JAPAN NRG WEEKLY

APRIL 18, 2022

JAPAN NRG WEEKLY

April 18, 2022

NEWS

TOP

- Japan to push for more upstream LNG investment, more coal from existing suppliers as substitutes for Russian commodities

- OCCTO: Tokyo power shortages will be more critical next winter; system operator stresses need to cut power consumption

- ENEOS and France’s TotalEnergies team up in bio fuel and solar; the two seek to commercialize SAF and invest in Asian solar farms

ENERGY TRANSITION & POLICY

- PM Kishida promotes pan-Asian green initiative outside of China

- Japan faces record climate shareholder resolutions this year

- Govt. to create nationwide bio jet fuel supply chain by 2023

- Mitsui and Pertamina to study CCUS potential in Indonesia

- Telco group KDDI brings forward net-zero target by 20 years

- Osaka Gas, Australia’s AQUA AEREM partner in hydrogen project

- Kawasaki Heavy, Airbus jointly to create hydrogen fuel ecosystem

- Fujitsu and Icelandic startup work to develop ammonia catalysts

ELECTRICITY MARKETS

- First-ever solar curtailment orders from Shikoku and Tohoku grids

- Hokuriku Electric forecasts wind capacity to surpass solar in 2030

- Tokyo’s power reserve shrinks due to delay in restarts post-quake

- Major utilities freeze new subscribers citing surge in requests as retailers continue to withdraw from the market

- Tokyo Gas, Green Power, Renova, KEPCO plan new offshore wind

- Pacifico Energy launches large solar project and sells its to a JV

- Japan rail operator tests wireless, solar powered phone charging

- Regulator tells Hokkaido Electric to step up nuclear safety measures

OIL, GAS & MINING

- Japan can’t afford to be outbid on LNG in tricky market: Kikkawa

- Opposition lawmakers call for reinstatement of gasoline tax relief

- Activist investor Murakami takes major stake in Cosmo Energy

- JGC and Kawasaki Kisen to reuse old tankers for floating LNG

- JX Nippon secures loan to start urban mining scheme for lithium

ANALYSIS

FRIEND OR FOE? HOW COMPETITION AUTHORITIES

IN JAPAN VIEW THE ENERGY TRANSITION

One difficulty of an energy transition is that often incumbent market players enjoy outsized influence thanks to decades of growth and consolidation. The move to a low-carbon economy promises profound structural changes in the industrial, social and financial sectors. But, how to make sure this process does not unduly favor the current industry majors? This is the question Japanese antitrust authorities are starting to grapple with as the energy transition accelerates.

Japan NRG Weekly sat down with former Japan Fair Trade Commission officials to discuss developments in the oil, gas, hydrogen, and power sectors.

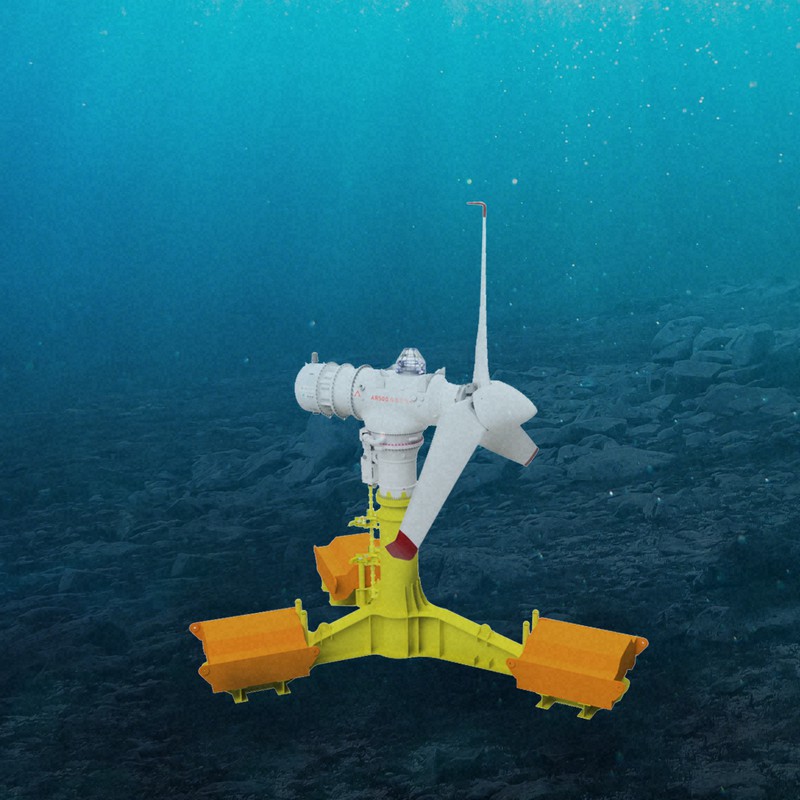

OCEAN ENERGY SHOWS PROGRESS AS PROJECTS MOVE TOWARDS THE MEGAWATT STAGE

Japan could generate nearly 170 TWh of electricity, or 20% of its annual needs, in the open seas through energy sources other than offshore wind power generation, according to government-backed research. After decades of theoretical analysis, close monitoring of water systems, R&D projects at home and abroad, Japanese marine energy tech is now maturing into sizable demonstration facilities, with a few aiming to reach commercial scale in the next two-three years. The strong push to develop offshore wind in Japan could also help to bring ocean energy into the mainstream.

GLOBAL VIEW

Global energy investments will reach a record $2.1 trillion this year. IEA updates oil market forecast to say no sign of major oil deficit this year. Denmark’s Orsted is boosting coal reserves ahead of next winter. Egypt asks Russia’s Rosatom to build its first nuclear power plant. South Korea reverses course on nuclear phase out. Details on these items and more in our global wrap.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Japan, Events)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Daniel Shulman (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com

For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

Kishida enthusiastic on pan-Asian green initiative

(Nikkei, April 14)

- CONTEXT: This opinion piece is by Shimizu Masato, a member of the editorial committee.

- Japan must balance energy security with the need to reduce carbon emissions.

- PM Kishida advocates creating an “Asia Zero Emissions Community”, in which Japan will share expertise in hydrogen, ammonia, and other green technologies with other Asian nations to help build green infrastructure and reduce carbon emissions.

- When asked if he saw China as a member, Kishida said he didn’t, and rather envisaged an ASEAN-centered community.

- Southeast Asia’s climate makes the region less suited to solar or wind generation. Meanwhile, exporting nuclear power plants would breach nuclear non-proliferation obligations. This is why PM Kishida is enthusiastic about ammonia and hydrogen.

- But ammonia and hydrogen supply chains have yet to be built, and controversy marks the carbon reduction levels required for a technology to be branded “green”.

TotalEnergies and ENEOS to explore Sustainable Aviation Fuel production in Japan

(New Energy Business News, April 15)

- ENEOS and France’s TotalEnergies will conduct a feasibility study for production of Sustainable Aviation Fuel (SAF) at ENEOS’ Negishi Refinery in Yokohama.

- The study will focus on commercialization of SAF production by utilizing idle production facilities and raw materials at the Negishi site, which include biomass, waste cooking oil and tallow.

- The two companies are considering a JV that might launch by 2025.

- The Negishi Refinery is close to major sites of aviation fuel demand, including the Narita and Haneda airports.

- SIDE DEVELOPMENT:ENEOS to partner with TotalEnergies on Asian solar(Sangyo Press, April 15)

- ENEOS plan shortly to launch a JV with French energy company TotalEnergies.

- The 50:50 venture between the two will seek over the next five years to establish 2 GW of solar capacity across Asia, including in Japan, India and Thailand.

- The electricity will be sold to local factories and commercial facilities under corporate power purchase agreements.

Japan faces record climate shareholder resolutions this year

(NPO Statement, April 13)

- This year, Japan faces a record number of climate-focused shareholder resolutions.

- Shareholders from civil society organizations announced four climate resolutions targeting SMBC Group, Mitsubishi Corp, and TEPCO and Chubu Electric, over their assets, which include the 50:50 JV, JERA.

