has been criticized as unattainable and unrealistic by some energy analysts in recent weeks. This is something Japan NRG Weekly will be focusing on in future editions.

Indonesia:

The Japanese prime minister offered a loan of $500 million to the Indonesian government last week following his first overseas trip as PM. Japan is a major investor in Indonesian energy and infrastructure.

Malaysia:

Goldman Sachs, the U.S. investment bank, announced a settlement of almost $5 billion last week in connection with the 1MDB Malaysian scandal surrounding former Prime Minister Najib Razak, one of the largest ever settlements by a private corporation. Almost $1 billion was found to have been remitted by the UAE, a major supplier of oil to Japan and Asia, to 1MDB bank accounts.

Thailand:

On Friday, the Thai prime minister ended the country’s state of emergency that had been announced on Oct. 15 in the wake of widespread civilian protests. Thailand is a major regional producer and importer of oil and natural gas, with Chevron and Japan’s Mitsui Oil being major energy investors in Thailand.

Middle East:

Following normalization of relations between the UAE and Israel, the prominent Arab energy producer has committed to ship oil via a pipeline that goes through Israel to the Mediterranean, thus bypassing the Suez Canal.

Africa:

Civil unrest in Nigeria could disrupt oil and natural gas exports from Africa’s largest oil producer. Nigeria produces 2 mbpd and is OPEC’s 7th largest producer. Japanese imports from Nigeria were $500 million in 2019.

Spain:

Iberdrola, Spain’s second largest company by market capitalization, and one of Europe’s largest utilities, agreed to buy PNM Resources in New Mexico, U.S. for $10 billion. PNM sells electricity in New Mexico and Texas.

Americas:

There were two large mergers announced in the shale oil and gas sector last week: Conoco’s acquisition of Concho for $10 billion and Pioneer’s acquisition of Parsley Energy for $5 billion, underlining the recent consolidation trend caused by lower oil prices.

STOCK MARKET PERFORMANCE

| As of close on October 23, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| INPEX CORP | 1605 JP | 790.24 | 0.20 | -51.59 | -5.18 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 105.56 | 8.01 | -35.68 | 13.19 | |

| ENEOS HOLDINGS INC | 5020 JP | 1186.81 | -1.37 | -21.83 | -4.33 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 649.05 | -1.04 | -23.82 | -4.93 | |

| COSMO ENERGY HOLD. | 5021 JP | 134.45 | 0.70 | -33.59 | 2.85 | |

| Industrials | ||||||

| JGC HOLDINGS CORP | 1963 JP | 247.29 | 0.63 | -44.89 | -12.56 | |

| CHIYODA CORP | 6366 JP | 63.52 | -0.81 | -13.78 | -5.06 | |

| MITSUBISHI CORP | 8058 JP | 3651.17 | -1.03 | -10.58 | -3.94 | |

| MITSUI & CO LTD | 8031 JP | 3098.53 | -0.08 | -2.88 | -2.64 | |

| Utilities | ||||||

| TOKYO ELECTRIC POWER | 9501 JP | 462.82 | -4.32 | -38.33 | -1.37 | |

| CHUBU ELECTRIC POWER | 9502 JP | 924.76 | -2.98 | -18.05 | -6.31 | |

| KANSAI ELECTRIC POWER | 9503 JP | 940.61 | -1.38 | -17.19 | -1.94 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 426.29 | -4.97 | -1.51 | -5.93 | |

