JAPAN NRG WEEKLY

JULY 25, 2022

JAPAN NRG WEEKLY

July 25, 2022

NEWS

TOP

- Govt. review of recent power crunch says forecasting a weak spot that is exposed by the shift to more intermittent sources

- Mitsui chair does not rule out abandoning Russia’s Sakhalin-2 LNG project if terms proposed by Moscow are “unacceptable”

- METI mulls freezing non-fossil target for wholesale electricity market as many new power retailers exit the market

ENERGY TRANSITION & POLICY

- Power and gas market guidelines updated to protect consumers

- Utilities industry group urges govt. to buy and stockpile LNG

- Mitsubishi Heavy to produce hydrogen with nuclear energy

- Toyota, ENEOS among group seeking to find next-gen biofuels

- Japanese university develops highly transparent solar panels

- Japan steelmakers lay out roadmap for hydrogen-electric future

- Sumitomo funds next-gen fusion reactor startup in the U.S.

- JAPEX to study potential for CCUS cluster in central Japan

ELECTRICITY MARKETS

- Thermal power plant glitches on the increase amid tight supply

- West Japan electricity shortages ease with two reactor restarts

- TEPCO and Chubu Electric seek 13th straight increase in tariffs

- Power utilities rush to issue bonds to secure cash as fuel costs bite

- Tokyu Land and Denmark’s CIP partner on offshore wind project

- Developer Tribay raises ¥1.4 billion for dozens of solar farms

- Eurus Energy plans large onshore wind farm in southern Hokkaido

OIL, GAS & MINING

- Nippon Steel buys LNG at highest price ever paid by Japan firm

- June crude and coal imports jump by about a fifth; LNG is flat

- Saudi tells Japan the kingdom will seek to stabilize oil markets

- Japan’s gasoline demand returns to pre-Covid level: PAJ Chair

- LNG stockpiles remain unchanged, below five-year average

ANALYSIS

CAN NEXT-GEN BATTERIES PROVIDE EVs WITH A BREAKTRHOUGH? OR WILL GEOPOLITICS INTERVENE?

The race for more durable and efficient all-solid-state batteries (ASSB) that could potentially replace lithium-ion batteries in powering electric vehicles is heating up. Japanese companies are competing vigorously against international rivals, with Toyota Motor the outright leader in next-generation battery patents worldwide.

If the Japanese makers succeed, then these innovations will significantly change the battery raw materials landscape. How Japan and others handle this shift will determine who controls the global shift to cleaner mobility.

AS JAPAN GEARS UP FOR OFFSHORE WIND,

WHAT CAN IT LEARN FROM THE UK MARKET?

As Japan struggles to lower the cost of offshore wind energy, fretting over its deep waters and less regular winds, the successful rollout of the technology elsewhere shows these factors are not the whole story. The UK’s offshore wind sector has installed almost 10 GW of capacity in the last decade and targets 50 GW by 2030. This is largely due to a consistent and effective policy framework, which has allowed for long-term planning and development of an extensive and large-scale supply chain. This, in turn, has cut costs. We look at what Japan needs to focus on now to kick start its own offshore wind development.

GLOBAL VIEW

TotalEnergies and ENI invest big in Algerian oil basin. Belgian hydrogen startup jumps in value. Gazprom resumes supplies to Europe. France to fully nationalize EDF. Guyana may emerge as a major oil supplier. And Mongolia gives update on Russia-China gas pipeline plans. Details on these and more in our global wrap.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Wilfried Goossens (Japan, Events)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Daniel Shulman (Japan)

Art & Design

22 Graphics Inc.

Events

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

NEWS: ENERGY TRANSITION & POLICY

As non-grid power operators exit market, METI mulls freezing non-fossil power target

(Government Data, July 20)

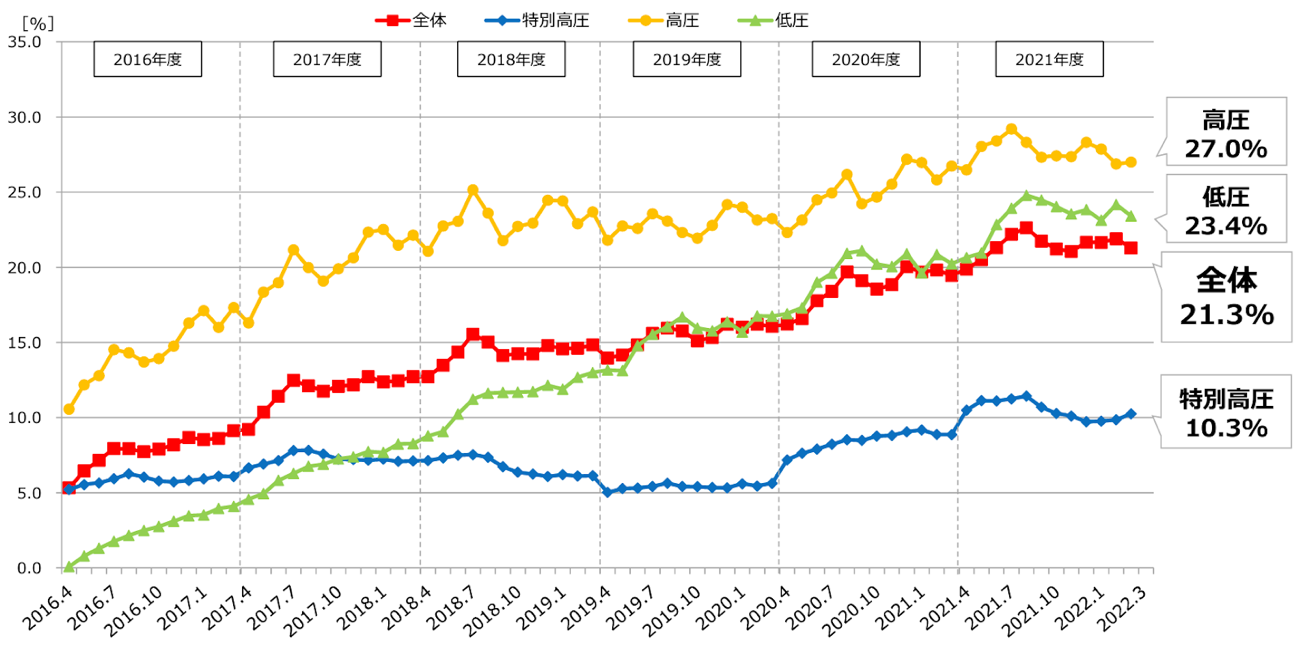

- Market share of power operators independent from regional grids has declined. Also, METI is is studying the idea of freezing its target of boosting the share of non-fossil power retailers in the market until an obvious increase in new non-fossil generation occurs.

