JAPAN NRG WEEKLY

FEBRUARY 22, 2021

JAPAN NRG WEEKLY

February 22, 2021

NEWS

TOP

- Cost of EVs in Japan down; oil major Idemitsu enters EV market and vows to sell electric autos for less than $10,000; first Idemitsu model to be shown in October and will go on sale next year

- Japan LNG stockpiles rebound to pre-winter levels with imports from the U.S. surging 136% in January; Coal imports also jumped

- Japan govt. co-liable for Fukushima accident compensation, according to a new court ruling

ENERGY TRANSITION & POLICY

- Japan mulls a hydrogen and CO2-based synthetic fuel as an alternative to gasoline

- Nippon Steel to close blast furnace to cut its emissions

- Cement firm to make lithium-ion batteries that charge faster

- Taisei to make concrete with CO2 drawn from the atmosphere

- Itochu to sell out of coal business

- Mitsubishi Heavy invests in venture offering hydrogen made from gas that doesn’t lead to carbon emissions

- ENEOS to install hydrogen pumps at existing gas stations

- Hitachi focuses on expanding its renewables energy business

- Marubeni, Mizuho ship first zero-emissions trailer … [MORE]

ELECTRICITY MARKETS

- Fukushima says 100% of its electricity will be renewable by 2025

- Quake off Fukushima coast shuts down at least 10 power plants

- Mutsu slams Kansai Electric idea to store nuclear waste locally

- String of errors jeopardize TEPCO’s Kashiwazaki NPP restart; TEPCO to hire 600 new employees next fiscal year

- Daiwa Securities facing major losses on energy investments

OIL, GAS & MINING

- Japan’s April-Dec fuel sales drop 11.5%; jet fuel down 57%

- Tokyo Gas CEO defends renewables push to nervous shareholders

- JGC wins gas separation contract in Kazakhstan

- INPEX shares tank as crude oil falls below $60

ANALYSIS

INTERVIEW WITH JARAND RYSTAD, CEO OF RYSTAD ENERGY ON OIL, GAS, RENEWABLES AND MORE

The founder of the well-known energy research and intelligence company discusses why the current oil prices can be sustained and even grow, what impact the new U.S. administration will have on shale output, why the U.S. has potential to become a renewables super-power, and what energy technologies hold most promise for the future.

Rystad also outlines his view of the best energy strategy for Japan and its wind capacity potential.

MYANMAR SITUATION LIKELY TO DETERIORATE,

FORCING A RETHINK IN JAPAN’S ENERGY STRATEGY

Japan potentially stands to lose out on a major energy and infrastructure market if the U.S. and others ramp up their sanctions against Myanmar in response to the deteriorating political situation in the country. This will impact Japanese oil and industrial investments, future LNG and power developments, and could threaten a key source of rare earths supply.

An Asia sanctions expert explains to Japan NRG readers what this situation will entail.

GLOBAL VIEW

We detail the extent of the Texas energy situation. The U.S. starts new sanctions against the Nord Stream 2 pipeline from Russia to Germany. The IEA sees the offshore wind market more than doubling in five years. And metals prices hit new records on renewables demand outlook. See this section for details on these and other global energy-related news.

EVENT REVIEW

Japan NRG held its “Nuclear Power in Asia” webinar.

2021 EVENT CALENDAR

Industry / political events related to Japan energy.

DATA Gas, power, and oil stats

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

Sponsored

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS: ENERGY TRANSITION & POLICY

Electric vehicles close price gap with gasoline competitors

(Nikkan Jidosha Shimbun, Feb. 19)

- Tesla reduced the price of its entry level Model 3 by ¥820,000, placing the car on a par with luxury gasoline sedans. When the Environment Ministry’s subsidy is added the Model 3’s effective retail price is around ¥3.5 million, which is significantly less than a Mercedes C class.

- Meanwhile, Japan’s Idemitsu Kosan has branched into the compact electric vehicle market as well, and aims to sell compact cars for between ¥1 and ¥1.5 million.

- In the past, the high cost of electric vehicles stymied their uptake. Now, however, more competitive pricing combined with government sanctions looks set to make electric cars competitive with their petrol counterparts.

- SIDE DEVELOPMENT:

Idemitsu to develop electric car priced below ¥1.5 million

(Sanyo News, Feb. 16)- Idemitsu Kosan announced on Feb. 16 that it was entering the electric vehicle market.

- Co. will unveil its EV in October, to go on sale next year.

- The micro-sized vehicle is aimed at elderly and inexperienced drivers, and will have a maximum speed of 60 km/h. The vehicle will be able to travel 120 km on an eight hour charge.

- The vehicles will be displayed at Idemitsu service stations around the country.

- Idemitsu hopes that revenue from EVs will help offset the projected fall in gasoline sales.

Japan mulls switching gasoline for synthetic fuels made from hydrogen in clean tech push

(Nikkei, Feb. 19)

- The govt. will consider the possibility of commercializing a fuel that is made by synthesizing CO2 with hydrogen, believing that in time it can become cheaper than oil-based fuels like gasoline.

- Synthetic fuel is manufactured by reusing CO2 emitted from factories and power plants. Although CO2 is emitted during driving, it can be reduced close to zero by offsetting the amount taken in during manufacturing.

- Although Japan announced a ban on new gasoline-engine car sales from 2035, a large number of gasoline vehicles will remain on the road for years to come.

- The new synthetic fuel could be cheaper than gasoline by around 2050, in the government’s preliminary estimate.

Nippon Steel to close furnace, cut capacity in effort to reduce emissions

(Nikkei, Feb. 18)

- Nippon Steel plans to stop production at a blast furnace at one of its factories near Tokyo, the Nikkei reported. Together with earlier decisions, this will cut domestic capacity by 20%.

- One reason is domestic overcapacity and sluggish demand for pipes used in shipbuilding and in the oil and gas industry. However, the Co. faces pressure to reduce its use of blast furnaces, which emit large amounts of carbon emissions.

- The closure will take place within several years.

- CONTEXT: Blast furnaces use coal-based coke for combustion and emit a large amount of CO2. The steel industry is Japan’s top emitter after the power generation plants. Nippon Steel’s use of blast furnaces for steelmaking makes it hard for the company to decarbonize.

Taiheiyo Cement to employ its tech for lithium-ion batteries to speed up EV charging

(Nikkei, Feb. 19)

- Taiheiyo Cement plans to use its technology to produce a new cathode material that is just 100 nanometers in diameter and which can be made without nickel or cobalt. This will improve lithium ions flow, which in turn helps batteries used in EVs charge faster.

- The technology should also triple the usable life of EV batteries, according to the Co.

- Taiheiyo will invest ¥1 billion ($9.4 million) in a demonstration plant, which should come online in fiscal 2021. The plant will produce annually 100 tons of the electrode material. Mass-production is expected as early as 2025.

Taisei to make concrete with CO2 drawn from the atmosphere

(Nikkei, Feb. 15)

- Taisei, a construction company, has developed a technology that captures atmospheric CO2 and uses it to produce calcium carbonate, which is a compound of CO2 and calcium. The compound is then turned into cement.

- This new method significantly reduces greenhouse gas emissions by capturing up to 170 kg of CO2 per cubic meter of concrete produced.

- The new process also emissions some CO2, but the extraction of the gas from the air during the production process should make the net amount negative, according to Co. calculations.

- Idemitsu, Ube Industries and JGC Holdings are involved in refining the new method and bringing down its cost.

- If all of Japan’s concrete production moved to the new method, the industry’s CO2 emissions are estimated to fall by as much as 430,000 kg.

- CONTEXT: Cement production is one of the most CO2-intensive industrial processes in the world.

Itochu to sell Colombia mine that accounts for 80% of coal business, fully exit coal by 2024

(Fuji Sankei Business, Feb. 19)

- Major Japanese trading companies are scrambling to divest from the coal industry, with Itochu Corp the latest to sell the majority of its interests in thermal coal to meet environmental, social, and governance (ESG) goals.

- Itochu plans to sell its interests in a Colombian coal mine before the end of the financial year. Producing 6.2 million metric tons of coal per year, the mine accounts for 80% of Itochu’s coal business.

- The remaining 20% comprises interests in two Australian coal mines, which Itochu plans to sell by the end of 2023/24.

- While Japan’s trading companies strategically lowered their exposure to energy and mining in response to the 2015 market crash, mining operations (including both coal and precious metals) still contribute significantly to their revenue. Trading companies are now hurrying to find an alternative source of income.

Mitsubishi Heavy invests in U.S. startup that had developed tech to produce carbon-free hydrogen from natural gas

(Company statement, Feb. 10)

- Mitsubishi Heavy Industries, Ltd. (MHI) today announced that it has invested in C-Zero, a hard tech startup located in Santa Barbara, Calif., to accelerate the first commercial-scale deployment of C-Zero’s drop-in decarbonization technology, which will allow industrial natural gas consumers to avoid producing CO2 in applications like electrical generation, process heating and the production of commodity chemicals like hydrogen and ammonia.

- C-Zero’s technology uses innovative thermocatalysis to split methane – the primary molecule in natural gas – into hydrogen and solid carbon in a process known as methane pyrolysis. The hydrogen can be used to help decarbonize a wide array of existing applications, including hydrogen production for fuel cell vehicles, while the carbon can be permanently sequestered. When renewable natural gas is used as the feedstock, C-Zero’s technology can even be carbon negative, effectively extracting carbon dioxide from the atmosphere and permanently storing it in the form of high-density solid carbon.

- Hydrogen produced via methane pyrolysis processes like C-Zero’s is increasingly referred to as “turquoise hydrogen,” as it combines the benefits of both “blue hydrogen,” (SMR with CO2 sequestration) and “green hydrogen” (produced by splitting water via electrolysis) with its low cost and low emissions, respectively.

ENEOS to install hydrogen pumps at existing gas stations from 2022

(Asia Nikkei, Feb. 14)

- Japan’s top oil supplier, ENEOS, will start adding hydrogen pumps to its gas station network across the country from spring 2022.

- The company has 13,000 stations in the country, and it will trial the plan at two stations – one in Kanagawa and one in Aichi prefectures.

- The move comes after METI relaxed measures for hydrogen pumps in January 2020, allowing them to be added even at downtown gas stations. The government will also provide ¥11 billion ($105 million) in the next fiscal year budget to companies building hydrogen stations.

- Iwatani, the biggest hydrogen producer in Japan, is also building six hydrogen filling stations around the country.

(Denki Shimbun; Feb. 15)

- Hitachi is focusing more on expanding its renewable energy business.

- Since December the company has carried out verification trials in Thailand for a voltage/reactive power online optimization control system, which analyzes power flow in transmission lines and operational data of substation equipment.

- The system analyzes data to forecast demand and plan optimal energy generation plans.

Marubeni and Mizuho Leasing ship first zero-emission refrigerated trailer

(New Energy Business News, Feb. 15)

- US-based rental service PLM Fleet LLC, which is partially owned by both Marubeni and the Mizuho Leasing Company, has begun shipping zero emission refrigerated trailer units.

- The units are designed and manufactured by Advanced Energy Machines and incorporate solar panels, charging units, and chiller units.

- Under an agency agreement with Advanced Energy Machines in 2020, PLM Machines has the rights to market the trailer to the U.S. market.

- Amidst increasing demand for zero emission technology, PLM’s client base is growing strongly.

TEPCO/Chubu Electric Power joint venture takes over vehicle recharging service

(New Energy Business News, Feb. 16)

- E-Mobility Power, a joint venture between TEPCO Holdings and the Chubu Electric Power Company, will take over the operations of Nippon Charge Service in April.

- Nippon Charge Service (NCS), which provides charging services for electric vehicles and affiliated services, was established in 2014 with the aim of promoting the uptake of EVs and plug-in hybrids. NCS is partially owned by Toyota, Honda, and Nissan, as well as TEPCO and the Chubu Electric Power Company.

- E-Mobility Power has aimed to absorb NCS since it was established in 2019. E-Mobility Power aims to be an economical and accessible recharging service.