| J-POWER | 9513 JP | 278.05 | -1.49 | -40.39 | -5.69 | |

| TOKYO GAS CO | 9531 JP | 1021.36 | -3.13 | -10.87 | -4.27 | |

| OSAKA GAS CO | 9532 JP | 815.03 | -2.93 | -4.20 | -5.51 | |

| TOHO GAS CO | 9533 JP | 548.10 | -2.81 | 17.58 | -0.07 | |

| SAIBU GAS CO | 9536 JP | 94.05 | -3.66 | 2.04 | -7.30 | |

| SHIZUOKA GAS CO | 9543 JP | 69.11 | -3.10 | -3.79 | -2.47 | |

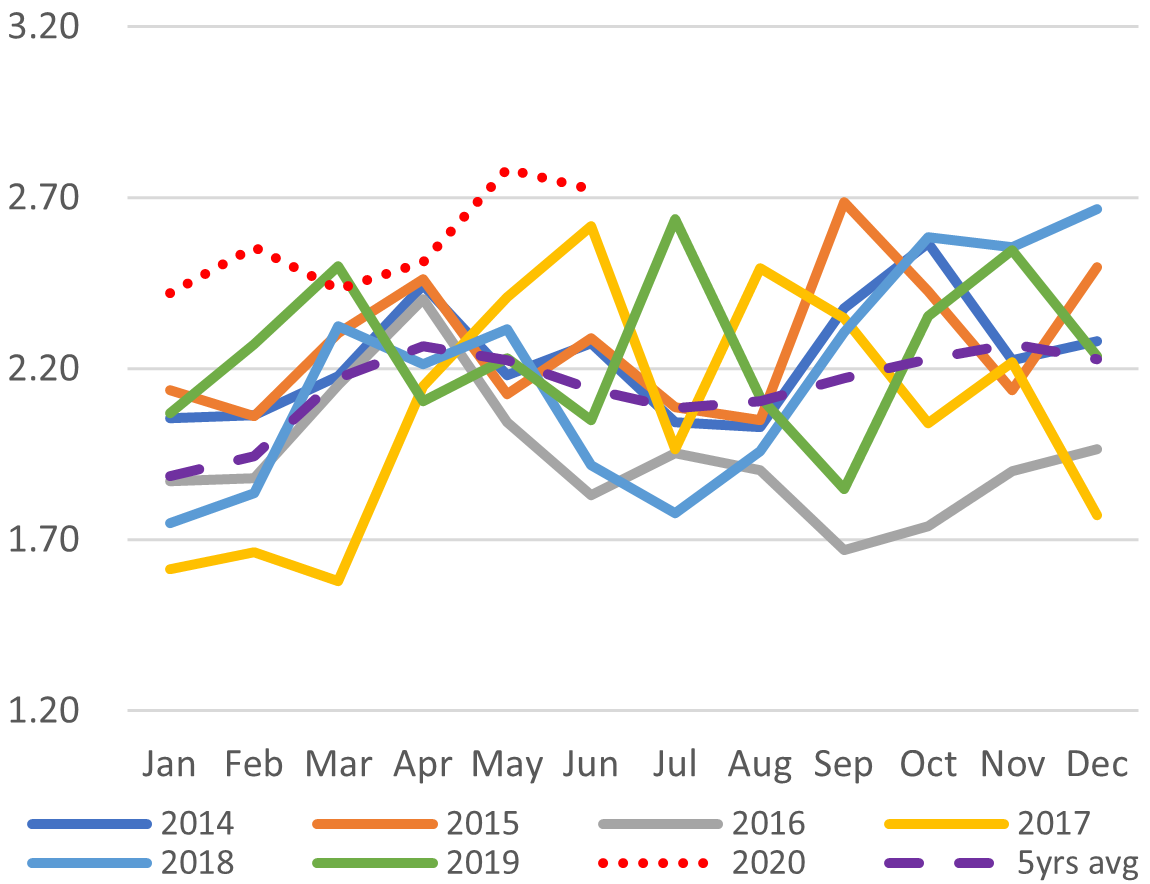

