JAPAN NRG WEEKLY

NOVEMBER 24, 2020

JAPAN NRG WEEKLY

November 24, 2020

TOP

- Japan releases FY2019 energy consumption numbers (prelim.); CO2 from the energy sector is down, so is total energy usage

- Environment Ministry to ask companies to disclose emissions on a per business unit basis, helping investors reward eco-friendly firms

- Telecom giant NTT downplays concern it will come to dominate Japan’s electricity industry, though admits plans to encroach

- Tokyo Gas, Marubeni to build ¥200 billion LNG-to-power plant in Vietnam in project that spans full gas supply chain

- Japan researchers invent alloy that turns impacts into electricity

OIL & GAS

- LNG price reaches one-year high on China, S. Korea demand

- Tokyo Gas walks away from Mexico LNG supply deal

- INPEX to lay second natural gas pipeline in central Japan

- Tokyo Gas likely to restart share buybacks from spring 2021: Bank

POWER & NUCLEAR

- No. of nuclear units online rises to three; two more close to restart

- EDITORIAL: Not enough debate on future of nuclear in Japan

- Kashiwazaki community looks for alternatives to nuclear power

- COVID hurts electricity revenues despite increase in consumption

- October Switching Data: decrease across all 10 areas in Japan

- TEPCO hydropower dam blamed for dry river

RENEWABLES, OTHER

- Japan needs ¥10 trillion ($96 billion) green fund: Govt. advisor

- Toyota Tsusho signs exclusive distribution deal for SFC fuel cells

- Idemitsu invests in Swiss clean tech fund Emerald Technologies

- Ministry scraps hydrogen station subsidy on fake renewable claim

- Tohoku Electric to build geothermal power plant in Akita by 2029

- SPARX invests in woody biomass power plant in Gifu; Osaka Gas says liquid CO2 plant goes online

INPEX FACES MAJOR CHALLENGES TO BRING

ONLINE ITS GIANT INDONESIAN LNG PROJECT

As INPEX pushes forward with engineering work at its Abadi LNG project in Indonesia, aiming for a final investment decision (FID) in 2022, new issues have come to the fore. A recent cap on gas prices set by Indonesia, and the announcement by project partner Shell of its desire to exit, mean that INPEX needs to secure support elsewhere. In theory, the government’s wish to keep Japan at the top of global LNG trade to ward off a Chinese ascendancy should bring other Japanese firms to the project. Still, even geopolitics come at a price. The question is, who will pay for the $20 billion Abadi development?

INSIDE VIEW: VENA ENERGY JAPAN CHAIRMAN SPEAKS ON SOLAR AND WIND INDUSTRY IN JAPAN

Vena Energy was one of the first to enter Japan’s renewable energy market after the introduction of the Feed-In Tariffs. Since arriving in Japan in 2013, the Singapore-based company has quickly grown into one of the country’s Top 5 solar and wind players. We spoke with Vena Energy’s Japan Chairman, Kameoka Nobuyuki, on why Japan is such an attractive market for renewables, what other investments the company is looking at, and what the declining FIT prices / switch to FIP means for the industry.

GLOBAL VIEW

As Tesla heads into the S&P500, the EV makers’ gap with Toyota and other Japanese automakers is only growing. The World Bank has cut mid-term oil price forecasts. Saudi Aramco raises funds via a bond sale. The U.K. unveiled an ambitious green energy plan. See details on these and other political and business events in our regular Global View column.

EVENT REVIEW: Japan – Canada

A review of the 2020 Japan-Canada Energy Partnership Forum.

JAPAN NRG WEEKLY

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Regular Contributors

Mayumi Watanabe

Daniel Shulman

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Group, which retains all copyright to the content of this report. Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS: OIL & GAS