- In March 2022, independent operators (i.e., those not affiliated with EPCos, the legacy regional utilities) accounted for 21.3% of the national power market, down from 21.7% in December 2021. Their share in low-voltage power – which is consumed by households, offices and small business facilities – slipped to 23.4% from 23.8%; for high-voltage power, consumed by industrial facilities, the share declined to 27% from 28.3%.

- CONTEXT: This is almost the first time since 2016 when “new electricity companies”, as the independent retailers are known, have given up market share to major power utilities. While EPCos run mostly thermal capacity, most new retailers are focused on renewables energy.

- The number of nationwide power retailers decreased to 738 in June, from 743 in April.

TAKEAWAY: One of the regions where independents gave up the most market share was Chubu, Japan’s automotive heartland. Together with Tokyo, Chubu is forecast to suffer power shortages in winter. This shows that supply security for major manufacturers is trumping any price savings expected from independents compared with the major utilities.

The government seems too busy with short-term energy issues to consider how they align with 2030 net-zero targets. That said, METI is not looking to revise the nation’s 2030 energy plan or weaken the emissions reduction goal, so the current situation should be considered in a crisis management context.

Wholesale Electricity Market Share Held by “New Power Retailers” (Non-EPCos)

Red: Total; Blue: Special High-Voltage; Yellow: High-Voltage; Low-Voltage

Source: METI

Source: METI

Power and gas market guidelines to be modified

(Japan NRG, July 20)

- METI plans to modify market guidelines for power and gas, respectively, to reflect fuel costs on power and gas service rates while protecting consumer interests. It plans to add a clause: “it is generally seen as good practice to appropriately reflect the cost changes on power rates, to maintain transparency of power rate setting and to increase benefit for the society as a whole.”

- The gas retail guidelines will be revised to clarify how consumers will be protected in a liberalized market. Gas retailers are advised to provide full detail of gas rate hikes, mechanisms on passing fuel costs to consumers and price menus to mitigate impacts, as well as clearly stating on contracts how the fuel surcharge price cap system works for consumers.

- The changes in the guidelines, after approval by the sub-committee on basic electricity and gas policies, will be open to public comments before the actual revision.

- CONTEXT: Initially, METI planned to require power operators to pass on the fuel cost changes in their rates, which met opposition from gas and power panel members as this would expose consumers to risks. Panelists suggested offering more choice to consumers including rates that directly reflect cost changes and those with different mechanisms. Forcing one pricing mechanism onto operators is also against the spirit of free market competition, one panelist said.

Power grid body urges METI to secure LNG

(Japan NRG, July 20)

- The Federation of Electric Power Companies (FEPC) urged METI to purchase and stockpile LNG to guarantee supply stability. Sasaki Toshiharu, the FEPC deputy chairman, told MET’s sub-committee on basic electricity and gas policy, that securing gas supply is increasingly challenging on the back of the Freeport accident and uncertainty over the Sakhalin 2 project.

- In order to secure the supply to survive winter, the government is urged to take direct roles in securing the fuel, Sasaki said.

Mitsubishi Heavy plans to produce hydrogen powered by nuclear energy

(Nikkei, July 19)

- In collaboration with the National Institute of Advanced Industrial Science and Technology, Mitsubishi Heavy Industries is developing a technology to produce hydrogen powered by nuclear energy on a commercial scale.

- Mitsubishi will leverage the solid oxide electrolysis process and the temperatures generated by a high temperature gas reactor (a type of nuclear reactor that operates at temperatures of up to 950° C), to produce up to 25 metric tons of hydrogen per hour.

- Unlike the steam reforming of methane or natural gas (the process often used to produce large quantities of hydrogen), using nuclear energy means there is no output of CO2 emissions.

TAKEAWAY: The technology refers to the HTTR nuclear program that Japan developed two decades ago. For a detailed look at the nuclear tech and its compatibility with hydrogen production, please see the Jan. 24, 2022 edition of Japan NRG.

ENEOS, Toyota and other automakers create group to find next-gen bio and synthetic fuels

(Sekiyu Tsushin, Company Statement, July 21)

- ENEOS, Suzuki, Subaru, Daihatsu, Toyota Motor, and Toyota Tsusho have established a Research Association of Biomass Innovation for Next Generation Automobile Fuels. The association chair is Koichi Nakata, general manager of Toyota Motor’s CN (carbon neutral Development Department.

- The group will research and develop next-gen fuels for cars and vehicles.

- The group confirms that hydrogen and synthetic fuels based on electricity from renewable energy sources, as well as bioethanol fuels, are all promising options. However, it’s essential to search for other solutions “throughout the manufacturing process”, and find raw material pathways for next-gen fuels.

- This association will promote technological research on the use of biomass, as well as the efficient production of bioethanol fuel for automobiles through the optimized circulation of hydrogen, oxygen, and CO2 during production.

Tohoku University develops highly transparent solar panel

(EE Times, July 19)

- Researchers at Tohoku University developed a solar cell that lets through 80% of visible light.

- The breakthrough is possible thanks to a substrate containing transition metal dichalcogenides (TMD) instead of the usual nickel or palladium.

- The cells are rated at 420 pW/ square centimeter.

Japan steelmakers lay out road map for a hydrogen-electric future

(Nikkei Asia, July 18)

- Major Japanese steelmakers unveiled a timeline through FY 2030 to develop technology for steel production using hydrogen and environmentally-friendly electric furnaces.

- Overall, decarbonizing Japan’s steelmaking is expected to cost ¥10 trillion ($72 billion). The Green Innovation Fund project will contribute ¥193 billion through fiscal 2030. The steel industry’s CO2 emissions account for 40% of Japan’s total industrial emissions.

- Nippon Steel and JFE Steel are building small trial furnaces in Ibaraki and Chiba prefectures, and will launch operations in FY2025 and FY2024, respectively.

Sumitomo invests in TAE Technologies; Funds next-gen fusion reactor

(Company press release, July 19)

- Sumitomo Corporation of Americas will invest in TAE Technologies, a fusion power company and world leader in hydrogen-boron fusion research. The investment will help fund the construction of TAE’s next research reactor, “Copernicus” and accelerate SCOA’s implementation of fusion power in Japan and Asia.

- Sumitomo established its Energy Innovation Initiative in April 2021, and has set “development and deployment of carbon-free energy” as one of the key strategies.

- Since 1998, TAE has worked toward delivering cost-competitive, environmentally benign hydrogen-boron fusion. Its fifth-generation reactor, Norman, was unveiled in 2017 and designed to keep plasma stable at 30 million degrees Celsius.