NEWS: POWER MARKETS

| No. of operable nuclear reactors | 33 | |||

| of which | applied for restart | 25 | ||

| approved by regulator | 16 | |||

| restarted | 9 | |||

| in operation today | 4 | |||

| able to use MOX fuel | 4 | |||

| No. of nuclear reactors under construction | 3 | |||

| No. of reactors slated for decommissioning | 27 | |||

| of which | completed work | 1 | ||

| started process | 4 | |||

| yet to start / not known | 22 | |||

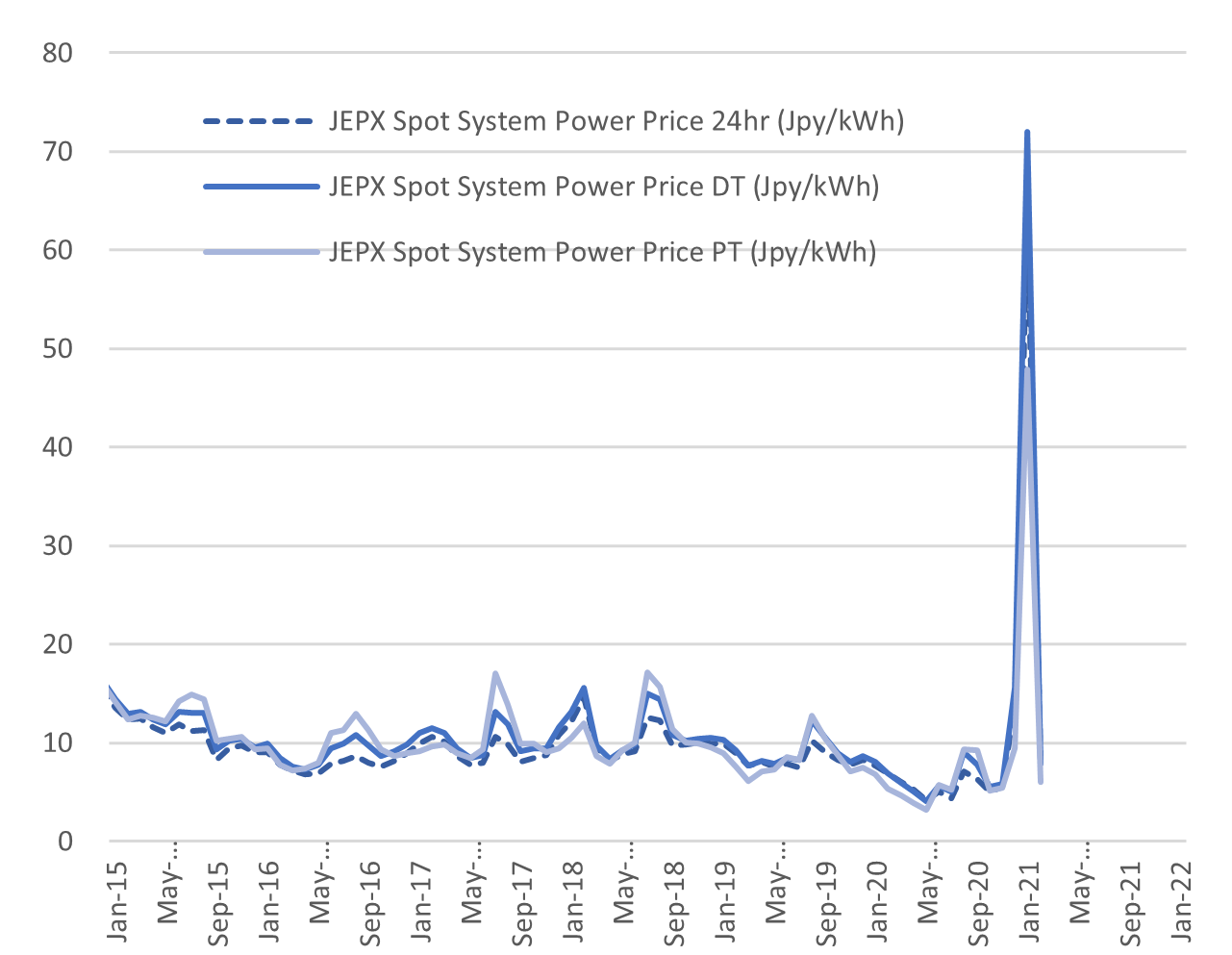

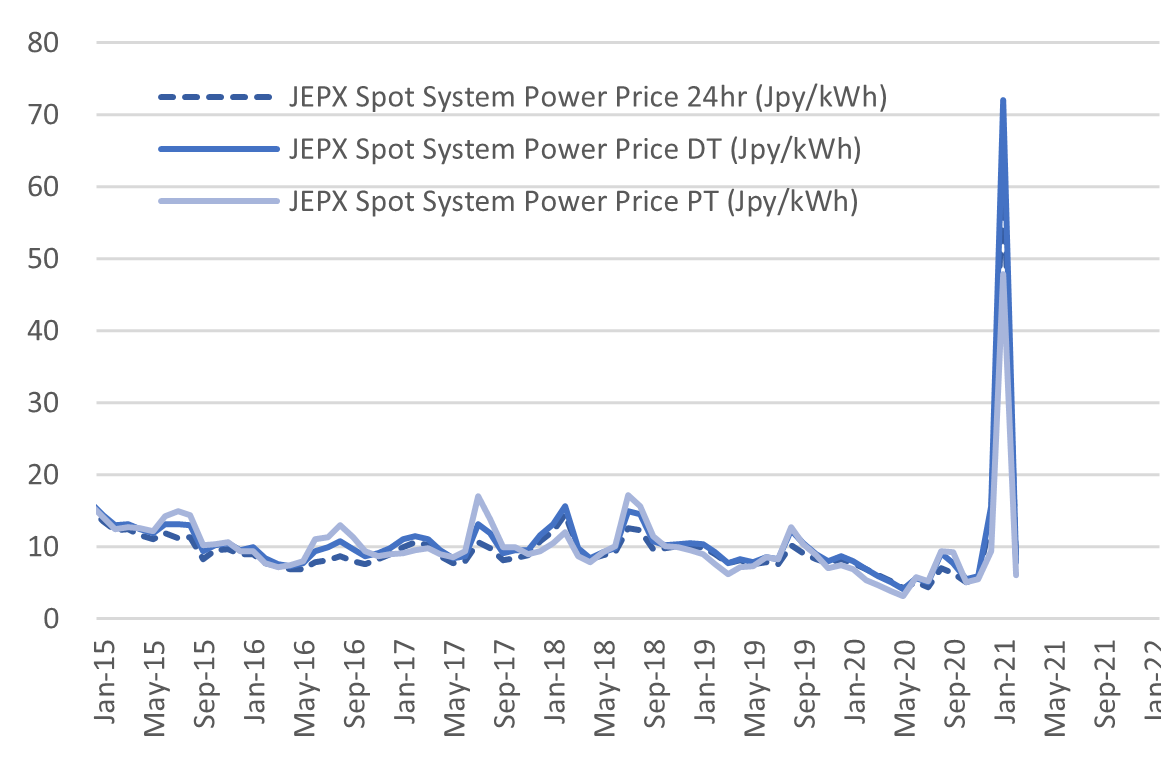

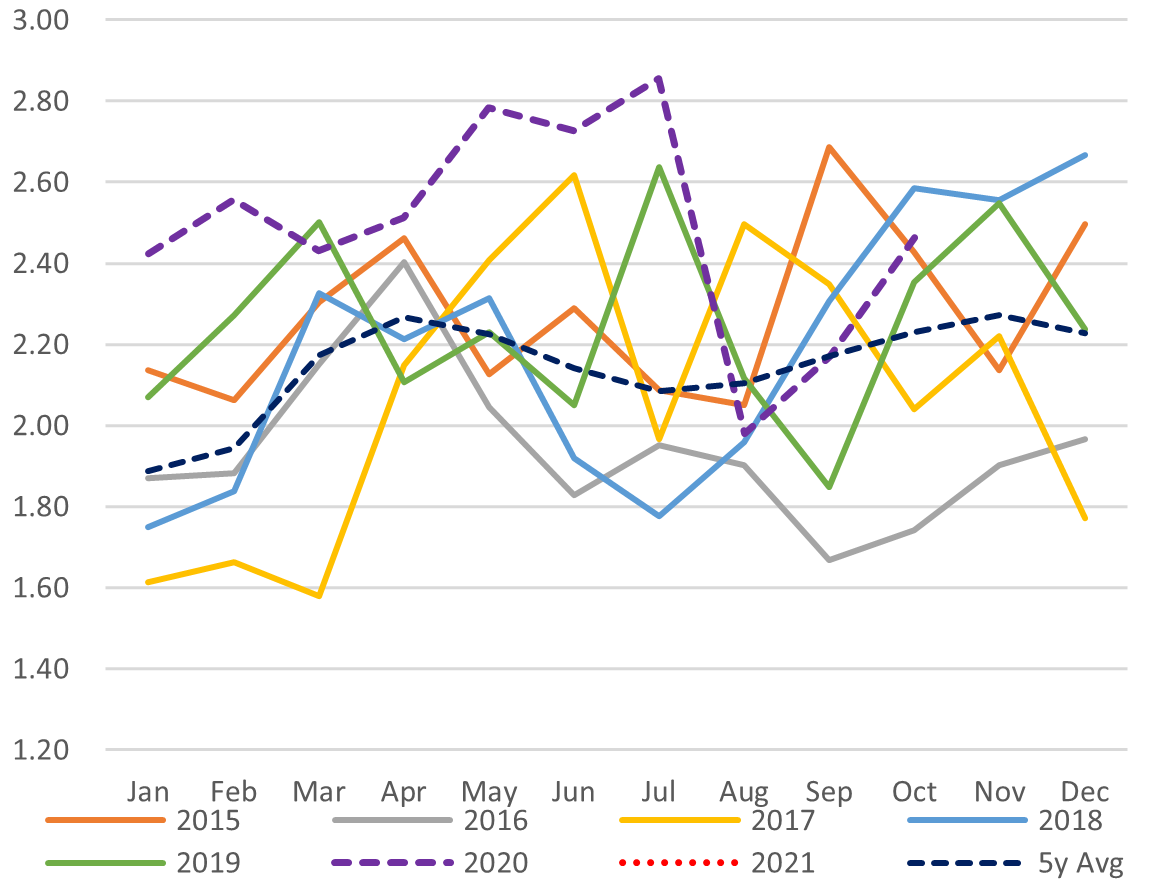

Spot Electricity Prices

Source: Company websites, JANSI and JAIF, as of Feb. 18, 2021

Court rules Japan government co-liable for Fukushima accident compensation

(Yomiuri Shimbun, Feb. 19)

- The Tokyo High Court has awarded damages to former residents of Fukushima who were forced to flee to Chiba after the 2011 nuclear disaster.

- Overturning a previous judgement that found sole liability to rest with TEPCO, the Court ordered both the government and TEPCO to pay compensation.

- This is the third of 30 lawsuits against TEPCO to go to appeal.

TAKEAWAY: The government is already paying money into TEPCO so that the company can pay the compensation due to citizens and business entities. In fact, TEPCO was kept afloat as an entity after the disaster partly out of the rationale that the company was needed to administer the payments. However, if the liability is placed equally on the government, it opens the possibility of individuals and entities being able to demand compensation from the state directly. Should that occur, it would at the very least put into question the need for the government to funnel the funds into TEPCO. In a more extreme scenario, it puts under question the rationale for keeping TEPCO as it is and may spur on an oft-rumored restructuring of the electricity utility.

Fukushima says electricity supply to be 100% renewable by 2025

(Nikkei, Feb. 16)

- Fukushima prefecture has set itself a target of generating 100% of its net electricity requirements from renewable sources by 2025.

- Fukushima erected dedicated transmission lines after the 2011 nuclear disaster using government aid, and these have facilitated its transition to renewable electricity.

- On paper, the prefecture will not have to rely at all on nuclear energy or fossil fuels after 2025.

- The capacity of the prefecture’s solar farms has grown 63% in the past year, and as of October stood at 870 MW.

Quake off the Fukushima coast shuts down power plants in the north-east

(Nikkei, Feb. 14)

- CONTEXT: A 7.3 magnitude earthquake off the coast Fukushima prefecture late on Saturday night (Feb. 13) and temporarily knocked power facilities offline, leaving close to 1 million households without electricity for several hours.

- A major earthquake centered off the coast of Fukushima on Feb. 13 forced Tohoku Electric and JERA to shut down at least 10 power stations.

- In addition to buying electricity from utilities in other regions, including 3.5 MW from TEPCO, Tohoku Electric weathered the shortage by restarting unit two of its Higashi-Niigata thermal plant, which had been idle.

- Some affected facilities, including units five and six of JERA’s Hirono thermal power station, are scheduled to be restarted on or after Feb. 15.

- Some 860,000 Tohoku Electric Power subscribers momentarily lost power after the quake.

- SIDE DEVELOPMENT:

Fukushima: earthquake causes water to slop from reactor pool

(Sankei Biz, Feb. 16)- TEPCO says the Feb. 13 earthquake caused water to overflow from pools located on top of Units 5 and 6 of the Fukushima Daiichi nuclear station.

- TEPCO says it is not aware of any spilled water leaking out of the reactor buildings and that there is no safety issue.

Mutsu officials say they never agreed to Kansai Electric’s nuclear waste idea

(Nikkei, Feb. 15)

- In a statement the municipality of Mutsu in Aomori condemned a Kansai Electric (KEPCO) proposal to Fukui Prefecture on Feb. 12 in which KEPCO would share access to the Mutsu nuclear waste storage facility as an option to store its spent nuclear fuel in the future.

- Mutsu never agreed to any such proposal, nor even discussed it, says the statement.

- Categorically ruling out Mutsu as potential destination for KEPCO’s waste, the statement says that Mutsu clearly told the Federation of Electric Power Companies that it would not engage in any discussion that assumed the shared use of the storage facility was an option.

TAKEAWAY: This could be a massive setback for Kansai Electric’s plans to restart as many as six reactors this spring and summer. However, we don’t expect this is the end of the discussion. Added incentives and pressure will try to persuade Mutsu to reconsider. The key, however, will be the reaction of the Fukui government to Mutsu’s statement. Do they pretend as if it does not matter and allow Kansai Electric to restart its NPPs, or do they dig in and demand an additional explanation from the utility? The next major pressure point from Kansai region’s electric supply perspective will likely be in July and August, giving the utility about 5 months to appease the Fukui government.

String of errors jeopardize restart of TEPCO’s Kashiwazaki nuclear plant

(Economist Online and NRA, Feb. 15-17)

- While the restart of the Kashiwazaki-Kariwa nuclear power plant is vital for TEPCO’s economic success, a spate of scandals looks likely to delay the restart.

- The regulatory authorities completed their safety audit of Unit 7, but it was recently revealed that an unauthorized worker entered the reactor’s control room in breach of security protocols. TEPCO also erroneously announced in January the completion of work to enhance the reactor’s safety when in fact it had not.

- The Governor of Niigata Prefecture has criticized the series of blunders, which he says damage confidence in TEPCO.

- The NRA Commissioner said on Feb. 17 in remarks streamed by the nuclear regulator that TEPCO should revise its current plan to load fuel into Unit 7 of the NPP.

- Even Kashiwazaki Mayor, and nuclear power proponent Sakurai Masahiro, believe the scandal will delay the restart date by several months.

- SIDE DEVELOPMENT:

TEPCO to hire 600 new employees in FY2021

(Okinawa Times, Feb. 19)- On Feb. 18, TEPCO announced its recruitment plans for the upcoming financial year, as well as the following financial year.

- The utility plans to hire 600 personnel (comprising 470 recent graduates and 130 mid-career hires) in 2021/22. To contribute to the Fukushima prefecture rebuild, 45 of the recent graduates will be from Fukushima.

- TEPCO plans to hire a similar number of personnel in 2022/2023.

Daiwa Securities lose big with energy investment: Now holding smoking bomb due to potential FSA investigation

(Sentaku, Feb. issue)

- IDI Infrastructures (an energy fund in which Daiwa Securities and IDI each have 50% ownership) saw its president ousted six months ago after a motion submitted by Araki Hideki (of Daiwa Securities), one of the fund’s directors.

- Many investors are indignant about this dismissal.

- In ousting the former president, Saitama Koji, Daiwa Securities unwittingly informed regulatory authorities about their risk assets, according to someone familiar with the matter.

- IDI Infrastructures (who manage power giant F Power) have been pushing forward with constructing a power plant that Daiwa is reluctant to support. Daiwa’s role in Saitama’s dismissal made clear the firm’s opposition to IDI, which wants shareholder contracts to be executed.

- IDI is suing Daiwa’s Araki and Matsui for damages exceeding ¥300m.

- Regardless of the lawsuit’s outcome, what is significant is the ¥50b impairment loss in the event of IDI Infrastructures going bankrupt. Past investments have not been included on Daiwa’s books because IDI Infrastructure is not consolidated even though it’s a Daiwa subsidiary.

- Japan’s FSA have noticed this off-book risk asset and are considering examining the matter.

- If consolidated, most of Daiwa’s net income of ¥32.8b for the first half of the fiscal year will go.

- F Power (which is managed by IDI Infrastructures) has seen large losses since 2017 due to the company failing to meet demand with its own power plants, which resulted in costs to procure energy to meet that demand shooting up.

- “Daiwa still has a culture of concealing ugly things and tried to scapegoat former-president Saitama to resolve this issue”, according to one person familiar with the matter.

KEPCO trade union demands ¥3,000 increase in base pay

(Sankei Biz, Feb. 19)

- On Feb. 18 the trade union for KEPCO employees demanded an across-the-board salary increase of ¥3,000 per month for its members.

- This is the fourth consecutive year that the union has demanded a pay rise.

- The union says COVID-19 and increased competition has made things tough for its members, and a pay rise is needed to boost morale.

NEWS: OIL, GAS & MINING

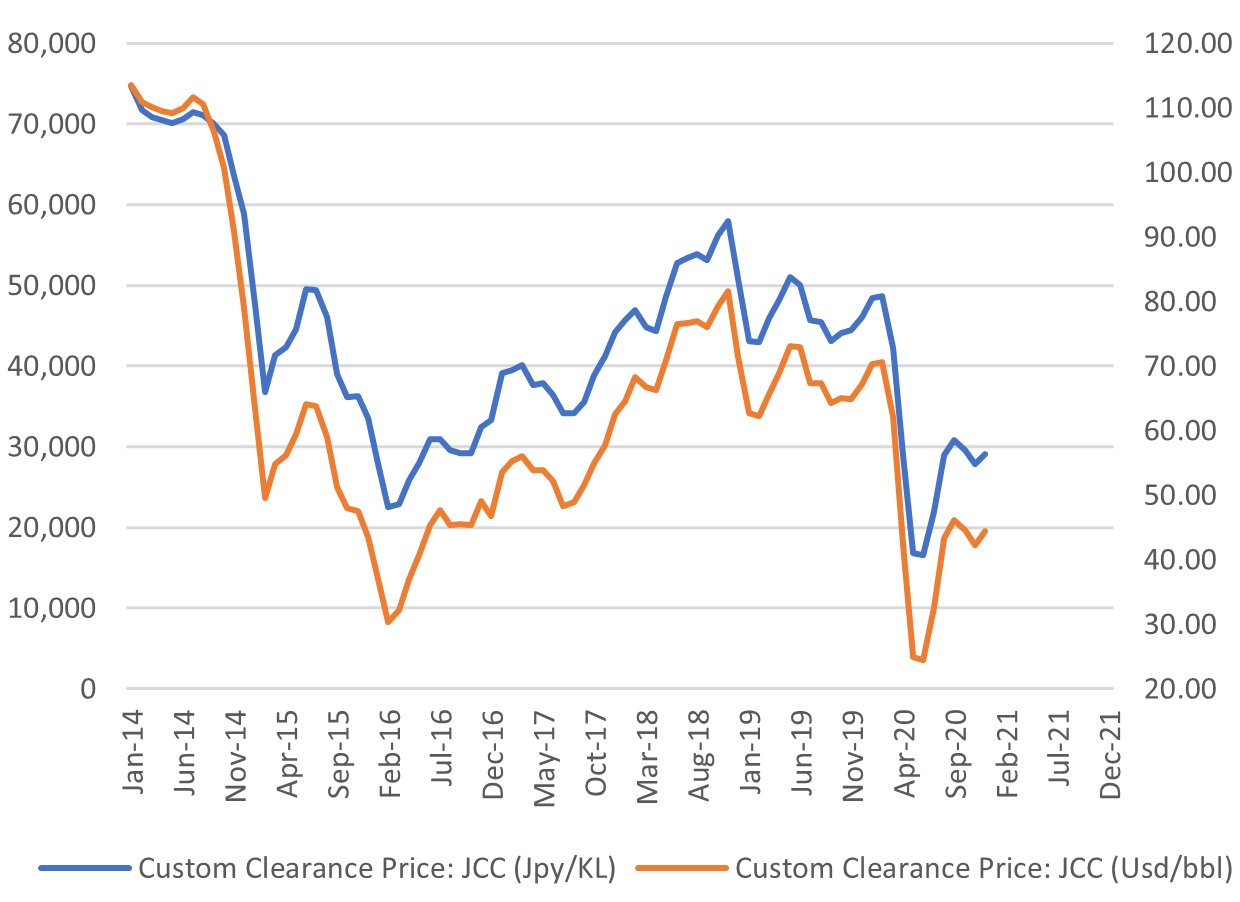

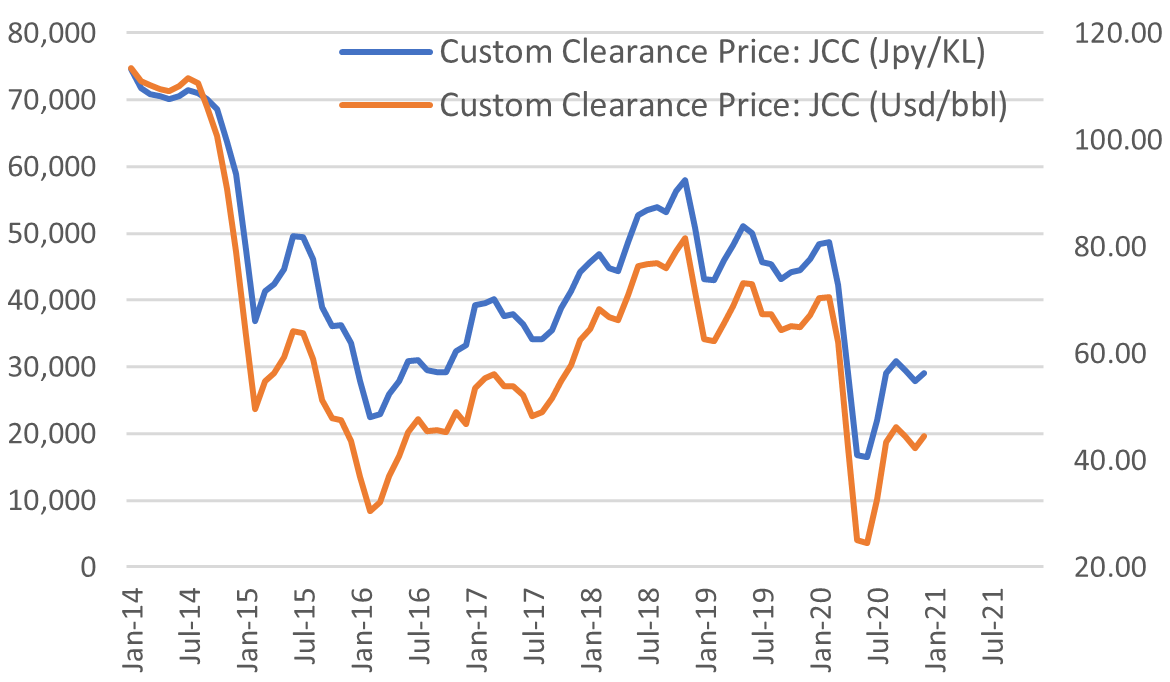

Japan Oil Price: $44.46/ barrel

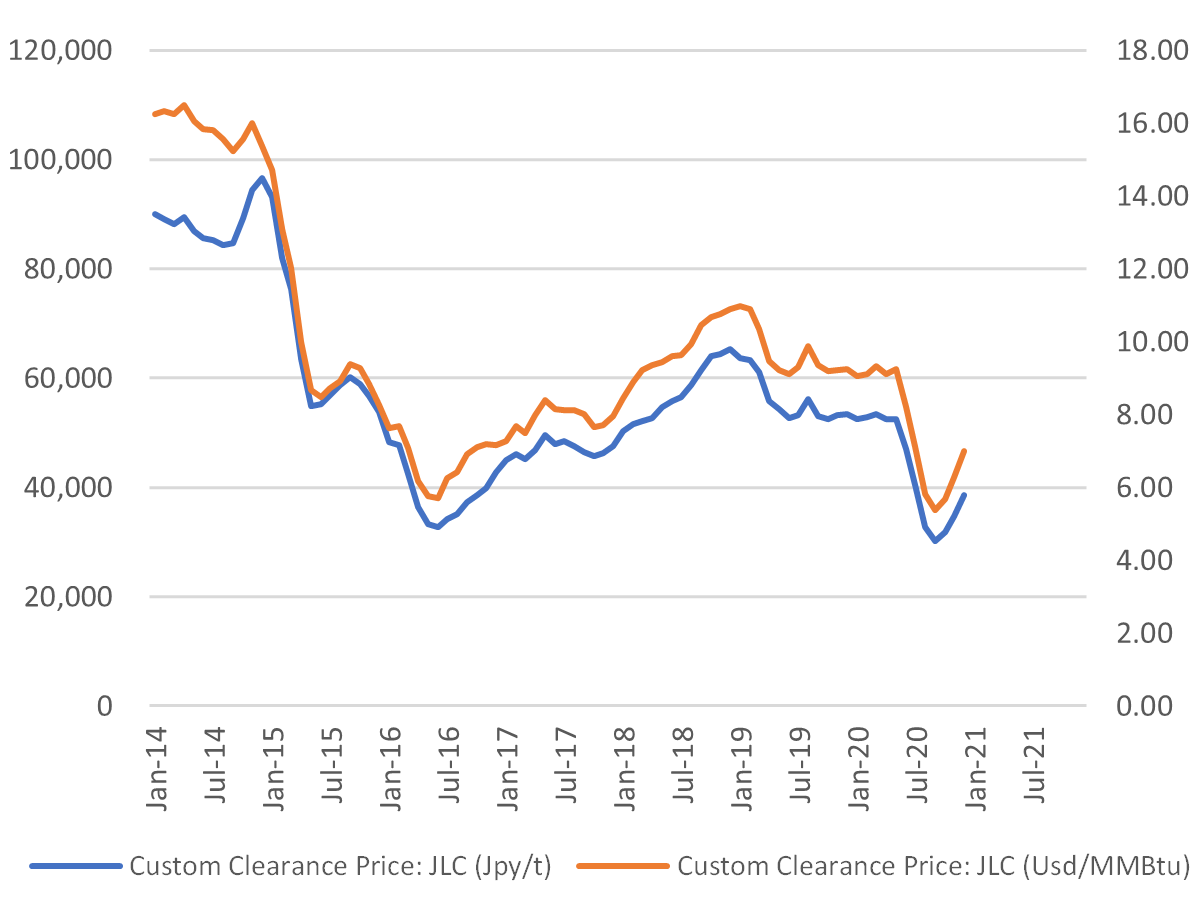

Japan (JLC) LNG Price: ¥45,383/ mmbtu

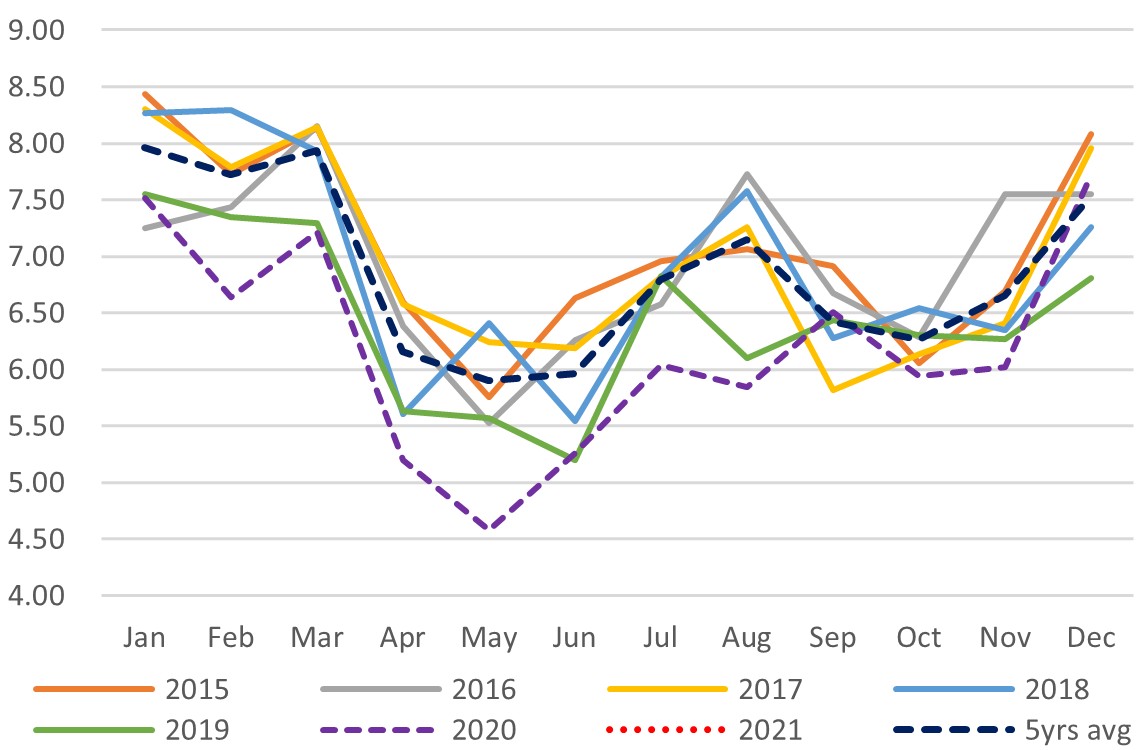

Japan’s LNG stocks have rebounded to above pre-winter levels: official data

(Bloomberg, Feb. 18)

- Japan’s major importers are potentially facing a glut after a series of panic buys in the spot market. The current level of stockpiles held by Japanese electricity companies has rebounded to 2.5 million tons, above its pre-winter level, data released in a one-off report by METI show.

- The change to milder temperatures since early February has also abated domestic demand.

- CONTEXT: Japanese LNG stockpiles hit a low around Jan. 10 due to the sudden snap in cold weather and other factors.

- Asia will likely be in a supply glut this spring as Chinese imports drop and warmer weather curbs demand for heating.

Japan’s April-Dec 2020 fuel sales drop 11.5% YoY due to lockdowns

(K.K. Sekiyu Tsushinsha, Fen. 15)

- Fuel oil sales in the last nine months of last calendar year, i.e., the first nine months of Japan’s fiscal year (April to December), totaled 81,048 kl, down 11.6% YoY, according to data compiled from the financial statements of the three oil wholesalers (ENEOS, Idemitsu, and Cosmo Energy).

- Gasoline sales dropped 9.2% to s 31.642 million kl. Naphtha sales dropped 22.5% to 6,592,000 kl.

- Kerosene sales were down just 2.3% due to the electricity shortages during a suddenly cold winter period.

- Jet fuel oil’s drop was the most drastic, falling 56.6% to 2,392,000 kl due to the restrictions on international travel.

Tokyo Gas CEO firm on decarbonization plans despite shareholder protests

(Nikkei, Feb. 16)

- Tokyo Gas CEO Uchida has responded to the government’s new energy policy by announcing a review of shareholder benefits in order to free up enough cash to finance the utility’s transition to renewable energy. The company’s shares fell 5% on the announcement.

- The gas utility had been known for its strong share price and generous dividends. The decision prompted protests from shareholders worried that Tokyo Gas will no longer be able to compete with shares of renewable energy companies.

- CEO Uchida has stood firm on his plans to reform the company, however, saying that it is only a matter of time before the move to decarbonize industry targets gas providers. If Tokyo Gas does not change it will not survive, he says.

JGC to design gas separation facility in Kazakhstan

(Chemical Daily, Feb. 15)

- JGC’s offshore engineering procurement and construction division won a contract to produce the basic design for a gas separation plant planned in Kazakhstan by state-owned KazMunayGas.

- JGC didn’t disclose the contract’s value, or say when the work will finish.

- The project involves the construction of a gas separation unit next to a gas processing plant that is operated by a joint venture between KazMunayGas, Exxon Mobil and Chevron.

INPEX shares tanks as crude falls below $60

(DZH Financial Research, Feb. 19)

- The INPEX share price tumbled nearly 6% on news that the price of March crude oil futures contracts traded on the New York Mercantile Exchange fell 1% the day before to $60.52. Crude futures continued to fall, ending up below the $60 mark.

ANALYSIS

BY TOM O’SULLIVAN

The future of oil & gas, and why the U.S. can dominate renewables: An interview with Jarand Rystad, CEO and founder, Rystad Energy

Last week Japan NRG interviewed Jarand Rystad and Artem Abramov of Rystad Energy to hear their views on recent developments in international energy markets. Below is a selection of their comments.

Rystad believes that current recovery in oil prices is sustainable in the short-term and may even feel stronger in a year as the impact of Covid-19 recedes and the fundamentals more firmly support prices. Last year’s production cuts by Saudi Arabia achieved their goal, although prices may fluctuate again after April as OPEC production gradually comes back online.

Rystad sees the oil price possibly spiking in 2022 as vaccinations are rolled out more broadly across the globe and international travel recovers.

In the short-term, the Biden administration’s policies could also be positive for oil consumption as economic stimulus is enacted and rolled out. Longer-term, the environment for the U.S. oil and gas industry will grow more challenging as the climate agenda gains momentum and more of the country’s emphasis is placed on renewable energy.

New Mexico may be the state most impacted by the moratorium on oil drilling on federal lands. Sixty-five percent of drilling acreage in the state is on federally owned lands. However, the negative impact on oil and natural gas production will be pushed back for some years because many local developers have stockpiled leases prior to the Nov. 3 election. Some companies accumulated more than 500 permits, enough to keep the current pace of drilling for the next four to five years. Offshore Gulf of Mexico oil leases will see a similarly negative impact in the mid-term for the same reasons.

Tax incentives for the U.S. fossil fuel industry are also expected to be gradually removed and the decarbonization of the power sector will be fast-tracked with the 2035 net-zero goal in place. This may be negative for smaller shale oil and gas players, spurring more concentration among super-majors and the shale independents. This situation could well turn out to be a positive for U.S. LNG exports to Asia as domestic reliance on natural gas is reduced.

Rystad sees the current strategy of global oil and gas companies split into three different approaches, largely delineated by geography. U.S. oil majors are transitioning to new energy sources at a slower pace than their counterparts in Europe or Asia. European oil majors including Total, BP, and Royal Dutch Shell have announced ambitious plans to re-balance their portfolios and Asian NOCs (national oil companies) and majors are reorienting toward natural gas. However, companies such as Exxon and Chevron are expected to accelerate their transition in coming years and may do so using acquisitions. Higher oil prices and significantly reduced capex will strengthen their cashflow generation. U.S. majors may also feel that greening their portfolios will be important in bolstering their share price, a key tool in M&A.

All oil and gas companies should accelerate carbon reduction strategies, including carbon capture and storage, and direct air capture.

Disruptive technologies will become increasingly relevant. Rystad believes there will be a complete international shift to EVs for transportation. Hydrogen will not be competitive with EV technology for ground transportation but could be a strong solution for aviation and shipping due to its high energy density. This may require a redesign of aircraft fuselages and the creation of hydrogen hubs around airports.

The U.S. may be the best place to produce hydrogen and, as a whole should end up being a renewable energy super-power. The country is blessed with the best natural resources for the next-generation of energy technologies, including batteries, according to Rystad.

For Japan, hydrogen and ammonia should create an important opportunity to reorientate its energy policies and infrastructure, and build more energy self-sufficiency.

Solar PV and battery technology are considered to be the most promising future technologies. Batteries will be extensively used for transportation and for peak electricity shaving and grid storage. Rystad believes nickel and iron phosphate will be used more extensively for batteries in the future.

Covid-19 could continue to negatively impact energy consumption for a few more months, with Rystad’s estimates of infections six times higher than the widely accepted numbers published by John Hopkins University. Rystad believes the real Covid-19 infection rate around the world is around 600 million people. John Hopkins cites 110 million global infections, based on official government numbers from around the world and media reports.

The pandemic’s impact on business travel may be structural as company management looks to get more done without extensive travel. This will have a long-term negative impact on jet fuel consumption.

As for Japan, the country’s reliance on renewable energy will grow and scale-up, particularly in wind energy. Japan has potential for 600 GW of wind power capacity and more extensive use of solar in un-utilized hydro reservoirs and on low-income farmland. Solar and wind should be natural hedges, and batteries should be more extensively used for grid back-up. Nuclear assets should be maintained and re-activated, but new nuclear may be uncompetitive.

Rystad Energy, founded in 2004, is an independent energy research and business intelligence company, headquartered out of Oslo, Norway. It provides data, tools, analytics and consultancy services to clients in the energy industry across the globe. Rystad’s capabilities within energy fundamentals, oil and gas markets, supply chains, renewables and energy transition facilitate their advisory work to clients enhancing decision-making across the energy sector around the world. Having become a sought-after voice in energy markets, Rystad is widely recognized for up-to-date, consistent and comprehensive data and insights.

Rystad ( https://www.rystadenergy.com/ ) has a Tokyo office run by Mr. Yosuke Uehara (yosuke.uehara@rystadenergy.com ).

ANALYSIS

Myanmar Coup Leaves Japan’s Southeast Asia LNG and

Industrial Anchor Strategy in Turmoil

Japan potentially stands to lose out on a major energy and infrastructure market if the U.S. and other jurisdictions strengthen their sanctions against Myanmar in response to a military coup in the Southeast Asian nation earlier this month.

Despite the initial view from Japan that the coup will not disrupt Japanese investments in Myanmar, the continuing escalation of the situation inside the country threatens a wave of more international actions that will make it extremely complicated to do business there. This places at risk not only Japan’s stake in one of Myanmar’s biggest gas fields and a future $2 billion LNG-to-power facility, but also several industrial complex developments and a big part of Japan’s strategy to develop the Southeast Asia LNG supply chain.

An expert in sanctions in Asia, Alexander Dmitrenko from Freshfields Bruckhaus Deringer, gives Japan NRG readers an outline of the impact that current and future sanctions will have on the energy business in Myanmar. (See next page)

| Japan-related Energy Investment in Myanmar | Companies Involved |

| Yetagun gas field accounts for about a quarter of Myanmar’s production, with volumes of about 60 million standard cubic feet per day. All of the gas from Yetagun is exported to Thailand. The field was due to stop production around 2023. | Petronas is the operator and holds a 40.75% stake. Nippon Oil and PTTEP have 19.4% each. State-owned Myanmar Oil and Gas Enterprise has 20.45% |

| The Thilawa 1.25 GW LNG-to-power project, was approved by the Ministry of Electricity and Energy (MoEE) last year. It would supply equivalent to 1/5th of Myanmar’s current power capacity. The plant was due to be operational by 2025, but construction is not due to start until around 2022. | Rival trading houses Marubeni, Mitsui and Sumitomo pooled resources and joined with local partner Eden Group to win the contract last summer. |

| The Thilawa Development is a special economic zone (SEZ) that contains the bulk of Japanese industrial investment in Myanmar. Judged to be a success, it was due to open up another SEZ, the Dawei, in the south of the country to Japanese investments. | Sumitomo, Marubeni, and Mitsubishi trading houses, plus the three Japanese mega-banks own 39% of the SEZ operating company. |

| Rare earth metals: While Japan is not known to be directly invested in rare earths mining in Myanmar, the latter is one of the world’s key suppliers of these elements and Japan is one of the biggest buyers. Myanmar was No. 3 (ahead of Australia, and just behind the U.S.) in terms of 2019 global rare earths mining output. Since China is the dominant supplier in the field, and Japan wants to lower its reliance on Chinese supply, Myanmar is a key strategic region. | Top Japanese buyers of rare earths include Hitachi Metals, Shin-Etsu Chemical, TDK and Showa Denko. Trading houses involved in the trade include Sojitz and Sumitomo. |

BY ALEXANDER DMITRENKO

FRESHFIELDS BRUCKHAUS DERINGER

The current U.S. sanctions targeting Myanmar may not have a direct immediate impact on the energy sector there, because none of the sanctioned entities are in the energy industry and all individuals were sanctioned in their private capacity. Also, the current sanctions apply primary, albeit not exclusively, to U.S. persons. However, there is a potential for further sanctions if the situation in Myanmar continues to escalate and/or the military does not cede power to the elected officials.

The U.S. and other governments will be monitoring for signs that the domestic situation is escalating into a violent crackdown of protests. According to media reports over this weekend, at least two people have been killed in protests and the police used live ammunition to disperse demonstrators. This indicates a high likelihood of further international action.

So far, President Joe Biden’s Executive Order granted wide authority to the Office of Foreign Assets Control (“OFAC”) of the U.S. Department of the Treasury for implementing further sanctions targeting “the defense sector of the Burmese economy or any other sector of the Burmese economy as may be determined by the Secretary of the Treasury, in consultation with the Secretary of State.”

From a historic perspective, prior U.S. sanctions targeted the Myanmar government (and, thus, all SOEs) until 2012. The U.S. government could adopt a similar approach by sanctioning the entire government of Myanmar or its specific ministries (e.g. defense and/or energy). This would mean that entities owned 50% or more by one or more of the targeted state bodies will also become sanctioned.

It is also possible that other jurisdictions (e.g. the UK and the EU) will implement their own sanctions targeting Myanmar, which may be different from the U.S. approach. This potential escalation would create a chilling effect, particularly on long-term projects and/or any projects with governmental entities (such as Myanmar Oil and Gas Enterprise).

Financial institutions will also add Myanmar to a “yellow flag” category, likely limiting long-term financing options and U.S. dollar payment transactions related to Myanmar.

The U.S. Commerce Department has already announced preliminary export restrictions against Myanmar, which may be expanded to include adding Myanmar persons to the Entity List and/or adding Myanmar to the Military End-Use rule. The current restrictions include a “presumption of denial” for U.S. export licenses to certain Burmese government entities.

In addition, the Commerce Department has suspended certain license exceptions previously available to Myanmar as a result of its current Country Group placement under the Export Administration Regulations, including Shipments to Country Group B countries (License Exception GBS) and Technology and Software under restriction (License Exception TSR).

To put it simply, these export controls changes may impact any energy projects that rely on U.S. technology or goods. This basically cuts off supply of certain key equipment due to a sufficient proportion of the said equipment / components being based on or incorporating U.S.-origin technology and/or software.

It is well known that U.S. technology is prevalent in the oil and gas industry, including in the LNG supply chain. Also, oil on international markets trade in USD, creating a further burden for Japanese investors in export-focused hydrocarbon projects in Myanmar.

In summary, while current sanctions lack real bite, it would be prudent to prepare for their escalation. For Japanese companies already involved or willing to consider business in Myanmar, this will mean a review of contracts to make sure they allow for risk mitigation, such as an ability to suspend or exit the venture entirely. These options need to be contractually permitted specifically based on a sanctions-escalation provision.

Despite the current events, Myanmar hasn’t closed for business. However, energy and other investments in the country will now need to be stress-tested to see if they can manage without the U.S. currency, financial institutions or technology. And that sets a high bar for achieving Japan’s energy business expansion in the Southeast Asian country.

EVENT REVIEW

Nuclear Power in Asia: New Tech, New Markets, New Impetus

Keynote: Francois Morin, Director at the World Nuclear Association (WNA)

Date: Feb. 17, 2021

Access: Online webinar

Last week, Japan NRG hosted the first of its “Japan NRG Transition 2050” series of online webinars. The virtual conference featured a keynote presentation by Francois Morin, a director at the WNA, to discuss the outlook for nuclear power in China, South Korea, and Taiwan. Mr. Morin is a French nuclear physicist with extensive experience in the nuclear industry, including 15 years in China.

The event included 40+ participants from the Americas, Asia, Europe, and Australia.

The WNA mainly represents the nuclear manufacturing industry with over 200 members, including three Japanese members. Last October, Ms. Sama Bilbao y León, a Spaniard, became the Director General of WNA. Previously, Ms. Bilbao y Leon was Head of the Division of Nuclear Technology Development and Economics at the OECD Nuclear Energy Agency.

WNA works closely with the World Association of Nuclear Operators (WANO) and the World Nuclear University that trains nuclear engineers.

PRESENTATION SUMMARY

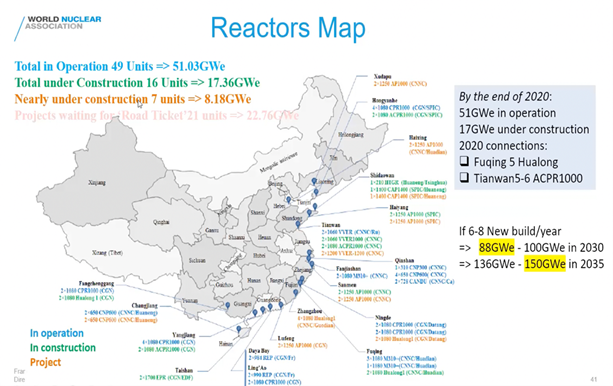

The 50 GW (49 units) of nuclear power units that are currently in operation around China currently generate around 290 TWh of power (equivalent to one third of Japan’s electricity consumption).

China may overtake the U.S. by 2028 in terms of nameplate nuclear generation capacity, exceeded 100 GW, becoming the world’s number one nuclear power generator. WNA expects per capita power consumption in China to grow 60% by 2040 to 8,000 kWh/ capita.

China’s nuclear power output may exceed Japan’s total electricity output (approx. 1,000 TWh) before 2030.

Meeting power consumption and the 2060 decarbonization goal may ultimately require the construction of 300 GW of nuclear capacity in China, including inland construction. WNA’s reference scenario for China for 2040 is almost 180 units, almost 4x current capacity.

In three provinces Zhejiang, Fujian, and Guangdong, nuclear output has already exceeded 20% of the electricity mix.

Last November, two new units at the Fuqing Plant, operated by CNNC, were connected to the grid. Construction times have been brought below six years and the costs per reactor are around $5 billion. The new reactors are now a fully Chinese model, the Hualong, with 50% more steel and concrete than pre-Fukushima construction, and 85% local content.

At another site, Tianwan, four Russian reactors, VVERs, have been constructed alongside two Chinese reactors, ACPR1000s.

China’s ‘go-out’ strategy involves the government working with various countries including India, Pakistan, Thailand, Vietnam, Cambodia, Kenya, Argentina, among others, on rolling out China’s nuclear technology.

WNA estimates that China could construct 8-10 reactors per year to meet national and international demand.

China is also building out its fast breeder and SMR capabilities with sites currently under construction in Fujian and Hainan, respectively.

Taiwan currently has two GE BWRs and two Westinghouse PWRs in operation on the northern and southern tips of the island, but was scheduled to phase out nuclear by 2025 following the accident at Fukushima. There will be a referendum in August this year to finally decide the matter.

South Korea has 24 reactors, all PWRs, built between 1983 and 2019. There was a plan to build 13 new reactors prior to the last presidential election in 2017, which would have taken the country’s nuclear share of electricity production to almost 30%.

President Moon, who won the election, campaigned on a policy of phasing out nuclear power over 40 years. However, this is now being reconsidered and two new reactors, at Ulchin, will be connected to the grid before May 2022. Two other reactors may also be built at that site. The government also recently approved the continued construction of Shin Kori reactors 5&6. South Korea recently successfully built four reactors in the UAE on time and under budget.

GLOBAL VIEW

BY TOM O’SULLIVAN

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

The Texas Freeze:

Electricity, natural gas, and water utilities suffered catastrophic and cascading outages across Texas last week as temperatures in the state approached -20 Celsius, a 126-year low, due to frigid polar vortex weather conditions. Temperatures in Austin were the lowest since 1909.

Over four million residents were without power and 14 million were without water.

Dozens of deaths have already been attributed to hypothermia and carbon monoxide poisoning. President Biden will sign a major disaster declaration for Texas when he visits over the next few days.

Economic damage is estimated to be at least $50 billion to the Texan economy which is worth almost $2 trillion. RWE, Germany’s largest power producer, which operates in the state, may suffer losses of $500 million due to the disruptions in Texas. General Motors and Ford also cut back production in Texas.

Outages impacted four million barrels of U.S. oil production capacity, 20% of U.S. refinery capacity, and 40% of Texan gas production. All of Conoco’s Permian and Eagle Ford shale oil output was halted. Natural gas prices at the Houston ship channel approached $400 mmbtu last week. Natural gas is used for electricity and heating across Texas aggravating the demand pressures.

Electricity prices were $9 kWh last week which is equivalent in energy terms to a $15,000 price per barrel of oil. The pre-Freeze power prices were 5 cents per kWh. A full Tesla charge would have cost $900 in Texas last week.

Power demand peaked as supply collapsed with over 30 GW of power generation assets disabled. Nuclear, coal, gas, wind, and solar generation assets were all impacted by the freeze. Gas pipelines into Mexico were also frozen, with efforts made to replace piped gas with LNG until the governor banned all LNG exports from Texas until yesterday. ERCOT, the local grid operator, is likely to be subject to a major investigation as scenario planning appears to have been deficient. Some are describing it as a ‘total failure’ of the Texas electricity infrastructure. The Texan grid is an electricity ‘island’.

Over 1,000 public water systems also suffered disruptions across the state.

Oil:

1). OPEC revised up demand for OPEC crude for 2021 by 0.3 mb/d from the previous month to stand at 27.5 mb/d, around 5.0 mb/d higher than in 2020.

2). JP Morgan and Goldman Sachs are now both predicting a super-cycle for oil once the pandemic abates.

3). Saudi Arabia is widely expected to reverse production cuts at next OPEC meeting.

Natural Gas:

EIA now predicts that annual U.S. LNG exports will exceed pipeline exports in 2022 and that natural gas will account for about 36% of U.S. electricity generation by 2050.

Pipelines:

The U.S. government has commenced a new sanctions-related review of the Nord Stream 2 natural gas pipeline that will link Russia to Germany, bypassing Ukraine.

Offshore Wind:

IEA projects that the annual offshore wind market is set to more than double in the next five years thanks to rapid cost declines supporting expansion in Asia and the U.S.

Metals:

Copper prices rose to their highest level since 2011 on Friday, to almost $9,000 a ton.

Nickel hit its highest level since 2014, and aluminum hit its highest level since 2018.

Tin prices have hit a seven-year high with prices at $23,400 per ton.

ESG:

European funds investing in specific ESG themes are now thought to exceed $1.3 trillion, with over 500 new funds launched in 2020.

EVs:

Ford will stop selling cars with ICE engines in Europe by 2030.

Shipping:

AP Moeller-Maersk will launch the first carbon-neutral container vessel by 2023, seven years ahead of schedule.

Air Travel:

1). IATA is reporting that flights in European airspace in February are at their lowest level in a single year.

2). Airbus announced losses of $1.2 billion for FY2020 and may cut 15,000 jobs.

3). Air France-KLM announced a loss of $8.5 billion for FY2020 and will need to apply for an additional round of state aid.

4). Two Board members of Boeing will step down, Susan Schwab and Arthur Collins.

Climate:

1). IEA believes that more work is needed to reduce emissions in chemicals, steel and cement as the huge amount of energy needed to produce them has serious implications for emissions. Steel production alone is thought to account for 9% of global CO2 emissions.

2). The U.S. Federal Reserve announced it will ramp up oversight work to ensure the U.S. financial system can deal with climate risks.

Covid ‘19:

Swiss Re announced business interruption claims of almost $4 billion for FY2020, resulting in a loss of $900 million.

China:

1). China is looking at new limits on exports of 17 rare metals where it controls 80% of global supply. This could impact EV and wind turbine production.

2). Jinko Solar announced a strategic cooperation agreement with Tongwei to build a high-purity crystalline silicone project with a capacity of 45,000 tons and a silicon wafer project of 15GW a year.

South Korea:

1). Last week the government passed the world’s first hydrogen law that outlines an infrastructure for a hydrogen economy.

2). A legal dispute between LG Chem and SK Innovation over trade secrets relating to battery production is impacting a production facility in Georgia, U.S. that could affect the EV rollout for the U.S. auto industry.

Singapore:

The government just released the ‘Singapore Green Plan 2030’, which is the blueprint for transitioning infrastructure to a more sustainable future over the next decade.

Indonesia:

1). IEA conducted a broad discussion with Indonesian energy officials on energy strategies.

2). Indonesia has picked Ridha Wirakusuah of Bank Permata to be the new head of its multi-billion sovereign wealth fund.

India:

1). Tesla is slated to start producing EVs in a suburb of Bangalore in 2021.

2). Disha Ravi, a climate activist, was arrested last week for sedition and could face life in prison.

Iran:

Iran will halt all IAEA independent inspections of its nuclear facilities from Feb. 23 in a clear break with the JCPOA agreement, unless international sanctions are lifted. The head of the IAEA has offered to visit Iran.

Georgia:

Block Energy commenced gas sales from its West Rustavi field last week.

Africa:

1). France’s President Macron has indicated a possible future withdrawal of French forces from the Sahel.

2). South Africa’s utility Eskom is moving forward with plans to close 25% of its coal capacity by 2030.

France

1). The French government has cancelled plans for a major $11 billion expansion of the Charles de Gaulle Airport due to environmental and climate concerns.

2). Renault announced a loss of almost $10 billion for FY2020.

United Kingdom:

1). UK power supplier, Aggreko, may be subject to a private equity takeover.

2). Jaguar Land Rover, owned by India’s Tata Motors, has announced it will halt production of ICE vehicles from 2025.

U.S.:

1). The U.S. rejoined the Paris Agreement on Friday.

2). Warren Buffet acquired a $4 billion stake in Chevron.

3). California is considering legislation that would ban fracking by 2027.

4). Janet Yellen has announced that a tax hike will be needed in the U.S. to finance President Biden’s climate plan.

