JAPAN NRG WEEKLY

DEC. 5, 2022

JAPAN NRG WEEKLY

Dec. 5, 2022

NEWS

TOP

- Top power utilities hit with massive antitrust penalty;

Chubu, Chugoku, and Kyushu face major impact on financials - Japan mulls setting up world’s first strategic LNG reserve

as a means to bolster energy security in the key fuel - Experts propose that Japan sets up a new hydrogen agency

to set technical and safety standards for the nascent industry

ENERGY TRANSITION & POLICY

- Kishida pushes GX Council for carbon pricing details

- ANRE reviews baseload power market as new players on the rise

- METI to start auction of green power capacity to help developers

- JERA expands hydrogen/ammonia buyers’ club to five utilities

- Lawmakers want old nuclear units to be replaced with new tech

- Transport Ministry to issue recommendations for motorway solar

- Officials want to establish EVs as a power-balancing tool

- ENEOS and local partner to create forest-based carbon credits

- Kawasaki gets approval for ammonia-powered ship design

ELECTRICITY MARKETS

- Five major power utilities ask for tariff bumps of as high as 46%

- Govt wants Japan to add 6 GW of gas-fired capacity this decade

- FIP solar capacity sold for as little as ¥9.65/ kWh in latest auction

- Three regional grids warn of curtailment of renewables next year

- New power retail players see market share decline close to 10%

- JERA secures more thermal power capacity ahead of winter peak

- Kansai Electric applies for reactor license extensions at Takahama

- Japan’s first commercial offshore wind farm has turbines installed

OIL, GAS & MINING

- Toyota Tsusho delays start of lithium materials plant until 2023

- LNG stockpiles decline over 3% in a week, remain high

- Japan imports no Russian crude in Oct; LNG retains 10% share

- BHP CEO: green hydrogen will be a local not global trade

ANALYSIS

GAP BETWEEN NET-ZERO AMBITIONS AND

MATERIALS AVAILABILITY SETS UP G7 CONUNDRUM

In a few weeks Japan will assume the G7 presidency for 2023, with energy at the top of the agenda. By the time the heads of the European and North American member states arrive in Hiroshima for the summit in May, Japan hopes to greatly expand previous discussions on critical minerals. Recent months have seen Japanese policymakers and analysts come to a consensus that decarbonization is threatened by material constraints, and will need much more robust and coordinated global policy responses.

TOKYO GAS AND UK’S OCTOPUS ENERGY

SEEK TO UPEND THE POWER RETAIL MARKET

With the energy retail market in disarray, a 130-year-old Japanese power company is teaming up with a 21st century British energy-tech startup. The unexpected alliance between a legacy utility and an innovative disruptor promises to shake up Japan’s power retail scene.

The alliance centers around a 30/70 joint venture that opened for business about a year ago under the name of TG Octopus Energy. As well as competing on price, the venture aims to turbocharge the development of a demand-response culture in Japan, where awareness of power conservation through lifestyle change is still at an early stage.

GLOBAL VIEW

China will “forge a closer partnership” with Russia

in energy; Shell will buy Nature Energy Biogas for

$2 billion; the EU is importing a record amount of seaborne Russian gas; the UAE’s state-owned ADNOC approved $150 billion to set up its gas subsidiary; and Chevron is allowed to resume oil exports from Venezuela. Details on these and more in our global wrap.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Yoshihisa Ohno (Japan)

Wilfried Goossens (Events, global)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Art & Design

22 Graphics Inc.

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

|

METI |

The Ministry of Energy, |

mmbtu |

Million British Thermal Units | |

|

MOE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

Kishida pushes GX Council for carbon pricing details to encourage GX investments

(Government statement, Nov. 29)

- PM Kishida asked the GX Council to specify details of carbon pricing, including the launch schedules, means to secure funds for GX Transition Bonds, initiatives that the bonds will finance, and the systems to deploy these strategies.

- Kishida also pushed for energy strategy proposals that have been well reviewed by experts and the ruling party, and a 10-year green transition roadmap that clarifies investment strategies for each sector.

TAKEAWAY: Observers say Kishida may seek speedy decisions to delay carbon-related issues; some media now report carbon pricing will be rolled out in 2030, instead of 2026. With the rollout timing uncertain, the GX Council is now pushing the idea of a carbon surcharge for fossil fuel importers that would start low and gradually increase. The surcharge and an emissions-trading system for high-emitters are on the table to get the GX fundraising started.

METI panel to set up a new hydrogen agency

(Japan NRG, Nov. 28)

- The study group on hydrogen safety advising METI will set up a third-party agency to set technical and safety standards for hydrogen, and enforce them.

- The new regulator is required since municipalities hosting hydrogen facilities may have varied rules and standards, and some might lack effective oversight.

- Hydrogen businesses will be asked to send experts to share their knowledge.

ANRE starts review of baseload market

(Japan NRG, Nov. 30)

- ANRE is reviewing the baseload power market as the share of non-grid independent operators exceeded 21% this year. The grids are required to supply to the baseload market until the non-grid share hits 30%.

- Some independent operators have exited the market, and the baseload market system needs to be revamped so they’ll have better access to power sources and make it possible for all suppliers to secure power on a multi-year basis.

METI to start auction of green power capacity to boost profit for developers

(Denki Shimbun, Dec. 1)

- To secure more business predictability for renewable energy developers, METI will start holding an annual auction of green power capacity.

- The first is scheduled in FY2023 where 4 GW will be put up for auction. The amount may change in later years, depending on the outcome.

- METI says 6 GW of new green power capacity must be added each year on average to replace all fossil fuel power sources by 2050.

- Also, METI believes that about 6 GW of new LNG / gas-fired power generation is needed over the coming years for peak balancing.

TAKEAWAY: See the Power Markets section of this issue for further details on the LNG capacity plans.

Five major utilities unite on hydrogen and ammonia procurement

(Denki Shimbun, Nov. 30)

- JERA, Kyushu, Chugoku, Shikoku and Tohoku power companies signed an MOU to collaborate on adopting hydrogen and ammonia as a power generation fuel.

- It includes joint procurement (import) of the energy sources in order to cut costs; there could be cooperation in transportation and storage.

- The MoU is based on a previous agreement by JERA, Kyushu and Chugoku in April 2022. This time, Shikoku and Tohoku were newly added.

TAKEAWAY: As JERA is a JV of TEPCO and Chubu Electric, 6 among 10 former regional utilities have joined this ammonia project. Also, Kansai, Hokuriku, Hokkaido and Tohoku power companies formed a project to import ammonia from Australia.

METI backs plan that extends rector life just once, but takes into account forced stoppages

(Denki Shimbun, Nov. 29)

- ANRE will retain the current system of awarding nuclear reactors a 40-year permit life with one possible extension of up to 20 years pending a successful review. However, the government won’t count the years spent idle due to forced stoppages as part of the operating life.

- At a previous meeting METI presented three options: 1) Keep the present rule, which set out a 40-year permit life with one possible extension of 20 years; 2) Switch to a system with no limit on the operating life, but make the facility apply for an extension every 10 years; and 3) Option 1, but exclude the years spent idled due to a forced stoppage.

- METI chose option 3. This matter will now pass to the GX Council later this month, which should make the final decision.

TAKEAWAY: At the previous session, it was believed that METI would favor option 3, due to the concerns of local residents and governments. METI also wants to replace the older reactors with new designs, so setting a finite operating life permit plays into this strategy.

- SIDE DEVELOPMENT:

LDP wants cabinet approval of nuclear reactor replacement built into GX

(Denki Shimbun, Dec. 1)- The Federation of LDP Diet Members for Promoting Replacement of Nuclear Reactors asked the GX Council to include replacing current units with next-gen reactors in the overall strategy and also require cabinet approval for this.

- The lawmakers explained that local residents prefer to see aged nuclear plants replaced with new ones with more advanced safety features rather than allowing lengthy extensions of existing facilities.

- The Federation wants decommissioning to happen alongside the replacement work. For example, Chugoku Electric could decommission unit 1 of Shimane NPP and at the same time build a more advanced station at Kamino-seki (which is now waiting for building permission).

TAKEAWAY: After the Fukushima disaster, politicians were hesitant to raise these kinds of issues in public for fear of losing elections. Kishida’s GX policy has completely changed the political climate of the LDP.

ANRE to establish EVs as power-balancing tool

(Japan NRG, Nov. 28)

- ANRE plans to establish EVs as a power supply and demand balancing tool, absorbing redundant supply by connecting to the grid network, and providing power to households in times of shortage.

- The goal is to resolve technological and regulatory issues to allow EVs to be a part of the power demand-supply adjusted market mechanism.

- Issues include reducing charging station installation costs, and unifying data and equipment management control standards.

- CONTEXT: EV sales are rising to account for 2.5% of total new vehicle sales in Q3, up from 0.8% for Q4 2021; but this is far below the EV share of nearly 20% in Europe.

TAKEAWAY: ANRE advisors stressed clear incentives are important to spread any form of demand response systems, since power saving is a “byproduct” of consumers’ day-to-day activities and only large businesses can dedicate resources to manage it.

Japan-India environmental week in January

(Government statement, Dec. 1)

- MoE and India’s Ministry of Environment, Forest and Climate Change will co-host Japan-India Environment Week (January 12-31) that will include policy dialogs, a business matching event and seminars.

- CONTEXT: The event aims to bring the two countries together as Japan will host the G7 summit and India the G20 summit in 2023.

Mitsubishi and ExxonMobil to collaborate on carbon capture

(Nikkei, Nov. 30)

- Mitsubishi Heavy Industries (MHI) and ExxonMobil will collaborate on development of technology for capturing CO2.

- MHI will initially license its carbon capture technology to ExxonMobil, which is involved in projects to store CO2 underground.

- To date, MHI has built 14 commercial carbon capture plants around the world, which currently capture over 1 million metric tons of CO2 annually.

Transport Ministry to issue recommendations for motorway solar

(Nikkei X-Tech, Nov. 29)

- The Ministry of Land, Infrastructure, Transport and Tourism is preparing guidelines for solar panels on and alongside motorways.

- So far, motorway solar panels tend to be on tollbooth roofs, etc.

- Guidelines will include recommendations on installing panels on median strips, above parking areas, and under bridges.

- The Ministry doesn’t recommend solar pavements due to the high costs of maintenance and replacement.

- Roadside solar now generates 13 GWh annually, which is tiny compared to the 3,060 GWh consumed by lighting and other road infrastructure.

Solar bylaw promises business opportunities

(Newswitch, Dec. 1)

- As Tokyo and Kawasaki will soon mandate solar panels on new houses, the construction industry hopes the solar bylaws will create new opportunities.

- The Tokyo bylaw will only apply to the largest 50 construction companies, which build around half of the 45,000 residential buildings that go up each year.

- However, the increasing cost of building materials means the cost of new housing is already on the rise, and solar panels are an additional expense.

- Construction companies that fall under the plan will need to convince buyers of the benefits of solar. Some are unsure about how to do this.

Itochu partners with French firm in solar panel recycling

(Japan NRG, Nov. 29)

- Itochu will join forces with France’s PV recycling company, ROSI SAS, by taking a stake through a private placement.

- ROSI’s recycling, which can recover silver, copper and silicon, more than halves the waste from discarded solar cells, and could be used in 2024.

- CONTEXT: There’s global concern about pending mass disposal of spent solar panels; each has a life of about 20 years. In Japan, mass disposal of solar panels will increase around 2030. ROSI has advanced technologies for high purity recovery and recycling of silver, copper and silicon, which are highly-valued materials in solar cells.

Kawasaki Kisen receives approval for ammonia-powered ship design

(LNews, Nov. 28)

- A design for an ammonia-powered ship by Nihon Shipyard – in collaboration with Kawasaki Kisen Kaisha, Itochu, Mitsui E&S Machinery, and NS United Kaiun Kaisha – received approval from maritime regulator ClassNK.

- While there are no international rules governing the use of ammonia-fueled ships, ClassNK concluded the design was as safe as a traditional vessel.

- The consortium aims to build its first ammonia-powered ship by 2026.

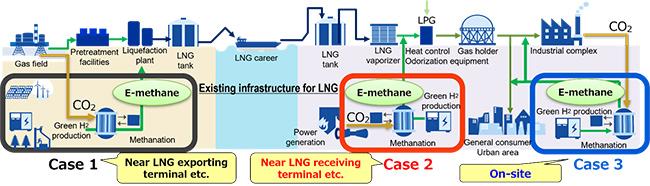

IHI to study e-methane project in Indonesia

(Company statement, Dec. 2)

- IHI Corp signed an MoU with PT Pertamina (Persero), Indonesia’s national energy company, for a feasibility study for local e-methane production.

- The goal is to produce e-methane near an existing LNG plant in Indonesia and sell it domestically and for export.

- Pertamina and IHI wish to start commercial e-methane operations in 2030.

- E-methane value chain

Source: IHI

- SIDE DEVELOPMENT:

IHI invests in ammonia developer

(Company statement, Nov. 22)- IHI has invested in Starfire Energy, an American startup that has developed green ammonia production and cracking technology.

- IHI seeks to accelerate technology acquisitions in Europe, the U.S., Japan and etc to bolster its carbon solutions, especially in synthetic hydrocarbons.

Itochu invests in U.S. biogas production startup

(Company statement, Nov. 28)

- Itochu invested in Impact Bioenergy, a U.S. startup that makes and sells equipment to produce biogas from food waste through anaerobic digestion.

- CONTEXT: The tightening of regulations on landfill waste, and the recent passing of the Inflation Reduction Act, is bolstering innovation in waste-to-energy projects. Impact Bioenergy develops, manufactures, and sells small- and medium-sized equipment that generates biogas through anaerobic methane fermentation of food and other organic waste. The biogas can be used for electricity and fuel. In August 2021, Itochu invested in Raven SR, a U.S. company that produces renewable hydrogen from solid waste.

Toray to join Siemens, Japanese partners in Scottish study of power-to-gas tech

(Company statement, Nov. 25)

- Toray Industries, Marubeni, Yamanashi Hydrogen Company, and Siemens Energy will jointly study in Scotland the feasibility of deploying power-to-gas (P2G) systems.

- The goal is to create a system that creates a green hydrogen supply chain that meets the heating needs of a cold urban area.

- CONTEXT: P2G technology uses electricity from solar and other renewable energy sources to produce hydrogen through electrolysis.

- The four companies are supported by NEDO in this project and are building on a plan that Marubeni has to set up a green hydrogen project in Scotland. The project is due to tap local renewables resources and employ a Siemens PEM electrolyzer for which Toray will provide a proprietary membrane.

ENEOS to work with Niigata partner to create forest-based carbon credits

(Kankyo Business, Nov. 30)

- ENEOS and Niigata Agriculture and Forestry Corp will create forest-based J-credits for the Shimoetsu region of Niigata Prefecture.

- The two will expand forest-based J-credits through a large project with an annual CO2 absorption volume of 10,000 tons and a 16-year certification period.

- ENEOS will purchase the forest-derived J-credits generated by the project to offset CO2 emissions in its business activities in Niigata and elsewhere.

Tokyo Gas to issue hybrid first hybrid transition bonds and loan

(Kankyo Business, Nov. 28)

- Tokyo Gas will issue ¥20 billion in hybrid (subordinated) bonds in the form of transition bonds for the first time. The bonds will raise funds for both decarbonization projects and to bolster the company’s finances.

- The company also plans to raise funds through a hybrid loan, which will have the same capital characteristics as the bonds, and expects to raise about ¥70 billion.

- The funds will support the development of cell stacks for low-cost water electrolysis, methanation demonstration tests, an onshore wind power project in Denmark, and a biomass power generation project.

TAKEAWAY: This is a significant amount to be raised under the banner of transition finance. It will be interesting to see what percentage of the money will go to clean energy projects and what will remain in company accounts to improve its finances.

Shinjuku gets hydrogen filling station

(New Energy News, Dec. 7)

- A relocatable hydrogen filling station recently opened in Shinjuku (Tokyo).

- It’s operated by Eneos in collaboration with a JV led by Toyota Tsusho, and is the first of its kind in Shinjuku.

- The Tokyo Metropolitan govt plans 150 such stations in Tokyo by 2030.

NEWS: POWER MARKETS

Chubu, Chugoku and Kyushu Electric hit with ¥100 billion FTC penalty

(Japan NRG, Dec. 1)

- The Fair Trade Commission accused Kansai Electric, Chugoku Electric, Kyushu Electric, and Chubu Electric of colluding to fix prices starting in 2018 in an effort to stay profitable after electricity market deregulation.

- The FTC made on-site inspections on suspicion of Anti-Monopoly Act violations in the high voltage power and extra-high voltage power markets.

- The total penalty will be about ¥100 billion. Chubu Electric will post a Q3 loss of about ¥27.6 billion; Chugoku Electric will have a Q3 loss of ¥70 billion.

- Each utility allegedly agreed with Kansai Electric not to enter its market area. However, since Kansai reported to the FTC on a voluntary basis, it wasn’t fined.

- Chubu Electric is also being investigated over allegations of similar arrangements with Toho Gas and other companies. The FTC is continuing its investigation.

TAKEAWAY: It’s believed that KEPCO’s penalty will be reduced because it was the first party to admit wrongdoing. KEPCO’s scandal around its nuclear facilities, which occurred just a few years ago, may have pushed the utility to be proactive in this case.

- According to one lawyer knowledgeable with the situation, the FTC probe will have a positive impact on power markets in the long run, but the fact that it took so long for the crackdown to take place is a shame. This puts the role of the Electricity and Power Market Surveillance body in question as it should have stepped in earlier. In order to ensure a level playing field for all, the Commission must engage in more data collection and stricter surveillance.

Utilities apply to METI for power rate hikes

(Japan NRG, Dec. 1)

- Hokuriku Electric, Shikoku Electric, Okinawa Electric, Chugoku Electric and Tohoku Electric filed appeals to METI for rate hikes to cover higher fuel costs.

|

EPCO (former regional utility) |

Average rate hike requested |

|

Hokuriku |

45.84% |

|

Shikoku |

28.08% |

|

Okinawa |

43.8% |

|

Chugoku |

31.33% |

|

Tohoku |

32.94% |

- CONTEXT: The Electricity and Gas Market Surveillance Commission will review the filings, and METI will then solicit public comments on the proposed rate hikes before approving the plans.

- Hokuriku Electric’s rate is the largest of the five power companies hoping to secure an increase. If approved, it will be Hokuriku’s first since increase since 1980, the time of the second oil crisis.

TAKEAWAY: Such a price increase would see the average Japanese household pay close to ¥10,000 per month. This is not something that METI or the govt in general wants to see, but the usual reason to refuse a utility’s plea to raise rates (i.e., you can cut internal expenses to offset rising operating costs) is no longer feasible. Fuel prices are double and triple the levels of a year ago and make up by far the largest cost item in the power price today.

Still, compared with many European countries, Japanese consumers are somewhat protected. Domestic firms are not able to pass-through rising costs as quickly and as fully as in Europe, which is putting Japanese power and gas firms under strain.

METI wants Japan to add 6 GW of gas-fired power capacity this decade

(Asia Nikkei, Dec. 4)

- METI wants to encourage companies to build an additional 6 GW of gas-fired power capacity this decade to help avoid power capacity shortages. This would translate into seven or eight new units and about 3% of the nation’s peak demand.

- The govt would be ready to support the building and investment costs as a way to compensate for uncertainty over future LNG prices and the context of such a move amid a push to decarbonize the power system.

- Companies will be recruited between fiscal 2023 and 2025.

- METI believes if the new gas-fired capacity replaces decommissioned coal power plants, it could even cut emissions.

TAKEAWAY: Japan faces the decommissioning of over 20 GW of thermal power capacity this decade and the majority of the country’s generation facilities are two years or older. So while this latest plan looks like an increase in thermal capacity, it would most likely act to replace old stations that are inefficient and likely higher in emissions than modern burners. That said, any large push into thermal power without a similar effort in expanding renewables capacity will both draw international criticism and make it even more difficult to reach the 2030 target to cut emissions by 46%.

FIP solar capacity sold at ¥9.65/ kWh in latest state auction

(OCCTO statement, Nov. 25)

- OCCTO announced results of the 14th solar PV auction (the third this fiscal year). The FIP results for capacity of 1 MW or more saw 11 successful bids secure 137.2 MW.

- The FIP auction had a ¥9.75/ kWh ceiling, but attracted a bid as low as ¥9.65; the average bid price was ¥9.73.

- FIT results for PV facilities of 250 kW and over, but less than 1 MW in capacity, attracted 17 successful bids, for 11.3 MW in total capacity.

- The FIT auction had a ¥9.75/ kWh ceiling, but attracted a bid as low as ¥9.50; the average bid price was ¥9.70.

Chubu, Hokuriku and Okinawa grids see renewables curtailments in 2023

(Japan NRG, Nov. 30)

- Power transmission units of grids in Chubu, Hokuriku and Okinawa regions say that curbs of 0.01-0.3% are likely in April 2023-March 2024 on renewable capacity increases, up from zero.

- Hokkaido and Shikoku, which saw negligible renewable capacity expansions in 2022, forecast a decline in the curb.

- Curbs are not expected in Tokyo and Kansai areas in 2023.

|

|

Hokkaido |

Tohoku |

Chubu |

Hokuriku |

Chugoku |

Shikoku |

Kyushu |

Okinawa |

|

2023 forecast |

0.01% |

0.56% |

0.01% |

0.02% |

0.67% |

0.48% |

4.8% |

0.34% |

|

2022 (March 2022- to date) |

0.03% |

0.36% |

0% |

0% |

0.16% |

0.58% |

3.0% |

0% |

TAKEAWAY: Power from storage batteries may also be subject to a curb when supply overwhelms demand.

Electricity sales of new market players declined 9.5% in August, YoY

(Denki Shimbun, Nov. 30)

- The Electricity and Gas Market Surveillance Commission said electricity sales in August 2022 by new market players dropped to 15.4 billion kWh, a 9.5% decrease YoY. The former regional utilities (EPCOs) added 59.7 billion kWh, up 2.3%.

- The market share of new players (shin-denryoku) was 20.5%, down 2.1%.

- New players lost a 3.5% market share in extra-high voltage contracts (greater than 20kV), and a 5.9% share in high voltage contracts (6kV or 7kV).

TAKEAWAY: This year, most new players that entered the market since 2016 took a hit from fuel price hikes and other costs. Only with their own power generation facilities that can sell at the market price did well.

JERA to secure 3 GW of additional power supply ahead of this winter

(Denki Shimbun, Nov. 30)

- JERA will bring five units online with 3 GW of total capacity this winter to ensure there is adequate supply in the system.

- These are units 5 and 6 of Anegasaki power plant (TEPCO area, LNG, each 600 MW); unit 5 of Chita power plant (Chubu Electric area, LNG, 700 MW); and units 4 and 5 at the Yotsuka-ichi power plant (Chubu Electric area, LNG, 234 MW).

- The company will also start the newly-built unit 1 of Anega-saki power plant (TEPCO area) in February 2023.

TAKEAWAY: Both Anegasaki and Chita started operations in the late 1970s, but they lost their price competitiveness due to age, so JERA stopped operations. Now it needs to restart those costly plants to secure enough power for peak demand.

Kansai Electric applies for license extension at Takahama NPP units 3 and 4

(Denki Shimbun, Nov. 28

- Kansai Electric will apply for a 20-year additional operation at units 3 and 4 of the Takahama NPP (both PWR, 870 MW). The units both passed a special inspection for longer operation, but Kansai Electric will still need to upgrade a steam generator.

- Unit 3 of Takahama turns 40 in January 2025, and unit 4 in June 2025.

- Kansai has already secured extensions for units 1 and 2 of Takahama (both PWR, 826MW) and unit 3 of Mihama NPP.

TAKEAWAY: Takahama unit 1 will restart in June 2023, and unit 2 in July 2023. In western Japan, Kyushu Electric applied for a 20-year extension of units 1 and 2 of Sendai NPP.

Renova considers a geothermal power plant in Hokkaido

(New Energy Business News, Dec. 2)

- Renova might develop a geothermal plant in Hakodate, Hokkaido. Tentatively named Keiyama Geothermal Power Project, it would have a 9.9 MW capacity.

- Daiwa Energy Infrastructure and Mitsubishi Materials are working with Renova on studying the area’s geothermal potential.

- The project area is about 3.8 ha, of which the power plant site is 2.8 ha. Construction will begin in April 2027, with operation from October 2028.

Japan’s first commercial offshore wind farm has turbines installed

(New Energy Business News, Nov. 28)

- Kajima and Sumitomo Electric Industries completed installation of 33 wind turbines (13 at Akita Port and 20 at Noshiro Port) as part of a project billed as the first commercial offshore wind farm in Japan. The turbines will now start trial operations.

- The 140 MW Akita Offshore Wind Farm, a project led by Marubeni and others, uses monopile foundations for its Vestas 4.2 MW turbines.

NEWS: OIL, GAS & MINING

Japan considers setting up strategic LNG reserve to bolster energy security

(Bloomberg, Dec. 2)

- Japan mulls the creation of a strategic LNG reserve to secure adequate supply of the key fuel.

- The government is working on a plan to create an LNG buffer under the umbrella of JOGMEC. Domestic firms can then buy LNG on short and long-term contracts without additional concern about being left with excess supply. The latter would be resold overseas during normal times and offered to domestic buyers in times of need.

- Any loss from the sale of LNG cargo to the strategic reserve would be reimbursed by JOGMEC.

- The govt’s immediate goal is to secure at least one cargo of LNG per month (usually ~70,000 tons) between December and February starting in 2023 through short-term contracts, and to secure at least 12 cargoes per year via mid- to long-term contracts over the course of this decade.

CONTEXT: Japanese end-users have let long-term contracts lapse with Qatar, UAE and Indonesia as the domestic demand picture becomes less certain. In contrast, growing supply issues globally have raised it to an issue of national security. - CONTEXT: This would be the world’s first such reserve.

TAKEAWAY: There is an obvious need for a strategic LNG stockpile in Japan given the importance of the fuel to its power and heating sectors. However, the nation lacks the infrastructure to create a physical storage hub of any size. How such a “stockpile” would function without long-term storage infrastructure is unclear. This is just one of many questions raised by this development, but it does at least indicate that Japan’s interest in the LNG market remains as strong as ever.

Expansion of Toyota Tsusho’s lithium carbonate plant delayed into 2023

(Japan NRG, Nov. 28)

- Expansion of Toyota Tsusho’s 17,500 tons/ year lithium carbonate plant in Argentina, initially planned for completion in 2020, won’t be completed this year.

- After the ramp up, the plant will have a 42,500 tons/ year capacity.

- CONTEXT: The Argentinian plant is a JV of Toyota Tsusho and Australia’s Allkem. It will supply carbonate feedstock to Japan’s first 10,000 tons/ year lithium hydroxide plant also owned by the two companies.

TAKEAWAY: Toyota Tsusho’s plan depends on how quickly the Argentinian carbonate plant completes its ramp up, as well as the market outlook of hydroxide and carbonate. Theoretically, hydroxide prices are higher than carbonate, but China’s massive appetite for carbonate is changing this.

LNG stocks fall to 2.53 million tons

(Government data, Dec. 1)

- LNG stocks of 10 power grids stood at 2.53 million tons as of Nov 27, down from 2.61 million tons a week earlier. The end-November stocks last year were 2.16 million tons. The five-year average for this time of year is 1.95 million tons.

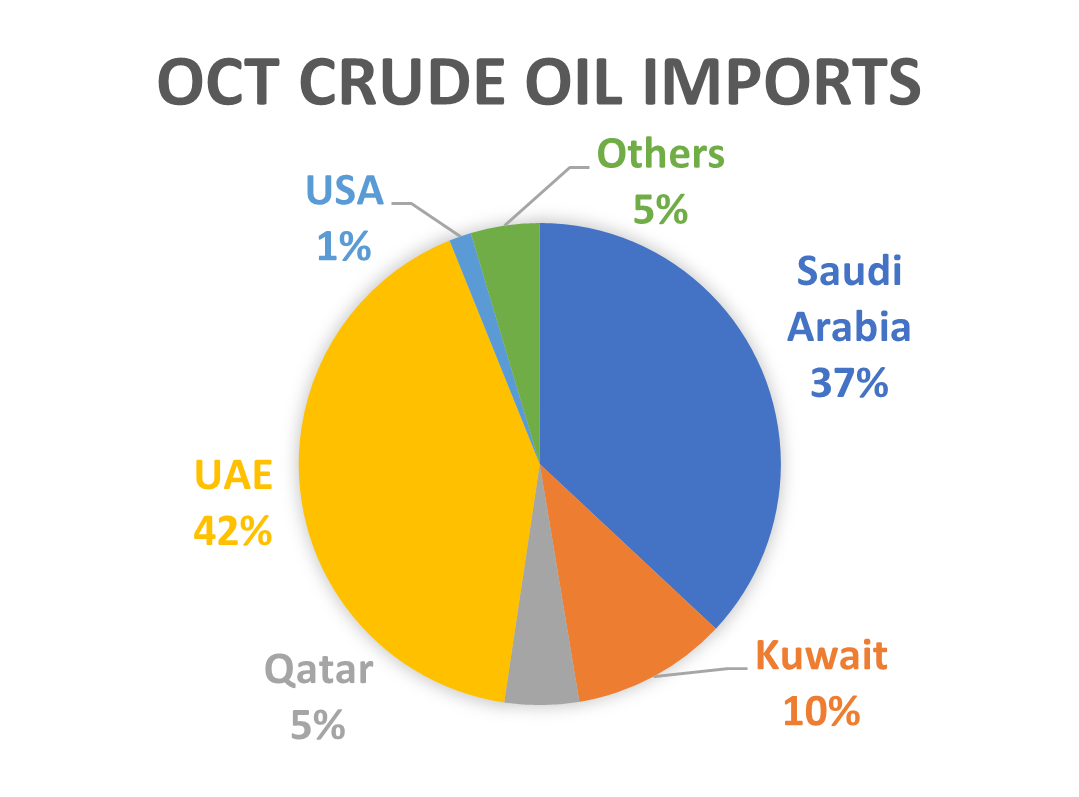

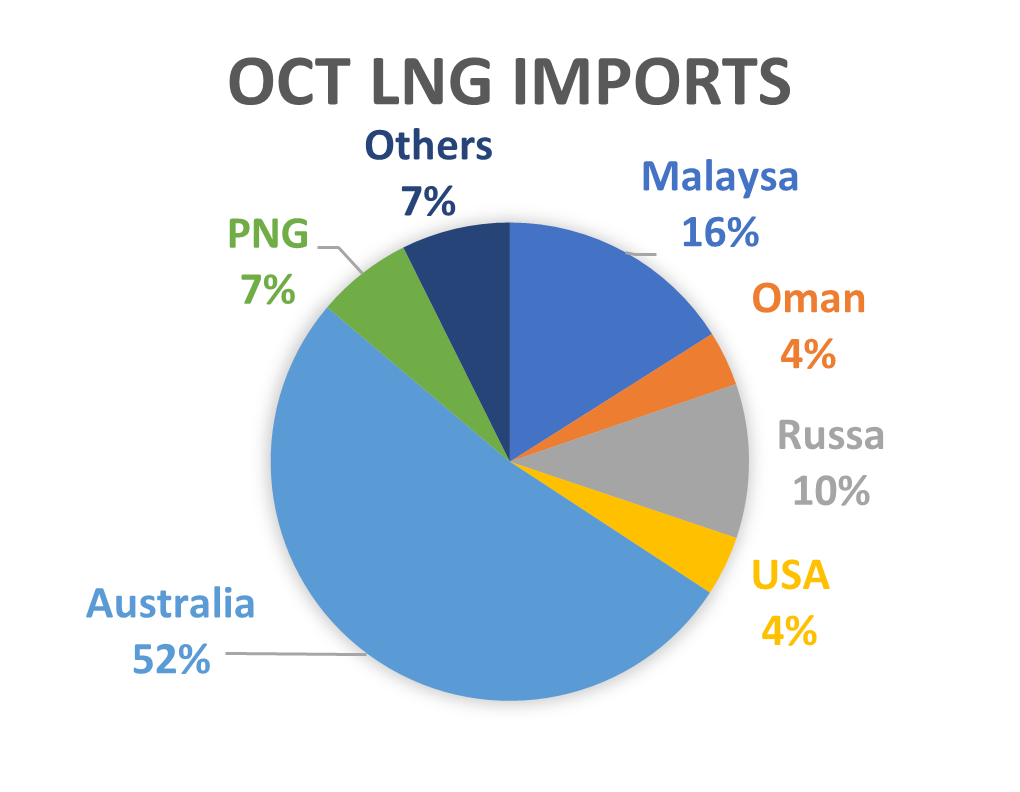

Japan imports zero Russian crude in Oct, but Russian LNG retains 10% share

(Government data, Nov. 29)

- Japan did not import any crude oil from Russia in October, but Russian LNG held 10% share of the total LNG imports, according to customs data.

- October crude oil imports were 12.6 million kiloliters, and the biggest supplier was the UAE with a 42% share followed by Saudi Arabia at 37%.

- October LNG imports were 5.1 million tons. Australia supplied 52%, Malaysia 16% and Russia 10%.

BHP CEO: Green hydrogen will have local uses, not traded globally

(Japan NRG, Nov. 31)

- BHP’s CEO Mike Henry said that green hydrogen will be used in certain industrial applications, such as steel and mining.

- But he doesn’t think green hydrogen will be used widely because of the costs and difficulty of transporting it around the world. In large part, green hydrogen will “more likely be produced and consumed domestically”.

- BHP is reading to use green hydrogen at its mining sites, but it’s not something that the company will pursue as a business opportunity because he doesn’t see the returns on investment to justify such operations.

- Instead, the company will focus on providing the critical minerals that the world needs for the energy transition.

- Mr. Henry spoke at the Reuters NEXT conference in New York (Nov 31-Dec 1).

ANALYSIS

BY JEREMY BOWDEN

Tokyo Gas and the UK’s Octopus

Seek to Upend Power Retail Market

With Japan’s energy retail market in disarray, a 130-year old Japanese power company is teaming up with a 21st century British energy-tech startup. The unexpected alliance between a legacy company and a young innovative business promises to shake up Japan’s power retail sector.

Almost two years have passed since Tokyo Gas purchased a 9.7% stake in the UK-based Octopus Energy for $200 million. The main factor driving the deal was Tokyo Gas’ need for a partner to develop its nascent power retail business in Japan and elsewhere. As the gas provider expanded into electricity, it saw the need to upgrade and adapt to digital technologies while harnessing new demand trends, such as for green power.

In Japan, the alliance centers around a 30/70 joint venture that opened for business about a year ago under the name of TG Octopus Energy. As well as competing on price, the venture aims to turbocharge the development of a demand-response culture in Japan, where awareness of power conservation through lifestyle change is still at an early stage.

As a large portion of the retail market struggles to stay afloat, the Japanese-British venture has the opportunity to gain significant market share. After all, that’s exactly what the UK startup has managed to do in its home market.

Grow the customer base

Next year, Octopus is set to grow its UK customer base by 60%, to about five million individual and corporate customers, pending its takeover of former rival, Bulb, which went into bankruptcy in November 2021. This will make Octopus the UK’s fourth biggest domestic supplier, after just seven years in operation. (In April 2018, Octopus had 200,000 customers).

While the UK liberalized its power market in 1999, Japan only did so in 2016, which means it has high potential for growth from this point. Tokyo Gas sees Octopus as an optimal partner because of its combined focus on digital technology, renewable power, and electricity retailing – it’s basically a green energy tech firm. Octopus says its mission is “to revolutionize energy globally.” In addition to Japan, Octopus has launched in the U.S. and Germany.

On the generation side, its portfolio includes more than 300 renewable energy projects across 11 countries, ranging from rooftop and ground-mount solar farms to wind farms and storage. In Europe, the company manages over £5 billion worth of assets with a total capacity of more than 3 GW.

Since the liberalization of Japan’s electricity market in 2016, Tokyo Gas, which mainly operates in the Tokyo Metropolitan Area, has turned its eye to energy retail by expanding its offering from gas to electrical power.

Going forward, Tokyo Gas wants to focus more on electricity retailing with opportunities opening outside its home region. It also understands the importance of leveraging its legacy gas business to develop a strong footprint in renewables and new services fit for the net-zero age. The UK market provides the perfect parable of what happens when a dominant gas utility fails to do so.

The UK’s top gas provider, British Gas, was privatized in the mid 1980s, and after a corporate restructuring in the late 1990s became known as Centrica. The upstream-focused company enjoyed strong growth until about 2013, but has lost as much as 90% of its market value since then. Today its shares trade for less than when it first listed in March 1995.

In contrast, after raising $900 million from investors earlier this year, Octopus Energy’s valuation approaches that of Centrica despite the startup boasting a fraction of the latter’s customer numbers.

Kraken unleashed

Tokyo Gas isn’t the only partner courting Octopus know-how. In July, Octopus secured a further $550 million investment to improve its technology platform, Kraken, as well as to drive renewable energy generation on a global scale. The turmoil in markets all around the world only spurred on the expansion, according to Octopus founder and CEO Greg Jackson.

Deregulated energy markets have to shift from “dozens of market stalls” to a model closer to supermarkets, “where a few chains offer distinctive products,” Jackson said.

Use of Kraken technology allows Octopus Energy Japan’s customers to trial flexible electricity options, enabling them to save money by driving usage toward times of high renewable generation.

One example is a new tariff in the Tokyo/ Kanto area called “EV Octopus” that includes a cheap and green electricity rate between 2-4 a.m. There are plans to expand this to other regions in the near future.

Another thing Octopus brings to the Japan power market is a firm belief in hedging market risk. While many domestic power retailers have struggled to include that in their business models and got burned by the volatility of electricity prices over the last year, Octopus is pushing regulators to make hedging mandatory. The UK firm says the failure of retailers should not fall on the shoulders of consumers.

Fan clubs and EV leasing

At home in the UK, Octopus has developed an innovative approach to speeding up planning permission, which could be directly applicable in Japan. Dubbed the ‘Fan Club’, it offers households close to one of its (Fan Club) wind turbines discounts of up to 50% on electricity rates when the wind is blowing. Octopus has three operating ‘Fans’ in the UK and plans to build 1,000 more by the decade’s end.

The company has also set up an online platform for developing more onshore wind turbines where people want them called ‘Winder (Tinder for wind).’ This brings together landowners, communities, grid availability and wind speed data. The eventual aim is to reduce the time it takes to build a wind turbine in the UK from an average of seven years to one year.

Another part of Octopus’s business model is an EV all-in-one service. Started in 2018, it offers car lease, charge point installation, and specialist EV energy tariffs. In Europe, the service has access to over 310,000 public charging points. Octopus says EV leasing is a big part of the puzzle for green energy suppliers, enabling optimized EV charging, demand response and storage when integrated into a broader supply system.

Importing overseas green energy tech

The Tokyo Gas stake in Octopus is not the only overseas foray by established Japanese energy companies. A common thread among Japanese firms is striking new alliances to tap into innovative know-how and technologies from the U.S. and Europe, where deregulated markets and high carbon taxes have encouraged innovation.

This will help secure revenue in the face of growing competition, while also decarbonizing their products and solutions. These investments sometimes appear isolated, unfocused and ambiguous, but they’re often part of a strategy to learn and then replicate the knowledge in the home market.

One such investment in early 2020 was in Dutch energy firm Eneco, for which trading house Mitsubishi Corp and Chubu Electric together paid €4.1 billion. Why such a major outlay made sense became apparent about 18 months later, when the two Japanese partners beat out experienced European rivals to win all three major offshore wind auctions at home.

Similarly, Mitsubishi used a 2016 investment in an Irish renewables trading firm, ElectroRoute, to build a sizable PPA business in Japan, booking core clients such as Amazon.

Tokyo Gas now hopes to emulate such success with Octopus. After the big power utilities, the gas firm has quickly grown to be a leading electricity retailer in Japan. However, at a time of great changes, it might be eyeing an even bigger place in the industry ranks.

ANALYSIS

BY ANDREW DEWIT

PROFESSOR OF ENERGY POLICY

SCHOOL OF ECONOMIC POLICY STUDIES

RIKKYO UNIVERSITY, TOKYO

Gap Between Net-Zero Ambitions and Materials Availability

Sets Up a G7 Conundrum

In a few weeks Japan will assume the G7 presidency for 2023, with energy at the top of the agenda. By the time the heads of the European and North American member states arrive in Hiroshima for the summit in May, Japan hopes to greatly expand previous discussions on critical minerals.

Virtually all of the global net-zero dialogue has focused on energy sources and technologies that could or should drive net-zero, and the impact they might have on emissions. Minimal attention has been directed at the key materials required to realize the various scenarios of energy transformation. Judging by recent price increases for several battery and other energy-transition materials, the upstream aspect of net-zero must be addressed.

Lithium prices are up an eye-watering 150% this year, with graphite prices also increasing 13% and set to “do a lithium” next year. Copper, aluminum, and tin have all hit records this year. The impact on the cost of clean energy projects has been dubbed ‘greenflation’, and further troubles appear inevitable due to inadequate mining investment and other factors impinging on constrained supplies of critical minerals.

Recent months have seen Japanese policymakers and analysts come to a consensus that decarbonization is threatened by material constraints, and will need much more robust and coordinated global policy responses. The G7 affords one platform for articulating this concern, aggressively building on its previous two years of recommendations that failed to elicit commensurate action.

Fundamentals behind the narrative

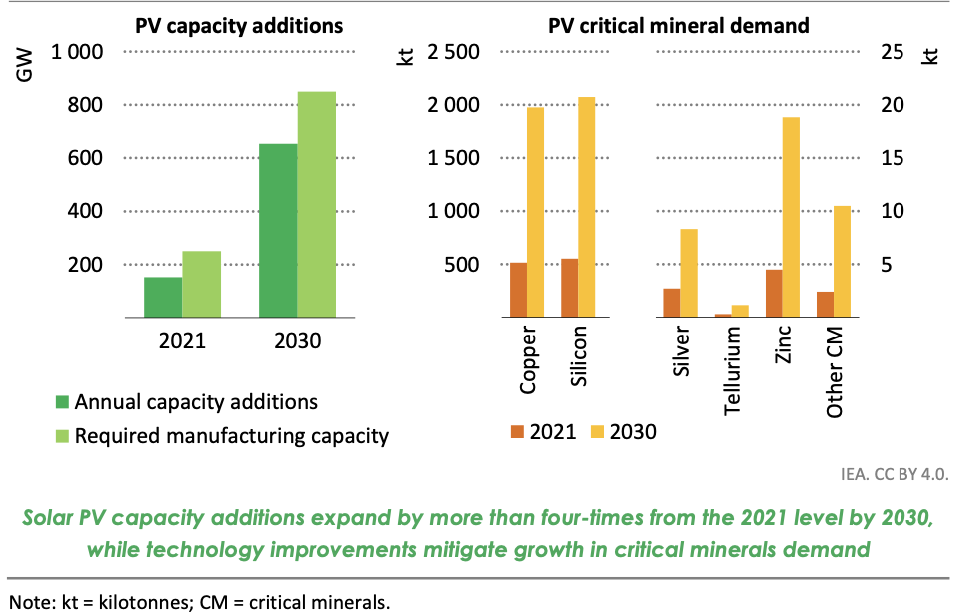

The main demand-side challenges to critical mineral supply are driven by material-intensive decarbonization via intermittent renewables and EVs, but also encompass high-tech digitization, defence, and other areas. One indication of the potential scale of critical mineral demand was seen in the IEA’s 2022 World Energy Outlook, which said that an aggressive net-zero emissions scenario implied 650 GW of new solar capacity by 2030, roughly quadruple the solar capacity added in 2021.

The IEA’s calculations anticipate efficiency gains in the use of critical minerals. Even so, their assessments suggest that for solar assemblies alone (ie, not including storage and transmission infrastructure), copper demand could quadruple over the 9 year-period.

They also point out that in 2021, solar already represented 11% of global silver demand, 6% of metallurgical‐grade silicon, and over 40% of refined tellurium. Though the IEA expects material efficiencies to lead to a 25% reduction in the volume of silver per solar assembly, in 2030 solar’s call on silver still rises to 35% of global production.

The IEA’s estimate of critical mineral demand for net-zero emissions solar capacity additions, 2021 vs 2030

Among similar jaw-dropping outlooks, Bloomberg New Energy Finance warns that global copper production needs to double over the next two decades, from about 21 million tons per year to roughly 40 million tons. This unprecedented increase is just to meet the demand for a 30% penetration of EVs, leaving aside the myriad other calls on copper.

Making matters worse, there are limited prospects for significantly increasing critical mineral mining and refining over the next decade. One major constraint is that average lead times for new mining projects is several years at the very least, with an average of about 16 years for copper. These long lead times are due to the exploration, permitting, infrastructure outlays, and other essential steps before any ore can be extracted from the ground.

An additional problem is the “boom and bust” mining industry’s reluctance to expand exploration and development in response to rising prices. A decade ago, the industry was severely burned when commodity prices dropped and they were compelled to rein in spending and focus on shareholders.

Geopolitical impact

To be sure, myriad analyses indicate that decarbonization and diversifying away from reliance on Russian and Chinese critical minerals promise a new and sustained boom. But as in past busts, the mining industry would again be left holding the bag were they to invest massively only to be surprised by unanticipated technical, geopolitical, or other changes.

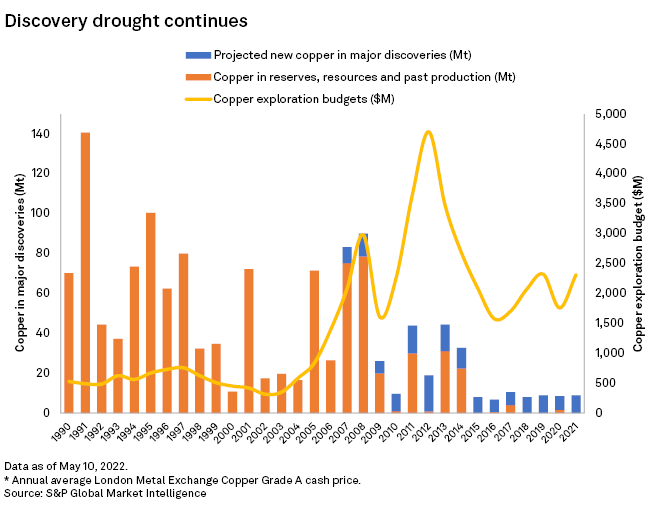

Another worrisome trend – seen in the figure from S&P – is that investments in copper exploration have not only flatlined over the past several years, but are also netting meager returns in new discoveries. Even massive exploration budgets in the mid-2010s led to declining new discoveries, so the industry’s reluctance to throw money at the challenge seems understandable. And what the figure doesn’t show is that depleting ore-grades are also making the business of mining each new ton of copper increasingly expensive.

The above developments don’t mean the sky is falling, but they suggest that many structural factors could further drive ‘greenflation’ increases for critical minerals. Even before the war in Ukraine, materials and other issues led to an historic reversal of long-declining renewable and battery costs, with wind and solar up 9% and 16%, respectively, in 2021.

Those costs continued rising this year, and are expected to balloon even more under demand pressure from the renewables and electrification projects of the U.S., EU and other countries. For Japan, the challenges are daunting since the country has no appreciable domestic mining of critical minerals. The possibility of seabed mining projects might only start in 2028.

Japan’s outlook

The Institute of Energy Economics Japan (IEEJ) and the Japan Organization for Metals and Energy Security (JOGMEC) collaborated on a critical minerals demand study that was released in early November. The IEEJ said the results underscore the need to analyze supply and price risks in light of the total system costs of intermittent renewables – by that, they mean the transmission, storage and other mineral-intensive infrastructure needed to connect and manage wind and solar capacity in the overall power system.

This should concern Japanese policymakers, as current plans call for 52 GW of new solar capacity during the 2020s and a 45 GW installation of offshore wind over the next 20 years. Those substantial numbers have a massive material footprint that Japan may struggle to meet as China, the U.S., the EU, and others also build renewable power generation.

These concerning developments have led Japan to further ramp up policy support for critical minerals. Japan’s 2020 New International Resource Policy stressed an enlarged state role in financing critical mineral projects overseas, in addition to expanding and fine-tuning strategic stockpiles of the commodities at home.

More recently, Japan has been expanding its policy ambitions through a proposed integration of industrial policy tools to encompass supply-chain security for critical minerals in 11 crucial areas, including batteries, permanent magnets, and microprocessors, where Japan keeps losing market share and now confronts resource constraints.

Japan’s bolstered tools range from increased resource-diplomacy and project financing to fostering the skilled human capital essential to these rapidly expanding industries. And this initiative is to be financed through over ¥1.3 trillion in emergency finance via a second supplementary budget for FY2022.

Japan seems likely to highlight its measures at the May G7 meeting in Hiroshima. In advance of taking over the G7 Presidency, Japan’s top policymakers and experts are compiling a credible list of recommendations for the increasingly fraught area of critical minerals. So, Japan is now one to watch in the vital area of matching ambitious decarbonization scenarios with the means to actually realize them.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Australia/ Wind power

Construction will soon begin on Golden Plains. The developer, TagEnergy, secured funding of A$2 billion ($1.3 billion) after years of delays. The first stage involves a 756 MW wind farm that will start generating in Q1 of 2025.

China/ Russia energy ties

China will “forge a closer partnership” with Russia in energy, helping the Kremlin skirt western sanctions. No details were given. Chinese leader Xi made the comment in a letter to the 4th China-Russia Energy Business Forum. In October, China’s energy purchases from Russia more than doubled, YoY, to $10.2 billion.

Denmark/ Biogas

Shell will buy Nature Energy Biogas from Davidson Kempner Capital for $2 billion, becoming the EU’s largest producer of renewable natural gas (RNG). Nature Energy plans expansion in the EU and North America.

EU/ Natural gas

The EU is importing a record amount of seaborne Russian gas. Imports of Russian LNG to the EU rose more than 40%, YoY, between January and October.

EU/ Oil price cap

To curb the Kremlin’s revenues, Brussels will enact a $60 ceiling on Russian oil. Poland, however, wants a cap of around $30. Dec 5 is the start of the ban on Russian seaborne oil shipments into the EU.

Germany/ Natural gas

Qatar will provide Germany with LNG under a long-term supply deal. About 2 million tons of LNG will be sent annually for at least 15 years; deliveries are expected to start in 2026.

Italy/ Oil refinery

Crossbridge Energy Partners is negotiating an agreement with Lukoil that would value the ISAB refinery in Sicily at €1bn to €1.5 billion. Global commodity trader Vitol will help to finance the deal.

Russia/ Gas infrastructure

Gazprom announced $35 billion in investment for 2023, a 15% YoY increase. The company is preparing to embark on major capital-intensive projects that may include new gas pipelines to China.

UAE/ Natural gas

State-owned ADNOC approved $150 billion for the next five years to set up its gas subsidiary and list its shares on the Abu Dhabi Securities Exchange. The new company, ADNOC Gas, will begin operations on January 1, 2023.

U.S./ Carbon costs

The EPA proposed a new value for the social cost of CO2 emissions, almost quadruple from the Obama Administration’s $51/ ton. The EPA now proposes $190/ ton, which would make new oil and gas projects very difficult.

Venezuela/ Oil shipments

Chevron is allowed to resume oil exports that were halted in 2019 when the U.S. increased sanctions against Venezuela. The first tanker carrying about 1 million barrels could set sail this month.

2022 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

|

January |

OPEC quarterly meeting; JCCP Petroleum Conference – Tokyo; EU Taxonomy Climate Delegated Act activates; Regional Comprehensive Economic Partnership (RCEP) Trade Agreement that includes ASEAN countries, China and Japan activates; Indonesia to temporarily ban coal exports for one month; Regional bloc developments: Cambodia assumes presidency of ASEAN; Thailand assumes presidency of APEC; Germany assumes presidency of G7; France assumes presidency of EU; Indonesia assumes presidency of G20; and Senegal assumes presidency of African Union; Japan-U.S. two-plus-two meeting; Japan’s parliament convenes on Jan. 17 for 150 days; Prime Minister Kishida visits Australia (tentative) |

|

February |

Chinese New Year (Jan. 31 to Feb. 6); Beijing Winter Olympics; South Korea joins RCEP trade agreement |

|

March |

Renewable Energy Institute annual conference; Smart Energy Week – Tokyo; Japan Atomic Industrial Forum annual conference – Tokyo; World Hydrogen Summit – Netherlands; EU New strategy on international energy engagement published; End of 2021/22 Japanese Fiscal Year; South Korean presidential election |

|

April |

Japan Energy Summit – Tokyo; MARPOL Convention on Emissions reductions for containerships and LNG carriers activates; Japan Feed-in-Premium system commences as Energy Resilience Act takes effect; Launch of Prime Section of Japan Stock Exchange with TFCD climate reporting requirement; Convention on Biological Diversity Conference for post-2020 biodiversity framework – China; Elections: French presidential election; Hungarian general election |

|

May |

World Natural Gas Conference WCG2022 – South Korea; Elections: Australian general election; Philippines general and presidential elections |

|

June |

Happo-Noshiro offshore wind project auction closes; Annual IEA Global Conference on Energy Efficiency – Denmark; UNEP Environment Day, Environment Ministers Meeting – Sweden; G7 meeting – Germany |

|

July |

Japan to finalize economic security policies as part of natl. security strategy review; China connects to grid 2nd 200 MW SMR at Shidao Bay Nuclear Plant, Shandong; Czech Republic assumes presidency of EU; Elections: Japan’s Upper House Elections; Indian presidential election |

|

August |

Japan: Africa (TICAD 8) Summit – Tunisia; Kenyan general election |

|

September |

IPCC to release Assessment and Synthesis Report; Clean Energy Ministerial and the Mission Innovation Summit – Pittsburg, U.S.; Japan LNG Producer/Consumer Conference – Tokyo; IMF/World Bank annual meetings – Washington; Annual UN General Assembly meetings; METI to set safety standards for ammonia and hydrogen-fired power plants; End of 1H FY2022 Fiscal Year in Japan; Swedish general election |

|

October |

EU Review of CO2 emission standards for heavy-duty vehicles published; Chinese Communist Party 20th quinquennial National Party Congress; G20 Meeting – Bali, Indonesia; Innovation for Cool Earth TCFD & Annual Forums – Tokyo; Elections: Okinawa gubernational election; Brazilian presidential election; |

|

November |

COP27 – Egypt; U.S. mid-term elections; Soccer World Cup – Qatar; |

|

December |

Germany to eliminate nuclear power from energy mix; Happo-Noshiro offshore wind project auction result released; Japan submits revised 2030 CO2 reduction goal following Glasgow’s COP26; Japan-Canada Annual Energy Forum (tentative); Tesla expected to achieve 1.3 million EV deliveries for full year 2022 |

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.