JAPAN NRG WEEKLY

FEB. 7, 2022

JAPAN NRG WEEKLY

Feb. 7, 2022

NEWS

TOP

- Japan cautions against its ability to help Europe with natural gas as Qatar cools on Japan energy relations after LNG contract spat

- JERA enters China’s LNG market with a Beijing office; importer looking to future trends and opportunities in the industry

- Japan to move bottom-fixed offshore wind entirely to new tariff; emerging sector is already seen ready to embrace market rates

ENERGY TRANSITION & POLICY

- Govt. to tighten inspection of mini-solar projects on safety worries

- Pilot liquified carbon transport to launch in 2024

- METI solicits participants for voluntary carbon exchange trial runs

- METI minister meets with IEA, UAE to discuss rising energy prices

- JAPEX, Petronas to study carbon capture and storage in Malaysia

- Trading houses join BP, Woodside in west Australia CCS project

- Kansai Electric, partners to develop ammonia FSRU units

- Japan nuclear fusion startup attracts investors for global push

- Honda to buy 2% of developer of a new type of lithium battery

ELECTRICITY MARKETS

- West HD, JERA plan to jointly develop 1.1 GW of solar in Japan

- Mitsubishi responds to claims of price dumping in wind tender

- Kansai Electric aims for Takahama NPP reactor restarts next year

- Japan’s top power and gas utilities say rates will rise in March

- Utilities used less LNG last year to cut costs, but earnings still dire

- First Chinese wind turbine maker wins a contract in Japan

- Japan group to develop floating substations to aid offshore wind

- Mitsui invests in Brazilian power trading company

OIL, GAS & MINING

- LNG stockpiles drop 28% in less than a month on colder winter; fuel oil stocks also down significantly at the end of last year

- Govt. says will not rule out tax relief scheme for gasoline

- FGE’s Fesharaki says oil could top $100; LNG to peak in 2040s

- Tokyo Gas, ENEOS announce “carbon neutral” LNG contracts

ANALYSIS

JAPAN’S “ALTERNATIVE ENERGY TRANSITION” WINS OVER SOUTHEAST ASIA AND BOOSTS BUSINESS

Japan’s government and major energy corporations are increasing their operations in Southeast Asia, seeing the region as sympathetic to their gradual approach to decarbonization. Southeast Asian economies are forecast to grow between 4% to 7% in the next few years, yet local governments have hesitated to put forward ambitious net-zero pledges. With nuclear power virtually non-existent in the region, and renewables development still at a nascent stage, Japan’s vision for a less disruptive energy transition that retains coal-fired plants is gaining attention, and opening up business opportunities.

JAPAN’S LNG ENERGY SECURITY HAS A COST:

ESTIMATING THE PRICE OF SUPPLY DIVERSITY

Cutting CO2 emissions and decarbonization was supposed to be the main topic in global LNG markets last year. Instead, energy security is again front and center, especially for purchasing countries. In the case of Japan, security of LNG supply is especially pressing because the fuel has an outsized influence on domestic electricity pricing. Assuming the government sticks to its decarbonization strategy, which says that Japan’s LNG demand for the power sector could drop 50% by 2030, retaining supply security through diversity of import sources could incur a significant monetary cost.

GLOBAL VIEW

EU ruling says nuclear and natural gas can be classified as “green” in some cases. California needs 53 GW of solar by 2045 and 37 GW of battery storage. Russia to develop two giant copper mines. Brazil’s wind power capacity jumps 26% in a year. Big tech firms drive the demand for more renewables. Details on these and more in our global wrap.

EVENT CALENDAR FOR 2022

Key political and business events in Japan and abroad.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Tom O’Sullivan (Japan, Middle East, Africa)

Mayumi Watanabe (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Daniel Shulman (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

Events

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Fixed foundation offshore wind to shift entirely to FIP in 2024

(Japan NRG, Jan. 28)

- Starting in 2024, fixed-foundation offshore wind power will shift to the Feed-in-Premium (FIP) system from the Feed-in-Tariff (FIT) for all farms, including those in Renewable Promotion Zones.

- CONTEXT: Under the FIP scheme, power operators sell electricity in the spot market and receive a premium on top of the spot price. Under the FIT system, the operators receive full payment of fees pre-set by auctions.

- FIP will not apply to floating offshore wind as the market is not yet mature.

- FIP will roll out earlier, in 2022, for onshore wind farms that have more players.

- In the initial phase, ¥1/kWh will be given to FIP operators to cover the spread between planned and actual power output. The fee will eventually be removed.

- In 2020, Japan had 4.2 GW of installed wind capacity, mostly onshore, generating 7.7 TWh.

FIP transition schedule

|

Offshore, fixed foundation |

FIP from 2024 |

Exchange trading unit: 330 kW |

|

Offshore, floating |

FIP will not apply |

— |

|

Onshore, over 50 kW |

In 2022, operators can choose between FIT or FIP, and shift to FIP from 2023 |

Exchange trading unit: 390 kW |

|

Onshore, below 50 kW |

FIP will not apply |

— |

TAKEAWAY: Solar is less variable than wind, and will shift to FIP earlier. From April 2022, solar capacity of over 1 MW will fall under FIP; and from April 2023, it will apply for any installation of over 50 kW. Solar dominates the current FIT licensees, accounting for 80% of the total.

The government has installed a very aggressive timeline to move the wind industry to a competitive landscape. This is partly due to “lessons learned” from the rollout of solar, which was seen as having received generous FIT licenses for longer than was necessary, and which is now weighing on the consumer power bills.

METI to tighten inspection of mini-solar projects

(Japan NRG, Jan. 28)

- There will be stricter oversight of solar power operators of less than 10 kW because some large operators are reportedly splitting operations into multiple small capacity units to avoid regulation.

- METI will require 0-10 kW power stations applying for the FIT to submit land and building registry documents, and will conduct on-site checks. Small power stations are not subjected to public service duties, such as providing power during emergencies.

- The number of FIT applications for 0-10 kW solar power stations jumped to 3,668 in 2020, from 937 a year earlier. From April 2021-January 2022, there were 2,643 applications, but only 834 were approved.

TAKEAWAY: Regulation of the solar industry is on the up. One of the reasons is that with available flat land few and far between, developers have at times cleared forests or build utility solar on slopes. In times of heavy rain, this has led to several accidents. The solution being proposed by many sides, including the govt., is to “communicate” more with the local community. In essence, this means share income with the local community ostensibly to cover potential damages from natural disaster. That makes sense as disaster mitigation. It doesn’t help to make solar in Japan cheaper. How the tension will be resolved is as yet unclear.

Pilot liquefied carbon transport to launch in 2024

(Japan NRG, Jan. 28)

- In 2024, METI will launch a pilot run for the transport of liquefied carbon by sea, in order to move the carbon to carbon capture and storage (CCS) sites. Together with Norway, Japan is developing technologies to liquefy carbon and store it in a low pressure, low temperature environment.

- Carbon from the Maizuru coal-fired power plant in Kyoto will be transported to the CCS site in Tomakomai, Hokkaido. The sea vessel will be built in 2023.

- Transport demand is expected because most emitting facilities are on the Pacific coast while potential CCS sites are on the Sea of Japan coast of the main Honshu island.

- METI sees the commercial launch of CCS around 2030, and plan to start feasibility studies in 2023. Japan’s CCS potential is 16 billion tons. METI will also establish a methodology to assess carbon reduction through CCS, in order to be used as voluntary carbon credits. A detailed CCS development roadmap will be released in May.

TAKEAWAY: The main actors in this project are Kansai Electric, operator of the Maizuru station, and Mitsubishi Heavy Industries (MHI), which is developing the ship to transport liquid carbon. However, many other large firms are involved including oil explorers such as JAPEX, which have a strong motivation to make CCS work so as to shift their core business from pumping oil to filling wells with carbon.

METI solicits participants of carbon exchange trial runs

(Japan NRG, Feb. 1)

- METI calls businesses to participate in the trial runs of a carbon exchange to be formally launched in April 2023. Applications close on March 31.

- The companies are asked to show their ambition to limit global temperature rise to 1.5 C, carbon neutrality initiatives throughout their supply chains, and how their activities contribute to carbon reductions.

- The pilot program participants will be dubbed “GX (Green Transformation) Basic Framework Supporters”. They were previously called “Top League Companies”.

TAKEAWAY: It may seem odd, but labels matter, especially in Japan. Once a rival company has a new “title” to add their presentations, others want in. METI’s biggest hurdle will be to get that initial momentum started.

METI minister talks oil prices with IEA and UAE; MoE minister promotes JCM

(Japan NRG, Feb. 2)

- METI minister Hagiuda held online talks with IEA’s secretary general Fatih Birol on Jan. 31, and with Ahmed Al Jaber, the UAE’s Minister of Industry and Advanced Technology on Feb. 2, to discuss rising energy prices.

- Hagiuda and Birol touched on Ukraine and balancing the energy transition with energy security, while the blue ammonia supply chain was brought up in the talks with Al Jaber.

- On Jan. 27, Environment Minister Yamaguchi joined the U.S.-led Major Economies Forum on Energy and Climate (MEF) on methane and other greenhouse gas reduction. Yamaguchi said that the forum plans to invite more nations to participate in the Joint Credit Mechanism (JCM).

- Currently, there are 17 countries in the JCM. Other diplomatic initiatives in January included signing bilateral energy partnerships with Indonesia, Thailand and Singapore.

JAPEX agrees with Petronas to jointly study CCS project in Malaysia

(Sekiyu Tsushin, Jan. 31)

- JAPEX signed an MoU with Petronas, Malaysia’s main energy company, to conduct a joint study on CO2 capture and storage (CCS) in Malaysia.

- JAPEX and Petronas will conduct a “site survey with a view to implement geological storage of CO2” and “technical studies,” including not only the capture and transport of CO2 from Petronas’ LNG terminal in Bintulu, Sarawak, but also “possibly “receiving CO2 from outside Malaysia”.

- The duration of the joint study will be about 20 months.

- CONTEXT: JAPEX aims to commercialize CCS in Japan by 2030.

Japanese trading houses partner with BP, Woodside on Australia carbon capture

(Nikkei, Feb. 3)

- Trading houses Mitsubishi Corp. and Mitsui & Co. are partnering with Australia’s Woodside Petroleum and oil major BP to assess areas for carbon capture and storage (CCS) off the Australian coast. Preparations for the survey will start as early as next month.

- Depleted gas fields off the coast of Western Australia are seen as potential sites for CCS.

- The two Japanese firms will work via their Australian LNG joint venture, MIMI.

- The goal is to start operating CCS facilities around 2030.

- CONTEXT: There are 135 CCS projects being developed worldwide, of which 27 are already in operation, according to the Australia-based Global CCS Institute. The projects span an estimated 150 million tons of sequestration capacity, more than double the total five years earlier.

Kansai Electric to develop ammonia FSRU units

(Denki Shimbun, Feb. 4)

- Kansai Electric will begin studies to develop and bring online an ammonia FSRU (floating storage and regasification unit).

- It signed an MoU to work on the technology with Mitsubishi Shipbuilding, a subsidiary of Mitsubishi Heavy Industries, and shipper Mitsui O.S.K.

- The companies want to reduce costs to shift to ammonia-based systems.

Nuclear fusion startup lures Japanese investors in global push

(Nikkei Asia, Feb. 2)

- Kyoto Fusioneering, a nuclear fusion startup, raised ¥2 billion ($17.3 mln) from Japanese investors and banks as it plans to take its supply chain global.

- Nuclear fusion creates energy by making atoms collide at extreme temperatures, the same process that powers the sun. Fusion has been studied for decades, but the R&D failed to advance substantially until recently.

- Kyoto Fusioneering was founded in 2019 by professor Konishi Satoshi of Kyoto University’s Institute of Advanced Energy, and Nagao Taka, who worked in space and energy startups. The company is active in engineering and equipment production for nuclear fusion plants. Last fall, it won a contract from the U.K. Atomic Energy Authority to supply a device called a gyrotron that will be used in its testing facility.

Honda to buy 2% of U.S. developer of a new type of lithium batteries for EVs

(New Energy Business News, Feb. 2)

- Honda signed a joint development agreement with SES Holdings, a U.S. firm that conducts R&D on lithium rechargeable batteries for electric vehicles (EVs).

- SES’s battery, which uses lithium metal as the anode, is said to have higher energy density than ordinary lithium-ion batteries that use carbon-based materials, and if it can be applied to EVs, it will extend the cruising range.

- SES plans to list on the New York Stock Exchange. Honda will acquire about 2% of the shares.

- CONTEXT: Honda is considering several options for the next generation of batteries, including all solid-state batteries, which it is developing on its own.

Toyota-Panasonic venture leads group to research battery resources and recycling

(Kankyo Business, Jan. 28)

- Prime Planet Energy & Solutions (PPES), a joint venture between Toyota and Panasonic will start joint research on battery resources and recycling with Panasonic, the trading house Toyota Tsusho, and the Institute of Industrial Science, University of Tokyo. The goal is to significantly reduce production costs throughout the battery supply chain through better integration, and to advance battery recycling processes.

- PPES is engaged in the development, manufacture, and sale of automotive lithium-ion batteries.

Toshiba to double power chip production with new plant in Japan

(Nikkei Asia, Feb. 4)

- As decarbonization gains momentum worldwide, Toshiba will build production capacity for power chips that save energy and contribute to lower emissions.

- Toshiba will spend around ¥100 billion to build a power semiconductor fabrication facility in Japan (Kaga Toshiba Electronics in Ishikawa Prefecture) to meet the rising demand for power chips used in autos and other equipment.

- Production is expected to begin March 2025.

One-Dot News

- Kyushu Electric completed construction of the 75 MW Shimonoseki Biomass Power Plant, while Kansai Electric completed a 75 MW woody biomass power generation project in Kanda Town, Fukuoka Prefecture. (New Energy Business News, Feb. 4)

- Siemens Gamesa Renewable Energy has established a Japanese subsidiary, Siemens Gamesa Renewable Energy Co. The Japanese business was previously operated by an Australian entity. It will now be incorporated in Japan, focusing on onshore and offshore wind turbines and related services. (New Energy Business News, Feb. 2)

NEWS: POWER MARKETS

JERA, West Holdings plan to jointly develop 1.1 GW of solar in Japan

(Nikkei, Feb. 1)

- JERA will develop more than 1 GW of solar capacity over the next five years with the help of solar power developer West Holdings. The two will also form a capital alliance in the first half of FY2022: JERA will buy some of West’s stock.

- JERA hopes to develop solar projects in about 7,000 locations, in part by using sites of former thermal power plants. It earmarked ¥160 billion for investment.

- The electricity generated will be sold to third parties, including through West’s retail business.

- JERA is considering pairing solar generation facilities with gas-fired power plants to maintain stable electricity supply when sunlight is not available.

- This will be JERA’s first foray into solar power generation in Japan. The two firms might also work jointly in Southeast Asia.

TAKEAWAY: West Holdings has now struck three major partnerships in the last six months or so, but this is the biggest one yet. The Hiroshima-based solar developer agreed to set up 450 solar sites for Amazon and Mitsubishi Corp (22 MW), and up to 2,000 sites for Sumitomo Mitsui Finance and Leasing Co. (200 MW). This suggests West HD has assumed the mantle of partner of choice for many large corporates that don’t have their own experience in the solar business but would like to enter the domain and scale quickly.

West HD is not yet a household name, yet the listed company is already worth more than some of the EPCos. In fact, its market value is now half that of Kyushu Electric, one of the big three regional utilities.

Wind tender: Mitsubishi responds to angry accusations of price dumping

(Diamond, Jan. 27)

- The Mitsubishi Corporation-led consortium that won government contracts to build offshore wind farms in Akita and Chiba has been accused of predatory pricing, amid skepticism that it can turn a profit at the agreed tariffs.

- The head of a major engineering company said the low tariffs destroy the incentive for potential engineering subcontractors to participate.

- Other rivals also doubt that Mitsubishi can establish a profitable supply chain, and say subcontractors will have to work at unprofitable rates. They add that Mitsubishi lacks experience with offshore wind projects.

- Mitsubishi countered by citing a 10-year collaboration with Dutch energy company Eneco, in which Mitsubishi staff are actively involved in project management.

TAKEAWAY: The storm over the first offshore wind tenders has yet to die down. What would help divert attention away from it is the announcement for another tender.

Kansai Electric aims for Takahama NPP reactor restarts next year

(Jiji, Jan. 31)

- Kansai Electric completed safety work on the No. 2 reactor at the Takahama Nuclear Power Plant in Fukui Prefecture. Due to industrial accidents and the pandemic, the work was delayed by almost two years.

- The company also submitted to the Nuclear Regulation Authority (NRA) a plan to restart the Takahama NPP No. 1 reactor on June 3, 2023, and the No. 2 reactor on July 15 of the same year.

Japan power and gas utilities to raise rates, citing LNG costs

(Kyodo News, Jan. 29)

- All 10 major power utilities, except Hokuriku Electric, will hike household electricity rates in March citing LNG’s rising cost.

- Power prices are at the highest level in the past five years.

- All four major city gas companies will hike prices for the seventh month in a row, straining household budgets as prices of daily necessities also rise.

- Biggest rate increase: Chubu Electric. Smallest rate increase: Kansai Electric.

- CONTEXT: Hokuriku Electric’s rates won’t change; they reached the top limit of the fuel cost adjustment system that reflects monthly fuel rate changes. The rates for March reflect the average fuel prices from October to December.

Utilities used less LNG last year to rein in costs

(Denki Shimbun, Feb. 2)

- Due to rising LNG prices, JERA and eight other major power companies saw LNG consumption in April to December 2021 drop 13.8% YoY, or 4.37 million tons; the total was below 30 million tons for the first time since 2010.

- Coal consumption exceeded 40 million tons for the first time in two years, up 5.33 million tons, 13.8% YoY; the fourth-highest total in the last decade.

- Heavy oil consumption increased for the first time in nine years. Although overall consumption was low, jumping 53.6% YoY.

- Only Chugoku and Okinawa EPCos didn’t report a decrease in LNG use.

- The largest annual declines were in the Kansai region (-36.5%), Hokkaido (-34.8%), and Kyushu (-30.3%) regions.

- CONTEXT: Kansai and Kyushu regions benefitted from high run rates of nuclear facilities last year.

- SIDE DEVELOPMENT:

EPCOs earnings worse than expected

(Nikkei, Jan. 31)- Japan’s 10 leading utilities released results for the three months to December.

- All downgraded earnings; Chubu Electric, Tohoku Electric, Hokuriku Electric and Shikoku Electric project losses for the fiscal year.

- Chugoku Electric, which mostly operates thermal plants, making it more exposed to fuel prices, forecasts a ¥37 billion loss for the year, up from a previously projected ¥14 billion loss.

- TEPCO, which had projected a ¥16 billion loss, now expects a ¥41 billion loss.

- While power companies are able to pass on higher fuel prices to domestic subscribers, there’s a time lag of a few months.

China wind turbine maker wins offshore project in Japan

(Nikkei Asia, Feb. 4)

- Mingyang Smart Energy Group won a contract to become the first Chinese player to supply turbines for an offshore wind farm in Japan, helped by its cheaper price tag.

- Mingyang will supply three 3-MW turbines for a wind power facility off the coast of Nyuzen, central Japan. The company will soon sign a formal contract with general contractor Shimizu Corp., and will seek third-party certification for its equipment.

- Venti Japan leads the Nyuzen project, which will start operation as early as next year.

- Founded in 2006, Mingyang ranked sixth in the world, and third in China, as a supplier of new wind turbines in 2020, according to the Global Wind Energy Council.

TAKEAWAY: Chinese producers will have a tougher time selling turbines in Japan’s offshore wind market than the one for solar panels. Installing turbines tends to give the manufacturers access to data on wind and ocean currents, something that would be viewed by the government as a security issue. On the other hand, Chinese firms tend to offer a lower price and minimizing the cost of decarbonization is key for PM Kishida’s government.

It’s reported that the Japanese and Chinese sides in the project agreed that no data collected during turbine installation and operation will be transferred to China. However, Japan’s government, and allied nations, will be sure to keep a close eye on Chinese wind turbine placements in Japanese waters.

Japan power utilities to develop offshore substation to aid wind turbines

(Nikkei, Jan. 30)

- Seven major power utilities, including TEPCO and Kansai Electric, will jointly develop a floating substation to help develop offshore wind energy.

- Substations must be near power generation sites to ensure supply without waste. A dedicated transmission cable for offshore wind has also been developed.

- TEPCO Renewable Power will lead the group to develop equipment that can work in a stable manner even in extreme weather conditions such as typhoons and heavy snowfall. The government will provide subsidies for the project.

Winter power shortages could become chronic

(Jiji, Jan. 30)

- The energy industry still warns that shortages of electricity are possible.

- Twice already this winter, utilities in regions where demand is high were forced to ask regional generators to send surplus power.

- While there are plans to upgrade the transmission grid to ease the sending of power between regions, the increase in renewably generated supply, which tends to be unreliable, means winter power shortages could become the norm.

Mitsui invests in Brazilian power trading company

(Kankyo Business, Jan. 31)

- Mitsui & Co. will invest in Stima Energia, a company engaged in the power trading business in Brazil. Mitsui will own 36% of Stima, which was established in 2017 and which also engages in price risk hedging services.

- Mitsui intends to help Stima add customers, expand trading volumes, while also improving its understanding of the Brazil power market, which is expected to grow on the back of market liberalization.

Panel cleaning robot promises to boost solar productivity

(Nikkei, Jan. 28

- At the DER/Microgrid Japan energy expo in Tokyo between Jan. 26 and 28, World Scan Project exhibited a robotic system for cleaning solar panels.

- The system, dubbed ‘Solar Sunva’, can clean all panels in a 1 MW solar farm in two or three days. A two-person crew is required to operate the system.

- Price for the system starts at ¥2.5 million.

Historic 1920s hydro plant grows capacity by 10%

(Nikkei, Feb. 3)

- The Yokokawa hydroelectric power station in Miyagi operated by Tohoku Electric Power Company has been generating electricity since 1928.

- A five-year upgrade is now complete; increasing output to 2 MW, up from 1.8 MW.

- This is an example of how all parts of the country’s infrastructure, no matter how small, are modernizing in order to meet national net-zero goals.

TAKEAWAY: On the face of it, a very small upgrade. However, it’s a good example of the kind of works many of the power plant owners are engaged in right now. Note that a significant part of Japan meeting its 2030 decarbonization targets relies on energy conservation and adaptation.

NEWS: OIL, GAS & MINING

JERA opens office in Beijing, to sell LNG directly to China

(Japan NRG, Feb. 4)

- JERA, Japan’s biggest power company and LNG importer, opened “Beijing JERA consulting Ltd”. Previously, JERA had no business operations in China.

- The new entity has several staff members from both China and Japan, and is part of the company’s plans to grow across Asia.

- The office will be led by an energy sector veteran, Akashi, who once worked in the Beijing office of Japan’s TEPCO. JERA is a JV of TEPCO and Chubu Electric.

- JERA said it “seeks opportunities in cultivating LNG value chain projects” in China, which is now the world’s biggest LNG purchaser.

TAKEAWAY: Last year, China imported 79 million tons of LNG; 30 million was on spot trading. Some of this came from Japan via one or more third-party trading houses. Thus, direct trade makes economic sense for both sellers and buyers.

Japan cautions about its ability to help Europe with gas

(Bloomberg, Feb. 4)

- METI head Hagiuda said Japan must ensure adequate fuel supplies before aiding Europe with LNG cargos in case supplies are disrupted due to conflict.

- “Japan is an energy importer, and we are resource-scarce,” said Hagiuda, adding that cold weather is forecasted, and Japan must look after its own needs before considering “what it can do to contribute to the international community.”

- CONTEXT: Japan does not have a national stockpile of natural gas. The reserves held by private companies amount to only about 2-3 weeks of demand.

- An executive from JERA, Japan’s top LNG importer and user, said that while diverting Japanese LNG cargos to Europe is not impossible, it will affect the domestic market and there is not much slack in the system.

TAKEAWAY: The government was reportedly considering how to divert some supplies to Europe in response to the U.S. administration’s call to allies to help in case conflict around Ukraine. Among the many problems with asking Japan to pitch in is that the government cannot easily commandeer supplies of private firms; it cannot put needs overseas above that of own population; and it would seek to avoid coming into direct conflict with Russia.

- SIDE DEVELOPMENT:

Qatar, upset by Japan’s long-term LNG contract snub, may not help in future

(Nikkei Views, Feb. 5)- JERA let a large, long-term contract for LNG deliveries from Qatar expire in December because it was unhappy with the conditions under which the supplier nation wanted to deliver the fuel. JERA wanted more flexibility in the terms that Qatar declined.

- Qatar is upset with JERA for not renewing the contract and not minded to help Japan in times of future crises. A boost in Qatari deliveries after the Fukushima disaster helped Japan secure fuel for additional thermal capacity.

- Japan’s govt. wonders if there wasn’t a smoother solution to the JERA-Qatari dispute.

- CONTEXT: The Ukraine-Russia standoff threatens gas supply disruptions. At this time, importers may need additional volumes.

LNG stocks fall to the four-year average level

(Japan NRG, Feb. 2)

- Stocks of LNG for power generation fell to 1.67 million tons on Jan. 30, from 1.76 million tons a week ago. The four-year average was just at 1.67 million tons.

- It stands higher than the 1.49 million tons logged a year ago, but is a noticeable drop from the stockpile at the start of the year (2.33 million tons).

- Japanese LNG imports fell about 14% YoY in January, Bloomberg reported, citing shipping data, which would be the lowest level for a peak demand month since 2011.

TAKEAWAY: As noted in our Feb. 4 Data Book report, the reason LNG purchases have been slower this winter is due to the fuel’s price rally and the ability of Japanese utilities to cover demand with coal-fired generation, among other ways.

End-December fuel oil stocks down 8.2% YoY

(Japan NRG, Jan. 31)

- Fuel oil stocks at the end of 2021 stood at 9.42 million kl, down 8.2% YoY. December production was 13.97 million kl, up 4.7% YoY, while domestic sales were 15.69 million kl, up 2.6% YoY.

- Imports were up 2.2% to 3.48 million kl, while exports dropped 4.6% to 2.04 million kl.

Government won’t rule out tax relief on gasoline

(Nikkei, Jan. 30)

- METI head Haguida said the govt. won’t rule out reinstating a scheme by the now defunct Democratic Party of Japan that reduces gasoline tax by ¥25.1/ liter.

- Under the scheme, tax relief would be triggered whenever the price of gasoline remained above ¥160/ liter for three consecutive months.

FGE’s Fesharaki says oil could top $100; LNG to peak in late 2040s

(Sekiyu Tsushin, Feb. 4)

- ENEOS and the Institute of Energy Economics, Japan held an international panel discussion on the energy market. Facts Global Energy chair Fereidun Fesharaki said that while a relaxation of output cuts imposed by OPEC Plus meant oil prices could reach $78 and $85 by spring, restrictions on upstream investment would most likely dictate future oil prices.

- Geopolitical risks could push the price of oil over $100, said Mr Fesharaki.

- IEEJ Chief Economist Koyama Ken said prices for all forms of energy were high at the moment, and there’s no end in sight to high gas prices.

- Fesharaki echoed this, saying that natural gas had an essential role to play in energy transition, and that LNG demand would peak in the late 2040s.

On high LNG prices, Tokyo Gas upgrades profit forecast 54%

(Nikkei, Jan. 29)

- Tokyo Gas expects a consolidated profit of ¥76 billion for the year to March.

- This represents a 54% increase on previous projections and is a result of high LNG prices that benefited the utility’s offshore development operations.

Tokyo Gas to supply Saibu Gas with “carbon neutral” LNG

(Denki Shimbun, Feb. 4)

- Tokyo Gas will supply Saibu Gas with “carbon neutral” LNG. The first cargo of about 70,000 tons arrived at the Hibiki LNG terminal in Kitakyushu on Feb. 2.

- This is the Kyushu area’s first “carbon neutral” LNG. The emissions from the LNG are offset by carbon credits.

ENEOS to supply “carbon neutral” LNG to Hachinohe Gas

(Japan Metal Bulletin, Feb. 4)

- Yokokawa ENEOS will supply “carbon neutral” gas to Hachinohe Gas.

- The gas will be used to power the utility’s residential gas supply operations as well as powering gas appliances and air-conditioners at its offices.

ANALYSIS

BY MASUTOMO TAKEHIRO

Japan’s Bold Bet on an “Alternative” Energy Transition

In Southeast Asia Promises Big Dividends

Japan’s government and major energy corporations are increasing their operations in Southeast Asia, seeing the region as sympathetic to their gradual approach to decarbonization.

Southeast Asian economies are forecast to grow between 4% to 7% in the next few years, yet local governments have hesitated to put forward ambitious net-zero pledges, fearing business curtailment. With nuclear power virtually non-existent in the region, and renewable energy development still at a nascent stage, Japan’s vision for a less disruptive energy transition that retains coal-fired plants in some form is gaining attention.

The political dimension also plays a role. Southeast Asia wishes to update its energy systems without handing all opportunities to China. Japan represents diversification and does not post a commercial or geopolitical threat. For Japan, good relations with resource-rich nations like Indonesia also help secure future materials supply.

That’s the context in which Japan is trying to sell low-carbon power solutions in the ASEAN region. Unable to scrap coal-fired generation at home, Japan is fending off international criticism by supporting the region’s hopes to adapt rather than eliminate thermal power.

While the EU, the U.S. and China are putting effort into promoting renewable energy in Southeast Asia, Japan is giving more attention to local projects around LNG, carbon capture, utilization and storage (CCUS), as well as building supply chain infrastructure for hydrogen and ammonia.

Background: Government initiatives for ASEAN

In the past year, Japan and Southeast Asia unveiled a number of bilateral initiatives in the energy sector. In May 2021, METI launched the Asia Energy Transition Initiative (AETI) for ASEAN. The main points are:

- Support for the development of energy transition roadmaps

- Presentation and promotion of the Asian version of transition finance

- $10 billion support for renewable energy, energy efficiency, LNG, and other projects

- Support for technology development and demonstration from the Green Innovation Fund

- Human resource development on decarbonization technologies and knowledge sharing through the Asia CCUS Network

In June, the first Japan-ASEAN Energy Minister Special Meeting was held online and the Japanese officially announced support with a $10 billion investment, which was meant to cover the introduction of some renewable energy and energy-saving technologies, as well as a shift to LNG-fired power. Also, on June 23, the Asia CCUS Network was officially launched.

Japan’s calls for a broader energy transition in Asia that includes LNG was criticized by U.S. special presidential envoy for climate, John Kerry, but Tokyo seems more attuned to the interests of the region than Washington.

Under the previous prime minister Suga, whose administration showed strong enthusiasm for renewable energy, Tokyo’s offer to set up a Japan-ASEAN ministerial-level meeting on the green economy went unanswered. Indonesia, the group’s heavyweight member, was cautious and the meeting didn’t take place. A few months later, the Indonesian energy minister accepted the invitation to an inaugural International Conference on Fuel Ammonia organized by Japan in October. Likewise, Brunei, Indonesia, Malaysia and Thailand joined the Japan-led Hydrogen meeting held that same month.

Part of the govt.’s plan

Japan’s Basic Energy Plan, revised in October, also emphasizes Asia. For example, it ambitiously mentions that “we will promote the AETI and strengthen our cooperation with ASEAN countries, and coordination with other Asian countries, the U.S., Canada, Australia, the Middle East to spread this idea throughout the world”. It stresses Japan’s outstanding presence in the LNG sector, vowing to “take the lead in resilience and realistic energy transitions in Asia as a whole.”

At COP26 in November, newly-elected Prime Minister Kishida, who is seen to have a stronger attachment towards Asia than the two previous PMs, reiterated his support for an Asia-specific clean energy transition. Among other actions, Japan plans to establish a common guideline for calculating emissions of individual companies from ASEAN countries in order to help reduce their greenhouse gas emissions (GHGs). The guideline is expected in the summer of 2022.

In January, despite concerns about the spread of the Omicron variant, METI Minister Hagiuda visited Thailand, Indonesia, and Singapore. Hagiuda and his Indonesian counterpart signed an MoU to cooperate in decarbonization. Mitsubishi Heavy Industries will conduct a study with Indonesia’s state-owned electric power company to use an ammonia-mixed fuel starting this April.

This is a new addition to Japan’s decarbonization projects in Indonesia. Both Mitsubishi Corp. and J-Power are separately conducting carbon capture and storage experiments in Southeast Asia’s most populous country, while Kyudenko Corp. is supporting the conversion of diesel power generation to renewable energy in remote islands outside Java.

Indonesia has said it wants to curtail or even ban exports of unprocessed raw materials, some of which are critical for clean energy technologies, in order to accelerate its own industrialization.

During Hagiuda’s tour, Japan also announced it will collaborate with Singapore to establish a local supply network for hydrogen and ammonia. Japan’s influence on regional net-zero pathways will extend to Thailand, which is due to seek advice from Tokyo on its decarbonization timetable.

A top official in charge of fossil fuel procurement at JOGMEC says, “I think the time has come for us to communicate a kind of code of conduct for Asia that includes carbon recycling, considerations around economic growth, and stable energy supply.”

METI director Kume told Japan NRG recently that the government will convey the message that the energy transition has to be done with a “sense of reality,” not just through the G7 but also through the G20, which includes Indonesia as a formal member.

Business expectations for ASEAN

Following the official direction, Japan’s private sector has begun to place greater emphasis on Southeast Asia. The case in point is JERA, Japan’s largest utility and the world’s largest handler of LNG. It has explicitly said that its goal is to help “decarbonize all of Southeast Asia”.

In September 2021, as its biggest investment to date, JERA decided to invest ¥175 billion in Aboitiz Power, a major Philippines power generation company, to acquire a 27% stake.

In a recent interview, JERA President Onoda said: “We will expand our overseas business, mainly in Southeast Asia. Naturally, the decarbonization strategy for Asia is different from that of Europe, where cheap renewable energy and power grids are in place and economic growth is moderate.”

Onoda added that CO2 emissions can be reduced by mixing coal-fired power with ammonia and gas-fired power with hydrogen. “Using thermal power to decarbonize is the answer to achieving economic growth and a stable energy supply. We will also be able to procure LNG flexibly and sell it to Asia, where demand is growing,” he said.

Other Japanese firms are also diving deep into the region. In August 2021, Mitsubishi and Chiyoda Corp., among others, announced they’ll supply hydrogen produced in Brunei to ENEOS. Last month, Nippon Steel said it will pay $763 million to acquire two major Thai electric furnaces, G Steel and GJ Steel, to capture growing demand in Southeast Asia.

Conclusion

Southeast Asia’s power systems remain wedded to coal-fired power and progress towards an entirely different network around renewables is likely to take decades. Japan’s approach is to push for a gradual transition that would also retain key energy infrastructure by replacing coal with gas, and where possible move from burning fossil fuels to ammonia or hydrogen-fired generation.

This strategy has met with criticism from other G7 nations, yet it has backing in the ASEAN. The U.S. and the EU now have to adjust to the region’s nuanced position. Japan appears to have already done so.

ANALYSIS

BY JIAXIN YANG, NING LIN and

ROBERT BROOKS

Japan’s LNG Energy Security Has a Cost:

Estimating the Price of Supply Diversity

Cutting CO2 emissions and decarbonization was supposed to be the main topic in global LNG markets last year. Instead, energy security is again front and center, especially for purchasing countries.

In the case of Japan, the security of LNG supply is especially pressing because the fuel has an outsized influence on domestic electricity pricing. Assuming the government sticks to its decarbonization strategy, which says that Japan’s LNG demand for the power sector could drop 50% by 2030, retaining supply security through diversity of import sources could incur a significant monetary cost.

Below we investigate the impact of diversification strategy on Japan and its neighbor, China, which last year emerged as the world’s biggest LNG importer for the first time.

The new “normal” in LNG

The events of 2021 tested both the resilience and flexibility of the global natural gas and LNG markets and demonstrated a new “normal” based on two points:

- LNG has evolved into a truly global market; Europe and Asia, as well as other parts of the world, compete for the same cargos, while local fundamentals such as gas storage levels and renewables output impact LNG prices the world over.

- Gas and LNG supply, even as a bridging fuel, is vital to national security and the broader economy.

In 2021, countries with limited diversity of gas supply were affected heavily by even tiny market fluctuations, demonstrating low price elasticity and a lack of flexibility in switching to alternatives. This led China to build three transnational pipelines and move forward with new LNG regasification terminals along its Southeast coast, while also allocating more funding to domestic gas production projects.

Simulating market change

A diversification strategy for LNG sourcing might be more expensive than a pure cost-base optimization strategy, but our calculations show the price difference may not be prohibitively expensive as the LNG market matures and becomes more competitive after 2030.

To simulate the cost changes, we implemented a scenario-based approach, testing against fundamental factors that determine LNG imports into Japan and China such as long-term gas demand and the potential emergence of new infrastructure options, such as the Power of Siberia 2 (PS2) pipeline from Russia into China.

We also set credible limitations on how big a market share each LNG supplier country could have in the portfolio of the import nation. These market share limitations are based on historical data gleaned from BP’s 2021 Statistical Review and then extended into the future along realistic minimum and maximum levels. The assumptions mirror the way that countries like Japan operate to retain a balanced supply portfolio.

Such “Destination Contraints” should not be confused with “Destination Restriction” clauses on some LNG contracts, which limit to where the cargo can be delivered.

How Japan’s LNG portfolio changes

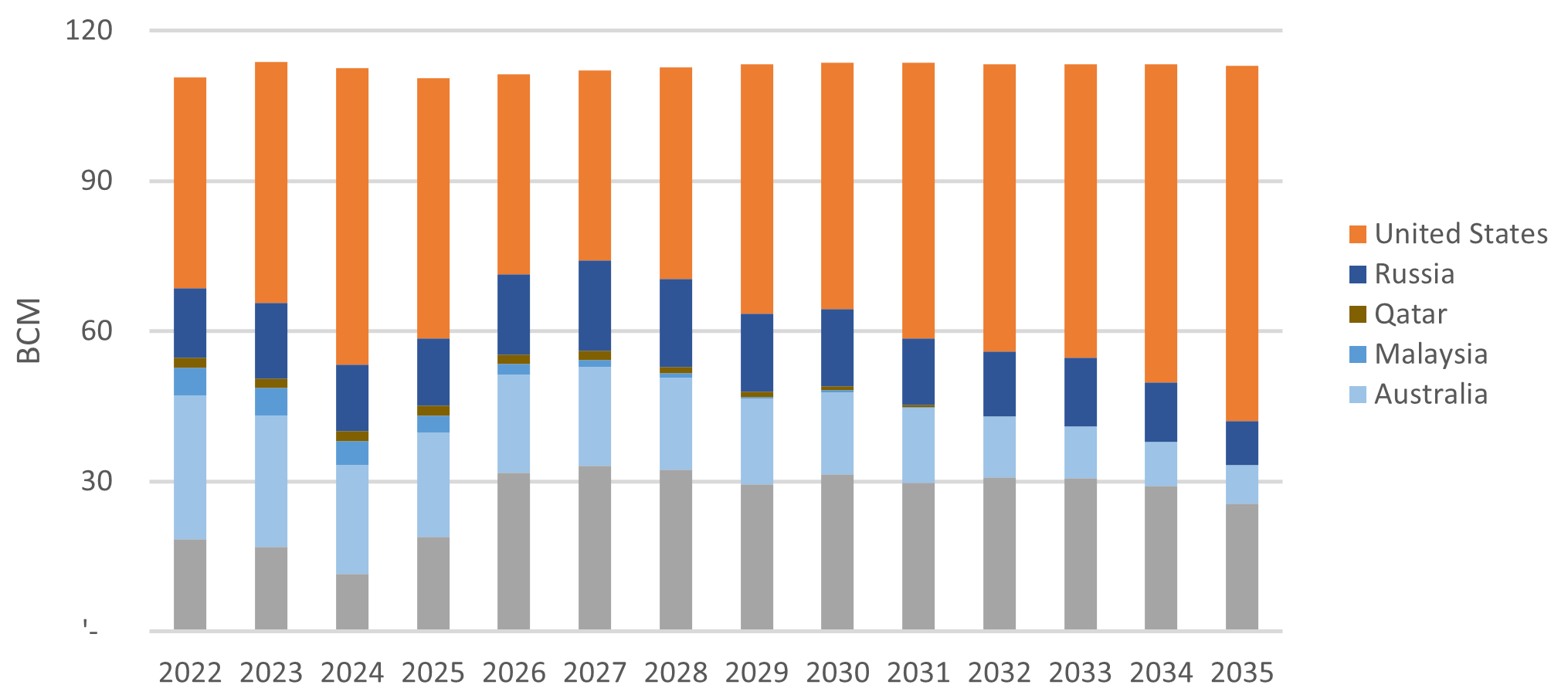

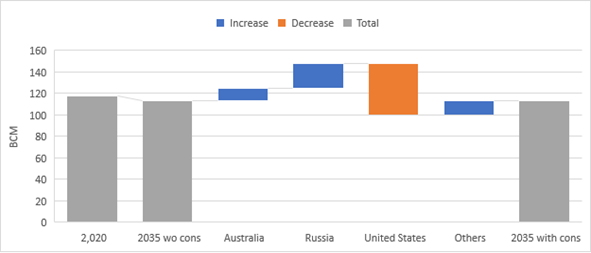

As the largest LNG importer until recently, Japan has always diversified supply sources. However, if today’s Japan employed an approach that only looked at cost, we estimate that half of its LNG imports would come from the U.S. Once our “Destination Constraints” are added to Japan’s purchasing model, imports from Russia and Australia gain greater prominence at the expense of the U.S.

Figure 1: Japan LNG Imports Under Base Demand without LNG Destination Constraints

Figure 2: Japan LNG Imports Under Base Demand after Adding LNG Destination Constraints

Japan’s impact on China LNG buying

Interestingly, as a result of Japan’s balancing strategy, U.S. producers are incentivized to build bridges with other Asian buyers, such as China and India, and to sell in other parts of the world.

In just the last two years, the U.S. has rapidly increased deliveries to China. In 2019, only 0.5% of China’s LNG imports came from the U.S. In 2020, it was 5% and last year they grew to 12%. This plays counter to the political narrative between the two.

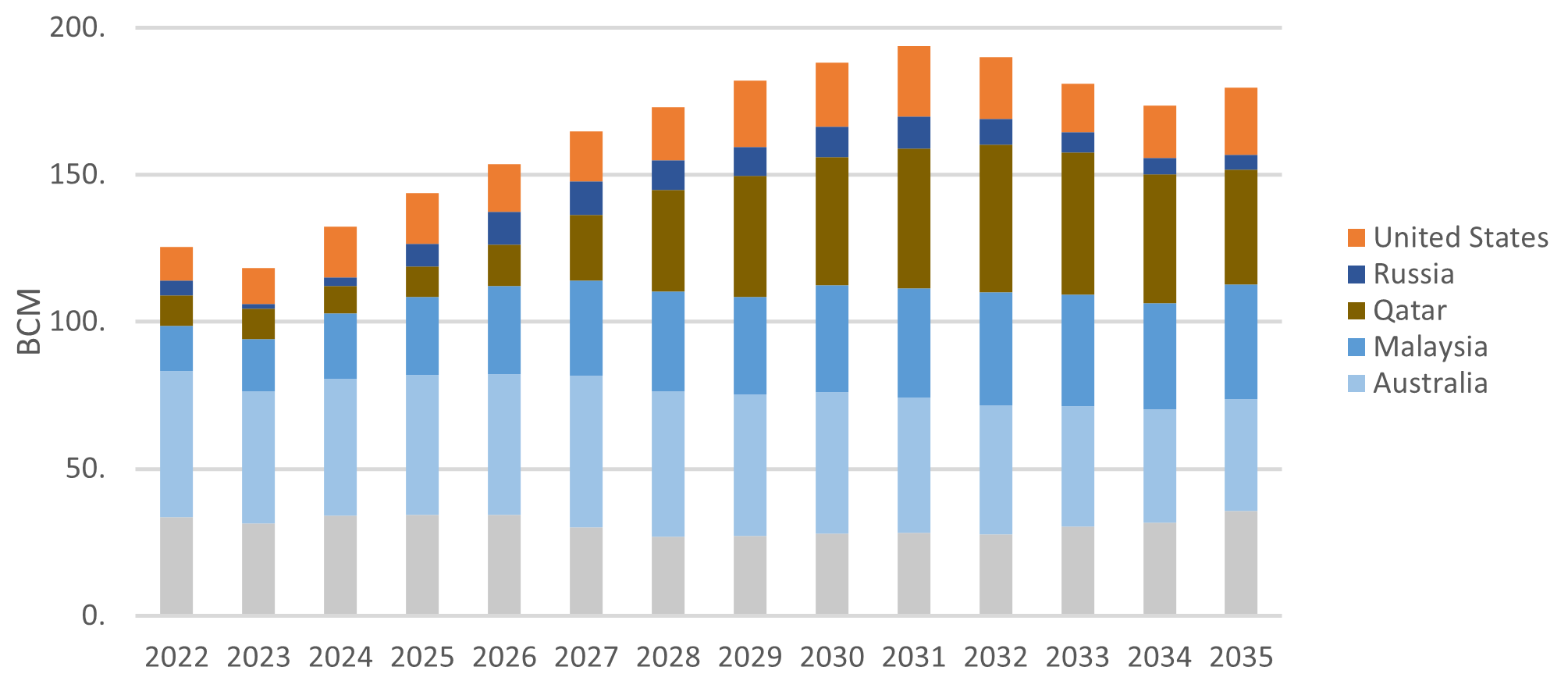

Were cost the only issue for China, then by 2035 our modeling shows that the main sources of supply are Australia (21%), Malaysia (22%) and Qatar (22%), while the U.S. only holds a small percentage of the market.

However, the recent flurry of long-term contracts signed by Chinese buyers with U.S. LNG suppliers indicates that China is also practicing a diversification rather than cost-only strategy. Last year, China’s CNOOC and ENN signed long-term contracts with American suppliers for a total of 14 million tons of cargo per year. That’s nearly 50% of all contracts China signed during 2021. Improving trade relations indicate that the U.S. share of the Chinese LNG market is unlikely to fall below the 2021 level.

This same diversification strategy makes it possible to model which countries China is going to likely buy from going forward. Based on China’s destination constraint, there are greater opportunities for suppliers from nations outside of Australia, Malaysia and Qatar, which are currently the main LNG sellers to China. That includes space for more LNG imports from the U.S.

Figure 3: China LNG Imports Under Base Demand with LNG Destination Constraints

What about decarbonization?

Two additional factors should be considered. The first is the potential impact of lower gas demand under a fast energy transition scenario.

In our “Base Demand” case, China’s gas demand grows at an annual average of 4% while Japan’s remains stable through 2035. In the “Advanced Technology” (fast energy transition) case, the average growth rate of Chinese gas consumption is 3%; Japanese gas consumption for power generation drops 3% per year.

For Japan, the latter fast-transition scenario would translate into lower import volumes and higher prices. In terms of supply sources, however, it would most affect LNG from the U.S. and Australia. Japanese buyers could find it difficult to justify long-term contracts with sellers in these countries if they feel uncertain about demand fundamentals.

The second assumption is impact from the proposed 50-billion-cubic-meter (bcm) PS2 pipeline from Russia to China. If it achieves FID and comes online in 2030, it would provide China with an alternative to higher LNG imports.

The pipeline would likely have little impact on LNG imports to Japan since growing demand from the emerging East Asia market would fill the gap left by China’s PS2 volumes. However, in China’s balanced portfolio approach, an active PS2 by 2030 is bad news for new U.S., Qatar and Malaysia volumes looking for long-term contracts.

The cost calculation

To achieve the kind of energy security rebalancing calculated above, countries should need to pay an economic cost. For Japan, under the Normal Demand scenario that also assumes an active PS2 pipeline in 2030, the cost of diversification could amount to a premium of about $0.04/ MMBtu in the average settled price of LNG into Japan. This is equivalent to about $1.4 million per bcm.

In total, Japan’s annual LNG bill goes up by $150 million to retain and increase energy security by diversifying supply sources[1]. This amounts to about 0.05% of the total cost of LNG supply, a small price to pay for a matter of national security. Meanwhile, the total annual premium for China, on average, would be around $270 million.

- Calculation details: 1 trillion = 10^6 million, 1 trillion btu = 0.029 BCM (according to BP), thus 1 MMBtu = 0.029 *10^(-6) BCM, thus 1 $/MMBtu = 1/(0.029 *10^(-6)) $/BCM = 34,000,000 $/BCM.

If Japan develops under the Advanced Technology scenario and faces decreasing gas demand, then the biggest impact would likely be on Australia and U.S. buyers, which would see their volumes decline. For China, the same scenario spells smaller volumes for Qatar and the U.S., a trend that would be exacerbated by the coming onstream of the PS2 project.

The emergence of a truly global gas and LNG market makes it more important than ever to fully understand such relationships between domestic and global markets. This understanding is enhanced through market simulations so as to identify the risks as well as best opportunities during the energy transition.

About the authors

- Dr. Robert Brooks is the President and founder of RBAC, a supplier of global and regional gas and LNG market simulation systems used to support investment, M&A and improve operations.

- Dr. Lin is an energy industry economist and leader of the global gas and LNG modeling team at RBAC. Before joining RBAC, Dr. Lin managed global market analysis capabilities for Shell Trading, KOCH Industries and Tenaska.

- Jiaxin Yang is a market research analyst with RBAC.

In the results, Asian LNG price without LNG destination constraints is $0.04 lower than that with LNG destination constraints. Thus 0.04$/MMBtu = 1,400,000 $/BCM.

Japan LNG imports in 2030 = 110 BCM, cost = 110 * 1,400,000 = $ 0.15 billion

China LNG imports in 2030 = 190 BCM, cost = 190 * 1,400,000 = $ 0.27 billion) ↑

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Brazil/ Wind power

Wind power grew 26%, YoY, and now totals 33.2 GW, which represents about 17% of the country’s total installed electricity capacity. Renewables account for 48% of Brazil’s energy mix. Going forward, the government said it will prioritize the development of offshore wind projects, of which the country currently has few.

China/ Energy storage

Swiss company Energy Vault (EV) signed a $50 million license and royalty agreement with US-based Atlas Renewable and its majority investor China Tianying to deploy EV’s gravity energy storage technology and management software platform in China, Hong Kong and Macau.

EU/ Nuclear and Natural gas

Nuclear power plants can now be labelled as “green” if countries provide plans for safe waste management and decommissioning. Also, gas-fired power plants can earn the “green” status if they emit less than 270 g of CO2 equivalent per kWh, or have annual emissions below 550 kg CO2e per kW. Climate activists vow to fight the decision.

Laos/ Wind power

Keppel Infrastructure Holdings signed a MoU with Thai renewables developer Impact Electrons Siam (IES) and China’s Envision Group to provide low-carbon electricity and storage. The three companies will leverage IES’ rights to develop the 1 GW expansion of the 600 MW Monsoon wind farm in Laos, which will be operational in 2025.

Renewable energy

In 2021, technology giants were the largest corporate buyers of renewable power. Amazon accounted for 20% (6.2 GW) of a record 31 GW of clean power bought by corporations, which also accounted for more than 10% of all renewable energy capacity added globally last year.

Romania/ Wind power

Leading German wind power developer, wpd, plans to build two wind energy projects with a combined capacity of 1.9 GW in the Black Sea. Wpd already has onshore wind projects under development in Romania with a total capacity of 1.3 GW.

Russia/ Clean energy metals

Over $15 billion will be spent to develop two Siberian copper mines that are betting big on the renewable energy transformation. Kaz Minerals will invest in the $8.5 billion Baimskaya mine that opens later this year; while USM Holdings will invest $7 billion in the Udokan mine expected to open in 2027.

Spain/ Hydrogen power

Copenhagen Infrastructure Partners (CIP) heads a consortium of partners, including Vestas, to build a 500 MW green hydrogen project in Spain. The first phase of Project Catalina will comprise 1.7 GW of wind and solar energy facilities, as well as a 500 MW electrolyser. Construction starts at the end of 2023.

U.S./ Energy transition

California’s energy transition needs 53 GW of solar PV by 2045, and the transmission system needs $30.5 billion in investment along with increases in energy storage. By 2045, the state will require 53 GW of utility-scale solar, 37 GW of battery energy storage systems, 4 GW of long-duration storage and 24 GW of wind power reserves.

U.S./ Oil and Gas

A federal judge cancelled the Biden Administration’s sale of an oil and gas field in the Gulf of Mexico, claiming it didn’t calculate climate change’s impact. This was the largest oil and gas lease in U.S. history. In related news, Chevron reported a 2021 Q4 net income of $5.1 billion, compared to a $665 million 2020 Q4 loss. Also, Tellurian will soon begin construction of its $16.8 billion Driftwood LNG plant in Louisiana.

UK/ Hydrogen power

Essar and Progressive Energy will develop a JV, known as Vertex Hydrogen, and create a £1 billion hydrogen production facility at Stanlow Manufacturing Complex. Vertex was formed to “provide the catalyst for the development of a hydrogen economy across North West England and North Wales”. The facility is planned to open in 2026.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

|

January |

OPEC quarterly meeting; JCCP Petroleum Conference – Tokyo; EU Taxonomy Climate Delegated Act activates; Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

|

February |

Chinese New Year (Jan. 31 to Feb. 6); Beijing Winter Olympics; South Korea joins RCEP trade agreement |

|

March |

Renewable Energy Institute annual conference; Smart Energy Week – Tokyo; Japan Atomic Industrial Forum annual conference – Tokyo; World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

|

April |

Japan Energy Summit – Tokyo; MARPOL Convention on Emissions reductions for containerships and LNG carriers activates; Japan Feed-in-Premium system commences as Energy Resilience Act takes effect; Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

|

May |

World Natural Gas Conference WCG2022 – South Korea; Elections: Australian general election; Philippines general and presidential elections |

|

June |

Happo-Noshiro offshore wind project auction closes; Annual IEA Global Conference on Energy Efficiency – Denmark; UNEP Environment Day, Environment Ministers Meeting – Sweden; G7 meeting – Germany |

|

July |

Japan to finalize economic security policies as part of natl. security strategy review; China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong; Czech Republic assumes presidency of EU; Elections: Japan’s Upper House Elections; Indian presidential election |

|

August |

Japan: Africa (TICAD 8) Summit – Tunisia; Kenyan general election |

|

September |

IPCC to release Assessment and Synthesis Report; Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.; Japan LNG Producer/Consumer Conference – Tokyo; IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

|

October |

EU Review of CO2 emission standards for heavy-duty vehicles published; Chinese Communist Party 20th quinquennial National Party Congress; G20 Meeting – Bali, Indonesia; Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

|

November |

COP27 – Egypt; U.S. mid-term elections; Soccer World Cup – Qatar; |

|

December |

Germany to eliminate nuclear power from energy mix; Happo-Noshiro offshore wind project auction result released; Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26; Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.