JAPAN NRG WEEKLY

APRIL 10, 2023

JAPAN NRG WEEKLY

April 10, 2023

NEWS

TOP

- At G7, Japan to call for precise CO2 rules for hydrogen, which would create definitions that go beyond colors

- METI starts enforcing rule to annul FIT for idled projects; more than 4 GW of solar, wind capacity could be affected

- Japan to stress the importance of LNG investments at Sapporo meeting of G7 ministers later this month

ENERGY TRANSITION & POLICY

- Agency ratifies guidelines for competition rules in clean energy

- IAEA says no need for further review of Fukushima water release

- Two major engineering firms join forces on domestic SAF projects

- Idemitsu and Chile’s HIF partner in e-fuel production and imports

- City starts to use FAME biodiesel as fuel for construction vehicles

- Osaka Gas and MHI to collaborate on CO2 value chain for CCUS

- Kansai Electric to study hydrogen, ammonia potential in Canada

- Toyota aims to sell 1.5 mn EVs by 2026, set up U.S. production

- Japanese aluminum firm says switching factories to renewables

ELECTRICITY MARKETS

- Kansai Electric to have 7 reactors online for summer demand peak

- Antitrust officials’ leniency to Kansai Electric breeds resentment

- METI delays power tariff increases sought by several EPCOs

- Niigata Port picked as next hub for offshore wind development

- Regulator issues notice to Chugoku Electric on JEPX trades

- METI announces first Long-Term Decarbonized Capacity auction

- NRA temporarily halts restart review of Japan Atomic’s reactor

- Sumitomo and partners finalize plans for offshore wind in France

OIL, GAS & MINING

- INPEX submits revised plan for Abadi LNG project in Indonesia

- Japan says closely monitoring China’s rare earths export policy

- JOGMEC, Canadian miner to explore new nickel ore deposits

- Tokyo Gas expands LNG trading resources with new London desk

ANALYSIS

CAN JAPAN RETURN TO THE SOLAR MARKET

WITH INNOVATIVE NEW TECH?

In the 2000s, the solar industry was dominated by Japanese engineering and innovation. Manufacturers like Sharp at one point garnered more than half of the global PV market. Fast forward to 2023, and Japan’s once vaunted solar panel industry, which was the envy of the green energy world, is barely hanging onto life. While demand for solar panels continues to boom, Japan’s firms are left with a tiny market share. But just as all seemed lost, a leap in innovation promises to usher in a next-generation solar power where Japan has a good chance of success.

JAPAN’S NEW EMISSIONS TRADING SYSTEM:

AIMING HIGH BUT WITH A SLOW ROLLOUT

Japan has finally launched its long-awaited CO2 emissions trading system (ETS). After an earlier five-month trial, last week the system began full-fledged operations on the Tokyo Stock Exchange. Initially, carbon trading will be conducted on a voluntary basis. The ETS will run in ‘phase-one’ mode for the next three years for companies that signed up. The idea is not only to cut CO2 levels but create a basis for a host of new energy technologies. But does the slow rollout undermine the process?

GLOBAL VIEW

A wrap of top energy news from around the world.

EVENTS SCHEDULE

A selection of events to keep an eye on in 2023.

JAPAN NRG WEEKLY

PUBLISHER

K. K. Yuri Group

Events

Editorial Team

Yuriy Humber (Editor-in-Chief)

John Varoli (Senior Editor, Americas)

Mayumi Watanabe (Japan)

Yoshihisa Ohno (Japan)

Wilfried Goossens (Events, global)

Kyoko Fukuda (Japan)

Filippo Pedretti (Japan)

Regular Contributors

Chisaki Watanabe (Japan)

Takehiro Masutomo (Japan)

SUBSCRIPTIONS & ADVERTISING

Japan NRG offers individual, corporate and academic subscription plans. Basic details are our website or write to subscriptions@japan-nrg.com

For marketing, advertising, or collaboration opportunities, contact sales@japan-nrg.com For all other inquiries, write to info@japan-nrg.com

OFTEN USED ACRONYMS

| METI | The Ministry of Energy, Trade and Industry | mmbtu | Million British Thermal Units | |

| MOE | Ministry of Environment | mb/d | Million barrels per day | |

| ANRE | Agency for Natural Resources and Energy | mtoe | Million Tons of Oil Equivalent | |

| NEDO | New Energy and Industrial Technology Development Organization | kWh | Kilowatt hours (electricity generation volume) | |

| TEPCO | Tokyo Electric Power Company | FIT | Feed-in Tariff | |

| KEPCO | Kansai Electric Power Company | FIP | Feed-in Premium | |

| EPCO | Electric Power Company | SAF | Sustainable Aviation Fuel | |

| JCC | Japan Crude Cocktail | NPP | Nuclear power plant | |

| JKM | Japan Korea Market, the Platt’s LNG benchmark | JOGMEC | Japan Organization for Metals and Energy Security | |

| CCUS | Carbon Capture, Utilization and Storage | |||

| OCCTO | Organization for Cross-regional Coordination of Transmission Operators | |||

| NRA | Nuclear Regulation Authority | |||

| GX | Green Transformation |

NEWS: ENERGY TRANSITION & POLICY

Japan to propose carbon intensity standard for hydrogen at G7

(Japan NRG, April 5)

- The govt will propose to set the definition and standard of carbon intensity of hydrogen at the upcoming G7 meeting. A global carbon intensity standard is essential to build mutual verification systems, to expand trade and to diversify supply sources.

- CONTEXT: Currently, hydrogen made from coal or natural gas is called “blue hydrogen”, and hydrogen made from renewable energy as “green hydrogen”. Hydrogen made from nuclear is “pink hydrogen”, and hydrogen made from methane is “turquoise hydrogen”. However, there is no definitive agreement on this issue. Japan seeks to place priority on CO2 numbers rather than colors.

- Japan is expected to propose 3.4 kg of CO2/ kg of hydrogen as low-carbon hydrogen, which is in line with the EU standard.

TAKEAWAY: METI has unveiled the outline of the revised hydrogen strategy which included a carbon intensity standardization, a new goal of 15 GW electrolysis capacity by 2030, and a new 2040 supply goal of 12 million tons. METI had a 2030 goal of 3 million tons and a 2050 goal of 20 million tons, but not for 2040.

- International agreement on this standard will help Japan import hydrogen and export manufacturing equipment.

- SIDE DEVELOPMENT:

Japan Gas Association urges rules on carbon footprint measurement of e-fuels

(JGA statement, April 6)- The Japan Gas Association sent a formal request to the MoE to speed up writing carbon footprint measurement rules for e-methane, SAF and other fuels made from recycled carbon.

- CONTEXT: The request comes ahead of the G7 Climate Ministers Meeting in Sapporo next week (April 15 and 16).

METI starts enforcement of new rule to annul idle FIT-approved projects

(Denki Shimbun, April 4)

- METI said it has started enforcing its new rule to cancel the FIT agreement for projects that have not started construction one year or more after their stated start of operations. The FIT contract is based on the project operator’s stated timeline.

- CONTEXT: Feed-in Tariff (FIT) guarantees payment for electricity generated at the power facility at a certain price level for a long period, usually 20 years. Some developers won an FIT contract at high prices in the early stage of the program but then did not go on to build the facilities.

- The revised FIT Law came into effect in April 2022.

- At the end of FY2022 (which is March 31, 2023), 50,000 projects to build 4 GW of capacity did not meet the revised law criteria and therefore could lose their FIT approval, according to METI.

- During FY2023, officials estimate that another 10,000 projects will face the same fate. The ministry will send out warning notices to the related parties.