- TAE’s approach differs from other nuclear fusion technologies in development because of its unique combination of plasma physics and accelerator physics.

JAPEX to study potential for CCUS cluster linking several CO2 storage sites

(Gas Energy News, July 18)

- JAPEX will conduct a feasibility study for a “hub and cluster CCUS (CO2 Capture, Utilization, and Storage) Project”, which would link multiple carbon emission sources and storage sites.

- The project will be carried out under the auspices of the Japan Oil, Gas and Metals National Corporation (JOGMEC) and with the cooperation of companies and business sites in the Niigata East Port area.

- The study will run for nine months, from June of this year to the end of February 2023. JAPEX will calculate how much CO2 can be separated, collected, and transported in the port area.

- CONTEXT: JAPEX operates the Higashi-Niigata gas field in Niigata East Port area. The company sees the Niigata area as one of the most promising to develop a carbon capture and storage business.

Mitsui OSK wins NEDO support for deep ocean energy project in Mauritius

(Company Statement, July 14)

- Mitsui O.S.K. Lines (MOL) won support from Japan’s state research hub, NEDO, for the development of a deep ocean energy generation system in Mauritius.

- The ocean thermal energy conversion (OTEC) project is conducted with Xenesys Inc. and Saga University.

- MOL has much knowledge in this field, participating since April in the operation of a 100 kW-class OTEC demo facility in Kumejima Town, Okinawa, which is operated and managed by Xenesys. It is the only such facility in Japan.

- CONTEXT: These initiatives aim to speed up the commercialization of ocean renewable energy.

UN finds no evidence of health effects from Fukushima disaster

(Yomiuri Shimbun, July 19)

- The UN Scientific Committee on the Effects of Atomic Radiation visited Japan and said it was unable to find any evidence of injury to health attributable to the Fukushima disaster.

- The Committee concluded that radiation exposure was low, and that the possibility of increases in cancer rates was also low.

- Saying the report was backed up by hard data, UNSCEAR Chair Gillian Hirth doesn’t think the Committee’s conclusions will change.

TAKEAWAY: Intentional or not, this will likely be used by the industry to promote a positive attitude towards nuclear power plants and restarts.

NEWS: POWER MARKETS

Thermal power plant glitches increase amid tight supply

(Japan NRG, July 20)

- Unplanned closures by thermal power stations are increasing amid tight power supply. From July 2 to July 7, METI data showed a total of 2.5 GW of power plants were taken offline, an increase of 1.4 GW from a year ago.

- METI said increases in variable renewable power are forcing thermal power plants to change run rates frequently, causing the glitches. Some old plants cannot cope with rampant run rate changes, METI reported.

METI judges how TEPCO coped with power crisis, forecasting questioned

(Japan NRG, July 20)

- METI’s sub-committee on basic electricity and gas policies met to assess Tokyo Electric’s management of the June power crisis and the lessons learnt, as well as the previous power crunch in March.

- Cold snap and heat waves unexpectedly hit in March and June, respectively, both before and after the peak demand period.

- In March, the major problem was a lack of communication between TEPCO and Tohoku Electric on the usage of linkage power transmission lines that potentially caused a blackout due to overflow of power.

- OCCTO (Organization for Cross-Regional Coordination of Transmission Operators) said the grids were working well together to cope with the July crisis. But a review of TEPCO actions in July also brought to light new issues, such as the need to improve forecasting.

- TEPCO data showed that fully automated, AI-driven power supply and demand forecasts missed the actuals by as much as 2 GWh. One sub-committee member, Prof. Matsuhashi Ryuji of Tokyo University, said that 10 years ago when the forecast was done manually with a simpler model, the gap was only 0.3 GWh.

- The forecasts have become less accurate despite advances in analytical systems, possibly due to increases in variable renewable in the power supply, and rampant temperature changes that are beyond AI’s capacity. The causes of forecast gaps need to be fully investigated, Matsuhashi said.

- TEPCO said solar power forecasts need to improve as the share of variable renewables increases. Temperature forecasts often miss by a measure of 2° Celsius, which could alter demand forecasts by over 2 GWh. TEPCO also pointed out that better communication within regional balancing groups of power retailers would also help the grid get a grasp on area-wide demand conditions.

- CONTEXT: As reported in the July 19 issue of Japan NRG, OCCTO urged the grids and Japan Meteorological Agency to work closer together to improve forecasting. Meanwhile, forecast and balancing group issues are relevant to all grids, not just TEPCO, METI said.

TAKEAWAY: One sub-committee member insisted on conducting a thorough investigation on forecast accuracy, but METI did not respond immediately to the suggestion. Even so, an informal review of demand and supply forecasting models may now take place. Several overseas suppliers of forecasting software have entered the Japanese market in recent years, but uptake for their services has been conservative. This may now change.

West Japan electricity shortage eases amid Ohi restart

(MBS News, July 17)

- On July 17, Ohi NPP Unit 4 (Kansai Electric) in Fukui Prefecture began supplying the grid.

- While it had been feared in recent months that the electricity supply in west Japan wouldn’t keep up with demand, the situation has improved, and the latest reactor restart will boost available capacity.

- Unit 4 was scheduled to restart in March, but the date was pushed back after leaks were found in plumbing.

- SIDE DEVELOPMENT:

Kansai Electric restarts Unit 3 of Takahama NPP, initially for tests

(Company Statement, July 22)- The 870 MW reactor concluded the bulk of its periodic inspection and is scheduled to restart on July 24.

- After that, various tests will be conducted as part of the final stage of the periodic inspection. On Aug. 19, a comprehensive load and performance inspection will be conducted, and full-scale power operations will resume.

TAKEAWAY: With the restart of the Takahama unit, Japan will have seven nuclear reactors online. After that, there’ll be just one more reactor restart, each by Kansai Electric and Kyushu Electric, before peak winter demand. Then the country will comfortably reach the nine-reactor target set by PM Kishida.

- SIDE DEVELOPMENT:

Generators’ federation says nine reactors still not enough

(Nikkei, July 15)- Federation of Electric Power Companies chair and Kyushu Electric CEO Ikebe Kazuhiro said that even with nine nuclear units operating, Japan is likely to face power shortages in winter.

- The comments came in response to a recent pledge by PM Kishida to have nine nuclear reactors running in time for winter.

- Ikebe said the restart of the nine units was already figured into projections and restarting shuttered coal-fired stations may be needed to ensure adequate supply.

TEPCO seeks price increase to power tariffs in September; Chubu also

(Nikkei Shimbun, July 21)

- TEPCO and Chubu Electric will ask the government to confirm a 13th monthly tariff increase until September on the back of high fuel costs. In this period of just over a year, power prices are up about 30-40%.

