JAPAN NRG WEEKLY

JANUARY 18, 2021

JAPAN NRG WEEKLY

January 18, 2021

NEWS

TOP

- Government considers emissions quotas, carbon tax

- Update on Japan’s “power emergency”: milder weather and expanding lockdown measures cooling energy demand, but scars likely to remain and impact decarbonization policies

- Govt. effectively sets ceiling on spot electricity price thru June

ENERGY TRANSITION & POLICY

- Green Ammonia Group set up to promote use of coal alternative

- Japan’s top shipper to switch auto cargo to railways to cut CO2

- Panasonic vows to make cobalt-free EV battery; Mitsubishi Chemical to boost battery liquid output 50%; China signals that it will tighten rare-earth materials’ export

- Ministry wants changes to Akita offshore wind farm project; KEPCO and Marubeni submit assessment for Yamagata wind farm

- Hyogo solar farm beats output target by 10% with air conditioners

- J-Power to issue its first green power bonds

ELECTRICITY MARKETS

- J-Power to run coal plant on fuel oil as power shortages bite

- Govt and utilities ask consumers to conserve electricity, turn to oil

- The reason govt. is reluctant to declare energy crisis: Lockdown

- Electricity retailers fight for survival amid spot price surge

- OPINION: Japan’s LNG over-dependence exposed and pivot to green power in question as cold weather shows structural issues

- Pipe damage found at Kansai Electric’s Takahama nuclear plant; Utility not learning from its nuclear energy mistakes

- Kansai Electric’s Ohi Unit 4 reactor starts to send power to grid, but resident group again tries to shut down Ohi nuclear station

- JERA tries to drum up business in Taiwan

UPSTREAM: OIL & GAS

- ENEOS cuts operations at refinery on falling jet fuel demand

- Marubeni looks to exit investments in U.K. North Sea oil and gas

- INPEX shuts Ichthys LNG facility for unplanned maintenance

- What caused the LNG shortage? View from Japan

ANALYSIS

JAPAN’S GREEN REVOLUTION PLANS FACE

CRITICAL RAW MATERIALS ISSUES

Along with dozens of other countries, in 2020 Japan committed to achieve net-zero in greenhouse-gas emissions by 2050. Japan’s decarbonization pledge is backed up by ambitions for a vast rollout of offshore wind, millions of tons of green hydrogen, and assertions that domestic automakers can establish net-zero emissions from the entire life cycle of a vehicle.

Japan may yet possess the innovative capacity to realize these goals. But one pertinent question is whether resource-scarce Japan has access to sufficient critical materials to make it happen. Equally important is asking whether Japan has a strategy to secure critical raw materials that conform to rapidly diffusing sustainability rules.

SYMBOL OF JAPAN’S “OLD ENERGY” EXCELLENCE SEEKS TO REINVENT ITSELF IN THE GREEN AGE

For most of the 20th century, Mitsubishi Heavy Industries (MHI) was a stalwart of Japan’s shipping, aviation, and energy industries. When the shift to renewables first started in earnest, MHI again sought to be at the forefront. By the early 2010s, it had developed the world’s top wind turbine by capacity and joined forces with a leading European wind power manufacturer, Vestas. And yet, a decade on, MHI’s pivot to green-age energy has yet to really take off, while its core business lines are underperforming. For Japan to meet its 2050 decarbonization commitments, its engineering powerhouse will need to turn things around and soon.

GLOBAL VIEW

Last year was the hottest on record. Investors want HSBC to stop financing fossil fuels. The U.S. hits CNOOC officials with sanctions for actions in the South China Sea. U.S. GMG emissions fell 10% last year. And Germany steps closer to deciding on who will replace Angela Merkel. See details on these and other political and business events.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Damon Evans (Indonesia)

Art & Design

22 Graphics Inc.

Sponsored

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS:

ENERGY TRANSITION & POLICY

Government considers emissions quotas, carbon tax

(Nikkei, Dec. 27)

- The Ministry of Economy, Trade and Industry is preparing to start charging carbon emitters, in a bid to achieve its pledge of becoming carbon neutral by 2050.

- While the government has thus far concentrated on technological innovations and greater use of nuclear energy as a way of achieving its goal, it believes that technological innovations alone will not be enough.

- Senior officials at the Ministry of Finance have stated the opinion that until a system of quotas or carbon taxes are imposed, big corporations will not make any effort to cut their emissions.

- The government will now decide whether the new regulations should take the form of a carbon tax, or a system of emissions quotas with penalties for exceeding those quotas.

- Several companies including Fujitsu and Ricoh have been calling on the government to introduce carbon pricing since 2018, saying that such a system is essential in order to improve the competitiveness of Japanese corporations internationally, even if it entails increased cost in the short term.

Green Ammonia Consortium aims to profit from green boom

(Nikkan Kogyo Shimbun, Dec. 30)

- The Tokyo-based Green Ammonia Consortium aims to establish a supply chain for the distribution in Japan of ammonia produced in the U.S. and Australia.

- Ammonia can be blended with the coal burned by power stations to reduce their carbon emissions. In future, there are also plans to build power stations fueled entirely by ammonia, and even ammonia-fueled ships.

- Established in 2019, the GAC has over 100 members from Japan and overseas.

- In future, the GAC plans to expand manufacturing and supply chains, and to begin sourcing ammonia from the Middle East and other new regions.

- The GAC forecasts domestic ammonia demand of 3 million to 5 million metric tons annually by the 2030s.

Nippon Yusen to deliver cars to Europe by train to cut emissions

(Nikkei, Jan. 14)

- Japanese marine shipper Nippon Yusen will send some of its exports by rail rather than sea freight to cut carbon emissions. Later this year it will start transporting Japanese cars to Europe using trains that cross mainland China.

- Nippon Yusen has a partnership with a Chinese railway operator.

- The Japanese firm can move cars by ship to the Chinese city of Dalian. From there, cargo will travel through Altynkol in Kazakhstan, over a total distance of 5,000 km.

- Until now, Nippon Yusen has been shipping cars from Japan to Turkey from where they enter Europe.

- The volume of autos that can be sent by rail is only half that of shipping. However, by rail it’s twice as fast and carbon emissions are half.

Panasonic vows to develop cobalt-free battery

(Asia Nikkei, Jan. 13)

- Co. aims to make cobalt-free batteries for Tesla’s electric vehicles in two to three years.

- Cobalt is blamed for the high price of EV’s lithium-ion batteries, which account for 30%-40% of the car’s cost. Cobalt is used in the cathode of lithium-ion batteries.

https://asia.nikkei.com/Business/Materials/Mitsubishi-Chemical-leads-charge-against-China-s-EV-battery-giants? - SIDE DEVELOPMENT:

Mitsubishi Chemical to raise global battery liquid output by 50%

(Asia Nikkei, Jan. 13)- Co. to invest ¥1 billion to increase output. It already has a 20% global share in the battery liquid material.

- SIDE DEVELOPMENT:

China tightens rare-earth regulations including in exports

(Nikkei Asia, Jan. 16)- The draft of the new law seeks to review the entire industrial chain of China’s mining, refining, product transport and export of important rare earth materials.

- The new rules may limit China’s exports of these critical raw materials.

- Japan wants to lower its reliance on Chinese imports of rare earths to 50% from 58% by 2025.

TAKEAWAY: See the analysis section for a deep dive on this topic and its implications for Japan.

Environment Minister calls for changes to Akita offshore wind farm over ecological concerns

(Kankyo Business Online, Jan. 6)

- The Environment Ministry has made a submission to METI on the environmental impact of an offshore wind farm project planned for Akita prefecture.

- The Environment Ministry is calling for changes to the Hihata 1 and Aramaki sections to reduce the impact on swans and other migratory birds. Officials are very concerned about the impact on bird populations from changes to migration routes and the availability of food.

KEPCO, Marubeni submit assessment for 500 MW Yamagata offshore wind farm

(New Energy Business News, Jan. 15)

- Kansai Electric (KEPCO) and Marubeni have filed with METI an environmental impact statement in relation to a proposed wind farm off the coast of Yuza (Yamagata).

- The proposal involves as many as 52 floating turbines with a capacity of up to 500 MW.

- In 2020 the area was designated as a focus area for renewable energy.

- KEPCO and Marubeni are the latest in a long list of companies that have already submitted environmental impact statements for the project, including the Chubu Electric, Cosmos Eco Power, JAPEX, Sumitomo Corporation, Japan Wind Development, and SB Energy.

Hyogo solar farm exceeds output target by 10% with special technique

(New Energy Business News, Jan. 15)

- The Delta Electronics Energy Park in Ako (Hyogo) is now five years old.

- By exercising highly granular panel control and using state of the art power conditioners, the 4 MW facility has been able to generate 2.7 MWh of electricity in its first five years of operation: 10% above initial projections.

J-Power to issue first green bonds

(Denki Shimbun, Jan. 14)

- J-Power will raise between ¥10 and ¥20 billion by issuing 10-year green bonds. The first bonds will be issued this month.

- Proceeds will be used to fund wind farm construction.

- CONTEXT: Heavily coal-reliant J-Power aims to bolster its renewable capacity to 1 GW by 2025.

NEWS:

POWER MARKETS

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 4 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

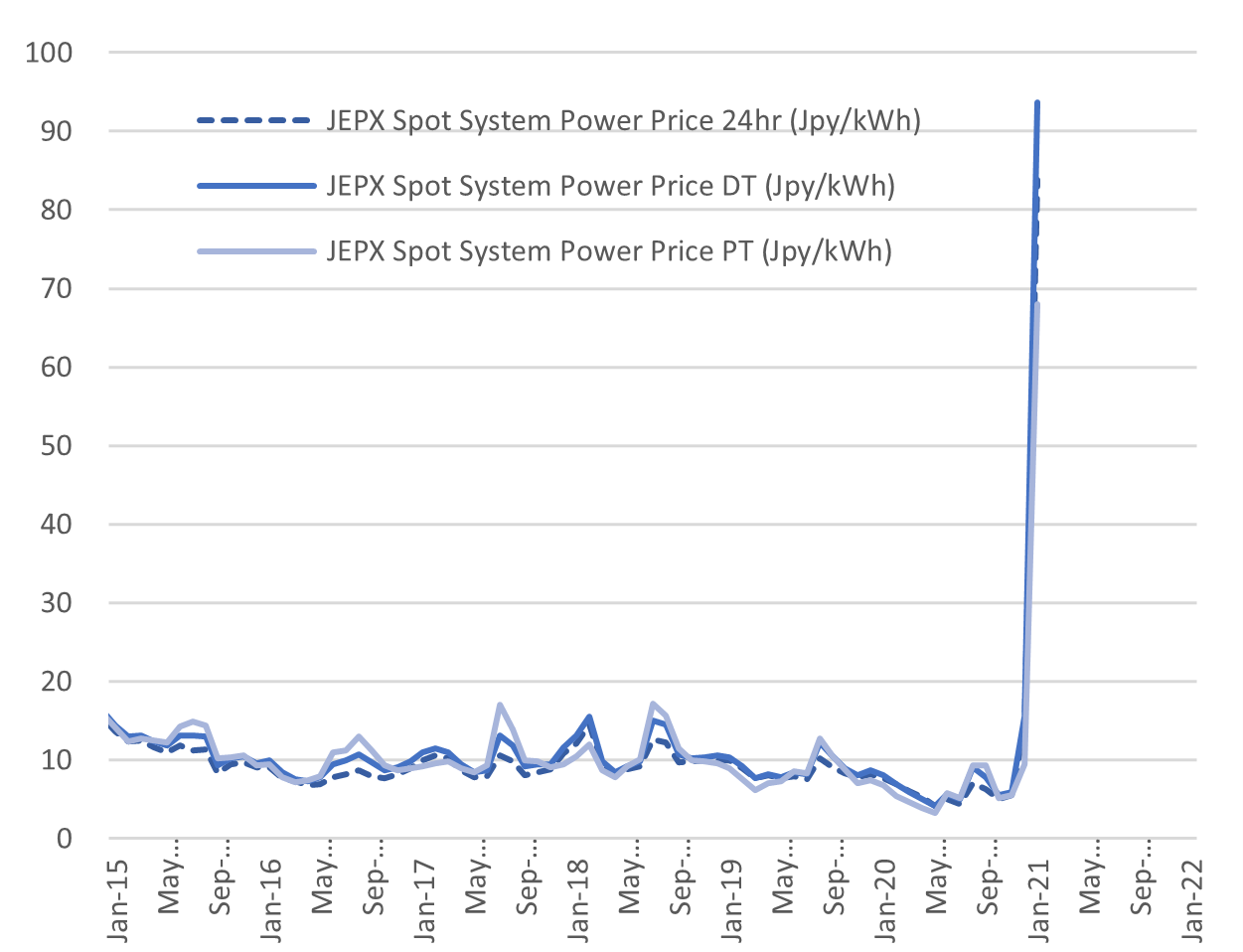

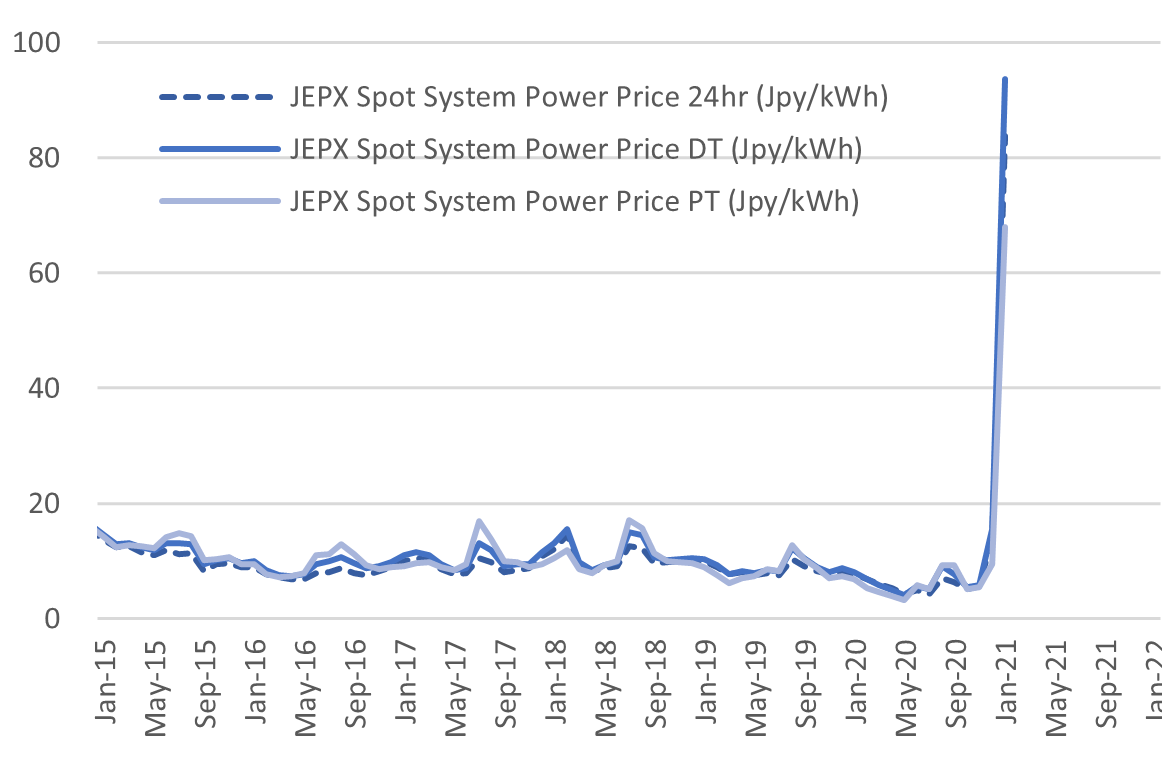

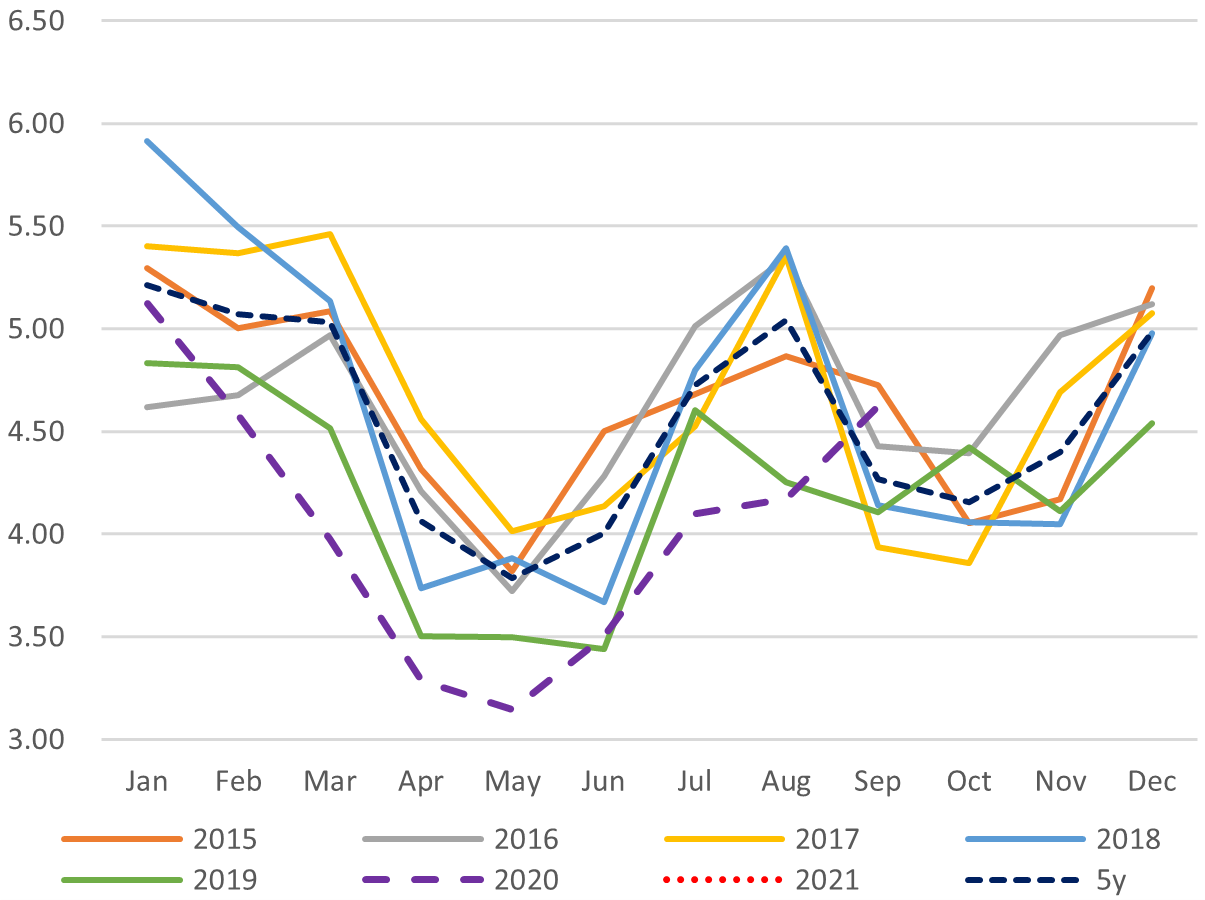

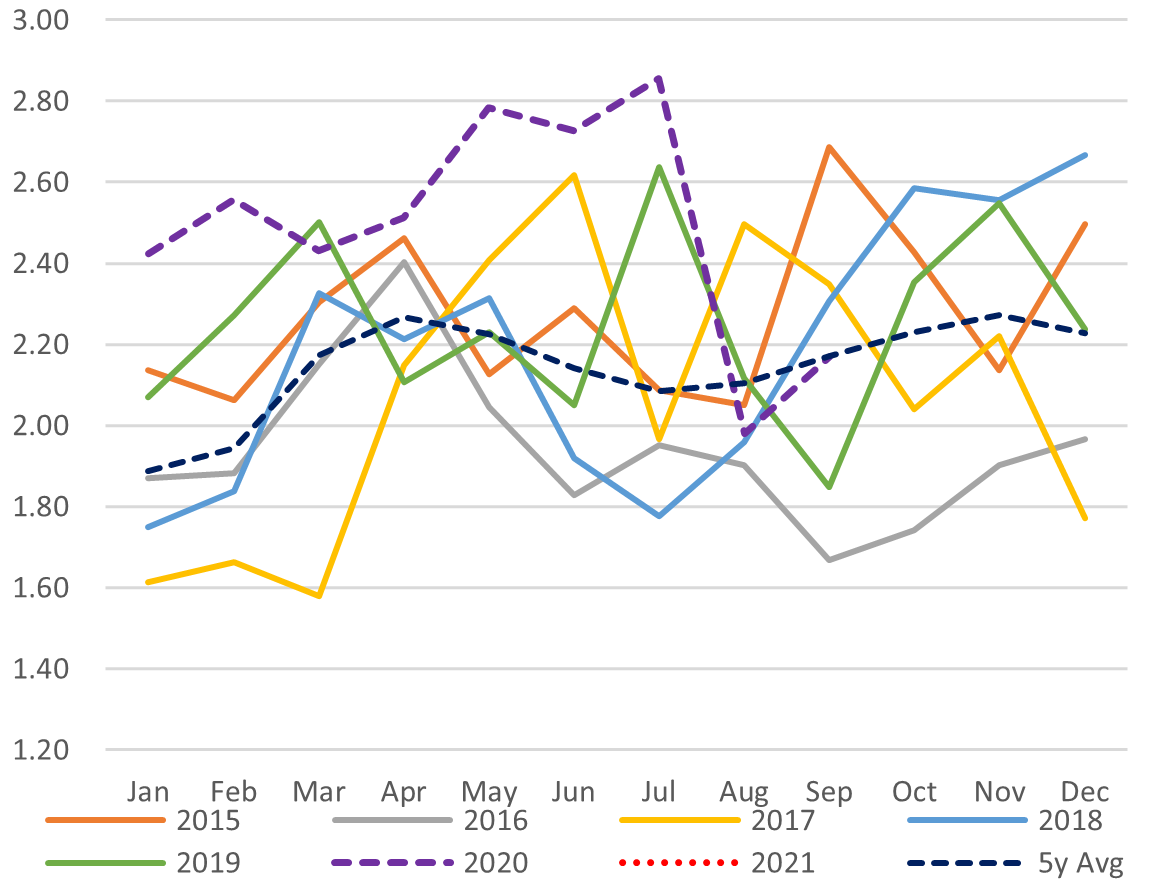

Spot Electricity Prices

Source: Company websites, JANSI and JAIF, as of Jan. 8, 2021

Update on Japan’s power shortages due to cold weather and LNG price spike

(Japan NRG, Jan. 17)

- Japan experienced a period of colder than average weather at the start of January. Snowfall in southern parts of Japan was particularly unusual and hampered the use of solar power, as well as other renewable generation, such as pumped storage hydro. It has led to power companies asking business and individual consumers to limit electricity use for the first time since 2011, when a major earthquake and tsunami struck, resulting in most of Japan’s nuclear capacity being taken offline.

- With a jump in COVID-19 cases at the end of December, and the expected announcement of a State of Emergency in parts of Japan, power utilities expected seasonal demand to be less than usual and did not jump into the spot market late in 2020 to secure additional LNG cargos. The result has been a spike in prices of LNG, and then electricity, to record levels.

- Below is a selection of the most pertinent news stories on this issue, as well as some data on the current load factor of power utilities.

TAKEAWAY: Two factors signal that the original “power emergency” may be over. One is a return to milder weather, with Tokyo, for example, seeing 16 degrees Celsius on Jan. 16. The second is the widening of the govt.’s State of Emergency (i.e., lockdown) to around half the country, in terms of the economy and population total. There is even talk of implementing the same for the entire nation, though Prime Minister Suga’s government seems keen to avoid going to an extreme to minimize the economic impact.

Admittedly, Japan’s lockdown, as detailed in the Jan. 12 edition of Japan NRG, is a mild version of measures imposed in other countries. However, it’s having a pronounced impact on swathes of businesses, such as restaurants and nightspots, all of which are closed from 8 p.m. We expect lockdown measures to last at least until the official target of Feb. 7.

It is clear that government and business discussions on what this power crunch means will continue for many months to come. The following items will be under particular scrutiny in light of the recent “energy emergency”:

- The new energy mix 2030 vision currently being drawn up by METI

- The pace of shutdown of the coal-fired power plants in Japan (should it slow down not to leave the nation too reliant on LNG)

- LNG storage issues (currently, Japan can only store the molecules for two weeks and thus has limited adjustment room for volumes)

- The idea of electrifying all consumer and industrial applications (as opposed to using petroleum products and other fossil fuels)

- The pace of nuclear reactor restarts

- Power price volatility and spot market mechanisms

- State funding to energy storage and battery development

- Whether it is “healthy” to have such a large number of power retail companies in the market (currently 700+ firms with a retail license)

Percentage of regional Electric Power Companies’ capacity in use

| Power utility | Peak Load on Jan. 12 (Monday) | Peak Load on Jan. 17 (Sunday) | Expected Peak Load on Jan. 18 (Monday) |

| Hokkaido Electric | 95% | 87% | 90% |

| Tohoku Electric | 97% | 89% | 92% |

| TEPCO | 93% | 85% | 92% |

| Chubu Electric | 95% | 82% | 91% |

| Hokuriku Electric | 94% | 93% | 97% |

| Kansai Electric | 99% | 88% | 92% |

| Chugoku Electric | 94% | 89% | 93% |

| Shikoku Electric | 98% | 94% | 97% |

| Kyushu Electric | 96% | 91% | 96% |

Govt. sets ¥200/ kWh limit for imbalance fees, effectively placing cap on electricity spot price

(Japan NRG, Jan. 15)

- On Jan. 15, METI announced the imbalance charge ceiling to begin from Jan. 17. The ministry said the ceiling is made in light of electricity prices exceeding ¥200/ kWh on the spot market in recent days and this has made it difficult for many market participants to procure power supply.

- The ministry said this was an urgent measure needed to protect the market and ensure a “stable electricity trading environment” that has a “degree of predictability”.

- The rule will stay in place until June 30 this year.

- CONTEXT: imbalance fee is charged when the amount of power supply doesn’t match the planned demand submitted by retailers. The measure has indeed put a ceiling of ¥200 on the spot electricity market as can be clear from intra-day pricing.

J-Power to run coal plant on fuel oil as power shortages bite

(Nikkei, Jan. 12)

- J-Power is due to restart the out-of-service Matsushima coal-fired power station in Nagasaki as early as Jan. 14 to combat fuel shortages.

- The plant’s number two boiler has not been operational since Jan. 7 due to broken coal crushing equipment. However, so dire are the current power shortages that J-Power will take the unusual step of using fuel oil to fire the boiler.

TAKEWAWAY: This is a very unusual move in that heavy oil tends to be used at such power plants to help with combustion when the station is restarted following an inspection. This time, the plant is running on oil only. Because of this and other factors, the plant is only able to work at about half its nameplate capacity of 500 MW.

Minister encourages efficient power use as cold snap causes shortages

(Tokyo Shimbun, Jan. 12)

- On Jan. 12 Minister for Economy, Trade and Industry Kajiyama Hiroshi called on consumers to be efficient in their electricity use in light of power shortages.

- The Minister said he’s not asking people to reduce electricity use per se, since hard-hit areas can be supplied with electricity from other regions. People can use heating normally, he said.

Kansai Electric pleads with consumers to conserve electricity

(NHK, Jan. 10)

- On Jan. 10, the Kansai Electric Power Co. began calling on domestic and commercial subscribers to reduce electricity use as cold weather causes power shortages.

- KEPCO calls on consumers to turn off lights and reduce non-essential electricity use.

- A large cold front saw demand for electricity in areas served by KEPCO hit record levels on Jan. 8. Electricity use remains above 95% of capacity as of 9 a.m. on Jan. 10.

- Recent LNG shortages, combined with the fact that KEPCO’s nuclear power stations are closed for maintenance, means resources are likely to remain strained for some time.

- SIDE DEVELOPMENT:

Japan power utilities asks oil firms for supply to burn in power plants - (Nikkei, Jan. 16)

- Power utilities all over the country are turning to the oil refineries such as ENEOS for help in providing fuel oil that can be burned in some power plants.

- Kansai Electric is among those in the most difficult situation needing to secure oil supplies.

- Chairman of the Federation of Electric Power Companies of Japan, Ikebe Kazuhiro, who is also head of Kyushu Electric, told the media that several bad events have overlapped to cause the current energy crisis and the situation remains unpredictable.

Why government doesn’t want to tell consumers to save power despite historic shortage

(Nikkei Business, Jan. 12)

- Despite not having been afflicted by a nuclear accident or major earthquake, Japan currently finds itself in the grips of its worst power shortage since the Fukushima disaster. Since Jan. 4, the government has walked a tightrope as utilities barely manage to stave off power outages.

- In an unprecedented move, on Jan. 6, the Organization for Cross-regional Coordination of Transmission Operators called on generators to crank up output to maximum levels and redirect all surplus electricity to the wholesale market.

- Power companies have called on subscribers to turn down their thermostats. However, sources in the power industry say that METI is reluctant to make a similar plea over fear of criticism, in view of the fact that the government recently declared a Covid-19 emergency. At a press conference on Jan. 8, METI Ministry Kajiyama said he didn’t envisage asking the public to save power.

Electricity retailers fight for survival amid skyrocketing spot prices

(Diamond Online, Jan. 14)

- The spot price for electricity traded on the wholesale market recorded a historical high of over ¥154 on Jan. 13, over eight times its level one year before.

- CONTEXT: This is still the peak closing price for 24-hour day-ahead pricing as of Jan. 17.

- Power retailers that lack their own generation capacity are burning through cash reserves as they sell electricity to clients at a significant loss.

- While the high prices are being blamed on an LNG shortage and cold weather, in reality, the culprit is the business model underpinning the wholesale electricity market.

- Industry insiders say exceptionally low spot prices in the first half of 2020 prompted many electricity retailers to pull out of long-term contracts with JERA and other legacy generators and source electricity on the spot market instead.

- The COVID-19 pandemic makes it difficult to forecast LNG demand, and power generators underestimated winter demand. At least one month is needed for any new LNG order to be delivered.

Cold snap: TEPCO EP offers special terms to hard-hit regions

(Denki Shimbun, Jan. 15)

- TEPCO Energy Partner, the retail company in the TEPCO Holding group, is discounting power bills and allowing special payment terms to residents of municipalities affected by the recent record snowfall.

- Subscribers need to apply to be eligible. Affected areas include Akita, Niigata, Toyama, and Fukui.

OPINION: Japan’s LNG dependence exposed and pivot to green power under question

(Nikkei, Jan. 13)

- CONTEXT: the writer Matsuo Hirofumi is a senior staff at Nikkei Shimbun. This is presented as an editorial.

- The current energy crisis shows the challenges of decarbonization for Japan and the many problems with the current energy system.

- Peak load for many regions hit 99% at times, with a record 140 cases when a utility was instructed to send power to a neighboring region to stave off shortages.

- Japan’s reliance on LNG has been exposed with this crisis. It takes about two months to get a cargo delivered from time of purchase. But, Japan has only two weeks of LNG storage built into the system.

- Oil-burning plants are less clean and more expensive, but oil can be stored for many months. It is also much easier and quicker to procure and transport.

- As the government has pushed for liberalization in the power market, oil-fueled power plants with high fixed costs and low-capacity factors were decommissioned one after another.

- A long-standing concern has materialized: Liberalizing the power markets is making it difficult to maintain generation capacity.

- The intermittency of renewable energy has also been shown up in this crisis as the situation in Kyushu region exemplified. Available solar power capacity dropped 42% during the cold snap, the equivalent of two nuclear reactors. Also, this solar capacity is often used to power pumped storage hydro. The lack of solar made it unusable.

- Japan has focused its energy policy discussions too much on zero-carbon aspirations and market liberalization. There needs to more thought about stable supply and how to meet that at minimum cost.

- LNG plants also need to become more resilient and the grid needs to be restructured to make the national system more flexible.

Pipe damage found at Kansai Electric’s Takahama nuclear plant

(Denki Shimbun, Jan. 15)

- KEPCO said on Jan. 14 that a scheduled inspection of the No. 4 reactor at the Takahama nuclear power plant had found damage to steam generator infrastructure. It appears that iron oxide scale has compromised the network of pipes that transport heat from the generator.

- The age of the plant is believed to be a factor.

- SIDE DEVELOPMENT:

- Kansai Electric not learning from its nuclear mistakes

- (President, Jan. 11)

- Kansai Electric (KEPCO) is known for being highly reliant on nuclear power plants (NPP), and has made the restarting of its three Fukui NPPs a top priority.

- CEO Morimoto’s indecisiveness on the issue of finding storage locations for nuclear waste, however, could mean the company finds itself in crisis.

- After 11th-hour negotiations between METI and the Federation of Electric Power Companies, it was proposed that KEPCO could share a new interim storage facility being built in Mutsu (Aomori).

- However, the enthusiasm expressed by Morimoto about sending waste to Mutsu has attracted criticism from within the Federation and KEPCO itself. Insiders say Morimoto showed his true colors with the remark.

- The statement sparked fierce protests from Mutsu officials, who accuse KEPCO of using its Federation membership as a back-door way of forcing its waste on the area. Mutsu officials say KEPCO has not directly informed the municipality of its intentions. KEPCO’s attitude is completely unacceptable, they say.

- This is not the first time KEPCO has angered the Aomori government. Back in 2017, then CEO Iwane told Mustu officials that KEPCO would have a long-term plan in place for dealing with its spent nuclear fuel by the end of 2018. When no plan eventuated, Iwane was forced to apologize to the governor of Aomori.

Kansai Electric’s Ohi No. 4 nuclear reactor to go fully online on Jan. 17

(Denki Shimbun, Jan. 15)

- KEPCO says the 1.2 GW Unit 4 at the Ohi nuclear power plant will be restarted on Jan. 15 and begin supplying electricity to the grid on Jan. 17.

- It is hoped that restarting the reactor will help alleviate the current electricity shortage.

- SIDE DEVELOPMENT:

- Residents call for suspension of Ohi permit

- (Mainichi Shimbun, Jan. 15)

- In a bid to force the shutdown of Units 3 and 4 at the Ohi NPP, the group of Fukui residents that successfully petitioned for the revocation of the original restart permit granted by the Nuclear Regulation Authority has now filed a petition demanding that the force of the permit be suspended until after the appeal process has concluded.

JERA Energy Taiwan drumming up business

(Denki Shimbun, Jan. 15)

- In a bid to boost its profile, JERA Energy’s Taiwanese subsidiary, JERA Energy Taiwan, launched its Chinese language website on Jan. 14.

- Established in June 2019, the company currently participates in three offshore wind farm projects in Taiwan as well as operating three gas-fired power stations.

- The Taiwanese government aims to source 50% of its electricity from natural gas and 25% from renewables by 2025.

Forest Energy to build 7MW biomass plant in Shizuoka

(New Energy Business News, Jan. 15)

- Forest Energy is planning a 7.1 MW wood biomass power station in Shizuoka.

- Forest Energy’s proposal has been approved by METI under the FIT (Feed-In Tariff) Act.

- Around 90,000 metric tons of feedstock, particularly branches, bark and logs, will be sourced annually from the local area.

NEWS:

OIL & GAS

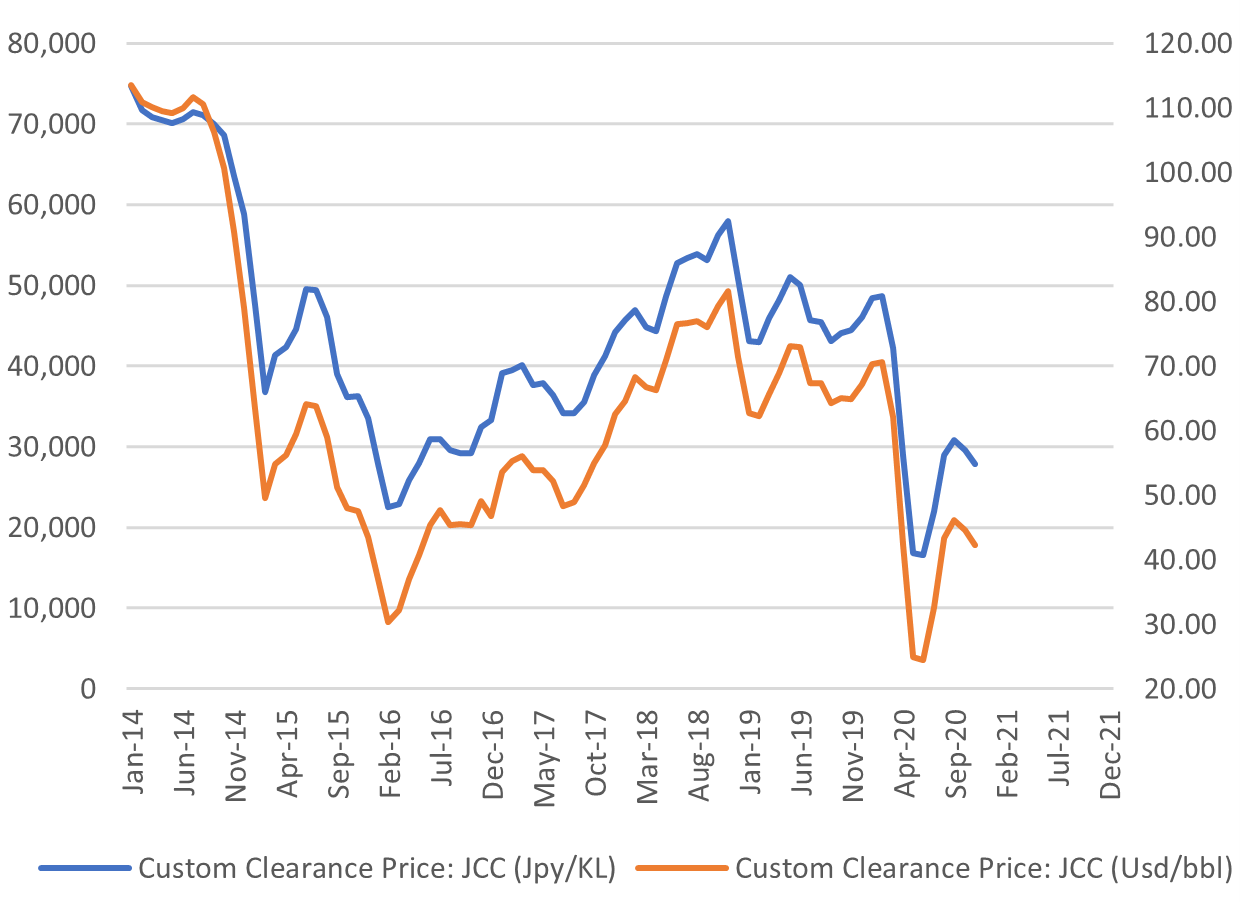

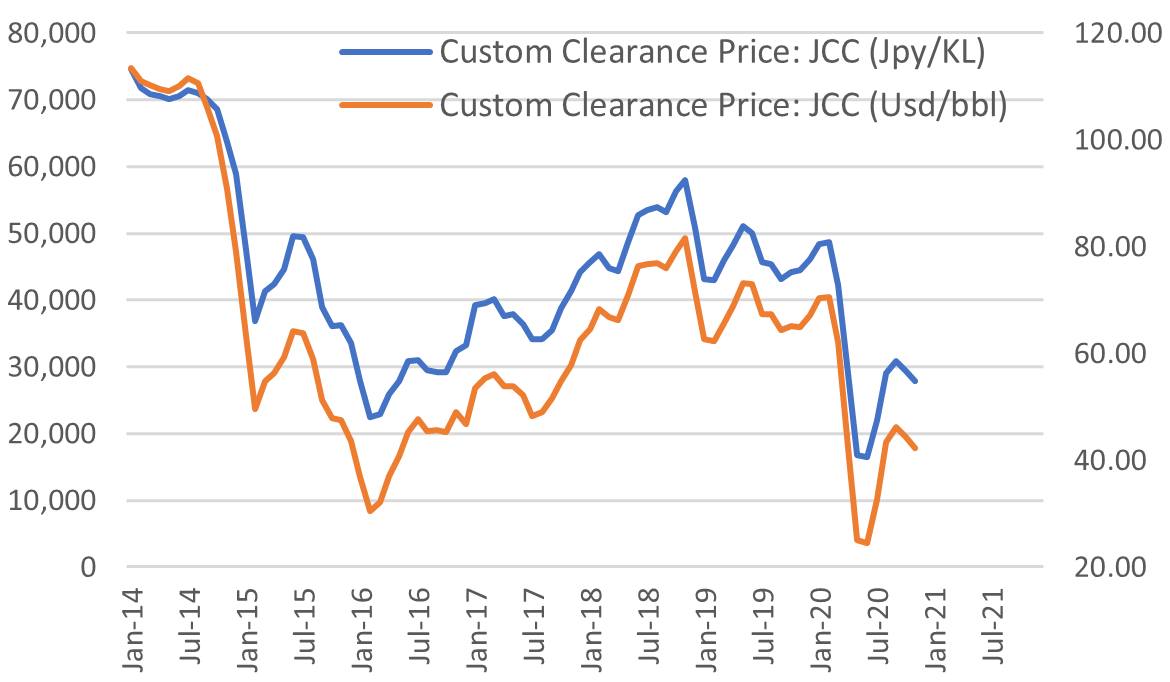

Japan Oil Price:

$42.28

/ barrel

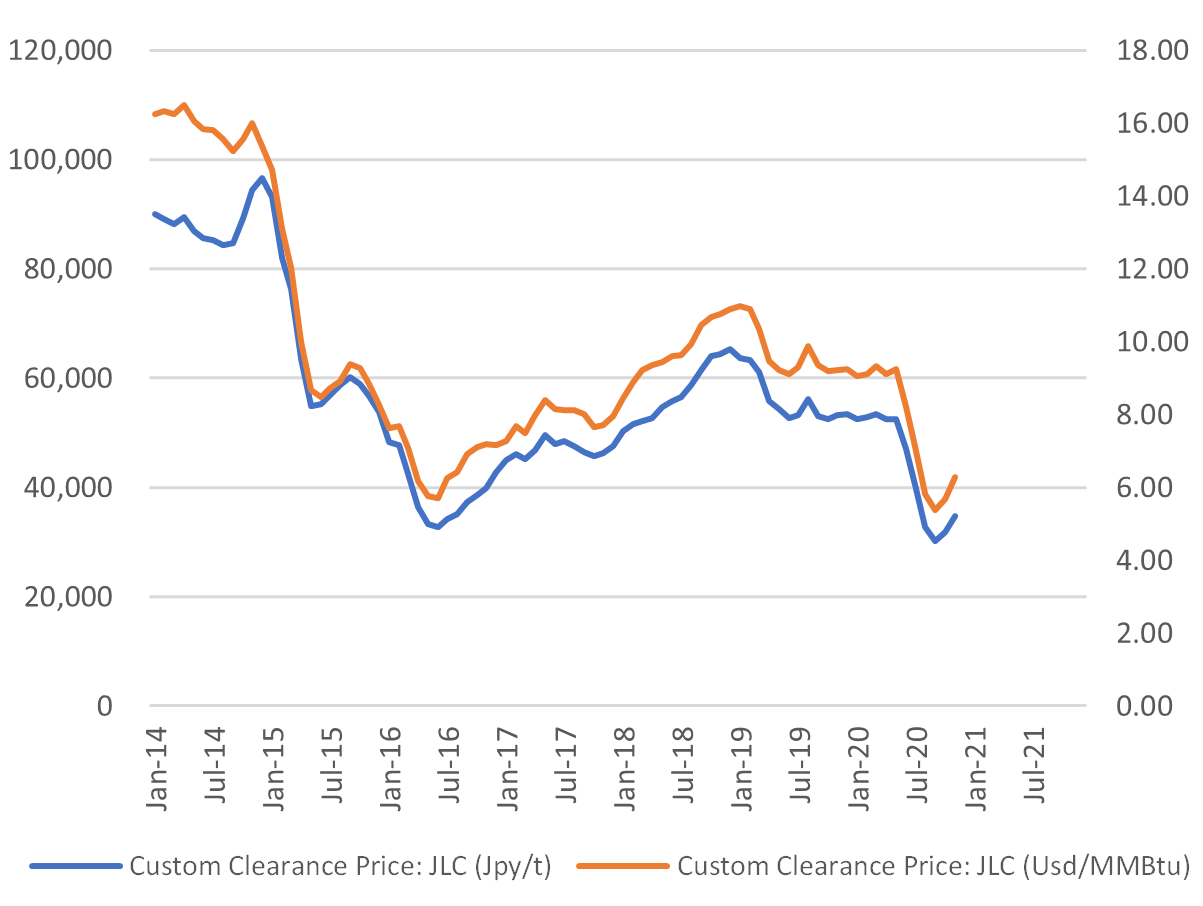

Japan (JLC) LNG Price:

$6.27

/ mmbtu

ENEOS scales back operations at Kanagawa refinery on falling jet demand

(Sekiyu Tsushin, Jan. 15)

- ENEOS said on Jan. 14 that in fall it will decommission part of the atmospheric distillation equipment at its Negishi refinery amid falling demand for jet fuel and other petroleum products.

- This will reduce the capacity of the refinery from 270,000 to 150,000 barrels per day.

- This represents a 6.4% reduction in the ENEOS Group’s total output.

Marubeni said to be planning exit from U.K. North Sea oil and gas

(Bloomberg News, Jan. 15)

- Marubeni is looking to sell its main oil and gas fields in the North Sea region of the U.K. Bids are due in March.

- The Japanese trader may be looking to focus on larger operations elsewhere.

- If the sale takes place, only JX Nippon Exploration and Mitsui & Co will be left among the Japanese investors in the region.

INPEX shuts Ichthys LNG facility for unplanned maintenance

(Bloomberg News, Jan. 14)

- On Jan. 12 the Japanese co. sent notice to Australia’s National Offshore Petroleum Safety and Environmental Management Authority that it will make repairs at the Ichthys LNG export facility.

What caused the LNG shortage? View from Japan

(Nikkei, Jan. 13)

- CONTEXT: This article from Japan’s biggest business media explained the background of the LNG shortage.

- An unexpected cold snap combined with congestion in the Panama Canal has resulted in major power shortages throughout Japan.

- LNG is currently in strong demand thanks to recent cold weather in China, South Korea and Taiwan. The situation has been exacerbated by Chinese manufacturers which are ramping up production now that China has successfully come out of the coronavirus pandemic.

- A series of maintenance and operational issues at LNG plants in Australia, Malaysia and Qatar 2020 has exacerbated supply difficulties. According to an analyst at Japan Oil, Gas and Metals National Corporation (JOGMEC), this is the first time that multiple production issues have arisen simultaneously in multiple locations.

ANALYSIS

BY ANDREW DEWIT

PROFESSOR OF ENERGY POLICY

SCHOOL OF ECONOMIC POLICY STUDIES

RIKKYO UNIVERSITY, TOKYO

Japan’s Green Tech Plans Face Critical Raw Material Issues

Along with dozens of other countries, in 2020 Japan committed to achieve net-zero in greenhouse-gas emissions by 2050. Japan’s decarbonization pledge is backed up by ambitions for a vast rollout of offshore wind, millions of tons of green hydrogen, and assertions that domestic automakers can establish net-zero emissions from the entire life cycle of a vehicle.

Japan may yet possess the innovative capacity to realize these goals. But one pertinent question is whether resource-scarce Japan has access to sufficient critical materials to make it happen. Equally important is asking whether Japan has a strategy to secure critical raw materials that conform to rapidly diffusing sustainability rules.

It’s a Material World

Concerns about decarbonization’s material demand went mainstream at the start of this year. On January 11, the International Energy Agency (IEA) announced a series of special projects for 2021, leading up to the May 18 release of The World’s Roadmap to Net Zero by 2050. Key among the IEA special reports will be what IEA director Fatih Birol correctly described as the first comprehensive and global study of the supply constraints, lifecycle costs, environmental justice, and related challenges confronting critical minerals used in electric vehicles, renewable energy equipment, and the myriad other elements of the clean energy transition. This IEA special report is tentatively titled The Role of Critical Minerals in Clean Energy Transitions, and is slated for publication in April.

According to Birol, copper, nickel, cobalt and rare earth metals will feature among the critical minerals under the IEA’s review. However, that itemization is not exhaustive. What constitutes a “critical raw material” (CRM) varies by country and is based on domestic economic importance, supply risk and related factors. The most recent CRM list from Australia contains 24 materials. As of 2018, the U.S. identifies 35 CRMs. And Japan’s list comprises 34 CRMs, up from 30 in 2012.

Interestingly, what is deemed a critical resource has largely evolved and expanded in line with the expansion of green energy. The EU is a notable example of this phenomenon. Its triennial review of CRMs identified 14 materials in 2014. As investments in renewable energy and other green tech have soared, the EU’s CRM list has ballooned. By 2017, it contained 27 materials. Last September, the number had grown to 30.

While most CRM lists converge on rare earths, cobalt, graphite, indium, and lithium, the view on other materials differs. For example, Japan has long determined copper to be critical, whereas the EU, U.S., Canada and Australia do not. Yet the global take on copper is rapidly moving closer to Japan’s position. Many experts and analysts are re-evaluating copper’s core contribution in the renewables space and – as Wood Mackenzie does – ranking it alongside aluminum, nickel, cobalt and lithium as an “energy transition metal.”

Driving concerns

There are several drivers for this deepening convergence of concern regarding CRMs. One is the rapidly increasing global commitment to “green deal,” “green recovery,” and similarly named transformative policies to “build back better” from the ravages of COVID-19. These policies are imperative lest China’s currently carbon-intensive recovery become the norm.

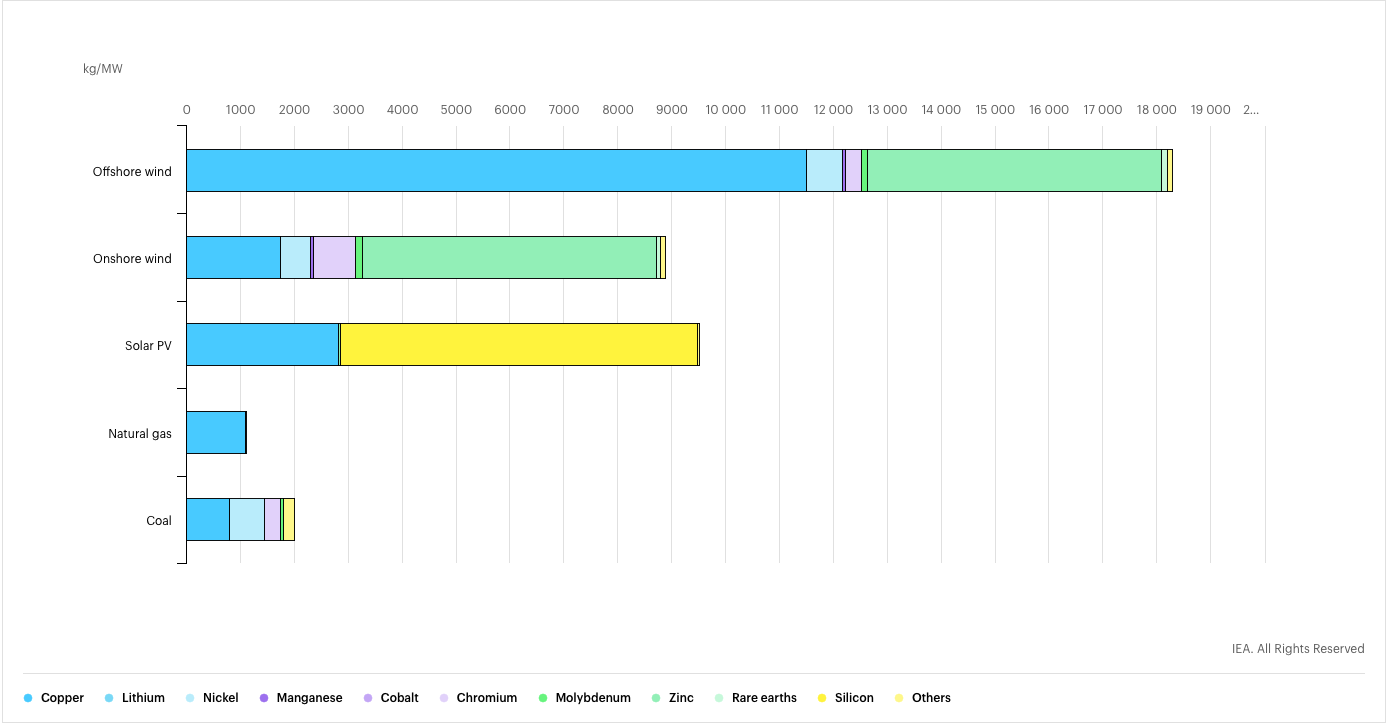

However, implementing the “green” future in power, mobility and other industries is not done via intangible new technologies and innovation. Greening requires a dramatically different mix of raw materials than what composes the grey, or carbon-intensive economy and society. For example, as seen in figure 1, data from a March 2020 IEA report indicate that building offshore wind capacity is well over ten times more copper-intensive than natural-gas and coal-fired fossil-fuel plant.

As for mobility, the same IEA publication points out that electric vehicles require roughly five times as much CRM as a conventional car.

Figure 1: Minerals used in selected power generation technologies

Source: IEA, 2020

Another driver of growing concern over CRMs supply is that no one is minding the store. The policy environment is in flux, the knowledge base concerning CRMs mining and processing is poor, and there are wildly optimistic assumptions regarding substitutability and recycling. Hence, our precarious present, where green-energy scenarios of “overbuild” and “electrify everything” assume a cornucopia of CRMs that analysts realize doesn’t exist.

Indeed, experts on the realities of lithium mining warn that battery-maker and other firms’ current planning for 2023 implies eight times more demand than any conceivable scenario for global supply.

Japan’s supply-chain vulnerabilities

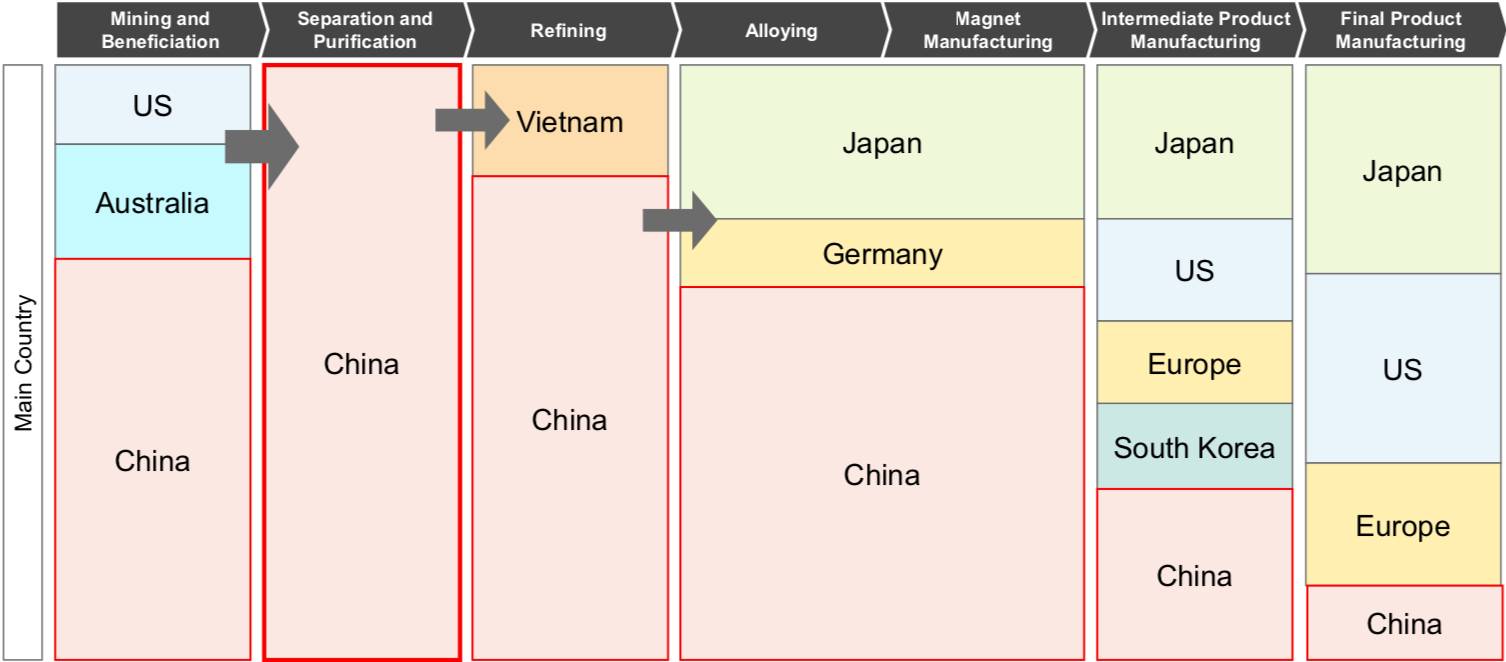

A more long-term set of issues for Japan, in particular, are supply-chain vulnerabilities. The country has had strong trade ties but, at times, a rocky political relationship with neighboring China. And yet, 58% of Japan’s rare earth imports came from China in 2019, according to the Center for Strategic and International Studies’ “China Power” project.

China dominates the mining and processing of CRMs. Last month, Japan’s Ministry of the Economy, Trade and Industry (METI) stated in its vision for the domestic offshore wind industry that Japan must aim to produce at least 60% of components locally in order to cut costs. At present, the viability of this goal depends heavily on China’s interest in continuing to export a large share of its CRMs to Japanese manufacturers. As the story of photovoltaic panels shows, that is not a given. The photovoltaic sector, once led by Japanese firms, is now dominated by Chinese peers.

Over the last decade, Japan has somewhat diversified its rare earths supply, wary of China’s demonstrated capacity to restrict exports. Yet as we see in Figure 2, a 2020 report from the Japan Oil, Gas and Metals National Corporation (JOGMEC) warns that China enjoys a continued monopoly in the separation and purification of rare earths. One reason is that China’s ability to bear the enormous environmental damage from mining and purifying rare earths allows it to weaken the investment incentives of would-be competitors.

Figure 2: Risks in the rare earths supply chain

Source: JOGMEC, 2020

What’s more, extracting and processing rare earths and other CRMs is very energy-intensive, with massive carbon footprints when undertaken in locales dependent on fossil-fuels, as China still is.

However, things are changing. The coal-fired power and lax environmental regulations that have helped make China a formidable player in CRMs, and by extension a major factor affecting Japan’s manufacturing and energy strategies, may soon work against it.

One major reason is the striking rise in prominence of environmental, social and governance (ESG) rules. These rules are now forcing firms to forego the business-as-usual approach in securing CRMs and obligating them to accept responsibility for the lifecycle environmental cost of products.

The upshot is that a Japanese manufacturer of, say, wind power equipment will need to factor in the additional “cost” of the environmental impacts of the CRMs they import. Put simply, in the choice between a bar of metal produced with clean energy and another with dirty energy, the former will become more attractive. At the very least, the cost of the metal will be assessed in terms of both production costs and ESG impacts. The resulting all-in cost may in time also include an emissions tax and similar measures.

This new trajectory of competition and price-discovery is already emerging in certain energy fields, such as LNG. Producers are being encouraged to offer carbon offsets as part of the sale, anticipating compulsory rules.

Similar trends are already emerging in the CRM space – not in spite of, but precisely because of the strategic importance of these materials.

Whither Japan?

As it stands, Japan’s laudable zero-carbon ambitions effectively commit it to a massive increase in imported CRMs. To date, resource-poor Japan has emphasized CRM recycling and substitution. But as the IEA and other initiatives show, those strategies are buckshot rather than silver-bullet solutions.

Japan has a weak mining industry, and will have to secure much larger volumes of CRMs in the midst of increasing resource nationalism, worsening ore-grades, and other complications. At the same time, life-cycle emission commitments will push Japan to be choosy: if it fails to procure ESG-conforming “green CRMs” rather than the environmentally costly “gray CRMs” that it currently sources, it risks forfeiting business in the midst of history’s biggest energy revolution.

Through its purchasing power, Japan finally has the chance to lead on CRMs – to be a rule-maker rather than a rule-taker. So far, Japan’s domestic resource and energy-environmental policy debates have yet to grapple with the dilemmas. But the IEA’s new initiative tells us this complacency has a short shelf life.

ANALYSIS

BY DANIEL SHULMAN

PRINCIPLE

SHULMAN ADVISORY

Symbol of Japan’s “Old Energy” Engineering Excellence

Seeks to Reinvent Itself for the Green Energy Age

For most of the 20th century, Mitsubishi Heavy Industries (MHI) was a stalwart of Japan’s shipping, aviation, and energy industries. It built the nation’s top jets, excelled in defense and commercial ships, and propelled Japanese rockets into space. In the energy sector, MHI crafted many of Japan’s top-selling gas and steam turbines, developed nuclear reactors, and produced ships to carry LNG, LPG and oil.

When the shift to renewables first started in earnest, MHI again sought to be at the forefront. By the early 2010s, it had developed the world’s top wind turbine by capacity and joined forces with a leading European wind power manufacturer, Vestas. And yet, a decade on, MHI’s pivot to green-age energy has yet to really take off, while its core business lines are badly underperforming. For Japan to meet its 2050 decarbonization commitments, its engineering powerhouse will need to turn things around and soon.

Last year was one to forget for MHI. The engineering conglomerate expected to turn things around after posting its first loss in two decades in 2019. Instead, losses mounted, spreading from its now-frozen Mitsubishi Regional Jet project to other core busines pillars. In a bullish year for Japanese stocks, MHI shares dropped 26%.

Crimped ambitions in the wind power market

Having contributed 39% of MHI’s total revenues in FY2019, Energy Systems is the company’s second largest business unit. Among other things, it includes production of gas-turbine combined cycle and nuclear power plants, wind turbines, and aircraft engine parts.

As the nuclear industry in Japan has floundered and nuclear export ambitions waned, Energy System saw profits turn to a loss. The segment had a ¥12.4 billion loss in 1H2020, with lower sales of steam power and aircraft engines also contributing.

More disappointing, perhaps, were the dim results of MHI’s wind power ambitions. Between FY2011 and FY2018, MHI participated in the Fukushima Offshore Wind Consortium, which included nine other private companies and universities in Japan. The METI-subsidized demonstration project sought to build the case for commercial floating offshore facilities in Japan, based on homegrown technology. After the Fukushima nuclear disaster, it was also a symbolic move to help rebuild Fukushima prefecture as a beacon for renewable energy.

The consortium installed three sets of turbines off the coast of Fukushima: 2 MW, 5 MW, and 7 MW capacity turbines. Of the first two, made by Hitachi, only one, the smallest, reached the target capacity factor of 30%. MHI was responsible for the 7 MW model. It performed the worst of the three, operating at just 2% capacity due to issues with the turbine’s hydraulic system.

Luckily for MHI, it had hedged its wind ambitions by partnering with Denmark’s Vestas in 2014. The Danish firm was on the brink of bankruptcy and MHI promised to work as equals in the 50-50 JV with its European partner.

Six years later and it’s the Danish partner rescuing MHI’s wind business. While MHI expected the MHI Vestas JV to help it gain valuable know-how in the off-shore wind turbine business, the majority of the ¥850 billion order pipeline that Vestas brought to the venture was from projects in Europe (and thus served by Vestas-manufactured turbines). MHI failed to generate any significant business for the JV in Japan.

With that, in November 2020, Mitsubishi Heavy announced that it will terminate the development of its own wind turbines and dissolve the MHI Vestas joint-venture. As part of the dissolution, however, MHI became a Vestas shareholder, taking a 2.5% stake. Those shares are now worth about $1.2 billion.

Trouble in traditional energy markets

MHI’s struggles in energy are not limited to the wind power market. The conglomerate has seen COVID-19 hurt demand across a number of industrial and infrastructure projects. It has also delayed a planned exit from LNG tanker production, announced in December 2019.

Photo credit: MHI Vestas.

MHI planned to sell one of its shipyards to Oshima Shipbuilding, Japan’s third-largest shipbuilder, by March 2020. This did not happen and a revised schedule for the sale remains unknown.

The October announcement by Prime Minister Suga that pledged to make Japan emissions net-zero by 2050 also casts doubt on MHI’s turbines business, much of which has been molded around thermal and nuclear power facilities. The nation’s decarbonization commitment looks set to strongly reduce demand for new thermal power capacity, while new nuclear plant construction is not on the agenda, according to Suga’s Chief Cabinet Secretary Kato.

A green turnaround?

By the end the year, MHI set out a plan to reorient its energy products to green energy. On November 26, 2020, MHI announced an “Energy Transition Strategy,” part of which involves investing ¥90 billion in energy transition-related projects over the next three years. By FY2023, the company aims for this segment to contribute ¥50 billion to total revenues, and it expects that amount to increase to ¥300 billion yen in FY2030.

As part of the new initiative, MHI plans to offer services that improve efficiency at gas and coal co-firing power plants, to develop turbines for hydrogen co-firing plants, and to invest in CO2 recovery and utilization technologies.

The company also expressed interest in investing in hydrogen and ammonia production projects, starting by acquiring a stake in Australia’s H2U Investments.

While domestic peer Kawasaki Heavy Industries has said it will sell all of its domestic nuclear business, MHI is not giving up on that segment. MHI said it believes it can grow its nuclear business by supporting the restart of Japan’s existing reactors and by developing technologies to produce clean hydrogen using nuclear power. Also, MHI says it plans to design a safer next-generation light water reactor.

With the levelized cost of electricity from nuclear rising from around $117/ MWh in 2015 to $155/ MWh at the end of 2019, and the world looking to shift from fossil fuel-burning power plants to renewables, MHI’s strategy seems risky. Its core emphasis remains on co-firing and nuclear.

Still, MHI’s focus also happens to be in line with the Japanese government’s focus on strengthening infrastructure exports as part of its “Infrastructure System Export Strategy.” What’s more, the conglomerate might finally turn around its fortunes in wind power after the government recently announced a target requiring at least 60% of offshore wind components to be made domestically.

MHI is also making headway in carbon capture, a technology for which the government and industry have particularly high expectations. In Sept. 2020, MHI began trials of carbon capture at a biomass power station in the U.K. operated by Drax Group. The target is to combine plant-based fuel and carbon capture to report negative net emissions.

MHI has already delivered 14 carbon capture facilities globally and has worked on this technology since the 1990s.

At the end of 2020, MHI issued so-called green bonds for the first time. The ¥25 billion amount is not small, but more than the money, it indicates the direction of the engineering conglomerate. MHI has said it will use the proceeds to support wind, hydrogen, and geothermal power projects.

GLOBAL VIEW

BY TOM O’SULLIVAN

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

LNG:

Extreme volatility in LNG pricing due to a record half-century plunge in temperatures in China, South Korea, and Japan saw LNG delivery prices rise to almost $40 mmbtu from a low of $2 mmbtu one year ago.

Oil:

1). Exxon is under investigation by the U.S. Securities and Exchange Commission, following an employee’s whistle-blower complaint for overvaluing one of its most important oil and gas holdings in the Permian Basin.

2). OPEC issued its latest global oil demand forecast for 2021 on Thursday showing consumption increasing by 5.9 mbpd YoY to average 96 mbpd in 2021.

Climate:

Copernicus, the EU monitoring center, has reported 2020 as the joint hottest year on record, along with 2016. In June 2020, temperatures of 38 Celsius (100.4 Fahrenheit) were recorded in the Russian town of Verkhoyansk in the Sakha Republic, which lies inside the Arctic Circle and is otherwise known as one of the coldest places on Earth.

ESG:

HSBC investors, Amundi and Man Group, have criticized the bank for fossil fuel financing activities and have filed a climate resolution ahead of the April HSBC AGM.

Hydropower:

1). Negotiations between Ethiopia, Sudan and Egypt over the 4 GW Grand Ethiopian Renaissance Dam on the Blue Nile broke down last week. Ethiopia had commenced filling the dam in July 2020.

2). China’s decision to hold back the Mekong River’s water flow by almost 50% at the Jinghong Hydropower Station dam for close to a month, until Jan. 24, has been criticized by Thai and Laos interest groups and could impact the livelihoods of up to 60 million people. The reason for the reduced water discharge was attributed to maintenance for power grid transmission lines.

EVs:

1). GM will launch a new electric-truck business focused on delivery services.

2). Tesla faces a 158,000 vehicle recall in the U.S. for its Model S and Model X sports utility models due to defects with its touch screen technology.

China:

1). The U.S. government has sanctioned CNOOC officials for harassing and threatening Vietnamese oil and gas exploration and extraction facilities in the South China Sea, although the sanctions don’t impact oil or natural gas trade.

2). China has placed travel restrictions on 23 million residents of Shijiazhuang, Xingtai and Lanfang in Hebei Province due to virus outbreaks, potentially stalling the country’s improving energy consumption. The World Bank now estimates that pandemic will cost the global economy more than $10 trillion in lost output in 2020 and 2021.

South Korea:

1). The share price of Hyundai Motor has soared over 25% since the publication of a report that it would sign an agreement with Apple to manufacture autonomous EVs.

2). Deputy Foreign Minister Choi Jong-Kun of South Korea (‘RoK’) has asked Qatar for “maximum support” to secure the release of the Hankuk Chemi oil tanker seized by Iran on Jan. 4 near Hormuz in the Persian Gulf. Choi visited Qatar from Tehran after talks with Iranian officials failed to secure the release of RoK sailors or the tanker.

Taiwan:

U.S. ambassador to U.N., Kelly Craft, abruptly cancelled a trip to Taiwan on Wednesday. The scheduled trip followed the announcement by the U.S. State Department that it would remove multi-year restrictions on engagement with Taiwanese diplomats. The announcement is thought to have infuriated China, potentially raising tensions in the seas around Taiwan.

Indonesia:

The 6.2 earthquake on Sulawesi Island in Indonesia on Friday caused significant power outages in West Sulawesi, which has a population of 15 million.

Australia:

Shell resumed LNG cargoes from its Prelude FLNG facility following a one-year technical disruption at the Browse Basin facility in Western Australia. The FLNG structure is estimated to have cost $13 billion and Japan’s INPEX holds a 17.5% stake in the project.

Kyrgyzstan:

Sadyr Japarov was elected president on Jan. 10 in a move welcomed by China and Russia. Russia is the major supplier of oil and gas with Gazprom operating the country’s gas network. Hydro and coal are the major sources of electricity and the country is thought to have $2 billion of Chinese debt coming due soon. Shinzo Abe was the first Japanese prime minister to ever visit the country in 2015. The U.S. embassy in Bishkek has not yet issued any comments on Japarov’s election.

Saudia Arabia:

1). The Saudi government launched the initiative, “Programme HQ”, to lure large oil services companies from Dubai to Riyadh. Inducements include a 50-year tax holiday.

2). The country also announced $40 billion of spending over five years by the Public Investment Fund on two futuristic projects on the Red Sea including one at Neom.

Iran:

1). Iran announced it will produce material from uranium used in nuclear warheads. This followed an announcement earlier in the month about uranium enrichment levels and stockpiles of low-enriched uranium, all of which exceed levels in the 2015 nuclear agreement.

2). Ayatollah Ali Khamenei banned all Covid-19 vaccines from the U.S. and the U.K. Iran is thought to have 1.3 million infections and has suffered 56,000 fatalities.

Africa:

The African Development Bank has committed $14 billion to build the ‘Great Green Wall’ project that will plant vegetation along an 8,000 km route across the Sahel from Senegal to Djibouti.

Turkey/Greece:

Both governments will meet in Istanbul on Jan. 25 to discuss oil and gas territorial disputes in the Aegean and the East Mediterranean. France had sent a military frigate to the region in August to back Greece’s claims after Greek and Turkish frigates collided.

Germany:

Armin Laschet was elected leader of the ruling CDU party on Saturday making him favorite to replace Angela Merkel as German chancellor after the federal election on Sept. 26. He is currently prime minister of North Rhine-Westphalia, which borders Holland and Belgium, and has been a member of the Bundestag since 1994 and is a committed European. There is likely to be no change in Germany’s policy of energy engagement with Russia or Germany’s 11 commercial engagement with China.

Mexico:

Pemex, the state oil monopoly, is facing a cash crunch due to low oil prices and a $110 billion debt mountain. It was forced to raise almost $5 billion from a government-refinancing program to meet a $2 billion debt repayment due this month.

Brazil:

Ford will cease auto manufacturing in Brazil with the loss of 5,000 jobs. The company is expected to lose almost $400m in South America in 2020.

United States:

1). In Texas output from wind energy exceeded output from coal projects for the first time ever in 2020. Wind output reached one quarter of total Texan output, with coal at 18%.

2). The operator of the Millennium Bulk Terminal coal project on the Columbia River in Washington State filed for bankruptcy last month. The project was meant to ship coal from the Power River Basin in Wyoming and Montana to Asia.

3). U.S. GHG emissions fell by 10% YoY in 2020, falling below 5.5 billion tons for the first time since the 1980.

4). Toyota paid a $180 million fine for breaching EPA reporting requirements.

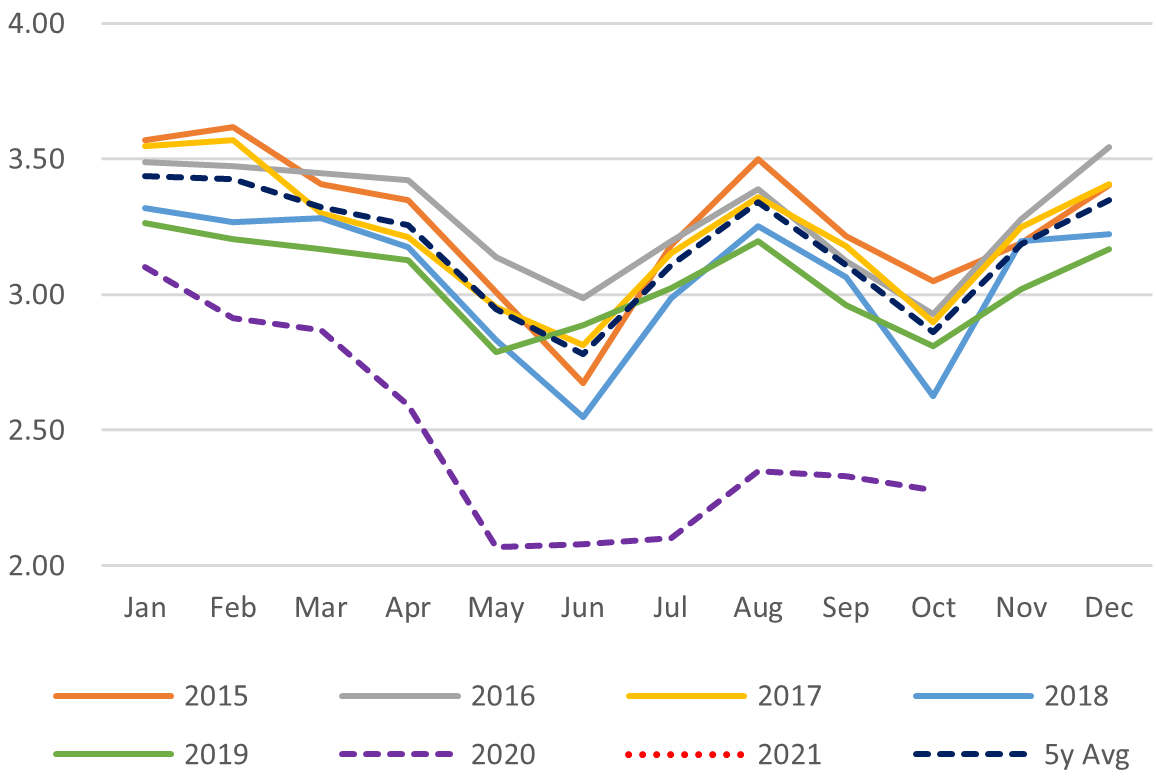

DATA

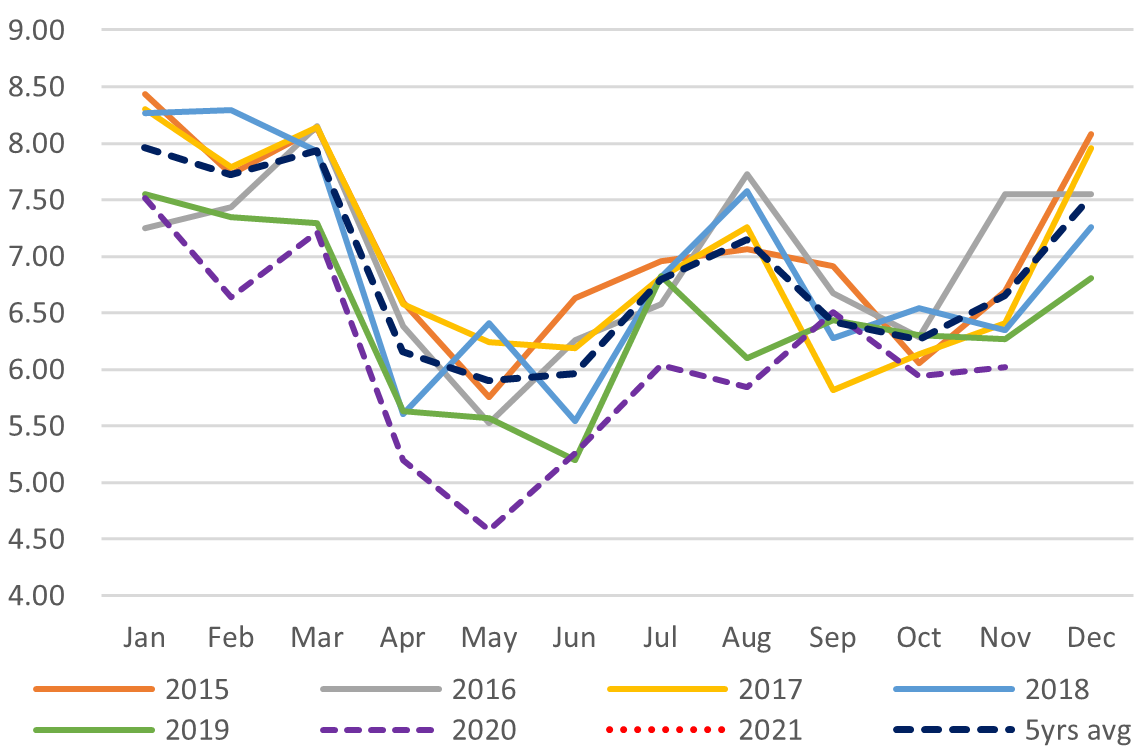

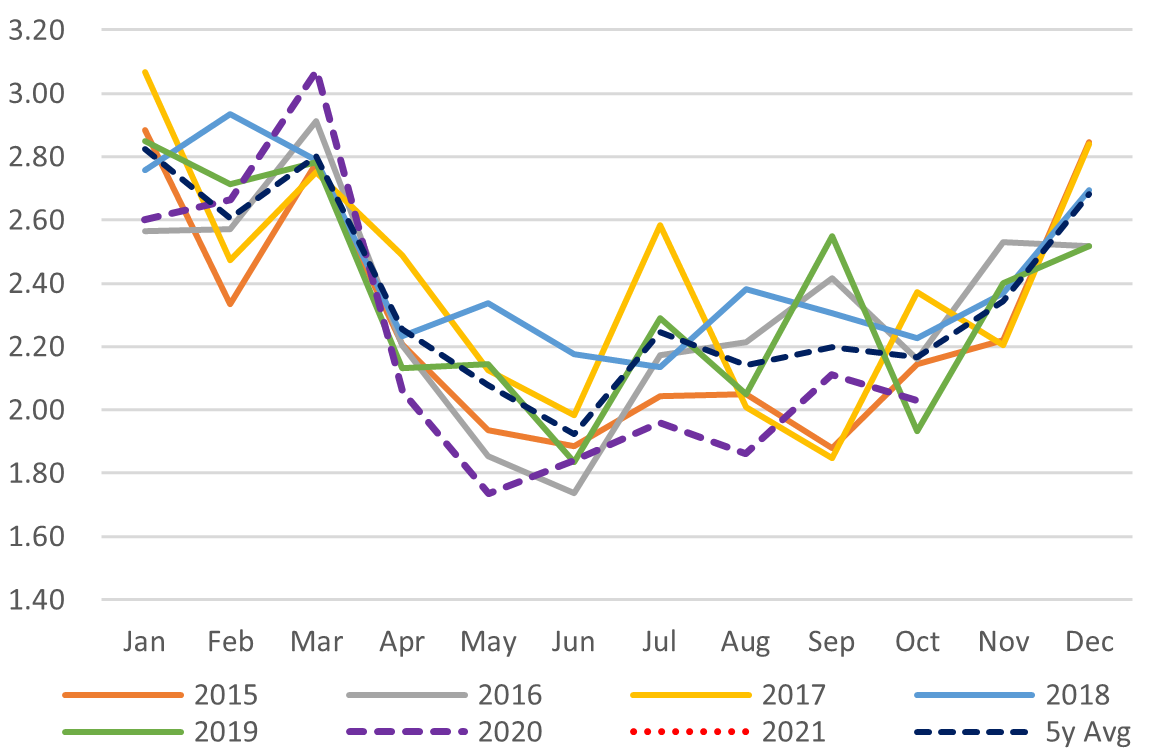

Japan Oil Price

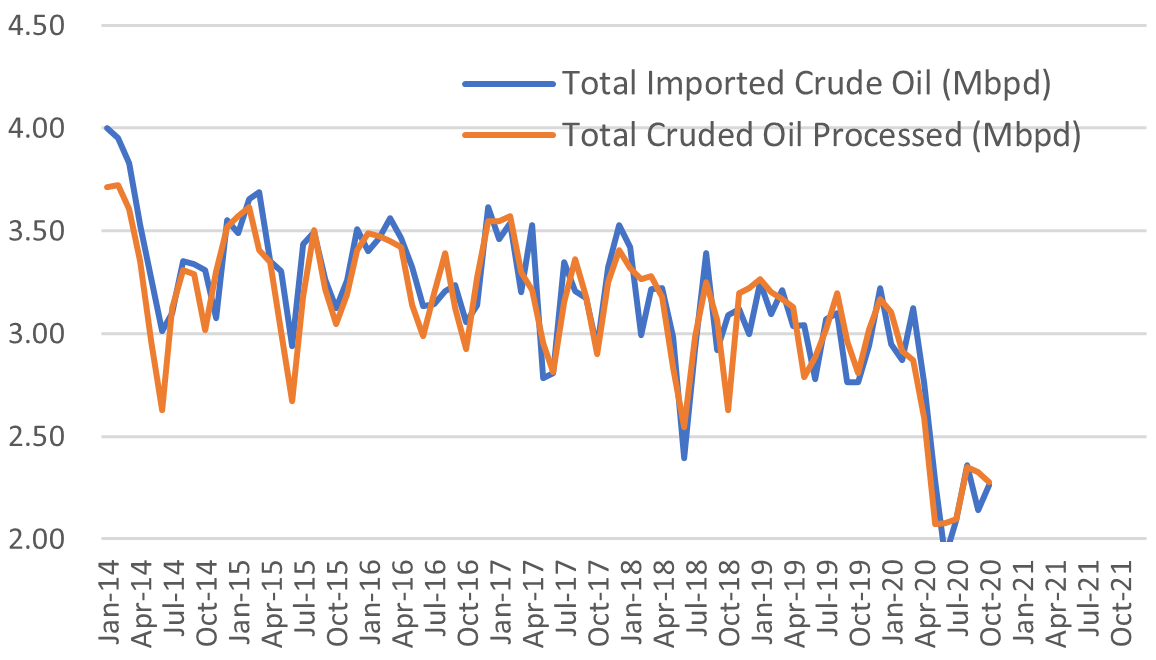

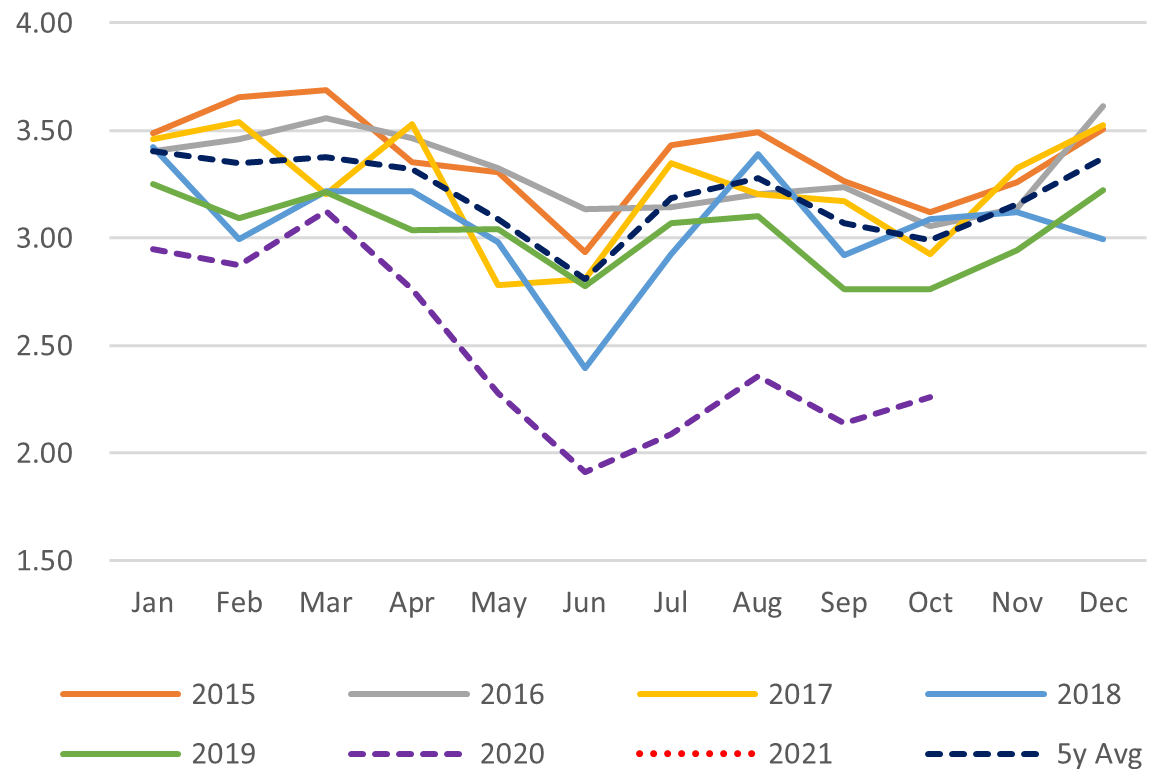

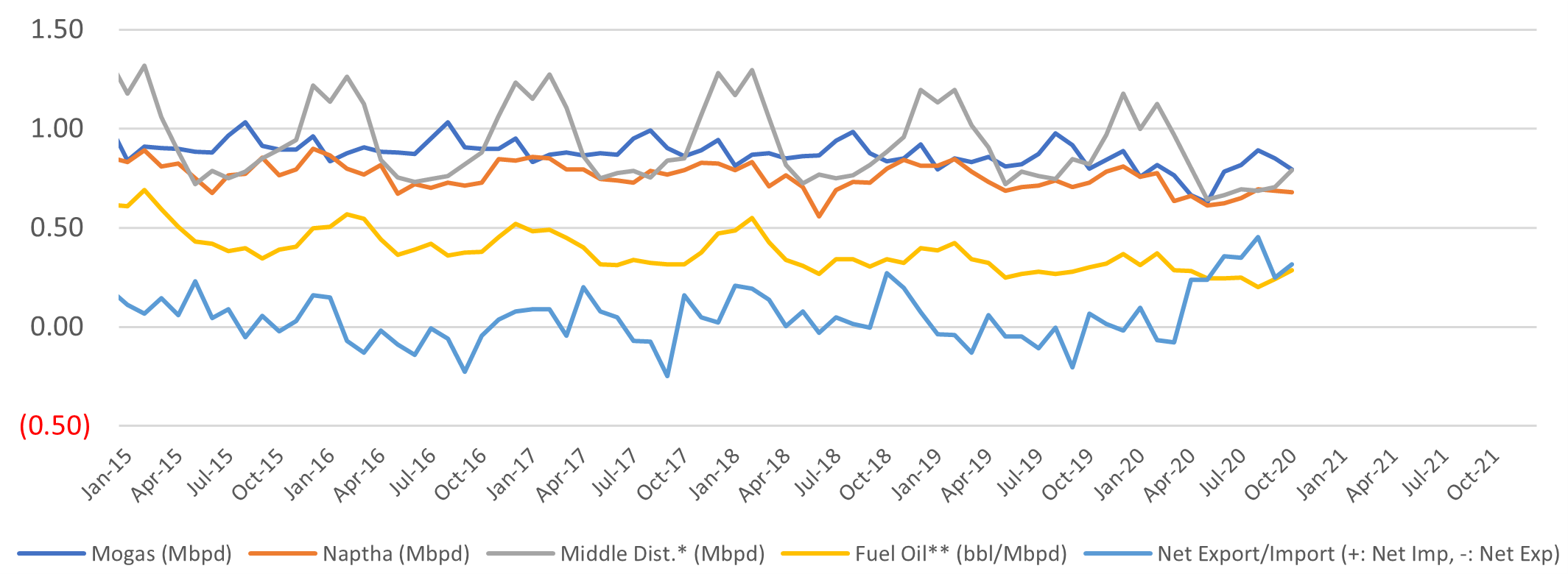

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

Domestic Fuel Sales

SOURCES: Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

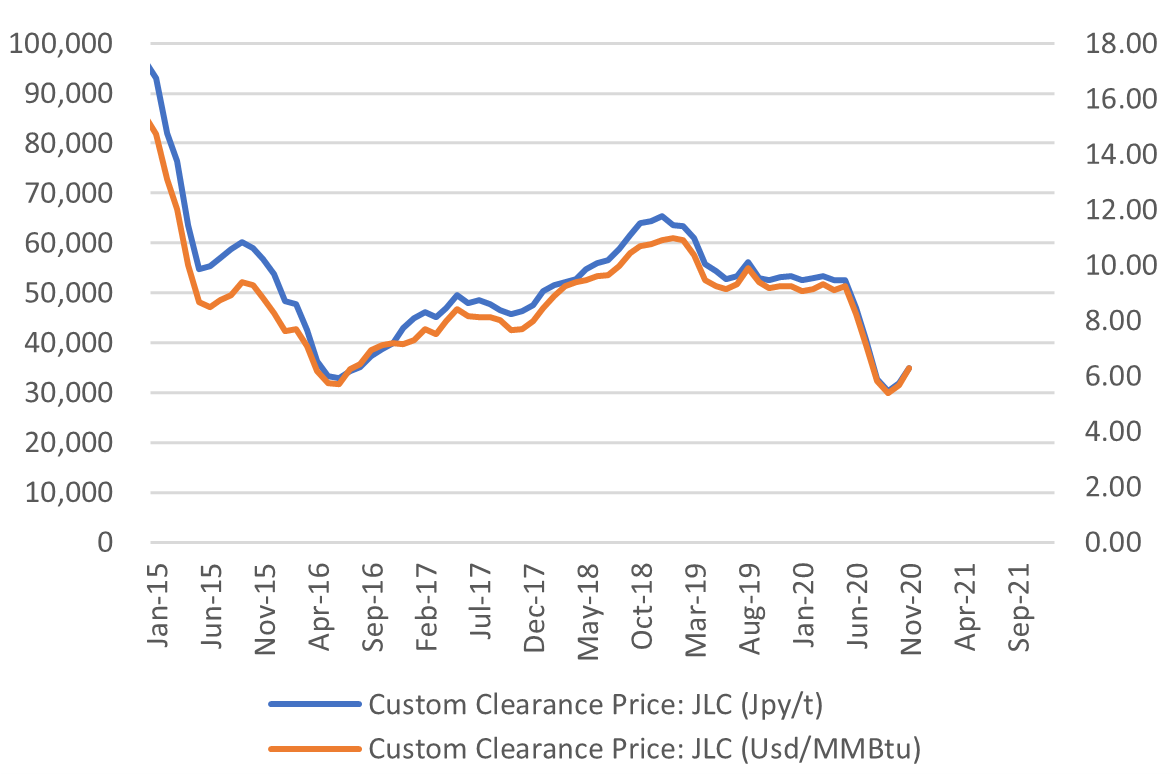

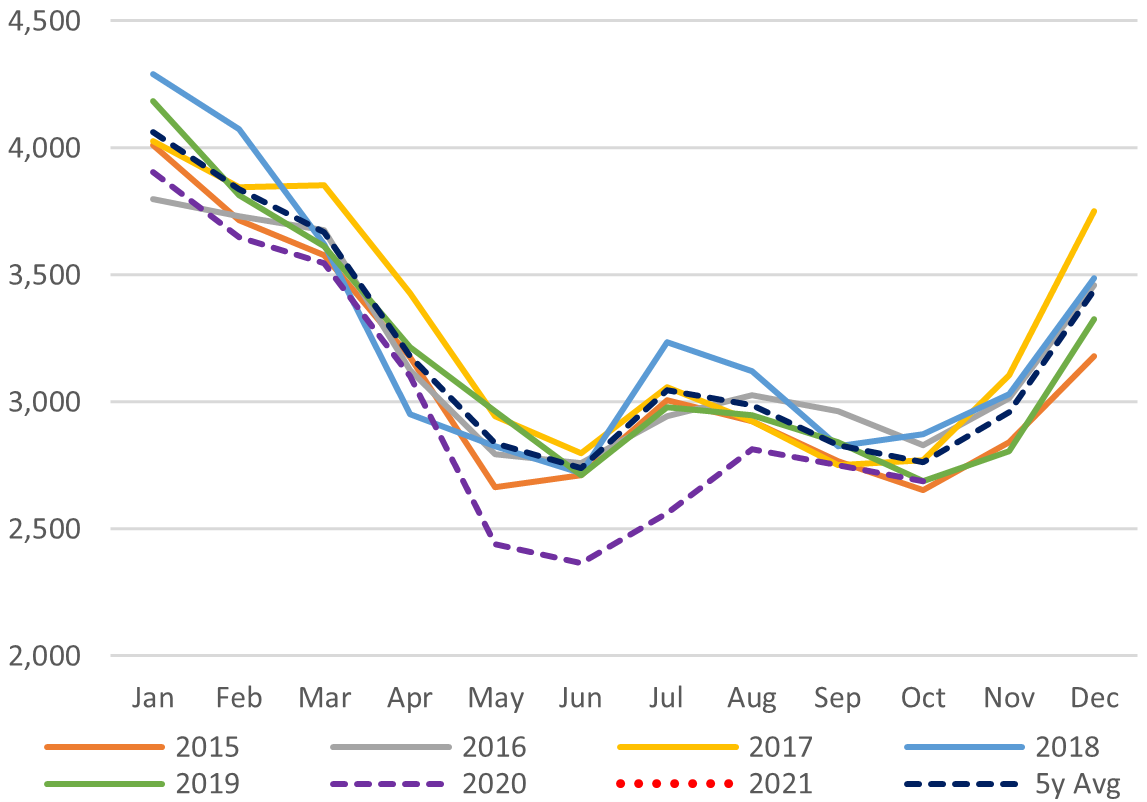

Japan LNG Price

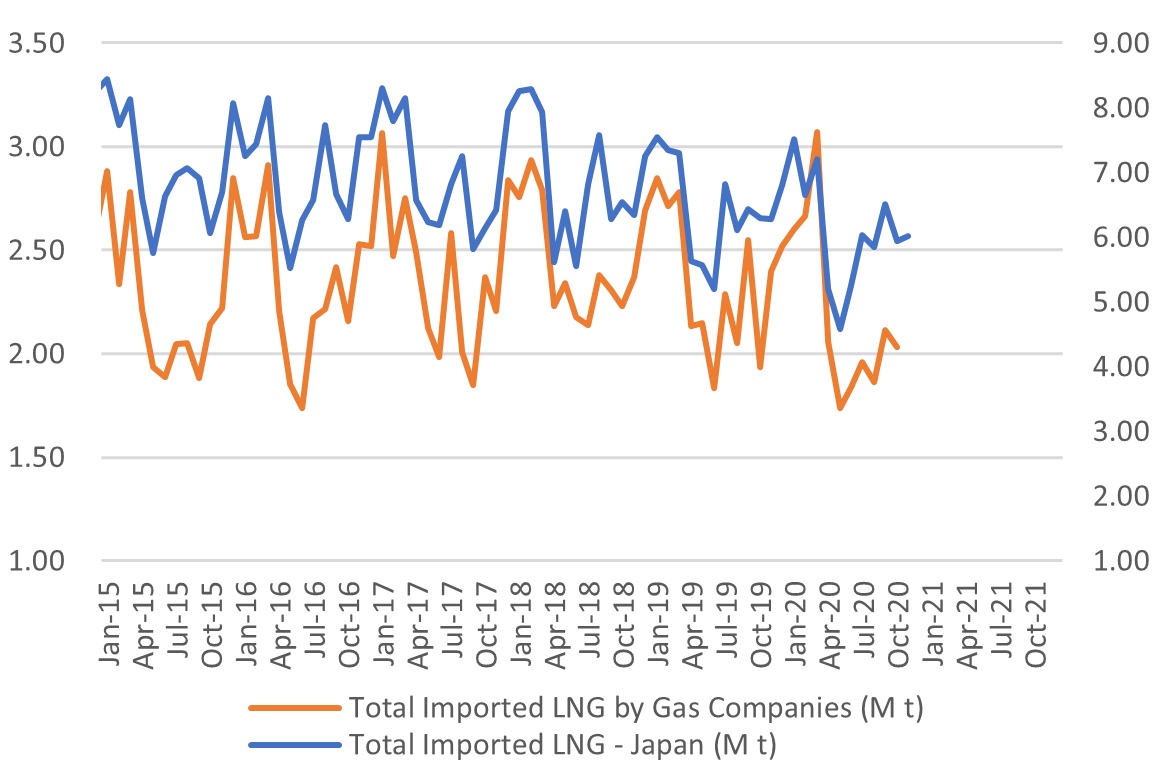

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

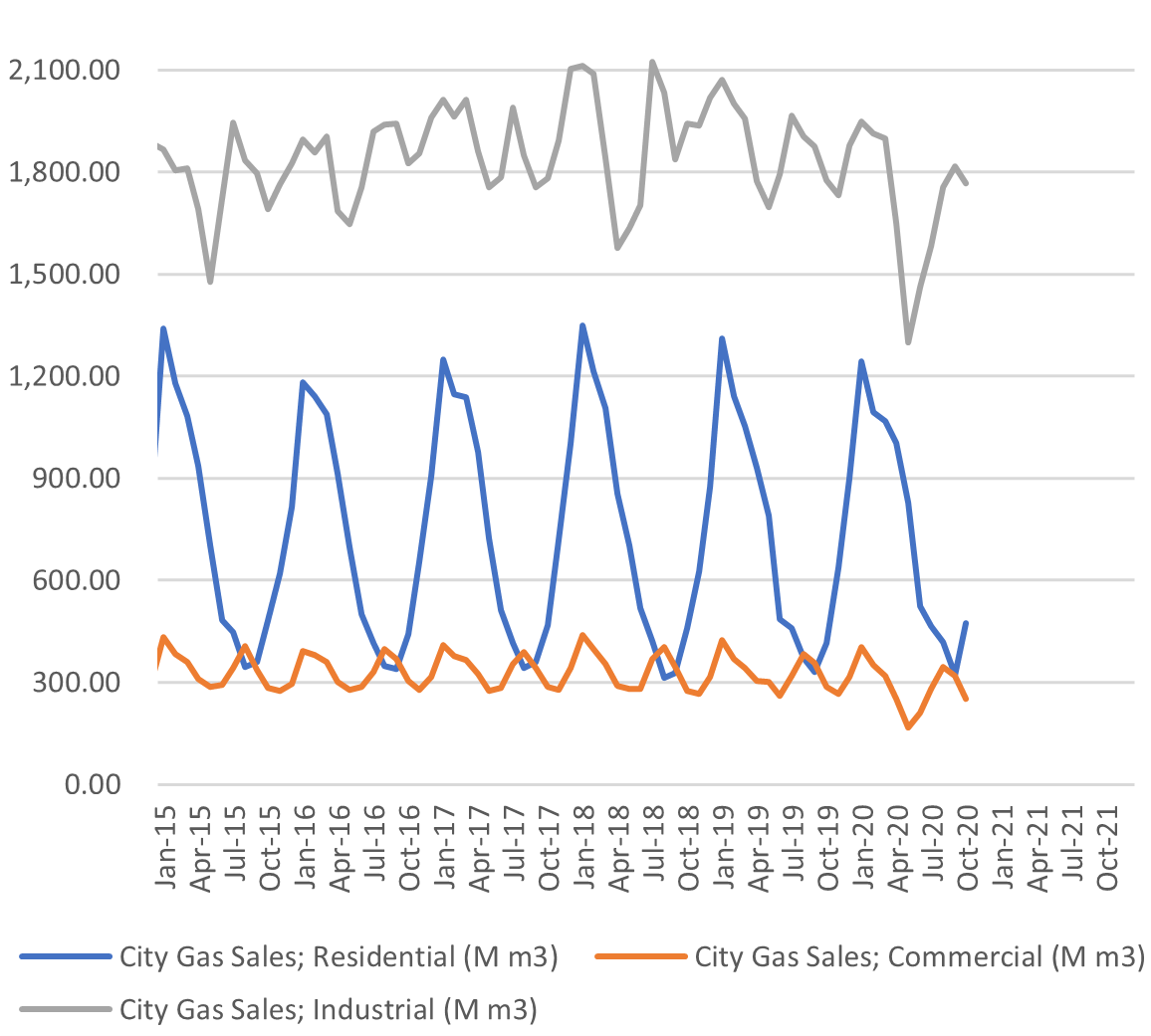

City Gas Sales – Total (M m3)

City Gas Sales by Sector (M m3)

SOURCES: Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

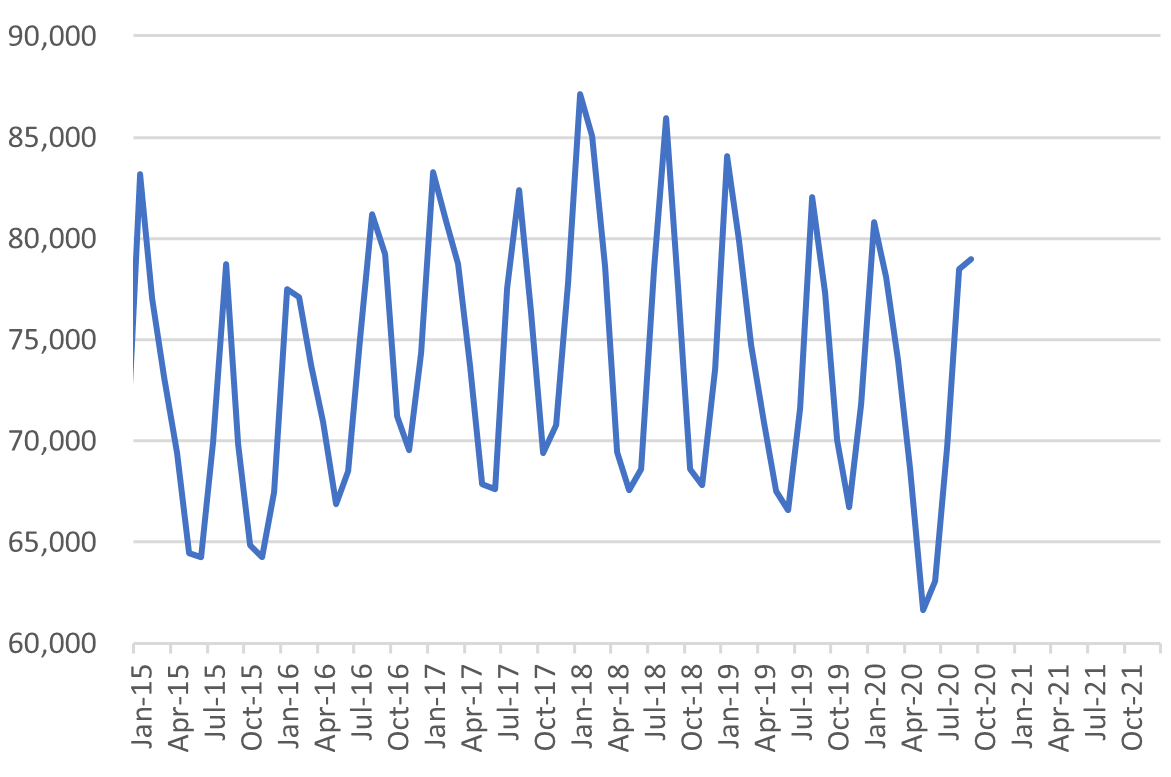

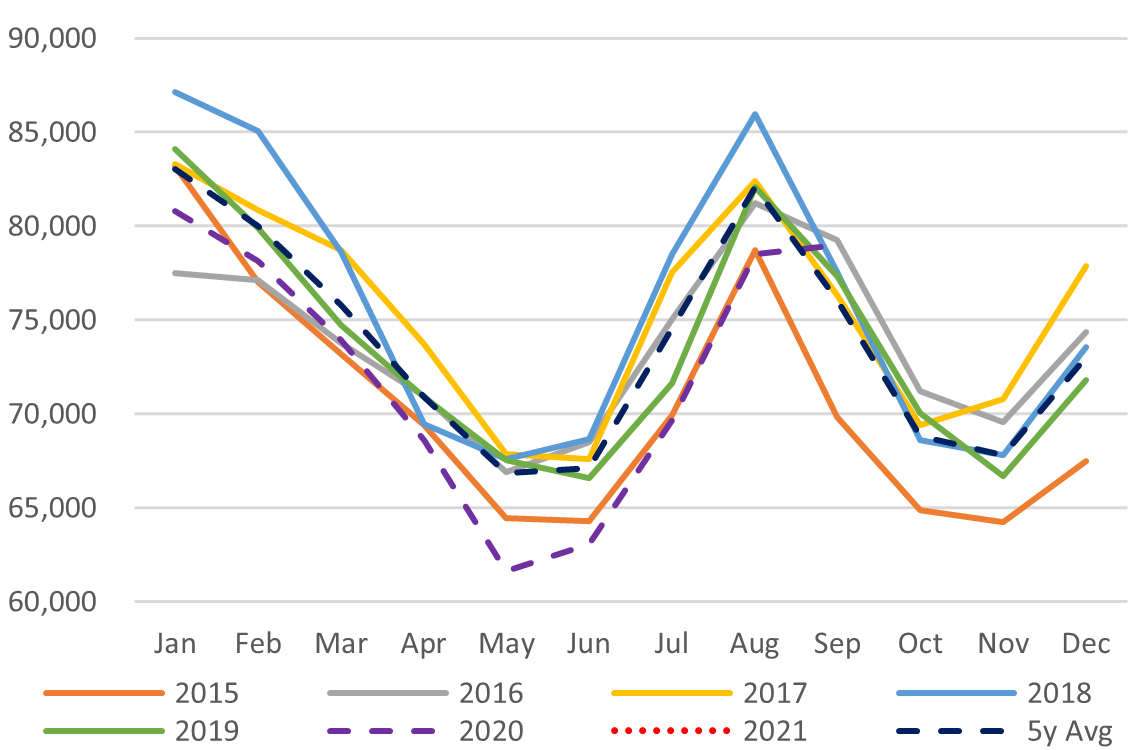

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

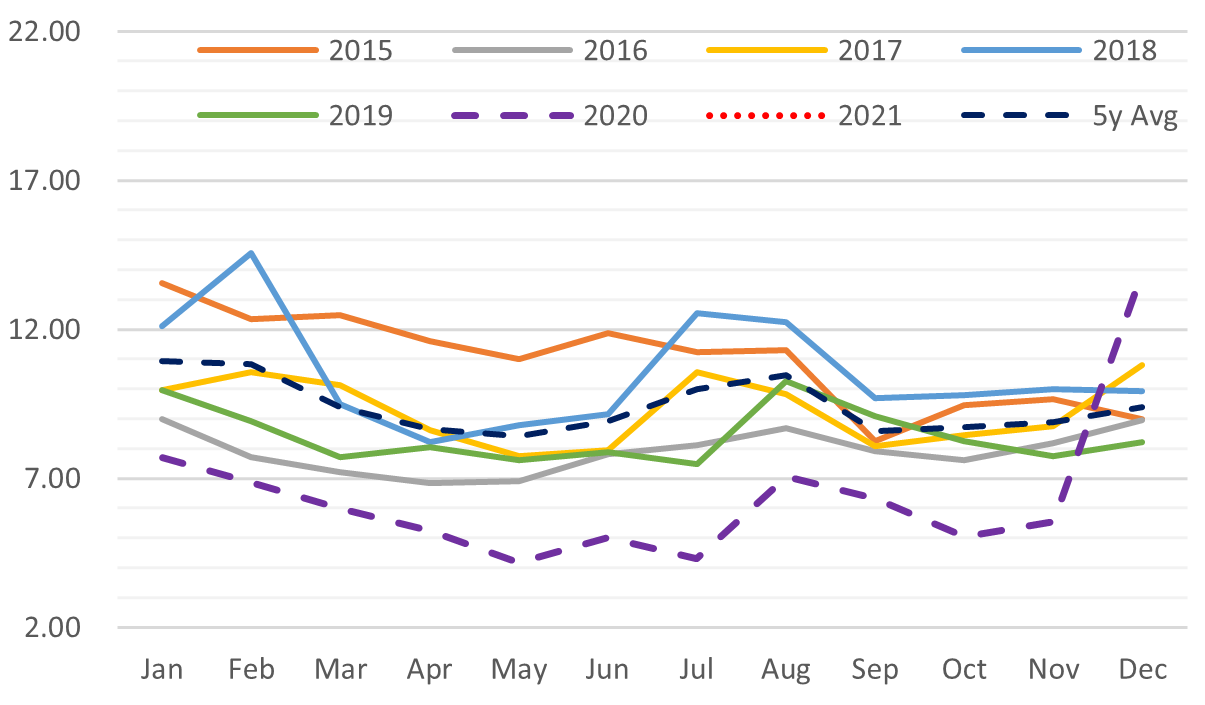

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange