PM Kishida says power subsidies may reach 80 million consumers and warns utilities not to use them to prop up corporate profits

Officials to review fees for renewables projects that add battery, seeking to expand on the new feed-in premium pricing system

METI suggests scrapping limit on nuclear reactor operating life provided that safety can be guaranteed

ENERGY TRANSITION & POLICY

Feed-in tariff (FIT) annual cost seen rising to ¥4.2 trillion

JOGMEC to update technical CCS guidelines to address leaks

ICEF releases roadmaps for low-carbon ammonia and blue carbon

TCFD updates guidance on climate-related financial disclosures

Antitrust authorities agree to clarify rules for net-zero businesses

Steelmakers estimate hydrogen demand at 20 million tons / year

NRA responds after reports that inspectors flouted security rules

Tokyo City to offer subsidies to businesses to conserve power

IHI tests small volume co-firing at an Indonesian power plant

ELECTRICITY MARKETS

Japan’s PPA market could grow 15-fold this decade: Yano study

Opposition calls for waiver of renewables levy to cut power bills

Vena Energy plans major offshore wind project in Hokkaido area

EPCOs involved in alleged pricing cartel scandal fear large fines

Osaka Gas to build several solar farms via offsite PPA; Hitachi Metals claims Japan’s largest PPA deal through TEPCO Ventures

Floating offshore wind group begins construction in Nagasaki

Hitachi Energy invests to expand transformer output in the U.S.

OIL, GAS & MINING

INPEX CEO warns energy crisis will likely last several more years

Ministry probes claims gas stations pocketed consumer subsidies

Japan urges Malaysia to minimize impact from gas pipeline leak

LNG stocks slip but remain well above the five-year average

ANALYSIS

POWER RETAILERS STRUGGLE TO KEEP LIGHTS ON AS LAW CHANGE ADDS TO MARKET WOES

This year’s electricity spot prices are around 60% higher on average than a year earlier. The increase is playing havoc with more than just household and business power bills. It’s also upending several market structures. The hallmark of Japan’s quick rollout of renewable energy over the last decade, which saw a tripling in solar capacity, was the feed-in tariff (FIT). The FIT’s fixed price made securing finance for new projects straightforward. And, the system was paid for by a surcharge in consumer electricity bills.

A law change to the FIT, however, introduced before this year’s energy crisis, is making current conditions even harder for many electricity retailers.

ENERGY JOBS IN JAPAN: CORPORATE PPAs SHOW QUICK GROWTH

Corporate PPAs are big business these days. Developers, offtakers, traders, and utilities are all in to secure long-term, price-stable electricity that’s generated from renewable energy. This means they need to hire people who can formulate, facilitate and structure CPPA deals.

The PPA sector is still a young industry, however, and there are a limited number of professionals with actual successful experience, which in turn has created high demand for specialists in a low-supply segment.

GLOBAL VIEW

Russia agrees to invest $40 billion in Iranian gas and proposes to send its Nord Stream volumes south. U.S. starts to expand LNG export capacity. France gets a new nuclear turbine deal, but struggles to keep utility staff content. Canada to invest in strategic metals. Details on these and more in our global wrap.

JAPAN NRG WEEKLY

PUBLISHER K. K. Yuri Group

Editorial Team Yuriy Humber (Editor-in-Chief) John Varoli (Senior Editor, Americas) Mayumi Watanabe (Japan) Yoshihisa Ohno (Japan) Wilfried Goossens (Events, global)

METI The Ministry of Energy, Trade and Industry

MOE Ministry of Environment

ANRE Agency for Natural Resources and Energy

NEDO New Energy and Industrial Technology Development Organization

TEPCO Tokyo Electric Power Company

KEPCO Kansai Electric Power Company

EPCO Electric Power Company

JCC Japan Crude Cocktail

JKM Japan Korea Market, the Platt’s LNG benchmark

CCUS Carbon Capture, Utilization and Storage

mmbtu Million British Thermal Units

mb/d Million barrels per day

mtoe Million Tons of Oil Equivalent

kWh Kilowatt hours (electricity generation volume)

The Power Tariff Committee that sets policies on renewable fees will discuss rules for solar operators that install storage batteries after participation in the Feed-in-Premium system.

The fees for solar power with and without storage systems are not the same, and the committee will determine the respective calculation methodologies.

The committee will also discuss expanding the FIP to include smaller solar operators as well as plans to drive solar system installations on roof tops, as well as wind, biomass, geothermal and consumption tax declaration issues.

The committee’s first meeting for FY2022 was held on Oct 12 and decisions will be made by the end of March 2023.

CONTEXT: The government’s goal is to accelerate the shift away from the FIT system to FIP and possibly other new systems such as user-driven agreements. A committee member, Akimoto Keigo, pointed out that hydro and geothermal power costs have stayed flat over the years and suggested their separation from the FIT system.