- Some TEPCO contracts will no longer be able to automatically pass on higher fuel prices to customers. If TEPCO is left with no financial leeway, it will stall investment in new power plants.

- TEPCO’s rates will likely rise about ¥8 to around ¥9,126 for the average household, while Chubu’s increase could be ¥360 to around ¥9,110, according to Nikkei calculations.

- CONTEXT: Under the fuel price adjustment system, power companies can only pass on to consumers up to 1.5 times the base price, no matter how much fuel prices rise. When prices gain more than that, the utilities must bear the costs.

- From early fall, most utilities will have hit the ceiling for how much they can increase tariffs.

- SIDE DEVELOPMENT:

Tokyo Gas to hike tariffs for 8.4 million subscribers

(NHK, July 21)- In October, Tokyo Gas will increase tariffs to reflect higher energy costs.

- The increase will be more than ¥280/ month for the average household.

As energy costs soar, Japan power utilities rush to secure cash

(Nikkei Asia, July 18)

- Japanese power utilities are increasing fundraising via bond sales as high prices for natural resources and a weak yen deplete their cash holdings; total bond offerings this fiscal year will rise 6% to ¥1.73 trillion ($12.4 billion).

- The amount of debt issued by 10 power utilities accounted for 23% of the total sum by Japanese companies in Q2, up 9% from fiscal 2021, according to Refinitiv.

- Tohoku Electric Power plans to issue a record ¥280 billion in debt, to help finance safety measures for the Onagawa NPP set to restart by February 2024.

- Tepco Power Grid, a unit of TEPCO, will raise ¥360 billion, 60% more than the amount slated to mature in FY2022. Kansai Electric plans to issue up to ¥400 billion.

- Shikoku Electric will issue ¥125 billion in bonds; “If our cash flow deteriorates further, we could increase the amount,” said a person in charge of bond offerings.

Tokyu Land and Denmark’s CIP partner in Aomori offshore wind project

(New Energy Business News, July 19)

- Tokyu Land and Copenhagen Infrastructure Partners (CIP) of Denmark have established a JV, Aomori South Offshore Wind Development G.K.

- The two companies will collaborate on an offshore wind power generation project in the Sea of Japan off the coast of Aomori Prefecture (south side).

- In March, the companies announced an environmental assessment study for a wind project off the Tsugaru City and Ajigasawa Town coast, Aomori Prefecture.

Eurus Energy plans 160 MW wind power plant in Hokkaido

(New Energy Business News, July 22)

- Eurus Energy will develop a 160 MW wind power plant in Hakodate, Hokkaido. Located in the southeastern area of Hakodate City, the project covers 6,616 hectares, and will install 37 wind turbines.

- Construction begins in April 2028, will be commissioned in November 2030, and operational starting April 2031.

Developer Tribay raises ¥1.4 billion for dozens of solar power plants

(New Energy Business News, July 20)

- Tribay, a Tokyo-based developer of solar power plants, raised ¥1.4 billion through a term loan with a commitment period for its portfolio assets consisting of 74 low-voltage solar power plants.

- The lender is Mizuho Bank and the borrower is East Japan Energy Development No. 2, an affiliate of Tribay.

- Tribay says the development of solar projects in mountain forests has become more complicated. The developer plans to diversify its portfolio in both the FIT and non-FIT markets.

Hitachi Energy to provide Petrofac with turbine power transmission systems

(Nikkan Kogyo Shimbun; July 15)

- Hitachi Energy signed an agreement with UK-based Petrofac. The two companies will supply high-voltage DC and AC transmission systems for offshore-wind applications.

- Hitachi’s high-voltage DC converters have applications in the offshore wind market.

NEWS: OIL, GAS & MINING

Mitsui does not rule out abandoning Russia’s Sakhalin-2

(Denki Shimbun, July 21)

- Yasunaga Tatsuo, chairman of Mitsui & Co., which owns shares in the current holding company for the Sakhalin-2 project, said: “We need to maintain our interests in order to continue supplying LNG to Japan.”

- CONTEXT: Russian President Putin signed a decree transferring Sakhalin II assets from a company in which Mitsui and Mitsubishi Corp have stakes, to a new Russian holding. Moscow said current investors in Sakhalin-2 need to reapply to keep their stakes and that it will have the final say on acceptance.

- Yasunaga said he has no information about the conditions for investment in the new company.

- Mitsui will consult with Japan’s government, but “if [Russian] conditions are unacceptable, then we may abandon” the project, Yasunaga said.

- SIDE DEVELOPMENT:

Japan should remain in Sakhalin: ENEOS chief say

(Denki Shimbun, July 21)- Japan should maintain its stake and ensure stable supply from Russia’s Sakhalin-2 LNG project in order to protect national interests, said head of refining major ENEOS Sugimori Tsutomu.

- SIDE DEVELOPMENT:

Why Japan needs to divest from Russian energy

(Asahi Shimbun, July 19)- CONTEXT: This is an editorial in one of Japan’s top five newspapers. Asahi is politically left-leaning.

- The government must not flinch in the face of Russian threats to seize Japanese interests in the Sakhalin-2 LNG project.

- Russia is requiring Japanese trading firms and other shareholders to consent to the transfer of assets to a new state entity established under presidential order.

- While Moscow cited “breach of contract” as reason for its actions, no basis was provided. In fact, Russia’s actions may violate an agreement on investor protection.

- Giving into Russia’s demands would play into their hands, and such a move would compromise solidarity between Japan, the U.S. and Europe, and reduce the efficacy of sanctions imposed on Russia.

- Instead, the government should assert legitimacy of its claims to Sakhalin-2 and work with the private sector to prepare for the possibility that Russia will cut off gas supplies in order to pressure Japan.

Nippon Steel buys LNG at highest price ever paid in Japan

(Reuters, July 20)

- Nippon Steel, Japan’s top steelmaker, bought a cargo for delivery in September for $40/ mmBtu, the most expensive cargo a Japanese buyer ever procured.

- The price shows the premium Japanese firms are willing to pay to avoid a power crunch amid growing fears of disruptions of LNG supplies from Russia.

- “Based on a standard LNGC (liquefied natural gas carrier) sized vessel, the cargo would cost between $132 – $135 million,” one source said.

Japan’s June crude imports up 22.1%, LNG up 1.7% and thermal coal up 17.7%

(Government Data, July 21)

- June crude oil imports were 12.1 million kiloliters, up 22.1% YoY, while their import value totaled ¥1.2 trillion, up 145.9%. LNG imports were 5.8 million tons, up 1.7%, but value soared to ¥586.8 billion, up 98.9%. Thermal coal imports were 8.8 million tons, up 17.7%, while their value rose 318.9% to ¥393.4 billion.

