JAPAN NRG WEEKLY

MARCH 27, 2023

JAPAN NRG WEEKLY

March 27, 2023

NEWS

TOP

- Govt announces additional ¥1.2 trillion package to curb inflation, will subsidizing LP gas users, consumers of high-voltage power

- EPCOs seek ways to prevent further unauthorized access, will add separate computer systems for power grid and retail operations

- Osaka Gas president hopes G7 climate and energy ministers meeting can set rules for CCU and methanation

ENERGY TRANSITION & POLICY

- OCCTO releases 2023 supply plan; Supply-demand imbalance of Tokyo Area still unresolved

- Trial GX carbon exchange logs 150,000 CO2 tons of credit trades

- Minister asks Siemens to join offshore wind, hydrogen projects

- Japan awards inaugural Hydrogen Municipality of the Year

- JGC Holdings to participate in Indonesia/ U.S. SMRs project

- GS Yuasa wins order for Li-ion storage battery system from Honda

- Marubeni demonstrates first green H2 injection in Portugal pipes

- Yamaha invests in microbial tech to remove CO2 from the air

- JGC to build green ammonia demo plant in Fukushima Pref

ELECTRICITY MARKETS

- JERA acquires Belgium’s leading offshore wind power company

- iGrid Solutions gets ¥10.3 billion loan for 200 MW onsite PPA

- Hokkaido Electric to halve loss thanks to decline in spot prices

- JERA to decommission 4.4 GW of thermal power capacity

- NRA accused JAEA of more faults, Tsuruga NPP restart at risk

- Kansai Electric to modernize facilities at LNG-fired power station

- Hokkaido firm installs Chinese wind turbine to demo effectiveness

- Kansai Electric restarts reactor at Takahama NPP after glitch

OIL, GAS & MINING

- Idemitsu CEO says crude oil’s prices to decline but not collapse

- LNG stockspiles at power utilities rise 7.1% from a week earlier

- NYK chief asks govt to cover potential losses from Russian LNG

- Toho Gas to supply “carbon neutral” gas, power to Aichi area

ANALYSIS

BASELOAD ELECTRICITY MARKET: EPCOS AND NEW PLAYERS VIE FOR CHEAP ELECTRICITY

The electricity market liberalization in 2016 allowed a variety of new players to enter the market. Many hoped to compete and profit by buying electricity and reselling it at prices lower than those offered by Japan’s 10 major power utilities. Seven years later, however, the logic of the new players’ business model – and liberalization itself – is questioned. The main question was and remains: Where can companies that don’t generate electricity acquire electricity to sell?

KAWASAKI CITY’S INDUSTRIAL CLUSTER AIMS TO TURN OIL REFINING HEARTLAND TO CLEAN ENERGY

In the mid-1950’s, Japan developed vast industrial complexes along its eastern coastline. This was a time when the nation’s focus on energy resources shifted from coal to oil. Today, these complexes face a herculean challenge to transition their fossil fuel-intensive industries to cleaner alternatives. An interesting example of the transformation is the port city of Kawasaki, which wants to gain recognition as a leader in efforts to decarbonize the traditional industrial sector.

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Yoshihisa Ohno (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Filippo Pedretti (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

|

METI |

The Ministry of Energy, |

mmbtu |

Million British Thermal Units | |

|

MOE |

Ministry of Environment |

mb/d |

Million barrels per day | |

|

ANRE |

Agency for Natural Resources and Energy |

mtoe |

Million Tons of Oil Equivalent | |

|

NEDO |

New Energy and Industrial Technology Development Organization |

kWh |

Kilowatt hours (electricity generation volume) | |

|

TEPCO |

Tokyo Electric Power Company |

FIT |

Feed-in Tariff | |

|

KEPCO |

Kansai Electric Power Company |

FIP |

Feed-in Premium | |

|

EPCO |

Electric Power Company |

SAF |

Sustainable Aviation Fuel | |

|

JCC |

Japan Crude Cocktail |

NPP |

Nuclear power plant | |

|

JKM |

Japan Korea Market, the Platt’s LNG benchmark |

JOGMEC |

Japan Organization for Metals and Energy Security | |

|

CCUS |

Carbon Capture, Utilization and Storage | |||

|

OCCTO |

Organization for Cross-regional Coordination of Transmission Operators | |||

|

NRA |

Nuclear Regulation Authority | |||

|

GX |

Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

Government announces additional ¥1.2 trillion package to curb inflation

(Government statement, March 22)

- The govt announced a ¥1.2 trillion package to curb inflation by subsidizing LP gas users as well as consumers of high-voltage power such as schools, hospitals, etc.

- ¥30,000 will be provided to low-income households exempted from residential tax.

- Renewable surcharges included in the electricity bills will be reduced from April bills, and power utilities seeking rate hikes are to reassess their plans.

- The Ministry of Agriculture, Forestry and Fisheries will cover 70% of the energy cost rise of farms under its energy conservation programs.

OCCTO releases 2023 supply plan; Supply-demand imbalance of Tokyo Area still unresolved

(Denki Shimbun, Mar. 24)

- OCCTO disclosed its supply plan for FY2023 through 2032 at the advisers council on March 22. The electric supply reliability of the Tokyo Area for FY2023 is less than required, and TEPCO might face difficulty in balancing demand and supply.

- Moreover, the reserve margin of the Tokyo Area in case of severe heat that’s forecasted once in a decade slightly surpassed 3%, a level that might cause a blackout if other facilities are in trouble.

- In addition, the grid oversight body noted concerns about a supply-demand mismatch in other areas over the next decade. In Hokkaido, there’s worry about the situation in 2027. In Tokyo, it’s the years 2025 and 2026; in Kyushu, it’s 2025 and 2027 to 2029; while in Okinawa, it is 2025 to 2026 and 2029 to 2032.

- OCCTO will soon submit a final report to the METI Minister.

TAKEAWAY: The report suggests a review of the Capacity Market is needed so that more power supply can be secured when demand-supply balance is tight. During FY2023, a total of 2.43 GW of thermal power capacity will stop operation. This suggests further market tightness in the near future.

Trial GX carbon exchange logs 150,000 CO2 tons of credit trades

(Government data, March 22)

- Carbon exchange under the Green Transformation (GX) logged J-Credit trades that amounted to around 150,000 tons of CO2 during its trial phase from September to Jan 31.

- There were 220 offers, 342 bids resulting in 163 transactions.

|

J-Credit type |

Turnover (CO2 tons) |

Average transacted price/ton |

|

Energy conservation |

73,619 |

¥1,431 |

|

Renewables |

75,255 |

¥2,953 |

|

Forestry |

59 |

¥14,571 |

- Among the 183 participating companies and municipalities, 21% check exchange prices on a daily basis, while 29% said less than once a week.

