PM Kishida gives green light to continue with fuel subsidies to counterbalance rising energy costs

Japan begins release of treated Fukushima water, safety levels observed

ENERGY TRANSITION & POLICY

Hydrogen economy lags on slow investment, policy: IGES

Japan, Mexico academia to collaborate on PSC, hydrogen tech

ANRE identified key GHG items to improve biomass disclosures

Japanese firms expand EV battery materials output in the U.S.

Battery startup PowerX successfully raises Series B round

Registration for JPX Carbon Credit Market closes this month

Japan, Australia firms develop large CO2 shipping solutions

Mitsubishi UBE Cement to invest ¥50 billion for waste plastic fuel

KEPCO studies hydrogen production using nuclear power

ELECTRICITY MARKETS

Chubu Electric, NTT Data to study renewables curtailment issues

MHI makes coils for experimental ITER fusion reactor in France

Hydropower facilities in Mie Pref in full operation

City of Kawasaki to form a new energy company

May power volumes dropped; New market players struggling

Abalance sets up factory to produce solar cells in Vietnam

Pacifico Energy to update plan for 135 MW solar plant in Mie

OIL, GAS & MINING

Hokkaido tests show liquid biomethane can replace city gas

Petrobras, Japanese partner on carbon capture at offshore rigs

Japan and ASEAN to recover critical metals from e-waste

INPEX takes stake in LNG project in Australia

ANALYSIS

ENHANCING CARBON CAPTURE MANAGEMENT: JAPAN SELECTS 7 CCS PROJECTS

This year, the government published its first concrete roadmap for the sector detailing where and at what cost CCS technology should be introduced. Still, even with broad global support, turning CCS into a commercially viable technology comes with a number of complications. While CCS has passed its technical tests in Japan, how it will work as a business has many guessing.

HOW TO KEEP AMMONIA SAFE: PART 2

Japan plans commercial operations of thermal power plants that burn coal and ammonia, side by side, from 2027-28. The technology, known as co-firing, is vital for Japan to cut CO2 emissions and wean itself off coal. It also poses several challenges. Among the biggest of these is how to move and store the ammonia fuel and create the right kind of tanks to contain it.

New Energy and Industrial Technology Development Organization

kWh

Kilowatt hours (electricity generation volume)

TEPCO

Tokyo Electric Power Company

FIT

Feed-in Tariff

KEPCO

Kansai Electric Power Company

FIP

Feed-in Premium

EPCO

Electric Power Company

SAF

Sustainable Aviation Fuel

JCC

Japan Crude Cocktail

NPP

Nuclear power plant

JKM

Japan Korea Market, the Platt’s LNG benchmark

JOGMEC

Japan Organization for Metals and Energy Security

CCUS

Carbon Capture, Utilization and Storage

OCCTO

Organization for Cross-regional Coordination of Transmission Operators

NRA

Nuclear Regulation Authority

GX

Green Transformation

NEWS: ENERGY TRANSITION & POLICY

Govt proposes multi-year GX budget of ¥2 trillion, Diet to approve in early 2024

(Government statement, Japan NRG, Aug 23)

The govt proposed a GX budget of ¥2 trillion over the next few years, as multi-year fiscal budgets are now possible with the recent passage of the GX Promotion Act.

Aug 31 is the deadline to file the FY2024 budget to the Finance Ministry. Then the relevant ministries will finalize the budget plan. Finally, it goes to the Diet in early 2024 for approval or further amendment.

By the end of FY2023, the govt will come up with sector-specific action plans for achieving carbon neutrality by 2050, which will build on the 22-sector investment strategy compiled earlier by the GX Implementation Council.

Among the top priorities are strategies for mass production of perovskite solar cells (PSC) and acceleration of next-gen grid development, as well as development of next-gen nuclear reactors.

(¥ Billions)

High Speed nuclear reactor R&D

¥ 52.3

¥ 152.1 in FY2024 to FY2026

Building local supply chain of breakthrough net zero products (electrolyzer, storage batteries, perovskite solar cells, offshore wind equipment, power semiconductors, etc)

¥ 820.7

¥ 1,200 in FY 2024 to FY2028

GX deep tech startup support

¥ 40.7

¥ 203 in FY2024 to FY2028

Energy conservation and energy transition at small and medium sized enterprises

¥ 91

¥ 192.5 in FY2024 to FY2028

Energy efficient homes

¥ 148.4

NA

Promoting FCV, EV and other green mobility solutions

¥ 141.7

NA

Others, including subsidies for hydrogen and ammonia supplies

NA

NA

PM eager to continue fuel subsidies to combat rising energy costs, ¥6.2 trillion spent to date

(Government statement, Aug 22)

PM Kishida has asked the head of the ruling party policy research council to hammer out policies to mitigate rising energy costs, including a review of fuel subsidies that end in September, as well as new economic packages.

A total of ¥6.2 trillion has been spent on fuel subsidies that ran from January 2022.

CONTEXT: Businesses are divided on extending fuel subsidies. Some say the govt spent too much on fossil fuel subsidies and more of the budget should go to carbon neutral solutions. Energy intensive sectors such as semiconductors are asking for more state support. A combination of programs may help balance different interests.

TAKEAWAY: The fuel subsidy amount is enormous, but it should be viewed in the context of high energy prices. Naturally, the higher the prices are, the most the state spends on subsidies. For comparison, the EU is estimated to have spent 39 billion euros on fossil fuel subsidies in 2021 alone, according to Climate Scorecard. That’s the same in yen terms as the Japanese spending.

Maintaining the subsidies is partly a political move since PM Kishida’s ratings are low at home and he’s not in a position to upset business lobbies. Still, with fuel prices down significantly from last year, an exit from some of the subsidies is likely early next year.

Tokyo GX Week: Ministers from various countries to convene in late Sept

(Japan NRG, Aug 21)

METI will organize “Tokyo GX Week,” a series of international conferences for energy and the environment, Sept 25 to Oct 5, 2023.

There’ll be nine meetings, such as the “Hydrogen Ministers’ Meeting” and the “Asia Green Growth Partnership Ministerial Meeting,” where countries will discuss energy security, climate change, etc.

Most meetings will be in Tokyo, but the “Asia CCUS Network Forum” on Sept 27 will be held in Hiroshima, focusing on project strategies for CCUS in collaboration with ASEAN.

After the opening plenary session on Sept 25, the following meetings will run on the following schedule:

Sept 25 (Monday):

Asia Green Growth Partnership Ministerial Meeting

Hydrogen Energy Ministerial Meeting

Sept 27

Asia CCUS Network Forum

International Conference on Carbon Recycling

Sept 29

International Conference on Fuel Ammonia

Oct 2

GGX x TCFD Summit focusing on energy transition financing

Oct 4

Innovation for Cool Earth Forum (ICEF): Day 1

Oct 5

ICEF: Day 2

Research & Development 20 for Clean Energy Technologies (RD20), Leaders Sessions

Hydrogen economy lags on slow investment and policy decisions: IGES

(Japan NRG, Aug 23)

The development of the hydrogen economy lags behind forecasts as investment and policy decisions remain slow, according to energy experts speaking at the Net-Zero Agenda Through Regional Cooperation in Green Hydrogen in Asia.

The event was hosted by the Institute for Global Environmental Strategies (IGES) in Kanagawa Pref; speakers included analysts from the IEA, the Asian Development Bank, IGES and Zero Carbon Hydrogen.

The International Energy Agency forecasts that global hydrogen demand in 2030 will double to 200 million tons from around 100 million tons in 2021. Water electrolysis will be the major production method, requiring 15,000 TWh of power.

CONTEXT: There are projects planned for 26 million tons of low-emission hydrogen by 2030, but only 5% have reached investment decisions. Asian countries are developing hydrogen economies at varied speeds, and govts need to coordinate to bring down production costs and create demand, speakers said.

The govts also need to accelerate implementation after the plan announcement stage, increase hydrogen demand, harmonize standards to boost international trades, and build up infrastructure for long-distance hydrogen transport.

Japan must scale up long distance hydrogen transport by building tankers that are 100 times larger than Suiso Frontier, Japan’s first hydrogen tanker with a capacity to load 1,250 cubic meters of liquefied hydrogen.

SIDE DEVELOPMENT: METI budget request to improve hydrogen and ammonia infrastructure (Denki Shimbun, Aug 25)

METI will ask for more budget funds in FY2024 for GX activities. For example, new funding of ¥10 billion will be allocated for investment in hydrogen production.

Another ¥3 billion will be requested for supply infrastructure. To promote renewable energy: an additional ¥12 billion.

The total budget request for actions designated as energy-related will increase by ¥800 billion compared to the initial FY2023 budget, and reach ¥7.82 trillion.

Subsidies to promote energy-saving facilities will be increased by ¥9.9 billion compared to the initial budget for FY2023, totaling ¥360 billion.

For advanced CCS projects, the requested amount will be doubled compared to the initial budget for FY2023, reaching ¥7 billion.

Japan, Mexico academia to collaborate on perovskite, hydrogen tech

(Japan NRG, Aug 24)

In September, the University of Hyogo and the University of Sonora in Mexico will launch five-year research on perovskite solar cell (PSC) and hydrogen fuel cell systems. This will be Mexico’s first hydrogen FC project.

The University of Hyogo developed screen print-based PSC production technology and seeks to apply it to FC production.

Mexico’s Sonora State has large solar power farms and plans to export green hydrogen. The two universities also will collaborate in lithium mining in Mexico.

CONTEXT: Other PSC production methods developed in Japan include roll-to-roll “printing”, spraying and/or sputtering the molecule paste on films.

SIDE DEVELOPMENT: Toppan starts production of CCM/MEA for hydrogen market (Company statement, Aug 17)

Toppan began production of catalyst coated membrane (CCM)/ membrane electrode assemblies (MEAs) at its factory in Kochi Pref.

CCM/MEAs are core components of electrolyzers to produce hydrogen. Those made by Toppan reduce electrical resistance and increase energy conversion efficiency.

CONTEXT: Toppan has been developing CCM/MEAs since 2004.

ANRE identified key GHG items to improve biomass disclosures

(Government statement, Aug 25)

ANRE identified items biomass power operators will now need to include in GHG emission reports. These are not mandatory but operators are encouraged to make the disclosure voluntarily.

ANRE proposes that biomass sector associations collect the GHG emission reports of its members for analysis. The association will also conduct annual follow-ups.

Disclosure rules

Items

Disclosure coverage

Equipment, ID, year of operational launch, output, efficiency, fuel category, fuel name, amount used, origin of fuel supplies, GJG calculation method, formulas used, third-party certifications, sustainability certification schemes, ideas on how to cut GHGs further

Amount of fuel

Fuel amounts from every supplier, rather than the total volume

GHGs

Plans to cut GHG

Term

April-March

Where to disclose

Operators’ respective websites

Reporting

In addition to website disclosures, operators file their reports to sector associations.

Mitsubishi Chem, Asahi Kasei, Zeon to expand EV battery material production in U.S.

(Nikkei, Aug 23)

To take advantage of the U.S. effort to establish a local EV supply chain, Japanese firms are expanding battery material production in North America.

Mitsubishi Chemical intends to set up a fresh North American production facility for anode material. This will leverage U.S. incentives and reduce reliance on China for raw materials.

Other Japanese companies, such as Zeon and Asahi Kasei, are also investing in EV-related manufacturing in the U.S.

CONTEXT: U.S. Inflation Reduction Act provides tax credits to EV buyers using domestically sourced battery materials, further incentivizing local production.

PowerX raised ¥4.62 billion in Series B round

(Company statement, Aug 17)

PowerX raised an additional ¥2.71 billion in the second half of its Series B round. Combined with the round’s first half, the company has raised a total of ¥4.62 billion.

Investors include Nippon Gas, Mori Trust, JAL Innovation fund, JAPEX, Yaskawa Electric, etc. Mitsubishi UFJ Morgan Stanley Securities was the financial advisor.

The funds will go to R&D of battery storage and for the production machinery needed at its battery module factory in Tamano city, Okayama Pref.

Registration for JPX Carbon Credit Market closes this month

(Japan NRG, Aug 25)

Registration for the JPX Carbon Credit Market is due by Aug 31. If the deadline is missed, one can register and participate gradually after the opening.

The schedule is as follows: application deadline, 8/31; ID and password issuance by 9/8; participant testing from 9/11 to 9/26; checklist submission deadline, 9/27; market opening and trading start in mid-October

CONTEXT: The TSE Carbon Credit Market will allow for trading on the exchange, replacing the previous methods of negotiated transactions or state-mediated bidding and selling of J-Credits. The market will feature J-Credits in six categories, each associated with specific applications like renewable energy and conservation.

TAKEAWAY: The launch of the carbon credit market is being done in stages. The current state has been given a fun-sounding name, the GX League, to give it a sense of prestige and coolness. The 500+ companies that have signed up either to trade carbon credits or be involved in the new market’s developments and rule-making are described as members of the GX League. The League and the carbon credits market are both voluntary. Those that join the GX League are also asked to seek GHG reductions of 46% by the end of this decade (compared with FY2013) to mirror the national CO2 reduction commitments. Emission reduction on top of that would be rewarded with credits that should be monetized on the exchange.

Japan, Australian companies to develop large-volume CO2 shipping solutions

(Company statement, Aug 23)

Osaka Gas, Mitsui OSK Lines, Low Emission Technology Australia, JX Nippon Oil & Gas Exploration, and Future Energy Exports CRC inked an agreement to develop technologies to ship CO2 in large volumes.

Low pressures of 7 bar and temperatures of -49°C are the best conditions to transport CO2 on ships. However, it has not been tested in real situations.

Presently, CO2 is transported in vessels with a pressure of 18 bar and – 26°C.

Toyota Tsusho supplies biofuel to cargo carrier at Kobe Port

(Company statement, Aug. 22)

Toyota Tsusho provided biodiesel fuel for a test voyage at Kobe Port to a cargo carrier for Kobe steel, owned by Asahi Shipping and NYK Line.

This biofuel was delivered using ship-to-ship bunkering and is produced by refining waste cooking oil collected from Toyota Group and Toyota Tsusho Group facilities.

CONTEXT: In April, Toyota Tsusho initiated Japan’s first continuous commercial supply of biodiesel blended fuel for ships at the Port of Nagoya.

Mitsubishi UBE Cement to invest ¥50 billion for waste plastic fuel

(Nikkei, Aug 23)

Mitsubishi UBE Cement plans to invest ¥50 billion by 2030 to enhance its waste plastic processing capacity to turn it into fuel for cement production.

The company will substitute waste plastics for coal, the primary fuel, increasing the waste plastic proportion from 20% to 50%. This move is projected to reduce CO2 emissions by 1.27 million tons by FY2030 compared to FY2022 levels.

They’ll set up processing facilities at various locations, including at the Kanda Cement Plant (Fukuoka Pref). Similar plans are in the works for the Kyushu (Fukuoka Pref) and Ube (Yamaguchi Pref) plants.

In 2021, the ceramics and stone industry, including cement, accounted for 7.4% of Japan’s industrial sector CO2 emissions.

Idemitsu joins with LOPS to develop SAF supply chain

(Company statement, Aug 24)

Idemitsu Kosan will work with LOPS Corp, which operates an oils and fats business, to procure feedstock for Sustainable Aviation Fuel (SAF).

By the late 2020s, the two companies will set up a procurement system for SAF feedstocks such as used cooking oil (UCO) in order to produce SAF domestically.

LOPS supplies oil and fat feedstocks for various applications backed by strong partnerships with producers and has a more than 50% share in the export of UCO.

CONTEXT: SAF is made from non-fossil-derived raw materials, but one challenge is to secure raw materials that are less competitive with food crops. Idemitsu plans a SAF production of 500,000 kiloliters per year by 2030. Starting FY2026, the company will supply and verify SAF produced from bioethanol at its Chiba facility. For SAF produced from waste cooking oil, the company is also progressing with facility preparations aimed at supply launch by the late 2020s.

KEPCO studies CO2-free hydrogen production using nuclear power

(Denki Shimbun, Aug 24)

KEPCO to consider using nuclear power to produce CO2-free hydrogen. In a recent project, the company successfully traced the flow of nuclear-derived hydrogen from generation to supply.

Hydrogen was produced and supplied to fuel-cell vehicles via a system in Tsuruga City. KEPCO plans to expand this project. It also utilized nuclear-generated electricity to produce hydrogen for use as a coolant.

While direct nuclear power usage is more efficient, converting it to hydrogen offers storage and transport benefits.

Asahi Kasei to develop technology for resin materials production from CO2 and water

(Nikkei, Aug 25)

Asahi Kasei is developing technology to produce resin materials from CO2 and water through electrolysis, aiming to reduce CO2 emissions during manufacturing.

The company plans to implement this in a pilot facility by 2026, utilizing renewable energy. The method involves creating “ethylene,” a resin component.

The goal is to establish large-scale production by 2030, with an annual target of several thousand tons of ethylene.

JFE Engineering will develop new CO2 separation technology

(Company statement, Aug 17)

JFE Engineering has been selected to develop “CO2 separation technology using cold heat” by NEDO’s “Program to Develop and Promote the Commercialization of Energy Conservation Technologies to Realize a Decarbonized Society”.

The company has been developing a technology, “GX-Crystal”, which will separate CO2 from LNG combustion exhaust gas, minimizing external energy input by using unused cold heat generated during LNG gasification.

Development is planned to run until March 2025, collecting and evaluating data through experiments. Commercialization is planned for 2027.

Marubeni, Peru LNG and Osaka Gas to conduct Pre-FEED study on e-methane

(Company statement, Aug 22)

Marubeni, Peru LNG, and Osaka Gas will conduct a pre-FEED study for a methanation project in Peru, to create e-methane using green hydrogen and CO2.

The initial study found that Peru’s renewable energy and CO2 availability can competitively produce 60,000 tons of e-methane annually. Discussions will cover material procurement, plant specs, and economic evaluations.

An investment decision is expected by 2025, targeting e-methane production by 2030.

NEWS: POWER MARKETS

Japan begins of Fukushima water release; safety maintained but international outcry persists

(Japan NRG, Aug 24)

As part of the decommissioning process, Japan began the release of treated water from Fukushima No. 1 NPP.

Initially, about 200-210 metric tons of water were discharged; the daily target is set at 460 tons. The plant currently holds about 1.3 million tons of treated water, which is hindering decommissioning.

Prior to release, the water underwent treatment to eliminate radionuclides and was mixed with seawater to dilute it. The main radioactive substance remaining in the water is tritium, which is almost impossible to remove. The safety of the water was confirmed by the IAEA, which verified that tritium levels are within acceptable limits.

CONTEXT: A financial aid package of ¥80 billion will be put in place to minimize potential harm and bolster the local fishing sector, which fears repercussions. The objective is to advocate for the removal of import limitations on Fukushima produce in countries that still have them. China and South Korea have pointed to safety issues.

TAKEAWAY: Despite the many months of carefully planning and safety inspections with international bodies and partners, a number of international media are capitalizing on the public’s uneasy attitude toward this issue. Many of the headlines around the release have played to people’s natural anxiety about radiation, rather than lay out the scientific research and context. It is well documented that many nuclear plants around the world, including in China, the most vocal critic of the release program, release water into tritium levels above that of Fukushima — without causing damage to marine life.

No matter the science, the unfortunate fact is that the treated water release in Fukushima is going to cause damage to Japan’s international reputation. While the treated water release is validated by the IAEA and Japan’s own nuclear regulator, the NRA, public distrust of TEPCO’s management due to the company’s past behavior remains. Japan’s allies, such as the U.S. and the EU, have expressed support.

MHI completes coils for experimental ITER fusion reactor in France

(Company statement, Aug 24)

MHI completed the manufacturing of the final toroidal field (TF) coil for the ITER experimental fusion reactor under construction in France.

MHI produced a total of five out of nine TF coils assigned to Japan for the project. These are massive superconducting components crucial for igniting fusion reactions. Each coil stands 16.5 meters high, 9 meters wide, and weighs 300 tons.

TF coils are essential to confine high-temperature plasma within the reactor. MHI is also involved in producing other critical components.

CONTEXT: ITER is a global effort to advance the development of fusion energy. Japan, the EU, the U.S., Russia, South Korea, China, and India are participating. Japan is responsible for core component development, including TF coils.

Chubu Electric, Chubu Electric PG and NTT Data to study renewable energy output control

(Denki Shimbun, Aug 23)

Chubu Electric and Chubu Electric Power Grid (PG) will collaborate with NTT Data to study controlling renewable energy output.

They plan to use decentralized energy resources (DER), such as EVs and storage batteries, for demand response (DR) in order to shift power demand from evening to morning when solar power generation is high. The goal is to be operational by 2027.

DER owners will be asked to help shift power consumption to daytime to match with surplus renewable energy, reducing the need for curtailments. NTT Data will assist with data utilization and IoT device control. The companies will conduct simulations in 2023 and begin verification in 2024.

Hydropower facilities in Mie Pref at full operational capacity

(Yomiuri Shimbun, Aug 22)

During high-demand summer months, hydroelectric power facilities in Mie Pref generate 10 times the power compared to winter.

Chubu Electric has six power plants in the region, with total power output reaching a maximum of 86.6 MW, the highest in the area. The company said the reserve rate within its region is at 7.8%.

On a side note, Chubu Electric’s Misedani Dam is also gaining attention as a tourist spot, participating in the phenomenon called “infrastructure tourism.’’

City of Kawasaki to form a new energy company

(New Energy Business, Aug 25)

In October, Kawasaki City will establish a new electric power company, Kawasaki Mirai Energy, in partnership with private companies. The new company will distribute excess energy derived from a local incineration plant to public buildings.

Shareholders are: NTT Anode Energy (18.5%), Tokyu (10%), Tokyu Power Supply (8.5%), Kawasaki Shinkin Bank (3%), JA Ceresa Kawasaki (3%), Kirabohi Bank (3%), and Yokohama Bank (3%). Kawasaki city will have the remaining 51%.

The city has three incineration plants; one is being modernized (capacity 200 tons x 3 furnaces per day). When completed, Kawasaki expects 120 MWh of excess electricity from the incineration plants that can be utilized through Kawasaki Mirai Energy.

May power sales down; New power market entrants struggle

(Denki Shimbun, Aug 21)

According to the EGC, the May volume of power sales was 57,132 GWh, a decrease of 4.2% YoY,(and a 4.2% decrease from the previous month).

New power providers (shin denryoku) saw a 25.5% drop in their volumes to 8,679 GWh, a consecutive double-digit decrease for eight months. This meant that the market share for the retailers that entered the business to compete with EPCOs fell to 15.2% in May, down 4.3 points YoY and down 0.7 points from the previous month.

Special high-voltage sales saw a 3.6-point drop to 4.8% (0.2-point drop from the previous month); high-voltage sales had an 8.4-point drop to 16.1% (0.4-point drop from the previous month).

Abalance sets up factory to produce solar cells in Vietnam

(Company statement, Aug 18)

Abalance and its subsidiary, Vietnam Sunergy (VSUN), set up Vietnam Sunergy Cell (VSC). VSUN plans to establish a supply chain of solar panel manufacturing by integrating a solar cell supplier within its group companies to reduce production costs.

VSC is a 100% subsidiary of VSUN established in Vietnam in Nov 2022 to produce cells for solar panels.

VSC is building a factory to produce cells for solar panels, investing $180 million (¥23.8 billion) that will be completed in Oct 2023. Once completed, the factory will produce 3 GW of cells per year.

Pacifico Energy to update its plan for 135 MW solar plant in Mie

(New Energy Business, Aug 22)

Pacifico Energy welcomed public feedback for its environmental assessment for the 135 MW Hakusan Mitsugano solar station. The governor of Mie Pref suggested the company review issues such as noise, water quality, and land stability.

Pacifico plans a 135 MW DC/ 93 MW AC solar power station at the ex-golf course site, with 24,800 solar panels and 29 units of 3.2 MW power conditioner systems. Construction starts in 2026; operation in 2028.

Environmental assessment for repowering 36 MW wind station in Aomori Pref

(Government statement, Aug 18)

The MoE submitted to METI its comment on “Rokkasho-mura Wind Power Station Replacement Project Environmental Assessment Report”. This project calls for demolishing the existing wind power station and replacing it. Japan Wind Development (JWD) is in charge.

The MoE summarized its comments: (1) minimize the influence of noise and shadow; (2) prevent birds from crashing into the wind turbines and not disturbing their migration routes; and (3) minimize endangering rare plant species.

The new station will have a 36 MW capacity (up to ten 3.6 to 4.2 MW turbines) to be built at Rokkasho-mura in Aomori Pref.

CONTEXT: This project dates to August 2020 when the first plan was drafted. After three years, METI and MoE are still reviewing the environmental assessment reports. Now the govt will ask JWD to update its plan, with reference to their comments.

NEWS: OIL, GAS & MINING

Hokkaido tests shows liquefied biomethane can be used for city gas

(Company statement, Aug 22)

In July, Hokkaido-based Obihiro Gas and Air Water studied the impact of liquefied biomethane (LBM) in the city gas supply system and concluded that it could be treated like LNG and could substitute the fossil fuel.

About 5 tons of LBM, which is made from cow manure, was mixed with city gas supplies. This was the first time a public utility supplied LBM to consumers.

Air Water’s LBM output capacity is 360 tons/ year. If 360 tons/ year of LNG were replaced by LBM, CO2 emissions would drop by 7,740 tons/ year, claims Air Water.

CONTEXT: LBM is produced by heat-treating cow manure to generate biogas that consists mainly of 60% methane and 40% CO2. Air Water uses heat exchangers to remove the CO2 from the gas, and liquefies it at -160°C. The liquefaction plant is in Obihiro City.

TAKEAWAY: Air Water claims LBM is “carbon neutral” but fossil energy is likely consumed during transport. Biogas plants are located in the Taiki Township, which is 50-60 km from the liquefaction plant.

SIDE DEVELOPMENT: Japan Gas Association panel to launch biogas life-cycle assessment (Japan NRG, Aug 22)

Japan Gas Association will launch a biogas life-cycle assessment in October to March 2024 ahead of the start of the Clean Gas Certificate system in FY2024.

The JGA plans to issue Clean Gas Certificates for synthetic methane (e-methane) and biogas, and the certificates will be tradeable in the marketplace.

CONTEXT: The MoE has guidelines on biogas LCA, but few assessments have been done. Those that were done related to the environmental impact of the gas in power generation. The JGA plans to standardize the LCA processes to make it relevant for gas supply.

TAKEAWAY: Biogas applications are spreading fast. In February, a group consisting of Mitsui OSK Lines, JERA and Air Water tested liquefied bio methane (LBM) to sail a ship, substituting LNG with LBM. In October, Interstellar Technologies plans to launch a rocket propelled solely by LBM, which is made by removing CO2 from biogas generated from livestock manure. The gas is around 60% methane and 40% CO2.

Petrobras and Kureha partner on carbon capture at offshore rigs

(Nikkei Asia, Aug 20)

Tokyo-based Kureha Corp, a leading diversified chemical products manufacturer, is partnering with Brazil’s Petrobras to develop carbon capture (CC) for offshore oil fields.

Kureha will develop a catalyst for CC together with the Kitami Institute of Technology. A prototype should be ready by 2024.

The technology will convert captured emissions into useful products, such as carbon nanotubes. The process involves capturing methane from natural gas and transforming it into a transportable powder. For 2023, the project received funding of ¥15 million.

Japan and ASEAN to recover critical metals from e-waste

(Nikkei Asia, Aug 25)

Japan will collaborate with ASEAN countries to extract valuable materials from discarded electronic devices such as smartphones.

With electronic waste in ASEAN reaching 3.5 million tons in 2019 and growing, the partnership will establish disposal rules to address environmental and health concerns.

Japan plans to help set up guidelines for waste disposal, including systems for registration and certification of collection and dismantling businesses.

CONTEXT: This initiative aligns with Japan’s strategy to secure critical minerals for EVs and batteries through recycling due to its limited natural metal resources. While Europe and the U.S. are aiming to retain these resources domestically, Japan is shifting its focus to cooperation with ASEAN.

INPEX takes stake in LNG project in Australia

(Company statement, Aug 21)

INPEX acquired a 74% stake in the LNG exploration project in the AC/ RL7 block in the Bonaparte Basin of Western Australia.

The seller was PTTEP Australasia. TotalEnergies will own the remaining 26%.

The block is located 250 km northeast of the INPEX Ichthys Gas Project.

LNG stocks slip to 1.81 million tons

(Government data, Aug 23)

LNG stocks of 10 power utilities stood at 1.81 million tons as of Aug 20, down 6.7% from 1.94 million tons a week earlier. The Aug 13 stocks were first reported at 1.98 million tons but METI corrected the figure.

The end-August stocks last year were 2.75 million tons. The five-year average for this time of year was 2 million tons.

ANALYSIS

BY FILIPPO PEDRETTI

Enhancing Carbon Capture Management:

Japan Selects 7 Sites for CCS Projects

A decade and a half ago, Japan embarked on its first CCS trial in a small northern port when carbon capture and storage seemed like a distant, highly experimental technology. Critics may say that little has changed for CCS in that time, but Japan’s top officials disagree.

This year, the government published its first concrete roadmap for the sector, which gives specific details on when, where and at what cost the technology should be introduced. There are designs for carbon storage sites at home and abroad, and a parallel development for a domestic carbon credits marketplace.

The confidence with which Japanese officials have outlined the emergence of CCS as a new sector that should be operational by 2030 owes a lot to that successful trial back in 2008. In fact, the same northern Hokkaido port has now been upgraded to an industry hub to carry the flag for CCS in Japan.

Still, even with broad global support, turning CCS into a commercially viable technology comes with a number of complications. While CCS has passed its technical tests in Japan, how it will work as a business has many guessing.

Japan’s blueprint for CCS

In early February, ANRE released a final CCS sector roadmap that calls for Japan to establish the facilities that can store between 6 to 12 million metric tons per annum (mtpa) of CO2 by 2030. This is equal to the annual emissions generated by two to three coal-fired power plants.

ANRE assesses the cost of isolating, recovering, transporting, and storing a ton of CO2 to be about ¥13,000 to ¥20,000. The top of that range is higher than the price at which a carbon credit for a ton of CO2 trades in most countries. The ETS in the EU, for example, has only once reached the 100-euro level (¥15,860) since January 2020. Thus, Japan’s roadmap outlines a target of reducing its initial cost range by 60% through 2050, mainly by improving the pipeline network.

Overall, the national strategy for CCS development is expected to be focused on six actions, as outlined by METI in a sector blueprint earlier this year.

State assistance for firms interested in becoming CCS operators

Initiatives to lower costs

Promotion of industry to raise public awareness

Sector expansion globally, aided by JOGMEC

Implementation of a ‘’CCS Business Act’’

Creation and refinement of a sector action strategy

In particular, the government is keen to put in place legislation to govern the new industry, something that METI has identified as holding back progress in the past. That’s why it’s working on the CCS Business Act, a draft version of which will face parliamentary debates in the coming weeks.

The Act should give more clarity on geological regulations and on the handling of oil and natural gas. There is some uncertainty around whether existing acts that cover mining and hydrocarbons can or should apply to the CCS business. Furthermore, rules are needed for the CCS value chain (CO2 separation, capture, transport, storage), as well as for gas handling and data provision, as well as other aspects.

Another key point in METI’s action plan is how CCS operators should communicate the sector’s safety issues to local communities.

Corporate response

So far, several domestic consortiums have shown interest in jumping into the carbon storage businesses. This is partly thanks to METI’s resolution to support a limited number of CCS projects (around four) through grants and tax breaks (similar to EU and U.S. practices).

Trading house Itochu announced a collaboration with Mitsubishi Heavy Industries, INPEX, and Taisei Corp to study the transport of CO2 by ship for storage within Japan. Oil refiner Idemitsu Kosan has teamed up with Hokkaido Electric and JAPEX to explore CCS and CO2 reuse projects in Tomakomai, the port in Hokkaido where Japan’s CCS industry was born.

Another oil wholesaler, ENEOS, established a research company in partnership with J-Power and JX Nippon Oil & Gas Exploration to prepare for carbon storage site selection in western Japan by 2030. The group’s plan involves storing CO2 captured at ENEOS oil refineries and J-Power electricity stations.

Shipper Kawasaki Kisen Kaisha has signed an MoU with Kansai Electric to assess marine transport and shipping costs associated with moving liquefied CO2. Kansai Electric will also work with trading house Mitsui to conduct a feasibility study on a CCS value chain. While Kansai Electric examines the potential to capture CO2 from its thermal power plants, Mitsui will focus on strategies to transport and store the emissions.

Japan’s advanced CCS projects

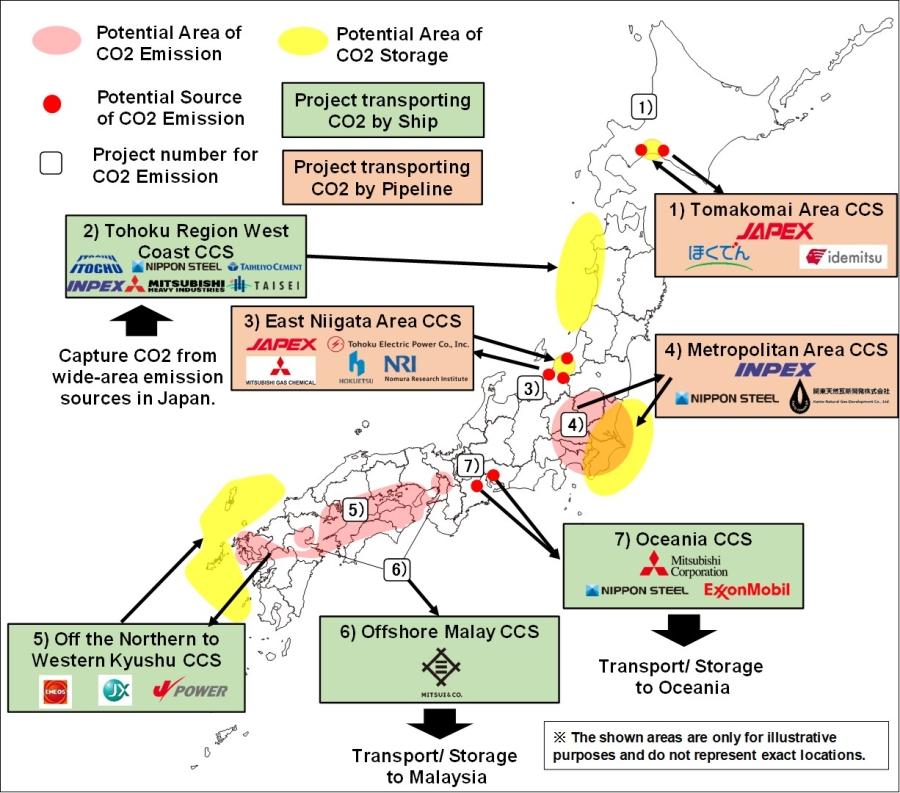

Perhaps the industry’s biggest catalyst, however, came in June when state energy company JOGMEC announced that it has picked seven sites – five in Japan, two abroad – for development as part of the first wave of Japanese CCS projects. These sites are projected to store around 13 mtpa of CO2, of which 30% would be then exported overseas.

JOGMEC envisages the development of more CCS projects outside Japan that would allow the storage of 120 to 240 mtpa of CO2 by 2050. According to METI’s calculations, this scale would require the introduction of up to 24 new injection wells every year.

Project

Companies

CO2 Storage Volume

Outline

Tomakomai Area CCS

JAPEX, Idemitsu Kosan, Hokkaido Electric

1.5 mtpa

CCUS project aimed to partner with “CCU/Carbon Recycling” for CO2 reuse and “BECCS” that combines CCS with a CO2 pipeline-connected biomass power plant.

Scalable project across diverse CO2 sources like steel and cement industries through CO2 shipping in a broad area.

East Niigata Area CCS

JAPEX, Tohoku Electric, Mitsubishi Gas, Hokuetsu, Nomura Research Institute

1.5 mtpa

Project anticipates added value, like decarbonized fuels and environmental benefits, using established oil and gas fields to store CO2 from chemical, pulp, electric power plants, and more.

Metropolitan Area CCS

INPEX, Nippon Steel, Kanto Natural Gas Development

1 mtpa

High scalability project targeting emission sources of industrial complex in metropolitan area

Offshore Malay CCS

Mitsui

2 mtpa

Cooperation project with Malaysian National Oil Company, interested in receiving CO2 from Japan

Oceania CCS

Mitsubishi, Nippon Steel, ExxonMobil Asia Pacific

2 mtpa

Project in offshore Oceania. It targets industries on Nagoya and Yokkaichi ports.

Off the Northern to Western Kyushu CCS

ENEOS, JX Nippon Oil & Gas Exploration, J-POWER

3 mtpa

Project with offshore CO2 storage targeting West Japan

Source: JOGMEC

The industry hub

Among the first wave of projects, the one in Tomakomai is seen as a flagship and an epicenter of CCUS technology progress. The port town is host to that first CCS project that Japan created as a pilot in 2008. The project is run by a JV of domestic companies called Japan CCS Corp, which started with a geophysical survey that was commissioned by METI in 2012. Over the course of four years, through 2019, it successfully captured and stored approximately 0.1 mt of CO2 per year from an Idemitsu oil refinery.

The CO2 was captured from the off-gas (50% CO2 content) emitted at the refinery using active amine technology. It was then injected into nearby offshore saline aquifers and continuously monitored. By late 2019, the project exceeded its target, capturing a total of 0.3 Mt of CO2. Since then, there’s been no leaks, no local impact from CO2 injections and no issues with earthquakes in the area.

To build on the pilot’s success, businesses are also considering ways to link the CCS facilities with other clean energy initiatives in the area. For example, JAPEX and Deloitte unveiled plans to create a pipeline network that will link the carbon storage site with manufacturers that need carbon, aiming to foster a carbon-sharing economy. With plans for green hydrogen production facilities in Hokkaido, the CCS hub of Tomakomai could also develop as a production center for synthetic fuels that bind hydrogen and CO2.

Source: JOGMEC

Conclusion

The realization of the CCS strategy could have a strong impact on Japan’s electricity mix. Director of ANRE’s CCUS policy, Saeki Norihiko, stated that by 2035 the domestic CCS framework should serve the power sector as well as big factories in the cement and chemical industries.

Still, the scale of CCS sector targets also raises questions. Realizing all seven projects in seven years seems unlikely and there’s scant evidence that an entirely new industry can be built in such a short time. Another schedule problem may arise when trying to pair CCS development with that of a national carbon credits market. The latter is set to be fully operational in 2026, four years ahead of the CCS timeline.

CCS projects will also require significant financing. While all seven of JOGMEC’s selected projects are due to get fundings from the state, at present only the Tomakomai development has received funds from another state body – NEDO. New financing sources, such as the issue of GX Bonds, will be necessary.

Most importantly, the success of domestic projects will play a big role in whether Japan can later execute its Asia-focused CCS strategy. After all, the small size of the Japanese sites indicates that the really big capacities will need to be secured elsewhere.

ANALYSIS

BY MAYUMI WATANABE

How to Keep Ammonia Safe: Part II

This is Part II of a two-part series examining the safety issues involved in using ammonia for power generation. The first story was published in the Aug. 21 Weekly report.

As several Japanese utilities prepare to start world-first trials of ammonia-fired power generation, most of the focus will be on the process of producing electricity. But a major challenge for companies pursuing this technology at gigawatt-scale will be in how to move and store the ammonia fuel.

Ammonia, a compound that includes hydrogen atoms, is a key component of Japan’s decarbonization strategy. It is seen as a versatile energy carrier that burns without emitting CO2, potentially offering another net-zero option to generate electricity.

Japan has already penciled in commercial operations of thermal power plants that burn coal and ammonia, side by side, from 2027-28. The technology, known as co-firing because it allows two fuels to be used, is seen as vital for Japan to cut CO2 emissions and wean itself off coal.

The current timescale leaves utilities with just four to five years to solve several significant logistical and safety standards issues. And among the biggest of these is creating the right kind of tanks to contain ammonia.

Source: Canva AI imagining of new ammonia storage tanks

Safety first

Tank safety requirements range from outlining specific levels of earthquake resistance to temperature and pressure controls. To meet such tough requirements, finding the right tank raw materials is key and a big challenge, according to the Japan Clean Fuel Ammonia Association. This is because ammonia exposes storage tanks to corrosion risks.

Tanks require high tensile material that withstands high pressure, low temperatures and stress corrosion cracks (SCC). Presently, most ammonia tanks in Japan are made of SLA (low temperature, aluminum-free) carbon steel.

Engineering firms are pursuing alternatives to SLA. They are also studying new tank shapes in addition to the conventional sphere-shaped structures. Stainless steel covered by a thin invisible film on the surface, which protects from corrosion, has emerged as a strong possibility.

Size matters

A power plant installed to co-fire (i.e., use both ammonia and coal as fuel) on a commercial basis would need to keep tens of thousands of tons of ammonia on site. That poses a problem, because regulations for large ammonia tanks are yet to be introduced.

“We cannot build their tanks because safety standards for ammonia tanks of such sizes are not clear,” an official for Toyo Tanka, a tank manufacturer, told Japan NRG.

Qatar hosts some of the world’s largest tanks for ammonia storage, each of which has a 50,000-ton capacity. In Japan, tanks of 40,000 tons and above are not permitted. This will be a serious bottleneck to grow the ammonia energy supply chain as utilities will need tanks that could hold 100,000 tons of the fuel. A single tank holding 100,000 tons is the ultimate goal. Several small tanks would take up space as each would have to be situated about 100 meters away from the others.

Engineering major IHI, which has a track record of building 15,000-ton tanks in Japan, said it discovered that stainless steel of the SUS821L1 specification could potentially hold up to 110,000 tons of ammonia. The company has also set its sights on ship-shaped membrane pressurized cargo tanks made from SUS304 stainless steel.

Some have suggested using LNG and LPG tanks, made of carbon steel or aluminum alloys, for ammonia storage. This would be a major cost saver for the utilities. Stainless steel, however, appears to be the most popular choice so far.

One industrial tank manufacturer said he believes that some of his customers are using small stainless steel storage tanks originally designed for other chemicals, but instead using them to hold ammonia, because they think stainless steel is a stronger material.

Using the right protection

All metals corrode, including stainless steel. Protective coating on a stainless steel surface cracks at high temperatures and when exposed to chlorine. Ammonia is stored at -30 Celsius, but some studies show stainless steel still suffers from slow pitting corrosion. Aluminum alloy, like stainless steel, has a film on its surface and is vulnerable to chlorine.

Potential SLA alternatives

CHEMICAL COMPOSITION

MANUFACTURERS

SUS821L1 stainless steel

21% chrome, 3% nickel, 3% manganese-copper, 0.17% nitrogen, remainder iron

When the coating dissolves and the surface cracks open, copper, nickel and other elements flow out and react with ammonia, creating new compounds that may impact the ammonia or the tank surface. Copper compounds in particular may cause explosions and Japanese regulations ban the use of any copper in ammonia storage or applications.

The Japan Society of Refrigerating and Air Conditioning Engineers found 3% of ammonia tanks cracked after three years of usage, possibly due to the tank manufacturing process used rather than the quality of the metal.

Corrosion also slows the development of ammonia fuel cell batteries, said one gas utility laboratory researcher. “The cell system may be perfect from the energy efficiency angle, but the ammonia causes the cell components to degrade fast…this is the biggest challenge toward cell commercialization,” he said.

Lacking data

Ammonia projects are also deadlocked by a lack of data. For example, all metals become thinner with time. The metal thickness of tanks needs to factor in abrasion. However, there are few if any studies that examine how fast stainless steel is worn away by ammonia. Most corrosion tests cover short periods of time, about 24 hours, since products are currently designed to keep ammonia only for a short period.

There is no data on how ammonia affects aluminum. There are ammonia-resistant zinc-plated steel products. These are also for limited ammonia exposures. Views on the safety of SUS304 are also divided. In general, researchers say more non-partisan analyses are needed.

Many industrial associations are not big enough to finance research and data collection, and at the end of the day, they rely on company research. The Japanese government’s Green Innovation Fund, managed by NEDO, is financing some of the R&D in this field and is expected to help fill some of the gaps in data. One of the upcoming pilot projects to co-fire ammonia at a coal power plant is done by power utility JERA with financing from NEDO.

What happens when coal and ammonia meet?

Another key area to explore will be what happens when ammonia and coal combust, and what impact this has on boilers, which are usually made from specialty steels. “There has been analysis on the impact of ammonia gas on machinery components, but that of the gas generated from the combined combustion of coal and ammonia is new,” said one laboratory official.

At least compared to tank material safety assessment, the combustion impact analysis is straightforward. The first step is to identify gases that are released during co-firing and to build scenarios to forecast their volume. Most boiler components are made of nickel-based superalloys with strong corrosion resistance, but they are not corrosion-free.

Metals are sensitive to NOx (nitrogen oxide), sulfur dioxide, nitrogen dioxide, hydrogen sulfide, and chlorine gases. Ammonia alone releases NO, NO2, and nitrous oxide (N2O), another type of greenhouse gas. The second step is to draft maintenance guidelines based on how the gases affect the metals, and identify required changes to current standards.

One of the gases released from ammonia combustion in particular has caught the attention of environmentalist activist groups. Ammonia does not emit CO2 when burned, but it does create NOx, a global warming gas. That said, the chemistry is not straightforward.

Ammonia has a dual property when it comes to NOx, which it releases when combusted but also acts as its reduction agent. Chugoku Electric’s 2017 co-firing demo showed that NOx intensity decreased when the ammonia ratio was increased to 0.8% from 0.6%. Increased understanding of ammonia’s reduction mechanism will help not only mitigate the gas emissions but also standardize methods to measure and forecast its environmental impact.

Meanwhile, Chugoku Electric said the temperatures of boiler components were not affected by ammonia, suggesting that the risk of suspending power generation due to temperature changes is low.

Rules for worst-case scenarios

ANRE, the agency under METI’s authority that’s responsible for policies on energy and natural resources, has started to draft version 3 of the sector-relevant Electricity Business Act Rulebook, which had been upgraded in December last year.

ANRE’s to-do list includes a review of some of the currently unrealistic rules, such as a 320-meter distancing requirement from the most immediate neighboring facilities. Officials also want more risk assessments and will likely draft guidelines for emergencies, such as how to manage contact lists and regular staff training.

Once version 3 of the Rulebook is completed, it will be put before the public for feedback and comments. Going forward, it will be updated often to reflect the findings of large-scale co-firing tests and to address operational management approaches.

Meanwhile, the Clean Fuel Ammonia Association is working on its own proposal for tank standards. It has not elaborated on when the proposal will be released. “Whether the gas dosage is small or large…it needs to be taken with utmost care,” IHI told Japan NRG.

Reliable safety codes will not only assure safety and well-being but they’re also essential for the growth of new industries. Ammonia is a highly hazardous and toxic chemical, and even the smallest leak can cause serious damage to the environment and human life.

Development of corrosion-resistant materials and reliable safety codes to clarify the proper use of materials are some of the essential actions required for the growth of new ammonia energy solutions ranging from co-firing, transport and fuel cells.

Reliable safety codes will not only assure safety and well-being; they’re also essential for the growth of new industries. Businesses should not be intimidated by safety risks. On the other hand, underestimating them can deter innovation. Companies studying a possible entry into the ammonia fuel cell business often learn about the severity of corrosion for the first time.

Some consider developing corrosion solutions on their own but give up due to high business risks. There are ideas for corrosion resistant plating materials or ways to convert ammonia into something else safer during long-term storage.

For robust research to drive the industry and permeate among its members, correct safety awareness and codes are needed. Once key safety issues are cleared, Japan will be ready to develop this into the forecast 50 million tons/ year ammonia market.

GLOBAL VIEW

BY JOHN VAROLI

Below are some of last week’s most important international energy developments monitored by the Japan NRG team because of their potential to impact energy supply and demand, as well as prices. We see the following as relevant to Japanese and international energy investors.

Australia/ LNG

Woodside Energy reached an in-principle agreement with unions at Australia’s largest LNG project, in the hopes of averting a supply disruption for one of the world’s biggest exporters of the fuel.

Brazil/ Fossil fuels

State-owned Petrobras pledged to maintain a balanced portfolio, continuing to produce oil for the next four decades, but still boosting investments in renewables. While the company sees global oil demand dropping in coming decades, it believes that fossil fuels demand will remain strong.

China/ LNG

China’s LNG gas importers are opening or expanding trading desks internationally to better manage growing supply portfolios in a global market that doubled in value last year. For example, PCI, a unit of PetroChina, is the country’s largest gas company, with traders and analysts in Beijing, Singapore, London, Dubai and Houston.

Germany/ LNG

Chemicals group BASF inked a deal to import 800,000 tons of LNG annually from the U.S., starting 2026 and running through 2043. The seller is Cheniere Energy, the biggest producer of LNG in the U.S. This is the latest in a string of LNG deals inked by German companies.

LNG/ Global markets

Global gas prices could rise in the short term if strikes at Australia’s LNG plants take place, but markets are well balanced now with inventory levels high in North Asia and Europe, a Shell executive said. Last week, gas prices jumped in Asia and Europe on concerns that industrial action could disrupt exports from Australia.

Mongolia/ CRMs

The U.S. wants Mongolia to deepen cooperation on mining rare earths and other minerals. Mongolia and the U.S. will seek “creative ways” to ensure that the country, which is landlocked by neighbors China and Russia, could get critical minerals onto the world market.

Norway/ Offshore wind

Equinor and partners launched the world’s largest floating offshore wind farm. Its 88 MW of capacity will cover about 35% of annual power demand for five platforms at North Sea oil and gas fields.

Saudi Arabia/ CRMs

By 2030, Saudi Arabia plans to attract nearly $200 billion in investments in its nascent mining sector. The country’s known mineral wealth is estimated to be worth $1.5 trillion.

Sweden/ Battery storage

Northvolt raised €1.2 billion in convertible bonds, including from BlackRock, as Europe’s biggest battery maker is boosting production to meet EV demand. The debt issuance comes as the Swedish start-up prepares to raise $5 billion in equity financing in the next few weeks.

U.S./ LNG

The U.S. will remain the world’s dominant LNG provider over the next four years. By 2027 the country will have 284 million tons of annual LNG liquefaction capacity. In that period, global liquefaction capacity is expected to rise from the current 487 million tons annually to 958 million tons annually.

2023 EVENTS CALENDAR

A selection of domestic and international events we believe will have an impact on Japanese energy

ASEAN-Japan summit to mark 50 years of cooperation

Last market trading day (December 30)

Disclaimer

This communication has been prepared for information purposes only, is confidential and may be legally privileged. This is a subscription-only service and is directed at those who have expressly asked K.K. Yuri Group or one of its representatives to be added to the mailing list. This document may not be onwardly circulated or reproduced without prior written consent from Yuri Group, which retains all copyright to the content of this report.

Yuri Group is not registered as an investment advisor in any jurisdiction. Our research and all the content express our opinions, which are generally based on available public information, field studies and own analysis. Content is limited to general comment upon general political, economic and market issues, asset classes and types of investments. The report and all of its content does not constitute a recommendation or solicitation to buy, sell, subscribe for or underwrite any product or physical commodity, or a financial instrument.

The information contained in this report is obtained from sources believed to be reliable and in good faith. No representation or warranty is made that it is accurate or complete. Opinions and views expressed are subject to change without notice, as are prices and availability, which are indicative only. There is no obligation to notify recipients of any changes to this data or to do so in the future. No responsibility is accepted for the use of or reliance on the information provided. In no circumstances will Yuri Group be liable for any indirect or direct loss, or consequential loss or damages arising from the use of, any inability to use, or any inaccuracy in the information.

JAPAN NRG WEEKLY AUG 28, 2023 JAPAN NRG WEEKLY Aug 28, 2023 NEWS TOP ENERGY TRANSITION & POLICY ELECTRICITY MARKETS OIL, GAS & MINING ANALYSIS ENHANCING CARBON CAPTURE MANAGEMENT: JAPAN SELECTS 7 CCS PROJECTS This year, the government published its first concrete roadmap for the sector detailing where and at what cost CCS technology […]