JAPAN NRG WEEKLY

JAN. 11, 2022

JAPAN NRG WEEKLY

Jan. 11, 2022

NEWS

TOP

- Mitsubishi and Chubu Electric unit snag all three offshore wind tenders in preliminary round; Amazon part of winning group

- China and Japan to launch joint “clean-coal technology” project;

China-based facility will utilize green hydrogen - Japan aims to introduce carbon capture tech before FY2030 and is monitoring U.S. experience with older nuclear plants: Minister

ENERGY TRANSITION & POLICY

- Japan to set rules for ammonia/hydrogen power plants by Sept.

- Parliament approves 2021 budget with METI to get ¥5.4 trillion; PM Kishida vows to upgrade grid; Perovskite R&D to get ¥20 bn

- METI starts wholesale review of current power market structures

- Japan-U.S. vow to work together on next-gen nuclear technology

- Japan restarts next-gen nuclear reactor, mulls use for hydrogen

- Toyota Tsusho to test hydrogen derived from manure as truck fuel

- 12,000 firms will be asked to set targets on use of green energy

ELECTRICITY MARKETS

- Town passes Japan’s first ever tax on business use of solar panels

- Spot electricity prices hold stable compared to volatility in Europe

- JERA temporarily restarts old thermal unit to meet winter demand

- TEPCO struggles to keep up with demand as Tokyo hit by snow

- Hokkaido Electric to start direct trading of power futures by April

- JERA focuses Asian strategy on switching coal plants to ammonia

- JERA to establish floating offshore wind firm with French partners

OIL, GAS & MINING

- Japan to limit access to rare earths mining to state-approved firms

- Battery costs rise as lithium demand outstrips supply

- Japan asks Indonesia for immediate removal of coal export ban; and signs accord to support nation’s switch from coal to ammonia

- Osaka Gas is first Japanese firm to enter India city gas market

- Oil company CEOs pessimistic about gasoline demand

- Further restructuring seen as unavoidable in petrochemical sector

TWO VIEWS OF ENERGY

THE YEAR 2021 AND COP26 SHOWED US THAT…

❶ THE FUTURE BELONGS TO RENEWABLES, BUT

JAPAN CONTINUES TO BUCK GLOBAL TREND

Tomas Kåberger, the Chair of Executive Board of Renewable Energy Institute (Japan), argues that the global progress in renewable energy is making fossil fuels obsolete, while the growing trend in carbon tax and similar instruments will make traditional energy uncompetitive with green sources. Japan’s current approach is betting on the wrong energy strategy.

❷ RUSHING THE GREEN AGENDA WILL BACKFIRE;

JAPAN EMBRACES ENERGY PRAGMATISM

Former COP negotiator, Arima Jun, now a professor at the University of Tokyo’s Graduate School of Public Policy, and Tezuka Hiroyuki, Chair of the WG on Global Environment Strategy at Keidanren (Japan Business Federation), say that the energy transition cannot occur at any cost. They explain how the climate agenda can be furthered without rushing, and possibly derailing, the overall process.

GLOBAL OUTLOOK 2022

To start the year, our Global Wrap column takes a look at all the main energy sources and sectors, and paints a brief outlook of their prospects for this year. With the world economy expected to see elevated growth after two years of pandemic-induced restrictions, fossil fuel usage in particular looks likely to stay strong.

JAPAN OUTLOOK 2022

A look at what this year holds in store for Japan care of the nation’s leading energy think tank: The Institute of Energy Economics in Japan (IEEJ).

EVENT CALENDAR FOR 2022

Key political and business events in Japan and abroad.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Tom O’Sullivan (Japan, Middle East, Africa)

Regular Contributors

Mayumi Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

Events

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Japan, China to launch joint clean-coal technology project in Shaanxi province

(Japan NRG, Dec. 27)

- At the 15th Japan-China Forum on Energy Conservation and Environment METI announced a plan to launch a “clean-coal technology” pilot project in China’s Shaanxi province. The Forum was held online on Dec. 26, with METI and MoE ministers, and key National Development Reform Commission officials from China delivering keynote addresses. Here are some major highlights from the forum:

- The Shaanxi project will be Japan’s first major coal methanation rollout overseas.

- Coal methanation converts carbon emitted from a coal-fired power plant into synthetic methane by combining carbon with green hydrogen. Methane can be a fuel for gas-fired power generators.

- Hitachi Zosen will provide the methanation and hydrogen manufacturing equipment. Project participants include the Japan Coal Frontier Organization (JCOAL), the Shaanxi regional government and Yulin Chemical.

- The plant’s methanation process will reduce emissions and is expected to run for several years.

- Ten other bilateral projects were agreed at the Japan-China forum in the fields of hydrogen, fuel cells, pollution control, and energy conservation. Still, this number of projects is lower than in previous years due to pandemic-related travel restrictions. About 700 participants joined the forum online.

- CONTEXT: In a bid to spread “clean coal” technology in Asia, METI established the Asia CCUS Network in June 2021. It does not include South Korea or China.

- CONTEXT: As JCOAL is an active member of the Asia CCUS Network, the Shaanxi project will possibly keep China connected to the Japanese initiatives to retain coal power while mitigating emissions.

TAKEAWAY: While bilateral ties in clean and green energy grow, PM Kishida’s government wants to regulate trade with China more closely by legislating the Economic Security Act. This will allow the government to check if components used for power and telecommunication infrastructure are sourced from suppliers with economic security implications.

The proposed act is expected to impact solar power operators as China has a dominant share in the production of panels, mounts and other components. The move may curb Chinese investment in Japan’s renewable sector. China’s Suntech runs 18 solar plants in Japan; total capacity of 37 MW.

Japan aims to introduce carbon capture technology before FY2030: Minister

(Nikkei, Jan. 7)

- METI minister Hagiuda said Japan will introduce technology to capture CO2 and bury it underground by 2030.

- He said thermal power generation is needed for a stable supply of electricity, and intends to maintain thermal power while reducing CO2 emissions in underground storage.

- So far, Japan has successfully stored 300,000 tons of CO2 in a demonstration project off the coast of Tomakomai City, Hokkaido.

- Hagiuda said many issues need to be addressed before commercialization of CCS, including cost reduction and development of suitable sites.

- METI will draw up a roadmap to work with the public and private sectors.

- Hagiuda also said that Japan is paying attention to the U.S. experience of operating nuclear reactors for 80 years. Japan’s reactors are currently only able to run to 60 years, but some want this period to be brought in line with the U.S.

METI to set safety standards for ammonia and hydrogen-fired power by September 2022

(Japan NRG, Dec. 21)

- By interviewing businesses in the industry, METI will set safety standards for ammonia and hydrogen-fired power plants by September 2022. Prospective players include former regional grids and smaller companies.

- The ammonia/hydrogen power plants will fall in the thermal power plant category and safety standards will be written in “government ordinances relevant to thermal power plant operations”. Licensing, approvals and reporting rules will be set at a later date.

- CONTEXT: Last year, JERA started ammonia co-firing on a trial basis at its 1 GW Hekinan-4 USC coal plant, and the ammonia ratio will be gradually raised to 20% in 2024. ANRE estimates co-firing will first spread among 28 USC coal plants with a total capacity of 22 GW.

Parliament approves 2021 supplementary budget

(Japan NRG, Dec. 20)

- The parliament on Dec. 20 approved the fiscal 2021 supplementary budget of over ¥35 trillion. METI’s budget was ¥5.4 trillion. Over half will support COVID-hit businesses.

- Major energy items:

|

¥90 billion |

Oil price rise measures |

|

¥47 billion |

Fukushima nuclear plant waste water release |

|

¥137 billion |

Fostering EVs, build charging stations and relevant facilities |

|

¥100 billion |

Storage battery manufacturing |

|

¥31 billion |

Renewable energy |

|

¥2 billion |

R&D on nuclear power |

|

¥4 billion |

Preliminary CCUS studies |

|

¥7 billion |

Ammonia/hydrogen storage centers |

- SIDE DEVELOPMENT:

PM promises to upgrade transmission infrastructure to foster renewables

(Nikkei, Jan. 4)- PM Kishida said his government is discussing an upgrade of the transmission infrastructure.

- SIDE DEVELOPMENT:

Government to invest ¥20 billion in perovskite

(Nikkei, Dec. 28)- The government-backed NEDO said it would invest ¥20 billion in the development of perovskite solar panel technology.

- Light and flexible, perovskite promises to halve solar panel prices.

- The funding comes from the ¥2-trillion Green Innovation fund that supports research by the likes of Toshiba, Sekisui Chemical and Tokyo University.

METI launches studies on power market reforms

(Japan NRG, Dec. 28)

- METI launched a group on power market structure in response to calls for reforms. It will review the wholesale and supply-demand adjustment market mechanisms to ensure efficient sourcing of power while increasing renewables.

- The review won’t affect METI’s plan to introduce power in-balancing rates in 2022 and a new capacity market in 2024.

- The group will look into a lack of supply in the wholesale spot market and disconnects between different market mechanisms. Usually, when power demand increases in winter, disconnects between power retailers and suppliers are common, as suppliers don’t know if retailers have enough supplies. In the end, suppliers must cover any deficit.

- Retailers need to increase risk awareness, and an effective demand response system must be established, said an official at the Transmission and Distribution Grid Council. The seven-member panel is chaired by Tsutomu Ohyama of the Organization for Cross-regional Coordination of Transmission Operators (OCCTO). The panel will report its findings to the Electricity and Gas Market Surveillance Commission.

TAKEAWAY: While the review doesn’t cover capacity auctions, Prof. Yumiko Iwafune of Tokyo University pointed out that the October capacity auction level was alarmingly low and may trigger plant closures.

METI Minister, US Energy Secretary agree to strengthen cooperation on nuclear

(Japan NRG, Jan. 6)

- During a Jan. 6 online meeting, METI Minister Koichi Hagiuda and U.S. Energy Secretary Jennifer Granholm agreed to strengthen bilateral initiatives to develop next-gen nuclear power technology. Japan will test SMRs and high-speed reactors developed by NuScale and other companies.

Japan restarts experimental nuclear reactor

(Nikkei, Jan. 5)

- JAEA restarted its experimental high temperature, gas-cooled nuclear reactor (HTGR) after 10 years idle. Media were given a tour.

- Geiger counters mounted on the reactor exterior read zero, showing that not even a minuscule amount of radiation escapes.

- HTGRs are safer than traditional reactors because the fuel rods have a melting point of over 2,500 C. The rods used in traditional reactors begin to melt when temperatures exceed 1,200 degrees.

- While Toshiba and Fujitsu are both developing HTGR technology, the Japanese government has yet to endorse it.

- SIDE DEVELOPMENT:

Nuclear-powered hydrogen generator unveiled to media

(Nikkei Xtech, Dec. 28)- The Japan Atomic Energy Agency (JAEA) unveiled a prototype of a system that uses heat from a nuclear reactor to generate hydrogen.

- The facility uses a multistage process, known as the IS process, which has temperatures as high as 900 C to reduce sulfuric acid and hydrogen iodide.

- While the prototype achieves the required temperatures with electric elements, the system is powered by a high-temperature gas reactor.

- The JAEA envisages systems capable of generating up to 1,000 m3 of hydrogen per hour, which may be possible by 2040.

- SIDE DEVELOPMENT:

Molten sodium from experimental reactor to be sent to UK

(NHK, Dec. 24)- The government says molten sodium recovered from the Monju experimental fast breeder reactor that’s being decommissioned will be sent to the UK for processing.

- A MoA was signed with Cavendish Nuclear and Jacobs on Dec. 21.

Surplus power from nuclear plants to produce hydrogen

(NHK, Dec. 23)

- In a first for Japan, Tsuruga City and Kansai Electric launched an initiative to use surplus power from local nuclear power stations to generate hydrogen.

- Hydrogen fueling stations will be built and Tsuruga City vehicles replaced with hydrogen vehicles.

- Tsuruga City wants to become carbon neutral.

Toyota Tsusho to test hydrogen derived from manure as truck fuel at U.S. port

(Asia Nikkei, Dec. 22)

- A Toyota Motor group member will start a 4-year test at one of the largest U.S. ports using cargo equipment powered by hydrogen derived from animal waste.

- The pilot program takes place at the Port of Los Angeles until March 2026 and will be run by Japanese commodity and equipment distributor Toyota Tsusho.

- It will involve seven pieces of machinery powered by fuel cells, including a crane, machines that offload containers, and trucks.

- The hydrogen will come from renewable natural gas or biomethane. Derived from farm manure improved to fuel-grade, this gas helps reduce CO2 emissions.

Idemitsu reorganizes agri-bio business for faster growth

(Japan NRG, Dec. 21)

- Oil refiner Idemitsu Kosan will spin off its agri-bio business unit in July 2022 for a merger with SDS Biotech, a subsidiary. SDS Biotech was a chemical joint venture between Showa Denko and Diamond Shamrock, which Idemitsu acquired in 2011.

- SDS Biotech will take over all Idemitsu agri-bio operations including manufacturing of cattle compound feed, which generated annual revenue of ¥2.6 billion ($22 million). Idemitsu and SDS Biotech want to maximize the potential of micro-organisms, and the merger will allow them to share manufacturing technologies and R&D results.

- Idemitsu’s Ruminup is Japan’s leading methane-reducing cattle compound feed, cutting methane emissions 20%. The product was first sold in 2011. Ruminup’s main ingredient is cashew nut shell liquid (CNSL) from Vietnam. CNSL helps cows’ stomachs reduce methane. Product inquiries started to increase after last summer due to growing concerns about GHGs. The product is exported across Asia.

- CONTEXT: Japan’s methane release was 28.2 million CO2 equivalent tons in FY2020; 21.9 million tons came from rice farming, livestock and other agricultural production. Methane release must be cut 30% by 2030, from 2020 levels. For the last two years, biomass power operators have lobbied for approval to use CNSL for power generation. Japan imports around 5,000 tons/year of CNSL and only 10-20% of the imports have been used for livestock feed production, according to market sources.

Two municipalities delist from Fukushima radioactivity monitoring areas; 86 remain

(Japan NRG, Dec. 27)

- Two municipalities were removed from the list of areas subject to regular radioactivity monitoring and decontamination programs in 2021. In March, Watari Town of Miyagi Prefecture, and effective Dec. 28, Otama Village, were removed since radioactivity measured below 0.23 microsieverts/ hour on average. The government and municipalities jointly measure radioactivity levels.

- Watari and Otawa are 60-70 km away from the Fukushima plant. 86 municipalities in Fukushima and seven surrounding prefectures remain under monitoring and local decontamination programs. The more severely affected Futaba Town, the plant site, and six adjacent municipalities are under separate programs of the central government.

TAKEAWAY: Radioactivity is measured 50-100 cm above ground using gamma ray instruments. Underground water, dioxin, sulfuric acid, and dust around waste treatment facilities are also monitored. The total population of the 86 municipalities under surveillance exceeds 1 million.

- SIDE DEVELOPMENT:

Fukushima worker may have been exposed to radiation

(FNN Prime Online, Jan. 6)- A worker at the Fukushima nuclear power plant is believed to have suffered internal radiation exposure from inhaled air.

- It’s unknown how the worker, who was wearing a mask, was exposed.

New garbage trucks to run on rubbish

(Newswitch, Dec. 24)

- Kawasaki City commissioned JFE Engineering to develop garbage trucks that will be powered by electricity generated from incinerating garbage.

- Rather than being recharged at charging stands, the trucks will have their batteries swapped for fully-charged ones.

- The system is dubbed the ‘Zero E’ garbage collection system.

Challenergy eyes cyclones as energy source

(Nikkei, Dec. 20)

- Tokyo-based Challenergy will build a prototype vertical wind turbine in Madagascar to generate electricity from winds of up to 40 m/sec.

- The 10-kW turbine will begin operating in or before 2023 and take advantage of the region’s high incidence of cyclones and typhoons.

- Challenergy already operates similar turbines in the Philippines.

Sony to set up mobility company for EV push

(Asia Nikkei, Jan. 5)

- Conglomerate unveils electric SUV at CES 2022.

12,000 companies in Japan obliged to set targets on adoption of green energy

(Yomiuri Shimbun Nikkei, Jan. 6)

- About 12,000 firms in Japan will be asked to set targets to switch to renewable energy as early as 2023, according to a new government policy to be submitted to parliament in the new session that starts this month. The policy is part of a revised Law on the Rational Use of Energy.

- Companies that consume energy equivalent to at least 1,500 kiloliters of crude oil annual will be subject to the policy. This is to encourage firms to switch from fossil fuels to CO2-free sources.

- METI will work out the exact rules, but it seems that firms will need to set targets based on a ratio that renewables will amount to in their total energy use.

- Companies will also need to submit an annual report to government to explain what efforts they are undertaking to use CO2-free energy.

One-Dot Wrap

- 20 companies to conduct joint assessment of offshore wind farm in Yusa, Yamagata Prefecture. (New Energy Business News, Dec. 28)

- Kansai Electric to revise some of its electricity rates, lowering daytime rates and raising nighttime rates due to increase in solar generation and lifestyle changes. (New Energy Business News, Jan. 7)

- Marubeni New Power Corporation will enter the capacity market as a DR aggregator after success in power supply auction. (New Energy Business News, Jan. 7)

- Sompo Japan and Charles Taylor Japan form alliance to deal with accidents in the offshore wind sector. (New Energy Business News, Jan. 6)

- Kawasaki Heavy Industries to start developing larger and more efficient hydrogen liquefiers as it wins first order for 5-MW cogeneration system in Malaysia. (New Energy Business News, Jan. 6)

- Next Energy and Resources forms a capital alliance with Toyota Tsusho to boost development of renewable energy. (New Energy Business News, Jan. 5)

- JA Mitsui Leasing signed a loan agreement with Canadian Solar to finance the development of a large-scale solar generation and storage battery project in Australia. (Kankyo Business, Jan. 5)

- Sumitomo Corporation will begin full-scale design and development of an ammonia-fueled dry bulk carrier in cooperation with Oshima Shipyard, one of its group firms. (Kankyo Business, Jan. 5)

- Ube Industries, Sumitomo Chemical, Mitsui Chemicals, and Mitsubishi Gas Chemical agreed to begin a joint study to secure stable supply of clean ammonia in Japan. (Kankyo Business, Dec. 28)

- Toshiba achieves the world’s highest power generation efficiency for transmissive copper oxide solar cells at 8.4%. The technology is due to be produced at a practical size by fiscal 2025. (New Energy Business News, Dec. 27)

- Five companies, including Nippon Koei, invest in a large-scale storage battery operation business in the UK with commercial operation to begin in spring 2023 with an output of approximately 100MW. (New Energy Business News, Dec. 22)

- INPEX invests in 85 MW Muara Labo Geothermal Power Project in Indonesia, which Sumitomo Corporation and others manage and which started operation in 2019. (New Energy Business News, Dec. 21)

- Okinawa Electric, Air Water and others will conduct a survey for the establishment of a hydrogen supply chain in the Okinawa area and have their application for funding approved by NEDO (Kankyo Business, Dec. 20)

NEWS: POWER MARKETS

Mitsubishi the big winner in Japan’s first commercial offshore wind tenders

(Japan NRG, Dec. 24)

- Three tender results announced:

819 MW Yurihonjo City wind farm offshore Akita Prefecture

No. of bidders: 5

Winning consortium: Mitsubishi Corporation Energy Solutions Ltd., Venti Japan Inc., C-Tech Corporation, and Mitsubishi Corporation

Project partners: Amazon.com, Inc, NTT Anode Energy Corporation, Kirin Holdings

Planned start of operations: December 2030

Winning tariff price: ¥13.26/ kWh

479 MW Noshiro City, Mitane Town, Oga City project, Akita Prefecture

No. of bidders: 5

Winning consortium: Mitsubishi Corporation Energy Solutions Ltd., C-Tech Corporation, and Mitsubishi Corporation

Project partners: Amazon.com, Inc, NTT Anode Energy Corporation, Kirin Holdings

Planned start of operations: December 2028

Winning tariff price: ¥11.99/ kWh

391 MW Choshi City project off Chiba Prefecture

No. of bidders: 2

Winning consortium: Mitsubishi Corporation Energy Solutions Ltd., C-Tech Corporation, and Mitsubishi Corporation

Project partners: Amazon.com, Inc, NTT Anode Energy Corporation, Kirin Holdings

Planned start of operations: September 2028

Winning tariff price: ¥16.49/ kWh

- All three projects will use GE Haliade-X wind turbines.

- In all three projects, the group led by Mitsubishi achieved a much higher rating from METI and the local government than its rivals groups.

- Note: the partners in each project are the same; according to the statement from the consortium, the partners will help with regional promotion strategy.

- CONTEXT: Mitsubishi is Japan’s biggest trading house and one of the top LNG importers. Mitsubishi Corporation Energy Solutions is one of its subsidiaries and handles overall energy management for customers.

- CONTEXT: C-Tech Corporation is part of Chubu Electric group, which is one of Japan’s top power utilities and owner of half of JERA Corp., the country’s biggest operator of thermal power plants and top buyer of LNG.

- CONTEXT: Venti Japan is a company focused on renewable energy in the Akita area.

TAKEAWAY: These results raised many eyebrows for different reasons. Some in the industry noted that handing the entire first batch of projects to the same two companies, moreover firms who have not built a single watt of offshore wind capacity in Japan or neighboring countries, smelled of favoritism. Especially since experience in developing offshore wind in Japan was supposed to be one of the selection criteria.

Price was one reason for picking the same winner. When tender conditions were first announced, the upper ceiling was set at ¥29/ kWh. Privately, some Japanese companies complained it was too low. Yet Mitsubishi and Chubu Electric won with proposed rates at less than half that level. Firms such as TEPCO and Obayashi Corp. envisaged much higher rates and must now reconsider how to compete. TEPCO hopes to develop at least 2 GW of offshore wind in Japan and overseas by FY2030.

The reason Mitsubishi and Chubu won at lower prices may well lie in their ability to lock in early off-site PPAs or secure other premiums from buyers such as Amazon, which believes they can pass on costs to their clients.

Also, Mitsubishi and METI believe that sourcing three projects at once brings economies of scale. It’s interesting that all three projects will use GE’s Haliade-X turbines. This both reduces costs and at the same time conveniently places an order for 1.7 GW of capacity to both GE and its new Japanese partner, Toshiba.

Incidentally, Toshiba is embroiled in a scandal over shareholder dealings which is at least partly the work of METI. Toshiba’s future is on the line. Winning a large bulk order as GE’s strategic partner to manufacture the turbines partly in Japan is potentially METI’s way to repay and support Toshiba, and as an extension, support the building of a domestic wind turbine supply chain led by GE-Toshiba.

Top European offshore wind operators that made bids will wonder why their know-how was ignored. They and others considered favorites, such as TEPCO and Renova, will get a chance later this year in a tender for a single area off the coast of Happo Town and Noshiro City in Akita Prefecture. However, they will need to pay attention to the winning price of the first three auctions.

Surprisingly, a few Japanese media described the winning rates as higher than expected. One way that could make sense is when we remember that METI has said several times that it hoped to bring the price of offshore wind to ¥8/ kWh by FY2030, just one-two years after these projects come online. The same media then suggested that the ¥8 level is now expected by 2035, subtly shifting the government narrative.

This means bids in new METI tenders that start around 2030 will still be accepted above the ¥8 level. The message seems to be: bid in the low 10s or walk away. So, the number of interested players will likely shrink.

It’s clear that METI wanted to deal with one familiar set of players to iron out any kinks before wider deployment of offshore wind. METI also needs to show that its efforts in renewables are on track and it’s not repeating the early years of Feed-In Tariff largess.

We expect competition for this year’s tender to be intense.

Local solar tax is a first for Japan

(Smart Japan, Dec. 23)

- Councilors of the town of Mimasaka (Okayama) approved a bylaw to tax commercial users of photovoltaic panels.

- Scheduled to take effect in 2023, the bylaw is a first for Japan.

- Operators of standalone solar farms rated at 10 kW or more will be taxed ¥50 per sq/m of panel area for five years after installation, but farms in areas that are not sloping or prone to landslides will be exempt from the tax.

- Japan Photovoltaic Energy Association (JPEA) came out against the tax, saying it will equal 2% of revenue earned by affected operators.

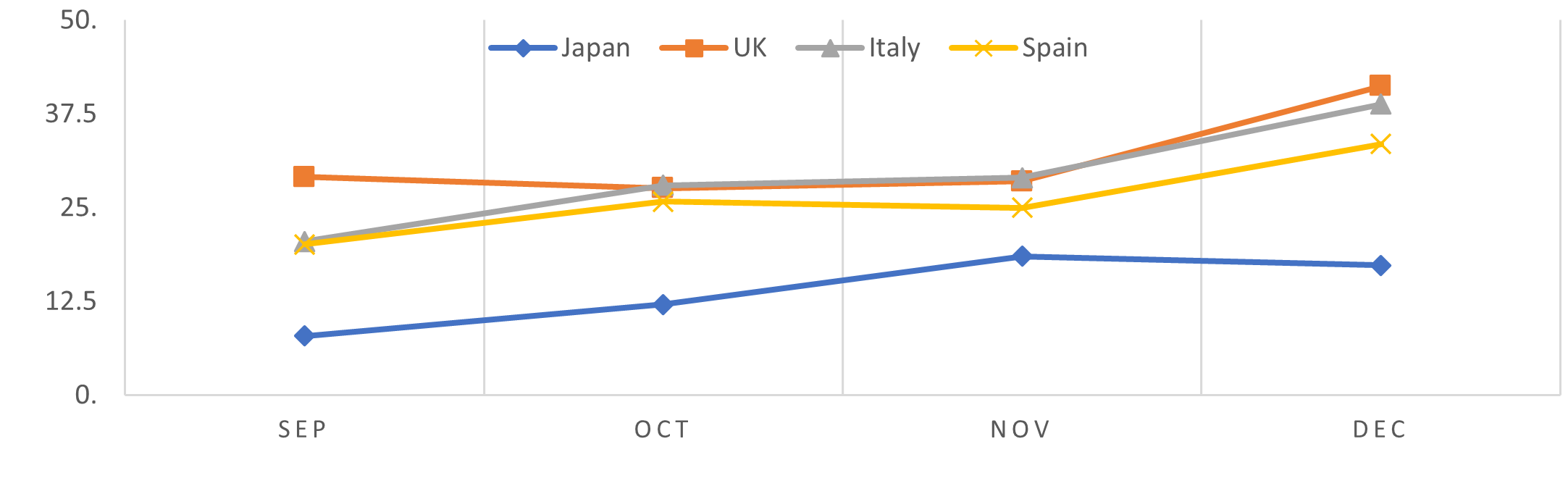

Japan’s spot power prices hold stable compared to Europe

(Japan NRG, Dec. 27)

- Japan’s spot power prices in December averaged ¥17.3/ kWh, up from ¥7.9/ kWh in September, but held stable compared to Europe. December prices averaged ¥41.2/ kWh in the UK, ¥38.8/ kWh in Italy and ¥33.5/ kWh in Spain.

- A cold spell hit the European continent earlier, and gas supplies from Russia appear to be limited. Japan may see soaring power prices as winter storms are soon expected.

- As of Dec. 23, Japan’s LNG stocks stood at 2.42 million tons, up from 2.16 million tons at end November. Tight supply conditions will continue into summer 2022 as Joban Joint Power’s 600 MW coal-fired power plant and JERA’s 1 GW coal plant went offline due to technical issues and may not recover before July.

- Meanwhile July-September demand is expected to rise this year as post-COVID business activities pick up and residential energy consumption rises as more workers work from home.

Sport power prices, monthly average (Yen/ kWh)

OCCTO releases October capacity auction results

(Japan NRG, Dec. 23)

- October’s auction for 165 GW to be supplied in 2025 finished at ¥3,495-¥5,242/ kW, said OCCTO. Auction participants included regional grids, gas utilities, municipalities and renewable operators.

JERA temporarily restarts old thermal power plant to meet demand during winter

(Nikkan Kogyo Shimbun, Jan. 4)

- JERA restarted Unit 5 at the Anesaki thermal power plant in Ichihara City after shuttering the entire six-unit station for decommissioning due to its age.

- The plant will run from January 4 to February 30, 2022.

- The six reactors were built in the 1960s and 1970s. Four have already been decommissioned, while units 5 and 6 were shut down in April 2021.

- The operator has not restarted the plant from scratch in all 44 years of its operation. More than 40 problems were found before the restart, including holes in ducts and broken steam pipes. Experienced operators were recalled because younger staff hadn’t dealt with such technical issues before.

TEPCO struggles to keep up with demand as Tokyo hit by snow

(ITmedia News, Jan. 6)

- TEPCO asked Hokkaido Electric, Tohoku Electric, Chubu Electric and KEPCO to send all available electricity to Tokyo as low temperatures saw demand reach 97% of capacity.

- TEPCO is asking subscribers to be efficient with energy use.

Hokkaido Electric to start direct trading of electricity futures by April

(Jiji News, Jan. 6)

- The northern power utility will participate directly in electricity futures trading both on the TOCOM exchange owned by JPX and the European Energy Exchange (EEX) platform in Japan. The company hopes to start trading on both exchanges by the end of this fiscal year.

- Hokkaido Electric has sent orders for off-auction TOCOM and EEX futures trading through trading companies and financial institutions since September 2020. The utility will continue to trade in this way, but it will also set up its own direct trading on the exchange.

- CONTEXT: JERA is another Japanese power major expected to start directly trading electricity futures. Tohoku Electric was the first of Japan’s major power utilities to trade futures contracts. The majority of the power futures volume is currently on the EEX.

JERA’s focus on fuel switch for thermal power offers Asia third way to decarbonize

(Nikkei Business, Jan. 5)

- The weekly ran a series of articles tracking the strategy of JERA, Japan’s biggest power company and top LNG importer; and how JERA persuaded its foreign directors, banks and others that decarbonization doesn’t need to be done only through renewables.

- The company’s message is that switching coal-fired power plants in Asia to burn ammonia or hydrogen, alongside introducing new renewables capacity, is a much more effective and realistic strategy for the region.

- A JERA official said: “If you focus solely on renewable energy, like European energy companies, you may indeed be able to increase your corporate value. However, if you look outside of Europe, such as in Asia, the reality is that you can’t just jump straight to renewable energy. This is where JERA, as the vanguard of Japan’s global energy companies, can contribute, and that’s where we should aim for new business.”

- SIDE DEVELOPMENT:

JERA and IHI start an ammonia co-firing demonstration project at Hekinan coal station

(Company statement, Jan. 7)- JERA and IHI Corporation had a grant application accepted by the Green Innovation Fund to develop technology that increases ammonia co-firing at coal power plants.

- JERA and IHI are working on a demonstration project that employs an ammonia co-firing rate of 20% at JERA’s Hekinan Thermal Power Station Unit 4.

- The goal is to develop a new ammonia co-firing burner and install it at Hekinan Station Unit 4 or Unit 5 to raise the ammonia co-firing rate to at least 50% by FY 2024.

JERA signs accord to establish floating offshore wind firm with two French partners

(Denki Shimbun, Jan. 7)

- JERA signed a final agreement with two French companies to establish a floating offshore wind power development company. BW Ideale and a government-owned investment firm, were in talks with JERA since June 2020.

- The three will establish a JV in France that will be 51% held by BW IDEOL, and 24.5% each by JERA and the investment company.

- The venture will utilize BW Ideol’s floating foundation technology and focus on business in the U.S., UK, France and other European countries; but not Japan.

- JERA aims to acquire know-how by developing floating offshore wind power projects from an early stage. It then hopes to apply that knowledge in Japan.

Shikoku Electric under fire over Vietnamese coal project

(NHK, Dec. 24)

- Shikoku Electric will participate in the construction of the Vung Ang 2 coal-fired station in Vietnam.

- The utility claims the project will enable existing, less efficient power stations to be retired, thereby reducing GHG emissions.

- However, environmental group Kiko Network criticized the announcement, saying that attitudes to climate change have changed since the project’s inception and it will take Vietnam further away from carbon neutrality.

NEWS: OIL, GAS & MINING

METI to set new rare earth mining licenses and expand JOGMEC functions

(Japan NRG, Dec. 21)

- METI plans to create a new mining license category for rare earths and expand the role of Japan Oil Gas and Metals National Corporation (JOGMEC) to strengthen the supply of metals vital for decarbonization. This will limit rare earth mining in offshore deposits within Japan’s exclusive economic zone access to state-approved miners.

- Japan has the regulatory framework for mining base metals such as copper, zinc, and lead, but not for rare earths that haven’t been mined in Japan.

- In 2020, a government team prospecting for deposits of rare earth, cobalt and nickel in the seas south of Tokyo successfully recovered cobalt and nickel, increasing the possibility of recovering rare earth.

- JOGMEC’s role, which is tasked to secure energy and metal resources overseas, will be expanded locally, and it will be more instrumental in enhancing refining capabilities of copper, zinc, lead, and nickel smelters in Japan, as well as metal recycling.

- CONTEXT: Currently, JOGMEC’s investment in upstream projects is limited to 50% but this threshold will be removed to finance high-risk operations. The changes will involve amendments to the Mining Act and the JOGMEC Act to be proposed to parliament when it convenes later this month.

TAKEAWAY: Among the 34 critical mineral resources in the national stockpile, the so-called battery metals — cobalt, lithium and nickel, and rare earths — are the focus in building stronger supply chains. Copper and rare earths are priority recycling items.

- SIDE DEVELOPMENT:

Battery costs rise as lithium demand outstrips supply

(Asia Nikkei, Jan. 3)- Carmakers scramble for raw materials in a bid to win global electric vehicle race.

- Price of batteries for electric vehicles looks set to rise in 2022 following a decade of sharp decline as supplies of lithium and other raw materials fail to keep up with ballooning demand.

- The increases are undermining the technological and efficiency gains of recent years. Chinese prices up five-fold in a year.

Japan Asks Indonesia for Immediate Coal Export Ban Removal

(Various, Jan. 5)

- Japan asked Indonesia to remove a ban on export of high-grade coal as several vessels loaded to ship the product from the Southeast Asian nation await departure permits.

- The world’s largest thermal coal exporter banned exports from this year to avoid falling short of the fuel domestically, causing power outages.

- Japan argues that the high-caloric coal it buys from Indonesia isn’t used by that country’s power plants.

- Japan imports most thermal coal from Australia; about 15% from Indonesia.

- Given high inventory levels at home, JERA and J-Power, which are Japan’s main buyers of coal for power generation, aren’t concerned by the ban.

- Japan has about one month of coal reserves in stocks, but some utilities may choose to utilize more gas-fired generation if coal reserves start to run low.

- SIDE DEVELOPMENT:

Japan agrees to support Indonesia’s switch from coal to ammonia power generation

(Nikkei, Jan. 10)- Japan agreed to supporting Indonesia’s efforts to decarbonize through a joint public-private project to use ammonia, which does not emit CO2 when burned, at coal-fired power plants in the Southeast Asian nation.

- METI minister Hagiuda is touring Indonesia, Thailand, and Singapore this week. On Jan 10, he signed a MoU with Indonesia to cooperate on a gradual transition to decarbonization.

- CONTEXT: Indonesia has set a net-zero emissions target set for 2060.

- Mitsubishi Heavy Industries is one of the Japanese firms embarking on ammonia generation projects in Indonesia. It will test co-firing at a Suraya coal-fired power plant. The project will receive financial support from Japan’s public and private sectors.

Osaka Gas becomes first Japanese firm to enter city gas business in India

(Company statement, Dec. 20)

- Osaka Gas will enter India’s gas distribution business, investing $120 million in a local unit of Atlantic, Gulf & Pacific International Holdings (AG&P), a Singapore-based infrastructure development company. The investment will be made with the Japan Overseas Infrastructure Investment Corporation for Transport & Urban Development.

- Osaka Gas is already an investor in the parent company, but the latest deal will give it a stake in the Indian vehicle that AG&P set up after it won licenses to operate in 12 city gas areas in South India and Rajasthan.

- AG&P aims to grow Indian gas sales to 3.5 billion m3 a year, which is approximately half of Osaka Gas’ city gas sales volume in Japan.

- Osaka Gas is Japan’s first participant in India’ city gas distribution sector.

Oil company CEOs pessimistic about gasoline demand

(NHK, Dec 27)

- The CEOs of Japan’s big three oil companies described an unprecedented sense of crisis over falling demand for petrochemical products.

- Describing the shift away from carbon as irreversible, ENEOS boss Ota Katsuyuki says there’s an increasing risk that demand for petrochemicals will decline faster than expected. Lower demand could cause oil producing nations to reduce supply, thereby causing oil prices to skyrocket.

- COSMO CEO Kiriyama Hiroshi echoed this, saying that as Japan is currently reliant on fossil fuels for over 80% of its primary energy needs, imposing sudden restrictions on fossil fuels will cause prices to rise.

- Idemitsu CEO Kito Shun’ichi said that while divestment from fossil fuels can boost renewables growth, power shortages may result if done too quickly.

Further restructuring unavoidable in petrochemical sector

(Asahi Shimbun, Jan. 2)

- 2021 saw a record number of mergers and acquisitions in Japan’s petrochemical sector, reflecting the global trend to divest from fossil fuels.

- Mitsubishi Chemical Holdings aims to spin off its petrochemical and carbon-products businesses by 2023.

- These businesses supply the raw materials for making plastics and steel, both of which are part of Mitsubishi Chemical’s core business.

- Its Okayama and Ibaraki plants make 730,000 metric tons of ethylene annually, but major investment is needed to reduce their carbon footprints.

- CEO Jean-Marc Gilson said further consolidation and restructuring in the Japanese market is unavoidable.

Toho Gas to supply carbon free gas to KIOXIA

(Denki Shimbun, Dec. 24)

- Toho Gas agreed with 10 companies, including Kioxia, to supply carbon-neutral city gas that offers carbon offset credits along with the gas itself. The total supply of gas during the contract period is expected to be about 30 million m3.

- The 10 companies will contribute to a reduction of about 80,000 tons of CO2.

- The deal brings the number of carbon neutral clients of Toho Gas to 26.

- Toho Gas will use 25,000 tons of carbon-neutral LNG to supply city gas to the 10 companies. Toho Gas is sourcing the LNG mostly from Sakhalin Energy.

Asian LNG prices plunge 30% as Europe supply worries ease

(Asia Nikkei, Jan. 6)

- Asian spot prices for LNG dropped by 30% in a span of a week, with Chinese and Japanese inventory pressures easing after a similar plunge in Europe.

- The weekly LNG spot price for the Asia region stood at $33.80 per mbtu around the start of the year, down from the record $48.30 logged on Dec. 23.

- Chinese and Japanese inventories slacken, but remain at elevated levels.

ANALYSIS

BY TOMAS KÅBERGER

The Future Belongs to Renewables, but

Japan’s Policies Continue to Buck Global Trends

Many felt disappointed by the outcomes of the United Nations Climate Change Conference (COP26) held last November in Glasgow. To me, the conference and 2021 as a whole only reinforced the strength of the decarbonization movement and the shift to renewables. The optimism of the COP26 meeting exceeded that of any previous COP summit.

There are several important trends to note from last year:

- The cost of renewables has dropped to the point where renewable electricity is economically attractive as a replacement for fossil fuels

- Business is welcoming the climate-neutral environment and several industry groups have presented joint plans to reduce emissions by shifting away from hydrocarbons to renewable energy sources in their supply chains

- Policies that set a price on CO2 emissions are spreading around the world and ideas such as the EU’s Climate Board-Adjustment Mechanism (CBAM) are proving popular as a way to ensure the competitiveness of industry in a net-zero-emissions environment

Let’s look at some numbers behind these trends.

In 2020, the International Energy Agency (IEA) called solar electricity the cheapest in history. In 2021, Saudi Arabia achieved a new record low when electricity from a solar farm was offered at only $0.0104/ kWh (about ¥1.16/ kWh). Even if countries in Europe, North America and Northeast Asia, where solar radiation is only half as intense as in Saudi Arabia and costs are double as a result, the price is still low enough to start outcompeting thermal power plants.

Not only solar has become cheap. Investments in wind generation have brought down costs to the point where onshore and offshore projects in Europe can compete without subsidies. Costs are around ¥3 to ¥4 per kWh and could fall further.

The most important achievement of renewable electricity is that its total cost now runs below the price of energy contained in crude oil. Renewable electricity is often cheaper per unit of energy than natural gas and, sometimes, can be a more profitable substitute to coal in industrial use. Thus, we can conclude that even without subsidies and taxes, electricity from renewable sources can start to replace fossil fuel systems. We already see this happening in the transport sector and, increasingly, in manufacturing.

Transport and Industry

For electricity to replace fuels, we inevitably need batteries or power to be stored in hydrogen or liquid fuels. The market share of battery electric vehicles (BEVs) is in the double-digits in several countries already; it is approaching 100% in Norway, which has also employed wind and hydro power to generate nearly all of its electricity.

Steel is often given as an example of a product that’s impossible to make without fossil fuels. In June 2021, Sweden’s Hybrit delivered the first sponge iron made from iron ore with electricity that came from renewable sources. In the ironmaking process, Hybrit (a joint venture of SSAB, LKAB and Vattenfall) replaced coal with green hydrogen. In August, SSAB had converted that sponge iron into steel, and in October, Volvo had used that steel to build a vehicle.

These advances in batteries and hydrogen systems make the task of replacing fossil fuels in power generation easier. Car batteries and hydrogen are examples of energy storage that could be topped up during times when renewable energy generation is abundant and cheap. In the hours of the day when the sun is not shining or the wind is blowing less, batteries aren’t charged and hydrogen is not produced. So, vehicles and industries operate with the energy stored. This basic concept makes it easier to phase out fossil fuels as a whole rather than just replacing them in the power sector.

COP26 and Carbon Pricing

At the COP26 summit a Coalition of First Movers and other industrial initiatives committed to go ahead and, in various ways, demand CO2-free supply chains from their vendors. They did this to prove their social responsibility and because they saw an opportunity to gain competitiveness as renewable energy becomes cheaper. But they also did this to reduce the risks for investors during the shift to new technologies.

In July 2021, the EU Commission adopted a proposal for a new Carbon Border Adjustment Mechanism that will put a carbon price on imported products. This is done to avoid putting first movers in decarbonization and adopters of carbon pricing at a competitive disadvantage.

Carbon pricing now exists in an increasing number of countries and this kind of mechanism will make it more difficult for others to continue with their fossil fuel systems, even if they are still cost-competitive domestically with renewable alternatives.

Japan’s Implausible Gambit

Japanese industry was once a leader in developing solar PV technologies. Japanese firms have been providing batteries for customers all over the world, and the country was where the idea of hydrogen as an energy carrier evolved.

Today, however, the political leadership in Tokyo seems lost when it comes to deciphering the global developments as described above.

Newly elected Prime Minister Kishida delivered a speech at COP26 that won yet another “Fossil of the Day” award from the Climate Action Network. The reason: His economically implausible idea that it’s fine to build more thermal power plants, because at some point in the future they can be fueled by imported hydrogen or ammonia, both of which could also be derived from fossil fuels while being offset with carbon capture and storage technology to reduce emissions. The premise seems dead from the start. When electricity from renewables is cheaper than from thermal generation, seeking to manufacture even more expensive fuels in order to burn them in power plants at home cannot be an economically credible solution.

In Japan, the cost of renewable power is coming down thanks to a build-up of industrial experience and the efforts of hundreds of companies.

If Japanese manufacturing is to stay cost-competitive on a global basis, the government has to remove administrative barriers to renewables and truly open up the power grid and the power market to new, progressive actors.

Deliberately wedding Japan to future imports of coal, LNG, uranium and expensive hydrogen or ammonia instead of utilizing cheap domestic renewable resources seems like a recipe for economic demise.

Such a policy seems to be diametrically opposite to the atmosphere of technological and economic progress that we saw at COP26.

Tomas Kåberger has been the Chair of Executive Board of Renewable Energy Institute (Japan) since its foundation in 2011. He is professor in International Sustainable Energy Systems at the International Institute for Industrial Environmental Economics at Lund University, and currently an affiliate Professor of Industrial Energy Policy at Chalmers University of Technology. He also serves on the Board of Directors of Vattenfall. He was also a member of the Swedish Climate Policy Council between 2018 and 2021.

ANALYSIS

BY JUN ARIMA AND

HIROYUKI TEZUKA

Rushing the Green Agenda Will Backfire!

Japan Embraces Energy Pragmatism

The message regularly put out by most developed western nations in 2021 was that the world must move towards a green energy transition at all costs. The economic reality, however, showed us that it cannot happen at any cost. If climate change is to be tackled in a truly global fashion, the solutions and processes cannot ignore current and future global needs. In this sense, the COP26 summit in November was a perfect example of how the message is starting to run away from the context.

We are not pessimistic about the challenge of carbon neutrality. Yet, as with all problems, we must be candid about the current situation and set realistic targets. We should also acknowledge that decarbonization will be an expensive and long-term process that much of the developing world cannot currently afford. Forcing a rushed climate agenda would likely backfire and there is already evidence for that.

Global Policy Rushes to Cancel Coal

The UK, EU and the U.S. have expedited the climate agenda in the last year, which has yielded more results than many realize. In the summer, as host of the G7, the UK succeeded in cementing the idea that global average temperatures should be restrained to an increase of 1.5°C. This was included in a G7 Summit Communiqué for the first time. Other firsts included a net-zero-emissions target by 2050 and an agreement to move away from “unabated” coal-fired generation. Calls by Western nations for G7 members to halt financing for coal projects abroad were also heeded.

The UK planned to have similar messages reflected in the G20 Leaders’ Declaration, yet its ideas were met with strong opposition from China, India, Saudi Arabia, Russia, and other countries. In the end, the G20 summit only reconfirmed the temperature targets of the Paris Agreement. The G20 did not agree to phase out domestic coal-fired capacity.

Despite the resistance at the G20, the UK pushed through the more ambitious targets at COP26 in November. The Glasgow Climate Pact adopted at COP26 includes:

- A resolution to pursue efforts to limit global temperature increase to 1.5°C;

- Recognition that limiting this rise in temperatures requires a 45% cut in global emissions by 2030 (compared with 2010 levels) and to reach net zero by mid-century;

- Calling for COP27 to adopt a working plan to scale up ambitions during the “critical decade” leading to 2030; and

- Request the parties to strengthen their nationally determined contributions (NDCs) as necessary to align with the Paris Agreement temperature goal by the end of 2022.

Most importantly, the Glasgow agreement includes the wording: “to accelerate the…phasedown of unabated coal power and phase-out of inefficient fossil fuel subsidies…” While toned down from the originally proposed “phase out,” this is the first time that such wording targeted a specific energy source.

The Cost of Expediting Net Zero

The proactive approach of the UK and like-minded western politicians has significantly altered the nature of the Paris Agreement, part of the appeal of which was its delicate balance between a top-down approach of setting global temperature targets and a bottom-up approach through which each country could set targets based on its own specific circumstances.

What does that mean in practice? By aiming for a 45% cut by 2030 and net zero by 2050 all around the world – at once – the scene is set for a fierce battle between the developed and developing nations over a limited carbon budget. It’s no wonder that India asked rich nations for $1 trillion in annual contributions. That’s the cost of expediting decades of development in the weaker economies while at the same time raising the NDCs.

Now that “coal phaseout” is officially accepted, the next global policy war will focus on the date by which this must be completed. The debate could well expand to setting similar dates for other fossil fuels. At COP26, we already saw over 40 countries, including the U.S. and EU, issue a joint declaration to end public financing for the entire fossil fuel sector. But such messages are disconnected from energy reality.

The ongoing energy crisis in the UK, parts of Europe and elsewhere is to a large extent caused by the supply-demand imbalance in fossil fuels that resulted from stagnant upstream oil and gas investment. So, while green policies call for an end to fossil fuels and claim that GHG cuts are the utmost priority, the top item on the daily agenda of many governments is cooling record high energy prices.

It seems clear that when there’s a risk to secure and affordable energy supply, which is the fundamental policy requirement, then the climate agenda can easily be set aside.

Why Japan is Not Rushing into Renewables at Full Speed

Last April, former Prime Minister Suga declared that Japan will cut GHG emissions 46% by FY2030, compared to the FY2013 level. It was a highly ambitious target since 85% of Japan’s energy currently comes from fossil fuels.

Between 2013 and 2018, Japan reduced CO2 emission 12%. How? Japan restarted nine nuclear reactors, which contributed 2.4 percentage points. The rollout of renewable energy, mostly solar that was supported by a Feed-In Tariff (FIT), offered the same. In total, nuclear restarts and renewables offered a 5% reduction in emissions. But the 2030 target requires Japan to cut another 38% from the 2018 level.

The good news is that Japan still has 18 reactors waiting for a restart. As well as cutting emissions, nuclear plants can suppress the increase in electricity cost caused by building more solar and other renewables through the FIT tariffs — the nation’s expenses on FIT jumped to ¥2.4 trillion, or ¥2.9/ kWh in 2018. That number inched up to ¥2.7 trillion in 2021 and if the share of renewables doubles over the next decade, as per the instruction from the new Basic Energy Plan, then the FIT number will swell to about ¥4.7 trillion.

Even at 2018 levels, the FIT surcharge translates into a carbon price of around $70/ ton of CO2. It could get much worse economically since the restart of reactors in Japan is currently a highly political and unpredictable process.

There are other constraints to renewables in Japan. The country already has the highest solar-panel cover density among major countries; twice the density of Germany when comparing flat land surfaces. This is one of the reasons for many local issues that plague the development of solar power and the growing local resistance to new projects.

Onshore wind farms face the same space issues, while offshore the relatively deeper ocean floor and 30% lower wind flow, compared with the North Sea in Europe, leads to cost disadvantages for Japan.

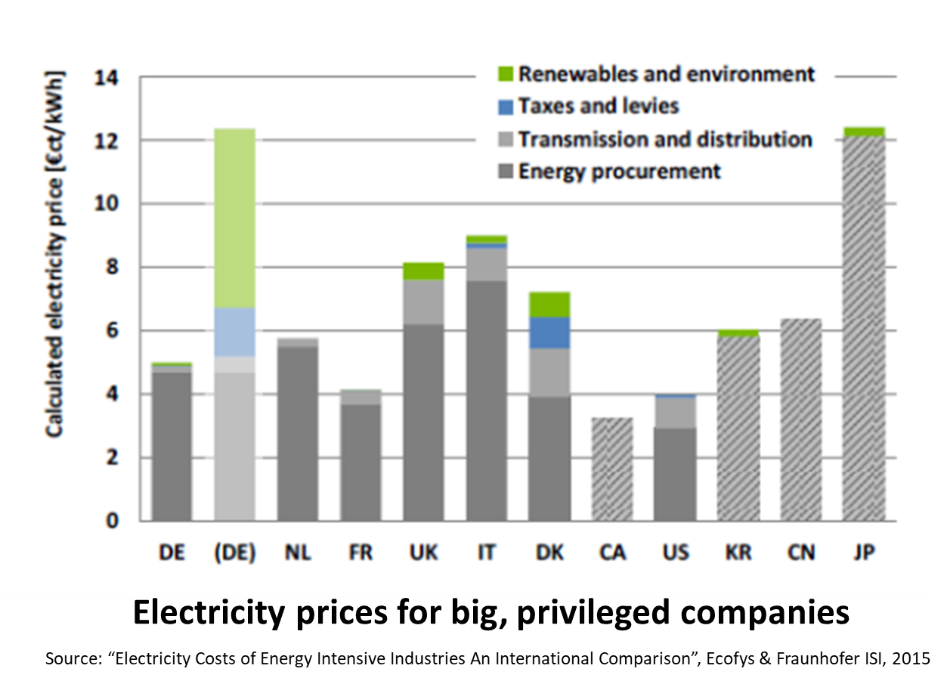

The cost of energy, electricity in particular, impacts competitiveness for Japan’s industry, which produces globally traded, energy-intensive products. According to a study by European think-tanks[1], Japan’s electricity cost for industry was among the highest in 2015. It is three times more expensive than the U.S. and Canada and almost double that of China and Korea. The study also revealed that the electricity cost in Germany was significantly reduced to the levels of France, where cheap nuclear is a major source of electricity, by exempting most of the policy charges such as EEG (the equivalent of FIT in Japan) and tax levies.

Therefore, we can suppose that high energy costs are one of the reasons for stagnant wages in Japan.

As things stand, Japan’s commitment to doubling its renewables quota to 36-38% of the energy mix by 2030 will inevitably push up the cost of electricity. Asking for an even higher percentage, with the current technologies and conditions, creates the risk of backfiring in the same way that developing nations pushed back against the G7 agenda in 2021.

What Japan needs most is a strategic industrial energy policy that looks to ensure global competitiveness for its industry, while also improving the environmental footprint. Ignoring the former to pursue the latter eliminates the vital connection between climate and the economy.

Jun Arima is a Project Professor at the Graduate School of Public Policy at the University of Tokyo, is a former METI official, and a former member of Japan’s COP negotiation team

Hiroyuki Tezuka is Chair of the Working Group on Global Environment Strategy at Keidanren and is a Fellow at JFE Steel Corporation

GLOBAL OUTLOOK 2022

BY JOHN VAROLI

In the Chinese tradition, 2022 is the Year of the Tiger. How fitting, because the global energy sector seems set to roar, especially in China whose economy grew 8% in 2021 and electricity consumption at 10%. The country is making large investments in renewable energy, as well as in nuclear power and the reactivation of coal-fired plants.

As demand increases, critical energy shortages are pushing many nations to put climate promises on hold. Greta Thunberg will be disappointed in 2022 — fossil fuels and nuclear power will enjoy a good year, if not a good several years. Fossil fuels and renewables will have to coexist and cooperate longer than environmentalists had hoped for.

Covid, of course, is the big unknown that could throw a wrench into the machinery of the global economy. However, pandemic fatigue is reaching a critical point, and governments will be pressured to invigorate the global economy rather than shut it down again.

Let’s take a look at each major energy sector and its prospects for 2022.

Nuclear

Since the Fukushima nuclear accident in 2011, nuclear power’s future has been bleak. But much has changed in the past six months. Many countries signed up to ambitious climate goals, and that’s unlikely to happen without carbon-free nuclear power. While Germany closed three of its remaining six nuclear plants on Dec 31, 2021, about half a dozen EU countries plan to build new reactors. The U.S. is also supportive of nuclear power to meet net-zero goals, while China’s nuclear program beguiles the mind — to build 150 reactors in the next 15 years. For its part, Japan is developing SMRs, most notably a GE-Hitachi project in Canada, and a $5 billion nuclear reactor with TerraPower in the U.S.

Oil

It’s going to be a good year for fossil fuels. As people get back on the road, oil demand will remain robust. The price of oil is a key indicator of national happiness in the U.S. and will impact the midterm elections in November. Thus, the Biden administration will do its best to keep oil prices stable. He’ll have to call on favors from OPEC countries and also make concessions to Big Oil at home. Oil prices are expected to stay within a range of $65 to $80 per barrel. What the oil companies do with those profits, however, will be a contentious issue. Will they invest in new fossil-fuel projects or finance the green energy transition?

LNG/ Gas

Likewise, LNG and natural gas will see another good year. Prices will remain high but likely stable. While natural gas faces condemnation from environmentalists, the European Union plans to classify some gas-fired plants as “transitional” under certain strict conditions. This is crucial for the EU’s leading economy, Germany, which more than ever is heavily dependent on gas. In general, about 25% of the EU’s total energy currently comes from gas, and replacing that capacity with renewable energy will take a decade or more. In Asia, countries such as South Korea are switching coal-fired power plants to gas. East Asian demand for LNG will grow this year and beyond.

Coal

Even though the U.S. and many West European countries are shutting their coal-fired power plants, global coal demand will hit another high this year — reaching 8,025 Mt in 2022, the highest ever. China and India will lead consumption growth, which will more than outpace the declines in other markets. Motivated by the need to power its industry, China is ignoring climate change impact for now and reigniting many of its coal-fired plants. Regarding coal, Japan is closer to China and India than Europe, but Tokyo vows to push on with developing co-firing generation that should see thermal plants also run on ammonia as well as coal to cut total emissions. In addition, China and Japan are planning to launch a “clean-coal” technology pilot project in China’s Shaanxi province.

Hydrogen

Despite setbacks to meeting net-zero targets as described above, the clean energy sector will continue to grow in giant leaps and bounds in 2022, especially in the hydrogen space. For example, Australia is fast-tracking the $10 billion, 10-GW Desert Bloom green hydrogen project that will use solar and wind. Economies of scale and improved technology have lowered the cost of hydrogen fuel cells by 60% over the past decade. What more, green hydrogen, which relies on renewables such as solar and wind, seems to be one of the few energy sources that makes everyone happy — from environmentalists to giant legacy energy companies eager to enhance their environmental credentials.

Solar

Solar will continue to shine in 2022, with an estimated 44 GW coming online globally,

nearly double 2021′s projected 23 GW, according to S&P. This increase in solar capacity is driven by the expansion of state-mandated renewable requirements and more tax credits. Energy storage is key for intermittent power sources like solar and S&P expects 8 GW of storage to be installed in 2022, around 600% more than in 2020. But there are bumps on the road to this bright future. Rystad Energy says that more than half of 2022′s global solar infrastructure projects will be hindered by rising raw material costs and supply chain woes. This means that 56% of an anticipated 90 GW of new utility-scale solar projects could face delays or be canceled.

Wind

New installed wind turbine capacity in 2022 will easily surpass the annual record of 16 GW set in 2020 and could be as much as double that number. This year, the UK will complete the world’s largest offshore wind farm — the 165 turbines of Hornsea Two, (8.4 MW each). The IEA believes that offshore wind has the potential to power all of global demand. Meanwhile, wind farms are bigger than ever. Four years ago, wind farms typically utilized 7- and 8-MW turbines with 70- to 90-meter-long blades. Soon, market leader Vesta plans to start selling 15-MW turbines with 115-meter-long blades.

Geothermal

While a niche, the global geothermal electricity market is expected to grow about 9%, from $5.5 billion in 2021 to $6 billion in 2022. The World Bank will loan Turkey $300 million to support its Geothermal Development Project to build 380 MW of capacity by tapping heat sources deep in the ground. There’s strong enthusiasm for more geothermal energy in Japan and Southeast Asia, as well as parts of Africa, though the technology’s application is of course limited by location and its complexity. One project in the U.S. is already bogged down in lawsuits. Last week, conservationists and tribal leaders sued the U.S. government to block construction of two geothermal plants in Nevada’s high desert that they say will destroy a sacred hot spring.

Biomass

The global biomass energy market will remain marginal but its value is forecasted to grow 10%, from $33.6 billion in 2021 to $37 billion in 2022. At the end of December, the UK government pledged £26 million to boost the use of materials such as grasses, hemp and seaweed as green energy solutions. One drawback with biomass fuels is that they can’t easily be scaled. Meeting demand for low-carbon aviation fuel offers much potential, but meeting that demand is problematic. For example, only about 26.4 million gallons of low-emission, sustainable aviation fuel (SAF) is produced annually, which is a fraction of the 18 billion gallons of fuel burned by U.S. carriers alone.

Green Finance

Sustainable finance, also known as green finance, will accelerate in 2022. Bloomberg predicts that this year about $2.5 trillion of green and ESG-oriented debt will be issued, up from $1.5 trillion in 2021. For the first time since the Paris Climate Accord in 2015, financial institutions are earning more fees from green-related bond sales and loans, a total of $3.4 billion last year; which slightly surpasses what they earned raising money for fossil-fuel companies: $3.3 billion. In 2020, those figures were $1.9 billion for green deals, and $3.7 billion for fossil fuel deals.

JAPAN OUTLOOK 2022

IEEJ Energy Forecasts for Japan for 2022: Zero-Emissions Power Sources Exceed 30% for the first time since 2011 and Household Energy Expenditures to hit $130 billion

The Institute of Energy Economics in Japan (‘IEEJ’) has released their domestic energy forecasts for FY2022. With the kind permission of the IEEJ, we’re providing a summary below.

The IEEJ is Japan’s leading non-profit energy think-tank with over 100 member firms. In 2020 the University of Pennsylvania ranked the IEEJ as a top three energy and resource policy think-tank in the world.

Japan Energy and Economic Forecasts for 2022

- Real GDP will hit a record high of ¥558 trillion in FY2022 (FY2019 was ¥551 trillion)

- Total energy consumption will be 429 million toe in FY2022 compared with 445 mtoe in FY2019, the pre-pandemic year, a decrease of 4%

- Household energy expenditures are expected to be ¥14.9 trillion (almost $130 billion) in FY2022, up 4% YoY and up 6% vs. FY2019, with most of the increase coming from electricity charges

- Two additional nuclear reactors will restart in FY2022, bringing the total number of units restarted to 12 since the Great East Japan Earthquake of March 2011

- Electricity prices will rise for the second successive year due to high renewable surcharges and higher fuel imports with prices for electricity for lighting hitting ¥29.7 (26 U.S. cents)/ kWh compared with ¥27.3/ kWh in FY2019

- Coal and oil consumption will marginally increase

- CO2 emissions will increase for the second successive year, which means only half of the 46% emissions cut (vs. FY2013) by 2030 will have been achieved; C02 emissions in FY2022 are expected to be 20% lower than in FY2013, the reference year; 75% of the reductions since FY2013 are now attributable to energy efficiencies and lower energy consumption per unit of GDP

- Sales of electricity are expected to increase to 840 TWh, up 1% YoY, and higher than FY2019 (836 TWh), but lower than FY2018 (853 TWh), due to business demand

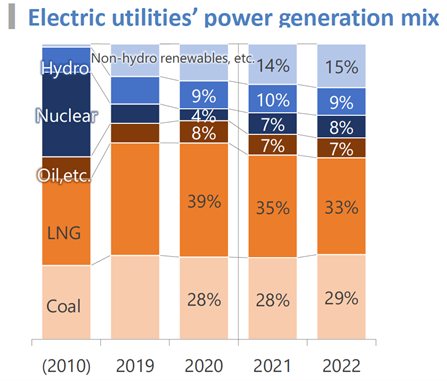

- Zero-emission power generation (renewables and nuclear) in FY2021 exceeded 30% of total generation for the first time since 2011; the trend will continue in FY2022

- Power generation from LNG will fall by 6% vs. FY2019

- Power generation from hydro will fall marginally YoY

- Total city sales of natural gas will increase marginally to 42 bcm vs. 41 bcm in FY2021 with sales to industry and commercial firms increasing, and residential sales flat

- Fuel oil sales in Japan will continue their decline and are expected to fall 1% YoY to 153 billion liters, with sales of naphtha contributing most of the decline

We are deeply grateful to Mr. Toshiyuki Sakamoto, Board Member, IEEJ and Mr. Ryo Eto, Senior Economist, for giving us permission to reprint these forecasts.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

| January | OPEC quarterly meeting;

JCCP Petroleum Conference – Tokyo; EU Taxonomy Climate Delegated Act activates; Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

| February | Chinese New Year (Jan. 31 to Feb. 6);

Beijing Winter Olympics; South Korea joins RCEP trade agreement |

| March | Renewable Energy Institute annual conference;

Smart Energy Week – Tokyo; Japan Atomic Industrial Forum annual conference – Tokyo; World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

| April | Japan Energy Summit – Tokyo;

MARPOL Convention on Emissions reductions for containerships and LNG carriers activates; Japan Feed-in-Premium system commences as Energy Resilience Act takes effect; Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

| May | World Natural Gas Conference WCG2022 – South Korea;

Elections: Australian general election; Philippines general and presidential elections |

| June | Happo-Noshiro offshore wind project auction closes;

Annual IEA Global Conference on Energy Efficiency – Denmark; UNEP Environment Day, Environment Ministers Meeting – Sweden; G7 meeting – Germany |

| July | Japan to finalize economic security policies as part of natl. security strategy review;

China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong; Czech Republic assumes presidency of EU; Elections: Japan’s Upper House Elections; Indian presidential election |

| August | Japan: Africa (TICAD 8) Summit – Tunisia;

Kenyan general election |

| September | IPCC to release Assessment and Synthesis Report;

Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.; Japan LNG Producer/Consumer Conference – Tokyo; IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

| October | EU Review of CO2 emission standards for heavy-duty vehicles published;

Chinese Communist Party 20th quinquennial National Party Congress; G20 Meeting – Bali, Indonesia; Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

| November | COP27 – Egypt;

U.S. mid-term elections; Soccer World Cup – Qatar; |

| December | Germany to eliminate nuclear power from energy mix;

Happo-Noshiro offshore wind project auction result released; Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26; Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

- https://publica.fraunhofer.de/eprints/urn_nbn_de_0011-n-3829110.pdf ↑