TAKEAWAY: The reasons why companies don’t begin operation before the deadline are numerous. Sometimes, it is because developers hope to get lower equipment prices by waiting. Others simply hope to flip the FIT permit to other parties at a profit. But delays cause problems for the grid, which must keep space in reserve for agreed FIT capacity. Also, delays impact Japan’s targets for the rollout of renewable energy.

JFTC formalizes green competition guidelines after revisions

(Japan NRG, March 31)

- The Japan Fair Trade Commission formalized green competition guidelines, reflecting public feedback.

- The changes include a clarification for initiatives to reduce Scope 3 emissions, asking transport service providers to cut emissions and excluding those with high emissions. This is unlikely to be anticompetitive behavior.

- CONTEXT: The guidelines clarify sustainability initiatives that are compliant (or not) with the Antimonopoly Act (AMA). They were opened for a month-long public consultation in January.

TAKEAWAY: Ruling party lawmaker Amari Akira and some govt officials have been asking for wider AMA exemptions, possibly by amending the AMA, saying companies need to collaborate, not compete to speed up large hydrogen and ammonia projects. Some critics describe the JFTC as “a mini-METI”. On the other hand, lawyers told Japan NRG that it failed to provide thought leadership for the future, as the guidelines were reprints of past case studies.

Govt calls for JCM project proposals

(Government statement, April 6)

- The govt calls for proposals of projects for the Joint Crediting Mechanism. The projects cover decarbonizing technologies, products, systems, services and infrastructure and other mitigation actions in developing countries.

- Applications close Nov 30. The govt budgeted ¥15 billion for JCM projects in 2023-2025. Since 2013, there have been 228 projects.

IAEA: No need for further technical review of Fukushima water release

(IAEA statement, April 5)

- No further review of TEPCO’s plan to release contaminated water into the sea is needed, the International Atomic Energy Agency said in its report of the November 2022 safety review mission to Fukushima NPP.

- The review assessed safety aspects of the systems for discharging the treated water.

- IAEA will publish its full conclusions before the water release.

TAKEAWAY: The discharge of treated water is scheduled for early this summer. But the IAEA will issue the final report only in a few months; thus, TEPCO might wait to execute the discharge until after the report’s publication.

Two major EPCs in Japan join forces on domestic SAF plants

(Company Statement, March 31)

- JGC and Toyo Engineering (TEC) will work on orders for front-end engineering design (FEED) and engineering, procurement and constructions (EPC) services for domestic sustainable aviation fuel (SAF) plants.

- JGC specializes in production supply planning, and TEC specializes in technology for SAF production. Both are experienced in building large oil refineries and chemical/petrochemical plants in Japan and overseas.

- CONTEXT: Japan has set a target to replace 10% of jet fuel used by domestic airlines with SAF by 2030. Domestic SAF demand is expected to grow from 300,000 kiloliters in 2025 to 171 million kiloliters in 2030 – nearly six-fold. Domestic oil refining companies and others plan to start construction of SAF plants between 2024 and 2027, investing several hundred billion yen from the government’s Green Innovation Fund.

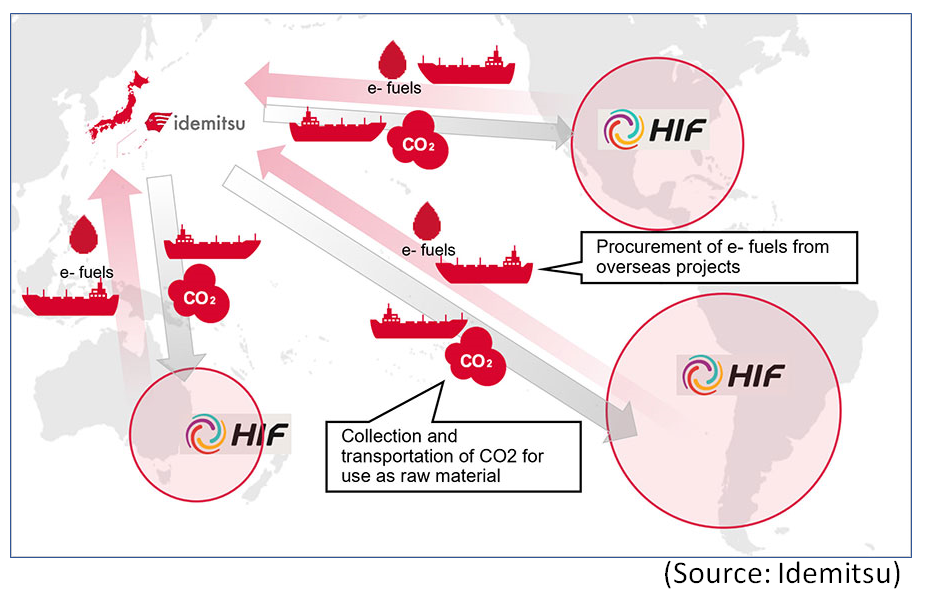

Idemitsu and Chile’s HIF Global partner in e-fuel production and imports

(Japan NRG, April 5)

- Idemitsu and HIF Global signed a MoU on imports and production of e-fuel supplies, including possible JVs to produce synthetic gasoline and SAF in Japan.

- Idemitsu plans to import synthetic methanol, the feed for synthetic gasoline and SAF, from the Americas and produce them in Japan.

- Sale of the e-fuel and production at Idemitsu refineries are planned for 2025.

- CONTEXT: Japan’s GX strategy calls for synthetic fuels to enter commercial operation by 2030.

TAKEAWAY: Idemitsu partnered with HIF because its technologies are almost ready for commercialization and are the quickest e-fuel solution, the company told Japan NRG. HIF production costs are believed to be above current gasoline price levels considering the cost of green hydrogen. Idemitsu may need government subsidies to commercialize e-fuel products.

HIF makes e-fuel from synthetic methanol produced from CO2 and green hydrogen. HIF’s technologies are different from the methanation-based technologies developed by Hitachi Zosen and IHI to produce e-methane, another type of e-fuel.

Idemitsu also told the media that the export of CO2 captured in Japan to HIF facilities overseas is also under discussion.

Itochu sets up domestic jet fuel blending supply chain and Neat SAF import, Japan’s first

(Company statement, March 30)

- Itochu started importing neat SAF from Finland’s Neste, and began supplying SAF to Chubu Centrair International Airport, the third airport where Itochu has SAF supply bases. The other two are Narita and Haneda.

- The SAF supply chain is blended with conventional fossil jet fuel from Fuji Oil.

- CONTEXT: Neat SAF is a jet fuel made from biomass materials. It requires blending with other jet fossil fuels and is mainly produced in Europe. Neste OYJ’s SAF can be blended up to 50%.

City of Saga uses FAME biodiesel fuel for construction vehicles

(New Energy Business News, April 3)

- Nishimatsu Construction and Saga City (Saga Pref) verified next-gen biodiesel fuel produced by an incineration plant that can be used for construction vehicles. This biodiesel fuel is equivalent to light (diesel) oil, processed through decarboxylation.

- Saga City has been using FAME biodiesel fuel (FAME = fatty acid methyl ester) for city buses since 2010.

- Nishimatsu and the city will continue work to expand use of next-gen biodiesel fuel.

Osaka Gas and MHI to collaborate on CO2 value chain for CCUS

(Company statement, March 31)

- Osaka Gas and MHI will study developing a carbon capture, utilization, and storage (CCUS) value chain. Captured CO2 will be transported by ship, also overseas.

- Both will study how to capture CO2 from industries such as steel, cement, chemicals and petrochemicals. The CO2 will be used for e-methane and underground storage.

- They will also study how to quantify the environmental value of CCUS through CO2NNEX, a digital platform being developed by MHI and IBM Japan.