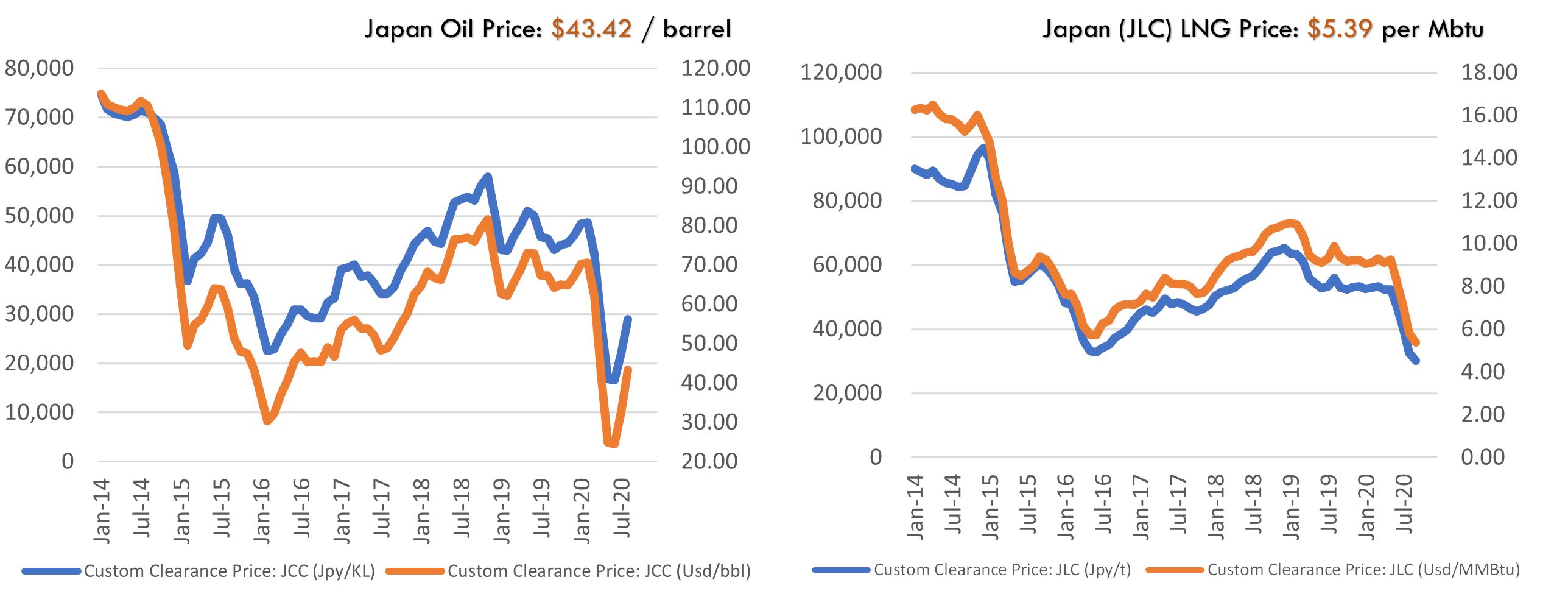

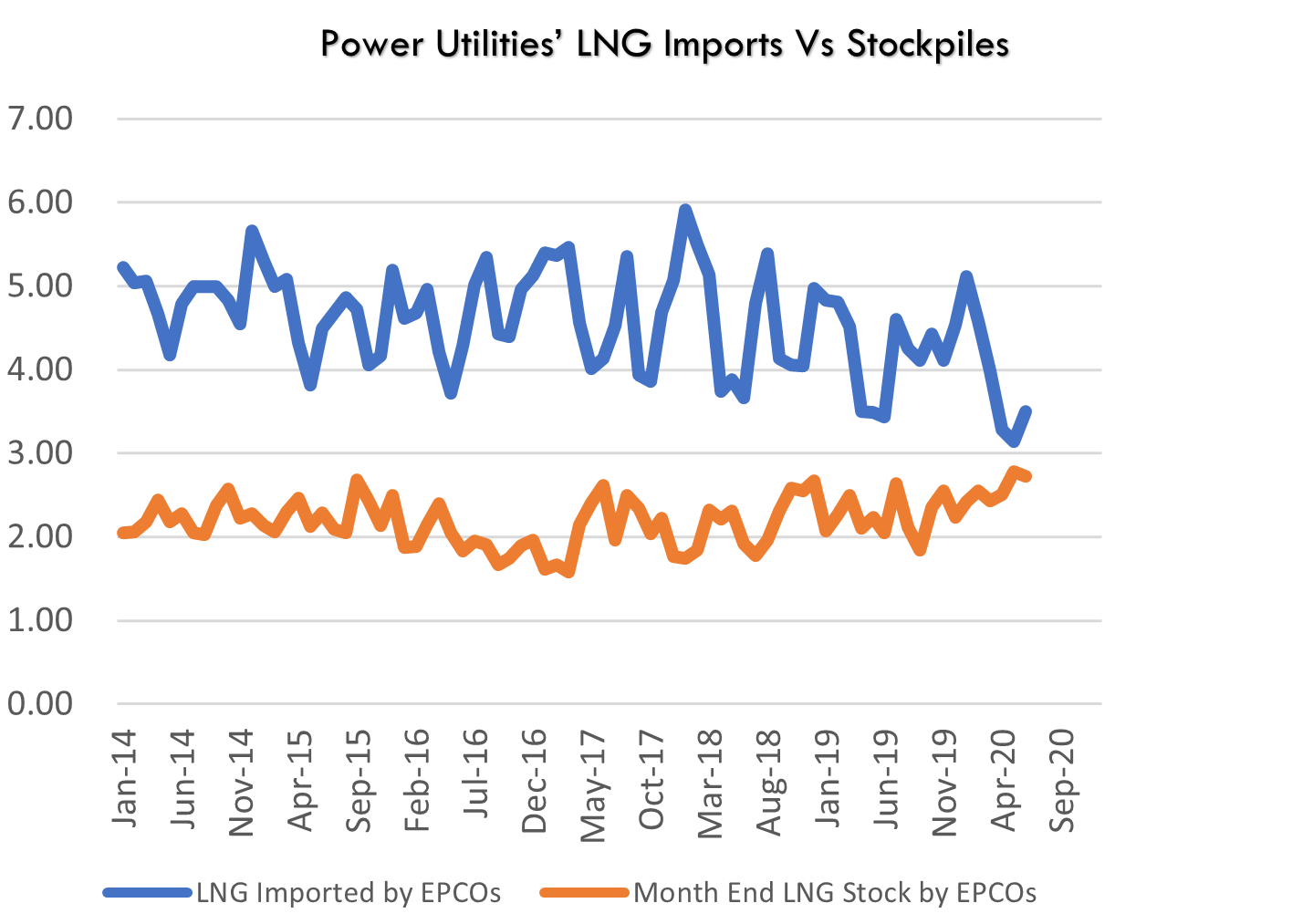

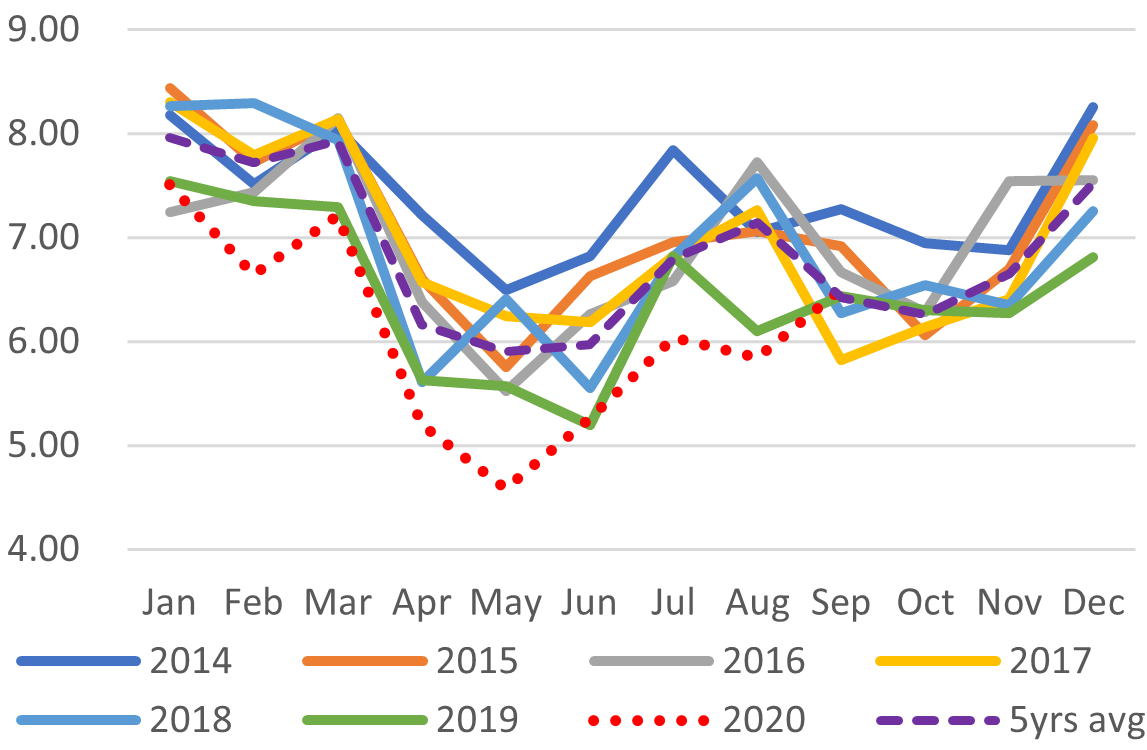

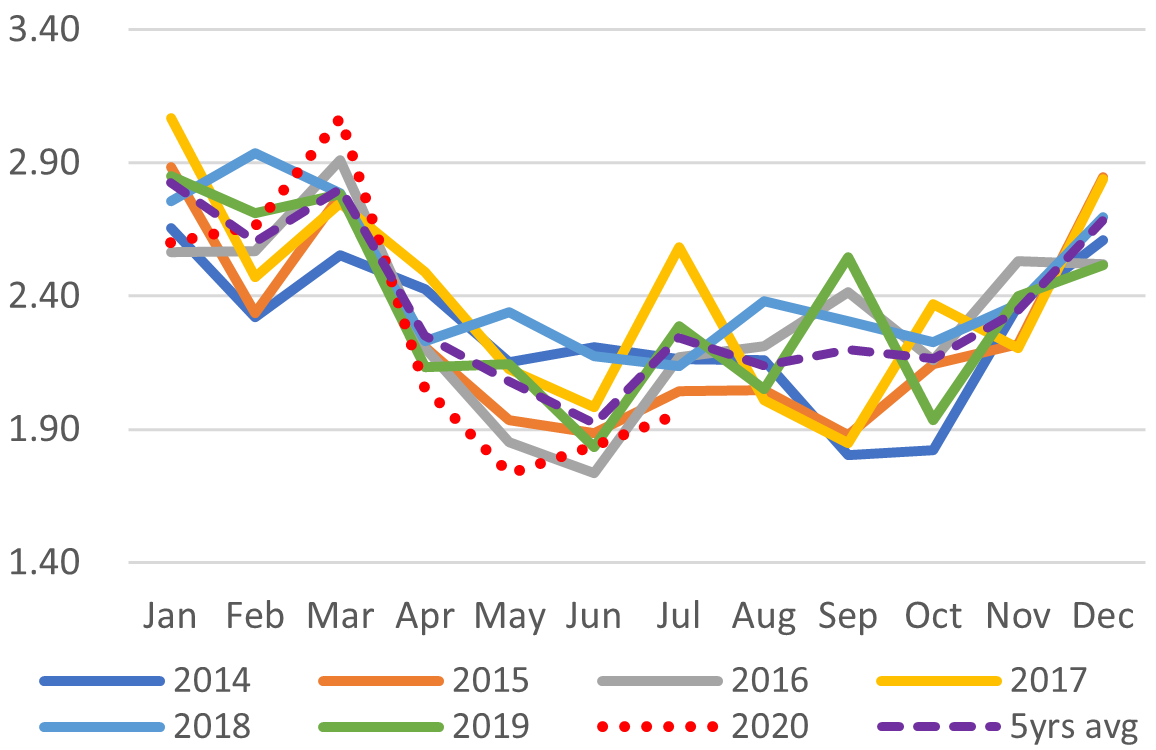

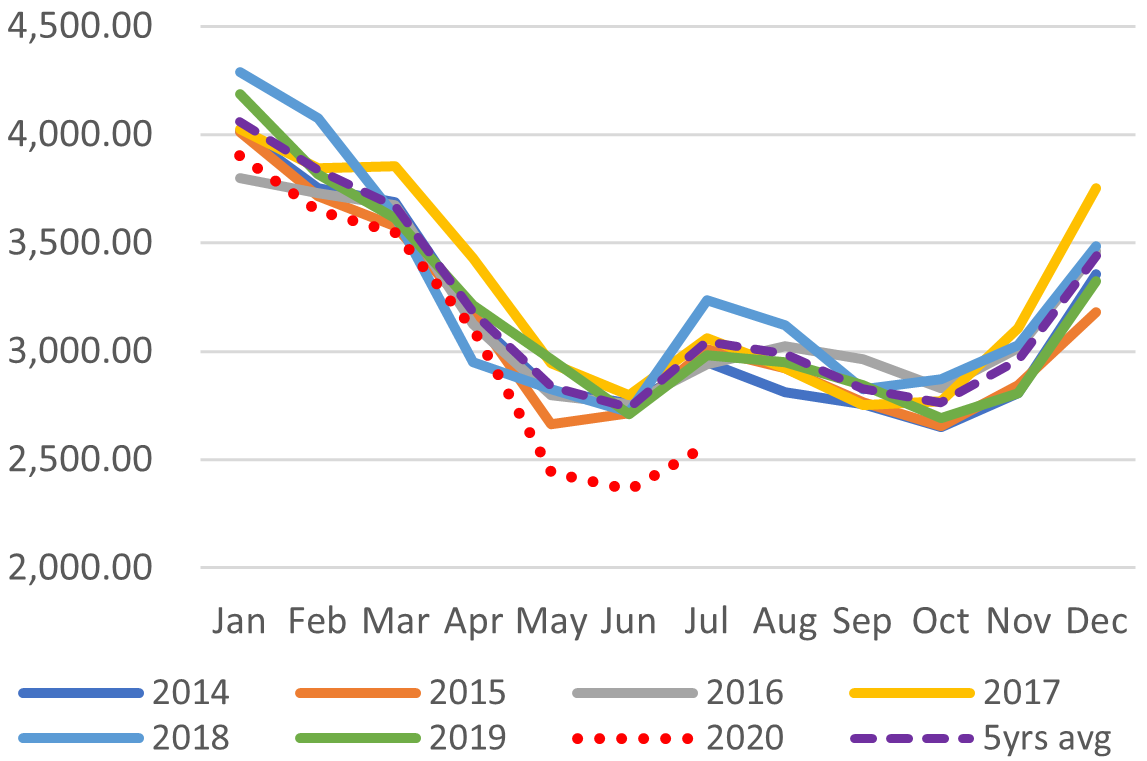

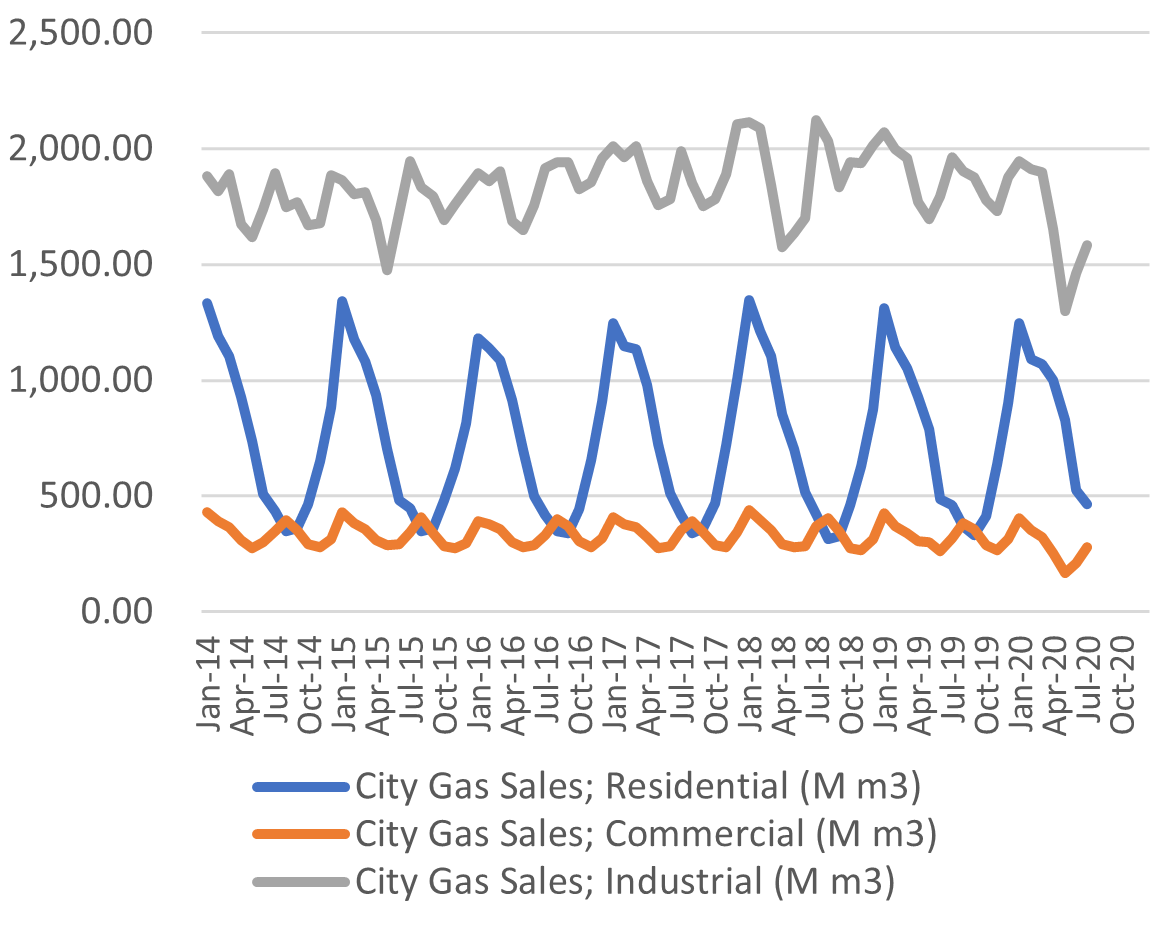