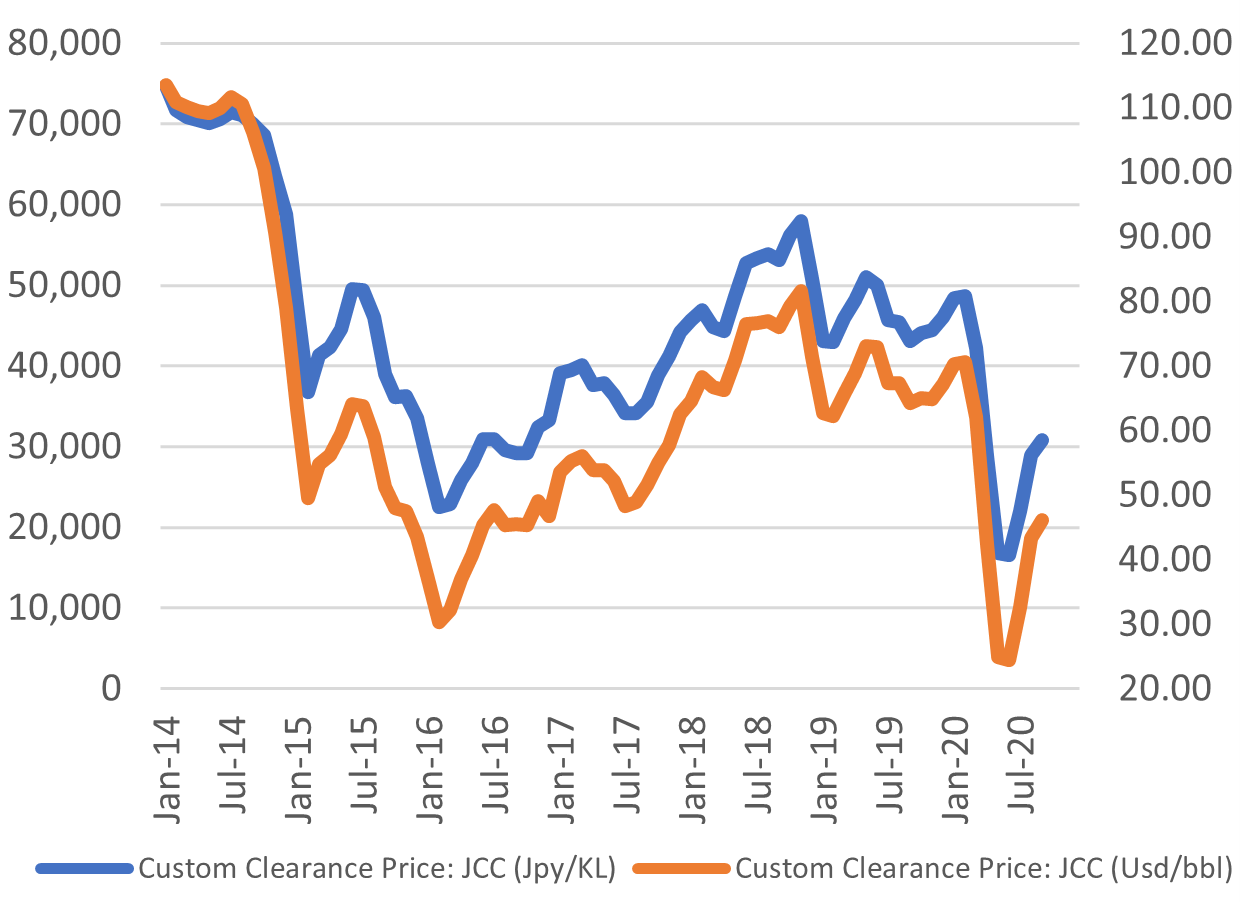

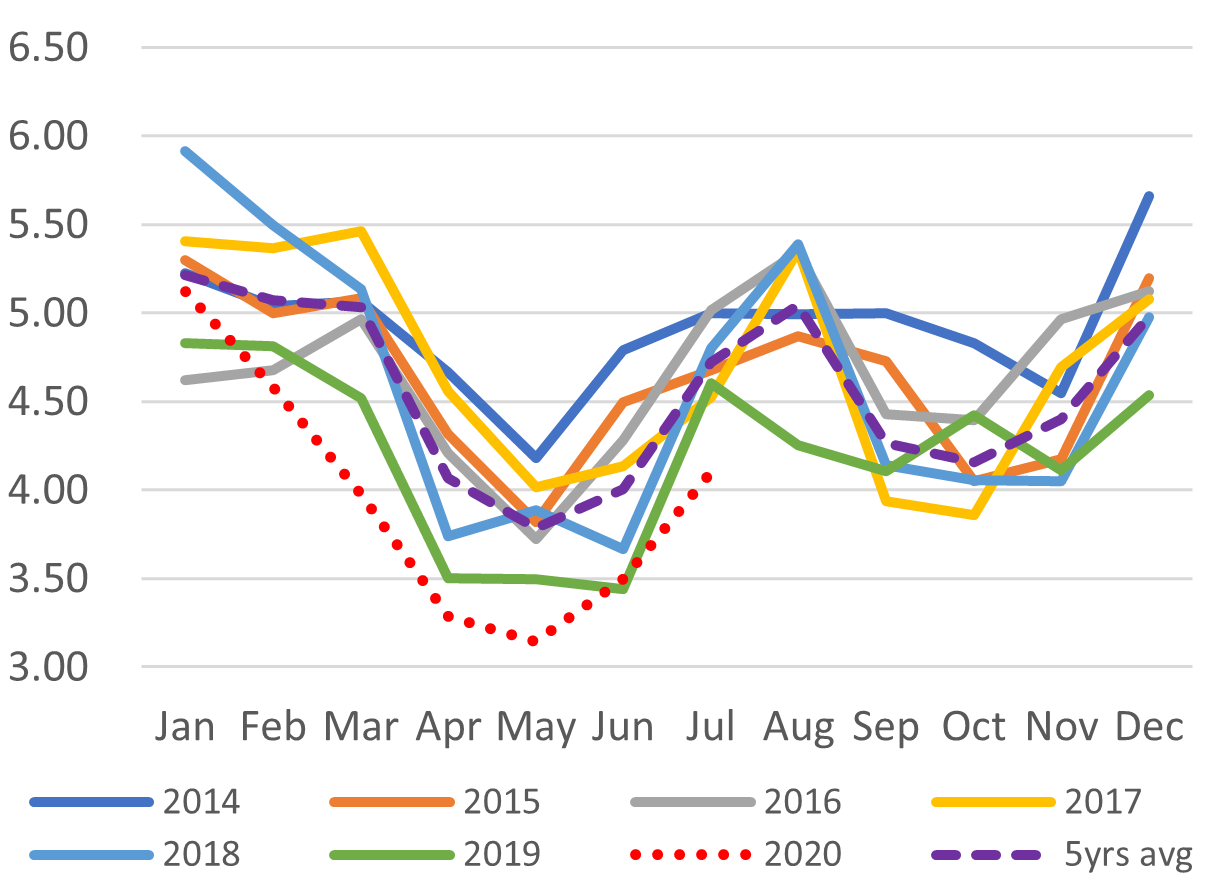

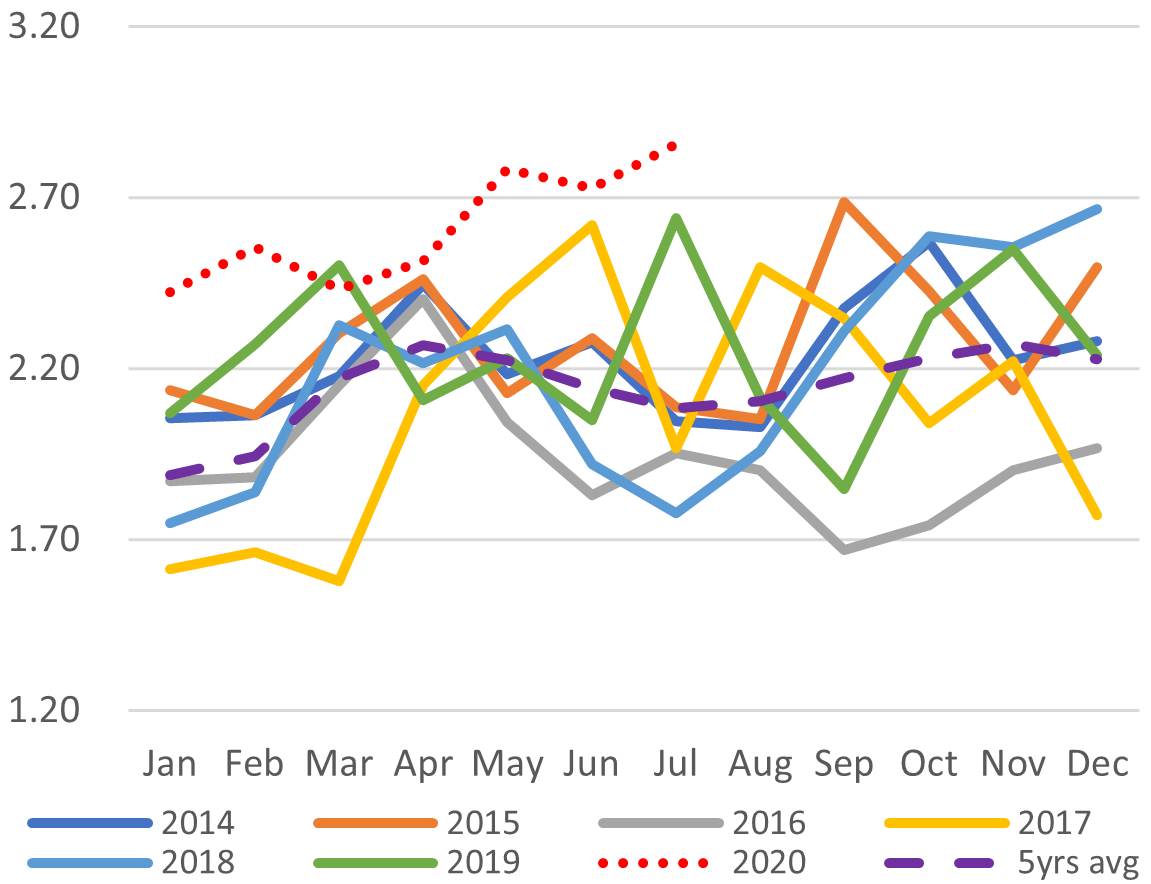

Japan Oil Price: $46.20 / barrel

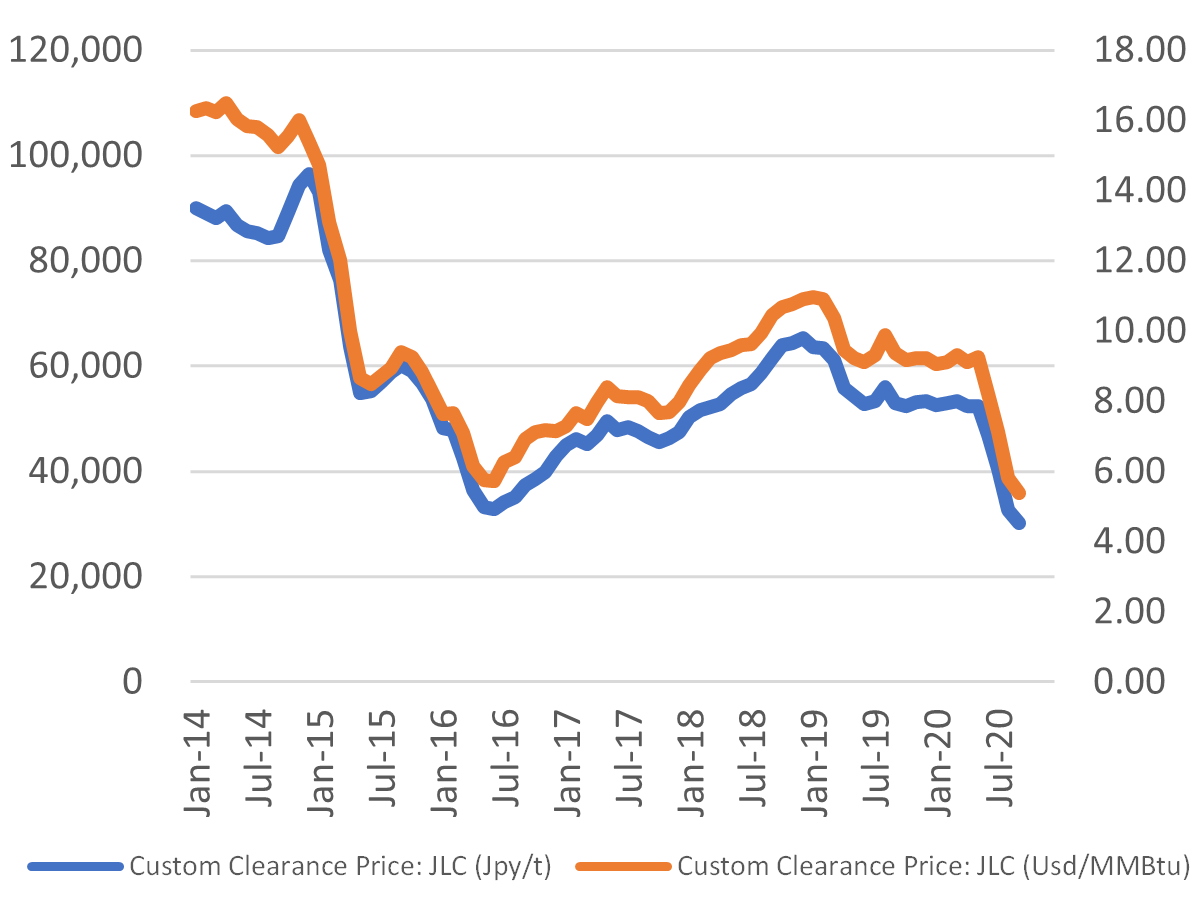

Japan (JLC) LNG Price: $5.39 per Mbtu

Tokyo Gas, Marubeni to build a ¥200 billion LNG-fired power plant in Vietnam

(Asia Nikkei, Nov. 19)

- Tokyo Gas and Marubeni signed a memorandum of understanding with Petrovietnam Power, a part of state-owned Vietnam Oil and Gas Group, and a local construction company. Total investment is expected to be around ¥200 billion ($1.93 billion).

- Feasibility study on the project in the coastal province of Quant Ninh is now due to begin, as well as power price talks. The partners aim to bring the 1,500 MW plant online in 2026.

- The project includes the building of an LNG receiving terminal and regasification facilities, as well as a pipeline to the power station.

- CONTEXT: This will be the first full-cycle LNG project for Tokyo Gas overseas. Several Japanese companies are trying to break into the energy markets in Vietnam, with the oil refiners the most advanced so far. Marubeni is working on similar LNG-to-power deals in Indonesia and Myanmar.

LNG price reaches one year high on Chinese/South Korean demand

(Nikkei Shimbun, Nov. 17)

- LNG spot markets in Asia hit their highest price in nearly a year amid increasing Chinese demand for LNG as a replacement for coal.

- South Korea also moved to procure additional LNG in preparation for a harsh winter.

- This comes as production issues in the supplier nations restrict throughput.

- The price paid in Japan for imported natural gas is also likely to rise.

TAKEAWAY: LNG prices in Asia have been on a tear since August, quickly rising on expectations of colder weather from some of the lowest levels ever seen. LNG cargoes on a DES-basis traded around $6.50 to $7 / mmbtu level last week, three times the level of spring when the global pandemic caused widespread lockdowns. However, since most of Japan’s LNG imports come via long-term contracts, most of which are still tied to oil prices, the change in LNG spot prices will only have a mild impact on the domestic import price.

Tokyo Gas walks away from Mexico LNG supply deal

(Bloomberg, Nov. 18)

- Co. stopped talks with the Energia Costa Azul LNG project in Mexico, a Tokyo Gas spokesperson said, without explaining the reasons.

- Co. had signed a preliminary accord with units of Sempra Energy in Nov. 2018 to buy as much as 800,000 tons per year for 20 years.

- CONTEXT: The 3.25-mtpa Energia Costa Azul project has just received green light from local regulators and will start to export LNG to China and Japan in the next year years. The project is able to transport LNG through Mexico’s west coast, thus bypassing the Panama Canal and cutting costs. According to BNEF, the project could export 2.5 mtpa to Asia, with Total and Mitsui & Co. the biggest traders of the fuel.

INPEX to lay second natural gas pipeline in central Japan

(Sekiyu Tsushin, Nov. 18)

- INPEX (International Petroleum Exploration Teikoku Oil) Corporation will install a second gas pipeline along some sections of its North-Kanto network, after projecting strong growth in demand.

- A second pipeline will be laid along a 6 km section of the 89 km Ryomo pipeline, between Tatebayashi (Gumma) and Sano (Tochigi).

- INPEX is also considering extending the 213 km New Tokyo pipeline by 16 km between Fujioka and Honjo.

- CONTEXT: Six different gas companies currently supply the Ryomo pipeline. The additional pipeline route is due to ensure better access to the distribution infrastructure for all the companies, which should improve the consistency of gas supply.

- SIDE DEVELOPMENT:

Tokyo Gas Ibaraki pipeline to go online in 2021

(Nikkan Kogyou, Nov. 20)- A new 92 km gas pipeline laid by Tokyo Gas between the Ibaraki cities of Hitachi and Kamisu will become operational in early 2021.

- Work began on the pipeline in January 2018 and was completed in October.

- The new pipeline will increase the utility’s supply capacity by around 10%.

- SIDE DEVELOPMENT:

Tokyo Gas orders random checks over revelations of fake renewables claims

(Kensetsu Kogyo Shimbun, Nov. 20)- Tokyo Gas has called on its construction contractors to perform random checks on subcontractors after revelations that contractors used non-approved filling materials to backfill trenches dug when laying gas pipes.

- The use of non-compliant materials can cause asphalt to crack and roads to be weakened. Tokyo Gas says it may order asphalt to be re-laid at some work sites.

Tokyo Gas likely to restart share buybacks from spring 2021: Mizuho

(DZH traders report)

- Mizuho bank analysts said they believe Tokyo Gas is likely to recommence its share buyback in or after Spring 2021.

- Mizuho raised its target price for Tokyo Gas shares from ¥2,650 to ¥2,900.

Tokyo Gas and Osaka Gas score highly in ranking of staff salaries

(Gendai Digital via Yahoo News, Nov. 18)

- Tokyo Gas is Japan’s largest household gas supplier, serving Tokyo, Kanagawa, Saitama, Chiba, Gumma, Ibaraki, and Tochigi with a 60,000 km network of pipes.

- Osaka Gas is Japan’s second-largest gas utility in terms of volume sold, and has a reputation for excelling in new technologies such as catalytic fuel cells.

- The average salary for a permanent employee at Tokyo Gas is ¥6.6 million, while employees at Osaka Gas earn an average of ¥6.5 million.

- These salaries are high by local standards, and employees of both utilities can expect to retire comfortably.

NEWS: POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 3 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

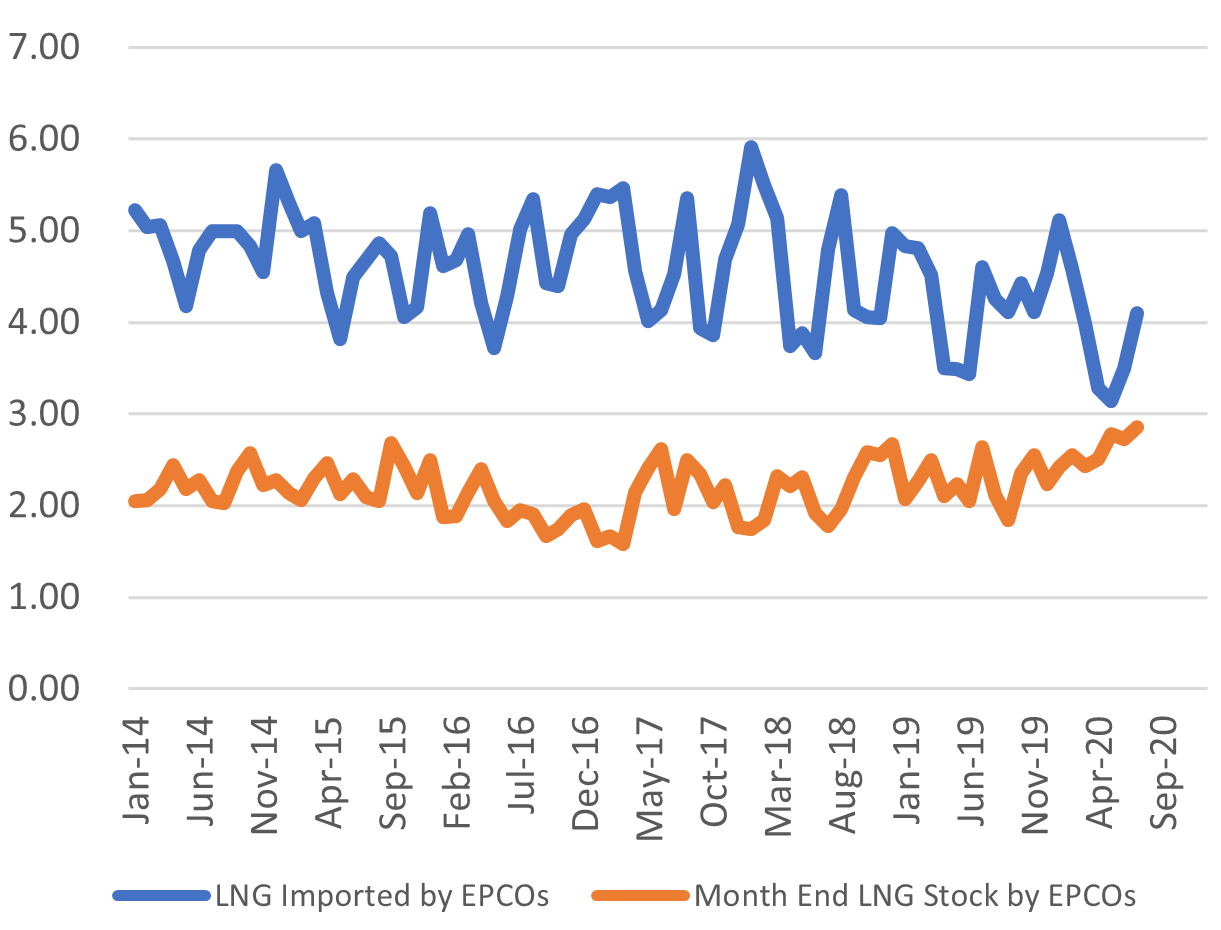

Power Utilities’ LNG Imports Vs Stockpiles

Source: Company websites, JANSI and JAIF, as of Nov. 22, 2020

Japan releases FY2019 energy consumption figures (preliminary)

(Japan NRG, Nov. 18)

- Total energy consumption dropped 2% YoY; of this, oil use was down 2.5%, coal – down 2%, gas – down 0.1%, electricity consumption – down 1.9%.

- Electricity consumption was down 4.1% among householders, mainly due to a warm winter; usage was down 1.1% for commercial and industrial users on lower steel and chemicals industry capacity.

- Primary energy supply was down 3.1% YoY; use of fossil fuels declined for a sixth consecutive year. Supply of renewables and nuclear power increased for a seventh consecutive year.

- Output of electricity from renewables (including unused generation) increased by 1.7% YoY, driven by solar and biomass power generation.

- Output of fossil fuels for thermal power generation, as well as use of petroleum for businesses and coal for industrial production, dropped by 3.8% YoY.

- The share of fossil fuels in the primary energy mix dropped to 85%, the lowest since the 2011 Great East Japan Earthquake and tsunami disaster.

- Total power generation was down 2.2% to 1.28 trillion kWh. The ratio of non-fossil fuels in electricity was at 24.2%, up 1.2% from the previous year.

- Electricity mix by energy source: renewables – 18% (up 1.2%), nuclear – 6.2% (flat), and thermal power (excluding biomass) – 75.8% (down 1.2%).

- Energy-derived CO2 emissions decreased by 3.4% from the previous year, decreasing for the sixth consecutive year to 1.03 billion tons. This is a 16.7% drop compared with the 2013 level.

- CO2 emissions per kilowatt hour of electricity improved by 2.6% from last year to 0.47kg of CO2 / kWh.

- CONTEXT: Emissions jumped by 2013 from two years earlier because Japan switched off its nuclear reactors in the aftermath of the earthquake and tsunami, which also caused a major accident at the Fukushima Dai-Ichi nuclear station. Emissions have since trended down as the ratio of nuclear power in the mix has risen and the country’s renewable energy industry has greatly expanded.

- CONTEXT: These figures will later be updated with the final numbers. However, it’s very unlikely that there will any notable changes.

- SIDE DEVELOPMENT:

Japan’s decarbonization fails to improve for 25 years(Asia Nikkei, Nov. 22)

- Japan’s carbon emissions per unit of GDP are flat since the 1990s. In that time, most European countries have reduced theirs by half to one-third using renewable energy.

Telecoms giant NTT plays down concerns that it will take control of the electricity market

(Diamond, Nov. 14)

- CONTEXT: NTT Group is Japan’s dominant telecommunications firm, which controls not only the fixed-line market but also owns the top mobile carrier in the country and is the main player in many domestic ICT business areas. The group created a renewable energy unit last year, named NTT Anode Energy Corp, and in June vowed to invest around $9 billion in green energy and the smart grid, while also forming a partnership with Mitsubishi Corp., the top Japanese trading house. This prompted concerns among power utilities that NTT was aiming to move into their market.

