JAPAN NRG WEEKLY

MAY 10, 2021

JAPAN NRG WEEKLY

May 10, 2021

NEWS

TOP

- METI minister hints at more support for nuclear energy while also promising to cut the cost of renewables in Japan considerably

- New power suppliers now account for 20% of Japan’s electricity market, but imbalances in the system grow; Govt. panel seeks to reform baseload and capacity markets

- Wind and geothermal power growth rate now higher than solar

ENERGY TRANSITION & POLICY

- Japan seeks to create an annual global hydrogen conference

- Top Japan trader to switch power portfolio in favor of renewables; Sumitomo Corp delays coal exit until late 2040s

- Sumitomo Corp partners with Norway firm to make ship batteries

- Mitsui Oil trials heat recovery tech for geothermal power plants

- Toho Gas creates a hydrogen-fired furnace for auto / metal plants

- Nippon Paper to develop battery that doesn’t use rare metals

- Toshiba’s new solar cell could be placed on EV car rooftops

- Toyota perfects artificial photosynthesis to cut CO2 at factories

- METI to spend $3.5B on supporting hydrogen infrastructure

- Kyuden Mirai creates biomass energy cycle …[MORE]

ELECTRICITY MARKETS

- Last remaining coal power plant project in Japan is canned

- Kyoto government calls on Kansai Electric to close coal plants; Kansai Electric sets up a new division focused on hydrogen

- Governor approves restart of Kansai Electric’s older nuclear units; Govt. offers extra grants for restart of 40yo+ reactors

- Regulator approves decommissioning of Fukushima Dai-Ni NPP

- New TEPCO chair vows focus on sweeping governance reforms

- Solar operator bankruptcies slightly down last year at 79 cases

- Inside story of the power utilities “cartel” …[MORE]

OIL, GAS & MINING

- Power producers’ LNG use drops to at 10-year low

- Trading companies ramp up procurement of rare metals, copper

ANALYSIS

THE IEA’S CRITICAL RAW MATERIALS REPORT, AND IMPLICATIONS FOR JAPAN’S DECARBONIZATION

Decarbonization and green technologies will not make the world an environmentally better place unless we closely monitor and control the supply of raw materials needed for this transition. And the metals and minerals that renewables, EVs, and other green tech require are vastly different in scale and composition from our current use. That’s the message of a landmark 285-page report from the International Energy Agency (IEA) published last week.

We break down what the report says, what impact decarbonization will have on mining and ESG, and what needs to be done. We also take a close look at what Japan is and isn’t doing in this arena, and make recommendations for a way forward.

JAPAN’S PATHWAYS TO A 46% DROP IN EMISSIONS: WHAT WILL THIS MEAN IN PRACTICE?

Last month, Prime Minister Suga declared a 46% reduction in greenhouse gas (GHG) emissions by FY2030 compared to FY2013 levels. According to PM Suga’s declaration, within nine years Japan needs to reduce greenhouse gas (GHG) emissions to about 800 million tons of CO2 equivalent. In FY2019, which ended March 31, 2020, Japan had annual emissions of 1.21 billion tons of CO2 equivalent. So, the country needs to cut emissions by 34% from current levels.

Such a major reduction will mean a lot more than simply adding renewables capacity and closing the coal-fired power plants. We look at the implications across the economy.

2021 EVENT CALENDAR

DATA SECTION

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Sponsored

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

METI Minister hints at further support for nuclear and lower cost for nonfossil power certs

(Asia Nikkei, April 27)

- METI Minister Kajiyama said Japan would help its companies access renewable energy at a lower price as global IT firms including Apple ask all their suppliers to run on green energy by 2030 or risk losing business.

- One aspect of this will involve lowering the cost of electricity generated from non-fossil fuel sources. Currently, companies buy a “nonfossil certificate” to prove that the power they buy was generated from renewable sources and is not contributing to greenhouse gas emissions.

- Kajiyama said METI plans to cut the government-mandated minimum price of the certificate to around ¥0.1 per kilowatt-hour from the current ¥1.3.

- The minister also signaled further support for nuclear energy. “We won’t consider any topic taboo” in terms of building or expanding nuclear power plants, he said.

- SIDE DEVELOPMENT:

Nuclear power: Gulf between ideals and reality frustrates economists a decade on

(Nikkei, May 3)- At a recent online forum on renewable energy and nuclear power hosted by the Japan Association of Corporate Executives, and which was attended by economists, students, journalists, and industry representatives, participants expressed frustration at the difficulty in achieving consensus on whether Japan should continue to pursue nuclear power. Despite years of debate, no progress had been made, complained participants.

- While the Association supports a reduction in the use of nuclear power, it believes nuclear will continue to be an essential energy source.

- Some attendees pointed out the challenges faced by Japan, in which land suitable for solar farms is more limited than overseas. Japan actually ranks highly in terms of installed generation capacity per square kilometer.

- Others were skeptical about the ability of solar and wind farms to match thermal power stations on consistency of supply, although representatives of green energy entities pointed out the example of Australia, which has successfully used storage batteries to smooth output from solar farms.

- Some commented that it was still difficult for members of the public to feel connected to these issues.

Power and Gas Policy Panel delivers interim report on power market reforms

(Japan NRG, April 28)

- The panel noted that fewer baseload deals were done in 2020 compared to 2019, and proposed a reform of capacity and baseload markets.

- Baseload reform proposals include cutting deposit fees to solicit more participation.

- Panel noted that current supply and demand are not matching.

- SIDE DEVELOPMENT:

New power suppliers now account for 20% of Japan’s power market

(Japan NRG, April 28)- New power companies, which mostly entered the market since liberalization in 2016, comprise 20% of Japan’s electricity markets as of December 2020, according to a report from the power and gas policy panel.

- The new power companies, many of which are focused on renewables, hold their highest share in the Tokyo market and their lowest share in Okinawa.

TAKEAWAY: The increase in renewable power volumes in Japan has created a number of balancing issues for the country’s grid, which we covered in detail in the April 26 edition of Japan NRG. Next week, we will look into how the rising friction between the grid companies and renewables operators may be resolved, at least temporarily, via the introduction of a new methodology for grid connections.

Japan seeks to create an annual international hydrogen conference

(Japan NRG, April 28)

- Japan needs to create an annual international hydrogen conference to reinforce its positions in this field and strengthen the country’s efforts to promote the industry according to a new hydrogen roadmap drafted by METI’s Green Innovation Strategy panel.

- The country also needs to revise regulations on hydrogen storage, which are not practical, and to invest more in supply chain R&D, according to the panel.

TAKEAWAY: Japan hosts one of the most influential conferences in the LNG market, the LNG Producer-Consumer Conference. As the world’s biggest buyer of the fuel, Japan is able to annually gather the industry’s top business and government officials and thus, in part, drive the narrative for the industry’s development. It would make sense to do the same in hydrogen, a space that Japan seeks to dominate.

Mitsubishi Corp. to increase investments in solar, wind to make renewables key power assets

(Nikkei, April 30)

- Trading house Mitsubishi Corp. will boost the share of renewables in its power generation business from the current 30% to over 60% by FY2030.

- By FY2030, the company will double the amount of power from renewable energy sources compared to 6.6 million kWh in FY2019.

- The company will increase investment in solar and wind power at home and abroad, while gradually reducing coal-fired power generation to zero by 2050.

- CONTEXT: Mitsubishi has a portfolio of 10.8 GW in power assets, including those under development.

- In the U.S. and Europe, Mitsubishi will promote development through its electric power subsidiary Eneco, a Dutch renewable energy power generator it bought in March 2020 in partnership with Chubu Electric, spending a total of ¥500 billion ($4.5bn).

- Mitsubishi Corp. is also seeking to expand its business in the U.S. through Nexamp, a Massachusetts solar power developer acquired in 2018..

- In Japan, the company has plans for offshore wind power projects in Chiba and Akita prefectures.

- By 2030, Mitsubishi expects to be involved with just three coal-fired power stations, including Vietnam’s planned Vung Ang 2.

- Mitsubishi plans to sell its share of gas-fired thermal power plants in North America and close old facilities.

- CONTEXT: Mitsubishi is the first Japanese trading company to announce a reduction in its use of gas-fired power plants.

- SIDE DEVELOPMENT:

Sumitomo Corp says will exit coal-fired plants by late 2040s

(Company statement, May 7)- Trading house lowers its 2035 expected share of coal in the power mix to 20% from 30% while increase natural gas’ share to 50% from 40%.

- Sumitomo vows not to enter new coal projects, but also says it is involved in a potential project to build two units in Bangladesh.

- SIDE DEVELOPMENT:

Mitsubishi Corporation to build data centers in U.S.

(Nikkei, May 7)- Mitsubishi Corporation announced on May 7 that it was entering the data center market and would build two data centers in the U.S. in conjunction with Tokyo Century, with plans to build five more by around 2030.

- The initial two centers will be located in Virginia and consume a total of 100 MW of electricity that will come from renewable sources.

- The cost of building the two data centers is estimated at ¥50 billion.

Sumitomo Corp partners with Corvus Energy on battery systems for ships

(New Energy Business News, April 26)

- Sumitomo Corporation signed a joint venture agreement with Norway’s Corvus Energy under which Sumitomo will market and maintain energy storage systems for ships.

- The joint venture is the latest development in the partnership between the two corporations, which began in 2019.

- The International Maritime Organization’s 2018 greenhouse gas reduction strategy calls for a 40% improvement in ship energy efficiency by 2030.

Mitsui Oil Exploration trials heat recovery technology in geothermal plant

(New Energy Business News, April 27)

- Mitsui Oil Exploration is harnessing a process patented by US-based Green Fire Energy to trial heat recovery in geothermal power plants.

- The closed loop heat exchanger process promises to improve the efficiency of Mitsui’s plants.

- Mitsui Oil Exploration entered the geothermal energy sector in 2012. In 2019, it opened the Matsuo Hachiman Taichi geothermal power station, in collaboration with partners JOGMEC, JFE Engineering, Japan Metals and Chemicals, and Geothermal Engineering.

Toho Gas develops hydrogen-fired furnace

(Kankyo Business, April 26)

- In a first for a Japanese company, Toho Gas said it converted a single-ended radiant tube burner of the type used in the automotive and metallurgical industries to run on hydrogen instead of natural gas.

- Because hydrogen burns at a higher temperature than natural gas, its use can lead to an increase in NOx emissions and accelerate burner wear. However, Toho says that its new burner has a NOx emission and durability profile comparable with natural gas burning units.

Nippon Paper to develop battery that is not reliant on rare metals

(Nikkei, April 26)

- Nippon Paper is working on a new high-performance battery that does not contain rare metals.

- The battery under development is paper-based and boasts 2.5 times the energy density of a conventional lithium-ion battery.

- Fuji Keizai estimates that worldwide demand for automobile batteries alone will increase more than seven-fold by 2035. There are concerns that rare metals could become prohibitively expensive or difficult to procure.

