Mitsui Fudosan to invest in U.S. tandem perovskite tech firm Caelux that will boost solar power efficiency

PM Kishida visits Fukushima seeking final buy-in for treated water release as the Swiss lift restrictions on Japan food imports

Japan’s oil and gas self-sufficiency rate dips on the back of demand recovery and geopolitical conditions

ENERGY TRANSITION & POLICY

Sekisui Chemical to mass produce PSC (next-gen solar) by 2030

MHI, Heidelberg work on world’s first CCUS for cement industry

MHI invests in U.S. startup to strengthen hydrogen value chain

ENEOS to launch VPP at oil refineries

Kyushu Electric and Mitsubishi to collaborate on energy storage

KEPCO, Toshiba to launch EV battery analysis service in FY2024

JAPEX acquires shares in storage battery startup PowerX

ELECTRICITY MARKETS

EPCOs see high-voltage contracts rise to highest since 2017

TOCOM power futures volumes drop, hedging demand wanes

erex gets hit hard, drops in spot price puts company in the red

Eurus Energy sets up fully-owned subsidiary in Vietnam

Mayor welcomes research for spent nuclear fuel storage

Police arrest copper cable thieves in Gunma Pref, as crimes rise

KEPCO’s Kanden Plant finishes first factory in Hyogo Pref

OIL, GAS & MINING

Delfin Midstream and MOL to launch first FLNG facility in the U.S.

ADNOC Gas and JAPEX sign 5-year deal on LNG supply

July LNG imports rise as Sakhalin 2 closes for maintenance

LNG stockpiles by power utilities jump WoW

ANALYSIS

HOW TO KEEP AMMONIA SAFE: NEW STANDARDS IN THE CO-FIRING ERA

Japan will soon see the start of two ammonia-and-coal co-firing pilot projects. The two fuels will be burned side by side at gigawatt-scale power generation facilities. Today’s regulations are made for ammonia’s current use in agriculture and industry. New safety standards are needed for power generation. Co-firing is in an early adaptation phase, but there’s more work before large-scale commercial use becomes a reality.

EFFORTS TO ENGAGE MUNICIPALITIES ON GREEN ENERGY PLANS STYMIED BY RESOURCES GAP

About a year after the MoE began encouraging municipalities to designate areas for renewables development, progress has been slow. Meanwhile, opposition to new solar and wind projects is rising. Complaints range from solar panels on steep slopes, to tree logging to make space for wind turbines. The government needs to work with localities to re-engage with renewables development

New Energy and Industrial Technology Development Organization

kWh

Kilowatt hours (electricity generation volume)

TEPCO

Tokyo Electric Power Company

FIT

Feed-in Tariff

KEPCO

Kansai Electric Power Company

FIP

Feed-in Premium

EPCO

Electric Power Company

SAF

Sustainable Aviation Fuel

JCC

Japan Crude Cocktail

NPP

Nuclear power plant

JKM

Japan Korea Market, the Platt’s LNG benchmark

JOGMEC

Japan Organization for Metals and Energy Security

CCUS

Carbon Capture, Utilization and Storage

OCCTO

Organization for Cross-regional Coordination of Transmission Operators

NRA

Nuclear Regulation Authority

GX

Green Transformation

NEWS: ENERGY TRANSITION & POLICY

Mitsui Fudosan to invest in U.S. tandem PSC tech firm Caelux that will boost solar efficiency

(Japan NRG, Aug 14)

Mitsui Fudosan will invest into Caelux, a U.S. tech startup developing tandem perovskite solar cells (PSC). The 31Ventures Global Innovation Fund II, which is controlled by Mitsui Fudosan, will make the investment.

Caelux held a Series A3 round, raising $12 million. Other investors included Temasek, Reliance New Energy, and Kosla Ventures.

Caelux will build a manufacturing facility in California to produce glass coated with perovskite-silicon film that consists of modules generating power at a 30% efficiency. The plant capacity will be up to 100 MW/ year.

CONTEXT: Solar modules with perovskite-structured compound layers will be cheaper than crystalline silicon modules since they’ll require much less energy to make. Caelux has created a tandem structure, applying the perovskite layer on silicon, which is far more efficient than traditional silicon modules. Current Japanese tech consists mostly of a stand-alone perovskite layer.

TAKEAWAY: Mitsui Fudosan is the second Japanese entity after travel agency HIS’ founder, Sawada Hideo, to invest in non-Japanese PSC tech. Sawada invested into Poland’s Saule Technologies, the world’s first company to commercialize inkjet-printed solar modules. In 2018, HIS installed Saule’s building-integrated modules at a facility in the House Tenbosu theme park, but the modules were removed last year after the park’s sale to a Hong Kong fund. The company, however, told Japan NRG that it still plans to produce Saule’s modules in Japan. It’s still not clear if Mitsui Fudosan will also import the PSC tech into Japan.

SIDE DEVELOPMENT: Sekisui Chemical to mass produce PSC by 2030 (Nikkei, Aug 18)

Sekisui Chemical will invest over ¥10 billion to mass produce PSC cells by 2030. The new plant will make “several tens of thousands square meters” of thin-film PSCs with a total power generation capacity of “several hundred MW/ year”.

China’s DaZheng Micro-Nano Technologies launched PSC commercial production last year and Sekisui is trying to catch up.

Sekisui will target outdoor applications since its PSC can last up to 10 years, much longer than that of competitors.

TAKEAWAY: China leads the world in the development of PSC with carbon electrodes, replacing the metallic perovskite crystal layer (that consists of lead, iodine, titanium among others) with cheaper carbon. Japan has been pushing metallic PSC development because the country has large iodine deposits.