- The NPOs include Market Forces, 350.org Japan, Friends of the Earth Japan, Kiko Network and Rainforest Action Network.

- NPOs said their shareholder action is focused on companies developing or financing new fossil fuel infrastructure.

Climate business lobby meets with PM to promote renewables, carbon pricing

(Kankyo Business, April 8)

- The Japan Climate Leaders Partnership (JCLP), which represents 206 companies, met with PM Kishida and gave him a “Position Paper on Overcoming the Climate Crisis through New Capitalism.”

- CONTEXT: Kishida came into power on a platform called “New Capitalism”, which promises more focus on income equality.

- The group said that for Japan to meet climate targets, action is needed that complies with the 1.5°C climate warming roadmap. Specifically, the country should (1) adjust its systems to give priority to renewable energy, and (2) introduce carbon pricing, to recognize the social costs of climate impact.

- The PM accepted the proposal and wants the JCLP to continue playing an important role in communicating its ideas to society.

Japan to create bio jet fuel supply chain in clean energy push

(Nikkei Asia, April 14)

- Japan will develop a supply network for bio jet fuel, to make the fuel available across the country next year. The government will take the lead in importing the eco-friendly fuel and building storage facilities.

- Infrastructure for handling sustainable aviation fuel (SAF) will first be built at Chubu Centrair International Airport in Aichi Prefecture. The hub will be used for a two-month trial of bio jet fuel. Later, SAF will spread to other airports.

- CONTEXT: Japanese airlines are under pressure to use SAF since it’s mandatory in other regions, but costs are several times higher than for conventional jet fuel.

- Itochu will import the fuel for the trials from Finland’s Neste.

KDDI, mobile and data conglomerate, brings forward net-zero pledge by 20 years

(Kankyo Business, April 8)

- KDDI aims for net-zero CO2 emissions by FY2030, which is 20 years ahead of its previous declaration. In addition, KDDI seeks to achieve zero CO2 emissions at its data centers globally by FY2026.

- KDDI’s energy consumption results in about 1 million tons of CO2 annually; 98% of which is due to electricity for cell phone base stations, telecom stations, and data centers. Those numbers will increase with the spread of 5G.

- KDDI will accelerate power saving initiatives.

- CONTEXT: KDDI is Japan’s No. 2 mobile operator.

Mitsui and Indonesia’s Pertamina to launch CCUS studies

(Company statement, April 7)

- Mitsui & Co, and Indonesian state-owned energy producer Pertamina will study the potential for CCUS in the oil and gas fields of Rokan Block in Central Sumatra.

- The study will evaluate the CO2 subsurface storage capacity of oil and gas fields whose production volume has been declining, and to examine the establishment of a CCUS value chain, including capture and transportation of CO2 emitted from industrial plants, power generation plants, and other facilities.

- This study will also look into receiving CO2 not only from within Indonesia but also from other nations, including Japan, via ship transportation, aiming to create a new low-carbon solution business in Indonesia.

Major Indonesian CCUS projects with Japanese involvement

| Partners | Location | Schedule |

| Pertamina, ExxonMobil | Gundih | Operational in 2026 |

| J-Power, METI, NEDO, JANUS, Pertamina | 2021-2025 feasibility study, subject to JCM credits | |

| Mitsubishi, Inpex, JX, KG Mitsui, LNG Japan, Sumitomo, Sojitz, CNOOC, BP | Tangguh | 2020-2025 feasibility study, operational in 2026 |

| JAPEX, Pertamina, LEMIGAS | Sukowati | 2020-2025 feasibility study, 2025 project starts, 2028 carbon injection, subject to JCM |

| `Chiyoda, Pertamina | Unspecified | MoU signed in January 2022 |

Can carbon storage overcome cost hurdles?

(Nikkei, April 13)

- The International Energy Agency says that in addition to the 27 carbon capture, use, and storage projects in operation globally, an unprecedented 163 are in the pipeline.

- The growth of the CCUS market is a boon for heavy industry, which is well-placed to provide the necessary separation, recovery, transport and pressurization services.

- Mitsubishi Heavy Industries, Kawasaki Heavy Industries and Toshiba are pursuing initiatives to recover CO2 produced by power stations and factories.

- JGC, INPEX, JAPEX, and Idemitsu are involved in initiatives to store CO2 underground or under the seafloor. Mitsui OSK Lines and Mitsubishi Shipbuilding are developing CO2 transport vessels.

- While enhanced oil recovery, which involves the injection of pressurized CO2 into depleted oil wells, is not new, the technique requires drilling injection borewells, and high costs meant few operators seriously pursued the technique until recently.

- While the technology remains expensive, competition in the global CCUS market is such that Japanese industry can’t afford to take a “wait-and-see” approach.

- A recent METI trial in Hokkaido reported costs of over ¥11,000 per metric ton of CO2 sequestered, half of which went to dig the bore well and inject the CO2.

- The IEA projects 6.9 billion tons of CO2 needs to be sequestered by 2070 to achieve carbon neutrality by 2050; the world will face astronomical CCUS bills unless ways are found to make the technology cheaper.

Mitsui invests in French green hydrogen startup via convertible notes

(Company Statement, April 13)

- Mitsui & Co invested €10 million, by way of convertible notes, in the French company Lhyfe, which produces green hydrogen using renewable energy.

- Lhyfe was created in 2017 by ex-employees of the French Alternative Energies and Atomic Energy Commission (CEA), with the aim to reduce GHG emissions via production of green hydrogen, connecting to renewables power plants.

- Lhyfe developed its first commercial plant to produce renewable green hydrogen using power from wind turbines. The company is active in 10 countries in Europe and has over 90 projects across 11 countries.

Osaka Gas, Australia’s AQUA AEREM partner in hydrogen

(Japan NRG, April 12)

- Osaka Gas and Australia’s AQUA AEREM will jointly produce green hydrogen using AQUA’s proprietary technology to produce hydrogen from water captured in air and solar energy. Osaka Gas, which in 2005 commercialized the hydrogen manufacturing equipment HYSERVE, will provide the know-how to build the hydrogen plant and gas storage. In 2023, AQUA AEREM plans to build a 400 ton/ year plant in Northern Territories of Australia, and will expand production to 400,000 tons/ year. Hydrogen will be supplied to Australian power stations and overseas. Osaka Gas, however, said it has no plans to export AQUA AEREM hydrogen to Japan.

- CONTEXT: Methanation, or synthetic methane that recycles carbon, is the main carbon neutrality project of gas utilities. Osaka Gas doesn’t seek to expand into the hydrogen supply business, but rather, to secure the means to produce green hydrogen for methanation.

Kawasaki Heavy partners with Airbus to develop hydrogen fuel ecosystem

(Company Statement, April 12)

- Airbus and Kawasaki Heavy Industries signed an MoU to develop an ecosystem for hydrogen fuel: from production to delivery to airports and aircraft.

- They’ll prepare a roadmap to define an advocacy plan on hydrogen aviation needs, and will pioneer the deployment of hydrogen infrastructure for aviation with a particular focus on the development of Airport Hydrogen Hubs.

Fujitsu teams up with Icelandic startup to develop new ammonia production catalysts

(New Energy Business News, April 15)

- Fujitsu and Atmonia, an Icelandic venture company that develops methods for synthesizing ammonia, teamed up to explore catalysts for the clean synthesis of ammonia. The two started a joint research project that utilizes high-performance computing (HPC) and AI, and which is due to finish by April 2023.

- Fujitsu and Atomonia will run high-speed quantum chemical simulations to determine the relationship between nitrogen and hydrogen and catalysts. This should help speed up the search for new catalyst materials.

Japan Bank for International Cooperation invests in U.S. nuclear startup NuScale

(Company Statement, April 4)

- The Japan Bank for International Cooperation (JBIC) paid about $110 million for a stake in NuScale Power. Participation will be made via a special purpose company established by JGC Holdings (JGC) and IHI Corporation.

- JBIC’s investment goes toward maintaining and improving the international competitiveness of the Japanese nuclear power industry.