- January-June crude imports were up 12.7% from a year ago to 77.2 million kl, while their import value rose 106.3% to ¥5.8 trillion. LNG import quantity was down 3.5% to 37.5 million tons, but value was up 94.1% to ¥3.5 trillion. Thermal coal import volumes were up 7.8% to 56 million tons, while value was up 207.2% to ¥1.7 trillion.

LNG stocks hold flat at 1.94 million tons

(Government Data, July 20)

- LNG stocks stood at 1.94 million tons as of July 17, unchanged from a week earlier. The end-July stocks last year were 2.26 million tons. The five-year average for this time of year is 2.03 million tons.

Saudi foreign minister says efforts will continue to stabilize oil market

(Government Statement, July 19)

- Saudi foreign minister Prince Faisal bin Farhan Al-Saud told the Japanese PM that Saudi Arabia will continue efforts to stabilize the global oil market.

- The Saudi minister was paying a courtesy call to the premier to express condolences on former prime minister Abe’s death.

- Faisal also said he’d like to continue multilateral cooperation with Japan in energy, finance, technology and cultural exchanges, as spelled out in the Japan-Saudi 2030 vision signed in March 2017.

- CONTEXT: In 2013, Abe signed a treaty with Saudi Arabia that helped drive Japanese investment in energy and manufacturing.

Japan’s gasoline demand returns to pre-Covid level

(Sekiyu Tsushin, July 21)

- The head of the Petroleum Association of Japan, Sugimori, said “demand for gasoline has returned to pre-Covid levels,” adding that oil refining major ENEOS, where he is also CEO, no longer expects demand impact from the pandemic.

- While there is a slight drop off in demand compared to three years ago, Sugimori said this was due to the spread of hybrid and EVs.

- Separately, ENEOS will try to boost output of fuel oil that can be burned in thermal power plants this winter, answering the government’s call for more thermal capacity to be available during a power crunch.

- CONTEXT: Demand for fuel oil from power utilities remains high due to record LNG prices.

ANALYSIS

BY MAYUMI WATANABE

Can Next-Generation Batteries provide EVs with a Breakthrough,

Or Will Geopolitics Stymie Progress?

The race for more durable and efficient all-solid-state batteries (ASSB) that could potentially replace lithium-ion batteries in powering electric vehicles is heating up. Japanese companies are competing vigorously against international rivals, with Toyota Motor the outright leader in next-generation battery patents worldwide.

If the Japanese makers succeed, then these innovations will significantly change the battery raw materials landscape. How Japan and others handle this shift will determine who controls the global shift to cleaner mobility.

The emergence of “green” geopolitics

ASSBs, which promise to cut EV charging times and boost driving range, are still at a prototype stage. Which means the jury is out on the materials that would be required for their key components – the cathode, anode and electrolyte. While much of the current conversation revolves around lithium, attempts are also being made to try new materials such as silicon metal, indium and others.

The chemical and metallic makeup of the technology matters not only from an environmental perspective. The mining, refining and processing of many of the materials currently slated for use in EV batteries takes place in China.

The grim irony of the green energy revolution for Japan is that unless it accelerates plans to secure critical raw materials elsewhere, it will find its current dependency on Middle Eastern oil replaced by another energy dependency on rival China.

Recently, awareness of the implications is rising in Japan. In the past few months, the government has signed pacts with the U.S. to create frameworks and systems that would challenge China’s top position in rare earths, allowing the allies to move forward with ASSB with confidence.

And just last month, Australian miner Lynas Rare Earths, which counts the Japanese government among its major backers, was awarded a $120 million contract by the U.S. Department of Defense to build a processing facility in Texas. Lynas has supply agreements with Japan, which has priority rights until 2038.

Geopolitical considerations aside, cost reductions in battery manufacturing are one key to a wider spread of EVs. This is where ASSB can play a pivotal role. This is where the development of new materials and more efficient and recyclable systems are needed.

Nissan’s big ambitions for ASSB

Scientists expect that the energy density of ASSB will be twice as powerful as the current liquid lithium-ion batteries, allowing for a 30% reduction in charging time. This would mean longer trips and less worry for drivers. Mass production of ASSBs, however, is still at least six years away.

In April, Nissan Motor unveiled its prototype ASSB cell as part of its long-term vision, “Nissan Ambition 2030”, by which the company aims to launch an EV with all-solid-state batteries by FY2028.

Nissan plans to establish a pilot production line at its Yokohama Plant in FY2024, and the company believes all-solid-state battery costs can drop to $75 per kWh in fiscal 2028 and subsequently to $65 per kWh. This would place EVs at the same cost level as gasoline-powered vehicles.

Nevertheless, there have been setbacks in effort to develop ASSBs. For example, Toyota Motor disappointed the industry last year when it failed to deliver the world’s first ASSB-powered taxi for the Tokyo Olympics.

EVs, in general, are struggling to secure market share in Japan. While the country’s EV sales hit a record high in March – 4,219 vehicles, that amount only represented a 5% market share. Meanwhile, hybrid vehicles proved far more successful, taking a 48% share. Gasoline vehicles still finished with 44% of the market.

Despite government subsidies equivalent to $4,000-6,000 for every EV purchased, sales are struggling. As consumer budgets downsize on energy and food inflation, dealers are not keen to sell EVs. The bitter truth is that lithium-ion batteries have failed customer expectations.

Advantages of ASSB

Lithium-ion in an electrolyte solution travels between cathode and anode to generate electricity. ASSB’s electrolyte is solid, removing the risk of solution leakages and fire.

Other advantages are:

— Easy to pack the modules and the cells are flexible to shape

— Longer lifecycle

— Able to operate in -40ºC to 100ºC temperatures

The major challenge is electrical resistance in the interface between the solid electrolyte and the cathode that hampers battery performance and speeds up battery component degradation. Solid electrolytes are vulnerable to moisture, but new materials that resist such drawbacks have been key to successful ASSB development.

Establishing low power and environmentally sustainable manufacturing of the materials has been equally important. An ideal version would be made of recycled materials and could itself be easily recycled. The volumes that would such ideals, however, are not yet there.

Flourishing ASSB projects

Various ASSB types have been developed so far, using different combinations of oxide and sulfides-based lithium, nickel, cobalt and manganese. There are also initiatives to test new material. Silicon metal and indium used for some anodes are electrically conductive materials that have track records in solar batteries.