- NTT Anode Energy CEO Takama Toru denies reports that his company will progressively impinge on the electricity generation, transmission, and retail sectors.

- Takama says NTT Anode Energy is an infrastructure company, the focus of which is construction of smart cities. While he conceded that in the process of establishing infrastructure, NTT Anode Energy might impinge to some extent on the territory of power companies, Takama insisted that NTT’s main focus is making the world more sustainable.

- Rather than fighting with power companies for market share, NTT Anode Energy will cooperate with the electricity industry, says Takama.

TAKEAWAY: It’s possible to overestimate the impact that NTT Group, no matter its size, would have on the electricity market. It is, after all, a new player in this field. Still, NTT is partly state-owned, and it’s often described as more of a ministry than a corporation. Given its firepower and administrative resource, NTT could become a state-guided instrument for disruption in the power market. NTT’s rival in the mobile carrier space, SoftBank, has already built a sizeable presence in power generation by creating solar and wind power stations. NTT may see opportunities to forge even further synergies between telco and power distribution in the increasingly IoT-driven, smart-grid cityscapes.

Japan’s operating nuclear reactor number rises to three; two more close to restart

(Japan NRG, Nov. 23)

- In the last five days, Kyushu Electric has restarted its Sendai NPP Unit 1 and the Genkai NPP Unit 3, to add to Genkai’s Unit 4, which was already in operation.

- The reactors were shut down for months so that Kyushu Electric could implement new measures to make the sites more resilient against terrorist attacks.

- Should Kyushu Electric restart Sendai NPP Unit 2 according to its plans around Dec. 26, the utility will have all its nuclear reactors operating at the end of this year.

- Kansai Electric is due to restart Takahama NPP Unit 3 around Dec. 22. This completes the reactor restarts expected during 2020.

- In addition, Kansai Electric met with local authorities in the town of Mihama, host of another of its NPPs, about restarting the facilities there. The meeting went well, without fundamental opposition to a restart, according to comments made by the chairman of the local committee on the matter that comprises bureaucrats and business leaders, as reported by Asahi Shimbun on Nov. 19.

- CONTEXT: Kansai Electric’s restarts are more complicated than those of Kyushu Electric because of the aftermath of a corporate scandal at Kansai. The utility has tried to rally public opinion in localities that host its nuclear assets, but with mixed results so far. The comments from Mihama locality are the most positive to date.

- SIDE DEVELOPMENT:

TEPCO has no choice but to abandon Kashiwazaki-Kariwa NPP(Gendai, Nov. 17)

TAKEAWAY: Should Kansai Electric manage to receive local political backing it could return online all seven of its reactors by mid-summer 2021. That, and the restart of TEPCO’s Unit 7 at the Kashiwazaki-Kariwa NPP, also expected in the next six months, would cardinally change the picture for nuclear power in Japan. However, Japan NRG is currently cautious about the possibility of this “best-case” scenario for nuclear power in Japan.

EDITORIAL: Not enough debate on future of nuclear power in Japan

(Nikkei, Nov. 17)

- There is consensus that to achieve its target of zero net carbon emissions by 2050 Japan will have to drastically reduce its use of coal and other fossil fuels. When it comes to the future of nuclear, however, commentators differ.

- The Institute for Global Environmental Strategies, a government think tank, has made no explicit statement on the future of nuclear power.

- The Institute’s modeling suggests Japan can use sustainably-generated electricity to supply 100% of demand, assuming a 62% reduction in total energy consumption over 2015, achieved by savings and optimization. However, fossil fuels will remain part of the picture to supply industrial demand, necessitating CO2 sequestration, says the Institute.

- While the non-governmental Renewable Energy Institute (REI) says Japan can source 100% of its energy from renewable sources by 2050, without relying on nuclear power or carbon sequestration, it fails to back up its claims with detailed analysis.

- CONTEXT: The REI is one of the main lobbyists for an expanded role for renewable energy in Japan and it has allies across the business and political spectrum. The institute’s representatives were part of the Japan Climate Initiative (JCI) delegation, which included CEOs from Sony, Ricoh and Kao, that met with Reform Ministry Kono Taro on Nov. 18 to submit a proposal for more usage of green electricity in the country.

TAKEAWAY: Backers of more renewable energy in Japan seem to be gaining more government attention and support since this summer. This may be due to the Japanese government starting to take notes of Europe’s energy policies more than those of the U.S., its traditional beacon. While there are many nuances and caveats, one major difference in the Western European approach is its lesser interest in nuclear power. The “old guard” in Japan are skeptical of following the European path of renewables-only and letting go of the country’s nuclear capacity. As the Nikkei editorial writer notes, the idea of how Japan can achieve decarbonization goals without turning to nuclear power has not yet been made clear by the government.

Kashiwazaki community explores ways to kick the nuclear habit

(Nikkei, Nov. 18)

- For over 100 years, Kashiwazaki in Niigata has prospered on the back of the oil and nuclear industries. Now, however, it is exploring new energy options.

- The city’s 2018 energy vision pledged to end reliance on nuclear power.

- One proposal involves building large solar and wind farms in the area, and transmitting the power to greater Tokyo, using the transmission lines built to carry nuclear-generated electricity.

- Projects to decommission disused reactors also promise to inject money into the local economy. It costs around ¥70 billion to decommission a single reactor.

TAKEAWAY: The localities of Kashiwazaki and Kariwa co-host a major nuclear power plant, which is operated by TEPCO. However, since the 2011 Fukushima disaster, all of the nuclear capacity owned by TEPCO has been shut down and / or slated for decommissioning. The utility has been particularly keen to restart the Kashiwazaki-Kariwa nuclear plant and last week’s local elections in both towns suggested local support for this action. However, even if the plant does restart, it seems highly likely that only two of its seven reactors will ever come back online. This leaves the revenues of the localities much lower than they once were, which is why the towns are looking at other energy options. This does not suggest the towns are opposed to restarting the Kashiwazaki-Kariwa nuclear station.

Covid-19: Domestic electricity revenue down despite increased consumption

(Denki Shimbun, Nov. 20)

- The Institute of Energy Economics has released the results of a survey of the effect of the coronavirus pandemic on domestic electricity consumption.

- The Institute found that despite increased electricity consumption by domestic subscribers since February, which is due to the increasing number of people working from home, falling electricity tariffs meant actual revenue continued to fall until June.

- It is possible that revenue will now start to increase due to higher fuel prices, the Institute said.

October Switching Data: decrease across all 10 areas in Japan

(Gas Energy News, Nov. 16)

- OCCTO published switching data for October. The number of applications for the month of October was 375,400, a decrease of about 60,000 from September, which was at a relatively high level of just under 440,000.

- The cumulative number of switching applications to date has reached 18,486,900.

TEPCO hydropower dam blamed for dry river

(Asahi Shimbun via Yahoo News, Nov. 19)

- The diversion of water from the Midono river (Nagano) to feed the Midono hydro lake, operated by the Tokyo Electric Power Company, is causing the river to dry up frequently.

- Environmental groups have called on TEPCO to take action, saying that fish are no longer able to travel upstream to spawn. This could have serious environmental consequences, they say.

- Pipes remove up to five metric tons of water from the river every second.

The little-known, turn-of-the-century battle for the electricity market

(Diamond, Nov. 15)

- The predecessor of TEPCO was established in 1883. By 1906, Japan had a total of 84 power companies.

- The advent of high-tension lines enabled power to be transmitted over longer distances. This enabled the construction of a hydro dam in Yamanashi in 1907.

- A battle for market share soon erupted between the “big five” players: (TEPCO predecessor) Tokyo Electric Light, Toho Electric Power, Ujigawa Denki, Great Consolidated, and Nippon Denryoku.

- Competition was so fierce that it was common for salespeople from rival power companies to brawl with each other on the street.

- This battle of attrition caused the financial performance of Tokyo Electric Light, Toho, and Ujigawa to suffer, eventually driving them to form a cartel—the Japan Electric Generation and Transmission Company—in 1932. The age of competition was over.

NEWS: RENEWABLES & OTHERS

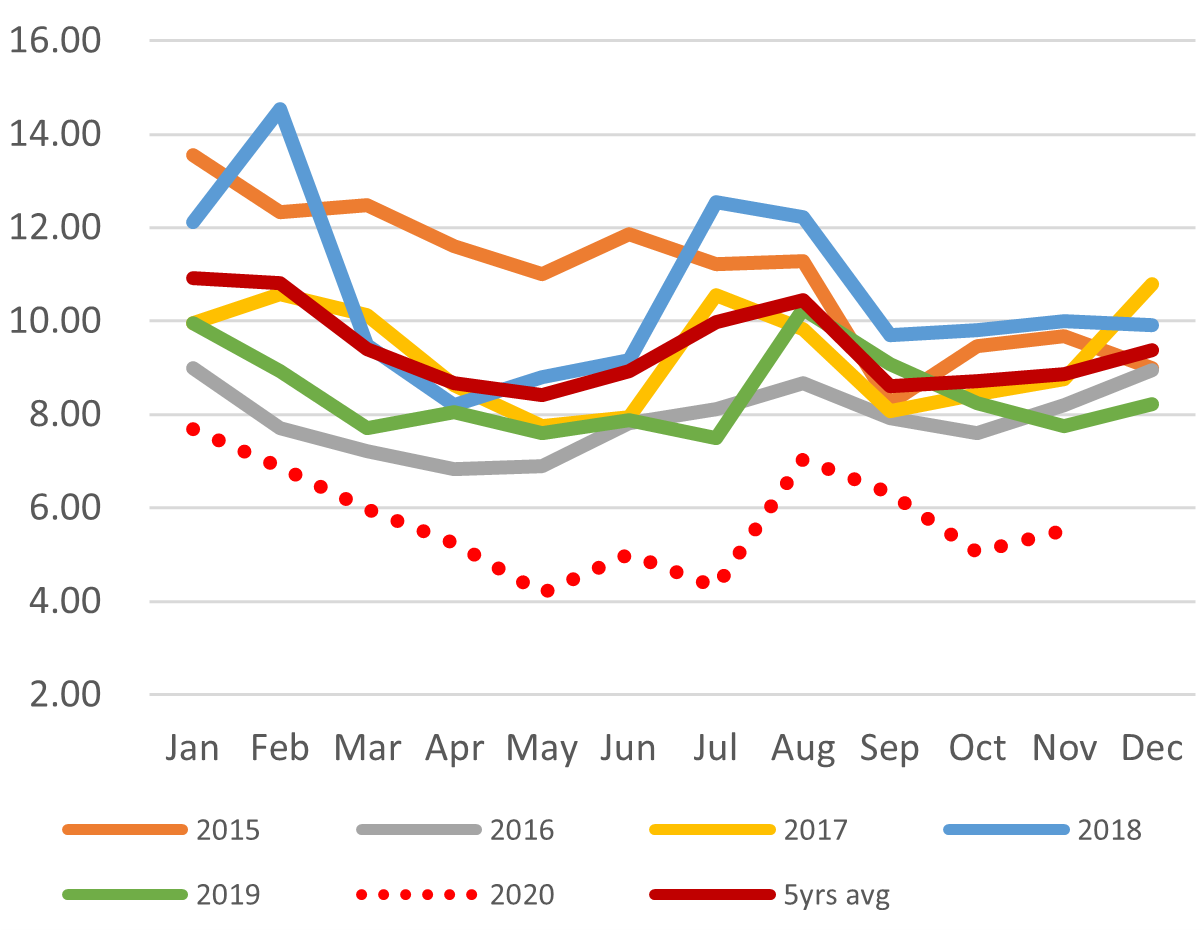

Spot Electricity Prices (24h)

Spot Electricity Prices (2020)

Environment Ministry pushes for Japan to disclose CO2 emissions per company unit

(Nikkei Shimbun, Nov. 22)

- Environment Minister Koizumi Shinjiro said Nov. 22 that he will put together a bill to amend the law to allow the government to push for the disclosure of CO2 emissions per company unit.

- The current system only requires emissions disclosure if the total exceeds a certain level. This will widen the application of the rule and ask for each firm to show emissions on a per business unit level.

- The idea is also to help investors understand the breakdown of emissions of companies and encourage companies to invest in better efficiency of their older environmentally unfriendly assets.

- Koizumi said he wants to help companies that make ESG initiatives get rewarded by the market.

- Koizumi said he will push for three areas to be supported by the next government budget: renewable energy, electric vehicles (EV) and fuel cell vehicles (FCV), as well as the decarbonization of housing.

- The minister also said renewable energy should be made the main power source for Japan and nuclear energy should be used as little as possible.

- Thermal power can improve its emissions by utilizing hydrogen and ammonia, he said. “Ultimately, we’d like to support thermal generation that does not produce emissions.”

Japan needs ¥10 trillion ($96 billion) green fund to support energy transition: Govt. Advisor

(Bloomberg, Nov. 18)

- Advisor to Prime Minister Suga tells Bloomberg that Japan needs a fund to invest in green technologies and digitalization, and the money may come from the third additional budget the government plans this year as part of the post-COVID economic revitalization measures.

- Kumagai Mitsumaru, chief economist at Daiwa Institute of Research, was appointed as one of the advisors to PM Suga last month. His comments hint that the government is serious in following up on PM Suga’s pledge to make Japan carbon-neutral by 2050.

- Kumagai cited an unidentified study that suggests Japan needs to invest ¥11 trillion each year of public and private funds to meet the 2050 target.

- SIDE DEVELOPMENT:

NEDO publishes report on IT innovation and climate change in light of President-Elect Biden

(TechCrunch Japan, Nov. 18)- State-backed research and development entity, New Energy and Industrial Technology Development Organization (NEDO), published report on what Japan needs to do to act on climate issues.

- The report mostly looks at the New Green Deal of President-Elect Joe Biden and finds what may be the equivalent policies in Japan, Europe and China. NEDO also points out that U.S. green policies will ramp up the nation’s spending on technical innovation to ¥23 trillion / year, which is less than China’s ¥30 trillion / year, but a lot more than Japan’s ¥5 trillion / year.

- SIDE DEVELOPMENT:

Survey of Japanese firms reducing CO2 emissions

(Asia Nikkei, Nov. 17)- Nikkei surveyed 731 major Japanese companies. Of these, 42% said they reduced direct greenhouse gas emissions in fiscal 2019.

- The leaders in the fight against climate change included Sapporo Holdings, Omron, and Ricoh.