DATA

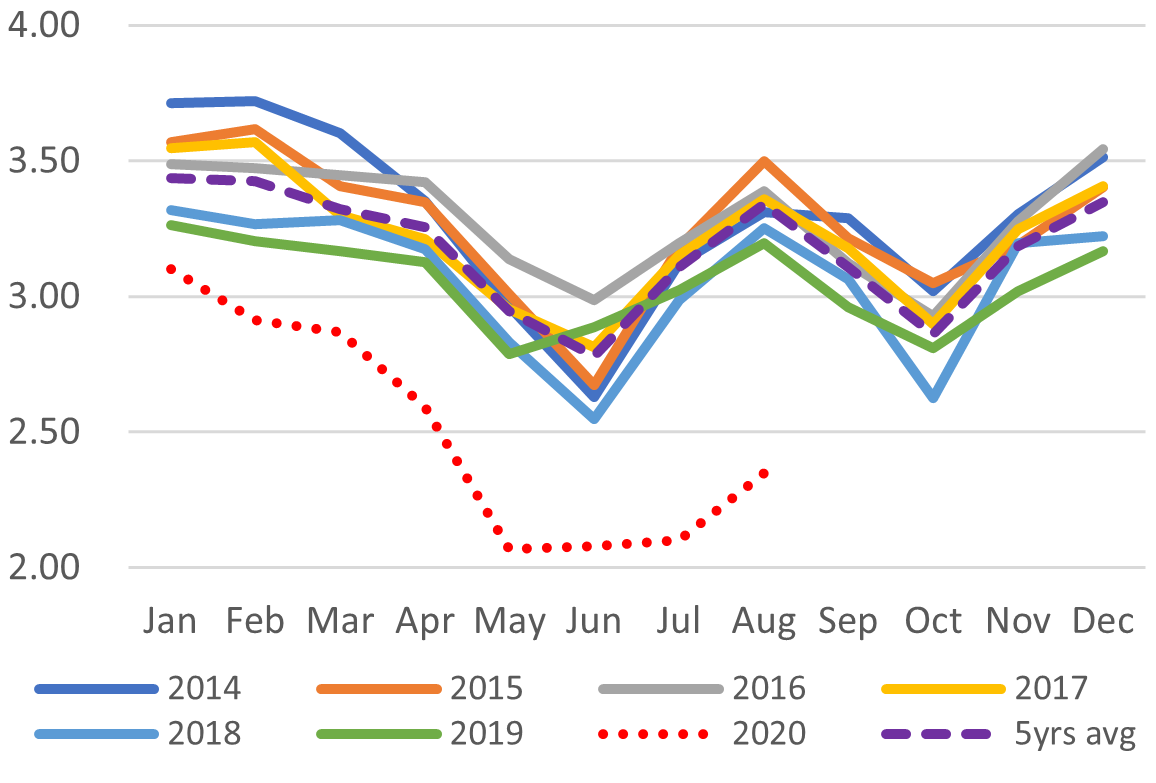

Japan Oil Price

Crude Imports Vs Processed Crude

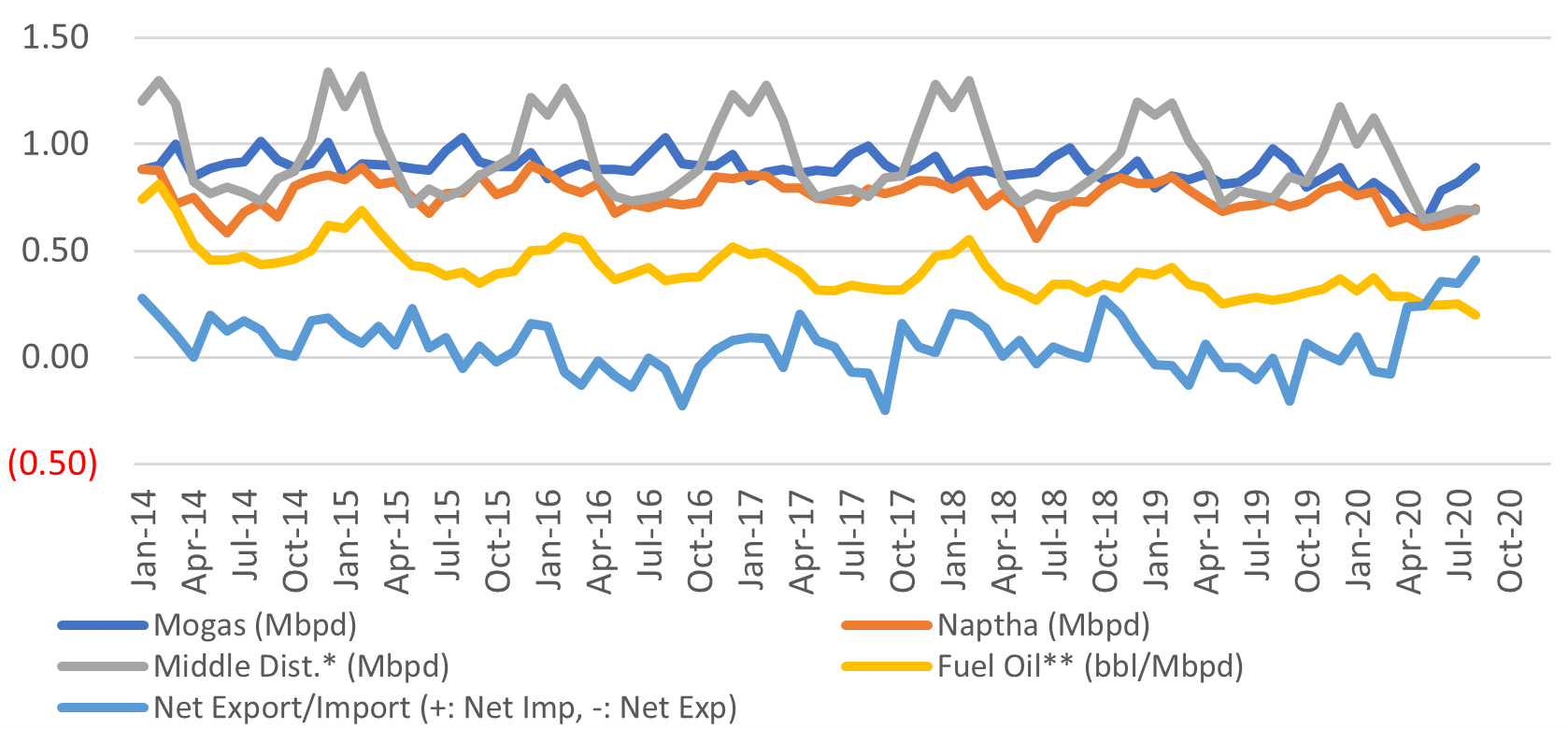

Monthry Oil Import Volume (Mbpd)

Monthry Crude Processed (Mbpd)

Domestic Fuel Sales

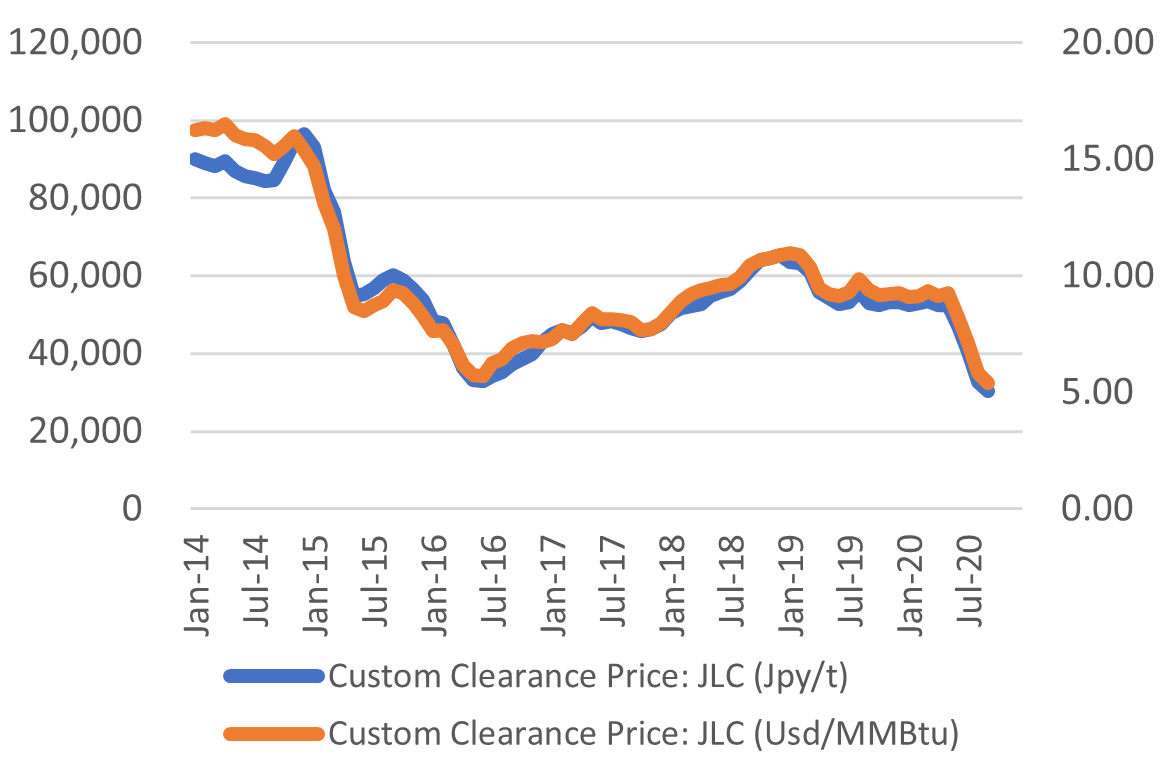

Japan LNG Price

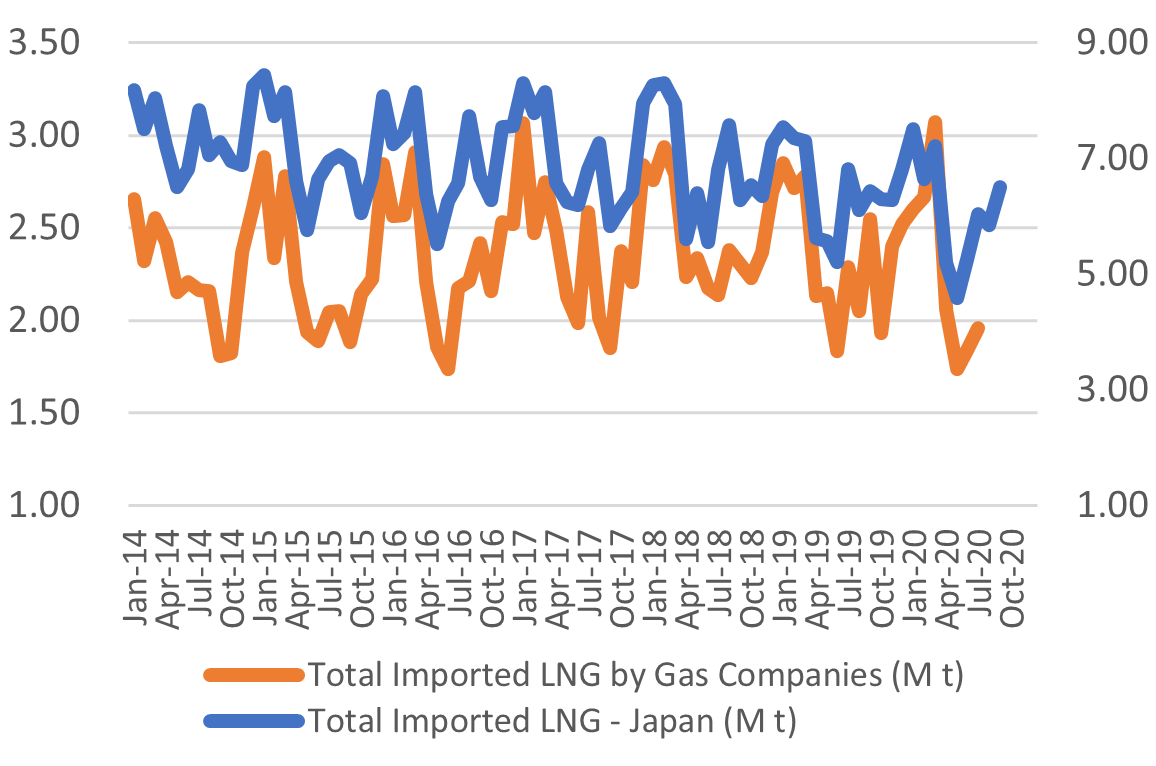

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

City Gas Sales – Total (M m3)

City Gas Sales by Sector (M m3)

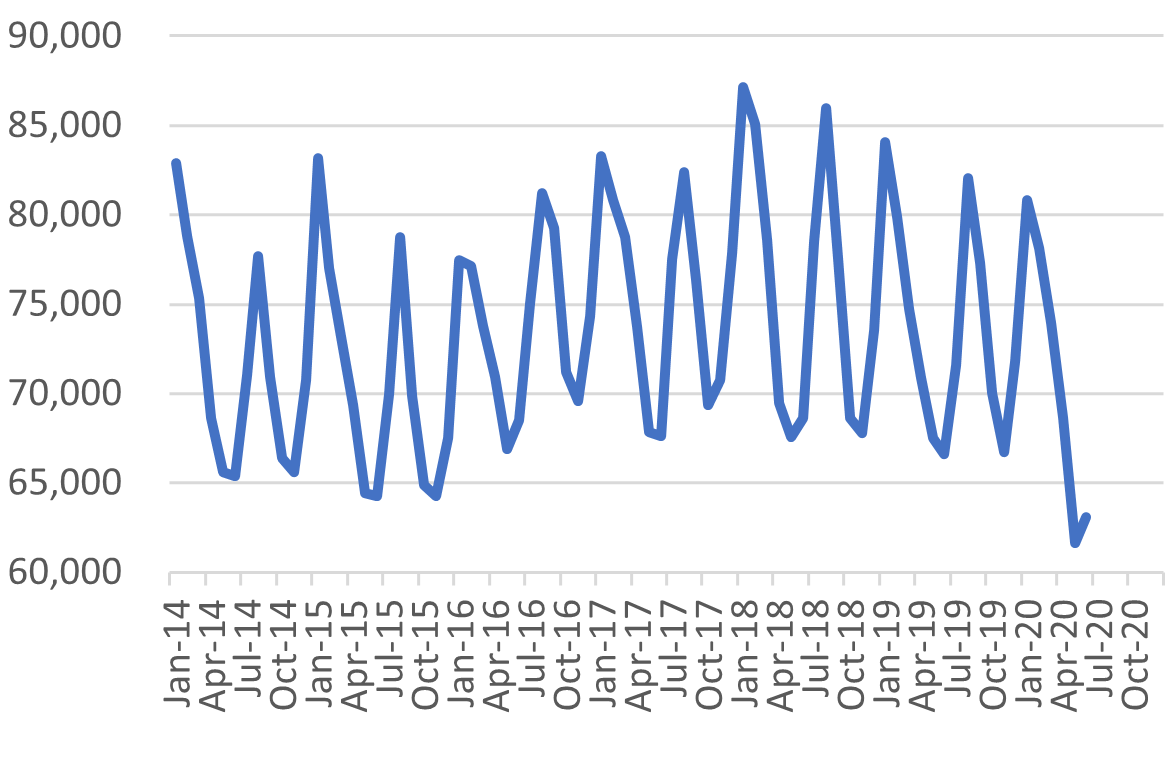

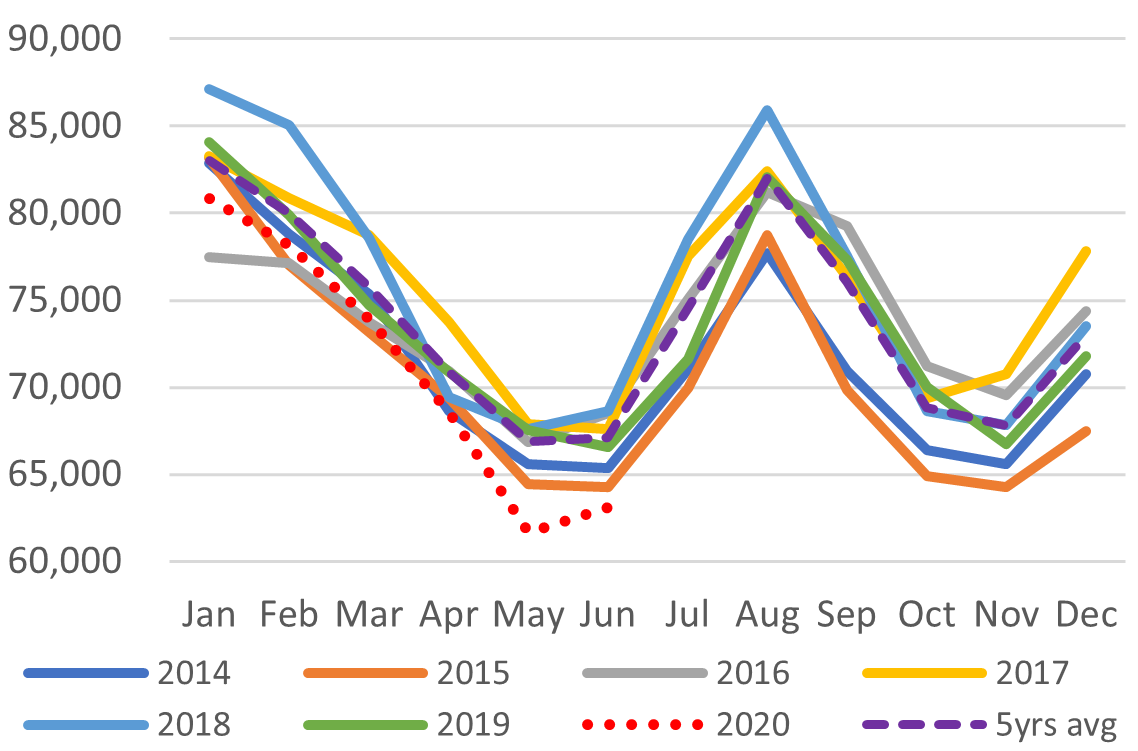

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