Toshiba’s tandem solar cell could enable cars that run on the power of the sun

(Nikkei X-Tech, April 28)

- Toshiba is developing what it calls a “tandem photovoltaic cell” that combines porous copper oxide with traditional silicon photovoltaic cell technology.

- Toshiba hopes to achieve efficiencies of over 30% using its copper oxide tandem cell, which could make electric vehicles powered solely by roof-mounted solar cells a reality.

- The copper oxide tandem cell is just the latest in a series of new solar cell designs developed by the corporation, including one based on perovskite.

Toyota perfects artificial photosynthesis

(Kankyo Business, April 23)

- Toyota Central R&D Labs said on April 21 that it had successfully performed “artificial” photosynthesis in a process that uses sunlight, CO2 and water to produce a useful compound (formic acid).

- Toyota’s 36 cm² photosynthetic cell achieved 7.2% efficiency, which is a world record.

- The goal is to use artificial photosynthesis to convert CO2 emissions from factories and other industrial sources into useful products.

Kyuden Mirai Energy aims to establish biomass cycle

(New Energy Business News, April 27)

- Kyuden Mirai Energy launched a new initiative aimed at establishing a “biomass energy cycle”.

- Most ash generated by biomass generation is sent to landfill. Kyuden Mirai Energy aims to convert these ash byproducts to fertilizer, which can then be shipped back to the overseas forests from which the biomass was sourced, to promote the growth of new trees.

- Kyuden aims to make this initiative commercially viable by 2023.

Japan’s industry ministry to invests ¥370 billion to support hydrogen projects

(Nikkei, April 28)

- The Ministry of Economy, Trade and Industry agreed on April 28 to award up to ¥370 billion of its ¥2 trillion decarbonization fund to hydrogen projects.

- The lion’s share of the funds (¥300 billion) are earmarked for hydrogen supply chain infrastructure, with the remainder being earmarked for projects to scale up equipment used to synthesize hydrogen from water.

- Project proposals will be accepted starting in May.

- METI aims to leverage economies of scale to reduce hydrogen transportation costs to 1/6 of current levels by 2030/2031.

Mitsui Sumitomo offers insurance for businesses issuing green power certificates

(Kankyo Business, May 8)

- The insurance would offer compensation when operation is stopped due to power supply issues. The product from Mitsui Sumitomo Insurance Co is called “Green Power Certificate Stable Supply Support Insurance”.

Sojitz invests in U.S. firms developing commercial hydrogen aircraft and fuel

(Kankyo Business, April 27)

- Sojitz Corp said it will invest in Universal Hydrogen Company (UH2), based in California. The U.S. firm is working on the development and commercialization of hydrogen-fueled aircraft and the hydrogen supply networks for aircraft. Sojitz will act as a strategic partner of UH2.

Kawasaki Heavy developing hydrogen engine for large vessels by 2025

(Kankyo Business, April 28)

- Kawasaki Heavy Industries, Yanmar Power Technology, and Japan Engine Corporation aim to be the first in the world to develop a hydrogen engine for large ocean and coastal vessels. The group aims to bring its product to market around 2025.

Suga plan for greener Japan stirs hope in wind energy sector

(Asia Nikkei, May 7)

- A summary of all the main developments in the offshore wind strategy over the last year or so. Companies involved in it, such as Marubeni, say they feel the development is finally going ahead and the government is committed to offshore wind.

NEWS: POWER MARKETS

| No. of operable nuclear reactors | 33 | |

| of which | applied for restart | 25 |

| approved by regulator | 16 | |

| restarted | 9 | |

| in operation today | 7 | |

| able to use MOX fuel | 4 | |

| No. of nuclear reactors under construction | 3 | |

| No. of reactors slated for decommissioning | 27 | |

| of which | completed work | 1 |

| started process | 4 | |

| yet to start / not known | 22 | |

Source: Company websites, JANSI and JAIF, as of April. 16, 2021

Wind and geothermal growth rate exceeds solar for the first time since 2012

(New Energy Business News, May 7)

- In a first, the growth rate of wind and geothermal power generation is now exceeding that of solar power since the introduction of the FIT system, according to research published by Professor Kurasaka of Chiba University and the NPO Institute for Environmental Energy Policy.

- Due to the FIT system that came into effect in July 2012, solar power, which has a short lead time to starting operation, has been the main source of new renewable electricity. However, in FY2019, large-scale projects in wind and geothermal generation started operating, overtaking the YoY growth rate of solar (6%). Wind was up 12%. Geothermal generation was up 13%.

- On the other hand, heat supply volume from renewables, which is not covered by the FIT system, decreased by 4% in FY2019. Both solar heat utilization and biomass heat utilization decreased by 5%, with the research calling for policies to promote renewable energy heat supply.

TAKEAWAY: Solar remains by far the biggest renewables energy source in Japan at this moment, but momentum has definitely shifted elsewhere and this latest report supports that evidence. There is more government policy focus on the wind sector at present and, while it’s hard to see geothermal capacity growing rapidly the fact that its rate of installation surpassed that of solar says a lot about the latter. If the government is to follow through on its emission cuts commitments by FY2030, this momentum in solar will need to be reversed. We expect this to begin with changes in land regulations over the course of the current fiscal year.

Last remaining coal project in Japan is canned

(NHK, April 27)

- Marubeni and KEPCO said it’s abandoning plans to build a 1.3 GW coal-fired power station in Akita.

- The announcement means that no new coal-fired power stations are planned anywhere in Japan. Increased awareness about the need to reduce carbon emissions means future new coal-fired plants look unlikely.

- Marubeni and KEPCO say they’re exploring the possibility of using the site to build a biomass fired plant instead.

- SIDE DEVELOPMENT:

Kyoto government calls on Kansai Electric to close coal plants

(Kiko Network, April 30)- The Kyoto prefectural govt, which owns a stake in KEPCO, has brought a shareholder resolution calling on KEPCO to decarbonize operations.

- This is the first time that a local body has taken such a course of action.

- In the resolution, the govt says there’s a need for industry to embrace the 1.5° warming target stipulated in the Paris Agreement, and that to achieve this, Japan needs to not only stop building coal-fired power stations, but also rapidly deploy carbon capture technology in existing coal-fired plants.

- Because carbon capture technology is not yet commercially viable, however, if Japan waits for carbon capture technology to arrive, it will miss its targets, argues the resolution. More drastic action is required to decarbonize industry, says the resolution.

- The resolution calls for a review of KEPCO’s agreement to buy electricity from the under-construction Kobelco Power Dai-Ni coal-fired plant.

- SIDE DEVELOPMENT:

Kansai Electric sets up hydrogen business division

(Denki Shimbun, May 6)- The new division inside the company will promote and coordinate the company’s mid-term plans in developing the hydrogen business in terms of power generation and hydrogen as a fuel for transport.

- Mori Nozomi, a managing executive officer, will be in charge of this division, which will initially have 30 staff.

- Another internal reorganization will pool more than 1,000 staff into a new renewables energy division that will focus primarily on offshore wind.

Fukui governor approves extension of Kansai Electric’s NPP reactor lifetimes

(Asahi Shimbun, April 28)

- In a nationwide first, Fukui governor Sugimoto Tatsuji said that he’d approve the restart of three KEPCO-operated nuclear power stations in Fukui.

- All three power stations now exceed their intended service life of 40 years.

- After a 2013 law change, nuclear plants can be operated for an additional 20 years beyond the end of their design life with the approval of the Nuclear Regulation Authority.

- This would be the first restart of reactors older than 40 years in Japan.

- SIDE DEVELOPMENT:

Government to offer localities ¥2.5 billion to restart older reactors

(Nikkan Kogyo, April 27)- METI Minister Kajiyama said the govt will make grants of up to ¥2.5 billion to the municipalities where nuclear reactors over 40 years old are restarted.

- The minister said the situation needs a different response from the normal restart since this is the first time that nuclear facilities over 40 years in service will be restarted.

TAKEAWAY: The restart process is expected to take about a month. It takes time to load fuel, start up the equipment and test things before the facility is generating electricity and is connected to the grid. However, on June 9 Takahama NPP’s units will need to shut down again because work on upgrading them with anti-terrorism measures will not be complete. Kansai Electric has already said as much. So, why does the utility want to restart its reactors for just a few days? For one, to make sure it can move forward before any other snag comes along, such as a court order or citizen protest or local government getting cold feet. But, also Kansai Electric needs to test the restart process of these 1) older reactors and 2) reactors that have been offline for a decade. The latter is an especially concerning part as it is not easy to restart power equipment that has been idle for so long. Having a “test run” restart is not such a bad thing from the utility’s perspective.

Fukushima Dai-Ni: Regulator approves decommissioning schedule

(NHK, April 28)

- The Nuclear Regulation Authority has formally approved TEPCO’s proposed timeline for decommissioning the Fukushima Dai-Ni nuclear power station.

- The four reactors at the power plant will be decommissioned in stages over a total of 44 years.

- It will take 22 years to remove the 10,000 used fuel rods from the power plant. A new dry cask storage facility will also be constructed to store fuel rods that are not sent for processing.

- The total cost of disposing of the 50 tons of radioactive material on the site is estimated at ¥280 billion.

- TEPCO’s current issues at the Kashiwazaki-Kariwa plant are no excuse for allowing Fukushima Dai-Ni decommissioning work to fall behind schedule, cautioned Authority chair Fuketa Toyoshi.

Hopes that new TEPCO chair will carry out sweeping reforms

(Denki Shimbun, May 7)

- Corporate heavyweight Kobayashi Yoshimitsu named as the new chair of TEPCO Holdings.

- Kobayashi was involved in a recent revamp of the corporation’s operations and it is hoped he’ll beef up the corporation’s governance, improve profitability, and make progress on decarbonization.

- However, Kobayashi has not commented on what stance he will take on support to residents affected by the Fukushima disaster, and concerns remain about the new chair’s ability to restore the trust of the community.

- The recent scandal at the Kashiwazaki-Kariwa nuclear power station is believed to be one reason for Kobayashi’s appointment. It’s said that upon learning of the security breach, he expressed strong fears about the corporation’s governance arrangements.

- While Kobayashi made no bones about the fact that the only reason TEPCO still exists is so it can make amends for the Fukushima disaster, he also said that the utility needs to become more profitable if it is to compensate residents.

Solar operator bankruptcies slightly lower at 79 cases last year: Survey

(New Energy Business News, May 7)

- There were 79 bankruptcies of solar power operators in FY2020, little changed from the 81 cases in FY2019. However, a few large companies failed, according to a survey from Teikoku Databank.

- The most bankruptcies (40.5%) occurred in the Kanto area of Japan.

- Since Teikoku started collecting data in April 2006, Japan has had 562 bankruptcies of solar operators. The overwhelming reason for the business failures has been “slow sales”.

- SIDE DEVELOPMENT:

Solar energy companies under investigation for fraud

(NHK, April 28)- Yokohama-based solar technology company Techno Systems and several of its trading partners are under investigation on suspicion of defrauding the Financial Services Agency of hundreds of millions of yen.

- Lender SBI Holdings stated in February that it had concerns about Techno Systems’ operations, which prompted the current investigation.

Inside the power utilities cartel

(Sentaku, May edition)

- CONTEXT: Last month, four electricity and one gas utility in western Japan were raided by antitrust officials looking for evidence of cartel-like behavior. The probe is led by Japan’s Fair Trade Commission (JFTC) and includes Kansai Electric, Chugoku Electric, Chubu Electric, and Toho Gas.

- The antitrust probe has so far discovered rifts in the Chubu Electric management. Chubu reportedly conducted its own internal probes before dawn raids by the officials.

- Kansai Electric’s aggressive sales strategy is possible what sparked the cartel’s formation.

- Kansai Electric might be accused of cartel behavior and of dumping.

- Chugoku Electric may be hit the hardest and is likely to cooperate with the JFTC.

- It seems that people in the renewables industry are tipping off the JFTC.

Kyushu Electric accused of bullying local retails to prevent competition

(Zaiten, May edition)

- No sooner had Nobeoka City in the Kyushu announced plans to establish its own local power company, which the city would fully own, that Kyushu Electric rolled out a smear campaign against the plans, aiming to prevent competition.

- A Kyushu Electric executive is said to have started a rumor by telling local council and business organization leaders that the new company will post major losses.

- Nobeoka’s government complained about the situation to Minister Kono Taro, who is in charge of Administrative Reform and who supports the wider rollout of renewable energy. The city claimed that Kyushu Electric is interfering with the local deregulation process.

- The city also lodged a complaint with the Agency of Natural Resources and Energy, which is under METI. The ministry looks favorably on Kyushu Electric because it’s one of only two utilities to have restarted nuclear reactors in Japan. But since the city has gone also to Kono, METI feels it can’t protect the regional utility.

- The markets regulator already issued Kyushu Electric with a verbal warning via an order for business improvement.

- A senior METI official said: “We understand that market liberalization is causing difficulties [for EPCos] as it shrinks the customer pool and increases raw material costs. But, it’s sad to see Kyushu Electric bullying small local power companies.”

Tohoku Electric announces plans to build 14.9 MW geothermal plant in Akita

(New Energy Business News, April 26)

- The utility released an environmental impact assessment for a project to build a 14.9 MW geothermal power plant in Yuzawa City, Akita prefecture. Named the Kijiyama Geothermal Power Plant, construction would begin in 2025, with operations to begin in 2029.

- The plant will have six production wells that extract geothermal steam from the ground.

Tohoku Electric delays restart of nuclear reactor by three years

(Nikkei Shimbun, April 28)

- Tohoku Electric will postpone the completion of safety measures for Higashidori NPP Unit 1 by three years from the previously planned 2021 to 2024. This will be the fifth postponement of the work.

- President Kojiro said the reason for the postponement was “based on current examination and progress of construction.”

Kyushu EPCO makes its 2050 net-zero pledge

(Company statement, April 28)

- Utility said it has already reduced its emissions by about 50% from the FY2013 level, which is more than the national target of reducing CO2 emissions by 46% by FY2030.

- Utility plans to invest about ¥500 billion in the next five years in decarbonization, including in maximizing the use of nuclear power, shifting thermal power plants to hydrogen and ammonia and adding carbon capture and storage technology, as well as some renewables capacity.

All major power utilities forecast worsening financial results this year

(Nikkan Kogyo Shimbun, May 3)

- Nine of the 10 major power utilities, EPCos, gave sales forecasts for the fiscal year ending March 22, and all saw a decline in revenue. Six of the eight firms to give an ordinary profit forecast expect worse figures this year.

- Profits are growing only for Shikoku Electric, whose Ikata NPP is due to restart in October, and Kyushu Electric, which has all its NPPs in operation.

- Worsening financials are due to the continued effects of the pandemic and its lower electricity sales, as well as intensifying competition in the market due to liberalization. Finally, a change in accounting standards from this year will mean that levies and grants related to FIT will be excluded from sales.

ENEOS participates in U.S. solar farm project

(Sekiyu Tsushin, May 7)

- ENEOS said that it would participate in a Texan solar development project headed by the Swiss corporation Advanced Power.

- The 140 MW solar farm will go online in late 2022, boosting ENEOS’ global generation capacity by 70 MW.

- The ENEOS Group aims to have 1 GW of renewable generation capacity in place around the world by 2022/23.

NEWS: OIL, GAS & MINING

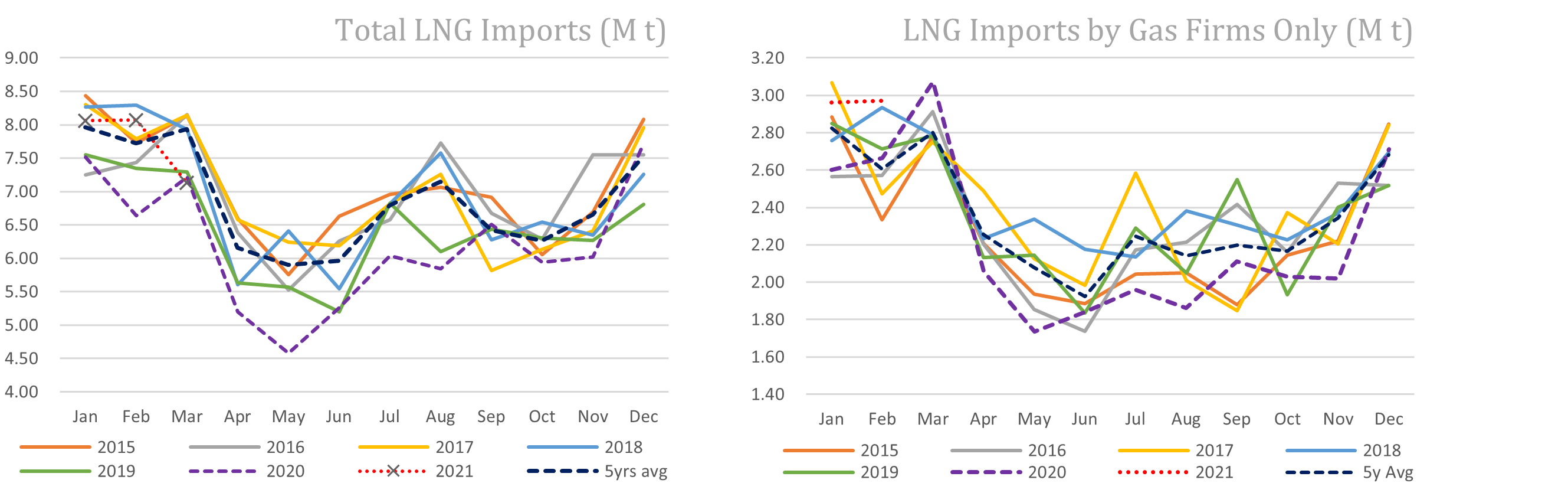

Power producers’ LNG use at 10 year low

(Denki Shimbun, May 7)

- Japan’s nine major electricity generators reported their lowest LNG usage in 10 years in the 12 months to March, with consumption down over 20% since peaking in 2014.

- LNG consumption dropped at four firms: Tohoku EPCo, JERA, Hokuriku EPCo and Chugoku EPCo.

- JERA’s consumption of LNG posted only one quarterly increase in 2020 during the fourth quarter (up 1.6% to 7.52 million tons).

- Kyushu EPCo’s LNG consumption jumped 86%, YoY, to about 1.9 million tons due to long shutdowns of nuclear reactors.

- Fuel oil consumption was also down and coal use dropped for a third year, with Chugoku EPCo posting the largest drop in coal use (-11.6% YoY)

- Consumption of crude oil, however, rose over 60% on the year before, with 70% of demand coming from KEPCO.

Trading companies ramp up procurement of rare metals, copper

(Sankei Biz, April 29)

- Major Japanese trading companies have started to stockpile rare metals and copper amid forecasts for increased demand for these commodities, both of which are required in the manufacture of electric vehicles.

- Competition for sought-after minerals is projected to become fierce In light of the China-U.S. trade war. Making the supply chain for such minerals more robust is a major issue for Japan-U.S. economic security.

- In 2022, Mitsubishi Corporation, in cooperation with its UK partner, plans to begin mining one of the world’s largest untouched mineral mines, located in Peru. Annual production is forecast at 300,000 metric tons.

- For its part, Marubeni plans to begin recycling vehicle batteries in 2022/23, recovering nickel and cobalt for reuse.

- While both companies earn significant revenue from minerals, market volatility means that exposure to these commodities carries significant risks of losses. Marubeni and Mitsubishi will probably need to diversify their portfolios to mitigate this risk.

- SIDE DEVELOPMENT:

Economic recovery, decarbonization boom buoy copper prices

(Nikkei, April 30)- Commodity prices are surging across the board as the global economy recovers, with the copper price exceeding $10,000 per metric ton for the first time in 10 years. Copper is an important component in electric vehicles.

- Prices of other metals, as well as lumber and agricultural produce, are also on the rise.

- Specifically, the price of silver, which is used in photovoltaic panels, is up 79%, platinum is up 44% and nickel, which is used in batteries, is up 35%.

- Rising commodity prices are impacting the price of automobiles, electronic appliances, and housing.

Osaka Gas profits up 90% last year

(NHK, April 27)

- Osaka Gas has released financial statements for the year to March.

- While the Covid 19 pandemic caused a reduction in business activity in Japan, resulting in lower domestic gas sales, the strong performance of Osaka Gas’ overseas operations enabled the corporation to post a final profit 90% larger than last year.

- The utility also benefited from electricity market deregulation, and an online marketing offensive enabled it to boost the volume of electricity sales during the year by 22%.

ENEOS reveals safety breach

(Chemical Daily, April 30)

- ENEOS revealed that it failed to perform legally-mandated inspections of high-pressure gas equipment at several of its refineries.

- Some statutory inspections of high-pressure gas valves at ENEOS’ Kawasaki, Sakai and Kurashiki refineries were not done for over two years.

- Upon reporting the breach to the Ministry of Economy, Trade and Industry, ENEOS was issued with a warning.

ANALYSIS

BY ANDREW DEWIT

PROFESSOR OF ENERGY POLICY

SCHOOL OF ECONOMIC POLICY STUDIES

RIKKYO UNIVERSITY, TOKYO

The IEA’s Critical Minerals Report and Implications for Japan

Decarbonization and green technologies will not make the world an environmentally better place unless we closely monitor and control the supply of raw materials needed for this transition. And the metals and minerals that renewables, EVs, and other green tech require are vastly different in scale and composition from our current use. That’s the message of a landmark 285-page report from the International Energy Agency (IEA) published last week.

“The Role of Critical Minerals in Clean Energy Transitions” (hereafter, “Critical Minerals”) is a key flagship study underpinning the IEA’s ambition later this year to outline the material, financial and other requirements for a global roadmap to decarbonization by 2050. Thus, Critical Minerals aggregates the best-available current evidence on the supply and demand for copper, nickel, lithium, cobalt, rare earths, silicon, and several other materials crucial to clean-energy technologies.

The report shows that current mineral supply chains are inadequate to meet the emerging tsunami of demand associated with decarbonization. This risks delays, rising costs and inefficiencies, as well as social injustices. But Critical Minerals also shows that these risks can be addressed through smart and global collaboration. It is a wake-up call to Japan, and all other countries committed to decarbonization, to undertake immediate and comprehensive policy changes.

Energy Transition Materials

Critical Minerals is clearly written because it seeks to communicate a message of utmost importance to a COVID-weary world seemingly inured by warnings of precarious supply-chains. The material basis of 21st century energy security is rapidly shifting from fossil fuels to a few dozen critical minerals that compose clean energy technology.

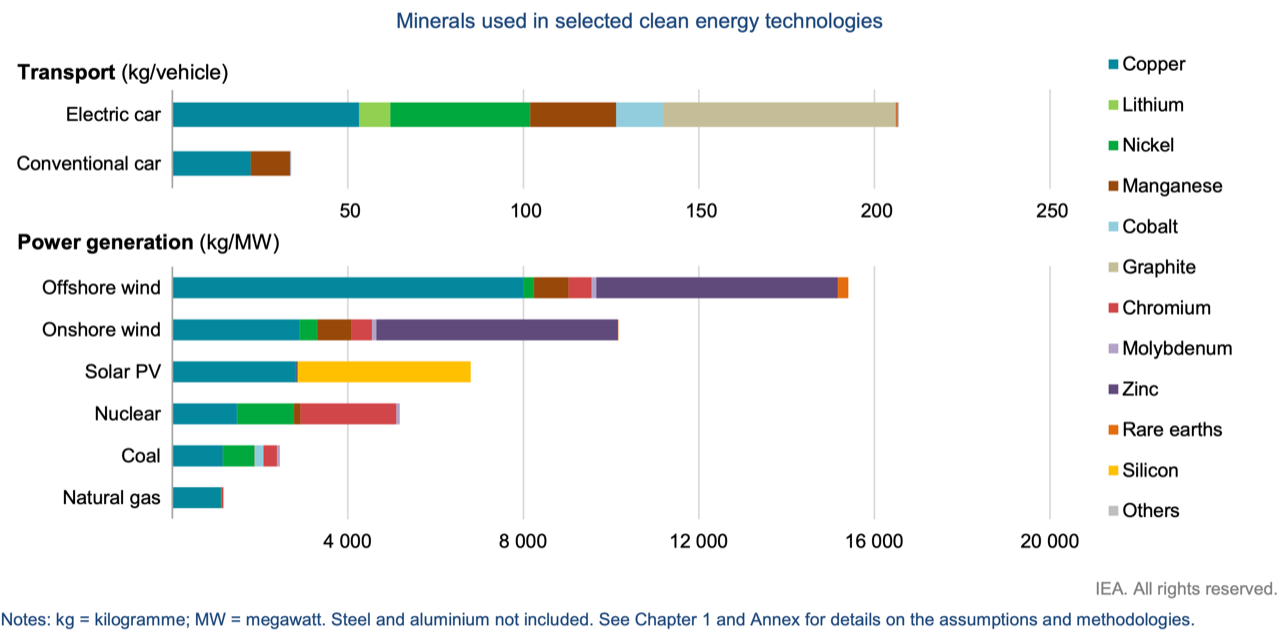

IEA’s analysis shows just how different the raw materials sensitivities will be by breaking down the mix needed for new and existing technologies.

Figure 1: Minerals used in selected clean energy technologies

Source: IEA, 2021

Figure 1 demonstrates that clean power and mobility technologies have significantly higher material-density, and a different composition. The aggregate per-MW amount of critical minerals, per MW, balloons from a couple of tons for a carbon-intensive natural gas plant to nearly 16 tons for a decarbonizing offshore wind array. Solar and wind demand vast quantities of zinc, rare earths and silicon, which thermal power barely uses. Even the copper component is very different.

On top of that, wind and solar have considerably lower capacity factors – meaning percent of actual power generation versus rated generation capacity – than fossil-fuel and nuclear plant. In consequence, the total volume of critical minerals required to produce a given amount of power with wind and solar versus the alternatives is even higher than expressed in the figure.

Yet quite unlike recent literature from fossil-fuel advocates, Critical Minerals does not argue that this higher material footprint negates the decarbonizing effect of electric vehicles and renewable energy. Its detailed assessments include, for example, the comparative lifecycle emissions for electric and conventional vehicles. The IEA’s work shows that even assuming GHG-intensive materials and electricity, an electric vehicle’s lifecycle emission are less than half of its conventional counterpart.

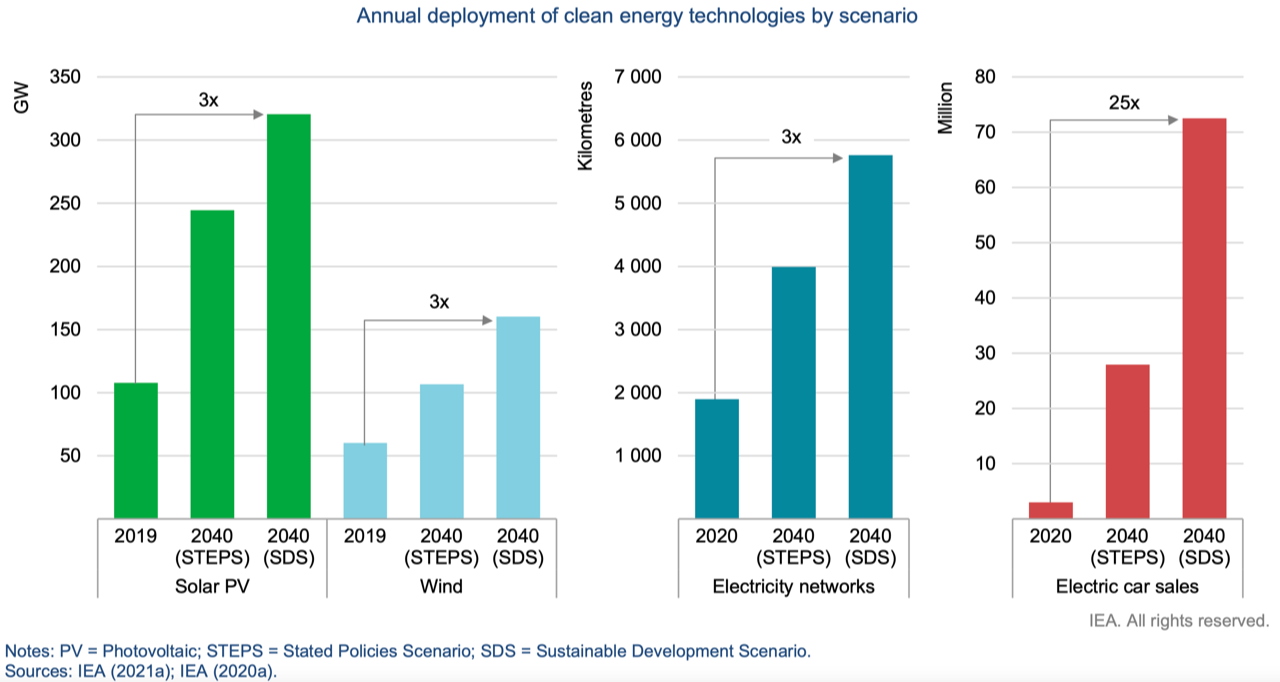

The Need for Unprecedented Volumes

With most countries adopting decarbonization by mid-century, the demand for new technologies is set to be overwhelming. Critical Minerals uses 2 basic scenarios: the Stated Policies Scenario (STEPS), which currently implies global warming of over 3 degrees Celsius, and the Sustainable Development Scenario (SDS), which aims to limit global warming to well below 2 degrees Celsius, and ideally to 1.5 degrees. The figure reveals that even under unambitious STEPS, solar deployment more than doubles between 2019 and 2040, with corresponding increases in wind, electricity networks and electric vehicles. But under the ideal of SDS, solar, wind, and electricity networks triple, while electric vehicles multiply an astounding 25 times.

Figure 2: Annual deployment of clean energy technologies by scenario

Source: IEA, 2021

The IEA concludes that the overall, undifferentiated demand for the 30-odd critical minerals essential to clean-energy technologies may increase by six-fold or more. Within that aggregate increase, depending on the 11 technological pathways used by Critical Minerals, individual materials confront varying demand profiles. For example, in utility scale storage under the SDS, between 2020 and 2040 nickel demand is projected to grow 140 times, cobalt by 70 times, and manganese by 58 times.

Markets and Mining

A neoclassical economist might argue that the prospect of such massive demand will – if we cut back state meddling – surely see market mechanisms deftly respond with capital allocation in more mining, greater efficiency, and substitution. Critical Materials concedes that history shows these market-driven responses do indeed happen, but add that the record reveals that relying on markets is “typically accompanied by price volatility, considerable times lags or some loss of performance or efficiency.” So the ramifications of waiting for market mechanisms to kick in will almost certainly be a more costly, delayed and inadequate decarbonization, particularly in difficult areas like steel, aviation, and agriculture.

If one accepts that global decarbonization is urgent, then it is imperative for robust policy to drive markets and other institutions towards that collective goal. After all, we did not wait for market mechanisms to produce vaccines against COVID.

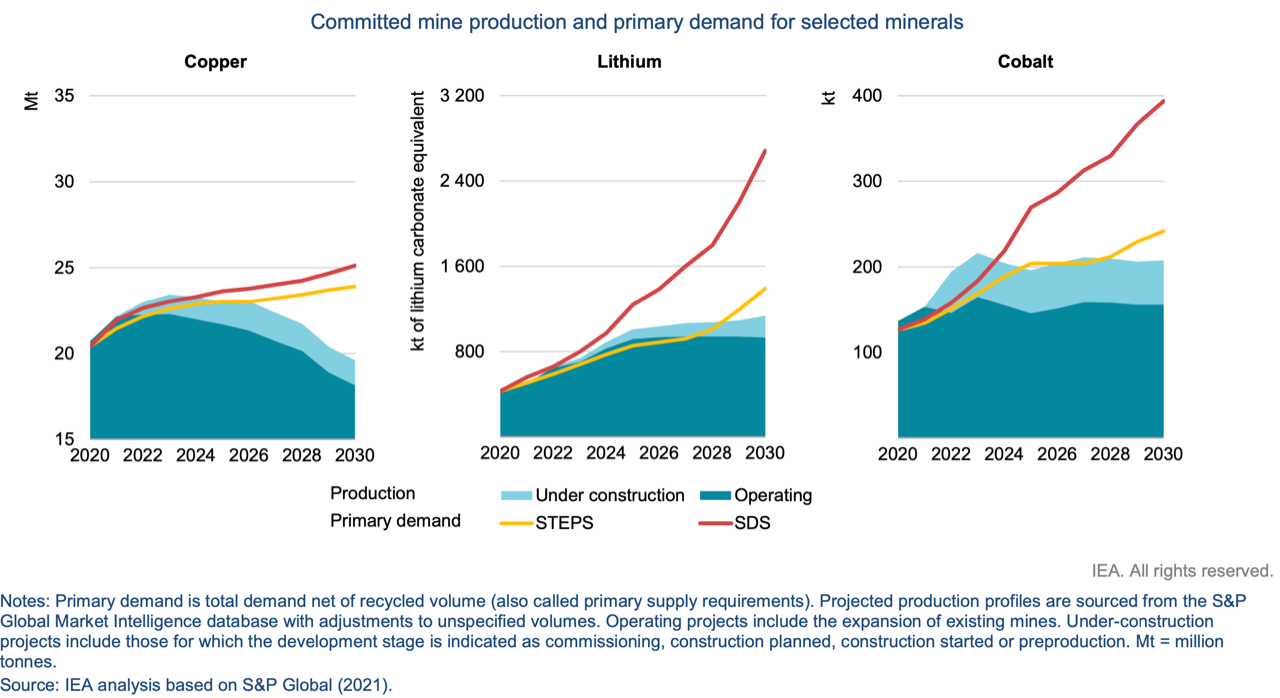

One proof of the IEA’s argument is seen in the data in figure 3. The figure shows the 2020-2030 clean-energy demand profiles for copper, lithium and cobalt under STEPS and SDS. Current and planned mining projects are clearly inadequate for these three materials alone, notwithstanding the enormous amount of attention they have received in recent years. Similar charts could be generated for graphite, nickel, rare earths, and the other critical minerals essential to energy transition.

Figure 3: Committed mine production and primary demand for selected minerals

Worse yet, securing more supply is not simply a matter of throwing more money at miners. One quandary here is the lengthy lead times for discovering, assessing and then developing mining projects. Critical Minerals highlights that between 2010-2019 the global average lead time – from discovery through to production – for the world’s top 35 critical mineral mining ventures was 16.5 years. The most blistering pace of projects the IEA identify is 4 years for a lithium mine in Australia. Even that speed seems plodding compared to figure 3’s exponential rate of increased lithium demand under SDS-decarbonization.

But it gets worse: the figure projects a massive supply gap for copper by 2030. Finding and developing copper mines takes well over a decade, and often closer to 2 decades.

The ESG Issues

Critical minerals are generally abundant, but the richest endowments and greatest ongoing exploitation are far more geographically concentrated than the fossil fuels we must displace. Many existing production sites have poor performance on governance, human rights, and other indicators, which puts them at loggerheads with the recent uptake of environment, social and governance (ESG) standards. And yet projects in the pipeline suggest that the geographical mix is very unlikely to change much over the next five years, according to the IEA.

There are no easy answers here. Child labor and other severe human rights concerns surrounding cobalt – 80% of which is mined in the Democratic Republic of the Congo – have led to global efforts to substitute for it. But as we saw in figure 3, the IEA anticipates clean-energy demand for the mineral to nearly quadruple between 2020 and 2030.

An additional matter of grave concern is that many critical minerals – particularly copper and lithium – are mined in areas with high water stress. Meanwhile, declining ore-grades for most critical minerals require more energy and water per unit of output.

Recycling and Substitution

Perhaps the most startling finding from Critical Minerals concerns the limits of recycling and substitution. Most work on energy transitions looks to recycling in “circular economy” strategies as the key means to reduce the need for newly mined copper, cobalt, rare earths and other metals and minerals. Substitution strategies complement this approach, by seeking new materials to replace the role of supply-constrained minerals used in batteries, solar panels, and the like.

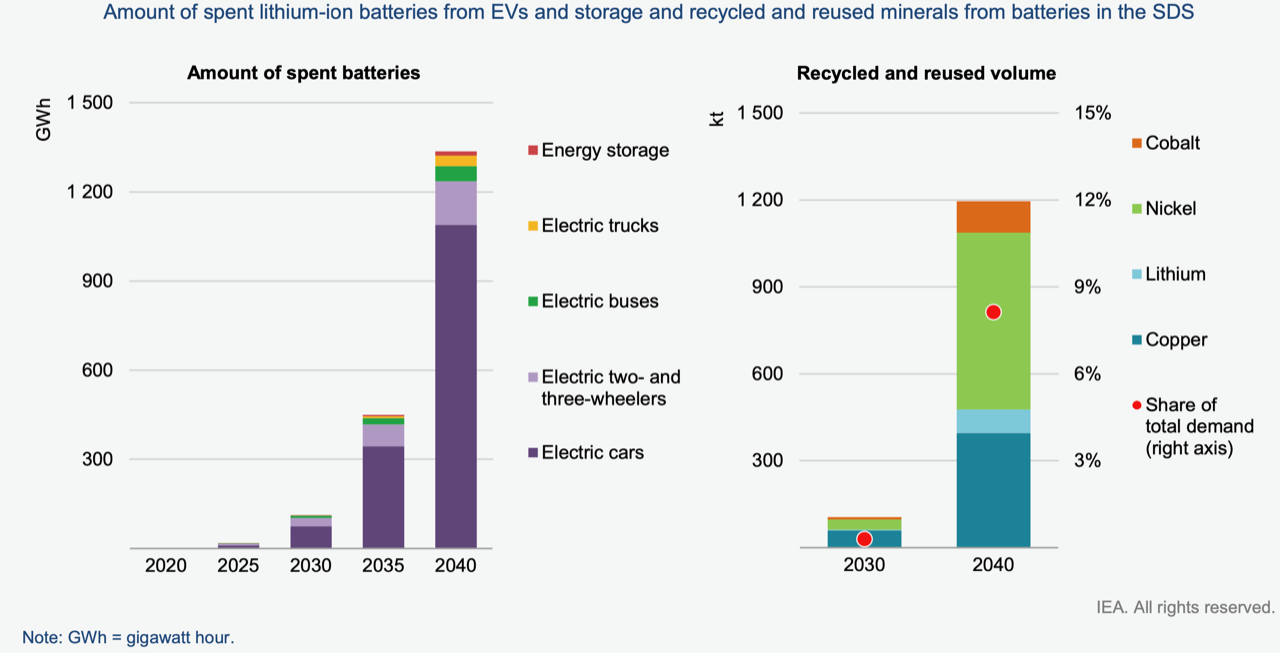

Recycling and substitution are key elements of Japan’s approach, with Panasonic’s 2170 lithium-ion batteries for Tesla, for example, cutting the proportion of problematic cobalt by increasing the share of nickel.

But figure 4 shows that the 2020 stock of spent lithium-ion batteries from cars and grid storage is negligible, meaning their recycling cannot meet any of the escalating SDS demand for battery storage. By 2030, recycled battery materials are at best a source of 1% of demand, and even as late as 2040, recycling provides only about 8% of demand.

Figure 4: Amount of spent lithium-ion batteries from EVs / storage / recycled / reused minerals from batteries in the SDS

Source: IEA, 2021

To be sure, Critical Minerals does not downplay the importance of recycling and substitution. On the contrary, the report spotlights recycling and substitution’s significant role in a broad, portfolio strategy of amplified investment, innovation, recycling, supply chain resilience and sustainability standards. Yet the upshot of the IEA analysis confounds the oft-repeated insistence that we can avoid hard choices by simply fostering the circular economy and harvesting the “urban mine” of discarded smart phones, appliances, and conventional cars.

To take a recent example, from 2017 Japan undertook a nationwide, 2-year project to collect and recycle about 80,000 tons of mobile phones and other e-waste, harvesting about 2 tons of copper for its Olympic medals. But in energy-transition terms, that collective effort secured only 1/4 the 8 tons of copper required for a single MW of offshore wind capacity.

What is to be Done?

So, while an intensive effort at recycling, substitution, and innovation is needed, Critical Minerals underscores the need for clear policy goals within decarbonization. Clear sectoral and technology targets are essential to reduce uncertainty and thereby alleviate the risks of critical minerals price volatility and other impediments to expanded supply.

In addition, the report stresses the need for a regime of ESG-compliant critical minerals, both to protect the environment and human wellbeing as well as to foster new supply. The latter aspect is a subtle way of saying that more diversified supply depends on reducing the dominance of producers whose ability to downplay ESG-related issues impedes the opportunity for cleaner, more community-engaged producers to enter the market.

A further recommendation is much stronger and integrated international governance. At present, a patchwork of international institutions and initiatives addresses various aspects of critical mineral mining and processing. But Critical Minerals details how these efforts, however laudable, are poorly coordinated and often lack adequate transparency. The IEA rightly suggests that its energy security framework for conventional fuels and their institutions could be of service.

And What is Japan Doing?

To its credit, Japan is already doing a few of the items that the IEA points to, and receives a degree of acknowledgement in the report. Japan does have comparatively good initiatives on critical mineral recycling and substitution. Since October 2011 Japan has played a role in the U.S.-Japan-EU Trilateral Workshop on Critical Raw Materials. Also, since 2013 Japanese specialists have been working with the U.S. Department of Energy’s Ames Institute on the “effective use of critical materials.” More recently, the March Quad summit between the U.S., Japan, Australia and India included attention to bolstering critical mineral supply chains.

As of March 2020, Japan instituted a New International Resource Strategy. This policy covers 34 critical minerals – referred to as “rare metals” – and includes increased and fine-tuned goals for stockpiling of emergency reserves and a greater ability for the state-controlled Japan Oil, Gas and Metals National Corporation (JOGMEC) to support private-sector mining and smelting initiatives. JOGMEC is also empowered to work with foreign firms in exploration activities.

After rare earth difficulties with China a decade ago, Japan reduced its dependence on that country to 58% by 2019. Japan also officially aims at 80% self-sufficiency (i.e., supply controlled by Japanese companies) by 2030 in base metals such as copper and nickel, and 50% in rare metals such as rare earths. And from 2028, Japan aims to undertake commercial exploitation of critical mineral resources on the seabed within its Exclusive Economic Zone.

And What is Japan Not Doing?

There is very little public debate or concern in Japan on this issue. As of this writing even Japan’s specialist media have paid scant attention to the IEA’s report. This curious lack of interest is consistent with Japan’s comparative inattention to the recent flood of critical-mineral scoping studies from G-20 governments, global think tanks like the Center for Strategic and International Studies, and credible private sector players like Benchmark Minerals and Goldman Sachs.

There has been plenty of domestic attention from media, academic and business to Suga’s commitment to a 46% cut in emissions by FY2030 from FY2013 levels, and to net-zero by 2050. No one has questioned how those targets will be met under the current base-metal and rare-metal supply scenarios even after Suga and Biden mentioned the need to bolster supply chains for critical and strategic minerals after their April 16 meeting.

Serious calculation of the mineral volumes required to meet Japan’s green ambitions has barely started in government. In March, METI released an outline draft of raw material components that Japan needs to meet its target of installing 10 GW of offshore wind capacity by 2030. The ministry noted that this portion of the Green Growth Strategy by itself would require about 10% of the copper and 20% of the niobium rare earth Japan consumed in 2018. The country’s offshore wind target for 2040 is 45 GW of capacity, but nobody seems to have down the math on critical minerals.

What Should Japan be Doing?

It is of prime importance that Japan’s decarbonization strategy – and the upcoming revision of the energy strategy, due this summer – include a Japan-based comprehensive critical minerals assessment. Even the METI calculation of copper requirements for offshore wind is derived from the IEA’s generalized data. But Japan’s offshore wind may be more material-intensive than average, due to its greater oceanic depths, further project distance from shore, and other factors such as high typhoon risk.

What’s more, Japan not only needs access to prodigious quantities of critical minerals, but also ESG-compliant materials. After all, another of prime minister Suga’s commitments is to bring lifecycle emissions from auto manufacturing and other industry to zero. That requires Japan to consider the emissions intensity of the minerals its imports for its auto plants. And, while Canada, Norway, Sweden and other countries are already moving to source “green” nickel, “green” copper and so on, this process has yet to begin in Japan.

Japan needs to put critical mineral-density at the heart of spatial planning for decarbonization while dramatically increasing support for new breakthrough developments in recycling and substitution. This can come in the form of policy recommendations for smart cities or more pointed actions that support less mineral-intense technology such as ultra-small EVs.

Here are five more outside-the-box ideas for Japan:

Join the new US-Canada-Australia “Earth MRI” (Earth Mapping Resource Initiative) alliance, which deploys the most advanced satellite, drone and other 3D mapping technologies to identify deposits of critical minerals and renewable energy resource potential;

Build on the recent Quad Summit and start working with India on exploring critical minerals (only 10% of India’s geology has been explored and both countries need abundant and secure supplies);

Accelerate seafloor mining of critical minerals (from current 2028 starting time) and show that deep-sea mining is potentially more ESG-compliant than terrestrial;

Push JOGMEC to collaborate with Canadian and other projects on mineralization to get more supply and help clean up the mining process, thus booking CO2 offsets under the Joint Crediting Mechanism;

Integrate mitigation and adaption strategies into decarbonization goals.

Reading the IEA’s disquieting work and taking appropriate action is a tall order. But being pro-active means creating opportunities as much as alleviating risks. Among other benefits, a broader portfolio of collaboration might help Japan balance its dependence on China for critical minerals, in addition to diversifying what Moody’s recently portrayed as the ongoing, nearly inescapable economic integration of Japan, China and South Korea.

Japanese policymakers need to find ways to finesse the critical mineral linchpin of the Asia’s difficult mix of industrial competition, national security, and climate mitigation-adaptation needs. Japan has a great opportunity to lead in the integrated spatial and functional planning to ensure equitable and sustainable deployment of critical minerals. Wasting the opportunity will leave Japan’s decarbonization plans (and its overall economy) dependent on actions elsewhere.

ANALYSIS

BY YURIY HUMBER

Japan’s Pathways to a 46% Emissions Reduction by End of Decade

Last month, Prime Minister Suga declared a 46% reduction in greenhouse gas (GHG) emissions by FY2030 compared to FY2013 levels. We look at what this means in practice.

According to PM Suga’s declaration, within nine years Japan needs to reduce greenhouse gas (GHG) emissions to about 800 million tons of CO2 equivalent. In FY2019, which ended March 31, 2020, Japan had annual emissions of 1.21 billion tons of CO2 equivalent. So, the country needs to cut emissions by 34% from current levels.

Japan’s Greenhouse Gas Emissions

| Year | Tons of CO2 equivalent |

| FY2013(April 1, 2013 – March 31, 2014) | 1.480 billion |

| FY2019(April 1, 2019 – March 31, 2020) | 1.212 billion |

| FY2030(April 1, 2030 – March 31, 2031) | 0.799 billion |

Source: Ministry of Environment

To achieve this, Japan needs to drastically restructure its energy sector, which emits 85% of total greenhouse gases (including methane and CFCs, etc.) and 93% of CO2. However, this can’t be done simply by shuttering coal plants and building more solar and wind farms. “Energy conversion” (which includes electricity generation and oil refining) accounted for only 433 million tons, or around 35.7% of Japan’s total emissions in FY2019.

Manufacturing contributed a further 279 million tons (23%), while transport emitted 199 million tons. Incidentally, transport’s CO2 footprint is almost unchanged since 1990. This is surprising since the current number of registered two and four-wheel vehicles totals 82.5 million units, compared to 58 million units three decades ago.

Unless Japan eliminates the entire CO2 output of its energy sector in nine years, which is impossible, it will have to use other means to meet the FY2030 numbers. We outline a few of those paths, as well as areas of potential reductions within the energy sector.

Main lines of attack / defense

Delivering the 2050 net-zero emissions pledge in October 2020, PM Suga hinted at the elements that will ultimately make up the country’s emission reduction strategy. These were:

1) energy conservation;

2) increased reliance on renewable energy;

3) continuation of the country’s nuclear policy;

4) phase out of coal-fired generation.

In practice, this could be translated as:

1) closing some capacity of high-emitting industries, especially in the steelmaking, oil refining, and cement-making industries;

2) creating a domestic offshore wind industry, promoting non-utility solar and a broader uptake of biomass;

3) restarting existing nuclear power plants and testing the waters for new construction;

4) transforming coal (and some gas) plants to burn ammonia / biomass / hydrogen.

In addition, Japan will seek to

5) switch its transport (autos, trains, ships, and aviation) to battery power / hydrogen fuel cells / synthetic fuels;

6) improve energy efficiency (especially utilization of waste heat) of buildings and non-power utilities;

7) buy carbon offsets at the company and country level.

Carbon offsets in particular may become a giant business, depending on what carbon pricing model the government adopts. That in turn is likely to be influenced by policy actions in the U.S, the EU, and China. In previous issues Japan NRG has covered Japan’s growing interest in getting more out of offset schemes such as the Joint Crediting Mechanism, J-Credits, and offsets for individual commodities such as LNG. We expect the scale and pricing of offsets to crystalize over the course of this year.

Shrinking Manufacturing

Sacrifices by Japan’s heavy industry are coming. The nation’s steelmakers accounted for 155 million tons of emissions in FY2019, three times as much as the next highest-emitting segment. Overall, steel mills contribute 40.2% of all manufacturing emissions, while their reduction of CO2 has been the smallest of all manufacturing sectors in the last 10-15 years.

Last year, Japan’s steel output dropped to its lowest volume in 50 years. While the reason was mainly the pandemic, the industry is said to carry 30% more capacity than is required for domestic needs, which leaves steel mills as the primary target for the government to curtail.

Nippon Steel reportedly plans to close four of its blast furnaces, cutting domestic capacity by 20% over several years. Japan’s largest steelmaker emitted 94 million tons of CO2 equivalent in FY2019, so its actions alone would reduce the emissions footprint of manufacturing by close to 7%. However, we expect Nippon Steel’s domestic peers to follow with cuts of at least on the same scale.

To compare, China has asked its steelmakers in major hubs, such as Tangshan, to curb output 30% to 50%, and is introducing measures to discourage steel exports.

Of course, steelmakers could try to preserve their output if they manage to switch production processes to hydrogen from coal. An experiment with hydrogen heat is taking place in Sweden, where Vattenfall, SSAB and LKAB started working on a pilot plant in 2017. However, the partners only expect full-scale fossil-free steelmaking to take place from 2035.

This indicates that the best option for Japan to meet its FY2030 target will be simply to reduce steel output. We expect an emissions reduction of around 40 million tons in steel.

Cement makers will likely be the second major target for capacity closures in Japan, as they produce around 3% to 4% of Japan’s CO2. The domestic industry is currently working with the technical and scientific community to refine new concrete production processes that promise both to recycle old concrete and capture the atmospheric CO2 released during manufacture.

Some optimistic estimates see a CO2 reduction of more than 60% from current levels, as well as a much lower use of energy in cement manufacture. Based on the idea of recycling old concrete, some even see a total emissions reduction of 20 million tons for the industry – by 2050.

However, with the new manufacturing processes yet to be commercialized, cement output will likely need to follow steelmakers and trim output first to deliver tangible results by FY2030. We expect the continued shrinking of the population, some materials substitution, and innovation to lower cement emissions by 8-10 million tons by the end of the decade.

Other sectors that will come under close scrutiny for emissions will be chemicals and machinery.

Lower Emissions in Transport

The sale of new gasoline cars in Japan will be banned from 2035. The Tokyo government said its deadline for the same is five years earlier, or 2030. Greater Tokyo accounts for a quarter of the country’s population and is the top market, which suggests domestic automakers will likely need to switch primarily to EVs and fuel cell cars as early as 2025/26.

METI estimates that 50% to 70% of autos sold in the country by 2030 will be emissions free. Assuming annual sales remain around 5 million units a year, an optimistic scenario would have 10% of the nation’s autos CO2-free in FY2030.

Other factors such as the rollout of MaaS and related services will reduce the number of vehicles on the road as more people choose to access cars on demand, rather than as regular owners.

Japan could also increase the ratio of biofuels in gasoline as a short-term solution to lower emissions.

Efforts to engineer trucks, trains, ships and airplanes that run on hydrogen, ammonia, or electric batteries is also under way. The commercialization of transport that does not use fossil fuels, however, is seen as unlikely before the end of this decade.

Taking all factors into consideration, an optimistic scenario will see transport emissions drop by 10%, or around 20 million tons of CO2 equivalent, by FY2030.

Changing the Fuel Mix

Overall, we expect manufacturing curtailments and the start of a shift away from fossil fuels in transport, as well as broader energy saving across the economy, to deliver a saving of up to 100 million tons of CO2 equivalent by FY2030. This suggests that the rest of the 400 million tons in cuts that Japan needs to make will come from the energy industry and carbon offsets.

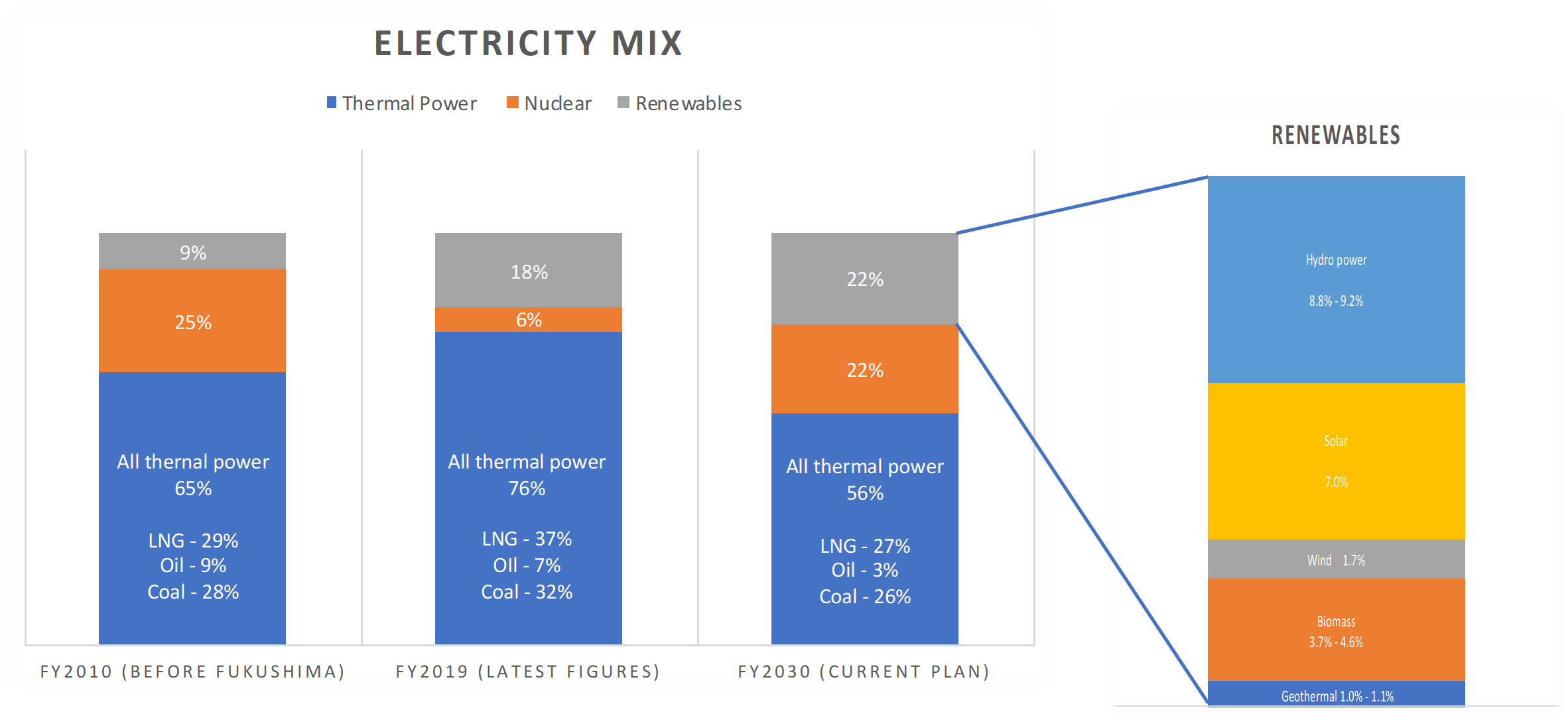

This is how the electricity mix looks today and according to the current FY2030 target.

The FY2030 composition will be changed in the new basic energy policy that Japan plans to publish this summer. An early draft of what it might look like was featured last month in the newspaper, Nikkei:

1) Renewables increased to 30%-40% of mix

2) Nuclear unchanged at 20%

3) Hydrogen/ammonia at least 1% (a new addition)

4) Fossil fuels lowered to 40%

In the last year, the share of renewables in electricity output has risen to about 23%. To add another 10 percentage points by FY2030, solar industry association ASPEn believes Japan needs to add 45 GW of solar capacity in the next 10 years.

The government has also outlined plans to add 10 GW of offshore wind by FY2030.

However, rather than simply adding capacity, the power industry will need to work on storage and grid management to improve the utilization rates of renewables.

Meanwhile, the hydrogen/ammonia component is likely to be higher than 1%. The latest hydrogen roadmap drafted by a METI panel published last month shows hydrogen-only firing generation will be at the commercial stage only from FY2031. However, hydrogen as second fuel at a thermal plant, in a co-firing capacity, will be tested and ready for mass rollout by FY2026.

A very optimistic view of the energy sector’s emissions based on the above and expected revisions to the electricity mix would see CO2 levels drop as much as 50% by FY2030. Add to this the forecast shuttering of 20% to 30% of Japan’s oil refining capacity, and the country may succeed in a saving of 200 million tons of CO2 equivalent.

This would still leave about 100 million tons in CO2 equivalent unaccounted for.

Carbon offsets: Big Opportunities

In the April 12 edition of Japan NRG, we described how Japan is ramping up the number of projects it certifies via the Joint Crediting Mechanism (JCM). To date, the country can count on 17.9 million tons of credits from JCM alone and the government hopes that could rise to as much as 100 million tons of CO2 equivalent by 2030.

While the JCM target from the government is highly optimistic, it highlights just how much Japan’s hopes for FY2030 will rest on offset mechanisms. Schemes such as JCM allow Japan to make bigger cuts to global emissions than it might achieve through incremental energy savings at home, while also being cheaper and protecting domestic manufacturing jobs.

Conclusion

While many of our estimates are very rough calculations, they indicate the scale of what could be possible (and what is unrealistic), as well as mapping the potential routes for the decarbonization strategy.

We expect every industry to fight for its share of the carbon budget, while privately pouring major resources into finding technological, operational, or financial solutions to lower its environmental footprint.

PM Suga has set a very ambitious emissions reduction target for Japan. Whether the country meets it exactly is uncertain, yet the process of getting there should act as a boost for Japan’s overall economic competitiveness.

EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy.

| February | Approval of Fiscal 2021 Budget by Japanese parliament including energy funding projects;CMC LNG Conference |

| March | 10th Anniversary of Fukushima Nuclear Accident;Smart Energy Week – Tokyo;

Quarterly OPEC Meeting; Japan LPG Annual Conference; Full completion of all aspects of the multi-year deregulation of Japan’s electricity market; End of 2020/21 Fiscal Year in Japan; |

| April | Japan Atomic Industrial Forum – Annual Nuclear Power Conference;38th ASEAN Annual Conference-Brunei;

Japan LNG & Gas Virtual Summit (DMG)-Tokyo Three crucial by-elections in Hokkaido, Nagano & Hiroshima – April 25th |

| May | Bids close in first tender for commercial offshore wind projects in Japan;Prime Minister Suga to visit the U.S.-tentative |

| June | Release of New Japan National Basic Energy Plan-2021;G7 Meeting – U.K.

Forum for China-Africa Cooperation Summit (Senegal) |

| July | Tokyo Metropolitan Govt. Assembly Elections;Commencement of 2020 Tokyo Olympics |

| August | Hydrogen Ministerial Conference in conjunction with IEA World Economic Forum in Singapore – Deferred from May |

| September | Ruling LDP Presidential Election;UN General Assembly Annual Meeting that is expected to address energy/climate challenges;

IMF/World Bank Annual Meetings (multilateral and central banks expected to take further action on emissions disclosures and lending to fossil fuel projects); End of H1 FY2021 Fiscal Year in Japan; Japan-Russia: Eastern Economic Forum (Vladivostok)-tentative |

| October | Last possible month for holding Japan’s 2021 General Election;METI Sponsored LNG Producer/Consumer Conference;

Innovation for Cool Earth Forum – Tokyo Conference; Task Force on Climate-Related Financial Disclosure (TCFD) – Tokyo Conference; G20 Meeting-Italy |

| November | COP26 (Glasgow);Asian Development Bank (‘ADB’) Annual Conference;

Japan-Canada Energy Forum; East Asia Summit (EAS) – Brunei |

| December | Asia Pacific Economic Cooperation (APEC) Forum – New Zealand;Final details expected from METI on proposed unbundling of natural gas pipeline network scheduled for 2022. |

DATA

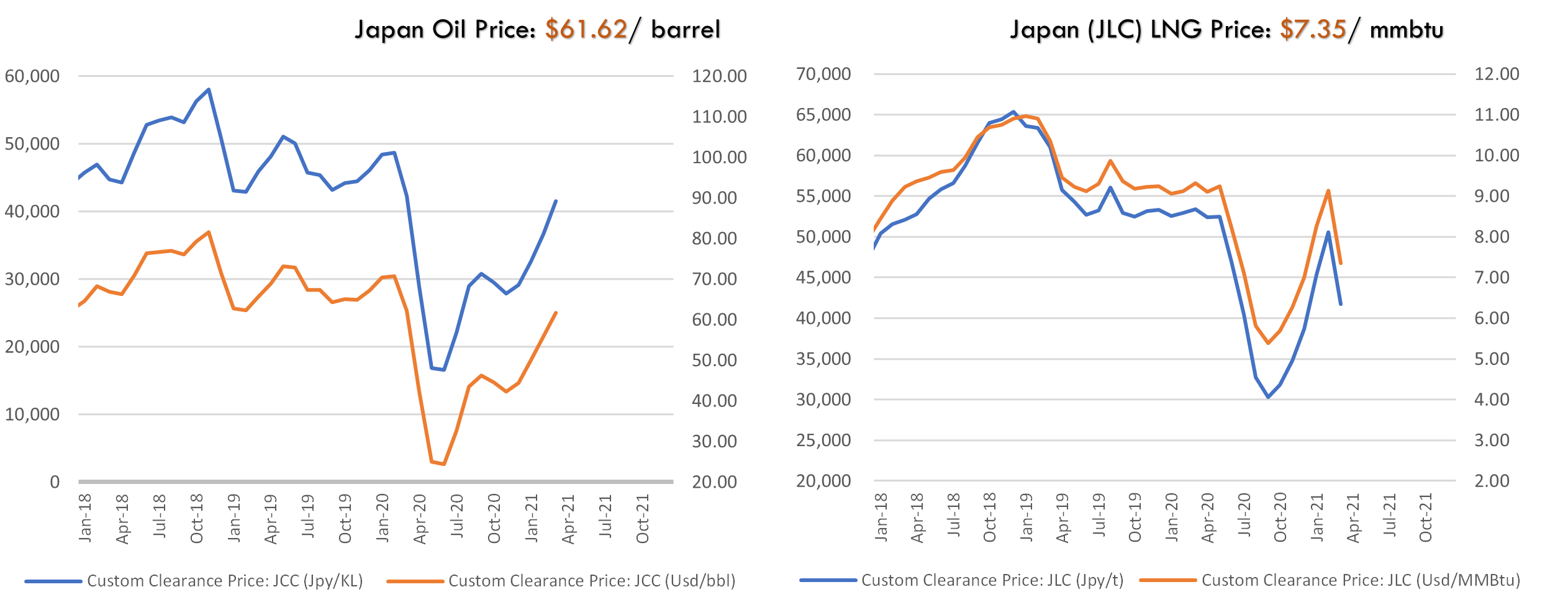

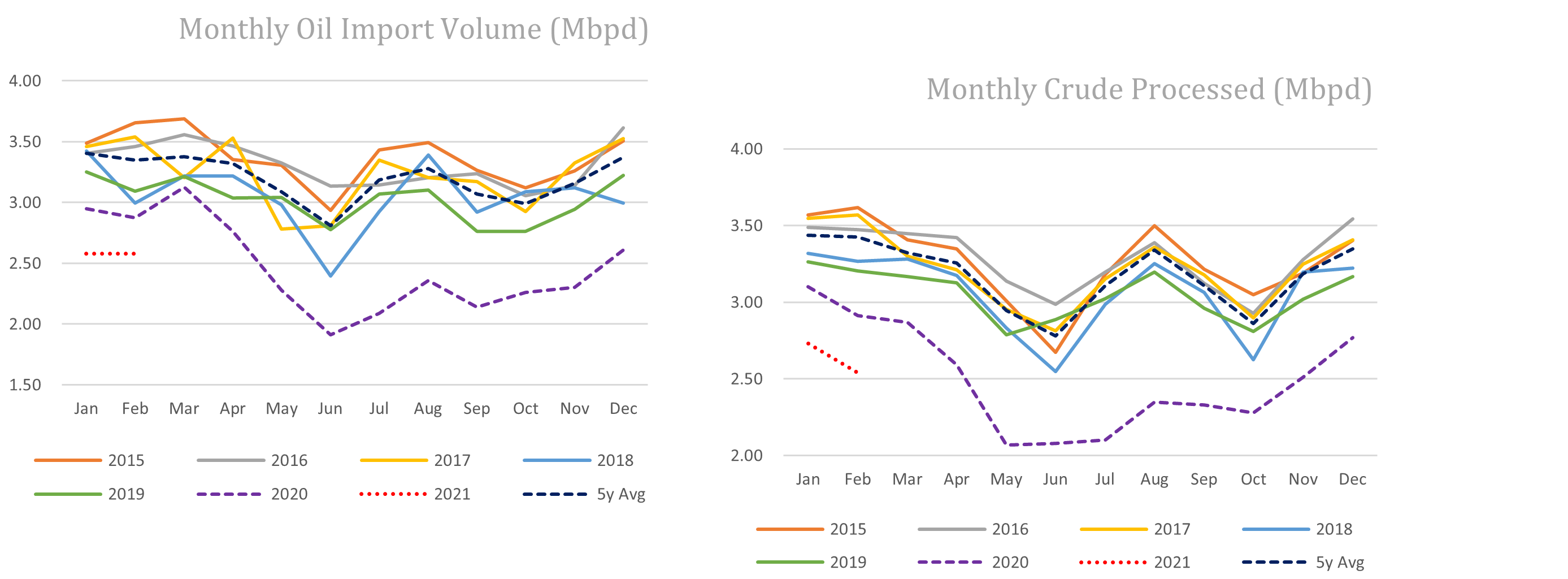

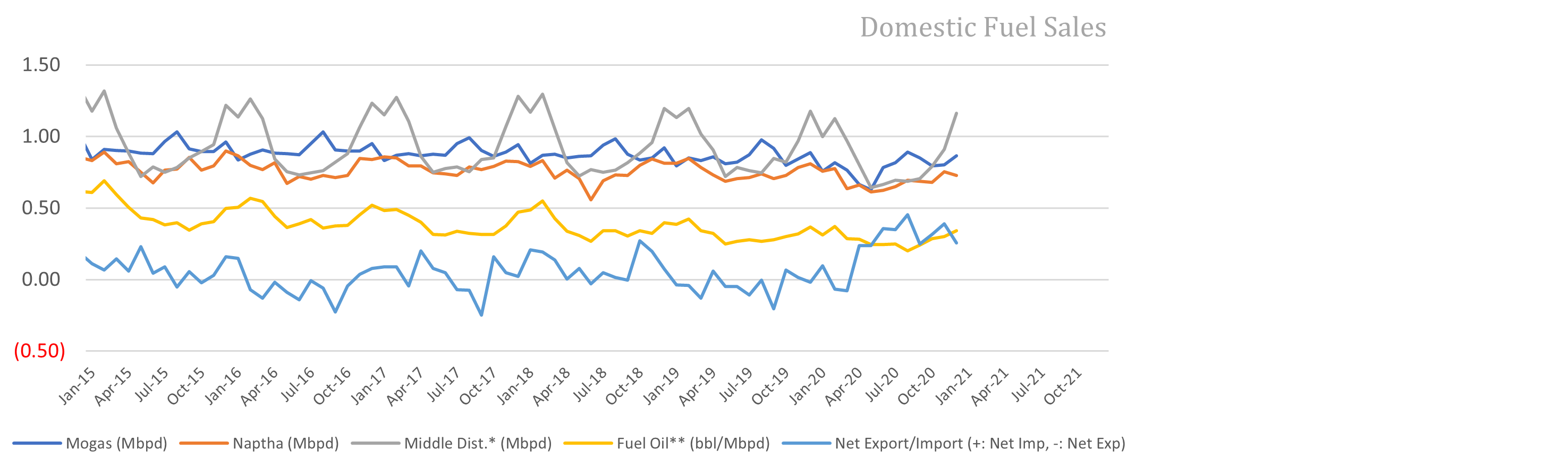

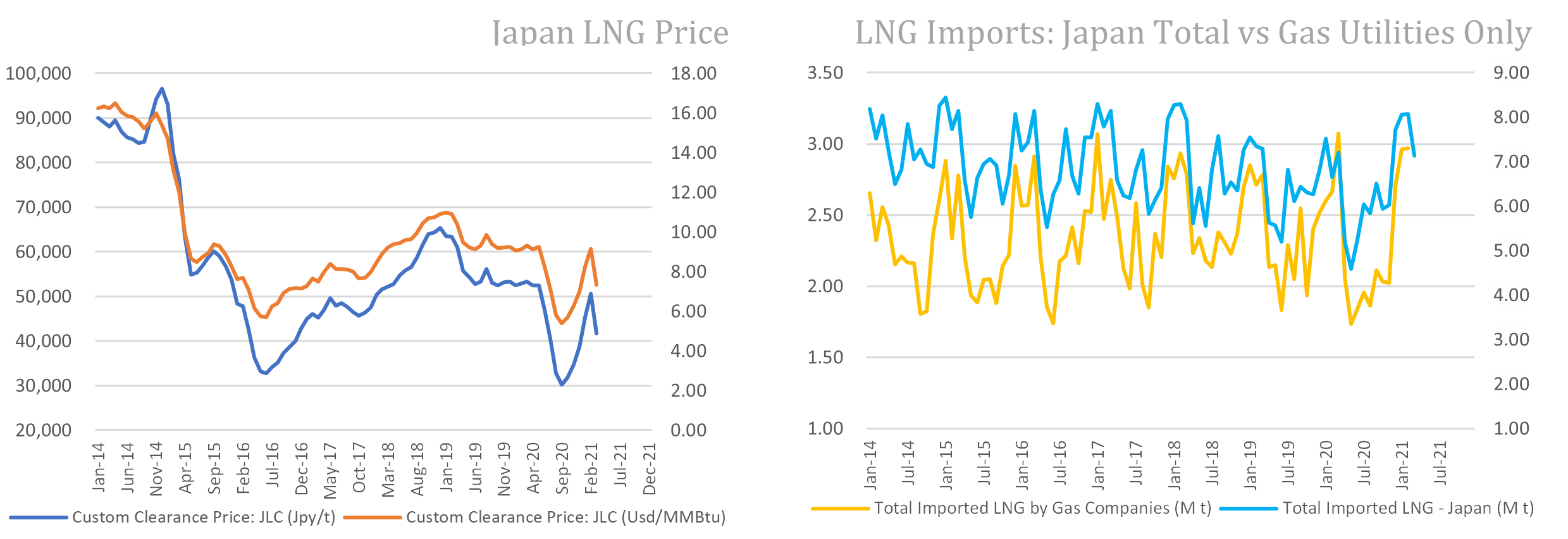

SOURCES: Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

SOURCES: Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

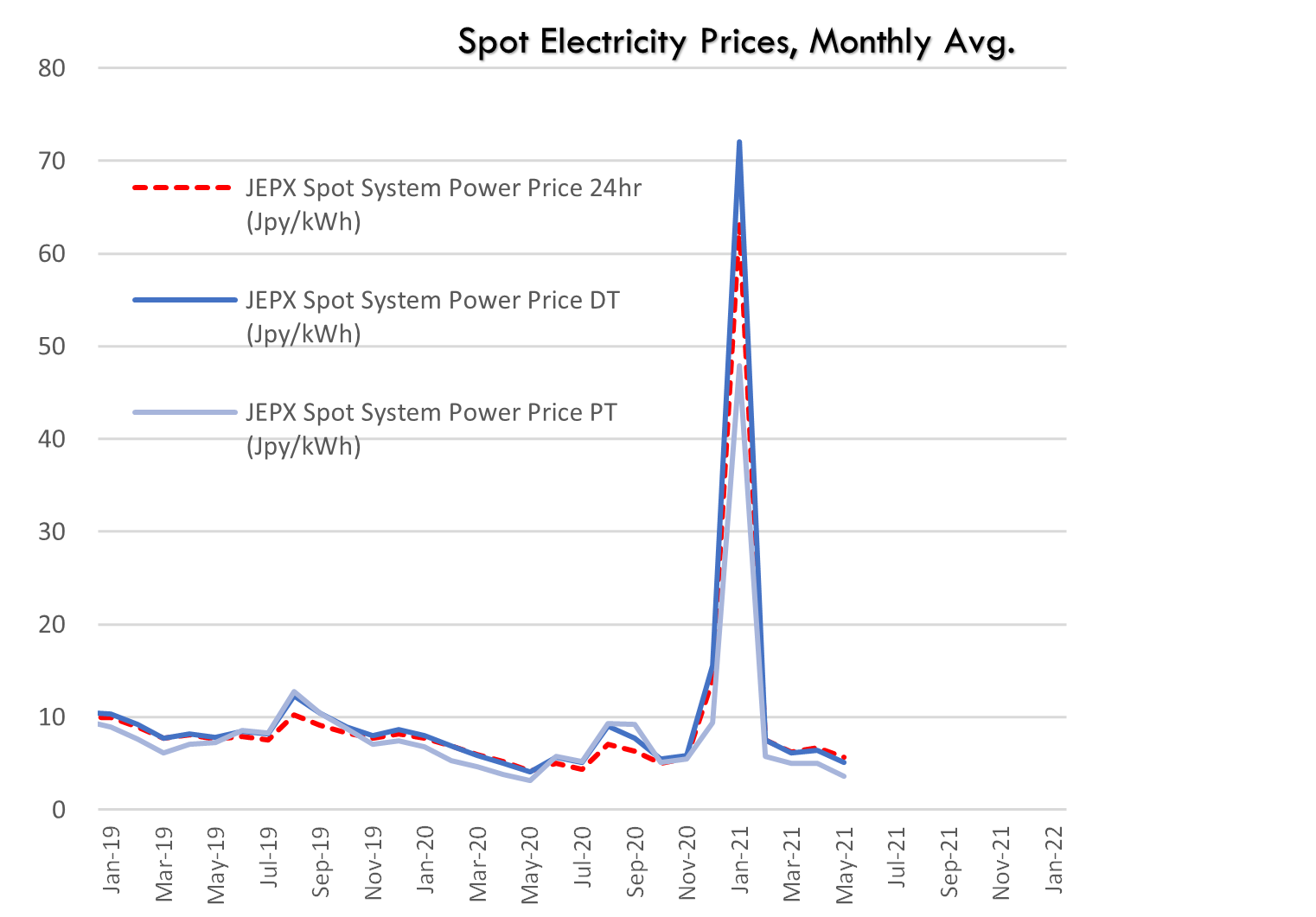

SOURCES: Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.