TAKEAWAY: As we noted in one of the top items in last week’s Japan NRG Weekly, Suga’s government is assembling resources to push for more public and private sector moves into energy efficiency and decarbonization. These moves will include tax break for renewable energy projects, making more land available for solar, wind and geothermal stations, including in national parks and on land currently classified as reserved for agriculture. The government also wants to support batteries, EVs, fuel cells, the hydrogen economy, and carbon capture technology development.

Universities invent alloy that turns impacts into electricity

(ITmedia, Nov. 16)

- Researchers at Tohoku University and Yamagata University have developed a material comprising cobalt iron and aluminum alloys that generates electricity when struck.

- The material could have applications in the manufacture of car parts and engine parts, where strength and durability are required.

- The researchers succeeded in greatly increasing the voltage and current generated by the material.

- SIDE DEVELOPMENT:

Japan works to cut cost of battery materials

(Nikkei Shimbun, Nov. 21)- Research is underway to increase the cost competitiveness of commercial storage batteries, which hold the key to the spread of renewable energy. Technologies for improving performance while using inexpensive sodium and lead are being developed one after another.

- The work is focused on finding alternatives to lithium-ion batteries, which are expensive because they use rare materials such as lithium and cobalt.

Toyota Tsusho signs exclusive distribution agreement for SFC fuel cell

(New Energy Business News, Nov. 17)

- Toyota Tsusho, a trading house, has bought exclusive rights to sell ethanol powered fuel cells manufactured by Germany’s SFC Energy in Japan.

- The fuel cells’ applications include powering wind monitoring stations in isolated areas, and as a portable backup power supply for use in emergencies.

- SFC has the largest share of the international market for fuel cells with an output of up to 500 Watt.

- The fuel cell generates electricity directly from ethanol and air using a patented catalytic technology, and is able to continue providing power for up to a month.

Idemitsu invests in Swiss clean tech fund Emerald Technology Ventures

(Company press release, Nov. 16)

- The open innovation fund operated by Emerald has a portfolio of industrial innovations such as material chemistry and clean tech that contribute to improving energy efficiency and solving social issues such as CO2 reduction.

- Idemitsu noted that Emerald has access to promising start-ups in North America, Europe and Israel.

- CONTEXT: While primarily an oil refining company, Idemitsu Kosan is developing high-performance materials such as lubricating oils, functional chemicals, electronic materials, agribios, and all-solid-state lithium-ion batteries to expand into more green energy businesses as part of its mid-term strategy.

Ministry scraps hydrogen station subsidy after discovering renewables condition not met

(Mega Solar Business News/Nikkei BP, Nov. 18)

- According to a report by the Board of Audit released on Nov. 10, the plug has been pulled on a Ministry of the Environment initiative to subsidize hydrogen filling stations in regional centers after it became clear that many operators were not using renewably-generated electricity.

- While the use of renewable electricity was a condition of receiving the grant, it was discovered that five out of the seven operators receiving subsidies sourced less than half of the electricity consumed by their operations from renewable sources.

- The scheme was launched in 2015.

Tohoku Electric to build new geothermal plant in Akita, opening set for 2029

(Denki Shimbun, Nov. 18)

- Tohoku Electric Power subsidiary Tohoku Sustainable and Renewable Energy said on Nov. 17 it will construct a 15 MW geothermal plant in Akita, and aims to have the plant running by 2029.

- Tohoku Sustainable began surveying the area’s geothermal resources in 2010.

- The plant will use “single flash” technology, and separate hot water from steam, with the steam being used to produce electricity while the hot water is reinjected into the ground.

- Work on the plant will begin in 2025.

SPARX to build 7.1 MW woody biomass power plant in Toki City, Gifu Prefecture

(New Energy Business News, Nov. 16)

- SPARX Green Energy & Technology will sell electricity to Chubu Electric using the FIT scheme.

- Investment is about ¥7 billion. Construction is due to start in Jan. 2021, and the plant should be operational two years later.

- The FIT price will depend on the fuel that the station uses, varying between ¥33 / kWh for scrap wood to ¥13 / kWh for recycled materials. About 65,000 tons of various types of wood chip fuel will be used.

Osaka Gas group’s liquid CO2 plant goes online

(Denki Shimbun, Nov. 17)

- Osaka Gas said on Nov. 16 its new liquefied CO2 plant in Niigata has begun commercial operation. New technologies for removing impurities from carbon dioxide gas mean the plant is capable of producing highly pure CO2.

- It is hoped that the plant, which aims to sell 50,000 metric tons of CO2 per day, will help relieve Japan’s chronic shortage of the commodity.

- Liquefied carbon dioxide has uses in welding, beverages, and dry ice production.

ANALYSIS

INDEPENDENT,

RESEARCH & ANALYSIS

Giant Indonesian LNG Project; May Need All-Japan Support

INPEX Corp. made a global name for itself by taking the lead on one of the world’s most expensive LNG projects, the $45 billion Ichthys development in Australia. Now, the state-backed Japanese company seeks to follow this up by taking on the giant Abadi LNG project in Indonesia.

As INPEX pushes forward with engineering work at Abadi, aiming for a final investment decision (FID) in 2022, new issues have come to the fore. A recent cap on gas prices in Indonesia, and the announcement by project partner Royal Dutch Shell of its desire to exit, mean that INPEX needs to secure support elsewhere. In theory, the Japanese government’s wish to keep Japan at the top of global LNG trade in the face of a rising China should bring other Japanese firms to the project. Still, even geopolitics come at a price. The question is, who will pay for the $20 billion Abadi development?

Abadi is in one of the world’s largest undeveloped gas resources and sits in close proximity to the fuel’s biggest buyers. The project in the Masela Block, off the coast of Indonesia, marks a huge resource opportunity for INPEX. There is plenty of corporate pride involved in having discovered and potentially developing a find of this magnitude.

The importance of Japan’s relationship with Indonesia was in clear view as both current Prime Minister Suga Yoshihide, and his predecessor Abe Shinzo, made the Southeast Asian country their first stop abroad. Energy and security are tightly interlinked in the relationship between the two countries with Indonesia among the top suppliers of coal and LNG to Japan. In fact, the world’s oldest LNG deal is between Indonesia and Japanese buyers.

So, why did Indonesian regulator SKK Migas announce in July that Shell plans to divest its 35% stake in Abadi, valued at up to $2.2 billion?

THE CHALLENGES TO BRINGING ABADI TO MARKET

Holding 360 billion cubic metres of gas, Abadi is one of the biggest gas fields discovered in Asia over the past 20 years. However, the cost of development is high relative to other global LNG projects. The breakeven LNG price, based on delivery to Asia, is estimated at around $8 per million British thermal units (MMBtu). At the very least, Abadi would need to sell gas for at least $6/MMBtu to make a 10% return. In comparison, Qatar projects can breakeven at around $4/MMBtu based on delivery to Asia.

There are also engineering challenges, and INPEX’s relatively small LNG project development history may be an issue for new investors. Development of Abadi’s proposed 9.5 million ton/year onshore liquefaction scheme will be technically challenging. The project includes a large FPSO unit capable of handling 51 million cm per day of gas and up to 36,000 barrels per day of condensate, as well as a deep-water trunk pipeline from the Abadi field to liquefaction facilities on Yamdena in the remote Tanimbar Islands.

What’s more, Indonesia is a thorny jurisdiction. Jakarta has surely tested INPEX and Shell’s patience following a history of delays and disagreements. The final development plan was only officially approved last year, 18 years after Abadi was discovered.

Ironically, the project could have been well advanced by now if Indonesian President Joko Widodo had not vetoed the previously proposed – and potentially cheaper – floating LNG (FLNG) concept in 2016. At that time, INPEX and Shell estimated the FLNG option to cost around $14 billion.

Shell’s withdrawal from the project comes as no surprise. The company originally entered the scheme on the premise of FLNG, a technology that Shell has pioneered. The company is likely frustrated with the glacial progress of the project to date.

Shell’s departure, however, leaves INPEX in the lurch. With an FID set for 2022, INPEX believed it could start to produce first gas by 2028. Now, this seems unrealistic. Shell’s divestment is expected to take at least 12-24 months. This suggests the FID is unlikely before 2023, with first gas more likely to come after 2030.

INPEX will hope a new partner can bring either the same technological capability as Shell, or similar LNG marketing experience. However, it is unlikely that other supermajors would be interested at this time.

Asia’s national oil companies, with ready access to home markets, might be a better fit. The Chinese, however, have recently signed up for minority stakes in Russia’s Arctic LNG2 project and are unlikely to be seeking further LNG exposure.

Under preliminary agreements, Indonesian utility PLN is projected to take 2 million to 3 million tons of LNG per year from Abadi, while Pupuk Indonesia is expected to buy 150 million cubic feet per day via pipeline.

Source: INPEX

The trouble with domestic sales will be Indonesia’s new gas price regulation, introduced in April 2020, which caps domestic gas sales at $6/MMBtu.

Indonesian industrial customers pay some of the highest gas prices in Southeast Asia, despite the country being the largest regional gas producer. Average domestic gas prices are over $9/MMBtu, higher than other neighboring countries, where average domestic gas prices range from $6 to $8/MMBtu.

Crucially, INPEX will need a much higher domestic gas price. Recent regulation only covers Indonesian prices up until 2025, and it’s unclear how it will evolve afterwards. INPEX will need to strike an agreement with the Indonesian government before starting production.

ALL-JAPAN TOGETHER NOW

Today, Japanese LNG investors and buyers have access to a much broader set of projects around the world, with significant new supply emerging in Mozambique and offers coming in continuously from U.S., Canadian, Russia, Australian and other projects. Still, the Abadi development carries weight, not only for INPEX, but also for Japan. Indonesia is one of Tokyo’s core partners in the Free and Open Indo-Pacific strategy, a concept that seeks to keep in check the rising maritime ambitions of China in the region.

For INPEX, Abadi is also the culmination of decades of work in the region and on this field in particular. Despite the above-mentioned hurdles, there has been notable progress at Abadi since the revised plan of development was approved last year. Site surveys are progressing as planned, the land acquisition process has started, and tenders for onshore LNG, FPSO, gas export pipeline and other items are underway.

While other Japanese firms have been content to take on minority stakes in overseas upstream and LNG projects, INPEX dared to take the lead on the Ichthys development in northwest Australia. Ichthys has developed into one of the most expensive capital projects of all time and recently necessitated a restructuring of INPEX’s debt.

The company sees Abadi as the next step in its development into a significant energy firm with access to major resources.

In today’s world, with few FIDs for LNG export projects on the horizon, there are even fewer opportunities to join projects with bitesize stakes. That could help INPEX persuade domestic utilities and energy trading firms to band together and make Abadi an all-Japan affair.

Still, given the billions of dollars needed to bring Abadi online, INPEX has to be careful not to place too much of its resources in one asset. Its outlay on Ichthys, the budget of which blew up by a third from initial estimates, calls for risk diversification.

Whether INPEX’s new partners are all Japanese or not is yet to be seen. Either way, INPEX is unlikely to take on the Abadi challenge by itself.

ANALYSIS

INSIDE VIEW: Solar and Wind Power in Japan

We spoke with Vena Energy’s Japan Chairman, Kameoka Nobuyuki on why Japan is such an attractive market for renewables, what other investments the company is looking at, and what the declining FIT prices / switch to FIP means for the industry.

BIOGRAPHY

Born in 1950, Kameoka Nobuyuki joined Sumitomo Bank after graduation and worked in their U.K. office in addition to stints in operations and the M&A department. After rising to the rank of Executive Officer of then Sumitomo Mitsui Banking Corp., he went to manage a major Japanese property developer, then switched back to banking to act as advisor and later managing director of Morgan Stanley Securities in Tokyo. Kameoka-san joined Vena Energy in 2018.

Recently, there has been more focus in Japan on wind than solar. Which of these is of greater interest for Vena Energy?

We are equally focused on expanding both our wind and solar activities. Japan is our main market, with over 1,000 megawatts of solar and wind projects under operation, construction and ready-to-build stage. We have an even larger number of megawatts under development in both technologies.

In addition, we continue to successfully participate in the solar tenders with our large-scale solar projects while, at the same time, we progress on the construction and development of onshore and offshore wind projects.

Did you consider any other energy investments in Japan outside of solar and wind?

We believe that the renewable sector will naturally evolve towards closer integration with energy storage systems, which would allow solar and wind generation profiles to become steady and programmable. Vena Energy has already developed energy storage projects in some of our other markets and we are currently building the largest battery energy storage system in the state of Queensland in Australia, with the ability to store up to 150 megawatt hours of energy.

We are also looking at other promising energy storage technologies, such as green hydrogen, which we expect to expand in the medium-long term. We will definitely also consider making such investments in Japan, as soon as a clear regulatory framework is established by the Japanese government.

What are your thoughts about the current levels of FIT? Is it possible to continue to invest in new solar and wind projects at current FIT levels?

The Japanese renewable energy sector began its expansion thanks to the introduction of the FIT system less than a decade ago following the Fukushima Dai-Ichi nuclear disaster. Despite the late start compared to many countries in Europe and North America, the Japanese FIT framework has successfully attracted numerous renewable energy players, and the Japanese renewable sector has rapidly become very sizeable.

The FIT level of solar and onshore wind projects has then progressively reduced over the years, reflecting the continuous cost reductions and economies of scale achieved across the renewable energy’s value chain. This has rendered the cost of renewable energy cheaper and more competitive, while also pushing the least efficient developers out of the market.

With the switch from FIT to tenders, the tariffs continue to reduce and some renewable developers may no longer be able to pursue new project developments at the current tariff levels. Only a handful of renewable energy companies have actively developed projects at these tariff levels and participated in the solar tenders with large-scale sites. Vena Energy has a fully integrated business model, with in-house development, construction, operations and maintenance capabilities. This allowed us to reduce our costs while retaining our quality, and to be competitive at the current tariff levels. In fact, just a few weeks ago we emerged as one of the winners of the latest solar tender, being awarded the largest project in the tender of approximately 70 megawatts.

What are your expectations for the Feed-In Premium? Will it help to transform renewables projects in Japan?

Similar to other system transitions, we believe that the outcome of the transition to FIP will depend on the details of its implementation. If the FIP model is properly implemented, we expect the economics of projects to be broadly preserved, hence we do not anticipate critical differences with the previous FIT model. We understand that this is another step towards a more structured electricity market, which can be seen as a positive signal for a high-potential energy market such as the one in Japan.

What is the biggest issue you face as a renewables developer in Japan right now?

This year the COVID-19 pandemic has probably been on top of the issues list for most businesses worldwide. For Vena Energy the main focus has been to preserve the health and safety of our team.

The operating solar and wind projects have demonstrated their resilience to potential disruptions related to the pandemic. These assets are generally self-sufficient and only require natural sun irradiation and wind. The absence of a supply chain helps minimize disruptions and risks for the employees that regularly operate and maintain the projects.

The development of new projects, however, usually requires physical meetings and interactions with local stakeholders, including community members, landowners and local authorities. These activities have generally progressed more slowly, due to the health and safety measures we took to protect both employees and local stakeholders from potential exposure to the virus.

However, no collective relief measure or organic extensions for FIT deadlines were provided by the authorities, as other markets may have provided during these unprecedented times.

Is Japan still an attractive market for new players / investors in solar and wind?

The Japanese renewable sector is generally considered more complex than other key markets. This is partly due to higher costs and risks associated with development and construction activities, mainly deriving from Japan’s unique geomorphological and land-related complexities. New players without an established presence, proven experience and a history of operations in the country may struggle to cope with the intrinsic difficulties of the sector.

We noticed that participants in the solar tenders rarely include new players for large-scale solar projects. In contrast, we noticed a high level of interest from foreign energy companies to partner with local developers and IPPs for the co-development of offshore wind projects.

Japan is the biggest revenue contributor to VENA. Why has it evolved this way and will it change?

We have an enduring focus on Japan since first establishing our operations in 2013, and we aim to continue to operate in Japan as a going concern indefinitely. More than one third of Vena Energy’s global team is based in Japan, in Tokyo and across our local offices in the country.

Over the past eight years we have progressively built solid relationships with host communities and local stakeholders across the country. They have welcomed us as a trusted long-term partner for the operations of our solar and wind projects, and they continue to support us on the development of new projects in neighboring areas.

From a macro perspective, Japan has credible policymakers and well-established off-takers, as well as a solid track-record of averting retroactive regulatory changes. Vena Energy is an investment-grade rated company and we aim to retain a strong financial standing and sound credit profile. Our significant exposure to Japanese cashflows is compatible with our credit risk targets, and we plan to maintain a similar exposure in the medium-long term.

Lastly, the Japanese energy market and growth prospects are sizeable across the technologies in which we are active: solar, onshore wind, and offshore wind. We are also hopeful about future integration of energy storage in the Japanese energy infrastructure.

Recently, both TOCOM and EEX started to offer electricity hedging contracts on their trading platforms. Are these useful developments from your perspective?

These new instruments are certainly valuable additions to the Japanese electricity market. We look forward to participating in a more structured and mature market that offers short and long-term balancing solutions, route-to-market agreements, etc.

Last year VENA conducted a USD-denominated Euro Note offering. This February you sold debut bonds, also in USD. Would you consider issuing JPY denominated bonds or notes in the future?

We registered our Euro Medium Term Note program on the Singapore Exchange in November 2019. The program is sized at $1 billion but it allows Vena Energy to issue bonds in different currencies, including JPY.

In February 2020 we issued our debut green bond as a benchmark issuance of $325 million. We have subsequently swapped this bond to JPY in order to align it with our cashflows, which are predominantly from Japanese projects and, therefore, also denominated in JPY. We expect to continue to issue green bonds under this EMTN program as Vena Energy continues to grow, and to add new projects across our active markets.

GLOBAL VIEW

BY TOM O’SULLIVAN

Below are some of last week’s most important international developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Tesla will enter the S&P500 U.S. stock market index on Dec. 21 in another major breakthrough for the electric car manufacturer and for the broader EV industry. With a market capitalization of $450 billion+ Tesla’s market valuation is now 2.5x Toyota’s. Other EV industry players in the U.S. also saw significant increases in market capitalizations last week, including Blink Charging, Lordstown Motors and Nikola. General Motors announced it would increase its EV investments by over 30% to $27 billion through 2025.

Shipping:

On Friday, the International Maritime Organization approved a ban on the use of heavy fuel oils by ships in Arctic waters starting in July 2024.

Oil:

In its Q3 Commodity Outlook Report published last week the World Bank cut its forecast for 2020 oil prices to $41, and reduced its forecast for 2021 to $44. In a major departure, the bank also indicated that it might reduce its long-range oil price forecast to $60 from $70. The bank also opined that the pandemic might have accelerated peak oil demand by a decade. John Baffes, the World Bank Commodities Economist, also expressed his view that the “writing is on the wall” for fossil fuel companies.

China:

Yongcheng Coal & Electricity Holdings Group Co. failed to repay a maturing debt of $150 million indicating some stresses in China’s local bond market. The power company had a triple-A local credit rating.

South Korea:

Korea Airlines will inject $1.4 billion in equity to Asiana, South Korea’s second largest airline, and acquire a 64% stake in a rescue effort coordinated by the Korean government. This should be a positive for jet fuel consumption in the region.

Taiwan:

The head of the U.S. Environmental Protection Agency, Andrew Wheeler, will visit Taiwan from Dec. 5.

Hong Kong/Singapore:

The opening of the world’s first quarantine-free travel corridor, due to start on Nov. 22 between the two cities, has been delayed by two weeks after a surge of new infections in Hong Kong. This continues to pressure the outlook for jet fuel consumption in East Asia. Singapore also said it will tighten borders with Malaysia and Japan.

Malaysia:

The local Japanese arm of the Malay LCC, Air Asia, filed for bankruptcy in Japan last Tuesday with debts of over $200 million.

Philippines:

A moratorium on the exploration of oil and gas fields in the South China Sea has been lifted with PXP Energy Corp., a Philippines upstream oil and gas company, expected to jointly develop oil and gas projects with China’s CNOOC.

Australia:

Prime Minister Morrison, who was in Japan last week, was the first foreign head of government to visit the country since Prime Minister Suga assumed power on Sept. 15. The countries signed a Reciprocal Access Defense Agreement that may also help to secure freedom of navigation rights in the international waters used to transport LNG and coal from Australia to Japan.

Middle East:

1). Saudi Arabia’s Aramco raised $8 billion in a bond offering last week as it struggles to meet dividend obligations due to low oil prices.

2). Saudi Arabia became the first Middle East country to host a G20 heads of government meeting on Sunday.

3). Iran is poised to further tighten Covid-19 lockdowns.

Africa:

The ongoing conflict in Ethiopia could threaten the construction of the 6 GW Grand Ethiopian Renaissance Dam on the Blue Nile River. Ethiopian Electric Power Corporation owns the project and it was supposed to supply electricity to the populations in the Horn of Africa region.

Norway:

Norwegian Air announced that it would file bankruptcy in a further blow to Europe’s international travel business and further clouding the outlook for jet fuel usage.

United Kingdom:

1). The U.K. prime minister announced a 10-point, $16 billion plan last week to advance use of clean energy. The plan included:

40 GW of offshore wind investments by 2030; 5 GW of low-carbon hydrogen production capacity by 2030; promotion of nuclear power by developing large and smaller-scale plants; the end for sales of new petrol and diesel cars by 2030; investment in zero-emission public transport; promoting advance use of zero-emission planes and ships; removal of 10 million tons of carbon dioxide by 2030; and

planting of 30,000 hectares of trees every year.

2). The U.K. government will issue its first sovereign green bonds in 2021.

Americas:

1). The Mexican president indicated last week that the U.S.-Canada-Mexico FTA may not apply to Mexico’s energy sector, potentially complicating investments into Mexico’s oil and gas and electricity markets that were opened up in 2014.

2). Jeff Bezos, the founder of Amazon, announced last week that he has given $790 million to 16 organizations working on fighting climate change as part of his Bezos Earth Fund, a $10 billion fund he established to fight climate change.

EVENT REPORT

The 2020 Japan-Canada Energy Partnership Forum

Last week Canada hosted its annual energy partnership forum with the Japanese government and energy industry with the focus mainly on LNG and propane. Energy ministers from the Canadian federal government and the British Columbia and Alberta provincial governments attended.

Senior METI and JOGMEC officials represented the Japanese government.

Energy industry representatives included Alta Gas, Astomas Energy, Prince Rupert Port Authority and the LNG Canada project.

The EIA ranks Canada #3 in terms of oil reserves and #17 in terms of gas reserves. Various projects are being developed in British Columbia to deliver gas to Asia including Japan with the primary advantage being the significantly shorter shipping routes compared to Gulf of Mexico projects.

Investments in LNG in British Columbia and Alberta could total $500 billion by mid-century. Japan is currently getting LNG from 14 countries but not yet from Canada. However, Japan does source propane and coal from Canada.

With regard to natural gas and oil, the problems Canada faces continue to be mainly around the construction of pipelines to deliver gas and oil to the west coast for onward delivery to Asia. The country is also preparing to enshrine a net-zero carbon emissions law into force that could further restrict its ability to construct more pipeline infrastructure.

A Biden administration could also frustrate Canada’s efforts to move oil and gas freely across the U.S.-Canadian border as well as placing restrictions on the construction of energy projects south of the border.

The other areas for energy cooperation between Japan and Canada are nuclear power including small modular reactors and carbon capture and storage projects where Canada is a world leader.

STOCK MARKET PERFORMANCE

| As of close on Nov 20, 2020 | Ticker | Market Cap | 1W (%) | MTD (%) | YTD (%) | |

| billions of yen | ||||||

| Energy | ||||||

| INPEX CORP | 1605 JP | 842.30 | 5.11 | -48.40 | 6.59 | |

| JAPAN PETROLEUM EXPL. | 1662 JP | 105.16 | 2.34 | -35.92 | -0.38 | |

| ENEOS HOLDINGS INC | 5020 JP | 1210.06 | 1.19 | -20.30 | 1.96 | |

| IDEMITSU KOSAN CO LTD | 5019 JP | 657.98 | 0.18 | -22.77 | 1.38 | |

| COSMO ENERGY HOLD. | 5021 JP | 149.96 | 0.68 | -25.93 | 11.54 | |

| Industrials | ||||||

| MITSUBISHI CORP | 8058 JP | 3728.42 | 0.54 | -8.69 | 2.12 | |

| MITSUI & CO LTD | 8031 JP | 3163.77 | 0.57 | -0.83 | 2.11 | |

| JGC HOLDINGS CORP | 1963 JP | 244.96 | 0.43 | -45.41 | -0.94 | |

| CHIYODA CORP | 6366 JP | 63.26 | -0.82 | -14.13 | -0.41 | |

| Utilities | ||||||

| TOKYO ELECTRIC POWER | 9501 JP | 464.43 | -2.69 | -38.12 | 0.35 | |

| CHUBU ELECTRIC POWER | 9502 JP | 989.57 | 2.92 | -12.31 | 7.01 | |

| KANSAI ELECTRIC POWER | 9503 JP | 934.41 | -0.24 | -17.73 | -0.66 | |

| KYUSHU ELECTRIC POWER | 9508 JP | 448.58 | 1.94 | 3.64 | 5.23 | |

| J-POWER | 9513 JP | 267.80 | -3.30 | -42.58 | -3.69 | |

| TOKYO GAS CO | 9531 JP | 1135.95 | -1.06 | -0.87 | 11.22 | |

| OSAKA GAS CO | 9532 JP | 916.28 | 0.37 | 7.70 | 12.42 | |

| TOHO GAS CO | 9533 JP | 726.57 | 8.69 | 55.87 | 32.56 | |

| SAIBU GAS CO | 9536 JP | 117.33 | 0.80 | 27.30 | 24.75 | |

| SHIZUOKA GAS CO | 9543 JP | 75.43 | 0.10 | 5.01 | 9.15 | |

DATA

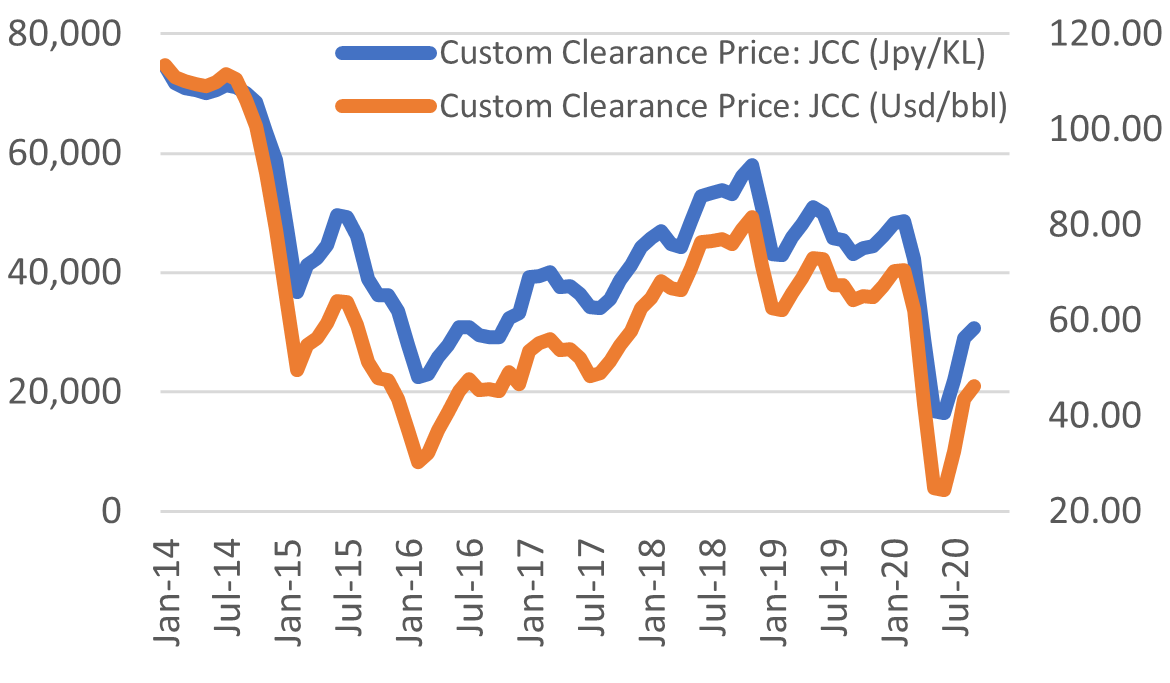

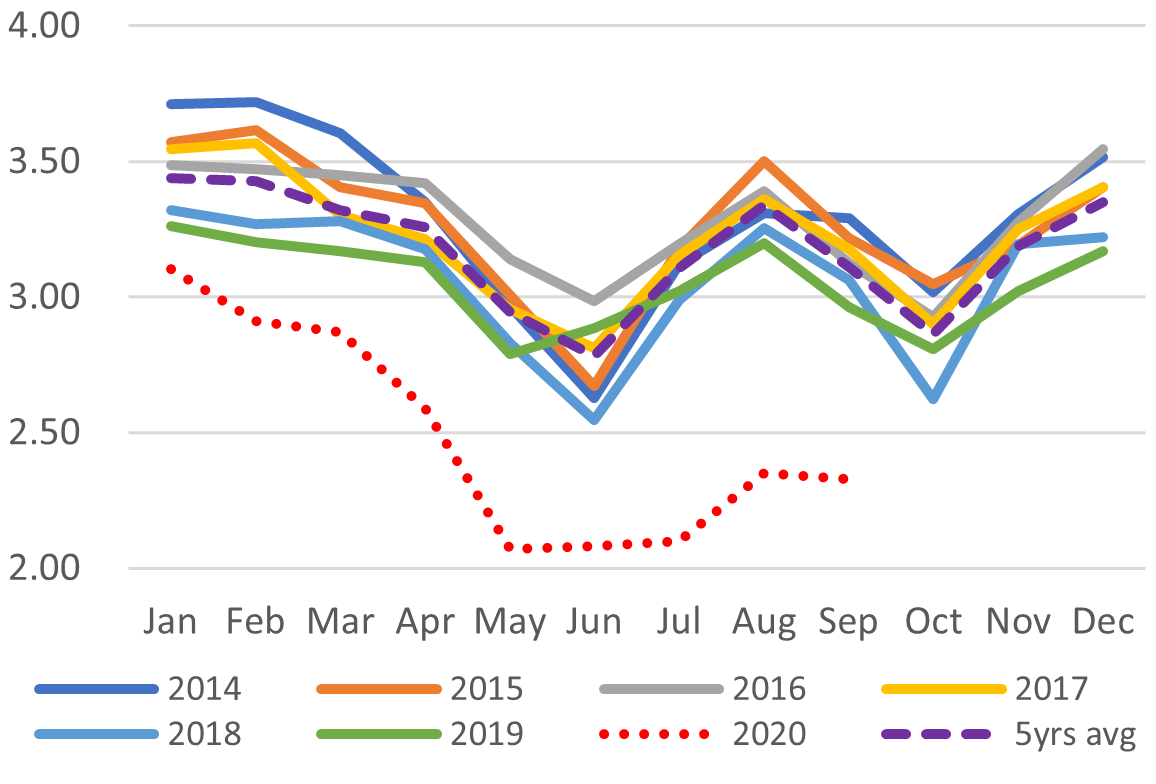

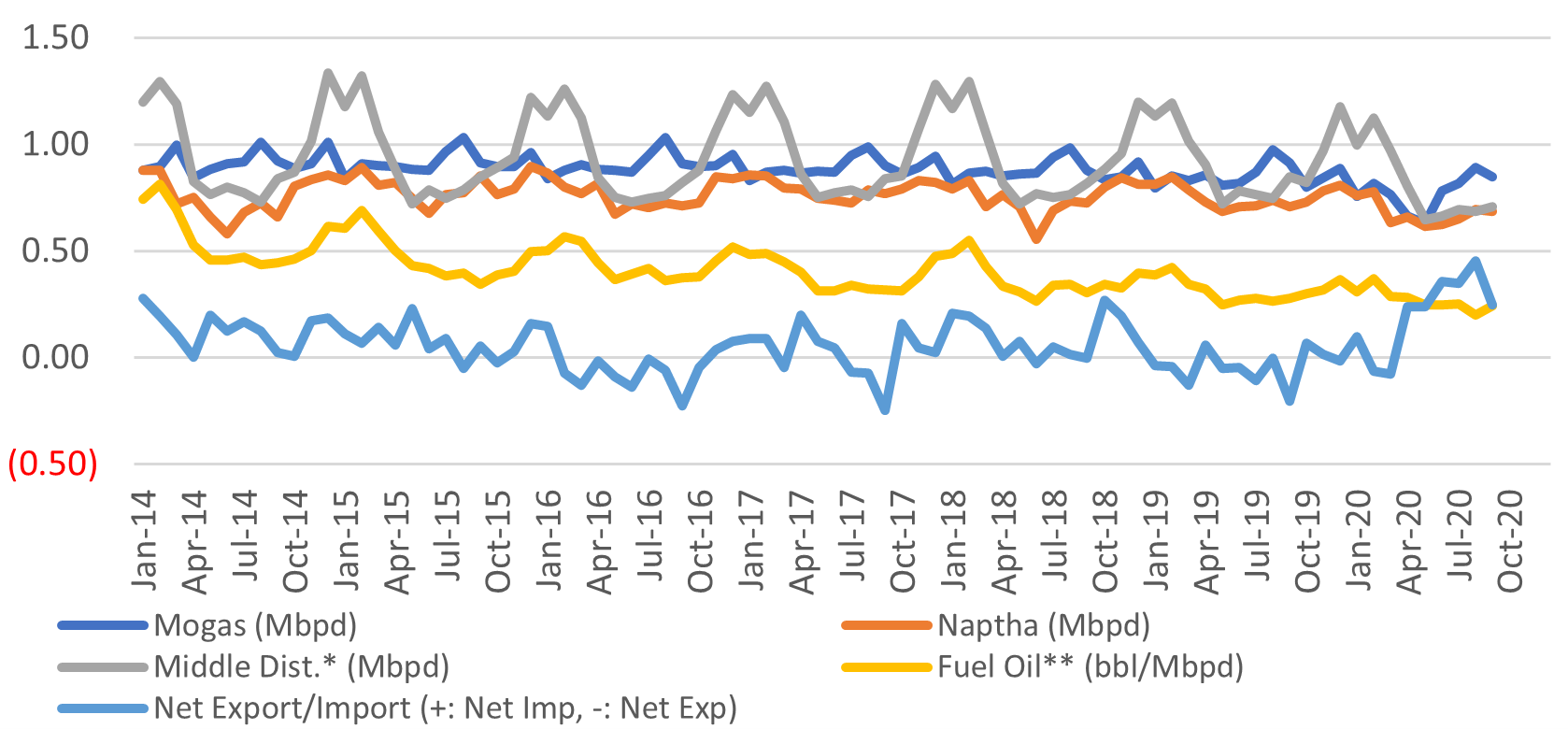

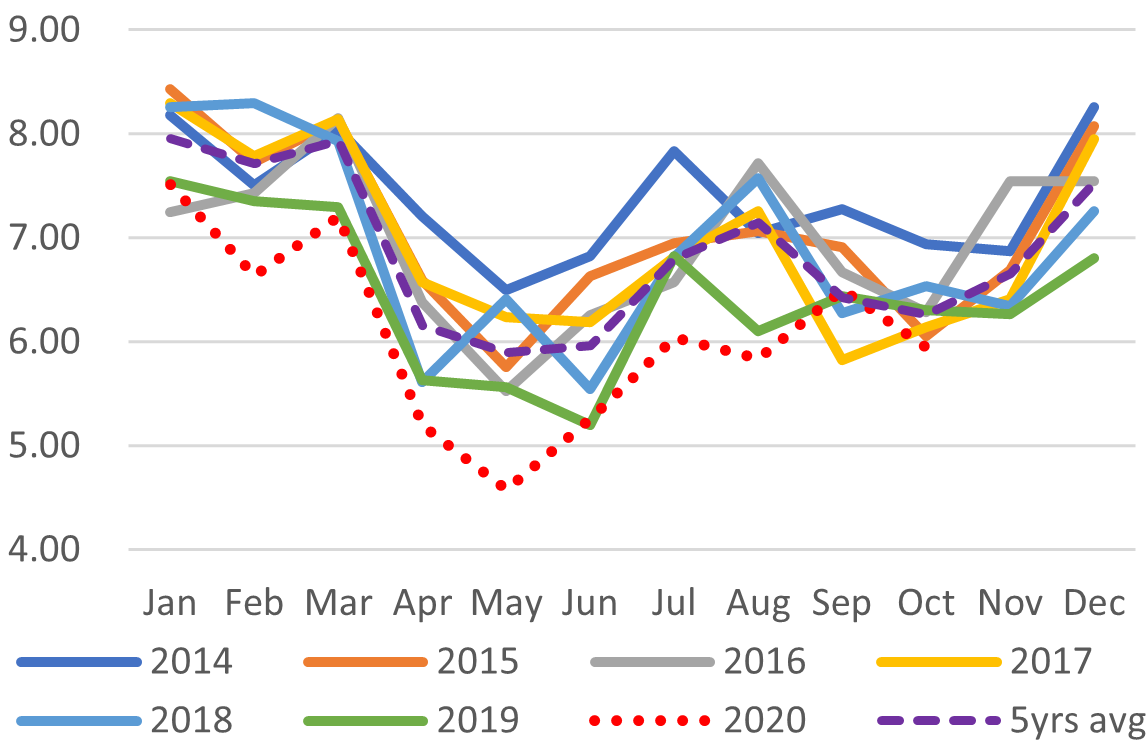

Japan Oil Price

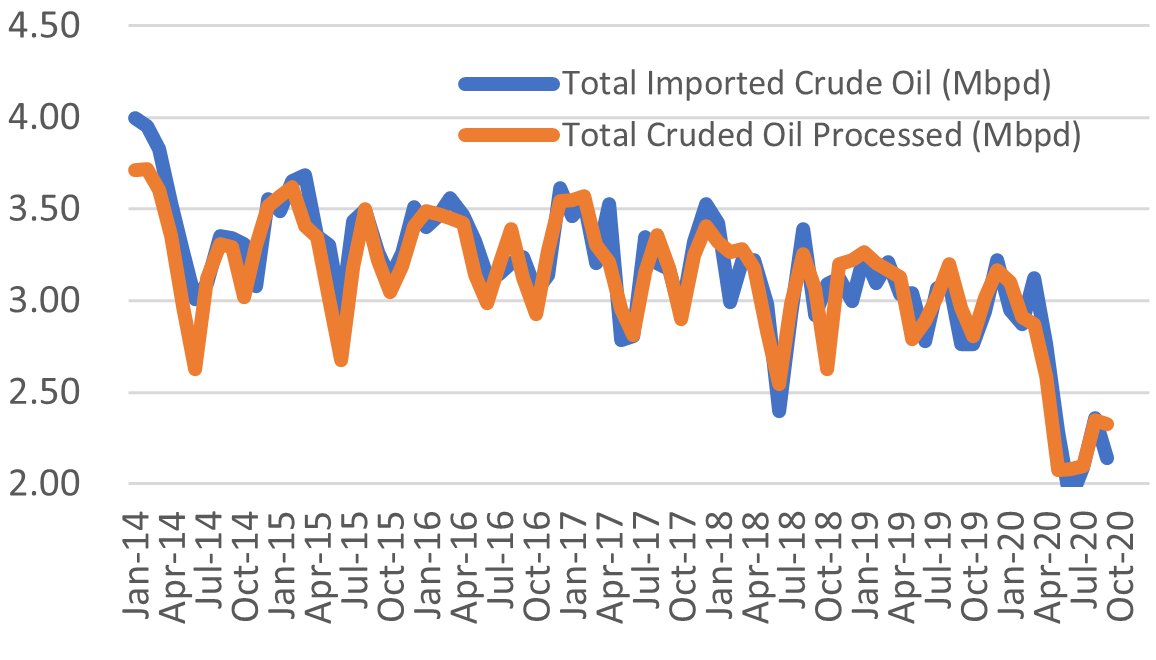

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

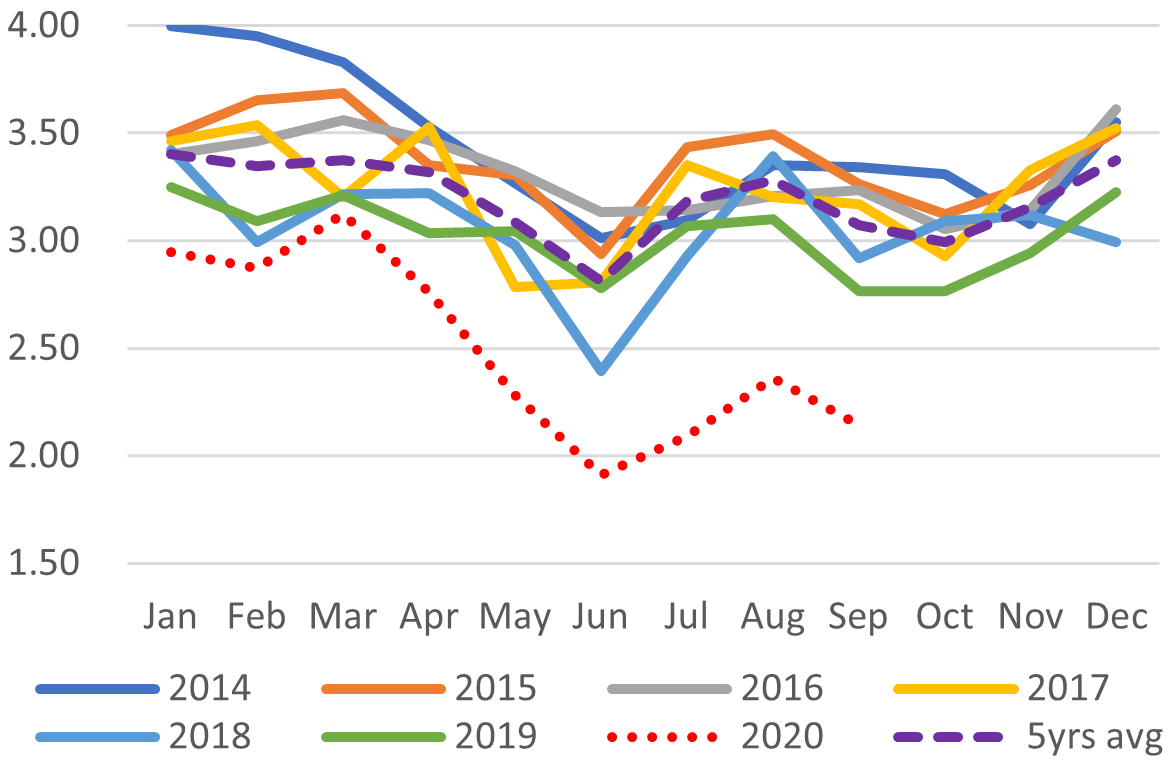

Domestic Fuel Sales

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

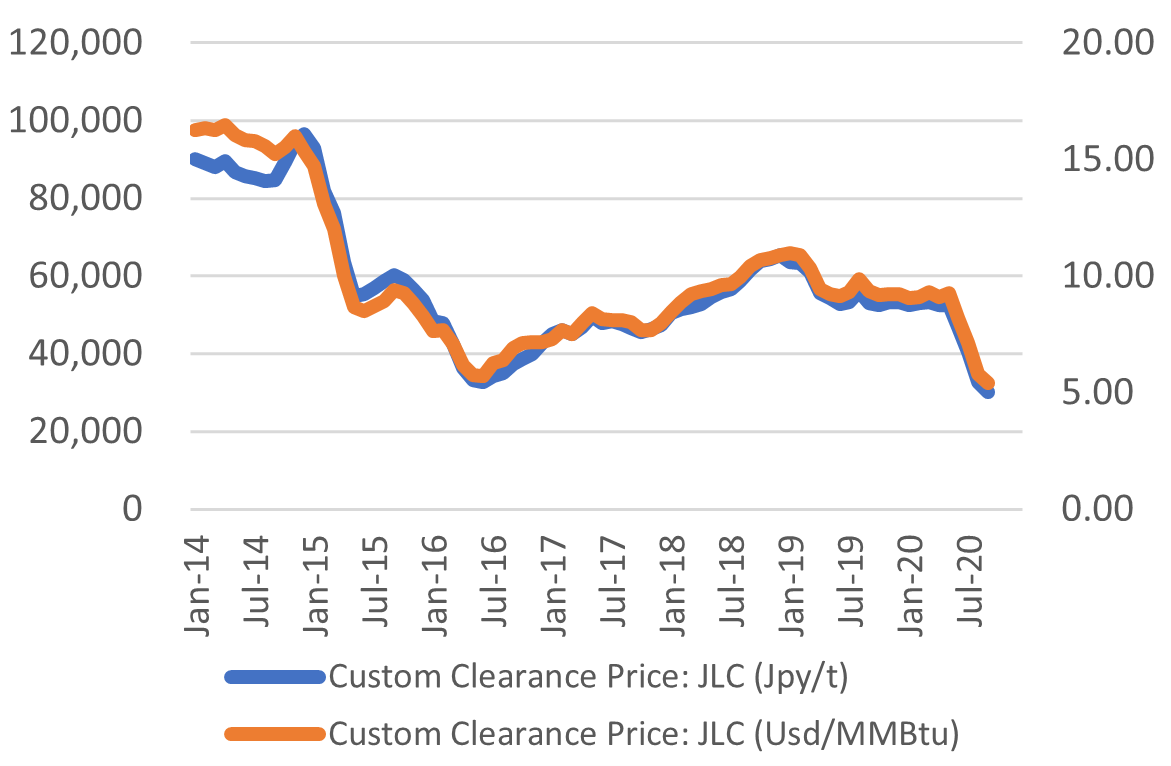

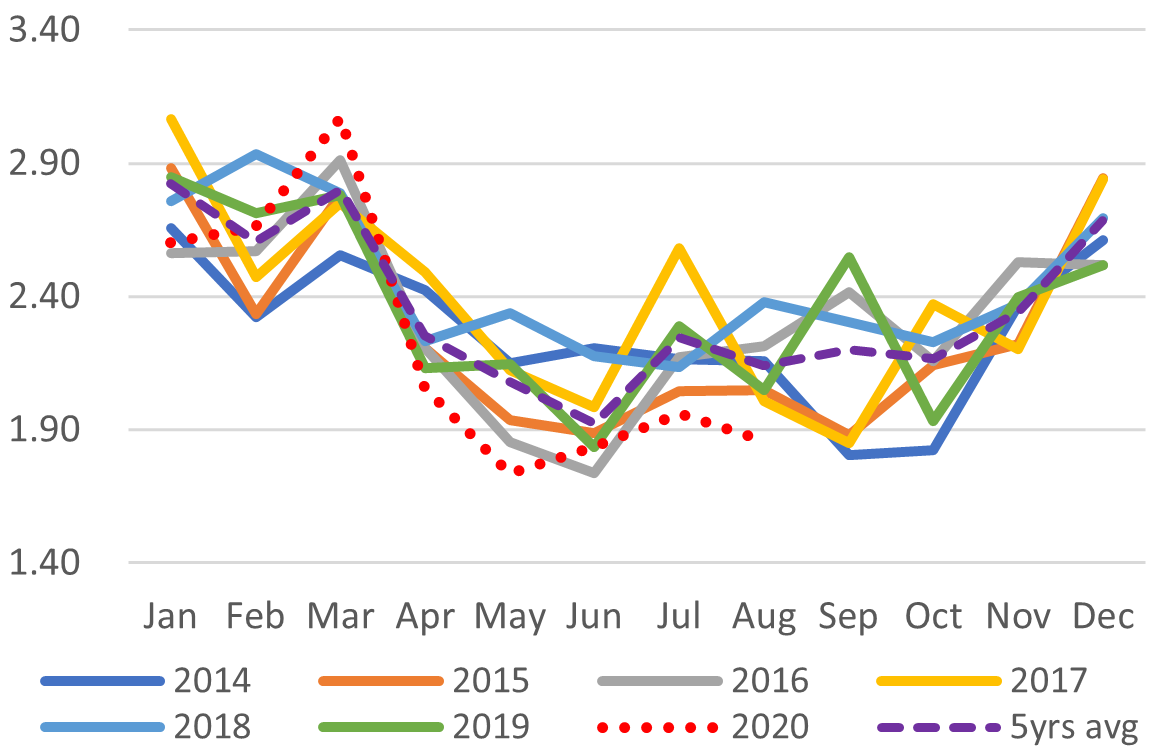

Japan LNG Price

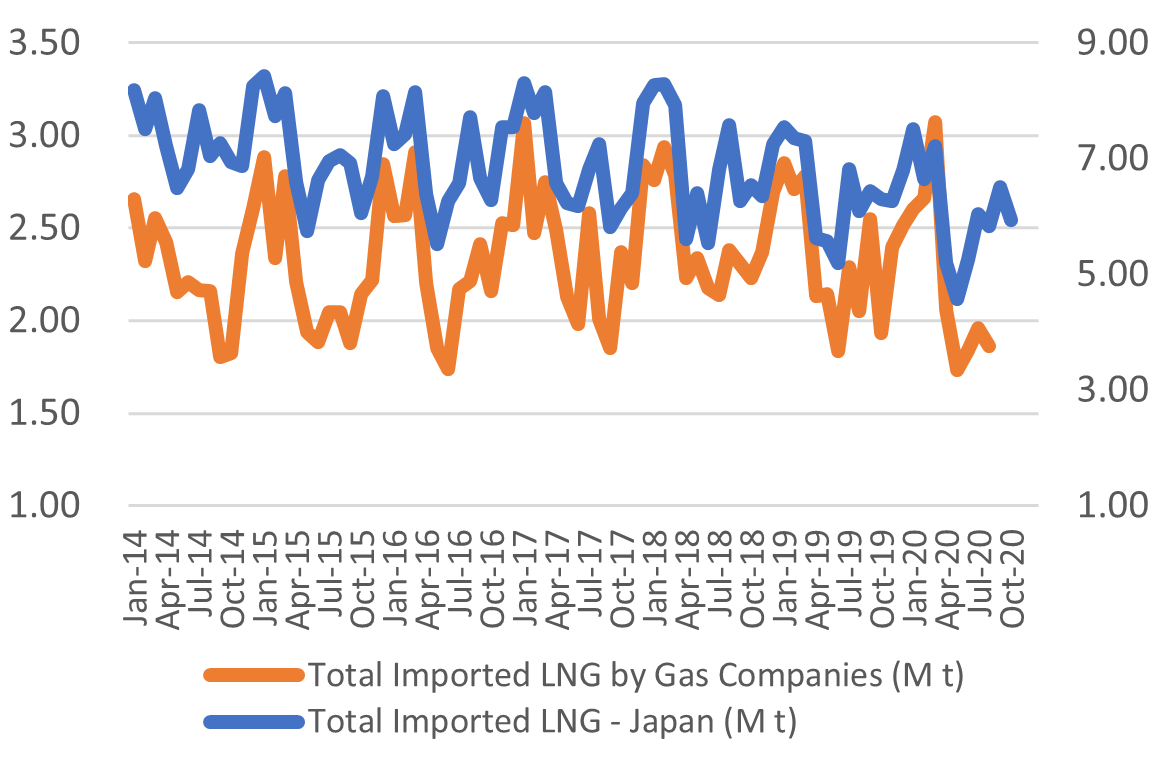

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

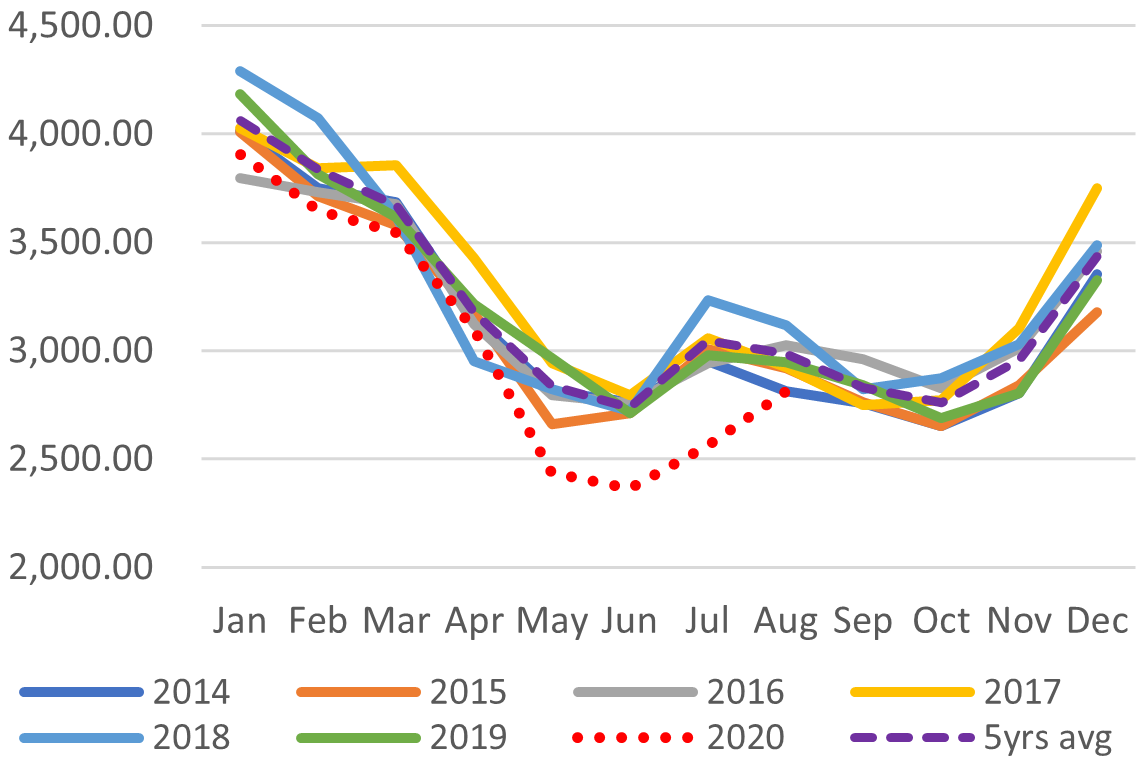

City Gas Sales – Total (M m3)

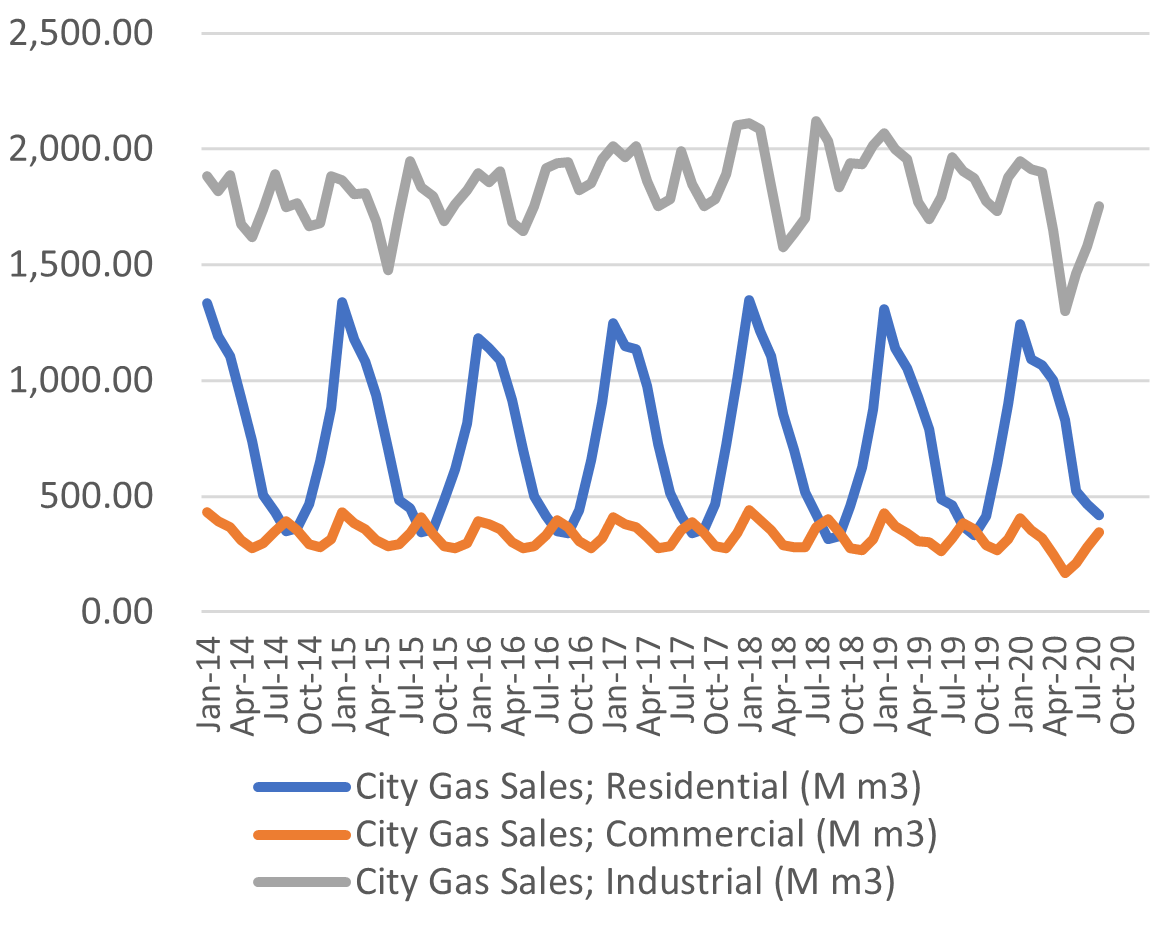

City Gas Sales by Sector (M m3)

SOURCES: the Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

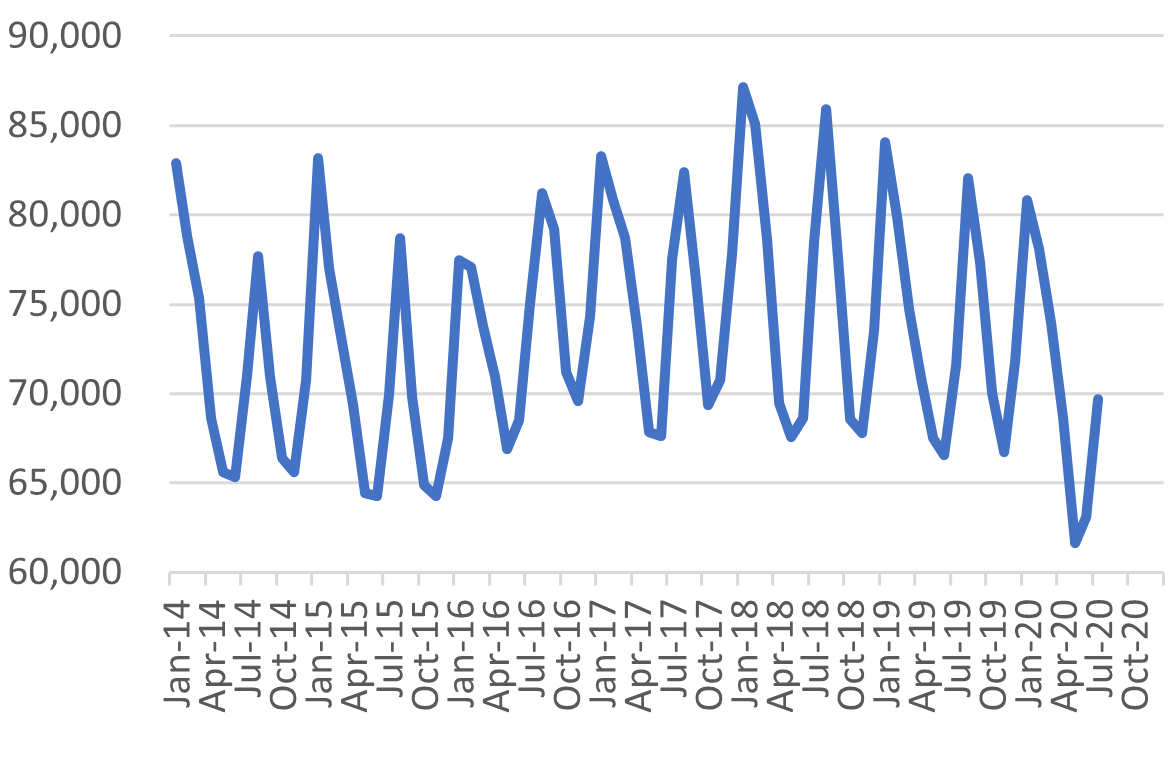

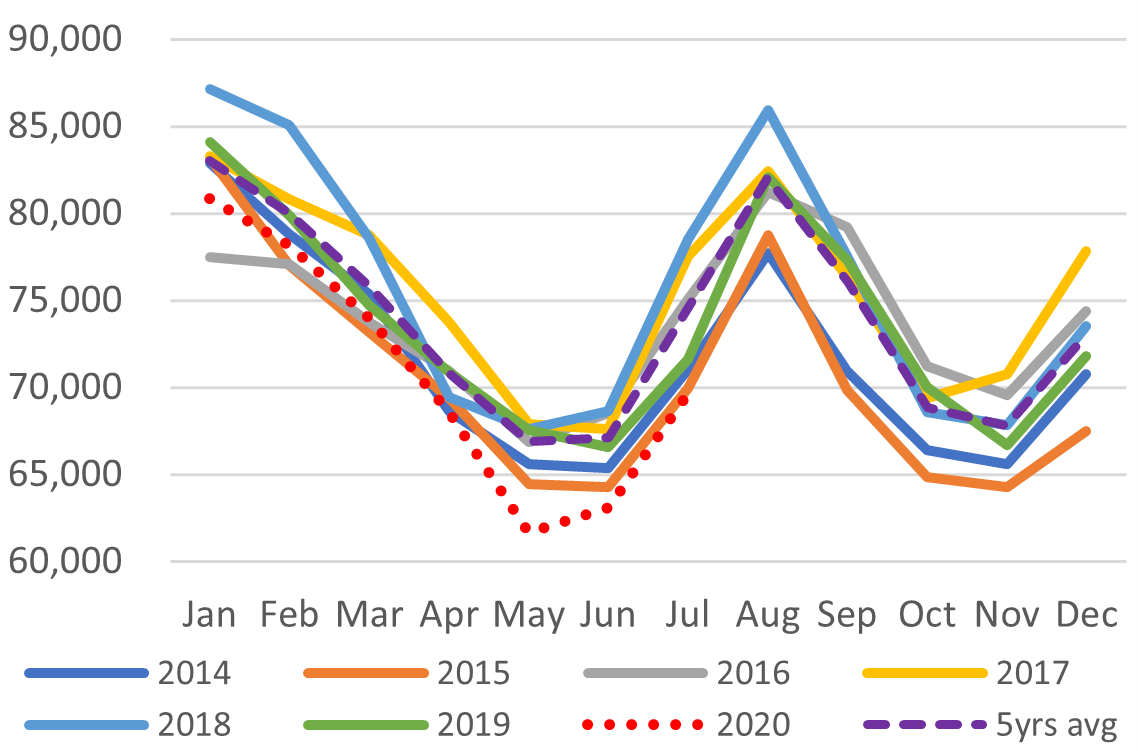

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

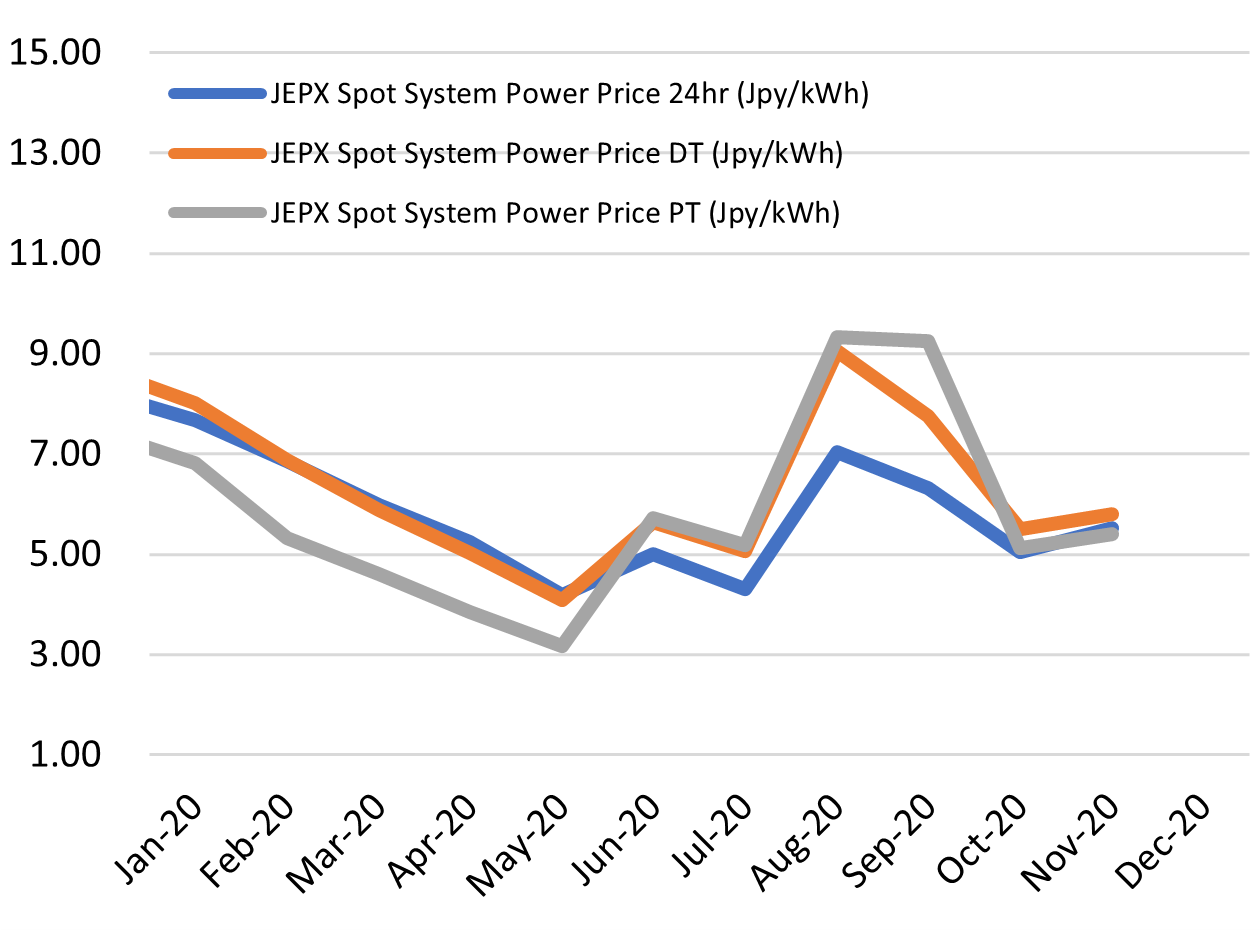

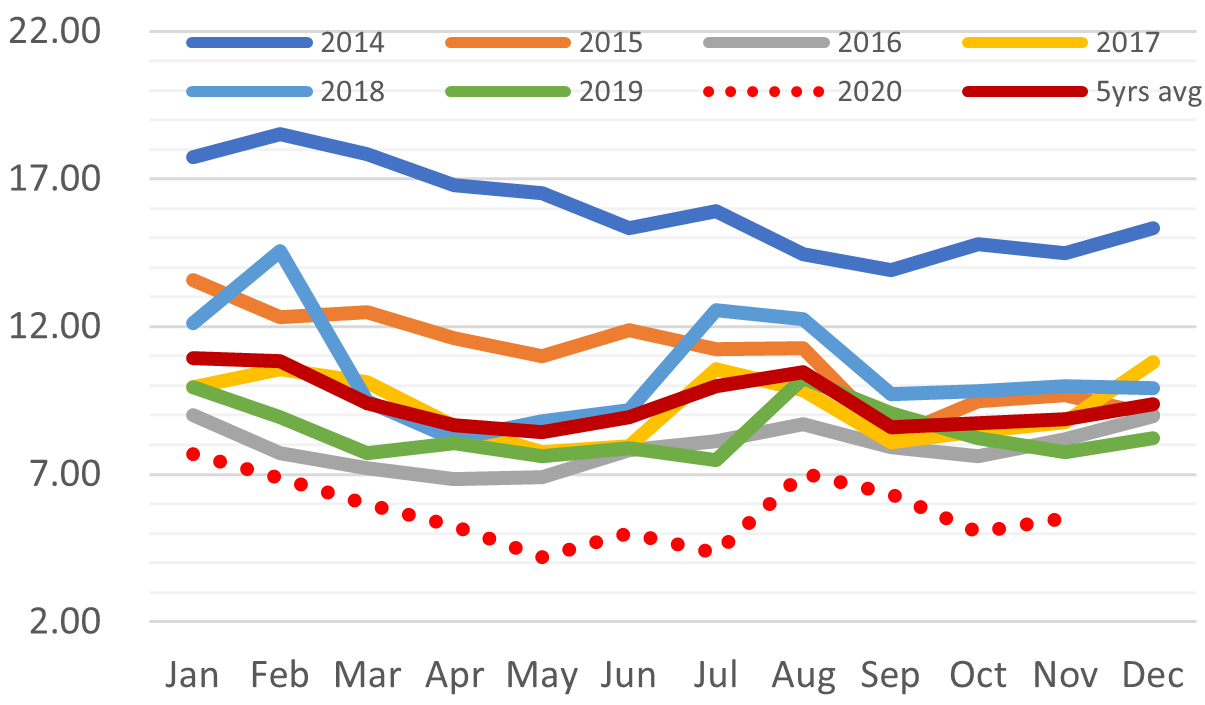

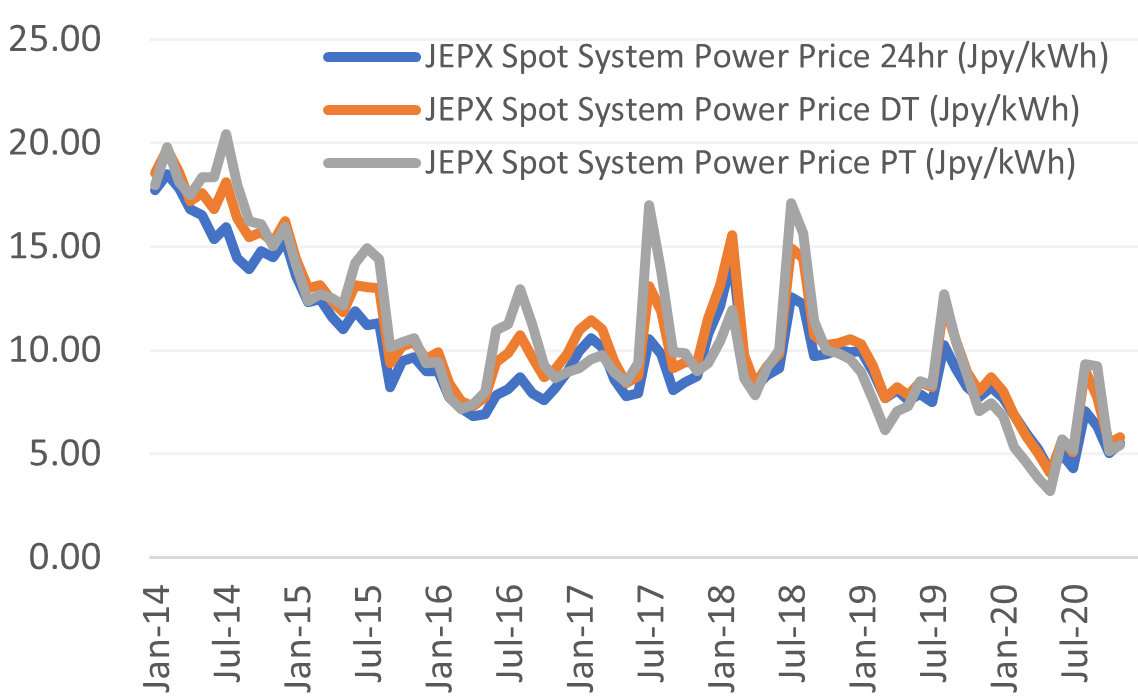

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchang