JAPAN NRG WEEKLY

MARCH 6, 2023

JAPAN NRG WEEKLY

Mar. 6, 2023

NEWS

TOP

- Task force calls for separation of transmission asset ownership to limit potential violations by EPCOs

- INPEX buys Mitsubishi Corporation’s 16.7% stake in 950 MW offshore wind farm in Scotland

- Mitsui subscribes to ¥6.4 bln in bonds for Norway’s Hexagon Purus, leading hydrogen tank manufacturer

ENERGY TRANSITION & POLICY

- Agency seeks to prevent unauthorized power data access as the scandal around major utilities attracts new govt. scrutiny

- JCM program to expand to multilateral GHG reduction projects

- J-Credit recognizes rice field drying as a GHG reduction method

- METI to promote overseas geothermal power generation

- Govt to order new strategy to accelerate nuclear fusion R&D

- Municipalities with net-zero pledge cover 99% of the population

- Tokyo Gas, Sumitomo develop Japan’s first H2 reheating burner

- Japan to test marine transport of liquid CO2 next year

- MOL, Methanex conduct first voyage fueled by bio-methanol

ELECTRICITY MARKETS

- Winter power demand down from last year on warmer weather

- METI to make utilities resubmit data for price hikes appeal

- Regulator ruling edges Hokuriku Electric closer to reactor restart

- Kyushu Electric to consolidate renewable energy assets

- METI considers baseload market contracts longer than 1-year

- ANRE mulls auction alternatives for backup power supply

- New power market players lost 19.7% of volume in retail market

- Tokyo Gas to allocate over ¥200 bln for wind power, clean tech

OIL, GAS & MINING

- LNG stockpiles at utilities rise to be at 25% above 5-year average

- Australia supplied 68% of Japan’s coal imports in Jan; Russia: 3%

- Middle East accounts for 95% of Japan’s oil imports in Jan

- NYK takes delivery of the first of four LNG-fueled car carriers

ANALYSIS

JAPAN’S ENERGY MARKET IN

THE NEW WORLD DISORDER

The tectonic geopolitical shifts in 2022 brought tremendous changes to global energy markets. While politics reshaped Japan’s energy sources, import data shows that the country also charted a pragmatic course. War in Ukraine has led to the creation of two major geopolitical blocs. Altering energy flows in line with political positions, however, has proved challenging. While the import of Russian coal and crude oil slowed, Japan’s purchases of Sakhalin LNG actually climbed.

Early trade data from this year indicates that energy pragmatism and security concerns remain Japan’s dominant government and corporate policy. Japan NRG analyzed trade data to see how the new global geopolitical landscape has influenced its energy sector.

NOTES FROM MAJOR SUMMITS LAST WEEK:

ALL EYES ON HOW TO DECARBONIZE

Several big events took place in Tokyo last week, among them the Asia Zero Emissions Community (AZEC) Public-Private Forum and the Japan Energy Summit. While LNG and thermal power featured prominently, almost all discussions and speeches focused on how to decarbonize energy systems and the great uncertainty in demand outlook for fossil fuels in the coming decades. How to bridge traditional and new energy technologies, while maintaining security of supply, remains a key conundrum. We list some of the big talking points from last week’s events.

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Yoshihisa Ohno (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Filippo Pedretti (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

| METI | The Ministry of Energy, Trade and Industry | mmbtu | Million British Thermal Units | |

| MOE | Ministry of Environment | mb/d | Million barrels per day | |

| ANRE | Agency for Natural Resources and Energy | mtoe | Million Tons of Oil Equivalent | |

| NEDO | New Energy and Industrial Technology Development Organization | kWh | Kilowatt hours (electricity generation volume) | |

| TEPCO | Tokyo Electric Power Company | FIT | Feed-in Tariff | |

| KEPCO | Kansai Electric Power Company | FIP | Feed-in Premium | |

| EPCO | Electric Power Company | SAF | Sustainable Aviation Fuel | |

| JCC | Japan Crude Cocktail | NPP | Nuclear power plant | |

| JKM | Japan Korea Market, the Platt’s LNG benchmark | JOGMEC | Japan Organization for Metals and Energy Security | |

| CCUS | Carbon Capture, Utilization and Storage | |||

| OCCTO | Organization for Cross-regional Coordination of Transmission Operators | |||

| NRA | Nuclear Regulation Authority | |||

| GX | Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

ANRE to prevent unauthorized data access by power operators, EGC also probes this issue

(Japan NRG, March 1)

- ANRE began work on measures to keep regional power companies from accessing the customer data of new market players connecting to the grid. Separate from ANRE, the Electricity and Gas Market Surveillance Commission (EGC) is probing this issue.

- ANRE is reviewing the effect of separations of different operational units, data management required, governance and market competition issues.

- Members of the Electricity and Gas Basic Policy Sub Committee called for more rigid separation between the power system operation and other units of regional utilities. One panelist urged a review of the EGC as well, since it failed to spot incompliance although it had been monitoring the activities of different units after the 2020 separation.

- SIDE DEVELOPMENT:

Task force calls to separate ownership of transmission companies from EPCOs, violators might see license revoked

(Denki Shimbun, March 3)- The Task Force for regulation of Renewable Energy, which is under the Cabinet, required EPCOs to separate ownership of their power transmission companies; this is in response to recent unlawful computer access issues by the EPCOs.

- With reference to the Electricity Business Act, the Task Force requested to cancel the license of power transmission companies that lack compliance.

- They also accused the Electricity and Gas Market Surveillance Commission (EGC) of failing to detect the issue beforehand.

TAKEAWAY: Separating transmission companies is a first important step to prevent further such abuses and unlawful access; but this might not be so feasible due to the proprietary right issue of power transmission equipment.

- SIDE DEVELOPMENT:

Tohoku Electric scandal: Unauthorized access to customer information worse than thought

(Nikkei, March 1)- Tohoku Electric said 214 people gained illegal access to customer data — on 36,980 occasions — from their power management company Tohoku Electric Power Network.

- Also, there were 9,402 incidents of illegal access by 75 employees at two contractors.

- In January the company said the number was 130, but then corrected that figure upon further investigation.

Cabinet submits proposed amendments of nuclear and renewable laws to parliament

(Government statement, Feb. 28)

- The Kishida Cabinet submitted to the Diet amendments for nuclear and renewable energy laws, to allow NPPS to operate beyond 40 years, to mandate renewable operators to communicate their plans with local stakeholders ahead of plant construction, etc.

TAKEAWAY: Kishida made it clear that the state will be responsible for satisfying demands of stakeholders in communities affected by nuclear projects. In contrast, renewable operators, including offshore wind stations in EEZ, are responsible for striking agreements with the various stakeholders themselves.

JCM to expand to multilateral GHG reduction projects

(Japan NRG, March 1)

- Joint Crediting Mechanism, a system to transfer carbon offset credits to Japan from overseas, will be expanded to include projects involving multiple countries.

- Takahashi Yasuo, the executive director of Institute for Global Environmental Strategy (IGES), told a sustainability law forum in Tokyo that governments are discussing rules on dividing the offset credits among several countries. Presently, credit transfers are bilateral undertakings between Japan and a partner country.

- JCM’s principle remains unchanged – providing decarbonizing tech to developing nations. The transfer of credits from industrialized economies to Japan will be implemented in a framework separate from JCM, Takahashi added.

- CONTEXT: Many carbon capture and storage and carbon recycling projects are planned in North America and Australia. Project participants have been seeking expansion of the JCM framework to include industrialized economies.

TAKEAWAY: Use of market mechanisms such as the JCM have been an important part of Japan’s GHG reduction strategy since the days of the Kyoto Protocol. One reason why Japan puts a strong focus on earning credits from decarbonization projects in developing economies is that project costs are likely to be lower there.

J-Credit recognizes rice field drying as GHG reduction method

(Government statement, March 1)

- The Ministry of Agriculture, Forestry and Fisheries said rice field drying was added to the GHG reduction methodology of the J-Credit carbon offset system.

- From mid-April, rice farmers that extend the field drying period by seven days or more from the past two-year period will be awarded GHG offset credits.

- CONTEXT: For one to two weeks, water in the rice fields is removed to prevent weeds growing and to strengthen the roots of rice plants. This process also cuts methane emissions. Rice fields account for over 40% of Japan’s total methane emissions.

METI drafts resource recycling action plan

(Japan NRG, Feb. 27)

- METI drafted a resource recycling action plan called the Growth Oriented and Self-sufficient Resource Economy Strategy to drive recycling.

| Challenges | Solutions |

| Quality improvement | Transparency throughout the value chain |

| Stabilizing available quantities | Setting up collection points and providing data |

| Pricing | Data systems for each secondary commodity |

| Expanding applications | Exploring resources that have not been recycled |

| Designing products to make it easier to recycle | Sharing information on raw materials used |

| Making one’s contribution to sustainable economy more visual | Possibly providing benefits to parties making significant contributions in circular economy |

- METI plans to strengthen surveys of critical resources and include ambitious recycling projects to the GX financing program.

- The goal is to double the recycling capacity of spent batteries and electronic scrap and plastics by 2030.

- CONTEXT: The size of the recycled materials market, dubbed “circular market”, is estimated to now be ¥50 trillion and will grow to ¥80 trillion by 2030, according to METI’s plan.

TAKEAWAY: Japan is a global technology leader in the recycling of platinum group metals, which are used as catalysts to speed up hydrogen and ammonia chemical reactions. However, due to high labor costs of collecting and sorting scrap, Japan relies on China, Southeast Asia and Russia for materials that are not as highly priced as platinum, such as recycled aluminum alloys.

Municipalities declaring net zero now cover 99% of country’s population

(Japan NRG, Feb. 28)

- The number of municipalities pledging to be carbon neutral by 2050 hit 831; they cover 99% of the Japanese population, according to the MoE.

- However, few municipalities have set detailed roadmaps to net zero and the MoE has launched a promotional zone program that will serve as a model for others.

- The municipalities in the program will set roadmaps by 2025. They are also required to name businesses operating in their areas as project partners.

TAKEAWAY: Community conflicts caused by renewable projects have resulted in tighter regulations on renewables operators, but the MoE plans to drive sustainable energy development at municipal levels.

METI to promote overseas geothermal power generation

(Nikkei, Feb. 26)

- METI will promote exploratory drilling companies participating in overseas projects, possibly in Indonesia and New Zealand, where INPEX is considering expansion of existing geothermal power plants and new geological surveys.

- ¥630 million is included in the FY2023 budget. JOGMEC will provide funding.

- The international cooperation will help METI to gain the knowledge and know-how necessary for geothermal power generation technology.

TAKEAWAY Many suitable sites for geothermal power are in national or national sponsored parks, and thus development is slow. According to METI, geothermal power related sources in Japan have a capacity potential of 23 GW, one of the world’s biggest. However, current geothermal power capacity is only 600 MW, 0.3% of Japan’s total power. This is why METI has been working to revise the regulation since 2021.

- SIDE DEVELOPMENT:

Japan to lend Indonesian utility PLN $200 mn for renewable energy

(Asia Nikkei, March 3)- Japanese banks are due to lend $200 million to Indonesian state-owned power utility PLN as part of a Tokyo-backed effort to speed a transition from coal to renewable energy.

- Nippon Export and Investment Insurance (NEXI) was due to sign an MoU with PLN as part of the Asia Zero Emission Community initiative.

- CONTEXT: PLN, or Perusahaan Listrik Negara, plans no new coal-fired power plants and will replace existing ones with solar and geothermal plants from 2025.

Government orders new strategy to accelerate development of nuclear fusion

(Denki Shimbun, Mar. 2)

- The Council of Advisers on How to Develop Nuclear Fusion Technology called for a strategy to develop nuclear fusion by April 2023.

- Next, the Cabinet will discuss more specific roadmaps both for nuclear fusion technology development and for suppliers.

- The government decided to “realize fusion power generation as early as possible” instead of the previous vague goal of “around 2050”.

TAKEAWAY: The GX calls for completing a detailed design for a prototype nuclear fusion reactor by 2030 and construction by 2050. Other nuclear tech, such as next-gen PWR / BWR, SMR, fast reactor and HTGR (high temperature gas-cooled reactor), are all scheduled to start operation before mid 2040s. Thus, nuclear fusion will be the last of the new technologies to start generating electricity.

Cabinet approves 60+ year operation of NPP reactors

(Nikkei, Feb. 28)

- The Cabinet approved laws to allow operation of NPP reactors for more than 60 years. A suite of laws, including the Electricity Business Act and Atomic Energy Fundamental A, would be amended under this cabinet decision.

- This is a big change to the rule that was decided after the Fukushima disaster, which set maximum operation years for reactors as “Originally 40 years, but can be extended for 20 years if approved by the NRA (40 + 20 = 60)”.

- Under the new rule, the original operation year is lessened to 30 years, but a three-time extension of 10 years each is possible. Moreover, the reactors are allowed to exclude the period of time they were forced to stop by the government; therefore, this is the equation being used: (30 + 10 + 10 + 10 + stopped years).

TAKEAWAY: While it’s true that this amendment offers relief for utilities, since many reactors are already aged, early replacement may be required for both sound management and stable supply.

Tokyo Gas and Sumitomo subsidiary developed Japan’s first H2-firing reheating burner

(Company statement, Feb. 28)

- Tokyo Gas and Sunray Reinetsu, a subsidiary of Sumitomo Electric, developed Japan’s first reheating burner for a hydrogen-firing gas turbine cogeneration system.

- By combining this product with a gas turbine that generates power using 100% hydrogen, it will realize zero CO2 emissions from the entire gas turbine cogeneration system. It also reduces NOx emissions to the same level as city gas.

- CONTEXT: Gas turbine cogeneration systems with a supplementary burner can increase the amount of steam generated by waste heat boilers by further heating its own exhaust.

CO2 marine transportation to be tested next year at Maizuru power station

(Yomiuri Shimbun, March 2)

- Japan’s first demo to transport liquefied CO2 by ship will begin in 2024 at KEPCO’s Maizuru thermal power station. The aim is to solve problems such as temperature control during transportation and establish stable transport technology by FY2026.

- CO2 storage facilities will be built at the Maizuru power station and in Tomakomai (Hokkaido). The facilities will be linked by cargo ship. Total cost is about ¥16 billion.

TAKEAWAY: Japan aims to put technology for capturing and storing CO2 into practical use by 2030. The storage sites are expected to be mainly underground on the seabed, but proper management of temperature and pressure will be necessary to safely transport liquefied CO2.

Mitsui subscribes to bond issue for Hexagon Purus, leading hydrogen tank manufacturer

(Company statement, March 2)

- Mitsui will subscribe to about ¥6.5 billion in convertible bonds of Norway’s Hexagon Purus, one of the world’s largest hydrogen tank manufacturers. The two companies will promote new businesses related to vehicle electrification.

- Hexagon Purus is a subsidiary of Hexagon Composites, in which Mitsui has invested since 2016.

- CONTEXT: Mitsui has developed compressed hydrogen that is used in Europe and the U.S. as fuel for fuel cell vehicles (FCEV) and for land transportation of hydrogen.

MOL and Methanex completed the first net-zero voyage fueled by bio-methanol

(Company statement, Feb. 28)

- Mitsui OSK Lines (MOL) and Methanex announced that the dual-fuel vessel, “Cajun Sun,” successfully completed the first-ever, net-zero trans-Atlantic voyage fueled by bio-methanol. (Video in English, link https://youtu.be/U9G4Ym9qNEg)

- The use of methanol as an alternative marine fuel was pioneered in 2016 by Waterfront Shipping partnering with Methanex, MOL, and others. A net-zero voyage means the total GHG emissions measured on a lifecycle basis, including the avoided emissions that occurred during bio-methanol production.

- MOL plans to further develop bio-methanol to decarbonize marine shipping.

- SIDE DEVELOPMENT:

MOL and Air Water studies use of liquefied bio-methane as marine fuel

(Company statement, Feb. 22)- Mitsui OSK Lines (MOL) and Air Water signed an MoU to study the use of liquefied bio-methane (LBM) that’s derived from cattle manure for use in LNG fueled vessels. Air Water produces LBM in Hokkaido and supplies MOL.

- This study is part of an LBM R&D program approved by the MoE. The two companies will verify if LBM can be transported, supplied, and used with the existing shore and onboard equipment. If successful, this will be Japan’s first use of LBM as marine fuel.

- Methane is the main component of LBM and LNG, and the current LNG supply chains can be used. LBM reduces CO2 emissions more than LNG does.

“K” LINE trials use of B24 marine biofuel supplied by BP to JFE Steel’s bulker

(Company statement, Feb. 22)

- Kawasaki Kisen (“K” LINE) conducted a trial use of B24 marine biofuel blended with very low sulfur fuel oil supplied by BP to the capesize bulker, “Cape Tsubaki” that’s chartered by JFE Steel Corp.

- The biofuel was stored for two months in a tank and used during the voyage from Ponta da Madeira to Japan. No problems were reported. The blended fuel is expected to achieve a 80-90% reduction in GHG emission from fuel generation to consumption, without changing current engine specifications.

IHI begins studies on green ammonia business in India

(Company statement, Feb. 21)

- IHI signed a MoU with ACME, a leading renewable energy company in India, to study the feasibility of producing and utilizing green ammonia derived from renewable energy.

- IHI is mulling green ammonia projects led by ACME, in Oman, India, the U.S., and Egypt. IHA is also studying ammonia co-firing in thermal power plants in India to contribute to early implementation of ammonia fuel and decarbonization.

NEWS: POWER MARKETS

Winter power demand down from last year on warmer temperatures, power saving

(Japan NRG, March 1)

- ANRE said power demand slid from December to February due to warmer temperatures and power saving efforts on the back of rising prices: December demand was down 1%; January down 5%; and the first three weeks of February were down 9%.

- On January 25-31, temperatures were the lowest in the last five years and power demand rose 6%. But there was no critical power shortage.

- Consumption by households and businesses decreased due to power conservation.

METI to make utilities resubmit data for price hikes appeal

(Asahi Shimbun, March 1)

- METI will review the latest data on foreign exchange rates and fuel import prices, which are the basis for the electricity prices increase. This will help to reduce the electricity price hikes that seven major power companies have requested.

- As the yen and fuel prices become more stable, METI believes it will be possible to limit the price increase and will ask companies to resubmit their most recent data.

- The electricity rates under discussion are ‘regulated fees’ that require government approval. Companies plan to raise rates by an average of 28-45%.

Regulator ruling helps Hokuriku Electric’s reactor move closer to a restart

(NHK, March 3)

- Nuclear regulator said that Hokuriku Electric’s Shika NPP does not sit on an active geological fault line. That is a shift in NRA’s opinion from seven years ago, when it stated it as a possibility and thus started a years-long review of the geology.

- CONTEXT: The NRA’s previous assessment required Unit 1 of the station to be decommissioned and Unit 2 to undergo major modifications.

- The utility presented evidence using a new evaluation method using the state of minerals in the soil to show they have not been disturbed by a fault. The data presented by Hokuriku Electric has convinced the NRA, the regulator said.

TAKEAWAY: Hokuriku Electric has not even applied to restart Unit 1 of Shika NPP, but it did do so for Unit 2 in 2014. This ruling suggests that a Unit 2 restart is now looking more likely. However, the NRA is yet to conclude a host of other reviews around the safety of the site, so the regulatory approval is still a way off.

Kyushu Electric will consolidate renewable energy capacity with subsidiary Kyuden Mirai

(Denki Shimbun, Feb. 28)

- Kyushu Electric will consolidate its renewable energy business with its subsidiary Kyuden Mirai Energy. Firstly, geothermal will be transferred in April 2024, and hydro capacity will follow.

- Kyuden Mirai owns a total of 100 MW of renewables capacity, including wind, solar and biomass power. After the consolidation, Kyushu says its renewable energy assets will total 1.6 GW, making it Japan’s second largest renewables operator. This capacity breaks down as follows: 50% hydro, 21% biomass, 14% wind, 9% geothermal, and 6% solar.

- By 2030, the company’s renewables capacity will almost double to 5 GW.

INPEX buys Mitsubishi’s 16.7% stake in 950 MW Scottish offshore wind farm

(Denki Shimbun, March 3)

- INPEX, Japan’s largest oil and gas exploration and production company, acquired Mitsubishi’s 16.7% stake in the Moray East offshore wind farm in Scotland, which began operation in April 2022 and consists of one hundred 9.5 MW wind turbines.

- Other Moral East shareholders include Kansai Electric, EDP Renewables and ENGIE.

TAKEAWAY: One reason why INPEX is keen to develop offshore wind is because the technology has much in common with drilling for oil and gas. This is the company’s third offshore wind project; the other two are in the Netherlands and were acquired last year.

Baseload power auction fetches higher prices

(Government data, Feb. 27)

- The Jan 31 baseload power auction closed at ¥25.30/ kWh for east Japan; and ¥20/ kWh for west Japan; compared to ¥14.87/ kWh and 14.50/ kWh a year ago. There was no settlement for the Hokkaido area.

- The transactions totaled 280 GWh for delivery in April 2023-March 2024, down from 510 GWh a year ago.

- CONTEXT: Baseload power auctions are held four times a year. This was the last auction for the current fiscal term.

TAKEAWAY: Out of the 280 GWh transacted, 270 GWh were in west Japan. East Japan is seeing limited activity possibly due to a lack of nuclear power online. If the restart of TEPCO’S Kashiwazaki Kariwa NPP Unit 7 is delayed after the October timeline set out by the company, it will have ripple effects beyond the Tokyo utility. The baseload market may not be functional at all.

METI to discuss baseload market contracts longer than 1-year

(Denki Shimbun, Feb. 28)

- At the System Design Working Group of the Advisory Committee METI said it began discussion around introducing contracts longer than one year for the baseload market.

- Under the present rule, baseload contracts cover following-year generation at nuclear, large hydro and coal-fired power plants owned by EPCOs. The main buyers are new power market players.

- If the contract term is extended beyond a year, then fuel price volatility could be higher. Thus, the working group presented two ideas to reduce risk: 1) allow fixing the price at the time when the year changes, and 2) add a system to adjust prices automatically.

TAKEAWAY: In 2019, Japan launched the baseload market to secure electricity at affordable cost and bridge the imbalance between EPCOs (which own large power plants) and new power market players (which often own small plants or none at all). The system was meant to ensure that EPCOs supply a certain amount of electricity to the baseload market. However, prices are not always as low as expected. Officials hope that a change to market design can improve its liquidity and operation.

ANRE mulls auction alternatives for backup power supplies

(Japan NRG, Feb. 27)

- ANRE seeks alternatives to auctions for securing backup power supplies, due to a lack of consistency in its availability.

- One possibility is to float a tender with a wide selection criterion including non-price factors, and another is selecting suppliers without a formal bidding process if potential suppliers are limited.

- CONTEXT: Backup power is positioned as a long-term source that complements the capacity market. The power type, size, launch schedules, management organization, and financial rules have yet to be decided.

Tokyo Gas allocates about ¥215 billion in investments for wind power, climate tech

(Company statement, Feb. 22)

- Tokyo Gas announced a ¥1 trillion investment plan for the FY2023-2025 period focused on green transformation (GX). Of that money, ¥650 billion will go into so-called growth investments.

- One-third of the growth investments are in decarbonization fields. In particular, the utility will focus on wind power; its capacity will reach 2.2 GW by 2025, up from the current level of 1.5 GW.

- The company plans an annual 12-million-ton reduction of CO2 by FY2025. This includes using more “carbon neutral LNG (CNL)” and developing a global e-methane supply chain on a commercial scale.

- CONTEXT: In early February, Tokyo Gas said it would start a study for a 30 MW floating wind farm off Fukushima Prefecture’s coast, aiming to start operations in 2027. In addition, Chiba and Ibaraki prefectures are also considered.

EPCOs still supply power to corporate clients that switched to new power market players

(Nikkei, Feb. 28)

- Around 41,000 corporate clients which had switched their power supplier from EPCOs to cheaper new market players, and saw those go bankrupt or withdraw from service, still haven’t found a replacement.

- This number peaked in October 2022 at 46,000 companies. Since then, only 10% have found new power suppliers. The remaining 41,000 now get electricity from EPCOs as “Final power supply security” customers, which must pay extra charges for the electricity.

- Complying with METI’s requirements, the EPCOs will accept their former clients as a “standard customer” starting April 2023.

TAKEAWAY: Many new power market players have stopped signing new contracts to sell electricity, because the more they sell the more they sink into the red. Corporate clients who once left EPCOs are having to return, but are now being asked to pay according to a new price menu. Some corporates can’t afford this, which is why they are listed as “Final power supply security” customers. So, METI has requested EPCOs to accept their former corporate clients at a cheaper standard pricing. EPCOs are complying, but limiting the rate at which they accept the return of their former customers. Due to a sharp hike in fuel costs, EPCOs can’t accept all customers that wish to buy power at the “standard” menu. This is why the number of stranded corporate clients remains high.

New power market players see retail market volume decline 19.7%

(Denki Shimbun, Mar. 2)

- According to the Electricity and Gas Market Surveillance Commission (EGC), the total amount of electric power sold by EPCOs was 48,639 GWh, while new market players sold 10,681 GWh.

- The monthly volume sold by EPCOs fell 2.5% YoY; new retail market players saw their volume decline 19.7%, the second consecutive month of double-digit loss.

- The market share of new power players for November was 18.0%, down 3.1% YoY.

TAKEAWAY: The market share held by new retail players is expected to decline further in December 2022 or January 2023.

Osaka Gas and Leapton Energy agree to buy power from FIP sources

(Company statement, March 1)

- Osaka Gas agreed with Leapton Energy, which installs solar power plants, for long-term power supplies from solar power plants that utilize FIP.

- Osaka Gas will buy 5 MW per year or more — at a fixed price.

- Osaka Gas targets 5 GW of renewable capacity in Japan and overseas by FY2030.

Hitachi Energy to build HVDC factory in India – fourth production base globally

(Denki Shimbun, March 2)

- In February, Hitachi Energy will open a plant in Chennai, India to make high voltage direct current (HVDC) transmission equipment. This is their fourth factory for HVDC t, following a new factory in Sweden last November.

- In reaction to the global trend of building large scale offshore wind farms, Hitachi Energy is receiving orders for HVDC transmission equipment. To date, Hitachi has a total of seven orders from India.

TAKEAWAY: Hitachi’s engineering know-how for HVDC equipment mostly depends on ABB’s grid business, which it fully took over in 2022. The origin of HVDC dates to 1954 when Asea (which represents the “A” of ABB) built the world’s first HVDC transmission system from mainland Sweden to Gotland Island.

NEWS: OIL, GAS & MINING

Middle East accounts for 95% of Japan’s oil imports in January

(Government data, Feb. 28)

- Japan imported 13.8 million kiloliters (86.8 million barrels) of crude oil in January, up 6.4% YoY. Imports from the Middle East accounted for 95%. Russia had a 1% share.

- LNG imports were 6.82 million tons, flat from 6.79 million tons a year ago; the top three sources were Australia with a 34% share, Malaysia at 16% and Russia at 10%.

LNG stocks rise to 2.4 million tons, about 25% over 5-year average

(Government data, March 1)

- LNG stocks of 10 power grids stood at 2.4 million tons as of Feb 26, up from 2.32 million tons a week earlier. METI initially reported the Feb 19 stocks were 2.57 million tons but corrected the figure.

- The end-February stocks last year were 1.69 million tons. The five-year average for this time of year is 1.98 million tons.

Australia accounts for 68% of Japan’s coal imports in Jan; Russia down to 3%

(Government data, March 1)

- Japan’s coal imports from Australia were 11.05 million tons; Indonesia’s stood at 2.53 million tons. Russia’s coal supplies were 509,500 tons, or 3% of the total.

- Australia took the lion’s share of Japan’s thermal coal imports, with 7.72 million tons, or 72% of Japan’s thermal coal imports. Imports from Russia were 495,710 tons.

NYK Line LNG-fueled car carrier arrives in Hiroshima Port, a first

(Company statement, March 1)

- Nippon Yusen (NYK) received its third LNG fueled car carrier on Feb 27. But this is the first time an LNG-fueled car carrier entered Hiroshima Port. It’s the first of four LNG-fueled car carriers ordered by NYK Line from China’s CSC Jinling.

- The vessel was supplied with LNG from Central LNG Marine Fuel’s vessel KAGUYA, in which NYK has a stake. It will transport vehicles, including for Mazda.

ANALYSIS

BY MAYUMI WATANABE

AND FILIPPO PEDRETTI

Japan’s Energy Market in the New World Disorder

The tectonic geopolitical shifts in 2022 brought tremendous changes to global energy markets. While politics reshaped Japan’s energy sources, import data shows that Asia’s second-largest economy also charted a pragmatic course, especially in relation to the purchase of Russian commodities.

The war in Ukraine has led to the creation of two major geopolitical blocs, with each side grouping consumers into categories of “friendly” and “unfriendly” nations. Japan stood with its G7 allies, denouncing Russia’s February 2022 incursion into Ukraine, and took swift action on sanctions.

Altering energy flows in line with political positions, however, has proved challenging, especially since the ensuing market disarray led to a steep rise in commodity prices. What’s more, inflation and rate increases in western markets significantly weakened the yen, restricting Tokyo’s room for maneuver. So, while the import of Russian coal and crude oil slowed, purchases of its LNG actually climbed.

Early trade data from this year indicates that energy pragmatism and security concerns remain Japan’s dominant government and corporate policy. Japan NRG analyzed trade data to see how the new global geopolitical landscape has influenced the energy sector.

LNG

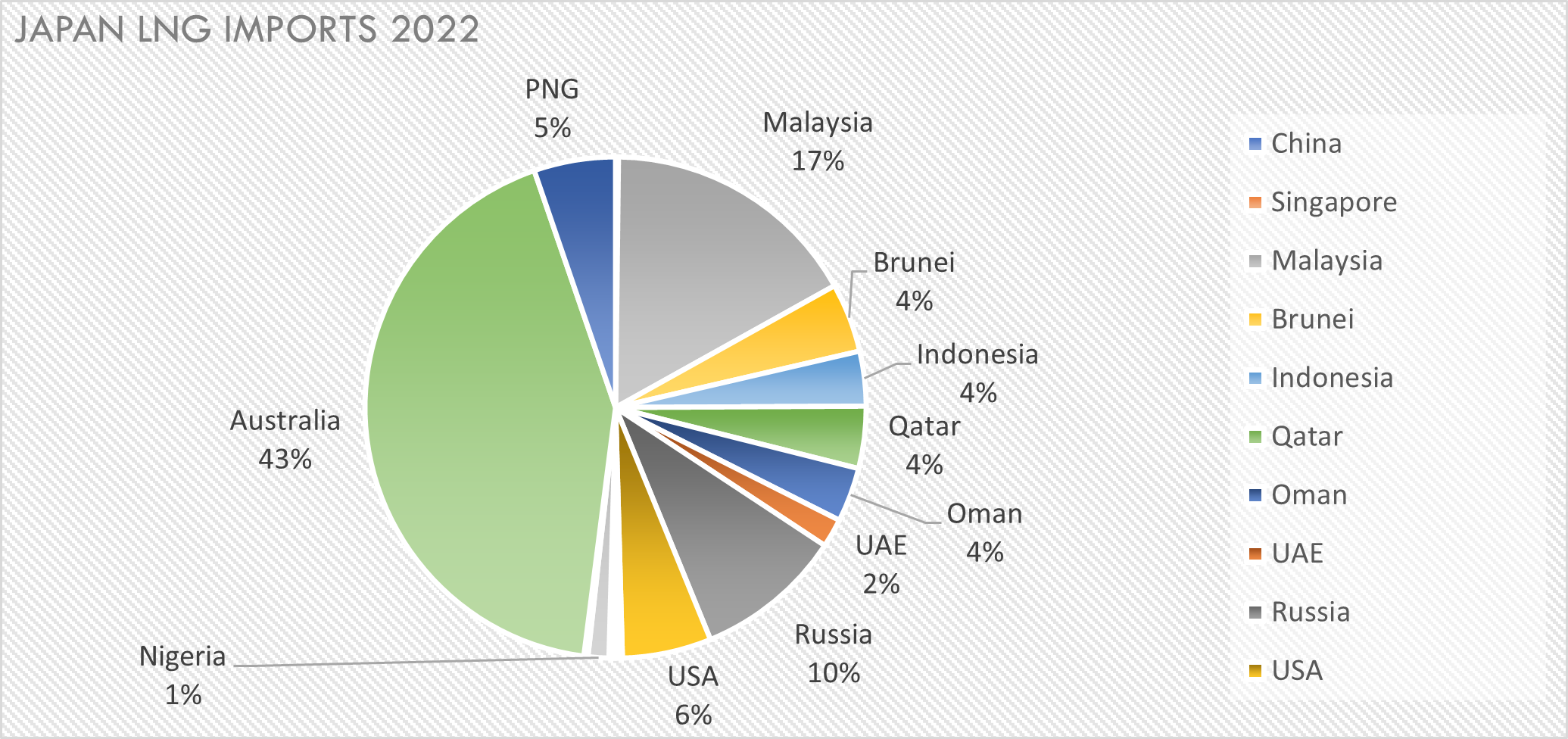

In 2022, the value of Japan’s LNG imports reached ¥8.5 trillion, doubling from ¥4.3 trillion in 2021. That’s despite import volumes declining only slightly to 72 million tons from 74 million tons a year earlier. With Chinese LNG purchase down significantly, Japan retained its crown as the world’s largest importer of the fuel.

Russia held on to its place as Japan’s third largest supplier, trailing Australia and Malaysia. Japan persuaded its G7 partners to exempt gas produced at Russia’s Sakhalin-2 LNG plant from sanctions; the country’s energy security hung in the balance and any damage could have ripple effects.

Russian LNG sales to Japan increased to 6.9 million tons from 6.6 million tons, bringing its share of Japan’s total to 9.5%, up from 8.8% a year earlier.

Nearly all of the Russian gas came from the Sakhalin-2 plant where Japanese trading companies Mitsubishi Corp and Mitsui & Co. continue to hold onto their stakes despite voices of unease both from allies and in Moscow. The reasons for that include decades of investment in Russian LNG infrastructure development and proximity of Sakhalin-2 to Japanese ports. In addition, the price for Russian gas averaged ¥98,640/ ton in 2022, below the overall average of ¥117,356/ ton at which Japan imported the molecules.

Meanwhile, imports from Qatar slumped to 2.9 million tons, from 9 million tons a year prior, reflecting JERA’s decision not to renew a 5.5 million ton/ year long-term contract that expired at the end of 2021. Imports from the U.S. decreased to 4.1 million tons, down from 7.1 million tons, mostly due to the lingering effects of the accident at the Freeport LNG facility in Texas. In late 2021, JERA, the world’s biggest LNG buyer, acquired a 25.7% stake in Freeport.

Australia, the top supplier to Japan, exported 31 million tons of LNG, up from 27 million tons a year ago. Malaysia exported 12 million tons despite a blast at the key Sabah-Sarawak gas pipeline, which has restricted the nation’s exports since October 2022. Supply from Indonesia, Papua New Guinea and Algeria also rose.

In January 2023, Russia accounted for 10% of total imports, behind Australia’s 34% and Malaysia’s 16%.

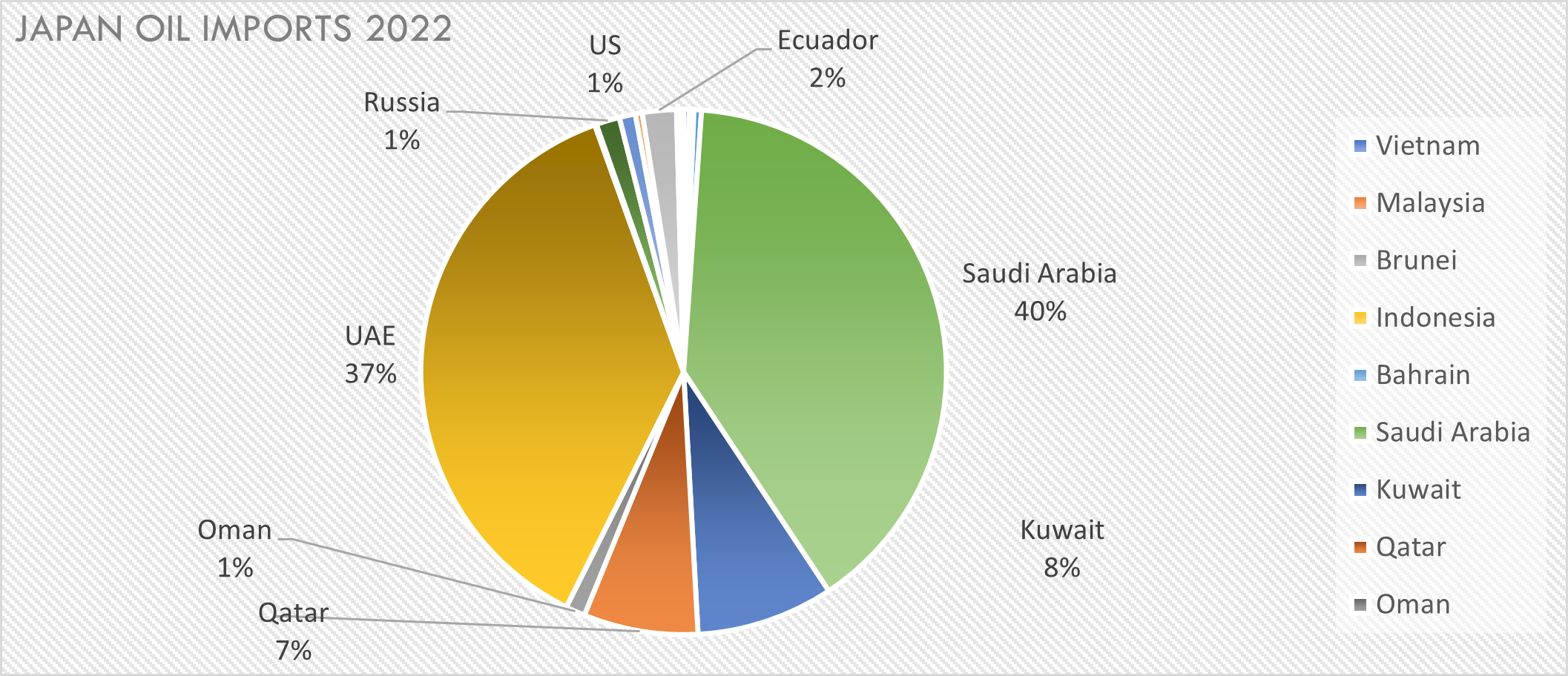

Crude oil

The 2022 total value of crude imports was ¥13.3 trillion, nearly double the previous annual amount of ¥6.9 trillion. By volume, Japan imported a total of 132 billion kiloliters of crude oil (830.28 billion barrels), up 8.6% from a year earlier.

Ironically, in 2022, Japan shifted back to the Middle East, which accounted for a total of 94.1% of crude imports; this compares to 68% in 1987 and 92.7% in 2021. This is a drastic about-face. In the 2010s, Japan specifically increased purchases of Russian crude to shift away from overt dependence on a historically volatile Middle East region.

Imports from Saudi Arabia, the biggest supplier, increased by 7.8% year-on-year to 59 billion kiloliters; and the U.A.E., the second biggest seller for Japan, rose 18% to 49 billion kiloliters. Omani crude surged 150% to 1.6 billion kiloliters.

Despite the smaller market share, Russia remains Japan’s second largest crude supplier outside the Middle East. In 2022, the share of Russian crude oil imports fell to 1.5% of Japan’s total, down from 3.6%, as imports from Sakhalin-1 were suspended. Those imports hit zero from September to December, but Japan will continue to receive Sakhalin-2 crude, a byproduct of LNG that’s exempted from U.S.-led sanctions. Japan has argued that the loss of the crude byproduct would alter the economics of LNG production.

The U.S. was a big winner as oil sales to Japan jumped more than three-fold to ¥144.9 billion. The U.S. expanded its share to 9.9%, up from 7.2%. The price of American oil averaged ¥110/ kiloliter, which was above the overall ¥100/ kiloliter average and the Russian average of ¥91/ kiloliter.

In January 2023, Russia accounted for 1% of Japan’s oil imports. The U.S. had 2%.

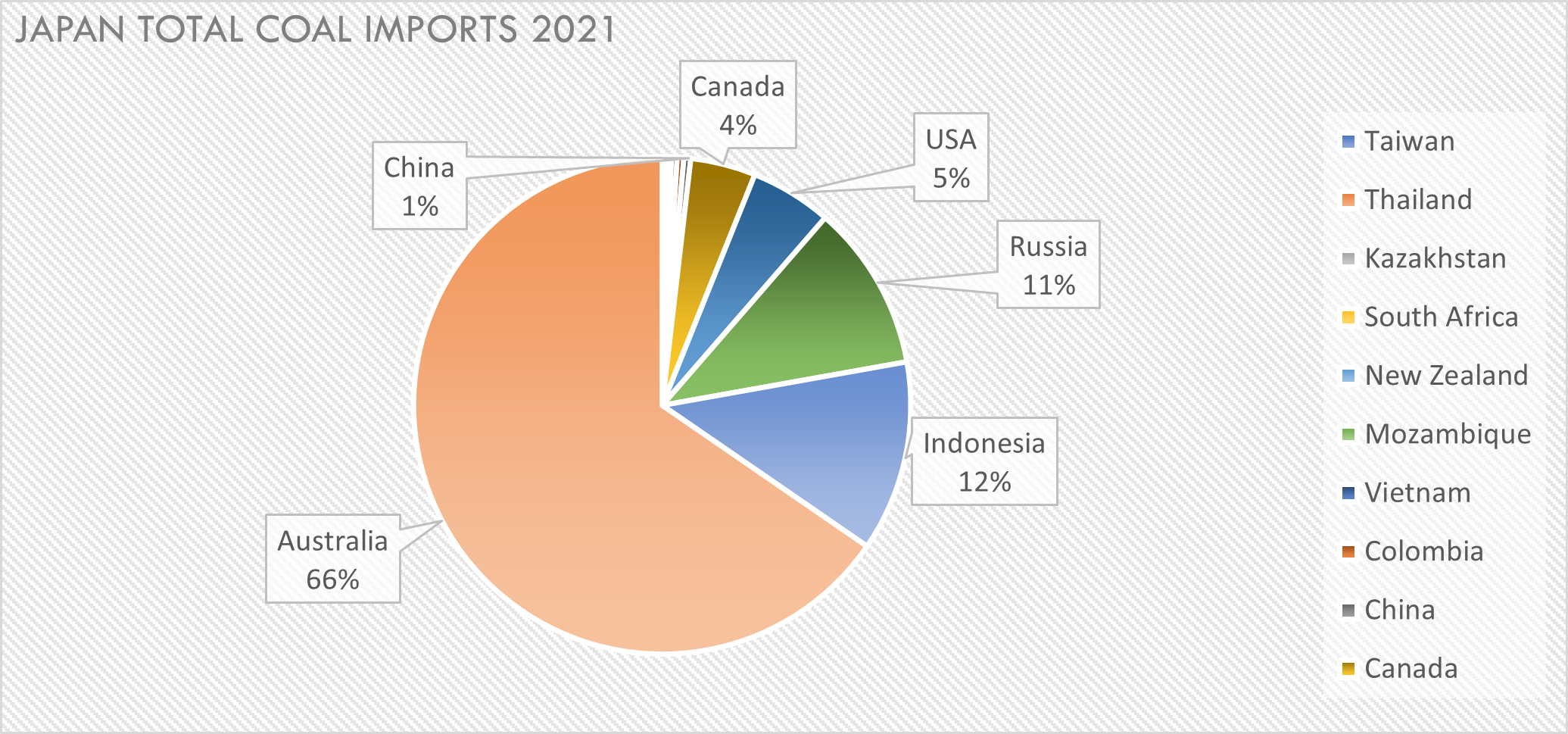

Coal

In terms of coal, 2022 was certainly a difficult year for Japan. While volumes were almost identical to 2021, at 183 million tons, the financial value of imports almost tripled to ¥7.79 trillion. Of the total, 115 million tons were in thermal coal for power generation, and 63 million tons were coking coal for steel production.

Last year, PM Kishida vowed to phase out Russian coal imports, without giving a timeline. Data shows that Japan has halved its dependence on coal from Russia, which accounted for 10.8% of total imports in 2021 and just 6.3% in 2022. Still, Russia remained the third-largest coal supplier after Australia and Indonesia. Canada crawled up to fourth place, thanks to a doubling of its thermal coal exports. Those three countries took market share away from Russia.

In terms of value, Russian thermal coal imports increased dramatically, by 76.7% and unlike LNG or crude oil, the price was not at a heavy discount to global markets, reflecting the challenge of replacing specific grades of the mineral. Russian imports averaged ¥42,936/ ton, less than the cost of Australian coal but higher than Canadian or Indonesian equivalents.

Australia confirmed its position as Japan’s largest coal source, accounting for 67% of total imports. However, Australian thermal coal cost jumped 201.5%, with the benchmark Newcastle price exceeding a record $400 per ton last year.

Although Australian coal is suitable for Japanese power plants due to its low ash and sulfur levels, many companies now intend to look for lower grade alternatives in order to shrink costs. Africa and South America are seen as interesting alternative sources for the fuel. Such strategic planning is even more necessary as China, a top coal importer, prepares for an economic recovery. As a result, Australia’s Newcastle benchmark regressed to just $179.57 per ton at the end of February.

Russian coal imports declined to 3% of Japan’s total in January 2023.

Limits to diversification’s effectiveness

The biggest energy drama of 2022 was likely in the LNG sector, which faced tight global supplies. With Russian pipeline volumes down significantly, cas-starved E.U. became the premium global market, bidding up LNG cargo prices to divert supply from Asia. In addition to this, Japanese buyers had to deal with LNG supply disruptions in the U.S. and Malaysia, and had walked away from new Qatari contracts.

Ironically, Russian LNG served as Japan’s safety net while supplies from the U.S. and Malaysia declined. Tokyo’s response was to launch a new national stockpile called the Strategic Buffer LNG, where importers can keep extra supplies in case of emergencies.

Japan reduced reliance on Russian crude oil but its decades-long strategy to depend less on the volatile Middle East fell apart. Ties with Southeast Asian oil producers look promising but those countries have less room to export because their domestic energy demand is rising. Japan’s answer to this conundrum was to deepen ties with Saudi Arabia, the U.A.E. and Oman, signing bilateral agreements on stabilizing fossil fuel supplies and in return helping them develop ammonia and hydrogen resources.

Last year showed that Japan’s strategy of locking supplies in long-term contracts, and diversifying supply sources to minimize dependency on high-risk regions is not always viable. That strategy worked well in a buyers’ market, but in today’s new geopolitical disorder, it leaves countries scrambling to secure fuel from any possible option.

For now, 2023 has started with a milder tone. Commodity prices have softened and the yen has strengthened against the dollar. But like the future of the war in Ukraine, the picture of future energy flows remains blurry. Businesses and governments will need to create more buffers, more risk-hedging strategies and even more diversification options to maintain balance.

ANALYSIS

BY KYOKO FUKUDA

AND YURIY HUMBER

Notes From Major Energy Summits Last Week:

All Eyes on How to Decarbonize

Several big events took place in Tokyo last week, among them the Asia Zero Emissions Community (AZEC) Public-Private Investment Forum and the Japan Energy Summit. While LNG and thermal power featured prominently, almost all discussions and speeches focused on how to decarbonize energy systems and the great uncertainty in demand outlook for fossil fuels in the coming decades. How to bridge traditional and new energy technologies, while maintaining security of supply, remains a key conundrum. We list some of the big talking points from last week’s events.

AZEC, March 3

The AZEC forum is supported both by the Japanese government (via METI) and big businesses (via the Keidanren lobby group). It aims to align Japan’s energy transition strategies with those of other nations in the region, especially those in Southeast Asia. With Japan already a major investor in energy and electricity facilities in Asia, achieving regional consensus on policies is good for business. So, while METI hosted top political leaders from Asia in Tokyo at the AZEC Ministerial Meeting, the Public-Private Investment Forum gave a chance for politicians to be joined by the chiefs of Japan’s biggest energy companies.

Attendees at the AZEC forum included the ministers responsible for energy in Indonesia, the Philippines, and Australia. Business speakers included the presidents of JERA, JOGMEC, IHI, Sumitomo Corporation, Erex and Shizen Energy, as well as senior executives from Tokyo Gas, MUFG Bank, Kawasaki Heavy and Mitsubishi Heavy.

Presentations by Japanese firms especially focused on technological advances and new projects in carbon capture (including the transportation of CO2 and its recycling), hydrogen (both from a green and blue perspective), e-methane as a future clean gas pathway, and energy storage systems. Speakers from MOE and NEDO, among others were also keen to point out that Japan has put aside significant public funds to advance these technologies and would look to sponsor projects that introduce them both at home and abroad.

Japan’s actions to cut emissions abroad (via its companies and technologies), and an ability to county part of the reduced volumes against its own CO2 reduction targets, is a big part of the national strategy, according to a presentation from the MOE official.

Finance officials were keen to show the sector was moving forward in forging clean investment rules that can apply to Asia while respecting the region’s unique position.

One sector that perhaps did not get as much attention, however, was renewable energy generation. Offshore wind is the main topic at a couple of other industry gatherings in Tokyo in early March, but it has yet to gain prominence at regional diplomacy showcases like the AZEC.

Japan Energy Summit, Feb 28-March 2

Japan Energy Summit & Exhibition was originally an event for the natural gas and LNG industry, but it has evolved in the last two years to include hydrogen, ammonia and other clean energy technologies. As such, many of the event’s 12 sessions involved discussions on how to incorporate these fuels into a net-zero world, with over 300 participants also joining in polls during panels to offer their perspectives.

The event featured keynote speeches from the director of the gas and petroleum division of METI, Soda Takeshi, the Secretary General of the International Energy Forum, Joseph McMonigle, and the Executive Director of the Hydrogen Council, Daryl Wilson. Panelists over the three days were senior executives from JERA, Tokyo Gas, Osaka Gas, JOGMEC, Venture Global LNG, JBIC, Kawasaki Heavy, PetroChina, Alaska LNG and Bosch Corp.

A brief summary of select sessions:

METI Keynote:

- Japan needs an additional 1,050 GW of renewable energy to achieve carbon neutrality by 2050, and METI is preparing for both the most optimistic and worst-case outcome based on IEA scenarios.

- Asian countries still need coal-fired power generation, but METI will support energy transition initiatives in Asia while promoting economic security.

International Energy Forum (IEF) Keynote:

- Half of the net-zero goals for 2050 can be met with existing technologies. For the rest, we need to rely on innovative technologies still in the R&D stage or even earlier.

Gas buyers panel:

- Japan needs to stabilize its gas reserves.

- War in Ukraine sent gas prices to levels that are beyond affordability in Asia, which is why the industry needs to have better contingency plans and work much harder on its pricing.

Hydrogen Council Keynote:

- Asia can be a hydrogen trade hub and Japan is one of the leaders in private sector development of the various steps in the supply chain of the fuel, with state support.

- Biggest challenge for hydrogen over the next 12-24 months is achieving international consensus on standardization and certification. The ability to track CO2 volumes across all steps of the supply chain and prioritize low carbon numbers over color (for example: green vs blue) is important to create a transparent global market for hydrogen.

Hydrogen panel:

- Many of Japan’s hydrogen technologies are valid but not yet economical.

- Ammonia is currently seen as the most likely way to transport hydrogen and store it. But, each hydrogen carrier pathway has its merits and will be able to appeal to its own consumer niche / geography.

- E-methane is gaining in recognition and there are U.S.-Japan projects starting to emerge in this niche.

Energy trading panel:

- As the price of LNG has been increased drastically, Japan needs measures to stabilize supply. This can be done through a stronger rollout of renewable energy or a more active restart of nuclear power plants.

- The market for electricity derivatives is growing rapidly, but is still relatively small. Futures volume is equal to about 5% of physical volume in Japan. In mature markets, derivatives volume is several times larger than physical volume.

Tech and infrastructure panel:

- Osaka Gas is focusing on methanation and building out low-cost e-methane supply chains to bring down the emissions from natural gas.

- Japanese startup Helical Fusion, in association with universities in Tokyo, Nagoya and Kyoto, aims to establish a working nuclear fusion energy facility in Japan by 2034.

- ABB sees wide scope to cut GHG in the LNG value chain.

International LNG cooperation panel:

- The EU became one of the world’s biggest LNG buyers last year, but it maintains its course to phase out fossil fuels over the mid-term and focus on renewable energy and hydrogen. However, in the meantime, Europe will need to engage in “LNG diplomacy”.

- Europe’s recent investments in LNG receiving infrastructure could be repurposed for clean fuels or moved for use elsewhere. So, the investment does not necessarily lock Europe into LNG use for the long term.

- New projects like the Alaska LNG development are already thinking about how they can be attractive to buyers by adding CCS tech and potential pathways into ammonia production.

- Africa’s natural gas industry could emerge as a major exporter over coming decade in addition to U.S. and Middle East supply.

Zero-emissions mobility panel:

- ENEOS operates 47 out of 160 hydrogen refueling stations in Japan, but struggles to maintain the facilities with only 5-6 customer a day.

- ChemOne produces sustainable aviation fuel from palm oil and used cooking oil. Japan aims to switch 10% of aviation fuel to SAF by 2030.

Maritime industry panel:

- By 2050, the world needs 110 times more vessels that operate on clean fuels such as ammonia or methanol.

- Companies are still looking at both pipeline and shipping technologies to move hydrogen.

CCS panel:

- Carbon capture (via CCS, CCUS and DAC) are seen as key to achieving net zero. This is the essential component of decarbonizing thermal power generation.

- Japan’s CCUS site in Tomakomai is a good example of a project that was well executed and showed no CO2 leakage. But now Japan must identify more sites (at home and abroad) in order to move the sector forward. Japan’s new CCS projects expected to start around 2030.

- Japan expects annual CCS storage needs to be between 120 and 240 million tons of CO2 by 2050. Transportation tech for the CO2 needs verification.

Carbon trading speeches and panels:

- Former IEA chief Tanaka Nobuo and METI official Nakayama Ryutaro discussed how Japan could achieve carbon neutrality by developing a domestic market for carbon.

- METI plans to implement Phase 1 of the Green Transformation over the next two-three years, which will see the gradual incorporation of carbon pricing in the broader economy.

- Recent focus on energy security has slowed investment in carbon credits and offsets, which has delayed work to introduce carbon trading mechanisms in Japan. But this momentum will pick up and, more importantly, it needs international cooperation to make sure carbon credit systems are inter-connected or that they share common standards and rules.

Energy policy panel:

- METI said it’s planning to upgrade Japan’s power grid to allow an 8-fold growth in renewable energy over time.

- At the same time, officials believe Japan must develop next-generation nuclear reactors to maintain energy security.

- Japan should learn from the U.S.’s IRA and EU’s Green Deal subsidy programs and work out its own plans. Equally, the government needs to motivate the population to change behavior in order to accelerate the move to carbon neutrality in Japan.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Canada/ LNG

Pipeline operator Enbridge will invest C$3.3 billion in natural gas and liquids infrastructure and in renewable power. The company will also buy a gas storage facility on the Gulf of Mexico to strengthen its LNG export business.

Carbon emissions

Global CO2 emissions from energy hit a record high last year, but increased slower than expected thanks to growth in renewable energy. The record 36.8 billion tons of CO2 emissions in 2022 was a rise of just under 1%, the IEA said. In 2021, that rise was 6%.

Energy Transition

In 2021, financing for energy totalled $1.9 trillion, $1 trillion of which went to fossil fuels and the rest to low-carbon energy projects. To reach energy transition goals for 2030, the world needs to invest $4 in renewable energy for every $1 invested in fossil fuels.

Europe/ Energy crisis

European countries’ bill to shield households and companies from soaring energy costs has climbed to nearly €800 billion, reported the Brussels-based think tank, Bruegel. Germany led the continent, spending about €280 billion.

India/ Solar power

Solar module makers, including Reliance Industries and Tata Power, are among bidders for $2.4 billion in incentives to expand domestic manufacturing and curb imports from China. The government’s goal is to boost the country’s module-making capacity to 90 GW.

Malaysia/ Renewable energy

Gentari, the clean energy arm of state oil firm Petronas, sees India and Australia as key markets for growth. In June, Petronas launched Gentari with the goal to build 40 GW in renewable energy capacity and produce up to 1.2 million tons of hydrogen annually by 2030.

Mozambique/ LNG

In July, Italy’s Saipem will restart its LNG project for TotalEnergies. Frozen in 2021 due to security issues, the project will be the first onshore LNG plant in Mozambique. The Saipem contract is €3.5 billion.

Solar power

By 2027 solar PV power will have the largest share of capacity of any generation source, according to the IEA. A decade ago, solar power had less than 1% of global energy capacity, the smallest share of any power source at that time.

Spain/ Offshore wind power

The government approved its first areas for wind farms on 5,000 km2 of maritime area that’s divided into 19 sectors. Spain has one of the largest expanses of sea in the EU.

UK/ Nuclear power

EDF’s new nuclear plant is likely to cost 30% more than its last budget estimate as inflation propels the price tag to almost £33 billion. The Hinkley Point C is Britain’s first new nuclear plant in two decades. EDF is building the plant with China’s CGN, which has a 33.5% stake.

UK/ North Sea energy

The windfall tax led to more than 90% of North Sea oil and gas producers cutting spending, with the policy “undermining” the country’s energy security, say critics. Meanwhile, the North Sea has potential for as much as £220 billion to be spent on oil and gas, offshore wind, CCS and hydrogen projects by 2030, said the head of the North Sea Transition Authority.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.