JAPAN NRG WEEKLY

APRIL 4, 2022

JAPAN NRG WEEKLY

April 4, 2022

NEWS

TOP

- Govt. sets out policies to move away from Russian commodities including natural gas and metals through a multiprong strategy

- Majority of Japanese now support nuclear reactor restarts, a survey by top business daily finds in first such result since 2011

- Japan’s top three banks to stop financing the mining of coal for power generation, lowering exposure to the sector over time

ENERGY TRANSITION & POLICY

- Govt. sets up new panel to plan advanced nuclear tech roadmaps

- ENEOS estimates cost of building hydrogen supply chain

- Japanese households emit 5.9% more carbon in 2020: MoE

- Used cooking oil prices soar as Japan exports more supply to Asia

- Japan coins first carbon credits from joint project with Bangladesh

- EV subsidies raised slightly to encourage transition from gasoline

- Toshiba part of group planning a hydrogen hub in Kawasaki

ELECTRICITY MARKETS

- High prices, volatility push more players to exit electricity retail

- Shipper Mitsui OSK seeks entry points into offshore wind market

- Kansai Electric begins study of giant offshore wind project in Saga

- Chubu Electric buys stake in Indian firm targeting off-grid users

- All of Japan’s top power and gas companies to raise rates in May

- TEPCO begins move of nuclear power unit to Kashiwazaki City

- JERA announces plans to decommission 3.82 GW of old capacity

OIL, GAS & MINING

- Japan joins G7 in rejecting Russia demand to pay for gas in rubles

- METI says Japan will not pull out of Arctic LNG 2 project in Russia

- Lawmakers call for reinstatement of special gasoline tax break

- METI forecasts 2022 jet fuel demand to surge on travel plans

- Battery-grade nickel demand to rise by a quarter this year: SMM

- Japan LNG stocks fall slightly from a week earlier

- Truck diesel consumption surging amid supply bottlenecks

ANALYSIS

LIMITED OPTIONS TIE JAPAN’S HAND

IN DEALING WITH LOOMING OIL SHOCK

Soaring LNG and crude oil prices, accelerated by Russia’s war with Ukraine, are starting to reverberate throughout the economy, inflicting a high toll on Japanese households and nearly all areas of commerce and industry. Some experts already refer to this situation as the Third Oil Shock, with the first such global energy shock having taken place in 1973, almost half a century ago. So far, state subsidies have been the main measure to combat energy-driven inflation. Last week Prime Minister Kishida ordered yet more of the same. But it’s increasingly clear that this won’t be enough and bolder steps will be needed.

PUTIN DEMANDS RUBLE PAYMENT FOR RUSSIAN GAS: DESPERATE PLOY OR START OF BIGGER CHANGES?

President Putin demanded that from April 1, all new energy contracts supplying Russian gas to “unfriendly” nations have to be settled in rubles. Japan, like other G7 nations, has rejected the notion. But the exchange rate of the ruble suggests this isn’t the end of the story. We lay out the potential mechanics of new “ruble-based” gas payments and show how this is part of a broader strategy Putin seeks to deploy in global commodity markets that may have much larger consequences.

GLOBAL VIEW

Chile to retire half of its coal-fired power plants. ING is the latest bank to stop financing new oil and gas deals. China’s top coal miner commits large portion of capex to renewables. The UK, Netherlands and U.S. plan new offshore wind auctions and investments. Details on these and more in our global wrap.

JOBS IN JAPAN’S ENERGY SECTOR

We begin a new monthly column that will examine trends in the labor market around Japan’s energy industry. This week: “The Great Talent Squeeze.”

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Japan, Events)

Events

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Daniel Shulman (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Japan’s top three banks to stop financing thermal coal mining

(Nikkei Asia, April 1)

- Japan’s three largest banks will stop financing coal excavation for power generation.

- Sumitomo Mitsui Financial Group and Mitsubishi UFJ Financial Group said they no longer will provide funding for new thermal coal mining projects. Mizuho Financial Group made a similar policy change last year.

- In Sumitomo’s case, this will extend to coal transport infrastructure.

- The three banks are estimated to have billions of dollars in outstanding loans for thermal coal mining.

New panel to write advanced nuclear reactor development roadmaps

(Japan MRG, March 28)

- METI plans to launch a new working group comprised of nuclear experts to design road maps to develop advanced nuclear reactors. The panel will be headed by Kyoto University Professor Kurosaki Ken.

- METI sees advanced nuclear reactors as technologies that go beyond power supplies, and which also have the means to produce zero emission hydrogen, and to complement variable renewables. Among the 73 types of small modular reactors in development globally, Japan is focused on high-temperature engineering of fast reactors that use recycled nuclear fuel.

TAKEAWAY: Most small modular reactor projects outside Russia and China are driven by equipment vendors, while power operators are cautious on cost.

In addition to building realistic cost scenarios, the METI working group is tasked to answer questions that range from identifying the sites of the new reactors, creating new regulatory framework for safety inspection of new technologies, and ensuring the safety of nuclear plants that are operating.

See the Electricity Markets section for results of a recent public opinion survey that favors the restart of existing nuclear reactors.

Top oil major gives estimate for Japan hydrogen supply chain capex

(Japan NRG, March 29)

- Oil refiner ENEOS met with the government to explain the outlook for building out the hydrogen supply chain to deliver both green and blue versions of the fuel to Japan.

- The company told the government’s ammonia and hydrogen subcommittee that capital expenditure for building a 40,000 ton/ year hydrogen supply chain overseas is ¥130 billion, while a 300,000-ton/ year facility will cost ¥440 billion.

- The government expects Japan will consume 2 to 3 million tons of hydrogen in 2030, and based on ENEOS’ model ¥1-1.5 trillion capital expenditure is required.

- Spending needs to increase 1-fold until 2040.

ENEOS hydrogen supply chain capex model (in billions of yen)

| Manufacturing green hydrogen | Cost of MCH conversion for transport | Transport (use existing vessels) | Local storage, delivery | Total | |

| Capex for 40,000 tons/ year output | 50 | 60 | 0 | 20 | 130 |

| Expansion to 300,000 tons/ year | 200 | 100 | 0 | 20 | 440 (includes 130 from the previous phase) |

- As the investment is massive, suppliers are wary if there’ll be enough demand and returns for the investment, ENEOS told the subcommittee.

TAKEAWAY: ENEOS and JERA are two of the top energy firms to have discussed the cost of hydrogen supply chain investments. Given the investment amounts estimates, there is now growing interest in re-opening the debate around building more green hydrogen production capacities in Japan, which would also allay energy security concerns.