ASSB materials

|

Research bodies |

Cathode |

Anode |

Electrolyte |

Status |

|

Hitachi Zosen |

Nickel oxide (NiO), cobalt oxide (Co2O3), manganese oxide (MnO2) and other transition metal oxides |

Graphite |

Sulfide-based solid |

Commercialized |

|

Toho Titanium |

NA |

NA |

Lithium lanthanum titanate LLTO (La0.57Li0.27TO3) |

Commercialized |

|

Solid Power (U.S.), Japan Sanoh Industrial, Ford, BMW, SK |

Nickel, manganese, cobalt |

Silicon metal or lithium metal |

Sulfide based solid |

Production possibly in 2024 |

|

Tokyo Institute of Technology, Softbank, Sumitomo Chemical, etc. |

Lithium-excess compounds |

Lithium metal |

Phosphorus sulfide (Li10GePS12) |

NA |

|

Tokyo Institute of Technology |

Lithium cobalt oxide |

Lithium |

Lithium phosphate (Li3PO4) |

NA |

|

Osaka Prefecture University |

Lithium sulfide (Li2S) |

Lithium-indium alloy |

Lithium phosphorus sulfide (Li3PS4) |

NA |

|

National Institute of Advanced Industrial Science and Technology (AIST) |

Lithium cobalt oxide (LiCoO2) |

Lithium |

Lithium phosphate (Li3PO4) |

NA |

|

AIST |

Lithium sulfide (Li2S) |

Silicon metal |

Oxide-based solid |

NA |

State-run research hub NEDO has an ASSB evolution scenario. The current version in development is the first generation. The second generation will be fluoride-ion ASSB, which replaces lithium with fluorine. Toyota Motor is developing this technology. The third generation would be zinc ASSB, whose key components will be made of zinc.

Raw material market

The choice of materials for battery components has been important not only for performance but also for controlling costs. Presently, batteries are said to account for 30% of EV production costs. Around 70% of battery costs come from raw materials; namely, lithium hydroxide and carbonate, nickel, manganese and cobalt for the cathode, lithium carbonate for the electrolyte, and graphite for the anode.

According to Goldman Sachs, lithium is the recent world volatility champion, rising eight-fold in the last two years from $8,000/ ton in 2020 to $60,000-70,000/ ton. The bank forecasts that prices will ease on the back of Chinese investments to increase supply, but will remain elevated at avoe pre-Covide levels.

Shifts to ASSB will unlikely affect demand for lithium, nickel, cobalt and manganese, as they will still be used but in different ways. One possibility is a decline in cobalt consumption, which automakers have been striving for and have achieved for some models.

NEDO forecasts this trend will continue, possibly by replacing cobalt with nickel. ASSB will also trigger usage of raw materials that were not used before. Mitsui Mining and Smelting has begun sample shipments of A-SOLiD, an argyrodite sulfide electrolyte.

Goldman Sachs forecast, US$/ton

|

|

May spot price |

2022 average |

2023 average |

|

Lithium |

$60,350 |

$53,982 |

$16,372 |

|

Cobalt |

$87,100 |

$78,500 |

$59,500 |

|

Nickel |

$20,000-30,000 |

$31,000 |

$30,250 |

Diversification of ASSB raw materials may mean more dependency on China. While lithium raw materials – brine and spodumene – are found in South America and Australia, China dominates production of their intermediate product, lithium metal.

With its abundant high-grade silica deposits, China is also a global silicon metal giant. Still, there are elements that Japan does not have to worry too much about. Indium is one. While China dominates primary indium production, Japanese recyclers have been recovering the metal from flat panel displays and other digital scrap, achieving 99.999% purity. Japan is also a leading producer of titanium products.

Also, in a bid to increase self-sufficiency of battery materials, the government is pushing battery-to-battery recycling. The latest recycling breakthrough came from Dowa Eco Systems, which established a process to separate lithium carbonate from scrap batteries.

It is not yet clear which material and which process will become the ASSB mainstream. The successful development of powerful and reliable ASSB will reduce battery sizes as well as per unit raw material consumption that may cut costs.

If Japan can successfully develop ASSB technology that will lower EV production costs, and secure sufficient metal supplies from its global allies, then the chances of EVs becoming more widespread will become a reality. If not, then a critical part of the green energy revolution will remain in doubt.

|

R&D description |

Companies |

|

All-solid-state battery, production processes |

Nissan Motor, Toyota Motor, Honda Motor |

|

Fluoride-ion ASSB |

Toyota Motor |

|

Water resistant solid electrolyte, cathode with minimum cobalt content, ASSB anode; mass battery production process |

GS Yuasa |

|

All polymer battery |

APB Corporation |

|

Cathode material for advanced storage battery |

Sumitomo Metal Mining |

|

Cathode material for oxide-based ASSB |

JX Nippon Mining and Metals |

|

Mass production process of lithium metal anode |

Ulvac |

|

Mass production process of proprietary A-SOLiD sulfide based solid electrolyte |

Mitsui Mining and Smelting |

|

Mass production process of sulfide based solid electrolyte |

Idemitsu Kosan |

|

High ion conductive polymer electrolyte |

Osaka Soda |

ANALYSIS

BY JEREMY BOWDEN

As Japan Gears Up for Offshore Wind Expansion,

What Can It Learn from the UK and Other Markets?

As Japan struggles to lower the cost of offshore wind energy, fretting over its deep waters and less regular winds, the successful rollout of the technology elsewhere shows these factors are not the whole story.

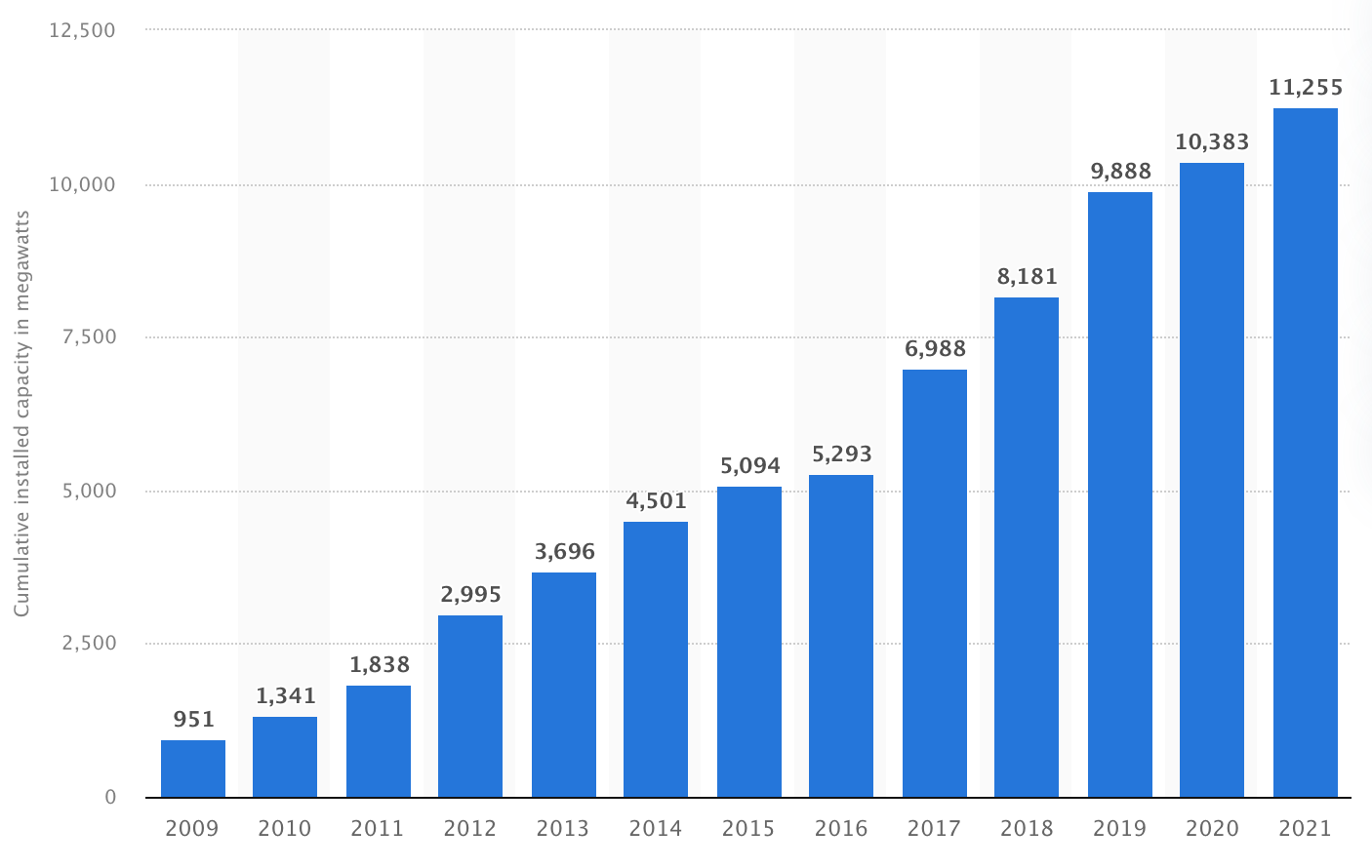

The UK’s offshore wind sector has installed almost 10 GW in the last decade and targets 50 GW by 2030 largely due to a consistent and effective policy framework. That has allowed for long-term planning and development of an extensive and large-scale supply chain in the UK, which in turn has driven down costs.

In contrast, Japan’s continued wrangling over rules for offshore wind auctions has already drawn major global turbine manufacturers to reconsider setting up local production. Yet without Japan-made components, the ability to reduce costs will be extremely hampered.

Should the rule-making issues get resolved, Japan has many of the key ingredients for success. Like the UK, Japan has a number of companies active in oil and gas exploration. It is that sector and the many engineering and support services companies involved that have since adapted to offshore wind.

After all, there are many crossovers. For example, Equinor’s floating wind substructures are cast in concrete using the same technology as the legs for its Troll natural gas platform.

With water depth also less of a factor in the UK as more of its projects move further offshore, Japan should take heart that geography won’t be a handicap.

Cumulative installed capacity of offshore wind in the UK

Source: © Statista 2022

Contracts for Difference

So, what did the UK do to make its offshore wind industry come alive in the last decade? One key starting point is the power purchasing scheme.

The UK government provides price guarantees for 15 years under its Contracts for Difference (CFD) auction scheme, which it awards based on the lowest price offered. This allows for competition and lowest possible prices, but does not inhibit investors with concerns about future revenue. In fact, after the Round 3 auctions in 2019, sector financings in the first half of 2020 totaled $35 billion.

Under CFDs, the government pays a top up between the market price and the guaranteed level, while the wind farm pays the government if the price goes above this level. This means that currently, with market prices at £200/ MWh and above, some wind farms are actually paying significant sums to the government.

Plants outside this support structure, (i.e. those that came in before it was introduced or the very new projects) are now making more money in spot sales. This is further encouraging business models that do not rely on CFDs, such as PPAs or direct sales to the electricity wholesale market.

Still, the revenue stability of a CFD is attractive, and other nations like Germany are considering adopting a similar system.

Oil and gas companies join utilities

Another catalyst for the UK wind market was the entry of international oil companies. Firms like Equinor were already present in the UK. To develop the new offshore wind sector, these oil majors partnered with UK utilities – a pattern that also seems to be emerging in Japan.

A change in 2021 to the lease-holding rules for offshore wind farms may encourage this further as it imposes higher leasing fees. Critics say only oil majors have deep enough pockets to cover them. Since the introduction of the new rule, TotalEnergies together with Green Investment Group, and BP in partnership with German utility EnBW, have secured more than half of the 8 GW of capacity on offer.

Still, even before the rule change, offshore wind projects needed large and long-term financing commitments that naturally favored big energy firms, which typically have roots in hydrocarbons.

The outlook for the maturing UK sector is for BP and Total to secure further capacity via CFDs and for Shell to be among the top bidders. These same companies show interest in Japanese offshore wind projects and will likely tie up with local utilities and other firms. The local groups that they’ll bid against will also feature Japanese utility blue chips like Tokyo Gas, JERA, and J-Power, as well as the trading houses.

The strong competition in the Japan market has shocked some local utilities and fueled lobbying efforts that now delay further auctions while rules are reviewed. Should the government cave in, and accept that price is no longer a key factor, then Japan’s offshore wind sector may have a short history. That competition is precisely what has brought UK wind power prices below those of fossil fuel generation, convincing consumers to switch.

Meanwhile, a CFD model could help prevent bidders that seek to delay the start of their work since the contracts have clearly defined timelines.

Latest UK auctions and prices

The latest UK CFD round (Round 4) secured 11 GW of renewables, including offshore wind, floating wind and tidal – all for delivery between 2023 and 2027. It began last December, and awards were made on July 7.

Of the total, offshore wind development accounted for 7 GW of capacity and saw new record low bids of £37.35/ MWh (inflation indexed to 2012 prices). That was the winning offer from Vattenfall for the 1.4 GW Norfolk Boreas farm, and the same from Orsted for the giant 2.9 GW Hornsea 3 project, the world’s largest. The lowest floating offshore wind award was at £87.30/ MWh.

