JAPAN NRG WEEKLY

MARCH 13, 2023

JAPAN NRG WEEKLY

March 13, 2023

NEWS

TOP

- PM Kishida decided to retain govt energy subsidies even as most inflation indicators show sign of slowing price growth

- Euglena plans a large biofuels factory in Malaysia with Petronas and Eni as partners to meet rising demand for clean fuels

- Japan venture to take stake in Australian rare earth miner for A$200 million to boost access to metals used in EVs, turbines

ENERGY TRANSITION & POLICY

- Lawmakers to debate GX draft law as METI talks up GX bonds

- ANRE asked to stop planned expansion of biomass feed rules

- Kishida says he’ll make final decision on Fukushima water release

- Honda and LG plan $4.4 billion EV battery plant in Ohio, U.S.

- Japan maker postpones production start of next-gen solar cells

- J-Power, Sumitomo team up on clean hydrogen, CCS in Australia

- Kawasaki-led group seeks to create liquid hydrogen supply chain

- JERA, Chevron will work together on CCS in Australia and U.S.

- Osaka Gas to collaborate with Santos on e-methane in Australia

ELECTRICITY MARKETS

- Nuclear regulator slams TEPCO, says restart approval in balance

- Toyota Tsusho takes 40% stake in large wind power IPP in Egypt

- UK’s SSE advises Japan to scale up offshore wind projects

- METI to set targets for floating offshore wind sector, including HR

- JOGMEC, local partner to develop Indonesian geothermal power

- Shizen Energy expands in Philippines, Thai renewables sectors

- Hokuriku Electric NPP restart to be debated at March 15 meeting

- Mitsubishi Power keeps top spot in global gas turbines market

OIL, GAS & MINING

- INPEX to develop oil field in Iraq with Russia’s LUKoil

- LNG stockpiles of Japan’s power utilities decline 5% in a week

- Saibu Gas to set up new unit for LNG business

- Japan’s top oil firms forecast bursting of the oil price “bubble”

ANALYSIS

OUTLOOK FOR LNG IN A TIME OF UNCERTAINTY;

AND IMPACT ON JAPAN

As natural gas prices recede from the wild surges of last year, more countries are flocking to use the fuel. Several will import LNG for the first time this year.

In Japan, the world’s biggest LNG importer, the national energy strategy calls for the use of gas in power generation to drop by half by 2030 in order to expand the use of renewables. At the same time, some officials still call for Japan’s LNG imports to increase. So, which course is the country really taking?

To get a perspective on the global gas sector and its development, we break down the five major trends in the industry and review the outlook for LNG among major buyers and sellers, including for Japan.

This is a double-header feature with input from some of the major voices in the global gas / LNG industry.

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Yoshihisa Ohno (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Filippo Pedretti (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

Events

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

|

METI |

The Ministry of Energy, |

mmbtu |

Million British Thermal Units | |

|

MOE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

Energy subsidy programs will continue, says Kishida

(Government statement, March 10)

- PM Kishida told ruling coalition party officials that programs to ease inflationary pressure on energy and food bills will continue as prices rise further.

- CONTEXT: On October 28 last year, the Kishida Cabinet decided to gradually reduce the subsidies, by setting a cap on the subsidy amount. The cap was to start decreasing from January. It is unclear whether there will be changes in this policy. Over ¥3 trillion in state money has already been spent on the subsidies so far, according to METI.

TAKEAWAY: Inflation has receded in the last month across a number of indices thanks to a slight strengthening of the yen last year and lower global fuel prices. Where energy prices will head next, however, remains uncertain and the yen has also resumed its weaker course against the U.S. dollar in the last month. This year, the range of energy sectors covered by state subsidies has increased to include household electricity and gas bills. Given that, it is in the state’s interest to start phasing out some of the subsidies, but Kishida also faces local government elections soon and will be wary of reigning in govt spending before the summer.

GX draft law taken up by lawmakers

(Denki Shimbun, March 10)

- The “Proposed Legislation of GX Promotion”, which aims to issue GX economy transition bonds and introduce a carbon pricing system, was put before lawmakers.

- METI Minister/ GX Promotion Minister Nishimura Yasutoshi explained at the Lower House plenary session that the GX economy transition bond will be used to develop decarbonizing tech, and carbon pricing will help companies’ green transformation.

- The total figure for the GX transition bonds will be about ¥20 trillion and they will be issued over the course of 10 years, from 2023 to 2032.

TAKEAWAY: In 2020, Japan paid about ¥11.3 trillion to import oil and gas. If ¥20 trillion can truly achieve a green transformation, at least in part, this could be considered money well spent.

Panel asks ANRE to shelve plan to add grain straw and husk to FIT biomass feed

(Japan NRG, March 9)

- ANRE’s working group on sustainable biomass proposed to shelve the plan to add rice straw, wheat straw and rice husk to biomass fuel that’s subsidized by the Feed-in-Tariff.

- The Ministry of Agriculture, Forestry and Fisheries reported these materials were used for animal feed, fertilizer and soil enhancement, and the country’s food security will be impacted if they are used for power generation.

- The working group recognized the need to study the use of each material. Gas generated during the processing of rice husk biochar may be collected and used as fuel.

- CONTEXT: Energy and food security issues are causing clashes between energy and farm communities, with both claiming the need to be more self-sufficient on their supplies.

TAKEAWAY: Some experts urge more flexibility on this issue rather than building a barrier between the farming and energy sectors. Blanket rules that ban the use of crop products for energy, or put energy requirements as a higher priority, will not allow the sectors to respond efficiently to changes. For example, there are some farm communities that use rice husks for their own power generation due to a rise in transport costs.

Euglena plans a biofuel factory in Malaysia; will produce 725,000 kl of biofuel annually

(Japan NRG, March 7)

- The Federation of LDP Diet Members for Carbon Neutrality by Promoting Domestic Biofuel and Synthetic Fuel hosted a session with leading biofuel suppliers.

- Euglena, the first start-up spun out from Tokyo University to then be listed in Tokyo, now has ¥44.4 billion in sales. It plans a large biofuel factory in Malaysia, in cooperation with Petronas and Eni, that will produce 725,000 kl of biofuel annually.

- Itochu introduced its pioneering efforts to promote GTL (Gas to Liquids) and Renewable Diesel (RD), and asked lawmakers to change the law related to synthetic fuels.

- Toyota said carbon neutrality is growing in motor sports, such as Formula 1 (10% second-gen biofuel), and World Rally Championship (100% second-gen biofuel).

Kishida says he will decide when to discharge treated water from Fukushima

(Fukushima Minpo, March 9)

- PM Kishida said he’ll decide the timing to discharge treated water from the Fukushima site. The decision will take into account the reputation risk that fishery produce from the prefecture may face and the government will seek to address rumors around safety both domestically and internationally.

- Kishida said he will seek public understanding that radioactivity above accepted norms has been removed from the water.

- Disposal of the water will start in spring or summer of 2023 and can’t be delayed, Kishida said.

TAKEAWAY: The government has discussed paying out compensation to large fishing ships for any decline in sales due to public concern over their produce. However, this measure would not cover all the Fukushima area fishermen since about two-thirds of the industry deploy small ships. Compensating every boat would increase both the outlay and administrative load. This is just one of the issues the government will need to address as it draws closer to the release of water from the Fukushima site. This is water that has been treated to remove excess radiation.

Hosiden postpones next-gen solar cell output to 2024

(Japan NRG, March 8)

- Hosiden plans to launch sales of perovskite solar cells (PSCs) in FY2024, rather than its previous goal of 2023, the company told Japan NRG. The pilot to produce PSCs started in 2021 and samples were sent to potential customers.

- In 2022, production facilities were installed at Hosiden FD’s plant in Shiga Pref; the company wants one more year for trials. Output of 100,000 units /month is planned.

- PSCs are thin, shaped like films, and consist of iodine and other chemical compounds. The cells can be formed in low temperatures and, manufacturers say, do not require critical raw materials.

- CONTEXT: In Japan, Sekisui Chemical, Toshiba, Panasonic, Kaneka, Aisin, Hosiden, Mitsubishi Materials and Ricoh are among the firms racing to lead in PSC development. Hosiden’s 2024 launch is still ambitious despite the delay. Sekisui Chemical will launch a demo project next month but commercialization is planned for 2025.

Honda and LG Energy Solution plan $4.4 billion EV battery plant in Ohio, to launch in 2024

(Company statement, March 1)

- Honda and LG Energy Solutions will build an EV battery plant near Jeffersonville, OH.

- The two will invest as much as $4.4 billion in the facility, which will launch in late 2024. Mass production is expected by the end of 2025.

- CONTEXT: The facility will supply lithium-ion batteries to Honda auto plants in North America. Honda will also spend $700 million to re-tool existing auto plants in Ohio to produce EVs.

TAKEAWAY: The U.S. has seen close to 20 new EV battery plant announcements in the last few years, a process that has accelerated since the passing of the Inflation Reduction Act of 2022. Tax credits and other support measures are making the U.S. a more attractive location for new clean tech manufacturing.

- Japanese automakers have been chastised of late for being slow to the EV trend. Part of the delay is said to have stemmed from doubts about the EV battery supply chain. The new factories, such as the one by Honda, should create the manufacturing capacity to alleviate such concerns. On the other hand, how all new battery plants will be able to source their raw materials remains unclear.

- SIDE DEVELOPMENT:

Honda’s zero-emission stationary fuel cell provides backup power to data center

(Company statement, March 6)- American Honda Motors in Torrance, CA, launched a stationary fuel cell power station as a first step toward commercialization of zero-emission backup power generation. This power station supplies clean emergency backup power to the data center on the campus.

- Honda will apply the next-gen stationary fuel cell system to its production facilities and data centers around the world, to achieve carbon neutrality by 2050.

- The future stationary FC units will power a fuel cell EV that’s modeled on the Honda CR-V and which will be unveiled in 2024.

J-Power considers hydrogen production from coal in Australia; up to 40,000 tons annually

(Nikkei, March 8)

- J-Power is considering producing hydrogen from coal in Australia. By 2030, the company plans to build a manufacturing plant to extract hydrogen from lignite.

- The company aims to produce 30,000 to 40,000 tons of hydrogen per year. If 70,000 tons of lignite coal is steamed, about 40,000 tons of hydrogen can be produced.

- The company hopes to supply methanol and fertilizer production in Australia. CO2 will be separated, captured and stored underground in Australia, in conjunction with Sumitomo. The company will also consider liquefying hydrogen and transporting it to Japan. The investment amount wasn’t disclosed.

TAKEAWAY Lignite has a higher moisture content and can be procured at a lower cost than high-grade bituminous coal. J-Power developed a technology to extract hydrogen from coal as a fuel for power generation, and operates a demo facility to produce hydrogen from lignite.

- SIDE DEVELOPMENT:

J-Power and Sumitomo team up on clean hydrogen and CCS project in Australia

(Company statement, March 8)- J-Power and Sumitomo signed an MoU to study clean hydrogen production from a gas field in Latrobe Valley, as well as carbon capture & storage (CCS) in Victoria, Australia.

- Drawing on J-Power’s experience at Osaki Cool Gen Project in collaboration with Chugoku Electric, which is supported by METI and NEDO, this latest project will study the pathway to commercialization for clean hydrogen production together with CCS.

- Also, the project will look at ways to commercialize a liquefied hydrogen supply chain, which is one of the focus areas at NEDO’s Green Innovation Fund.

LH2 supply chain commercialization demo

(Company statement, March 8)

- KHI, NEDO, Japan Suiso Energy (JSE), Iwatani, and ENEOS will collaborate on liquefied hydrogen supply chain commercialization demo projects.

- The goal is to establish sea transport of liquefied clean hydrogen from the production site at Port of Hastings, Australia to the Kawasaki Coastal Area, Kanagawa Pref, which has a large industrial complex; hydrogen supply cost is estimated at ¥30/Nm3 by 2030.

- As a part of the Green Innovation Fund, the project plans to establish an international liquefied hydrogen supply chain.

JERA and Chevron will work together on CCS in Australia and the U.S.

(Company statement, March 8)

- Chevron and JERA signed a MoU for CCS projects in Australia and the U.S.

- This MoU has the potential to expand the significant LNG relationship that Chevron and JERA already have.

- In November 2022 the companies announced co-development of low carbon fuel in Australia and the study of liquid organic hydrogen carriers (LOHC) in the U.S.

Osaka Gas will collaborate with Santos in e-methane production in Australia

(Company statement, March 7)

- Osaka Gas will begin studies to produce synthetic methane in Australia as an alternative to LNG. The goal is to export about 60,000 tons per year from 2030.

- Synthetic methane is made from CO2 and green hydrogen. Osaka Gas will work with Santos to find a location for production and to procure CO2. An investment decision will be made in 2025. The synthetic methane is slated for export to Japan, etc.

- Osaka Gas also conducts e-methane studies in Australia, U.S., South America, etc.

- CONTEXT: Osaka Gas last week announced a new 2030 strategy, which aims to cut the group’s total CO2 emissions from 32 million tons in FY2017 to 27 million tons in FY2030 by introducing synthetic methane (e-methane) and other measures. The company maintained the goal of making e-methane account for 1% of its gas sales volumes in FY30.

MOL to build a clean hydrogen/ ammonia value chain in Thailand

(Company statement, March 6)

- Mitsui O.S.K. Lines will build a clean hydrogen and ammonia value chain from renewable energy sources in Thailand. An MoU was signed with the Electricity Generation Authority of Thailand, Mitsubishi’s Thai subsidiary and Chiyoda Corp.

- In south Thailand, they’ll build supply networks for clean hydrogen and ammonia production, transportation and use. They’ll also provide supply for export.

TAKEAWAY: In January 2022, PM Kishida announced the Asia Zero Emission Community (AZEC) concept to promote decarbonization in Asia. Thailand is a key nation in AZEC.

Astomos and NYK Line complete marine biofuel demo on LPG carrier

(Company statement, March 6)

- Astomos Energy, a subsidiary of Idemitsu Kosan, and Nippon Yusen (NYK) completed a pilot on an LPG carrier bunkering FAME B24 marine biofuel in Singapore. FAME stands for the biofuel “fatty acid methyl ester”. B24 refers to a 24% blending ratio (so, fuel containing 24% FAME).

- The demo contributes to a project announced in 2022 for establishing a framework that provides transparency in the supply chain of sustainable biofuels from upstream to downstream. The project involves a consortium of 19 industry partners and 13 vessels bunkering in five different supply chains.

TAKEAWAY: Despite generating CO2 when combusted, biofuels are considered carbon-neutral since they’re made from biomass and feedstock, such as waste cooking oil. They don’t require any modification to the ship’s existing engines.

Toyota demonstrates hydrogen production device using FCV technology

(Nikkei, March 9)

- Toyota developed hydrogen production equipment using fuel cell vehicle (FCV) technology. The company will install it at the Denso Fukushima Plant and will begin a demo in March. The hydrogen produced will be used for the plant’s gas furnace.

- The device can produce 8 kg of hydrogen per hour, and it takes 53 kWh of electricity to produce one kilo of hydrogen. The company aims to commercialize it in the future.

- The hydrogen production equipment will run on renewable energy. The LP gas used in the afterburner furnace, which detoxifies the emitted gas, will be replaced with hydrogen.

Tokyo Gas to develop non-iridium catalyst for hydrogen production with H2U Technologies

(Nikkei, March 9)

- Tokyo Gas and H2U Technologies, which is based in California, will develop a low-cost catalyst for hydrogen production that’s made of inexpensive elements.

- The two sides will create sample/test catalysts and rate their reactivity and efficiency. According to Tokyo Gas, it takes three to four days to produce a single catalyst sample using a conventional method. But with a system developed by H2U, a new catalyst can be tested and analyzed in about 10 minutes.

- CONTEXT: Tokyo Gas is developing technology to synthesize methane by mixing hydrogen and CO2. This is one part of the process of lowering costs for that technology.

TAKEAWAY Polymer electrolyte membrane (PEM) electrolyzers use the rare and expensive metal iridium. South Africa accounts for about 87% of global iridium production. If an inexpensive replacement for iridium can be found, the cost of producing hydrogen can be reduced significantly.

Sumitomo to partner with Israel’s H2Pro on production of green hydrogen and ammonia

(Denki Shimbun, March 10)

- Sumitomo Corp will partner with Israeli hydrogen tech venture company H2Pro to form a partnership to produce green hydrogen and green ammonia.

- Sumitomo will integrate H2Pro’s 95% efficient E-TAC electrolyzer system at a scale of hundreds of MW, primarily for use in green ammonia projects.

- In the initial phase, Sumitomo and partners will collaborate with H2Pro on its technology pilot and demo, and will supply H2Pro with manufacturing equipment.

Idemitsu Kosan plans to study growing plant material for SAF in Australia

(Denki Shimbun, March 10)

- Idemitsu Kosan will team up with J-Oil Mills and Australian NGO Burnett Mary Regional Group to study setting up a sustainable aviation fuel (SAF) supply chain by planting Pongamia pinnata trees, a non-edible oil feedstock, in Queensland.

- SAF is produced from non-fossil fuel derived raw materials, and one of the challenges is to secure raw materials that are less competitive with food crops.

- Pongamia pinnata, a legume grown in Southeast Asia and Oceania, is a non-edible oil feedstock with high oil yield efficiency and could be leveraged as an SAF feedstock.

Mitsui Fudosan to power properties with in-house solar energy

(Nikkei Asia, March 7)

- Mitsui Fudosan will power part of its large-scale commercial properties with electricity from own solar plants.

- The company recently acquired land in Hokkaido and other locations with the aim of operating solar farms by the end of 2023. Total power generation will be about 23 GWh. CO2 emissions will be reduced by 10,000 tons per year.

- At the moment, Mitsui Fudosan’s five operating solar plants produce electricity sold under the FIT program. However, the new plants will send power to the company’s properties through a self-consignment system. This will help cut electricity bills.

TAKEAWAY: Mitsui Fudosan aims to build up to 30 solar power plants by FY2030. The goal is to generate 380 GWh of renewable energy.

NEWS: POWER MARKETS

NRA says TEPCO doesn’t follow advice, can’t allow Kashiwazaki-Kariwa NPP restart

(Sankei Shimbun, Mar. 8)

- NRA Chairman Yamanaka Shinsuke said that since TEPCO hasn’t been following 27 pieces of advice regarding security, it will be difficult to lift the ban on transporting nuclear fuel at the site.

- In the wake of safety equipment failures, such as a malfunction of the intrusion detector, in April 2021 the NRA issued an injunction against transporting nuclear fuel within the site. In September 2022, the NRA listed a total of 27 requirements to lift the ban, but TEPCO still hasn’t complied with six of those.

- In mid-May, the NRA will make a final decision on whether to lift the ban.

TAKEAWAY: This news is not positive for TEPCO or its electricity users. TEPCO recently won approval for power price hikes from June 2022. But even these increases are based on the idea that it will be able to restart Unit 7 of the Kashiwazaki-Kariwa NPP in October 2023. In case the utility cannot do so, its flagging finances means the Tokyo area electricity price will most likely rise further.

Toyota Tsusho takes 40% stake in 500 MW wind power IPP in Egypt

(Company statement, March 6)

- Toyota Tsusho will take part in a wind power project in Egypt with a 500 MW capacity. Operation starts in August 2025. The cost is about ¥86 billion.

- The company set up an Independent Power Producer (IPP) with its subsidiary Eurus Energy and four others. Toyota Tsusho Group owns 40%; France’s Engie, 35%; and Egypt’s Orascom Construction, 25%.

- CONTEXT: Egypt’s electricity demand is growing steadily. The government’s plan is to achieve 42% of total power generation from renewable energy by 2035. In Egypt, Toyota Tsusho has been participating in power plant and substation construction projects since the 1990s. In 2017, it invested in the country’s first wind power IPP.

UK’s SSE Renewables advises Japan to scale up offshore wind projects

(Denki Shimbun, March 8)

- At a session of the Federation of LDP Diet Members for Promoting Renewable Energy, Paul Cooley, the head of global offshore wind for SSE Renewables, said that scaling up projects is key to develop offshore wind farms and bring down the electricity costs.

- Citing their own offshore wind project that’s scheduled to start operation in 2026 in the UK, the unit price of generated electricity is expected to be ¥6.5/ kWh, but it took 10 years to reach that low price. Japan also needs time to achieve such levels.

- Cooley said his company negotiated with the UK government to simplify approval procedures to start offshore projects. Also, the UK offers courses about offshore wind at universities to increase awareness and encourage young people to enter the profession.

- CONTEXT: In 2021, SSE Renewables announced plans to start business in Japan, and it’s now developing offshore wind projects in cooperation with Pacifico Energy.

Floating Offshore Wind Power Council will discuss political obstacles

(Denki Shimbun, March 8)

- The Floating Offshore Wind Power Council, which is composed of six companies such as JGC and Toda, hosted the Floating Offshore Wind Power conference on March 7.

- The latest policy and industry trends were discussed. The head of METI’s wind policy said the government will set a target to develop floating offshore wind power, not only to develop the market, but also to foster human resources and new technology.

- The MLIT’s Maritime Bureau introduced some ways to reduce the cost of offshore wind power. It also announced issuing a guideline for technological issues in March 2023.

JOGMEC and Geo Dipa Energi will develop geothermal energy in Indonesia

(Company statement, March 6)

- During the Asia Zero Emissions Community (AZEC), JOGMEC and PT Geo Dipa Energi signed an MoU to develop geothermal energy in Indonesia.

- JOGMEC hopes that the partnership will help it to obtain know-how and technologies for geothermal energy development in Japan.

- CONTEXT: JOGMEC also announced signing two other MoUs this past week. One was with PetroVietnam for a CCS/CCUS project in Vietnam. Another one was with Petronas to work on carbon-neutral fields in Malaysia including projects related to hydrogen/ ammonia fuel, CCS, and GHG emissions reduction. Both projects show JOGMEC’s ambitions to achieve net zero goals through international cooperation, especially in Asia.

Shizen’s Ganubis Renewable Energy to develop 96 MW onshore wind power in Philippines

(Company statement, March 3)

- Ganubis Renewable Energy, a consortium in which Shizen Energy and its subsidiary Shizen International participate, signed an MoU for development of a 96 MW onshore wind power generation project in the Philippines.

- Another partner, Isla Gran Viento, provides local development, grid access and permits. Shizen provides technical support and financing.

- The power plant will be built on Guimaras Island; feasibility studies begin this month. If favorable results are obtained, construction begins January 2024. Electricity will be supplied to utilities and retail operators in Luzon and Visayas regions.

- If completed, it will be one of Southeast Asia’s largest onshore wind farms.

- SIDE DEVELOPMENT:

Shizen International develops 60 MW of renewable energy in Thailand

(Company statement, March 7)- Sena Solar Energy and Shizen International, a Shizen Energy Group company, signed an MoU to explore opportunities in Thailand’s renewable energy market.

- The two hope to develop floating/rooftop hybrid solar projects over 60 MW.

- Shizen International has a total power generation capacity of 12.6 MW, but this will rise to 24 MW in the near future once other projects are completed.

Hokuriku Electric Shika NPP fate may be decided at a March 15 meeting

(Denki Shimbun, March 9)

- NRA member Dr. Ishiwatari Akira, who is in charge of earthquake-proof certification, concluded that Hokuriku Electric’s Shika NPP does not sit on an active geological fault.

- Dr. Ishiwatari pointed out that his conclusion contradicts the decision from April 2016 by the NRA that the possibility of active geological faults can’t be denied.

- The NRA will compare the two decisions at a regular meeting on March 15.

TAKEAWAY: The 2016 conclusion is unlikely to prevail because it was based on a smaller data sample than the recent decision by Dr. Ishiwatari.

Daiwa Securities buys into U.K. offshore wind farm

(Asia Nikkei, March 11)

- The Daiwa Securities group will invest in the Hornsea One offshore wind power project in the UK, the brokerage firm’s first investment in the sector.

- Daiwa will buy a minority interest in the project form a British infrastructure fund for about $100 million.

- The 1.2 GW Hornsea One project is operated by Denmark’s Orsted. It is already in operation.

Mitsubishi Power achieves top spot for global gas turbines in 2022

(Company statement, March 9)

- In 2022, Mitsubishi Power led the global gas turbine market with a 33% share in terms of megawatts sold, and also had a 49% market share in the advanced-class gas turbine market, said McCoy Power Reports.

- Mitsubishi Power’s latest JAC (J-Series Air-Cooled) gas turbines is a world leader in efficiency, which is greater than 64%.

- Low carbon features are another reason for the company’s standing. All heavy-duty gas turbines are equipped with hydrogen co-firing capability. They can run on a mixture of up to 30% hydrogen and 70% natural gas, and will be capable of 100% hydrogen firing in the future.

TAKEAWAY: Mitsubishi Power combines the thermal power businesses of Mitsubishi Heavy Industries (turbines) and Hitachi (turbines, generators). In 2024, the company also plans to add Mitsubishi Electric’s thermal power business (generators), which should help it to maintain a strong position in the global market.

NEWS: OIL, GAS & MINING

Japan venture to take a stake in Australian rare earth miner Lynas for A$200 million

(Japan NRG, March 7)

- Japan Australia Rare Earth (JARE), a subsidiary of Sojitz and JOGMEC, will take about a 3% stake in Australian rare earth miner Lynas for A$200 million, which will build a concentrator and facilities to extract dysprosium and terbium from ores at its Mount Weld mine.

- Lynas produces 26,500 tons/ year of rare earth oxide, mainly neodymium-praseodymium. To date, it has not extracted dysprosium and terbium from the ores.

- Japanese customers will take up to 65% of Lynas’ dysprosium and terbium, said METI. The two elements are used to make magnetic motors mounted on EVs and wind turbines.

- CONTEXT: Presently, Lynas ships the ores to Malaysia for processing. Last month, Malaysia banned Lynas from importing radioactive lanthanide rare earth concentrate, starting July 2023. Lynas appealed this decision. Dysprosium and terbium deposits contain radioactive thorium and they may be banned in Malaysia.

- The companies and JOGMEC declined to elaborate on where the new dysprosium-terbium concentrator will be located, as well as details of the technique used.

TAKEAWAY: While Japan has secured dysprosium and terbium resources, it’s not clear where, when and how much will be available. A lack of transparency in the supply chain may lead to uncertainties in regulators’ decisions. Finding applications for thorium is another challenge.

INPEX to develop oil field in Iraq with Russia’s LUKoil

(Nikkei, March 8)

- INPEX is conducting a study with Russian oil giant LUKoil for developing the Eridu oil field in Iraq. The companies’ target is to produce 250,000 bpd. LUKoil will hold 60% of the concession and INPEX will hold 40% through its subsidiary.

- LUKoil got approval for the draft plan from the Iraqi National Oil Co. A detailed plan will be submitted and, if approved, a final decision will be made.

LNG stocks fall to 2.23 million tons, down 5% from last week

(Government data, March 8)

- LNG stocks of 10 power grids stood at 2.23 million tons as of March 5, down 5% from 2.34 million tons a week earlier. METI initially reported that the March 1 stocks were 2.4 million tons but then corrected the figure.

- The end-March stocks last year were 1.63 million tons. The five-year average for this time of year is 2.07 million tons.

Saibu Gas to set up new unit for LNG business development

(Yomiuri Shimbun, March 9)

- Saibu Gas will establish a new department, the LNG Business Department, in April to centralize the procurement and supply-demand management of LNG. In part this is a reaction to the turmoil in the LNG market since Russia’s invasion of Ukraine in Feb 2022.

- CONTEXT: Prior to the incursion last year, Saibu Gas partnered with Russian gas producer Novatek and aspired to jointly develop LNG sales to the Chinese gas market. Saibu Gas secures a portion of its LNG from Sakhalin-2 project in Russia operated by Gazprom.

- Saibu’s new 20-person department will be in charge of LNG sales both domestically and internationally, and is expected to optimize supply and demand management.

Japan’s major oil firms get ready for bursting of the “oil price bubble”

(Diamond, March 8)

- Japan’s largest oil companies saw a significant revenue increase, between 30% to 60%, in the last three months of last year thanks to high crude oil prices. INPEX earnings grew around 58%, while ENEOS and Idemitsu both posted growth of around 35% also due to a period of particular yen weakness.

- However, earnings growth is now stalling and oil prices have receded since their 2022 peaks. INPEX announced that it expects both sales and profits to decline in 2023, while ENEOS and Idemitsu have also revised their forecasts downward in the period.

- The oil price “bubble” or recent months looks set to burst.

ANALYSIS

BY YURIY HUMBER

Outlook for LNG in a Time of Uncertainty; and Impact on Japan

Commodity | Price Range (2020 to 2023) |

|

Crude oil / (WTI) |

-$33 to $122 |

|

LNG / (JKM) |

$2 to $54 |

|

Coal / (Newcastle) |

$50 to $475 |

|

Electricity, Japan / (JEPX, monthly) |

¥4 to ¥63 |

|

USD to JPY |

¥108 to ¥150 |

The last three years have seen extreme events roil energy markets. Global gas and the LNG industry have been impacted most of all. The price range for LNG has seen the biggest swings of all major energy sources.

As natural gas prices recede from the wild surges of last year, a number of new countries are flocking to use the fuel. Germany welcomed its first LNG cargo in January. Vietnam and Hong Kong are among those seeking to debut as LNG importers later in 2023. But even as the gas market expands, questions grow louder about its longevity and place in a net-zero world.

In Japan, the world’s biggest LNG importer, national strategy claims that domestic use of the fuel in power generation will drop by half by 2030 in order to expand the use of renewables. At the other end of the spectrum, Pakistan is among countries ditching gas / LNG in favor of coal because of recent price volatility.

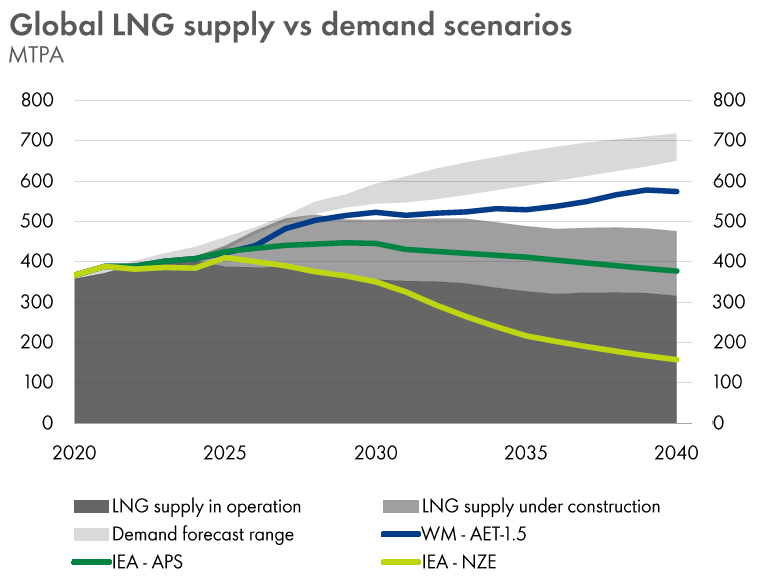

At a time of great uncertainty, forecasting the future of the LNG market is tricky. Yet, over the last decade, it’s become one of the most important global commodities. So, in order to get a perspective on the sector and its development, we break down the five major trends carrying the industry and review the outlook for LNG among major buyers and sellers.

Source: Shell LNG Outlook 2023

Background

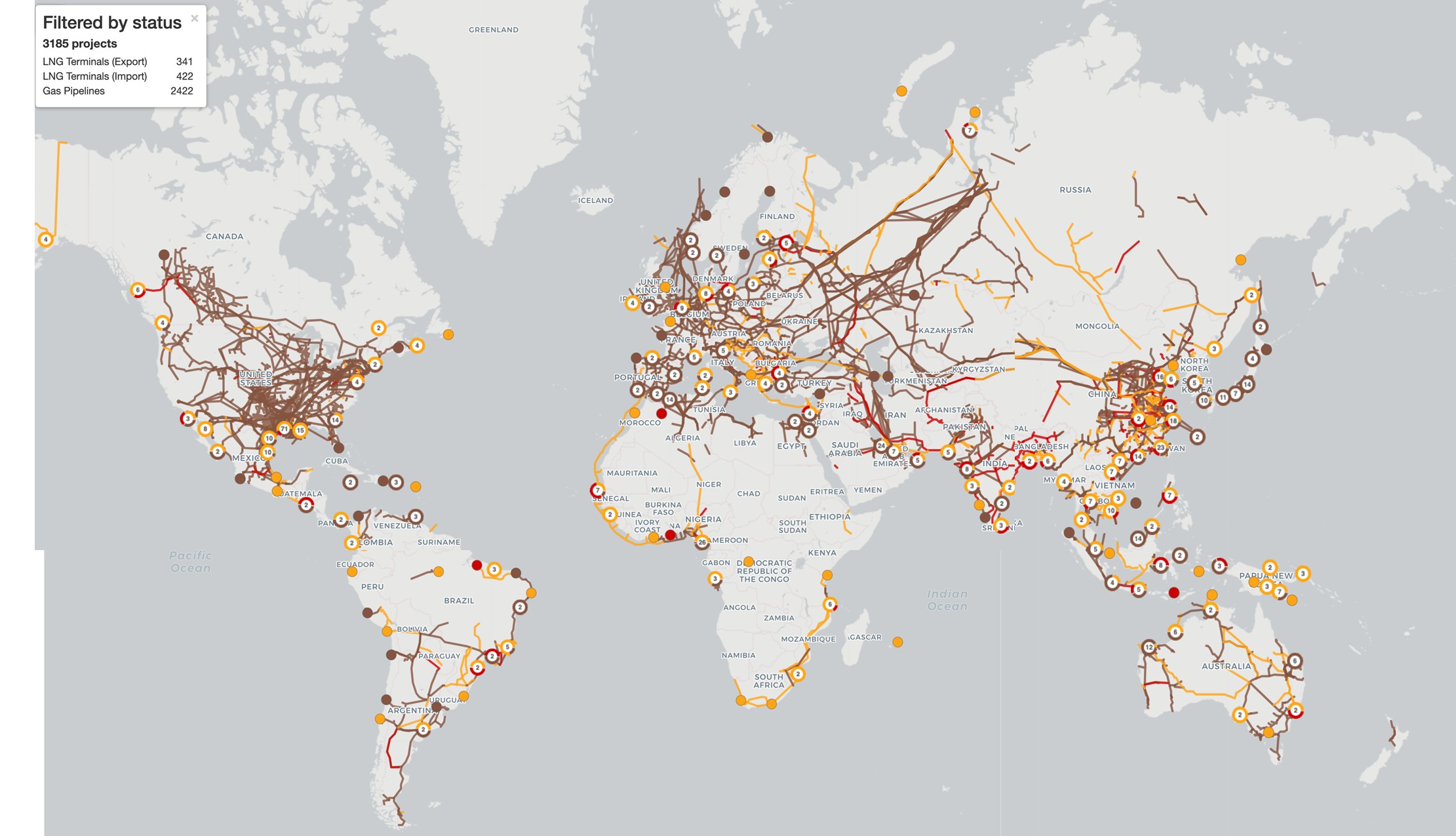

Despite increasing criticism by environmental groups, the gas industry is growing rapidly and its outlook is bullish. There are already over 150 LNG export and over 180 LNG import terminals active around the world and many more in the works.

Source: Global Energy Monitor

Historically, gas developed as a local commodity, which traveled by pipelines and was consumed close to where it was produced. In the map above, you can see the congestion of pipelines in the south of the U.S., which is where the distribution center called Henry Hub is also located. It only emerged in the 1950s and until most of the U.S. started to export LNG in 2016, Henry Hub had relatively little impact on global gas markets.

In Europe, production from the giant Groningen field was the driver for the creation of the Title Transfer Facility (TTF) gas benchmark. In the UK, gas production in the North Sea inspired the creation of the National Balancing Point (NBP).

And of course, in Asia, the dominant pricing point is the Japan Korea Marker (JKM) created by Platts as recently as in 2009.

These four major gas pricing points were largely unconnected until the start of the previous decade, when the IEA forecast that the world will enter the Golden Age of Gas. But as more gas is sent by ship rather than pipeline, the market has become truly global and very connected. About a quarter of gas is now traded, not just sold in bilateral deals based on pipelines. That’s less than for crude oil, around half of which is traded on an exchange, but a big change from 10 years ago.

Also of note is how resilient global gas demand remained during the Covid-19 pandemic. It increased by 5% in 2021 – double the annual growth rate of the past decade.

Russia’s incursion into Ukraine in February 2022 pushed globalization of the gas industry even further as Europe sought to swap its “local” pipeline supplier (Russia) for global LNG input. In the process, it aligned global gas benchmarks ever closer, while magnifying local market fundamentals onto the global stage.

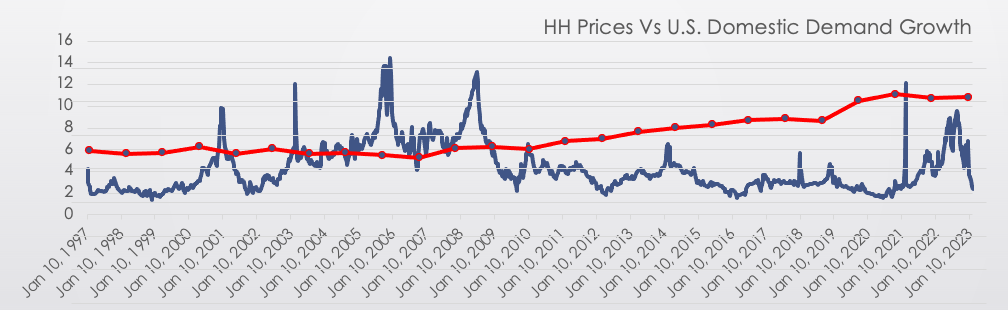

Of course, the dependence on Russian gas was different across nations, and that muddied the correlation among benchmarks for a time. The jump in U.S. gas prices, for example, was less pronounced last year than in Europe. But U.S. price increases were certainly affected by events in Europe while also being drive by domestic factors, such as a cold snap in parts of the country.

Source: ICE and EIA data

The red line above shows domestic U.S. natural gas demand. It is definitely higher in 2021/22 than in 2006/07, which was the last time that gas prices spiked in the U.S. But the increase in demand has been gradual. Also, there is no major volatility in the Henry Hub benchmark after 2016, when the U.S. started LNG exports from the lower 48 states.[1]

U.S. prices start to react more to global prices as natural gas exports from the country start to offer LNG contracts with no fixed destination clause. In 2019, 90% of all LNG contracts signed did not have a fixed destination clause, according to the IEA. Just two years before, only 15% of global LNG contracts were signed without a destination clause. This is one of the biggest drivers of connectivity between global price benchmarks.

With U.S. domestic fundamentals becoming more and more important for gas prices globally, it pays to look at their drivers. According to forecasts by Wood Mackenzie, among others, Domestic U.S. gas production will continue to rise this year, which will keep Henry Hub prices below $5/ mmbtu in the near term.

Mega Trend 1: Local → Global

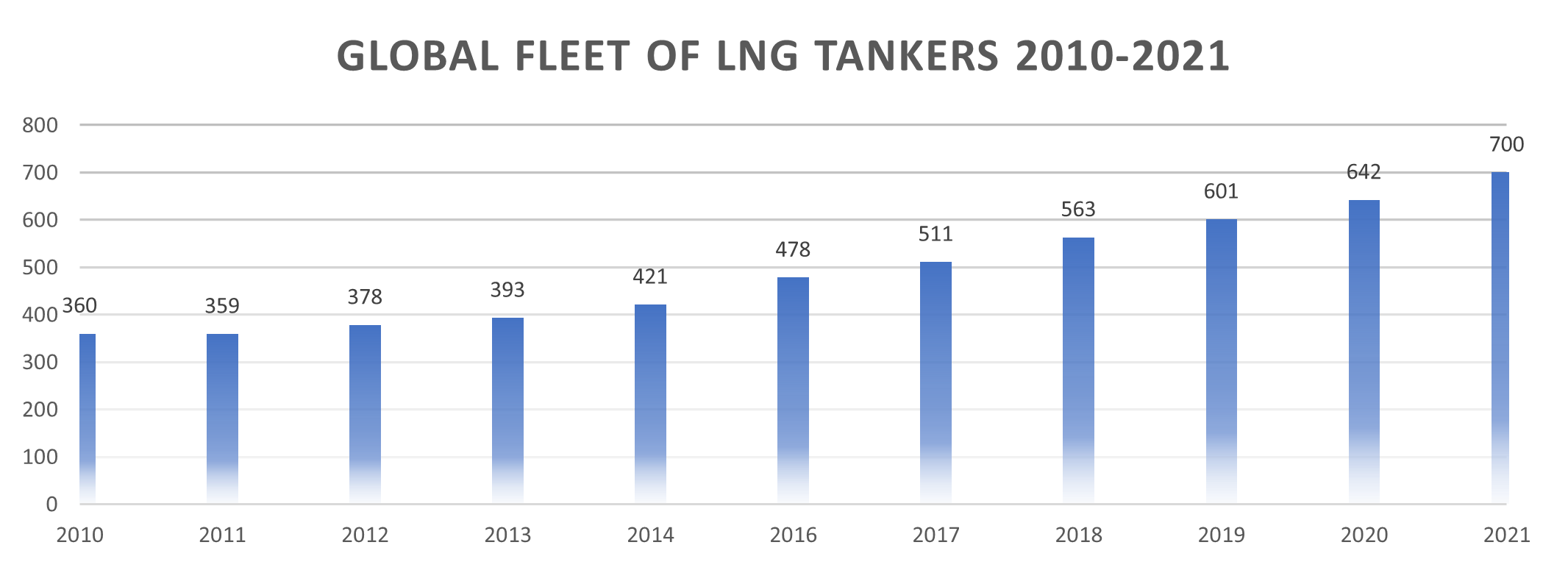

In the last five years or so, the gas market has transformed into an LNG market, which has made it more global. LNG export volumes have tripled in the last 20 years.

Last year, an average of 3 new LNG carriers were ordered. That suggests that gas will travel further than before and will start to mirror the crude oil market in some respects.

Importantly, we should remember that chilling natural gas and moving it around the world requires a lot of energy and it is expensive. A new LNG carrier costs about $200 million.

As the world consumes more LNG and installs more Floating Storage and Regasification Units (FSRUs), we should expect gas prices to continue to rise on average.

Source: GIIGNL, May 2022

- The first commercial liquefaction facility was built in Cleveland, Ohio, in 1941 and the first transportation of a large LNG cargo across the ocean took place in 1959, from Lake Charles, Louisiana, to Canvey Island, UK. Japan imported its first LNG cargo, from the now shuttered Alaska LNG facility, in 1969. However, the Lower 48 states of the U.S. did not start exports of LNG until February 2016. ↑

Mega Trend 2: Contract Model Changes

As more gas travels by ship, naturally it becomes a traded commodity. Henry Hub, and BNP and TTF were created as a way to price gas for local markets. Now, they are used to create global prices and there are clearly some limitations. Consumers in markets where gas prices were traditionally low will start to get more frustrated. This could push more governments to create two-tier systems, splitting the domestic market from the export market.

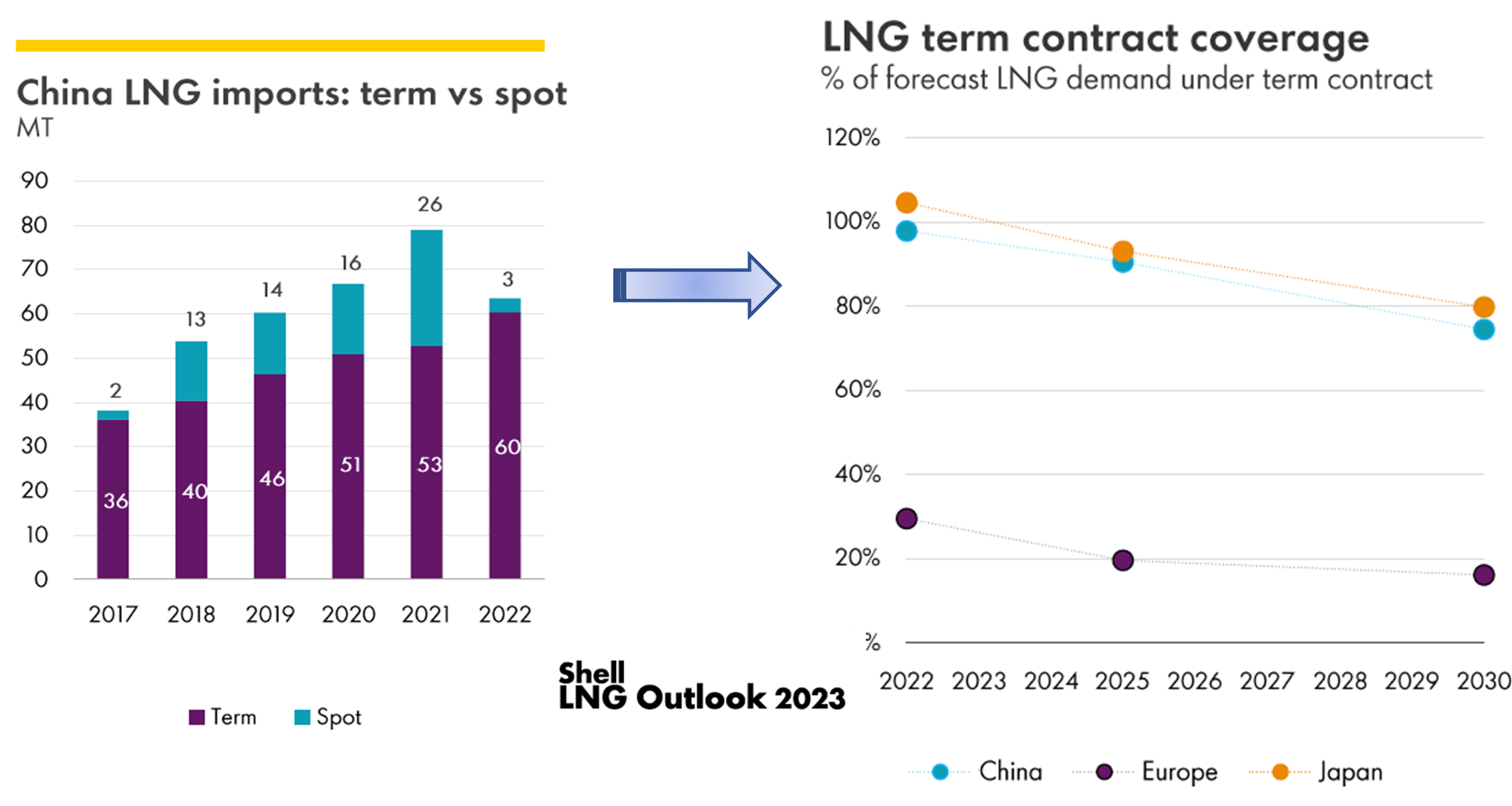

Recent market tightness has pushed buyers in Japan and China and elsewhere to sign new long-term LNG deals. Now, everyone is concerned about “energy security”. But that feels like a short-term reaction. Risk-averse sentiment is unlikely to continue for too long in the face of other mega-trends in the industry. Many expect the ratio of long-term contracts across the world to decline in a couple of years.

Of course, every LNG importing nation has a different risk tolerance level. So, it’s likely that the ratio of long-term contracts in Japan will stay much higher than in Europe. But it’s difficult to see Japan continuing to buy 85% or more of its LNG based on long-term contracts.

Shell said in a recent report that it expects global buyers to pursue three pricing models. One based on Henry Hub prices. One based on Brent oil. And one based on spot rates.

While Japan’s decline in long-term contract volumes is partly driven by national strategy to phase down the use of LNG in power generation, growth in China’s LNG market is still at an early stage. Only 22% of its gas is used for power, and most of the LNG China imports does not get used to make electricity. That gives Chinese buyers more certainty to strike long-term deals now in a tight market and then return to spot trading once global supply returns to a surplus around 2025/26.

Source: RBAC Inc.

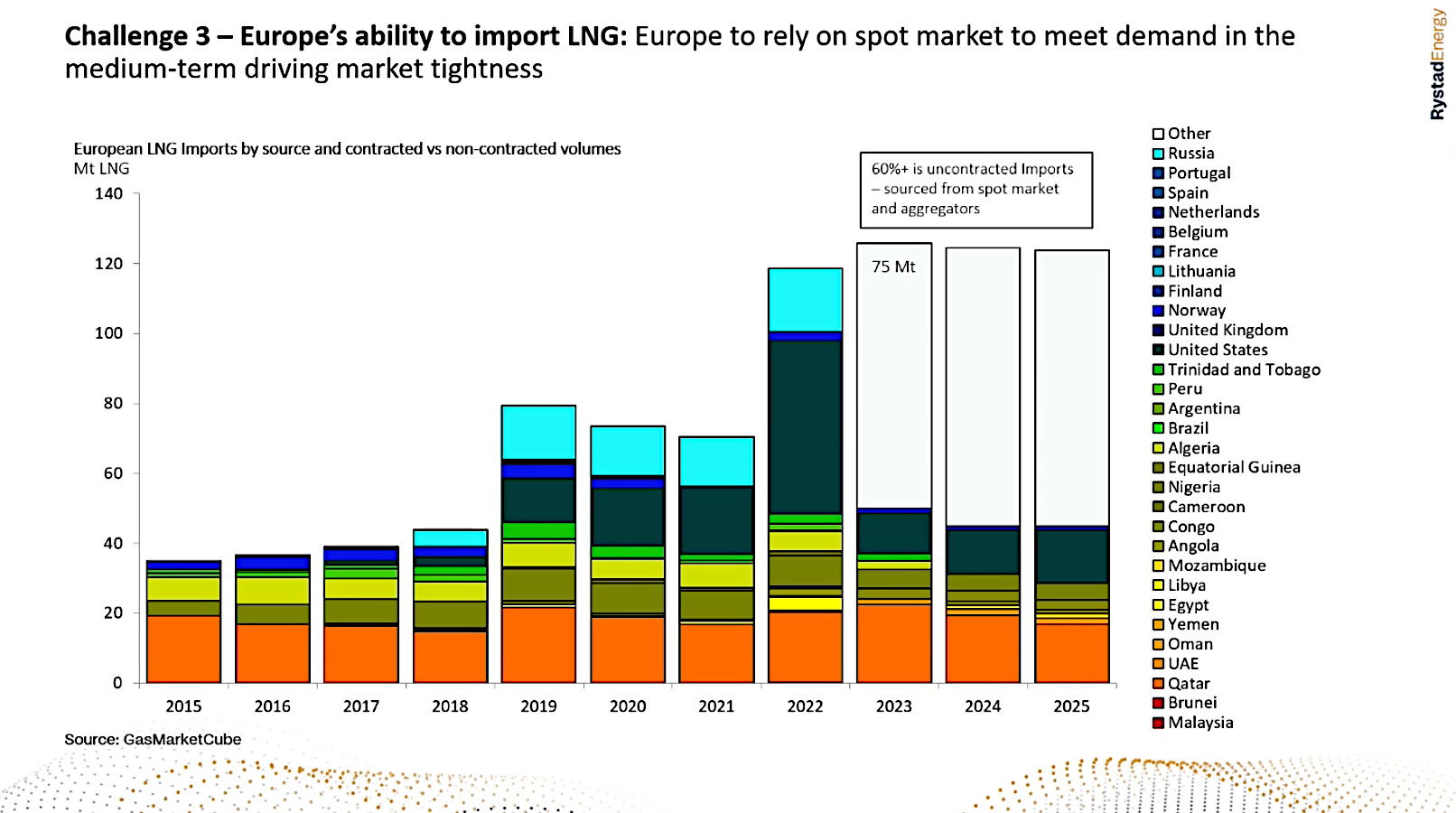

In Europe, political will and rulemaking dictate that natural gas is a short-term, transitory solution, which is why buyers there prefer to rely on the spot market. As such, Europe is expected to be a major spot cargo buyer in the coming years.

Source: Rystad Energy

At the moment, European gas storage is at almost record high levels thanks to a mild winter. It means the region could manage without any Russian pipeline gas until spring 2024, according to Rystad Energy. However, one of the ways that Europe managed in 2022 was by asking industries to cut gas consumption. Such frugality cannot last, otherwise manufacturers of fertilizer, steel, chemicals, and other products will look to move production elsewhere.

Last year, Russian gas pipeline exports to Europe fell 70% (82 bcm), but European demand also fell 10% (50 bcm), while LNG imports surged (up 60 bcm).

Europe is also investing heavily in new LNG receiving infrastructure. There are at least 15 new regasification projects being carried out in 12 European countries. Germany has ordered 6 FRSUs and will have the world’s fourth-largest import capacity by the end of the decade.

Will China fill Europe’s place?

So, what will happen to Russian gas that used to go to Europe? One answer is: some of it will be delivered to Europe via LNG (as it was last year) and those volumes will probably grow further unless political actions curtail the trend.

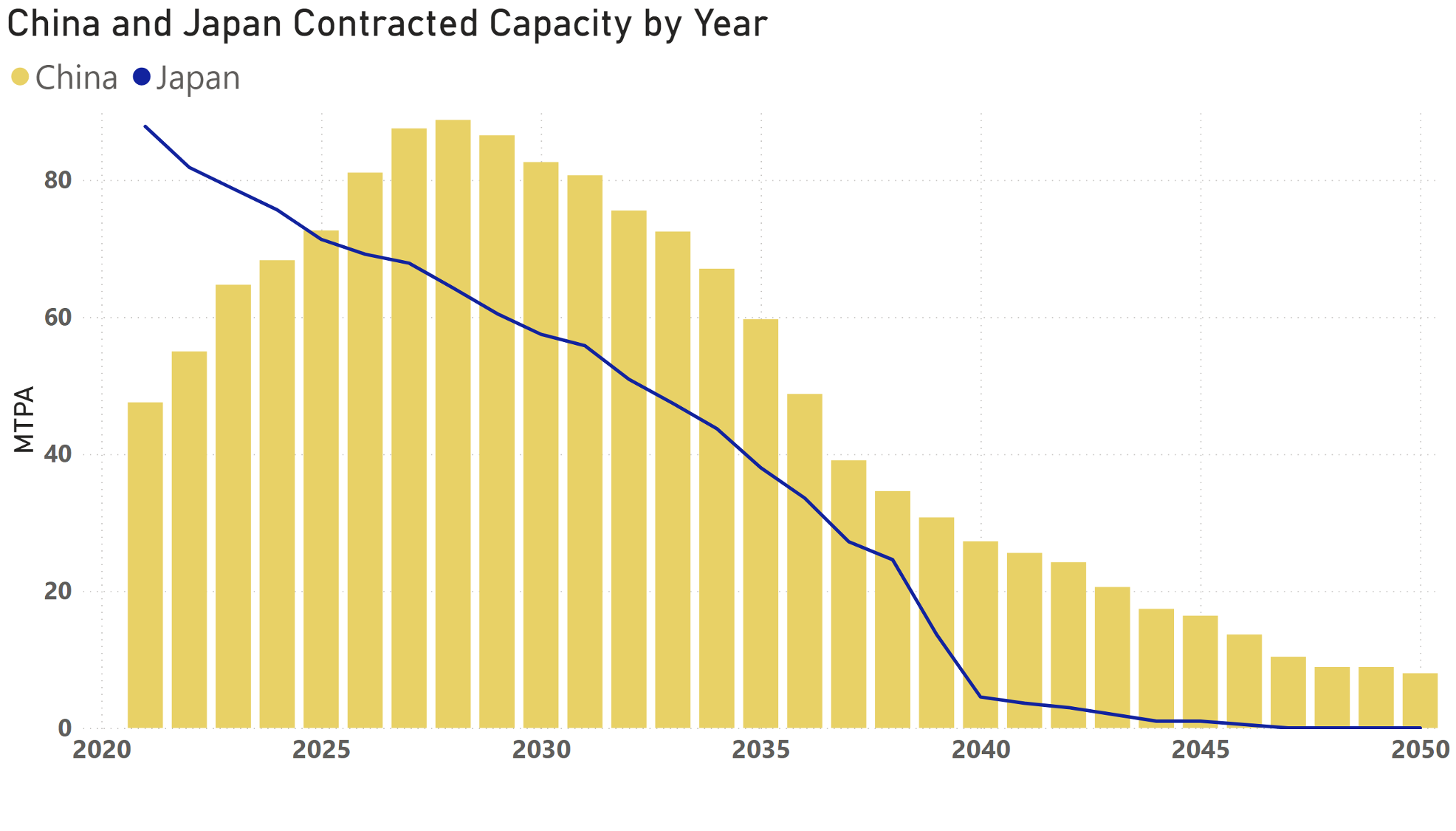

Russia has articulated a strategy to shift its gas supply from Europe to Asia, but this will not be straightforward. The obvious buyer would seem to be China. There is, however, just one major gas pipeline between the two countries. The Power of Siberia is already working but below capacity. It’ll deliver 38 bcm a year by 2025, when it hits full capacity.

In the meantime, Russian state gas company, Gazprom, wants to build a second Power of Siberia line to China with 50 bcm of capacity. That project won’t start operating until 2030 at the earliest.

For China, relying on one seller is risky and it has other pipeline suppliers, such as Turkmenistan.

Meanwhile, China has increased domestic gas production by 14% since 2020. In the same period, it has also increased gas storage by a third and added 19% more regasification capacity. This gives China a lot more flexibility about when and where it buys gas / LNG.

Outside of gas, China is setting global records for how much solar and wind capacity it is installing. It may have the world’s largest nuclear power fleet by 2030.

So, China has alternatives to Russian gas. But there are risks in China’s energy system. The condition of its giant hydropower plants seems to be deteriorating and there are drought concerns. That’s why China is likely to continue signing long-term LNG deals with the U.S. and the Middle East, while paying close attention to opportunities to invest in LNG facilities in Russia too.

Mega Trend 3: Russia decouples from Europe

Russian gas sales fell 25% in 2022. Export pipelines to China will take many more years to build. Therefore, it is likely that Russia will be very aggressive in trying to market its LNG to new clients, mainly in emerging Asia economies.

Russia still plans to boost its annual LNG output to at least 80 mtpa from 35 mtpa by 2035. It claims that the volume could even reach 140 mtpa. That would represent 20% of the world’s LNG market.

Those ambitions will depend on the war in Ukraine and geopolitics. For now, Russia will likely try to maintain good trade relations with its most profitable LNG client in Asia – Japan. Even that, however, is not enough in terms of sales, which is why Russia has started LNG exports talks with at least half a dozen other Asian buyers from India to Vietnam and Thailand.

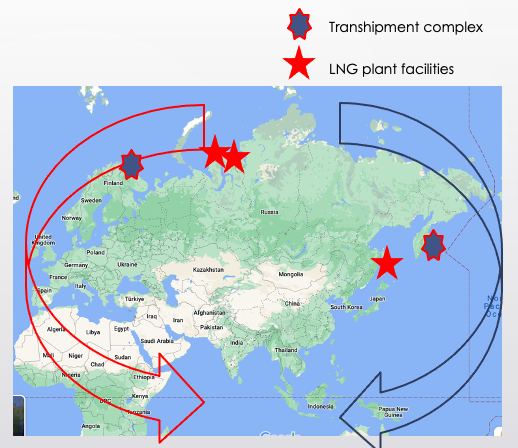

Russia hopes to send LNG via the Northern Sea Route and has plans to create facilities in the East and the West of the country to help its ships travel further. Of course, this will mean the cost of Russian LNG will rise and it will take longer to deliver. Still, with demand in Asia growing it will likely find buyers. We may also see Chinese traders resell Russia cargoes.

Will Japan turn away from Russian LNG?

For Japan, Russian LNG is hard to replace. It’s cheaper than other suppliers and the Sakhalin-2 project is the closest producer to Japan, able to deliver a cargo in less than half the time of other LNG plants. Which makes a big difference for a country with limited gas storage facilities: Japan can only store LNG for 2-3 weeks.

This makes gas analysts including RBAC Inc believe Japan will buy more, not less, Russian LNG in the future.

Of course, Japan is also looking at options elsewhere. But these are not straightforward. Politicians in Australia have called for fewer LNG exports to leave more gas for the local market. Similarly, Indonesia sees itself turning into a net importer from exporter in the coming years.

Canada could become a major new supplier for Japan, but beyond its first export project in British Columbia, due to start shipping in 2025, the pipeline of new projects is unclear.

The future of Japan’s biggest overseas LNG investment in Mozambique is entirely up in the air due to attacks from local terrorist groups. And while the Middle East offers plentiful gas resources and a history of good diplomatic ties, the strict contract terms of the region’s exporters leave Japanese buyers frustrated.

The most popular option of late has been to sign contracts with U.S. players. Yet even there, risks remain. The accident at the Freeport LNG site last year knocked out exports from the plant for close to a year. Meanwhile, 95% of U.S. LNG export projects are located in the same two states, creating a risk of over-concentration.

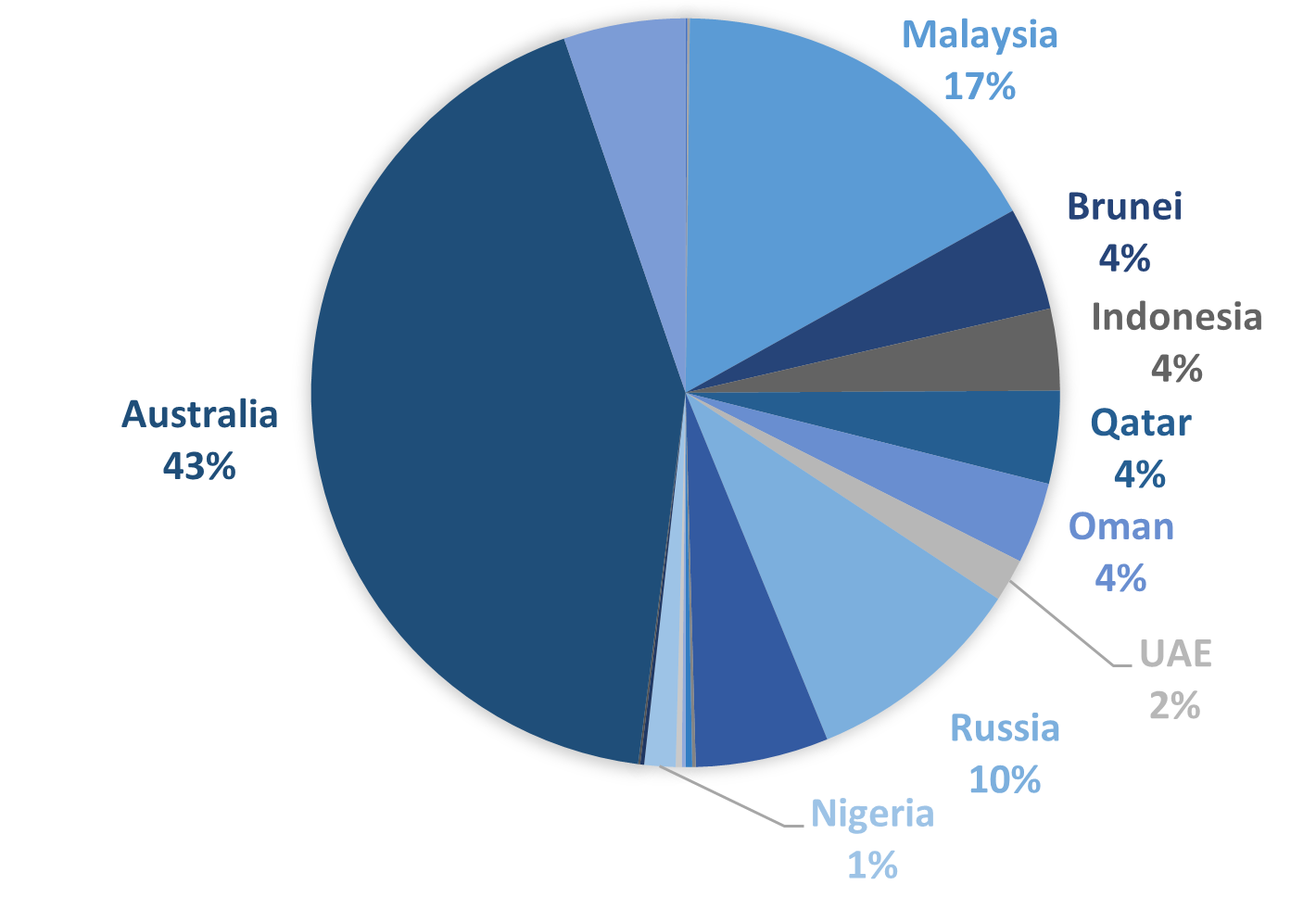

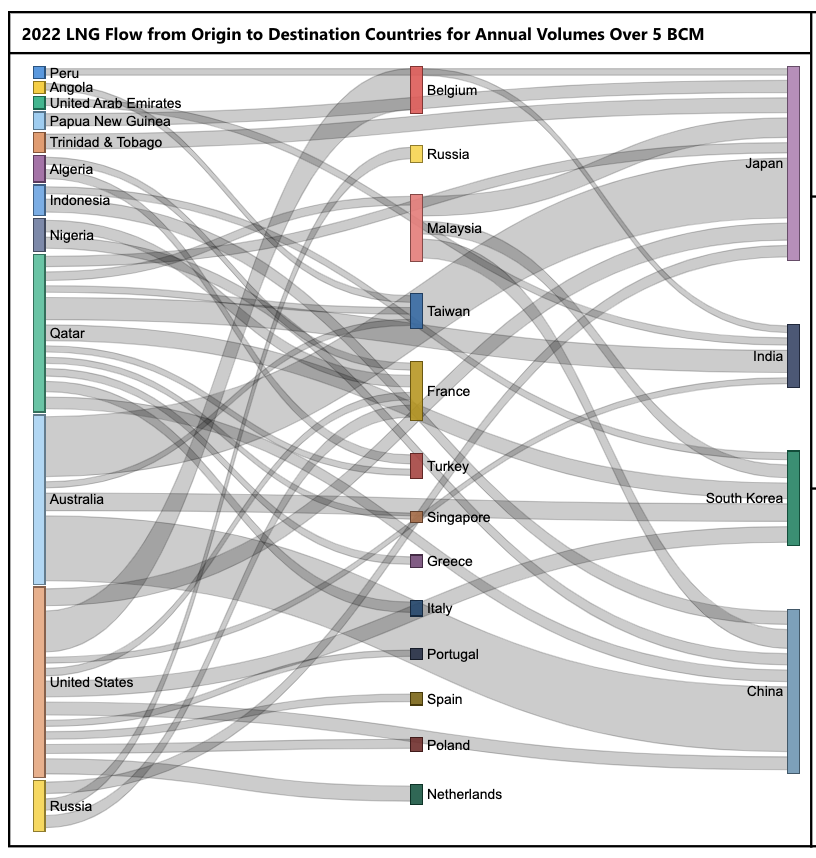

Japan LNG Imports in 2022

Source: Customs data

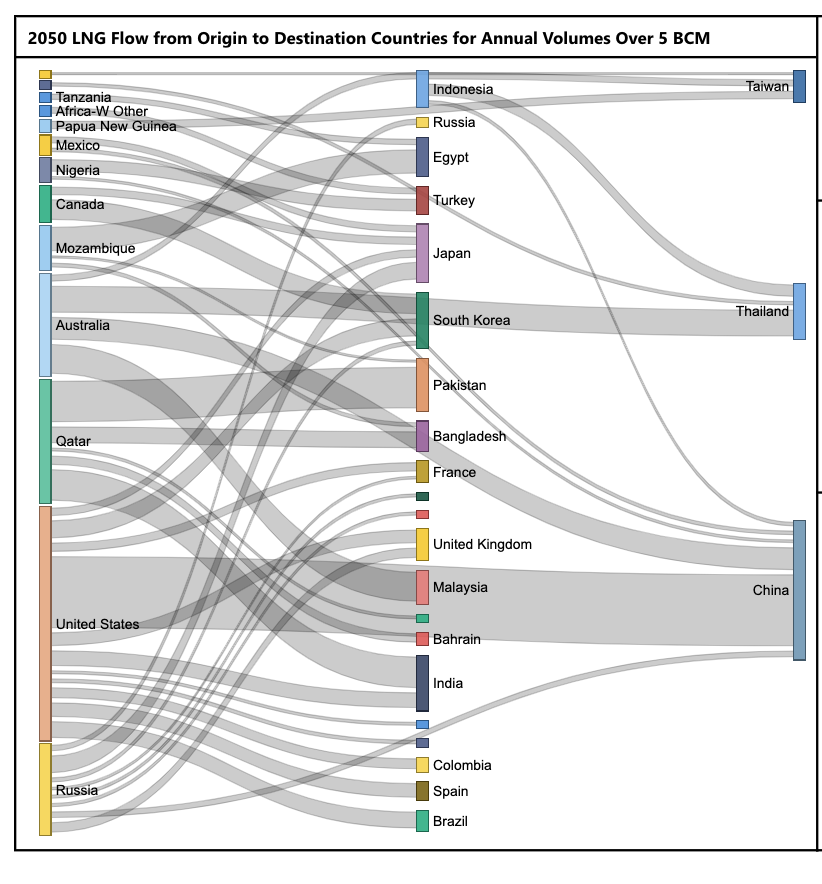

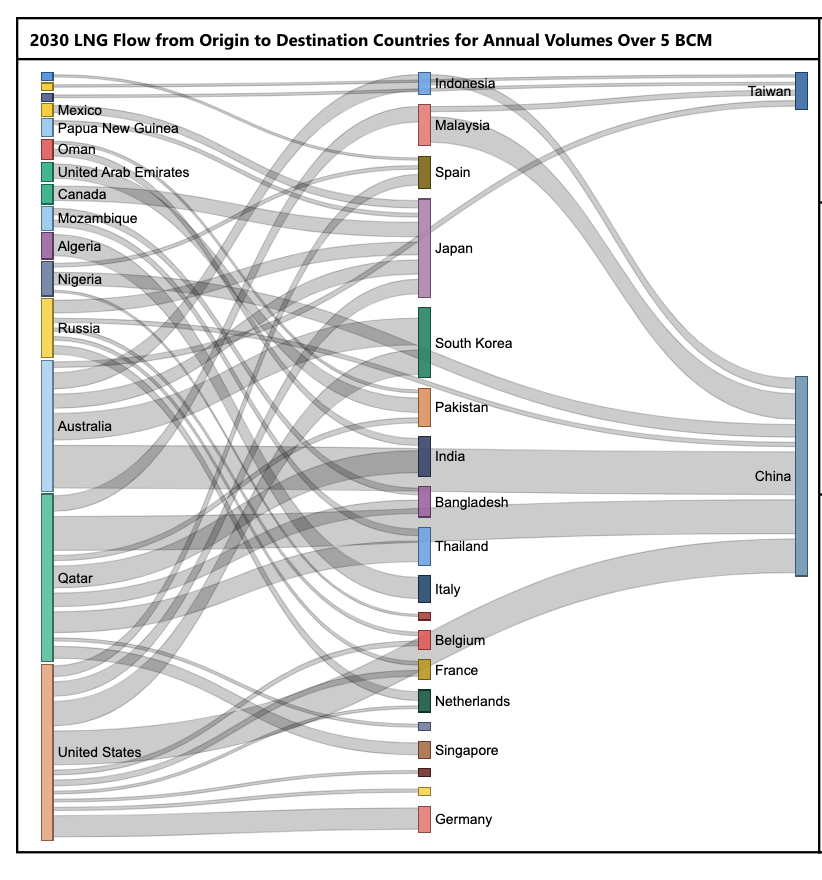

Mega Trend 4: Markets Grow More Crowded

So, how will the global LNG market develop until 2050? The simple answer is: there will be more buyers and more sellers. This level of market complexity also suggests that more flexibility in contract terms will be needed, as well as more LNG trade on exchanges and with more liquidity in the derivatives markets.

Source: RBAC

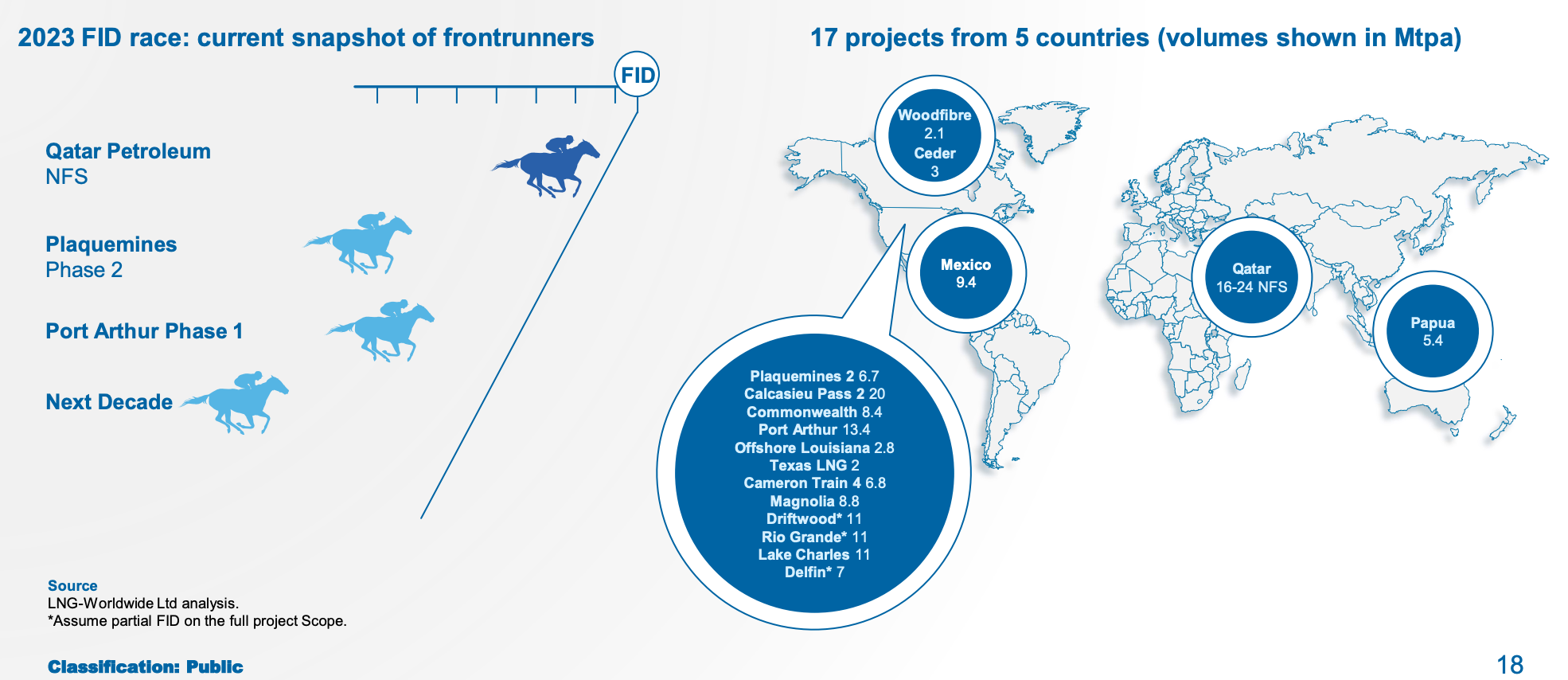

On the supply side, there are great expectations for new projects to win their FID (Final investment decision) this year in the U.S., Qatar, Mexico and Papua New Guinea. There is around 150 mtpa of new capacity under consideration, according to Tullett Prebon.

By the end of the decade, U.S. capacity alone could hit 280 mtpa, according to industry forecasts.

Source: Tullett Prebon

Still, less than half of the proposed projects may actually go ahead. Last year, only a quarter of those seeking FID attained it. As a result, this year only 9 mtpa of new global capacity (all from the U.S.) is expected to come online.

Mega-Trend 5: Decarbonization

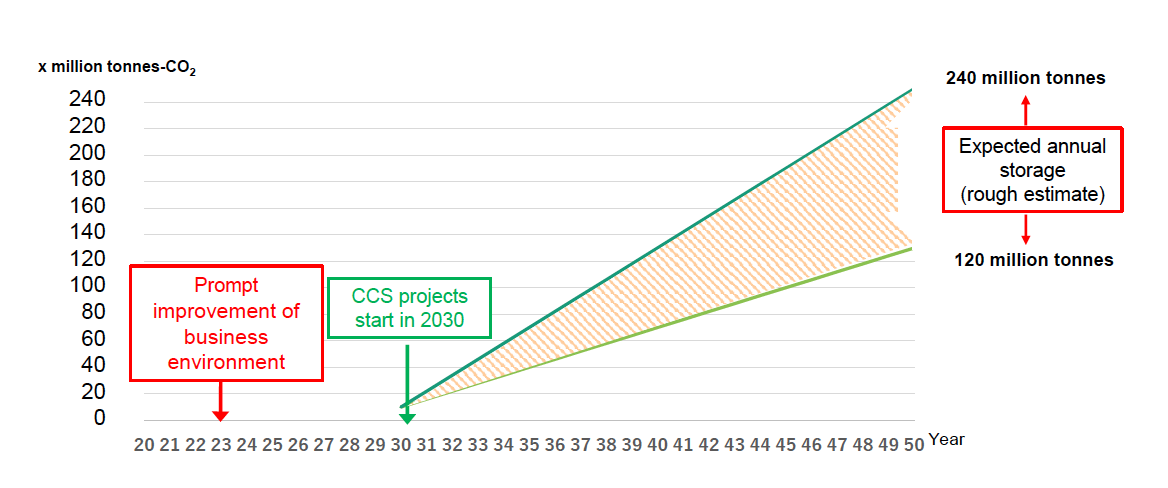

Decarbonization commitments are now enshrined in law in Japan and many other countries. How will the LNG industry cope? There are a few options. One is to install carbon capture technology, which is still at an early stage of development and expensive. There are also questions about how long-term carbon storage will work in practice. But there is no doubt that new government subsidies, such the Inflation Reduction Act in the U.S., will support investment in new CCS projects this year.

Japan is exploring CCS options in Malaysia and Indonesia, and also looking at several domestic sites. A recent forecast by JOGMEC sees Japan starting to utilize CCS on a commercial level from 2030 with volumes rising to between 120 and 240 million tons of CO2 per year.

Source: Japan CCS Co.

It is too early to say whether CCS alone will allow LNG to keep its place in the long-term pantheon of energy, but history shows that cheaper, easier alternatives need to be available to displace it. At present, non-fossil energy sources are facing their own challenges in Japan. Meanwhile, some of the low carbon solutions on the table today rely on natural gas as a feedstock.

This leads many to say that natural gas is guaranteed growth for several more decades as LNG displaces coal in the power mix. The U.S. Energy Information Administration, for example, forecasts domestic gas consumption to grow at least until 2050.

Japan’s energy policies remain a contradiction for now. The government target for 2030 calls for a halving of LNG’s role in the power mix. But while the shuttering of old thermal power plants will see a net loss of 9.2 GW of LNG-fired generation capacity this decade, this is nowhere near a 50% drop. Will utilities simply use gas-fired plants less despite an acknowledged power crunch in the country?

At the same time, Japan’s rollout of renewables has slowed rather than accelerated in part due to grid constraints and a growing local opposition. On the other hand, there’s frustration among many in offshore wind around the slow pace of industry development in Japan and anxiety among solar developers about their future business models after a guaranteed tariffs price system (FIT) was replaced with one with more emphasis on the market (FIP).

The fuel most likely to rival LNG in Japan in the future could be ammonia. With Japan’s coal plants relatively young compared to those in Europe or the U.S., many could convert to co-fire ammonia and eventually work entirely on the clean-burning fuel. JERA will trial co-firing at its Hekinan Thermal Power Plant in FY2023 and believes it could move to 100% ammonia-burning power plants as early as the first half of the next decade.

Environmental groups, however, don’t agree with Japan’s co-firing strategy, claiming it is too expensive and less efficient than renewable energy. What’s more, the growing number of RE100 firms in Japan could find ammonia generation at odds with their commitments to global clients and partners.

Conclusion

Last year was tough, but in the end, the global natural gas and LNG industry re-balanced. What it needs to be mindful of are prices, however, since LNG will lose its position in the global energy mix if it is seen as a luxury commodity.

China will undoubtedly become a major force in the Asian and global LNG market. For Japan, this can be an opportunity, not just a challenge. Finding ways to boost Japan-China LNG trade could help deliver more liquidity to the regional market, and in turn help to balance Asian demand with Europe’s needs.

While the global LNG market remains tight, most buyers will play it safe, retaining contracts linked to crude oil. But more and more new pricing models will emerge, including those that seek to link LNG prices with electricity. Thus, the fundamentals of local markets will play a bigger role on global LNG pricing and supply-demand balances.

Finally, opportunities in LNG derivatives will also diversify. Without a more liquid and active futures market, LNG buyers and sellers will need to assume ever-rising risks. While LNG futures trading has struggled to take off in Japan to date, a wind change may well be just around the corner.

A special thanks to the good people at Tullett Prebon, Rystad Energy, RBAC, ICIS and Japan CCS, among others for sharing their thoughts on the market in recent weeks.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Argentina/ Natural gas

Next year, state-controlled energy company YPF and Malaysia’s Petronas will make a final decision on a $60 billion natural gas project that would integrate production, storage, pipelines and liquefaction. The project is key for Argentina’s efforts to monetize its vast reserves and become an LNG exporter.

Commodities trading

ADNOC’s potential acquisition of energy trading house Gunvor has stalled. It hopes to acquire all of Gunvor, or at least take a majority stake, but CEO Torbjörn Törnqvist won’t give up his 90% stake. He’ll only sell a minority stake to raise funds to drive growth.

Europe/ Natural gas

The 80% drop in Russian natural gas sales to the EU has given high-priced LNG exports from the U.S. a crucial place in the global economy, says Torbjörn Törnqvist, head of Gunvor. Meanwhile, the EU will struggle over the next two winters to replace gas supplies as China’s demand recovers, said Törnqvist.

France/ Renewable energy

The UK’s Octopus Energy will invest €1 billion in the French green energy sector over the next two years that will generate low-carbon power to supply 300,000 households. Octopus entered the French market in January 2022 with its acquisition of Plüm énergie.

Germany/ EV batteries

Volkswagen has put on hold a planned battery plant in Eastern Europe in order to prioritize a similar facility in North America. The company estimates that it could receive €10 billion in U.S. incentives under the Inflation Reduction Act.

Italy/ Biofuels

Energy group Eni signed a two-year contract with Spinelli to power its trucks with a diesel fuel made from 100% renewable raw materials such as waste raw materials, vegetable residue and oils processed in Eni’s bio refineries.

Italy/ Nuclear fusion

Eni and U.S.-based Commonwealth Fusion System will cooperate on a series of projects aimed at launching a nuclear fusion power plant, with the goal of feeding electricity into the grid in the early 2030s.

Oil prices

As the shale revolution stalls, OPEC is back in the driver’s seat. This is what many energy execs said at CERAWeek in Houston. Thin global supply capacity means prices might again surge, and the return of China’s economy will put more pressure on supply.

South Korea/ Coal

Thermal coal imports in Q1 are on track to hit a five-year high as heating demand rose during a cold snap and as industrial demand recovers after the pandemic. South Korea is Asia’s fifth-largest coal consumer.

Tanzania/ LNG

Norway’s Equinor and Shell agreed with the government on a $30 billion LNG terminal that will be built near natural gas discoveries in deep waters off Tanzania’s south coast. In 2025, the government expects to make the final investment decision on the terminal.

U.S./ Energy transition

The oil industry is eager to claim billions of dollars of tax credits under the Inflation Reduction Act for investments in renewable power generation. This includes incentives for lower-carbon technologies, CO2 capture and storage, revamping refineries for biofuels, and producing low-emission hydrogen.

U.S./ Offshore oil and gas

President Biden’s offshore oil and gas lease plan will be even later as the Interior Department argues it needs until December to finalize the plan. There’s still no active offshore leasing program for new lease sales despite the Outer Continental Shelf Lands Act mandating that the Secretary of the Interior “shall prepare” this program to “meet national energy needs.”

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.