EVENTS CALENDAR

Below is a selection of domestic and international events that we believe will have an impact on the Japanese energy and electricity industry.

| February | Approval of Fiscal 2021 Budget by Japanese parliament including energy funding projects;

CMC LNG Conference |

| March | 10th Anniversary of Fukushima Nuclear Accident;

Smart Energy Week – Tokyo; Quarterly OPEC Meeting; Japan LPG Annual Conference; Full completion of all aspects of the multi-year deregulation of Japan’s electricity market; End of 2020/21 Fiscal Year in Japan; |

| April | Japan Atomic Industrial Forum – Annual Nuclear Power Conference;

38th ASEAN Annual Conference-Brunei; Japan LNG & Gas Virtual Summit (DMG)-Tokyo Three crucial by-elections in Hokkaido, Nagano & Hiroshima – April 25th |

| May | Bids close in first tender for commercial offshore wind projects in Japan;

Prime Minister Suga to visit the U.S.-tentative |

| June | Release of New Japan National Basic Energy Plan-2021;

G7 Meeting – U.K. Forum for China-Africa Cooperation Summit (Senegal) |

| July | Tokyo Metropolitan Govt. Assembly Elections;

Commencement of 2020 Tokyo Olympics |

| August | Hydrogen Ministerial Conference in conjunction with IEA World Economic Forum in Singapore – Deferred from May |

| September | Ruling LDP Presidential Election;

UN General Assembly Annual Meeting that is expected to address energy/climate challenges; IMF/World Bank Annual Meetings (multilateral and central banks expected to take further action on emissions disclosures and lending to fossil fuel projects); End of H1 FY2021 Fiscal Year in Japan; Japan-Russia: Eastern Economic Forum (Vladivostok)-tentative |

| October | Last possible month for holding Japan’s 2021 General Election;

METI Sponsored LNG Producer/Consumer Conference; Innovation for Cool Earth Forum – Tokyo Conference; Task Force on Climate-Related Financial Disclosure (TCFD) – Tokyo Conference; G20 Meeting-Italy |

| November | COP26 (Glasgow);

Asian Development Bank (‘ADB’) Annual Conference; Japan-Canada Energy Forum; East Asia Summit (EAS) – Brunei |

| December | Asia Pacific Economic Cooperation (APEC) Forum – New Zealand;

Final details expected from METI on proposed unbundling of natural gas pipeline network scheduled for 2022. |

DATA

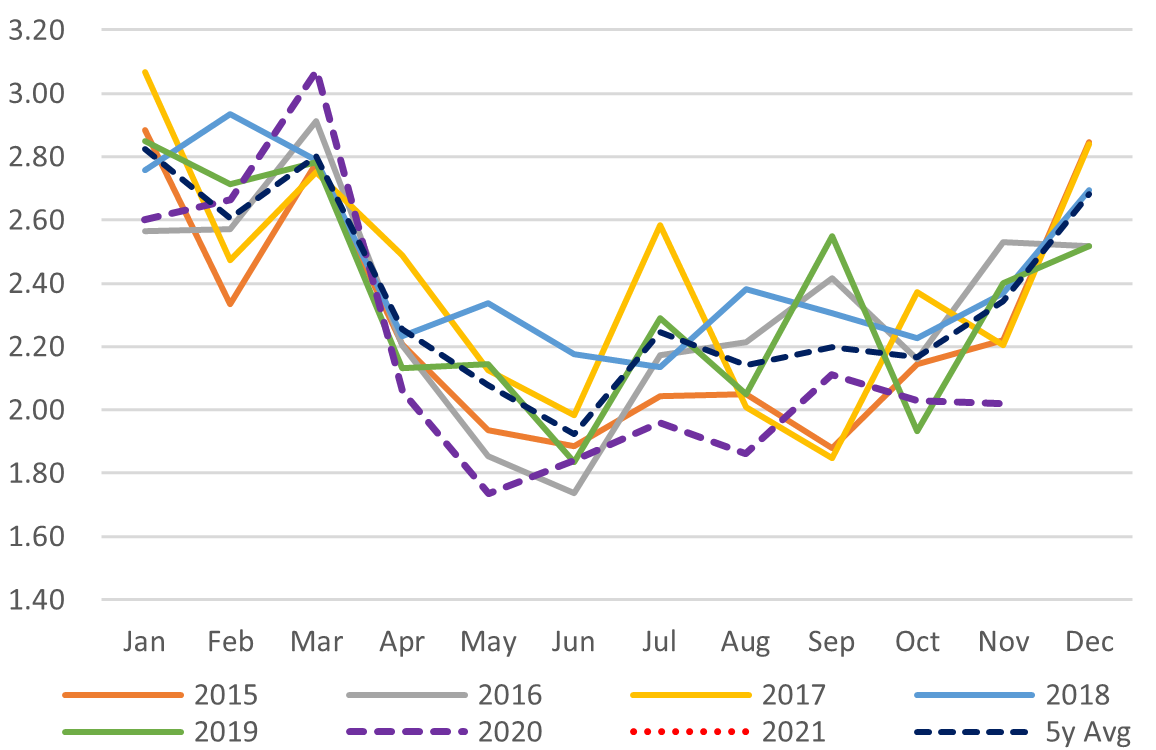

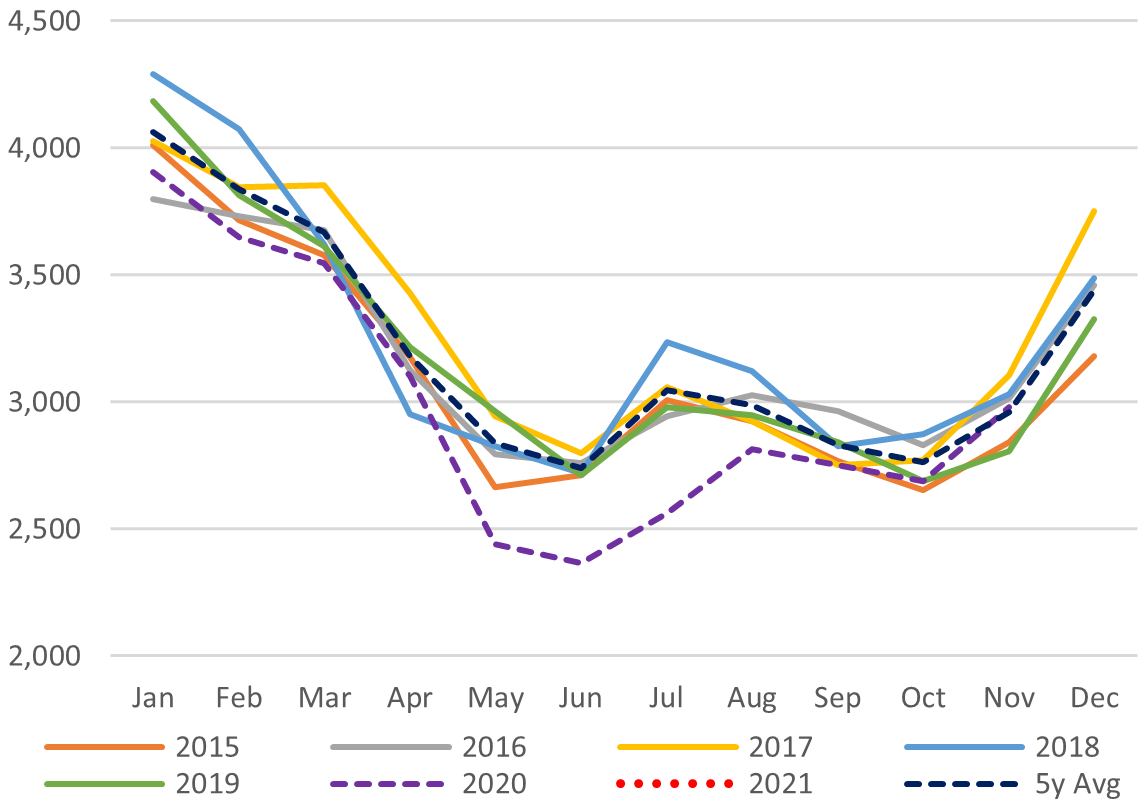

Japan Oil Price

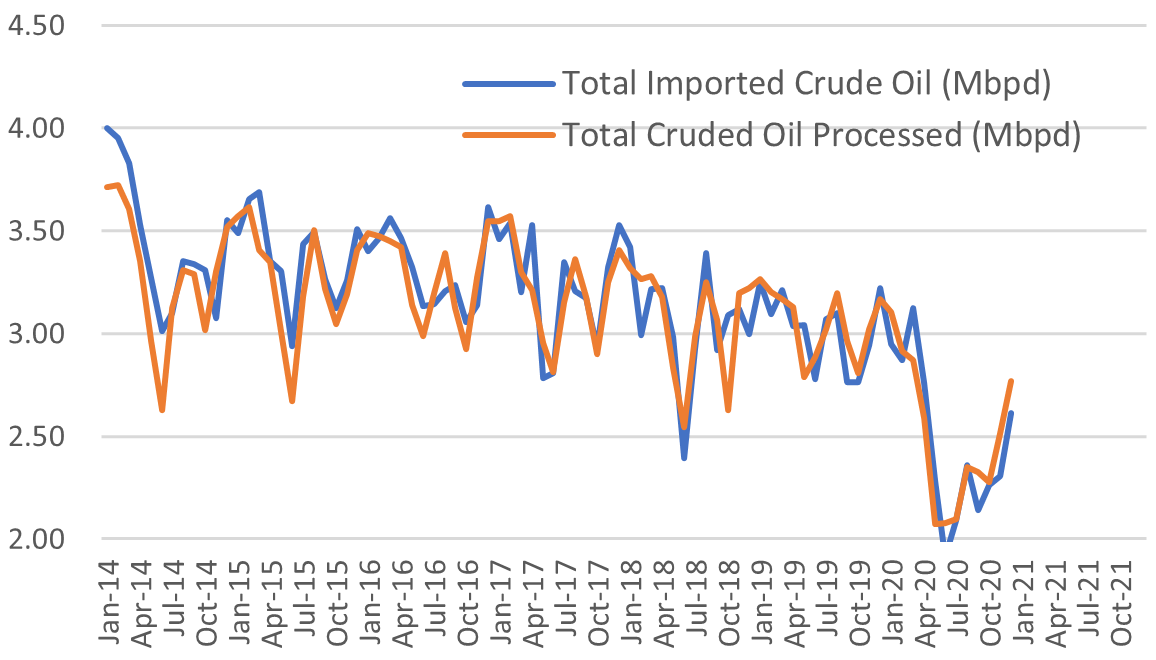

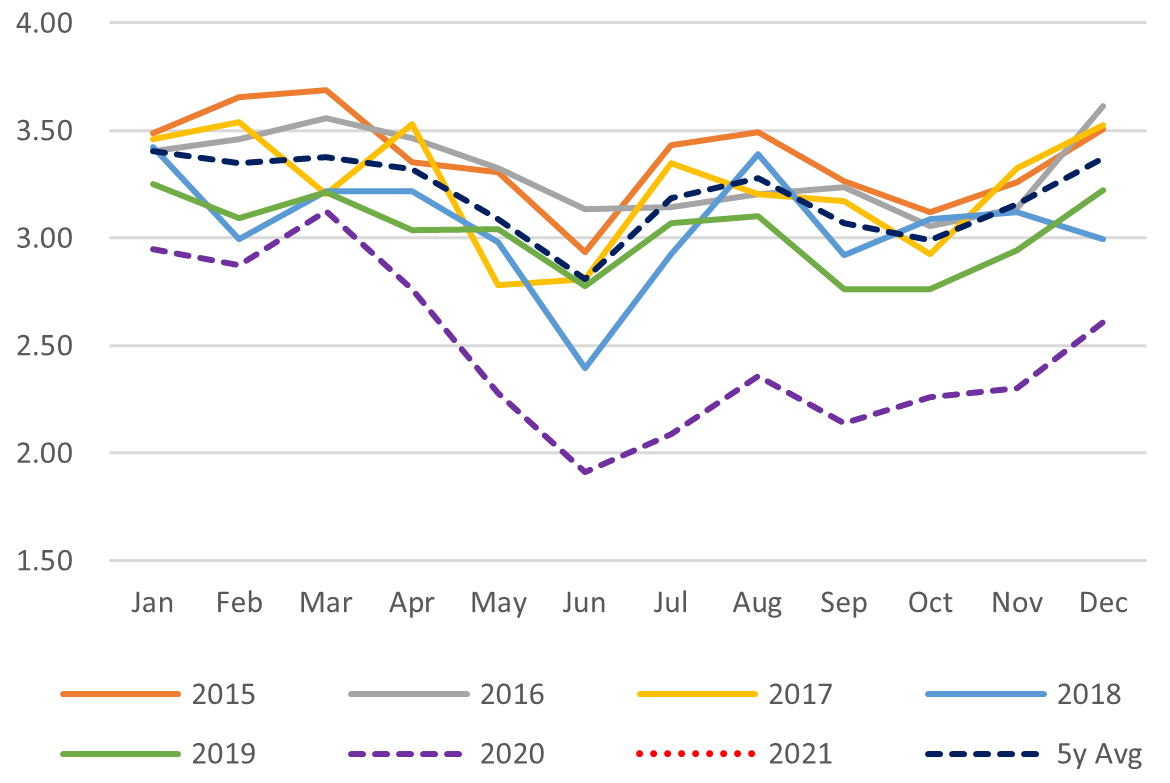

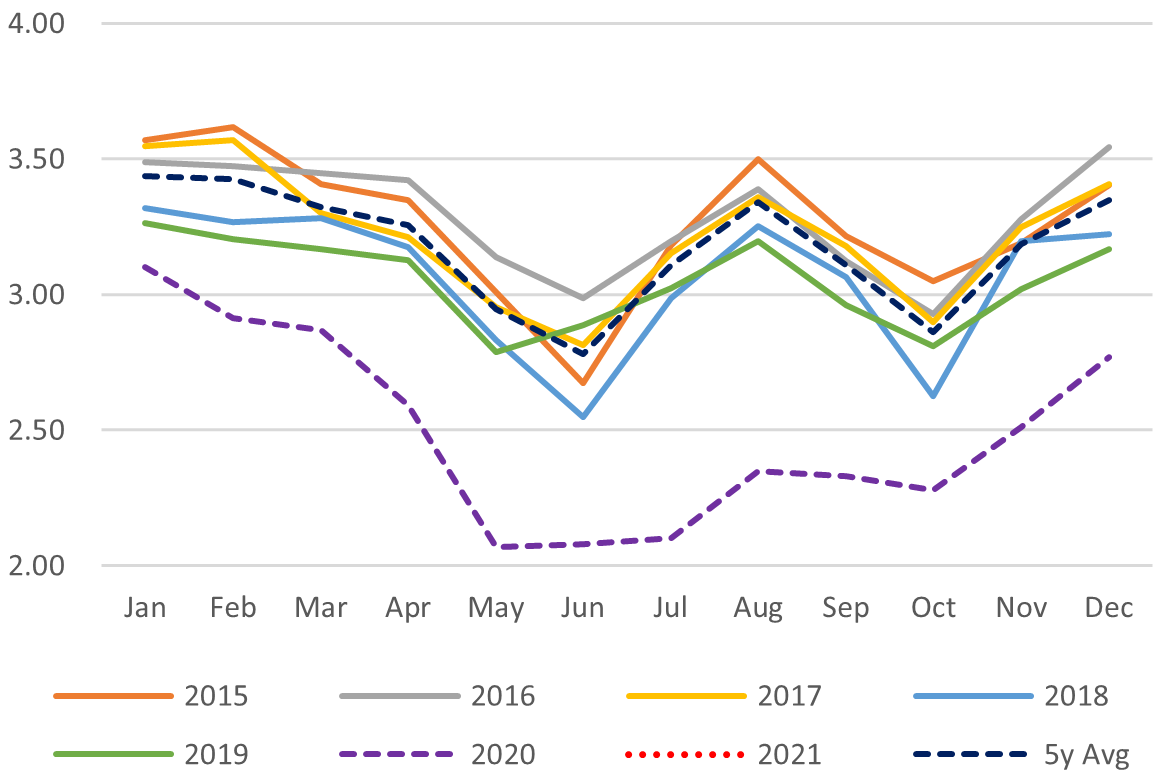

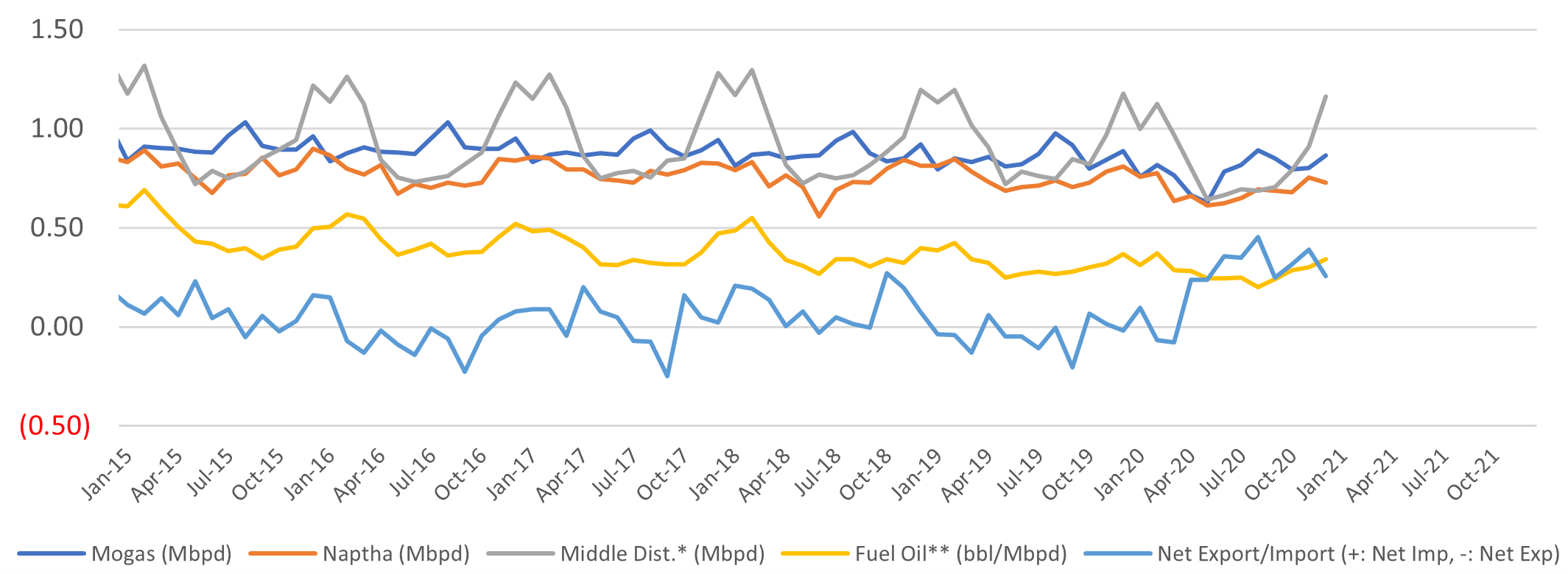

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

Domestic Fuel Sales

SOURCES: Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

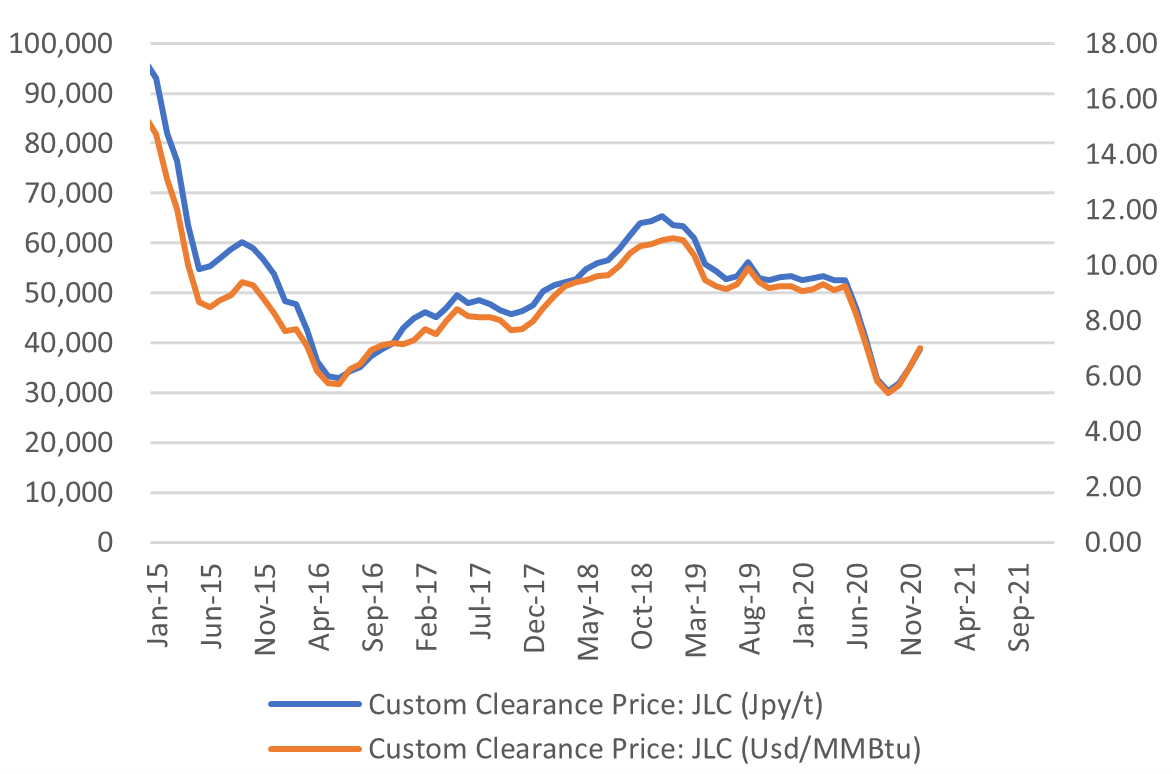

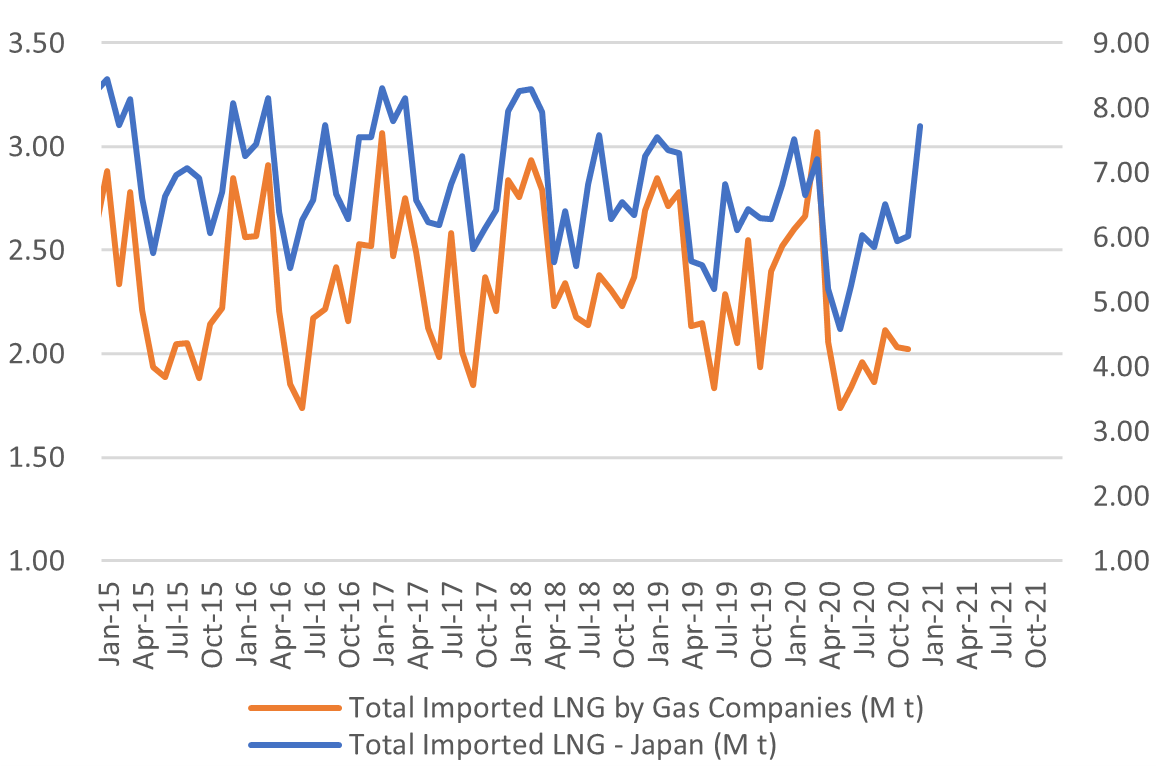

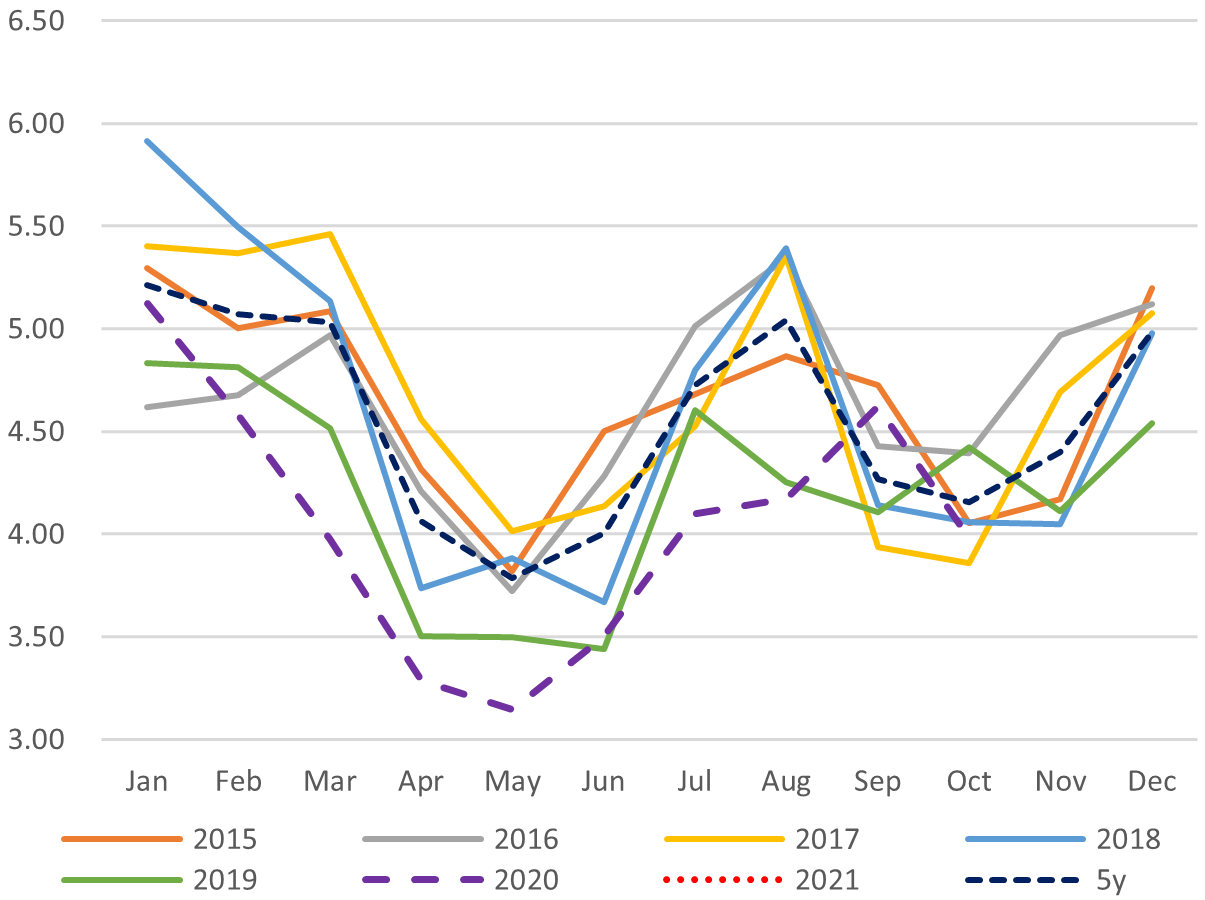

Japan LNG Price

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

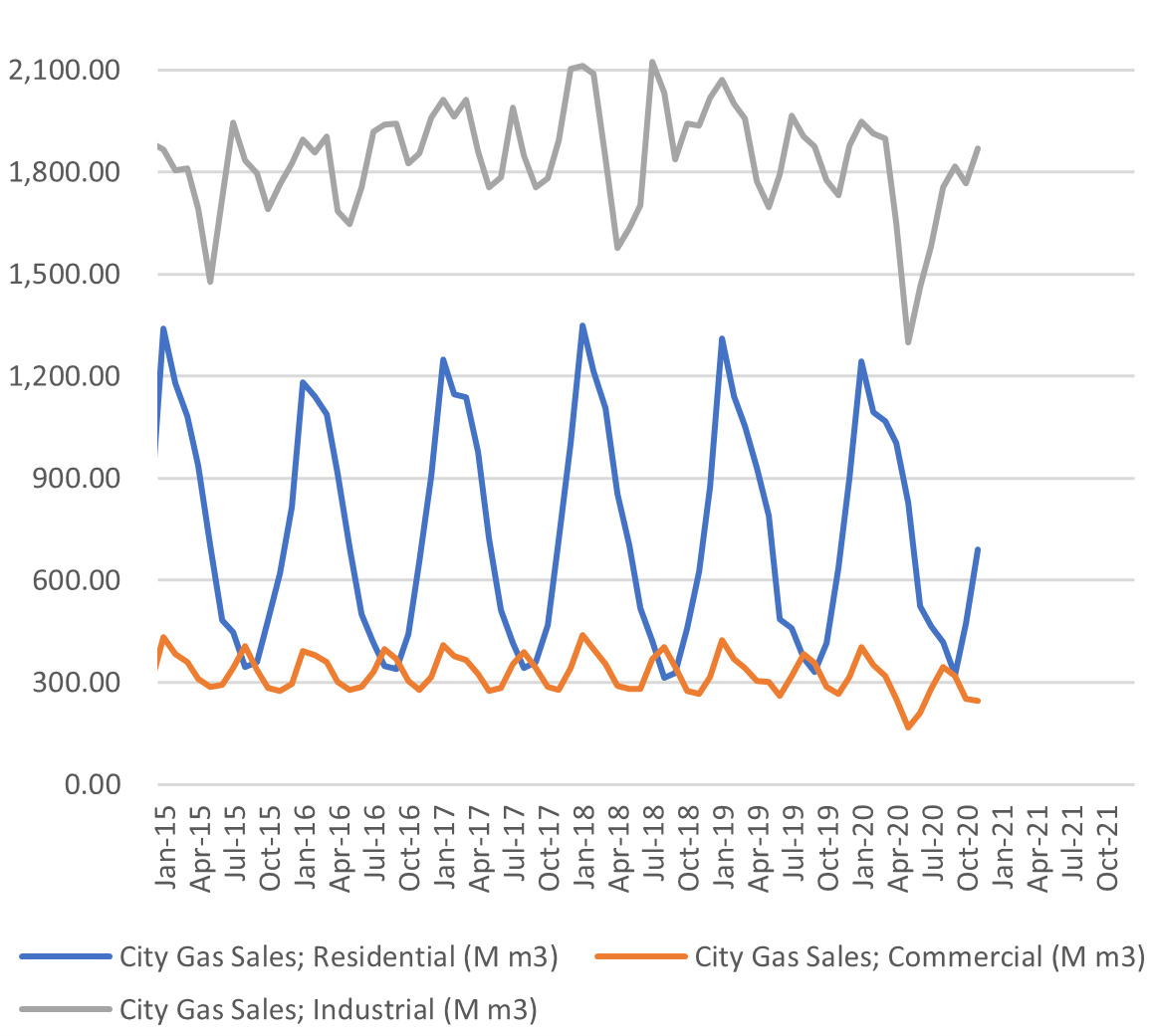

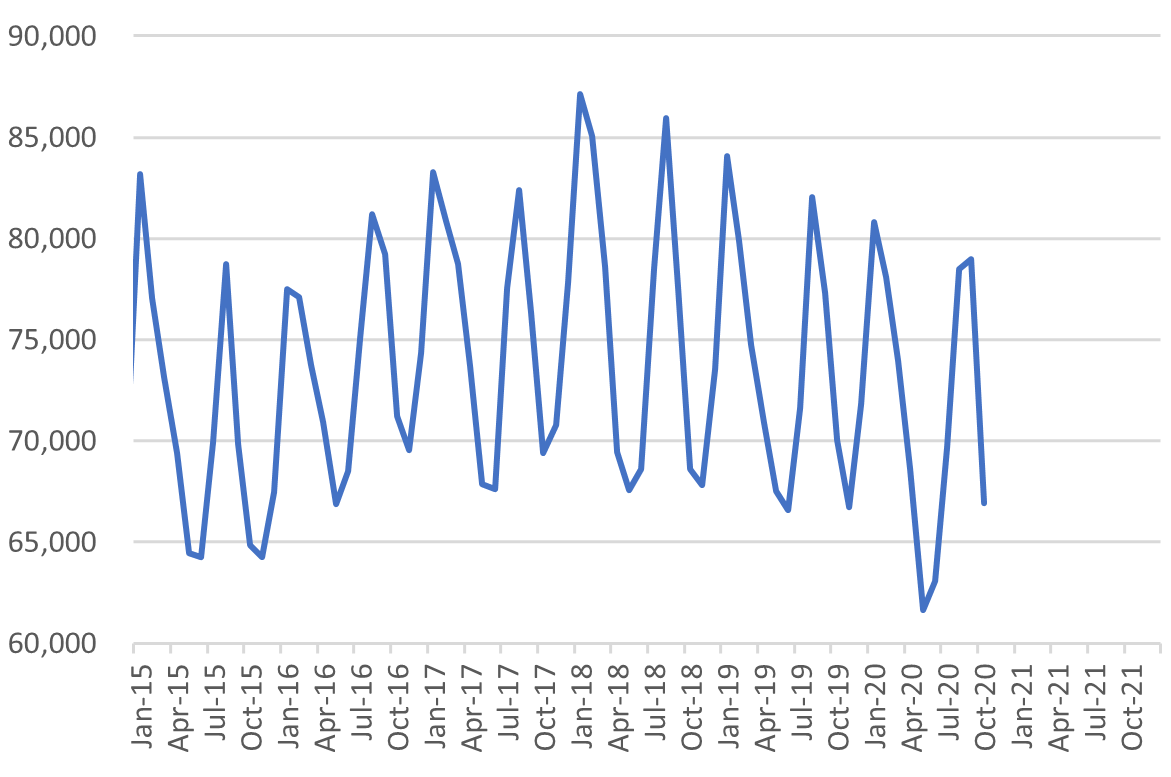

City Gas Sales – Total (M m3)

City Gas Sales by Sector (M m3)

SOURCES: Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

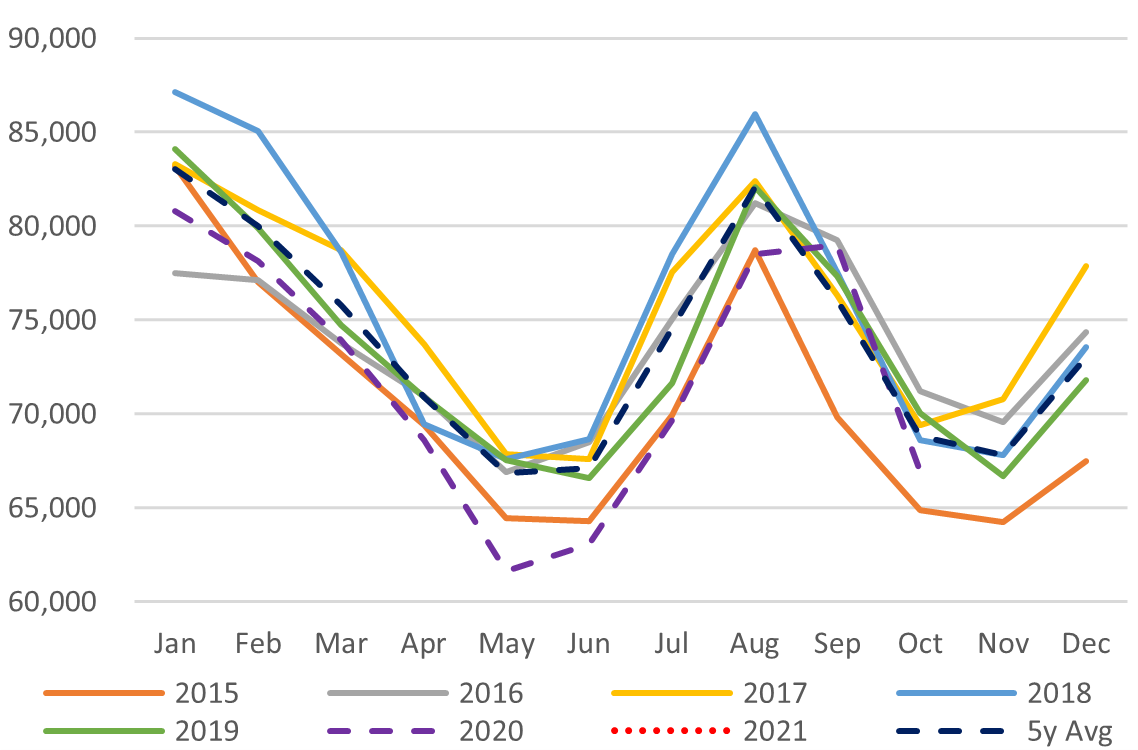

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

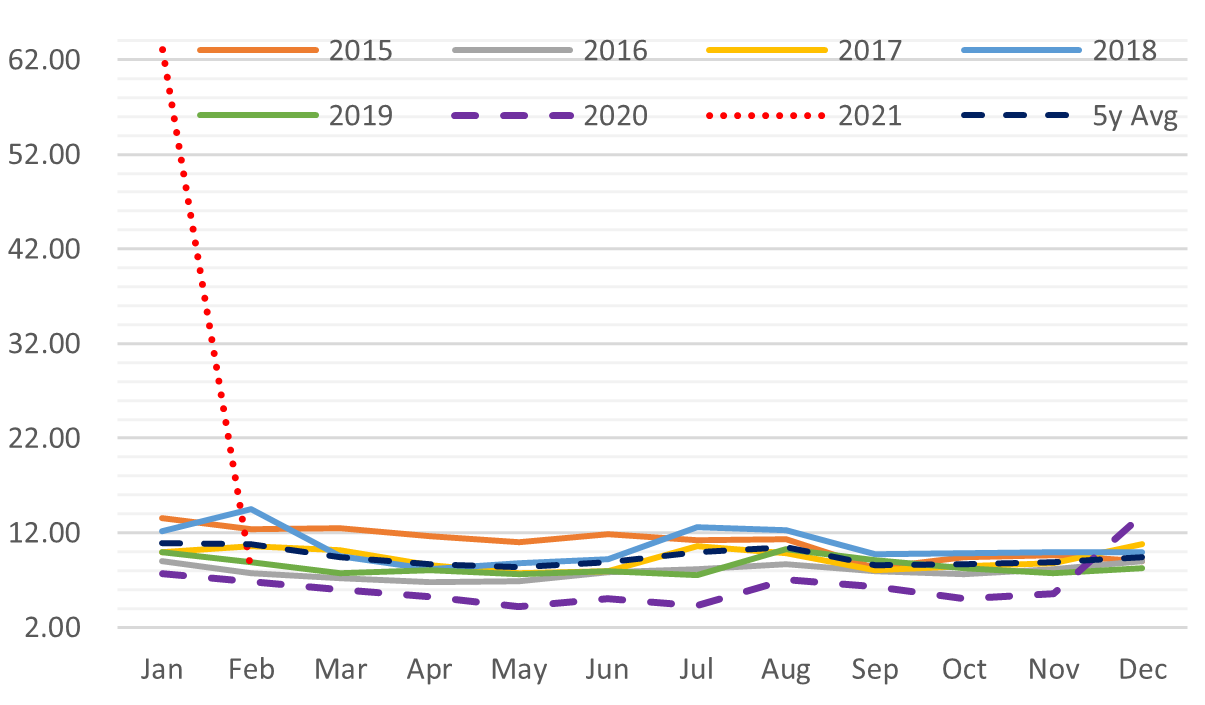

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

ACRONYMS

| METI | The Ministry of Energy, Trade and Industry | mmbtu | Million British Thermal Units |

| ANRE | Agency for Natural Resources and Energy | mb/d | Million barrels per day |

| TEPCO | Tokyo Electric Power Company | mtoe | Million Tons of Oil Equivalent |

| KEPCO | Kansai Electric Power Company | kWh | Kilowatt hours (electricity generation volume) |

| EPCO | Electricity power company, refers to the 10 regional utilities that used to control all parts of the Japanese power industry | ||

| NEDO | New Energy and Industrial Technology Development Organization | ||

| JCC | Japan Crude Cocktail | ||

| JKM | Japan Korea Market, the Platt’s LNG benchmark | ||

| CCUS | Carbon Capture, Utilization and Storage | ||

| CCUR | Carbon Capture, Utilization and |