JAPAN NRG WEEKLY

NOVEMBER 30, 2020

JAPAN NRG WEEKLY

November 30, 2020

TOP

- IHI blends “blue” ammonia with natural gas to generate electricity as Japan looks for decarbonization options in the power sector; MHI invests in green hydrogen/ammonia company in Australia

- Kawasaki Heavy becomes latest major brand to exit nuclear sector with sale of all nuclear operations to a private domestic company

- Japan proposes the creation of Asia CCUS Network to share know-how on carbon capture technology and promote its use

- Nissan’s new hybrid spells the beginning of the end for the gasoline engine as Japanese carmaker shifts focus to EVs

OIL & GAS

- ANA completes first flight utilizing sustainable biofuel

- Tokyo Gas invests ¥10 billion in Indonesian gas distributor

- Idemitsu to unify gasoline service stations in goodbye to “Shell”

POWER & NUCLEAR

- Power grid oversight entity told to grow distance from utilities

- Kansai Electric delays restart of Takahama NPP Unit 4, but wins local support for bringing online older units; Shikoku Electric says it expects ruling on the restart of Ikata NPP in March

- Decommissioning bill for nuclear fuel plant seen at ¥1 trillion

- Cyberattack on nuclear regulator still disrupting staff’s daily work

- Local politicians push METI, J-Power to upgrade coal power plant

- Fukushima contaminated water release still hotly debated

RENEWABLES, OTHER

- NEDO announces funding for energy-saving projects and support for Osaka Gas, CRIEPI development of CO2 sequestration tech

- Lithium-ion battery, rare earth firms among the winners of state subsidies for supporting supply chain resilience

- Toshiba develops world’s first nonflammable lithium-ion battery

- Tokyo Gas joins Chiba offshore wind project; invests in U.S. distributed energy startup Heila Technologies

- Solar panel shipments drop 22% in July-Sept due to COVID-19

- JERA trials storage batteries to encourage renewable energy

- ENEOS issues green bonds to finance biomass power plant

THE CASE FOR MOVING FROM U.S. DOLLAR TO YEN SETTLEMENT IN REGIONAL ENERGY CONTRACTS

The time has come for Japan, and Asia more broadly, to price energy trades in the home currency. One of the world’s biggest buyers of LNG, crude oil, and coal, Japan has traditionally used the U.S. dollar to settle commodity contracts. That dollar hegemony helped standardize trade. Today, it’s creating a new systemic risk for the global financial system. In the last two years, China has already moved to price some oil and copper sales in RMB. If Japan wants to retain influence in global energy markets, it should do the same. We lay out the case for Japan and why it would also benefit the U.S. and its oil industry.

CORPORATE PPAs LAND IN JAPAN AS GOVERNMENT

BACKS NEW FORM OF PRICING FOR RENEWABLES

There are two uncomfortable facts about renewable energy in Japan. One is that despite the tripling of solar capacity in less than a decade on the back of a specialized tariff scheme, the cost of green electricity in Japan remains high. The other is a lack of adequate supply – even for companies willing to pay a premium to score ESG points with investors. There is now a mechanism that could improve the situation for both and it’s just starting to gain traction in Japan, aided by state funding. Corporate power purchase agreements (PPAs) create a direct long-term contract between an electricity generator and a big business user, thus mimicking the function of the specialized Feed-in Tariff (FIT) that the government introduced in 2012. To date, the application of PPAs in Japan was cumbersome and, because of that, costly. That is now changing.

GLOBAL VIEW

The UAE is threatening to leave OPEC. Exxon finally succumbed and lowered long-term oil price forecasts to a level that may even less than its break even. The Czechs have frozen nuclear plant tenders due to security concerns around Russian and Chinese bidders. And China is using its economic muscle to punish Australia, which has pushed down the price of Australian coal by 25%. See details on these and other political and business events in our regular Global View column.

JAPAN NRG WEEKLY

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Regular Contributors

Mayumi Watanabe

Daniel Shulman

Damon Evans

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without the prior written consent of Yuri Group, which retains all copyright to the content of this report. Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content of our reports express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS: OIL & GAS

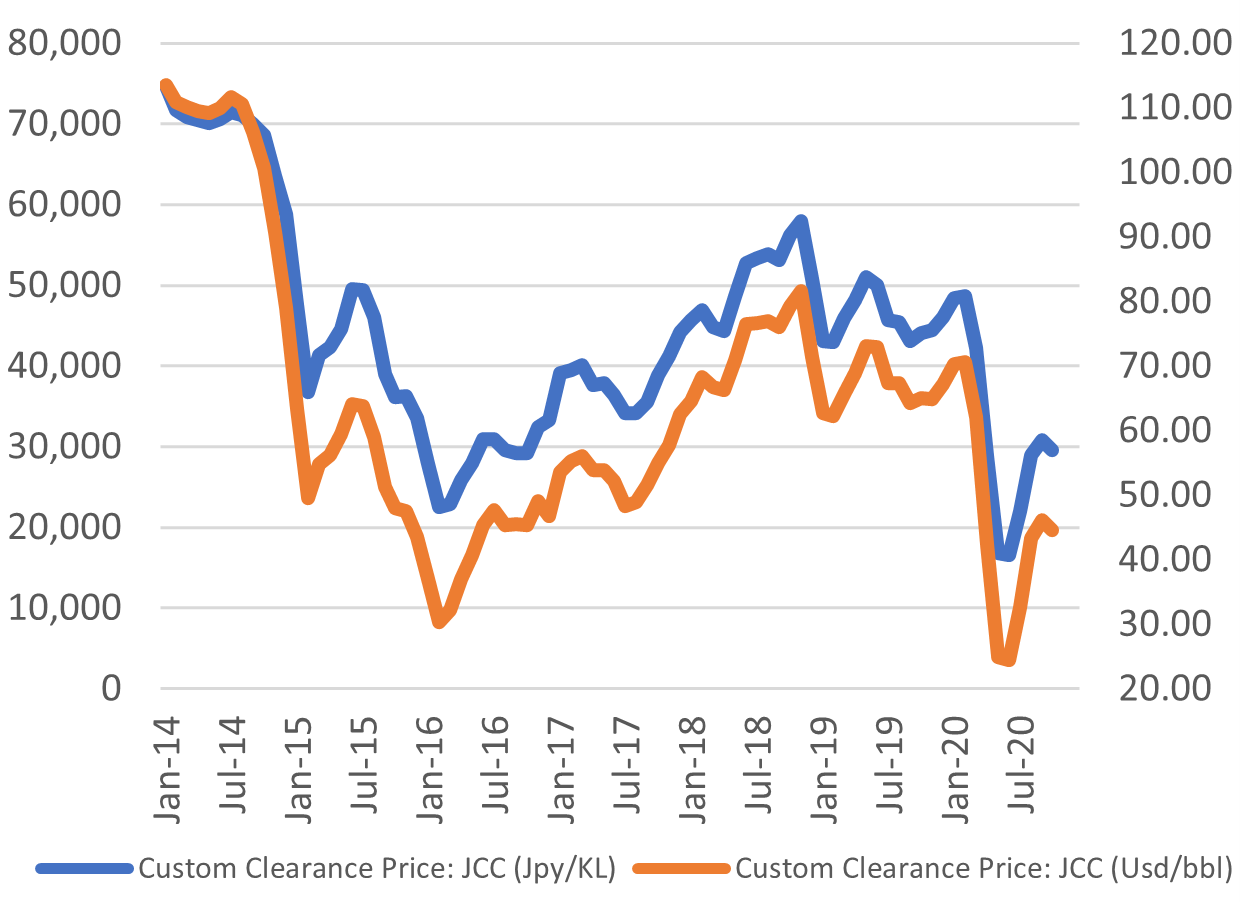

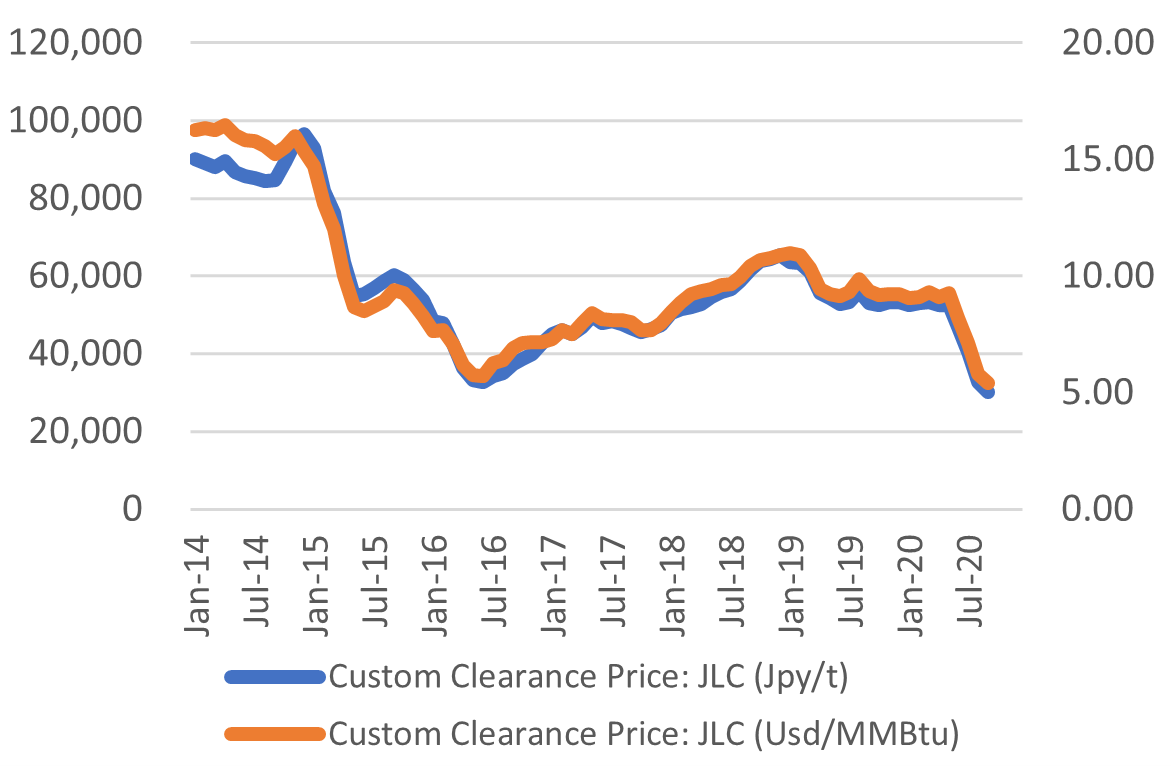

Japan Oil Price: $44.51 / barrel

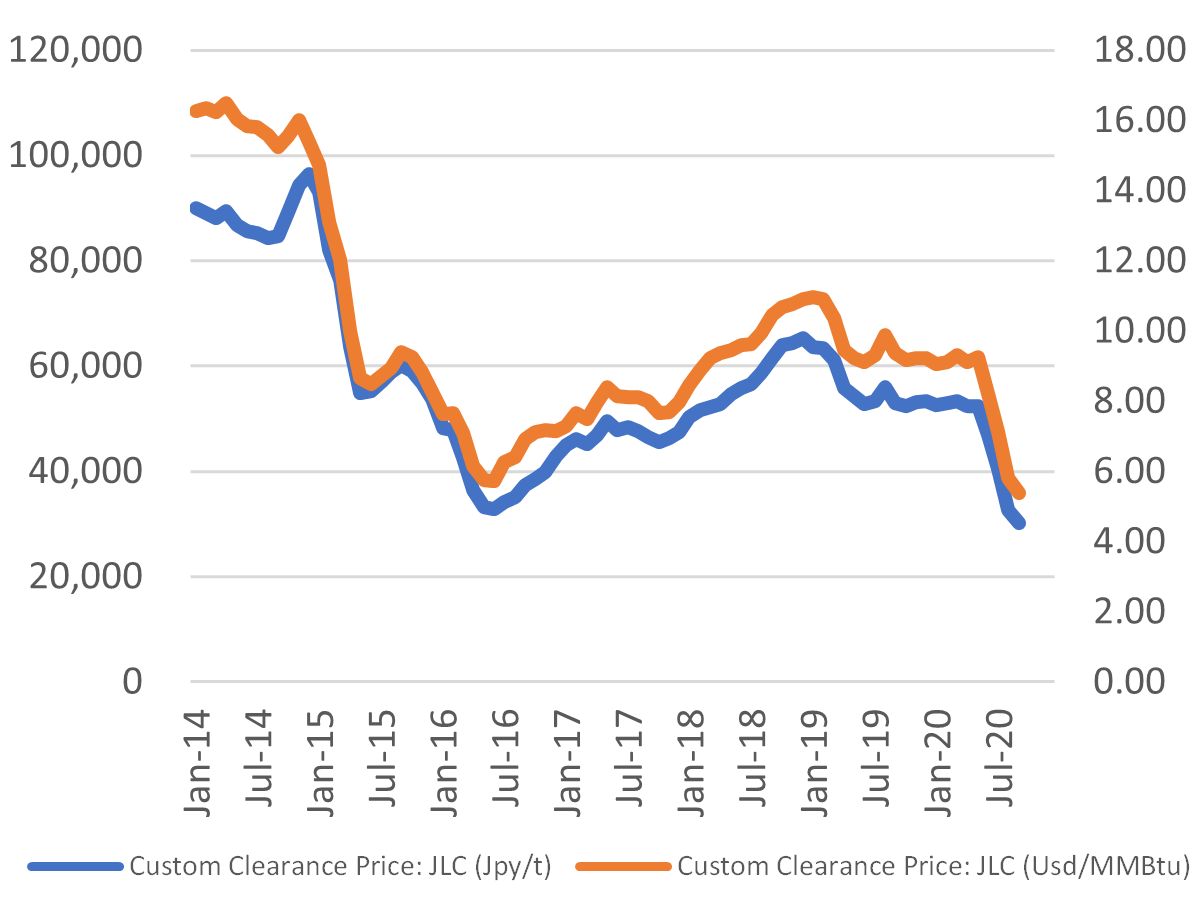

Japan (JLC) LNG Price: $5.39 per Mbtu

IHI trials “blue ammonia” blend to generate electricity

(Nikkan Sangyo Shimbun, Nov. 23)

- In a world-first, engineering company IHI is trialing “blue ammonia”— the material synthesized from natural gas using carbon sequestration technology. It will be blended with natural gas to power a 2 MW gas turbine.

- The trial is being assisted by the Institute of Energy Economics and Saudi Aramco, which will assess the viability of the blue ammonia supply chain.

- Taking place at IHI’s Yokohama plant, the trial will use 36 metric tons of ammonia.

- CONTEXT: Saudi Aramco sent the world’s first shipment of blue ammonia to Japan in September, providing the fuel for this trial. Blue ammonia is known as feedstock for blue hydrogen. Hydrogen and ammonia manufactured with electricity from renewable energy facilities is labeled as “green.”

TAKEAWAY: As discussed in detail in the Japan NRG of Oct. 19, ammonia and hydrogen are seen by Japan as one of the main solutions in decarbonizing the power sector, which is the biggest emitter of CO2. The general idea is to start by blending ammonia / hydrogen with gas and use both to fire the power turbines. The end goal is to switch thermal generation to ammonia or hydrogen only. Provided that hydrogen is at least blue or green, it would allow thermal power to be classified as carbon-neutral.

- SIDE DEVELOPMENT:

Mitsubishi Heavy invests in green hydrogen and ammonia business in Australia

(New Energy Business News, Nov. 30) - Mitsubishi Heavy Industries agreed to invest in H2U Investments, the holding of Hydrogen Utility (H2U), which is an Australian company that develops green hydrogen and ammonia business lines.

- H2U plans to build a hydrogen production plant using water electrolysis and renewable energy-derived electricity, such as offshore wind and solar power. It also plans an ammonia production plant and a hydrogen gas turbine demonstration project on the Eyre Peninsula in south-west Australia. It expects to start producing green hydrogen and ammonia at the end of 2022.

- Mitsubishi Heavy Industries, Ltd. will participate in the study from the design specification stage and promote the project with a view to supplying major equipment such as hydrogen gas turbines and hydrogen compressors.

- Future export of green hydrogen and ammonia to Japan and other countries is on the agenda.

ANA makes first flight with sustainable fuel

(Mainavi News via Yahoo News, Nov. 25)

- All Nippon Airways completed its first flight powered by biofuel, making it the first Asian airline to do so.

- The flight, a delivery of a Boeing 787 from the American manufacturer’s Everett factory to Narita Airport, was powered by Neste MY sustainable aviation fuel.

TAKEAWAY: In the Nov. 9 edition of Japan NRG, we detailed the efforts of ANA to secure what is known as sustainable aviation fuel (SAF). The airliner has signed contracts with at least three potential suppliers of biofuel and is working to meet global aviation regulations that seek decarbonization for the industry.

Tokyo Gas invests ¥10 billion in Indonesian CNG industry

(Nikkan Kogyo Shimbun, Nov. 27)

- Tokyo Gas said on Nov. 26 that it had acquired a 33.4% stake in Super Energy, a subsidiary of Super Capital Indonesia, and an 18% stake in Super Energy subsidiary Energy Mina Abadi.

- The purchase is valued at around ¥10 billion and represents the largest ever investment in an overseas gas utility by a Japanese company.

- Super Energy supplies 50 million cubic meters of CNG every year, but the company plans to eventually increase this amount to 250 million cubic meters.

- CONTEXT: This is the fifth overseas investment into a gas distribution firm by Tokyo Gas. The company opened an office in Indonesia in 2015 and has been looking to expand aggressively in the local market due to its fast demand growth for natural gas.

Idemitsu to integrate gasoline stations branding

(Nikkei, Nov. 25)

- Beginning in April, Idemitsu Kosan will rebrand all of its service stations using the “apollostation” brand.

- Since absorbing Showa Shell in 2019, Idemitsu’s network of 6,400 gasoline service stations has been characterized by mixed branding, with some using the face of Apollo, the Greek god of the sun and light, and others the red and yellow “Shell” logo.

NEWS: POWER & NUCLEAR

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 3 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

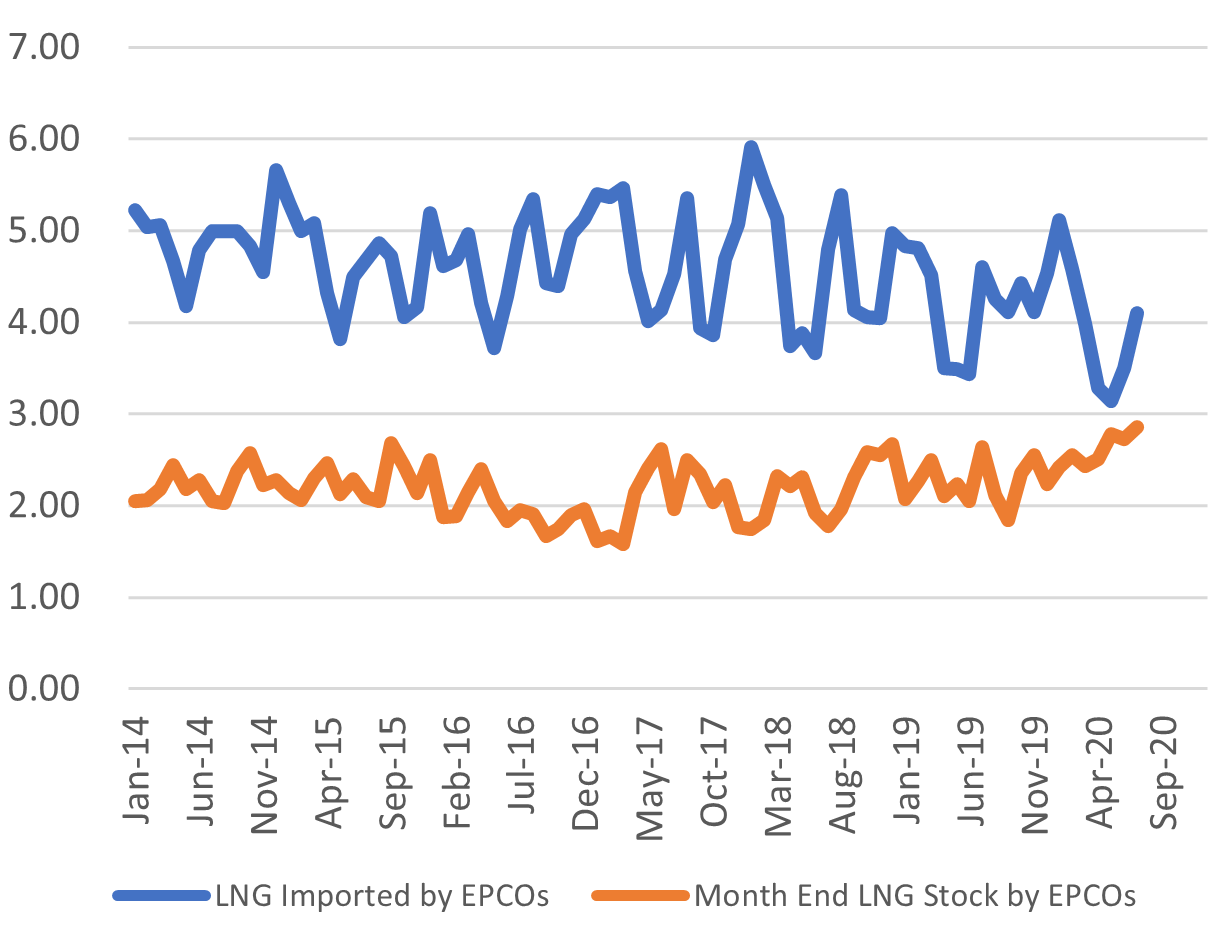

Power Utilities’ LNG Imports Vs Stockpiles

Source: Company websites, JANSI and JAIF, as of Nov. 25, 2020

Kawasaki Heavy engineering giant says it will sell all nuclear operations

(SankeiBiz, Nov. 25)

- Since Kawasaki Heavy Industries announced on Nov. 24 the sale of its nuclear power operations to Tokyo-based Atox for an undisclosed sum.

- Kawasaki does not disclose how much revenue it earns from nuclear operations.

- While Kawasaki provides design and maintenance services to the nuclear industry, its offerings are uncompetitive. Kawasaki will now focus on the hydrogen sector, which is projected to grow.

- Kawasaki Heavy Industries began serving the nuclear power industry in 1969. Kawasaki equipment has been used in many nuclear power stations, including Japan’s first commercial nuclear power station, the Tokai station.

- CONTEXT: Atox began life as a maintenance firm for nuclear facilities and is now an integrated engineering company, dealing both in a broad range of nuclear services, including fuel reprocessing, and in medical equipment related to radiology. The company has offices adjacent to most nuclear power plants in Japan.

TAKEAWAY: At first glance, this is the story of another famous Japanese engineering brand giving up on the nuclear business, joining Toshiba, IHI, and others. Another way to look at it, however, is as a transfer of nuclear assets away from listed companies to private firms that face less scrutiny from the public and the investment community, and which have less pressure on short-term earnings. For a listed firm like Kawasaki Heavy, it’s more profitable to deliver investors a growth narrative around hydrogen as the company pioneers ships to transport the fuel. This does not necessarily mean the future of the nuclear business is over. Still, it is also true that spending on nuclear plant upgrades in Japan is down (-5% during fiscal 2019 versus a year earlier). The initial spurt of investment by the power utilities to upgrade NPPs so that they can be restarted is over and there is little compulsion for the plant operators to keep spending unless more NPPs come online. While Japan’s nuclear industry, for now, retains its staff and resources, the vast majority of the people involved see the outlook as “bad”, according to a recent survey by the Japan Atomic Industrial Forum Inc (JAIF). What the same survey showed was that the Japanese nuclear industry wants clear direction and support from the government in order to continue. The unveiling of the new Japan energy mix target around spring will show whether Kawasaki Heavy’s decision was justified.

Grid oversight entity told to become more independent, draw distance with utilities

(Japan NRG, Nov. 29)

- CONTEXT: The electricity grid is overseen by a private entity rather than a regulatory authority. The Organization for Cross Regional Coordination of Transmission Operators (OCCTO) is, however, enshrined in the Electricity Business Act and has the authority over the transmission grid across the private utilities’ respective operational areas. OCCTO also coordinates power supply and demand nationwide, and promotes the construction of infrastructure to move electricity across Japan’s various separate grid systems. OCCTO was set up in 2015 and took over from the Electric Power System Council of Japan.

- A working group at OCCTO turned in its assessment of the entity’s activities and this was published by METI.

- The group suggested that OCCTO appoints an audit firm to conduct annual reviews and reduce its seconded staff from power utilities to assure neutrality, among other recommendations.

Takahama Unit 4 restart delayed by over a month on finding faults

(Nikkei, Nov. 27)

- The Kansai Electric Power Companies said on Nov. 25 that cracks had been found in four pipes connected to the steam generator of Unit 4 at the Takahama Nuclear Power Plant (NPP).

- Anomalies suggested during preliminary testing were confirmed by camera inspection.

- Further inspections are now required, meaning the restarting of the reactor, initially scheduled for January, will be delayed by at least a month.

- SIDE DEVELOPMENT:

Takahama NPP wins locals support as 40+ age limit of reactors extended

(Nikkei, Nov. 25)- The government of Takahama, the town where the Takahama nuclear power station is located, agreed on October 25 to allow the plant’s oldest two reactors to be restarted (Units 1 and 2), a nationwide first for reactors aged over 40.

- Japanese law allows reactors to operate for an additional 20 years after the end of their 40-year design life if they are deemed to be safe.

- CONTEXT: To achieve the government target of procuring at least 20% of the nation’s electricity from nuclear facilities by 2030-31, 90% of the country’s 35 operable reactors (this figure includes units still under construction) would need to be operating by 2030.

TAKEAWAY: As Japan NRG forecast earlier this month in our nuclear reactor status table, Takahama NPP’s Unit 1 will not be generating electricity until March and unit 2 not until late May or June. With Unit 4 also now delayed until around March, Kansai Electric is coming to a make-or-break moment. If the local support the company gained at the municipality level in Takahama is repeated at the prefectural government level, then it will be able to have all four units of Takahama NPP, as well as its Mihama NPP and Ohi NPP, all online and generating electricity by the summer of 2021. This would drastically change the company’s profit and its CO2 emissions levels, as we described in the Nov. 16 Japan NRG edition. The problem, however, is that to date the comments from prefectural level have been hostile. We expect intense lobbying on nuclear over the next few months.

- SIDE DEVELOPMENT:

Shikoku Electric says ruling on restart of Ikata NPP may come by March

(Asahi Shimbun, Nov. 25)- Co. said on Nov. 24 that it will go ahead with works to add plant upgrades based on new counterterrorism regulations even without a final decision in its court proceedings over the restart of the Ikata NPP Unit 3 still ongoing.

- Co. said it expects to hear a ruling from the Hiroshima High Court in March. If the utility wins the case, it still needs to complete the plant upgrades before the nuclear reactor can restart operations.

- CONTEXT: the utility’s operations of the NPP was frozen by a court ruling at the start of 2020 based on citizen concerns over safety.

One-trillion-yen bill for decommissioning of Tokaimura nuclear fuel plant

(Mainichi Shimbun, Nov. 23)

- While the Tokaimura reprocessing plant, which was operated by Japan Nuclear Fuel until 2007, was only operational for 25 years, the decommissioning of the plant is projected to take over seventy years and cost over ¥1 trillion.

- The plant was built to reprocess high-level nuclear waste as part of a “recycling” policy promoted by the government at the time.

Nuclear Regulator’s top-secret documents “unlikely” to have been accessed but system remains shut down

(Yomiuri Shimbun, Nov. 27)

- The police investigation into last month’s cyberattack on Japan’s Nuclear Regulation Authority revealed that the intruders got access to undisclosed meeting materials. Who is behind the attack is not yet known.

- According to the police investigation, the attackers got access to a system used to send and receive emails of the agency’s 1,200 staff and to shared business files. Private meeting notes and accounting materials, such as instructional documents, and government information security standards were stored in those areas.

- However, the attack on Nov. 26 did not compromise the top-secret materials such as nuclear power plant blueprints and crisis management systems, which are stored in a separate system. It is “unlikely” that the intruders got access to those materials.

- The full extent of the damage and the manner of the intrusion is still not known. As of this month, the system has remained shut off, and regulatory officials have been unable to access the internet or external emails, and have been communicating by phone or fax.

TAKEAWAY: Apart from the obvious security concerns that such a cyber-attack raises, the question for the nuclear industry will be how well the NRA can continue to do its job and whether there will be any delays in ongoing plant restart assessments due to agency staff not having access to their usual work systems.

Local politicians push METI to prompt J-Power to upgrade coal power plant

(Nagasaki Shimbun, Nov. 20)

- Nagasaki Deputy Governor Hirata Ken visited the Ministry of Economy, Trade and Industry on Nov. 19, along with the mayors of three cities in the prefecture, to request the replacement of Units 1 and 2 at the Matsushima coal-fired power station, which is operated by J-Power.

- The four politicians presented METI official Ando Hisayoshi with a letter that stressed their strong desire for action. A J-Power spokesperson said on Oct. 30 that the utility is considering replacing the units.

- The local bodies have asked that the older units are replaced with integrated coal gasification combined cycle technology, which is more efficient and less pollutant. There is also concern about the future of the 500 workers employed at the plants.

TAKEAWAY: Japan has said it will phase out inefficient coal-fired power plants by 2030 to cut CO2 emissions. This move by local politicians is a way to preserve the power plant and the jobs there by switching it to more efficient thermal generation, which would pass the new METI criteria.

Despite reassurances, concerns remain about Fukushima contaminated water release

(Mainichi Shimbun, Nov. 26)

- In an October Diet hearing, Abe Tomoko, a Diet member affiliated with a nonpartisan group of politicians that lobbies to end nuclear power, asked Ministry of Economy, Trade and Industry officials about the effect of tritium (a radioactive isotope of hydrogen) on the environment, and called for data to be published on how much tritium specifically was being discharged into the sea.

- While a decontamination system operated by TEPCO is able to reduce the concentration of strontium and other radioactive isotopes contained in contaminated water at the reactor site, it is not able to remove tritium.

- METI responded by saying that even if the entire 860 trillion Becquerel of tritium currently stored in tanks at the reactor site were to be released over the course of a year, it would amount to less than 1/1000th of natural background radiation.

- SIDE DEVELOPMENT:

Fukushima 10 years on: we look at the radiation levels in Tokyo Bay

(Tokyo Shimbun, Nov. 25)- Periodic testing of core samples taken in Tokyo Bay and the Hanami River have found that levels of radioactive cesium 134, which has a relatively short half-life, are now 30 times lower than they were immediately after the accident.

- Most of the radioactive cesium detected in core samples now comprises cesium 137, which has a half-life of 30 years. While radioactive cesium levels fell rapidly in the years after the accident, the curve is now more gradual.

- Results show that seabed contamination extends to a depth of at least 35 cm.

TEPCO subscribers complain about the utility’s sudden move to paperless billing

(Toyo Keizai, Nov. 25)

- TEPCO abruptly phased out physical power bills in December, in a move designed solely to suit itself. Subscribers only received one warning of the change, in October, and many overlooked this notice, only to receive a shock as December approaches. Even TEPCO’s website contains little helpful information.

- Many subscribers have taken to social media to criticize the change, and the Tokyo Metropolitan Government’s consumer protection center has also received many complaints.

NEWS: RENEWABLES & OTHERS

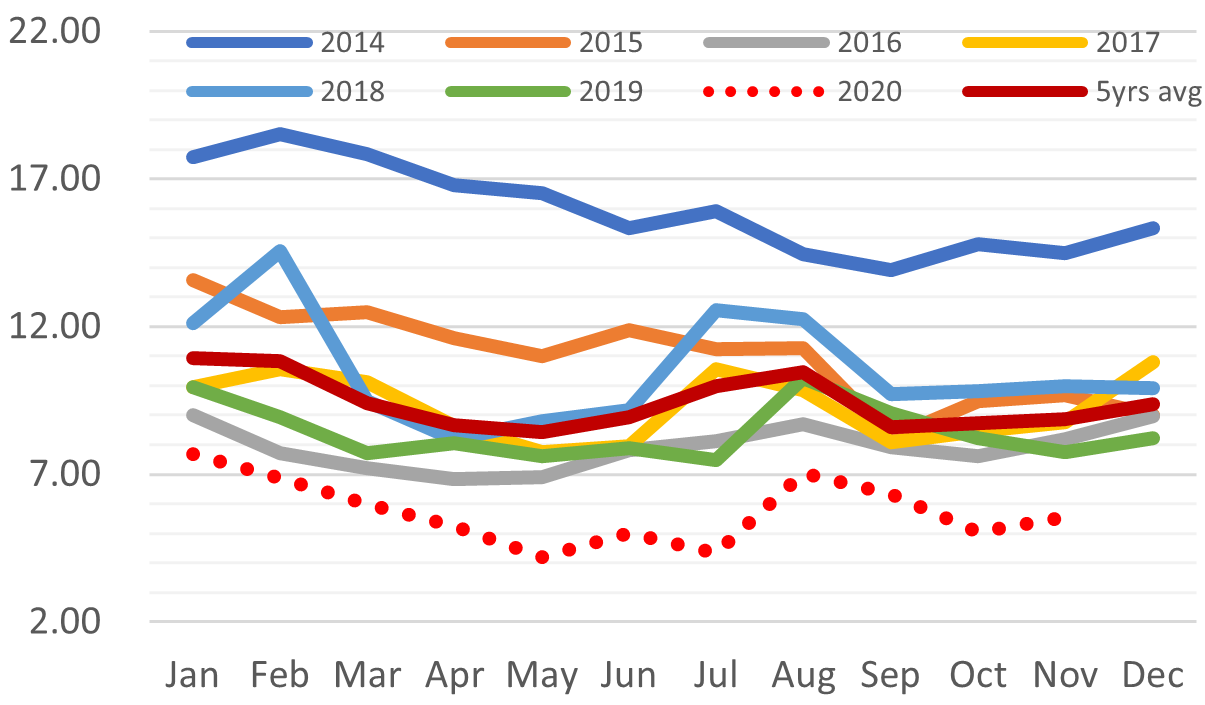

Spot Electricity Prices (24h)

Spot Electricity Prices (2020)

Japan proposes creation of Asia CCUS Network to share know-how on carbon capture

(Japan NRG, Nov. 29)

- Japan took part in the energy ministers’ meeting of the ASEAN+3, also known as the East Asia Summit (EAS). The meeting, which was held online for the first time, was attended by 10 ASEAN countries, as well as representatives from Japan, China, South Korea, Australia, India, New Zealand, Russia, and the U.S. Japan’s delegation was led by Minister of Economy, Trade and Industry Kajiyama. Below comes from the joint statement, as published by METI.

- Japan’s research projects through the Distributed Generation Initiative, as well as efforts to realize decarbonization of the hydrogen and transportation sectors, were welcomed by other ASEAN ministers.

- Japan also proposed construction of the “Asia CCUS Network” as a platform for sharing knowledge and improving the environment for the utilization of CCUS throughout the region, and each country welcomed it.

Lithium-ion battery maker and rare-earths firm among winners of state subsidies for supply chain resilience

(Japan NRG, Nov. 29)

- List of subsidies published by METI. Japan vowed to increase support for industries vital to the supply chain after the COVID-19 pandemic cut supplies from overseas companies.

- Medical and healthcare goods manufacturers, including makers of masks and alcohol disinfectant dominate the list.

- Envision AESC Japan Co., Ltd. won state support for its lithium-ion battery business.

- Shin-Etsu Chemical Co., Ltd. won subsidies for making products from rare earth materials.

NEDO announces extraordinary green technology grants for energy-saving

(New Energy Business News, Nov. 25)

- The New Energy and Industrial Technology Development Organization says it will fund 11 new projects to conduct further research into energy-saving technologies.

- The additional projects were selected on an emergency basis in response to the changes in society and industry brought about by the coronavirus pandemic.

- Mabuchi Engineering received a grant to research low-cost electricity generation systems that apply scroll compressor technology.

- U-MAP will develop new thermo-conducting materials that will enable power modules to be installed more densely.

- SIDE DEVELOPMENT:

NEDO to fund CRIEPI, Osaka Gas to develop sequestration technologies

(New Energy Business News, Nov. 27)- NEDO is funding the Central Research Institute of Electric Power Industry to develop CO2 recovery polygeneration technologies that work with a diverse range of fuels.

- NEDO will also fund an Osaka Gas/JCOAL projects to develop CO2 separation and recovery technology.

- A total of ¥3 billion will be allocated to the projects.

- The projects aim to boost efficiency by integrating the gasification, separation, and recovery processes.

TAKEAWAY: NEDO investments can be seen as a precursor to commercialization of a technology in Japan. Not all the projects that the state-backed entity supports make the cut, but it does give a useful indication of what policies are in favor and which are progressing towards mass utilization.

Nissan’s new hybrid spells beginning of the end of gasoline-engine

(Asia Nikkei, Nov. 26)

- Nissan unveiled a revamp of its bestselling car in Japan, the Note, and said it will be available only as a hybrid.

- Unlike the hybrid technology of Toyota, which uses both electric and gasoline power to run the engine, Nissan’s hybrid technology uses the gasoline engine only to generate electricity. Nissan’s motor is electric-powered, which makes it closer to an EV.

- Nissan executives said at the launch that the company will focus all resources on electrification. This begins the phase-out of the internal-combustion engine and the race by Nissan to bring down EV costs to that of gasoline cars.

- The new Note goes 60% further on a tank of gas than the current gasoline version.

- Nissan wants the ratio of EVs and hybrids to be 60% of all vehicles its sells in Japan within three years. In China, the carmaker will switch all models to EV or hybrid.

Toshiba develops world’s first nonflammable lithium-ion battery

(New Energy Business News, Nov. 24)

- In a world-first, Toshiba has developed a rechargeable, water-based lithium-ion battery that can operate at temperatures as low as -30°C.

- Toshiba’s battery contains no flammable substances, allowing it to be used in a wider range of applications than conventional lithium-ion batteries.

- Each cell in the battery is capable of developing 2.4 V. This is still lower than the 3.7 V achieved by conventional cells.

Tokyo Gas joins Chiba offshore wind project

(New Energy Business News, Nov. 26)

- Tokyo Gas has joined the Chiba offshore wind project established by Canadian renewables firm Northland Power and Shizen Energy Inc.

- To make the windfarm project possible, a team of 30 staff from the two companies is working to have the area off the coast of Chiba classified as a redevelopment area by the local government.

- CONTEXT: Tokyo Gas has a goal of having 5 GW of renewable generation capacity worldwide by 2030.

- SIDE DEVELOPMENT:

Tokyo Gas invests in U.S. distributed energy startup Heila Technologies

(Company press release, Nov. 20)- Acario Investment One, a unit of Tokyo Gas, made the investment.

- Heila Technologies develops and sells integrated DER (Distributed Energy Resources) control systems for energy micro-grids.

- Tokyo Gas said the investment will help it acquire expertise in supply and demand adjustment and operations through the integrated control of DERs, and will allow the company to develop new energy businesses, such as micro-grids that utilize DERs, in Japan and abroad.

- CONTEXT: This is the fourth investment by Tokyo Gas in an overseas start-up.

Solar panel shipments drop 22% in Japan during July-Sept. due to the pandemic

(Nikkei Shimbun, Nov. 27)

- Figures released by the Japan Solar Power Association show a drop in both the panels for larger projects and rooftop units. The biggest demand drop came from SMEs, which have been hit hard by the COVID-19 pandemic.

JERA trials storage batteries to encourage renewables use

(Nikkei, Nov. 25)

- JERA, a joint venture between TEPCO and the Chubu Electric, said on Nov. 25 that it had commenced a trial to analyze utilization of storage batteries by commercial customers.

- The trial will take place in a manufacturing plant in Aichi prefecture.

- During the trial, JERA will publicize information on the times of the day during which battery capacity is at a surplus, and make proposals to its commercial clients about ways to make smarter use of electricity.

Residents of Japan’s most nuclear-heavy area are skeptical about premise of wind power

(Fukui Shimbun, Nov. 24)

- A recent feature on an offshore windfarm plan for Fukui has generated a skeptical response from Fukui Shimbun readers, who doubt that renewables will be able to replace Fukui’s aging nuclear power plants.

- The proposed wind farm would radically change the skyline, as the turbines could be as high as 260 m, which is three times higher than Fukui’s tallest building.

- Two proposals are currently being considered, one from Hokuriku Electric Power, Chubu Electric Power and OSCF, and the other from J-Power and Mitsui Fudosan.

- CONTEXT: Fukui has the biggest concentration of nuclear power plants of all Japanese prefectures. It is home to all of Kansai Electric’s nuclear facilities.

ENEOS issues green bonds to finance biomass power plant in Hokkaido

(Sekiyu Tsushin, Nov. 27)

- ENEOS Holdings said on Nov. 25 that it was issuing a third tranche of unsecured green bonds to finance a biomass fired power plant to be constructed in Hokkaido.

- A total of ¥15 billion worth of bonds will be issued in denominations of ¥100 million. The bonds pay interest of 0.02% and mature on Dec. 1, 2023.

Work begins on 50MW Kamisu biomass power station

(Kensetsu Tsushin Shimbun, Nov. 27)

- Kamisu Biomass Hatsudensho GK, a joint venture between the Chubu Electric, Mitsubishi UFJ Lease, Solariant Capital, and Biofuel Co., began work on the construction of its Kamisu Biomass power plant on Nov. 25.

- The contract to build the station has gone to a venture between Hitachi Zosen and Okamuragumi.

- The 50 MW plant will be fueled by palm kernels.

ANALYSIS

TOM O’SULLIVAN

In Regional Oil & Gas Energy Trading

The time has come for Japan, and Asia more broadly, to price energy trades in the home currency. One of the world’s biggest buyers of LNG, crude oil, and coal, Japan has traditionally used the U.S. dollar to settle commodity contracts. That dollar hegemony helped standardize trade. Today, it’s creating a new systemic risk for the global financial system.

In the last two years, China has moved to price some oil deals in RMB. Earlier this month it started copper futures trading in RMB. If Japan wants to retain influence in global energy markets, it should do the same.

Historically, the dollar-based WTI and Brent oil indices have been used to price crude oil transactions in Asia as well as around the world. The Japan LNG price index, JCC, is linked to crude oil prices. Most oil and natural gas trades in the Asian time zone are settled in U.S. dollars. This is sometimes referred to as the petrodollar cycle.

This cycle can create an excess of dollars in oil and gas producing countries that flows back to U.S. capital markets, sometimes creating financial instability. The 2007-2008 global financial crisis was widely attributed to an overflow of Middle-East petrodollars creating an excess of liquidity and an underestimation of credit risk. Credit derivatives and other financial instruments were not the cause of the financial crisis but a by-product of excess dollar liquidity coupled with high oil prices.

Continuing with dollar hegemony, in place since at least the 1971 collapse of the Bretton Woods Agreement, we risk another financial crisis as a cyclical recurrence.

Moreover, the dollar link is no longer supported by the energy market fundamentals. Asia and the Pacific already consume over half the world’s energy, and since 2000 Asia alone has accounted for about 70% of the growth in global energy consumption. Demographic and wealth forecasts suggest this skew to Asia will only accelerate, and it makes sense for energy contracts to reflect the dynamics of the buyers’ markets.

A few months ago, Japan’s LNG buyers asked producer nations and companies to start moving pricing to benchmarks that better reflect Japanese domestic market fundamentals. We expect to see similar calls in other commodifies and from other Asian countries.

The benefits to introducing multi-currency settlement for Asian energy trading would be felt globally, not just in Asia itself. These upsides include:

- An increase in global financial stability;

- Greater multi-currency liquidity, which motivates more global trade;

- Closer alignment between price indices and real consumption, which helps to improve energy efficiency;

- A knock-on effect of decreasing excess volatility in commodity prices.

A break between the dollar and oil trade would put a circuit-breaker in the established trend of oil prices weakening when the U.S. currency is strong, which is an impediment to growth of the U.S.’s own oil industry.

Furthermore, a multi-currency settlement regime would beneficially weaken the U.S. dollar by helping to restore the competiveness of U.S. manufacturing. The exorbitant privilege of one dominant currency typically has a price associated with it: the weakening of ‘Main Street’ and the prosperity of ‘Wall Street’ exacerbating income inequality. The growing U.S. debt globally has not been matched by the U.S.’s share of global output, which continues to decline.

Indo-Pacific and the Japanese Yen

A Free and Open Indo-Pacific (‘FOIP’) has become an important diplomatic goal for Japan. This goal can only be achieved through actual policies such as trade, defense and greater use of regional currencies. The Regional Comprehensive Economic Partnership (‘RCEP’) trade agreement was signed recently. In the area of currencies, RCEP lacks proper implementation tools. Promotion of internationalization of the Japanese Yen could be used to promote FOIP.

With regard to LNG, we see scope for several specific measures.

- Japan could contribute to Asian economic development by providing yen-based loans to the 10 ASEAN countries.

- ASEAN nations can then accumulate yen based on sales of LNG and use the accumulated Japanese currency to repay the Japanese loans.

- The broader roles of the Japan Stock Exchange, which now includes the Tokyo Commodity Exchange and yen bond markets, could be achieved through promoting the usage of the yen along with yen settlement of LNG trades.

Non-U.S. commodity producers have periodically discussed moving pricing to their own currency with little to no success. Ultimately, energy consumers chose not to take on the additional currency risks of the Russian ruble, for example, since the economic condition of the producer bares little relation and impact on the consumer’s needs.

The purchaser’s economy and currency environment, however, directly affects what energy must be acquired and how. It is not surprising then that when Russian oil companies tried to move away from the greenback, they accepted the currency of the buyer – China – as their settlement basis.

While China has bought some oil from Russia via contracts denominated in the RMB since late 2015, the world’s biggest oil importer only moved to create yuan-denominated oil futures in 2018, launching the contracts on the Shanghai exchange. At first, the move was viewed as national vanity and mostly ignored. And yet, by the summer of 2020, Shanghai International Energy Exchange (INE) had gained a 10.5 percent share of the global crude oil contracts, according to Bloomberg data.

China’s clout in oil markets allowed this foray. Japan’s even stronger clout in LNG indicates the country should follow suit to protect its global economic position.

There may always be geopolitics involved in currency and the energy trade. This time the economic rationale is even stronger. And, the U.S. has as much to gain from the shift to a multi-currency settlement regime as Asian buyers.

IMPACT ON THE U.S. SECTOR

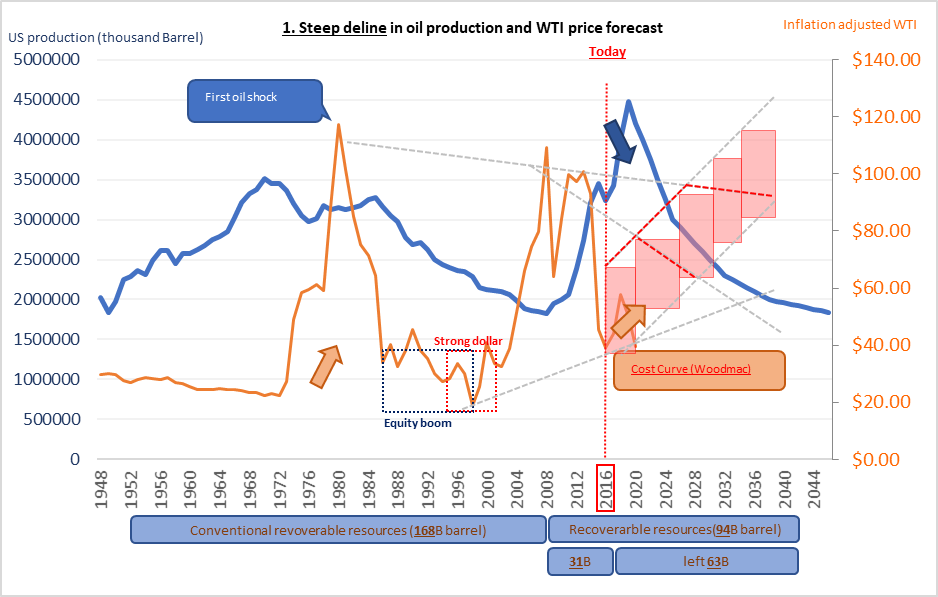

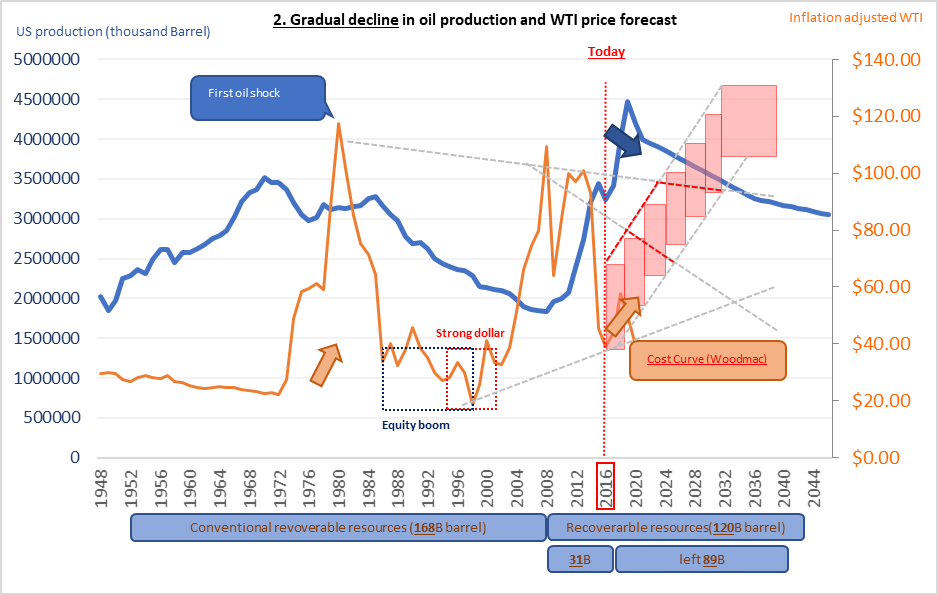

This year, several developments with currencies shed light on the future of the oil price. By May, U.S. onshore production dropped by almost a quarter compared with the end of last year, and some predict that these volumes will never return. Hence, the recent spate of M&A in the oil sector in the U.S. The question is how much will the oil price accommodate the pace of decline in U.S. production. We looked at two scenarios, below, which consider oil prices based on the cost of U.S. shale production and reserves data. Without the de-linking of the U.S. dollar to oil contracts, our calculations suggest that the U.S. might need to have oil prices at around $80 / barrel in 2028 and $100 / barrel in around 2034 to avert further output declines.

ANALYSIS

New Government Support to Spur Uptake Amid Renewables Push

There are two uncomfortable facts about renewable energy in Japan. One is that despite the tripling of solar capacity in less than a decade on the back of a specialized tariff scheme, the cost of green electricity in Japan remains high. The other is the lack of adequate supply – even for companies willing to pay a premium to score ESG points with investors.

There is a mechanism that could improve the situation for both and it’s just starting to gain traction in Japan, aided by state funding. Corporate power purchase agreements (PPAs) create a direct long-term contract between an electricity generator and a big business user, thus mimicking the function of the specialized Feed-in Tariff (FIT) that the government introduced in 2012. To date, the application of PPAs in Japan has been cumbersome and, because of that, costly. That, however, is now changing.

More than eight years since the launch of FIT, the goal of promoting wider use of renewable energy in Japan has been met. Investment has poured in to drive the supply side. However, the premise that this would result in a lower levelized cost of electricity (LCOE) for solar, wind and other renewables has not been realized.

The government’s spending on FIT, and Japanese consumers’ electricity bill surcharges to cover it, have ballooned tenfold. The average “green” surcharge per household is up to ¥767 / month compared with ¥57 / month in the year before FIT was introduced.

As a result, the government plans to phase out FIT and move to the less costly, but also less investor-friendly, feed-in-premium (FIP) program which will come into effect in April 2022. This shift pushes renewables power operators to look at other options for securing steady long-term revenue and predictable returns on investment. PPAs offer just that.

Corporate PPAs are a Growing Global Trend

Corporate PPAs are generally 10- to 25-year power supply contracts. As a scheme, they have been around for over a decade, yet they only started to gain popularity globally around 2014. By last year, 19.5 GW of capacity was signed via corporate PPAs, most of this in the Americas.

One key factor behind the growth has been the rapid decline in the LCOE of renewables across the world. In 2010, the LCOE of onshore wind and solar power was, on average, higher than that of nuclear, coal, and combined-cycle gas. Just a year later, in 2011, the LCOE of onshore wind dropped below all three. The LCOE of solar reached that point four years later, in 2015.

This made smaller renewable power generators competitive with conventional power plants operated by major utilities and allowed them to sign PPAs directly with corporate consumers, bypassing the traditional channels. These long-term contracts

help power generators and investors build predictable revenue streams, and allow customers to hedge against future electricity price fluctuations.

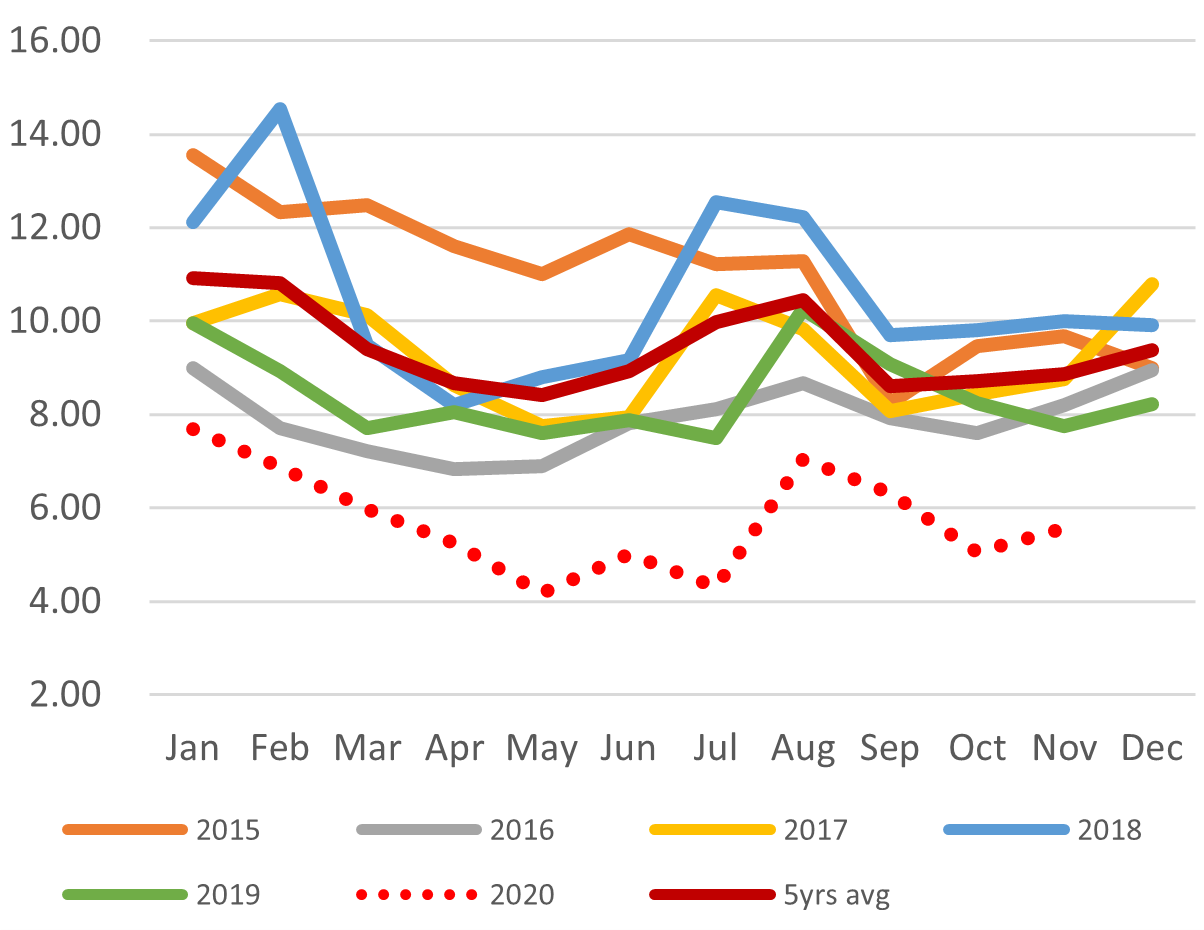

Global volume of PPAs (GW)

Source: BloombergNEF

The PPAs can be both physical and virtual. The former work as a regular supply contract with the buyer directly securing the volumes for which they signed up. This can be either via the usual power line transmission (offsite PPAs) or by adding generation equipment on the end-user’s property (e.g. solar panels on a shopping mall’s rooftop). The latter is called onsite PPA.

Virtual corporate PPAs, on the other hand, are derivatives. In this arrangement, the power firm sells its electricity volume into the wholesale market while the corporate consumer gets their power from a traditional retailer. The virtual PPA acts as a contract for the difference.

The extra benefit of the virtual PPA is that the buyer can claim the environmental value of the contracted electricity, regardless of how the power they actually receive was produced. Put simply, the buyer can say they buy 100% green electricity, because that’s what they paid for, while the actual power they receive may be from a coal plant. (Naturally, the consumer of that green electricity, if different from the virtual PPA client, cannot make the same claim.)

The Emergence of Corporate PPAs in Japan

In Japan, the corporate PPA market is in its infancy for two reasons: a relatively high LCOE of renewables, and (until recently) the availability of an attractive government-run FIT program.

Instead, Japan has up to now relied on a similar mechanism, known as offsite self-wheeling. Companies like Sony and Kyocera have used offsite self-wheeling to operate their own power facilities and supply themselves with electricity from the grid without having a retail license, and without paying a renewables levy. However, this mechanism requires businesses to pay for a wheeling charge and to submit daily generation forecasts to the Organization for Cross-regional Coordination of Transmission Operators (OCCTO). Furthermore, in case of major discrepancies between forecasts and actual generation, the companies are required to pay imbalance fees.

The corporate PPA offers an easier scheme, and power generators and investors are starting to see them as a viable alternative to FIT. After all, corporate PPAs can, when signed with a reputable counterparty, secure a long-term and steady revenue stream – the same as a FIT contract. Corporate PPAs are also less vulnerable to changes in government policy and resulting issues.

The problem for offsite PPAs in Japan to date has been the need for users to pay a renewables levy, as well as wheeling charges. Another reason is the need to involve a licensed power retailer in such an arrangement. Combined, these two factors make offsite PPAs relatively expensive.

Onsite PPAs, on the other hand, do not pose the same problems, and they are starting to gain the attention of major Japanese brands, which see the potential to lock in long-term power supply and price while also answering the growing calls for more ESG compliance from investors. So far, Altenergy and Nissan Chemical, as well as Hitachi Green Energy and Bourbon, have signed onsite PPAs.

Another example is the retail giant Aeon, which announced last year that it would introduce an onsite PPA model at 200 facilities including shopping centers, supermarkets, pharmacies, and convenience stores. Since then, it has entered into such arrangements with companies including MUL Utility Innovation, a subsidiary of Mitsubishi UFJ Lease & Finance.

The Future of Corporate PPAs in Japan

We expect the momentum for PPAs in Japan to grow. The government has started actively promoting this model through subsidies and other mechanisms.

For example, a subsidy program supporting PPAs and similar arrangements as a means to turn renewables into Japan’s main energy source and to strengthen the country’s power supply resilience is expected to receive ¥18.6 billion of the national budget in FY2021, nearly five times the amount it received in FY2020. The subsidy offsets a portion of equipment costs (solar panels, storage batteries, energy management systems, etc.).

Furthermore, with all non-fossil generation now eligible for trading in the environmental value market, Japan has the infrastructure necessary for implementing virtual PPAs.

As the FIT scheme transforms to FIP in 2022, the momentum for virtual PPAs should grow.

In theory, it would also allow power generators to trade environmental value separately from generated electricity. However, new regulatory changes due later in 2020 could nix that option, unbundling environmental value from actual power delivered. So, this aspect of the PPAs is uncertain.

What is clear is the need for a better solution both for government, big business, and the green energy industry. As Minister for Administrative Reform, Kono Taro, told the FT last week, large corporates like Sony have threatened to move factories abroad unless they can procure stable, affordable long-term supply of renewable energy in Japan. That pressure is motivating the government to be more proactive, Kono said.

Channeling budgetary funds to support PPAs is the first step. With the use of PPAs also able to boost demand for energy storage solutions, other steps should follow.

Energy Measures Due to Receive Support in the Next Budget

(Based on Environmental Ministry requests)

| Item | Requested Budget |

| Special measures in energyThe above is split into four main areas1) building “resilient and comfortable communities and lifestyles through decarbonization”

2) “accelerating technological innovation for decarbonization” 3) “realizing a virtuous cycle of green finance and corporate decarbonization, and creating socio-economic system innovation.” 4) supporting the decarbonization of developing countries through the promotion of the bilateral credit system (JCM) and verification of emissions by satellite. | ¥225.4 billion |

| ¥138.4 billion |

| Of which, support for PPAs | ¥18.6 billion |

| ¥41.4 billion |

| ¥21.8 billion |

| ¥23.3 billion |

Source: Ministry of the Environment

GLOBAL VIEW

BY TOM O’SULLIVAN

Below are some of last week’s most important international developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Oil prices rebounded sharply last week on global vaccine developments with WTI @ $45 and Brent @ $48, up $3 / barrel or 7% week-on-week. However, gasoline prices at the pump in the U.S. hit a five-year low at Thanksgiving at $1.66 per gallon due to continued impact of lockdowns and over-capacity at refineries.

Also, Exxon lowered its outlook for oil prices for the next decade by over 10% due to the impact of the pandemic and competition from renewable energy sources. Previously, the company had forecast Brent oil prices @ $60 by 2027 but this may now be lowered to $55. Exxon’s breakeven oil price may be closer to $60, although the company is maintaining a $15 billion dividend for 2020.

Biofuels:

Global production of biofuels for transportation are expected to decline by 12% in 2020, according to the IEA. This is the first fall in 20 years, mainly due to the pandemic and competition from low oil prices.

Nuclear Power:

1). CEZ, the Czech power utility, has delayed tenders for a 1.2 GW nuclear power plant due to national security concerns over Russian and Chinese bidders.

2). EdF expedited the closure of its U.K. Hinkley Point reactors by two years amid concerns about lack of U.K. government support for traditional large-scale nuclear power projects.

China:

1). Ongoing geopolitical tensions between China and Australia continue to impact commodity prices with Australian coking coal prices losing around $40 a ton or 25% since the coal ban was implemented earlier in 2020. Up to seven million tons of Australian thermal and coking coal is stuck at ports in Hebei Province due to the ban.

2). Chinese Foreign Minister Wang Yi visited Tokyo for meetings with the Japanese prime minister and foreign ministers last week, indicating an improvement in economic relations between Asia’s two largest economies and the region’s two largest energy importers.

South Korea:

SK Group, the $200 billion Korean energy, chemicals and telecommunications conglomerate, has committed to end new overseas oil and gas investments, and will cut CO2 emissions by two-thirds over the next three years.

Middle East:

1). The UAE is indicating that it may exit OPEC, the oil-producing cartel, due to concerns over breaches of production quotas. UAE is the world’s eight largest oil producer and the fourth largest OPEC producer, and is a major oil supplier to Japan.

2). Yemeni Houthi rebels struck two oil production targets last week in Western Saudi Arabia, one at a petroleum distribution center in Jeddah operated by Aramco, and the other a Maltese-flagged oil tanker that had just delivered a cargo to a facility 60 km north of the city of Jazan on the Red Sea. The attack on the oil tanker may have been similar to the one that struck a Japanese vessel in the Gulf of Oman in 2019 while the Japanese prime minister was visiting Tehran.

3). The assassination of Mohsen Fakhrizadeh in Tehran on Friday could inflame tensions in the region and disrupt oil supplies. Fakhrizadeh was the head of Iran’s nuclear weapons program and a senior officer in the IRGC, as well as the fourth Iranian nuclear scientist to be assassinated. It may also complicate President-elect Biden’s plans to re-engage with Iran and the re-start of Iranian oil exports.

Sweden:

LKAB, the Swedish government-owned mining company, plans to invest $47 billion in the production of carbon-free iron ore that will require electricity equivalent to one-third of Sweden’s national supply.

Spain:

Respol, the Spanish oil and refining company, announced plans for a fivefold, $22 billion, increase in renewable energy generation capacity by 2025.

Italy:

Enel, the Italian multinational electricity company, announced plans to triple its renewable energy capacity to 120 GW by 2030.

U.K.:

Centrica, the British electricity and gas company, will dispose of its LNG supply portfolio and other LNG assets. Its 20-year gas contract with Cheniere in the U.S. may have no intrinsic value due to lower spreads between U.K. and U.S. gas prices. Tokyo Gas has a long-term contract with Centrica to jointly purchase 2.6 million tons of Mozambique LNG.

Americas:

Six U.S. Citgo Petroleum executives were found guilty of corruption in a Venezuelan court last week and sentenced to between eight and 14 years in prison.

DATA

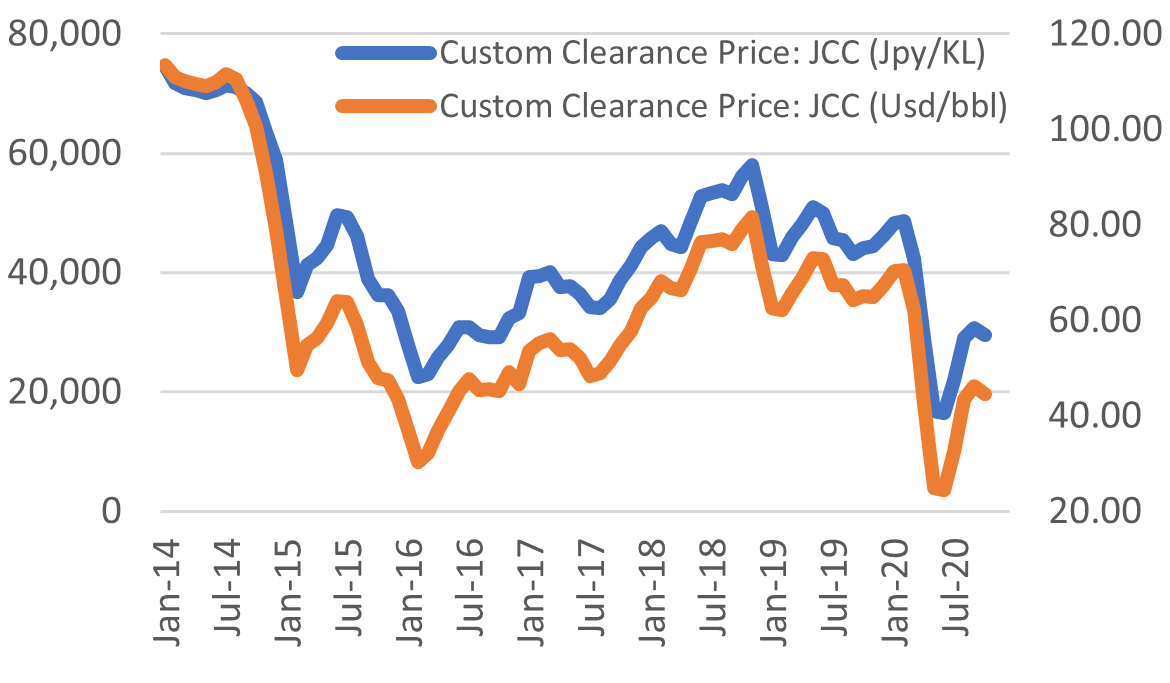

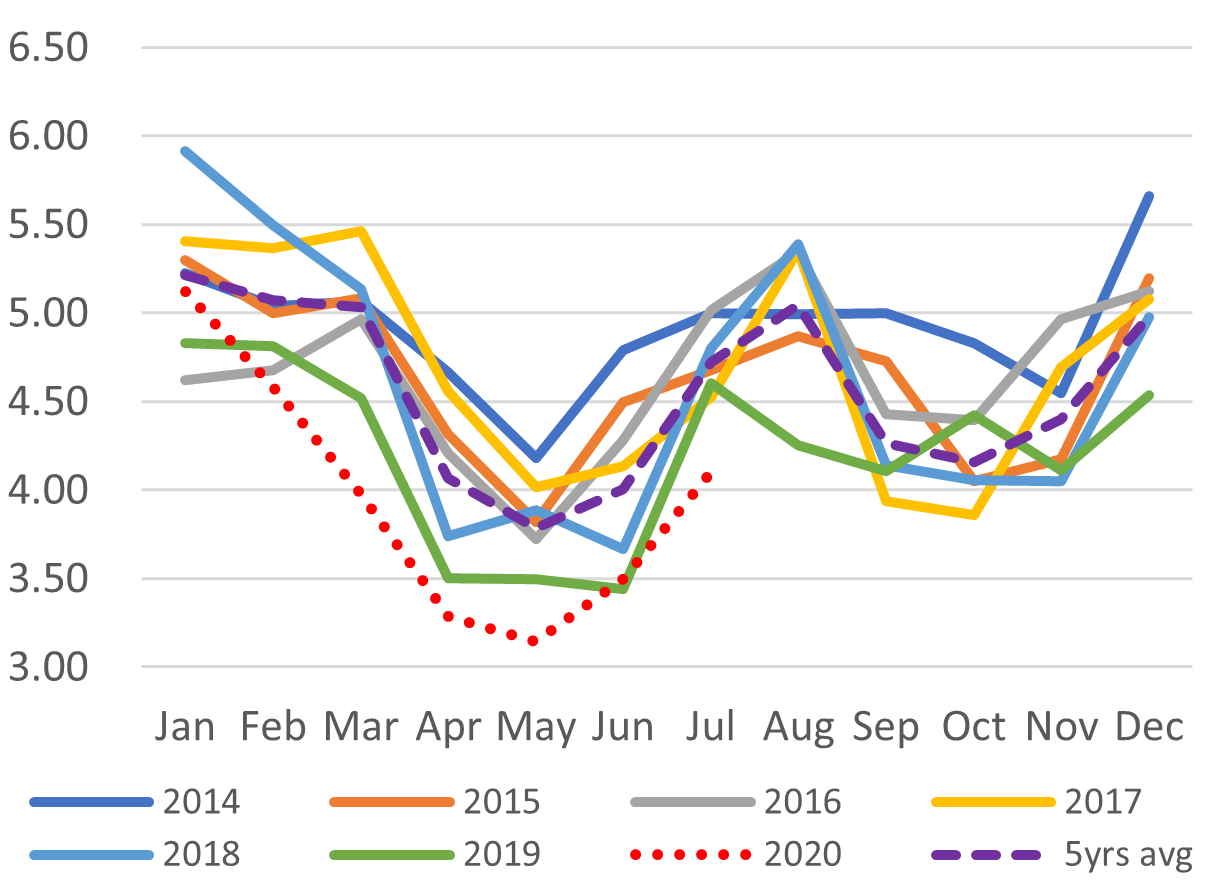

Japan Oil Price

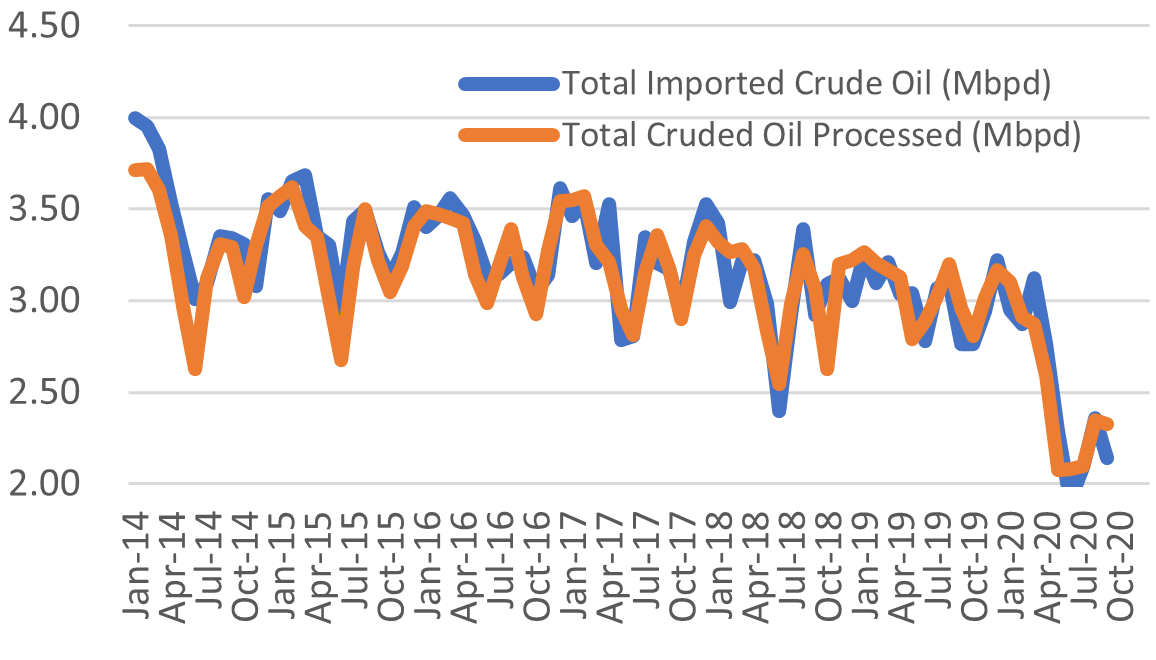

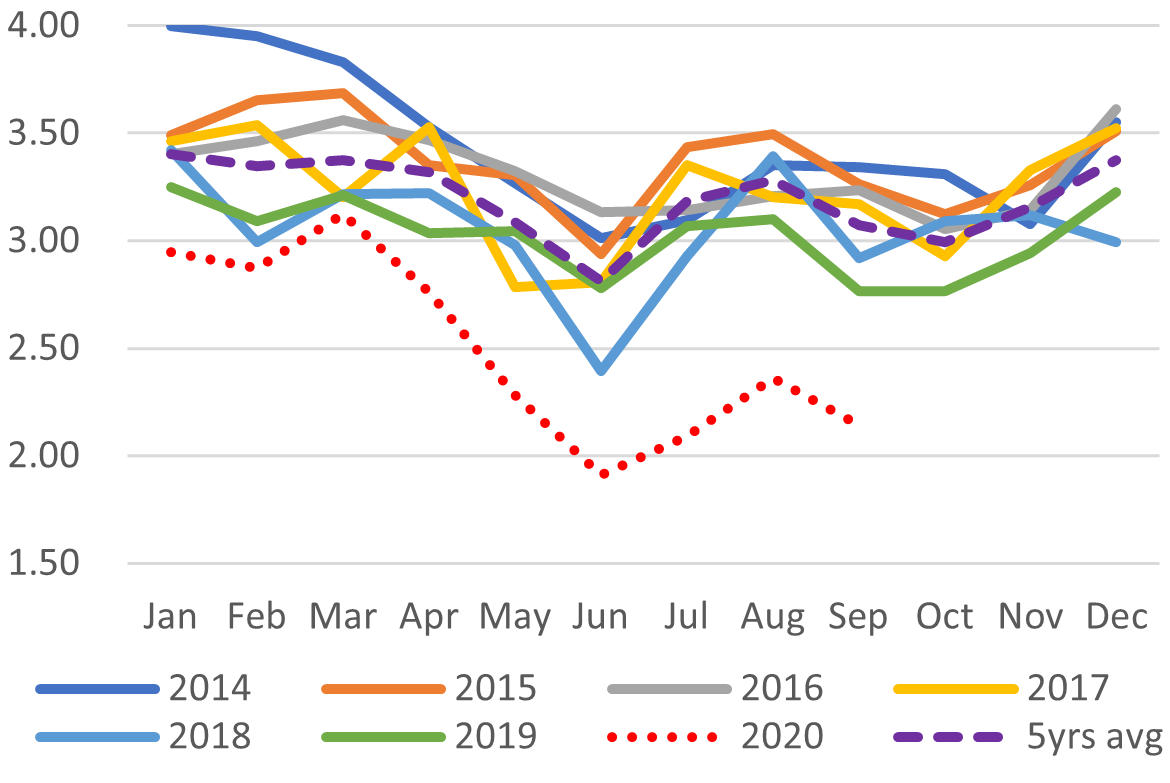

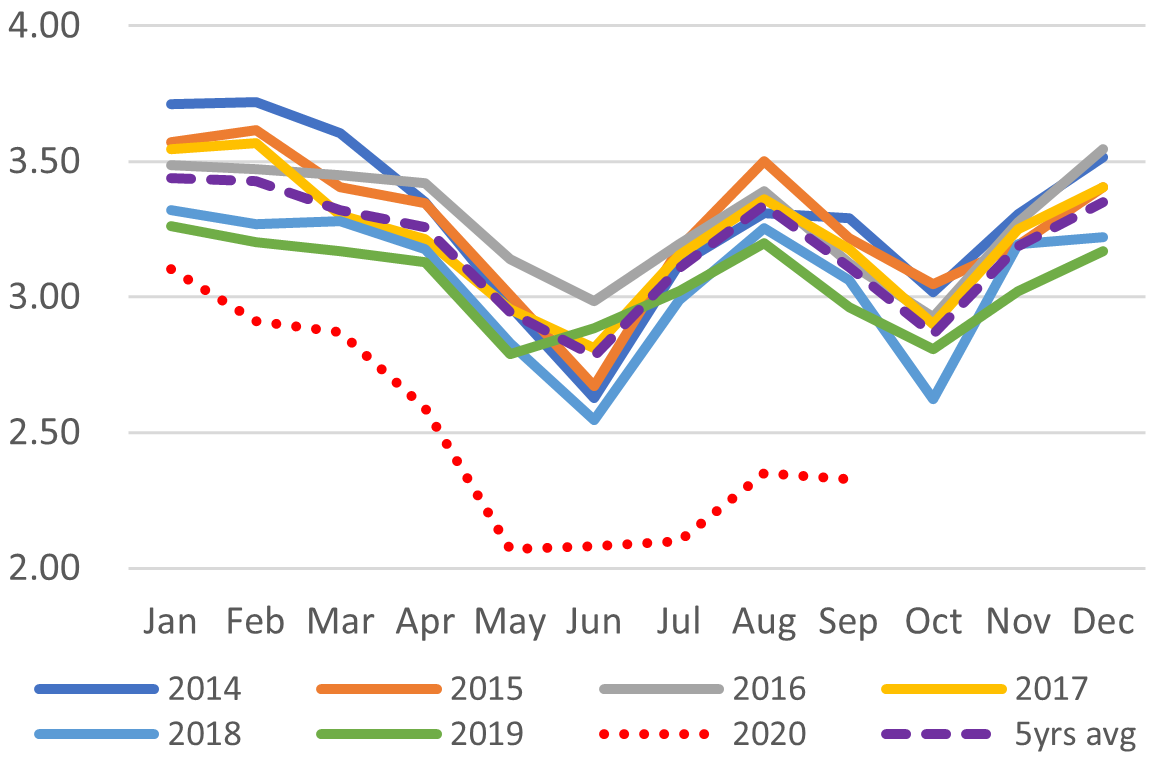

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

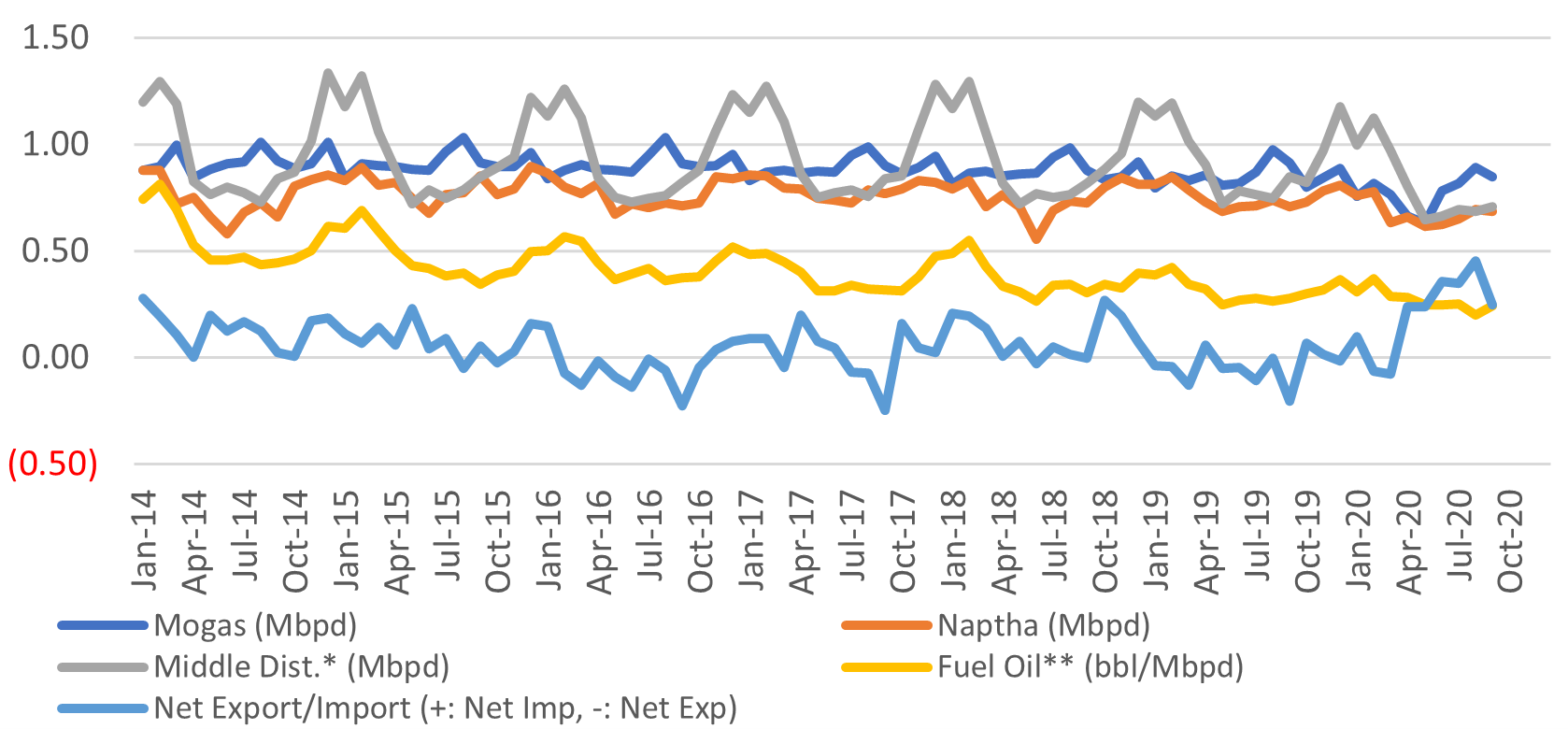

Domestic Fuel Sales

SOURCES: the Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

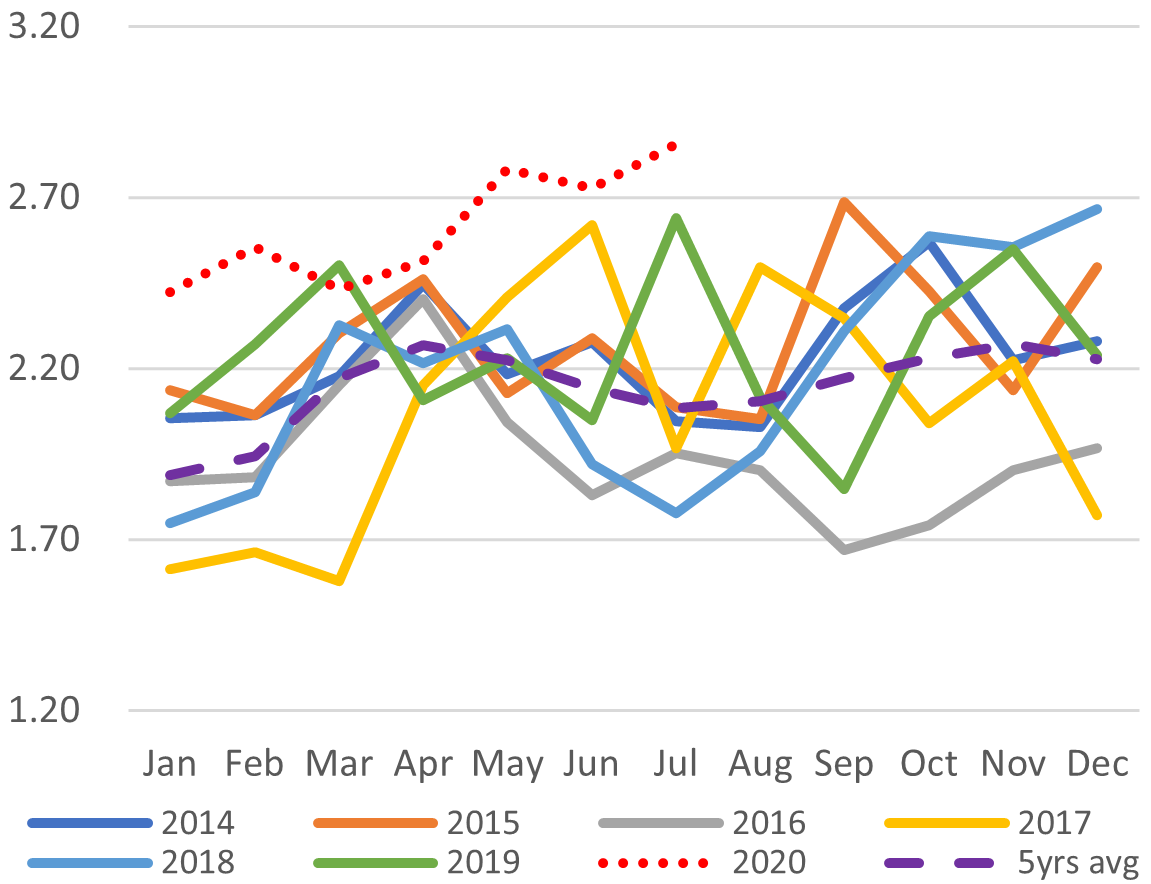

Japan LNG Price

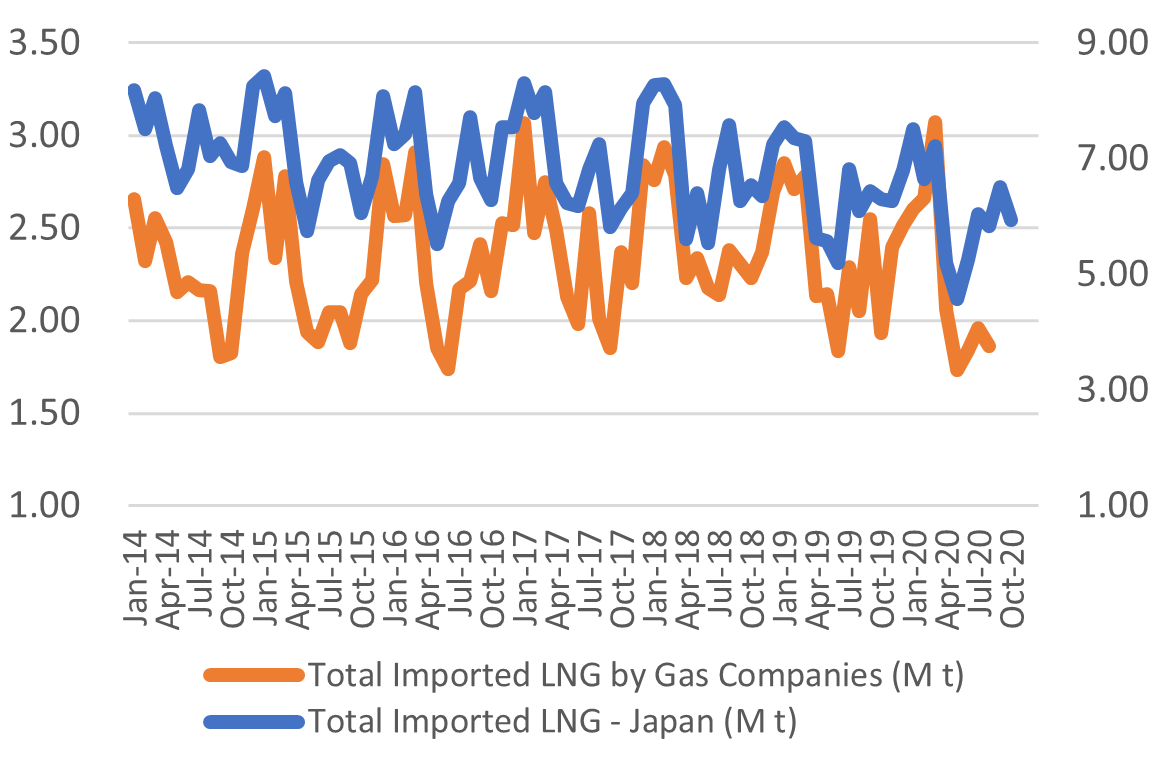

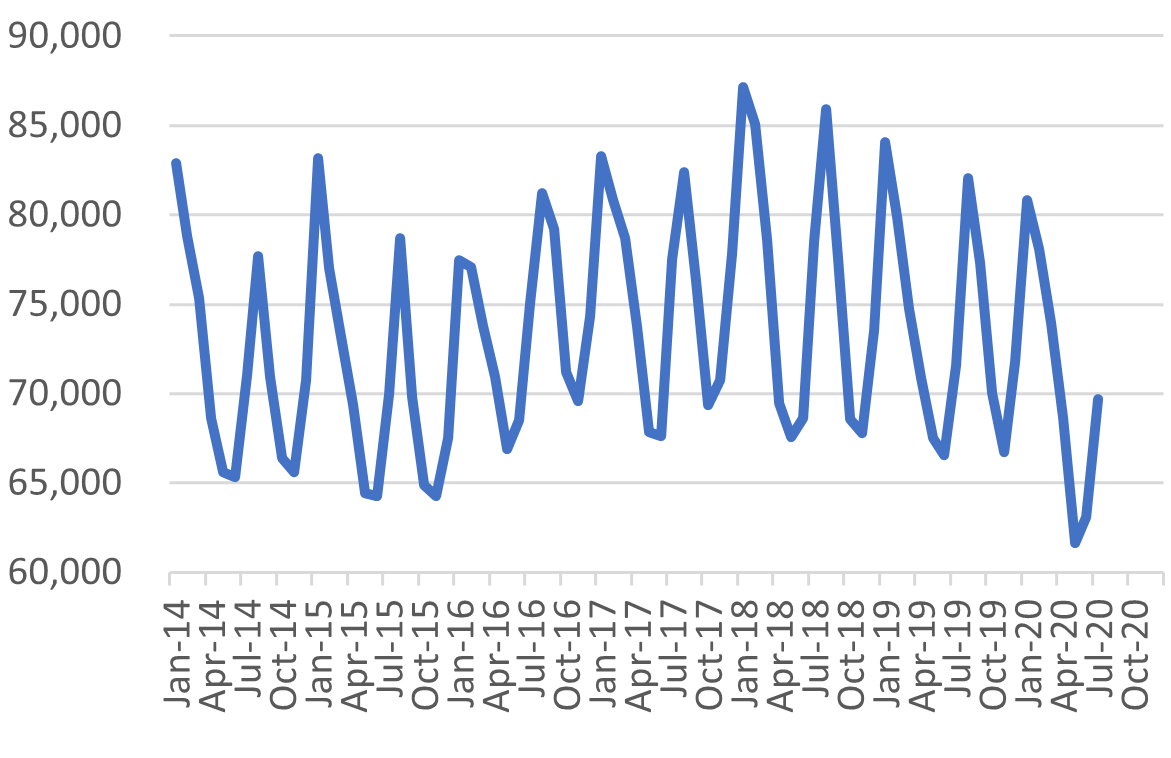

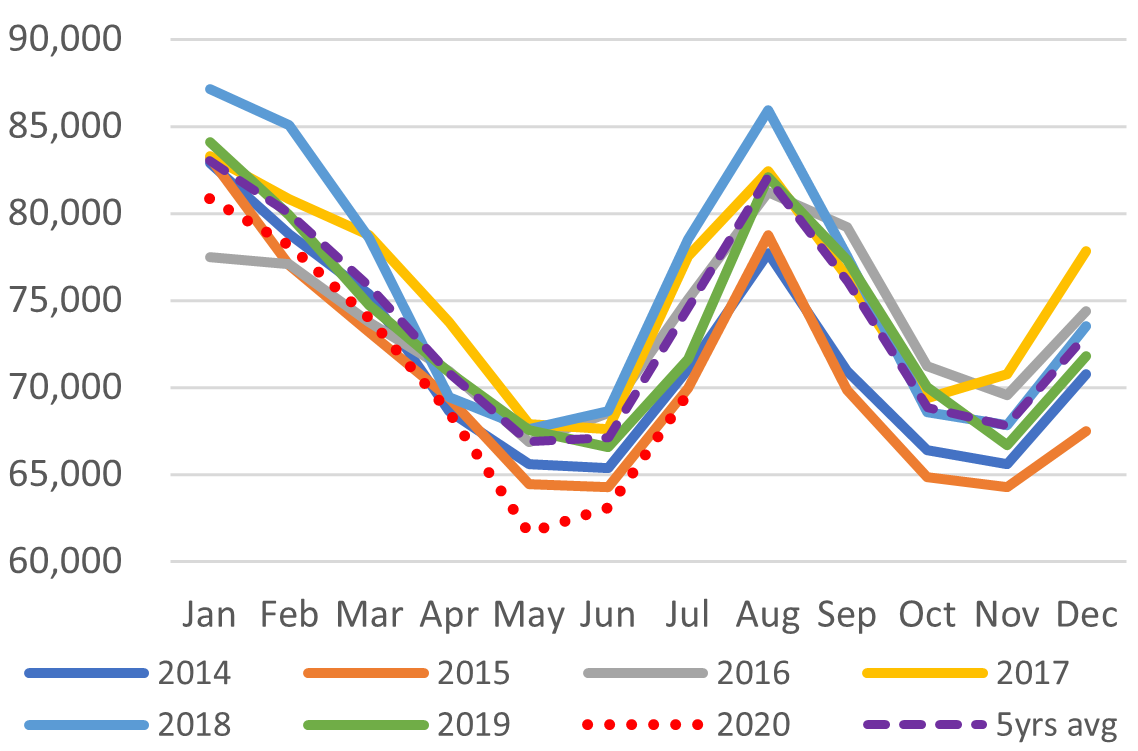

LNG Imports: Japan Total vs Gas Utilities Only

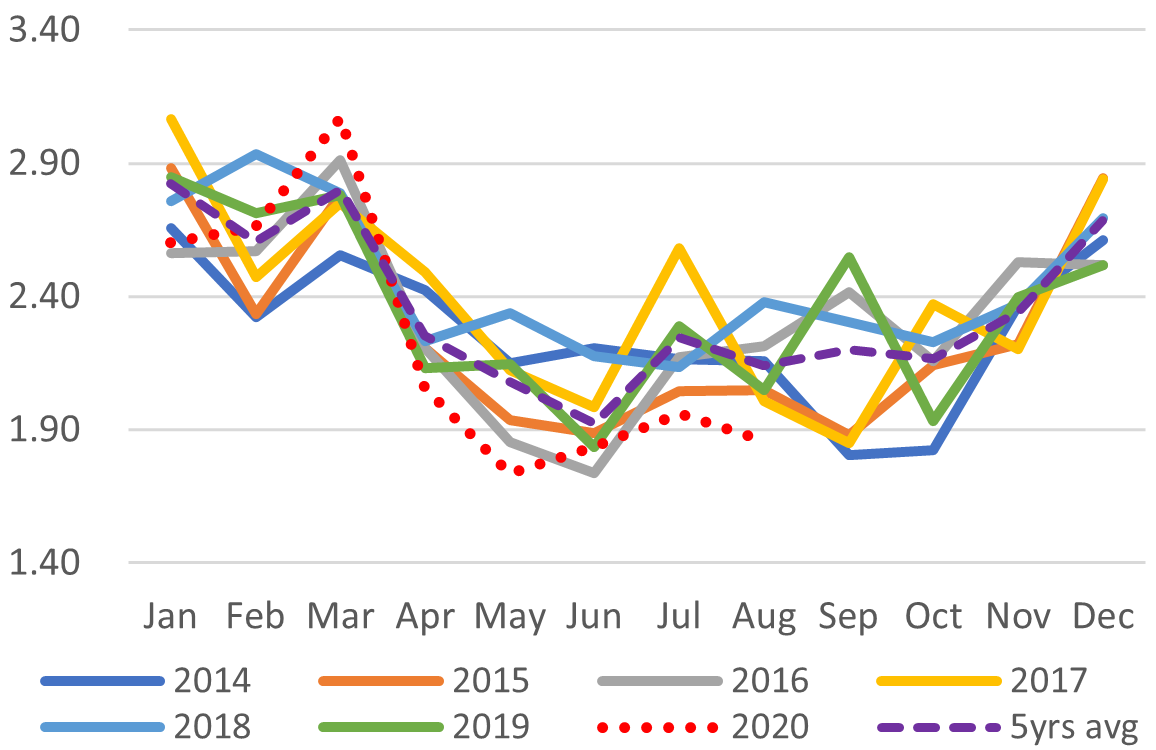

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

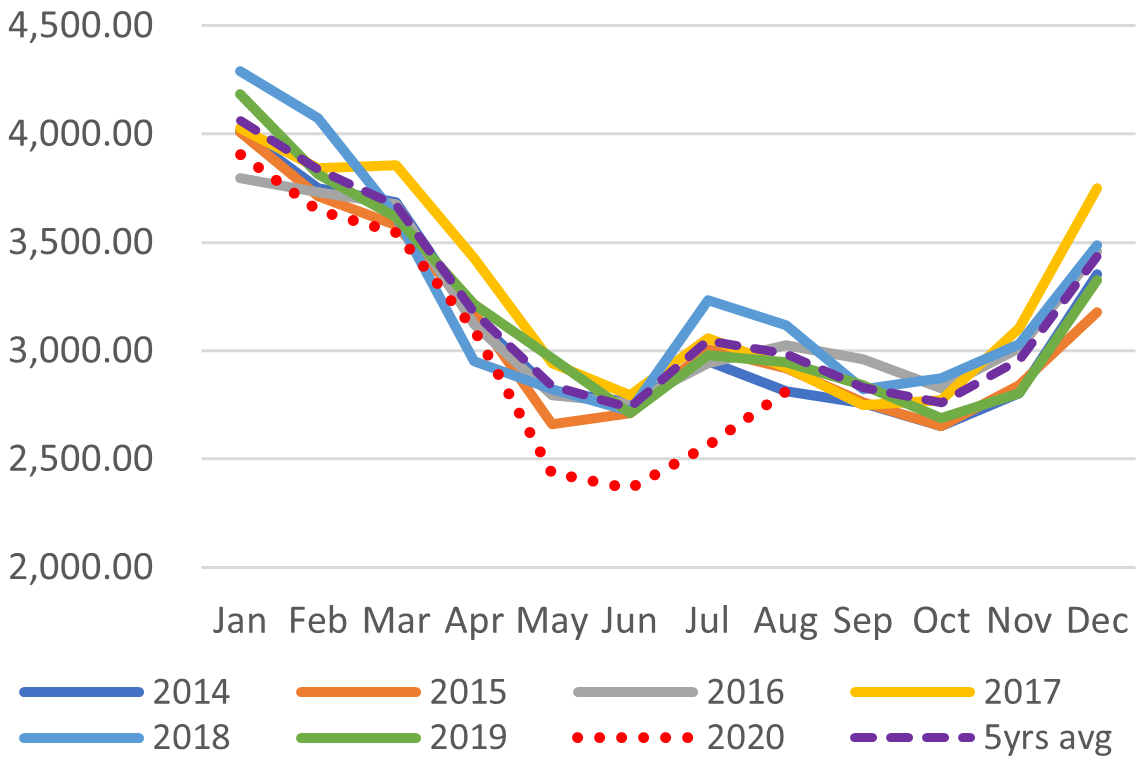

City Gas Sales – Total (M m3)

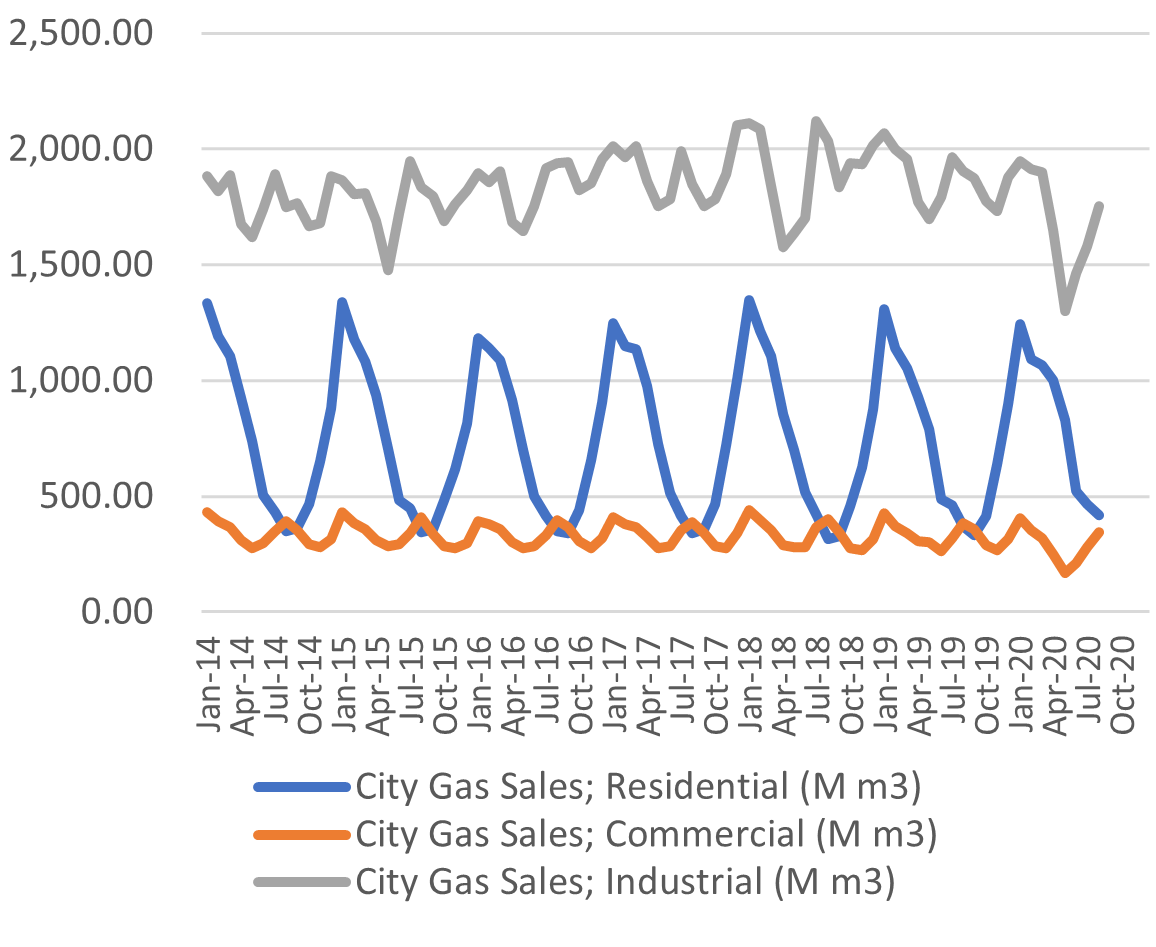

City Gas Sales by Sector (M m3)

SOURCES: the Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

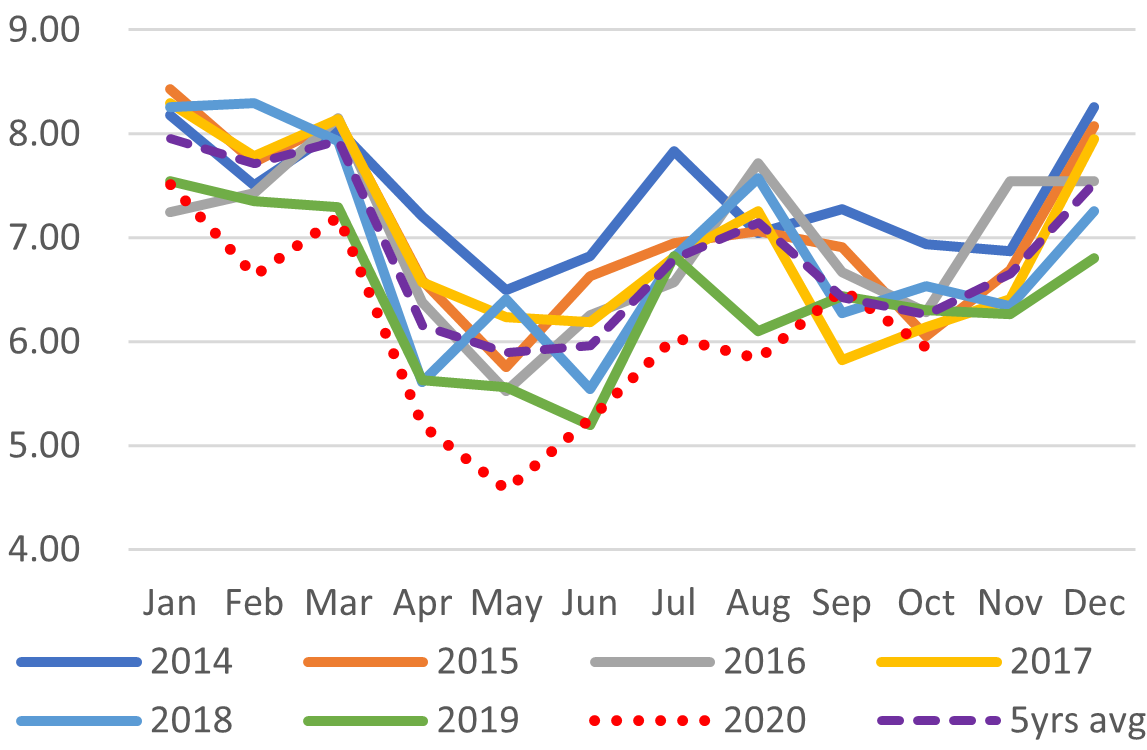

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

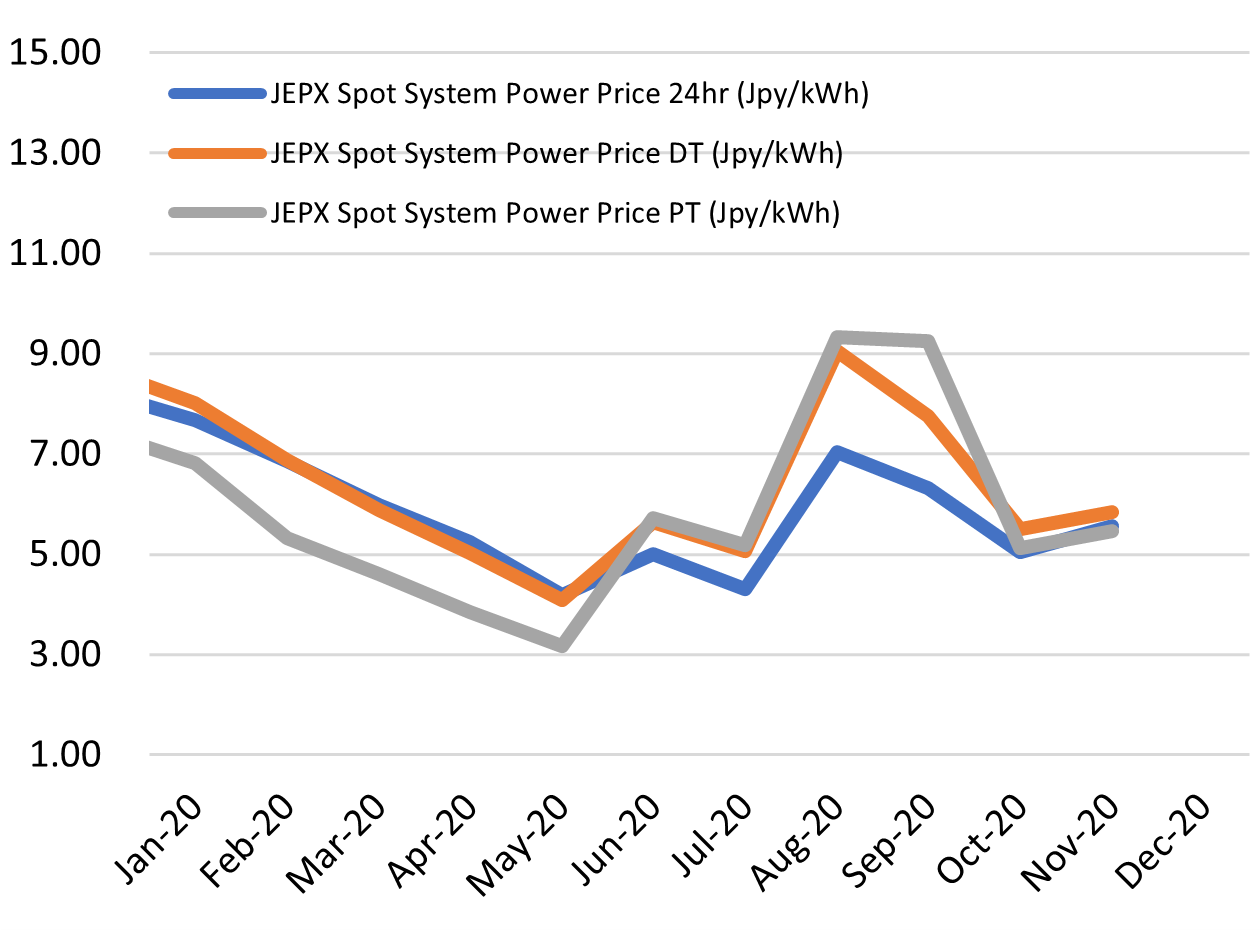

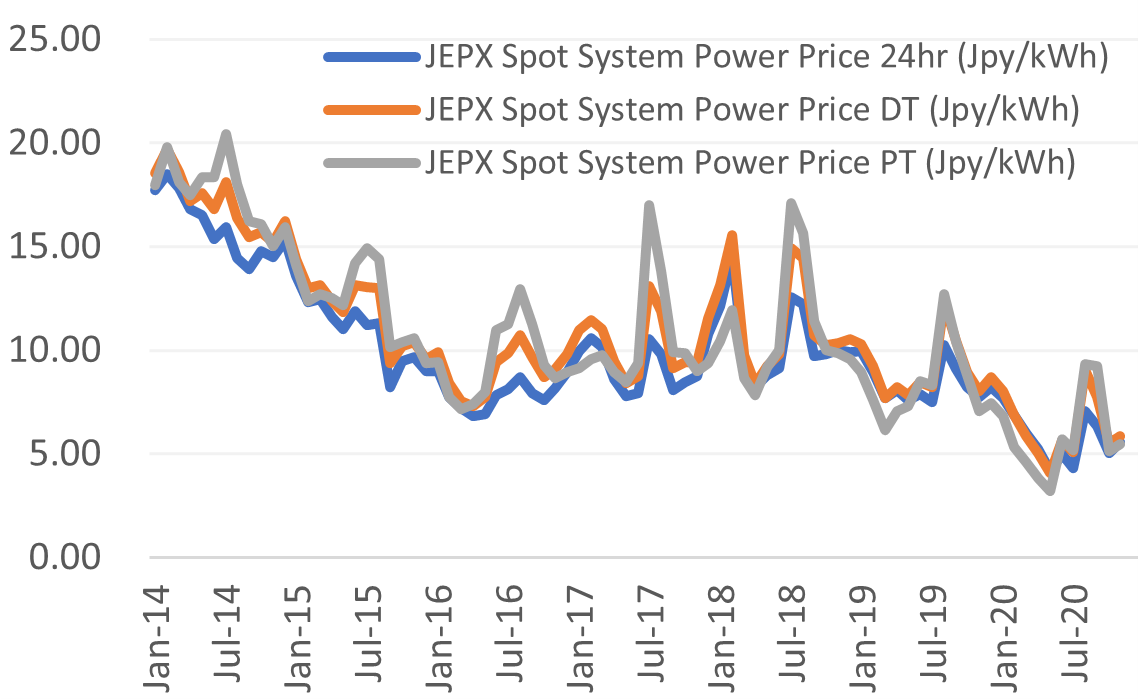

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: the Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange