JAPAN NRG WEEKLY

AUGUST 2, 2021

JAPAN NRG WEEKLY

August 2, 2021

NEWS

TOP

- Group unveils plans for Japan’s biggest green hydrogen plant; offshore wind as power source; manufacture to start by 2024?

- Japan moves up timeline for cutting hydrogen costs, introduction of other decarbonization technologies by a decade

- Regulator calls out J-Atomic for allegedly rewriting data; officials say Tsuruga NPP No. 2 data affected, may spawn a broader probe

ENERGY TRANSITION & POLICY

- Study of undersea cables for offshore wind due by March 2022

- METI task force sets 2030 storage battery development goals

- Japan firms to begin commercial jet biofuel production in 2025

- Solar panels to be fitted to at least 60% of new houses by 2030

- METI to expand energy efficiency benchmarks to auto makers

- Tokyo govt. says 50% of city’s power will be renewable by 2030

- Mitsubishi buys into Australian carbon emissions trading market

- Japan tests ammonia supply chains in Russia, Australia, and UAE

- Nippon Paper to invest in Brazilian wood chips on tight supply

- Kawasaki Heavy trials gas-solar-battery hybrid generation system

- Oil-producing plankton discovered in Arctic Ocean … [MORE]

ELECTRICITY MARKETS

- Residents go to court to challenge operation of coal-fired plants

- Tohoku Electric picks partners for rooftop solar and storage offer

- METI offers mark to renewables projects that support local region

- TEPCO submits ¥3T plan for decarbonization via wind, nuclear

- JFE Engineering to set up wind turbine monopiles manufacture

- Western Tokyo leads the way in proving worth of VPP initiative

- Canadian Solar reveals details of recent tender wins … [MORE]

OIL, GAS & MINING

- ENEOS to boost polyethylene output to meet renewables demand

- Toho Gas, Keiyo Gas and Osaka Gas start supplying carbon-neutral LNG to industrial clients in their respective regions

- TOCOM to launch yen-denominated LNG futures in 1Q of 2023

ANALYSIS

JAPAN’S NEW BASIC ENERGY PLAN DRAFT: A SPRINGBOARD TO A MORE VIABLE ROADMAP?

Japan policymakers have unveiled a draft version of the Sixth Basic Energy Plan. Like previous iterations of the triennial planning initiative, the goals are both comprehensive and controversial. Unlike previous versions, this draft’s ambitions are crafted as much to address international decarbonization commitments as to appease domestic advocacy coalitions. The problem is that, as it stands, the Plan cannot deliver on its main goal: decarbonization. Could it pave the way to a more credible roadmap?

SOLAR’S WILD WEST ERA ENDS AS INDUSTRY

STANDS ON THE VERGE OF ITS 2.0 REVAMP

The era of cowboys in Japan solar is over. The rich Feed-in Tariff (FIT) that opened the country to a solar PV boom from 2012 attracted a hotchpotch crowd. Some simply monetized their earlier land-grab via FIT without much knowledge or interest in energy. Some used solar farms as a tax write-off. A few did little more than flash their business card to secure financing and pick up a tidy fee. Since the initial tariff dropped by 75% over a decade, that era has closed. The next one is just emerging, and the kind of companies that will compete – can compete – in a Japan where solar is heading to ¥8/ kWh will be quite different. Solar 2.0 will feature a different kind of industry player.

GLOBAL VIEW

The U.S. edges towards approving Biden’s $1.2T infrastructure bill. G20 ministers agree to limit global warming but not coal use. M&A in U.S. shale jumps. U.S. faces jet fuel shortages. China commits to circular economy for EV batteries. Singapore to build one of world’s largest solar farms. U.K. seeks to remove China from nuclear power project.

Details on these and more in our global wrap.

EVENT CALENDAR / DATA SECTION

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

Tom O’Sullivan (Japan, Middle East, Africa)

John Varoli (Americas)

Sponsored

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Offshore wind project to power Japan’s biggest green hydrogen plant

(Asia Nikkei, Company Statements, July 27-28)

- As early as the fiscal year ending March 2024, Japan plans to begin operation of its largest hydrogen plant powered by offshore wind. The plant will manufacture about 550 tons of hydrogen a year, enough to fuel more than 10,000 hydrogen vehicles.

- The facility will be based on the coastal city of Ishikari, Hokkaido, and powered by a 110 MW wind farm. The locality already provides almost 2,000 tons of hydrogen a year.

- Participating in the project are Hokkaido Electric, renewable energy developer Green Power Investment, Nippon Steel Engineering, industrial gas supplier Air Water, an ICT and energy engineering unit of Kyocera, and Imoto Lines, a domestic shipping firm.

- The project envisions selling the hydrogen in Hokkaido and also shipping it to other parts of the country.

- The key to making the project a success will be lowering the cost of green hydrogen production, which in Japan is double that of the EU and three times that of the U.S.

- Hokkaido Electric will study / work on implementing the project from August 2021 through February 2023.

TAKEAWAY: This is not only the biggest but also one of only a few green hydrogen projects announced in Japan. The scale is bigger than a pilot, but smaller than a typical commercial-scale venture, which makes sense in that the project is trying to create a market rather than fill an immediate need.

There are several points of interest. One is that pairing hydrogen with offshore wind in Hokkaido is one way to solve the mismatch between where Japan has lots of offshore wind potential but low electricity demand (compared with the central Kanto area). The transmission of power from offshore Hokkaido to Kanto would be an expensive exercise that involves building almost a whole new grid system that would need to stretch about 1,000 km. Using the power locally to make hydrogen partially alleviates wind power’s intermittency and allows the energy to be carried to peak demand areas in a more flexible manner. This makes the project’s distribution part potentially the most important phase.

Another curiosity is the parties involved. Hokkaido Electric, as the local utility, is an obvious choice. Air Water’s hydrogen expertise makes sense. The presence of Nippon Steel, however, indicates that the hydrogen may eventually go to the company’s furnaces, something that needs to happen as the steelmaking giant moves away from burning coal.

Finally, a major question is how this offshore wind farm will be green-lighted. So far, the government said that all offshore wind projects must enter auctions. Only four auctions have taken place so far and results are yet to be announced for three. At the current pace it’s hard to imagine how an offshore wind project in Japan could receive government approval, complete all the environmental assessments, win local community approval, and be built in time to start operations by March 2024. That means either a new fast lane for green hydrogen projects will be created, or this project’s timelines are wildly optimistic.

METI moves up timeline for cutting hydrogen cost, other decarbonization technologies

(Japan NRG, July 26)

- Japan updated its Carbon Recycling Technology Development Roadmap, moving up target timelines to implement decarbonization technologies.

- Japan’s timeline for cutting hydrogen retail cost to ¥20/ nm3 and eliminating sales of gasoline-fueled cars was expedited to the 2040’s from 2050’s. The 2030 near-term targets are unchanged.

- METI also added to the Roadmap new technologies such as DAC (direct air capture) and synthetic fuel made from CO2 and hydrogen. International partnerships, such as with the U.S., Australia and the United Arab Emirates, were also included for the first time.

Underwater power transmission network studies due by March 2022

(Japan NRG, July 29)

- Feasibility studies for the 8 GW high-voltage direct current (HVDC) submarine cable power transmission network connecting Hokkaido and the main island of Japan (Honshu) will be completed by March 2022, the Agency for Natural Resources and Energy said.

- The studies will identify potential cable routes and costs. There are two possible routes, via the Sea of Japan and via the Pacific Ocean.

- In addition to narrowing down the cost estimate, initially seen between ¥1.5 – ¥2.2 trillion, the studies will look into efficient cable and equipment production systems, issues related to property rights and financing of the project.

Green Innovation Task Force sets 2030 storage battery development goals

(Japan NRG, July 30)

- The Green Innovation Task Force under the METI Industrial Structure Council has set storage battery development goals for 2030. The group has set numerical performance targets for vehicle storage batteries at 700-800 Wh/L per pack, or 2,000-2,500 W/kg or 200-300 Wh/pack depending on the battery type.

- Price targets were not set as they depend on the material used.

- Recycling goals for critical raw materials were also set. Target lithium recovery rate from spent batteries was set at 70%, and nickel and cobalt at 95%. Motor manufacturers should aim for 85% performance efficiencies, the group said.

Japan firms to begin commercial jet biofuel production in 2025

(Nikkei, July 30)

- Engineering firm JGC Holdings and oil refining major Cosmo plan to become the first to make commercial jet biofuel in Japan, starting production in Osaka in 2025.

- Biofuel is also known as sustainable aviation fuel (SAF) and is made from waste plastics or biomass such as algae and wood chips. SAF does not reduce emissions to zero, but is widely adopted in Europe and elsewhere.

- JGC and Cosmo will use waste cooking oil from restaurants and food factories. The two are investing billions of yen to build a factory at Cosmo’s oil plant in Osaka’s Sakai City to produce up to 30,000 kiloliters of jet biofuel per year. NEDO will provide subsidies.

- Top domestic airlines Japan Airlines and All Nippon Airways have both already started using SAF, and hope to boost orders going further to meet net zero goals.

- Eventually, JGC and Cosmo aim to supply 30% of Japan’s domestic needs in biofuel. The government estimates the total domestic market to reach 5.6 million kiloliters in 2030.

TAKEAWAY: Apart from being at least double the price, SAF’s lack of supply has been one of the biggest constraints for its wider use in Japan. At a recent webinar held by the Brazil embassy in Japan, METI officials spoke of their desire for biofuels to make a significant impact in decarbonizing Japanese aviation.

Solar panels to be fitted to 60% of new houses by 2030

(Nikkei, July 27)

- The govt. is discussing a goal of 60% of new houses to have solar panels on roofs by 2030.

- METI says that while solar panels are fitted to nearly 50% of houses built by major construction companies, smaller construction companies generally do not fit solar panels.

- METI wants to see major construction companies fitting solar panels to 90% of new builds, and smaller construction companies fitting panels to at least half of new builds.

METI to expand energy conservation benchmarks to car manufacturing

(Japan NRG, July 30)

- METI will expand energy conservation benchmark systems applied to steel, chemical, ceramics and retail sectors, to less energy-intensive sectors including car manufacturing.

- The system identifies energy conservation goals and requires companies to report energy consumption levels. In addition to 26 car manufacturing plants, semiconductor chip makers, gas compressors and LPG makers, plastics makers, synthetic fiber makers and aluminum rolling mills and alloy makers are sectors that will come under the benchmark system.

METI and the Ministry of Environment jointly approach global warning, on paper

(Japan NRG, July 26)

- While METI and MoE sometimes clash on coal-fired power and carbon tax policies, they co-published a report on global warming approaches. METI’s Industry Structure Council and MoE’s Central Environment Council authored it.

- The paper stressed that carbon cuts will primarily be driven by voluntary engagements, adding that Japan was successful in cutting CO2 by 10.9% over the 2013 to 2019 period without regulatory enforcement. Periodical government reviews of sectoral reduction programs will endorse the cuts.

- In Japan, 114 business sectors already report decarbonization programs. The govt. hopes to expand the program to SMEs.

- Carbon pricing schemes should propel economic growth while cutting carbon. There are pros and cons to carbon taxes and the government will pursue more discussions, seeking to strike a balance with other forms of energy taxes and the Feed-in Tariff program.

Tokyo government says 50% of city’s power will come from renewables by 2030

(Kankyo Business, July 21)

- The Tokyo Metropolitan government pledged to halve the prefecture’s greenhouse gas emissions by 2030 as part of an important milestone towards carbon neutrality.

- The new target is outlined in a recent update to the government’s zero emission strategy.

- By 2030, the government also aims to:

- source 50% of electricity from renewable sources

- cut Tokyo’s total energy consumption by 50% (against 2000 levels)

- have 1.3 GW of solar generation capacity in place across the prefecture

- source 100% of electricity used by government buildings from renewables

- require all new cars and trucks to be hybrid or electric

- require 50% of all new cars to be zero-emission

- install 1 million domestic storage batteries

- install 3 MW of industrial and commercial fuel cells

- deploy 300 zero emission buses

- build 150 hydrogen filling stations.

- Hydrogen plays an important role in the strategy, which includes new subsidies for fuel cell vehicles and measures to encourage the creation of a hydrogen supply chain.

Mitsubishi Corp buys into Australia’s carbon emissions trading market

(Asia Nikkei, July 29)

- Trading house Mitsubishi Corp. will enter Australia’s carbon emissions trading market after buying a 40% stake in Australian Integrated Carbon (AIC) for an undisclosed sum, becoming the top shareholder.

- AIC helps livestock farmers turn grazing land back into native forests, showing them how to regrow native vegetation lost due to deforestation. Regrowth of native vegetation requires less expense than revegetation.

- AIC uses satellite image analysis to estimate carbon absorption volumes. The volume of CO2 displaced has to be approved by the Australian government before credits are issued.

- Australia formed a scheme for purchasing carbon credits in 2015. Credits worth 16 million tons of emissions are traded yearly, with projects protecting plants accounting for 80%.

- Mitsubishi aims to tap AI Carbon’s know-how and launch a similar service in North America.

Ammonia supply chains tested in Russia, Australia and Abu Dhabi

(New Energy Business News, Various, July 29)

- Japanese firms are looking through plans to construct ammonia supply chains in at least three locations around the world.

- INPEX and JERA, as well as state-backed JOGMEC, are working with the Abu Dhabi National Oil Co. to conduct a feasibility study for a clean ammonia production project in the United Arab Emirates (UAE).

- Marubeni, Hokuriku Electric and Kansai Electric are working with Woodside Energy of Australia, and again JOGMEC, to jointly conduct a commercialization survey on the construction of a clean-ammonia supply chain from Australia to Japan. This project would include carbon capture of CO2 from gas-based ammonia production and tree planting measures to reduce environmental impact.

- Meanwhile, Itochu and Toyo Engineering have embarked on the second phase of a project led by Russia’s Irkutsk Oil Co. and JOGMEC to establish another “blue ammonia” value chain from eastern Siberia to Japan. The parties will produce a master plan that includes conceptual designs for the plant that will synthesize hydrogen and ammonia from natural gas sourced from Irkutsk’s East Siberian oil wells.

- CONTEXT: All three projects focus on blue ammonia and how to utilize the captured CO2 for enhanced oil recovery.

Nippon Paper to invest in Brazilian wood chips

(New Energy Business News, July 26)

- Nippon Paper is heavily reliant on imported wood chips. Supply is likely to become constrained in the future for conservation reasons, and this has prompted the manufacturer to invest in Brazilian feedstock.

- By purchasing an additional 10,000 ha of eucalyptus forest in Brazil, Nippon Paper will increase its annual dry woodchip supply by up to 700,000 tons.

- Japan Bank for International Cooperation is financing the.investment.

Iwatani and KEPCO selected to develop fuel cell technology

(Kankyo Business, July 27)

- A group comprising KEPCO, Iwatani, the Tokyo University of Marine Science and Technology, and shipbuilder Namura has been commissioned by government-backed New Energy and Industrial Technology Development Organization (NEDO) to research ways of overcoming some of the challenges that currently beset fuel cell technology.

- The project will run until 2025.

Kawasaki Heavy Industries trials gas-solar hybrid generation system

(Kankyo Business, July 21)

- Kawasaki Heavy Industries is trialing a hybrid generation system to provide electricity at its Akashi factory.

- The system comprises 5 kW of photovoltaic cells, a 1,800 kW gas turbine, and 35 kWh of storage batteries, and is able to switch automatically between power sources without interrupting the supply.

Researchers discover petrol-producing plankton

(NHK, July 26)

- In a world first, researchers from the Japan Agency for Marine-Earth Science and Technology discovered a variety of plankton in the Arctic Ocean that synthesizes chemicals found in gasoline.

- Researchers initially assumed the samples had been contaminated by oil, and they only realised after repeated testing that the petroleum compounds observed had been synthesised by the plankton themselves.

Grants for development of zero emissions technology, automated ships

(Kankyo Business, July 28)

- METI is offering grants to shipbuilders to develop zero emission power plants, autopilot systems and other innovations.

- Daihatsu diesel and Mitsui E&S Machinery were selected to develop zero emissions engine technology.

- Also, a subsidiary of NYK was selected to develop an autopilot system for testing on ships.

NEWS: POWER MARKETS

| No. of operable nuclear reactors | 33 | |

| of which | applied for restart | 25 |

| approved by regulator | 17 | |

| restarted | 10 | |

| in operation today | 9 | |

| able to use MOX fuel | 4 | |

| No. of nuclear reactors under construction | 3 | |

| No. of reactors slated for decommissioning | 27 | |

| of which | completed work | 1 |

| started process | 4 | |

| yet to start / not known | 22 | |

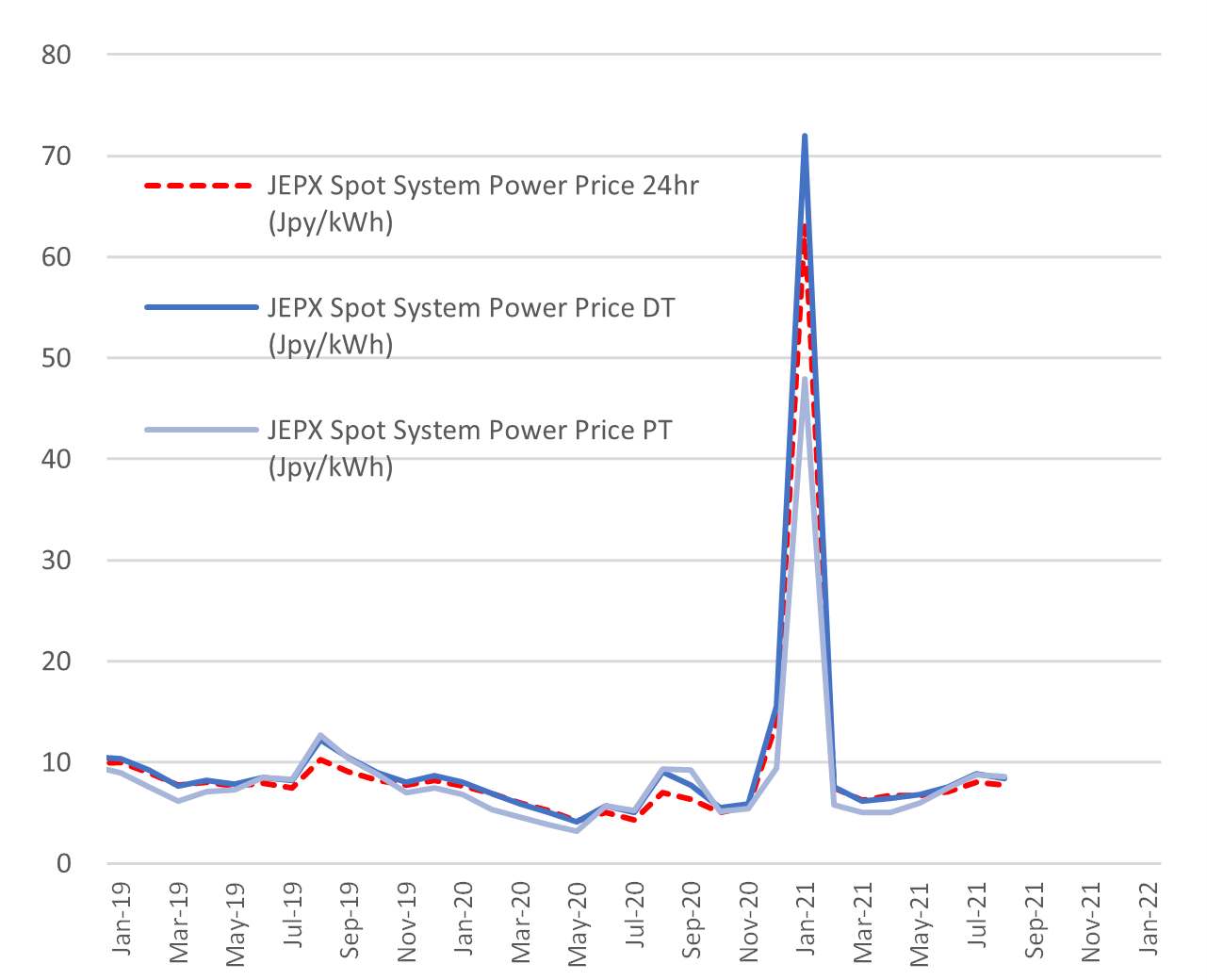

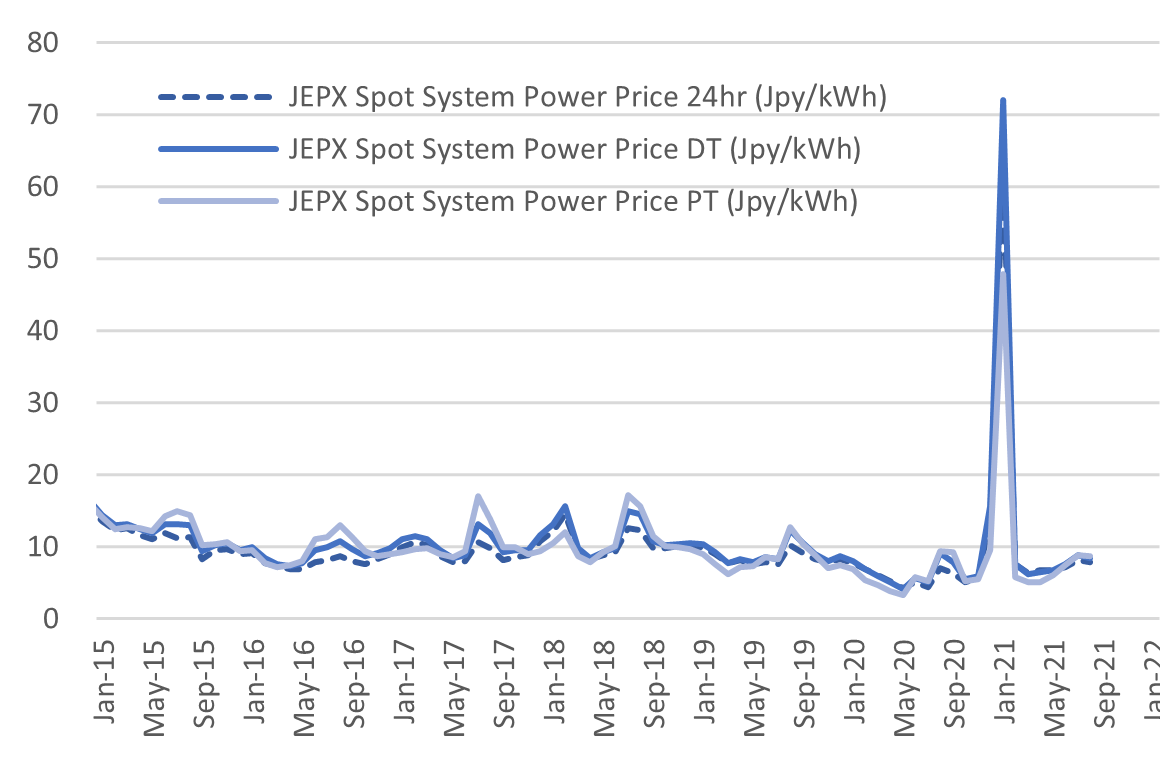

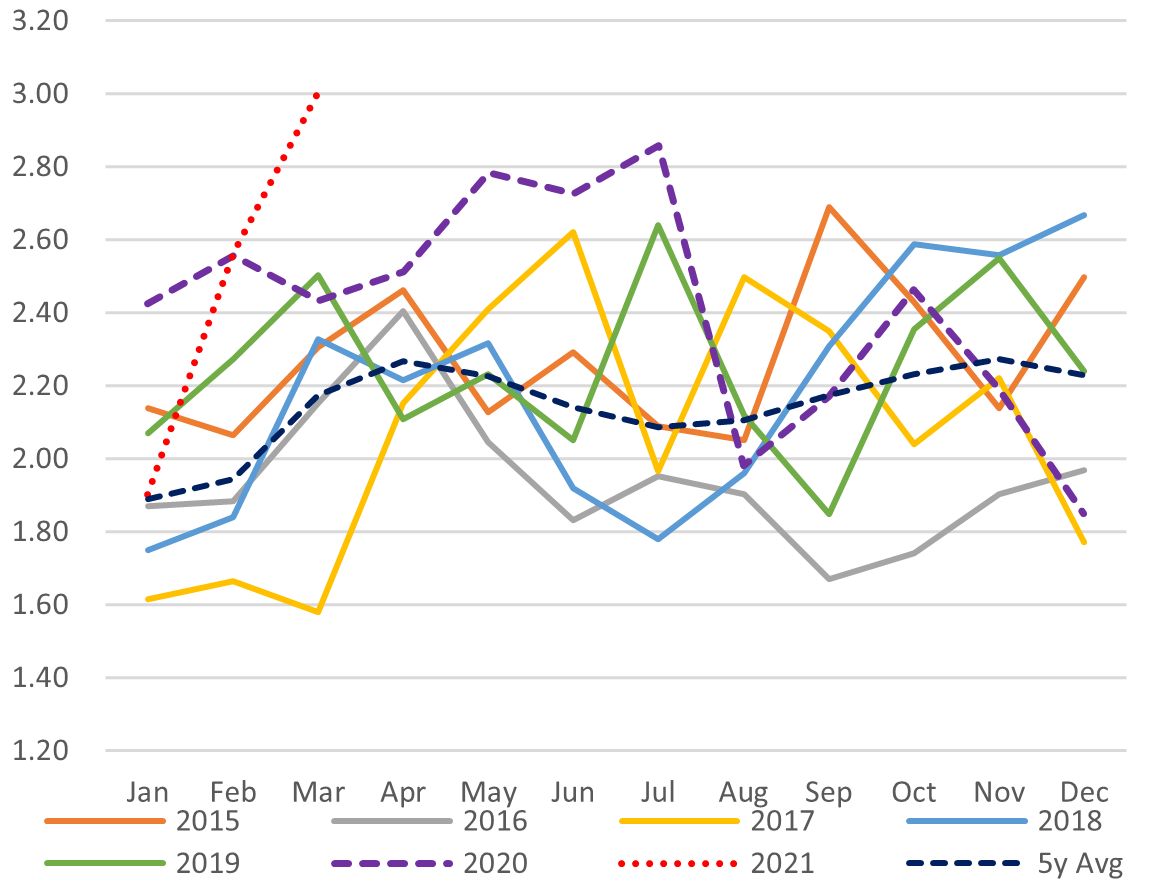

Spot Electricity Prices, Monthly Avg.

Source: Company websites, JANSI and JAIF, as of July 28, 2021

Nuclear regulator calls out J-Atomic for rewriting geological data

(Kyodo News, July 28)

- The Nuclear Regulation Authority (NRA) said at a regular meeting that it suspects that staff at Japan Atomic Power Co. rewrote some of the data on the geological attributes of the site of its Tsuruga NPP Unit 2.

- The regulator believes the alteration of data was inappropriate and will discuss an adequate response at a meeting soon.

- Based on this, the NRA will stop examining the reactor’s application for a restart.

- NRA chair Fuketa Toyoshi said the problem did not appear during the examination of the geological data at Japan Atomic’s Tokai No. 2 reactor, which recently passed its checks. Another NRA official said he wants to examine whether this is a “company-wide” problem and if that’s the case then Tokai No. 2 will also be involved.

- Japan Atomic said it merely sought to improve the ease of reading the data and that it wasn’t an attempt at falsification.

- The debate centers on the idea that the Tsuruga Unit 2 may sit on an active fault line.

TAKEAWAY: This is potentially a very negative development for the nuclear energy sector, working against the recent momentum it had built in restarts and license extensions. Whatever the truth, Japan Atomic will have a tough time convincing the public that its actions were “clean”.

It’s unfortunate because the latest Basic Energy Plan draft is currently in review and open for public comment. The comments by the NRA will likely be employed by anti-nuclear parties to argue that the industry has no realistic chance to meet 20% of the Plan.

Meanwhile, nuclear power continues to be attacked by a significant portion of the media for rising cost of operation and other factors.

- SIDE DEVELOPMENT:

Debunking the nuclear myths

(Business Journal, July 28)- CONTEXT: Although presented in the news rather than the opinion section, this is an example of the anti-nuclear commentaries across various media published after the release of the latest draft of the Basic Energy Plan.

- Before the Fukushima disaster, nuclear power was widely believed to be safer, cheaper, cleaner and more reliable than other means of generation. Even after the Three Mile Island and Chernobyl disasters, Japan’s nuclear lobby continued to claim that Japanese nuclear power plants were safer than their overseas counterparts.

- However, a recent government report estimates that the cost of electricity sourced from Japanese nuclear power stations will reach over ¥11.5 per kilowatt hour between by 2030, making it more expensive than solar power, which can be as cheap as ¥8 per kilowatt hour.

- Nuclear’s environmental claims are also disputed. While it’s true that nuclear reactors do not emit CO2, they have a significant effect on the marine environment: every second, a typical 1 GW nuclear power station heats 70 metric tons of seawater by 7°C.

- The only area in which nuclear still has the edge over renewable sources is its ability to reliably generate a constant output, 24 hours a day, 365 days a year.

- As Japan transitions to a more decentralized generation network, legacy utilities, which have invested in a highly centralized grid structure, are likely to lose money. This has driven many utilities to anti-competitive practices, as evidenced by recent Japan Fair Trading Commission investigations into Kyushu Electric, KEPCO, Chugoku Electric, and Kyuden Mirai Energy.

- Also, the centralized grid structure favored by operators of nuclear plants is more vulnerable to outages, as seen after recent typhoons in Chiba, Okinawa and Kyushu.

Resident groups file challenges against coal-fired power stations

(Asahi Shimbun, July 26)

- Resident activist groups in Kobe, Kanagawa, Tokyo and Sendai have filed multiple legal challenges to the continued operation of coal-fired power plants by KEPCO and Kobelco.

- While a recent challenge at the Osaka District Court was rejected, the court noted in its judgement that under current legislation, operators of thermal power plants are not required to obtain advanced permission from the authorities, and stated that this makes it difficult to restrict the building of new plants.

- While KEPCO and JERA state they plan to convert coal-fired stations to ammonia fuel, the technology for achieving this is not yet viable.

Tohoku Electric picks partners to offer rooftop solar and battery storage

(Kankyo Business, July 28)

- A unit of Tohoku Electric will partner with Kitashu, a housing manufacturer, and a third-party solar and storage battery service to promote the service to its clients.

- The service offers installation of solar panels and a power storage system at no initial cost, with clients paying only a monthly fee. The service mainly targets new detached houses.

- This is the first partnership of the kind for Tohoku Electric.

TAKEAWAY: As we noted previously, it’s interesting to see how Japan’s biggest power utilities attempt to enter the renewables space over the next decade. With renewables now allotted the lion’s share of the 2030 energy mix, it really is a case of “how” rather than “if”. Still, we don’t expect EPCos to immediately embark on a major building spree with new land-based utility-scale solar and wind installations. Gaining experience in residential rooftop solar seems like a smart move for Tohoku Electric, just as the government signals Japan will increasingly need to utilize rooftop locations and the MoE advocates for public buildings to install PVs.

New government service mark to raise profile of regional renewable operators

(Kankyo Business, July 27)

- On July 21 METI began accepting applications to use the ‘regional cooperation mark’, which will identify renewable energy service providers whose operations help local regions.

- To use the mark, operators must show that they support regional economies, provide a stable supply of electricity in emergencies, or have a long-term growth strategy in place.

- Issues of dumping of disused solar panels and visual pollution have plagued renewable energy developments in Japan’s regions. The new service mark will help local governments and consumers identify good corporate citizens.

TEPCO submits ¥3 trillion plan for decarbonization, drafts nuclear restart schedule

(Denki Shimbun, Mainichi, July 26)

- TEPCO, the Tokyo-based electric power utility, submitted a revised strategy to the govt. under which it plans to invest up to ¥3 trillion by fiscal 2030 for decarbonization.

- As part of the plan, which the state-controlled utility says will aim for net-zero emissions by 2050, TEPCO sees the restart of its Kashiwazaki-Kariwa NPP after FY2022.

- Among other key measures, TEPCO plans to:

- expand its EV charger network to 1 million members by 2030

- allocate ¥1 trillion to development of renewable energy, especially wind power;

- become more active in the power transmission market after the distribution licensing system comes into effect from FY2022, investing as much as ¥2 trillion in that and the nuclear power plant segment of its business;

- bolster its hydropower output by 100 million kWh in FY23 vs FY18

- The company’s latest business plan included an outlook for future revenue and expenditures, assuming that the Kashiwazaki-Kariwa No. 7 reactor would be restarted in October 2022 at the earliest and the No. 6 reactor in April 2024. It also expressed hope that one of the first five units would be restarted in 2028.

JFE Engineering will build wind turbine monopiles in Japan

(Kankyo Business, July 26)

- JFE Engineering will build a new plant on the grounds of its Okayama steelworks to manufacture monopiles for wind turbines.

- The factory will be the first of its kind in Japan.

- The considerable length and weight (over 1000 tons) of monopiles makes them difficult to manufacture using conventional facilities.

- JFE will also make additional investment in facilities to manufacture the “transition pieces” that link monopiles to towers.

Western Tokyo leads way with virtual power plant initiative

(Kankyo Business, July 28)

- The neighbourhood of Minami-Osawa in West Tokyo established a virtual power plant (VPP) as a proof of concept for localized sharing of renewably-generated electricity.

- By centrally controlling electric car batteries, storage batteries, photovoltaic panels, hydrogen stations and other infrastructure, the VPP can absorb supply and demand imbalances.

- TEPCO subsidiary TN Cross was selected to provide aggregation services by public tender.

- Between 2022 and 2024, the operators will attempt to define optimum utilisation patterns for both normal and emergency conditions.

Canadian Solar wins tender to build 9 MW of capacity

(Kankyo Business, July 27)

- Canadian Solar revealed details of its three solar projects that won tenders.

- The company will build an 80 MW solar farm in Miyagi, a 3 MW farm in Aomori, and another 3 MW farm in Fukushima. The Miyagi site will supply both direct and alternating current.

- The farms will begin supplying the grid by no later than 2026.

Kansai Electric failed to declare ¥270 million in tax

(Mainichi Shimbun, July 27)

- The Osaka taxation bureau has ordered KEPCO to pay ¥270 million in tax in response to revelations that the utility made undisclosed payments to former directors.

- The tax bill includes ¥32 million in fines.

NEWS: OIL, GAS & MINING

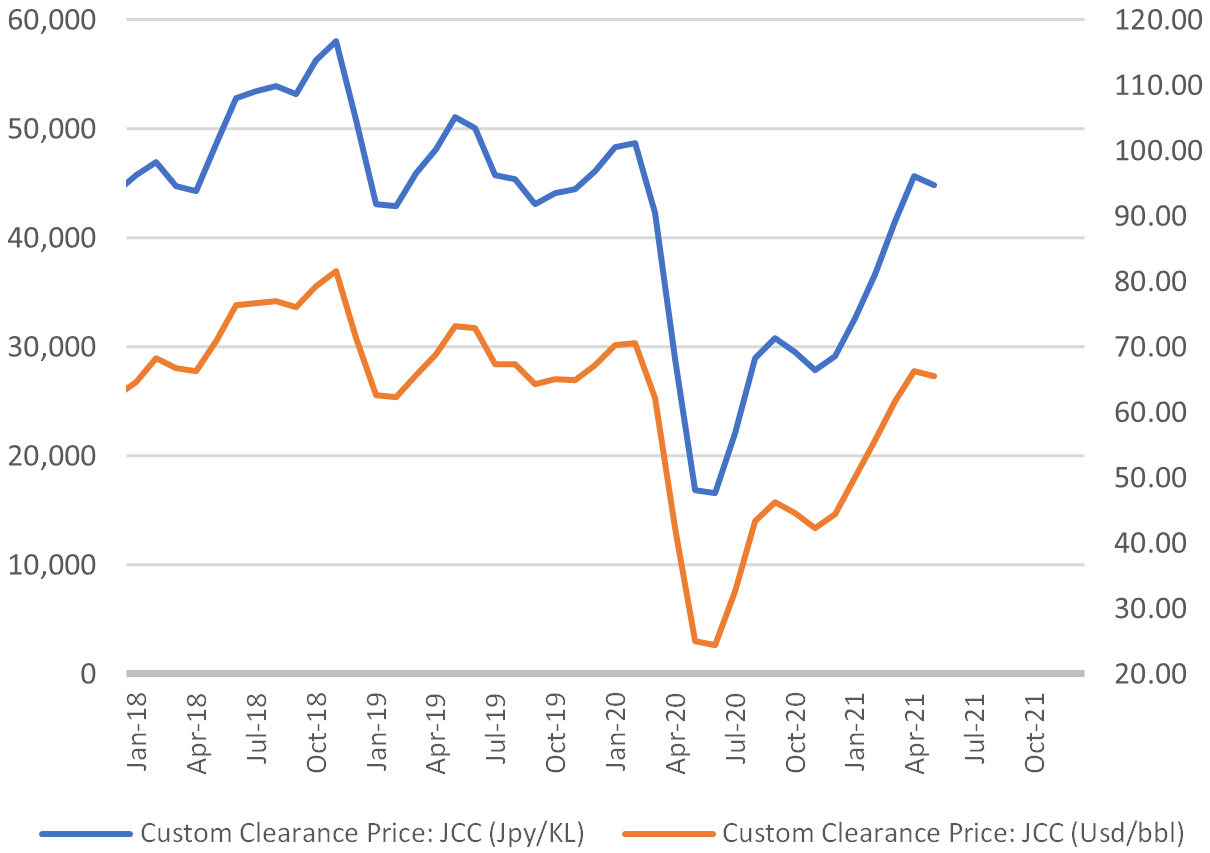

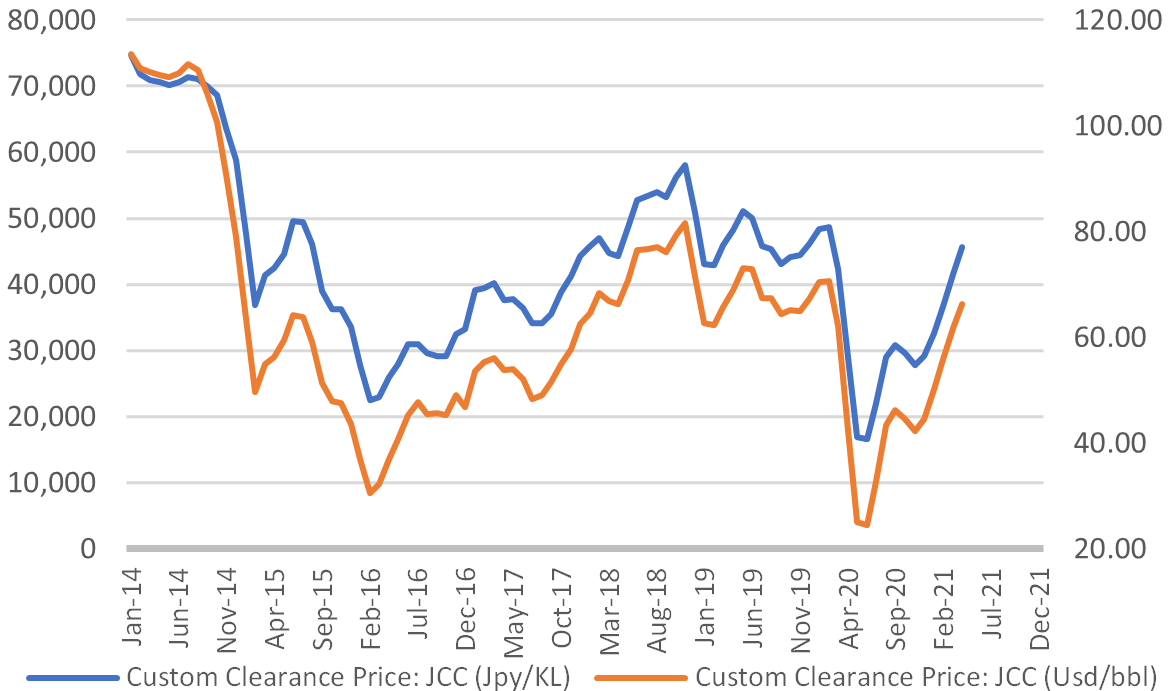

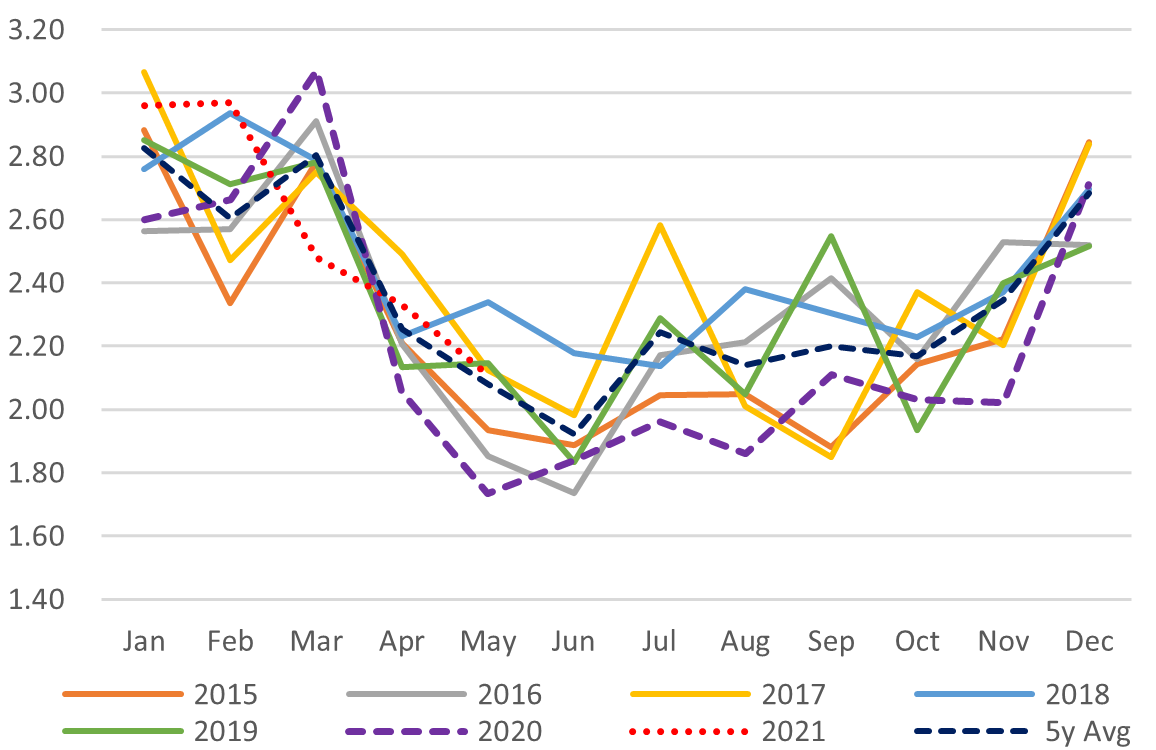

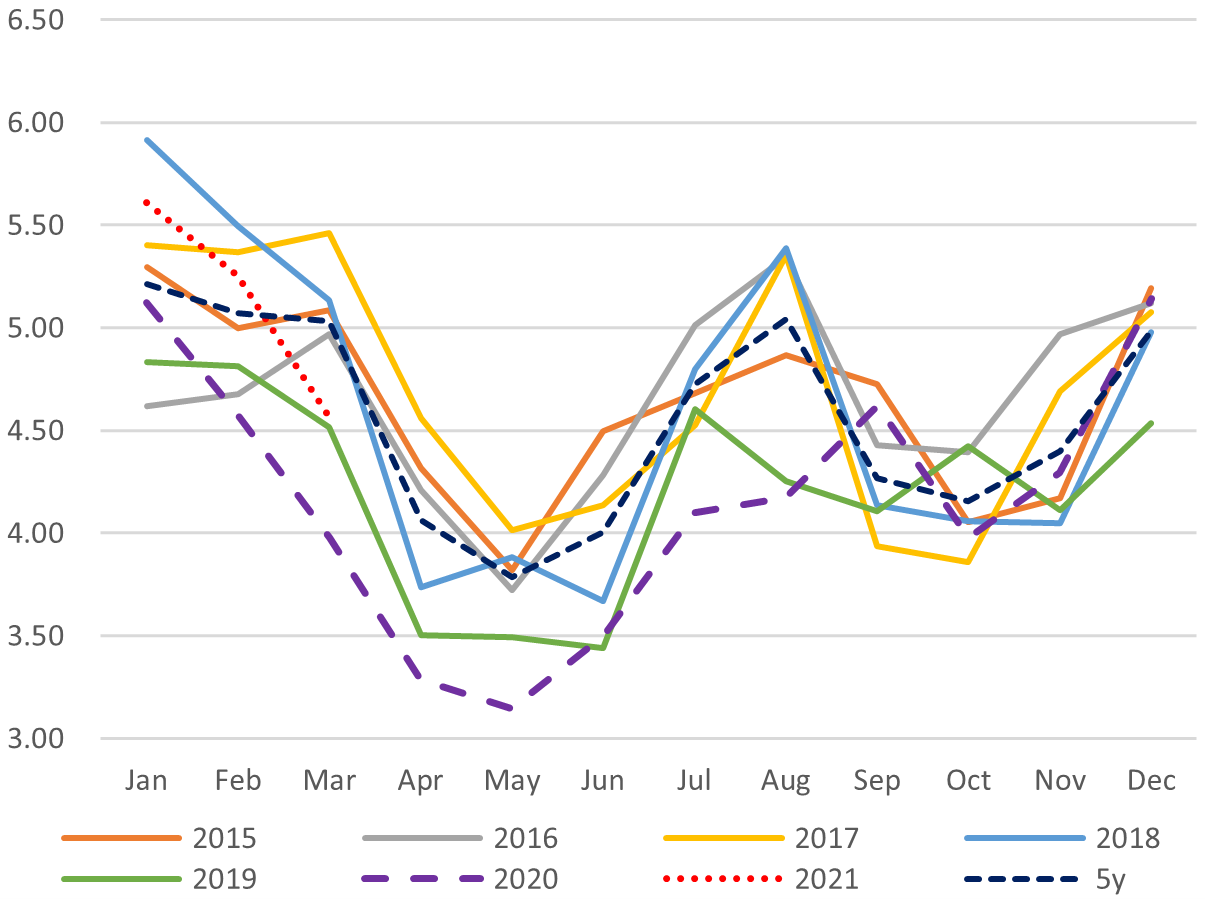

Japan Oil Price: $65.45/ barrel

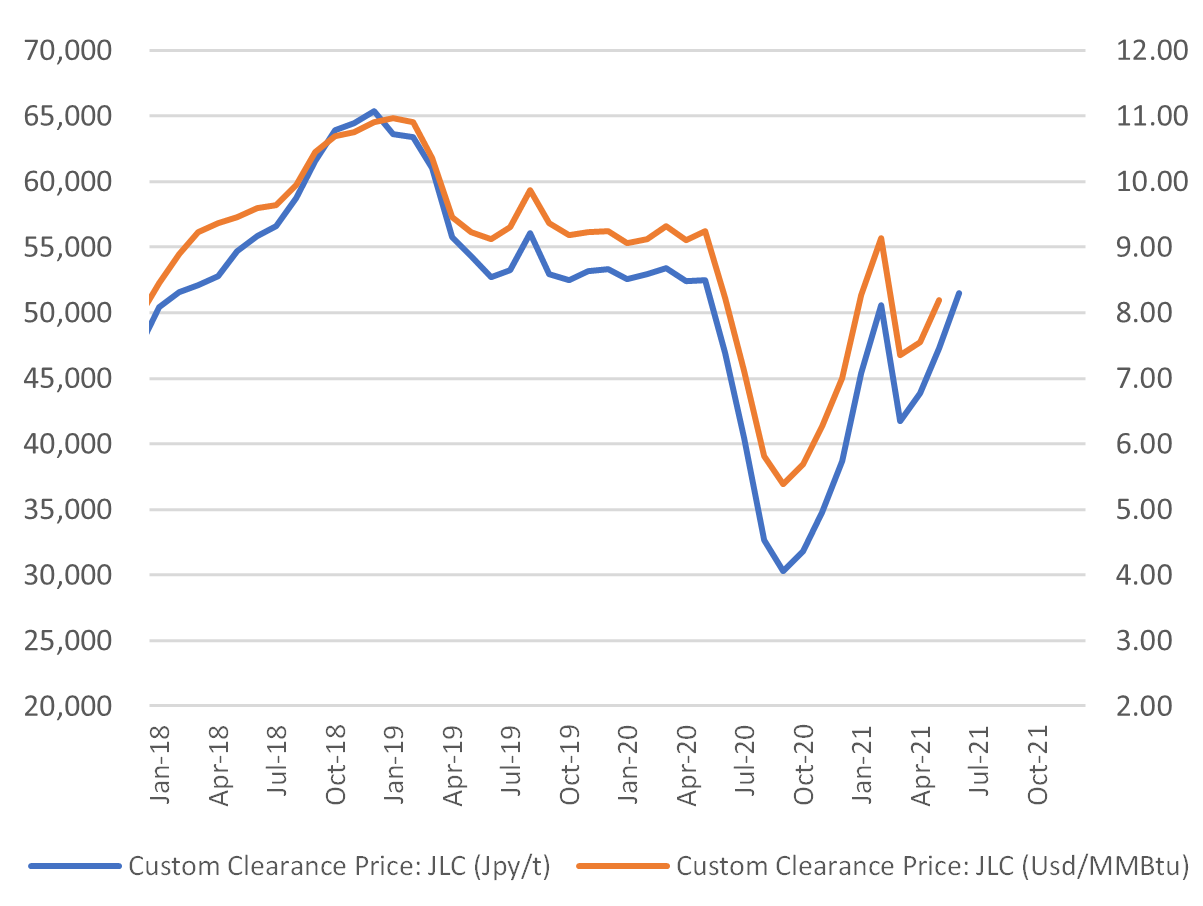

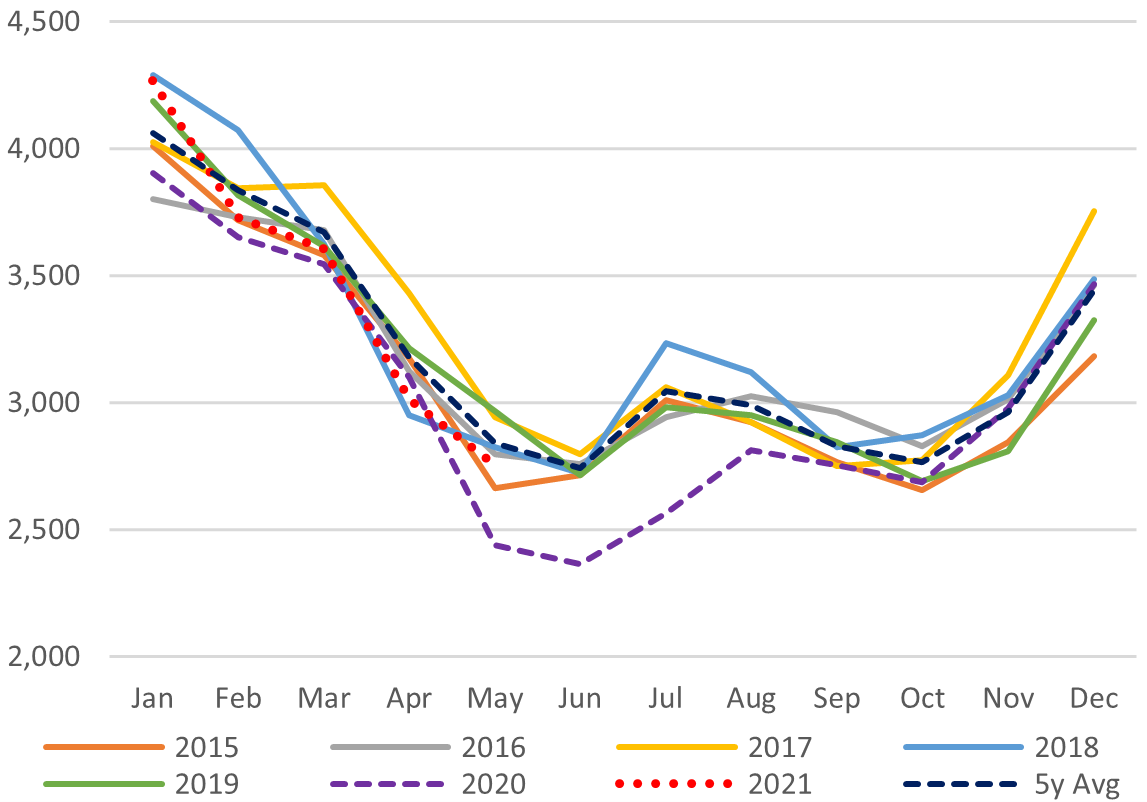

Japan (JLC) LNG Price: $8.19/ mmbtu

ENEOS to boost polyethylene production amid increased demand for renewable electricity

(Nikkan Chemical News, July 30)

- ENEOS subsidiary ENEOS NUC will increase annual capacity to manufacture polyethylene for use as insulation for high-tension lines by 30,000 metric tons.

- To this end, ENEOS NUC is investing ¥12 billion in new manufacturing facilities that will go online in 2023.

- Growth in the renewable energy sector has generated increased demand for high-tension lines.

Toho Gas starts to supply carbon-neutral LNG to 6 Japanese manufacturers

(New Energy Business News, July 27)

- Toho Gas agreed with Showa Densen Holdings, Sumitomo Dainippon Pharma, Denso, Tokai Rika, NGK and its group firm NGK Ceramic Devices to start the supply of carbon-neutral city gas from August 2021.

- The contracts are expected to offset about 200,000 tons of CO2 for the six companies from August 2021 to September 2026.

- Toho Gas plans to focus future business on city gas, LPG gas, hydrogen, and electricity.

- SIDE DEVELOPMENT:

Keiyo Gas now supplying carbon neutral gas

(Company statement, June 30)- As of July 1, Keiyo Gas is supplying carbon neutral reticulated natural gas to subscribers.

- Carbon credits offset the carbon emissions generated in manufacture and use of the gas.

- SIDE DEVELOPMENT:

Osaka Gas to supply carbon neutral gas to industrial clients

(New Energy Business News, July 27)- Under an agreement with Singapore-based Shell Eastern Trading, Osaka Gas has accepted delivery of its first shipment of carbon-neutral LNG.

- The natural gas comprising the shipment was extracted and liquefied in Brunei.

- From August 1, Osaka Gas will supply Koatsu Chemical and three other industrial clients with the carbon-neutral gas.

- Osaka Gas also signed a basic agreement with several regional gas companies, including Okayama Gas and Shikoku Gas, concerning the supply of carbon-neutral gas.

TOCOM to launch yen-denominated LNG future based on JKM in 2022

(Platt’s, July 29)

- Tokyo Commodity Exchange (TOCOM) plans to launch a cash-settled LNG futures contract based in Yen, using the Platts JKM for settlement.

- The launch is set for 1Q of fiscal year ending March 2023.

ANALYSIS

BY ANDREW DEWIT

PROFESSOR OF ENERGY POLICY

SCHOOL OF ECONOMIC POLICY STUDIES

RIKKYO UNIVERSITY, TOKYO

Debating Japan’s Draft Basic Energy Plan

On July 21 Japanese policymakers unveiled a draft version of the country’s Sixth Basic Energy Plan. Much like previous iterations of the triennial planning initiative, the goals are both comprehensive and controversial. Unlike previous versions, this draft’s ambitions are crafted as much to address international decarbonization commitments as to appease domestic advocacy coalitions.

The plan aggregates what is deemed to be the best-available evidence on current and mid-term energy costs, strategic options, and myriad other parameters relevant to shaping policy for a resource-poor industrial economy with the world’s fifth largest energy appetite. The current draft is subject to public comment through August. Formal adoption by the cabinet is only expected after a general election that must be held by Oct. 22 of this year. Hence, its details may change.

The assessment of energy costs and economic opportunities is more wide-ranging than in the past. Policies to accelerate smart electrification for decarbonization and disaster resilience have been ramped up. Overall, the initiative was framed by Prime Minister Suga’s commitment to a 46% reduction of Japan’s greenhouse gas emissions by 2030 and net-zero by 2050.

Key Goals

Proposed changes to the previous plan’s vision of Japan’s 2030 power mix have received the most attention. Table 1 compares the two plans. The Fifth Plan in 2018 conceded to making solar, wind, biomass and other renewables 20-22% of the 2030 power mix. But by 2020 renewables were already about 18% of Japan’s power mix, amidst the accelerating global diffusion of ever-cheapening solar, wind and storage. The draft renewable target has thus been raised to 36-38%.

Also attracting much commentary was the decision to maintain the target of having nuclear power compose 20-22% of electricity generation, building on the current level of roughly 6%. There is also a new commitment to generate about 1% of power via burning hydrogen and/or ammonia. This first-ever quantified role for the “hydrogen society” in the power mix is expected to help boost Japan’s zero-carbon electricity to 59% of the power mix, compared to the aim of 44% in the 2018 plan.

The big losers in the draft are fossil-fuel thermal generation, including liquid natural gas (LNG), coal, and oil-fired power. In 2019, these sources composed 76% of Japan’s power mix, with respective shares of 37% (LNG), 32% (coal), and 7% (oil). LNG is now projected to drop to 20% by 2030, a far steeper cut than the previous scenario of a decline to 27%.

| Table 1: Comparing Japan’s Proposed 2030 Power Mixes (Units: %) | |||

| 2018 5th Basic Energy Plan | 2021 6th Basic Energy Plan (Draft) | ||

| Renewable | 22-24 | Renewable | 36-38 |

| Nuclear | 20-22 | Nuclear | 20-22 |

| Hydrogen-Ammonia | 0 | Hydrogen-Ammonia | 1 |

| LNG | 27 | LNG | 20 |

| Coal | 26 | Coal | 19 |

| Oil | 3 | Oil | 2 |

| Total Generation

(billion kWh) | 1,065 | Total Generation

(billion kWh) | 930-940 |

| Source: METI, 2021 | |||

Though coal-fired generation is about twice as dirty than LNG, its rate of decline is less precipitous, down to 19% versus the 26% envisioned in the Fifth Plan. Changes to the role of oil-fired power are minimal, with a previously projected 3% share falling to 2%. Overall, the draft plan foresees fossil-fueled power totaling 41% of the 2030 power mix, down from the 56% share envisioned in the Fifth Plan.

One item not adequately addressed in the debate is Japan’s ambition for energy efficiency. The Sixth Plan anticipates Japan’s power needs to decline to about 930-940 billion kWh, compared to 2019’s level of 1,024 billion kWh. The Fifth Plan, by contrast, expected Japan’s power demand to increase to 1,065 billion kWh.

Renewables

The new goals have led to an unprecedented volume of domestic debate. Criticism of the renewable targets is polarized between disappointment that they’re not much higher and worries that they may be unrealistically ambitious.

Advocates of much higher renewable numbers insist that Japan has the opportunity to retake the leadership role it enjoyed decades ago. They assert that building robust domestic renewable industries – especially in offshore wind, hydrogen, and smart-energy management – could help the country play a stronger role in global greening. Many of these advocates argue that the draft plan should target well over 40% renewables by 2030, declaring this would lead to lower power costs by 2030.

Naturally, Japan’s dwindling band of critics of renewable energy counter that the raised renewable targets can only be met with expensive (in Japan) solar and wind, and thus increase energy poverty while undermining the country’s competitiveness. But concerns about renewables are no longer restricted to these stalwart critics. Japan’s center-left media also scrutinize renewables’ pecuniary and environmental costs. Attention has been directed particularly at utility-scale solar. In mid-July Japan’s national broadcaster NHK released a survey revealing roughly 10% of Japan’s 500 kW+ solar arrays are in areas of significant landslide risk. The NHK’s work increased the spotlight on a large risk-governance gap, where lax rules leave local communities vulnerable to worsened disaster risks in the name of greening. Related commentary highlights that local governments are increasingly compelled to implement ordinances, as residents band together and oppose projects they perceive as harmful to local environmental amenities.

Moreover, debate on the draft points to the need to factor in transmission, storage and system costs of solar and other intermittent renewables, including the need for back-up by thermal power. The draft plan and related work has yet to calculate these costs in specific terms for Japan. But they’re likely to be significant.

Nuclear

The decision to keep striving for 20-22% nuclear in the 2030 power mix also satisfies no one. Since the Fukushima disaster Japanese public opinion has been cool towards restarting existing nuclear capacity, let alone building more. Advocates of 100% renewables fought to have nuclear eliminated from the 2030 mix, while proponents of keeping or increasing nuclear were handicapped by memories of Fukushima coupled with continuing safety and other slip-ups by the industry.

Nuclear power’s critics argue that costs have increased due to safety measures and the difficulties of decommissioning. These facts are undeniable, as is the stubbornly negative public opinion. Critics also stress a narrative that nuclear has no future, drawing heavily on debates from within the EU.

In formulating the current draft, the anti-nuclear position was bolstered by several factors. Most important perhaps are the impending general election and PM Suga’s abysmal rankings in the polls. Another item is an increasing split within the governing Liberal Democrat Party (LDP) on nuclear, with MoE Minister Koizumi Shinjiro advocating its reduction in alliance with other LDPers and the LDP coalition partner, the Komei Party. These factors enabled anti-nuclear advocates to remove from this draft any commitments to new nuclear construction.

Advocates of nuclear power also base their case on costs, in addition to the imperative of decarbonization. They concede that costs have increased, but note that Japan’s recent permitting of over 40-year lifetimes for extant plant implies reduced costs over extended lifecycles. They also highlight nuclear’s provision of clean baseload power to complement intermittent wind and solar.

Another point of emphasis is that restarting Japan’s roughly 30 viable reactors is the fastest and cheapest way to secure significant cuts in greenhouse gases. Both proponents and opponents caution that Japan is unlikely to reach the draft plan’s 20-22% target for 2030 without accelerated progress on reactor restarts. Advocates also warn of a disturbing lack of investment in training new nuclear engineers.

Potentially one of the most important interventions in Japan’s public debate on nuclear came on June 28 from International Energy Agency (IEA) Executive Director Fatih Birol. Birol noted in comments to Japan’s biggest newspaper that the country’s topographic and other challenges essentially required that nuclear restarts and new build complement renewables and efficiency. Birol argues in remarks also posted on the IEA website that were Japan to rely on solar PV and batteries, “an additional land area equivalent to 12 times the entire Tokyo metropolitan region would need to be covered by solar panels, and storage capacity equivalent to 40 times the world’s current largest battery project.”

Thermal

Renewable advocacy coalitions declared Japan’s ambition to reduce thermal to 41% of the power mix to be inadequate in light of accelerating climate change. Japan’s aim of reducing coal to 19% from the current 32% of the mix has received faint applause from any quarter. North American and European/UK coal power is in steep decline, often to single digits, and the perception is that Japan should be in a similar position.

Yet, Japan’s coal fleet is younger than its counterparts among the G-7, and the country lacks the continental power-trading or cheap natural gas that have enabled the EU and the U.S. to drive a lot of coal from their power mixes.

The aim of nearly halving the role of LNG from 37% currently to 20% by 2030 mainly caught the attention of experts alert to potential signaling effects. They’re concerned that LNG (and to some extent coal) exporters might take the numbers seriously and reduce their reliance on Japan in favor of other consuming countries. The worry is that reduced bargaining power could impair energy security and lead to yet higher prices.

Interestingly, some of Japan’s most ambitious renewable scenarios actually rely on LNG increasing to roughly half of the 2030 power mix in order to eliminate both coal and nuclear. Those scenarios are perhaps the most telling evidence that – at least in energy – there is a limit on the number of big things that can be done in a decade.

In short, Japan’s draft energy plan is completely inadequate for achieving the decarbonization targets while maintaining economic vitality, environmental justice, and other amenities. Compromises must clearly be made, without sacrificing the decarbonization goals. Fortunately, Japan’s vigorous public and expert debate on the draft generally recognizes that key point. So perhaps the ensuing months will see Japan make headway with this draft towards a more credible roadmap.

ANALYSIS

BY ESWAR MANI

MANAGING PARTNER

MANI KAPITAL

Solar’s Wild West Era Ends

As Industry Stands on the Verge of its 2.0 Revamp

The era of cowboys in Japan solar is over. The rich Feed-in Tariff (FIT) that opened the country to a solar PV boom from 2012 attracted a hotchpotch crowd. Some simply monetized their earlier land-grab via FIT without much knowledge or interest in energy. Some used solar farms as a tax write-off. A few did little more than flash their business card to secure financing and pick up a tidy fee.

Since the initial tariff dropped by 75% over a decade, that era has closed. The next one is just emerging, and the kind of companies that will compete – can compete – in a Japan where solar is heading to ¥8/ kWh will be quite different.

How companies will structure and operate the 30-50 GW of solar capacity that Japan’s government expects to come online over the next 10 years will be different to the similar amount added since 2012.

This next phase of the industry’s development, call it Solar 2.0, will likely create companies of notable size in terms of assets, diversification, and knowledge. The winners will likely become publicly listed and hold considerable clout in policy circles.

The Wild West days of solar in Japan are all but over. The bigger battles are just starting.

Calling all cowboys

Setting the world’s highest solar tariff is one way to get global attention. As solar developments in other countries slumped, post-Fukushima Japan pushed through a major reform of financing for renewable energy projects. Then the ruling Democratic Party of Japan (DPJ) agreed on a system in which regional electricity utilities backed by the government would subsidize payments for power generated from renewable sources.

The idea, in part, was to find an alternative to nuclear, while also supporting Japanese solar panel makers such as Sharp and Panasonic, which were starting to lose their once dominant position to Chinese rivals.

For solar, the FIT started at ¥40/ kWh.

To DPJ’s credit, the green policy attracted fanfare and significant foreign players to Japan. As an additional incentive, individuals and corporates that developed and owned these solar plants were able to enjoy a one-year accelerated depreciation for the total expense of the generation facility. This attracted profitable companies and investors into the fold, even those that had zero interest in sustainability.

The principal investors at one leading investment bank started a lucrative solar investment business initially based on offsetting their own personal tax liabilities.

The early winners in solar FIT were those with ready access to land. A nefarious community of 70’s land grab cowboys, known as jiageya (地上屋), made quick profits. Golf courses under distress were converted to solar power plants, and bankable general contractors who managed the construction took the lion’s share of the costs.

The Ministry of Economy, Trade, and Infrastructure (METI) issued IDs with the FIT certificate that initially cost less than ¥2 million to apply for, including legal and documentation fees. Solar took off as projects were modular and you could start a solar plant with a single 250-watt panel. Individuals used this subsidy for their home rooftop solar panels. Interestingly, 90% of the initial METI IDs were for these small-scale “plants”.

As a result, some 90 GWs of certificates were quickly distributed by METI. And yet, today even the largest solar player in Japan is just shy of 1 GW in operating assets.

The backlash

After a brisk start came the backlash. Many of the cowboy developers were unscrupulous in their use of land, willing to sell plots in hard-to-reach mountainous areas that were less protected in times of heavy rain and mudslides. The profitability of solar projects perversely encouraged natural destruction.

While local governments struggled to process all newcomers and worried over land management, the buyers of the renewable energy – the major regional utilities – decided that they were placing too much money and effort into assets that were (mildly) competing with their own power plants. Kyushu and Hokkaido electric companies were the first to rebel, pressuring to curtail solar generation, and thus avoid paying for renewable electricity that they didn’t need. The utilities said they needed to cut the solar generation they received to balance the local grid system, which incidentally they also controlled.

With regional utilities unwilling to buy more green electricity at elevated prices, and local politics adding to problems, the national government started putting downward pressure on FIT prices and clawed back some developer benefits and policy certainties. The FIT went from ¥40 to ¥36, then ¥32, had a brief stop at ¥29, before falling again to ¥27. As solar project pricing moved to an auction system, it tumbled from ¥19 to ¥16, then ¥12, and most recently to ¥10.

Naoshima Island, Kagawa, Japan.

Photo by Susan Q Yin on Unsplash

The price slide is not over. METI last month stated its objective to have solar at ¥8 by 2030. In a separate Green Growth Strategy paper, the ministry forecast offshore wind would also drop to ¥8 by 2030. You best believe that METI expects solar to be cheaper than wind by 2030.

The New Look of the Solar Business

The existing business models and technology in Japan will need to innovate to reach ¥8. It will also require quite a lot of change in how things get done.

First, banks will need to change their financing schemes, which currently favor lending only to blue-chip general contractors. The latter are not usually the ones that do the work, passing it down the food chain to much smaller outfits, with each stage taking a margin. In Japan, there’s no limit to the number of subcontractors on a project. These smaller construction firms will need to be recognized by banks for costs to shrink.

Operations will need to start including more sophisticated modeling, risk and management systems – something that naturally favors bigger industry players. This will likely spur a wave of consolidation, especially as the earliest FIT certificates start to run out of their 20-year life-span towards the latter half of this decade.

There will be new and cheaper technological solutions, such as bi-facial solar panels with tracking to enhance the kwh delivered per square meter. Dashboards and remote operations and maintenance services will help companies beat expected generation and support earnings.

There will be business model solutions: combining solar with wind, storage and other energy sources to maximize gains from project space. This requires operators that are comfortable across several renewable energy technologies. We’re already seeing many of the bigger solar players venture into wind, biomass, and even hydrogen. Pairing with storage is being tested by small and major industrial players. A typical Solar 2.0 player will be an energy company, not a solar company per se.

Further combinations will be tested in solar sharing: placing panels above agricultural land, unused water reservoirs, on walls of buildings, car roof tops, and other currently untapped spaces. Part of this will require technological solutions. But a lot of it will require scale to manage, attract financing, and have vision that only larger companies can generally deliver.

The Ministry of Environment’s recently unveiled plans to add solar panels to at least half of the nation’s public buildings is another 10 GW business opportunity open to firms of scale that are nimble enough to innovate.

That said, Solar 2.0 is unlikely to be a bastion for today’s blue chips. Those were the winners of Solar 1.0, when brand reputation and trust factor with banks played a role, as did your land bank or a pan-Japan sales network. The next generation of industry winners will be ground-up solar startups with a track record of participating in auctions and which have exemplified grit by fine-tuning their operating model like a factory. They will use global best-in class technology, business, and financing models.

The multiple-energy-source aspect of Solar 2.0 opens the door for Japan’s large energy companies in oil and gas to join the renewables party. Some, like Tokyo Gas, seem keen. Many others are testing the waters. They will need to prove that they can compete irrespective of energy policies, that they can bring something to the table – like an excellence in procurement or a diverse staff skill.

The litmus test for a Solar 2.0 participant will be simple. Can you run your operations at ¥8/ kWh as standard? If not, it’s time to pack up and leave the market.

GLOBAL VIEW

BY TOM O’SULLIVAN

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

U.S. Infrastructure Bill:

The U.S. Senate agreed last Wednesday to begin deliberation on the Biden Administration’s $1.2 trillion infrastructure bill.

The draft bill includes $73 billion of investments in U.S. power grid infrastructure, $11 billion in electric car/bus infrastructure, and $16 billion to clean up orphaned oil and gas wells. The bill also includes $66 billion of investments in passenger freight rail, and $39 billion in public transit.

G20 Environment Ministers:

G20 environment ministers, including Japan, agreed at a summit in Naples, to adopt new climate targets within three months ahead of COP26 in Glasgow in November. The ministers committed to try to limit global warming to 1.5C. However, no agreement was reached to phase out coal usage or termination of fossil fuel subsidies due to objections from China, Russia, India, and Saudi Arabia.

Nuclear Power:

China General Nuclear will temporarily shut unit 1 of the Taishan nuclear power plant in Guangdong province, west of Hong Kong, to replace damaged fuel rods. An increase in the concentration of noble gases in the primary circuit of the European Pressurized Reactor (EPR) in June was attributed to the damaged fuel rods. France’s EDF has a 30% stake in Taishan. It is the only plant in the world to currently operate an EPR, although another one is under construction at Hinkley Point in Somerset, UK.

Oil/Gas:

1). Over $30 billion of M&A consolidations were closed in Q2 in the U.S. shale oil sector, the highest level in around eight quarters. The deals included Pioneer’s acquisition of DoublePoint for $6.4 billion. A minimum capitalization of $10 billion may now be required for shale producers to survive.

2). Shell announced a $2 billion share buyback following strong Q2 results with Brent oil closing @ $76 a barrel on Friday.

3). Natural gas prices in almost all geographies are also hitting multi-year highs as demand for electricity around the world surges. Spot prices in Asia hit $15 mmbtu last week. In the UK prices are at their highest level since 2005. In Europe prices have hit a record high of E4 cents kWh.

Batteries:

Redwood Materials, the EV battery start-up founded by JB Straubel, the Tesla co-founder, raised $700 million in a funding round last week. Redwood, based in Nevada, is seeking to create a closed-loop supply chain for EV batteries that could eliminate the need for mining rare metals.

Power Cables:

PG&E, California’s largest utility, plans to bury 16,000 km of power lines to reduce wildfire risk at an estimated cost of $20 billion.

Power Turbines:

In Q2, GE reported $5 billion of orders for gas power turbines, up almost 70% qoq, and almost 40 orders for mobile power units. GE orders for wind turbines in Q2 increased 7% qoq to over $3 billion.

Aviation/U.S. Jet Fuel Shortages:

A resurgence in domestic U.S. travel coupled with a requirement for jet fuel to fight wildfires in California and Oregon is creating jet fuel shortages across the Western U.S. This has been compounded by manpower shortages and lack of pipeline availability to airports. At some U.S. aviation hubs, up to 20% of flights have been cancelled due to fuel shortages. American Airlines is warning pilots that fuel stops may need to be added to certain domestic U.S. routes.

EVs:

1). In Q2 Tesla’s profit exceeded $1 billion for the first time on revenues of $12 billion. It sold over 200,000 vehicles in the quarter. Tesla’s market capitalization on Friday was $680 billion, almost three times Toyota’s. Tesla also sold over $350 million in regulatory credits to rival automakers in Q2.

2). Lucid, the EV-maker, listed on Nasdaq on Monday through a SPAC, achieving a market capitalization of almost $40 billion.

3). The founder of Nikola, the EV truck company, was charged by U.S. prosecutors with securities fraud and released on $100 million of bail. Trevor Milton was also served with an SEC civil complaint for defrauding investors.

4). The European Automobiles Manufacturers Association estimates that Europe will ultimately need six million EV charging points when petrol and diesel cars are banned, around 30x the current level.

China:

The National Development and Reform Commission, in its five-year plan, has committed to create a circular economy for batteries for EVs.

South Korea:

1). Hyundai Motor’s Q2 profits of $1.6 billion were at their highest level in seven years due to improved sales of EVs, including the Ioniq 5.

2). LG Electronics has committed to shift to 100% renewable energy by 2050. U.S. operations will be 100% RE by the end of 2021; other overseas production bases will follow by the end of 2025. LG is also targeting 60% RE by 2030, and 90% by 2040.

Mongolia/Copper:

The UK regulator, the FCA, is investigating Rio Tinto in connection with disclosures on its $7 billion copper investment in the Oya Tolgai mine in the Gobi Desert in Mongolia. The project has been subject to delays and cost overruns. Oya Tolgai was expected to be one of the largest copper mines in the world, producing 500,000 tons per annum.

Singapore:

1). Singapore’s Sembcorp has built one of the largest floating solar power farms in the world that covers an area equivalent to 45 soccer pitches. It is made up of 122,000 panels, based at the Tengeh Reservoir, and will produce electricity to operate five water treatment plants. Singapore plans to quadruple solar power output by 2025.

2). TotalEnergies has agreed to buy Singapore’s largest EV charging network from France’s Bollore Group.

Iran:

Water shortages in the Iranian province of Khuzestan are causing serious electricity outages in hydroelectric plants that generate around 15% of Iranian electricity. Iranian experts warn about ‘water bankruptcy’. On Wednesday, Ebrahim Raisi will take over as Iran’s 8th president since the 1979 revolution.

Israel:

Two sailors were killed on Thursday when an Israeli-managed petroleum product tanker was attacked by drones off Oman. Israel is blaming Iran. The vessel was sailing under the escort of a U.S. naval vessel.

Lebanon:

The government signed a barter agreement with Iraq to buy one million tons of heavy fuel oil to be sold to Lebanese companies to ease fuel shortages. Lebanon is offering health services and agricultural consultancy services instead of cash for the Iraqi oil.

Nigeria:

A Glencore employee pleaded guilty in the U.S. to bribing Nigerian government officials to procure oil at favorable terms and at higher grades. U.S. prosecutors are also investigating Glencore’s activities in Venezuela and the DRC.

Angola:

A Dutch court ruled this week that Isabel dos Santos, daughter of Angola’s former president and Africa’s onetime richest woman, must return to Angola her shares in Portugal’s Galp Energy worth $500 million. Dos Santos is accused of diverting billions from state companies during her father’s Jose Eduardo dos Santos’s nearly 40-year rule of oil-rich Angola. Dos Santos’ business assets have been frozen since 2019. The shares must be returned to Angola’s national Sonangol energy group, which she previously chaired.

Sweden:

Volvo Cars, owned By China’s Geely, is now expected to IPO in 2021 as it focuses on EV and distribution strategies. Geely bought Volvo from Ford in 2010 for $1.8 billion.

Germany:

Mercedes-Benz has formulated plans to double EV sales by 2025 and to make 100% of vehicle sales EVs by 2030. It plans to invest $47 billion in battery-driven vehicles between 2022 and 2030. Eight EV models will be made at seven Mercedes-Benz locations across three continents by the end of 2022. The German company also plans to leverage Shell’s 30,000 EV charge points in Europe, China and the Americas. It’s also acquiring a UK-based electric-motor company to augment manufacturing and development.

Holland:

The Dutch EV charging company, Allego, will go public via a SPAC later this year at an expected valuation of around $3 billion. The company is backed by Apollo Global Management, the private equity firm.

Switzerland:

ABB announced the $3 billion sale of its mechanical power transmission business, Dodge, to U.S.-based RBC Bearings as it focuses its strategy on electrification. ABB is planning another $5 billion+ of disposals.

France:

The planned restructuring of EDF, which owns all of France’s nuclear power infrastructure, has been delayed due to a dispute between the French government and the European Commission. Project Hercules, which was meant to overhaul EDF, would have allowed the company to expand its global nuclear and renewables footprints.

UK:

1). The government is seeking to remove China General Nuclear’s (CGN) involvement in the Sizewell and Bradwell nuclear power projects. CGN was planning to install its Hualong HPR1000 reactor technology at Bradwell. CGN is on a US export blacklist for allegedly stealing U.S. nuclear technology for use in military applications. However, the UK is thought to need 10 GW of new nuclear capacity by 2050 to meet its climate commitments. France’s EDF leads the Hinkley and Sizewell projects with CGN as junior partner.

2). UK weather extremes will occur more frequently owing to climate change, according to a Met Office report released last week, which found that 2020 was one of the warmest, and one of the wettest and sunniest, on record. 2020 was the first in the top 10 for heat, rain and hours of sunshine, in records stretching back more than a century. Moderate UK weather is rapidly becoming a thing of the past, according to the climate scientists who authored the report.

U.S.:

1). A U.S. start-up based in Massachusetts has developed iron-air batteries that are capable of long-duration utility-scale power storage. Form Energy Inc. is backed by investments from Bill Gates, Amazon, and India’s ArcelorMittal.

2). First Energy Corp. has agreed to pay a $230 million fine to resolve charges relating to the bribery of Ohio state officials in connection with the bailout of two nuclear power plants owned by a subsidiary, Energy Harbor.

3). President Biden is requesting that all U.S. automakers voluntarily commit that 40% of vehicle sales will be EVs by 2030.

EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy.

| February | Approval of Fiscal 2021 Budget by Japanese parliament including energy funding projects;

CMC LNG Conference |

| March | 10th Anniversary of Fukushima Nuclear Accident;

Smart Energy Week – Tokyo; Quarterly OPEC Meeting; Japan LPG Annual Conference; Full completion of all aspects of the multi-year deregulation of Japan’s electricity market; End of 2020/21 Fiscal Year in Japan; |

| April | Japan Atomic Industrial Forum – Annual Nuclear Power Conference;

38th ASEAN Annual Conference-Brunei; Japan LNG & Gas Virtual Summit (DMG)-Tokyo Three crucial by-elections in Hokkaido, Nagano & Hiroshima – April 25th |

| May | Bids close in first tender for commercial offshore wind projects in Japan;

Prime Minister Suga to visit the U.S. |

| June | Release of New Japan National Basic Energy Plan-2021;

G7 Meeting – U.K. Presidents Biden and Putin are due to meet at a summit in Geneva Forum for China-Africa Cooperation Summit (Senegal) |

| July | Tokyo Metropolitan Govt. Assembly Elections;

Commencement of 2020 Tokyo Olympics |

| August | Hydrogen Ministerial Conference in conjunction with IEA |

| September | Ruling LDP Presidential Election;

UN General Assembly Annual Meeting that is expected to address energy/climate challenges; IMF/World Bank Annual Meetings (multilateral and central banks expected to take further action on emissions disclosures and lending to fossil fuel projects); End of H1 FY2021 Fiscal Year in Japan; Japan-Russia: Eastern Economic Forum (Vladivostok)-tentative |

| October | Last possible month for holding Japan’s 2021 General Election;

METI Sponsored LNG Producer/Consumer Conference; Innovation for Cool Earth Forum – Tokyo Conference; Task Force on Climate-Related Financial Disclosure (TCFD) – Tokyo Conference; G20 Meeting-Italy |

| November | COP26 (Glasgow);

Asian Development Bank (‘ADB’) Annual Conference; Japan-Canada Energy Forum; East Asia Summit (EAS) – Brunei |

| December | Asia Pacific Economic Cooperation (APEC) Forum – New Zealand;

Final details expected from METI on proposed unbundling of natural gas pipeline network scheduled for 2022. |

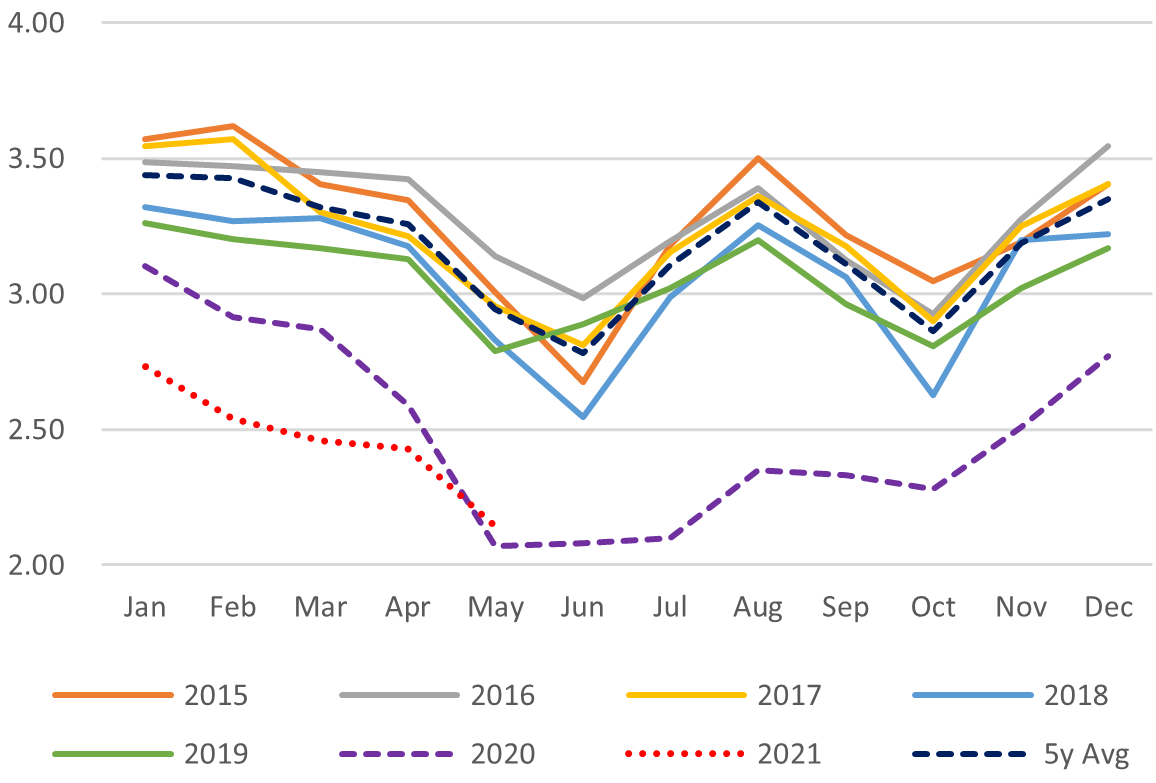

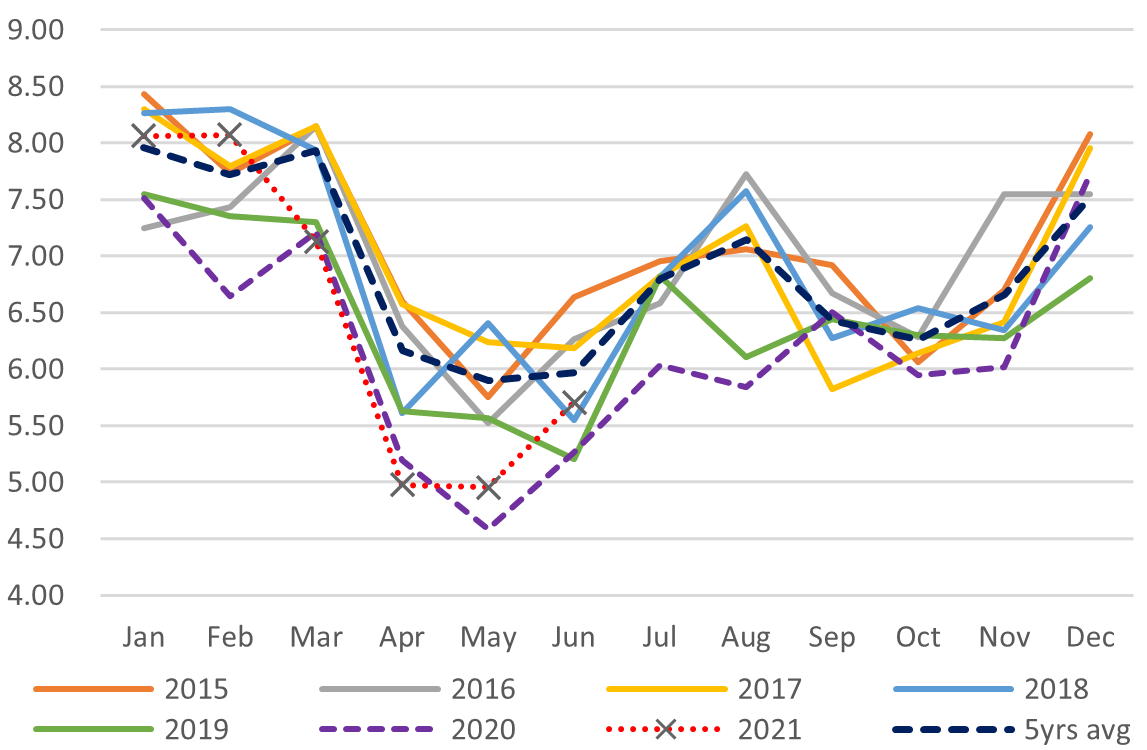

DATA

Japan Oil Price

Crude Imports Vs Processed Crude

Monthly Oil Import Volume (Mbpd)

Monthly Crude Processed (Mbpd)

Domestic Fuel Sales

SOURCES: Ministry of Economy, Trade, and Industry (METI), Ministry of Finance, and the Petroleum Association of Japan

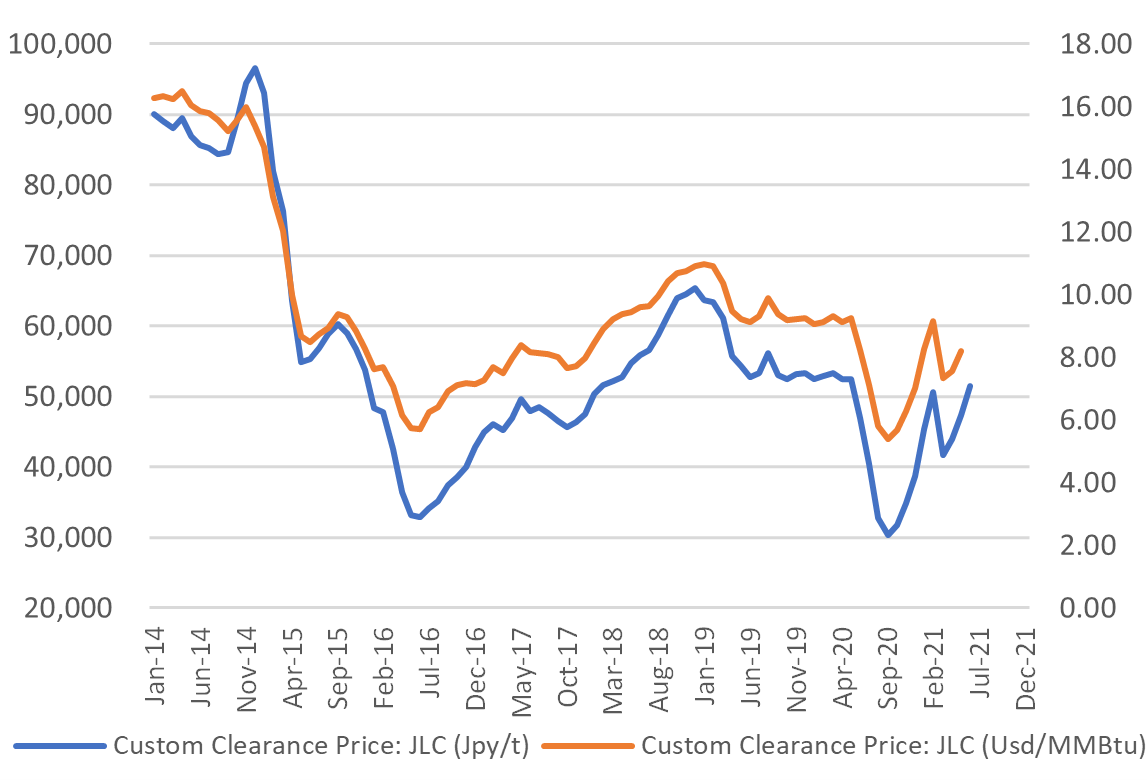

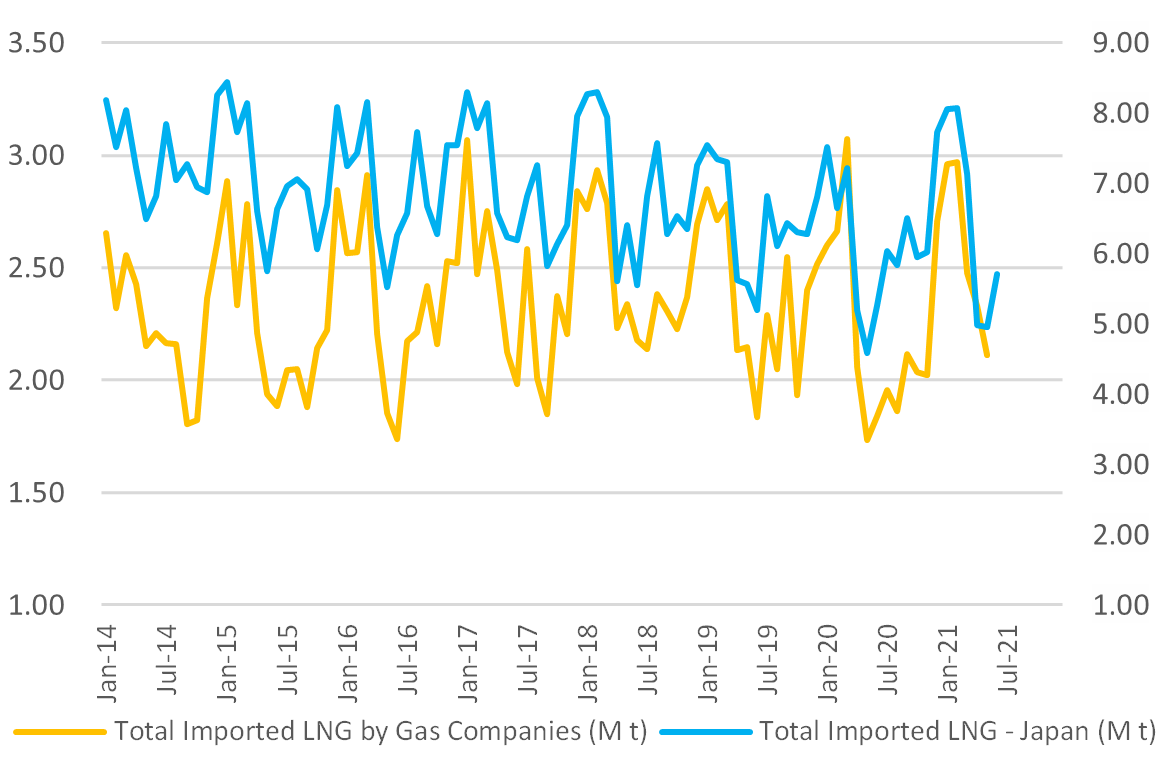

Japan LNG Price

LNG Imports: Japan Total vs Gas Utilities Only

Total LNG Imports (M t)

LNG Imports by Gas Firms Only (M t)

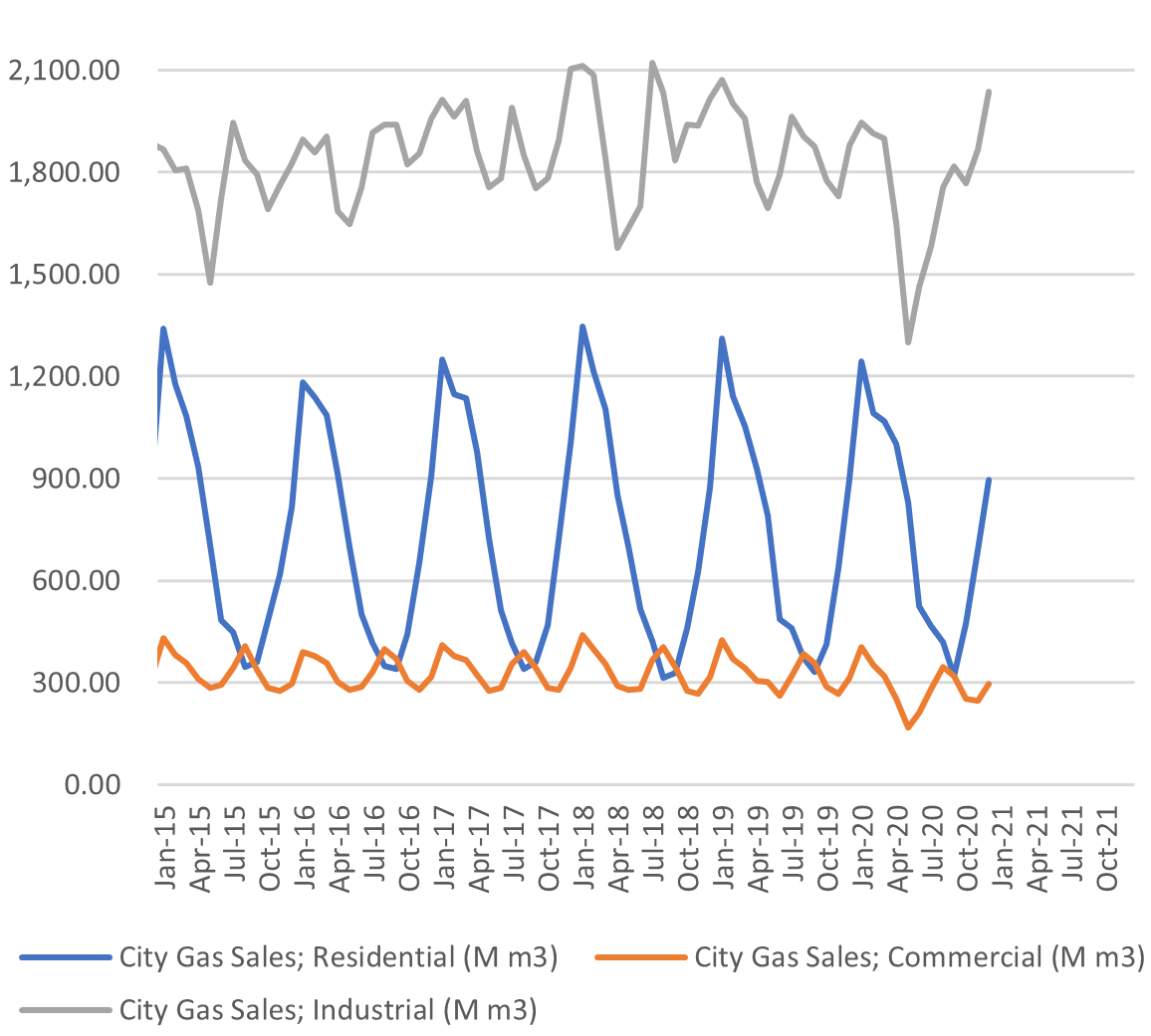

City Gas Sales – Total (M m3)

City Gas Sales by Sector (M m3)

SOURCES: Ministry of Economy, Trade, and Industry (METI),

Ministry of Finance

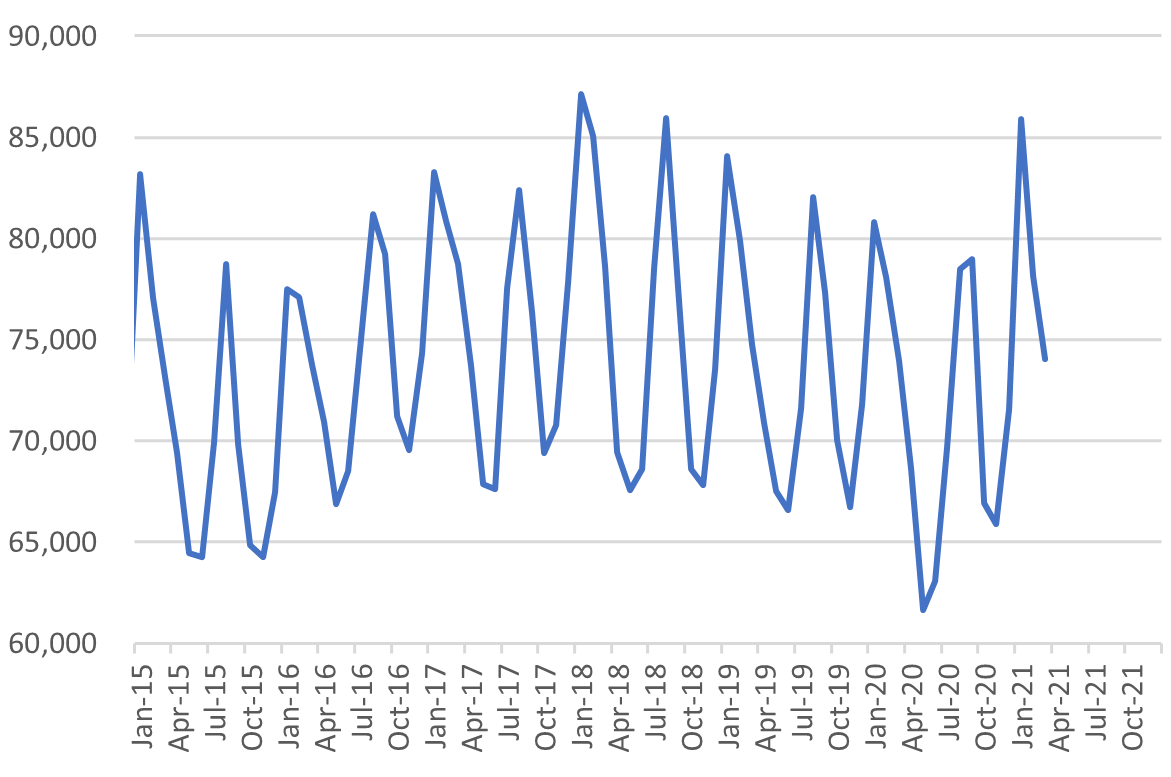

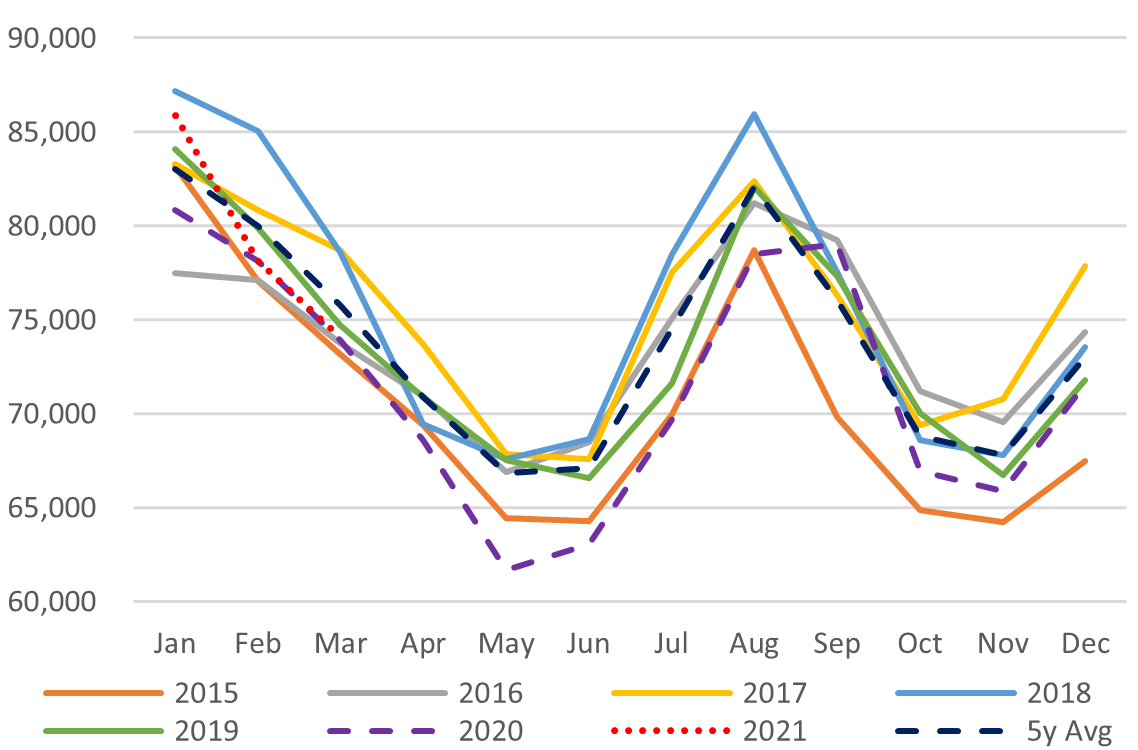

Japan Total Power Demand (GWh)

Current Vs Historical Demand (GWh)

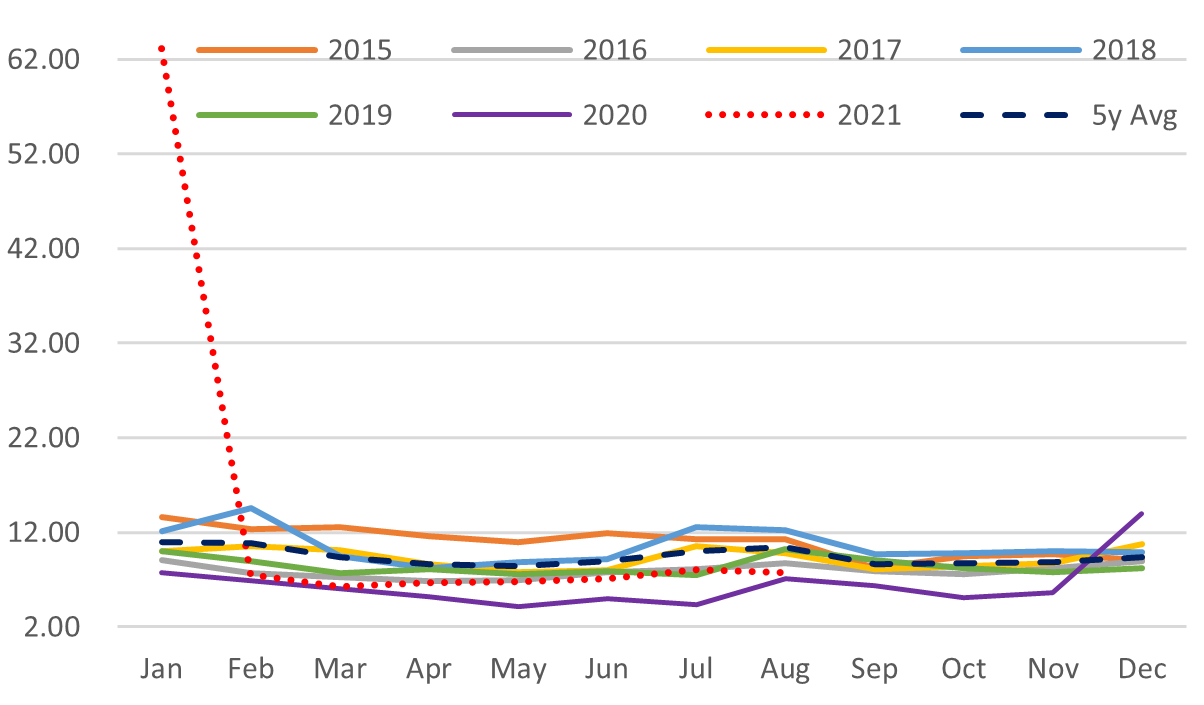

Day-Ahead Spot Electricity Prices

Day-Ahead Vs Day Time Vs Peak Time

LNG Imports by Electricity Utilities

LNG Stockpiles of Electricity Utilities

SOURCES: Ministry of Economy, Trade, and Industry (METI), and the Japan Electric Power Exchange

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.