For comparison, the lowest winning bids from Mitsubishi Corp. in the Japanese offshore auctions last year came at around £75-80/ MWh.

The prices of UK’s offshore wind projects have declined rapidly since the auctions began. In the previous Round 3, from September 2019, the lowest bid was £39.65/MWh, much less than the government forecast. That bid in 2019 was 30% lower than in the previous Round 2 (2017) and a whole 70% less than in Round 1 (2015).

Round 5 is due in March 2023 with plans for larger floating wind farms, more tidal and the opening up of new offshore provinces such as the Celtic Sea.

Other price reduction tools

Some projects in Germany and the Netherlands are proceeding without price guarantees – partly due to the provision of grid connections, which cuts costs compared to UK projects. Should Japan proceed with a mooted plan to build subsea cables from its northern Hokkaido areas to the northeast of the main island, it could lower the cost of generation while increasing the overall energy security of its fragmented grid.

Other factors contributing to drastic cuts in UK wind prices over the last seven years owe to the introduction of larger turbines and the winning locations’ high wind speeds. Project extensions close to existing wind farms are also allowing developers to share costs across projects. Meanwhile, as the market matures, the efficiency of installations improves and utilities lean on suppliers to reduce prices.

The final, and perhaps most vital input, is the cost of financing. While the UK, like many other nations, is raising interest rates to combat inflation, Japan appears determined to stick to its low-interest rate environment. Of course, rising raw materials prices and the weak yen will surely impact the financial models of bidders, but the chance to access low-interest loans should cool some of the cost inflation.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Algeria/ Oil

Algeria’s Sonatrach, in partnership with Occidental, TotalEnergies and ENI, will invest $4 billion dollars in the Berkine basin in order to produce nearly 1 billion of oil equivalent barrels when it’s operational.

Belgium/ Hydrogen energy

Tree Energy Solutions, a hydrogen energy start-up, secured €65 million in its latest funding round. Among the investors are HSBC, UniCredit and Germany’s Eon. The funding means that Tree Energy Solutions is valued at about €700 million.

Europe/ Gas pipeline

Gazprom resumed gas supplies through Nord Stream 1 after weeks of repair issues that threatened a total stoppage. However, Gazprom warned EU customers that in theory gas supplies still could be disrupted due to an “act of God”. Such a clause releases a party from legal obligations. This doesn’t mean Gazprom will stop deliveries, but rather that it won’t feel responsible if it fails to meet contract terms.

France/ Nuclear power

The government will fully nationalize debt-laden EDF, offering to pay €9.7 billion to take full control of the utility that is also Europe’s biggest nuclear power operator. EDF’s minority shareholders will be offered €12/ share, a 53% premium over the closing price on July 5.

Germany/ Nuclear power

The government might continue operating three remaining nuclear power plants, in contradiction to former Chancellor Merkel’s promise in 2011 to phase out nuclear energy following Japan’s Fukushima accident that same year. Germany’s nuclear plants are scheduled to be shut by end of 2022.

Guyana/ Oil

Bound by contracts with oil firms that are said to be “too one-sided”, the government shelved plans for a state-run oil company. A group led by Exxon Mobil, Hess Corp and CNOOC has found about 11 billion barrels of oil in the country’s waters. They expect to pump 1.2 mbpd in 2027, putting Guyana ahead of Venezuela in production.

Iran/ Russia/ Oil

On the occasion of President Vladimir Putin’s visit to Tehran, the National Iranian Oil Company signed a $4 billion oil deal with Gazprom, the biggest such deal ever with Moscow. Iran says it needs “$160 billion in investment in its oil and natural gas industries in the coming years”.

Italy/ Oil corruption case

Italian prosecutors dropped a legal challenge to the acquittal of Eni and Shell in a corruption case over a deal in Nigeria. The trial is one of the oil industry’s biggest corruption cases, involving the $1.3 billion purchase of a Nigerian oilfield in 2012.

Mongolia/ Gas pipeline

The country’s PM said that in two years Russia will go ahead with the “Power of Siberia 2” gas pipeline, which will for the first time connect the Siberian gas fields to China, via Mongolia. The PM also said Rio Tinto’s Oyu Tolgoi copper and gold mine project was on schedule.

Oil/ Prices

Oil prices have fallen and stabilized on fears that a global economic slowdown will lessen oil demand. By July 20, Brent crude prices for September fell 43 cents to settle at $106.92 a barrel, in part due to lower summer demand in the U.S., where the price of gasoline now is about $4.25 to $4.60/ gallon, down from $5/ gallon in early July.

Russia/ Oil payments

Russia seeks payment in the United Arab Emirates’ currency, dirhams, to pay for oil export deals to Indian customers. This is part of Moscow’s plans to move away from the U.S. dollar in order to insulate the country from Western sanctions.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

|

January |

OPEC quarterly meeting; JCCP Petroleum Conference – Tokyo; EU Taxonomy Climate Delegated Act activates; Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

|

February |

Chinese New Year (Jan. 31 to Feb. 6); Beijing Winter Olympics; South Korea joins RCEP trade agreement |

|

March |

Renewable Energy Institute annual conference; Smart Energy Week – Tokyo; Japan Atomic Industrial Forum annual conference – Tokyo; World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

|

April |

Japan Energy Summit – Tokyo; MARPOL Convention on Emissions reductions for containerships and LNG carriers activates; Japan Feed-in-Premium system commences as Energy Resilience Act takes effect; Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

|

May |

World Natural Gas Conference WCG2022 – South Korea; Elections: Australian general election; Philippines general and presidential elections |

|

June |

Happo-Noshiro offshore wind project auction closes; Annual IEA Global Conference on Energy Efficiency – Denmark; UNEP Environment Day, Environment Ministers Meeting – Sweden; G7 meeting – Germany |

|

July |

Japan to finalize economic security policies as part of natl. security strategy review; China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong; Czech Republic assumes presidency of EU; Elections: Japan’s Upper House Elections; Indian presidential election |

|

August |

Japan: Africa (TICAD 8) Summit – Tunisia; Kenyan general election |

|

September |

IPCC to release Assessment and Synthesis Report; Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.; Japan LNG Producer/Consumer Conference – Tokyo; IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

|

October |

EU Review of CO2 emission standards for heavy-duty vehicles published; Chinese Communist Party 20th quinquennial National Party Congress; G20 Meeting – Bali, Indonesia; Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

|

November |

COP27 – Egypt; U.S. mid-term elections; Soccer World Cup – Qatar; |

|

December |

Germany to eliminate nuclear power from energy mix; Happo-Noshiro offshore wind project auction result released; Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26; Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.