MHI and Heidelberg Materials cooperate on world’s first CCUS for cement industry

(Company statement, Aug 17)

MHI and Heidelberg Materials have joined forces to create a carbon capture system at their cement plant in Edmonton, Canada. The goal is to set up the first large-scale carbon capture, utilization, and storage (CCUS) solution for the cement industry.

It will be operational by late 2026 and will capture over 1 million tons of CO2 annually from both the cement plant and its heat and power facility.

The captured CO2 will be sent via pipeline for permanent storage. MHI’s will provide remote support via its monitoring system.

SIDE DEVELOPMENT: MHI invests in U.S. startup to strengthen hydrogen value chain (Company statement, Aug 17)

MHI invested in Advanced Ionics, a startup in Milwaukee that specializes in innovative low-temperature water vapor electrolysis technology.

The core focus revolves around development of a water-vapor electrolysis apparatus that utilizes low-temperature steam (100°C) to yield hydrogen, leading to a 30% reduction in energy consumption compared to conventional water electrolyzers.

By harnessing existing industrial heat to generate steam, this approach holds promise as an efficient decarbonization remedy for steel, ammonia, and oil refining.

ENEOS to launch VPP at oil refineries

(Japan NRG, Aug 17)

ENEOS started a virtual power plant (VPP) operation at its Negishi oil refinery. The system consists of a 342 MW thermal power plant and a 5 MW Tesla storage battery on the refinery premises, as well as outside power suppliers.

Power from the ENEOS thermal unit and other suppliers are pooled into the batteries. Then, an AI-based control unit, which ENEOS has developed, remotely manages the refinery’s power storage and consumption. Excess power will be sold on the market.

ENEOS plans to start VPPs at its Muroran refinery by late March 2024 and at its Chiba refinery by late March 2026. The Muroran storage unit will have a 50 MW capacity and the one in Chiba a 100 MW capacity.

CONTEXT: ENEOS’ eleven refineries have self-generators with a total capacity of 2.11 GW, but only the power station at the Kawasaki refinery operates on a commercial basis.

NTT Anode Energy, Kyushu Electric and Mitsubishi collaborate on energy storage

(Dempa Shimbun, Aug 15)

NTT Anode Energy, Kyushu Electric, and Mitsubishi set up a 1.4 MW/ 4.2 MWh energy storage system in Kawara, Fukuoka Pref.

Their goal is to reduce the curtailment of renewable energy. Surplus energy control is crucial, with around 740 GWh needed for output control in Kyushu this year.

The project will manage this surplus, using grid-connected energy storage. NTT Anode Energy’s trial achieved 260,000 kWh with 47 cycles at the Tagawa Energy Storage Plant. Capacity market contributions are expected to start in 2025.

KEPCO and Toshiba to launch EV battery analysis service in FY2024

(Nikkei, Aug 18)

KEPCO and Toshiba Energy System will begin a service in FY2024 to analyze the deterioration of EV storage batteries and offer advice on vehicle updates by assessing charging data such as voltage, current, and temperature.

They’re targeting transport companies with many vehicles. An initial free analysis of 100 EV batteries owned by transport companies will refine the diagnosis process.

This effort aims to extend battery lifespan and improve the accuracy of used EV pricing. The technology may also be applied to grid-use storage batteries that connect to power lines for charging and discharging.

PM Kishida is nearing a conclusion regarding the release of treated wastewater from the Fukushima No. 1 NPP into the Pacific Ocean. He made a visit to the plant site on Aug 20.

Kishida was due to hold discussions with the top executives of TEPCO to ensure their dedication to decommissioning and reconstructing the site. He refrained from specifying a discharge timetable.

Despite opposition, he aims to secure support from fisheries cooperatives for the release plan. An official decision on the date of the ocean release might be reached as early as Aug 22.

SIDE DEVELOPMENT: Switzerland, Liechtenstein lift restrictions on Japanese food imports (Fukushima Minyu Shimbun, Aug 16)

Switzerland and Liechtenstein have lifted import restrictions on Japanese food products, including those from Fukushima, that were put in place after the 2011 nuclear disaster.

The Ministry of Agriculture plans to establish an “Export Support Platform” in Brussels to promote exports and accurate information.

CONTEXT: This move corresponds with the actions of the EU, as well as Norway and Iceland, which also lifted their import restrictions in collaboration with the European Free Trade Association (EFTA). Import limitations remain in effect for China, South Korea, Taiwan, Hong Kong, Macau, French Polynesia, and Russia.

TAKEAWAY: The lifting of Japanese food restrictions in multiple nations is positive news for PM Kishida as Japan is poised to release treated water from Fukushima. This news reveals growing trust in Japan, contrasted with others — China, for instance — that persist in their disapproval.

JAPEX acquires shares in storage battery startup PowerX

(Company statement, Aug 17)

JAPEX acquired a stake in a storage battery startup PowerX via a third party allotment of new shares issued in the Series B round.

PowerX’s focus includes development and production of energy storage system solutions, vessels with storage batteries to transfer power from offshore wind power stations, and EV charging stations.