- CONTEXT: Environmental value refers to a certified reduction of emissions that can be packaged into a sellable product, such as a carbon credit. Buyers use such products to cut their own emissions total.

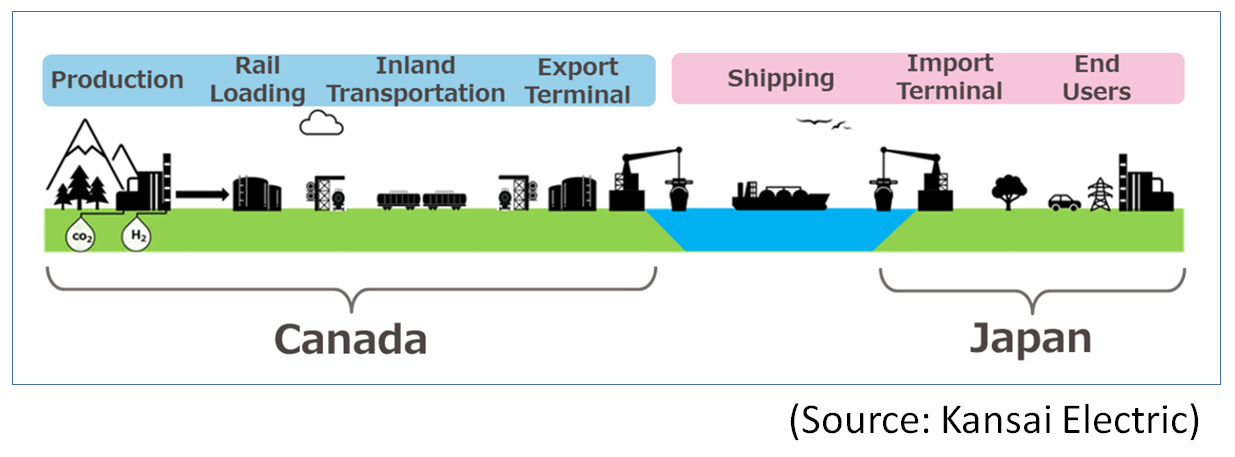

KEPCO to study whether to develop hydrogen or ammonia with Canada

(Nikkei Asia, April 7)

- Kansai Electric is partnering with Canada’s ATCO to conduct a feasibility study on the production, transportation and import of either hydrogen or ammonia from Canada.

- Details on the investment and the fuel amount to be purchased are not yet known; the decision whether hydrogen or ammonia will be based on production cost, etc.

- After the feasibility study finishes later this year, production facilities could start up on a trial basis in 2029. KEPCO is also conducting a study on importing Australian-made hydrogen to be burnt with natural gas at a power plant in Hyogo Pref in 2030.

- CONTEXT: Kansai Electric will start a study to procure hydrogen or ammonia from Canadian energy infrastructure company ATCO. While ATCO undertakes the production, Kansai Electric would be in charge of transportation, import facility and final use.

Toyota to sell 1.5 million EV by 2026, produce in the U.S.

(Nikkei, April 7)

- Toyota will introduce 10 new EV models by 2026, bringing its annual global sales to 1.5 million units. The company will begin local production in the U.S. in 2025.

- The company will produce a three-row SUV in the U.S. It plans to build a new battery plant and increase production.

- In addition to hybrid vehicles (HVs), the company will maintain FCVs (fuel cell vehicles) and hydrogen engine vehicles in its strategy. Toyota will also accelerate its EV strategy.

- CONTEXT: Toyota’s EV strategy has so far been to sell 3.5 million units in 30 years and to introduce 30 new models, and this is a sign of the progress it has made along the way.

e-Mobility Power to set up 1,100 EV chargers at service/ parking areas on highways by 2025

(Company statement, March 29)

- e-Mobility Power and three of NEXCO Group’s companies plan to double the number of EV/PHEV chargers at service and parking areas on highways by 2025.

- The company has 500 sites for EV chargers, and that will grow to 1,100 in two years.

Chiyoda and Samsung sign MoU on SPERA Hydrogen in Korea

(Company statement, March 31)

- Chiyoda signed an MoU with Samsung C&T to explore opportunities with Chiyoda’s SPERA Hydrogen Technology in Korea, and to expand the business in global markets.

- SPERA Hydrogen or Methylcyclohexane (MCH) is made from toluene and hydrogen, and allows hydrogen to be stored and transported at ambient temperature and pressure.

Japanese aluminum firm switches power at 17 factories to renewables

(Company statement, March 27)

- From April 2023, UACJ, a Japanese aluminum group, decided to purchase 220 GWh of electricity from 100% renewable sources for use at its 17 manufacturing plants in Japan. As a result, 63% of UACJ’s operations in Japan achieved RE100 for Scope 2 emissions.

- In addition, the group plans to cut CO2 output by 100,000 tons a year.

TAKEAWAY: This appears to be a major power purchasing agreement. However, the processing of aluminum raw materials, which is what UACJ does, involves re-melting metal. For that, LNG is traditionally used as the main source of heat. The initiatives UACJ will take to reduce gas-derived emissions would certainly be of interest to industry stakeholders working to cut down the carbon footprint of the aluminum value chain. Meanwhile, rising energy and labor costs will need to be passed onto product prices. The question is, will business models of low-margin products, such as aluminum sheets used to make beverage cans, allow for prices to be raised?

German Pharma plant in Yamagata Pref to end fossil fuel use

(Gas Energy News, April 3)

- Kirsch Energy Service, a company co-owned by JAPEX and Yamagata Gas, began providing energy services to the Yamagata Plant in Yamagata Pref. The plant is owned by German pharmaceutical company Boehringer Ingelheim (BIS).

- This is the first energy service locally to use a gas cogeneration system, which is expected to reduce CO2 emissions by up to 21%.

- Kirsch built an energy center on the BIS site, with three 700 kW gas engines.

JOGMEC’s reckless expansion into decarbonization

(Sentaku, April-2023 issue)

- CONTEXT: Sentaku is a popular monthly magazine that covers business and politics. It often covers the chatter inside government organizations and big companies and likes to wade in on controversial topics. This is not an editorial, but many of its articles convey a strong opinion.

- The METI-affiliated Japan Organization for Metals and Energy Security (JOGMEC) has recklessly expanded its business scope to carbon capture and storage (CCS) facilities, hydrogen production, and offshore wind power.

- By rushing into such risky sectors, in which it has little experience, JOGMEC will likely amass bad assets just like Japan National Oil Corp did decades back.

- CCS isn’t the trump card for decarbonization hailed by the media and government. Serious questions hang over its technology and economic viability.

- Helping METI to survive is a big factor behind JOGMEC’s expansion. Many METI projects concern procuring or using CO2, which contrasts with the decarbonization efforts of other agencies. METI fears these agencies will take lead roles in the future.

- It’s possible that a JOGMEC-supported structure is set up in which trading houses and companies bring risky CCS and hydrogen-production projects to Japan.

NEWS: POWER MARKETS

Kansai Electric set to have 7 reactors online for 2023 summer peak demand, first since 2011

(Denki Shimbun, April 5)

- Kansai Electric said that with Takahama NPP Units 1 and 2 ready to supply power from June 3 and July 15, respectively, it is counting on being able to operate seven reactors during the summer 2023 peak demand period.

- The utility expects to have all four units at Takahama NPP online, as well as Units 3 and 4 at Ohi NPP, and Units 3 of Mihama NPP.

- This is the first time Kansai Electric will operate seven reactors in 12 years since the Fukushima accident. The seven have a total capacity of 6.58 GW. The utility expects a capacity factor of 78.4% for the facilities, the first time since 2010 that the ratio has exceeded 70%.

- Five of the seven reactors are scheduled to shut down for periodic inspection after the peak demand period.

- Ohi Unit 4 stops in August 2023

- Takahama Unit 3 in September 2023

- Mihama Unit 3 in October 2023

- Takahama Unit 4 in December 2023

- Ohi Unit 3 in February 2024.

- The remaining two reactors – Takahama Units 1 and 2 – will operate beyond this period since they would only have restarted in June and July of 2023.

TAKEAWAY: In Japan, reactors must undergo a regular inspection every 13 months. Utilities try to manage their operating schedules so as to have the nuclear stations online during the peak summer and winter periods. Inspection times differ depending on the age and condition of the facility with some taking less than 60 days while others more than 150 days.

Cartel leniency triggers resentment against Kansai Electric

(Japan NRG, Diamond Online, April 4)

- Many power operators are unhappy with the Japan Fair Trade Commission’s (JFTC) decision to exempt from penalties accused cartel member Kansai Electric (KEPCO). The big players in the collusion have more information to offer to the authorities and escape penalties, several lawyers told Japan NRG.

- Kansai Electric acknowledges violating the antitrust law and will report to the Electricity and Gas Market Surveillance Commission (EGC) on how it plans to improve compliance.

- Rivalry between Kansai Electric and Chubu Electric is intense; KEPCO’s information was partly the basis of charges against Chubu. KEPCO has a cost advantage thanks to a large nuclear power fleet and may poach Chubu’s customers.

- CONTEXT: On March 30, the JFTC charged Chugoku Electric, Kyushu Electric, Chubu Electric and subsidiaries of the latter two companies with forming a cartel on power rates for business users.

TAKEAWAY: Some lawyers who do not serve the power sector also say that the present leniency system has flaws.

METI delays power tariff increase sought by EPCOs until after June

(Nikkei, April 6)

- The electricity price hike requested by Tohoku, Hokuriku, Chugoku, Shikoku and Okinawa power companies, which was to start from April, will be pushed back until after June, because METI asked the companies to recalculate their fuel costs.

- METI will decide on the start and the level of the tariff hikes together with the Consumer Affairs Agency. The utilities initially asked for the higher tariffs to be in place from April or May.

TAKEAWAY: Power companies are suffering from steep fuel cost increases. But PM Kishida has put pressure on companies to rein in price increases in part because of local elections this month.

Still, the govt’s position seems inconsistent. On the one hand it espouses a fully liberalized power market and strongly encourages competition, but on the other hand it keeps a partial tariff system in place through which it can regulate certain power prices.

MLIT designates Niigata Port as Japan’s fifth offshore “wind base port”

(Denki Shimbun, April 7)

- The Subcommittee on Developing Offshore Wind Power designated Niigata as an offshore “wind base port” that can assemble and maintain offshore wind equipment.

- Niigata is the fifth port in Japan to have such a status, after Akita Port, Noshiro Port, (Akita Pref), Kashima Port (Ibaraki Pref), and Kita-Kyushu Port (Fukuoka Pref).

- Niigata Port will invest ¥ 9.1 billion to improve the port facilities, so that 15 MW class wind turbines can be assembled. Niigata Pref plans two offshore wind projects, at Murakami City and Tainai City.

EGC issues advisory to Chugoku Electric on JEPX trades

(Government statement, March 31)

- The Electricity and Gas Market Surveillance Commission (EGC) issued an advisory to Chugoku Electric after the latter did not disclose a decrease in output at three of its power stations as required by the Electricity Business Act. The cuts directly impact trading on the Japan Electric Power Exchange (JEPX).

- The company lowered the output because it was running low on fuel stocks, and sourced additional volumes of power from the spot market at high prices.

- The company will submit a compliance follow-up report to the EGC by April 30.

- CONTEXT: The Japan Fair Trade Commission (JFTC) said its recent probe discovered that unnamed EPCOs (former regional power monopolies) were manipulating JEPX prices. The JFTC handed over the case to the EGC.

TAKEAWAY: The EGC has received complaints around JEPX transactions in the past, but had insisted there were no problems to address. Antitrust authorities seem to disagree and the JFTC continues to point out issues to the EGC. Later this year, JFTC plans to release the full results of a fact-finding survey around spot power trades. The survey was launched in December last year. While a survey cannot lead to penalties for corporate misconduct, it does push companies to act to correct their behavior.

There are mixed views in the market on how the situation will develop. A lawyer advising EPCOs believes ANRE/METI will look to seize the initiatives and rewrite power sector rules, which should expand the authorities of the EGC and give them more enforcement powers. Whether the antitrust officials continue to be a catalyst for change, or hand the initiative over to METI, is also unclear.

Since the EGC is relatively new, when it was formed it was comprised mostly of ANRE officials. The EGC continues to recruit staff from ANRE and METI, as well as from the JFTC. Staff from those government entities stay at the EGC for several years before returning to their original ministries and agencies. Some experts say this weakens the ability of the EGC to act as a strong sector oversight body.

METI to hold first Long-Term Decarbonized Power Source Auction in Jan 2024

(Denki Shimbun, April 6)

- The govt will hold its first Long-Term Decarbonized Power Source Auction in January next year. The new auction system will be operated by OCCTO and slot in as part of the greater Capacity Market system.

- CONTEXT: The purpose of the Long-Term Decarbonized Power Source Auction is to support investment in non-fossil generation. The auction system was created so that operators can have a certain guarantee around future revenue, while giving power retailers a chance to lock in future supplies.

- The first auction will offer as much as 4 GW of non-fossil power capacity. The size of future auction rounds will depend on interest from the industry.

TAKEAWAY: Investment in new power capacity in Japan has slowed, both in thermal and renewables generation. This is one attempt to reverse the trend. In addition to this new system, METI wants an auction system to part-fund 6 GW of new LNG-fired capacity within three years, which it sees as important to balance Japan’s power system.

NRA to temporary halt review of JAPC’s Tsuruga NPP Unit 2 restart

(Nikkei, April 5)

- The NRA suspended its review of whether JAPC’s Tsuruga NPP Unit 2 is fit to restart. The regulator said the suspension is in force until the company rectifies its issues. JAPC has been given until late August to do so.

- Should JAPC fail to meet the deadline, the NRA will stop the review entirely. This will mean the reactor will have to be decommissioned.

- CONTEXT: JAPC applied in November 2015 for a review to restart Tsuruga Unit 2. The main point of contention was whether the facility sits on top of an active fault. In 2019, the NRA claimed that the utility failed to provide answers for over 1,000 points that it raised and in 2020 the regulator said the geological data it received from JAPC had been tampered with.

- The NRA only restarted this review after a two-year suspension in December 2022. The nuclear operator is on its last chance to salvage the review and restart process.

TAKEAWAY: Even if JAPC gets NRA approval to restart Unit 2, its track record suggests that it will be very difficult to get approval for a restart from the local govt. That then puts into question the viability of other JAPC plants and future construction projects.

Marubeni and Chubu Electric start operation of wood-fueled biomass power plant

(Company statement, April 3)

- Marubeni Corp and Chubu started operating the Godo Biomass Power Plant in Gifu Pref.

- This is their first biomass power plant involving consumption of locally produced fuel.

- The plant mainly uses locally-sourced surplus wood thinnings and has a power generation output of 7.5 MW. Estimated power generation is 53 GWh

- CONTEXT: The companies also operate the Tsuruga Green Power Plant, a wood-fueled biomass power plant in Fukui Pref.

Starting in 2025, Sumitomo to operate offshore wind power in France

(Company statement, Nikkei, April 5)

- Sumitomo will start offshore wind power generation at two sites in the Bay of Biscay, France between 2025 and 2026. Construction begins later this month. Total generating capacity will be 1 GW.

- Construction was expected to cost ¥500 billion, but due to soaring material costs, that’s now expected to be up to ¥800 billion. Funds will come from Japanese banks, including the Japan Bank for International Cooperation.

- CONTEXT: In 2018, Sumitomo acquired a 29.5% stake in French offshore wind projects in cooperation with French Engie and Madrid-based EDP Renewables (EDPR).

- Sumitomo’s partners are Ocean Winds and Vendée Energie. The project has a long-term power purchase agreement to provide power for about 800,000 people.

Toho Gas to invest ¥70 billion in FY2023, most ever; invest in renewables

(Denki Shimbun, April 3)

- Toho Gas plans to invest ¥70.4 billion in FY2023; 70% will be for pipeline construction, while ¥15 billion will be for renewables such as biomass and onshore wind power. Electricity sales volume is expected to be 2,540 GWh, up 5.4% from FY2022.

- The company plans to handle 250 MW of renewable power sources by FY2025 and 500 MW by FY2030. It also plans to invest in Southeast Asia and Australia.

- City gas sales are expected to be 3.67 bcm in 2023, up 2.5% from FY2022 forecast.

- CONTEXT: This is expected to be Toho Gas’ biggest investment ever for a single fiscal year, surpassing FY2021 investments of ¥60.3 billion.

J-Power re-started operation of Miyagi geothermal power station

(Company statement, April 3)

- On April 2, J-Power started operation of Onikobe Geothermal Power Station (14.9 MW) in Osaki city, Miyagi Pref. after completing renovations. The power station first started operation in 1975 and was shut down for renovations in 2017.

- The turbine and generator are decorated to look as a naruko kokeshi doll, a local traditional handicraft, in respect to the nearby community.

NEWS: OIL, GAS & MINING

Minister Nishimura to stress importance of investments in LNG at G7 Sapporo meeting

(Bloomberg, April 5)

- Nishimura said he’ll call for supporting upstream investments in LNG development and production at the upcoming G7 meeting on climate, energy and environment.

- He said that G7 countries agree on LNG’s importance as a transition energy source. However, there are different views regarding the transition period. Nishimura believes that 10 to 15 years will be necessary.

- Japan set up a framework for LNG interchange with countries such as Thailand, Malaysia and Singapore. It also plans a similar mechanism for cooperation at the G7.

- CONTEXT: Japan will chair the upcoming G7 meeting, April 15-16 in Sapporo. U.S. and UK officials criticized an initial draft communique, claiming that there was not enough emphasis on efforts for climate action.

INPEX Submits Revised Plan for Abadi LNG Project with added CCS component

(Company statement, April 5)

- INPEX Masela, an INPEX and Shell joint venture, has incorporated CCS into the Abadi LNG project. The company filed the revised development plan to the Indonesian government, before proceeding to the feasibility study phase.

- A govt review could take several weeks. In March, Indonesia enacted the Ministerial Regulation of Energy and Mineral Resources on Carbon Capture, Utilization and Storage to increase fossil fuel production while cutting GHGs.

- The Abadi output is expected at 9.5 million tons/ year of LNG, which is 10% of Japan’s demand. The CCS will completely neutralize GHGs at Abadi, INPEX said.

TAKEAWAY: With Ichthys LNG in Australia, INPEX is the only Japanese company to operate a major LNG production and export facility. The Abadi project is their attempt to build a second such facility, but the situation is highly complicated as Shell has publicly said that it wants to exit the development while the Indonesian government has demanded a portion of the gas to be sold domestically at reduced prices.

Govt closely monitors China’s export ban policy: Chief Cabinet Sec

(Government statement, April 5)

- The govt is closely monitoring China’s move to ban the export of rare earth-containing magnet technologies and to restrict the export of silicon solar panel technologies, Chief Cabinet Secretary Matsuno said.

TAKEAWAY: A rare earth trader told Japan NRG that the possibility of China banning the export of magnet technologies has been discussed since last year. Japan’s rare earth imports have been smooth and not impacted at all by political tensions.

JOGMEC, Canada’s FPX to explore nickel-iron awaruite deposits

(JOGMEC statement, April 5)

- JOGMEC and Canada’s exploration firm FPX Nickel will explore awaruite deposits in British Columbia and eventually worldwide. Awaruite ores contain nickel and iron. JOGMEC will provide C$2.3 million ($1.7 million) for the next three years.

- CONTEXT: Among the various ores that contain the nickel element, miners sought sulfide and laterite ores, but not awaruite as its ore processing technologies were not established. FPX is capable of retrieving high-purity nickel suitable for batteries from awaruite and claims its processes release less GHG than conventional technologies.

Tokyo Gas to expand LNG trading resources in London

(Nikkan Kogyo, April 6)

- Tokyo Gas has set up an LNG trading base in the U.K. and began 24-hour trading in the fuel. The London office links up to the company’s teams in Tokyo and Singapore.

- The company’s LNG imports in FY2021 hit 12.61 million tons. The amount is set to grow to 20 million tons by 2030. Of this, 5 million tons will come from trading.

- CONTEXT: The global trading center for LNG is Singapore, where JERA is among the firms to have already set up 24 hours capabilities.

Saudi Aramco to lower price of LPG sold to Japan in April

(Nikkei, April 5)

- Saudi Aramco will lower the April price of LPG exported to Japan. It’s the second consecutive month of price cuts and the lowest in 22 months.

- The crude oil price, which affects LPG prices, plunged amid financial instability in the U.S. and EU. There has also been a decline in LPG demand.

- Propane used for hot water and heating was $555 a ton, $165, 23% lower than the March loading. Butane for use in petrochemicals was $545 a ton, $195, 26% lower. Both are the lowest prices since June 2021.

LNG stocks rise to 2.4 million tons

(Government data, April 5)

- LNG stocks of 10 power grids stood at 2.4 million tons as of April 2, up 4% from 2.3 million tons a week earlier. METI previously reported the March 29 stocks as 2.29 million tons but revised the figure.

- The end-April stocks last year were 1.96 million tons. The five-year average for this time of year was 1.95 million tons.

ANALYSIS

BY YOSHIHISA OHNO

PART I:

Can Japan Return to the Market with Innovative Solar Technology?

In the 2000s, the solar industry was dominated by Japanese engineering and innovation. Solar manufacturers such as Sharp, Kyocera, Sanyo (now Panasonic) and Mitsubishi Electric were leading suppliers worldwide, and they garnered more than half of the global market.

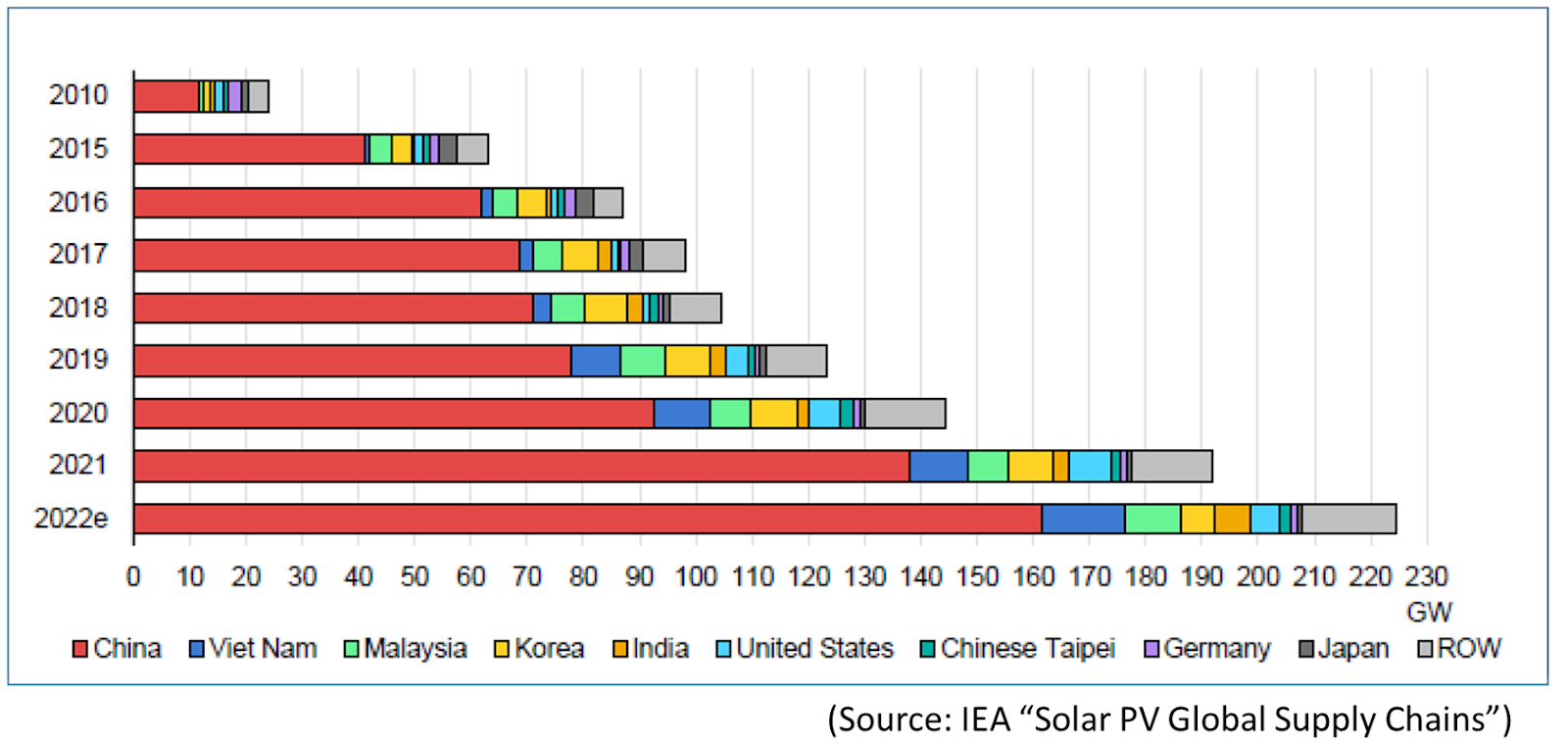

Fast forward to 2023, and Japan’s once vaunted solar panel industry, which was the envy of the green energy world, is in the doldrums, barely hanging onto life. While the overall volume of the global solar market has increased exponentially, Japan’s left with a tiny market share as Chinese manufacturers race ahead.

While Sharp Corp still produces solar cells, in 2016 it was acquired by Taiwan’s Hon Hai Precision Industry. Panasonic stopped production of solar panels in 2021; Kyocera also stopped domestic production in 2017. Mitsubishi Electric started to use imported solar cells from 2018. In fact, as of 2022, only one small Japanese firm makes conventional monocrystalline silicon solar cells.

This sad state of affairs recently culminated with the announcement by energy major Idemitsu that its subsidiary Solar Frontier will stop manufacturing solar equipment. Solar Frontier was the last active Japanese player in the solar equipment space, and its exit basically means that Japan has raised the white flag on the solar tech that’s currently in commercial exploitation.

Given this precarious situation, it might be easy to write off Japan as a solar market player. Indeed, how could it possibly catch up with China and India, both of whom are making massive investments in solar R&D and manufacturing, and which enjoy a big advantage thanks to lower labor costs, state support, and a huge domestic market.

But just when it seemed that all was lost, a leap in innovation has led to breakthroughs in next-generation solar power. According to patent data and a survey of industry participants, Japanese manufacturers believe they could stage a comeback.

The historical context: Japan as a solar pioneer

Today, there is only one maker of conventional (monocrystalline silicon) solar cells in Japan: Choshu Industry Co. But there are at least nine Japanese firms pioneering next-gen tech known as the perovskite solar cell (PSC).

PSC is expected by its supporters to turbo charge the energy transition in Japan and globally. And according to data by Energy Monitor, the leading solar PV patent publishers in recent years are from Japan.

If the PSC makers are successful, this would make some return to form for Japan’s solar industry, whose story has seen many ups and downs since it began some 70 years ago.

In 1954, the Tokyo-based Nippon Electronics Corporation (NEC) was the first in Japan to develop and launch the use of monocrystalline silicon cells, which are the most commonly used in commercially available solar panels. Japan’s first solar system was installed at the wireless station of Tohoku Electric in 1958.

In those early years, visionaries were able to find ways to create and utilize solar products, such as wireless base stations in remote areas. As early as 1963, Sharp began large-scale production of solar equipment.

The solar industry made a very slow start due to high costs, low reliability, and low power generation capacity per cell. There was meager demand for solar products except in remote places. The world was then flush with cheap and plentiful crude oil, and the global population was under 4 billion. Only a small number of countries were highly industrialized. Energy demand was simply much less compared to today.

Then, in the wake of the Arab-Israeli war, the Middle Eastern oil crisis hit in October 1973. In circumstances somewhat similar to 2022, crude oil prices quickly rose 300% by March 1974. This was followed by a second oil crisis in 1979. Both oil shocks left economic depression and inflation in their wake, making the 1970s a lost decade.

During years of cheap oil before 1973, Japan’s electrical system had been largely dependent on oil-burning thermal power plants. The oil shock convinced Japanese industry and policymakers that alternative energy sources were needed, and that the country had to work on better energy efficiency. In a sense, the 1970s oil shock paved the way for the Japanese auto industry to win over international markets in the 1980s, thanks to its cutting-edge fuel efficiency.

Eternal sunshine of the MITI mind

One major solar initiative to emerge from the 1970s oil crisis was the Sunshine Project launched in late 1974 at the National Institute of Advanced Industrial Science and Technology under the auspices of METI’s predecessor, MITI (Ministry of International Trade and Industry). This national program sought to develop alternative energy such as solar, geothermal, and hydrogen.

Results came quickly. Anyone old enough to remember can’t forget the feeling of awe when, in 1976, Sharp unveiled the world’s first electronic calculator fully powered by solar energy.

After some time, however, as oil prices stabilized, the impetus to develop solar plateaued. At the Sunshine Project, there were plans to develop solar equipment affordable for households within 20 years. Finally, it was achieved but the idea never translated into commercial reality.

In 1993, after 20 years, the first solar equipment for households reached the market. The price was ¥15 million for a 4 kW system, far from affordable. However, undeterred, MITI then embarked on a “New Sunshine Program”.

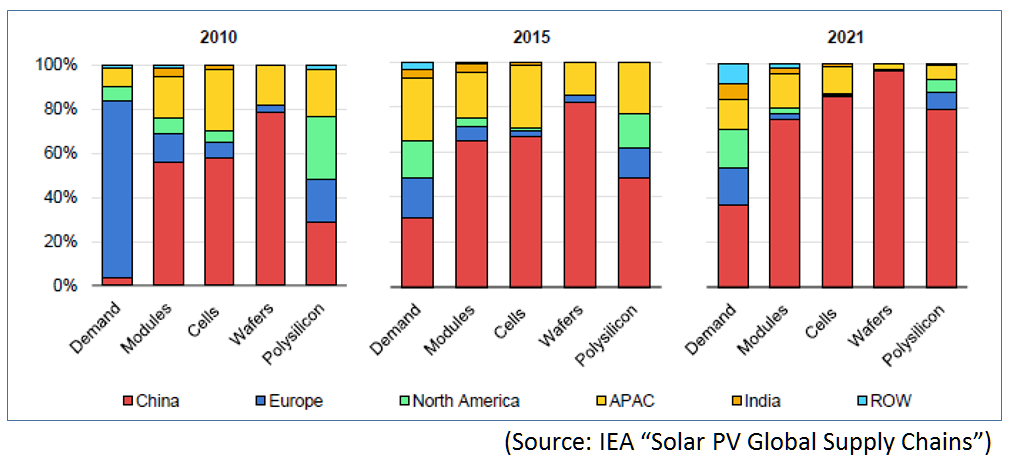

By 2000, Japanese PV manufacturers led the nascent global solar market. In 2005, Japan produced almost half (48.2%) of the world’s solar panels. Among the world’s top five solar panel producers, four were Japanese, according to Renewable Energy World.

1. Sharp (428 MW)

2. Q-Cells (166 MW)

3. Kyocera (142 MW)

4. Sanyo (125 MW)

5. Mitsubishi Electric (100 MW)

China pushes aside Japan’s dominance

Years of Japanese dominance came to an end by the end of the 2000s, first slowly and then at a rapid pace thanks to the accelerating pace of development by suppliers in other countries. None were more active than the Chinese manufacturers, using state support to leap from big local players to global majors. Today, firms like Jinko Solar, JA Solar, Trina Solar and LONGi Solar control most of the Japanese solar PV market.

Chinese firms enjoy lower labor costs than Japanese peers, but they also leveraged the power of government-affiliated financial institutions such as China Development Bank to surge ahead. The bank backed the construction of both manufacturing facilities and mega solar projects across the globe.

Such a public-private partnership helped China surge ahead to develop both the most cost-competitive and technically proficient solar equipment on the market, making the country a vital part of the global PV supply chain.

After more than a decade of mourning the loss of their market share, Japanese companies seem finally ready to offer a new competitive proposition for the solar industry. They believe that the sector is ready for a technological shift to PSC, a radically different and innovative product, in which Japan’s makers currently have an edge. And this time, support from the government in Tokyo will be a crucial factor in the strategy.

Part 2 to follow in the next issue of Japan NRG

ANALYSIS

BY FILIPPO PEDRETTI

Japan’s New Emissions Trading System:

Aiming High, but Going Slow

Japan has finally launched its long-awaited CO2 emissions trading system (ETS). After an earlier five-month trial, last week the system began full-fledged operations on the Tokyo Stock Exchange.

Initially, carbon trading will be conducted on a voluntary basis. The ETS will run in ‘phase-one’ mode for the next three years for companies that signed up. The government has dubbed the early adopters as the GX League, and entry to this club is open until April 28.

The last two governments ranked carbon trading as a priority for Japan to meet emission reduction targets, and Prime Minister Kishida has brought it to fruition. His clean energy strategy, called the Green Transformation (GX), sees the ETS as the basis for a range of other initiatives in carbon capture, hydrogen, synthetic fuels, and energy efficiency, etc. It’s even seen as a platform to help develop renewables and revive the nuclear sector.

Last week, the House of Representatives approved the GX League bill to push the world’s No. 5 polluter closer to counting its emission costs. But while Kishida promises to use GX to attract ¥150 trillion of investments into decarbonization efforts, how much of a role will the CO2 trading mechanism actually play?

Past trials and future roadmap

Last year, a group of more than 400 companies and other entities signed up to the GX League. These pioneers spent several months debating what a nationwide carbon trading market should look like. While many of the bigger issues remained outstanding, it was decided to move to a test phase of actual trading of contracts on an exchange.

From September 2022 to January 2023, the Tokyo Stock Exchange ran a trial on a new platform set up for carbon credits. The main goals were to check what liquidity the market could attract and ensure that exchange prices could work based on market signals. For the sake of simplicity and uniformity, the trading was in J-Credits, a domestic CO2 credits program set up a decade ago.

Over those five months, J-Credits equivalent to 150,000 tons of CO2 were traded. There were 163 transactions between 183 participants. The number of offers (220) was notably lower than the volume of bids (342).

GX ETS Trial Data (Sept 2022-Jan. 2023)

| J-Credit type | Trading volume in CO2 ton equivalent | Average transacted price/ ton of CO2 |

| Energy conservation | 73,619 | ¥1431 |

| Renewables | 75,255 | ¥2953 |

| Forestry | 59 | ¥14,571 |

This trial wasn’t the first time that Japan embarked on efforts to build an ETS. Local cap and trade systems have been in place in Tokyo and Saitama since 2010 and 2011, respectively. Yet, these were limited to their regions, with the credits negotiated on a bilateral basis or sold via a basic auction, rather than offered on an exchange. Such factors made it difficult to establish a universal market price.

Market rules

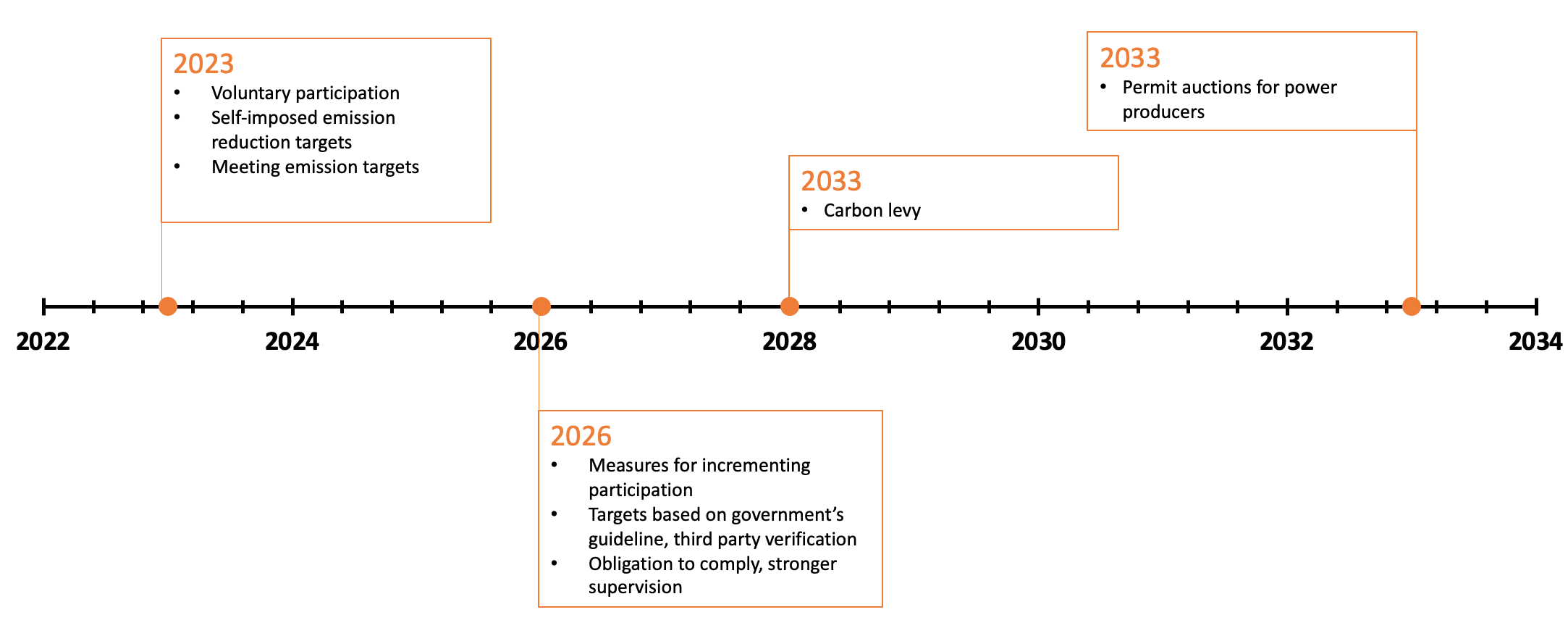

The first three years of credits trading will be used to build a fair and effective overall framework, as well as to collect data from the companies involved. Further improvements will follow in FY2026.

Then, the platform is expected to move to the next stage once Japan introduces a carbon levy from FY2028. Initially, the levy will be limited to the heavy polluter, broadening to include power producers only in 2033. Until that time, carbon credit trading will remain on a voluntary basis.

Still, even with a voluntary approach, a company interested in participating has to fulfill certain criteria. For example, participants must send data to the GX League about their emissions reduction, and set annual emission targets for FY2025 and FY2030. The baseline for company targets will be FY2013.

The GX League will divide participating companies into two groups, those that emitted more than 100,000 tons of CO2e in FY2021 (Group G), and those who emitted less than that in the same period (Group X).

Failures and Options

Companies that don’t meet GHG emission targets must abide by an “explain or comply’’ principle. They’ll have to buy eligible carbon credits or explain the reasons for failing to reach targets. For the first three-year period of trading, all participating companies will need to have an emissions target, but only Scope 1 emissions will be traded in the ETS.

Companies that manage to cut their CO2 equivalent at a faster rate than Japan’s national goal (as defined in the NDC sent to the United Nations) will also be eligible to receive additional credits. Japan’s NDC targets a 46% emission reduction by 2030, compared to 2013; that assumes a drop of 27.0% by FY2023; 29.7% by FY2024; and 32.4% by FY2025.

The credits themselves will mainly come from Japan’s domestic programs, the J-Credit and the Joint Crediting Mechanism (JCM). However, this year, the GX League plans to establish a working group that will consider eligibility of other types of carbon credits.

What this means is, credits that reflect efforts toward the removal / capture of carbon may also be eligible, in addition to credits coined from reducing emissions. This opens the door to the trading of J-Blue credits (which certify CO2 that’s absorbed by marine and coastal ecosystems, such as seagrass) and others.

Carbon credits that reflect the reduction of global emissions, however, would be ineligible for the Japanese platform. To trade in Tokyo, the credit needs to be based on a change in emissions affecting Japan.

Doubts and uncertainty

Many questions remain around Japan’s ETS, which is lagging similar developments in other major Asian economies. China and South Korea already have carbon trading schemes. Europe, which has one of the world’s largest ETS platforms, will also introduce a Carbon Border Adjustment Mechanism (CBAM) this fall. In that respect, Japan’s goal of fully embedding the ETS into its economy by 2033 seems too distant.

On the corporate side, many worry about limited trading volumes, claiming that JCM and J-Credits programs alone will be insufficient to supply the market. Therefore, the business world is calling to allow the use of foreign credits. But the government looks resolute in focusing on Japan’s emissions only (and, thus, limiting the outflow of money overseas).

The number of participating companies may also be a problem. Currently, GX League counts around 700 members, but it’s not clear how many of them will actually join in the trading and do so at a substantial level. The GX number also looks small when compared to countries like Thailand, whose ETS has attracted 12,000 firms.

Businesses that endorse the GX League are said to account for 40% of Japan’s total emissions. Yet, participation in the ETS will probably be much smaller.

How to benefit?

Some critics believe that too much focus on trading will do little to address decarbonization itself and call for the ETS to play only a side role in Japan’s net-zero strategy.

Historically, trading has also been a minor part of Japan’s business and market environment outside of a few energy commodities with the number of specialist traders in the country low. It’s notable that when Tokyo City introduced its local cap-and trade system, only 15% of the participants went on to participate in emission trading during 2015-2019. Most managed to reach reduction targets through other means, such as energy conservation.

What will stimulate companies outside the initial GX League list to embrace change is not clear. Japan’s carbon levy and trading roadmap is less aggressive than in other countries. The government hopes that a voluntary approach will foster a culture of climate accountability without coming across like a climate tax. Such an approach has worked well with corporate governance reform in the country.

However, with the pace of change abroad much faster, Japanese firms with international exposure will struggle to remain competitive if they are seen to dither at home. There’s a risk also that international rules will be indirectly imposed on Japan by first-movers elsewhere.

PM Kishida’s government will need to demonstrate to companies at home how this voluntary market will benefit them while contributing to the lowering of Japan’s emissions as a whole. Officials will have much less than their roadmap suggests to make that happen.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

China/ Energy deals

France and China signed nuclear and wind energy deals during Macron’s visit to China. French state utility EDF and Chinese utility CGN, both major NPP operators, renewed their long-standing partnership. Deals were also signed between EDF and China Energy Investment Corp for offshore wind.

Europe/ Oil imports

The EU is benefiting from India’s record high imports of Russian crude oil, boosting diesel and jet fuel exports to the EU which has banned Russian products. Access to cheap Russian crude has boosted output and profits at Indian refineries, enabling them to export refined products competitively to the EU and take bigger market share.

France/ Nuclear power

The UK’s Competition and Markets Authority is investigating a deal by French power operator EDF to buy a nuclear turbine maker from General Electric. EDF agreed to buy GE’s nuclear components business in February; the acquisition was hailed as a way of securing French control of turbine technology as EDF plans to build new reactors.

Germany/ Clean energy infrastructure

From 2026 to 2030, the deep water port of Wilhelmshaven will spend €5 billion to build clean energy infrastructure needed for hydrogen and ammonia imports, hydrogen production and offshore carbon storage. Energy Hub Port Wilhelmshaven comprises 30 companies, which include Wintershall Dea, Uniper , E.ON, and RWE.

India/ Renewable energy

By March 2028, India will issue tenders for 250 GW of green energy capacity, looking to cut national emissions 45% from 2005 levels. After missing a target to build 175 GW in renewables capacity by 2022, India seeks to boost non-fossil capacity to 500 GW by 2030.

India/ Electricity

Last fiscal year, National power generation grew at the fastest pace in over three decades, reported Reuters. This has fueled a major surge in GHG emissions as output from both coal-fired and renewable plants hit record highs.

Iraq/ Oil deal

Baghdad agreed to a smaller 30% stake in TotalEnergies long-delayed $27 billion project, reviving a deal that could lure back foreign investment. Signed in 2021, the deal called for TotalEnergies to build four oil, gas and renewables projects with an initial investment of $10 billion in southern Iraq over 25 years.

Mexico/ Electricity

The government will buy 13 power plants from Spanish energy giant Iberdrola in a $6 billion deal to be completed within five months. Mexico’s president hailed it as a “new nationalization” of the electricity market that will strengthen state control.

Russia/ Oil deals

Russia is making ship-to-ship transfers of diesel near African ports, with an eye to transatlantic sales. For example, as a result of the EU ban on Russian fuel that started Feb. 5, tankers carrying oil products such as gasoline, diesel, jet fuel and naphtha travel up to 18 days to bring Russian supplies to Brazil. The result is more GHG emissions from ships.

Venezuela/ Oil exports

Oil exports rose to the highest monthly average since August, boosted by resumption of loadings after an export freeze and by more cargoes assigned to Chevron. State oil company PDVSA reinstated two export contracts: a medium-term contract with Hangzhou Energy, and another with Portugal’s Adinius Sociedade de Servicios.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

K.K. Yuri Group: Oonoya Building 8F, Yotsuya 1-18, Shinjuku-ku, Tokyo, Japan, 160-0004.