Honda to invest $40bn in EVs as it aims to go all-electric by 2040

(Asia Nikkei, April 12)

- Honda Motor will invest ¥5 trillion yen (~$40 billion) in the development of EVs over the next decade and plans to release 30 EV models by 2030.

Sumitomo Corp sets up second renewables investment fund

(Kankyo Business, April 11)

- Sumitomo Corp established a second renewable energy fund through Spring Infrastructure Capital (SIC), a renewable energy fund management company jointly owned by Sumitomo Mitsui Banking Corporation (SMBC) and the Development Bank of Japan (DBJ).

- The fund targets solar power projects in Japan. The company secured investment commitments totaling ¥13 billion from a number of institutional investors.

- As its first investment, the fund acquired from Sumitomo 50% of the shares of two solar projects in Minamisoma, Fukushima Prefecture (total 92.2 MW).

Yamaha Motor to bring biofuel motorcycles to Asia

(Asia Nikkei, April 11)

- Yamaha Motor aims to bring synthetic-fuel motorcycles to Asia “very soon,” but it’s more cautious about ramping up its offerings of electric two-wheelers in the region.

- Synthetic fuels are made from bioethanol and other raw materials, and their use in passenger vehicles is seen as a step on the road to decarbonization.

NEWS: POWER MARKETS

OCCTO warns Tokyo’s power shortage will be more critical next winter

(Japan NRG, April 12)

- The Organization for Cross-Regional Coordination of Transmission Operators (OCCTO), which is METI’s agency for power transmission, warned that Tokyo’s power shortage will be more critical next winter as demand exceeds supply by 2.5 GW in a worst weather scenario.

- Supply will be limited as Shinchi No. 1 (1 GW) and No. 2 (1 GW) coal power stations, which suffered damages from the March earthquake, will remain closed. The closure, until next January-February, of Genkai No. 3 (1.18 GW) and No.4 (1.18 W) nuclear plants in Kyushu will also tighten national power supply.

- Tokyo’s power reserve rate would be -1.7% in January and -1.5% in February, way below the minimum requirement of 3%.

- Newly constructed thermal power plants in soft runs, and IGCC coal plants under care and maintenance could be brought on-stream. But it is risky to count them as reliable power sources, OCCTO said, adding that demand-side efforts to cut power consumption are required.

Power reserve rate (%) in worst case scenarios

| July 2022 | August | January 2023 | February | |

| Hokkaido | 21.4 | 12.5 | 6 | 6.1 |

| Tohoku | 3.1 | 4.9 | 3.2 | 3.4 |

| Tokyo | 3.1 | 4.9 | -1.7 | -1.5 |

| Chubu | 3.1 | 4.9 | 2.2 | 2.5 |

| Hokuriku | 5 | 4.9 | 2.2 | 2.5 |

| Kansai | 5 | 4.9 | 2.2 | 2.5 |

| Chugoku | 5 | 4.9 | 2.2 | 2.5 |

| Shikoku | 5 | 4.9 | 2.2 | 2.5 |

| Kyushu | 5 | 4.9 | 2.2 | 2.5 |

| Okinawa | 31.6 | 34.3 | 42.0 | 43.6 |

- Of the eight power plants impacted by the earthquake, the Haramachi No.2 (1 GW) coal power station is expected to restart in mid-July. The restart dates of seven others, in the table below, have not been determined.

| Name | Capacity | Operator |

| Haramachi No. 1 | 1 GW coal | Tohoku Electric |

| Shin Sendai 3-1 | 523 MW LNG | Tohoku Electric |

| Sendai Power Station | 112 MW coal | Sendai Power Station |

| Soma Coal Biomass | 112 MW coal | Soma Energy Park |

| Shinchi No. 1 | 1 GW coal | Soma Kyodo Power Station |

| Hirono No. 6 | 600 MW coal | JERA |

| Shinchi No. 2 (was offline during quake) | 1 GW coal | Soma Kyodo Power Station |

J-Power’s Isogo No. 2 coal power station to restart on Sept 30

(Japan NRG, April 12)

- J-Power’s 600 MW Isogo No. 2 coal power station that closed on March 20, following a transformer problem, will restart on Sept. 30, the company reported to OCCTO.

- CONTEXT: Tokyo will lose capacity of 400-500 MW this coming summer due to the Isogo plant closure. The area’s power reserve rate is 3.1% in July and 4.9% in August.

First ever solar curtailment orders from Shikoku Electric and Tohoku Electric

(Japan NRG, April 11)

- For the first time ever, Shikoku Electric and Tohoku Electric utilities limited the amount of wind and solar energy that can be fed into their network, citing risks of widespread power cuts if supply outstrips demand.

- Shikoku put 150 MW of power capacity on output control during peak supply period from 12:30-13:00. That’s how much supply outstripped demand. Of the 4.65 GW of capacity online at the time, 2.45 GW was from renewable energy.

- Tohoku Electric put 110 MW of capacity from 21 power generators on output control for 11:30-12:00, less than curtailment plans reported a day earlier due to lower than forecast output from solar and wind generators.

- CONTEXT: Curtailment of renewables operators in Kyushu has occurred for the last five years, but this is a first in other regions. Grid operators say they need to ask renewables operators to cut back during peak supply times to balance the system.

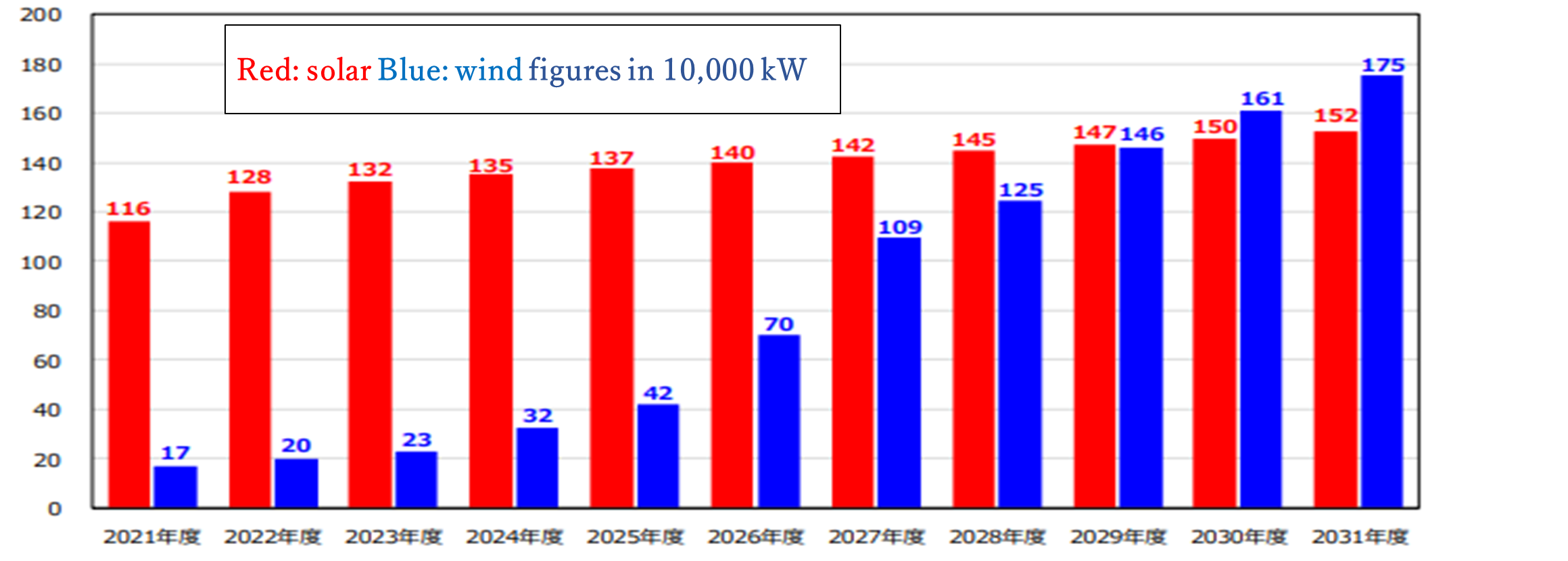

Hokuriku Electric forecasts wind capacity to surpass solar in 2030

(Japan NRG, April 12)

- Hokuriku Electric will have more wind capacity than solar by 2030, as more onshore wind power stations are built in north Ishikawa Prefecture. By 2030, wind power capacity will reach 1.61 GW; solar capacity will reach 1.5 GW. By end of 2031, wind will grow to 1.75 GW; solar will reach 1.52 GW. Currently, solar is the region’s main renewable power source, with 1.16 GW capacity, while wind has 170 MW.