- CONTEXT: The first trial phase will be followed by a second after April. The goals of the first were to monitor liquidity, and to check if exchange prices effectively serve as market signals, and if credits of varied types could trade simultaneously on a single trading platform.

Siemens Energy asked by METI Minister to join offshore wind and hydrogen projects

(Denki Shimbun, March 20)

- Siemens Energy CEO Dr Christian Bruch met METI Minister Nishimura on March 17.

- While Mr Nishimura asked Siemens about offshore wind power and hydrogen, Dr Bruch replied: “As the world faces a big challenge for energy issues, and as great change is required, we wish to join hands”.

- Dr Bruch showed interest in expanding to Japan, and asked Mr Nishimura about offshore wind and hydrogen policy.

TAKEAWAY: Siemens Energy’s hydrogen project in Yamanashi Pref was selected for the Green Innovation Fund, along with TEPCO and Toray. Also, Siemens Gamesa was selected as turbine supplier at Ishikari Bay of Hokkaido and Kagoshima Port of Ibaraki Pref.

Shikaoi Township in Hokkaido awarded “Hydrogen Municipality of the Year”

(Government statement, March 20)

- Shikaoi Township in Hokkaido was awarded the inaugural Hydrogen Municipality of the Year Award for building a hydrogen supply chain system utilizing livestock manure.

- In April 2022, the town (pop. 5,600) launched hydrogen production using biogas from livestock manure. The hydrogen is used mainly for fuel cell vehicles.

- Yamanashi Pref, Kawasaki City, the Hyogo prefecture-Kobe City team, and Namie Twp in Fukushima Pref were also awarded. For several years, they’ve already worked with the central government on Power-to-Gas and hydrogen projects.

- MoE and Japan Hydrogen Association organized the award.

IPCC report emphasizes the need to speed up direct carbon removal

(Japan NRG, March 22)

- The Intergovernmental Panel on Climate Change (IPCC) released its sixth assessment calling to accelerate development and use of carbon removal technology. 30 scholars from Japan participated as lead authors and editors.

- CONTEXT: The Research Institute of Innovative Technology for the Earth (RITE), a METI organization, participates in standardization of carbon capture and storage at ISO. NEDO supports direct air capture (DAC) development through moonshot R&D funding.

TAKEAWAY:While the global technology development focus is on massive carbon removal, the Japanese research aims to establish DAC of various sizes, from installations at large fossil power plants to small ones on buildings due to the country’s space constraints. Japanese researchers also position carbon re-use as an integral part of DAC systems.

GS Yuasa received order for 2.6 MW Li-ion storage battery system for Honda Motor

(Company statement, March 16)

- GS Yuasa received an order for a lithium-ion (Li-ion) storage battery system from Tokyo Gas Engineering Solutions (TGES) to be installed at Honda Motors’ Kumamoto Plant. GS Yuasa will deliver the system in FY2023; Honda will use it starting April 2024.

- The storage system has the output of 2.6 MW, or the capacity of 20 MWh. This is, as of March 1, 2023, Japan’s biggest storage battery system. Honda will use this system in association with the energy service that TGES delivered.

- The excess energy generated through solar PV systems will be saved to the storage battery and used when electricity from renewables falls short due to weather conditions. The storage battery system helps Honda reduce 3,300 tons of CO2 per year.

- CONTEXT: Honda Motors Kumamoto Plant installed 2 MW of solar PV in 2022, and plans to install 1.2 MW of solar PV in FY2023. Together with the existing solar capacity of 3.8 MW, Honda will have 7 MW of power generation capacity from renewable energy by 2024.

Central Glass plans sodium-ion cell electrolyte production

(Japan NRG, March 23)

- Central Glass confirmed to Japan NRG that it will launch production of electrolyte solution for sodium-ion batteries, which are the new vehicle batteries replacing lithium-ion cells, once there is customer demand.

- There’s no need to build a new plant, however, as existing lithium-ion raw material plants can be used to produce sodium-ion electrolytes.

- Reports of a plan to produce 1 GW-worth of the cell material in 2024 are unfounded, the company said.

Hitachi Zosen to install South Asia’s first sodium sulfide storage battery system

(Company statement, March 22)

- Hitachi Zosen, Male Water & Sewer Company and Renewable Energy Maldives will install a 1.45 MWh sodium sulfide (NAS) storage battery in the Gulhifalhu island of Maldives in spring 2024.

- The battery system will be located at a desalination plant that runs on solar power. The batteries store excess power. This will be the first NAS system in South Asia.

- CONTEXT: The NAS storage battery system, developed by Japan’s NGK Insulators, is one of the lithium-ion battery alternatives. Both NAS and lithium-ion cells have temperature issues. NAS systems need to be maintained in systems of 300 C. Optimal temperatures for lithium-ion systems are below 20 degrees C.

Marubeni demonstrates first green H2 injection in Portugal

(Company statement, March 17)

- Marubeni launched the first green hydrogen injection demo in Portugal’s natural gas distribution network through its investment in Floene Energias, a gas distribution system operator in which Marbeni holds a 22.5% stake through a JV with Toho Gas.

- In this project, Floene transports green hydrogen through its newly-constructed hydrogen pipeline, injecting it into an existing natural gas network. Floene plans to increase the injection ratio up to 20% during a two-year demo period to meet the 2030 Portuguese government’s target of having 10% to 15% of the total gas in the pipelines be hydrogen.

JGC to build green ammonia demo plant in Fukushima Pref

(Denki Shimbun, Mar. 23)

- Engineering company JGC Holdings will construct a demo plant to make green ammonia at Namie Town, Fukushima Pref, along with chemical company Asahi Kasei Corp.

- This project was selected by NEDO’s Green Innovation Fund that aims to develop technology for reducing overall GHG emissions to zero by 2050. The ammonia for this project will be fueled by hydrogen produced by 100% solar power.

- Construction starts in autumn of 2023, and operation to begin in FY2024. Each day, four tons of ammonia will be produced.

Yamaha Motor invests in microbial tech to remove CO2 from the air

(Company statement, March 17)

- Yamaha Motor invested in Andes Ag, a startup pursuing research into microbial technologies to remove CO2 from the air. This is the first investment made through the $100 million sustainability fund established in June 2022.

- Yamaha Motor, in its management plan (2022-2024), will strengthen sustainability efforts and explore new technologies and business models to reach carbon neutrality goals.

- The investment will help Yamaha acquire more knowledge about carbon credits/offsets and about natural sources of scalable carbon removal that can be applied in agriculture.

Marubeni sells biomethane from cow manure in the U.S.

(Company statement, March 23)

- Marubeni started producing and selling biomethane derived from cow manure at the Bio Town Biogas facility in Reynolds, Indiana through a joint venture with Green Rock Energy Partners.

- The company collects manure from 23,000 cows at nearby dairy farms to generate biogas, and biomethane, and uses it as fuel for compressed natural gas (CNG) vehicles.

- The project will earn environmental credits by preventing the release of methane.

PowerX launched “Chiku-den-sho AI” first software product

(Company statement, March 14)

- PowerX released its first software product, “Chiku-den-sho AI”, which applies AI to grid battery operation. The company’s algorithm helps to automate grid battery operation (electricity trading and charge/discharge control).

- AI creates arbitrage trading strategies that maximize profits, taking into account storage battery capacity and power input. It automatically generates bidding plans that anticipate JEPX price forecasts.

- The company predicts that operational profit will improve 76%, or earn gains of ¥78 million to ¥138 million, as a result of its simulation based on a 30 MWh grid battery.

- This software can be installed with PowerX grid and other batteries, as well as other energy management systems or virtual power plant platforms.

Japan’s JGC to participate in Indonesia/ U.S. SMRs project

(World Nuclear News, March 20)

- The U.S. and Indonesia announced a partnership to develop the Indonesian nuclear energy program. The U.S. Trade and Development Agency awarded a grant to PLN Indonesia Power for assistance in establishing a NPP in the country.

- Indonesia Power selected NuScale Power for assisting in the project, in partnership with a subsidiary of Fluor Corporation and Japan’s JGC Corporation. It plans a 462 MW facility and will utilize NuScale’s SMR (small modular reactor) technology.

NEWS: POWER MARKETS

JERA buys Parkwind, Belgium’s top offshore wind firm, to build global renewables platform

(Company statement, March 22)

- JERA agreed to buy all of Parkwind, Belgium’s leading offshore wind power producer, from Virya Energy for an equity value of close to €1.55 billion. The Japanese utility said it hopes to use the acquisition to build a platform for a global renewable energy business focused on offshore wind.

- In addition, JERA and Virya will explore the possibility for Virya to re-invest in a minority stake in Parkwind’s Belgian wind farm projects and discuss collaboration on more opportunities within Belgium.

- CONTEXT: Virya operates four offshore wind projects in Belgium, with 771 MW total capacity (Virya’s share is 420 MW). It’s also developing projects in Germany with a 257 MW capacity (Virya’s share is 180 MW); this makes for a total 4.5 GW capacity in Europe.

- The Parkwind acquisition will be completed by late 2023.

TAKEAWAY: JERA’s renewable energy assets at the end of 2022 totalled 2.2 GW capacity, but it plans to grow its renewables assets to 5 GW by 2025, including offshore wind investments in the UK and Taiwan. JERA recently sold its stake in Taiwan’s Formosa 3 wind project, but it is expected to be one of the bidders in the current round of offshore wind auctions in Japan.

Federation of EPCOs seeks ways to prevent further unauthorized access

(Denki Shimbun, Mar. 20)

- The Federation of Electric Power Companies (FEPC), an alliance of 10 EPCOs (not including Electric Power Development Co., or J-POWER) hosted a corporate ethical committee to discuss how to improve compliance, responding to recent cases of unauthorized access gained by member EPCOs.

- The companies decided to physically separate the computer systems used for the power grid business run by EPCOs from those used in the utilities’ retail operations.

- They also set up a task force on judicial reform led by an FEPC vice president.

TAKEAWAY: In the wake of several consecutive incidents of unlawful computer access, the govt is discussing how to separate transmission and distribution assets from those in the power retail sector. After market deregulation in 2016, the EPCOs unbundled their generation, T&D and retail assets, but in most cases they all sit inside the same holding structure.

iGrid Solutions obtained additional ¥10.3 billion for onsite PPA for 200 MW

(Company statement, March 14)

- VPP Japan, a subsidiary of iGrid Solutions, secured a ¥10.3 billion syndicate loan from ten banks led by Mizuho Bank. Since 2020, the company has raised ¥20.3 billion.

- The funds will help expedite solar power installation; the power will be locally generated and consumed.

- Participating banks are: Mizuho, Kagoshima, Chiba, Chiba Kogyo, Yamanashi Chuo, Shoko Chukin, Fukuoka, Shiga, and Nishi Nippon City.

- VPP Japan aims to build 1000 facilities to generate 200 MW of power by late March 2024. As of January, 510 facilities are in operation generating 107 MW of power.

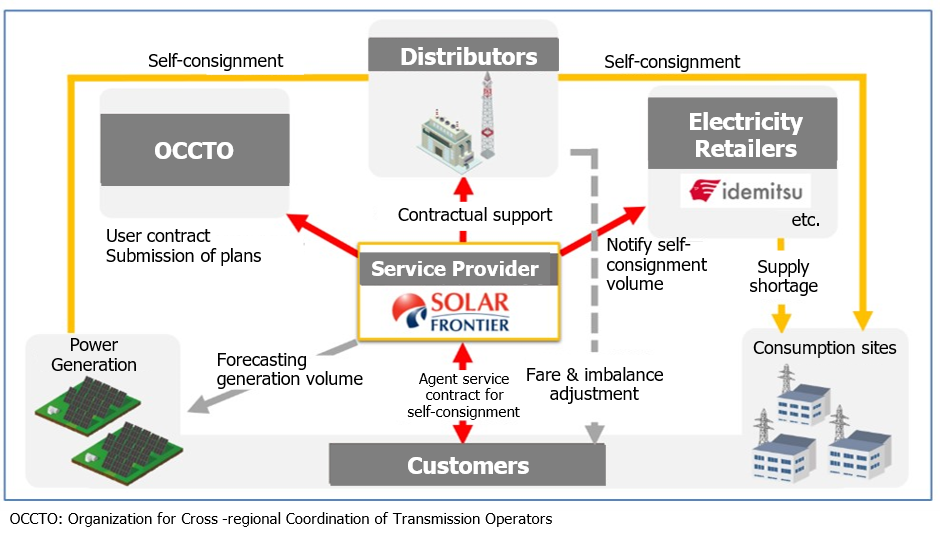

Idemitsu and Solar Frontier start self-consignment service of solar power

(Company statement, March 15)

- Idemitsu and its 100% subsidiary Solar Frontier began a one-stop agent service to process contracting and operation of power self-consignment from solar power plants to consumption sites located at a far distance.

- A self-consignment service uses a network to distribute power generated from a company’s plant to its consumption site(s). This allows a company to use renewable energy even when there’s no space to install solar PV at the site when it needs the power.

- Solar Frontier takes care of all contractual processes and other issues related to self-consignment. Solar Frontier offers to rectify power imbalances inherent in intermittent sources.

Hokkaido Electric improves full year forecast thanks to decline in JEPX prices

(Company statement and media reports, March 23)

- Hokkaido Electric announced an upward revision to its earnings forecast for fiscal year 2022, in large part due to a decline in JEPX wholesale power market prices.

- The operating loss is expected to drop by ¥27 billion to ¥24 billion (from the ¥51 billion number announced in January). However, revenue was also revised down by ¥24 billion to ¥897 billion, driven by more electricity sales to retailers and to the JEPX.

- This year, wholesale electricity prices have cooled in line with the drop in fuel prices and power demand.

- The utility said that a shorter construction period to upgrade its Tomato-Atsuma coal-fired power plant, and an increase in hydro power output, also contributed to the improved financial performance.

TAKEAWAY: Hokkaido Electric has pinned its hopes on improving the financial performance on the restart of its three-unit Tomari NPP. The nuclear station has not operated since May 2012 and it has been under NRA review for close to a decade. Recently, there seemed to be some progress in the regulator’s review of Tomari’s preparedness against earthquakes, but when any of the reactors are given the green light to restart remains unclear.

JERA to decommission six units at Kashima power station; loss of 4.4 GW capacity

(Company statement, March 17)

- On March 31, JERA will decommission Units 1 to 6 at Kashima thermal power station. They began operation in the first half of the 1970s.

- Units 1 to 4 have been shut since 2014, while Units 5 and 6 shut in 2020. Units 1-6 were fueled by heavy oil and crude oil, and had a 4.4 GW capacity.

- The company also makes upgrades at other thermal power plants that will have a total capacity of 4.9 GW.

KEPCO to modernize facilities at LNG-fired Nanko power station

(Company statement, March 20)

- KEPCO plans to modernize its LNG-fired Nanko thermal power station (Osaka).

- The company will introduce a combined cycle power generation system that combines gas and steam turbines. This will increase the power generation efficiency ratio by 40% and cut CO2 emissions.

- Installation starts in FY2026, and operation starts in FY2029.

- CONTEXT Nanko power station is KEPCO’s oldest LNG thermal power station. It consists of three Units (600 MW each, total capacity of 1.8 GW); operations started in 1990 and 1991.

- SIDE DEVELOPMENT:

KEPCO to restart Unit 2 of Maizuru power plant after recent fire

(Company statement, March 20)- KEPCO will restart the coal/ biomass-fired Maizuru power plant’s Unit 2, after a fire hit the plant on March 14. It has two units and a 1.8 GW total capacity.

- The fire started in a biomass fuel supply facility. Investigation into the cause continues.

The NRA accused JAEA of seven additional faults at Tsuruga Unit 2 – restart now at risk

(Denki Shimbun, Mar. 20)

- New problems have been discovered that might delay the restart of Tsuruga NPP Unit 2.

- At the previous meeting, the NRA said plant operator Japan Atomic Power Company (JAEA) didn’t comply with protocol for taking samples on earthquake protection performance. Now, the NRA found seven more issues in the document submitted by JAEA at the last meeting. These concern the procedures used to take samples of geological data.

- Committee member Mr. Naito said JAEA’s sloppiness was “extremely regrettable”; another committee member, Dr. Ishiwatari, said the NRA will meet in April to discuss whether to continue the review of Tsuruga NPP Unit 2 or not.

TAKEAWAY: The decommissioning of Tsuruga NPP Unit 1 started in April 2015, not long after the Fukushima accident. Now, only Unit 2 is operable (after a restart was certified by the NRA), but two new units, namely Unit 3 and 4 are planned at this site. Therefore, if JAEA doesn’t get a green light for restart of Unit 2, the construction of Unit 3 and 4 might be endangered. That would be a nightmare for Mitsubishi Heavy Industries, which began work on those two units.

Hokutaku installs Chinese wind turbine in Fukushima to demonstrate effectiveness

(New Energy Business, March 22)

- Hokutaku, a multi-vendor wind turbine maintenance company, began construction of a 2.5 MW wind turbine in Iwaki city, Fukushima Pref. The turbine comes from Gold Wind, China. Hokutaku will use the power generated in-house and sell it via the FIT at ¥19/Kwh.

- The turbine will also be used for operation and maintenance training and to demonstrate its effectiveness to officials and other companies.

- Hokutaku awarded the engineering, procurement, and construction work to Toko Denki. Locally procured components such as the turbine tower and bolts will be used. The wind turbine arrives in Sept 2023.

- CONTEXT: Hokutaku won the operation & maintenance contract for the Abukuma wind power farm being built in Namie Town, Fukushima Pref.

Kansai Electric’s Takahama NPP Unit 4 has restarted operations after glitch

(Sankei Shimbun, Mar. 24)

- Kansai Electric restarted Unit 4 at its Takahama NPP on March 24.

- The facility made an unplanned shutdown in late January due to a problem with a coil in the control rod system. After Kansai Electric switched off power to the coil to investigate, the reactor automatically shut down.

- Kansai Electric concluded that the cause of the stoppage was an issue with an electrical circuit in the driving mechanism of the control rod.

TAKEAWAY: With the restart, Kansai Electric will now have 870 MW of capacity back online. The company has faced financial losses since Unit 4 stopped during winter peak power demand.

Hiroshima High Court throws out appeal to stop Shikoku Electric’s Ikata NPP Unit 3

(Yomiuri Shimbun, March 24)

- The Hiroshima High Court threw out an immediate appeal by seven residents in both Hiroshima and Ehime Pref to stop operation of Shikoku Electric’s Ikata NPP Unit 3.

- Previously, the Hiroshima Local Court rejected residents’ appeal for a temporary injunction to stop Ikata Unit 3 in Nov 2021, but residents immediately filed an appeal.

- The biggest issue for this lawsuit was anti-earthquake measures, which Shikoku Electric claimed to be sufficient, a claim the residents disputed.

TAKEAWAY: This is the 12th case of a citizen group applying for a temporary injunction to stop Ikata NPP’s Unit 3 from operating. Already, 10 cases have been thrown out by the court. Unit 3 (890 MW, PWR) is currently under scheduled maintenance, but Shikoku Electric plans a restart on May 25.

- SIDE DEVELOPMENT:

Osaka court rejects appeal to stop operation of Mihama NPP Unit 3

(Denki Shimbun, Mar. 23)- On March 30, the Osaka District Court dismissed an appeal by two residents of Fukui and Saitama Pref to stop operation of Mihama NPP Unit 3.

- The two alleged in May 2022 that their rights are at risk of violation due to a possible accident of Kansai Electric’s Mihama NPP Unit 3, caused by earthquake or terrorism.

- However the District Court ruled that it found neither direct nor serious risk of damage for the two plaintiffs. In particular the plaintiff who lives in Saitama Pref was judged to be too distant to suffer from any possible accident at Mihama NPP Unit 3.

Enblue starts 1 MW solar sharing operation in Tochigi

(Company statement, March 14)

- Enblue develops and operates renewable energy plants for small-to-medium enterprises. The company began commercial operation of agrivoltaic solar sharing in Nasu Shiobara, Tochigi Pref for 1 MW. The annual power generation volume is about 1.2 MWh that will be sold through the FIT at ¥32/kWh.

- The plant is built on 16 km2 of farm land that grows barley. The solar panels are set on a pedestal 2.8 meters high to give sufficient solar rays to the barley.

NEWS: OIL, GAS & MINING

Osaka Gas president hopes G7 Sapporo meeting can set rules for CCU and methanation

(Gas Energy Shimbun, March 20)

- Fujiwara Masataka, president of Osaka Gas, spoke about global LNG supply and demand, the weak yen and the impact of the Ukraine war. During the G7 ministers meeting on Climate and Energy to be held in Sapporo (April 15-16), Fujiwara hopes that international rules for the calculation of CCU (CO2 capture and utilization) reduction, including methanation, could be formulated.

- Fujiwara stressed the importance of switching to natural gas in coal and oil using factories for reducing CO2. He also said that the company set a renewable energy development target of 5 GW by 2030, and already reached 1.95 GW.

- Regarding methanation, he explained that manufacturing could take place in North America, South America, Southeast Asia, Australia, the Middle East, and other places.

Idemitsu CEO says crude oil’s prices to decline but not collapse

(Nikkei, March 20)

- Petroleum Association of Japan’s Chairman Kito Shunichi (who is also the President of oil refining major Idemitsu Kosan) said on March 20 that crude oil’s sales, whose prices are on a downward trend, “may continue for the time being”.

- He explained that the bankruptcy of Silicon Valley Bank (SVB) and the mismanagement of Credit Suisse Group have increased uncertainty about the economic outlook.

- He added, “I don’t think we will see a slithering downward trend,” mainly due to strong demand in emerging markets. He forecasted crude oil prices at $70-$85 per barrel.

- CONTEXT: Middle East-produced Dubai crude oil was at $75/ barrel as of March 17, down from $127 in March 2022. The price now holds steady despite global economic problems. There are also speculations that OPEC and “OPEC+,” which consists of non-members such as Russia, will cut production in order to support prices, and uncertainty remains strong.

LNG stocks rise to 2.56 million tons, up 7.1% from a week earlier

(Government data, March 22)

- LNG stocks of 10 power grids stood at 2.56 million tons as of March 19, up 7.1% from 2.39 million tons a week earlier. METI initially reported the March 12 stocks were 2.38 million tons but corrected the figure.

- The end-March stocks last year were 1.63 million tons. The five-year average for this time of year is 2.07 million tons.

New head of NYK asks govt to cover potential losses for Russian LNG vessels

(Bloomberg, March 22)

- The new head of NYK Soga Takaya is lobbying the govt for compensation in case of an incident on a Russian LNG-carrying vessel that might leave shipping companies liable.

- Soga said insurance conditions for vessels operating in Russian waters are stricter, and insurance might suddenly be canceled.

- Soga said the Sakhalin-2 LNG plant accounts for a significant part of LNG procurement among domestic power and gas companies, and problems could arise if supplies were to stop.

- CONTEXT: Late last year, three major Japanese non-life insurance companies said they’d stop providing insurance to compensate for damage caused by the war from January. However, subsequent negotiations have allowed them to continue providing insurance.

Toho Gas to supply CO2-free electricity and carbon neutral gas in Aichi Pref

(Company statement, March 17)

- Starting April, Toho Gas will supply CO2-free electricity and carbon neutral gas to city hall, schools and other public facilities in Anjo, Aichi Pref.

- Toho Gas estimates this will help reduce CO2 emissions by 4,700 tons a year. Anjo will be the first municipality in Aichi Pref to have carbon neutral electricity and gas.

ANALYSIS

BY YOSHIHISA OHNO

Baseload Electricity Market: EPCOs and New Market Players

Vie for Cheap Electricity Volumes

The full liberalization of the electricity market in 2016 was one of Japan’s most significant developments of the past decade. That process has allowed a wide variety of new players to enter the market, including firms from the oil, telecommunications and other sectors.

Many of the new entrants believed they could compete and profit by buying electricity and reselling it at prices lower than those offered by Japan’s 10 major power utilities collectively known as the EPCOs. Seven years later, however, the logic of the new players’ business model – and by extension the liberalization itself – is being questioned by some in the industry and the media. After all, current results differ from the picture painted by officials prior to 2016.

The main question was and remains: Where can companies that don’t generate electricity acquire electricity to sell? New players, often referred to as shin denryoku (“new power companies”) who do not have enough of their own power generation capacity to cover the needs of their customers largely depend on buying power directly from generators or on the wholesale market. For the former, new players need to offer better terms than those that the generators can secure themselves. Meanwhile, the latter option is limited by the volume that the power generation companies are willing to feed to the market.

For a while, during a period of declining electricity prices, the EPCOs found it profitable to sell some output on the wholesale market. In the last two years, the price trend has reversed and grown more volatile while a growing capacity crunch has made power generators cautious about sharing volumes.

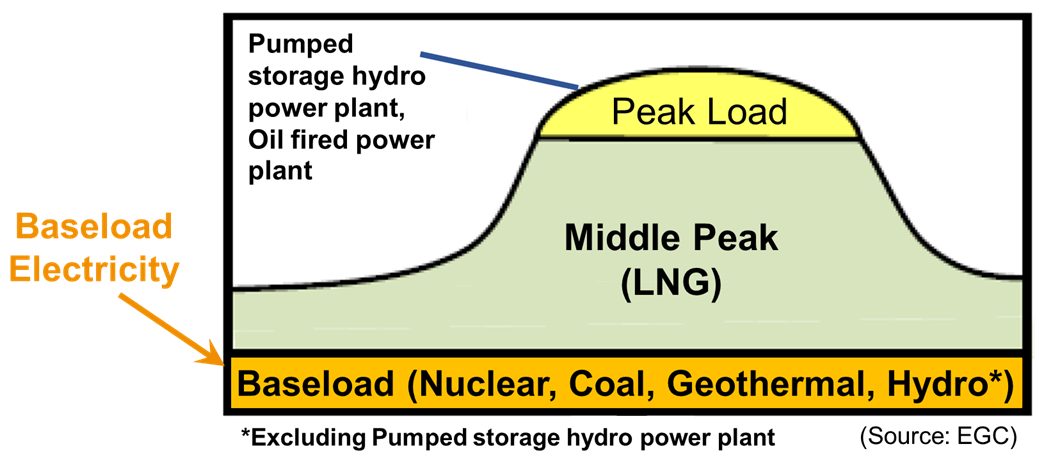

What makes the situation even more complicated is the bifurcation of the power market by energy source. Most new capacity is solar or wind; it’s sold through elevated state tariffs; and, it’s owned by smaller generators. But the bulk of Japan’s power system is propped up by thermal, nuclear, and hydro power plants, which are known as baseload capacity, and which are almost entirely owned by the EPCOs.

For shin denryoku to compete, they need more baseload power to be available on the market, especially because it includes some of the cheapest power facilities in the country. But EPCOs feel that this capacity has been paid for with their sweat (and blood), and should remain their competitive advantage.

As the government seeks to find a solution between the warring sides, it knows that finding the right model for sharing baseload power will be key to fostering competition.

What’s at stake

The EPCOs spent many years and tremendous amounts of investment to build the nation’s energy infrastructure. In some cases, this came at a human cost. For example, construction of the Kurobe Dam (Kurobe No. 4 Hydropower Plant) owned by Kansai Electric claimed 171 victims by the time it was completed in 1963.

Given the history, the EPCOs don’t want to part with their hard-earned baseload electricity and hand it over to the new power market players. For their part, new power market players believe that the current system has been manipulated by the deeply entrenched EPCOs, which can count on old relationships to manipulate regulations and markets.

The impasse between the two feuding sides has been a factor slowing the growth in Japan’s power generation sector. With EPCOs the owners of most of the thermal and all of nuclear generation, and solar and wind facilities in the hands of other generators, the split extends to battles over Japan’s vision for its future power mix.

And so, everyone agrees that METI urgently needs to reform the system. The challenge is to accommodate the interests of the EPCOs and the ambitions of new power market players, with both sides currently criticizing the system as unfair.

Towards that goal, in July 2019 METI set up the Baseload Electricity Market. It was meant to invigorate the electricity retail market by obliging EPCOs to sell a portion of their baseload output on the wholesale JEPX market. This effectively opened the gate for coal, hydro (but not pumped storage), and geothermal and nuclear power plants to operate on open market terms. It also bridged the gap for retailers that only had access to electricity from renewable sources during peak demand times of the day.

Baseload auction system

A baseload contract runs for up to 12 consecutive months, providing power each day over 24 hours.

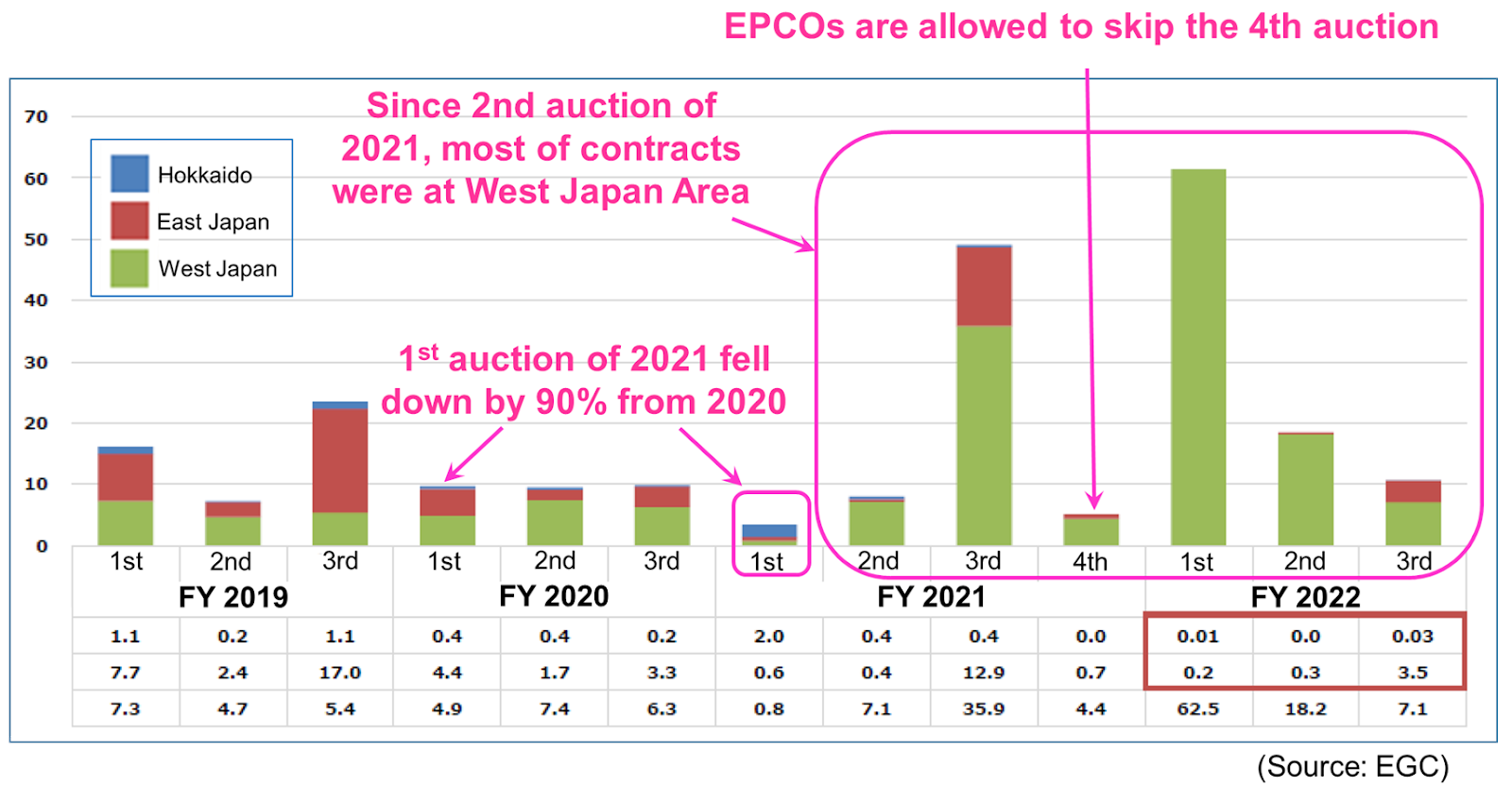

During the first two years after the introduction of this market segment, baseload power was sold via an auction, which was held three times a year. Today, auctions are held four times a year: in July, September, November and January; but, the EPCOs are allowed to skip the fourth auction. Each auction trades electricity for the following year, they’re held in three regions: Hokkaido; East Japan; and West Japan. Okinawa is the only region excluded from this market.

The EPCOs are required to sell a proportion of their baseload power according to a formula that calculates their power mix, and the rate of switched customers. In October 2017, METI unveiled a preliminary calculation for how much of their total volume the EPCOs must sell to the baseload market.

|

Hokkaido |

Tohoku |

Tokyo |

Chubu |

Hokuriku |

Kansai |

Chugoku |

Shikoku |

Kyushu |

|

4.88% |

8.26% |

36.85% |

11.11% |

2.61% |

19.92% |

5.27% |

2.41% |

8.69% |

Source: EGC

At the start, METI said it would operate the Baseload Electricity Market until the new players (shin denryoku) controlled about 30% of all power sold in Japan. And, until about two years ago, the industry was heading in that direction. New players gained about 22% of the power market.

The trend stalled as a series of energy crises since the 2020 onset of the Covid pandemic has roiled markets. But there was trouble even before that.

At the first Baseload Electricity Market held in July 2019, the prices posted by the EPCOs were much higher than what new power market players expected. The price for the Tokyo Area Baseload Electricity Market auction was ¥9.77/ kWh. This was as much as a fifth less than the JEPX spot market price at the time, but almost double what some new market players said they expected.

With such a mismatch, TEPCO and Tohoku Electric ended up selling only 1.6 TWh of electricity in the 2019 auction, which was just 2% of the total volume executed at this auction. To put another way, only 2% of baseload electricity sold by Tohoku Electric and TEPCO was considered affordable by the new power market players.

The Baseload Market remained in this steady if anemic state for two years, but in 2021 volumes fell 90% compared to the year before as rising fossil fuel prices filtered into the cost of electricity. The market regained some momentum during the third auction of 2021, but most of the contracts were signed for the Kansai Area, which largely reflected the improving power capacity situation there due to a restart of several nuclear reactors.

A similar story continued with auctions since then. As East Japan (including the Tokyo area) and Hokkaido face a capacity crunch, the prices asked by EPCOs have failed to entice buyers and volumes have shrunk even further. Only in West Japan has baseload contract trading increased, again arguably due to the availability of nuclear power.

Ripe for a change

Noting the auctions situation, in 2022 METI began discussions to reform the Baseload Electricity Market. During the most recent government meeting on this issue, held on Feb 20, some experts pointed out that one of the issues affecting the mechanism is an unclear process for fuel cost calculations. It was also noted that the EPCOs seem to sell electricity volumes to affiliated power retailers at prices that reflect the variable cost of fuel.

Meanwhile, the EPCOs offer baseload electricity contracts at prices that appear to factor the upper range of fuel costs. Also, those at the meeting discussed the potential to extend baseload contract terms beyond a year.

There are a few ways that METI can tackle the perceived discrepancy. One option is to ask the EPCOs to clarify their fuel cost calculations. Another is to add an adjustment mechanism to Baseload prices to reflect volatility in fuel costs. Yet another option, suggested by experts on a METI panel overseeing the issue, is to fix the price based on the one that the EPCOs use to sell surplus power to their affiliated retail companies.

After hearing various export and industry views, METI proposed to follow the second option: add a mechanism to adjust baseload contract prices in line with fuel costs. The ministry has yet to provide further details on how this will be introduced.

Squaring the circle

The latest development by METI reflects the difficulty of marrying two very different sets of industry players. The EPCOs were responsible for almost the entirety of Japan’s electricity network until liberalization and they’ve spent decades creating the system as it exists today. They feel that new market entrants are getting a free ride on the back of their assets, which are relatively cheap to operate today thanks to massive investments in the past.

New players naturally ask for rules that can help them compete. Otherwise, they argue, what was the point of introducing market competition in Japan?

Without a way to incentivise the transfer of electricity between the two sets of players, Japan risks returning to an oligopoly of 10 major regional utilities. And while METI is tweaking the Baseload Electricity Market system, it’s unclear whether the changes would address the key question posed earlier: What will make asset-lite new market entrants more competitive than the power generators from which they secure volumes?

The answer possibly lies in the two “Transformations” that the government has set as a target for Japan: Green (GX) and Digital (DX). The rapidly expanding local power derivatives market will also play a big role. The two warring sides may find that in the nexus of these three trends they can offer each other solutions, not only competition.

ANALYSIS

BY CHISAKI WATANABE

Kawasaki City’s Industrial Cluster Aims to Turn Oil Refining Heartland into Clean Energy Hub

In the mid-1950’s, Japan began developing vast industrial complexes along its eastern coastline to support the development of the country’s petroleum, petrochemical and steel industries during a post-WWII boom. This was also a time when the nation’s focus on energy resources shifted from coal to oil.

More than a half century later, these complexes face a herculean challenge to transition their fossil fuel-intensive industries to cleaner alternatives all the while trying to maintain international competitiveness.

An interesting example of how the transformation may turn out lies in Kawasaki, a port city just south of Tokyo. The city hosts one of Japan’s major petrochemical industrial clusters. Now, Kawasaki wants to gain recognition as a leader in efforts to decarbonize the traditional industrial sector.

In January, Kawasaki City became Japan’s first industrial cluster to join an initiative launched by the World Economic Forum (WEF) and Accenture and the Electric Power Research Institute. Named the Transition Industrial Clusters Towards Net Zero, the project supports industrial clusters in their efforts to achieve net zero emissions.

The WEF’s initiative so far includes 17 industrial clusters in the Netherlands, the U.S., Belgium, the U.K., Spain, Australia, Indonesia, China and Japan. Eventually, it aims to sign on 100 industrial clusters globally in a collective effort that would reduce 1.6 billion metric tons of CO2 emissions, possibly contributing $2.5 trillion to global GDP.

Decarbonizing major industries worldwide is crucial because they’re responsible for 30% of global CO2 emissions. Yet, there’s still no consensus on the most effective clean technologies to reach net-zero for industry. Among the top candidates are carbon capture and hydrogen, both of which require significant investments.

Kawasaki City’s GHG emissions

Kawasaki City’s main industries are oil, chemicals and steel, with ENEOS, Kao, and Asahi Kasei among its largest enterprises. Emissions from the top 30 companies operating in its industrial cluster account for 73% of Kawasaki City’s total emissions.

Kawasaki City’s entry into the WEF project followed plans for a carbon neutral industrial cluster that was launched in March 2022. The city also set up a private-public council, which has 71 member companies, in order to push through measures to achieve carbon neutrality.

According to the city’s carbon neutrality plans, the main focus will be development in three key areas:

1) A supply base for carbon neutral energy centered on hydrogen

2) An industrial cluster around the carbon cycle

3) A competitive industrial area with optimized use of energy.

Source: Kawasaki City

1) Hydrogen Push:

Kawasaki City is betting on hydrogen thanks to the area’s expertise as an early adopter of hydrogen technologies. The city was ahead of other municipalities when it put together a hydrogen strategy in 2015, and it has been conducting pilot programs with the government and companies. It is home to hydrogen-related industries, such as manufacturers of fuel cells and parts for hydrogen stations.

Furthermore, the cluster’s supply and demand for hydrogen accounts for about 10% of Japan’s total. The area has one of Japan’s longest pipe networks to deliver hydrogen, which is commonly used in manufacturing.

|

Goals to 2030 |

|

|

Goals for 2030~2050 |

|

Source: Kawasaki City

Now, Kawasaki City aims to expand supply and consumption of the fuel further. In order to keep its status as energy supplier for Tokyo and the surrounding regions, Kawasaki City needs to serve as a receiving terminal for imported hydrogen.

The city also notes the need to develop a supply system for both imported and locally produced “CO2-free” hydrogen, referring to green hydrogen (generated using renewable power sources) and blue hydrogen (produced from natural gas with carbon capture technology). The city has three objectives to boost hydrogen use: 1) Build a system to supply CO2-free hydrogen; 2) Expand demand for CO2-free hydrogen; and 3) Improve social acceptance of CO2-free hydrogen.

2) Improving the carbon cycle:

Kawasaki City has a high concentration of recycling businesses, including for plastic. Some of the plastic waste is incinerated, which increases GHG emissions. Therefore, the city plans to expand plastic recycling and also to expand the use of CO2 captured from nearby factories. The city’s objectives are: 1) Expand the scope of recycling of CO2 and plastic; 2) Introduce innovative recycling measures; and 3) Promote understanding among citizens and companies

|

~2030 |

|

|

2030~2050 |

|

Source: Kawasaki City

3) Optimizing energy use

One of Kawasaki’s biggest challenges is to decarbonize the cluster’s energy use. The city’s port serves as a major import hub for crude oil and LNG, accounting for about 10% of Japan’s total imports. The area has more than 8 GW of power generation capacity, including three commercial gas-fired power plants, and a city gas production facility, making it a major energy supplier. The city also has renewable power plants (biomass, solar, wind) and two oil refineries.

The following are some of the challenges.

- Low potential for local renewables capacity: According to Kawasaki City’s estimates, renewable energy could supply 1,655 GWh by 2050, but that is only 9% of current power consumption. The chart below shows estimates of the city’s renewable energy capacity and potential.

- There is an increasing need to decarbonize the entire supply chain starting with sourcing of materials, as well as during manufacturing and post-manufacturing.

- Most CO2 emissions come from heat production, but there’s a lack of established methods to decarbonize it; possible measures include electrification (i.e., installation of electrical furnaces), switching to hydrogen and ammonia fuels (i.e., installation of hydrogen and ammonia boilers), as well as synthetic fuels/gasses.

- The city has many power generation facilities owned and operated by non-utility companies. Unlike major power companies that already have plans to decarbonize their electricity supply, individual non-utilities need their own measures.

|

2022 estimated capacity |

2022 estimated generation |

2050 estimated potential capacity |

2050 estimated potential generation |

2019 city-wide consumption | |

|

Residential solar |

41,854 kW |

51 GWh |

320,611 kW |

387 GWh | |

|

Non-residential Solar |

51,924 kW |

57 GWh |

490,401 kW |

592 GWh | |

|

Onshore wind |

2,003 kW |

4 GWh |

2,003 kW |

4 GWh | |

|

Offshore wind |

0 |

0 |

0 |

0 | |

|

Hydropower |

314 kW |

2 GWh |

314 kW |

1 GWh | |

|

Geothermal |

0 |

0 |

0 |

0 | |

|

Biomass |

108,800 kW |

571 GWh |

122,300 kW |

671 GWh | |

|

Total |

204,895 kW |

683 GWh |

935,629 kW |

1,655 GWh |

18,410 GWh |

Source: Kawasaki City Global Warming Basic Plan 2022

The Kawasaki cluster will seek to optimize its energy use through:

(1) Optimization of local electricity production

(2) Optimization of local heat production

(3) Expansion of effective utilization of CO2 and materials

|

~2030 |

|

|

2030 ~ 2050 |

|

Source: Kawasaki City

Beacon to the rest of Japan?

Kawasaki City’s efforts follow in the wake of the central government’s push for “carbon neutral ports,” which will serve as import and storage facilities for hydrogen and fuel ammonia, improve port functions and coordinate with local industries to achieve zero GHG emissions. Kawasaki’s experience could serve as a guide for other major ports around Japan, with discussions around “carbon neutral ports” also taking place in Yamaguchi and Ibaraki prefectures.

Meanwhile, Japan has seven other petrochemical industrial complexes, which face the equally challenging prospect of finding ways to decarbonize and may look to copy Kawasaki’s playbook.

One issue that all these places may face, however, is cost. Many of the measures under consideration in Japan’s industrial heartlands at present revolve around hydrogen. But prices for the clean-burning fuel are too high for widespread adoption and the production of hydrogen itself is not always done without generating emissions.

So it’s not surprising that at this stage, Kawasaki City’s clean industry plans lack details on the scope of emissions that will be cut, the investments required, or a detailed roadmap to net zero. It will be up to companies to join the local efforts and help plot a more precise course.

For its part, the city will need to step up efforts to ensure close coordination with the private sector so that everyone is on the same page and the energy transition proceeds with minimal disruptions and dislocation.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

China/ Russian energy imports

Since March 1, 2022, China has imported from Russia oil, gas and coal to the tune of $88 billion; this is about 60% more YoY. The rise reflects both increased volumes and higher prices for the commodities.

Commodities trading

Energy trader Gunvor seeks to expand its oil trading and develop power trading. Gunvor traditionally focuses on oil and gas, metals and bulk commodities, but it has in recent years also begun trading power in Europe. The company set up a power desk last year in the U.S. and will start gasoline blending operations there.

EU/ Nuclear power

Last Energy, a startup developing small nuclear power plants, signed four deals worth $18.9 billion to build 34 reactors in the EU. The U.S. company expects to install the first of its 20-MW systems in 2025.

France/ Strikes

Several refineries were still blocked after two weeks of strikes, disrupting production and power supply. Strategic reserves of fuel have had to be utilised. Also, due to strikes, at least 14 nuclear reactors in EDF’s fleet of 56 suffered delay in their maintenance plans.

India/ Energy transition

India can attain energy independence by 2047, says a study by the U.S. Department of Energy. But India’s energy infrastructure requires $3 trillion in investments over the next several decades.

Scotland/ Pumped hydro

UK power generator SSE will invest £100 million in a pumped hydro plan that could boost energy storage capacity. Pumped hydro plants work by pumping water uphill to a reservoir before releasing it; the flow downhill through turbines produces electricity.

UK/ Carbon capture

Power generator Drax will pause its £2 billion investment in bioenergy with carbon capture and storage (BECCS) until it receives clarity on state support. Drax needs a commitment to BECCS before it will install the technology at its 2.6 GW biomass power plant in Yorkshire.

UN/ Climate change

The UN Intergovernmental Panel on Climate Change issued a report seen as a final warning to act swiftly on climate change. Global warming will “more likely than not” exceed 1.5 C in the near-term. Current policies put the world on track for warming of 3.2 C by 2100.

U.S. / EV chargers

Manufacturers and operators of EV chargers are bracing for a slowdown in production and deployment as they scramble to comply with “Made in America” terms of a $7.5 billion federal program meant to accelerate the industry. Companies warn that the country lacks the domestic production capacity – particularly on high-speed chargers.

U.S./ LNG

Sempra Energy greenlighted its $13 billion Port Arthur LNG terminal on the Gulf Coast. The 13.5 million ton per year “phase 1” facility — to come online by 2028 — will add another roughly 10% to the capacity of existing projects and those under construction.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.