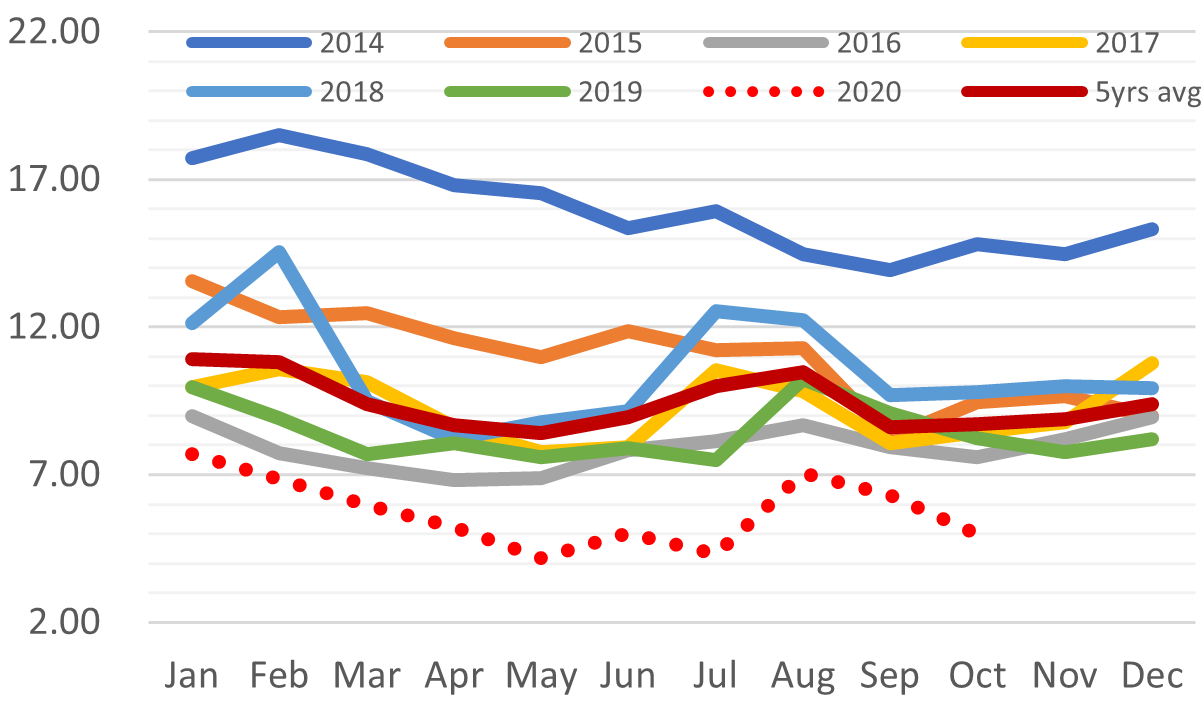

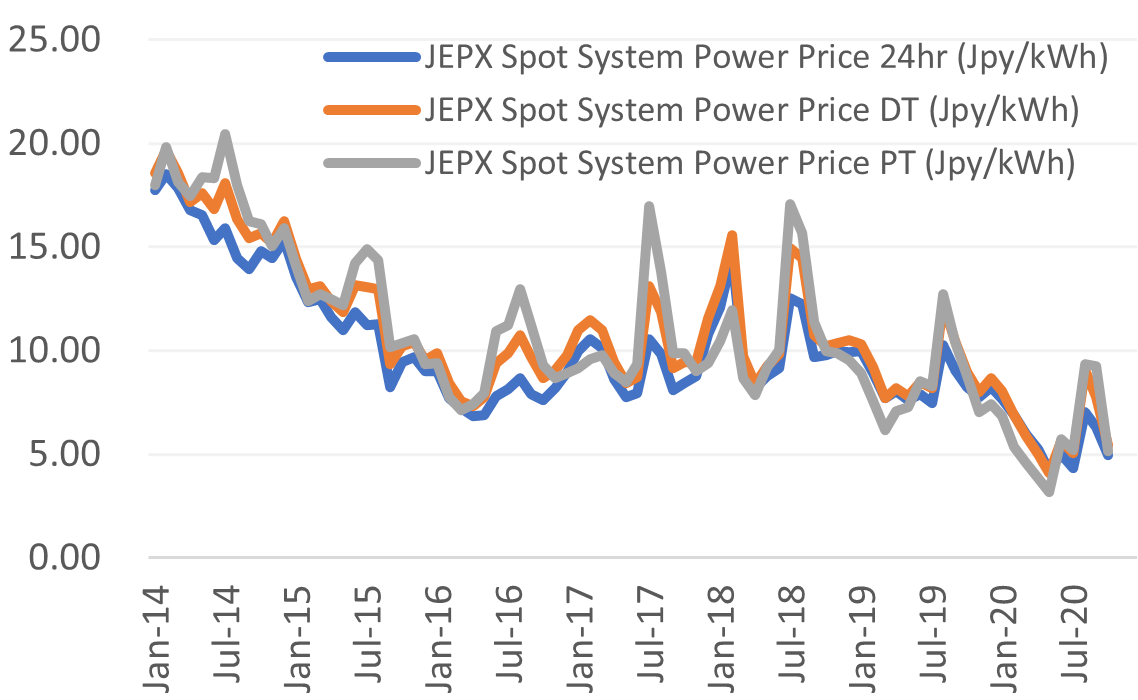

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities