JAPAN NRG WEEKLY

DEC. 20, 2021

JAPAN NRG WEEKLY

Dec. 20, 2021

NEWS

TOP

- MoE asks J-Power to add abatement options to coal plant; and warns that the aging station should close if this cannot be done

- METI wants to build regulatory, market rules for storage batteries; but ministry experts say fixing power markets is more urgent

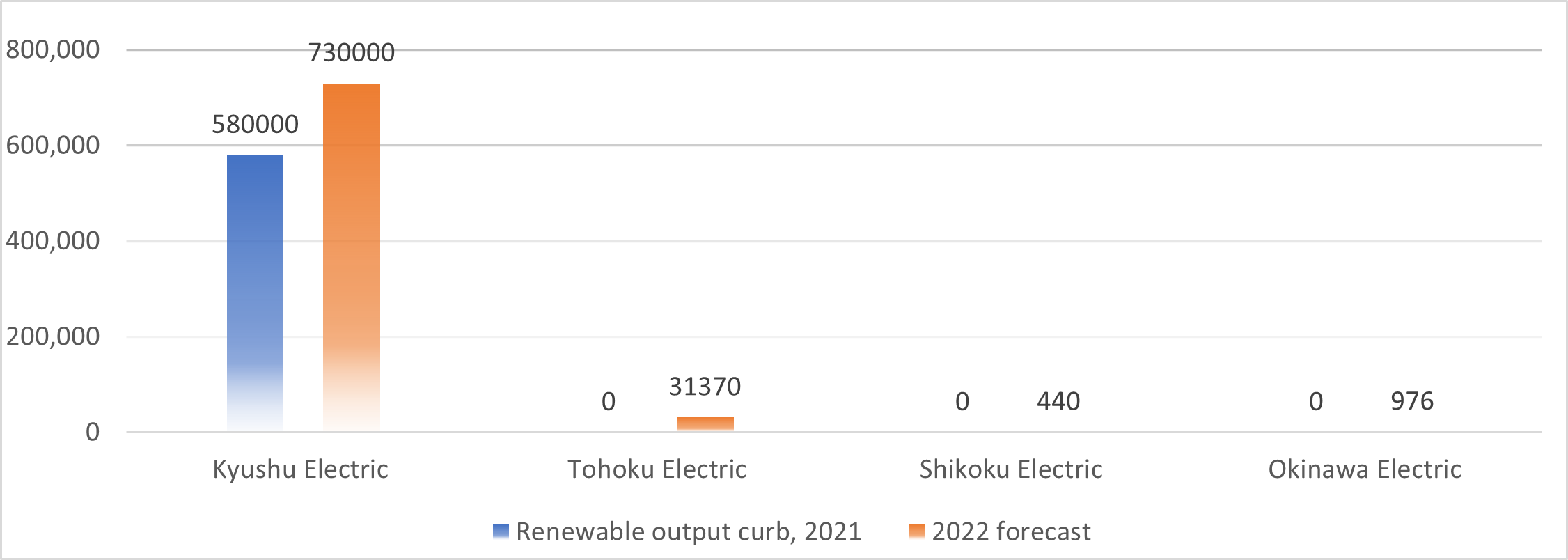

- Kyushu Electric says it may curtail 730 GWh of renewables power next year as METI tells local grids to limit thermal plants’ output

ENERGY TRANSITION & POLICY

- Japan seeks to make TCFD part of corporate governance system

- Peccell Tech to launch Japan’s first mass output of perovskite solar

- Green Innovation Fund adds six more research projects to review

- NTT unit, Sumitomo Mitsui Trust start $1 bn fund for renewables

- Japan’s top two airlines vow to use SAF for 10% of fuel by 2030

- New Mitsubishi Corporation CEO pledges to boost renewables

- Kawasaki Heavy in talks with RWE to build hydrogen-only turbine

- Kansai Electric to electrify biomass fuel supply vessel … [MORE]

ELECTRICITY MARKETS

- Japan launches another offshore wind power tender in Akita

- Kyushu Electric restarts Unit 1 at Sendai nuclear power plant

- Tokyo Gas: 2 GW gas/hydrogen co-firing plant to start in 2028; Co. to invest ¥40 billion intro storage battery R&D this decade

- Japan may guarantee income of hydrogen/ammonia generators

- JERA renegotiates power purchasing contract with TEPCO EP; and hastens restart of aging gas plant to avert capacity shortages

- Power bills to remain at highest in years through February

- Mitsubishi strikes one of Japan’s biggest offsite PPA with Lawson

- Tokyu Land increases stake in solar developer Renewable Japan

- Toshiba develops AI for power market trading … [MORE]

OIL, GAS & MINING

- High LNG prices cause fuel oil orders to triple in Japan

- Osaka Gas to enter India’s city gas market, seeks local partner

- Mitsui OSK, Vopak to jointly operate FSRU at new LNG terminal

ANALYSIS

2021: A YEAR IN ENERGY,

SUMMARY OF MAIN EVENTS ACROSS SECTORS

We look back at some of the year’s key events in the major energy sectors.

COAL On the brink of exit, but stays a strong part of the energy mix, even as major changes beckon

HYDROGEN Interest grows exponentially as tech edges closer to commercial levels

LNG Often slammed as one more fossil fuel, gas has also been a rock for the economy that won’t disappear

NUCLEAR Best year for industry in over a decade as restarts are followed by deals and state financing

SOLAR A difficult year for the industry as tariffs drop but costs rise amid pivotal changes for top players

WIND Most popular sector by far, but deadlines for project development are already starting to slide

BIOMASS Once driven by power generation, it is now seen as the savior for aviation and waste management

GEOTHERMAL Interest is there; opportunities not so much as potential is still stifled by procedures

OTHER Batteries, CCS, EVs and FCVs, and Direct Air Capture have all had a breakout year in Japan

GLOBAL VIEW

France shuts down 6 GW of nuclear capacity on pipe corrosion. German gas inventories drop to record low. HSBC tells clients to exit coal. EU emissions credits hit another record. Australia fast-tracks $10 billion green hydrogen project. Turkey gets loan for 380 MW of new geothermal capacity. More details and other stories in our global wrap.

WEATHER OUTLOOK

Japan weather forecasters say expect higher-than-average snowfall mid-December to mid-January and a temperature drop across most of the country from around Dec. 23.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Tom O’Sullivan (Japan, Middle East, Africa)

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

Sponsored

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYM

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

METI proposes new thermal power plants run at 20-30% to avoid curbs of renewables

(Japan NRG, Dec.15)

- New and upgraded thermal power plants will run at rates of 20-30% during low demand days to minimize curtailment of output from renewable energy sources, METI told the power transmission systems working group.

- Older plants will be asked to run at 30-50%, but power plants inside factory complexes (in-house power generation) won’t be restricted. Plant run rates will be disclosed in the event that renewable operators curb output.

- Kyushu Electric Power Transmission and Distribution, which has curtailed output from renewable power plants the most of any utility in Japan, asked solar and wind generators to curb output 44 times so far in 2021. This resulted in total output curtailment of 580 GWh, or 4.6% of the region’s total renewable output. The company forecasts that it may curtail as much as 730 GWh of green electricity in 2022 due to expanding solar capacities.

- This year, other regions didn’t experience renewable output curbs but major utilities say it’s possible this will occur in 2022.

- Kyushu Electric said if its thermal plants ran at 20% operational capacity, then renewables would be asked to curb 1% less output. This would also result in a CO2 reduction of 70,000 tons and ¥800 million in saved fuel costs.

- METI stressed that renewable operators with online connections to the grid transmission systems will face less risk of output curbs as they’ll be able to react quicker when conditions change.

TAKEAWAY: This is quite a big victory for the non-EPCo sector in Japan. Regional grids previously told METI that older thermal and nuclear power plants couldn’t be flexible with run rates. Gas turbine combined-cycle (GTCC) LNG plants with high energy efficiencies are designed to run at minimum 50% rates. Critics, however, said that allowing older thermal plants to operate without restriction would discourage new green investments in Japan, leaving the country struck in a cycle of having to rely on those older plants to the end of their life cycle. Aside from the environmental issues, it was argued to METI that this is not healthy in terms of energy security.

Volume of Renewable Output Curbs (in MWh)

METI to build regulatory and market frameworks for power from storage batteries

(Japan NRG, Dec. 15)

- METI plans to build regulatory and market frameworks for power supplies that become redundant in times of low demand, so that they can be stores in batteries until demand picks up, a METI official told the power transmission systems working group.

- The scope and specifications of battery-stored power will be defined in the Electricity Business Act. METI will also configure market mechanisms to sell the power.

- A working group member and Tokyo University Professor Matsumura Toshihiro said METI could change priorities. There are flaws in the present market mechanisms that need to be addressed, notably the disconnects between the wholesale and retail markets. This must come first before building a scheme for storage batteries.

TAKEAWAY: Prof. Matsumura is not alone in raising concerns that METI may possibly be neglecting immediate issues while focusing on future big-budget projects. Various current electricity “market mechanisms” (such as a capacity market) were artificially created by METI rather than building on existing trade practices. This leaves the ministry continually fine-tuning the market rules and mechanisms based on close exchange of views with market stakeholders.

That said, creating rules within which standalone batteries could operate and be part of the energy system would welcome new entrants to the market and help offset grid disbalances.

Japan needs to move fast in batteries or see another sector become reliant on overseas suppliers. In November, Tesla launched sales of Powerwall storage battery systems for Japanese homes, at ¥1 million for 13.5 kWh, or one third the price of local products. Tesla also plans to build a battery-based power station in Hokkaido.

TCFD’s growing role in Japan’s corporate governance

(Japan NRG, Dec. 16)

- Climate impact reports according to the Taskforce for Climate Financial Disclosure (TCFD) format are becoming mandatory rather than voluntary, said Nagamura Masaaki of Tokio Marine Holdings at the De-Carbon Management Forum of the MoE.

- Financial authorities are pushing a wider rollout of TFCD to Japanese businesses beyond the biggest listed companies.

- The Bank of Japan and the Financial Services Agency aim to make the TFCD system a part of Japanese corporate governance.

- CONTEXT: Over 500 companies have endorsed TCFD as of November 2021, making Japan the system’s world’s largest supporter. Also, Scope 3 emissions are increasingly important in the disclosures. Banks will be required to disclose emissions of companies and projects they’re financing; and insurance companies will have to disclose the emissions of customers’ insurance policies.

Peccell Technologies to launch Japan’s first mass production of perovskite solar cells

(Japan NRG, Dec. 16)

- Yokohama-based Peccell Technologies will launch Japan’s first mass production of perovskite solar cells in spring 2022.

- It will make customized table-cloth sized modules with an initial production run planned for up to 1 GW in total output.

- The modules can be installed in buildings, such as in walls. They look similar to Poland’s Saule inkjet-printed products that were commercialized earlier this year. But the Peccell modules have different structures and their energy efficiency is 15% higher than those from Saule, a company official said.

- CONTEXT: Polish firm Saule Technologies, the world’s first company to commercialize perovskite solar cells, has actually received funding from Sawada Hideo, the chairman of HIS Co., one of Japan’s largest travel and hospitality companies.

- SIDE DEVELOPMENT:

- Robotics to revolutionize perovskite cell production

- (Nikkei X-Tech, Dec. 14)

- While the invention of the perovskite solar cell was a major breakthrough, inventor Miyasaka Tsutomu says manufacture on a commercial scale is difficult, as the slightest variation can impact cell efficiency.

- Earlier this year, Miyasaka invented a robotic system able to uniformly deposit perovskite films, thereby ensuring reproducibility and high efficiency. Cells manufactured using the technique have an efficiency of over 15%.

Green Innovation Fund adds six projects to review

(Japan NRG, Dec. 14)

- METI is reviewing six potential new research projects for the Green Innovation Fund to develop breakthrough decarbonization technologies: producing fuel from carbon, carbon separation and collection, computing systems to improve vehicle energy efficiency, smart mobility systems, reducing carbon in industrial waste treatment, and carbon absorption and reduction in food supply chains.

- To fund the new projects, the Green Innovation Fund’s reserve, set aside for potential game changers, will be decreased to 20% from 30% of the total ¥2 trillion allocated to the Fund. An experts panel will decide by March 2022 whether to go ahead with the above projects.

- Allocated already is ¥1.33 trillion for 11 projects that include hydrogen steel, offshore wind, perovskite solar cells, ammonia and hydrogen supply chains, green cement and concrete, and next-generation storage batteries. Funding is for the next 10 years but will be cut if projects fail to meet milestones; accelerating research is the key goal.

TAKEAWAY: Changing Japan’s food supply chains by reducing Scope 3 emissions, improving process efficiency and using more local supplies are all relevant to Japan’s commitment to the Inter-governmental Science Policy Panel on Biodiversity (IPBES), which will update its goals in 2022. Japan ranks second after the U.S. as the country generating most harm to global nature through food imports, according to the Institute of Global Environment Studies (IGES).

NTT unit, Sumitomo Mitsui Trust start $1 Bn fund for renewables

(Kankyo Business, Dec. 15)

- NTT Anode Energy, a unit of telco giant NTT Group, Century Tokyo Corp, Sumitomo Mitsui Trust Bank, and Sumitomo Mitsui Trust Investment jointly established a fund to acquire renewable energy projects worth a total of ¥100 billion.

- The fund’s official name is NTT, TC, SuMi Green Energy No.1 Investment Business Ltd Partnership.

- NTT Anode Energy promotes locally-produced and locally-consumed energy by using NTT Group’s ICT and DC power supply technology and assets such as telecom buildings.

Japan’s two major airlines pledge to use SAF for 10% of all aviation fuel by 2030

(Zaiten, December edition)

- ANA and JAL, Japan’s two major airlines, joined the “Clean Skies for Tomorrow Coalition” in September, which aims for a wider rollout of Sustainable Aviation Fuel (SAF). The two companies signed the pledge to have SAF account for 10% of total fuel by 2030, up from just 0.03% now.

- CONTEXT: CO2 emissions from SAF are about 80% lower than the fuel now used by the airlines.

- ANA and JAL estimate that to reach net-zero by 2050, they need at least 23 million kl a year. At present, domestic production of SAF is negligible, which makes it hard for the airliners to introduce it into operations. Thus, they want to speed up SAF production.

- At present, ANA uses SAF on a freight flight between Narita and Frankfurt. The supplier is Nestle, working with Nippon Express, Kintetsu World Express and Yusen Logistics.

“Clean Energy Strategy” panel hold inaugural meeting

(Japan NRG, Dec. 16)

- METI advisors on “Clean Energy Strategy” held their first meeting on Dec. 16, which was joined by members of the Green Transformation Panel and 2050 Carbon Neutrality Panel of ANRE. The Clean Strategy will come up with technology transition scenarios on both the supply and demand sides to meet carbon neutrality goals.

- Companies lack the financial resources to achieve green transformation and so it needs to be done in stages, one of the advisors urged.

- The meeting agendas includes:

- Building global ammonia supply chains partnering with countries heavily dependent on coal power,

- Structural changes in the manufacturing sector,

- Households developing diversified energy sources, more resilient to power cuts,

- Pass on the costs of new energy infrastructure without straining stakeholders and consumers

New Mitsubishi CEO pledges to boost renewables

(Jiji, Dec. 17)

- Nakanishi Katsuya was appointed CEO of Mitsubishi Corporation. Former CEO Kakiuchi Takehiko moves to the position of chairman.

- Nakanishi says he’ll ramp up efforts to restructure the company and bolster its renewable energy business.

Kawasaki preparing to run power station on pure hydrogen

(Kankyo Business, Dec. 13)

- Kawasaki Heavy Industries is in talks with Germany’s RWE Generation to construct a 30 MW gas turbine to be powered entirely by hydrogen.

- The trial would be the first of its type in the world.

- The parties aim to fire up the turbine in 2024.

Kansai Electric plans to electrify biomass fuel supply ship for its generation unit

(Denki Shimbun, Dec. 15)

- Kansai Electric will introduce an electric propulsion ship to transport fuel for its Aioi Biomass Plant.

- The plant is converting its No. 2 reactor from fuel oil and crude oil to wood pellets, and is scheduled to start operation in January 2023.

- In conjunction with the conversion, one of the four vessels used to bring supplies to the plant will be an EV hybrid. This will be the world’s first electrified biomass fuel carrier.

Sojitz gets MoE funding for hydrogen project in Queensland

(New Energy Business News, Dec. 16)

- MoE selected Sojitz to receive state subsidies to develop hydrogen projects overseas.

- Sojitz will work with the local government on a project to produce hydrogen from renewable energy in Queensland, Australia, and will also develop mobile hydrogen stations, hydrogen storage alloys to transport the fuel, and stationary small fuel cells and hydrogen fueled ships in Palau, Western Pacific.

- This project will be subsidized by Japan’s MoE in order to promote the bilateral credit system (JCM), which aims to cut emissions in developing countries with the latest decarbonization technologies and obtain carbon offsets under the JCM scheme.

SoftBank co-develops lithium battery with 2x capacity of lithium-ion

(Nikkei; Dec. 15)

- SoftBank Corp. and Japan’s National Institute for Materials Science have developed a lithium-air battery with approximately twice the capacity of current lithium-ion batteries.

- These batteries are a promising option for drones and other applications as the tech is easy to miniaturize.

- They plan to bring the battery to market in the next five to 10 years.

Japan Renewable Energy Corp’s CEO says more needs to be done to meet climate targets

(Bloomberg, Dec. 16)

- Japan’s government isn’t doing enough to meet 2030 and 2050 climate targets and policies lack clarity, said CEO Takeuchi of Japan Renewable Energy Corp.

- The govt. should ease the permit process and help clean energy firms gain access to land.

- CONTEXT: JRE was acquired by ENEOS this summer for $1.8 billion.

- Takeuchi hopes JRE will develop synergies with ENEOS’s retail electricity and battery storage businesses.

Obayashi moves New Zealand hydrogen project to early commercial stage

(New Energy Business News, Dec. 16)

- Obayashi Corporation started test sales of the fuel produced by its 1.5 MW hydrogen plant in New Zealand, to be offered to public transport and vehicles in logistics facilities, as well as for industry.

- The hydrogen plant is powered by geothermal energy and can produce 100 tons of green hydrogen per year (equivalent to 1,000 fuel cell vehicle tanks).

Nippon Steel mulls acquiring Thai steel mills in bid to go green

(Nikkei, Dec. 13)

- In 2022, Nippon Steel is considering buying major Thai steel manufacturers G Steel and GJ Steel in a deal worth as much as ¥100 billion.

- G Steel and GJ Steel use electric arc furnaces with less CO2 emissions than the blast furnaces that now produce 90% of Nippon Steel’s output.

- G Steel and GJ Steel have combined annual output of over 3 million tons, which is more than what’s produced by Japan’s largest arc furnace operator (Tokyo Steel).

Toyota ramps up EV plans, aims for 3.5 million units sold in 2030

(Nikkei, Dec. 14)

- Toyota Motor expects to sell 3.5 million EVs globally in 2030, marketing 30 models.

- The automaker will allocate ¥8 trillion ($70.4 billion) this decade to R&D as well as capital investment in electric, hybrid and fuel cell vehicles. Half will be spent on EVs, the first time Toyota has earmarked funding for this purpose.

- This target exceeds original plans for 2-million-unit sales in 2030 and 15 EV models.

- Toyota’s luxury brand Lexus will accelerate the move to EVs as there is strong demand in the market’s high end. Lexus will be centered on battery EVs.

- By 2030, battery production capacity will rise to 280 GWh, 40% more than previous plans.

- Toyota said it secured enough supplies of battery raw materials including lithium to meet its needs until 2030 via associated trading house Toyota Tsusho.

Japan fashion industry looks for a green makeover

(Asia Nikkei, Dec. 14)

- The fashion industry will embrace recycled materials, thinner shoe midsoles, and slash the amount of water used to make clothes and accessories.

- CONTEXT: The fashion sector is ranked as the world’s second most polluting industry, sucking up water for processes like dyeing and generating waste such as unused fabric.

TEPCO investment unit sets up second fund targeting drinks companies

(Denkin Shimbun, Dec. 15)

- TEPCO Timeless Capital, an investment unit in the TEPCO group, will invest about ¥27.8 billion over 7.5 years into SMEs in the drinks and bottled water sector.

- So far, Timeless Capital has acquired Cosmo Life, which manufactures and delivers natural water under the Cosmo Water brand, and operates a water purification business.

OPINION: Essential perspectives in understanding Japan’s energy security

(Toyo Keizai opinion, Dec. 13)

- CONTEXT: Toyo Keizai is one of the best-selling business weeklies.

- At COP26, PM Kishida didn’t commit to the abolition of coal-fired power stations due to concerns about energy security. Despite reliance on imports, many in Japan still don’t grasp energy security.

- Japan needs to learn from Europe’s experience where a recent power shortage was due to poor output from wind farms and other renewables.

- EU Commission President Ursula von de Leyen said that nuclear energy and natural gas are needed to solve the European energy crisis, and that both could be categorized as clean forms of energy.

- By failing to take a clear position on nuclear energy, Japan has lost the chance to participate in the debate over its future. While China and Russia are implementing state-led projects to develop small modular reactors (SMR), in Japan the development of this technology has been left to the private sector, causing it to lag behind

- Energy policy is crucial to a nation’s existence and should involve the pooling of both public and private sector resources. The Fukushima disaster shows how top-down bureaucracy jeopardizes a nation’s energy security.

OPINION: Solar developments responsible for deforestation, landslides

(Nikkei opinion, Dec. 13)

- CONTEXT: Nikkei is Japan’s biggest business daily.

- In August, work to prepare a solar farm site in Kumamoto triggered a landslide after the contractor failed to build a mandatory retention basin. Up to 10,000 m3 of earth was dislodged in the incident.

- The landslide was the latest in a string of such incidents since the feed-in tariff (FIT) scheme began for solar generators.

- NEDO plans to issue guidelines to ensure better drainage on solar farms built on inclined land. But understanding of these issues is limited and it remains to be seen whether the guidelines will be properly implemented.

One-Dot News:

- Idemitsu took delivery of ammonia derived from natural gas from producer Abu Dhabi National Oil Company (ADNOC). The ammonia was transported in an ISO tank container and is part of plans to build a blue ammonia supply chain between UAE and Japan. (Denki Shimbun, Dec. 14)

- INPEX bought a 9.9% stake in a geothermal power generation business in Indonesia. The 85 MW Muara Labo geothermal power plant is in the Sumatra area and began operating in December 2019. The acquisition price is not disclosed. (Denki Shimbun, Dec. 17)

- Nippon Koei will enter the wind power business in American Samoa. The company seeks to install a 42 MW onshore wind power facility and storage batteries (40 MWh) in the western part of Tutuila Island, a major island in American Samoa, in cooperation with Renova, a Japanese developer and operator of renewable energy. (Kankyo Business, Dec. 15)

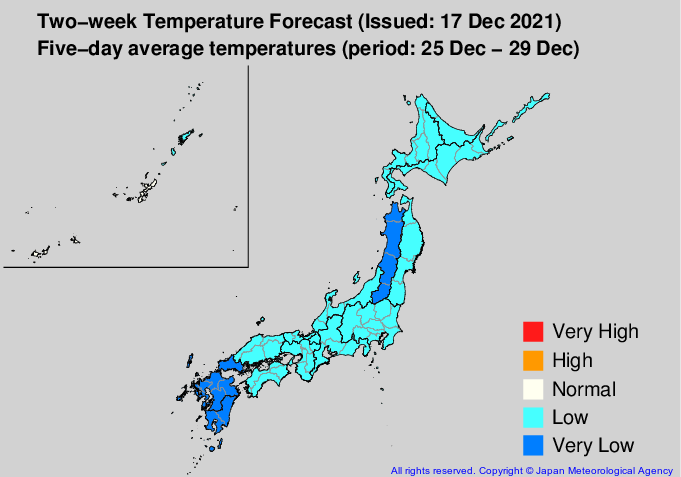

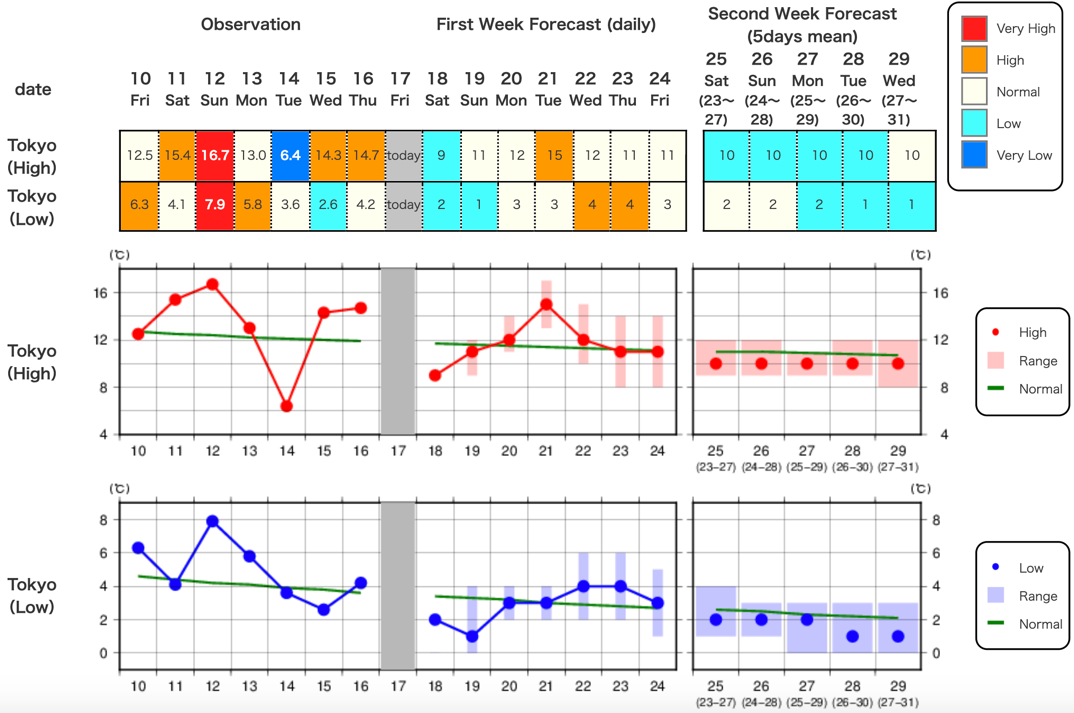

WEATHER OUTLOOK

TWO-WEEK TEMPERATURE FORECASTS (DEC. 17~ DEC. 29)

Nation-wide

Tokyo area

- North/ West Japan: Lower-than-average temperatures for the next 2 weeks, but especially cold from Dec. 23. Heavy snowfall in the Sea of Japan side from Dec. 23.

- Kanto/ Tokai/ North Japan/ Okinawa/ Amami Region: Very cold temperatures from Dec. 23.

- Winter Forecast: Japan’s Metrological Agency (JMA) said it expects higher-than-average snowfall in northern, eastern, and western Japan on the Sea of Japan side from mid-December to mid-January.

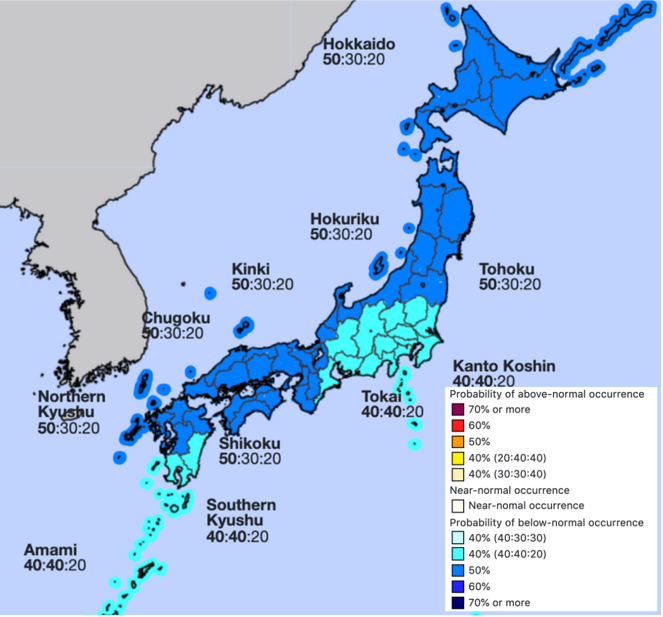

ONE-MONTH SEASONAL FORECAST (DEC. 18~ JAN. 17)

NEWS: POWER MARKETS

|

No. of operable nuclear reactors |

33 |

Electricity Price |

Friday, Dec. 17 |

% Change WoW | ||

|

Of which |

restarted |

10 |

JEPX 24-Hour Spot |

¥16.74/ kWh |

-7.87% | |

|

in operation today |

9 |

TOCOM Jan. baseload (Tokyo area) |

¥25.33/ kWh | |||

Source: Company websites, JANSI and JAIF, as of Dec 20, 2021

Environment Ministry asks J-Power to add abatement options to coal plant in Kyushu

(Denki Shimbun, Dec. 17)

- MoE urged METI to consider environmental grounds when reviewing plans from J-Power to upgrade its coal-fired Matsushima station in Saikai City, Nagasaki Prefecture.

- CONTEXT: This is the first time in three years that MoE submitted an opinion on coal-fired power plants. It previously stopped making such suggestions after industry push back.

- CONTEXT: Matsushima Thermal Power Plant is one of the oldest coal-fired power plants in Japan. It began operation in 1981.

- MoE recommends J-Power to introduce fuels that don’t emit CO2 when burned into the Matsushima station’s fuel mix. This refers to biomass or ammonia and the MoE says it should be done as soon as possible.

- The MoE also said that “all options” should be considered, including decommissioning the plant if it can’t be operated in line with Japan’s GHG emission reduction plans.

- J-Power plans a coal gasification facility for Matsushima, construction to begin in 2024.

TAKEAWAY: Given Japan’s commitments at COP26 and before, it would be a surprise if METI and J-Power push against MoE’s suggestions. In fact, J-Power suggested that it would burn ammonia together with coal at one of the two units of the 1 GW Matsushima station from around 2026/27. However, MoE’s comments may be trying to accelerate the timeframe. J-Power’s reaction is worth monitoring.

Japan launches offshore wind tender in Akita Prefecture

(Kankyo Business, Dec. 15)

- METI and the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) launched a tender to develop offshore wind power projects in Akita Prefecture.

- Application deadline is June 10, 2022. Results will be announced in December 2022.

- An online session will be held Dec. 23 to explain submission guidelines.

- The lower limit capacity to be developed in the area is 285 MW and the upper limit is 356 MW. The price ceiling is ¥28/ kWh with a guaranteed purchasing period of 20 years.

- Wind turbines are expected to be mounted to the seabed.

Sendai NPP to start sending power to the grid on December 20

(NHK, Dec. 14)

- Shikoku Electric will restart its Sendai Unit 1 reactor on Dec. 18 and begin power transmission on Dec. 20.

- The plant went offline for regular inspection on Oct. 17. The reactor finished most of its inspection on Dec. 14.

- The operator will increase output and plans to resume normal operation in Jan 2022. The plant reaches its 40-year operation license in July 2024.

- Meanwhile, a special inspection is scheduled for its Unit 2 reactor in late Feb 2022. Unit 2 will reach its 40-year operation license in 4 years.

Tokyo Gas: 2 GW Chiba gas and hydrogen co-firing plant to start as early as 2028

(Nikkei, Dec. 15)

- Tokyo Gas and the Kyushu Electric said their planned LNG-fired power station in Chiba might start generating electricity in 2028.

- The new power station will have an output of 2 GW.

- The plant will have co-firing with hydrogen or ammonia to reduce GHGs.

- Tokyo Gas CEO Uchida said he planned to progressively replace all of the utility’s Japanese and overseas assets.

- He also said that technological breakthroughs will be needed if Tokyo Gas is to achieve its zero emissions goal by 2050.

- While Tokyo Gas strives to be a majority stakeholder in solar and onshore wind ventures, Uchida said that in offshore wind it will only be a minority investor due to a lack of experience with the technology.

- SIDE DEVELOPMENT:

- Tokyo Gas to invest ¥40 billion over this decade into new storage battery R&D

- (Yomiuri Shimbun, Dec. 15)

- Tokyo Gas plans to invest around ¥40 billion to develop storage batteries by 2030.

- Storage batteries are essential for the spread of renewable energy, and Tokyo Gas wants to work with overseas firms on R&D in this area.

- This decade, Tokyo Gas plans to invest ¥600 billion in renewables in Japan and overseas.

- SIDE DEVELOPMENT:

- METI to guarantee income of hydrogen, ammonia generators

- (Nikkei, Dec. 14)

- METI is discussing a plan to guarantee operators of hydrogen and ammonia fired power stations a minimum level of revenue for at least 10 years.

- The plan, slated for introduction in 2023/24, will foster investment in these technologies, thereby avoiding power shortages while reducing Japan’s carbon footprint.

- This in effect creates a capacity market for plants that work on hydrogen/ ammonia fuel.

- The government is also considering whether to cover investments to decarbonize existing thermal plants and to extend the operating life of existing nuclear power plants.

- Currently, new nuclear plant construction or the rebuilding of nuclear plants at existing sites is still not on the government’s agenda.

TAKEAWAY: Nothing kickstarts a sector’s growth like guaranteed income. We expect Tokyo Gas to be joined by a string of other utilities in announcing commercial-scale co-firing power stations over the next year.

JERA and TEPCO renegotiate purchasing agreement to avoid power shortages

(Nikkei Energy Next, Dec. 14)

- JERA head Noguchi Takashi says last winter’s electricity price spike led to renegotiating its power purchase agreement with TEPCO Energy Partners.

- Noguchi explains that deregulation means roughly a third of TEPCO EP subscribers have since switched to independent electricity retailers, making it more difficult for JERA to forecast demand trends in greater Tokyo.

- Since JERA is the region’s largest supplier it absorbs blips in supply or demand, but the many unknown variables mean this is no longer the case, says Noguchi.

- Under its previous agreement with JERA, TEPCO EP could order additional electricity in an hour’s notice. (While lead time on an LNG order is 2-3 months.)

- To sell surplus electricity on the exchange to consumers in greater Tokyo, JERA previously went through TEPCO, unable to supply the market directly.

- Under the revised PPA, TEPCO EP must inform JERA of requirements for a given day before the start of bidding on the energy spot market the day before. This allows JERA to release all surplus capacity to the spot market.

- Noguchi is critical of the state of the JEPX spot market. You could spend ¥10 billion buying LNG on the spot market, but it would only yield ¥5 billion worth of electricity, he says.

- To avoid a repeat of last year’s power shortages, power producers must alert the market before LNG becomes scarce again, says Noguchi.

- SIDE DEVELOPMENT:

- JERA to restart aging station amid fears of power shortages

- (Nikkei, Dec. 16)

- JERA carried out repairs on the long-idle Unit 5 at its Anegasaki power plant in Chiba, which it plans to restart in January to avert power shortages.

- The 600 MW unit can power 1.7 million households.

Top utilities like Chubu Electric are marketing local green electricity to local businesses

(Zaiten, December edition)

- CONTEXT: This article shows how the big power utilities, EPCos, are trying to tap into the local-power-for-local-people dynamic promoted by the government, while also using that to move a little more into renewables.

- In March 2020, Chubu Electric launched the “Shinshu Green Electricity Project,” which aims to raise the value of local companies by helping them procure locally-sourced electricity from renewables, thus lowering their CO2 footprint.

- In August, Chubu Electric offered “green” electricity plans in Mie Prefecture, followed by Shizuoka Prefecture in September and Gifu Prefecture in November.

- Much of Chubu Electric’s green electricity plans are based on local hydropower.

- The first company to buy green electricity in Gifu was Jyuroku Financial Group, which claims that powering its HQ with renewables reduced annual CO2 emission by 754 tons.

TAKEAWAY: While we often focus on the supply side, it’s important to keep an eye on consumers who are literally buying into the “green revolution” in Japan. The initial wave over the last 1-2 years was from large corporates. Now, the rollout of green electricity plans by big utilities is bringing local firms and SMEs into the space. Those firms make up a far larger part of Japan’s economy and therefore can be a far bigger driver for demand for electricity from renewable sources.

Power bills to remain high through February

(Nikkei, Dec. 17)

- The high price of LNG means electricity tariffs set by Japan’s three largest utilities are projected to rise around 4% between January and February.

- The average TEPCO Holdings subscriber can expect to pay ¥330 more in February for using the same amount of electricity.

Mitsubishi strikes one of Japan’s largest offsite PPAs with Lawson convenience stores

(Kensetsu Tsushin Shimbun, Dec.14)

- Mitsubishi Corporation struck one of Japan’s largest off-site PPA deals to supply 3,600 convenience stores of Lawson, Inc. with renewable energy.

- Mitsubishi will commission West Holdings (Hiroshima City) to build new solar power generation facilities and supply renewable energy to the stores.

- CONTEXT: Mitsubishi is Lawson’s biggest shareholder.

Tokyu Land Corporation increases stake in Renewable Japan

(Nikkei, Dec. 15)

- Tokyu Land Corporation (TLC) grew its stake in solar developer Renewable Japan after its listing on the Tokyo Stock Exchange’s Mothers market.

- This brings TLC closer to its sustainable development goals.

Toshiba develops AI for power-market trading

(jiji; Dec. 15)

- Toshiba developed AI to optimize renewable energy trading in wholesale power markets.

- The tech can predict the amounts of power generated and market prices, and propose strategies for selling energy.

- METI is testing the AI, and Toshiba plans to commercialize it depending on test results.

Subscription-based plan lowers bar to rooftop solar

(Kankyo Business, Dec. 16)

- Xsol, Power Next, and Osumi Hanto Smart Energy will collaborate to offer a subscription-based plan that allows subscribers to have rooftop solar panels and storage batteries installed for zero upfront expenditure.

- Subscribers pay less than ¥10,000/ month for the first 400 kW of electricity.

ENEOS invests in Vietnamese solar

(Sekiyu Tsushin, Dec. 15)

- ENEOS will invest in Vietnam’s first large-scale solar farm.

- It will acquire a 19% stake in the VKT-Hoa An Solar Plant.

- The 35-MW farm began feeding the grid last year.

NUCLEAR REACTOR WRAP:

- NRA releases images of Fukushima Units 1 and 3

- (NRA/YouTube, Dec. 10)

- The Nuclear Regulation Authority released images filmed inside the reactor buildings of Units 1 and 3 at Fukushima Dai-Ichi nuclear power plant.

- LINK and LINK to videos.

- SIDE DEVELOPMENT:

- Accident leaves two workers injured at the Genkai nuclear reactor

- (NHK, Dec. 11)

- A 10-meter-long reinforcing bar that weighs about 90kg fell from a crane at a construction site for the new “Emergency Response Building” at the Genaki reactor (Kyushu Electric). Two workers were slightly injured.

- The operator halted construction for the “Emergency Response Building”.

- Last month saw a fire at a building site for work on anti-terrorism measures.

- The date on when the construction will resume is unknown.

- SIDE DEVELOPMENT:

- Mayor asks for preventive measures after scandals at Genkai reactor

- (NHK, Dec. 13)

- Following a series of scandals at Genkai nuclear reactor (Kyushu Electric) the local mayor requested the operator to investigate the cause.

- SIDE DEVELOPMENT:

- Takahama nuclear to extend its work on safety measures: No impact on the restart

- (Mainichi Shimbun, Dec. 15)

- Kyushu Electric will extend safety measure work for Takahama Unit 2 reactor.

- The new end-date will be Jan 2022. The original plan was for December.

- Work on safety measures was temporarily hauled for 3 weeks in August, due to rising COVID-19 cases among workers.

- Operator says this will not affect the plant’s restart scheduled for July 2023.

- SIDE DEVELOPMENT:

- Nuclear disaster prevention drill to be held in Feb 2022 at Onagawa

- (NHK, Dec. 10)

- The national nuclear disaster prevention drill, postponed due to the pandemic, will be held at Onagawa nuclear power plant (Tohoku Electric) on Feb 2022. The drill was originally planned for last year.

- It will be held in the same situation as the 2011 Earthquake, considering both a natural disaster and nuclear accident.

- The operator will restart the plant when safety upgrades are complete.

TEPCO reports to METI on plans to release treated water from Fukushima

(Japan NRG, Dec. 14)

- Tokyo Electric Power Company (TEPCO) plans to construct an undersea tunnel to release treated water from its Fukushima nuclear plant, the company told the MoE panel monitoring the water release.

- The tunnel will be 1 km below sea level so that the sea water used for diluting the ALPS water will not mix with the released water.

- CONTEXT: Although processed by Advanced Liquid Processing System (ALPS) to remove radioactive elements, the water will still contain tritium.

- The ALPS water will be diluted to 1,500 becquerel/ liter of tritium contamination. TEPCO will also engage third-party inspectors to measure the water. The total tritium release will be under 22 trillion becquerel/ year.

- TEPCO will also grow olive flounder, sea shells and sea weeds in the area and will report how the ALPS water impacts the local ecology.

TAKEAWAY: The radioactivity level of the water is well below most international norms, but it is causing much consternation both at the local level and among some of Japan’s neighbors.

NEWS: OIL, GAS & MINING

Japan Oil Price: $76.81/ barrel

Japan (JLC) LNG Price: $11.61/ mmbtu

LNG prices causes fuel oil orders to triple

(Denki Shimbun, Dec. 17)

- Sugimori Tsutomu, chair of Petroleum Association of Japan and ENEOS, said it has three times the usual level of bids for heavy fuel oil used in power generation.

- This reflects high LNG prices, says Sugimori, because at current prices fuel oil is a cheaper source of electricity than LNG bought on the spot market.

Osaka Gas to enter India’s city gas market to tap decarbonization trend

(Reuters, Dec. 15)

- Osaka Gas plans to enter India’s city gas market as a part of efforts to expand overseas.

- It’ll be the first Japanese firm in India’s gas market. It could supply gas using trucks and pipelines, with vehicles, homes and industries as the end client.

- India is promoting wider use of natural gas to move away from coal. This includes giving operators exclusive marketing rights and infrastructure ownership for a certain period.

Mitsui OSK and Vopak to jointly operate FSRU at a new LNG terminal in Hong Kong

(Company statements, Dec. 16)

- Shipper Mitsui OSK and Dutch tank storage firm Vopak will own and operate a floating storage and regasification unit (FSRU) at a new LNG terminal in Hong Kong.

- Vopak will acquire 49.99% of the vessel owning company of Mitsui OSK (MOL) that owns the FSRU unit. The two companies will work together to provide jetty operations & maintenance and port services for the new FSRU-based offshore LNG terminal.

- The move will contribute to Hong Kong’s energy transition as they explore downstream opportunities for local bunkering of LNG.

- CONTEXT: The FSRU terminal is under construction and will be operational mid-2022.

ANALYSIS

BY YURIY HUMBER

2021: Summary of a Year Across Key Energy Industries

Japan started the year with an electricity price crisis, but also a new Green Growth Strategy that outlined new priorities in energy for many sectors. Since then, the prime minister and the Cabinet have changed, and a new Basic Energy Plan was published. As winter comes around, however, the same concerns about electricity shortages and prices have returned.

Below we look back at some of the year’s key events in the major energy sectors. With so much going on, we could not highlight all major events, but we hope this helps you review some of the important narratives in each sector.

Coal

After making a splash in summer of 2020 by signaling the closure of the majority of Japan’s coal-fired power plants within a decade, METI has largely failed to move forward with its plans. First came resistance from manufacturers, which own more coal-fired units than power utilities. Makers of chemicals, steel, concrete and other industrial goods claimed that shutting the in-house coal plants would leave them exposed to market prices for electricity, slashing profitability and increasing energy supply security risks.

Government panels and experts then spent months debating the best way to decide which coal plants should be closed. As things stand, very few coal plants will close soon. In fact, for all the coal capacity to be shuttered in coming years, more new capacity will be added. Proponents claim that the new coal-fired plants are cleaner and necessary to maintain power price stability, which in turn helps provide economic security for the country.

Adding carbon capture technology to coal-fired power plants is something engineering firms like Mitsubishi Heavy Industries are very keen to promote. Kansai Electric is one of the most enthusiastic utilities in this space.

This year a new direction for coal took root — the switching of coal power plants to co-firing ammonia or hydrogen. Japan’s government and big business are most comfortable with these solutions. Moving the fuel mix to 40% ammonia/ 60% coal can lower a power station’s CO2 emissions to the same level as if it were running on natural gas, and test are already under way in Japan and the U.S. While many questions remain, one thing seems certain — despite the wishes of many at COP26, coal will not be making an exit any time soon.

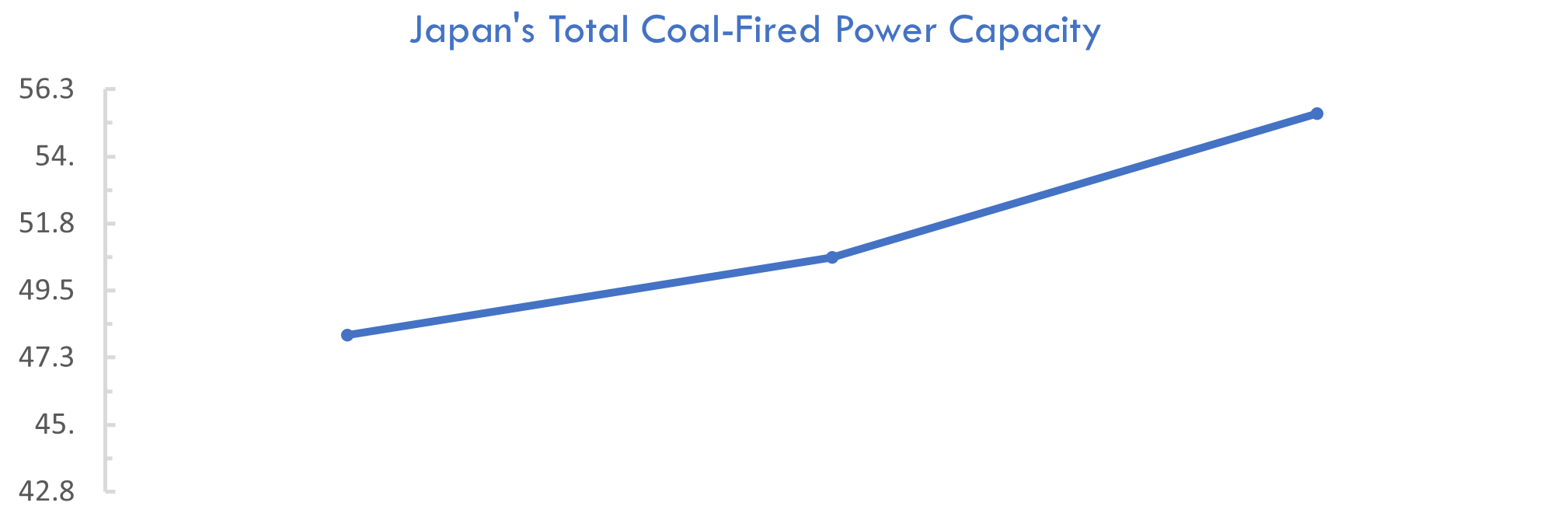

48 GW

July 2020

50.6 GW

July 2021

55.4 GW

December 2024

Hydrogen / Ammonia

The hydrogen industry has grown exponentially in the last year. Japan’s belief in hydrogen has always been strong, but it was solidified in the Green Growth Strategy and the Basic Energy Plan. The former called for ammonia to “dilute” the fuel mix at thermal power plants by 20% at the decade’s end. The latter claimed that hydrogen or ammonia will make up 1% of Japan’s power mix by 2030 – suggesting that roughly 3 GW of hydrogen-fired capacity would be online by that time.

The policies have been followed by quick action from the private sector. Power retailer Erex, which has ambitions of becoming a clean energy generation company, will launch Japan’s first hydrogen-fired power plant by April 2022. The 300 kW facility near Mt. Fuji is expected to deliver electricity to TEPCO Power Grid on a commercial basis, while also testing a new hydrogen production process that extracts it from rocks at ambient temperature.

On the transport side, Toyota launched an updated fuel cell electric vehicle; Tokyo city started to trial fuel cell buses, trucks and even garbage collection vehicles; and, major logistics companies began considering a fuel switch.

Hydrogen, however, has yet to find broad support for which form it should be produced in (MCH, ammonia, liquid hydrogen or other). Also, there are debates over which power sources should be used to manufacture it. Proponents of renewables only want ‘green’ sources to be used. Many in industry and METI prefer “blue” hydrogen made from coal or natural gas, with the CO2 sequestered and stored deep underground.

Hydrogen’s main challenge, however, is to establish a “normal” environment for transport and utilization, which also means how to store it. Kawasaki Heavy has prepared the world’s first hydrogen carriers. Iwatani is developing solutions for handling hydrogen at refueling stations. And Mitsubishi Heavy is working on a project in the U.S. to store 150 GW hours’ worth of energy in the form of hydrogen gas in an underground cavern carved into salt.

It’s certain that hydrogen will become mainstream this decade. It would be too much, however, to bet on the color and source of hydrogen. That’s why Japan’s strategy so far has been to diversify the geography of supply and manufacturing method as much as possible.

Countries That Signed Agreements with Japan to Deliver Hydrogen

LNG

Arguably the biggest beneficiary of the energy transition so far has been natural gas and its adjacent LNG industry. Once intrinsically tied to oil, this year natural gas evolved into a truly global market as weaker-than-expected performance from wind and hydro generation assets in Europe and in Brazil, among others, boosted demand.

In contrast, Japan’s LNG industry is in a confused state, ceding to China its title of top importer. The government’s latest Basic Energy Plan envisages cutting the use of LNG in power generation by half this decade. Even longer-term, the influential Gas Study Group at METI believes natural gas must seek decarbonization either through hydrogen co-firing, or methanation, or (where possible) carbon capture.

Lower purchasing volumes means less influence on global LNG markets, endangering energy security if rivals such as China lock up supplies with long-term deals. Experts warn that China’s impact on Japan’s LNG purchasing strategies can lead to higher prices.

Still, Japan’s position in LNG is not lost. METI forecasts that LNG purchases will grow 50% to 100 million tons by 2030. This is based on the idea that Japanese companies will control LNG infrastructure and end-users in other parts of Asia and will buy supply for the region.

Meanwhile, JERA last month flexed its muscle by rejecting a massive 5.5-million ton a year contract with Qatar, allegedly because of the latter’s unwillingness to allow the Japanese firm to divert cargos to other destinations. JERA has ambitions to be a major LNG trader as well as importer for Japanese consumers, and needs to manage its portfolio accordingly.

Other Middle Eastern suppliers who have been inflexible on where cargos are delivered have seen Japan’s LNG purchases decline in recent years. But, Qatar quickly found an alternative buyer in China, which puts JERA’s gamble into question.

Today, LNG costs translate into almost 60% of Japan’s electricity price. Until other generation sources increase output, LNG will be a bellwether for the Japanese market and electricity traders will pay as much attention to it as power market fundamentals.

The year’s big story for LNG was supposed to be the industry’s decarbonization. Japan was one of the top voices calling for a cleanup of methane emissions at production and transportation stages, and has been an enthusiastic supporter of the “carbon neutral” LNG market. However, the net-zero story has been overtaken by concerns about energy supply.

Nuclear

Japan’s nuclear industry had its best year in over a decade. Eight reactors (over 7 GW of capacity) restarted between mid-December 2020 and this summer. While the total number of units in operation is still in single-digits, last week’s bringing back online the first unit of Kyushu Electric’s Sendai NPP puts the number at nine.

A further three units could restart next year, as well as two or three more in 2023, but only if the facilities avoid further troubles and the fallout from ongoing scandals at TEPCO. In a best-case scenario, we might see 15 nuclear reactors operating in Japan in late 2023 and almost 20 units by mid-decade.

An even bigger boost for the industry was the restart of state funding for new nuclear technology, which included a 14% rise in nuclear R&D budgets for 2022. This money will mostly go to the Small Modular Reactor (SMR) program and the High Temperature Engineering Test Reactor (HTTR).

While building new nuclear power stations or replacing aging facilities with modern ones remains literally ‘radioactive’ for politicians, the contract won by GE-Hitachi earlier this month to supply its first ever SMR unit to a Canadian utility was a watershed. This was Japan’s first commercial win for next-generation nuclear technologies and raised expectations for greater acceptance of SMRs in Japan.

With the U.S., Canada, and parts of Europe moving to a much more favorable stance towards nuclear in the last six months, Japan’s ambivalence on the technology begins to look like the odd man out. While previous PM Suga kept a distance from nuclear in order to pursue a clean energy agenda more fixed on renewables, the new Kishida government has welcomed back some familiar faces known to be pro-nuclear.

|

No. of operable nuclear reactors |

33 | |

|

of which |

applied for restart |

25 |

|

approved by regulator |

17 | |

|

restarted |

10 | |

|

in operation today |

9 | |

|

No. of nuclear reactors under construction |

3 | |

|

No. of reactors slated for decommissioning |

27 | |

|

of which |

completed work |

1 |

|

started process |

4 | |

|

|

yet to start / not known |

22 |

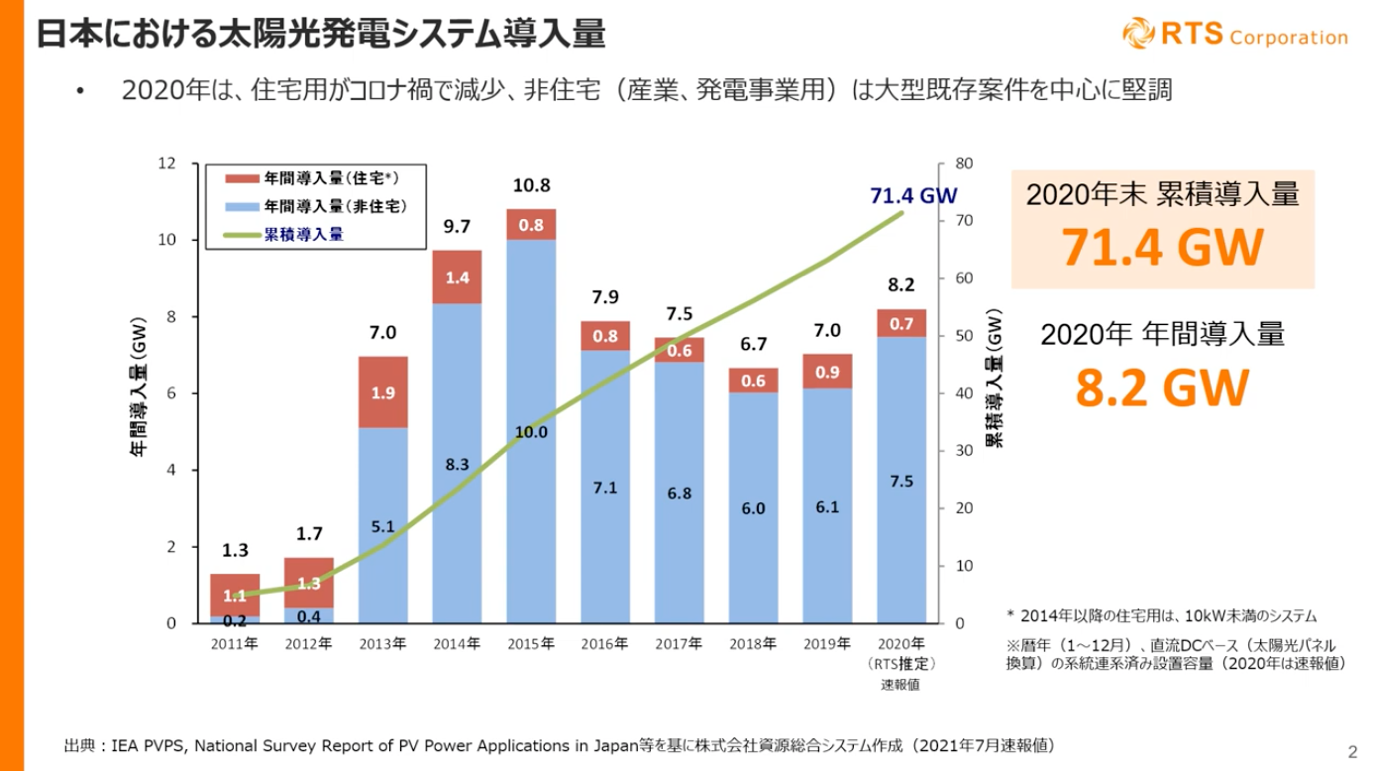

Solar

The solar industry struggled more than most this year. After a tripling of capacity in the last decade, new growth slowed due to the ever-lowering Feed-In Tariffs, which hit an average of just ¥10.31/ kWh in the November tender.

The industry’s competitive nature, the rising number of municipalities objecting to new solar construction, and a general rise in costs, have all impacted Japan’s solar power industry. Uncertainty ahead of the April 2022 switch to the Feed-In Premium (FIP) system, which is supposed to encourage the addition of a storage component but offers less guarantees on price, has also left some market participants nervous.

Goldman Sachs was one of the prominent names to exit Japan’s solar space this year, selling its stake in Japan Renewable Energy (JRE) to ENEOS for about ¥200 billion. The deal marked a changing of the guard, a moment in which the initial “cowboy” era of the solar industry in Japan ended and a new generation began. Those likely to thrive in the new era are comfortable with working at lower power prices. They are nimble, more sophisticated technologists and engineers, and comfortable with hybrid energy systems.

Of course, how firms like JRE compete in the new environment once they are under the umbrella of large, traditional Japanese corporates like ENEOS is yet to be seen, but the latter also bring something vital to the table: better government relations and traditional domestic clients.

Another type of solar investor starting to emerge as a serious force in Japan this year is the “white-label” energy provider. West Holding is the most prominent example after it inked deals to supply Amazon (via Mitsubishi Corp) with 450 mini solar farms and then a further 200 MW of solar capacity to Sumitomo Finance. Also, Itochu Corp, one of Japan’s sharpest trading houses, invested in another domestic solar developer and now plans to build 5,000 mini solar farms around the country by 2025.

While the above are drivers pushing private development, the MoE’s drastically increased budget for next year indicates that the government too will play its part by installing solar on rooftops of public facilities. For those looking for the next game-changer in solar, the answer will likely lie in batteries and a shift to perovskite cell technology. Both areas are major recipients of financing from the Green Innovation Fund.

Japan Solar Capacity (by year and in total)

Legend: red bars represent household solar capacity and blue the rest (utility)

Source: RTS Corporation

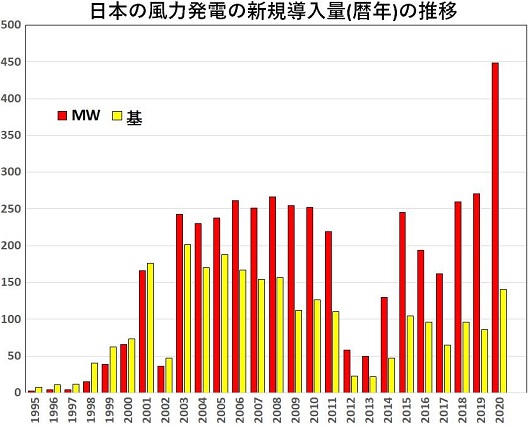

Wind

Japan’s most popular energy sector by far is wind, especially offshore. Membership of the Japan Wind Power Association (JWF) surpassed 500 last month. The most active include overseas firms Ørsted, Vestas, and Copenhagen Infrastructure Partners (Denmark); RWE (Germany); and Shell and SSE (UK); other prominent voices include Equinor and Macquarie.

TEPCO, Kansai, Chubu, Kyushu and Tohoku Electric, J-Power and JERA are Japan’s major power industry veterans vying for market entry, but there are also a large number of non-electricity firms from the trading houses (Mitsubishi, Marubeni) to transport firms (JR East) and oil and gas specialists (JAPEX, INPEX, Cosmo, ENEOS).

So far, there’s only been one tender concluded for a commercial-scale offshore wind zone, off the coast of Nagasaki. An all-Japan consortium of eight firms is pooling knowledge and resources to develop floating turbine technology that has yet to be fully tamed anywhere in the world.

Earlier this month, bids for one more offshore wind zone (Happo-Noshiro) opened on a deadline of June 10, 2022; the winners will be announced by December that year. Many are concerned that the tender process is simply too long and slow.

One change that’s likely to improve the offshore wind process is the recently planned shift in early-stage data collection. A METI subcommittee proposed to centralize the collection of wind and meteorological data, as well as undersea geography and transport capacity.

The wind sector today is still about 99% onshore and over the next decade the biggest growth will continue to be on land. Onshore wind capacity could quadruple to about 16 GW in 2030, while offshore will only reach about 3.7 GW. That’s quite a come down from the announced 10 GW of offshore wind capacity by 2030 in the Green Growth Strategy.

An undersea power grid that will connect Hokkaido and other northern offshore wind farms to central Japan is the most prominent item of infrastructure now under consideration (with initial estimates for the plan due in spring 2022).

![]()

![]()

![]()

![]() Annual Wind Power Capacity Additions, Japan

Annual Wind Power Capacity Additions, Japan

![]()

![]()

![]()

Source: Japan Wind Power Association (JWPA) via Shin Energy Shimpo

Units

Biomass

Bigger expectations are set aside for biomass, both via liquid and dry fuel and biogas facilities. Biomass came to prominence in recent years thanks to power generation and it already occupies a bigger share of the energy mix than wind and geothermal. However, expectations from the government are focused on transport.

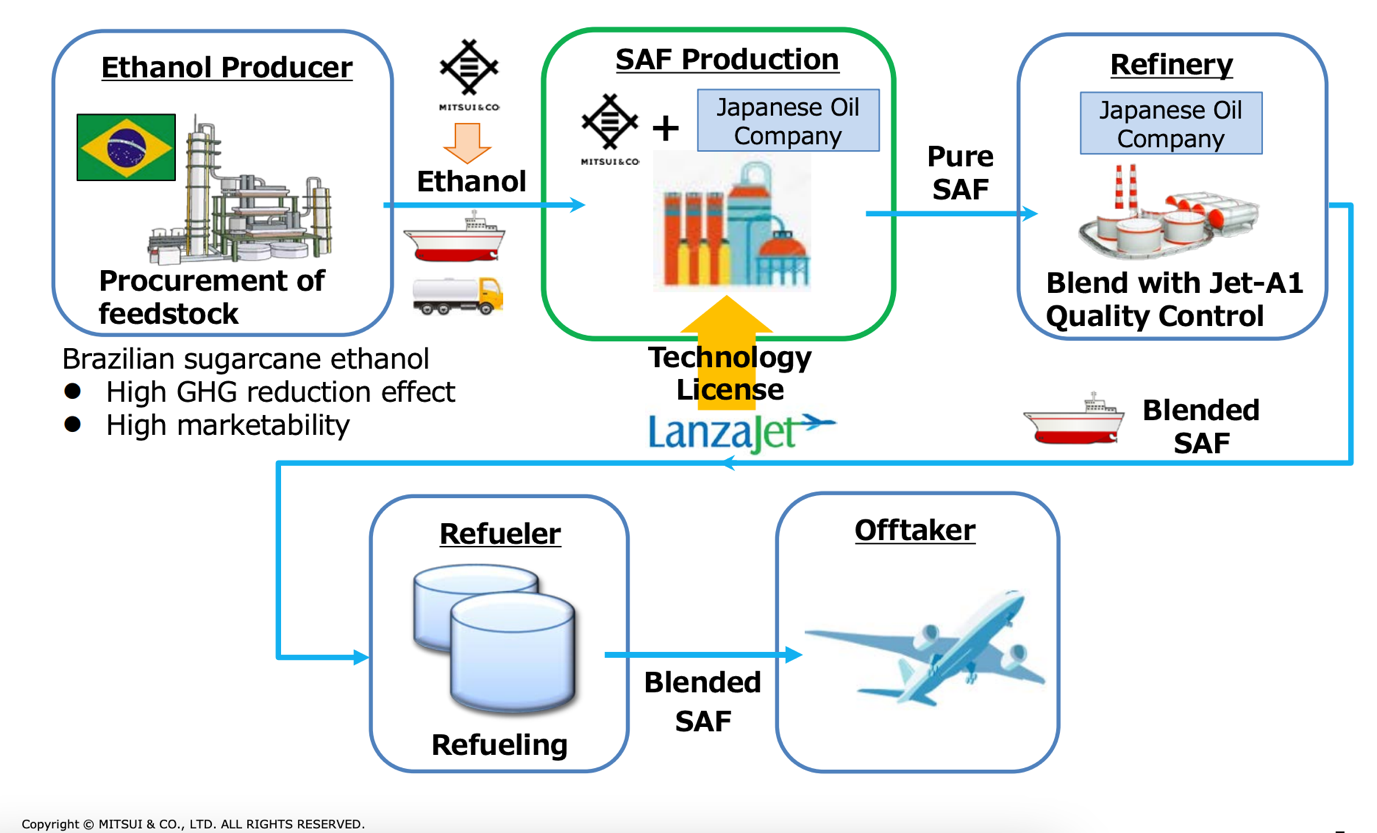

There are several paths for biofuels to develop. Mitsui & Co. is betting on ethanol and the ability to convert that into SAF thanks to its stake in U.S. biomass startup LanzaJet. With Brazil as a major supplier of sugarcane ethanol, Mitsui hopes to bring LanzaJet’s SAF manufacturing technology to Japan by 2025.

Meanwhile, Euglena Inc. continues to tout the potential of algae-based biofuel. Once Japan’s hottest startup, the company struggles to bring manufacturing costs to levels that could compete with regular oil-based fuel. Over the last year, however, it moved forward with testing of biofuels in buses and other transport.

The latest steps are thanks to a more flexible approach to source material; for example, mixing algae-based oils with those from used cooking oils and animal fats, which opens up a much wider market.

Arguably the most creative energy niche in Japan is biogas. Many projects involve taking food, animal, and human waste and then processing that into a potent gas, high in methane, for heating and cooling systems, as well as industrial purposes. The so-called Renewable Natural Gas industry in Japan is still small, but it’s grown in the last five years.

As of March 2020, there were 228 biogas power generation facilities under the state-supported feed-in-tariff (FIT) scheme, with total capacity of 86 MW. That’s almost a quadrupling compared with 2012 levels. The appeal is largely financial: Biogas-generated power can claim an FIT of ¥39, which is more than triple that of solar.

Biogas has the potential to displace a lot of the natural gas Japan currently imports. As one small step, Japanese industrial gas firm, Air Water, plans to set up liquified biomethane production from cow dung at Hokkaido farms and says it could produce the equivalent of half the LNG needed by Hokkaido factories.

These kinds of plans previously carried little weight given the high costs involved. However, as LNG prices jump into the $40/ mmbtu range again this winter, a level unimaginable a couple of years ago, the attractiveness of researching local biogas resources grows.

Geothermal

Every few years, there’s a wave of interest in geothermal energy and the same questions pop up: Why does a country with the world’s third-largest potential fail to capitalize on it, especially when you consider that many top manufacturers of geothermal power equipment are also Japanese? The latest surge in enthusiasm appeared this year.

Most problems faced by geothermal energy developers are: access to land; winning local approval; long lead time for site exploration; environmental surveys; small scale; and other preliminary work. The truth is: over the course of a decade needed to develop most geothermal projects, 10-times the power capacity can be added in offshore wind.

Japan has about 0.5 GW of geothermal capacity. That may double or even triple this decade, but with few companies willing to stake a claim as an industry leader it’s hard to see strong momentum.

A boost for geothermal could come from Japanese projects overseas. JERA’s $1.6 billion acquisition of Philippines clean energy utility Aboitz Power includes geothermal assets. The development of next-generation geothermal turbines that sit deeper and are more efficient is led by U.S. startups, and Japanese firms have started to invest in them. The fact that geothermal is also the only major renewables source that counts as baseload power could promote this energy source further in coming years.

Notable Geothermal Projects in Japan

|

Companies involved |

Project details |

|

J-Power), Mitsubishi Materials, and Mitsubishi Gas Chemical |

46 MW double flash Wasabizawa station, based in Akita Prefecture. Commenced operation in May 2019. |

|

J-Power), Mitsubishi Materials, and Mitsubishi Gas Chemical |

15 MW plant in Hachimantai, also in Akita Pref. Expected to go online in 2024. |

|

Idemitsu, INPEX, and Mitsui Oil Exploration |

Environmental assessment ongoing for a 15 MW plant at Katatsumuri Mountain, Akita. Aims to start operation in 2024. |

|

ORIX Corp, Ormat Technologies (U.S.) |

Orix acquired a stake in Nevada-based Ormat, which is building a geothermal plant in Hakodate, Hokkaido. Operation due to start in spring 2022. It will be one of the largest binary power plants in Japan. Orix also conducting drilling surveys in neaby Aomori Prefecture and near Tokyo Bay. |

|

Nippon Heavy Industries, Geothermal Engineering, JFE Engineering, Mitsui Oil Exploration, and JOGMEC |

7-MW plant started operating in January 2019 in Hachimantai, Iwate Prefecture |

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Australia/ Hydrogen

The government wants to fast-track the $10 billion, 10 GW Desert Bloom green hydrogen project being developed by Aqua Aerem. Huge solar-powered arrays will both source water and produce hydrogen through electrolysis. The first fuel is expected in 2023, and in 2027 it will reach a maximum capacity of 400,000 tons of hydrogen.

Brazil/ Solar power

Brazilian natural gas and power utility Eneva is acquiring renewable energy firm Focus Energia for $160 million, resulting in that company again going private just 10 months after it held an IPO. Focus Energia is building over 3 GW of solar power capacity.

China/ Offshore wind power

EDF and China Energy Investment Corporation commissioned the 200 MW Dongtai 5 offshore wind farm north of Shanghai. Together with the 300 MW at Dongtai 4, the JV now has 125 turbines with a total of 500 MW in offshore wind capacity in China.

Europe/ Carbon price

Carbon prices in the EU’s emissions trading system soared above €90 per ton, more than double the value in July. Higher carbon prices improve the case for investment in new technologies such as carbon capture and green hydrogen.

Fossil Fuels/ Investment

The International Energy Forum and IHS Markit said in a joint report that global annual upstream investment needs to increase by as much as 50%, to $525 billion, if the global oil market is to avert a severe supply shortage. This year, upstream investment is estimated at $340 billion, almost 25% below 2019 levels.

France/ Nuclear power

Safety concerns forced EDF to shut two nuclear power plants, Civaux and Chooz, each with two reactors. Corrosion of reactor pipes is to blame. The four reactors have a combined capacity of 6 GW. Analysts said the shutdown will continue into next year.

Germany/ Natural gas

Natural gas storage inventory dropped below 60% for the first time in many years, according to the German Association of Underground Gas Storage Operators. This “historical low” is seen as a troubling development as winter begins.

Green finance/ HSBC

Europe’s top banker to Asia wants clients to have a plan to exit fossil fuels by late 2023. Following its pledge not to finance new coal-fired power plants or coal mines, HSBC will cut exposure to thermal coal financing 25% by 2025, and 50% by 2030. However, non-EU clients could be funded until a global phase-out by 2040.

India/ Solar power

Adani Green Energy inked a deal with state-run Solar Energy Corp to sell 4.7 GW of solar power. Adani now has buyers for 6 GW of the 8 GW of its planned solar capacity. Adani will invest $70 billion in renewables by 2030, and it wants to be the world’s largest renewables company by 2030. Currently, Adani ranks No. 30, says Bloomberg.

Spain/ Wind power

For the first time, wind power overtook nuclear power in the national energy mix. Experts say that wind will eventually dominate the Spanish electricity grid as installed capacity of wind turbines is expected to double between now and 2030.

Turkey/ Geothermal power

The World Bank will loan Ankara $300 million to support the country’s Geothermal Development Project that will build 380 MW of capacity by tapping heat sources deep in the ground.

U.S./ Coal

By late 2028, American Electric Power Co. will shut both units at the 2.6 GW Rockport coal-fired plant in Indiana. By 2024, which is 15 years earlier than planned, Ameren Corp. will close its 1.3 GW Rush Island coal-fired power plant near St Louis. The company doesn’t want to install pollution controls that would cost $1 billion.

U.S./ Clean energy

Biden ordered state agencies to stop financing new fossil fuel projects overseas and to instead promote net-zero goals and clean energy projects across the globe. This order, however, can be sidestepped when fossil fuel projects are vital to national security.

EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy.

|

February |

Approval of Fiscal 2021 Budget by Japanese parliament including energy funding projects; CMC LNG Conference |

|

March |

10th Anniversary of Fukushima Nuclear Accident; Smart Energy Week – Tokyo; Quarterly OPEC Meeting; Japan LPG Annual Conference; Full completion of all aspects of the multi-year deregulation of Japan’s electricity market; End of 2020/21 Fiscal Year in Japan; |

|

April |

Japan Atomic Industrial Forum – Annual Nuclear Power Conference; 38th ASEAN Annual Conference-Brunei; Japan LNG & Gas Virtual Summit (DMG)-Tokyo Three crucial by-elections in Hokkaido, Nagano & Hiroshima – April 25th |

|

May |

Bids close in first tender for commercial offshore wind projects in Japan; Prime Minister Suga to visit the U.S. |

|

June |

Release of New Japan National Basic Energy Plan-2021; G7 Meeting – U.K. Presidents Biden and Putin are due to meet at a summit in Geneva Forum for China-Africa Cooperation Summit (Senegal) |

|

July |

Tokyo Metropolitan Govt. Assembly Elections; Commencement of 2020 Tokyo Olympics |

|

August |

METI committee approves draft of Japan’s 6th Basic Energy Plan |

|

September |

Ruling LDP Presidential Election; UN General Assembly Annual Meeting that is expected to address energy/climate challenges; IMF/World Bank Annual Meetings (multilateral and central banks expected to take further action on emissions disclosures and lending to fossil fuel projects); End of H1 FY2021 Fiscal Year in Japan; Japan-Russia: Eastern Economic Forum (Vladivostok)-tentative |

|

October |

Potentially, Japan’s 2021 General Election; METI Sponsored LNG Producer/Consumer Conference; Innovation for Cool Earth Forum – Tokyo Conference; Task Force on Climate-Related Financial Disclosure (TCFD) – Tokyo Conference; G20 Meeting-Italy |

|

November |

COP26 (Glasgow); Asian Development Bank (‘ADB’) Annual Conference; Japan-Canada Energy Forum; East Asia Summit (EAS) – Brunei |

|

December |

Asia Pacific Economic Cooperation (APEC) Forum – New Zealand; Final details expected from METI on proposed unbundling of natural gas pipeline network scheduled for 2022. |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.