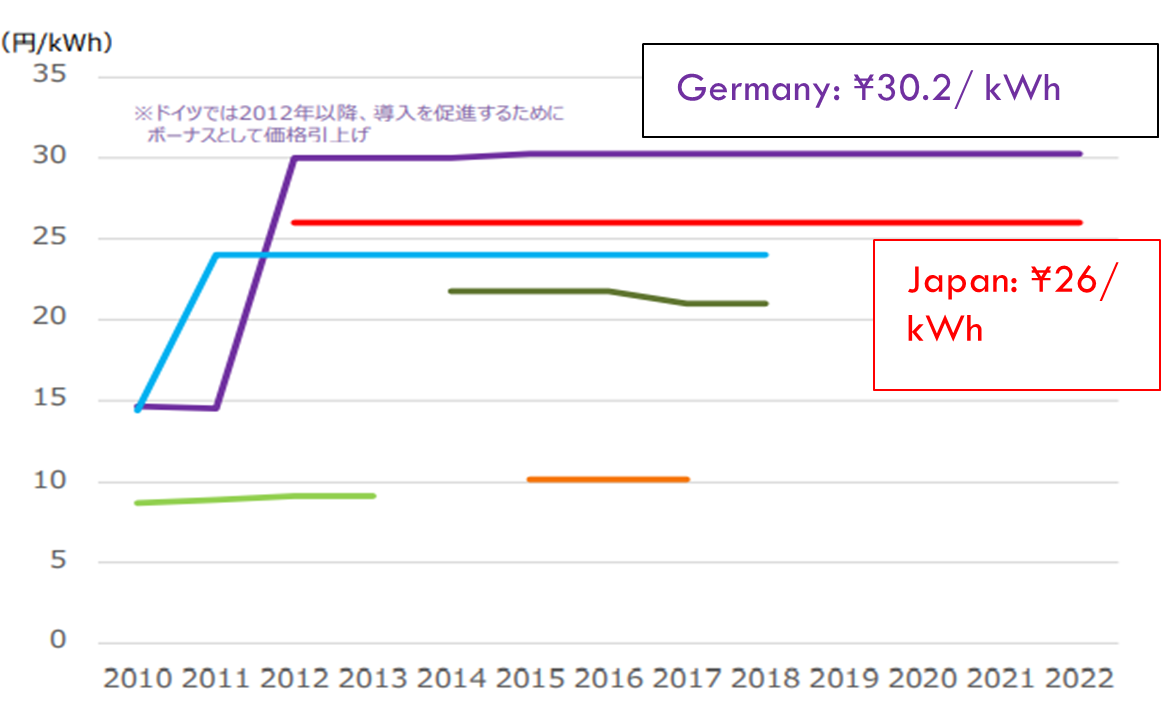

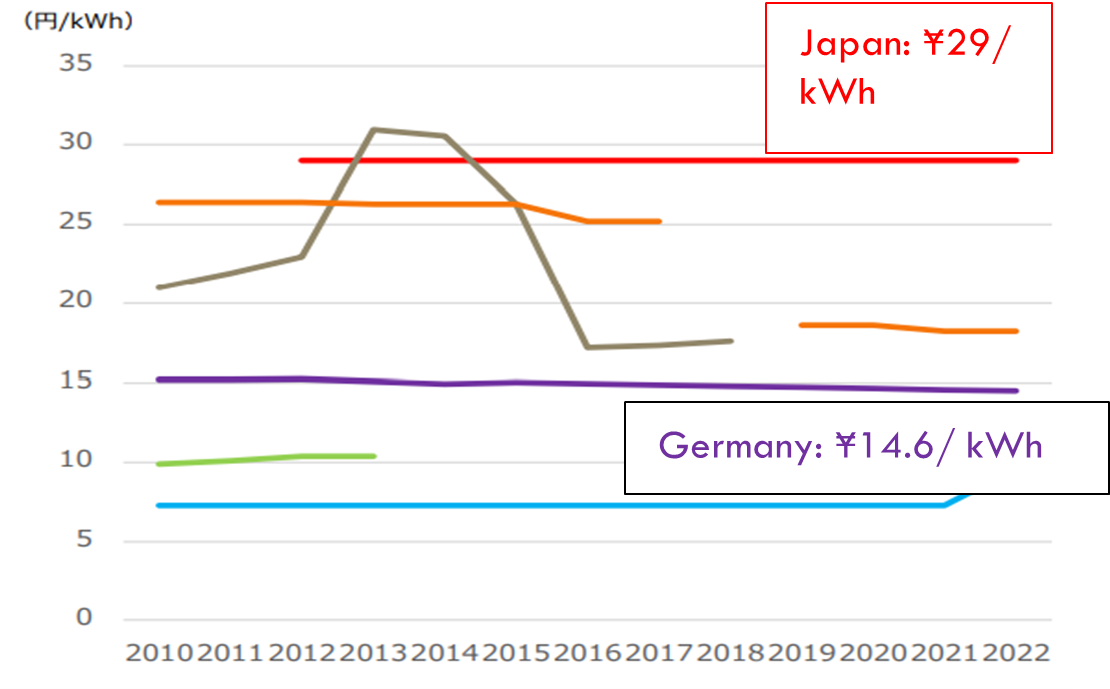

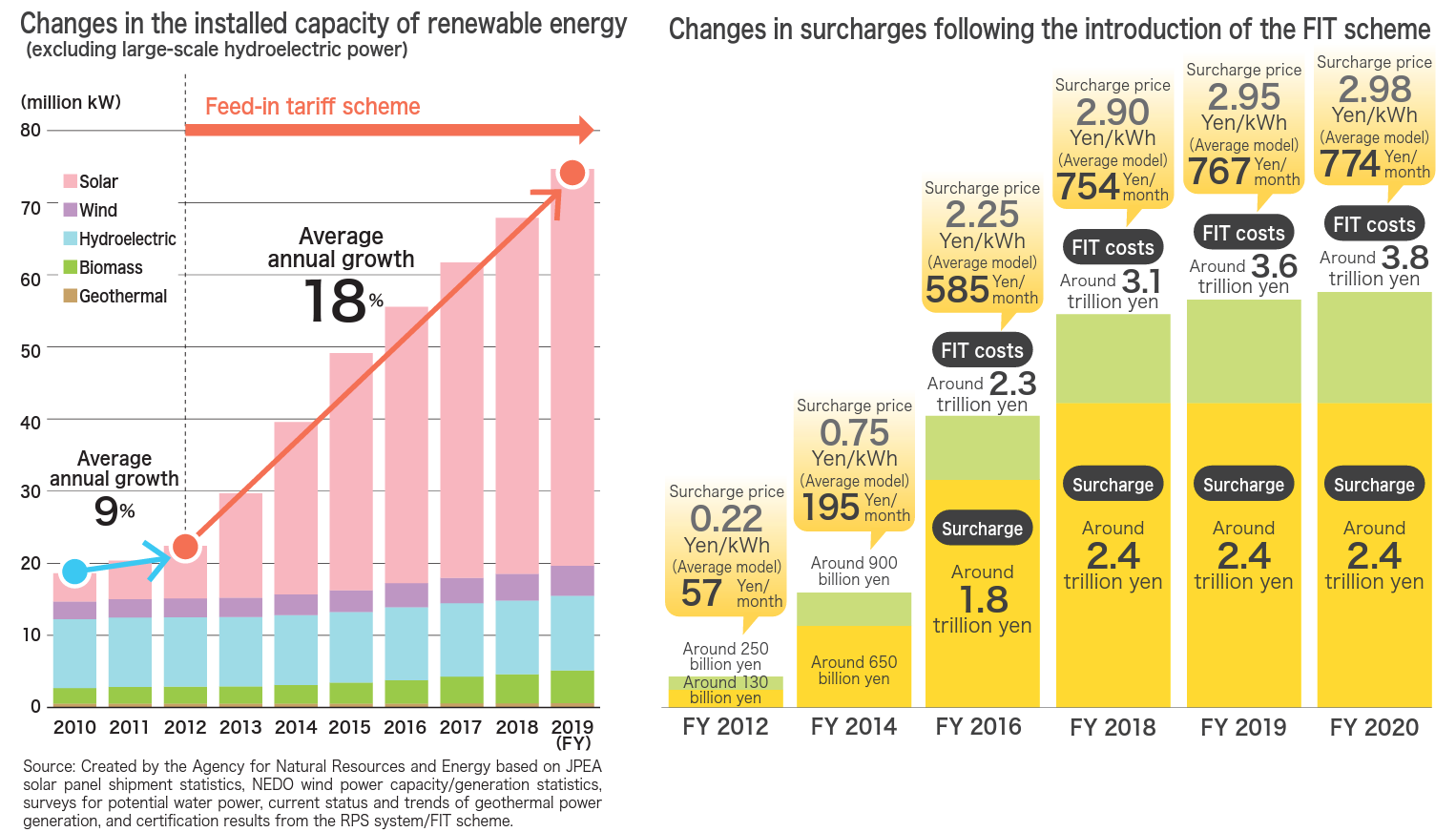

Total annual Feed-in-Tariff (FIT) fees paid to renewable operators are forecast to reach ¥4.2 trillion in by end of FY2022, up from ¥3.8 trillion in the previous term.

Of the ¥4.2 trillion, ¥2.7 trillion are paid by consumers automatically, since the renewable promotion surcharge is included in electricity bills.

In 1H of 2022, solar power cost ¥12/ kWh, more than double the global average of ¥5.2/ kWh; onshore wind was ¥14.9/ kWh, almost three times the global average of ¥5.2/ kWh.

Breakdown of FIT costs (¥ trillion)

Solar

3.0

Wind

0.2

Geothermal

0.02

Small and medium sized hydro

0.1

Biomass

0.7

Adjustment fee

0.1

TAKEAWAY: See this week’s Analysis section for a deep dive into how the FIT system has impacted the market, especially the retail companies, this year.

JOGMEC plans to update the guidelines for the technical aspects of Carbon Capture and Storage projects, released May this year.

Version 2 of the guidelines will address methane leakages, actual examples of carbon capture capacity calculations, approaches to primary and secondary data, as well as accounting methods for synthetic methane, said Shimouch Makoto, a JOGMEC official, at the Green Hydrogen Conference.

The May guidelines showed how to quantify and verify carbon and greenhouse gas volumes, and defined steps on planning CCS projects, evaluating storage capacities and calculating the offset volumes.

JOGMEC will apply its methodology for an ammonia plant. JGC Corp will conduct measurements including carbon intensity of ammonia.

CONTEXT: The project guidelines aim to show the operational processes of starting and running CCS projects, and do not address regulatory requirements. Japan does not yet have a CCS regulatory framework that defines licensing, liabilities of project operators and the scope of regulator’s authority. METI is presently studying examples in the U.S., Canada and in the EU.

The updated guidance of the Task Force for Climate-related Financial Disclosures reflects the 2050 carbon neutrality goals and the revision of the corporate governance code last year.

It also aims to support companies expanding disclosure efforts.

The new guidance also provides sector-specific case studies.

Global TCFD participants increased by 1,290 organizations, YoY, to 3,819.

The Japan Fair Trade Commission will set up a panel to write new guidelines for decarbonization initiatives, clarifying how competing companies can collaborate, share information and facilities while complying with anti-monopoly regulations.

CONTEXT: Idemitsu, among other companies in ammonia/ hydrogen projects, have been asking for competition guidelines.

TAKEAWAY: The key issue is standardizing infrastructure and service specifications, where the first players potentially gain advantages in setting the standards.

Nippon Steel told ANRE’s sub-panels on hydrogen and ammonia policies that the steel sector’s hydrogen demand is forecasted at 20 million tons/ year by 2050. Steelmakers need hydrogen at ¥8/ nm3 in order to stay competitive.

The steel sector will consume 33% of annual hydrogen supplies by 2050.

METI’s price scenario of ¥20/ nm3 in 2050 is untenable, and financial support is needed to build new infrastructure and run it, said Nippon Steel.

TAKEAWAY: The sub-panels will set funding criteria for various sectors, as well as a process to determine the base hydrogen/ ammonia prices. Safety, energy security, economic efficiency, reliability and wider economic impact are suggested criterions.

The NRA will centralize authorization of inspector access to nuclear facilities and revise operational manuals.

CONTEXT: This comes in the aftermath of a scandal that appeared in the media about three nuclear security inspectors entering reactor and fuel facilities without entry passes this year.

Tokyo City to offer subsidies for electricity conservation

(Kankyo Business, Oct. 13)

City government to offer ¥200,000 per business establishment as an incentive.

The subsidies will be open to power retailers and also projects to install energy management systems, among other options.

CONTEXT: Japan was the largest aid donor nation to Sri Lanka from 1980 to 2009.

IHI small volume ammonia co-firing at Indonesian power plant

(Denki Shimbun, Oct. 14)

IHI Corp completed a small-volume cofiring of ammonia test at Unit 1 of the Gresik Gas-Fired Power Plant, together with PT Pembangkitan Jawa-Bali (PJB), a subsidiary of Indonesia’s state-owned power company, PLN.

IHI and PJB will conduct studies on boilers with a view to ammonia not only co-firing but also mono-firing down the line.

Indonesia, PLN, and PJB look to employ carbon-neutral fuels at thermal power plants to attain net-zero greenhouse gas emissions by 2060.

IHI will draw on this work to showcase ways to attain carbon neutrality across ASEAN countries. By offering diverse models for tapping carbon-neutral fuels, IHI seeks to promote ammonia fuel and other carbon-neutral fuels.

TAKEAWAY: On August 19, IHI also announced plans to explore ammonia co-firing at a thermal power plant in India as part of a project led by state research hub NEDO, together with Kowa Company. These cases show IHI seeks to be the leading Japanese player in ammonia projects in Asia.

Kansai Electric and Shell sign MOU for liquid hydrogen supply chains

(Denki Shimbun, October 14)

Kansai Electric and Shell signed a MoU to cooperate in liquid hydrogen supply chains in order to promote decarbonization.

The agreement includes: 1. production of decarbonized hydrogen; 2. deployment of hydrogen liquefaction, storage and shipping technology by Shell; and receiving and use of hydrogen at KEPCO thermal power plants.

KEPCO aims to develop a hydrogen supply chain by collaborating with a wide range of stakeholders.

Tohoku Electric and Mitsui launch freighter with innovative Wind Challenger sail

(Denki Shimbun, Oct. 11)

Tohoku Electric and Mitsui O.S.K. Lines said a coal carrier equipped with Wind Challenger (a hard sail wind power propulsion system) started on Oct 7.

The Shofu Maru is the world’s first vessel equipped with Wind Challenger, and will transport coal mainly from Australia, Indonesia, and North America as a dedicated vessel for Tohoku Electric.

Use of Wind Challenger is expected to reduce GHG emissions about 5% on a Japan-Australia voyage and about 8% on a Japan-North America West Coast voyage, compared to a conventional vessel of the same type.

Bulk carrier featuring the Wind Challenger Sail system Source: Tohoku Electric

METI investing in subsea cables

(Nikkan Kogyo Shimbun, Oct. 10)

In the 2023/24 provisional budget, METI earmarked an additional ¥3 billion for investment in technology for laying subsea cables.

METI says early investment in technology will benefit a project to lay 900 km of subsea cable between Hokkaido and Greater Tokyo in the early 2030s.

While only 900 MW can now be sent between Hokkaido and Honshu, the government plans to increase capacity to 1.2 GW by 2027/28.

This figure will more than triple with the planned subsea cable.

SB Energy will collaborate across seven industries (gaming, data analysis, real estate, etc.) to encourage people to be active outside of home. There’ll be incentives (e.g., points for completing games outside, coupons) to save energy.

It’s rare for various industries to collaborate in an effort to change consumer behavior to save electricity.

About 60% of 17–19-year-olds support more nuclear energy

(Denki Shimbun, Oct. 11)

The Nippon Foundation conducted the 48th installment of its Awareness Survey. of 1,000 respondents aged 17 to 19. The teenagers were asked about energy shortages and policy in light of the government’s request for reduced electricity consumption in the summer and plans for a full-fledged restart of nuclear power.

When asked: “Do you agree to increase the percentage of nuclear power to achieve the 20%-22% nuclear energy target contained in the Sixth Strategic Energy Plan or want a higher figure?”, 61.2% answered “Yes”.

However, 23.7% of young people want less nuclear power, and 15.1% think Japan should stop using nuclear power altogether.

PM Kishida met with power sector representatives, urging them to secure more capacity by bringing online thermal plants that were taken offline, procuring more fuel, and maximizing the use of nuclear generation facilities provided there is local community support and that safety is guaranteed.

Kishida asked power retailers to be flexible as he plans programs to ease power rate hikes on consumers. Such programs will be designed to affect 80 million consumers.

METI minister Nishimura said ruling party lawmakers are asking for similar schemes for city gas, adding that gas rate hikes won’t be as high as power price increases since gas utilities source LNG on long term contracts.

SIDE DEVELOPMENT: PM warns power companies about using state subsidies for own gain (Denki Shimbun, Oct. 13)

PM Kishida met with TEPCO Holdings CEO Kobayakawa to discuss the electricity market and the govt’s plan for a subsidy.

Kishida emphasized that the substantial state payments to power companies aren’t intended to subsidize their businesses.

Power companies will have to show how the funds were used to reduce subscriber power bills.

SIDE DEVELOPMENT: Opposition party calls for waiver of renewables levy to reduce power bills (Nikkei, Oct. 13)

The Democratic Party for the People is calling for legislation to temporarily waive the renewable energy levy imposed on electricity consumers under the feed-in tariff (FIT) scheme.

State subsidies should compensate for the revenue shortfall, says the DPP.

PPA market to see massive expansion this decade: Yano Research forecast

(New Energy Business News, Oct. 14)

The domestic market for Power Purchase Agreement (PPA) schemes is expected to grow from ¥3.8 billion in FY2021 to ¥70 billion in FY2030, according to a study done by the Yano Research Institute.

In Japan, PPA contracts were not strongly promoted due to the FIT fixed pricing system. However, the latter has decreased over the years, and some clients prefer to consumer renewable energy on-site rather than sell it under the FIT.

Interest in PPAs in the Japanese market began to show around FY2020 and it has taken off strongly since then.

SIDE DEVELOPMENT: Hitachi Metal sets up nation’s largest PPA deal (Kankyo Business, Oct. 7)

The company will build a 10 MW solar farm, one of the largest on-site solar generation facilities in Japan, in the Kumagaya area near one of Hitachi Metal’s manufacturing bases.

TEPCO Ventures will be responsible for the planning and operation of this generation facility and another 2.7 MW project at a Hitachi Metal plant in the Tochigi area. For both projects, the electricity sales will be structured through the TPO/PPA model (power purchase agreement based on third-party ownership).

The Kumagaya site is scheduled to begin operation in September 2023.

Minister pledges decision on reactor extensions as officials asks to scrap term limits

(Nikkei, Denki Shimbun, Oct.11-14)

The government is considering whether to extend the term limits for nuclear reactors, which are currently pegged at 40 years of operating life. Today’s system allows for a one-time extension of 20-years to be granted pending a full review by the regulator. However, METI officials are proposing to scrap term limits altogether, making operating life indefinite as long as the equipment is deemed safe.

The issue is under consideration by the NRA, a part of the MoE, and also the Agency for Natural Resources and Energy that’s under METI.

Recently retired NRA chair Fuketa said that the 60-year cap does not have a technical rationale and would leave many reactors retired at the same time. Each one should be reviewed separately on its own merits, he said.

METI Minister Nishimura said a decision is expected by the year’s end and may need law changes.

TAKEAWAY: The 20-year extension cap was introduced after the Fukushima accident. While all reactors that applied for the extension were approved, it is a lengthy process. Some reactors have been under NRA review for almost a decade. Since all stations, including those that had no issues, were forced to stop after the Fukushima accident, many utilities face losses unless they are able to operate them for longer than the current term limits and recoup their costs, as well as earn enough revenue to pay for facility decommissioning.

SIDE DEVELOPMENT: Kyushu Electric to extend use of Unit 1 and 2 at Sendai NPP (Kyodo News, Oct. 12)

Kyushu Electric applied to the NRA to extend the lifespan of Unit 1 and 2 of Sendai NPP for another 20 years.

Previously, Kansai Electric submitted applications to extend use of Unit 1 and 2 of Takahama NPP, Unit 3 of Mihama NPP, and Japan Atomic Power Company for Tokai No. 2 NPP.

If the NRA rules against extension, Sendai Units 1 and 2 must be shut down in July 2024 and November 2025, respectively.

TAKEAWAY: In light of stricter safety standards after the Fukushima disaster, Kyushu Electric had to invest more than $6.7 billion to upgrade its NPPs. For the company, it’s crucial to secure the operating life extension and make a return on those investments.

Vena Energy plans offshore wind farm in Hokkaido area

(New Energy Business News, Oct. 11)

Vena Energy plans to develop an offshore wind farm off the coast of Shimamaki Village, in Hokkaido. The maximum output would be 600 MW.

The project area is approximately 169 square kilometers, which would house up to 50 wind turbines. The foundation will be a ground-mounted type, and the construction period is expected to be up to three years.

The area off Shimamaki coast is considered to be “at a certain stage of preparation” under the law. MHI and Eco Power are also conducting assessments in the area.

Major utilities involved in cartel scandal fear large fines

(Sentaku, October 2022)

The Fair Trade Commission will soon rule on alleged cartel behavior of four power companies: KEPCO, Chubu Electric, Kyushu Electric, and Chugoku Electric. The fines might be the highest ever ordered.

CONTEXT: The four companies are charged with forming a cartel to sell power to corporate customers after 2018.

The fines for cartel behavior may be as much as 10% of earnings. KEPCO earned ¥2.21 trillion in FY2018, of which 70% came from corporate customers. In addition, company management would be subject to a shareholder lawsuit.

Power utilities fear the ruling will affect their hopes to increase power rates to cover rising fuel costs. All four utilities are expected to post losses this year.

Chugoku Electric won’t pay a dividend for the first time, as the other three.

KEPCO has been cooperating with the investigation and a source close to the company suggests this may reduce the fines.

Osaka Gas to build 8 solar farms via off-site PPA

(Nikkan Kogyo Shimbun, Oct. 13)

A group of five companies including Osaka Gas and Tokyu Corp will build 8 solar farms, each with a capacity of 1 MW, to supply electricity to various Tokyu Group properties under an off-site corporate PPP.

The farms will begin feeding the grid in June 2023.

Construction begins on Nagasaki floating wind farm

(Nikkei, Oct. 12)

A consortium of six companies led by Toda Corp began assembling wind turbines in the sea off Nagasaki.

A total of 8 floating turbines will be anchored, generating up to 17 MW.

CONTEXT: This project is one of the four first commercial offshore wind tenders held by Japan. The tender results were announced last summer.

FEPC sets up body to improve NPP management and safety

(Denki Shimbun, Oct. 14)

The Federation of Electric Power Companies (FEPC) will establish Japan’s first collective system uniting all power companies that operate nuclear power plants in order to share organization management and to improve nuclear safety.

All the regional power utilities apart from Okinawa Electric (which doesn’t have a nuclear facility) will be involved. In addition, J-Power (which is building its first nuclear plant), Japan Atomic Power Co. or J-Atomic, and Japan Nuclear Fuel Limited / JNFL (the firm in charge of uranium enrichment, processing and storage) will be involved.

TAKEAWAY: Decommissioning work for all Japanese reactors is due to be consolidated in one new company.

Hitachi Energy invests $37 million to expand transformer production facility in U.S.

(Denki Shimbun, Oct. 14)

Hitachi Energy plans to invest $37 million in the expansion and modernization of its power transformer manufacturing facility in South Boston, Virginia to address rapid demand from utility customers for renewable energy and data centers.

This facility produces both distribution and power transformers for the power grid, commercial buildings, and industrial facilities, as well as traction transformers for use in railway applications.

These latest investments call for the manufacturing of larger transformers specifically designed for utility and renewable energy markets.

TAKEAWAY: Hitachi has invested considerably in its energy business in the last five or so years, building out its T&D division after the acquisition of assets from ABB and through its nuclear JV with GE. The Japanese engineering firms is also actively recruiting unemployed engineers from recently bankrupt competitors.

Toshiba to commercialize inspection robots for turbine generators

(Company Statement, Oct. 12)

Toshiba Energy Systems & Solutions (Toshiba ESS) launched its inspection robot services for turbine generators in power plants.

There are two types of robots: “ultra-thin” for use in medium-to-big generators and also small generators; and “multi-functional” that can overcome barriers to provide a range of inspection services for power plants.

The ultra-thin robots have been used at overseas nuclear power plants, while the multi-functional robots will conduct inspections in Japan.

TAKEAWAY: This technology might also be utilized for various operations presently required at nuclear plants, especially for reactor decommissioning.

Meidensha’s China subsidiary ships 10,000 surge arresters for gas-insulated switchgear

(Denki Shimbun, Oct. 13)

Meiden Zhengzhou Electric, a part of Meidensha Corp, had total shipments of 10,000 surge arresters for gas-insulated switchgear (GIS) in June. China-based MZE has helped build infrastructure in local regions and industries with the manufacturing and sales of various surge arresters, including those used in power grids and electric railways.

NEWS: OIL, GAS & MINING

Finance Ministry investigates claims that service stations pocket fuel subsidies

(Response, Oct.11)

Some service stations have used state fuel subsidies to pay for improvements to facilities rather than pass them on to consumers.

A Finance Ministry survey of service stations found that of the ¥558 billion in subsidies between March and July, ¥11 billion wasn’t passed on to consumers.

The most common reason for not passing on subsidies was based on local prices not always requiring the full amount of the government payment.

INPEX CEO warns of lengthy energy crisis

(NNA Asia, Oct. 13)

During an address to the Australia-Japan Business Cooperation Committee, INPEX CEO Kitamura Toshiaki said the energy crisis is due to lower investment amounts in coal, oil and gas since 2015, and it will continue for at least five more years.

Kitamura said that since fossil fuels account for 80% of energy, sufficient supply capacity must be maintained.

Japan urges Malaysia to minimize impact in wake of Petronas leak

(Jiji, Oct. 11)

While commenting on a gas pipeline leak that has curtailed Malaysia’s LNG output, METI minister Nishimura made a strongly-worded request on Oct 11 for Malaysia to quickly restore capacity and minimize impact on supply to Japan.

Petronas declared the event a force majeure.

TAKEAWAY: Japan is applying political pressure to make sure the force majeure declaration does not leave it contingent on buying LNG cargos on the spot market, a costly and uncertain venture in today’s conditions. How Malaysia responds will be interesting not only from the point of view of current relations, but also to test the theory proposed by METI that Asia could create LNG hubs around the region and share supplies in times of emergency as a form of energy security.

LNG stocks of 10 power grids stood at 2.49 million tons as of Oct 9, down from 2.68 million tons a week earlier. The end-October stocks last year were 2.07 million tons. The five-year average for this time of year is 1.84 million tons.

ANALYSIS

BY YOSHIHISA OHNO

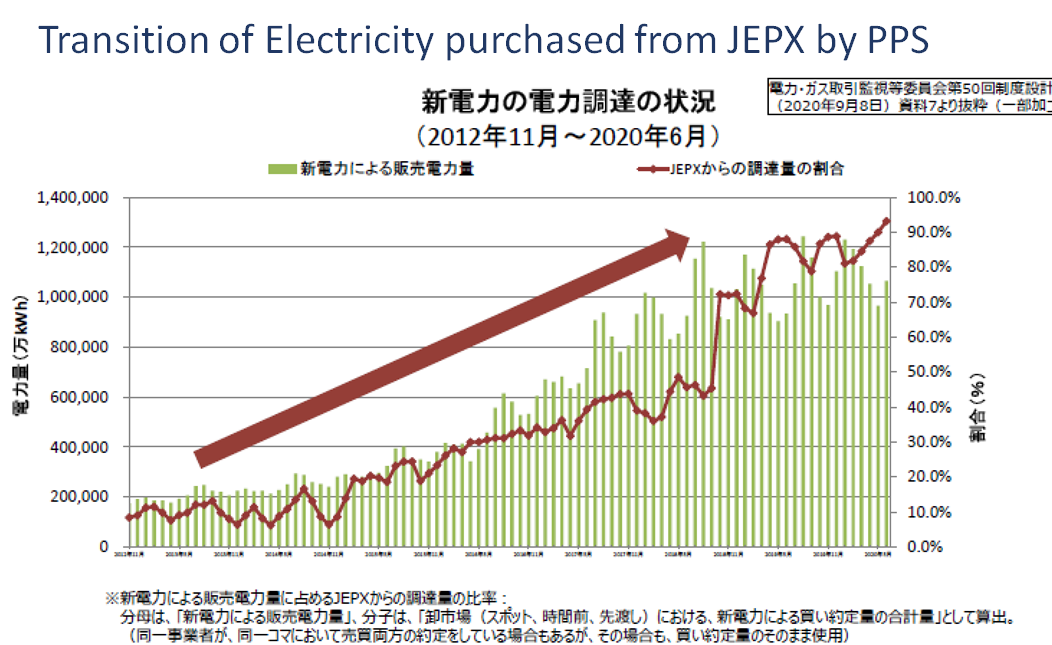

Power Retailers Struggle to Keep the Lights On

as Law Change Adds to Market Woes

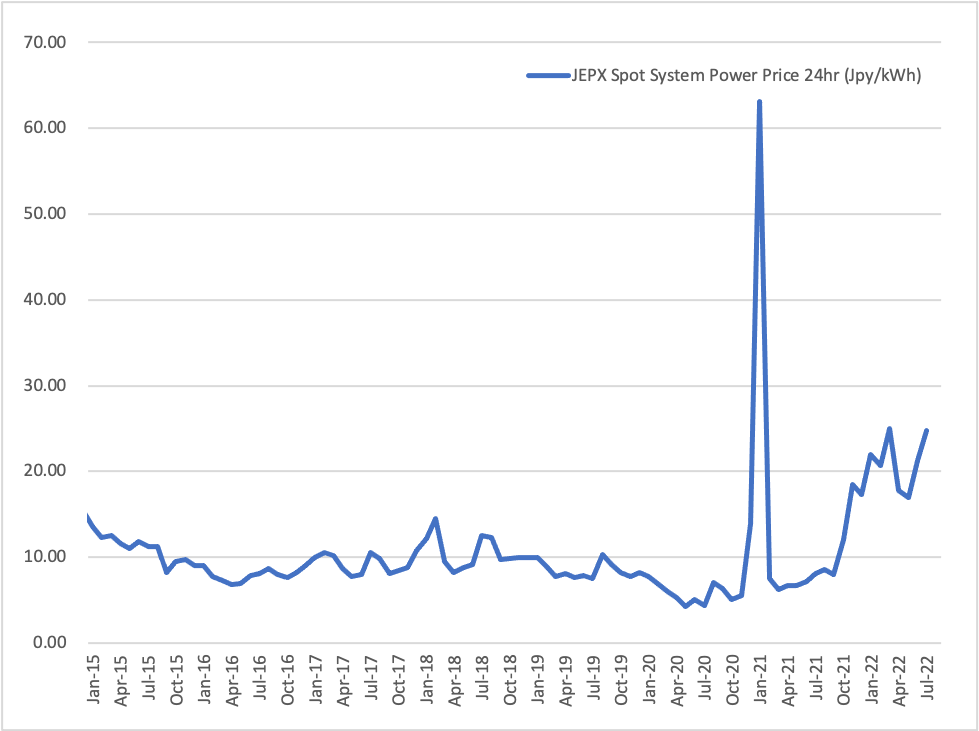

This year’s electricity spot prices are around 60% higher on average than a year earlier. The increase is playing havoc with more than just household and business power bills. It’s also upending several market structures.

The hallmark of Japan’s quick rollout of renewable energy over the last decade, which saw a tripling in solar capacity, was the feed-in tariff (FIT). The FIT’s fixed price made securing finance for new projects straightforward. And, the system was paid for by a surcharge in consumer electricity bills.

For years, the FIT was higher than the wholesale power price, leaving the consumers to bridge the gap between green policy support and market realities through ever-larger bills. To prevent this from spiraling, METI always meant to flip the narrative, gradually moving renewables to market-based pricing. As such, the officials amended the FIT law to set the wheels in motion for change from spring 2021.

This year’s energy crisis, however, has greatly accelerated the structural shift. And while developers recalibrate to new conditions, companies that signed up to sell more green electricity than they can generate are caught off-balance. The FIT law change forces them to buy extra volumes at market prices. In contrast, legacy regional utilities are largely unaffected.

In a worst-case scenario, the power market could move back towards an oligopoly.

Unforeseen circumstances The process of moving the sale of electricity generated by renewables from a fixed tariff system to a variable and market-based one was meant to take place over several years. In a way, it was the logical continuation of METI’s 2016 power market liberalization.

And so, from this April, FIT for businesses started to be phased out in in favor of the variable Feed-In Premium (FIP). The latter is a way to offer more upside for proactive asset managers. In turn, it makes the project cash flow less predictable.

This was not the only price structural change METI has planned for renewables. A May 2016 amendment of FIT Law, also mandated that electricity generated by FIT-permitted projects should start to be offered on the wholesale (JEPX) market in line with spot rates. The ministry allowed for a few years of adjustment, but envisioned that from FY2021 more and more of the FIT-supported electricity volumes should be sold based on the JEPX price.

The idea was to lessen the burden on consumers from the surcharge. After all, FIT was introduced in 2012 at a rate of ¥40/ kWh (+ tax for FIT energy suppliers with a total output of over 10 kW). At the time of the April 2016 market liberalization, new FIT projects could still command at least ¥24 + tax and for smaller systems as much as ¥33. On the JEPX, the average price for April 2016 was just ¥6.83.

The dynamics have shifted even as new industry entrants, often referred to as PPS firms, gained market share at the expense of the legacy utilities.

This year, new FIT projects can expect only around ¥10/ kWh (for solar projects with total output of more than 50 kW). Yet, the wholesale market averages around ¥22, and it has jumped to the ¥200 ceiling in isolated time slots due to a nationwide power capacity crunch and rising fuel prices.

For power generators selling their electricity under FIT, there is little impact; their volumes get the same fixed price.

For regional transmission and distribution firms there is also little impact. They sell the FIT-sponsored electricity on the spot market and take a small margin as a fee.

The large utilities with captive generation have relatively few renewables facilities and are also largely untouched by the changes.

For the PPS firms, however, it is a different story.

How PPS are affected As renewables capacity has increased, the surcharge covered by Japan’s consumers has also. It was set at ¥3.45/ kWh for the Tokyo area for FY2022, over 50% higher than in FY2016, when the market was liberalized.

Source: METI

The surcharge supported the generators. But it also benefited the sellers of electricity, who fueled their own growth in part thanks to more electricity being made available in the spot market.

From the middle of the last decade, the spot price of electricity in Japan declined, making it attractive for retailers to buy wholesale and cover their customer contract demand.

The downward price trend was often attributed to market liberalization. Rather than regional utilities fixing the price, it could be determined by the market.

The trend gave METI enough confidence to push through reform of FIT law, expecting the market trend also to help chisel down the price of electricity from renewable energy sources.

METI gave the power sellers a five-year notice to adjust, marking FY2021 as the time when electricity from FIT projects would shift to “market-linked prices”. The ministry reiterated the necessity and fairness of the move in October 2020, pointing to high renewables surcharges and the large market share that PPS firms had managed to build up.

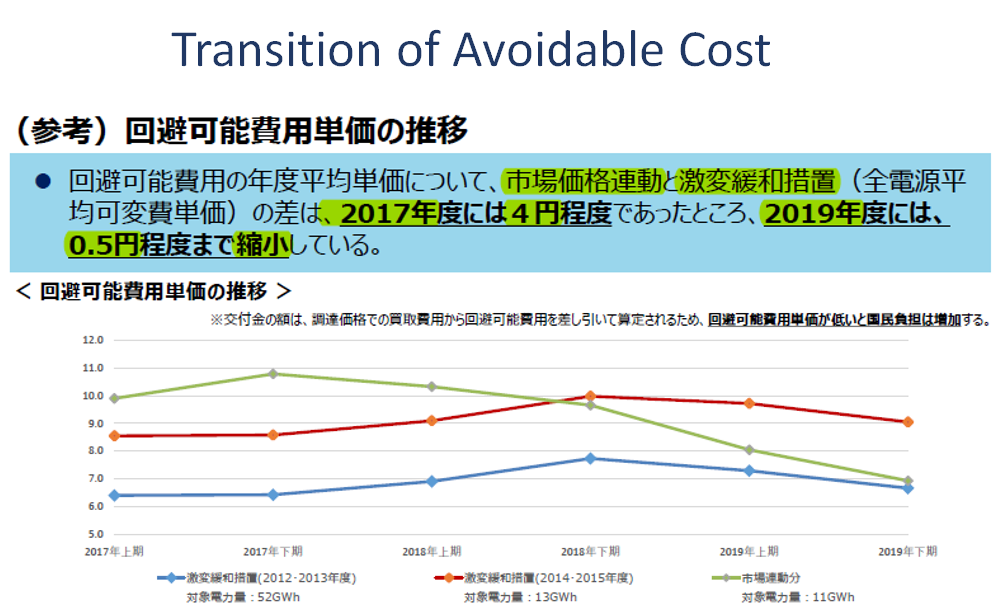

In turn, the so-called “avoidable cost” of not using thermal power, a metric used to determine the renewables surcharge, shrunk to ¥0.5 in FY2019 from ¥4 in FY2017.

Can’t PPS firms stop buying FIT electricity?

PPS firms are not obliged to purchase electricity from FIT-backed generators. They can simply use their own generation capacity, if they own such facilities.

However, as a differentiation factor, many PPS won over customers by promising to provide a certain percentage of green electricity. That’s particularly important for industrial firms that need to meet certain emissions targets or abide by rules of their clients that specify the use of green electricity.

With more and more of the FIT and non-FIT renewables-generated electricity sold on the wholesale market, PPS firms have little choice but to buy expensive power to meet contract obligations, or face exiting the business altogether.

Major power utilities that have sold similar green electricity plans to clients have more options at their disposal given their large and varied asset base.

Back to oligopoly?

When METI begin forcing the shift to market pricing, it likely did not foresee the energy price escalation of the past year or so. It also gave a lengthy period for adjustment. So, it’s hard to see this as a METI plan to roll back on market liberalization.

However, the government cannot allow the PPS sector implosion to continue. It would severely dent international interest in the Japanese electricity market, thus robbing it of liquidity, and would also likely hamper the development of new renewables capacity. The ministry’s own target calls for renewable energy to account for 36-38% of the power mix in FY2030 and that requires at least 7 GW of new solar projects a year from now on.

How METI will steady the market is not yet clear. However, the re-introduction of a more predictable pricing structure, such as FIT used to provide, should not be ruled out. In that respect, METI’s recent order to OCCTO to design a new auction system for decarbonized capacity should be worth paying close attention.

ANALYSIS

BY ANDREW STATTER

Corporate PPAs: the Ultimate Shortage of Professional Talent

Corporate PPAs are big business these days. Developers, offtakers, traders, and utilities are all in to secure long-term, price-stable electricity that’s generated from renewable energy. First and foremost, this means they need to hire people who can formulate, facilitate and structure CPPA deals.

The PPA sector is still a young industry, however, and there are a limited number of professionals with actual successful experience, which in turn has created high demand for top specialists in a low supply market. Let’s take a look at the kinds of roles and backgrounds that are most in demand.

Offtakers

Large, publicly-listed companies have long been chasing renewable energy as part of their ESG strategy. Japan is home to more RE100 companies (firms committing to using 100% renewable energy) than any other country, with the exception of the U.S.

Advanced software platforms, such as SAP Product Footprint Management, allow large companies to record and track the behavior of their supply chain and measure Scope 3 emissions. The result is that suppliers of materials, parts, and services to large manufacturers, such as Toyota, are now under the microscope and feel the pressure to procure clean energy.

The current energy crisis with LNG shortages, and spot electricity prices on occasion hitting ¥200/ kWh, are further intensifying demand for corporate power purchasing deals, or CPPA, which all support energy security, especially for critical infrastructure such as data centers. Essentially, there has never been more demand for the clean, long-term, secure energy supply that a CPPA provides.

These companies seek talent who understand energy procurement, have a network of developers/ suppliers, and who possess strong negotiating skills to secure the best possible terms for the deal.

Developers

All but the most stubborn developers agree that the Feed-in Tariff (FIT) is dead for PV solar plants. We’re seeing the more sophisticated players look at establishing a retail business, entering into the Feed-in Premium (FIP) auctions, or pursuing CPPAs.

The latter option is certainly gaining the most favor from power producers as it gives less exposure to market volatility, and secures long-term, predictable revenue, which makes for more bankable projects.

Developers and investors need candidates who have a solid understanding of the financials of renewable projects, know the development process timeline, risks, etc., and also have the negotiation skills to secure solid terms.

Let’s look at one case study. Once we had a company that was eager to hire a PPA Manager. Like many IPPs, this firm is transitioning from the FIT model to the CPPA and needed to hire a dedicated person to facilitate and structure offtake agreements and make projects bankable.

After a search, a successful candidate was found due to the wealth of their experience in infrastructure investments and finance for PV projects at a large trading house in Tokyo. The person had since moved into decarbonization strategy consulting for a Big 4 advisory firm, gaining new experience in carbon credits. She had never dealt with CPPA directly, but the building blocks of her career made her a great fit for the new role.

Sources: Pixabay

Trading companies

Japanese powerhouse trading firms and global specialists in CPPAs are very interested in this market and playing matchmaker between the supply and demand side. With their global reach and networks, they’re in a position to provide offtakers with clean energy procurement solutions, not only for Japan’s domestic energy needs but also to provide CPPA or other options for corporate energy needs at the site of their manufacturing facilities, often throughout Southeast Asia.

Trading companies are neither the buyer, nor the seller. Therefore, they tend to put a high focus on talent which brings excellent communication and consultative sales skills to the table. An understanding of the development process, finance and power markets is still highly sought after in a candidate. However, high value is placed on soft skills.

For the renewable power sector, the demand far outweighs the supply, and it’s very competitive in the current environment. On the talent side, the supply/ demand ratio is even more stressed, as every company needs people who can facilitate CPPA deals.

Here’s another case study. Once we worked with a global trading firm based in the U.S. that was hiring the head of CPPA/ VPPA solutions for the APAC region. Due to Japan’s high number of RE100 companies, and with operations across the region, this U.S. company decided to base its APAC director in Tokyo rather than Singapore.

The successful Japanese candidate was young (mid 30s), and had a background in electricity retail, as well as corporate decarbonization/ ESG strategy. He had spent a few years working as a renewables developer and understood the development and financing side of solar projects. He also had experience in structuring PPAs in India, though none in Japan.

Getting yourself into the CPPA business, and successfully structuring a couple of deals, is the career value equivalent of buying Tesla stock early on when they only had the original Tesla Roadster.

Now, as Japan is in the early stages of the CPPA business, there’s more need for people than talent available with exact skills and a successful track record. The career path is wide open for those with transferable skills such as:

Renewable power plant development and financing experience

Experience working in an electricity retailer, or in corporate sales in an EPCO

Consultants working on ESG or corporate decarbonization strategies

Those with M&A experience in the renewable sector

Experience in negotiation of long-term service agreements in power sector

As with the rapid development of any sector of the economy, this window of opportunity won’t last forever. Once the market matures, more people will have CPPA success cases and experience on their CVs.

Also, the big trading houses, utilities and powerful offtakers will have trained up more staff and the result will be a higher barrier to entry for those who are new to this sector. For now, however, both potential candidates and corporations active in this sector will face a very interesting and challenging next few years.

Andrew Statter is Partner, Head of Titan GreenTech, a Tokyo-based human capital and executive search firm with a focus on renewables and clean tech.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Canada/ Strategic metals

Rio Tinto and the Canadian govt will invest C$737 million over 8 years to modernize a 70-year-old facility in Quebec to counter Chinese control of the supply of strategic metals. Rio Tinto plans 12 tons annual output of titanium and quadruple scandium oxide, both are essential to aerospace and fuel cells.

EU/ Energy crisis

Member countries agreed to impose emergency levies on energy company’s windfall profits, and began talks on further measures to tackle the energy crisis – possibly a bloc-wide gas price cap.

EU/ EVs

Amazon will invest more than €1 billion over the next five years in electric vans, trucks and low-emission hubs across Europe. The news came just as Amazon-backed Rivian, the California-based EV company, is recalling all its vehicles to tighten a loose fastener in the front suspension.

France/ Labor unrest

The govt told TotalEnergies to raise wages and end the two-week strike that has seen oil depot and refinery output fall by more than 60%, leaving one in three gas stations struggling for fuel. Labor unrest spread this week to other energy companies, such as nuclear power group EDF

France/ Nuclear power

EDF renegotiated a deal to buy a nuclear turbine maker from GE, cutting its offer price by 10-20% off the deal value, originally set at about $200 million. The deal is seen as a way of recovering French control of nuclear technology as EDF prepares to build new reactors.

Iran/ Natural gas

Tehran signed a MoU with Russia to invest $40 billion to develop natural gas pipelines and LNG facilities. The deal was discussed at the Caspian Economic Forum in Moscow, Oct 5-6. Iran has the world’s second largest known natural gas reserves but lacks infrastructure to increase exports because of western sanctions.

Nuclear power

In a $7.9 billion deal, Westinghouse Electric will be bought by Brookfield Renewable Partners, one of the world’s largest clean energy investors, and Cameco, a supplier of uranium fuel. The group makes technology used in about half the world’s 440 nuclear reactors.

Poland/ Oil pipeline

Repairs to a pipeline carrying Russian oil to Germany are underway. The leak is believed to be due to material fatigue and there’s no indication of sabotage, Polish officials said, adding that oil bound for Germany will resume to “full levels” as soon as possible.

Spain/ Hydrogen energy

Oil and gas group Cepsa signed a deal with the port of Rotterdam to ship green hydrogen from southern Spain. Cepsa is diversifying into green energy and wants to take advantage of cheap solar energy in the sunny region of Andalusia to boost hydrogen production up to 4.6 million tons by 2030.

Turkey/Natural gas

Energy Minister Fatih Donmez said it was too early to comment on Vladimir Putin’s proposal for a European gas hub in Turkey, but added that the issue should be discussed. During Energy Week in Moscow, Putin said that Russia could redirect supplies intended for Nord Stream pipelines to the Black Sea.

U.S./ LNG

Work began on the third stage of Cheniere Energy’s new LNG plant, expected to be finished in 2025. The work is estimated to cost $8 billion and will add to the already-built $17 billion facility. Cheniere is the largest U.S. exporter of LNG.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

January

OPEC quarterly meeting;

JCCP Petroleum Conference – Tokyo;

EU Taxonomy Climate Delegated Act activates;

Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates;

Indonesia to temporarily ban coal exports for one month;

Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union;

Japan-U.S. two-plus-two meeting;

Japan’s parliament convenes on Jan. 17 for 150 days;

Prime Minister Kishida visits Australia (tentative)

February

Chinese New Year (Jan. 31 to Feb. 6);

Beijing Winter Olympics;

South Korea joins RCEP trade agreement

March

Renewable Energy Institute annual conference;

Smart Energy Week – Tokyo;

Japan Atomic Industrial Forum annual conference – Tokyo;

World Hydrogen Summit – Netherlands;

EU New strategy on international energy engagement published;

End of 2021/22 Japanese Fiscal Year;

South Korean presidential election

April

Japan Energy Summit – Tokyo;

MARPOL Convention on Emissions reductions for containerships and LNG carriers activates;

Japan Feed-in-Premium system commences as Energy Resilience Act takes effect;

Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement;

Convention on Biological Diversity Conference for post-2020 biodiversity framework – China;

Elections: French presidential election; Hungarian general election

May

World Natural Gas Conference WCG2022 – South Korea;

Elections: Australian general election; Philippines general and presidential elections

Germany to eliminate nuclear power from energy mix;

Happo-Noshiro offshore wind project auction result released;

Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26;

Japan-Canada Annual Energy Forum (tentative);

Tesla expected to achieve 1.3 million EV deliveries for full year 2022

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.

NEWS

・PM Kishida says power subsidies may reach 80 million consumers and warns utilities not to use them to prop up corporate profits

・Officials to review fees for renewables projects that add battery, seeking to expand on the new feed-in premium pricing system

・METI suggests scrapping limit on nuclear reactor operating life provided that safety can be guaranteed