Chubu Electric freezes new commercial subscriptions amid surging costs

(NHK, April 14)

- The Chubu Electric suspended contracts to new commercial subscribers.

- The utility says it was forced to act after inundated by requests from customers whose power providers went out of business.

- Chubu says the surge in the price of LNG, coal and wholesale electricity means it’s too costly to sign new commercial subscribers on its standard tariff plan.

- SIDE DEVELOPMENT:

Tohoku Electric stops accepting commercial subscriptions

(To-o Nippo, April 14)- Citing high wholesale energy prices, the Tohoku Electric Power Co. stopped accepting requests from businesses wanting to switch to the company.

- The utility is sending those making enquiries to the website of the Agency for Natural Resources and Energy, which lists retail electricity providers.

- SIDE DEVELOPMENT:

Kansai Electric suspends commercial subscriptions

(NHK, April 13)- Kansai Electric Power Co. has stopped accepting requests from commercial clients wanting to switch electricity providers.

- A spate of energy start-ups leaving the market has stranded many subscribers.

- In a situation unprecedented in the history of Japan’s deregulated electricity market, stranded subscribers are turned away by legacy power companies.

- SIDE DEVELOPMENT:

Retailer winds down power service in face of high prices

(IT Media News, April 11)- IoT gadget manufacturer, Nature Inc., will discontinue its electricity retail service, and it instructed subscribers to switch to other utilities by May 11.

- Subscribers that fail to switch by the end of June will see power cut.

- The Japan Electric Power Exchange says wholesale electricity prices will remain high, and this means operations have little chance of turning a profit.

Tokyo Gas offshore wind venture to build 500 MW project near Chiba

(New Energy Business News, April 14)

- Chiba Offshore Wind Power — a JV between Tokyo Gas, Shizen Energy, and Canada’s Northland Power — plans to launch a wind power project off the coast of Isumi City, Chiba Prefecture with a capacity potential of 500 MW.

- The area will cover 87 km2. Up to 40 wind turbines, each with outputs of 12 MW to 16 MW, will be installed. Construction is expected to be about 50 months.

Green Power Investment plans 630 MW offshore wind project near Chiba

(New Energy Business News, April 15)

- Green Power Investment will develop a 630 MW wind farm off the coast of Isumi City, Chiba Prefecture.

- The area covers about 8,450 hectares; there are 45 wind turbines, each with 14 MW output. Construction starts in 2029 and to be operational in 2032.

- CONTEXT: Green Power Investment was founded by Hori Toshio, a former top exec at Tomen Corporation (now part of Toyota Tsusho), and the founder and Chairman of Eurus Energy Holdings. Shareholders include the Development Bank of Japan and Sumitomo Mitsui Finance and Leasing Company.

Renova plans 450 MW offshore wind project near Chiba

(New Energy Business News, April 14)

- MoE submitted its opinion on the Environmental Assessment Consideration Statement for Renova’s 450 MW “Offshore Wind Power Generation Project off the coast of Isumi City, Chiba Prefecture”. The ministry asked to avoid or minimize the alteration of seaweed beds to lessen impact on marine life.

- Renova wants to install up to 47 wind turbines, each with an output of 9.5 MW to 15 MW, in an area of 15,500 hectares.

Kansai Electric explores building 676 MW offshore wind plant near Saga

(New Energy Business News, April 12)

- Kansai Electric plans 676 MW of wind power generation off the coast of Karatsu City, Saga Prefecture. The company made an Environmental Assessment Consideration Report.

- The area is about 14,300 hectares; 46 to 63 wind turbines, each with outputs ranging from 9.5 MW to 14.7 MW, will be installed.

Pacifico Energy starts 111 MW solar project and sells it to Kansai Electric group

(New Energy Business News, April 12)

- Pacific Energy started operations at the 111 MW Pacific Energy Wakayama Mega Solar Power Plant in Kamitonda-cho, Wakayama Prefecture. It’s expected to generate approximately 1.5 million kWh of electricity a year.

- It was sold to a 50-50 JV of Kansai Electric and Mitsubishi HC Capital Energy.

- CONTEXT: The solar plant has an 18-year FIT of ¥32/ kWh, according to METI project approval documentation.

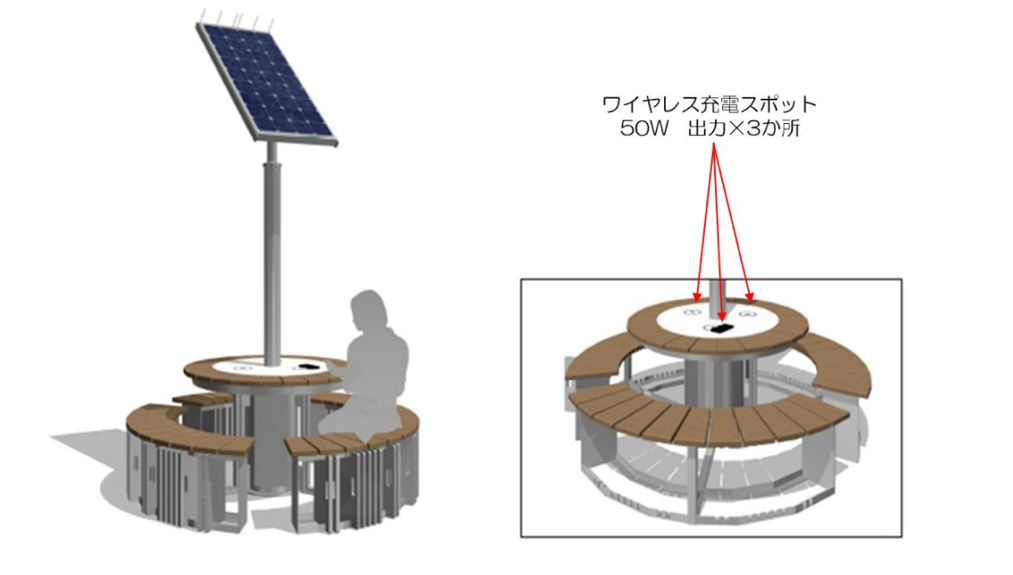

Japan rail operator starts wireless, solar powered phone charging at station

(Company Statement, April 8)

- East Japan Railway Company and Bell Design, a startup based in Saitama City, started a demonstration experiment of an outdoor charging spot using renewable energy and wireless power transfer technology.

- One outdoor recharging spot will operate until Aug. 31; it’s a round table that seats six, equipped with a 90W solar panel; the table has built-in storage batteries (38Ah x 3 units). The tables and benches are made of recycled wood.

Source: Bell Design

Hitachi Energy wins Danish transmission lines contract

(NNA Europe; April 13)

- Hitachi Energy (formerly Hitachi ABB Power Grid) was commissioned by Danish energy company Energinet to lay gas-insulated transmission lines in Denmark.

- The 420 kV lines will be isolated using an environmentally-friendly gas mixture that doesn’t contain sulfur hexafluoride.

Nuclear regulator pushes Hokkaido Electric to step up safety measures

(Japan NRG, April 13)

- The Nuclear Regulation Authority chief told Hokkaido Electric that the Kashiwa nuclear power plant inspection needs to improve communications. “There are issues that need a lot of focus and we want them to let us know if they’ve caught the ball that we threw… it will be a waste of time if they come to us after completing a procedure and we tell them, ‘this is not what we meant’,” NRA chief Fuketa told reporters.

- He added that the grid needs to increase the number of safety staff. “Nuclear safety is not a process that gets done when they clear regulatory requirements, but it’s a continual process to brace for potential earthquakes,” he added.

- Fuketa met with Hokkaido Electric’s CEO earlier.

Nearly 100,000 Niigata residents sign petition demanding voice in nuclear restart

(NHK, April 11)

- A Niigata-based group submitted a petition that calls for the prefectural government to respect the wishes of Niigata locals when deciding whether to approve the restart of the Kashiwazaki-Kariwa nuclear power station.

- The group stresses the importance of public opinion, be it for or against the restart.

- Over 980,000 residents signed the petition.

NEWS: OIL, GAS & MINING

WAR IN UKRAINE:

Russia launches cruise missiles into Sea of Japan

(Nikkan Gendai, April 15)

- Russia’s Defense Ministry announced that two submarines of its Pacific Fleet conducted a launch exercise of the “Kalibr” cruise missile and hit a target in the Sea of Japan. The Petropavlovsk-Kamchatsky and Volkhov, the newest diesel submarines, fired the missiles, and more than 15 ships of the Pacific Fleet supported the exercise.

- The Kalibr is a subsonic missile also used by the Russian military in its invasion of Ukraine. Some types have a maximum range of up to 2,000 kilometers. It can carry both a conventional and a nuclear warhead.

Japan to push more upstream LNG investment: METI minister

(Japan NRG, April 15)

- METI minister Hagiuda said Japan will push for more upstream gas investment including capacity expansion of gas fields currently in production. JOGMEC will provide financing.

- Separately, METI told the Green Transformation Panel that it will strictly monitor coal imports to phase out Russian coal, which accounts for 11% of Japan’s supply. It will urge Australia and Indonesian coal suppliers to guarantee supply to Japan.

- Separately, METI told the Green Transformation Panel on April 14 that it will closely monitor coal imports and speed up efforts to find substitutes to Russian coal, and will modify the power generation framework to allow quick restarts of idled thermal power plants. A severe power shortage is forecast for next winter, so some businesses are constructing their own solar and battery-based generation plants, the minister said, adding that it will be regrettable if regional grids aren’t transparent about their supply situation, which has confused retailers.

- SIDE DEVELOPMENT:

Japan Boosts Effort to Secure LNG Supply Through Next Winter

(Bloomberg, April 11)- Japan is buying LNG as global competition increases for the super-chilled fuel. JERA, the world’s top LNG buyer, purchased at least 10 spot cargoes for delivery from June 2022 to February 2023, according to traders with knowledge of the matter.

- Several other Japanese utilities are seeking additional cargoes or swap shipments beyond their contracted supply, the traders said.

- Europe and Japan will be competing in a very tight market as the former seeks alternatives to Russian gas supplies.

- SIDE DEVELOPMENT:

April 10 LNG stocks flat at 1.66 million tons

(METI statement, April 13)- Japan’s LNG stocks stood at 1.66 million tons as of April 10, flat from 1.65 million tons a week ago. The end-April stocks last year were 2.01 million tons, and the four-year average was 1.90 million tons.

Japan can’t afford to be outbid on LNG: Kikkawa

(Nikkei Business, April 14)

- This is an interview with Kikkawa Takeo, Vice Chancellor of the International University of Japan and a commentator on energy issues.

- Kikkawa says Japan has traditionally been favored by LNG suppliers, since it pays a premium on LNG spot contracts.

- However, LNG producers are well aware that Japan’s latest basic energy plan didn’t mention LNG, and are less inclined to guarantee contracts to Japanese buyers.

- While the government did not explicitly mention the importance of LNG in its latest energy plan, LNG has absorbed the disparity between reality and the government’s targets for renewable- and nuclear-generated electricity.

- Japan must remain invested in the Sakhalin 1 project to ensure it doesn’t run out of gas. While Exxon said it will pull out of Sakhalin 1, this has yet to happen.

- The situation around Sakhalin 2 most affects Hiroshima Gas, which will be exposed to the volatile spot market if forced to pull out of its long-term purchase agreements.

- Regarding nuclear energy, Kikkawa notes that units six and seven of the Kashiwazaki-Kariwa nuclear power station are both advanced boiling water reactors, and hold the potential to greatly relieve Japan’s energy crisis.

- But the community won’t support the restarts as long as TEPCO is in charge.

- If Kashiwazaki-Kariwa restarts, then it needs to be taken over by Tohoku Electric or the Japan Atomic Power Co.

DPFP calls for reinstatement of “trigger clause” or equivalent measures

(NHK, April 8)

- The Democratic Party for the People has called on the government to reinstate the “trigger clause” — a scheme that imposes tax relief on gasoline if prices at the pump do not go below ¥160 per liter for three months.

- The DPFP said that if it was not possible to reinstate the trigger clause, the government should implement measures with similar effect.

- The DPFP, which splintered off the now-defunct Democratic Party of Japan, was invited to join sessions held by the LDP-Komei coalition to debate gasoline prices.

- SIDE DEVELOPMENT:

Government postpones decision on trigger clause, cites disruption

(Kyodo, April 9)- The ruling coalition decided against immediate reinstatement of the gasoline “trigger clause” over fears that motorists will put off buying gasoline until the clause took effect.

- Instead, the government might increase the maximum subsidy that can be paid to petrochemical companies, to ¥25/ liter.

Activist investor Murakami buys more Cosmo shares

(Nikkei; April 8)

- City Index Eleventh acquired 5.24m shares (6.13% of outstanding stock) of Cosmo Energy Holdings; and a Murakami family member, Ms. Nomura Aya, acquired 810,000 stock of convertible bonds in the company.

- On March 31 their combined stake was 7.09%. In an April 5 disclosure, it was 5.81%.

- City Index Eleventh is a leading shareholder of Fuji Oil, with a stake of around 10% as of Dec. 2021. It’s rumored that this might trigger restructuring in the oil sector.

JGC and Kawasaki Kisen to reuse old LNG tankers into floating LNG bases

(Nikkei Shimbun, April 13)

- JGC Holdings and Kawasaki Kisen Kaisha have developed a method of reusing old LNG tankers as floating LNG (FLNG) storage tanks. This should cut the cost of creating FLNG platforms by 30%.

- CONTEXT: The aim is to make it cheaper to move gas from extraction on the seafloor to land. Currently, pipelines are cheaper, but with gas supply tight it’s desirable to expand production sites in waters difficult to access by pipelines.

- FLNG often costs more than onshore facilities, with about ¥100 billion investment required. The two firms believe they can provide a cheaper and faster solution.

JX Nippon Mining to ‘dig’ for lithium in old batteries

(Asia Nikkei, April 14)

- JX Nippon Mining & Metals will install lithium recovery equipment at subsidiary JX Metals Circular Solutions. The aim is to launch the recycling business soon, tapping its expertise for recovering high-purity lithium from batteries.

- JX Nippon Mining will supply samples from as early as the current fiscal year. It initially expects annual output of several tons; this could expand in FY2023.

- SIDE DEVLEOPMENT:

JX Metals secures €9 million green loan for recycling lithium-ion batteries

(Company statement, April 11)- JX Metals secured a loan of €9 million from Mizuho Bank for recycling automotive lithium-ion batteries.

- CONTEXT: Lithium, nickel, cobalt and copper recovered from used batteries are utilized for steel and alloy products. Purity is a major challenge to achieve battery-to-battery recycling.

TAKEAWAY: Germany has an organized used battery collection system and has relatively large recyclable supplies. This is a main advantage for Germany-based recyclers, as vehicle batteries are heavy and costly to transport.

The EU plans to require a recycling quota for batteries to increase resource re-use, and Japan plans a similar regulation.

ANALYSIS

BY MAYUMI WATANABE

Friend or Foe?

How Competition Authorities in Japan View the Energy Transition

One difficulty of an energy transition is that incumbent market players enjoy outsized influence thanks to decades of growth and consolidation. The move to a low-carbon economy promises profound structural changes in the industrial, social and financial sectors. But, how to make sure this process does not unduly favor the existing players, thus replicating their domination in the clean energy sector?

This is the question Japanese antitrust authorities are starting to grapple with as the energy transition accelerates. Supporting any and all innovation that will help Japan reach carbon neutrality is seen as imperative. Yet allowing today’s top players to benefit the most simply due to their extensive resources would put into question the oft-stated goal of making the energy transition inclusive and fair.

The issue is especially pertinent in Japan, where energy corporations look to repurpose legacy fossil fuel infrastructure, such as oil terminals and thermal power plants, for hydrogen, ammonia and other constituents of a low-carbon economy. If Japan follows its gradual trajectory towards green energy, will it also mean that new players will be largely shut out from the transition? Or, will owners of existing fossil fuel infrastructure be made to compete on a level playing field?

Japan NRG Weekly sat down with former Japan Fair Trade Commission (JFTC) officials to discuss the developments in the oil and gas, hydrogen, and power sectors.

More consolidation in the oil sector?

In 1980, Japan had 17 oil refineries, but eventually they were consolidated inside three groups: ENEOS, Idemitsu and Cosmo Energy. The era of M&A within the sector looked over until this month. Earlier in April, an activist investment fund led by former state bureaucrat Murakami Yoshiaki acquired an 8.28% stake in Cosmo Energy, spurring talks of further industry consolidation.

METI’s most recent long-term oil demand forecast shows that industry is moving away from fossil fuels at a faster rate than expected, creating redundant refining capacity. The national fuel oil demand forecast is for a decrease of 7.1% by 2026 over 2021 levels, dropping to 142 million kiloliters. The previous five-year forecast was for a 5.7% demand decline by 2025 versus 2021.

The new forecast equals 2.4 million barrels/ day; yet, Japan’s refining capacity is 3.5 million barrels/ day. This means, within five years 1/3 of the nation’s refining capacity will be redundant; and by 2030, unused capacity will increase to more than half.

The 3.5 million barrels/ day breaks down as follows: 50% for ENEOS; 27% for Idemitsu; and 11% for Cosmo Energy. The remaining 12% is claimed by small local refineries – Fuji Oil, Taiyo Oil, and Seibu Oil.

The possibility of small independent refineries joining one of the bigger three would have negligible competition impact. Meanwhile, thoughts of a merger among any of the top three or even all three joining to form a single oil company, simply won’t be possible, experts say.

The JFTC, upon reviewing the merger plans of JX with Tonen General (to form today’s ENEOS) and Idemitsu with Showa Shell in 2016, warned that a decrease in the number of players will restrain oil market competition and harm consumers. The refineries are already in a commoditized market where differentiation is not easy.

In the end, the JFTC cleared the mergers mentioned above, but not unconditionally. The refineries had to commit to programs that foster competition. For example, in a bid to create alternative supply flows, they have to support outside traders and distributors when it comes to importing and stockpiling oil products.

Antitrust views on the hydrogen supply chain

Antitrust authority decisions are deeply impacted by how markets, potential substitutes and competition pressures are defined.

Five years from now, the emergence of renewable alternatives to gasoline and other oil products will likely revamp the market structures. Among the changes will be multiple hydrogen and ammonia co-firing pilot projects. Also, the first offshore wind projects are expected to begin operations in 2028.

This increase in the availability of substitutes to fossil fuels will impact JFTC decisions.

As co-firing generation takes off, import of hydrogen and ammonia is expected to pick up from 2028. Hydrogen from Australia and the Middle East will provide competition for locally sourced supply, and also to fossil fuel energy. Players like Iwatani Corp, the largest Japanese hydrogen producer, will do both – manufacture domestically and import from Australia, bolstering the number of supply options on the market.

ENEOS, Idemitsu and Cosmo plan to convert their oil desulfurization and processing units, tanks and terminals into hydrogen/ammonia supply bases, and their oil and chemical tankers into carriers of liquefied hydrogen. A dehydrogenation unit and an oil desulfurization unit could run side-by-side in a single refinery.

The refineries, however, aren’t evenly spread across the country. Rather, they’re concentrated in industrial zones such as the Tokyo, Sakai and the Yokkaichi bay areas. The islands of Kyushu and Hokkaido each have one refinery, run by ENEOS and Idemitsu, respectively.

So, this raises the question: If ENEOS, which doesn’t have a refinery in Hokkaido, reaches out to Idemitsu to use its facility to supply green hydrogen from Australia, will this cause competition issues? And will the move restrain other players from supplying hydrogen/ammonia to Hokkaido? How about Cosmo, which partners with the biggest Japanese hydrogen producer Iwatani – will it be able to join such initiatives?

A former JFTC official says it’s possible that refineries could be allowed to share facilities. The main concern, however, is that the alliance must be rigidly defined. Outside those alliances, the refineries and traders must continue to compete.

Antitrust authorities will need to see how the market develops before they can define what may constitute anti-competitive behavior. After all, being an oil refinery does not mean it will automatically take a major position in the hydrogen supply market, notes attorney Matsuda Serina.

Based on company disclosures, for example, it appears Iwatani is taking the lead in terms of hydrogen volumes, while ENEOS has the most diversified project pipeline. Meanwhile, the technologies to produce, store and transport hydrogen are still in development and the molecule supply chain structure will likely fluctuate for a while.

In an immature market, industry players hedge strategies. ENEOS is developing a proprietary Direct Methylcyclohexane (MCH) hydrogen transport process, but it’s also collaborating with Kawasaki Heavy Industries and Iwatani on supply chains based on transporting liquid hydrogen.

Selection of major hydrogen projects

| Tier 1 supplier (location) | Local supplier | Volume |

| Iwatani Corporation (Japan) | Iwatani/Cosmo | 10,000-11,000 tons/year |

| Stanwell/Iwatani/Kawasaki Heavy/Kansai Electric/Marubeni (Australia) | Iwatani, etc? | 30,000-40,000 tons/year by 2026 |

| Mitsubishi/Chiyoda (Brunei) | ENEOS | 40,000 tons/year by 2030? |

| Origin (Australia) | ENEOS | |

| Fortescue (Australia) | ENEOS | |

| SEDC/Sumitomo/ENEOS (Malaysia) | ENEOS/Sumitomo? | |

| Petronas (Malaysia) | ENEOS | |

| Saudi Aramco (Saudi Arabia) | ENEOS | |

| New Castle Port/Macquarie/Idemitsu (Australia) | Idemitsu? | NA |

| AQUA AEREM/Osaka Gas (Australia) | TBD | Up to 400,000 tons/year but not exclusively to Japan |

| Nel ASA/Itochu (US) | Itochu? | NA |

Antitrust view of the co-firing sector

JERA is now a key player in ammonia-coal co-firing after last year embarking on 20% ammonia co-firing trials and eyeing a commercial launch in 2024 in Aichi Prefecture. In February, JERA opened an international tender for up to 500,000 tons/ year of ammonia to be supplied from 2027 through the 2040s, thereby making the company Japan’s largest ammonia importer and supplier. JERA also has 30% of Japan’s coal-fired power capacity.

Rival J-Power, with a 20% coal-fired capacity share, plans to commercialize coal-biomass-ammonia co-firing by 2026, at its Matsushima power station. It’s also partnering with Chugairo, an ammonia burner maker, Osaka University, the Central Research Institute of Electric Power Industry and government research institutes.

With co-firing processes at a very early stage, the industry approach in Japan is generally based on collaboration. Over time, this may need to change.

Japanese Antimonopoly Act guidelines generally ban joint research and development by two potential competitors as this could restrict future competition. Still, even a very concentrated field could be expanded through the entry of startups that offer new ammonia and related co-firing technologies. The startups themselves may become natural targets for the utilities, but such acquisitions have a chance of going through, provided the antitrust authorities see evidence that there are multiple entities with breakthrough technologies, said one lawyer.

Attorney Matsuda says there are several approaches the antitrust authorities could take to frame the market. One would be to see this as a technology development market. Or, officials could treat the operators of power services that employ ammonia-thermal co-firing as a separate market.

“The power generation market may not necessarily be defined as a single nationwide market,” she said.

In March, METI launched an energy and competition expert group to identify regulations that block the growth of a climate-resilient economy. This was a response to calls for more flexible competition rules to help companies to work together on carbon neutrality projects, specifically in building supply chain infrastructure for the manufacture, transport and storage of hydrogen and ammonia.

The group will first study regulatory trends overseas in order to better align Japanese policies with the global community, and may discuss specific issues at a later stage.

How lenient will the officials be?

In the past, a number of industries have asked authorities to be more lenient on competition rules in the face of structural challenges.

In November 2020, the regional bus transport and bank sectors were exempted from the Antimonopoly Act strictures, allowing flexible mergers and joint operations for a period of 10 years. Those sectors are essential for regional economies, many of which are facing a declining population.

So far, this is the only standout, despite regular lobbying for relaxed antimonopoly rules from several other industries. What would make a more lenient approach for the energy transition even more unusual is the fact that clean energy is a growing industry with bright prospects.

The questions that Japan’s antitrust authorities now face include: How will industrial growth policy and market competition policy interplay? And, if greater leniency is provided to players involved in decarbonization, how long should this last and what is the basis to end this approach?

The debates in government and business circles are just beginning, but they are certain to last months and years, and are sure to be closely followed – especially by new entrants in the power and energy markets. Renewable operators claim the unbundling of regional power monopolies was superficial, leaving legacy players with undue advantages in the liberalized electricity market. Will the same be true in the age of hydrogen and gigawatt-scale renewables?

ANALYSIS

BY YURIY HUMBER

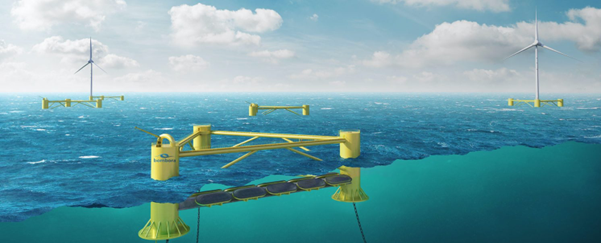

Ocean Energy Shows Progress

As Projects Start to Move to the `Megawatt’ Stage

Japan could generate nearly 170 TWh of electricity, or 20% of its annual needs, in the open seas through energy sources other than offshore wind power generation, according to government-backed research suggesting the nation can do more to harness marine energy.

After decades of theoretical analysis, close monitoring of water systems, R&D projects at home and abroad, Japanese marine energy tech is now maturing into sizable demonstration facilities, with a few aiming to reach commercial scale in the next two-three years.

National strategy sees the application of generation systems that rely on ocean currents, tides and sea waves as naturally suited for smaller, remote parts of the Japan archipelago, which boasts over 6,000 islands.

The strong push to develop offshore wind in Japan, however, could also bring ocean energy into the mainstream as developers look at ways to maximize the effectiveness of their sea areas through hybrid, multi-technology arrays.

Background

Ocean energy is a renewable power source that’s seen little development despite decades of research. There’s only 517 MW of installed capacity globally among the 22 countries that form the International Energy Agency’s Ocean Energy Systems program (IEA-OES). Most of that capacity is from two tidal range dams: one in France and the other in South Korea.

Japan was one of the earliest members of IEA-OES, joining in 2002, but it doesn’t even provide regular updates for the group’s annual report, unlike other members that include the U.S., China, India, Denmark, the UK, and Singapore.

In part, this may be because after an initial wave of enthusiasm in marine energy following the 2011 Fukushima accident, progress stalled as more mature technologies such as solar and wind power caught the popular imagination. When Japan’s first Green Growth Strategy was announced in late 2020, ocean energy wasn’t even mentioned.

Since then, technical progress and innovation has revived business attention. In FY2018, state-backed research hub NEDO launched a three-year, grant funding program to accelerate R&D and set ocean energy on course to roll out commercially viable technologies by 2030. The program was succeeded by targeted funding for both startups and large companies.

A similar approach was taken by the Ministry of Environment (MoE), which secured funding for a 500-kW tidal current power generation project off the Goto Islands, Nagasaki Prefecture. The one-year project, started in 2021 and led by a unit of Kyushu Electric, involved installing, operating and decommissioning a tidal turbine shipped from the U.K.

Incidentally, the Goto area is also the site of Japan’s first commercial-scale floating offshore wind turbines tender awarded to a group of eight domestic companies. The group aims to deliver 16.8 MW of capacity, more than the size of current ocean energy projects, but considerably less than the established fixed-bottom offshore wind turbine technology.

As ocean energy projects gain in size and deliver positive results over long-term demonstrations in open seas, the sector could be in line to switch from the current grant-based model to tariff-based revenue support, much like the way solar, wind and biomass energy developed with the introduction of the Feed-In Tariff (FIT).

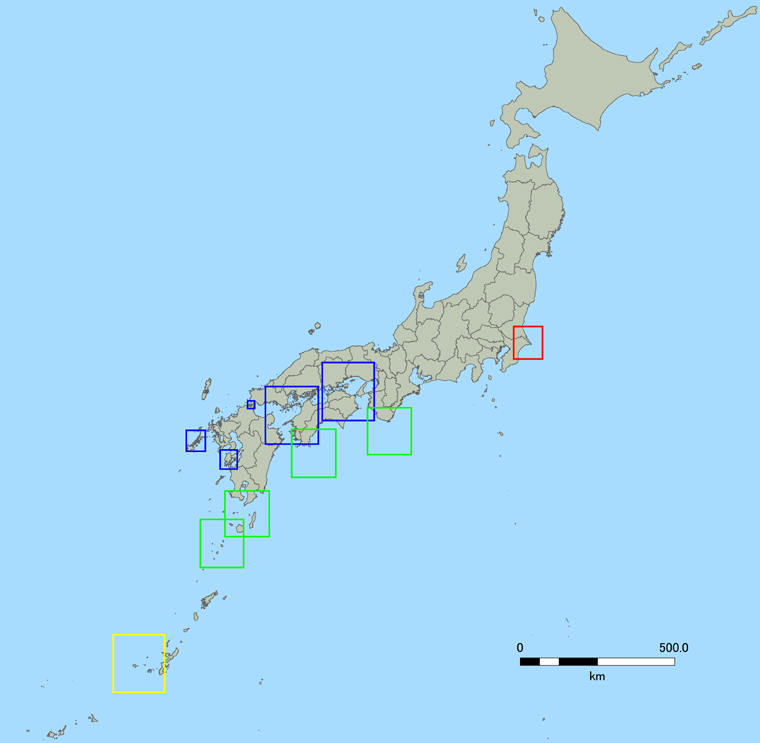

Main types of ocean energy pursued in Japan

Japan has spent decades surveying its waters. Data on wave, tide and seawater temperature patterns span at least two or three decades, and much of it can be accessed on government websites. Japan’s Basic Plan on Ocean Policy, last updated in 2018, focuses on ocean energy for remote islands, where electricity costs are high and supply options limited.

| Marine Power Type | How It Works | Annual Electricity Potential in Japan |

| Ocean Current | Strong ocean current in the open sea rotates turbine | 10 – 37 TWh |

| Tidal Current | Tidal flow in a strait, or similar water channel, turns turbine rotors | 6 TWh |

| Wave | Vertical motion of the wave pushes the rotor | 19 – 87 TWh |

| Ocean Thermal (Temperature Difference) Energy | Harness the difference in temperatures at the sea surface and in deep water, for example, by employing a device with liquid ammonia: the boiling point of the gas is raised by adjusting pressure; warm seawater is used to cause evaporation of the ammonia that turns the turbine; the steam is then cooled using cold seawater | 15 – 47 TWh |

Source: NEDO, Shin Energy Shimpo, IEA-OES, Japan NRG

- Red box: Wave power potential (off the coast of Choshi, Chubu Prefecture)

- Blue box: Tidal current potential (eastern Seto Inland Sea, western Seto Inland Sea, Kanmon Strait, Ariake Sea/Yatsushiro Sea, Goto Islands)

- Green box: Ocean current potential (Tokara Strait, Osumi Strait, off Ashizurimisaki and off Shiomisaki)

- Yellow box: Ocean thermal energy potential map (off Kumejima Island)

Source: NEDO

SELECT PROJECTS

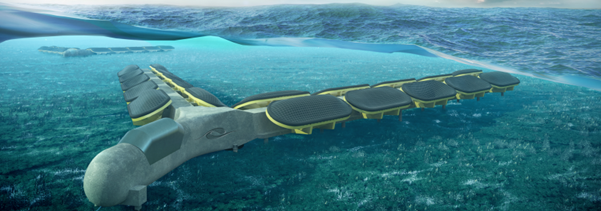

We review several standout projects close to commercial use.

1. The startup Global Energy Harvest Co. (formerly SoundPower) is building a circulation-type wave power pumped storage. Toyo Denki said late last year that it received an order for a 300-kW system from the company, and that it’ll work with Austria’s Andritz Group on the project. Andritz has equipped some of the world’s biggest tidal power facilities.

Source: Global Energy Harvest

The system designed by Global Energy Harvest is said to be unique. It doesn’t directly use the energy from waves, but instead funnels the water into a pump which then releases it, and with that motion drives the generator. It’s similar to how hydropower-pumped storage systems release water from an elevated dam.

Combining pumping action with wave power avoids the need for multiple rotors that could interfere with sea life. It also makes the system more durable, and can even hold up in a typhoon, says Global Energy Harvest, which wants to launch a 332-kW circulation-type wave power pumped storage generation system by next year. The facility may be located in Kumejima Island, Okinawa Prefecture.

Global Energy Harvest believes its hybrid system could achieve a power generation cost of ¥20/ kWh, which would make it competitive with offshore wind projects. It’s also enough to recoup the invested money within four years, less than half the time for a solar project. Other advantages are that it can be installed near existing infrastructure, and it doesn’t require much maintenance, unlike most marine energy systems.

In the last two years, Global Energy Harvest has raised close to ¥300 million from companies including ENEOS, Daiwa House, Edge Labs, and Japan Green Power Development Co. The startup is also one of the recipients of NEDO ocean energy program funding.

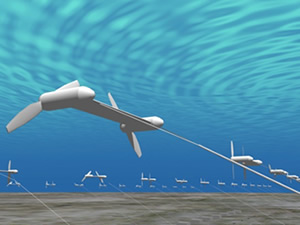

Source: Bombora Wave Power

2. Mitsui OSK Lines (MOL), a shipping firm, will launch a large facility with ocean thermal energy conversion tech by around 2025. The 1 MW station will cost several billion yen. Before that, the company will conduct demonstrations in Okinawa Prefecture.

The shipping firm plans to use existing pipes built for fishing to lower the cost of creating a new ocean energy facility, which the company hopes will allow it to cut the cost to ¥20/ kWh by mid-decade. If the plans materialize, Mitsui OSK sees the potential to install more ocean energy plants in both Japan and abroad, such as in Indonesia.

The shipping firm also invested earlier this year in Bombora Wave Power, an Australian firm operating in the UK, which seeks to commercialize wave energy with a 1.5 MW validation project during 2022.

Aside from MOL, ocean thermal energy conversion systems are researched by the team at Saga University, which hopes to combine the electricity generation aspect of the technology with capability to desalinate seawater. The university will participate in an experiment of the Ocean Thermal Energy Conversion (OTEC) system in Malaysia around 2024.

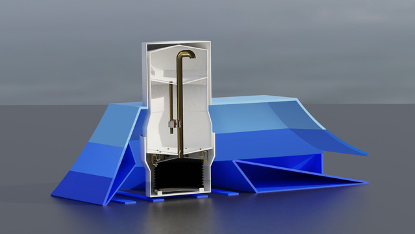

3. NEDO’s initial three-year ocean energy project helped IHI hold a demo experiment of the world’s first floating type ocean current turbine called the Kairyu. The 100-kW turbine was lowered 50 m below sea level off the coast of Kuchinoshima Island in the path of the Kuroshio Current. The project did generate electricity, validating the concept and collecting key data, but saw its second phase delayed by the pandemic.

Source: IHI Corporation

4. The MoE funded a wave power generator developed by the Institute of Industrial Science, University of Tokyo, which was installed in front of the Hiratsuka Shinko breakwater in Kanagawa Prefecture, and which was connected to the grid. Kawasaki Heavy Industries was one of the firms involved in the one-year demonstration project.

The ministry also selected Kyuden Mirai, a unit of Kyushu Electric, to run a tidal current power generation demonstration this year as part of its regional decarbonization funding program. The project will run a 1 MW generator, reaching the start of commercial scale.

Source: Mainichi Shimbun, image courtesy of Kyuden Mirai Energy Co.

Conclusion

Given the slow pace of technological development, in part due to the need to test long-term impact on the ocean environment, it can be easy to disregard ocean energy’s potential. Yet, a clear trend in renewable energy has been the stacking of different technologies within a project to maximize the total efficiency and returns. Ocean energy systems have the potential to do that for offshore wind power projects.

Finally, as a hallmark of how far the sector has come, one of Japan’s top insurers, Sompo, has begun to offer comprehensive insurance policies for tidal power generation. This apparently small detail is a strong indicator that the mechanics of ocean energy is no longer only an academic discussion.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Argentina/ Renewable energy

Energy company Genneia will invest $200 million to build 1 GW of renewable capacity — 222 MW of solar and 878 MW of wind energy, to be distributed in 11 parks across the country. Over the last five years, Genneia invested $1.2 billion in renewable capacity.

Denmark/ Coal power

Power company Ørsted will boost its coal reserves in anticipation of increased usage of the fuel next winter. The move is a surprise because Ørsted is one of the world’s biggest developers of offshore wind farms and seen as a champion of green energy.

Egypt/ Nuclear power

The country’s first nuclear power plant will be built at El Dabaa on the Mediterranean Sea, in partnership with Russia’s nuclear power developer Rosatom. The 4.8 GW facility will start operation in 2028 and has a $60 billion total price tag.

Energy Transition

In 2022, global energy investment will reach a record $2.1 trillion, a level not seen since 2014, said Rystad Energy. Upstream oil and gas spending will grow 16%, or $142 billion; global green capacity will grow by 250 GW as spending rises 24%, or $125 billion. In 2021, renewables accounted for 38% of total global power, making up a record 81% of new global capacity, according to the International Renewable Energy Agency.

Germany/ Nuclear power

Energy company Eon won’t extend the life of its nuclear power plant, one of the country’s three remaining nuclear sites. “There’s no future for nuclear in Germany,” said CEO Leo Birnbaum. “It’s too emotional.” Eon’s Isar 2 plant will go offline at the end of 2022.

Italy and Algeria/ Natural gas

PM Mario Draghi visits Algeria next week to sign a gas deal. Algeria is Italy’s second-largest supplier, providing 21 billion c/m — 31% of annual gas consumption. The Trans-Mediterranean pipeline that links the countries is operating only at 66% of its annual capacity of 33 billion c/m.

India/ Renewable energy

Abu Dhabi-based conglomerate, International Holding Company (IHC), will invest $2 billion in green energy companies belonging to India’s Adani Group, which has diversified from ports and coal-fired power plants into renewable energy.

Oil

The International Energy Agency says the global oil market won’t have a major deficit this year because emergency stock releases and slower Chinese demand will offset lower Russian production. The world fuel consumption forecast is 99.4 million bpd, as opposed to the previous forecast of 99.7 million bpd before the war began in Ukraine.

South Korea/ Nuclear power

The new government will reverse an earlier plan to phaseout nuclear power. South Korea is one of the world’s top-five fossil fuels importers, but also the fifth-largest nuclear power producer. Nuclear accounted for 26% of its total electricity generation. South Korea has the world’s highest density of nuclear reactors, with most of its 24 reactors located at two complexes.

UK/ Electricity markets

Contracts worth over £1.5 billion were awarded for the NeuConnect project, which is an interconnector project linking Germany and the U.K. The project includes 725 km of subsea cables that will enable 1.4 GW of electricity to pass in both directions between the two countries.

U.S./ LNG

Excelerate Energy, which operates a fleet of floating natural gas import terminals around the world, raised $384 million in an IPO, valuing the Texas-based LNG company at about $2.5 billion. The deal was the first oil and gas IPO in more than a year.

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.