NEWS: POWER MARKETS

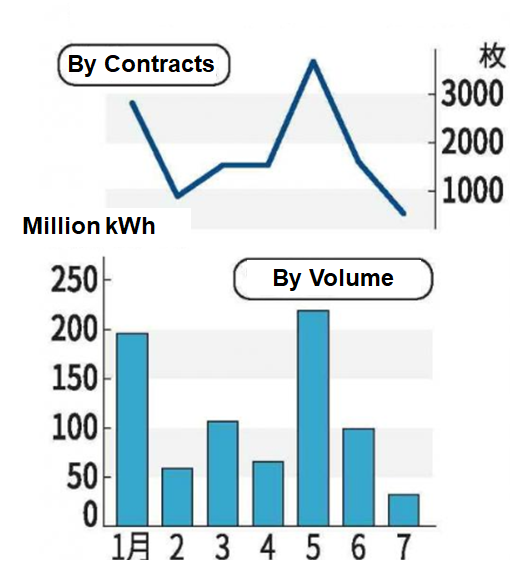

TOCOM power futures trading volume plummet, hedging demand wanes

(Denki Shimbun, Japan NRG, Aug 17)

The electricity futures market on the Tokyo Commodity Exchange (TOCOM) has been sluggish. Trading volume in July fell to 32.36 GWh, down 67.4% from June.

This is due to factors such as spot pricing remaining calm despite the current heatwave nationwide. A market insider said: “The soaring spot price in 2022 has been a big lesson. Risk hedging will continue to be important.”

On a volume basis, transactions in July totaled 533 contracts, almost the same level as in August 2021. The average system price in July was ¥10.13, down ¥14 from the same period last year when tight supply-demand led to a rally.

In contrast, volumes on the EEX, which commands the bigger share of the power futures market in Japan, were up in July. Monthly traded contracts number jumped to 1,704 from 1,263, representing about 1,320 GWh of electricity volume. This was a gain from June’s volume of 985 GWh and four times more than the year-earlier 265 GWh number.

TAKEAWAY: TOCOM has gained ground in the last six months or so after seeing EEX take a very dominant position in the electricity futures market. However, the summer lull has affected the former more than the latter. This may be partly due to the slightly different mix of trading participants on each exchange. Big domestic power utilities have tended to use TOCOM more.

Source: Denki Shimbun

Major utilities see special high-voltage contract number rise to highest since 2016

(Denki Shimbun, Aug 16)

Japan’s biggest power utilities, known as EPCOs, saw their number of high-voltage contracts reach the highest in five and a half years (since Oct 2017) and the number of special high-voltage contracts exceed 10,000 for the first time since April 2016.

The wave of new contracts come as EPCOs resume accepting new clients on their standard pricing menu. Around spring, EPCOs stopped new applications after being overwhelmed by the wave of switching from new market players (shin denryoku). A jump in market prices and other factors had made it difficult for many new market players to continue providing their service.

Since spring, EPCOs had to service clients without a power provider as a seller of last resort. But now, consumers are able to switch officially, which is what is driving up the numbers.

Biomass specialist and power trader erex hit hard by drops in spot price

(Denki Shimbun, Aug 15)

erex’s performance has declined rapidly. The company, which specializes in biomass power generation and electricity trading, saw its consolidated ordinary income for Q1 (April to June) fall to a loss of ¥4.1 billion (from ¥2.1 billion in profit a year earlier). The main cause is a drop in spot prices on the Japan Electric Power Exchange (JEPX).

The company expected spot prices to remain around last year’s highs and secured additional electricity volumes through bilateral deals. However, after some customer outflows, erex had to sell some of these volumes in the spot market, where prices are around half that of 2022 levels.

In recent years, erex had managed to secure a relatively large volumes of power via bilateral deals as a risk hedge against rising spot prices. Last fiscal year, it sold the surplus in the spot market and posted record high profits. The Tokyo area base load futures hit highs of around ¥30-37/ kWh during August to December 2022.

This year’s spot prices have dipped back into single digits, averaging ¥9.21 since April. The futures price for the full year of FY2011 fell to ¥14.37 as of July.

erex said it will seek new clients by pitching CO2-free high-voltage plans, among other measures, and expects to reduce its power procurement volumes. It sees more low-voltage retailers switching to rate plans that reflect spot prices.

Eurus Energy sets up fully-owned subsidiary in Vietnam

(Company statement, Aug 14)

Eurus Energy HD set up a fully-owned subsidiary, Eurus Energy Vietnam, to develop and operate solar and wind power stations in the country.

This is Eurus Energy’s first subsidiary in Southeast Asia. Eurus chose Vietnam due to its economic growth and rising energy demand.

CONTEXT: Vietnam has great potential for wind power generation, and the govt plans for 22 GW of onshore wind power by 2030 and 60 GW by 2050.

Mayor welcomes Chugoku Electric, KEPCO research for spent nuclear fuel storage

(Nikkei, Aug 18)

Kaminosaki Mayor Tetsuo Nishi (Yamaguchi Pref) welcomed research by Chugoku Electric and KEPCO into building an interim spent nuclear fuel storage locally.

Chugoku Electric and KEPCO will do an excavation survey over the next six months to determine if it’s feasible to construct an interim storage facility. If deemed feasible, a plan will be presented to the town.

CONTEXT: About 80% of Japan’s storage capacity for spent nuclear fuel is full. Since launch of the delay-plagued Rokkasho nuclear fuel reprocessing plant (Aomori Pref) has been pushed back to 2024 – and even that date is likely to be further postponed – there’s an urgent need to set up a new interim storage facility.

Copper cable thieves arrested in Gunma Pref, such crimes on the rise

(NHK, Aug 14)

The Gunma Pref police arrested five Cambodian nationals for allegedly cutting down and stealing copper cables from a solar power station in Fujioka City. The stolen cables were 1.4 km in length, with a market value of about ¥17.6 million.

From January to the end July, solar power stations in Gunma reported a total of 487 copper cable thefts with damages totaling ¥726 million.

CONTEXT: Used copper cables are sold in the market as scrap; their prices are usually lower than new production. However, in China last year, prices of used clean copper wire fetched higher prices than new cathodes due to excessively high demand.