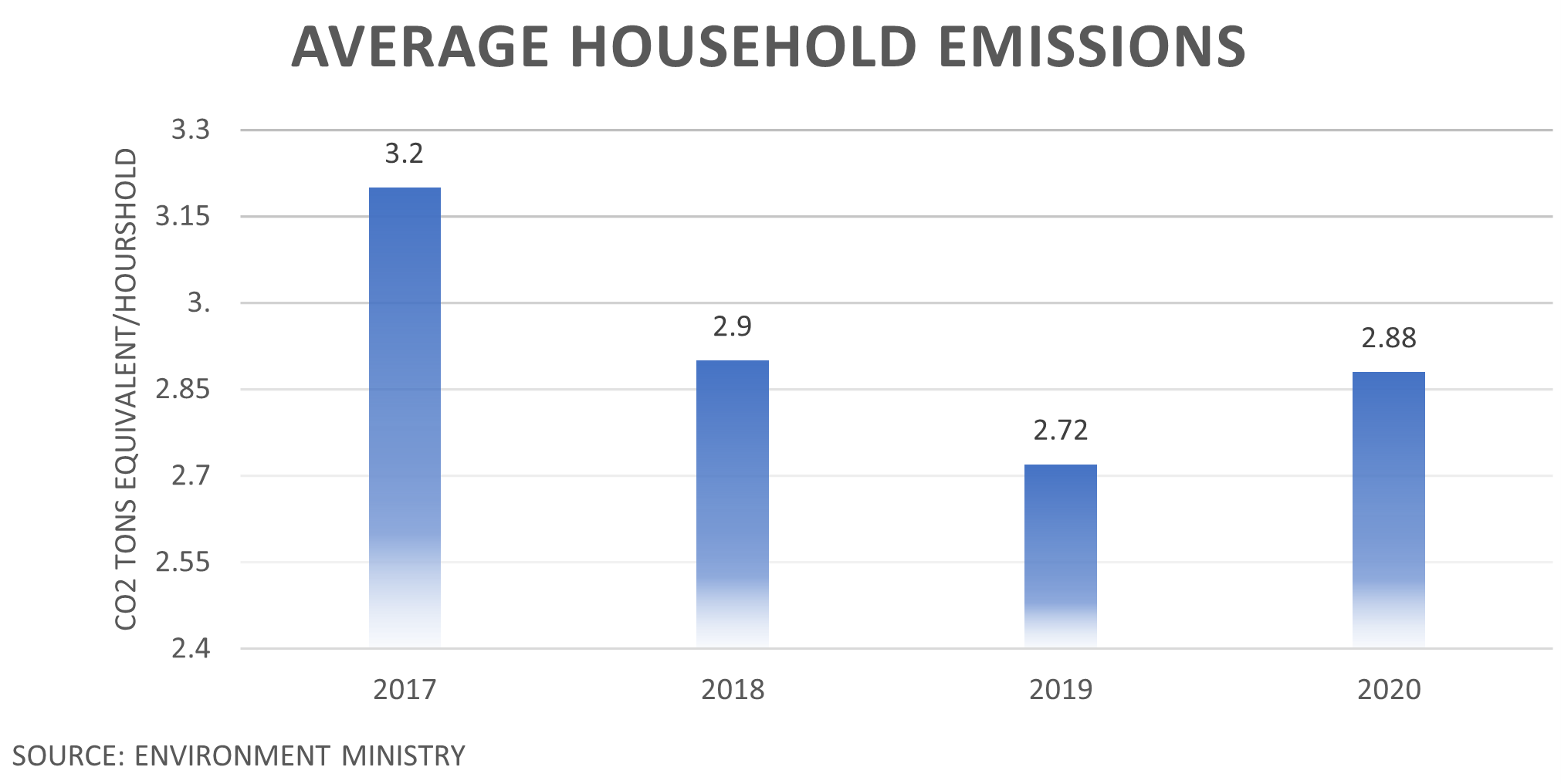

Japanese households emit 5.9% more carbon in 2020: MoE

(Japan NRG, March 29)

- The average Japanese household emitted 2.88 tons of carbon in 2020, up 5.9% from the previous year. When broken down — 1.88 tons were from electricity consumption, 0.44 tons from city gases, 0.17 tons from LP gases, and 0.39 tons from kerosene.

- The regional breakdown showed Hokkaido households topped at 4.65 tons, due to high consumption of kerosene and electricity for heating. Senior households aged over 65 emit 3.02 tons, while those below 29 only 1.59 tons.

Japan’s used cooking oil export price soars on clean oil demand in Asia

(Japan NRG, March 30)

- Food supplies for animals in Japan are diminishing as used cooking oil, one of the key ingredients of animal nutrition products, is exported in larger volumes on strong demand for low emission oil.

- Japan’s export price surged to ¥140/ kl, to the level of local diesel oil retail prices that are at multi-year highs. The cooking oil is usually exported at ¥75-85/ kg.

- Used cooking oil export volume has also swelled. The 2021 exports totaled 109,374 tons, up from 75,675 tons in 2018. The February export volume was 7,602 tons.

- Used cooking oil is used as clean fuel in Asian countries. Singapore is the top buyer, followed by South Korea and Malaysia.

TAKEAWAY: Higher grain and corn prices propelled by the Ukraine conflict, as well as soaring crude oil that triggered the rise in palm oil prices, are causing clashes between energy and food players in some markets. The junior partner in the ruling coalition, the Komeito Party, has pressed PM Kishida for more decisive measures to strengthen Japan’s food supply chain.

First carbon credit issued for Japan-Bangladeshi joint crediting mechanism project

(Japan NRG, March 31)

- 251 tons of compliance credits were issued to Japan, and 238 tons to Bangladesh for improving energy efficiency at a plant and installing solar/diesel hybrid power generation system at a fastener factory.

Japan to boost EV subsidies marginally to encourage transition

(Kyodo, March 25)

- METI will raise the maximum subsidy to EV car buyers to ¥850,000, an increase of ¥50,000 on the ¥800,000 announced in November’s supplemental budget.

- METI says the boost was prompted by high energy prices and will encourage drivers to transition away from fossil fuels.

- The maximum subsidy payable to buyers of plug-in hybrids and fuel cell vehicles will increase by the same amount, to ¥550,000 and ¥2.55 million, respectively.

Seven-party consortium plans hydrogen hub for Kawasaki waterfront

(Company Statement, March 30)

- A consortium comprising Asahi Kasei, Ajinomoto, ENEOS, JR East, Showa Denko, Toshiba Energy Systems plans to make Kawasaki a hydrogen hub.

- The consortium will build new pipelines as well as utilize existing pipelines and other infrastructure to provide hydrogen services to a wide range of industries in the area, including factories and power plants.

- The consortium wants to avoid a “Catch-22” situation where demand never increases due to a lack of supply and vice versa.

- SIDE DEVELOPMENT:

Local governments foster private/public groups to promote decarbonization

(Nikkei, March 29)- A number of cities around Japan are building public-private consortiums to promote decarbonization, including the rollout of a hydrogen economy. The oldest example of such a scheme is in Fukuoka, western Japan.

- The Fukuoka Strategy Conference for Hydrogen Energy was established in 2004, making it one of Japan’s longest-running alternative energy groups. It has over 700 businesses affiliated with it, as well as local bodies and academics.

- In the latest move in promoting hydrogen, the Fukuoka government will create a liaison office to handle inquiries from manufacturers interested in producing hydrogen-related systems or fuel cells.

- Similar initiatives are also underway in Yokohama and Tottori. The Tokyo Metropolitan Government is establishing an innovation fund for private/public partnerships expected to be worth over ¥12 billion.

Panasonic sets aside almost $5 billion for shift to batteries and hydrogen

(Asia Nikkei, April 1)

- Panasonic will invest ¥600 billion ($4.9 billion) in the next three years in automotive batteries, hydrogen energy and software.

- Growth areas such as automotive batteries, supply chain software and air-conditioning, would get two-thirds of the capital while the rest will go into new technologies like hydrogen energy and workplace digitization.

INPEX to join nuclear fusion race with startup investments

(Nikkei Asia, April 1)

- INPEX aims to invest in several startups in Japan that will allow the oil and gas company to move into the emerging technology of nuclear fusion as early as this year. Investments include into Kyoto Fusioneering in Kyoto, EX-Fusion in Osaka, and Helical Fusion in Tokyo. INPEX is also in talks with overseas startups.

- These would mark the first investments by a major Japanese company in a nuclear fusion developer. Inpex plans to invest several hundred millions of yen in each company and gradually raise the amount of funds up to tens of billions of yen.

- Japan’s government aims to commercialize nuclear fusion generation in the 2040s and Inpex shares this target.

- SIDE DEVELOPMENT:

INPEX, ANZ and Qantas to work on carbon farming and biofuels project in Australia

(Company Statement, March 31)- INPEX, ANZ and Qantas have entered an MoU to progress the evaluation of a project which brings together carbon farming and renewable biofuels in the Wheatbelt region of Western Australia.

- The project provides an opportunity to support reforestation and decarbonization using drought-resilient native tree crops, integrated with existing farming systems.

- The parties will undertake a more detailed feasibility study into the harvesting and processing of native biomass crops and selected agricultural waste residues, to produce low-carbon renewable biofuels. Under the MoU, the first planting of native trees is expected to take place in the winter of 2023.

Kansai Electric unveils plans to halve CO2 emissions from power generation by 2025

(Kankyo Business, March 30)

- Kansai Electric unveiled a “Zero Carbon Road Map”, which calls for halving CO2 emissions from power generation by fiscal 2025, compared with FY2013 levels. That would mean a drop of 25 million tons of CO2 or more.

- The power utility plans to achieve this without reducing power output.

- The target includes a goal for making renewable energy one of its core sources of power. With a ¥1 trillion investment plan for the Japan market, the utility plans to grow its domestic renewables portfolio to 5 GW by 2040. Globally, the renewables assets would amount to 9 GW by then.

- Other ways to reduce emissions envision efficiencies, nuclear restarts, and an eventual move into hydrogen.

Nuclear power’s hidden carbon intensity: Opinion

(Asahi Ronza, March 28)

- CONTEXT: This opinion piece is by Ryukoku University lecturer Oshima Ken’ichi in a magazine published by Asahi Shimbun, one of the top national dailies.

- In February, the EU taxonomy for sustainable activities, a “green” classification system, officially categorized nuclear energy as “sustainable”. However, according to the IEA, only 3% of the $359 billion invested in energy in 2020 went to the nuclear sector.

- The situation in Japan is no different, with less than 5% of total electricity needs supplied by nuclear power stations in 2020. Nuclear plants are no longer a major source of electricity, or even a source of baseload electricity.

- Such concerns about the future of Japan’s nuclear power industry have encouraged pundits to paint nuclear as a green source of energy.

- However, nuclear plants are dependent on external electricity supplies for safety, and the mining, refining, processing and transport of uranium, as well as the construction and decommissioning of power plants, are all carbon intensive.

- While the Central Research Institute of Electric Power Industry puts the life-cycle carbon footprint associated with nuclear power generation at a mere 19 g/ kWh, a Stanford University analysis introduces the concept of “opportunity cost emissions” for the long time taken to construct nuclear plants compared with renewable energy plants, and estimates total carbon emissions associated with each kWh generated by a nuclear plant at over 100 g. This is 30 times higher than for offshore wind.

NEWS: POWER MARKETS

Majority of Japanese now want nuclear plants restarted

(Nikkei, March 28)

- A survey by Nikkei Shimbun found that 53% of respondents think idle nuclear plants that passed safety checks should be restarted. This is up from 44% in September.

- 38% of respondents were opposed to restarting nuclear plants, down from 46%.

- When asked about “nuclear sharing” — an arrangement under which U.S. nuclear weapons would be stationed in Japan and the government consulted on their use — 23% of respondents supported establishing such an arrangement with the U.S., while 17% did not. A further 56% were opposed to nuclear sharing but supported the matter being discussed.

TAKEAWAY: This is possibly the first media survey in Japan to show the majority of the respondents being supporting of nuclear restarts since the Fukushima accident in March 2011. The numbers also tally closely with a poll conducted in March by the left-leaning (and largely anti-nuclear) Asahi Shimbun, which showed 48% of the respondents behind restarts. Should the mood continue, PM Kishida will feel safer about discussing pro-nuclear initiatives including government backing for new reactor designs. Still, given how long the public has been anti-nuclear and how much depends on matters outside the control of the national government, we do not expect the restart process to accelerate suddenly.

High costs drive Lpio and West Holdings out of electricity retail market

(Smart Japan, March 28)

- Electricity retailer Lpio is discontinuing all retail electricity services.

- Lpio said high wholesale energy prices made its operations unsustainable.

- Founded as a supplier of LPG in 1965, Lpio launched its electricity retail business in 2016. In November, Lpio supplied 37 GWh to an estimated 140,000 subscribers.

- West Holdings also announced its withdrawal from power retail as prices soar due to high fossil fuel costs and tight domestic supply.

TAKEAWAY: Lpio and West join Hope Energy in exiting power retail in recent weeks. Other companies have also been named in the media as taking similar steps. There remain more than 700 power retailers in Japan and clearly the majority do not have the resources to become serious players in the now changed electricity market, in which there is greater volatility and prices are rising. It would probably benefit Japan to have the number of retailers shrink, but unless the process is smoothly managed it will cause disruptions for households and businesses. Were that to occur on a noticeable scale in the near future, expect the government to quickly bring out tougher regulations on power retail.

Shipper Mitsui O.S.K. looks for entry points into offshore wind

(Dempa Publications, March 29)

- Mitsui O.S.K. Lines (MOL), a major shipping company, has begun full-fledged efforts to move into the business of offshore wind power generation.

- Earlier in March, the company announced its participation in an offshore wind farm jointly with a major energy company, and also established a fund to invest in related businesses in Japan. MOL is the first major Japanese shipping company to move into offshore wind power generation.

- The company has also begun discussions with a construction company with a track record in offshore construction to see how it can use its ships in this business area.

- MOL, together with Toho Gas and Hokuriku Electric, are due to participate in Formosa 1, the first commercial-scale offshore wind farm in Taiwan.

Kansai Electric looks at 676.3 MW offshore wind project in Saga prefecture

(Denki Shimbun, March 31)

- Kansai Electric has begun studying the development of a landing-type offshore wind farm off the coast of Karatsu City, Saga Prefecture.

- The company submitted the first stage of the environmental assessment to METI and the head of the local government.

- The facility is expected to have a maximum capacity of 676.2 MW, which would be one of Japan’s biggest. The output of a single turbine will range from 9,500 to 14,700 kilowatts.

Chubu Electric invests in Indian energy company targeting off-grid consumers

(Nikkei, March 28)

- Chubu Electric plans to purchase a 20% stake of Indian-based OMC Power in a deal believed to be worth several billion yen.

- Founded by Telecommunications mogul Rohit Chandra in 2011, OMC operates around 200 small power stations and offers mini-grid services to rural consumers.

- SIDE DEVELOPMENT:

Chubu Electric plans to develop 86 MW wind power plant near Shitara Town, Aichi

(Kensetsu Tsushin Shimbun, March 39)- Chubu Electric’s partner is Tokyo-based OSCF Co.

All of Japan’s major power and gas companies due to raise rates in May

(Yomiuri Shimbun, March 31)

- All 10 major electric power companies and the four major city gas companies announced increased rates for May citing rising LNG and coal prices due to Russia’s invasion of Ukraine.

- The largest increase among the electric utilities was announced by TEPCO. The rates are now up by more than ¥1,600 in the last year to ¥8,505 (including consumption tax) for the average household. Prices are at their highest in five years, the period for which comparable data is available.

- May will be the ninth consecutive month that all major gas companies will raise their prices.

- CONTEXT: Electricity and gas rates are subject to a national system that automatically reflects fluctuations in the prices of fuels and raw materials in rates. In order to reduce the burden on consumers, there is a cap on the amount that can be passed on, and five power companies, including Kansai Electric and Shikoku Electric have already reached it.

- SIDE DEVELOPMENT:

Chubu Electric downgrades earnings guidance again amid high fossil fuel prices

(Asahi Shimbun, March 25)- Chubu Electric revised investor earnings guidance for the fourth time.

- Chubu projected a ¥45 billion loss in the fiscal year to March, but revised its projected loss to ¥50 billion in response to high wholesale energy prices.

TEPCO begins move of nuclear power unit to Kashiwazaki city

(Denki Shimbun, March 31)

- Tokyo Electric (TEPCO) Holdings has begun relocating its nuclear power business headquarters to Kashiwazaki City, Niigata Prefecture, which will eventually see 300 staff moved there.

- Approximately 70 people involved in quality, safety, and facility diagnostics will be assigned to the new office in April.

- The company plans to split the roles of chief of its Nuclear Energy & Safety division and director of its Kashiwazaki-Kariwa NPP to create a structure that allows the company to focus on the power plant. A former Chubu Electric employee will be appointed as an assistant director.

TAKEAWAY: Kashiwazaki-Kariwa NPP is TEPCO’s only operable nuclear power plant and this is a step towards building better local relations to allow for its restart at some point in the future. At the earliest, it would be 2H 2022.

JERA announces plans to decommission 3.82 GW of capacity

(Nikkan Kogyo Shimbun, April 1)

- JERA will decommission nine units at three thermal power plants with a total capacity of about 3.83 GW.

- These include the first three units at the oil-fired Oi power plant in central Tokyo; units 5 and 6 at the LNG-fired Yokohama power plant; and the first four units at the Chita thermal power plant.

- All the units had been in operation for around 50 years and were already idled several years ago.

NEWS: OIL, GAS & MINING

WAR IN UKRAINE:

METI announces policies to move away from Russian gas, oil, palladium

(Japan NRG, March 31)

- METI will be more active in securing oil, coal, LNG, palladium, ferrosilicon, low-carbon ferrochrome and gases for semiconductor manufacturing. It will:

- Ask non-Russian producers to increase output, starting with Kuwait on March 31. Japan is providing financial support to Kuwait.

- Collaborate with other oil consuming nations

- Directly engage with the private sector’s LNG procurement activities

- Monitor local LNG and coal stocks

- Decrease consumption of coal, palladium and other resources and find substitutes

- Support upstream projects through JOGMEC

- Deploy mega solar-storage battery systems, cut the number of gasoline cars on the road

- Push ambitious energy conservation/transition programs

- Newly-established Strategic Material and Energy Supply Chain will coordinate the actions.

TAKEAWAY: Japanese companies purchase raw materials on long-term contracts, often paying premiums over spot prices. This has worked out in their favor so far and may further help when negotiating new deals amid tight market conditions. As in the Kuwaiti case, supply guarantees may be packaged with financial aid and hydrogen/ammonia technology transfers.

There is also a risk, however, that a mentality to hoard supplies will see the government protecting too many raw materials, even those that are less critical or for which there are ready alternatives. Example: It is questionable if the ferrosilicon supply chain requires government support. Japanese steelmakers increased purchases from Russian Ferro Alloys and Mechel over the last two years for economic reasons, not because Russian companies were the only suppliers on the market. There are plenty of substitutes. On the other hand, Russia does have strong market power over low-carbon ferrochrome, used for specialty steel, and palladium.

Japan joins G7 in rejecting Russia’s demand to pay in rubles

(Japan NRG, March 29)

- METI Minister Hagiuda told the G7 that Japan won’t accept the Russian government unilaterally changing contract terms between private companies. Such behavior discourages stability of deals between companies, he said.

Hagiuda says Japan will not pull out of Arctic LNG

(Jiji, Japan NRG, Apr 1)

- Underlining the importance placed by the government on energy security, METI minister Hagiuda said Japan won’t pull out of the Arctic LNG 2 project.

- “We have secured long-term claimants,” and “in the current situation of sudden energy price increases, we can procure energy at prices cheaper than the market price. This is extremely important for energy security,” Hagiuda said.

- JOGMEC and Mitsui & Co. are the Japanese corporations that hold interests in the project, which operates within the Arctic circle. Japanese banks had previously committed funding to the project.

- The EU passed legislation banning additional European participation in Arctic LNG 2.

TAKEAWAY: In the last week, both PM Kishida and METI minister Hagiuda have said for the first time in a clear fashion that Japan will not exist Russian oil and gas interests. Without U.S. pressure for Japan to exit, the government is able to stick to its position that letting go of the rights Japanese firms hold in Russia will not help contain the war in Ukraine but will benefit either Russia or China. For now, it looks like the operating projects in Russia’s Sakhalin will continue to send their products to Japan, but new developments like Arctic LNG 2 will be frozen. At some point, that position too will become untenable. President Putin may well decide to push forward with Arctic LNG 2 regardless and label those partners that obstruct the process (or conversely do not help with financing and engineering know-how) to be “unfriendly”. When that point comes, Japan will need to act. But for now, the onus on Japanese energy buyers will be to search for alternative sources and prepare for a Plan B.

METI will not ban export of strategically critical energy and metal supplies

(Japan NRG, April 1)

- METI’s Strategic Material and Energy Supply Chain headquarters confirmed that there won’t be export bans on strategically critical oil and metal products.

- Japan exported 2.4 million kl of refined oil products in February, up 42% from a year ago.

- METI will focus on the diversification of resource bases while promoting a shift to alternative supplies where possible.

Ruling coalition’s junior partner calls for reinstatement of gasoline ‘trigger clause’

(NHK, Mar 28)

- Representatives of the LDP’s coalition partner, the New Komeito, called on PM Kishida to reinstate the ‘trigger clause’ (a gasoline tax relief scheme), and include additional funding for gasoline subsidies in the upcoming supplemental budget.

- Komeito Diet members hope to debate the matter with the LDP in April.

- If the trigger clause is activated, tax breaks will cause prices at the pump to fall by ¥25/ liter whenever the average retail price for gasoline exceeds ¥160/ liter.

TAKEAWAY: See the Analysis section for a deep dive on this issue.

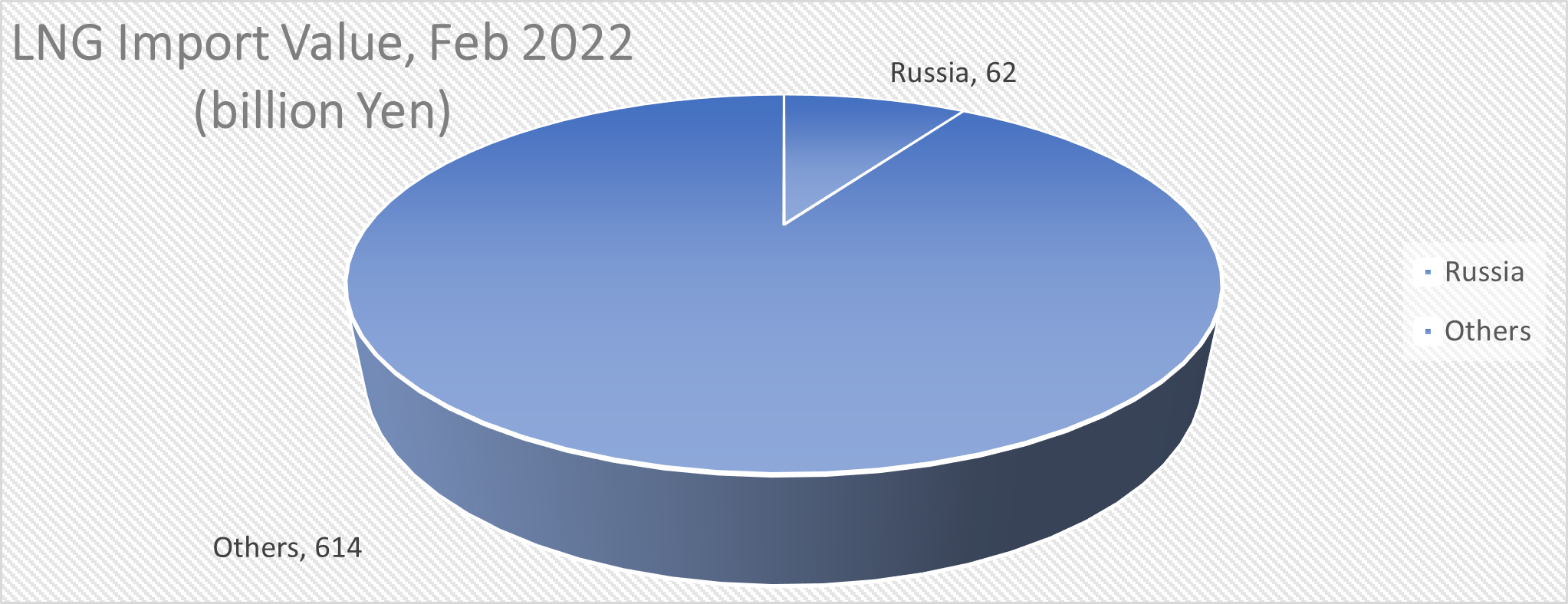

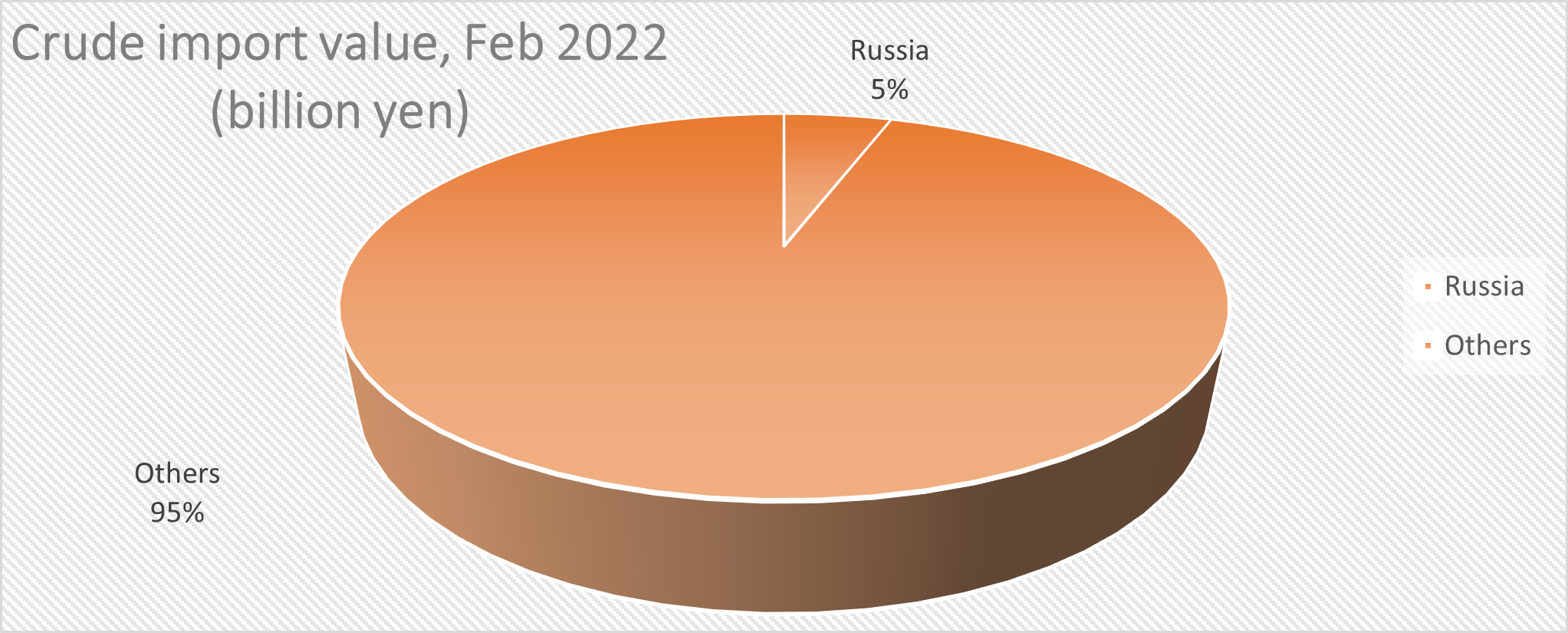

Japan imports 652,809 tons of LNG, 660,560 kl of crude from Russia in Feb

(Japan NRG, March 30)

- Japan imported 652,809 tons of LNG from Russia in February, out of a total 7.1 million tons. The Russian imports were worth ¥62 billion, out of the total ¥676 billion. Imports of Russian crude oil were 660,560 kiloliters, out of the 13 million kiloliters total. Russian oil was valued at ¥43 billion. The total crude oil import value was ¥808 billion.

LNG stocks fall to 1.66 million tons

(Japan NRG, March 31)

- LNG stocks stood at 1.66 million tons as of March 27, down from 1.68 million tons a week earlier and the lowest since 1.63 million tons of Feb. 6. The end-March stocks last year were 2.41 million tons and the four-year average was 2.19 million tons.

METI forecasts 2022 jet fuel demand to surge by 16.1%

(Japan NRG, March 29)

- METI released preliminary refined oil products demand forecasts for 2022-2026. In 2022, jet fuel demand is expected to surge by 16.1% to 4,072,000 kiloliters, while heavy fuel oil for non-utility consumers will fall 6.8% to 4,894,000 kl.

- Kerosene demand will decline 3.2% to 13,486,000 kl. Gasoline and kerosene demand is expected to edge up, by 0.4%, to 45,382,000 kl, and 1.6% to 32, 650,000 kl, respectively.

- In 2026, jet fuel demand will rise 27.9% over 2021, but demand for other products will fall. The diesel demand decrease will be marginal, at 0.3%, while heavy fuel oil will decline by 23%.

Battery-grade nickel demand to rise 24.2% in 2022: Sumitomo Metal Mining

(Tekko Shimbun, March 29)

- Demand for Class-1 nickel for batteries will rise 24.2% to 410,000 tons in 2022, and there could be a shortage of around 60,000-70,000 tons, according to Sumitomo Metal Mining forecast. The total 2022 global nickel demand is seen to increase by 8.4% while supply also increases 11.4%, mainly in Indonesia.

- CONTEXT: Indonesian nickel matte supplies, which are battery-grade material converted from stainless-grade nickel, will swing the supply demand balance. Production could increase if Chinese stainless-steel production slows due to lockdowns. Wood Mackenzie forecasts 100,000 tons of matte may be available in 2022, while SMM sees the matte emergence to be slower.

Anglo-Mitsubishi copper mine to build desalination plant in Chile

(Bloomberg, March 29)

- CONTEXT: Mines in Chile, the world’s top copper producer, are required to cut consumption of water from glaciers, rivers and lakes to 10% of the total by 2030, and 5% by 2050, as well as to provide full traceability of their water consumption.

- Anglo American, which runs the Los Bronces copper mine in Chile together with Mitsubishi Corporation, plans to build a desalination plant to be self-sufficient on water used for production of copper and hydrogen fuel for haulage trucks. The Bronces mine uses 85% recycled water from its operations as well as industrial and sewer waste water.

TAKEAWAY: Chile’s copper miners have commissioned seven desalination projects so far, many delayed as COVID slowed plant construction. The Chilean government is also promoting hydrogen-fueled equipment at mine sites.

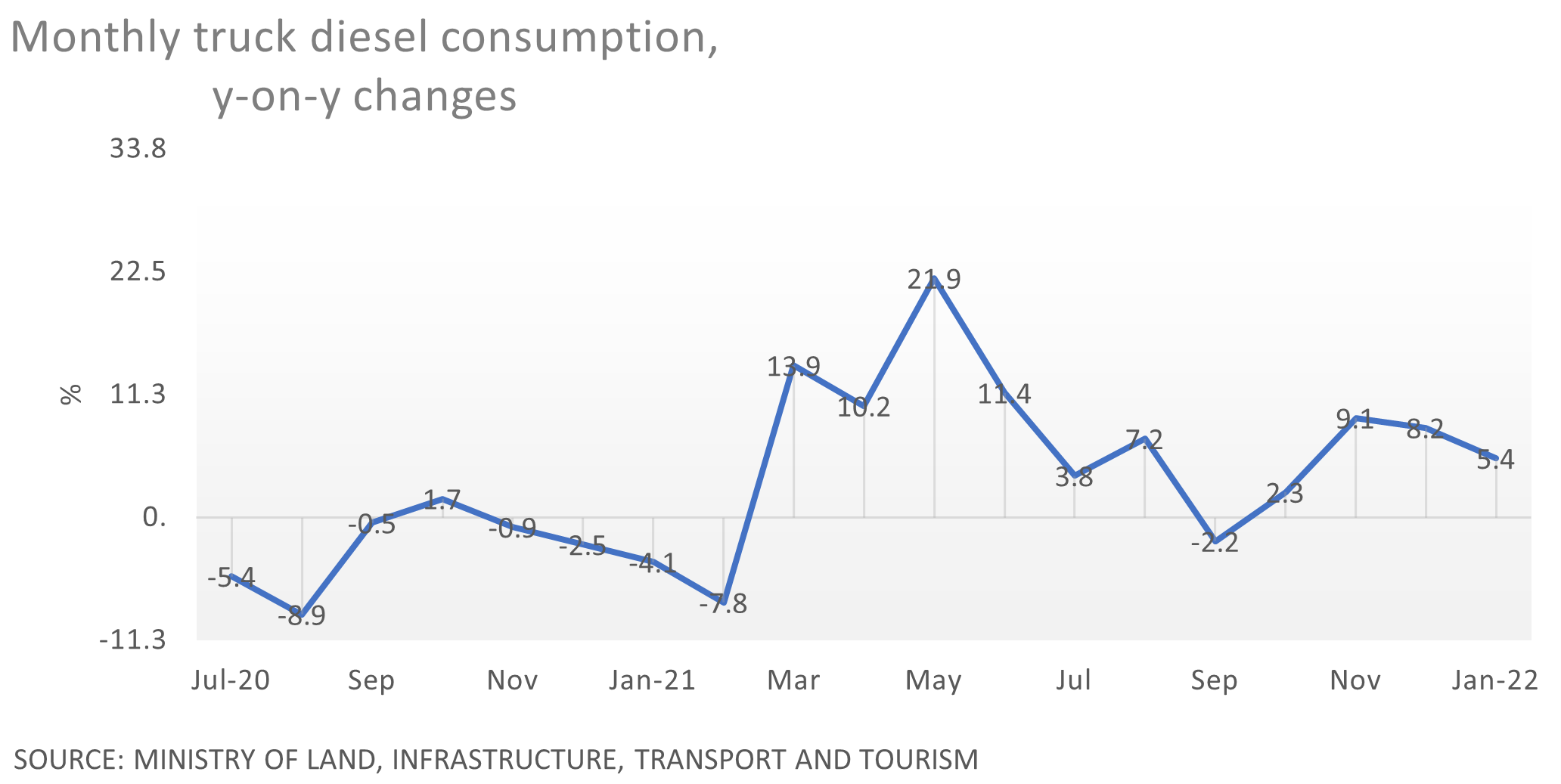

Truck diesel consumption trends up

(Japan NRG, March 30)

- Diesel oil consumption in the truck transport sector has been trending up since March 2021 when the monthly figure ticked up to 1,330,000 kiloliters, up 13.9% YoY. Double digit increases continued into June. Demand has stabilized but January 2022 consumption was a strong 1,325,000 kl, up 5.4% from last January.

- CONTEXT: Oceangoing vessels notably from Europe and the U.S. have been avoiding minor Japanese ports on the back of container shortages, increasing demand for transports from the main ports. In December, container cargo traffic at the five largest ports increased by 4.2-7.4% YoY, while ports ranking sixth and below saw over 6% declines. The five largest ports are Tokyo, Yokohama, Nagoya, Osaka and Kobe.

JERA says establishing Singapore unit to maximize global LNG portfolio value

(Company Statement, April 1)

- JERA established JERA LNG Portfolio Strategy Pte. Ltd. in Singapore as a strategic base to maximize the value of JERA’s LNG portfolio.

- To achieve a stable supply of affordable energy, JERA aims to maximize the value of its LNG portfolio by building an optimal LNG portfolio that takes into account stability, economic efficiency, and flexibility. This will require access to talent and resources that are readily available in Singapore.

ANALYSIS

BY MASUTOMO TAKEHIRO

Limited Options Tie Japanese Government’s Hands

Dealing with Looming Oil Shock

Soaring LNG and crude oil prices, accelerated by Russia’s war with Ukraine, are starting to reverberate throughout the economy, inflicting a high toll on Japanese households and nearly all areas of commerce and industry. Some experts already refer to this situation as the Third Oil Shock, with the first such global energy shock having taken place in 1973, almost half a century ago.

So far, state subsidies have been the main measure to combat energy-driven inflation. Last week Prime Minister Kishida ordered yet more of the same in an effort to shield consumers and seniors, in particular, from higher food bills. But it’s increasingly clear that this won’t be enough and bolder steps will be needed in the coming months, likely tying up more of the national budget, weakening the yen, and likely delaying the energy transition.

Unlike the 1970s, Japan’s government, as well as those of its western allies, are more experienced and in a better position to tackle the negative fallout from rapidly rising energy prices. However, many of the tools available to the state and the monetary authorities in Japan are already deployed or even tapped out after three years of dealing with the Covid-19 pandemic as well as long-term structural issues.

With only three months or so before upper house election the premier will be walking a political and economic tightrope. Deft handling of the energy dilemma could help Kishida’s administration secure a strong political platform for years. How much control the government can exercise over energy markets will be severally tested in the next three to four months.

It all starts with a full tank

Nationwide, retail gasoline prices have risen to a 13-year high. Without existing countermeasures, the price would have surpassed the record high of ¥185/ liter reached in 2008. Some experts even foresee the price going beyond ¥200.

If crude oil prices remain at an average of ¥120/ barrel, the burden on households will grow by about ¥44,000 this year and the same next year, according to estimates. Inevitably, this would lead directly to a painful dip in disposable income. Additionally, the cost for kerosene purchases in cold weather regions will be of particular concern from about October this year.

The Consumer Price Index (CPI) for February indicates that gasoline, as well as electricity, and gas prices rose 22.2%, 19.7%, and 22.9%, respectively, the steepest YoY increase for energy in 41 years.

Soaring fuel costs are putting pressure on agriculture and fisheries, which use heavy oil for fuel, and the transportation and cleaning industries are also said to be hit hard.

Power utilities are having a rough time, in part due to the fact that it takes three to five months to pass on rising fuel costs to electricity bills. To make matters worse, in order to protect consumers there’s a system in place that prevents an upward adjustment if the average fuel price exceeds 1.5 times over a certain base price. Indeed, Hokuriku Electric faced this upper limit for February, and four more utilities are heading for the same for March.

Already in the 3Q of 2021, all of the major power companies, except for Kyushu Electric, saw a YoY decline of 30-80% in income, pushing four of the 10 into the red. Six of the companies, including TEPCO and Chubu Electric, are expected to post losses for the fiscal year that ended in March.

Subsidies vs tax cuts

PM Kishida, who appears to favor the pork-barrel approach, last week instructed government to start work on a new stimulus package, rumored to be as large as ¥2 trillion, ready for late April. That will aim to combat high oil prices and shield households from rising food prices, while also supporting SMEs.

Until the new stimulus arrives, Kishida will hope to placate public ire mainly by subsidizing gasoline. Since January, the government has been subsidizing the portion of the pump price above ¥172/ liter, sending funds to oil wholesalers to compensating for their rising costs.

The subsidy cap was initially set at ¥5/ liter, but raised to ¥25 on March 4 after the Russian incursion into Ukraine. To implement this policy from January to March, ¥430 billion ($3.5 billion) was appropriated from the FY2021 budget reserve.

This measure was supposed to be time-limited until the end of March, but the government has decided to extend it to the end of April as chaotic scenes around gas stations could emerge if it was suddenly discontinued.

Further subsidies are more targeted to industry and seek to cool prices for kerosene, diesel, and fuel oil.

There are other policy tools PM Kishida could deploy. One is a so-called “trigger clause” introduced when the current opposition parties were in power over a decade ago. This option temporarily lowers a type of tax on gasoline.

Gasoline is subject to a “gasoline tax” of ¥53.8/ liter, as well as a “petroleum and coal tax” of ¥2.8/ liter. A 10% consumption tax is applied at the moment of sale. Originally, the gasoline tax rate was fixed at ¥28.7/ liter, but in the 1970s an additional ¥25.1/ liter was added to finance road construction. Today, this additional portion serves as a general revenue source.

What a “trigger clause” does is reduce the overall gasoline price by halting this additional ¥25.1 tax when the price of gasoline exceeds ¥160/ liter for three consecutive months. The trigger clause was frozen following the 2011 Japan Earthquake to secure financial resources for reconstruction.

On March 4, when asked about measures to be taken after April, Chief Cabinet Secretary Matsuno Hirokazu, admitted: “The government will consider all options, including the trigger clause”.

Lifting the freeze requires new legislation, which is why this method is politically charged. Introducing a trigger clause would lower tax revenue by ¥130 billion per month. Supposing it’s in effect for 12 months, then the missed revenue would amount to ¥1.6 trillion. Since the gasoline tax is inclusive of a local gasoline tax portion, this option would also hurt local municipality budgets.

Additional efforts

In addition to the demand-side measures, the government has been active in trying to raise supply. In response to a request from the U.S., Japan has been releasing oil reserves. At the end of 2021, Japan’s national stockpile had 146 days’ worth of domestic demand. The Oil Stockpiling Act does not permit the sale of oil for price suppression measures, but the government got around this by claiming that the main purpose is replacement of the liquid in the tanks.

The three-stage release is due to total about 660,000 kiloliters. The sale of 100,000 kiloliters (630,000 barrels) of oil in February and a further 260,000 kiloliters in March were done via public tenders. The remaining 300,000 kiloliters is approved for distribution after May 20 in the third and final round of tenders.

Diplomatic efforts are also in play. On March 15, Kishida spoke with the UAE’s Crown Prince Muhammad and confirmed that the two sides will work together to stabilize the oil market. Shortly thereafter, Foreign Minister Hayashi visited the UAE.

Japan’s top three banks are also part of a western consortium that recently agreed to loan $1 billion to Kuwait Petroleum Corp. to help it expand output.

In the meantime, the oil shock is replacing another one related to nuclear energy. Potentially for the first time since the 2011 Fukushima disaster, the majority of respondents to a survey by a national newspaper said they favor the restart of more nuclear reactors in the country. The Nikkei survey from late March had 53% of people calling for restarts. (For more on Japan’s nuclear debates, see the March 14 edition)

There are also national efforts around energy efficiency and conservation.

Conclusion

If history is any indication, the Japanese economy, along with the entire global economy, could well be entering a period of recession and accompanying difficulties. The year after the 1973 Oil Crisis, for example, Japan posted negative growth for the first time in the postwar era – an 8.2% plunge in GDP growth over 12 months.

Precisely because of that past experience, however, Japan and allied governments are more able and knowledgeable when it comes to mitigating the impact of an impending energy crisis. The economic fallout after the Lehman Shock, for example, was staggered over two years and saw a 7% drop in GDP growth over 24 months.

The biggest problems for PM Kishida will be the events that he cannot control and sudden supply shocks. With President Putin determined to strike back against Western sanctions, the chance of both of those occurring are not small.

ANALYSIS

BY JOHN VAROLI

Putin’s Rubles-for-Gas Threat:

Desperate Measure or Start of Bigger Changes?

The global energy community was initially bewildered by Moscow’s threats last week demanding ruble payment for energy sales. Russian President Vladimir Putin set an April 1 deadline for the measure, which left some wondering whether it was a mischievous geopolitical prank. That certainly wasn’t the case.

The threat was real and aimed at “unfriendly nations” which includes Japan, the U.S., Australia, Canada, Britain, New Zealand, South Korea, and all EU member states. With Europe’s economy dependent on Russia for about 40% of gas imports and 25% of oil, EU leaders began to prepare for possible disruption of energy supplies that would have had catastrophic consequences.

Germany’s finance minister was the first to reject the notion, saying that energy contracts can’t be altered. Other EU countries quickly followed suit. Since Russian energy exports to Japan are much smaller, METI Minister Hagiuda waited a few days before telling the G7 that Japan won’t accept Russia unilaterally changing contract terms between private companies.

The political standoff will not surface in energy flows just yet since commodities already paid for will be delivered as agreed, according to Russia. But from the middle of April, the impact will start to be seen. With the ruble’s recent rebound, President Putin is seeking to build on his gambit to subvert the dollar-bound commodity world order. For the Kremlin, ruble-priced gas is just the beginning.

Brief history of recent events

First, some background. For eight years, Russia and the West have stared each other down over control of Ukraine, Europe’s largest country after Russia. In the early 2010s, Ukraine’s government negotiated a political and free trade agreement with the EU, but in late 2013 then President Viktor Yanukovich made a sudden decision to walk away from the deal. This sparked protests, which turned violent and resulted in deadly clashes with the police. By early 2014, Yanukovich fled from Ukraine to Russia and a new government was formed.

Russia called the ousting of Yanukovich an illegal coup. The U.S. backed the insurrection, which brought to power a pro-western group. Ethnic Russian separatists living in the heavily-industrialized eastern Ukraine region of Donbas, however, vowed not to support the new government and formed a militia. The new Ukrainian regime engaged in a military campaign against the separatists.

Moscow responded by sending unmarked troops into Crimea and annexing the predominantly ethnic Russian region. It also sent forces to help the pro-Russian Donbas militia. The latter’s standoff with the Ukrainian military ground to a stalemate after six months. The annexation of Crimea sparked a wave of sanctions, though Japan’s measures against Russia were relatively mild as then Prime Minister Abe sought to improve Russo-Japanese relations. Western countries also helped to arm and train Ukraine’s military.

Fast forward to Feb. 24, 2022 when Russia invaded Ukraine, claiming it was a preemptive strike to outwit an alleged planned Ukrainian offensive against the besieged Donbas region. (Kiev and NATO deny these charges). On Feb. 26, western allies announced far-reaching sanctions against Russia, the most wide-reaching of which was freezing the country’s $640 billion in foreign-exchange reserves.

That sent the ruble plunging from 84 rubles to almost 135 rubles per dollar in early March. White House officials claimed that they had devastated the Russian economy and reduced the ruble “to rubble”.

Faced with this humiliation, the Kremlin sought to shore up domestic reserves and stabilize the economy. Russia’s Central Bank raised interest rates to 20% and enacted capital controls on exchanging rubles for dollars or euros. Until at least the end of June, the ruble is backed by gold (at a fixed 5,000 rubles per gram).

After the initial wobble, Putin decided to go on the offensive, unleashing a broadside against the U.S. dollar’s dominance in global trade. Leveraging Europe’s dependence on energy imports to its advantage, Putin demanded that all “unfriendly” countries pay Gazprom, the state-controlled gas giant, in rubles. The Kremlin has signaled that a similar move to rubles will follow for other commodities that Russia exports.

How will rubles-for-gas work?

Except for the UK, where Gazprombank faces sanctions, energy companies can continue to buy Russian gas and oil in euros, according to Paul Goncharoff, an American business consultant based in Moscow. The only change is that foreign gas buyers will need to set up a ruble account in Gazprombank and link it to their euro account. Then, they’ll have to instruct Gazprombank to transfer the euro payment to their new ruble account.

“Russian banks have been sanctioned from the western banking and payment system, rendering it unusable,” said Mr. Goncharoff. “Russia will honor its supply contracts, receiving from the buyers the same USD or Euro sums due, but converted and paid in rubles. Now buyers can use the same payment paths that a host of countries like India, China, and others successfully have done and do.”

As existing contracts run down, western buyers may be asked to pay directly in rubles for future supplies. In theory, this could still be accommodated if a middleman firm registered in a neutral, “Russia-friendly” or even offshore jurisdiction was set up to bridge the currency issue. While such a scheme would be open to many weaknesses, not least of which is currency risk, it could also keep the flow of gas intact, albeit at a higher price.

Russia’s government would like to present the situation as not just a sanctions workaround, but the start of a new world order in international trade. Deputy Foreign Minister Sergei Ryabkov said that BRICS — Brazil, Russia, India, China and South Africa — will try to create their own economic order, and that the demand for rubles is meant “to protect Russian interests”, but “not a change in the terms of energy contracts.”

India has already declared that it has and will continue to buy Russian commodities as this is a matter of energy security. Russia has reportedly offered India oil at a discount to global market prices.

Furthermore, Russia is talking with its allies to create a new “basket of commodities” to partially, or wholly back, the ruble.

“This probably would include oil, gas, gold, and grains in a formula based on monthly settlement prices on globally recognized exchanges,” said Mr. Goncharoff. “It may well turn out to be quite advantageous to conduct business in rubles, a hard asset-backed currency. Time will tell.”

Russia’s offensive on the U.S. dollar has sympathies in some non-Western countries. The IMF and Goldman Sachs have also warned that U.S. sanctions are damaging the dollar’s leading position because many countries now see Washington as weaponizing the American currency far too often.

Meanwhile, the ruble has bounced back from its initial post-invasion collapse. As of April 3, it was at 83.5 to the USD, close to levels before Russia’s incursion into Ukraine. Putin’s battle to force a change in the payment currency for key commodities, initially rejected by the G7, is far from over.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Chile/ Solar power

Atlas Renewable Energy switched on its new 244 MW solar farm, now one of the country’s largest. Spread over 479 hectares, the plant will generate 714 GWh annually. Chile plans to retire and/or convert half of its coal-fired power plants by 2025.

China/ Renewable energy

China Shenhua Energy Co. will spend about 40% of its annual capital expenditures on renewable energy by 2030, reaching peak GHG emissions by 2025 and carbon neutrality by 2060. Shenhua is a subsidiary of state-owned China Energy Investment Corp., the country’s biggest coal miner, but also the world’s second-biggest renewable power developer.

Germany/ Hydrogen power

E.ON and Australia’s Fortescue agreed to develop a hydrogen supply chain. Fortescue plans to produce and export green hydrogen to Germany to replace about one third of Russian gas imports. The plan requires $50 billion in investment to produce 5 million tons of hydrogen.

India/ Renewable energy

Steel giant ArcelorMittal will partner with Greenko Group to develop a 975 MW around-the-clock wind and solar project. Power from the $600 million project will go to the company’s JV, ArcelorMittal Nippon Steel India, and will be fully operational by mid-2024.

Mexico/ Solar power

A $20 million roof-top solar power project will cover Mexico City’s massive outdoor market, La Central de Abasto. With about 18 MW of generating capacity, the project is a rare green initiative for the government of President Lopez Obrador, who prioritizes fossil fuel power generation.

Netherlands/ Fossil fuel financing

ING Group will stop financing new oil and gas projects, becoming the largest bank to commit to climate change measures. While ING won’t finance projects approved after Dec. 31, 2021, it will still fund energy firms. Also, ING plans a 50% increase in lending for renewable energy projects by 2025. In 2021, ING loaned €7.3 billion to renewable energy development.

Netherlands/ Wind power

The Netherlands will double offshore wind farm capacity to about 10 GW by 2030. The additional power will particularly help large industrial concerns, such as chemical and steel plants, switch to sustainable energy.

UK/ Renewables infrastructure

In the next 10 years, Shell UK will invest £20 to £25 billion in the British energy system; mostly to fund offshore wind, hydrogen energy, carbon capture utilization and storage (CCUS) and electric mobility. In related news, BP will spend £1 billion on EV infrastructure by 2030, building 300 kW and 150 kW ultra-fast charging points to provide EV drivers with a range of 100 miles in 10 minutes of charging.

UK/ Wind and solar power

The government proposed tripling solar panels and doubling onshore wind power by 2030. Solar would increase from its current capacity of 14 GW to 50 GW; offshore wind from 11 GW to 50 GW; and onshore wind from 15 GW to 30 GW. In related news, work began on the first phase of the 3.6 GW Dogger Bank Wind Farm owned by SSE Renewables, Equinor, and Eni. Also, Ørsted will sell, for £3 billion, its 50% stake in the 1.3 GW Hornsea 2 Offshore Wind Farm. The buyer is a group that includes AXA IM Alts and Crédit Agricole Assurances.

U.S./ LNG

A subsidiary of New Fortress Energy will scrap its proposed LNG plant in Pennsylvania due to an environmental group’s lawsuit seeking to terminate the company’s emissions permit. The $800 million plant was intended to liquify natural gas from the Marcellus Shale gas field.

U.S./ Wind power

The first wind energy lease sale for areas off the coast of North and South Carolina will be held in May. The Interior Department will offer two areas covering 110,000 acres in the Carolina Long Bay area that could generate as much as 1.3 GW of offshore wind energy.

JOBS IN JAPAN’S ENERGY SECTOR

BY ANDREW STATTER

The Great Energy Talent Squeeze

As Japan and the world transitions their energy mix from fossil fuels to renewables and new fuels, the workforce is transitioning as well.

With new sectors such as offshore wind and hydrogen growing quickly, companies need to hire more people than experienced professionals exist in the market. With highly competitive tender processes and immature markets, this creates the challenge of a market short in qualified candidates.

A clear example of this is seen in the nascent offshore wind industry, where multiple developers form a consortium, and multiple consortiums compete over the same project. While there’s only one eventual winner, all of them need to hire qualified talent to develop proposals. The challenge is compounded by the fact that Japan is going from <0.1GW to 10 GW of capacity by 2030, and the experienced talent pool is very thin. The same will be true for years to come.

As offshore wind developers grow and need more people, they are turning to other renewable sectors in the hunt for staff. Talent in onshore wind, solar power, as well as real estate and large Japanese trading firms is in high demand.

Many companies are putting emphasis on transferable skills, coupled with a flexible mindset. This is great news for professionals from other sectors, who can leverage relevant experience to move into a high-growth market. Skills in particularly high demand are project management, negotiation with local stakeholders (landowners, local business, fisheries, municipal governments etc.) commercial negotiations, and financial acumen.

With the right motivation and attitude, as well as support from the employer, members of the workforce can catch up quickly and learn new industry specifics.

The PV market is in transition, and has plenty of talent experienced in local stakeholder management. As the oil & gas industry plateaus, we will see more talent adept at complex commercial negotiations, supply chain management and contract work transition into the renewables sector.

The energy transition demands flexibility from the government, incumbent companies and the grid. Companies driving the transition need to show the same flexibility in hiring in what is currently a developing market.

About the author

Andrew Statter is Partner and Head of GreenTech at Titan GreenTech, a Tokyo-based human capital and executive search firm with a focus on renewable energy and clean technology markets. Titan supports global companies with Japan market entry, as well as scale-up and key hiring.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.