TAKEAWAY: There are 96 solar power operators in Gunma. This is less than the nearby Ibaraki and Fukushima Pref, which have over 150. The figures suggest that, on average, the Gunma operators have suffered ¥7.6 million in theft damages.

KEPCO’s Kanden Plant finishes first factory in Hyogo Pref

(Denki Shimbun, Aug 17)

Kanden Plant, part of KEPCO group, completed construction on its inaugural factory in Hyogo Pref. It is responsible for the maintenance and construction of nuclear and thermal facilities.

The factory will focus on equipment fabrication and maintenance. Located on the former site of Takasago Power Plant, it features an office and factory building with specialized equipment.

Previously outsourced tasks will now be managed in-house, streamlining operations.

NEWS: OIL, GAS & MINING

Japan’s oil and gas self-sufficiency rate dips due to economic recovery and geopolitics

(Government data, Aug 15)

In FY2022, Japan’s oil and gas “self-sufficiency rate” fell to 33.4%, the lowest since 29.4% in FY 2018. Japanese companies’ share of the uptake of fossil-fuel projects decreased on the back of demand recovery from COVID and geopolitical conditions.

The self-sufficiency rate was 40.1% in FY2021.

The govt’s goal is for the rate to reach over 50% in FY2030 and 60% in FY2040.

CONTEXT: The self-sufficiency rate includes oil and gas volumes that Japanese companies receive but then sell in local and overseas markets. Thus, the 33.4% self-sufficiency does not directly correspond to the volume of oil and gas that Japan imports from projects in which its firms have ownership or uptake agreements.

TAKEAWAY: It should be noted that Japan’s oil and gas demand is falling even faster than “the self-sufficiency rate”. Imports are down by over 10% in the last four years. This means an increasing share of Japanese uptake volumes is delivered to global markets, especially to its Asian neighbors. This puts into question the need for METI to stick to its 50-60% “self-sufficiency goals”.

METI, however, believes Asian consumers buying more fossil fuel from Japanese companies helps to strengthen the country’s energy value chain. Earlier this month, JAPEX (36% owned by the government), launched a feasibility study on LNG end-user applications in northern Vietnam. This symbolizes stronger emphasis on the downstream part of the gas value chain by Japanese businesses while seeking more upstream projects to cater to Asia’s LNG growing demand.

Key LNG value chain investments in Asia

Vietnam

Toho Gas, JERA, Tokyo Gas, JAPEX

LNG terminals, local distribution, gas-fired power plant and other end-user applications

Thailand

Tokyo Gas, Osaka Gas, Shizuoka Gas

LNG terminals, local distribution, end-user applications

India

Osaka Gas

Gas utility services

Philippines

Tokyo Gas

LNG terminals

Bangladesh

Tokyo Gas

LNG terminals

Delfin Midstream and MOL to launch first FLNG facility in the U.S.

(Nikkei, Aug 17)

Delfin Midstream, in conjunction with Mitsui O.S.K. Lines (MOL), plans the first Floating Liquefied Natural Gas (FLNG) vessel in the U.S. by 2027. They hope to reduce construction costs by 10-15% thanks to lower labor costs in Asian shipyards.

The project is focused on offshore LNG projects in Louisiana that will process shale gas and then export LNG to Europe and Asia.

The first unit is almost fully contracted, and negotiations for the second are underway, including talks with Japanese firms. Total cost is about ¥750 billion.

The plan calls for four vessels that will have a total of 13 million tons production capacity, which is comparable to large onshore plants.

CONTEXT: In June, MOL and Delfin began to strengthen Delfin’s low-cost floating liquefaction solution thanks to MOL’s marine expertise. The agreement allows MOL to invest directly in Delfin’s FLNG vessels and assist in construction and operation.

TAKEAWAY: FLNG plants help in capitalizing on gas reserves in remote or challenging regions, but there are disadvantages regarding automation and operational complexities. For instance, FLNG installations face issues related to restricted spatial availability, deterioration from weather conditions, capacity limitations due to vessel dimensions, and shorter leasing periods (10-12 years) compared to onshore LNG terminals. Also, FLNG projects often face rising costs and schedule delays.

ADNOC Gas and JAPEX sign 5-year deal on LNG supply

(Reuters, Aug 17)

ADNOC Gas signed a five-year agreement with Japex on LNG supply, valued at $450-$550 million. The LNG volume and starting date have not been revealed.

This comes after PM Kishida’s visit to the UAE in July. Japan is ADNOC’s largest international buyer of oil and gas.

CONTEXT: Japan imports about 25% of its crude from the UAE. Kishida’s goal while visiting the UAE and Gulf states was to cement energy supplies.

July LNG imports rise above 5 mln tons as Sakhalin-2 closes for maintenance

(Japan NRG, Aug 17)

In July, Japan imported 5.09 million tons of LNG, the first month since March that the number exceeded 5 million tons. It was up 12.4% compared to June, but down 17.4% YoY.

July imports from Russia were 0.26 million tons, down 53.6% YoY as Sakhalin-2 closed for maintenance.

The total LNG import value was ¥453 billion, down 42.3% YoY.

Crude oil imports were 11.15 million kiloliters (70 million barrels), down 2.9% YoY. The total import value was ¥803 billion, down 29.7%.

Thermal coal imports were 8.68 million tons, down 7% YoY; while the value was ¥257 billion, down 46.5%.

Total coal imports, including coking coal, were 14.1 million tons, down 9% YoY, and the import value ¥443 billion, down 44.8%.

TAKEAWAY: Japan’s volumes were subdued this summer despite multi-month LNG stocks at below 2 million tons, tight coal supplies and Saudi Arabia’s output cuts. Also, Japan’s energy sector got a boost from more generation volume coming from nuclear power plants. However, Japan might have to step up LNG imports ahead of winter if Sakhalin-2 doesn’t restart as scheduled.

LNG stocks edge up to 1.98 million tons

(Government data, Aug 16)

LNG stocks of 10 power utilities stood at 1.98 million tons as of Aug 13, up 6.5% from 1.86 million tons a week earlier. The Aug 6 stocks were first reported at 1.87 million tons but METI corrected the figure.

The end-August stocks last year were 2.75 million tons. The five-year average for this time of year was 2 million tons.

ANALYSIS

BY MAYUMI WATANABE

How to Keep Ammonia Safe: New Standards in the Co-Firing Era

In the coming months, Japan will see the start of two ammonia-and-coal co-firing pilot projects. The two fuels will be burned side by side at gigawatt-scale power generation facilities. If all goes well, the utilities envision commercial operations beginning in 2027-2028.

The premise is massive. Japan is betting that gradually replacing coal with ammonia as the fuel of thermal power plants will lead to reduced emissions. Once coal is phased out entirely, and ammonia becomes the only fuel, the generation of electricity should be free of any CO2 footprint.

What’s more, switching existing coal-fired power plants to burning ammonia would allow utilities to retain legacy power stations and transmission lines operational, thereby saving costs, avoiding job losses and painful accounting write downs of major assets. And, unlike hydrogen, ammonia can be fed directly into boilers without conversion.

This neat vision for a CO2-free alternative to renewables energy does, however, carry several challenges. The ones often discussed by environmental groups are concerns over the cost of ammonia-fired generation and thus its ability to compete with renewables. Procuring clean ammonia in sufficient quantities, without impeding on existing demand for ammonia in farming, is another point of debate.

But there is another area that will need quick resolutions if Japan’s ammonia plans are to succeed. Today’s regulations are made for ammonia’s current use in agriculture and industry. The safety standards will need to evolve to encompass the new demand center in power generation. Co-firing is entering the phase of early adaptation, but there are more stairs to climb before large-scale commercial use can become a reality.

Current safety measures

The obstacles to growing the scale of the ammonia-coal co-firing industry are many, ranging from logistics to regulations and safety standards. For example, currently, Japan does not allow construction of ammonia tanks with storage capacity of over 40,000 tons due to safety concerns.

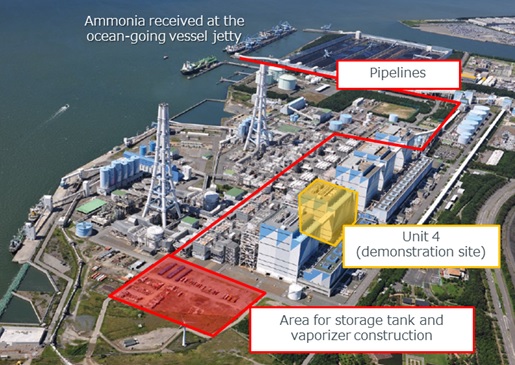

Power stations, however, would need larger tanks to manage operations. JERA, Japan’s biggest thermal power utility, has calculated that it requires about 500,000 tons of fuel ammonia a year to cover a 20% co-firing rate at Unit 4 (1 GW) of its Hekinan power station. The co-firing rate refers to 80% of the power output coming from burning coal and the rest from combusting ammonia.

Another risk for utilities is the scarce data available on ammonia’s impact when combusted with coal, because the fuel has not traditionally been used this way. Most ammonia today is turned into urea, which is one of the three key fertilizers for crops.

The biggest drawback for many, however, is the potential risk of handling ammonia, which is classified as a hazardous gas. It can cause health problems when inhaled or in direct eye or skin contact. In large doses, it can lead to death; it’s flammable and may explode in temperatures of 650°C or when reacting with a large dose of oxygen.

Hazardous substance communication standard requires anything containing over 0.2% ammonia to be clearly labeled. In contrast, hydrogen and methane don’t have this requirement.

That said, Japan’s power sector has been a long-time user of ammonia for other reasons.

Ammonia has long been used in a process called denitrification – breaking up nitrogen oxide (NOx) in the flue gas generated from thermal power generation. Some thermal plants use ammonia for boiler water treatment. The total usage volume is usually a few hundred tons/ year in total.

Japan already has over 15 regulations that spell out the safe handling of ammonia, covering everything from labor safety, fire control, and facility management to storage and transport. The Electricity Business Act Rulebook, and the High-Pressure Gas Safety Act are the most relevant to power utilities.

Still, the volumes currently processed by the power sector are miniscule compared to even today’s 1 million tons/ year of national consumption. And these volumes are due to at least double by 2030 and then grow several times larger in the following decade if the upcoming trials bear fruit.

Pilot projects

In 2017, Chugoku Electric held Japan’s first ammonia co-firing test at its 156 MW Mizushima power station, which is one of the country’s smallest coal power plants operated by an electricity company. The Mizushima site was chosen since it had a facility that treated boil-off gas released from LNG, and ammonia was used as its fuel. JERA and Kyushu Electric followed up with tests at bigger plants.

Due to a lack of co-firing safety standards, temporary expert panels were set up to review and approve safety plans. As the process was simply spraying a small amount of ammonia onto the burner in the boiler, co-firing was classified as a type of internal combustion where coal was the major fuel.

In December 2022, METI revised the Electricity Business Act Rulebook to adapt to larger scale co-firing demonstrations. The new rules clarify that co-firing is not “a self-propelled internal combustion.” This change and others mandate that power companies seeking to practice co-firing must:

Install gas leak detection and alarm systems

Install emergency spray and other ammonia absorber devices

Name a chief boiler/ turbine engineer before construction of co-firing units, and report the appointment to METI; the engineers require their track records to be certified by METI.

The updated rules apply to any use in which ammonia or hydrogen is above 0% of total, which effectively means all and any co-firing processes.

Interestingly, bureaucrats also added mention of ammonia fuel cells to the scope of the new Rulebook, hinting at the upcoming development of solid oxide fuel cells (SOFC).

Co-firing test schedule

Time

Power plant

Capacity

Ammonia ratio

July 2017

Chugoku Electric Mizushima No. 2

156 MW

0.6-0.8%

April 2019

Chubu Electric Chita LNG plant

300 kW

100%

October 2021- March 2022

JERA Hekinan Unit No. 5

1 GW

0.02%

June 2022

IHI Yokohama R&D facility

2 MW

100%

Dec 2022

METI tightens ammonia safety rules

April 2023

Kyushu Electric Reihoku Unit No. 1

700 MW

20%

Fall 2023

Kyushu Electric Matsuura Unit No. 2

1 GW

20%

March-April 2024

JERA Hekinan Unit No. 4

1 GW

20%

TBD

Tohoku Electric Niigata Unit No. 5, Noshiro ?

333-600 MW

TBD

2027-2028

JERA to commercialize co-firing operations

1 GW?

20%?

In the next eight months, Kyushu Electric and JERA each plan a 20% co-firing run at coal power stations that have a capacity of 1 GW.

Chugoku Electric’s ammonia consumption was 450 kg/ hour for several hours over the July 3-9 testing period, which calculates as a few tons. JERA’s 2021 test consumed 200 tons of ammonia. For the 2024 pilot co-firing, JERA is building a larger 2,000 cubic meter tank that’s 18 meters high, capable of storing over 4,000 tons. It’s also building pipelines to transport ammonia offloaded from ships to the storage site.

Source: JERA website

Welding shut the risks

Asked by Japan NRG about its safety approach, a JERA spokesman said: “Blocking leakage, early leak detection and the prevention of its spread are at the core of pipeline construction. The pipe joints will be welded to eliminate any possibility of leaks; gas detectors will be installed and gas flow will stop in case of emergencies.”

For power utilities, ammonia slips pose a bigger threat than explosions. That’s because the chances of slips are likely to be higher than fire or explosion caused by unexpected electricity sparks.

Co-firing to trigger paradigm shift

Co-firing will possibly massively expand Japan’s ammonia demand, especially after 2027 when JERA is expected to commercialize co-firing. As already mentioned, JERA’s estimate for ammonia fuel volumes needed to maintain 20% co-firing at a 1-GW generator would by itself add 50% to Japan’s total ammonia consumption. Demand from the power sector alone is seen reaching 2 million tons by 2030.

Other hard-to-abate sectors, such as chemical manufacturers, are also looking into ammonia as fuel to run their plants. If three 1-million ton/ year capacity naphtha crackers started to use ammonia, about 6.7 million tons/ year of ammonia would be required, according to METI.

Shipping companies are also emerging as potential consumers. The first ammonia-fueled tug boat of NYK Line is set to sail in 2024, and by 2050 the government hopes ammonia will consist of around half of the fuel demand of ocean-going ships.

Safety approach comparisons

Power units

Industrial complexes

Major risks

Ammonia slips; Power generating units may trigger unexpected electricity discharge and temperature changes, which may cause ammonia to catch fire

Explosions and fire from slips; Other flammable substances may be in use in the vicinity.

Requirement for pipes

Joints need to be welded

Joints need to be welded and pipes double layered

Tank locations

No ammonia tanks allowed in nuclear power plant premises; Large tanks of several 10,000 cubic meters need to keep a 320 meter distance from another facility

Equipment layouts are regulated if gas and oil units are in the same premise

Currently, 10 to 30 ammonia incidents are reported every year. Most occur at chemical and food processing plants. In the last four years, none were in the power sector. However, as volumes rise, so will the likelihood of incidents.

In this context, METI, power utilities that utilize coal-fired stations, and all other relevant stakeholders will need to move fast to create and implement safety standards that take into account the greater quantities of ammonia that will be moved around Japan to cover electricity sector needs. METI is rewriting the co-firing Rulebook it updated in December last year, and the Japan Clean Ammonia Fuel Association and high-pressure gas sector organizations are working to identify the infrastructure requirements to ensure safety.

Since ammonia’s application in energy is new, there are many unknowns and reliable data still needs to be collected. Thus, complete safety guidelines cannot be created overnight, and will need to be developed in several stages.

A failure to write coherent rules through transparent discussions could result in consequences that will make further development of co-firing untenable. That would immediately put into question Japan’s CO2 emission cut targets and its technology export aspirations.

Japan NRG ammonia demand forecast

Total demand

Details

Today

1 mln tons

Chemical manufacturing demand dominates; Power demand is at a few hundred tons

2024-2030

Up to 2.3 mln tons

1.3 million tons for 20% co-firing at two 1 GW plants and three 100 MW plants; the balance comes from non-power-sector demand; First ammonia-fueled ship may sail in 2024

2030

3-10 mln tons

3 million tons/ year if 1% of Japan’s electricity is generated through ammonia co-firing; Additional 0-7 million tons/ year from the chemical and other sectors; SOFC in early commercialization phase

2050

30-50 mln tons

Minimum 30 million tons/ year if 10% of power is generated by ammonia; as much as 20 million tons of demand from the other sectors

Note: This is a rough forecast adding up figures from public data

In Part II of this article, to be published next week, we outline the challenges in scaling up ammonia storage capacities and data collection, and how these are being addressed in Japan.

ANALYSIS

BY CHISAKI WATANABE

Rollout of Local Decarbonization Plans Has Been Slow; Efforts to Engage Municipalities Faces Resources Gap

Originally, the program was designed to be part of the government’s sweeping regional decarbonization efforts to expedite the deployment of renewables. However, a year after the Ministry of the Environment (MoE) launched the initiative, which encourages municipalities to designate local areas for renewables development, progress has been slow.

The program aimed at a unique bottom-up approach, seeking to empower local areas to declare themselves as net-zero leaders. The idea was to have communities take charge of clean energy developments to balance out the top-down national decarbonization agenda.

More than a year after the start of the program, however, only 12 renewables promotion zones have been designated by municipalities. Meanwhile, community opposition to new solar and wind projects is on the rise.

Complaints range from solar panels placed on slopes that are too steep and too close to homes, to tree logging carried out to make space for wind turbines. The national government may now need to adjust its approach for localities to re-engage with new renewables development.

Program Terms

In April 2022, the MoE launched its program, “Regional Decarbonization Promotion Projects,” following an amendment to the Act on the Promotion of Global Warming Countermeasures. Under this program, each municipality (city/town/village) can designate areas as “promotion zones (促進区域)” to welcome new clean energy projects.

The program emphasized that projects should “co-exist harmoniously” with host communities, seeking to address the tensions that have built up in some areas between the locals and developers. Applicable projects for promotion zones are classified under four broad categories:

Renewable energy sources that generate electricity or heat (i.e., solar PV, solar heat, wind, small hydro, geothermal, and biomass)

Additional initiatives to the above aimed at reducing emissions (i.e., EV charging stations, municipally funded renewables power companies that provide green electricity for local use, and educational programs)

Efforts to protect the local environment (i.e., protection of rare animals and plants, efforts to minimize project impact on local landscape)

Efforts for sustainable development of the local economy and society (i.e., local job creation and training opportunities)

A developer planning a renewables project in such a promotion zone must receive the municipality’s approval. Once approved, developers benefit from:

A simpler process to receive permits:the municipality on behalf of the developer applies for the various necessary permits from governors or the central government as related to the national parks law, hot springs law, and others;

An exemption from the first step of the EIA: The developer is exempt from submitting a “document on primary environmental impact consideration,” which is required before turning in an actual plan for the EIA”;

Better business prospects due to improved clarity on the above and other issues.

Designated promotion zones also provide benefits to hosting municipalities. These include:

Consensus building: a council is set up to bring together residents and developers to discuss renewable projects in order to help build consensus among stakeholders;

Environmental protection: the process promotes the development of projects that would benefit host communities and avoid environmental destruction;

Contributions to local society and economy: A municipality can ask developer to create jobs and allow residents to use the facility in case of natural disaster.

Results so far

The program was introduced largely to promote the use of renewable electricity and cut Japan’s reliance on fossil fuels, thus also improving its energy security and meeting national decarbonization targets. But a year on, as of August 8, there are only 12 promotion zones.

There are 1,741 municipalities of varying population sizes across Japan. Almost all of the 12 promotion zones designated by municipalities so far involve solar, with plans to install panels on rooftops and public land. This underlines the limitations of public initiatives.

Parallel efforts to boost renewables

In June 2021, the national government adopted a roadmap for local decarbonization that set a target of creating more than 100 “decarbonization model areas” (脱炭素先行地域) by 2025. This is a parallel initiative, focused more directly on renewables power generation and energy efficiency measures for the residential and commercial sectors, and it seems to have fared better in attracting local government attention.

In this initiative, the MoE picks the so-called “decarbonization model area” via a public solicitation process. So far, 62 model areas have been selected after three rounds of solicitations.

The definition of “area” covered by this program is flexible and wide-ranging. It could cover an entire municipality, or just parts of a municipality such as a residential area, an airport, a natural park, or a cluster of facilities.

Many of the proposals for the first 46 areas picked last year were jointly submitted with partners such as NTT Anode Energy, universities, and utilities including TEPCO and KEPCO. During the third round of solicitation earlier this year, it became mandatory for proposals to be submitted jointly with commercial or academic partners.

Promotion zones in Japan

Municipality

Renewables

Areas, locations

1

Minowa town, Nagano

Solar

Rooftop of town facilities, town-owned site, industry hub

2

Odawara city, Kanagawa

Solar

Designated areas in the city

3

Karatsu city, Saga

Solar, Wind, Small Hydro, Green hydrogen

Public facilities and land

4

Iruma city, Saitama

Solar

Public facilities

5

Ena city, Gifu

Solar

Rooftop

6

Fukuoka city, Fukuoka

Solar

Rooftop, public land

7

Atsugi city, Kanagawa

Solar

Rooftop, other areas

8

Misato town, Shimane

Solar

Rooftop (town-owned buildings), town-owned land, farming land

9

Maibara city, Shiga

Solar

Part of business areas near Maibara Station

10

Anan city, Tokushima

Solar

Public facilities and land

11

Matsuyama city, Ehime

Solar

Areas near an airport, parts of islands, public land

12

Toyama city, Toyama

Solar

Areas excluding landslide-prone areas and others

Source: MOE presentation, municipal government websites

Local expertise shortage

These various MoE efforts are intended to strike a balance between the deployment of renewables and environmental protection. The ministry also wants local governments to get involved more in choosing future sites of new renewables facilities.

Municipalities, however, have been slow to follow national guidance due to the frequent problems of manpower shortages and a lack of expertise in making green action plans.

The compiling of such plans – which outline the local vision on how to reduce GHG emissions in two sections, one for government operations and the other for area-wide emissions – is actually stipulated by law, in Article 21 of the Global Warming Act. So far, most local governments have compiled plans to cut emissions at public facilities, but are yet to do the same for area-wide emissions.

As the table below shows, the smaller the municipality, the less likely it’s to compile an action plan for decarbonization. In addition to lacking staff, municipalities say they have a shortage of knowledge about climate change measures and face difficulty in securing budgets for measures that such an action plan would propose.

Breakdown of completion rate for local action plans by the size of local government

Designating promotion zones is even tougher for municipalities. As of December 2022, a majority – 52.9%, or 860 of municipalities – have no plans to designate promotion zones in their jurisdictions, according to a survey by the MoE. Only 0.2% (4 municipalities) said they have determined a promotion zone. Another 6.2% (101) said they’re working on it and a further 40.6% (660) said they plan to work on designating zones but haven’t started yet.

The central government is in charge of setting national environmental standards for the zones, while each prefectural government sets regional environmental standards that are aligned with local natural and social requirements.

National response

Against this backdrop, in April the MoE started an expert panel to discuss how to accelerate regional decarbonization and improve the ministry’s programs in this area.

WWF Japan delivered a presentation to the panel in May, saying the system of state support programs and subsidies is too diverse and complex, complicating their use by municipalities. It suggested funneling everything through a one-stop shop and focusing support more on renewables projects developed by municipalities. Those projects are more likely to gain local acceptance and their profits would go back into the community.

The WWF also suggested creating a portal site for companies to express a willingness to source locally produced green electricity. This could give more clarity to municipalities about their business prospects. In the draft released in August experts suggested the government consider the following points:

Provide stronger incentives to project developers, such as tax breaks

Allow prefectures to jointly designate promotion zones with municipalities

Create demand and set promotion zones for next-generation solar panels, such as perovskites and solar windows/walls

The panel also suggested that further consideration be given to power grid development in the promotion zones.

In line with panel suggestions for a streamlined approach amid strained local resources, the MoE may go one step further and look to consolidate its own programs – the “promotion zones” and “decarbonization model areas” – or at least find ways for the two to work together better.

Encouraging municipalities to take charge of clean energy developments in their area makes sense because they know their communities best. The national government can help by taking upon itself all issues related to the administrative burden and provide municipalities with the IT and knowledge resources they need to make the green action plans work.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Africa/ Oil

Carlyle Group will sell its Gabon-focused oil and gas company, Assala Energy, to French producer Maurel & Prom for $730 million. Carlyle International Energy Partners (CIEP), the fund’s non-U.S. energy arm, first invested in Assala in 2017 when it acquired Shell’s aging operations in Gabon for $628 million.

Brazil/ Oil

In August, Brazil is set to increase purchases of Russian petroleum products by 25% over July, with imports set to reach record levels this month, helping Russia overtake the U.S. as Brazil’s top foreign fuel supplier, said energy analytics firm Kpler. The discount on Russian diesel to Brazil is estimated at $10 to $15 a barrel.

EU/ Cleantech

EU cleantech startups have attracted less than half the investment as their U.S. counterparts since the $390 billion package of climate subsidies and tax credits was passed a year ago, (Inflation Reduction Act). The EU spent a total of $8.7 billion on startups in areas such as carbon storage and EVs; while $21.7 billion was committed to such projects in the U.S.

Indonesia/ Energy transition

Citing insufficient data, Indonesia has pushed back until later this year its plans to launch investments from a fund of $20 billion pledged by rich countries and global lenders to speed the energy transition. The initiative aims to help Indonesia close coal power plants, adopt green sources of power and reach peak emissions in 2030.

Ireland/ Critical raw materials

Dublin-based TechMet raised $200 million in equity that will go towards investment in mining for nickel, lithium and other metals that will help the West counter China’s dominance of critical minerals supplies for clean energy technologies and infrastructure.

Offshore wind power

Global targets to increase wind power installations five-fold annually by 2030 are unrealistic and would require $27 billion in investment in the supply chain by 2026, Wood Mackenzie said, adding that annual capacity is more likely to increase by 30 GW a year by 2030, well below the 80 GW per year target that’s been set by the global community.

Saudi Arabia/ Oil exports

Saudi Arabia’s crude oil exports fell for a third straight month in June to their lowest since September 2021, as big Asian buyers favor cheaper Russian oil. Saudi crude exports totalled 6.8 mbpd in June, down about 1.8% from 6.93 mbpd in May.

Venezuela/ Oil

Venezuela opposes a court-ordered auction of shares in the parent of Citgo Petroleum to pay creditors seeking $10 billion from expropriations and debt defaults. Some 20 creditors with arbitration awards or lawsuits against Venezuela’s state oil company PDVSA asked a Delaware court to register their cases so they can join the October auction.

U.S./ Carbon capture

Occidental Petroleum will buy startup Carbon Engineering for $1.1 billion, hoping to profit from its CCS technology at the Stratos project in Texas, which will be the world’s largest direct air capture plant by 2025.

U.S./ Oil and gas pipelines

Pipeline operator Energy Transfer will buy rival Crestwood Equity Partners for about $7.1 billion. This will give Energy Transfer a larger share of energy transport in three top shale basins. This year, consolidation in the oil and gas pipeline sector has accelerated as U.S. production grows.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

ASEAN-Japan summit to mark 50 years of cooperation

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.